UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): October 22, 2024

Boot Barn Holdings, Inc.

(Exact name of registrant as specified in its charter)

Delaware |

001-36711 |

90-0776290 |

(State or other jurisdiction |

(Commission |

(I.R.S. Employer |

15345 Barranca Parkway, Irvine, California |

92618 |

(Address of principal executive offices) |

(Zip Code) |

(949) 453-4400

(Registrant’s telephone number, including area code)

Not Applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol |

Name of each exchange on which registered |

Common Stock, $0.0001 par value |

BOOT |

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to section 13(a) of the Exchange Act. ☐

Item 2.02 Results of Operations and Financial Condition

On October 28, 2024, Boot Barn Holdings, Inc. (the “Company”) issued a press release announcing certain financial results for its fiscal second quarter ended September 28, 2024. The press release is attached hereto as Exhibit 99.1 and incorporated into this Item 2.02 by reference.

The information provided in this Item 2.02, including Exhibit 99.1, is intended to be “furnished” and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that section, nor shall it be deemed incorporated by reference into any other filing under the Securities Act of 1933, as amended (the “Securities Act”), or the Exchange Act, except as expressly set forth by specific reference in such filing.

Item 5.02 Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain Officers; Compensatory Arrangements of Certain Officers.

On October 22, 2024, James G. Conroy notified the Company of his intent to resign as the Company’s President and Chief Executive Officer and as a member of the Company’s Board of Directors (the “Board”) to pursue a different opportunity, with such resignation to be effective as of November 22, 2024 (the “Effective Date”). Mr. Conroy’s resignation is not the result of any disagreement with the Company on any matter relating to the Company’s operations, policies, or practices.

In connection with Mr. Conroy’s resignation, on October 23, 2024, the Board appointed the Company’s current Chief Digital Officer, John Hazen, as Interim Chief Executive Officer and the Company’s “principal executive officer,” with such appointment to be effective as of the Effective Date. Mr. Hazen will serve in such position while the Board conducts an internal and external executive search before making a permanent decision on its next Chief Executive Officer. In addition, to assist in the transition, Peter Starrett, the Chairman of the Board, will become Executive Chairman.

Mr. Hazen’s biographical information (as required by Item 401(b) of Regulation S-K) and business experience (as required by Item 401(e) of Regulation S-K) is set forth on page 19 of the Definitive Proxy Statement on Schedule 14A filed by the Company with the Securities and Exchange Commission on July 18, 2024 and is incorporated herein by reference. There are no family relationships between Mr. Hazen and any director or executive officer of the Company, and the Company has not entered into any transactions with Mr. Hazen that are reportable pursuant to Item 404(a) of Regulation S-K. There are no arrangements or understandings between Mr. Hazen and any other persons pursuant to which he was selected as the Company’s Interim Chief Executive Officer.

Any material changes or amendments to Mr. Hazen’s compensation arrangements in connection with his appointment to Interim Chief Executive Officer have not yet been determined. In accordance with Instruction 2 to Item 5.02 of Form 8-K, the Company intends to file an amendment to this Current Report on Form 8-K if and when such information is available.

Item 7.01 Regulation FD Disclosure.

The Company is furnishing this Current Report on Form 8-K in connection with the disclosure of information contained in a supplemental financial presentation (the “Presentation”) to be used by the Company at various meetings with institutional investors and analysts. This information may be amended or updated at any time and from time to time through another Current Report on Form 8-K or other means. A copy of the Presentation is furnished herewith as Exhibit 99.2 and is incorporated into this Item 7.01 by reference.

The information furnished in this Item 7.01, including Exhibit 99.2, is being furnished and shall not be deemed to be “filed” for the purposes of Section 18 of the Exchange Act or otherwise subject to the liabilities of that section, nor shall it be deemed to be incorporated by reference into any other filing under the Securities Act or the Exchange Act, except as expressly set forth by specific reference in such filing.

The Company expressly disclaims any obligation to update or revise any of the information contained in the Presentation.

The Presentation is available on the Company’s investor relations website located at investor.bootbarn.com, although the Company reserves the right to discontinue that availability at any time. The website address included herein is an inactive textual reference only. The information contained on such website is not incorporated into this Current Report on Form 8-K.

Item 9.01. Financial Statements and Exhibits.

Exhibit Number |

Description |

||

Exhibit 99.1 |

|||

Exhibit 99.2 |

|||

Exhibit 104 |

The cover page of this Current Report on Form 8-K, formatted in Inline XBRL. |

||

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

BOOT BARN HOLDINGS, INC. |

|

Date: October 28, 2024 |

By: |

/s/ James M. Watkins |

|

|

Name: James M. Watkins |

|

|

Title: Chief Financial Officer and Secretary |

Exhibit 99.1

Boot Barn Holdings, Inc. Announces Second Quarter Fiscal Year 2025

Financial Results and CEO Transition

IRVINE, California – October 28, 2024 – Boot Barn Holdings, Inc. (NYSE: BOOT) (the “Company”) today announced its financial results for the second fiscal quarter ended September 28, 2024. A Supplemental Financial Presentation is available at investor.bootbarn.com.

In addition, the Company announced that Jim Conroy plans to step down as the Company’s Chief Executive Officer (CEO) and President and as a member of the Company’s Board of Directors, effective November 22, 2024, to pursue an opportunity as CEO of Ross Stores, Inc (NASDAQ: ROST).

CEO Transition

The Company further announced that John Hazen, the Company’s current Chief Digital Officer, will assume the role of Interim CEO, effective November 22, 2024. Mr. Hazen joined the Company in 2018 with responsibility for e-commerce, marketing, and the customer experience. Additionally, Peter Starrett, the Company’s current Chairman of the Board of Directors, will assume the role of Executive Chairman, effective November 22, 2024. Mr. Conroy will remain with the Company through November 22, 2024 to assist with an orderly transition.

Mr. Starrett stated, “John Hazen is very highly regarded within the Boot Barn organization and has a diverse background that includes brand building, digital, and store roles. He has a strong track record of growing sales and profits both at Boot Barn and prior to joining the Company. He also has been extremely instrumental in advancing Boot Barn’s customer-facing technology capabilities including many industry-leading applications of artificial intelligence. I am confident in his ability to step into the role as Interim CEO. Personally, I am looking forward to providing oversight and mentorship as Executive Chairman while the Board conducts an internal and external search before making a permanent decision on our next CEO.”

John Hazen commented, "I am deeply honored to step into this role and incredibly grateful to Jim for his visionary leadership and unwavering support. I also want to express my heartfelt thanks to the Board for their trust and to every member of this incredible team for their dedication that makes this Company exceptional. Together, we will continue building on the strong foundation that we have created and will move forward with confidence, tenacity, and purpose.”

Mr. Starrett added, “The Board recognizes the great contributions Jim has made during his tenure as Boot Barn’s CEO. When he assumed the CEO reins 12 years ago, Boot Barn was one of several regional retail chains specializing in western and work products. His focused approach on the execution of our strategic initiatives has led to one of the most exceptional growth stories in the retail industry. Today, Boot Barn is a national chain of 426 stores and the industry leader by a wide margin. On behalf of all Boot Barn partners, we wish Jim continued success in his next endeavor.”

Mr. Conroy commented, “After 12 incredible years, I am filled with immense gratitude for this Company and the extraordinary people who have been by my side throughout this journey. Together, we’ve built something truly special, and I will forever cherish the shared successes, challenges, and memories we created. Thank you for your trust, dedication, and passion—I leave with a heart full of pride and appreciation for every one of you.”

1

Second Quarter Fiscal Year 2025 Financial Results

For the quarter ended September 28, 2024 compared to the quarter ended September 30, 2023:

| ● | Net sales increased 13.7% over the prior-year period to $425.8 million. |

| ● | Same store sales increased 4.9% compared to the prior-year period, comprised of an increase of 4.3% in retail store same store sales and an increase of 10.1% in e-commerce same store sales. |

| ● | Net income was $29.4 million, or $0.95 per diluted share, compared to $27.7 million, or $0.90 per diluted share, in the prior-year period. |

| ● | The Company opened 15 new stores, bringing its total store count to 425. |

Jim Conroy, President and Chief Executive Officer said, "Our fiscal second quarter saw broad-based growth in same store sales, the addition of 15 new stores and a healthy beat to guidance in earnings per diluted share. Our team's excellent execution has driven improving trends across all channels, store geographies, and major merchandise classifications, positioning us well for the upcoming holiday season. As we manage through an orderly transition over the next month, I feel great about the condition of the business and am confident in the team’s ability, under John’s leadership, to execute on the four strategic initiatives and to drive future growth in sales and earnings."

Operating Results for the Second Quarter Ended September 28, 2024 Compared to the Second Quarter Ended September 30, 2023

| ● | Net sales increased 13.7% to $425.8 million from $374.5 million in the prior-year period. Consolidated same store sales increased 4.9%, with retail store same store sales increasing 4.3% and e-commerce same store sales increasing 10.1%. The increase in net sales was the result of incremental sales from new stores and the increase in consolidated same store sales. |

| ● | Gross profit was $152.9 million, or 35.9% of net sales, compared to $133.9 million, or 35.8% of net sales, in the prior-year period. Gross profit increased primarily due to an increase in sales and merchandise margin, partially offset by the occupancy costs of new stores. The increase in gross profit rate of 10 basis points was driven primarily by a 70 basis-point increase in merchandise margin rate, partially offset by 60 basis points of deleverage in buying, occupancy and distribution center costs. The increase in merchandise margin rate was primarily the result of supply chain efficiencies, while the deleverage in buying, occupancy and distribution center costs was driven by the occupancy costs of new stores. |

| ● | Selling, general and administrative expenses were $112.9 million, or 26.5% of net sales, compared to $95.3 million, or 25.5% of net sales, in the prior-year period. The increase in selling, general and administrative expenses, as compared to the prior-year period, was primarily a result of higher store payroll and store-related expenses associated with operating more stores, incentive-based compensation, marketing expenses, and legal expenses in the current year. Selling, general and administrative expenses as a percentage of net sales increased by 100 basis points primarily as a result of higher incentive-based compensation, legal expenses, and marketing expenses in the current year, partially offset by lower store payroll expenses. |

| ● | Income from operations increased $1.4 million to $40.0 million, or 9.4% of net sales, compared to $38.6 million, or 10.3% of net sales, in the prior-year period, primarily due to the factors noted above. |

| ● | Net income was $29.4 million, or $0.95 per diluted share, compared to net income of $27.7 million, or $0.90 per diluted share, in the prior-year period. The increase in net income is primarily attributable to the factors noted above. |

2

Operating Results for the Six Months Ended September 28, 2024 Compared to the Six Months Ended September 30, 2023

| ● | Net sales increased 12.0% to $849.2 million from $758.2 million in the prior-year period. Consolidated same store sales increased 3.1%, with retail store same store sales increasing 2.5% and e-commerce same store sales increasing 8.4%. The increase in net sales was the result of incremental sales from new stores and the increase in consolidated same store sales. |

| ● | Gross profit was $309.6 million, or 36.5% of net sales, compared to $275.9 million, or 36.4% of net sales, in the prior-year period. Gross profit increased primarily due to an increase in sales and merchandise margin, partially offset by the occupancy costs of new stores. The increase in gross profit rate of 10 basis points was driven primarily by an 80 basis-point increase in merchandise margin rate, partially offset by 70 basis points of deleverage in buying, occupancy and distribution center costs. The increase in merchandise margin rate was the result of supply chain efficiencies, while the deleverage in buying, occupancy and distribution center costs was driven primarily by the occupancy costs of new stores. |

| ● | Selling, general and administrative expenses were $219.4 million, or 25.8% of net sales, compared to $191.1 million, or 25.2% of net sales, in the prior-year period. The increase in selling, general and administrative expenses, as compared to the prior-year period, was primarily a result of higher store payroll and store-related expenses associated with operating more stores, marketing expenses, and incentive-based compensation in the current year. Selling, general and administrative expenses as a percentage of net sales increased by 60 basis points primarily as a result of higher incentive-based compensation and marketing expenses in the current year, partially offset by lower store payroll and store-related expenses. |

| ● | Income from operations increased $5.4 million to $90.2 million, or 10.6% of net sales, compared to $84.8 million, or 11.2% of net sales, in the prior-year period, primarily due to the factors noted above. |

| ● | Net income was $68.3 million, or $2.21 per diluted share, compared to net income of $61.9 million, or $2.03 per diluted share, in the prior-year period. The increase in net income is primarily attributable to the factors noted above. |

Sales by Channel

The following table includes total net sales growth, same store sales (“SSS”) growth/(decline) and e-commerce as a percentage of net sales for the periods indicated below.

|

|

Thirteen Weeks |

|

|

|

|

|

|

|

|

|

Preliminary |

|

|

|

Ended |

|

|

Four Weeks |

|

Four Weeks |

|

Five Weeks |

|

|

Four Weeks |

|

|

|

September 28, 2024 |

|

|

Fiscal July |

|

Fiscal August |

|

Fiscal September |

|

|

Fiscal October |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Net Sales Growth |

|

13.7 |

% |

|

8.8 |

% |

14.7 |

% |

16.8 |

% |

|

14.6 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Retail Stores SSS |

|

4.3 |

% |

|

(0.9) |

% |

5.3 |

% |

7.5 |

% |

|

4.3 |

% |

E-commerce SSS |

|

10.1 |

% |

|

5.0 |

% |

12.1 |

% |

12.2 |

% |

|

12.5 |

% |

Consolidated SSS |

|

4.9 |

% |

|

(0.3) |

% |

6.0 |

% |

8.0 |

% |

|

5.1 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E-commerce as a % of Net Sales |

|

9.5 |

% |

|

9.2 |

% |

9.4 |

% |

9.9 |

% |

|

9.3 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3

Balance Sheet Highlights as of September 28, 2024

| ● | Cash of $37 million. |

| ● | Zero drawn under the $250 million revolving credit facility. |

| ● | Average inventory per store increased approximately 10.5% on a same store basis compared to September 30, 2023. |

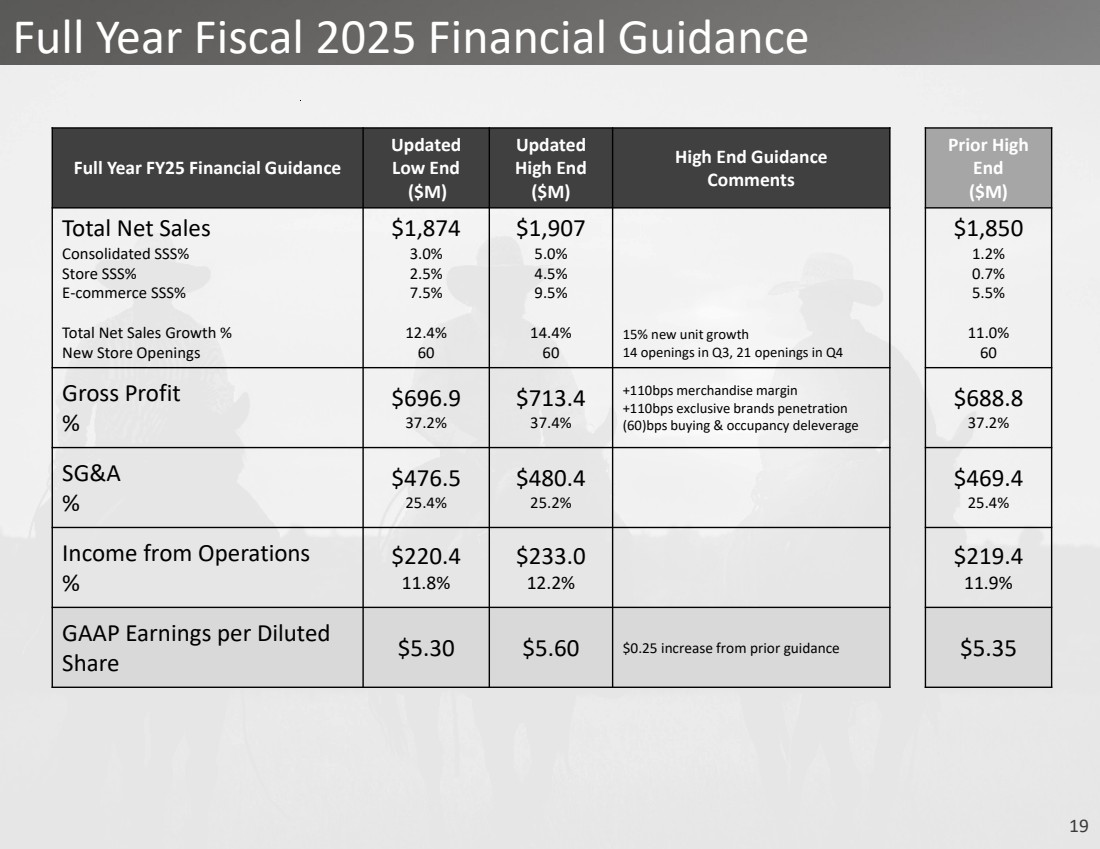

Fiscal Year 2025 Outlook

The Company is providing updated guidance for the fiscal year ending March 29, 2025, superseding in its entirety the previous guidance issued in its first quarter earnings report on August 7, 2024. Please note that the Company’s guidance excludes any benefits and costs related to the CEO transition.

For the fiscal year ending March 29, 2025 the Company now expects:

| ● | To open a total of 60 new stores. |

| ● | Total sales of $1.874 billion to $1.907 billion, representing growth of 12.4% to 14.4% over the prior year. |

| ● | Same store sales growth of approximately 3.0% to 5.0%, with retail store same store sales growth of approximately 2.5% to 4.5% and e-commerce same store sales growth of approximately 7.5% to 9.5%. |

| ● | Gross profit between $696.9 million and $713.4 million, or approximately 37.2% to 37.4% of sales. |

| ● | Selling, general and administrative expenses between $476.5 million and $480.4 million, or approximately 25.4% to 25.2% of sales. |

| ● | Income from operations between $220.4 million and $233.0 million, or approximately 11.8% to 12.2% of sales. |

| ● | Effective tax rate of 26.6% for the remaining six months of the fiscal year. |

| ● | Net income of $164.4 million to $173.7 million. |

| ● | Net income per diluted share of $5.30 to $5.60, based on 31.0 million weighted average diluted shares outstanding. |

| ● | Capital expenditures between $115.0 million and $120.0 million, which is net of estimated landlord tenant allowances of $30.2 million. |

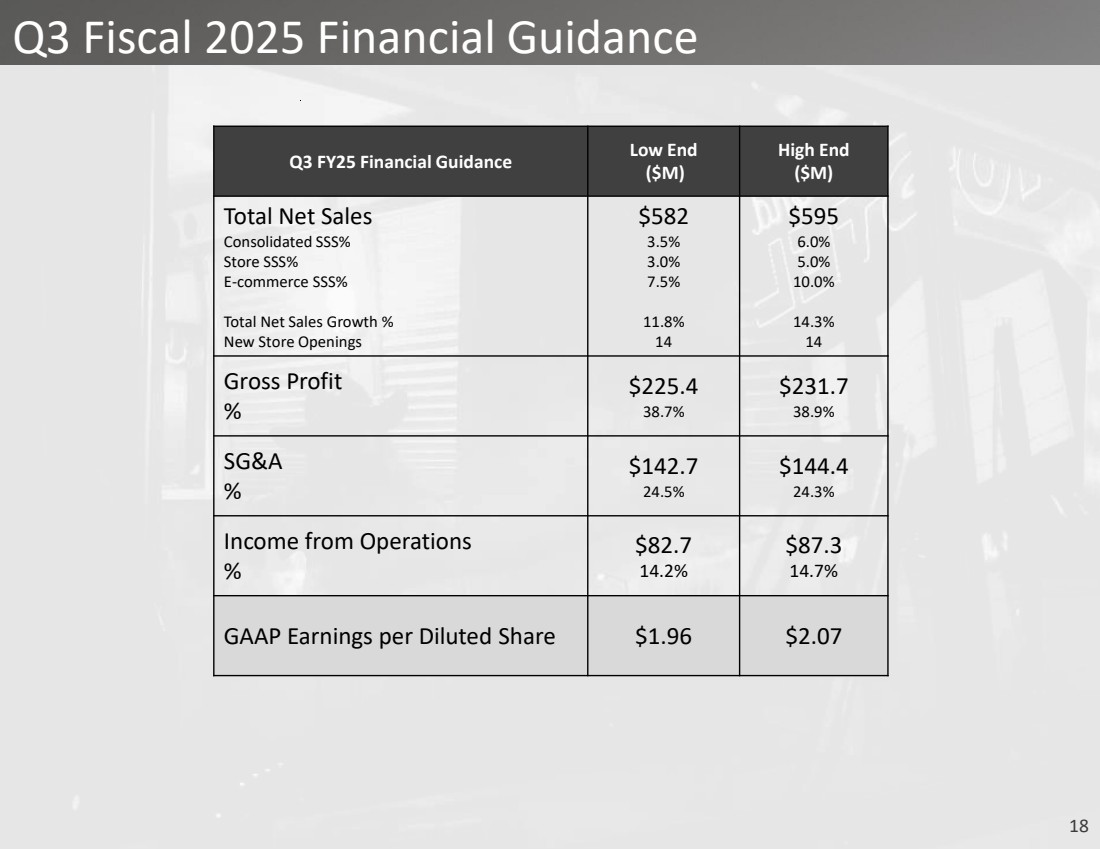

For the fiscal third quarter ending December 28, 2024, the Company now expects:

| ● | Total sales of $582 million to $595 million, representing growth of 11.8% to 14.3% over the prior-year period. |

| ● | Same store sales growth of approximately 3.5% to 6.0%, with retail store same store sales growth of approximately 3.0% to 5.0% and e-commerce same store sales growth of approximately 7.5% to 10.0%. |

| ● | Income from operations between $82.7 million and $87.3 million, or approximately 14.2% to 14.7% of sales. |

| ● | Net income per diluted share of $1.96 to $2.07, based on 31.0 million weighted average diluted shares outstanding. |

Conference Call Information

A conference call to discuss the financial results for the second quarter of fiscal year 2025 is scheduled for today, October 28, 2024, at 4:30 p.m. ET (1:30 p.m. PT). Investors and analysts interested in participating in the call are invited to dial (844) 481-2552. The conference call will also be available to interested parties through a live webcast at investor.bootbarn.com. Please visit the website and select the “Events and Presentations” link at least 15 minutes prior to the start of the call to register and download any necessary software. A Supplemental Financial Presentation is also available on the investor relations section of the Company’s website. A telephone replay of the call will be available until November 28, 2024, by dialing (844) 512-2921 (domestic) or (412) 317-6671 (international) and entering the conference identification number: 10193684. Please note participants must enter the conference identification number in order to access the replay.

4

About Boot Barn

Boot Barn is the nation’s leading lifestyle retailer of western and work-related footwear, apparel and accessories for men, women and children. The Company offers its loyal customer base a wide selection of work and lifestyle brands. As of the date of this release, Boot Barn operates 426 stores in 46 states, in addition to an e-commerce channel www.bootbarn.com. The Company also operates www.sheplers.com, the nation’s leading pure play online western and work retailer and www.countryoutfitter.com, an e-commerce site selling to customers who live a country lifestyle. For more information, call 888-Boot-Barn or visit www.bootbarn.com.

Forward Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this press release are forward-looking statements. Forward-looking statements refer to the Company’s current expectations and projections relating to, by way of example and without limitation, the Company’s financial condition, liquidity, profitability, results of operations, margins, plans, objectives, strategies, future performance, business and industry. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. These statements may include words such as “anticipate”, “estimate”, “expect”, “project”, “plan“, “intend”, “believe”, “may”, “might”, “will”, “could”, “should”, “can have”, “likely”, “outlook” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events, but not all forward-looking statements contain these identifying words. These forward-looking statements are based on assumptions that the Company’s management has made in light of their industry experience and on their perceptions of historical trends, current conditions, expected future developments and other factors that they believe are appropriate under the circumstances. As you consider this press release, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (some of which are beyond the Company’s control) and assumptions. These risks, uncertainties and assumptions include, but are not limited to, the following: decreases in consumer spending due to declines in consumer confidence, local economic conditions or changes in consumer preferences; the Company’s ability to effectively execute on its growth strategy; and the Company’s failure to maintain and enhance its strong brand image, to compete effectively, to maintain good relationships with its key suppliers, and to improve and expand its exclusive product offerings. The Company discusses the foregoing risks and other risks in greater detail under the heading “Risk factors” in the periodic reports filed by the Company with the Securities and Exchange Commission. Although the Company believes that these forward-looking statements are based on reasonable assumptions, you should be aware that many factors could affect the Company’s actual financial results and cause them to differ materially from those anticipated in the forward-looking statements. Because of these factors, the Company cautions that you should not place undue reliance on any of these forward-looking statements. New risks and uncertainties arise from time to time, and it is impossible for the Company to predict those events or how they may affect the Company. Further, any forward-looking statement speaks only as of the date on which it is made. Except as required by law, the Company does not intend to update or revise the forward-looking statements in this press release after the date of this press release.

Investor Contact:

ICR, Inc.

Brendon Frey, 203-682-8216

BootBarnIR@icrinc.com

or

Company Contact:

Boot Barn Holdings, Inc.

Mark Dedovesh, 949-453-4489

Senior Vice President, Investor Relations & Financial Planning

BootBarnIRMedia@bootbarn.com

5

Boot Barn Holdings, Inc.

Consolidated Balance Sheets

(In thousands, except per share data)

(Unaudited)

|

|

September 28, |

|

March 30, |

||

|

|

2024 |

|

2024 |

||

Assets |

|

|

|

|

|

|

Current assets: |

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

37,377 |

|

$ |

75,847 |

Accounts receivable, net |

|

|

7,886 |

|

|

9,964 |

Inventories |

|

|

712,991 |

|

|

599,120 |

Prepaid expenses and other current assets |

|

|

48,851 |

|

|

44,718 |

Total current assets |

|

|

807,105 |

|

|

729,649 |

Property and equipment, net |

|

|

368,289 |

|

|

323,667 |

Right-of-use assets, net |

|

|

429,020 |

|

|

390,501 |

Goodwill |

|

|

197,502 |

|

|

197,502 |

Intangible assets, net |

|

|

58,677 |

|

|

58,697 |

Other assets |

|

|

6,184 |

|

|

5,576 |

Total assets |

|

$ |

1,866,777 |

|

$ |

1,705,592 |

Liabilities and stockholders’ equity |

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

Accounts payable |

|

$ |

153,564 |

|

$ |

132,877 |

Accrued expenses and other current liabilities |

|

|

134,302 |

|

|

116,477 |

Short-term lease liabilities |

|

|

70,540 |

|

|

63,454 |

Total current liabilities |

|

|

358,406 |

|

|

312,808 |

Deferred taxes |

|

|

41,267 |

|

|

42,033 |

Long-term lease liabilities |

|

|

446,068 |

|

|

403,303 |

Other liabilities |

|

|

4,378 |

|

|

3,805 |

Total liabilities |

|

|

850,119 |

|

|

761,949 |

|

|

|

|

|

|

|

Stockholders’ equity: |

|

|

|

|

|

|

Common stock, $0.0001 par value; September 28, 2024 - 100,000 shares authorized, 30,824 shares issued; March 30, 2024 - 100,000 shares authorized, 30,572 shares issued |

|

|

3 |

|

|

3 |

Preferred stock, $0.0001 par value; 10,000 shares authorized, no shares issued or outstanding |

|

|

— |

|

|

— |

Additional paid-in capital |

|

|

244,931 |

|

|

232,636 |

Retained earnings |

|

|

791,363 |

|

|

723,026 |

Less: Common stock held in treasury, at cost, 298 and 228 shares at September 28, 2024 and March 30, 2024, respectively |

|

|

(19,639) |

|

|

(12,022) |

Total stockholders’ equity |

|

|

1,016,658 |

|

|

943,643 |

Total liabilities and stockholders’ equity |

|

$ |

1,866,777 |

|

$ |

1,705,592 |

6

Boot Barn Holdings, Inc.

Consolidated Statements of Operations

(In thousands, except per share data)

(Unaudited)

|

|

Thirteen Weeks Ended |

|

Twenty-Six Weeks Ended |

||||||||

|

|

September 28, |

|

September 30, |

|

September 28, |

|

September 30, |

||||

|

|

2024 |

|

2023 |

|

2024 |

|

2023 |

||||

Net sales |

|

$ |

425,799 |

|

$ |

374,456 |

|

$ |

849,185 |

|

$ |

758,151 |

Cost of goods sold |

|

|

272,941 |

|

|

240,540 |

|

|

539,578 |

|

|

482,272 |

Gross profit |

|

|

152,858 |

|

|

133,916 |

|

|

309,607 |

|

|

275,879 |

Selling, general and administrative expenses |

|

|

112,879 |

|

|

95,338 |

|

|

219,406 |

|

|

191,056 |

Income from operations |

|

|

39,979 |

|

|

38,578 |

|

|

90,201 |

|

|

84,823 |

Interest expense |

|

|

384 |

|

|

463 |

|

|

735 |

|

|

1,486 |

Other income (loss), net |

|

|

949 |

|

|

(50) |

|

|

1,545 |

|

|

174 |

Income before income taxes |

|

|

40,544 |

|

|

38,065 |

|

|

91,011 |

|

|

83,511 |

Income tax expense |

|

|

11,116 |

|

|

10,385 |

|

|

22,674 |

|

|

21,578 |

Net income |

|

$ |

29,428 |

|

$ |

27,680 |

|

$ |

68,337 |

|

$ |

61,933 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per share: |

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

$ |

0.96 |

|

$ |

0.92 |

|

$ |

2.24 |

|

$ |

2.06 |

Diluted |

|

$ |

0.95 |

|

$ |

0.90 |

|

$ |

2.21 |

|

$ |

2.03 |

Weighted average shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

|

30,510 |

|

|

30,137 |

|

|

30,471 |

|

|

30,029 |

Diluted |

|

|

30,899 |

|

|

30,627 |

|

|

30,859 |

|

|

30,540 |

7

Boot Barn Holdings, Inc.

Consolidated Statements of Cash Flows

(In thousands)

(Unaudited)

|

|

Twenty-Six Weeks Ended |

||||

|

|

September 28, |

|

September 30, |

||

|

|

2024 |

|

2023 |

||

Cash flows from operating activities |

|

|

|

|

|

|

Net income |

|

$ |

68,337 |

|

$ |

61,933 |

Adjustments to reconcile net income to net cash provided by operating activities: |

|

|

|

|

|

|

Depreciation |

|

|

29,540 |

|

|

22,597 |

Stock-based compensation |

|

|

10,864 |

|

|

7,833 |

Amortization of intangible assets |

|

|

20 |

|

|

27 |

Noncash lease expense |

|

|

32,229 |

|

|

26,487 |

Amortization and write-off of debt issuance fees and debt discount |

|

|

54 |

|

|

54 |

Loss on disposal of assets |

|

|

134 |

|

|

298 |

Deferred taxes |

|

|

(766) |

|

|

2,993 |

Changes in operating assets and liabilities: |

|

|

|

|

|

|

Accounts receivable, net |

|

|

2,097 |

|

|

3,046 |

Inventories |

|

|

(113,871) |

|

|

3,921 |

Prepaid expenses and other current assets |

|

|

(4,397) |

|

|

9,243 |

Other assets |

|

|

(608) |

|

|

1,302 |

Accounts payable |

|

|

19,722 |

|

|

7,051 |

Accrued expenses and other current liabilities |

|

|

9,897 |

|

|

13,600 |

Other liabilities |

|

|

573 |

|

|

510 |

Operating leases |

|

|

(20,283) |

|

|

(15,435) |

Net cash provided by operating activities |

|

$ |

33,542 |

|

$ |

145,460 |

Cash flows from investing activities |

|

|

|

|

|

|

Purchases of property and equipment |

|

|

(65,403) |

|

|

(64,687) |

Net cash used in investing activities |

|

$ |

(65,403) |

|

$ |

(64,687) |

Cash flows from financing activities |

|

|

|

|

|

|

Payments on line of credit, net |

|

|

— |

|

|

(66,043) |

Repayments on debt and finance lease obligations |

|

|

(423) |

|

|

(428) |

Tax withholding payments for net share settlement |

|

|

(7,617) |

|

|

(2,412) |

Proceeds from the exercise of stock options |

|

|

1,431 |

|

|

8,582 |

Net cash used in financing activities |

|

$ |

(6,609) |

|

$ |

(60,301) |

Net (decrease)/increase in cash and cash equivalents |

|

|

(38,470) |

|

|

20,472 |

Cash and cash equivalents, beginning of period |

|

|

75,847 |

|

|

18,193 |

Cash and cash equivalents, end of period |

|

$ |

37,377 |

|

$ |

38,665 |

|

|

|

|

|

|

|

Supplemental disclosures of cash flow information: |

|

|

|

|

|

|

Cash paid for income taxes |

|

$ |

17,770 |

|

$ |

2,822 |

Cash paid for interest |

|

$ |

677 |

|

$ |

1,399 |

Supplemental disclosure of non-cash activities: |

|

|

|

|

|

|

Unpaid purchases of property and equipment |

|

$ |

24,061 |

|

$ |

14,103 |

8

Boot Barn Holdings, Inc.

Store Count

|

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

|

September 28, |

|

June 29, |

|

March 30, |

|

December 30, |

|

September 30, |

|

July 1, |

|

April 1, |

|

December 24, |

|

|

2024 |

|

2024 |

|

2024 |

|

2023 |

|

2023 |

|

2023 |

|

2023 |

|

2022 |

Store Count (BOP) |

|

411 |

|

400 |

|

382 |

|

371 |

|

361 |

|

345 |

|

333 |

|

321 |

Opened/Acquired |

|

15 |

|

11 |

|

18 |

|

11 |

|

10 |

|

16 |

|

12 |

|

12 |

Closed |

|

(1) |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

Store Count (EOP) |

|

425 |

|

411 |

|

400 |

|

382 |

|

371 |

|

361 |

|

345 |

|

333 |

Boot Barn Holdings, Inc.

Selected Store Data

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fourteen |

|

Thirteen |

|

||||

|

|

Thirteen Weeks Ended |

|

Weeks |

|

Weeks |

|

||||||||||||||||||

|

|

September 28, |

|

June 29, |

|

March 30, |

|

December 30, |

|

September 30, |

|

July 1, |

|

April 1, |

|

December 24, |

|

||||||||

|

|

2024 |

|

2024 |

|

2024 |

|

2023 |

|

2023 |

|

2023 |

|

2023 |

|

2022 |

|

||||||||

Selected Store Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Same Store Sales growth/(decline) |

|

|

4.9 |

% |

|

1.4 |

% |

|

(5.9) |

% |

|

(9.7) |

% |

|

(4.8) |

% |

|

(2.9) |

% |

|

(5.5) |

% |

|

(3.6) |

% |

Stores operating at end of period |

|

|

425 |

|

|

411 |

|

|

400 |

|

|

382 |

|

|

371 |

|

|

361 |

|

|

345 |

|

|

333 |

|

Comparable stores operating during period(1) |

|

|

363 |

|

|

349 |

|

|

335 |

|

|

322 |

|

|

312 |

|

|

302 |

|

|

290 |

|

|

280 |

|

Total retail store selling square footage, end of period (in thousands) |

|

|

4,720 |

|

|

4,547 |

|

|

4,371 |

|

|

4,153 |

|

|

4,027 |

|

|

3,914 |

|

|

3,735 |

|

|

3,598 |

|

Average retail store selling square footage, end of period |

|

|

11,105 |

|

|

11,063 |

|

|

10,929 |

|

|

10,872 |

|

|

10,855 |

|

|

10,841 |

|

|

10,825 |

|

|

10,806 |

|

Average sales per comparable store (in thousands)(2) |

|

$ |

952 |

|

$ |

980 |

|

$ |

917 |

|

$ |

1,256 |

|

$ |

950 |

|

$ |

1,014 |

|

$ |

1,092 |

|

$ |

1,424 |

|

| (1) | Comparable stores have been open at least 13 full fiscal months as of the end of the applicable reporting period. |

| (2) | Average sales per comparable store is calculated by dividing comparable store trailing three-month sales for the applicable period by the number of comparable stores operating during the period. |

9

|

0 Supplemental Financial Presentation October 2024 Offering everyone a piece of the American spirit—one handshake at a time. |

|

1 Important Information Forward-Looking Statements This presentation contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this presentation are forward-looking statements. You can identify forward-looking statements by the fact that they generally include words such as "anticipate," "estimate," "expect," "project," "plan,“ "intend," "believe," “outlook” and other words of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events but not all forward-looking statements contain these identifying words. These forward-looking statements are based on assumptions that Boot Barn Holdings, Inc.’s (the “Company,” “we,” “us,” and “our”) management has made in light of their industry experience and on their perceptions of historical trends, current conditions, expected future developments and other factors that they believe are appropriate under the circumstances. As you consider this presentation, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (some of which are beyond the Company’s control) and assumptions. These risks, uncertainties and assumptions include, but are not limited to, the following: decreases in consumer spending due to declines in consumer confidence, local economic conditions or changes in consumer preferences; the Company’s ability to effectively execute on its growth strategy; and the Company’s failure to maintain and enhance its strong brand image, to compete effectively, to maintain good relationships with its key suppliers, and to improve and expand its exclusive product offerings. The Company discusses the foregoing risks and other risks in greater detail under the heading “Risk factors” in the periodic reports filed by the Company with the Securities and Exchange Commission. Although the Company believes that these forward-looking statements are based on reasonable assumptions, you should be aware that many factors could affect the Company’s actual financial results and cause them to differ materially from those anticipated in the forward-looking statements. Because of these factors, the Company cautions that you should not place undue reliance on any of these forward-looking statements. New risks and uncertainties arise from time to time, and it is impossible for the Company to predict those events or how they may affect the Company. Further, any forward-looking statement speaks only as of the date on which it is made. Except as required by law, the Company does not intend to update or revise the forward-looking statements in this presentation after the date of this presentation. Industry and Market Information Statements in this presentation concerning our industry and the markets in which we operate, including our general expectations and competitive position, business opportunity and market size, growth and share, are based on information from independent industry organizations and other third-party sources, data from our internal research and management estimates. Management estimates are derived from publicly available information and the information and data referred to above and are based on assumptions and calculations made by us based upon our interpretation of such information and data. The information and data referred to above are imprecise and may prove to be inaccurate because the information cannot always be verified with complete certainty due to the limitations on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties. As a result, please be aware that the data and statistical information in this presentation may differ from information provided by our competitors or from information found in current or future studies conducted by market research institutes, consultancy firms or independent sources. Recent Developments Our business and opportunities for growth depend on consumer discretionary spending, and as such, our results are particularly sensitive to economic conditions and consumer confidence. Inflation and other challenges affecting the global economy could impact our operations and will depend on future developments, which are uncertain. These and other effects make it more challenging for us to estimate the future performance of our business, particularly over the near-to-medium term. For further discussion of the uncertainties and business risks affecting the Company, see the sections captioned “Risk factors” in our periodic reports filed with the Securities and Exchange Commission. |

|

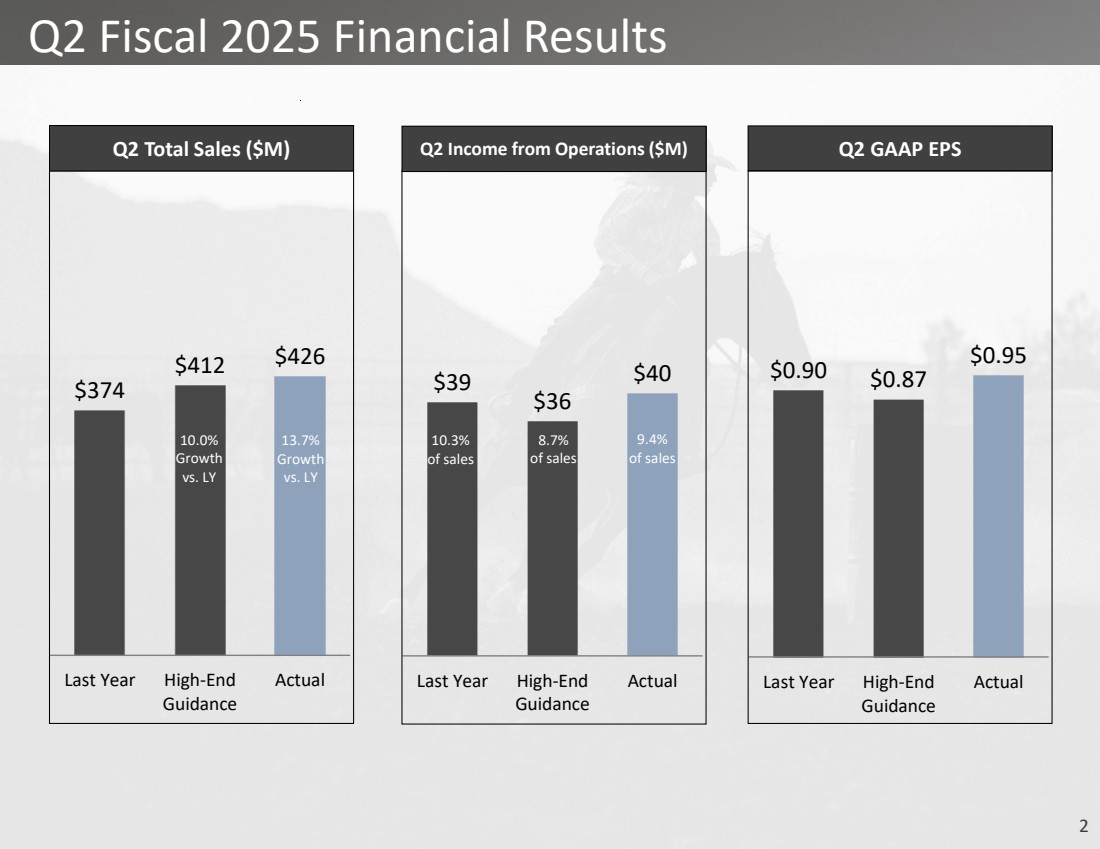

2 $374 $412 $426 Last Year High-End Guidance Actual Q2 Fiscal 2025 Financial Results Q2 Total Sales ($M) Q2 GAAP EPS $0.90 $0.87 $0.95 Last Year High-End Guidance Actual $39 $36 $40 Last Year High-End Guidance Actual Q2 Income from Operations ($M) 10.3% of sales 8.7% of sales 9.4% of sales 10.0% Growth vs. LY 13.7% Growth vs. LY |

|

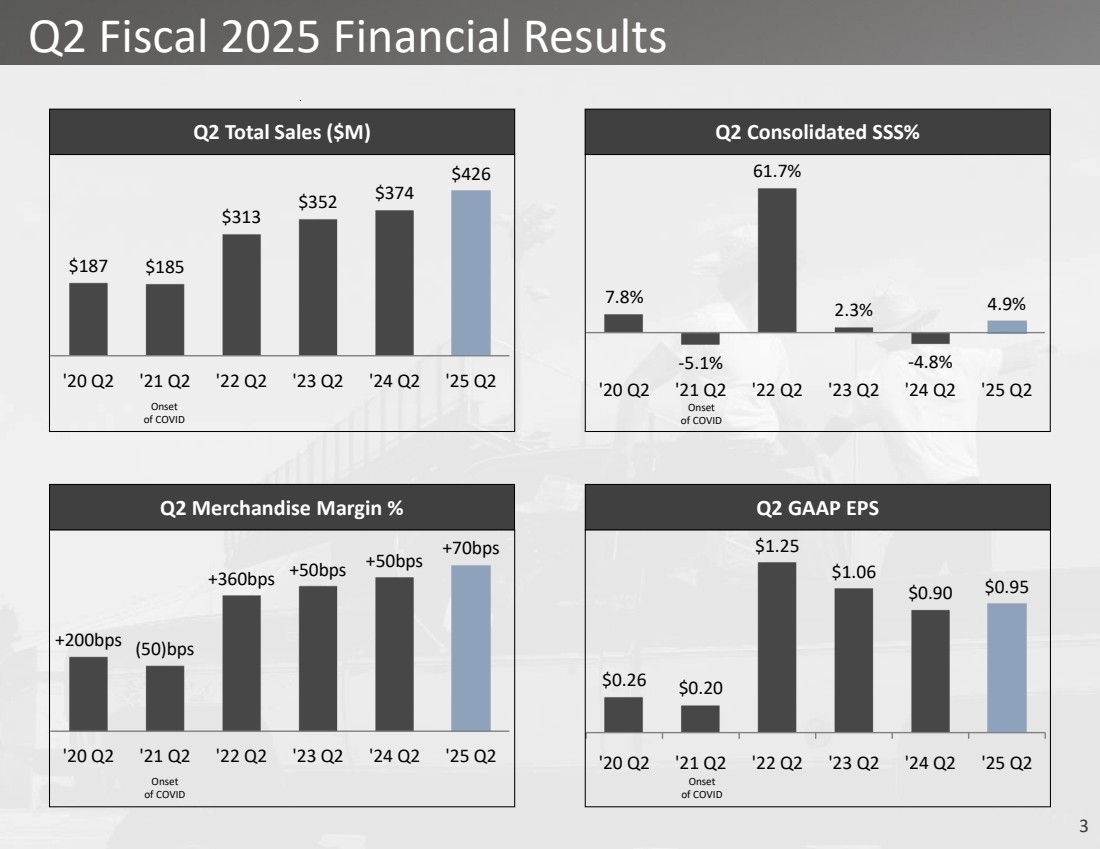

3 Q2 Fiscal 2025 Financial Results $187 $185 $313 $352 $374 $426 '20 Q2 '21 Q2 '22 Q2 '23 Q2 '24 Q2 '25 Q2 Q2 Total Sales ($M) 7.8% -5.1% 61.7% 2.3% -4.8% 4.9% '20 Q2 '21 Q2 '22 Q2 '23 Q2 '24 Q2 '25 Q2 Q2 Consolidated SSS% +200bps (50)bps +360bps +50bps +50bps +70bps '20 Q2 '21 Q2 '22 Q2 '23 Q2 '24 Q2 '25 Q2 Q2 Merchandise Margin % $0.26 $0.20 $1.25 $1.06 $0.90 $0.95 '20 Q2 '21 Q2 '22 Q2 '23 Q2 '24 Q2 '25 Q2 Q2 GAAP EPS Onset of COVID Onset of COVID Onset of COVID Onset of COVID |

|

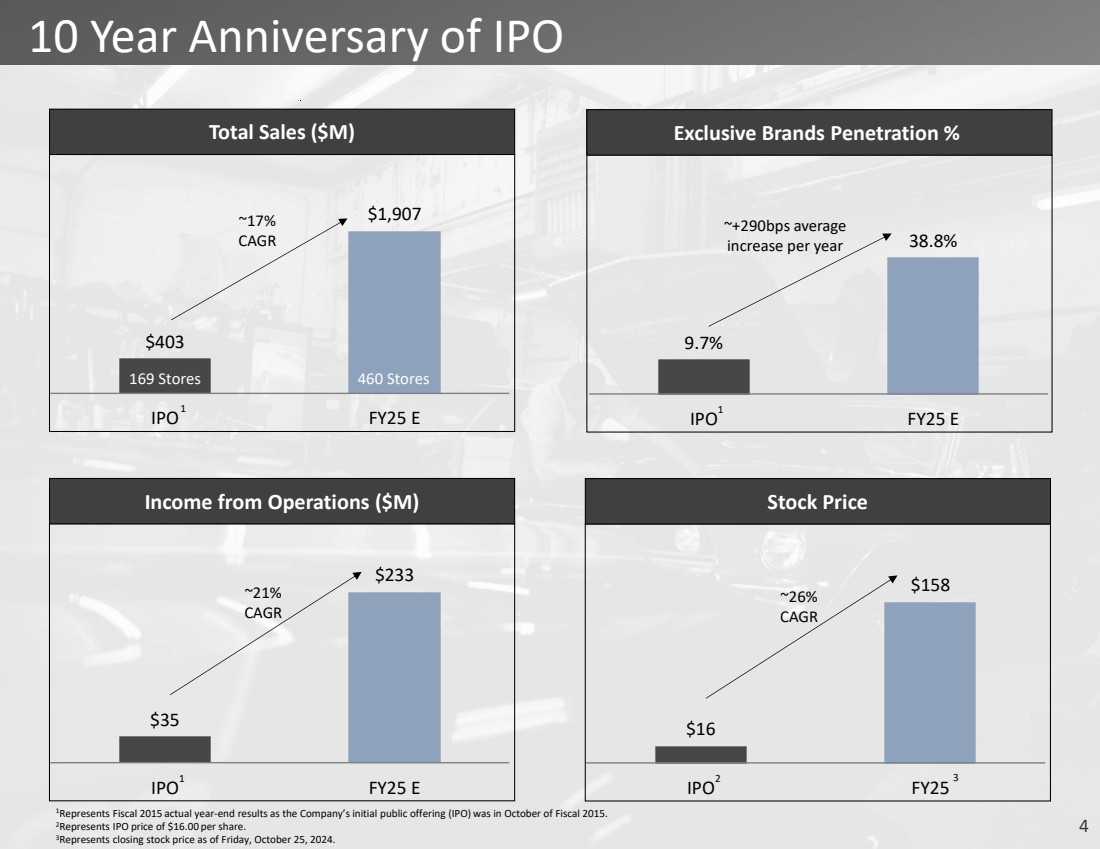

4 10 Year Anniversary of IPO $403 $1,907 IPO FY25 E Total Sales ($M) ~17% CAGR 9.7% 38.8% IPO FY25 E Exclusive Brands Penetration % $16 $158 IPO FY25 Stock Price ~26% CAGR ~+290bps average increase per year 1 1 2 1Represents Fiscal 2015 actual year-end results as the Company’s initial public offering (IPO) was in October of Fiscal 2015. 2Represents IPO price of $16.00 per share. 3Represents closing stock price as of Friday, October 25, 2024. 169 Stores 460 Stores $35 $233 IPO FY25 E Income from Operations ($M) ~21% CAGR 1 3 |

|

5 Strategic Initiatives Update 1 2 3 4 New Stores Same Store Sales Omni-Channel Merchandise Margin & Exclusive Brands |

|

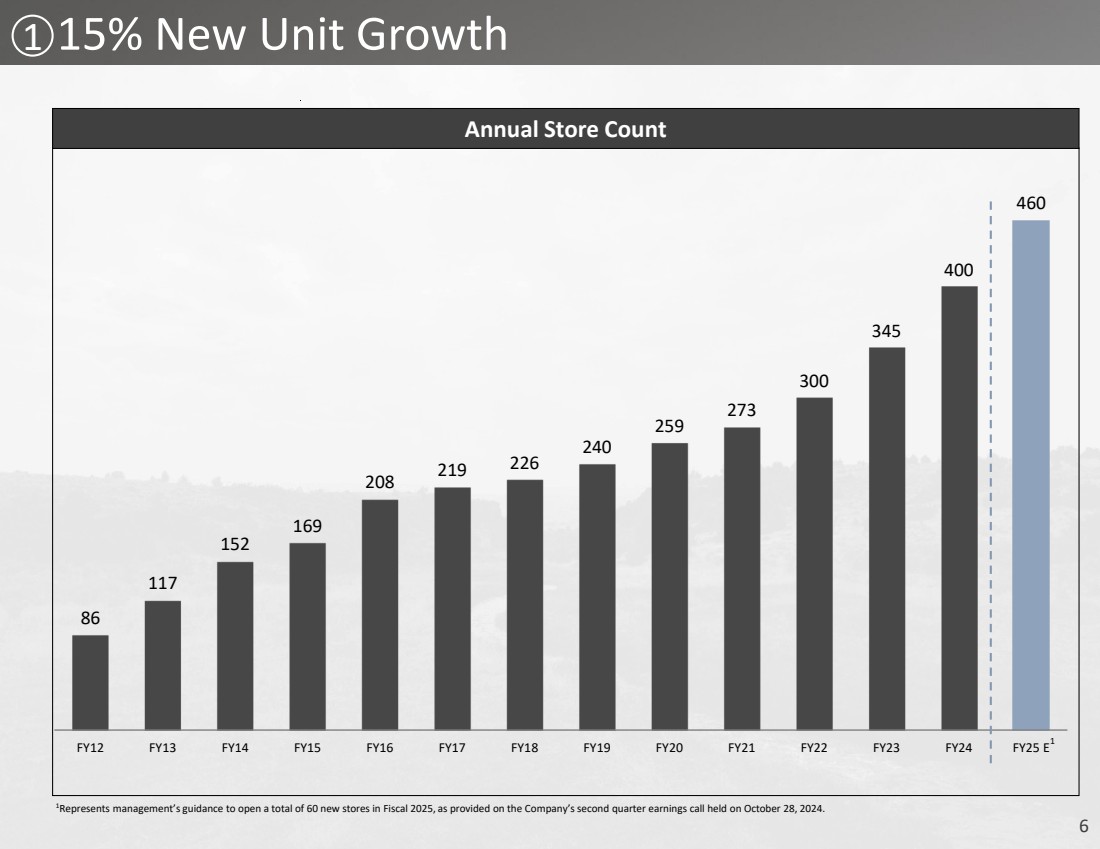

6 15% New Unit Growth 86 117 152 169 208 219 226 240 259 273 300 345 400 460 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 E Annual Store Count 1 1Represents management’s guidance to open a total of 60 new stores in Fiscal 2025, as provided on the Company’s second quarter earnings call held on October 28, 2024. 1 |

|

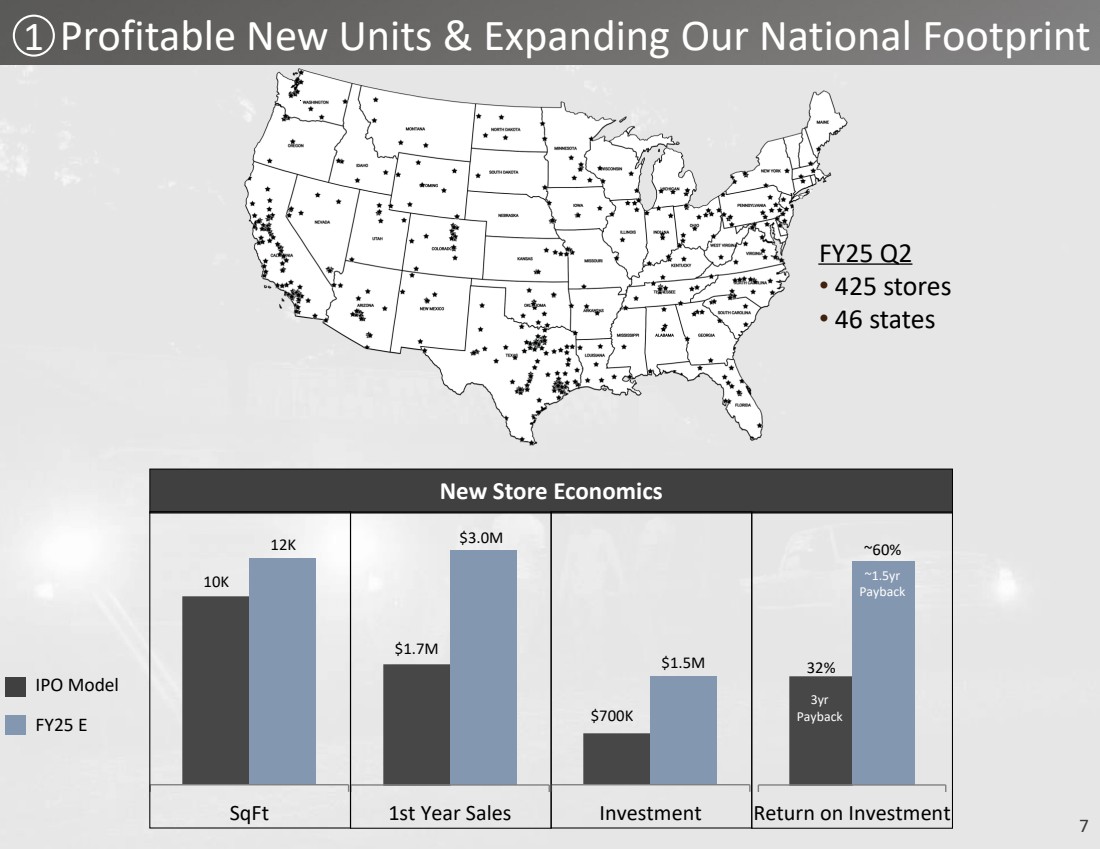

7 1 Profitable New Units & Expanding Our National Footprint FY25 Q2 • 425 stores • 46 states New Store Economics SqFt $1.7M $3.0M 1st Year Sales $700K Investment Return on Investment FY25 E 3yr Payback ~1.5yr Payback IPO Model $1.5M 32% 12K ~60% 10K |

|

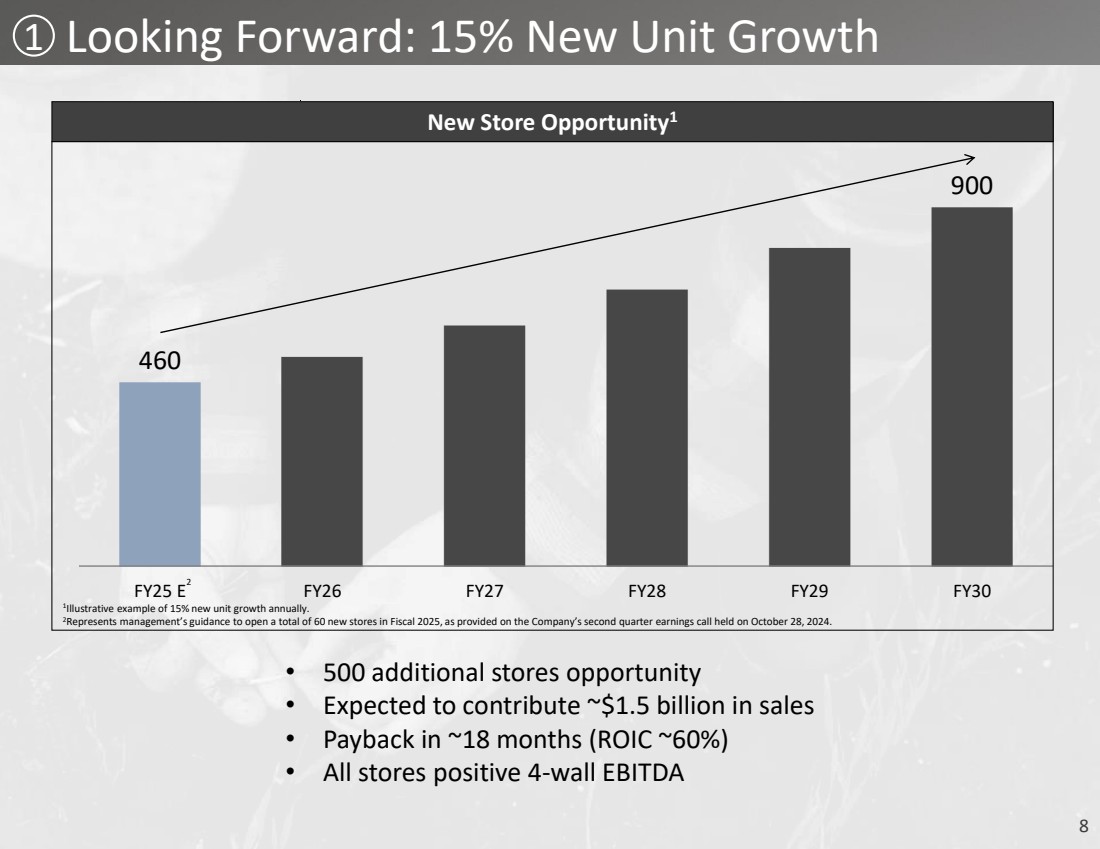

8 460 900 FY25 E FY26 FY27 FY28 FY29 FY30 1 Illustrative example of 15% new unit growth annually. 2Represents management’s guidance to open a total of 60 new stores in Fiscal 2025, as provided on the Company’s second quarter earnings call held on October 28, 2024. New Store Opportunity1 Looking Forward: 15% New Unit Growth • 500 additional stores opportunity • Expected to contribute ~$1.5 billion in sales • Payback in ~18 months (ROIC ~60%) • All stores positive 4-wall EBITDA 1 2 |

|

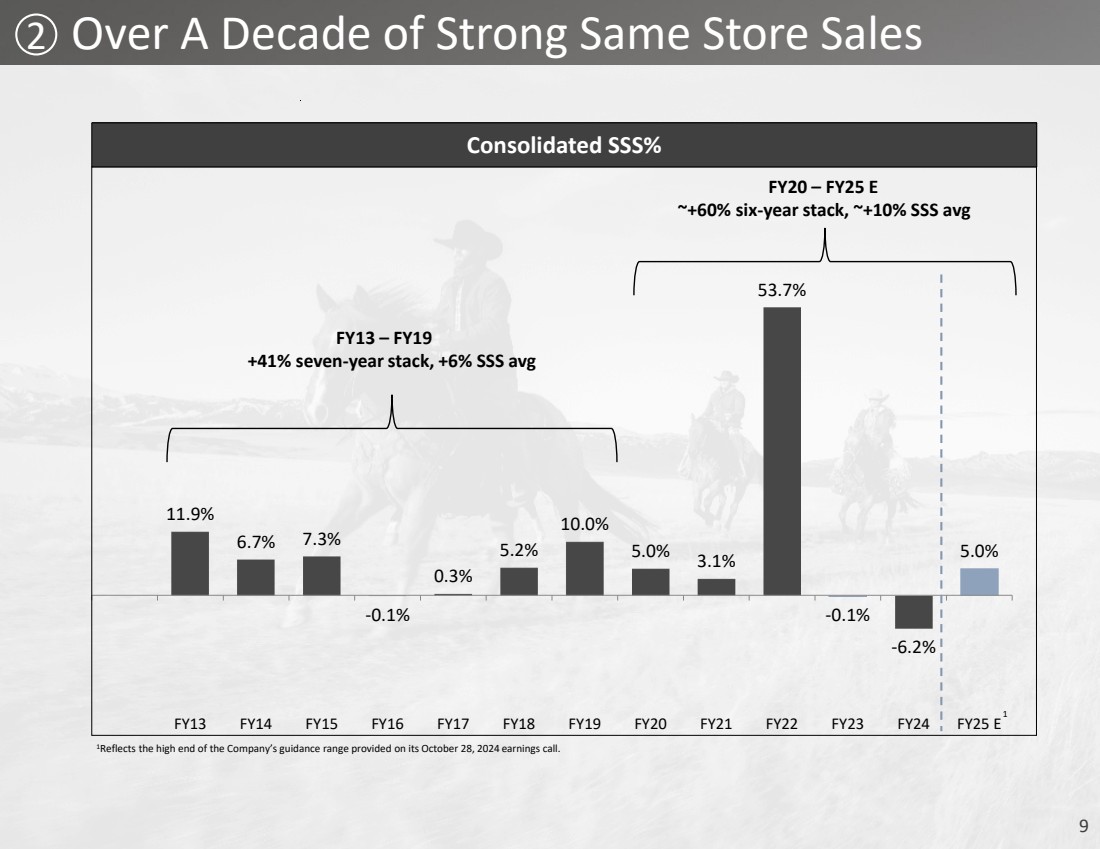

9 11.9% 6.7% 7.3% -0.1% 0.3% 5.2% 10.0% 5.0% 3.1% 53.7% -0.1% -6.2% 5.0% FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 E Consolidated SSS% 2 Over A Decade of Strong Same Store Sales FY13 – FY19 +41% seven-year stack, +6% SSS avg FY20 – FY25 E ~+60% six-year stack, ~+10% SSS avg 1 1Reflects the high end of the Company’s guidance range provided on its October 28, 2024 earnings call. |

|

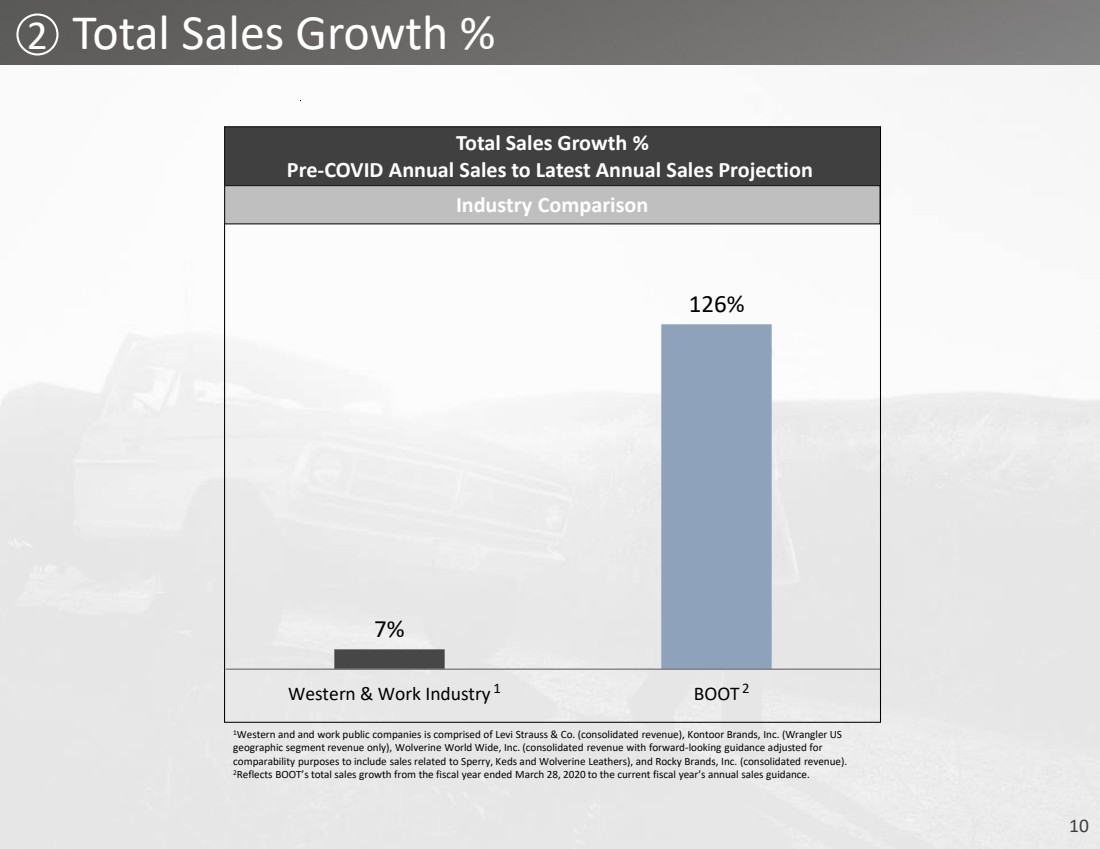

10 2 Total Sales Growth % 7% 126% Western & Work Industry BOOT Total Sales Growth % Pre-COVID Annual Sales to Latest Annual Sales Projection +55% five-year SSS% stack 1 1Western and and work public companies is comprised of Levi Strauss & Co. (consolidated revenue), Kontoor Brands, Inc. (Wrangler US geographic segment revenue only), Wolverine World Wide, Inc. (consolidated revenue with forward-looking guidance adjusted for comparability purposes to include sales related to Sperry, Keds and Wolverine Leathers), and Rocky Brands, Inc. (consolidated revenue). 2Reflects BOOT’s total sales growth from the fiscal year ended March 28, 2020 to the current fiscal year’s annual sales guidance. 2 Industry Comparison |

|

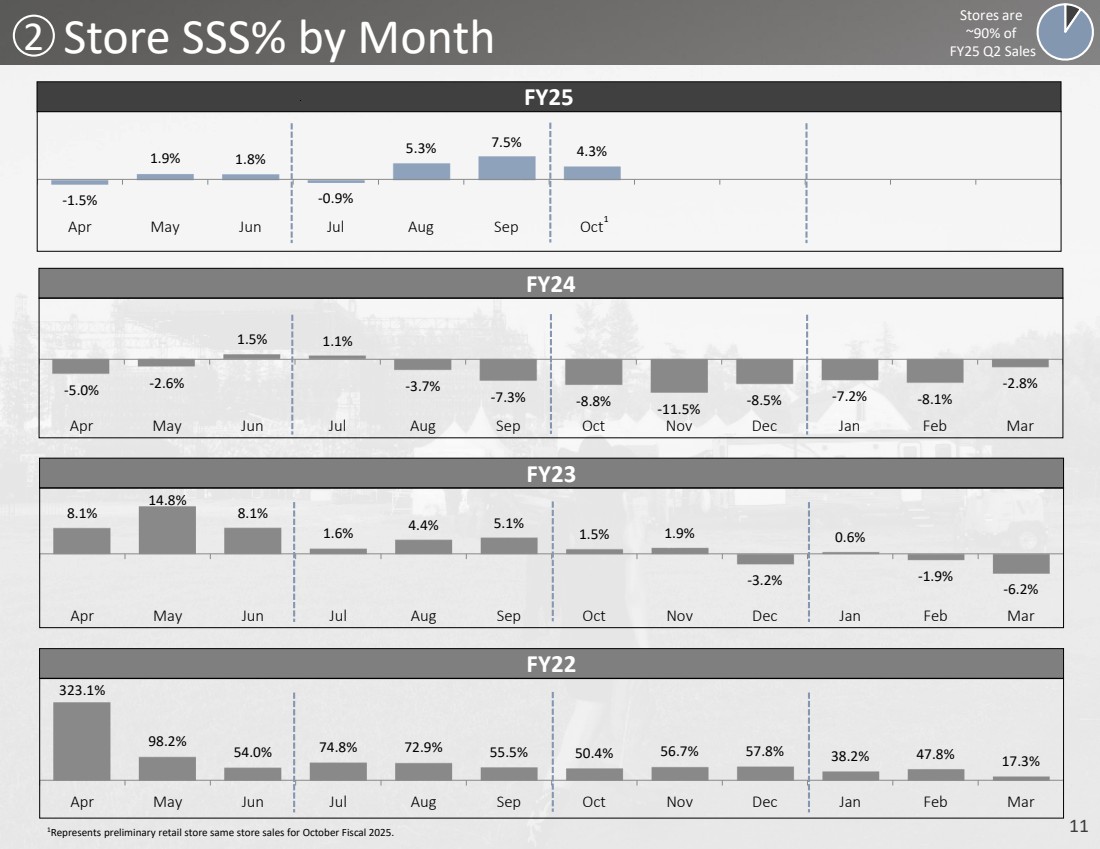

11 -1.5% 1.9% 1.8% -0.9% 5.3% 7.5% 4.3% Apr May Jun Jul Aug Sep Oct 2 Store SSS% by Month FY24 -5.0% -2.6% 1.5% 1.1% -3.7% -7.3% -8.8% -11.5% -8.5% -7.2% -8.1% -2.8% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 FY23 8.1% 14.8% 8.1% 1.6% 4.4% 5.1% 1.5% 1.9% -3.2% 0.6% -1.9% -6.2% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Stores are ~90% of FY25 Q2 Sales 1Represents preliminary retail store same store sales for October Fiscal 2025. FY22 323.1% 98.2% 54.0% 74.8% 72.9% 55.5% 50.4% 56.7% 57.8% 38.2% 47.8% 17.3% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 1 |

|

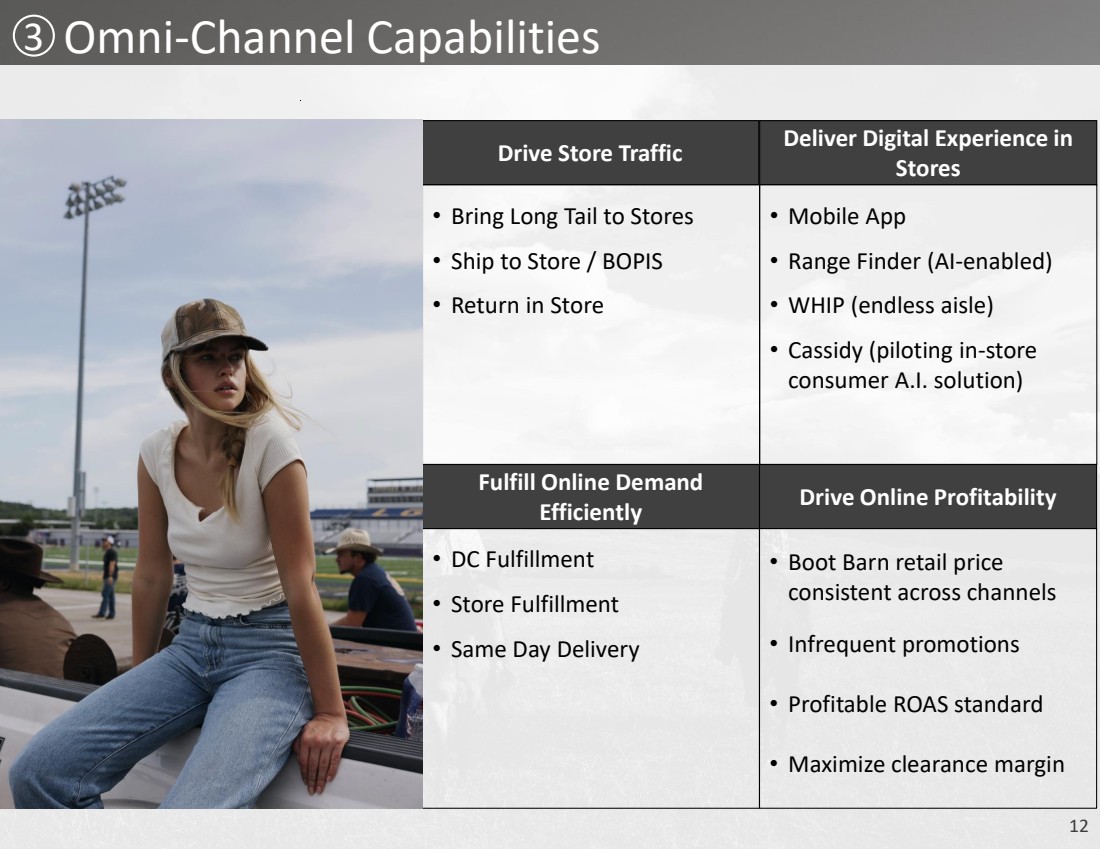

12 3 Omni-Channel Capabilities Drive Store Traffic • Bring Long Tail to Stores • Ship to Store / BOPIS • Return in Store Deliver Digital Experience in Stores • Mobile App • Range Finder (AI-enabled) • WHIP (endless aisle) • Cassidy (piloting in-store consumer A.I. solution) Fulfill Online Demand Efficiently • DC Fulfillment • Store Fulfillment • Same Day Delivery Drive Online Profitability • Boot Barn retail price consistent across channels • Infrequent promotions • Profitable ROAS standard • Maximize clearance margin |

|

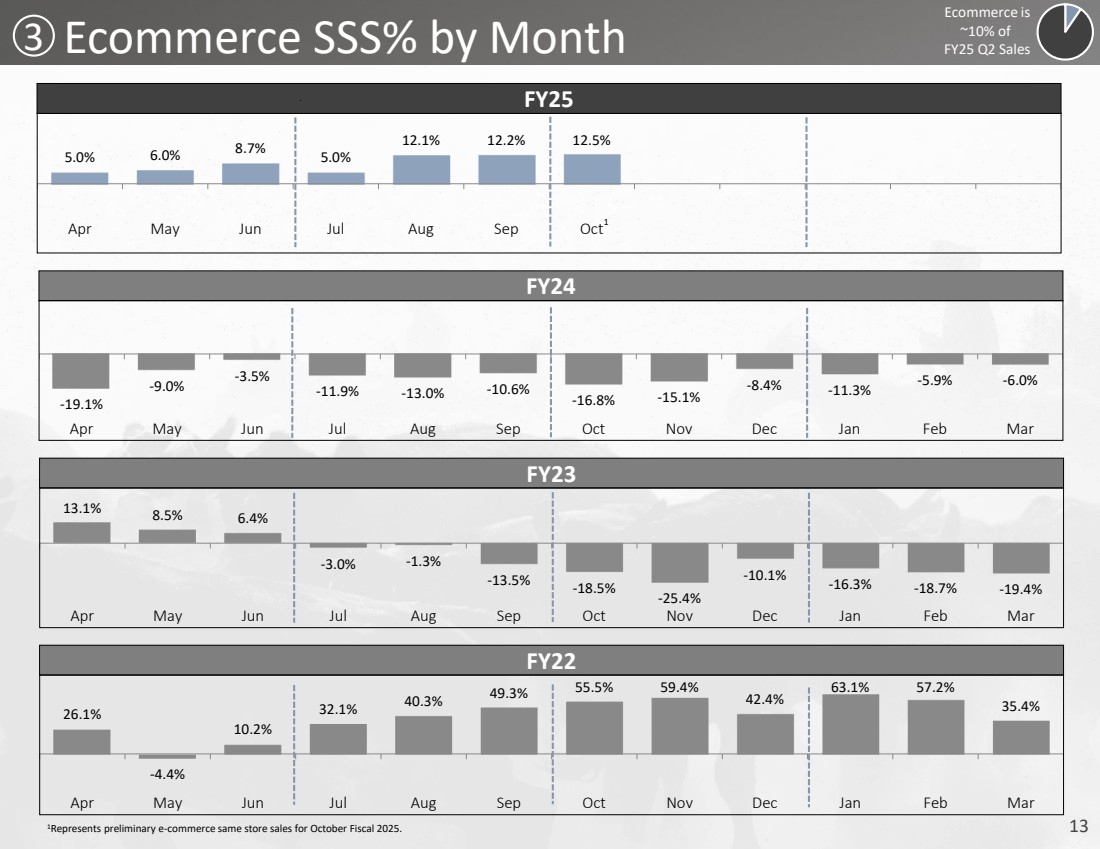

13 3 Ecommerce SSS% by Month 5.0% 6.0% 8.7% 5.0% 12.1% 12.2% 12.5% Apr May Jun Jul Aug Sep Oct FY24 -19.1% -9.0% -3.5% -11.9% -13.0% -10.6% -16.8% -15.1% -8.4% -11.3% -5.9% -6.0% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 FY23 13.1% 8.5% 6.4% -3.0% -1.3% -13.5% -18.5% -25.4% -10.1% -16.3% -18.7% -19.4% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Ecommerce is ~10% of FY25 Q2 Sales 1Represents preliminary e-commerce same store sales for October Fiscal 2025. FY22 26.1% -4.4% 10.2% 32.1% 40.3% 49.3% 55.5% 59.4% 42.4% 63.1% 57.2% 35.4% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 1 |

|

14 WESTERN COUNTRY ARTIST INSPIRED WORK RANCH & RODEO 4 Exclusive Brands Portfolio PREMIUM VALUE |

|

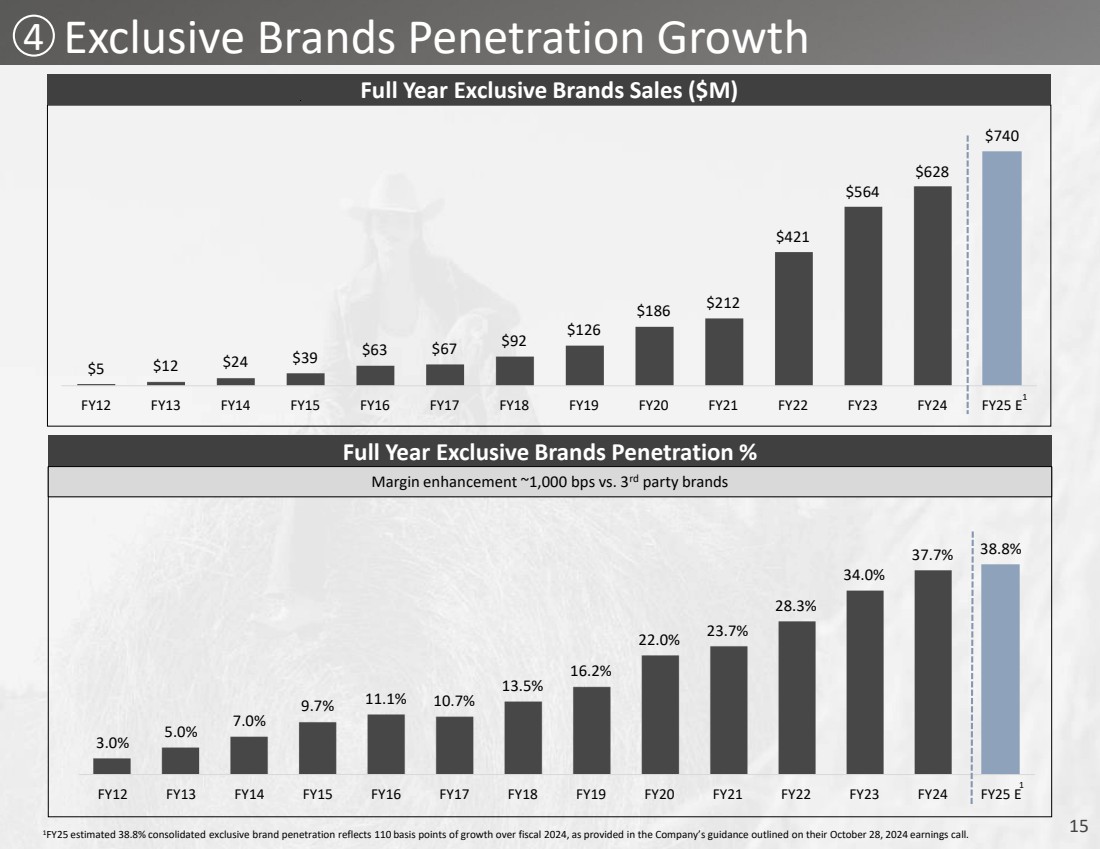

15 3.0% 5.0% 7.0% 9.7% 11.1% 10.7% 13.5% 16.2% 22.0% 23.7% 28.3% 34.0% 37.7% 38.8% FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 E Full Year Exclusive Brands Penetration % Margin enhancement ~1,000 bps vs. 3rd party brands $5 $12 $24 $39 $63 $67 $92 $126 $186 $212 $421 $564 $628 $740 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 E Full Year Exclusive Brands Sales ($M) 4 1FY25 estimated 38.8% consolidated exclusive brand penetration reflects 110 basis points of growth over fiscal 2024, as provided in the Company’s guidance outlined on their October 28, 2024 earnings call. 1 1 Exclusive Brands Penetration Growth |

|

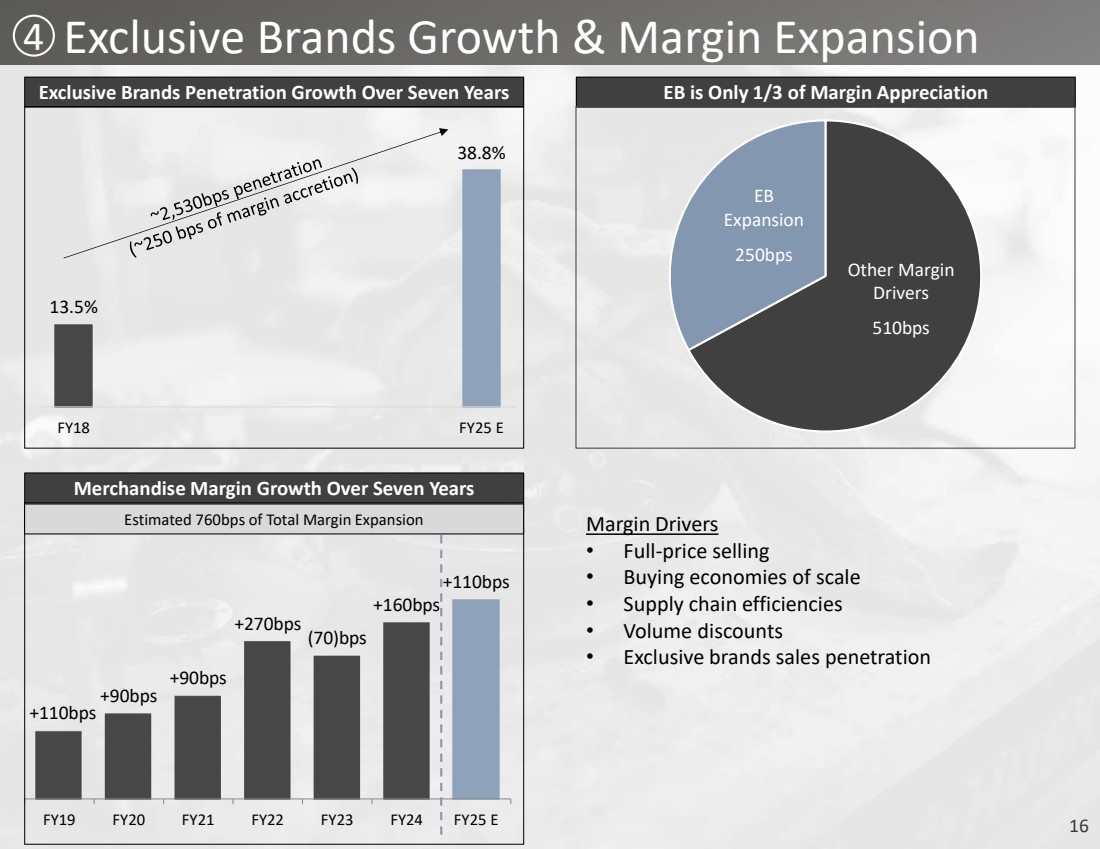

16 Margin Drivers • Full-price selling • Buying economies of scale • Supply chain efficiencies • Volume discounts • Exclusive brands sales penetration Exclusive Brands Penetration Growth Over Seven Years 13.5% 38.8% FY18 FY25 E EB is Only 1/3 of Margin Appreciation EB Expansion 250bps Other Margin Drivers 510bps +110bps +90bps +90bps +270bps (70)bps +160bps +110bps FY19 FY20 FY21 FY22 FY23 FY24 FY25 E Merchandise Margin Growth Over Seven Years 4 Estimated 760bps of Total Margin Expansion Exclusive Brands Growth & Margin Expansion |

|

17 FY25 Guidance |

|

18 Q3 Fiscal 2025 Financial Guidance Q3 FY25 Financial Guidance Low End ($M) High End ($M) Total Net Sales Consolidated SSS% Store SSS% E-commerce SSS% Total Net Sales Growth % New Store Openings $582 3.5% 3.0% 7.5% 11.8% 14 $595 6.0% 5.0% 10.0% 14.3% 14 Gross Profit % $225.4 38.7% $231.7 38.9% SG&A % $142.7 24.5% $144.4 24.3% Income from Operations % $82.7 14.2% $87.3 14.7% GAAP Earnings per Diluted Share $1.96 $2.07 |

|

19 Full Year Fiscal 2025 Financial Guidance Full Year FY25 Financial Guidance Updated Low End ($M) Updated High End ($M) High End Guidance Comments Total Net Sales Consolidated SSS% Store SSS% E-commerce SSS% Total Net Sales Growth % New Store Openings $1,874 3.0% 2.5% 7.5% 12.4% 60 $1,907 5.0% 4.5% 9.5% 14.4% 60 15% new unit growth 14 openings in Q3, 21 openings in Q4 Gross Profit % $696.9 37.2% $713.4 37.4% +110bps merchandise margin +110bps exclusive brands penetration (60)bps buying & occupancy deleverage SG&A % $476.5 25.4% $480.4 25.2% Income from Operations % $220.4 11.8% $233.0 12.2% GAAP Earnings per Diluted Share $5.30 $5.60 $0.25 increase from prior guidance Prior High End ($M) $1,850 1.2% 0.7% 5.5% 11.0% 60 $688.8 37.2% $469.4 25.4% $219.4 11.9% $5.35 |

|

20 National Leader in Attractive Market • Leading player in estimated $40 billion industry • Brick-and-mortar presence in 46 states and online sales in all 50 states plus international • Pressure-tested model World Class Omni-Channel Capabilities • Strong variety of omni-channel offerings in place • Ability to drive incremental traffic to stores • Improved customer satisfaction with added convenience and quicker delivery Strong New Unit Growth Opportunities • Proven ability to open stores in both new and existing markets • Store-preferred shopping experience • Minimal sales cannibalization from new stores Lifestyle Brand with Loyal Customer • Genuine lifestyle retail brand • Extremely loyal customers seeking authenticity • Lifestyle experience across stores, e-commerce and events Profit Enhancement Opportunities • Proven ability to drive merchandise margin expansion • Economies of scale in purchasing & ability to leverage expenses Investment Considerations Exclusive Brands • 1,000bps margin enhancement vs. 3rd party brands • Differentiated assortment to satisfy all customer segments • Proven supply chain reliability |

|

21 investor.bootbarn.com |