| Maryland | 000-54691 | 27-1106076 | ||||||||||||

| (State or other jurisdiction of incorporation) |

(Commission File Number) | (IRS Employer Identification No.) |

||||||||||||

|

11501 Northlake Drive

Cincinnati, Ohio

|

45249 | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

(513) 554-1110 | ||

| (Registrant’s telephone number, including area code) | ||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

| Common Stock $0.01 par value per share |

PECO | The Nasdaq Global Select Market | ||||||||||||

| Exhibit Number | Description of Exhibit | |||||||

| 99.1 | ||||||||

| 99.2 | ||||||||

| 104 | Cover Page Interactive Data File (formatted as inline XBRL) | |||||||

| PHILLIPS EDISON & COMPANY, INC. | ||||||||

| Dated: August 1, 2023 | By: | /s/ Jennifer L. Robison | ||||||

| Jennifer L. Robison | ||||||||

| Chief Accounting Officer and Senior Vice President (Principal Accounting Officer) |

||||||||

| (in thousands, except per share amounts) | 2Q YTD |

Updated Full Year

2023 Guidance

|

Previous Full Year

2023 Guidance

|

||||||||||||||

| Results: | |||||||||||||||||

| Net income per share | $0.26 | $0.51 - $0.55 | $0.47 - $0.52 | ||||||||||||||

| Nareit FFO per share | $1.15 | $2.27 - $2.32 | $2.23 - $2.29 | ||||||||||||||

| Core FFO per share | $1.18 | $2.30 - $2.36 | $2.28 - $2.34 | ||||||||||||||

| Same-Center NOI growth | 5.1% | 3.75% - 4.50% | 3.00% - 4.00% | ||||||||||||||

| Portfolio Activity: | |||||||||||||||||

| Acquisitions (net of dispositions) | $72,400 | $200,000 - $300,000 | $200,000 - $300,000 | ||||||||||||||

| Development and redevelopment spend | $20,444 | $35,000 - $45,000 | $50,000 -$60,000 | ||||||||||||||

| Other: | |||||||||||||||||

| Interest expense, net | $40,141 | $85,000 - $90,000 | $85,000 - $90,000 | ||||||||||||||

| G&A expense | $23,219 | $44,000 - $48,000 | $44,000 - $48,000 | ||||||||||||||

Non-cash revenue items(1) |

$8,314 | $16,000 - $19,000 | $14,000 - $19,000 | ||||||||||||||

| Adjustments for collectibility | $1,313 | $3,000 - $4,000 | $3,500 - $4,500 | ||||||||||||||

| (Unaudited) | Low End | High End | |||||||||

| Net income | $ | 0.51 | $ | 0.55 | |||||||

| Depreciation and amortization of real estate assets | 1.74 | 1.75 | |||||||||

| Adjustments related to unconsolidated joint ventures | 0.02 | 0.02 | |||||||||

| Nareit FFO | $ | 2.27 | $ | 2.32 | |||||||

| Depreciation and amortization of corporate assets | 0.01 | 0.02 | |||||||||

| Transactions and other | 0.02 | 0.02 | |||||||||

| Core FFO | $ | 2.30 | $ | 2.36 | |||||||

| June 30, 2023 | December 31, 2022 | ||||||||||

| ASSETS | |||||||||||

| Investment in real estate: | |||||||||||

| Land and improvements | $ | 1,703,349 | $ | 1,674,133 | |||||||

| Building and improvements | 3,653,088 | 3,572,146 | |||||||||

| In-place lease assets | 477,974 | 471,507 | |||||||||

| Above-market lease assets | 72,350 | 71,954 | |||||||||

| Total investment in real estate assets | 5,906,761 | 5,789,740 | |||||||||

| Accumulated depreciation and amortization | (1,429,070) | (1,316,743) | |||||||||

| Net investment in real estate assets | 4,477,691 | 4,472,997 | |||||||||

| Investment in unconsolidated joint ventures | 26,064 | 27,201 | |||||||||

| Total investment in real estate assets, net | 4,503,755 | 4,500,198 | |||||||||

| Cash and cash equivalents | 5,564 | 5,478 | |||||||||

| Restricted cash | 4,352 | 11,871 | |||||||||

| Goodwill | 29,066 | 29,066 | |||||||||

| Other assets, net | 198,274 | 188,879 | |||||||||

| Total assets | $ | 4,741,011 | $ | 4,735,492 | |||||||

| LIABILITIES AND EQUITY | |||||||||||

| Liabilities: | |||||||||||

| Debt obligations, net | $ | 1,951,186 | $ | 1,896,594 | |||||||

| Below-market lease liabilities, net | 108,190 | 109,799 | |||||||||

| Accounts payable and other liabilities | 98,187 | 113,185 | |||||||||

| Deferred income | 21,700 | 18,481 | |||||||||

| Total liabilities | 2,179,263 | 2,138,059 | |||||||||

| Equity: | |||||||||||

Preferred stock, $0.01 par value per share, 10,000 shares authorized, zero shares issued and outstanding at June 30, 2023 and December 31, 2022 |

— | — | |||||||||

Common stock, $0.01 par value per share, 1,000,000 shares authorized, 117,443 and 117,126 shares issued and outstanding at June 30, 2023 and December 31, 2022, respectively |

1,174 | 1,171 | |||||||||

| Additional paid-in capital | 3,387,764 | 3,383,978 | |||||||||

| Accumulated other comprehensive income | 21,059 | 21,003 | |||||||||

| Accumulated deficit | (1,204,714) | (1,169,665) | |||||||||

| Total stockholders’ equity | 2,205,283 | 2,236,487 | |||||||||

| Noncontrolling interests | 356,465 | 360,946 | |||||||||

| Total equity | 2,561,748 | 2,597,433 | |||||||||

| Total liabilities and equity | $ | 4,741,011 | $ | 4,735,492 | |||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Revenues: | |||||||||||||||||||||||

| Rental income | $ | 148,980 | $ | 137,230 | $ | 296,708 | $ | 275,978 | |||||||||||||||

| Fees and management income | 2,546 | 4,781 | 5,024 | 7,242 | |||||||||||||||||||

| Other property income | 611 | 505 | 1,469 | 1,459 | |||||||||||||||||||

| Total revenues | 152,137 | 142,516 | 303,201 | 284,679 | |||||||||||||||||||

| Operating Expenses: | |||||||||||||||||||||||

| Property operating | 24,674 | 22,852 | 49,736 | 46,172 | |||||||||||||||||||

| Real estate taxes | 18,397 | 16,473 | 36,453 | 33,964 | |||||||||||||||||||

| General and administrative | 11,686 | 11,376 | 23,219 | 22,908 | |||||||||||||||||||

| Depreciation and amortization | 59,667 | 60,769 | 118,165 | 117,995 | |||||||||||||||||||

| Total operating expenses | 114,424 | 111,470 | 227,573 | 221,039 | |||||||||||||||||||

| Other: | |||||||||||||||||||||||

| Interest expense, net | (20,675) | (17,127) | (40,141) | (35,326) | |||||||||||||||||||

| Gain on disposal of property, net | 75 | 2,793 | 1,017 | 4,161 | |||||||||||||||||||

| Other expense, net | (904) | (1,457) | (1,659) | (5,822) | |||||||||||||||||||

| Net income | 16,209 | 15,255 | 34,845 | 26,653 | |||||||||||||||||||

| Net income attributable to noncontrolling interests | (1,758) | (1,727) | (3,775) | (3,046) | |||||||||||||||||||

| Net income attributable to stockholders | $ | 14,451 | $ | 13,528 | $ | 31,070 | $ | 23,607 | |||||||||||||||

| Earnings per share of common stock: | |||||||||||||||||||||||

Net income per share attributable to stockholders - basic and diluted |

$ | 0.12 | $ | 0.12 | $ | 0.26 | $ | 0.21 | |||||||||||||||

| Three Months Ended June 30, | Favorable (Unfavorable) | Six Months Ended June 30, | Favorable (Unfavorable) | ||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | $ Change | % Change | 2023 | 2022 | $ Change | % Change | ||||||||||||||||||||||||||||||||||||||||

| Revenues: | |||||||||||||||||||||||||||||||||||||||||||||||

Rental income(1) |

$ | 102,927 | $ | 98,497 | $ | 4,430 | $ | 206,508 | $ | 197,183 | $ | 9,325 | |||||||||||||||||||||||||||||||||||

| Tenant recovery income | 33,567 | 30,063 | 3,504 | 67,461 | 63,210 | 4,251 | |||||||||||||||||||||||||||||||||||||||||

Reserves for uncollectibility(2) |

(357) | 177 | (534) | (1,269) | (661) | (608) | |||||||||||||||||||||||||||||||||||||||||

| Other property income | 568 | 466 | 102 | 1,368 | 1,366 | 2 | |||||||||||||||||||||||||||||||||||||||||

| Total revenues | 136,705 | 129,203 | 7,502 | 5.8 | % | 274,068 | 261,098 | 12,970 | 5.0 | % | |||||||||||||||||||||||||||||||||||||

| Operating expenses: | |||||||||||||||||||||||||||||||||||||||||||||||

| Property operating expenses | 20,396 | 19,186 | (1,210) | 41,934 | 39,866 | (2,068) | |||||||||||||||||||||||||||||||||||||||||

| Real estate taxes | 17,341 | 16,054 | (1,287) | 34,670 | 33,333 | (1,337) | |||||||||||||||||||||||||||||||||||||||||

| Total operating expenses | 37,737 | 35,240 | (2,497) | (7.1) | % | 76,604 | 73,199 | (3,405) | (4.7) | % | |||||||||||||||||||||||||||||||||||||

| Total Same-Center NOI | $ | 98,968 | $ | 93,963 | $ | 5,005 | 5.3 | % | $ | 197,464 | $ | 187,899 | $ | 9,565 | 5.1 | % | |||||||||||||||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

Net income |

$ | 16,209 | $ | 15,255 | $ | 34,845 | $ | 26,653 | ||||||||||||||||||

| Adjusted to exclude: | ||||||||||||||||||||||||||

| Fees and management income | (2,546) | (4,781) | (5,024) | (7,242) | ||||||||||||||||||||||

Straight-line rental income(1) |

(3,284) | (3,319) | (5,864) | (5,128) | ||||||||||||||||||||||

| Net amortization of above- and below- market leases | (1,262) | (1,078) | (2,490) | (2,080) | ||||||||||||||||||||||

| Lease buyout income | (74) | (176) | (429) | (2,141) | ||||||||||||||||||||||

| General and administrative expenses | 11,686 | 11,376 | 23,219 | 22,908 | ||||||||||||||||||||||

| Depreciation and amortization | 59,667 | 60,769 | 118,165 | 117,995 | ||||||||||||||||||||||

| Interest expense, net | 20,675 | 17,127 | 40,141 | 35,326 | ||||||||||||||||||||||

| Gain on disposal of property, net | (75) | (2,793) | (1,017) | (4,161) | ||||||||||||||||||||||

| Other expense, net | 904 | 1,457 | 1,659 | 5,822 | ||||||||||||||||||||||

| Property operating expenses related to fees and management income | 711 | 1,287 | 1,026 | 2,357 | ||||||||||||||||||||||

| NOI for real estate investments | 102,611 | 95,124 | 204,231 | 190,309 | ||||||||||||||||||||||

Less: Non-same-center NOI(2) |

(3,643) | (1,161) | (6,767) | (2,410) | ||||||||||||||||||||||

| Total Same-Center NOI | $ | 98,968 | $ | 93,963 | $ | 197,464 | $ | 187,899 | ||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Calculation of Nareit FFO Attributable to Stockholders and OP Unit Holders | |||||||||||||||||||||||

Net income |

$ | 16,209 | $ | 15,255 | $ | 34,845 | $ | 26,653 | |||||||||||||||

| Adjustments: | |||||||||||||||||||||||

| Depreciation and amortization of real estate assets | 59,115 | 59,849 | 117,068 | 116,169 | |||||||||||||||||||

| Gain on disposal of property, net | (75) | (2,793) | (1,017) | (4,161) | |||||||||||||||||||

| Adjustments related to unconsolidated joint ventures | 645 | (1,186) | 1,343 | (481) | |||||||||||||||||||

| Nareit FFO attributable to stockholders and OP unit holders | $ | 75,894 | $ | 71,125 | $ | 152,239 | $ | 138,180 | |||||||||||||||

| Calculation of Core FFO Attributable to Stockholders and OP Unit Holders | |||||||||||||||||||||||

| Nareit FFO attributable to stockholders and OP unit holders | $ | 75,894 | $ | 71,125 | $ | 152,239 | $ | 138,180 | |||||||||||||||

| Adjustments: | |||||||||||||||||||||||

| Depreciation and amortization of corporate assets | 552 | 920 | 1,097 | 1,826 | |||||||||||||||||||

| Change in fair value of earn-out liability | — | — | — | 1,809 | |||||||||||||||||||

| Transaction and acquisition expenses | 1,261 | 2,035 | 2,599 | 4,080 | |||||||||||||||||||

| (Gain) loss on extinguishment or modification of debt and other, net | (9) | 129 | (9) | 1,029 | |||||||||||||||||||

| Amortization of unconsolidated joint venture basis differences | 7 | 175 | 8 | 219 | |||||||||||||||||||

Realized performance income(1) |

— | (2,546) | (75) | (2,742) | |||||||||||||||||||

| Core FFO attributable to stockholders and OP unit holders | $ | 77,705 | $ | 71,838 | $ | 155,859 | $ | 144,401 | |||||||||||||||

| Nareit FFO/Core FFO Attributable to Stockholders and OP Unit Holders per Diluted Share | |||||||||||||||||||||||

| Weighted-average shares of common stock outstanding - diluted | 131,887 | 129,117 | 132,004 | 128,857 | |||||||||||||||||||

| Nareit FFO attributable to stockholders and OP unit holders per share - diluted | $ | 0.58 | $ | 0.55 | $ | 1.15 | $ | 1.07 | |||||||||||||||

| Core FFO attributable to stockholders and OP unit holders per share - diluted | $ | 0.59 | $ | 0.56 | $ | 1.18 | $ | 1.12 | |||||||||||||||

| Three Months Ended June 30, |

Six Months Ended June 30, |

Year Ended December 31, | |||||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | 2022 | |||||||||||||||||||||||||

Calculation of EBITDAre |

|||||||||||||||||||||||||||||

Net income |

$ | 16,209 | $ | 15,255 | $ | 34,845 | $ | 26,653 | $ | 54,529 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Depreciation and amortization | 59,667 | 60,769 | 118,165 | 117,995 | 236,224 | ||||||||||||||||||||||||

| Interest expense, net | 20,675 | 17,127 | 40,141 | 35,326 | 71,196 | ||||||||||||||||||||||||

| Gain on disposal of property, net | (75) | (2,793) | (1,017) | (4,161) | (7,517) | ||||||||||||||||||||||||

| Impairment of real estate assets | — | — | — | — | 322 | ||||||||||||||||||||||||

| Federal, state, and local tax expense | 119 | 97 | 237 | 194 | 806 | ||||||||||||||||||||||||

| Adjustments related to unconsolidated joint ventures | 918 | (885) | 1,884 | 134 | 1,987 | ||||||||||||||||||||||||

EBITDAre |

$ | 97,513 | $ | 89,570 | $ | 194,255 | $ | 176,141 | $ | 357,547 | |||||||||||||||||||

Calculation of Adjusted EBITDAre |

|||||||||||||||||||||||||||||

EBITDAre |

$ | 97,513 | $ | 89,570 | $ | 194,255 | $ | 176,141 | $ | 357,547 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Change in fair value of earn-out liability | — | — | — | 1,809 | 1,809 | ||||||||||||||||||||||||

| Transaction and acquisition expenses | 1,261 | 2,035 | 2,599 | 4,080 | 10,551 | ||||||||||||||||||||||||

| Amortization of unconsolidated joint venture basis differences | 7 | 175 | 8 | 219 | 220 | ||||||||||||||||||||||||

Realized performance income(1) |

— | (2,546) | (75) | (2,742) | (2,742) | ||||||||||||||||||||||||

Adjusted EBITDAre |

$ | 98,781 | $ | 89,234 | $ | 196,787 | $ | 179,507 | $ | 367,385 | |||||||||||||||||||

| June 30, 2023 | December 31, 2022 | ||||||||||

| Net debt: | |||||||||||

| Total debt, excluding discounts, market adjustments, and deferred financing expenses | $ | 1,990,378 | $ | 1,937,142 | |||||||

| Less: Cash and cash equivalents | 5,863 | 5,740 | |||||||||

| Total net debt | $ | 1,984,515 | $ | 1,931,402 | |||||||

| Enterprise value: | |||||||||||

| Net debt | $ | 1,984,515 | $ | 1,931,402 | |||||||

Total equity market capitalization(1)(2) |

4,484,144 | 4,178,204 | |||||||||

| Total enterprise value | $ | 6,468,659 | $ | 6,109,606 | |||||||

| June 30, 2023 | December 31, 2022 | ||||||||||

Net debt to Adjusted EBITDAre - annualized: |

|||||||||||

| Net debt | $ | 1,984,515 | $ | 1,931,402 | |||||||

Adjusted EBITDAre - annualized(1) |

384,665 | 367,385 | |||||||||

Net debt to Adjusted EBITDAre - annualized |

5.2x | 5.3x | |||||||||

| Net debt to total enterprise value: | |||||||||||

| Net debt | $ | 1,984,515 | $ | 1,931,402 | |||||||

| Total enterprise value | 6,468,659 | 6,109,606 | |||||||||

| Net debt to total enterprise value | 30.7% | 31.6% | |||||||||

| Table of Contents | |||||

Earnings Release |

|||||

Consolidated Statements of Operations (Quarterly) |

|||||

FFO, Core FFO, and Adjusted FFO (Quarterly) |

|||||

Joint Venture Summary and Financials |

|||||

Summary of Outstanding Debt

|

|||||

Covenant Disclosures |

|||||

| INVESTOR INFORMATION | |||||

| Phillips Edison & Company |

2

|

|||||||

| Introductory Notes | ||||||||

SUPPLEMENTAL INFORMATION | ||

| CAUTIONARY NOTE ABOUT FORWARD-LOOKING STATEMENTS | ||

| NOTICE REGARDING NON-GAAP FINANCIAL MEASURES | ||

| Phillips Edison & Company |

3

|

|||||||

| Introductory Notes | ||||||||

PRO RATA FINANCIAL INFORMATION | ||

| Phillips Edison & Company |

4

|

|||||||

| FINANCIAL RESULTS | ||

Quarter Ended June 30, 2023 | ||

|

Earnings Release

Unaudited

| ||||||||

| Phillips Edison & Company |

6

|

|||||||

|

Earnings Release

Unaudited

| ||||||||

| Phillips Edison & Company |

7

|

|||||||

|

Earnings Release

Unaudited

| ||||||||

| (in thousands, except per share amounts) | 2Q YTD |

Updated Full Year

2023 Guidance

|

Previous Full Year

2023 Guidance

|

||||||||||||||

| Results: | |||||||||||||||||

| Net income per share | $0.26 | $0.51 - $0.55 | $0.47 - $0.52 | ||||||||||||||

| Nareit FFO per share | $1.15 | $2.27 - $2.32 | $2.23 - $2.29 | ||||||||||||||

| Core FFO per share | $1.18 | $2.30 - $2.36 | $2.28 - $2.34 | ||||||||||||||

| Same-Center NOI growth | 5.1% | 3.75% - 4.50% | 3.00% - 4.00% | ||||||||||||||

| Portfolio Activity: | |||||||||||||||||

| Acquisitions (net of dispositions) | $72,400 | $200,000 - $300,000 | $200,000 - $300,000 | ||||||||||||||

| Development and redevelopment spend | $20,444 | $35,000 - $45,000 | $50,000 -$60,000 | ||||||||||||||

| Other: | |||||||||||||||||

| Interest expense, net | $40,141 | $85,000 - $90,000 | $85,000 - $90,000 | ||||||||||||||

| G&A expense | $23,219 | $44,000 - $48,000 | $44,000 - $48,000 | ||||||||||||||

Non-cash revenue items(1) |

$8,314 | $16,000 - $19,000 | $14,000 - $19,000 | ||||||||||||||

| Adjustments for collectibility | $1,313 | $3,000 - $4,000 | $3,500 - $4,500 | ||||||||||||||

| Phillips Edison & Company |

8

|

|||||||

|

Earnings Release

Unaudited

| ||||||||

| (Unaudited) | Low End | High End | |||||||||

| Net income | $ | 0.51 | $ | 0.55 | |||||||

| Depreciation and amortization of real estate assets | 1.74 | 1.75 | |||||||||

| Adjustments related to unconsolidated joint ventures | 0.02 | 0.02 | |||||||||

| Nareit FFO | $ | 2.27 | $ | 2.32 | |||||||

| Depreciation and amortization of corporate assets | 0.01 | 0.02 | |||||||||

| Transactions and other | 0.02 | 0.02 | |||||||||

| Core FFO | $ | 2.30 | $ | 2.36 | |||||||

| Phillips Edison & Company |

9

|

|||||||

|

Earnings Release

Unaudited

| ||||||||

| Phillips Edison & Company |

10

|

|||||||

|

Overview of Results

Unaudited, in thousands (excluding per share and per square foot amounts)

| |||||||||||||||||||||||

| Three Months Ended June 30, |

Six Months Ended June 30, |

||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| SUMMARY FINANCIAL RESULTS | |||||||||||||||||||||||

Total revenues (page 14) |

$ | 152,137 | $ | 142,516 | $ | 303,201 | $ | 284,679 | |||||||||||||||

Net income attributable to stockholders (page 14) |

14,451 | 13,528 | 31,070 | 23,607 | |||||||||||||||||||

Net income per share - basic and diluted (page 14) |

$ | 0.12 | $ | 0.12 | $ | 0.26 | $ | 0.21 | |||||||||||||||

Same-Center NOI (page 20) |

98,968 | 93,963 | 197,464 | 187,899 | |||||||||||||||||||

Adjusted EBITDAre (page 18) |

98,781 | 89,234 | 196,787 | 179,507 | |||||||||||||||||||

Nareit FFO (page 16) |

75,894 | 71,125 | 152,239 | 138,180 | |||||||||||||||||||

Nareit FFO per share - diluted (page 16) |

$ | 0.58 | $ | 0.55 | $ | 1.15 | $ | 1.07 | |||||||||||||||

Core FFO (page 16) |

77,705 | 71,838 | 155,859 | 144,401 | |||||||||||||||||||

Core FFO per share - diluted (page 16) |

$ | 0.59 | $ | 0.56 | $ | 1.18 | $ | 1.12 | |||||||||||||||

| SUMMARY OF FINANCIAL AND OPERATING RATIOS | |||||||||||||||||||||||

Same-Center NOI margin (page 20) |

72.4 | % | 72.7 | % | 72.0 | % | 72.0 | % | |||||||||||||||

Same-Center NOI change (page 20)(1) |

5.3 | % | 4.3 | % | 5.1 | % | 5.5 | % | |||||||||||||||

| LEASING RESULTS | |||||||||||||||||||||||

Comparable rent spreads - new leases (page 40)(2) |

25.1 | % | 39.0 | % | 26.1 | % | 36.6 | % | |||||||||||||||

Comparable rent spreads - renewals (page 40)(2) |

17.7 | % | 14.4 | % | 17.0 | % | 14.6 | % | |||||||||||||||

| Portfolio retention rate | 93.8 | % | 92.1 | % | 94.4 | % | 90.6 | % | |||||||||||||||

| As of June 30, | |||||||||||||||||||||||

| 2023 | 2022 | ||||||||||||||||||||||

| OUTSTANDING STOCK AND PARTNERSHIP UNITS | |||||||||||||||||||||||

| Common stock outstanding | 117,443 | 115,782 | |||||||||||||||||||||

| Operating Partnership (OP) units outstanding | 14,134 | 14,560 | |||||||||||||||||||||

SUMMARY PORTFOLIO STATISTICS(2) |

|||||||||||||||||||||||

| Number of properties | 274 | 269 | |||||||||||||||||||||

GLA (page 42) |

31,378 | 30,935 | |||||||||||||||||||||

Leased occupancy (page 36) |

97.8 | % | 96.8 | % | |||||||||||||||||||

Economic occupancy (page 36) |

97.2 | % | 96.2 | % | |||||||||||||||||||

Leased ABR PSF (page 36) |

$ | 14.64 | $ | 14.06 | |||||||||||||||||||

Leased Anchor ABR PSF (page 36) |

$ | 9.97 | $ | 9.83 | |||||||||||||||||||

Leased Inline ABR PSF (page 36) |

$ | 23.95 | $ | 22.66 | |||||||||||||||||||

| Phillips Edison & Company |

11

|

|||||||

| FINANCIAL SUMMARY | ||

Quarter Ended June 30, 2023 | ||

|

Consolidated Balance Sheets

Condensed and Unaudited, in thousands (excluding per share amounts)

| |||||||||||

| June 30, 2023 | December 31, 2022 | ||||||||||

| ASSETS | |||||||||||

| Investment in real estate: | |||||||||||

| Land and improvements | $ | 1,703,349 | $ | 1,674,133 | |||||||

| Building and improvements | 3,653,088 | 3,572,146 | |||||||||

| In-place lease assets | 477,974 | 471,507 | |||||||||

| Above-market lease assets | 72,350 | 71,954 | |||||||||

| Total investment in real estate assets | 5,906,761 | 5,789,740 | |||||||||

| Accumulated depreciation and amortization | (1,429,070) | (1,316,743) | |||||||||

| Net investment in real estate assets | 4,477,691 | 4,472,997 | |||||||||

| Investment in unconsolidated joint ventures | 26,064 | 27,201 | |||||||||

| Total investment in real estate assets, net | 4,503,755 | 4,500,198 | |||||||||

| Cash and cash equivalents | 5,564 | 5,478 | |||||||||

| Restricted cash | 4,352 | 11,871 | |||||||||

| Goodwill | 29,066 | 29,066 | |||||||||

| Other assets, net | 198,274 | 188,879 | |||||||||

| Total assets | $ | 4,741,011 | $ | 4,735,492 | |||||||

| LIABILITIES AND EQUITY | |||||||||||

| Liabilities: | |||||||||||

| Debt obligations, net | $ | 1,951,186 | $ | 1,896,594 | |||||||

| Below-market lease liabilities, net | 108,190 | 109,799 | |||||||||

| Accounts payable and other liabilities | 98,187 | 113,185 | |||||||||

| Deferred income | 21,700 | 18,481 | |||||||||

| Total liabilities | 2,179,263 | 2,138,059 | |||||||||

| Equity: | |||||||||||

Preferred stock, $0.01 par value per share, 10,000 shares authorized as of June 30, 2023 and December 31, 2022 |

— | — | |||||||||

|

Common stock, $0.01 par value per share, 1,000,000 shares authorized,

117,443 and 117,126 shares issued and outstanding at June 30, 2023 and December 31, 2022, respectively

|

1,174 | 1,171 | |||||||||

| Additional paid-in capital | 3,387,764 | 3,383,978 | |||||||||

| Accumulated other comprehensive income | 21,059 | 21,003 | |||||||||

| Accumulated deficit | (1,204,714) | (1,169,665) | |||||||||

| Total stockholders’ equity | 2,205,283 | 2,236,487 | |||||||||

| Noncontrolling interests | 356,465 | 360,946 | |||||||||

| Total equity | 2,561,748 | 2,597,433 | |||||||||

| Total liabilities and equity | $ | 4,741,011 | $ | 4,735,492 | |||||||

| Phillips Edison & Company |

13

|

|||||||

|

Consolidated Statements of Operations

Condensed and Unaudited, in thousands (excluding per share amounts)

| |||||||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| REVENUES | |||||||||||||||||||||||

| Rental income | $ | 148,980 | $ | 137,230 | $ | 296,708 | $ | 275,978 | |||||||||||||||

| Fees and management income | 2,546 | 4,781 | 5,024 | 7,242 | |||||||||||||||||||

| Other property income | 611 | 505 | 1,469 | 1,459 | |||||||||||||||||||

| Total revenues | 152,137 | 142,516 | 303,201 | 284,679 | |||||||||||||||||||

| OPERATING EXPENSES | |||||||||||||||||||||||

| Property operating | 24,674 | 22,852 | 49,736 | 46,172 | |||||||||||||||||||

| Real estate taxes | 18,397 | 16,473 | 36,453 | 33,964 | |||||||||||||||||||

| General and administrative | 11,686 | 11,376 | 23,219 | 22,908 | |||||||||||||||||||

| Depreciation and amortization | 59,667 | 60,769 | 118,165 | 117,995 | |||||||||||||||||||

| Total operating expenses | 114,424 | 111,470 | 227,573 | 221,039 | |||||||||||||||||||

| OTHER | |||||||||||||||||||||||

| Interest expense, net | (20,675) | (17,127) | (40,141) | (35,326) | |||||||||||||||||||

| Gain on disposal of property, net | 75 | 2,793 | 1,017 | 4,161 | |||||||||||||||||||

Other expense, net |

(904) | (1,457) | (1,659) | (5,822) | |||||||||||||||||||

Net income |

16,209 | 15,255 | 34,845 | 26,653 | |||||||||||||||||||

Net income attributable to noncontrolling interests |

(1,758) | (1,727) | (3,775) | (3,046) | |||||||||||||||||||

Net income attributable to stockholders |

$ | 14,451 | $ | 13,528 | $ | 31,070 | $ | 23,607 | |||||||||||||||

| EARNINGS PER SHARE OF COMMON STOCK | |||||||||||||||||||||||

Net income per share attributable to stockholders - basic and diluted |

$ | 0.12 | $ | 0.12 | $ | 0.26 | $ | 0.21 | |||||||||||||||

| Phillips Edison & Company |

14

|

|||||||

|

Consolidated Statements of Operations

Condensed and Unaudited, in thousands (excluding per share amounts)

| |||||||||||||||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| June 30, 2023 |

March 31, 2023 |

December 31, 2022 | September 30, 2022 |

June 30, 2022 |

|||||||||||||||||||||||||

| REVENUES | |||||||||||||||||||||||||||||

| Rental income | $ | 148,980 | $ | 147,728 | $ | 141,703 | $ | 142,857 | $ | 137,230 | |||||||||||||||||||

| Fees and management income | 2,546 | 2,478 | 2,218 | 2,081 | 4,781 | ||||||||||||||||||||||||

| Other property income | 611 | 858 | 1,118 | 716 | 505 | ||||||||||||||||||||||||

| Total revenues | 152,137 | 151,064 | 145,039 | 145,654 | 142,516 | ||||||||||||||||||||||||

| OPERATING EXPENSES | |||||||||||||||||||||||||||||

| Property operating | 24,674 | 25,062 | 26,098 | 23,089 | 22,852 | ||||||||||||||||||||||||

| Real estate taxes | 18,397 | 18,056 | 15,859 | 18,041 | 16,473 | ||||||||||||||||||||||||

| General and administrative | 11,686 | 11,533 | 11,484 | 10,843 | 11,376 | ||||||||||||||||||||||||

| Depreciation and amortization | 59,667 | 58,498 | 58,216 | 60,013 | 60,769 | ||||||||||||||||||||||||

| Impairment of real estate assets | — | — | 322 | — | — | ||||||||||||||||||||||||

| Total operating expenses | 114,424 | 113,149 | 111,979 | 111,986 | 111,470 | ||||||||||||||||||||||||

| OTHER | |||||||||||||||||||||||||||||

| Interest expense, net | (20,675) | (19,466) | (18,301) | (17,569) | (17,127) | ||||||||||||||||||||||||

| Gain (loss) on disposal of property, net | 75 | 942 | 3,366 | (10) | 2,793 | ||||||||||||||||||||||||

| Other expense, net | (904) | (755) | (2,422) | (3,916) | (1,457) | ||||||||||||||||||||||||

| Net income | 16,209 | 18,636 | 15,703 | 12,173 | 15,255 | ||||||||||||||||||||||||

| Net income attributable to noncontrolling interests | (1,758) | (2,017) | (2,025) | (1,135) | (1,727) | ||||||||||||||||||||||||

| Net income attributable to stockholders | $ | 14,451 | $ | 16,619 | $ | 13,678 | $ | 11,038 | $ | 13,528 | |||||||||||||||||||

| EARNINGS PER SHARE OF COMMON STOCK | |||||||||||||||||||||||||||||

| Net income per share attributable to stockholders - basic and diluted | $ | 0.12 | $ | 0.14 | $ | 0.12 | $ | 0.09 | $ | 0.12 | |||||||||||||||||||

| Phillips Edison & Company |

15

|

|||||||

|

Nareit FFO, Core FFO, and Adjusted FFO

Unaudited, in thousands (excluding per share amounts)

| |||||||||||||||||||||||

| Three Months Ended June 30, |

Six Months Ended June 30, |

||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| CALCULATION OF NAREIT FFO ATTRIBUTABLE TO STOCKHOLDERS AND OP UNIT HOLDERS | |||||||||||||||||||||||

Net income |

$ | 16,209 | $ | 15,255 | $ | 34,845 | $ | 26,653 | |||||||||||||||

| Adjustments: | |||||||||||||||||||||||

| Depreciation and amortization of real estate assets | 59,115 | 59,849 | 117,068 | 116,169 | |||||||||||||||||||

| Gain on disposal of property, net | (75) | (2,793) | (1,017) | (4,161) | |||||||||||||||||||

| Adjustments related to unconsolidated joint ventures | 645 | (1,186) | 1,343 | (481) | |||||||||||||||||||

| Nareit FFO attributable to stockholders and OP unit holders | $ | 75,894 | $ | 71,125 | $ | 152,239 | $ | 138,180 | |||||||||||||||

| CALCULATION OF CORE FFO ATTRIBUTABLE TO STOCKHOLDERS AND OP UNIT HOLDERS | |||||||||||||||||||||||

| Nareit FFO attributable to stockholders and OP unit holders | $ | 75,894 | $ | 71,125 | $ | 152,239 | $ | 138,180 | |||||||||||||||

| Adjustments: | |||||||||||||||||||||||

| Depreciation and amortization of corporate assets | 552 | 920 | 1,097 | 1,826 | |||||||||||||||||||

| Change in fair value of earn-out liability | — | — | — | 1,809 | |||||||||||||||||||

| Transaction and acquisition expenses | 1,261 | 2,035 | 2,599 | 4,080 | |||||||||||||||||||

| (Gain) loss on extinguishment or modification of debt and other, net |

(9) | 129 | (9) | 1,029 | |||||||||||||||||||

| Amortization of unconsolidated joint venture basis differences | 7 | 175 | 8 | 219 | |||||||||||||||||||

Realized performance income(1) |

— | (2,546) | (75) | (2,742) | |||||||||||||||||||

| Core FFO attributable to stockholders and OP unit holders | $ | 77,705 | $ | 71,838 | $ | 155,859 | $ | 144,401 | |||||||||||||||

| CALCULATION OF ADJUSTED FFO ATTRIBUTABLE TO STOCKHOLDERS AND OP UNIT HOLDERS | |||||||||||||||||||||||

| Core FFO attributable to stockholders and OP unit holders | $ | 77,705 | $ | 71,838 | $ | 155,859 | $ | 144,401 | |||||||||||||||

| Adjustments: | |||||||||||||||||||||||

| Net amortization of above-market contracts | (125) | — | (250) | — | |||||||||||||||||||

| Straight-line rent and above- and below-market leases | (4,520) | (4,406) | (8,314) | (7,226) | |||||||||||||||||||

| Non-cash debt adjustments | 1,632 | 1,443 | 3,195 | 2,831 | |||||||||||||||||||

Capital expenditures and leasing commissions(2) |

(15,533) | (11,898) | (28,674) | (25,674) | |||||||||||||||||||

| Non-cash share-based compensation expense | 2,700 | 2,005 | 4,705 | 4,238 | |||||||||||||||||||

| Adjustments related to unconsolidated joint ventures | (256) | (139) | (394) | (231) | |||||||||||||||||||

| Adjusted FFO attributable to stockholders and OP unit holders | $ | 61,603 | $ | 58,843 | $ | 126,127 | $ | 118,339 | |||||||||||||||

| NAREIT FFO/CORE FFO ATTRIBUTABLE TO STOCKHOLDERS AND OP UNIT HOLDERS PER DILUTED SHARE | |||||||||||||||||||||||

| Weighted-average shares of common stock outstanding - diluted | 131,887 | 129,117 | 132,004 | 128,857 | |||||||||||||||||||

| Nareit FFO attributable to stockholders and OP unit holders per share - diluted | $ | 0.58 | $ | 0.55 | $ | 1.15 | $ | 1.07 | |||||||||||||||

| Core FFO attributable to stockholders and OP unit holders per share - diluted | $ | 0.59 | $ | 0.56 | $ | 1.18 | $ | 1.12 | |||||||||||||||

| Phillips Edison & Company |

16

|

|||||||

|

Nareit FFO, Core FFO, and Adjusted FFO

Unaudited, in thousands (excluding per share amounts)

| |||||||||||||||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| June 30, 2023 |

March 31, 2023 |

December 31, 2022 |

September 30, 2022 |

June 30, 2022 |

|||||||||||||||||||||||||

| CALCULATION OF NAREIT FFO ATTRIBUTABLE TO STOCKHOLDERS AND OP UNIT HOLDERS | |||||||||||||||||||||||||||||

| Net income | $ | 16,209 | $ | 18,636 | $ | 15,703 | $ | 12,173 | $ | 15,255 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Depreciation and amortization of real estate assets | 59,115 | 57,953 | 57,266 | 59,136 | 59,849 | ||||||||||||||||||||||||

| Impairment of real estate assets | — | — | 322 | — | — | ||||||||||||||||||||||||

| (Gain) loss on disposal of property, net | (75) | (942) | (3,366) | 10 | (2,793) | ||||||||||||||||||||||||

| Adjustments related to unconsolidated joint ventures | 645 | 698 | 661 | 662 | (1,186) | ||||||||||||||||||||||||

| Nareit FFO attributable to stockholders and OP unit holders | $ | 75,894 | $ | 76,345 | $ | 70,586 | $ | 71,981 | $ | 71,125 | |||||||||||||||||||

| CALCULATION OF CORE FFO ATTRIBUTABLE TO STOCKHOLDERS AND OP UNIT HOLDERS | |||||||||||||||||||||||||||||

| Nareit FFO attributable to stockholders and OP unit holders | $ | 75,894 | $ | 76,345 | $ | 70,586 | $ | 71,981 | $ | 71,125 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Depreciation and amortization of corporate assets | 552 | 545 | 950 | 877 | 920 | ||||||||||||||||||||||||

| Transaction and acquisition expenses | 1,261 | 1,338 | 2,731 | 3,740 | 2,035 | ||||||||||||||||||||||||

| (Gain) loss on extinguishment or modification of debt and other, net | (9) | — | — | (4) | 129 | ||||||||||||||||||||||||

| Amortization of unconsolidated joint venture basis differences | 7 | 1 | — | 1 | 175 | ||||||||||||||||||||||||

Realized performance income(1) |

— | (75) | — | — | (2,546) | ||||||||||||||||||||||||

| Core FFO attributable to stockholders and OP unit holders | $ | 77,705 | $ | 78,154 | $ | 74,267 | $ | 76,595 | $ | 71,838 | |||||||||||||||||||

| CALCULATION OF ADJUSTED FFO ATTRIBUTABLE TO STOCKHOLDERS AND OP UNIT HOLDERS | |||||||||||||||||||||||||||||

| Core FFO attributable to stockholders and OP unit holders | $ | 77,705 | $ | 78,154 | $ | 74,267 | $ | 76,595 | $ | 71,838 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Net amortization of above-market contracts | (125) | (125) | — | — | — | ||||||||||||||||||||||||

| Straight-line rent and above- and below-market leases | (4,520) | (3,794) | (4,377) | (5,022) | (4,406) | ||||||||||||||||||||||||

| Non-cash debt adjustments | 1,632 | 1,563 | 1,529 | 1,524 | 1,443 | ||||||||||||||||||||||||

Capital expenditures and leasing commissions(2) |

(15,533) | (13,141) | (13,512) | (17,296) | (11,898) | ||||||||||||||||||||||||

| Non-cash share-based compensation expense | 2,700 | 2,005 | 2,488 | 2,502 | 2,005 | ||||||||||||||||||||||||

| Adjustments related to unconsolidated joint ventures | (256) | (138) | (146) | (236) | (139) | ||||||||||||||||||||||||

| Adjusted FFO attributable to stockholders and OP unit holders | $ | 61,603 | $ | 64,524 | $ | 60,249 | $ | 58,067 | $ | 58,843 | |||||||||||||||||||

| NAREIT FFO/CORE FFO ATTRIBUTABLE TO STOCKHOLDERS AND OP UNIT HOLDERS PER DILUTED SHARE | |||||||||||||||||||||||||||||

| Weighted-average shares of common stock outstanding - diluted | 131,887 | 131,943 | 131,781 | 131,593 | 129,117 | ||||||||||||||||||||||||

| Nareit FFO attributable to stockholders and OP unit holders per share - diluted | $ | 0.58 | $ | 0.58 | $ | 0.54 | $ | 0.55 | $ | 0.55 | |||||||||||||||||||

| Core FFO attributable to stockholders and OP unit holders per share - diluted | $ | 0.59 | $ | 0.59 | $ | 0.56 | $ | 0.58 | $ | 0.56 | |||||||||||||||||||

| Phillips Edison & Company |

17

|

|||||||

|

EBITDAre Metrics

Unaudited, in thousands

| ||||||||||||||||||||||||||

| Three Months Ended June 30, |

Six Months Ended June 30, |

|||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

CALCULATION OF EBITDAre |

||||||||||||||||||||||||||

Net income |

$ | 16,209 | $ | 15,255 | $ | 34,845 | $ | 26,653 | ||||||||||||||||||

| Adjustments: | ||||||||||||||||||||||||||

| Depreciation and amortization | 59,667 | 60,769 | 118,165 | 117,995 | ||||||||||||||||||||||

| Interest expense, net | 20,675 | 17,127 | 40,141 | 35,326 | ||||||||||||||||||||||

| Gain on disposal of property, net | (75) | (2,793) | (1,017) | (4,161) | ||||||||||||||||||||||

| Federal, state, and local tax expense | 119 | 97 | 237 | 194 | ||||||||||||||||||||||

| Adjustments related to unconsolidated joint ventures | 918 | (885) | 1,884 | 134 | ||||||||||||||||||||||

EBITDAre |

$ | 97,513 | $ | 89,570 | $ | 194,255 | $ | 176,141 | ||||||||||||||||||

CALCULATION OF ADJUSTED EBITDAre |

||||||||||||||||||||||||||

EBITDAre |

$ | 97,513 | $ | 89,570 | $ | 194,255 | $ | 176,141 | ||||||||||||||||||

| Adjustments: | ||||||||||||||||||||||||||

| Change in fair value of earn-out liability | — | — | — | 1,809 | ||||||||||||||||||||||

| Transaction and acquisition expenses | 1,261 | 2,035 | 2,599 | 4,080 | ||||||||||||||||||||||

| Amortization of unconsolidated joint venture basis differences | 7 | 175 | 8 | 219 | ||||||||||||||||||||||

Realized performance income(1) |

— | (2,546) | (75) | (2,742) | ||||||||||||||||||||||

Adjusted EBITDAre |

$ | 98,781 | $ | 89,234 | $ | 196,787 | $ | 179,507 | ||||||||||||||||||

| Phillips Edison & Company |

18

|

|||||||

|

EBITDAre Metrics

Unaudited, in thousands

| |||||||||||||||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| June 30, 2023 |

March 31, 2023 |

December 31, 2022 |

September 30, 2022 |

June 30, 2022 |

|||||||||||||||||||||||||

CALCULATION OF EBITDAre |

|||||||||||||||||||||||||||||

| Net income | $ | 16,209 | $ | 18,636 | $ | 15,703 | $ | 12,173 | $ | 15,255 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Depreciation and amortization | 59,667 | 58,498 | 58,216 | 60,013 | 60,769 | ||||||||||||||||||||||||

| Interest expense, net | 20,675 | 19,466 | 18,301 | 17,569 | 17,127 | ||||||||||||||||||||||||

| (Gain) loss on disposal of property, net | (75) | (942) | (3,366) | 10 | (2,793) | ||||||||||||||||||||||||

| Impairment of real estate assets | — | — | 322 | — | — | ||||||||||||||||||||||||

| Federal, state, and local tax expense | 119 | 118 | 433 | 179 | 97 | ||||||||||||||||||||||||

| Adjustments related to unconsolidated joint ventures | 918 | 966 | 926 | 927 | (885) | ||||||||||||||||||||||||

EBITDAre |

$ | 97,513 | $ | 96,742 | $ | 90,535 | $ | 90,871 | $ | 89,570 | |||||||||||||||||||

CALCULATION OF ADJUSTED EBITDAre |

|||||||||||||||||||||||||||||

EBITDAre |

$ | 97,513 | $ | 96,742 | $ | 90,535 | $ | 90,871 | $ | 89,570 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Transaction and acquisition expenses | 1,261 | 1,338 | 2,731 | 3,740 | 2,035 | ||||||||||||||||||||||||

| Amortization of unconsolidated joint venture basis differences | 7 | 1 | — | 1 | 175 | ||||||||||||||||||||||||

Realized performance income(1) |

— | (75) | — | — | (2,546) | ||||||||||||||||||||||||

Adjusted EBITDAre |

$ | 98,781 | $ | 98,006 | $ | 93,266 | $ | 94,612 | $ | 89,234 | |||||||||||||||||||

| Phillips Edison & Company |

19

|

|||||||

|

Same-Center Net Operating Income

Unaudited, in thousands

| |||||||||||||||||||||||||||||||||||

| Three Months Ended June 30, |

Favorable (Unfavorable) % Change |

Six Months Ended June 30, |

Favorable (Unfavorable) % Change |

||||||||||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||||||||||||||

SAME-CENTER NOI(1) |

|||||||||||||||||||||||||||||||||||

| Revenues: | |||||||||||||||||||||||||||||||||||

Rental income(2) |

$ | 102,927 | $ | 98,497 | $ | 206,508 | $ | 197,183 | |||||||||||||||||||||||||||

| Tenant recovery income | 33,567 | 30,063 | 67,461 | 63,210 | |||||||||||||||||||||||||||||||

Reserves for uncollectibility(3) |

(357) | 177 | (1,269) | (661) | |||||||||||||||||||||||||||||||

| Other property income | 568 | 466 | 1,368 | 1,366 | |||||||||||||||||||||||||||||||

| Total revenues | 136,705 | 129,203 | 5.8% | 274,068 | 261,098 | 5.0 | % | ||||||||||||||||||||||||||||

| Operating expenses: | |||||||||||||||||||||||||||||||||||

| Property operating expenses | 20,396 | 19,186 | 41,934 | 39,866 | |||||||||||||||||||||||||||||||

| Real estate taxes | 17,341 | 16,054 | 34,670 | 33,333 | |||||||||||||||||||||||||||||||

| Total operating expenses | 37,737 | 35,240 | (7.1)% | 76,604 | 73,199 | (4.7) | % | ||||||||||||||||||||||||||||

| Total Same-Center NOI | $ | 98,968 | $ | 93,963 | 5.3% | $ | 197,464 | $ | 187,899 | 5.1 | % | ||||||||||||||||||||||||

| Same-Center NOI margin | 72.4% | 72.7% | 72.0% | 72.0% | |||||||||||||||||||||||||||||||

|

(1)Same-Center NOI represents the NOI for the 262 properties that were wholly-owned and operational for the entire portion of all comparable reporting periods.

(2)Excludes straight-line rental income, net amortization of above- and below-market leases, and lease buyout income.

(3)Includes billings that will not be recognized as revenue until cash is collected or the Neighbor resumes regular payments and/or we deem it appropriate to resume recording revenue on an accrual basis, rather than on a cash basis.

| |||||||||||||||||||||||||||||||||||

| Three Months Ended June 30, |

Six Months Ended June 30, |

||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

RECONCILIATION OF NET INCOME TO NOI AND SAME-CENTER NOI |

|||||||||||||||||||||||

Net income |

$ | 16,209 | $ | 15,255 | $ | 34,845 | $ | 26,653 | |||||||||||||||

| Adjusted to exclude: | |||||||||||||||||||||||

| Fees and management income | (2,546) | (4,781) | (5,024) | (7,242) | |||||||||||||||||||

Straight-line rental income(1) |

(3,284) | (3,319) | (5,864) | (5,128) | |||||||||||||||||||

| Net amortization of above- and below-market leases | (1,262) | (1,078) | (2,490) | (2,080) | |||||||||||||||||||

| Lease buyout income | (74) | (176) | (429) | (2,141) | |||||||||||||||||||

| General and administrative expenses | 11,686 | 11,376 | 23,219 | 22,908 | |||||||||||||||||||

| Depreciation and amortization | 59,667 | 60,769 | 118,165 | 117,995 | |||||||||||||||||||

| Interest expense, net | 20,675 | 17,127 | 40,141 | 35,326 | |||||||||||||||||||

| Gain on disposal of property, net | (75) | (2,793) | (1,017) | (4,161) | |||||||||||||||||||

Other expense, net |

904 | 1,457 | 1,659 | 5,822 | |||||||||||||||||||

| Property operating expenses related to fees and management income | 711 | 1,287 | 1,026 | 2,357 | |||||||||||||||||||

| NOI for real estate investments | 102,611 | 95,124 | 204,231 | 190,309 | |||||||||||||||||||

Less: Non-same-center NOI(2) |

(3,643) | (1,161) | (6,767) | (2,410) | |||||||||||||||||||

| Total Same-Center NOI | $ | 98,968 | $ | 93,963 | $ | 197,464 | $ | 187,899 | |||||||||||||||

|

(1)Includes straight-line rent adjustments for Neighbors for whom revenue is being recorded on a cash basis.

(2)Includes operating revenues and expenses from non-same-center properties which includes properties acquired or sold and corporate activities.

| |||||||||||||||||||||||

| Phillips Edison & Company |

20

|

|||||||

|

Joint Venture Portfolio and Financial Summary

Unaudited, dollars and square feet in thousands

| |||||||||||||||||||||||||||||||||||

| UNCONSOLIDATED JOINT VENTURE PORTFOLIO SUMMARY | |||||||||||||||||||||||||||||||||||

| As of June 30, 2023 | |||||||||||||||||

| Joint Venture | Investment Partner | Ownership Percentage | Number of Shopping Centers | ABR | GLA | ||||||||||||

| Grocery Retail Partners I LLC ("GRP I") | The Northwestern Mutual Life Insurance Company | 14% | 20 | $31,350 | 2,213 | ||||||||||||

| UNCONSOLIDATED JOINT VENTURE FINANCIAL SUMMARY | |||||||||||||||||||||||||||||||||||

| As of June 30, 2023 | |||||||||||||||||

| GRP I | NRP(1) |

||||||||||||||||

| Total assets | $ | 370,558 | $ | 628 | |||||||||||||

| Gross debt | 174,026 | — | |||||||||||||||

| Pro rata share of debt | 24,358 | — | |||||||||||||||

| Six Months Ended June 30, 2023 |

|||||||||||||||||

| GRP I | NRP(1) |

||||||||||||||||

Pro rata share of Nareit FFO(2) |

$ | 1,425 | $ | (15) | |||||||||||||

Pro rata share of NOI(2) |

2,046 | — | |||||||||||||||

| Phillips Edison & Company |

21

|

|||||||

|

Supplemental Balance Sheets Detail

Unaudited, in thousands

| |||||||||||

| June 30, 2023 | December 31, 2022 | ||||||||||

| OTHER ASSETS, NET | |||||||||||

| Deferred leasing commissions and costs | $ | 51,652 | $ | 49,687 | |||||||

Deferred financing expenses(1) |

8,984 | 8,984 | |||||||||

| Office equipment, capital lease assets, and other | 23,385 | 23,051 | |||||||||

| Corporate intangible assets | 6,685 | 6,692 | |||||||||

| Total depreciable and amortizable assets | 90,706 | 88,414 | |||||||||

| Accumulated depreciation and amortization | (50,473) | (47,483) | |||||||||

| Net depreciable and amortizable assets | 40,233 | 40,931 | |||||||||

Accounts receivable, net(2) |

43,017 | 37,274 | |||||||||

| Accounts receivable - affiliates | 798 | 513 | |||||||||

Deferred rent receivable, net(3) |

57,954 | 52,141 | |||||||||

| Derivative assets | 25,231 | 25,853 | |||||||||

| Prepaid expenses and other | 12,638 | 14,575 | |||||||||

| Investment in third parties | 9,901 | 9,800 | |||||||||

| Investment in marketable securities | 8,502 | 7,792 | |||||||||

| Total other assets, net | $ | 198,274 | $ | 188,879 | |||||||

| ACCOUNTS PAYABLE AND OTHER LIABILITIES | |||||||||||

| Accounts payable trade and other accruals | $ | 29,380 | $ | 34,431 | |||||||

| Accrued real estate taxes | 29,037 | 30,979 | |||||||||

| Security deposits | 14,500 | 14,170 | |||||||||

| Distribution accrual | 1,062 | 1,048 | |||||||||

| Accrued compensation | 8,349 | 14,210 | |||||||||

| Accrued interest | 9,138 | 8,192 | |||||||||

| Capital expenditure accrual | 6,684 | 9,834 | |||||||||

| Accrued income taxes and deferred tax liabilities, net | 37 | 321 | |||||||||

| Total accounts payable and other liabilities | $ | 98,187 | $ | 113,185 | |||||||

| Phillips Edison & Company |

22

|

|||||||

|

Supplemental Statements of Operations Detail

Unaudited, in thousands

| |||||||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| REVENUES | |||||||||||||||||||||||

Rental income(1) |

$ | 109,149 | $ | 101,395 | $ | 218,032 | $ | 202,527 | |||||||||||||||

Recovery income(1) |

35,760 | 31,199 | 71,504 | 65,044 | |||||||||||||||||||

| Straight-line rent amortization | 3,148 | 3,170 | 5,591 | 4,865 | |||||||||||||||||||

| Amortization of lease assets | 1,249 | 1,062 | 2,465 | 2,054 | |||||||||||||||||||

| Lease buyout income | 74 | 177 | 429 | 2,141 | |||||||||||||||||||

Adjustments for collectibility(2)(3) |

(400) | 227 | (1,313) | (653) | |||||||||||||||||||

| Fees and management income | 2,546 | 4,781 | 5,024 | 7,242 | |||||||||||||||||||

| Other property income | 611 | 505 | 1,469 | 1,459 | |||||||||||||||||||

| Total revenues | $ | 152,137 | $ | 142,516 | $ | 303,201 | $ | 284,679 | |||||||||||||||

|

(1)Includes income related to lease payments before assessing for collectibility.

(2)Includes revenue adjustments for non-creditworthy Neighbors.

(3)Contains general reserves but excludes reserves for straight-line rent amortization; includes recovery of previous revenue reserved.

| |||||||||||||||||||||||

| INTEREST EXPENSE, NET | |||||||||||||||||||||||

| Interest on unsecured term loans and senior notes, net | $ | 11,538 | $ | 9,512 | $ | 22,830 | $ | 19,428 | |||||||||||||||

| Interest on secured debt | 4,666 | 5,147 | 9,554 | 10,678 | |||||||||||||||||||

| Interest on revolving credit facility, net | 2,756 | 521 | 4,324 | 768 | |||||||||||||||||||

Non-cash amortization and other(1) |

1,724 | 1,818 | 3,442 | 3,423 | |||||||||||||||||||

(Gain) loss on extinguishment or modification of debt and other, net(2) |

(9) | 129 | (9) | 1,029 | |||||||||||||||||||

| Total interest expense, net | $ | 20,675 | $ | 17,127 | $ | 40,141 | $ | 35,326 | |||||||||||||||

|

(1)Amortization of debt-related items includes items such as deferred financing expenses, assumed market debt, and derivative adjustments, net.

(2)Includes defeasance fees related to early repayments of debt.

| |||||||||||||||||||||||

OTHER EXPENSE, NET |

|||||||||||||||||||||||

| Transaction and acquisition expenses | $ | (1,261) | $ | (2,035) | $ | (2,599) | $ | (4,080) | |||||||||||||||

| Federal, state, and local income tax expense | (119) | (97) | (237) | (194) | |||||||||||||||||||

| Equity in net income of unconsolidated joint ventures | 105 | 1,228 | 195 | 1,174 | |||||||||||||||||||

| Increase in fair value of earn-out liability | — | — | — | (1,809) | |||||||||||||||||||

| Other | 371 | (553) | 982 | (913) | |||||||||||||||||||

Total other expense, net |

$ | (904) | $ | (1,457) | $ | (1,659) | $ | (5,822) | |||||||||||||||

| Phillips Edison & Company |

23

|

|||||||

|

Capital Expenditures

Unaudited, in thousands

| |||||||||||||||||||||||

| Three Months Ended June 30, |

Six Months Ended June 30, |

||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

CAPITAL EXPENDITURES FOR REAL ESTATE(1)(2) |

|||||||||||||||||||||||

| Capital improvements | $ | 6,081 | $ | 3,025 | $ | 9,790 | $ | 4,822 | |||||||||||||||

| Tenant improvements | 6,429 | 4,664 | 12,848 | 11,924 | |||||||||||||||||||

| Redevelopment and development | 8,467 | 14,596 | 20,444 | 22,590 | |||||||||||||||||||

| Total capital expenditures for real estate | $ | 20,977 | $ | 22,285 | $ | 43,082 | $ | 39,336 | |||||||||||||||

| Corporate asset capital expenditures | 128 | 1,167 | 493 | 2,085 | |||||||||||||||||||

Capitalized indirect costs(3) |

969 | 886 | 2,183 | 1,525 | |||||||||||||||||||

| Total capital spending activity | $ | 22,074 | $ | 24,338 | $ | 45,758 | $ | 42,946 | |||||||||||||||

| Cash paid for leasing commissions | $ | 1,948 | $ | 1,811 | $ | 3,254 | $ | 3,921 | |||||||||||||||

| Phillips Edison & Company |

24

|

|||||||

|

Active Capital Projects

Unaudited, dollars in thousands

| |||||||||||||||||||||||

Project |

Location |

Description |

Target Stabilization Quarter(1) |

Incurred to Date | Future Spend | Total Estimated Costs | Estimated Project Yield | ||||||||||||||||

GROUND UP EXPANSION DEVELOPMENT |

|||||||||||||||||||||||

| Cinco Ranch at Market Center | Katy, TX | Construction of a 7K SF multi-tenant outparcel 100% leased with Chipotle, Floyd's 99 Barbershop, Cup Bop, Handel's Ice Cream | Q3 2023 | $ | 3,589 | $ | 573 | $ | 4,163 | ||||||||||||||

| Sunset Shopping Center | Corvallis, OR | Construction of a 2K SF single tenant outparcel 100% leased with Starbucks | Q4 2023 | 1,505 | 359 | 1,865 | |||||||||||||||||

| New Prague Commons | New Prague, MN | Construction of a 5K SF inline expansion 75% leased with Edward Jones, New Prague Tobacco | Q4 2023 | 1,178 | 298 | 1,476 | |||||||||||||||||

| Shasta Crossroads | Redding, CA | Construction of a 4K SF multi-tenant outparcel 100% leased with Panera | Q4 2023 | 428 | 2,334 | 2,762 | |||||||||||||||||

| Oak Mill Plaza | Niles, IL | Construction of a 5K SF multi-tenant outparcel 74% leased with Starbucks, Buffalo Wild Wings Go | Q1 2024 | 2,755 | 718 | 3,473 | |||||||||||||||||

| Southern Palms | Tempe, AZ | Construction of a 2K SF single tenant outparcel 100% leased with Starbucks | Q2 2024 | 566 | 1,339 | 1,905 | |||||||||||||||||

| Northstar Marketplace | Ramsey, MN | Construction of a 7K SF multi-tenant outparcel | Q4 2024 | 2,385 | 749 | 3,134 | |||||||||||||||||

| Total | $ | 12,406 | $ | 6,370 | $ | 18,778 | 7%-9% | ||||||||||||||||

| Phillips Edison & Company |

25

|

|||||||

|

Active Capital Projects

Unaudited, dollars in thousands

| |||||||||||||||||||||||

Project |

Location |

Description |

Target Stabilization Quarter(1) |

Incurred to Date | Future Spend | Total Estimated Costs | Estimated Project Yield | ||||||||||||||||

REDEVELOPMENT |

|||||||||||||||||||||||

| Shoregate Town Center | Willowick, OH | Remerchandise former Pat Catans with Goodwill | Q3 2023 | $ | 674 | $ | 1,173 | $ | 1,847 | ||||||||||||||

| Loganville Town Center | Loganville, GA | Purchase and repositioning of single tenant outparcel into multi-tenant. 100% leased with First Watch, Sage Dental | Q3 2023 | 3,032 | 434 | 3,466 | |||||||||||||||||

| The Oaks | Hudson, FL | Multi-phase Repositioning project with EOS Fitness, Ross, Five Below | Q4 2023 | 3,794 | 6,442 | 10,236 | |||||||||||||||||

| Duck Creek Plaza | Bettendorf, IA | Remerchandise former Schnuck's with Malibu Jacks | Q1 2024 | 1,340 | 1,821 | 3,161 | |||||||||||||||||

| Total | $ | 8,840 | $ | 9,870 | $ | 18,710 | 9%-15% | ||||||||||||||||

| Active Projects Total | $ | 21,246 | $ | 16,240 | $ | 37,488 | 9%-12% | ||||||||||||||||

2023 STABILIZED PROJECTS |

7 | $21,415 | 10% | ||||||||||||||||||||

| Phillips Edison & Company |

26

|

|||||||

|

Capitalization and Debt Ratios

Unaudited, in thousands (excluding per share amounts and leverage ratios)

| |||||||||||

| June 30, 2023 |

December 31, 2022 |

||||||||||

| EQUITY CAPITALIZATION | |||||||||||

| Common stock outstanding | 117,443 | 117,126 | |||||||||

| OP units outstanding | 14,134 | 14,099 | |||||||||

| Total shares and units outstanding | 131,577 | 131,225 | |||||||||

Share price |

$ | 34.08 | $ | 31.84 | |||||||

| Total equity market capitalization | $ | 4,484,144 | $ | 4,178,204 | |||||||

| DEBT | |||||||||||

| Debt obligations, net | $ | 1,951,186 | $ | 1,896,594 | |||||||

| Add: Discount on notes payable | 6,654 | 7,001 | |||||||||

| Add: Market debt adjustments, net | 1,314 | 1,226 | |||||||||

| Add: Deferred financing expenses, net | 6,866 | 7,963 | |||||||||

| Total debt - gross | 1,966,020 | 1,912,784 | |||||||||

| Less: Cash and cash equivalents | 5,564 | 5,478 | |||||||||

| Total net debt - consolidated | 1,960,456 | 1,907,306 | |||||||||

| Add: Prorated share from unconsolidated joint ventures | 24,059 | 24,096 | |||||||||

| Total net debt | $ | 1,984,515 | $ | 1,931,402 | |||||||

| ENTERPRISE VALUE | |||||||||||

| Total net debt | $ | 1,984,515 | $ | 1,931,402 | |||||||

| Total equity market capitalization | 4,484,144 | 4,178,204 | |||||||||

| Total enterprise value | $ | 6,468,659 | $ | 6,109,606 | |||||||

| FINANCIAL LEVERAGE RATIOS | |||||||||||

Net debt to Adjusted EBITDAre - annualized: |

|||||||||||

| Net debt | $ | 1,984,515 | $ | 1,931,402 | |||||||

Adjusted EBITDAre - annualized(1) |

384,665 | 367,385 | |||||||||

Net debt to Adjusted EBITDAre - annualized |

5.2x | 5.3x | |||||||||

| Net debt to total enterprise value: | |||||||||||

| Net debt | $ | 1,984,515 | $ | 1,931,402 | |||||||

| Total enterprise value | 6,468,659 | 6,109,606 | |||||||||

| Net debt to total enterprise value | 30.7% | 31.6% | |||||||||

| Phillips Edison & Company |

27

|

|||||||

|

Summary of Outstanding Debt

Unaudited, dollars in thousands

| |||||||||||||||||

| Outstanding Balance | Contractual Interest Rate |

Maturity Date | Percent of Total Indebtedness | ||||||||||||||

| SECURED DEBT | |||||||||||||||||

| Individual property mortgages | $ | 97,564 | 3.45% - 6.43% | 2024 - 2031 | 5% | ||||||||||||

| Secured pool due 2027 (15 assets) | 195,000 | 3.52% | 2027 | 10% | |||||||||||||

| Secured pool due 2030 (16 assets) | 200,000 | 3.35% | 2030 | 10% | |||||||||||||

| Total secured debt | $ | 492,564 | 25% | ||||||||||||||

| UNSECURED DEBT | |||||||||||||||||

Revolving credit facility(1)(3) |

$ | 168,000 | SOFR + 1.14% | 2026 | 9% | ||||||||||||

Term loan due 2025(1) |

240,000 | SOFR + 1.29% | 2025 | 12% | |||||||||||||

Term loan due 2026(1) |

240,000 | SOFR + 1.29% | 2026 | 12% | |||||||||||||

Term loan due 2026(2)(3) |

161,750 | SOFR + 1.35% | 2026 | 8% | |||||||||||||

Term loan due 2027(2) |

165,000 | SOFR + 1.35% | 2027 | 8% | |||||||||||||

Term loan due 2027(2) |

158,000 | SOFR + 1.35% | 2027 | 8% | |||||||||||||

| Senior unsecured note due 2031 | 350,000 | 2.63% | 2031 | 18% | |||||||||||||

Total unsecured debt(2) |

$ | 1,482,750 | 75% | ||||||||||||||

| Finance leases, net | 456 | ||||||||||||||||

Total debt obligations(2) |

$ | 1,975,770 | |||||||||||||||

| Assumed market debt adjustments, net | $ | (1,314) | |||||||||||||||

| Discount on notes payable | (6,654) | ||||||||||||||||

| Deferred financing expenses, net | (12,776) | ||||||||||||||||

| Debt obligations, net | $ | 1,955,026 | |||||||||||||||

| Notional Amount | Fixed Rate | ||||||||||

SOFR INTEREST RATE SWAPS(4) |

|||||||||||

| Interest rate swap expiring September 2023 | 255,000 | 1.30 | % | ||||||||

| Interest rate swap expiring October 2024 | 200,000 | 2.19 | % | ||||||||

| Interest rate swap expiring September 2024 | 175,000 | 2.17 | % | ||||||||

| Interest rate swap expiring November 2025 | 125,000 | 2.94 | % | ||||||||

| Total notional amount | $ | 755,000 | |||||||||

| Phillips Edison & Company |

28

|

|||||||

|

Debt Overview and Schedule of Maturities

Unaudited, dollars in thousands

| ||||||||||||||||||||||||||||||||||||||||||||||||||

| Secured Debt | Unsecured Debt | |||||||||||||||||||||||||||||||||||||||||||||||||

| Maturity Year | Scheduled Mortgage Principal Payments | Mortgage Loans | Secured Portfolio Loans | Unsecured Term Loans | Senior Unsecured Notes | Revolving Line of Credit | Total Consolidated Debt | Pro Rata Share of JV Debt | Total Debt | Weighted-Average Interest Rate(1) |

||||||||||||||||||||||||||||||||||||||||

| 2023 | $ | 1,883 | $ | — | $ | — | $ | — | $ | — | $ | — | $ | 1,883 | $ | — | $ | 1,883 | — | % | ||||||||||||||||||||||||||||||

| 2024 | 2,996 | 25,130 | — | — | — | — | 28,126 | — | 28,126 | 5.1 | % | |||||||||||||||||||||||||||||||||||||||

| 2025 | 1,956 | 35,680 | — | 240,000 | — | — | 277,636 | — | 277,636 | 3.7 | % | |||||||||||||||||||||||||||||||||||||||

| 2026 | 1,908 | — | — | 240,000 | — | — | 241,908 | 24,358 | 266,266 | 5.9 | % | |||||||||||||||||||||||||||||||||||||||

| 2027 | 1,905 | 3,690 | 195,000 | 323,000 | — | 168,000 | 691,595 | — | 691,595 | 4.0 | % | |||||||||||||||||||||||||||||||||||||||

| 2028 | 767 | 16,600 | — | 161,750 | — | — | 179,117 | — | 179,117 | 3.2 | % | |||||||||||||||||||||||||||||||||||||||

| 2029 | 805 | — | — | — | — | — | 805 | — | 805 | — | % | |||||||||||||||||||||||||||||||||||||||

| 2030 | 844 | — | 200,000 | — | — | — | 200,844 | — | 200,844 | 3.4 | % | |||||||||||||||||||||||||||||||||||||||

| 2031 | 560 | 2,840 | — | — | 350,000 | — | 353,400 | — | 353,400 | 2.7 | % | |||||||||||||||||||||||||||||||||||||||

| Net debt market adjustments / discounts / issuance costs | — | — | — | — | — | — | (20,744) | (642) | (21,386) | N/A | ||||||||||||||||||||||||||||||||||||||||

| Finance leases | — | — | — | — | — | — | 456 | — | 456 | N/A | ||||||||||||||||||||||||||||||||||||||||

Total(2) |

$ | 13,624 | $ | 83,940 | $ | 395,000 | $ | 964,750 | $ | 350,000 | $ | 168,000 | $ | 1,955,026 | $ | 23,716 | $ | 1,978,742 | 3.9 | % | ||||||||||||||||||||||||||||||

| Weighted-Average | |||||||||||||||||||||||||||||

| Total Debt | Percent of Total Indebtedness | Effective Interest Rate(1) |

Years to Maturity(2) |

||||||||||||||||||||||||||

Fixed rate debt(1) |

$ | 1,597,564 | 79.9% | 3.2% | 6.4 | ||||||||||||||||||||||||

| Variable rate debt | 377,750 | 18.9% | 6.5% | 3.4 | |||||||||||||||||||||||||

| Net debt premiums / issuance costs | (20,744) | N/A | N/A | N/A | |||||||||||||||||||||||||

| Finance leases | 456 | N/A | N/A | N/A | |||||||||||||||||||||||||

| Total consolidated debt | $ | 1,955,026 | 98.8% | 3.9% | 4.6 | ||||||||||||||||||||||||

| Pro rata share of JV Debt | 24,358 | 1.2% | 3.6% | 3.3 | |||||||||||||||||||||||||

| Net debt premiums / issuance costs of JV Debt | (642) | N/A | N/A | N/A | |||||||||||||||||||||||||

| Total consolidated + JV debt | $ | 1,978,742 | 100.0% | 3.9% | 4.6 | ||||||||||||||||||||||||

| Phillips Edison & Company |

29

|

|||||||

|

Debt Covenants

Unaudited, dollars in thousands

| |||||||||||||||||

| UNSECURED CREDIT FACILITY AND TERM LOANS DUE 2024, 2025, AND 2026 | |||||||||||||||||

| Covenant | June 30, 2023 |

||||||||||||||||

| LEVERAGE RATIO | |||||||||||||||||

| Total Indebtedness | $1,978,981 | ||||||||||||||||

| Total Asset Value | $6,471,301 | ||||||||||||||||

| Leverage Ratio | =<60% | 30.6% | |||||||||||||||

| SECURED LEVERAGE RATIO | |||||||||||||||||

| Total Secured Indebtedness | $517,379 | ||||||||||||||||

| Total Asset Value | $6,471,301 | ||||||||||||||||

| Secured Leverage Ratio | =<35% | 8.0% | |||||||||||||||

| FIXED CHARGE COVERAGE RATIO | |||||||||||||||||

| Adjusted EBITDA | $360,266 | ||||||||||||||||

| Total Fixed Charges | $77,185 | ||||||||||||||||

| Fixed Charge Coverage Ratio | >1.5x | 4.67x | |||||||||||||||

| MAXIMUM UNSECURED INDEBTEDNESS TO UNENCUMBERED ASSET VALUE | |||||||||||||||||

| Total Unsecured Indebtedness | $1,486,833 | ||||||||||||||||

| Unencumbered Asset Value | $5,174,803 | ||||||||||||||||

| Unsecured Indebtedness to Unencumbered Asset Value | =<60% | 28.7% | |||||||||||||||

| MINIMUM UNENCUMBERED NOI TO INTEREST EXPENSE | |||||||||||||||||

| Unencumbered NOI | $336,565 | ||||||||||||||||

| Interest Expense for Unsecured Indebtedness | $51,716 | ||||||||||||||||

| Unencumbered NOI to Interest Expense | >=1.75x | 6.51x | |||||||||||||||

| DIVIDEND PAYOUT RATIO | |||||||||||||||||

| Distributions | $147,368 | ||||||||||||||||

| Funds From Operations | $307,386 | ||||||||||||||||

| Dividend Payout Ratio | <95% | 47.9% | |||||||||||||||

| SENIOR UNSECURED NOTES DUE 2031 | |||||||||||||||||

| Covenant | June 30, 2023 |

||||||||||||||||

| AGGREGATE DEBT TEST | |||||||||||||||||

| Total Indebtedness | $1,978,791 | ||||||||||||||||

| Total Asset Value | $5,843,551 | ||||||||||||||||

| Aggregate Debt Test | <65% | 33.9% | |||||||||||||||

| SECURED DEBT TEST | |||||||||||||||||

| Total Secured Indebtedness | $493,021 | ||||||||||||||||

| Total Asset Value | $5,843,551 | ||||||||||||||||

| Secured Debt Test | <40% | 8.4% | |||||||||||||||

| DEBT SERVICE TEST | |||||||||||||||||

| Consolidated EBITDA | $381,936 | ||||||||||||||||

| Annual Debt Service Charge | $70,464 | ||||||||||||||||

| Debt Service Test | >1.5x | 5.42x | |||||||||||||||

| MAINTENANCE OF TOTAL UNENCUMBERED ASSETS | |||||||||||||||||

| Unencumbered Asset Value | $4,825,177 | ||||||||||||||||

| Total Unsecured Indebtedness | $1,485,771 | ||||||||||||||||

| MAINTENANCE OF TOTAL UNENCUMBERED ASSETS | >150% | 325% | |||||||||||||||

| Note: Calculations are per covenant definitions as set forth in the applicable debt agreements. | |||||||||||||||||

| Phillips Edison & Company |

30

|

|||||||

| TRANSACTIONAL SUMMARY | ||

Quarter Ended June 30, 2023 | ||

|

Acquisition Summary

Unaudited, dollars in thousands

| ||||||||||||||||||||||||||||||||||||||

| Date | Property Name | Location | Total GLA | Contract Price | Leased Occupancy at Acquisition | Grocery Anchor | ||||||||||||||||||||||||||||||||

| 1/19/2023 | Providence Commons | Mt. Juliet, TN | 110,137 | $27,100 | 100.0% | Publix | ||||||||||||||||||||||||||||||||

| 3/16/2023 | Village Shoppes at Windermere | Suwanee, GA | 73,442 | 19,550 | 93.2% | Publix | ||||||||||||||||||||||||||||||||

| 3/27/2023 | Town Center at Jensen Beach | Jensen Beach, FL | 109,326 | 17,200 | 83.8% | Publix | ||||||||||||||||||||||||||||||||

| 3/27/2023 | Shops at Sunset Lakes | Miramar, FL | 70,288 | 14,800 | 96.8% | Publix | ||||||||||||||||||||||||||||||||

| Total acquisitions | 363,193 | $78,650 | ||||||||||||||||||||||||||||||||||||

Weighted-average cap rate(1) |

6.3 | % | ||||||||||||||||||||||||||||||||||||

|

Disposition Summary

Unaudited, dollars in thousands

| ||||||||||||||||||||||||||||||||||||||

| Date | Property Name | Location | Total GLA | Sale Price | Leased Occupancy at Disposition | Grocery Anchor | ||||||||||||||||||||||||||||||||

| 5/9/2023 | Greentree McDonald's | Racine, WI | 4,130 | $1,000 | 100.0% | N/A | ||||||||||||||||||||||||||||||||

| 6/9/2023 | Towne & Country (B&O) | Hamilton, OH | 79,896 | 4,800 | 98.6% | N/A | ||||||||||||||||||||||||||||||||

| 6/16/2023 | Broadway Promenade Condo Unit 2102 | Sarasota, FL | 2,417 | 450 | N/A | N/A | ||||||||||||||||||||||||||||||||

| Total dispositions | 86,443 | $6,250 | ||||||||||||||||||||||||||||||||||||

| Weighted-average cap rate | 8.7 | % | ||||||||||||||||||||||||||||||||||||

| Phillips Edison & Company |

32

|

|||||||

| PORTFOLIO SUMMARY | ||

Quarter Ended June 30, 2023 | ||

|

Wholly-Owned Portfolio Summary

Unaudited, dollars and square feet in thousands (excluding per square foot amounts)

| |||||

| As of June 30, 2023 |

|||||

| PORTFOLIO OVERVIEW: | |||||

| Number of shopping centers | 274 | ||||

| Number of states | 31 | ||||

| Total GLA | 31,378 | ||||

| Average shopping center GLA | 115 | ||||

| Total ABR | $ | 449,314 | |||

Total ABR from necessity-based goods and services(1) |

70.9 | % | |||

| Percent of ABR from non-grocery anchors | 13.5 | % | |||

| Percent of ABR from inline spaces | 54.3 | % | |||

| GROCERY METRICS: | |||||

Percent of ABR from omni-channel grocery-anchored shopping centers |

97.4 | % | |||

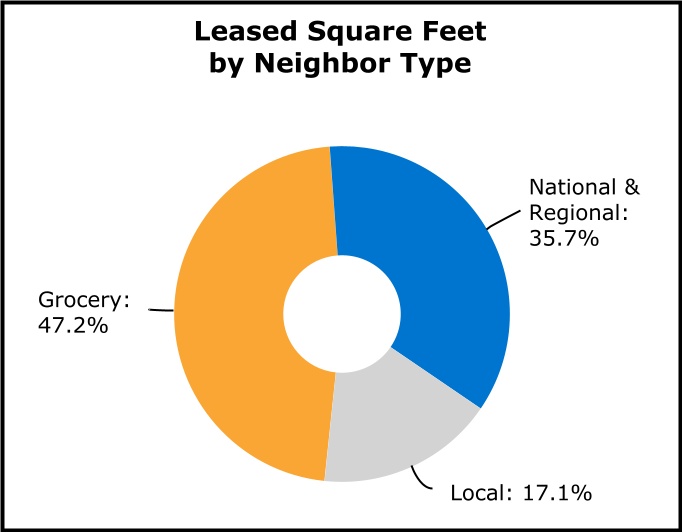

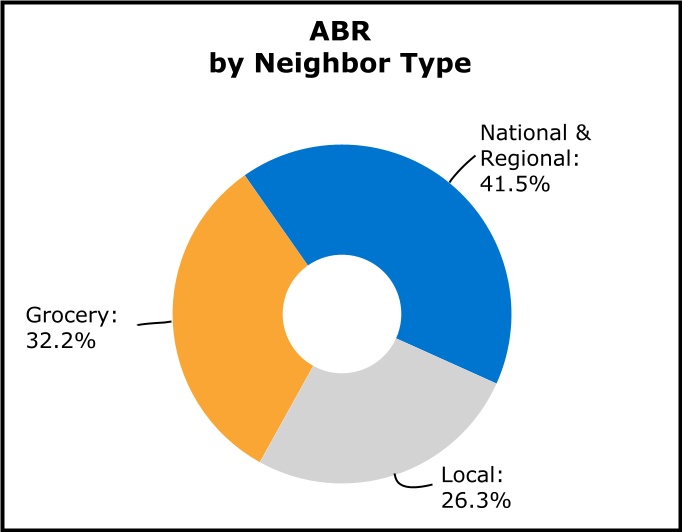

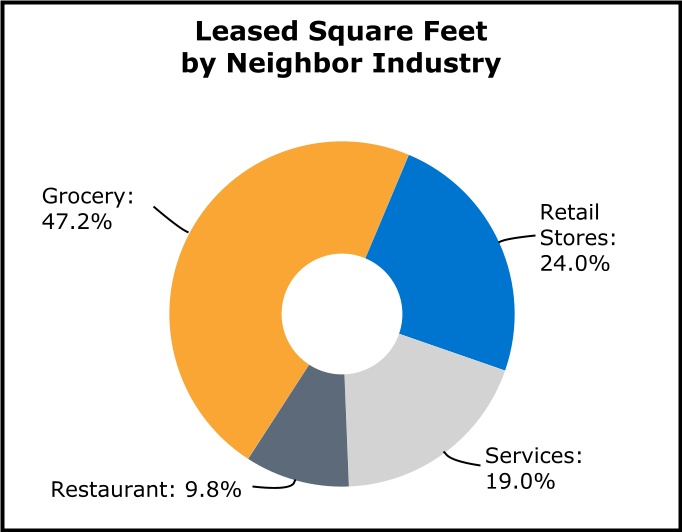

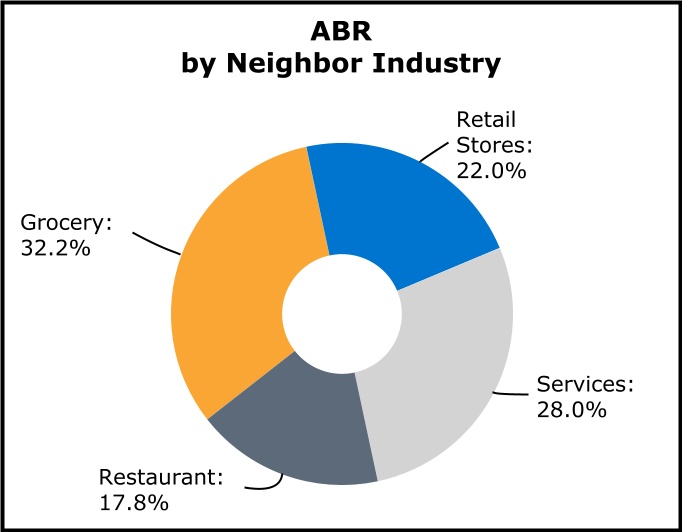

| Percent of ABR from grocery anchors | 32.2 | % | |||

| Percent of occupied GLA leased to grocery Neighbors | 47.2 | % | |||

Grocer health ratio(2) |

2.3 | % | |||

| Percent of ABR from centers with grocery anchors that are #1 or #2 by sales | 86.5 | % | |||

| Average annual sales per square foot of reporting grocers | $ | 668 | |||

| LEASED OCCUPANCY AS A PERCENTAGE OF RENTABLE SQUARE FEET: | |||||

| Total portfolio | 97.8 | % | |||

| Anchor spaces | 99.4 | % | |||

| Inline spaces | 94.8 | % | |||

AVERAGE REMAINING LEASE TERM (IN YEARS):(3) |

|||||

| Total portfolio | 4.5 | ||||

| Grocery anchor spaces | 4.6 | ||||

| Non-grocery anchor spaces | 5.0 | ||||

| Inline spaces | 4.1 | ||||

PORTFOLIO RETENTION RATE:(4) |

|||||

| Total portfolio | 93.8 | % | |||

| Anchor spaces | 100.0 | % | |||

| Inline spaces | 86.3 | % | |||

| AVERAGE ABR PER SQUARE FOOT: | |||||

| Total portfolio | $ | 14.64 | |||

| Anchor spaces | $ | 9.97 | |||

| Inline spaces | $ | 23.95 | |||

| Phillips Edison & Company |

34

|

|||||||

|

ABR by Neighbor Category

Unaudited

| |||||

| As of June 30, 2023 | |||||

| NECESSITY RETAIL AND SERVICES | |||||

| Grocery | 32.2 | % | |||

| Quick service - Restaurant | 10.9 | % | |||

| Medical | 6.1 | % | |||

| Beauty & Hair Care | 5.1 | % | |||

| Banks, insurance, and government services | 3.7 | % | |||

| Dollar stores | 2.3 | % | |||

| Pet supply | 1.8 | % | |||

| Hardware/automotive | 1.5 | % | |||

| Telecommunications/cell phone services | 1.5 | % | |||

| Wine, Beer, & Liquor | 1.5 | % | |||

| Education & Training | 1.6 | % | |||

| Pharmacy | 0.8 | % | |||

| Other Necessity-based | 1.9 | % | |||

| Total ABR from Necessity-based goods and services | 70.9 | % | |||

| OTHER RETAIL STORES | |||||

Soft goods(1) |

13.0 | % | |||

| Full service - restaurant | 6.9 | % | |||

Fitness and lifestyle services(2) |

5.5 | % | |||

Other retail(3) |

3.7 | % | |||

| Total ABR from other retail stores | 29.1 | % | |||

| Total ABR | 100.0 | % | |||

| Phillips Edison & Company |

35

|

|||||||

|

Occupancy and ABR

Unaudited

| |||||||||||||||||||||||||||||

| Quarter Ended | |||||||||||||||||||||||||||||

| June 30, 2023 |

March 31, 2023 |

December 31, 2022 |

September 30, 2022 |

June 30, 2022 |

|||||||||||||||||||||||||

| OCCUPANCY | |||||||||||||||||||||||||||||

| Leased Basis | |||||||||||||||||||||||||||||

| Anchor | 99.4 | % | 99.3 | % | 99.3 | % | 98.9 | % | 98.7 | % | |||||||||||||||||||

| Inline | 94.8 | % | 94.3 | % | 93.8 | % | 93.6 | % | 93.2 | % | |||||||||||||||||||

| Total leased occupancy | 97.8 | % | 97.5 | % | 97.4 | % | 97.1 | % | 96.8 | % | |||||||||||||||||||

| Economic Basis | |||||||||||||||||||||||||||||

| Anchor | 99.0 | % | 98.4 | % | 98.4 | % | 98.4 | % | 98.1 | % | |||||||||||||||||||

| Inline | 93.8 | % | 93.5 | % | 92.5 | % | 92.7 | % | 92.5 | % | |||||||||||||||||||

| Total economic occupancy | 97.2 | % | 96.7 | % | 96.4 | % | 96.4 | % | 96.2 | % | |||||||||||||||||||

| ABR | |||||||||||||||||||||||||||||

| Leased Basis - $ | |||||||||||||||||||||||||||||

| Anchor | $ | 203,645 | $ | 203,525 | $ | 200,926 | $ | 198,873 | $ | 197,449 | |||||||||||||||||||

| Inline | 245,669 | 242,086 | 234,786 | 230,132 | 223,570 | ||||||||||||||||||||||||

| Total ABR | $ | 449,314 | $ | 445,611 | $ | 435,712 | $ | 429,005 | $ | 421,019 | |||||||||||||||||||

| Leased Basis - PSF | |||||||||||||||||||||||||||||

| Anchor | $ | 9.97 | $ | 9.95 | $ | 9.92 | $ | 9.85 | $ | 9.83 | |||||||||||||||||||

| Inline | $ | 23.95 | $ | 23.66 | $ | 23.39 | $ | 23.00 | $ | 22.66 | |||||||||||||||||||

| Total ABR PSF | $ | 14.64 | $ | 14.52 | $ | 14.39 | $ | 14.21 | $ | 14.06 | |||||||||||||||||||

| Phillips Edison & Company |

36

|

|||||||

|

Top 25 Neighbors by ABR

Dollars and square footage amounts in thousands

| |||||||||||||||||||||||

| Number of Locations | |||||||||||||||||||||||

| Neighbor | Banners Leased at PECO Centers | Wholly-Owned | Joint Ventures | ABR(1) |

% ABR(1) |

Leased SF(1) |

|||||||||||||||||

| 1 | Kroger | Kroger, Ralphs, Smith’s, King Soopers, Fry's Food Stores, Quality Food Centers, Harris Teeter, Pick ‘n Save, Mariano’s, Food 4 Less, Metro Market | 56 | 6 | $ | 27,831 | 6.1 | % | 3,411 | ||||||||||||||

| 2 | Publix | Publix | 52 | 9 | 26,567 | 5.9 | % | 2,519 | |||||||||||||||

| 3 | Albertsons | Albertsons, Safeway, Vons, Jewel-Osco, Shaw's Supermarket, Tom Thumb, United Supermarkets, Market Street United, Randalls | 29 | 2 | 18,343 | 4.0 | % | 1,709 | |||||||||||||||

| 4 | Ahold Delhaize | Giant, Stop & Shop, Food Lion, Martin's | 23 | — | 17,738 | 3.9 | % | 1,249 | |||||||||||||||

| 5 | Walmart | Walmart, Walmart Neighborhood Market | 13 | — | 8,971 | 2.0 | % | 1,770 | |||||||||||||||

| 6 | Giant Eagle | Giant Eagle | 9 | 1 | 7,384 | 1.6 | % | 760 | |||||||||||||||

| 7 | Sprouts Farmers Market | Sprouts Farmers Market | 14 | — | 6,566 | 1.5 | % | 421 | |||||||||||||||

| 8 | TJX Companies | T.J. Maxx, HomeGoods, Marshalls, Sierra Trading | 18 | — | 6,201 | 1.4 | % | 516 | |||||||||||||||

| 9 | Raley's | Raley's | 5 | — | 4,592 | 1.0 | % | 288 | |||||||||||||||

| 10 | Dollar Tree | Dollar Tree, Family Dollar | 31 | 4 | 3,519 | 0.8 | % | 343 | |||||||||||||||

| 11 | SUPERVALU | Cub Foods | 5 | — | 3,280 | 0.7 | % | 336 | |||||||||||||||

| 12 | Starbucks Corporation | Starbucks | 32 | — | 2,586 | 0.6 | % | 57 | |||||||||||||||

| 13 | Lowe's | Lowe's | 3 | 1 | 2,469 | 0.5 | % | 369 | |||||||||||||||

| 14 | Subway Group | Subway | 60 | 2 | 2,409 | 0.5 | % | 90 | |||||||||||||||

| 15 | Anytime Fitness, Inc. | Anytime Fitness | 27 | 2 | 2,368 | 0.5 | % | 140 | |||||||||||||||

| 16 | Food 4 Less (PAQ) | Food 4 Less | 2 | — | 2,305 | 0.5 | % | 118 | |||||||||||||||

| 17 | Pet Supplies Plus | Pet Supplies Plus | 19 | — | 2,253 | 0.5 | % | 148 | |||||||||||||||

| 18 | United Parcel Service | The UPS Store | 57 | 8 | 2,245 | 0.5 | % | 82 | |||||||||||||||

| 19 | Kohl's Corporation | Kohl's | 4 | — | 2,241 | 0.5 | % | 365 | |||||||||||||||

| 20 | Office Depot | Office Depot, OfficeMax | 8 | — | 2,237 | 0.5 | % | 179 | |||||||||||||||

| 21 | Save Mart | Save Mart Supermarkets, FoodMaxx, Lucky Supermarkets | 5 | — | 2,194 | 0.5 | % | 258 | |||||||||||||||

| 22 | H&R Block, Inc. | H&R Block | 51 | 2 | 2,168 | 0.5 | % | 92 | |||||||||||||||

| 23 | Great Clips, Inc. | Great Clips | 61 | 7 | 2,125 | 0.5 | % | 77 | |||||||||||||||

| 24 | Petco Animal Supplies, Inc. | Petco | 9 | 1 | 2,044 | 0.5 | % | 115 | |||||||||||||||

| 25 | Planet Fitness | Planet Fitness | 8 | — | 2,021 | 0.5 | % | 176 | |||||||||||||||

| Total | 601 | 45 | $ | 162,657 | 36.0 | % | 15,588 | ||||||||||||||||

| Phillips Edison & Company |

37

|

|||||||

|

Neighbors by Type and Industry(1)(2)

Unaudited

| ||

| Phillips Edison & Company |

38

|

|||||||

|

Properties by State(1)

Dollars and square footage amounts in thousands (excluding per square foot amounts)

| |||||||||||||||||||||||

| State | ABR | % ABR | ABR / Leased SF | GLA | % GLA | % Leased | Number of Properties | ||||||||||||||||

| Florida | $ | 56,624 | 12.5 | % | $ | 14.43 | 4,088 | 12.6 | % | 96.0 | % | 51 | |||||||||||

| California | 48,800 | 10.8 | % | 20.76 | 2,403 | 7.6 | % | 97.8 | % | 25 | |||||||||||||

| Georgia | 39,360 | 8.7 | % | 13.51 | 2,935 | 9.4 | % | 99.3 | % | 30 | |||||||||||||

| Texas | 36,301 | 8.0 | % | 17.44 | 2,115 | 6.7 | % | 98.4 | % | 18 | |||||||||||||

| Ohio | 25,354 | 5.6 | % | 11.01 | 2,331 | 7.6 | % | 98.8 | % | 19 | |||||||||||||

| Illinois | 24,894 | 5.5 | % | 16.08 | 1,637 | 5.0 | % | 94.6 | % | 14 | |||||||||||||

| Colorado | 24,829 | 5.5 | % | 18.01 | 1,408 | 4.5 | % | 97.9 | % | 12 | |||||||||||||

| Virginia | 22,225 | 4.9 | % | 16.94 | 1,363 | 4.2 | % | 96.3 | % | 13 | |||||||||||||

| Minnesota | 18,169 | 4.0 | % | 14.97 | 1,265 | 3.9 | % | 96.0 | % | 12 | |||||||||||||

| Massachusetts | 16,565 | 3.7 | % | 14.81 | 1,146 | 3.5 | % | 97.5 | % | 9 | |||||||||||||

| Nevada | 13,705 | 3.0 | % | 22.47 | 623 | 2.0 | % | 97.9 | % | 5 | |||||||||||||

| Pennsylvania | 12,193 | 2.7 | % | 12.41 | 1,001 | 3.2 | % | 98.2 | % | 6 | |||||||||||||

| Wisconsin | 12,045 | 2.7 | % | 11.51 | 1,057 | 3.4 | % | 99.1 | % | 9 | |||||||||||||

| Arizona | 10,633 | 2.3 | % | 14.65 | 736 | 2.3 | % | 98.6 | % | 6 | |||||||||||||