| Maryland | 001-32268 | 11-3715772 | ||||||

| Delaware | 333-202666-01 | 20-1453863 | ||||||

| (State or other jurisdiction of incorporation) | (Commission File Number) | (IRS Employer Identification Number) | ||||||

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||

| Common Shares, $0.01 par value per share | KRG | New York Stock Exchange | ||||||||||||

| Exhibit No. | Description | |||||||

| 99.1 | ||||||||

| 99.2 | ||||||||

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document) | |||||||

| KITE REALTY GROUP TRUST | ||||||||

| Date: July 30, 2025 | By: | /s/ HEATH R. FEAR | ||||||

| Heath R. Fear | ||||||||

| Executive Vice President and | ||||||||

| Chief Financial Officer | ||||||||

| KITE REALTY GROUP, L.P. | ||||||||

| By: Kite Realty Group Trust, its sole general partner | ||||||||

| By: | /s/ HEATH R. FEAR | |||||||

| Heath R. Fear | ||||||||

| Executive Vice President and | ||||||||

| Chief Financial Officer | ||||||||

| Exhibit 99.1 | ||||||||

| Low | High | ||||||||||

| Net income | $ | 0.75 | $ | 0.79 | |||||||

| Realized gain on sales of operating properties, net | (0.46) | (0.46) | |||||||||

| Depreciation and amortization | 1.77 | 1.77 | |||||||||

| NAREIT FFO | $ | 2.06 | $ | 2.10 | |||||||

| Non-cash items | (0.04) | (0.04) | |||||||||

| Core FFO | $ | 2.02 | $ | 2.06 | |||||||

| June 30, 2025 |

December 31, 2024 |

||||||||||

| Assets: | |||||||||||

| Investment properties, at cost | $ | 7,423,024 | $ | 7,634,191 | |||||||

| Less: accumulated depreciation | (1,661,279) | (1,587,661) | |||||||||

| Net investment properties | 5,761,745 | 6,046,530 | |||||||||

| Cash and cash equivalents | 182,044 | 128,056 | |||||||||

|

Tenant and other receivables, including accrued straight-line rent

of $69,042 and $67,377, respectively

|

125,289 | 125,768 | |||||||||

| Restricted cash and escrow deposits | 5,566 | 5,271 | |||||||||

| Deferred costs, net | 208,683 | 238,213 | |||||||||

| Short-term deposits | — | 350,000 | |||||||||

| Prepaid and other assets | 96,278 | 104,627 | |||||||||

| Investments in unconsolidated subsidiaries | 390,827 | 19,511 | |||||||||

| Assets associated with investment properties held for sale | 87,908 | 73,791 | |||||||||

| Total assets | $ | 6,858,340 | $ | 7,091,767 | |||||||

| Liabilities and Equity: | |||||||||||

| Liabilities: | |||||||||||

| Mortgage and other indebtedness, net | $ | 3,022,496 | $ | 3,226,930 | |||||||

| Accounts payable and accrued expenses | 180,564 | 202,651 | |||||||||

| Deferred revenue and other liabilities | 227,807 | 246,100 | |||||||||

| Liabilities associated with investment properties held for sale | 4,949 | 4,009 | |||||||||

| Total liabilities | 3,435,816 | 3,679,690 | |||||||||

| Commitments and contingencies | |||||||||||

| Limited Partners’ interests in the Operating Partnership | 102,891 | 98,074 | |||||||||

| Equity: | |||||||||||

|

Common shares, $0.01 par value, 490,000,000 shares authorized,

219,858,193 and 219,667,067 shares issued and outstanding at

June 30, 2025 and December 31, 2024, respectively

|

2,198 | 2,197 | |||||||||

| Additional paid-in capital | 4,867,036 | 4,868,554 | |||||||||

| Accumulated other comprehensive income | 28,397 | 36,612 | |||||||||

| Accumulated deficit | (1,579,915) | (1,595,253) | |||||||||

| Total shareholders’ equity | 3,317,716 | 3,312,110 | |||||||||

| Noncontrolling interests | 1,917 | 1,893 | |||||||||

| Total equity | 3,319,633 | 3,314,003 | |||||||||

| Total liabilities and equity | $ | 6,858,340 | $ | 7,091,767 | |||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | ||||||||||||||||||||

| Revenue: | |||||||||||||||||||||||

| Rental income | $ | 211,182 | $ | 205,836 | $ | 430,354 | $ | 411,649 | |||||||||||||||

| Other property-related revenue | 1,360 | 3,146 | 3,525 | 4,457 | |||||||||||||||||||

| Fee income | 853 | 3,452 | 1,278 | 3,767 | |||||||||||||||||||

| Total revenue | 213,395 | 212,434 | 435,157 | 419,873 | |||||||||||||||||||

| Expenses: | |||||||||||||||||||||||

| Property operating | 28,881 | 28,564 | 58,707 | 56,645 | |||||||||||||||||||

| Real estate taxes | 26,651 | 26,493 | 54,412 | 53,027 | |||||||||||||||||||

| General, administrative and other | 13,390 | 12,966 | 25,648 | 25,750 | |||||||||||||||||||

| Depreciation and amortization | 97,887 | 99,291 | 196,118 | 199,670 | |||||||||||||||||||

| Impairment charges | — | 66,201 | — | 66,201 | |||||||||||||||||||

| Total expenses | 166,809 | 233,515 | 334,885 | 401,293 | |||||||||||||||||||

| Other (expense) income: | |||||||||||||||||||||||

| Interest expense | (34,052) | (30,981) | (67,006) | (61,345) | |||||||||||||||||||

| Income tax expense of taxable REIT subsidiaries | (199) | (132) | (209) | (290) | |||||||||||||||||||

| Gain (loss) on sales of operating properties, net | 103,022 | (1,230) | 103,113 | (1,466) | |||||||||||||||||||

| Equity in loss of unconsolidated subsidiaries | (3,238) | (174) | (3,845) | (594) | |||||||||||||||||||

| Gain on sale of unconsolidated property, net | — | — | — | 2,325 | |||||||||||||||||||

| Other income, net | 480 | 4,295 | 4,538 | 7,923 | |||||||||||||||||||

| Net income (loss) | 112,599 | (49,303) | 136,863 | (34,867) | |||||||||||||||||||

| Net (income) loss attributable to noncontrolling interests | (2,281) | 665 | (2,815) | 385 | |||||||||||||||||||

| Net income (loss) attributable to common shareholders | $ | 110,318 | $ | (48,638) | $ | 134,048 | $ | (34,482) | |||||||||||||||

| Net income (loss) per common share – basic and diluted | $ | 0.50 | $ | (0.22) | $ | 0.61 | $ | (0.16) | |||||||||||||||

| Weighted average common shares outstanding – basic | 219,835,322 | 219,622,059 | 219,775,829 | 219,561,586 | |||||||||||||||||||

| Weighted average common shares outstanding – diluted | 219,949,868 | 219,622,059 | 219,888,939 | 219,561,586 | |||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | ||||||||||||||||||||

| Net income (loss) | $ | 112,599 | $ | (49,303) | $ | 136,863 | $ | (34,867) | |||||||||||||||

| Less: net income attributable to noncontrolling interests in properties | (81) | (74) | (151) | (141) | |||||||||||||||||||

| Less/add: (gain) loss on sales of operating properties, net | (103,022) | 1,230 | (103,113) | 1,466 | |||||||||||||||||||

| Less: gain on sale of unconsolidated property, net | — | — | — | (2,325) | |||||||||||||||||||

| Add: impairment charges | — | 66,201 | — | 66,201 | |||||||||||||||||||

|

Add: depreciation and amortization of consolidated and unconsolidated entities,

net of noncontrolling interests

|

104,469 | 99,433 | 203,146 | 199,993 | |||||||||||||||||||

NAREIT FFO of the Operating Partnership(1) |

113,965 | 117,487 | 236,745 | 230,327 | |||||||||||||||||||

| Less: Limited Partners’ interests in FFO | (2,466) | (1,946) | (4,929) | (3,768) | |||||||||||||||||||

FFO attributable to common shareholders(1) |

$ | 111,499 | $ | 115,541 | $ | 231,816 | $ | 226,559 | |||||||||||||||

| FFO, as defined by NAREIT, per share of the Operating Partnership – basic | $ | 0.51 | $ | 0.53 | $ | 1.05 | $ | 1.03 | |||||||||||||||

| FFO, as defined by NAREIT, per share of the Operating Partnership – diluted | $ | 0.51 | $ | 0.53 | $ | 1.05 | $ | 1.03 | |||||||||||||||

| Weighted average common shares outstanding – basic | 219,835,322 | 219,622,059 | 219,775,829 | 219,561,586 | |||||||||||||||||||

| Weighted average common shares outstanding – diluted | 219,949,868 | 220,013,860 | 219,888,939 | 219,957,009 | |||||||||||||||||||

| Weighted average common shares and units outstanding – basic | 224,684,910 | 223,329,063 | 224,451,187 | 223,219,523 | |||||||||||||||||||

| Weighted average common shares and units outstanding – diluted | 224,799,456 | 223,720,864 | 224,564,297 | 223,614,946 | |||||||||||||||||||

Reconciliation of NAREIT FFO to Core FFO(2) |

|||||||||||||||||||||||

NAREIT FFO of the Operating Partnership(1) |

$ | 113,965 | $ | 117,487 | $ | 236,745 | $ | 230,327 | |||||||||||||||

| Add: | |||||||||||||||||||||||

| Amortization of deferred financing costs | 1,751 | 987 | 3,395 | 1,916 | |||||||||||||||||||

| Non-cash compensation expense and other | 3,048 | 2,906 | 5,564 | 5,628 | |||||||||||||||||||

| Less: | |||||||||||||||||||||||

| Straight-line rent – minimum rent and common area maintenance | 2,835 | 3,651 | 5,413 | 6,776 | |||||||||||||||||||

| Market rent amortization income | 1,879 | 2,390 | 5,421 | 4,657 | |||||||||||||||||||

| Amortization of debt discounts, premiums and hedge instruments | 890 | 3,734 | 3,646 | 7,490 | |||||||||||||||||||

| Core FFO of the Operating Partnership | $ | 113,160 | $ | 111,605 | $ | 231,224 | $ | 218,948 | |||||||||||||||

| Core FFO per share of the Operating Partnership – diluted | $ | 0.50 | $ | 0.50 | $ | 1.03 | $ | 0.98 | |||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||||||||||||||

| 2025 | 2024 | Change | 2025 | 2024 | Change | ||||||||||||||||||||||||||||||

Number of properties in Same Property Pool for the period(1) |

175 | 175 | 175 | 175 | |||||||||||||||||||||||||||||||

| Leased percentage at period end | 93.2 | % | 94.8 | % | 93.2 | % | 94.8 | % | |||||||||||||||||||||||||||

| Economic occupancy percentage at period end | 90.3 | % | 91.6 | % | 90.3 | % | 91.6 | % | |||||||||||||||||||||||||||

Economic occupancy percentage(2) |

90.4 | % | 91.3 | % | 91.1 | % | 91.2 | % | |||||||||||||||||||||||||||

| Minimum rent | $ | 150,706 | $ | 147,190 | $ | 301,765 | $ | 293,361 | |||||||||||||||||||||||||||

| Tenant recoveries | 41,704 | 40,364 | 84,876 | 81,361 | |||||||||||||||||||||||||||||||

| Bad debt reserve | (1,521) | (1,562) | (3,469) | (2,072) | |||||||||||||||||||||||||||||||

| Other income, net | 2,488 | 2,169 | 4,685 | 4,766 | |||||||||||||||||||||||||||||||

| Total revenue | 193,377 | 188,161 | 387,857 | 377,416 | |||||||||||||||||||||||||||||||

| Property operating | (24,195) | (24,001) | (49,626) | (49,028) | |||||||||||||||||||||||||||||||

| Real estate taxes | (25,078) | (24,648) | (50,328) | (49,350) | |||||||||||||||||||||||||||||||

| Total expenses | (49,273) | (48,649) | (99,954) | (98,378) | |||||||||||||||||||||||||||||||

Same Property NOI(3) |

$ | 144,104 | $ | 139,512 | 3.3 | % | $ | 287,903 | $ | 279,038 | 3.2 | % | |||||||||||||||||||||||

|

Reconciliation of Same Property NOI to most

directly comparable GAAP measure:

|

|||||||||||||||||||||||||||||||||||

| Net operating income – same properties | $ | 144,104 | $ | 139,512 | $ | 287,903 | $ | 279,038 | |||||||||||||||||||||||||||

Net operating income – non-same activity(4) |

12,906 | 14,413 | 32,857 | 27,396 | |||||||||||||||||||||||||||||||

| Total property NOI | 157,010 | 153,925 | 2.0 | % | 320,760 | 306,434 | 4.7 | % | |||||||||||||||||||||||||||

| Other (expense) income, net | (2,104) | 7,441 | 1,762 | 10,806 | |||||||||||||||||||||||||||||||

| General, administrative and other | (13,390) | (12,966) | (25,648) | (25,750) | |||||||||||||||||||||||||||||||

| Impairment charges | — | (66,201) | — | (66,201) | |||||||||||||||||||||||||||||||

| Depreciation and amortization | (97,887) | (99,291) | (196,118) | (199,670) | |||||||||||||||||||||||||||||||

| Interest expense | (34,052) | (30,981) | (67,006) | (61,345) | |||||||||||||||||||||||||||||||

| Gain (loss) on sales of operating properties, net | 103,022 | (1,230) | 103,113 | (1,466) | |||||||||||||||||||||||||||||||

| Gain on sale of unconsolidated property, net | — | — | — | 2,325 | |||||||||||||||||||||||||||||||

|

Net (income) loss attributable to noncontrolling

interests

|

(2,281) | 665 | (2,815) | 385 | |||||||||||||||||||||||||||||||

| Net income (loss) attributable to common shareholders | $ | 110,318 | $ | (48,638) | $ | 134,048 | $ | (34,482) | |||||||||||||||||||||||||||

| Three Months Ended June 30, 2025 |

|||||

| Net income | $ | 112,599 | |||

| Depreciation and amortization | 97,887 | ||||

| Interest expense | 34,052 | ||||

| Income tax expense of taxable REIT subsidiaries | 199 | ||||

| EBITDA | 244,737 | ||||

| Unconsolidated EBITDA, as adjusted | 5,689 | ||||

| Gain on sales of operating properties, net | (103,022) | ||||

| Other income and expense, net | 2,758 | ||||

| Noncontrolling interests | (210) | ||||

Pro forma adjustments(1) |

(2,280) | ||||

| Adjusted EBITDA | $ | 147,672 | |||

Annualized Adjusted EBITDA(2) |

$ | 590,690 | |||

| Company share of Net Debt: | |||||

| Mortgage and other indebtedness, net | $ | 3,022,496 | |||

| Add: Company share of unconsolidated joint venture debt | 190,841 | ||||

| Add: debt discounts, premiums and issuance costs, net | 3,082 | ||||

Less: Partner share of consolidated joint venture debt(3) |

(9,777) | ||||

| Company’s consolidated debt and share of unconsolidated debt | 3,206,642 | ||||

| Less: cash, cash equivalents and restricted cash | (201,796) | ||||

| Company share of Net Debt | $ | 3,004,846 | |||

| Net Debt to Adjusted EBITDA | 5.1x | ||||

| Exhibit 99.2 | ||||||||

| Earnings Press Release | |||||

| Contact Information | |||||

| Results Overview | |||||

| Consolidated Balance Sheets | |||||

| Consolidated Statements of Operations | |||||

| Same Property Net Operating Income | |||||

| Net Operating Income and Adjusted EBITDA by Quarter | |||||

| NAREIT Funds From Operations | |||||

| Joint Venture Summary | |||||

| Key Debt Metrics | |||||

| Summary of Outstanding Debt | |||||

| Maturity Schedule of Outstanding Debt | |||||

| Acquisitions and Dispositions | |||||

| Development and Redevelopment Projects | |||||

| Geographic Diversification – ABR by Region and State | |||||

| Top 25 Tenants by ABR | |||||

| Retail Leasing Spreads | |||||

| Lease Expirations | |||||

| Components of Net Asset Value | |||||

| Non-GAAP Financial Measures | |||||

i |

|||||

ii |

|||||

| Low | High | ||||||||||

| Net income | $ | 0.75 | $ | 0.79 | |||||||

| Realized gain on sales of operating properties, net | (0.46) | (0.46) | |||||||||

| Depreciation and amortization | 1.77 | 1.77 | |||||||||

| NAREIT FFO | $ | 2.06 | $ | 2.10 | |||||||

| Non-cash items | (0.04) | (0.04) | |||||||||

| Core FFO | $ | 2.02 | $ | 2.06 | |||||||

iii |

|||||

iv |

|||||

| Investor Relations Contact | Analyst Coverage | Analyst Coverage | ||||||||||||

| Tyler Henshaw | Robert W. Baird & Co. | Jefferies LLC | ||||||||||||

| Senior Vice President, Capital Markets and IR | Mr. Wes Golladay | Ms. Linda Tsai | ||||||||||||

| (317) 713-7780 | (216) 737-7510 | (212) 778-8011 | ||||||||||||

| thenshaw@kiterealty.com | wgolladay@rwbaird.com | ltsai@jefferies.com | ||||||||||||

| Matt Hunt | Bank of America/Merrill Lynch | J.P. Morgan | ||||||||||||

| Senior Director, Capital Markets and IR | Mr. Jeffrey Spector/Mr. Samir Khanal | Mr. Michael W. Mueller/Mr. Hongliang Zhang | ||||||||||||

| (317) 713-7646 | (646) 855-1363/(646) 855-1497 | (212) 622-6689/(212) 622-6416 | ||||||||||||

| mhunt@kiterealty.com | jeff.spector@bofa.com/ | michael.w.mueller@jpmorgan.com/ | ||||||||||||

| samar.khanal@bofa.com | hongliang.zhang@jpmorgan.com | |||||||||||||

| Transfer Agent | BTIG | KeyBanc Capital Markets | ||||||||||||

| Broadridge Financial Solutions | Mr. Michael Gorman | Mr. Todd Thomas | ||||||||||||

| Ms. Kristen Tartaglione | (212) 738-6138 | (917) 368-2286 | ||||||||||||

| 2 Journal Square, 7th Floor | mgorman@btig.com | tthomas@keybanccm.com | ||||||||||||

| Jersey City, NJ 07306 | ||||||||||||||

| (201) 714-8094 | Citigroup Global Markets | Piper Sandler | ||||||||||||

| Mr. Craig Mailman | Mr. Alexander Goldfarb | |||||||||||||

| (212) 816-4471 | (212) 466-7937 | |||||||||||||

| craig.mailman@citi.com | alexander.goldfarb@psc.com | |||||||||||||

| Stock Specialist | ||||||||||||||

| GTS | Compass Point Research & Trading, LLC | Raymond James | ||||||||||||

| 545 Madison Avenue, 15th Floor | Mr. Ken Billingsley | Mr. RJ Milligan | ||||||||||||

| New York, NY 10022 | (202) 534-1393 | (727) 567-2585 | ||||||||||||

| (212) 715-2830 | kbillingsley@compasspointllc.com | rjmilligan@raymondjames.com | ||||||||||||

| Green Street | Wells Fargo | |||||||||||||

| Ms. Paulina Rojas Schmidt | Mr. James Feldman | |||||||||||||

| (949) 640-8780 | (212) 215-5328 | |||||||||||||

| projasschmidt@greenstreet.com | james.feldman@wellsfargo.com | |||||||||||||

| UBS | ||||||||||||||

| Mr. Michael Goldsmith | ||||||||||||||

| (212) 713-2951 | ||||||||||||||

| michael.goldsmith@ubs.com | ||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 1 |

||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| Summary Financial Results | 2025 | 2024 | 2025 | 2024 | |||||||||||||||||||

| Total revenue (page 4) | $ | 213,395 | $ | 212,434 | $ | 435,157 | $ | 419,873 | |||||||||||||||

| Net income (loss) attributable to common shareholders (page 4) | $ | 110,318 | $ | (48,638) | $ | 134,048 | $ | (34,482) | |||||||||||||||

| Net income (loss) per diluted share (page 4) | $ | 0.50 | $ | (0.22) | $ | 0.61 | $ | (0.16) | |||||||||||||||

| Net operating income (NOI) (page 6) | $ | 157,010 | $ | 153,925 | $ | 320,760 | $ | 306,434 | |||||||||||||||

| Adjusted EBITDA (page 6) | $ | 144,473 | $ | 144,411 | $ | 296,390 | $ | 284,451 | |||||||||||||||

| NAREIT Funds From Operations (FFO) (page 7) | $ | 113,965 | $ | 117,487 | $ | 236,745 | $ | 230,327 | |||||||||||||||

| NAREIT FFO per diluted share (page 7) | $ | 0.51 | $ | 0.53 | $ | 1.05 | $ | 1.03 | |||||||||||||||

| Core FFO (page 7) | $ | 113,160 | $ | 111,605 | $ | 231,224 | $ | 218,948 | |||||||||||||||

| Core FFO per diluted share (page 7) | $ | 0.50 | $ | 0.50 | $ | 1.03 | $ | 0.98 | |||||||||||||||

| Dividend payout ratio (as % of NAREIT FFO) | 53 | % | 47 | % | 51 | % | 49 | % | |||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Summary Operating and Financial Ratios | June 30, 2025 |

March 31, 2025 |

December 31, 2024 |

September 30, 2024 |

June 30, 2024 |

||||||||||||||||||||||||

| NOI margin (page 6) | 74.0 | % | 74.2 | % | 74.6 | % | 74.5 | % | 73.8 | % | |||||||||||||||||||

| NOI margin – retail (page 6) | 74.4 | % | 74.7 | % | 75.1 | % | 75.2 | % | 74.3 | % | |||||||||||||||||||

| Same Property NOI performance (page 5) | 3.3 | % | 3.1 | % | 4.8 | % | 3.0 | % | 1.8 | % | |||||||||||||||||||

| Total property NOI performance (page 5) | 2.0 | % | 7.4 | % | 4.9 | % | 1.2 | % | 0.1 | % | |||||||||||||||||||

| Net debt to Adjusted EBITDA, current quarter (page 9) | 5.1x | 4.7x | 4.7x | 4.9x | 4.8x | ||||||||||||||||||||||||

| Recovery ratio of retail operating properties (page 6) | 92.0 | % | 91.4 | % | 92.1 | % | 91.2 | % | 91.6 | % | |||||||||||||||||||

| Recovery ratio of consolidated portfolio (page 6) | 87.8 | % | 86.5 | % | 87.4 | % | 86.6 | % | 87.8 | % | |||||||||||||||||||

| Outstanding Classes of Stock | |||||||||||||||||||||||||||||

| Common shares and units outstanding (page 18) | 224,707,781 | 224,661,888 | 223,859,664 | 223,626,166 | 223,361,957 | ||||||||||||||||||||||||

| Summary Portfolio Statistics | |||||||||||||||||||||||||||||

| Number of properties | |||||||||||||||||||||||||||||

Operating retail/mixed-use(1) |

179 | 180 | 179 | 179 | 178 | ||||||||||||||||||||||||

Standalone office(2) |

2 | 2 | 2 | 1 | 1 | ||||||||||||||||||||||||

| Development and redevelopment projects (page 13) | 1 | 1 | 2 | 3 | 2 | ||||||||||||||||||||||||

Owned retail operating gross leasable area (GLA)(3) |

27.8 | M | 27.8 | M | 27.7 | M | 27.7 | M | 27.6 | M | |||||||||||||||||||

| Owned office GLA | 2.0 | M | 1.5 | M | 1.5 | M | 1.4 | M | 1.4 | M | |||||||||||||||||||

Number of multifamily units(4) |

2,187 | 1,405 | 1,405 | 1,405 | 1,405 | ||||||||||||||||||||||||

| Percent leased – total | 92.7 | % | 93.0 | % | 94.2 | % | 94.6 | % | 94.3 | % | |||||||||||||||||||

| Percent leased – retail | 93.3 | % | 93.8 | % | 95.0 | % | 95.0 | % | 94.8 | % | |||||||||||||||||||

| Anchor (≥ 10,000 sq. ft.) | 94.2 | % | 95.1 | % | 97.1 | % | 97.0 | % | 96.8 | % | |||||||||||||||||||

| Small shop (< 10,000 sq. ft.) | 91.6 | % | 91.3 | % | 91.2 | % | 91.2 | % | 90.8 | % | |||||||||||||||||||

| Retail annualized base rent (ABR) per square foot | $ | 22.02 | $ | 21.49 | $ | 21.15 | $ | 21.01 | $ | 20.90 | |||||||||||||||||||

| Total new and renewal lease GLA (page 16) | 1,214,631 | 843,829 | 1,214,390 | 1,651,986 | 1,153,766 | ||||||||||||||||||||||||

| New lease cash rent spread (page 16) | 31.3 | % | 15.6 | % | 23.6 | % | 24.9 | % | 34.8 | % | |||||||||||||||||||

| Non-option renewal lease cash rent spread (page 16) | 19.7 | % | 20.1 | % | 14.4 | % | 11.9 | % | 14.3 | % | |||||||||||||||||||

| Option renewal lease cash rent spread (page 16) | 8.2 | % | 7.0 | % | 6.8 | % | 7.7 | % | 6.0 | % | |||||||||||||||||||

| Total new and renewal lease cash rent spread (page 16) | 17.0 | % | 13.7 | % | 12.5 | % | 11.1 | % | 15.6 | % | |||||||||||||||||||

| 2025 Guidance | Current (as of 7/30/25) |

Previous (as of 4/29/25) |

Original (as of 2/11/25) |

||||||||||||||

| NAREIT FFO per diluted share | $2.06 to $2.10 | $2.04 to $2.10 | $2.02 to $2.08 | ||||||||||||||

| Core FFO per diluted share | $2.02 to $2.06 | $2.00 to $2.06 | $1.98 to $2.04 | ||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 2 |

||||

| June 30, 2025 |

December 31, 2024 |

||||||||||

| Assets: | |||||||||||

| Investment properties, at cost | $ | 7,423,024 | $ | 7,634,191 | |||||||

| Less: accumulated depreciation | (1,661,279) | (1,587,661) | |||||||||

| Net investment properties | 5,761,745 | 6,046,530 | |||||||||

| Cash and cash equivalents | 182,044 | 128,056 | |||||||||

|

Tenant and other receivables, including accrued straight-line rent

of $69,042 and $67,377, respectively

|

125,289 | 125,768 | |||||||||

| Restricted cash and escrow deposits | 5,566 | 5,271 | |||||||||

| Deferred costs, net | 208,683 | 238,213 | |||||||||

| Short-term deposits | — | 350,000 | |||||||||

| Prepaid and other assets | 96,278 | 104,627 | |||||||||

| Investments in unconsolidated subsidiaries | 390,827 | 19,511 | |||||||||

| Assets associated with investment properties held for sale | 87,908 | 73,791 | |||||||||

| Total assets | $ | 6,858,340 | $ | 7,091,767 | |||||||

| Liabilities and Equity: | |||||||||||

| Liabilities: | |||||||||||

| Mortgage and other indebtedness, net | $ | 3,022,496 | $ | 3,226,930 | |||||||

| Accounts payable and accrued expenses | 180,564 | 202,651 | |||||||||

| Deferred revenue and other liabilities | 227,807 | 246,100 | |||||||||

| Liabilities associated with investment properties held for sale | 4,949 | 4,009 | |||||||||

| Total liabilities | 3,435,816 | 3,679,690 | |||||||||

| Commitments and contingencies | |||||||||||

Limited Partners’ interests in the Operating Partnership |

102,891 | 98,074 | |||||||||

| Equity: | |||||||||||

|

Common shares, $0.01 par value, 490,000,000 shares authorized,

219,858,193 and 219,667,067 shares issued and outstanding at

June 30, 2025 and December 31, 2024, respectively

|

2,198 | 2,197 | |||||||||

| Additional paid-in capital | 4,867,036 | 4,868,554 | |||||||||

| Accumulated other comprehensive income | 28,397 | 36,612 | |||||||||

| Accumulated deficit | (1,579,915) | (1,595,253) | |||||||||

| Total shareholders’ equity | 3,317,716 | 3,312,110 | |||||||||

| Noncontrolling interests | 1,917 | 1,893 | |||||||||

| Total equity | 3,319,633 | 3,314,003 | |||||||||

| Total liabilities and equity | $ | 6,858,340 | $ | 7,091,767 | |||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 3 |

||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | ||||||||||||||||||||

| Revenue: | |||||||||||||||||||||||

| Rental income | $ | 211,182 | $ | 205,836 | $ | 430,354 | $ | 411,649 | |||||||||||||||

| Other property-related revenue | 1,360 | 3,146 | 3,525 | 4,457 | |||||||||||||||||||

| Fee income | 853 | 3,452 | 1,278 | 3,767 | |||||||||||||||||||

| Total revenue | 213,395 | 212,434 | 435,157 | 419,873 | |||||||||||||||||||

| Expenses: | |||||||||||||||||||||||

| Property operating | 28,881 | 28,564 | 58,707 | 56,645 | |||||||||||||||||||

| Real estate taxes | 26,651 | 26,493 | 54,412 | 53,027 | |||||||||||||||||||

| General, administrative and other | 13,390 | 12,966 | 25,648 | 25,750 | |||||||||||||||||||

| Depreciation and amortization | 97,887 | 99,291 | 196,118 | 199,670 | |||||||||||||||||||

| Impairment charges | — | 66,201 | — | 66,201 | |||||||||||||||||||

| Total expenses | 166,809 | 233,515 | 334,885 | 401,293 | |||||||||||||||||||

| Other (expense) income: | |||||||||||||||||||||||

| Interest expense | (34,052) | (30,981) | (67,006) | (61,345) | |||||||||||||||||||

| Income tax expense of taxable REIT subsidiaries | (199) | (132) | (209) | (290) | |||||||||||||||||||

| Gain (loss) on sales of operating properties, net | 103,022 | (1,230) | 103,113 | (1,466) | |||||||||||||||||||

| Equity in loss of unconsolidated subsidiaries | (3,238) | (174) | (3,845) | (594) | |||||||||||||||||||

| Gain on sale of unconsolidated property, net | — | — | — | 2,325 | |||||||||||||||||||

| Other income, net | 480 | 4,295 | 4,538 | 7,923 | |||||||||||||||||||

| Net income (loss) | 112,599 | (49,303) | 136,863 | (34,867) | |||||||||||||||||||

| Net (income) loss attributable to noncontrolling interests | (2,281) | 665 | (2,815) | 385 | |||||||||||||||||||

| Net income (loss) attributable to common shareholders | $ | 110,318 | $ | (48,638) | $ | 134,048 | $ | (34,482) | |||||||||||||||

| Net income (loss) per common share – basic and diluted | $ | 0.50 | $ | (0.22) | $ | 0.61 | $ | (0.16) | |||||||||||||||

| Weighted average common shares outstanding – basic | 219,835,322 | 219,622,059 | 219,775,829 | 219,561,586 | |||||||||||||||||||

| Weighted average common shares outstanding – diluted | 219,949,868 | 219,622,059 | 219,888,939 | 219,561,586 | |||||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 4 |

||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||||||||||||||

| 2025 | 2024 | Change | 2025 | 2024 | Change | ||||||||||||||||||||||||||||||

Number of properties in Same Property Pool for the period(1) |

175 | 175 | 175 | 175 | |||||||||||||||||||||||||||||||

| Leased percentage at period end | 93.2 | % | 94.8 | % | 93.2 | % | 94.8 | % | |||||||||||||||||||||||||||

| Economic occupancy percentage at period end | 90.3 | % | 91.6 | % | 90.3 | % | 91.6 | % | |||||||||||||||||||||||||||

Economic occupancy percentage(2) |

90.4 | % | 91.3 | % | 91.1 | % | 91.2 | % | |||||||||||||||||||||||||||

| Minimum rent | $ | 150,706 | $ | 147,190 | $ | 301,765 | $ | 293,361 | |||||||||||||||||||||||||||

| Tenant recoveries | 41,704 | 40,364 | 84,876 | 81,361 | |||||||||||||||||||||||||||||||

| Bad debt reserve | (1,521) | (1,562) | (3,469) | (2,072) | |||||||||||||||||||||||||||||||

| Other income, net | 2,488 | 2,169 | 4,685 | 4,766 | |||||||||||||||||||||||||||||||

| Total revenue | 193,377 | 188,161 | 387,857 | 377,416 | |||||||||||||||||||||||||||||||

| Property operating | (24,195) | (24,001) | (49,626) | (49,028) | |||||||||||||||||||||||||||||||

| Real estate taxes | (25,078) | (24,648) | (50,328) | (49,350) | |||||||||||||||||||||||||||||||

| Total expenses | (49,273) | (48,649) | (99,954) | (98,378) | |||||||||||||||||||||||||||||||

Same Property NOI(3) |

$ | 144,104 | $ | 139,512 | 3.3 | % | $ | 287,903 | $ | 279,038 | 3.2 | % | |||||||||||||||||||||||

|

Reconciliation of Same Property NOI to most

directly comparable GAAP measure:

|

|||||||||||||||||||||||||||||||||||

| Net operating income – same properties | $ | 144,104 | $ | 139,512 | $ | 287,903 | $ | 279,038 | |||||||||||||||||||||||||||

Net operating income – non-same activity(4) |

12,906 | 14,413 | 32,857 | 27,396 | |||||||||||||||||||||||||||||||

| Total property NOI | 157,010 | 153,925 | 2.0 | % | 320,760 | 306,434 | 4.7 | % | |||||||||||||||||||||||||||

| Other (expense) income, net | (2,104) | 7,441 | 1,762 | 10,806 | |||||||||||||||||||||||||||||||

| General, administrative and other | (13,390) | (12,966) | (25,648) | (25,750) | |||||||||||||||||||||||||||||||

| Impairment charges | — | (66,201) | — | (66,201) | |||||||||||||||||||||||||||||||

| Depreciation and amortization | (97,887) | (99,291) | (196,118) | (199,670) | |||||||||||||||||||||||||||||||

| Interest expense | (34,052) | (30,981) | (67,006) | (61,345) | |||||||||||||||||||||||||||||||

| Gain (loss) on sales of operating properties, net | 103,022 | (1,230) | 103,113 | (1,466) | |||||||||||||||||||||||||||||||

| Gain on sale of unconsolidated property, net | — | — | — | 2,325 | |||||||||||||||||||||||||||||||

|

Net (income) loss attributable to noncontrolling

interests

|

(2,281) | 665 | (2,815) | 385 | |||||||||||||||||||||||||||||||

| Net income (loss) attributable to common shareholders | $ | 110,318 | $ | (48,638) | $ | 134,048 | $ | (34,482) | |||||||||||||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 5 |

||||

| Three Months Ended | |||||||||||||||||||||||||||||

| June 30, 2025 |

March 31, 2025 |

December 31, 2024 |

September 30, 2024 |

June 30, 2024 |

|||||||||||||||||||||||||

| Revenue: | |||||||||||||||||||||||||||||

| Minimum rent | $ | 149,092 | $ | 150,150 | $ | 149,331 | $ | 145,971 | $ | 144,617 | |||||||||||||||||||

| Minimum rent – ground leases | 10,450 | 10,644 | 10,750 | 10,758 | 10,492 | ||||||||||||||||||||||||

| Lease termination income | 2,725 | 7,390 | 152 | 800 | 832 | ||||||||||||||||||||||||

| Straight-line rent | 2,129 | 2,266 | 1,592 | 2,902 | 3,278 | ||||||||||||||||||||||||

| Non-cash market rent | 1,569 | 3,538 | 3,158 | 2,264 | 2,389 | ||||||||||||||||||||||||

| Tenant reimbursements | 45,103 | 46,213 | 44,058 | 42,453 | 44,422 | ||||||||||||||||||||||||

| Bad debt reserve | (1,625) | (2,076) | (1,755) | (1,468) | (1,544) | ||||||||||||||||||||||||

Other property-related revenue(1) |

870 | 1,640 | 3,843 | 1,402 | 2,701 | ||||||||||||||||||||||||

| Overage rent | 1,738 | 1,048 | 2,680 | 1,253 | 1,350 | ||||||||||||||||||||||||

| Total revenue | 212,051 | 220,813 | 213,809 | 206,335 | 208,537 | ||||||||||||||||||||||||

| Expenses: | |||||||||||||||||||||||||||||

Property operating – recoverable(2) |

24,849 | 25,798 | 24,913 | 23,961 | 24,257 | ||||||||||||||||||||||||

Property operating – non-recoverable(2) |

3,700 | 3,661 | 3,972 | 3,469 | 4,005 | ||||||||||||||||||||||||

| Real estate taxes | 26,492 | 27,604 | 25,495 | 25,083 | 26,350 | ||||||||||||||||||||||||

| Total expenses | 55,041 | 57,063 | 54,380 | 52,513 | 54,612 | ||||||||||||||||||||||||

| NOI | 157,010 | 163,750 | 159,429 | 153,822 | 153,925 | ||||||||||||||||||||||||

| Other (expense) income: | |||||||||||||||||||||||||||||

| General, administrative and other | (13,390) | (12,258) | (13,549) | (13,259) | (12,966) | ||||||||||||||||||||||||

| Fee income | 853 | 425 | 441 | 455 | 3,452 | ||||||||||||||||||||||||

| Total other (expense) income | (12,537) | (11,833) | (13,108) | (12,804) | (9,514) | ||||||||||||||||||||||||

| Adjusted EBITDA | 144,473 | 151,917 | 146,321 | 141,018 | 144,411 | ||||||||||||||||||||||||

| Impairment charges | — | — | — | — | (66,201) | ||||||||||||||||||||||||

| Depreciation and amortization | (97,887) | (98,231) | (97,009) | (96,656) | (99,291) | ||||||||||||||||||||||||

| Interest expense | (34,052) | (32,954) | (32,706) | (31,640) | (30,981) | ||||||||||||||||||||||||

| Equity in (loss) earnings of unconsolidated subsidiaries | (3,238) | (607) | 43 | (607) | (174) | ||||||||||||||||||||||||

| Income tax (expense) benefit of taxable REIT subsidiaries | (199) | (10) | 186 | (35) | (132) | ||||||||||||||||||||||||

| Loss on extinguishment of debt | — | — | (180) | — | — | ||||||||||||||||||||||||

| Interest income | 493 | 4,049 | 5,453 | 4,333 | 4,364 | ||||||||||||||||||||||||

| Other (expense) income, net | (13) | 9 | 122 | 38 | (69) | ||||||||||||||||||||||||

| Gain (loss) on sales of operating properties, net | 103,022 | 91 | — | 602 | (1,230) | ||||||||||||||||||||||||

| Net income (loss) | 112,599 | 24,264 | 22,230 | 17,053 | (49,303) | ||||||||||||||||||||||||

Net (income) loss attributable to noncontrolling interests |

(2,281) | (534) | (406) | (324) | 665 | ||||||||||||||||||||||||

| Net income (loss) attributable to common shareholders | $ | 110,318 | $ | 23,730 | $ | 21,824 | $ | 16,729 | $ | (48,638) | |||||||||||||||||||

| NOI/Revenue – Retail properties | 74.4 | % | 74.7 | % | 75.1 | % | 75.2 | % | 74.3 | % | |||||||||||||||||||

| NOI/Revenue | 74.0 | % | 74.2 | % | 74.6 | % | 74.5 | % | 73.8 | % | |||||||||||||||||||

Recovery Ratios(3) |

|||||||||||||||||||||||||||||

| – Retail properties | 92.0 | % | 91.4 | % | 92.1 | % | 91.2 | % | 91.6 | % | |||||||||||||||||||

| – Consolidated | 87.8 | % | 86.5 | % | 87.4 | % | 86.6 | % | 87.8 | % | |||||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 6 |

||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | ||||||||||||||||||||

| Net income (loss) | $ | 112,599 | $ | (49,303) | $ | 136,863 | $ | (34,867) | |||||||||||||||

| Less: net income attributable to noncontrolling interests in properties | (81) | (74) | (151) | (141) | |||||||||||||||||||

| Less/add: (gain) loss on sales of operating properties, net | (103,022) | 1,230 | (103,113) | 1,466 | |||||||||||||||||||

| Less: gain on sale of unconsolidated property, net | — | — | — | (2,325) | |||||||||||||||||||

| Add: impairment charges | — | 66,201 | — | 66,201 | |||||||||||||||||||

|

Add: depreciation and amortization of consolidated and unconsolidated entities,

net of noncontrolling interests

|

104,469 | 99,433 | 203,146 | 199,993 | |||||||||||||||||||

NAREIT FFO of the Operating Partnership(1) |

113,965 | 117,487 | 236,745 | 230,327 | |||||||||||||||||||

Less: Limited Partners’ interests in FFO |

(2,466) | (1,946) | (4,929) | (3,768) | |||||||||||||||||||

FFO attributable to common shareholders(1) |

$ | 111,499 | $ | 115,541 | $ | 231,816 | $ | 226,559 | |||||||||||||||

| FFO, as defined by NAREIT, per share of the Operating Partnership – basic | $ | 0.51 | $ | 0.53 | $ | 1.05 | $ | 1.03 | |||||||||||||||

| FFO, as defined by NAREIT, per share of the Operating Partnership – diluted | $ | 0.51 | $ | 0.53 | $ | 1.05 | $ | 1.03 | |||||||||||||||

| Weighted average common shares outstanding – basic | 219,835,322 | 219,622,059 | 219,775,829 | 219,561,586 | |||||||||||||||||||

| Weighted average common shares outstanding – diluted | 219,949,868 | 220,013,860 | 219,888,939 | 219,957,009 | |||||||||||||||||||

| Weighted average common shares and units outstanding – basic | 224,684,910 | 223,329,063 | 224,451,187 | 223,219,523 | |||||||||||||||||||

| Weighted average common shares and units outstanding – diluted | 224,799,456 | 223,720,864 | 224,564,297 | 223,614,946 | |||||||||||||||||||

Reconciliation of NAREIT FFO to Core FFO(2) |

|||||||||||||||||||||||

NAREIT FFO of the Operating Partnership(1) |

$ | 113,965 | $ | 117,487 | $ | 236,745 | $ | 230,327 | |||||||||||||||

| Add: | |||||||||||||||||||||||

| Amortization of deferred financing costs | 1,751 | 987 | 3,395 | 1,916 | |||||||||||||||||||

| Non-cash compensation expense and other | 3,048 | 2,906 | 5,564 | 5,628 | |||||||||||||||||||

| Less: | |||||||||||||||||||||||

| Straight-line rent – minimum rent and common area maintenance | 2,835 | 3,651 | 5,413 | 6,776 | |||||||||||||||||||

| Market rent amortization income | 1,879 | 2,390 | 5,421 | 4,657 | |||||||||||||||||||

| Amortization of debt discounts, premiums and hedge instruments | 890 | 3,734 | 3,646 | 7,490 | |||||||||||||||||||

| Core FFO of the Operating Partnership | $ | 113,160 | $ | 111,605 | $ | 231,224 | $ | 218,948 | |||||||||||||||

| Core FFO per share of the Operating Partnership – diluted | $ | 0.50 | $ | 0.50 | $ | 1.03 | $ | 0.98 | |||||||||||||||

Reconciliation of Core FFO to Adjusted Funds From Operations (“AFFO”)(2) |

|||||||||||||||||||||||

| Core FFO of the Operating Partnership | $ | 113,160 | $ | 111,605 | $ | 231,224 | $ | 218,948 | |||||||||||||||

| Less: | |||||||||||||||||||||||

| Maintenance capital expenditures | 9,195 | 6,927 | 15,493 | 12,665 | |||||||||||||||||||

Tenant-related capital expenditures(3) |

22,273 | 25,226 | 53,595 | 43,644 | |||||||||||||||||||

| Total Recurring AFFO of the Operating Partnership | $ | 81,692 | $ | 79,452 | $ | 162,136 | $ | 162,639 | |||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 7 |

||||

| Consolidated Investments | ||||||||||||||||||||||||||

| Investments | Total Debt |

Partner Economic

Ownership Interest(1)

|

Partner Share of Debt |

Partner Share of Annual EBITDA |

||||||||||||||||||||||

| Delray Marketplace | $ | 13,400 | 2 | % | $ | 268 | $ | — | ||||||||||||||||||

| One Loudoun – Pads G&H Residential | 95,095 | 10 | % | 9,509 | 838 | |||||||||||||||||||||

| Total | $ | 108,495 | $ | 9,777 | $ | 838 | ||||||||||||||||||||

| Unconsolidated Investments | ||||||||||||||||||||

| Investments | Total GLA | Multifamily Units |

Economic Ownership Interest |

|||||||||||||||||

| Nuveen Portfolio | 416,011 | — | 20 | % | ||||||||||||||||

| Embassy Suites at Eddy Street Commons | — | — | 35 | % | ||||||||||||||||

| Glendale Center Apartments | — | — | 11.5 | % | ||||||||||||||||

| The Corner – IN | 23,852 | 285 | 50 | % | ||||||||||||||||

| Legacy West | 785,564 | 782 | 52 | % | ||||||||||||||||

| GIC Portfolio | 921,280 | — | 52 | % | ||||||||||||||||

| Total | 2,146,707 | 1,067 | ||||||||||||||||||

| Total Unconsolidated Investments | ||||||||||||||||||||

| Investment as of June 30, 2025 | $ | 390,827 | ||||||||||||||||||

| Three Months Ended June 30, 2025 |

||||||||

| EBITDA | $ | 5,689 | ||||||

| Depreciation and amortization | (6,932) | |||||||

| Interest expense | (2,185) | |||||||

| Other income, net | 190 | |||||||

| KRG share of net loss | $ | (3,238) | ||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 8 |

||||

| June 30, 2025 |

Debt Covenant

Threshold(1)

|

||||||||||

| Senior Unsecured Notes Covenants | |||||||||||

| Total debt to undepreciated assets | 39% | <60% | |||||||||

| Secured debt to undepreciated assets | 4% | <40% | |||||||||

| Undepreciated unencumbered assets to unsecured debt | 266% | >150% | |||||||||

| Debt service coverage | 4.5x | >1.5x | |||||||||

| Unsecured Credit Facility Covenants | |||||||||||

| Maximum leverage | 34% | <60% | |||||||||

| Minimum fixed charge coverage | 4.2x | >1.5x | |||||||||

| Secured indebtedness | 3.8% | <45% | |||||||||

| Unsecured debt interest coverage | 4.1x | >1.75x | |||||||||

| Unsecured leverage | 33% | <60% | |||||||||

| Senior Unsecured Debt Ratings | |||||||||||

| Fitch Ratings | BBB/Positive | ||||||||||

| Moody's Investors Service | Baa2/Stable | ||||||||||

| Standard & Poor's Rating Services | BBB/Stable | ||||||||||

| Liquidity | |||||||||||

| Cash and cash equivalents | $ | 182,044 | |||||||||

| Availability under unsecured credit facility | 1,095,500 | ||||||||||

| $ | 1,277,544 | ||||||||||

| Unencumbered Consolidated NOI as a % of Total Consolidated NOI | 95 | % | |||||||||

| Net Debt to Adjusted EBITDA | |||||||||||

| Mortgage and other indebtedness, net | $ | 3,022,496 | |||||||||

| Add: Company share of unconsolidated joint venture debt | 190,841 | ||||||||||

| Add: debt discounts, premiums and issuance costs, net | 3,082 | ||||||||||

| Less: Partner share of consolidated joint venture debt | (9,777) | ||||||||||

| Company's consolidated debt and share of unconsolidated debt | 3,206,642 | ||||||||||

| Less: cash, cash equivalents and restricted cash | (201,796) | ||||||||||

| Company share of Net Debt | $ | 3,004,846 | |||||||||

| Q2 2025 Adjusted EBITDA, Annualized: | |||||||||||

| – Consolidated Adjusted EBITDA | $ | 577,892 | |||||||||

| – Unconsolidated Adjusted EBITDA | 22,756 | ||||||||||

– Minority interest Adjusted EBITDA(2) |

(838) | ||||||||||

– Pro forma adjustments(3) |

(9,120) | 590,690 | |||||||||

| Ratio of Company share of Net Debt to Adjusted EBITDA | 5.1x | ||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 9 |

||||

| Total Outstanding Debt | Amount Outstanding |

Ratio | Weighted Average Interest Rate |

Weighted Average Years to Maturity |

|||||||||||||||||||

Fixed rate debt(1) |

$ | 2,857,178 | 89 | % | 4.28 | % | 4.9 | ||||||||||||||||

Variable rate debt(2) |

168,400 | 5 | % | 7.63 | % | 1.2 | |||||||||||||||||

| Debt discounts, premiums and issuance costs, net | (3,082) | N/A | N/A | N/A | |||||||||||||||||||

| Total consolidated debt | 3,022,496 | 94 | % | 4.46 | % | 4.7 | |||||||||||||||||

| KRG share of unconsolidated debt | 190,841 | 6 | % | 4.38 | % | 4.7 | |||||||||||||||||

| Total | $ | 3,213,337 | 100 | % | 4.46 | % | 4.7 | ||||||||||||||||

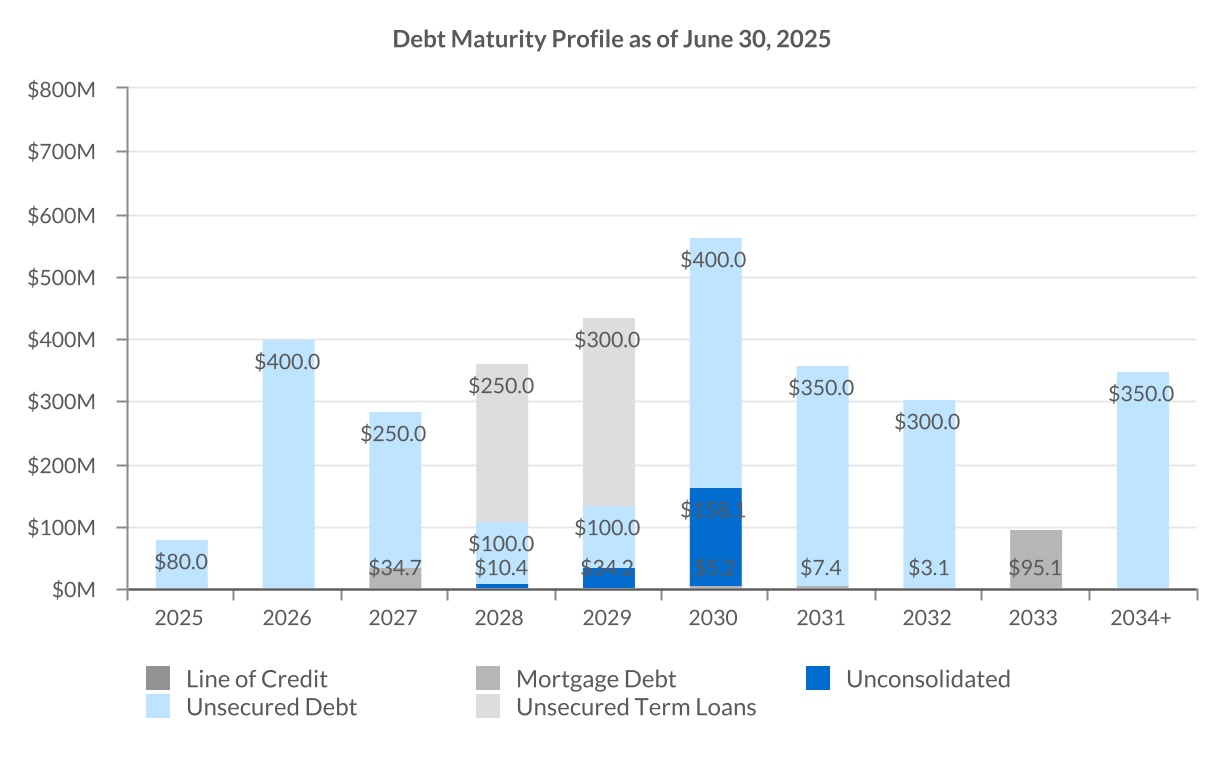

| Schedule of Maturities by Year | |||||||||||||||||||||||||||||||||||

| Secured Debt | |||||||||||||||||||||||||||||||||||

| Scheduled Principal Payments |

Term Maturities |

Unsecured Debt |

Total Consolidated Debt |

Total Unconsolidated Debt |

Total Debt Outstanding |

||||||||||||||||||||||||||||||

| 2025 | $ | 2,641 | $ | — | $ | 80,000 | $ | 82,641 | $ | — | $ | 82,641 | |||||||||||||||||||||||

| 2026 | 4,581 | — | 400,000 | 404,581 | — | 404,581 | |||||||||||||||||||||||||||||

| 2027 | 3,120 | 10,600 | 250,000 | 263,720 | — | 263,720 | |||||||||||||||||||||||||||||

| 2028 | 3,757 | — | 350,000 | (3) |

353,757 | 10,378 | 364,135 | ||||||||||||||||||||||||||||

| 2029 | 4,324 | — | 400,000 | 404,324 | 34,197 | 438,521 | |||||||||||||||||||||||||||||

| 2030 and beyond | 23,767 | 92,788 | 1,400,000 | 1,516,555 | 158,080 | 1,674,635 | |||||||||||||||||||||||||||||

| Debt discounts, premiums and issuance costs, net | — | 843 | (3,925) | (3,082) | (11,814) | (14,896) | |||||||||||||||||||||||||||||

| Total | $ | 42,190 | $ | 104,231 | $ | 2,876,075 | $ | 3,022,496 | $ | 190,841 | $ | 3,213,337 | |||||||||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 10 |

||||

| Description |

Contractual

Interest Rate(1)

|

Swapped

Interest Rate(1)

|

Maturity Date |

Balance as of June 30, 2025 |

% of Total Outstanding |

|||||||||||||||||||||||||||

| Senior Unsecured Notes | 4.47% | SOFR + 3.65% | 9/10/2025 | $ | 80,000 | |||||||||||||||||||||||||||

| 2025 Debt Maturities | 4.47% | 7.68% | 80,000 | 3 | % | |||||||||||||||||||||||||||

| Senior Unsecured Notes | 4.08% | 4.08% | 9/30/2026 | 100,000 | ||||||||||||||||||||||||||||

| Senior Unsecured Notes | 4.00% | 4.00% | 10/1/2026 | 300,000 | ||||||||||||||||||||||||||||

| 2026 Debt Maturities | 4.02% | 4.02% | 400,000 | 12 | % | |||||||||||||||||||||||||||

| Senior Unsecured Exchangeable Notes | 0.75% | 0.75% | 4/1/2027 | 175,000 | ||||||||||||||||||||||||||||

| Northgate North | 4.50% | 4.50% | 6/1/2027 | 21,329 | ||||||||||||||||||||||||||||

Delray Marketplace(2) |

SOFR + 2.15% | SOFR + 2.15% | 8/4/2027 | 13,400 | ||||||||||||||||||||||||||||

| Senior Unsecured Notes | 4.57% | SOFR + 3.75% | 9/10/2027 | 75,000 | ||||||||||||||||||||||||||||

| 2027 Debt Maturities | 2.31% | 3.15% | 284,729 | 9 | % | |||||||||||||||||||||||||||

Unsecured Term Loan(3) |

SOFR + 0.95% | 3.94% | 10/24/2028 | 250,000 | ||||||||||||||||||||||||||||

| Senior Unsecured Notes | 4.24% | 4.24% | 12/28/2028 | 100,000 | ||||||||||||||||||||||||||||

| 2028 Debt Maturities | 5.07% | 4.03% | 350,000 | 11 | % | |||||||||||||||||||||||||||

| Senior Unsecured Notes | 4.82% | 4.82% | 6/28/2029 | 100,000 | ||||||||||||||||||||||||||||

| Unsecured Term Loan | SOFR + 1.25% | 3.72% | 7/29/2029 | 300,000 | ||||||||||||||||||||||||||||

Unsecured Credit Facility(4) |

SOFR + 1.15% | SOFR + 1.15% | 10/3/2029 | — | ||||||||||||||||||||||||||||

| 2029 Debt Maturities | 5.48% | 3.99% | 400,000 | 12 | % | |||||||||||||||||||||||||||

| Rampart Commons | 5.73% | 5.73% | 6/10/2030 | 5,231 | ||||||||||||||||||||||||||||

| Senior Unsecured Notes | 4.75% | 4.75% | 9/15/2030 | 400,000 | ||||||||||||||||||||||||||||

| The Shoppes at Union Hill | 3.75% | 3.75% | 6/1/2031 | 7,387 | ||||||||||||||||||||||||||||

| Senior Unsecured Notes | 4.95% | 4.95% | 12/15/2031 | 350,000 | ||||||||||||||||||||||||||||

| Nora Plaza Shops | 3.80% | 3.80% | 2/1/2032 | 3,136 | ||||||||||||||||||||||||||||

| Senior Unsecured Notes | 5.20% | 5.20% | 8/15/2032 | 300,000 | ||||||||||||||||||||||||||||

| One Loudoun – Pads G&H Residential | 5.36% | 5.36% | 5/1/2033 | 95,095 | ||||||||||||||||||||||||||||

Senior Unsecured Notes(5) |

4.60% | 4.60% | 3/1/2034 | 350,000 | ||||||||||||||||||||||||||||

| 2030 and beyond Debt Maturities | 4.89% | 4.89% | 1,510,849 | 47 | % | |||||||||||||||||||||||||||

| Debt discounts, premiums and issuance costs, net | (3,082) | |||||||||||||||||||||||||||||||

| Total debt per consolidated balance sheet | 4.62% | 4.46% | $ | 3,022,496 | 94 | % | ||||||||||||||||||||||||||

| KRG share of unconsolidated debt | ||||||||||||||||||||||||||||||||

| Nuveen Portfolio | 4.09% | 4.09% | 7/1/2028 | $ | 10,378 | |||||||||||||||||||||||||||

The Corner – IN(6) |

SOFR + 2.86% | SOFR + 2.86% | 11/25/2029 | 34,197 | ||||||||||||||||||||||||||||

| Legacy West | 3.80% | 3.80% | 5/1/2030 | 158,080 | ||||||||||||||||||||||||||||

| KRG share of unconsolidated debt | 4.38% | 4.38% | 202,655 | |||||||||||||||||||||||||||||

| KRG share of debt discounts and issuance costs, net | (11,814) | |||||||||||||||||||||||||||||||

| Total KRG share of unconsolidated debt | 190,841 | 6 | % | |||||||||||||||||||||||||||||

| Total consolidated and KRG share of unconsolidated debt | 4.60% | 4.46% | $ | 3,213,337 | ||||||||||||||||||||||||||||

| Interest Rate Swaps | Swap Maturity Date |

KRG Receives | KRG Pays | Aggregate Notional | ||||||||||||||||||||||

| Interest rate swap on Term Loan Due 7/29/2029 | 8/1/2025 | 1-month SOFR (4.32%) | 2.47% | $ | 300,000 | |||||||||||||||||||||

| Interest rate swap on Term Loan Due 10/24/2028 | 10/24/2025 | 1-month SOFR (4.32%) | 2.99% | 250,000 | ||||||||||||||||||||||

| Interest rate swap to be assigned to Term Loan Due 7/29/2029 effective August 1, 2025 | 7/17/2026 | 1-month SOFR (4.32%) | 1.68% | 150,000 | ||||||||||||||||||||||

| $ | 700,000 | |||||||||||||||||||||||||

| Reverse interest rate swap on Notes Due 9/10/2025 | 9/10/2025 | 4.47% | 3-month SOFR + 3.65% (7.68%) | $ | 80,000 | |||||||||||||||||||||

| Reverse interest rate swap on Notes Due 9/10/2027 | 9/10/2025 | 4.57% | 3-month SOFR + 3.75% (7.78%) | 75,000 | ||||||||||||||||||||||

| $ | 155,000 | |||||||||||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 11 |

||||

| Property Name | Acquisition Date | Metropolitan Statistical Area (“MSA”) |

Grocery Anchor | Retail GLA |

Office GLA |

Acquisition Price – at KRG’s share |

||||||||||||||||||||||||||||||||

| Village Commons | January 15, 2025 | Miami | Publix | 170,976 | — | $ | 68,400 | |||||||||||||||||||||||||||||||

Legacy West(1) |

April 28, 2025 | Dallas/Ft. Worth | N/A | 342,011 | 443,553 | 408,200 | ||||||||||||||||||||||||||||||||

| Total acquisitions | 512,987 | 443,553 | $ | 476,600 | ||||||||||||||||||||||||||||||||||

| Property Name | Disposition Date | MSA | Grocery Anchor | GLA | Sales Price | |||||||||||||||||||||||||||

| Stoney Creek Commons | April 4, 2025 | Indianapolis | N/A | 84,094 | $ | 9,500 | ||||||||||||||||||||||||||

| Fullerton Metrocenter | June 25, 2025 | Los Angeles | Sprouts, Target | 241,027 | 118,500 | |||||||||||||||||||||||||||

Denton Crossing(2) |

June 27, 2025 | Dallas/Ft. Worth | Kroger (shadow) | 343,345 | 39,263 | |||||||||||||||||||||||||||

Parkway Towne Crossing(2) |

June 27, 2025 | Dallas/Ft. Worth | Target (shadow) | 180,736 | 27,743 | |||||||||||||||||||||||||||

The Landing at Tradition(2) |

June 27, 2025 | Port St. Lucie, FL | The Fresh Market, Target (shadow) | 397,199 | 45,114 | |||||||||||||||||||||||||||

| Humblewood Shopping Center | July 21, 2025 | Houston | N/A | 85,682 | 18,250 | |||||||||||||||||||||||||||

| Total dispositions | 1,332,083 | $ | 258,370 | |||||||||||||||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 12 |

||||

| Project | MSA | KRG Ownership % |

Projected

Completion Date(1)

|

Total Owned GLA |

Total Multifamily Units |

Total Project Costs – at KRG's Share |

KRG Equity Requirement |

KRG Remaining Spend |

Estimated Stabilized NOI to KRG |

Estimated

Remaining NOI

to Come Online(2)

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

| Active Projects | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

One Loudoun Expansion(3) |

Washington, D.C./Baltimore | 100% | Q4 2026– Q2 2027 |

119,000 | — | $81.0M–$91.0M | $65.0M–$75.0M | $58.0M–$68.0M | $4.7M–$6.2M | $2.0M–$3.5M | ||||||||||||||||||||||||||||||||||||||||||||||||||||

Future Opportunities(4) |

||||||||||||||

| Project | MSA | Project Description | ||||||||||||

| Hamilton Crossing Centre – Phase II | Indianapolis, IN | Addition of mixed-use (multifamily, office and retail) components adjacent to the Republic Airways headquarters. | ||||||||||||

| Carillon | Washington, D.C./Baltimore | Potential of 1.2 million square feet of commercial GLA and 3,000 multifamily units for additional expansion. | ||||||||||||

| One Loudoun Hotel | Washington, D.C./Baltimore | Potential for 1.7 million square feet remaining following the planned approximately 170-room hotel. | ||||||||||||

| One Loudoun Residential | Washington, D.C./Baltimore | Potential for approximately 1,300 multifamily units remaining following the planned 400 additional multifamily units. | ||||||||||||

| Main Street Promenade | Chicago, IL | Potential of 16,000 square feet of commercial GLA for additional expansion. | ||||||||||||

| Downtown Crown | Washington, D.C./Baltimore | Potential of 42,000 square feet of commercial GLA for additional expansion. | ||||||||||||

| Edwards Multiplex – Ontario | Los Angeles, CA | Potential redevelopment of existing Regal Theatre. | ||||||||||||

| Glendale Town Center | Indianapolis, IN | Potential of 200 multifamily units for additional expansion. | ||||||||||||

| The Shops at Legacy East | Dallas/Ft. Worth, TX | Potential of 285 multifamily units for additional expansion. | ||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 13 |

||||

| Region/State |

Number of

Properties(1)

|

Owned GLA(2) |

Total

Weighted

ABR(3)

|

% of

Weighted

ABR(3)

|

||||||||||||||||||||||

| South | ||||||||||||||||||||||||||

| Texas | 44 | 8,644 | $ | 185,070 | 29.2 | % | ||||||||||||||||||||

| Florida | 31 | 3,717 | 71,415 | 11.2 | % | |||||||||||||||||||||

| Virginia | 7 | 1,307 | 37,726 | 5.9 | % | |||||||||||||||||||||

| Maryland | 9 | 1,535 | 34,873 | 5.5 | % | |||||||||||||||||||||

| North Carolina | 8 | 1,532 | 34,203 | 5.4 | % | |||||||||||||||||||||

| Georgia | 11 | 1,849 | 30,904 | 4.9 | % | |||||||||||||||||||||

| Oklahoma | 3 | 505 | 8,606 | 1.4 | % | |||||||||||||||||||||

| Tennessee | 3 | 580 | 8,490 | 1.3 | % | |||||||||||||||||||||

| South Carolina | 2 | 262 | 3,815 | 0.6 | % | |||||||||||||||||||||

| Total South | 118 | 19,931 | 415,102 | 65.4 | % | |||||||||||||||||||||

| West | ||||||||||||||||||||||||||

| Washington | 10 | 1,651 | 32,080 | 5.1 | % | |||||||||||||||||||||

| Nevada | 5 | 846 | 28,670 | 4.5 | % | |||||||||||||||||||||

| Arizona | 5 | 714 | 16,009 | 2.5 | % | |||||||||||||||||||||

| Utah | 2 | 388 | 8,494 | 1.3 | % | |||||||||||||||||||||

| California | 1 | 292 | 4,478 | 0.7 | % | |||||||||||||||||||||

| Total West | 23 | 3,891 | 89,731 | 14.1 | % | |||||||||||||||||||||

| Midwest | ||||||||||||||||||||||||||

| Indiana | 16 | 1,940 | 39,234 | 6.2 | % | |||||||||||||||||||||

| Illinois | 7 | 1,222 | 27,252 | 4.3 | % | |||||||||||||||||||||

| Michigan | 1 | 308 | 6,840 | 1.1 | % | |||||||||||||||||||||

| Missouri | 1 | 453 | 4,356 | 0.7 | % | |||||||||||||||||||||

| Ohio | 1 | 236 | 2,152 | 0.3 | % | |||||||||||||||||||||

| Total Midwest | 26 | 4,159 | 79,834 | 12.6 | % | |||||||||||||||||||||

| Northeast | ||||||||||||||||||||||||||

| New York | 7 | 889 | 27,708 | 4.4 | % | |||||||||||||||||||||

| New Jersey | 4 | 342 | 11,533 | 1.8 | % | |||||||||||||||||||||

| Massachusetts | 1 | 264 | 4,888 | 0.8 | % | |||||||||||||||||||||

| Connecticut | 1 | 206 | 4,075 | 0.6 | % | |||||||||||||||||||||

| Pennsylvania | 1 | 136 | 1,982 | 0.3 | % | |||||||||||||||||||||

| Total Northeast | 14 | 1,837 | 50,186 | 7.9 | % | |||||||||||||||||||||

Total(4) |

181 | 29,818 | $ | 634,853 | 100.0 | % | ||||||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 14 |

||||

| Credit Ratings | |||||||||||||||||||||||||||||||||||||||||||||||

| Tenant | Primary DBA/ Number of Stores |

Number

of Stores(1)

|

Total

Leased

GLA(2)

|

ABR(3) |

% of

Weighted ABR(4)

|

S&P | Moody’s | ||||||||||||||||||||||||||||||||||||||||

| 1 | The TJX Companies, Inc. | T.J. Maxx (18), Marshalls (13), HomeGoods (11), Homesense (4), Sierra (3), T.J. Maxx & HomeGoods combined (2) | 51 | 1,469 | $ | 16,279 | 2.6 | % | A | A2 | |||||||||||||||||||||||||||||||||||||

| 2 | Ross Stores, Inc. | Ross Dress for Less (32), dd’s DISCOUNTS (1) | 33 | 937 | 11,342 | 1.8 | % | BBB+ | A2 | ||||||||||||||||||||||||||||||||||||||

| 3 | PetSmart, Inc. | 31 | 638 | 10,452 | 1.7 | % | B+ | B2 | |||||||||||||||||||||||||||||||||||||||

| 4 | Best Buy Co., Inc. | Best Buy (14), Pacific Sales (1) | 15 | 593 | 9,002 | 1.4 | % | BBB+ | A3 | ||||||||||||||||||||||||||||||||||||||

| 5 | Dick’s Sporting Goods, Inc. | Dick’s Sporting Goods (12), Golf Galaxy (1) | 13 | 625 | 7,977 | 1.3 | % | BBB | Baa2 | ||||||||||||||||||||||||||||||||||||||

| 6 | Gap Inc. | Old Navy (25), The Gap (3), Athleta (3), Banana Republic (2) | 33 | 448 | 7,899 | 1.2 | % | BB | Ba2 | ||||||||||||||||||||||||||||||||||||||

| 7 | Michaels Stores, Inc. | Michaels | 27 | 606 | 7,745 | 1.2 | % | B- | B3 | ||||||||||||||||||||||||||||||||||||||

| 8 | Publix Super Markets, Inc. | 15 | 720 | 7,724 | 1.2 | % | N/A | N/A | |||||||||||||||||||||||||||||||||||||||

| 9 | Ulta Beauty, Inc. | 29 | 299 | 6,364 | 1.0 | % | N/A | N/A | |||||||||||||||||||||||||||||||||||||||

| 10 | Total Wine & More | 15 | 355 | 6,093 | 1.0 | % | N/A | N/A | |||||||||||||||||||||||||||||||||||||||

| 11 | BJ’s Wholesale Club, Inc. | 3 | 115 | 5,892 | 0.9 | % | BB+ | N/A | |||||||||||||||||||||||||||||||||||||||

| 12 | The Kroger Co. | Kroger (6), Harris Teeter (2), QFC (1), Smith’s (1) |

10 | 356 | 5,892 | 0.9 | % | BBB | Baa1 | ||||||||||||||||||||||||||||||||||||||

| 13 | Lowe’s Companies, Inc. | 6 | — | 5,838 | 0.9 | % | BBB+ | Baa1 | |||||||||||||||||||||||||||||||||||||||

| 14 | Five Below, Inc. | 31 | 282 | 5,299 | 0.8 | % | N/A | N/A | |||||||||||||||||||||||||||||||||||||||

| 15 | Fitness International, LLC | LA Fitness (4), XSport Fitness (1) | 5 | 206 | 5,098 | 0.8 | % | B | B2 | ||||||||||||||||||||||||||||||||||||||

| 16 |

Petco Health and Wellness

Company, Inc.

|

19 | 274 | 5,059 | 0.8 | % | B | B3 | |||||||||||||||||||||||||||||||||||||||

| 17 | Kohl’s Corporation | 7 | 265 | 5,033 | 0.8 | % | BB- | B2 | |||||||||||||||||||||||||||||||||||||||

| 18 | Trader Joe's | 12 | 150 | 5,031 | 0.8 | % | N/A | N/A | |||||||||||||||||||||||||||||||||||||||

| 19 | Nordstrom, Inc. | Nordstrom Rack | 9 | 272 | 4,750 | 0.8 | % | BB | Ba2 | ||||||||||||||||||||||||||||||||||||||

| 20 | KnitWell Group | Chico’s (7), Talbots (7), LOFT (5), Soma (4), Ann Taylor (4), White House Black Market (4) | 31 | 134 | 4,635 | 0.7 | % | N/A | N/A | ||||||||||||||||||||||||||||||||||||||

| 21 | The Container Store Group, Inc. | 7 | 151 | 4,627 | 0.7 | % | N/A | N/A | |||||||||||||||||||||||||||||||||||||||

| 22 | Burlington Stores, Inc. | 11 | 435 | 4,619 | 0.7 | % | BB+ | N/A | |||||||||||||||||||||||||||||||||||||||

| 23 | Dollar Tree, Inc. | 28 | 321 | 4,616 | 0.7 | % | BBB | Baa2 | |||||||||||||||||||||||||||||||||||||||

| 24 | Albertsons Companies, Inc. | Safeway (3), Tom Thumb (2), Jewel-Osco (1) | 6 | 281 | 4,198 | 0.7 | % | BB+ | Ba1 | ||||||||||||||||||||||||||||||||||||||

| 25 | Designer Brands Inc. | DSW Designer Shoe Warehouse | 15 | 295 | 4,164 | 0.7 | % | N/A | N/A | ||||||||||||||||||||||||||||||||||||||

| Total Top Tenants | 462 | 10,227 | $ | 165,628 | 26.1 | % | |||||||||||||||||||||||||||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 15 |

||||

Comparable Space(1)(2) |

||||||||||||||||||||||||||||||||||||||||||||||||||

|

Category

|

Total

Leases(1)

|

Total

Sq. Ft.(1)

|

Leases | Sq. Ft. | Prior Rent PSF(3) |

New Rent PSF(4) |

Cash Rent Spread |

TI, LL Work,

Lease Commissions PSF(5)

|

||||||||||||||||||||||||||||||||||||||||||

| New Leases – Q2 2025 | 64 | 342,658 | 38 | 219,271 | $ | 19.65 | $ | 25.80 | 31.3 | % | ||||||||||||||||||||||||||||||||||||||||

| New Leases – Q1 2025 | 58 | 169,703 | 26 | 76,021 | 32.89 | 38.02 | 15.6 | % | ||||||||||||||||||||||||||||||||||||||||||

| New Leases – Q4 2024 | 48 | 233,043 | 23 | 97,594 | 25.32 | 31.29 | 23.6 | % | ||||||||||||||||||||||||||||||||||||||||||

| New Leases – Q3 2024 | 63 | 284,580 | 35 | 136,874 | 24.11 | 30.11 | 24.9 | % | ||||||||||||||||||||||||||||||||||||||||||

| Total | 233 | 1,029,984 | 122 | 529,760 | $ | 23.75 | $ | 29.68 | 25.0 | % | $ | 84.72 | ||||||||||||||||||||||||||||||||||||||

| Non-Option Renewals – Q2 2025 | 63 | 223,294 | 52 | 159,247 | $ | 27.12 | $ | 32.47 | 19.7 | % | ||||||||||||||||||||||||||||||||||||||||

| Non-Option Renewals – Q1 2025 | 91 | 331,781 | 67 | 232,071 | 23.57 | 28.30 | 20.1 | % | ||||||||||||||||||||||||||||||||||||||||||

| Non-Option Renewals – Q4 2024 | 93 | 447,352 | 69 | 323,610 | 20.67 | 23.65 | 14.4 | % | ||||||||||||||||||||||||||||||||||||||||||

| Non-Option Renewals – Q3 2024 | 81 | 477,515 | 59 | 236,747 | 23.69 | 26.50 | 11.9 | % | ||||||||||||||||||||||||||||||||||||||||||

| Total | 328 | 1,479,942 | 247 | 951,675 | $ | 23.21 | $ | 26.97 | 16.2 | % | $ | 4.31 | ||||||||||||||||||||||||||||||||||||||

| Option Renewals – Q2 2025 | 43 | 648,679 | 43 | 648,679 | $ | 12.72 | $ | 13.76 | 8.2 | % | ||||||||||||||||||||||||||||||||||||||||

| Option Renewals – Q1 2025 | 33 | 342,345 | 33 | 342,345 | 17.15 | 18.36 | 7.0 | % | ||||||||||||||||||||||||||||||||||||||||||

| Option Renewals – Q4 2024 | 29 | 533,995 | 29 | 533,995 | 13.24 | 14.14 | 6.8 | % | ||||||||||||||||||||||||||||||||||||||||||

| Option Renewals – Q3 2024 | 61 | 889,891 | 61 | 889,891 | 16.51 | 17.79 | 7.7 | % | ||||||||||||||||||||||||||||||||||||||||||

| Total | 166 | 2,414,910 | 166 | 2,414,910 | $ | 14.86 | $ | 15.98 | 7.5 | % | $ | — | ||||||||||||||||||||||||||||||||||||||

| Total – Q2 2025 | 170 | 1,214,631 | 133 | 1,027,197 | $ | 16.43 | $ | 19.23 | 17.0 | % | ||||||||||||||||||||||||||||||||||||||||

| Total – Q1 2025 | 182 | 843,829 | 126 | 650,437 | 21.28 | 24.20 | 13.7 | % | ||||||||||||||||||||||||||||||||||||||||||

| Total – Q4 2024 | 170 | 1,214,390 | 121 | 955,199 | 16.99 | 19.11 | 12.5 | % | ||||||||||||||||||||||||||||||||||||||||||

| Total – Q3 2024 | 205 | 1,651,986 | 155 | 1,263,512 | 18.68 | 20.75 | 11.1 | % | ||||||||||||||||||||||||||||||||||||||||||

| Total | 727 | 4,924,836 | 535 | 3,896,345 | $ | 18.11 | $ | 20.52 | 13.3 | % | $ | 12.57 | ||||||||||||||||||||||||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 16 |

||||

| Operating Portfolio | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Expiring GLA(2) |

Expiring Retail ABR per Sq. Ft.(3) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Number of

Expiring

Leases(1)

|

Shop Tenants |

Anchor Tenants |

Office Tenants |

Expiring ABR (Pro rata) |

Expiring Ground Lease ABR (Pro rata) |

% of Total ABR (Pro rata) |

Shop Tenants |

Anchor Tenants |

Total | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2025 | 176 | 366,073 | 188,579 | 79,733 | $ | 18,159 | $ | 1,091 | 3.0 | % | $ | 32.60 | $ | 20.11 | $ | 28.35 | ||||||||||||||||||||||||||||||||||||||||||||||

| 2026 | 496 | 1,123,486 | 1,833,687 | 117,996 | 63,583 | 3,689 | 10.6 | % | 30.86 | 14.95 | 21.00 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2027 | 589 | 1,284,207 | 2,253,802 | 133,479 | 75,928 | 5,477 | 12.8 | % | 34.55 | 14.19 | 21.58 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2028 | 612 | 1,311,507 | 2,589,240 | 325,926 | 90,934 | 6,638 | 15.4 | % | 36.35 | 15.00 | 22.18 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2029 | 585 | 1,236,333 | 2,919,517 | 182,070 | 91,231 | 3,581 | 14.9 | % | 36.09 | 15.24 | 21.44 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2030 | 445 | 1,079,852 | 2,000,847 | 124,030 | 63,652 | 4,710 | 10.8 | % | 32.51 | 13.12 | 19.92 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2031 | 229 | 565,079 | 959,650 | 196,290 | 38,406 | 2,131 | 6.4 | % | 38.74 | 13.93 | 23.13 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2032 | 204 | 494,522 | 1,131,795 | 176,704 | 36,344 | 466 | 5.8 | % | 32.74 | 14.79 | 20.25 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2033 | 217 | 552,019 | 689,378 | 108,240 | 33,040 | 4,156 | 5.9 | % | 38.00 | 15.58 | 25.55 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2034 | 187 | 384,400 | 689,269 | 86,112 | 28,906 | 2,225 | 4.9 | % | 40.64 | 17.10 | 25.53 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Beyond | 296 | 619,446 | 1,684,665 | 158,900 | 55,586 | 4,920 | 9.5 | % | 37.89 | 16.76 | 22.90 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 4,036 | 9,016,924 | 16,940,429 | 1,689,480 | $ | 595,769 | $ | 39,084 | 100.0 | % | $ | 35.25 | $ | 14.97 | $ | 22.02 | |||||||||||||||||||||||||||||||||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 17 |

||||

| Cash Net Operating Income (“NOI”) | Page | Other Assets(1) |

Page | |||||||||||||||||

| GAAP property NOI (incl. ground lease revenue) | $ | 157,010 | 6 | Cash, cash equivalents and restricted cash | $ | 187,610 | 3 | |||||||||||||

| Lease termination income | (2,725) | 6 | Tenant and other receivables (net of SLR) | 56,247 | 3 | |||||||||||||||

| Non-cash revenue adjustments | (4,714) | Prepaid and other assets | 96,278 | 3 | ||||||||||||||||

| Other property-related revenue | (870) | 6 | ||||||||||||||||||

| Ground lease (“GL”) revenue | (10,450) | 6 | ||||||||||||||||||

| Consolidated Cash Property NOI (excl. GL) | $ | 138,251 | ||||||||||||||||||

|

Annualized Consolidated Cash Property NOI

(excl. ground leases)

|

$ | 553,004 | ||||||||||||||||||

| Adjustments to Normalize Annualized Cash NOI | Liabilities | |||||||||||||||||||

Remaining NOI to come online from development and redevelopment projects(2) |

$ | 2,750 | 13 | Mortgage and other indebtedness, net | $ | (3,025,578) | 10 | |||||||||||||

| Unconsolidated Adjusted EBITDA | 22,756 | Pro rata adjustment for joint venture debt | (181,064) | |||||||||||||||||

Pro forma adjustments(3) |

(9,120) | 9 | Accounts payable and accrued expenses | (180,564) | 3 | |||||||||||||||

| General and administrative expense allocable to property management activities included in property expenses ($4.0 million in Q2) | 16,000 | 6, note 2 | Other liabilities | (227,807) | 3 | |||||||||||||||

| Total Adjustments | 32,386 | Projected remaining under construction development/redevelopment(4) |

(63,000) | 13 | ||||||||||||||||

|

Annualized Normalized Portfolio Cash NOI

(excl. ground leases)

|

$ | 585,390 | ||||||||||||||||||

| Annualized ground lease NOI | 41,800 | |||||||||||||||||||

Total Annualized Portfolio Cash NOI(5) |

$ | 627,190 | Common shares and Units outstanding | 224,707,781 | ||||||||||||||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 18 |

||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 19 |

||||

| 2nd Quarter 2025 Supplemental Financial and Operating Statistics | 20 |

||||