UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d)

of The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): October 30, 2024

![]()

Smurfit Westrock plc

(Exact name of registrant as specified in its charter)

| Ireland (State or other jurisdiction of incorporation) |

001-42161 (Commission |

98-1776979 (I.R.S. Employer Identification No.) |

Beech Hill, Clonskeagh

Dublin 4, D04 N2R2

Ireland

(Address of principal executive offices, including Zip Code)

+353 1 202 7000

(Registrant’s telephone phone number, including area code)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Ordinary shares, par value $0.001 per share | SW | New York Stock Exchange (NYSE) |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Item 2.02. Results of Operations and Financial Condition.

On October 30, 2024, Smurfit Westrock plc (the “Company”) issued a press release announcing the financial results for the third quarter ended September 30, 2024. Due to the timing of the completion of the combination of Smurfit Kappa Group plc and WestRock Company (“WestRock”) on July 5, 2024, these results do not include the results of legacy WestRock for the first five days of July. The press release is furnished as Exhibit 99.1 and is incorporated into this Item 2.02 by reference.

The information furnished in this Item 2.02, including the exhibit described above, is being “furnished” and shall not be deemed “filed” hereunder for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or incorporated by reference in any filing under the Securities Act of 1933, as amended (the “Securities Act”), or the Exchange Act, except as shall be expressly set forth by specific reference in any such filings.

Item 7.01. Regulation FD Disclosure.

On October 30, 2024, the Company will host a conference call during which it will discuss the Company’s financial results for the third quarter ended September 30, 2024. The presentation to be used in connection with the conference call is attached as Exhibit 99.2.

The information provided pursuant to this Item 7.01, including Exhibit 99.2, is being “furnished” and shall not be deemed to be “filed” with the SEC or incorporated by reference in any filing under the Securities Act or the Exchange Act, except as shall be expressly set forth by specific reference in any such filings.

Item 9.01. Financial Statements and Exhibits.

| (d) | Exhibits |

| 99.1 | Third Quarter 2024 Earnings Press Release dated October 30, 2024 |

| 99.2 | Third Quarter 2024 Earnings Presentation |

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document) |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Smurfit Westrock plc | ||

| /s/ Ken Bowles | ||

| Name: | Ken Bowles | |

| Title: | Executive Vice President and Chief Financial Officer | |

Date: October 30, 2024

Exhibit 99.1

www.smurfitwestrock.com

| Smurfit Westrock Reports Third Quarter 2024 Financial Results |

Dublin – October 30, 2024 – Smurfit Westrock plc (NYSE: SW, LSE: SWR) today announced the financial results for the third quarter ended September 30, 2024.

Key points:

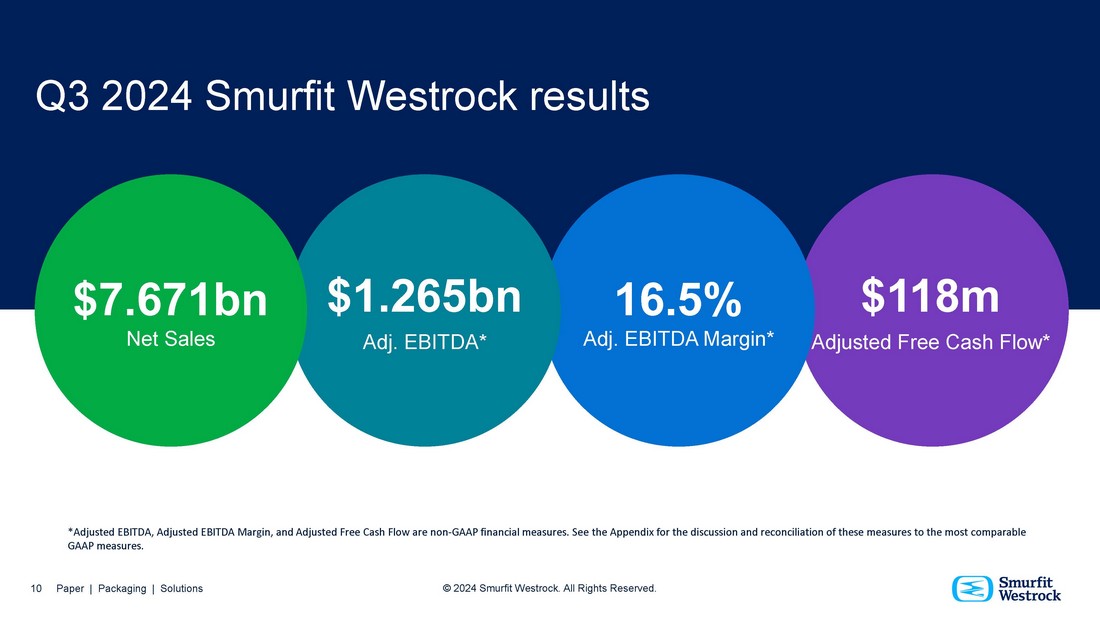

| · | Net Sales of approx. $7.7 billion |

| · | Net Loss of $150 million, with a Net Income Margin of negative 2.0% |

| · | Adjusted EBITDA1 of $1,265 million, with an Adjusted EBITDA Margin1 of 16.5% |

| · | Continuing focus on asset optimization |

| · | Previously announced quarterly dividend of $0.3025 per ordinary share |

Smurfit Westrock plc’s performance for the three months ended September 30, 2024 and September 30, 2023 (in millions, except margin percentages):

| September 30, 20242 | September 30, 20233 | |||||||

| Net Sales | $ | 7,671 | $ | 2,915 | ||||

| Net (Loss) Income | $ | (150 | ) | $ | 229 | |||

| Net Income Margin | (2.0 | %) | 7.8 | % | ||||

| Adjusted EBITDA1 | $ | 1,265 | $ | 525 | ||||

| Adjusted EBITDA Margin1 | 16.5 | % | 18.0 | % | ||||

| Net Cash provided by Operating Activities | $ | 320 | $ | 378 | ||||

| Adjusted Free Cash Flow1 | $ | 118 | $ | 214 | ||||

Tony Smurfit, President and CEO, commented:

“I am pleased to report an excellent performance for the third quarter, the first for Smurfit Westrock. The Net Loss for the quarter of $150 million was primarily due to transaction related expenses and purchase accounting adjustments totalling approximately $500 million. With Adjusted EBITDA1 of $1,265 million and an Adjusted EBITDA Margin1 of 16.5%, these results are a strong foundation to build upon.

“Our established track record of delivering value to our customers through service, quality and innovation is already beginning to yield results. Equally, we believe our focus on plant level autonomy, operational improvement and profitability will deliver in time, benefits at least equal to the stated synergy target of $400 million.

“Our third quarter performance, combined with our deeper knowledge of the Combination and continuing asset optimization, clearly points to the opportunities ahead for Smurfit Westrock. We are at the start of our journey to build the ‘go-to’ sustainable packaging partner of choice, a global leader with an unrivalled scale, geographic reach and product portfolio. Having spent the last number of months visiting our plants, it is also clear that our people are excited and motivated to be a part of this journey.

“We expect 2024 Full Year Combined Adjusted EBITDA4 of approximately $4.7 billion and we are increasingly excited by our immediate and longer-term prospects.”

1 Adjusted EBITDA, Adjusted EBITDA Margin and Adjusted Free Cash Flow are non-GAAP measures. See the “Non-GAAP Financial Measures and Reconciliations” below for the discussion and reconciliation of these measures to the most comparable GAAP measures.

2 All results reported for the three months ended September 30, 2024 do not include the financial results of legacy WestRock Company (“WestRock”) for the first five days of July due to the closing of the combination between Smurfit Kappa Group plc and WestRock Company on July 5, 2024.

3 All results reported for the three months ended September 30, 2023 reflect the historical financial results of legacy Smurfit Kappa Group plc, which is considered the accounting acquirer in the combination between Smurfit Kappa Group plc and WestRock, which closed on July 5, 2024 (the “Combination”).

4 2024 Full Year Combined Adjusted EBITDA is a non-GAAP financial measure. We have not reconciled Adjusted EBITDA outlook to the most comparable GAAP outlook because it is not possible to do so without unreasonable efforts due to the uncertainty and potential variability of reconciling items, which are dependent on future events and often outside of management’s control and which could be significant. Because such items cannot be reasonably predicted with the level of precision required, we are unable to provide an outlook for the comparable GAAP measure (net income).

Page

Third Quarter 2024 | Financial Performance

Smurfit Westrock’s net sales increased by $4,756 million, to $7,671 million in the third quarter of 2024 from $2,915 million in the third quarter of 2023. This increase was primarily due to the positive impact from acquisitions of $4,693 million, of which $4,684 million related to the acquisition of WestRock, and a net positive volume impact of $98 million (excluding the impact of acquisitions), primarily driven by an increase in corrugated volumes. The above increases were partially offset by the net negative impact of a lower selling price/mix of $30 million and a net negative currency impact of $5 million.

Net income decreased by $379 million, to a net loss of $150 million, with a net income margin of negative 2.0% in the third quarter of 2024, from net income of $229 million, with a net income margin of 7.8% in the third quarter of 2023. This decrease was primarily due to a $4,148 million increase in cost of goods sold (including an expense of $227 million for the amortization of the fair value step up on inventory recognized on WestRock’s inventory acquired) and a $657 million increase in selling, general and administrative (“SG&A”) expenses, both driven by additional costs related to the acquisition of WestRock. Additionally, transaction and integration-related expenses associated with the Combination increased by $250 million. These increased costs were partially offset by the increase in net sales.

Adjusted EBITDA1 for the Company was $1,265 million, with an Adjusted EBITDA Margin1 of 16.5% in the third quarter of 2024, compared to Adjusted EBITDA1 of $525 million, with an Adjusted EBITDA Margin1 of 18.0% in the third quarter of 2023.

The Company’s interest expense, net increased by $128 million, to $167 million in the third quarter of 2024, from $39 million in the third quarter of 2023 primarily due to increased debt in connection with the Combination partially offset by higher interest income on cash balances.

Other expense, net increased to $13 million from $4 million in the third quarter of last year primarily due to a $12 million expense recorded in the third quarter in connection with the sale of receivables under an accounts receivable monetization program acquired as a result of the Combination and partially offset by other movements.

Income tax expense decreased by $40 million to $33 million in the third quarter of 2024, from $73 million in the third quarter of 2023, primarily due to the loss in 2024 compared to a profit in 2023, the change in the geographical mix of earnings and the significant impact of transaction and integration-related expenses associated with the Combination which are only partly deductible for tax.

Net cash provided by operating activities decreased by $58 million, to $320 million in the third quarter of 2024, from $378 million in the third quarter of 2023. The decrease was primarily due to an increase in tax payments of $29 million, an increase in net cash interest paid of $162 million and a negative working capital change of $272 million, partly offset by an increase in consolidated net income adjusted for non-cash items.

Including capital expenditure of $512 million in the third quarter of 2024, and $202 million in the same period last year, free cash flow was an outflow of $192 million in the third quarter of 2024 and an inflow of $176 million in the third quarter of 2023. Excluding transaction, integration and restructuring costs of $310 million (net of tax) in the third quarter of 2024, Adjusted Free Cash flow for the period was an inflow of $118 million. Adjusted Free Cash Flow1 in the third quarter of 2023 was an inflow of $214 million.

Adjusted EBITDA5 for our Europe, MEA and APAC segment remained at $411 million in the third quarter of 2024, consistent with the same period in 2023. This was primarily due to a $37 million positive impact from the acquisition of WestRock offset by a reduction in Adjusted EBITDA (excluding the impact of acquisitions) primarily due to an increase in raw material, payroll and distribution costs, partially offset by an increase in net sales and a decrease in energy costs. The Adjusted EBITDA Margin in the Europe, MEA and APAC segment was 15.5% in the third quarter of 2024, compared to 18.8% in the third quarter of 2023.

5 For the three months ended September 30, 2024, Adjusted EBITDA and Adjusted EBITDA Margin for the segments are our measures of segment profitability because they are used by our chief decision-maker (“CODM”) to make decisions regarding allocation of resources and to assess segment performance in accordance with Accounting Standards Codification 280. These financial measures comply with GAAP when used in that context. For the three months ended September 30, 2023, segment information reflects performance of legacy Smurfit Kappa Group plc.

Page

Adjusted EBITDA5 for our North America segment increased by $714 million, to $780 million in the third quarter of 2024, from $66 million for the third quarter of 2023. This increase was primarily due to a $724 million positive impact from the acquisition of WestRock partially offset by a $10 million decrease in Adjusted EBITDA (excluding the impact of acquisitions) primarily due to an increase in raw material costs. The Adjusted EBITDA Margin in the North America segment was 16.8% in the third quarter of 2024, compared to 16.4% in the third quarter of 2023.

Adjusted EBITDA5 for our LATAM segment increased by $42 million, to $116 million in the third quarter of 2024, from $74 million for the third quarter of 2023. This increase was primarily due to a positive impact of $56 million from the acquisition of WestRock partially offset by a reduction in Adjusted EBITDA (excluding the impact of acquisitions) primarily due to an increase in payroll and other costs. The Adjusted EBITDA Margin in the LATAM segment was 23.1% in the third quarter of 2024, compared to 22.0% in the third quarter of 2023.

Page

Earnings Call

Management will host an earnings conference call today at 7:30 AM ET / 11:30 AM GMT to discuss Smurfit Westrock’s financial results. The conference call will be accessible through a live webcast. Interested investors and other individuals can access the webcast, earnings release, and earnings presentation via the Company’s website at www.smurfitwestrock.com. The webcast will be available at https://investors.smurfitwestrock.com/overview and a replay of the webcast will be available on the website shortly after the call.

Forward Looking Statements

This press release includes certain “forward-looking statements” (including within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) regarding, among other things, the plans, strategies, outcomes, outlooks, and prospects, both business and financial, of Smurfit Westrock, the expected benefits of the completed combination of Smurfit Kappa Group plc and WestRock Company (the “Combination”), including, but not limited to, synergies, and any other statements regarding the Company's future expectations, beliefs, plans, objectives, results of operations, financial condition and cash flows, or future events, outlook or performance. Statements that are not historical facts, including statements about the beliefs and expectations of the management of the Company, are forward-looking statements. Words such as “may”, “will”, “could”, “should”, “would”, “anticipate”, “intend”, “estimate”, “project”, “plan”, “believe”, “expect”, “target”, “prospects”, “potential”, “commit”, “forecasts”, “aims”, “considered”, “likely”, “estimate” and variations of these words and similar future or conditional expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. While the Company believes these expectations, assumptions, estimates and projections are reasonable, such forward-looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond the control of the Company. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend upon future circumstances that may or may not occur. Actual results may differ materially from the current expectations of the Company depending upon a number of factors affecting its business, including risks associated with the integration and performance of the Company following the Combination. Important factors that could cause actual results to differ materially from such plans, estimates or expectations include: economic, competitive and market conditions generally, including macroeconomic uncertainty, customer inventory rebalancing, the impact of inflation and increases in energy, raw materials, shipping, labor and capital equipment costs; the impact of public health crises, such as pandemics (including the COVID-19 pandemic) and epidemics and any related company or governmental policies and actions to protect the health and safety of individuals or governmental policies or actions to maintain the functioning of national or global economies and markets; reduced supply of raw materials, energy and transportation, including from supply chain disruptions and labor shortages; developments related to pricing cycles and volumes; intense competition; the ability of the Company to successfully recover from a disaster or other business continuity problem due to a hurricane, flood, earthquake, terrorist attack, war, pandemic, security breach, cyber-attack, power loss, telecommunications failure or other natural or man-made events, including the ability to function remotely during long-term disruptions such as the COVID-19 pandemic; the Company's ability to respond to changing customer preferences and to protect intellectual property; the amount and timing of the Company's capital expenditures; risks related to international sales and operations; failures in the Company's quality control measures and systems resulting in faulty or contaminated products; cybersecurity risks, including threats to the confidentiality, integrity and availability of data in the Company's systems; works stoppages and other labor disputes; the Company’s ability to establish and maintain effective internal controls over financial reporting in accordance with SOX, and remediate any weaknesses in controls and processes; the Company's ability to retain or hire key personnel; risks related to sustainability matters, including climate change and scarce resources, as well as the Company's ability to comply with changing environmental laws and regulations; the Company's ability to successfully implement strategic transformation initiatives; results and impacts of acquisitions by the Company; the Company's significant levels of indebtedness; the impact of the Combination on the Company's credit ratings; the potential impairment of assets and goodwill; the availability of sufficient cash to distribute dividends to the Company's shareholders in line with current expectations; the scope, costs, timing and impact of any restructuring of operations and corporate and tax structure; evolving legal, regulatory and tax regimes; changes in economic, financial, political and regulatory conditions in Ireland, the United Kingdom, the United States and elsewhere, and other factors that contribute to uncertainty and volatility, natural and man-made disasters, civil unrest, pandemics (such as the COVID-19 pandemic), geopolitical uncertainty, and conditions that may result from legislative, regulatory, trade and policy changes associated with the current or subsequent Irish, US or UK administrations; legal proceedings instituted against the Company; actions by third parties, including government agencies; the Company's ability to promptly and effectively integrate Smurfit Kappa's and WestRock's businesses; the Company's ability to achieve the synergies and value creation contemplated by the Combination; the Company's ability to meet expectations regarding the accounting and tax treatments of the Combination, including the risk that the Internal Revenue Service may assert that the Company should be treated as a US corporation or be subject to certain unfavorable US federal income tax rules under Section 7874 of the Internal Revenue Code of 1986, as amended, as a result of the Combination; other factors such as future market conditions, currency fluctuations, the behavior of other market participants, the actions of regulators and other factors such as changes in the political, social and regulatory framework in which the Company's group operates or in economic or technological trends or conditions, and other risk factors included in the Company's filings with the Securities and Exchange Commission. Neither the Company nor any of its associates or directors, officers or advisers provides any representation, assurance or guarantee that the occurrence of the events expressed or implied in any such forward-looking statements will actually occur. You are cautioned not to place undue reliance on these forward-looking statements. Other than in accordance with its legal or regulatory obligations (including under the UK Listing Rules, the Disclosure Guidance and Transparency Rules, the UK Market Abuse Regulation and other applicable regulations), the Company is under no obligation, and the Company expressly disclaims any intention or obligation, to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise.

Page

About Smurfit Westrock

Smurfit Westrock is a leading provider of paper-based packaging solutions in the world, with approximately 100,000 employees across 40 countries.

| Contacts | |

|

Ciarán Potts Smurfit Westrock T: +353 1 202 71 27 E: ir@smurfitwestrock.com |

FTI Consulting

T: +353 1 765 0800 E: smurfitwestrock@fticonsulting.com |

Page

Condensed Consolidated Statements of Operations

| in $ millions, except share and per share data | ||||||||||||||||

| Three months ended | Nine months ended | |||||||||||||||

|

September 30, 2024 |

September 30, 2023 |

September 30, 2024 |

September 30, 2023 |

|||||||||||||

| Net sales | $ | 7,671 | $ | 2,915 | $ | 13,570 | $ | 9,231 | ||||||||

| Cost of goods sold | (6,321 | ) | (2,173 | ) | (10,817 | ) | (6,878 | ) | ||||||||

| Gross profit | 1,350 | 742 | 2,753 | 2,353 | ||||||||||||

| Selling, general and administrative expenses | (1,028 | ) | (371 | ) | (1,797 | ) | (1,144 | ) | ||||||||

| Transaction and integration-related expenses associated with the Combination | (267 | ) | (17 | ) | (350 | ) | (17 | ) | ||||||||

| Operating profit | 55 | 354 | 606 | 1,192 | ||||||||||||

| Pension and other postretirement non-service benefit (expense), net | 8 | (9 | ) | (31 | ) | (29 | ) | |||||||||

| Interest expense, net | (167 | ) | (39 | ) | (225 | ) | (109 | ) | ||||||||

| Other expense, net | (13 | ) | (4 | ) | (13 | ) | (19 | ) | ||||||||

| (Loss) income before income taxes | (117 | ) | 302 | 337 | 1,035 | |||||||||||

| Income tax expense | (33 | ) | (73 | ) | (164 | ) | (258 | ) | ||||||||

| Net (loss) income | (150 | ) | 229 | 173 | 777 | |||||||||||

| Less: Net (loss) income attributable to noncontrolling interests | - | - | - | - | ||||||||||||

| Net (loss) income attributable to common stockholders | $ | (150 | ) | $ | 229 | $ | 173 | $ | 777 | |||||||

| Basic (loss) earnings per share attributable to common stockholders | $ | (0.30 | ) | $ | 0.89 | $ | 0.51 | $ | 3.01 | |||||||

| Diluted (loss) earnings per share attributable to common stockholders | $ | (0.30 | ) | $ | 0.88 | $ | 0.50 | $ | 3.00 | |||||||

Page

Segment Information

Following the completion of the Combination we reassessed our operating segments due to changes in our organizational structure and how our chief operating decision maker (“CODM”) makes key operating decisions, allocates resources and assesses the performance of our business. The CODM is determined to be the executive management team, comprising the President and Chief Executive Officer Anthony Smurfit and the Executive Vice President and Group Chief Financial Officer Ken Bowles. The CODM is responsible for assessing performance, allocating resources and making strategic decisions.

During the three months ended September 30, 2024, we identified three operating segments, which are also our reportable segments:

| i. | Europe, the Middle East and Africa (MEA), and Asia-Pacific (APAC). |

| ii. | North America, which includes operations in the U.S., Canada and Mexico. |

| iii. | Latin America (“LATAM”), which includes operations in Central America and Caribbean, Argentina, Brazil, Chile, Colombia, Ecuador and Peru. |

These changes reflect how we manage our business following the completion of the Combination. No operating segments have been aggregated for disclosure purposes. Prior period comparatives have been restated to reflect the change in segments.

In the identification of the operating and reportable segments, we considered the level of integration of our different businesses as well as our objective to develop long-term customer relationships by providing customers with differentiated packaging solutions that enhance the customer’s prospects of success in their end markets.

The Europe, MEA and APAC, North America, and LATAM segments are each highly integrated within the segment and there are many interdependencies within these operations. They each include a system of mills and plants that primarily produce a full line of containerboard that is converted into corrugated containers within each segment, or is sold to third parties.

In addition, the Europe, MEA and APAC segment also produces types of paper, such as solid board, sack kraft paper, machine glazed and graphic paper; and other paper-based packaging, such as honeycomb, solid board packaging, folding cartons, inserts and labels; and bag-in-box packaging (located in Europe, Argentina, Canada, Mexico and the U.S.).

The North America segment also produces paperboard and specialty grades; other paper-based packaging, such as folding cartons, inserts, labels; and displays and also engages in the assembly of displays as well as the distribution of packaging products.

The LATAM segment also comprises forestry; types of paper, such as boxboard and sack paper; and paper-based packaging, such as folding cartons, honeycomb and paper sacks.

Inter-segment transfers or transactions are entered into under normal commercial terms and conditions that would also be available to unrelated third parties.

Segment profit is measured based on Adjusted EBITDA, defined as (loss) income before income taxes, unallocated corporate costs, depreciation, depletion and amortization, amortization of fair value step up on inventory, transaction and integration-related expenses associated with the Combination, interest expense, net, pension and other postretirement non-service benefit (expense), net, share-based compensation expense, other expense, net. restructuring costs, legislative or regulatory fines and reimbursements, losses at closed facilities and impairment of goodwill and other assets.

Page

Segment Information (continued)

Financial information by segment is summarized below and in the schedules with this release.

| in $ millions, except Adjusted EBITDA Margin and share and per share data | ||||||||||||||||

| Three months ended | Nine months ended | |||||||||||||||

|

September 30, 2024 |

September 30, 2023 |

September 30, 2024 |

September 30, 2023 |

|||||||||||||

| Net sales (aggregate) | ||||||||||||||||

| Europe, MEA and APAC | $ | 2,651 | $ | 2,191 | $ | 7,056 | $ | 7,047 | ||||||||

| North America | 4,649 | 401 | 5,499 | 1,239 | ||||||||||||

| LATAM | 506 | 341 | 1,187 | 1,000 | ||||||||||||

| Total | $ | 7,806 | $ | 2,933 | $ | 13,742 | $ | 9,286 | ||||||||

| Less net sales (intersegment) | ||||||||||||||||

| Europe, MEA and APAC | $ | 5 | $ | 3 | $ | 13 | $ | 9 | ||||||||

| North America | 118 | - | 119 | - | ||||||||||||

| LATAM | 12 | 15 | 40 | 46 | ||||||||||||

| Total | $ | 135 | $ | 18 | $ | 172 | $ | 55 | ||||||||

| Net sales (unaffiliated customers) | ||||||||||||||||

| Europe, MEA and APAC | $ | 2,646 | $ | 2,188 | $ | 7,043 | $ | 7,038 | ||||||||

| North America | 4,531 | 401 | 5,380 | 1,239 | ||||||||||||

| LATAM | 494 | 326 | 1,147 | 954 | ||||||||||||

| Total | $ | 7,671 | $ | 2,915 | $ | 13,570 | $ | 9,231 | ||||||||

| Adjusted EBITDA | ||||||||||||||||

| Europe, MEA and APAC | $ | 411 | $ | 411 | $ | 1,158 | $ | 1,330 | ||||||||

| North America | 780 | 66 | 900 | 209 | ||||||||||||

| LATAM | 116 | 74 | 257 | 217 | ||||||||||||

| Total | $ | 1,307 | $ | 551 | $ | 2,315 | $ | 1,756 | ||||||||

|

Adjusted EBITDA Margin Adjusted EBITDA/Net sales (aggregate) |

||||||||||||||||

| Europe, MEA and APAC | 15.5 | % | 18.8 | % | 16.4 | % | 18.9 | % | ||||||||

| North America | 16.8 | % | 16.4 | % | 16.4 | % | 16.9 | % | ||||||||

| LATAM | 23.1 | % | 22.0 | % | 21.6 | % | 21.7 | % | ||||||||

Page

Condensed Consolidated Balance Sheets

| in $ millions, except share and per share data | ||||||||

| As of | ||||||||

|

September 30, 2024 |

December 31, 2023 |

|||||||

| Assets | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents, including restricted cash (amounts related to consolidated variable interest entities of $3 million and $3 million at September 30, 2024 and December 31, 2023, respectively) | $ | 951 | $ | 1,000 | ||||

| Accounts receivable (amounts related to consolidated variable interest entities of $823 million and $816 million at September 30, 2024 and December 31, 2023, respectively) | 4,613 | 1,806 | ||||||

| Inventories | 3,585 | 1,203 | ||||||

| Other current assets | 1,396 | 561 | ||||||

| Total current assets | 10,545 | 4,570 | ||||||

| Property plant and equipment, net | 23,206 | 5,791 | ||||||

| Goodwill | 7,215 | 2,842 | ||||||

| Intangibles, net | 1,094 | 218 | ||||||

| Prepaid pension asset | 615 | 29 | ||||||

| Other non-current assets (amounts related to consolidated variable interest entities of $390 million and $- million at September 30, 2024 and December 31, 2023, respectively) | 2,354 | 601 | ||||||

| Total assets | $ | 45,029 | $ | 14,051 | ||||

| Liabilities and Equity | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | 3,357 | $ | 1,728 | ||||

| Accrued expenses | 813 | 278 | ||||||

| Accrued compensation and benefits | 954 | 438 | ||||||

| Current portion of debt | 745 | 78 | ||||||

| Other current liabilities | 1,257 | 484 | ||||||

| Total current liabilities | 7,126 | 3,006 | ||||||

| Non-current debt due after one year (amounts related to consolidated variable interest entities of $337 million and $20 million at September 30, 2024 and December 31, 2023, respectively) | 13,174 | 3,669 | ||||||

| Deferred tax liabilities | 3,682 | 280 | ||||||

| Pension liabilities and other postretirement benefits, net of current portion | 788 | 537 | ||||||

| Other non-current liabilities (amounts related to consolidated variable interest entities of $334 million and $- at September 30, 2024 and December 31, 2023, respectively) | 2,267 | 385 | ||||||

| Total liabilities | 27,037 | 7,877 | ||||||

| Equity: | ||||||||

| Preferred stock; $0.001 par value; 500,000,000 and Nil shares authorized; 10,000 shares and Nil outstanding at September 30, 2024 and December 31, 2023, respectively | - | - | ||||||

| Common stock; $0.001 par value; 9,500,000,000 and 9,910,931,085 shares authorized; 520,056,084 and 260,354,342 shares outstanding at September 30, 2024 and December 31, 2023, respectively | 1 | - | ||||||

| Deferred shares, €1 par value; 25,000 shares and 25,000 shares authorized; 25,000 and 100 shares outstanding at September 30, 2024 and December 31, 2023, respectively | - | - | ||||||

| Treasury stock, at cost (2,037,589, and 1,907,129 common stock at September 30, 2024, and December 31, 2023, respectively) | (93 | ) | (91 | ) | ||||

| Capital in excess of par value | 15,890 | 3,575 | ||||||

| Accumulated other comprehensive loss | (1,011 | ) | (847 | ) | ||||

| Retained earnings | 3,178 | 3,521 | ||||||

| Total stockholders’ equity | 17,965 | 6,158 | ||||||

| Noncontrolling interests | 27 | 16 | ||||||

| Total equity | 17,992 | 6,174 | ||||||

| Total liabilities and equity | $ | 45,029 | $ | 14,051 | ||||

Page

Condensed Consolidated Statements of Cash Flows

| in $ millions, except share and per share data | ||||||||||||||||

| Three months ended | Nine months ended | |||||||||||||||

|

September 30, 2024 |

September 30, 2023 |

September 30, 2024 |

September 30, 2023 |

|||||||||||||

| Operating activities: | ||||||||||||||||

| Consolidated net (loss) income | $ | (150 | ) | $ | 229 | $ | 173 | $ | 777 | |||||||

| Adjustments to reconcile consolidated net income to net cash provided by operating activities: | ||||||||||||||||

| Depreciation, depletion and amortization | 564 | 147 | 872 | 430 | ||||||||||||

| Cash surrender value increase in excess of premiums paid | (14 | ) | - | (14 | ) | - | ||||||||||

| Share-based compensation expense | 123 | 7 | 154 | 43 | ||||||||||||

| Deferred income tax benefit | (89 | ) | 8 | (99 | ) | (4 | ) | |||||||||

| Pension and other postretirement funding more than cost | (26 | ) | (10 | ) | (30 | ) | (35 | ) | ||||||||

| Other | 17 | (8 | ) | 16 | (4 | ) | ||||||||||

| Change in operating assets and liabilities, net of acquisitions and divestitures: | ||||||||||||||||

| Accounts receivable | (186 | ) | 93 | (422 | ) | 63 | ||||||||||

| Inventories | 140 | 29 | 120 | 161 | ||||||||||||

| Other assets | 74 | 34 | (31 | ) | 21 | |||||||||||

| Accounts payable | (214 | ) | (110 | ) | (226 | ) | (438 | ) | ||||||||

| Income taxes | (29 | ) | (55 | ) | 34 | (46 | ) | |||||||||

| Accrued liabilities and other | 110 | 14 | 155 | (20 | ) | |||||||||||

| Net cash provided by operating activities | 320 | 378 | 702 | 948 | ||||||||||||

| Investing activities: | ||||||||||||||||

| Capital expenditures | (512 | ) | (202 | ) | (897 | ) | (661 | ) | ||||||||

| Cash paid for purchase of businesses, net of cash acquired | (688 | ) | (29 | ) | (716 | ) | (29 | ) | ||||||||

| Proceeds from corporate owned life insurance | 2 | - | 2 | - | ||||||||||||

| Proceeds from sale of property, plant and equipment | 12 | 10 | 15 | 11 | ||||||||||||

| Other | 1 | 4 | 1 | 2 | ||||||||||||

| Net cash used for investing activities | (1,185 | ) | (217 | ) | (1,595 | ) | (677 | ) | ||||||||

| Financing activities: | ||||||||||||||||

| Additions to debt | 315 | 8 | 3,127 | 77 | ||||||||||||

| Repayments of debt | (1,607 | ) | (76 | ) | (1,640 | ) | (120 | ) | ||||||||

| Revolving credit facilities repayments, net | - | - | (4 | ) | (4 | ) | ||||||||||

| Changes in commercial paper, net | (33 | ) | - | (33 | ) | - | ||||||||||

| Other debt additions, net | 17 | - | 17 | - | ||||||||||||

| Repayments of lease liabilities | (11 | ) | - | (12 | ) | (2 | ) | |||||||||

| Debt issuance costs | (15 | ) | - | (44 | ) | - | ||||||||||

| Tax paid in connection with shares withheld from employees | (21 | ) | - | (21 | ) | - | ||||||||||

| Purchases of treasury stock | - | - | (27 | ) | (30 | ) | ||||||||||

| Cash dividends paid to stockholders | (158 | ) | - | (493 | ) | (299 | ) | |||||||||

| Other | - | - | (1 | ) | - | |||||||||||

| Net cash provided by (used for) financing activities | $ | (1,513 | ) | $ | (68 | ) | $ | 869 | $ | (378 | ) | |||||

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | 4 | (32 | ) | (25 | ) | (5 | ) | |||||||||

| (Decrease) increase in cash, cash equivalents and restricted cash | $ | (2,374 | ) | $ | 61 | $ | (49 | ) | $ | (112 | ) | |||||

| Cash, cash equivalents and restricted cash at beginning of period | 3,325 | 668 | 1,000 | 841 | ||||||||||||

| Cash, cash equivalents and restricted cash at end of period | $ | 951 | $ | 729 | $ | 951 | $ | 729 | ||||||||

Page

Non-GAAP Financial Measures and Reconciliations

Smurfit Westrock plc (“Smurfit Westrock”) reports its financial results in accordance with accounting principles generally accepted in the United States ("GAAP"). However, management believes certain non-GAAP financial measures provide Smurfit Westrock’s board of directors, investors, potential investors, securities analysts and others with additional meaningful financial information that should be considered when assessing our ongoing performance. Management also uses these non-GAAP financial measures in making financial, operating and planning decisions, and in evaluating company performance. Non-GAAP financial measures should be viewed in addition to, and not as an alternative for, the GAAP results. The non-GAAP financial measures we present may differ from similarly captioned measures presented by other companies. Smurfit Westrock uses the non-GAAP financial measures “Adjusted EBITDA,” “Adjusted EBITDA Margin,” and “Adjusted Free Cash Flow.” We discuss below details of the non-GAAP financial measures presented by us and provide reconciliations of these non-GAAP financial measures to the most directly comparable financial measures calculated in accordance with GAAP.

Definitions

Smurfit Westrock uses the non-GAAP financial measures “Adjusted EBITDA” and “Adjusted EBITDA Margin” to evaluate its overall performance. The composition of Adjusted EBITDA is not addressed or prescribed by GAAP. Smurfit Westrock defines Adjusted EBITDA as (loss) income before income taxes, depreciation, depletion and amortization, amortization of fair value step up on inventory, transaction and integration-related expenses associated with the Combination, interest expense, net, pension and other postretirement non-service (benefit) expense, net, share-based compensation expense, other expense, net, restructuring costs, legislative or regulatory fines and reimbursements, losses at closed facilities and impairment of goodwill and other assets. Smurfit Westrock views Adjusted EBITDA as an appropriate and useful measure used to compare financial performance between periods. Adjusted EBITDA Margin is calculated as Adjusted EBITDA divided by Net Sales.

Management believes Adjusted EBITDA and Adjusted EBITDA Margin measures provide Smurfit Westrock’s management, board of directors, investors, potential investors, securities analysts and others with useful information to evaluate Smurfit Westrock’s performance because, in addition to income tax expense, depreciation, depletion and amortization expense, interest expense, net, pension and other postretirement non-service (benefit) expense, net, and share-based compensation expense, Adjusted EBITDA also excludes restructuring costs, impairment of goodwill and other assets and other specific items that management believes are not indicative of the operating results of the business. Smurfit Westrock and its board of directors use this information in making financial, operating and planning decisions and when evaluating Smurfit Westrock’s performance relative to other periods.

Smurfit Westrock uses the non-GAAP financial measure “Adjusted Free Cash Flow”. Smurfit Westrock defines Adjusted Free Cash Flow as net cash provided by operating activities as adjusted for capital expenditures and to exclude certain costs not reflective of underlying operations. Management utilizes this measure in connection with managing Smurfit Westrock’s business and believes that Adjusted Free Cash Flow is useful to investors as a liquidity measure because it measures the amount of cash generated that is available, after reinvesting in the business, to maintain a strong balance sheet, pay dividends, repurchase stock, service debt and make investments for future growth. It should not be inferred that the entire free cash flow amount is available for discretionary expenditures. By adjusting for certain items that are not indicative of Smurfit Westrock’s underlying operational performance, Smurfit Westrock believes that Adjusted Free Cash Flow also enables investors to perform meaningful comparisons between past and present periods.

Page

Reconciliations to Most Comparable GAAP Measure

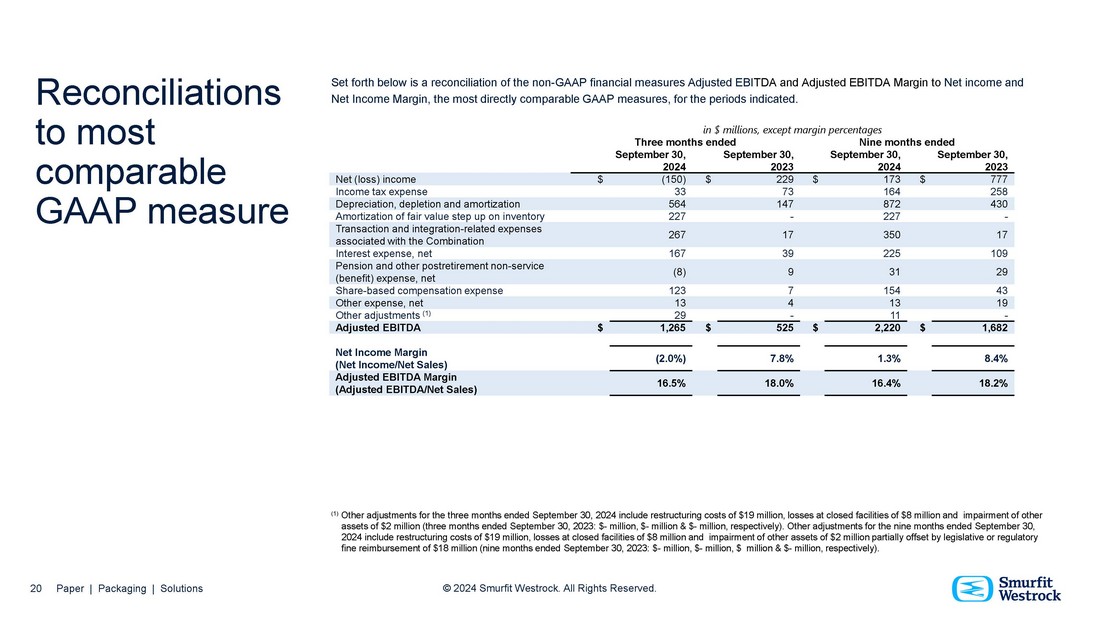

Set forth below is a reconciliation of the non-GAAP financial measures Adjusted EBITDA and Adjusted EBITDA Margin to Net income and Net Income Margin, the most directly comparable GAAP measures, for the periods indicated.

| in $ millions, except margin percentages | ||||||||||||||||

| Three months ended | Nine months ended | |||||||||||||||

|

September 30, 2024 |

September 30, 2023 |

September 30, 2024 |

September 30, 2023 |

|||||||||||||

| Net (loss) income | $ | (150 | ) | $ | 229 | $ | 173 | $ | 777 | |||||||

| Income tax expense | 33 | 73 | 164 | 258 | ||||||||||||

| Depreciation, depletion and amortization | 564 | 147 | 872 | 430 | ||||||||||||

| Amortization of fair value step up on inventory | 227 | - | 227 | - | ||||||||||||

| Transaction and integration-related expenses associated with the Combination | 267 | 17 | 350 | 17 | ||||||||||||

| Interest expense, net | 167 | 39 | 225 | 109 | ||||||||||||

| Pension and other postretirement non-service (benefit) expense, net | (8 | ) | 9 | 31 | 29 | |||||||||||

| Share-based compensation expense | 123 | 7 | 154 | 43 | ||||||||||||

| Other expense, net | 13 | 4 | 13 | 19 | ||||||||||||

| Other adjustments (1) | 29 | - | 11 | - | ||||||||||||

| Adjusted EBITDA | $ | 1,265 | $ | 525 | $ | 2,220 | $ | 1,682 | ||||||||

|

Net Income Margin (Net Income/Net Sales) |

(2.0 | %) | 7.8 | % | 1.3 | % | 8.4 | % | ||||||||

|

Adjusted EBITDA Margin (Adjusted EBITDA/Net Sales) |

16.5 | % | 18.0 | % | 16.4 | % | 18.2 | % | ||||||||

(1) Other adjustments for the three months ended September 30, 2024 include restructuring costs of $19 million, losses at closed facilities of $8 million and impairment of other assets of $2 million (three months ended September 30, 2023: $- million, $- million & $- million, respectively).

Other adjustments for the nine months ended September 30, 2024 include restructuring costs of $19 million, losses at closed facilities of $8 million and impairment of other assets of $2 million partially offset by legislative or regulatory fine reimbursement of $18 million (nine months ended September 30, 2023: $- million, $- million, $- million & $- million, respectively).

Page

Reconciliations to Most Comparable GAAP Measure (continued)

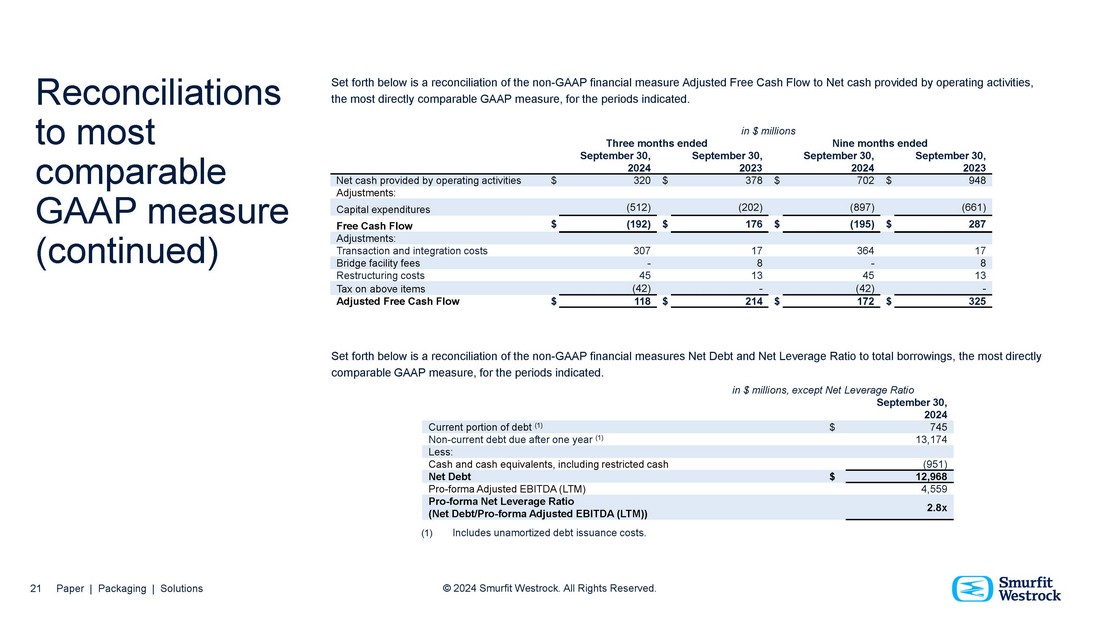

Set forth below is a reconciliation of the non-GAAP financial measure Adjusted Free Cash Flow to Net cash provided by operating activities, the most directly comparable GAAP measure, for the periods indicated.

| in $ millions | ||||||||||||||||

| Three months ended | Nine months ended | |||||||||||||||

|

September 30, 2024 |

September 30, 2023 |

September 30, 2024 |

September 30, 2023 |

|||||||||||||

| Net cash provided by operating activities | $ | 320 | $ | 378 | $ | 702 | $ | 948 | ||||||||

| Adjustments: | ||||||||||||||||

| Capital expenditures | (512 | ) | (202 | ) | (897 | ) | (661 | ) | ||||||||

| Free Cash Flow | $ | (192 | ) | $ | 176 | $ | (195 | ) | $ | 287 | ||||||

| Adjustments: | ||||||||||||||||

| Transaction and integration costs | 307 | 17 | 364 | 17 | ||||||||||||

| Bridge facility fees | - | 8 | - | 8 | ||||||||||||

| Restructuring costs | 45 | 13 | 45 | 13 | ||||||||||||

| Tax on above items | (42 | ) | - | (42 | ) | - | ||||||||||

| Adjusted Free Cash Flow | $ | 118 | $ | 214 | $ | 172 | $ | 325 | ||||||||

Page

Exhibit 99.2

Paper | Packaging | Solutions 2024 Third Quarter Results Forward Looking Statements The presentation includes certain “forward - looking statements” (including within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) regarding, among other things, the plans, strategies, outcomes, outlooks, and prospects, both business and financial, of Smurfit Westrock, the expected benefits of the completed Combination (including, but not limited to, synergies), and any other statements regarding the Company's future expectations, beliefs, plans, objectives, results of operations, financial condition and cash flows, or future events or performance. Statements that are not historical facts, including statements about the beliefs and expectations of the management of the Company, are forward - looking statements. Words such as “may”, “will”, “could”, “should”, “would”, “anticipate”, “intend”, “estimate”, “project”, “plan”, “believe”, “expect”, “target”, “prospects”, “potential”, “commit”, “forecasts”, “aims”, “considered”, “likely”, “estimate” and variations of these words and similar future or conditional expressions are intended to identify forward - looking statements but are not the exclusive means of identifying such statements. While the Company believes these expectations, assumptions, estimates and projections are reasonable, such forward - looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond the control of the Company. By their nature, forward - looking statements involve risk and uncertainty because they relate to events and depend upon future circumstances that may or may not occur. Actual results may differ materially from the current expectations of the Company depending upon a number of factors affecting its business, including risks associated with the integration and performance of the Company following the Combination. Important factors that could cause actual results to differ materially from such plans, estimates or expectations include: economic, competitive and market conditions generally, including macroeconomic uncertainty, customer inventory rebalancing, the impact of inflation and increases in energy, raw materials, shipping, labor and capital equipment costs; the impact of public health crises, such as pandemics (including the COVID - 19 pandemic) and epidemics and any related company or governmental policies and actions to protect the health and safety of individuals or governmental policies or actions to maintain the functioning of national or global economies and markets; reduced supply of raw materials, energy and transportation, including from supply chain disruptions and labor shortages; developments related to pricing cycles and volumes; intense competition; the ability of the Company to successfully recover from a disaster or other business continuity problem due to a hurricane, flood, earthquake, terrorist attack, war, pandemic, security breach, cyber - attack, power loss, telecommunications failure or other natural or man - made events, including the ability to function remotely during long - term disruptions such as the COVID - 19 pandemic; the Company's ability to respond to changing customer preferences and to protect intellectual property; the amount and timing of the Company's capital expenditures; risks related to international sales and operations; failures in the Company's quality control measures and systems resulting in faulty or contaminated products; cybersecurity risks, including threats to the confidentiality, integrity and availability of data in the Company's systems; works stoppages and other labor disputes; the Company's ability to retain or hire key personnel; risks related to sustainability matters, including climate change and scarce resources, as well as the Company's ability to comply with changing environmental laws and regulations; the Company's ability to successfully implement strategic transformation initiatives; results and impacts of acquisitions by the Company; the Company's significant levels of indebtedness; the impact of the Combination on the Company's credit ratings; the potential impairment of assets and goodwill; the availability of sufficient cash to distribute dividends to the Company's shareholders in line with current expectations; the scope, costs, timing and impact of any restructuring of operations and corporate and tax structure; evolving legal, regulatory and tax regimes; changes in economic, financial, political and regulatory conditions in Ireland, the United Kingdom, the United States and elsewhere, and other factors that contribute to uncertainty and volatility, natural and man - made disasters, civil unrest, pandemics (such as the COVID - 19 pandemic), geopolitical uncertainty, and conditions that may result from legislative, regulatory, trade and policy changes associated with the current or subsequent Irish, US or UK administrations; legal proceedings instituted against the Company; actions by third parties, including government agencies; the Company's ability to promptly and effectively integrate Smurfit Kappa's and WestRock's businesses; the Company's ability to achieve the synergies and value creation contemplated by the Combination; the Company's ability to meet expectations regarding the accounting and tax treatments of the Combination, including the risk that the Internal Revenue Service may assert that the Company should be treated as a US corporation or be subject to certain unfavorable US federal income tax rules under Section 7874 of the Internal Revenue Code of 1986, as amended, as a result of the Combination; other factors such as future market conditions, currency fluctuations, the behavior of other market participants, the actions of regulators and other factors such as changes in the political, social and regulatory framework in which the Company's group operates or in economic or technological trends or conditions, and other risk factors included in the Company's filings with the Securities and Exchange Commission. Neither the Company nor any of its associates or directors, officers or advisers provides any representation, assurance or guarantee that the occurrence of the events expressed or implied in any such forward - looking statements will actually occur. You are cautioned not to place undue reliance on these forward - looking statements. Other than in accordance with its legal or regulatory obligations (including under the UK Listing Rules, the Disclosure Guidance and Transparency Rules, the UK Market Abuse Regulation and other applicable regulations), the Company is under no obligation, and the Company expressly disclaims any intention or obligation, to update or revise publicly any forward - looking statements, whether as a result of new information, future events or otherwise. 2 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

Non - GAAP Financial Measures and Reconciliations Smurfit Westrock plc (“Smurfit Westrock”) reports its financial results in accordance with accounting principles generally accepted in the United States ("GAAP"). However, management believes certain non - GAAP financial measures provide Smurfit Westrock’s board of directors, investors, potential investors, securities analysts and others with additional meaningful financial information that should be considered when assessing our ongoing performance. Management also uses these non - GAAP financial measures in making financial, operating and planning decisions, and in evaluating company performance. Non - GAAP financial measures should be viewed in addition to, and not as an alternative for, the GAAP results. The non - GAAP financial measures we present may differ from similarly captioned measures presented by other companies. Smurfit Westrock uses the non - GAAP financial measures “Adjusted EBITDA,” “Adjusted EBITDA Margin,” and “Adjusted Free Cash Flow”, “Net Debt” and “Net Leverage Ratio.” We discuss below details of the non - GAAP financial measures presented by us and provide reconciliations of these non - GAAP financial measures to the most directly comparable financial measures calculated in accordance with GAAP. Definitions Smurfit Westrock uses the non - GAAP financial measures “Adjusted EBITDA” and “Adjusted EBITDA Margin” to evaluate its overall performance. The composition of Adjusted EBITDA is not addressed or prescribed by GAAP. Smurfit Westrock defines Adjusted EBITDA as (loss) income before income taxes, depreciation, depletion and amortization, amortization of fair value step up on inventory, transaction and integration - related expenses associated with the Combination, interest expense, net, pension and other postretirement non - service (benefit) expense, net, share - based compensation expense, other expense, net, restructuring costs, legislative or regulatory fines and reimbursements, losses at closed facilities and impairment of goodwill and other assets. Smurfit Westrock views Adjusted EBITDA as an appropriate and useful measure used to compare financial performance between periods. Adjusted EBITDA Margin is calculated as Adjusted EBITDA divided by Net Sales. Management believes Adjusted EBITDA and Adjusted EBITDA Margin measures provide Smurfit Westrock’s management, board of directors, investors, potential investors, securities analysts and others with useful information to evaluate Smurfit Westrock’s performance because, in addition to income tax expense, depreciation, depletion and amortization expense, interest expense, net, pension and other postretirement non service (benefit) expense, net, and share - based compensation expense, Adjusted EBITDA also excludes restructuring costs, impairment of goodwill and other assets and other specific items that management believes are not indicative of the operating results of the business. Smurfit Westrock and its board of directors use this information in making financial, operating and planning decisions and when evaluating Smurfit Westrock’s performance relative to other periods. Smurfit Westrock uses the non - GAAP financial measure “Adjusted Free Cash Flow”. Smurfit Westrock defines Adjusted Free Cash Flow as net cash provided by operating activities as adjusted for capital expenditures and to exclude certain costs not reflective of underlying operations. Management utilizes this measure in connection with managing Smurfit Westrock’s business and believes that Adjusted Free Cash Flow is useful to investors as a liquidity measure because it measures the amount of cash generated that is available, after reinvesting in the business, to maintain a strong balance sheet, pay dividends, repurchase stock, service debt and make investments for future growth. It should not be inferred that the entire free cash flow amount is available for discretionary expenditures. By adjusting for certain items that are not indicative of Smurfit Westrock’s underlying operational performance, Smurfit Westrock believes that Adjusted Free Cash Flow also enables investors to perform meaningful comparisons between past and present periods. Smurfit Westrock uses the non - GAAP financial measures “Net Debt” and “Net Leverage Ratio” as useful measures to highlight the overall movement resulting from its operating and financial performance and its overall leverage position. Management believes these measures provide Smurfit Westrock’s board of directors, investors, potential investors, securities analysts and others with useful information to evaluate Smurfit Westrock’s repayment of debt relative to other periods. Smurfit Westrock defines Net Debt as borrowings net of cash and cash equivalents. Smurfit Westrock defines Net Leverage Ratio as Net Debt divided by last twelve months (“LTM”) Adjusted EBITDA. 3 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

Introduction 4 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

What we’ve said Creating the global leader in sustainable packaging • Delivering problem solving, value adding packaging through the most innovative approach in the industry • Leveraging the deepest data sets, across an unrivalled geographic footprint, to further develop our unparalleled product diversity • Improved operating efficiency – providing quality and service for the customer, delivering commercial excellence • Owner operator management team with a proven track record of delivery – our culture is performance - driven, fostering teamwork, accountability, and a dedication to customer satisfaction • Disciplined capital allocation is the foundation of our success, creating value for our shareholders 5 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

Opportunities we’ve identified • Already excellent market positions • Experienced and motivated people at operational level • Opportunity for growth and cost - reducing capital allocation is significant • Opportunity to develop sharper commercial focus across the organization • Opportunity to promote and develop innovative approach for both a new and existing customer base • Opportunity to prioritize value over volume • Opportunity to increase operating efficiency, retaining and winning business through quality and service improvement Paper | Packaging | S olution s 6 6 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

What we’ve done so far First 100 days • Aligned leadership teams around culture and operating model • Senior management have visited 85% of the SWNA paper capacity • Fostering a sharper commercial focus – prioritizing value over volume • Identified opportunities to drive greater operational efficiency • Reducing SG&A costs and eliminating reliance on external consultants – contributing significant savings • Headcount – recent reduction of >800 people 7 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

Strategic asset optimization Ongoing business improvement Over the last 22 months we have: Europe, MEA & APAC North America • Closed one mill • Closed six packaging facilities • Closed 10 corrugated packaging facilities • Closed 13 consumer packaging facilities • Closed two mills • Divested four mills Enhance focus on core facilities leads to better resource allocation Achieve cost savings by reducing redundant facilities Improve operational efficiency through strategic closures Paper | Packaging | S olution s 8 8 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

Financials 9 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

$7.671bn 10 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved. Net Sales $1.265bn Adj. EBITDA* 16.5% Adj. EBITDA Margin* $118m Adjusted Free Cash Flow* Q3 2024 Smurfit Westrock results *Adjusted EBITDA, Adjusted EBITDA Margin, and Adjusted Free Cash Flow are non - GAAP financial measures. See the Appendix for the discussion and reconciliation of these measures to the most comparable GAAP measures.

Q3 2024 Operating segments LATAM Europe, MEA & APAC North America $0.5 billion $2.7 billion $4.6 billion Net sales (aggregate) $116 million $411 million $780 million Adjusted EBITDA* 23.1% 15.5% 16.8% Adjusted EBITDA margin* *Adjusted EBITDA and Adjusted EBITDA margin are our GAAP measures of segment profitability because they are used by our chief operating decision maker to make decisions regarding allocation of resources and to assess segment performance. 11 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

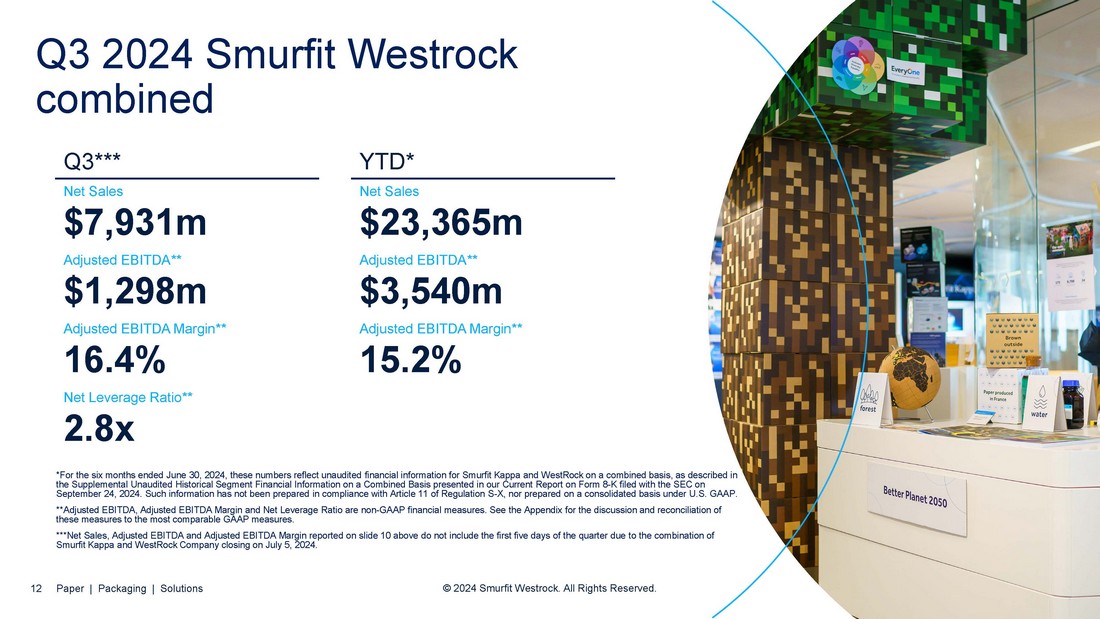

Option A NEED TO ADJUST FOR THE FIRST TRADING WEEK Q3 2024 Smurfit Westrock combined Q3*** Net Sales $7,931m Adjusted EBITDA** $1,298m Adjusted EBITDA Margin** 16.4% Net Leverage Ratio** 2.8x 12 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved. YTD* Net Sales $23,365m Adjusted EBITDA** $3,540m Adjusted EBITDA Margin** 15.2% *For the six months ended June 30, 2024, these numbers reflect unaudited financial information for Smurfit Kappa and WestRock on a combined basis, as described in the Supplemental Unaudited Historical Segment Financial Information on a Combined Basis presented in our Current Report on Form 8 - K filed with the SEC on September 24, 2024. Such information has not been prepared in compliance with Article 11 of Regulation S - X, nor prepared on a consolidated basis under U.S. GAAP. **Adjusted EBITDA, Adjusted EBITDA Margin and Net Leverage Ratio are non - GAAP financial measures. See the Appendix for the discussion and reconciliation of these measures to the most comparable GAAP measures. ***Net Sales, Adjusted EBITDA and Adjusted EBITDA Margin reported on slide 10 above do not include the first five days of the quarter due to the combination of Smurfit Kappa and WestRock Company closing on July 5, 2024.

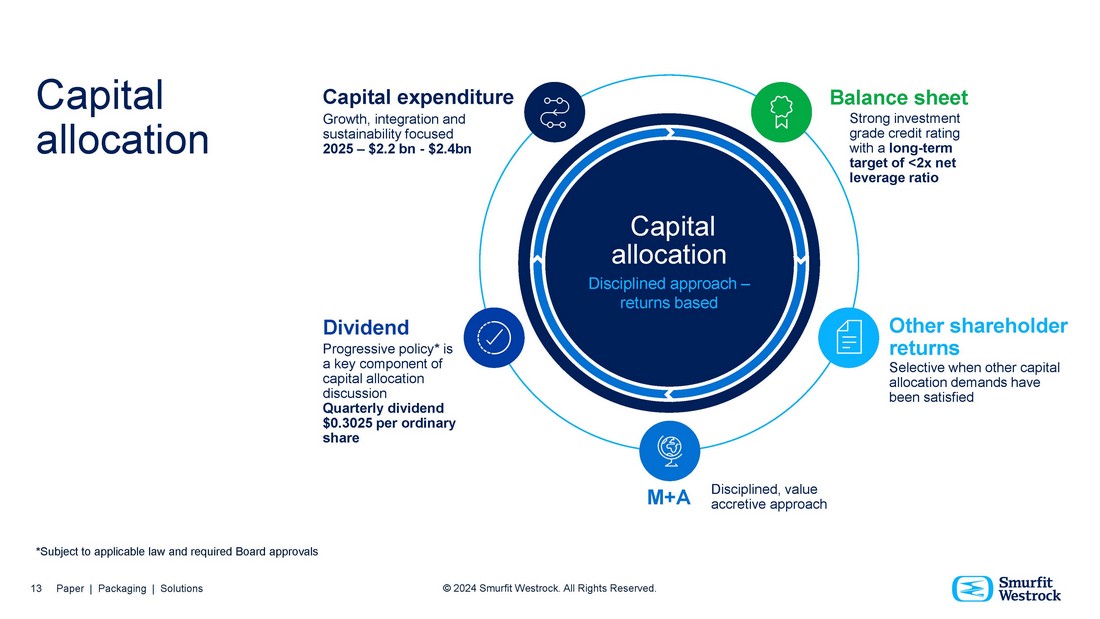

Capital expenditure Growth, integration and sustainability focused 2025 – $2.2 bn - $2.4bn Dividend Progressive policy* is a key component of capital allocation discussion Quarterly dividend $0.3025 per ordinary share Balance sheet Strong investment grade credit rating with a long - term target of <2x net leverage ratio Other shareholder returns Selective when other capital allocation demands have been satisfied Capital allocation Disciplined approach – returns based Disciplined, value accretive approach 13 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved. M+A Capital allocation *Subject to applicable law and required Board approvals Conclusion 14 Paper | Packaging | Solutions © 2024 Smurfit Westrock.

All Rights Reserved.

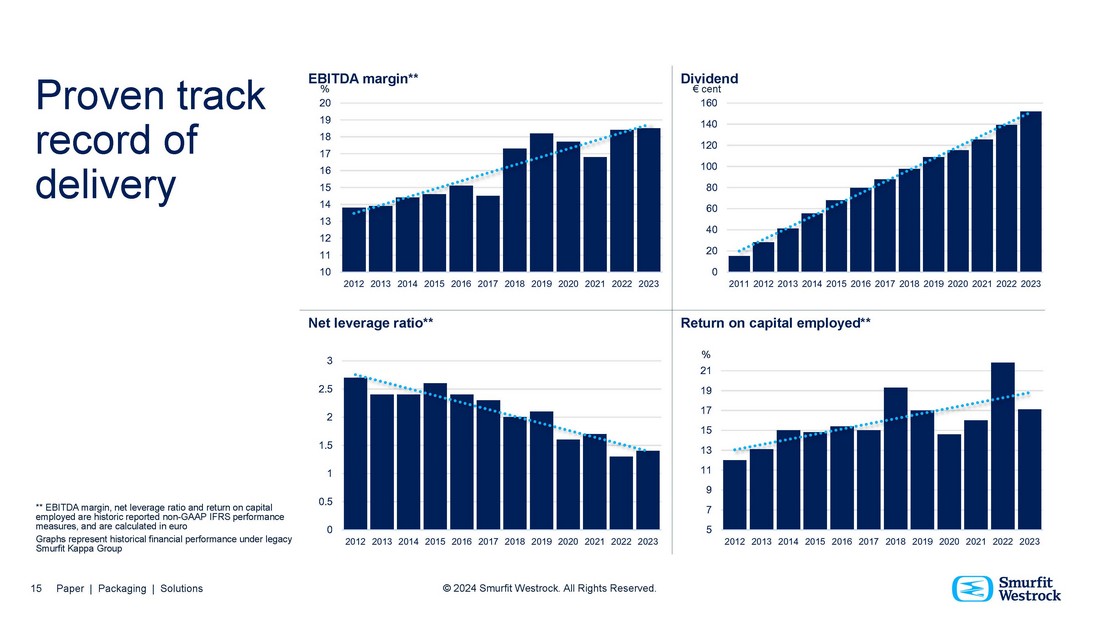

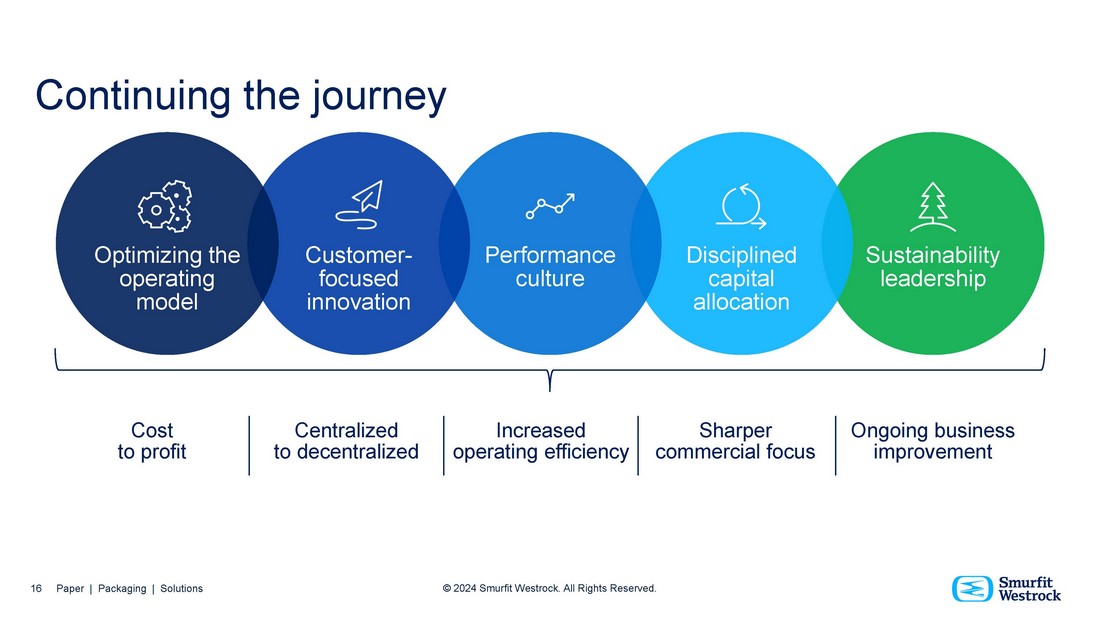

EBITDA margin** Net leverage ratio** Return on capital employed** 19 18 17 16 15 14 13 12 11 10 15 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved. 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 0 0.5 1 1.5 2 2.5 3 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 140 120 100 80 60 40 20 0 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 % 21 19 17 15 13 11 9 7 5 % 20 Dividend € cent 160 ** EBITDA margin, net leverage ratio and return on capital employed are historic reported non - GAAP IFRS performance measures, and are calculated in euro Graphs represent historical financial performance under legacy Smurfit Kappa Group Proven track record of delivery Disciplined capital allocation Optimizing the operating model Customer - focused innovation Performance culture Sustainability leadership Centralized to decentralized Increased operating efficiency Sharper commercial focus Cost to profit Continuing the journey Ongoing business improvement 16 Paper | Packaging | Solutions © 2024 Smurfit Westrock.

All Rights Reserved.

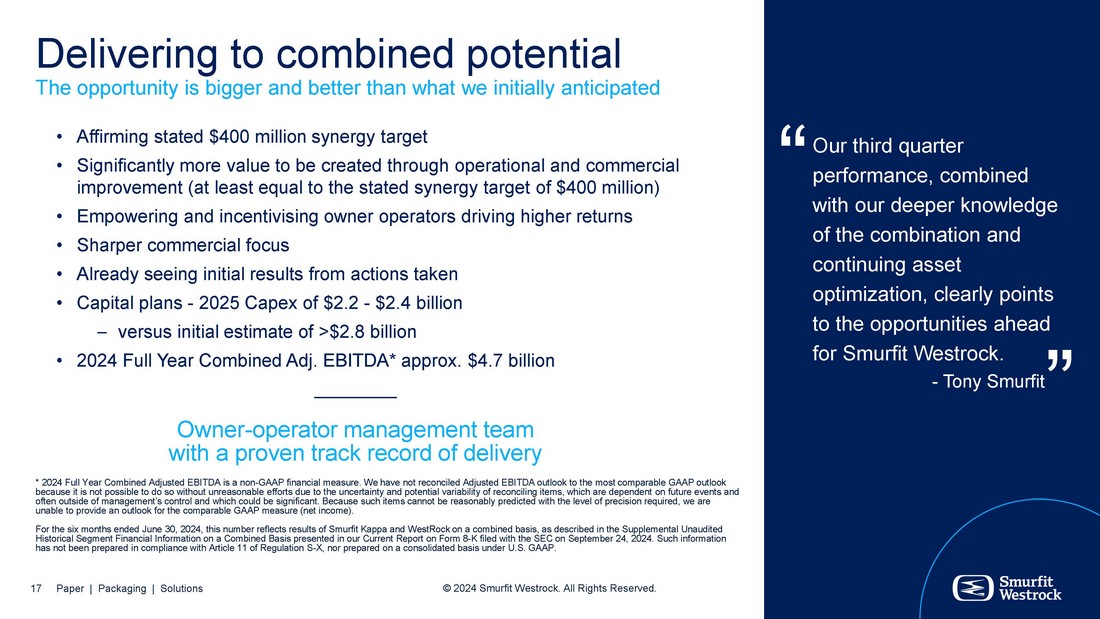

Delivering to combined potential The opportunity is bigger and better than what we initially anticipated • Affirming stated $400 million synergy target • Significantly more value to be created through operational and commercial improvement (at least equal to the stated synergy target of $400 million) • Empowering and incentivising owner operators driving higher returns • Sharper commercial focus • Already seeing initial results from actions taken • Capital plans - 2025 Capex of $2.2 - $2.4 billion – versus initial estimate of >$2.8 billion • 2024 Full Year Combined Adj. EBITDA* approx. $4.7 billion Our third quarter performance, combined with our deeper knowledge of the combination and continuing asset optimization, clearly points to the opportunities ahead for Smurfit Westrock. - Tony Smurfit “ “ Owner - operator management team with a proven track record of delivery * 2024 Full Year Combined Adjusted EBITDA is a non - GAAP financial measure. We have not reconciled Adjusted EBITDA outlook to the most comparable GAAP outlook because it is not possible to do so without unreasonable efforts due to the uncertainty and potential variability of reconciling items, which are dependent on future events and often outside of management’s control and which could be significant. Because such items cannot be reasonably predicted with the level of precision required, we are unable to provide an outlook for the comparable GAAP measure (net income). For the six months ended June 30, 2024, this number reflects results of Smurfit Kappa and WestRock on a combined basis, as described in the Supplemental Unaudited Historical Segment Financial Information on a Combined Basis presented in our Current Report on Form 8 - K filed with the SEC on September 24, 2024. Such information has not been prepared in compliance with Article 11 of Regulation S - X, nor prepared on a consolidated basis under U.S. GAAP. 17 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

Appendices 18 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved.

~$0.7 billion Cash interest ~$0.7 billion Cash tax ~26% Effective tax rate ~$2.1 – $2.3 billion Capital expenditure ~ $4.7 billion 2024 Full Year Combined Adjusted EBITDA* 19 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved. 2024 Full Year Guidance (combined) *2024 Full Year Combined Adjusted EBITDA is a non - GAAP financial measure. We have not reconciled the Adjusted EBITDA outlook to the most comparable GAAP outlook because it is not possible to do so without unreasonable efforts due to the uncertainty and potential variability of reconciling items, which are dependent on future events and often outside of management’s control and which could be significant. Because such items cannot be reasonably predicted with the level of precision required, we are unable to provide an outlook for the comparable GAAP measure (net income). For the six months ended June 30, 2024, this number reflects the results of Smurfit Kappa and WestRock on a combined basis, as described in the Supplemental Unaudited Historical Segment Financial Information on a Combined Basis presented in our Current Report on Form 8 - K filed with the SEC on September 24, 2024. Such information has not been prepared in compliance with Article 11 of Regulation S - X, nor prepared on a consolidated basis under U.S. GAAP.

Reconciliations to most comparable GAAP measure 20 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved. Set forth below is a reconciliation of the non - GAAP financial measures Adjusted EBI TDA and Adjusted EBITDA Margin to Net income and Net Income Margin, the most directly comparable GAAP measures, for the periods indicated. (1) Other adjustments for the three months ended September 30, 2024 include restructuring costs of $19 million, losses at closed facilities of $8 million and impairment of other assets of $2 million (three months ended September 30, 2023: $ - million, $ - million & $ - million, respectively). Other adjustments for the nine months ended September 30, 2024 include restructuring costs of $19 million, losses at closed facilities of $8 million and impairment of other assets of $2 million partially offset by legislative or regulatory fine reimbursement of $18 million (nine months ended September 30, 2023: $ - million, $ - million, $ million & $ - million, respectively). in $ millions, except margin percentages Nine months ended Three months ended September 30, 2024 September 30, 2023 September 30, 2024 173 $ 229 $ (150) $ Net (loss) income 164 73 33 Income tax expense 872 147 564 Depreciation, depletion and amortization 227 - 227 Amortization of fair value step up on inventory 350 17 267 Transaction and integration - related expenses associated with the Combination 225 39 167 Interest expense, net 31 9 (8) Pension and other postretirement non - service (benefit) expense, net 154 7 123 Share - based compensation expense 13 4 13 Other expense, net 11 - 29 Other adjustments (1) 2,220 $ 525 $ 1,265 $ Adjusted EBITDA 1.3% 7.8% (2.0%) Net Income Margin (Net Income/Net Sales) 16.4% 18.0% 16.5% Adjusted EBITDA Margin (Adjusted EBITDA/Net Sales)

Reconciliations to most comparable GAAP measure (continued) 21 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved. Set forth below is a reconciliation of the non - GAAP financial measure Adjusted Free Cash Flow to Net cash provided by operating activities, the most directly comparable GAAP measure, for the periods indicated. Set forth below is a reconciliation of the non - GAAP financial measures Net Debt and Net Leverage Ratio to total borrowings, the most directly comparable GAAP measure, for the periods indicated. (1) Includes unamortized debt issuance costs. in $ millions, except Net Leverage Ratio September 30, 2024 745 $ Current portion of debt (1) 13,174 Non - current debt due after one year (1) Less: (951) Cash and cash equivalents, including restricted cash 12,968 $ Net Debt 4,559 Pro - forma Adjusted EBITDA (LTM) 2.8x Pro - forma Net Leverage Ratio (Net Debt/Pro - forma Adjusted EBITDA (LTM)) in $ millions Nine months ended Three months ended September 30, 2023 September 30, 2024 September 30, 2023 September 30, 2024 948 $ 702 $ 378 $ 320 $ Net cash provided by operating activities Adjustments: (661) (897) (202) (512) Capital expenditures 287 $ (195) $ 176 $ (192) $ Free Cash Flow Adjustments: 17 364 17 307 Transaction and integration costs - 8 - Bridge facility fees 13 45 13 45 Restructuring costs - (42) - (42) Tax on above items 325 $ 172 $ 214 $ 118 $ Adjusted Free Cash Flow Reconciliations to most comparable GAAP measure for combined Adjusted EBITDA 22 Paper | Packaging | Solutions © 2024 Smurfit Westrock.

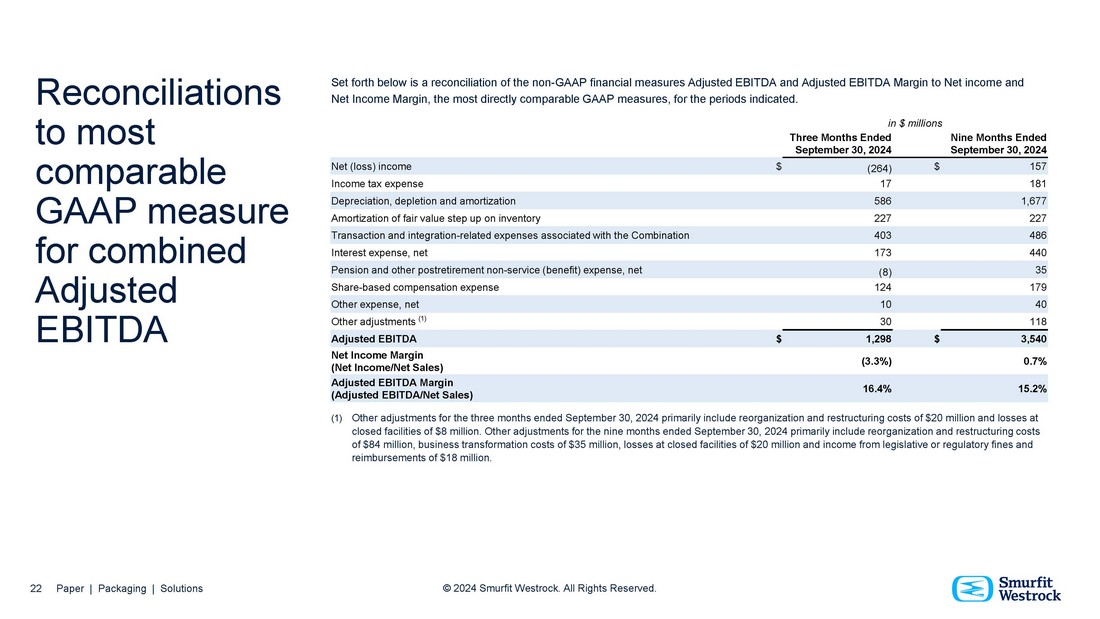

All Rights Reserved. Set forth below is a reconciliation of the non - GAAP financial measures Adjusted EBITDA and Adjusted EBITDA Margin to Net income and Net Income Margin, the most directly comparable GAAP measures, for the periods indicated. (1) Other adjustments for the three months ended September 30, 2024 primarily include reorganization and restructuring costs of $20 million and losses at closed facilities of $8 million. Other adjustments for the nine months ended September 30, 2024 primarily include reorganization and restructuring costs of $84 million, business transformation costs of $35 million, losses at closed facilities of $20 million and income from legislative or regulatory fines and reimbursements of $18 million. in $ millions Nine Months Ended September 30, 2024 Three Months Ended September 30, 2024 157 $ (264) $ Net (loss) income 181 17 Income tax expense 1,677 586 Depreciation, depletion and amortization 227 227 Amortization of fair value step up on inventory 486 403 Transaction and integration - related expenses associated with the Combination 440 173 Interest expense, net 35 (8) Pension and other postretirement non - service (benefit) expense, net 179 124 Share - based compensation expense 40 10 Other expense, net 118 30 Other adjustments (1) 3,540 $ 1,298 $ Adjusted EBITDA 0.7% (3.3%) Net Income Margin (Net Income/Net Sales) 15.2% 16.4% Adjusted EBITDA Margin (Adjusted EBITDA/Net Sales)

Our purpose 23 Paper | Packaging | Solutions © 2024 Smurfit Westrock. All Rights Reserved. Create Protect Care 24 Paper | Packaging | Solutions © 2024 Smurfit Westrock.

All Rights Reserved.