UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported): April 23, 2024

First United Corporation

(Exact name of registrant as specified in its charter)

| Maryland | 0-14237 | 52-1380770 | ||

| (State or other jurisdiction of | (Commission file number) | (IRS Employer | ||

| incorporation or organization) | Identification No.) |

19 South Second Street, Oakland, Maryland 21550

(Address of principal executive offices) (Zip Code)

(301) 334-9471

(Registrant’s telephone number, including area code)

N/A

(Former Name or Former Address, if Changed Since Last Report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligations of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbols | Name of each exchange on which registered |

| Common Stock | FUNC | Nasdaq Stock Market |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR §230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR §240.12b-2).

Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

INFORMATION TO BE INCLUDED IN THE REPORT

Item 2.02. Results of Operation and Financial Condition.

On April 23, 2024, First United Corporation (the “Corporation”) issued a press release describing its financial results for the three months ended March 31, 2024. A copy of the press release is furnished herewith as Exhibit 99.1.

The information contained in this Item 2.02 shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or incorporated by reference in any filing under the Securities Act of 1933, as amended (the “Securities Act”), or the Exchange Act, except as shall be expressly set forth by specific reference in such a filing.

Item 7.01. Regulation FD Disclosure.

On April 24, 2024, the Corporation published an investor presentation that discusses certain aspects of its financial results for the three-months ended March 31, 2024. A copy of the presentation is furnished herewith as Exhibit 99.2.

The information contained in this Item 7.01 shall not be deemed “filed” for purposes of Section 18 of the Exchange Act or incorporated by reference in any filing under the Securities Act or the Exchange Act, except as shall be expressly set forth by specific reference in such a filing.

Item 9.01. Financial Statements and Exhibits.

(d) Exhibits.

The exhibits filed or furnished with this report are listed in the following Exhibit Index:

| Exhibit No. | Description | |

| 99.1 | Press release dated April 23, 2024 (furnished herewith) | |

| 99.2 | Investor presentation dated April 24, 2024 (furnished herewith) | |

| 104 | Cover page interactive data file (embedded within the iXBRL document) |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| FIRST UNITED CORPORATION | ||

| Dated: April 24, 2024 | By: | /s/ Tonya K. Sturm |

| Tonya K. Sturm | ||

| Senior Vice President & CFO | ||

Exhibit 99.1

FIRST UNITED CORPORATION ANNOUNCES

FIRST QUARTER 2024 FINANCIAL RESULTS

OAKLAND, MARYLAND— April 23, 2024: First United Corporation (the “Corporation, “we”, “us”, and “our”) (NASDAQ: FUNC), a bank holding company and the parent company of First United Bank & Trust (the “Bank”), today announced financial results for the three-month period ended March 31, 2024. Consolidated net income was $3.7 million for the first quarter of 2024, or $0.56 per diluted share, compared to $4.4 million, or $0.65 per diluted share, for the first quarter of 2023 and $1.8 million, or $0.26 per diluted share, for the fourth quarter of 2023.

According to Carissa Rodeheaver, Chairman, President and CEO, “The first quarter of 2024 was a solid quarter with stable net income impacted slightly by the slowing of loan growth, stabilization of the net interest margin and the final costs associated with the branch consolidation announced last quarter. We experienced positive growth in our wealth management income spurred by improving market conditions and growth in new relationships and we successfully managed our core operating expenses. Our associates remain committed to working with our customers as they adjust to the higher interest rate and inflationary cost environment.”

First Quarter Financial Highlights:

| · | Total assets at March 31, 2024 increased by $7.1 million, or 0.4%, when compared to December 31, 2023. Significant changes during the first quarter included: |

| o | Cash balances increased by $37.2 million. |

| o | Investment securities decreased by $32.8 million due primarily to the maturity of $30.0 million of held-to-maturity (“HTM”) U.S. Treasury Bonds during the quarter. |

| o | Gross loans increased by $5.7 million as: |

| § | commercial balances increased by $5.6 million; |

| § | mortgage balances increased by $2.1 million; and |

| § | consumer loans decreased by $2.1 million. |

| o | Deposits increased by $12.5 million as: |

| § | non-interest-bearing deposits decreased by $4.9 million; |

| § | interest-bearing demand deposits increased by $26.9 million; |

| § | savings and money market accounts increased by $4.9 million; and |

| § | time deposits decreased by $14.4 million. |

| o | Short-term borrowings increased by $34.1 million as the Bank borrowed $40.0 million from the Federal Reserve’s Bank Term Funding Program (“BTFP”) in January 2024, which was partially offset by a decrease of $5.9 million in other short-term borrowings due to fluctuations in municipal customer balances in overnight investment sweep products. Long-term borrowings decreased by $40.0 million as a $40.0 million Federal Home Loan Bank (“FHLB”) advance matured in March 2024 and was fully repaid. |

| · | For the first quarter of 2024, consolidated net income was $3.7 million, inclusive of $0.4 million, net of tax, of accelerated depreciation expenses related to the closure of four branches in February 2024. |

| o | Net interest margin, on a non-GAAP, fully tax equivalent (“FTE”) basis, was 3.12% for the first quarter of 2024 compared to 3.53% for the first quarter of 2023 and 3.13% for the fourth quarter of 2023. |

| o | Non-interest income, excluding net gains and losses, remained stable in the first quarter of 2024 when compared to the fourth quarter of 2023 and increased by $0.5 million when compared to the first quarter of 2023 due primarily to increases in wealth management income. |

| o | Non-interest expense increased by $0.6 million when compared to the fourth quarter of 2023 due to increased salaries and benefits of $0.8 million and a $0.5 million increase in other real estate owned (“OREO”) expenses. The increase in salaries and benefits was related to increases in full-time salaries, incentive compensation, life and health insurance, and executive officer long-term and short-term expense, partially offset by a decrease in stock compensation expense and 401(k) plan expense. OREO expense increased due to a credit to expense in the fourth quarter of 2023 from gain on sales. The foregoing increases were offset primarily by reductions in occupancy associated with the accelerated lease expense in the fourth quarter of 2023 related to closure of four branches in the first quarter of 2024, as well as reductions in data processing, marketing and professional services expenses. When compared to the first quarter of 2023, the increases were primarily due to accelerated depreciation expenses associated with the branch closures, partially offset by reduced salaries and benefits. |

Income Statement Overview

On a GAAP basis, net income for the first quarter of 2024 was $3.7 million, inclusive of $0.4 million, net of tax, accelerated depreciation expenses related to branch closures. This compares to $4.4 million for the first quarter of 2023 and $1.8 million, inclusive of a $3.3 million, net of tax, loss on the sale of securities and $0.5 million, net of tax, accelerated depreciation and lease termination expenses related to the branch closures, for the fourth quarter of 2023.

| Q1 2024 | Q4 2023 | Q1 2023 | ||||||||||

| Net Income, non-GAAP (millions) | $ | 4.1 | $ | 5.5 | $ | 4.4 | ||||||

| Net Income, GAAP (millions) | $ | 3.7 | $ | 1.8 | $ | 4.4 | ||||||

| Basic net income per share, non-GAAP | $ | 0.62 | $ | 0.82 | $ | 0.66 | ||||||

| Diluted net income per share, non-GAAP | $ | 0.62 | $ | 0.82 | $ | 0.65 | ||||||

| Basic net income per share, GAAP | $ | 0.56 | $ | 0.26 | $ | 0.66 | ||||||

| Diluted net income per share, GAAP | $ | 0.56 | $ | 0.26 | $ | 0.65 | ||||||

The $0.7 million decrease in net income year over year was primarily driven by a $0.7 million decrease in net interest income and a $0.4 million increase in provision for credit losses. Two large commercial relationships with combined loan balances of $12.1 million were moved to non-accrual status during the first quarter of 2024, which resulted in a reversal of $0.4 million in accrued interest income and fees during the quarter. Additionally, interest expense increased at a slightly faster pace than interest income comparing year over year. The provision for credit loss also increased year over year due to increased qualitative risk factors associated with the non-accrual loan balances. Management is actively managing these credits, which we anticipate will lead to normal collection procedures such as returning the credits to accrual or moving loans through the foreclosure process over the next year. Other activity comparing the first quarter of 2024 to the same period in 2023 was a $0.4 million increase in wealth management income year over year due to improving market conditions and growth of new relationships and an increase in operating expenses of $0.2 million. The provision for income tax expense was down $0.2 million when comparing the two quarters due to decreased net income before tax.

Compared to the linked quarter, net income increased by $1.9 million due primarily to $4.2 million in recognized losses from the restructuring of the investment portfolio. This was partially offset by the $0.4 million decrease in net interest income and the $0.5 million increase in provision expense when compared to the prior quarter. Comparing the linked quarters, interest income was impacted by the $0.4 million reversal of accrued interest, and provision expense increased by $0.1 million due to increased qualitative factors associated with the increase in non-accrual loans described above. Operating expenses increased by $0.6 million due primarily to increased salary and employee benefits and net OREO expenses offset by decreases in occupancy marketing and professional services.

Net Interest Income and Net Interest Margin

Net interest income, on a non-GAAP, FTE basis, decreased by $0.9 million for the first quarter of 2024 when compared to the first quarter of 2023. This decrease was driven by an increase of $4.8 million in interest expense due to an increase of 133 basis points on interest paid on deposit accounts. The average balances decreased by $39.4 million when compared to the first quarter of 2023 due primarily to the increased deposit pricing pressures that began in the first quarter of 2023 as a result of the bank failures in March 2023 and liquidity fears in the market. Interest income increased by $3.9 million. Interest income on loans increased by $3.8 million due to the increase of 59 basis points in overall yield on the loan portfolio as new loans were booked at higher rates as well as adjustable-rate loans repricing in correlation to the rising rate environment and an increase in average balances of $128.3 million. Investment income decreased by $0.4 million due to a decrease of $64.4 million in average balances related to the balance sheet restructuring of our investment portfolio in the fourth quarter of 2023 and the maturity of $30.0 million of U.S. Treasury bonds. The net interest margin for the three months ended March 31, 2024 was 3.12% compared to 3.53% for the three months ended March 31, 2023. Excluding the reversal of $0.4 million of interest and fees on loans related to the movement of $12.1 million of loans to non-accrual, the net interest margin would have been 3.21%.

Comparing the first quarter of 2024 to the fourth quarter of 2023, net interest income, on a non-GAAP, FTE basis, decreased by $0.4 million. This decrease was driven by a decrease of $0.3 million in interest income and an increase of $0.1 million in interest expense. Interest income on loans decreased by $0.1 million related to the reversal of $0.4 million in accrued interest and loan fees related to the non-accrual loans in the first quarter of 2024 offset by an overall increase of 1 basis point in the yield and an increase of $9.5 million in average loan balances. Interest expense on deposits decreased by $0.2 million due to a decrease in average deposit balances of $98.7 million during the quarter. Interest expense on short-term borrowings increased by $0.4 million due to the Corporation’s decision to borrow $40.0 million from the BTFP in the first quarter of 2024.

Non-Interest Income

Other operating income, including net gains/(losses), for the first quarter of 2024 increased by $0.5 million when compared to the same period of 2023. The growth was driven by an increase of $0.4 million in wealth management income due to improving market conditions and growth in new and existing customer relationships.

On a linked quarter basis, other operating income, including net losses, increased by $4.3 million due primarily to the $4.2 million in losses related to the sale of available-for-sale (“AFS”) securities in the fourth quarter of 2023 related to the Corporation’s balance sheet restructuring. Additionally, debit card income decreased by $0.2 million when compared to the previous quarter. These decreases were partially offset by a $0.2 million increase in wealth management income.

Non-Interest Expense

Operating expenses increased by $0.2 million in the first quarter of 2024 when compared to the first quarter of 2023. The increase was largely driven by a $0.3 million increase in equipment and occupancy expense due to the accelerated depreciation expenses recognized in the first quarter of 2024 in conjunction with the announced branch closures in February 2024. This increase was partially offset by a $0.1 million decrease in salaries and employee benefits year over year due to unusually high health insurance premiums recognized in the first quarter of 2023 offset by higher salaries and benefits associated with normal merit increases effective April 1, 2023.

Non-interest expense increased by $0.6 million when compared to the linked quarter due to increased salaries and benefits of $0.8 million and increased OREO expense of $0.5 million. The increase in salaries and benefits was related to increases in full-time salaries, incentive compensation, life and health insurance, and executive officer long-term and short-term expense, partially offset by decreases in stock compensation expense and 401(k) plan expense. OREO expense increased due to a credit to expense in the fourth quarter of 2023 from gain on sales. These increases were offset by reductions in occupancy, data processing, marketing and professional service expenses.

The effective income tax rates as a percentage of income for the three-month periods ended March 31, 2024 and March 31, 2023 were 23.9% and 23.6%, respectively.

Balance Sheet Overview

Total assets at March 31, 2024 were $1.9 billion, representing a $7.1 million increase since December 31, 2023. During the first quarter of 2024, cash and interest-bearing deposits in other banks increased by $37.2 million. The investment portfolio decreased by $32.8 million due to the maturities of $30.0 million of U.S. Treasury bonds during the quarter and normal principal amortization. Gross loans increased by $5.7 million. Other assets, including deferred taxes, premises and equipment, and accrued interest receivable, remained stable.

Total liabilities at March 31, 2024 were $1.7 billion, representing a $3.5 million increase since December 31, 2023. Total deposits increased by $12.5 million when compared to December 31, 2023. The increase in deposits was primarily attributable to the shift of $10.0 million in overnight investment sweep balances to the IntraFi Cash Service (“ICS”) product, as a result of management’s strategy to release pledging of investment securities for municipalities to increase available liquidity. Short term borrowings increased by $34.1 million since December 31, 2023 due primarily to the Bank’s utilization of the BTFP to obtain $40.0 million in borrowings during January 2024 at a rate of 4.87% with a one-year maturity. There are no prepayment penalties associated with early payments on the BTFP. Long-term borrowings decreased by $40.0 million in the first quarter of 2024 when compared to December 31, 2023 due to the repayment of $40.0 million in FHLB borrowings.

Total AFS and HTM securities totaled $278.7 million at March 31, 2024, representing a $32.8 million decrease when compared to December 31, 2023. In the first quarter of 2024, $30.0 million in U.S. Treasury bonds matured and were reinvested into cash at the Federal Reserve in anticipation of the $40.0 million maturing FHLB advance. Additionally, there were $2.5 million of other principal amortizations in the portfolio during the quarter.

Outstanding loans of $1.4 billion at March 31, 2024 reflected growth of $5.7 million for the first quarter of 2024. Since December 31, 2023, commercial real estate loans decreased by $0.9 million and acquisition and development loans increased by $6.4 million. Commercial and industrial loans increased by $0.1 million. Residential mortgage loans increased $2.1 million, offset by a decline of $2.1 million in the consumer loan portfolio related to new production offset by monthly amortization.

New commercial loan production for the three months ended March 31, 2024 was approximately $28.3 million. The pipeline of commercial loans as of March 31, 2024 was $30.9 million. At March 31, 2024, unfunded, committed commercial construction loans totaled approximately $8.2 million. Commercial amortization and payoffs were approximately $35.5 million through March 31, 2024, due primarily to pay-offs of short-term commercial loans as well as normal amortizations of the commercial loan portfolio.

New consumer mortgage loan production for the first quarter of 2024 was approximately $11.2 million, with most of this production comprised of in-house mortgages. The pipeline of in-house, portfolio loans as of March 31, 2024 was $9.8 million. The residential mortgage production level declined in the first quarter of 2024 due to the higher interest rates and seasonality of this line of business. Unfunded commitments related to residential construction loans totaled $13.9 million at March 31, 2024. Management has chosen to shift activity to the secondary market in the first quarter of 2024 to preserve liquidity.

Total deposits at March 31, 2024 increased by $12.5 million when compared to December 31, 2023. During the quarter, non-interest-bearing deposits decreased by $4.9 million. Interest-bearing demand deposits increased by $26.9 million, primarily related to the shift of $10.0 million in overnight investment sweep balances into the ICS product to maintain FDIC insurance due to management’s strategy to release pledging of investment securities for municipalities to increase available liquidity. Money market accounts increased by $7.3 million due primarily to the expansion of current relationships and new relationships during the quarter. Traditional savings accounts decreased by $2.4 million and time deposits decreased by $14.4 million. The decrease in time deposits was primarily due to the maturing of a nine-month CD product that was offered by the Bank in 2023 at higher rates. The Bank has worked closely with customers as these CDs mature to transition them to other deposit and wealth management products offered by the Bank.

Short-term borrowings increased by $34.1 million as the Bank borrowed $40.0 million from the BTFP in January 2024, which was partially offset by a decrease of $5.9 million in other short-term borrowings due to fluctuations in municipal customer balances in overnight investment sweep products. Long-term borrowings decreased by $40.0 million as a $40.0 million FHLB advance matured in March 2024 and was fully repaid.

The book value of the Corporation’s common stock was $24.89 per share at March 31, 2024 compared to $24.38 per share at December 31, 2023. At March 31, 2024, there were 6,648,645 of basic outstanding shares and 6,657,239 of diluted outstanding shares of common stock. The increase in the book value at March 31, 2024 was due to the undistributed net income of $2.4 million for the first quarter of 2024.

Asset Quality

The allowance for credit losses (“ACL”) was $18.0 million at March 31, 2024 compared to $16.9 million recorded at March 31, 2023 and $17.5 million at December 31, 2023. The provision for credit losses was $0.9 million for the quarter ended March 31, 2024 compared to $0.5 million for the quarter ended March 31, 2023 and $0.4 million for the fourth quarter of 2023. The increased provision expense recorded in 2024 was primarily related to increases in qualitative risk factors of our commercial and industrial portfolio, as two large relationships moved to non-accrual status during the quarter. Net charge-offs of $0.5 million were recorded for the quarter ended March 31, 2024 compared to net charge-offs of $0.2 million for the quarter ended March 31, 2023. The ratio of the ACL to loans outstanding was 1.27% at March 31, 2024 compared to 1.24% at December 31, 2023 and 1.31% at March 31, 2023.

The ratio of net charge offs to average loans was 0.13% for the quarter ended March 31, 2024, and 0.08% for the quarter ended March 31, 2023. The commercial and industrial portfolio had net charge offs of 0.12% for the quarter ended March 31, 2024 compared to a net recovery of 0.01% for the quarter ended March 31, 2023. This shift was due to charge offs of equipment loan balances on two commercial relationships during the first quarter of 2024. The increase in net charge offs in consumer loans in the first quarter of 2024 was primarily driven by approximately $0.3 million in charge offs of overdrawn demand deposit balances during the quarter. Details of the ratios, by loan type, are shown below. Our special assets team continues to actively collect on charged-off loans, resulting in overall low net charge-off ratios.

| Ratio of Net (Charge Offs)/Recoveries to Average Loans | ||||||||

| 3/31/2024 | 3/31/2023 | |||||||

| Loan Type | (Charge Off) / Recovery | (Charge Off) / Recovery | ||||||

| Commercial Real Estate | 0.03 | % | 0.00 | % | ||||

| Acquisition & Development | 0.01 | % | 0.03 | % | ||||

| Commercial & Industrial | (0.12 | %) | 0.01 | % | ||||

| Residential Mortgage | 0.01 | % | 0.01 | % | ||||

| Consumer | (2.89 | %) | (1.79 | %) | ||||

| Total Net (Charge Offs)/Recoveries | (0.13 | %) | (0.08 | %) | ||||

Non-accrual loans totaled $16.0 million at March 31, 2024 compared to $4.0 million at December 31, 2023. The increase in non-accrual balances at March 31, 2024 was related to two commercial and industrial loan relationships that were moved to non-accrual during the first quarter. Management believes that these loans are marked appropriately, and our credit department is actively working with these borrowers on work-out plans.

Non-accrual loans that have been subject to partial charge-offs totaled $0.1 million at both March 31, 2024 and December 31, 2023. Loans secured by 1-4 family residential real estate properties in the process of foreclosure totaled $1.8 million at both March 31, 2024 and December 31, 2023. As a percentage of the loan portfolio, accruing loans past due 30 days or more was 0.40% at March 31, 2024 compared to 0.24% at December 31, 2023 and 0.17% as of March 31, 2023.

ABOUT FIRST UNITED CORPORATION

First United Corporation is a Maryland corporation chartered in 1985 and a financial holding company registered with the Board of Governors of the Federal Reserve System under the Bank Holding Company Act of 1956, as amended, that elected financial holding company status in 2021. The Corporation’s primary business is serving as the parent company of the Bank, First United Statutory Trust I (“Trust I”) and First United Statutory Trust II (“Trust II” and together with Trust I, “the Trusts”), both Connecticut statutory business trusts. The Trusts were formed for the purpose of selling trust preferred securities that qualified as Tier 1 capital. The Bank has two consumer finance company subsidiaries- Oak First Loan Center, Inc., a West Virginia corporation, and OakFirst Loan Center, LLC, a Maryland limited liability company – and two subsidiaries that it uses to hold real estate acquired through foreclosure or by deed in lieu of foreclosure – First OREO Trust, a Maryland statutory trust, and FUBT OREO I, LLC, a Maryland limited liability company. In addition, the Bank owns 99.9% of the limited partnership interests in Liberty Mews Limited Partnership, a Maryland limited partnership formed for the purpose of acquiring, developing and operating low-income housing units in Garrett County, Maryland, and a 99.9% non-voting membership interest in MCC FUBT Fund, LLC, an Ohio limited liability company formed for the purpose of acquiring, developing and operating low-income housing units in Allegany County, Maryland (the “MCC Fund”). The Corporation’s website is www.mybank.com.

FORWARD-LOOKING STATEMENTS

This press release contains forward-looking statements as defined by the Private Securities Litigation Reform Act of 1995. Forward-looking statements do not represent historical facts, but are statements about management's beliefs, plans and objectives about the future, as well as its assumptions and judgments concerning such beliefs, plans and objectives. These statements are evidenced by terms such as "anticipate," "estimate," "should," "expect," "believe," "intend," and similar expressions. Although these statements reflect management's good faith beliefs and projections, they are not guarantees of future performance and they may not prove true. The beliefs, plans and objectives on which forward-looking statements are based involve risks and uncertainties that could cause actual results to differ materially from those addressed in the forward-looking statements. For a discussion of these risks and uncertainties, see the section of the periodic reports that First United Corporation files with the Securities and Exchange Commission entitled "Risk Factors". In addition, investors should understand that the Corporation is required under generally accepted accounting principles to evaluate subsequent events through the filing of the consolidated financial statements included in its Quarterly Report on Form 10-Q for the quarter ended March 31, 2024 and the impact that any such events have on our critical accounting assumptions and estimates made as of March 31, 2024, which could require us to make adjustments to the amounts reflected in this press release.

FIRST UNITED CORPORATION

Oakland, MD

Stock Symbol : FUNC

Financial Highlights - Unaudited

| (Dollars in thousands, except per share data) | ||||||||

| Three Months Ended | ||||||||

| March 31, | March 31, | |||||||

| 2024 | 2023 | |||||||

| Results of Operations: | ||||||||

| Interest income | $ | 21,898 | $ | 17,829 | ||||

| Interest expense | 8,086 | 3,311 | ||||||

| Net interest income | 13,812 | 14,518 | ||||||

| Provision for credit losses | 946 | 543 | ||||||

| Other operating income | 4,793 | 4,339 | ||||||

| Net gains | 82 | 54 | ||||||

| Other operating expense | 12,881 | 12,638 | ||||||

| Income before taxes | $ | 4,860 | $ | 5,730 | ||||

| Income tax expense | 1,162 | 1,355 | ||||||

| Net income | $ | 3,698 | $ | 4,375 | ||||

| Per share data: | ||||||||

| Basic net income per share | $ | 0.56 | $ | 0.66 | ||||

| Diluted net income per share | $ | 0.56 | $ | 0.65 | ||||

| Adjusted Basic net income (1) | $ | 0.62 | $ | 0.66 | ||||

| Adjusted Diluted net income (1) | $ | 0.62 | $ | 0.65 | ||||

| Dividends declared per share | $ | 0.20 | $ | 0.20 | ||||

| Book value | $ | 24.89 | $ | 22.85 | ||||

| Diluted book value | $ | 24.86 | $ | 22.81 | ||||

| Tangible book value per share | $ | 23.08 | $ | 21.01 | ||||

| Diluted Tangible book value per share | $ | 23.05 | $ | 20.96 | ||||

| Closing market value | $ | 22.91 | $ | 16.89 | ||||

| Market Range: | ||||||||

| High | $ | 23.85 | $ | 20.41 | ||||

| Low | $ | 21.21 | $ | 16.75 | ||||

| Shares outstanding at period end: Basic | 6,648,645 | 6,688,710 | ||||||

| Shares outstanding at period end: Diluted | 6,657,239 | 6,703,252 | ||||||

| Performance ratios: (Year to Date Period End, annualized) | ||||||||

| Return on average assets | 0.76 | % | 0.94 | % | ||||

| Adjusted return on average assets (1) | 0.85 | % | 0.97 | % | ||||

| Return on average shareholders' equity | 9.07 | % | 11.87 | % | ||||

| Adjusted return on average shareholders' equity (1) | 10.11 | % | 11.50 | % | ||||

| Net interest margin (Non-GAAP), includes tax exempt income of $57 and $227 | 3.12 | % | 3.53 | % | ||||

| Net interest margin GAAP | 3.10 | % | 3.48 | % | ||||

| Efficiency ratio - non-GAAP (1) | 65.71 | % | 67.02 | % | ||||

(1) Efficiency ratio is a non-GAAP measure calculated by dividing total operating expenses by the sum of tax equivalent net interest income and other operating income, less gains/(losses) on sales of securities and/or fixed assets.

| March 31, | December 31 | |||||||

| 2024 | 2023 | |||||||

| Financial Condition at period end: | ||||||||

| Assets | $ | 1,912,953 | $ | 1,905,860 | ||||

| Earning assets | $ | 1,695,962 | $ | 1,725,236 | ||||

| Gross loans | $ | 1,412,327 | $ | 1,406,667 | ||||

| Commercial Real Estate | $ | 492,819 | $ | 493,703 | ||||

| Acquisition and Development | $ | 83,424 | $ | 77,060 | ||||

| Commercial and Industrial | $ | 274,722 | $ | 274,604 | ||||

| Residential Mortgage | $ | 501,990 | $ | 499,871 | ||||

| Consumer | $ | 59,372 | $ | 61,429 | ||||

| Investment securities | $ | 278,716 | $ | 311,466 | ||||

| Total deposits | $ | 1,563,453 | $ | 1,550,977 | ||||

| Noninterest bearing | $ | 422,759 | $ | 427,670 | ||||

| Interest bearing | $ | 1,140,694 | $ | 1,123,307 | ||||

| Shareholders' equity | $ | 165,481 | $ | 161,873 | ||||

| Capital ratios: | ||||||||

| Tier 1 to risk weighted assets | 14.58 | % | 14.42 | % | ||||

| Common Equity Tier 1 to risk weighted assets | 12.60 | % | 12.44 | % | ||||

| Tier 1 Leverage | 11.48 | % | 11.30 | % | ||||

| Total risk based capital | 15.83 | % | 15.64 | % | ||||

| Asset quality: | ||||||||

| Net charge-offs for the quarter | $ | (459 | ) | $ | (195 | ) | ||

| Nonperforming assets: (Period End) | ||||||||

| Nonaccrual loans | $ | 16,007 | $ | 3,956 | ||||

| Loans 90 days past due and accruing | 120 | 543 | ||||||

| Total nonperforming loans and 90 day past due | $ | 16,127 | $ | 4,499 | ||||

| Other real estate owned | $ | 4,402 | $ | 4,493 | ||||

| Allowance for credit losses to gross loans | 1.27 | % | 1.24 | % | ||||

| Allowance for credit losses to non-accrual loans | 112.34 | % | 441.86 | % | ||||

| Allowance for credit losses to non-performing assets | 87.59 | % | 194.40 | % | ||||

| Non-performing and 90 day past due loans to total loans | 1.14 | % | 0.32 | % | ||||

| Non-performing loans and 90 day past due loans to total assets | 0.84 | % | 0.24 | % | ||||

| Non-accrual loans to total loans | 1.13 | % | 0.28 | % | ||||

| Non-performing assets to total assets | 1.07 | % | 0.47 | % | ||||

FIRST UNITED CORPORATION

Oakland, MD

Stock Symbol : FUNC

Financial Highlights - Unaudited

| March 31, | December 31, | September 30, | June 30, | March 31, | ||||||||||||||||

| (Dollars in thousands, except per share data) | 2024 | 2023 | 2023 | 2023 | 2023 | |||||||||||||||

| Results of Operations: | ||||||||||||||||||||

| Interest income | $ | 21,898 | $ | 22,191 | $ | 21,164 | $ | 19,972 | $ | 17,829 | ||||||||||

| Interest expense | 8,086 | 7,997 | 7,180 | 5,798 | 3,311 | |||||||||||||||

| Net interest income | 13,812 | 14,194 | 13,984 | 14,174 | 14,518 | |||||||||||||||

| Provision for credit losses | 946 | 419 | 263 | 395 | 543 | |||||||||||||||

| Other operating income | 4,793 | 4,793 | 4,716 | 4,483 | 4,339 | |||||||||||||||

| Net gains/(losses) | 82 | (4,184 | ) | 182 | 86 | 54 | ||||||||||||||

| Other operating expense | 12,881 | 12,309 | 12,785 | 12,511 | 12,638 | |||||||||||||||

| Income before taxes | $ | 4,860 | $ | 2,075 | $ | 5,834 | $ | 5,837 | $ | 5,730 | ||||||||||

| Income tax expense | 1,162 | 317 | 1,321 | 1,423 | 1,355 | |||||||||||||||

| Net income | $ | 3,698 | $ | 1,758 | $ | 4,513 | $ | 4,414 | $ | 4,375 | ||||||||||

| Per share data: | ||||||||||||||||||||

| Basic net income per share | $ | 0.56 | $ | 0.26 | $ | 0.67 | $ | 0.66 | $ | 0.66 | ||||||||||

| Diluted net income per share | $ | 0.56 | $ | 0.26 | $ | 0.67 | $ | 0.66 | $ | 0.65 | ||||||||||

| Adjusted basic net income (1) | $ | 0.62 | $ | 0.66 | $ | 0.66 | $ | 0.66 | $ | 0.66 | ||||||||||

| Adjusted diluted net income (1) | $ | 0.62 | $ | 0.65 | $ | 0.65 | $ | 0.65 | $ | 0.65 | ||||||||||

| Dividends declared per share | $ | 0.20 | $ | 0.20 | $ | 0.20 | $ | 0.20 | $ | 0.20 | ||||||||||

| Book value | $ | 24.89 | $ | 24.38 | $ | 23.08 | $ | 23.12 | $ | 22.85 | ||||||||||

| Diluted book value | $ | 24.86 | $ | 24.33 | $ | 23.03 | $ | 23.07 | $ | 22.81 | ||||||||||

| Tangible book value per share | $ | 23.08 | $ | 22.56 | $ | 21.27 | $ | 21.29 | $ | 21.01 | ||||||||||

| Diluted Tangible book value per share | $ | 23.05 | $ | 22.51 | $ | 21.22 | $ | 21.25 | $ | 20.96 | ||||||||||

| Closing market value | $ | 22.91 | $ | 23.51 | $ | 16.23 | $ | 14.26 | $ | 16.89 | ||||||||||

| Market Range: | ||||||||||||||||||||

| High | $ | 23.85 | $ | 23.51 | $ | 17.34 | $ | 17.01 | $ | 20.41 | ||||||||||

| Low | $ | 21.21 | $ | 16.12 | $ | 13.70 | $ | 12.56 | $ | 16.75 | ||||||||||

| Shares outstanding at period end: Basic | 6,648,645 | 6,639,888 | 6,715,170 | 6,711,422 | 6,688,710 | |||||||||||||||

| Shares outstanding at period end: Diluted | 6,657,239 | 6,653,200 | 6,728,482 | 6,724,734 | 6,703,252 | |||||||||||||||

| Performance ratios: (Year to Date Period End, annualized) | ||||||||||||||||||||

| Return on average assets | 0.76 | % | 0.78 | % | 0.93 | % | 0.95 | % | 0.94 | % | ||||||||||

| Adjusted return on average assets (1) | 0.85 | % | 0.94 | % | 0.94 | % | 0.94 | % | 0.94 | % | ||||||||||

| Return on average shareholders' equity | 9.07 | % | 9.68 | % | 11.44 | % | 11.43 | % | 11.87 | % | ||||||||||

| Adjusted return on average shareholders' equity (1) | 10.11 | % | 11.87 | % | 11.87 | % | 11.87 | % | 11.87 | % | ||||||||||

| Net interest margin (Non-GAAP), includes tax exempt income of $57 and $227 | 3.12 | % | 3.26 | % | 3.30 | % | 3.39 | % | 3.53 | % | ||||||||||

| Net interest margin GAAP | 3.10 | % | 3.22 | % | 3.25 | % | 3.34 | % | 3.48 | % | ||||||||||

| Efficiency ratio - non-GAAP (1) | 65.71 | % | 65.12 | % | 66.41 | % | 66.00 | % | 67.02 | % | ||||||||||

(1) Efficiency ratio is a non-GAAP measure calculated by dividing total operating expenses by the sum of tax equivalent net interest income and other operating income, less gains/(losses) on sales of securities and/or fixed assets.

| March 31, | December 31, | September 30, | June 30, | March 31, | ||||||||||||||||

| 2024 | 2023 | 2023 | 2023 | 2023 | ||||||||||||||||

| Financial Condition at period end: | ||||||||||||||||||||

| Assets | $ | 1,912,953 | $ | 1,905,860 | $ | 1,928,201 | $ | 1,928,393 | $ | 1,937,442 | ||||||||||

| Earning assets | $ | 1,695,962 | $ | 1,725,236 | $ | 1,717,244 | $ | 1,707,522 | $ | 1,652,688 | ||||||||||

| Gross loans | $ | 1,412,327 | $ | 1,406,667 | $ | 1,380,019 | $ | 1,350,038 | $ | 1,289,080 | ||||||||||

| Commercial Real Estate | $ | 492,819 | $ | 493,703 | $ | 491,284 | $ | 483,485 | $ | 453,356 | ||||||||||

| Acquisition and Development | $ | 83,424 | $ | 77,060 | $ | 79,796 | $ | 79,003 | $ | 76,980 | ||||||||||

| Commercial and Industrial | $ | 274,722 | $ | 274,604 | $ | 254,650 | $ | 249,683 | $ | 241,959 | ||||||||||

| Residential Mortgage | $ | 501,990 | $ | 499,871 | $ | 491,686 | $ | 475,540 | $ | 456,198 | ||||||||||

| Consumer | $ | 59,372 | $ | 61,429 | $ | 62,603 | $ | 62,327 | $ | 60,587 | ||||||||||

| Investment securities | $ | 278,716 | $ | 311,466 | $ | 330,053 | $ | 350,844 | $ | 357,061 | ||||||||||

| Total deposits | $ | 1,563,453 | $ | 1,550,977 | $ | 1,575,069 | $ | 1,579,959 | $ | 1,591,285 | ||||||||||

| Noninterest bearing | $ | 422,759 | $ | 427,670 | $ | 429,691 | $ | 466,628 | $ | 468,554 | ||||||||||

| Interest bearing | $ | 1,140,694 | $ | 1,123,307 | $ | 1,145,378 | $ | 1,113,331 | $ | 1,122,731 | ||||||||||

| Shareholders' equity | $ | 165,481 | $ | 161,873 | $ | 154,990 | $ | 155,156 | $ | 152,868 | ||||||||||

| Capital ratios: | ||||||||||||||||||||

| Tier 1 to risk weighted assets | 14.58 | % | 14.42 | % | 14.60 | % | 14.40 | % | 14.90 | % | ||||||||||

| Common Equity Tier 1 to risk weighted assets | 12.60 | % | 12.44 | % | 12.60 | % | 12.40 | % | 12.82 | % | ||||||||||

| Tier 1 Leverage | 11.48 | % | 11.30 | % | 11.25 | % | 11.25 | % | 11.47 | % | ||||||||||

| Total risk based capital | 15.83 | % | 15.64 | % | 15.81 | % | 15.60 | % | 16.15 | % | ||||||||||

| Asset quality: | ||||||||||||||||||||

| Net (charge-offs)/recoveries for the quarter | $ | (459 | ) | $ | (195 | ) | $ | (83 | ) | $ | (398 | ) | $ | (245 | ) | |||||

| Nonperforming assets: (Period End) | ||||||||||||||||||||

| Nonaccrual loans | $ | 16,007 | $ | 3,956 | $ | 3,479 | $ | 2,972 | $ | 3,258 | ||||||||||

| Loans 90 days past due and accruing | 120 | 543 | 145 | 160 | 87 | |||||||||||||||

| Total nonperforming loans and 90 day past due | $ | 16,127 | $ | 4,499 | $ | 3,624 | $ | 3,132 | $ | 3,345 | ||||||||||

| Modified/restructured loans | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||

| Other real estate owned | $ | 4,402 | $ | 4,493 | $ | 4,878 | $ | 4,482 | $ | 4,598 | ||||||||||

| Allowance for credit losses to gross loans | 1.27 | % | 1.24 | % | 1.24 | % | 1.25 | % | 1.31 | % | ||||||||||

| Allowance for credit losses to non-accrual loans | 112.34 | % | 441.86 | % | 492.84 | % | 568.81 | % | 517.83 | % | ||||||||||

| Allowance for credit losses to non-performing assets | 87.59 | % | 194.40 | % | 473.12 | % | 539.79 | % | 212.40 | % | ||||||||||

| Non-performing and 90 day past due loans to total loans | 1.14 | % | 0.32 | % | 0.26 | % | 0.23 | % | 0.26 | % | ||||||||||

| Non-performing loans and 90 day past due loans to total assets | 0.84 | % | 0.24 | % | 0.19 | % | 0.16 | % | 0.17 | % | ||||||||||

| Non-accrual loans to total loans | 1.13 | % | 0.28 | % | 0.25 | % | 0.22 | % | 0.25 | % | ||||||||||

| Non-performing assets to total assets | 1.07 | % | 0.47 | % | 0.44 | % | 0.39 | % | 0.41 | % | ||||||||||

| (Dollars in thousands - Unaudited) | March 31, 2024 |

December 31, 2023 |

||||||

| Assets | ||||||||

| Cash and due from banks | $ | 85,578 | $ | 48,343 | ||||

| Interest bearing deposits in banks | 1,354 | 1,410 | ||||||

| Cash and cash equivalents | 86,932 | 49,753 | ||||||

| Investment securities – available for sale (at fair value) | 95,580 | 97,169 | ||||||

| Investment securities – held to maturity (at cost) | 183,136 | 214,297 | ||||||

| Restricted investment in bank stock, at cost | 3,390 | 5,250 | ||||||

| Loans held for sale | 175 | 443 | ||||||

| Loans | 1,412,327 | 1,406,667 | ||||||

| Unearned fees | (314 | ) | (340 | ) | ||||

| Allowance for credit losses | (17,982 | ) | (17,480 | ) | ||||

| Net loans | 1,394,031 | 1,388,847 | ||||||

| Premises and equipment, net | 30,268 | 31,459 | ||||||

| Goodwill and other intangible assets | 12,021 | 12,103 | ||||||

| Bank owned life insurance | 47,933 | 47,607 | ||||||

| Deferred tax assets | 10,736 | 11,948 | ||||||

| Other real estate owned, net | 4,402 | 4,493 | ||||||

| Operating lease asset | 1,299 | 1,367 | ||||||

| Accrued interest receivable and other assets | 43,050 | 41,124 | ||||||

| Total Assets | $ | 1,912,953 | $ | 1,905,860 | ||||

| Liabilities and Shareholders’ Equity | ||||||||

| Liabilities: | ||||||||

| Non-interest bearing deposits | $ | 422,759 | $ | 427,670 | ||||

| Interest bearing deposits | 1,140,694 | 1,123,307 | ||||||

| Total deposits | 1,563,453 | 1,550,977 | ||||||

| Short-term borrowings | 79,494 | 45,418 | ||||||

| Long-term borrowings | 70,929 | 110,929 | ||||||

| Operating lease liability | 1,484 | 1,556 | ||||||

| Allowance for credit loss on off balance sheet exposures | 858 | 873 | ||||||

| Accrued interest payable and other liabilities | 29,925 | 32,904 | ||||||

| Dividends payable | 1,329 | 1,330 | ||||||

| Total Liabilities | 1,747,472 | 1,743,987 | ||||||

| Shareholders’ Equity: | ||||||||

| Common Stock – par value $0.01 per share; Authorized 25,000,000 shares; issued and outstanding 6,715,170 shares at September 30, 2023 and 6,666,428 at December 31, 2022 | 66 | 66 | ||||||

| Surplus | 23,865 | 23,734 | ||||||

| Retained earnings | 176,272 | 173,900 | ||||||

| Accumulated other comprehensive loss | (34,722 | ) | (35,827 | ) | ||||

| Total Shareholders’ Equity | 165,481 | 161,873 | ||||||

| Total Liabilities and Shareholders’ Equity | $ | 1,912,953 | $ | 1,905,860 | ||||

| 2024 | 2023 | |||||||||||||||||||

| Q1 | Q4 | Q3 | Q2 | Q1 | ||||||||||||||||

| In thousands | (Unaudited) | |||||||||||||||||||

| Interest income | ||||||||||||||||||||

| Interest and fees on loans | $ | 19,218 | $ | 19,290 | $ | 18,055 | $ | 16,780 | $ | 15,444 | ||||||||||

| Interest on investment securities | ||||||||||||||||||||

| Taxable | 1,744 | 1,834 | 1,792 | 1,779 | 1,768 | |||||||||||||||

| Exempt from federal income tax | 53 | 53 | 123 | 268 | 270 | |||||||||||||||

| Total investment income | 1,797 | 1,887 | 1,915 | 2,047 | 2,038 | |||||||||||||||

| Other | 883 | 1,014 | 1,194 | 1,145 | 347 | |||||||||||||||

| Total interest income | 21,898 | 22,191 | 21,164 | 19,972 | 17,829 | |||||||||||||||

| Interest expense | ||||||||||||||||||||

| Interest on deposits | 6,266 | 6,498 | 5,672 | 4,350 | 2,678 | |||||||||||||||

| Interest on short-term borrowings | 461 | 54 | 33 | 29 | 31 | |||||||||||||||

| Interest on long-term borrowings | 1,359 | 1,445 | 1,475 | 1,419 | 602 | |||||||||||||||

| Total interest expense | 8,086 | 7,997 | 7,180 | 5,798 | 3,311 | |||||||||||||||

| Net interest income | 13,812 | 14,194 | 13,984 | 14,174 | 14,518 | |||||||||||||||

| Credit loss expense/(credit) | ||||||||||||||||||||

| Loans | 961 | 530 | 322 | 434 | 414 | |||||||||||||||

| Debt securities held to maturity | — | — | 45 | — | — | |||||||||||||||

| Off balance sheet credit exposures | (15 | ) | (111 | ) | (104 | ) | (39 | ) | 129 | |||||||||||

| Provision for credit losses | 946 | 419 | 263 | 395 | 543 | |||||||||||||||

| Net interest income after provision for credit losses | 12,866 | 13,775 | 13,721 | 13,779 | 13,975 | |||||||||||||||

| Other operating income | ||||||||||||||||||||

| Net losses on investments, available for sale | — | (4,214 | ) | — | — | — | ||||||||||||||

| Gains on sale of residential mortgage loans | 82 | 59 | 182 | 86 | 54 | |||||||||||||||

| Losses on disposal of fixed assets | — | (29 | ) | — | — | — | ||||||||||||||

| Net gains/(losses) | 82 | (4,184 | ) | 182 | 86 | 54 | ||||||||||||||

| Other Income | ||||||||||||||||||||

| Service charges on deposit accounts | 556 | 567 | 569 | 546 | 516 | |||||||||||||||

| Other service charges | 215 | 223 | 230 | 244 | 232 | |||||||||||||||

| Trust department | 2,188 | 2,148 | 2,139 | 2,025 | 1,970 | |||||||||||||||

| Debit card income | 932 | 1,120 | 995 | 1,031 | 955 | |||||||||||||||

| Bank owned life insurance | 326 | 325 | 320 | 311 | 305 | |||||||||||||||

| Brokerage commissions | 495 | 360 | 245 | 258 | 297 | |||||||||||||||

| Other | 81 | 50 | 218 | 68 | 64 | |||||||||||||||

| Total other income | 4,793 | 4,793 | 4,716 | 4,483 | 4,339 | |||||||||||||||

| Total other operating income | 4,875 | 609 | 4,898 | 4,569 | 4,393 | |||||||||||||||

| Other operating expenses | ||||||||||||||||||||

| Salaries and employee benefits | 7,157 | 6,390 | 6,964 | 6,870 | 7,296 | |||||||||||||||

| FDIC premiums | 269 | 268 | 254 | 277 | 193 | |||||||||||||||

| Equipment | 923 | 912 | 718 | 747 | 780 | |||||||||||||||

| Occupancy | 954 | 1,169 | 745 | 742 | 785 | |||||||||||||||

| Data processing | 1,318 | 1,384 | 1,388 | 1,306 | 1,306 | |||||||||||||||

| Marketing | 134 | 311 | 242 | 160 | 120 | |||||||||||||||

| Professional services | 486 | 631 | 488 | 520 | 494 | |||||||||||||||

| Contract labor | 183 | 170 | 155 | 157 | 134 | |||||||||||||||

| Telephone | 109 | 125 | 115 | 116 | 110 | |||||||||||||||

| Other real estate owned | 86 | (370 | ) | 139 | 18 | 124 | ||||||||||||||

| Investor relations | 53 | 65 | 74 | 123 | 83 | |||||||||||||||

| Contributions | 32 | 12 | 74 | 79 | 64 | |||||||||||||||

| Other | 1,177 | 1,242 | 1,429 | 1,396 | 1,149 | |||||||||||||||

| Total other operating expenses | 12,881 | 12,309 | 12,785 | 12,511 | 12,638 | |||||||||||||||

| Income before income tax expense | 4,860 | 2,075 | 5,834 | 5,837 | 5,730 | |||||||||||||||

| Provision for income tax expense | 1,162 | 317 | 1,321 | 1,423 | 1,355 | |||||||||||||||

| Net Income | $ | 3,698 | $ | 1,758 | $ | 4,513 | $ | 4,414 | $ | 4,375 | ||||||||||

| Basic net income per common share | $ | 0.56 | $ | 0.26 | $ | 0.67 | $ | 0.66 | $ | 0.66 | ||||||||||

| Diluted net income per common share | $ | 0.56 | $ | 0.26 | $ | 0.67 | $ | 0.66 | $ | 0.65 | ||||||||||

| Weighted average number of basic shares outstanding | 6,642 | 6,649 | 6,714 | 6,704 | 6,675 | |||||||||||||||

| Weighted average number of diluted shares outstanding | 6,655 | 6,663 | 6,728 | 6,718 | 6,697 | |||||||||||||||

| Dividends declared per common share | $ | 0.20 | $ | 0.20 | $ | 0.20 | $ | 0.20 | $ | 0.20 | ||||||||||

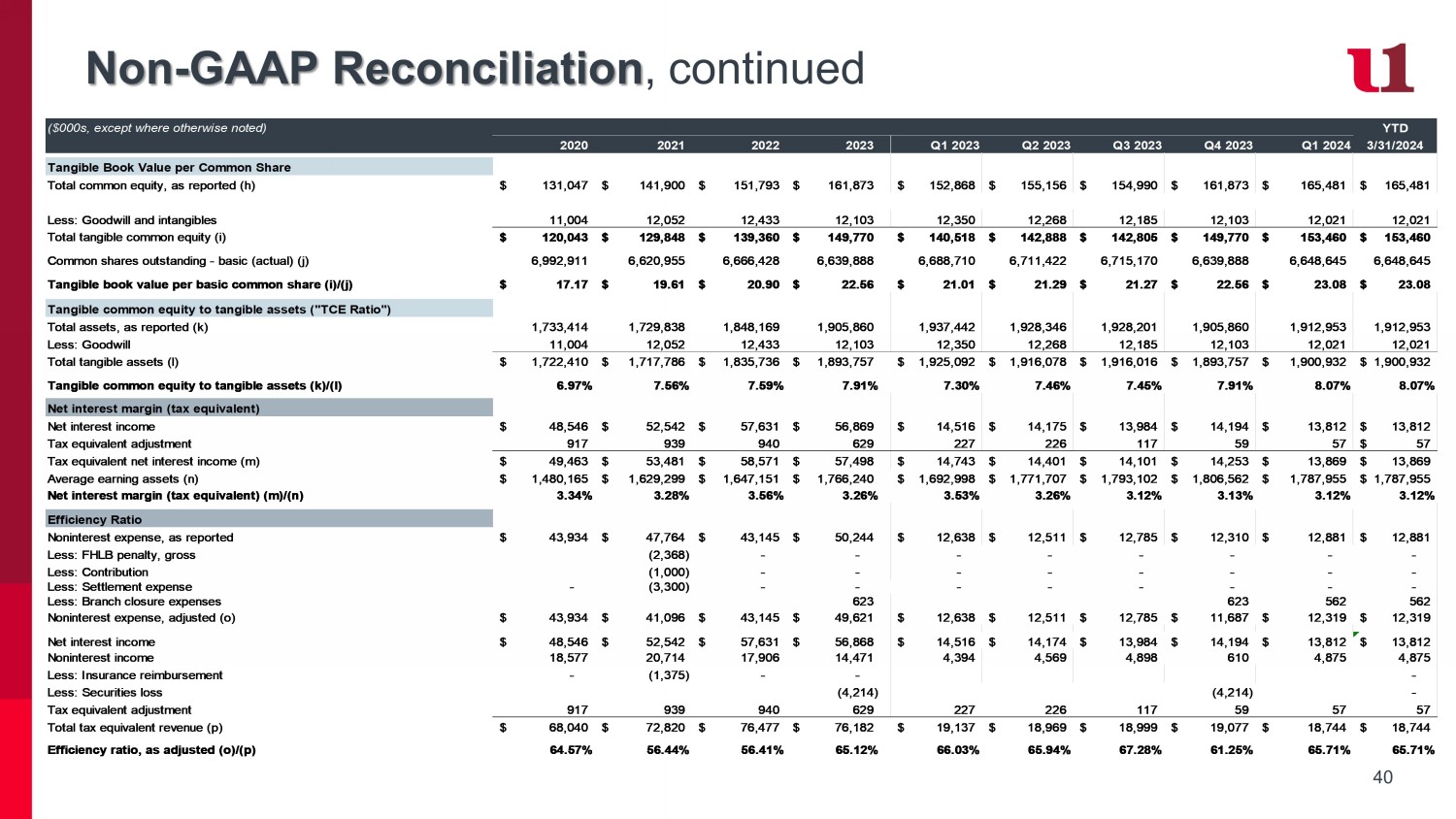

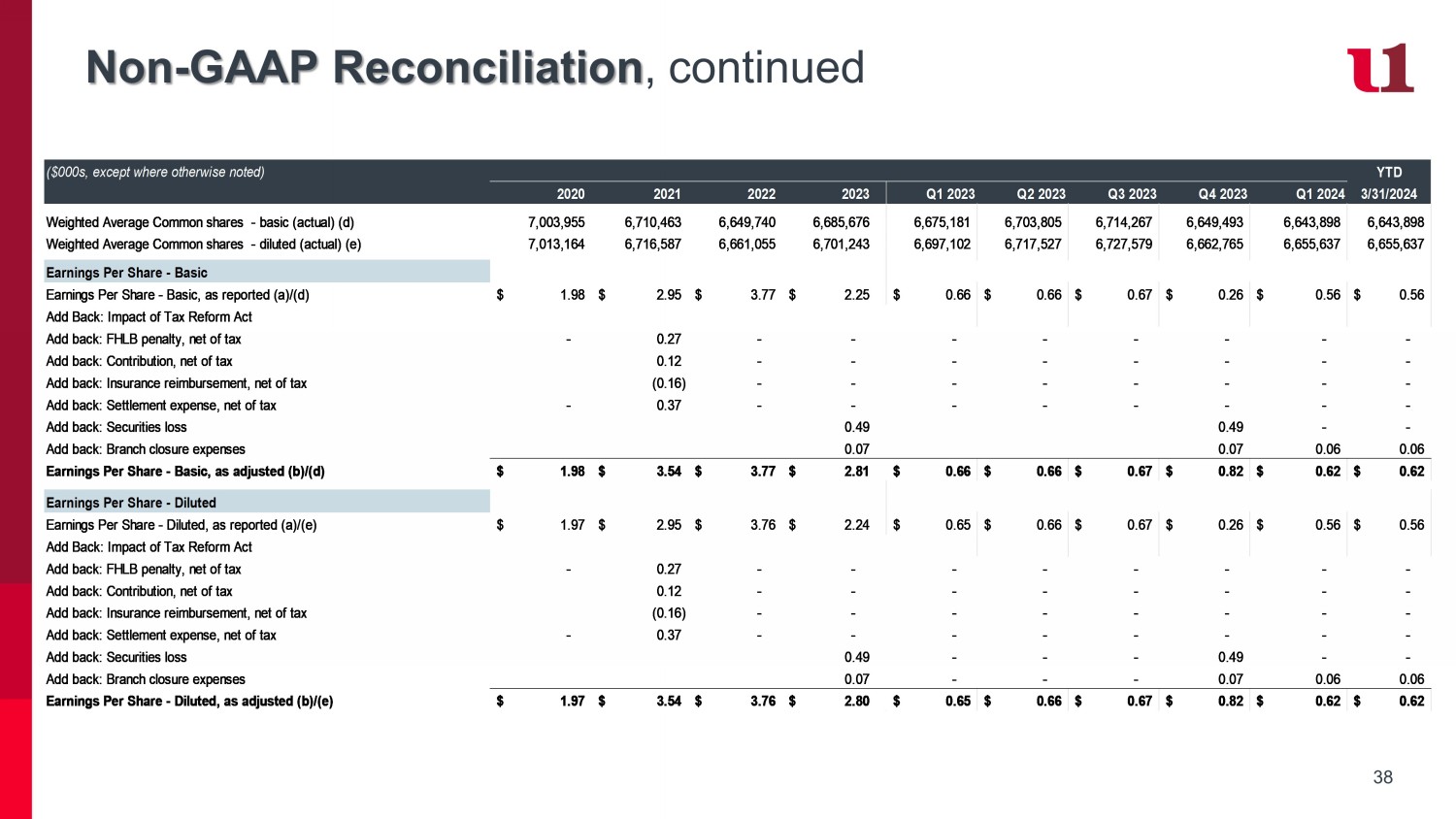

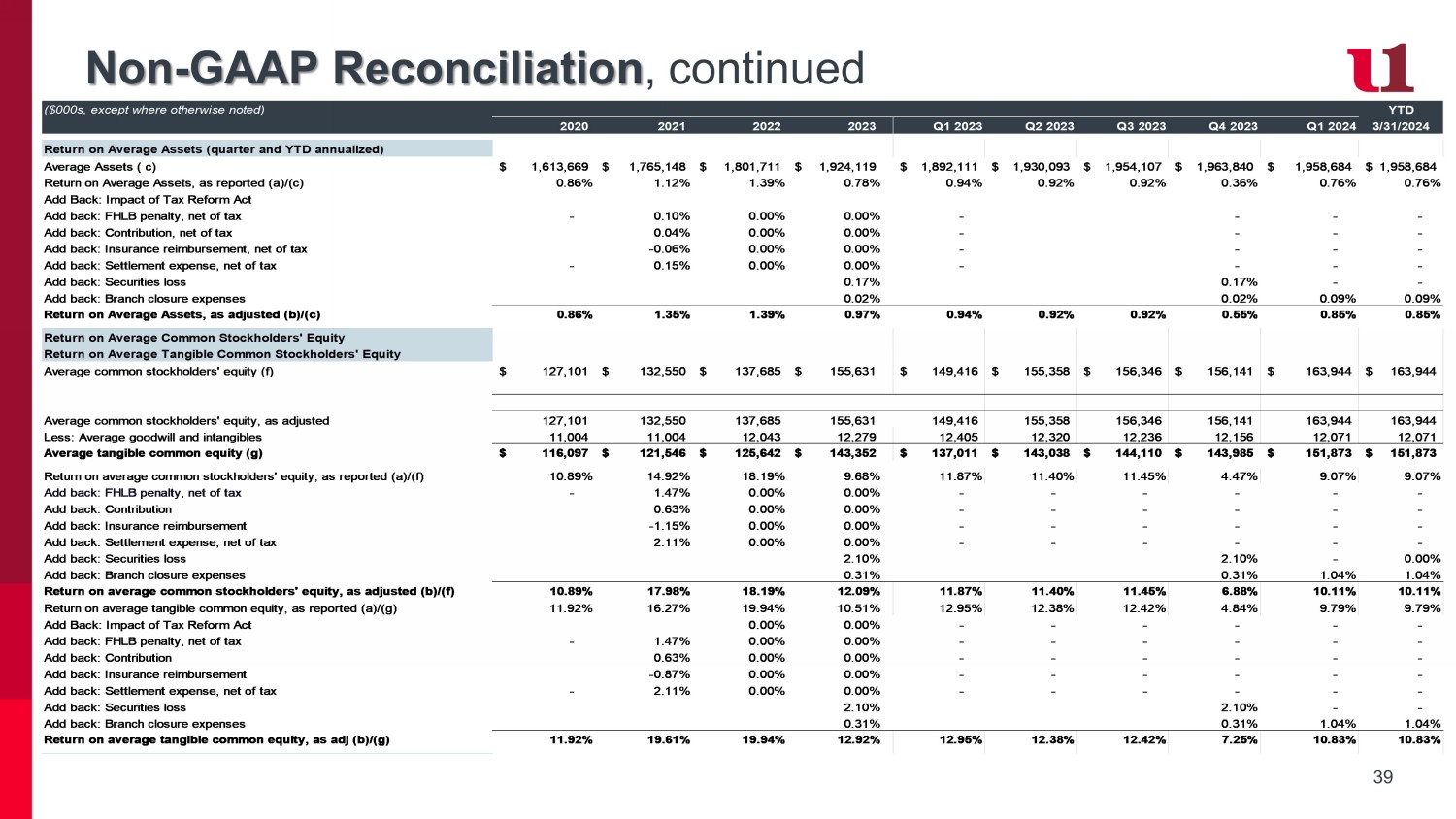

Non-GAAP Financial Measures (unaudited)

Reconciliation of as reported (GAAP) and non-GAAP financial measures

The following tables below provide a reconciliation of certain financial measures calculated under generally accepted accounting principles ("GAAP") (as reported) and non-GAAP. A non-GAAP financial measure is a numerical measure of historical or future financial performance, financial position or cash flows that excludes or includes amounts that are required to be disclosed in the most directly comparable measure calculated and presented in accordance with GAAP in the United States. The Company’s management believes the presentation of non-GAAP financial measures provide investors with a greater understanding of the Company’s operating results in addition to the results measured in accordance with GAAP. While management uses these non-GAAP measures in its analysis of the Company’s performance, this information should not be viewed as a substitute for financial results determined in accordance with GAAP or considered to be more important than financial results determined in accordance with GAAP.

The following non-GAAP financial measures exclude accelerated depreciation expenses related to the branch closures.

| Three months ended March 31, | ||||||||

| (in thousands, except for per share amount) | 2024 | 2023 | ||||||

| Net income - as reported | $ | 3,698 | $ | 4,376 | ||||

| Adjustments: | ||||||||

| Accelerated depreciation expenses | 562 | — | ||||||

| Income tax effect of adjustments | (137 | ) | — | |||||

| Adjusted net income (non-GAAP) | $ | 4,123 | $ | 4,376 | ||||

| Diluted earnings per share - as reported | $ | 0.56 | $ | 0.65 | ||||

| Adjustments: | ||||||||

| Accelerated depreciation expenses | 0.08 | — | ||||||

| Income tax effect of adjustments | (0.02 | ) | — | |||||

| Adjusted basic and diluted earnings per share (non-GAAP) | $ | 0.62 | $ | 0.65 | ||||

| As of or for the three months ended |

||||||||

| March 31, | ||||||||

| (in thousands, except per share data) | 2024 | 2023 | ||||||

| Per Share Data | ||||||||

| Basic net income per share (1) - as reported | $ | 0.56 | $ | 0.66 | ||||

| Basic net income per share (1) - non-GAAP | 0.62 | 0.66 | ||||||

| Diluted net income per share (1) - as reported | $ | 0.56 | $ | 0.65 | ||||

| Diluted net income per share (1) - non-GAAP | 0.62 | 0.65 | ||||||

| Basic book value per share | $ | 24.89 | $ | 22.85 | ||||

| Diluted book value per share | $ | 24.86 | $ | 22.81 | ||||

| Significant Ratios: | ||||||||

| Return on Average Assets (1) - as reported | 0.76 | % | 0.94 | % | ||||

| Accelerated depreciation expenses | 0.12 | % | — | |||||

| Income tax effect of adjustments | (0.03 | %) | — | |||||

| Adjusted Return on Average Assets (1) (non-GAAP) | 0.85 | % | 0.94 | % | ||||

| Return on Average Equity (1) - as reported | 9.07 | % | 11.87 | % | ||||

| Accelerated depreciation expenses | 1.38 | % | — | |||||

| Income tax effect of adjustments | (0.34 | %) | — | |||||

| Adjusted Return on Average Equity (1) (non-GAAP) | 10.11 | % | 11.87 | % | ||||

(1) See reconcilation of this non-GAAP financial measure provided elsewhere herein.

| Three Months Ended | ||||||||||||||||||||||||

| March 31 | ||||||||||||||||||||||||

| 2024 | 2023 | |||||||||||||||||||||||

| (dollars in thousands) | Average Balance |

Interest | Average Yield/Rate |

Average Balance |

Interest | Average Yield/Rate |

||||||||||||||||||

| Assets | ||||||||||||||||||||||||

| Loans | $ | 1,407,886 | $ | 19,234 | 5.49 | % | $ | 1,279,547 | $ | 15,457 | 4.90 | % | ||||||||||||

| Investment Securities: | ||||||||||||||||||||||||

| Taxable | 294,526 | 1,744 | 2.38 | % | 340,622 | 1,768 | 2.11 | % | ||||||||||||||||

| Non taxable | 7,806 | 94 | 4.84 | % | 26,104 | 484 | 7.52 | % | ||||||||||||||||

| Total | 302,332 | 1,838 | 2.45 | % | 366,726 | 2,252 | 2.49 | % | ||||||||||||||||

| Federal funds sold | 63,843 | 758 | 4.78 | % | 40,092 | 307 | 3.11 | % | ||||||||||||||||

| Interest-bearing deposits with other banks | 8,787 | 31 | 1.42 | % | 5,001 | 26 | 2.11 | % | ||||||||||||||||

| Other interest earning assets | 5,107 | 94 | 7.40 | % | 1,632 | 14 | 3.48 | % | ||||||||||||||||

| Total earning assets | 1,787,955 | 21,955 | 4.94 | % | 1,692,998 | 18,056 | 4.33 | % | ||||||||||||||||

| Allowance for credit losses | (17,696 | ) | (14,816 | ) | ||||||||||||||||||||

| Non-earning assets | 188,425 | 213,929 | ||||||||||||||||||||||

| Total Assets | $ | 1,958,684 | $ | 1,892,111 | ||||||||||||||||||||

| Liabilities and Shareholders’ Equity | ||||||||||||||||||||||||

| Interest-bearing demand deposits | $ | 348,998 | $ | 1,441 | 1.66 | % | $ | 353,072 | $ | 888 | 1.02 | % | ||||||||||||

| Interest-bearing money markets | 322,965 | 3,260 | 4.06 | % | 340,128 | 1,298 | 1.55 | % | ||||||||||||||||

| Savings deposits | 189,572 | 48 | 0.10 | % | 246,708 | 79 | 0.13 | % | ||||||||||||||||

| Time deposits - retail | 157,678 | 1,118 | 2.85 | % | 118,667 | 281 | 0.96 | % | ||||||||||||||||

| Time deposits - brokered | 30,000 | 399 | 5.35 | % | 10,180 | 132 | 5.26 | % | ||||||||||||||||

| Short-term borrowings | 73,351 | 461 | 2.53 | % | 57,364 | 31 | 0.22 | % | ||||||||||||||||

| Long-term borrowings | 103,017 | 1,359 | 5.31 | % | 43,373 | 602 | 5.63 | % | ||||||||||||||||

| Total interest-bearing liabilities | 1,225,581 | 8,086 | 2.65 | % | 1,169,492 | 3,311 | 1.15 | % | ||||||||||||||||

| Non-interest-bearing deposits | 534,413 | 545,215 | ||||||||||||||||||||||

| Other liabilities | 34,746 | 27,988 | ||||||||||||||||||||||

| Shareholders’ Equity | 163,944 | 149,416 | ||||||||||||||||||||||

| Total Liabilities and Shareholders’ Equity | $ | 1,958,684 | $ | 1,892,111 | ||||||||||||||||||||

| Net interest income and spread | $ | 13,869 | 2.29 | % | $ | 14,745 | 3.18 | % | ||||||||||||||||

| Net interest margin | 3.12 | % | 3.53 | % | ||||||||||||||||||||

Exhibit 99.2

MyBank.com INVESTOR PRESENTATION First Quarter 2024

2 Forward looking statements This presentation contains forward - looking statements as defined by the Private Securities Litigation Reform Act of 1995 . Forward - looking statements do not represent historical facts, but are statements about management's beliefs, plans and objectives about the future, as well as its assumptions and judgments concerning such beliefs, plans and objectives . These statements are evidenced by terms such as "anticipate," "estimate," "should," "expect," "believe," "intend," and similar expressions . Although these statements reflect management's good faith beliefs and projections, they are not guarantees of future performance and they may not prove true . The beliefs, plans and objectives on which forward - looking statements are based involve risks and uncertainties that could cause actual results to differ materially from those addressed in the forward - looking statements . For a discussion of these risks and uncertainties, see the section of the periodic reports that First United Corporation files with the Securities and Exchange Commission entitled "Risk Factors . Whether actual results will conform to expectations and predictions is subject to known and unknown risks and uncertainties . Actual results could be materially different from management’s expectations . This presentation should be read in conjunction with our Annual Report on Form 10 - K, as amended, for the year ended December 31 , 2023 , including the sections of the report entitled “Risk Factors”, as well as the reports and other documents that we subsequently file with the Securities and Exchange Commission (“SEC”), which are available on the SEC’s website at www . sec . gov or at our website at www . mybank . com . Except as required by law, we do not intend to publish updates or revisions of any forward - looking statements we make to reflect new information, future events or otherwise .

3 I. II. II. Corporate Overview Financial Performance Appendices Pg. 4 Pg. 9 Pg. 30 Table of Contents Our Mission To enrich the lives of our associates, customers, communities and shareholders through uncommon commitment to service and customized financial solutions.

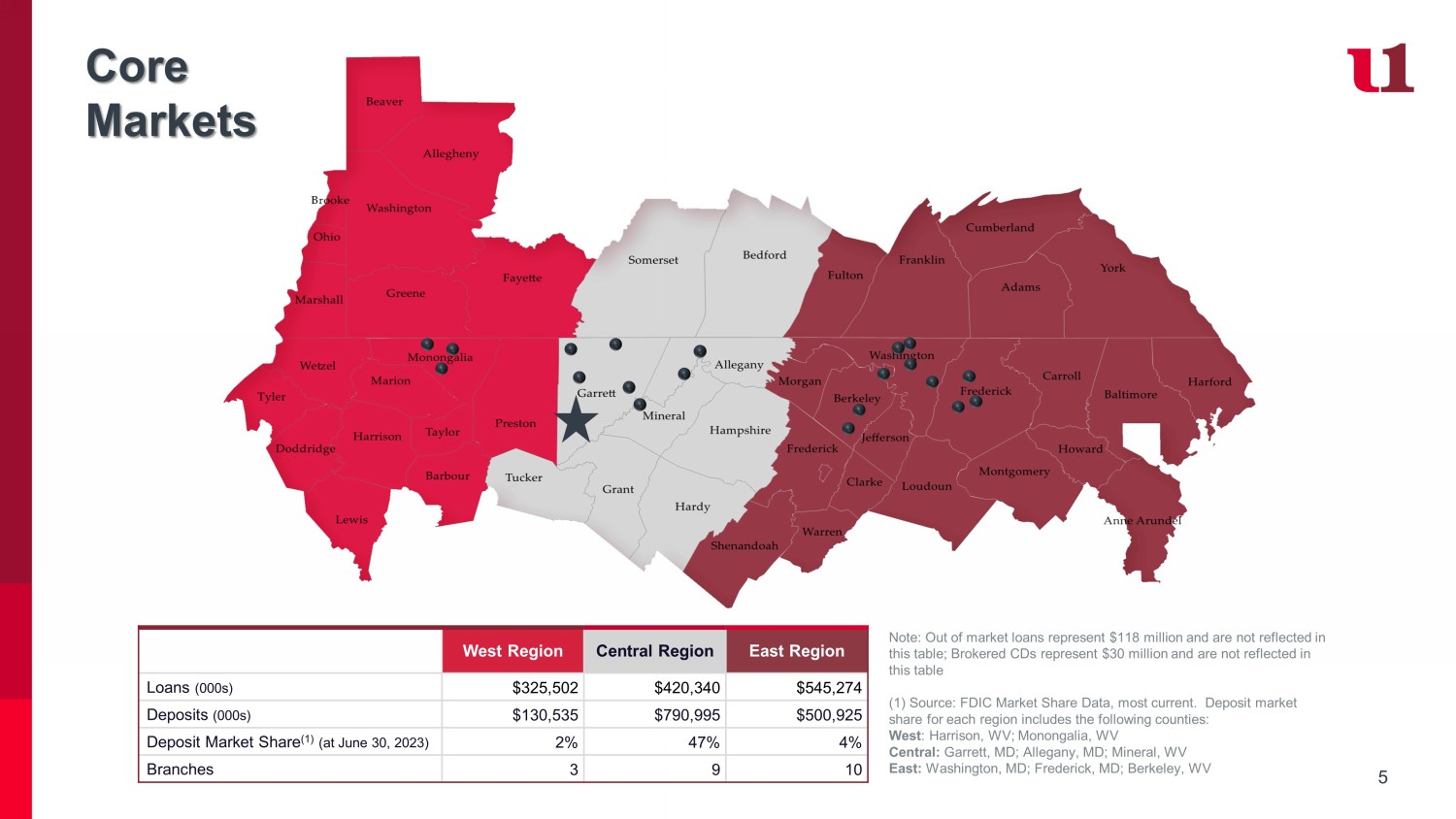

Corporate Overview Founded: 1900 Headquarters: Oakland, MD Locations: 22 branches Business Lines: ▪ Commercial & Retail Banking ▪ Trust Services ▪ Wealth Management Ticker: FUNC (Nasdaq) Website: www.MyBank.com Overview West Virginia Maryland • Pittsburgh, PA • Washington, DC • Columbus, OH • Baltimore, MD • Richmond, VA Morgantown, WV භ • Philadelphia, PA • Harrisburg, PA Winchester, VA භ Star denotes Oakland, Maryland Headquarters 4 5 West Region Central Region East Region Loans (000s) $325,502 $420,340 $545,274 Deposits (000s) $130,535 $790,995 $500,925 Deposit Market Share (1) (at June 30, 2023) 2% 47% 4% Branches 3 9 10 Note: Out of market loans represent $118 million and are not reflected in this table; Brokered CDs represent $30 million and are not reflected in this table (1) Source: FDIC Market Share Data, most current.

Deposit market share for each region includes the following counties: West : Harrison, WV; Monongalia, WV Central: Garrett, MD; Allegany, MD; Mineral, WV East: Washington, MD; Frederick, MD; Berkeley, WV Core Markets 6 Core Strengths ▪ Diversified revenue stream driven by trust and brokerage fee income provides protection during times of low interest rates Diversified Revenue Stream ▪ Stable legacy markets produce steady low - cost funding ▪ Technology and business relationships drive growth Core Deposit Franchise ▪ Diverse and experienced Board with the skills to oversee risks, strategic initiatives and governance best practices ▪ Ongoing Board succession strategy Engaged & Diverse Leadership ▪ Supporting local causes with financial education, consultation and robust products and services ▪ Knowledgeable associates committed to helping clients & the communities we serve Culture of Engagement ▪ Well - established operational infrastructure will support future growth ▪ Expense management focus, hybrid work environment and technology drive cost savings Expense Structure ▪ Strong underwriting guidelines and risk management framework ▪ Focus on risk mitigation, loan concentration management and information security Robust Enterprise Risk Management ▪ Innovative and dynamic approach to attracting and retaining clients ▪ Investment in FinTech funds provides early exposure to new technology Forward - Thinking Approach ▪ Regulatory capital ratios significantly above regulatory requirements ▪ Significant access to liquidity sources Financial Strength 7 Risk Management, Monitoring & Mitigation Underlies all Strategic Priorities ▪ Low net charge - offs and stable asset quality resulting from conservative and proactive credit culture ▪ ACL level of 1.27%; future provisioning based on loan growth, economic environment and asset quality changes ▪ Diversified commercial loan portfolio and geographic footprint ▪ Disciplined loan growth strategy, concentration management, stress testing and exception tracking and monitoring ▪ Well - defined loan approval levels ▪ Centralized risk rating and monitoring of risk rating migration and delinquency trends ▪ Robust annual third - party loan review ▪ Maintaining a slightly asset sensitive balance sheet and positioning for down rate environment ▪ Limiting longer - term investment exposure and actively managing loan and deposit terms ▪ Focused on capturing core, low - cost deposits ▪ Monitoring dynamic and static rate ramp scenarios ▪ Board regularly briefed on cyber - security matters ▪ Robust information security training programs for associates and Board ▪ Regular third - party review and testing of information security, compliance processes and cybersecurity controls ▪ No security breaches to - date ▪ Adaptive fraud detection and management ▪ Strong capital levels well above regulatory “well - capitalized” definition ▪ Conservative dividend payout policy to improve TCE and maintain capital during this turbulent economic environment ▪ Capital stress tests indicate Bank is well positioned to absorb potential losses ▪ Loan to deposit ratio of 90% ▪ Liquidity contingency plan in place and funds position monitored daily ▪ Liquidity stress testing performed quarterly with strong liquidity under various scenarios ▪ Available borrowing capacity of $365 million through correspondent lines of credit, FHLB and the Federal Reserve ▪ Strong, stable low - cost core deposit franchise of 88% of total deposit portfolio Cyber - Security & Fraud Monitoring Asset Quality Capital Liquidity Management Interest Rate Sensitivity Strategic Pillars & Key Objectives Culture & Human Capital ▪ Attract and hire passionate, diverse talent to engage with clients and prospects across broader geographics.

▪ Drive associate retention and foster career development through mentoring initiatives, leadership programs, and educational opportunities. ▪ Expand associate engagement , cross - functional collaboration , and communication . ▪ Enhance succession plan by fostering forward - thinking strategies that promote innovation and long - term growth. Product & Service Revenue Diversification ▪ Increase non - interest income as a percentage of revenue to reduce dependence on net interest margin. ▪ Expand business development training and outreach efforts to drive strategic sales growth and deepen community - oriented business owner relationships . ▪ Revamp customer segmentation to focus on expanding product and service utilization by the existing customer base. ▪ Improve brand awareness in growth markets. Resource Optimization ▪ Optimize balance sheet mix to maximize profitability. ▪ Expand net interest margin through a disciplined approach to loan and deposit portfolio repricing. ▪ Effectively manage Capital through repurchase opportunities and effective investor communication . ▪ Improve efficiency by utilizing technology, leveraging data, artificial intelligence, and digital alternatives. ▪ Reduce monetary loss and administrative costs associated with cyber security and fraud. ▪ Allocate resources to enhance market share and execute tactics to optimize geographic presence. ▪ Cultivate relationships for potential future bank and wealth expansion. Effective use of technology, marketing and communications, and an environmental focus underlies all strategic priorities. 8 First Quarter Financial Highlights $4.1 Million Net Income (1) $0.62 Diluted EPS (1) 0.85% * ROAA (1) 10.11% * ROATCE (1) 3.12% NIM ▪ Total assets increased $7.1 million compared to December 31, 2023 ▪ Consolidated net income (1) of $4.1 million in 1Q24 compared to $4.4 million in 1Q23 and $5.5 million in linked quarter; pre - provision net revenue of $6.4 million compared to $6.3 million and $7.3, respectively ▪ Net interest income, on a non - GAAP, FTE basis* decreased by 2.69% in 1Q24 compared to 4Q23, driven by a 1.33% decrease in interest income and a 1.09% increase in interest expense, primarily resulting from the reversal of interest and fees on two non - accrual loan relationships and the continued competitive deposit landscape ▪ Asset quality remains strong with the ratio of the allowance for credit losses (“ACL”) to loans outstanding at 1.27% in 1Q24 and 1.24% in the linked quarter ▪ Efficiency ratio of 65.71% (1) for the first quarter of 2024 compared to 61.25% for the linked quarter; increase primarily related to reduced net interest income, increased salaries and benefits and gains on sales of OREO properties in the fourth quarter of 2023 (1) See Appendix for a reconciliation of these non - GAAP financial measure * 1Q2024 Annualized 9

10 Long - Term Growth Pre - Provision Net Revenue ($ in millions) (1) $23.2 $30.8 $32.5 $25.9 $6.40 2020 2021 2022 2023 1Q2024 +5.5% YoY (1) See Appendix for a reconciliation of these non - GAAP financial measures $1.97 $3.54 $3.76 $2.80 $0.62 2020 2021 2022 2023 1Q2024 +6.2% YoY Diluted Earnings per Share (1) Total Deposits ($ in millions) $1,422 $1,469 $1,571 $1,551 $1,563 2020 2021 2022 2023 1Q2024 +6.9% YoY Total Gross Loans, including PPP ($ in millions) $1,168 $1,154 $1,279 $1,407 $1,412 2020 2021 2022 2023 1Q2024 +10.8% YoY $114 PPP $8 PPP 11 Solid Profitability (1) See Appendix for a reconciliation of these non - GAAP financial measures 11.92% 19.78% 19.94% 12.92% 10.11% 2020 2021 2022 2023 1Q2024 Long - term Strategic Target 13% - 15% 0.86% 1.35% 1.39% 0.97% 0.85% 2020 2021 2022 2023 1Q2024 Long - term Strategic Target 1.25% - 1.60% Core ROAA (non - GAAP (1) ) Core ROATCE (non - GAAP (1) )

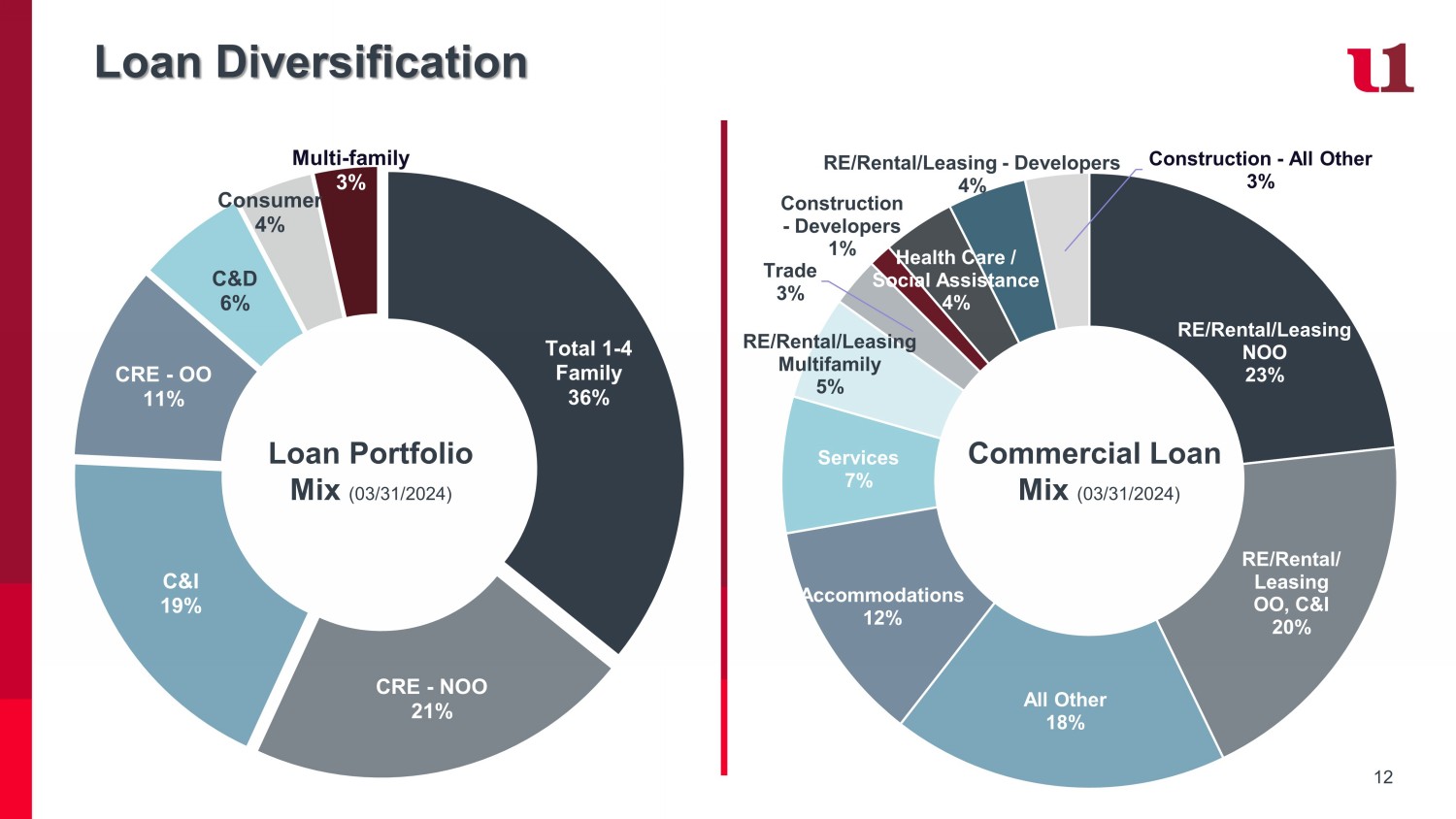

12 Total 1 - 4 Family 36% CRE - NOO 21% C&I 19% CRE - OO 11% C&D 6% Consumer 4% Multi - family 3% Loan Diversification Loan Portfolio Mix (03/31/2024) RE/Rental/Leasing NOO 23% RE/Rental/ Leasing OO, C&I 20% All Other 18% Accommodations 12% Services 7% RE/Rental/Leasing Multifamily 5% Trade 3% Construction - Developers 1% Health Care / Social Assistance 4% RE/Rental/Leasing - Developers 4% Construction - All Other 3% Commercial Loan Mix (03/31/2024)

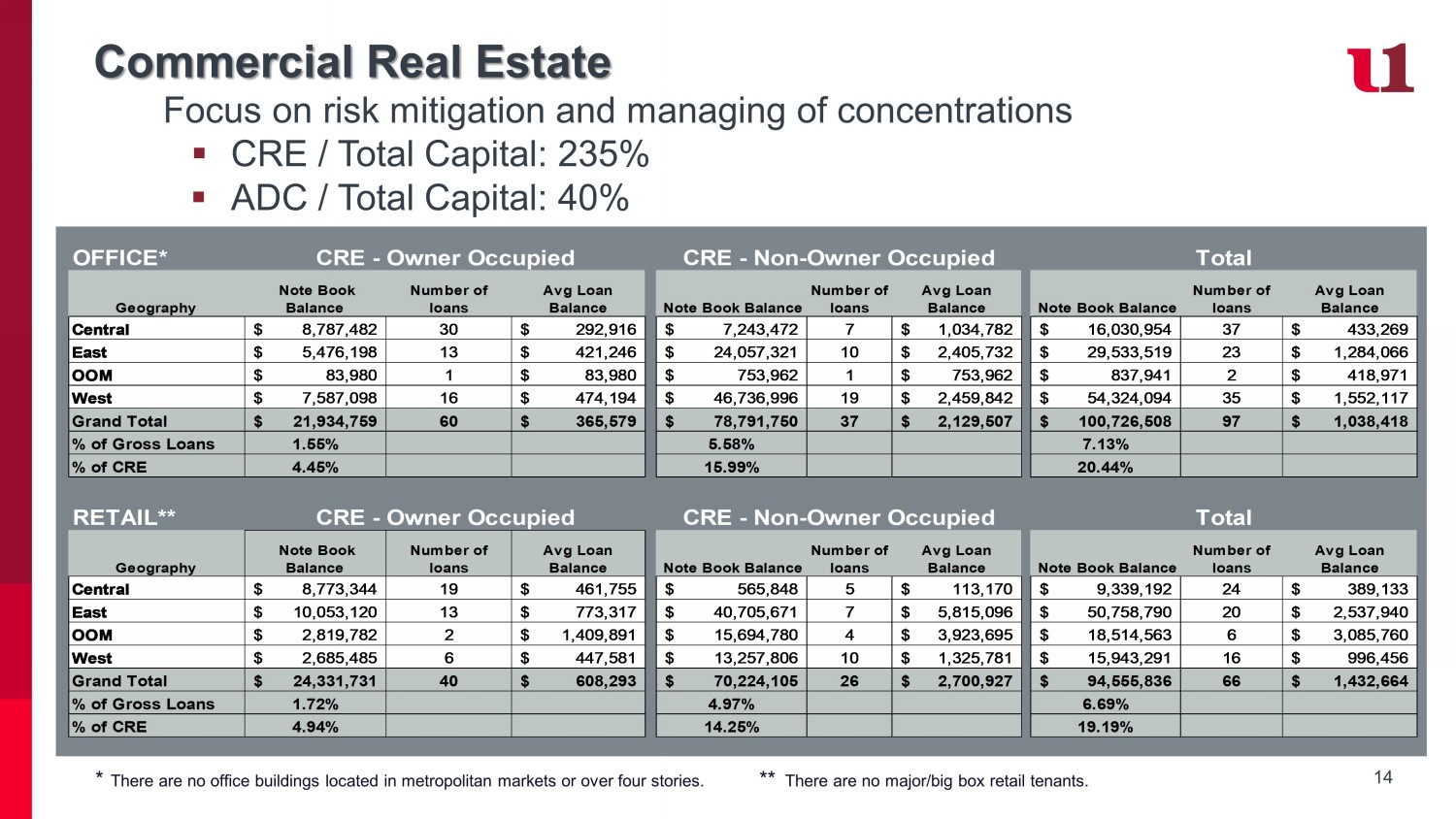

13 Commercial Industry Mix by Origination Year Commercial Industry Mix by Origination Prior to 2000 2000 - 2005 2006 - 2010 2011 - 2015 2016 - 2020 2021 - Current Total RE / Rental / Leasing - NOO -$ 4,421,846$ 3,072,508$ 12,117,472$ 86,379,551$ 102,222,237$ 208,213,614$ RE / Rental / Leasing - OO, C&I 17,036 33,712 1,292,299 8,036,116 50,084,263 115,718,222 175,181,649 RE / Rental / Leasing - Multifamily - 68,279 2,189,013 9,767,575 16,236,615 21,106,491 49,367,973 RE / Rental / Leasing - Developers - 73,434 78,567 - 3,157,347 33,732,433 37,041,781 Construction - All Other 36,249 83,388 112,482 1,827,468 8,176,626 19,479,990 29,716,203 Construction - Developers - - 2,283,871 81,485 1,191,725 7,595,098 11,152,179 Accommodations - 1,447,880 3,890,403 10,750,875 48,121,052 21,749,054 85,959,264 Services - 2,258,665 497,985 9,503,482 14,368,114 37,718,380 64,346,626 Health Care / Social Assistance - 1,969,994 5,053,420 8,662,776 18,172,300 33,858,490 Trade - 109,973 253,324 1,312,242 10,044,115 11,574,983 23,294,637 All Other 38,247 302,412 1,240,201 881,185 28,317,174 127,425,277 158,204,496 Totals 91,532$ 8,799,589$ 16,880,647$ 59,331,320$ 274,739,358$ 516,494,465$ 876,336,912$ 14 Commercial Real Estate Focus on risk mitigation and managing of concentrations ▪ CRE / Total Capital: 235% ▪ ADC / Total Capital: 40% * There are no office buildings located in metropolitan markets or over four stories.

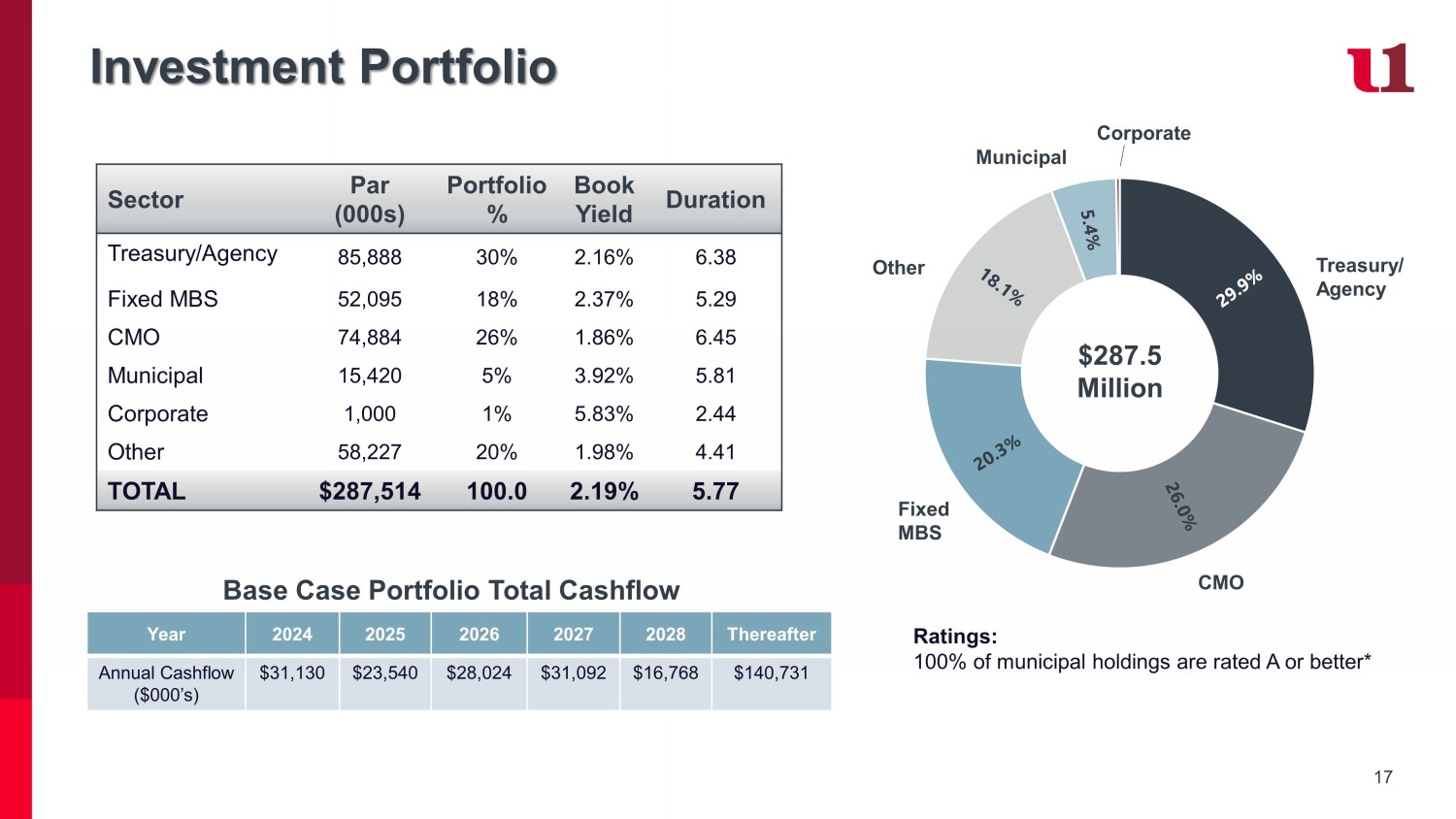

** There are no major/big box retail tenants. OFFICE* Geography Note Book Balance Number of loans Avg Loan Balance Note Book Balance Number of loans Avg Loan Balance Note Book Balance Number of loans Avg Loan Balance Central 8,787,482$ 30 292,916$ 7,243,472$ 7 1,034,782$ 16,030,954$ 37 433,269$ East 5,476,198$ 13 421,246$ 24,057,321$ 10 2,405,732$ 29,533,519$ 23 1,284,066$ OOM 83,980$ 1 83,980$ 753,962$ 1 753,962$ 837,941$ 2 418,971$ West 7,587,098$ 16 474,194$ 46,736,996$ 19 2,459,842$ 54,324,094$ 35 1,552,117$ Grand Total 21,934,759$ 60 365,579$ 78,791,750$ 37 2,129,507$ 100,726,508$ 97 1,038,418$ % of Gross Loans 1.55% 5.58% 7.13% % of CRE 4.45% 15.99% 20.44% RETAIL** Geography Note Book Balance Number of loans Avg Loan Balance Note Book Balance Number of loans Avg Loan Balance Note Book Balance Number of loans Avg Loan Balance Central 8,773,344$ 19 461,755$ 565,848$ 5 113,170$ 9,339,192$ 24 389,133$ East 10,053,120$ 13 773,317$ 40,705,671$ 7 5,815,096$ 50,758,790$ 20 2,537,940$ OOM 2,819,782$ 2 1,409,891$ 15,694,780$ 4 3,923,695$ 18,514,563$ 6 3,085,760$ West 2,685,485$ 6 447,581$ 13,257,806$ 10 1,325,781$ 15,943,291$ 16 996,456$ Grand Total 24,331,731$ 40 608,293$ 70,224,105$ 26 2,700,927$ 94,555,836$ 66 1,432,664$ % of Gross Loans 1.72% 4.97% 6.69% % of CRE 4.94% 14.25% 19.19% CRE - Owner Occupied CRE - Non-Owner Occupied Total CRE - Owner Occupied CRE - Non-Owner Occupied Total 15 Variable Rate Loans and Repricing * Includes personal lines of credit and home equity lines Loan Type Reprices Monthly % to Total Type Repricing Repricing 2024 % to Total Type Repricing Repricing 2025 % to Total Type Repricing Repricing 2026 + % to Total Type Repricing Grand Total Commercial Loans 19,511,032$ 11.1% 36,084,763$ 52.7% 12,354,586$ 46.0% 94,718,338$ 31.2% 162,668,718$ Commercial Lines of Credit 68,379,208 38.9% - 0.0% - 0.0% 414,293 0.1% 68,793,501 Commercial Floor Plans 32,939,120 18.7% - 0.0% - 0.0% - 0.0% 32,939,120 Mortgage - 0.0% 32,370,739 47.3% 14,520,735 54.0% 208,557,738 68.7% 255,449,212 Home Equity Lines (no Locks) 11,806,596 6.7% - 0.0% - 0.0% - 0.0% 11,806,596 Other Consumer Lines* 43,067,208 24.5% - 0.0% - 0.0% - 0.0% 43,067,208 Totals 175,703,165$ 100.0% 68,455,502$ 100.0% 26,875,320$ 100.0% 303,690,369$ 100.0% 574,724,355$

16 Credit Quality ALL / ACL Trends (Net Charge - Offs)/Average Loans 0.13% - 0.02% - 0.02% - 0.07% - 0.13% 2020 2021 2022 2023 1Q2024 Nonaccrual Loans / Total Loans 0.35% 0.21% 0.27% 0.28% 1.13% 2020 2021 2022 2023 1Q2024 NPAs / Total Assets 0.99% 0.60% 0.46% 0.48% 1.07% 2020 2021 2022 2023 1Q2024 1.41% 1.38% 1.14% 1.24% 1.27% 2020 2021 2022 2023 1Q2024 17 Investment Portfolio Sector Par (000s) Portfolio % Book Yield Duration Treasury/Agency 85,888 30% 2.16% 6.38 Fixed MBS 52,095 18% 2.37% 5.29 CMO 74,884 26% 1.86% 6.45 Municipal 15,420 5% 3.92% 5.81 Corporate 1,000 1% 5.83% 2.44 Other 58,227 20% 1.98% 4.41 TOTAL $287,514 100.0 2.19% 5.77 Ratings: 100% of municipal holdings are rated A or better* $287.5 Million Year 2024 2025 2026 2027 2028 Thereafter Annual Cashflow ($000’s) $31,130 $23,540 $28,024 $31,092 $16,768 $140,731 Base Case Portfolio Total Cashflow Treasury/ Agency CMO Fixed MBS Other Municipal Corporate 18 Shocked Investment Portfolio Unrealized Gains / Losses Capital Impact Intent Dn200 Dn100 BaseCase Up100 Up200 Up300 Up400 AFS - 9,883 - 13,645 - 17,450 - 21,349 - 25,135 - 28,724 - 31,774 HTM - 10,411 - 20,617 - 30,956 - 39,778 - 48,656 - 56,969 - 64,033 Total - 20,294 - 34,262 - 48,406 - 61,127 - 73,791 - 85,693 - 95,807 Corp As Reported Corp Pro - Forma AFS + HTM Sale Corp Difference Bank As Reported Bank Pro - Forma AFS + HTM Sale Bank Difference Federal Reserve Minimum RBC Thresholds Regulatory Well - Capitalized Thresholds Corp Excess Above Well - Capitalized (After Proforma Sale) Tier 1 Capital 220,761 178,797 (41,964) 191,343 149,379 (41,964) Total Risk Based Capital (RBC) 239,645 197,175 (42,470) 209,871 167,357 (42,514) CET 1 Ratio 12.60% 10.12% (2.48%) 12.91% 10.39% (2.52%) 4.50% 6.50% 3.62% Tier 1 Ratio 14.58% 12.17% (2.41%) 12.91% 10.39% (2.52%) 6.00% 8.00% 4.17% Total RBC Ratio 15.83% 13.42% (2.41%) 14.16% 11.64% (2.52%) 8.00% 10.00% 3.42% Leverage Ratio 11.48% 9.30% (2.18%) 10.08% 7.87% (2.21%) 4.00% 5.00% 4.30% Locally held TIF bond of $1.7 million and Trust Preferred securities of $18.7 million have been excluded from the sale impact 19 Deposits 30% 34% 32% 28% 27% 14% 16% 23% 23% 24% 40% 39% 36% 37% 37% 16% 11% 8% 10% 10% 0% 0% 0% 2% 2% 2020 2021 2022 2023 1Q2024 NIB Demand IB Demand MMA & Savings CDs - Retail CDs - Brokered $1.57 $1.55 $1.42 $1.56 $1.57 Deposit Composition ($ in billions as of 03/31/2024) 82% 79% 81% 91% 90% Loan to Deposit Ratio 2020 2021 2022 2023 2024 Overall deposit levels increased $12.1 million primarily due to a shift of a municipal account moving from the Overnight Investment Sweep product during the quarter.

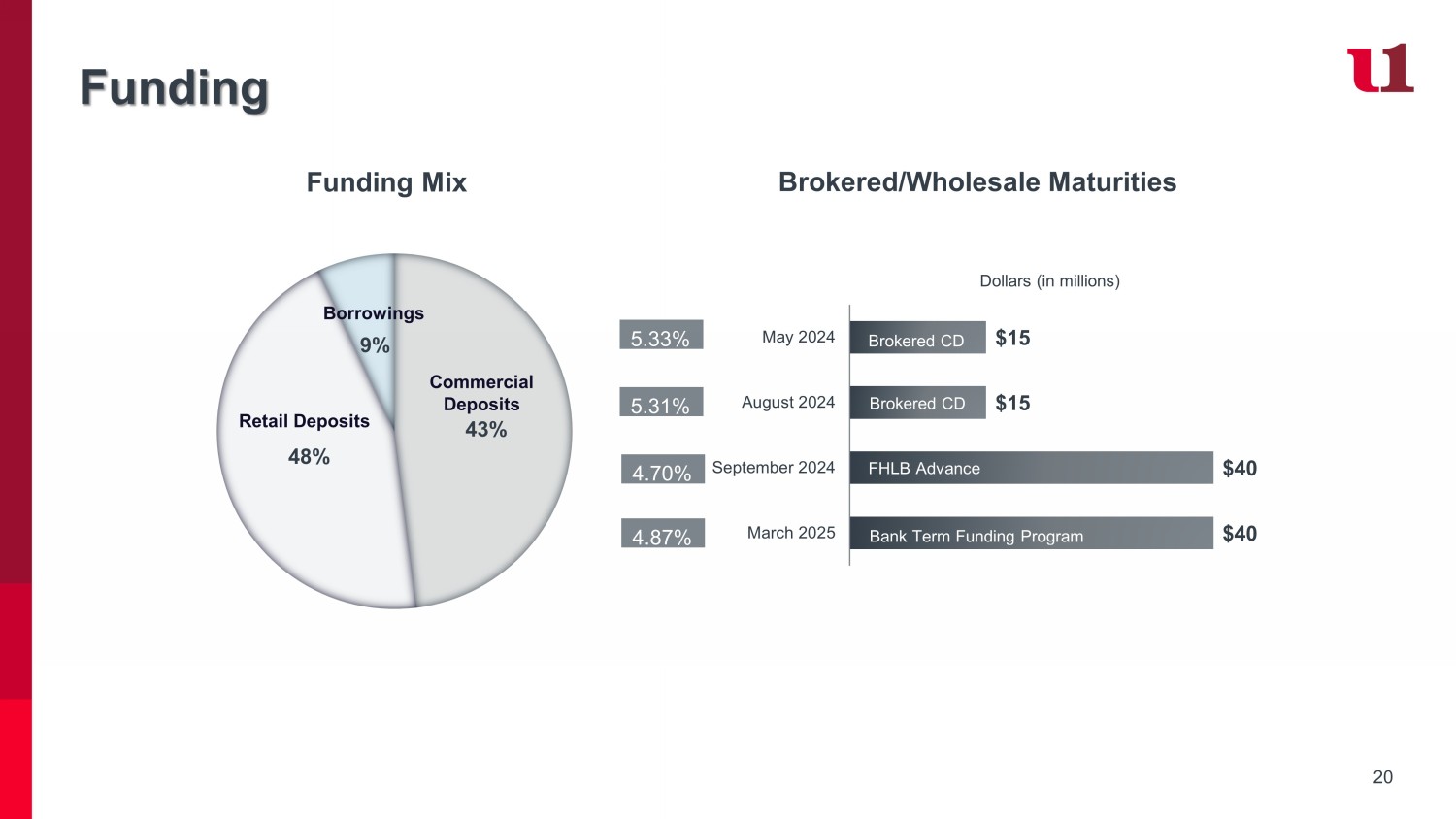

Deposit Type Balance % Insured Deposits $1,198,898,299 77% Uninsured – Uncollateralized Deposits $283,283,796 18% Uninsured - Collateralized Deposits $81,270,638 5% Deposit Type Balance (MMs) % Retail Deposits $820,953,593 49% Business Deposits $730,023,313 51% 20 Funding 43% 48% 9% Commercial Deposits Retail Deposits Borrowings Funding Mix Brokered/Wholesale Maturities $40 $40 $15 $15 March 2025 September 2024 August 2024 May 2024 Dollars (in millions) Bank Term Funding Program FHLB Advance FHLB Advance 4.87% 5.33% 5.31% 4.70% Brokered CD Brokered CD

21 Net Interest Margin (1) See Appendix for a reconciliation of these non - GAAP financial measures 3.99% 3.63% 3.85% 4.63% 4.94% 0.91% 0.51% 0.44% 1.92% 2.65% 3.34% 3.28% 3.56% 3.26% 3.12% 0.49% 0.24% 0.21% 1.16% 1.51% -0.5% 0.5% 1.5% 2.5% 3.5% 4.5% 2020 2021 2022 2023 1Q2024 Yield on Earning Assets Cost of Interest-bearing Liabilities Net Interest Margin Cost of Deposits 22 Diversified Fee Income (1) See Appendix for a reconciliation of these non - GAAP financial measures Composition Trust and Brokerage 55% Service Charges 16% Net Gain on Loan Sales 2% Debit Card Income 19% Bank - owned Life Insurance 7% Other Noninterest Income 1% Non - Interest Income Mix 1Q2024 $1,377 $1,482 $1,359 $1,532 $1,573 2020 2021 2022 2023 1Q2024 Trust & Brokerage Assets Under Management (MMs) ▪ First United’s non - interest income (1) comprised 26% of operating revenue for the first quarter of 2024 ▪ Fee - based business provides stable growth and a diversified revenue stream not directly tied to interest rates, as well as opportunities to build client relationships ▪ First United’s diverse array of products provides opportunities to fully engage with customers and produce stable increases to earnings 23 Committed to Efficiency & Innovation 64.6% 57.5% 56.4% 65.1% 65.7% 2020 2021 2022 2023 1Q2024 (1) See Appendix for a reconciliation of these non - GAAP financial measures Efficient operational platforms and fraud protection ▪ Mortgage Bot ▪ SecureLOCK Premium Debit Card Fraud ▪ Credit Insights/ Savvy Money Cross Marketing Tool ▪ ProfitStars forecasting model ▪ Automated Loan Booking ▪ Vericast Consumer Loan Lead Generator ▪ Customer Service Center Enhancements ▪ U1 - Connect Customer Relationship Management Software Efficiency Ratio (1) Strategic Target 53% - 58% FinTech Investments ▪ Provision IAM ▪ FinTech Funds Planned solutions for a seamless and secure client experience: ▪ Zelle for Business ▪ Online Banking External Transfer ▪ New Customer Relationship Management Tool ▪ Consumer Online and Mobile Banking Digital Platform Upgrade ▪ Business Online and Mobile Banking Digital Platform Upgrade ▪ Check Fraud Prevention Solution Slight increase in the first quarter of 2024 is primarily due to reduced net interest income primarily driven by the reversal of the non - accrual interest and fees on two loan relationships.

24 Liquidity Position Liquidity Sources (03/31/2024) Amount Available ($ in thousands) Amount Used ($ in thousands) Net Availability ($ in thousands) Internal Sources Excess Cash $79,521 $79,521 Unpledged Securities (BV) $35,757 $35,757 External Sources Federal Reserve (Discount Window) $31,776 $31,776 Correspondent Unsecured Lines of Credit FHLB Bank Term Funding Program* $140,000 $235,475 $40,000 $42,914 $40,000 $140,000 $192,561 $0 Total Funding Sources $562,529 $82,914 $479,615 25 Interest Rate Risk (1) Standard Model Assumptions Interest Rate Risk Sensitivity ▪ The Bank’s interest rate risk position is stress tested under three interest rate ramp scenarios to determine the impact on net interest income, net income and capital under dynamic and static balance sheet conditions.

▪ The Bank’s net interest income position at a slightly asset sensitive position. ▪ The Bank’s largest risk from an interest rate risk perspective is falling rate scenarios but has improved from prior quarter. ▪ Assumptions regarding offering rates, loan and investment prepayment speeds, beta and decay rates are reviewed and adjusted on a quarterly basis. Management Outlook & Strategy ▪ Disciplined loan pricing ▪ Manage deposit pricing on relationship and exception basis ▪ Deposit acquisition through short - term CD promotions and adjustable - rate money market products for businesses, municipalities and consumers ▪ $30 million brokered CD in two $15 million brokered CDs with maturities in second and third quarters ▪ $80 million in FHLB advances with $40 million maturing in March and $40 million in August - 400 - 300 - 200 - 100 Flat +100 +200 +300 +400 Net Interest Income (03/31/24) (13.5%) (9.6%) (6.4%) (2.5%) 2.3% 4.8% 5.4% 4.9% Net Interest Income (12/31/23) (13.2%) (8.6%) (5.1%) (2.1%) 1.9% 3.7% 5.5% 7.3% EVE (12/31/23) (19.4%) (9.9%) (3.9%) (1.5%) (4.3%) (8.3%) (11.5%) (14.5%) 12 Month Sensitivity Shock (1) Standard Model Assumptions 26 Capital Management 16.08% 15.89% 16.12% 15.64% 15.83% 2020 2021 2022 2023 1Q2024 10.36% 10.80% 11.46% 11.30% 11.48% 2020 2021 2022 2023 1Q2024 12.61% 12.50% 12.96% 12.44% 12.60% 2020 2021 2022 2023 1Q2024 14.83% 14.64% 15.06% 14.42% 14.58% 2020 2021 2022 2023 1Q2024 CET1 Ratio Leverage Ratio Tier 1 Ratio Total Risk - Based Capital Ratio Regulatory Well - Capitalized 10% 5% 8% 6.5%

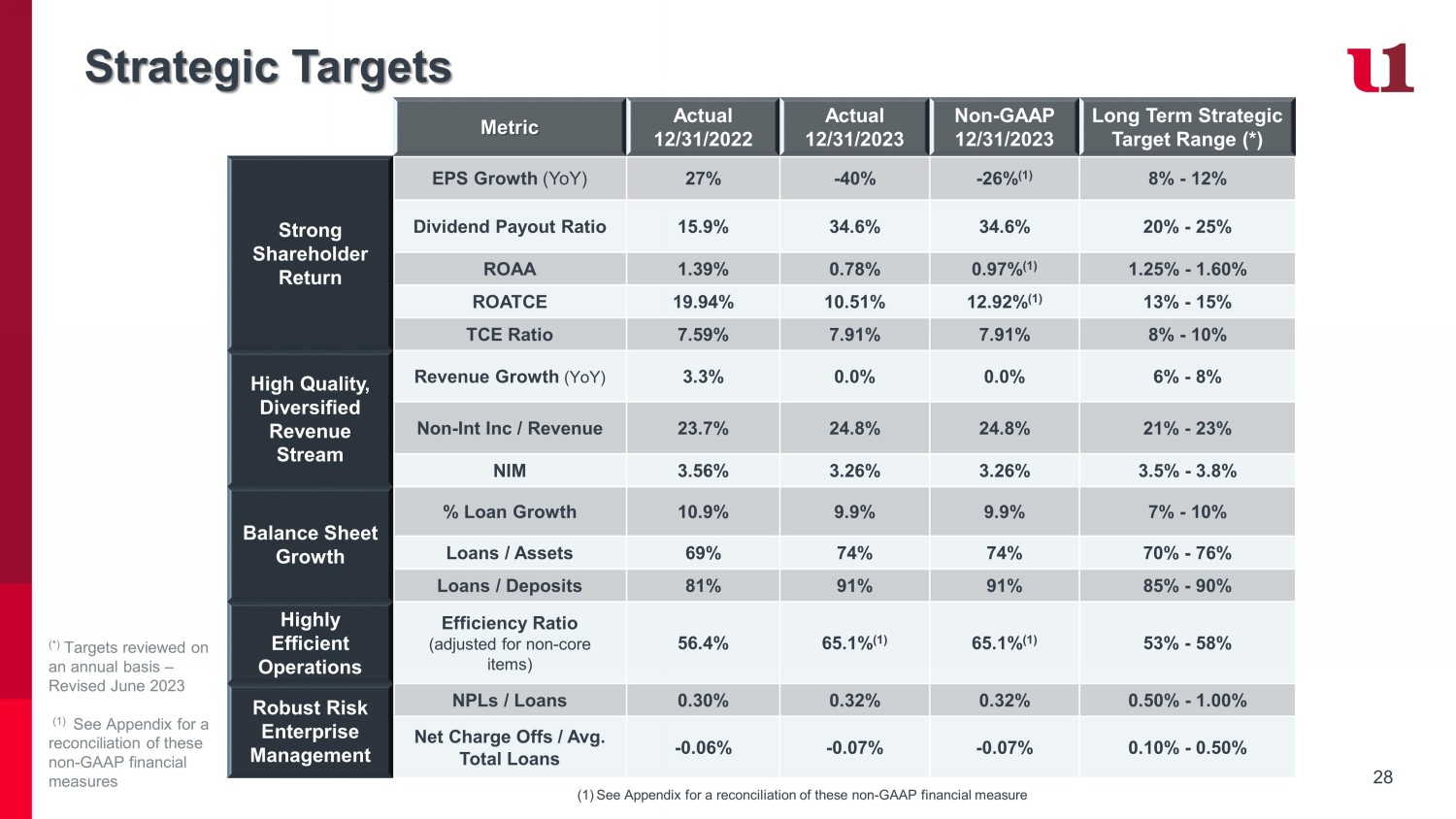

27 Capital Management $17.17 $19.61 $20.90 $22.56 $23.08 2020 2021 2022 2023 1Q2024 6.97% 7.56% 7.59% 7.91% 8.07% 2020 2021 2022 2023 1Q2024 Tangible Book Value / Share TCE Ratio 28 Strategic Targets Metric Actual 12/31/2022 Actual 12/31/2023 Non - GAAP 12/31/2023 Long Term Strategic Target Range (*) Strong Shareholder Return EPS Growth (YoY) 27% - 40% - 26% (1) 8% - 12% Dividend Payout Ratio 15.9% 34.6% 34.6% 20% - 25% ROAA 1.39% 0.78% 0.97% (1) 1.25% - 1.60% ROATCE 19.94% 10.51% 12.92% (1) 13% - 15% TCE Ratio 7.59% 7.91% 7.91% 8% - 10% High Quality, Diversified Revenue Stream Revenue Growth (YoY) 3.3% 0.0% 0.0% 6% - 8% Non - Int Inc / Revenue 23.7% 24.8% 24.8% 21% - 23% N IM 3.56% 3.26% 3.26% 3.5% - 3.8% Balance Sheet Growth % Loan Growth 10.9% 9.9% 9.9% 7% - 10% Loans / Assets 69% 74% 74% 70% - 76% Loans / Deposits 81% 91% 91% 85% - 90% Highly Efficient Operations Efficiency Ratio (adjusted for non - core items) 56.4% 65.1% (1) 65.1% (1) 53% - 58% Robust Risk Enterprise Management NPLs / Loans 0.30% 0.32% 0.32% 0.50% - 1.00% Net Charge Offs / Avg. Total Loans - 0.06% - 0.07% - 0.07% 0.10% - 0.50% (*) Targets reviewed on an annual basis – Revised June 2023 (1) See Appendix for a reconciliation of these non - GAAP financial measures (1) See Appendix for a reconciliation of these non - GAAP financial measure Strong Investor Relations & Shareholder Engagement Members of the Board and senior management routinely engage with shareholders and other stakeholders, and management regularly updates the Board in the context of ongoing investor discussions.