0001857154FY2023FALSEhttp://fasb.org/us-gaap/2023#OtherOperatingIncomeExpenseNethttp://fasb.org/us-gaap/2023#OtherOperatingIncomeExpenseNethttp://fasb.org/us-gaap/2023#OtherOperatingIncomeExpenseNethttp://fasb.org/us-gaap/2023#PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortizationhttp://fasb.org/us-gaap/2023#PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortizationhttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsCurrenthttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsCurrenthttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationshttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsP1YP1YP1YP1YP1Y45800018571542023-01-022023-12-3100018571542023-07-02iso4217:USD00018571542024-02-15xbrli:shares00018571542023-12-3100018571542023-01-010001857154us-gaap:ProductMember2023-01-022023-12-310001857154us-gaap:ProductMember2022-01-032023-01-010001857154us-gaap:ProductMember2021-01-042022-01-020001857154us-gaap:RoyaltyMember2023-01-022023-12-310001857154us-gaap:RoyaltyMember2022-01-032023-01-010001857154us-gaap:RoyaltyMember2021-01-042022-01-0200018571542022-01-032023-01-0100018571542021-01-042022-01-020001857154us-gaap:NonrelatedPartyMember2023-01-022023-12-310001857154us-gaap:NonrelatedPartyMember2022-01-032023-01-010001857154us-gaap:NonrelatedPartyMember2021-01-042022-01-020001857154us-gaap:RelatedPartyMember2023-01-022023-12-310001857154us-gaap:RelatedPartyMember2022-01-032023-01-010001857154us-gaap:RelatedPartyMember2021-01-042022-01-02iso4217:USDxbrli:shares0001857154us-gaap:CommonStockMember2021-01-030001857154us-gaap:AdditionalPaidInCapitalMember2021-01-030001857154dnut:ReceivablesFromStockholderNotesReceivableMember2021-01-030001857154us-gaap:AccumulatedTranslationAdjustmentMember2021-01-030001857154us-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2021-01-030001857154us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-01-030001857154us-gaap:RetainedEarningsMember2021-01-030001857154us-gaap:NoncontrollingInterestMember2021-01-0300018571542021-01-030001857154us-gaap:RetainedEarningsMember2021-01-042022-01-020001857154us-gaap:NoncontrollingInterestMember2021-01-042022-01-020001857154us-gaap:AccumulatedTranslationAdjustmentMember2021-01-042022-01-020001857154us-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2021-01-042022-01-020001857154us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-01-042022-01-020001857154us-gaap:CommonStockMember2021-01-042022-01-020001857154us-gaap:AdditionalPaidInCapitalMember2021-01-042022-01-020001857154dnut:ReceivablesFromStockholderNotesReceivableMember2021-01-042022-01-020001857154us-gaap:CommonStockMember2022-01-020001857154us-gaap:AdditionalPaidInCapitalMember2022-01-020001857154dnut:ReceivablesFromStockholderNotesReceivableMember2022-01-020001857154us-gaap:AccumulatedTranslationAdjustmentMember2022-01-020001857154us-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2022-01-020001857154us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2022-01-020001857154us-gaap:RetainedEarningsMember2022-01-020001857154us-gaap:NoncontrollingInterestMember2022-01-0200018571542022-01-020001857154us-gaap:RetainedEarningsMember2022-01-032023-01-010001857154us-gaap:NoncontrollingInterestMember2022-01-032023-01-010001857154us-gaap:AccumulatedTranslationAdjustmentMember2022-01-032023-01-010001857154us-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2022-01-032023-01-010001857154us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2022-01-032023-01-010001857154us-gaap:CommonStockMember2022-01-032023-01-010001857154us-gaap:AdditionalPaidInCapitalMember2022-01-032023-01-010001857154dnut:ReceivablesFromStockholderNotesReceivableMember2022-01-032023-01-010001857154us-gaap:CommonStockMember2023-01-010001857154us-gaap:AdditionalPaidInCapitalMember2023-01-010001857154dnut:ReceivablesFromStockholderNotesReceivableMember2023-01-010001857154us-gaap:AccumulatedTranslationAdjustmentMember2023-01-010001857154us-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2023-01-010001857154us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-01-010001857154us-gaap:RetainedEarningsMember2023-01-010001857154us-gaap:NoncontrollingInterestMember2023-01-010001857154us-gaap:RetainedEarningsMember2023-01-022023-12-310001857154us-gaap:NoncontrollingInterestMember2023-01-022023-12-310001857154us-gaap:AccumulatedTranslationAdjustmentMember2023-01-022023-12-310001857154us-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2023-01-022023-12-310001857154us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-01-022023-12-310001857154us-gaap:CommonStockMember2023-01-022023-12-310001857154us-gaap:AdditionalPaidInCapitalMember2023-01-022023-12-310001857154dnut:ReceivablesFromStockholderNotesReceivableMember2023-01-022023-12-310001857154us-gaap:CommonStockMember2023-12-310001857154us-gaap:AdditionalPaidInCapitalMember2023-12-310001857154dnut:ReceivablesFromStockholderNotesReceivableMember2023-12-310001857154us-gaap:AccumulatedTranslationAdjustmentMember2023-12-310001857154us-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2023-12-310001857154us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-12-310001857154us-gaap:RetainedEarningsMember2023-12-310001857154us-gaap:NoncontrollingInterestMember2023-12-31dnut:segmentdnut:storednut:country0001857154dnut:CompanyOwnedShopsMemberdnut:KrispyKremeU.S.Member2023-12-310001857154dnut:CompanyOwnedShopsMemberdnut:KrispyKremeInternationalMember2023-12-310001857154dnut:CompanyOwnedShopsMemberdnut:MarketDevelopmentSegmentMember2023-12-310001857154dnut:CompanyOwnedShopsMember2023-12-310001857154dnut:CompanyOwnedCookieBakeriesMemberdnut:KrispyKremeU.S.Member2023-12-310001857154dnut:CompanyOwnedCookieBakeriesMemberdnut:MarketDevelopmentSegmentMember2023-12-310001857154dnut:CompanyOwnedCookieBakeriesMember2023-12-310001857154us-gaap:FranchiseMemberdnut:MarketDevelopmentSegmentMember2023-12-310001857154us-gaap:FranchiseMember2023-12-310001857154dnut:KrispyKremeU.S.Member2023-12-310001857154dnut:KrispyKremeInternationalMember2023-12-310001857154dnut:MarketDevelopmentSegmentMember2023-12-310001857154us-gaap:IPOMember2021-07-012021-07-010001857154us-gaap:IPOMemberus-gaap:CommonStockMember2021-07-010001857154us-gaap:SecuredDebtMemberdnut:TermLoanFacilityMemberdnut:KrispyKremeHoldingsIncKKHIMember2021-06-100001857154us-gaap:SecuredDebtMemberdnut:TermLoanFacilityMemberdnut:KrispyKremeHoldingsIncKKHIMember2021-06-172021-06-170001857154us-gaap:SecuredDebtMemberdnut:TermLoanFacilityMemberdnut:KrispyKremeHoldingsIncKKHIMember2021-06-170001857154us-gaap:SecuredDebtMemberdnut:TermLoanFacilityMember2021-07-072021-07-070001857154us-gaap:SecuredDebtMemberdnut:TermLoanFacilityMember2021-07-070001857154us-gaap:NoncontrollingInterestMember2021-06-282021-06-2800018571542021-06-282021-06-2800018571542021-06-302021-06-30xbrli:pure0001857154us-gaap:NotesPayableOtherPayablesMember2021-07-040001857154us-gaap:NotesPayableOtherPayablesMember2021-04-052021-07-0400018571542021-04-052021-07-040001857154dnut:ExecutiveOfficersSharesRepurchasedAtPricePaidByUnderwritersMember2021-07-052021-08-170001857154dnut:ExecutiveOfficersShareRepurchasedForPaymentOfWithholdingTaxesMember2021-07-052021-08-170001857154us-gaap:OverAllotmentOptionMember2021-08-022021-08-0200018571542021-07-012021-08-020001857154us-gaap:ShippingAndHandlingMember2023-01-022023-12-310001857154us-gaap:ShippingAndHandlingMember2022-01-032023-01-010001857154us-gaap:ShippingAndHandlingMember2021-01-042022-01-020001857154us-gaap:FranchiseMember2023-01-022023-12-310001857154us-gaap:AdvertisingMember2023-01-022023-12-310001857154us-gaap:AdvertisingMember2022-01-032023-01-010001857154us-gaap:AdvertisingMember2021-01-042022-01-020001857154dnut:GiftCardsMember2023-12-310001857154dnut:GiftCardsMember2023-01-010001857154dnut:BreakageRevenueMember2023-12-310001857154dnut:BreakageRevenueMember2023-01-010001857154dnut:CustomerLoyaltyProgramMember2023-12-310001857154dnut:CustomerLoyaltyProgramMember2023-01-010001857154us-gaap:BuildingMembersrt:MinimumMember2023-12-310001857154srt:MaximumMemberus-gaap:BuildingMember2023-12-310001857154srt:MinimumMemberus-gaap:MachineryAndEquipmentMember2023-12-310001857154srt:MaximumMemberus-gaap:MachineryAndEquipmentMember2023-12-310001857154srt:MinimumMemberus-gaap:SoftwareAndSoftwareDevelopmentCostsMember2023-12-310001857154srt:MaximumMemberus-gaap:SoftwareAndSoftwareDevelopmentCostsMember2023-12-310001857154dnut:StrategicInitiativesMember2023-01-022023-12-310001857154dnut:KrispyKremeIncKKIMember2023-01-022023-12-31dnut:franchisee0001857154dnut:KrispyKremeFranceMember2023-10-022023-12-310001857154dnut:KrispyKremeFranceMemberdnut:KrispyKremeFranceMember2023-01-010001857154dnut:KrispyKremeUSShops2022Member2022-07-042022-10-020001857154dnut:KrispyKremeUSShops2022Member2022-10-020001857154dnut:KrispyKremeUSShops2022Memberdnut:U.S.SegmentMember2023-01-010001857154dnut:KrispyKremeUSShops2022Memberdnut:U.S.SegmentMember2022-01-020001857154dnut:KrispyKremeUSShops2022Member2022-01-032023-01-010001857154dnut:KrispyKremeFranceMember2022-07-042022-10-020001857154dnut:KrispyKremeCanadaShops2021Member2021-10-040001857154dnut:KrispyKremeCanadaShops2021Member2021-10-042021-10-040001857154dnut:KrispyKremeCanadaShopsMember2021-10-040001857154dnut:KrispyKremeUnitedStatesShops2021Member2021-01-042021-04-040001857154dnut:KrispyKremeUnitedStatesShops2021Member2021-04-040001857154dnut:KrispyKremeCanadaShops2021Memberdnut:U.S.SegmentMember2021-04-040001857154dnut:KrispyKremeUnitedStatesShops2021Memberdnut:U.S.SegmentMember2021-04-040001857154dnut:KrispyKremeUSAndCanada2021Member2021-04-040001857154dnut:KrispyKremeCanadaShops2021Memberdnut:U.S.SegmentMember2022-01-020001857154dnut:KrispyKremeUnitedStatesShops2021Memberdnut:U.S.SegmentMember2022-01-020001857154dnut:KrispyKremeUSAndCanada2021Member2022-01-020001857154dnut:KrispyKremeCanadaShops2021Memberdnut:U.S.SegmentMember2021-01-030001857154dnut:KrispyKremeUnitedStatesShops2021Memberdnut:U.S.SegmentMember2021-01-030001857154dnut:KrispyKremeUSAndCanada2021Member2021-01-030001857154dnut:KrispyKremeUSAndCanada2021Member2021-01-042022-01-020001857154us-gaap:LandMember2023-12-310001857154us-gaap:LandMember2023-01-010001857154us-gaap:BuildingMember2023-12-310001857154us-gaap:BuildingMember2023-01-010001857154us-gaap:LeaseholdImprovementsMember2023-12-310001857154us-gaap:LeaseholdImprovementsMember2023-01-010001857154us-gaap:MachineryAndEquipmentMember2023-12-310001857154us-gaap:MachineryAndEquipmentMember2023-01-010001857154us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2023-12-310001857154us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2023-01-010001857154us-gaap:ConstructionInProgressMember2023-12-310001857154us-gaap:ConstructionInProgressMember2023-01-010001857154dnut:U.S.SegmentMember2022-01-020001857154dnut:InternationalSegmentMember2022-01-020001857154dnut:MarketDevelopmentSegmentMember2022-01-020001857154dnut:U.S.SegmentMember2022-01-032023-01-010001857154dnut:InternationalSegmentMember2022-01-032023-01-010001857154dnut:MarketDevelopmentSegmentMember2022-01-032023-01-010001857154dnut:U.S.SegmentMember2023-01-010001857154dnut:InternationalSegmentMember2023-01-010001857154dnut:MarketDevelopmentSegmentMember2023-01-010001857154dnut:U.S.SegmentMember2023-01-022023-12-310001857154dnut:InternationalSegmentMember2023-01-022023-12-310001857154dnut:MarketDevelopmentSegmentMember2023-01-022023-12-310001857154dnut:U.S.SegmentMember2023-12-310001857154dnut:InternationalSegmentMember2023-12-310001857154dnut:MarketDevelopmentSegmentMember2023-12-310001857154us-gaap:TradeNamesMember2023-12-310001857154us-gaap:TradeNamesMember2023-01-010001857154us-gaap:FranchiseRightsMember2023-12-310001857154us-gaap:FranchiseRightsMember2023-01-010001857154us-gaap:CustomerRelationshipsMember2023-12-310001857154us-gaap:CustomerRelationshipsMember2023-01-010001857154dnut:ReacquiredFranchiseRightsMember2023-12-310001857154dnut:ReacquiredFranchiseRightsMember2023-01-010001857154us-gaap:ComputerSoftwareIntangibleAssetMember2023-12-310001857154us-gaap:ComputerSoftwareIntangibleAssetMember2023-01-010001857154us-gaap:AccountsPayableMember2023-12-310001857154us-gaap:AccountsPayableMember2023-01-010001857154dnut:StructuredPayablesMember2023-12-310001857154dnut:StructuredPayablesMember2023-01-010001857154dnut:KrispyKremeIncKKIMemberdnut:SupplyChainFinancingProgramsMember2023-01-022023-12-310001857154dnut:SupplyChainFinancingProgramsMemberdnut:VendorsUnderSCFProgramMember2023-01-022023-12-310001857154us-gaap:SecuredDebtMemberdnut:A2023FacilityMember2023-12-310001857154us-gaap:SecuredDebtMemberdnut:A2023FacilityMember2023-01-010001857154us-gaap:LineOfCreditMemberdnut:A2023FacilityMemberus-gaap:RevolvingCreditFacilityMember2023-12-310001857154us-gaap:LineOfCreditMemberdnut:A2023FacilityMemberus-gaap:RevolvingCreditFacilityMember2023-01-010001857154us-gaap:LineOfCreditMember2023-12-310001857154us-gaap:LineOfCreditMember2023-01-010001857154us-gaap:SecuredDebtMemberdnut:A2019FacilityMember2023-12-310001857154us-gaap:SecuredDebtMemberdnut:A2019FacilityMember2023-01-010001857154dnut:A2019FacilityMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2023-12-310001857154dnut:A2019FacilityMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2023-01-010001857154dnut:A2023FacilityMemberus-gaap:RevolvingCreditFacilityMember2023-03-310001857154us-gaap:SecuredDebtMemberdnut:A2023FacilityMember2023-03-310001857154dnut:A2023FacilityMember2023-12-310001857154dnut:A2023FacilityMemberus-gaap:RevolvingCreditFacilityMember2023-12-310001857154dnut:A2019FacilityMember2023-01-022023-12-310001857154dnut:A2019FacilityMember2023-01-010001857154dnut:CreditSpreadAdjustmentMemberdnut:A2023FacilityMember2023-01-022023-12-310001857154dnut:SecuredOvernightFinancingRateSOFRMemberdnut:LeverageRatioEqualToOrExceeds400To100Memberdnut:A2023FacilityMember2023-01-022023-12-310001857154dnut:SecuredOvernightFinancingRateSOFRMemberdnut:LeverageRatioLessThan400To100ButGreaterThanOrEqualTo300To100Memberdnut:A2023FacilityMember2023-01-022023-12-310001857154dnut:SecuredOvernightFinancingRateSOFRMemberdnut:LeverageRatioLessThan300To100Memberdnut:A2023FacilityMember2023-01-022023-12-310001857154dnut:SecuredOvernightFinancingRateSOFRMemberdnut:A2023FacilityMember2023-12-310001857154dnut:SecuredOvernightFinancingRateSOFRMemberdnut:A2019FacilityMember2023-01-010001857154srt:MinimumMemberdnut:A2023FacilityMemberus-gaap:RevolvingCreditFacilityMember2023-01-022023-12-310001857154srt:MaximumMemberdnut:A2023FacilityMemberus-gaap:RevolvingCreditFacilityMember2023-01-022023-12-310001857154dnut:A2023FacilityMemberus-gaap:RevolvingCreditFacilityMember2023-01-022023-12-310001857154dnut:A2019FacilityMemberus-gaap:RevolvingCreditFacilityMember2021-01-042022-01-020001857154dnut:A2019FacilityMemberus-gaap:RevolvingCreditFacilityMember2022-01-032023-01-010001857154us-gaap:LineOfCreditMember2023-09-012023-09-30dnut:agreement0001857154us-gaap:LineOfCreditMember2023-09-300001857154dnut:SecuredOvernightFinancingRateSOFRMemberus-gaap:LineOfCreditMember2023-09-012023-09-300001857154dnut:A2019FacilityMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2021-07-072021-07-070001857154us-gaap:SecuredDebtMemberdnut:TermLoanFacilityMember2023-01-022023-12-31dnut:day0001857154us-gaap:SecuredDebtMemberdnut:TermLoanFacilityMemberdnut:KrispyKremeHoldingsIncKKHIMember2021-01-042022-01-020001857154us-gaap:SecuredDebtMemberdnut:TermLoanFacilityMemberdnut:KrispyKremeHoldingsIncKKHIMember2022-01-020001857154us-gaap:SellingGeneralAndAdministrativeExpensesMember2023-01-022023-12-310001857154us-gaap:SellingGeneralAndAdministrativeExpensesMember2022-01-032023-01-010001857154us-gaap:SellingGeneralAndAdministrativeExpensesMember2021-01-042022-01-020001857154us-gaap:OperatingExpenseMember2023-01-022023-12-310001857154us-gaap:OperatingExpenseMember2022-01-032023-01-010001857154us-gaap:OperatingExpenseMember2021-01-042022-01-0200018571542022-12-31dnut:property00018571542021-12-310001857154us-gaap:FairValueInputsLevel1Memberus-gaap:InterestRateContractMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001857154us-gaap:FairValueInputsLevel2Memberus-gaap:InterestRateContractMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001857154us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001857154us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2023-12-310001857154us-gaap:FairValueInputsLevel1Memberus-gaap:ForeignExchangeContractMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001857154us-gaap:ForeignExchangeContractMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001857154us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2023-01-010001857154us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2023-01-010001857154us-gaap:FairValueInputsLevel1Memberus-gaap:ForeignExchangeContractMemberus-gaap:FairValueMeasurementsRecurringMember2023-01-010001857154us-gaap:ForeignExchangeContractMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2023-01-010001857154us-gaap:FairValueInputsLevel1Memberus-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2023-01-010001857154us-gaap:CommodityContractMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2023-01-010001857154us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2023-01-010001857154us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2023-12-310001857154us-gaap:NondesignatedMemberus-gaap:CommodityContractMember2023-01-012023-01-01utr:gal0001857154us-gaap:NondesignatedMemberus-gaap:CommodityContractMember2022-01-022022-01-020001857154us-gaap:NondesignatedMemberus-gaap:CommodityContractMember2023-12-310001857154us-gaap:NondesignatedMemberus-gaap:CommodityContractMember2023-01-010001857154us-gaap:InterestRateContractMember2019-06-300001857154us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2019-06-300001857154dnut:InterestRateContractFebruary2020SwapAgreementMemberus-gaap:DesignatedAsHedgingInstrumentMember2020-02-290001857154us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2018-11-300001857154dnut:InterestRateContractNewInterestRateSwapAgreementMemberus-gaap:DesignatedAsHedgingInstrumentMember2020-02-290001857154us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2020-02-290001857154us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2022-12-3100018571542022-12-012022-12-310001857154dnut:InterestRateContractNewInterestRateSwapAgreementMemberus-gaap:DesignatedAsHedgingInstrumentMember2022-12-310001857154us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-04-0200018571542023-01-022023-04-020001857154dnut:InterestRateContractNewInterestRateSwapAgreementMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-04-020001857154us-gaap:SecuredDebtMemberdnut:A2023FacilityMember2023-04-020001857154us-gaap:CashFlowHedgingMemberus-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-12-310001857154us-gaap:CashFlowHedgingMemberus-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-01-010001857154us-gaap:ForeignExchangeContractMemberus-gaap:NondesignatedMember2023-12-310001857154us-gaap:ForeignExchangeContractMemberus-gaap:NondesignatedMember2023-01-010001857154us-gaap:PrepaidExpensesAndOtherCurrentAssetsMemberus-gaap:NondesignatedMemberus-gaap:CommodityContractMember2023-12-310001857154us-gaap:PrepaidExpensesAndOtherCurrentAssetsMemberus-gaap:NondesignatedMemberus-gaap:CommodityContractMember2023-01-010001857154us-gaap:NondesignatedMember2023-12-310001857154us-gaap:NondesignatedMember2023-01-010001857154dnut:AccruedLiabilitiesCurrentMemberus-gaap:ForeignExchangeContractMemberus-gaap:NondesignatedMember2023-12-310001857154dnut:AccruedLiabilitiesCurrentMemberus-gaap:ForeignExchangeContractMemberus-gaap:NondesignatedMember2023-01-010001857154dnut:AccruedLiabilitiesCurrentMemberus-gaap:NondesignatedMemberus-gaap:CommodityContractMember2023-12-310001857154dnut:AccruedLiabilitiesCurrentMemberus-gaap:NondesignatedMemberus-gaap:CommodityContractMember2023-01-010001857154us-gaap:PrepaidExpensesAndOtherCurrentAssetsMemberus-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-12-310001857154us-gaap:PrepaidExpensesAndOtherCurrentAssetsMemberus-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-01-010001857154us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:OtherAssetsMember2023-12-310001857154us-gaap:InterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:OtherAssetsMember2023-01-010001857154us-gaap:DesignatedAsHedgingInstrumentMember2023-12-310001857154us-gaap:DesignatedAsHedgingInstrumentMember2023-01-010001857154dnut:InterestIncomeExpenseMemberus-gaap:InterestRateContractMember2023-01-022023-12-310001857154dnut:InterestIncomeExpenseMemberus-gaap:InterestRateContractMember2022-01-032023-01-010001857154dnut:InterestIncomeExpenseMemberus-gaap:InterestRateContractMember2021-01-042022-01-020001857154us-gaap:ForeignExchangeContractMemberus-gaap:OtherNonoperatingIncomeExpenseMember2023-01-022023-12-310001857154us-gaap:ForeignExchangeContractMemberus-gaap:OtherNonoperatingIncomeExpenseMember2022-01-032023-01-010001857154us-gaap:ForeignExchangeContractMemberus-gaap:OtherNonoperatingIncomeExpenseMember2021-01-042022-01-020001857154us-gaap:CommodityContractMemberus-gaap:OtherNonoperatingIncomeExpenseMember2023-01-022023-12-310001857154us-gaap:CommodityContractMemberus-gaap:OtherNonoperatingIncomeExpenseMember2022-01-032023-01-010001857154us-gaap:CommodityContractMemberus-gaap:OtherNonoperatingIncomeExpenseMember2021-01-042022-01-020001857154dnut:A401kPlanMember2023-01-022023-12-310001857154dnut:A401kPlanMemberdnut:MatchingContributionTrancheOneMember2023-01-022023-12-310001857154dnut:MatchingContributionTrancheTwoMemberdnut:A401kPlanMember2023-01-022023-12-310001857154dnut:KKUKAndIrelandContributionPlansMember2023-01-022023-12-310001857154dnut:InsomniaCookiesContributionPlanMember2023-01-022023-12-310001857154dnut:AustraliaPlanMember2023-01-022023-12-310001857154dnut:NewZealandPlanMember2023-01-022023-12-310001857154dnut:CanadaPlanMember2023-01-022023-12-310001857154dnut:A401kMirrorPlanMembersrt:ExecutiveOfficerMember2023-12-310001857154dnut:A401kMirrorPlanMembersrt:ExecutiveOfficerMember2023-01-010001857154dnut:MexicoSeniorityPremiumPlanMember2023-01-022023-12-310001857154dnut:MexicoTerminationIndemnityPlanMember2023-01-022023-12-310001857154dnut:RestrictedStockUnitsRSUsFiftyFourMonthVestingMember2023-01-022023-12-310001857154dnut:RestrictedStockUnitsRSUsSixtyMonthVestingPeriodMember2023-01-022023-12-310001857154us-gaap:ShareBasedCompensationAwardTrancheOneMemberdnut:RestrictedStockUnitsRSUsSixtyMonthVestingPeriodMember2023-01-022023-12-310001857154us-gaap:ShareBasedCompensationAwardTrancheTwoMemberdnut:RestrictedStockUnitsRSUsSixtyMonthVestingPeriodMember2023-01-022023-12-310001857154us-gaap:ShareBasedCompensationAwardTrancheThreeMemberdnut:RestrictedStockUnitsRSUsSixtyMonthVestingPeriodMember2023-01-022023-12-310001857154srt:MaximumMemberdnut:PerformanceStockUnitsPSUsMember2023-01-022023-12-310001857154dnut:PerformanceStockUnitsPSUsMembersrt:MinimumMember2023-01-022023-12-310001857154dnut:RestrictedStockUnitsRSUsFiftyFourMonthVestingMember2022-03-212022-03-210001857154us-gaap:ShareBasedCompensationAwardTrancheOneMemberdnut:RestrictedStockUnitsRSUsFiftyFourMonthVestingMember2022-03-212022-03-210001857154dnut:RestrictedStockUnitsRSUsFiftyFourMonthVestingMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-03-212022-03-210001857154dnut:RestrictedStockUnitsRSUsFiftyFourMonthVestingMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2022-03-212022-03-210001857154dnut:RestrictedStockUnitsRSUsFiftyFourMonthVestingMember2022-03-222022-03-22dnut:grantee0001857154dnut:RestrictedStockUnitsRSUsAndPerformanceStockUnitsPSUsMemberdnut:KrispyKremeIncKKIMember2022-01-020001857154dnut:RestrictedStockUnitsRSUsAndPerformanceStockUnitsPSUsMemberdnut:KrispyKremeIncKKIMember2022-01-032023-01-010001857154dnut:RestrictedStockUnitsRSUsAndPerformanceStockUnitsPSUsMemberdnut:KrispyKremeIncKKIMember2023-01-010001857154dnut:RestrictedStockUnitsRSUsAndPerformanceStockUnitsPSUsMemberdnut:KrispyKremeIncKKIMember2023-01-022023-12-310001857154dnut:RestrictedStockUnitsRSUsAndPerformanceStockUnitsPSUsMemberdnut:KrispyKremeIncKKIMember2023-12-310001857154dnut:KrispyKremeHoldingUKLtdKKUKMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-020001857154dnut:KrispyKremeHoldingUKLtdKKUKMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-032023-01-010001857154dnut:KrispyKremeHoldingUKLtdKKUKMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-010001857154dnut:KrispyKremeHoldingUKLtdKKUKMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-022023-12-310001857154dnut:KrispyKremeHoldingUKLtdKKUKMemberus-gaap:RestrictedStockUnitsRSUMember2023-12-310001857154dnut:InsomniaCookiesHoldingsLLCInsomniaCookiesMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-020001857154dnut:InsomniaCookiesHoldingsLLCInsomniaCookiesMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-032023-01-010001857154dnut:InsomniaCookiesHoldingsLLCInsomniaCookiesMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-010001857154dnut:InsomniaCookiesHoldingsLLCInsomniaCookiesMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-022023-12-310001857154dnut:InsomniaCookiesHoldingsLLCInsomniaCookiesMemberus-gaap:RestrictedStockUnitsRSUMember2023-12-310001857154dnut:KrispyKremeHoldingsPtyLtdKKAustraliaMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-020001857154dnut:KrispyKremeHoldingsPtyLtdKKAustraliaMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-032023-01-010001857154dnut:KrispyKremeHoldingsPtyLtdKKAustraliaMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-010001857154dnut:KrispyKremeHoldingsPtyLtdKKAustraliaMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-022023-12-310001857154dnut:KrispyKremeHoldingsPtyLtdKKAustraliaMemberus-gaap:RestrictedStockUnitsRSUMember2023-12-310001857154dnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-020001857154dnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-032023-01-010001857154dnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-010001857154dnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-022023-12-310001857154dnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMemberus-gaap:RestrictedStockUnitsRSUMember2023-12-310001857154dnut:RestrictedStockUnitsRSUsAndPerformanceStockUnitsPSUsMember2023-01-022023-12-310001857154dnut:RestrictedStockUnitsRSUsAndPerformanceStockUnitsPSUsMember2022-01-032023-01-010001857154dnut:RestrictedStockUnitsRSUsAndPerformanceStockUnitsPSUsMember2021-01-042022-01-020001857154dnut:KrispyKremeIncKKIMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-022023-12-310001857154dnut:KrispyKremeIncKKIMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-032023-01-010001857154dnut:KrispyKremeIncKKIMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-042022-01-020001857154dnut:KrispyKremeHoldingUKLtdKKUKMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-042022-01-020001857154dnut:InsomniaCookiesUSCanadaMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-032023-01-010001857154dnut:InsomniaCookiesUSCanadaMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-042022-01-020001857154dnut:KrispyKremeHoldingsPtyLtdKKAustraliaMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-042022-01-020001857154dnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-042022-01-020001857154us-gaap:EmployeeStockOptionMember2023-01-022023-12-310001857154us-gaap:ShareBasedCompensationAwardTrancheOneMemberus-gaap:EmployeeStockOptionMember2023-01-022023-12-310001857154us-gaap:EmployeeStockOptionMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2023-01-022023-12-310001857154us-gaap:ShareBasedCompensationAwardTrancheThreeMemberus-gaap:EmployeeStockOptionMember2023-01-022023-12-310001857154us-gaap:EmployeeStockOptionMemberdnut:KrispyKremeIncKKIMember2023-01-022023-12-310001857154us-gaap:EmployeeStockOptionMemberdnut:KrispyKremeIncKKIMember2022-01-032023-01-010001857154dnut:KrispyKremeIncKKIMember2022-01-020001857154dnut:KrispyKremeIncKKIMember2022-01-032023-01-010001857154dnut:KrispyKremeIncKKIMember2023-01-010001857154dnut:KrispyKremeIncKKIMember2023-01-022023-12-310001857154dnut:KrispyKremeIncKKIMember2023-12-310001857154us-gaap:EmployeeStockOptionMember2022-01-032023-01-010001857154us-gaap:EmployeeStockOptionMember2021-01-042022-01-020001857154us-gaap:EmployeeStockOptionMemberdnut:KrispyKremeIncKKIMember2023-12-310001857154us-gaap:OtherNoncurrentAssetsMember2023-12-310001857154us-gaap:OtherNoncurrentAssetsMember2023-01-010001857154dnut:DeferredIncomeTaxLiabilitiesNetMember2023-12-310001857154dnut:DeferredIncomeTaxLiabilitiesNetMember2023-01-010001857154us-gaap:StateAndLocalJurisdictionMember2023-12-310001857154us-gaap:DomesticCountryMember2023-12-310001857154us-gaap:StateAndLocalJurisdictionMember2023-01-010001857154us-gaap:DomesticCountryMember2023-01-010001857154us-gaap:ForeignCountryMember2023-12-310001857154us-gaap:ForeignCountryMember2023-01-010001857154srt:MinimumMember2023-12-310001857154srt:MaximumMember2023-12-310001857154dnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMember2023-12-310001857154dnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMember2023-01-0100018571542019-12-302021-01-030001857154dnut:TSWFoodsLitigationMember2022-07-142022-07-140001857154dnut:KremeWorksUSALLCMember2023-12-310001857154dnut:KremeWorksUSALLCMember2023-01-010001857154dnut:KremeWorksCanadaLPMember2023-12-310001857154dnut:KremeWorksCanadaLPMember2023-01-010001857154dnut:KrispyKremeFranceMember2023-12-310001857154us-gaap:EquityMethodInvesteeMember2023-12-310001857154us-gaap:EquityMethodInvesteeMember2023-01-010001857154us-gaap:EquityMethodInvesteeMemberdnut:SalesOfIngredientsAndEquipmentToFranchiseesMember2023-01-022023-12-310001857154us-gaap:EquityMethodInvesteeMemberdnut:SalesOfIngredientsAndEquipmentToFranchiseesMember2022-01-032023-01-010001857154us-gaap:EquityMethodInvesteeMemberdnut:SalesOfIngredientsAndEquipmentToFranchiseesMember2021-01-042022-01-020001857154us-gaap:EquityMethodInvesteeMemberdnut:RoyaltyRevenuesFromFranchiseesMember2023-01-022023-12-310001857154us-gaap:EquityMethodInvesteeMemberdnut:RoyaltyRevenuesFromFranchiseesMember2022-01-032023-01-010001857154us-gaap:EquityMethodInvesteeMemberdnut:RoyaltyRevenuesFromFranchiseesMember2021-01-042022-01-020001857154dnut:LicensingRevenuesMembersrt:AffiliatedEntityMemberdnut:KeurigDrPepperIncKDPMember2023-01-022023-12-310001857154dnut:LicensingRevenuesMembersrt:AffiliatedEntityMemberdnut:KeurigDrPepperIncKDPMember2022-01-032023-01-010001857154dnut:LicensingRevenuesMembersrt:AffiliatedEntityMemberdnut:KeurigDrPepperIncKDPMember2021-01-042022-01-020001857154dnut:BDTCapitalPartnersLLCBDTMemberdnut:AdvisoryServicesAgreementMembersrt:AffiliatedEntityMember2022-01-032023-01-010001857154dnut:BDTCapitalPartnersLLCBDTMemberdnut:AdvisoryServicesAgreementMembersrt:AffiliatedEntityMember2021-01-042022-01-020001857154dnut:BDTCapitalPartnersLLCBDTMemberdnut:AdvisoryServicesAgreementMembersrt:AffiliatedEntityMember2023-01-022023-12-310001857154dnut:ValuationAssistanceInPreparationForIPOMemberdnut:BDTCapitalPartnersLLCBDTMembersrt:AffiliatedEntityMember2021-01-042022-01-020001857154dnut:ValuationAssistanceInPreparationForIPOMemberdnut:BDTCapitalPartnersLLCBDTMembersrt:AffiliatedEntityMember2023-01-022023-12-310001857154dnut:ValuationAssistanceInPreparationForIPOMemberdnut:BDTCapitalPartnersLLCBDTMembersrt:AffiliatedEntityMember2022-01-032023-01-010001857154dnut:KrispyKremeGPKKGPMembersrt:AffiliatedEntityMemberus-gaap:UnsecuredDebtMemberdnut:SeniorUnsecuredNoteTheOriginalAgreementMember2017-12-310001857154dnut:KrispyKremeGPKKGPMemberdnut:SeniorUnsecuredNoteTheAdditionalAgreementMembersrt:AffiliatedEntityMemberus-gaap:UnsecuredDebtMember2019-04-300001857154dnut:KrispyKremeGPKKGPMembersrt:AffiliatedEntityMemberus-gaap:UnsecuredDebtMember2021-01-030001857154dnut:KrispyKremeGPKKGPMembersrt:AffiliatedEntityMemberus-gaap:UnsecuredDebtMember2021-01-042022-01-020001857154dnut:KrispyKremeGPKKGPMembersrt:AffiliatedEntityMemberus-gaap:UnsecuredDebtMember2023-01-022023-12-310001857154dnut:KrispyKremeGPKKGPMembersrt:AffiliatedEntityMemberus-gaap:UnsecuredDebtMember2022-01-032023-01-010001857154srt:AffiliatedEntityMember2023-12-310001857154srt:AffiliatedEntityMember2023-01-010001857154dnut:FinishedProductInShopsMember2023-01-022023-12-310001857154dnut:FinishedProductInShopsMember2022-01-032023-01-010001857154dnut:FinishedProductInShopsMember2021-01-042022-01-020001857154dnut:MixAndEquipmentRevenueFromFranchiseesMember2023-01-022023-12-310001857154dnut:MixAndEquipmentRevenueFromFranchiseesMember2022-01-032023-01-010001857154dnut:MixAndEquipmentRevenueFromFranchiseesMember2021-01-042022-01-0200018571542024-01-012023-12-3100018571542024-12-302023-12-3100018571542025-12-292023-12-3100018571542027-01-042023-12-3100018571542028-01-032023-12-3100018571542029-01-012023-12-310001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:KrispyKremeIncKKIMember2023-01-022023-12-310001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:KrispyKremeIncKKIMember2022-01-032023-01-010001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:KrispyKremeIncKKIMember2021-01-042022-01-020001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:KrispyKremeHoldingUKLtdKKUKMember2023-01-022023-12-310001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:KrispyKremeHoldingUKLtdKKUKMember2022-01-032023-01-010001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:KrispyKremeHoldingUKLtdKKUKMember2021-01-042022-01-020001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:InsomniaCookiesUSCanadaMember2023-01-022023-12-310001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:InsomniaCookiesUSCanadaMember2022-01-032023-01-010001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:InsomniaCookiesUSCanadaMember2021-01-042022-01-020001857154dnut:KrispyKremeHoldingsPtyLtdKKAustraliaMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-022023-12-310001857154dnut:KrispyKremeHoldingsPtyLtdKKAustraliaMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-032023-01-010001857154dnut:KrispyKremeHoldingsPtyLtdKKAustraliaMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-042022-01-020001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMember2023-01-022023-12-310001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMember2022-01-032023-01-010001857154us-gaap:RestrictedStockUnitsRSUMemberdnut:KrispyKremeMexicoSDeRLDeCVKKMexicoMember2021-01-042022-01-020001857154dnut:KrispyKremeIncKKIMemberus-gaap:EmployeeStockOptionMember2023-01-022023-12-310001857154dnut:KrispyKremeIncKKIMemberus-gaap:EmployeeStockOptionMember2022-01-032023-01-010001857154us-gaap:OperatingSegmentsMemberdnut:U.S.SegmentMember2023-01-022023-12-310001857154us-gaap:OperatingSegmentsMemberdnut:U.S.SegmentMember2022-01-032023-01-010001857154us-gaap:OperatingSegmentsMemberdnut:U.S.SegmentMember2021-01-042022-01-020001857154us-gaap:OperatingSegmentsMemberdnut:InternationalSegmentMember2023-01-022023-12-310001857154us-gaap:OperatingSegmentsMemberdnut:InternationalSegmentMember2022-01-032023-01-010001857154us-gaap:OperatingSegmentsMemberdnut:InternationalSegmentMember2021-01-042022-01-020001857154dnut:MarketDevelopmentSegmentMemberus-gaap:OperatingSegmentsMember2023-01-022023-12-310001857154dnut:MarketDevelopmentSegmentMemberus-gaap:OperatingSegmentsMember2022-01-032023-01-010001857154dnut:MarketDevelopmentSegmentMemberus-gaap:OperatingSegmentsMember2021-01-042022-01-020001857154us-gaap:CorporateNonSegmentMember2023-01-022023-12-310001857154us-gaap:CorporateNonSegmentMember2022-01-032023-01-010001857154us-gaap:CorporateNonSegmentMember2021-01-042022-01-020001857154dnut:StrategicShopExitsMember2023-01-022023-12-310001857154dnut:TSWFoodsLitigationMember2022-01-032023-01-010001857154country:US2023-01-022023-12-310001857154country:US2022-01-032023-01-010001857154country:US2021-01-042022-01-020001857154country:GB2023-01-022023-12-310001857154country:GB2022-01-032023-01-010001857154country:GB2021-01-042022-01-020001857154dnut:AustraliaNewZealandMember2023-01-022023-12-310001857154dnut:AustraliaNewZealandMember2022-01-032023-01-010001857154dnut:AustraliaNewZealandMember2021-01-042022-01-020001857154country:MX2023-01-022023-12-310001857154country:MX2022-01-032023-01-010001857154country:MX2021-01-042022-01-020001857154dnut:AllOtherMember2023-01-022023-12-310001857154dnut:AllOtherMember2022-01-032023-01-010001857154dnut:AllOtherMember2021-01-042022-01-020001857154country:US2023-12-310001857154country:US2023-01-010001857154country:US2022-01-020001857154country:GB2023-12-310001857154country:GB2023-01-010001857154country:GB2022-01-020001857154dnut:AustraliaNewZealandMember2023-12-310001857154dnut:AustraliaNewZealandMember2023-01-010001857154dnut:AustraliaNewZealandMember2022-01-020001857154country:MX2023-12-310001857154country:MX2023-01-010001857154country:MX2022-01-020001857154dnut:AllOtherMember2023-12-310001857154dnut:AllOtherMember2023-01-010001857154dnut:AllOtherMember2022-01-020001857154us-gaap:SubsequentEventMember2024-02-082024-02-0800018571542023-10-022023-12-310001857154dnut:MichaelTattersfieldMember2023-10-022023-12-310001857154dnut:MichaelTattersfieldMember2023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________

FORM 10-K

_________________________

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____ to ____

Commission file number: 001-40573

Krispy Kreme, Inc.

(Exact name of registrant as specified in its charter)

|

|

|

|

|

|

| Delaware |

37-1701311 |

(State or other jurisdiction of incorporation) |

(IRS Employer Identification No.) |

2116 Hawkins Street, Charlotte, North Carolina 28203

(Address of principal executive offices)

(800) 457-4779

(Registrant's telephone number, including area code)

_________________________

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

Common stock, $0.01 par value per share |

|

DNUT |

|

Nasdaq Global Select Market |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

|

|

|

|

|

|

|

Large accelerated filer |

☒ |

Accelerated filer |

☐ |

Non-accelerated filer |

☐ |

Smaller reporting company |

☐ |

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Exchange Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of voting stock held by non-affiliates of the registrant as of the end of the registrant’s most recently completed second fiscal quarter, based on the closing price of $14.73 for shares of the registrant’s common stock as reported by the Nasdaq Global Select Market, was approximately $1.3 billion. Shares of common stock beneficially owned by each executive officer, director, and holder of more than 10% of our common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The registrant had outstanding 168.7 million shares of common stock as of February 15, 2024.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement for the registrant’s Annual Meeting of Shareholders, which will be filed with the SEC no later than 120 days after December 31, 2023, have been incorporated by reference into Part III of this Annual Report on Form 10-K.

Table of Contents

PART I

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K includes forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. The words “plan,” “believe,” “may,” “could,” “will,” “should,” “would,” “anticipate,” “estimate,” “expect,” “intend,” “objective,” “seek,” “strive” or similar words, or the negative of these words, identify forward-looking statements. Such forward-looking statements are based on certain assumptions and estimates that we consider reasonable but are subject to various risks and uncertainties and assumptions relating to our operations, financial results, financial conditions, business, prospects, growth strategy and liquidity. Accordingly, there are, or will be, important factors that could cause our actual results to differ materially from those indicated in these statements including, without limitation, those described under the heading “Risk Factors” in this Annual Report on Form 10-K. The inclusion of this forward-looking information should not be regarded as a representation by us that the future plans, estimates or expectations contemplated by us will be achieved. Our actual results could differ materially from the forward-looking statements included herein. These forward-looking statements are made only as of the date of this document, and we do not undertake any obligation, other than as may be required by applicable law, to update or revise any forward-looking or cautionary statement to reflect changes in assumptions, the occurrence of events, unanticipated or otherwise, or changes in future operating results over time or otherwise. We are including this Cautionary Note to make applicable and take advantage of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 for forward-looking statements. We expressly disclaim any obligation to update or revise any forward-looking statements after the date of this report as a result of new information, future events, or other developments, except as required by applicable laws and regulations.

Item 1. Business

The Joy of Krispy Kreme

Krispy Kreme, Inc. (“KKI”) and its subsidiaries (collectively, the “Company” or “Krispy Kreme”) is one of the most beloved and well-known sweet treat brands in the world. Our iconic Original Glazed® doughnut is universally recognized for its fresh, hot-off-the-line, melt-in-your-mouth experience. Over its 86-year history, Krispy Kreme has developed a broad consumer base globally and currently operates in 39 countries through its unique network of fresh Doughnut Shops, partnerships with leading retailers, and a rapidly growing Ecommerce and delivery business. Our purpose of touching and enhancing lives through the joy that is Krispy Kreme guides how we operate every day and is reflected in the love we have for our people, our communities, and the planet.

We are a global omni-channel business with more than 14,000 Global Points of Access, creating awesome fresh doughnut experiences via (1) our Hot Light Theater and Fresh Shops, (2) Delivered Fresh Daily (“DFD”) branded cabinets and merchandising units within high traffic grocery and convenience stores, Quick Service Restaurant (“QSR”), club membership, and drug stores (“DFD Doors”), and (3) Ecommerce. We have a capital-efficient Hub and Spoke model, which leverages our Hot Light Theater Shops’ production capabilities and Doughnut Factories to deliver fresh doughnuts daily to local Fresh Shops, DFD Doors, and through Ecommerce channels. We seek to increase our Sales per Hub through innovation, marketing campaigns, and increasing physical availability to our fresh doughnuts from our Hubs to new Points of Access, primarily DFD Doors. Additionally, our convenient Ecommerce platform and delivery capability are significant enablers of our omni-channel growth.

In addition to creating awesome, fresh doughnut experiences, we create “cookie magic” through Insomnia Cookies, which specializes in warm, delicious cookies delivered right to the doors of its consumers, along with an innovative portfolio of cookie cakes, ice cream, cookie-wiches, and brownies. Insomnia Cookies is a digital-first concept with over 45% of its sales driven through Ecommerce in fiscal 2023. Targeting affordable, high-quality emotional indulgence experiences is at the heart of both the Krispy Kreme and Insomnia Cookies brands.

Our current business model, which focuses on fresh daily premium quality doughnuts produced by the capital-efficient Hub and Spoke model, primarily via Company controlled shops is in contrast to the Krispy Kreme operating model prior to 2016, which was focused on retail and legacy wholesale channels (including discounted long shelf-life doughnuts and coffeehouse execution), a capital-heavy Hot Light Theater Shop production model, and primarily via franchisee controlled shops. In addition to our core offerings such as the Original Glazed doughnut, we now also focus on limited time offerings (“LTOs” or “specialty doughnuts”) and seasonal occasions to generate buzz for our premium products. A taste of our offerings includes:

The Ingredients of Our Success

We believe the following competitive differentiators position us to generate significant growth as we continue towards our goal of becoming the most loved sweet treat brand in the world.

Beloved Global Brand with Ubiquitous Appeal

We believe that our brand love and ubiquitous appeal differentiate us from the competition. We believe that Krispy Kreme is an iconic, globally recognized brand with rich history that is epitomized by our fresh Original Glazed doughnut. We are one of the most loved sweet treat retailers in the U.S. and many markets around the world. We are the most loved sweet treat brand in several key countries already in fiscal 2023, such as the U.S., the U.K., and Australia, based on the results of Krispy Kreme’s Annual Global Brand Tracking Survey conducted by Service Management Group based on over 22,000 consumer responses with Krispy Kreme achieving the highest percentage of consumers indicating they rank our brand as a “ten: absolutely love the brand for sweet treats” on a ten point scale. We have an extremely loyal, energetic, and emotionally connected consumer base.

We continuously seek to understand what consumers are celebrating or experiencing in their lives and actively engage our passionate followers to activate this emotional connection through memorable, sharable moments – our “Acts of Joy” – which we believe further fuel our brand love.

Creating Awesome Experiences

We provide authentic indulgent experiences, delivering joy through high quality doughnuts made from our own proprietary formulations. Our strict quality standards and uniform production systems ensure the consumer’s interaction with Krispy Kreme is consistent with our brand promise, no matter where in the world they experience it. We aim to create product experiences that align with seasonal and trending consumer interests and make positive connections through simple, frequent, brand-focused offerings that encourage shared experiences.

We utilize seasonal innovations, alongside the expansion of our core product offering, to inspire consumer wonder and keep our consumers engaged with the brand and our products. Our sweet treat assortment begins with our iconic Original Glazed doughnut inspired by our founder’s classic yeast-based recipe that serves as the canvas for our product innovation and ideation. Using the Original Glazed doughnut as our foundation, we have expanded our offerings to feature everyday classic items such as our flavor glazes and “minis,” which lend themselves well to gifting occasions such as birthdays and school activities. Our “Original Filled” rings offer the benefits of a filled shell doughnut without the mess. Our seasonal items create unique assortments centered on holidays and events, with Valentine’s Day, St. Patrick’s Day, Easter, the Fourth of July, Halloween, and Christmas, all examples of holidays for which we routinely innovate. We also maintain brand relevance by participating in significant cultural moments. We strategically launch offerings tied to these historic moments to gain mind share, grow brand love, and help drive sales.

Leveraging our Omni-Channel Model to Expand Our Reach

We believe our omni-channel model, enabled by our Hub and Spoke approach and Ecommerce, allows us to maximize our market opportunity while ensuring control and quality across our suite of products. Our goal is to provide our fresh doughnuts to consumers as conveniently and efficiently as possible. We apply a tailored approach across a variety of distinct shop formats to grow in discrete, highly attractive, and diverse markets, and maintain brand integrity and scarcity value while capitalizing on significant untapped consumer demand. Many of our shops offer drive-thrus, which also expand their off-premises reach. Our Hot Light Theater Shops’ production capacity allow us to leverage our investment by efficiently expanding to our consumers wherever they may be — whether in a local Fresh Shop, in a grocery or convenience store, on their commute home or directly to their doorstep via home delivery.

Hub and Spoke

•Hot Light Theater Shops and other Hubs: Immersive and interactive experiential shops which provide unique and differentiated consumer experiences while serving as local production facilities for our network. The average capital investment for a Hot Light Theater Shop is $2 million to $5 million.

•Fresh Shops: Smaller doughnut shops and kiosks, without manufacturing capabilities, selling fresh doughnuts delivered daily from Hub locations. The average capital investment for a Fresh Shop is $0.1 million to $1 million.

•Delivered Fresh Daily: Krispy Kreme branded doughnut cabinets within high traffic grocery and convenience locations, QSR, club membership, and drug stores, selling fresh doughnuts delivered daily to more than 11,900 doors from Hub locations. The average capital investment for a DFD Door is $2,000 to $10,000.

•Ecommerce and Delivery: Fresh doughnuts for pickup or delivery, ordered via our branded Ecommerce platforms or through third-party digital channels.

The Hub and Spoke approach is applied globally and is currently most developed in our international Company-owned markets such as the U.K. and Australia. We are in process of applying lessons learned in those international markets to the U.S., and particularly to expansion in top growth areas such as population-dense greenfield markets, which we expect to be a significant driver of margin expansion in the U.S., as well as in Canada, Japan, and in new countries we plan to enter in the future.

Insomnia Cookies

Insomnia Cookies has expanded our sweet treat platform to include a complementary brand rooted in the belief that indulgent experiences are better enjoyed together. Insomnia Cookies delivers warm, delicious cookies right to the doors of individuals and companies alike.

Our Segments

We conduct our business through the following three reported segments:

•U.S.: Includes all our Company-owned operations in the U.S., including our Krispy Kreme-branded shops and Insomnia Cookies Bakeries, DFD, and the recently exited Branded Sweet Treats business;

•International: Includes all our Krispy Kreme Company-owned operations in the U.K., Ireland, Australia, New Zealand, and Mexico; and

•Market Development: Includes our franchise operations across the globe, as well as our Company-owned operations in Japan and Canada.

The following table presents our Global Points of Access as of December 31, 2023:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Global Points of Access (1) |

|

Hot Light Theater Shops |

|

Fresh Shops |

|

Cookie Bakeries |

|

Carts, Food Trucks, and Other |

|

DFD Doors |

|

Total |

|

Company-Owned (%) |

| U.S. |

229 |

|

|

70 |

|

|

265 |

|

|

— |

|

|

6,808 |

|

|

7,372 |

|

|

100 |

% |

| International |

35 |

|

|

413 |

|

|

— |

|

|

16 |

|

|

3,693 |

|

|

4,157 |

|

|

100 |

% |

Market Development (2) |

125 |

|

|

1,038 |

|

|

2 |

|

|

30 |

|

|

1,423 |

|

|

2,618 |

|

|

14 |

% |

| Total Global Points of Access |

389 |

|

|

1,521 |

|

|

267 |

|

|

46 |

|

|

11,924 |

|

|

14,147 |

|

|

84 |

% |

(1)Excludes the recently exited Branded Sweet Treats distribution points.

(2)Includes Japan and Canada locations, which are Company-owned.

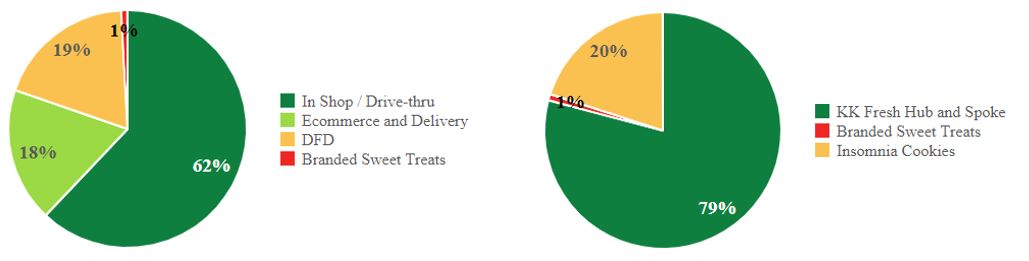

Total fiscal 2023 revenue of $1,686.1 million consisted of the following revenue by reporting segment:

The U.S. segment’s fiscal 2023 revenue of $1,104.9 million consisted of:

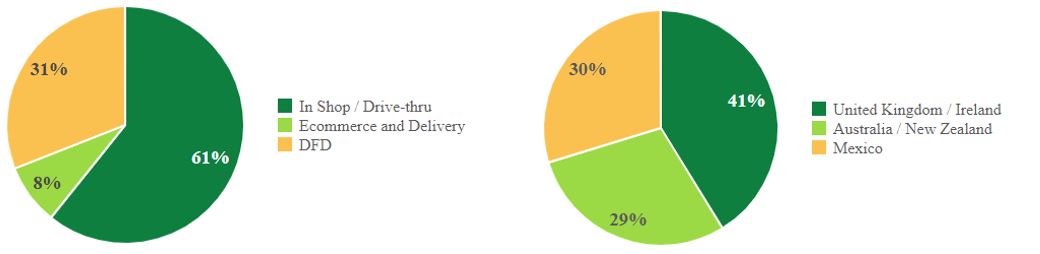

The International segment’s fiscal 2023 revenue of $401.8 million consisted of:

The Market Development segment’s fiscal 2023 revenue of $179.4 million consisted of:

Our Growth Strategies

We have made investments in our brand, our people, and our infrastructure and believe we are well positioned to drive sustained growth as we execute on our strategy. Across our global organization, we have built a team of talented and highly engaged Krispy Kremers and Insomnia employees (or “Insomniacs”). Over the past several years we have taken increased control of the U.S. operations to enable execution of our omni-channel strategy, including accelerating growth across our doughnut shops, DFD, and Ecommerce. Globally, we have developed an operating model that sets the foundation for continued expansion in both existing and new geographies. As a result, we believe we are able to combine a globally recognized and loyalty-inspiring brand with a leading management team and we aim to unlock increased growth in sales and profitability through the following strategies:

• Increase purchase frequency;

• Expand availability;

• Drive operating leverage; and

• Maximize capital returns.

Increase purchase frequency

Almost all consumers desire an occasional indulgence, and when they indulge, they want a high quality, emotionally differentiated experience. We believe we have significant runway to be part of a greater number of shared indulgence occasions. On average, U.S. consumers visit Krispy Kreme less than three times per year, creating a significant frequency opportunity. The success of recently launched products, including filled rings and minis, seasonal favorites, limited time buzz-worthy offerings, and flavored glazes, affirms our belief that our innovations create additional opportunities for consumers to engage with our brand. We intend to strengthen our product portfolio by centering further innovation around seasonal and societal events, and through the development of new innovation platforms to drive sustained baseline growth. Our strategy of linking product launches with relevant events has allowed us to effectively increase consumption occasions while meaningfully engaging with our communities and consumers.

Our marketing and innovation efforts have expanded the number of incremental consumer use cases for Krispy Kreme doughnuts. For example, our gifting value proposition makes doughnuts an ideal way to celebrate everyday occasions like birthdays and holidays, through gifting sleeves and personalized gift messaging. Our gifting value proposition fulfills distinct consumption occasions and will continue to make our brand and products more accessible and allow us to participate with greater frequency in small and large indulgent occasions, from impromptu daily gatherings with family and friends to holidays and weddings, and everything in between.

Expand availability

We believe there are opportunities to continue to grow in new and existing markets in which we currently operate by further capitalizing on our strong brand awareness as we deploy our Hub and Spoke model. We apply a deliberate approach to growing these discrete, highly attractive markets and maintain our brand integrity and scarcity value while unlocking significant consumer demand. We focus on increasing Global Points of Access through low cost DFD Doors, including in new channels like QSR and club membership, as well as investments in Fresh Shops with a limited number of investments in our experiential Hot Light Theater shops to implement the Hub and Spoke model in new and existing markets. We expect this to lead to growth in our key Sales per Hub metric as we further leverage the production capacity of existing Hubs.

We believe our omni-channel strategy, empowered by our Hub and Spoke model, will allow us to effectively seize expansion opportunities both domestically and internationally. Despite our high brand awareness, we have a limited presence in certain key, population-dense U.S. markets, and have yet to build a presence in key U.S. cities, including Boston and Minneapolis. We also believe we have a significant opportunity to increase our presence in our existing international markets such as Mexico, Japan, and Ireland where we have a less developed Hub and Spoke system. We believe this provides us ample opportunity to grow within markets in which we are already present. We also view Hub and Spoke expansion to other international markets where we do not currently have a presence as a major growth driver for the future. We have identified key international whitespace market opportunities such as China, Brazil, and parts of Western Europe. Our goal is to open in at least three new countries per year; in fiscal 2023, we opened shops in seven new countries. Our proven track record of entering new, diverse markets across multiple continents and deploying the capital-efficient Hub and Spoke approach demonstrates our ability to effectively penetrate a broad range of market types. New markets will either consist of Company-owned shops or entered via franchise operations (sometimes with us holding a minority equity interest), to be determined on a case-by-case basis.

Drive operating leverage

We are making focused investments in our omni-channel strategy to expand our presence efficiently while driving top-line growth, margin expansion, and capital efficiency. The Hub and Spoke model enables an integrated approach to operations, which is designed to bring efficiencies in production, distribution, and supervisory management while ensuring product freshness and quality are consistent with our brand promise no matter where consumers experience our doughnuts. By expanding Points of Access such as new local DFD Doors to existing Hubs, we increase not just total Sales per Hub, but also profitability and capital efficiency because the production Hubs have largely fixed costs including rent, utilities, and even labor.

To support the Hub and Spoke model in the U.S., we have implemented labor management systems and processes in our shops and delivery route optimization technology to support our DFD logistics chain. In addition, we employ a demand planning system that is intended to improve service and to deliver both waste and labor efficiencies across all our business channels. We are also investing in automation in the doughnut production process, including filling and icing doughnuts, which are primarily done manually today. By streamlining these operations across our platform, we believe we can continue to deliver on our brand promise and provide joy to our consumers while continuing to drive efficiencies across our platform.

Maximize capital returns

We believe we have a strong runway to grow while maximizing capital returns, supported by the capital-efficient Hub and Spoke model. We intend to maximize capital returns both by leveraging existing capacity and making selective investments in geographies which currently have limited access to our products.

Responsibility

We are committed to making a positive impact on the world — to touch and enhance lives through the joy that is Krispy Kreme — and our ambition is to Be Sweet in All That We Do, which represents our Responsibility platform. With this platform, we focus on our greatest opportunities for positive social and environmental impact with our people, our communities, and our planet. We are committed to transparency and disclosure of our Responsibility strategies, programs, and governance. Progress along our Responsibility strategy is regularly reported to our senior management leadership team (“the Global Leadership Team”) and our Board of Directors, which also has oversight of our environmental, social, and governance strategy. We published our first ever Be Sweet Responsibility Report during fiscal 2023 outlining our journey, progress through fiscal 2022, and future ambitions. To read the full report, visit krispykreme.com/responsibility-report.

•Loving our Krispy Kremers: We create opportunities for our Krispy Kremers to achieve their dreams — building the most engaged, inclusive workforce.

We are committed to diversity, equity, and inclusion throughout our organization, from our Board room to our shops. We have established a Be Sweet Working Group (sponsored by members of the Global Leadership Team) with a core focus on Belonging, and six U.S. Employee Resource Groups. We are focused on gender parity globally and increasing our U.S. people of color representation. We are also developing a comprehensive, global total rewards framework to drive pay equity and access for our Krispy Kremers.

•Loving our Communities: We bring joy to others — engaging locally to support and uplift communities globally.

Our brand purpose truly shines through our Acts of Joy and community fundraising initiatives. Whether through providing financial support to third-party organizations focused on children in need, or through our offer of free doughnuts to graduating seniors, we bring joy to others while doing good. In fiscal 2023, we raised more than $40 million to support local community causes across the U.S. We also engage with numerous local philanthropic organizations in the communities that we serve around the world.

•Loving our Planet: We respect our planet — using sustainable practices and reducing our environmental impacts.

We are committed to advancing sustainable business throughout our operations. During fiscal 2023, we progressed our efforts to address climate change and build the resilience of our business and supply chain. We conducted a multi-year global emissions assessment to establish our emissions baseline, using this foundation to soon set goals for greenhouse gas emission reductions.

We made progress on our responsible sourcing commitment across our global supply chain. Krispy Kreme has set a goal of using 100% cage-free eggs by 2025. One important action was a strategic product line exit during the first quarter of fiscal 2023, which represented 70% of our egg use. We are committed to progress on sourcing sustainable palm oil that supports a deforestation-free supply chain. As global awareness of food waste increases, so does our focus on food waste reduction, with a goal to divert at least 50% of food waste from landfills by 2025. We took steps in fiscal 2023 to increase landfill diversion and increase our use of food-to-feed initiatives across our business.

We are also committed to significantly increasing the recyclability of our packaging, with a goal to reach 80% recyclable or compostable packaging across our operations by 2025. In the near future, we are focusing on the commercialization of recyclable grease-resistant DFD cartons, 100% paper-based coffee cups, and a reduction in our single-use plastic consumption to reach our goal.

Team Members and Human Capital Resources

Investing in, developing, and maintaining human capital is critical to our success. Globally, we employ approximately 22,800 employees as of December 31, 2023, including approximately 19,400 at Krispy Kreme locations that we refer to as our “Krispy Kremers.” We are not a party to any collective bargaining agreement, although we have experienced occasional unionization initiatives.

We depend on our Krispy Kremers to provide great customer service, to make our products in adherence to our high-quality standards and to maintain the consistency of our operations and logistics chain. While we continue to operate in a competitive market for talent, we believe that our culture, policies, and practices contribute to our strong relationship with our Krispy Kremers, which we feel is instrumental to our business model. Our culture is best captured by our Leadership Mix, which are the dozen behaviors that guide us every day. The Leadership Mix was developed based on the beliefs of our founder, incorporating years of learning on what makes Krispy Kreme such a special organization. These cultural behaviors are shared with Krispy Kremers globally, through an internally developed Leadership Mix training program.

The Leadership Mix is what keeps our consumers at the center of everything we do and ensures that our Krispy Kremers are empowered to do the right thing for our consumers and for the business. We pride ourselves on being an entrepreneurial and innovative team that is not afraid to take smart risks in service of creating awesome doughnut experiences.

Consistent with our Leadership Mix ingredients, we pride ourselves on attracting a diverse team of Krispy Kremers and Insomniac team members from a wide range of backgrounds. As of December 31, 2023, our U.S. Krispy Kreme Company-owned operations include approximately 10,600 employees, of which 96% are field-based employees and the remaining 4% are corporate employees. 69% of such employees are people of color and 52% of such employees are female. We believe our diverse team drives the entrepreneurial culture that is at the center of our success. The success of our business is fundamentally connected to the well-being of our Krispy Kremers. Accordingly, we are committed to their health, safety, and wellness.

Our Total Rewards platform provides Krispy Kremers and their families with access to a variety of competitive, innovative, flexible, and convenient pay, health, and wellness programs. Our total package of pay and benefits is designed to support the physical, mental, and financial health of our people and includes medical, dental, vision, employee assistance program, life insurance and retirement benefits as well as disability benefits and assistance with major life activities, such as educational reimbursement and adoption.

Many of these benefits are available to our part-time Krispy Kremers; we believe that offering select benefits to our part-time Krispy Kremers offers us a competitive advantage in recruiting and retaining talent. We have also rolled out employee equity ownership plans across the organization, including for our shop general managers, to effectively align Krispy Kremers’ incentives with the Company’s long-term strategic goals.

Marketing and Innovation

Our marketing strategy is as unique and innovative as our brand. Krispy Kreme’s marketing strategy is to participate in culture through “Acts of Joy,” deliver new product experiences that align with seasonal and trending consumer and societal interests and to create positive connections through simple, frequent, brand-focused offerings that encourage shared experiences. The tactics which support this strategy are also distinct. In the U.S., Krispy Kreme’s paid media strategy is 100% digital with a heavy focus on social media where our passionate consumer base engages and shares our marketing programs far and wide through their own networks. Earned media is also an important part of our media mix. We create promotions and products that attract media outlets to our brand. Through the widespread dissemination of our programs through pop culture, entertainment, and news outlets, we believe we can achieve disproportionately large attention relative to our spend in a media environment populated by brands with far larger media budgets. During fiscal 2023 we generated over 40 billion media impressions reflecting how well our fresh and innovative doughnuts resonated with consumers. We believe our marketing strategy, supported with non-traditional media tactics, has proven to be a potent combination that simultaneously drives sales while growing brand love. By drawing inspiration from important societal events, we create a unique way for our consumers to celebrate and engage. Our ability to create this connection between our consumers and our brand is what has helped make the Krispy Kreme brand iconic, and helps to solidify our position in popular culture.

Limited time seasonal innovation and permanent innovations are used to create consumer wonder and are an essential ingredient in keeping our consumers engaged with the brand and the products. Our specialty doughnuts are anticipated by consumers and the media alike and generate significant social sharing amongst our fans and media coverage. The impact of limited time seasonal offerings goes well beyond the sales of the innovations themselves; they drive traffic and create additional sales of our core product offering.

Krispy Kreme has a strong brand presence across both emerging and well-established social media platforms, including Facebook, Instagram, X, YouTube, and Tik-Tok. These channels enable us to engage with our consumers on a personal level, while spreading the global brand of Krispy Kreme, including communicating promotional activity, featured products, new shop openings, and highlighting core equities of the brand. Social media allows precise geo-targeting around our shops and effective targeting of consumers likely to be interested in our messages.

Supply Chain

Sourcing and Supplies

We are committed to sourcing the best ingredients available for our products. The principal ingredients to manufacture our products include flour, shortening, and sugar which are used to formulate our proprietary doughnut mix and concentrate at our Winston-Salem manufacturing facility. We procure the raw materials for these products from different vendors. Although most raw materials we require are typically readily available from multiple vendors, we currently have approximately 20 main vendors in addition to our own mix plant.

We manufacture our doughnut mix at our mix plant in Winston-Salem, North Carolina and a third-party facility in Pico Rivera, California, domestically, and at several locations internationally, where we produce the doughnut mix used to make our doughnuts across the U.S. and internationally. In support of international markets, we produce a concentrate exclusively at our Winston-Salem facility for shipping efficiency. The concentrate is mixed with commodity ingredients in local markets to get to a finished doughnut mix. Throughout the process, the recipe for what makes a Krispy Kreme doughnut remains known only to the Company.

At an additional facility in Winston-Salem, North Carolina, we manufacture our proprietary doughnut making equipment for shipment to new shops and Doughnut Factories around the world. We manufacture a range of doughnut making lines, with different capacities to support the needs of different shop types.

In addition, we provide other ingredients, packaging and supplies, principally to Company-owned and domestic franchise shops. Our Krispy Kreme shop-level replenishments generally occur on a weekly basis, working with one national distribution partner. In addition, we serve New York City with a regional distribution partner to best serve our needs in that market.

In the U.S., we operate four Doughnut Factories located in Indianapolis, Indiana, Monroe, Ohio, New York, New York, and Fort Lauderdale, Florida. Internationally, we operate 37 Doughnut Factories, of which 23 are operated by franchisees. Each Doughnut Factory is staffed by Krispy Kremers and supports multiple business channels for Krispy Kreme. Each Doughnut Factory manufactures fresh doughnuts daily, powering the Hub and Spoke model by producing product for Spoke locations such as Fresh Shops and Carts and Food Trucks. In addition, they also provide DFD finished products to support local and regional markets. We operate DFD routes out of each Doughnut Factory to ensure our DFD doughnuts are delivered fresh, every day, and maintain our highest standards of quality and brand experience.

Insomnia Cookies operates a nationwide supply chain, supported by third-party logistic providers which bring ingredients and supplies to Insomnia Cookies Bakeries to create their warm, delicious products.

Quality Control

We operate an integrated supply chain to help maintain the consistency and quality of products. Our business model is centered on ensuring consistent quality of our products. We manufacture doughnut mixes at our facility in Winston-Salem, North Carolina. Additionally, we also manufacture doughnut mix concentrates, which are blended with flour and other ingredients by contract mix manufacturers to produce finished doughnut mix. We have an agreement with an independent food company to manufacture certain doughnut mixes using concentrate for domestic regions outside the southeastern U.S. and to provide backup mix production capability in the event of a business disruption at the Winston-Salem facility. In-process quality checks are performed throughout the production process, including ingredients, moisture percentage, fat percentage, sieve size, and metal checks. We provide specific instructions to franchise partners for storing and cooking our products. All products are transported and stored at ambient temperature.

Competition

We compete in the fragmented indulgence industry. Our domestic and international competitors include a wide range of retailers of doughnuts and other sweet treats, coffee shops, and other café and bakery concepts. We compete with snacks sold through convenience stores, supermarkets, restaurants, Ecommerce, and retail stores in the U.S. The number, size and strength of competitors vary by region and by category. We also compete against retailers who sell sweet treats such as cookies, cupcakes, and ice cream shops. We compete on elements such as food quality, freshness, convenience, accessibility, customer service, price, and value. We view our brand engagement, overall consumer experience and the uniqueness of our Original Glazed doughnut as important factors that distinguish our brand from competitors, both in the doughnut and broader indulgence categories. See “Risk Factors — Risks Related to Executing Our Business Strategy – Our success depends on our ability to compete with many food service businesses.”

Intellectual Property

Our doughnut shops are operated under the Krispy Kreme® trademark, and we use many federally and internationally registered trademarks and service marks, including Original Glazed®, Hot Krispy Kreme Original Glazed Now®, Insomnia Cookies®, and the logos associated with these marks. We have registered various trademarks in over 65 other countries, and we generally license the use of these trademarks to our franchisees for the operation of their doughnut shops. We have also licensed our marks for other consumer goods. We believe that our trademarks and service marks have significant value and are important to our brand. To better protect our brand, we have registered and maintain numerous Internet domain names.