0001766478falseFY202313400017664782023-01-012023-12-3100017664782023-06-30iso4217:USD00017664782024-03-15xbrli:shares0001766478aomr:LoansReceivableResidentialMember2023-12-310001766478aomr:LoansReceivableResidentialMember2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMember2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMember2022-12-310001766478us-gaap:ResidentialMortgageBackedSecuritiesMember2023-12-310001766478us-gaap:ResidentialMortgageBackedSecuritiesMember2022-12-310001766478us-gaap:USTreasurySecuritiesMember2023-12-310001766478us-gaap:USTreasurySecuritiesMember2022-12-3100017664782023-12-3100017664782022-12-310001766478us-gaap:NonrecourseMember2023-12-310001766478us-gaap:NonrecourseMember2022-12-310001766478us-gaap:NonrelatedPartyMember2023-12-310001766478us-gaap:NonrelatedPartyMember2022-12-310001766478srt:AffiliatedEntityMember2023-12-310001766478srt:AffiliatedEntityMember2022-12-31iso4217:USDxbrli:shares00017664782022-01-012022-12-310001766478us-gaap:NonrelatedPartyMember2023-01-012023-12-310001766478us-gaap:NonrelatedPartyMember2022-01-012022-12-310001766478srt:AffiliatedEntityMember2023-01-012023-12-310001766478srt:AffiliatedEntityMember2022-01-012022-12-310001766478us-gaap:PreferredStockMember2021-12-310001766478us-gaap:CommonStockMember2021-12-310001766478us-gaap:AdditionalPaidInCapitalMember2021-12-310001766478us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001766478us-gaap:RetainedEarningsMember2021-12-3100017664782021-12-310001766478us-gaap:PreferredStockMember2022-01-012022-12-310001766478us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001766478us-gaap:RetainedEarningsMember2022-01-012022-12-310001766478us-gaap:CommonStockMember2022-01-012022-12-310001766478us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001766478us-gaap:PreferredStockMember2022-12-310001766478us-gaap:CommonStockMember2022-12-310001766478us-gaap:AdditionalPaidInCapitalMember2022-12-310001766478us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001766478us-gaap:RetainedEarningsMember2022-12-310001766478us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001766478us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001766478us-gaap:RetainedEarningsMember2023-01-012023-12-310001766478us-gaap:PreferredStockMember2023-12-310001766478us-gaap:CommonStockMember2023-12-310001766478us-gaap:AdditionalPaidInCapitalMember2023-12-310001766478us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-310001766478us-gaap:RetainedEarningsMember2023-12-3100017664782022-05-312022-05-3100017664782022-03-312022-03-3100017664782022-08-312022-08-3100017664782022-11-302022-11-3000017664782023-05-312023-05-3100017664782023-03-312023-03-3100017664782023-11-302023-11-3000017664782023-08-312023-08-31aomr:segment0001766478aomr:VestingPeriodOneMemberus-gaap:PerformanceSharesMember2023-01-012023-12-31xbrli:pure0001766478aomr:VestingPeriodTwoMemberus-gaap:PerformanceSharesMember2023-01-012023-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMemberaomr:SecuritizationDebtMemberus-gaap:NonrecourseMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMemberaomr:SecuritizationDebtMemberus-gaap:NonrecourseMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMemberus-gaap:NonrecourseMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMemberus-gaap:NonrecourseMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMemberaomr:RatedAndNonRatedCertificatesMember2023-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMemberaomr:RatedAndNonRatedCertificatesMember2022-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-01-012023-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-01-012022-12-310001766478us-gaap:BondsMember2023-12-310001766478us-gaap:BondsMember2022-12-310001766478us-gaap:BondsMember2023-01-012023-12-310001766478us-gaap:BondsMember2022-01-012022-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMember2023-12-310001766478us-gaap:AssetBackedSecuritiesSecuritizedLoansAndReceivablesMember2022-12-310001766478us-gaap:NonrecourseMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001766478us-gaap:NonrecourseMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-31aomr:loan0001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMezzanineMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMezzanineMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustSubordinateMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustSubordinateMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustInterestOnlyExcessMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustInterestOnlyExcessMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustRetainedMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustRetainedMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyFannieMaeMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyFannieMaeMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyFreddieMacMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyFreddieMacMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyMember2023-12-310001766478us-gaap:ResidentialMortgageBackedSecuritiesMember2023-12-310001766478srt:ConsolidationEliminationsMemberaomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustRetainedMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustSeniorMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustSeniorMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMezzanineMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMezzanineMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustSubordinateMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustSubordinateMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustInterestOnlyExcessMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustInterestOnlyExcessMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustRetainedMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustRetainedMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesOtherNonAgencySubordinateMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesOtherNonAgencySubordinateMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesOtherNonAgencyInterestOnlyExcessMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesOtherNonAgencyInterestOnlyExcessMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesOtherNonAgencyMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesOtherNonAgencyMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyFannieMaeMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyFannieMaeMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyFreddieMacMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyFreddieMacMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesWholePoolAgencyMember2022-12-310001766478us-gaap:ResidentialMortgageBackedSecuritiesMember2022-12-310001766478us-gaap:USTreasurySecuritiesMember2023-01-012023-12-310001766478us-gaap:CollateralPledgedMember2023-12-310001766478us-gaap:CollateralPledgedMember2022-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:MultinationalBank1Membersrt:MinimumMember2023-01-012023-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MaximumMemberaomr:MultinationalBank1Member2023-01-012023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:MultinationalBank1Member2023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:MultinationalBank1Member2022-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MinimumMemberaomr:MultinationalBank2Member2023-01-012023-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MaximumMemberaomr:MultinationalBank2Member2023-01-012023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:MultinationalBank2Member2023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:MultinationalBank2Member2022-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank1Membersrt:MinimumMember2023-01-012023-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MaximumMemberaomr:GlobalInvestmentBank1Member2023-01-012023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank1Member2023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank1Member2022-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank2Membersrt:MinimumMember2023-01-012023-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MaximumMemberaomr:GlobalInvestmentBank2Member2023-01-012023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank2Member2023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank2Member2022-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Membersrt:MinimumMember2023-01-012023-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MaximumMemberaomr:GlobalInvestmentBank3Member2023-01-012023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Member2023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Member2022-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberaomr:InstitutionalInvestorsAAndBMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001766478aomr:InstitutionalInvestorsAAndBMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMember2023-12-310001766478aomr:InstitutionalInvestorsAAndBMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMember2022-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MinimumMemberaomr:RegionalBank1Member2023-01-012023-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MaximumMemberaomr:RegionalBank1Member2023-01-012023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:RegionalBank1Member2023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:RegionalBank1Member2022-12-310001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:RegionalBank2Member2023-01-012023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:RegionalBank2Member2023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:RegionalBank2Member2022-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMember2023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMember2022-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:MultinationalBank1Member2022-04-130001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:MultinationalBank1Member2022-04-132022-04-130001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:MultinationalBank1Member2022-08-040001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:MultinationalBank1Member2023-07-252023-07-250001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:MultinationalBank1Member2023-12-152023-12-150001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank2Member2022-02-042022-02-040001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank2Membersrt:MinimumMember2022-02-042022-02-040001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MaximumMemberaomr:GlobalInvestmentBank2Member2022-02-042022-02-040001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank2Memberaomr:FormerLondonInterbankOfferedRateLIBORMembersrt:MinimumMember2022-02-032022-02-030001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MaximumMemberaomr:GlobalInvestmentBank2Memberaomr:FormerLondonInterbankOfferedRateLIBORMember2022-02-032022-02-030001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Member2022-01-012022-01-010001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Memberaomr:FormerLondonInterbankOfferedRateLIBORMember2021-12-312021-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Member2022-12-190001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Member2022-12-192022-12-190001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Member2022-12-192022-12-190001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Member2023-11-070001766478aomr:SecuredOvernightFinancingRateSOFRMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Member2023-11-072023-11-070001766478aomr:SecuredOvernightFinancingRateSOFRIndexSpreadMemberus-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:GlobalInvestmentBank3Member2023-11-072023-11-070001766478aomr:InstitutionalInvestorsAAndBMemberaomr:MasterRepurchaseAgreementsMember2022-10-04aomr:facilityaomr:lender0001766478aomr:InstitutionalInvestorsAAndBMemberaomr:MasterRepurchaseAgreementsMember2022-10-042022-10-04aomr:extension0001766478us-gaap:CollateralPledgedMemberaomr:InstitutionalInvestorsAAndBMemberaomr:MasterRepurchaseAgreementsMember2022-12-310001766478us-gaap:CollateralPledgedMemberaomr:InstitutionalInvestorsAAndBMemberaomr:MasterRepurchaseAgreementsMember2023-12-310001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:RegionalBank1Member2022-03-070001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:RegionalBank1Member2022-03-060001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMemberaomr:FormerLondonInterbankOfferedRateLIBORMembersrt:MinimumMemberaomr:RegionalBank1Member2022-03-062022-03-060001766478us-gaap:NotesPayableToBanksMemberus-gaap:LineOfCreditMembersrt:MaximumMemberaomr:FormerLondonInterbankOfferedRateLIBORMemberaomr:RegionalBank1Member2022-03-062022-03-060001766478us-gaap:CashAndCashEquivalentsMember2023-12-310001766478us-gaap:CashAndCashEquivalentsMember2022-12-310001766478us-gaap:ResidentialMortgageBackedSecuritiesMember2023-01-012023-12-310001766478us-gaap:ResidentialMortgageBackedSecuritiesMember2022-01-012022-12-310001766478aomr:InterestRateFutureMember2023-12-310001766478aomr:InterestRateFutureMember2022-12-310001766478aomr:ToBeAnnouncedTBAsMember2023-12-310001766478aomr:ToBeAnnouncedTBAsMember2022-12-310001766478us-gaap:NondesignatedMemberaomr:InterestRateFutureMember2023-12-31aomr:contract0001766478us-gaap:LongMemberus-gaap:NondesignatedMemberaomr:InterestRateFutureMember2023-12-310001766478us-gaap:ShortMemberus-gaap:NondesignatedMemberaomr:InterestRateFutureMember2023-12-310001766478us-gaap:NondesignatedMemberaomr:ToBeAnnouncedTBAsMember2023-12-310001766478us-gaap:LongMemberus-gaap:NondesignatedMemberaomr:ToBeAnnouncedTBAsMember2023-12-310001766478us-gaap:ShortMemberus-gaap:NondesignatedMemberaomr:ToBeAnnouncedTBAsMember2023-12-310001766478us-gaap:NondesignatedMemberaomr:InterestRateFutureMember2022-12-310001766478us-gaap:LongMemberus-gaap:NondesignatedMemberaomr:InterestRateFutureMember2022-12-310001766478us-gaap:ShortMemberus-gaap:NondesignatedMemberaomr:InterestRateFutureMember2022-12-310001766478us-gaap:NondesignatedMemberaomr:ToBeAnnouncedTBAsMember2022-12-310001766478us-gaap:LongMemberus-gaap:NondesignatedMemberaomr:ToBeAnnouncedTBAsMember2022-12-310001766478us-gaap:ShortMemberus-gaap:NondesignatedMemberaomr:ToBeAnnouncedTBAsMember2022-12-310001766478us-gaap:NondesignatedMemberaomr:InterestRateFutureMember2023-01-012023-12-310001766478us-gaap:NondesignatedMemberaomr:ToBeAnnouncedTBAsMember2023-01-012023-12-310001766478us-gaap:NondesignatedMemberaomr:InterestRateFutureMember2022-01-012022-12-310001766478us-gaap:NondesignatedMemberaomr:ToBeAnnouncedTBAsMember2022-01-012022-12-310001766478us-gaap:FairValueInputsLevel1Memberaomr:LoansReceivableResidentialMember2023-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:FairValueInputsLevel2Member2023-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialMortgageLoansInSecuritizationTrustsMemberus-gaap:FairValueInputsLevel1Member2023-12-310001766478aomr:LoansReceivableResidentialMortgageLoansInSecuritizationTrustsMemberus-gaap:FairValueInputsLevel2Member2023-12-310001766478aomr:LoansReceivableResidentialMortgageLoansInSecuritizationTrustsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialMortgageLoansInSecuritizationTrustsMember2023-12-310001766478us-gaap:FairValueInputsLevel1Memberaomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMember2023-12-310001766478us-gaap:FairValueInputsLevel2Memberaomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMember2023-12-310001766478aomr:ResidentialMortgageBackedSecuritiesAngelOakMortgageTrustMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:FairValueInputsLevel1Memberaomr:AgencyWholePoolLoanSecuritiesMember2023-12-310001766478us-gaap:FairValueInputsLevel2Memberaomr:AgencyWholePoolLoanSecuritiesMember2023-12-310001766478aomr:AgencyWholePoolLoanSecuritiesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:AgencyWholePoolLoanSecuritiesMember2023-12-310001766478us-gaap:FairValueInputsLevel1Memberus-gaap:USTreasurySecuritiesMember2023-12-310001766478us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueInputsLevel2Member2023-12-310001766478us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:FairValueInputsLevel1Member2023-12-310001766478us-gaap:FairValueInputsLevel2Member2023-12-310001766478us-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:FairValueInputsLevel1Memberus-gaap:FutureMember2023-12-310001766478us-gaap:FutureMemberus-gaap:FairValueInputsLevel2Member2023-12-310001766478us-gaap:FutureMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:FutureMember2023-12-310001766478us-gaap:FairValueInputsLevel1Memberaomr:ToBeAnnouncedTBAsMember2023-12-310001766478us-gaap:FairValueInputsLevel2Memberaomr:ToBeAnnouncedTBAsMember2023-12-310001766478us-gaap:FairValueInputsLevel3Memberaomr:ToBeAnnouncedTBAsMember2023-12-310001766478aomr:ToBeAnnouncedTBAsMember2023-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2023-12-310001766478aomr:LoansReceivableResidentialMembersrt:MaximumMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialMembersrt:WeightedAverageMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2023-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:MeasurementInputLossSeverityMemberaomr:LoansReceivableResidentialMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2023-12-310001766478us-gaap:MeasurementInputLossSeverityMemberaomr:LoansReceivableResidentialMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:MeasurementInputLossSeverityMemberaomr:LoansReceivableResidentialMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:MeasurementInputExpectedTermMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2023-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:MeasurementInputExpectedTermMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:MeasurementInputExpectedTermMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMembersrt:MaximumMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMembersrt:WeightedAverageMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2023-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialSecuritizationTrustMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialSecuritizationTrustMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputLossSeverityMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputLossSeverityMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputLossSeverityMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputExpectedTermMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputExpectedTermMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputExpectedTermMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2023-12-310001766478us-gaap:CarryingReportedAmountFairValueDisclosureMember2023-12-310001766478us-gaap:EstimateOfFairValueFairValueDisclosureMember2023-12-310001766478us-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310001766478us-gaap:EstimateOfFairValueFairValueDisclosureMember2022-12-310001766478us-gaap:FairValueInputsLevel1Memberaomr:LoansReceivableResidentialMember2022-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:FairValueInputsLevel2Member2022-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialMortgageLoansInSecuritizationTrustsMemberus-gaap:FairValueInputsLevel1Member2022-12-310001766478aomr:LoansReceivableResidentialMortgageLoansInSecuritizationTrustsMemberus-gaap:FairValueInputsLevel2Member2022-12-310001766478aomr:LoansReceivableResidentialMortgageLoansInSecuritizationTrustsMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialMortgageLoansInSecuritizationTrustsMember2022-12-310001766478us-gaap:FairValueInputsLevel1Memberaomr:ResidentialMortgageBackedSecuritiesIssuedByPrivateEnterprisesMember2022-12-310001766478us-gaap:FairValueInputsLevel2Memberaomr:ResidentialMortgageBackedSecuritiesIssuedByPrivateEnterprisesMember2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesIssuedByPrivateEnterprisesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:ResidentialMortgageBackedSecuritiesIssuedByPrivateEnterprisesMember2022-12-310001766478us-gaap:FairValueInputsLevel1Memberaomr:AgencyWholePoolLoanSecuritiesMember2022-12-310001766478us-gaap:FairValueInputsLevel2Memberaomr:AgencyWholePoolLoanSecuritiesMember2022-12-310001766478aomr:AgencyWholePoolLoanSecuritiesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:AgencyWholePoolLoanSecuritiesMember2022-12-310001766478us-gaap:FairValueInputsLevel1Memberus-gaap:FutureMember2022-12-310001766478us-gaap:FutureMemberus-gaap:FairValueInputsLevel2Member2022-12-310001766478us-gaap:FutureMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478us-gaap:FutureMember2022-12-310001766478us-gaap:FairValueInputsLevel1Memberaomr:ToBeAnnouncedTBAsMember2022-12-310001766478us-gaap:FairValueInputsLevel2Memberaomr:ToBeAnnouncedTBAsMember2022-12-310001766478us-gaap:FairValueInputsLevel3Memberaomr:ToBeAnnouncedTBAsMember2022-12-310001766478aomr:ToBeAnnouncedTBAsMember2022-12-310001766478us-gaap:FairValueInputsLevel1Member2022-12-310001766478us-gaap:FairValueInputsLevel2Member2022-12-310001766478us-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2022-12-310001766478aomr:LoansReceivableResidentialMembersrt:MaximumMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialMembersrt:WeightedAverageMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2022-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478us-gaap:MeasurementInputLossSeverityMemberaomr:LoansReceivableResidentialMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2022-12-310001766478us-gaap:MeasurementInputLossSeverityMemberaomr:LoansReceivableResidentialMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478us-gaap:MeasurementInputLossSeverityMemberaomr:LoansReceivableResidentialMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:MeasurementInputExpectedTermMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2022-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:MeasurementInputExpectedTermMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialMemberus-gaap:MeasurementInputExpectedTermMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMembersrt:MaximumMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMembersrt:WeightedAverageMemberus-gaap:MeasurementInputPrepaymentRateMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2022-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialSecuritizationTrustMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478us-gaap:MeasurementInputDefaultRateMemberaomr:LoansReceivableResidentialSecuritizationTrustMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputLossSeverityMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputLossSeverityMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputLossSeverityMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputExpectedTermMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMember2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputExpectedTermMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478aomr:LoansReceivableResidentialSecuritizationTrustMemberus-gaap:MeasurementInputExpectedTermMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Member2022-12-310001766478srt:AffiliatedEntityMemberaomr:LoansReceivableResidentialMemberaomr:LoansPurchasedFromAffiliatesMember2023-01-012023-12-310001766478srt:AffiliatedEntityMemberaomr:LoansReceivableResidentialMemberaomr:LoansPurchasedFromAffiliatesMember2023-12-310001766478srt:AffiliatedEntityMemberaomr:LoansReceivableResidentialMemberaomr:LoansPurchasedFromAffiliatesMember2022-01-012022-12-310001766478srt:AffiliatedEntityMemberaomr:LoansReceivableResidentialMemberaomr:LoansPurchasedFromAffiliatesMember2022-12-310001766478srt:AffiliatedEntityMemberaomr:ManagementAgreementMember2021-06-21aomr:calendarQuarter0001766478aomr:ChiefExecutiveOfficerAndPresidentMember2022-09-280001766478us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2022-12-310001766478us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2021-12-310001766478us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2023-01-012023-12-310001766478us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2022-01-012022-12-310001766478us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2023-12-310001766478aomr:LoansReceivableCommercialMember2023-12-310001766478aomr:LoansReceivableCommercialMember2022-12-310001766478us-gaap:CommercialMortgageBackedSecuritiesMember2023-12-310001766478us-gaap:CommercialMortgageBackedSecuritiesMember2022-12-310001766478aomr:AOMT20231Memberus-gaap:InvestmentAffiliatedIssuerControlledMember2023-12-310001766478us-gaap:InvestmentAffiliatedIssuerControlledMemberaomr:AOMT20235Member2023-12-310001766478aomr:AOMT20237Memberus-gaap:InvestmentAffiliatedIssuerControlledMember2023-12-310001766478us-gaap:RestrictedStockMember2023-01-012023-12-310001766478us-gaap:StockCompensationPlanMember2022-01-012022-12-310001766478aomr:EquityIncentivePlan2021Member2021-06-210001766478aomr:EquityIncentivePlan2021Member2023-12-310001766478us-gaap:PerformanceSharesMember2023-12-310001766478us-gaap:RestrictedStockMember2023-12-310001766478aomr:EquityIncentivePlan2021Member2023-01-012023-12-310001766478aomr:EquityIncentivePlan2021Member2022-01-012022-12-310001766478us-gaap:RestrictedStockMemberaomr:EquityIncentivePlan2021Member2023-12-310001766478us-gaap:RestrictedStockMemberaomr:EquityIncentivePlan2021Member2023-01-012023-12-310001766478us-gaap:RestrictedStockMember2021-12-310001766478us-gaap:RestrictedStockMember2022-01-012022-12-310001766478us-gaap:RestrictedStockMember2022-12-310001766478us-gaap:RestrictedStockMember2023-01-012023-12-310001766478us-gaap:PerformanceSharesMember2023-01-012023-12-310001766478us-gaap:SubsequentEventMember2024-02-072024-02-070001766478aomr:ContributedLoansMemberus-gaap:SubsequentEventMember2024-03-150001766478us-gaap:SubsequentEventMemberus-gaap:ResidentialMortgageBackedSecuritiesMember2024-03-1500017664782023-10-012023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2023

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

Commission file number 001-40495

Angel Oak Mortgage REIT, Inc.

(Exact name of registrant as specified in its charter)

|

|

|

|

|

|

|

|

|

|

|

|

| Maryland |

|

37-1892154 |

| (State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

3344 Peachtree Road Northeast, Suite 1725, Atlanta, Georgia 30326

(Address of Principal Executive Offices and Zip Code)

404-953-4900

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

|

|

|

|

| Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

| Common stock, $0.01 par value |

AOMR |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☒ Non-accelerated filer ☐ Smaller reporting company ☒ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of June 30, 2023 (the last business day of the registrant’s most recently completed second fiscal quarter) the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $185.7 million based on the closing sale price as reported on the New York Stock Exchange.

The number of shares of the registrant’s common stock outstanding on March 15, 2024 was 24,965,274.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement to be filed with the Securities and Exchange Commission under Regulation 14A within 120 days after the end of registrant’s fiscal year covered by this Annual Report are incorporated by reference into Part III.

ANGEL OAK MORTGAGE REIT, INC.

Form 10-K

Table of Contents

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART I |

|

| ITEM 1. |

|

|

| ITEM 1A. |

|

|

| ITEM 1B. |

|

|

ITEM 1C. |

|

|

| ITEM 2. |

|

|

| ITEM 3. |

|

|

| ITEM 4. |

|

|

|

PART II |

|

| ITEM 5. |

|

|

| ITEM 6. |

|

|

| ITEM 7. |

|

|

| ITEM 7A. |

|

|

| ITEM 8. |

|

|

| ITEM 9. |

|

|

| ITEM 9A. |

|

|

| ITEM 9B. |

|

|

| ITEM 9C. |

|

|

|

PART III |

|

| ITEM 10. |

|

|

| ITEM 11. |

|

|

| ITEM 12. |

|

|

| ITEM 13. |

|

|

| ITEM 14. |

|

|

|

PART IV |

|

| ITEM 15. |

|

|

| ITEM 16. |

|

|

|

|

|

Unless otherwise indicated, the terms “Angel Oak Mortgage REIT, Inc.,” “we,” “us,”“our,” “our company,” and “the Company” refer to Angel Oak Mortgage REIT, Inc. and its subsidiaries including Angel Oak Mortgage Operating Partnership, LP (our “operating partnership”), through which we hold substantially all of our assets and conduct our operations. Unless otherwise indicated, the term “Angel Oak” refers collectively to Angel Oak Capital Advisors, LLC (“Angel Oak Capital”) and its affiliates, including Falcons I, LLC, our external manager (our “Manager”), Angel Oak Companies, LP (“Angel Oak Companies”), and the proprietary mortgage lending platform of affiliates Angel Oak Mortgage Solutions LLC (together with other non-operational affiliated originators, “Angel Oak Mortgage Lending”).

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K for the year ended December 31, 2023 contains forward-looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve numerous risks and uncertainties. Our actual results may differ from our beliefs, expectations, estimates, and projections and, consequently, you should not rely on these forward-looking statements as predictions of future events. Forward-looking statements are not historical in nature and can be identified by words such as “anticipate,” “estimate,” “will,” “should,” “expect,” “believe,” “intend,” “seek,” “plan” and similar expressions or their negative forms, or by references to strategy, plans, or intentions. These forward-looking statements are subject to risks and uncertainties, including, among other things, those described in “Item 1A. Risk Factors” of this Annual Report on Form 10-K. Other risks, uncertainties, and factors that could cause actual results to differ materially from those projected may be described from time to time in reports we file with the Securities and Exchange Commission (the “SEC”). We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

Factors that could have a material adverse effect on future results and performance relative to those set forth in or implied by the related forward-looking statements, as well as on our business, financial condition, liquidity, results of operations and prospects, include, but are not limited to:

•the effects of adverse conditions or developments in the financial markets and the economy upon our ability to acquire target assets such as non-qualified residential mortgage (“non-QM”) loans, particularly those sourced from Angel Oak’s proprietary mortgage lending platform, Angel Oak Mortgage Lending;

•the level and volatility of prevailing interest rates and credit spreads;

•changes in our industry, inflation, interest rates, business strategies, target assets, the debt or equity markets, the general economy (or in specific regions) or the residential real estate finance and real estate markets specifically;

•general volatility of the markets in which we invest;

•changes in the availability of attractive loans and other investment opportunities, including non-QM loans sourced from Angel Oak Mortgage Lending;

•the ability of our Manager to locate suitable investments for us, manage our portfolio, and implement our strategy;

•our ability to profitably execute securitization transactions;

•our ability to obtain and maintain financing arrangements on favorable terms, or at all;

•the adequacy of collateral securing our investments and a decline in the fair value of our investments;

•the timing of cash flows, if any, from our investments;

•the operating performance, liquidity, and financial condition of borrowers;

•increased rates of default and/or decreased recovery rates on our investments;

•changes in prepayment rates on our investments;

•the departure of any of the members of senior management of our company, our Manager, or Angel Oak;

•the availability of qualified personnel;

•conflicts with Angel Oak, including our Manager and its personnel, including our officers, and entities managed by Angel Oak;

•events, contemplated or otherwise, such as acts of God, including hurricanes earthquakes, and other natural disasters, including those resulting from global climate change, pandemics, acts of war or terrorism, the initiation or escalation of military conflicts (such as the Russian invasion of Ukraine), and others that may cause unanticipated and uninsured performance declines, disruptions in markets, and/or losses to us or the owners and operators of the real estate securing our investments;

•impact of and changes in governmental regulations, tax laws and rates, accounting principles and policies and similar matters;

•the level of governmental involvement in the U.S. mortgage market;

•future changes with respect to the Federal National Mortgage Association (“Fannie Mae”) or Federal Home Loan Mortgage Corporation (“Freddie Mac” and together with Fannie Mae, the “GSEs”) in the mortgage market and related events, including the lack of certainty as to the future roles of these entities and the U.S. Government in the mortgage market and changes to legislation and regulations affecting these entities;

•effects of hedging instruments on our target assets and our returns, and the degree to which our hedging strategies may or may not protect us from interest rate volatility;

•our ability to make distributions to our stockholders in the future at the level contemplated by our stockholders or the market generally, or at all;

•our ability to continue to qualify as a real estate investment trust (a “REIT”) for U.S. federal income tax purposes; and

•our ability to maintain our exclusion from regulation as an investment company under the Investment Company Act of 1940, as amended (the “Investment Company Act”).

When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this Annual Report on Form 10-K and in the other reports we file with the SEC. Readers are cautioned not to place undue reliance on any of these forward-looking statements, which reflect our management's views only as of the date such statements are made. The risks described in “Item 1A. Risk Factors” of this Annual Report on Form 10-K could cause actual results and performance to differ materially from those set forth in or implied by our forward-looking statements. New risks and uncertainties arise over time, and it is not possible for us to predict those events or how they may affect us.

IMPORTANT INFORMATION REGARDING OUR DISCLOSURE TO INVESTORS

We may use our website (www.angeloakreit.com) to communicate with our investors and disclose company information. The information disclosed through our website may be considered material, so investors should monitor our website in addition to press releases, SEC filings and public conference calls and webcasts. The contents of our website referenced herein are not incorporated by reference into this Annual Report on Form 10-k.

GLOSSARY

This glossary highlights some of the industry and other terms that we use elsewhere in this Annual Report on Form 10-K and is not a complete list of all the defined terms used herein.

“ABS” means securities collateralized by a pool of assets, such as loans, credit card debt, royalties or receivables, but typically excluding mortgages.

“Agency” means a U.S. Government agency, such as Ginnie Mae, or a federally chartered corporation, such as Fannie Mae or Freddie Mac, which guarantees payments of principal and interest on mortgage-backed securities.

“Agency RMBS” means residential mortgage-backed securities for which an Agency guarantees payments of principal and interest on the securities.

“Alt-A mortgage loans” mean residential mortgage loans made to borrowers whose qualifying mortgage characteristics do not conform to Agency underwriting guidelines, but whose borrower characteristics may. Generally, Alt-A mortgage loans allow homeowners to qualify for a mortgage loan with reduced or alternate forms of documentation. The credit quality of an Alt-A borrower generally exceeds the credit quality of subprime borrowers.

“A-Note” means a senior interest in a mortgage loan secured by a first mortgage on a single large commercial property or group of related commercial properties. A-Notes have a senior right to receive interest and principal related to the mortgage loan.

“ATR rules” means the Ability-to-Repay rules under the Truth-in-Lending Act established by the CFPB pursuant to authority granted under the Dodd-Frank Act, which rule, among other matters, requires lenders to make a reasonable and good faith determination of a borrower’s ability to repay when underwriting a new mortgage, including documenting and verifying income and assets, as well as other factors.

“B-Note” means an interest in a loan secured by a first mortgage on a single large commercial property or group of related commercial properties and that is subordinated in right of payment on an A-Note, which is a senior interest in such loan.

“CFPB” means the Consumer Financial Protection Bureau, an agency of the U.S. Government responsible for consumer protection in the financial sector.

“CMBS” means mortgage-backed securities that are secured by interests in a single commercial mortgage loan or a pool of mortgage loans secured by commercial properties.

“Commercial bridge loans” mean, generally, floating rate whole loans secured by first priority mortgage liens on commercial real estate made to borrowers seeking short-term capital (typically with terms of up to five years) to be used in the acquisition, construction or redevelopment of commercial properties. This type of bridge financing enables the borrower to secure short-term financing while improving the commercial property and avoid burdening it with restrictive long-term debt.

“Commercial mortgage loans” mean, with respect to our target assets, senior mortgage loans, commercial bridge loans, mezzanine loans, B-Notes, construction loans, and small balance commercial mortgage loans.

“Conforming residential mortgage loans” mean residential mortgage loans that conform to the underwriting guidelines of a GSE.

“Construction loans” mean short-term mortgage loans secured by first priority mortgage liens on real estate used to finance the cost of construction or rehabilitation of commercial properties, and are typically disbursed over time as construction progresses.

“Consumer loans” mean loans made to individuals for personal, family or household purposes (such as auto loans, credit cards and student loans).

“CRT securities” mean risk-sharing instruments issued by GSEs, or similarly structured transactions arranged by third-party market participants, that transfer a portion of the risk associated with credit losses within pools of conventional residential mortgage loans to investors such as us. Unlike Agency RMBS, full repayment of the original principal balance of CRT securities is not guaranteed by a GSE; rather, “credit risk transfer” is achieved by writing down the outstanding principal balance of the CRT securities if credit losses on the related pool of loans exceed certain thresholds. By reducing the amount that issuers are obligated to repay to holders of CRT securities, the issuers of CRT securities are able to offset credit losses on the related pool of loans.

“Dodd-Frank Act” means the Dodd-Frank Wall Street Reform and Consumer Protection Act.

“DTI” means debt-to-income ratio, which is calculated as a borrower’s monthly debt payments, divided by the borrower’s monthly gross income.

“EU/UK Securitization Rules” means the legislation in effect in the European Union or, as applicable, in the United Kingdom that, in each case, requires institutional investors, prior to investing in a securitization, to verify compliance with certain conditions, including that the originator, the original lender or the sponsor retains, on an ongoing basis, a material net economic interest in the relevant securitization of not less than 5% in the form of the retention of certain specified credit risk tranches or asset exposures.

“Ginnie Mae” means the Government National Mortgage Association, a wholly-owned corporate instrumentality of the United States within the U.S. Department of Housing and Urban Development.

“GSE” means a government-sponsored enterprise. When we refer to a GSE, we mean Fannie Mae or Freddie Mac.

“Investment property loans” mean mortgage loans made on portfolios of residential rental properties.

“Jumbo prime mortgage loans” mean residential mortgage loans that may not conform to GSE underwriting guidelines for a variety of reasons, such as exceeding GSE loan limits.

“LTV" means loan-to-value ratio, which is calculated for purposes of this Annual Report on Form 10-K as the outstanding principal amount of a loan plus any financing that is pari passu with or senior to such loan at the time of acquisition, divided by the applicable real estate value at acquisition of such loan. The real estate value reflects the results of third-party appraisals obtained by the selling mortgage companies prior to the loan closing.

“MBS” means mortgage-backed securities that are secured by interests in a pool of mortgage loans secured by property.

“Mezzanine loans” mean loans made to commercial property owners that are secured by pledges of the borrowers’ ownership interests, in whole or in part, in entities that directly or indirectly own the properties, such loans being subordinate to whole loans secured by first or second mortgage liens on the properties themselves. Mezzanine loans may be structured as preferred equity investments which provide substantively the same rights for the lender but involve the lender holding actual equity interests with preferential rights over the common equity.

“Mortgage loans” mean loans secured by real estate with a right to receive the payment of principal and interest on the loans (including servicing fees).

“MSRs” mean mortgage servicing rights. MSRs represent the right to service mortgage loans, which involves activities such as collecting mortgage payments, escrowing, and paying taxes and insurance premiums and forwarding principal and interest payments to the mortgage lender. In return for providing these services, the holder of an MSR is entitled to receive a servicing fee, typically specified as a percentage (expressed in basis points) of the serviced loan’s unpaid principal balance. An MSR is made up of two components: a basic fee and an “excess MSR.” The basic fee is the amount of compensation for the performance of servicing duties (including advance obligations), and the excess MSR is the amount that exceeds the basic fee.

“non-Agency RMBS” means RMBS that are not issued or guaranteed by an Agency or a GSE.

“non-QM loans” mean residential mortgage loans that do not satisfy the requirements for QM loans, including “exempt loans,” such as “Investor” loans made to real estate investors that do not need to meet the ATR rules.

“QM loans” mean residential mortgage loans that comply with the ATR rules and related guidelines of the CFPB.

“Residential bridge loans” mean short-term residential mortgage loans secured by a first priority security interest in non-owner occupied single family or multi-family residences, which loans are typically used in the acquisition and re-development of the residences with a view to the borrowers selling the residences.

“Residential mortgage loans” mean, with respect to our target assets, non-QM loans, QM loans, conforming residential mortgage loans, second lien mortgage loans, residential bridge loans, investment property loans, jumbo prime mortgage loans, Alt-A mortgage loans, and subprime residential mortgage loans.

“RMBS” means mortgage-backed securities that are secured by interests in a pool of mortgage loans secured by residential property. RMBS may be senior, subordinate, interest-only, principal-only, investment-grade, non-investment grade, or unrated.

“Second lien mortgage loans” mean residential mortgage loans that are subordinate to the primary or first lien mortgage loans on a residential property.

“Senior mortgage loans” mean commercial mortgage loans secured by first mortgage liens on commercial properties, which loans may vary in duration, may bear interest at fixed or floating rates and may amortize, and typically require balloon payments of principal at maturity.

“Small balance commercial mortgage loans” mean commercial mortgage loans that typically range in original principal amounts of between $250,000 and $15 million.

“Subprime residential mortgage loans” mean residential mortgage loans that do not conform to GSE underwriting guidelines. These lower standards permit loans to be made to borrowers having low credit scores and/or imperfect or impaired credit histories (including outstanding judgments or prior bankruptcies), loans with no income disclosure or verification and loans with high LTVs.

“TBAs” mean “To be Announced” forward-settling of MBS trades. The actual MBS that will be delivered to fulfill a TBA trade is not designated at the time the trade is made. These securities are announced 48 hours prior to the established trade settlement date. Net settlement typically occurs before settlement and physical delivery of the securities takes place.

“U.S. Risk Retention Rules” mean the credit risk retention rules of the SEC that generally require the sponsor of asset-backed securities to retain not less than 5% of the credit risk of the assets collateralizing the issuer’s securities.

“U.S. Treasury Securities” mean a short-term U.S. government debt obligation backed by the Treasury Department with a maturity of one year or less.

“UPB” means unpaid principal balance of a mortgage loan.

“VIE” means variable interest entity.

“Whole loans” mean direct investments in whole residential mortgage loans, as opposed to investments in other structured products that are backed by such loans.

PART I

Item 1. Business

The Company

Angel Oak Mortgage REIT, Inc. is a real estate finance company focused on acquiring and investing in first lien non-QM loans and other mortgage-related assets in the U.S. mortgage market. Our strategy is to make credit-sensitive investments primarily in newly-originated first lien non-QM loans that are primarily made to higher-quality non-QM loan borrowers and primarily sourced from Angel Oak’s proprietary mortgage lending platform, Angel Oak Mortgage Lending, which currently operates primarily through a wholesale channel and has a national origination footprint. We also may invest in other residential mortgage loans, RMBS, and other mortgage-related assets, which, collectively with non-QM loans, we refer to as our target assets. Further, we may identify and acquire our target assets through the secondary market when market conditions and asset prices are conducive to making attractive purchases. Our objective is to generate attractive risk-adjusted returns for our stockholders, through cash distributions and capital appreciation, across interest rate and credit cycles.

We are a Maryland corporation and commenced operations in September 2018. On June 21, 2021, we completed an initial public offering (“IPO”) of our common stock on the New York Stock Exchange (“NYSE”). Our common stock is traded on the NYSE under the symbol “AOMR.” We are externally managed and advised by our Manager pursuant to a management agreement (the “Management Agreement”).

We have elected to be taxed as a REIT for U.S. federal income tax purposes commencing with our taxable year ended December 31, 2019. Commencing with our taxable year ended December 31, 2019, we believe that we have been organized and operated, and we intend to continue to operate in conformity with the requirements for qualification and taxation as a REIT under the Internal Revenue Code of 1986 (the “Code”). Our qualification as a REIT, and maintenance of such qualification, depends on our ability to meet, on a continuing basis, various complex requirements under the Code relating to, among other things, the sources of our gross income, the composition and values of our assets, our distribution levels and the concentration of ownership of our stock. We also intend to operate our business in a manner that will allow us to maintain our exclusion from regulation as an investment company under the Investment Company Act.

Our Manager

We are externally managed and advised by our Manager, Falcons I, LLC, a registered investment adviser under the Investment Advisers Act of 1940 and an affiliate of Angel Oak Capital, a leading alternative credit manager with market leadership in mortgage credit that includes asset management, lending, and capital markets. Angel Oak Capital was established in 2009 and is a market leader in non-QM loan production via its Angel Oak Mortgage Lending affiliates. Angel Oak Mortgage Trust (“AOMT”), Angel Oak’s securitization platform, is a leading programmatic issuer of non-QM securities, and is among the largest issuers of such securities.

Our Investment Strategy

Our investment strategy is to make credit-sensitive investments primarily in newly-originated first lien non-QM loans that are primarily made to higher-quality non-QM loan borrowers and primarily sourced from Angel Oak Mortgage Lending, which primarily operates through a wholesale channel and has a national origination footprint. We also may invest in other target assets as described below. Further, we may identify and acquire our target assets through the secondary market when market conditions and asset prices are conducive to making attractive purchases. We often finance these target assets through various financing lines on, primarily, a short-term basis and ultimately seek to secure long-term securitization funding for substantially all of our non-QM loans. Our objective is to generate attractive risk-adjusted returns for our stockholders, through cash distributions and capital appreciation, across interest rate and credit cycles.

Subject to maintaining our qualification as a REIT under the Code, and maintaining our exclusion from regulation as an investment company under the Investment Company Act, we also expect to continue to utilize various derivative instruments and other hedging instruments to mitigate interest rate risk, credit risk, and other risks. For example, we may enter into hedging transactions with respect to interest rate exposure on one or more of our assets or liabilities. Any such hedging transactions could take a variety of forms, including the use of derivative instruments such as interest rate swap contracts, index swap contracts, interest rate cap or floor contracts, futures or forward contracts, and options.

Our Investment Guidelines

Our Board of Directors has approved the following investment guidelines:

•No investment shall be made that would cause us to fail to qualify as a REIT under the Code;

•No investment shall be made that would cause us or any of our subsidiaries to be regulated as an investment company under the Investment Company Act;

•Our investments will be predominantly in our target assets;

•Prior to the deployment of capital into our target assets, our Manager may cause our capital to be invested in any short-term investments in money market funds, bank accounts, overnight repurchase agreements with primary U.S. Federal Reserve Bank dealers collateralized by direct U.S. Government obligations, and other instruments or investments determined by our Manager to be of high quality; and

•The acquisition of any of our target assets by us or any of our subsidiaries from Angel Oak Mortgage Lending or other affiliate of our Manager shall require the pricing approval of our affiliated transactions committee, which is comprised of three of our independent directors.

These investment guidelines may be amended, restated, modified, supplemented, or waived by our Board of Directors (which must include a majority of our independent directors) from time to time without the approval of, or prior notice to, our stockholders.

Our Target Assets

Our target assets include:

|

|

|

|

|

|

| Target assets, Investments Backed by: |

Examples: |

|

|

| Residential properties |

Non-QM loans |

|

Non-Agency RMBS |

|

|

| Commercial real estate properties |

Senior mortgage loans |

|

Commercial bridge loans |

|

Small balance commercial mortgage loans |

|

|

| Other investments |

Agency RMBS |

|

Second lien mortgage loans |

|

Mezzanine loans |

|

Construction loans |

|

B-notes |

|

QM loans |

|

Conforming residential mortgage loans |

|

Residential bridge loans |

|

Subprime residential mortgage loans |

|

Alt-A mortgage loans |

|

CRT securities |

|

CMBS |

|

MSRs and excess MSRs |

|

Certain non-real estate related assets, including ABS and consumer loans |

Our strategy is adaptable to changing market environments, subject to our ability to maintain our qualification as a REIT for U.S. federal income tax purposes and to maintain our exclusion from regulation as an investment company under the Investment Company Act. Our investment and asset management decisions depend on prevailing market conditions. Accordingly, our strategy and target assets may vary over time in response to market conditions. Our Manager is authorized to follow very broad investment guidelines and, as a result, we cannot predict our portfolio composition. We may change our strategy and policies without a vote of our stockholders.

Our Portfolio and Securitizations

Since the commencement of our operations in September 2018 through December 31, 2023, we have focused on the acquisition of our target assets, including residential mortgage loans, a substantial portion of which were sourced by Angel Oak Mortgage Lending. As of December 31, 2023, we have participated in thirteen rated securitization transactions.

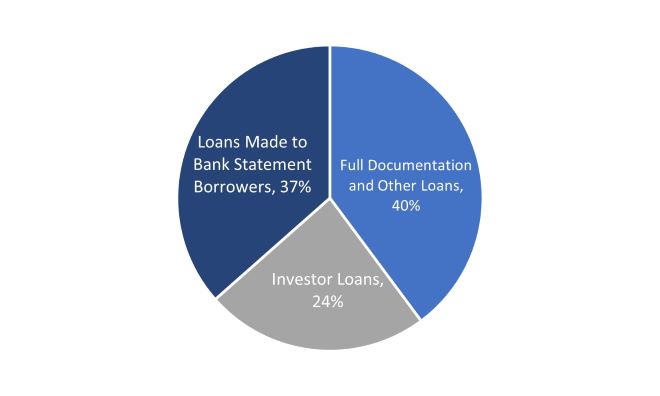

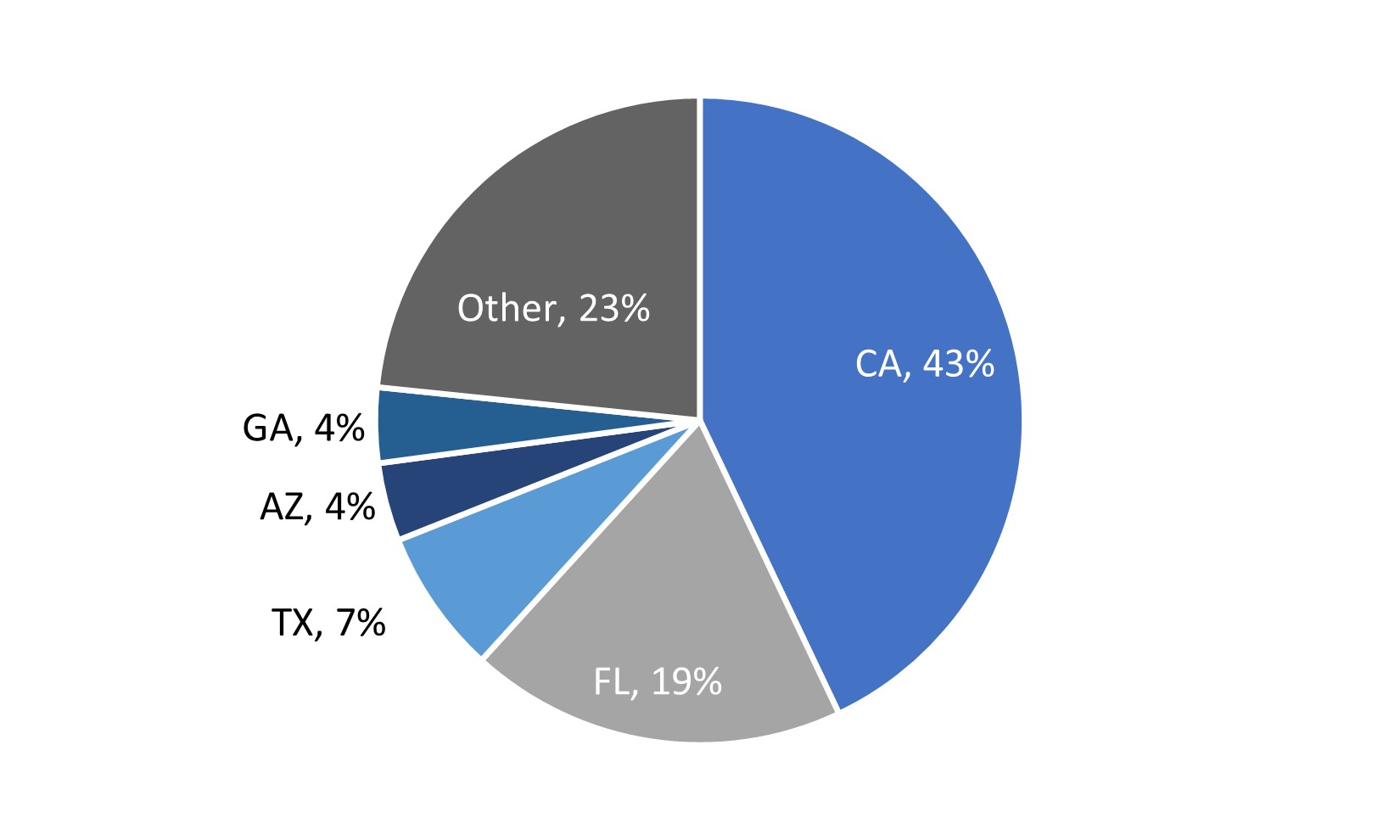

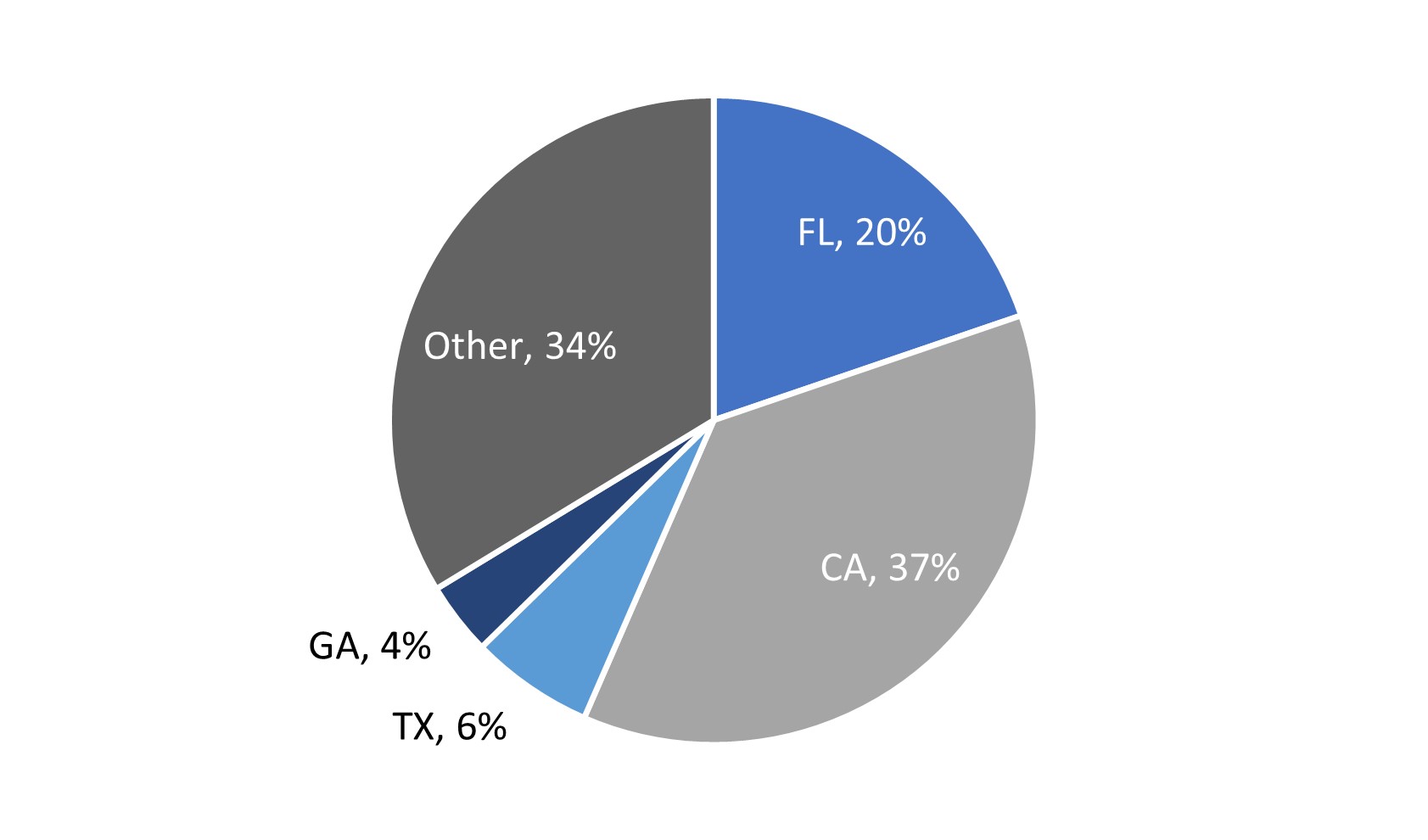

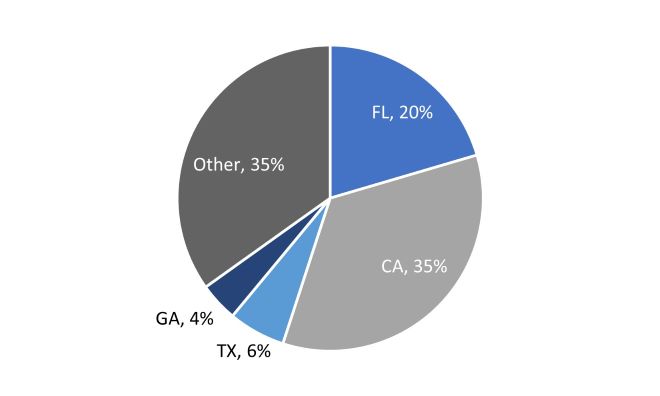

We believe that our portfolio validates our strategy of making credit-sensitive investments primarily in newly-originated first lien non-QM loans that are primarily made to higher-quality non-QM loan borrowers and substantially sourced from Angel Oak’s proprietary mortgage lending platform, Angel Oak Mortgage Lending.

As of December 31, 2023, our approximately $2.3 billion portfolio of total assets consisted predominantly of residential mortgage loans owned directly, residential mortgage loans held in securitization trusts, and RMBS. For additional information regarding our portfolio as of December 31, 2023, see Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Our Portfolio”.

Our Financing Strategy and Use of Leverage

We finance our assets with what we believe to be a prudent amount of leverage, which will vary from time to time based upon the particular characteristics of our portfolio, availability of financing and market conditions. We expect to use loan financing lines to finance the acquisition and accumulation of mortgage loans or other mortgage-related assets pending their eventual securitization. Upon accumulating an appropriate amount of assets, we expect to finance a substantial portion of our mortgage loans utilizing fixed rate term securitization funding that provides long-term financing for our mortgage loans and locks in our cost of funding, regardless of future interest rate movements.

In addition to our existing loan financing lines, we employ short-term repurchase facilities to borrow against U.S. Treasury Securities, securities issued by AOMT, and other securities we may acquire in accordance with our investment guidelines.

Our use of leverage, especially in order to increase the quantity of assets supported by our capital base, may have the effect of increasing losses when these assets underperform. The amount of leverage employed on our assets will depend on our Manager’s assessment of the credit, liquidity, price volatility and other risks and availability of particular types of financing at any given time. Moreover, our charter, third amended and restated bylaws (our “bylaws”) and investment guidelines require no minimum or maximum leverage and our Manager will have the discretion, without the need for further approval by our Board of Directors, to change both our overall leverage and the leverage used for individual asset classes. Because our strategy is flexible, dynamic, and opportunistic, our overall leverage and the leverage used for individual asset classes will vary over time.

Competition and Regulatory Considerations

We are engaged in a competitive business. In our investing activities, we compete for opportunities with a variety of institutional investors, including other REITs, specialty finance companies, public and private funds (including funds that Angel Oak or its affiliates may sponsor, advise and/or manage), commercial and investment banks, commercial finance and insurance companies, and other financial institutions. Several other REITs have raised, or may raise, significant amounts of capital, and may have investment objectives that overlap with ours, which may create additional competition for investment opportunities. Some competitors may have a lower cost of funds and access to funding sources that are not available to us. Many of our competitors are not subject to the operating constraints associated with REIT compliance or maintenance of an exclusion from registration under the Investment Company Act. In addition, some of our competitors may have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of loans and investments, offer more attractive pricing or other terms and establish more relationships than us. Furthermore, competition for originations of and investments in our target asset classes may lead to the yields of such assets decreasing, which may further limit our ability to generate satisfactory returns.

In addition, changes in the financial regulatory regime could decrease the current restrictions on banks and other financial institutions and allow them to compete with us for investment opportunities that were previously not available to them.

Human Capital Resources

We have no employees. All of our executive officers, and our dedicated or partially dedicated personnel, which include our Chief Executive Officer, Chief Financial Officer, accounting staff, in-house legal counsel, and other personnel providing services to us were employees of our Manager or one or more of our Manager’s affiliates as of December 31, 2023.

Available Information

Our website address is www.angeloakreit.com. We make available on our website under “Investors,” free of charge, this Annual Report on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K and any other reports that we file with the SEC as soon as reasonably practicable after we electronically file or furnish such materials to the SEC. Information on our website, however, is not part of or incorporated by reference into this Annual Report on Form 10-K. In addition, all our filed reports can be obtained at the SEC’s website at www.sec.gov.

Item 1A. Risk Factors

An investment in our common stock involves significant risks. Before making a decision to invest in our common stock, you should carefully consider the following risks in addition to the other information contained in this Annual Report on Form 10-K. The risks discussed in this Annual Report on Form 10-K can materially adversely affect our business, financial condition, liquidity, results of operations and prospects and our ability to make distributions to our stockholders (which we refer to collectively as “materially and adversely affecting us” or having “a material adverse effect on us,” and comparable phrases). This could cause the market price of our common stock to decline significantly, and you could lose all or part of your investment in our common stock. Some statements in this Annual Report on Form 10-K, including statements in the following risk factors, constitute forward-looking statements. Please refer to the section entitled “Special Note Regarding Forward-Looking Statements.”

Summary Risk Factors

We are subject to a number of risks that, if realized, could materially and adversely affect our business, financial condition, liquidity, results

of operations and prospects and our ability to make distributions to our stockholders. Some of our more significant challenges and risks

include, but are not limited to, the following, which are described in greater detail below:

•We are dependent on our Manager and certain key personnel of Angel Oak who are or may be provided to us through our Manager, and may not find a suitable replacement if our Manager terminates the Management Agreement or such key personnel are no longer available to us.

•There are conflicts of interest in our relationship with Angel Oak, including our Manager, and we may compete with existing and future managed entities of Angel Oak, which may present various conflicts of interest that restrict our ability to pursue certain investment opportunities or take other actions that are beneficial to our business and result in decisions that are not in the best interests of our stockholders.

•We rely on Angel Oak Mortgage Lending to source non‑QM loans and other target assets for acquisition by us and it is under no contractual obligation to sell to us any loans that it originates.

•Our Manager’s fee structure may not create proper incentives or may induce our Manager and its affiliates to make certain loans or other investments, including speculative investments, which increase the risk of our portfolio.

•The Management Agreement with our Manager was not negotiated on an arm’s‑length basis and may not be as favorable to us as if it had been negotiated with an unaffiliated third party and may be costly and difficult to terminate. Our Manager’s liability is limited under the Management Agreement, and we have agreed to indemnify our Manager against certain liabilities.

•Our operating results are dependent upon our Manager’s ability to source a large volume of desirable non‑QM loans and other target assets for our investment on attractive terms.

•Difficult conditions in the residential mortgage and residential real estate markets as well as general market concerns, including macroeconomic events, may adversely affect the value of residential mortgage loans, including non‑QM loans, and other target assets in which we invest.

•Non-QM loans that are underwritten pursuant to less stringent underwriting guidelines could experience higher rates of delinquencies, defaults and foreclosures than those experienced by loans underwritten to more stringent underwriting guidelines.

•Angel Oak Mortgage Lending is subject to extensive licensing requirements and regulation, which could materially and adversely affect us if Angel Oak Mortgage Lending does not comply with these requirements.

•Currently, we are focused on acquiring and investing in non‑QM loans, which may subject us to legal, administrative, regulatory, and other risks, which could materially and adversely affect us.

•Prepayment rates may adversely affect the value of our portfolio.

•Our investment in lower rated non‑Agency RMBS resulting from the securitization of our assets or otherwise exposes us to the first loss on the mortgage assets held by the securitization vehicle. Additionally, the principal and interest payments on non‑Agency RMBS are not guaranteed by any entity, including any government entity or GSE, and therefore are subject to increased risks, including credit risk.

•Mortgage loan modification programs and future legislative action may adversely affect the value of, and the returns on, our target assets, which could materially and adversely affect us.

•We are highly dependent on information systems, and system failures could significantly disrupt our business, which may, in turn, have a material adverse effect on us.

•Our industry is highly regulated and we or Angel Oak, including our Manager, may be subject to adverse legislative or regulatory changes.

•Maintenance of our exclusion from regulation as an investment company under the Investment Company Act imposes significant limitations on our operations.

•Our significant debt subjects us to increased risk of loss, and our charter and bylaws contain no limitation on the amount of debt we may incur.

•Our access to financing sources, which may not be available on favorable terms, or at all, may be limited, and this may materially and adversely affect us.

•Market conditions and other factors may affect our ability to securitize assets, which could increase our financing costs and materially and adversely affect us.

•We may be unable to profitably execute securitization transactions, which could materially and adversely affect us.

•Interest rate fluctuations could increase our financing costs, which could materially and adversely affect us.

•Our significant stockholders and their respective affiliates have significant influence over us and their actions might not be in your best interest as a stockholder.

•Legislative or other actions affecting REITs could materially and adversely affect us.

•Our failure to qualify as a REIT would subject us to U.S. federal income tax and potentially increased state and local taxes, which would reduce the amount of our income available for distribution to our stockholders.

•Complying with REIT requirements and avoiding a prohibited transaction tax may force us to hold a significant portion of our assets and conduct a significant portion of our activities through a taxable REIT subsidiary (“TRS”), and a significant portion of our income may be earned through a TRS.