false2023FY0001728205http://fasb.org/us-gaap/2023#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2023#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2023#OtherLiabilitiesCurrenthttp://fasb.org/us-gaap/2023#OtherLiabilitiesCurrent100017282052023-01-012023-12-3100017282052023-06-30iso4217:USD00017282052024-02-23xbrli:shares00017282052023-10-012023-12-3100017282052022-01-012022-12-3100017282052021-07-012021-12-3100017282052020-07-012021-06-30iso4217:USDxbrli:shares00017282052023-12-3100017282052022-12-3100017282052021-12-3100017282052021-06-3000017282052020-06-300001728205us-gaap:CommonStockMember2020-06-300001728205us-gaap:AdditionalPaidInCapitalMember2020-06-300001728205us-gaap:RetainedEarningsMember2020-06-300001728205us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-06-300001728205us-gaap:CommonStockMember2020-07-012021-06-300001728205us-gaap:AdditionalPaidInCapitalMember2020-07-012021-06-300001728205us-gaap:RetainedEarningsMember2020-07-012021-06-300001728205us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-07-012021-06-300001728205us-gaap:CommonStockMember2021-06-300001728205us-gaap:AdditionalPaidInCapitalMember2021-06-300001728205us-gaap:RetainedEarningsMember2021-06-300001728205us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-06-300001728205us-gaap:AdditionalPaidInCapitalMember2021-07-012021-12-310001728205us-gaap:CommonStockMember2021-07-012021-12-310001728205us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-07-012021-12-310001728205us-gaap:RetainedEarningsMember2021-07-012021-12-310001728205us-gaap:CommonStockMember2021-12-310001728205us-gaap:AdditionalPaidInCapitalMember2021-12-310001728205us-gaap:RetainedEarningsMember2021-12-310001728205us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001728205us-gaap:CommonStockMember2022-01-012022-12-310001728205us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001728205us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001728205us-gaap:RetainedEarningsMember2022-01-012022-12-310001728205us-gaap:CommonStockMember2022-12-310001728205us-gaap:AdditionalPaidInCapitalMember2022-12-310001728205us-gaap:RetainedEarningsMember2022-12-310001728205us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001728205us-gaap:CommonStockMember2023-01-012023-12-310001728205us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001728205us-gaap:RetainedEarningsMember2023-01-012023-12-310001728205us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001728205us-gaap:CommonStockMember2023-12-310001728205us-gaap:AdditionalPaidInCapitalMember2023-12-310001728205us-gaap:RetainedEarningsMember2023-12-310001728205us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-310001728205srt:MinimumMember2023-01-012023-12-310001728205srt:MaximumMember2023-01-012023-12-310001728205pll:SayonaMiningLimitedMember2023-01-012023-12-310001728205us-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMemberpll:ThreeLargestCustomersMember2023-01-012023-12-31xbrli:pure0001728205pll:StockIncentivePlanMember2023-01-012023-12-310001728205pll:StockIncentivePlanMember2023-12-310001728205pll:ExplorationCostsMember2023-01-012023-12-310001728205pll:ExplorationCostsMember2022-01-012022-12-310001728205pll:ExplorationCostsMember2021-07-012021-12-310001728205pll:ExplorationCostsMember2020-07-012021-06-300001728205us-gaap:SellingGeneralAndAdministrativeExpensesMember2023-01-012023-12-310001728205us-gaap:SellingGeneralAndAdministrativeExpensesMember2022-01-012022-12-310001728205us-gaap:SellingGeneralAndAdministrativeExpensesMember2021-07-012021-12-310001728205us-gaap:SellingGeneralAndAdministrativeExpensesMember2020-07-012021-06-300001728205srt:MinimumMember2022-01-012022-12-310001728205srt:MaximumMember2022-01-012022-12-310001728205srt:MinimumMember2020-07-012021-06-300001728205srt:MaximumMember2020-07-012021-06-300001728205pll:MilestonePRAsMember2023-12-310001728205pll:TSRPRAsMember2023-12-310001728205us-gaap:PerformanceSharesMember2023-12-310001728205pll:TSRPRAsMembersrt:MinimumMember2023-12-310001728205pll:TSRPRAsMembersrt:MaximumMember2023-12-310001728205pll:TSRPRAsMembersrt:MinimumMember2023-01-012023-12-310001728205pll:TSRPRAsMembersrt:MaximumMember2023-01-012023-12-310001728205pll:TSRPRAsMember2023-01-012023-12-310001728205us-gaap:RestrictedStockUnitsRSUMember2020-06-300001728205us-gaap:PerformanceSharesMember2020-06-300001728205us-gaap:RestrictedStockUnitsRSUMember2020-07-012021-06-300001728205us-gaap:PerformanceSharesMember2020-07-012021-06-300001728205us-gaap:RestrictedStockUnitsRSUMember2021-06-300001728205us-gaap:PerformanceSharesMember2021-06-300001728205us-gaap:RestrictedStockUnitsRSUMember2021-07-012021-12-310001728205us-gaap:PerformanceSharesMember2021-07-012021-12-310001728205us-gaap:RestrictedStockUnitsRSUMember2021-12-310001728205us-gaap:PerformanceSharesMember2021-12-310001728205us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001728205us-gaap:PerformanceSharesMember2022-01-012022-12-310001728205us-gaap:RestrictedStockUnitsRSUMember2022-12-310001728205us-gaap:PerformanceSharesMember2022-12-310001728205us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001728205us-gaap:PerformanceSharesMember2023-01-012023-12-310001728205us-gaap:RestrictedStockUnitsRSUMember2023-12-310001728205us-gaap:EmployeeStockOptionMember2023-01-012023-12-310001728205us-gaap:EmployeeStockOptionMember2022-01-012022-12-310001728205us-gaap:EmployeeStockOptionMember2021-07-012021-12-310001728205us-gaap:EmployeeStockOptionMember2020-07-012021-06-300001728205us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001728205us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001728205us-gaap:RestrictedStockUnitsRSUMember2021-07-012021-12-310001728205us-gaap:RestrictedStockUnitsRSUMember2020-07-012021-06-300001728205us-gaap:PerformanceSharesMember2023-01-012023-12-310001728205us-gaap:PerformanceSharesMember2022-01-012022-12-310001728205us-gaap:PerformanceSharesMember2021-07-012021-12-310001728205us-gaap:PerformanceSharesMember2020-07-012021-06-300001728205us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-12-310001728205us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-12-310001728205us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-06-300001728205us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-06-300001728205us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2023-01-012023-12-310001728205us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-01-012022-12-310001728205us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-07-012021-12-310001728205us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-07-012021-06-300001728205us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2023-12-310001728205us-gaap:DomesticCountryMember2023-12-310001728205us-gaap:DomesticCountryMember2022-12-310001728205us-gaap:StateAndLocalJurisdictionMember2023-12-310001728205us-gaap:StateAndLocalJurisdictionMember2022-12-310001728205us-gaap:ForeignCountryMemberus-gaap:AustralianTaxationOfficeMember2023-12-310001728205us-gaap:ForeignCountryMemberus-gaap:AustralianTaxationOfficeMember2022-12-310001728205pll:ForeignTaxAuthorityOtherMemberus-gaap:AustralianTaxationOfficeMember2023-12-310001728205pll:ForeignTaxAuthorityOtherMemberus-gaap:AustralianTaxationOfficeMember2022-12-310001728205us-gaap:MiningPropertiesAndMineralRightsMember2023-12-310001728205us-gaap:MiningPropertiesAndMineralRightsMember2022-12-310001728205us-gaap:MineDevelopmentMember2023-12-310001728205us-gaap:MineDevelopmentMember2022-12-310001728205us-gaap:LandMember2023-12-310001728205us-gaap:LandMember2022-12-310001728205us-gaap:LeaseholdImprovementsMember2023-12-310001728205us-gaap:LeaseholdImprovementsMember2022-12-310001728205us-gaap:WellsAndRelatedEquipmentAndFacilitiesMember2023-12-310001728205us-gaap:WellsAndRelatedEquipmentAndFacilitiesMember2022-12-310001728205us-gaap:ConstructionInProgressMember2023-12-310001728205us-gaap:ConstructionInProgressMember2022-12-310001728205pll:SayonaMiningLimitedMember2021-06-300001728205pll:SayonaQuebecIncMember2021-06-300001728205pll:AtlanticLithiumMember2021-06-300001728205pll:VinlandLithiumMember2021-06-300001728205pll:AtlanticLithiumMember2021-07-012021-12-310001728205pll:SayonaMiningLimitedMember2021-07-012021-12-310001728205pll:SayonaQuebecIncMember2021-07-012021-12-310001728205pll:SayonaMiningAndSayonaQuebecMember2021-07-012021-12-310001728205pll:SayonaMiningLimitedMember2021-12-310001728205pll:SayonaQuebecIncMember2021-12-310001728205pll:AtlanticLithiumMember2021-12-310001728205pll:VinlandLithiumMember2021-12-310001728205pll:SayonaMiningLimitedMember2022-01-012022-12-310001728205pll:SayonaQuebecIncMember2022-01-012022-12-310001728205pll:SayonaMiningAndSayonaQuebecMember2022-01-012022-12-310001728205pll:AtlanticLithiumMember2022-01-012022-12-310001728205pll:SayonaMiningLimitedMember2022-12-310001728205pll:SayonaQuebecIncMember2022-12-310001728205pll:AtlanticLithiumMember2022-12-310001728205pll:VinlandLithiumMember2022-12-310001728205pll:VinlandLithiumMember2023-01-012023-12-310001728205pll:SayonaQuebecIncMember2023-01-012023-12-310001728205pll:AtlanticLithiumMember2023-01-012023-12-310001728205pll:SayonaMiningSayonaQuebecAndAtlanticLithiumMember2023-01-012023-12-310001728205pll:SayonaMiningLimitedMember2023-12-310001728205pll:SayonaQuebecIncMember2023-12-310001728205pll:AtlanticLithiumMember2023-12-310001728205pll:VinlandLithiumMember2023-12-310001728205pll:SayonaMiningLimitedMemberpll:SayonaQuebecIncMember2023-12-310001728205pll:NorthAmericanLithiumMiningMemberpll:SayonaQuebecIncMember2023-12-310001728205pll:SayonaQuebecIncMember2023-12-31utr:tiso4217:USDutr:t0001728205pll:NorthAmericanLithiumMiningMemberpll:SayonaQuebecIncMember2023-01-012023-12-310001728205pll:NorthAmericanLithiumMiningMemberpll:SayonaQuebecIncMember2023-12-31iso4217:USDpll:Tonne0001728205pll:AtlanticLithiumMember2023-12-310001728205pll:KillickLithiumMember2023-12-310001728205pll:SayonaMiningLimitedMember2023-01-012023-12-310001728205pll:SayonaQuebecIncMember2023-01-012023-12-310001728205pll:AtlanticLithiumMember2023-01-012023-12-310001728205pll:SayonaMiningLimitedMember2023-12-310001728205pll:SayonaQuebecIncMember2023-12-310001728205pll:AtlanticLithiumMember2023-12-310001728205pll:SayonaMiningLimitedMember2022-01-012022-12-310001728205pll:SayonaQuebecIncMember2022-01-012022-12-310001728205pll:AtlanticLithiumMember2022-01-012022-12-310001728205pll:SayonaMiningLimitedMember2022-12-310001728205pll:SayonaQuebecIncMember2022-12-310001728205pll:AtlanticLithiumMember2022-12-310001728205pll:SayonaMiningLimitedMember2021-07-012021-12-310001728205pll:SayonaQuebecIncMember2021-07-012021-12-310001728205pll:AtlanticLithiumMember2021-07-012021-12-310001728205pll:SayonaMiningLimitedMember2021-12-310001728205pll:SayonaQuebecIncMember2021-12-310001728205pll:AtlanticLithiumMember2021-12-310001728205pll:SayonaMiningLimitedMember2020-07-012021-06-300001728205pll:SayonaMiningLimitedMember2021-06-300001728205pll:GhanaProjectMember2023-12-31pll:phase0001728205pll:GhanaProjectPhaseOneMember2023-12-310001728205pll:GhanaProjectPhaseTwoMember2023-12-310001728205pll:EwoyaaProjectMember2023-12-310001728205pll:KillickLithiumMember2023-01-012023-12-310001728205pll:EwoyaaProjectMember2023-01-012023-12-310001728205pll:EwoyaaProjectMember2022-01-012022-12-310001728205pll:EwoyaaProjectMember2021-07-012021-12-31pll:option0001728205srt:MinimumMember2023-12-310001728205srt:MaximumMember2023-12-310001728205pll:PiedmontAustraliaMember2023-12-310001728205pll:PiedmontLithiumMember2021-05-1700017282052021-05-1600017282052021-05-170001728205pll:AdvanceOfFundingObligationsToKillickLithiumProjectMember2023-11-012023-11-300001728205pll:AdvanceOfFundingObligationsToKillickLithiumProjectMember2023-11-300001728205pll:VinlandLithiumMemberpll:AdvanceOfFundingObligationsToKillickLithiumProjectMember2023-11-012023-11-300001728205pll:LGChemMember2023-02-012023-02-280001728205pll:LGChemMember2023-02-280001728205pll:ShelfRegistrationProgramMember2022-03-012022-03-310001728205pll:ShelfRegistrationProgramMember2022-03-310001728205pll:USPublicOfferingProgramMember2022-03-012022-03-3100017282052021-09-240001728205pll:ShelfRegistrationProgramMember2023-12-310001728205pll:AustraliaSharePlacementsAndUSPublicOfferingsMember2020-08-012020-08-310001728205pll:AustraliaSharePlacementsAndUSPublicOfferingsMember2020-08-31iso4217:AUDxbrli:shares0001728205pll:AustraliaSharePlacementsAndUSPublicOfferingsMember2020-10-012020-10-310001728205pll:AustraliaSharePlacementsAndUSPublicOfferingsMember2020-10-3100017282052021-03-012021-03-3100017282052022-03-31pll:segment00017282052023-09-08pll:action00017282052023-05-3100017282052023-07-012023-07-3100017282052023-10-012023-10-3100017282052023-05-012023-05-310001728205pll:AtlanticLithiumMemberus-gaap:SubsequentEventMember2024-01-012024-02-270001728205pll:AtlanticLithiumMemberus-gaap:SubsequentEventMember2024-02-270001728205us-gaap:SubsequentEventMemberpll:SayonaMiningLimitedMember2024-01-012024-02-270001728205us-gaap:SubsequentEventMemberpll:SayonaMiningLimitedMember2024-02-270001728205us-gaap:SubsequentEventMemberpll:SayonaMiningLimitedMembersrt:MinimumMember2024-01-012024-02-270001728205us-gaap:SubsequentEventMemberpll:SayonaMiningLimitedMembersrt:MaximumMember2024-01-012024-02-270001728205us-gaap:SubsequentEventMemberpll:A2024CostSavingsPlanMember2024-02-012024-02-270001728205us-gaap:SubsequentEventMemberpll:A2024CostSavingsPlanMember2024-01-012024-02-270001728205us-gaap:SubsequentEventMemberpll:A2024CostSavingsPlanMemberus-gaap:EmployeeSeveranceMember2024-02-27

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________

FORM 10-K

________________________________

|

|

|

|

|

|

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2023

OR

|

|

|

|

|

|

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______ to ________

Commission File Number 001-38427

___________________________________________________________

Piedmont Lithium Inc.

(Exact name of Registrant as specified in its Charter)

_________________________________________________________________________________________

|

|

|

|

|

|

| Delaware |

36-4996461 |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

42 E Catawba Street

Belmont, North Carolina

|

28012 |

| (Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (704) 461-8000

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Title of each class |

|

Trading Symbol |

|

Name of each exchange on which registered |

| Common stock, $0.0001 par value per share |

|

PLL |

|

The Nasdaq Capital Market |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Securities Exchange Act.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Large accelerated filer |

☒ |

Accelerated filer |

☐ |

Emerging growth company |

☐ |

|

|

|

|

|

|

| Non-accelerated filer |

☐ |

Smaller reporting company |

☐ |

|

|

☐ If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Securities Exchange Act.

☒ Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

☐ If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

☐ Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

☐ Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act).

As of June 30, 2023, the aggregate market value of voting and non-voting common stock held by non-affiliates of the registrant (based on the closing price of the registrant's common shares on the Nasdaq Stock Market for June 30, 2023) was approximately $1,107,794,754. For the purposes of the foregoing calculation only, all directors and executive officers of the registrant have been deemed affiliates.

As of February 23, 2024, there were 19,360,939 shares of the Registrant’s common stock outstanding.

Table of Contents

GLOSSARY OF TERMS AND DEFINITIONS

When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below:

|

|

|

|

|

|

| 401(k) Plan |

Piedmont Lithium 401(k) Plan |

| ADS |

American depositary shares |

| Air Permit |

Conditional Major Non-Title V Construction and Operating Air Permit |

| Annual Report |

Annual Report on Form 10-K |

| ASC |

Accounting Standards Codification |

| ASX |

Australian Securities Exchange |

| Atlantic Lithium |

Atlantic Lithium Limited |

| Atlantic Lithium Ghana |

Atlantic Lithium’s Ghanaian-based lithium portfolio companies |

| ATVM |

Advanced Technology Vehicles Manufacturing |

| Authier |

Authier Lithium project |

| BAPE |

Bureau d’Audiences Publiques Sur l’Environnement |

| Carolina Lithium |

Carolina Lithium project |

| CDI |

CHESS Depository Interest |

| CERCLA |

Comprehensive Environmental Response, Compensation, and Liability Act |

| CIF |

cost, insurance and freight |

| CODM |

Chief Operating Decision Maker |

| COSO |

Committee of Sponsoring Organizations of the Treadway Commission |

| CWA |

Clean Water Act |

| DAP |

delivered at place |

| DEMLR |

Department of Energy, Mineral and Land Resources |

| DFS |

definitive feasibility study |

| dmt |

dry metric ton |

| DOE |

U.S. Department of Energy |

|

|

| EPA |

U.S. Environmental Protection Agency |

| EPC |

engineer, procure, and construct |

| ESG |

environmental, social and governance |

| Ewoyaa |

Ewoyaa Lithium project |

| Exchange Act |

Securities Exchange Act of 1934 |

| FCPA |

U.S. Foreign Corrupt Practices Act |

| FDIC |

Federal Deposit Insurance Corporation |

| FEED |

front-end engineering and design |

|

|

| FOB |

free on board |

| IRA |

Inflation Reduction Act of 2022 |

|

|

| JORC Code |

2012 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves |

| Killick Lithium |

Killick Lithium Inc. |

| Lac Albert |

Lac Albert Lithium project |

| LCE |

lithium carbonate equivalent |

| LG Chem |

LG Chem, Ltd. |

Li2O |

lithium oxide |

LiOH·H2O |

lithium hydroxide monohydrate |

|

|

| MIIF |

Minerals Income Investment Fund of Ghana |

| Milestone PRAs |

PRAs that could be earned based upon achievement of certain specified milestones |

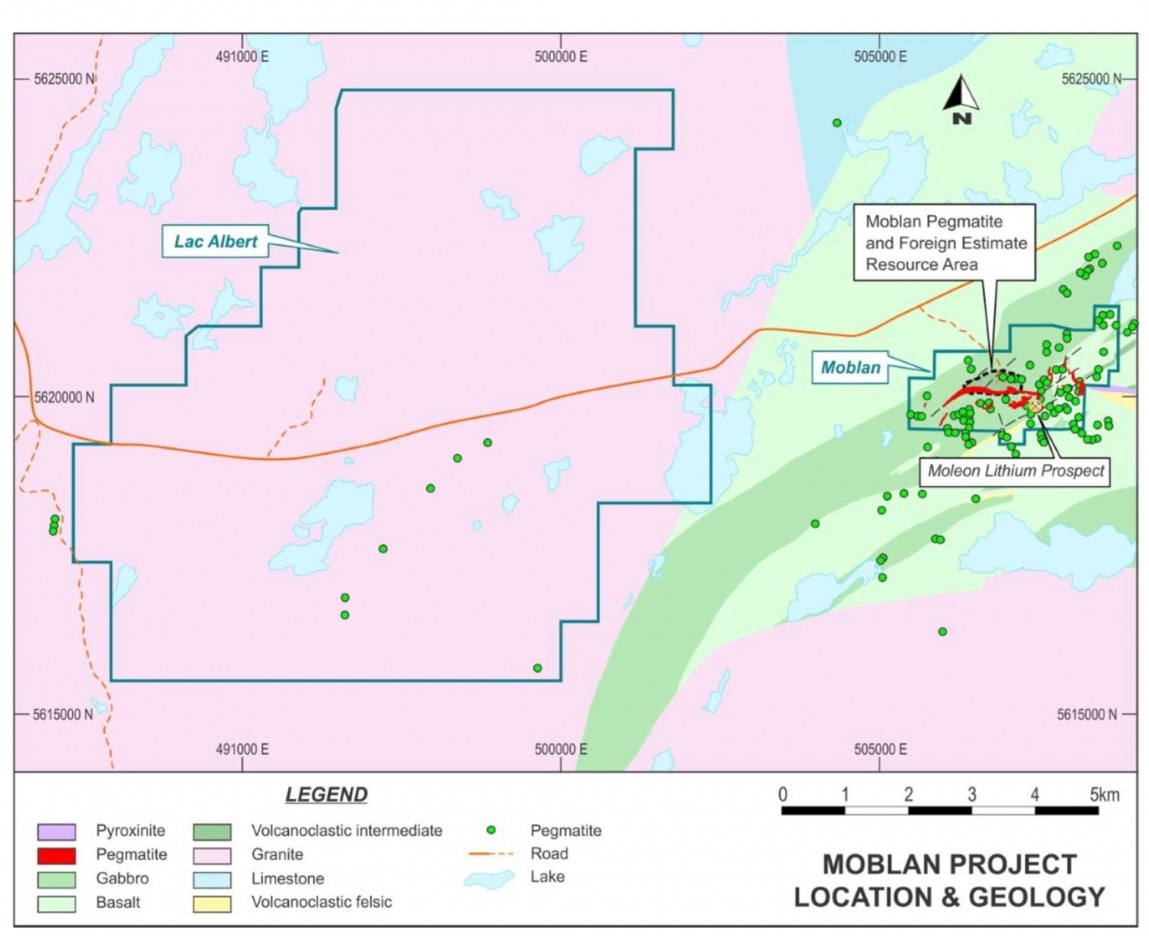

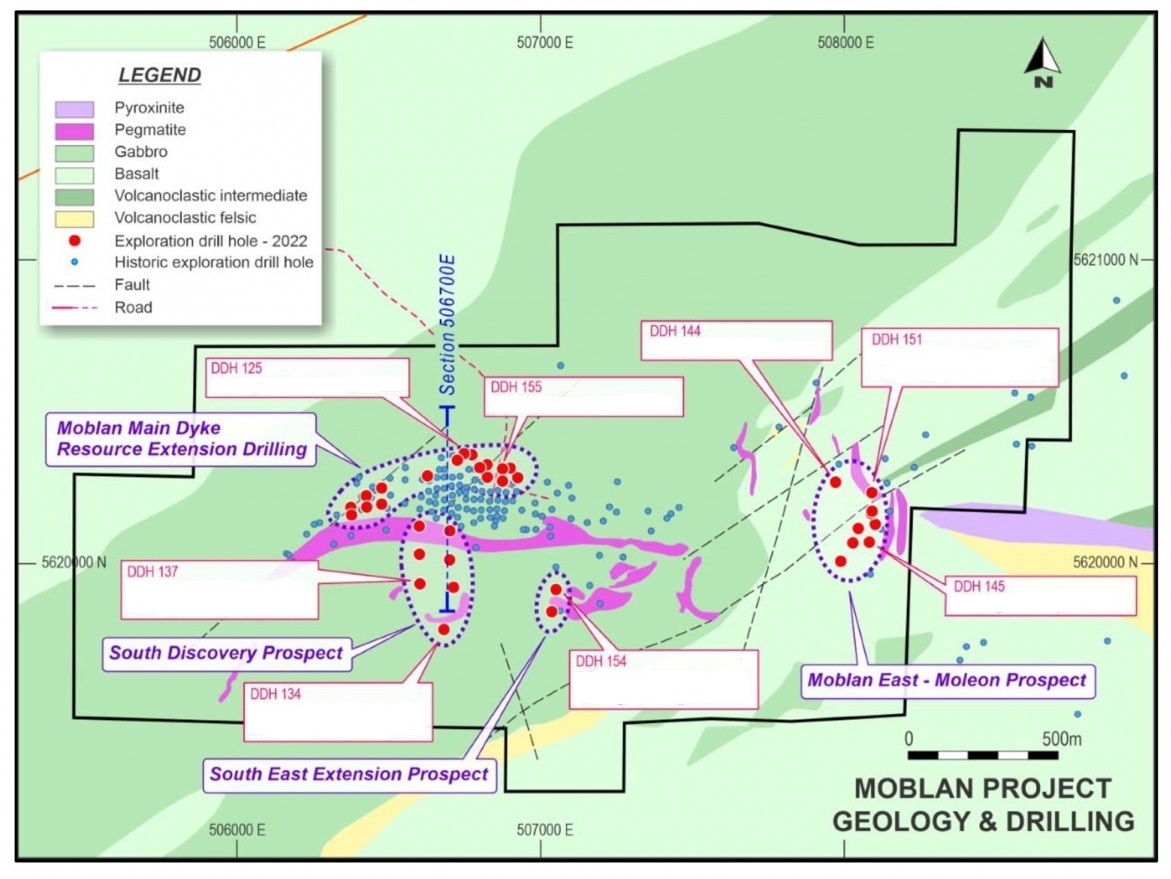

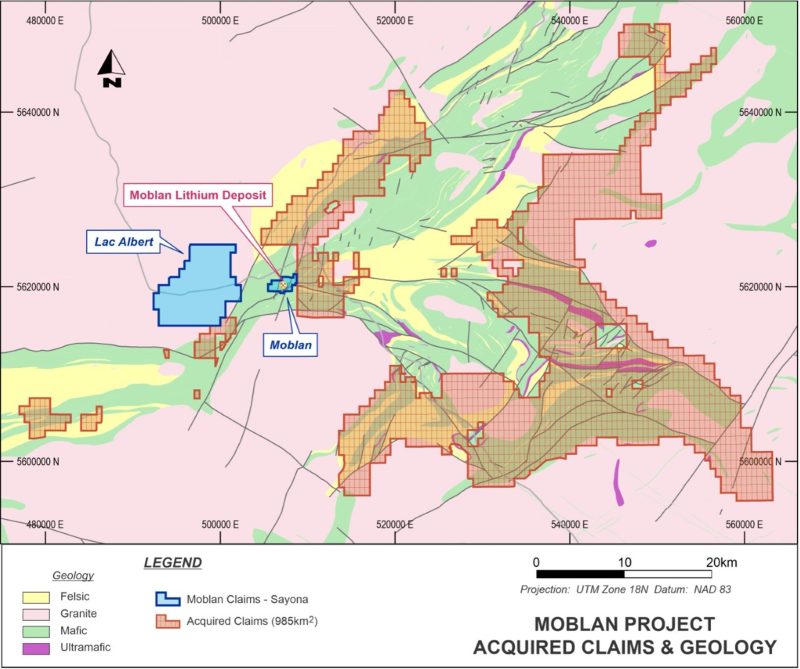

| Moblan |

Moblan Lithium project |

|

|

|

|

|

|

| Morella |

Morella Corporation Limited |

| MT |

million metric tons |

| NAL |

North American Lithium Inc. |

| Nasdaq |

Nasdaq Capital Market |

| NCDEQ |

North Carolina Department of Environmental Quality |

| NCDOT |

North Carolina Department of Transportation |

| NEPA |

National Environmental Protection Act |

| PFS |

prefeasibility study |

| Piedmont Australia |

Piedmont Lithium Pty Ltd (formerly named Piedmont Lithium Limited) |

|

|

| PRAs |

performance rights awards |

| Proxy Statement |

definitive Proxy Statement for our 2024 Annual Meeting of Stockholders to be held on or about June 14, 2024 |

| QP |

Qualified Person, as defined in Regulation S-K, Subpart 1300, under the Securities Act of 1933, as amended |

| RCRA |

Resource Conservation and Recovery Act |

| Ricca |

Ricca Resources Limited |

| ROU |

right-of-use |

| RSUs |

restricted stock units |

| Sayona Mining |

Sayona Mining Limited |

| Sayona Quebec |

Sayona Quebec Inc. |

| SEC |

Securities and Exchange Commission |

| SEH |

safety, environment and health |

| S-K 1300 |

Regulation S-K, Subpart 1300, under the Securities Act of 1933, as amended |

| spodumene concentrate |

spodumene concentrate or SC[X] where “X” represents the lithium content of the concentrate on an Li2O% basis |

| Stock Incentive Plan |

Piedmont Lithium Inc. Stock Incentive Plan adopted by our board in March 2021 |

| Tansim |

Tansim Lithium project |

| TDEC |

Tennessee Department of Environment and Conservation |

| Tennessee Lithium |

Tennessee Lithium project |

| Title V Permit |

Title V Prevention of Significant Deterioration Permit |

| TSR PRAs |

PRAs related to market goals based on a comparison of the Company's total shareholder return relative to the total shareholder return of a pre-determined set of peer group companies for the performance periods |

| U.S. |

United States of America |

| U.S. GAAP |

U.S. generally accepted accounting principles |

| Vallée |

Vallée Lithium project |

| Vinland Lithium |

Vinland Lithium Inc. |

Item 1. BUSINESS

Overview

Piedmont Lithium Inc. (“Piedmont Lithium,” “we,” “us,” “our,” “Company”) is a U.S.-based, development-stage company advancing a multi-asset, integrated lithium business in support of a clean energy economy and U.S. and global energy security. We plan to supply lithium hydroxide to the electric vehicle and battery manufacturing supply chains in North America by processing spodumene concentrate produced from assets we own or in which we have an economic interest.

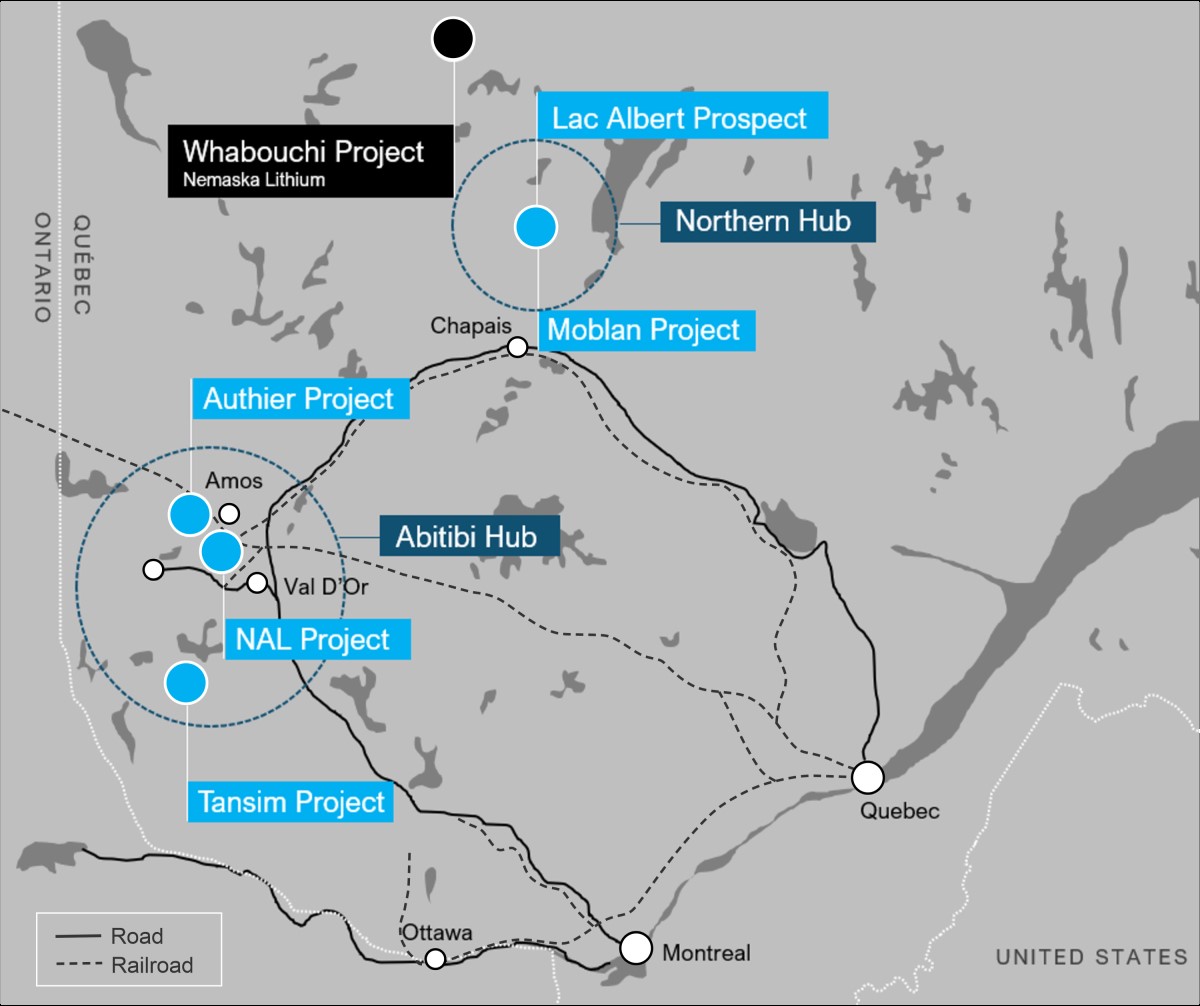

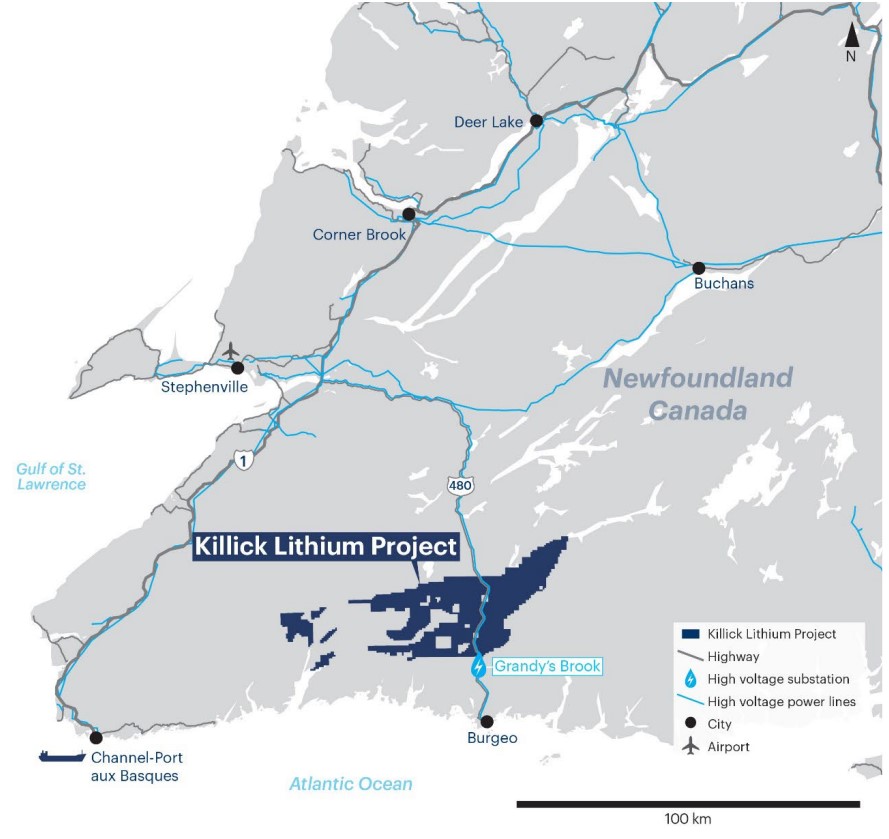

Our portfolio of wholly-owned projects includes Carolina Lithium, a proposed fully integrated spodumene ore-to-lithium hydroxide project in Gaston County, North Carolina, and Tennessee Lithium, a proposed merchant lithium hydroxide manufacturing plant in McMinn County, Tennessee. The balance of our project portfolio includes strategic investments in lithium assets in Quebec, Canada, including the now operating NAL mine; in Ghana, West Africa with Atlantic Lithium, including Ewoyaa; and in Newfoundland, Canada with Vinland Lithium, including the Killick Lithium project.

Piedmont Lithium is incorporated in the State of Delaware. We maintain executive offices at 42 E Catawba Street, Belmont, NC, 28012, and our telephone number is (704) 461-8000. Our website address is www.piedmontlithium.com. Shares of our common stock, par value $0.0001 per share, are traded on the Nasdaq under the symbol “PLL” and our CDIs, each representing 1/100th of a share of our common stock, are traded on the Australian Securities Exchange, also under the symbol “PLL.”

Foreign Currencies

Our consolidated financial statements have been presented in our reporting currency, U.S. dollars.

Gains and losses arising from translations or settlements of foreign currency denominated transactions or balances are included in the determination of income. Foreign currency translation adjustments resulting from the change in functional currency are included in “Other comprehensive income (loss), net of tax,” and gains and losses resulting from foreign currency transactions are presented in “(Loss) gain from foreign exchange” in the consolidated financial statements.

Unless otherwise indicated, all references to “$” are to U.S. dollars, all references to “AUD” are to Australian dollars, all references to “CAD” are to Canadian dollars, and all references to “GBP” are to Pound Sterling.

Our Segment

We have one operating segment, which is also our reportable segment. Our Chief Operating Decision Maker, who is also our CEO, manages our operations on a consolidated basis for purposes of allocating resources.

Strategy

Our strategic goal is to become a leading producer of lithium hydroxide in North America, supplied by geographically diverse and sustainable spodumene assets. North American demand for large vehicles and the custom of driving relatively long distances, combined with automakers’ plans for and commitments to electric vehicle production, should continue to expand the demand for North American manufactured lithium hydroxide. We believe our global portfolio of hard rock lithium assets should support a level of estimated lithium hydroxide production that will dramatically increase current production of lithium hydroxide in the United States.

Our plan is to produce battery-grade lithium hydroxide from spodumene concentrate. We believe spodumene concentrate represents the lowest-risk and most commercially scalable raw material source for the production of lithium hydroxide. Within our production process, we expect to use the innovative Metso:Outotec Pressure Leach Technology as well as a number of manufacturing processes commonly used in the lithium industry today. We plan, as part of our sustainability goals within our overall ESG strategy, to develop our greenfield operations in North Carolina and Tennessee as two of the most sustainable lithium hydroxide production operations in the world.

Our portfolio of projects and strategic equity investments are being developed on a measured timeline to optimize both near-term cash flow and long-term value maximization. At production, we expect to have an estimated lithium hydroxide manufacturing capacity of 60,000 metric tons per year, as compared to the current total estimated U.S. lithium hydroxide production capacity of approximately 20,000 metric tons per year. In support of our strategy, we continue to evaluate opportunities to further expand our resource base and production capacity.

Developing an Integrated Lithium Production Business—Key Projects

Quebec

Piedmont Lithium owns an equity interest of 25% in Sayona Quebec, which owns full interests in the NAL, Authier, Tansim and Vallée properties. These projects are located in the Abitibi region of Quebec, Canada. Additionally, as of December 31, 2023, we owned an equity interest of approximately 12% in Sayona Mining, which owns 75% of Sayona Quebec. We also hold an offtake agreement with Sayona Quebec for the greater of 113,000 dmt per year or 50% of spodumene concentrate production at market prices, subject to a price floor of $500 per dmt and a price ceiling of $900 per dmt for 6.0% spodumene concentrate equivalent, on a life-of-mine basis.

NAL restarted production of spodumene concentrate in March 2023 and began delivering shipments in August 2023. From July 1, 2023, to December 31, 2023, NAL produced 65,723 dmt of spodumene concentrate, of which 43,200 dmt were delivered to Piedmont Lithium in accordance with our offtake agreement. We, in turn, shipped 43,200 dmt to our own customers whom we supply through offtake and purchase agreements, all of which contain market-based pricing mechanisms. A shipment of 13,104 dmt of spodumene concentrate was originally scheduled for late December 2023, but was delayed due to the effect of inclement weather on port logistics and did not ship until January 2024.

In October 2023, Sayona Mining provided a forecast for the one-year period July 1, 2023, through June 30, 2024, projecting production of 140,000 to 160,000 dmt and shipments of 160,000 to 180,000 dmt. This target assumes NAL reaches full production levels during the second quarter of 2024. NAL completed construction of its tailings storage facility in the first quarter of 2024 and plans to complete a new crushed-ore dome in the first half of 2024. The dome is expected to be key in achieving full run-rate production throughput at NAL, allowing for improved overall availability in the operation and resulting in meaningfully lower unit production costs.

In addition to spodumene mining and concentrate production, NAL’s complex also includes a partially completed lithium carbonate facility, which was developed by a prior operator of NAL. In the event both we and Sayona Mining decide to jointly construct and operate a lithium conversion plant through our jointly-owned entity, Sayona Quebec, then spodumene concentrate produced from NAL would be preferentially delivered to that conversion plant upon commencement of conversion operations. Any remaining spodumene concentrate not delivered to a jointly-owned conversion plant would first be delivered to Piedmont Lithium up to our offtake right and then to third parties.

In February 2024, we sold approximately 1,249.8 million shares of Sayona Mining for an average of $0.03 per share. The shares sold represented approximately 12% of Sayona Mining’s outstanding shares and resulted in approximately $41.4 million in net proceeds. The sale of these shares has no impact on Piedmont Lithium’s joint venture or offtake rights with Sayona Quebec. See Note 16—Subsequent Events to our Consolidated Financial Statements for additional information.

Ghana

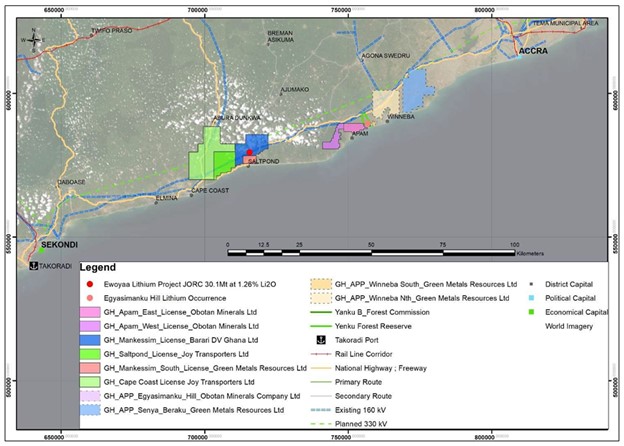

As of December 31, 2023, we owned an equity interest of approximately 9% in Atlantic Lithium and have the ability to earn a 50% equity interest in Atlantic Lithium Ghana. Additionally, we hold an offtake agreement for 50% of annual production of spodumene concentrate from Ewoyaa at market prices on a life-of-mine basis, subject to our satisfaction of certain development cost requirements. Ewoyaa is Atlantic Lithium’s flagship project in the Cape Coast region of Ghana and located approximately 70 miles from a major port via a national highway. We anticipate the development of the Ewoyaa project to be key for delivering spodumene concentrate to our planned Tennessee Lithium plant for conversion into lithium hydroxide.

In October 2023, Atlantic Lithium announced that Ghana’s Ministry of Lands and Natural Resources granted a mining lease for Ewoyaa. The mining lease provides exclusive rights to carry out lithium mining and commercial production activities for an initial 15-year period and is renewable in accordance with Ghanaian legislation. The issuance of the mining lease is subject to ratification by the Ghanaian parliament, approval by the Environmental Protection Agency of Ghana, and other statutory requirements. The mining lease provides the Government of Ghana a 13% free-carried interest and a 10% royalty in Ewoyaa. A final investment decision for Ewoyaa is anticipated upon receipt of the mining lease ratification and all environmental permits required for the construction and operation of Ewoyaa. Piedmont Lithium currently estimates these milestones will be achieved by 2025.

In September 2023, Atlantic Lithium announced that the Minerals Income Investment Fund of Ghana plans to invest (1) $27.9 million to acquire a 6% stake in Ewoyaa and (2) $5 million in Atlantic Lithium’s common stock to help further, in part, the development of Ewoyaa. MIIF completed the $5 million investment in Atlantic Lithium’s common stock in January 2024. As part of these investments, MIIF intends to fund 6% of all future exploration and development costs within Atlantic Lithium Ghana.

These funds are expected to equally reduce Piedmont Lithium’s and Atlantic Lithium’s capital expenditure contributions for Ewoyaa.

In August 2023, we exercised our option, subject to government approval, to acquire an initial 22.5% equity interest in Atlantic Lithium Ghana, which includes Ewoyaa. We expect to earn an additional 27.5% equity interest subject to funding the first $70 million of capital expenditures for Ewoyaa. Once our equity interests are acquired, and if both the mining lease is ratified and the agreement with MIIF is executed, Piedmont Lithium and Atlantic Lithium expect to each own 40.5% equity interest in Ewoyaa. As of December 31, 2023, we have not received any shares in Atlantic Lithium Ghana.

In February 2024, we sold 24.5 million shares of Atlantic Lithium, after which we retained shares representing approximately a 5% ownership interest. In connection with the sale of these shares, we no longer hold a board seat with Atlantic Lithium. See Note 16— Subsequent Events to our consolidated financial statements for additional information.

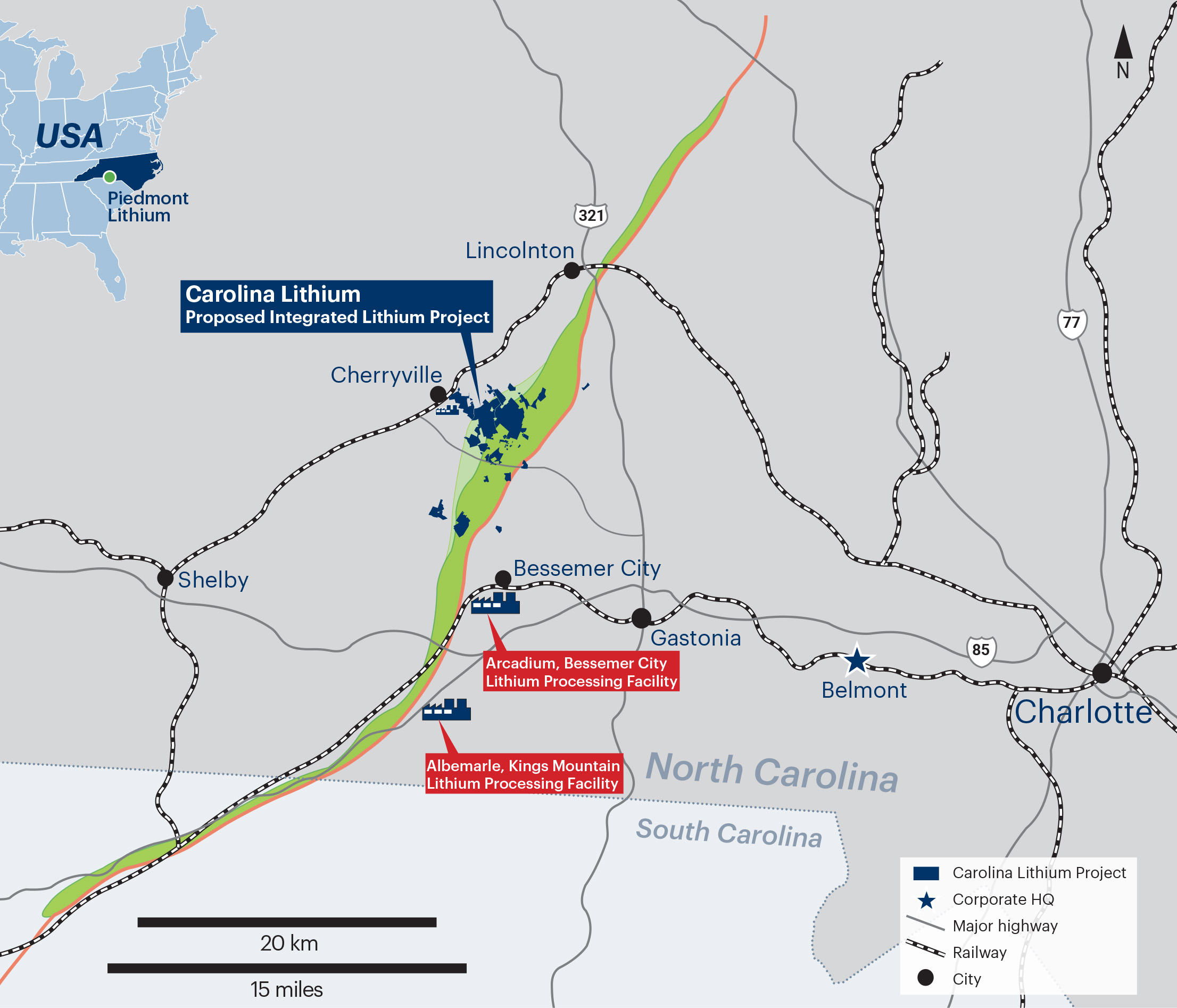

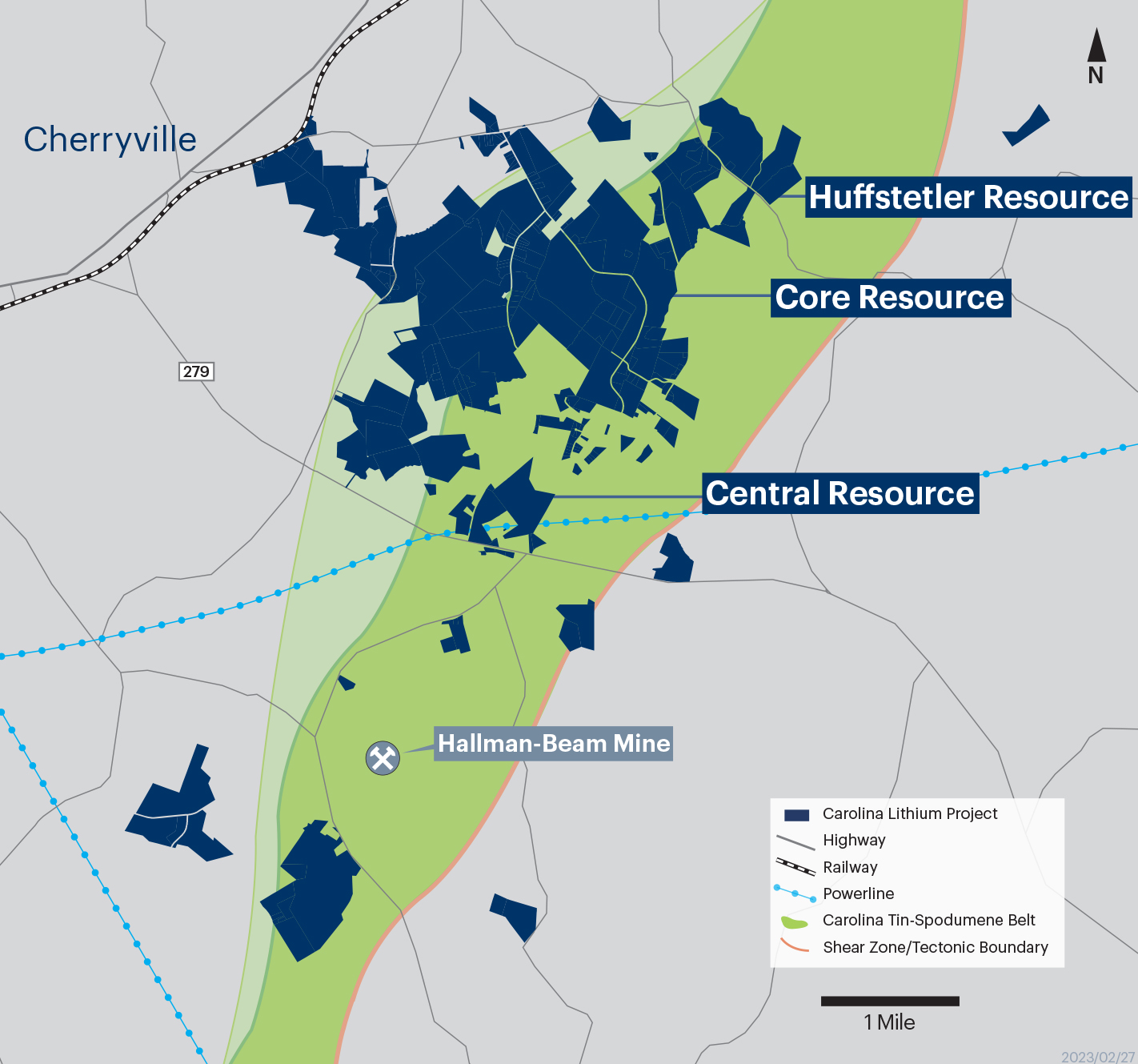

Carolina Lithium

Carolina Lithium is a development stage, hard rock lithium project located within the renowned Carolina Tin-Spodumene Belt of North Carolina and in close proximity to lithium markets. Carolina Lithium is expected to consist of a mining operation, a concentrator, and a lithium hydroxide conversion plant. In December 2021, we completed a DFS, inclusive of potential recovery of byproduct mineral resources, which estimated a project capital investment requirement of approximately $1 billion. The project is expected to produce 30,000 metric tons of lithium hydroxide per year at full capacity. Due to the expected quality of this hard rock lithium asset, integration of the operation, existing infrastructure, and proximity to lithium and byproduct markets, we believe Carolina Lithium will be one of the lowest cost lithium hydroxide manufacturing operations in the world.

We are currently engaged in permitting activities with state and local agencies for Carolina Lithium. In August 2021, we submitted a mining permit application to the NCDEQ’s DEMLR. Since our submission, we have responded to a series of additional information requests made by DEMLR. In February 2024, DEMLR issued their fourth Additional Information Request. We have 180 days in which to respond to this most recent information request. We estimate that we will submit our response by the end of the first quarter of 2024. A Prevention of Significant Deterioration – Title V Air Permit application has been submitted to the NCDEQ Division of Air Quality and was deemed complete in February 2023. Additionally, we continue to work with the North Carolina Division of Water Resources on our National Pollutant Discharge Elimination System permits for the site.

Our goal in 2024 is to obtain the necessary material state permits for Carolina Lithium. Thereafter, we expect to proceed with rezoning activities and anticipate construction to commence upon receipt of all required permits, rezoning, local approvals, and project financing activities.

Tennessee Lithium

Tennessee Lithium is a proposed merchant lithium hydroxide manufacturing plant located within McMinn County near Etowah, Tennessee. The plant is expected to produce 30,000 metric tons per year of lithium hydroxide, well surpassing the current estimated U.S. production capacity of 20,000 metric tons per year. The plant is expected to be one of the most sustainable lithium hydroxide operations in the world utilizing the innovative Metso:Outotec Pressure Leach Technology. Use of this technology is expected to reduce solid waste, create fewer emissions, lower carbon intensity, and improve capital and operating costs relative to incumbent technologies.

In July 2023, the Tennessee Department of Environment and Conservation issued a Conditional Major Non-Title V Construction and Operating Air Permit for Tennessee Lithium. As a result, we now have all material permits required to proceed with construction.

In 2023, we engaged advisors to support our funding strategy for the construction of Tennessee Lithium. In consultation with the DOE, we have decided to pursue an ATVM loan with the DOE’s Loan Programs Office, rather than complete the previously announced $141.7 million grant under the Bipartisan Infrastructure Law. The ATVM loan, if awarded, is expected to cover a significantly larger share of the capital required for the project, strengthening the opportunity for strategic parties to partner with us on the project. We expect the DOE and strategic funding processes to take several months to complete and is dependent on numerous factors, including prevailing market conditions.

In October 2023, we acquired a 132-acre disposal facility adjacent to the proposed Tennessee Lithium plant site for the purpose of disposing tailings from our operations if we do not establish a commercial plan to create value through the sale of this material. We maintain this facility in care and maintenance at this time. Additionally, we have entered into a purchase agreement to acquire an existing industrial facility in close proximity to our proposed Tennessee Lithium project site.

In December 2023, our option agreement to purchase the proposed site for Tennessee Lithium in the North Etowah Industrial Park in McMinn County, Tennessee expired. We are currently in discussions with county officials to extend the option.

Strengths

We believe that we are well-positioned to successfully execute our business strategies primarily due to our following competitive strengths:

•U.S.-based company—As a U.S. domiciled and listed company, Piedmont Lithium can benefit from U.S. policies aimed at supporting growth in the domestic battery supply chain and reducing reliance on foreign nations. These policies include the IRA’s Advanced Manufacturing Production Credit (Section 45X), which is available only to U.S. taxpayers and provides certain tax incentives for the production of applicable critical minerals. The IRA’s Clean Vehicle Tax Credit (Section 30D) for qualifying light electric vehicle purchases requires escalating usage of domestic critical minerals, which we expect to supply. These credits are in addition to the opportunities available through the DOE’s ATVM loan program.

•Revenue generation from NAL—We hold an offtake agreement with Sayona Quebec for the greater of 113,000 dmt per year or 50% of spodumene concentrate production from NAL at market prices, subject to a price floor of $500 per metric ton and a price ceiling of $900 per metric ton, on a life-of-mine basis. We, in turn, sell spodumene concentrate procured under our NAL offtake to Piedmont Lithium’s own customers at market-based prices. NAL remains a highly strategic asset as the only operating spodumene mine in all of North America.

•Scale and diversification of resources—We own or hold equity investments in three significant spodumene resources located in Quebec, Ghana, and North Carolina. Since January 2021, we have made investments in key spodumene resources and have established strategic partnerships with Sayona Mining and Atlantic Lithium. We continue to pursue opportunities to complement our business through additional acquisitions, joint ventures, strategic alliances, and investments.

•Advantageous locations and infrastructure—NAL is located in a well-established mining district within the Abitibi region of Quebec, Canada. The region provides access to infrastructure and is geopolitically advantageous. NAL is near the major mining town of Val-d’Or, Quebec, with access to rail, hydropower, and a skilled labor workforce. NAL has a partially completed lithium carbonate facility on site, which was developed by a previous operator. Ewoyaa is located in the Cape Coast region of Ghana with available power infrastructure nearby and direct highway access to Accra, which is approximately 60 miles from Ewoyaa. Ewoyaa also is approximately 70 miles from the deep-water Port of Takoradi, providing reasonable transport of spodumene concentrate as the feedstock for our planned Tennessee Lithium operation. Carolina Lithium is well situated in a historical lithium region within the developing “Battery Belt.” The area features access to road and rail infrastructure, a highly skilled labor force, low-cost and low-carbon sources of baseload grid power, and research and development centers for lithium manufacturing. Tennessee Lithium is expected to be located within the North Etowah Industrial Park in McMinn County, Tennessee. The region is home to a manufacturing workforce as well as power infrastructure, rail, highways, and nearby riverways.

•Strategic funding—We are evaluating a variety of funding options to support development objectives aimed at maintaining shareholder value in the capital markets. In February 2023, we received $75 million from LG Chem in exchange for common shares in Piedmont Lithium in conjunction with a multi-year spodumene concentrate offtake agreement. In October of 2022, we were selected for a $141.7 million grant from the DOE to support construction at our planned Tennessee Lithium project. However, in consultation with the DOE, we have decided to pursue an ATVM loan for Tennessee Lithium with the DOE’s Loan Programs Office, rather than complete the previously announced grant. We also intend to pursue ATVM loan funding for Carolina Lithium. The ATVM loans, if awarded, are expected to cover a significant share of the capital required for each project, thereby strengthening the opportunity for strategic parties at each project. Strategic partnerships, offtake prepayments, mineral royalties, and other opportunities are being considered to support the development of our projects and equity investments.

•Greenfield opportunities—Carolina Lithium and Tennessee Lithium are being designed as new operations, which offer the opportunity to leverage modern technologies, systems, and procedures. We expect to utilize the innovative Metso:Outotec Pressure Leach Technology to convert spodumene concentrate to lithium hydroxide at both U.S. projects. This technology is expected to provide a relative advantage in capital and operating costs and supports our ESG strategy to create a more sustainable operating profile as compared to other hard rock lithium conversion methods.

•Highly experienced management team—Our leadership team includes professionals with core skills and experience in management, operations, sales, and marketing of lithium manufacturing. The team has broad backgrounds and a long history of acquiring, developing, financing, and operating mining, energy, lithium, and chemical projects.

Marketing, Sales, and Principal Markets

We have a strategic partnership with Ion Carbon & Mineral, LLC to form Pronto Minerals, LLC for the purpose of marketing and selling byproducts, specifically quartz, feldspar, and mica, produced by our proposed Carolina Lithium project. We continue to explore potential strategic partnership and sales, offtake, and marketing agreements that will benefit the development of the Company’s assets as well as the U.S. electric vehicle supply chain.

Customers

On January 2, 2023, we entered into an amended offtake agreement with Tesla, Inc. to supply 125,000 dmt of spodumene concentrate from NAL. The term of the agreement is three years, beginning on January 2, 2023, through the end of 2025. Pricing is determined by a market-based mechanism. The three-year term can be extended for an additional three years upon mutual agreement.

On February 16, 2023, we entered into a spodumene concentrate offtake agreement with LG Chem. In the contract, we agree to sell 200,000 dmt of spodumene concentrate from our NAL offtake agreement. The term of the agreement expires four years from the date of first shipment, or upon the delivery 200,000 dmt. Pricing is determined by a market-based mechanism.

In addition to our offtake customers, we have entered into a series of purchase agreements with a major international trading company to facilitate individual sales. These purchase agreements provided for the delivery of spodumene concentrate on an FOB vessel basis (Incoterms 2020) and included a partial prepayment convention.

Competition and Market Barriers

We compete with other mineral and chemical processing companies in connection with the acquisition of suitable exploration properties and the engagement of qualified personnel. Many of our competitors possess greater financial resources and technical facilities than Piedmont Lithium. Although we aspire to be a leading lithium hydroxide producer in North America, the lithium mining and chemical industries are fragmented. We are one of many participants in these sectors. Many of our competitors, as compared to us, have been in business longer, have established more strategic partnerships and relationships, and have greater financial accessibility.

While we compete with other exploration companies in acquiring suitable properties, we believe there will be readily available purchasers of lithium chemical products or other industrial minerals if they are produced from any of our owned or leased properties. The price of our planned products may be affected by factors beyond our control, including fluctuations in the market prices for lithium, supplies of lithium, demand for lithium, and mining activities of others.

If we identify lithium mineralization that is determined to be of economic grade and in sufficient quantity to justify production, additional capital would be required to develop, mine, and sell such production. Our strategic partners, in which we have equity investments, face similar challenges as discussed above.

Government Regulations

Overview

Exploration and development activities for our projects are subject to extensive laws and regulations, which are overseen and enforced by multiple U.S. federal, state, and local authorities as well as foreign jurisdictions. These applicable laws govern exploration, development, production, exports, various taxes, labor standards, occupational and mine health and safety, waste disposal, protection and remediation of the environment, protection of endangered and protected species, and other matters. Various permits from government bodies are required for drilling, mining, or manufacturing operations to be undertaken, and we cannot be assured such permits will be received. Environmental laws and regulations may also, in addition to other requirements;

•require notice to stakeholders of proposed and ongoing exploration, drilling, environmental studies, mining, or production activities;

•require the installation of pollution control equipment;

•restrict the types, quantities and concentrations of various substances that can be released into the environment in connection with exploration, drilling, mining, lithium hydroxide manufacturing, or other production activities;

•limit or prohibit drilling, mining, lithium manufacturing or other production activities on lands located within wetlands, areas inhabited by endangered species and other protected areas, or otherwise restrict or prohibit activities that could impact the environment, including water resources;

•impose substantial liabilities for pollution resulting from current or former operations on or for any preexisting environmental impacts from our projects;

•require significant reclamation obligations in the future as a result of our mining and chemical operations; and

•require preparation of an environmental assessment or an environmental impact statement.

Compliance with environmental laws and regulations may impose substantial costs on us, subject us to significant potential liabilities, and have an adverse effect on our capital expenditures, results of operations, and competitive position. Violations and liabilities with respect to these laws and regulations could result in significant administrative, civil, and criminal penalties, remedial clean-ups, natural resource damages, permit modifications and/or revocations, operational interruptions and/or shutdowns, and other liabilities, as well as reputational harm, including damage to our relationships with customers, suppliers, investors, governments and other stakeholders. The costs of remedying such conditions may be significant, and remediation obligations could adversely affect our business, results of operations, and financial condition. Federal, state, and local legislative bodies and agencies frequently revise environmental laws and regulations, and any changes in these regulations, or the interpretations thereof, could require us to expend significant resources to comply with new laws or regulations or changes to current requirements and could have a material adverse effect on our business operations. As of the date of this Annual Report, other than with respect to the permitting activities of Carolina Lithium and Tennessee Lithium, we have not been required to spend material amounts on compliance regarding environmental regulations.

Permits

Obtaining and renewing governmental permits are complex and time-consuming processes and involves numerous jurisdictions, public hearings, and possibly costly undertakings. The timeliness and success of permitting efforts are contingent upon many variables not within our control, including the interpretation of permit approval requirements administered by the applicable permitting authority. We may not be able to obtain or renew permits that are necessary for our planned operations, or the cost and time required to obtain or renew such permits may exceed our expectations. Any unexpected delays or costs associated with the permitting process could delay the exploration, development and/or operation of our projects. For additional information, refer to Part I, Item 1A, “Risk Factors—We will be required to obtain governmental permits in order to conduct development and mining operations, a process that is often costly and time-consuming. There is no certainty that all necessary permits and approvals for our planned operations will be granted.”

Carolina Lithium

In November 2019, we were granted a CWA Section 404 Standard Individual Permit from the U.S. Army Corps of Engineers for our integrated Carolina Lithium project. We received an updated preliminary jurisdictional determination in March 2022 based on updated footprint of the integrated site.

In July 2022, we received an updated Clean Water Act Section 401 Individual Water Quality Certificate from the NCDEQ Division of Water Resources for our Carolina Lithium project.

In August 2021, we submitted a mining permit application to the NCDEQ’s DEMLR. Since our submission, we have responded to a series of additional information requests made by DEMLR. On February 9, 2024, DEMLR issued their fourth Additional Information Request. We have 180 days to respond to this latest information request.

In September 2021, the Gaston County Board of Commissioners updated its Unified Development Ordinance which, in part, defines operational requirements for new mines and quarries in the county and provides the parameters for the requisite conditional district zoning. At this time, we remain in pre-application consultation with Gaston County staff members and have not submitted a conditional district rezoning application.

We hold a Synthetic Minor Construction and Operation Permit issued by the NCDEQ’s Division of Air Quality for our property in Kings Mountain, NC. In June 2022, we submitted an application to modify the received air permit to incorporate the use of Metso:Outotec’s Pressure Leach Technology. Our application is currently on hold as further refinements to the process are being made.

In January 2022, we submitted a determination request to NCDEQ’s Division of Air Quality in connection with Carolina Lithium. In March 2022, we received a response to this request informing us that Carolina Lithium would require a Title V Permit. In August 2022, we submitted our Title V Permit application, which was deemed complete in February 2023, and is subject to ongoing review.

In January 2022, we received guidance that Carolina Lithium was not eligible for a North Carolina General Stormwater Permit. After further evaluation and testing, it was determined that the site would be covered by a National Pollutant Discharge Elimination System permit. In December 2022, we submitted applications to the NCDEQ Division of Water Resources for two permits, one covering the mine and concentration operations, and one covering the lithium hydroxide conversion plant. Both permit applications are currently under review. In June 2023, we received an additional information request for both permits. We continue to work with the Division of Water Resources to provide thorough responses for these additional information requests.

Exploration and evaluation activities for our Carolina Lithium project included drilling, which is authorized under a general permit initially approved in 2017 by the NCDEQ and updated in April 2019, October 2019, and June 2021. We have reclamation obligations under this permit, requiring us to reclaim all disturbed drill pads and temporary roads to the approximate original contours, including the seeding of grass and straw to stabilize any disturbances. Generally, we are required to affect such reclamation within 14 days following drilling. We have concluded that this cost of reclamation obligations is immaterial.

We may be required to obtain additional permits and approvals for Carolina Lithium including, but not limited to, a municipal wastewater permit by the City of Gastonia Wastewater Treatment, a road abandonment approved by the NCDOT and Gaston County under North Carolina General Statute 136-63, an encroachment permit for an at-grade rail crossing issued by the NCDOT, various driveway permits issued by the NCDOT, a Gaston County Watershed Permit approved by the Gaston County Planning Department, various building permits approved by the Gaston County Planning Department, explosives permits approved by the U.S. Bureau of Alcohol, Tobacco, and Firearms, and hazardous chemical permits issued by Gaston County Fire Officials.

Tennessee Lithium

In July 2023, the TDEC issued a Conditional Major Non-Title V Construction and Operating Air Permit for Tennessee Lithium. As a result, we have now obtained all material permits required to begin construction. Prior to operation, additional permits for our Tennessee Lithium project will be required, including, but not limited to, a municipal wastewater permit by Etowah Utilities, various driveway permits issued by McMinn County, and waste disposal permits. The building permit process will include design reviews by the McMinn County Economic Development Authority.

In October 2023, we purchased a 132 acre disposal facility adjacent to the proposed Tennessee Lithium plant site for the placement of inert tailings produced as part of the innovative alkaline pressure leach process. We currently hold a Solid Waste Disposal Permit for this disposal facility.

U.S. Federal Legal Framework

Carolina Lithium and Tennessee Lithium will be required to comply with applicable environmental protection laws and regulations and licensing and permitting requirements. The material environmental, health, and safety laws and regulations that we must comply with include, among others, the following U.S. federal laws and regulations:

•NEPA, which requires careful evaluation of the environmental impacts of mining and lithium manufacturing operations that require federal approvals;

•Clean Air Act and its amendments, which governs air emissions;

•CWA, which governs discharges to and excavations within the waters of the U.S.;

•RCRA, which governs the management of solid waste;

•CERCLA, which imposes liability where hazardous substances have been released into the environment (commonly known as Superfund); and

•Federal Mine Safety and Health Act, which established the primary safety and health standards regarding working conditions of employees engaged in mining, related operations, and preparation and milling of the minerals extracted, as well as the Occupation Safety and Health Act, which regulates the protection of the health and safety of workers in lithium manufacturing operations.

Our operations will also be subject to state environmental laws and regulations, including, but not limited to, laws and regulations related to the reclamation of mined lands, which may require reclamation bonds to be acquired prior to the commencement of mining operations and may require substantial financial guarantees to cover the cost of future reclamation activities.

Solid and Hazardous Waste

RCRA, and comparable state statutes, affect our operations by imposing regulations on the generation, transportation, treatment, storage, disposal, and cleanup of hazardous wastes and on the disposal of non-hazardous wastes. Under the auspices of the EPA, individual states administer some or all of the provisions of RCRA, sometimes in conjunction with their own, more stringent requirements.

In addition, CERCLA can impose joint and several liability without regard to fault or legality of conduct on classes of persons who are statutorily responsible for the release of a hazardous substance into the environment. These persons can include the current and former owners, lessees, or operators of a site where a release occurs, and anyone who disposes or arranges for the disposal of a hazardous substance. Under CERCLA, such persons may be subject to strict, joint, and several liability for the entire cost of cleaning up hazardous substances that have been released into the environment and for other costs, including response costs, alternative water supplies, damage to natural resources and for the costs of certain health studies. Moreover, it is not uncommon for neighboring landowners, workers, and other third parties to file claims for personal injury and property damage allegedly caused by hazardous substances released into the indoor or outdoor environment. Each state also has environmental cleanup laws analogous to CERCLA. Hazardous wastes may have been previously handled, disposed of, or released on or under properties currently or formerly owned or leased by us or on or under other locations to which we sent waste for disposal. These properties and any materials disposed or released on them may subject us to liability under CERCLA, RCRA, and analogous state laws. Under such laws, we could be required to remove or remediate disposed wastes or property contamination, contribute to remediation costs, and perform remedial activities to prevent future environmental harm.

Air Emissions

The federal Clean Air Act and comparable state laws restrict the emission of air pollutants from numerous sources through the issuance of permits and the imposition of other requirements. Major sources of air pollutants are subject to more stringent, federally imposed permitting requirements. Air pollution regulations may require us to obtain pre-approval for the construction or modification of certain projects or facilities expected to produce or significantly increase air emissions, obtain air permits, and comply with stringent permit requirements or utilize specific equipment or technologies to control emissions of certain pollutants. The need to obtain permits has the potential to delay our operations, and we may be required to incur capital expenditures for air pollution control equipment or other air emissions related obligations. Administrative enforcement actions for failure to strictly comply with air pollution regulations or permits are generally resolved by payment of monetary fines and correction of any identified deficiencies. Alternatively, regulatory agencies could require us to forego construction, modification, or operation of certain air emission sources.

Clean Water Act

The CWA imposes restrictions and strict controls regarding the pollution of protected waters, including mineral processing wastes, into waters of the U.S., a term broadly defined to include, among other things, certain wetlands. Permits must be obtained to discharge pollutants into federal waters. The CWA provides for civil, criminal, and administrative penalties for unauthorized discharges, both routine and accidental, of pollutants. It imposes substantial potential liability for the costs of removal or remediation associated with discharges of oil or hazardous substances. State laws governing discharges to water also provide varying civil, criminal, and administrative penalties, and impose liabilities in the case of a discharge of petroleum or its derivatives, or other hazardous substances, into state waters. In addition, the EPA has promulgated regulations that require permits to discharge storm water runoff, including discharges associated with construction activities. In the event of an unauthorized discharge of waste, we may be liable for penalties and costs.

Pursuant to these laws and regulations, we may also be required to develop and implement spill prevention, control, and countermeasure plans in connection with on-site storage of significant quantities of oil. Some states also maintain groundwater protection programs that require permits for discharges or operations that may impact groundwater conditions. The CWA also prohibits the discharge of fill materials to regulated waters, including wetlands, without a permit from the U.S. Army Corps of Engineers.

In May 2015, the EPA issued a final rule that attempted to clarify the federal jurisdictional reach over waters of the U.S. The EPA repealed this rule in September 2019 and replaced it in April 2020 with the Navigable Water Protection Rule, which narrowed federal jurisdictional reach relative to the 2015 rule. The repeal and replacement of the 2015 rule is currently subject to litigation, and the scope of the jurisdictional reach of the CWA may, therefore, remain uncertain for several years, with a patchwork of legal guidelines applicable to various states potentially developing. We could incur increased costs and delays with respect to obtaining permits for dredge and fill activities in wetland areas to the extent they are required.

NEPA

NEPA requires federal agencies to evaluate major agency actions having the potential to significantly impact the environment. The NEPA process involves public input through comments, which can alter the nature of a proposed project either by limiting the scope of the project or requiring resource-specific mitigation. NEPA decisions can be appealed through the court system by process participants. This process may result in delaying the permitting and development of projects or increase the costs of permitting and developing some facilities.

Endangered Species Act

The federal Endangered Species Act restricts activities that may affect endangered and threatened species or their habitats. Some of our operations may be located in areas that are designated as habitats for endangered or threatened species. A critical habitat designation could result in further material restrictions to federal and private land use and could delay or prohibit land access or development. The U.S. Fish and Wildlife Service continues its effort to make listing decisions and critical habitat designations where necessary. To date, the Endangered Species Act has not had a significant impact on our operations. However, the designation of previously unprotected species as being endangered or threatened could cause us to incur additional costs or become subject to operating restrictions in areas where the species are known to exist.

Foreign Legal Framework

Our projects with Sayona Mining, Atlantic Lithium, and Vinland Lithium are required to comply with all environmental laws and regulations in Quebec, Canada, Ghana, West Africa, and Newfoundland, Canada, respectively.

U.S. Foreign Corrupt Practices Act

The U.S. Foreign Corrupt Practices Act generally prohibits U.S. companies and their intermediaries from making corrupt payments to foreign officials for the purpose of obtaining or keeping business or otherwise obtaining favorable treatment and requires companies to maintain appropriate record-keeping and internal accounting practices to accurately reflect the transactions of the company. The FCPA applies to companies, individual directors, officers, employees and agents. Under the FCPA, U.S. companies may be held liable for actions taken by agents or local partners or representatives. If we or our intermediaries fail to comply with the requirements of the FCPA or the anti-corruption laws of other countries, governmental authorities in the U.S. or other countries could seek to impose civil and criminal penalties, which could have a material adverse effect on our business.

Human Capital Management

Our employees are driven by our core values:

•Teamwork. We work collaboratively in a transparent manner with all stakeholders.

•Optimism. We believe in a better future and see opportunities to improve our communities and the world.

•Pride. We are proud of our people, our mission, our commitment to safety, environment, health, and the delivery of our products, and our support of the clean energy economy.

•Innovation. We continuously look for creative ways to improve our business and the solutions we offer customers.

•Care. We understand the inherent worth and dignity of all people and care deeply about our team members, our neighbors, and our impact on the environment.

By living our core values every day, we are working to create a culture of excellence that inspires our employees to achieve their full potential and drive the success of our organization.

Employees

As of December 31, 2023, we had 63 employees, all of which were located in the U.S. with the exception of two, who were located in Canada. None of our employees are subject to any union or collective bargaining agreement. We believe that we have a good relationship with our employees.

Contractors

We rely on specialized skills and knowledge to be able to gather, interpret and process geological and geophysical data; successfully permit, design, build, and operate production facilities; and engage in additional activities required as part of the mine-to-lithium hydroxide process. We have employed, and expect to continue to employ, a strategy of contracting consultants and other service providers who have specialized skills and knowledge to supplement the skills and knowledge of our permanent workforce to undertake our lithium operations effectively.

Safety, Environment, and Health

SEH is a cornerstone of Piedmont Lithium. Our commitment to the health and welfare of every person involved in our projects is built into every aspect of our organization and is engrained in our company’s culture. We endeavor to implement safety programs and develop risk management processes covering our project activities to promote a behavior-based safety culture, ensure compliance with applicable environmental regulations and international standards, and raise environmental awareness among our employees and partners. Our SEH vision is to conduct operations with safety and the environment as a top priority. We work to promote the “Piedmont Promise,” which recognizes our obligation to our employees, neighbors, stakeholders, and the communities in which we live, work, and play.

Diversity, Equity, and Inclusion

Diversity, equity, and inclusion are embedded in our values and integrated into our strategies. Our Business Code of Conduct and Ethics commits us to fair treatment and non-discrimination. Our policy is to treat each employee and job applicant without regard to race, color, age, sex, religion, national origin, citizenship, sexual orientation, gender identity, ancestry, veteran status, or any other category protected by law. We believe in allocating resources and establishing, in an equitable manner, policies and procedures that are fair, impartial, and just. We believe that we will become better and achieve growth by intentionally creating a culture through acquiring and retaining a diverse workforce. We recognize it takes unique gifts, talents, varied perspectives, backgrounds, and experiences to deliver innovative, high-quality products and services. To provide a diverse and inclusive workplace, we focus our efforts on creating a culture where all employees can contribute their skills and talents and be themselves. In furtherance of that mission, we adopted a DEI policy in 2023 to establish clear guidelines and expectations for promoting diversity, equity, and inclusion within our organization.

Compensation and Benefits

Our compensation and benefits program is designed to attract and retain talented employees in the industry by offering competitive compensation and benefits. We use a combination of fixed and variable compensation, which includes base salary, incentive bonuses with pay for performance elements, and merit increases. As part of our long-term incentive plan for executive management and certain key employees, we provide long-term equity awards tied to the value of our stock price, some of which are performance based and time based. Additionally, all employees are eligible for an annual discretionary cash bonus and a long-term equity grant. We are focused on the health and wellness of our employees. As such, we offer eligible employees comprehensive medical plans, dental and vision coverage, short-term and long-term disability insurance, term life insurance, flexible work schedules, an employee assistance program, remote and hybrid work options, paid time off, new parent leave, and a 401(k) plan with employer-matching contributions.

Commitment to Values and Ethics

In connection with our core values, we act in accordance with our Code of Business Conduct and Ethics, which requires a commitment from employees, officers, and directors of Piedmont Lithium to conduct business honestly and ethically. This code discusses the responsibility that team members have to each other, the Company, stakeholders, our customers, and communities in which we operate. We have an anonymous hotline for employees to call in the event of ethical concerns or suspected instances of misconduct.

Protecting the Rights of Workers

We are an Equal Opportunity Employer committed to providing our employees with a safe, non-discriminatory work environment that promotes open and honest communication and embraces dignity, respect, and diversity in all aspects of its business operations. We expect our partners, suppliers, and contractors to uphold these same commitments. We maintain policies designed to support the elimination of all forms of forced labor including prison labor, forcibly indentured labor, bonded labor, slavery, and servitude. We condemn all forms of child exploitation. We do not recruit child labor, and we support the standard covering the prohibition on child labor in accordance with the International Labor Organization Minimum Age Convention. We support laws enacted to prevent and punish the crime of sexual exploitation of children, and we will cooperate fully with law enforcement authorities in these matters.

We will work with our partners at Atlantic Lithium, Sayona Mining, and Vinland Lithium to ensure appropriate policies are in place within the businesses and projects in which we have invested.

Anti-Human Trafficking

We are committed to a work environment that is free from human trafficking and slavery, which includes forced labor and unlawful child labor. We will not tolerate or condone human trafficking or slavery in any part of our global organization.

Human Rights and Relationships with Indigenous People

We are committed to respecting human rights and providing a positive contribution in the communities where we operate and plan to operate. We expect our partners, suppliers, and contractors to uphold the same commitment. We respect the cultures, customs, and values of people in the communities where we operate and plan to operate and take into account their needs, concerns, and aspirations.

Equal Opportunity and Zero Discrimination

We recognize, respect, and embrace the cultural differences found in the worldwide marketplace. Our goal is to attract, develop, promote, and retain the best people from all cultures and segments of the population, based on ability. We maintain a policy of zero tolerance for discrimination or harassment of any kind. We have implemented policies regarding the reporting and investigation of discrimination, harassment, sexual harassment, retaliation, and abusive behavior and provide our employees training to foster full compliance with our policies.

Community Involvement

We are committed to making a measurable impact in the communities in which we operate and have project investments through our charitable giving. In December 2021, we created Piedmont Lithium Foundation – Power for Life, Inc., to provide scholarships to science, technology, engineering and mathematics students and financial support to our schools and communities.

We have devoted tremendous time and effort to engaging community stakeholders regarding Carolina Lithium and have begun similar engagement with stakeholders surrounding Tennessee Lithium.

Through in-person meetings, phone calls, social media, and information shared with the media via press releases and interviews, we work to keep the community residents and local businesses informed of our plans and activities. Our goal is to develop relationships with residents near the sites of Carolina Lithium and Tennessee Lithium and communicate our commitment to responsibly developing two of the world’s most sustainable lithium hydroxide operations. Further, we are committed to working with our investment partners, Sayona Mining, Atlantic Lithium, and Vinland Lithium, all of whom have several mechanisms in place for engaging with local communities regarding their projects, including addressing concerns and sharing information about employment opportunities.

Sustainability

We are committed to contributing to the transition to a net zero carbon world and the creation of a clean energy economy in North America through the products we sell and the way we produce products, operate our business, and work with our customers, vendors, and stakeholders. We are evaluating our emission profiles in a pre-operational state while establishing systems and tools to allow us to manage data easily and efficiently as we continue to grow.

We released our inaugural sustainability report in June 2023, affirming our commitment to being a responsible, respectful steward of the planet, people, and the communities where we plan to operate our wholly-owned projects, Carolina Lithium and Tennessee Lithium. A copy of our sustainability report can be found under the “Sustainability” tab of our website: www.piedmontlithium.com. The information on our website, including, without limitation, the information in our inaugural sustainability report, should not be deemed incorporated by reference into this Annual Report on Form 10-K or otherwise “filed” for purposes of Section 18 of the Exchange Act, as amended, or otherwise subject to the liabilities of that section.

Governance

Audit Committee

The primary responsibilities of our Audit Committee are to monitor the integrity of our consolidated financial statements, the independence and qualifications of our independent auditors, the performance of our accounting staff and independent auditors, our compliance with legal and regulatory requirements, supervising our cybersecurity policies, and the effectiveness of our internal controls. The Audit Committee is responsible for selecting, retaining (subject to stockholder approval), evaluating, setting the compensation of, and if appropriate, recommending the termination of our independent auditors.

Leadership and Compensation Committee

The primary purpose of our Leadership and Compensation Committee is to assist our Board in discharging its responsibilities related to the compensation of the Company’s executive officers and directors and overseeing the Company’s overall compensation philosophy, policies, and programs.

Nominating and Corporate Governance Committee

The primary purpose of our Nominating and Corporate Governance Committee is to identify individuals qualified to become members of the Company’s Board, make recommendations on candidates for election at the annual meeting of stockholders, and perform a leadership role in shaping the Company’s corporate governance, including the implementation of our ESG principles. The Nominating and Corporate Governance Committee is responsible for preparing the report required by the SEC for the Company’s annual proxy statement.

Corporate Information