FALSE00016914212025FYhttp://fasb.org/us-gaap/2025#OtherAssetshttp://fasb.org/us-gaap/2025#OtherAssetshttp://fasb.org/us-gaap/2025#AccruedLiabilitiesAndOtherLiabilitieshttp://fasb.org/us-gaap/2025#AccruedLiabilitiesAndOtherLiabilities1169iso4217:USDxbrli:sharesiso4217:USDxbrli:shareslmnd:securityxbrli:purelmnd:segmentlmnd:claimlmnd:directorlmnd:floor00016914212025-01-012025-12-3100016914212025-06-3000016914212026-02-2400016914212025-10-012025-12-3100016914212025-12-3100016914212024-12-3100016914212024-01-012024-12-3100016914212023-01-012023-12-310001691421us-gaap:CommonStockMember2022-12-310001691421us-gaap:AdditionalPaidInCapitalMember2022-12-310001691421us-gaap:RetainedEarningsMember2022-12-310001691421us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-3100016914212022-12-310001691421us-gaap:CommonStockMember2023-01-012023-12-310001691421us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001691421us-gaap:RetainedEarningsMember2023-01-012023-12-310001691421us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001691421us-gaap:CommonStockMember2023-12-310001691421us-gaap:AdditionalPaidInCapitalMember2023-12-310001691421us-gaap:RetainedEarningsMember2023-12-310001691421us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-3100016914212023-12-310001691421us-gaap:CommonStockMember2024-01-012024-12-310001691421us-gaap:AdditionalPaidInCapitalMember2024-01-012024-12-310001691421us-gaap:CommonStockMember2025-01-012025-12-310001691421us-gaap:RetainedEarningsMember2024-01-012024-12-310001691421us-gaap:AccumulatedOtherComprehensiveIncomeMember2024-01-012024-12-310001691421us-gaap:CommonStockMember2024-12-310001691421us-gaap:AdditionalPaidInCapitalMember2024-12-310001691421us-gaap:RetainedEarningsMember2024-12-310001691421us-gaap:AccumulatedOtherComprehensiveIncomeMember2024-12-310001691421us-gaap:AdditionalPaidInCapitalMember2025-01-012025-12-310001691421us-gaap:RetainedEarningsMember2025-01-012025-12-310001691421us-gaap:AccumulatedOtherComprehensiveIncomeMember2025-01-012025-12-310001691421us-gaap:CommonStockMember2025-12-310001691421us-gaap:AdditionalPaidInCapitalMember2025-12-310001691421us-gaap:RetainedEarningsMember2025-12-310001691421us-gaap:AccumulatedOtherComprehensiveIncomeMember2025-12-310001691421us-gaap:ComputerEquipmentMember2025-12-310001691421lmnd:FurnitureAndEquipmentMember2025-12-310001691421us-gaap:SoftwareDevelopmentMember2025-12-310001691421us-gaap:EmployeeStockOptionMember2025-01-012025-12-310001691421us-gaap:CorporateDebtSecuritiesMember2025-12-310001691421us-gaap:USGovernmentAgenciesDebtSecuritiesMember2025-12-310001691421us-gaap:AssetBackedSecuritiesMember2025-12-310001691421us-gaap:ForeignGovernmentDebtSecuritiesMember2025-12-310001691421us-gaap:CorporateDebtSecuritiesMember2024-12-310001691421us-gaap:USGovernmentAgenciesDebtSecuritiesMember2024-12-310001691421us-gaap:AssetBackedSecuritiesMember2024-12-310001691421us-gaap:ForeignGovernmentDebtSecuritiesMember2024-12-310001691421us-gaap:FixedIncomeSecuritiesMember2025-12-310001691421us-gaap:FixedIncomeSecuritiesMember2024-12-310001691421us-gaap:CashAndCashEquivalentsMember2025-01-012025-12-310001691421us-gaap:CashAndCashEquivalentsMember2024-01-012024-12-310001691421us-gaap:CashAndCashEquivalentsMember2023-01-012023-12-310001691421us-gaap:DebtSecuritiesMember2025-01-012025-12-310001691421us-gaap:DebtSecuritiesMember2024-01-012024-12-310001691421us-gaap:DebtSecuritiesMember2023-01-012023-12-310001691421us-gaap:ShortTermInvestmentsMember2025-01-012025-12-310001691421us-gaap:ShortTermInvestmentsMember2024-01-012024-12-310001691421us-gaap:ShortTermInvestmentsMember2023-01-012023-12-310001691421lmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421lmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:DElmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:DElmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:NYlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:NYlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:WAlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:WAlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:COlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:COlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:VAlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:VAlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:NMlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:NMlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:OHlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:OHlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:NJlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:NJlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:NClmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:NClmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:NVlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:NVlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:ARlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:ARlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:FLlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:FLlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:MAlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:MAlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:KSlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:KSlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:KYlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:KYlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421stpr:GAlmnd:DepositWithStateInsuranceDepartmentMember2025-12-310001691421stpr:GAlmnd:DepositWithStateInsuranceDepartmentMember2024-12-310001691421us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2025-12-310001691421us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2025-12-310001691421us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2025-12-310001691421us-gaap:USGovernmentAgenciesDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2025-12-310001691421us-gaap:USGovernmentAgenciesDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2025-12-310001691421us-gaap:USGovernmentAgenciesDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2025-12-310001691421us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel1Member2025-12-310001691421us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel2Member2025-12-310001691421us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel3Member2025-12-310001691421us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2025-12-310001691421us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2025-12-310001691421us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2025-12-310001691421us-gaap:FairValueInputsLevel1Member2025-12-310001691421us-gaap:FairValueInputsLevel2Member2025-12-310001691421us-gaap:FairValueInputsLevel3Member2025-12-310001691421us-gaap:WarrantMemberus-gaap:FairValueInputsLevel1Member2025-12-310001691421us-gaap:WarrantMemberus-gaap:FairValueInputsLevel2Member2025-12-310001691421us-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2025-12-310001691421us-gaap:WarrantMember2025-12-310001691421us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2024-12-310001691421us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2024-12-310001691421us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2024-12-310001691421us-gaap:USGovernmentAgenciesDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2024-12-310001691421us-gaap:USGovernmentAgenciesDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2024-12-310001691421us-gaap:USGovernmentAgenciesDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2024-12-310001691421us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel1Member2024-12-310001691421us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel2Member2024-12-310001691421us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel3Member2024-12-310001691421us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2024-12-310001691421us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2024-12-310001691421us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2024-12-310001691421us-gaap:FairValueInputsLevel1Member2024-12-310001691421us-gaap:FairValueInputsLevel2Member2024-12-310001691421us-gaap:FairValueInputsLevel3Member2024-12-310001691421us-gaap:WarrantMemberus-gaap:FairValueInputsLevel1Member2024-12-310001691421us-gaap:WarrantMemberus-gaap:FairValueInputsLevel2Member2024-12-310001691421us-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2024-12-310001691421us-gaap:WarrantMember2024-12-310001691421Reinsurance Program2024-07-012024-07-0100016914212023-07-012023-07-010001691421Proportional Reinsurance Contracts2023-07-012023-07-010001691421srt:MaximumMemberProperty Per Risk Excess of Loss Reinsurance2023-07-012023-07-010001691421Property Per Risk Excess of Loss Reinsurance2023-07-012023-07-010001691421lmnd:LemonadeInsuranceCompanyMemberAutomatic Facultative Property Per Risk Excess of Loss2024-06-302024-06-300001691421lmnd:LemonadeInsuranceCompanyMemberAutomatic Facultative Property Per Risk Excess of Loss Reinsurance2024-06-302024-06-300001691421Excess of Loss Reinsurance Contract2023-07-012023-07-010001691421lmnd:HannoverRueckSEMembersrt:AMBestAPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:HannoverRueckSEMembersrt:AMBestAPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:MAPFREReCompaniaDeReasegurosSAMembersrt:AMBestARatingMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:MAPFREReCompaniaDeReasegurosSAMembersrt:AMBestARatingMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:SwissReinsuranceAmericaCorporationMembersrt:AMBestAPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:SwissReinsuranceAmericaCorporationMembersrt:AMBestAPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:AvivaInsuranceLimitedMembersrt:AMBestAPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:AvivaInsuranceLimitedMembersrt:AMBestAPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:LloydsUnderwriterSyndicateNo2791MAPMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:LloydsUnderwriterSyndicateNo2791MAPMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:TokioMarineNichidoFireInsuranceCompanyLimitedMembersrt:AMBestAPlusPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:TokioMarineNichidoFireInsuranceCompanyLimitedMembersrt:AMBestAPlusPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:LloydsUnderwriterSyndicateNo1084CSLMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:LloydsUnderwriterSyndicateNo1084CSLMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:TheTravellersIndemnityCompanyMembersrt:AMBestAPlusPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:TheTravellersIndemnityCompanyMembersrt:AMBestAPlusPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:OdysseyReinsuranceCompanyMembersrt:AMBestAPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:OdysseyReinsuranceCompanyMembersrt:AMBestAPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:LloydsUnderwriterSyndicateNo2001AMLMembersrt:AMBestAPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:LloydsUnderwriterSyndicateNo2001AMLMembersrt:AMBestAPlusRatingMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:TopReinsurersMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:TopReinsurersMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:OtherReinsurersMemberus-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421lmnd:OtherReinsurersMemberus-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421us-gaap:CededCreditRiskUnsecuredMember2025-12-310001691421us-gaap:CededCreditRiskUnsecuredMember2024-12-310001691421lmnd:ComputerEquipmentAndSoftwareMember2025-12-310001691421lmnd:ComputerEquipmentAndSoftwareMember2024-12-310001691421us-gaap:LeaseholdImprovementsMember2025-12-310001691421us-gaap:LeaseholdImprovementsMember2024-12-310001691421lmnd:FurnitureAndEquipmentMember2024-12-310001691421lmnd:InsuranceLicensesMember2025-12-310001691421lmnd:InsuranceLicensesMember2024-12-310001691421us-gaap:TrademarksMember2025-12-310001691421us-gaap:TrademarksMember2024-12-310001691421lmnd:TechnologyMember2025-01-012025-12-310001691421lmnd:TechnologyMember2025-12-310001691421lmnd:TechnologyMember2024-12-310001691421lmnd:ValueOfBusinessAcquiredMember2025-01-012025-12-310001691421lmnd:ValueOfBusinessAcquiredMember2025-12-310001691421lmnd:ValueOfBusinessAcquiredMember2024-12-310001691421lmnd:CaliforniaWildfiresMember2025-01-012025-12-310001691421lmnd:CaliforniaWildfiresMember2025-03-012025-03-310001691421lmnd:HurricaneHeleneMember2024-01-012024-12-310001691421lmnd:HurricaneBerylMember2024-01-012024-12-310001691421lmnd:WinterStormElliotMember2023-01-012023-12-310001691421lmnd:TexasHailStormMember2023-01-012023-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2016-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2017-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2018-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2019-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2020-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2021-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2022-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2023-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2024-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2025-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2017-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2018-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2019-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2020-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2021-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2022-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2023-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2024-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2025-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2018-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2019-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2020-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2021-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2022-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2023-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2024-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2025-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2019-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2020-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2021-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2022-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2023-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2024-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2025-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2020-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2021-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2022-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2023-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2024-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2025-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2021-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2022-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2023-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2024-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2025-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2022-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2023-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2024-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2025-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2023-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2024-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2025-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2024Member2024-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2024Member2025-12-310001691421us-gaap:PropertyInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2025Member2025-12-310001691421us-gaap:PropertyInsuranceProductLineMember2025-12-310001691421us-gaap:PropertyInsuranceProductLineMember2023-12-310001691421us-gaap:PropertyInsuranceProductLineMember2022-12-310001691421us-gaap:PropertyInsuranceProductLineMember2020-12-310001691421us-gaap:PropertyInsuranceProductLineMember2024-12-310001691421us-gaap:PropertyInsuranceProductLineMember2016-12-310001691421us-gaap:PropertyInsuranceProductLineMember2017-12-310001691421us-gaap:PropertyInsuranceProductLineMember2019-12-310001691421us-gaap:PropertyInsuranceProductLineMember2021-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2020-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2021-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2022-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2023-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2024-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2025-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2021-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2022-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2023-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2024-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2025-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2022-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2023-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2024-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2025-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2023-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2024-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2025-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2024Member2024-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2024Member2025-12-310001691421lmnd:PetInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2025Member2025-12-310001691421lmnd:PetInsuranceMember2025-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2016-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2017-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2018-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2019-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2020-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2021-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2022-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2023-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2024-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2025-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2017-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2018-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2019-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2020-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2021-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2022-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2023-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2024-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2025-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2018-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2019-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2020-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2021-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2022-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2023-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2024-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2025-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2019-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2020-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2021-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2022-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2023-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2024-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2025-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2020-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2021-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2022-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2023-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2024-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2025-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2021-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2022-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2023-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2024-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2025-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2022-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2023-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2024-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2025-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2023-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2024-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2025-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2024Member2024-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2024Member2025-12-310001691421lmnd:CarInsuranceMemberus-gaap:ShortDurationInsuranceContractAccidentYear2025Member2025-12-310001691421lmnd:CarInsuranceMember2025-12-310001691421lmnd:CustomerInvestmentAgreementMemberus-gaap:LineOfCreditMember2023-06-280001691421lmnd:CustomerInvestmentAgreementMemberus-gaap:LineOfCreditMember2023-06-282023-06-280001691421lmnd:AmendedAndRestatedCustomerInvestmentAgreementMemberus-gaap:LineOfCreditMember2024-01-080001691421lmnd:AmendedAndRestatedCustomerInvestmentAgreementMemberus-gaap:LineOfCreditMember2025-02-030001691421lmnd:GCCustomerValueArrangerLLCMemberlmnd:CustomerInvestmentAgreementMemberus-gaap:LineOfCreditMember2023-06-282023-06-280001691421lmnd:CustomerInvestmentAgreementMemberus-gaap:LineOfCreditMember2025-12-310001691421lmnd:CustomerInvestmentAgreementMemberus-gaap:LineOfCreditMember2024-12-310001691421lmnd:CustomerInvestmentAgreementMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001691421lmnd:CustomerInvestmentAgreementMemberus-gaap:LineOfCreditMember2024-01-012024-12-310001691421lmnd:CustomerInvestmentAgreementMemberus-gaap:LineOfCreditMember2023-01-012023-12-310001691421lmnd:LemonadeFoundationMembersrt:AffiliatedEntityMember2020-01-012020-12-310001691421lmnd:LemonadeInc.Membersrt:AffiliatedEntityMemberlmnd:LemonadeFoundationMember2024-12-310001691421lmnd:LemonadeInc.Membersrt:AffiliatedEntityMemberlmnd:LemonadeFoundationMember2025-12-310001691421lmnd:OmnibusAgreementMemberus-gaap:WarrantMember2022-12-310001691421lmnd:OmnibusAgreementMember2022-12-310001691421lmnd:OmnibusAgreementMember2022-01-012022-12-310001691421lmnd:OmnibusAgreementMemberus-gaap:WarrantMember2025-04-040001691421lmnd:IncentiveCompensationPlan2020Member2020-07-020001691421lmnd:IncentiveCompensationPlan2020Member2020-07-022020-07-020001691421lmnd:IncentiveCompensationPlan2020Member2025-12-310001691421lmnd:EmployeeStockPurchasePlan2020Member2020-07-020001691421lmnd:EmployeeStockPurchasePlan2020Member2020-07-022020-07-020001691421lmnd:EmployeeStockPurchasePlan2020Member2025-12-310001691421lmnd:IncentiveShareOptionPlan2015Memberus-gaap:EmployeeStockOptionMember2015-07-012015-07-310001691421lmnd:IncentiveShareOptionPlan2015Member2015-07-310001691421lmnd:IncentiveShareOptionPlan2015Member2025-12-310001691421lmnd:IncentiveStockPlan2021Member2022-01-012022-12-310001691421lmnd:IncentiveCompensationPlan2020Memberus-gaap:SubsequentEventMember2026-01-012026-01-010001691421lmnd:EmployeeSharePurchasePlanESPPMember2026-01-012026-01-010001691421us-gaap:EmployeeStockOptionMember2024-01-012024-12-310001691421us-gaap:RestrictedStockUnitsRSUMember2024-12-310001691421us-gaap:RestrictedStockUnitsRSUMember2025-01-012025-12-310001691421us-gaap:RestrictedStockUnitsRSUMember2025-12-310001691421lmnd:ClaimsAndClaimsAdjustmentExpenseMember2025-01-012025-12-310001691421lmnd:ClaimsAndClaimsAdjustmentExpenseMember2024-01-012024-12-310001691421lmnd:ClaimsAndClaimsAdjustmentExpenseMember2023-01-012023-12-310001691421lmnd:OtherInsuranceExpenseMember2025-01-012025-12-310001691421lmnd:OtherInsuranceExpenseMember2024-01-012024-12-310001691421lmnd:OtherInsuranceExpenseMember2023-01-012023-12-310001691421us-gaap:SellingAndMarketingExpenseMember2025-01-012025-12-310001691421us-gaap:SellingAndMarketingExpenseMember2024-01-012024-12-310001691421us-gaap:SellingAndMarketingExpenseMember2023-01-012023-12-310001691421us-gaap:ResearchAndDevelopmentExpenseMember2025-01-012025-12-310001691421us-gaap:ResearchAndDevelopmentExpenseMember2024-01-012024-12-310001691421us-gaap:ResearchAndDevelopmentExpenseMember2023-01-012023-12-310001691421us-gaap:GeneralAndAdministrativeExpenseMember2025-01-012025-12-310001691421us-gaap:GeneralAndAdministrativeExpenseMember2024-01-012024-12-310001691421us-gaap:GeneralAndAdministrativeExpenseMember2023-01-012023-12-310001691421us-gaap:WarrantMember2025-01-012025-12-310001691421us-gaap:WarrantMember2024-01-012024-12-310001691421us-gaap:WarrantMember2023-01-012023-12-310001691421us-gaap:EmployeeStockOptionMember2023-01-012023-12-310001691421us-gaap:RestrictedStockUnitsRSUMember2024-01-012024-12-310001691421us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001691421us-gaap:EmployeeStockOptionMember2025-12-310001691421lmnd:OmnibusAgreementMemberus-gaap:WarrantMember2022-01-012022-12-310001691421lmnd:OmnibusAgreementMemberus-gaap:WarrantMember2024-04-300001691421country:IL2025-01-012025-12-310001691421country:IL2024-01-012024-12-310001691421country:IL2023-01-012023-12-310001691421us-gaap:ForeignTaxJurisdictionOtherMember2025-01-012025-12-310001691421us-gaap:ForeignTaxJurisdictionOtherMember2024-01-012024-12-310001691421country:US2025-01-012025-12-310001691421country:US2024-01-012024-12-310001691421country:US2023-01-012023-12-310001691421country:NL2025-01-012025-12-310001691421country:NL2024-01-012024-12-310001691421country:NL2023-01-012023-12-310001691421us-gaap:DomesticCountryMember2025-12-310001691421us-gaap:StateAndLocalJurisdictionMember2025-12-310001691421us-gaap:EmployeeStockOptionMember2025-01-012025-12-310001691421us-gaap:EmployeeStockOptionMember2024-01-012024-12-310001691421us-gaap:EmployeeStockOptionMember2023-01-012023-12-310001691421us-gaap:RestrictedStockMember2025-01-012025-12-310001691421us-gaap:RestrictedStockMember2024-01-012024-12-310001691421us-gaap:RestrictedStockMember2023-01-012023-12-310001691421us-gaap:WarrantMember2025-01-012025-12-310001691421us-gaap:WarrantMember2024-01-012024-12-310001691421us-gaap:WarrantMember2023-01-012023-12-310001691421lmnd:MetromileMember2024-01-012024-12-310001691421lmnd:MetromileMember2025-01-012025-12-310001691421lmnd:MetromileMember2023-01-012023-12-310001691421us-gaap:RelatedPartyMember2025-12-310001691421lmnd:LemonadeFoundationMembersrt:AffiliatedEntityMember2025-01-012025-12-310001691421lmnd:LemonadeFoundationMembersrt:AffiliatedEntityMember2025-12-310001691421lmnd:LemonadeFoundationMembersrt:AffiliatedEntityMember2024-12-310001691421us-gaap:PropertyLeaseGuaranteeMember2025-12-310001691421lmnd:CaliforniaWildfiresMember2025-02-280001691421stpr:NY2025-01-012025-12-310001691421lmnd:AmsterdamMember2025-01-012025-12-310001691421lmnd:TelAvivMember2025-01-012025-12-310001691421lmnd:SanFranciscoMember2025-01-012025-12-310001691421stpr:NY2023-09-300001691421stpr:NY2024-01-012024-12-310001691421stpr:NY2023-01-012023-12-310001691421lmnd:SanFranciscoMember2024-01-012024-12-310001691421lmnd:SanFranciscoMember2023-01-012023-12-310001691421lmnd:LemonadeInsuranceCompanyMember2025-12-310001691421lmnd:LemonadeInsuranceCompanyMember2024-12-310001691421lmnd:MetromileInsuranceCompanyMember2025-12-310001691421lmnd:MetromileInsuranceCompanyMember2024-12-310001691421lmnd:ReportableSegmentMember2025-01-012025-12-310001691421lmnd:ReportableSegmentMember2024-01-012024-12-310001691421lmnd:ReportableSegmentMember2023-01-012023-12-310001691421us-gaap:DomesticCountryMemberlmnd:CARESActERCProgramMember2025-01-012025-12-310001691421stpr:NY2024-01-012024-12-310001691421lmnd:MetromileMember2023-12-310001691421stpr:CA2025-01-012025-12-310001691421stpr:CAus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421stpr:CA2024-01-012024-12-310001691421stpr:CAus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421stpr:CA2023-01-012023-12-310001691421stpr:CAus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421stpr:TX2025-01-012025-12-310001691421stpr:TXus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421stpr:TX2024-01-012024-12-310001691421stpr:TXus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421stpr:TX2023-01-012023-12-310001691421stpr:TXus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421stpr:NY2025-01-012025-12-310001691421stpr:NYus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421stpr:NYus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421stpr:NY2023-01-012023-12-310001691421stpr:NYus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421stpr:WA2025-01-012025-12-310001691421stpr:WAus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421stpr:WA2024-01-012024-12-310001691421stpr:WAus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421stpr:WA2023-01-012023-12-310001691421stpr:WAus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421stpr:IL2025-01-012025-12-310001691421stpr:ILus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421stpr:IL2024-01-012024-12-310001691421stpr:ILus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421stpr:IL2023-01-012023-12-310001691421stpr:ILus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421stpr:NJ2025-01-012025-12-310001691421stpr:NJus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421stpr:NJ2024-01-012024-12-310001691421stpr:NJus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421stpr:NJ2023-01-012023-12-310001691421stpr:NJus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421stpr:CO2025-01-012025-12-310001691421stpr:COus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421stpr:CO2024-01-012024-12-310001691421stpr:COus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421stpr:CO2023-01-012023-12-310001691421stpr:COus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421stpr:FL2025-01-012025-12-310001691421stpr:FLus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421stpr:FL2024-01-012024-12-310001691421stpr:FLus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421stpr:FL2023-01-012023-12-310001691421stpr:FLus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421stpr:PA2025-01-012025-12-310001691421stpr:PAus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421stpr:PA2024-01-012024-12-310001691421stpr:PAus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421stpr:PA2023-01-012023-12-310001691421stpr:PAus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421stpr:AZ2025-01-012025-12-310001691421stpr:AZus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421stpr:AZ2024-01-012024-12-310001691421stpr:AZus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421stpr:AZ2023-01-012023-12-310001691421stpr:AZus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421lmnd:AllOtherStatesMember2025-01-012025-12-310001691421lmnd:AllOtherStatesMemberus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421lmnd:AllOtherStatesMember2024-01-012024-12-310001691421lmnd:AllOtherStatesMemberus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421lmnd:AllOtherStatesMember2023-01-012023-12-310001691421lmnd:AllOtherStatesMemberus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421country:US2025-01-012025-12-310001691421country:USus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421country:US2024-01-012024-12-310001691421country:USus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421country:US2023-01-012023-12-310001691421country:USus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421lmnd:EuropeAndUintedKindomMember2025-01-012025-12-310001691421lmnd:EuropeAndUintedKindomMemberus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421lmnd:EuropeAndUintedKindomMember2024-01-012024-12-310001691421lmnd:EuropeAndUintedKindomMemberus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421lmnd:EuropeAndUintedKindomMember2023-01-012023-12-310001691421lmnd:EuropeAndUintedKindomMemberus-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421us-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2025-01-012025-12-310001691421us-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2024-01-012024-12-310001691421us-gaap:GeographicConcentrationRiskMemberlmnd:PremiumsWrittenGrossBenchmarkMember2023-01-012023-12-310001691421us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2024-12-310001691421us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2025-01-012025-12-310001691421us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2025-12-310001691421us-gaap:AllowanceForUncollectiblePremiumsReceivableMember2024-12-310001691421us-gaap:AllowanceForUncollectiblePremiumsReceivableMember2025-01-012025-12-310001691421us-gaap:AllowanceForUncollectiblePremiumsReceivableMember2025-12-310001691421us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2023-12-310001691421us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2024-01-012024-12-310001691421us-gaap:AllowanceForUncollectiblePremiumsReceivableMember2023-12-310001691421us-gaap:AllowanceForUncollectiblePremiumsReceivableMember2024-01-012024-12-310001691421lmnd:OfficerTradingArrangementMember2025-01-012025-12-310001691421lmnd:MayaProsorMember2025-10-012025-12-310001691421lmnd:MayaProsorMember2025-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2025

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

for the transition period from to

Commission file number: 001-39367

Lemonade, Inc.

(Exact name of Registrant as specified in its charter)

|

|

|

|

|

|

|

|

|

|

|

|

| Delaware |

|

|

32-0469673 |

|

(State or other jurisdiction of

incorporation or organization)

|

|

|

(I.R.S. Employer

Identification No.)

|

5 Crosby Street, 3rd Floor

New York, New York 10013

(Address of principal executive offices) (Zip Code)

(844) 733-8666

(Registrant’s telephone number including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

| Common Stock, $0.00001 par value per share |

|

LMND |

|

The New York Stock Exchange |

|

|

|

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☑ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☑ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☑ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Large accelerated filer |

☑ |

|

Accelerated filer |

☐ |

| Non-accelerated filer |

☐ |

|

Smaller reporting company |

☐ |

|

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☑ No

The aggregate market value of the common stock held by non-affiliates of the registrant, based on the closing sales price of $43.81 on June 30, 2025, was approximately $2,880,712,049.

Registrant had 76,383,438 shares of common stock outstanding as of February 24, 2026.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive Proxy Statement relating to its 2026 Annual Meeting of Stockholders, to be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates, are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated.

|

|

|

|

|

|

|

|

|

|

|

Page |

| Part I |

|

|

|

|

|

|

|

| Item 1 |

|

|

| Item 1A. |

|

|

| Item 1B. |

|

|

Item 1C. |

|

|

| Item 2. |

|

|

| Item 3. |

|

|

| Item 4. |

|

|

|

|

|

| Part II |

|

| Item 5. |

|

|

| Item 6. |

|

|

| Item 7. |

|

|

| Item 7A. |

|

|

| Item 8. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Item 9. |

|

|

| Item 9A. |

|

|

| Item 9B. |

|

|

| Item 9C. |

|

|

| Part III |

|

| Item 10. |

|

|

| Item 11. |

|

|

| Item 12. |

|

|

| Item 13. |

|

|

| Item 14. |

|

|

| Part IV |

|

| Item 15. |

|

|

|

|

|

| Item 16. |

|

|

|

|

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (the “Annual Report”) contains forward-looking statements. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements other than statements of historical fact contained in this Annual Report are forward-looking statements, including without limitation, statements regarding our future results of operations and financial position, our ability to expand our business, our ability to effectively manage the growth of our business, our ability to achieve profitability, our ability to attract, retain and expand our customer base, our ability to operate under and maintain our business model, our ability to maintain and enhance our brand and reputation, the effects of seasonal trends on our results of operations, the impact of catastrophe events or natural disasters on our results of operations, our ability to attain greater value from each customer, our ability to compete effectively in our industry, the future performance of the markets in which we operate, our ability to maintain reinsurance contracts, the adequacy of our loss and loss adjustment reserves, the impact of the evolving conflict in Israel and surrounding region, the potential effects of macroeconomic conditions including inflation, changes in trade policy and tariffs on our claims costs and results of operations, our ability to develop and deploy artificial intelligence and technology, our ability to expand into new products and geographic markets, anticipated benefits of and our ability to maintain our financing arrangements, the impact of current and future laws and regulations including tax legislation, the sufficiency of our capital and liquidity, and the plans and objectives of management for future operations and capital expenditures. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential”, or “continue” or the negative of these terms or other similar expressions. The forward-looking statements in this Annual Report are only predictions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements speak only as of the date of this Annual Report and are subject to a number of important factors that could cause actual results to differ materially from those in the forward-looking statements, including the factors described under the sections in this Annual Report titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

You should read this Annual Report and the documents that we reference in this Annual Report completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise.

In this Annual Report, unless we indicate otherwise or the context otherwise requires, "Lemonade," the “Company," "we," "our," "ours" and "us" refer to Lemonade, Inc. and its consolidated subsidiaries, including Lemonade Insurance Company, Lemonade Insurance Agency, LLC, Metromile, Inc. and Metromile Insurance Company.

SUMMARY RISK FACTORS

Our business is subject to numerous risks and uncertainties, including those described in Part I Item 1A. “Risk Factors” in this Annual Report. You should carefully consider these risks and uncertainties, together with all of the other information contained in this Annual Report, when investing in our common stock. The principal risks and uncertainties affecting our business include the following:

•We have a history of losses and we may not achieve or maintain profitability in the future.

•Our success and ability to grow our business depend on retaining and expanding our customer base.

•Denial of claims or our failure to accurately and timely pay claims could materially and adversely affect our business, financial condition, results of operations, and prospects.

•Our future revenue growth depends on our ability to increase the lifetime value of our customers and attaining greater value from each customer.

•Intense competition in the segments of the insurance industry in which we operate could negatively affect our ability to attain or increase profitability.

•Our proprietary artificial intelligence algorithms may not operate properly or as we expect them to which could cause us to write policies we should not write, price those policies inappropriately or overpay claims that are made by our customers.

•Failure to maintain our risk-based capital at the required levels could adversely affect the ability of our insurance subsidiaries to maintain regulatory authority to conduct our business.

•If we are unable to maintain and implement relationships with third-party service providers, or renew contracts with them on favorable terms, or if those parties are adversely impacted by financial, reputational, regulatory and other tasks, our prospects for future growth and our business may be adversely affected.

•If we are unable to expand our product offerings, or penetrate new markets, our future growth may be limited.

•We rely on artificial intelligence, telematics, mobile technology, and our digital platforms to collect data and any legal or regulatory requirements that prohibit or restrict our ability to collect or use this data could adversely affect our business.

•If we are unable to underwrite risks accurately and charge competitive yet profitable rates our business will be adversely affected.

•Our pricing model for self-driving technologies and reliance on direct vehicle telemetry may not function as expected.

•We may require additional capital to grow our business, which may not be available on terms acceptable to us or at all.

•Interruptions or delays in the services provided by our sole provider of third-party data centers could impair the operability of our website.

•Security incidents or real or perceived errors, failures or bugs in our systems could impair our operations.

•We are periodically subject to examinations by our primary state insurance regulators, which could result in adverse examination findings and necessitate remedial actions.

•Reinsurance may be unavailable at current levels and prices, which may limit our ability to write new business and impact our capital needs.

•We may face particular privacy, data security, and data protection risks as we continue to expand into Europe and the UK in connection with the GDPR and other data protection regulations.

•We may be unable to prevent or address the misappropriation of our data.

•If our customers were to claim that the policies they purchased failed to provide adequate or appropriate coverage, we could face claims.

•Our product development cycles are complex and subject to regulatory approval, and we may incur significant expenses before we generate revenues.

•Litigation and legal proceedings filed by or against us and our subsidiaries could have a material adverse effect.

•The "Lemonade" brand may not become as widely known as incumbents' brands or the brand may become tarnished.

•Our expansion within the United States and any future international expansion strategy will subject us to additional costs and risks.

•There may be an adverse impact of the Customer Investment Agreement.

•We are subject to extensive insurance industry regulations.

•Severe weather events and other catastrophes are inherently unpredictable and may have a material adverse effect on our financial results and financial condition.

•We rely on data from our customers and third parties for pricing and underwriting our insurance policies handling claims and maximizing automation, the unavailability or inaccuracy of which could limit the functionality of our products and disrupt our business.

•Our results of operations and financial condition may be adversely affected due to limitations in the analytical models used to assess and predict our exposure to catastrophe losses.

•Our actual incurred losses may be greater than our loss and loss adjustment expense reserves, which could have a material adverse effect on our financial condition and results of operations.

•Our insurance subsidiaries are subject to minimum capital and surplus requirements, and our failure to meet these requirements could subject us to regulatory action.

PART I

Item 1. Business

Overview

Lemonade is rebuilding insurance from the ground up on a digital substrate and an innovative business model. By leveraging technology, data, artificial intelligence, contemporary design, and social impact, we believe we are making insurance more delightful, more affordable, and more precise. To that end, we have built a vertically-integrated company with wholly-owned insurance carriers in the United States and Europe, including the UK, and the full technology stack to power them.

A brief chat with our bot, AI Maya, is all it takes to get covered with renters, homeowners, pet, car or life insurance, and we expect to offer a similar experience for other insurance products over time. Claims are filed by chatting with another bot, AI Jim, who pays claims in as little as two seconds. This breezy experience belies the extraordinary technology that enables it: a state-of-the-art platform that spans marketing to underwriting, customer care to claims processing, finance to regulation. Our architecture melds artificial intelligence with the human kind, and learns from the prodigious data it generates to become ever better at delighting customers and evaluating risk.

In addition to digitizing insurance end-to-end, we also reimagined the underlying business model to minimize volatility while maximizing trust and social impact. To lessen the volatility inherent in an industry directly impacted by the weather, we utilize several forms of reinsurance, with the goal of reducing the impact on our gross margin.

Our Business Model

At the foundation of our business model is a direct, digital, customer-centric experience that enables rapid growth and strong retention. Our customer-centricity runs deep, and our underlying business model is designed to align interests between us and our customers. This technology-first customer acquisition and retention strategy, combined with our unconflicted business model, results in a highly attractive financial model.

We leverage technology in everything we do. AI Maya and our APIs sell 98% of Lemonade's policies. Homeowners insurance policies in the United States are sold primarily via agents, making a platform that finds, onboards, and digitally serves consumers end-to-end very much an outlier. Our digital substrate enables us to integrate marketing and onboarding with underwriting and claims processing, collecting and deploying data throughout, to constantly drive efficient customer acquisition, enhance the customer experience, and mitigate risk. This approach results in significant, rapid scaling coupled with high customer satisfaction.

To align our interests with those of our customers, encourage good behavior and build a long-term relationship based on mutual trust, we endeavor to decouple our financial incentives from variability in claims. Unlike many of our competitors, we work to minimize incentives to deny legitimate claims as we aim to give back, rather than keep the remaining monies. Our reinsurance contracts lessen the volatility in our operating results, as a portion of claims are borne by our reinsurance partners. See "Risk Factors - Risks Relating to Our Business”. In the future, reinsurance may be unavailable at current levels and prices, which may limit our ability to write new business and impact our capital needs. Furthermore, reinsurance subjects us to counterparty risk and may not be adequate to protect us against losses, which could have a material effect on our results of operations and financial condition.

After our customers purchase a policy, we ask them to designate a charitable cause for us to support. As a result, we believe customers are less inclined to embellish claims as they could be hurting a nonprofit they care about, rather than an insurance company they do not.

Strong retention rates and a subscription-based model create highly-recurring and naturally-growing revenue streams, and provide visibility into our topline results. Our reinsurance construct, in turn, mitigates the volatility inherent in traditional insurance companies, where profits quite literally depend on the weather. With our reinsurance agreements reducing the impact of excess claims, and our Giveback policy, we have two powerful ballasts that reduce volatility, while creating an aligned, trustful, and values-rich relationship with our customers.

This combination of a customer-focused onboarding experience, a customer-aligned business model, and a revenue stream that grows along with our customers' insurance needs, has created a sustainable financial model that we are proud of. Over time, we believe our platform will continue to efficiently acquire new customers and give us the ability to service their growing needs at a lower cost, and with higher satisfaction levels, than the industry at large.

Our Technology

Data Advantage

Our proprietary and entirely integrated technology stack is a key enabler of our strategy and business model. Interactions with our customers across our platform generate a trove of data, which in turn improves interactions with our customers across our platform.

AI Maya

AI Maya, our playful onboarding and customer experience bot, uses natural language to guide customers through an easy and fun process of joining Lemonade. Maya handles everything from collecting information and personalizing coverage to creating quotes and facilitating payments securely. By asking customers a limited number of high-impact questions, and adapting based on their responses, AI Maya is able to dramatically reduce onboarding times while still collecting and utilizing the data that is central to our continuous improvement.

AI Jim

AI Jim is our claims bot, and, as of December 31, 2025, 96% of the time, it is AI Jim that will take the first notice of loss from a Lemonade customer without human intervention (and with zero claims overhead, known as loss adjustment expense, or “LAE”). As of December 31, 2025, roughly 55% of our claims were automated, resulting in instant or near-instant processing from start to finish. AI Jim triages and assigns claims he is not authorized to settle, or ones where he identifies concerns, to human claims experts, analyzing each expert's specialty, qualifications, workload, and schedule to determine to whom to assign the claim. Even where human escalation is needed, AI Jim will have done much of the heavy lifting so our team can settle claims and support customers in their hour of need as quickly and smoothly as possible.

The claims process represents the most acute pain point in the insurance experience, and it is where animosity toward the industry is most commonly cultivated. Re-imagining claims for the benefit of the customer, by aligning interests and incentives and by endeavoring to remove friction, hassle, cost, and delays, is therefore a key driver of our leadership in customer satisfaction.

CX.AI

CX.AI is our bot platform built to understand and resolve customer requests without human intervention. Currently, over half of Lemonade’s customer inquiries are handled this way. Customers often require assistance pre- or post-purchase, ranging from coverage questions to making changes to their policy, such as adding a spouse, updating coverage amounts, changing payment methods, or adding newly purchased items. CX.AI uses Natural Language Processing to analyze and understand customers' requests, helping them perform a growing set of tasks.

Our customer-facing technologies, AI Maya, AI Jim, and CX.AI deliver a superior experience at a fraction of the cost, all the while collecting and utilizing far more data than their human counterparts. A similar construct powers the rest of the Company.

Our 'behind the scenes technology' is structured within three proprietary applications: Forensic Graph, Blender, and Cooper.

Forensic Graph

Forensic Graph utilizes the combined power of behavioral economics, big data, and AI to predict, deter, detect, and block fraud throughout the customer engagement. Insurance fraud is a complicated problem to solve for traditional insurers, mostly due to data paucity. Forensic Graph tracks untold signals and analyzes relationships between things which may appear trivial or invisible to humans, but in which our machine learning uncovers complex multivariate links that have helped us avoid millions of dollars' worth of potential losses.

Blender

Blender is a robust insurance management platform that we built with customer centricity and exponential efficiency in mind. This is a built-from-scratch, cutting edge backend system, designed as a single, cohesive, and streamlined management tool for our customer experience, underwriting, claims, growth, marketing, finance, and risk teams. When a claims experience specialist logs in to Blender, for example, they instantly see all claims assigned to them by AI Jim. Blender then provides them with instructions for next steps, and when possible, includes coverage determinations, and alerts of suspicious activity. Critically, they will also see an extraordinary amount of information about the users' behavior patterns and their claim, background information, risk indicators, insurance history, and much more. If a vendor is needed, for example, to assess the damage, all appropriate suppliers will appear in Blender, and can be dispatched to the field, and paid, at the push of a button. Blender brings similar integrated, customer-centric, and focused workflows to the other Lemonade teams as well.

Cooper

Cooper is our internal bot (we like to think of him as our own Jarvis) who runs important parts of our Company. Cooper handles complex as well as repetitive tasks, from helping our customer experience team handle lengthy, manual processes such as processing paper checks, to automatically running tens of thousands of tests on each release of our software. Cooper continuously analyzes spectrometry imaging beamed from NASA's satellites, identifying wildfires in real time and blocking ads and sales in the affected areas; Cooper collates and formats materials for our regulatory filings; and he even handles most of our engineering task allocation, code deployment, QA, and more. Cooper makes our team dramatically more efficient and keeps evolving and learning with time.

Blender, Forensic Graph and Cooper, together with AI Maya, AI Jim, and CX.AI, run atop our Customer Cortex. The Customer Cortex, like a central nervous system, is the place where all data about our customers is transmitted, continuously analyzed, and then used by all six applications.

Growth Opportunities

Acquire more customers

We recently passed 3 million customers, proof that people are ready for insurance to work differently. We are well positioned to continue to grow our customer base by continuing to attract first time buyers, an underserved population that continually replenishes.

Our delightful experience and competitive pricing also attract customers who switch from their existing carriers. Our bot automatically files the necessary paperwork to cancel a customer's old policy, removing what is typically a barrier to switching. As we continue to strengthen brand recognition and execute our marketing strategy, we will look to increase the number of customers migrating to the Lemonade platform.

Grow within our existing customer base

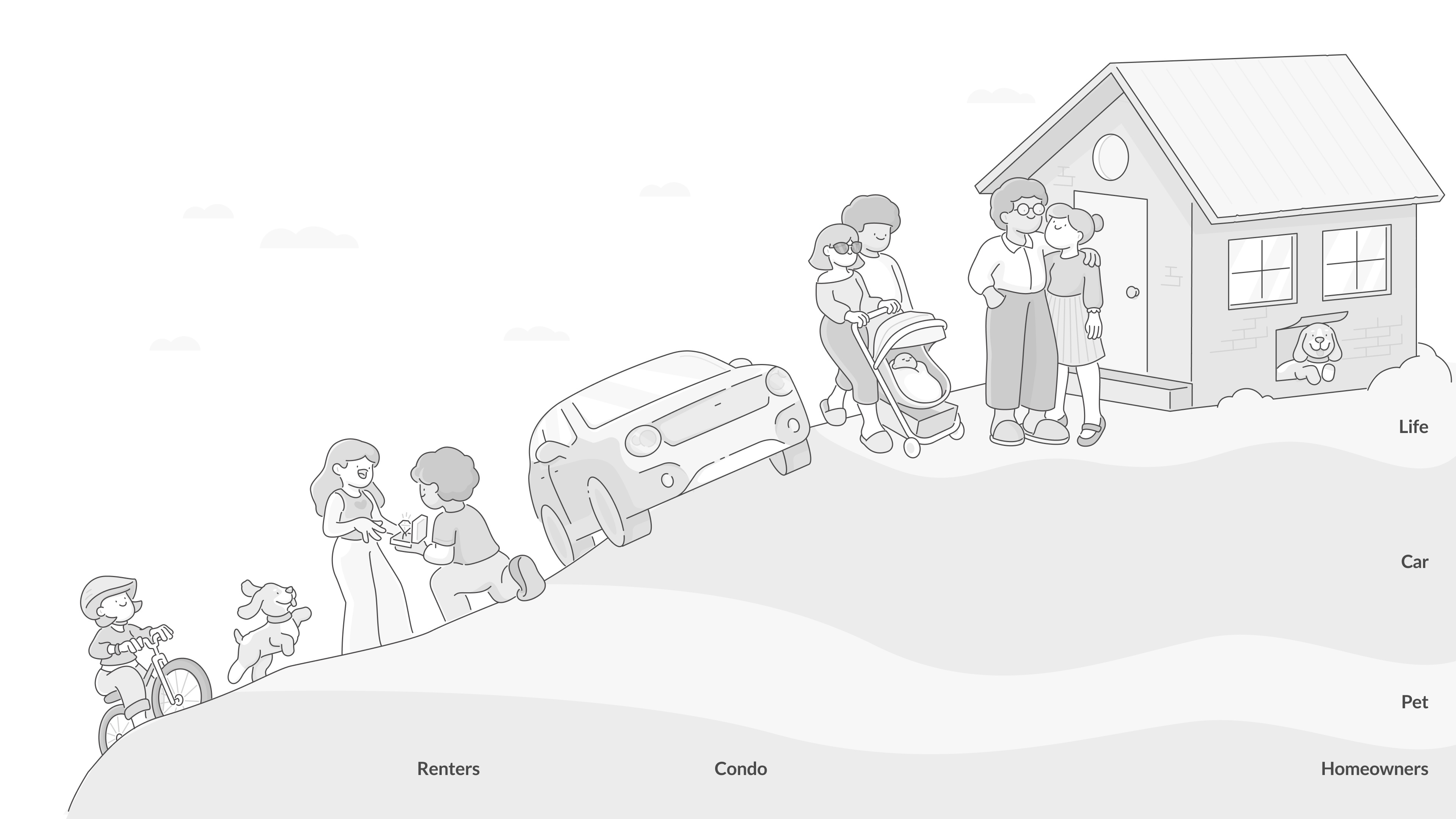

As our customers move up the economic ladder and through lifecycle events, their insurance needs evolve to higher value products: renters typically acquire more property and frequently upgrade to successively larger homes. Growing households often need car, pet, and life insurance, and additional coverage. These progressions regularly trigger orders of magnitude jumps in insurance premiums, and within states that offer all of Lemonade’s “suite of products” - Renters, Home, Car, Pet, and Life - we see a growing proportion of customers with multiple Lemonade policies and see ripe opportunities for the business. For instance, we see a significant opportunity for Lemonade Car in selling to our existing customers, allowing us to acquire customers at little or no cost. Of the approximately 3,000,000 customers we have today, about 1.9 million already have car insurance—that translates to a potential multi-billion dollar opportunity in car premiums at nearly zero acquisition costs. We aim to provide an unmatched user experience in order to retain customers throughout their lifespan, expanding their lifetime value without incurring any incremental costs of acquisition.

Expand to new products

Our strategy of growing with our customers also lends itself to expanding into new lines of insurance, as lifecycle events trigger the need for additional insurance products.

Our regulatory framework, technology stack, and brand are all extensible to new lines of insurance, and we anticipate that these will contribute to our growth in the future. In the last five years, we have added life, pet and car insurance to our growing portfolio of offerings, and have expanded product offerings in certain countries in Europe and the UK.

Expand to new geographies

The Lemonade platform is inherently multilingual and agile by design, so that we can efficiently expand into new markets and new product offerings both within the United States and internationally. We are licensed to sell renters, homeowners, pet and/or car insurance policies in 50 states of the United States and Washington, D.C. As of December 31, 2025, we operate in 41 of those states and Washington, D.C., which collectively represent approximately 95% of the U.S. population. Our strong brand and unique business model drive rapid growth and allow us to quickly gain share in new markets. We also hold a pan-European license, enabling us to passport into and sell in 30 countries across Europe. We currently operate in Germany, the Netherlands, France and the UK and will continue to expand our product offerings in other countries.

Our Product Offerings

Renters and Homeowners Insurance

We offer our products to renters and homeowners in the United States, France, the Netherlands and the UK (in addition to liability insurance) and contents and liability insurance in Germany. The insurance we offer in the United States covers stolen or damaged property, and personal liability, which protects our customers if they are responsible for an accident or damage to another person or their property. In a number of states, we also offer landlord insurance policies to condo and co-op owners who rent out their property less than five times a year.

In the past two years, we expanded our offerings to include Buildings insurance in the UK, the Netherlands and France, giving homeowners the ability to purchase extensive coverage for their home and belongings. Both expansions in the UK and France were supported by existing partnerships with Aviva in the UK and BNP Paribas Cardif in France, providing coverage options unique to each locale through our fully digital experience.

The full Lemonade experience is available through our iOS and Android apps, as well as through our website. Before a customer purchases one of our policies, we allow the customer to review a summary of their coverage and a sample policy. We also enable the customer to reconfigure their coverage and other policy settings, such as the deductible and start date. After payment via a credit or debit card, we instantly issue the customer their policy documents and send it to them via email. From start to finish, the entire process is completed digitally.

In the U.S., our products automatically cover all residents of a household who are related to the customer by marriage, blood, or adoption. In addition to the base coverage we offer for personal property, electronics, furniture, and clothing, our customers can purchase extra coverage to protect against accidental loss, damage, and theft, worldwide, of their jewelry, fine art, and other personal property.

Pet Insurance

We currently offer pet insurance that covers diagnostics, procedures, medication, accidents or illness. Even our basic pet insurance offering covers blood tests, urinalysis, X-rays, MRIs, lab work, and CT scans. We also offer two optional add-ons to the basic plan, a wellness package and an extended accident and illness package. These provide additional coverage for preventative care costs, including annual exams and vaccines, and recovery treatments, including physical therapy and hydrotherapy.

We believe our expansion into pet insurance will allow us to further achieve our long-term strategy of growing with our young customer base by offering new insurance experiences to customers as they progress in their lifecycles. Our leadership in leveraging AI has also allowed us to create a highly-efficient business. Our Pet book of business has increased more than 35x (in IFP), dropped 39 points from the loss ratio, and increased efficiencies by 78%, driving down the cost per claim from $65 to $14. About 87% of our pet insurance policies were sold to new customers, and about 5% of those have already added a renters or homeowners policy to their pet policy as of December 31, 2025. Customers that bundle our insurance offerings typically save money. The remaining 13% or so of pet insurance policies were sold to existing customers, whose median premium per customer grew roughly 3.8x with little to no incremental customer acquisition costs.

Car Insurance

We offer car insurance in a number of states. Lemonade Car insurance covers car accidents, weather damage, theft and vandalism, damage from fire, trees, or animals, glass and windshield repair, liability for bodily injury and property damage, medical expenses, roadside assistance, and reimburses drivers for expenses relating to temporary transportation when a car is being repaired, subject to certain exceptions.

Recently, we have integrated a pricing model in certain markets that utilizes direct vehicle telemetry to distinguish between human-driven and autonomous miles. This allows us to offer specialized rates for self-driving technologies specifically pricing autonomous miles at significant discount to reflect the differing risk profiles of AI-assisted driving.

Life Insurance

Lemonade also provides life insurance through a partnership arrangement with a third-party carrier, Legal & General Group. With Lemonade’s term life insurance offering individuals can apply online for up to $1.5 million or more in coverage, for a term of 10 to 40 years. Applicants use Lemonade’s interface to receive an initial quote estimate and then are transferred to our partner to complete their final application.

Giveback Feature

Giveback is a distinctive Lemonade policy to which the Company continues to have a deep commitment. Each year, we aim to donate funds to cause our customers care about. After our customers purchase a policy, we ask them to select from a list of charitable causes categories to support. We determine the annual Giveback based on our review of the Company’s financial performance and our customers’ chosen causes, and aim to donate funds quarterly.

The Giveback is paid only if payment is authorized by our board of directors in its sole discretion and consistent with its duty of care. See "Risk Factors — We could be forced to modify or eliminate our Giveback, which could undermine our business model and have a material adverse effect on our results of operations and financial condition." Since 2017, we have donated over $12 million to causes chosen by our customers under our Giveback program. The Giveback is not a contractual obligation to any customer or to any cause, and customers may not take a tax deduction related to the donations.

Although a new and untested concept, we believe that donating funds to causes our customers care about will discourage fraud and promote greater trust between us and our customers. The Giveback program, and its underlying ethos, has also helped build an honest relationship with our consumers. They trust us, and they also become part of a community; our policyholders are helping others while protecting their valuables, insuring their home, or making sure their pet can afford vital medical care.

Our Vertically Integrated Platform