Document

MANAGEMENT'S DISCUSSION AND ANALYSIS

OF FINANCIAL POSITION AND RESULTS OF OPERATIONS

First Quarter Ended March 31, 2025

INDEX

|

|

|

|

|

|

| Introduction |

|

About IAMGOLD |

|

| Highlights |

|

| Operating and Financial Results |

|

| Outlook |

|

| Environmental, Social and Governance |

|

|

|

| Operations |

|

|

|

|

|

| Côté Gold |

|

| Westwood |

|

| Essakane |

|

| Other Projects |

|

| Exploration |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Financial Condition |

|

|

|

| Liquidity and Capital Resources |

|

| Contractual Obligations |

|

| Cash Flow |

|

|

|

| Financial Instruments |

|

|

|

| Shareholders’ Equity |

|

| Quarterly Financial Review |

|

| Disclosure Controls and Procedures and Internal Control over Financial Reporting |

|

| Critical Judgments, Estimates and Assumptions |

|

|

|

| New Accounting Standards |

|

| Risks and Uncertainties |

|

| Non-GAAP Financial Measures |

|

| Cautionary Statement on Forward-Looking Information |

|

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

1 |

INTRODUCTION

The following Management’s Discussion and Analysis (“MD&A”) of IAMGOLD Corporation (“IAMGOLD” or the “Company”), dated May 6, 2025, should be read in conjunction with IAMGOLD's unaudited condensed consolidated interim financial statements and related notes for the three months ended March 31, 2025 ("consolidated interim financial statements"). This MD&A should be read in conjunction with IAMGOLD's audited annual consolidated financial statements and related notes as at and for the fiscal year ended December 31, 2024, and the related MD&A included in the 2024 annual report. All figures in this MD&A are in U.S. dollars and tabular dollar amounts are in millions, unless stated otherwise. Additional information on IAMGOLD can be found at www.iamgold.com. However, the information on the website is not in any way incorporated in or made a part of this MD&A.

ABOUT IAMGOLD

IAMGOLD is an intermediate gold producer and developer based in Canada with three operating mines: Côté Gold (Canada), Westwood (Canada) and Essakane (Burkina Faso). Côté Gold ("Côté") commenced production on March 31, 2024. The Company has an established portfolio of early stage and advanced exploration projects within highly prospective mining districts in Canada.

IAMGOLD employs approximately 3,700 people and is committed to maintaining its culture of accountable mining through high standards of Environmental, Social and Governance (“ESG”) practices. IAMGOLD is listed on the New York Stock Exchange (NYSE:IAG) and the Toronto Stock Exchange (TSX:IMG).

HIGHLIGHTS

Operating and financial results

•Attributable gold production was 161,000 ounces in the first quarter.

•Côté produced 51,000 attributable ounces (73,000 ounces on a 100% basis) in the first quarter. During March, Côté achieved an average mill throughput rate of 90% of nameplate design capacity and produced 26,500 attributable ounces (37,900 ounces on a 100% basis). Subsequent to quarter end, the plant continued to demonstrate good availability and utilization with throughput averaging 96% of nameplate over the last 30 days.

•Production is expected to be higher quarter over quarter through 2025 as Côté ramps up to design capacity by the end of 2025 and the grade at Essakane increases during the second half of the year based on the mining sequence. At Westwood, underground throughput and grade is expected to increase compared to the first quarter.

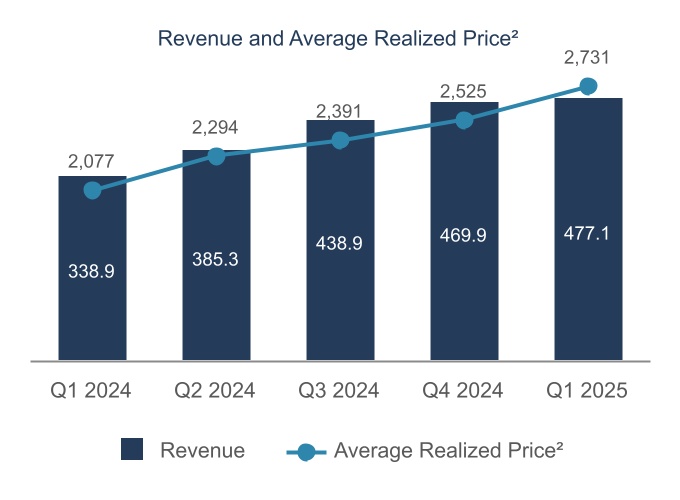

•Revenues were $477.1 million from sales of 174,000 ounces at an average realized gold price1 of $2,731 per ounce for the quarter2.

•Cost of sales per ounce sold was $1,465, cash cost1 per ounce sold was $1,459 and all-in-sustaining cost1 ("AISC")1 per ounce sold was $1,908.

•Net earnings and adjusted net earnings per share attributable to equity holders1 for the first quarter of $0.07 and $0.10, respectively.

•Net cash from operating activities was $74.3 million for the first quarter, net of the impact of delivering 37,500 ounces into gold prepay obligations. Net cash from operating activities, before movements in working capital and non-current ore stockpiles1, was $104.9 million for the first quarter, net of the impact of delivering 37,500 ounces into gold prepay obligations.

•Earnings before interest, income taxes, depreciation and amortization (“EBITDA”)1 was $195.2 million for the first quarter and adjusted EBITDA1 was $204.5 million.

•Mine-site free cash flow1 was $139.6 million during the first quarter.

•The Company has available liquidity1 of $745.8 million, mainly comprised of cash and cash equivalents of $316.6 million and the available balance of the revolving credit facility (“Credit Facility”) of $428.5 million as at March 31, 2025.

•In health and safety, the Company reported a TRIFR (total recordable injuries frequency rate) of 0.67, tracking slightly above the prior year performance.

Corporate

•During the first quarter of 2025, the Company delivered 37,500 ounces into the 2024 gold prepay arrangements and a further 12,500 ounces during April 2025, reducing the outstanding balance of remaining prepay arrangements to 25,000 ounces as at April 30, 2025. Deliveries into the gold prepayment arrangement will be complete by the end of the second quarter 2025.

•On March 21, 2025, the Company received an updated credit rating from Fitch which upgraded the corporate credit rating from B- to B+ with a stable outlook.

____________________________

1.This is a non-GAAP financial measure. See “Non-GAAP Financial Measures".

2.The average realized gold price in the first quarter 2025, excluding the impact of the 2024 Prepay Arrangement (as defined below), was $2,909 per ounce.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

2 |

•On February 3, 2025, Annie Torkia Lagacé joined IAMGOLD as Chief Legal and Strategy Officer, and as part of this strategic realignment, Tim Bradburn, SVP, General Counsel and Corporate Secretary and Stephen Eddy, SVP, Business Development departed IAMGOLD.

•On February 20, 2025, Dorena Quinn was appointed as Chief People Officer, having joined the Company in 2018 and most recently serving as Senior Vice President, People.

•On May 6, 2025, the Company released its 2024 Sustainability Report. The report draws upon various ESG frameworks and standards and internationally recognized methodologies such as the Global Reporting Initiative (“GRI”) and Sustainability Accounting Standards Board (“SASB”).

OPERATING AND FINANCIAL RESULTS

For more details and the Company's overall outlook for 2025, see “Outlook”, and for individual mines performance, see “Operations”. The following table summarizes certain operating and financial results for the three months ended March 31, 2025 (Q1 2025) and March 31, 2024 (Q1 2024) and certain measures of the Company's financial position as at December 31, 2024.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Q1 2025 |

Q1 2024 |

|

|

|

Key Operating Statistics ($ millions) |

|

|

|

|

|

| Gold production – attributable (000s oz) |

161 |

|

151 |

|

|

|

|

- Côté Gold1 |

51 |

|

1 |

|

|

|

|

| - Westwood |

24 |

|

32 |

|

|

|

|

| - Essakane |

86 |

|

118 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold sales – attributable (000s oz) |

165 |

|

150 |

|

|

|

|

- Côté Gold1 |

52 |

|

— |

|

|

|

|

| - Westwood |

27 |

|

33 |

|

|

|

|

| - Essakane |

86 |

|

117 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cost of sales2 ($/oz sold) – attributable |

$ |

1,465 |

|

$ |

1,056 |

|

|

|

|

- Côté Gold1 |

$ |

1,264 |

|

$ |

— |

|

|

|

|

| - Westwood |

$ |

1,547 |

|

$ |

1,243 |

|

|

|

|

| - Essakane |

$ |

1,560 |

|

$ |

1,004 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash costs3 ($/oz sold) – attributable |

$ |

1,459 |

|

$ |

1,053 |

|

|

|

|

- Côté Gold1 |

$ |

1,260 |

|

— |

|

|

|

|

| - Westwood |

$ |

1,527 |

|

$ |

1,236 |

|

|

|

|

| - Essakane |

$ |

1,557 |

|

$ |

1,002 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

AISC3 ($/oz sold) – attributable |

$ |

1,908 |

|

$ |

1,493 |

|

|

|

|

- Côté Gold1 |

$ |

1,643 |

|

$ |

— |

|

|

|

|

| - Westwood |

$ |

2,124 |

|

$ |

1,836 |

|

|

|

|

| - Essakane |

$ |

1,846 |

|

$ |

1,312 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average realized gold price3,4 ($/oz) |

$ |

2,731 |

|

$ |

2,077 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.Attributable portion for Côté Gold is based on IAMGOLD’s ownership of 70%; prior to November 30, 2024, IAMGOLD’s ownership was 60.3% (refer to Côté Gold section below for more details).

2.Throughout this MD&A, cost of sales, excluding depreciation, is disclosed in the segment note in the consolidated interim financial statements.

3.Refer to the “Non-GAAP Financial Measures” disclosure at the end of this MD&A for a description and calculation of these measures.

4.The average realized gold price in the first quarter 2025, excluding the impact of the 2024 Prepay Arrangement (as defined below), was $2,909 per ounce.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Q1 2025 |

Q1 2024 |

|

|

|

Financial Results ($ millions) |

|

|

|

|

|

| Revenues |

$ |

477.1 |

|

$ |

338.9 |

|

|

|

|

|

|

|

|

|

|

| Gross profit |

$ |

141.2 |

|

$ |

105.7 |

|

|

|

|

EBITDA1 |

$ |

195.2 |

|

$ |

154.1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted EBITDA1 |

$ |

204.5 |

|

$ |

152.5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net earnings (loss) attributable to equity holders |

$ |

39.7 |

|

$ |

54.8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted net earnings (loss) attributable to equity holders1 |

$ |

55.2 |

|

$ |

53.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net earnings (loss) per share attributable to equity holders |

$ |

0.07 |

|

$ |

0.11 |

|

|

|

|

Adjusted net earnings (loss) per share attributable to equity holders1 |

$ |

0.10 |

|

$ |

0.11 |

|

|

|

|

Net cash from operating activities before changes in working capital1 |

$ |

104.9 |

|

$ |

142.8 |

|

|

|

|

| Net cash from operating activities |

$ |

74.3 |

|

$ |

77.1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mine-site free cash flow1 |

$ |

139.6 |

|

$ |

46.2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Capital expenditures1,2 – sustaining |

$ |

61.7 |

|

$ |

55.1 |

|

|

|

|

Capital expenditures1,2 – expansion |

$ |

5.3 |

|

$ |

115.2 |

|

|

|

|

|

March 31 |

December 31 |

|

|

|

|

2025 |

2024 |

|

|

|

Financial Position ($ millions) |

|

|

|

|

|

| Cash and cash equivalents |

$ |

316.6 |

|

$ |

347.5 |

|

|

|

|

| Long-term debt |

$ |

1,022.3 |

|

$ |

1,028.9 |

|

|

|

|

Net cash (debt)1 |

$ |

(882.3) |

|

$ |

(859.3) |

|

|

|

|

| Available Credit Facility |

$ |

428.5 |

|

$ |

418.5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.Refer to the “Non-GAAP Financial Measures” disclosure at the end of this MD&A for a description and calculation of these measures.

2.Sustaining and expansion capital expenditures represent incurred expenditures for property, plant and equipment and exploration and evaluation assets, and exclude right-of-use assets and working capital impacts.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

4 |

____________________________

1.Cost of sales, including depreciation, cash costs and AISC are expressed on an attributable ounce sold basis (excluding the non-controlling interests of 10% at Essakane).

2.This is a non-GAAP financial measure. See “Non-GAAP Financial Measures”.

3.Côté capital expenditures reflect the proportionate interest in Côté Gold UJV on an incurred basis.

4.All-in sustaining cost and sustaining capital expenditures for the third quarter 2024 for Côté Gold represent the two-month period following achievement of commercial production.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

5 |

OUTLOOK

Production (000 oz)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Actual Q1 2025 |

Full Year Guidance 2025 |

|

|

| Côté Gold – (70%) |

51 |

250 – 280 |

|

|

| Westwood – (100%) |

24 |

125 – 140 |

|

|

| Essakane – (90%) |

86 |

360 – 400 |

|

|

|

|

|

|

|

|

|

|

|

|

| Total attributable production (000s oz) |

161 |

735 – 820 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total attributable production for IAMGOLD in 2025 is expected to be in the range of 735,000 to 820,000 ounces. Production is expected to be higher quarter over quarter through 2025 as Côté ramps up to design capacity by the end of 2025 and the grade at Essakane increases during the second half of the year based on the mining sequence. At Westwood, underground throughput and grade is expected to increase from the first quarter through underground process improvements. For further details, refer to the operations section of each mine below.

Costs

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Actual Q1 2025 |

Full Year Guidance 2025 |

|

|

| Côté Gold |

|

|

|

|

| Cash costs ($/oz sold) |

$1,260 |

$950 – $1,100 |

|

|

| AISC ($/oz sold) |

$1,643 |

$1,350 – $1,500 |

|

|

| Westwood |

|

|

|

|

| Cash costs ($/oz sold) |

$1,527 |

$1,175 – $1,325 |

|

|

| AISC ($/oz sold) |

$2,124 |

$1,675 – $1,825 |

|

|

| Essakane |

|

|

|

|

| Cash costs ($/oz sold) |

$1,557 |

$1,400 – $1,550 |

|

|

| AISC ($/oz sold) |

$1,846 |

$1,675 – $1,825 |

|

|

| Consolidated |

|

|

|

|

Cost of sales1 ($/oz sold) |

$1,465 |

$1,200 – $1,350 |

|

|

Cash costs1,2 ($/oz sold) |

$1,459 |

$1,200 – $1,350 |

|

|

AISC1,2 ($/oz sold) |

$1,908 |

$1,625 – $1,800 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.Consists of Côté Gold, Westwood and Essakane on an attributable basis of 70%, 100% and 90%, respectively.

2.This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

Cash costs on a consolidated basis are expected to be in the range of $1,200 to $1,350 per ounce sold, a slight increase from last year primarily as a result of an increase in expected cash costs at Essakane. AISC for the Company is expected to be in the range of $1,625 and $1,800 per ounce sold, in line with 2024 as a result of the ramp-up of Côté Gold and reduced capitalized waste stripping at Essakane. In line with production levels, unit costs are expected to decrease corresponding with higher production volumes throughout the year.

The full year guidance is based on the following 2025 full year assumptions, before the impact of hedging: average realized gold price of $2,500 per ounce, USDCAD exchange rate of 1.35, EURUSD exchange rate of 1.11, average Brent oil price of $75 per barrel and WTI price of $70 per barrel. For expected impacts from fluctuation in these assumptions, refer to the Sensitivity Impact table included in the Financial Condition section.

Capital Expenditures

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Actual Q1 20251 |

Full Year Guidance 20252 |

|

| ($ millions) |

Sustaining |

Expansion |

Total |

Sustaining |

Expansion |

Total |

|

|

|

Côté Gold (IMG share) |

$ |

18.2 |

|

$ |

3.1 |

|

$ |

21.3 |

|

$ |

110 |

|

$ |

15 |

|

$ |

125 |

|

|

|

|

| Westwood |

$ |

15.1 |

|

$ |

— |

|

$ |

15.1 |

|

$ |

70 |

|

$ |

— |

|

$ |

70 |

|

|

|

|

| Essakane |

27.9 |

|

2.2 |

|

30.1 |

|

110 |

|

5 |

|

115 |

|

|

|

|

|

$ |

61.2 |

|

$ |

5.3 |

|

$ |

66.5 |

|

$ |

290 |

|

$ |

20 |

|

$ |

310 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Corporate |

0.5 |

|

— |

|

0.5 |

|

— |

|

— |

|

— |

|

|

|

|

Total3 |

$ |

61.7 |

|

$ |

5.3 |

|

$ |

67.0 |

|

$ |

290 |

|

$ |

20 |

|

$ |

310 |

|

|

|

|

1.100% basis, for Westwood and Essakane, and reflects IAMGOLD’s 70% interest in Côté Gold UJV on an incurred basis.

2.Capital expenditures guidance (±5%).

3.Includes $11 million of capitalized exploration and evaluation expenditures also included in the Exploration Outlook guidance table.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

6 |

Capital expenditures in 2025 are expected to total $310 million, of which $290 million is categorized as sustaining capital. Capital expenditures are lower than 2024, as a result of the completion of expansion capital outlays as Côté Gold construction and commissioning was completed earlier in the year. Sustaining capital estimates are expected to decline going forward, as Côté completes the construction of the full tailings dam footprint and related earthworks projects and as capitalized waste stripping declines at Essakane based on the current mine plan.

Exploration Outlook

Exploration expenditures for 2025 are expected to be approximately $38 million, the majority of which will be expensed. The largest exploration spend will be at Côté Gold of approximately $13 million attributable to IAMGOLD including the Gosselin resource delineation drilling program, Essakane at approximately $7 million, followed by Nelligan/Monster Lake at approximately $6 million.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Actual Q1 2025 |

Full Year Guidance 2025 |

| ($ millions) |

Capitalized |

Expensed |

Total |

Capitalized |

Expensed |

Total |

| Exploration projects – greenfield |

$ |

0.2 |

|

$ |

5.5 |

|

$ |

5.7 |

|

$ |

— |

|

$ |

25 |

|

$ |

25 |

|

| Exploration projects – brownfield |

1.9 |

|

0.6 |

|

2.5 |

|

11 |

|

2 |

|

13 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

2.1 |

|

$ |

6.1 |

|

$ |

8.2 |

|

$ |

11 |

|

$ |

27 |

|

$ |

38 |

|

Income Taxes Paid and Depreciation Outlook

The Company expects to pay cash taxes in the range of $120 to $130 million during 2025. Cash tax payments do not occur evenly by quarter, as amounts paid in a quarter can include payments of the final balance of the prior year taxes and payments of instalments for the current year, both required to be made at times as prescribed by different countries. There are no significant cash taxes expected in respect of the new global minimum top-up taxes ("GloBE"). The income taxes paid guidance does not include cash tax obligations arising from asset sales.

Depreciation expense for 2025 is expected to be $450 million (±5%) with increased depreciation expense due to the increase in the value of depreciable property, plant and equipment following the completion of construction and commencement of commercial operations at Côté Gold and the 2024 impairment reversal at the Westwood cash generating unit ("CGU"). In line with production levels, depreciation expense is expected to be higher in the second half of the year due to the large proportion of depreciable assets that are depreciated on a units of production basis.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ($ millions) |

Actual Q1 2025 |

Full Year Guidance 2025 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Depreciation expense |

$79.7 |

$450 (±5%) |

|

|

| Income taxes paid |

$15.2 |

$120 – $130 |

|

|

ENVIRONMENTAL, SOCIAL AND GOVERNANCE

The Company released its 2024 Sustainability Report on May 6, 2025. The report draws upon various ESG frameworks and standards and internationally recognized methodologies such as the Global Reporting Initiative (“GRI”) and Sustainability Accounting Standards Board (“SASB”).

Health and Safety

The TRIFR was 0.67 as at March 31, 2025, (compared to 0.61 as at March 31, 2024), and tracking above the Company's tolerance of 0.57. IAMGOLD is continuing to advance its critical risk management and visible leadership to improve safety and reduce high-potential incidents. This includes the integration of contractors in the critical risk management program.

The Company continues to track a range of leading indicators around critical risk management, contractor management, and incident investigation quality, reported annually.

Environmental

There were zero significant environmental incidents reported for the quarter1.

Indigenous Relations

As a Canadian business committed to responding to the Truth and Reconciliation Commission of Canada’s Calls to Action2, IAMGOLD launched a company-wide initiative in the first quarter 2025, that will help the Company articulate how it works with Indigenous peoples beyond reconciliation, towards a future that builds upon the Company’s experiences and reflects its values. This work will lead to the creation of a coherent vision for reconciliation and a roadmap to help guide the Company’s actions as an organization.

__________________________

1.IAMGOLD defines significant incidents as those assessed as Level 4 or 5 based on the Company's risk matrix, and/or resulting in fines greater than US$100,000. The Company's risk matrix includes a consequence matrix to determine incident severity that considers environmental, health and safety, social, and financial aspects.

2.The Truth and Reconciliation Commission of Canada (2015) released its Calls to Action report, which included a call to the Canadian corporate sector to support reconciliation

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

7 |

Social Performance

During the first quarter 2025, IAMGOLD renewed its partnership with Laurentian University, creating the IAMGOLD President’s Fund for Innovation at Canada’s Mining University. This five-year, C$2.5 million fund will allow the university to support initiatives that will drive innovation in education and research at the university, fostering greater engagement with the university and providing solutions to the mining industry.

Equity, Diversity and Inclusion

IAMGOLD includes annual objectives to support its efforts in integrating EDI into the strategy and corporate scorecard, for the annual objectives, and tracks EDI metrics in site and corporate reports for visibility and measurement. As of March 31, 2025, IAMGOLD’s executive leadership group has 40% female representation.

For the third consecutive year, IAMGOLD has been recognized as a Greater Toronto Top Employer for its commitment to inclusion, employee engagement, and workplace culture. The Company has also been honoured for a third consecutive year by the Canadian HR Awards for excellence in the category of Financial, Physical, and Mental Wellness.

Governance

The Board of Directors of IAMGOLD (the “Board”) adopted diversity and renewal guidelines in 2021, reflecting governance best practices. Membership should comprise, at a minimum, the greater of (i) two and (ii) 30% female directors, the average tenure of the Board should not exceed ten years, and no director should serve as the chair of the Board or the chair of any committee for more than ten consecutive years.

Currently, women represent 44% of the directors and 50% of the independent directors. The average tenure of directors on the Board is approximately three years.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

8 |

OPERATIONS

Côté Gold, Canada

The Côté District is located 125 kilometres southwest of Timmins and 175 kilometres north of Sudbury, Ontario, Canada. The mine is being operated through an unincorporated joint venture (the "Côté Gold UJV" or "UJV") between IAMGOLD, as the operator, and Sumitomo Metal Mining Co. Ltd. (“Sumitomo” or “SMM”). On November 30, 2024, the Company repurchased a 9.7% temporarily transferred interest (the “Funding Agreement with Sumitomo”) which returned IAMGOLD to its full 70% interest in the Côté Gold UJV (see “Funding Agreement with Sumitomo” below).

Côté Gold Mine (IAMGOLD interest – 70% for Q1 2025, 60.3% for Q1 2024)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Q1 2025 |

|

Q1 2024 |

|

|

Key Operating Statistics (100% basis, unless otherwise stated) |

|

|

|

|

|

| Ore mined (000s t) |

3,115 |

|

|

1,944 |

|

|

|

| Grade mined (g/t) |

0.78 |

|

|

0.72 |

|

|

|

| Operating waste mined (000s t) |

5,667 |

|

|

3,208 |

|

|

|

| Capital waste mined (000s t) |

1,973 |

|

|

2,445 |

|

|

|

|

|

|

|

|

|

| Material mined (000s t) – total |

10,755 |

|

|

7,597 |

|

|

|

Strip ratio1 |

2.5 |

|

|

2.9 |

|

|

|

| Ore milled (000s t) |

2,097 |

|

|

48 |

|

|

|

| Head grade (g/t) |

1.17 |

|

|

0.81 |

|

|

|

| Recovery (%) |

93 |

|

|

80 |

|

|

|

| Gold production (000s oz) – 100% |

73 |

|

|

1 |

|

|

|

| Gold production (000s oz) – attributable |

51 |

|

|

1 |

|

|

|

| Gold sales (000s oz) – 100% |

74 |

|

|

— |

|

|

|

| Gold sales (000s oz) – attributable |

52 |

|

|

— |

|

|

|

Average realized gold price2,3 ($/oz) |

$ |

2,925 |

|

|

$ |

— |

|

|

|

Financial Results ($ millions – attributable interest) |

|

|

|

|

|

Revenues4 |

$ |

151.2 |

|

|

$ |

— |

|

|

|

Cost of sales4 |

65.2 |

|

|

— |

|

|

|

| Production costs |

56.4 |

|

|

0.8 |

|

|

|

| (Increase)/decrease in finished goods |

(0.8) |

|

|

(0.8) |

|

|

|

Royalties5 |

9.6 |

|

|

— |

|

|

|

Cash costs2 |

65.1 |

|

|

— |

|

|

|

Sustaining capital expenditures2,6 |

18.2 |

|

|

— |

|

|

|

Expansion capital expenditures2,6 |

3.1 |

|

|

118.8 |

|

|

|

Total sustaining and expansion capital expenditures2,6 |

21.3 |

|

|

118.8 |

|

|

|

| Earnings from operations |

49.7 |

|

|

— |

|

|

|

Mine site free cash flow2 |

57.6 |

|

|

— |

|

|

|

Unit costs per tonne2 |

|

|

|

|

|

| Mine costs per operating tonne mined |

$ |

3.49 |

|

|

$ |

3.33 |

|

|

|

Mill costs per tonne milled2 |

$ |

20.18 |

|

|

$ |

— |

|

|

|

G&A costs per tonne milled2 |

$ |

8.89 |

|

|

$ |

— |

|

|

|

Operating costs per ounce7 |

|

|

|

|

|

| Cost of sales excluding depreciation ($/oz sold) |

$ |

1,264 |

|

|

$ |

— |

|

|

|

Cash costs2 ($/oz sold) |

$ |

1,260 |

|

|

$ |

— |

|

|

|

AISC2,7 ($/oz sold) |

$ |

1,643 |

|

|

$ |

— |

|

|

|

1.Strip ratio is calculated as waste mined divided by ore mined.

2.This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

3.Average gold price realized on the attributable portion of sales excludes the impact of gold delivered into prepayment arrangements.

4.As per note 25 of the consolidated interim financial statements for revenues and cost of sales. Cost of sales is net of depreciation expense.

5.Includes 7.5% net profit interest payment.

6.All-in sustaining cost and sustaining capital expenditure for 2024 are $nil as commercial production was achieved starting August 1, 2024. Expansion capital expenditures include Project Expenditures.

7.Cost of sales, cash costs and AISC per ounce sold may not be calculated based on amounts presented in this table due to rounding.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

9 |

Operational Insights

•Attributable gold production was 51,000 ounces (73,000 ounces on a 100% basis) in the first quarter 2025 as the mine continues to ramp-up following the start of production on March 31, 2024. Production was impacted by maintenance and repair activities in the quarter; however, the operation achieved a record monthly throughput of 1.0 million tonnes in March, representing an average monthly processing rate of 90% of design capacity. Subsequent to quarter end, the plant continued to demonstrate good availability and utilization with throughput averaging 34,500 tpd or 96% over the last 30 days.

•Mining activity totaled 10.8 million tonnes in the first quarter 2025, an increase over the prior year period, with ore tonnes mined increasing to 3.1 million tonnes and an associated strip ratio of 2.5:1 waste to ore. The average grade of mined ore was 0.78 g/t in the first quarter 2025, in line with the updated mining schedule, as mining activities expand the pit and increase the volume of blasted ore in the pit to provide greater flexibility in supporting the planned mill feed with reduced rehandling.

•Mill throughput in the first quarter 2025 totaled 2.1 million tonnes. In March 2025, the plant processed approximately 1.0 million tonnes. Total quarterly throughput was lower in January and February due to maintenance and repair activities described below. Head grades of 1.17 g/t were in line with guidance, with feed material comprised of a combination of direct-feed ore and stockpiles. Recoveries in the plant averaged 93% in the quarter. The gravity circuit is now operational. The reconciliation between the reserve models, grade control models and mill feed continues in line with expected tolerances.

•During the quarter, the HPGR rollers demonstrated accelerated wear necessitating a changeover ahead of schedule and limiting the secondary crushing capacity in January. The changeover of the HPGR rolls was completed in February 2025 with operating and maintenance procedures adjusted to maximize lifespan and optimize future changeover windows. Inside the plant, the grinding circuit was also impacted early in the quarter, due to repairs required on one of the Vertimills following a faulty start-up post-maintenance. Prevention and mitigation procedures have been put in place. Plant throughput was lower in the first two months of the quarter as a result of the impact of the timing of these maintenance issues, with record monthly throughput achieved in March following these repairs.

•The target is to achieve the steady-state nameplate throughput rate of 36,000 tonnes per day ("tpd") by the end of 2025.

Financial Highlights (attributable basis) – Q1 2025

•Revenue and cost of sales were recognized in accordance with IAMGOLD's ownership level of 70% for the first quarter 2025, following the November 30, 2024, repurchase of the 9.7% transferred interest from SMM.

•Production costs of $56.4 million were incurred during the three months ended March 31, 2025.

•Mining cost was $3.49 per tonne mined during the three months ended March 31, 2025. Costs are expected to decrease over the course of the year as mining operations continue to ramp-up and rehandling is reduced. The price of explosives and diesel were higher than planned in the quarter, partially offset by lower overall consumption.

•Milling cost was $20.18 per tonne milled during the three months ended March 31, 2025. Unit costs were higher in the first quarter due to lower throughput during the first two months of the quarter, higher parts and contractor costs from the increased maintenance activities and frequency, and costs associated with the refeed circuit to support the mill feed during the periods of sustained maintenance. Unit costs are expected to decrease over the course of the year as throughput increases towards nameplate capacity, and as operations and maintenance processes stabilize. Mill availability is expected to increase with the installation of the additional secondary crusher that should reduce the use of the refeed circuit and related costs.

•G&A cost was $8.89 per tonne milled during the three months ended March 31, 2025. Unit costs remained higher than expected as the average throughput during the quarter was below plan due to the maintenance activities. Unit costs are expected to further decrease as throughput increases over the course of the year.

•Cost of sales, excluding depreciation, during the three months ended March 31, 2025, totaled $65.2 million. Cost of sales includes $9.6 million of royalties and net profit interests for the three months ended March 31, 2025. Cost of sales per ounce sold, excluding depreciation, was $1,264 for the three months ended March 31, 2025.

•Cash costs during the three months ended March 31, 2025, totaled $65.1 million and cash cost per ounce sold was $1,260.

•AISC per ounce sold was $1,643 for the quarter.

•Capital expenditures, on a 100% and incurred basis, totaled $30.2 million in the first quarter 2025. Sustaining capital expenditures totaled $25.8 million ($18.2 million on a 70% basis), including $11.7 million of capital projects related to operational improvements and ramp-up, $7.2 million of capitalized stripping, $3.5 million of tailings expansion and related earthworks, $3.3 million of mobile equipment and critical spares and $0.1 million of other capital projects. Expansion capital of $4.4 million ($3.1 million on a 70% basis) was primarily associated with the progress on the additional secondary crusher being installed later in the year and completion of the truck shop expansion.

2025 Outlook

Production at Côté Gold is expected to be in the range of 360,000 to 400,000 ounces on a 100% basis (250,000 to 280,000 ounces on an attributable basis). The primary focus continues to be the ramp-up of the processing plant towards the goal of achieving nameplate mill design capacity of 36,000 tpd by the end of the year.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

10 |

Mining activities are expected to increase throughout the year, averaging approximately 12 million tonnes in the fourth quarter, with a declining strip ratio throughout the year as ore mined increases. Plant throughput is expected to total approximately 11 to 12 million tonnes in 2025 with processing rates expected to increase quarter over quarter, particularly in the second quarter, following the winter season and first quarter maintenance, and in the fourth quarter with the installation of the additional secondary crusher. The additional secondary crusher will provide further capacity and redundancy in the dry side of the plant in support of the operation and potential future expansions. The installation of the crusher will require a multi-day shutdown in the fourth quarter, which is accounted for in current guidance estimates. Plant head grades are expected to average approximately 1.1 to 1.2 g/t Au, as mining and stockpiling activities shift towards a more efficient mine plan to reduce rehandling of stockpiled ore and optimized for potential future expansions. Gold production is expected to be lowest in the first quarter of the year and increase sequentially as plant throughput increases throughout the year.

Cash costs are expected to be in the range of $950 to $1,100 per ounce sold and AISC to be in the range of $1,350 to $1,500 per ounce sold. The cash cost guidance reflects the cost levels experienced in the first year of operations, including higher levels of maintenance, contractor support and continuous improvement consultants. Costs are expected to be lower in the second half of the year as targeted improvements are deployed and as production increases.

Sustaining capital expenditures guidance (±5%) attributable to IAMGOLD is approximately $110 million ($157 million on a 100% basis) and continues to be higher than the life-of-mine average as the mine progresses the completion of construction of the full tailings dam footprint and related earthworks projects and incurs higher capital waste spending of approximately $20 million ($28 million on a 100% basis) to complete the final year of the initial pit pushback. Expansion capital of $15 million ($21 million on a 100% basis) is primarily associated with the planned installation of the additional secondary crusher in the fourth quarter of this year.

Exploration

The Gosselin zone is located immediately to the northeast of the Côté zone. Following the expansion and delineation diamond drilling program completed in 2024, the 2025 drilling plan entails the continuation of the ongoing diamond drilling program to increase the confidence of the existing resource and convert a large part of the Inferred Resource category to the Indicated category. A total of 45,000 metres is planned and approximately 12,000 metres were completed in the first quarter. In addition, 6,500 metres is planned this year to test high potential targets along the favourable structural corridor towards the Jack Rabbit area to the north-east of the Gosselin zone and develop models and targets within the larger Côté District at Swayze West - Jerome area.

Technical studies are progressing to advance metallurgical testing, conduct mining and infrastructure studies to review options for potential inclusion of the Gosselin deposit into a future Côté Gold LOM plan.

Côté Zone Drilling

An infill drilling program of 20,000 metres is also planned on the Côté zone and will start early in the second quarter of 2025. This infill drilling program is planned to improve resource confidence within the northeastern extension of the Côté deposit and convert other areas of Inferred Resources into the Indicated Resources category.

Funding Agreement with Sumitomo

On December 19, 2022, the Company announced it had entered into the JV Funding and Amending Agreement with SMM (“JV Funding Agreement”), whereby SMM contributed the Company's funding obligations to the Côté Gold UJV and as a result, the Company transferred 9.7% of its interest in Côté Gold to SMM with a right to repurchase these transferred interests to return to its full 70% interest in the Côté Gold Mine.

On November 30, 2024, the Company exercised its right to repurchase the 9.7% interest in Côté Gold returning IAMGOLD to its full 70% interest in Côté Gold.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

11 |

Westwood Complex, Canada

The Westwood Complex is located 35 kilometres northeast of Rouyn-Noranda and 80 kilometres west of Val d'Or in southwestern Québec, Canada. The Westwood Complex includes the Westwood underground mine and the Grand Duc open pit mine.

Westwood Complex (IAMGOLD interest – 100%)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Q1 2025 |

Q1 2024 |

|

|

|

| Key Operating Statistics |

|

|

|

|

|

| Underground lateral development (metres) |

1,147 |

|

1,307 |

|

|

|

| Ore mined (000s t) – underground |

89 |

|

83 |

|

|

|

|

| Ore mined (000s t) – open pit |

192 |

|

120 |

|

|

|

|

| Ore mined (000s t) – total |

281 |

|

203 |

|

|

|

|

| Grade mined (g/t) – underground |

6.29 |

|

8.90 |

|

|

|

|

| Grade mined (g/t) – open pit |

1.31 |

|

2.28 |

|

|

|

|

| Grade mined (g/t) – total |

2.89 |

|

5.00 |

|

|

|

|

| Ore milled (000s t) |

282 |

|

249 |

|

|

|

|

| Head grade (g/t) – underground |

6.28 |

|

8.78 |

|

|

|

|

| Head grade (g/t) – open pit |

1.37 |

|

2.21 |

|

|

|

|

| Head grade (g/t) – total |

2.89 |

|

4.27 |

|

|

|

|

| Recovery (%) |

91 |

|

94 |

|

|

|

|

| Gold production (000s oz) |

24 |

|

32 |

|

|

|

|

| Gold sales (000s oz) |

27 |

|

33 |

|

|

|

|

Average realized gold price1,2 ($/oz) |

$ |

2,914 |

|

$ |

2,088 |

|

|

|

|

Financial Results ($ millions) |

|

|

|

|

|

Revenues3 |

$ |

79.8 |

|

$ |

68.9 |

|

|

|

|

Cost of sales3 |

42.1 |

|

40.9 |

|

|

|

|

| Production costs |

41.0 |

|

38.6 |

|

|

|

|

| (Increase)/decrease in finished goods |

1.1 |

|

2.0 |

|

|

|

|

| Royalties |

— |

|

0.3 |

|

|

|

|

Cash costs1 |

41.6 |

|

40.7 |

|

|

|

|

Sustaining capital expenditures1 |

15.1 |

|

19.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Earnings/(loss) from operations |

21.1 |

|

16.1 |

|

|

|

|

Mine site free cash flow1 |

16.6 |

|

10.5 |

|

|

|

|

Unit costs per tonne1 |

|

|

|

|

|

| Underground mining cost per tonne mined |

$ |

274.75 |

|

$ |

247.22 |

|

|

|

|

| Open pit mining cost per operating tonne mined |

$ |

7.24 |

|

$ |

13.29 |

|

|

|

|

| Milling cost per tonne milled |

$ |

23.26 |

|

$ |

24.65 |

|

|

|

|

| G&A cost per tonne milled |

$ |

22.70 |

|

$ |

20.56 |

|

|

|

|

Operating costs per ounce4 |

|

|

|

|

|

| Cost of sales excluding depreciation ($/oz sold) |

$ |

1,547 |

|

$ |

1,243 |

|

|

|

|

Cash costs1 ($/oz sold) |

$ |

1,527 |

|

$ |

1,236 |

|

|

|

|

AISC1 ($/oz sold) |

$ |

2,124 |

|

$ |

1,836 |

|

|

|

|

1.This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

2.Average realized gold price excludes the impact of gold delivered into prepayment arrangements.

3.As per note 25 of the consolidated interim financial statements for revenues and cost of sales. Cost of sales is net of depreciation expense.

4.Cost of sales, cash costs and AISC per ounce sold may not be calculated based on amounts presented in this table due to rounding.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

12 |

Operational Insights

•Production in the first quarter 2025 was 24,000 ounces, lower by 8,000 ounces or 25% compared with the same prior year period, primarily due to lower grades from both the underground and open pit mines.

•Mining activity in the first quarter 2025 of 281,000 tonnes of ore was higher by 78,000 tonnes or 38% from the same prior year period. The underground mine averaged 987 tpd as production from the underground operation continued to increase compared to the prior year, with eight active mining zones in the quarter. Grade mined from the underground mine was lower than the prior year period due to temporary equipment challenges impacting blasting efficiency that required stope re- sequencing, combined with increased dilution in certain stopes. The amount of stopes that are drilled and loaded have doubled over the last year.

•Lateral underground development of 1,147 metres in the first quarter 2025 was lower by 160 metres or 12% compared to the same prior year period, as the mine has successfully developed multiple mining zones in the prior periods.

•Mill throughput in the first quarter 2025 was 282,000 tonnes, at an average head grade of 2.89 g/t, 13% higher and 32% lower than the same prior year period, respectively.

•The mill achieved recoveries of 91% in the first quarter 2025, slightly lower than the same prior year period. Plant availability in the quarter of 94% was higher than the same prior year period of 85%.

Financial Performance – Q1 2025 Compared to Q1 2024

•Production costs of $41.0 million were higher by $2.4 million or 6% than the same prior year period primarily due to increased labour costs, increased explosives and tire costs at the mine, as well as increased rental cost of a mobile ore crusher supporting higher mill throughput. Administration costs increased due to consulting support for decarbonization initiatives, and increased insurance costs resulting from a higher insurable baseline revenue expectation for Westwood.

•Cost of sales, excluding depreciation, of $42.1 million was slightly higher than the same prior year period due to higher production costs. Cost of sales per ounce sold, excluding depreciation, of $1,547, was higher by $304 or 24% primarily due to lower production and sales volumes.

•Cash costs of $41.6 million were $0.9 million or 2% higher than the prior year period. Cash costs per ounce sold of $1,527 were higher by $291 or 24%, primarily due to lower production and sales volumes.

•AISC per ounce sold of $2,124 was higher by $288 or 16%, primarily due to higher cash costs per ounce sold and lower production and sales volumes, partially offset by lower sustaining capital.

•Sustaining capital expenditures of $15.1 million included underground development and rehabilitation of $8.9 million, mill and mobile equipment of $3.0 million, and other sustaining capital projects of $3.2 million.

2025 Outlook

Westwood production is expected to be in the range of 125,000 to 140,000 ounces in 2025, as underground mining rates target 1,000 tpd from multiple active mining zones. Underground throughput and grade is expected to increase from the first quarter through underground process improvements. Open pit activities from Grand Duc are currently planned to be completed by the fourth quarter of 2025, though Grand Duc stockpiled material will contribute to the mill feed into 2027. The Company is investigating the potential for an expansion and extension of the pit, with a decision to be made later in the year.

Cash costs at Westwood are expected to be in the range of $1,175 to $1,325 per ounce sold and AISC in the range of $1,675 to $1,825 per ounce sold. Unit costs are expected to decrease from 2024 levels, in line with increased production levels.

Capital expenditures guidance is $70 million (±5%), primarily consisting of underground development and rehabilitation in support of the 2025 mine plan, the continued renewal of the mobile fleet and equipment overhauls, and certain asset integrity projects at the Westwood mill.

Brownfield Exploration

During the three months ended March 31, 2025, approximately 7,300 metres of underground diamond drilling (including approximately 800 metres of geotechnical drilling) were completed to support the continued ramp-up of underground mining operations.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

13 |

Essakane, Burkina Faso

The Essakane District is located in north-eastern Burkina Faso, West Africa approximately 330 km northeast of the capital, Ouagadougou. The Essakane District includes the Essakane Mine and the surrounding mining lease and exploration concessions totaling approximately 600 square kilometres. The Company owns a 90% interest in the Essakane mine with the remaining 10% held by the government of Burkina Faso.

Essakane Mine (IAMGOLD interest – 90%)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Q1 2025 |

Q1 2024 |

|

|

|

Key Operating Statistics1 |

|

|

|

|

|

| Ore mined (000s t) |

2,447 |

|

3,458 |

|

|

|

|

| Grade mined (g/t) |

1.21 |

|

1.54 |

|

|

|

|

| Operating waste mined (000s t) |

5,667 |

|

3,132 |

|

|

|

|

| Capital waste mined (000s t) |

2,747 |

|

4,750 |

|

|

|

|

|

|

|

|

|

|

| Material mined (000s t) – total |

10,861 |

|

11,340 |

|

|

|

|

Strip ratio2 |

3.4 |

|

2.3 |

|

|

|

|

| Ore milled (000s t) |

3,112 |

|

3,039 |

|

|

|

|

| Head grade (g/t) |

1.08 |

|

1.52 |

|

|

|

|

| Recovery (%) |

88 |

|

89 |

|

|

|

|

| Gold production (000s oz) – 100% |

95 |

|

131 |

|

|

|

|

| Gold production (000s oz) – attributable 90% |

86 |

|

118 |

|

|

|

|

| Gold sales (000s oz) – 100% |

95 |

|

130 |

|

|

|

|

Average realized gold price3,4 ($/oz) |

$ |

2,898 |

|

$ |

2,092 |

|

|

|

|

Financial Results ($ millions)1 |

|

|

|

|

|

Revenues5 |

$ |

276.9 |

|

$ |

272.3 |

|

|

|

|

Cost of sales5 |

148.9 |

|

130.5 |

|

|

|

|

| Production costs |

127.7 |

|

110.9 |

|

|

|

|

| (Increase)/decrease in finished goods |

1.8 |

|

1.3 |

|

|

|

|

| Royalties |

19.4 |

|

18.3 |

|

|

|

|

Cash costs3 |

148.6 |

|

130.2 |

|

|

|

|

Sustaining capital expenditures3 |

27.9 |

|

36.0 |

|

|

|

|

Expansion capital expenditures3 |

2.2 |

|

0.5 |

|

|

|

|

Total sustaining and expansion capital expenditures3 |

30.1 |

|

36.5 |

|

|

|

|

| Earnings from operations |

94.8 |

|

91.5 |

|

|

|

|

Mine site free cash flow3 |

65.4 |

|

35.7 |

|

|

|

|

Unit costs per tonne3 |

|

|

|

|

|

| Open pit mining cost per operating tonne mined |

$ |

5.57 |

|

$ |

5.48 |

|

|

|

|

| Milling cost per tonne milled |

$ |

17.56 |

|

$ |

18.23 |

|

|

|

|

| G&A cost per tonne milled |

$ |

10.28 |

|

$ |

9.08 |

|

|

|

|

Operating costs per ounce6 |

|

|

|

|

|

| Cost of sales excluding depreciation ($/oz sold) |

$ |

1,560 |

|

$ |

1,004 |

|

|

|

|

Cash costs3 ($/oz sold) |

$ |

1,557 |

|

$ |

1,002 |

|

|

|

|

AISC3 ($/oz sold) |

$ |

1,846 |

|

$ |

1,312 |

|

|

|

|

1.100% basis, unless otherwise stated.

2.Strip ratio is calculated as waste mined divided by ore mined.

3.This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

4.Average realized gold price excludes the impact of gold delivered into prepayment arrangements.

5.As per note 25 of the consolidated interim financial statements for revenues and cost of sales. Cost of sales is net of depreciation expense.

6.Cost of sales, cash costs and AISC per ounce sold may not be calculated based on amounts presented in this table due to rounding.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

14 |

Operational Insights

•Essakane produced 86,000 ounces of attributable production, a decrease of 32,000 ounces or 27%, compared to the same prior year period, primarily due to a decrease in the grade as the mining activities sequenced through the upper benches of Phase 7 compared to the same prior year period when the mine was mining at the bottom of Phase 5. Grades tend to reconcile slightly below the reserve model during the earlier stages of mining a new phase, and conversely to the positive as mining moves deeper into a phase, as was experienced in the first half of 2024 when mining activities were on the later stages of phase 5.

•Mining activity totaled 10.9 million tonnes mined in the first quarter 2025, lower by 0.5 million tonnes or 4% compared to the same prior year period.

•Mill throughput in the first quarter 2025 was 3.1 million tonnes at an average head grade of 1.08 g/t, 2% higher and 29% lower than the same prior year period, respectively.

•The security situation in Burkina Faso continues to be a focus for the Company. Security-related incidents are still occurring in the country, the immediate region of the Essakane mine and, more broadly, the West African region. The security situation in Burkina Faso and its neighboring countries continues to apply pressures to supply chains, although with a reduced impact and there was no related business interruption during 2024 and the first quarter 2025. The Company continues to take proactive measures to ensure the safety and security of in-country personnel and is constantly adjusting its protocols and the activity levels at the site according to the security environment. The Company continues to invest in the security and supply chain infrastructure in the region and at the mine site. It is also incurring additional costs to bring employees, contractors, supplies and inventory to the mine. The situation has placed the Government of Burkina Faso under significant financial constraint due to the high cost of funding its initiatives to defend itself against the militant attacks (see “Risks and Uncertainties”).

Financial Performance – Q1 2025 Compared to Q1 2024

•Production costs of $127.7 million were higher by $16.8 million or 15%, resulting from higher expensed mining costs primarily due to a lower proportion of capitalized waste in the period, higher maintenance activities, and slightly higher administrative costs, offset by lower realized consumable costs including diesel, grinding media and cyanide.

•Cost of sales, excluding depreciation, of $148.9 million was higher by $18.4 million or 14% primarily due to higher production costs and higher royalties. Cost of sales per ounce sold, excluding depreciation, of $1,560 was higher by $556 or 55% primarily due to lower production and sales volumes and higher royalties. Royalties were $203 per ounce, an increase of $62 per ounce due to higher realized gold prices, partially offset by lower sales volume.

•Cash costs of $148.6 million were higher by $18.4 million or 14%, primarily due to higher cost of sales and higher royalties. Cash costs per ounce sold of $1,557 were higher by $555 or 55%, primarily due to lower production and sales volumes and higher royalties.

•AISC per ounce sold of $1,846 was higher by $534 or 41% primarily due to lower production and sales volumes, partially offset by a decrease in sustaining capital expenditures compared to the prior period.

•Total capitalized stripping of $14.4 million was lower by $11.3 million or 44%, as the mine fleet sequenced through mining phases with higher life of phase strip ratios, resulting in a higher proportion of waste tonnes classified as operating waste consistent with the 2025 mine plan.

•Sustaining capital expenditures, excluding capitalized stripping, of $13.5 million included capital spares of $5.5 million, resource development of $1.9 million, tailings management of $1.6 million, generator overhaul of $0.9 million, mobile and mill equipment of $0.4 million, and other sustaining projects of $3.2 million. Expansion capital expenditures of $2.2 million were incurred in fulfillment of the community village resettlement commitment.

2025 Outlook

Essakane attributable production is expected to be in the range of 360,000 to 400,000 ounces (400,000 to 440,000 ounces at 100%). The mill is expected to operate at throughput and head grades in line with the current life of mine plan (detailed in the December 2023 43-101 Technical Report), though as mining moves into the primary zones of Phase 6 and 7 in the second half of the year, grades are expected to reconcile positively over this period.

Cash costs at Essakane are expected to be in the range of $1,400 to $1,550 per ounce sold and AISC to be in the range of $1,675 to $1,825 per ounce sold. The cost guidance for 2025 is higher than the 2024 cost guidance ranges due to lower production and higher local spending including regional security expenditures, increased community programs, permit fees and taxes. A decrease in capitalized waste mining is expected to result in a lower proportion of waste stripping costs being capitalized in 2025 and therefore a higher proportion of costs included in cash costs.

Capital expenditures guidance is approximately $115 million (±5%), including approximately $40 million on capitalized waste stripping to progress into Phases 6 and 7, as well as the ongoing replacement of certain equipment to improve efficiency and maintenance costs at Essakane.

Continued security incidents or related concerns could have a material adverse impact on future operating performance. The Company continues to actively work with authorities and suppliers to mitigate potential impacts and manage continuity of supply due to the security situation noted above while also investing in additional infrastructure and supply inventory levels appropriate to secure operational continuity (see "Risks and Uncertainties").

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

15 |

Brownfield Exploration

During the three months ended March 31, 2025, approximately 7,750 metres of diamond drilling were completed as part of a step-out and infill drilling program to extend known mineralization and improve resource confidence within selected areas of Essakane North, Essakane Main Zone and the Lao satellite deposit and southern extension. The deposits remain open along strike and at depth. Exploration activities on concessions surrounding the mine lease continue to be suspended due to regional security constraints.

Other Projects

Chibougamau District, Canada

The Chibougamau District includes the Nelligan Gold Project, the Monster Lake Project and the Anik Gold Project.

Nelligan Gold Project

The Company holds a 100% interest in the Nelligan Gold Project ("Nelligan") located approximately 45 kilometres south of the Chapais Chibougamau area in Québec.

On February 20, 2025, the Company announced its updated Mineral Resources for the Nelligan Project of 3.1 million Indicated gold ounces in 102.8 million tonnes (“Mt”) at 0.95 grams per tonne gold (“g/t Au”), and 5.2 million Inferred ounces (166.4 Mt at 0.96 g/t Au). This represents a 56% increase in Indicated ounces, or 1.1 million ounces, with an accompanying 13% increase in grade; as well as a 33% increase in Inferred ounces, or 1.3 million ounces, with a similar 14% increase in grade. Nelligan mineralization remains open along strike and at depth.

A diamond drilling program of 13,000 metres of expansion and delineation drilling is planned for 2025, of which approximately 8,000 metres were completed in the first quarter 2025.

Monster Lake Gold Project

The Company holds a 100% interest in the Monster Lake Gold Project, which is located approximately 15 kilometres north of the Nelligan Gold Project in the Chapais Chibougamau area in Québec.

In the fourth quarter 2024, the Company reported an updated Mineral Resource Estimate of 239,000 tonnes of Indicated Mineral Resources averaging 11.0 g/t Au for 84,000 ounces of gold, and 1,053,000 tonnes of Inferred Mineral Resources averaging 14.4 g/t Au for 489,000 ounces of gold (see news release dated October 23, 2024).

A diamond drilling program of 17,000 metres of exploration drilling is planned for 2025 and approximately 6,300 metres were completed in the first quarter 2025, testing exploration targets along the main Monster Lake Shear Zone structural corridor and known gold mineralized lateral and depth extensions.

Anik Gold Project

The Anik Gold Project is wholly owned by Kintavar Exploration Inc. (“Kintavar”) and is contiguous with Nelligan to the north and east. IAMGOLD has entered into an option agreement on May 20, 2020, to acquire 80% of the interests in this project.

A diamond drilling program of 1,800 metres was planned for 2025 and was slightly increased to approximately 2,100 metres which were completed in the first quarter 2025, testing different target areas.

Exploration

In the first quarter 2025, drilling activities on active projects and mine sites totaled approximately 43,500 metres. For additional information regarding the brownfield and greenfield exploration projects, see "Operations". The Company's exploration expenditures guidance for 2025 is $38 million.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ($ millions) |

Q1 2025 |

Q1 2024 |

|

|

|

| Exploration projects – greenfield |

$ |

5.7 |

|

$ |

4.0 |

|

|

|

|

Exploration projects – brownfield1 |

2.5 |

|

2.1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total – all operations |

$ |

8.2 |

|

$ |

6.1 |

|

|

|

|

1.Exploration projects – brownfield for the first quarter 2025 included near-mine exploration and resource development of $1.9 million (first quarter 2024 - $1.2 million) which are capitalized.

FINANCIAL CONDITION

Liquidity and Capital Resources

As at March 31, 2025, the Company had $316.6 million in cash and cash equivalents and net debt of $882.3 million. The Company has $210.0 million drawn on the Credit Facility and approximately $428.5 million remains available, resulting in liquidity at March 31, 2025, of approximately $745.8 million.

Within cash and cash equivalents, $46.9 million (70% basis) was held by the Côté Gold UJV, $200.2 million was held by Essakane and $60.6 million was held in the corporate treasury. The Côté Gold UJV requires its joint venture partners to fund, in advance, two months of future expenditures and cash calls are made at the beginning of each month, resulting in the month end cash balance approximating the following month's expenditure.

|

|

|

|

|

|

|

IAMGOLD CORPORATION

First Quarter 2025 Management's Discussion and Analysis

|

16 |

The Company uses dividends and intercompany loans to repatriate funds from its operations and the timing of dividends may impact the timing and amount of required financing at the corporate level, including the Company's drawdowns under the Credit Facility. Excess cash at Essakane is mainly repatriated through dividend payments, of which the Company will receive its share based on its ownership, net of dividend taxes. The size of the dividend is dependent on cash held and the projected cash generation at Essakane. There is a risk that the Company may not receive full or partial refunds or be able to sell the outstanding VAT balances during 2025 which would impact the cash available for dividends paid during 2025 and future years (see “Risks and Uncertainties”).

On February 5, 2025, the Company concluded the disposition of its interest in the Yatela mine, initiated in 2019, by way of issuing the final closure payment of $18.2 million releasing the Company of all obligations.