| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

| Title of each class | Trading symbols | Name of each exchange on which registered | ||||||||||||

| American Depositary Shares | ING | New York Stock Exchange | ||||||||||||

| Ordinary shares | New York Stock Exchange(i) |

|||||||||||||

| 3.950% Fixed Rate Senior Notes due 2027 | ING27 | New York Stock Exchange | ||||||||||||

| 4.550% Fixed Rate Senior Notes due 2028 | ING28 | New York Stock Exchange | ||||||||||||

| 4.050% Fixed Rate Senior Notes due 2029 | ING29 | New York Stock Exchange | ||||||||||||

| 1.726% Callable Fixed-to-Floating Rate Senior Notes due 2027 | ING27A | New York Stock Exchange | ||||||||||||

| 2.727% Callable Fixed-to-Floating Rate Senior Notes due 2032 | ING32 | New York Stock Exchange | ||||||||||||

| Callable Floating Rate Senior Notes due 2027 | ING27B |

New York Stock Exchange | ||||||||||||

| 4.017% Callable Fixed-to-Floating Rate Senior Notes due 2028 | ING28A | New York Stock Exchange | ||||||||||||

| 3.869% Callable Fixed-to-Floating Rate Senior Notes due 2026 | ING26 | New York Stock Exchange | ||||||||||||

| 4.252% Callable Fixed-to-Floating Rate Senior Notes due 2033 | ING33 | New York Stock Exchange | ||||||||||||

| Callable Floating Rate Senior Notes due 2026 | ING26A | New York Stock Exchange | ||||||||||||

| 6.083% Callable Fixed-to-Floating Rate Senior Notes due 2027 | ING27C | New York Stock Exchange | ||||||||||||

| $500,000,000 Callable Floating Rate Senior Notes due 2027 | ING27D | New York Stock Exchange | ||||||||||||

| $1,250,000,000 6.114% Callable Fixed-to-Floating Rate Senior Notes due 2034 | ING34 | New York Stock Exchange | ||||||||||||

| 5.335% Callable Fixed-to-Floating Rate Senior Notes due 2030 | ING30 | New York Stock Exchange | ||||||||||||

| 5.550% Callable Fixed-to-Floating Rate Senior Notes due 2035 | ING35 | New York Stock Exchange | ||||||||||||

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. | ||||

| U.S. GAAP☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ |

Other ☐ | ||||||||||||

ING Groep N.V. Bijlmerdreef 106 1102 CT Amsterdam P.O. Box 1800, 1000 BV Amsterdam The Netherlands | ||

| Telephone +31 20 563 9111 | ||

|

ING Financial Holdings Corporation

1133 Avenue of the Americas New York, NY 10036 United States of America

| ||

| Telephone +1 646 424 6000 | ||

| Our values and behaviours | Main ING policies and procedures |

|||||||||||||

| Business Conduct Framework | ||||||||||||||

The Orange Code is a manifesto that describes our way of working. It is comprised of our values and behaviours |

Orange Code |

ING Global Code

of Conduct

|

Whistleblower Policy | |||||||||||

| Global Investigations Charter | ||||||||||||||

Zero tolerance on corruption and bribery |

Anti-bribery and Corruption Policy | ABC High-Risk Roles Guidance | Global Event Management Procedure | |||||||||||

Values |

Behaviours |

||||

We are honest |

You take it on and make it happen. | ||||

We are prudent |

You help others to be successful. | ||||

We are responsible |

You are always a step ahead. | ||||

| Total operations | |||||||||||||||||||||||

|

1 January to 31 December 2024

in EUR million

|

Retail Banking Netherlands |

Retail Banking Belgium |

Retail Banking Germany |

Retail Other |

Wholesale Banking |

Corporate Line |

Total | ||||||||||||||||

| Income: | |||||||||||||||||||||||

| - Net interest income | 3,027 | 1,959 | 2,647 | 3,817 | 3,259 | 315 | 15,023 | ||||||||||||||||

| - Net fee and commission income | 1,049 | 603 | 433 | 609 | 1,317 | -3 | 4,008 | ||||||||||||||||

| - Total investment and other income | 835 | 189 | -173 | 263 | 2,405 | 66 | 3,584 | ||||||||||||||||

| Total income | 4,910 | 2,751 | 2,906 | 4,688 | 6,981 | 378 | 22,615 | ||||||||||||||||

| Expenditure: | |||||||||||||||||||||||

| - Operating expenses | 2,124 | 1,811 | 1,303 | 2,792 | 3,558 | 533 | 12,121 | ||||||||||||||||

| - Additions to loan loss provision | -8 | 134 | 149 | 291 | 627 | 1 | 1,194 | ||||||||||||||||

| Total expenditure | 2,117 | 1,944 | 1,452 | 3,083 | 4,185 | 534 | 13,315 | ||||||||||||||||

| Result before taxation | 2,793 | 807 | 1,455 | 1,605 | 2,796 | -156 | 9,300 | ||||||||||||||||

| Taxation | 723 | 210 | 505 | 381 | 693 | 138 | 2,650 | ||||||||||||||||

| Non-controlling interests | 1 | 221 | 35 | 258 | |||||||||||||||||||

| Net result IFRS-EU | 2,070 | 597 | 949 | 1,002 | 2,068 | -294 | 6,392 | ||||||||||||||||

| Adjustment of the EU 'IAS 39 carve-out' | -1,058 | -1,058 | |||||||||||||||||||||

| Net result IFRS-IASB | 2,070 | 597 | 949 | 1,002 | 1,010 | -294 | 5,334 | ||||||||||||||||

| Total operations | |||||||||||||||||||||||

|

1 January to 31 December 2023

in EUR million

|

Retail Banking Netherlands |

Retail Banking Belgium |

Retail Banking Germany |

Retail Other |

Wholesale Banking |

Corporate Line |

Total | ||||||||||||||||

| Income: | |||||||||||||||||||||||

| - Net interest income | 3,096 | 2,063 | 2,862 | 3,437 | 4,028 | 489 | 15,976 | ||||||||||||||||

| - Net fee and commission income | 959 | 502 | 357 | 519 | 1,259 | -1 | 3,595 | ||||||||||||||||

| - Total investment and other income | 945 | 117 | -67 | 277 | 1,771 | -38 | 3,005 | ||||||||||||||||

| Total income | 5,001 | 2,683 | 3,152 | 4,233 | 7,057 | 450 | 22,575 | ||||||||||||||||

| Expenditure: | |||||||||||||||||||||||

| - Operating expenses | 2,135 | 1,852 | 1,243 | 2,479 | 3,313 | 542 | 11,564 | ||||||||||||||||

| - Additions to loan loss provision | 5 | 169 | 119 | 313 | -92 | 5 | 520 | ||||||||||||||||

| Total expenditure | 2,140 | 2,022 | 1,362 | 2,792 | 3,222 | 547 | 12,084 | ||||||||||||||||

| Result before taxation | 2,861 | 661 | 1,790 | 1,441 | 3,836 | -97 | 10,492 | ||||||||||||||||

| Taxation | 740 | 182 | 631 | 359 | 900 | 158 | 2,970 | ||||||||||||||||

| Non-controlling interests | 174 | 61 | 235 | ||||||||||||||||||||

| Net result IFRS-EU | 2,121 | 479 | 1,159 | 908 | 2,875 | -255 | 7,287 | ||||||||||||||||

| Adjustment of the EU 'IAS 39 carve-out' | -3,147 | -3,147 | |||||||||||||||||||||

| Net result IFRS-IASB | 2,121 | 479 | 1,159 | 908 | -272 | -255 | 4,140 | ||||||||||||||||

| Total operations | |||||||||||||||||||||||

|

1 January to 31 December 2022

in EUR million

|

Retail Banking Netherlands |

Retail Banking Belgium |

Retail Banking Germany |

Retail Other |

Wholesale Banking |

Corporate Line |

Total | ||||||||||||||||

| Income: | |||||||||||||||||||||||

| - Net interest income | 2,888 | 1,668 | 1,666 | 2,725 | 4,260 | 550 | 13,756 | ||||||||||||||||

| - Net fee and commission income | 892 | 511 | 437 | 535 | 1,217 | -6 | 3,586 | ||||||||||||||||

| - Total investment and other income | 417 | -32 | 69 | 377 | 849 | -460 | 1,219 | ||||||||||||||||

| Total income | 4,196 | 2,147 | 2,172 | 3,637 | 6,325 | 84 | 18,561 | ||||||||||||||||

| Expenditure: | |||||||||||||||||||||||

| - Operating expenses | 2,115 | 1,786 | 1,140 | 2,509 | 3,114 | 535 | 11,199 | ||||||||||||||||

| - Additions to loan loss provision | 67 | 139 | 131 | 302 | 1,220 | 2 | 1,861 | ||||||||||||||||

| Total expenditure | 2,182 | 1,924 | 1,271 | 2,812 | 4,334 | 537 | 13,060 | ||||||||||||||||

| Result before taxation | 2,014 | 223 | 901 | 825 | 1,991 | -453 | 5,502 | ||||||||||||||||

| Taxation | 540 | 72 | 202 | 254 | 581 | 76 | 1,725 | ||||||||||||||||

| Non-controlling interests | 3 | 47 | 52 | 1 | 102 | ||||||||||||||||||

| Net result IFRS-EU | 1,474 | 151 | 696 | 525 | 1,358 | -530 | 3,674 | ||||||||||||||||

| Adjustment of the EU 'IAS 39 carve-out' | 8,451 | 8,451 | |||||||||||||||||||||

| Net result IFRS-IASB | 1,474 | 151 | 696 | 525 | 9,810 | -530 | 12,126 | ||||||||||||||||

| Retail Netherlands | |||||||||||

| in EUR million | 2024 | 2023 | 2022 | ||||||||

| Income: | |||||||||||

| Net interest income | 3,027 | 3,096 | 2,888 | ||||||||

| Net fee and commission income | 1,049 | 959 | 892 | ||||||||

| Investment income and other income | 835 | 945 | 417 | ||||||||

| Total income | 4,910 | 5,001 | 4,196 | ||||||||

| Expenditure: | |||||||||||

| Operating expenses | 2,124 | 2,135 | 2,115 | ||||||||

| Additions to the provision for loan losses | -8 | 5 | 67 | ||||||||

| Total expenditure | 2,117 | 2,140 | 2,182 | ||||||||

| Result before tax | 2,793 | 2,861 | 2,014 | ||||||||

| Taxation | 723 | 740 | 540 | ||||||||

| Non-controlling interests | 0 | 0 | 0 | ||||||||

| Net result IFRS-IASB | 2,070 | 2,121 | 1,474 | ||||||||

| Retail Belgium | |||||||||||

| in EUR million | 2024 | 2023 | 2022 | ||||||||

| Income: | |||||||||||

| Net interest income | 1,959 | 2,063 | 1,668 | ||||||||

| Net fee and commission income | 603 | 502 | 511 | ||||||||

| Investment income and other income | 189 | 117 | -32 | ||||||||

| Total income | 2,751 | 2,683 | 2,147 | ||||||||

| Expenditure: | |||||||||||

| Operating expenses | 1,811 | 1,852 | 1,786 | ||||||||

| Additions to the provision for loan losses | 134 | 169 | 139 | ||||||||

| Total expenditure | 1,944 | 2,022 | 1,924 | ||||||||

| Result before tax | 807 | 661 | 223 | ||||||||

| Taxation | 210 | 182 | 72 | ||||||||

| Net result IFRS-IASB | 597 | 479 | 151 | ||||||||

| Retail Germany | |||||||||||

| in EUR million | 2024 | 2023 | 2022 | ||||||||

| Income: | |||||||||||

| Net interest income | 2,647 | 2,862 | 1,666 | ||||||||

| Net fee and commission income | 433 | 357 | 437 | ||||||||

| Investment income and other income | -173 | -67 | 69 | ||||||||

| Total income | 2,906 | 3,152 | 2,172 | ||||||||

| Expenditure: | |||||||||||

| Operating expenses | 1,303 | 1,243 | 1,140 | ||||||||

| Additions to the provision for loan losses | 149 | 119 | 131 | ||||||||

| Total expenditure | 1,452 | 1,362 | 1,271 | ||||||||

| Result before tax | 1,455 | 1,790 | 901 | ||||||||

| Taxation | 505 | 631 | 202 | ||||||||

| Non-controlling interests | 1 | 0 | 3 | ||||||||

| Net result IFRS-IASB | 949 | 1,159 | 696 | ||||||||

| Retail Other | |||||||||||

| in EUR million | 2024 | 2023 | 2022 | ||||||||

| Income: | |||||||||||

| Net interest income | 3,817 | 3,437 | 2,725 | ||||||||

| Net fee and commission income | 609 | 519 | 535 | ||||||||

| Investment income and other income | 263 | 277 | 377 | ||||||||

| Total income | 4,688 | 4,233 | 3,637 | ||||||||

| Expenditure: | |||||||||||

| Operating expenses | 2,792 | 2,479 | 2,509 | ||||||||

| Additions to the provision for loan losses | 291 | 313 | 302 | ||||||||

| Total expenditure | 3,083 | 2,792 | 2,812 | ||||||||

| Result before tax | 1,605 | 1,441 | 825 | ||||||||

| Taxation | 381 | 359 | 254 | ||||||||

| Non-controlling interests | 221 | 174 | 47 | ||||||||

| Net result IFRS-IASB | 1,002 | 908 | 525 | ||||||||

| Wholesale Banking | |||||||||||

| in EUR million | 2024 | 2023 | 2022 | ||||||||

| Income: | |||||||||||

| Net interest income | 3,259 | 4,028 | 4,260 | ||||||||

| Net fee and commission income | 1,317 | 1,259 | 1,217 | ||||||||

| Investment income and other income | 2,405 | 1,771 | 849 | ||||||||

| Total income | 6,981 | 7,057 | 6,325 | ||||||||

| Expenditure: | |||||||||||

| Operating expenses | 3,558 | 3,313 | 3,114 | ||||||||

| Additions to the provision for loan losses | 627 | -92 | 1,220 | ||||||||

| Total expenditure | 4,185 | 3,222 | 4,334 | ||||||||

| Result before tax | 2,796 | 3,836 | 1,991 | ||||||||

| Taxation | 693 | 900 | 581 | ||||||||

| Non-controlling interests | 35 | 61 | 52 | ||||||||

| Net result IFRS-EU | 2,068 | 2,875 | 1,358 | ||||||||

| Adjustment of the EU 'IAS 39 carve-out' | -1,058 | -3,147 | 8,451 | ||||||||

| Net result IFRS-IASB | 1,010 | -272 | 9,810 | ||||||||

| Customer lending IFRS-IASB versus Customer lending IFRS-EU and Net core lending growth by business line | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retail Netherlands | Retail Belgium | Retail Germany | Retail Other | Wholesale Banking | Corporate Line | Total | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| in EUR billion | 2024 | 2023 | change | 2024 | 2023 | change | 2024 | 2023 | change | 2024 | 2023 | change | 2024 | 2023 | change | 2024 | 2023 | change | 2024 | 2023 | change | ||||||||||||||||||||||||||||||||||||||||||||

Customer lending IFRS-IASB 1 |

164.3 | 152.8 | 11.4 | 98.3 | 94.3 | 4.0 | 110.2 | 102.9 | 7.3 | 117.2 | 109.8 | 7.4 | 199.2 | 192.9 | 6.3 | 0.3 | 0.3 | 0.0 | 689.4 | 652.9 | 36.5 | ||||||||||||||||||||||||||||||||||||||||||||

| IFRS-EU 'IAS 39 carve out' impact | -3.4 | -4.9 | 1.5 | -3.4 | -4.9 | 1.5 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Customer lending IFRS-EU | 164.3 | 152.8 | 11.4 | 98.3 | 94.3 | 4.0 | 110.2 | 102.9 | 7.3 | 117.2 | 109.8 | 7.4 | 195.8 | 188.0 | 7.8 | 0.3 | 0.3 | 0.0 | 686.1 | 648.0 | 38.0 | ||||||||||||||||||||||||||||||||||||||||||||

| Exclude: FX impact | 0.0 | 0.0 | 0.0 | 0.9 | -4.7 | -3.8 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exclude: Change in fair value of macro hedged loans | 0.0 | 0.0 | 0.0 | 0.0 | -1.5 | -1.5 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exclude: Treasury, run-off portfolios and other | -1.9 | -0.4 | -2.9 | -0.2 | 0.2 | 0.0 | -5.1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net core lending growth | 9.6 | 3.7 | 4.4 | 8.2 | 1.8 | 0.0 | 27.7 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Customer deposits IFRS-IASB versus Customer deposits IFRS-EU and Net core deposits growth by business line | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retail Netherlands | Retail Belgium | Retail Germany | Retail Other | Wholesale Banking | Corporate Line | Total | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| in EUR billion | 2024 | 2023 | change | 2024 | 2023 | change | 2024 | 2023 | change | 2024 | 2023 | change | 2024 | 2023 | change | 2024 | 2023 | change | 2024 | 2023 | change | ||||||||||||||||||||||||||||||||||||||||||||

| Customer deposits IFRS-IASB | 200.7 | 199.7 | 1.0 | 97.1 | 91.2 | 5.9 | 151.1 | 143.6 | 7.5 | 163.2 | 151.0 | 12.1 | 79.6 | 64.8 | 14.9 | 0.0 | 0.0 | 0.0 | 691.7 | 650.3 | 41.4 | ||||||||||||||||||||||||||||||||||||||||||||

| IFRS-EU 'IAS 39 carve out' impact | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Customer deposits IFRS-EU | 200.7 | 199.7 | 1.0 | 97.1 | 91.2 | 5.9 | 151.1 | 143.6 | 7.5 | 163.2 | 151.0 | 12.1 | 79.6 | 64.8 | 14.9 | 0.0 | 0.0 | 0.0 | 691.7 | 650.3 | 41.4 | ||||||||||||||||||||||||||||||||||||||||||||

| Exclude: FX impact | 0.0 | 0.0 | 0.0 | 0.6 | -0.4 | 0.3 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exclude: Treasury, run-off portfolios and other | 4.0 | 0.5 | 0.0 | -0.1 | 1.3 | 0.0 | 5.8 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net core deposits growth | 5.0 | 6.4 | 7.5 | 12.7 | 15.8 | 0.0 | 47.4 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Customer lending IFRS-IASB versus Customer lending IFRS-EU and Net core lending growth by business line | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retail Netherlands | Retail Belgium | Retail Germany | Retail Other | Wholesale Banking | Corporate Line | Total | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| in EUR billion | 2023 | 2022 | change | 2023 | 2022 | change | 2023 | 2022 | change | 2023 | 2022 | change | 2023 | 2022 | change | 2023 | 2022 | change | 2023 | 2022 | change | ||||||||||||||||||||||||||||||||||||||||||||

Customer lending IFRS-IASB 1 |

152.8 | 153.6 | -0.7 | 94.3 | 91.7 | 2.6 | 102.9 | 98.3 | 4.6 | 109.8 | 108.2 | 1.6 | 192.9 | 198.9 | -6.1 | 0.3 | 0.2 | 0.1 | 652.9 | 650.9 | 2.1 | ||||||||||||||||||||||||||||||||||||||||||||

| IFRS-EU 'IAS 39 carve out' impact | -4.9 | -9.4 | 4.5 | -4.9 | -9.4 | 4.5 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Customer lending IFRS-EU | 152.8 | 153.6 | -0.7 | 94.3 | 91.7 | 2.6 | 102.9 | 98.3 | 4.6 | 109.8 | 108.2 | 1.6 | 188.0 | 189.5 | -1.6 | 0.3 | 0.2 | 0.1 | 648.0 | 641.5 | 6.5 | ||||||||||||||||||||||||||||||||||||||||||||

| Exclude: FX impact | 0.0 | 0.0 | 0.0 | 0.3 | 2.6 | 2.9 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exclude: Change in fair value of macro hedged loans | 0.0 | 0.0 | 0.0 | 0.0 | -4.5 | -4.5 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exclude: Treasury, run-off portfolios and other | 3.0 | -1.2 | -2.9 | 2.4 | 2.3 | -0.1 | 3.6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net core lending growth | 2.3 | 1.4 | 1.7 | 4.3 | -1.2 | 0.0 | 8.6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Customer deposits IFRS-IASB versus Customer deposits IFRS-EU and Net core deposits growth by business line | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retail Netherlands | Retail Belgium | Retail Germany | Retail Other | Wholesale Banking | Corporate Line | Total | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| in EUR billion | 2023 | 2022 | change | 2023 | 2022 | change | 2023 | 2022 | change | 2023 | 2022 | change | 2023 | 2022 | change | 2023 | 2022 | change | 2023 | 2022 | change | ||||||||||||||||||||||||||||||||||||||||||||

| Customer deposits IFRS-IASB | 199.7 | 201.1 | -1.4 | 91.2 | 91.5 | -0.3 | 143.6 | 135.9 | 7.7 | 151.0 | 137.7 | 13.3 | 64.8 | 74.6 | -9.8 | 0.0 | 0.0 | 0.0 | 650.3 | 640.8 | 9.5 | ||||||||||||||||||||||||||||||||||||||||||||

| IFRS-EU 'IAS 39 carve out' impact | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Customer deposits IFRS-EU | 199.7 | 201.1 | -1.4 | 91.2 | 91.5 | -0.3 | 143.6 | 135.9 | 7.7 | 151.0 | 137.7 | 13.3 | 64.8 | 74.5 | -9.8 | 0.0 | 0.0 | 0.0 | 650.3 | 640.8 | 9.5 | ||||||||||||||||||||||||||||||||||||||||||||

| Exclude: FX impact | 0.0 | 0.0 | 0.0 | -0.4 | 0.3 | -0.1 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exclude: Treasury, run-off portfolios and other | -0.2 | -1.0 | 0.8 | 0.0 | 1.6 | 0.0 | 1.2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net core deposits growth | -1.6 | -1.3 | 8.5 | 12.9 | -7.9 | 0.0 | 10.6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ING Group Consolidated Cash Flows | |||||||||||

| cash and cash equivalents | |||||||||||

| in EUR million | 2024 | 2023 | 2022 | ||||||||

| Treasury bills and other eligible bills included in securities at AC | 37 | 0 | 1 | ||||||||

| Deposits from banks | -6,303 | -5,132 | -6,172 | ||||||||

| Loans and advances to banks | 4,982 | 7,931 | 13,948 | ||||||||

| Cash and balances with central banks | 70,353 | 90,214 | 87,614 | ||||||||

| Cash and cash equivalents at end of year | 69,069 | 93,012 | 95,391 | ||||||||

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||

|

Steven van Rijswijk (CEO)

Born: 1970

Nationality: Dutch

|

Tanate Phutrakul (CFO)

Born: 1965

Nationality: Thai

|

Ljiljana Čortan (CRO)

Born: 1971

Nationality: Croatian

|

Pinar Abay

Born: 1977

Nationality: Turkish

|

Andrew Bester

Born: 1965

Nationality: British/South African

|

Marnix van Stiphout (COO)

Born: 1970

Nationality: Dutch

|

Daniele Tonella (CTO)

Born: 1971

Nationality: Swiss

|

||||||||||||||||||||||||||||||||||||||||||||

|

Steven has been a member of the Executive Board since May 2017. He has been CEO and chairperson of this Board since July 2020. Prior to his appointment as CEO and chairperson of this Board, he was the chief risk officer.

Steven is responsible for ING's strategy including ESG and sustainability, decision- making, results, governance, culture, branding, reputation and people.

|

Tanate was appointed as chief financial officer and member of the Management Board Banking in February 2019. Subsequently, Tanate was appointed as a member of the Executive Board of ING Groep at the Annual General Meeting in April 2019.

Tanate is responsible for ING's financial strategy, budgeting, cost control and the financing of the company.

|

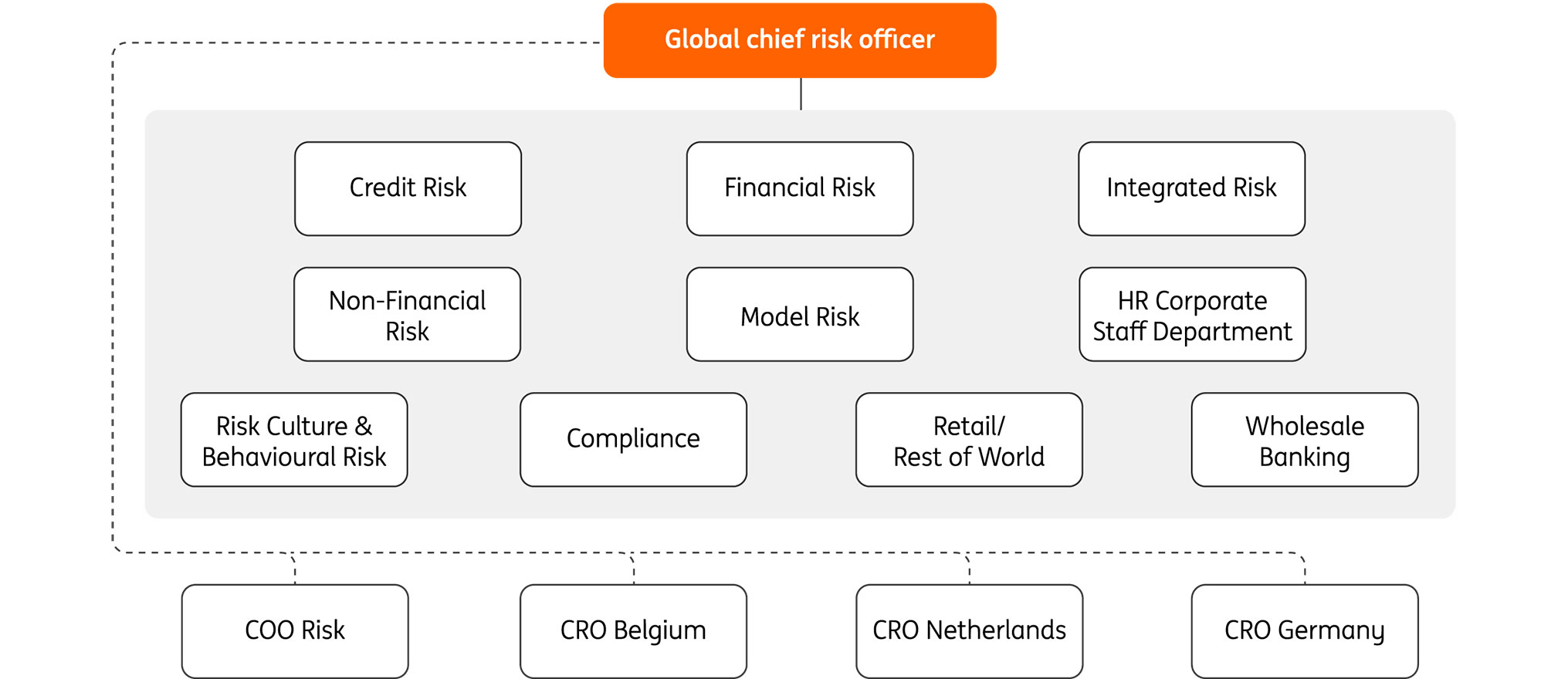

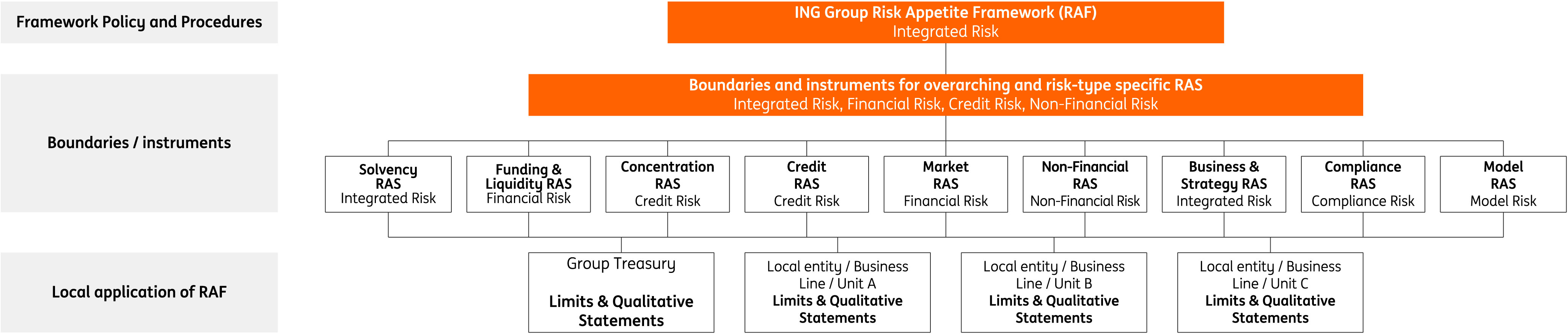

Ljiijana was appointed as chief risk officer and a member of the Management Board Banking effective January 2021. Ljiijana was appointed as a member of the Executive Board At the Annual General Meeting in April 2021.

Ljiijana is responsible for ING's risk activities including formulating our risk framework and risk appetite, risk culture and awareness, risk governance and policies and compliance.

|

Pinar was appointed a member of the Management Board Banking in January 2020. She is also head of Retail, Market Leaders and Challengers & Growth Markets. She was appointed as non-executive member of the board of ING in Belgium in March 2021 and was chairperson of that board from May 2022 until December 2023. In May 2023, Pinar was appointed a member of the supervisory board of ING-DiBa AG.

Pinar is responsible for defining strategy and priorities for global retail banking and driving performance, operations and compliance of retail, market leaders and challengers & growth markets.

|

Andrew was appointed as a member of the Management Board Banking and head of Wholesale Banking in April 2021.

Andrew is responsible for ING's wholesale banking activities globally.

|

Marnix was appointed as a member of the Management Board Banking and chief operations officer in September 2021.

Marnix is responsible for translating, overseeing and implementing ING's strategies into a strategy for the operations function.

|

Daniele joined ING's Management Board Banking as chief technology officer on 5 August 2024.

Daniele is responsible for overseeing and managing the total IT landscape and advising on technology-driven business opportunities.

|

||||||||||||||||||||||||||||||||||||||||||||

|

Relevant CRD IV position(s)

CEO and chairperson of the

EB and MBB

Other ancillary positions

▪Member of the Management Board of the Nederlandse Vereniging van Banken (NVB)

▪Member of the Cyber Security Council (CSR)

|

Relevant CRD IV position(s)

CFO and member of the EB and the MBB

Other ancillary positions

▪None

|

Relevant CRD IV position(s)

CRO and member of the EB and the MBB

Other ancillary positions

▪None

|

Relevant CRD IV position(s)

Member of the MBB, non-executive member of the board of ING Belgium N.V./S.A. and member of the supervisory board of ING-DiBa A.G.

Other ancillary positions

▪Member of the board of EPI Company SE

|

Relevant CRD IV position(s)

Member of the MBB

Other ancillary positions

▪None

|

Relevant CRD IV position(s)

Member of the MBB

Other ancillary positions

▪None

|

Relevant CRD IV position(s)

Member of the MBB

Other ancillary positions

▪None

|

||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||

|

Karl Guha (chairperson)

Born: 1964

Nationality: Dutch

Term expires: 2027

|

Mike Rees (vice-chairperson)

Born: 1956

Nationality: British

Term expires: 2027

|

Juan Colombás

Born: 1962

Nationality: Spanish

Term expires: 2028

|

Margarete Haase

Born: 1953

Nationality: Austrian

Term expires: 2025

|

Lodewijk Hijmans van den Bergh

Born: 1963

Nationality: Dutch

Term expires: 2025

|

Herman Hulst

Born: 1955

Nationality: Dutch

Term expires: 2028

|

Harold Naus

Born: 1969

Nationality: Dutch

Term expires: 2028

|

Alexandra Reich

Born: 1963

Nationality: Austrian

Term expires: 2027

|

Herna Verhagen

Born: 1966

Nationality: Dutch

Term expires: 2027

|

||||||||||||||||||||||||||||||||||||||||||

|

Karl was appointed chairperson of the SB at the General Meeting in April 2023. He started in July 2023.

Karl is chairperson of the

Nomination and Corporate

Governance Committee

and member of the Remuneration Committee,

the Risk Committee, the

Audit Committee, the ESG Committee and the Technology & Operations Committee.

|

Mike was appointed a member of the SB at the General Meeting in April 2019.

Mike is vice-chairperson of the SB, chairperson of the Risk Committee and member of the Nomination and Corporate Governance Committee and the Audit Committee.

|

Juan was appointed a member of the SB at the General Meeting in April 2020. He started in October 2020.

Juan is chairperson of the Technology & Operations Committee and member of the Risk Committee, the Audit Committee and the ESG Committee.

|

Margarete was appointed a member of the SB at the General Meeting in May 2017.

Margarete is chairperson of the Audit Committee and member of the Risk Committee and the Remuneration Committee.

|

Lodewijk was appointed a member of the SB at the General Meeting in April 2021.

Lodewijk is chairperson of the ESG Committee and member of the Risk Committee.

|

Herman was appointed a member of the SB at the General Meeting in April 2020.

Herman is member of the Audit Committee, the Risk Committee and the ESG Committee.

|

Harold was appointed a member of the SB at the General Meeting in April 2020.

Harold is member of the

Remuneration Committee,

the Risk Committee and the Technology & Operations Committee.

|

Alexandra was appointed a member of the SB at the General Meeting in April 2023.

Alexandra is member of the

Risk Committee, the Technology & Operations Committee and the ESG

Committee.

|

Herna was appointed a member of the SB at the General Meeting in April 2019, and started in October 2019.

Herna is chairperson of the

Remuneration Committee and

member of the Nomination and Corporate Governance

Committee.

|

||||||||||||||||||||||||||||||||||||||||||

|

Former position:

CEO of Van Lanschot Kempen

Relevant CRD IV position(s)

▪Chairperson of the SB

▪Member of the supervisory board of SHV Holdings N.V.

Other ancillary positions

▪Member of the supervisory board of Rijksmuseum Fonds

|

Former position:

Deputy CEO of Standard Chartered Bank PLC.

Relevant CRD IV position(s)

▪Vice-chairperson of the SB

▪Non-executive chairperson of the board of directors of Travelex International Limited

▪Non-executive chairperson of the board of directors of Midlands Mindforge

Other ancillary positions

▪Non-executive chairperson of the board of directors of Mauritius Africa FinTech Hub

|

Former position:

Chief operations officer and executive board member of the board of directors of Lloyds Banking Group

Relevant CRD IV position(s)

▪Member of the SB

▪Non-executive member of the board of directors of Azora Capital S.L.

▪Non-executive chairperson of the board of directors of Bluserena Spa

Other ancillary positions

▪Member of the global alumni advisory board of the Institute de Empresa (IE) Business School

|

Former position:

CFO of Deutz AG

Relevant CRD IV position(s)

▪Member of the SB

▪Chairperson of the supervisory board of ams-OSRAM AG

▪Member of the supervisory board of Fraport AG

Other ancillary positions

▪Chairperson of the employers association of Kölnmetall

▪Member of the German Corporate Governance Commission

|

Former position:

Partner/member of the management committee of De Brauw Blackstone Westbroek N.V.

Relevant CRD IV position(s)

▪Member of the SB

▪Deputy chairperson of the supervisory board of HAL Holding N.V.

▪Member of the supervisory board of Heineken N.V.

Other ancillary positions

▪Chairperson of the board of Utrecht University Fund (the Netherlands)

▪Chairperson of the executive committee of Vereniging Aegon

|

Former position:

Global vice-chairperson EY Japan

Relevant CRD IV position(s)

▪Member of the SB

Other ancillary positions

▪None

|

Former position:

Global head of Trading Risk Management and general manager Market Risk of ING Bank

Relevant CRD IV position(s)

▪Member of the SB

▪CEO of Cardano Asset Management N.V.

▪CEO of Cardano Risk Management B.V.

▪Member of the executive board of Cardano Holding Limited

Other ancillary positions

▪None

|

Former position:

CEO of Telenor Thailand

Relevant CRD IV position(s)

▪Member of the SB

▪Member of the non-executive board of directors of Cellnex Telecom S.A.

▪Member of the non-executive board of directors of Salt Mobile S.A.

▪Member of the non-executive board of directors of DELTA Fiber

Other ancillary positions

▪None

|

Former position:

Member of the supervisory board of SNS Reaal N.V. (now: SRH N.V.)

Relevant CRD IV position(s)

▪Member of the SB

▪CEO of PostNL N.V.

▪Member of the supervisory board of Koninklijke Philips N.V.

Other ancillary positions

▪Member of the supervisory board of Het Concertgebouw N.V.

▪Member of the advisory council of Goldschmeding Foundation

|

||||||||||||||||||||||||||||||||||||||||||

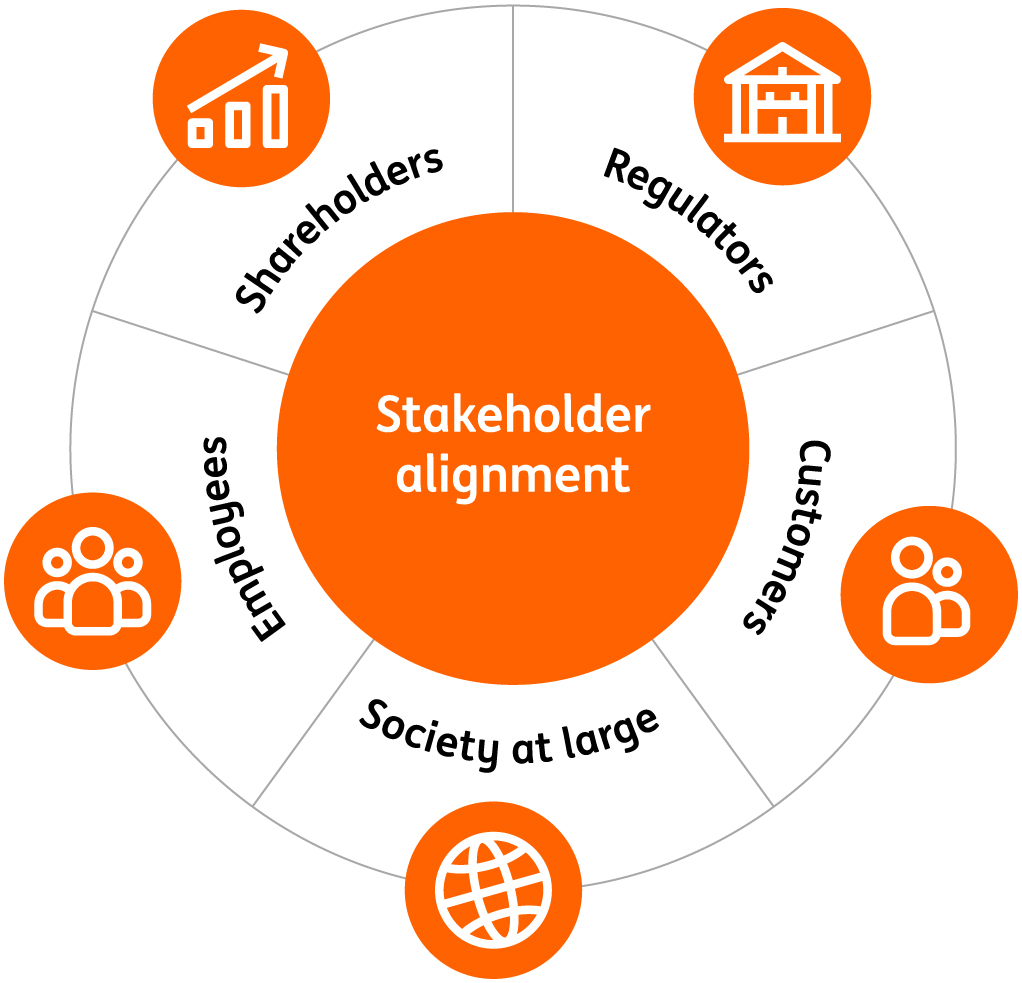

| Stakeholder alignment | Employees | Shareholders | Regulators | Customers | Society at large | ||||||||||||||||||||||||

|

▪The Executive Board remuneration policy is aligned with the remuneration principles that apply to all ING employees.

▪Salaries for the EB are reviewed in the context of salary developments across ING's wider workforce.

▪EB members' variable remuneration is determined using a multi-step and integrated process, which is closely aligned to the approach used to determine variable remuneration for the wider workforce.

▪We communicate with our employees through our ongoing engagement with the Works Council in the Netherlands on EB remuneration.

▪In recent years, this stakeholder group has focused on ensuring EB remuneration levels and decisions are acceptable to society at large.

|

▪Remuneration outcomes take into account performance against stretching financial and non-financial targets that are consistent with ING's strategy.

▪Variable remuneration for EB members is deferred fully into ING Group shares.

▪In recent years, shareholders continuously expressed their concerns about the low variable remuneration and low total remuneration levels of EB members.

▪Alignment of EB performance targets and variable remuneration serves as an important driver of the Company’s strategic priorities and long-term shareholder value creation.

|

▪Variable remuneration outcomes reflect ex-ante and ex-post risk performance.

▪Variable remuneration pay structures are aligned with regulatory requirements, including deferral, malus and clawback.

|

▪Through our qualitative survey we engaged with and listened to the views of our customers on a range of executive compensation topics, which was used to inform our remuneration policy and decision-making.

▪Variable remuneration is designed with appropriate consideration of the views and interest of customers and clients, ensuring this is represented in the Executive Board remuneration policy and decision-making.

|

▪In recent years, customers are increasingly interested in the way EB remuneration is linked to environmental and social objectives.

▪Environmental and social objectives within variable remuneration for the EB reflects ING's wider purpose and strategy.

▪Variable remuneration includes measures to drive our diversity and gender ambitions.

|

||||||||||||||||||||||||

| Executive Board remuneration principles | ||

Consistent with ING’s strategy and the promotion of sound and effective risk management; | ||

Being able to attract, motivate and retain leaders with the ability, experience, skills, values and behaviours to fulfil our role as a global bank; | ||

| The interest of EB members to receive fair, consistent and balanced remuneration; | ||

| Maintaining a sustainable balance between the short and long-term interests of our clients, shareholders, employees, society at large and other stakeholders, and encouraging sustainable long-term value creation; | ||

Complying with all applicable regulatory requirements. | ||

| Remuneration component | Operation |

||||

| Base salary |

▪Base salary is set to reflect the individual's role, responsibilities, and experience, and to reward ongoing contribution to the role.

▪Base salary is fully paid out in cash.

▪Base salary is reviewed annually by the SB with potential increases normally applying from January.

|

||||

| Pension |

▪Participation in ING's general collective defined contribution (CDC) pension plan in the same way as all employees working in the Netherlands.

▪Same approach to all participants in the Dutch CDC pension plan who earn a salary above the maximum allowed pensionable salary, the EB members are compensated for the lack of pension accrual by means of a monthly individual savings allowance.

|

||||

| Benefits |

▪Benefits are offered if considered appropriate by the SB in the context of the executive’s role, specific individual circumstances and benefits offered to the wider workforce, and for comparable roles in ING’s peer group.

▪Benefits may include reimbursement of costs related to travel and accident insurance, expatriate allowances, banking and insurance benefits from ING, tax and financial planning services, and the use of a company car or driver service.

|

||||

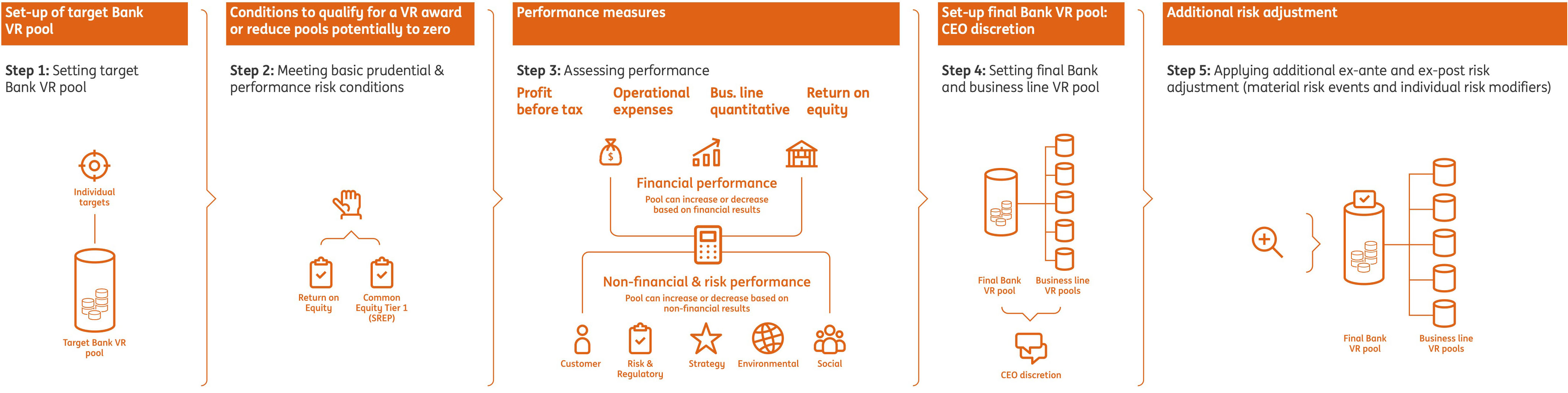

| Variable remuneration |

▪The maximum annual variable remuneration opportunity is 20 percent of annual base salary. In case of achievement of target performance, variable remuneration of 16 percent of annual base salary will be awarded.

▪Variable remuneration is delivered fully in ING Group shares.

▪The amount of variable remuneration is based on performance as measured against agreed financial, non-financial and risk objectives. At least 50 percent of variable remuneration metrics must be based on non-financial targets. At the beginning of each performance year, the Supervisory Board determines the performance measures and targets applicable for determining variable remuneration that year.

▪Variable remuneration awards are paid 40 percent upfront and 60 percent is deferred. The deferred portion vests in equal annual tranches over five years plus an additional retention year as of the vesting date.

|

||||

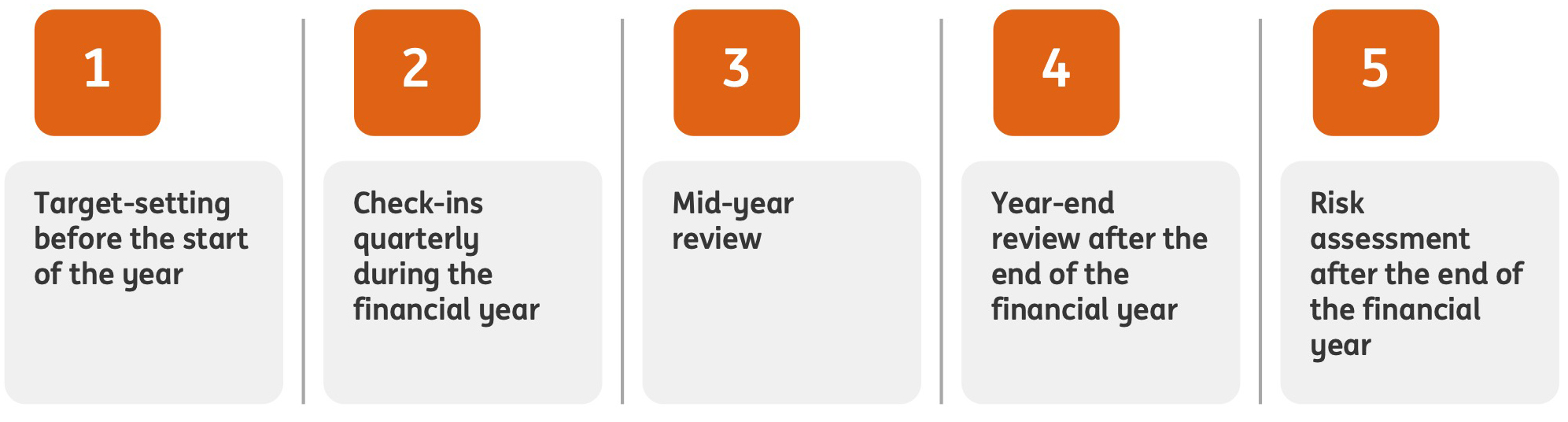

Variable remuneration is awarded taking into consideration performance over the prior year. |

100% | ||||||||||||||||||||||||||||||||||

| Delivery fully in shares | Upfront shares are awarded and vest on the same date and have a five-year retention period. |

40% | |||||||||||||||||||||||||||||||||

| 60% | |||||||||||||||||||||||||||||||||||

Deferred shares are awarded on the same date but vest in five tranches. There is a holding period requirement of five years from the award date plus a minimum retention period of 12 months post vesting. |

12% | ||||||||||||||||||||||||||||||||||

| 12% | |||||||||||||||||||||||||||||||||||

| 12% | |||||||||||||||||||||||||||||||||||

| 12% | |||||||||||||||||||||||||||||||||||

| 12% | |||||||||||||||||||||||||||||||||||

Holdback |

Unvested tranches are subject to holdback provision. |

||||||||||||||||||||||||||||||||||

Clawback |

Vested tranches remain subject to clawback provision. Clawback provision applies during the maximum limitation period as permitted by applicable law. |

||||||||||||||||||||||||||||||||||

Guiding principle |

Short description |

||||

Size |

ING acknowledges the importance of including companies that are broadly comparable in terms of size and complexity. |

||||

Governance framework |

ING is subject to the Dutch (financial services) regulatory framework and operates within a Dutch stakeholder environment. | ||||

Geography |

ING is a leading European universal bank with a global presence and is headquartered in the Netherlands. | ||||

Talent market |

ING is increasingly experiencing a cross-pollination of talent across sectors/industries, not limited to traditional banking competitors. | ||||

Balancing |

ING acknowledges the importance of not losing sight of relevant peer companies that do not match on the other criteria. |

||||

|

▪ABN AMRO

▪Aegon1

▪Ahold Delhaize

▪ASML

▪Banco Santander

|

▪BBVA

▪BNP Paribas

▪Commerzbank

▪Crédit Agricole

▪Deutsche Bank

|

▪Heineken

▪Intesa Sanpaolo

▪KBC

▪Lloyds Banking Group

▪NatWest

|

▪NN Group

▪Philips

▪Rabobank

▪Société Générale

▪UniCredit

|

||||||||

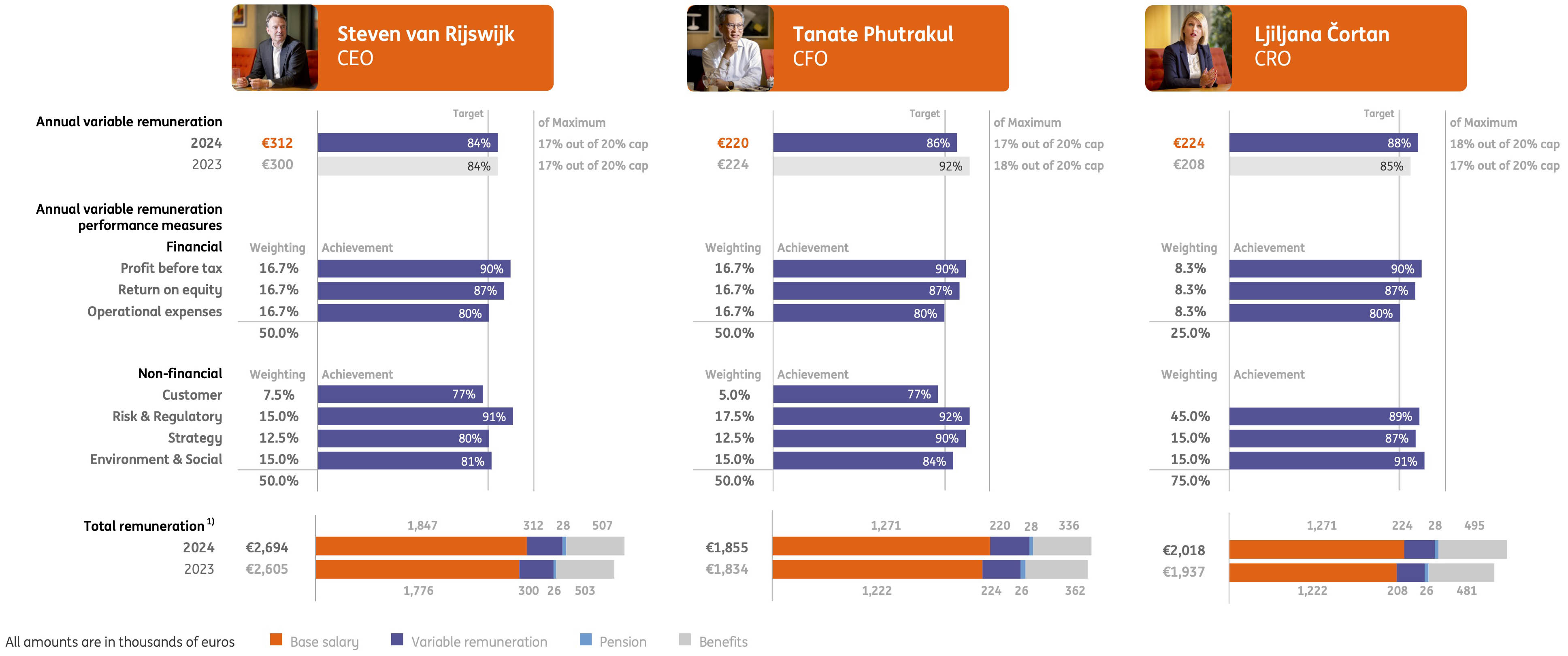

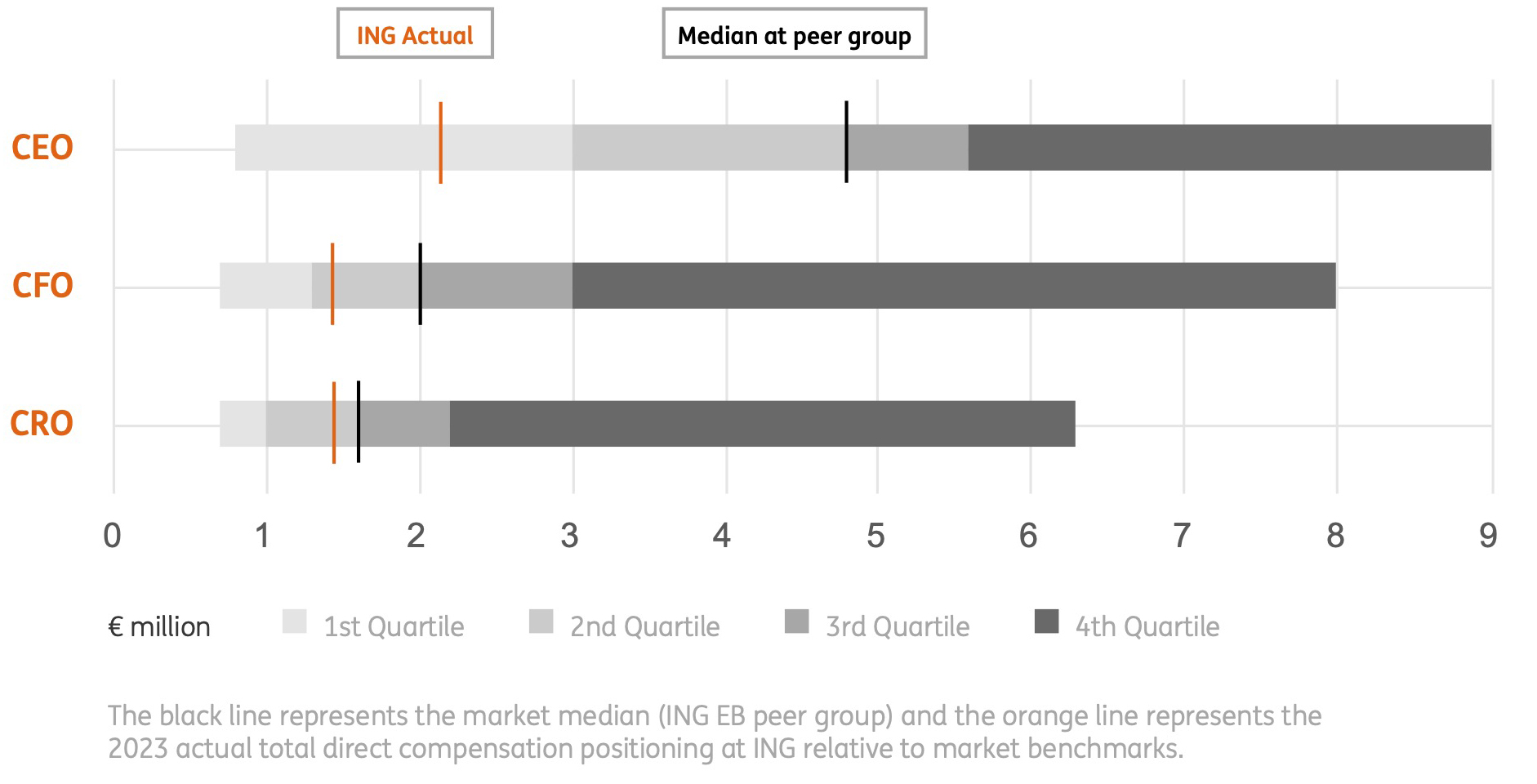

| 1. 2024 variable remuneration outcomes | ||||||||||||||||||||||||||||||||||||||||||||

|

Target –

Minimum

|

Target |

Target –

Maximum

|

Performance | Steven van Rijswijk (CEO) | Tanate Phutrakul (CFO) | Ljiljana Čortan (CRO) | ||||||||||||||||||||||||||||||||||||||

| Weighting | Assessment | Outcome | Weighting | Assessment | Outcome | Weighting | Assessment | Outcome | ||||||||||||||||||||||||||||||||||||

| Financial | Profit before tax | 6,790 | 8,488 | 10,185 | 9,300 | 16.7 | % | 90 | % | 15 | % | 16.7 | % | 90 | % | 15 | % | 8.3 | % | 90 | % | 7 | % | |||||||||||||||||||||

| Return on equity | 9.7 | % | 12.2 | % | 14.6 | % | 13.0 | % | 16.7 | % | 87 | % | 14 | % | 16.7 | % | 87 | % | 14 | % | 8.3 | % | 87 | % | 7 | % | ||||||||||||||||||

| Operational expenses | 12,731 | 12,125 | 11,519 | 12,121 | 16.7 | % | 80 | % | 13 | % | 16.7 | % | 80 | % | 13 | % | 8.3 | % | 80 | % | 7 | % | ||||||||||||||||||||||

| Non-financial | Customer | Performance against non-financial measures are organised around these target areas. Please see the following pages for more details on the non-financial performance of each Executive Board member. |

7.5 | % | 77 | % | 6 | % | 5.0 | % | 77 | % | 4 | % | NA |

NA | NA | |||||||||||||||||||||||||||

Risk & Regulatory |

15.0 | % | 91 | % | 14 | % | 17.5 | % | 92 | % | 16 | % | 45.0 | % | 89 | % | 40 | % | ||||||||||||||||||||||||||

| Strategy | 12.5 | % | 80 | % | 10 | % | 12.5 | % | 90 | % | 11 | % | 15.0 | % | 87 | % | 13 | % | ||||||||||||||||||||||||||

Environment & Social |

15.0 | % | 81 | % | 12 | % | 15.0 | % | 84 | % | 13 | % | 15.0 | % | 91 | % | 14 | % | ||||||||||||||||||||||||||

| Total | 100 | % | 84 | % | 100 | % | 86 | % | 100 | % | 88 | % | ||||||||||||||||||||||||||||||||

| Final 2024 variable remuneration outcomes | 84 | % | 86 | % | 88 | % | ||||||||||||||||||||||||||||||||||||||

Payout out of 20 percent variable remuneration cap (16 percent is at target variable remuneration) |

17 | % | 17 | % | 18 | % | ||||||||||||||||||||||||||||||||||||||

|

Steven van Rijswijk

CEO

|

|||||||||||||||||||||||||||||||||||||||||||

| Customer | Risk & Regulatory | Strategy | Environment | Social | ||||||||||||||||||||||||||||||||||||||||

|

▪Increase number of primary customers

▪Increase customer satisfaction of Retail and Wholesale customers by increasing NPS

|

▪Manage financial risk within risk appetite with a specific focus on the revision of the use of internal models

▪Manage non-financial risk within risk appetite with a specific focus on identity and access management and operational resilience

▪Deliver on regulatory programmes, including KYC

|

▪Increase digitisation and STP rate of customer processes

|

▪Increase sustainable volume mobilised

▪Support the transition of the most carbon-intensive sectors in Wholesale Banking (being power generation, oil & gas, cement, steel, automotive, aviation, shipping, and commercial real estate) towards a better carbon performance, in line with our 2030 decarbonisation target

|

▪Strengthen organisational health with a focus on four priority areas:

–Strategic clarity

–Role clarity

–Customer focus

–Operational discipline

▪Increase gender balance in ING's leadership cadre

|

||||||||||||||||||||||||||||||||||||||||

|

▪Earning 'primary relationships' with customers is an important driver for profitable growth. In 2024, the number of primary customers increased by 0.8 to 16.2 million. This is slightly below target.

▪In 2024, ING ranked number one in five of our Retail markets: Australia, Poland, Germany, Romania and Spain, which was in line with target. ING ranks in the top three in another two markets: Italy and the Netherlands.

▪In Wholesale Banking the NPS score exceeded target, as it increased to 74, up from 72 in 2023, with clients recognising ING's sector expertise, global reach and local experts.

|

▪Credit, financial and non-financial risk were managed well within ING’s risk appetite.

▪The delivery of credit risk models in 2024 was in line with the defined multi-year plan for redevelopment of credit models.

▪Continued improvement of identity and access management (IAM) by standardisation and harmonisation of processes, workflows and automation of IAM controls, as well as the further rollout of supporting global tooling.

▪Implementation of the Digital Operational Resilience Act (DORA), which aims to further strengthen the digital operational resilience.

▪The bank’s KYC activities further matured and maintained a sustainable level of operational effectiveness during 2024.

|

▪Developed and rolled out the next phase of ING’s strategy, 'Growing the difference', aimed at being the best European bank by accelerating growth, increasing impact and delivering value.

▪In 2024, the digitalisation of key customer journeys developed in line with target to create the foundation for providing a superior customer experience which is easy, instant, personal, and relevant.

–Customer friction has been further decreased. This is measured by the percentage of customer journeys that is handled without manual intervention, which went up from 71 percent year-end 2023 to 77 percent year-end 2024.

– Improved customer experience through the use of our GenAI chatbot, which also led to higher chat deflection.

–Continuous investment in AI to further strengthen ING's position as one of the leaders in the AI and analytics space by, among others, the launch of personalised marketing for specific retail segments.

|

▪Increased the sustainable finance volume mobilised to more than €130 bn in 2024, up from €115 bn in 2023, with 835 sustainable deals supported in 2024.

▪Sharpened relationship management approach towards our clients to be able to perform tighter monitoring and tracking of our clients' sustainability progress and a deeper risk-based analysis. During the year, engagement with Wholesale Banking clients has taken place on their transition plans.

▪ING uses the 'Terra' approach to steer our portfolios in high-emitting sectors towards net-zero alignment by 2050. The transition of the most carbon-intensive Wholesale Banking sectors was measured using eight sector indicators. Overall, we demonstrated good progress, and most sectors showed significant advancement. Two sectors, cement and steel, did not meet their targets. The sectors experienced slower progress, requiring further technological advancements and close collaboration among multiple stakeholders to stay on track for their targets.

|

▪In 2024, we held two OHI surveys, and 80 percent of our workforce provided feedback – the highest response rate ever. There is sustained engagement among ING's employees and feedback showed that the employees continue to value and appreciate their colleagues, the ability to work hybrid, and the opportunities that support their wellbeing.

▪Female representation in senior management increased in line with expectations from 31 percent at the end of 2023 to 32 percent at the end of 2024, with progress in nearly all domains.

|

||||||||||||||||||||||||||||||||||||||||

|

Tanate Phutrakul

CFO

|

|||||||||||||||||||||||||||||||||||||||||||

| Customer | Risk & Regulatory | Strategy | Environment | Social | ||||||||||||||||||||||||||||||||||||||||

|

▪Increase number of primary customers

▪Increase customer satisfaction of Retail and Wholesale customers by increasing NPS

|

▪Manage financial risk within risk appetite with a specific focus on the revision of the use of internal models

▪Manage non-financial risk within risk appetite with a specific focus on identity and access management and operational resilience

|

▪Increase efficiency of finance processes while maintaining the effectiveness of controls |

▪Prepare for Corporate Sustainability Reporting Directive (CSRD) disclosure requirements |

▪Strengthen organisational health with a focus on four priority areas:

–Strategic clarity

–Role clarity

–Customer focus

–Operational discipline

▪Increase gender balance in ING's leadership cadre

|

||||||||||||||||||||||||||||||||||||||||

|

▪Earning 'primary relationships' with customers is an important driver for profitable growth. In 2024, the number of primary customers increased by 0.8 to 16.2 million. This is slightly below target.

▪In 2024, ING ranked number one in five of our Retail markets: Australia, Poland, Germany, Romania and Spain, which was in line with target. ING ranks in the top three in another two markets: Italy and the Netherlands.

▪In Wholesale Banking the NPS score exceeded target, as it increased to 74, up from 72 in 2023, with clients recognising ING's sector expertise, global reach and local experts.

|

▪Credit, financial and non-financial risk were managed well within ING’s risk appetite.

▪The delivery of credit risk models in 2024 was in line with the defined multi-year plan for redevelopment of credit models.

▪Continued improvement of identity and access management (IAM) by standardisation and harmonisation of processes, workflows, and automation of IAM controls as well as the further rollout of supporting global tooling.

▪Implementation of the Digital Operational Resilience Act (DORA), which aims to further strengthen the digital operational resilience.

|

▪Developed and rolled out the next phase of ING’s strategy, 'Growing the difference', aimed at being the best European bank by accelerating growth, increasing impact and delivering value.

▪Increased efficiency of finance processes while maintaining overall effectiveness of the financial reporting control environment by: improving control efficiency across processes; further automation of manual controls and processes; and focusing on first time right for new and remediated controls in design and execution.

|

▪Enhanced the internal controls supporting the preparation of the 2024 sustainability disclosures (CSRD/ESRS):

–Installed proper governance to prepare, review, and approve disclosures.

–Implemented improved controls around receiving external climate data from vendors.

–Implemented improved controls in reporting processes with respective data and disclosure owners.

|

▪In 2024, we held two OHI surveys, and 80 percent of our workforce provided feedback - the highest response rate ever. There is sustained engagement among ING's employees, and feedback showed that the employees continue to value and appreciate their colleagues, the ability to work hybrid, and the opportunities that support their wellbeing.

▪Female representation in senior management increased in line with expectations from 31 percent at the end of 2023 to 32 percent at the end of 2024 with progress in nearly all domains.

|

||||||||||||||||||||||||||||||||||||||||

|

Ljiljana Čortan

CRO

|

|||||||||||||||||||||||||||||||||||||||||||

| Risk & Regulatory | Strategy | Environment | Social | |||||||||||||||||||||||||||||||||||||||||

|

▪Manage financial risk within risk appetite with a specific focus on the revision of the use of internal models

▪Manage non-financial risk within risk appetite with a specific focus on identity and access management and operational resilience

▪Deliver on regulatory programmes including KYC

|

▪Increase efficiency of risk processes while maintaining the effectiveness of controls

|

▪Implementation of ESG risk assessment methodology following CSRD requirements |

▪Strengthen organisational health with a focus on four priority areas:

–Strategic clarity

–Role clarity

–Customer focus

–Operationally disciplined

▪Increase gender balance in ING's leadership cadre

|

|||||||||||||||||||||||||||||||||||||||||

|

▪Credit, financial and non-financial risk were managed well within ING’s risk appetite.

▪The delivery of credit risk models in 2024 was in line with the defined multi-year plan for redevelopment of credit models.

▪Ongoing improvement of identity and access management (IAM) by standardisation and harmonisation of processes, workflows, and automation of IAM controls as well as the further rollout of supporting global tooling.

▪Implementation of the Digital Operational Resilience Act (DORA), which aims to further strengthen the digital operational resilience.

▪Maintained a sustainable level of operational effectiveness of KYC through oversight and challenge as the second line of defence, as the bank's KYC activities have matured.

|

▪Developed the next phase of ING’s strategy, 'Growing the difference', aimed at being the best European bank by accelerating growth, increasing impact, and delivering value.

▪Contributed to the digitalisation of lending processes by delivering on the defined automation milestones in risk processes of the retail and business banking lending journeys beyond expectation.

▪Improved the non-financial risk control processes in line with target while maintaining the effectiveness.

|

▪Exceeding expectations by implementing multiple initiatives to support the climate and environmental risk assessment process, among which:

–Enhancing the climate stress-testing methodology to assess the impact of climate risks on corporate and mortgage exposures from a credit risk perspective;

–Development and implementation of a transition risk scorecard, which is used to quantify transition risk with a scorecard approach at client level in order to identify the pool of high-risk clients within specific sectors;

–Developed a tool to measure and assign a level of physical risk for four chronic and nine acute physical risks across the short, medium and long term for portfolios and geographies in which ING operates; and

–Developed a new ESG risk assessment approach which considers the (climate and) environmental, social and governance risk factors, negative impacts and dependencies of ING's Wholesale Banking customers, and fully integrates the previous ESR framework. Tooling was developed to support the implementation of the assessment approach in the credit granting process. The new approach was gradually rolled out in 2024.

|

▪In 2024, we held two OHI surveys and 80 percent of our workforce provided feedback – the highest response rate ever. There is sustained engagement among ING's employees and feedback showed that the employees continue to value and appreciate their colleagues, the ability to work hybrid, and the opportunities that support their wellbeing.

▪Female representation in senior management increased in line with expectations from 31 percent at the end of 2023 to 32 percent at the end of 2024 with progress in nearly all domains.

|

|||||||||||||||||||||||||||||||||||||||||

| 2. 2024 remuneration outcomes | ||||||||||||||||||||||||||||||||

| 1. Fixed remuneration | 2. Variable remuneration | 3. Extraordinary items | 4. Pension benefits | 5. Total remuneration | 6. Proportion of fixed and variable remuneration | |||||||||||||||||||||||||||

| Amounts in euros (rounded figures) |

Base salary | Fees | Other benefits | One-year variable1 |

Multi-year variable | |||||||||||||||||||||||||||

| Steven van Rijswijk (CEO) | 2024 | 1,847,300 | — | 507,200 | 311,800 | — | — | 27,900 | 2,694,200 | 88.4% / 11.6% | ||||||||||||||||||||||

| 2023 | 1,776,300 | — | 503,300 | 299,600 | — | — | 26,100 | 2,605,200 | 88.5% / 11.5% | |||||||||||||||||||||||

| Tanate Phutrakul (CFO) | 2024 | 1,270,500 | — | 336,100 | 219,700 | — | — | 27,900 | 1,854,300 | 88.2% / 11.8% | ||||||||||||||||||||||

| 2023 | 1,221,700 | — | 362,300 | 224,100 | — | — | 26,100 | 1,834,200 | 87.8% / 12.2% | |||||||||||||||||||||||

| Ljiljana Čortan (CRO) | 2024 | 1,270,500 | — | 495,000 | 223,600 | — | — | 27,900 | 2,017,100 | 88.9% / 11.1% | ||||||||||||||||||||||

| 2023 | 1,221,700 | — | 481,400 | 208,000 | — | — | 26,100 | 1,937,200 | 89.3% / 10.7% | |||||||||||||||||||||||

| 3. Breakdown of benefits paid in 2024 | |||||||||||

| Amounts in euros (rounded figures) | Steven van Rijswijk (CEO) | Tanate Phutrakul (CFO) | Ljiljana Čortan (CRO) |

||||||||

| Contribution individual savings plans | 64,700 | 44,500 | 44,500 | ||||||||

| Individual savings allowance | 378,100 | 250,500 | 250,500 | ||||||||

| Travel and accident insurance | 15,000 | 15,000 | 15,000 | ||||||||

Other benefits1 |

49,400 | 26,100 | 185,000 | ||||||||

| Total | 507,200 | 336,100 | 495,000 | ||||||||

| 4. Share-based remuneration for Executive Board members | ||||||||||||||||||||||||||||||||||||||||||||

| The main conditions of share award plans | Information regarding the reported financial year | |||||||||||||||||||||||||||||||||||||||||||

| Opening balance | During the year | Closing balance | ||||||||||||||||||||||||||||||||||||||||||

| 1 | 2 | 3 | 4 | 5 | 6A | 6B | 6C | 7 | 8 | 9 | 10 | 11A | 11B | |||||||||||||||||||||||||||||||

Specification of plan1 |

Performance period | Granting/ offering date | Vesting date | End of retention period | Shares held at the beginning of the year | Shares subject to retention at the beginning of the year | Shares sold-to-cover2 |

Shares granted/ offered | Shares vested |

Shares subject to a performance condition | Shares granted/ offered and unvested at year-end | Shares subject to a retention period | Vested shares sold-to-cover2 |

|||||||||||||||||||||||||||||||

| Steven van Rijswijk (CEO) | LSPP Deferred Shares Idnt | 2017 | 27/03/2018 | 27/03/2023 | 27/03/2024 | - | 179 | 167 | - | - | - | - | - | - | ||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2017 | 10/05/2018 | 11/05/2023 | 11/05/2024 | - | 410 | 380 | - | - | - | - | - | - | |||||||||||||||||||||||||||||||

| LSPP Upfront Shares | 2019 | 11/05/2020 | 11/05/2020 | 11/05/2025 | - | 4,193 | 3,350 | - | - | - | - | 4,193 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2019 | 11/05/2020 | 11/05/2021 | 11/05/2025 | - | 1,241 | 1,022 | - | - | - | - | 1,241 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2019 | 11/05/2020 | 11/05/2022 | 11/05/2025 | - | 1,224 | 1,039 | - | - | - | - | 1,224 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2019 | 11/05/2020 | 11/05/2023 | 11/05/2025 | - | 1,202 | 1,061 | - | - | - | - | 1,202 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2019 | 11/05/2020 | 11/05/2024 | 11/05/2025 | 2,263 | - | - | - | 2,263 | - | - | 1,174 | 1,089 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2019 | 11/05/2020 | 11/05/2025 | 11/05/2026 | 2,263 | - | - | - | - | - | 2,263 | - | - | |||||||||||||||||||||||||||||||

| LSPP Upfront Shares | 2021 | 09/05/2022 | 09/05/2022 | 09/05/2027 | - | 5,108 | 4,082 | - | - | - | - | 5,108 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2023 | 09/05/2027 | - | 1,512 | 1,245 | - | - | - | - | 1,512 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2024 | 09/05/2027 | 2,757 | - | - | - | 2,757 | - | - | 1,491 | 1,266 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2025 | 09/05/2027 | 2,757 | - | - | - | - | - | 2,757 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2026 | 11/05/2027 | 2,757 | - | - | - | - | - | 2,757 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2027 | 11/05/2028 | 2,757 | - | - | - | - | - | 2,757 | - | - | |||||||||||||||||||||||||||||||

| LSPP Upfront Shares | 2022 | 11/05/2023 | 11/05/2023 | 11/05/2028 | - | 4,846 | 3,872 | - | - | - | - | 4,846 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2024 | 11/05/2028 | 2,615 | - | - | - | 2,615 | - | - | 1,434 | 1,181 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2025 | 11/05/2028 | 2,615 | - | - | - | - | - | 2,615 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2026 | 11/05/2028 | 2,615 | - | - | - | - | - | 2,615 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2027 | 11/05/2028 | 2,615 | - | - | - | - | - | 2,615 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2028 | 11/05/2029 | 2,618 | - | - | - | - | - | 2,618 | - | - | |||||||||||||||||||||||||||||||

| LSPP Upfront Shares | 2023 | 10/05/2024 | 10/05/2024 | 10/05/2029 | - | - | - | 9,742 | 9,742 | - | - | 5,415 | 4,327 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2025 | 10/05/2029 | - | - | - | 2,922 | - | - | 2,922 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2026 | 10/05/2029 | - | - | - | 2,922 | - | - | 2,922 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2027 | 10/05/2029 | - | - | - | 2,922 | - | - | 2,922 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2028 | 11/05/2029 | - | - | - | 2,922 | - | - | 2,922 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2029 | 11/05/2030 | - | - | - | 2,925 | - | - | 2,925 | - | - | |||||||||||||||||||||||||||||||

| Total | 28,632 | 19,915 | 16,218 | 24,355 | 17,377 | - | 35,610 | 28,840 | 7,863 | |||||||||||||||||||||||||||||||||||

| 4. Share-based remuneration for Executive Board members – continued | ||||||||||||||||||||||||||||||||||||||||||||

| The main conditions of share award plans | Information regarding the reported financial year | |||||||||||||||||||||||||||||||||||||||||||

| Opening Balance | During the year | Closing balance | ||||||||||||||||||||||||||||||||||||||||||

| 1 | 2 | 3 | 4 | 5 | 6A | 6B | 6C | 7 | 8 | 9 | 10 | 11A | 11B | |||||||||||||||||||||||||||||||

Specification of plan1 |

Performance period | Granting/ offering date | Vesting date | End of retention period | Shares held at the beginning of the year | Shares subject to retention at the beginning of the year | Shares sold-to-cover2 |

Shares granted/ offered | Shares vested | Shares subject to a performance condition | Shares granted/ offered and unvested at year-end | Shares subject to a retention period | Vested shares sold-to-cover2 |

|||||||||||||||||||||||||||||||

| Tanate Phutrakul (CFO) | LSPP Deferred Units Idnt (Equity settled) | 2016 | 27/03/2017 | 27/03/2023 | NULL | - | 238 | 247 | - | - | - | - | - | - | ||||||||||||||||||||||||||||||

| LSPP Deferred Units Idnt (Equity settled) | 2017 | 27/03/2018 | 27/03/2023 | NULL | - | 197 | 200 | - | - | - | - | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Units Idnt (Equity settled) | 2017 | 27/03/2018 | 27/03/2024 | NULL | 401 | - | - | - | 401 | - | - | 200 | 201 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2018 | 27/03/2019 | 27/03/2023 | 27/03/2024 | - | 117 | 110 | - | - | - | - | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2018 | 27/03/2019 | 27/03/2024 | 27/03/2025 | 227 | - | - | - | 227 | - | - | 117 | 110 | |||||||||||||||||||||||||||||||

| LSPP Upfront Shares | 2019 | 11/05/2020 | 11/05/2020 | 11/05/2025 | - | 3,934 | 3,144 | - | - | - | - | 3,934 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2019 | 11/05/2020 | 11/05/2021 | 11/05/2025 | - | 1,164 | 959 | - | - | - | - | 1,164 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2019 | 11/05/2020 | 11/05/2022 | 11/05/2025 | - | 1,148 | 975 | - | - | - | - | 1,148 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2019 | 11/05/2020 | 11/05/2023 | 11/05/2025 | - | 1,127 | 996 | - | - | - | - | 1,127 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2019 | 11/05/2020 | 11/05/2024 | 11/05/2025 | 2,123 | - | - | - | 2,123 | - | - | 1,102 | 1,021 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2019 | 11/05/2020 | 11/05/2025 | 11/05/2026 | 2,124 | - | - | - | - | - | 2,124 | - | - | |||||||||||||||||||||||||||||||

| LSPP Upfront Shares | 2021 | 09/05/2022 | 09/05/2022 | 09/05/2027 | - | 3,700 | 2,956 | - | - | - | - | 3,700 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2023 | 09/05/2027 | - | 1,095 | 902 | - | - | - | - | 1,095 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2024 | 09/05/2027 | 1,997 | - | - | - | 1,997 | - | - | 1,080 | 917 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2025 | 09/05/2027 | 1,997 | - | - | - | - | - | 1,997 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2026 | 11/05/2027 | 1,997 | - | - | - | - | - | 1,997 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2027 | 11/05/2028 | 1,997 | - | - | - | - | - | 1,997 | - | - | |||||||||||||||||||||||||||||||

| LSPP Upfront Shares | 2022 | 11/05/2023 | 11/05/2023 | 11/05/2028 | - | 3,351 | 2,678 | - | - | - | - | 3,351 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2024 | 11/05/2028 | 1,808 | - | - | - | 1,808 | - | - | 991 | 817 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2025 | 11/05/2028 | 1,808 | - | - | - | - | - | 1,808 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2026 | 11/05/2028 | 1,808 | - | - | - | - | - | 1,808 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2027 | 11/05/2028 | 1,808 | - | - | - | - | - | 1,808 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2028 | 11/05/2029 | 1,811 | - | - | - | - | - | 1,811 | - | - | |||||||||||||||||||||||||||||||

| LSPP Upfront Shares | 2023 | 10/05/2024 | 10/05/2024 | 10/05/2029 | - | - | - | 7,288 | 7,288 | - | - | 4,051 | 3,237 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2025 | 10/05/2029 | - | - | - | 2,186 | - | - | 2,186 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2026 | 10/05/2029 | - | - | - | 2,186 | - | - | 2,186 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2027 | 10/05/2029 | - | - | - | 2,186 | - | - | 2,186 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2028 | 11/05/2029 | - | - | - | 2,186 | - | - | 2,186 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2029 | 11/05/2030 | - | - | - | 2,188 | - | - | 2,188 | - | - | |||||||||||||||||||||||||||||||

| Total | 21,906 | 16,071 | 13,167 | 18,220 | 13,844 | - | 26,282 | 23,060 | 6,303 | |||||||||||||||||||||||||||||||||||

| 4. Share-based remuneration for Executive Board members – continued | ||||||||||||||||||||||||||||||||||||||||||||

| The main conditions of share award plans | Information regarding the reported financial year | |||||||||||||||||||||||||||||||||||||||||||

| Opening Balance | During the year | Closing balance | ||||||||||||||||||||||||||||||||||||||||||

| 1 | 2 | 3 | 4 | 5 | 6A | 6B | 6C | 7 | 8 | 9 | 10 | 11A | 11B | |||||||||||||||||||||||||||||||

Specification of plan1 |

Performance period | Granting/ offering date | Vesting Date | End of retention period | Shares held at the beginning of the year | Shares subject to retention at the beginning of the year | Shares sold-to-cover2 |

Shares granted/ offered | Shares vested | Shares subject to a performance condition | Shares granted/ offered and unvested at year-end | Shares subject to a retention period | Vested shares sold-to-cover2 |

|||||||||||||||||||||||||||||||

| Ljiljana Cortan (CRO) | LSPP Upfront Shares | 2021 | 09/05/2022 | 09/05/2022 | 09/05/2027 | - | 4,478 | 1,936 | - | - | - | - | 4,478 | - | ||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2023 | 09/05/2027 | - | 1,331 | 593 | - | - | - | - | 1,331 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2024 | 09/05/2027 | 1,924 | - | - | - | 1,924 | - | - | 1,319 | 605 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2025 | 09/05/2027 | 1,924 | - | - | - | - | - | 1,924 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2026 | 11/05/2027 | 1,924 | - | - | - | - | - | 1,924 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2021 | 09/05/2022 | 11/05/2027 | 11/05/2028 | 1,925 | - | - | - | - | - | 1,925 | - | - | |||||||||||||||||||||||||||||||

| LSPP Upfront Shares | 2022 | 11/05/2023 | 11/05/2023 | 11/05/2028 | - | 4,419 | 1,911 | - | - | - | - | 4,419 | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2024 | 11/05/2028 | 1,899 | - | - | - | 1,899 | - | - | 1,313 | 586 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2025 | 11/05/2028 | 1,899 | - | - | - | - | - | 1,899 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2026 | 11/05/2028 | 1,899 | - | - | - | - | - | 1,899 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2027 | 11/05/2028 | 1,899 | - | - | - | - | - | 1,899 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2022 | 11/05/2023 | 11/05/2028 | 11/05/2029 | 1,899 | - | - | - | - | - | 1,899 | - | - | |||||||||||||||||||||||||||||||

| LSPP Upfront Shares | 2023 | 10/05/2024 | 10/05/2024 | 10/05/2029 | - | - | - | 6,766 | 6,766 | - | - | 4,724 | 2,042 | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2025 | 10/05/2029 | - | - | - | 2,029 | - | - | 2,029 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2026 | 10/05/2029 | - | - | - | 2,029 | - | - | 2,029 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2027 | 10/05/2029 | - | - | - | 2,029 | - | - | 2,029 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2028 | 11/05/2029 | - | - | - | 2,029 | - | - | 2,029 | - | - | |||||||||||||||||||||||||||||||

| LSPP Deferred Shares Idnt | 2023 | 10/05/2024 | 11/05/2029 | 11/05/2030 | - | - | - | 2,033 | - | - | 2,033 | - | - | |||||||||||||||||||||||||||||||

| Total | 17,192 | 10,228 | 4,440 | 16,915 | 10,589 | - | 23,518 | 17,584 | 3,233 | |||||||||||||||||||||||||||||||||||

| 5. ING shares held by Executive Board members | ||||||||

| Numbers of shares | 2024 | 2023 | ||||||

| Steven van Rijswijk (CEO) | 101,908 | 92,394 | ||||||

| Tanate Phutrakul (CFO) | 33,160 | 25,619 | ||||||

| Ljiljana Čortan (CRO) | 17,584 | 10,228 | ||||||

| 6. 2025 Target areas | CEO | CFO | CRO | ||||||||||||||

| Weighting | Weighting | Weighting | |||||||||||||||

| Financial | Profit before tax | 16.7% | 16.7% | 8.3% | |||||||||||||

| Return on equity | 16.7% | 16.7% | 8.3% | ||||||||||||||

| Operational expenses | 16.7% | 16.7% | 8.3% | ||||||||||||||

| 50% | 50% | 25% | |||||||||||||||

| Non-financial | Customer |

▪Increase number of mobile primary customers as this leads to deeper relationships, greater customer satisfaction, and ultimately customers choosing ING for more of their financial needs

▪Increase customer satisfaction of Retail and Wholesale by increasing NPS

|

7.5% | 5% | NA | ||||||||||||

| Risk & Regulatory |

▪Manage financial risk within risk appetite, with a specific focus on the revision of the use of internal models

▪Manage non-financial risk within risk appetite, with a specific focus on the IT risk management

▪Maintain operational effectiveness of KYC

|

15% | 17.5% | 45% | |||||||||||||

| Strategy | ▪Increase digitisation and straight-through-processing (STP) rate of customer processes |

12.5% | |||||||||||||||

▪Increase efficiency of finance processes while maintaining the effectiveness of controls |

12.5% | ||||||||||||||||

▪Increase efficiency of risk processes while maintaining the effectiveness of controls |

15% | ||||||||||||||||

| Environment |

▪Increase sustainable volume mobilised

▪Support the transition of the most carbon-intensive sectors in Wholesale Banking towards a better carbon performance, in line with our 2030 decarbonisation target

|

10% | |||||||||||||||

▪Continuous refinement of CSRD disclosures |

10% | ||||||||||||||||

▪Continuous refinement of ESG risk assessment methodology |

10% | ||||||||||||||||

| Social |

▪Strengthen organisational health with a focus on five priority areas: strategic clarity, role clarity, customer orientation, data driven decision making, talent development

▪Increase gender balance in ING's leadership cadre

|

5% | 5% | 5% | |||||||||||||

| 50% | 50% | 75% | |||||||||||||||

| Total | 100% | 100% | 100% | ||||||||||||||

| 7. Internal ratio for CEO | All ING staff | ||||

| 2024 | 1:24 | ||||

| 2023 | 1:24 | ||||

| 2022 | 1:25 | ||||

| 2021 | 1:28 | ||||

| 2020 | 1:31 | ||||

| 8. Development of directors’ remuneration, company performance and employee remuneration ¹ | |||||||||||||||||||||||||||||||||||

| Amount in thousands of euros unless otherwise stated | FY 2024 | FY 2024 vs FY 2023 | FY 2023 vs FY 2022 | FY 2022 vs FY 2021 | FY 2021 vs FY 2020 | FY 2020 vs FY 2019 | |||||||||||||||||||||||||||||

Directors' remuneration (Executive Board) 2, 3, 4, 5 | |||||||||||||||||||||||||||||||||||

| Steven van Rijswijk (CEO) | 2,159 | 83 | 4.0% | 23 | 1.1% | -24 | -1.2% | 578 | 38.6% | 100 | 7.2% | ||||||||||||||||||||||||

| Tanate Phutrakul (CFO) | 1,490 | 44 | 3.0% | 33 | 2.3% | -27 | -1.9% | 218 | 17.9% | - | - | ||||||||||||||||||||||||

Ljiljana Čortan (CRO) |

1,494 | 64 | 4.5% | 7 | 0.5% | - | - | - | - | - | - | ||||||||||||||||||||||||

Directors' remuneration (Supervisory Board) 6 | |||||||||||||||||||||||||||||||||||

Karl Guha (chairperson) |

206 | - | - | - | - | - | - | - | - | - | - | ||||||||||||||||||||||||

Mike Rees (vice-chairperson) |

158 | 7 | 4.6% | 12 | 8.8% | 10 | 7.8% | 0 | 0% | - | - | ||||||||||||||||||||||||

| Juan Colombás | 141 | 18 | 14.7% | 21 | 20.4% | 8 | 8.5% | - | - | - | - | ||||||||||||||||||||||||

| Margarete Haase | 128 | 11 | 9.3% | 6 | 4.9% | 8 | 7.7% | -1 | -1.0% | 7 | 7.1% | ||||||||||||||||||||||||

| Lodewijk Hijmans van den Bergh | 111 | 4 | 3.4% | 11 | 10.8% | - | - | - | - | - | - | ||||||||||||||||||||||||

| Herman Hulst | 111 | 4 | 3.4% | 8 | 7.5% | 5 | 5.0% | - | - | - | - | ||||||||||||||||||||||||

| Harold Naus | 106 | 8 | 8.7% | 6 | 6.0% | -3 | -2.9% | - | - | - | - | ||||||||||||||||||||||||

| Alexandra Reich | 118 | - | - | - | - | - | - | - | - | - | - | ||||||||||||||||||||||||

| Herna Verhagen | 111 | 4 | 3.4% | 6 | 5.4% | 2 | 2.0% | -21 | -17.4% | - | - | ||||||||||||||||||||||||

| Company’s performance | |||||||||||||||||||||||||||||||||||

| Retail primary relationships (in mln) | 16.2 | 0.9 | 6% | 0.7 | 5% | 0.3 | 2% | 0.4 | 3% | 0.6 | 5% | ||||||||||||||||||||||||

| Profit before tax ING Group (in mln) | 9,300 | -1,192 | -11% | 4,990 | 91% | -1,280 | -19% | 2,973 | 78% | -3,025 | -44% | ||||||||||||||||||||||||

| Return on equity based on IFRS-EU equity | 13% | -1.8% | -12% | 7.6% | 106% | -2% | -22% | 4.4% | 92% | -4.6% | -49% | ||||||||||||||||||||||||

Average employee remuneration | |||||||||||||||||||||||||||||||||||

| Average fixed and annual variable remuneration | 81 | 3.8 | 4.9% | 4.8 | 6.5% | 2.4 | 3.5% | 2.7 | 4.0% | - | - | ||||||||||||||||||||||||

| Remuneration component | Operation | ||||

| Annual remuneration, committee fees and attendance fees |

▪SB members receive fees for their service on the SB as set out in the remuneration structure table below. The remuneration is awarded to the SB members by the General Meeting.

▪The remuneration structure reflects the roles and responsibilities of individual SB members.

▪All fees are paid out fully in cash. No variable remuneration is provided to ensure that the SB members can maintain independence and provide objective stewardship of ING, thereby contributing to the long-term performance of the company.

▪The fees of SB members may be indexed annually based on the salary increases for the wider workforce within ING for that relevant year.

▪Any adjustments in fee levels other than those following from the indexation will be subject to the approval of the General Meeting.

▪Any changes in the fee levels will be presented in ING’s Annual Report for the relevant year.4

|

||||

| Expenses | ▪SB members are reimbursed for their travel and business-related expenses incurred in their capacity as SB members. |

||||

| 9. ING shares held by Supervisory Board members | ||||||||

| Numbers of shares | 2024 | 2023 | ||||||

| Herman Hulst | 3,650 | 3,650 | ||||||

| Harold Naus | 1,645 | 1,645 | ||||||

| 10. Supervisory Board remuneration | ||||||||

| Amounts in euros | 2024 | 2025 | ||||||

| Annual remuneration | ||||||||

| Chairperson | 131,700 | 138,500 | ||||||

| Vice-chairperson | 100,100 | 105,300 | ||||||

| Member | 73,700 | 77,500 | ||||||

| Committee fees (annual amounts) | ||||||||

| Committee chairperson | 21,000 | 22,000 | ||||||

| Committee member | 10,500 | 11,000 | ||||||

| Attendance fees (per meeting) | ||||||||

| Attendance fee outside country of residence | 2,000 | 2,100 | ||||||

| Attendance fee outside continent of residence | 7,500 | 7,800 | ||||||

Remuneration principles | ||

Attract and retain to deliver ING's strategic goals Support ING's ambition to be the best European bank by attracting, retaining, and rewarding qualified employees who have the desired values, skills, behaviours, and knowledge to deliver this goal with market competitive pay. | ||

Pay for performance Define a clear link between the group, business line, and employee performance and individual remuneration, motivating, recognising, and rewarding long-term sustainable value. | ||

|

Fair and transparent