Document

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023 Exhibit 19.15.7

__________________________________________________________________________________

Technical Report Summary

Obuasi

A Life of Mine Summary Report

Effective date: 31 December 2023

As required by § 229.601(b)(96) of Regulation S-K as an exhibit to AngloGold Ashanti's Annual Report on Form 20-F pursuant to Subpart 229.1300 of Regulation S-K - Disclosure by Registrants Engaged in Mining Operations (§ 229.1300 through § 229.1305).

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

Date and Signatures Page

This report is effective as of 31 December 2023.

Where the registrant (AngloGold Ashanti plc) has relied on more than one Qualified Person to prepare the information and documentation supporting its disclosure of Mineral Resource or Mineral Reserve, the section(s) prepared by each qualified person has been clearly delineated.

AngloGold Ashanti has recognised that in preparing this report, the Qualified Person(s) may have, when necessary, relied on information and input from others, including AngloGold Ashanti. As such, the table below lists the technical specialists who provided the relevant information and input, as necessary, to the Qualified Person to include in this Technical Report Summary. All information provided by AngloGold Ashanti has been identified in Section 25: Reliance on information provided by the registrant in this report.

The registrant confirms it has obtained the written consent of each Qualified Person to the use of the person's name, or any quotation from, or summarisation of, the Technical Report summary in the relevant registration statement or report, and to the filing of the Technical Report Summary as an exhibit to the registration statement or report. The written consent only pertains to the particular section(s) of the Technical Report Summary prepared by each Qualified Person. The written consent has been filed together with the Technical Report Summary exhibit and will be retained for as long as AngloGold Ashanti relies on the Qualified Person’s information and supporting documentation for its current estimates regarding Mineral Resource or Mineral Reserve.

MINERAL RESOURCE QUALIFIED PERSON Eric Kofi Owusu Acheampong

Sections prepared: 1 - 11, 20 - 25 /s/ Eric Kofi Owusu Acheampong

MINERAL RESERVE QUALIFIED PERSON Douglas Atanga

Sections prepared: 1, 12-19, 21 - 25 /s/ Douglas Atanga

Responsibility Technical Specialist

Estimation Linda Acheampong

Evaluation QA/QC Samuel Fianko

Exploration Raymond Trornu

Geological Model Samuel Fianko

Geology QA/QC Bruno Ansah

Geotechnical Engineering Dawuda Konadu

Hydrogeology Philip Nyoagbe

Mineral Resource Classification Linda Acheampong

Environmental and Permitting George Owusu-Ansah

Financial Model Ishmael Kusi

Infrastructure Eric Broni

Legal Araba Attua-Afari

Metallurgy Kwaku Buahin

Mine Planning Douglas Atanga

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

Consent of Qualified Person

Mineral Reserve Classification Douglas Atanga I, Eric Kofi Owusu Acheampong, in connection with the Technical Report Summary for “Obuasi, A Life of Mine Summary Report” dated 31 December 2023 (the “Technical Report Summary”) as required by Item 601(b)(96) of Regulation S-K and filed as an exhibit to AngloGold Ashanti plc’s (“AngloGold Ashanti”) annual report on Form 20-F for the year ended 31 December 2023 and any amendments or supplements and/or exhibits thereto (collectively, the “Form 20-F”) pursuant to Subpart 1300 of Regulation S-K promulgated by the U.S. Securities and Exchange Commission (“1300 Regulation S-K”), consent to:

▪the public filing and use of the Technical Report Summary as an exhibit to the Form 20-F;

▪the use of and reference to my name, including my status as an expert or “Qualified Person” (as defined in 1300 Regulation S-K) in connection with the Form 20-F and Technical Report Summary;

▪any extracts from, or summary of, the Technical Report Summary in the Form 20-F and the use of any information derived, summarised, quoted or referenced from the Technical Report Summary, or portions thereof, that is included or incorporated by reference into the Form 20-F; and

▪the incorporation by reference of the above items as included in the Form 20-F into AngloGold Ashanti's registration statement on Form S-8 (Registration No. 333-274681) (and any amendments or supplements thereto).

Date: 25 April 2024

Eric Kofi Owusu Acheampong

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

Consent of Qualified Person

/s/ Eric Kofi Owusu Acheampong I, Douglas Atanga, in connection with the Technical Report Summary for “Obuasi, A Life of Mine Summary Report” dated 31 December 2023 (the “Technical Report Summary”) as required by Item 601(b)(96) of Regulation S-K and filed as an exhibit to AngloGold Ashanti plc’s (“AngloGold Ashanti”) annual report on Form 20-F for the year ended 31 December 2023 and any amendments or supplements and/or exhibits thereto (collectively, the “Form 20-F”) pursuant to Subpart 1300 of Regulation S-K promulgated by the U.S. Securities and Exchange Commission (“1300 Regulation S-K”), consent to:

▪the public filing and use of the Technical Report Summary as an exhibit to the Form 20-F;

▪the use of and reference to my name, including my status as an expert or “Qualified Person” (as defined in 1300 Regulation S-K) in connection with the Form 20-F and Technical Report Summary;

▪any extracts from, or summary of, the Technical Report Summary in the Form 20-F and the use of any information derived, summarised, quoted or referenced from the Technical Report Summary, or portions thereof, that is included or incorporated by reference into the Form 20-F; and

▪the incorporation by reference of the above items as included in the Form 20-F into AngloGold Ashanti's registration statement on Form S-8 (Registration No. 333-274681) (and any amendments or supplements thereto).

Date: 25 April 2024

/s/ Douglas Atanga

Douglas Atanga

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

Table of Contents

|

|

|

|

|

|

| 1 Executive Summary |

|

| 1.1 Property description including mineral rights |

|

| 1.2 Ownership |

|

| 1.3 Geology and mineralisation |

|

| 1.4 Status of exploration, development and operations |

|

| 1.5 Mining methods |

|

| 1.6 Mineral processing |

|

| 1.7 Mineral Resource and Mineral Reserve estimates |

|

| 1.8 Summary capital and operating cost estimates |

|

| 1.9 Permitting requirements |

|

| 1.10 Conclusions and recommendations |

|

| 2 Introduction |

|

| 2.1 Disclose registrant |

|

| 2.2 Terms of reference and purpose for which this Technical Report Summary was prepared |

|

| 2.3 Sources of information and data contained in the report / used in its preparation |

|

| 2.4 Qualified Person(s) site inspections |

|

| 2.5 Purpose of this report |

|

| 3 Property description |

|

| 3.1 Location of the property |

|

| 3.2 Area of the property |

|

| 3.3 Legal aspects (including environmental liabilities) and permitting |

|

| 3.4 Agreements, royalties and liabilities |

|

| 4 Accessibility, climate, local resources, infrastructure and physiography |

|

| 5 History |

|

| 6 Geological setting, mineralisation and deposit |

|

| 6.1 Geological setting |

|

| 6.2 Geological model and data density |

|

| 6.3 Mineralisation |

|

| 7 Exploration |

|

| 7.1 Nature and extent of relevant exploration work |

|

| 7.2 Drilling techniques and spacing |

|

| 7.3 Results |

|

| 7.4 Locations of drill holes and other samples |

|

| 7.5 Hydrogeology |

|

| 7.6 Geotechnical testing and analysis |

|

| 8 Sample preparation, analysis and security |

|

| 8.1 Sample preparation |

|

| 8.2 Assay method and laboratory |

|

| 8.3 Sampling governance |

|

| 8.4 Quality Control and Quality Assurance |

|

| 8.5 Qualified Person's opinion on adequacy |

|

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

|

|

|

|

|

|

| 9 Data verification |

|

| 9.1 Data verification procedures |

|

| 9.2 Limitations on, or failure to conduct verification |

|

| 9.3 Qualified Person's opinion on data adequacy |

|

| 10 Mineral processing and metallurgical testing |

|

| 10.1 Mineral processing / metallurgical testing |

|

| 10.2 Laboratory and results |

|

| 10.3 Qualified Person's opinion on data adequacy |

|

| 11 Mineral Resource estimates |

|

| 11.1 Reasonable basis for establishing the prospects of economic extraction for Mineral Resource |

|

| 11.2 Key assumptions, parameters and methods used |

|

| 11.3 Mineral Resource classification and uncertainty |

|

| 11.4 Mineral Resource summary |

|

| 11.5 Qualified Person's opinion |

|

| 12 Mineral Reserve estimates |

|

| 12.1 Key assumptions, parameters and methods used |

|

| 12.2 Cut-off grades |

|

| 12.3 Mineral Reserve classification and uncertainty |

|

| 12.4 Mineral Reserve summary |

|

| 12.5 Qualified Person’s opinion |

|

| 13 Mining methods |

|

| 13.1 Requirements for stripping, underground development and backfilling |

|

| 13.2 Mine equipment, machinery and personnel |

|

| 13.3 Final mine outline |

|

| 14 Processing and recovery methods |

|

| 15 Infrastructure |

|

| 16 Market studies |

|

| 17 Environmental studies, permitting plans, negotiations, or agreements with local individuals or groups |

|

| 17.1 Permitting |

|

| 17.2 Requirements and plans for waste tailings disposal, site monitoring and water management |

|

| 17.3 Socio-economic impacts |

|

| 17.4 Mine closure and reclamation |

|

| 17.5 Qualified Person's opinion on adequacy of current plans |

|

| 17.6 Commitments to ensure local procurement and hiring |

|

| 18 Capital and operating costs |

|

| 18.1 Capital and operating costs |

|

| 18.2 Risk assessment |

|

| 19 Economic analysis |

|

| 19.1 Key assumptions, parameters and methods |

|

| 19.2 Results of economic analysis |

|

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

|

|

|

|

|

|

| 19.3 Sensitivity analysis |

|

| 20 Adjacent properties |

|

| 21 Other relevant data and information |

|

| 21.1 Inclusive Mineral Resource |

|

| 21.2 Inclusive Mineral Resource by-products |

|

| 21.3 Mineral Reserve by-products |

|

| 21.4 Inferred Mineral Resource in annual Mineral Reserve design |

|

| 21.5 Additional relevant information |

|

| 21.5.1 Tracking of the conversion of Inferred to Indicated Mineral Resource between years |

|

21.5.2 Reconciling mined Inferred Mineral Resource to Grade Control |

|

| 21.5.3 Additional relevant information |

|

| 21.6 Certificate of Qualified Person(s) |

|

| 22 Interpretation and conclusions |

|

| 23 Recommendations |

|

| 24 References |

|

| 24.1 References |

|

| 24.2 Mining terms |

|

| 24.3 Abbreviations and acronyms |

|

| 25 Reliance on information provided by the registrant |

|

List of Figures

|

|

|

|

|

|

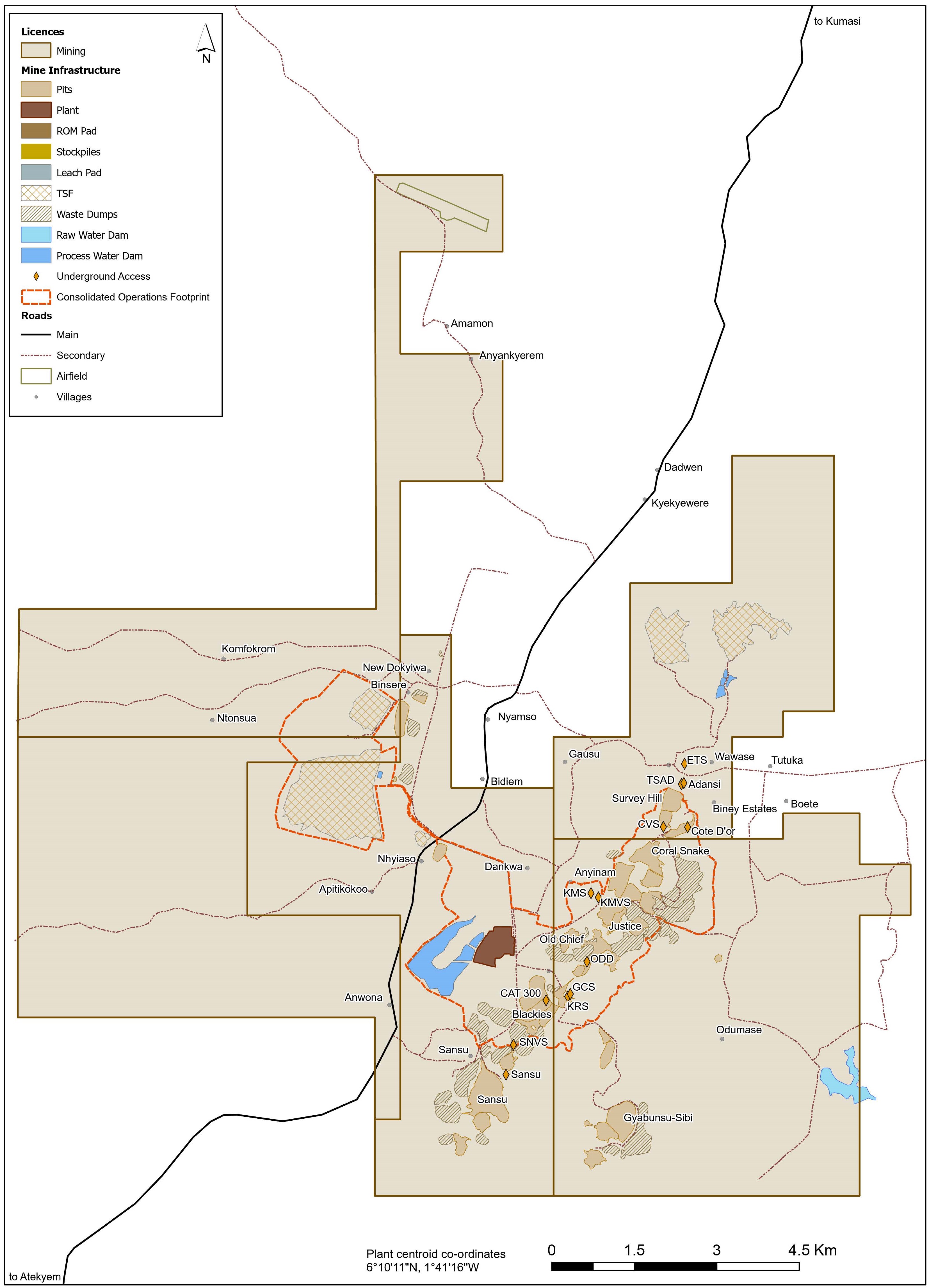

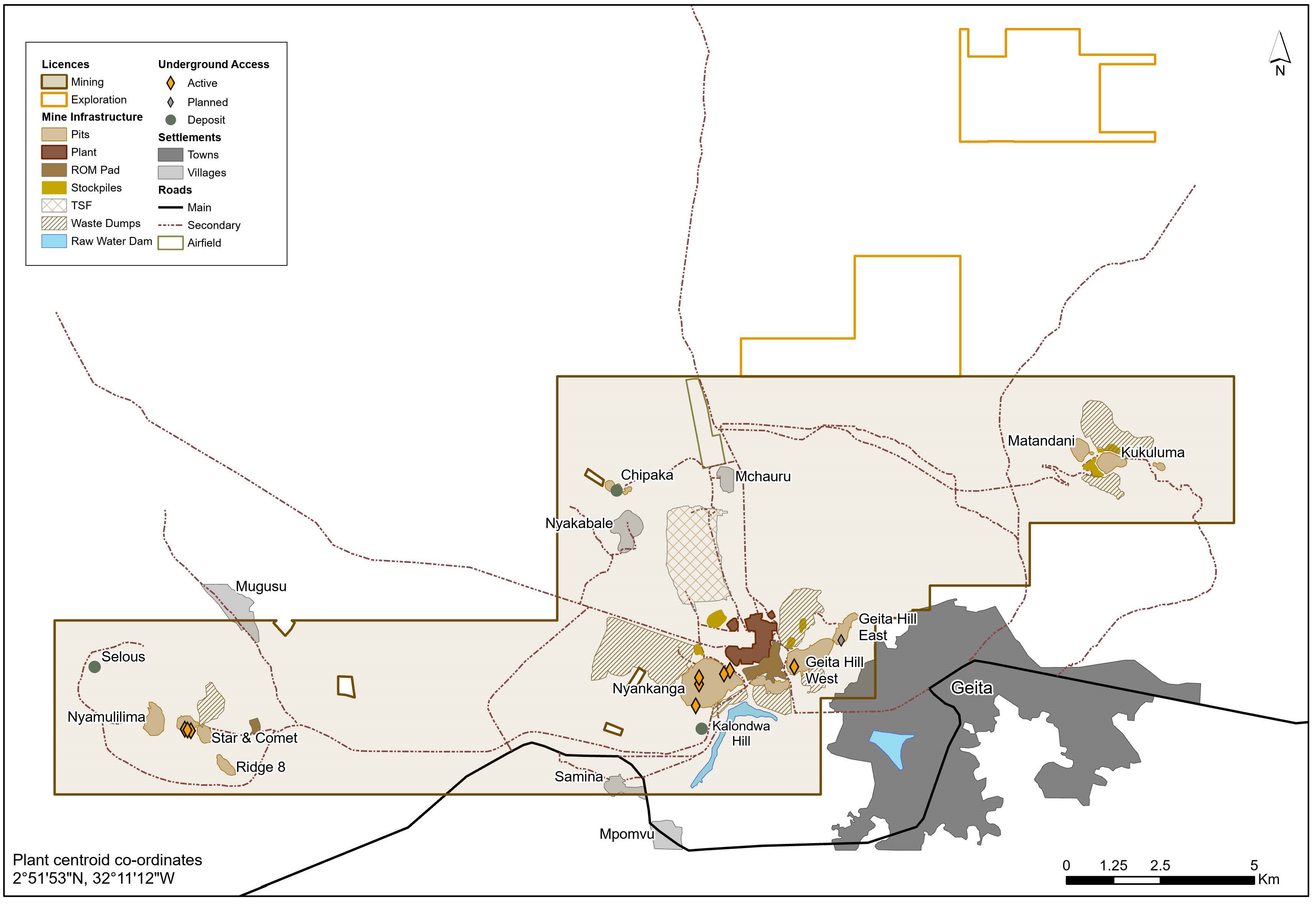

| Map showing the location, infrastructure and mining licence area for Obuasi gold mine. The coordinates of the mine, as represented by the plant, are depicted on the map and are in the geographic coordinate system. |

|

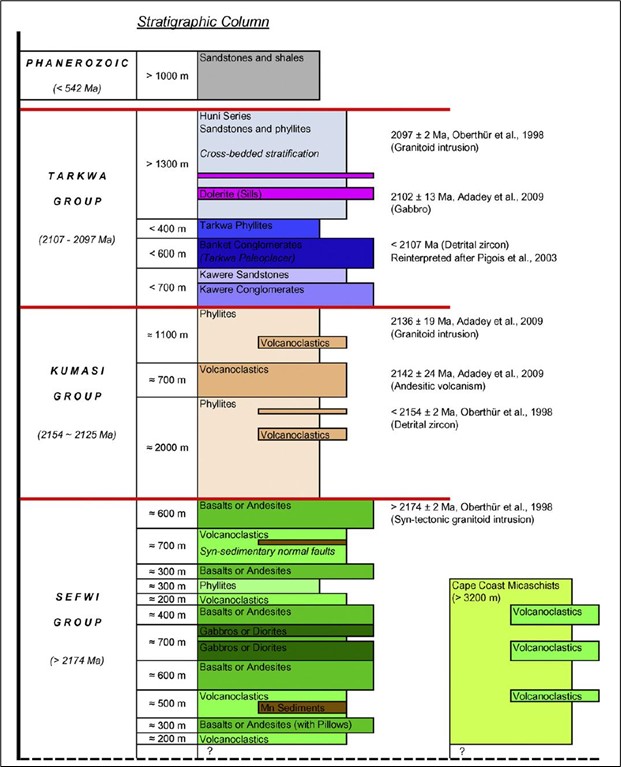

Stratigraphic column of the southwest part of Ghana (Perrouty et al., 2012) |

|

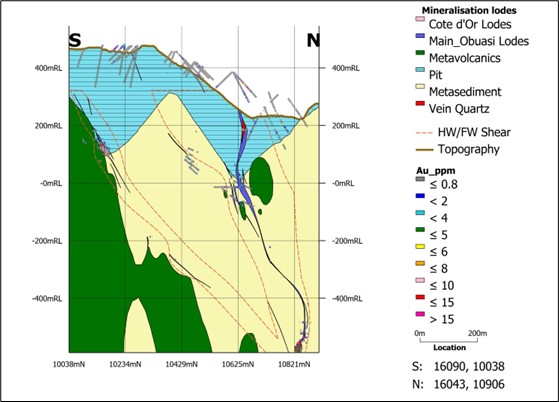

| A typical S-N geological cross-section (looking West) of Obuasi mine’s Block 2, through Anyinam and Côte d’Or pit, showing Côte d’Or and Obuasi Main lodes, elevation in metres Relative Level (mRL) |

|

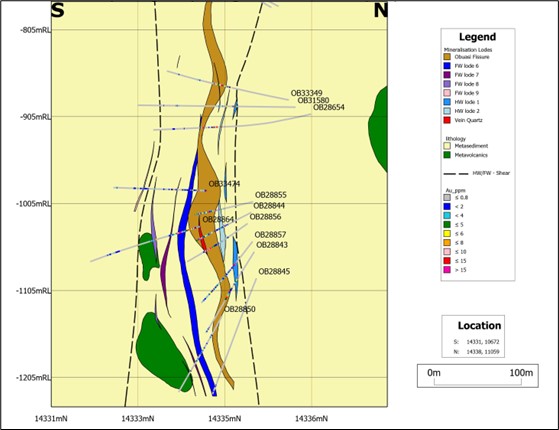

| A typical S-N geological cross-section (Looking West) through Obuasi mine’s Block 10 deposit, elevation in mRL |

|

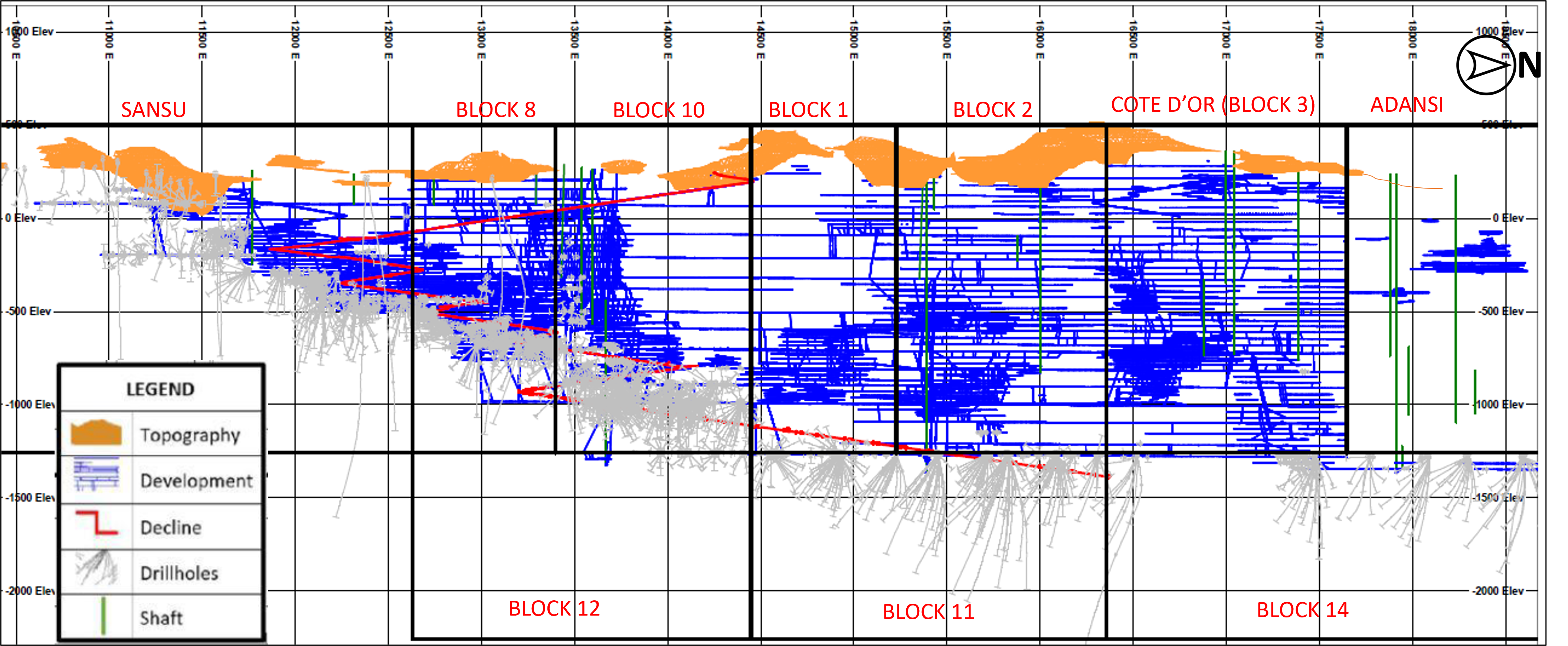

| S-N Section showing the underground areas with the locations of drill holes, shafts, declines and development (in local grid, looking west). |

|

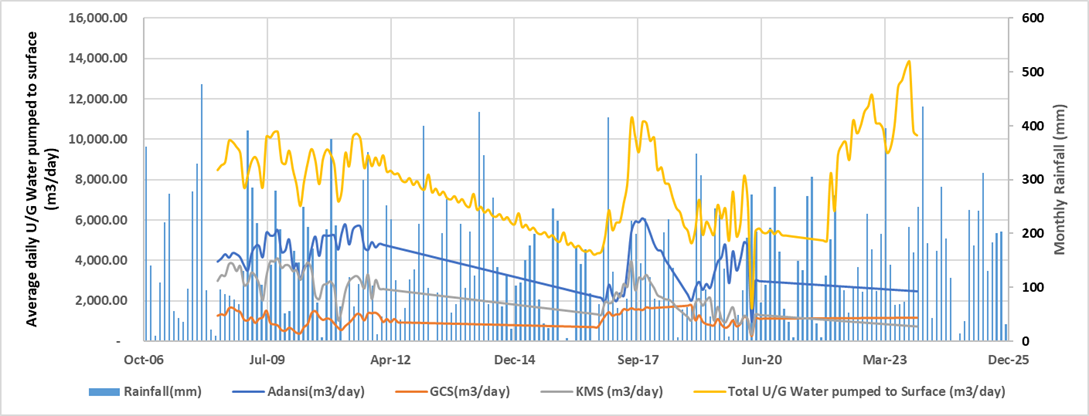

| Rainfall and pumping |

|

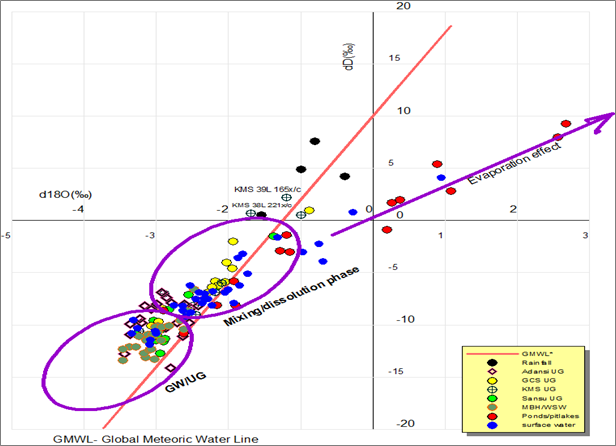

| Underground isotopic plots |

|

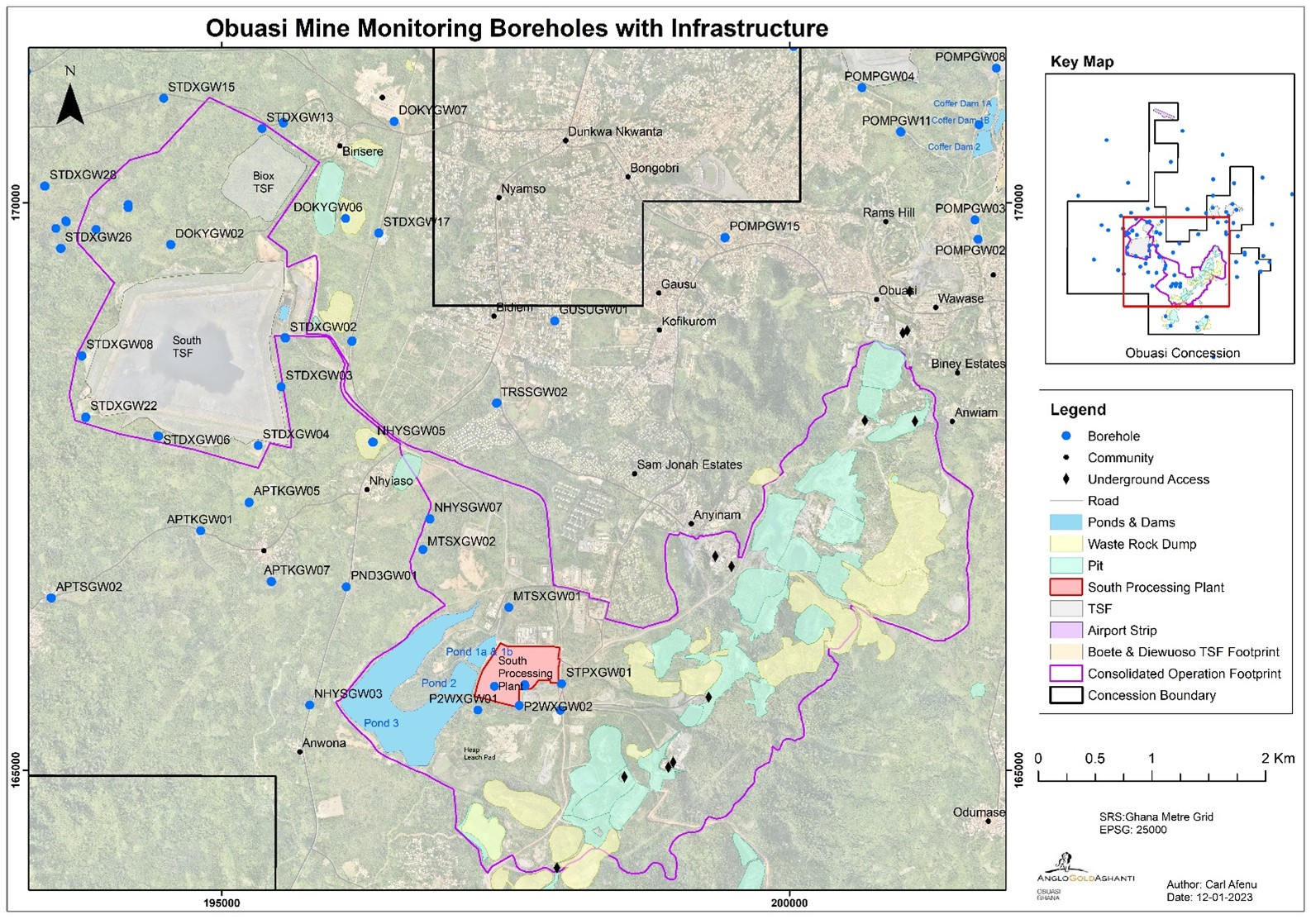

| Obuasi monitoring wells and infrastructure |

|

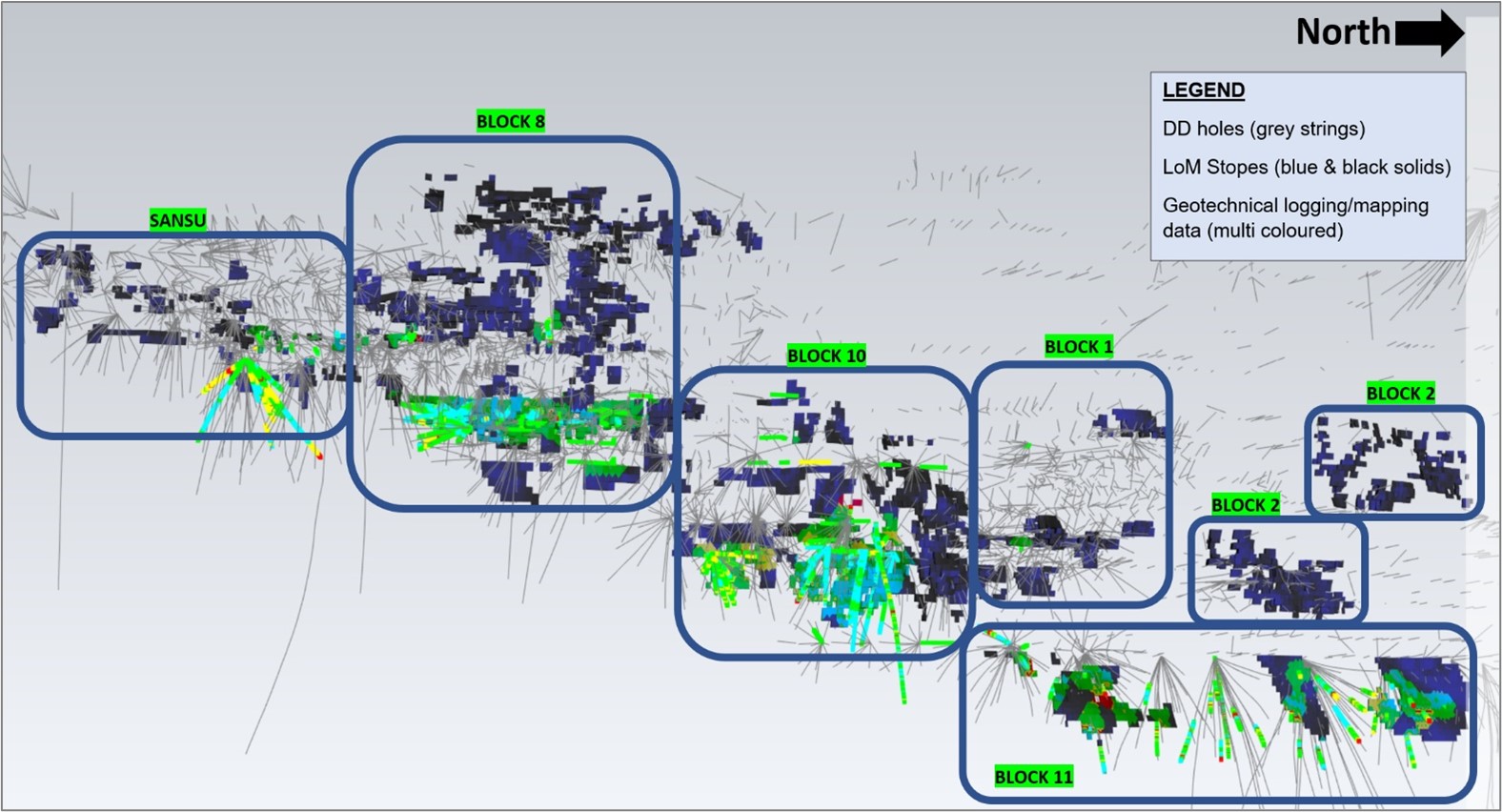

| Geotechnical logging/mapping data coverage within the mining blocks (long section looking true west) |

|

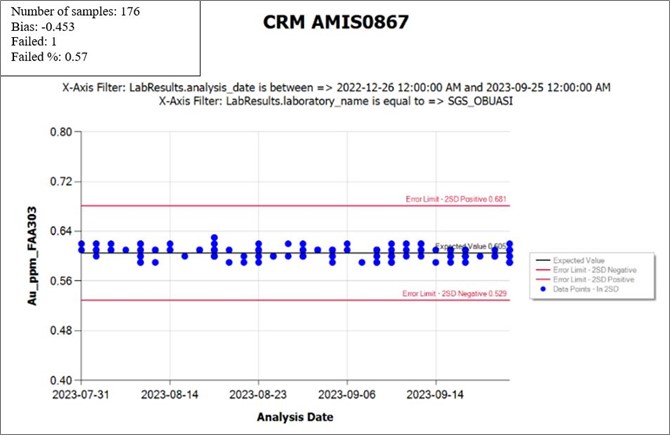

| Certified reference material AMIS0867 (2023) |

|

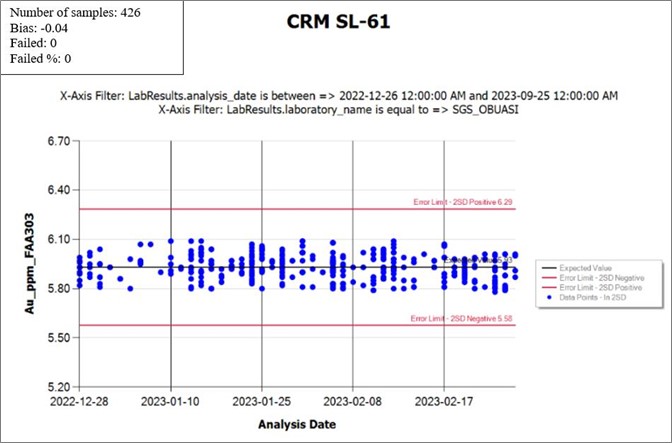

| Certified reference material SL-61 (2023) |

|

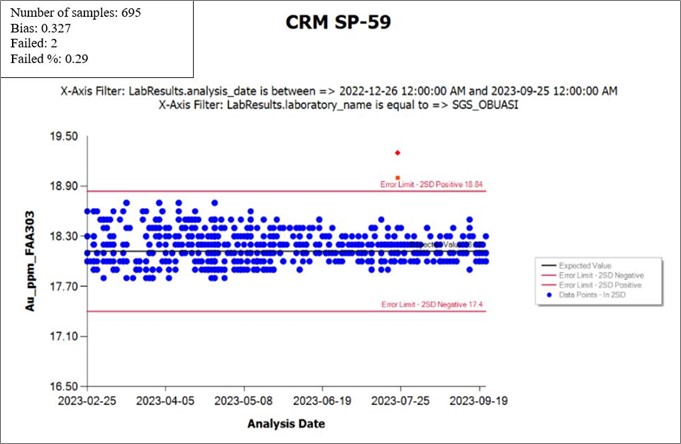

| Certified reference material SP-59 (2023) |

|

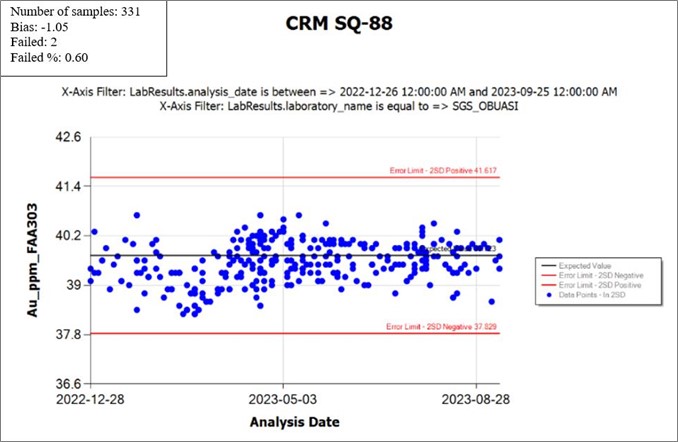

| Certified reference material SQ-88 (2023) |

|

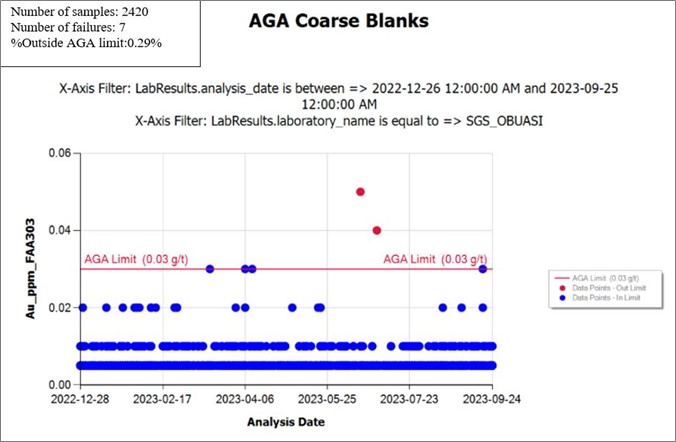

| Coarse blank material (2023) |

|

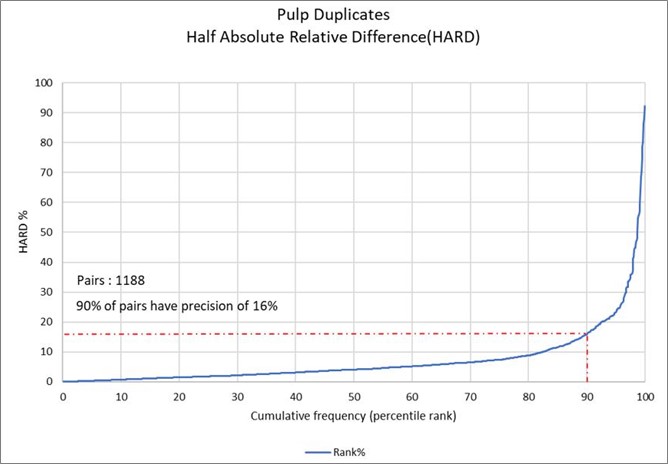

| Pulp duplicate HARD graph |

|

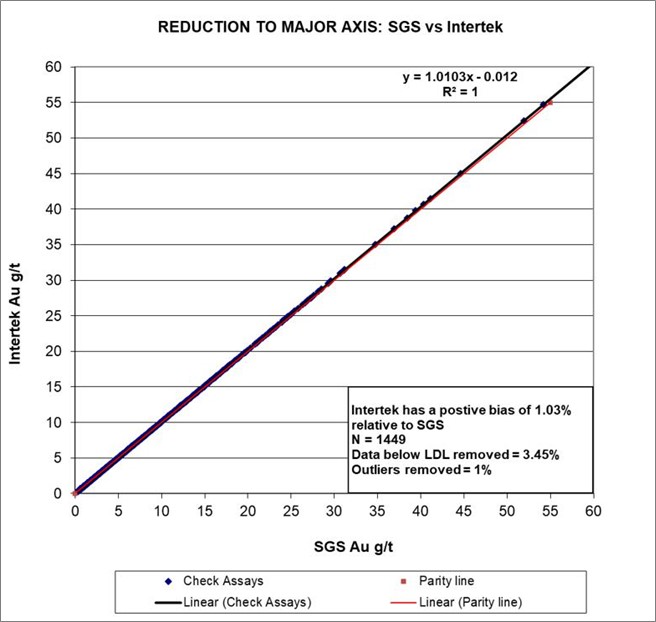

| Check assay graph (SGS Laboratory vs Intertek Laboratory) |

|

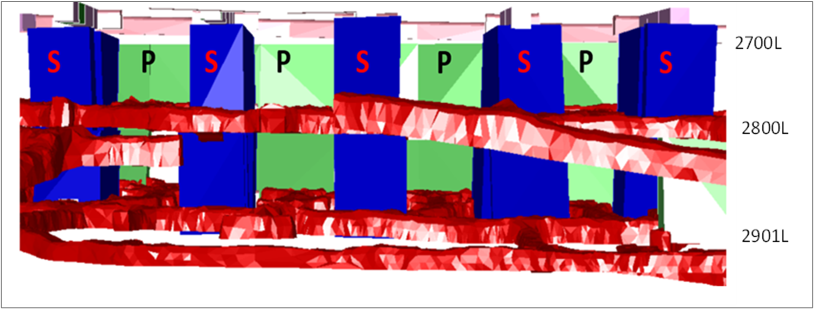

| Example of TOS Design for Block 8L: S-Secondary Stope, P-Primary Stope - long section view |

|

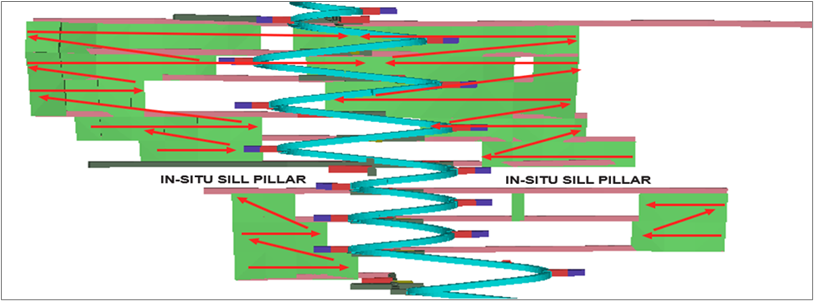

| Example of LRS design in Block 1 - long section view |

|

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

|

|

|

|

|

|

| Example of MSLOS in Block 11 – isometric view |

|

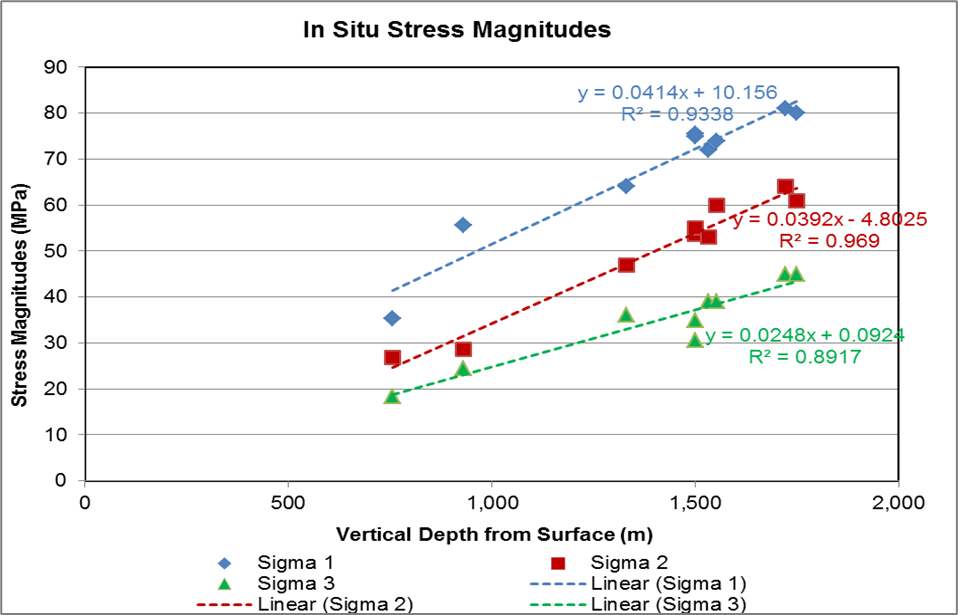

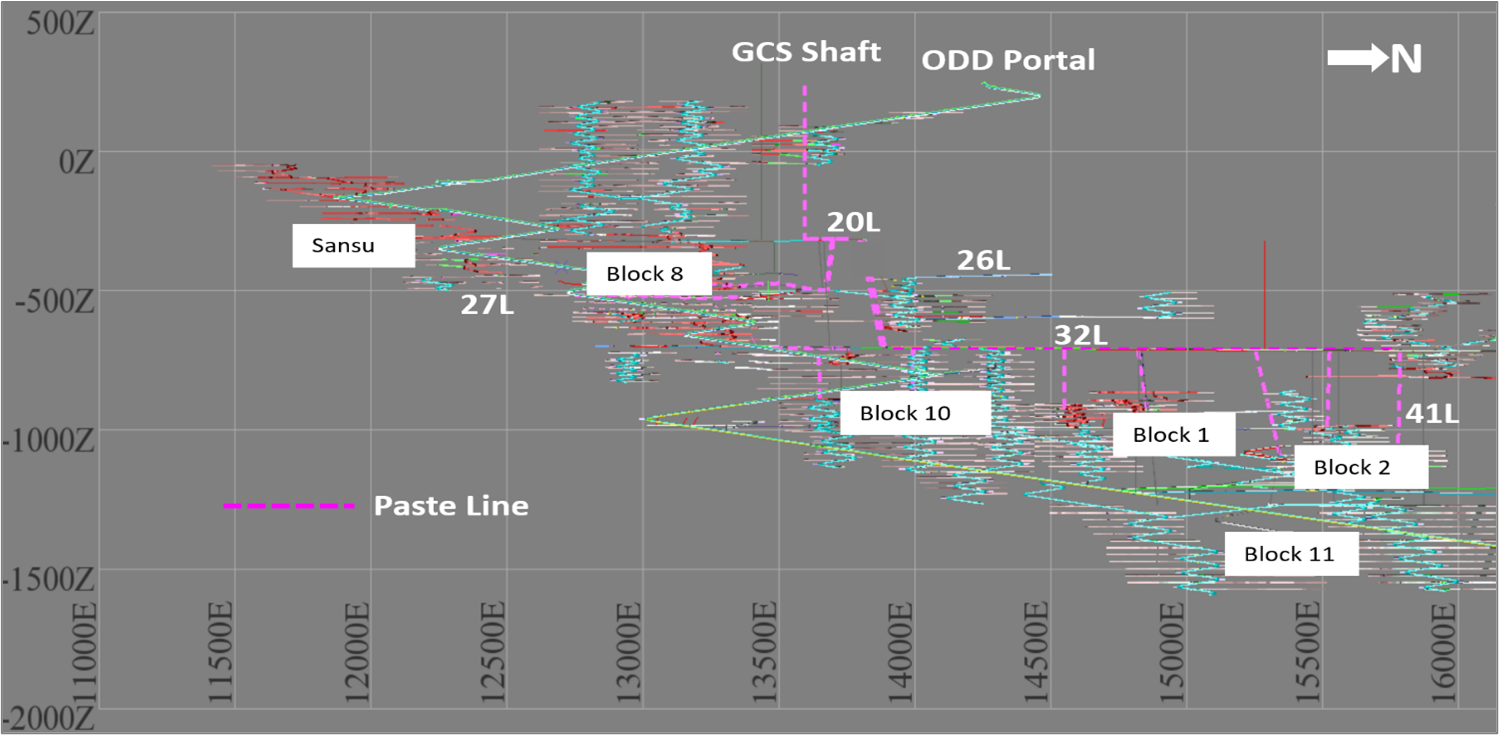

Obuasi in situ stress measurement locations – long section view (looking in a true west direction) |

|

| Relationship of principal stress with depth |

|

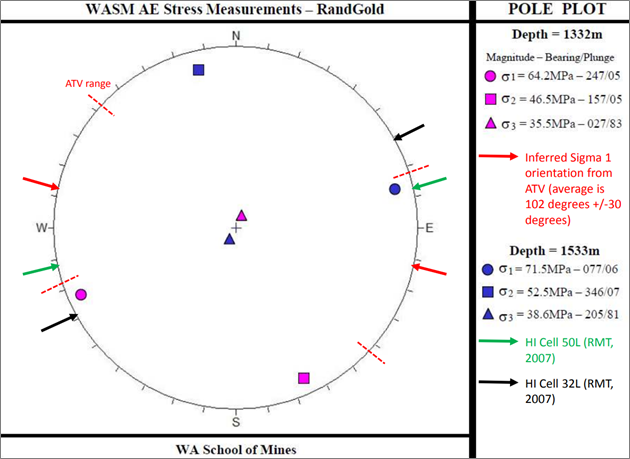

| WASM AE stress measurements: pole plot |

|

| Underground pastefill reticulation geometry – long section view (looking true west) |

|

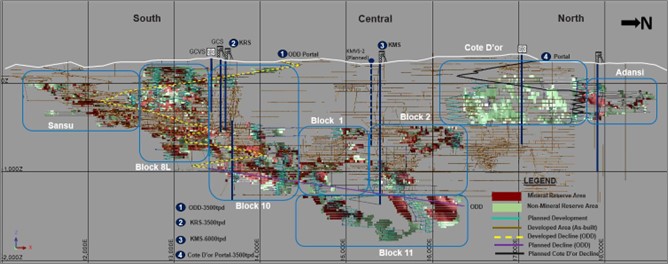

| Obuasi mine outline – long section view (looking true west) |

|

| A schematic representation of the South Treatment Plant |

|

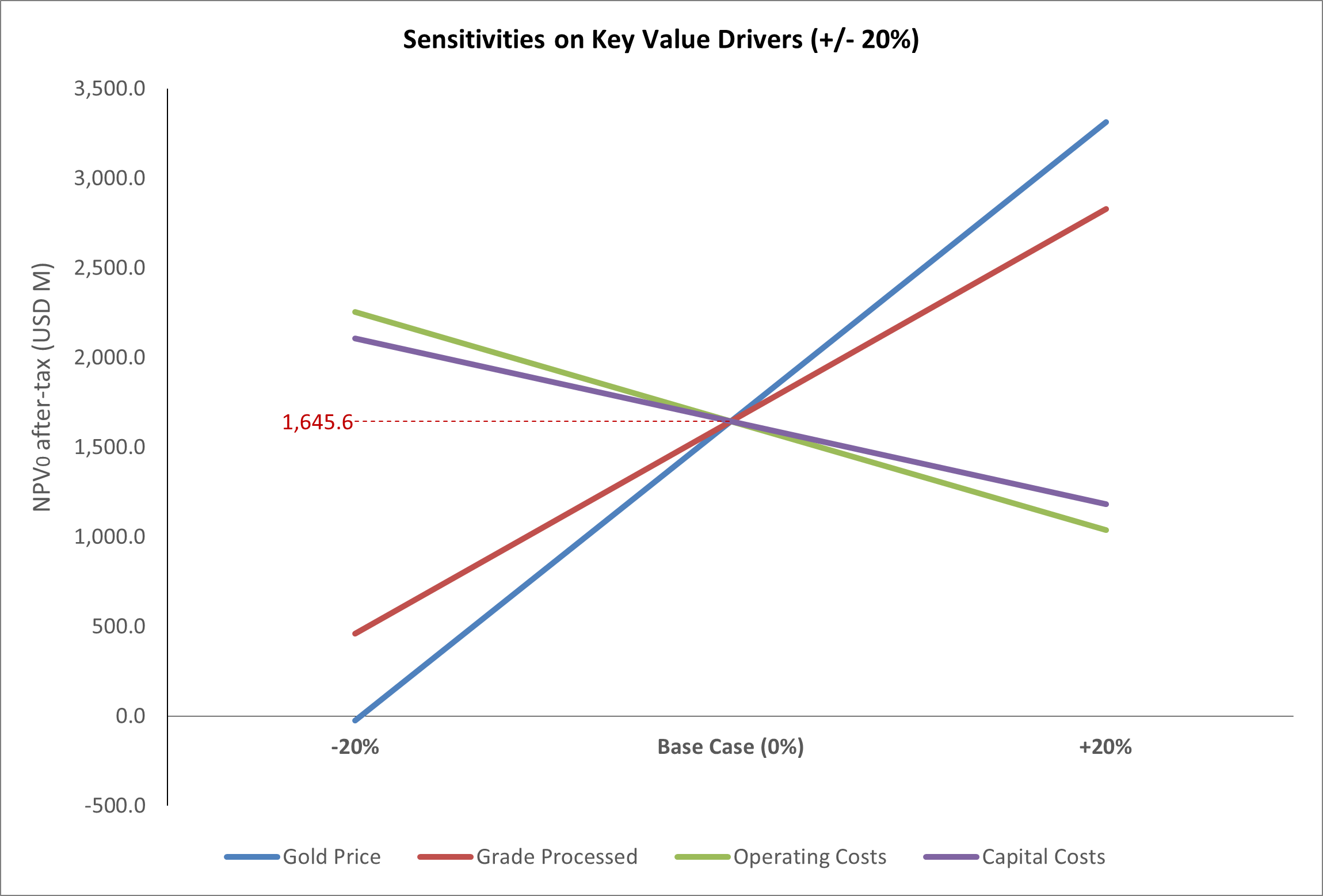

| Obuasi Mineral Reserve sensitivity on key value drivers |

|

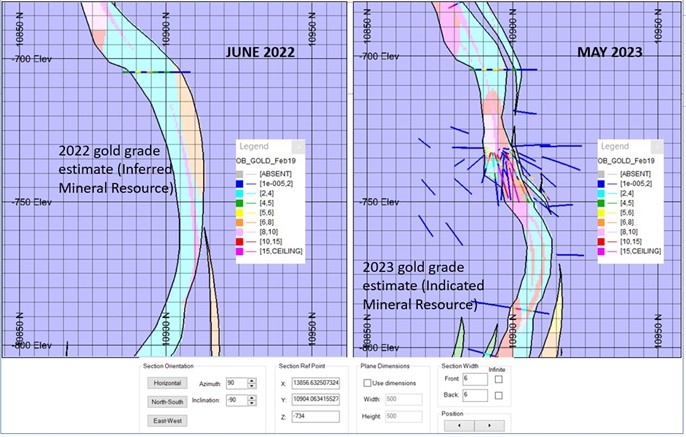

| A typical S-N vertical section (in local coordinates) for Block 10 comparing the 2022 gold grade estimates (left) with the 2023 gold grade estimates (right) for an area upgraded from Inferred to Indicated Mineral Resource |

|

List of Tables

|

|

|

|

|

|

| Exclusive gold Mineral Resource |

|

| Gold Mineral Reserve |

|

| Historical ounce production table from 1897 to 2023 |

|

| Reconciliation of produced gold for 2020, 2021, 2022 and 2023 |

|

| Details of average drill hole spacing and type in relation to Mineral Resource classification |

|

| Summary of major hydrochemical parameters of samples |

|

| Hydraulic conductivities of main hydrogeologic units |

|

| Recharge estimates from previous studies |

|

| Example of geotechnical rock mass core logging parameters |

|

| Summary of rock properties test results for the active mining blocks |

|

| Block 8L master composite confirmatory test: flotation conditions |

|

| Master composite confirmatory test: gravity recoverable gold test |

|

| Summary master composite confirmatory test |

|

| Master composite confirmatory test: products |

|

| Block 8L master composite: diagnostic leach test |

|

| Parameters used for generating the Underground Mineral Resource |

|

| Exclusive gold Mineral Resource |

|

| Mineral Reserve modifying factors |

|

| P300 FS stope design dimensions and modifying factors recommendations |

|

| Gold Mineral Reserve |

|

| External dilution recommendations |

|

| Capital budget in financial model |

|

| Key operational costs |

|

| Obuasi cash flow analysis (Mineral Reserve material only) |

|

Sensitivity analysis for key value drivers (numbers as after-tax NPV0, in $M) |

|

| Inclusive gold Mineral Resource |

|

| Inferred gold Mineral Resource in annual Mineral Reserve design |

|

| Inferred to Indicated Mineral Resource Conversion for 2023 |

|

| The following local prices of gold were used as a basis for estimation in the declaration as of 31 December 2023, unless otherwise stated |

|

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

1.Executive Summary

1.1Property description including mineral rights

The Obuasi gold mine (Obuasi) is 100% owned by AngloGold Ashanti plc (AngloGold Ashanti) and is a production stage property. All required mineral rights to the property are held by the Company. The mine, which is an underground operation, has been in operation since 1897 (more than 120 years). AngloGold Ashanti assumed ownership and operation of the mine since 2004.

The mine is in the Obuasi municipality, in the Ashanti region of Ghana and is about 240km northwest of the capital, Accra, and 60km south of Kumasi. The coordinates for the Obuasi South Processing Plant are 197,605.31E 165,901.46N (in Ghana metre grid). Refer to Section 3.1 for a map showing the location, infrastructure and mining licence area for Obuasi gold mine.

With a mining history dating back to 1897, the Obuasi mine has seen various owners and operators over the years. In 2004, the current operator took charge after the merger of AngloGold Limited of South Africa and the Ashanti Goldfields Company Limited of Ghana. However, the mine faced challenges in the years leading up to 2014, as outdated methodologies and deteriorating infrastructure hindered its performance.

In November 2014, the mine entered a limited operating phase recognising the need for significant infrastructure improvements to enhance productivity and utilisation metrics. At this time, a FS was initiated that aimed to determine more optimum mining methods and schedules based on modern mechanised mining methods and refurbishment of underground, surface, and process plant infrastructure. It was recognised that a significant rationalisation and/or replacement of the current infrastructure was needed to enable the delivery of improved utilisation and productivity metrics.

During this period, the mine operated in a limited capacity, primarily focusing on the development of the Obuasi deeps decline (ODD) and underground drilling. AngloGold Ashanti (Ghana) declared force majeure on 9 February 2016 with the incursion of Illegal mining activities on 5 February 2016, but law and order were restored with the arrival of the military and police in October 2016. The force majeure condition was lifted in mid-February 2017, and it is deemed that there is a low probability of this re-occurring. The FS progressed, and in 2017, a positive assessment was completed, indicating strong technical and economic viability for a 20-year lifespan. In 2018, approval was granted by the AngloGold Ashanti board and the government of Ghana to proceed with the project.

Redevelopment efforts commenced in late 2018, and by the fourth quarter of 2019, the mine achieved its first gold pour. Phase 1 of the redevelopment project, focusing on construction and mine development, was completed by September 2020, enabling the mine to begin commercial production on 1 October 2020. Phase 2, which concentrated on further construction and development, concluded in 2021. Currently, Phase 3 is in progress, aiming to establish the necessary infrastructure to support the planned increase in production. Phase 1 of production saw a ramp-up to 2,000 tonnes per day (tpd) in 2020. However, the planned increase to 4,000tpd in 2021 faced setbacks due to the suspension of underground mining activities following a fatality resulting from a sill pillar failure in May 2021.

In response to this incident, a thorough examination of the mining and ground management plans was undertaken by an internal team, supported by independent third-party Australian Mining Consultants (AMC). This review led to the implementation of a comprehensive set of protocols to enhance the existing operating procedures. As a result, underground ore mining was able to resume in October 2021. Since then, production has steadily progressed, with an average underground ore delivery to the processing plant of over 3,000tpd recorded during the second half of 2022. During 2023 ore production averaged 2,680tpd with significant effort geared towards mitigating difficult ground conditions and improving on mine development to create the needed production flexibility.

The Obuasi concession previously covered an area of 474.27km2 and had 80 communities within a 30km radius of the mine. This was reduced to 201km2 in March 2016 and subsequently reduced to 141.22km2 in January 2021. This 141.22km2 comprises three mining leases including the Obuasi mining lease covering 87.48km2, the Binsere 1 mining lease covering 29.03km2 and the Binsere 2 mining lease covering 24.71km2. The Obuasi mining lease will expire on 4 March 2054 and the Binsere leases on 8 April 2028.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

The leases are covered by a development agreement and tax concession agreement with the Government of Ghana, and all leases are renewable.

1.2Ownership

Obuasi is owned and operated by AngloGold Ashanti (Ghana) Limited (AngloGold Ashanti (Ghana)), which is a wholly-owned subsidiary of AngloGold Ashanti plc.

1.3Geology and mineralisation

Situated in the southwestern region of Ghana, the mine is located within the Obuasi concession area. It lies along the northeasterly Ashanti volcanic belt, which is recognised as one of the most notable Proterozoic gold belts uncovered thus far. The Ashanti belt is predominantly composed of sedimentary and volcanic rocks, making it the most prominent among the five Birimian Supergroup gold belts found in Ghana.

Approximately two billion years ago, the Birimian underwent deformation, metamorphism, and intrusion by syn- and post-tectonic granitoids during the Eburnean tectonothermal event. The dominant folding trends within this geological formation are oriented towards the north-northeast to the northeast. Amidst the Birimian system, elongated basins formed during the syn-Birimian period and were subsequently filled with Tarkwaian molasse sediments, primarily consisting of conglomerates, quartzose and arkosic sandstones, as well as minor shale units. Extensive faulting has occurred along these same trends. The Lower Birimian metasediments and metavolcanics are characterised by argillaceous and fine to intermediate arenaceous rocks. This includes phyllites, metasiltstones, metagreywackes, tuffaceous sediments, ash tuffs, and hornstones, listed in decreasing order of significance. In the vicinity of shear zones, these rocks are replaced by sericitic, chloritic, and carbonaceous schists, occasionally exhibiting graphitic features. Multiple lodes are commonly observed within this geological context. Mineralised shears are found near the contact zone between harder metamorphosed and metasomatically altered intermediate to basic Upper Birimian volcanics. The contrast in competency between the more rigid metavolcanic rocks to the east and the more argillaceous rocks to the west is believed to have created a zone of weakness. This zone subsequently underwent shearing and thrusting during periods of compressional phases within the crustal movement.

Gold mineralisation is associated with, and occurs within graphite-chlorite-sericite fault zones. These shear zones are commonly associated with pervasive silica, carbonate and sulphide hydrothermal alteration and occur in tightly folded Lower Birimian schists, phyllites, metagreywackes, and tuffs, along the eastern limb of the Kumasi anticlinorium.

Two main ore types are present, namely quartz vein and sulphide ore. The quartz vein type consists mainly of quartz with free gold in association with lesser amounts of various metal sulphides containing iron, zinc, lead and copper. This ore type is generally non-refractory. The sulphide ore type is characterised by the inclusion of gold in the crystal structure of arsenopyrite minerals. Higher gold grades tend to be associated with finer-grained arsenopyrite crystals. The sulphide ore is generally refractory.

1.4Status of exploration, development and operations

Obuasi is a production stage property. Exploration, development, and operations recommenced in 2019 as part of the redevelopment project and production ramped up to 2,000tpd in 2020. These activities were temporarily halted in May 2021 due to the sill pillar failure incident. Development and exploration were gradually restarted again in August 2021 and underground ore mining steadily resumed in October 2021. In 2022, production gradually ramped up to 4,000tpd, and exploration activities continued as planned. Surface exploration drilling activities targeting underground Mineral Resource in the Côte d'Or reef (at the eastern flank of the Obuasi main system) have been undertaken throughout 2023 together with extensive underground Mineral Resource conversion (Inferred to Indicated Mineral Resource) drilling at Sansu, Block 8 and Block 10.

1.5Mining methods

Obuasi is an underground operation utilising both vertical shafts and declines as main access routes to the underground workings. The mine has seen extensive historical mining activities with varying applications of different mining methods to date. The current life of mine (LOM) design employs mostly the long hole open stoping (LHOS) mining method for ore extraction.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

LHOS is a highly selective and productive method of mining that can be employed for orebodies of varying thicknesses and dips. The main distinct variations of the LHOS used at Obuasi are longitudinal retreat stoping (LRS), and transverse open stoping (TOS). The blind upper stoping (BUS) is a form of LRS or TOS used for partial sill pillar recovery. In the TOS mining method, the primary stopes are designed to be filled with paste enabling the secondary stopes to be blasted against competent ground thus minimising dilution, while the secondary stopes are to be filled preferably with unconsolidated waste rock. The secondary stopes can also be filled with paste, however, the use of unconsolidated waste rock allows for co-disposing of underground development waste with the added benefit of cost savings from trucking waste to the surface.

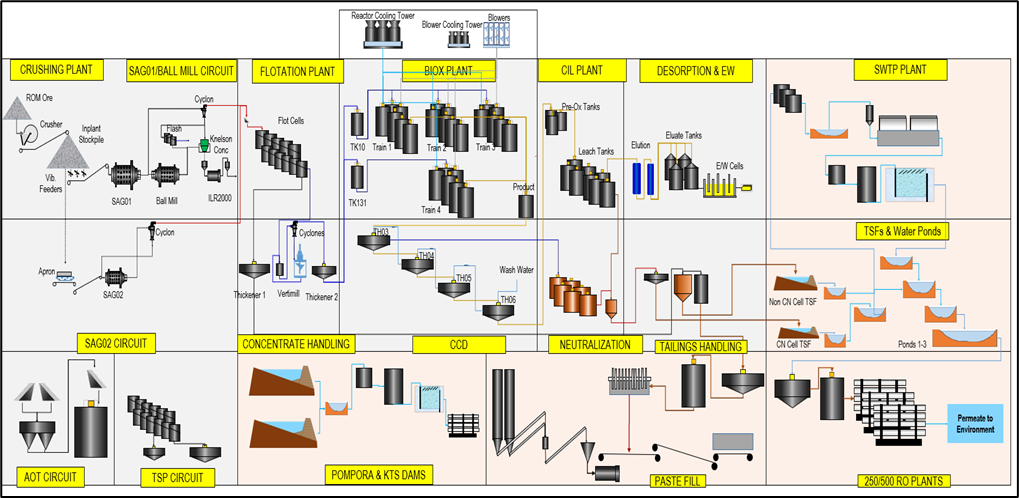

1.6Mineral processing

Existing infrastructure includes a 2.2Mtpa processing plant with flotation and Bacterial Oxidation (BIOX®) process for double refractory ore. A single-stage primary jaw crushing with the product feeding a primary semi-autogenous grinding (SAG) and ball mills via a transfer emergency stockpile station fitted with underneath feeders. The milling circuit is in a close circuit with the cyclones whose overflow feeds the conventional flotation while the underflow is split into three streams feeding the gravity, flash flotation, and third portion bleeding off back to the Ball mill.

A regrind Vertimill® is incorporated to further increase the surface area of the flash flotation concentrate product. The combined flotation concentrates are subjected to the BIOX process before leaching at the carbon-in-leach (CIL). The elution and gold room process then follows the BIOX process with conventional leaching for the carbon adsorption and desorption process.

The gravity gold recovery system is also integrated with Knelson concentrators and inline leach reactors (ILR). The BIOX-washed waste liquor with its low pH and arsenic content is stabilised through a double-stage lime neutralisation process before joining the CIL residues to the BIOX tailings storage facility (BTSF). A portion of the cyanide-free tailings from the conventional flotation circuit is processed through the pastefill plant for underground void backfilling and the excess is stored separately in the Sansu South Tailings storage facility (STSF). Decant return water from both tailings storage facilities (TSFs) is treated to a regulatory-compliant level before discharge.

1.7Mineral Resource and Mineral Reserve estimates

The exclusive Mineral Resource is reported as exclusive of the in situ component of the Mineral Reserve and includes that portion of the Mineral Resource which was not converted to Mineral Reserve. Further study and design, change in costs and/or gold price is required to develop economic extraction plans for the exclusive Mineral Resource. A large proportion of the exclusive Mineral Resource is Inferred Mineral Resource and will require Mineral Resource definition drilling to upgrade to an Indicated Mineral Resource.

As per AngloGold Ashanti’s Guidelines for the reporting of the Mineral Resource and Mineral Reserve (hereinafter referred to as the Guidelines for Reporting), the exclusive Mineral Resource is defined as the inclusive Mineral Resource less the Mineral Reserve before dilution and other factors are applied.

The exclusive Mineral Resource at Obuasi is comprised of 7% open pit and 93% underground. Of the underground exclusive Mineral Resource, Côte d’Or makes up 30% of which 100% is Inferred Mineral Resource. Block 2 makes up 15% of the underground exclusive Mineral Resource, of which 85% of the exclusive Mineral Resource is classified as Indicated Mineral Resource. Block 8 makes up 12% of the underground exclusive Mineral Resource, of which 87% is classified as Indicated and Measured Mineral Resource. Blocks 1, 11, 14, Adansi and Sansu account for the remaining 36% of the underground exclusive Mineral Resource at Obuasi.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

Exclusive gold Mineral Resource

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Obuasi |

Tonnes |

Grade |

Contained gold |

| at 31 December 2023 |

Category |

million |

g/t |

tonnes |

Moz |

|

Measured |

3.47 |

7.77 |

26.97 |

0.87 |

| Indicated |

28.83 |

6.95 |

200.23 |

6.44 |

| Measured & Indicated |

32.30 |

7.03 |

227.20 |

7.30 |

| Inferred |

35.37 |

8.48 |

299.94 |

9.64 |

Notes:

Rounding of numbers may result in computational discrepancies in the Mineral Resource tabulations. All figures are expressed on an attributable basis unless otherwise indicated. To reflect that figures are not precise calculations and that there is uncertainty in their estimation, AngloGold Ashanti reports tonnage, grade and content for gold to two decimals. All ounces are Troy ounces. “Moz” refers to million ounces.

1.All disclosure of Mineral Resource is exclusive of Mineral Reserve. The Mineral Resource exclusive of Mineral Reserve is defined as the inclusive Mineral Resource less the Mineral Reserve before dilution and other factors are applied.

2.“Tonnes” refers to a metric tonne which is equivalent to 1,000 kilograms.

3.The Mineral Resource tonnages and grades are reported in situ and stockpiled material is reported as broken material.

4.Property currently in a production stage.

5.Based on a gold price of $1,750/oz.

6.In 2023, a metallurgical recovery factor of 88% was applied to the underground.

7.In 2023, a cut-off grade of 1.07g/t was applied to the open pit, and a cut-off grade range from 3.79g/t to 4.49g/t (varying according to area) was applied to the underground.

The Mineral Reserve for Obuasi at 31 December 2023 totals 22.83Mt at 9.68g/t for 7.11Moz, consisting of 3.79Mt at 10.12g/t for 1.23Moz Proven Mineral Reserve, and 19.03Mt at 9.60g/t for 5.87Moz Probable Mineral Reserve.

Gold Mineral Reserve

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Obuasi |

Tonnes |

Grade |

Contained gold |

| at 31 December 2023 |

Category |

million |

g/t |

tonnes |

Moz |

|

Proven |

3.79 |

10.12 |

38.40 |

1.23 |

| Probable |

19.03 |

9.60 |

182.63 |

5.87 |

| Total |

22.83 |

9.68 |

221.03 |

7.11 |

Notes:

Rounding of numbers may result in computational discrepancies in the Mineral Reserve tabulations. All figures are expressed on an attributable basis unless otherwise indicated. To reflect that figures are not precise calculations and that there is uncertainty in their estimation, AngloGold Ashanti reports tonnage, grade and content for gold to two decimals. All ounces are Troy ounces. “Moz” refers to million ounces.

1.“Tonnes” refers to a metric tonne which is equivalent to 1,000 kilograms.

2.The Mineral Reserve tonnages and grades are estimated and reported as delivered to the plant (i.e., the point where material is delivered to the processing facility).

3.Property currently in a production stage.

4.Based on a gold price of $1,400/oz.

5.In 2023, a metallurgical recovery factor of 88% was applied to the underground.

6.In 2023, a cut-off grade range from 4.74g/t to 5.61g/t was applied to the underground (varying according to area).

1.8Summary capital and operating cost estimates

The key capital cost expenditure relates to Ore Reserve development (ORD), surface and underground infrastructure development, mining fleet replacement, new TSF, Brownfield exploration and site process water improvement projects. Total capital cost is estimated at $2,128M. non-sustaining capital expenditure of about $176M is associated with the Dokyiwaa TSF, the ODD and the Obuasi Phase 3 redevelopment project items.

Mining costs are based on the 2022 second half-year agreed rates with the mining contractor, Underground Mining Alliance (UMA), with variable cost reduced by 5%, as advised by group procurement and include owner geology and mine technical costs. Mining operating cost averages about $77.77/t for the first five years but an overall average of $59.31/t over the LOM. However, this varies from block to block depending on location and mining method. Processing costs have been determined based on the total material to be milled and include fixed costs associated with the operations of the processing plant. The milling cost is estimated to be $35.04/t over the LOM. General and administration (G&A) costs are calculated based on per tonne milled and were estimated at $35.46/t.

The closure cost is estimated at $210M. This is inclusive of a total security provision of $50.2M ($20.2M cash deposit and $30M bank guarantee).

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

A royalty payable to the government of Ghana of between 3% and 5% of gold produced is applied for the stabilised period. AngloGold Ashanti (Ghana) (Obuasi) signed a tax concession agreement and a development agreement with the government of Ghana in 2017 and 2018 respectively. In these agreements, a sliding scale royalty rate of between 3% and 5% based on the gold price and a corporate tax rate of 32.5% apply during the stabilised period. Obuasi is stabilised for 10 years, with a possibility to extend for a further five years if Obuasi meets certain criteria. Beyond the stabilised period, standard rates of 5% and 35% apply for royalty and income tax respectively. An agreed schedule of input duties is applicable for an initial period of six years ending 31 December 2023.

1.9Permitting requirements

The Obuasi Mineral Resource and Mineral Reserve are constrained within the three mining leases including the Obuasi mining lease, the Binsere 1 mining lease and Binsere 2 mining lease and AngloGold Ashanti (Ghana) has the surface rights to the necessary portions of the mining license required for mining and infrastructure. The main permits (although there are others required by Ghanaian Law) related to conducting mining operations in Ghana are the mining lease and environmental permits.

The mining lease entitles the holder and its authorised persons to extract, process, transport and manage specified minerals within a specified area, along with associated activities per approved plans and permits; and the environmental permits are required before the commencement of the activity specified in the permit.

In terms of permitting requirements, there are no significant current or future encumbrances affecting the property. Obuasi holds valid mining leases and environmental permits for its mining operations.

1.10Conclusions and recommendations

Obuasi has been in operation since 1897 and all available, appropriate data has been used for Mineral Resource and Mineral Reserve compilation. This includes the geological and survey data collected over several decades prior to the merger of AngloGold and Ashanti Goldfields in 2004. The risk associated with the inclusion of this data has been mitigated by a comprehensive data validation project completed between 2015 and 2018 (for geological data) and by reduced Mineral Resource confidence (such as the downgrades of Indicated to Inferred Mineral Resource for Côte d’Or). The verification of historical survey data, used for depletion and sterilisation, is an ongoing project and will continue as areas become accessible and further infill drilling and verification work becomes possible.

A gold price of $1,750/oz, provided by the registrant, was used for the estimation of the Mineral Resource.

The Obuasi Mineral Reserve was derived from the complete LOM plan which is based on a full mine design review and production schedule. The mine design and production schedule have considered the required infrastructure and all relevant mining constraints to arrive at appropriate productivities. The mine plan is designed to optimise ounces produced as early as possible and with due regard to geotechnical considerations and available infrastructure. This is in alignment with the Obuasi Project 300 (P300)FS which provided the basis for the project redevelopment.

The key economic parameters including capital and operating costs have been considered in completing the Mineral Reserve estimates. These economic factors and costs have been reviewed and accepted, they reflect the latest available information of the operations and are in line with best industry practices.

All permitting requirements and regulatory approvals have been obtained for the operations and there are no significant outstanding permits that would cause a material impact on the Mineral Reserve estimate.

A Mineral Reserve gold price of $1,400/oz used to represent the long-term price was provided by the registrant and is seen to be sound and reasonable.

The socio-economic and/or political factors in the local and general community are acceptably managed. The Obuasi sustainability department runs several community projects within its catchment area and there are regular engagements with community leaders.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

In the opinion of the Qualified Persons, the Obuasi Mineral Resource and Mineral Reserve statement is sound, and the Qualified Persons are not aware of any information that materially will affect the outcome of this work.

2.Introduction

2.1Disclose registrant

This Technical Report Summary was prepared for AngloGold Ashanti plc, the registrant.

2.2Terms of reference and purpose for which this Technical Report Summary was prepared

The purpose of this Technical Report Summary is to report the Mineral Resource and Mineral Reserve for Obuasi.

The Technical Report Summary aims to reduce complexity and therefore does not include large amounts of technical or other project data, either in the report or as appendices to the report, as stipulated in Subpart 229.1300 and 1301, Disclosure by Registrants Engaged in Mining Operations and 229.601 (Item 601) Exhibits, and General Instructions. The qualified person must draft the summary to conform, to the extent practicable, with the plain English principles set forth in § 230.421. Should more detail be required they will be furnished on request.

The terms of reference follow AngloGold Ashanti’s Mineral Resource and Mineral Reserve Reporting Group Standard (hereinafter referred to as the Standard for Reporting) and the Guideline for the reporting of the Mineral Resource and Mineral Reserve (hereinafter referred to as the Guideline for Reporting) and based on public reporting requirements as per Subpart 229.1300 of Regulation S-K (Regulation S-K 1300 or 1300 Regulation S-K).

The Mineral Resource and Mineral Reserve is quoted at 31 December 2023.

The following should be noted in respect of the Technical Report Summary:

•All figures are expressed on an attributable basis unless otherwise indicated.

•Unless otherwise stated, $, USD or dollar refers to United States dollars.

•AngloGold Ashanti, Group and Company are used interchangeably.

•Mine, operation, business unit and property are used interchangeably.

•Rounding of numbers may result in computational discrepancies.

•To reflect that figures are not precise calculations and that there is uncertainty in their estimation, AngloGold Ashanti reports tonnage and content for gold to two decimals.

•Metric tonnes (t) are used throughout this report and all ounces are Troy ounces.

•Abbreviations used in this report: gold - Au.

•The reference coordinate system used for the location of properties as well as infrastructure and licences maps/plans are latitude-longitude geographic coordinates in various formats or relevant Universal Transverse Mercator (UTM) projection.

AngloGold Ashanti requires that the Mineral Reserve that is an outcome of the business planning process is generated at a minimum of a Pre-Feasibility Study (PFS) level.

2.3Sources of information and data contained in the report / used in its preparation

This report has been prepared for AngloGold Ashanti, based on information provided by technical specialists and Qualified Persons.

Sources of information include internal information generated as part of the mine's business planning process (which is the overarching process to generate Mineral Resource and Mineral Reserve at the operation), as well as various reports and publications (as cited in Section 24.1 of this report).

Most data used in the preparation of this report comes from drilling and other non-drilling geological data collected over several decades by both the previous owners of the mine and AngloGold Ashanti (owners since 2004). A comprehensive data validation project was undertaken between 2015 and 2018 to improve confidence in the historical data and to demonstrate that the database is an accurate representation of the data collected.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

2.4Qualified Person(s) site inspections

The Qualified Person for Mineral Resource and the Qualified Person for Mineral Reserve are both employed by AngloGold Ashanti (Ghana) and are based at the mine site.

2.5Purpose of this report

The Technical Report Summary for Obuasi was first filed in 2021 (Obuasi Mine, A Life of Mine Summary Report dated 31 December 2021). The reporting in this Technical Report Summary is related to the updated Mineral Resource and Mineral Reserve for Obuasi, effective 31 December 2023.

3.Property description

3.1Location of the property

Obuasi is in the municipality of Obuasi in the Ashanti region of Ghana, 260km northwest of the capital Accra and 60km south of Kumasi, the regional capital. The closest town is Obuasi (the mine is within 5km of the centre of town).

Ghana is an English-speaking country in West Africa that is bounded by the Gulf of Guinea (Atlantic Ocean) to the south, and the countries of Ivory Coast, Burkina Faso, and Togo to the west, north and east respectively. Ghana has a population of approximately 34 million people (Worldometer info, 2023) and its capital is Accra which is located on the coast. Other major towns include Kumasi, Takoradi, and Obuasi. Ghana has two seaports, the largest at Tema (25km from Accra) which has 12 deep water berths, one oil tanker berth and can support facilities for cargo traffic. Takoradi is the secondary port in Ghana but is still a major facility handling most of the export traffic from Ghana. Ghana is divided into 16 administrative regions and 275 districts of which Obuasi is part of the Obuasi West district in the Ashanti Region.

Ghana is a stable presidential constitutional democracy with multi-party politics that is dominated by two parties: the National Democratic Congress and the New Patriotic Party. Nana Akufo-Addo of the New Patriotic Party was elected and then appointed president of Ghana in 2017 and was re-elected president in 2020 (BBC News, December 2020).

Ghana’s climate is tropical with two main seasons: a wet and a dry season with the south experiencing its wet season from March to mid-November.

Ghana is a resource-rich country and has significant gold mining, agricultural (cocoa) and oil resources. According to GlobalData, Ghana was the world's eleventh-largest producer of gold in 2022, with output up by 9% on 2021 levels. Domestic gold production was 3.7Moz, propelling the country to the summit as Africa's largest producer of the precious yellow metal. It’s 2023 the estimated gross domestic product (GDP) is $80B with a per capita GDP of $2,430. Its currency is the Cedi which, at September, 2023 had an exchange rate to the $ of 14.6549:1. Ghana has an emerging economy however there is a rapid increase in the deficit and public debt and there are infrastructure challenges e.g., energy and transport.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

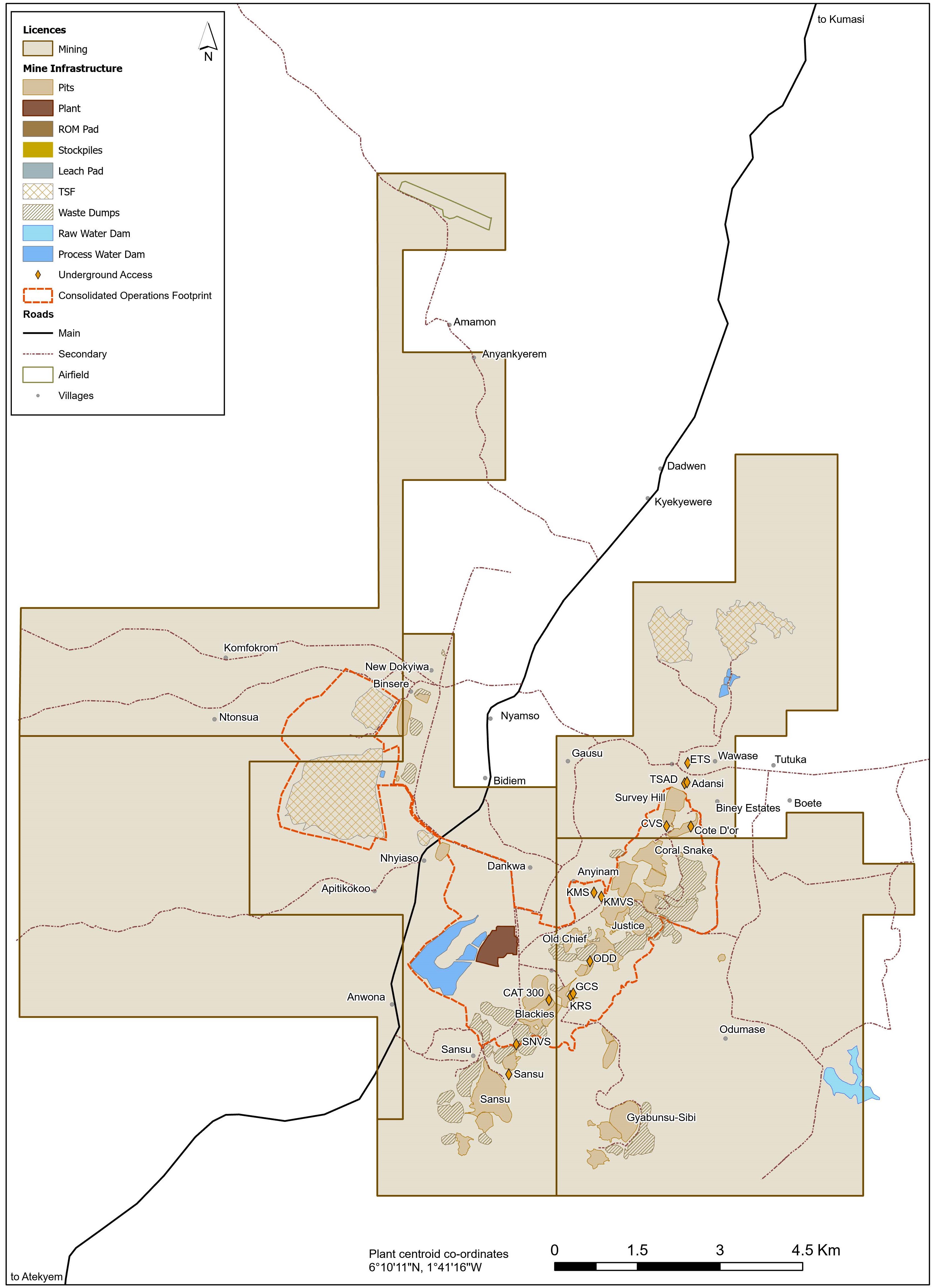

Map showing the location, infrastructure and mining licence area for Obuasi gold mine. The coordinates of the mine, as represented by the plant, are depicted on the map and are in the geographic coordinate system.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

3.2Area of the property

The concession area of the current property is 141.22km2.

3.3Legal aspects (including environmental liabilities) and permitting

The Constitution of Ghana, as well as the Minerals and Mining Act, 2006 (Act 703) (GMM Act), provides that all minerals in Ghana in their natural state are the property of the state, and title to them is vested in the President on behalf of and in trust for the people of Ghana, with rights of reconnaissance, prospecting, recovery, and associated land usage being granted under license or lease.

The grant of a mining lease by the Ghana Minister of Lands and Natural Resources (LNR Minister) upon the advice of the Minerals Commission is subject to parliamentary ratification unless the mining lease falls into a class of transactions exempted by the Ghanaian Parliament.

The LNR Minister has the power to object to a person becoming or remaining a controller of a company that has been granted a mining lease if the LNR Minister believes, on reasonable grounds, that the public interest would be prejudiced by the person concerned becoming or remaining such a controller. Except as otherwise provided in a specific mining lease, all immovable assets of the holder of a mining lease vest in the state upon termination, as does all moveable property that is fully depreciated for tax purposes. Moveable property that is not fully depreciated is to be offered to the state at the depreciated cost. A holder must exercise his rights subject to such limitations relating to surface rights as the LNR Minister may prescribe.

The concession previously covered an area of 474.27km2 and had 80 communities within a 30km radius of the mine. This was reduced to 201km2 in March 2016. In January 2021 a further reduction was approved by the Minister, bringing the total size of the lease to 141.22km2. The Obuasi Mineral Resource and Mineral Reserve are constrained within these mining leases and AngloGold Ashanti (Ghana) has the surface rights to the necessary portions of the mining license required for mining and infrastructure.

Following the latest reduction of the lease area, Obuasi holds three mining leases including the Obuasi mining lease covering 87.48km2, the Binsere 1 mining lease covering 29.03km2 and the Binsere 2 mining lease covering 24.71km2.

At the time of compiling this report, there were no known risks that could result in the loss of ownership in part, or whole, of the Mineral Resource and Mineral Reserve. The Obuasi mining lease will expire on 4 March 2054 and the Binsere 1 and 2 leases are valid until 8th April 2028. All the leases are renewable.

In terms of existing agreements, Obuasi is wholly owned by AngloGold Ashanti. There is no known heritage or environmental impediment over the leases and all required permits are in place. AngloGold Ashanti (Ghana) declared force majeure on 9 February 2016 with the incursion of Illegal mining activities on 5 February 2016, but law and order were restored with the arrival of the military and police in October 2016. The force majeure condition was lifted in mid-February 2017, and it is deemed that there is a low probability of this re-occurring.

The Company has a security agreement with the Government of Ghana, under which the government provides security for the mine, especially against illegal mining.

The tenure is secure at the time of reporting. Any future permits are reasonably expected to be granted and there are no known impediments to obtaining or retaining the right to operate in the area.

There are no known legal proceedings pending or threatened against AngloGold Ashanti (Ghana) that may influence the rights to prospect or mine. All mining leases have been duly granted and are valid and enforceable.

All government/statutory requirements have been met. All permits required for operations are valid, and future permits can be reasonably expected to be obtained.

3.4Agreements, royalties and liabilities

Per the Development Agreement between the Government of Ghana and AngloGold Ashanti (Ghana), royalties are payable by AngloGold Ashanti (Ghana) to the Republic of Ghana on a sliding scale ranging from 3% to 5% of the total revenue from minerals obtained, based on the gold price per ounce.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

The property is not owned or operated by a party other than the registrant.

The AngloGold Ashanti closure planning standard and Ghanaian mining law require that the company (i) considers rehabilitation and closure liabilities and includes them in its mine closure costs and plans; and (ii) post a reclamation bond based on the approved work plan for reclamation. Currently, the liability estimate for reclamation and decommissioning works is approx. $189.9M, out of which the company must post a reclamation bond of $50M split into a cash deposit of $20M held in an escrow account and a bank guarantee of $30M. The bank guarantee is currently provided by Standard Chartered Bank Ghana ($7M); Stanbic Bank ($8M) and United Bank for Africa (UBA) ($15M).

4.Accessibility, climate, local resources, infrastructure and physiography

Obuasi is located in the municipality of Obuasi in the Ashanti Region of Ghana, near the town of Obuasi, which has a population of approximately 200,000 people. The area has a rich mining history and a good supply of skilled mining personnel. The mine can be easily accessed through a well-connected paved road network from Kumasi, and it is also accessible by road or chartered air transport from the capital city, Accra.

The topography of the Obuasi area is primarily shaped by the Ashanti gold belt, leading to the formation of hills that stretch for 18km in a northeast-to-southwest direction within the concession area. The lowest point of the concession area is 50m above sea level, while the highest point reaches 540m above sea level. There are low-lying areas in the south, southwest, and west portions of the concession, but the topography does not hinder mining activities.

The climate in the region where the mine is located is classified as equatorial savannah. It is characterised by consistently high temperatures and humidity throughout the year. There are two distinct wet seasons: the main wet season occurs from mid-March to the end of July, followed by a shorter wet season with light rains between September and November. These wet seasons are separated by a relatively brief dry period in July and August, with the main dry season lasting from December to March. Monthly average temperatures range from 24°C to 33°C, with February being the hottest month. Over the past 69 years, the average annual precipitation is 1,600mm, ranging between 1,089mm and 2,240mm.

Power is supplied to the mine by the Volta River Authority and Ghana Grid Company Limited (GRIDCo). In addition to the electricity that the mine receives from the national grid there are also emergency diesel-powered generators installed as backup. The mine is authorised by the Water Resources Commission to extract water from the Jimi Dam, which is treated for domestic use. Additionally, underground water is extracted for operational purposes.

There is sufficient land area available for the expansion of facilities, such as TSFs and waste dumps.

Overall, the surface rights are deemed adequate for mining operations, and it is expected that none of the conditions, such as topography, property access, and climate, will significantly impact mining activities.

5.History

The Obuasi deposit was discovered in 1897 and has a long history of successful commercial gold production (over 120 years). It has been owned and operated by various operators during this time. The current operator became involved in 2004 following the merger of the former AngloGold Limited of South Africa and the Ashanti Goldfields Company Limited of Ghana.

The historical ounce production from the mine is presented below. It is separated into tailings, open pit, underground or plant cleaning sources. The plant cleaning was undertaken from 2015 to 2017 during the limited operating phase and the gold mainly came from carbon sludge. In total more than 34Moz has been produced from the deposit.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

Historical ounce production table from 1897 to 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1897 - 2001 |

2002 |

2003 |

2004 |

2005 |

2006 |

2007 |

2008 |

|

| Tailings |

797 |

42 |

44 |

31 |

32 |

41 |

36 |

34 |

|

| Open pit |

3,430 |

23 |

34 |

30 |

29 |

9 |

29 |

30 |

|

| Underground |

24,400 |

472 |

435 |

343 |

331 |

318 |

296 |

293 |

|

| Plant cleaning |

— |

— |

— |

— |

— |

— |

— |

— |

|

| Total |

28,627 |

537 |

513 |

404 |

392 |

368 |

361 |

357 |

|

| |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

|

| Tailings |

34 |

18 |

— |

— |

4 |

24 |

— |

— |

|

| Open pit |

9 |

6 |

3 |

10 |

14 |

— |

— |

— |

|

| Underground |

339 |

293 |

309 |

270 |

221 |

148 |

— |

— |

|

| Plant cleaning |

— |

— |

— |

— |

— |

— |

53 |

2 |

|

| Total |

382 |

317 |

312 |

280 |

239 |

172 |

53 |

2 |

|

| |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

Total |

Proportion of production (%) |

| Tailings |

— |

— |

2 |

— |

28 |

7 |

9 |

1,182 |

3.5 |

| Open pit |

— |

— |

— |

— |

— |

— |

— |

3,656 |

10.7 |

| Underground |

— |

— |

— |

127 |

80 |

243 |

215 |

29,134 |

85.6 |

| Plant cleaning |

2 |

— |

— |

— |

— |

— |

— |

57 |

0.2 |

| Total |

2 |

— |

2 |

127 |

108 |

250 |

224 |

34,029 |

100 |

However, the mine faced challenges in the years leading up to 2014, as outdated methodologies and deteriorating infrastructure hindered its performance. In November 2014, the mine entered a limited operating phase recognising the need for significant infrastructure improvements to enhance productivity and utilisation metrics. At this time, a FS was initiated that aimed to determine more optimum mining methods and schedules based on modern mechanised mining methods and refurbishment of underground, surface, and process plant infrastructure. It was recognised that a significant rationalisation and/or replacement of the current infrastructure was needed to enable the delivery of improved utilisation and productivity metrics.

During this period, the mine operated in a limited capacity, primarily focusing on the development of the ODD and underground drilling. AngloGold Ashanti (Ghana) declared force majeure on 9 February 2016 with the incursion of Illegal mining activities on 5 February 2016, but law and order were restored with the arrival of the military and police in October 2016. The force majeure condition was lifted in mid-February 2017, and it is deemed that there is a low probability of this re-occurring. The FS progressed, and in 2017, a positive assessment was completed, indicating strong technical and economic viability for a 20-year lifespan. In 2018, approval was granted by the AngloGold Ashanti board and the government of Ghana to proceed with the project.

The Obuasi redevelopment project commenced in 2019, and the first gold was poured in December 2019. With the first gold pour, the reconciliation of produced grade and tonnage resumed. The Mineral Resource and Mineral Reserve estimates and performance statistics on actual production for 2020, 2021, 2022 and 2023 are presented below.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

Reconciliation of produced gold for 2020, 2021, 2022 and 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year |

| Reconciliation entity |

2020 |

2021 |

2022 |

2023 |

| Mineral Resource model (oz) |

184,895 |

119,553 |

224,002 |

213,434 |

| Grade control model (oz) |

184,174 |

122,271 |

236,218 |

214,247 |

| Percentage (%) |

99.6 |

102.3 |

105.5 |

100.4 |

|

|

|

|

|

|

Year |

| Reconciliation entity |

2020 |

2021 |

2022 |

2023 |

| Mining Feed (oz) |

161,381 |

126,124 |

243,806 |

244,551 |

| Plant Accounted (oz) |

148,326 |

131,096 |

287,877 |

261,638 |

| Percentage (%) |

92.0 |

104.0 |

118.0 |

107.0 |

The current Mineral Resource and Mineral Reserve estimates are deemed to be satisfactory. The Mineral Resource estimates align favourably with the grade control estimates, indicating a strong performance. In 2023, the plant accounted for 107% of the mining feed on ounces. The mining feed is calculated based on the grade control estimates.

6.Geological setting, mineralisation and deposit

6.1Geological setting

Obuasi is located in the Ashanti Region of Ghana and lies in the eastern margin of the Pre-Cambrian West African craton. This craton consists of Lower Proterozoic volcanic and flysch sediments which make up the Birimian system and is overlain in part by the molasse sediments of the Middle Proterozoic Tarkwaian. The Ashanti belt is the most prominent of the five Birimian Supergroup gold belts in Ghana and is a 300km wrench fault system that propagated from Dixcove in the southwest to beyond Konongo in the north-east. In the vicinity of Obuasi is the Paleoproterozoic rocks which consist of volcano-sedimentary rocks of Birimian and Tarkwaian Series. The Birimian Series consists of the Sefwi group in the bottom of the stratigraphic column and the Kumasi group above it. These rocks are cut by voluminous intrusives, mostly granitoids of different ages. The Sefwi group forms the Lower Birimian Ashanti greenstone belt and consists mostly of andesites and basalts interlayered with metasediments and gabbros (WAXI II, 2017). A syntectonic granitoid intrusion dated at 2,170Ma is being considered as a minimum age for the Sefwi group, while the maximum age is still a matter of discussion. The Kumasi group contains mainly metaturbidites with graphitic interlayers and minor metavolcanics. Detrital and magmatic zircon geochronology revealed that sedimentation of this group is associated with minor volcanism during the Upper Birimian and is between 2,154Ma and 2,125Ma (WAXI II, 2017). The youngest Paleoproterozoic Tarkwaian Series consists mostly of metasediments (meta-conglomerates, quartzites) and phyllites interlayered with dolerite sills in the upper part. The Tarkwaian Series rocks lie unconformably on the Sefwi Group within the Ashanti greenstone belt. The occurrence of Tarkwaian Series rocks on Kumasi basin sediments has not been reported. Re-interpretation of zircon geochronology revealed that the deposition of the Tarkwaian Series occurred in a short period between 2,107 and 2,097Ma. It is also constrained by intrusions of metagabbro sills dated at 2,102 13Ma (Adadey et al., 2009) and by granitoids at 2,097 ± 2Ma (Oberthur et al., 1998). The Paleoproterozoic granitoids are usually divided into belt-type of Lower Birimian age (e.g. Sekondi granitoid, 2,174 2Ma and Dixcove suite) and basin-type of Upper Birimian age emplaced from 2,116 2Ma to 2,088 ± 1Ma (Hirdes et al., 1992; Davis et al., 1994). Hydrothermally altered and auriferous basin-type granitoids are ubiquitous in the vicinity of Obuasi along the western flank of the Ashanti belt, at Anyankyerim, Nhyiaso, Yao Mensakrom and Esuajah (Ayanfuri); all have intrusion ages within error of 2,105 ±2 Ma. Geochemistry shows that the belt-type granitoids are juvenile additions to the Paleoproterozoic crust, while the basin-type granitoids are a result of crustal recycling and partial melting of an existing crust (WAXI II, 2013). Apart from some late granitoids and dolerite dykes, all other lithologies have undergone regional metamorphism that generally does not exceed upper greenschist facies. Muscovite, chlorite, actinolite and epidote define a general metamorphic assemblage (Oberthur et al. 1994). Calculated Pressure-Temperature (P-T) ranges imply conditions of 340°C to 460°C at 2kb to 5kb based on the stability of the mineral assemblage (Schwartz et al.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

1992). Peak metamorphic conditions occurred along the Ashanti Fault and have been estimated at 520°C and 5.4kb (John et al., 1999). The metamorphism has been dated on metamorphic titanites within the basin-type granitoids at 2,092 ± 3Ma (Oberthur et al., 1998).

The Obuasi deposit comprises three identifiable trends, namely the Main trend, the Binsere trend about 5km to the northwest of the Main trend and the Gyabunsu trend about 3km to the southeast of the Main trend. The bulk of the auriferous deposits occur in the Main trend.

Five major shear zones have been identified within the Main trend with the Obuasi Fissure being the most prominent extending roughly NE-SW over a strike length of about 8km and mainly dipping towards the northwest at 65° to 90°. The other identifiable mineralised structures within the Main trend are the Côte d’Or, the Ashanti, the Insintsiam, the 12/74 and various footwall and hangingwall mineralised structures. These secondary shears branch off the main shear in an anastomosing structural pattern.

Gold mineralisation is associated with, and occurs within, graphite-chlorite-sericite fault zones. These shear zones are commonly associated with pervasive silica, carbonate and sulphide hydrothermal alteration and occur in tightly folded Upper Birimian schists, phyllites, meta-greywackes, and tuffs, along the eastern limb of the Kumasi anticlinorium (i.e., the Kumasi Group). They are found near the contact with harder metamorphosed and metasomatically altered intermediate to basic Lower Birimian volcanics (the Sefwi Group). The contact between the harder metavolcanic rocks to the east and the more argillaceous rock to the west is thought to have formed a plane of weakness. This is because of the contrast in competency at the contact between the lithological units. During crustal movement, this plane became a zone of shearing and thrusting coeval with the compressional phases. There are two broad styles of gold mineralisation at Obuasi which include free-milling quartz vein gold and sulphur-rich disseminated gold lodes which form alteration haloes around the quartz vein lodes.

6.2Geological model and data density

The geological model is constructed using geological data that has been obtained through underground geological mapping, crosscut and reef drive sampling, exploration, and grade control drilling. This information is then used to build an understanding of the local geology of the deposit and to extrapolate the models to depth and beyond data to guide the exploration programme. A combination of geology comprising the main rock types (metavolcanics, metasediments, quartz, graphite) shear boundaries, mineralised lodes within the shears, and geometallurgical data is used to define the geological model.

The mine has been exploited for over 120 years and the amount of geological data available is substantial and varied. The data has been collected over many years and the data density varies from close spaced grade control sampling (around 10m x 10m to 20m x 20m) to wider spaced exploration drilling ranging from about 50m x 50m up to 200m x 200m. Prior to 2014, all available data was converted to digital format and imported into a Datamine Fusion™ (Fusion) database. A review of the Obuasi Fusion database was undertaken in 2014 to ascertain the level of error associated with the database. The conclusions drawn were that the errors were varied and systematic and would necessitate a methodical approach to rectify the issues identified. A comprehensive data validation project commenced and in the ensuing years (2015 to 2018), the hard copy records were sourced, and a detailed validation exercise was undertaken. This, together with mine reconciliation records and a comprehensive Quality Assurance and Quality Control (QA/QC) programme, implemented since 2005, improves confidence in the pre-2014 data. For all newly collected data, QA/QC procedures are in place to ensure quality and reliability (as described in the following sections) both at the collection and at the laboratory. The data density, distribution and reliability of information are considered sufficient to support statements concerning the mineralisation.

The Obuasi deposit is an orogenic gold deposit and the geological concepts being applied, and forming the basis of the exploration programme, centres around this and the shear-hosted nature of the deposit. The first broad zone marks the boundaries of gold occurrence within which the shearing has occurred resulting in the Main Fissure and other hangingwall and footwall mineralised lodes. These are further separated into quartz and sulphides as deemed appropriate. Most of the shearing is parallel to the general strike of the deposit. The mineralisation dips steeply which informs the drilling orientations so that they are appropriate (attempts are made to intercept mineralisation perpendicularly). Mineralisation models are extrapolated beyond data along strike and depth (as deemed appropriate and representative of the geological concepts).

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

Extrapolations beyond 100m are not included in the Mineral Resource estimates but are rather deemed exploration upside (not declared as Mineral Resource, but only used internally by the company to represent an exploration target or upside potential).

Stratigraphic column of the southwest part of Ghana (Perrouty et al., 2012)

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

A typical S-N geological cross-section (looking West) of Obuasi mine’s Block 2, through Anyinam and Côte d’Or pit, showing Côte d’Or and Obuasi Main lodes, elevation in metres Relative Level (mRL)

A typical S-N geological cross-section (Looking West) through Obuasi mine’s Block 10 deposit, elevation in mRL

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

6.3Mineralisation

The mineralisation is classified into two types: sulphide-hosted, and quartz-lode hosted. Sulphide-hosted mineralisation is dominated by arsenopyrite (60 to 95% of all sulphides) with lesser amounts of pyrite, pyrrhotite, marcasite, chalcopyrite, and micrograins of native gold (Oberthur et al., 1994). This ore type has been responsible for half the gold production at Obuasi (Milesi et al., 1991). The larger arsenopyrite grains are zoned with gold-poor cores, gold-rich inner rims, and gold-poor outer rims. Gold within the sulphide mineralisation is refractory and locked in the sulphide lattice. The quartz lode hosted mineralisation is associated with spatially variable but exceptionally high-grade visible gold in quartz veins/lodes (up to 4m widths). The visible gold is within microfractures overprinting the quartz lodes. These lodes mainly comprise quartz but also minor amounts of ankerite and host rock fragments. The mineralised microfractures contain muscovite, gold, graphite and accessory minerals like galena, chalcopyrite, sphalerite, bournonite, boulangerite, and aurostibine (Oberthur et al., 1994).

The mineralised zones have a strike length of approximately 8km and extend to depths ranging from about 1,000m in the south of the mine (near Sansu) to 2,200m in the north of the mine (Blocks 11 and 14). The width of the mineralisation varies across the deposit. It is thicker in the south (20 to 40m) than in the north (10 to 20m) and narrows with depth where it is around 2 to 8m thick. The mineralisation is associated with, and occurs within, graphite-chlorite-sericite fault zones. These shear zones are commonly associated with pervasive silica, carbonate and sulphide hydrothermal alteration and occur in tightly folded Lower Birimian schists, phyllites, meta-greywackes, and tuffs. The most significant mineralised zone encountered on the property is called the Obuasi Fissure. It is steeply dipping and strikes for approximately 8km. Although the structure itself has high continuity, it is variably mineralised with the best mineralisation plunging at about 45° to the north. Various hangingwall and footwall mineralised lodes splay off the Obuasi Fissure.

They can be very well mineralised (especially close to the Obuasi Fissure), but their continuity decreases with distance away from the Fissure and generally eventually pinch out. Other identifiable and more continuous mineralised structures within the Main Trend are the Côte d’Or, the Ashanti and the Insintsiam. However, these secondary shears branch off the main Obuasi Fissure in an anastomosing structural pattern. These mineralised lodes are persistent and deep seated, forming in shear zones controlled by thrust faulting along the contact between the Lower Birimian phyllites and Upper Birimian metavolcanics. The mineralised zones generally comprise of quartz mineralisation surrounded by sulphides. In the south and at shallower levels, the sulphide mineralisation dominates. It is thick and well developed surrounding less continuous and narrower quartz zones. Towards the north, and at depth, the mineralisation narrows, and quartz start to dominate especially at depth, where it is much more continuous with little surrounding sulphides.

7.Exploration

7.1Nature and extent of relevant exploration work

A substantial amount of exploration work has been carried out for the mine over several decades. An in-house drilling department carried out underground diamond drilling (DD) prior to the redevelopment of the mine in 2019. Drilling was combined with systematic underground mapping and extensive reef drive and crosscut channel sampling but after the redevelopment, only the underground mapping is being done while crosscuts and reef drive sampling are stopped. All samplings have been fully replaced by diamond drill sampling which is being done by drilling contractors Boart Longyear™ and Westfield Drilling Limited™ (Westfield).

In 2023, lower confidence material drilling, and infill drilling to upgrade Inferred Mineral Resource to Indicated Mineral Resource, as well as Indicated to Measured Mineral Resource (grade control), continued underground at 26, 32, and 34 Levels (L).

The focus during 2023 was to upgrade areas in Sansu, Block 8L and 10 from Inferred to Indicated Mineral Resource and ultimately prepare it for mining by completing the last phase of grade control drilling. The strategy remains using the 32L as the main drilling platform to target the area below 32L. Drilling at 41L targeting areas below 41L will re-commence sometime in 2025 after rehabilitation works are completed.

AngloGold Ashanti Obuasi Technical Report Summary - effective date 31 December 2023

__________________________________________________________________________________

The Block 10 area being drilled lies along the trend of a flat-plunging shoot of approximately 380m vertical extent, where the current geological interpretation shows wider mineralisation with multiple lodes. A total of about 20,000m is still to be drilled on 41L. The results so far from the drilling show that the dip of the Obuasi Fissure, which is the main drill target, appears to steepen and roll over an easterly plunging felsic igneous body. High-grade mineralised quartz veins seem to be concentrated around the margins of this felsic igneous body creating a drill target at depth. Where tighter-spaced drilling has already been done into the area, elevated metal content has been observed.

The shear zone, within which the mineralisation in Block 8 is focused, is around the 12/74 Fissure which links the Obuasi Fissure to the east with a network of carbonaceous shears on the margin of the Sansu dyke to the west. The Obuasi and 12/74 Fissures splay apart at the eastern end of Block 8 with the Obuasi Fissure continuing in a WNW direction. A total of over 33,000m is being drilled from the 32L platforms targeting the mineralisation below the platform. Results show a continuous Obuasi Fissure as well as the east lode below 32L but with a strong display of pinch and swell characteristics.