Document

Management’s Discussion and Analysis

Exhibit 99.2

Index

|

|

|

|

|

|

|

|

|

|

|

|

| 6 |

Overview of the Business

|

34 |

Critical Accounting Estimates

|

| 8 |

Our Strategy

|

37 |

Adoption of New Accounting Standards |

| 10 |

Financial Highlights

|

37 |

Anticipated Changes to International Financial Reporting Standards |

| 10 |

Production Summary

|

37 |

Non-GAAP Measures

|

| 12 |

How We Analyze Our Business

|

39 |

Quarterly Financial Data (Unaudited)

|

| 12 |

Financial Results

|

39 |

Selected Annual Information

|

| 18 |

Liquidity and Capital Resources

|

40 |

Controls and Procedures

|

| 24 |

Risk Factors and Risk Management

|

41 |

Forward-Looking Statements

|

This Management’s Discussion and Analysis ("MD&A") is dated March 8, 2024, and should be read in conjunction with our consolidated financial statements and the accompanying notes for the year ended December 31, 2023. Except where otherwise noted, the financial information presented in this MD&A is prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board (the "IASB"). We use the United States dollar as our reporting currency and, except where otherwise noted, all currency amounts are stated in United States dollars. In this MD&A, a reference to the "Company" refers to Methanex Corporation and a reference to "Methanex," "we," "our" and "us" refers to the Company and its subsidiaries or any one of them as the context requires, as well as their respective interests in joint ventures and partnerships.

Throughout this document we use non-GAAP measures and ratios that do not have any standardized meaning prescribed by GAAP and therefore are unlikely to be comparable to similar measures presented by other companies. Refer to the Non-GAAP Measures section on page 37 for a description of each non-GAAP measure and reconciliations to the most comparable GAAP measures.

Some of the historical price data and supply and demand statistics for methanol and certain other industry data contained in this MD&A are derived by the Company from industry consultants or from recognized industry reports regularly published by independent consulting and data compilation organizations in the methanol industry, including Chemical Market Analytics by OPIS, a Dow Jones company, Tecnon OrbiChem Ltd., Argus, ICIS, S&P Global Platts and Methanol Market Services Asia. Industry consultants and industry publications generally state that the information provided has been obtained from sources believed to be reliable. We have not independently verified any of the data from third-party sources nor have we ascertained the underlying economic assumptions relied upon in these reports.

As at March 7, 2024 we had 67,387,492 common shares issued and outstanding and stock options exercisable for 1,478,353 additional common shares.

Additional information relating to Methanex, including our Annual Information Form, is available on our website at www.methanex.com, the Canadian Securities Administrators’ SEDAR+ website at www.sedarplus.ca and on the United States Securities and Exchange Commission’s EDGAR website at www.sec.gov.

OVERVIEW OF THE BUSINESS

Methanol is a clear liquid commodity chemical that is produced from natural gas and is also produced from coal, particularly in China. Traditional chemical demand, which represents approximately 50% of global methanol demand, is used to produce traditional chemical derivatives, including formaldehyde, acetic acid and a variety of other chemicals that form the basis of a wide variety of industrial and consumer products. Demand for energy-related applications, which represents over 30% of global methanol demand, includes several applications including methyl tertiary-butyl ether ("MTBE"), fuel applications (including vehicle fuel, marine fuel and other thermal applications), di-methyl ether and biodiesel. Demand into methanol-to-olefins ("MTO") represents over 15% of global methanol demand. MTO plants produce light olefins which have wide applications in packaging, textiles, plastic parts and automotive components.

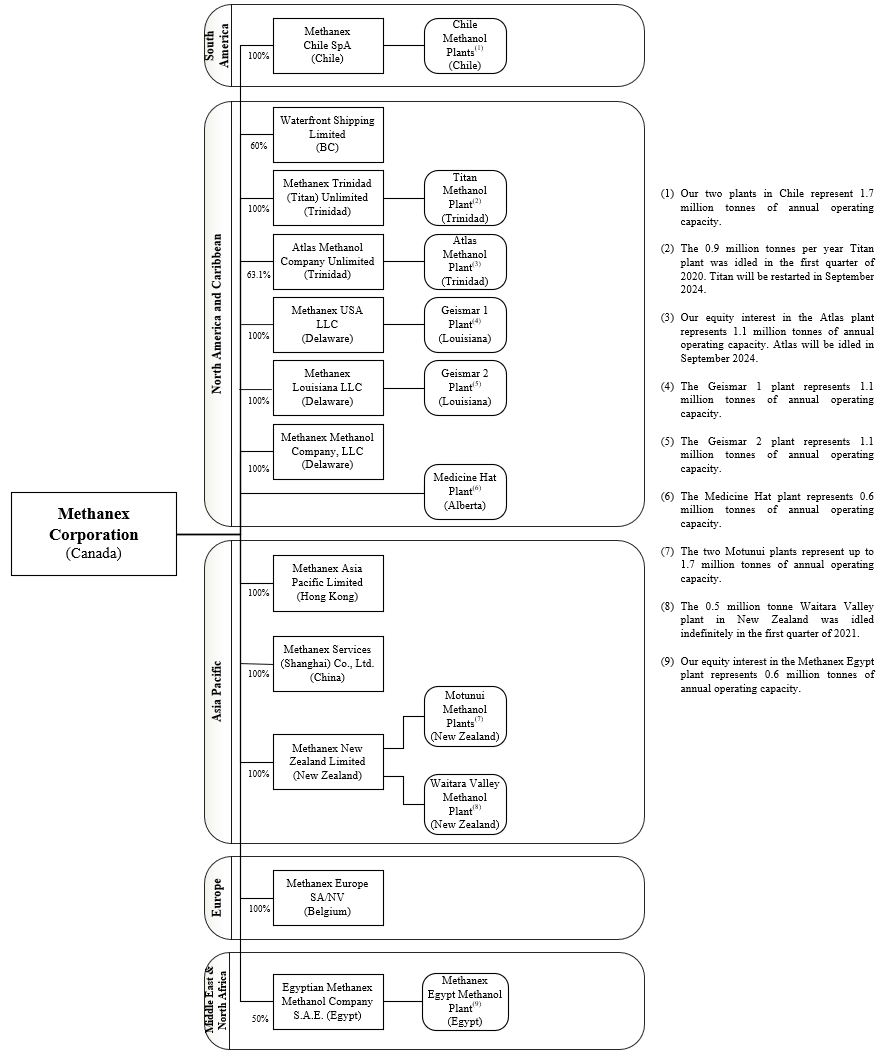

We are the world’s largest producer and supplier of methanol to the major international markets in Asia Pacific, North America, Europe and South America. Our total annual operating capacity, including Methanex's interests in jointly owned plants, is currently 9.3 million tonnes and is located in the United States, New Zealand, Trinidad and Tobago, Chile, Egypt, and Canada. In addition to the methanol produced at our sites, we purchase methanol produced by others under methanol offtake contracts and on the spot market. This gives us flexibility in managing our supply chain while continuing to meet customer needs and support our marketing efforts.

We have marketing rights for 100% of the production from the jointly-owned plants in Trinidad and Tobago and in Egypt, which provides us with an additional 1.3 million tonnes per year of methanol offtake supply when the plants are operating at full capacity.

Refer to the Production Summary section on page 10 for more information.

2023 Industry Overview & Outlook

Methanol is a global commodity and our earnings are significantly affected by fluctuations in the price of methanol, which is directly impacted by changes in methanol supply and demand. Based on the diversity of end products in which methanol is used, demand for methanol is driven by a number of factors, including: the strength of global and regional economies, industrial production levels, energy prices, pricing of end products, downstream capacity additions and government regulations and policies. Methanol industry supply is impacted by the cost of production, methanol industry operating rates and new methanol industry capacity additions.

Demand

We estimate that global methanol demand increased to approximately 91 million tonnes in 2023 driven primarily by growth in China. Outside of China, traditional demand decreased slightly due to ongoing macro-economic headwinds and the impact of inflation and the resulting monetary policy actions on the rate of industrial activity. This was offset by growing demand in China from traditional chemical derivatives driven by higher GDP growth as compared to 2022, higher demand from energy-related applications with increased global mobility, and strong operating rates in the second half of the year from the methanol-to-olefins (MTO) sector.

Over the long term, we believe that traditional chemical demand is influenced by the strength of global and regional economies and industrial production levels. We believe that demand for energy-related applications will be influenced by energy prices, pricing of end products, and government policies that are playing an increasing role in encouraging new applications for methanol due to its emissions benefits as a fuel. The future operating rates and methanol consumption of MTO producers will depend on a number of factors, including pricing for their various final products, the degree of downstream integration of these units with other products, the impact of olefin industry feedstock costs, including naphtha, on relative competitiveness and plant maintenance schedules.

Ongoing regulatory changes as part of the global energy transition along with other factors have led to a growing interest in methanol as a fuel due to its cleaner-burning attributes and potential to reduce greenhouse gas emissions.

There is growing interest in methanol as a marine fuel given its environmental benefits, wide availability, cost competitiveness and ease of use. When made from renewable sources, methanol can be carbon neutral on a life-cycle basis, providing a future-proof pathway to meet the decarbonization goals of the shipping industry. The demand outlook for methanol as marine fuel continues to grow with orders for dual-fueled vessels and retrofits. The current vessels operating coupled with the order book for new builds and retrofits represents over 250 dual-fueled ships. Actual methanol consumption from marine applications will depend on regulations, relative economics versus other fuels, and other factors.

Methanol is also being used as a vehicle fuel in China. Methanol can be blended with gasoline in low quantities and used in existing vehicles and can be used in high-proportion blends such as M85 in flex-fuel vehicles or M100 in dedicated methanol-fueled vehicles. There is significant interest in high-level methanol fuel blends for M100 taxis and trucks (able to run on 100% methanol fuel) in China. There are approximately 30,000 taxis and methanol hybrid passenger cars and 4,000 heavy-duty trucks in China, running on M100 fuel, representing approximately one million tonnes of annual methanol demand. Other countries are in the assessment or near-commercial stage for using methanol as a vehicle fuel.

In China, stricter air quality emissions regulations in several provinces are leading to a phase-out of coal-fueled commercial boilers, kilns, and cooking stoves in favour of cleaner fuels, creating a growing market for methanol as an alternative fuel. We estimate that this demand segment represents approximately seven million tonnes of methanol demand. We continue to support various pilot projects and the development of operational and safety standards to support the commercialization of methanol as a thermal fuel for industrial boilers, kilns and cooking stoves.

Supply

Methanol is predominantly produced from natural gas and is also produced from coal, particularly in China. The cost of production is influenced by the availability and cost of raw materials, including coal and natural gas, freight costs, other operating and maintenance costs and government policies. An increase in economically competitive methanol supply, all else equal, can displace supply from higher cost producers and have a negative impact on methanol price.

In 2023, approximately two to three million tonnes of new production capacity was added in China. In Iran, a new plant was commissioned at the end of 2023 but plant operating rates continue to be uncertain and challenged due to the impact of sanctions, plant technical issues and seasonal natural gas constraints. The methanol industry ran at similar rates in 2023 compared to 2022.

In North America, we expect our new 1.8 million tonne Geismar 3 facility, which will be our third plant in Louisiana, to reach commercial production in 2024. In Malaysia, a 1.8 million tonne plant is under construction with a scheduled start up in 2024. We expect to see increased supply from new capacities to be partially offset by rationalization of existing supply in the market in 2024.

With the shut down of Atlas and the restart of Titan in September 2024 the overall production in Trinidad will be lower by approximately 1 million tonnes annually and we continue to monitor other factors that could further impact supply such as the announced gas diversion from methanol to LNG in Equatorial Guinea. In China, there are planned capacity additions over the near-to-medium term which we expect will be somewhat offset by the closure of some small-scale, inefficient and older plants. New capacity built in China is expected to be consumed domestically as China requires methanol imports to meet growing demand.

Price

The methanol business is a highly competitive commodity industry and future methanol prices will ultimately depend on the strength of global demand and methanol industry supply. Methanol demand and industry supply are driven by several factors as described above. Methanol prices have historically been, and are expected to continue to be, characterized by cyclicality.

Methanex’s average realized price in 2023 was $333 per tonne compared to $397 per tonne in 2022.

OUR STRATEGY

Our primary objective is to create value through our leadership in the global production, marketing and delivery of methanol to customers. To achieve this objective we have a simple, clearly defined strategy: leadership, low cost and operational excellence. We pride ourselves in being a leader in Responsible Care (an operating ethic and set of principles for sustainability developed by the Chemistry Industry Association of Canada and recognized by the United Nations) and having a strategic focus on managing risks and proactive plans relating to personnel health and safety, environmental protection, community involvement, social responsibility, sustainability, security and emergency preparedness. Our brand differentiator "The Power of Agility®" defines our culture of flexibility, responsiveness and creativity that allows us to capitalize on opportunities quickly as they arise, and swiftly respond to customer needs.

Leadership

Leadership is a key element of our strategy. We are focused on creating value through our position as the leading producer and supplier in the global methanol industry, improving our ability to cost-effectively deliver methanol to customers and supporting both traditional and energy-related global methanol demand growth.

We are the leading producer and supplier of methanol to the major international markets in Asia Pacific, North America, Europe and South America. Our 2023 sales volume of 11.2 million tonnes of methanol represented approximately 12% of global methanol demand. This scale allows us the flexibility to meet customer needs across international markets. Our leadership position has also enabled us to play an important role in the methanol industry, which includes publishing Methanex reference prices that are used in each major market as the basis of pricing for our customer contracts.

The geographically diverse locations of our production sites allow us to deliver methanol cost-effectively to customers in all major global markets. We continue to invest in global distribution and supply infrastructure, which includes the world's largest methanol ocean tanker fleet and terminal capacity in all major international markets, enabling us to enhance value to customers by providing reliable and secure supply.

Another key component of our global leadership strategy is our ability to supplement methanol production with methanol purchased from third parties to give us flexibility in our supply chain to meet customer commitments. We purchase methanol through a combination of methanol offtake contracts and spot purchases. We manage the cost of purchased methanol by taking advantage of our global supply chain infrastructure, which allows us to purchase methanol in the most cost-effective region while still maintaining overall security of supply.

China and Asia continue to lead global methanol demand growth. We have storage capacity in China, South Korea, Japan and Singapore that allows us to cost-effectively manage supply to customers and we have offices in Shanghai, Beijing, Hong Kong, Tokyo, and Seoul to ensure customer service and industry positioning in the region. This enables us to participate in and improve our knowledge of the evolving and growing methanol markets in China and other Asian countries including the use of methanol as a cleaner burning fuel.

Low Cost

A low cost structure is an important competitive advantage in a commodity industry and is a key element of our strategy. Our approach to major business decisions is guided by a drive to improve our cost structure and create value for shareholders. The most significant components of total costs are natural gas for feedstock and distribution costs associated with delivering methanol to customers.

We manage our natural gas costs in two ways: through gas contracts linked to methanol price and through fixed price contracts. Our production facilities outside North America are largely underpinned by natural gas purchase agreements where the natural gas price is linked to methanol prices. This pricing relationship enables these facilities to be competitive throughout the methanol price cycle. In North America, we have fixed price contracts and hedges in place targeting minimum operating rate requirements of approximately 70% in the near term.

We purchase our remaining North American gas requirements through the spot market.

Our production facilities are well located to supply global methanol markets and we take a long-term approach to contracting shipping capacity to meet customer needs. Nonetheless, the cost to distribute methanol from production locations to customers is a significant component of total operating costs. These include costs for ocean shipping, in-market storage facilities and in-market distribution. We focus on identifying initiatives to reduce these costs, including optimizing the use of our shipping fleet, third-party backhaul arrangements and taking advantage of prevailing conditions in the shipping market by varying the type and term of ocean vessel contracts. We also look for opportunities to leverage our global asset position by entering into geographic product exchanges with other methanol producers to reduce distribution and transportation costs.

Operational Excellence

We maintain a focus on operational excellence in all aspects of our business. This includes excellence in manufacturing and supply chain processes, marketing and sales, Responsible Care and financial management.

To differentiate ourselves from competitors, we strive to be the best operator and the preferred supplier to customers. We believe that reliability of supply is critical to the success of our customers’ businesses and our goal is to deliver methanol reliably and cost-effectively. Our commitment to Responsible Care drives our adherence to the highest principles of health, safety, environmental stewardship, and social responsibility. We believe this commitment helps us achieve an excellent overall environmental and safety record and aligns our community involvement and social investments with our core values.

Product stewardship is a vital component of a Responsible Care culture and guides our actions through the complete life cycle of our product. We aim for the highest safety standards to minimize risk to employees, customers and suppliers as well as to the environment and the communities in which we do business. We promote the proper use and safe handling of methanol at all times through a variety of internal and external health, safety and environmental initiatives, and we work with industry colleagues to improve safety standards. We readily share technical and safety expertise with key stakeholders (including customers, end-users, suppliers, and logistics providers) through direct communication and active participation in local and international industry associations, seminars and conferences and online education initiatives.

In 2023, our strategy of operational excellence in financial management supported the construction of the Geismar 3 project to be funded from our cash balance, while continuing to allocate any excess cash to shareholders through share repurchases and a regular dividend. At December 31, 2023, we remain in a strong liquidity position with $458 million in cash and $300 million of undrawn back-up liquidity through our revolving credit facility, leaving us in position to fund the remaining costs for the Geismar 3 project fully with cash on hand. Our intent remains to repay rather than re-finance the $300 million bond due at the end of 2024. We have no other significant debt maturities in the near term. We actively manage our liquidity and capital structure in light of changes to economic conditions, the underlying risks inherent in our operations and the capital requirements of our business.

Sustainability

We have embedded sustainability into our long-term strategy alongside our commitment to Responsible Care. We prioritize the sustainability topics that are most relevant to our business and stakeholders. In a sustainability context, material topics are those environmental, social or governance topics that can significantly impact our business success and are of interest to our key stakeholders. In 2023, we conducted a materiality assessment with external stakeholder outreach to inform whether we were prioritizing the right topics. Our top material sustainability topics were confirmed as greenhouse gas ("GHG") emissions, transition to a low-carbon economy, employee and contractor safety and process safety.

Our executive leadership team has overall responsibility for ensuring our material sustainability topics are being effectively evaluated and managed. These include climate-related risks and opportunities associated with our GHG emissions and the transition to a low-carbon economy. The Executive Leadership Team incorporates these matters into our strategic and business planning activities to support the long-term sustainability of our business.

We believe that having a diverse team, equitable people practices and an inclusive workplace leads to a better culture, better decisions and a better company. Our Equity, Diversity and Inclusion (EDI) Vision is to have an inclusive culture where diversity is valued, differences are embraced and everyone has the opportunity to contribute, develop and advance. The Global EDI Council, made up of senior leaders from around the globe, supports the development and execution of our EDI strategy and its integration into the business. In 2023, we made significant strides towards achieving our vision, including a global roll-out of our foundational EDI learning module to all team members, the development of a Guide to Equitable Succession Planning, and the launch of an Employee Resource Group (ERG) Toolkit to support team members in forming new ERGs.

In March 2024, we issued our 2023 Sustainability Report, aligned with the Sustainability Accounting Standards Board (SASB) and the Task-Force on Climate-related Financial Disclosures (TCFD). Our 2023 Sustainability Report is available at https://www.methanex.com/sustainability.

FINANCIAL HIGHLIGHTS

|

|

|

|

|

|

|

|

|

($ Millions, except as noted) |

2023 |

2022 |

Production (thousands of tonnes) (attributable to Methanex shareholders) |

6,642 |

|

6,118 |

|

Sales volume (thousands of tonnes) |

|

|

Methanex-produced methanol |

6,455 |

|

6,141 |

|

Purchased methanol |

3,527 |

|

3,688 |

|

Commission sales |

1,187 |

|

945 |

|

Total sales volume 1 |

11,169 |

|

10,774 |

|

|

|

|

Methanex average non-discounted posted price ($ per tonne) 2 |

434 |

|

503 |

|

Average realized price ($ per tonne) 3 4 |

333 |

|

397 |

|

|

|

|

Revenue |

3,723 |

|

4,311 |

|

Net income (attributable to Methanex shareholders) |

174 |

|

354 |

|

Adjusted net income 4 |

153 |

|

343 |

|

Adjusted EBITDA 4 |

622 |

|

932 |

|

Cash flows from operating activities |

660 |

|

987 |

|

|

|

|

Basic net income per common share ($ per share) |

2.57 |

|

4.95 |

|

Diluted net income per common share ($ per share) |

2.57 |

|

4.86 |

|

Adjusted net income per common share ($ per share) 4 |

2.25 |

|

4.79 |

|

|

|

|

Common share information (millions of shares) |

|

|

Weighted average number of common shares |

68 |

|

71 |

|

Diluted weighted average number of common shares |

68 |

|

72 |

|

Number of common shares outstanding, end of year |

67 |

|

69 |

|

1 Methanex-produced methanol represents our equity share of volume produced at our facilities and excludes volume marketed on a commission basis related to 36.9% of the Atlas facility and 50% of the Egypt facility that we do not own.

2 Methanex average non-discounted posted price represents the average of our non-discounted posted prices in North America, Europe, China and Asia Pacific weighted by sales volume. Current and historical pricing information is available at www.methanex.com.

3 The Company has used Average realized price ("ARP") throughout this document. ARP is calculated as revenue divided by the total sales volume. It is used by management to assess the realized price per unit of methanol sold, and is relevant in a cyclical commodity environment where revenue can fluctuate widely in response to market prices.

4 The Company has used the terms Adjusted net income, Adjusted net income per common share, and Adjusted EBITDA throughout this document. These items are non-GAAP measures and ratios that do not have any standardized meaning prescribed by GAAP and therefore are unlikely to be comparable to similar measures presented by other companies. Refer to the Non-GAAP Measures section on page 37 for a description of each non-GAAP measure and reconciliations to the most comparable GAAP measures.

PRODUCTION SUMMARY

The following table details the annual operating capacity and actual production at our facilities in 2023 and 2022:

|

|

|

|

|

|

|

|

|

|

|

|

(Thousands of tonnes) |

Annual operating

capacity 1 |

2023

Production |

2022

Production |

USA (Geismar) 2 |

2,200 |

|

2,142 |

|

2,041 |

|

New Zealand 3 |

2,200 |

|

1,381 |

|

1,230 |

|

Trinidad (Methanex interest) 4 |

1,960 |

|

1,074 |

|

981 |

|

Chile |

1,700 |

|

993 |

|

888 |

|

Egypt (50% interest) |

630 |

|

504 |

|

385 |

|

Canada (Medicine Hat) |

600 |

|

548 |

|

593 |

|

|

9,290 |

|

6,642 |

|

6,118 |

|

1 The annual operating capacity of our production facilities may be higher or lower than original nameplate capacity as, over time, these figures have been adjusted to reflect ongoing operating efficiencies. Actual production for a facility in any given year may be higher or lower than operating capacity due to a number of factors, including natural gas availability, feedstock composition, the age of the facility's catalyst, turnarounds and access to CO2 from external suppliers for certain facilities. We review and update the operating capacity of our production facilities on a regular basis based on historical performance.

2 The operating capacity of USA (Geismar) does not include the incremental capacity from the Geismar 3 plant (1.8 million tonnes) that is starting up in 2024.

3 The operating capacity of New Zealand is made up of the two Motunui facilities and the Waitara Valley facility. The Waitara Valley facility is idled indefinitely due to natural gas constraints.(Refer to the New Zealand section below.)

4 The operating capacity of Trinidad is made up of the Titan (100% interest) and Atlas (63.1% interest) facilities. (Refer to the Trinidad and Tobago section below.)

United States

Our Geismar plants in Louisiana produced 2.1 million tonnes of methanol in 2023, compared with 2.0 million in 2022. Production at the Geismar site was higher in 2023 due an unplanned outage in late 2022 as the utilities supplier for the Geismar site experienced a loss of power due to a failed transformer. Refer to the Risk Factors and Risk Management – United States section on page 28 for more information.

New Zealand

In New Zealand, we produced 1.4 million tonnes of methanol in 2023 compared with 1.2 million tonnes in 2022. Production for 2023 was higher than 2022 due to higher gas deliveries in 2023. We operate the two Motunui plants in New Zealand with our smaller Waitara Valley plant idled indefinitely since the beginning of 2021 due to natural gas constraints.

We estimate production for 2024 to be between 1.0 - 1.1 million tonnes. 2024 natural gas supply is expected to be impacted by a combination of our suppliers' planned natural gas infrastructure maintenance outages as well as lower than expected output from existing wells. While upstream investment has been made by our gas suppliers in New Zealand over the past two years, recent gas production results have been lower than originally expected which has contributed to the revised forecast for lower production in 2024 as compared to 2023. Refer to the Risk Factors and Risk Management – New Zealand section on page 28 for more information.

Trinidad and Tobago

We operate our fully-owned Titan facility, which is currently idled, and the Atlas facility, in which we have a 63.1% economic interest and marketing rights for 100% of the production. Together, the two facilities represent 2.0 million tonnes of annual operating capacity. The Atlas facility produced 1.1 million tonnes of methanol (Methanex share) in 2023, compared with 1.0 million tonnes in 2022. Production in Trinidad was higher in 2023 due to unplanned outages in the fourth quarter of 2022. In October, Methanex signed a two-year natural gas supply agreement with the National Gas Company of Trinidad and Tobago (NGC) for its currently idled, wholly owned, Titan methanol plant (875,000 tonnes per year capacity) to restart operations in September 2024. Simultaneously, the Atlas plant (Methanex interest 63.1% or 1,085,000 tonnes per year capacity) will be idled in September 2024, when its legacy 20-year natural gas supply agreement expires. Refer to the Risk Factors and Risk Management – Trinidad and Tobago section on page 28 for more information.

Chile

The Chile facilities produced 1.0 million tonnes of methanol in 2023 compared with 0.9 million tonnes in 2022. Production in Chile was higher in 2023 due to higher gas availability from Argentina. Both plants are expected to run at full rates from the end of September 2023 through April 2024, the Southern hemisphere summer months. We estimate production for 2024 will be between 1.1 - 1.2 million tonnes. This production is underpinned by year-round natural gas supply from Chile for about 30 – 35% of our requirements with the remaining 65 – 70% from Argentina during the non-winter period allowing us to operate both plants at full rates. Natural gas development and related infrastructure investments in Argentina continue to progress and we are working with our Argentine natural gas suppliers on extending the period of full gas availability to our plants. Refer to the Risk Factors and Risk Management – Chile section on page 28 for more information.

Egypt

We operate the 1.3 million tonne per year methanol facility in Egypt, in which we have a 50% economic interest and marketing rights for 100% of the production. We produced 1.0 million tonnes of methanol (Methanex share of 0.5 million) in Egypt in 2023 compared to 0.8 million tonnes (Methanex share of 0.4 million) in 2022. We had lower levels of production from Egypt in 2022 as we completed an extended planned turnaround. 2023 production in Egypt was impacted by an unplanned outage in mid-October caused by a mechanical failure in the synthesis gas compressor. The unit was removed from service and repaired on an expedited schedule at the manufacturer overseas. The repairs were completed and the plant restarted in February 2024. Refer to the Risk Factors and Risk Management – Egypt section on page 29 for more information.

Canada

Medicine Hat produced 0.5 million tonnes of methanol in 2023 compared with 0.6 million tonnes in 2022. Production was lower in 2023 compared to 2022 due to unplanned outages in 2023. Refer to the Risk Factors and Risk Management – Canada section on page 29 for more information.

HOW WE ANALYZE OUR BUSINESS

Our operations consist of a single operating segment: the production and sale of methanol. We review our financial results by analyzing changes in the components of Adjusted EBITDA, mark-to-market impact of share-based compensation, depreciation and amortization, finance costs, finance income and other, and income taxes.

The Company has used the terms Adjusted net income, Adjusted net income per common share, and Adjusted EBITDA throughout this document. These items are non-GAAP measures and ratios that do not have any standardized meaning prescribed by GAAP and therefore are unlikely to be comparable to similar measures presented by other companies. Refer to the Non-GAAP Measures section on page 37 for a description of each non-GAAP measure and reconciliations to the most comparable GAAP measures.

In addition to the methanol that we produce at our facilities, we also purchase and resell methanol produced by others and we sell methanol on a commission basis. We analyze the results of all methanol sales together, excluding commission sales volume. The key drivers of changes in Adjusted EBITDA are average realized price, cash costs and sales volume, which are defined and calculated as follows:

|

|

|

|

|

|

| PRICE |

The change in Adjusted EBITDA as a result of changes in average realized price is calculated as the difference from period to period in the selling price of methanol multiplied by the current period total methanol sales volume, excluding commission sales volume. |

CASH

COSTS |

The change in Adjusted EBITDA as a result of changes in cash costs is calculated as the difference from period to period in cash costs per tonne multiplied by the current period total methanol sales volume, excluding commission sales volume in the current period. The cash costs per tonne is the weighted average of the cash cost per tonne of Methanex-produced methanol and the cash cost per tonne of purchased methanol. The cash cost per tonne of Methanex-produced methanol includes absorbed fixed cash costs per tonne and variable cash costs per tonne. The cash cost per tonne of purchased methanol consists principally of the cost of methanol itself. In addition, the change in Adjusted EBITDA as a result of changes in cash costs includes the changes from period to period in unabsorbed fixed production costs, consolidated selling, general and administrative expenses and fixed storage and handling costs. |

| SALES VOLUME |

The change in Adjusted EBITDA as a result of changes in sales volume is calculated as the difference from period to period in total methanol sales volume, excluding commission sales volume, multiplied by the margin per tonne for the prior period. The margin per tonne for the prior period is the weighted average margin per tonne of Methanex-produced methanol and margin per tonne of purchased methanol. The margin per tonne for Methanex-produced methanol is calculated as the selling price per tonne of methanol less absorbed fixed cash costs per tonne and variable cash costs per tonne. The margin per tonne for purchased methanol is calculated as the selling price per tonne of methanol less the cost of purchased methanol per tonne. |

We own 63.1% of the Atlas methanol facility and market the remaining 36.9% of its production through a commission offtake agreement, both of which we recognize as revenue on a gross basis. A contractual agreement between us and our partners establishes joint control over Atlas. As a result, we account for this investment using the equity method of accounting, which results in 63.1% of the net assets and net earnings of Atlas being presented separately in the consolidated statements of financial position and consolidated statements of income, respectively. For the purpose of analyzing our business, Adjusted EBITDA, Adjusted net income and Adjusted net income per common share include an amount representing our 63.1% equity share in Atlas. Our analysis of depreciation and amortization, finance costs, finance income and other, and income taxes is consistent with the presentation of our consolidated statements of income and excludes amounts related to Atlas.

We own 50% of the Egypt methanol facility and market the remaining 50% of its production through a commission offtake agreement. We own 60% of Waterfront Shipping, which provides service to Methanex for the ocean freight component of our distribution and logistics costs. We consolidate both Egypt and Waterfront Shipping, which results in 100% of the financial results being included in our financial statements. Non-controlling interests are included in the Company’s consolidated financial statements and represent the non-controlling shareholders’ interests in the Egypt methanol facility and Waterfront Shipping. For the purpose of analyzing our business, Adjusted EBITDA, Adjusted net income and Adjusted net income per common share exclude the amounts associated with non-controlling interests.

FINANCIAL RESULTS

For the year ended December 31, 2023, we reported a net income attributable to Methanex shareholders of $174 million ($2.57 net income per common share on a diluted basis), compared with a net income attributable to Methanex shareholders of $354 million ($4.86 net income per common share on a diluted basis) for the year ended December 31, 2022. Net income attributable to Methanex shareholders for the year ended December 31, 2023 is lower compared to the year ended December 31, 2022, primarily due to a lower average realized price and the non-recurring Egypt gas redirection and sale proceeds which occurred in 2022, partially offset by higher sales of Methanex-produced methanol and proceeds from a gas contract settlement that occurred in 2023.

For the year ended December 31, 2023, we reported Adjusted EBITDA of $622 million and Adjusted net income of $153 million ($2.25 Adjusted net income per common share), compared with Adjusted EBITDA of $932 million and Adjusted net income of $343 million ($4.79 Adjusted net income per common share) for the year ended December 31, 2022.

We calculate Adjusted EBITDA and Adjusted net income by including amounts related to our equity share of the Atlas facility (63.1% interest) and by excluding the non-controlling interests' share, the mark-to-market impact of share-based compensation as a result of changes in our share price, the impact of the Egypt gas contract revaluation included in finance income and other and the impact of certain items associated with specific identified events. For 2023, the settlement of a historical dispute under an existing gas contract was excluded from Adjusted EBITDA and Adjusted net income due to the one-time nature of the settlement and to better reflect the operating performance of the Company's business. For 2022, there were no specifically identified events impacting Adjusted EBITDA or Adjusted net income.

A reconciliation from net income attributable to Methanex shareholders to Adjusted net income and the calculation of Adjusted diluted net income per common share is as follows:

|

|

|

|

|

|

|

|

|

($ Millions, except number of shares and per share amounts) |

2023 |

2022 |

Net income attributable to Methanex shareholders |

$ |

174 |

|

$ |

354 |

|

Mark-to-market impact of share-based compensation, net of tax |

13 |

|

(6) |

|

Gas contract settlement, net of tax |

(31) |

|

— |

|

Impact of Egypt gas contract revaluation, net of tax |

(3) |

|

(5) |

|

Adjusted net income |

$ |

153 |

|

$ |

343 |

|

Diluted weighted average shares outstanding (millions) |

68 |

|

72 |

|

Adjusted net income per common share |

$ |

2.25 |

|

$ |

4.79 |

|

A summary of our consolidated statements of income for 2023 and 2022 is as follows:

|

|

|

|

|

|

|

|

|

($ Millions) |

2023 |

2022 |

Consolidated statements of income: |

|

|

Revenue |

$ |

3,723 |

|

$ |

4,311 |

|

Cost of sales and operating expenses |

(3,068) |

|

(3,446) |

|

Egypt gas redirection and sale proceeds |

— |

|

118 |

|

Mark-to-market impact of share-based compensation |

16 |

|

(7) |

|

| Adjusted EBITDA attributable to associate |

135 |

|

151 |

|

Amounts excluded from Adjusted EBITDA attributable to non-controlling interests |

(184) |

|

(195) |

|

| Adjusted EBITDA |

622 |

|

932 |

|

|

|

|

Mark-to-market impact of share-based compensation |

(16) |

|

7 |

|

Depreciation and amortization |

(392) |

|

(372) |

|

| Gas contract settlement, net of tax |

31 |

|

— |

|

Finance costs |

(117) |

|

(131) |

|

Finance income and other |

40 |

|

25 |

|

Income tax expense |

(1) |

|

(120) |

|

Earnings of associate adjustment 1 |

(67) |

|

(74) |

|

Non-controlling interests adjustment 1 |

74 |

|

87 |

|

Net income attributable to Methanex shareholders |

$ |

174 |

|

$ |

354 |

|

Net income |

$ |

284 |

|

$ |

462 |

|

1 These adjustments represent depreciation and amortization, finance costs, finance income and other and income taxes associated with our 63.1% interest in the Atlas methanol facility and the non-controlling interests.

Revenue

There are many factors that impact our global and regional revenue. The methanol business is a global commodity industry affected by supply and demand fundamentals. Based on the diversity of end products in which methanol is used, demand for methanol is driven by a number of factors, including: strength of global and regional economies, industrial production levels, energy prices, pricing of end products and government regulations and policies. Revenue was $3.7 billion in 2023 compared to $4.3 billion in 2022. The lower revenue reflects a lower average realized price, partially offset by higher sales volume in 2023 compared to 2022.

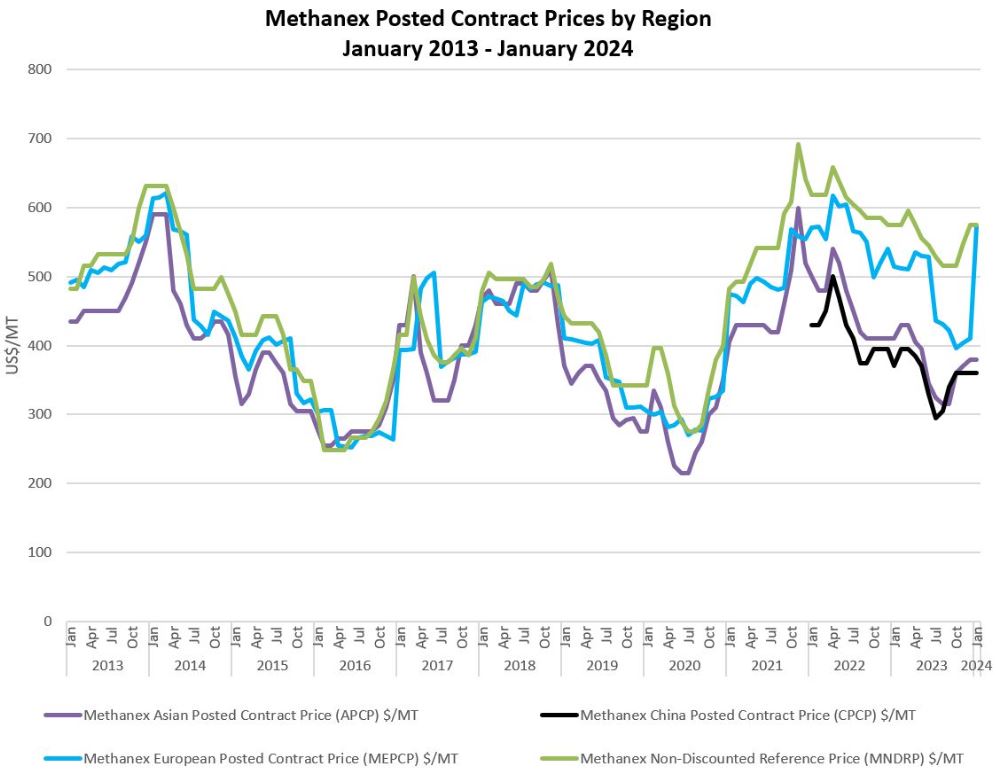

We publish regional non-discounted reference prices for each major methanol market and these posted prices are reviewed and revised monthly or quarterly based on industry fundamentals and market conditions. Most of our customer contracts use published Methanex reference prices as a basis for pricing, and we offer discounts to customers based on various factors. Our average non-discounted published reference price in 2023 was $434 per tonne compared with $503 per tonne in 2022.

Our average realized price in 2023 was $333 per tonne compared to $397 per tonne in 2022.

Distribution of Revenue

The geographic distribution of revenue by customer location for 2023 was comparable to 2022. Details are as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

($ Millions, except where noted) |

2023 |

2022 |

|

|

|

|

China |

$ |

1,043 |

28% |

$ |

1,106 |

26% |

|

|

|

|

Europe |

722 |

19% |

830 |

19% |

|

|

|

|

United States |

575 |

15% |

657 |

15% |

|

|

|

|

South America |

429 |

12% |

459 |

11% |

|

|

|

|

South Korea |

392 |

11% |

543 |

13% |

|

|

|

|

| Other Asia |

387 |

10% |

519 |

12% |

|

|

|

|

Canada |

175 |

5% |

197 |

4% |

|

|

|

|

|

$ |

3,723 |

100% |

$ |

4,311 |

100% |

|

|

|

|

Adjusted EBITDA (Attributable to Methanex Shareholders)

2023 Adjusted EBITDA was $622 million compared with 2022 Adjusted EBITDA of $932 million, a decrease of $310 million. The key drivers of change in our Adjusted EBITDA are average realized price, sales volume and cash costs as described below (refer to the How We Analyze Our Business section on page 12 for more information).

|

|

|

|

|

|

($ Millions) |

2023 vs. 2022 |

Average realized price |

$ |

(657) |

|

Sales volume |

16 |

|

Total cash costs |

331 |

|

|

|

Decrease in Adjusted EBITDA |

$ |

(310) |

|

Average Realized Price

Our average realized price for the year ended December 31, 2023, was $333 per tonne compared to $397 per tonne for 2022, and this decreased Adjusted EBITDA by $657 million (refer to the Financial Results – Revenue section on page 13 for more information).

Sales Volume

Methanol sales volume, excluding commission sales volume, for the year ended December 31, 2023, increased to 10.0 million tonnes from 9.8 million tonnes in 2022, and this increased Adjusted EBITDA by $16 million. Including commission sales volume from the Atlas and Egypt facilities, our total methanol sales volume was 11.2 million tonnes in 2023 compared with 10.8 million tonnes in 2022. Sales volume may vary year to year depending on customer requirements and inventory levels as well as the available commission sales volume.

Total Cash Costs

The primary drivers of change in our total cash costs are changes in the cost of Methanex-produced methanol and changes in the cost of methanol we purchase from others ("purchased methanol"). We supplement our production with methanol produced by others through methanol offtake contracts and purchases on the spot market to meet customer needs and support our marketing efforts in major global markets.

We apply the first-in, first-out method of accounting for inventories and it generally takes between 30 and 60 days to sell the methanol we produce or purchase. Accordingly, the changes in Adjusted EBITDA as a result of changes in Methanex-produced and purchased methanol costs primarily depend on changes in methanol pricing and the timing of inventory flows.

In a rising price environment, our margins at a given price are higher than in a stable price environment as a result of methanol purchases and production versus sales. Generally, the opposite applies when methanol prices are decreasing.

The changes in Adjusted EBITDA due to changes in total cash costs for 2023 compared with 2022 were due to the following:

|

|

|

|

|

|

($ Millions) |

2023 vs. 2022 |

Methanex-produced methanol costs |

$ |

199 |

|

Proportion of Methanex-produced methanol sales |

18 |

|

Purchased methanol costs |

207 |

|

Logistics costs |

(18) |

|

Egypt gas redirection and sale proceeds |

(58) |

|

Other, net |

(17) |

|

Increase in Adjusted EBITDA due to changes in total cash costs |

$ |

331 |

|

Methanex-Produced Methanol Costs

Natural gas is the primary feedstock at our methanol facilities and is the most significant component of Methanex-produced methanol costs. Through 2023, we purchased natural gas for more than half of our production under natural gas purchase agreements where the unique terms of each contract include a base price and a variable price component linked to methanol price to reduce our commodity price risk exposure. The variable price component of each gas contract is adjusted by a formula linked to methanol sales prices above a certain level. We also purchase natural gas in North America and are exposed to natural gas spot price fluctuations for the unhedged portion of our gas needs in the region. Methanex-produced methanol costs were lower in 2023 compared with 2022 by $199 million, primarily due to the impact of changes in realized methanol prices on the variable portion of our natural gas cost, changes in spot gas prices which impact the unhedged portion of our North American operations, timing of inventory flows and changes in the mix of production sold from inventory. For additional information regarding our natural gas supply agreements, refer to the Liquidity and Capital Resources – Summary of Contractual Obligations and Commercial Commitments section on page 21.

Proportion of Methanex-Produced Methanol Sales

The cost of purchased methanol is directly linked to the selling price for methanol at the time of purchase and the cost of purchased methanol is generally higher than the cost of Methanex-produced methanol. Accordingly, an increase in the proportion of Methanex-produced methanol sales results in a decrease in our overall cost structure for a given period, while a decrease in the proportion of Methanex-produced methanol will increase our cost structure. The proportion of Methanex-produced methanol sales increased in 2023 due to higher production and this decreased costs and increased Adjusted EBITDA by $18 million for 2023 compared with 2022.

Purchased Methanol Costs

A key element of our corporate strategy is global leadership and, as such, we have built a leading market position in each of the major global markets where methanol is sold. We supplement our production with purchased methanol through methanol offtake contracts and on the spot market to meet customer needs and support our marketing efforts within the major global markets. In structuring purchase agreements, we look for opportunities that provide synergies with our existing supply chain that allow us to purchase methanol in the most cost-effective region. The cost of purchased methanol consists principally of the cost of the methanol itself, which is directly related to the price of methanol at the time of purchase. Lower methanol prices in 2023 and the timing of inventory flows and purchases decreased the cost of purchased methanol per tonne and this increased Adjusted EBITDA by $207 million compared with 2022.

Logistics Costs

Our investment in global distribution and supply infrastructure includes a dedicated fleet of ocean-going vessels. We utilize these vessels to enhance value to customers by providing reliable and secure methanol supply. Additionally we carry third-party backhaul cargoes, when available, to optimize supply chain costs overall. Logistics costs can also vary from period to period primarily depending on the levels of production from each of our production facilities, the resulting impact on our supply chain, and variability in bunker fuel costs. Higher logistics costs in 2023 decreased Adjusted EBITDA by $18 million compared to 2022. Logistics costs increased in 2023 compared to 2022 primarily due to the mix of production from various plants and the impact of longer supply routes, with the outage in Egypt and preparation for Geismar 3 causing increased costs in the fourth quarter of 2023.

Egypt Gas Redirection and Sale Proceeds

In the third quarter of 2022, we entered into an agreement to redirect and sell the Egypt plant's contracted natural gas during an extended turnaround for a three-month period. Adjusted EBITDA for the year ended December 31, 2022 includes $58 million (attributable to Methanex) from this transaction which did not recur in 2023.

Other, Net

Other, net relates to unabsorbed fixed costs, selling, general and administrative expenses and other operational items. For the year ended December 31, 2023 compared with the same period in 2022, other costs were higher by $17 million mainly due to the organization build-up of costs relating to the start-up of Geismar 3 plant.

Mark-to-Market Impact of Share-Based Compensation

We grant share-based awards as an element of compensation. Share-based awards granted include stock options, share appreciation rights, tandem share appreciation rights, deferred share units, restricted share units and performance share units. For all share-based awards, share-based compensation is recognized over the related vesting period for the proportion of the service that has been rendered at each reporting date. Share-based compensation includes an amount related to the grant date value and a mark-to-market impact as a result of subsequent changes in the fair value of the share-based awards primarily driven by the Company’s share price. The grant date value amount is included in Adjusted EBITDA and Adjusted net income. The mark-to-market impact of share-based compensation as a result of changes in our share price is excluded from Adjusted EBITDA and Adjusted net income and is analyzed separately.

|

|

|

|

|

|

|

|

|

($ Millions, except share price) |

2023 |

2022 |

Methanex Corporation share price 1 |

$ |

47.36 |

|

$ |

37.86 |

|

Grant date fair value expense included in Adjusted EBITDA and Adjusted net income |

19 |

|

22 |

|

Mark-to-market impact 2 |

16 |

|

(7) |

|

Total share-based compensation expense, before tax |

$ |

35 |

|

$ |

15 |

|

1 U.S. dollar share price of Methanex Corporation as quoted on the NASDAQ Global Select Market on the last trading day of the respective period.

2 For the periods presented, the mark-to-market impact on share-based compensation is primarily due to changes in the Methanex Corporation share price.

For stock options, the cost is measured based on an estimate of the fair value at the grant date using the Black-Scholes option pricing model, and this grant date fair value is recognized as compensation expense over the related vesting period with no subsequent re-measurement to fair value.

Share appreciation rights ("SARs") are non-dilutive units that grant the holder the right to receive a cash payment upon exercise for the difference between the market price of the Company’s common shares and the exercise price that is determined at the grant date. Tandem share appreciation rights ("TSARs") give the holder the choice between exercising a regular stock option or a SAR. The fair value of SARs and TSARs are re-measured each quarter using the Black-Scholes option pricing model, which considers the market value of the Company’s common shares on the last trading day of each quarter.

Deferred, restricted and performance share units are grants of notional common shares that are redeemable for cash based on the market value of the Company’s common shares and are non-dilutive to shareholders. Performance share units granted annually reflect a long-term incentive plan where units are redeemable for cash based on the market value of the Company's common shares and are non-dilutive to shareholders. Units vest over three years and include two performance factors: (i) relative total shareholder return of Methanex shares versus a specific market index, and (ii) the three-year average return on capital employed. The relative total shareholder performance factor is measured by the Company at the grant date and each reporting date using a Monte-Carlo simulation model to determine fair value. The three-year average return on capital employed performance factor reflects the actual return on capital employed for historical periods and management's best estimate for forecast periods to determine the expected number of units to vest.

For deferred, restricted and performance share units, the cost of the service received as consideration is initially measured based on the market value of the Company’s common shares at the date of grant. The grant date fair value is recognized as compensation expense over the vesting period with a corresponding increase in liabilities. Deferred, restricted and performance share units are re-measured at each reporting date based on the market value of the Company’s common shares with changes in fair value recognized as compensation expense for the proportion of the service that has been rendered at that date.

The price of the Company’s common shares as quoted on the NASDAQ Global Select Market Composite increased from $37.86 per share at December 31, 2022, to $47.36 per share at December 31, 2023. As a result of the increase in the share price and the resulting impact on the fair value of the outstanding units, we recorded a $16 million mark-to-market expense related to share-based compensation during 2023.

Depreciation and Amortization

Depreciation and amortization was $392 million for the year ended December 31, 2023, and is higher than $372 million for the year ended December, 31 2022 due to the higher cost base of depreciable property, plant and equipment driven by additional capitalized maintenance costs and ocean going vessel additions.

Finance Costs

|

|

|

|

|

|

|

|

|

($ Millions) |

2023 |

2022 |

Finance costs before capitalized interest |

$ |

173 |

|

$ |

167 |

|

|

|

|

Less capitalized interest |

(55) |

|

(36) |

|

Finance costs |

$ |

117 |

|

$ |

131 |

|

Finance costs are primarily comprised of interest on borrowings and lease obligations and were $117 million for the year ended December 31, 2023, compared to $131 million for the year ended December 31, 2022. Finance costs are lower primarily due to higher capitalized interest. Capitalized interest relates to interest costs capitalized for the Geismar 3 project. Refer to the Liquidity and Capital Resources section of page 18 for more information.

Finance Income and Other

Finance income and other were $40 million for the year ended December 31, 2023, compared to $25 million for the year ended December 31, 2022. Finance income and other were higher during the year ended December 31, 2023 compared to the same period in 2022 primarily due to higher interest income.

Income Taxes

A summary of our income taxes for 2023 compared with 2022 is as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

($ Millions, except where noted) |

2023 |

2022 |

|

|

|

|

|

|

Per consolidated statement of income |

Adjusted 1 2 3 4 |

Per consolidated statement of income |

Adjusted 1 2 3 4 |

Net income before income tax |

$ |

286 |

|

$ |

199 |

|

$ |

582 |

|

$ |

482 |

|

Income tax expense |

(2) |

|

(46) |

|

(120) |

|

(139) |

|

Net income after income tax |

$ |

284 |

|

$ |

153 |

|

$ |

462 |

|

$ |

343 |

|

Effective tax rate |

1% |

23% |

21% |

29% |

1 Adjusted net income before income tax reflects amounts required for the inclusion of 63.1% of Atlas income, 50% of Egypt and 60% of Waterfront Shipping, as well as amounts required to exclude the mark-to-market impact of share-based-compensation expense or recovery, the impact of the Egypt gas contract revaluation, and the impact of the settlement of a historical dispute under an existing gas contract. The most directly comparable measure in the financial statements is net income before tax.

2 Adjusted income tax expense reflects amounts required for the inclusion of 63.1% of Atlas income, 50% of Egypt and 60% of Waterfront Shipping, as well as amounts required to exclude the tax impact of mark-to-market impact of share-based-compensation expense or recovery, the impact of the Egypt gas contract revaluation, and the impact of the settlement of a historical dispute under an existing gas contract calculated at the appropriate applicable tax rate for their respective jurisdictions. The most directly comparable measure in the financial statements is income tax expense.

3 Adjusted effective tax rate is a non-GAAP ratio and is calculated as adjusted income tax expense or recovery, divided by adjusted net income before tax.

4 Adjusted net income before income tax and Adjusted income tax (expense) recovery are non-GAAP measures. Adjusted effective tax rate is a non-GAAP ratio. These do not have any standardized meaning prescribed by GAAP and therefore are unlikely to be comparable to similar measures presented by other companies. Management uses these to assess the effective tax rate. These measures and ratios are useful as they are a better measure of our underlying tax rate across the jurisdictions in which we operate.

We earn the majority of our income in the United States, New Zealand, Trinidad and Tobago, Chile, Egypt and Canada. Including applicable withholding taxes, the statutory tax rate applicable to Methanex in the United States is 23%, New Zealand is 28%, Trinidad and Tobago is 38%, Chile is 35%, Egypt is 30% and Canada is 24.5%. We accrue for taxes that will be incurred upon distributions from our subsidiaries when it is probable that the earnings will be repatriated. As the Atlas entity is accounted for using the equity method, any income taxes related to Atlas are included in earnings of associate and therefore excluded from total income taxes but included in the calculation of Adjusted net income.

The effective tax rate based on Adjusted net income was an expense of 23% for the year ended December 31, 2023, compared to 29% for the year ended December 31, 2022. Adjusted net income represents the amount that is attributable to Methanex shareholders and excludes the mark-to-market impact of share-based compensation and the impact of certain items associated with specific identified events. The effective tax rate differs from period to period depending on the source of earnings (losses) and the impact of foreign exchange fluctuations against the United States dollar on our tax balances. In periods with low income levels or losses, the distribution of income and loss between jurisdictions can result in income tax rates that are not indicative of the longer-term corporate tax rate. In addition, the effective tax rate is impacted by changes in tax legislation in the jurisdictions in which we operate.

The following table shows a reconciliation of Net income to Adjusted net income before tax, and of Income tax expense to Adjusted income tax expense:

|

|

|

|

|

|

|

|

|

($ Millions, except where noted) |

2023 |

2022 |

| Net income |

$ |

284 |

|

$ |

462 |

|

| Adjusted for: |

|

|

| Income tax expense |

1 |

|

120 |

|

| Earnings from associate |

(99) |

|

(77) |

|

| Share of associate's income before tax |

152 |

|

120 |

|

| Net income before tax of non-controlling interests |

(103) |

|

(130) |

|

| Mark-to-market impact of share-based compensation |

16 |

|

(7) |

|

| Gas contract settlement |

(47) |

|

— |

|

| Impact of Egypt gas contract revaluation |

(5) |

|

(6) |

|

| Adjusted net income before tax |

$ |

199 |

|

$ |

482 |

|

|

|

|

| Income tax expense |

$ |

(1) |

|

$ |

(120) |

|

| Adjusted for: |

|

|

| Inclusion of our share of associate's adjusted tax expense |

(37) |

|

(43) |

|

| Removal of non-controlling interest's share of tax (recovery) expense |

(7) |

|

22 |

|

| Tax (recovery) expense on mark-to-market impact of share-based compensation |

(3) |

|

1 |

|

| Tax on impact of Egypt gas contract revaluation |

2 |

|

1 |

|

| Adjusted income tax expense |

$ |

(46) |

|

$ |

(139) |

|

For additional information regarding income taxes, refer to note 16 of our 2023 consolidated financial statements.

LIQUIDITY AND CAPITAL RESOURCES

A summary of our consolidated statements of cash flows is as follows:

|

|

|

|

|

|

|

|

|

($ Millions) |

2023 |

2022 |

Cash flows from/(used in) operating activities: |

|

|

Cash flows from operating activities before changes in non-cash working capital |

$ |

719 |

|

$ |

933 |

|

Changes in non-cash working capital related to operating activities |

(59) |

|

54 |

|

|

660 |

|

987 |

|

Cash flows from/(used in) financing activities: |

|

|

Payments for the repurchase of shares |

(86) |

|

(253) |

|

Dividend payments to Methanex Corporation shareholders |

(49) |

|

(44) |

|

Interest paid |

(169) |

|

(162) |

|

| Repayment of long-term debt and financing fees |

(12) |

|

(9) |

|

| Repayment of lease obligations |

(118) |

|

(106) |

|

|

|

|

| Distributions to non-controlling interests |

(185) |

|

(85) |

|

Proceeds on issue of shares on exercise of stock options |

1 |

|

1 |

|

|

|

|

| Restricted cash for debt service accounts |

(1) |

|

(1) |

|

| Sale of partial interest in subsidiary |

— |

|

149 |

|

Changes in non-cash working capital relating to financing activities |

69 |

|

2 |

|

|

|

|

|

(551) |

|

(508) |

|

Cash flows from/(used in) investing activities: |

|

|

Property, plant and equipment |

(178) |

|

(146) |

|

Geismar plant under construction |

(270) |

|

(432) |

|

|

|

|

|

|

|

|

|

|

Changes in non-cash working capital relating to investing activities |

(60) |

|

24 |

|

|

(509) |

|

(553) |

|

Decrease in cash and cash equivalents |

(400) |

|

(74) |

|

Cash and cash equivalents, end of year |

$ |

458 |

|

$ |

858 |

|

Cash Flow Highlights

Cash Flows from Operating Activities

Cash flows from operating activities for the year ended December 31, 2023 were $660 million compared with $987 million for the year ended December 31, 2022. The decrease in cash flows from operating activities is primarily due to lower earnings and differences in non-cash working capital changes, offset by lower tax payments and higher dividends received from the Atlas joint venture.

The following table provides a summary of these items for 2023 and 2022:

|

|

|

|

|

|

|

|

|

($ Millions) |

2023 |

2022 |

Net income |

$ |

284 |

|

$ |

462 |

|

Deduct earnings of associate |

(99) |

|

(77) |

|

Add dividends received from associate |

112 |

|

97 |

|

Add (deduct) non-cash items: |

|

|

Depreciation and amortization |

392 |

|

372 |

|

| Income tax expense |

1 |

|

120 |

|

Share-based compensation expense |

35 |

|

15 |

|

Finance costs |

117 |

|

131 |

|

Interest received |

22 |

|

10 |

|

Income taxes paid |

(82) |

|

(164) |

|

Other |

(63) |

|

(33) |

|

Cash flows from operating activities before changes in non-cash working capital |

719 |

|

933 |

|

Changes in non-cash working capital: |

|

|

Trade and other receivables |

(33) |

|

38 |

|

Inventories |

16 |

|

33 |

|

Prepaid expenses |

(19) |

|

(3) |

|

Accounts payable and accrued liabilities |

(23) |

|

(14) |

|

|

(59) |

|

54 |

|

Cash flows from operating activities |

$ |

660 |

|

$ |

987 |

|

For a discussion of the changes in net income, depreciation and amortization, income tax expense, share-based compensation expense (recovery) and finance costs, refer to the Financial Results section on page 12.

Changes in non-cash working capital decreased cash flows from operating activities by $59 million for the year ended December 31, 2023, compared with an increase of $54 million for the year ended December 31, 2022. Trade and other receivables increased in 2023 and this decreased cash flows from operating activities by $33 million, primarily due to timing of invoices and payments by customers by the end of 2023 compared to 2022. Inventories decreased primarily due to the lower cost of production in the fourth quarter of 2023 compared to the fourth quarter of 2022 driven by the impact of lower methanol prices on our natural gas costs, which increased cash flows from operating activities by $16 million. Accounts payable and accrued liabilities decreased in 2023 compared to 2022 due to the impact of lower gas costs and lower methanol prices on purchased methanol at the end of 2023 compared to at the end of 2022, which decreased cash flows from operating activities by $23 million.

Cash Flows from Financing Activities

In 2023, we repurchased 1,894,711 common shares under a normal course issuer bid for approximately $86 million, compared to 5,551,751 common shares repurchased in 2022 for approximately $253 million.

Total dividend payments in 2023 were $49 million compared with $44 million in 2022 as a result of an increase in quarterly dividends in 2023. Our quarterly dividend was increased from $0.175 per share to $0.185 per share in April of 2023.

Total interest payments increased from $162 million in 2022 to $169 million in 2023 as a result of an increase in leases held in 2023. The Company has no debt maturities until December 2024, other than normal course obligations for principal repayments related to our other limited recourse debt facilities.

Distributions to non-controlling interests, including the 50% ownership of the Egypt entity and the 40% ownership of Waterfront Shipping not attributable to Methanex, were $185 million in 2023 compared to $85 million in 2022 and include amounts accrued but unpaid during 2023. The higher distributions to non-controlling interests for 2023 compared to 2022 were primarily due to the timing of distribution accruals and changes in earnings of Egypt and Waterfront Shipping.

In 2022, the Company completed the sale of a 40% equity interest in Waterfront Shipping Limited for cash proceeds of $145 million, excluding final purchase price adjustments.

Cash Flows from Investing Activities

During 2023, we incurred cash outflows on capital expenditures relating to our consolidated operations of $178 million (2022 - $146 million) primarily related to planned turnarounds in Geismar, New Zealand and Chile. The 2022 capital expenditures were primarily related to planned turnarounds in New Zealand and Egypt as well as refurbishment work in Chile. In addition, we incurred cash outflows on capital expenditures of $270 million (2022 - $432 million) related to the construction of the Geismar 3 project.

Liquidity and Capitalization

Our objective in 2023 in managing liquidity and capital was to provide financial capacity and flexibility to meet our strategic objectives, with a focus on cash preservation and liquidity. Our intent remains to repay rather than re-finance the $300 million bond due at the end of 2024 and under current market conditions and pricing levels we will be prioritizing excess cash towards this repayment.

The following table provides information on our liquidity and capitalization position as at December 31, 2023, and December 31, 2022:

|

|

|

|

|

|

|

|

|

($ Millions, except where noted) |

2023 |

2022 |

Liquidity: |

|

|

Cash and cash equivalents |

$ |

458 |

|

$ |

858 |

|

Undrawn credit facility |

300 |

|

300 |

|

Undrawn G3 construction facility |

— |

|

300 |

|

Total liquidity 1 |

$ |

758 |

|

$ |

1,458 |

|

Capitalization: |

|

|

Unsecured notes, including current portion |

1,986 |

|

1,983 |

|

Other limited recourse debt facilities, including current portion |

156 |

|

168 |

|

Total debt |

2,142 |

|

2,151 |

|

Non-controlling interests |

242 |

|

317 |

|

Shareholders’ equity |

1,931 |

|

2,112 |

|

Total capitalization |

$ |

4,315 |

|

$ |

4,580 |

|

Total debt to capitalization 2 |

50% |

47% |

Net debt to capitalization 3 |

44% |

35% |

1 Total liquidity consists of cash and cash equivalents, as well as any undrawn amounts from facilities. Total liquidity is a non-GAAP capital management measure, see Non-GAAP Measures on page 37 for more information.

2 Defined as total debt (including other limited recourse debt facilities) divided by total capitalization.

3 Net debt to capitalization is defined as total debt (including other limited recourse debt facilities) less cash and cash equivalents divided by total capitalization less cash and cash equivalents. Net debt to capitalization is a non-GAAP capital management measure. See Non-GAAP Measures on page 37 for more information.

We manage our liquidity and capital structure in light of changes to economic conditions, the underlying risks inherent in our operations and the capital requirements for the business. Total liquidity is useful because it illustrates the extent to which management has immediate access to cash for operational and construction purposes, and is indicative of our flexibility should uses for these facilities immediately arise. Net debt to capitalization is useful because it illustrates the relative risk of our financing structure to potential lenders and investors. The strategies we have employed in managing our liquidity and capital structure include the issue or repayment of general corporate debt, the issue of project debt, the payment of dividends and the repurchase of shares.

We are not subject to any statutory capital requirements and have no commitments to sell or otherwise issue common shares except pursuant to outstanding employee stock options and TSARs.

We operate in a highly competitive commodity industry and believe that it is appropriate to maintain a strong balance sheet and maintain financial flexibility. As at December 31, 2023, we had a cash balance of $458 million, including $79 million of cash related to Egypt and $46 million of cash related to Waterfront Shipping entities consolidated on a 100% basis. We invest our cash only in highly rated instruments that have maturities of three months or less to ensure preservation of capital and appropriate liquidity.

As at December 31, 2023, we have access to a $300 million committed revolving credit facility expiring in July 2026. The facility is with a syndicate of highly rated financial institutions. During the year ended December 31, 2023, we cancelled the non-revolving construction facility for the Geismar 3 project. At the time of cancellation, the construction facility was undrawn.

We have covenant and default provisions under our long-term debt obligations and we also have certain covenants that could restrict access to our credit facilities. The covenants governing the unsecured notes, which are specified in an indenture, apply to the Company and its subsidiaries, excluding the Egypt entity and the Atlas joint venture entity, and include restrictions on liens, sale and lease-back transactions, a merger or consolidation with another corporation or sale of all or substantially all of our assets. The indenture also contains customary default provisions. The significant covenants and default provisions under the credit facility include:

a) the obligation to maintain an EBITDA to interest coverage ratio of greater than or equal to 2:1 calculated on a four-quarter trailing basis and a debt to capitalization ratio of less than or equal to 60%, both calculated in accordance with definitions in the credit agreement that include adjustments related to the limited recourse subsidiaries;

b) a default if payment is accelerated by a creditor on any indebtedness of $50 million or more of the Company and its subsidiaries, except for the limited recourse subsidiaries; and

c) a default if a default occurs that permits a creditor to demand repayment on any other indebtedness of $50 million or more of the Company and its subsidiaries, except for the limited recourse subsidiaries.

The credit facility is secured by certain assets of the Company, and also includes other customary covenants including restrictions on the incurrence of additional indebtedness.