2

Asset Quality

•

The

allowance

for

credit

losses

(“ACL”)

increased

by

$1.4

million

to

$26.1

million

at

March 31,

2026

from

$24.7

million

at

March 31, 2025.

•

The ACL represented 1.16% of total loans at March 31, 2026 and 1.22%

of total loans at March 31, 2025.

•

The provision for credit

loss was $801 thousand

for the quarter ended

March 31, 2026, an increase

of $120 thousand compared

to

$681 thousand for the same period in 2025.

•

The ratio of non-performing loans to

total loans was 0.16% for the quarter

ended March 31, 2026 and 0.20% for the

quarter ended

March 31, 2025. Non-performing loans totaled $3.6 million at March 31,

2026 and $4.2 million at March 31, 2025.

Non-interest Income and Non-interest Expense

•

Non-interest income was $4.2

million for the three

months ended March 31, 2026,

an increase of

$434 thousand or 11.7% compared

to $3.7 million for the same period in 2025.

•

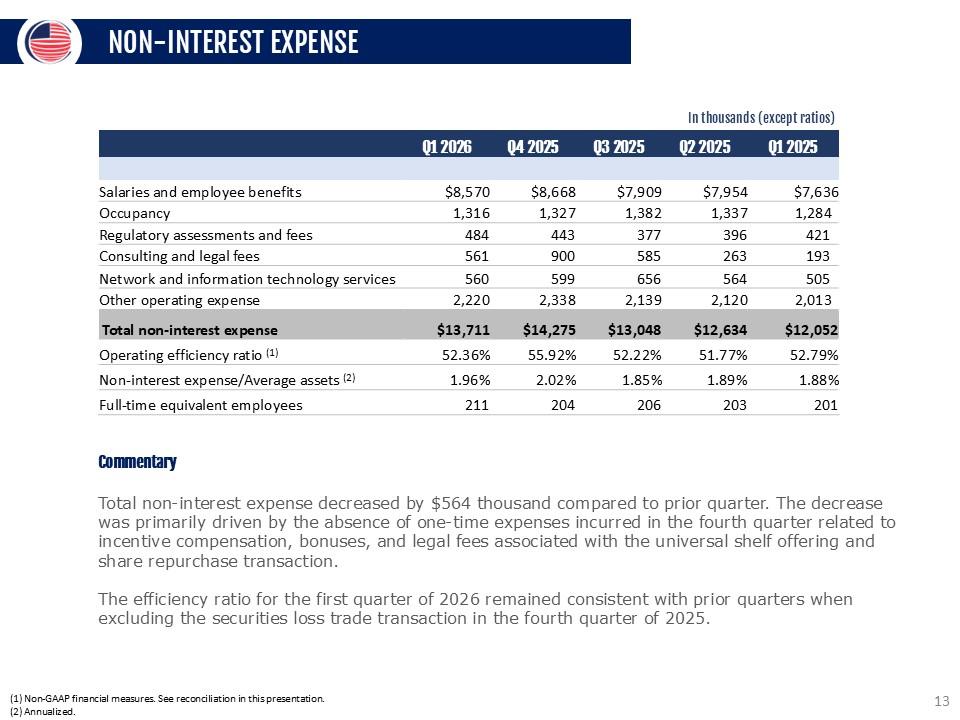

Non-interest expense was $13.7 million for the

three months ended March 31, 2026, an

increase of $1.7 million or

13.8% compared

to $12.1 million for the three months ended March 31, 2025.

•

On April

20, 2026,

the Company’s

Board of

Directors declared

a quarterly

cash dividend

of $0.125

per share

of the

Company’s

Class A

common stock.

The dividend

will be paid

on June 5,

2026 to

shareholders of

record at

the close

of business

on May

15,

2026.

•

As of March 31, 2026,

total risk-based capital ratios for the Company and the Bank were 14.09% and 13.96%, respectively, well in

excess of regulatory requirements (only applicable to the Bank currently)

.

•

Tangible book value per common

share (non-GAAP financial measure) was $12.23 at March 31, 2026, representing an increase of

$1.00 or 8.9% from $11.23 at March 31, 2025. At March 31, 2026,

tangible book value per common share was negatively affected

by ($1.72) per

share due to

an accumulated other

comprehensive loss of

$31.3 million mostly

due to changes

in the market

value

of the Company’s

available for sale securities. At March 31, 2025,

tangible book value per common share was negatively

affected

by ($2.05) per share due to an accumulated other comprehensive loss of $41.1

million.

Conference Call and Webcast

The Company

will host

a conference

call on

Friday,

April 24,

2026, at

11:00

a.m. Eastern Time

to discuss

the Company’s

unaudited

financial results for the quarter ended March 31,

2026. To access the conference call, dial (833) 816-1416 (U.S. toll-free) and

ask to join

the USCB Financial Holdings Call.

Additionally,

interested

parties can

listen to

a live

webcast

of the

call in

the “Investor

Relations” section

of the

Company’s

website

at www.uscentury.com

.

An archived version of the webcast will be available in the same location shortly after

the live call has ended.

About USCB Financial Holdings, Inc.

USCB Financial Holdings, Inc.

is the bank holding company for

U.S. Century Bank. Established in

2002, U.S. Century Bank is one

of

the largest

community banks

headquartered

in Miami,

and one

of the

largest community

banks in

the State

of Florida.

U.S. Century

Bank is rated 5-Stars by BauerFinancial, the nation’s leading independent

bank rating firm. U.S. Century Bank offers customers a wide

range of

financial products

and services

and supports

numerous community

organizations,

including

the Greater

Miami Chamber

of

Commerce, the South Florida Hispanic Chamber of Commerce, and ChamberSouth. For more information about us

or to find a banking

center near you, please call (305) 715-5200 or visit www.uscentury.com.

Forward-Looking Statements

This earnings release

may contain statements

that are not

historical in nature

and are intended

to be, and

are hereby identified

as, forward-

looking

statements

for

purposes

of

the

safe

harbor

provided

by

Section

21E

of

the

Securities

Exchange

Act

of

1934,

as

amended.

Forward-looking statements are

those that are

not historical facts.

The words “may,”

“will,” “anticipate,” “could,”

“should,” “would,”

“believe,” “contemplate,” “expect,” “aim,” “plan,” “estimate,” “seek,” “continue,” and “intend,”, the negative of these terms, as well as

other similar words

and expressions of

the future, are

intended to identify

forward-looking statements. These forward-looking statements

include, but are not limited

to, statements related to our

projected growth, anticipated future

financial performance, and management’s