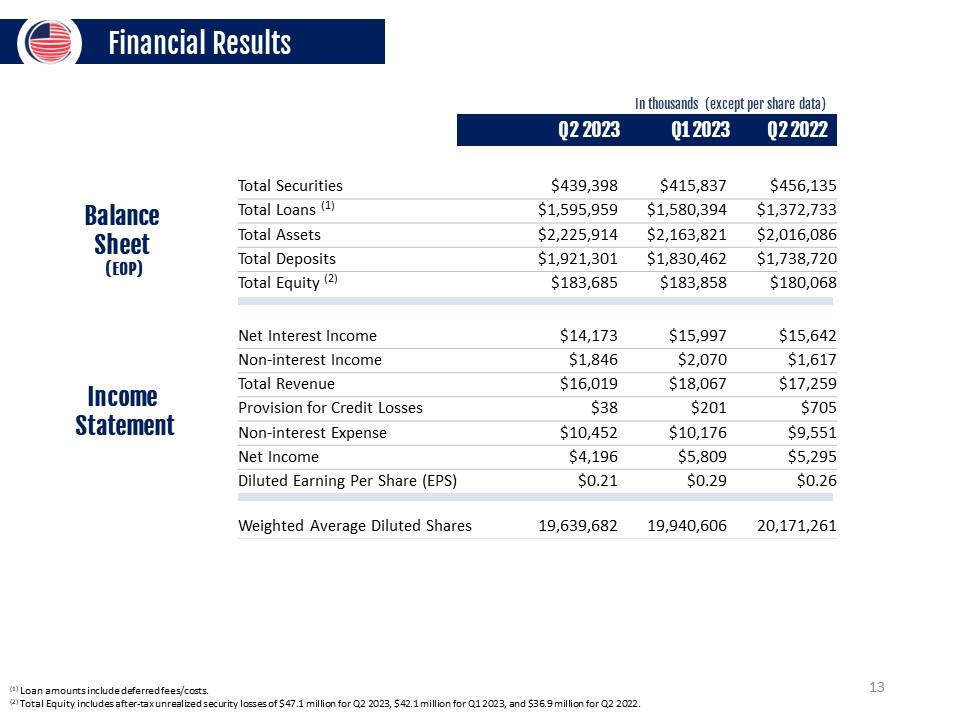

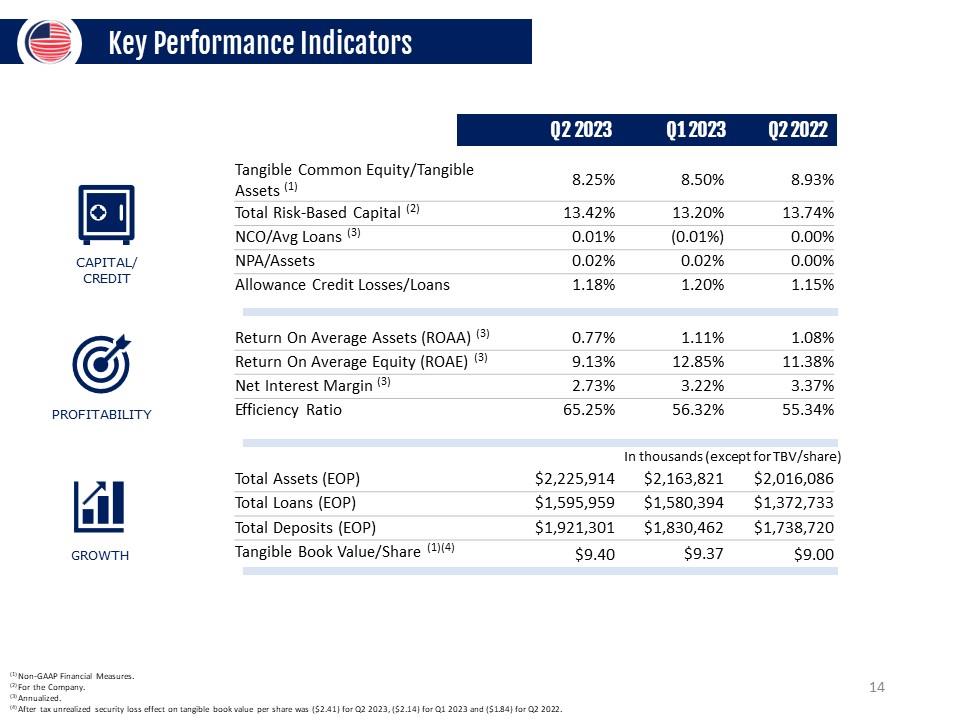

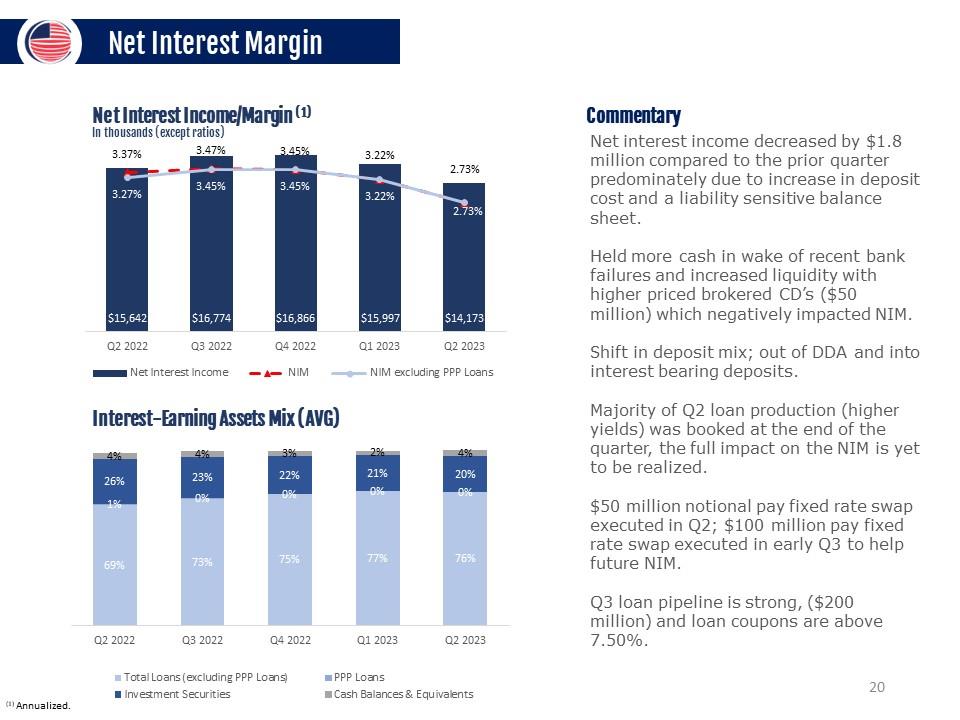

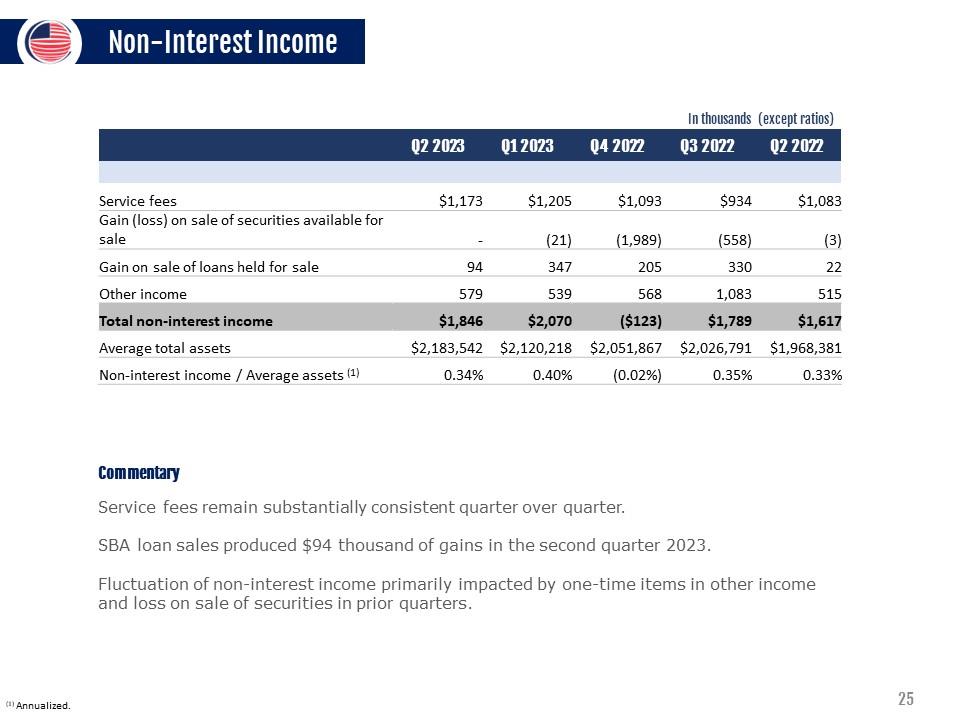

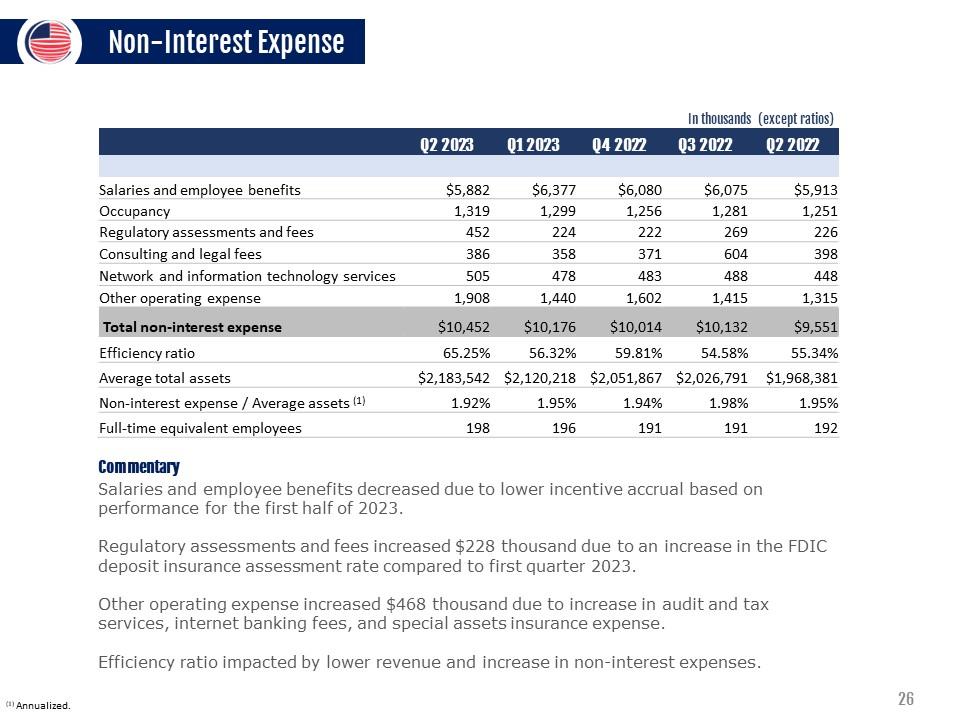

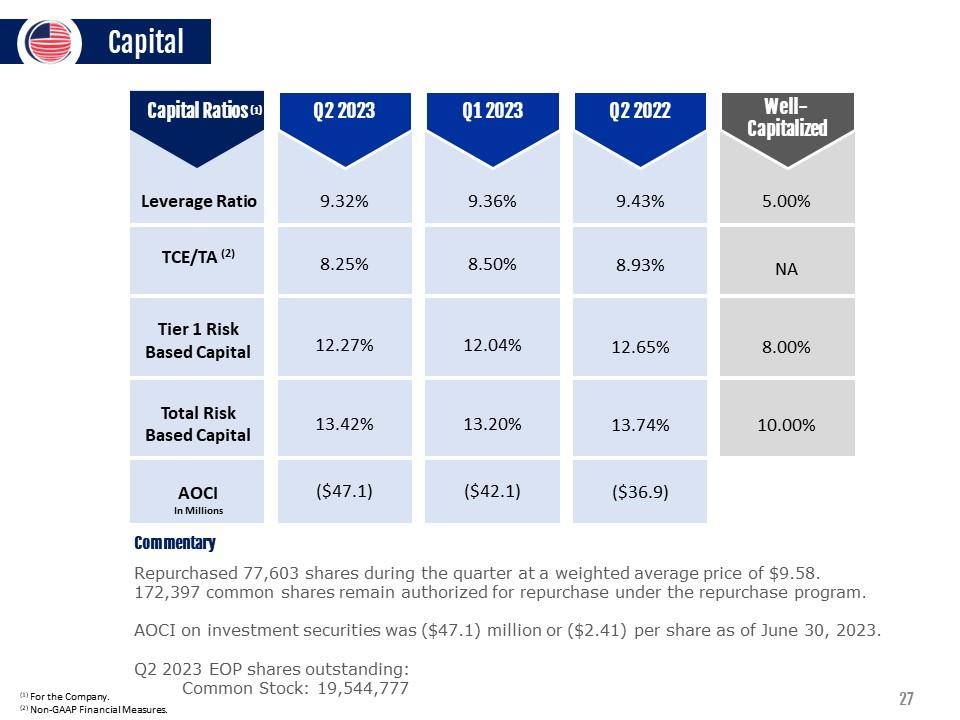

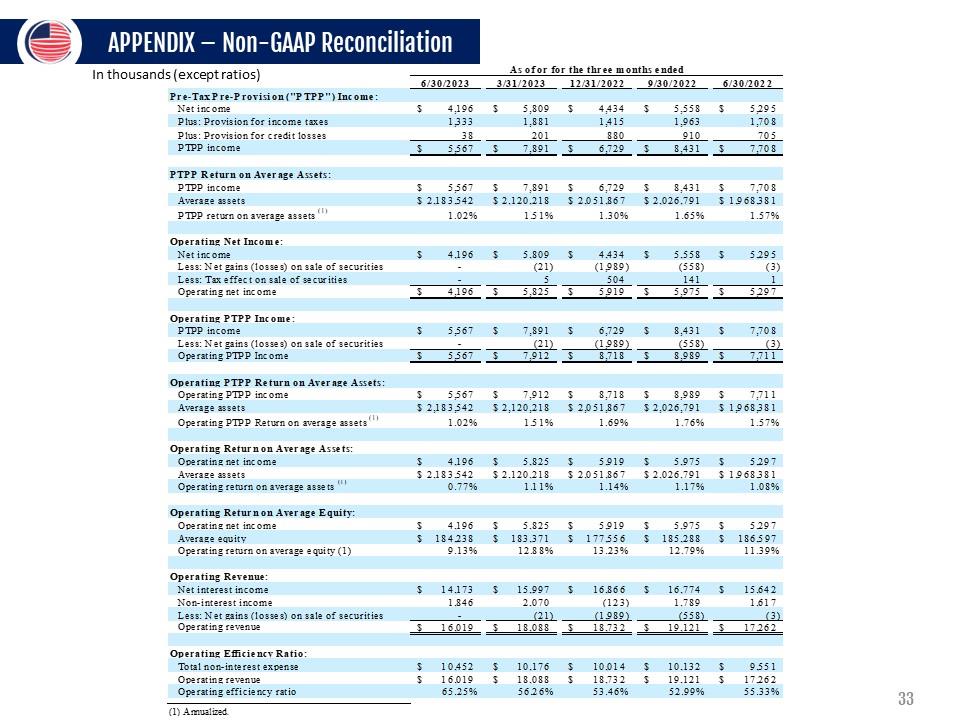

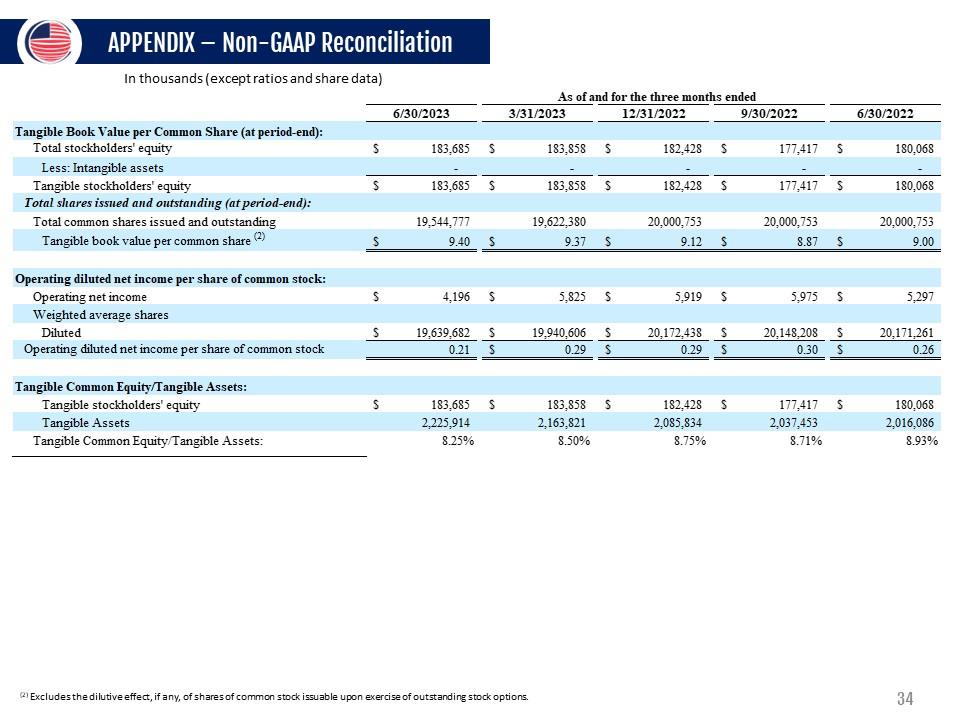

Operating revenue$16,019 Operating Efficiency Ratio: Total non -interest expense S 10,452 Operating revenue S 16,019 Operating efficiency ratio 65.25% (1) Annualized. S 7,912 S 2,120,218 1.51% S 8,718 S 2,051,867 1.69% S 8,989 S 2,026,791 1.76% S 7,711 S 1,968,381 1.57% S 5,825 S 2,120,218 1.11% S 5,919 S 2,051,867 1.14% S 5,975 S 2,026,791 1.17% S 5,297 S 1,968,381 1.08% S 5,825 S 5,919 S 5,975 S 5,297 S 183,371$177,556$185,288$186,597 12.88% 13.23% 12.79% 11.39% S 15,997$16,866$16,774$15,642 2,070 (123) 1,789 1,617 (21) (1:989) (558) (3) S 18,088$18,732$19,121$17,262 S 10,176 S 18,088 56.26% S 10,014 S 18,732 53.46% S 10,132 S 19,121 52.99% S 9,551 S 17,262 55.33% (1) Annualized. 33 APPENDIX – Non-GAAP Reconciliation In thousands (except ratios and share data) 6/30/2023 Tangible Book Value per Common Share (at period-end): Total stockholders 'equity$183:685 Less: Intangible assets - Tangible stockholders 'equity$183:685 Total shares issued and outstanding (at period-end): Total common shares issued and outstanding 19:544:777 Tangible book value per common shareS 9.40 Operating diluted net income per share of common stock: Operating net income$4:196 Weighted average shares Diluted$19;639;682 Operating diluted net income per share of common stock 0.21 Tangible Common Equity/Tangible Assets: Tangible stockholders 'equity$183:685 Tangible Assets 2:225:914 Tangible Common Equity /Tangible Assets: 8.25% As of and for the three months ended 3/31/2023 12/31/2022 9/30/2022 6/30/2022 S 183,858$181428$177,417$180:068 S 183,858$181428$177,417$180,068 19,622,380 20,000,753 20,000,753 20,000,753 S 9.37 $ 9.12$8.87 $ 9.00 S 5,825$5,919$5,975$5197 S 19,940,606 S 20,172,438 S 20,148,208 S 20,171161 S 0.29$0.29$0.30$0.26 S 183,858$182,428$177,417$180,068 2,163,821 8.50% 2,085,834 8.75% 2,037,453 8.71% 2,016,086 8.93% (2) Excludes the dilutive effect, if any, of shares of common stock issuable upon exercise of outstanding stock options. 34 CONTACT INFORMATION LOU DE LA AGUILERA Chairman, President & CEO (305) 715-5186 EH laguilera@uscentury.com ROB ANDERSON EVP, CHIEF FINANCIAL OFFICER (305) 715-5393 rob.anderson@uscentury.com INVESTOR RELATIONS InvestorRelations@uscentury.com 35