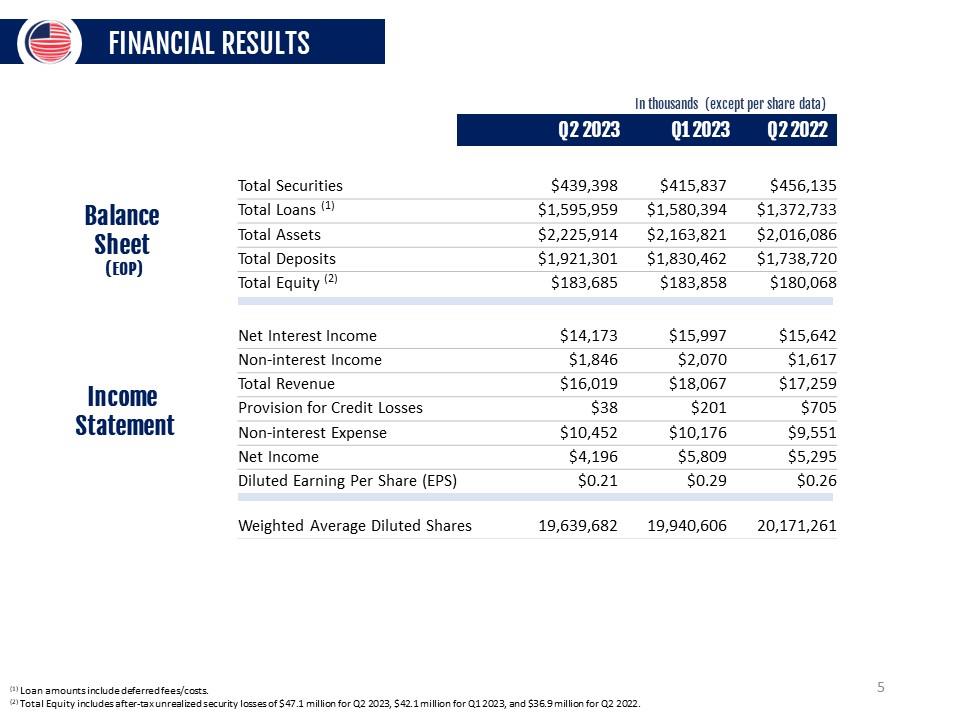

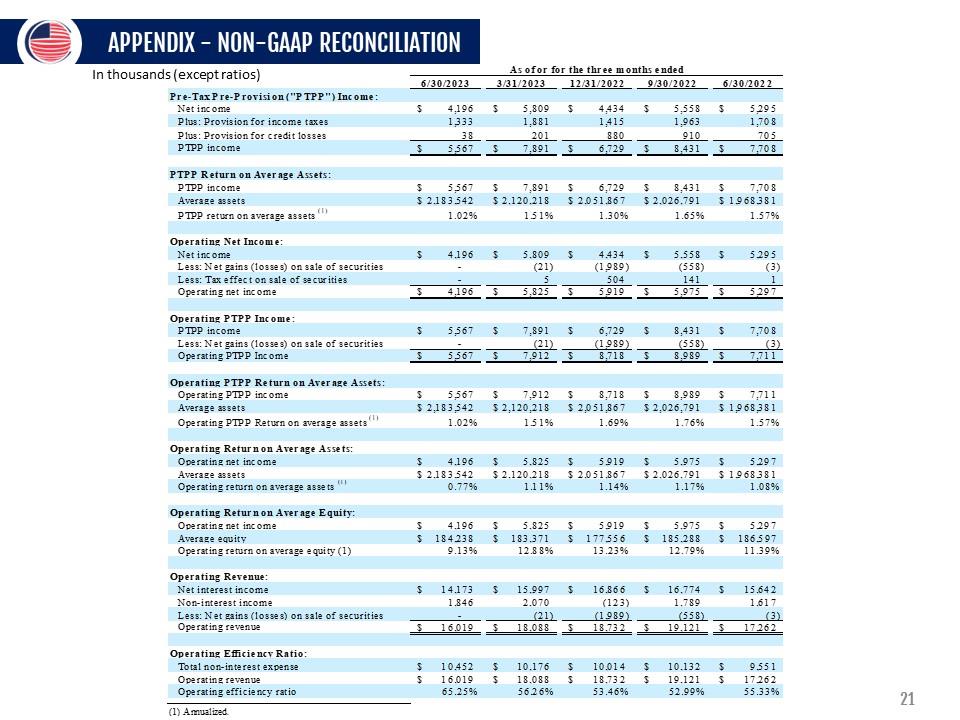

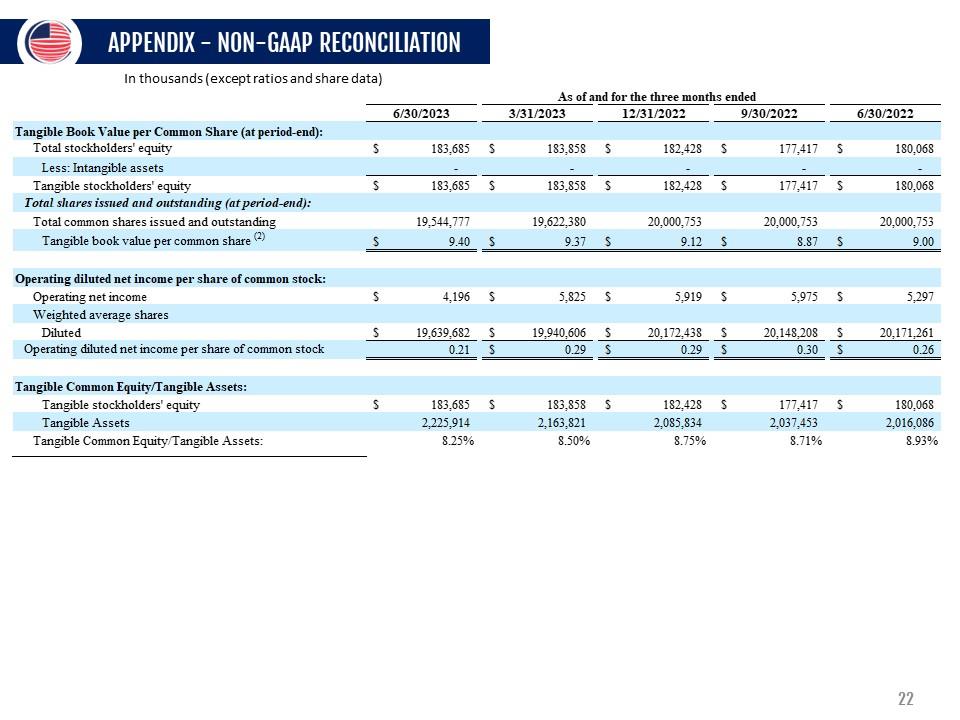

APPENDIX - NON-GAAP RECONCILIATION In thousand$(except

ratios) A$of or for the three month$ended 6/30/2023 3/31/2023

12/31/2022 9/30/2022 6/30/2022 U/JUí _u¿o Pre-Tax Pre-Provision

("PTPP") Income: Net income $4:196 Plus: Provision for income

taxe$1:333 Plus: Provision for credit losse$ 3S_ PTPP income $5.567

PTPP Return on Average Assets: PTPP income $5:567 Average

asset$$2,183,542 PTPP return on average asset$1 1.02% Operating Net

Income: Net income $4:196 Less: Net gain$(losses) on sale

of securities Less: Tax effect on sale of securitie$ - Operating

net income $4,196 Operating PTPP Income: PTPP income $5:567

Less: Net gain$(losses) on sale of securitie$ - Operating PTPP Income

$ 5,567 Operating PTPP Return on Average Assets: Operating

PTPP income $5,567 Average asset$$2,183,542 Operating PTPP

Return on average asset$‘ 1.02% Jl J II íí! O ÍI¿.V $5,809 $4,434

$5,558 $5,295 1,881 1,415 1,963 1,708 201 880 910 705 $7,891 $6,729

$8,431 $7,708 $7,891 $2,120,218 1.51% $6,729 $2,051,867

1.3 0% $8,431 $2,026,791 1.65% $7,708 $1,968,381 1.57% $5,809

$4,434 $5,558 $5,295 (21) (1,9 89) (558) (3) 5 504 141 1_

$5,825 $5,919 $5,975 $5,297 $7,891 $6,729 $8,431 $7,708 ^211

(1Î989) (558) _Q1 $7,912 $8,718 $8,989 $7,711 $7,912 $8,718

$8,989 $7,711 $2,120,218 $2,051,867 $2,026,791 $1,968,381 1.51%

1.57% 1.69% 1.76% Operating Return on Average Assets: Operating

net income $4:196 Average asset$$2,183,542 Operating

return on average asset$<1J 0.77% Operating Return on Average

Equity: Operating net income $4:196 Average equity $184,238

Operating return on average equity (1) 9.13% Operating Revenue:

Net interest income $14,173 Non-interest income 1,846 Less: Net

gain$(losses) on sale of securitie$ - Operating revenue

$16,019 Operating Efficiency Ratio: Total non-interest expense

$10,452 Operating revenue

$16,019 Operating efficiency ratio 65.25% (1) Annualized.