UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of September 2025 (Report No. 2)

Commission File Number: 001-41339

Swvl Holdings Corp

The Offices 4, One Central

Dubai World Trade Centre

Dubai, United Arab Emirates

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

CONTENTS

Interim Financial Statements

This Report of Foreign Private Issuer on Form 6-K consists of Swvl Holdings Corp (“Swvl”): (i) Unaudited Interim Condensed Consolidated Financial Statements as of and for the six months ended June 30, 2025, which are attached hereto as Exhibit 99.1; (ii) Management’s Discussion and Analysis of Financial Condition and Results of Operation as of and for the six months ended June 30, 2025, which is attached hereto as Exhibit 99.2; (iii) an investor presentation, which is attached hereto as Exhibit 99.3; and (iv) press release titled: “Swvl Announces H1 2025 Results, Delivering 26% Revenue Growth (49% in Constant Currency), 26% Gross Margin Growth, and Net Income of $0.43 Million”, which is attached hereto as Exhibit 99.4.

Exhibits 99.1, 99.2. and the first two paragraphs and the sections titled “Key Highlights” and “Forward Looking Statements” in exhibit 99.4 are incorporated by reference into Swvl’s Registration Statement on Form F-3 (Registration No. 333-279918) and Form S-8 (Registration No. 333-265464) filed with the Securities and Exchange Commission, to be a part thereof from the date on which this Report of Foreign Private Issuer on Form 6-K is submitted, to the extent not superseded by documents or reports subsequently filed or furnished.

EXHIBIT INDEX

Exhibit |

|

Description of Exhibit |

|

|

|

99.1 |

|

Swvl’s Unaudited Interim Condensed Consolidated Financial Statements as of June 30, 2025. |

99.2 |

|

|

99.3 |

|

|

99.4 |

|

|

101 |

|

The following financial information from the Registrant’s Interim Condensed Financial Statements as of June 30, 2025, formatted in XBRL (eXtensible Business Reporting Language): (i) Interim Condensed Statements of Financial Position, (ii) Interim Condensed Statements of Comprehensive Loss, (iii) Interim Condensed Statements of Changes in Shareholders’ Equity; (iv) Interim Condensed Statements of Cash Flows, and (v) Notes to the Unaudited Interim Condensed Financial Statements. |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

SWVL HOLDINGS CORP |

|

|

|

|

Date: September 8, 2025 |

By: |

/s/ Mostafa Kandil |

|

Name: |

Mostafa Kandil |

|

Title: |

Chief Executive Officer |

Exhibit 99.1

Swvl Holdings Corp and its subsidiaries

Condensed interim consolidated financial statements (unaudited)

For the six-month periods ended 30 June 2025 and 2024

Swvl Holdings Corp and its subsidiaries

Condensed interim consolidated financial statements (unaudited)

For the six-month periods ended 30 June 2025 and 2024

|

|

Page(s) |

|

|

|

Condensed interim consolidated statement of financial position |

|

2 |

|

|

|

Condensed interim consolidated statement of comprehensive profit or loss |

|

3 |

|

|

|

Condensed interim consolidated statement of changes in equity |

|

4 |

|

|

|

|

5 |

|

|

|

|

Notes to the condensed interim consolidated financial statements |

|

6 - 19 |

Swvl Holdings Corp and its subsidiaries

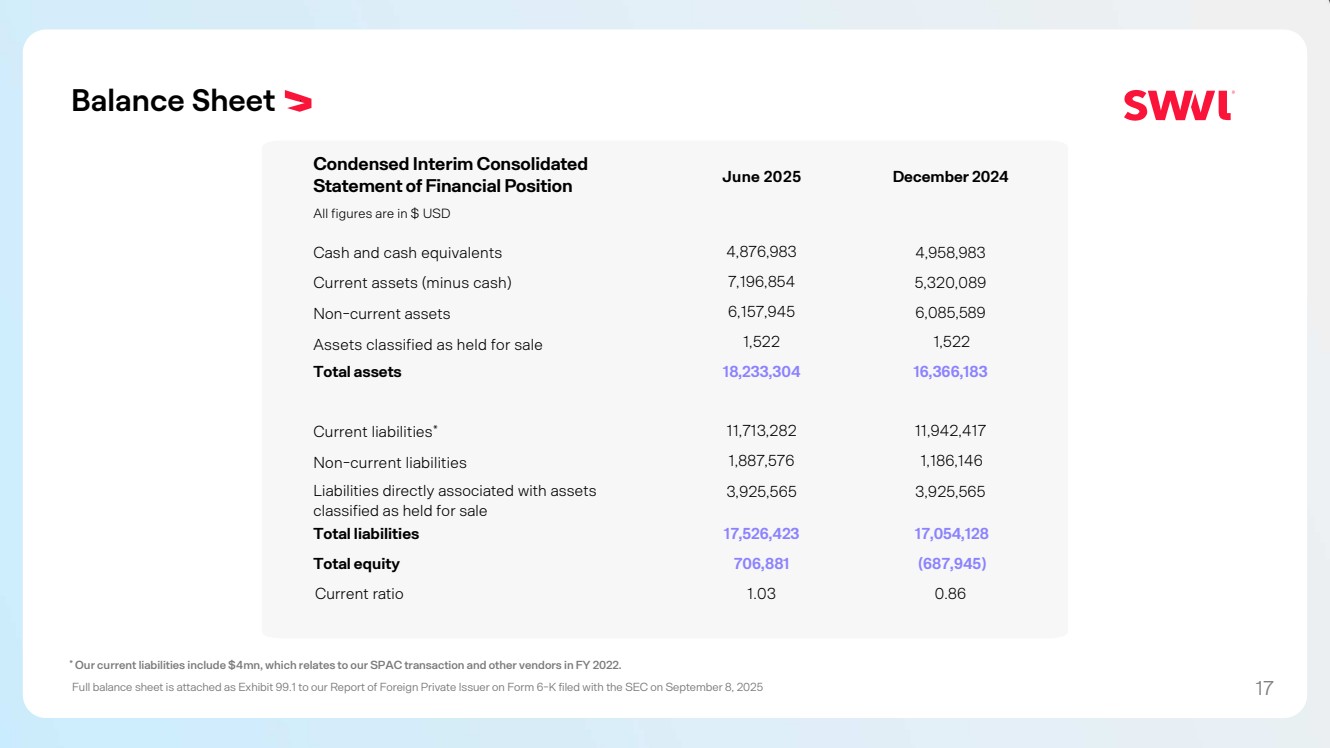

Condensed interim consolidated statement of financial position – As of 30 June 2025

(All amounts are shown in USD unless otherwise stated)

|

|

|

|

(Unaudited) |

|

(Audited) |

|

|

|

|

At 30 June |

|

At 31 December |

|

|

Note |

|

2025 |

|

2024 |

ASSETS |

|

|

|

|

|

|

Non-current assets |

|

|

|

|

|

|

Property and equipment |

|

4 |

|

460,752 |

|

457,802 |

Intangible assets |

|

5 |

|

92,900 |

|

106,262 |

Right-of-use assets |

|

|

|

190,675 |

|

232,612 |

Deferred tax assets |

|

18 |

|

5,413,618 |

|

5,288,913 |

|

|

|

|

6,157,945 |

|

6,085,589 |

|

|

|

|

|

|

|

Current assets |

|

|

|

|

|

|

Prepaid expenses and other current assets |

|

6 |

|

1,323,137 |

|

1,310,807 |

Trade and other receivables |

|

7 |

|

5,873,717 |

|

4,009,282 |

Cash and cash equivalents |

|

8 |

|

4,876,983 |

|

4,958,983 |

|

|

|

|

12,073,837 |

|

10,279,072 |

Assets classified as held for sale |

|

|

|

1,522 |

|

1,522 |

Total assets |

|

|

|

18,233,304 |

|

16,366,183 |

|

|

|

|

|

|

|

EQUITY AND LIABILITIES |

|

|

|

|

|

|

EQUITY |

|

|

|

|

|

|

Share capital |

|

9 |

|

24,912 |

|

24,746 |

Share premium |

|

9 |

|

354,179,327 |

|

353,883,768 |

Employee share scheme reserve |

|

10 |

|

631,629 |

|

564,127 |

Foreign currency translation reserve |

|

|

|

(18,004,387) |

|

(16,603,786) |

Reserve of disposal groups classified as held for sale |

|

|

|

2,372,514 |

|

2,372,514 |

Other reserves |

|

|

|

3,886,000 |

|

1,886,000 |

Accumulated losses |

|

|

|

(339,412,841) |

|

(339,845,041) |

Equity attributable to equity holders of the Parent Company |

|

|

|

3,677,154 |

|

2,282,328 |

|

|

|

|

|

|

|

Non-controlling interests |

|

|

|

(2,970,273) |

|

(2,970,273) |

Total equity/(deficit) |

|

|

|

706,881 |

|

(687,945) |

|

|

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

|

Non-current liabilities |

|

|

|

|

|

|

Provision for employees' end of service benefits |

|

|

|

58,348 |

|

45,957 |

Derivative warrant liabilities |

|

|

|

1,505,540 |

|

669,156 |

Accounts payable, accruals and other payables |

|

11 |

|

— |

|

30,850 |

Lease liabilities |

|

|

|

323,688 |

|

440,183 |

|

|

|

|

1,887,576 |

|

1,186,146 |

|

|

|

|

|

|

|

Current liabilities |

|

|

|

|

|

|

Accounts payable, accruals and other payables |

|

11 |

|

9,511,409 |

|

9,351,406 |

Deferred purchase price |

|

12 |

|

646,678 |

|

1,148,013 |

Current tax liabilities |

|

|

|

1,069,663 |

|

836,117 |

Lease liabilities |

|

|

|

485,532 |

|

606,881 |

|

|

|

|

11,713,282 |

|

11,942,417 |

Liabilities directly associated with assets classified as held for sale |

|

|

|

3,925,565 |

|

3,925,565 |

Total liabilities |

|

|

|

17,526,423 |

|

17,054,128 |

Total equity and liabilities |

|

|

|

18,233,304 |

|

16,366,183 |

op

The accompanying notes are an integral part of these condensed interim consolidated financial statements. |

(2) |

Swvl Holdings Corp and its subsidiaries

Condensed interim consolidated statement of comprehensive profit or loss - For the period ended 30 June 2025

(All amounts are shown in USD unless otherwise stated)

|

|

|

|

(Unaudited) |

|

(Unaudited) |

|

|

Note |

|

2025 |

|

2024 |

Continuing operations |

|

|

|

|

|

|

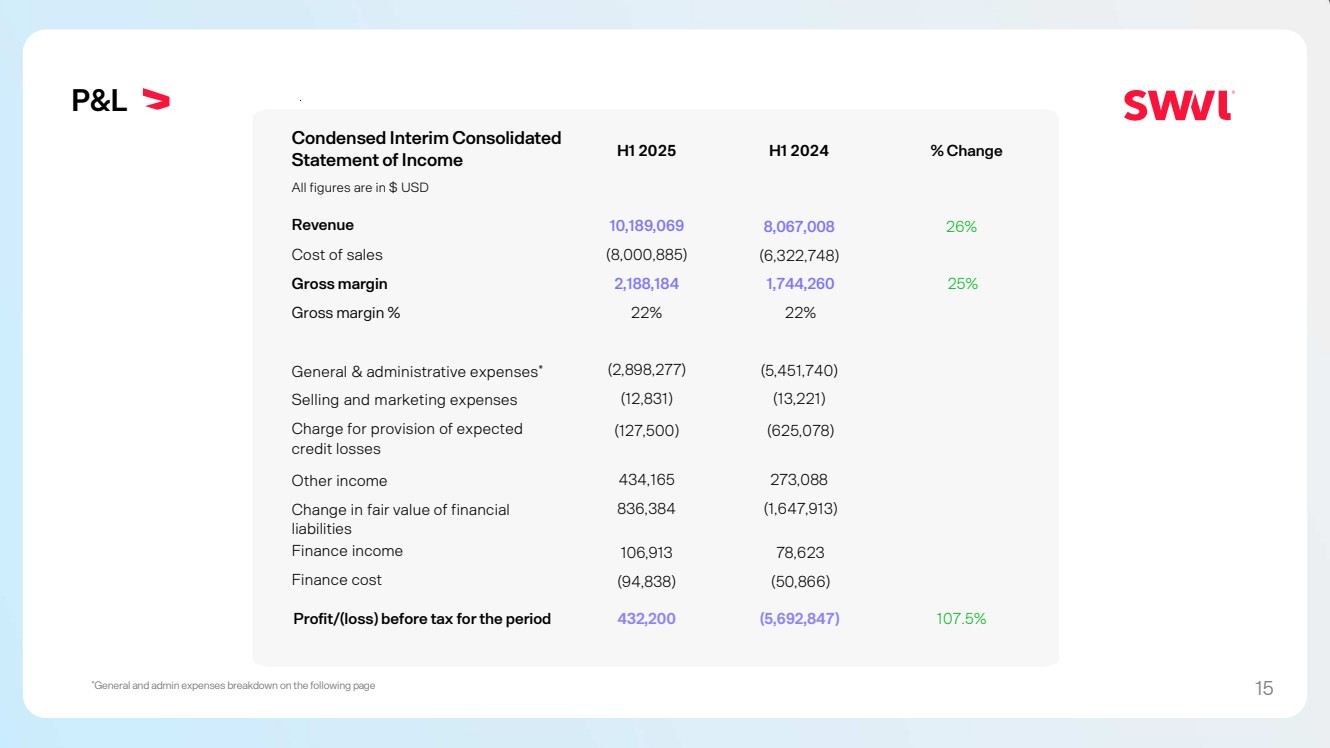

Revenue |

|

13 |

|

10,189,069 |

|

8,067,008 |

Cost of sales |

|

14 |

|

(8,000,885) |

|

(6,322,748) |

Gross income |

|

|

|

2,188,184 |

|

1,744,260 |

|

|

|

|

|

|

|

General and administrative expenses |

|

15 |

|

(2,898,277) |

|

(5,451,740) |

Selling and marketing costs |

|

|

|

(12,831) |

|

(13,221) |

Other expenses |

|

16 |

|

(127,500) |

|

(625,078) |

Other income |

|

17 |

|

434,165 |

|

273,088 |

Operating loss |

|

|

|

(416,259) |

|

(4,072,691) |

|

|

|

|

|

|

|

Change in fair value of financial liabilities |

|

|

|

836,384 |

|

(1,647,913) |

Finance income |

|

|

|

106,913 |

|

78,623 |

Finance cost |

|

|

|

(94,838) |

|

(50,866) |

Profit/(loss) before tax from continuing operations |

|

|

|

432,200 |

|

(5,692,847) |

|

|

|

|

|

|

|

Income tax benefit |

|

18 |

|

— |

|

— |

Profit/(loss) for the period from continuing operations |

|

|

|

432,200 |

|

(5,692,847) |

|

|

|

|

|

|

|

Discontinued operations |

|

|

|

|

|

|

Profit/(loss) for the period from discontinued operations |

|

|

|

— |

|

— |

Profit/(loss) for the period |

|

|

|

432,200 |

|

(5,692,847) |

|

|

|

|

|

|

|

Attributable to: |

|

|

|

|

|

|

Equity holders of the Parent Company |

|

|

|

432,200 |

|

(5,692,847) |

Non-controlling interests |

|

|

|

— |

|

— |

|

|

|

|

432,200 |

|

(5,692,847) |

|

|

|

|

|

|

|

Profit/(loss) per share attributable to equity holders of the Parent Company |

|

|

|

|

|

|

Basic |

|

19 |

|

0.04 |

|

(0.67) |

Diluted |

|

19 |

|

0.04 |

|

(0.67) |

|

|

|

|

|

|

|

Other comprehensive income |

|

|

|

|

|

|

Items that may be reclassified subsequently to profit or loss: |

|

|

|

|

|

|

Exchange differences on translation of foreign operations, net of tax |

|

|

|

(1,400,601) |

|

(4,713,527) |

Total comprehensive loss for the period |

|

|

|

(968,401) |

|

(10,406,374) |

|

|

|

|

|

|

|

Attributable to: |

|

|

|

|

|

|

Equity holders of the Parent Company |

|

|

|

(968,401) |

|

(10,406,374) |

Non-controlling interests |

|

|

|

— |

|

— |

|

|

|

|

(968,401) |

|

(10,406,374) |

op

The accompanying notes are an integral part of these condensed interim consolidated financial statements. |

(3) |

Swvl Holdings Corp and its subsidiaries

Condensed interim consolidated statement of changes in equity – As of 30 June 2025

(All amounts are shown in USD unless otherwise stated)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reserve for |

|

Foreign |

|

|

|

|

|

attributable to |

|

|

|

|

|

|

|

|

|

|

|

|

Share-based |

|

disposal |

|

currency |

|

|

|

|

|

equity holders |

|

Non- |

|

|

|

|

|

|

Share |

|

Share |

|

compensation |

|

group held |

|

translation |

|

Other |

|

Accumulated |

|

of the Parent |

|

controlling |

|

Total |

|

|

Note |

|

capital |

|

premium |

|

reserve |

|

for sale |

|

reserve |

|

reserve |

|

losses |

|

Company |

|

interests |

|

equity/(deficit) |

As at 1 January 2024 (Audited) |

|

|

|

16,979 |

|

347,295,152 |

|

507,677 |

|

2,106,737 |

|

(11,466,066) |

|

— |

|

(329,506,304) |

|

8,954,175 |

|

(3,039,317) |

|

5,914,858 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total comprehensive loss for the period |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loss for the period |

|

|

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

(5,692,847) |

|

(5,692,847) |

|

— |

|

(5,692,847) |

Other comprehensive loss for the period |

|

|

|

— |

|

— |

|

— |

|

98,234 |

|

(4,811,761) |

|

— |

|

— |

|

(4,713,527) |

|

— |

|

(4,713,527) |

|

|

|

|

— |

|

— |

|

— |

|

98,234 |

|

(4,811,761) |

|

— |

|

(5,692,847) |

|

(10,406,374) |

|

— |

|

(10,406,374) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Issuance of shares |

|

9 |

|

6,006 |

|

2,396,351 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

2,402,357 |

|

— |

|

2,402,357 |

Employee share scheme reserve |

|

10 |

|

— |

|

— |

|

(40,614) |

|

— |

|

— |

|

— |

|

— |

|

(40,614) |

|

— |

|

(40,614) |

As at 30 June 2024 (Unaudited) |

|

|

|

22,985 |

|

349,691,503 |

|

467,063 |

|

2,204,971 |

|

(16,277,827) |

|

— |

|

(335,199,151) |

|

909,544 |

|

(3,039,317) |

|

(2,129,773) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As at 1 January 2025 (Audited) |

|

|

|

24,746 |

|

353,883,768 |

|

564,127 |

|

2,372,514 |

|

(16,603,786) |

|

1,886,000 |

|

(339,845,041) |

|

2,282,328 |

|

(2,970,273) |

|

(687,945) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total comprehensive loss for the period |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Profit for the period |

|

|

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

432,200 |

|

432,200 |

|

— |

|

432,200 |

Other comprehensive loss for the period |

|

|

|

— |

|

— |

|

— |

|

— |

|

(1,400,601) |

|

— |

|

— |

|

(1,400,601) |

|

— |

|

(1,400,601) |

|

|

|

|

— |

|

— |

|

— |

|

— |

|

(1,400,601) |

|

— |

|

432,200 |

|

(968,401) |

|

— |

|

(968,401) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Issuance of shares |

|

9 |

|

166 |

|

295,559 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

295,725 |

|

— |

|

295,725 |

Other reserves |

|

|

|

— |

|

— |

|

— |

|

— |

|

— |

|

2,000,000 |

|

— |

|

2,000,000 |

|

— |

|

2,000,000 |

Employee share scheme reserve |

|

10 |

|

— |

|

— |

|

67,502 |

|

— |

|

— |

|

— |

|

— |

|

67,502 |

|

— |

|

67,502 |

As at 30 June 2025 (Unaudited) |

|

|

|

24,912 |

|

354,179,327 |

|

631,629 |

|

2,372,514 |

|

(18,004,387) |

|

3,886,000 |

|

(339,412,841) |

|

3,677,154 |

|

(2,970,273) |

|

706,881 |

op

The accompanying notes are an integral part of these condensed interim consolidated financial statements. |

(4) |

Swvl Holdings Corp and its subsidiaries

Condensed interim consolidated statement of cash flows - For the period ended 30 June 2025

(All amounts are shown in USD unless otherwise stated)

|

|

For the six-month period ended |

||

|

|

30 June |

||

|

|

(Unaudited) |

|

(Unaudited) |

|

|

2025 |

|

2024 |

Profit/(loss) before tax from continued operations |

|

432,200 |

|

(5,692,847) |

Profit before tax from discontinued operations |

|

— |

|

— |

Profit/(loss) for the period before tax |

|

432,200 |

|

(5,692,847) |

|

|

|

|

|

Adjustments to reconcile profit/(loss) before tax to net cash flows: |

|

|

|

|

Depreciation of property and equipment |

|

— |

|

130,529 |

Depreciation of right-of-use assets |

|

58,297 |

|

92,603 |

Amortization of intangible assets |

|

15,594 |

|

19,916 |

Other non – cash loss/(income) |

|

(90,910) |

|

2,478,195 |

Change in fair value of financial liabilities |

|

836,384 |

|

1,647,913 |

Provision for employees’ end of service benefits |

|

12,391 |

|

— |

|

|

1,263,956 |

|

(1,323,691) |

Changes in working capital: |

|

|

|

|

Trade and other receivables |

|

(1,864,435) |

|

1,180,067 |

Prepaid expenses and other current assets |

|

(12,330) |

|

625,002 |

Due to related party |

|

— |

|

(131,523) |

Accounts payable, accruals and other payables |

|

129,153 |

|

(699,808) |

Current tax liabilities |

|

233,546 |

|

(162,934) |

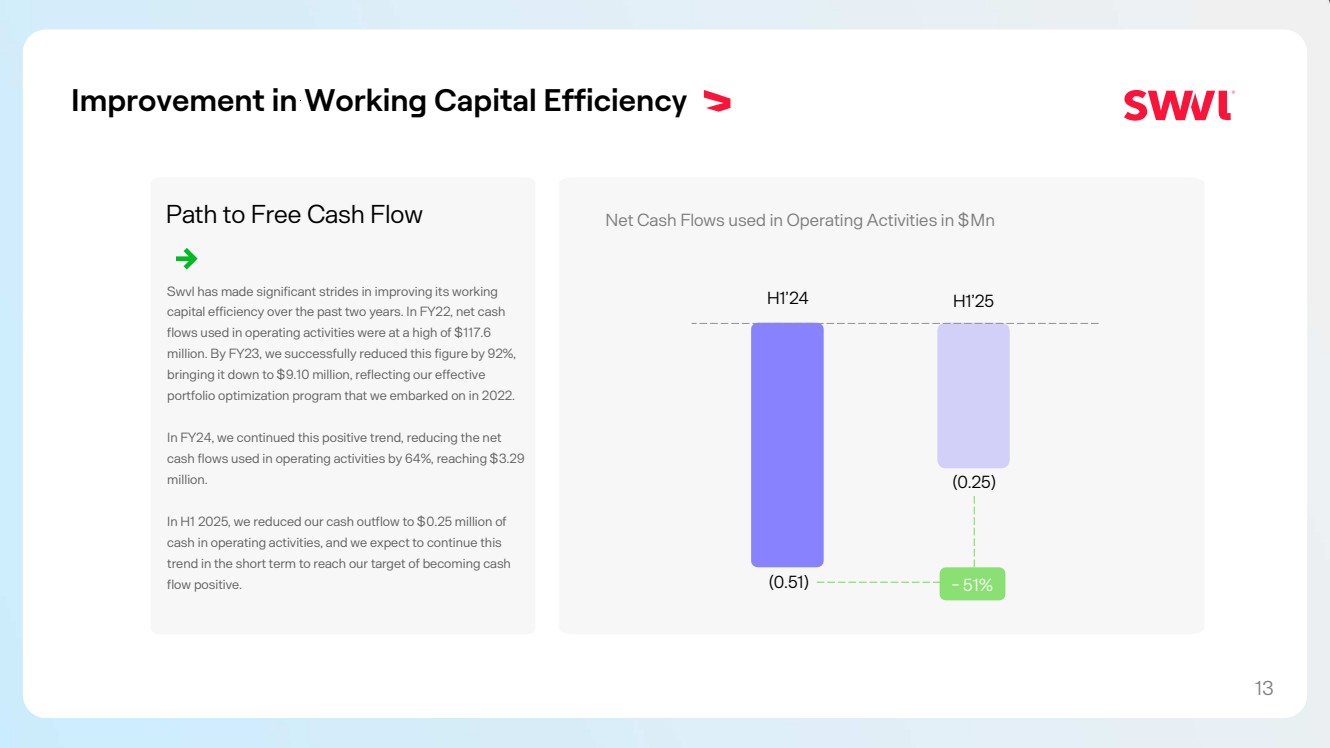

Net cash flows used in operating activities |

|

(250,110) |

|

(512,887) |

|

|

|

|

|

Cash flows from investing activities |

|

|

|

|

Sublease rentals received |

|

— |

|

366,785 |

Purchase of property and equpiment |

|

(2,950) |

|

— |

Net cash flows (used in)/generated from investing activities |

|

(2,950) |

|

366,785 |

|

|

|

|

|

Cash flows from financing activities |

|

|

|

|

Proceeds from issuance of share capital |

|

— |

|

— |

Proceeds from issuance of other instruments |

|

2,000,000 |

|

— |

Repayment of loan from related party |

|

— |

|

— |

Repayment of external loan |

|

— |

|

— |

Finance lease liabilities paid, net of accretion |

|

(236,844) |

|

(339,540) |

Net cash flows generated from/(used in) financing activities |

|

1,763,156 |

|

(339,540) |

|

|

|

|

|

Net increase/(decrease) in cash and cash equivalents |

|

1,510,096 |

|

(485,642) |

Cash and cash equivalents at the beginning of the period |

|

4,958,983 |

|

2,924,016 |

Effects of exchange rate changes on cash and cash equivalents |

|

(1,592,096) |

|

(1,254,584) |

Cash and cash equivalents at the end of the period |

|

4,876,983 |

|

1,183,790 |

op

The accompanying notes are an integral part of these condensed interim consolidated financial statements. |

(5) |

1 |

Establishment and operations |

Swvl Holdings Corp (the “Parent Company”) (formerly known as “Pivotal Holdings Corp”) is a business company limited by shares incorporated under the laws of the British Virgin Islands and was registered on 23 July 2021. The registered office of the Company is at P.O. Box 173, Kingston Chambers, Road Town, Tortola, the British Virgin Islands.

The condensed interim consolidated financial statements as at and for the six-month period ended 30 June 2025 consist of the Parent Company and its subsidiaries (together referred to as the “Group”). The Group’s principal head office is located in The Offices 4, One Central, Dubai World Trade Centre, Street 1, Dubai, United Arab Emirates.

Swvl Inc. was founded on 17 May 2017. Swvl Holdings Corp was incorporated as a direct wholly-owned subsidiary of Swvl Inc. As a result of various legal entity reorganization transactions undertaken in March 2022, Swvl Holdings Corp became the holding company of the Group, and the then-stockholders of Swvl Inc. became the stockholders of Swvl Holdings Corp. Swvl Inc. is the predecessor of Swvl Holdings Corp for financial reporting purposes.

The Group operates multimodal transportation networks that offer access to transportation options through the Group’s platform and mobile-based application. The Group also licenses its technology to transport operators to manage their service. The Group operates a technology platform that uses a widespread transportation network. The Group uses leading technology, operational excellence and product expertise to operate transportation services on predetermined routes. The Group develops and operates proprietary technology applications supporting a variety of offerings on its platform (“platform(s)” or “Platform(s)”). The Group provides transportation services through contracting with other service providers (or transportation operators). Riders are collectively referred to as “end-user(s)” or “consumer(s)”. The drivers are referred to as “captain(s)”.

1.1 |

Consolidated subsidiaries |

Subsidiaries are all entities over which the Group has control. The Group controls an entity when the Group is exposed, or has right to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. Subsidiaries are consolidated from the date on which control is transferred to the Group. They are deconsolidated from the date that control ceases.

As of 30 June 2025, the Group still maintained control for all subsidiaries, however, certain subsidiaries were decided to be held for sale or to be discontinued, subsidiaries listed below will be presented with the same alignment.

| i) | Continued operations |

|

|

Country of |

|

Legal ownership % |

|

Principal |

||

Company name |

|

incorporation |

|

30-Jun-25 |

|

31-Dec-24 |

|

business activities |

Swvl Inc. |

|

British Virgin Islands |

|

100 |

% |

100 |

% |

Holding company |

Swvl Group Corp |

|

British Virgin Islands |

|

100 |

% |

100 |

% |

Holding company |

Swvl Holdco Corp |

|

British Virgin Islands |

|

100 |

% |

100 |

% |

Dormant entity |

Pivotal Merger Sub Company I |

|

Cayman Islands |

|

100 |

% |

100 |

% |

Merger entity |

Swvl for Smart Transport Applications and Services LLC |

|

Egypt |

|

99.80 |

% |

99.80 |

% |

Technology platform |

Swvl Saudi for Information Technology |

|

Kingdom of Saudi Arabia |

|

100 |

% |

100 |

% |

Technology platform |

Swvl Saudi Regional Headquarters |

|

Kingdom of Saudi Arabia |

|

100 |

% |

100 |

% |

Technology platform |

Smart Mobility Solutions for Transportation Services (i) |

|

Kingdom of Saudi Arabia |

|

— |

% |

— |

% |

Technology platform |

Swvl for Mobility Solutions FZE (i) |

|

United Arab Emirates |

|

— |

% |

— |

% |

Technology platform |

(6)

1.1 |

Consolidated subsidiaries (continued) |

| ii) | Discontinued operations |

|

|

Country of |

|

Legal ownership % |

|

Principal |

||

Company name |

|

incorporation |

|

30-June-25 |

|

31-Dec-24 |

|

business activities |

Swvl NBO Limited |

|

Kenya |

|

100 |

% |

100 |

% |

Technology platform |

Swvl Technologies Ltd. |

|

Kenya |

|

100 |

% |

100 |

% |

Technology platform |

Smart Way Transportation LLC (ii) |

|

Jordan |

|

— |

% |

— |

% |

Technology platform |

Swvl My For Information Technology SDN BHD |

|

Malaysia |

|

100 |

% |

100 |

% |

Technology platform |

Viapool Inc. |

|

Delaware, USA |

|

51 |

% |

51 |

% |

Technology platform |

Movilidad Digital SAS, a subsidiary of Viapool, Inc. |

|

Argentina |

|

51 |

% |

51 |

% |

Holding company |

Viapool SRL, a subsidiary of Viapool, Inc. |

|

Argentina |

|

51 |

% |

51 |

% |

Technology platform |

Viapool SPA, a subsidiary of Viapool, Inc. |

|

Chile |

|

51 |

% |

51 |

% |

Technology platform |

Swvl Brasil Tecnologia LTDA, a subsidiary of Viapool, Inc. |

|

Brazil |

|

51 |

% |

51 |

% |

Technology platform |

Door2Door GmbH, a subsidiary of Swvl Germany GmbH |

|

Germany |

|

100 |

% |

100 |

% |

Technology platform |

Swvl Germany GmbH (formerly "Blitz B22-203 GmbH") |

|

Germany |

|

100 |

% |

100 |

% |

Holding company |

Swvl Global FZE |

|

United Arab Emirates |

|

— |

% |

— |

% |

Headquarters |

The Group, in certain cases, is required to have a resident as one of the shareholders besides the Parent Company to comply with local laws and regulations. However, in such cases, the Group continues to remain the economic beneficiary of the shareholding held by such resident shareholder and therefore is said to have a “beneficial ownership” of such non-controlling interests. Legal ownership and beneficial ownership are the same except as indicated below.

| (i) | The Parent Company’s subsidiary’s Swvl for Mobility Solutions FZE and Smart Mobility Solutions for Transportation Services were incorporated during the year ended 31 December 2024. The subsidiaries are currently legally owned by a member of the Group’s management and are in the process of a legal ownership transfer to the Group. The subsidiaries have been consolidated based on the beneficial ownership and effective control. |

| (ii) | The Parent Company’s subsidiary Smart Way Transportation LLC was incorporated during the year ended 31 December 2021. The subsidiary is currently legally owned by a member of the Group’s management. During 2022, the Group’s board of directors resolved to discontinue the subsidiary’s operations. As of 30 June 2025, the company is still in liquidation process. The subsidiary has been consolidated based on the beneficial ownership and effective control. |

2 |

Basis of preparation |

i) |

Compliance with International Financial Reporting Standards (“IFRS”) |

These condensed interim consolidated financial statements are for the six-month periods ended 30 June 2025 and 2024 and are presented in United States Dollars (“USD” or “$”), which is the functional currency of the Parent Company. They have been prepared in accordance with IAS 34 ‘Interim Financial Reporting’.

These condensed interim consolidated financial statements do not include all of the information required in annual consolidated financial statements in accordance with IFRS and should be read in conjunction with the consolidated financial statements for the year ended 31 December 2024. However, selected explanatory notes are included to explain events and transactions that are significant to an understanding of the changes in the Group’s financial position and performance since the last annual financial statements.

(7)

ii) |

Historical cost convention |

These condensed interim consolidated financial statements have been prepared under the historical cost convention except for the following:

- |

Certain financial assets, derivative warrant liabilities, derivative liabilities, convertible notes, and earnouts liabilities that are measured at fair value. |

- |

Income and expenses that have been accounted for using the accrual basis. |

2Basis of preparation (continued)

ii)Historical cost convention (continued)

The consolidated financial statements have been presented in US Dollars (“USD”, “$”) which is the reporting currency of the Group.

2.1 |

Going concern |

These condensed interim consolidated financial statements have been prepared on a going concern basis, which assumes that the Group will be able to discharge its liabilities in the ordinary course of business. The Group incurred a profit of $432,200 for the six-month period ended 30 June 2025 (loss of $5,692,847 for the six-month period ended 30 June 2024), had accumulated losses of $339.4 million as at 30 June 2025 ($ 339.8 million as at 31 December 2024), and had negative operating cash flows of $0.25 million for the six-month period ended 30 June 2025 (negative operating cash flows of $ 0.5 million for the six-month period ended 30 June 2024). Notwithstanding these results, Management believes there are no events or conditions that give rise to doubt the ability of the Group to continue as a going concern for a period of twelve months after the preparation of the consolidated financial statements.

2.2 |

Amended standards adopted by the Group |

A number of amended standards became applicable for the current reporting period. The Group did not have to change its accounting policies or make retrospective adjustments as a result of adopting these amended standards.

2.3Accounting policies

The accounting policies used for the condensed interim consolidated financial statements for the six-month period ended 30 June 2025 are consistent with those used in the annual consolidated financial statements for the year ended 31 December 2024.

3Critical accounting judgments and estimates

When preparing the condensed interim consolidated financial statements, management undertakes a number of judgements, estimates and assumptions about recognition and measurement of assets, liabilities, income and expenses. The actual results may differ from the judgements, estimates and assumptions made by management, and will seldom equal the estimated results. The judgements, estimates and assumptions applied in the condensed interim consolidated financial statements for the six-month period ended 30 June 2025 and 2024, including the key sources of estimation uncertainty, were the same as those applied in the Group’s annual consolidated financial statements for the year ended 31 December 2024.

(8)

4Property and equipment

The property and equipment net book value consists of the following:

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Leasehold improvements |

|

421,210 |

|

420,601 |

Furniture, fittings and equipment |

|

39,542 |

|

37,201 |

Property and equipment, net |

|

460,752 |

|

457,802 |

5Intangible assets

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

Net book value |

|

Net book value |

|

|

USD |

|

USD |

Licenses |

|

92,900 |

|

106,262 |

|

|

92,900 |

|

106,262 |

In May 2023 the Group obtained a smart transportation operating license in Egypt in collaboration with Land Transport Regulatory Authority (LTRA) which granted the Egyptian entity a five-year operating license commencing on May 16, 2023 and expires on May 15, 2028.

6Prepaid expenses and other current assets

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Withholding tax receivables |

|

1,166,732 |

|

983,770 |

Other assets |

|

140,458 |

|

134,826 |

Refundable deposits |

|

— |

|

160,902 |

Prepaid expenses |

|

15,947 |

|

31,309 |

|

|

1,323,137 |

|

1,310,807 |

(9)

7Trade and other receivables

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Trade receivables |

|

3,646,592 |

|

2,614,945 |

Accrued income |

|

1,577,598 |

|

1,318,327 |

Customer wallet receivables |

|

1,679,273 |

|

1,585,645 |

Less: provision for expected credit losses |

|

(1,029,746) |

|

(1,514,586) |

|

|

5,873,717 |

|

4,004,331 |

|

|

|

|

|

Other receivables |

|

— |

|

4,951 |

|

|

5,873,717 |

|

4,009,282 |

8Cash and bank balances

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Cash at banks |

|

4,876,982 |

|

4,958,983 |

Cash in hand |

|

— |

|

— |

|

|

4,876,982 |

|

4,958,983 |

For the purpose of the cash flow statement, cash and cash equivalents comprise the following:

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Cash attributable to continued operations |

|

4,876,982 |

|

4,958,983 |

Cash attributable to discontinued operations |

|

1,522 |

|

1,522 |

|

|

4,878,504 |

|

4,960,505 |

9Share capital

a. Share capital:

In 2023, the Group restructured its authorized shares and issued ordinary shares as detailed below:

| (a) | The number of ordinary shares which the Group is authorized to issue has been decreased to 20,000,000 ordinary shares by the consolidation of every 25 ordinary shares of US$0.0001 par value each currently in issue into 1 ordinary share of US$0.0025 par value each; and |

| (b) | the issued ordinary shares have been combined into a small number of shares, resulting in every 25 issued ordinary share being combined into 1 ordinary share with a par value of US$0.0025 each. |

Following the restructuring, the Group is authorized to issue 20,000,000 ordinary shares and 55,000,000 preference shares. The restructuring was approved on 4 January 2023 and became effective on 25 January 2023.

(10)

9Share capital (Continued)

a. Share capital: (Continued)

The below table sets out the Group’s share structure during the period ended 30 June 2025 and the year ended 31 December 2024:

|

|

At 30 June 2025 |

|

At 31 December 2024 |

||||

|

|

Authorized |

|

Issued |

|

Authorized |

|

Issued |

Class A ordinary shares |

|

20,000,000 |

|

9,964,344 |

|

20,000,000 |

|

9,898,516 |

Preferred shares |

|

55,000,000 |

|

— |

|

55,000,000 |

|

— |

|

|

75,000,000 |

|

9,964,344 |

|

75,000,000 |

|

9,898,516 |

|

|

At 30 June 2025 |

|

At 31 December 2024 |

||||

|

|

Number |

|

Share |

|

Number |

|

Share |

|

|

of shares |

|

capital |

|

of shares |

|

capital |

Issuance of shares in the normal course of business |

|

5,191,300 |

|

12,978 |

|

5,125,472 |

|

12,812 |

Issuance of shares to Swvl Inc. shareholders |

|

3,411,410 |

|

8,529 |

|

3,411,410 |

|

8,529 |

Issuance of shares to SPAC shareholders |

|

557,960 |

|

1,395 |

|

557,960 |

|

1,395 |

Conversion of convertible notes |

|

645,018 |

|

1,613 |

|

645,018 |

|

1,613 |

Issuance of shares to PIPE investors |

|

158,656 |

|

397 |

|

158,656 |

|

397 |

Other shares |

|

— |

|

— |

|

— |

|

0 |

|

|

9,964,344 |

|

24,912 |

|

9,898,516 |

|

24,746 |

b. Share premium:

|

|

At 30 June 2025 |

|

|

Share Premium |

Issuance of shares to shareholders |

|

88,873,188 |

Conversion of convertible notes |

|

145,952,505 |

Issuance of share to PIPE investors |

|

39,663,603 |

Recapitalization costs |

|

121,077,329 |

Other shares issued during the period |

|

— |

|

|

395,566,625 |

Less: |

|

|

Costs attributable to the issuance of shares in connection with the business combination |

|

(8,467,766) |

Fair value of earnout shares |

|

(75,550,455) |

|

|

311,548,404 |

Issuance of shares in the normal course of business |

|

42,630,923 |

|

|

354,179,327 |

|

|

At 31 December 2024 |

|

|

Share Premium |

Issuance of shares to shareholders |

|

88,873,188 |

Conversion of convertible notes |

|

145,952,505 |

Issuance of share to PIPE investors |

|

39,663,603 |

Recapitalization costs |

|

121,077,329 |

|

|

395,566,625 |

Less: |

|

|

Costs attributable to the issuance of shares in connection with the business combination |

|

(8,467,766) |

Fair value of earnout shares |

|

(75,550,455) |

|

|

311,548,404 |

Issuance of shares in the normal course of business |

|

42,335,364 |

|

|

353,883,768 |

(11)

10Employee share scheme reserve

At 30 June 2025, the employee share scheme reserve balance was $631,629 (at 31 December 2024: $564,127).

Total expense arising from share-based payment transactions recognized in the consolidated statement of comprehensive income as part of employee benefit were $67,502 for the six-month period ended 30 June 2025 (reversal of $40,614 for the six-month period ended 30 June 2024).

11Accounts payable, accruals and other payables

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Financial items |

|

|

|

|

Accounts payables |

|

6,872,144 |

|

5,709,577 |

Captain payables |

|

91,573 |

|

367,436 |

Salaries payable |

|

277,906 |

|

372,034 |

Accrued expenses |

|

2,123,118 |

|

2,592,446 |

Credit facility |

|

17,226 |

|

158,203 |

LTRA payable |

|

— |

|

78,125 |

Other payables |

|

154,468 |

|

98,745 |

|

|

9,536,435 |

|

9,376,566 |

LTRA payable non-current portion |

|

(30,850) |

|

(30,850) |

|

|

9,505,585 |

|

9,345,716 |

Non-financial items |

|

|

|

|

Advances from individual customers (e-wallets) (i) |

|

5,824 |

|

5,690 |

Total accounts payable, accruals and other payables |

|

9,511,409 |

|

9,351,406 |

| (i) | Advances from individual customers (e-wallets) are used by customers against future bookings. |

12Deferred purchase price

The movement in the deferred purchase price is as follows:

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Opening balance |

|

1,148,013 |

|

1,207,682 |

Change in fair value |

|

(205,610) |

|

1,865,274 |

Issuance of shares |

|

(295,725) |

|

(1,924,943) |

Ending balance |

|

646,678 |

|

1,148,013 |

The deferred purchase price consists of outstanding cash payments and share issuances. The change in fair value is a result of revaluing the shares outstanding to reflect share price as per the purchase agreements. Management has not used any complex assumptions in arriving at the fair value of the deferred purchase price.

(12)

12Deferred purchase price (Continued)

The deferred purchase price is detailed as follows:

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Shotl Transportation, S.L. |

|

627,158 |

|

627,158 |

Urbvan Mobility Ltd. |

|

— |

|

491,344 |

Door2Door |

|

19,520 |

|

29,511 |

|

|

646,678 |

|

1,148,013 |

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

Maturity analysis |

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Less than one year (current) |

|

646,678 |

|

1,148,013 |

|

|

646,678 |

|

1,148,013 |

13Revenue

The Group derives its revenue principally from end-users who use the Group’s platform to access routes predetermined by the Group. Revenue for transport services represents the total amount of fees charged to the end user for these services.

Disaggregated revenue information

|

|

(Unaudited) For the six-month |

||

|

|

period ended 30 June |

||

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Business to business |

|

8,676,762 |

|

6,001,062 |

Business to customers |

|

1,512,307 |

|

2,065,946 |

|

|

10,189,069 |

|

8,067,008 |

Revenue by geographical location

|

|

(Unaudited) For the six-month |

||

|

|

period ended 30 June |

||

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

|

|

|

|

|

Egypt |

|

6,752,936 |

|

6,636,048 |

Kingdom of Saudi Arabia |

|

2,576,607 |

|

1,430,960 |

United Arab Emirates |

|

859,526 |

|

— |

|

|

10,189,069 |

|

8,067,008 |

14Cost of sales

|

|

(Unaudited) For the six-month |

||

|

|

period ended 30 June |

||

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Captain costs |

|

8,035,494 |

|

6,347,514 |

Captain bonuses |

|

10,113 |

|

22,045 |

Captain deductions |

|

(44,722) |

|

(48,930) |

Tolls and fines |

|

— |

|

2,119 |

|

|

8,000,885 |

|

6,322,748 |

(13)

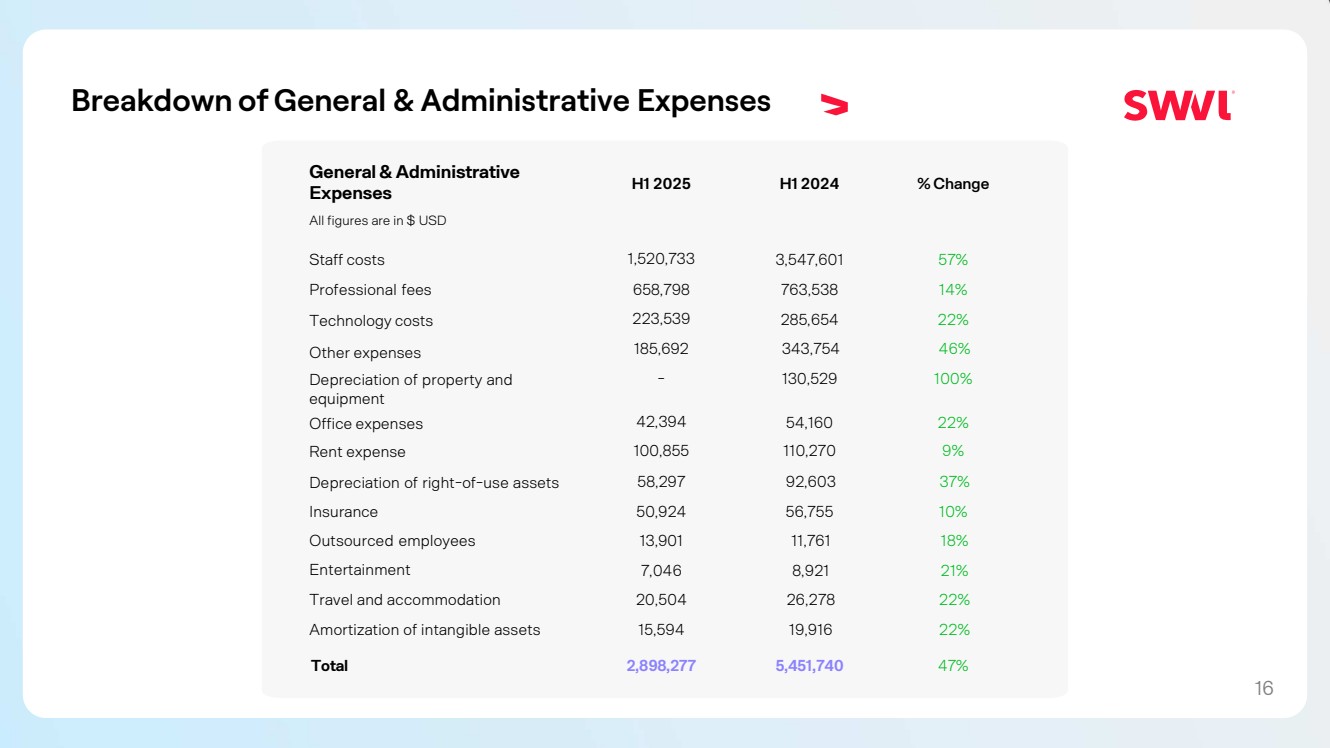

15General and administrative expenses

|

|

(Unaudited) For the six-month |

||

|

|

period ended 30 June |

||

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Staff costs |

|

1,520,733 |

|

3,547,601 |

Professional fees |

|

658,798 |

|

763,538 |

Technology costs |

|

223,539 |

|

285,654 |

Other expenses |

|

185,692 |

|

343,754 |

Depreciation of property and equipment |

|

— |

|

130,529 |

Rent expense |

|

100,855 |

|

110,270 |

Depreciation of right-of-use assets |

|

58,297 |

|

92,603 |

Insurance |

|

50,924 |

|

56,755 |

Office expenses |

|

42,394 |

|

54,160 |

Travel and accommodation |

|

20,504 |

|

26,278 |

Amortization of intangible assets |

|

15,594 |

|

19,916 |

Outsourced employees |

|

13,901 |

|

11,761 |

Entertainment |

|

7,046 |

|

8,921 |

|

|

2,898,277 |

|

5,451,740 |

16 |

Other expenses |

|

|

(Unaudited) For the six-month |

||

|

|

period ended 30 June |

||

|

|

2025 |

|

2024 |

Listing costs |

|

127,500 |

|

625,078 |

|

|

127,500 |

|

625,078 |

(14)

17 |

Other Income |

|

|

(Unaudited) For the six-month |

||

|

|

period ended 30 June |

||

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Other income |

|

434,165 |

|

273,088 |

|

|

434,165 |

|

273,088 |

18Taxes

18.1Deferred tax asset

Deferred income taxes reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes at the enacted rates. The significant components of the Group’s deferred tax assets as of the six-month period ended 30 June 2025 indicated below were as follows:

|

|

(Unaudited) For |

|

|

|

|

the six-month |

|

(Audited) For the |

|

|

period ended 30 |

|

year ended 31 |

|

|

30 June |

|

31 December |

|

|

USD |

|

USD |

Deferred tax asset movement |

|

|

|

|

|

|

|

|

|

Opening balance |

|

5,288,913 |

|

9,468,808 |

Foreign currency adjustments |

|

124,705 |

|

(3,616,186) |

Expiration |

|

— |

|

(563,709) |

Transfers to assets held for sale |

|

— |

|

— |

Income tax benefit |

|

— |

|

— |

Closing balance |

|

5,413,618 |

|

5,288,913 |

(15)

19Earnings/(loss) per share

Basic earnings/(loss) per share is computed by dividing the net profit/(loss) attributable to ordinary shareholders by the weighted average number of ordinary shares outstanding during the period.

15 million Earnout Shares have been excluded from the calculation of weighted average shares outstanding, as they are contingently issuable subject to achieving certain milestones on the trading price and volume of our Class A ordinary shares on NASDAQ.

During the six-month period ended 30 June 2024, the Group was loss making, therefore, all potentially dilutive instruments have an anti-dilutive impact and have been excluded in the calculation of diluted weighted average number of ordinary shares outstanding. These instruments include certain outstanding equity awards, warrants, share options and convertible loans and could potentially dilute earnings per share in the future.

The following table sets forth the computation of basic and dilutive earnings/(loss) from the continued operations per share attributable to the Group’s ordinary shareholders:

|

|

(Unaudited) |

|

(Unaudited) |

|

|

For the six- |

|

For the six- |

|

|

month period |

|

month period |

|

|

ended 30 |

|

ended 30 |

|

|

June 2025 |

|

June 2024 |

Profit/(loss) from continuing operations for the period attributable to equity holders of the Parent Company |

|

432,200 |

|

(5,692,847) |

Profit from discontinued operations for the period attributable to equity holders of the Parent Company |

|

— |

|

— |

|

|

|

|

|

Weighted average number of ordinary shares outstanding during the period |

|

9,964,344 |

|

8,528,466 |

|

|

|

|

|

Profit/(loss) per share attributable to equity holders of the Parent Company from continuing operations – basic earnings/(loss) per share |

|

0.04 |

|

(0.67) |

Profit/(loss) per share attributable to equity holders of the Parent Company – basic earnings/(loss) per share |

|

0.04 |

|

(0.67) |

|

|

|

|

|

|

|

|

|

|

Weighted average number of ordinary shares outstanding during the period adjusted for the effect of dilution |

|

10,218,200 |

|

8,528,466 |

|

|

|

|

|

Profit/(loss) per share attributable to equity holders of the Parent Company from continuing operations – diluted earnings/(loss) per share |

|

0.04 |

|

(0.67) |

Profit/(loss) per share attributable to equity holders of the Parent Company – diluted earnings/(loss) per share |

|

0.04 |

|

(0.67) |

20Related party transactions and balances

Parties are considered to be related if one party has the ability to control the other party or exercise significant influence over the other party in making financial and operating decisions. Related parties include associates, parent, subsidiaries, and key management personnel or their close family members. The terms and conditions of these transactions have been mutually agreed between the Group and the related parties. To determine significance, the Group considers various qualitative and quantitative factors including whether transactions with related parties are conducted in the ordinary course of business.

Interest in subsidiaries

The details of interests in the subsidiaries with whom the Group had entered into transactions or had agreements or arrangements in place during the period are disclosed in Note 1 of the condensed interim consolidated financial statements.

(16)

20Related party transactions and balances (continued)

Compensation of key management personnel

Key management personnel of the Group comprise the Parent Company’s directors and senior management of the Group.

|

|

(Unaudited) For the six-month |

||

|

|

period ended 30 June |

||

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Compensation and short-term employee benefits |

|

231,108 |

|

2,196,693 |

|

|

231,108 |

|

2,196,693 |

On December 26, 2023, the Board of Directors of Swvl approved a grant of 2,196,693 Restricted Stock Units (“RSUs”) to Swvl’s senior management vesting on March 31, 2024, pursuant to their respective employment agreements, and issued in consideration for services provided to the Group.

Balances with related parties

The following balances are outstanding at the end of the reporting periods:

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Balances with related parties |

|

— |

|

— |

|

|

— |

|

— |

Transactions with related parties

Details of transactions with related parties during the period, other than those which have been disclosed elsewhere in these condensed interim consolidated financial statements, are as follows:

|

|

(Unaudited) For the six-month |

||

|

|

period ended 30 June |

||

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Transactions with related parties |

|

— |

|

— |

(17)

21Financial instruments by category

Financial assets as per statement of financial position

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

At amortised cost |

|

|

|

|

Trade and other receivables |

|

5,224,190 |

|

4,009,282 |

Cash and cash equivalents |

|

4,876,982 |

|

4,958,983 |

|

|

10,101,172 |

|

8,968,265 |

Financial liabilities as per statement of financial position

|

|

(Unaudited) |

|

(Audited) |

|

|

At 30 June |

|

At 31 December |

|

|

2025 |

|

2024 |

|

|

USD |

|

USD |

Accounts payable, accruals and other payables excluding non-financial items |

|

9,536,435 |

|

9,376,566 |

Deferred purchase price |

|

646,678 |

|

1,148,013 |

Lease liabilities |

|

809,220 |

|

1,047,064 |

Current tax liabilities |

|

1,069,663 |

|

836,117 |

Derivative warrant liabilities |

|

1,505,540 |

|

669,156 |

Due to related parties |

|

— |

|

— |

|

|

13,567,536 |

|

13,076,916 |

(18)

22Fair value of financial instruments

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The fair value measurement is based on the presumption that the transaction to sell the asset or transfer the liability takes place either:

| ● | in the principal market for the asset or liability; or |

| ● | in the absence of a principal market, in the most advantageous market for the asset or liability. |

The principal or the most advantageous market must be accessible to the Group. The fair value of an asset or liability is measured using the assumptions that market participants would use when pricing the asset or liability, assuming that market participants act in their economic best interest.

A fair value measurement of a non-financial asset takes into account a market participant’s ability to generate economic benefits by using the asset in its highest and best use or by selling it to another market participant that would use the asset in its highest and best use.

The Group uses valuation techniques that are appropriate in the circumstances and for which sufficient data are available to measure fair value, maximising the use of relevant observable inputs and minimising the use of unobservable inputs.

In addition, for financial reporting purposes, fair value measurements are categorised into Level 1, 2 or 3 based on the degree to which the inputs to the fair value measurement are observable and the significance of the inputs to the fair value measurement in its entirety, which are described as follows:

Level 1: quoted market price (unadjusted) in an active market for identical assets or liabilities that the entity can access at the measurement date.

Level 2: inputs other than quoted prices included within Level 1 that are observable for the asset or liability; either directly or indirectly.

Level 3: inputs that are unobservable inputs for the asset or liability.

The carrying amounts of the financial assets and financial liabilities approximate their fair values.

(19)

Exhibit 99.2

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our financial condition and results of operations provides information that we believe to be relevant to an assessment and understanding of our results of operations and financial condition for the periods described. You should read the following discussion and analysis of our financial condition and results of operations together in conjunction with our interim consolidated financial statements and the notes to such financial statements, which are included in this Report of Foreign Private Issuer on Form 6-K (this “Report”). In addition, the information in this Report should also be read in conjunction with the information contained in our Annual Report on Form 20-F for the year ended December 31, 2024 (the “Annual Report”), including the consolidated annual financial statements as of December 31, 2024, and their accompanying notes include therein, filed with the Securities and Exchange Commission (the “SEC”) on April 2, 2025.

We report financial information under International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”) and related interpretations issued by the IFRS Interpretations Committee. None of the financial statements were prepared in accordance with generally accepted accounting principles in the United States.

Unless otherwise indicated, all references to the terms, “Swvl”, “we”, “us”, “our”, or the “Group” or “Company” refer to the business of Swvl Holdings Corp and its subsidiaries, “H1 2025” refers to the six-month period ending June 30, 2025, “H1 2024” refers to the six-month period ending 30 June 2024, “FY 2024” refers to the fiscal year of Swvl ended December 31, 2024, “FY 2023” refers to the fiscal year of Swvl ended December 31, 2023.

References to “U.S. dollars,” “USD” and “$” are to currency of the United States of America, and references to “EGP” are to the Egyptian Pound.

Forward-Looking Statements

The following discussion contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and other securities laws. Forward-looking statements are often characterized by the use of forward-looking terminology such as “may,” “will,” “expect,” “anticipate,” “estimate,” “continue,” “believe,” “should,” “intend,” “project” or other similar words, but are not the only way these statements are identified. These forward-looking statements may include, but are not limited to, statements relating to our objectives, plans and strategy for our business, statements that contain projections of results of operation or of financial condition, risks and uncertainties expected capital needs and expenses, statements relating to the research, development, completion and use of our products, and all statements (other than statements of historical facts) that address activities, events or developments that we intend, expect, project, believe or anticipate will or may occur in the future. Forward-looking statements are not guarantees of future performance and are subject to risks and uncertainties. We have based these forward-looking statements on assumptions and assessments made by our management in light of their experience and their perception of historical trends, current conditions, expected future developments and other factors they believe to be appropriate and are subject to a number of factors and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements.

Please see the sections titled “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements” for a discussion of the risks, uncertainties and assumptions associated with these statements and for a discussion of important factors that could cause actual results to differ materially from the results described in or implied by the forward-looking statements contained in the following discussion and analysis. Our historical results are not necessarily indicative of the results that may be expected for any period in the future.

These statements are only current predictions and are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from those anticipated by the forward-looking statements. We discuss many of these risks in our Annual Report. You should not rely upon forward-looking statements as predictions of future events.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, performance, or achievements. Except as required by law, we are under no duty to update or revise any of the forward-looking statements, whether as a result of new information, future events or otherwise, after the date of this Report.

Overview

We are a technology-driven disruptive mobility company that aims to provide reliable, safe, cost-effective and environmentally responsible mass transit solutions. Our mission is to identify and solve inefficiencies associated with low-quality or sometimes non-existent public transportation infrastructure in urban areas that are in critical need of such services. Our technology and services provide commuters, travelers and businesses with a valuable alternative to traditional public transportation, taxi companies or other ridesharing companies. Through our Swvl platform, we provide thousands of riders per day with dynamic routing and a self-optimizing network of minibuses and other vehicles, helping people get where they need to go.

Components of Results of Operations

Revenue

Our revenue consists of two components: (i) a business-to-customer (“B2C”) component, representing the gross amount of fares charged to end-users of our platform, not including reductions of end-user discounts and promotions, sales refunds, uncollected cash and Sales waivers (as defined below); and (ii) a business-to-business (“B2B”) component representing contractual smart transportation services for our corporate customer’s employees through the Swvl application, which is referred to as ‘Transport as a service’ (“TaaS”) and ‘Software as a service’ (“SaaS”), which enables corporate customers to manage their own fleets more efficiently. For further details on our revenue recognition, please see the Revenue details in the subsection “Critical Accounting Estimates”.

Cost of Sales

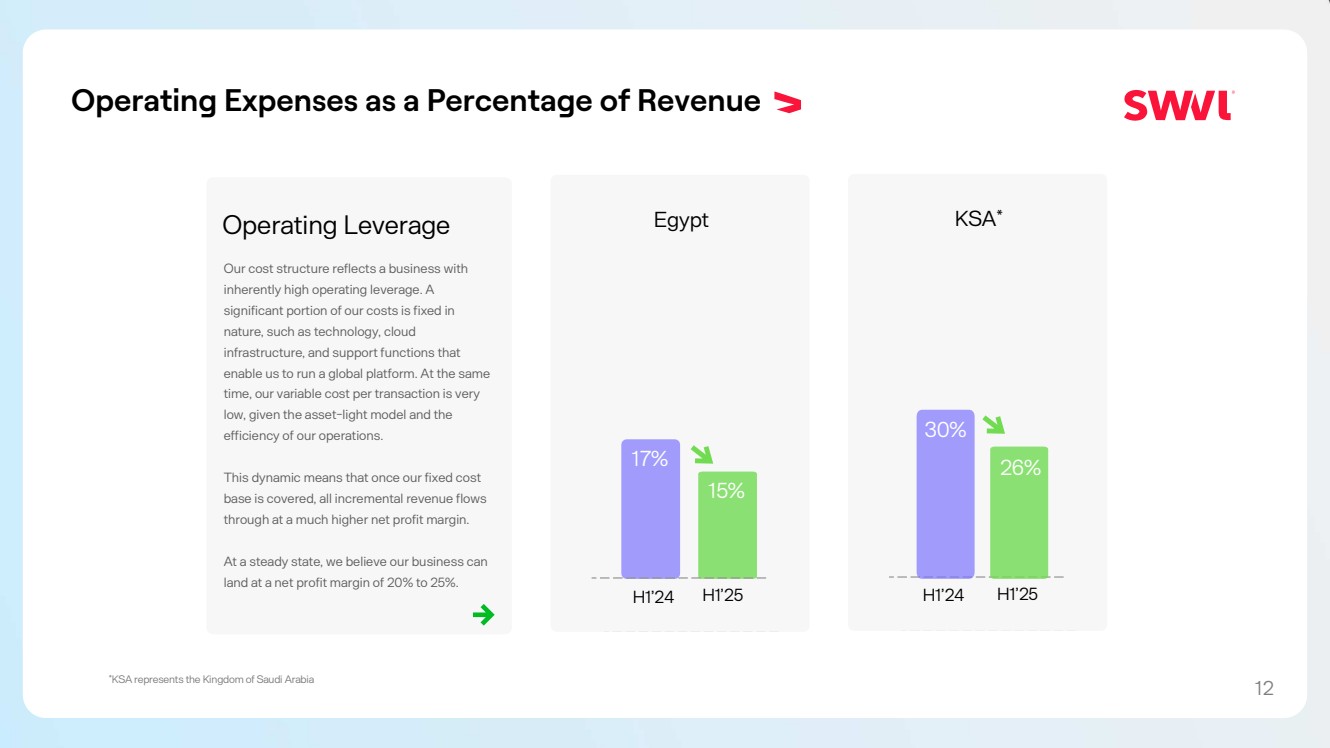

Our cost of sales consists of costs directly related to delivering transportation services, which include payments to captains for operating our routes (net of any deductions, including any amount charged to captains on account of breach of terms of service), bonuses payable to captains, tolls and fines paid by Swvl. Our cost of sales does not include any depreciation or amortization expenses. Our depreciation and amortization expenses are almost exclusively attributable to non-revenue generating activities, including depreciation of our facilities and equipment which support our back-office operations and depreciation of right-of-use assets associated with corporate leases.

General and Administrative Expenses

Our general and administrative expenses primarily consist of personnel-related compensation costs including employee share scheme charges, professional services fees, technology costs, office costs, travel costs, depreciation, insurance, rent, bank fees, foreign exchange losses/gains, utilities, communication and other corporate costs. Our general and administrative expenses are expensed as incurred.

Sales and Marketing Costs

Our sales and marketing expenses primarily consist of growth marketing expenses, offline marketing expenses, personnel compensation expenses and the costs of credits offered to riders for referring new riders. Our sales and marketing costs are expensed as incurred.

Other Income/(expenses)

Our other income consists primarily of recovery of previously written off asset that were not expected to be recovered and rental incomea. Other expenses consist primarily of indirect tax expenses and other expenses not categorized elsewhere.

Finance Income and Finance Costs

Our finance income consists primarily of dividend interest income from bank deposits. Our finance costs consist primarily of lease finance charges and interest expense on financial liabilities.

Changes in Fair Value of Financial Liabilities

Changes in fair value of financial liabilities consist of the change in the fair value of the Group’s earnouts liabilities, certain warrant liabilities and change in fair value of deferred purchase price resulting from the acquisition of certain subsidiaries by the Group.

Income Tax Benefit

Income tax benefit primarily relates to the deferred tax asset created on tax losses incurred by the Company, which can be set off against future taxable income. We have deferred tax asset balances in Egypt as carried forward losses from the early years of operation, planned to be utilized against future taxable income.

Impact of Foreign Currency Translation

As we have operations in countries with different currencies, foreign currencies have an impact on our results of operations. The main impact of foreign currency fluctuations on us is from the change.

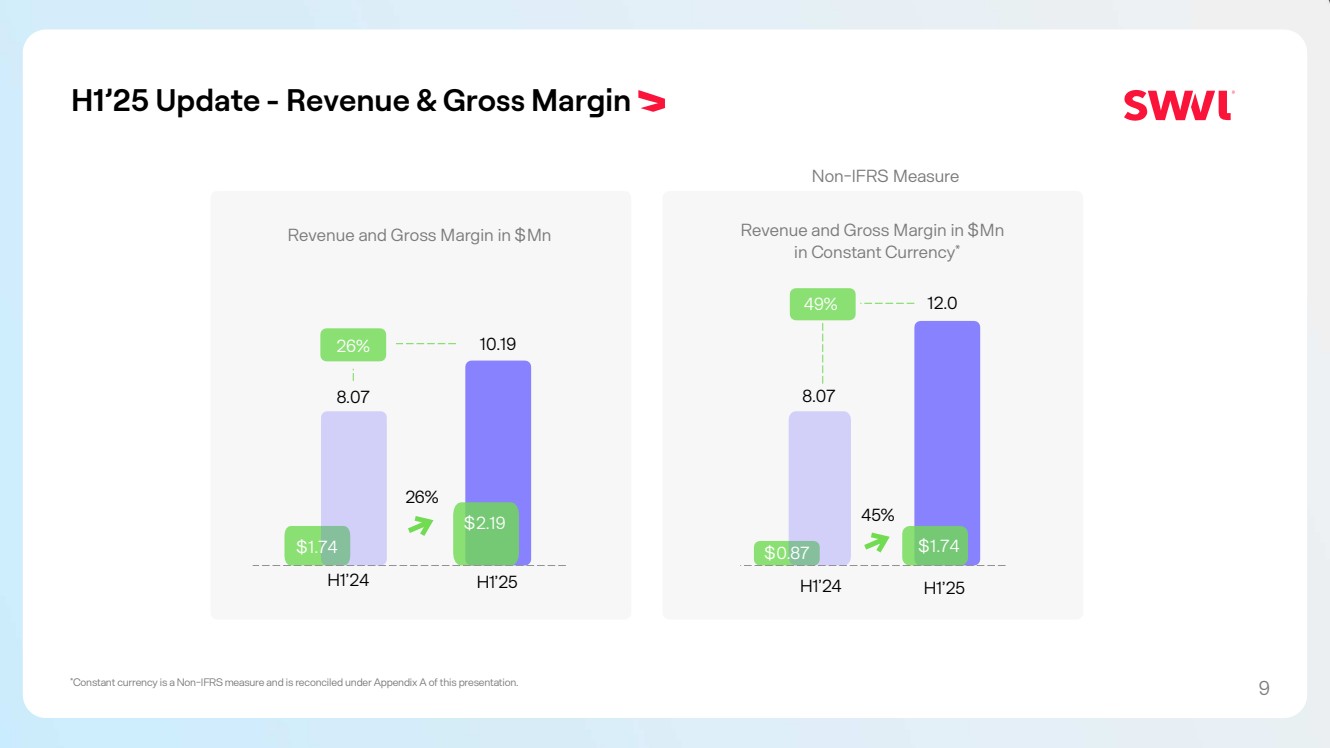

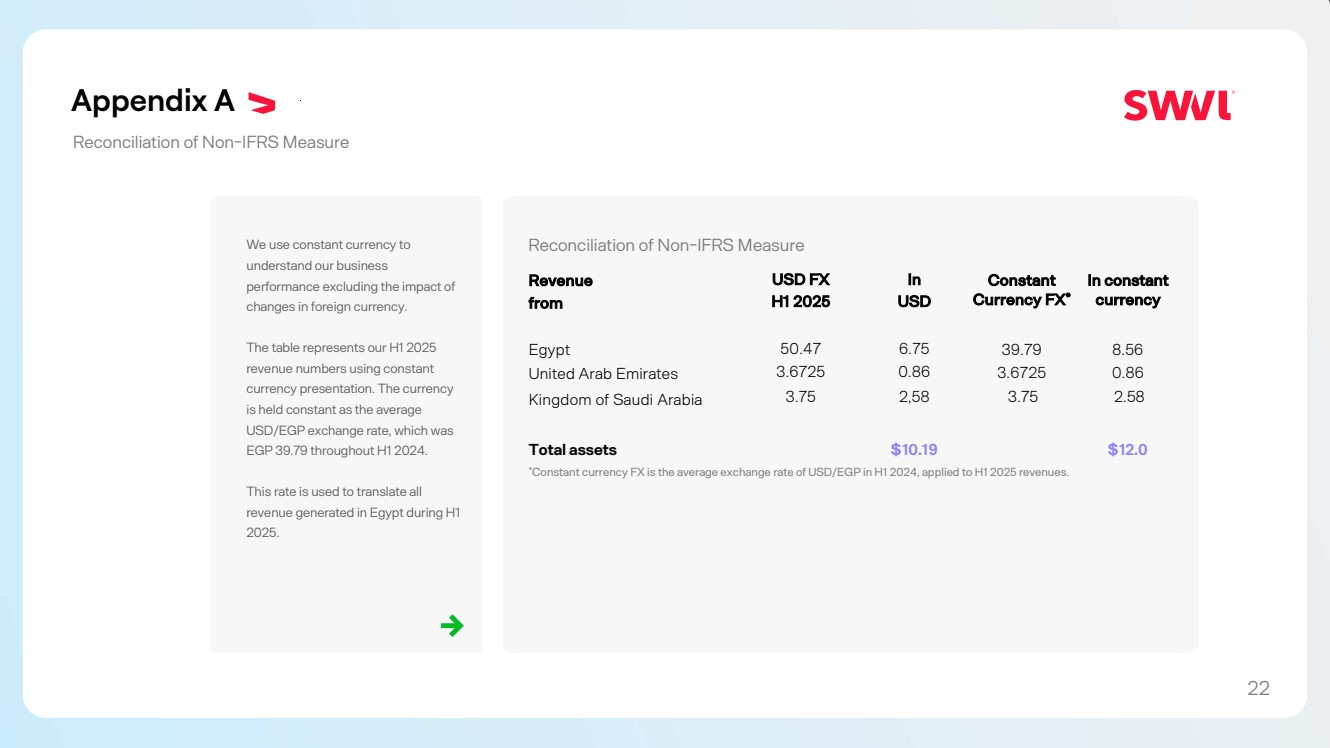

In our results of operations discussion below, we have provided certain comparisons both on an as reported and on a constant currency basis. The constant currency presentation, which is a non-IFRS measure, excludes the impact of fluctuations in foreign currency exchange rates. We believe that providing constant currency information provides valuable supplemental information regarding our results of operations and also provides a framework for assessing how our underlying business performed, excluding the effects of foreign currency rate fluctuations. We calculate constant currency percentages by converting our current period local currency financial results using the prior period exchange rates from the corresponding prior period, and compare these adjusted amounts to its prior period reported results. Amounts may not foot due to rounding.

A. Operating Results

Results of Operations

The following selected consolidated financial data is derived from the unaudited financial statements of the Company for H1 2025 and H1 2024, and should be read in conjunction with the information contained in our Annual Report for the year ended December 31, 2024, including the consolidated annual financial statements as of December 31, 2024, and their accompanying notes include therein, filed with SEC on April 2, 2025.

Our historical results are not necessarily indicative of the results of future operations. For a comparison of FY 2023 to the year ended December 31, 2022, see our Annual Report on Form 20-F for the fiscal year ending December 31, 2023 and the amendment thereto, filed with the SEC on April 30, 2024.

|

|

For the period ended 30 June |

||

($million) |

|

2025 |

|

2024 |

Continued operations |

|

|

|

|

Revenue |

|

10.19 |

|

8.07 |

Cost of sales |

|

(8.00) |

|

(6.32) |

Gross profit |

|

2.19 |

|

1.74 |

General and administrative expenses |

|

(2.90) |

|

(5.45) |

Selling and marketing expenses |

|

(0.01) |

|

(0.01) |

Other expenses |

|

(0.13) |

|

(0.54) |

Other income |

|

0.43 |

|

0.27 |

Operating loss |

|

(0.42) |

|

(4.07) |

Change in fair value of financial liabilities |

|

0.84 |

|

(1.65) |

Finance income |

|

0.11 |

|

0.08 |

Finance cost |

|

(0.09) |

|

(0.05) |

Profit/(loss) for the period before tax from continuing operations |

|

0.43 |

|

(5.69) |

Income tax benefit |

|

— |

|

— |

Profit/(loss) for the period from continuing operations |

|

0.43 |

|

(5.69) |

|

|

|

|

|

Other comprehensive income |

|

|

|

|

Exchange difference on translations of foreign operations |

|

(1.40) |

|

(4.71) |

Total comprehensive loss for the period |

|

(0.97) |

|

(10.41) |

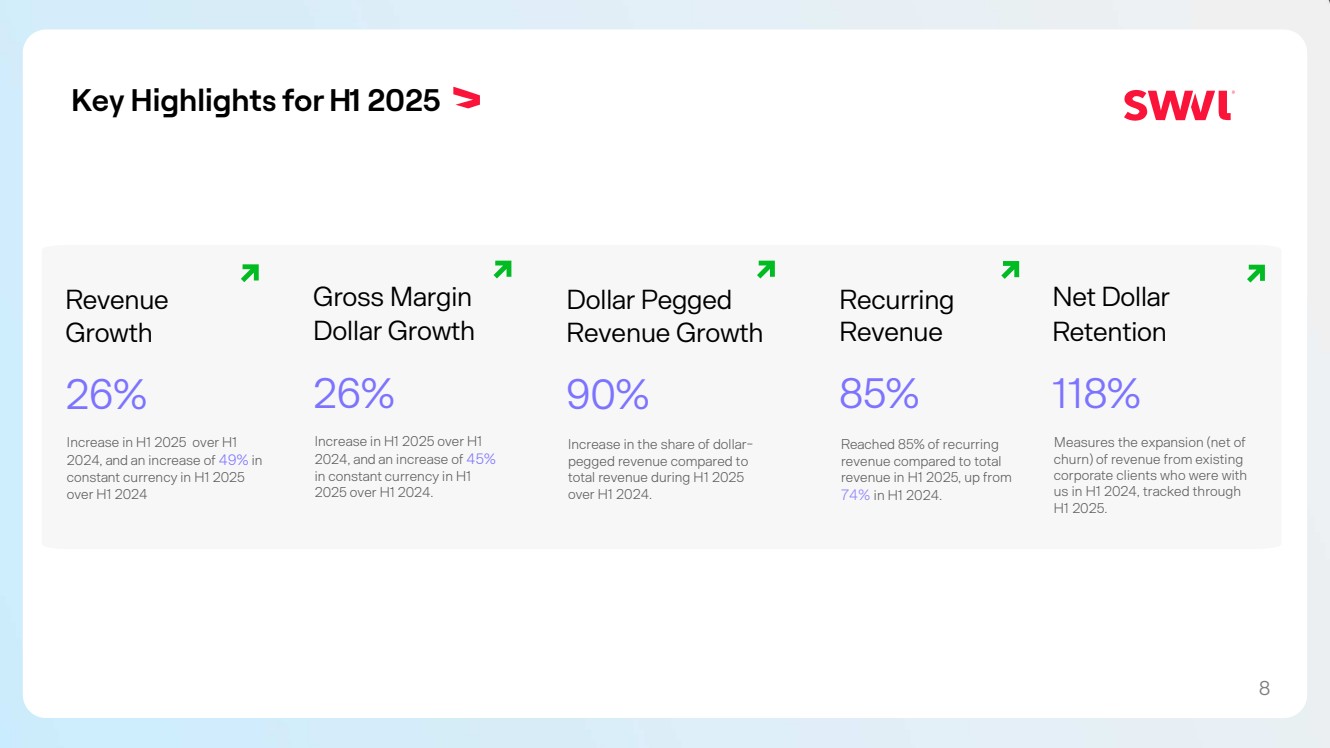

H1 2025 Compared to H1 2024

|

|

For the period ended June 30, |

|

|

|

||||

|

|

|

|

|

|

|

|

H1 2024 - H1 2025 |

|

($ million) |

|

2025 |

|

2024 |

|

% Change |

|

||

Total Revenue |

|

$ |

10.19 |

|

$ |

8.07 |

|

26 |

% |

Disaggregated by |

|

|

|

|

|

|

|

|

|

Business to customer |

|

$ |

1.5 |

|

$ |

2.07 |

|

(27) |

% |

Business to business |

|

$ |

8.69 |

|

$ |

6.0 |

|

45 |

% |

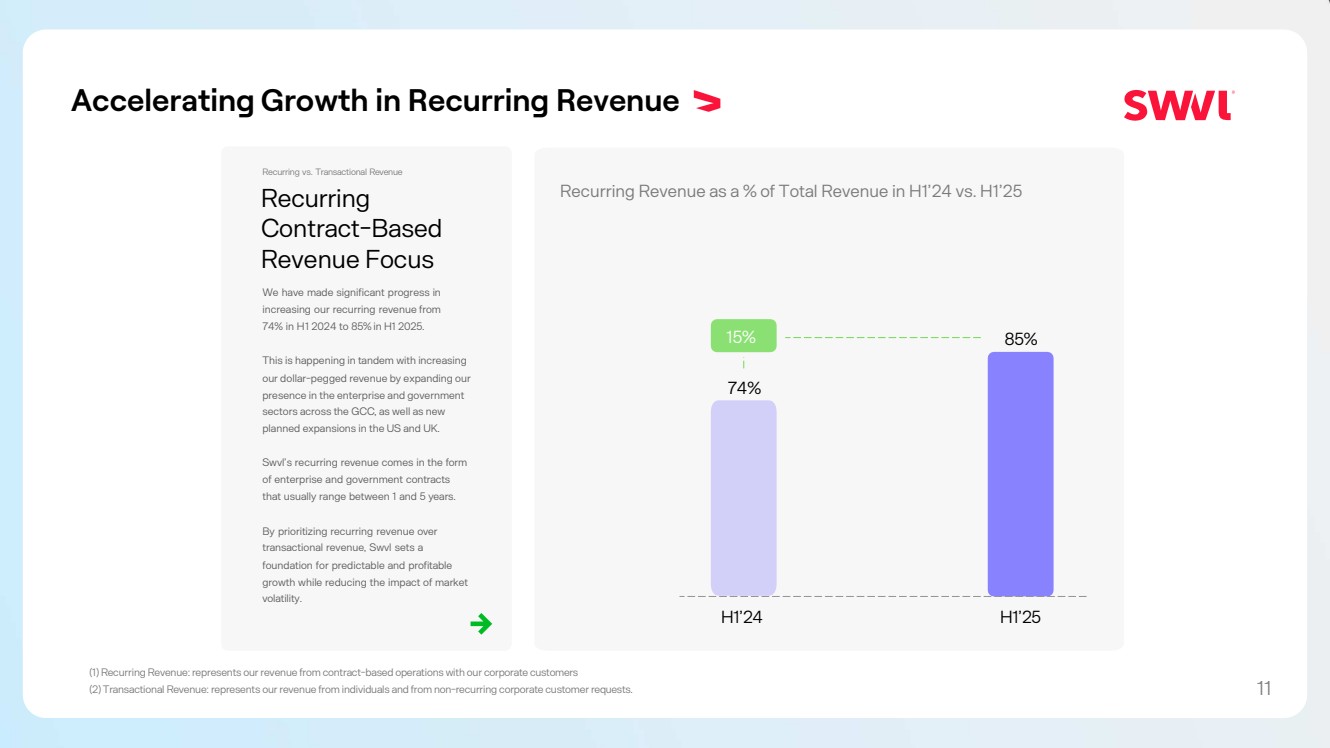

We disaggregate revenue by the type of customer served as follows: Revenue from Swvl Retail and Swvl Travel together is considered as B2C, and revenue from both TaaS and SaaS together is considered as B2B.

Revenues from B2C for H1 2025 were approximately $1.5 million, a decrease of approximately $0.56 million, or 27%, compared to H1 2024. The reason for the decrease was primarily due to the second quarter of FY 2024 having more public holidays, which serve as high volume days, further the devaluation of the EGP compared to the USD has negatively impacted our total revenue generated, as we have operated this business exclusively inside Egypt during both periods presented.

Revenues from B2B for H1 2025 were approximately $8.69 million, an increase of approximately $2.69 million, or 45%, compared to H1 2024. The increase was due to securing new client contracts across Egypt, Saudi Arabia and the United Arab Emirates, as part of our continued strategy that focuses on profitability and sustainable operations.

Further Analysis Using Constant Currency