UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): May 14, 2025

Boot Barn Holdings, Inc.

(Exact name of registrant as specified in its charter)

Delaware |

001-36711 |

90-0776290 |

(State or other jurisdiction |

(Commission |

(I.R.S. Employer |

17100 Laguna Canyon Road, Irvine, California |

92618 |

(Address of principal executive offices) |

(Zip Code) |

(949) 453-4400

(Registrant’s telephone number, including area code)

Not Applicable

(Former Address)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol |

Name of each exchange on which registered |

Common Stock, $0.0001 par value |

BOOT |

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to section 13(a) of the Exchange Act. ☐

Item 2.02 Results of Operations and Financial Condition

On May 14, 2025, Boot Barn Holdings, Inc. (the “Company”) issued a press release announcing certain financial results for its fiscal fourth quarter and fiscal year ended March 29, 2025. The press release is attached hereto as Exhibit 99.1 and incorporated into this Item 2.02 by reference.

The information provided in this Item 2.02, including Exhibit 99.1, is intended to be “furnished” and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that section, nor shall it be deemed incorporated by reference into any other filing under the Securities Act of 1933, as amended (the “Securities Act”), or the Exchange Act, except as expressly set forth by specific reference in such filing.

Item 7.01 Regulation FD Disclosure.

The Company is furnishing this Current Report on Form 8-K in connection with the disclosure of information contained in a supplemental financial presentation (the “Presentation”) to be used by the Company at various meetings with institutional investors and analysts. This information may be amended or updated at any time and from time to time through another Current Report on Form 8-K or other means. A copy of the Presentation is furnished herewith as Exhibit 99.2 and is incorporated into this Item 7.01 by reference.

The information furnished in this Item 7.01, including Exhibit 99.2, is being furnished and shall not be deemed to be “filed” for the purposes of Section 18 of the Exchange Act or otherwise subject to the liabilities of that section, nor shall it be deemed to be incorporated by reference into any other filing under the Securities Act or the Exchange Act, except as expressly set forth by specific reference in such filing.

The Company expressly disclaims any obligation to update or revise any of the information contained in the Presentation.

The Presentation is available on the Company’s investor relations website located at investor.bootbarn.com, although the Company reserves the right to discontinue that availability at any time. The website address included herein is an inactive textual reference only. The information contained on such website is not incorporated into this Current Report on Form 8-K.

Item 9.01. Financial Statements and Exhibits.

Exhibit Number |

Description |

||

Exhibit 99.1 |

|||

Exhibit 99.2 |

|||

Exhibit 104 |

The cover page of this Current Report on Form 8-K, formatted in Inline XBRL. |

||

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

BOOT BARN HOLDINGS, INC. |

|

Date: May 14, 2025 |

By: |

/s/ James M. Watkins |

|

|

Name: James M. Watkins |

|

|

Title: Chief Financial Officer and Secretary |

Exhibit 99.1

Boot Barn Holdings, Inc. Announces Fourth Quarter and Fiscal Year 2025

Financial Results and $200 Million Share Repurchase Program

IRVINE, California – May 14, 2025 – Boot Barn Holdings, Inc. (NYSE: BOOT) (the “Company”) today announced its financial results for the fourth fiscal quarter and fiscal year ended March 29, 2025 (“Fiscal Year 2025”). A Supplemental Financial Presentation is available at investor.bootbarn.com.

For the quarter ended March 29, 2025 compared to the quarter ended March 30, 2024:

| ● | Net sales increased 16.8% over the prior-year period to $453.7 million. |

| ● | Same store sales increased 6.0%, with retail store same store sales increasing 5.5% and e-commerce same store sales increasing 9.8%. |

| ● | Net income was $37.5 million, or $1.22 per diluted share, compared to $29.4 million, or $0.96 per diluted share, in the prior-year period. |

| ● | The Company opened 21 new stores, bringing its total store count to 459 as of the quarter end. |

For the fiscal year ended March 29, 2025 compared to the fiscal year ended March 30, 2024:

| ● | Net sales increased 14.6% over Fiscal Year 2024 to $1.911 billion. |

| ● | Same store sales increased 5.5%, with retail store same store sales increasing 5.0% and e-commerce same store sales increasing 9.7%. |

| ● | Net income was $180.9 million, or $5.88 per diluted share in Fiscal Year 2025, compared to $147.0 million, or $4.80 per diluted share, in Fiscal Year 2024. |

| ● | The Company opened 60 new stores, bringing its total store count to 459 as of the fiscal year end. |

John Hazen, Chief Executive Officer, commented, “Our team delivered a solid finish to fiscal year 2025 highlighted by 15% annual total sales growth and 23% growth in earnings per diluted share, underscoring the ongoing resilience of our core consumer despite broader market uncertainties. The continued strength across major merchandise categories, channels, and geographies reaffirms the broad appeal of our brand and the effectiveness of our strategic initiatives. As we look ahead, we remain confident in our ability to navigate the current tariff environment through our diversified sourcing capabilities and established vendor partnerships. The fundamentals of our business remain strong, and we are well-positioned to continue generating value for our shareholders.”

Share Repurchase Program

The Company’s Board of Directors has authorized the Company to repurchase up to $200 million of its common stock (the “Repurchase Program”). Repurchases under the Repurchase Program may be made through a variety of methods, which could include open market purchases, which may or may not be pursuant to Rule 10b5-1 trading plans, privately negotiated transactions, block trades, accelerated share repurchase plans, or any combination of such methods. The timing and amount of shares repurchased will depend on the stock price, business and market conditions, corporate and regulatory requirements, alternative investment opportunities, acquisition opportunities, and other factors. The Company is not obligated to repurchase any specific amount of shares of common stock, and the repurchase authorization does not have an expiration date and may be amended or terminated by the Board of Directors at any time without prior notice.

1

Operating Results for the Fourth Quarter Ended March 29, 2025 Compared to the Fourth Quarter Ended March 30, 2024

| ● | Net sales increased 16.8% to $453.7 million from $388.5 million in the prior-year period. Consolidated same store sales increased 6.0%, with retail store same store sales increasing 5.5% and e-commerce same store sales increasing 9.8%. The increase in net sales was the result of incremental sales from new stores and the increase in consolidated same store sales. |

| ● | Gross profit was $168.6 million, or 37.1% of net sales, compared to $139.4 million, or 35.9% of net sales, in the prior-year period. The increase in gross profit was primarily due to an increase in sales and merchandise margin, partially offset by the occupancy costs of new stores. The 130 basis-point increase in gross profit rate was driven primarily by a 210 basis-point increase in merchandise margin rate, partially offset by 80 basis points of deleverage in buying, occupancy and distribution center costs. The increase in merchandise margin rate was primarily the result of supply chain efficiencies, lower shrink expense, better buying economies of scale, and growth in exclusive brand penetration. The deleverage in buying, occupancy and distribution center costs was driven by the occupancy costs of new stores. |

| ● | Selling, general and administrative expenses were $118.9 million, or 26.2% of net sales, compared to $101.2 million, or 26.1% of net sales, in the prior-year period. The increase in selling, general and administrative expenses compared to the prior-year period was primarily the result of higher store payroll and store-related expenses associated with operating more stores, and corporate general and administrative expenses in the current-year period. Selling, general and administrative expenses as a percentage of net sales increased by 10 basis points primarily as a result of higher legal expenses and store payroll in the current-year period partially offset by marketing expenses. |

| ● | Income from operations increased $11.4 million to $49.7 million, or 11.0% of net sales, compared to $38.2 million, or 9.8% of net sales, in the prior-year period, primarily due to the factors noted above. |

| ● | Income tax expense was $12.4 million, or a 24.8% effective tax rate, compared to $9.4 million, or a 24.3% effective tax rate, in the prior-year period. The increase in effective tax rate was primarily due to a decrease in stock-based compensation tax benefits in the current-year period when compared to the prior-year period. |

| ● | Net income was $37.5 million, or $1.22 per diluted share, compared to $29.4 million, or $0.96 per diluted share, in the prior-year period. The increase in net income is primarily attributable to the factors noted above. |

Operating Results for the Fiscal Year Ended March 29, 2025 Compared to the Fiscal Year Ended March 30, 2024

| ● | Net sales increased 14.6% to $1.911 billion from $1.667 billion in Fiscal Year 2024. Consolidated same store sales increased 5.5%, with retail store same store sales increasing 5.0% and e-commerce same store sales increasing 9.7%. The increase in net sales was the result of incremental sales from new stores and the increase in consolidated same store sales. |

| ● | Gross profit was $717.0 million, or 37.5% of net sales, compared to $614.4 million, or 36.9% of net sales, in Fiscal Year 2024. The increase in gross profit was primarily due to an increase in sales and merchandise margin, partially offset by the occupancy costs of new stores. The 70 basis-point increase in gross profit rate was driven primarily by a 130 basis-point increase in merchandise margin rate partially offset by 60 basis points of deleverage in buying, occupancy and distribution center costs. The increase in merchandise margin rate was primarily the result of supply chain efficiencies, lower shrink expense, better buying economies of scale, and growth in exclusive brand penetration. The deleverage in buying, occupancy and distribution center costs was driven by the occupancy costs of new stores. |

| ● | Selling, general and administrative expenses were $477.7 million, or 25.0% of net sales, compared to $416.2 million, or 25.0% of net sales, in Fiscal Year 2024. The increase in selling, general and administrative expenses as compared |

2

| to Fiscal Year 2024 was primarily the result of higher store payroll and store-related expenses associated with operating more stores, corporate general and administrative expenses, and marketing expenses in Fiscal Year 2025. Selling, general and administrative expenses as a percentage of net sales was flat when compared to Fiscal Year 2024. |

| ● | Income from operations increased $41.1 million to $239.4 million, or 12.5% of net sales, compared to $198.2 million, or 11.9% of net sales, in Fiscal Year 2024, primarily due to the factors noted above. |

| ● | Income tax expense was $59.2 million, or a 24.6% effective tax rate, compared to $50.4 million, or a 25.4% effective tax rate, in Fiscal Year 2024. The decrease in effective tax rate was primarily due to reductions in nondeductible expenses, as well as an increase in pretax book income, partially offset by reduced stock-based compensation tax benefits. |

| ● | Net income was $180.9 million, or $5.88 per diluted share, compared to net income of $147.0 million, or $4.80 per diluted share, in Fiscal Year 2024. The increase in net income is primarily attributable to the factors noted above. |

Sales by Channel

The following table includes total net sales growth, same store sales (“SSS”) growth/(decline) and e-commerce as a percentage of net sales for the periods indicated below.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preliminary |

|

|

|

Thirteen Weeks |

|

|

|

|

|

|

|

|

|

Preliminary |

|

|

Two Weeks |

|

|

|

Ended |

|

|

Four Weeks |

|

Four Weeks |

|

Five Weeks |

|

|

Four Weeks |

|

|

Ended |

|

|

|

March 29, 2025 |

|

|

Fiscal January |

|

Fiscal February |

|

Fiscal March |

|

|

Fiscal April |

|

|

May 10, 2025 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Net Sales Growth |

|

16.8 |

% |

|

18.8 |

% |

12.7 |

% |

18.5 |

% |

|

18.3 |

% |

|

19.2 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Retail Stores SSS |

|

5.5 |

% |

|

7.0 |

% |

0.9 |

% |

8.0 |

% |

|

9.8 |

% |

|

8.4 |

% |

E-commerce SSS |

|

9.8 |

% |

|

17.1 |

% |

9.0 |

% |

5.1 |

% |

|

(0.4) |

% |

|

15.9 |

% |

Consolidated SSS |

|

6.0 |

% |

|

8.1 |

% |

1.8 |

% |

7.7 |

% |

|

8.7 |

% |

|

9.1 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E-commerce as a % of Net Sales |

|

9.9 |

% |

|

11.2 |

% |

10.3 |

% |

8.8 |

% |

|

8.4 |

% |

|

9.3 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance Sheet Highlights as of March 29, 2025

| ● | Cash of $70 million. |

| ● | Zero drawn under the $250 million revolving credit facility. |

| ● | Average inventory per store increased approximately 5.7% on a same store basis compared to March 30, 2024. |

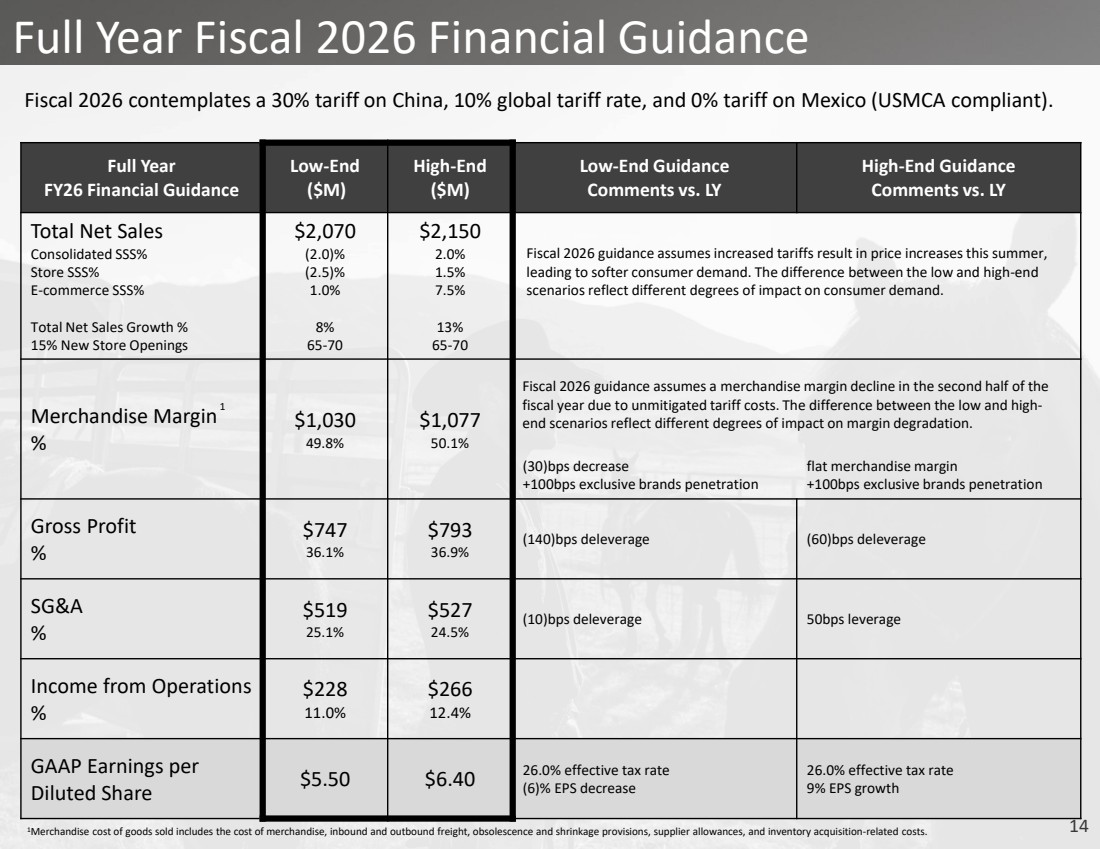

Fiscal Year 2026 Outlook

The Company is providing guidance for what it can reasonably expect at this time. For the fiscal year ending March 28, 2026 the Company expects:

| ● | To open between 65 and 70 new stores. |

| ● | Total sales of $2.070 billion to $2.150 billion, representing growth of 8% to 13% over Fiscal Year 2025. |

| ● | Same store sales declines of (2.0)% to growth of approximately 2.0%, with retail store same store sales declines of (2.5)% to growth of approximately 1.5% and e-commerce same store sales growth of approximately 1.0% to 7.5%. |

| ● | Merchandise margin between $1.030 billion and $1.077 billion, or approximately 49.8% to 50.1% of sales. |

| ● | Gross profit between $747 million and $793 million, or approximately 36.1% to 36.9% of sales. |

3

| ● | Selling, general and administrative expenses between $519 million and $527 million, or approximately 25.1% to 24.5% of sales. |

| ● | Income from operations between $228 million and $266 million, or approximately 11.0% to 12.4% of sales. |

| ● | Net income of $169 million to $197 million. |

| ● | Net income per diluted share of $5.50 to $6.40, based on 30.8 million weighted average diluted shares outstanding. |

| ● | Effective tax rate of 26.0%. |

| ● | Capital expenditures between $115.0 million and $120.0 million, which is net of estimated landlord tenant allowances of $35.5 million. |

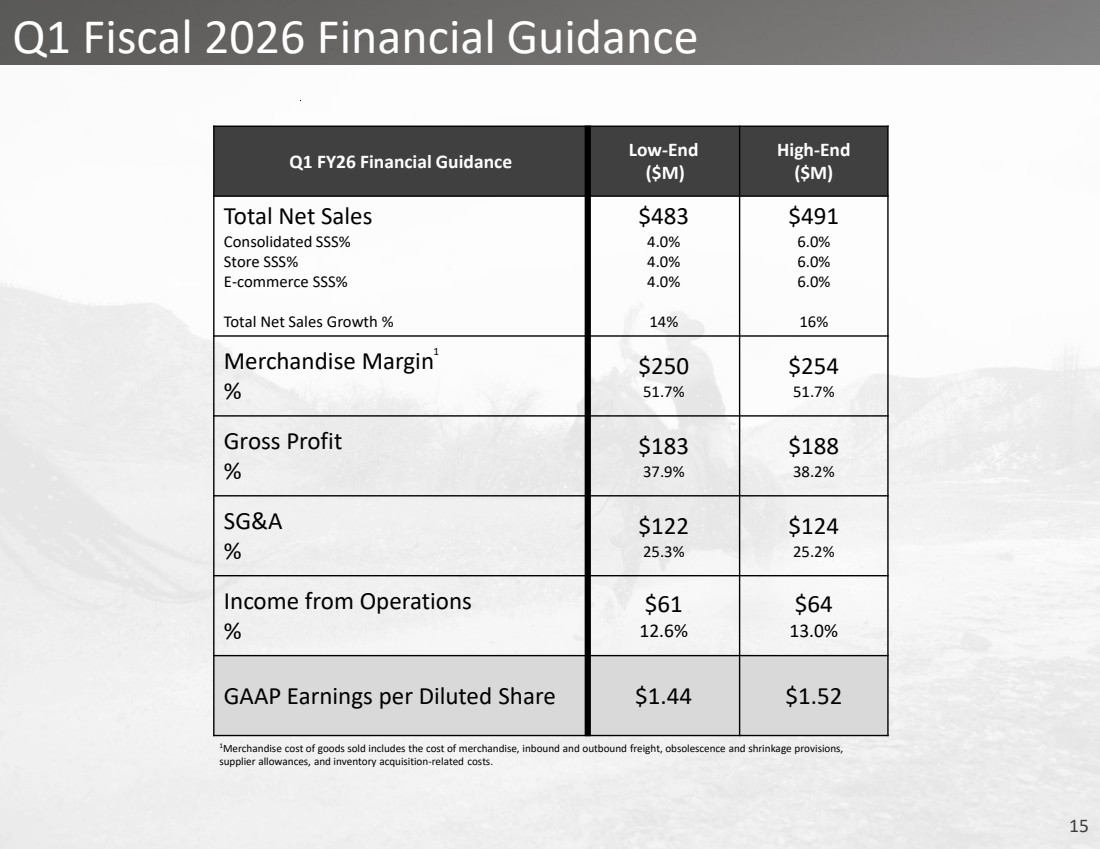

For the first fiscal quarter ending June 28, 2025, the Company expects:

| ● | Total sales of $483 million to $491 million, representing growth of 14% to 16% over the prior-year period. |

| ● | Same store sales growth of approximately 4.0% to 6.0%, with retail store same store sales growth of approximately 4.0% to 6.0% and e-commerce same store sales growth of approximately 4.0% to 6.0%. |

| ● | Merchandise margin between $250 million and $254 million, or approximately 51.7% of sales. |

| ● | Gross profit between $183 million and $188 million, or approximately 37.9% to 38.2% of sales. |

| ● | Selling, general and administrative expenses between $122 million and $124 million, or approximately 25.3% to 25.2% of sales. |

| ● | Income from operations between $61 million and $64 million, or approximately 12.6% to 13.0% of sales. |

| ● | Net income per diluted share of $1.44 to $1.52, based on 30.9 million weighted average diluted shares outstanding. |

Conference Call Information

A conference call to discuss the financial results for the fourth fiscal quarter and fiscal year ended March 29, 2025, is scheduled for today, May 14, 2025, at 4:30 p.m. ET (1:30 p.m. PT). Investors and analysts interested in participating in the call are invited to dial (866) 652-5200. The conference call will also be available to interested parties through a live webcast at investor.bootbarn.com. Please visit the website and select the “Events and Presentations” link at least 15 minutes prior to the start of the call to register and download any necessary software. A Supplemental Financial Presentation is also available on the investor relations section of the Company’s website. A telephone replay of the call will be available until June 12, 2025, by dialing (844) 512-2921 (domestic) or (412) 317-6671 (international) and entering the conference identification number: 10199545. Please note participants must enter the conference identification number in order to access the replay.

About Boot Barn

Boot Barn is the nation’s leading lifestyle retailer of western and work-related footwear, apparel and accessories for men, women and children. The Company offers its loyal customer base a wide selection of work and lifestyle brands. As of the date of this release, Boot Barn operates 465 stores in 49 states, in addition to an e-commerce channel www.bootbarn.com. The Company also operates www.sheplers.com, the nation’s leading pure play online western and work retailer and www.countryoutfitter.com, an e-commerce site selling to customers who live a country lifestyle. For more information, call 888-Boot-Barn or visit www.bootbarn.com.

Forward Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this press release are forward-looking statements. Forward-looking statements refer to the Company’s current expectations and projections relating to, by way of example and without limitation, the Company’s financial condition, liquidity, profitability, results of operations, margins, plans, objectives, strategies, future performance, business and industry. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts.

4

These statements may include words such as “anticipate”, “estimate”, “expect”, “project”, “plan“, “intend”, “believe”, “may”, “might”, “will”, “could”, “should”, “can have”, “likely”, “outlook” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events, but not all forward-looking statements contain these identifying words. These forward-looking statements are based on assumptions that the Company’s management has made in light of their industry experience and on their perceptions of historical trends, current conditions, expected future developments and other factors that they believe are appropriate under the circumstances. As you consider this press release, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (some of which are beyond the Company’s control) and assumptions. These risks, uncertainties and assumptions include, but are not limited to, the following: decreases in consumer spending due to declines in consumer confidence, local economic conditions or changes in consumer preferences; the Company’s ability to effectively execute on its growth strategy; and the Company’s failure to maintain and enhance its strong brand image, to compete effectively, to maintain good relationships with its key suppliers, and to improve and expand its exclusive product offerings. The Company discusses the foregoing risks and other risks in greater detail under the heading “Risk factors” in the periodic reports filed by the Company with the Securities and Exchange Commission. Although the Company believes that these forward-looking statements are based on reasonable assumptions, you should be aware that many factors could affect the Company’s actual financial results and cause them to differ materially from those anticipated in the forward-looking statements. Because of these factors, the Company cautions that you should not place undue reliance on any of these forward-looking statements. New risks and uncertainties arise from time to time, and it is impossible for the Company to predict those events or how they may affect the Company. Further, any forward-looking statement speaks only as of the date on which it is made. Except as required by law, the Company does not intend to update or revise the forward-looking statements in this press release after the date of this press release.

Investor Contact:

ICR, Inc.

Brendon Frey, 203-682-8216

BootBarnIR@icrinc.com

or

Company Contact:

Boot Barn Holdings, Inc.

Mark Dedovesh, 949-453-4489

Senior Vice President, Investor Relations & Financial Planning

BootBarnIRMedia@bootbarn.com

5

Boot Barn Holdings, Inc.

Consolidated Balance Sheets

(In thousands, except per share data)

(Unaudited)

|

|

March 29, |

|

March 30, |

||

|

|

2025 |

|

2024 |

||

Assets |

|

|

|

|

|

|

Current assets: |

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

69,770 |

|

$ |

75,847 |

Accounts receivable, net |

|

|

10,263 |

|

|

9,964 |

Inventories |

|

|

747,191 |

|

|

599,120 |

Prepaid expenses and other current assets |

|

|

36,736 |

|

|

44,718 |

Total current assets |

|

|

863,960 |

|

|

729,649 |

Property and equipment, net |

|

|

422,079 |

|

|

323,667 |

Right-of-use assets, net |

|

|

469,461 |

|

|

390,501 |

Goodwill |

|

|

197,502 |

|

|

197,502 |

Intangible assets, net |

|

|

58,677 |

|

|

58,697 |

Other assets |

|

|

6,342 |

|

|

5,576 |

Total assets |

|

$ |

2,018,021 |

|

$ |

1,705,592 |

Liabilities and stockholders’ equity |

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

Accounts payable |

|

$ |

134,450 |

|

$ |

132,877 |

Accrued expenses and other current liabilities |

|

|

146,038 |

|

|

116,477 |

Short-term lease liabilities |

|

|

72,861 |

|

|

63,454 |

Total current liabilities |

|

|

353,349 |

|

|

312,808 |

Deferred taxes |

|

|

39,317 |

|

|

42,033 |

Long-term lease liabilities |

|

|

490,182 |

|

|

403,303 |

Other liabilities |

|

|

4,116 |

|

|

3,805 |

Total liabilities |

|

|

886,964 |

|

|

761,949 |

|

|

|

|

|

|

|

Stockholders’ equity: |

|

|

|

|

|

|

Common stock, $0.0001 par value; March 29, 2025 - 100,000 shares authorized, 30,892 shares issued; March 30, 2024 - 100,000 shares authorized, 30,572 shares issued |

|

|

3 |

|

|

3 |

Preferred stock, $0.0001 par value; 10,000 shares authorized, no shares issued or outstanding |

|

|

— |

|

|

— |

Additional paid-in capital |

|

|

246,725 |

|

|

232,636 |

Retained earnings |

|

|

903,968 |

|

|

723,026 |

Less: Common stock held in treasury, at cost, 298 and 228 shares at March 29, 2025 and March 30, 2024, respectively |

|

|

(19,639) |

|

|

(12,022) |

Total stockholders’ equity |

|

|

1,131,057 |

|

|

943,643 |

Total liabilities and stockholders’ equity |

|

$ |

2,018,021 |

|

$ |

1,705,592 |

6

Boot Barn Holdings, Inc.

Consolidated Statements of Operations

(In thousands, except per share data)

(Unaudited)

|

|

Thirteen Weeks Ended |

|

Thirteen Weeks Ended |

|

Fifty-Two Weeks Ended |

|

Fifty-Two Weeks Ended |

||||

|

|

March 29, |

|

March 30, |

|

March 29, |

|

March 30, |

||||

|

|

2025 |

|

2024 |

|

2025 |

|

2024 |

||||

Net sales |

|

$ |

453,749 |

|

$ |

388,459 |

|

$ |

1,911,104 |

|

$ |

1,667,009 |

Cost of goods sold |

|

|

285,187 |

|

|

249,021 |

|

|

1,194,066 |

|

|

1,052,585 |

Gross profit |

|

|

168,562 |

|

|

139,438 |

|

|

717,038 |

|

|

614,424 |

Selling, general and administrative expenses |

|

|

118,875 |

|

|

101,194 |

|

|

477,686 |

|

|

416,210 |

Income from operations |

|

|

49,687 |

|

|

38,244 |

|

|

239,352 |

|

|

198,214 |

Interest expense |

|

|

346 |

|

|

230 |

|

|

1,497 |

|

|

2,238 |

Other income net |

|

|

607 |

|

|

871 |

|

|

2,262 |

|

|

1,396 |

Income before income taxes |

|

|

49,948 |

|

|

38,885 |

|

|

240,117 |

|

|

197,372 |

Income tax expense |

|

|

12,409 |

|

|

9,446 |

|

|

59,175 |

|

|

50,376 |

Net income |

|

$ |

37,539 |

|

$ |

29,439 |

|

$ |

180,942 |

|

$ |

146,996 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per share: |

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

$ |

1.23 |

|

$ |

0.97 |

|

$ |

5.93 |

|

$ |

4.87 |

Diluted |

|

$ |

1.22 |

|

$ |

0.96 |

|

$ |

5.88 |

|

$ |

4.80 |

Weighted average shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

|

30,593 |

|

|

30,317 |

|

|

30,524 |

|

|

30,167 |

Diluted |

|

|

30,771 |

|

|

30,717 |

|

|

30,773 |

|

|

30,611 |

7

Boot Barn Holdings, Inc.

Consolidated Statements of Cash Flows

(In thousands)

(Unaudited)

|

|

Fiscal Year Ended |

|||||||

|

|

March 29, |

|

March 30, |

|

April 1, |

|||

|

|

2025 |

|

2024 |

|

2023 |

|||

Cash flows from operating activities |

|

|

|

|

|

|

|

|

|

Net income |

|

$ |

180,942 |

|

$ |

146,996 |

|

$ |

170,553 |

Adjustments to reconcile net income to net cash provided by operating activities: |

|

|

|

|

|

|

|

|

|

Depreciation |

|

|

62,462 |

|

|

49,531 |

|

|

35,883 |

Stock-based compensation |

|

|

10,978 |

|

|

12,935 |

|

|

9,711 |

Amortization of intangible assets |

|

|

20 |

|

|

54 |

|

|

62 |

Impairment of intangible assets |

|

|

— |

|

|

2,000 |

|

|

— |

Noncash lease expense |

|

|

66,994 |

|

|

55,148 |

|

|

47,869 |

Amortization and write-off of debt issuance fees and debt discount |

|

|

108 |

|

|

108 |

|

|

130 |

Loss on disposal of property and equipment |

|

|

299 |

|

|

660 |

|

|

334 |

Deferred taxes |

|

|

(2,716) |

|

|

8,773 |

|

|

6,365 |

Changes in operating assets and liabilities, net of acquisition: |

|

|

|

|

|

|

|

|

|

Accounts receivable, net |

|

|

(240) |

|

|

3,282 |

|

|

(2,716) |

Inventories |

|

|

(148,071) |

|

|

(9,626) |

|

|

(115,194) |

Prepaid expenses and other current assets |

|

|

7,664 |

|

|

3,515 |

|

|

(11,276) |

Other assets |

|

|

(766) |

|

|

613 |

|

|

(2,874) |

Accounts payable |

|

|

210 |

|

|

425 |

|

|

(2,636) |

Accrued expenses and other current liabilities |

|

|

17,989 |

|

|

(6,208) |

|

|

(18,541) |

Other liabilities |

|

|

311 |

|

|

1,057 |

|

|

516 |

Operating leases |

|

|

(48,644) |

|

|

(33,183) |

|

|

(29,299) |

Net cash provided by operating activities |

|

$ |

147,540 |

|

$ |

236,080 |

|

$ |

88,887 |

Cash flows from investing activities |

|

|

|

|

|

|

|

|

|

Purchases of property and equipment |

|

$ |

(148,293) |

|

$ |

(118,782) |

|

$ |

(124,534) |

Proceeds from sale of property and equipment |

|

|

55 |

|

|

— |

|

|

— |

Net cash used in investing activities |

|

$ |

(148,238) |

|

$ |

(118,782) |

|

$ |

(124,534) |

Cash flows from financing activities |

|

|

|

|

|

|

|

|

|

(Payments)/borrowings on line of credit - net |

|

$ |

— |

|

$ |

(66,043) |

|

$ |

37,494 |

Repayments on debt and finance lease obligations |

|

|

(873) |

|

|

(863) |

|

|

(838) |

Tax withholding payments for net share settlement |

|

|

(7,617) |

|

|

(2,475) |

|

|

(4,689) |

Proceeds from the exercise of stock options |

|

|

3,111 |

|

|

9,737 |

|

|

1,199 |

Net cash (used in)/provided by financing activities |

|

$ |

(5,379) |

|

$ |

(59,644) |

|

$ |

33,166 |

Net (decrease)/increase in cash and cash equivalents |

|

|

(6,077) |

|

|

57,654 |

|

|

(2,481) |

Cash and cash equivalents, beginning of period |

|

|

75,847 |

|

|

18,193 |

|

|

20,674 |

Cash and cash equivalents, end of period |

|

$ |

69,770 |

|

$ |

75,847 |

|

$ |

18,193 |

|

|

|

|

|

|

|

|

|

|

Supplemental disclosures of cash flow information: |

|

|

|

|

|

|

|

|

|

Cash paid for income taxes |

|

$ |

59,929 |

|

$ |

57,157 |

|

$ |

60,171 |

Cash paid for interest |

|

$ |

1,381 |

|

$ |

2,385 |

|

$ |

5,835 |

Supplemental disclosure of non-cash activities: |

|

|

|

|

|

|

|

|

|

Unpaid purchases of property and equipment |

|

$ |

29,584 |

|

$ |

17,269 |

|

$ |

21,487 |

8

Boot Barn Holdings, Inc.

Store Count

|

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

Quarter Ended |

|

|

March 29, |

|

December 28, |

|

September 28, |

|

June 29, |

|

March 30, |

|

December 30, |

|

September 30, |

|

July 1, |

|

|

2025 |

|

2024 |

|

2024 |

|

2024 |

|

2024 |

|

2023 |

|

2023 |

|

2023 |

Store Count (BOP) |

|

438 |

|

425 |

|

411 |

|

400 |

|

382 |

|

371 |

|

361 |

|

345 |

Opened/Acquired |

|

21 |

|

13 |

|

15 |

|

11 |

|

18 |

|

11 |

|

10 |

|

16 |

Closed |

|

— |

|

— |

|

(1) |

|

— |

|

— |

|

— |

|

— |

|

— |

Store Count (EOP) |

|

459 |

|

438 |

|

425 |

|

411 |

|

400 |

|

382 |

|

371 |

|

361 |

Boot Barn Holdings, Inc.

Selected Store Data

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Thirteen Weeks Ended |

|

||||||||||||||||||||||

|

|

March 29, |

|

December 28, |

|

September 28, |

|

June 29, |

|

March 30, |

|

December 30, |

|

September 30, |

|

July 1, |

|

||||||||

|

|

2025 |

|

2024 |

|

2024 |

|

2024 |

|

2024 |

|

2023 |

|

2023 |

|

2023 |

|

||||||||

Selected Store Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Same Store Sales growth/(decline) |

|

|

6.0 |

% |

|

8.6 |

% |

|

4.9 |

% |

|

1.4 |

% |

|

(5.9) |

% |

|

(9.7) |

% |

|

(4.8) |

% |

|

(2.9) |

% |

Stores operating at end of period |

|

|

459 |

|

|

438 |

|

|

425 |

|

|

411 |

|

|

400 |

|

|

382 |

|

|

371 |

|

|

361 |

|

Comparable stores operating at end of period(1) |

|

|

382 |

|

|

374 |

|

|

363 |

|

|

349 |

|

|

335 |

|

|

322 |

|

|

312 |

|

|

302 |

|

Total retail store selling square footage, end of period (in thousands) |

|

|

5,133 |

|

|

4,877 |

|

|

4,720 |

|

|

4,547 |

|

|

4,371 |

|

|

4,153 |

|

|

4,027 |

|

|

3,914 |

|

Average retail store selling square footage, end of period |

|

|

11,183 |

|

|

11,134 |

|

|

11,105 |

|

|

11,063 |

|

|

10,929 |

|

|

10,872 |

|

|

10,855 |

|

|

10,841 |

|

Average sales per comparable store (in thousands)(2) |

|

$ |

926 |

|

$ |

1,301 |

|

$ |

952 |

|

$ |

980 |

|

$ |

917 |

|

$ |

1,256 |

|

$ |

950 |

|

$ |

1,014 |

|

| (1) | Comparable stores have been open at least 13 full fiscal months as of the end of the applicable reporting period. |

| (2) | Average sales per comparable store is calculated by dividing comparable store trailing three-month sales for the applicable period by the number of comparable stores operating during the period. |

9

|

0 Supplemental Financial Presentation May 2025 Offering everyone a piece of the American spirit—one handshake at a time. |

|

1 Important Information Forward-Looking Statements This presentation contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this presentation are forward-looking statements. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. These statements may include words such as "anticipate," "estimate," "expect," "project," "plan,“ "intend," "believe," “outlook” and other words of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events, but not all forward-looking statements contain these identifying words. These forward-looking statements are based on assumptions that the Boot Barn Holdings, Inc.’s (the “Company,” “Boot Barn,” “BOOT,” “we,” “us,” and “our,”) management has made in light of their industry experience and on their perceptions of historical trends, current conditions, expected future developments and other factors that they believe are appropriate under the circumstances. As you consider this presentation, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (some of which are beyond the Company’s control) and assumptions. These risks, uncertainties and assumptions include, but are not limited to, the following: decreases in consumer spending due to declines in consumer confidence, local economic conditions or changes in consumer preferences; the impact that import tariffs and other trade restrictions imposed by the U.S., China or other countries have had, and may continue to have, on our product costs and changes to U.S. or other countries’ trade policies and tariff and import/export regulations, including, without limitation, uncertainty with respect to the U.S. – China tariff deal; the Company’s ability to effectively execute on its growth strategy; and the Company’s failure to maintain and enhance its strong brand image, to compete effectively, to maintain good relationships with its key suppliers, and to improve and expand its exclusive product offerings. The Company discusses the foregoing risks and other risks in greater detail under the heading “Risk factors” in the periodic reports filed by the Company with the Securities and Exchange Commission. Although the Company believes that these forward-looking statements are based on reasonable assumptions, you should be aware that many factors could affect the Company’s actual financial results and cause them to differ materially from those anticipated in the forward-looking statements. Because of these factors, the Company cautions that you should not place undue reliance on any of these forward-looking statements. New risks and uncertainties arise from time to time, and it is impossible for the Company to predict those events or how they may affect the Company. Further, any forward-looking statement speaks only as of the date on which it is made. Except as required by law, the Company does not intend to update or revise the forward-looking statements in this presentation after the date of this presentation. Industry and Market Information Statements in this presentation concerning our industry and the markets in which we operate, including our general expectations and competitive position, business opportunity and market size, growth and share, are based on information from independent industry organizations and other third-party sources, data from our internal research and management estimates. Management estimates are derived from publicly available information and the information and data referred to above and are based on assumptions and calculations made by us based upon our interpretation of such information and data. The information and data referred to above are imprecise and may prove to be inaccurate because the information cannot always be verified with complete certainty due to the limitations on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties. As a result, please be aware that the data and statistical information in this presentation may differ from information provided by our competitors or from information found in current or future studies conducted by market research institutes, consultancy firms or independent sources. Recent Developments Our business and opportunities for growth depend on consumer discretionary spending, and as such, our results are particularly sensitive to economic conditions and consumer confidence. Inflation, changes to U.S. or other countries’ trade policies and tariff and import/export regulations, and other challenges affecting the global economy could impact our operations and will depend on future developments, which are uncertain. These and other effects make it more challenging for us to estimate the future performance of our business, particularly over the near-to-medium term. For further discussion of the uncertainties and business risks affecting the Company, see the sections captioned “Risk factors” in our periodic reports filed with the Securities and Exchange Commission. |

|

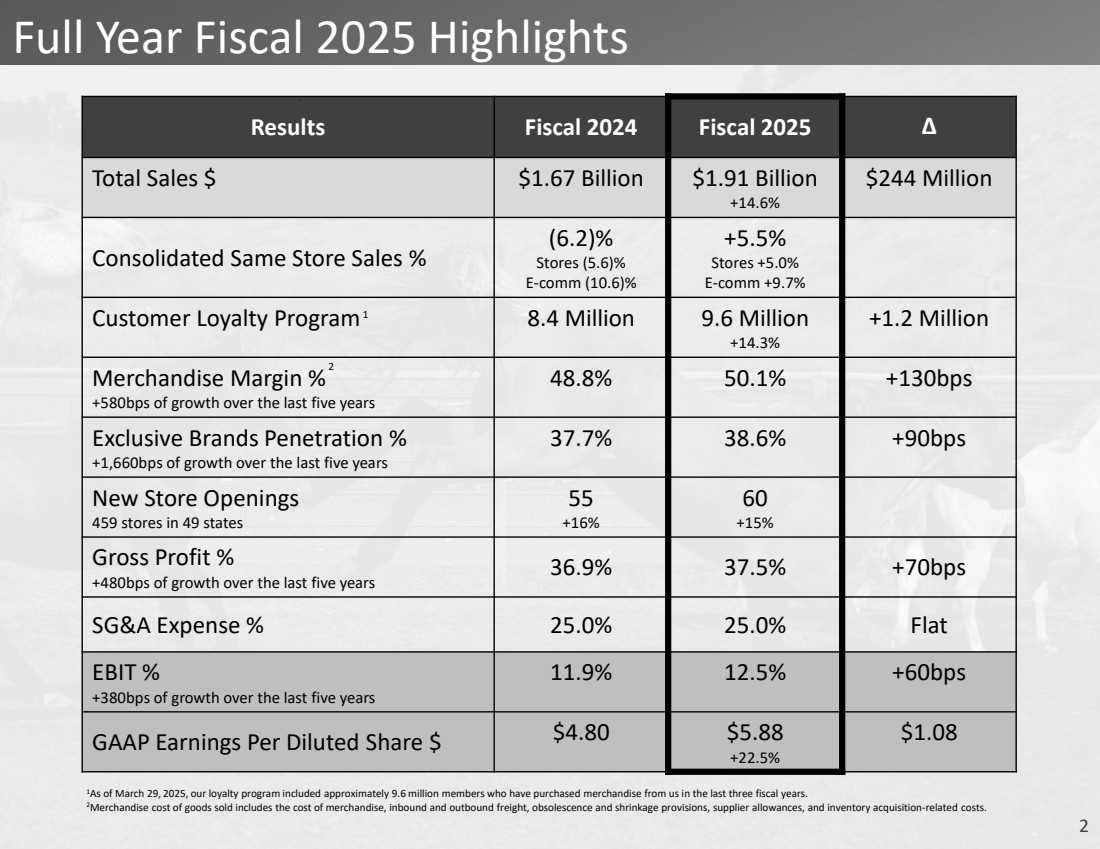

2 Full Year Fiscal 2025 Highlights Results Fiscal 2024 Fiscal 2025 Δ Total Sales $ $1.67 Billion $1.91 Billion +14.6% $244 Million Consolidated Same Store Sales % (6.2)% Stores (5.6)% E-comm (10.6)% +5.5% Stores +5.0% E-comm +9.7% Customer Loyalty Program 8.4 Million 9.6 Million +14.3% +1.2 Million Merchandise Margin % +580bps of growth over the last five years 48.8% 50.1% +130bps Exclusive Brands Penetration % +1,660bps of growth over the last five years 37.7% 38.6% +90bps New Store Openings 459 stores in 49 states 55 +16% 60 +15% Gross Profit % +480bps of growth over the last five years 36.9% 37.5% +70bps SG&A Expense % 25.0% 25.0% Flat EBIT % +380bps of growth over the last five years 11.9% 12.5% +60bps GAAP Earnings Per Diluted Share $ $4.80 $5.88 +22.5% $1.08 2 1As of March 29, 2025, our loyalty program included approximately 9.6 million members who have purchased merchandise from us in the last three fiscal years. 2Merchandise cost of goods sold includes the cost of merchandise, inbound and outbound freight, obsolescence and shrinkage provisions, supplier allowances, and inventory acquisition-related costs. 1 |

|

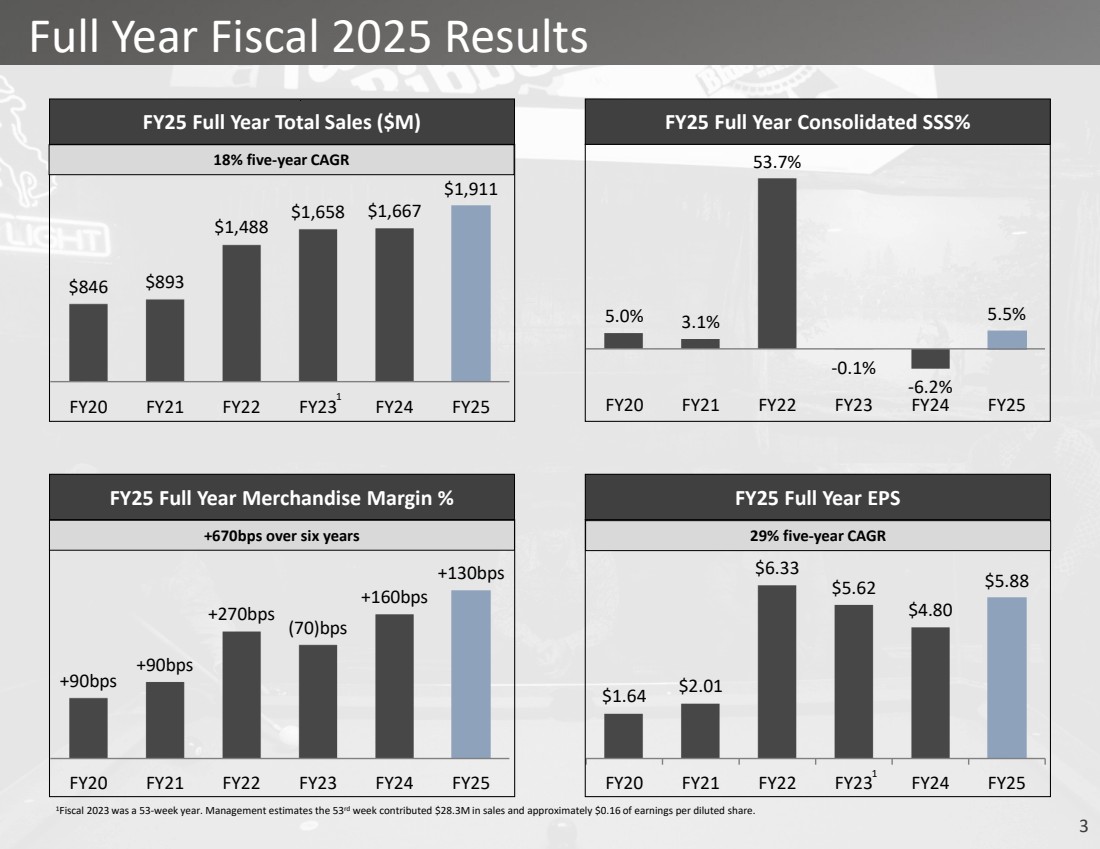

3 Full Year Fiscal 2025 Results 1Fiscal 2023 was a 53-week year. Management estimates the 53rd week contributed $28.3M in sales and approximately $0.16 of earnings per diluted share. $846 $893 $1,488 $1,658 $1,667 $1,911 FY20 FY21 FY22 FY23 FY24 FY25 FY25 Full Year Total Sales ($M) 5.0% 3.1% 53.7% -0.1% -6.2% 5.5% FY20 FY21 FY22 FY23 FY24 FY25 FY25 Full Year Consolidated SSS% +90bps +90bps +270bps (70)bps +160bps +130bps FY20 FY21 FY22 FY23 FY24 FY25 FY25 Full Year Merchandise Margin % $1.64 $2.01 $6.33 $5.62 $4.80 $5.88 FY20 FY21 FY22 FY23 FY24 FY25 FY25 Full Year EPS 18% five-year CAGR +670bps over six years 29% five-year CAGR 1 1 |

|

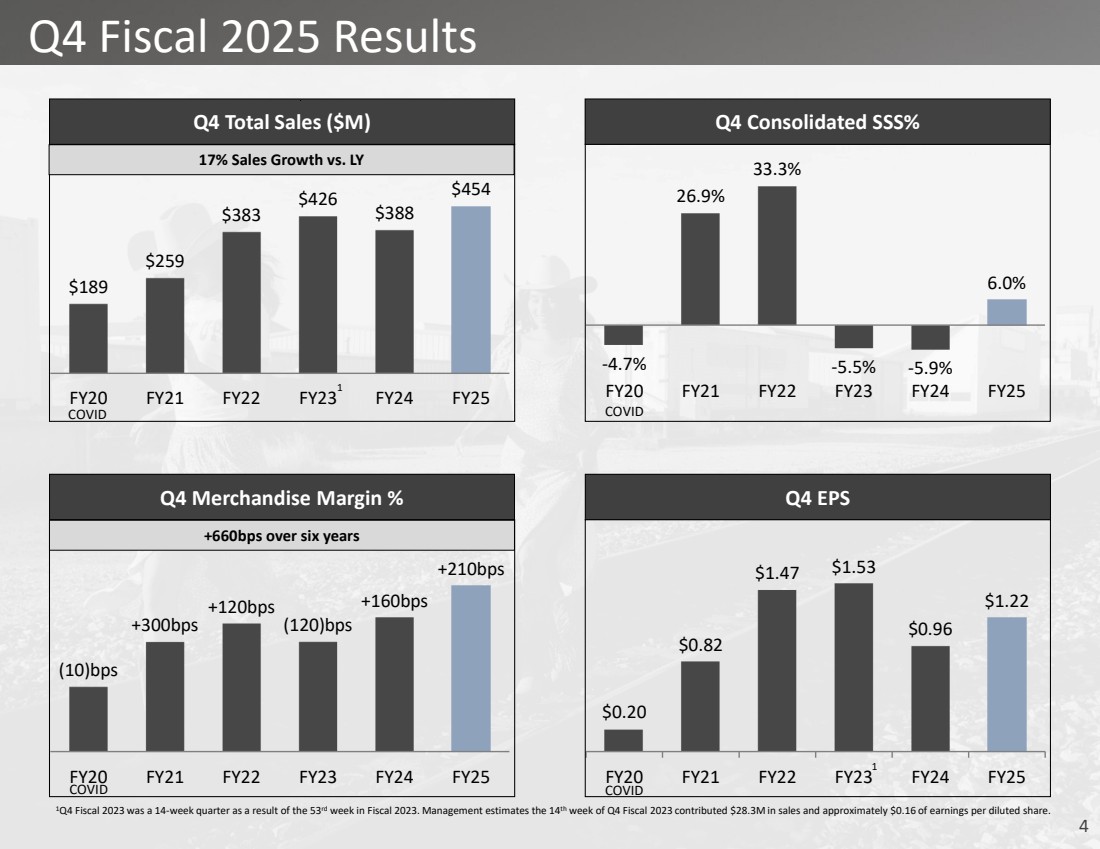

4 Q4 Fiscal 2025 Results 1Q4 Fiscal 2023 was a 14-week quarter as a result of the 53rd week in Fiscal 2023. Management estimates the 14th week of Q4 Fiscal 2023 contributed $28.3M in sales and approximately $0.16 of earnings per diluted share. $189 $259 $383 $426 $388 $454 FY20 FY21 FY22 FY23 FY24 FY25 Q4 Total Sales ($M) -4.7% 26.9% 33.3% -5.5% -5.9% 6.0% FY20 FY21 FY22 FY23 FY24 FY25 Q4 Consolidated SSS% (10)bps +300bps +120bps (120)bps +160bps +210bps FY20 FY21 FY22 FY23 FY24 FY25 Q4 Merchandise Margin % $0.20 $0.82 $1.47 $1.53 $0.96 $1.22 FY20 FY21 FY22 FY23 FY24 FY25 Q4 EPS 1 COVID COVID COVID COVID 17% Sales Growth vs. LY +660bps over six years 1 |

|

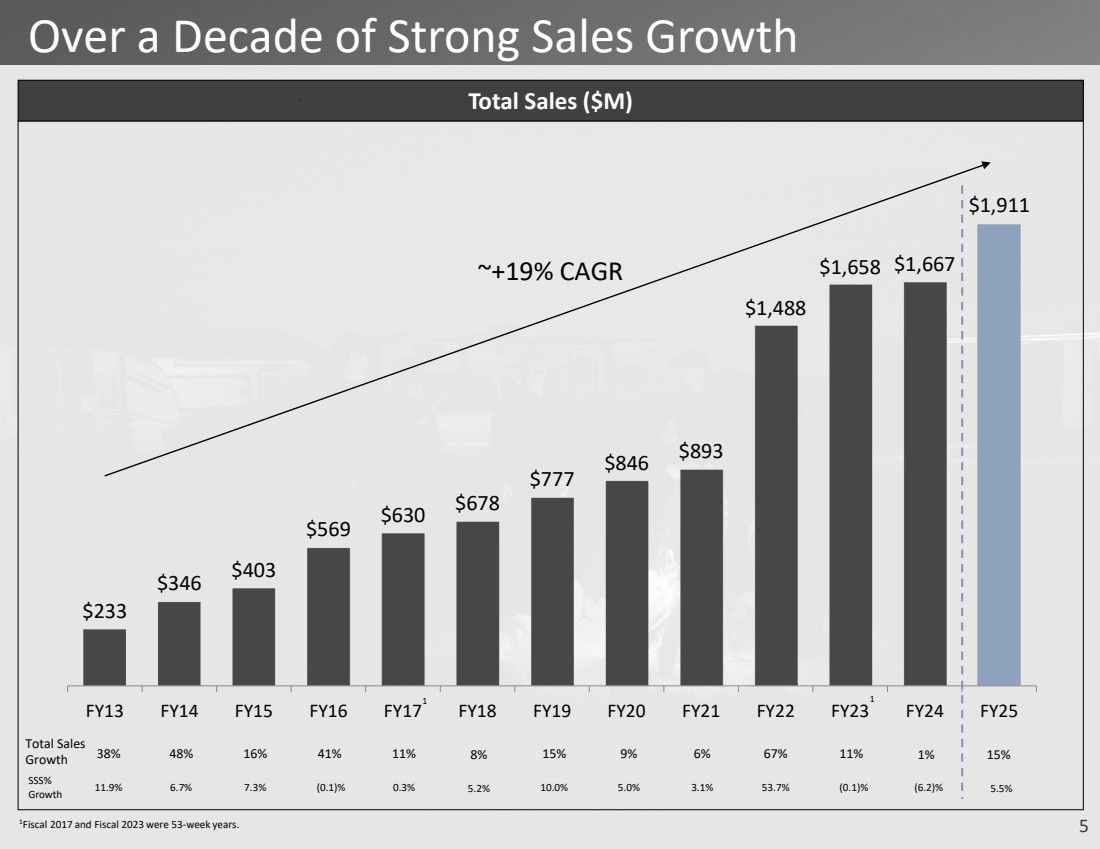

5 $233 $346 $403 $569 $630 $678 $777 $846 $893 $1,488 $1,658 $1,667 $1,911 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 Total Sales ($M) Total Sales Growth 38% 48% 16% 41% 11% 8% 15% 9% 6% 67% 11% Over a Decade of Strong Sales Growth 1 1 1Fiscal 2017 and Fiscal 2023 were 53-week years. 1% ~+19% CAGR SSS% Growth 11.9% 6.7% 7.3% (0.1)% 0.3% 5.2% 10.0% 5.0% 3.1% 53.7% (0.1)% (6.2)% 15% 5.5% |

|

6 Strategic Initiatives Update 1 2 3 4 New Stores Same Store Sales Omni-Channel Merchandise Margin & Exclusive Brands |

|

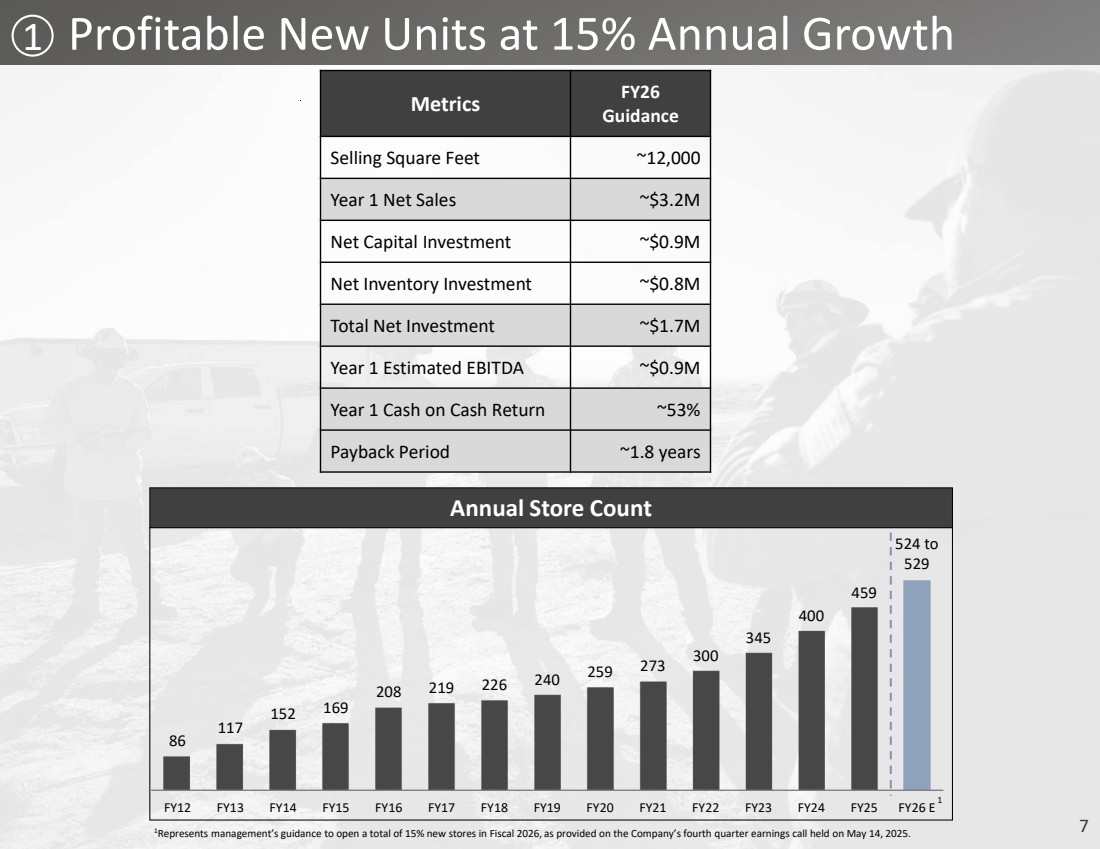

7 Profitable New Units at 15% Annual Growth 86 117 152 169 208 219 226 240 259 273 300 345 400 459 524 to 529 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 FY26 E Annual Store Count 1 1Represents management’s guidance to open a total of 15% new stores in Fiscal 2026, as provided on the Company’s fourth quarter earnings call held on May 14, 2025. 1 Metrics FY26 Guidance Selling Square Feet ~12,000 Year 1 Net Sales ~$3.2M Net Capital Investment ~$0.9M Net Inventory Investment ~$0.8M Total Net Investment ~$1.7M Year 1 Estimated EBITDA ~$0.9M Year 1 Cash on Cash Return ~53% Payback Period ~1.8 years |

|

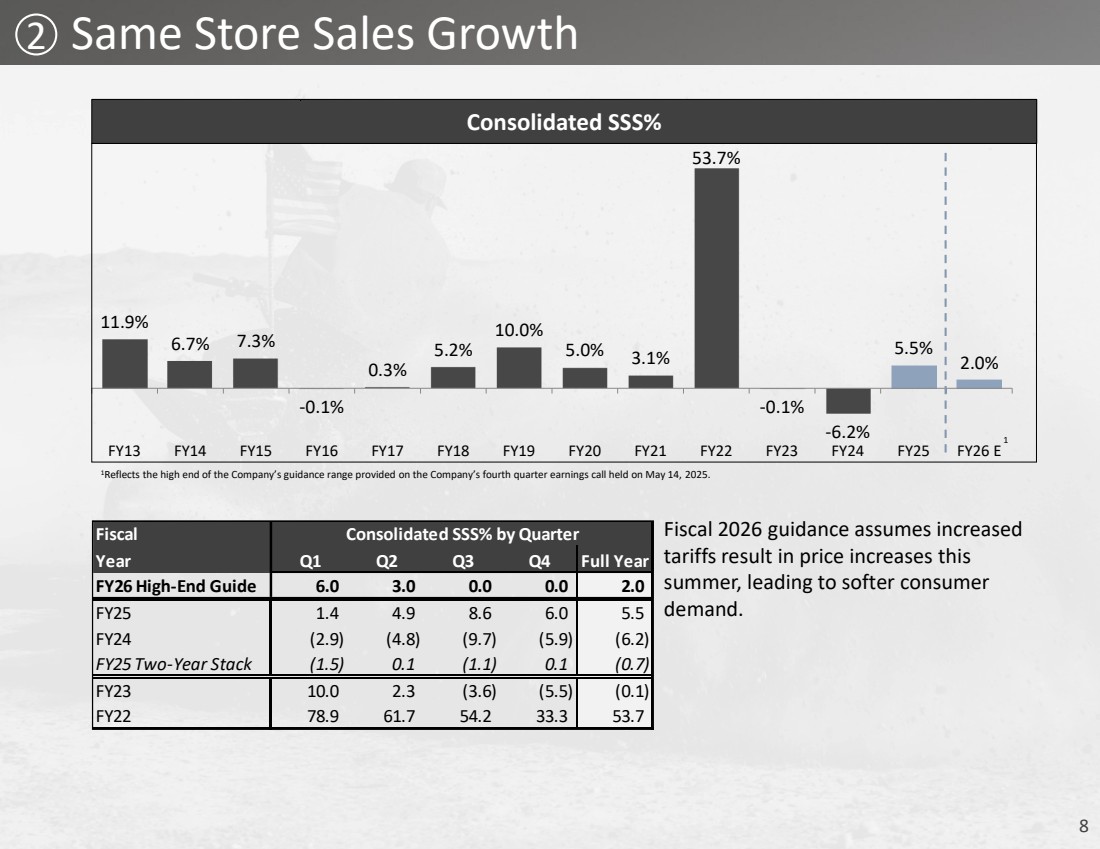

8 11.9% 6.7% 7.3% -0.1% 0.3% 5.2% 10.0% 5.0% 3.1% 53.7% -0.1% -6.2% 5.5% 2.0% FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 FY26 E Consolidated SSS% 2 Same Store Sales Growth 1 1Reflects the high end of the Company’s guidance range provided on the Company’s fourth quarter earnings call held on May 14, 2025. Fiscal 2026 guidance assumes increased tariffs result in price increases this summer, leading to softer consumer demand. Fiscal Consolidated SSS% by Quarter Year Q1 Q2 Q3 Q4 Full Year FY26 High-End Guide 6.0 3.0 0.0 0.0 2.0 FY25 1.4 4.9 8.6 6.0 5.5 FY24 (2.9) (4.8) (9.7) (5.9) (6.2) FY25 Two-Year Stack (1.5) 0.1 (1.1) 0.1 (0.7) FY23 10.0 2.3 (3.6) (5.5) (0.1) FY22 78.9 61.7 54.2 33.3 53.7 |

|

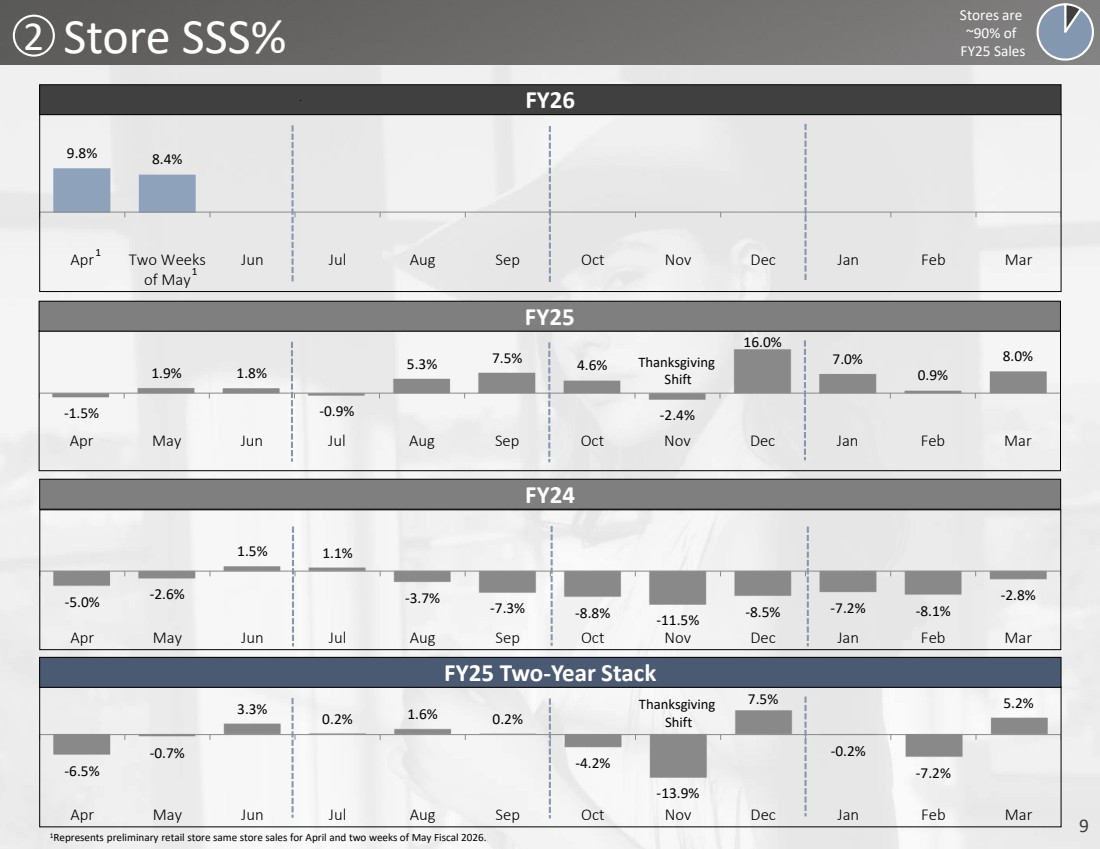

9 2 Store SSS% Stores are ~90% of FY25 Sales 1Represents preliminary retail store same store sales for April and two weeks of May Fiscal 2026. 9.8% 8.4% Apr Two Weeks of May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY26 -6.5% -0.7% 3.3% 0.2% 1.6% 0.2% -4.2% -13.9% 7.5% -0.2% -7.2% 5.2% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 Two-Year Stack Thanksgiving Shift 1 1 -1.5% 1.9% 1.8% -0.9% 5.3% 7.5% 4.6% -2.4% 16.0% 7.0% 0.9% 8.0% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 Thanksgiving Shift FY24 -5.0% -2.6% 1.5% 1.1% -3.7% -7.3% -8.8% -11.5% -8.5% -7.2% -8.1% -2.8% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar |

|

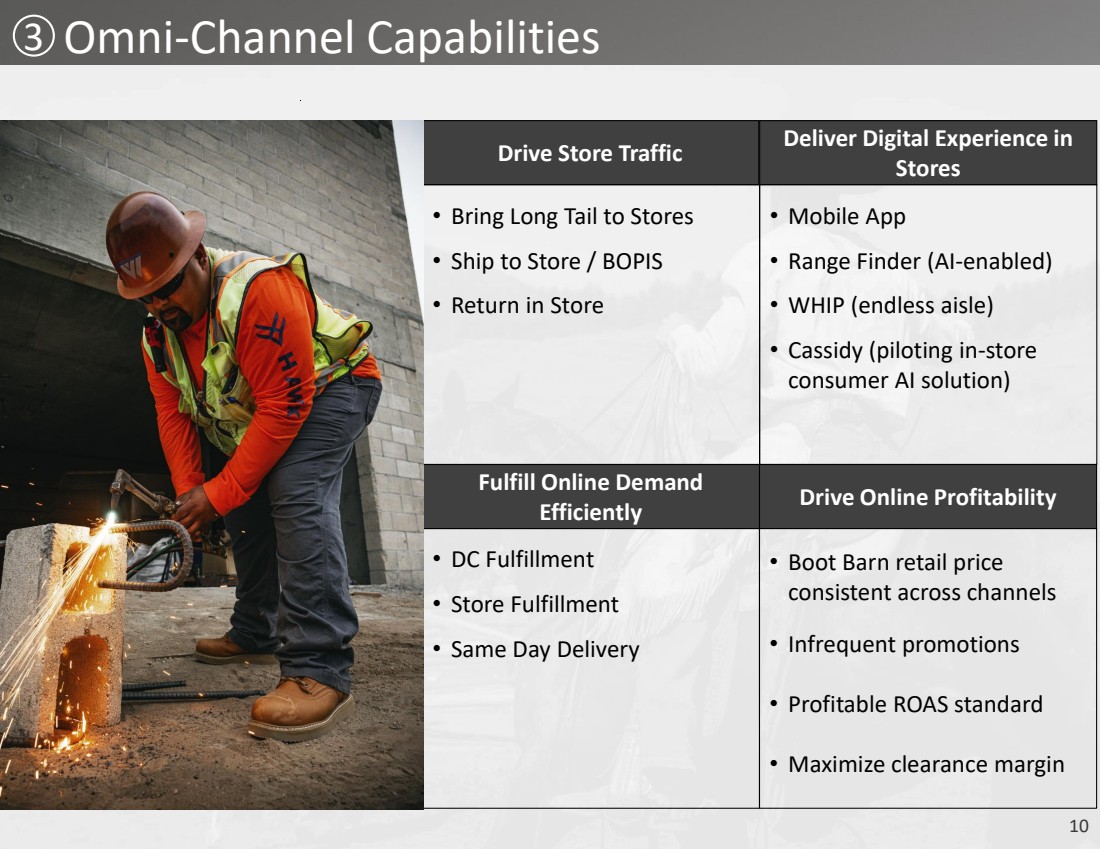

10 3 Omni-Channel Capabilities Drive Store Traffic • Bring Long Tail to Stores • Ship to Store / BOPIS • Return in Store Deliver Digital Experience in Stores • Mobile App • Range Finder (AI-enabled) • WHIP (endless aisle) • Cassidy (piloting in-store consumer AI solution) Fulfill Online Demand Efficiently • DC Fulfillment • Store Fulfillment • Same Day Delivery Drive Online Profitability • Boot Barn retail price consistent across channels • Infrequent promotions • Profitable ROAS standard • Maximize clearance margin |

|

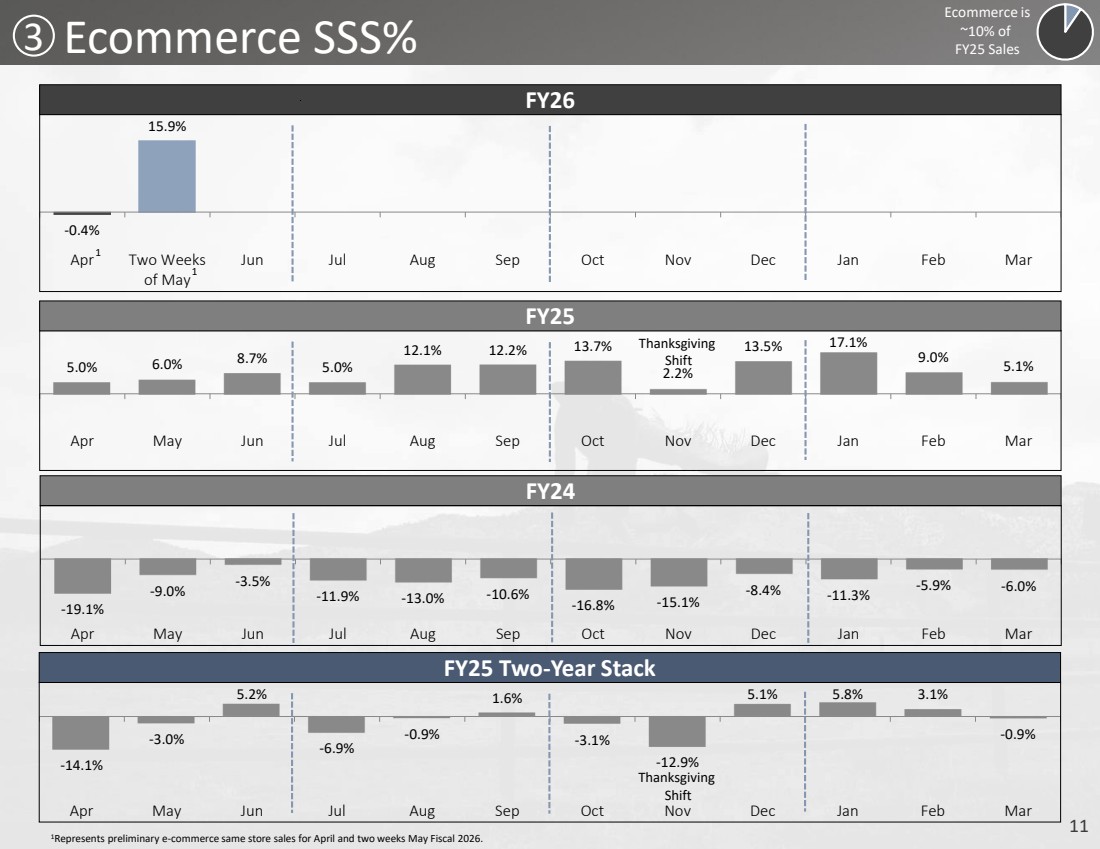

11 3 Ecommerce SSS% Ecommerce is ~10% of FY25 Sales 1Represents preliminary e-commerce same store sales for April and two weeks May Fiscal 2026. -0.4% 15.9% Apr Two Weeks of May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY26 -14.1% -3.0% 5.2% -6.9% -0.9% 1.6% -3.1% -12.9% 5.1% 5.8% 3.1% -0.9% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 Two-Year Stack Thanksgiving Shift 1 1 5.0% 6.0% 8.7% 5.0% 12.1% 12.2% 13.7% 2.2% 13.5% 17.1% 9.0% 5.1% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 Thanksgiving Shift FY24 -19.1% -9.0% -3.5% -11.9% -13.0% -10.6% -16.8% -15.1% -8.4% -11.3% -5.9% -6.0% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar |

|

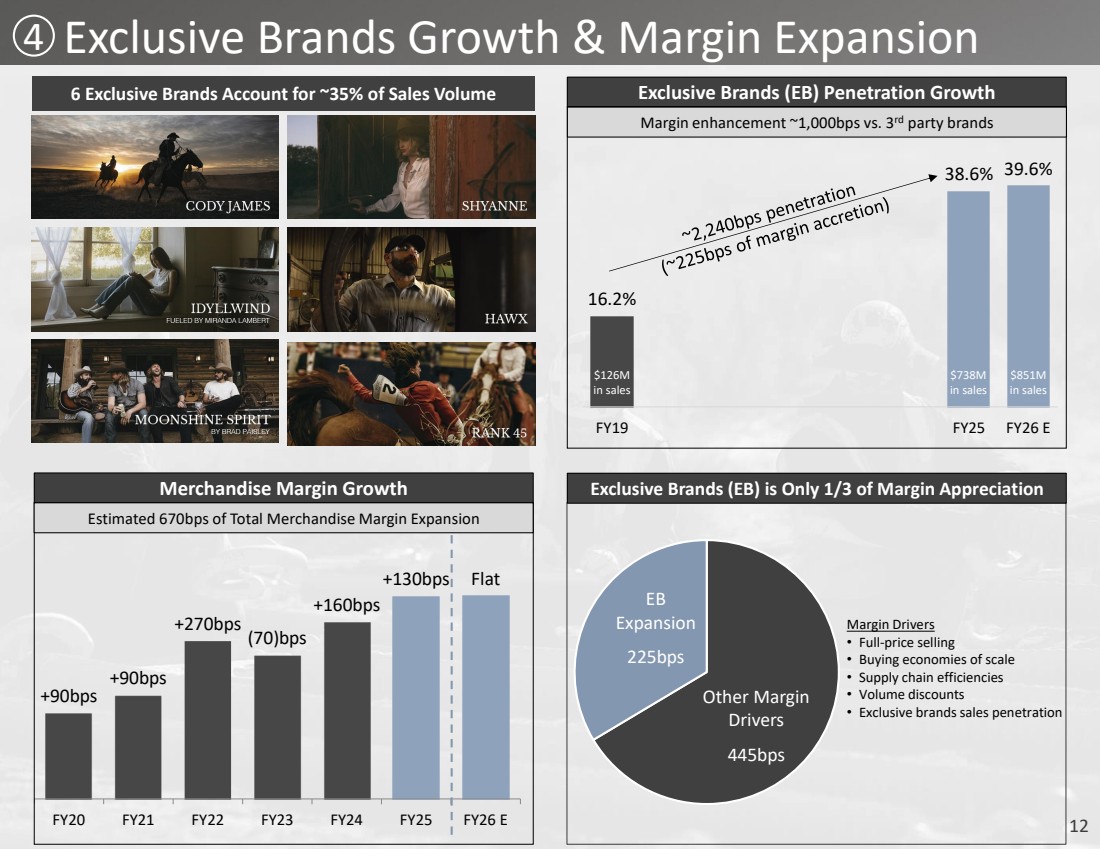

12 Margin Drivers • Full-price selling • Buying economies of scale • Supply chain efficiencies • Volume discounts • Exclusive brands sales penetration Exclusive Brands (EB) Penetration Growth 16.2% 38.6% 39.6% FY19 FY25 FY26 E Exclusive Brands (EB) is Only 1/3 of Margin Appreciation EB Expansion 225bps Other Margin Drivers 445bps +90bps +90bps +270bps (70)bps +160bps +130bps Flat FY20 FY21 FY22 FY23 FY24 FY25 FY26 E Merchandise Margin Growth 4 Estimated 670bps of Total Merchandise Margin Expansion Exclusive Brands Growth & Margin Expansion 6 Exclusive Brands Account for ~35% of Sales Volume $851M in sales $738M in sales $126M in sales Margin enhancement ~1,000bps vs. 3rd party brands |

|

13 FY26 Guidance |

|

14 Full Year Fiscal 2026 Financial Guidance Full Year FY26 Financial Guidance Low-End ($M) High-End ($M) Low-End Guidance Comments vs. LY High-End Guidance Comments vs. LY Total Net Sales Consolidated SSS% Store SSS% E-commerce SSS% Total Net Sales Growth % 15% New Store Openings $2,070 (2.0)% (2.5)% 1.0% 8% 65-70 $2,150 2.0% 1.5% 7.5% 13% 65-70 Merchandise Margin % $1,030 49.8% $1,077 50.1% (30)bps decrease +100bps exclusive brands penetration flat merchandise margin +100bps exclusive brands penetration Gross Profit % $747 36.1% $793 36.9% (140)bps deleverage (60)bps deleverage SG&A % $519 25.1% $527 24.5% (10)bps deleverage 50bps leverage Income from Operations % $228 11.0% $266 12.4% GAAP Earnings per Diluted Share $5.50 $6.40 26.0% effective tax rate (6)% EPS decrease 26.0% effective tax rate 9% EPS growth 1 1Merchandise cost of goods sold includes the cost of merchandise, inbound and outbound freight, obsolescence and shrinkage provisions, supplier allowances, and inventory acquisition-related costs. Fiscal 2026 guidance assumes increased tariffs result in price increases this summer, leading to softer consumer demand. The difference between the low and high-end scenarios reflect different degrees of impact on consumer demand. Fiscal 2026 guidance assumes a merchandise margin decline in the second half of the fiscal year due to unmitigated tariff costs. The difference between the low and high-end scenarios reflect different degrees of impact on margin degradation. Fiscal 2026 contemplates a 30% tariff on China, 10% global tariff rate, and 0% tariff on Mexico (USMCA compliant). |

|

15 Q1 Fiscal 2026 Financial Guidance Q1 FY26 Financial Guidance Low-End ($M) High-End ($M) Total Net Sales Consolidated SSS% Store SSS% E-commerce SSS% Total Net Sales Growth % $483 4.0% 4.0% 4.0% 14% $491 6.0% 6.0% 6.0% 16% Merchandise Margin % $250 51.7% $254 51.7% Gross Profit % $183 37.9% $188 38.2% SG&A % $122 25.3% $124 25.2% Income from Operations % $61 12.6% $64 13.0% GAAP Earnings per Diluted Share $1.44 $1.52 1 1Merchandise cost of goods sold includes the cost of merchandise, inbound and outbound freight, obsolescence and shrinkage provisions, supplier allowances, and inventory acquisition-related costs. |

|

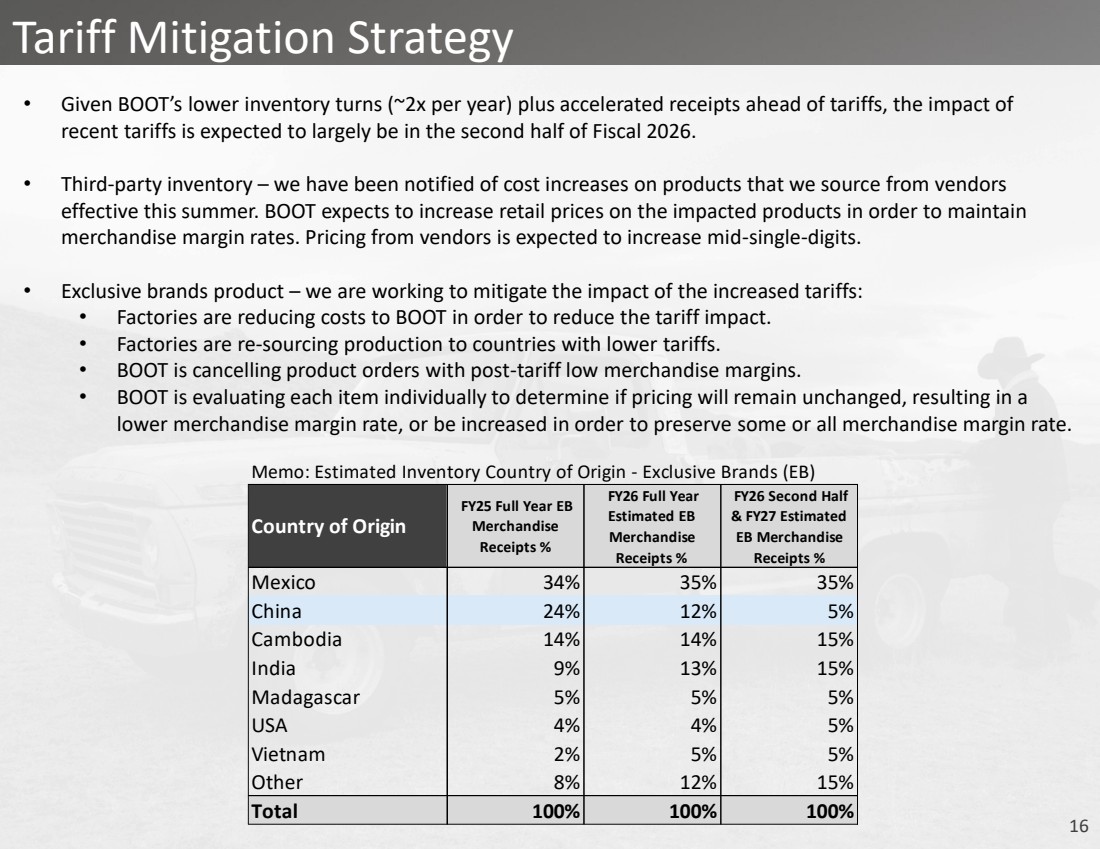

16 Tariff Mitigation Strategy • Given BOOT’s lower inventory turns (~2x per year) plus accelerated receipts ahead of tariffs, the impact of recent tariffs is expected to largely be in the second half of Fiscal 2026. • Third-party inventory – we have been notified of cost increases on products that we source from vendors effective this summer. BOOT expects to increase retail prices on the impacted products in order to maintain merchandise margin rates. Pricing from vendors is expected to increase mid-single-digits. • Exclusive brands product – we are working to mitigate the impact of the increased tariffs: • Factories are reducing costs to BOOT in order to reduce the tariff impact. • Factories are re-sourcing production to countries with lower tariffs. • BOOT is cancelling product orders with post-tariff low merchandise margins. • BOOT is evaluating each item individually to determine if pricing will remain unchanged, resulting in a lower merchandise margin rate, or be increased in order to preserve some or all merchandise margin rate. Memo: Estimated Inventory Country of Origin - Exclusive Brands (EB) Country of Origin FY25 Full Year EB Merchandise Receipts % FY26 Full Year Estimated EB Merchandise Receipts % FY26 Second Half & FY27 Estimated EB Merchandise Receipts % Mexico 34% 35% 35% China 24% 12% 5% Cambodia 14% 14% 15% India 9% 13% 15% Madagascar 5% 5% 5% USA 4% 4% 5% Vietnam 2% 5% 5% Other 8% 12% 15% Total 100% 100% 100% |

|

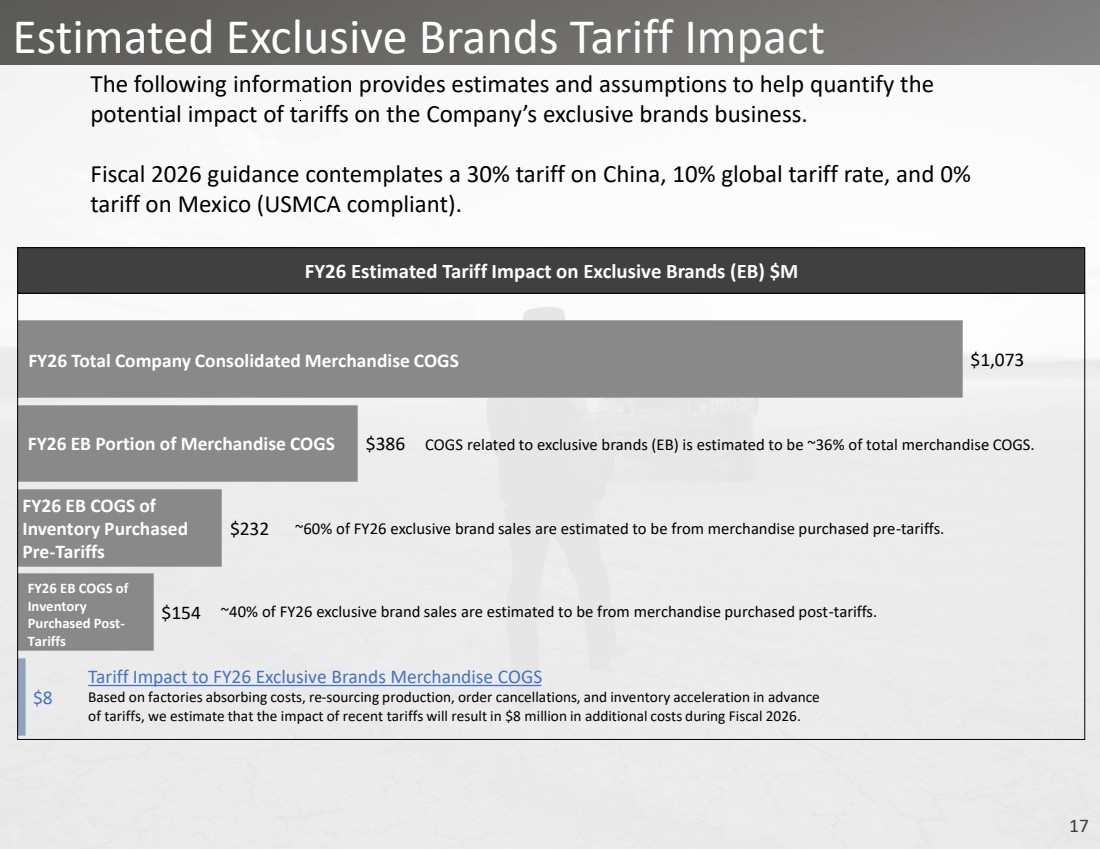

17 Estimated Exclusive Brands Tariff Impact The following information provides estimates and assumptions to help quantify the potential impact of tariffs on the Company’s exclusive brands business. Fiscal 2026 guidance contemplates a 30% tariff on China, 10% global tariff rate, and 0% tariff on Mexico (USMCA compliant). $8 $154 $232 $386 $1,073 FY26 Estimated Tariff Impact on Exclusive Brands (EB) $M FY26 Total Company Consolidated Merchandise COGS FY26 EB Portion of Merchandise COGS FY26 EB COGS of Inventory Purchased Pre-Tariffs FY26 EB COGS of Inventory Purchased Post-Tariffs COGS related to exclusive brands (EB) is estimated to be ~36% of total merchandise COGS. ~60% of FY26 exclusive brand sales are estimated to be from merchandise purchased pre-tariffs. ~40% of FY26 exclusive brand sales are estimated to be from merchandise purchased post-tariffs. Tariff Impact to FY26 Exclusive Brands Merchandise COGS Based on factories absorbing costs, re-sourcing production, order cancellations, and inventory acceleration in advance of tariffs, we estimate that the impact of recent tariffs will result in $8 million in additional costs during Fiscal 2026. |

|

18 Share Repurchase Program The Company’s Board of Directors has authorized the Company to repurchase up to $200 million of its common stock. We plan to execute a quarter of the total authorization this fiscal year, with the spend roughly consistent by quarter and this has been factored into our guidance. |

|

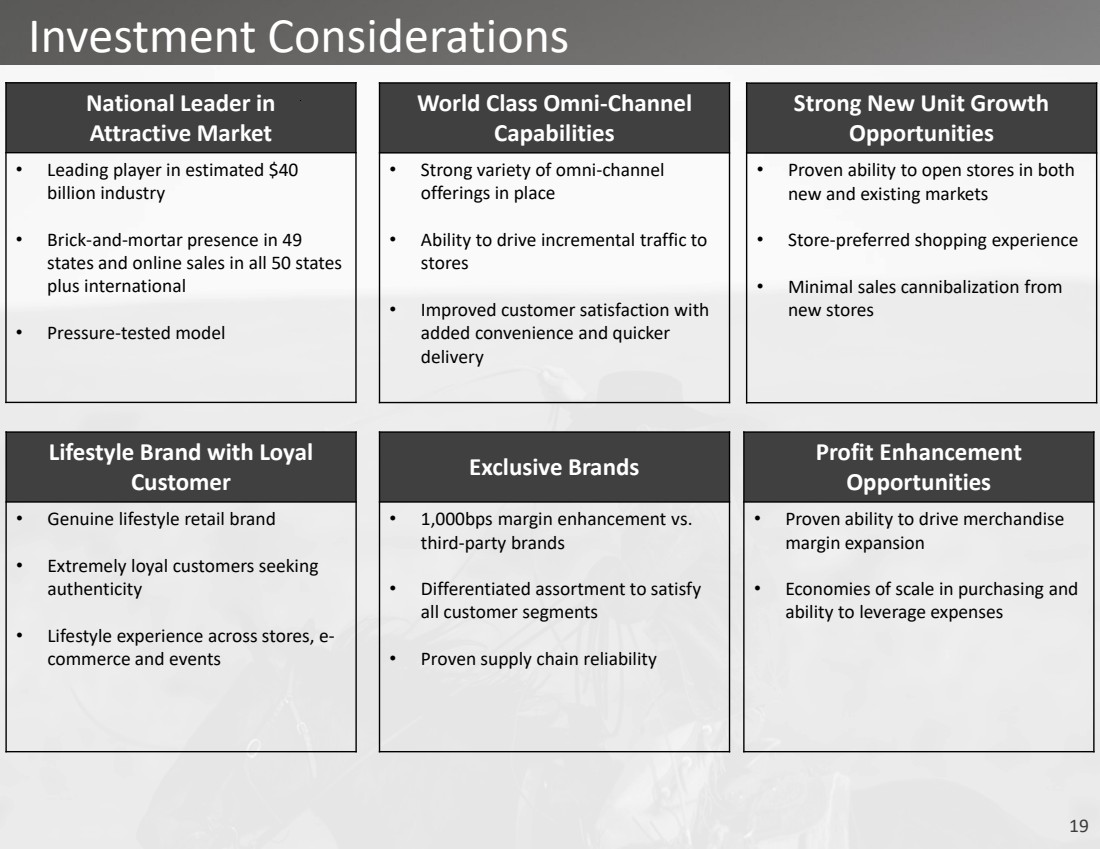

19 National Leader in Attractive Market • Leading player in estimated $40 billion industry • Brick-and-mortar presence in 49 states and online sales in all 50 states plus international • Pressure-tested model World Class Omni-Channel Capabilities • Strong variety of omni-channel offerings in place • Ability to drive incremental traffic to stores • Improved customer satisfaction with added convenience and quicker delivery Strong New Unit Growth Opportunities • Proven ability to open stores in both new and existing markets • Store-preferred shopping experience • Minimal sales cannibalization from new stores Lifestyle Brand with Loyal Customer • Genuine lifestyle retail brand • Extremely loyal customers seeking authenticity • Lifestyle experience across stores, e-commerce and events Profit Enhancement Opportunities • Proven ability to drive merchandise margin expansion • Economies of scale in purchasing and ability to leverage expenses Investment Considerations Exclusive Brands • 1,000bps margin enhancement vs. third-party brands • Differentiated assortment to satisfy all customer segments • Proven supply chain reliability |

|

20 investor.bootbarn.com |