UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of May 2025

Commission File Number: 001-36298

GeoPark Limited

(Exact name of registrant as specified in its charter)

Calle 94 N° 11-30 Piso 8

Bogota, Colombia

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F |

X |

|

Form 40-F |

GEOPARK LIMITED

TABLE OF CONTENTS

ITEM

1. |

Interim Condensed Consolidated Financial Statements and Explanatory Notes for the three-month periods ended March 31, 2025 and 2024. |

Item 1

GEOPARK LIMITED

INTERIM CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS

AND EXPLANATORY NOTES

For the three-month periods ended March 31, 2025 and 2024

Page |

|

|

|

3 |

|

4 |

|

5 |

|

6 |

|

7 |

|

8 |

Explanatory Notes to the Interim Condensed Consolidated Financial Statements |

2

CONDENSED CONSOLIDATED STATEMENT OF INCOME

|

|

|

|

Three-month |

|

Three-month |

|

|

|

|

period ended |

|

period ended |

|

|

|

|

March 31, 2025 |

|

March 31, 2024 |

Amounts in US$ '000 |

|

Note |

|

(Unaudited) |

|

(Unaudited) |

REVENUE |

|

3 |

|

137,349 |

|

167,416 |

Production and operating costs |

|

5 |

|

(35,437) |

|

(38,540) |

Geological and geophysical expenses |

|

6 |

|

(2,453) |

|

(2,738) |

Administrative expenses |

|

7 |

|

(9,056) |

|

(9,963) |

Selling expenses |

|

8 |

|

(2,168) |

|

(4,140) |

Depreciation |

|

|

|

(32,045) |

|

(28,659) |

Write-off of unsuccessful exploration efforts |

|

11 |

|

(5,883) |

|

— |

Other income (expenses), net |

|

|

|

109 |

|

579 |

OPERATING PROFIT |

|

|

|

50,416 |

|

83,955 |

Financial expenses |

|

9 |

|

(24,836) |

|

(11,137) |

Financial income |

|

9 |

|

3,224 |

|

2,083 |

Foreign exchange (loss) profit |

|

9 |

|

(3,288) |

|

164 |

PROFIT BEFORE INCOME TAX |

|

|

|

25,516 |

|

75,065 |

Income tax expense |

|

10 |

|

(12,447) |

|

(44,873) |

PROFIT FOR THE PERIOD |

|

|

|

13,069 |

|

30,192 |

Earnings per share (in US$). Basic |

|

|

|

0.25 |

|

0.55 |

Earnings per share (in US$). Diluted |

|

|

|

0.25 |

|

0.54 |

The above condensed consolidated statement of income should be read in conjunction with the accompanying notes.

3

CONDENSED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

|

|

Three-month |

|

Three-month |

|

|

period ended |

|

period ended |

|

|

March 31, 2025 |

|

March 31, 2024 |

Amounts in US$ '000 |

|

(Unaudited) |

|

(Unaudited) |

Profit for the period |

|

13,069 |

|

30,192 |

Other comprehensive income |

|

|

|

|

Items that may be subsequently reclassified to profit or loss: |

|

|

|

|

Currency translation differences |

|

19 |

|

(386) |

Gain (Loss) on cash flow hedges (a) |

|

802 |

|

(3,943) |

Income tax (expense) benefit relating to cash flow hedges |

|

(498) |

|

1,971 |

Other comprehensive profit (loss) for the period |

|

323 |

|

(2,358) |

Total comprehensive profit for the period |

|

13,392 |

|

27,834 |

| (a) | Unrealized result on commodity risk management contracts designated as cash flow hedges. See Note 4. |

The above condensed consolidated statement of comprehensive income should be read in conjunction with the accompanying notes.

4

CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION

|

|

Note |

|

At March 31, |

|

Year ended |

|

|

|

|

2025 |

|

December 31, |

Amounts in US$ '000 |

|

|

|

(Unaudited) |

|

2024 |

ASSETS |

|

|

|

|

|

|

NON CURRENT ASSETS |

|

|

|

|

|

|

Property, plant and equipment |

|

11 |

|

709,360 |

|

740,491 |

Right-of-use assets |

|

|

|

22,371 |

|

24,451 |

Prepayments and other receivables |

|

12 |

|

3,635 |

|

2,650 |

Other financial assets |

|

|

|

1,072 |

|

1,020 |

Deferred income tax asset |

|

|

|

6,719 |

|

1,332 |

TOTAL NON CURRENT ASSETS |

|

|

|

743,157 |

|

769,944 |

CURRENT ASSETS |

|

|

|

|

|

|

Inventories |

|

|

|

7,956 |

|

10,567 |

Trade receivables |

|

|

|

45,862 |

|

40,211 |

Prepayments and other receivables |

|

12 |

|

82,357 |

|

79,731 |

Derivative financial instrument assets |

|

17 |

|

4,404 |

|

2,764 |

Other financial assets |

|

|

|

— |

|

20,088 |

Cash and cash equivalents |

|

|

|

307,993 |

|

276,750 |

Assets held for sale |

|

|

|

6,227 |

|

— |

TOTAL CURRENT ASSETS |

|

|

|

454,799 |

|

430,111 |

TOTAL ASSETS |

|

|

|

1,197,956 |

|

1,200,055 |

EQUITY |

|

|

|

|

|

|

Equity attributable to owners of the Company |

|

|

|

|

|

|

Share capital |

|

13 |

|

51 |

|

51 |

Share premium |

|

|

|

74,501 |

|

73,750 |

Translation reserve |

|

|

|

(11,571) |

|

(11,590) |

Reserves |

|

|

|

15,357 |

|

15,053 |

Retained earnings |

|

|

|

132,353 |

|

126,027 |

TOTAL EQUITY |

|

|

|

210,691 |

|

203,291 |

LIABILITIES |

|

|

|

|

|

|

NON CURRENT LIABILITIES |

|

|

|

|

|

|

Borrowings |

|

14 |

|

638,432 |

|

492,007 |

Lease liabilities |

|

|

|

17,733 |

|

17,318 |

Provisions and other long-term liabilities |

|

15 |

|

21,865 |

|

31,952 |

Deferred income tax liability |

|

|

|

77,075 |

|

86,814 |

TOTAL NON CURRENT LIABILITIES |

|

|

|

755,105 |

|

628,091 |

CURRENT LIABILITIES |

|

|

|

|

|

|

Borrowings |

|

14 |

|

18,996 |

|

22,326 |

Lease liabilities |

|

|

|

8,425 |

|

8,605 |

Derivative financial instrument liabilities |

|

17 |

|

— |

|

464 |

Current income tax liability |

|

|

|

80,959 |

|

57,329 |

Trade and other payables |

|

16 |

|

110,948 |

|

279,949 |

Liabilities associated with assets held for sale |

|

|

|

12,832 |

|

— |

TOTAL CURRENT LIABILITIES |

|

|

|

232,160 |

|

368,673 |

TOTAL LIABILITIES |

|

|

|

987,265 |

|

996,764 |

TOTAL EQUITY AND LIABILITIES |

|

|

|

1,197,956 |

|

1,200,055 |

The above condensed consolidated statement of financial position should be read in conjunction with the accompanying notes.

5

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

|

|

Attributable to owners of the Company |

||||||||||

|

|

Share |

|

Share |

|

Translation |

|

Other |

|

Retained |

|

|

Amount in US$ '000 |

|

Capital |

|

Premium |

|

Reserve |

|

Reserve |

|

earnings |

|

Total |

Equity at January 1, 2024 |

|

55 |

|

111,281 |

|

(9,962) |

|

45,116 |

|

29,530 |

|

176,020 |

Comprehensive income: |

|

|

|

|

|

|

|

|

|

|

|

|

Profit for the three-month period |

|

— |

|

— |

|

— |

|

— |

|

30,192 |

|

30,192 |

Other comprehensive profit for the period |

|

— |

|

— |

|

(386) |

|

(1,972) |

|

— |

|

(2,358) |

Total comprehensive profit for the period ended March 31, 2024 |

|

— |

|

— |

|

(386) |

|

(1,972) |

|

30,192 |

|

27,834 |

Transactions with owners: |

|

|

|

|

|

|

|

|

|

|

|

|

Share-based payment |

|

— |

|

4,615 |

|

— |

|

— |

|

(2,987) |

|

1,628 |

Cash distribution |

|

— |

|

— |

|

— |

|

(7,520) |

|

— |

|

(7,520) |

Total transactions with owners for the period ended March 31, 2024 |

|

— |

|

4,615 |

|

— |

|

(7,520) |

|

(2,987) |

|

(5,892) |

Balance at March 31, 2024 (Unaudited) |

|

55 |

|

115,896 |

|

(10,348) |

|

35,624 |

|

56,735 |

|

197,962 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance at January 1, 2025 |

|

51 |

|

73,750 |

|

(11,590) |

|

15,053 |

|

126,027 |

|

203,291 |

Comprehensive income: |

|

|

|

|

|

|

|

|

|

|

|

|

Profit for the three-month period |

|

— |

|

— |

|

— |

|

— |

|

13,069 |

|

13,069 |

Other comprehensive profit for the period |

|

— |

|

— |

|

19 |

|

304 |

|

— |

|

323 |

Total comprehensive profit for the period ended March 31, 2025 |

|

— |

|

— |

|

19 |

|

304 |

|

13,069 |

|

13,392 |

Transactions with owners: |

|

|

|

|

|

|

|

|

|

|

|

|

Share-based payment |

|

— |

|

751 |

|

— |

|

— |

|

782 |

|

1,533 |

Cash distribution |

|

— |

|

— |

|

— |

|

— |

|

(7,525) |

|

(7,525) |

Total transactions with owners for the period ended March 31, 2025 |

|

— |

|

751 |

|

— |

|

— |

|

(6,743) |

|

(5,992) |

Balance at March 31, 2025 (Unaudited) |

|

51 |

|

74,501 |

|

(11,571) |

|

15,357 |

|

132,353 |

|

210,691 |

The above condensed consolidated statement of changes in equity should be read in conjunction with the accompanying notes.

6

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOW

|

|

Three-month |

|

Three-month |

|

|

period ended |

|

period ended |

|

|

March 31, 2025 |

|

March 31, 2024 |

Amounts in US$ '000 |

|

(Unaudited) |

|

(Unaudited) |

Cash flows from operating activities |

|

|

|

|

Profit for the period |

|

13,069 |

|

30,192 |

Adjustments for: |

|

|

|

|

Income tax expense |

|

12,447 |

|

44,873 |

Depreciation |

|

32,045 |

|

28,659 |

Loss on disposal of property, plant and equipment |

|

29 |

|

— |

Write-off of unsuccessful exploration efforts |

|

5,883 |

|

— |

Borrowings cancellation costs |

|

6,240 |

|

— |

Amortization of other long-term liabilities |

|

(23) |

|

(30) |

Accrual of borrowing interests |

|

11,767 |

|

7,747 |

Unwinding of long-term liabilities |

|

1,449 |

|

1,407 |

Accrual of share-based payment |

|

1,533 |

|

1,628 |

Foreign exchange loss (gain) |

|

3,288 |

|

(164) |

Income tax paid (a) |

|

(4,880) |

|

(6,917) |

Change in working capital (b) (c) |

|

(161,610) |

|

(19,774) |

Cash flows (used in) from operating activities – net |

|

(78,763) |

|

87,621 |

Cash flows from investing activities |

|

|

|

|

Purchase of property, plant and equipment |

|

(22,614) |

|

(48,807) |

Proceeds from divestment of long-term assets (d) |

|

15,939 |

|

2,158 |

Cash flows used in investing activities – net |

|

(6,675) |

|

(46,649) |

Cash flows from financing activities |

|

|

|

|

Proceeds from borrowings |

|

550,000 |

|

— |

Debt issuance costs paid |

|

(5,034) |

|

— |

Principal paid |

|

(405,333) |

|

— |

Interest paid |

|

(14,555) |

|

(13,750) |

Lease payments |

|

(1,489) |

|

(1,857) |

Repurchase of shares |

|

— |

|

— |

Cash distribution |

|

(7,525) |

|

(7,520) |

Cash flows from (used in) financing activities - net |

|

116,064 |

|

(23,127) |

Net increase in cash and cash equivalents |

|

30,626 |

|

17,845 |

Cash and cash equivalents at January 1 |

|

276,750 |

|

133,036 |

Currency translation differences |

|

617 |

|

(160) |

Cash and cash equivalents at the end of the period |

|

307,993 |

|

150,721 |

Ending Cash and cash equivalents are specified as follows: |

|

|

|

|

Cash at bank and bank deposits |

|

307,981 |

|

150,711 |

Cash in hand |

|

12 |

|

10 |

Cash and cash equivalents |

|

307,993 |

|

150,721 |

| (a) | Includes self-withholding taxes of US$ 4,880,000 and US$ 6,743,000 during the three-month periods ended March 31, 2025 and 2024, respectively. |

| (b) | Includes partial repayment of an advance payment drawn from the offtake and prepayment agreement with Vitol for US$ 132,769,000 during the three-month period ended March 31, 2025. See Note 30.1 to the annual consolidated financial statements as of and for the year ended December 31, 2024. |

| (c) | Includes withholding taxes from clients of US$ 4,536,000 and US$ 8,106,000 during the three-month periods ended March 31, 2025 and 2024, respectively. |

| (d) | Net cash received from the divestment of the Llanos 32 Block and the Manati gas field in Colombia and Brazil, respectively, in 2025, and the Chilean business in 2024. See Note 19 to these interim condensed consolidated financial statements and Note 35.3 to the annual consolidated financial statements as of and for the year ended December 31, 2024. |

The above condensed consolidated statement of cash flow should be read in conjunction with the accompanying notes.

7

EXPLANATORY NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 1

General information

GeoPark Limited (the “Company”) is a company incorporated under the laws of Bermuda. The Registered Office address is Clarendon House, 2 Church Street, Hamilton HM11, Bermuda.

The principal activity of the Company and its subsidiaries (the “Group” or “GeoPark”) is the exploration, development and production for oil and gas reserves in Latin America.

These interim condensed consolidated financial statements were authorized for issue by the Board of Directors on May 6, 2025.

Basis of Preparation

The interim condensed consolidated financial statements of GeoPark Limited are presented in accordance with IAS 34 “Interim Financial Reporting”. They do not include all of the information required for full annual financial statements and should be read in conjunction with the annual consolidated financial statements as of and for the year ended December 31, 2024, which have been prepared in accordance with IFRS.

The interim condensed consolidated financial statements have been prepared in accordance with the accounting policies applied in the most recent annual consolidated financial statements. The Group has not early adopted any standard, interpretation or amendment that has been issued but is not yet effective. The amendments and interpretations detailed in the annual consolidated financial statements as of and for the year ended December 31, 2024, that apply for the first time in 2025, do not have an impact on the interim condensed consolidated financial statements of the Group.

Whenever necessary, certain comparative amounts have been reclassified to conform to changes in presentation in the current period.

Taxes on income in the interim periods are accrued using the tax rate that would be applicable to expected total annual profit or loss.

The activities of the Group are not subject to significant seasonal changes.

Estimates

The preparation of interim financial information requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Group’s accounting policies. Actual results may differ from these estimates.

In preparing these interim condensed consolidated financial statements, the significant judgements made by management in applying the Group’s accounting policies and the key sources of estimation uncertainty were the same as those that applied to the annual consolidated financial statements as of and for the year ended December 31, 2024.

Financial risk management

The Group’s activities expose it to a variety of financial risks: currency risk, price risk, credit risk concentration, funding and liquidity risk, interest risk and capital risk. The interim condensed consolidated financial statements do not include all the financial risk management information and disclosures required in the annual consolidated financial statements and should be read in conjunction with the Group’s annual consolidated financial statements as of and for the year ended December 31, 2024.

8

Note 1 (Continued)

Financial risk management (Continued)

The Group is continually reviewing its exposure to the current market conditions and adjusting its capital expenditures program which remains flexible and quickly adaptable to different oil price scenarios. GeoPark also continues to add new oil hedges, increasing its price risk protection within the upcoming fifteen months.

The Group maintained a cash position of US$ 307,993,000 as of March 31, 2025. In addition, GeoPark has access to up to US$ 100,000,000 of committed funding from Trafigura (see Note 30.2 to the annual consolidated financial statements as of and for the year ended December 31, 2024), a US$ 100,000,000 senior unsecured credit agreement with Banco BTG Pactual S.A. and Banco Latinoamericano de Comercio Exterior S.A., and US$ 281,273,000 in uncommitted credit lines (including US$ 167,450,000 in Argentina). Additionally, GeoPark Argentina S.A., the Group’s Argentinian subsidiary, holds approval from the Argentinian securities regulator to issue up to US$ 500,000,000 in debt securities.

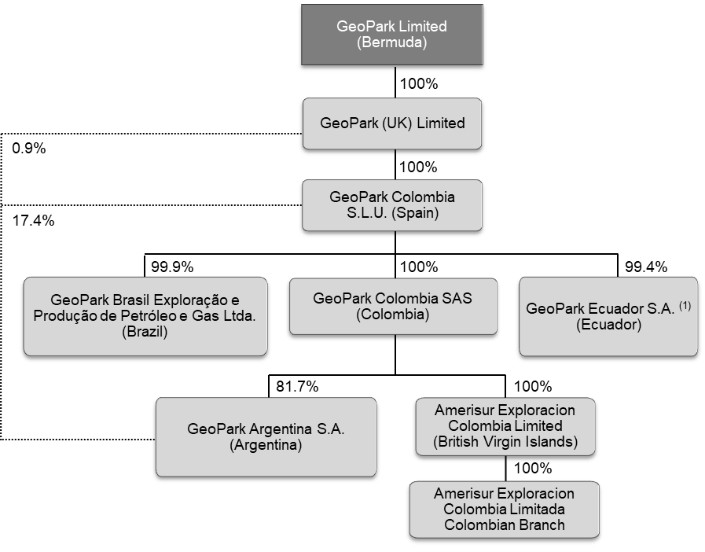

Subsidiary undertakings

The following chart illustrates the main companies of the Group structure as of March 31, 2025:

| (1) | GeoPark Ecuador S.A. holds 50% working interest in the consortiums that operate the Espejo and Perico Blocks. |

Details of the subsidiaries and joint operations of the Group are set out in Note 20 to the annual consolidated financial statements as of and for the year ended December 31, 2024.

During the three-month period ended March 31, 2025, the following changes took place:

| ● | On February 11, 2025, the Panamanian subsidiaries GPK Panama, S.A. and GPRK Holding Panama, S.A. finalized a merger process, with GPK Panama, S.A. being the surviving company. |

9

Note 2

Segment information

Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision-maker. The chief operating decision-maker, who is responsible for allocating resources and assessing performance of the operating segments, has been identified as the Executive Committee. This committee is integrated by the Chief Executive Officer, Chief Financial Officer, Chief Exploration and Development Officer, Chief Operating Officer, Chief Strategy, Sustainability and Legal Officer and Chief People Officer. This committee reviews the Group’s internal reporting to assess performance and allocate resources. Management has determined the operating segments based on these reports. The committee considers the business from a geographic perspective.

The Executive Committee assesses the performance of the operating segments based on a measure of Adjusted EBITDA. Adjusted EBITDA is defined as profit (loss) for the period (determined as if IFRS 16 Leases has not been adopted), before net finance results, income tax, depreciation, amortization, certain non-cash items such as impairments and write-offs of unsuccessful exploration efforts, accrual of share-based payment, unrealized result on commodity risk management contracts, geological and geophysical expenses allocated to capitalized projects, and other non-recurring events. Other information provided to the Executive Committee is measured in a manner consistent with that in the consolidated financial statements.

Three-month period ended March 31, 2025:

Amounts in US$ '000 |

|

Total |

|

Colombia |

|

Ecuador |

|

Brazil (a) |

|

Argentina |

|

Corporate |

Revenue |

|

137,349 |

|

129,869 |

|

7,061 |

|

— |

|

— |

|

419 |

Sale of crude oil |

|

137,145 |

|

130,084 |

|

7,061 |

|

— |

|

— |

|

— |

Sale of purchased crude oil |

|

419 |

|

— |

|

— |

|

— |

|

— |

|

419 |

Commodity risk management contracts designated as cash flow hedges |

|

(215) |

|

(215) |

|

— |

|

— |

|

— |

|

— |

Production and operating costs |

|

(35,437) |

|

(31,471) |

|

(2,644) |

|

(1,005) |

|

— |

|

(317) |

Royalties in cash |

|

(1,191) |

|

(1,191) |

|

— |

|

— |

|

— |

|

— |

Economic rights in cash |

|

(846) |

|

(846) |

|

— |

|

— |

|

— |

|

— |

Share-based payment |

|

(158) |

|

(132) |

|

(26) |

|

— |

|

— |

|

— |

Operating costs |

|

(33,242) |

|

(29,302) |

|

(2,618) |

|

(1,005) |

|

— |

|

(317) |

Depreciation |

|

(32,045) |

|

(29,692) |

|

(2,107) |

|

(246) |

|

— |

|

— |

Adjusted EBITDA |

|

87,944 |

|

88,389 |

|

3,393 |

|

(1,487) |

|

(1,241) |

|

(1,110) |

Three-month period ended March 31, 2024:

Amounts in US$ '000 |

|

Total |

|

Colombia |

|

Ecuador |

|

Brazil (a) |

|

Other (b) |

|

Corporate |

Revenue |

|

167,416 |

|

160,472 |

|

1,800 |

|

2,945 |

|

398 |

|

1,801 |

Sale of crude oil |

|

162,187 |

|

160,273 |

|

1,800 |

|

114 |

|

— |

|

— |

Sale of purchased crude oil |

|

1,801 |

|

— |

|

— |

|

— |

|

— |

|

1,801 |

Sale of gas |

|

3,513 |

|

284 |

|

— |

|

2,831 |

|

398 |

|

— |

Commodity risk management contracts designated as cash flow hedges |

|

(85) |

|

(85) |

|

— |

|

— |

|

— |

|

— |

Production and operating costs |

|

(38,540) |

|

(33,957) |

|

(1,212) |

|

(1,391) |

|

(437) |

|

(1,543) |

Royalties in cash |

|

(1,204) |

|

(966) |

|

— |

|

(226) |

|

(12) |

|

— |

Economic rights in cash |

|

(1,467) |

|

(1,467) |

|

— |

|

— |

|

— |

|

— |

Share-based payment |

|

(144) |

|

(143) |

|

(1) |

|

— |

|

— |

|

— |

Operating costs |

|

(35,725) |

|

(31,381) |

|

(1,211) |

|

(1,165) |

|

(425) |

|

(1,543) |

Depreciation |

|

(28,659) |

|

(27,680) |

|

(429) |

|

(544) |

|

(5) |

|

(1) |

Adjusted EBITDA |

|

111,543 |

|

113,405 |

|

(279) |

|

796 |

|

(696) |

|

(1,683) |

| (a) | Production in the Manati gas field, which is in process of divestment (see Note 19), was temporarily suspended since mid-March 2024 due to maintenance activities. |

| (b) | Includes Argentina and Chile segments. The Chilean business was divested in January 2024. |

10

Note 2 (Continued)

Segment information (Continued)

Total Assets |

|

Total |

|

Colombia |

|

Ecuador |

|

Brazil |

|

Argentina |

|

Corporate |

March 31, 2025 |

|

1,197,956 |

|

915,915 |

|

47,219 |

|

14,083 |

|

216,109 |

|

4,630 |

December 31, 2024 |

|

1,200,055 |

|

885,438 |

|

48,333 |

|

14,040 |

|

215,755 |

|

36,489 |

A reconciliation of total Adjusted EBITDA to total Profit before income tax is provided as follows:

|

|

Three-month |

|

Three-month |

|

|

period ended |

|

period ended |

|

|

March 31, 2025 |

|

March 31, 2024 |

Adjusted EBITDA |

|

87,944 |

|

111,543 |

Depreciation (a) |

|

(32,045) |

|

(28,659) |

Write-off of unsuccessful exploration efforts |

|

(5,883) |

|

— |

Share-based payment |

|

(1,533) |

|

(1,628) |

Lease accounting - IFRS 16 |

|

1,489 |

|

1,857 |

Others (b) |

|

444 |

|

842 |

Operating profit |

|

50,416 |

|

83,955 |

Financial expenses |

|

(24,836) |

|

(11,137) |

Financial income |

|

3,224 |

|

2,083 |

Foreign exchange (loss) gain |

|

(3,288) |

|

164 |

Profit before income tax |

|

25,516 |

|

75,065 |

Income tax expense |

|

(12,447) |

|

(44,873) |

Profit for the period |

|

13,069 |

|

30,192 |

| (a) | Net of capitalized costs for oil stock included in Inventories. |

| (b) | Includes allocation to capitalized projects. |

Note 3

Revenue

|

|

Three-month |

|

Three-month |

|

|

period ended |

|

period ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

March 31, 2024 |

Sale of crude oil |

|

137,145 |

|

162,187 |

Sale of purchased crude oil |

|

419 |

|

1,801 |

Sale of gas |

|

— |

|

3,513 |

Commodity risk management contracts designated as cash flow hedges (a) |

|

(215) |

|

(85) |

|

|

137,349 |

|

167,416 |

| (a) | Realized result on commodity risk management contracts designated as cash flow hedges. See Note 4. |

11

Note 4

Commodity risk management contracts

The Group has entered into derivative financial instruments to manage its exposure to oil price risk. These derivatives are zero-premium collars and were placed with major financial institutions and commodity traders. The Group entered into the derivatives under ISDA Master Agreements and Credit Support Annexes, which provide credit lines for collateral posting thus alleviating possible liquidity needs under the instruments and protect the Group from potential non-performance risk by its counterparties.

The Group’s derivatives are designated and qualify as cash flow hedges. The effective portion of changes in the fair values of these derivative contracts are recognized in Other Reserve within Equity. The gain or loss relating to the ineffective portion, if any, is recognized immediately as gains or losses in the results of the periods in which they occur. The amount accumulated in Other Reserves is reclassified to profit or loss as a reclassification adjustment in the same period or periods during which the hedged cash flows affect profit or loss as part of the Revenue line item in the Condensed Consolidated Statement of Income.

The following table summarizes the Group’s production hedged during the three-month period ended March 31, 2025, and for the following periods as a consequence of the derivative contracts in force as of March 31, 2025:

|

|

|

|

|

|

Volume |

|

Average |

Period |

|

Reference |

|

Type |

|

bbl/d |

|

price US$/bbl |

January 1, 2025 - March 31, 2025 |

|

ICE BRENT |

|

Zero Premium Collars |

|

19,500 |

|

69.79 Put 82.48 Call |

April 1, 2025 - June 30, 2025 |

|

ICE BRENT |

|

Zero Premium Collars |

|

19,000 |

|

69.26 Put 79.02 Call |

July 1, 2025 - September 30, 2025 |

|

ICE BRENT |

|

Zero Premium Collars |

|

17,500 |

|

68.69 Put 78.59 Call |

October 1, 2025 - December 31, 2025 |

|

ICE BRENT |

|

Zero Premium Collars |

|

16,000 |

|

68.25 Put 77.50 Call |

January 1, 2026 - March 31, 2026 |

|

ICE BRENT |

|

Zero Premium Collars |

|

1,000 |

|

68.00 Put 77.40 Call |

Note 5

Production and operating costs

|

|

Three-month |

|

Three-month |

|

|

period ended |

|

period ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

March 31, 2024 |

Staff costs |

|

3,375 |

|

3,496 |

Share-based payment |

|

158 |

|

144 |

Royalties in cash |

|

1,191 |

|

1,204 |

Economic rights in cash |

|

846 |

|

1,467 |

Well and facilities maintenance |

|

5,288 |

|

5,651 |

Operation and maintenance |

|

1,432 |

|

2,370 |

Consumables |

|

7,725 |

|

9,946 |

Equipment rental |

|

1,843 |

|

1,428 |

Transportation costs |

|

1,217 |

|

1,802 |

Field camp |

|

1,246 |

|

1,494 |

Safety and insurance costs |

|

671 |

|

940 |

Personnel transportation |

|

623 |

|

975 |

Consultant fees |

|

530 |

|

853 |

Gas plant costs |

|

359 |

|

543 |

Non-operated blocks costs |

|

5,791 |

|

4,993 |

Crude oil stock variation |

|

1,954 |

|

(1,056) |

Purchased crude oil |

|

317 |

|

1,543 |

Other costs |

|

871 |

|

747 |

|

|

35,437 |

|

38,540 |

12

Note 6

Geological and geophysical expenses

|

|

Three-month |

|

Three-month |

|

|

period ended |

|

period ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

March 31, 2024 |

Staff costs |

|

1,871 |

|

1,750 |

Share-based payment |

|

83 |

|

111 |

Allocation to capitalized project |

|

(335) |

|

(263) |

Other services |

|

834 |

|

1,140 |

|

|

2,453 |

|

2,738 |

Note 7

Administrative expenses

|

|

Three-month |

|

Three-month |

|

|

period ended |

|

period ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

March 31, 2024 |

Staff costs |

|

6,564 |

|

6,339 |

Share-based payment |

|

1,290 |

|

1,369 |

Consultant fees |

|

1,360 |

|

2,091 |

Safety and insurance costs |

|

775 |

|

819 |

Travel expenses |

|

89 |

|

373 |

Non-operated blocks expenses |

|

252 |

|

411 |

Director fees and allowance |

|

100 |

|

149 |

Communication and IT costs |

|

658 |

|

663 |

Allocation to joint operations |

|

(2,559) |

|

(3,105) |

Other administrative expenses |

|

527 |

|

854 |

|

|

9,056 |

|

9,963 |

Note 8

Selling expenses

|

|

Three-month |

|

Three-month |

|

|

period ended |

|

period ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

March 31, 2024 |

Staff costs |

|

124 |

|

116 |

Share-based payment |

|

2 |

|

4 |

Transportation (a) |

|

1,050 |

|

3,245 |

Selling taxes and other |

|

992 |

|

775 |

|

|

2,168 |

|

4,140 |

| (a) | The fluctuation in transportation costs is mainly attributed to deliveries at different sales points in the CPO-5 Block in Colombia. Sales at the wellhead incur no selling costs but yield lower revenue, while transportation expenses for sales to alternative delivery points are recognized as selling expenses. |

13

Note 9

Financial results

|

|

Three-month |

|

Three-month |

|

|

period ended |

|

period ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

March 31, 2024 |

Financial expenses |

|

|

|

|

Bank charges and other financial costs (a) |

|

(5,380) |

|

(1,983) |

Borrowings cancellation costs (b) |

|

(6,240) |

|

— |

Interest and amortization of debt issue costs |

|

(11,767) |

|

(7,747) |

Unwinding of long-term liabilities |

|

(1,449) |

|

(1,407) |

|

|

(24,836) |

|

(11,137) |

Financial income |

|

|

|

|

Interest received |

|

3,224 |

|

2,083 |

|

|

3,224 |

|

2,083 |

Foreign exchange gains and losses |

|

|

|

|

Foreign exchange (loss) gain |

|

(4,589) |

|

164 |

Unrealized result on currency risk management contracts (c) |

|

1,301 |

|

— |

|

|

(3,288) |

|

164 |

Total financial results |

|

(24,900) |

|

(8,890) |

| (a) | During the three-month period ended March 31, 2025, includes financial costs of US$ 1,415,000 associated with the advance payment drawn from the offtake and prepayment agreements with Vitol. See Note 16. |

| (b) | One-off non-cash charge related to the accelerated amortization of deferred issuance costs that were originally capitalized at the inception of the Notes due 2027 and were being amortized over its expected term. For further information on the partial repurchase of the Notes due 2027, see Note 14. |

| (c) | In November 2024, GeoPark entered into a derivative financial instrument (zero-premium collars) with a local bank in Colombia, for an amount equivalent to US$ 50,000,000, in order to anticipate any currency fluctuation with respect to a portion of the estimated income taxes to be paid in May and June 2025. |

Note 10

Income tax

The Group calculates income tax expense using the tax rate that would be applicable to the expected total annual earnings. The main components of income tax expense in the Condensed Consolidated Statement of Income are:

|

|

Three-month |

|

Three-month |

|

|

period ended |

|

period ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

March 31, 2024 |

Current income tax expense |

|

(27,984) |

|

(46,395) |

Deferred income tax benefit |

|

15,537 |

|

1,522 |

|

|

(12,447) |

|

(44,873) |

The effective tax rate was 49% and 60% for the three-month periods ended March 31, 2025 and 2024, respectively.

As of March 31, 2025 and 2024, the statutory income tax rate in Colombia was 35%, though a tax surcharge is also applicable, impacting companies engaged in the extraction of crude oil like GeoPark. The tax surcharge varies from zero to 15%, depending on different Brent oil prices. The Group currently estimates a tax surcharge of 5% for 2025, and therefore, the applicable statutory income tax rate in Colombia for 2025 would be 40%.

The Group’s consolidated effective tax rate of 49% for the three-month period ended March 31, 2025, which is higher than the statutory income tax rate in Colombia as noted above, was mainly driven by non-deductible tax losses in non-taxable jurisdictions, including a one-off non-cash charge related to the accelerated amortization of deferred issuance costs following the early extinguishment of a portion of the Notes due 2027. See Note 9.

14

Note 11

Property, plant and equipment

|

|

|

|

Furniture, |

|

|

|

|

|

|

|

Exploration |

|

|

|

|

|

|

equipment |

|

Production |

|

Buildings |

|

|

|

and |

|

|

|

|

Oil & gas |

|

and |

|

facilities and |

|

and |

|

Construction |

|

evaluation |

|

|

Amounts in US$ '000 |

|

properties |

|

vehicles |

|

machinery |

|

improvements |

|

in progress |

|

assets |

|

Total |

Cost at January 1, 2024 |

|

920,660 |

|

13,133 |

|

169,787 |

|

4,047 |

|

15,781 |

|

80,579 |

|

1,203,987 |

Additions |

|

1,603 |

(a) |

311 |

|

— |

|

— |

|

34,294 |

|

14,202 |

|

50,410 |

Transfers |

|

28,315 |

|

91 |

|

5,073 |

|

— |

|

(27,196) |

|

(6,283) |

|

— |

Currency translation differences |

|

(1,502) |

|

(20) |

|

(127) |

|

(4) |

|

— |

|

(10) |

|

(1,663) |

Cost at March 31, 2024 |

|

949,076 |

|

13,515 |

|

174,733 |

|

4,043 |

|

22,879 |

|

88,488 |

|

1,252,734 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cost at January 1, 2025 |

|

1,034,846 |

|

14,231 |

|

192,502 |

|

4,363 |

|

24,117 |

|

100,955 |

|

1,371,014 |

Additions |

|

327 |

(a) |

465 |

|

— |

|

4 |

|

12,499 |

|

9,646 |

|

22,941 |

Write-offs |

|

— |

|

— |

|

— |

|

— |

|

— |

|

(5,883) |

(b) |

(5,883) |

Transfers |

|

15,014 |

|

— |

|

11,501 |

|

— |

|

(26,388) |

|

(127) |

|

— |

Currency translation differences |

|

3,023 |

|

38 |

|

253 |

|

7 |

|

20 |

|

8 |

|

3,349 |

Disposals |

|

— |

|

(538) |

|

— |

|

(94) |

|

— |

|

— |

|

(632) |

Divestment of long-term assets (Note 19) |

|

(69,699) |

|

— |

|

(8,148) |

|

— |

|

(329) |

|

— |

|

(78,176) |

Cost at March 31, 2025 |

|

983,511 |

|

14,196 |

|

196,108 |

|

4,280 |

|

9,919 |

|

104,599 |

|

1,312,613 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation and write-down at January 1, 2024 |

|

(430,145) |

|

(10,467) |

|

(73,481) |

|

(3,070) |

|

— |

|

— |

|

(517,163) |

Depreciation |

|

(25,158) |

|

(381) |

|

(3,035) |

|

(45) |

|

— |

|

— |

|

(28,619) |

Currency translation differences |

|

1,357 |

|

19 |

|

119 |

|

3 |

|

— |

|

— |

|

1,498 |

Depreciation and write-down at March 31, 2024 |

|

(453,946) |

|

(10,829) |

|

(76,397) |

|

(3,112) |

|

— |

|

— |

|

(544,284) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation and write-down at January 1, 2025 |

|

(529,718) |

|

(11,809) |

|

(85,759) |

|

(3,237) |

|

— |

|

— |

|

(630,523) |

Depreciation |

|

(26,598) |

|

(386) |

|

(3,363) |

|

(63) |

|

— |

|

— |

|

(30,410) |

Currency translation differences |

|

(2,665) |

|

(37) |

|

(235) |

|

(7) |

|

— |

|

— |

|

(2,944) |

Disposals |

|

— |

|

509 |

|

— |

|

94 |

|

— |

|

— |

|

603 |

Divestment of long-term assets (Note 19) |

|

52,523 |

|

— |

|

7,498 |

|

— |

|

— |

|

— |

|

60,021 |

Depreciation and write-down at March 31, 2025 |

|

(506,458) |

|

(11,723) |

|

(81,859) |

|

(3,213) |

|

— |

|

— |

|

(603,253) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Carrying amount at March 31, 2024 |

|

495,130 |

|

2,686 |

|

98,336 |

|

931 |

|

22,879 |

|

88,488 |

|

708,450 |

Carrying amount at March 31, 2025 |

|

477,053 |

|

2,473 |

|

114,249 |

|

1,067 |

|

9,919 |

|

104,599 |

|

709,360 |

| (a) | Corresponds to the effect of the change in the estimate of asset retirement obligations. |

| (b) | Corresponds to one exploration well drilled in the PUT-8 Block in Colombia. |

15

Note 12

Prepayments and other receivables

|

|

At |

|

Year ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

December 31, 2024 |

V.A.T. |

|

4,010 |

|

3,734 |

Income tax payments in advance |

|

2,671 |

|

1,112 |

Other prepaid taxes |

|

326 |

|

227 |

To be recovered from co-venturers |

|

9,017 |

|

9,740 |

Prepayments and other receivables |

|

15,884 |

|

13,484 |

Advance payment for business transaction in Argentina (a) |

|

54,084 |

|

54,084 |

|

|

85,992 |

|

82,381 |

Classified as follows: |

|

|

|

|

Current |

|

82,357 |

|

79,731 |

Non-current |

|

3,635 |

|

2,650 |

|

|

85,992 |

|

82,381 |

| (a) | This advance payment was composed of US$ 38,000,000 for the acquisition of working interests in four unconventional blocks and US$ 16,084,000 for the acquisition of midstream capacity. See Note 35.1 to the annual consolidated financial statements as of and for the year ended December 31, 2024. |

Note 13

Equity

Share capital

|

|

At |

|

Year ended |

Issued share capital |

|

March 31, 2025 |

|

December 31, 2024 |

Common stock (US$ '000) |

|

51 |

|

51 |

The share capital is distributed as follows: |

|

|

|

|

Common shares, of nominal US$ 0.001 |

|

51,317,816 |

|

51,247,287 |

Total common shares in issue |

|

51,317,816 |

|

51,247,287 |

|

|

|

|

|

Authorized share capital |

|

|

|

|

US$ per share |

|

0.001 |

|

0.001 |

|

|

|

|

|

Number of common shares (US$ 0.001 each) |

|

5,171,949,000 |

|

5,171,949,000 |

Amount in US$ |

|

5,171,949 |

|

5,171,949 |

GeoPark’s share capital only consists of common shares. The authorized share capital consists of 5,171,949,000 common shares, par value US$ 0.001 per share. All of the Company’s issued and outstanding common shares are fully paid and nonassessable.

Cash distributions

In March 2025, the Company’s Board of Directors declared cash dividends of US$ 0.147 per share which were paid on March 31, 2025.

16

Note 13 (Continued)

Equity (Continued)

Other reserves

GeoPark applies hedge accounting for the derivative financial instruments entered to manage its exposure to oil price risk. Consequently, the Group’s derivatives are designated and qualify as cash flow hedges and, therefore, the effective portion of changes in the fair values of these derivative contracts and the income tax relating to those results are recognized in Other Reserve within Equity. The amount accumulated in Other Reserves is reclassified to profit or loss as a reclassification adjustment in the same period or periods during which the hedged cash flows affect profit or loss. During the three-month period ended March 31, 2025, a realized loss of US$ 215,000 on commodity risk management contracts was reclassified to the Condensed Consolidated Statement of Income.

Note 14

Borrowings

The outstanding amounts are as follows:

|

|

At |

|

Year ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

December 31, 2024 |

Notes due 2030 |

|

553,123 |

|

— |

Notes due 2027 |

|

94,400 |

|

504,535 |

Promissory note |

|

9,905 |

|

9,798 |

|

|

657,428 |

|

514,333 |

Classified as follows:

Current |

|

18,996 |

|

22,326 |

Non-Current |

|

638,432 |

|

492,007 |

On January 31, 2025, the Company successfully placed an aggregate principal amount of US$ 550,000,000 senior notes (the “Notes due 2030”) which were offered in a private placement to qualified institutional buyers in accordance with Rule 144A under the Securities Act of 1933, as amended (the “Securities Act”), and outside the United States to non U.S. persons in accordance with Regulation S under the Securities Act. The Notes due 2030 are fully and unconditionally guaranteed jointly and severally by GeoPark Colombia S.L.U., GeoPark Colombia S.A.S., and GeoPark Argentina S.A. The Notes due 2030 were priced at 100% and carry a coupon of 8.75% per annum (yield 8.75% per annum). The debt issuance cost for this transaction amounted to US$ 5,034,000 (debt issuance effective rate: 8.98%). Final maturity of the Notes due 2030 will be January 31, 2030.

The indenture governing the Notes due 2030 includes incurrence test covenants that provide among other things, that, the Net Debt to Adjusted EBITDA ratio should not exceed 3.5 times and the Adjusted EBITDA to Interest ratio should exceed 2.5 times. Failure to comply with the incurrence test covenants does not trigger an event of default. However, this situation may limit the Company’s capacity to incur additional indebtedness, as specified in the indenture governing the Notes due 2030. Incurrence covenants as opposed to maintenance covenants must be tested by the Company before incurring additional debt or performing certain corporate actions including but not limited to dividend payments, restricted payments and others.

The net proceeds from the Notes due 2030 were used by the Company to repurchase part of its Notes due 2027 for a nominal amount of US$ 405,333,000 through a concurrent tender offer, to repay up to US$ 152,000,000 of outstanding prepayments due under an offtake and prepayment agreement with Vitol (see Notes 29 and 30 to the annual consolidated financial statements as of and for the year ended December 31, 2024) and, the remainder for general corporate purposes, including capital expenditures.

17

Note 15

Provisions and other long-term liabilities

The outstanding amounts are as follows:

|

|

At |

|

Year ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

December 31, 2024 |

Assets retirement obligation (a) |

|

9,738 |

|

20,887 |

Deferred income |

|

547 |

|

603 |

Other (a) |

|

11,580 |

|

10,462 |

|

|

21,865 |

|

31,952 |

| (a) | The liabilities associated with the Manati gas field for US$ 12,832,000 were classified as held for sale. See Note 19. |

Note 16

Trade and other payables

The outstanding amounts are as follows:

|

|

At |

|

Year ended |

Amounts in US$ '000 |

|

March 31, 2025 |

|

December 31, 2024 |

Trade payables |

|

69,710 |

|

93,435 |

To be paid to co-venturers |

|

790 |

|

1,829 |

Customer advance payments (a) |

|

19,231 |

|

152,000 |

Other short-term advance payments (b) |

|

500 |

|

— |

Outstanding commitments in Chile (c) |

|

— |

|

3,320 |

Staff costs to be paid |

|

14,438 |

|

11,563 |

Royalties to be paid |

|

688 |

|

723 |

V.A.T. |

|

248 |

|

8,842 |

Taxes and other debts to be paid |

|

5,343 |

|

8,237 |

|

|

110,948 |

|

279,949 |

Classified as follows:

Current |

|

110,948 |

|

279,949 |

Non-Current |

|

— |

|

— |

| (a) | Advance payment of US$ 152,000,000 under the offtake and prepayment agreement with Vitol drawn in November 2024. See Note 30.1 to the annual consolidated financial statements as of and for the year ended December 31, 2024. Between February and March 2025, GeoPark repaid US$ 126,370,000 in cash and US$ 6,399,000 in kind from that amount and, as of March 31, 2025, US$ 19,231,000 remained outstanding. |

| (b) | Advance payment collected in relation with the divestment of the Manati gas field in Brazil. See Note 19. |

| (c) | Investment commitments in the Campanario and Isla Norte Blocks as a result of the divestment of the Chilean business. See Note 35.3 to the annual consolidated financial statements as of and for the year ended December 31, 2024. |

18

Note 17

Fair value measurement of financial instruments

Fair value hierarchy

The following table presents the Group’s financial assets and financial liabilities measured and recognized at fair value as of March 31, 2025, and December 31, 2024, on a recurring basis:

|

|

|

|

|

|

As of |

Amounts in US$ '000 |

|

Level 1 |

|

Level 2 |

|

March 31, 2025 |

Assets |

|

|

|

|

|

|

Derivative financial instrument assets |

|

|

|

|

|

|

Commodity risk management contracts |

|

— |

|

4,404 |

|

4,404 |

Total Assets |

|

— |

|

4,404 |

|

4,404 |

|

|

|

|

|

|

As of |

Amounts in US$ '000 |

|

Level 1 |

|

Level 2 |

|

December 31, 2024 |

Assets |

|

|

|

|

|

|

Derivative financial instrument assets |

|

|

|

|

|

|

Commodity risk management contracts |

|

— |

|

2,764 |

|

2,764 |

Total Assets |

|

— |

|

2,764 |

|

2,764 |

Liabilities |

|

|

|

|

|

|

Derivative financial instrument liabilities |

|

|

|

|

|

|

Commodity risk management contracts |

|

— |

|

464 |

|

464 |

Total Liabilities |

|

— |

|

464 |

|

464 |

There were no transfers between Level 2 and 3 during the period. The Group did not measure any financial assets or financial liabilities at fair value on a non-recurring basis as of March 31, 2025.

Fair values of other financial instruments (unrecognized)

The Group also has a number of financial instruments which are not measured at fair value in the balance sheet. For the majority of these instruments, the fair values are not materially different to their carrying amounts, since the interest receivable/payable is either close to current market rates or the instruments are short-term in nature.

Borrowings are comprised of fixed rate debt and are measured at their amortized cost. The Group estimates that the fair value of its financial liabilities is approximately 94.9% of its carrying amount, including interest accrued as of March 31, 2025. Fair value was calculated based on market price for the Notes and is within Level 1 of the fair value hierarchy.

19

Note 18

Capital commitments

Capital commitments are detailed in Note 33.2 to the annual consolidated financial statements as of December 31, 2024. The following updates have taken place during the three-month period ended March 31, 2025:

The Group incurred investments of US$ 6,397,000 to fulfill its commitments, at GeoPark’s working interest.

Colombia

Two of the three committed exploratory wells were drilled in the PUT-8 Block.

Chile

Total investments needed to fulfill the commitments in the Campanario and Isla Norte Blocks have already been completed. Final approval of the Ministry of Energy and the subsequent release of guarantees are pending.

Note 19

Business transactions

Divestment of non-operated working interest in the Llanos 32 Block in Colombia

On March 14, 2025, GeoPark agreed to transfer, subject to regulatory approval, its non-operated working interest in the Llanos 32 Block in Colombia to its joint operation partner for a total consideration of US$ 19,000,000, minus working capital adjustment of US$ 3,660,000. As of the date of these interim condensed consolidated financial statements, GeoPark has received the net proceeds from the transaction, which are subject to final settlement.

Divestment of non-operated working interest in the Manati gas field in Brazil

On March 27, 2025, GeoPark entered into an agreement to sell its 10% non-operated working interest in the Manati gas field in Brazil for a total consideration of US$ 1,000,000, subject to working capital adjustment, plus a contingent payment of an additional US$ 1,000,000, subject to the field’s future cash flow or its potential conversion into a natural gas storage facility. As of the date of these interim condensed consolidated financial statements, GeoPark has collected an advance payment of US$ 500,000. Closing of the transaction is pending customary regulatory approvals.

As of March 31, 2025, the amount of Property, plant and equipment and Right-of-use assets corresponding to the Manati gas field and the liabilities associated to it have been classified as held for sale for US$ 6,227,000 and US$ 12,832,000, respectively.

Note 20

Cost efficiency measures

In March 2025, the Group implemented cost efficiency measures which include the immediate reduction of the workforce. These measures were undertaken to enhance cost efficiency and better align the organizational structure with the Group’s strategic objectives and operational challenges. In connection with these measures, the Group incurred termination costs of approximately US$ 1,550,000, which were charged to the ‘Other income (expenses), net’ line item in the Condensed Consolidated Statement of Income.

20

Note 21

Subsequent events

Oil price volatility

Beginning in early April 2025, international crude oil prices experienced a significant decline, driven by a combination of geopolitical tensions and macroeconomic concerns. As of March 31, 2025, the Brent crude oil price was approximately US$ 74 per barrel. However, during the first week of April, Brent fell by more than 20%, reaching levels below US$ 60 per barrel, the lowest level since mid-2021. Following this initial decline, oil prices partially recovered, and during the second half of April, Brent fluctuated between US$ 60 and US$ 68 per barrel.

This abrupt downturn was primarily triggered by escalating trade tensions between the United States and major global trading partners, notably China, following the U.S. administration’s announcement of increased import tariffs. These actions intensified concerns about a potential global economic slowdown, thereby weakening the outlook for oil demand. Concurrently, certain OPEC+ members unexpectedly increased production in early April, further exacerbating the downward pressure on international crude oil benchmarks.

The Group is actively monitoring the recent volatility in international crude oil prices and its potential implications on the business. While the ultimate impact of these developments cannot be determined at this stage, the Group has included a sensitivity analysis in Note 36 to its annual consolidated financial statements as of and for the year ended December 31, 2024, that illustrates its approach to assessing the potential effects of changes in key macroeconomic assumptions on the recoverable value of its assets.

Currency risk management contracts

In April 2025, GeoPark entered into new derivative financial instruments (zero-premium collars) with local banks in Colombia, for a notional amount of US$ 30,000,000 (allocated at US$ 5,000,000 per month during the second half of 2025). The objective of these instruments is to mitigate potential currency fluctuations and protect the Group’s exposure to the Colombian Peso arising from its regular business operations.

Appointment of new Chief Executive Officer

On April 24, 2025, GeoPark announced the appointment of Felipe Bayon as its new Chief Executive Officer (“CEO”) and a member of the Board of Directors, effective June 1, 2025.

Mr. Bayon is recognized as one of the most effective energy executives in Latin America with more than three decades of accomplishments in the international oil and gas industry. From 2017 to 2023, Mr. Bayon was CEO of Ecopetrol, one of the most important energy groups in Latin America, where he led 18,000 employees, oversaw production of approximately 700,000 boepd and revenues of over US$ 30 billion, and delivered record financial, operational, and safety results. He is a proven and disciplined dealmaker who brought Ecopetrol into the unconventional Permian Basin in the U.S. in partnership with Oxy, a project that grew from 0 to ca. 150,000 bpd gross in 4 years, into the Brazilian ultra-deep water pre-salt play in partnership with Shell, as well as into a leading position in the Latin American power transmission sector and focused investments in renewable energies, water management, and nature-based climate solutions.

Mr. Bayon is a mechanical engineer who began his career in 1991 with Shell in field operations and projects and then moved to BP where he worked for 21 years in increasingly important operational and management roles in Colombia, Argentina, Brazil, Bolivia, the U.S. and the U.K., including his tenure as CEO of Pan American Energy, one of the leading private hydrocarbon producers in Argentina, from 2005 to 2010. Mr. Bayon has served on multiple Boards of Directors across the energy, utilities, education, and technology sectors.

21

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

GeoPark Limited |

|

|

|

|

|

|

|

|

|

|

|

By: |

/s/ Jaime Caballero Uribe . |

|

|

Name: Jaime Caballero Uribe |

|

|

Title: Chief Financial Officer |

Date: May 7, 2025

22