UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of Earliest Event Reported): April 24, 2025

HarborOne Bancorp, Inc.

(Exact Name of Registrant as Specified in its Charter)

Massachusetts |

001-38955 |

81-1607465 |

(State or other jurisdiction |

(Commission |

(IRS Employer |

of incorporation) |

File Number) |

Identification Number |

770 Oak Street, Brockton, Massachusetts 02301

(Address of principal executive offices)

(508) 895-1000

(Registrant’s telephone number, including area code)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☐Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

☐Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

☐Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

☐Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Title of each Class |

Trading Symbol |

Name of each exchange on which registered |

Common Stock, $0.01 par value |

HONE |

The NASDAQ Stock Market, LLC |

Item 2.02 |

Results of Operations and Financial Condition |

On April 24, 2025, HarborOne Bancorp, Inc. (the “Company”), the holding company for HarborOne Bank, issued a press release announcing its financial results for the quarter ended March 31, 2025. The Company’s press release is included as Exhibit 99.1 to this report.

The information set forth in this Item 2.02 and in the attached Exhibit 99.1 is deemed to be “furnished” and shall not be deemed to be “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that Section.

Item 7.01 |

Regulation FD Disclosure |

The Company has prepared an investor presentation about the Company’s operations and performance that management intends to use from time to time on and after April 24, 2025. The investor presentation is attached as Exhibit 99.2 to this report.

The information set forth in this Item 7.01 and in the attached Exhibit 99.2 shall not be deemed “filed” for purposes of Section 18 of the Exchange Act, or otherwise subject to the liabilities under that Section.

Item 9.01Financial Statements and Exhibits

(d)Exhibits

Number |

|

Description |

|

|

|

99.1 |

|

|

99.2 |

|

|

104 |

|

Cover Page Interactive Data File (formatted as inline XBRL) |

EXHIBIT INDEX

Number |

|

Description |

|

|

|

99.1 |

|

|

99.2 |

|

|

104 |

|

Cover Page Interactive Data File (formatted as inline XBRL) |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunder duly authorized.

|

HARBORONE BANCORP, INC. |

||

|

|

||

By: |

/s/ Joseph F. Casey |

|

|

|

Name: |

Joseph F. Casey |

|

|

Title: |

President and |

|

|

|

Chief Executive Officer |

|

|

|

|

|

Date: April 24, 2025 |

|

|

|

Exhibit 99.1

HarborOne Bancorp, Inc. Announces 2025 First Quarter Results

Contact: Stephen W. Finocchio, EVP and CFO

Brockton, Massachusetts (April 24, 2025): HarborOne Bancorp, Inc. (the “Company” or “HarborOne”) (NASDAQ: HONE), the holding company for HarborOne Bank (the “Bank”), announced net income of $5.5 million, or $0.14 per diluted share, for the quarter ended March 31, 2025, a decrease of $3.4 million, or 38.1%, compared to net income of $8.9 million, or $0.21 per diluted share, for the quarter ended December 31, 2024.

First Quarter Financial Highlights:

| ● | Net income of $5.5 million, or $0.14 per diluted share; the quarter-over-quarter decrease primarily reflects a $2.9 million decrease in mortgage banking income |

| ● | Net interest margin of 2.39%, up 3 basis-points on a quarter-over-quarter basis |

| ● | Noninterest expense was flat at $32.9 million |

| ● | Deposits, excluding brokered deposits, increased $79.6 million, or 1.9%, quarter-over-quarter |

| ● | The loans-to-deposits ratio improved 225 basis points during the quarter, from 106.63% to 104.38% |

| ● | Credit loss provision of $1.4 million, a $542,000 decrease compared to the fourth quarter of 2024 |

| ● | The quarterly dividend increased 12.5%; executed 513,855 in share repurchases |

“The first quarter represents a solid start to the year,” commented Joseph F. Casey, President & CEO. “Our Bank team achieved continued strong commercial and industrial loan growth of $33 million, decreased commercial real estate balances, lower loan delinquencies, and a reduction of 15 basis points in the cost of deposits, excluding brokered deposits. Our residential mortgage team delivered an 11.8% increase in year-over-year loan closings during the slowest quarter seasonally for that business, against a backdrop of elevated mortgage rates.”

Net Interest Income

Quarter-over-quarter, net interest and dividend income declined $358,000 from $31.8 million to $31.5 million, while net interest margin improved 3 basis points to 2.39%, impacted by:

| ● | Yield on loans declined 8 basis points as floating-rate assets repriced during the quarter, and average loan balances decreased $30.0 million. Yield on loans was also negatively impacted by a decline in prepayment fees of $277,000. |

| ● | Cost of deposits, excluding brokered deposits, decreased 15 basis points, and average deposit balances, excluding brokered deposits, decreased $33.2 million, primarily due to seasonal decreases in savings and DDA accounts in the first two months of the quarter that were largely recovered in March. |

| ● | Borrowing costs improved 6 basis points, and average borrowings declined $20.0 million. |

Noninterest Income

Quarter-over-quarter, total noninterest income decreased $3.8 million, or 27.7%, to $9.9 million, from $13.7 million, Total noninterest expense was flat at $32.9 million; quarter-over-quarter variances of note were:

1

impacted by:

| ● | HarborOne Mortgage, LLC (“HarborOne Mortgage”) realized a $2.7 million gain on loan sales from mortgage closings of $114.1 million in the first quarter of 2025, compared to $4.0 million from mortgage loan closings of $179.1 million in the fourth quarter, as an uptick in mortgage rates, and low for-sale inventory constrained loan demand. |

| ● | The mortgage servicing rights (“MSR”) valuation decreased $1.2 million compared to an increase of $2.3 million for the fourth quarter of 2024, including the impact of principal payments on the underlying mortgages of $782,000 and $1.0 million for the quarters ended March 31, 2025 and December 31, 2024, respectively. The first quarter MSR valuation loss of $1.1 million was offset by a $561,000 economic hedging gain, whereas the fourth quarter of 2024 included a MSR valuation gain of $2.2 million offset by a $1.3 million hedging loss. |

| ● | Deposit account fees decreased $871,000, primarily as a result of a decrease in debit card interchange fees of $493,000 due to a catch-up adjustment in the fourth quarter for the annual VISA volume incentive, and a $181,000 seasonal decrease in debit card interchange income. |

Noninterest Expense

| ● | Occupancy and equipment expense increased $150,000 primarily due to seasonal increases for snow removal and heating costs. |

| ● | Loan expenses decreased $94,000, consistent with lower loan originations in the first quarter of 2025. |

| ● | Deposit insurance decreased $113,000, reflecting a decrease in the assessment base. |

| ● | Other expenses increased $183,000, primarily reflecting an increase in cloud computing expenses as we continue to evolve our technology stack and fees charged for FHLB letters of credit to secure municipal deposits. |

Balance Sheet

Quarter-over-quarter, total assets decreased $52.8 million, or 0.9%, to $5.70 billion, from $5.75 billion, impacted by:

| ● | Loans declined $31.5 million, or 0.7%, to $4.82 billion, from $4.85 billion the prior quarter. Commercial real estate and construction loans decreased $44.5 million, favoring payoffs over renewals for loans secured by commercial real estate that are not included in our strongest customer relationships. Commercial and industrial loans increased $33.0 million. Residential real estate and consumer loans decreased $20.0 million, partly reflecting a decrease in loan purchases from HarborOne Mortgage during the quarter. |

| ● | Available-for-sale securities increased $1.7 million to $265.6 million from the prior quarter. The unrealized loss on securities available for sale decreased to $58.8 million, as compared to $65.2 million in the prior quarter. Securities held to maturity were steady at $19.2 million. |

| ● | Total deposits increased $68.0 million to $4.62 billion from $4.55 billion the prior quarter. Non-certificate accounts increased $73.2 million and term certificate accounts increased $6.4 million. Brokered deposits decreased $11.6 million. As of March 31, 2025, FDIC-insured deposits were approximately 74% of total deposits, including Bank subsidiary deposits. |

2

| ● | Borrowed funds decreased $117.0 million to $399.5 million compared to $516.6 million at the prior quarter end. As of March 31, 2025, the Bank had $1.42 billion in available borrowing capacity across multiple relationships. |

| ● | Total stockholders’ equity was $576.0 million, compared to $575.0 million at the prior quarter end. Stockholders’ equity increased 0.2% when compared to the prior quarter, as net income and an increase in the fair value of available-for-sale securities were partially offset by share repurchases and dividend payments. |

| ● | The tangible-common-equity-to-tangible-assets ratio(1) was 9.15% at March 31, 2025, compared to 9.05% at December 31, 2024. Book value per share and tangible book value per share(1) increased modestly quarter over quarter from $13.15 to $13.27 and from $11.78 to $11.90, respectively. |

(1) Non-GAAP financial measure. Refer to the Reconciliation of Non-GAAP Financial Measures.

Asset Quality and Allowance for Credit Losses

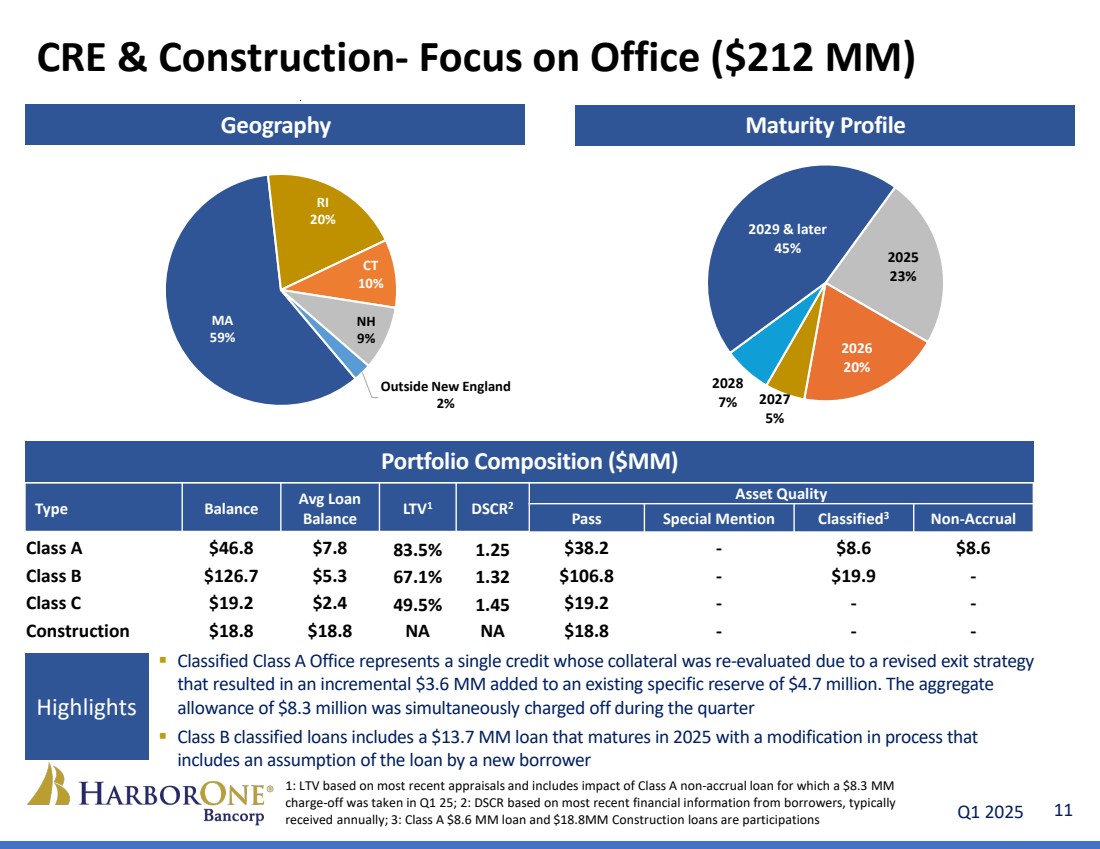

The Company recorded a $1.4 million provision for credit losses for the quarter ended March 31, 2025. The provision for loan credit losses was $1.9 million and the provision for unfunded commitments was a negative $506,000. The provision for loan credit losses was primarily due to a further specific reserve allocation for a previously identified classified commercial real estate loan, partially offset by a decrease in loan balances and qualitative factor adjustments. The specific reserve allocation recorded on the commercial real estate loan noted above was $3.6 million based on the re-evaluation of collateral due to a revised exit strategy, adding to a specific reserve allocation of $4.7 million. The aggregate allowance of $8.3 million was charged off in the first quarter of 2025. Net charge-offs totaled $8.7 million, or 0.72% of average loans outstanding on an annualized basis for the quarter ended March 31, 2025. For the quarter ended December 31, 2024, the Company had recorded a provision for credit losses of $1.9 million, reflecting a further specific reserve allocation for a previously identified classified commercial real estate loan, partially offset by qualitative factor adjustments, and a decrease in loan balance. Net charge-offs totaled $58,000 for the quarter ended December 31, 2024.

The ACL on loans was $49.3 million, or 1.02% of total loans, at March 31, 2025, compared to $56.1 million, or 1.16% of total loans, at December 31, 2024. The ACL on unfunded commitments, included in other liabilities on the unaudited Consolidated Balance Sheet, amounted to $3.0 million at March 31, 2025, compared to $3.5 million at December 31, 2024. Total nonperforming assets were $30.9 million and 0.54% of total assets at March 31, 2025, compared to $29.5 million and 0.51% of total assets at December 31, 2024. As of March 31, 2025 and December 31, 2024, total criticized and classified commercial loans amounted to $187.1 million and $178.6 million, respectively. The quarterly increase in total criticized and classified commercial loans primarily reflects the addition of three new credits in the special mention category as a result of continued pressure on commercial real estate values, offset by the charge-off noted above. In the quarter ended March 31, 2025, non-performing commercial real estate loans decreased $7.8 million, primarily a result of the charge-off noted above. Non-performing commercial and industrial loans increased $8.3 million, primarily the result of a single credit included in the healthcare segment.

About HarborOne Bancorp, Inc.

HarborOne Bancorp, Inc. is the holding company for HarborOne Bank, a Massachusetts-chartered trust company. HarborOne Bank serves the financial needs of consumers, businesses, and municipalities throughout Eastern Massachusetts and Rhode Island through a network of 30 full-service banking centers located in Massachusetts and Rhode Island, and commercial lending offices in Boston, Massachusetts and Providence, Rhode Island. HarborOne Bank also provides a range of educational resources through “HarborOne U,” with free digital content, webinars, and recordings for small business and personal financial education. HarborOne Mortgage, LLC, a subsidiary of HarborOne Bank, provides mortgage lending services throughout New England and other states.

3

Forward Looking Statements

Certain statements herein constitute forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Exchange Act and are intended to be covered by the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. We may also make forward-looking statements in other documents we file with the Securities and Exchange Commission (“SEC”), in our annual reports to shareholders, in press releases and other written materials, and in oral statements made by our officers, directors or employees. Such statements may be identified by words such as “believes,” “will,” “would,” “expects,” “project,” “may,” “could,” “developments,” “strategic,” “launching,” “opportunities,” “anticipates,” “estimates,” “intends,” “plans,” “targets” and similar expressions. These statements are based upon the current beliefs and expectations of the Company’s management and are subject to significant risks and uncertainties. Actual results may differ materially from those set forth in the forward-looking statements as a result of numerous factors. Factors that could cause such differences to exist include, but are not limited to, changes in general business and economic conditions (including, the impact of recently imposed tariffs by the U.S. Administration and foreign governments, inflation and concerns about liquidity) on a national basis and in the local markets in which the Company operates, including changes that adversely affect borrowers’ ability to service and repay the Company’s loans; changes in interest rates; changes in customer behavior; ongoing turbulence in the capital and debt markets and the impact of such conditions on the Company’s business activities; increases in loan default and charge-off rates; decreases in the value of securities in the Company’s investment portfolio; fluctuations in real estate values; the possibility that future credit losses may be higher than currently expected due to changes in economic assumptions, customer behavior or adverse economic developments; the adequacy of loan loss reserves; decreases in deposit levels necessitating increased borrowing to fund loans and investments; competitive pressures from other financial institutions; cybersecurity incidents, fraud, natural disasters, war, terrorism, civil unrest, and future pandemics; changes in regulation; changes in accounting standards and practices; the risk that goodwill and intangibles recorded in the Company’s financial statements will become impaired; demand for loans in the Company’s market area; the Company’s ability to attract and maintain deposits; risks related to the implementation of acquisitions, dispositions, and restructurings; the risk that the Company may not be successful in the implementation of its business strategy; changes in assumptions used in making such forward-looking statements and the risk factors described in the Annual Report on Form 10-K and Quarterly Reports on Form 10-Q as filed with the SEC, which are available at the SEC’s website, www.sec.gov. Should one or more of these risks materialize or should underlying beliefs or assumptions prove incorrect, HarborOne’s actual results could differ materially from those discussed. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this release. The Company disclaims any obligation to publicly update or revise any forward-looking statements to reflect changes in underlying assumptions or factors, new information, future events or other changes, except as required by law.

Use of Non-GAAP Measures

In addition to results presented in accordance with generally accepted accounting principles (“GAAP”), this press release contains certain non-GAAP financial measures including: “core net income,” “core earnings per common share,” “core return on average earning assets,” “core return on average earning equity,” “efficiency ratio,” “core efficiency ratio,” “tax equivalent efficiency ratio,” “tax equivalent core efficiency ratio,” “total adjusted noninterest expense”, “core noninterest expense,” “tax equivalent net interest and dividend income,” “total core noninterest income,” “tax equivalent total core revenue,” “tangible common equity,” “average tangible common equity,” “tangible assets,” “tangible book value per share,” “tangible common equity to tangible assets,” “return on average tangible common equity,” “core return on average tangible common equity” and certain ratios derived from these measures. Non-GAAP measures are utilized by management, regulators and market analysts to evaluate the Company’s financial position and therefore such information is useful to investors.

4

The tax equivalent basis adjusts for the tax-favored status from certain loans held by the Bank that are not taxable for federal income tax purposes.

Core net income, core noninterest income and core noninterest expense exclude certain items that management does not consider indicative of ongoing financial performance or enhances comparability of results with prior periods. These adjustments include gain or loss on the sale of certain assets and release of reserves for uncertain tax positions.

These disclosures should not be viewed as a substitute for financial results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures which may be presented by other companies. Because non-GAAP financial measures are not standardized, it may not be possible to compare these financial measures with other companies’ non-GAAP financial measures having the same or similar names.

5

HarborOne Bancorp, Inc.

Selected Financial Highlights

(Unaudited)

|

|

For the Quarters Ended |

|

|||||||||||||

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|

|||||

|

|

2025 |

|

2024 |

|

2024 |

|

2024 |

|

2024 |

|

|||||

|

|

(Dollars in thousands) |

||||||||||||||

Earnings data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest and dividend income |

|

$ |

31,469 |

|

$ |

31,827 |

|

$ |

31,893 |

|

$ |

31,350 |

|

$ |

30,582 |

|

Noninterest income |

|

$ |

9,891 |

|

$ |

13,689 |

|

$ |

10,568 |

|

$ |

11,919 |

|

$ |

10,741 |

|

Total revenue |

|

$ |

41,360 |

|

$ |

45,516 |

|

$ |

42,461 |

|

$ |

43,269 |

|

$ |

41,323 |

|

Noninterest expense |

|

$ |

32,850 |

|

$ |

32,873 |

|

$ |

32,268 |

|

$ |

33,144 |

|

$ |

31,750 |

|

Pre-tax, pre-provision income (loss) |

|

$ |

8,510 |

|

$ |

12,643 |

|

$ |

10,193 |

|

$ |

10,125 |

|

$ |

9,573 |

|

Provision for credit (benefits) losses |

|

$ |

1,385 |

|

$ |

1,927 |

|

$ |

5,903 |

|

$ |

615 |

|

$ |

(168) |

|

Income (loss) before income taxes |

|

$ |

7,125 |

|

$ |

10,716 |

|

$ |

4,290 |

|

$ |

9,510 |

|

$ |

9,741 |

|

Net income (loss) |

|

$ |

5,500 |

|

$ |

8,887 |

|

$ |

3,924 |

|

$ |

7,296 |

|

$ |

7,300 |

|

Core net income (1) |

|

$ |

5,500 |

|

$ |

8,341 |

|

$ |

3,924 |

|

$ |

6,689 |

|

$ |

7,300 |

|

Per-share data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per share, diluted |

|

$ |

0.14 |

|

$ |

0.21 |

|

$ |

0.10 |

|

$ |

0.18 |

|

$ |

0.17 |

|

Core earnings per share, diluted(1) |

|

$ |

0.14 |

|

$ |

0.20 |

|

$ |

0.10 |

|

$ |

0.16 |

|

$ |

0.17 |

|

Book value per share |

|

$ |

13.27 |

|

$ |

13.15 |

|

$ |

13.24 |

|

$ |

12.99 |

|

$ |

12.82 |

|

Tangible book value per share(1) |

|

$ |

11.90 |

|

$ |

11.78 |

|

$ |

11.88 |

|

$ |

11.63 |

|

$ |

11.48 |

|

Profitability |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on average assets |

|

|

0.39 |

% |

|

0.62 |

% |

|

0.27 |

% |

|

0.50 |

% |

|

0.50 |

% |

Core return on average assets(1) |

|

|

0.39 |

% |

|

0.58 |

% |

|

0.27 |

% |

|

0.45 |

% |

|

0.50 |

% |

Return on average equity |

|

|

3.79 |

% |

|

6.08 |

% |

|

2.69 |

% |

|

5.07 |

% |

|

5.00 |

% |

Core Return on average equity(1) |

|

|

3.79 |

% |

|

5.71 |

% |

|

2.69 |

% |

|

4.54 |

% |

|

5.00 |

% |

Return on average tangible common equity(1) |

|

|

4.23 |

% |

|

6.78 |

% |

|

3.00 |

% |

|

5.67 |

% |

|

5.57 |

% |

Core return on average tangible common equity(1) |

|

|

4.23 |

% |

|

6.36 |

% |

|

3.00 |

% |

|

5.19 |

% |

|

5.57 |

% |

Net interest margin on a fully tax equivalent basis(1) |

|

|

2.39 |

% |

|

2.36 |

% |

|

2.36 |

% |

|

2.31 |

% |

|

2.25 |

% |

Cost of total deposits |

|

|

2.48 |

% |

|

2.62 |

% |

|

2.68 |

% |

|

2.53 |

% |

|

2.49 |

% |

Efficiency ratio(1) |

|

|

78.97 |

% |

|

71.81 |

% |

|

75.55 |

% |

|

76.16 |

% |

|

76.38 |

% |

Core efficiency ratio(1) |

|

|

78.97 |

% |

|

71.81 |

% |

|

75.55 |

% |

|

77.54 |

% |

|

76.38 |

% |

Tax equivalent efficiency ratio(1) |

|

|

78.09 |

% |

|

71.09 |

% |

|

74.75 |

% |

|

75.72 |

% |

|

75.92 |

% |

Tax equivalent core efficiency ratio(1) |

|

|

78.09 |

% |

|

71.09 |

% |

|

74.75 |

% |

|

77.08 |

% |

|

75.92 |

% |

Balance Sheet |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets |

|

$ |

5,700,330 |

|

$ |

5,753,133 |

|

$ |

5,775,967 |

|

$ |

5,787,035 |

|

$ |

5,862,222 |

|

Total loans |

|

$ |

4,821,033 |

|

$ |

4,852,499 |

|

$ |

4,879,503 |

|

$ |

4,839,232 |

|

$ |

4,776,685 |

|

Total deposits |

|

$ |

4,618,721 |

|

$ |

4,550,753 |

|

$ |

4,536,177 |

|

$ |

4,458,297 |

|

$ |

4,394,024 |

|

Total loans / total deposits |

|

|

104.38 |

% |

|

106.63 |

% |

|

107.57 |

% |

|

108.54 |

% |

|

108.71 |

% |

Asset quality |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Allowance for credit losses ("ACL") |

|

$ |

49,323 |

|

$ |

56,101 |

|

$ |

54,004 |

|

$ |

49,139 |

|

$ |

48,185 |

|

Nonperforming assets |

|

$ |

30,908 |

|

$ |

29,473 |

|

$ |

28,408 |

|

$ |

9,766 |

|

$ |

12,201 |

|

Non-performing loans to total loans |

|

|

0.64 |

% |

|

0.61 |

% |

|

0.58 |

% |

|

0.20 |

% |

|

0.25 |

% |

Allowance for credit losses on loans to non-performing loans |

|

|

159.61 |

% |

|

190.41 |

% |

|

190.10 |

% |

|

503.16 |

% |

|

396.26 |

% |

Allowance for credit losses on loans to total loans |

|

|

1.02 |

% |

|

1.16 |

% |

|

1.11 |

% |

|

1.02 |

% |

|

1.01 |

% |

Net loans charged off as a percentage of average loans outstanding |

|

|

0.72 |

% |

|

- |

% |

|

0.02 |

% |

|

0.02 |

% |

|

0.01 |

% |

Capital adequacy |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stockholders' equity / assets |

|

|

10.10 |

% |

|

9.99 |

% |

|

10.11 |

% |

|

9.98 |

% |

|

9.85 |

% |

Tangible common equity / tangible assets(1) |

|

|

9.15 |

% |

|

9.05 |

% |

|

9.17 |

% |

|

9.03 |

% |

|

8.92 |

% |

Common equity tier 1 ratio ("CET1")(1) |

|

|

11.86 |

% |

|

11.79 |

% |

|

11.67 |

% |

|

11.73 |

% |

|

11.97 |

% |

Risk weighted assets |

|

$ |

4,738,746 |

|

$ |

4,795,304 |

|

$ |

4,827,022 |

|

$ |

4,822,128 |

|

$ |

4,727,354 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1)Non-GAAP financial measure. Refer to the Reconciliation of Non-GAAP Financial Measures |

|

|||||||||||||||

6

HarborOne Bancorp, Inc.

Consolidated Balance Sheet Trend

(Unaudited)

|

|

Period ended |

|||||||||||||

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|||||

(in thousands) |

|

2025 |

|

2024 |

|

2024 |

|

2024 |

|

2024 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and due from banks |

|

$ |

44,383 |

|

$ |

44,090 |

|

$ |

39,668 |

|

$ |

48,097 |

|

$ |

36,340 |

Short-term investments |

|

|

186,109 |

|

|

186,981 |

|

|

184,611 |

|

|

186,965 |

|

|

357,101 |

Total cash and cash equivalents |

|

|

230,492 |

|

|

231,071 |

|

|

224,279 |

|

|

235,062 |

|

|

393,441 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Securities available for sale, at fair value |

|

|

265,644 |

|

|

263,904 |

|

|

276,817 |

|

|

269,078 |

|

|

291,008 |

Securities held to maturity, at amortized cost |

|

|

19,211 |

|

|

19,627 |

|

|

19,625 |

|

|

19,725 |

|

|

19,724 |

Federal Home Loan Bank stock, at cost |

|

|

18,330 |

|

|

23,277 |

|

|

17,476 |

|

|

25,311 |

|

|

26,565 |

Asset held for sale |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

348 |

Loans held for sale, at fair value |

|

|

19,304 |

|

|

36,768 |

|

|

28,467 |

|

|

41,814 |

|

|

16,434 |

Loans: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial real estate |

|

|

2,272,480 |

|

|

2,280,309 |

|

|

2,321,148 |

|

|

2,380,881 |

|

|

2,355,672 |

Commercial construction |

|

|

216,013 |

|

|

252,691 |

|

|

270,389 |

|

|

233,926 |

|

|

234,811 |

Commercial and industrial |

|

|

627,480 |

|

|

594,453 |

|

|

549,908 |

|

|

499,043 |

|

|

471,215 |

Total commercial loans |

|

|

3,115,973 |

|

|

3,127,453 |

|

|

3,141,445 |

|

|

3,113,850 |

|

|

3,061,698 |

Residential real estate |

|

|

1,689,681 |

|

|

1,707,556 |

|

|

1,719,882 |

|

|

1,706,678 |

|

|

1,695,686 |

Consumer |

|

|

15,379 |

|

|

17,490 |

|

|

18,176 |

|

|

18,704 |

|

|

19,301 |

Loans |

|

|

4,821,033 |

|

|

4,852,499 |

|

|

4,879,503 |

|

|

4,839,232 |

|

|

4,776,685 |

Less: Allowance for credit losses on loans |

|

|

(49,323) |

|

|

(56,101) |

|

|

(54,004) |

|

|

(49,139) |

|

|

(48,185) |

Net loans |

|

|

4,771,710 |

|

|

4,796,398 |

|

|

4,825,499 |

|

|

4,790,093 |

|

|

4,728,500 |

Mortgage servicing rights, at fair value |

|

|

42,620 |

|

|

44,500 |

|

|

43,067 |

|

|

46,209 |

|

|

46,597 |

Goodwill |

|

|

59,042 |

|

|

59,042 |

|

|

59,042 |

|

|

59,042 |

|

|

59,042 |

Other intangible assets |

|

|

568 |

|

|

757 |

|

|

947 |

|

|

1,136 |

|

|

1,326 |

Other assets |

|

|

273,409 |

|

|

277,789 |

|

|

280,748 |

|

|

299,565 |

|

|

279,237 |

Total assets |

|

$ |

5,700,330 |

|

$ |

5,753,133 |

|

$ |

5,775,967 |

|

$ |

5,787,035 |

|

$ |

5,862,222 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Liabilities and Stockholders' Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deposits: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Demand deposit accounts |

|

$ |

703,736 |

|

$ |

690,647 |

|

$ |

713,379 |

|

$ |

689,800 |

|

$ |

677,152 |

NOW accounts |

|

|

340,194 |

|

|

298,337 |

|

|

296,322 |

|

|

308,016 |

|

|

305,071 |

Regular savings and club accounts |

|

|

908,136 |

|

|

895,232 |

|

|

926,192 |

|

|

989,720 |

|

|

1,110,404 |

Money market deposit accounts |

|

|

1,200,600 |

|

|

1,195,209 |

|

|

1,162,930 |

|

|

1,100,215 |

|

|

1,061,145 |

Term certificate accounts |

|

|

1,076,195 |

|

|

1,069,844 |

|

|

1,063,672 |

|

|

985,293 |

|

|

852,326 |

Brokered deposits |

|

|

389,860 |

|

|

401,484 |

|

|

373,682 |

|

|

385,253 |

|

|

387,926 |

Total deposits |

|

|

4,618,721 |

|

|

4,550,753 |

|

|

4,536,177 |

|

|

4,458,297 |

|

|

4,394,024 |

Borrowings |

|

|

399,547 |

|

|

516,555 |

|

|

539,364 |

|

|

619,372 |

|

|

754,380 |

Other liabilities and accrued expenses |

|

|

106,095 |

|

|

110,814 |

|

|

116,224 |

|

|

132,037 |

|

|

136,135 |

Total liabilities |

|

$ |

5,124,363 |

|

$ |

5,178,122 |

|

$ |

5,191,765 |

|

$ |

5,209,706 |

|

$ |

5,284,539 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common stock |

|

|

598 |

|

|

598 |

|

|

598 |

|

|

598 |

|

|

598 |

Additional paid-in capital |

|

|

490,327 |

|

|

489,532 |

|

|

488,983 |

|

|

487,980 |

|

|

487,277 |

Unearned compensation - ESOP |

|

|

(23,488) |

|

|

(23,947) |

|

|

(24,407) |

|

|

(24,866) |

|

|

(25,326) |

Retained earnings |

|

|

375,710 |

|

|

373,861 |

|

|

368,222 |

|

|

367,584 |

|

|

363,591 |

Treasury stock |

|

|

(221,516) |

|

|

(215,138) |

|

|

(210,197) |

|

|

(205,944) |

|

|

(199,853) |

Accumulated other comprehensive loss |

|

|

(45,664) |

|

|

(49,895) |

|

|

(38,997) |

|

|

(48,023) |

|

|

(48,604) |

Total stockholders' equity |

|

$ |

575,967 |

|

$ |

575,011 |

|

$ |

584,202 |

|

$ |

577,329 |

|

$ |

577,683 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total liabilities and stockholders' equity |

|

$ |

5,700,330 |

|

$ |

5,753,133 |

|

$ |

5,775,967 |

|

$ |

5,787,035 |

|

$ |

5,862,222 |

7

HarborOne Bancorp, Inc.

Consolidated Statements of Net Income - Trend

(Unaudited)

|

|

Quarters Ended |

|||||||||||||

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|||||

(dollars in thousands, except share data) |

|

2025 |

|

2024 |

|

2024 |

|

2024 |

|

2024 |

|||||

Interest and dividend income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest and fees on loans |

|

$ |

59,872 |

|

$ |

62,415 |

|

$ |

63,595 |

|

$ |

61,512 |

|

$ |

59,937 |

Interest on loans held for sale |

|

|

296 |

|

|

517 |

|

|

546 |

|

|

347 |

|

|

243 |

Interest on securities |

|

|

1,993 |

|

|

1,996 |

|

|

1,965 |

|

|

2,121 |

|

|

2,065 |

Other interest and dividend income |

|

|

2,278 |

|

|

2,591 |

|

|

2,928 |

|

|

3,971 |

|

|

4,659 |

Total interest and dividend income |

|

|

64,439 |

|

|

67,519 |

|

|

69,034 |

|

|

67,951 |

|

|

66,904 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest expense: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest on deposits |

|

|

27,643 |

|

|

29,963 |

|

|

29,969 |

|

|

27,272 |

|

|

26,899 |

Interest on borrowings |

|

|

5,327 |

|

|

5,729 |

|

|

7,172 |

|

|

9,329 |

|

|

9,423 |

Total interest expense |

|

|

32,970 |

|

|

35,692 |

|

|

37,141 |

|

|

36,601 |

|

|

36,322 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest and dividend income |

|

|

31,469 |

|

|

31,827 |

|

|

31,893 |

|

|

31,350 |

|

|

30,582 |

Provision (benefit) for credit losses |

|

|

1,385 |

|

|

1,927 |

|

|

5,903 |

|

|

615 |

|

|

(168) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest and dividend income, after provision (benefit) for credit losses |

|

|

30,084 |

|

|

29,900 |

|

|

25,990 |

|

|

30,735 |

|

|

30,750 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mortgage banking income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gain on sale of mortgage loans |

|

|

2,716 |

|

|

3,952 |

|

|

3,752 |

|

|

3,143 |

|

|

2,013 |

Changes in mortgage servicing rights fair value |

|

|

(1,372) |

|

|

(19) |

|

|

(2,641) |

|

|

(1,098) |

|

|

54 |

Other |

|

|

2,108 |

|

|

2,431 |

|

|

2,390 |

|

|

2,356 |

|

|

2,276 |

Total mortgage banking income |

|

|

3,452 |

|

|

6,364 |

|

|

3,501 |

|

|

4,401 |

|

|

4,343 |

Deposit account fees |

|

|

5,153 |

|

|

6,024 |

|

|

5,370 |

|

|

5,223 |

|

|

4,983 |

Income on retirement plan annuities |

|

|

119 |

|

|

121 |

|

|

122 |

|

|

141 |

|

|

145 |

Gain on sale of asset held for sale |

|

|

- |

|

|

- |

|

|

- |

|

|

1,809 |

|

|

- |

Loss on sale of securities |

|

|

- |

|

|

- |

|

|

- |

|

|

(1,041) |

|

|

- |

Bank-owned life insurance income |

|

|

743 |

|

|

769 |

|

|

777 |

|

|

758 |

|

|

746 |

Other income |

|

|

424 |

|

|

411 |

|

|

798 |

|

|

628 |

|

|

524 |

Total noninterest income |

|

|

9,891 |

|

|

13,689 |

|

|

10,568 |

|

|

11,919 |

|

|

10,741 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Compensation and benefits |

|

|

18,785 |

|

|

18,853 |

|

|

18,551 |

|

|

18,976 |

|

|

17,636 |

Occupancy and equipment |

|

|

4,627 |

|

|

4,477 |

|

|

4,628 |

|

|

4,636 |

|

|

4,781 |

Data processing |

|

|

2,625 |

|

|

2,626 |

|

|

2,711 |

|

|

2,375 |

|

|

2,479 |

Loan expense |

|

|

431 |

|

|

525 |

|

|

457 |

|

|

461 |

|

|

371 |

Marketing |

|

|

588 |

|

|

599 |

|

|

549 |

|

|

1,368 |

|

|

816 |

Professional fees |

|

|

1,382 |

|

|

1,451 |

|

|

1,292 |

|

|

1,236 |

|

|

1,457 |

Deposit insurance |

|

|

1,050 |

|

|

1,163 |

|

|

1,028 |

|

|

993 |

|

|

1,164 |

Other expenses |

|

|

3,362 |

|

|

3,179 |

|

|

3,052 |

|

|

3,099 |

|

|

3,046 |

Total noninterest expenses |

|

|

32,850 |

|

|

32,873 |

|

|

32,268 |

|

|

33,144 |

|

|

31,750 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income before income taxes |

|

|

7,125 |

|

|

10,716 |

|

|

4,290 |

|

|

9,510 |

|

|

9,741 |

Income tax provision |

|

|

1,625 |

|

|

1,829 |

|

|

366 |

|

|

2,214 |

|

|

2,441 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income |

|

$ |

5,500 |

|

$ |

8,887 |

|

$ |

3,924 |

|

$ |

7,296 |

|

$ |

7,300 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per common share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

$ |

0.14 |

|

$ |

0.21 |

|

$ |

0.10 |

|

$ |

0.18 |

|

$ |

0.17 |

Diluted |

|

$ |

0.14 |

|

$ |

0.21 |

|

$ |

0.10 |

|

$ |

0.18 |

|

$ |

0.17 |

Weighted average shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

|

40,344,922 |

|

|

40,700,783 |

|

|

40,984,857 |

|

|

41,293,787 |

|

|

41,912,421 |

Diluted |

|

|

40,605,799 |

|

|

41,062,421 |

|

|

41,336,985 |

|

|

41,370,289 |

|

|

42,127,037 |

8

HarborOne Bancorp, Inc.

Asset Quality

(Unaudited)

|

|

As of or for the Three Months Ended |

|

|||||||||||||

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|

|||||

|

|

2025 |

|

2024 |

|

2024 |

|

2024 |

|

2024 |

|

|||||

Non-performing Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nonaccruing loans: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial real estate and construction |

|

$ |

8,610 |

|

$ |

16,836 |

|

$ |

17,171 |

|

$ |

- |

|

$ |

1,496 |

|

Commercial and industrial |

|

|

10,538 |

|

|

2,204 |

|

|

1,743 |

|

|

1,773 |

|

|

1,744 |

|

Residential mortgages, construction, and HELOC |

|

|

11,705 |

|

|

10,409 |

|

|

9,451 |

|

|

7,949 |

|

|

8,866 |

|

Consumer |

|

|

49 |

|

|

14 |

|

|

43 |

|

|

44 |

|

|

54 |

|

Total nonaccruing loans |

|

|

30,902 |

|

|

29,463 |

|

|

28,408 |

|

|

9,766 |

|

|

12,160 |

|

Other real estate owned |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

Repossessed assets |

|

|

6 |

|

|

10 |

|

|

- |

|

|

- |

|

|

41 |

|

Total nonperforming assets |

|

$ |

30,908 |

|

$ |

29,473 |

|

$ |

28,408 |

|

$ |

9,766 |

|

$ |

12,201 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total nonperforming loans to total loans |

|

|

0.64 |

% |

|

0.61 |

% |

|

0.58 |

% |

|

0.20 |

% |

|

0.25 |

% |

Total nonperforming assets to total assets |

|

|

0.54 |

% |

|

0.51 |

% |

|

0.49 |

% |

|

0.17 |

% |

|

0.21 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Allowance for credit losses on loans |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Beginning balance |

|

$ |

56,101 |

|

$ |

54,004 |

|

$ |

49,139 |

|

$ |

48,185 |

|

$ |

47,972 |

|

Net (charge-offs) recoveries: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial real estate and construction |

|

|

(8,300) |

|

|

40 |

|

|

3 |

|

|

- |

|

|

100 |

|

Commercial and industrial |

|

|

(362) |

|

|

(57) |

|

|

(146) |

|

|

(184) |

|

|

(182) |

|

Residential mortgages and HELOC |

|

|

10 |

|

|

1 |

|

|

- |

|

|

5 |

|

|

3 |

|

Consumer |

|

|

(17) |

|

|

(42) |

|

|

(39) |

|

|

(16) |

|

|

(46) |

|

Total net charge-offs: |

|

|

(8,669) |

|

|

(58) |

|

|

(182) |

|

|

(195) |

|

|

(125) |

|

Provision for loan credit losses |

|

|

1,891 |

|

|

2,155 |

|

|

5,047 |

|

|

1,149 |

|

|

338 |

|

Ending balance |

|

$ |

49,323 |

|

$ |

56,101 |

|

$ |

54,004 |

|

$ |

49,139 |

|

$ |

48,185 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Allowance for credit losses on loans to total loans |

|

|

1.02 |

% |

|

1.16 |

% |

|

1.11 |

% |

|

1.02 |

% |

|

1.01 |

% |

Allowance for credit losses on loans to nonaccruing loans |

|

|

159.61 |

% |

|

190.41 |

% |

|

190.10 |

% |

|

503.16 |

% |

|

396.26 |

% |

Annualized net charge-offs (recoveries)/average loans |

|

|

0.72 |

% |

|

0.00 |

% |

|

0.02 |

% |

|

0.02 |

% |

|

0.01 |

% |

Provision (credit) for unfunded commitments |

|

$ |

(506) |

|

$ |

(228) |

|

$ |

856 |

|

$ |

(534) |

|

$ |

(506) |

|

Allowance for unfunded commitments |

|

$ |

3,000 |

|

$ |

3,506 |

|

$ |

3,734 |

|

$ |

2,878 |

|

$ |

3,412 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Delinquency |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total delinquent loans |

|

$ |

29,821 |

|

$ |

37,427 |

|

$ |

21,325 |

|

$ |

12,990 |

|

$ |

12,160 |

|

Total delinquent loans to total loans |

|

|

0.62 |

% |

|

0.77 |

% |

|

0.44 |

% |

|

0.27 |

% |

|

0.25 |

% |

9

HarborOne Bancorp, Inc.

Average Balances and Yield Trend

(Unaudited)

|

|

Quarters Ended |

|

||||||||||||||||||||||

|

|

March 31, 2025 |

|

December 31, 2024 |

|

March 31, 2024 |

|

||||||||||||||||||

|

|

Average |

|

|

|

|

|

Average |

|

|

|

|

|

Average |

|

|

|

|

|

||||||

|

|

Outstanding |

|

|

|

Yield/ |

|

Outstanding |

|

|

|

Yield/ |

|

Outstanding |

|

|

|

Yield/ |

|

||||||

|

|

Balance |

|

Interest |

|

Cost (8) |

|

Balance |

|

Interest |

|

Cost (8) |

|

Balance |

|

Interest |

|

Cost (8) |

|

||||||

|

|

(dollars in thousands) |

|

||||||||||||||||||||||

Interest-earning assets: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment securities (1) |

|

$ |

346,902 |

|

$ |

1,993 |

|

2.33 |

% |

$ |

350,041 |

|

$ |

1,996 |

|

2.27 |

% |

$ |

372,787 |

|

$ |

2,065 |

|

2.23 |

% |

Other interest-earning assets |

|

|

213,400 |

|

|

2,278 |

|

4.33 |

|

|

203,695 |

|

|

2,591 |

|

5.06 |

|

|

356,470 |

|

|

4,659 |

|

5.26 |

|

Loans held for sale |

|

|

17,237 |

|

|

296 |

|

6.96 |

|

|

31,358 |

|

|

517 |

|

6.56 |

|

|

14,260 |

|

|

243 |

|

6.85 |

|

Loans |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial loans (2)(3) |

|

|

3,125,369 |

|

|

41,796 |

|

5.42 |

|

|

3,139,356 |

|

|

43,845 |

|

5.56 |

|

|

3,040,835 |

|

|

41,653 |

|

5.51 |

|

Residential real estate loans (3)(4) |

|

|

1,696,444 |

|

|

18,243 |

|

4.36 |

|

|

1,711,481 |

|

|

18,685 |

|

4.34 |

|

|

1,700,694 |

|

|

18,175 |

|

4.30 |

|

Consumer loans (3) |

|

|

16,601 |

|

|

294 |

|

7.18 |

|

|

17,583 |

|

|

343 |

|

7.76 |

|

|

20,539 |

|

|

358 |

|

7.01 |

|

Total loans |

|

|

4,838,414 |

|

|

60,333 |

|

5.06 |

|

|

4,868,420 |

|

|

62,873 |

|

5.14 |

|

|

4,762,068 |

|

|

60,186 |

|

5.08 |

|

Total interest-earning assets |

|

|

5,415,953 |

|

|

64,900 |

|

4.86 |

|

|

5,453,514 |

|

|

67,977 |

|

4.96 |

|

|

5,505,585 |

|

|

67,153 |

|

4.91 |

|

Noninterest-earning assets |

|

|

290,734 |

|

|

|

|

|

|

|

295,057 |

|

|

|

|

|

|

|

299,153 |

|

|

|

|

|

|

Total assets |

|

$ |

5,706,687 |

|

|

|

|

|

|

$ |

5,748,571 |

|

|

|

|

|

|

$ |

5,804,738 |

|

|

|

|

|

|

Interest-bearing liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Savings accounts |

|

$ |

908,434 |

|

|

3,050 |

|

1.36 |

|

$ |

924,514 |

|

|

3,339 |

|

1.44 |

|

$ |

1,186,201 |

|

|

5,523 |

|

1.87 |

|

NOW accounts |

|

|

303,719 |

|

|

127 |

|

0.17 |

|

|

292,332 |

|

|

110 |

|

0.15 |

|

|

289,902 |

|

|

75 |

|

0.10 |

|

Money market accounts |

|

|

1,190,811 |

|

|

9,648 |

|

3.29 |

|

|

1,184,006 |

|

|

10,565 |

|

3.55 |

|

|

994,353 |

|

|

9,313 |

|

3.77 |

|

Certificates of deposit |

|

|

1,060,313 |

|

|

11,343 |

|

4.34 |

|

|

1,075,594 |

|

|

12,391 |

|

4.58 |

|

|

855,070 |

|

|

8,554 |

|

4.02 |

|

Brokered deposits |

|

|

387,294 |

|

|

3,475 |

|

3.64 |

|

|

376,154 |

|

|

3,558 |

|

3.76 |

|

|

356,459 |

|

|

3,434 |

|

3.87 |

|

Total interest-bearing deposits |

|

|

3,850,571 |

|

|

27,643 |

|

2.91 |

|

|

3,852,600 |

|

|

29,963 |

|

3.09 |

|

|

3,681,985 |

|

|

26,899 |

|

2.94 |

|

Total borrowings |

|

|

493,206 |

|

|

5,327 |

|

4.38 |

|

|

512,802 |

|

|

5,729 |

|

4.44 |

|

|

764,623 |

|

|

9,423 |

|

4.96 |

|

Total interest-bearing liabilities |

|

|

4,343,777 |

|

|

32,970 |

|

3.08 |

|

|

4,365,402 |

|

|

35,692 |

|

3.25 |

|

|

4,446,608 |

|

|

36,322 |

|

3.29 |

|

Noninterest-bearing liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest-bearing deposits |

|

|

677,314 |

|

|

|

|

|

|

|

697,364 |

|

|

|

|

|

|

|

654,436 |

|

|

|

|

|

|

Other noninterest-bearing liabilities |

|

|

105,747 |

|

|

|

|

|

|

|

101,371 |

|

|

|

|

|

|

|

119,289 |

|

|

|

|

|

|

Total liabilities |

|

|

5,126,838 |

|

|

|

|

|

|

|

5,164,137 |

|

|

|

|

|

|

|

5,220,333 |

|

|

|

|

|

|

Total stockholders' equity |

|

|

579,849 |

|

|

|

|

|

|

|

584,433 |

|

|

|

|

|

|

|

584,405 |

|

|

|

|

|

|

Total liabilities and stockholders' equity |

|

$ |

5,706,687 |

|

|

|

|

|

|

$ |

5,748,571 |

|

|

|

|

|

|

$ |

5,804,738 |

|

|

|

|

|

|

Tax equivalent net interest income |

|

|

|

|

|

31,930 |

|

|

|

|

|

|

|

32,285 |

|

|

|

|

|

|

|

30,831 |

|

|

|

Tax equivalent interest rate spread (5) |

|

|

|

|

|

|

|

1.78 |

% |

|

|

|

|

|

|

1.71 |

% |

|

|

|

|

|

|

1.62 |

% |

Less: tax equivalent adjustment |

|

|

|

|

|

461 |

|

|

|

|

|

|

|

458 |

|

|

|

|

|

|

|

249 |

|

|

|

Net interest income as reported |

|

|

|

|

$ |

31,469 |

|

|

|

|

|

|

$ |

31,827 |

|

|

|

|

|

|

$ |

30,582 |

|

|

|

Net interest-earning assets (6) |

|

$ |

1,072,176 |

|

|

|

|

|

|

$ |

1,088,112 |

|

|

|

|

|

|

$ |

1,058,977 |

|

|

|

|

|

|

Net interest margin (7) |

|

|

|

|

|

|

|

2.36 |

% |

|

|

|

|

|

|

2.32 |

% |

|

|

|

|

|

|

2.23 |

% |

Tax equivalent effect |

|

|

|

|

|

|

|

0.03 |

|

|

|

|

|

|

|

0.04 |

|

|

|

|

|

|

|

0.02 |

|

Net interest margin on a fully tax equivalent basis |

|

|

|

|

|

|

|

2.39 |

% |

|

|

|

|

|

|

2.36 |

% |

|

|

|

|

|

|

2.25 |

% |

Ratio of interest-earning assets to interest-bearing liabilities |

|

|

124.68 |

% |

|

|

|

|

|

|

124.93 |

% |

|

|

|

|

|

|

123.82 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental information: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total deposits, including demand deposits |

|

$ |

4,527,885 |

|

$ |

27,643 |

|

|

|

$ |

4,549,964 |

|

$ |

29,963 |

|

|

|

$ |

4,336,421 |

|

$ |

26,899 |

|

|

|

Cost of total deposits |

|

|

|

|

|

|

|

2.48 |

% |

|

|

|

|

|

|

2.62 |

% |

|

|

|

|

|

|

2.49 |

% |

Total funding liabilities, including demand deposits |

|

$ |

5,021,091 |

|

$ |

32,970 |

|

|

|

$ |

5,062,766 |

|

$ |

35,692 |

|

|

|

$ |

5,101,044 |

|

$ |

36,322 |

|

|

|

Cost of total funding liabilities |

|

|

|

|

|

|

|

2.66 |

% |

|

|

|

|

|

|

2.80 |

% |

|

|

|

|

|

|

2.86 |

% |

|

(1) Includes securities available for sale and securities held to maturity. (2) Tax-exempt income on industrial revenue bonds is included in commercial loans on a tax-equivalent basis. (3) Includes nonaccruing loan balances and interest received on such loans. (4) Includes the basis adjustments of certain loans included in fair value hedging relationships. (5) Net interest rate spread represents the difference between the yield on average interest-earning assets and the cost of average interest-bearing liabilities. |

(6) Net interest-earning assets represents total interest-earning assets less total interest-bearing liabilities. |

|

(7) Net interest margin represents net interest income divided by average total interest-earning assets. (8) Annualized |

10

HarborOne Bancorp, Inc.

Segments Key Financial Data

(Unaudited)

|

|

Quarters Ended |

|

|||||||||||||

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|

|||||

Statements of Net Income for HarborOne Bank Segment: |

|

2025 |

|

2024 |

|

2024 |

|

2024 |

|

2024 |

|

|||||

|

|

(Dollars in thousands) |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest and dividend income |

|

$ |

31,315 |

|

$ |

31,681 |

|

$ |

31,780 |

|

$ |

31,098 |

|

$ |

30,485 |

|

Provision (benefit) for credit losses |

|

|

1,385 |

|

|

1,927 |

|

|

5,903 |

|

|

615 |

|

|

(168) |

|

Net interest and dividend income, after provision for credit losses |

|

|

29,930 |

|

|

29,754 |

|

|

25,877 |

|

|

30,483 |

|

|

30,653 |

|

Mortgage banking income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Intersegment loss |

|

|

(81) |

|

|

(161) |

|

|

(357) |

|

|

(464) |

|

|

(236) |

|

Changes in mortgage servicing rights fair value |

|

|

(134) |

|

|

80 |

|

|

(220) |

|

|

(74) |

|

|

(32) |

|

Other |

|

|

167 |

|

|

169 |

|

|

175 |

|

|

180 |

|

|

180 |

|

Total mortgage banking (loss) income |

|

|

(48) |

|

|

88 |

|

|

(402) |

|

|

(358) |

|

|

(88) |

|

Other noninterest income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deposit account fees |

|

|

5,153 |

|

|

6,024 |

|

|

5,370 |

|

|

5,223 |

|

|

4,983 |

|

Income on retirement plan annuities |

|

|

119 |

|

|

121 |

|

|

122 |

|

|

141 |

|

|

145 |

|

Gain on sale of asset held for sale |

|

|

- |

|

|

- |

|

|

- |

|

|

1,809 |

|

|

- |

|

Loss on sale of securities |

|

|

- |

|

|

- |

|

|

- |

|

|

(1,041) |

|

|

- |

|

Bank-owned life insurance income |

|

|

743 |

|

|

769 |

|

|

777 |

|

|

758 |

|

|

746 |

|

Other income |

|

|

425 |

|

|

383 |

|

|

798 |

|

|

624 |

|

|

517 |

|

Total noninterest income |

|

|

6,392 |

|

|

7,385 |

|

|

6,665 |

|

|

7,156 |

|

|

6,303 |

|

Total noninterest expenses |

|

|

28,185 |

|

|

27,400 |

|

|

26,752 |

|

|

27,791 |

|

|

27,407 |

|

Income before income taxes |

|

|

8,137 |

|

|

9,739 |

|

|

5,790 |

|

|

9,848 |

|

|

9,549 |

|

Provision for income taxes |

|

|

1,903 |

|

|

2,015 |

|

|

875 |

|

|

2,310 |

|

|

2,386 |

|

Net income |

|

$ |

6,234 |

|

$ |

7,724 |

|

$ |

4,915 |

|

$ |

7,538 |

|

$ |

7,163 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Efficiency ratio (Non-GAAP) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest expense, as presented (GAAP) |

|

$ |

28,185 |

|

$ |

27,400 |

|

$ |

26,752 |

|

$ |

27,791 |

|

$ |

27,407 |

|

Less: Amortization of other intangible assets |

|

|

190 |

|

|

190 |

|

|

190 |

|

|

189 |

|

|

189 |

|

Total adjusted noninterest expense(non-GAAP) |

(A) |

$ |

27,995 |

|

$ |

27,210 |

|

$ |

26,562 |

|

$ |

27,602 |

|

$ |

27,218 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest and dividend income (GAAP) |

|

$ |

31,315 |

|

$ |

31,681 |

|

$ |

31,780 |

|

$ |

31,098 |

|

$ |

30,485 |

|

Plus: tax equivalent adjustment |

|

|

461 |

|

|

458 |

|

|

452 |

|

|

256 |

|

|

249 |

|

Tax equivalent net interest and dividend income (non-GAAP) |

(B) |

$ |

31,776 |

|

$ |

32,139 |

|

$ |

32,232 |

|

$ |

31,354 |

|

$ |

30,734 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|