F

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

☒ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

For the quarterly period ended September 30, 2024 |

|

|

|

OR |

|

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file no: 001-38719

MEDALIST DIVERSIFIED REIT, INC.

(Exact name of registrant as specified in its charter)

Maryland |

|

47-5201540 |

|

(State or other jurisdiction of incorporation or organization) |

|

(IRS Employer Identification No.) |

P. O. Box 8436

Richmond, VA 23226

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (804) 338-7708

Securities registered pursuant to section 12(b) of the Act:

Title of Each Class |

|

|

Trading |

Name of each Exchange |

Common Stock, $0.01 par value per share |

|

|

MDRR |

The Nasdaq Capital Market |

8.0% Series A Cumulative Redeemable Preferred Stock, $0.01 par value per share |

|

|

MDRRP |

The Nasdaq Capital Market |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ⌧ ◻ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ⌧ Yes No ◻

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

◻ |

Accelerated filer |

◻ |

|

|

|

|

Non-accelerated filer |

☒ |

Smaller reporting company |

☒ |

|

|

|

|

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ ☒ No

The number of shares of Common Stock, $0.01 par value per share, of the registrant outstanding at November 12, 2024 was 1,115,260.

Medalist Diversified REIT, Inc.

Quarterly Report on Form 10-Q

For the Quarter Ended September 30, 2024

Table of Contents

|

||

|

|

|

|

||

Condensed Consolidated Balance Sheets as of September 30, 2024 (unaudited) and December 31, 2023 |

||

|

|

|

|

||

|

|

|

|

||

|

|

|

|

Notes to Condensed Consolidated Financial Statements (unaudited) |

|

|

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

||

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2

PART I.FINANCIAL INFORMATION

Item 1. Financial Statements

Medalist Diversified REIT, Inc. and Subsidiaries

Condensed Consolidated Balance Sheets

|

|

|

September 30, 2024 |

|

|

December 31, 2023 |

|

|

|

(Unaudited) |

|

|

|

||

ASSETS |

|

|

|

|

|

|

|

Investment properties, net |

|

$ |

65,155,785 |

|

$ |

64,577,376 |

|

Cash |

|

|

3,121,333 |

|

|

2,234,603 |

|

Restricted cash |

|

|

1,847,326 |

|

|

1,575,002 |

|

Rent and other receivables, net of allowance of $31,145 and $13,413, as of September 30, 2024 and December 31, 2023, respectively |

|

|

215,532 |

|

|

292,618 |

|

Assets held for sale |

|

|

— |

|

|

9,707,154 |

|

Unbilled rent |

|

|

1,077,746 |

|

|

1,109,782 |

|

Intangible assets, net |

|

|

2,448,365 |

|

|

2,716,546 |

|

Other assets |

|

|

741,398 |

|

|

532,935 |

|

Total Assets |

|

$ |

74,607,485 |

|

$ |

82,746,016 |

|

|

|

|

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

|

|

Accounts payable and accrued liabilities |

|

$ |

1,291,987 |

|

$ |

1,095,049 |

|

Intangible liabilities, net |

|

|

1,736,263 |

|

|

1,865,310 |

|

Line of credit, short term, net |

|

|

— |

|

|

1,000,000 |

|

Mortgages payable, net |

|

|

50,219,369 |

|

|

50,772,773 |

|

Mortgages payable, net, associated with assets held for sale |

|

|

— |

|

|

9,588,888 |

|

Mandatorily redeemable preferred stock, net |

|

|

4,890,196 |

|

|

4,693,575 |

|

Total Liabilities |

|

$ |

58,137,815 |

|

$ |

69,015,595 |

|

|

|

|

|

|

|

|

|

EQUITY |

|

|

|

|

|

|

|

Common stock, 1,115,260 and 1,109,405 shares issued and outstanding at September 30, 2024 and December 31, 2023, respectively |

|

$ |

11,153 |

|

$ |

11,094 |

|

Additional paid-in capital |

|

|

51,577,572 |

|

|

51,525,303 |

|

Offering costs |

|

|

(3,350,946) |

|

|

(3,350,946) |

|

Accumulated deficit |

|

|

(35,678,971) |

|

|

(35,864,693) |

|

Total Stockholders' Equity |

|

|

12,558,808 |

|

|

12,320,758 |

|

Noncontrolling interests - Hanover Square Property |

|

|

— |

|

|

119,140 |

|

Noncontrolling interests - Parkway Property |

|

|

419,725 |

|

|

453,203 |

|

Noncontrolling interests - Operating Partnership |

|

|

3,491,137 |

|

|

837,320 |

|

Total Equity |

|

$ |

16,469,670 |

|

$ |

13,730,421 |

|

Total Liabilities and Equity |

|

$ |

74,607,485 |

|

$ |

82,746,016 |

|

See notes to condensed consolidated financial statements

3

Medalist Diversified REIT, Inc. and Subsidiaries

Condensed Consolidated Statements of Operations

(Unaudited)

|

|

Three Months Ended |

|

Nine Months Ended |

|

||||||||

|

|

September 30, |

|

September 30, |

|

||||||||

|

|

2024 |

|

2023 |

|

2024 |

|

2023 |

|

||||

REVENUE |

|

|

|

|

|

|

|

|

|

|

|

|

|

Retail center property revenues |

|

$ |

1,565,896 |

|

$ |

1,874,188 |

|

$ |

4,955,305 |

|

$ |

5,557,045 |

|

Flex center property revenues |

|

|

676,754 |

|

|

658,246 |

|

|

2,008,056 |

|

|

1,839,675 |

|

Single tenant net lease property revenues |

|

|

94,275 |

|

|

56,306 |

|

|

246,359 |

|

|

168,897 |

|

Total Revenue |

|

$ |

2,336,925 |

|

$ |

2,588,740 |

|

$ |

7,209,720 |

|

$ |

7,565,617 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

OPERATING EXPENSES |

|

|

|

|

|

|

|

|

|

|

|

|

|

Retail center property operating expenses |

|

$ |

374,016 |

|

$ |

459,132 |

|

$ |

1,193,838 |

|

$ |

1,489,602 |

|

Flex center property operating expenses |

|

|

162,800 |

|

|

180,164 |

|

|

491,586 |

|

|

535,065 |

|

Single tenant net lease property operating expenses |

|

|

8,188 |

|

|

7,696 |

|

|

23,697 |

|

|

23,174 |

|

Bad debt expense |

|

|

15,423 |

|

|

5,669 |

|

|

37,643 |

|

|

49,868 |

|

Share based compensation expenses |

|

|

— |

|

|

— |

|

|

277,500 |

|

|

— |

|

Legal, accounting and other professional fees |

|

|

261,670 |

|

|

237,562 |

|

|

941,244 |

|

|

1,228,262 |

|

Corporate general and administrative expenses |

|

|

238,189 |

|

|

162,649 |

|

|

748,928 |

|

|

364,868 |

|

Management restructuring expenses |

|

|

— |

|

|

1,452,904 |

|

|

— |

|

|

1,846,329 |

|

Loss on impairment |

|

|

— |

|

|

— |

|

|

— |

|

|

50,859 |

|

Depreciation and amortization |

|

|

973,367 |

|

|

1,149,664 |

|

|

2,979,142 |

|

|

3,459,262 |

|

Total Operating Expenses |

|

|

2,033,653 |

|

|

3,655,440 |

|

|

6,693,578 |

|

|

9,047,289 |

|

Gain on disposal of investment property |

|

|

— |

|

|

— |

|

|

2,819,502 |

|

|

— |

|

Loss on extinguishment of debt |

|

|

— |

|

|

— |

|

|

(51,837) |

|

|

— |

|

Operating Income (Loss) |

|

|

303,272 |

|

|

(1,066,700) |

|

|

3,283,807 |

|

|

(1,481,672) |

|

Interest expense |

|

|

730,922 |

|

|

900,182 |

|

|

2,331,030 |

|

|

2,612,642 |

|

Net (Loss) Income from Operations |

|

|

(427,650) |

|

|

(1,966,882) |

|

|

952,777 |

|

|

(4,094,314) |

|

Other income |

|

|

14,824 |

|

|

20,522 |

|

|

40,486 |

|

|

52,249 |

|

Other expense |

|

|

105,123 |

|

|

— |

|

|

76,985 |

|

|

— |

|

Net (Loss) Income |

|

|

(517,949) |

|

|

(1,946,360) |

|

|

916,278 |

|

|

(4,042,065) |

|

Less: Net (loss) income attributable to Hanover Square Property noncontrolling interests |

|

|

(399) |

|

|

(225) |

|

|

453,928 |

|

|

(1,482) |

|

Less: Net (loss) income attributable to Parkway Property noncontrolling interests |

|

|

(16,397) |

|

|

2,199 |

|

|

(9,178) |

|

|

10,081 |

|

Less: Net income (loss) attributable to Operating Partnership noncontrolling interests |

|

|

25,843 |

|

|

493 |

|

|

162,828 |

|

|

(2,878) |

|

Net (Loss) Income Attributable to Medalist Common Stockholders |

|

$ |

(526,996) |

|

$ |

(1,948,827) |

|

$ |

308,700 |

|

$ |

(4,047,786) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per common share - basic |

|

$ |

— |

|

$ |

— |

|

$ |

0.28 |

|

$ |

— |

|

Weighted-average number of shares - basic |

|

|

— |

|

|

— |

|

|

1,117,099 |

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per common share - diluted |

|

$ |

— |

|

$ |

— |

|

$ |

0.28 |

|

$ |

— |

|

Weighted-average number of shares - diluted |

|

|

— |

|

|

— |

|

|

1,123,249 |

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loss per common share - basic and diluted |

|

$ |

(0.47) |

|

$ |

(1.76) |

|

$ |

— |

|

$ |

(3.65) |

|

Weighted-average number of shares - basic and diluted |

|

|

1,116,391 |

|

|

1,109,405 |

|

|

— |

|

|

1,109,631 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dividends paid per common share |

|

$ |

0.05 |

|

$ |

— |

|

$ |

0.11 |

|

$ |

0.32 |

|

See notes to condensed consolidated financial statements

4

Medalist Diversified REIT, Inc. and Subsidiaries

Condensed Consolidated Statements of Stockholders’ Equity

For the nine months ended September 30, 2024 and 2023

(Unaudited)

|

|

For the nine months ended September 30, 2024 |

|||||||||||||||||||||||||||

|

|

Common Stock |

|

|

|

|

|

|

|

|

|

|

|

|

|

Noncontrolling Interests |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

Hanover |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional |

|

|

Offering |

|

Accumulated |

|

|

Stockholders' |

|

|

Square |

|

|

Parkway |

|

|

Operating |

|

|

|

||

|

|

Shares |

|

Par Value |

|

Paid in Capital |

|

|

Costs |

|

Deficit |

|

|

Equity |

|

|

Property |

|

|

Property |

|

|

Partnership |

|

|

Total Equity |

|||

Balance, January 1, 2024 |

|

1,109,405 |

|

$ |

11,094 |

|

$ |

51,525,303 |

|

$ |

(3,350,946) |

|

$ |

(35,864,693) |

|

$ |

12,320,758 |

|

$ |

119,140 |

|

$ |

453,203 |

|

$ |

837,320 |

|

$ |

13,730,421 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common stock repurchases |

|

(2,830) |

|

$ |

(28) |

|

$ |

(32,439) |

|

$ |

— |

|

$ |

— |

|

$ |

(32,467) |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

(32,467) |

Share based compensation |

|

8,910 |

|

|

89 |

|

|

87,411 |

|

|

— |

|

|

— |

|

|

87,500 |

|

|

— |

|

|

— |

|

|

190,000 |

|

|

277,500 |

Redemption of operating partnership units |

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

(77,226) |

|

|

(77,226) |

Retire fractional shares resulting from reverse stock split |

|

(225) |

|

|

(2) |

|

|

(2,703) |

|

|

— |

|

|

— |

|

|

(2,705) |

|

|

— |

|

|

— |

|

|

— |

|

|

(2,705) |

Net income (loss) |

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

308,700 |

|

|

308,700 |

|

|

453,928 |

|

|

(9,178) |

|

|

162,828 |

|

|

916,278 |

Dividends and distributions |

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

(122,978) |

|

|

(122,978) |

|

|

(516,596) |

|

|

(24,300) |

|

|

(21,785) |

|

|

(685,659) |

Non-controlling interests |

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

(56,472) |

|

|

— |

|

|

2,400,000 |

|

|

2,343,528 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, September 30, 2024 |

|

1,115,260 |

|

$ |

11,153 |

|

$ |

51,577,572 |

|

$ |

(3,350,946) |

|

$ |

(35,678,971) |

|

$ |

12,558,808 |

|

$ |

— |

|

$ |

419,725 |

|

$ |

3,491,137 |

|

$ |

16,469,670 |

|

|

For the nine months ended September 30, 2023 |

|||||||||||||||||||||||||||

|

|

Common Stock |

|

|

|

|

|

|

|

|

|

|

|

|

|

Noncontrolling Interests |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

Hanover |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional |

|

|

Offering |

|

Accumulated |

|

|

Stockholders' |

|

|

Square |

|

|

Parkway |

|

|

Operating |

|

|

|

||

|

|

Shares |

|

Par Value |

|

Paid in Capital |

|

|

Costs |

|

Deficit |

|

|

Equity |

|

|

Property |

|

|

Property |

|

|

Partnership |

|

|

Total Equity |

|||

Balance, January 1, 2023 |

|

1,109,902 |

|

$ |

11,099 |

|

$ |

51,530,298 |

|

$ |

(3,350,946) |

|

$ |

(30,939,020) |

|

$ |

17,251,431 |

|

$ |

127,426 |

|

$ |

470,685 |

|

$ |

842,898 |

|

$ |

18,692,440 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Retire fractional shares resulting from reverse stock split |

|

(497) |

|

$ |

(5) |

|

$ |

(2,495) |

|

$ |

— |

|

$ |

— |

|

$ |

(2,500) |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

(2,500) |

Net (loss) income |

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

(4,047,786) |

|

|

(4,047,786) |

|

|

(1,482) |

|

|

10,081 |

|

|

(2,878) |

|

|

(4,042,065) |

Dividends and distributions |

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

(354,394) |

|

|

(354,394) |

|

|

(16,000) |

|

|

— |

|

|

(4,271) |

|

|

(374,665) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, September 30, 2023 |

|

1,109,405 |

|

$ |

11,094 |

|

$ |

51,527,803 |

|

$ |

(3,350,946) |

|

$ |

(35,341,200) |

|

$ |

12,846,751 |

|

$ |

109,944 |

|

$ |

480,766 |

|

$ |

835,749 |

|

$ |

14,273,210 |

5

Medalist Diversified REIT, Inc. and Subsidiaries

Condensed Consolidated Statements of Stockholders’ Equity

For the three months ended September 30, 2024 and 2023

(Unaudited)

|

|

For the three months ended September 30, 2024 |

|||||||||||||||||||||||||||

|

|

Common Stock |

|

|

|

|

|

|

|

|

|

|

|

|

|

Noncontrolling Interests |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

Hanover |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional |

|

|

Offering |

|

|

Accumulated |

|

Stockholders' |

|

|

Square |

|

|

Parkway |

|

|

Operating |

|

|

|

||

|

|

Shares |

|

Par Value |

|

Paid in Capital |

|

|

Costs |

|

Deficit |

|

|

Equity |

|

|

Property |

|

|

Property |

|

|

Partnership |

|

|

Total Equity |

|||

Balance, July 1, 2024 |

|

1,118,315 |

|

$ |

11,183 |

|

$ |

51,612,714 |

|

$ |

(3,350,946) |

|

$ |

(35,096,071) |

|

$ |

13,176,880 |

|

$ |

8,339 |

|

$ |

436,122 |

|

$ |

3,477,004 |

|

$ |

17,098,345 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common stock repurchases |

|

(2,830) |

|

$ |

(28) |

|

$ |

(32,439) |

|

$ |

— |

|

$ |

— |

|

$ |

(32,467) |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

(32,467) |

Retire fractional shares resulting from reverse stock split |

|

(225) |

|

|

(2) |

|

|

(2,703) |

|

|

— |

|

|

— |

|

|

(2,705) |

|

|

— |

|

|

— |

|

|

— |

|

|

(2,705) |

Net (loss) income |

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

(526,996) |

|

|

(526,996) |

|

|

(399) |

|

|

(16,397) |

|

|

25,843 |

|

|

(517,949) |

Dividends and distributions |

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

(55,904) |

|

|

(55,904) |

|

|

(7,940) |

|

|

— |

|

|

(11,710) |

|

|

(75,554) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, September 30, 2024 |

|

1,115,260 |

|

$ |

11,153 |

|

$ |

51,577,572 |

|

$ |

(3,350,946) |

|

$ |

(35,678,971) |

|

$ |

12,558,808 |

|

$ |

— |

|

$ |

419,725 |

|

$ |

3,491,137 |

|

$ |

16,469,670 |

|

|

For the three months ended September 30, 2023 |

|||||||||||||||||||||||||||

|

|

Common Stock |

|

|

|

|

|

|

|

|

|

|

|

|

|

Noncontrolling Interests |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

Hanover |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional |

|

|

Offering |

|

|

Accumulated |

|

Stockholders' |

|

|

Square |

|

|

Parkway |

|

|

Operating |

|

|

|

||

|

|

Shares |

|

Par Value |

|

Paid in Capital |

|

|

Costs |

|

Deficit |

|

|

Equity |

|

|

Property |

|

|

Property |

|

|

Partnership |

|

|

Total Equity |

|||

Balance, July 1, 2023 |

|

1,109,405 |

|

$ |

11,094 |

|

$ |

51,527,803 |

|

$ |

(3,350,946) |

|

$ |

(33,392,373) |

|

$ |

14,795,578 |

|

$ |

110,169 |

|

$ |

478,567 |

|

$ |

835,256 |

|

$ |

16,219,570 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net (loss) income |

|

— |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

(1,948,827) |

|

$ |

(1,948,827) |

|

$ |

(225) |

|

$ |

2,199 |

|

$ |

493 |

|

$ |

(1,946,360) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, September 30, 2023 |

|

1,109,405 |

|

$ |

11,094 |

|

$ |

51,527,803 |

|

$ |

(3,350,946) |

|

$ |

(35,341,200) |

|

$ |

12,846,751 |

|

$ |

109,944 |

|

$ |

480,766 |

|

$ |

835,749 |

|

$ |

14,273,210 |

See notes to condensed consolidated financial statements

6

Medalist Diversified REIT, Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows

(Unaudited)

|

|

Nine months ended September 30, |

||||

|

|

2024 |

|

2023 |

||

CASH FLOWS FROM OPERATING ACTIVITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income (Loss) |

|

$ |

916,278 |

|

$ |

(4,042,065) |

|

|

|

|

|

|

|

Adjustments to reconcile consolidated net loss to net cash flows from operating activities |

|

|

|

|

|

|

Depreciation |

|

|

2,500,529 |

|

|

2,768,969 |

Amortization |

|

|

478,613 |

|

|

690,293 |

Loan cost amortization |

|

|

71,299 |

|

|

80,967 |

Mandatorily redeemable preferred stock issuance cost and discount amortization |

|

|

196,621 |

|

|

180,303 |

Amortization of lease incentives |

|

|

2,223 |

|

|

— |

Above (below) market lease amortization, net |

|

|

(193,398) |

|

|

(211,904) |

Bad debt expense |

|

|

37,643 |

|

|

49,868 |

Share-based compensation |

|

|

277,500 |

|

|

— |

Loss on extinguishment of debt |

|

|

51,837 |

|

|

50,859 |

Gain on disposal of investment property |

|

|

(2,819,502) |

|

|

— |

|

|

|

|

|

|

|

Changes in assets and liabilities |

|

|

|

|

|

|

Rent and other receivables, net |

|

|

39,443 |

|

|

257,784 |

Unbilled rent |

|

|

(62,487) |

|

|

(84,852) |

Other assets |

|

|

(208,463) |

|

|

(82,962) |

Accounts payable and accrued liabilities |

|

|

122,833 |

|

|

758,343 |

Net cash flows from operating activities |

|

|

1,410,969 |

|

|

415,603 |

|

|

|

|

|

|

|

CASH FLOWS FROM INVESTING ACTIVITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment property acquisitions |

|

|

(145,345) |

|

|

— |

Capital expenditures |

|

|

(664,264) |

|

|

(1,144,354) |

Cash received from disposal of investment properties, net |

|

|

3,110,149 |

|

|

— |

Net cash flows from investing activities |

|

|

2,300,540 |

|

|

(1,144,354) |

|

|

|

|

|

|

|

CASH FLOWS FROM FINANCING ACTIVITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

Dividends and distributions paid |

|

|

(685,659) |

|

|

(374,665) |

Repayment of line of credit, short term |

|

|

(1,000,000) |

|

|

— |

Operating partnership unit redemption |

|

|

(77,226) |

|

|

— |

Proceeds from line of credit, short term |

|

|

— |

|

|

1,000,000 |

Repayment of mortgages payable |

|

|

(754,398) |

|

|

(804,282) |

Repurchases of common stock, including costs and fees |

|

|

(32,467) |

|

|

— |

Retire fractional shares resulting from reverse stock split |

|

|

(2,705) |

|

|

(4,999) |

Net cash flows from financing activities |

|

|

(2,552,455) |

|

|

(183,946) |

|

|

|

|

|

|

|

INCREASE (DECREASE) IN CASH, CASH EQUIVALENTS AND RESTRICTED CASH |

|

|

1,159,054 |

|

|

(912,697) |

CASH, CASH EQUIVALENTS AND RESTRICTED CASH, beginning of period |

|

|

3,809,605 |

|

|

5,662,853 |

CASH, CASH EQUIVALENTS AND RESTRICTED CASH, end of period |

|

$ |

4,968,659 |

|

$ |

4,750,156 |

|

|

|

|

|

|

|

CASH AND CASH EQUIVALENTS, end of period, shown in condensed consolidated balance sheets |

|

|

3,121,333 |

|

|

3,015,859 |

RESTRICTED CASH including assets restricted for capital and operating reserves and tenant deposits, end of period, shown in condensed consolidated balance sheets |

|

|

1,847,326 |

|

|

1,734,297 |

CASH, CASH EQUIVALENTS AND RESTRICTED CASH, end of period shown in the condensed consolidated statements of cash flows |

|

$ |

4,968,659 |

|

$ |

4,750,156 |

|

|

|

|

|

|

|

Supplemental Disclosures and Non-Cash Activities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Other cash transactions: |

|

|

|

|

|

|

Interest paid |

|

$ |

2,236,271 |

|

$ |

2,148,248 |

|

|

|

|

|

|

|

Non-cash transactions: |

|

|

|

|

|

|

Issuance of operating partnership units for Citibank Acquisition |

|

$ |

2,400,000 |

|

$ |

— |

Capital expenditures accrued as of September 30, 2024 |

|

|

74,105 |

|

|

— |

See notes to condensed consolidated financial statements

7

Medalist Diversified REIT, Inc. and Subsidiaries

Notes to Unaudited Condensed Consolidated Financial Statements

1. Organization and Basis of Presentation and Consolidation

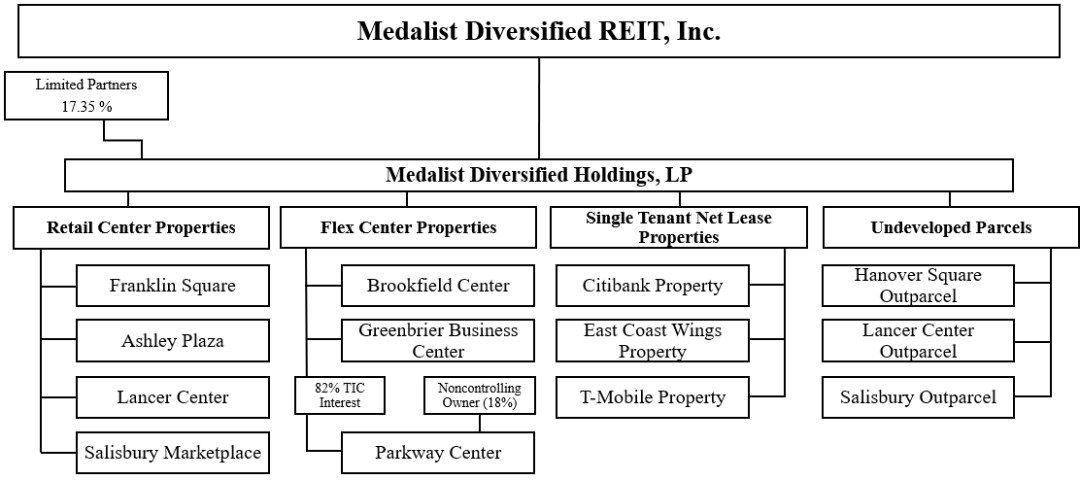

Medalist Diversified Real Estate Investment Trust, Inc. (the “REIT”) is a Maryland corporation formed on September 28, 2015. Beginning with the taxable year ended December 31, 2017, the REIT has elected to be taxed as a real estate investment trust for federal income tax purposes. The REIT serves as the general partner of Medalist Diversified Holdings, LP (the “Operating Partnership”) which was formed as a Delaware limited partnership on September 29, 2015. As of September 30, 2024, the REIT, through the Operating Partnership, owned and operated 10 developed properties consisting of four retail center properties, three flex center properties, and three single tenant net lease (“STNL”) properties, and three undeveloped parcels.

The use of the word “Company” refers to the REIT and its consolidated subsidiaries, except where the context otherwise requires. The Company includes the REIT, the Operating Partnership and wholly-owned limited liability companies which own or operate the properties.

The Company owns four retail center properties consisting of (i) the Shops at Franklin Square, a 134,239 square foot retail property located in Gastonia, North Carolina (the “Franklin Square Property”), (ii) the Ashley Plaza Shopping Center, a 156,012 square foot retail property located in Goldsboro, North Carolina (the “Ashley Plaza Property”), (iii) the Lancer Center, a 181,590 square foot retail property located in Lancaster, South Carolina (the “Lancer Center Property”), and (iv) the Salisbury Marketplace Shopping Center, a 79,732 square foot retail property located in Salisbury, North Carolina (the “Salisbury Marketplace Property”).

On March 13, 2024, the Company, and its tenant in common partner, sold the Shops at Hanover Square North, a 73,440 square foot retail property located in Mechanicsville, Virginia (the “Hanover Square Shopping Center Property”). The Company and its tenant in common partner retained ownership of the 0.86 acre outparcel (the “Hanover Square Outparcel” and together with the Hanover Square Shopping Century Property, the “Hanover Square Property”). The Company owned 84% of the Hanover Square Shopping Center Property and the Hanover Square Outparcel as a tenant in common with a noncontrolling owner which owned the remaining 16% interest. On March 25, 2024, the Company purchased its tenant in common partner’s 16% interest in the Hanover Square Outparcel (see Note 3, below). Collectively, the sale of the Hanover Square Shopping Center and the acquisition of the tenant in common partner’s 16% interest in the Hanover Square Outparcel are referenced herein as the “Hanover Square Transactions”.

The Company owns three flex center properties consisting of (i) Brookfield Center, a 64,880 square foot mixed-use industrial/office property located in Greenville, South Carolina (the “Brookfield Center Property”), (ii) the Greenbrier Business Center, an 89,280 square foot mixed-use industrial/office property located in Chesapeake, Virginia (the “Greenbrier Business Center Property”), and (iii) the Parkway Property, a 64,109 square foot mixed-use industrial office property located in Virginia Beach, Virginia (the "Parkway Property”), in which the Company owns an 82% tenant in common interest with a noncontrolling owner which owns the remaining 18% interest.

8

The Company owns three STNL properties consisting of (i) the Citibank Property, a 4,350 square foot single tenant building on 0.45 acres located in Chicago, Illinois, (ii) the East Coast Wings building, a 5,000 square foot single tenant building on approximately 0.89 acres located in Goldsboro, North Carolina (the “East Coast Wings Property”), and (iii) the T-Mobile building, a 3,000 square foot single tenant building on approximately 0.78 acres located in Goldsboro, North Carolina (the “T-Mobile Property”). The East Coast Wings Property and the T-Mobile Property are both located on outparcels adjacent to the Ashley Plaza Property. Prior to January 1, 2024, the Company included the East Coast Wings Property and the T-Mobile Property as part of the Ashley Plaza Property.

The Company also owns three undeveloped parcels which are currently being marketed for use as STNL properties including (i) an outparcel at its Lancer Center Property consisting of approximately 1.80 acres (the “Lancer Outparcel”), (ii) an outparcel at its Salisbury Marketplace Property consisting of approximately 1.20 acres (the “Salisbury Outparcel”) (the exact size of the Lancer Outparcel and Salisbury Outparcel will not be determined until a user is identified), and (iii) the Hanover Square Outparcel consisting of approximately 0.86 acres located adjacent to the Hanover Square Shopping Center Property, which the Company sold on March 13, 2024.

The Company prepared the accompanying condensed consolidated financial statements in accordance with accounting principles generally accepted in the United States of America (“GAAP”). References to the condensed consolidated financial statements and references to individual financial statements included herein, reference the condensed consolidated financial statements or the respective individual financial statement. All material balances and transactions between the consolidated entities of the Company have been eliminated.

The Company was formed to acquire, reposition, renovate, lease and manage income-producing properties, with a primary focus, as of September 30, 2024, on commercial properties, including retail properties and flex-industrial properties in secondary and tertiary markets in the southeastern part of the United States, with an expected concentration in Virginia, North Carolina, South Carolina, Georgia, Florida and Alabama, and STNL assets with an expected national focus. The Company may also pursue, in an opportunistic manner, other real estate-related investments, including, among other things, equity or other ownership interests in entities that are the direct or indirect owners of real property, indirect investments in real property, such as those that may be obtained in a joint venture. While these types of investments are not intended to be a primary focus, the Company may make such investments at the discretion of the Company’s Board of Directors (the “Board”).

For all periods prior to July 18, 2023, the Company was externally managed by Medalist Fund Manager, Inc. (the “Manager”). On July 18, 2023, the Company and the Manager entered into an agreement (the “Termination Agreement”) terminating that certain Management Agreement, dated as of March 15, 2016, among the Company, the Operating Partnership and the Manager, as amended (the “Management Agreement”). Until the termination of the Management Agreement, the Manager made all investment decisions for the Company, which were approved by the Board’s Acquisition Committee. In addition, until the termination of the Management Agreement, the Manager oversaw the Company’s overall business and affairs and had broad discretion to make operating decisions on behalf of the Company. Since the termination of the Management Agreement, the Company has been managed internally as directed by the Board. The Company’s stockholders are not involved in its day-to-day affairs.

2. Summary of Significant Accounting Policies

Investment Properties

The Company has adopted Accounting Standards Update (“ASU”) 2017-01, Business Combinations (Topic 805), which clarifies the framework for determining whether an integrated set of assets and activities meets the definition of a business. The revised framework establishes a screen for determining whether an integrated set of assets and activities is a business and narrows the definition of a business, which is expected to result in fewer transactions being accounted for as business combinations. Acquisitions of integrated sets of assets and activities that do not meet the definition of a business are accounted for as asset acquisitions. As a result, all of the Company’s acquisitions to date qualified as asset acquisitions and the Company expects future acquisitions of operating properties to qualify as asset acquisitions. Accordingly, third-party transaction costs associated with these acquisitions have been and will be capitalized, while internal acquisition costs will continue to be expensed.

9

Accounting Standards Codification (“ASC”) 805 mandates that “an acquiring entity shall allocate the cost of an acquired entity to the assets acquired and liabilities assumed based on their estimated fair values at date of acquisition.” ASC 805 results in an allocation of acquisition costs to both tangible and intangible assets associated with income producing real estate. Tangible assets include land, buildings, site improvements, tenant improvements and furniture, fixtures and equipment, while intangible assets include the value of in-place leases, lease origination costs (leasing commissions and tenant improvements), legal and marketing costs and leasehold assets and liabilities (above or below market leases), among others.

The Company uses independent, third-party consultants to assist management with its ASC 805 evaluations. The Company determines fair value based on accepted valuation methodologies including the cost, market, and income capitalization approaches. The purchase price is allocated to the tangible and intangible assets identified in the evaluation.

The Company records depreciation on buildings and improvements utilizing the straight-line method over the estimated useful life of the asset, generally 4 to 42 years. The Company reviews depreciable lives of investment properties periodically and makes adjustments to reflect a shorter economic life, when necessary. Capitalized leasing commissions and tenant improvements incurred and paid by the Company subsequent to the acquisition of the investment property are amortized utilizing the straight-line method over the term of the related lease. Amounts allocated to buildings are depreciated over the estimated remaining life of the acquired building or related improvements.

Acquisition and closing costs are capitalized as part of each tangible asset on a pro rata basis. Improvements and major repairs and maintenance are capitalized when the repair and maintenance substantially extend the useful life, increase capacity or improve the efficiency of the asset. All other repair and maintenance costs are expensed as incurred.

Assets Held for Sale

The Company may decide to sell properties that are held as investment properties. The accounting treatment for the disposal of long-lived assets is covered by ASC 360. Under this guidance, the Company records the assets associated with these properties, and any associated mortgages payable, as held for sale when management has committed to a plan to sell the assets, actively seeks a buyer for the assets, and the consummation of the sale is considered probable and is expected within one year. Delays in the time required to complete a sale do not preclude a long-lived asset from continuing to be classified as held for sale beyond the initial one-year period if the delay is caused by events or circumstances beyond an entity’s control and there is sufficient evidence that the entity remains committed to a qualifying plan to sell the long-lived asset.

Properties classified as held for sale are reported at the lower of their carrying value or their fair value, less estimated costs to sell. When the carrying value exceeds the fair value, less estimated costs to sell, an impairment charge is recognized. The Company determines fair value based on the three-level valuation hierarchy for fair value measurement. Level 1 inputs are quoted prices in active markets for identical assets or liabilities. Level 2 inputs are quoted prices for similar assets or liabilities in active markets; quoted prices for identical or similar assets in markets that are not active; and inputs other than quoted prices. Level 3 inputs are unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities.

During November 2023, the Company committed to a plan to sell an asset group associated with the Hanover Square Shopping Center Property that included the land, site improvements, building, building improvements and tenant improvements. As a result, as of December 1, 2023, the Company reclassified these assets, and the related mortgage payable, net, for the Hanover Square Shopping Center Property as assets held for sale and liabilities associated with assets held for sale, respectively. Under ASC 360, depreciation of assets held for sale is discontinued, so no further depreciation or amortization was recorded subsequent to December 1, 2023. The Company believed that the fair value, less estimated costs to sell, exceeded the Company’s carrying cost, so the Company did not record any impairment of assets held for sale related to the Hanover Square Shopping Center Property for any periods, including the three months ended March 31, 2024 and the year ended December 31, 2023, the periods during which the Hanover Square Shopping Center Property was classified as assets held for sale. The Company sold the Hanover Square Shopping Center on March 13, 2024.

10

Intangible Assets and Liabilities, net

The Company determines, through the ASC 805 evaluation, the above and below market lease intangibles upon acquiring a property. Intangible assets (or liabilities) such as above or below-market leases and in-place lease value are recorded at fair value and are amortized as an adjustment to rental revenue or amortization expense, as appropriate, over the remaining terms of the underlying leases. The Company amortizes amounts allocated to tenant improvements, in-place lease assets and other lease-related intangibles over the remaining life of the underlying leases. The analysis is conducted on a lease-by-lease basis.

Details of the deferred costs, net of amortization, arising from the Company’s purchases of its retail center properties, flex center properties and STNL properties are as follows:

|

|

|

September 30, 2024 |

|

|

|

|

|

|

|

(unaudited) |

|

December 31, 2023 |

|

|

Intangible Assets, net |

|

|

|

|

|

|

|

Leasing commissions |

|

$ |

843,627 |

|

$ |

912,040 |

|

Legal and marketing costs |

|

|

79,358 |

|

|

104,791 |

|

Above market leases |

|

|

71,502 |

|

|

106,907 |

|

Net leasehold asset |

|

|

1,453,878 |

|

|

1,592,808 |

|

|

|

$ |

2,448,365 |

|

$ |

2,716,546 |

|

|

|

|

|

|

|

|

|

Intangible Liabilities, net |

|

|

|

|

|

|

|

Below market leases |

|

$ |

(1,736,263) |

|

$ |

(1,865,310) |

|

Capitalized above-market lease values are amortized as a reduction of rental income over the remaining terms of the respective leases. Capitalized below-market lease values are amortized as an increase to rental income over the remaining terms of the respective leases. Adjustments to rental revenue related to the above and below market leases during the three and nine months ended September 30, 2024 and 2023, respectively, were as follows:

|

|

For the three months ended |

|

For the nine months ended |

|

||||||||

|

|

September 30, |

|

September 30, |

|

||||||||

|

|

|

2024 |

|

|

2023 |

|

|

2024 |

|

|

2023 |

|

|

|

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

Amortization of above market leases |

|

$ |

(7,074) |

|

$ |

(23,717) |

|

$ |

(35,405) |

|

$ |

(75,437) |

|

Amortization of below market leases |

|

|

71,241 |

|

|

88,586 |

|

|

228,803 |

|

|

287,341 |

|

|

|

$ |

64,167 |

|

$ |

64,869 |

|

$ |

193,398 |

|

$ |

211,904 |

|

Amortization of lease origination costs, leases in place and legal and marketing costs represent a component of depreciation and amortization expense. Amortization related to these intangible assets during the three and nine months ended September 30, 2024 and 2023, respectively, were as follows:

|

|

For the three months ended |

|

For the nine months ended |

|

||||||||

|

|

September 30, |

|

September 30, |

|

||||||||

|

|

|

2024 |

|

|

2023 |

|

|

2024 |

|

|

2023 |

|

|

|

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

Leasing commissions |

|

$ |

(42,887) |

|

$ |

(53,754) |

|

$ |

(135,097) |

|

$ |

(165,542) |

|

Legal and marketing costs |

|

|

(8,276) |

|

|

(14,745) |

|

|

(30,375) |

|

|

(46,406) |

|

Net leasehold asset |

|

|

(94,735) |

|

|

(147,788) |

|

|

(313,141) |

|

|

(478,345) |

|

|

|

$ |

(145,898) |

|

$ |

(216,287) |

|

$ |

(478,613) |

|

$ |

(690,293) |

|

As of September 30, 2024 and December 31, 2023, the Company’s accumulated amortization of lease origination costs, leases in place and legal and marketing costs totaled $2,092,772 and $2,204,404, respectively. During the three and nine months ended September 30, 2024, the Company wrote off $196,103 and $590,245, respectively, in accumulated amortization related to fully amortized intangible assets, and $0 and $0, respectively, in accumulated amortization related to the write off of intangible assets related to the early terminated leases, discussed below.

11

Future amortization of above and below market leases, lease origination costs, leases in place, legal and marketing costs and tenant relationships is as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

remaining three |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

months ending |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

December 31, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2024 |

|

2025 |

|

2026 |

|

2027 |

|

2028 |

|

2029-2041 |

|

Total |

|||||||

Intangible Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leasing commissions |

|

$ |

41,246 |

|

$ |

154,496 |

|

$ |

116,510 |

|

$ |

97,592 |

|

$ |

76,167 |

|

$ |

357,616 |

|

$ |

843,627 |

Legal and marketing costs |

|

|

7,064 |

|

|

24,456 |

|

|

13,842 |

|

|

8,599 |

|

|

5,886 |

|

|

19,511 |

|

|

79,358 |

Above market leases |

|

|

5,445 |

|

|

21,292 |

|

|

15,629 |

|

|

14,543 |

|

|

10,114 |

|

|

4,479 |

|

|

71,502 |

Net leasehold asset |

|

|

89,357 |

|

|

318,667 |

|

|

223,495 |

|

|

177,171 |

|

|

128,963 |

|

|

516,225 |

|

|

1,453,878 |

|

|

$ |

143,112 |

|

$ |

518,911 |

|

$ |

369,476 |

|

$ |

297,905 |

|

$ |

221,130 |

|

$ |

897,831 |

|

$ |

2,448,365 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Intangible Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Below market leases |

|

$ |

(67,407) |

|

$ |

(227,108) |

|

$ |

(192,535) |

|

$ |

(175,625) |

|

$ |

(153,615) |

|

$ |

(919,973) |

|

$ |

(1,736,263) |

Impairment

No loss on impairment was recorded during the three and nine months ended September 30, 2024. During the three and nine months ended September 30, 2023, the Company recorded a loss on impairment of $0 and $50,859, respectively, resulting from the events described below.

Investment Properties

The Company reviews its investment properties for impairment on a property-by-property basis whenever events or changes in circumstances indicate that the carrying value of investment properties may not be recoverable, but at least annually. These circumstances include, but are not limited to, declines in the property’s cash flows, occupancy and fair market value. The Company measures any impairment of an investment property when the estimated undiscounted cash flows plus its residual value is less than the carrying value of the property. To the extent impairment has occurred, the Company charges to income the excess of the carrying value of the property over its estimated fair value. The Company estimates fair value using unobservable data such as projected future operating income, estimated capitalization rates, or multiples, leasing prospects and local market information. The Company may decide to sell properties that are held for use and the sale prices of these properties may differ from their carrying values. The Company did not record any impairment adjustments to its investment properties resulting from events or changes in circumstances during the three and nine months ended September 30, 2024 and 2023, that would result in the projected value of the Company’s investment properties being below their carrying value.

However, during the nine months ended September 30, 2023, a tenant defaulted on its lease and abandoned its premises. The Company determined that the carrying value of capitalized leasing commissions associated with this lease which were recorded as a component of investment properties on the Company’s condensed consolidated balance sheets should be written off, and the Company recorded a loss on impairment of $5,873 for the nine months ended September 30, 2023. Additionally, during the nine months ended September 30, 2023, the Company agreed to allow a second tenant to terminate its lease early. The Company determined that the carrying value of capitalized tenant improvements associated with this lease which were recorded as a component of investment properties on the Company’s condensed consolidated balance sheets should be written off, and the Company recorded a loss on impairment of $8,655 for the nine months ended September 30, 2023. These amounts are included in the loss on impairment reported on the Company’s condensed consolidated statement of operations for the nine months ended September 30, 2023. No such loss on impairment was recorded for the three months ended September 30, 2023 or for the three and nine months ended September 30, 2024.

Intangible Assets

The Company also reviews its intangible assets for impairment whenever events or changes in circumstances indicate that the carrying value of its intangible assets may not be recoverable, but at least annually. During the nine months ended September 30, 2023, the tenant discussed in the paragraph immediately above terminated its lease early. The Company determined that the carrying value of the intangible assets and liabilities, net, associated with this lease that were recorded as part of the purchase of this property should be written off. As a result, for the nine months ended September 30, 2023, the Company recorded a loss on impairment related to intangible assets of $26,896.

12

This amount is included in the loss on impairment reported on the Company’s condensed consolidated statement of operations for the nine months ended September 30, 2023. No such loss on impairment was recorded for the three months ended September 30, 2023 or for the three and nine months ended September 30, 2024.

Unbilled Rent

The Company also reviews the unbilled rent asset recorded on the Company’s condensed consolidated balance sheets for impairment to determine if any amounts may not be recoverable. During the nine months ended September 30, 2023, the Company wrote off $9,435 in unbilled rent related to the two tenants discussed above. These amounts are included in the loss on impairment reported on the Company’s condensed consolidated statement of operations for the nine months ended September 30, 2023. No such amounts were recorded for the three months ended September 30, 2023 or for the three and nine months ended September 30, 2024.

Conditional Asset Retirement Obligation

A conditional asset retirement obligation represents a legal obligation to perform an asset retirement activity in which the timing and/or method of settlement depends on a future event that may or may not be within the Company’s control. Currently, the Company does not have any conditional asset retirement obligations. However, any such obligations identified in the future would result in the Company recording a liability if the fair value of the obligation can be reasonably estimated. Environmental studies conducted at the time the Company acquired its properties did not reveal any material environmental liabilities, and the Company is unaware of any subsequent environmental matters that would have created a material liability.

The Company believes that its properties are currently in material compliance with applicable environmental, as well as non-environmental, statutory and regulatory requirements. The Company did not record any conditional asset retirement obligation liabilities during the three and nine months ended September 30, 2024 and 2023, respectively.

Cash and Cash Equivalents and Restricted Cash

The Company considers all highly liquid investments purchased with an original maturity of 90 days or less to be cash and cash equivalents. Cash equivalents are carried at cost, which approximates fair value. Cash equivalents consist primarily of bank operating accounts and money markets. Financial instruments that potentially subject the Company to concentrations of credit risk include its cash and equivalents and its trade accounts receivable.

The Company places its cash and cash equivalents and any restricted cash held by the Company on deposit with financial institutions in the United States which are insured by the Federal Deposit Insurance Corporation (“FDIC”) up to $250,000. The Company’s credit loss in the event of failure of these financial institutions is represented by the difference between the FDIC limit and the total amounts on deposit. Management monitors the financial institutions’ credit worthiness in conjunction with balances on deposit to minimize risk. As of September 30, 2024, the Company held four cash accounts at a single financial institution with combined balances that exceeded the FDIC limit by $2,245,752. As of December 31, 2023, the Company held two cash accounts at a single financial institution with combined balances that exceeded the FDIC limit by $1,366,872.

Restricted cash represents amounts held by the Company for tenant security deposits, escrow deposits held by lenders for real estate tax, insurance, and operating reserves, and capital reserves held by lenders for investment property capital improvements.

Tenant security deposits are restricted cash balances held by the Company to offset potential damages, unpaid rent or other unmet conditions of its tenant leases. As of September 30, 2024 and December 31, 2023, the Company reported $248,110 and $260,898, respectively, in security deposits held as restricted cash.

Escrow deposits are restricted cash balances held by lenders for real estate taxes and insurance premiums. As of September 30, 2024 and December 31, 2023, the Company reported $427,960 and $191,139, respectively, in escrow deposits.

13

Capital reserves are restricted cash balances held by lenders for capital improvements, leasing commissions and tenant improvements. As of September 30, 2024 and December 31, 2023, the Company reported $1,171,256 and $1,122,965, respectively, in capital property reserves.

|

|

September 30, 2024 |

|

December 31, |

|

||

Property and Purpose of Reserve |

|

(unaudited) |

|

2023 |

|

||

Ashley Plaza Property – maintenance and leasing cost reserve |

|

|

514,547 |

|

|

439,404 |

|

Brookfield Center Property – maintenance and leasing cost reserve |

|

|

124,737 |

|

|

91,491 |

|

Franklin Square Property – leasing costs |

|

|

531,972 |

|

|

441,360 |

|

Hanover Square Property – operating reserve |

|

|

— |

|

|

150,710 |

|

Total |

|

$ |

1,171,256 |

|

$ |

1,122,965 |

|

Share Retirement

ASC 505-30-30-8 provides guidance on accounting for share retirement and establishes two alternative methods for accounting for the purchase price paid in excess of par value. The Company has elected the method by which the excess between par value and the purchase price, including costs and fees, is recorded to additional paid in capital on the Company’s condensed consolidated balance sheets. During the three and nine months ended September 30, 2024, the Company repurchased 2,830 shares of common stock, $0.01 par value per share (“Common Shares”) at a total cost of $32,467, including $62 in fees associated with this transaction, and at an average price of $11.45 per Common Share (excluding the impact of fees). Of the total repurchase price, $28 was recorded to Common Shares and the difference, $32,439, was recorded to additional paid in capital on the Company’s condensed consolidated balance sheet. No such amounts were recorded during the three and nine months ended September 30, 2023.

Revenue Recognition

Retail, Flex Center and STNL Property Revenues

The Company recognizes minimum rents from its retail center properties, flex center properties and STNL properties on a straight-line basis over the terms of the respective leases which results in an unbilled rent asset being recorded on the condensed consolidated balance sheets. As of September 30, 2024 and December 31, 2023, the Company reported $1,077,746 and $1,109,782, respectively, in unbilled rent.

The Company’s leases generally require the tenant to reimburse the Company for a substantial portion of its expenses incurred in operating, maintaining, repairing, insuring and managing the shopping center and common areas (collectively defined as Common Area Maintenance or “CAM” expenses). The Company includes these reimbursements, along with other revenue derived from late fees and seasonal events, on the condensed consolidated statements of operations under the captions “Retail center property revenues”, “Flex center property revenues”, and “Single tenant net lease asset revenues”. (See Recent Accounting Pronouncements, below.) This significantly reduces the Company’s exposure to increases in costs and operating expenses resulting from inflation or other outside factors. The Company accrues reimbursements from tenants for recoverable portions of all these expenses as revenue in the period the applicable expenditures are incurred. The Company calculates the tenant’s share of operating costs by multiplying the total amount of the operating costs by a fraction, the numerator of which is the total number of square feet being leased by the tenant, and the denominator of which is the average total square footage of all leasable buildings at the property. The Company also receives payments for these reimbursements from substantially all its tenants on a monthly basis throughout the year.

The Company recognizes differences between previously estimated recoveries and the final billed amounts in the year in which the amounts become final. Since these differences are determined annually under the leases and accrued as of December 31 in the year earned, no such revenues were recognized during the three and nine months ended September 30, 2024 and 2023.

The Company recognizes lease termination fees in the period that the lease is terminated and collection of the fees is reasonably assured. Upon early lease termination, any unrecovered intangibles and other assets are written off as a loss on impairment. (See Impairment, above.) The Company did not receive any lease termination fees during the three and nine months ended September 30, 2024 and 2023.

14

Management Restructuring Expenses

On July 18, 2023, the Company and the Operating Partnership entered into a Termination Agreement with the Manager, William R. Elliott and Thomas E. Messier, which provided for the immediate termination of the Management Agreement and, among other things, aggregate payments of $1,602,717 in settlement of all amounts payable under the Management Agreement (consisting of a $1,250,000 termination fee and a $352,717 deferred acquisition fee which represented acquisition fees that had been earned during 2022, but deferred under a deferral agreement). For the three and nine months ended September 30, 2023, the Company recorded $1,452,904 and $1,846,329 in management restructuring expenses, which included the payment of the termination fee, and legal and other expenses associated with the Board’s Special Committee’s (consisting of the Board’s independent directors) exploration of strategic alternatives, as management restructuring expenses on its condensed consolidated statement of operations in accordance with ASC 420-10-S99. The payment of the deferred acquisition fee was recorded as a reduction in accounts payable and accrued liabilities on the Company’s condensed consolidated balance sheet. For the three and nine months ended September 30, 2023, the Company recorded $151,917 and $545,342, respectively, in legal fees associated with the work of the Special Committee as management restructuring expenses and for the three and nine months ended September 30, 2023, the Company recorded $50,987 in expenses associated with the guaranty substitutions (see note 5, below) as management restructuring expenses. No such expenses were recorded for the three and nine months ended September 30, 2024.

Rent and other receivables

Rent and other receivables include tenant receivables related to base rents and tenant reimbursements. Rent and other receivables do not include receivables attributable to recording rents on a straight-line basis, which are included in unbilled rent, discussed above. The Company determines an allowance for the uncollectible portion of accrued rents and accounts receivable based upon customer credit worthiness (including expected recovery of a claim with respect to any tenants in bankruptcy), historical bad debt levels, and current economic trends. The Company considers a receivable past due once it becomes delinquent per the terms of the lease. A past due receivable triggers certain events such as notices, fees and other allowable and required actions per the lease. As of September 30, 2024 and December 31, 2023, the Company’s allowance for uncollectible rent totaled $31,145 and $13,413, respectively, which are comprised of amounts specifically identified based on management’s review of individual tenants’ outstanding receivables. Management determined that no additional general reserve is considered necessary as of September 30, 2024 and December 31, 2023, respectively.

Income Taxes

Beginning with the Company’s taxable year ended December 31, 2017, the REIT has elected to be taxed as a real estate investment trust for federal income tax purposes under Sections 856 through 860 of the Internal Revenue Code and applicable Treasury regulations relating to REIT qualification. In order to maintain this REIT status, the regulations require the Company to distribute at least 90% of its taxable income to stockholders and meet certain other asset and income tests, as well as other requirements. If the Company fails to qualify as a REIT, it will be subject to tax at regular corporate rates for the years in which it fails to qualify. If the Company loses its REIT status it could not elect to be taxed as a REIT for five years unless the Company’s failure to qualify was due to reasonable cause and certain other conditions were satisfied.

Management has evaluated the effect of the guidance provided by GAAP on Accounting for Uncertainty of Income Taxes and has determined that the Company had no uncertain income tax positions.

Use of Estimates

The Company has made estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements, and revenues and expenses during the reported period. The Company’s actual results could differ from these estimates.

15

Noncontrolling Interests

The ownership interests not held by the REIT are considered noncontrolling interests. There are three elements of noncontrolling interests in the capital structure of the Company. These noncontrolling interests have been reported in equity on the condensed consolidated balance sheets but separate from the Company’s equity. On the condensed consolidated statements of operations, the subsidiaries are reported at the consolidated amount, including both the amount attributable to the Company and noncontrolling interests. The Company’s condensed consolidated statements of changes in stockholders’ equity includes beginning balances, activity for the period and ending balances for stockholders’ equity, noncontrolling interests and total equity.