UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 8-K

CURRENT REPORTPURSUANT TO

SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of report (Date of earliest event reported): April 24, 2024

Alerus Financial Corporation

(Exact Name of Registrant as Specified in Charter)

Delaware |

001-39036 |

45-0375407 |

(State or Other Jurisdiction of Incorporation) |

(Commission File Number) |

(IRS Employer Identification No.) |

401 Demers Avenue

Grand Forks, North Dakota 58201

(Address of Principal Executive Offices) (Zip Code)

Registrant's telephone number, including area code: (701) 795-3200

N/A

(Former Name or Former Address, if Changed Since Last Report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

☐Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

☐Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

☐Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange

Act (17 CFR 240.14d-2(b))

☐Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange

Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading symbol |

|

Name of each exchange on which registered |

Common Stock, $1.00 par value per share |

|

ALRS |

|

The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§ 230.405 of this chapter) or Rule 12b–2 of the Securities Exchange Act of 1934 (§ 240.12b–2 of this chapter).

Emerging growth company ☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 2.02. Results of Operations and Financial Condition.

On April 24, 2024, Alerus Financial Corporation (the “Company”) issued a press release announcing its financial results for the three months ended March 31, 2024. A copy of the press release is attached as Exhibit 99.1 to this Form 8-K and is incorporated herein by reference.

The information in Item 2.02 of this Current Report on Form 8-K, and the related Exhibit 99.1, attached hereto is being “furnished” and will not, except to the extent required by applicable law or regulation, be deemed “filed” by the Company for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that section, nor will any of such information or exhibits be deemed incorporated by reference to any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as may be expressly set forth by specific reference in such filing.

Item 7.01. Regulation FD Disclosure.

On April 24, 2024, the Company posted a presentation to the Company’s investor relations website, located at investors.alerus.com. The presentation is also attached hereto as Exhibit 99.2.

The information in Item 7.01 of this Current Report on Form 8-K, and the related Exhibit 99.2, attached hereto is being “furnished” and will not, except to the extent required by applicable law or regulation, be deemed “filed” by the Company for purposes of Section 18 of the Exchange Act, or otherwise subject to the liabilities of that section, nor will any of such information or exhibits be deemed incorporated by reference to any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as may be expressly set forth by specific reference in such filing.

Item 9.01. Financial Statements and Exhibits.

(d) Exhibits

Exhibit No. |

|

Description |

99.1 |

|

Press Release of Alerus Financial Corporation, dated April 24, 2024 |

|

99.2 104 |

|

Investor Presentation of Alerus Financial Corporation Cover Page Interactive Data File (embedded within the Inline XBRL document) |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

Date: April 24, 2024 |

Alerus Financial Corporation |

|

|

|

|

|

|

|

|

By: |

/s/ Katie A. Lorenson |

|

Name: |

Katie A. Lorenson |

|

Title: |

President and Chief Executive Officer |

|

|

|

Exhibit 99.1

|

FOR RELEASE (04.24.2024) |

Alan A. Villalon, Chief Financial Officer 952.417.3733 (Office) |

ALERUS FINANCIAL CORPORATION REPORTS

FIRST QUARTER 2024 NET INCOME OF $6.4 MILLION

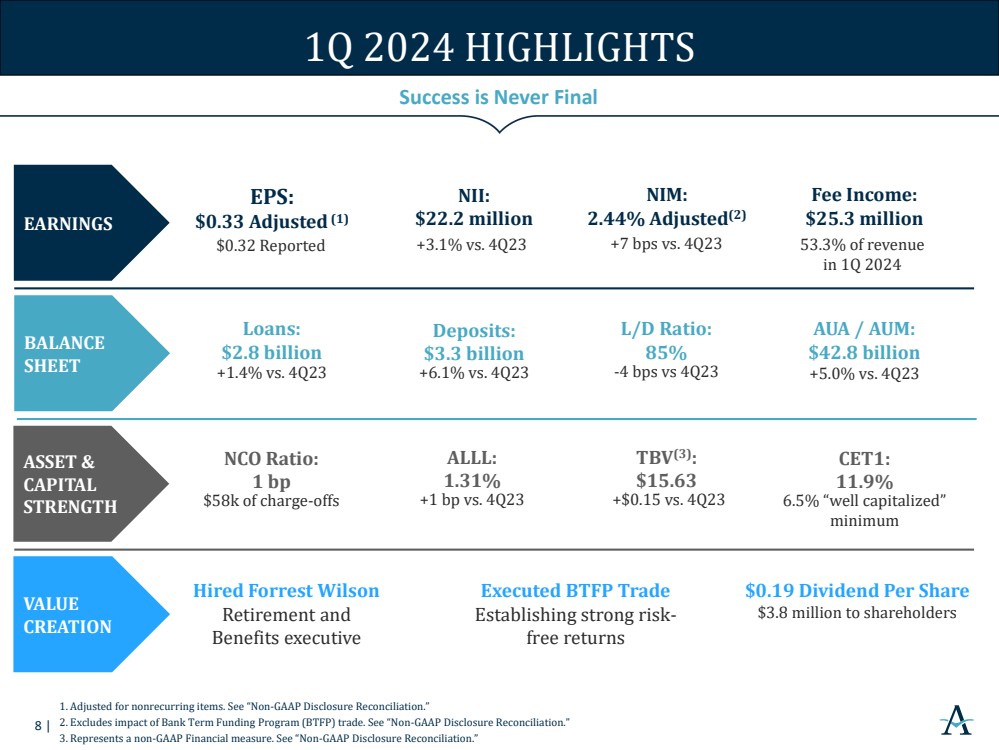

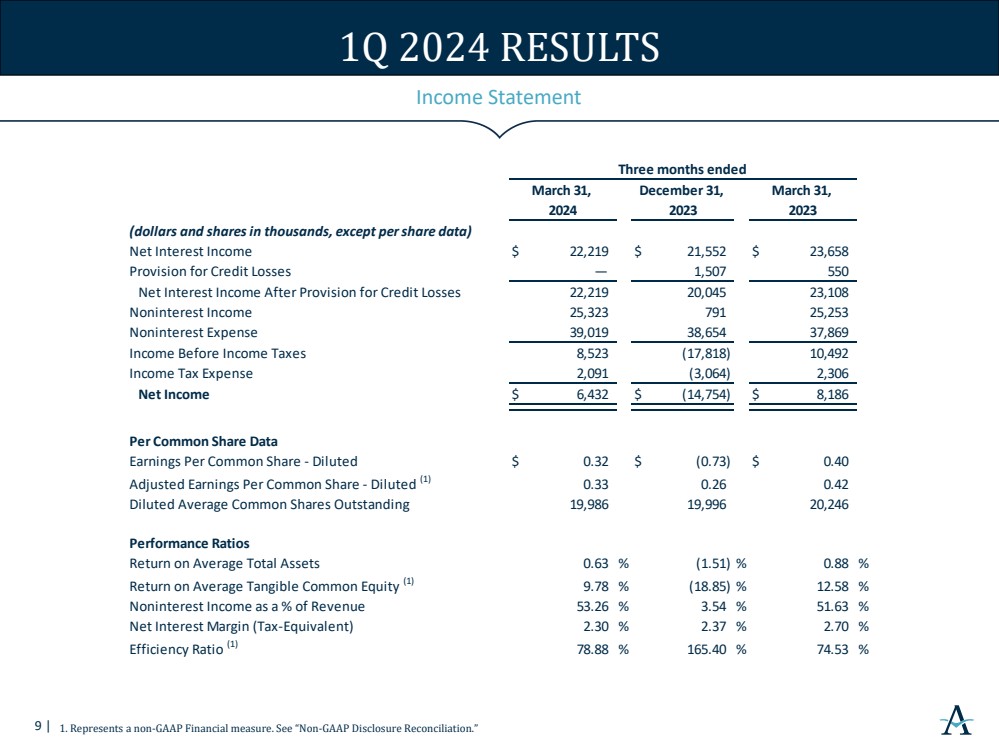

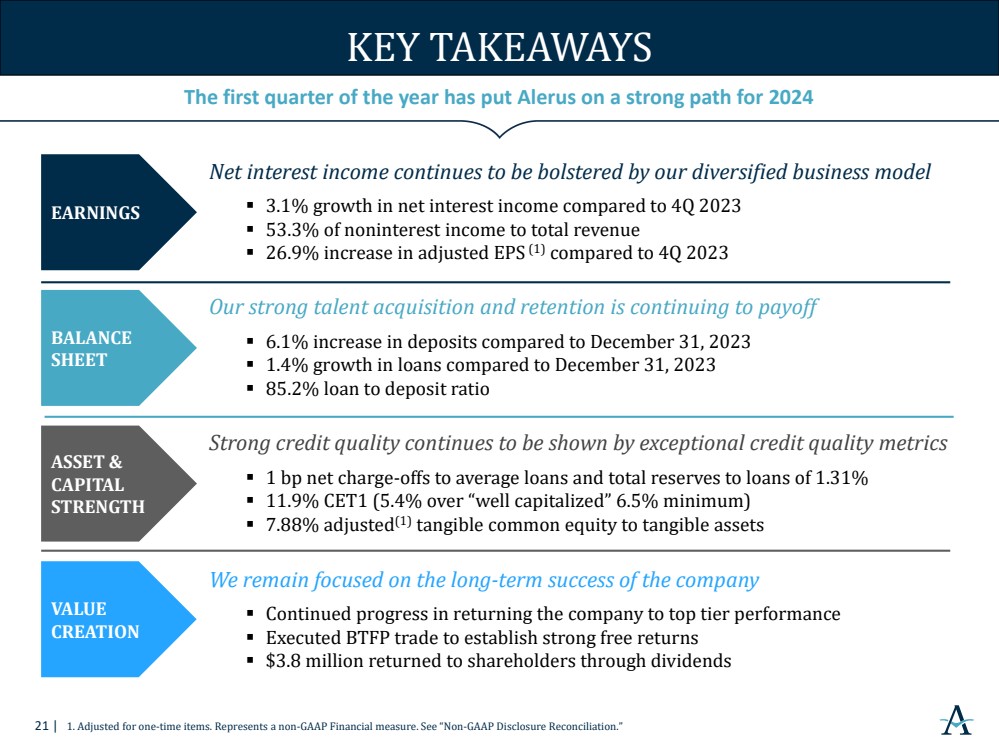

MINNEAPOLIS, MN (April 24, 2024) – Alerus Financial Corporation (Nasdaq: ALRS), or the Company, reported net income of $6.4 million for the first quarter of 2024, or $0.32 per diluted common share, compared to a net loss of $14.8 million, or ($0.73) per diluted common share, for the fourth quarter of 2023, and net income of $8.2 million, or $0.40 per diluted common share, for the first quarter of 2023.

CEO Comments

President and Chief Executive Officer Katie Lorenson said, “Our momentum continues into 2024 as we started the year with strong production and client acquisition in our commercial wealth bank and national retirement businesses. Deposit growth and inflows were robust at over 6%, adjusted net interest margin expanded another 7 basis points and our loan to deposit ratio trended down to 85.2%. We leveraged the Bank Term Funding Program as a strategic arbitrage which was additive to net interest income during the quarter and helped drive over 3% sequential growth. The company’s fee income, which accounted for 53.3% of total revenues, increased across each diversified business line. Our adjusted efficiency ratio decreased slightly, despite the inflationary headwinds, as we continue to manage expenses prudently. Maintaining our fortress balance sheet remained a priority and we ended the quarter with an allowance for credit losses to total loans of 1.31%, a CET1 capital ratio of 11.86%, and growth in tangible book value per common share of 7.8% over the prior year. We continue to make progress in returning the company to top tier performance and remain focused on the long-term success of the company. I would like to thank our team members for all they do to create value for our clients, our communities, and our shareholders.”

First Quarter Highlights

| ◾ | Total deposits were $3.3 billion as of March 31, 2024, an increase of $189.4 million, or 6.1%, from December 31, 2023 |

| ◾ | Total loans were $2.8 billion as of March 31, 2024, an increase of $39.9 million, or 1.4%, from December 31, 2023 |

| ◾ | The loan to deposit ratio as of December 31, 2024 was 85.2%, compared to 89.1% as of December 31, 2023; brokered deposits remained at $0 |

| ◾ | Net interest margin (on a tax equivalent basis) was 2.30% in the first quarter of 2024, compared to 2.37% in the fourth quarter of 2023. Adjusted net interest margin (on a tax-equivalent basis) (non-GAAP) increased 7 basis points from 2.37% in the fourth quarter of 2023 to 2.44% in the first quarter of 2024 |

| ◾ | Net interest income increased 3.1%, from $21.6 million in the fourth quarter of 2023 to $22.2 million in the first quarter of 2024 |

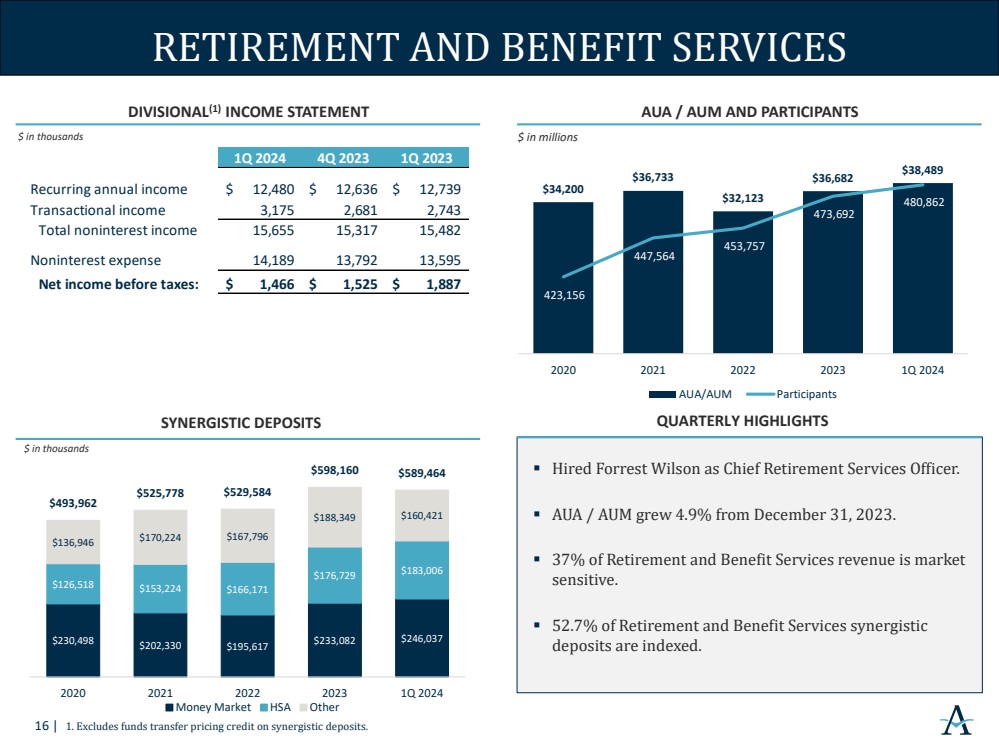

| ◾ | Total assets under administration/management at March 31, 2024 were $42.7 billion, a 5.0% increase from December 31, 2023 |

| ◾ | Net charge-offs to average loans of 0.01% for the first quarter of 2024, compared to net recoveries to average loans of 0.04% for the fourth quarter of 2023 |

| ◾ | Total nonperforming assets were $7.3 million as of March 31, 2024, a decrease of $1.4 million, or 16.2%, from December 31, 2023 |

| ◾ | Allowance for credit losses to nonperforming loans increased from 410% as of December 31, 2023 to 498% as of March 31, 2024 |

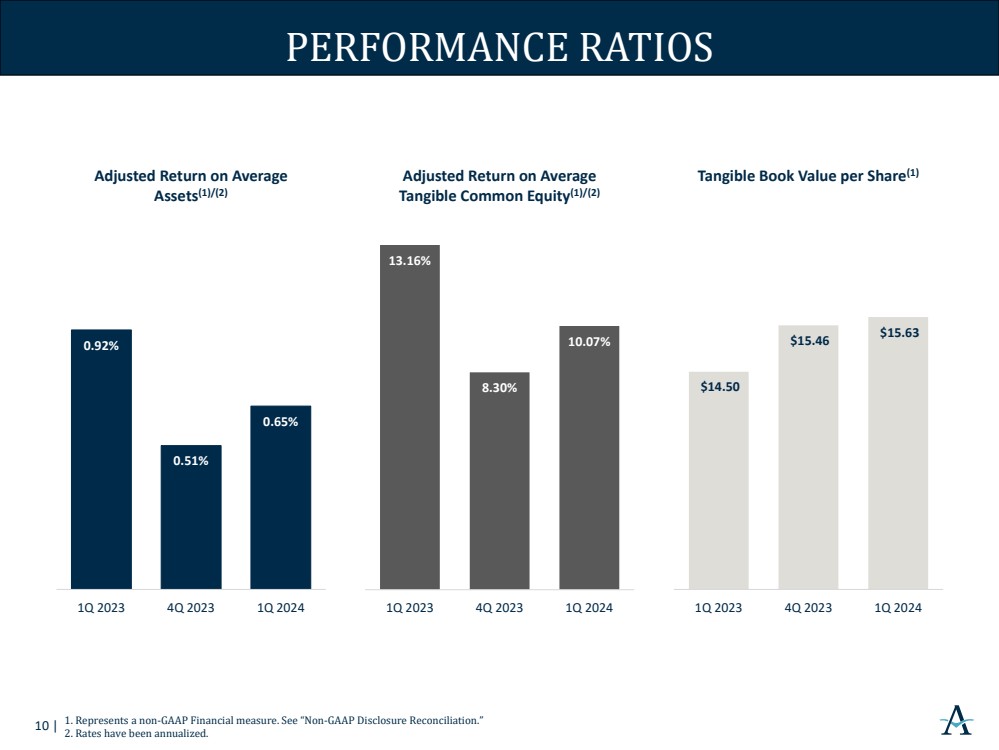

| ◾ | Tangible book value per common share (non-GAAP) was $15.63 as of March 31, 2024, a 1.1% increase from December 31, 2023 |

| ◾ | Common equity tier 1 capital to risk weighted assets as of March 31, 2024 was 11.86%, compared to 11.82% as of December 31, 2023, and continues to be well above the minimum threshold to be “well capitalized” of 6.50% |

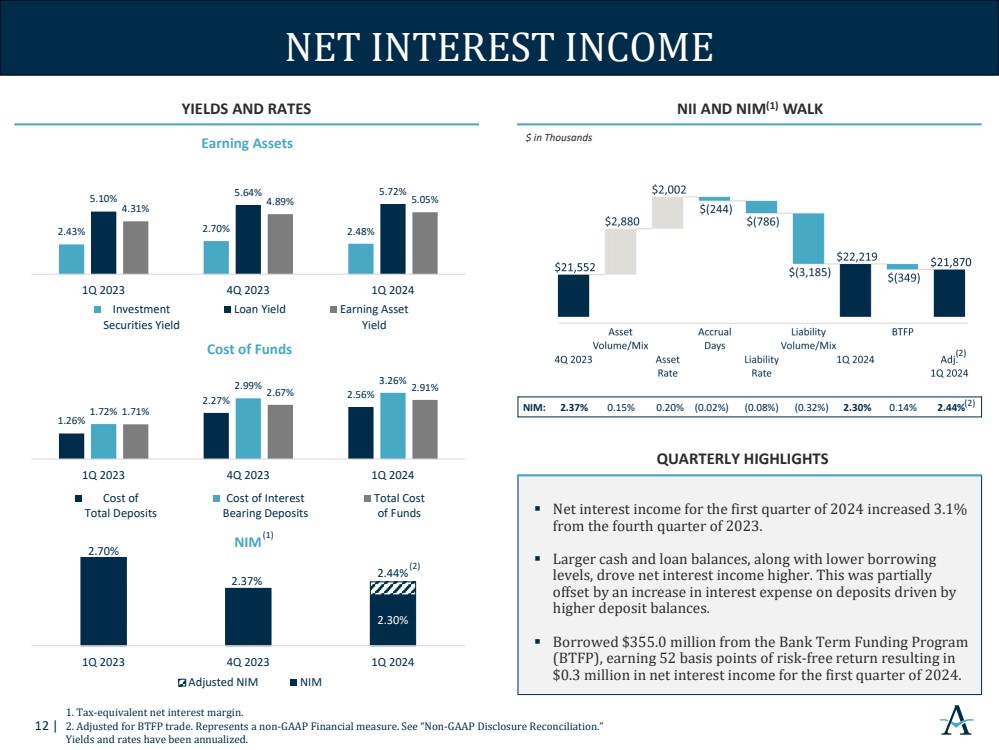

| ◾ | Borrowed $355.0 million from the Bank Term Funding Program (“BTFP”), earning 52 basis points of risk free return resulting in $0.3 million in net interest income for the first quarter of 2024 |

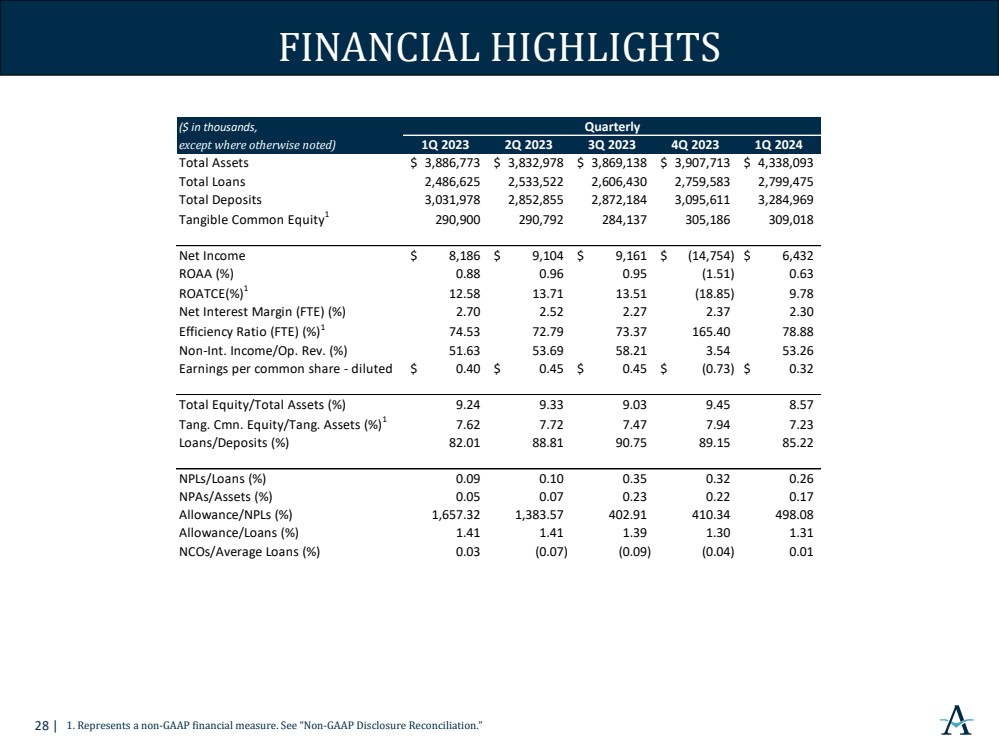

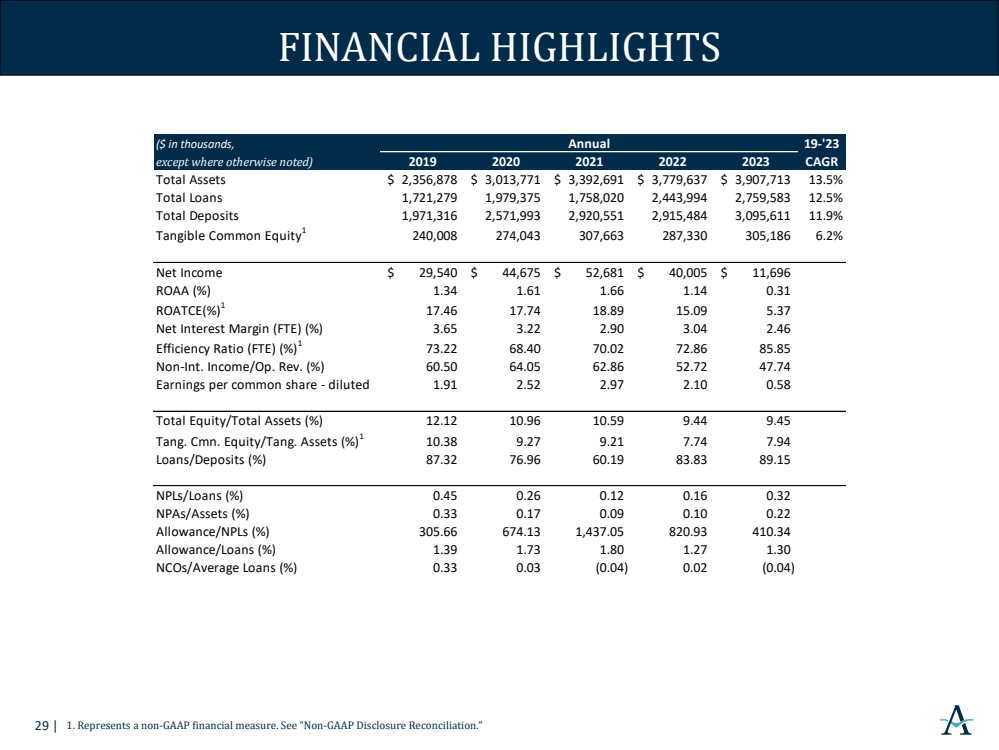

Selected Financial Data (unaudited)

|

|

As of and for the |

|

|||||||

|

|

Three months ended |

|

|||||||

|

|

March 31, |

|

December 31, |

|

March 31, |

|

|||

(dollars and shares in thousands, except per share data) |

|

2024 |

|

2023 |

|

2023 |

|

|||

Performance Ratios |

|

|

|

|

|

|

|

|

|

|

Return on average total assets |

|

|

0.63 |

% |

|

(1.51) |

% |

|

0.88 |

% |

Return on average common equity |

|

|

7.04 |

% |

|

(16.75) |

% |

|

9.17 |

% |

Return on average tangible common equity (1) |

|

|

9.78 |

% |

|

(18.85) |

% |

|

12.58 |

% |

Noninterest income as a % of revenue |

|

|

53.26 |

% |

|

3.54 |

% |

|

51.63 |

% |

Net interest margin (tax-equivalent) |

|

|

2.30 |

% |

|

2.37 |

% |

|

2.70 |

% |

Adjusted net interest margin (tax-equivalent) (1) |

|

|

2.44 |

% |

|

2.37 |

% |

|

2.70 |

% |

Efficiency ratio (1) |

|

|

78.88 |

% |

|

165.40 |

% |

|

74.53 |

% |

Adjusted efficiency ratio (1) |

|

|

78.88 |

% |

|

79.07 |

% |

|

74.53 |

% |

Net charge-offs/(recoveries) to average loans |

|

|

0.01 |

% |

|

(0.04) |

% |

|

0.03 |

% |

Dividend payout ratio |

|

|

59.38 |

% |

|

(26.03) |

% |

|

45.00 |

% |

Per Common Share |

|

|

|

|

|

|

|

|

|

|

Earnings per common share - basic |

|

$ |

0.32 |

|

$ |

(0.74) |

|

$ |

0.41 |

|

Earnings per common share - diluted |

|

$ |

0.32 |

|

$ |

(0.73) |

|

$ |

0.40 |

|

Dividends declared per common share |

|

$ |

0.19 |

|

$ |

0.19 |

|

$ |

0.18 |

|

Book value per common share |

|

$ |

18.79 |

|

$ |

18.71 |

|

$ |

17.90 |

|

Tangible book value per common share (1) |

|

$ |

15.63 |

|

$ |

15.46 |

|

$ |

14.50 |

|

Average common shares outstanding - basic |

|

|

19,739 |

|

|

19,761 |

|

|

20,028 |

|

Average common shares outstanding - diluted |

|

|

19,986 |

|

|

19,996 |

|

|

20,246 |

|

Other Data |

|

|

|

|

|

|

|

|

|

|

Retirement and benefit services assets under administration/management |

|

$ |

38,488,523 |

|

$ |

36,682,425 |

|

$ |

33,404,342 |

|

Wealth management assets under administration/management |

|

$ |

4,242,408 |

|

$ |

4,018,846 |

|

$ |

3,675,684 |

|

Mortgage originations |

|

$ |

54,101 |

|

$ |

65,488 |

|

$ |

77,728 |

|

Results of Operations

Net Interest Income

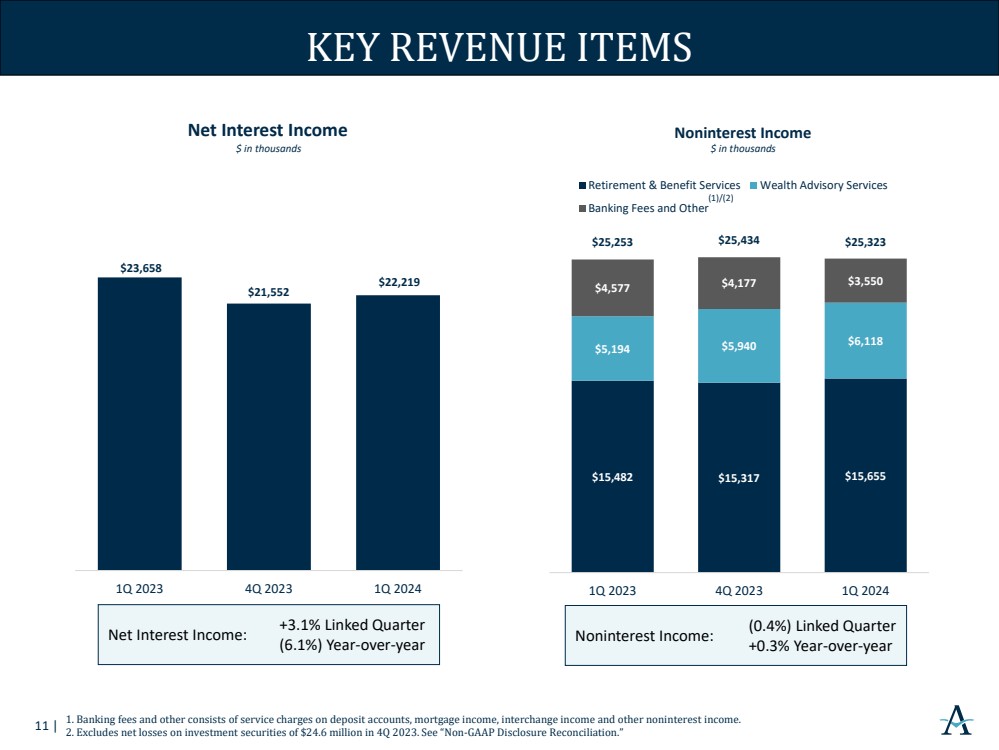

Net interest income for the first quarter of 2024 was $22.2 million, a $667.0 thousand, or 3.1%, increase from the fourth quarter of 2023. The increase was due to interest income on increased cash balances from deposit growth and BTFP borrowings, as well as increased loan balances and lower interest expense on borrowings due to lower borrowing balances. The increase was partially offset by an increase in interest expense on deposits, driven by higher deposit balances.

Net interest income decreased $1.4 million, or 6.1%, from $23.7 million for the first quarter of 2023 due to heightened deposit competition, the impact of higher short-term interest rates on indexed money market deposits, and clients moving deposits out of noninterest bearing products into interest-bearing products. Interest income increased $11.2 million, or 29.7%, from the first quarter of 2023, primarily driven by higher yields on new loans and strong organic loan growth, in addition to interest income on higher cash balances due to the Company’s excess cash position. The increase in interest income was offset by a $12.7 million, or 89.5%, increase in interest expense, primarily due to an increase in rates paid on interest-bearing deposits and higher short-term borrowing balances.

Net interest margin (on a tax-equivalent basis), was 2.30% for the first quarter of 2024, a 7 basis point decrease from 2.37% for the fourth quarter of 2023, and a 40 basis point decrease from 2.70% for the first quarter of 2023. The decrease in net interest margin (on a tax-equivalent basis) was mainly attributable to higher earning assets at lower yields resulting from the BTFP opportunity. Adjusted net interest margin (on a tax-equivalent basis) (non-GAAP), which excludes BTFP borrowings, was 2.44% for the first quarter of 2024, a 7 basis point increase from 2.37% for the fourth quarter of 2023, and a 26 basis point decrease from 2.70% for the first quarter of 2023. The increase in adjusted net interest margin (on a tax-equivalent basis) (non-GAAP) from the prior quarter reflected higher yields on new loans, partially offset by higher cost of funds from continued growth on interest-bearing deposits.

2

Noninterest Income

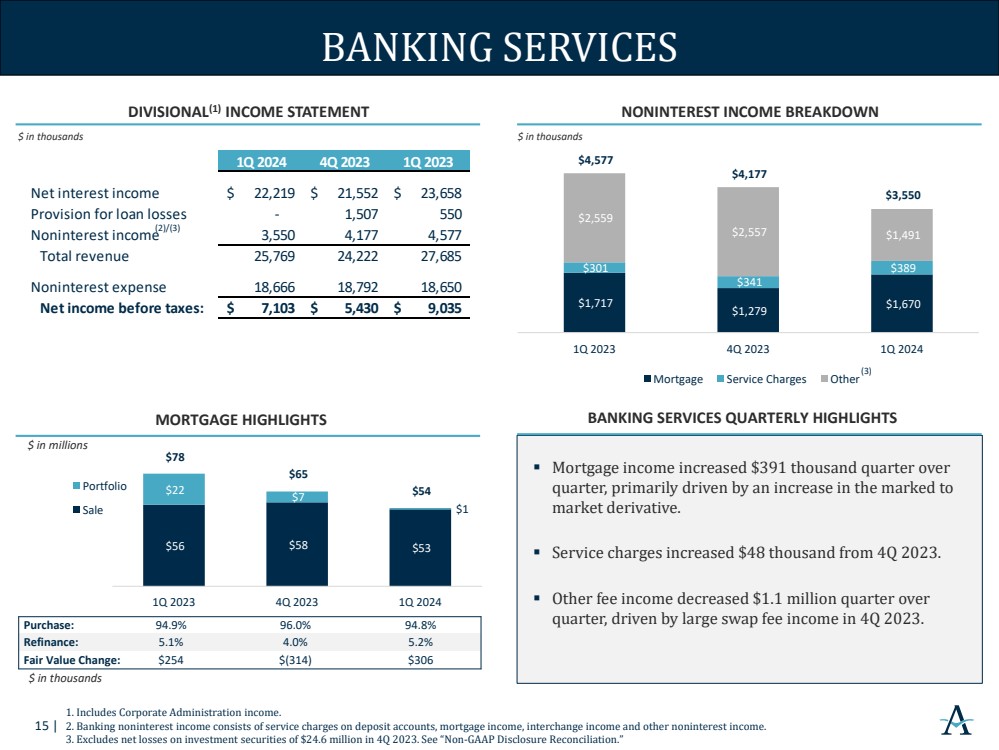

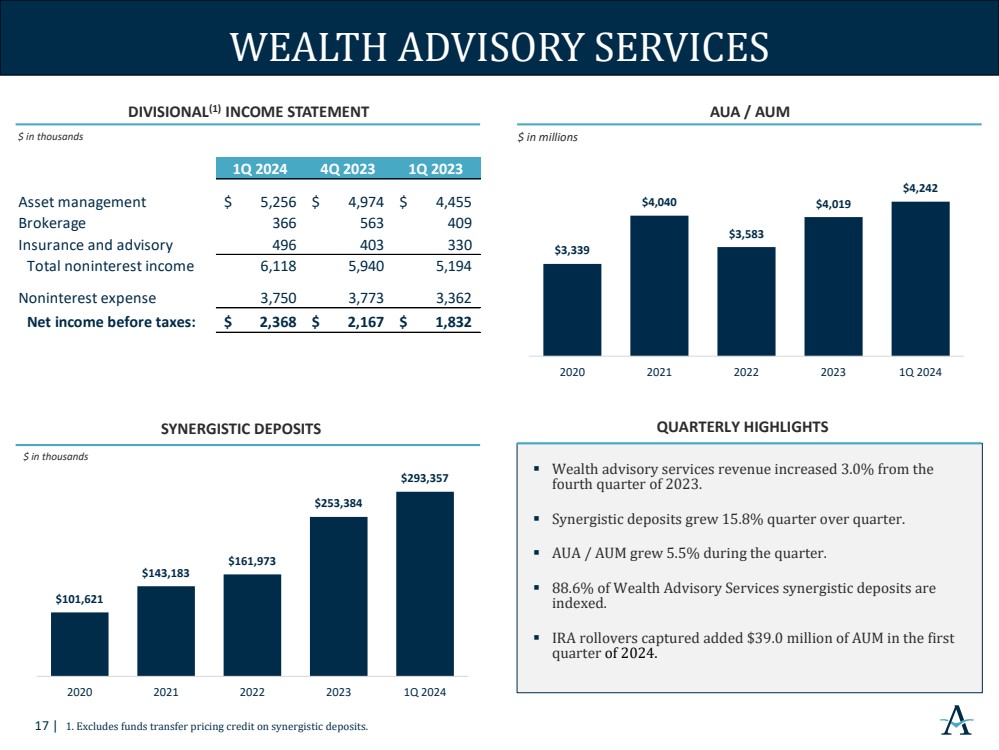

Noninterest income for the first quarter of 2024 was $25.3 million, a $24.5 million increase from the fourth quarter of 2023. The quarter over quarter increase was primarily driven by the balance sheet repositioning in the fourth quarter of 2023. Adjusted noninterest income (non-GAAP) for the first quarter of 2024 was $25.3 million, a 0.4% decrease from the fourth quarter of 2023. Retirement and benefit services revenue increased $0.3 million, a 2.2% increase from fourth quarter of 2023 results, primarily due to the growth in both asset-based revenue and transaction-based revenue. Assets under administration/management in retirement and benefit services increased 4.9% from December 31, 2023, due to improved equity and bond markets. Wealth management revenues increased $0.2 million during the first quarter of 2024, a 3.0% increase from the fourth quarter of 2023, as assets under administration/management increased 5.6% during that same period. Mortgage saw a $0.4 million increase in mortgage banking revenue with mortgage originations of $54.1 million for the first quarter of 2024, compared to originations of $65.5 million in the fourth quarter of 2023, primarily driven by an increase in the marked to market derivative.

Noninterest income for the first quarter of 2024 was $25.3 million, an increase of $71 thousand, or 0.3%, from the first quarter of 2023. While overall noninterest income was stable year over year, wealth management revenues increased $0.9 million, or 17.8%, in the first quarter of 2024 as assets under administration/management increased 15.4% during that same period. Offsetting this increase, other revenue decreased $1.1 million, or 41.7%, from $2.6 million in the first quarter of 2023, primarily due to $1.2 million in proceeds received on a bank-owned life insurance claim in the first quarter of 2023.

Noninterest Expense

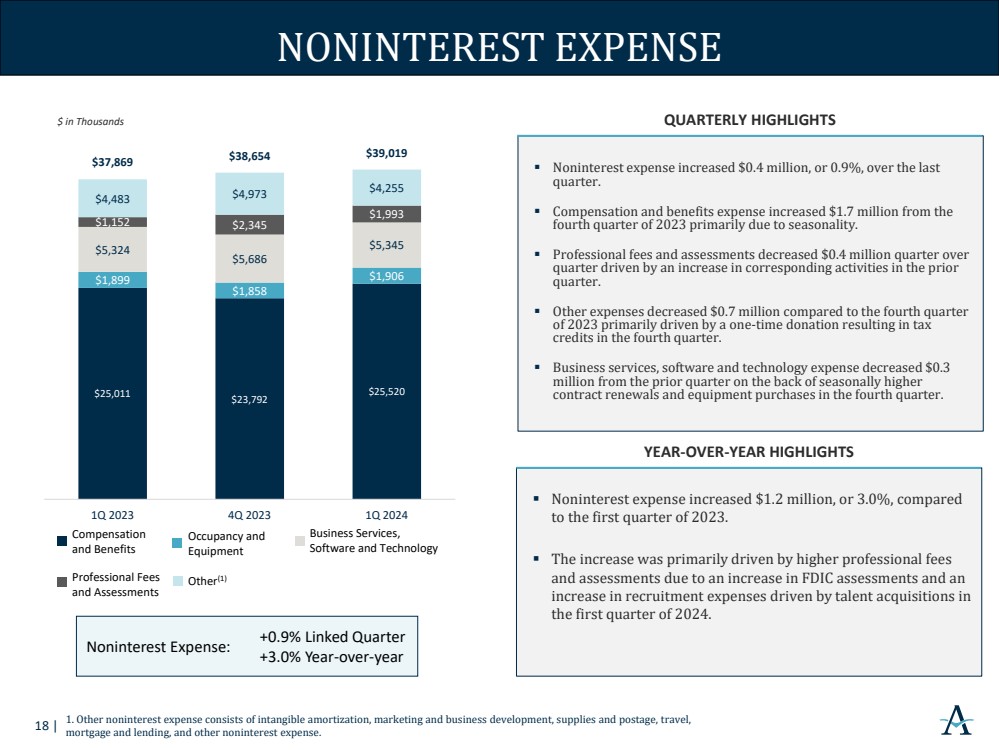

Noninterest expense for the fourth quarter of 2024 was $39.0 million, a $0.4 million, or 0.9%, increase from the fourth quarter of 2023. Employee taxes and benefits expense increased $1.6 million, a 35.2% increase from the fourth quarter of 2023, primarily due to seasonality. This was partially offset by decreases in professional fees and assessments, business services, software and technology expense, and marketing and business development expense totaling $1.0 million compared to the fourth quarter of 2023. Professional fees and assessments expense decreased $0.4 million, or 15.0%, from the fourth quarter of 2023, primarily driven by higher fees resulting from increased audit, examination, and other professional fees in the fourth quarter of 2023. Business services, software and technology expense decreased $0.3 million, or 6.0%, from the fourth quarter of 2023, primarily driven by seasonally higher contract renewals due to inflationary pressures and equipment purchases in the fourth quarter of 2023. Marketing and business development expense decreased $0.3 million, or 31.6%, from the fourth quarter of 2023 due to a one-time donation resulting in tax credits in the fourth quarter of 2023.

Noninterest expense for the first quarter of 2024 increased $1.2 million, or 3.0%, from $37.9 million in the first quarter of 2023. The increase was primarily driven by higher professional fees and assessments due to an increase in Federal Deposit Insurance Corporation (“FDIC”) assessments and an increase in recruitment expense driven by talent acquisitions in the first quarter of 2024.

Financial Condition

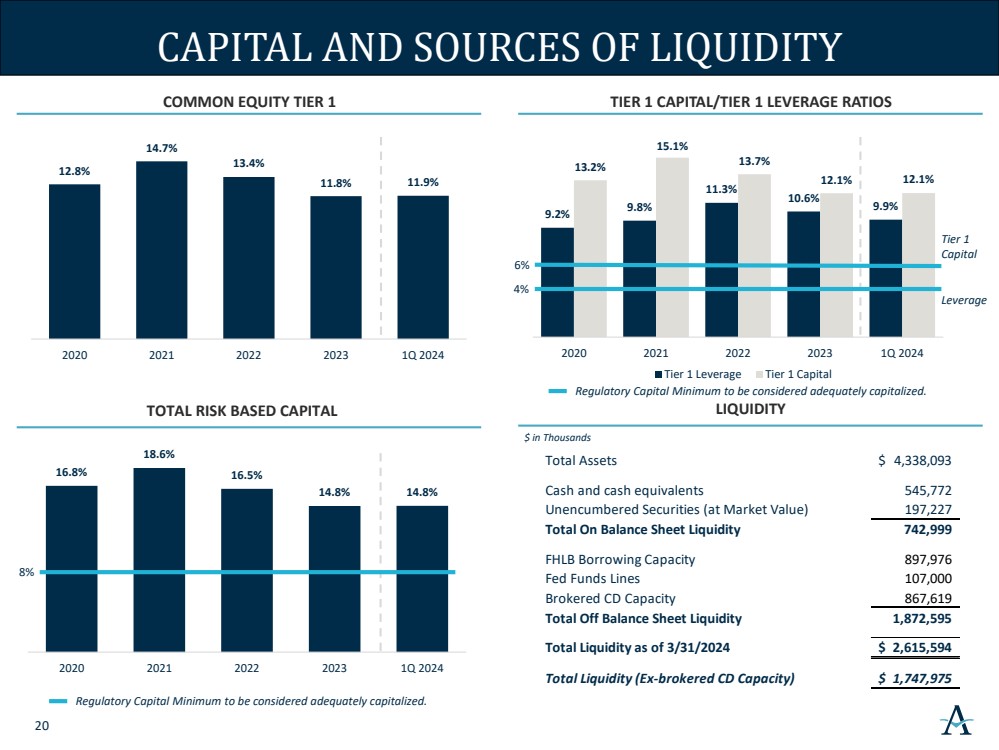

Total assets were $4.3 billion as of March 31, 2024, an increase of $430.4 million, or 11.0%, from December 31, 2023. The increase was primarily due to a $415.9 million increase in cash and cash equivalents and a $39.9 million increase in loans, partially offset by a decrease of $17.5 million in investment securities. The increase in cash and cash equivalents was primarily driven by the proceeds from BTFP borrowings.

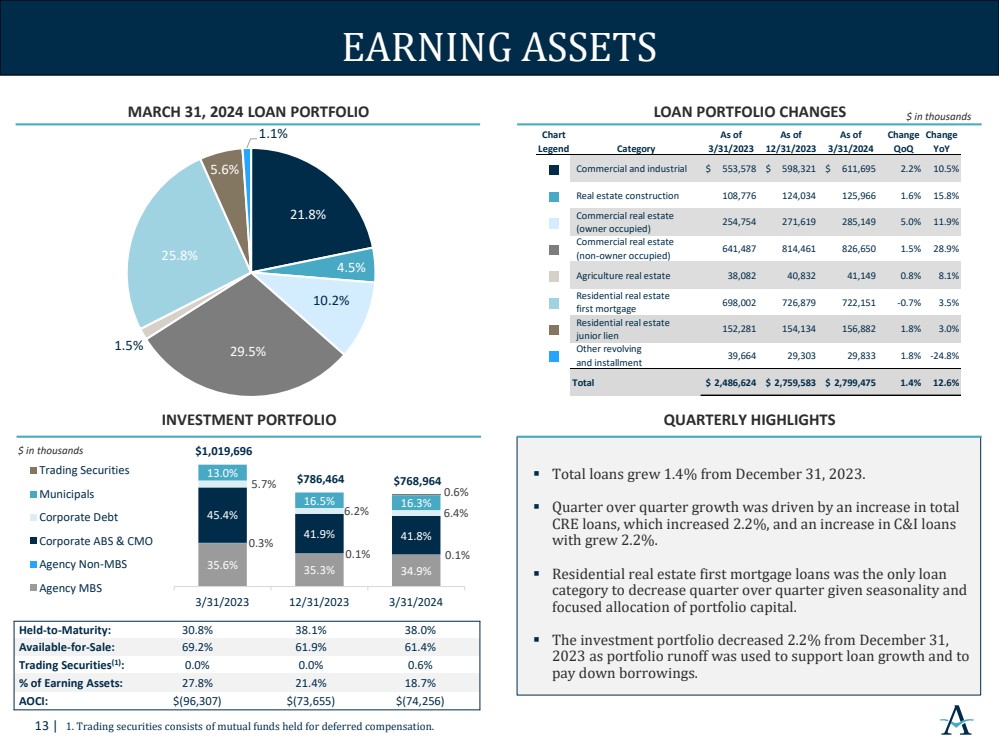

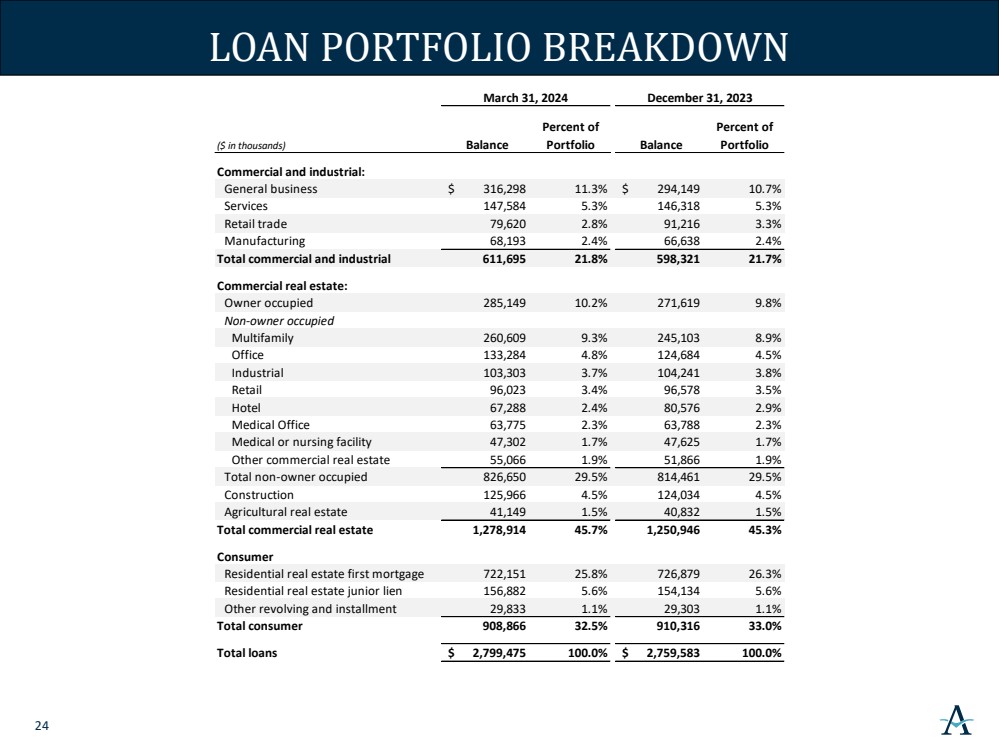

Loans

Total loans were $2.8 billion as of March 31, 2024, an increase of $39.9 million, or 1.4%, from December 31, 2023. The increase was primarily driven by a $26.0 million increase in commercial real estate loans, a $13.4 million increase commercial and industrial loans, a $2.7 million increase in residential real estate junior lien loans, and a $1.9 million increase in real estate construction loans, partially offset by a $4.7 million decrease in residential real estate first mortgage loans.

3

The following table presents the composition of our loan portfolio as of the dates indicated:

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|||||

(dollars in thousands) |

|

2024 |

|

2023 |

|

2023 |

|

2023 |

|

2023 |

|||||

Commercial |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial and industrial |

|

$ |

611,695 |

|

$ |

598,321 |

|

$ |

582,387 |

|

$ |

551,860 |

|

$ |

553,578 |

Real estate construction |

|

|

125,966 |

|

|

124,034 |

|

|

97,742 |

|

|

78,428 |

|

|

108,776 |

Commercial real estate |

|

|

1,152,948 |

|

|

1,126,912 |

|

|

1,025,014 |

|

|

1,003,821 |

|

|

934,324 |

Total commercial |

|

|

1,890,609 |

|

|

1,849,267 |

|

|

1,705,143 |

|

|

1,634,109 |

|

|

1,596,678 |

Consumer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Residential real estate first mortgage |

|

|

722,151 |

|

|

726,879 |

|

|

717,793 |

|

|

707,630 |

|

|

698,002 |

Residential real estate junior lien |

|

|

156,882 |

|

|

154,134 |

|

|

152,677 |

|

|

157,231 |

|

|

152,281 |

Other revolving and installment |

|

|

29,833 |

|

|

29,303 |

|

|

30,817 |

|

|

34,552 |

|

|

39,664 |

Total consumer |

|

|

908,866 |

|

|

910,316 |

|

|

901,287 |

|

|

899,413 |

|

|

889,947 |

Total loans |

|

$ |

2,799,475 |

|

$ |

2,759,583 |

|

$ |

2,606,430 |

|

$ |

2,533,522 |

|

$ |

2,486,625 |

Deposits

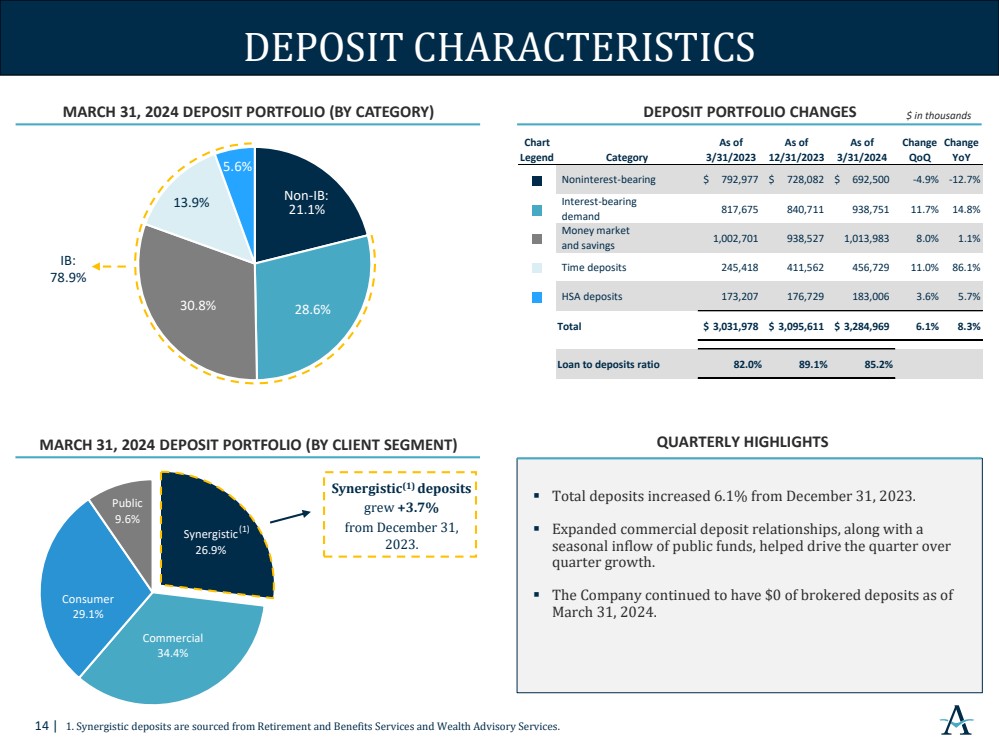

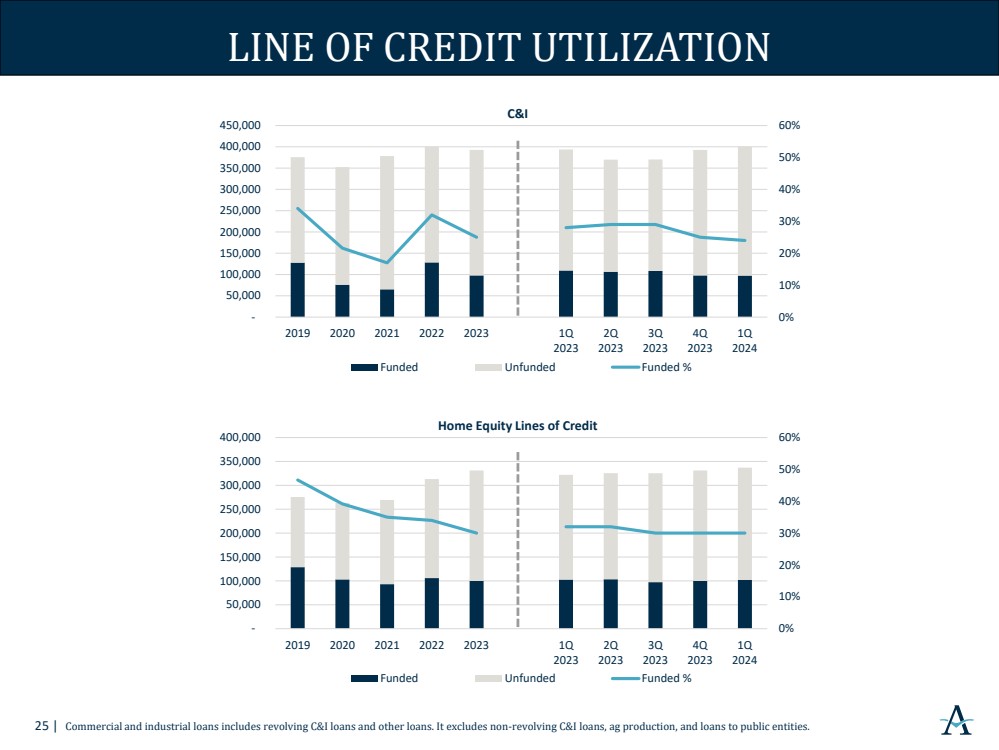

Total deposits were $3.3 billion as of March 31, 2024, an increase of $189.4 million, or 6.1%, from December 31, 2023. Interest-bearing deposits increased $224.9 million, while noninterest-bearing deposits decreased $35.6 million, from December 31, 2023. The increase in total deposits was due to both seasonal inflows of public funds deposit balances and expanded commercial deposit relationships, along with time deposit and synergistic deposit growth. Synergistic deposits were $882.8 million as of March 31, 2024, an increase of $31.3 million, or 3.7%, from December 31, 2023. The Company continued to have $0 of brokered deposits as of March 31, 2024.

The following table presents the composition of our deposit portfolio as of the dates indicated:

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|||||

(dollars in thousands) |

|

2024 |

|

2023 |

|

2023 |

|

2023 |

|

2023 |

|||||

Noninterest-bearing demand |

|

$ |

692,500 |

|

$ |

728,082 |

|

$ |

717,990 |

|

$ |

715,534 |

|

$ |

792,977 |

Interest-bearing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing demand |

|

|

938,751 |

|

|

840,711 |

|

|

759,812 |

|

|

753,194 |

|

|

817,675 |

Savings accounts |

|

|

82,727 |

|

|

82,485 |

|

|

88,341 |

|

|

93,557 |

|

|

99,742 |

Money market savings |

|

|

1,114,262 |

|

|

1,032,771 |

|

|

959,106 |

|

|

986,403 |

|

|

1,076,166 |

Time deposits |

|

|

456,729 |

|

|

411,562 |

|

|

346,935 |

|

|

304,167 |

|

|

245,418 |

Total interest-bearing |

|

|

2,592,469 |

|

|

2,367,529 |

|

|

2,154,194 |

|

|

2,137,321 |

|

|

2,239,001 |

Total deposits |

|

$ |

3,284,969 |

|

$ |

3,095,611 |

|

$ |

2,872,184 |

|

$ |

2,852,855 |

|

$ |

3,031,978 |

Asset Quality

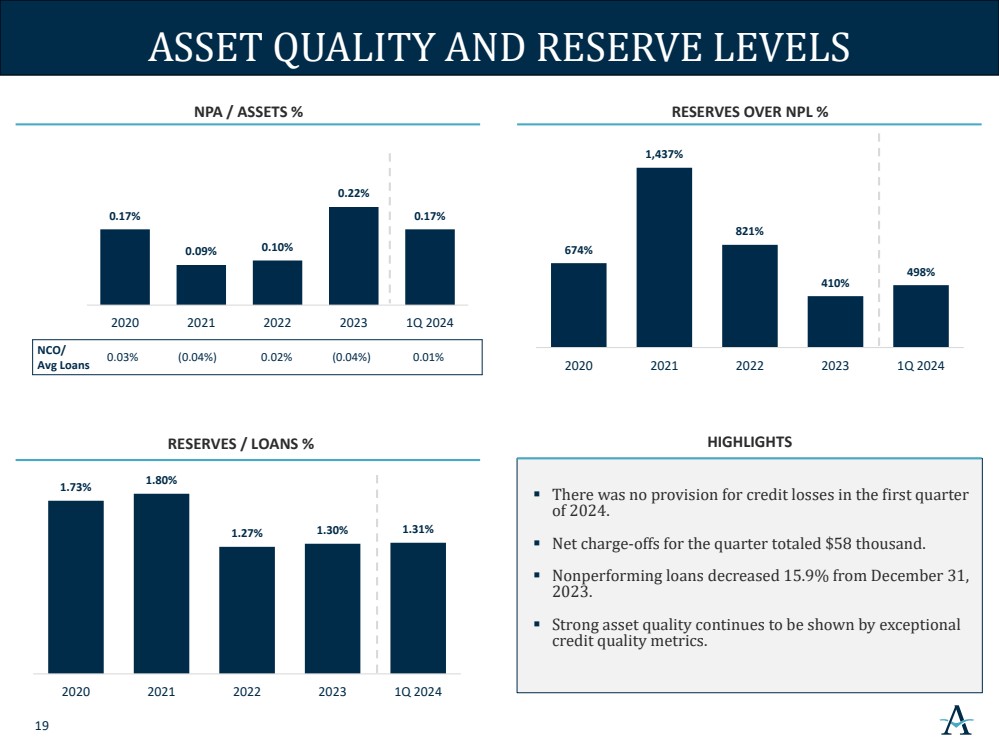

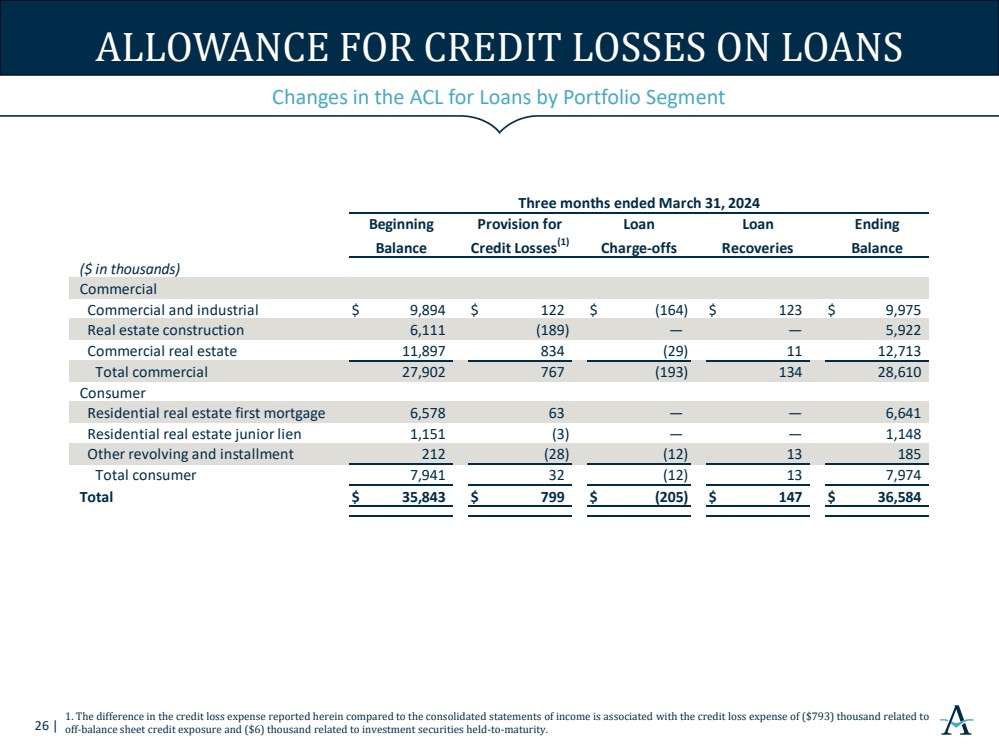

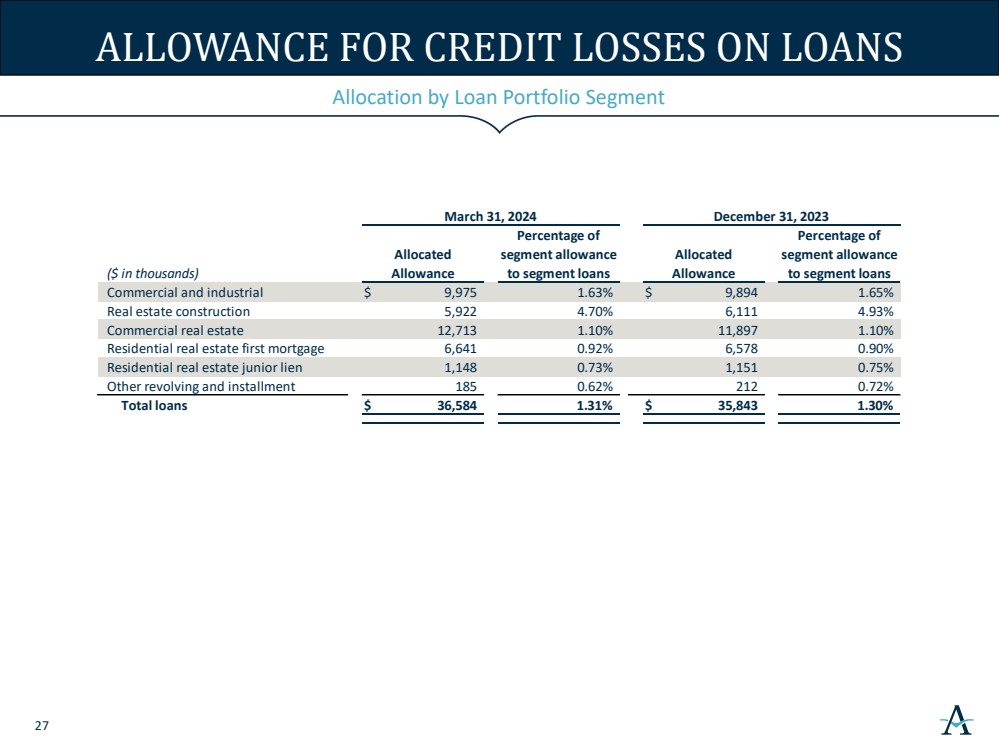

Total nonperforming assets were $7.3 million as of March 31, 2024, a decrease of $1.4 million, or 16.2%, from December 31, 2023. As of March 31, 2024, the allowance for credit losses on loans was $36.6 million, or 1.31% of total loans, compared to $35.8 million, or 1.30% of total loans, as of December 31, 2023.

4

The following table presents selected asset quality data as of and for the periods indicated:

|

|

As of and for the three months ended |

|

|||||||||||||

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|

|||||

(dollars in thousands) |

|

2024 |

|

2023 |

|

2023 |

|

2023 |

|

2023 |

|

|||||

Nonaccrual loans |

|

$ |

7,345 |

|

$ |

8,596 |

|

$ |

9,007 |

|

$ |

2,233 |

|

$ |

2,118 |

|

Accruing loans 90+ days past due |

|

|

— |

|

|

139 |

|

|

— |

|

|

347 |

|

|

— |

|

Total nonperforming loans |

|

|

7,345 |

|

|

8,735 |

|

|

9,007 |

|

|

2,580 |

|

|

2,118 |

|

OREO and repossessed assets |

|

|

3 |

|

|

32 |

|

|

3 |

|

|

— |

|

|

— |

|

Total nonperforming assets |

|

$ |

7,348 |

|

$ |

8,767 |

|

$ |

9,010 |

|

$ |

2,580 |

|

$ |

2,118 |

|

Net charge-offs/(recoveries) |

|

|

58 |

|

|

(238) |

|

|

(594) |

|

|

(403) |

|

|

170 |

|

Net charge-offs/(recoveries) to average loans |

|

|

0.01 |

% |

|

(0.04) |

% |

|

(0.09) |

% |

|

(0.07) |

% |

|

0.03 |

% |

Nonperforming loans to total loans |

|

|

0.26 |

% |

|

0.32 |

% |

|

0.35 |

% |

|

0.10 |

% |

|

0.09 |

% |

Nonperforming assets to total assets |

|

|

0.17 |

% |

|

0.22 |

% |

|

0.23 |

% |

|

0.07 |

% |

|

0.05 |

% |

Allowance for credit losses on loans to total loans |

|

|

1.31 |

% |

|

1.30 |

% |

|

1.39 |

% |

|

1.41 |

% |

|

1.41 |

% |

Allowance for credit losses on loans to nonperforming loans |

|

|

498 |

% |

|

410 |

% |

|

403 |

% |

|

1,384 |

% |

|

1,657 |

% |

For the first quarter of 2024, the Company had net charge-offs of $58 thousand, compared to net recoveries of $238 thousand for the fourth quarter of 2023 and net charge-offs of $170 thousand for the first quarter of 2023.

The Company recorded no provision for credit losses for the first quarter of 2024, compared to a provision of $1.5 million for the fourth quarter of 2023 and a provision of $550 thousand for the first quarter of 2023. The unearned fair value adjustments on the acquired Metro Phoenix Bank loan portfolio were $4.7 million as of March 31, 2024, $5.2 million as of December 31, 2023, and $6.9 million as of March 31, 2023.

Capital

Total stockholders’ equity was $371.6 million as of March 31, 2024, an increase of $2.5 million from December 31, 2023. This change was primarily driven by an increase in retained earnings of $2.7 million. Tangible book value per common share (non-GAAP) increased to $15.63 as of March 31, 2024, from $15.46 as of December 31, 2023. Tangible common equity to tangible assets (non-GAAP) decreased to 7.23% as of March 31, 2024, from 7.94% as of December 31, 2023. Common equity tier 1 capital to risk weighted assets increased to 11.86% as of March 31, 2024, from 11.82% as of December 31, 2023.

The following table presents our capital ratios as of the dates indicated:

|

|

March 31, |

|

December 31, |

|

March 31, |

|

|||

|

|

2024 |

|

2023 |

|

2023 |

|

|||

Capital Ratios(1) |

|

|

|

|

|

|

|

|

|

|

Alerus Financial Corporation Consolidated |

|

|

|

|

|

|

|

|

|

|

Common equity tier 1 capital to risk weighted assets |

|

|

11.86 |

% |

|

11.82 |

% |

|

13.30 |

% |

Tier 1 capital to risk weighted assets |

|

|

12.13 |

% |

|

12.10 |

% |

|

13.60 |

% |

Total capital to risk weighted assets |

|

|

14.79 |

% |

|

14.76 |

% |

|

16.51 |

% |

Tier 1 capital to average assets |

|

|

9.89 |

% |

|

10.57 |

% |

|

11.00 |

% |

Tangible common equity / tangible assets (2) |

|

|

7.23 |

% |

|

7.96 |

% |

|

7.62 |

% |

|

|

|

|

|

|

|

|

|

|

|

Alerus Financial, N.A. |

|

|

|

|

|

|

|

|

|

|

Common equity tier 1 capital to risk weighted assets |

|

|

11.71 |

% |

|

11.40 |

% |

|

12.67 |

% |

Tier 1 capital to risk weighted assets |

|

|

11.71 |

% |

|

11.40 |

% |

|

12.67 |

% |

Total capital to risk weighted assets |

|

|

12.87 |

% |

|

12.51 |

% |

|

13.87 |

% |

Tier 1 capital to average assets |

|

|

9.30 |

% |

|

9.92 |

% |

|

10.24 |

% |

| (1) | Capital ratios for the current quarter are to be considered preliminary until the Call Report for Alerus Financial, N.A. is filed. |

| (2) | Represents a non-GAAP financial measure. See “Non-GAAP to GAAP Reconciliations and Calculation of Non-GAAP Financial Measures.” |

5

Conference Call

The Company will host a conference call at 11:00 a.m. Central Time on Thursday, April 25, 2024, to discuss its financial results. The call can be accessed via telephone at 1-(833)-470-1428, using access code 557480. A recording of the call and transcript will be available on the Company’s investor relations website at investors.alerus.com following the call.

About Alerus Financial Corporation

Alerus Financial Corporation (Nasdaq: ALRS) is a commercial wealth bank and national retirement services provider with corporate offices in Grand Forks, North Dakota, and the Minneapolis-St. Paul, Minnesota metropolitan area. Through its subsidiary, Alerus Financial, National Association, Alerus provides diversified and comprehensive financial solutions to business and consumer clients, including banking, wealth services, and retirement and benefits plans and services. Alerus provides clients with a primary point of contact to help fully understand the unique needs and delivery channel preferences of each client. Clients are provided with competitive products, valuable insight, and sound advice supported by digital solutions designed to meet the clients’ needs. Alerus has banking and wealth offices in Grand Forks and Fargo, North Dakota, the Minneapolis-St. Paul, Minnesota metropolitan area, and Phoenix and Scottsdale, Arizona. Alerus Retirement and Benefits serves advisors, brokers, employers, and plan participants across the United States.

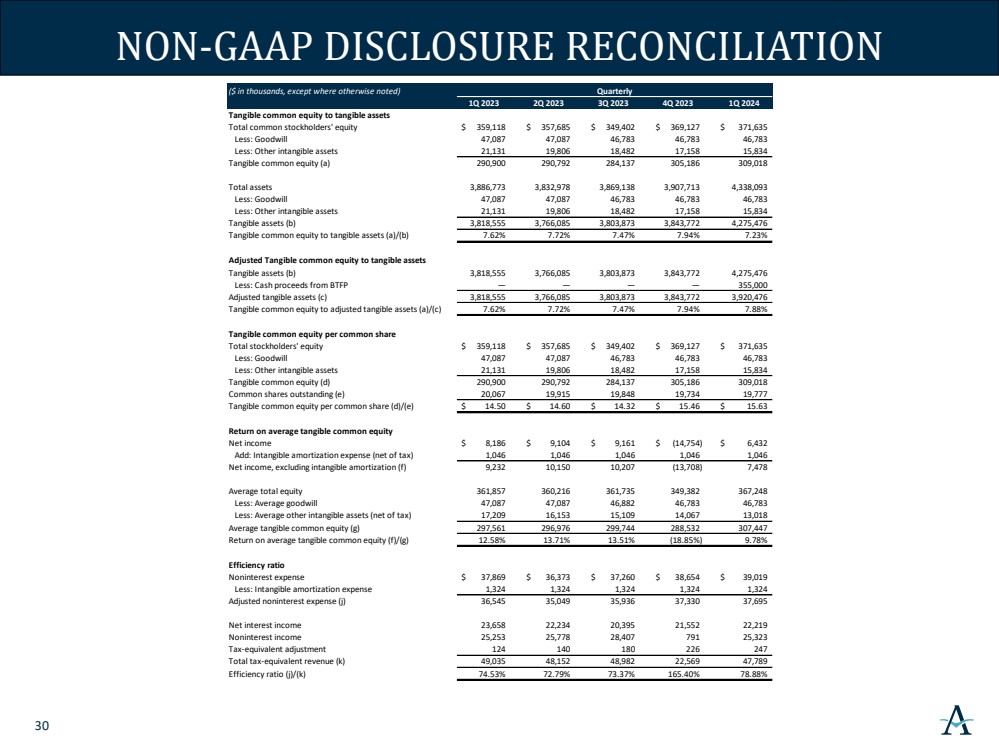

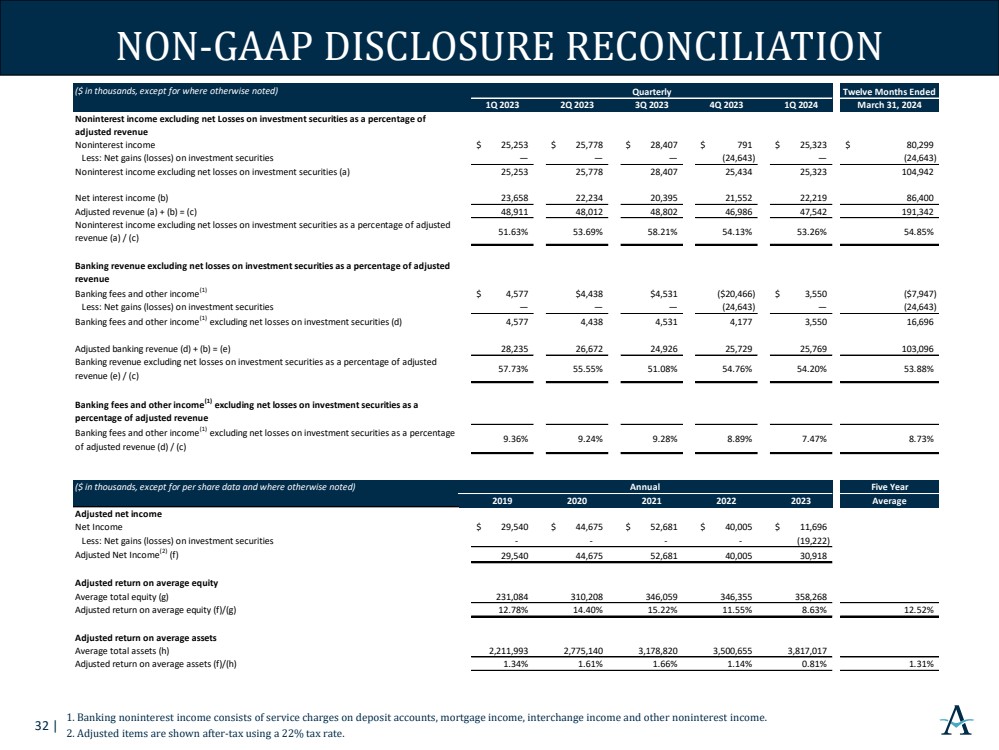

Non-GAAP Financial Measures

Some of the financial measures included in this press release are not measures of financial performance recognized by U.S. Generally Accepted Accounting Principles, or GAAP. These non-GAAP financial measures include the ratio of tangible common equity to tangible assets, adjusted tangible common equity to tangible assets, tangible book value per common share, return on average tangible common equity, efficiency ratio, adjusted efficiency ratio, adjusted noninterest income, net interest margin (tax-equivalent), and adjusted net interest margin (tax-equivalent). Management uses these non-GAAP financial measures in its analysis of its performance, and believes financial analysts and investors frequently use these measures, and other similar measures, to evaluate capital adequacy and financial performance. Reconciliations of non-GAAP disclosures used in this press release to the comparable GAAP measures are provided in the accompanying tables. Management, banking regulators, many financial analysts and other investors use these measures in conjunction with more traditional bank capital ratios to compare the capital adequacy of banking organizations with significant amounts of goodwill or other intangible assets, which typically stem from the use of the purchase accounting method of accounting for mergers and acquisitions.

These non-GAAP financial measures should not be considered in isolation or as a substitute for total stockholders’ equity, total assets, book value per share, return on average assets, return on average equity, or any other measure calculated in accordance with GAAP. Moreover, the manner in which the Company calculates these non-GAAP financial measures may differ from that of other companies reporting measures with similar names.

Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements include, without limitation, statements concerning plans, estimates, calculations, forecasts and projections with respect to the anticipated future performance of Alerus Financial Corporation. These statements are often, but not always, identified by words such as “may”, “might”, “should”, “could”, “predict”, “potential”, “believe”, “expect”, “continue”, “will”, “anticipate”, “seek”, “estimate”, “intend”, “plan”, “projection”, “would”, “annualized”, “target” and “outlook”, or the negative version of those words or other comparable words of a future or forward-looking nature. Examples of forward-looking statements include, among others, statements the Company makes regarding our projected growth, anticipated future financial performance, financial condition, credit quality, management’s long-term performance goals and the future plans and prospects of Alerus Financial Corporation.

6

Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in forward-looking statements. Therefore, you should not rely on any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those indicated in forward-looking statements include, among others, the following: interest rate risk, including the effects of significant rate increases by the Federal Reserve since 2020; our ability to successfully manage credit risk and maintain an adequate level of allowance for credit losses; new or revised accounting standards; business and economic conditions generally and in the financial services industry, nationally and within our market areas, including high rates of inflation and possible recession; the effects of recent developments and events in the financial services industry, including the large-scale deposit withdrawals over a short-period of time that resulted in recent bank failures; the overall health of the local and national real estate market; concentrations within our loan portfolio; the level of nonperforming assets on our balance sheet; our ability to implement our organic and acquisition growth strategies, including the integration of Metro Phoenix Bank which the Company acquired in 2022; the impact of economic or market conditions on our fee-based services; our ability to continue to grow our retirement and benefit services business; our ability to continue to originate a sufficient volume of residential mortgages; the occurrence of fraudulent activity, breaches or failures of our or our third party vendors’ information security controls or cybersecurity-related incidents, including as a result of sophisticated attacks using artificial intelligence and similar tools; interruptions involving our information technology and telecommunications systems or third-party servicers; potential losses incurred in connection with mortgage loan repurchases; the composition of our executive management team and our ability to attract and retain key personnel; rapid technological change in the financial services industry; increased competition in the financial services industry from non-banks such as credit unions and Fintech companies, including digital asset service providers; our ability to successfully manage liquidity risk, including our need to access higher cost sources of funds such as fed funds purchased and short-term borrowings; the concentration of large deposits from certain clients, who have balances above current FDIC insurance limits; the effectiveness of our risk management framework; the commencement and outcome of litigation and other legal proceedings and regulatory actions against us or to which the Company may become subject; potential impairment to the goodwill the Company recorded in connection with our past acquisitions, including the acquisition of Metro Phoenix Bank; the extensive regulatory framework that applies to us; the impact of recent and future legislative and regulatory changes, including in response to recent bank failures; fluctuations in the values of the securities held in our securities portfolio, including as a result of changes in interest rates; governmental monetary, trade and fiscal policies; risks related to climate change and the negative impact it may have on our customers and their businesses; severe weather, natural disasters, widespread disease or pandemics; acts of war or terrorism, including the ongoing Israeli-Palestinian conflict and the Russian invasion of Ukraine, or other adverse external events; any material weaknesses in our internal control over financial reporting; changes to U.S. or state tax laws, regulations and guidance, including the 1.0% excise tax on stock buybacks by publicly traded companies; potential changes in federal policy and at regulatory agencies as a result of the upcoming 2024 presidential election; talent and labor shortages and employee turnover; our success at managing the risks involved in the foregoing items; and any other risks described in the “Risk Factors” sections of the reports filed by Alerus Financial Corporation with the Securities and Exchange Commission.

Any forward-looking statement made by us in this press release is based only on information currently available to us and speaks only as of the date on which it is made. The Company undertakes no obligation to publicly update any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future developments or otherwise.

7

Alerus Financial Corporation and Subsidiaries

Consolidated Balance Sheets

(dollars in thousands, except share and per share data)

|

|

March 31, |

|

December 31, |

||

|

|

2024 |

|

2023 |

||

Assets |

|

(Unaudited) |

|

(Audited) |

||

Cash and cash equivalents |

|

$ |

545,772 |

|

$ |

129,893 |

Investment securities |

|

|

|

|

|

|

Trading, at fair value |

|

|

4,553 |

|

|

— |

Available-for-sale, at fair value |

|

|

472,272 |

|

|

486,736 |

Held-to-maturity, at amortized cost (with an allowance for credit losses on investments of $207 and $213, respectively) |

|

|

291,932 |

|

|

299,515 |

Loans held for sale |

|

|

10,625 |

|

|

11,497 |

Loans |

|

|

2,799,475 |

|

|

2,759,583 |

Allowance for credit losses on loans |

|

|

(36,584) |

|

|

(35,843) |

Net loans |

|

|

2,762,891 |

|

|

2,723,740 |

Land, premises and equipment, net |

|

|

18,162 |

|

|

17,940 |

Operating lease right-of-use assets |

|

|

5,112 |

|

|

5,436 |

Accrued interest receivable |

|

|

16,149 |

|

|

15,700 |

Bank-owned life insurance |

|

|

33,396 |

|

|

33,236 |

Goodwill |

|

|

46,783 |

|

|

46,783 |

Other intangible assets |

|

|

15,834 |

|

|

17,158 |

Servicing rights |

|

|

1,983 |

|

|

2,052 |

Deferred income taxes, net |

|

|

34,796 |

|

|

34,595 |

Other assets |

|

|

77,833 |

|

|

83,432 |

Total assets |

|

$ |

4,338,093 |

|

$ |

3,907,713 |

Liabilities and Stockholders’ Equity |

|

|

|

|

|

|

Deposits |

|

|

|

|

|

|

Noninterest-bearing |

|

$ |

692,500 |

|

$ |

728,082 |

Interest-bearing |

|

|

2,592,469 |

|

|

2,367,529 |

Total deposits |

|

|

3,284,969 |

|

|

3,095,611 |

Short-term borrowings |

|

|

555,000 |

|

|

314,170 |

Long-term debt |

|

|

58,985 |

|

|

58,956 |

Operating lease liabilities |

|

|

5,420 |

|

|

5,751 |

Accrued expenses and other liabilities |

|

|

62,084 |

|

|

64,098 |

Total liabilities |

|

|

3,966,458 |

|

|

3,538,586 |

Stockholders’ equity |

|

|

|

|

|

|

Preferred stock, $1 par value, 2,000,000 shares authorized: 0 issued and outstanding |

|

|

— |

|

|

— |

Common stock, $1 par value, 30,000,000 shares authorized: 19,776,786 and 19,734,077 issued and outstanding |

|

|

19,777 |

|

|

19,734 |

Additional paid-in capital |

|

|

150,740 |

|

|

150,343 |

Retained earnings |

|

|

275,374 |

|

|

272,705 |

Accumulated other comprehensive loss |

|

|

(74,256) |

|

|

(73,655) |

Total stockholders’ equity |

|

|

371,635 |

|

|

369,127 |

Total liabilities and stockholders’ equity |

|

$ |

4,338,093 |

|

$ |

3,907,713 |

8

Alerus Financial Corporation and Subsidiaries

Consolidated Statements of Income

(dollars and shares in thousands, except per share data)

|

|

Three months ended |

|||||||

|

|

March 31, |

|

December 31, |

|

March 31, |

|||

|

|

2024 |

|

2023 |

|

2023 |

|||

Interest Income |

|

(Unaudited) |

|

(Unaudited) |

|

(Unaudited) |

|||

Loans, including fees |

|

$ |

39,294 |

|

$ |

37,731 |

|

$ |

30,933 |

Investment securities |

|

|

|

|

|

|

|

|

|

Taxable |

|

|

4,568 |

|

|

6,040 |

|

|

5,951 |

Exempt from federal income taxes |

|

|

174 |

|

|

182 |

|

|

190 |

Other |

|

|

5,002 |

|

|

742 |

|

|

735 |

Total interest income |

|

|

49,038 |

|

|

44,695 |

|

|

37,809 |

Interest Expense |

|

|

|

|

|

|

|

|

|

Deposits |

|

|

20,152 |

|

|

17,169 |

|

|

9,104 |

Short-term borrowings |

|

|

5,989 |

|

|

5,292 |

|

|

4,393 |

Long-term debt |

|

|

678 |

|

|

682 |

|

|

654 |

Total interest expense |

|

|

26,819 |

|

|

23,143 |

|

|

14,151 |

Net interest income |

|

|

22,219 |

|

|

21,552 |

|

|

23,658 |

Provision for credit losses |

|

|

— |

|

|

1,507 |

|

|

550 |

Net interest income after provision for credit losses |

|

|

22,219 |

|

|

20,045 |

|

|

23,108 |

Noninterest Income |

|

|

|

|

|

|

|

|

|

Retirement and benefit services |

|

|

15,655 |

|

|

15,317 |

|

|

15,482 |

Wealth management |

|

|

6,118 |

|

|

5,940 |

|

|

5,194 |

Mortgage banking |

|

|

1,670 |

|

|

1,279 |

|

|

1,717 |

Service charges on deposit accounts |

|

|

389 |

|

|

341 |

|

|

301 |

Net gains (losses) on investment securities |

|

|

— |

|

|

(24,643) |

|

|

— |

Other |

|

|

1,491 |

|

|

2,557 |

|

|

2,559 |

Total noninterest income |

|

|

25,323 |

|

|

791 |

|

|

25,253 |

Noninterest Expense |

|

|

|

|

|

|

|

|

|

Compensation |

|

|

19,332 |

|

|

19,214 |

|

|

19,158 |

Employee taxes and benefits |

|

|

6,188 |

|

|

4,578 |

|

|

5,853 |

Occupancy and equipment expense |

|

|

1,906 |

|

|

1,858 |

|

|

1,899 |

Business services, software and technology expense |

|

|

5,345 |

|

|

5,686 |

|

|

5,324 |

Intangible amortization expense |

|

|

1,324 |

|

|

1,324 |

|

|

1,324 |

Professional fees and assessments |

|

|

1,993 |

|

|

2,345 |

|

|

1,152 |

Marketing and business development |

|

|

685 |

|

|

1,002 |

|

|

686 |

Supplies and postage |

|

|

528 |

|

|

521 |

|

|

460 |

Travel |

|

|

292 |

|

|

313 |

|

|

248 |

Mortgage and lending expenses |

|

|

441 |

|

|

501 |

|

|

497 |

Other |

|

|

985 |

|

|

1,312 |

|

|

1,268 |

Total noninterest expense |

|

|

39,019 |

|

|

38,654 |

|

|

37,869 |

Income (loss) before income tax expense (benefit) |

|

|

8,523 |

|

|

(17,818) |

|

|

10,492 |

Income tax expense (benefit) |

|

|

2,091 |

|

|

(3,064) |

|

|

2,306 |

Net income (loss) |

|

$ |

6,432 |

|

$ |

(14,754) |

|

$ |

8,186 |

Per Common Share Data |

|

|

|

|

|

|

|

|

|

Earnings (loss) per common share |

|

$ |

0.32 |

|

$ |

(0.74) |

|

$ |

0.41 |

Diluted earnings (loss) per common share |

|

$ |

0.32 |

|

$ |

(0.73) |

|

$ |

0.40 |

Dividends declared per common share |

|

$ |

0.19 |

|

$ |

0.19 |

|

$ |

0.18 |

Average common shares outstanding |

|

|

19,739 |

|

|

19,761 |

|

|

20,028 |

Diluted average common shares outstanding |

|

|

19,986 |

|

|

19,996 |

|

|

20,246 |

9

Alerus Financial Corporation and Subsidiaries

Non-GAAP to GAAP Reconciliations and Calculation of Non-GAAP Financial Measures (unaudited)

(dollars and shares in thousands, except per share data)

|

|

March 31, |

|

December 31, |

|

March 31, |

|

|||

|

|

2024 |

|

2023 |

|

2023 |

|

|||

Tangible Common Equity to Tangible Assets |

|

|

|

|

|

|

|

|

|

|

Total common stockholders’ equity |

|

$ |

371,635 |

|

$ |

369,127 |

|

$ |

359,118 |

|

Less: Goodwill |

|

|

46,783 |

|

|

46,783 |

|

|

47,087 |

|

Less: Other intangible assets |

|

|

15,834 |

|

|

17,158 |

|

|

21,131 |

|

Tangible common equity (a) |

|

|

309,018 |

|

|

305,186 |

|

|

290,900 |

|

Total assets |

|

|

4,338,093 |

|

|

3,907,713 |

|

|

3,886,773 |

|

Less: Goodwill |

|

|

46,783 |

|

|

46,783 |

|

|

47,087 |

|

Less: Other intangible assets |

|

|

15,834 |

|

|

17,158 |

|

|

21,131 |

|

Tangible assets (b) |

|

|

4,275,476 |

|

|

3,843,772 |

|

|

3,818,555 |

|

Tangible common equity to tangible assets (a)/(b) |

|

|

7.23 |

% |

|

7.94 |

% |

|

7.62 |

% |

Adjusted Tangible Common Equity to Tangible Assets |

|

|

|

|

|

|

|

|

|

|

Tangible assets (b) |

|

$ |

4,275,476 |

|

$ |

3,843,772 |

|

$ |

3,818,555 |

|

Less: Cash proceeds from BTFP |

|

|

355,000 |

|

|

— |

|

|

— |

|

Adjusted tangible assets (c) |

|

|

3,920,476 |

|

|

3,843,772 |

|

|

3,818,555 |

|

Adjusted tangible common equity to tangible assets (a)/(c) |

|

|

7.88 |

% |

|

7.94 |

% |

|

7.62 |

% |

Tangible Book Value Per Common Share |

|

|

|

|

|

|

|

|

|

|

Total common stockholders’ equity |

|

$ |

371,635 |

|

$ |

369,127 |

|

$ |

359,118 |

|

Less: Goodwill |

|

|

46,783 |

|

|

46,783 |

|

|

47,087 |

|

Less: Other intangible assets |

|

|

15,834 |

|

|

17,158 |

|

|

21,131 |

|

Tangible common equity (d) |

|

|

309,018 |

|

|

305,186 |

|

|

290,900 |

|

Total common shares issued and outstanding (e) |

|

|

19,777 |

|

|

19,734 |

|

|

20,067 |

|

Tangible book value per common share (d)/(e) |

|

$ |

15.63 |

|

$ |

15.46 |

|

$ |

14.50 |

|

|

|

Three months ended |

|

|||||||

|

|

March 31, |

|

December 31, |

|

March 31, |

|

|||

|

|

2024 |

|

2023 |

|

2023 |

|

|||

Return on Average Tangible Common Equity |

|

|

|

|

|

|

|

|

|

|

Net income (loss) |

|

$ |

6,432 |

|

$ |

(14,754) |

|

$ |

8,186 |

|

Add: Intangible amortization expense (net of tax) |

|

|

1,046 |

|

|

1,046 |

|

|

1,046 |

|

Net income (loss), excluding intangible amortization (f) |

|

|

7,478 |

|

|

(13,708) |

|

|

9,232 |

|

Average total equity |

|

|

367,248 |

|

|

349,382 |

|

|

361,857 |

|

Less: Average goodwill |

|

|

46,783 |

|

|

46,783 |

|

|

47,087 |

|

Less: Average other intangible assets (net of tax) |

|

|

13,018 |

|

|

14,067 |

|

|

17,209 |

|

Average tangible common equity (g) |

|

|

307,447 |

|

|

288,532 |

|

|

297,561 |

|

Return on average tangible common equity (f)/(g) |

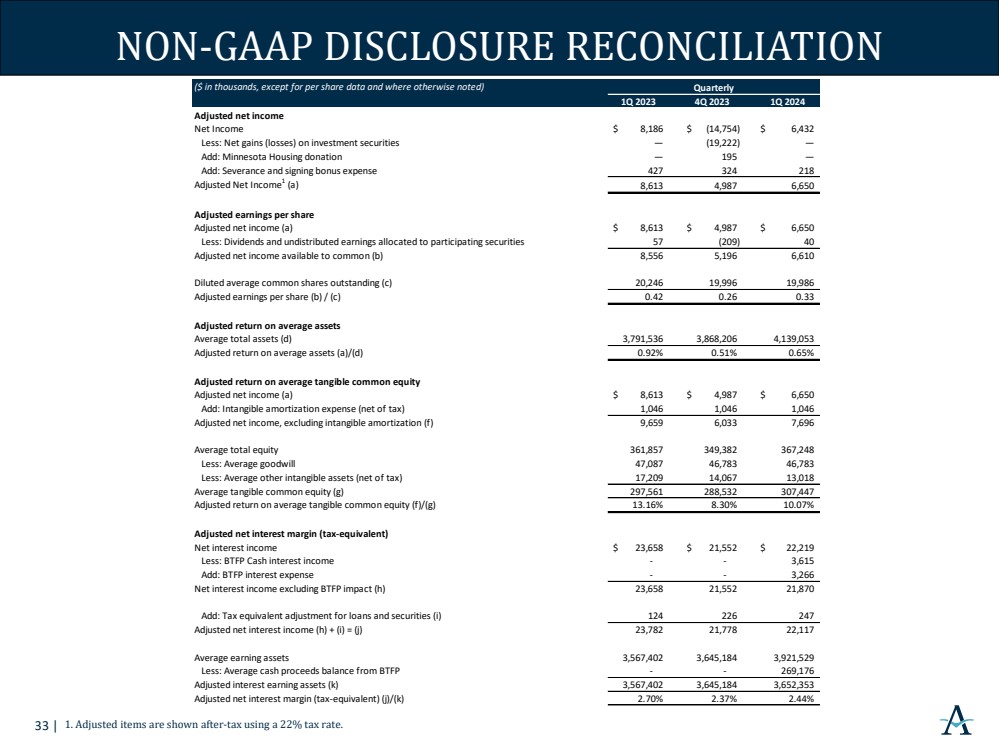

|

|

9.78 |

% |

|

(18.85) |

% |

|

12.58 |

% |

Efficiency Ratio |

|

|

|

|

|

|

|

|

|

|

Noninterest expense |

|

$ |

39,019 |

|

$ |

38,654 |

|

$ |

37,869 |

|

Less: Intangible amortization expense |

|

|

1,324 |

|

|

1,324 |

|

|

1,324 |

|

Adjusted noninterest expense (h) |

|

|

37,695 |

|

|

37,330 |

|

|

36,545 |

|

Net interest income |

|

|

22,219 |

|

|

21,552 |

|

|

23,658 |

|

Noninterest income |

|

|

25,323 |

|

|

791 |

|

|

25,253 |

|

Tax-equivalent adjustment |

|

|

247 |

|

|

226 |

|

|

123 |

|

Total tax-equivalent revenue (i) |

|

|

47,789 |

|

|

22,569 |

|

|

49,034 |

|

Efficiency ratio (h)/(i) |

|

|

78.88 |

% |

|

165.40 |

% |

|

74.53 |

% |

Adjusted Efficiency Ratio |

|

|

|

|

|

|

|

|

|

|

Noninterest expense |

|

$ |

39,019 |

|

$ |

38,654 |

|

$ |

37,869 |

|

Less: Intangible amortization expense |

|

|

1,324 |

|

|

1,324 |

|

|

1,324 |

|

Adjusted noninterest expense (j) |

|

|

37,695 |

|

|

37,330 |

|

|

36,545 |

|

Net interest income |

|

|

22,219 |

|

|

21,552 |

|

|

23,658 |

|

Noninterest income |

|

|

25,323 |

|

|

791 |

|

|

25,253 |

|

Tax-equivalent adjustment |

|

|

247 |

|

|

226 |

|

|

123 |

|

Less: Net gains (losses) on investment securities |

|

|

— |

|

|

(24,643) |

|

|

— |

|

Total tax-equivalent revenue (k) |

|

|

47,789 |

|

|

47,212 |

|

|

49,034 |

|

Adjusted efficiency ratio (j)/(k) |

|

|

78.88 |

% |

|

79.07 |

% |

|

74.53 |

% |

10

Alerus Financial Corporation and Subsidiaries

Non-GAAP to GAAP Reconciliations and Calculation of Non-GAAP Financial Measures (unaudited)

(dollars and shares in thousands, except per share data)

|

|

Three months ended |

|

|||||||

|

|

March 31, |

|

December 31, |

|

March 31, |

|

|||

|

|

2024 |

|

2023 |

|

2023 |

|

|||

Adjusted Noninterest Income |

|

|

|

|

|

|

|

|

|

|

Noninterest income |

|

$ |

25,323 |

|

$ |

791 |

|

$ |

25,253 |

|

Add: Net gains (losses) on investment securities |

|

|

— |

|

|

(24,643) |

|

|

— |

|

Adjusted noninterest income |

|

$ |

25,323 |

|

$ |

25,434 |

|

$ |

25,253 |

|

Adjusted Net Interest Margin (Tax-Equivalent) |

|

|

|

|

|

|

|

|

|

|

Net interest income |

|

$ |

22,219 |

|

$ |

21,552 |

|

$ |

23,658 |

|

Less: BTFP cash interest income |

|

|

3,615 |

|

|

— |

|

|

— |

|

Add: BTFP interest expense |

|

|

3,266 |

|

|

— |

|

|

— |

|

Net interest income excluding BTFP impact |

|

|

21,870 |

|

|

21,552 |

|

|

23,658 |

|

Add: Tax equivalent adjustment for loans and securities |

|

|

247 |

|

|

226 |

|

|

124 |

|

Adjusted net interest income (l) |

|

$ |

22,117 |

|

$ |

21,778 |

|

$ |

23,782 |

|

Interest earning assets |

|

|

3,921,529 |

|

|

3,645,184 |

|

|

3,567,402 |

|

Less: Average cash proceeds balance from BTFP |

|

|

269,176 |

|

|

— |

|

|

— |

|

Adjusted interest earning assets (m) |

|

$ |

3,652,353 |

|

$ |

3,645,184 |

|

$ |

3,567,402 |

|

Adjusted net interest margin (tax-equivalent) (l)/(m) |

|

|

2.44 |

% |

|

2.37 |

% |

|

2.70 |

% |

|

|

|

|

|

|

|

|

|

|

|

11

Alerus Financial Corporation and Subsidiaries

Analysis of Average Balances, Yields, and Rates (unaudited)

(dollars in thousands)

|

|

Three months ended |

||||||||||||||||

|

|

March 31, 2024 |

|

December 31, 2023 |

|

March 31, 2023 |

||||||||||||

|

|

|

|

|

Average |

|

|

|

|

Average |

|

|

|

|

Average |

|||

|

|

Average |

|

Yield/ |

|

Average |

|

Yield/ |

|

Average |

|

Yield/ |

||||||

|

|

Balance |

|

Rate |

|

Balance |

|

Rate |

|

Balance |

|

Rate |

||||||

Interest Earning Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing deposits with banks |

|

$ |

352,038 |

|

5.33 |

% |

|

$ |

33,920 |

|

3.22 |

% |

|

$ |

41,947 |

|

3.23 |

% |

Investment securities (1) |

|

|

775,305 |

|

2.48 |

|

|

|

921,555 |

|

2.70 |

|

|

|

1,034,288 |

|

2.43 |

|

Loans held for sale |

|

|

9,014 |

|

5.67 |

|

|

|

11,421 |

|

6.01 |

|

|

|

10,345 |

|

4.98 |

|

Loans |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial and industrial |

|

|

599,456 |

|

6.93 |

|

|

|

573,174 |

|

6.89 |

|

|

|

559,416 |

|

6.09 |

|

Real estate construction |

|

|

127,587 |

|

8.04 |

|

|

|

117,765 |

|

8.12 |

|

|

|

103,099 |

|

6.56 |

|

Commercial real estate |

|

|

1,134,540 |

|

5.58 |

|

|

|

1,053,812 |

|

5.47 |

|

|

|

911,634 |

|

4.95 |

|

Total commercial |

|

|

1,861,583 |

|

6.18 |

|

|

|

1,744,751 |

|

6.12 |

|

|

|

1,574,149 |

|

5.46 |

|

Consumer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Residential real estate first mortgage |

|

|

723,315 |

|

4.05 |

|

|

|

724,110 |

|

4.00 |

|

|

|

688,754 |

|

3.76 |

|

Residential real estate junior lien |

|

|

154,781 |

|

7.86 |

|

|

|

155,137 |

|

7.86 |

|

|

|

149,720 |

|

7.21 |

|

Other revolving and installment |

|

|

28,835 |

|

6.43 |

|

|

|

29,510 |

|

6.33 |

|

|

|

44,531 |

|

5.86 |

|

Total consumer |

|

|

906,931 |

|

4.77 |

|

|

|

908,757 |

|

4.73 |

|

|

|

883,005 |

|

4.45 |

|

Total loans (1) |

|

|

2,768,514 |

|

5.72 |

|

|

|

2,653,508 |

|

5.64 |

|

|

|

2,457,154 |

|

5.10 |

|

Federal Reserve/FHLB stock |

|

|

16,658 |

|

8.14 |

|

|

|

24,780 |

|

7.48 |

|

|

|

23,668 |

|

6.87 |

|

Total interest earning assets |

|

|

3,921,529 |

|

5.05 |

|

|

|

3,645,184 |

|

4.89 |

|

|

|

3,567,402 |

|

4.31 |

|

Noninterest earning assets |

|

|

217,524 |

|

|

|

|

|

223,022 |

|

|

|

|

|

224,134 |

|

|

|

Total assets |

|

$ |

4,139,053 |

|

|

|

|

$ |

3,868,206 |

|

|

|

|

$ |

3,791,536 |

|

|

|

Interest-Bearing Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing demand deposits |

|

$ |

869,060 |

|

1.97 |

% |

|

$ |

798,634 |

|

1.65 |

% |

|

$ |

746,660 |

|

0.87 |

% |

Money market and savings deposits |

|

|

1,186,900 |

|

3.77 |

|

|

|

1,092,656 |

|

3.53 |

|

|

|

1,165,269 |

|

2.17 |

|

Time deposits |

|

|

431,679 |

|

4.46 |

|

|

|

383,715 |

|

4.27 |

|

|

|

231,959 |

|

2.23 |

|

Fed funds purchased and Bank Term Funding Program |

|

|

282,614 |

|

4.99 |

|

|

|

189,568 |

|

5.71 |

|

|

|

290,187 |

|

4.85 |

|

Short-term borrowings |

|

|

200,000 |

|

4.99 |

|

|

|

200,000 |

|

5.09 |

|

|

|

80,000 |

|

4.69 |

|

Long-term debt |

|

|

58,971 |

|

4.62 |

|

|

|

58,943 |

|

4.59 |

|

|

|

58,858 |

|

4.51 |

|

Total interest-bearing liabilities |

|

|

3,029,224 |

|

3.56 |

|

|

|

2,723,516 |

|

3.37 |

|

|

|

2,572,933 |

|

2.23 |

|

Noninterest-Bearing Liabilities and Stockholders' Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest-bearing deposits |

|

|

675,926 |

|

|

|

|

|

719,895 |

|

|

|

|

|

789,134 |

|

|

|

Other noninterest-bearing liabilities |

|

|

66,655 |

|

|

|

|

|

75,413 |

|

|

|

|

|

67,612 |

|

|

|

Stockholders’ equity |

|

|

367,248 |

|

|

|

|

|

349,382 |

|

|

|

|

|

361,857 |

|

|

|

Total liabilities and stockholders’ equity |

|

$ |

4,139,053 |

|

|

|

|

$ |

3,868,206 |

|

|

|

|

$ |

3,791,536 |

|

|

|

Net interest income (1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest rate spread |

|

|

|

|

1.49 |

% |

|

|

|

|

1.52 |

% |

|

|

|

|

2.08 |

% |

Net interest margin, tax-equivalent (1) |

|

|

|

|

2.30 |

% |

|

|

|

|

2.37 |

% |

|

|

|

|

2.70 |

% |

| (1) | Taxable-equivalent adjustment was calculated utilizing a marginal income tax rate of 21.0%. |

12

|

INVESTOR PRESENTATION 1Q 2024 NASDAQ: ALRS |

|

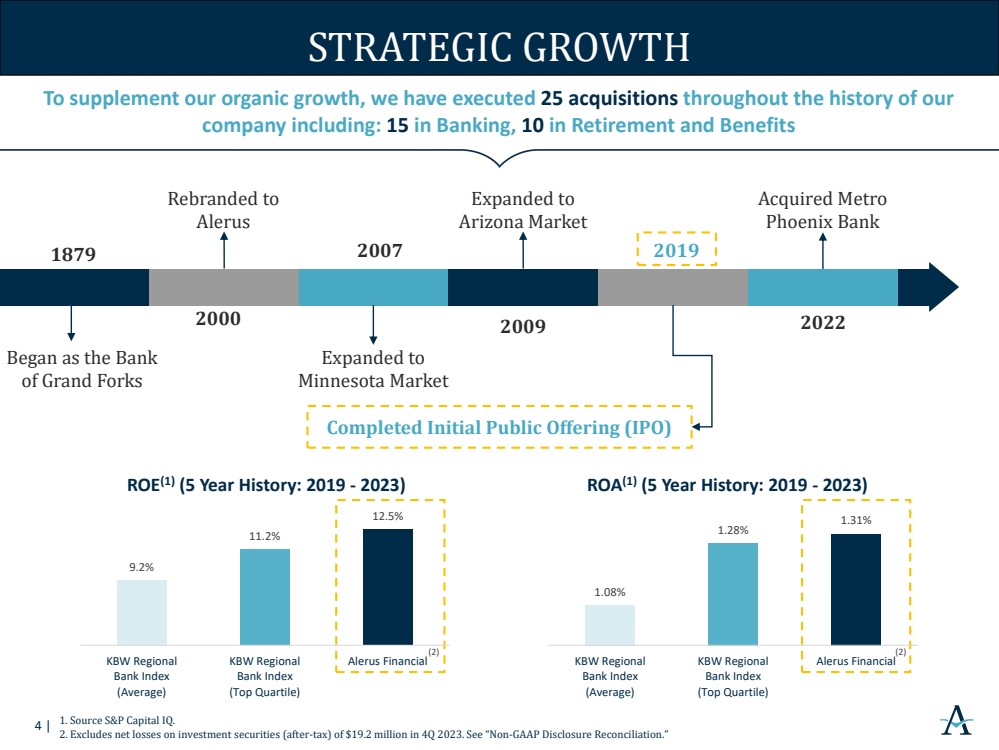

DISCLAIMERS Forward-Looking Statements This presentation contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements include, without limitation, statements concerning plans, estimates, calculations, forecasts and projections with respect to the anticipated future performance of Alerus Financial Corporation. These statements are often, but not always, identified by words such as “may”, “might”, “should”, “could”, “predict”, “potential”, “believe”, “expect”, “continue”, “will”, “anticipate”, “seek”, “estimate”, “intend”, “plan”, “projection”, “would”, “annualized”, “target” and “outlook”, or the negative version of those words or other comparable words of a future or forward-looking nature. Examples of forward-looking statements include, among others, statements we make regarding our projected growth, anticipated future financial performance, financial condition, credit quality, management’s long-term performance goals and the future plans and prospects of Alerus Financial Corporation. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in forward-looking statements. Therefore, you should not rely on any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those indicated in forward-looking statements include, among others, the following: interest rate risk, including the effects of significant rate increases by the Federal Reserve since 2020; our ability to successfully manage credit risk and maintain an adequate level of allowance for credit losses; new or revised accounting standards; business and economic conditions generally and in the financial services industry, nationally and within our market areas, including high rates of inflation and possible recession; the effects of recent developments and events in the financial services industry, including the large-scale deposit withdrawals over a short-period of time that resulted in recent bank failures of those institutions; the overall health of the local and national real estate market; concentrations within our loan portfolio; the level of nonperforming assets on our balance sheet; our ability to implement our organic and acquisition growth strategies, including the integration of Metro Phoenix Bank which we acquired in 2022; the impact of economic or market conditions on our fee-based services; our ability to continue to grow our retirement and benefit services business; our ability to continue to originate a sufficient volume of residential mortgages; the occurrence of fraudulent activity, breaches or failures of our or our third-party vendors’ information security controls or cybersecurity-related incidents, including as a result of sophisticated attacks using artificial intelligence and similar tools; interruptions involving our information technology and telecommunications systems or third-party servicers; potential losses incurred in connection with mortgage loan repurchases; the composition of our executive management team and our ability to attract and retain key personnel; rapid technological change in the financial services industry; increased competition in the financial services industry from non-banks such as credit unions and Fintech companies, including digital asset service providers; our ability to successfully manage liquidity risk, including our need to access higher cost sources of funds such as fed funds purchased and short-term borrowings; the concentration of large deposits from certain clients, who have balances above current Federal Deposit Insurance Corporation (“FDIC”) insurance limits; the effectiveness of our risk management framework; the commencement and outcome of litigation and other legal proceedings and regulatory actions against us or to which we may become subject; potential impairment to the goodwill we recorded in connection with our past acquisitions, including the acquisition of Metro Phoenix Bank; the extensive regulatory framework that applies to us; the impact of recent and future legislative and regulatory changes, including in response to the recent bank failures; fluctuations in the values of the securities held in our securities portfolio, including as a result of changes in interest rates; governmental monetary, trade and fiscal policies; risks related to climate change and the negative impact it may have on our customers and their businesses; severe weather, natural disasters, widespread disease or pandemics; acts of war or terrorism, including the ongoing Israeli-Palestinian conflict and the Russian invasion of Ukraine, or other adverse external events; any material weaknesses in our internal control over financial reporting; changes to U.S. or state tax laws, regulations and guidance, including the 1.0% excise tax on stock buybacks by publicly traded companies; potential changes in federal policy and at regulatory agencies as a result of the upcoming 2024 presidential election; talent and labor shortages and employee turnover; our success at managing the risks involved in the foregoing items; and any other risks described in the “Risk Factors” sections of the reports filed by Alerus Financial Corporation with the Securities and Exchange Commission. Any forward-looking statement made by us in this presentation is based only on information currently available to us and speaks only as of the date on which it is made. We undertake no obligation to publicly update any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future developments or otherwise. Non-GAAP Financial Measures This presentation includes certain ratios and amounts that do not conform to U.S. Generally Accepted Accounting Principles, or GAAP. Management uses certain non-GAAP financial measures to evaluate financial performance and business trends from period to period and believes that disclosure of these non-GAAP financial measures will help investors, rating agencies and analysts evaluate the financial performance and condition of Alerus Financial Corporation. This presentation includes a reconciliation of each non-GAAP financial measure to the most comparable GAAP equivalent. Miscellaneous Except as otherwise indicated, this presentation speaks as of the date hereof. The delivery of this presentation shall not, under any circumstances, create any implication that there has been no change in the affairs of Alerus Financial Corporation after the date hereof. Certain of the information contained herein may be derived from information provided by industry sources. We believe that such information is accurate and that the sources from which it has been obtained are reliable. We cannot guarantee the accuracy of such information, however, and we have not independently verified such information. 1 |

|