UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

January 24, 2024

Date of Report

(Date of earliest event reported)

BRIDGEWATER BANCSHARES, INC.

(Exact name of registrant as specified in its charter)

|

Minnesota (State or other jurisdiction of incorporation) |

001-38412 (Commission File Number) |

26-0113412 (I.R.S. Employer Identification No.) |

|

4450 Excelsior Boulevard, Suite 100 St. Louis Park, Minnesota (Address of principal executive offices) |

55416 (Zip Code) |

Registrant’s telephone number, including area code: (952) 893-6868

Not Applicable

(Former name or former address, if changed since last report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

Title of each class: |

|

Trading Symbol |

|

Name of each exchange on which registered: |

|

Common Stock, $0.01 Par Value Depositary Shares, each representing a 1/100th interest in a share of 5.875% Non-Cumulative Perpetual Preferred Stock, Series A |

|

BWB BWBBP |

|

The NASDAQ Stock Market LLC The NASDAQ Stock Market LLC |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 2.02 Results of Operations and Financial Condition.

On January 24, 2024, Bridgewater Bancshares, Inc. (the “Company”) issued a press release announcing its financial results for the three and twelve months ended December 31, 2023. A copy of the press release is attached as Exhibit 99.1 to this Current Report on Form 8-K and is incorporated herein by reference.

The information furnished in this item of this Form 8-K, and the related exhibits, shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as may be expressly set forth by specific reference in such filing.

Item 7.01 Regulation FD Disclosure.

The Company hereby furnishes the Investor Presentation attached hereto as Exhibit 99.2.

The information furnished in this item of this Form 8-K, and the related exhibits, shall not be deemed “filed” for purposes of Section 18 of the Exchange Act, or incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as may be expressly set forth by specific reference in such filing.

Item 8.01 Other Events.

On January 24, 2024, in its 2023 fourth quarter earnings release, the Company announced that its Board of Directors had declared a quarterly cash dividend on its 5.875% Non-Cumulative Perpetual Preferred Stock, Series A (“Series A Preferred Stock”). The quarterly cash dividend of $36.72 per share, equivalent to $0.3672 per depository share, each representing a 1/100th interest in a share of the Series A Preferred Stock (Nasdaq: BWBBP), is payable on March 1, 2024, to shareholders of record of the Series A Preferred Stock at the close of business on February 15, 2024.

Item 9.01 Financial Statements and Exhibits.

(d) Exhibits

Exhibit 99.1 |

Exhibit 99.2 |

Exhibit 104 |

Cover Page Interactive Data File (embedded within the Inline XBRL document) |

2

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

|

Bridgewater Bancshares, Inc. |

|

|

|

|

Date: January 24, 2024 |

|

|

By: /s/ Jerry Baack |

|

Name: Jerry Baack |

|

Title: Chairman, Chief Executive Officer and President |

3

Exhibit 99.1

Investor Contact: |

|

January 24, 2024

Bridgewater Bancshares, Inc. Announces Fourth Quarter 2023 Net Income

of $8.9 Million, $0.28 Diluted Earnings Per Common Share

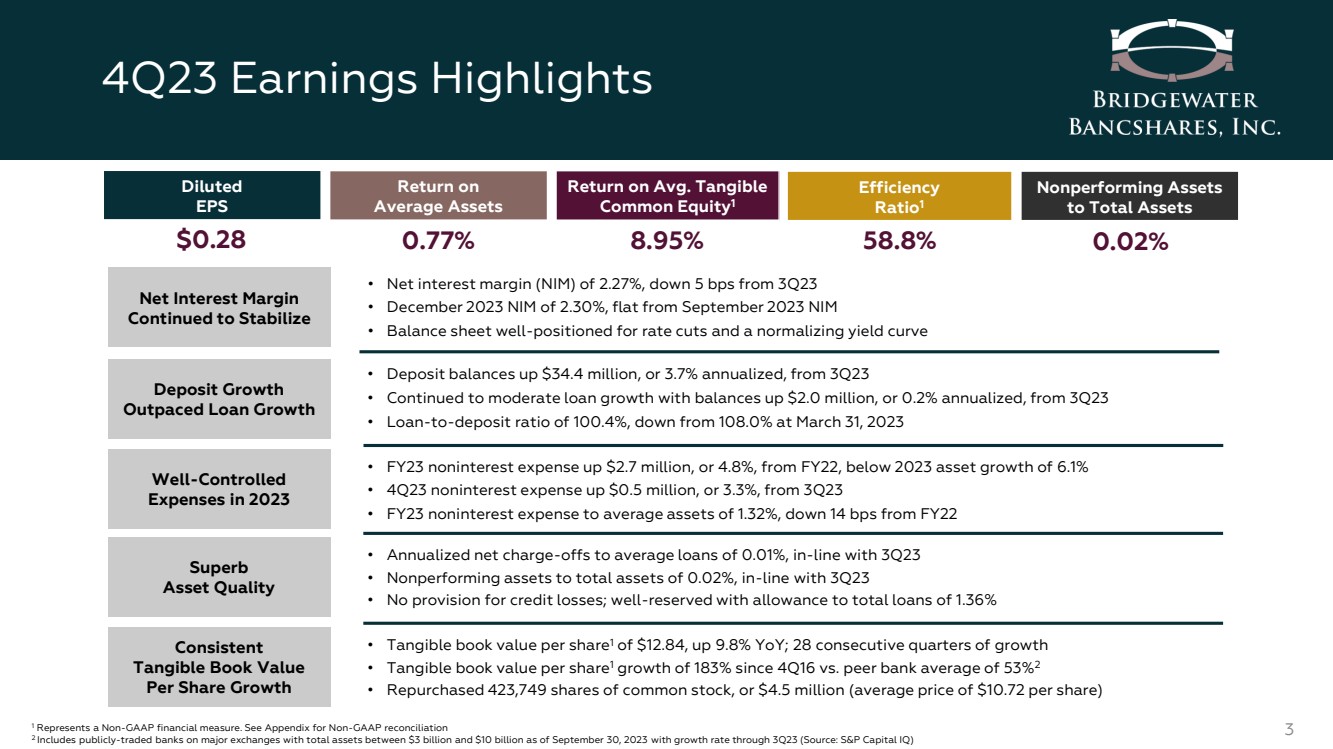

Fourth Quarter 2023 Highlights

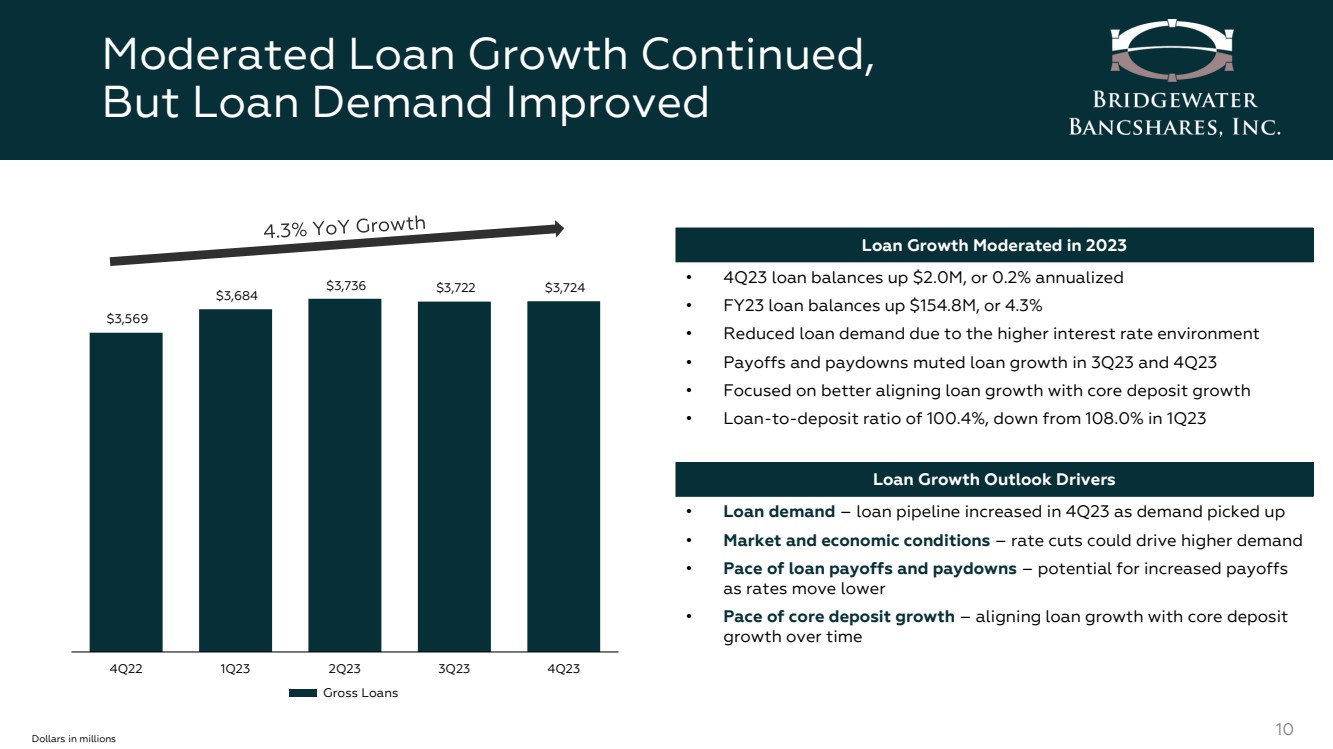

| ● | Deposit growth of $34.4 million, or 3.7% annualized, from the third quarter of 2023, exceeded gross loan growth which remained relatively stable from the third quarter of 2023, lowering the loan-to-deposit ratio to 100.4%. |

| ● | Net interest margin (on a fully tax-equivalent basis) of 2.27%, compared to 2.32% in the third quarter of 2023. |

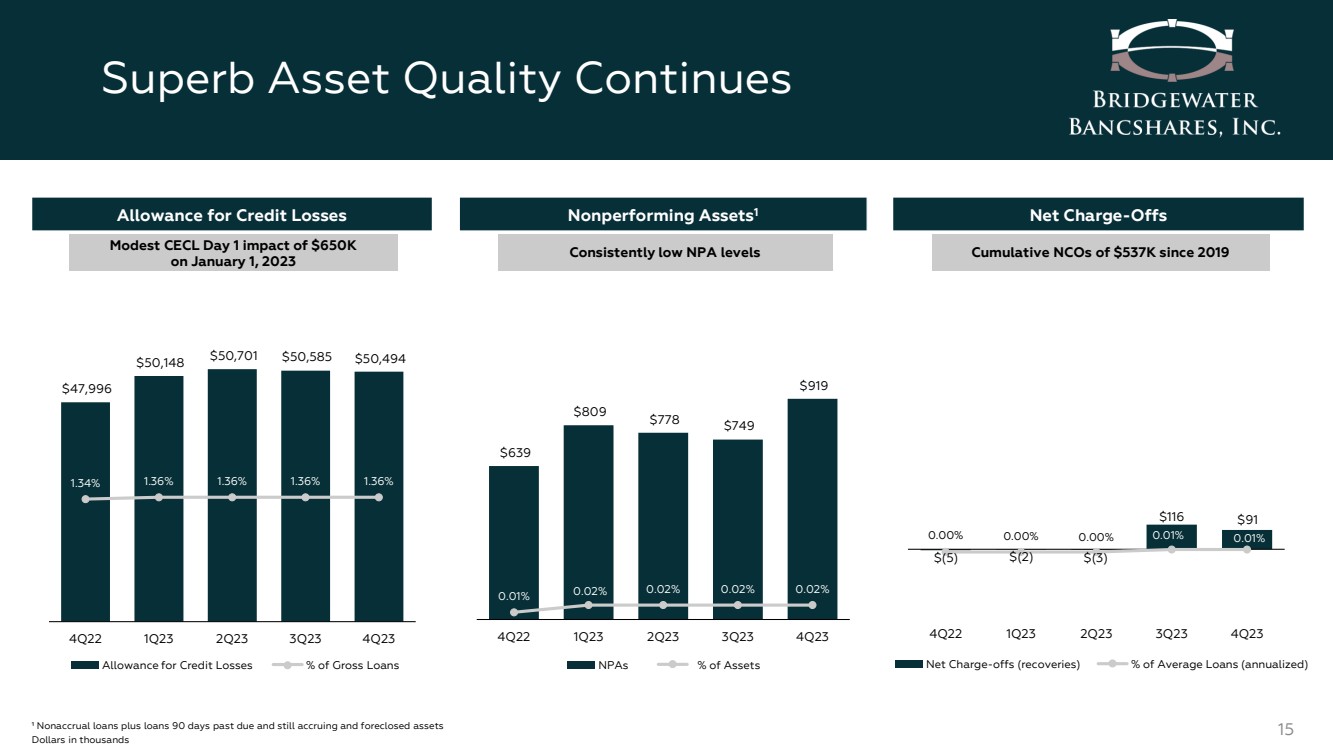

| ● | No provision for credit losses on loans was recorded in the fourth quarter of 2023. The allowance for credit losses on loans to total loans was 1.36% at December 31, 2023 and September 30, 2023, respectively. |

| ● | Nonperforming assets to total assets of 0.02% at December 31, 2023 and September 30, 2023. |

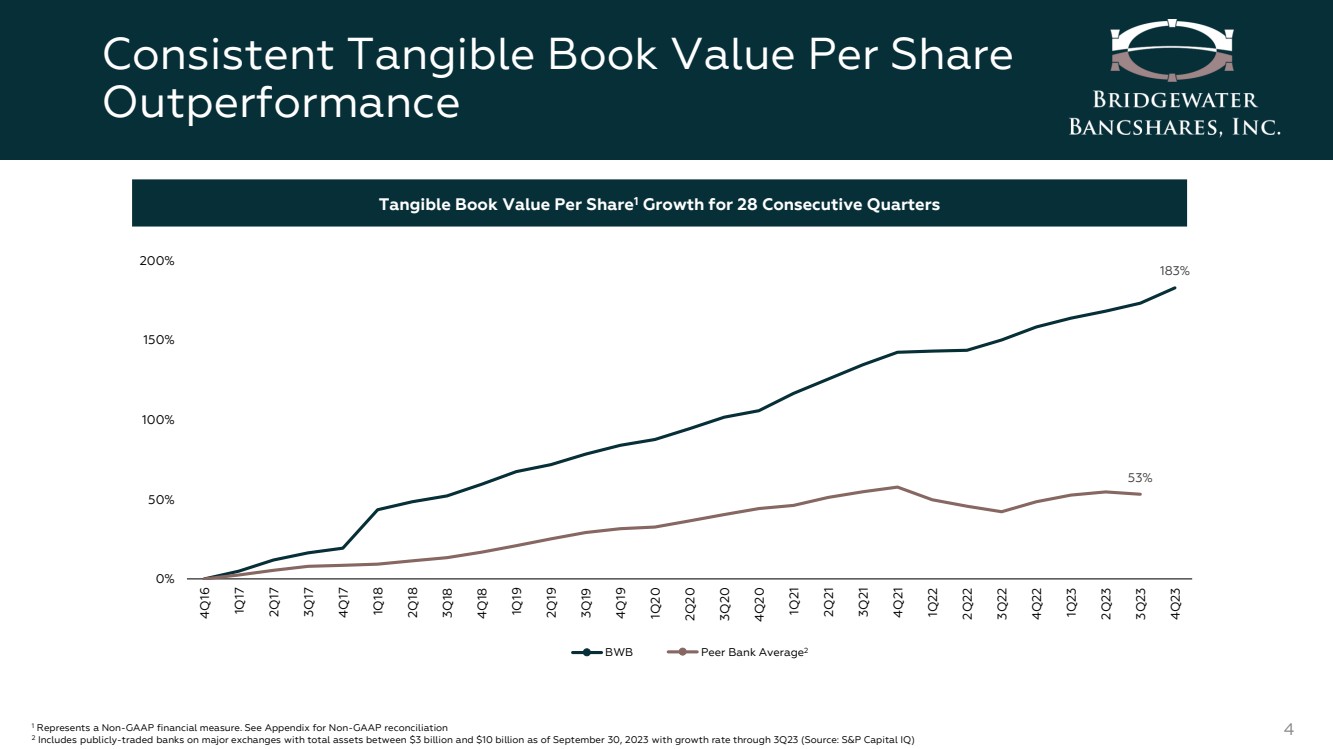

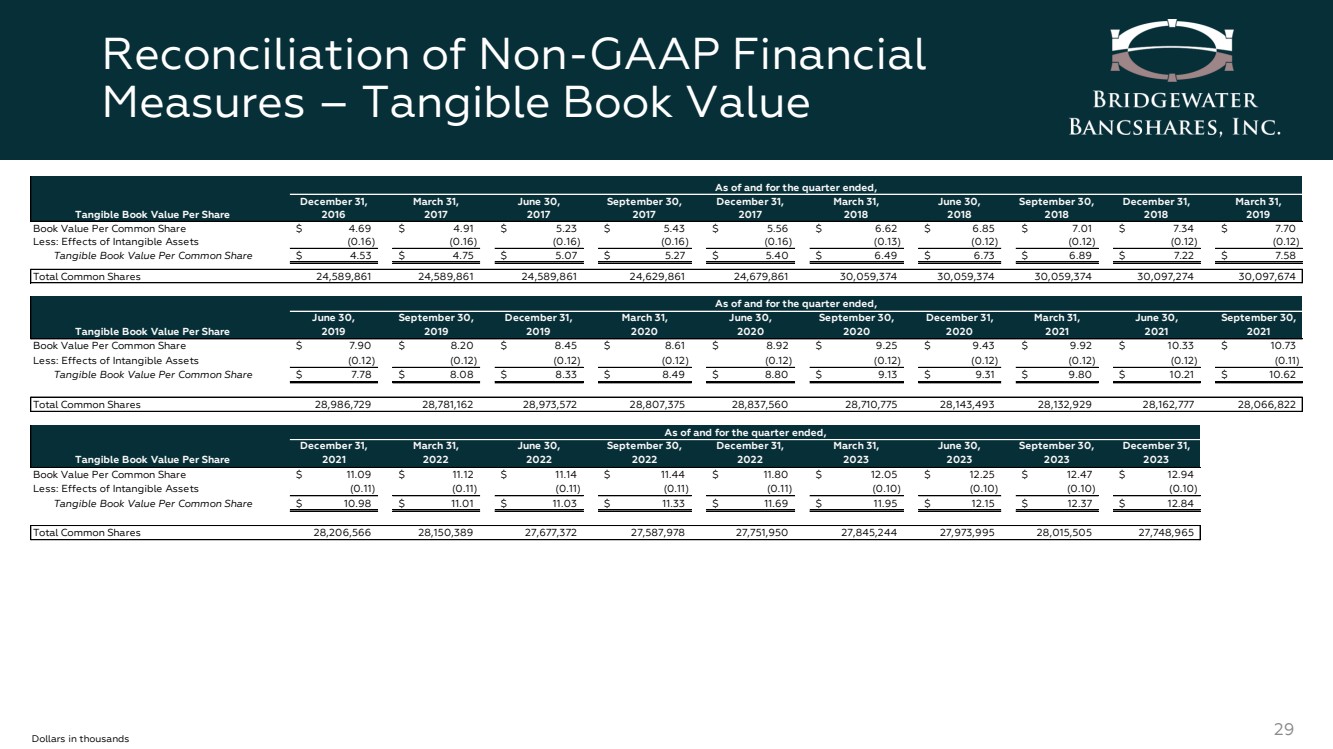

| ● | Tangible book value per share(1) of $12.84 at December 31, 2023, an increase of $0.46, or 14.9% annualized, compared to $12.37 at September 30, 2023. |

| ● | Repurchased 423,749 shares of common stock at a weighted average price of $10.72, for a total of $4.5 million. |

| ● | Early adopted ASU 2023-02 applying the modified retrospective method which reclassified noninterest expense to income tax expense effective January 1, 2023, which may impact comparability to prior 2023 filings. |

Annual 2023 Highlights

| ● | Diluted earnings per common share for the year ended December 31, 2023 were $1.27, compared to $1.72 for the year ended December 31, 2022. |

| ● | Asset growth of 6.1% compared to December 31, 2022 exceeded 2023 full-year noninterest expense growth of 4.8% compared to the full year of 2022. |

| ● | Deposit growth of $293.4 million, or 8.6%, in 2023 exceeded gross loan growth of $154.8 million, or 4.3%. |

| ● | Net loan charge-offs (recoveries) as a percentage of average loans were 0.01% for the year ended December 31, 2023, compared to (0.01)% for the year ended December 31, 2022. |

| ● | Tangible book value per share(1) increased $1.15, or 9.8%, to $12.84 at December 31, 2023, compared to $11.69 at December 31, 2022. |

| ● | Common Equity Tier 1 Risk-Based Capital Ratio was 9.16% at December 31, 2023, compared to 8.40% at December 31, 2022. |

| (1) | Represents a non-GAAP financial measure. See "Non-GAAP Financial Measures" for further details. |

Page 1 of 17

St. Louis Park, MN – Bridgewater Bancshares, Inc. (Nasdaq: BWB) (the Company), the parent company of Bridgewater Bank (the Bank), today announced net income of $8.9 million for the fourth quarter of 2023, compared to $9.6 million for the third quarter of 2023, and $13.7 million for the fourth quarter of 2022. Earnings per diluted common share were $0.28 for the fourth quarter of 2023, compared to $0.30 for the third quarter of 2023, and $0.45 for the fourth quarter of 2022.

“Bridgewater finished 2023 strong with the continuation of several positive trends as net interest margin continued to stabilize, deposit growth outpaced loan growth, and asset quality remained superb,” said Chairman, Chief Executive Officer, and President, Jerry Baack. “We also returned capital to shareholders by opportunistically repurchasing shares of common stock during the fourth quarter, while tangible book value per share increased for the 28th consecutive quarter.

“As we enter 2024, we are optimistic about our outlook as our balance sheet is well-positioned to benefit as the yield curve normalizes. In addition, our loan pipeline has begun to grow once again as loan demand has started to increase. By moderating our loan growth and reducing our loan-to-deposit ratio over the past few quarters, we believe we can continue to gain market share by deploying capital into more profitable loan growth as the interest rate environment improves.”

Key Financial Measures

|

|

As of and for the Three Months Ended |

|

|

As of and for the Year Ended |

|

|||||||||||

|

|

December 31, |

|

September 30, |

|

December 31, |

|

|

December 31, |

|

December 31, |

|

|||||

|

|

2023 |

|

2023 |

|

2022 |

|

|

2023 |

|

2022 |

|

|||||

Per Common Share Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic Earnings Per Share |

|

$ |

0.28 |

|

$ |

0.31 |

|

$ |

0.46 |

|

|

$ |

1.29 |

|

$ |

1.78 |

|

Diluted Earnings Per Share |

|

|

0.28 |

|

|

0.30 |

|

|

0.45 |

|

|

|

1.27 |

|

|

1.72 |

|

Book Value Per Share |

|

|

12.94 |

|

|

12.47 |

|

|

11.80 |

|

|

|

12.94 |

|

|

11.80 |

|

Tangible Book Value Per Share (1) |

|

|

12.84 |

|

|

12.37 |

|

|

11.69 |

|

|

|

12.84 |

|

|

11.69 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Financial Ratios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on Average Assets (2) |

|

|

0.77 |

% |

|

0.85 |

% |

|

1.28 |

% |

|

|

0.89 |

% |

|

1.38 |

% |

Pre-Provision Net Revenue Return on Average Assets (1)(2) |

|

|

0.96 |

|

|

1.01 |

|

|

1.82 |

|

|

|

1.15 |

|

|

2.06 |

|

Return on Average Shareholders' Equity (2) |

|

|

8.43 |

|

|

9.23 |

|

|

14.06 |

|

|

|

9.73 |

|

|

13.90 |

|

Return on Average Tangible Common Equity (1)(2) |

|

|

8.95 |

|

|

9.92 |

|

|

15.86 |

|

|

|

10.53 |

|

|

15.69 |

|

Net Interest Margin (3) |

|

|

2.27 |

|

|

2.32 |

|

|

3.16 |

|

|

|

2.42 |

|

|

3.45 |

|

Core Net Interest Margin (1)(3) |

|

|

2.21 |

|

|

2.24 |

|

|

3.05 |

|

|

|

2.34 |

|

|

3.27 |

|

Cost of Total Deposits |

|

|

3.19 |

|

|

2.99 |

|

|

1.31 |

|

|

|

2.73 |

|

|

0.75 |

|

Cost of Funds |

|

|

3.23 |

|

|

3.10 |

|

|

1.67 |

|

|

|

2.92 |

|

|

0.99 |

|

Efficiency Ratio (1) |

|

|

58.8 |

|

|

56.1 |

|

|

43.8 |

|

|

|

53.0 |

|

|

41.5 |

|

Noninterest Expense to Average Assets (2) |

|

|

1.37 |

|

|

1.34 |

|

|

1.42 |

|

|

|

1.32 |

|

|

1.46 |

|

Tangible Common Equity to Tangible Assets (1) |

|

|

7.73 |

|

|

7.61 |

|

|

7.48 |

|

|

|

7.73 |

|

|

7.48 |

|

Common Equity Tier 1 Risk-based Capital Ratio (Consolidated) (4) |

|

|

9.16 |

|

|

9.07 |

|

|

8.40 |

|

|

|

9.16 |

|

|

8.40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance Sheet and Asset Quality (dollars in thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Assets |

|

$ |

4,611,990 |

|

$ |

4,557,070 |

|

$ |

4,345,662 |

|

|

$ |

4,611,990 |

|

$ |

4,345,662 |

|

Total Loans, Gross |

|

|

3,724,282 |

|

|

3,722,271 |

|

|

3,569,446 |

|

|

|

3,724,282 |

|

|

3,569,446 |

|

Deposits |

|

|

3,709,948 |

|

|

3,675,509 |

|

|

3,416,543 |

|

|

|

3,709,948 |

|

|

3,416,543 |

|

Loan to Deposit Ratio |

|

|

100.4 |

% |

|

101.3 |

% |

|

104.5 |

% |

|

|

100.4 |

% |

|

104.5 |

% |

Net Loan Charge-Offs (Recoveries) to Average Loans (2) |

|

|

0.01 |

|

|

0.01 |

|

|

0.00 |

|

|

|

0.01 |

|

|

(0.01) |

|

Nonperforming Assets to Total Assets (5) |

|

|

0.02 |

|

|

0.02 |

|

|

0.01 |

|

|

|

0.02 |

|

|

0.01 |

|

Allowance for Credit Losses to Total Loans |

|

|

1.36 |

|

|

1.36 |

|

|

1.34 |

|

|

|

1.36 |

|

|

1.34 |

|

| (1) | Represents a non-GAAP financial measure. See "Non-GAAP Financial Measures" for further details. |

| (2) | Annualized. |

| (3) | Amounts calculated on a tax-equivalent basis using the statutory federal tax rate of 21%. |

| (4) | Preliminary data. Current period subject to change prior to filings with applicable regulatory agencies. |

| (5) | Nonperforming assets are defined as nonaccrual loans plus 90 days past due and still accruing plus foreclosed assets. |

Page 2 of 17

Income Statement

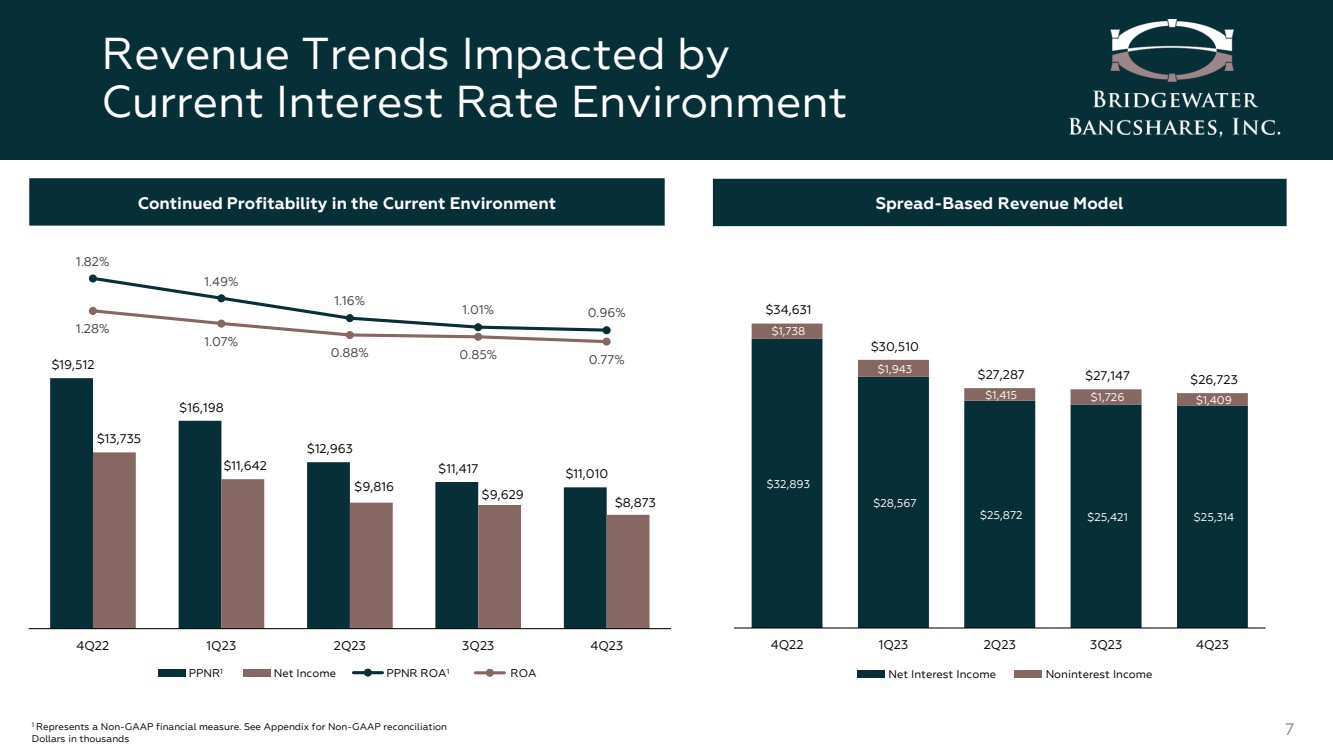

Net Interest Margin and Net Interest Income

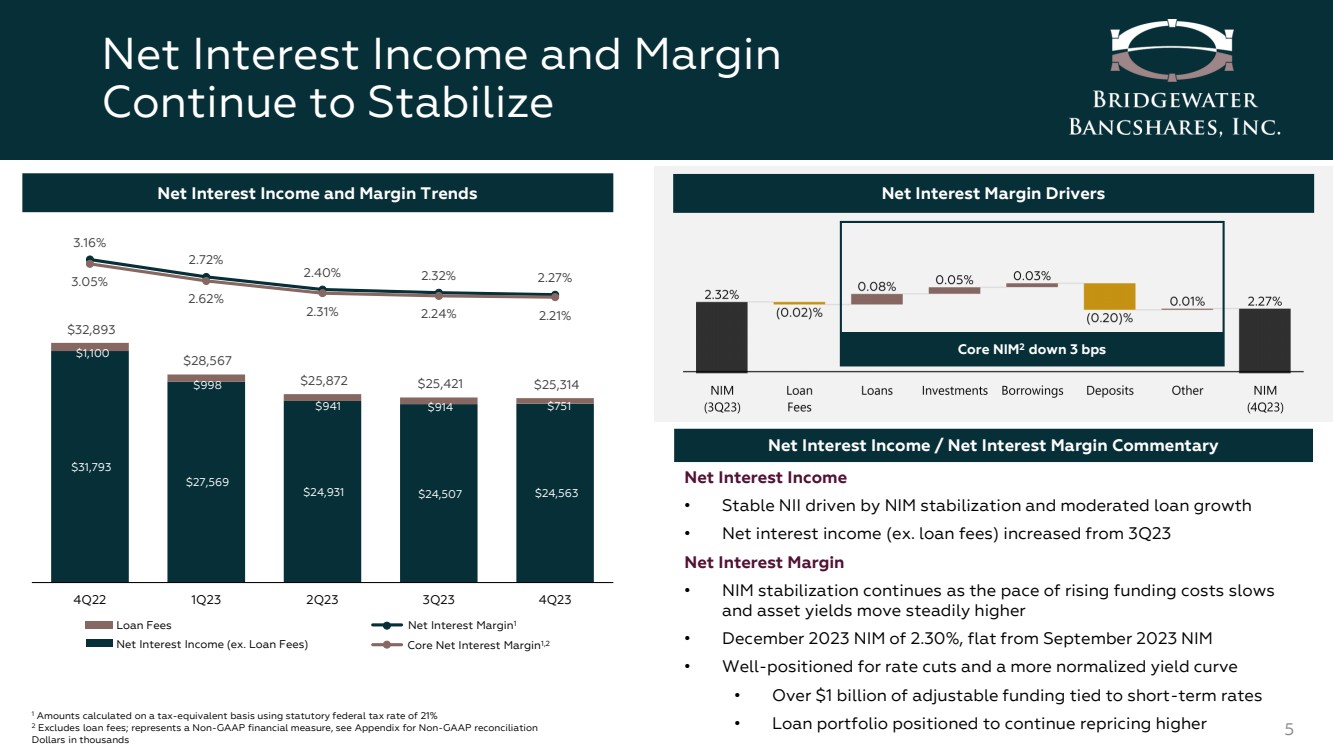

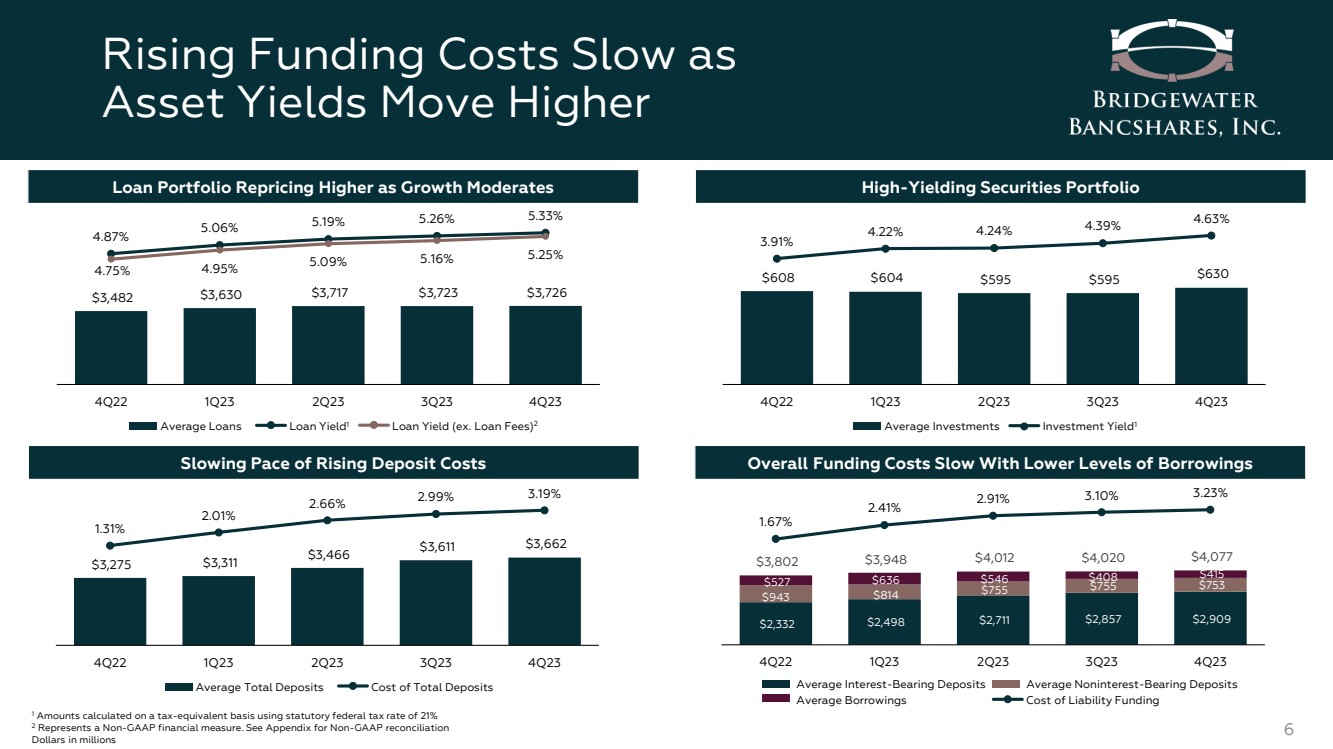

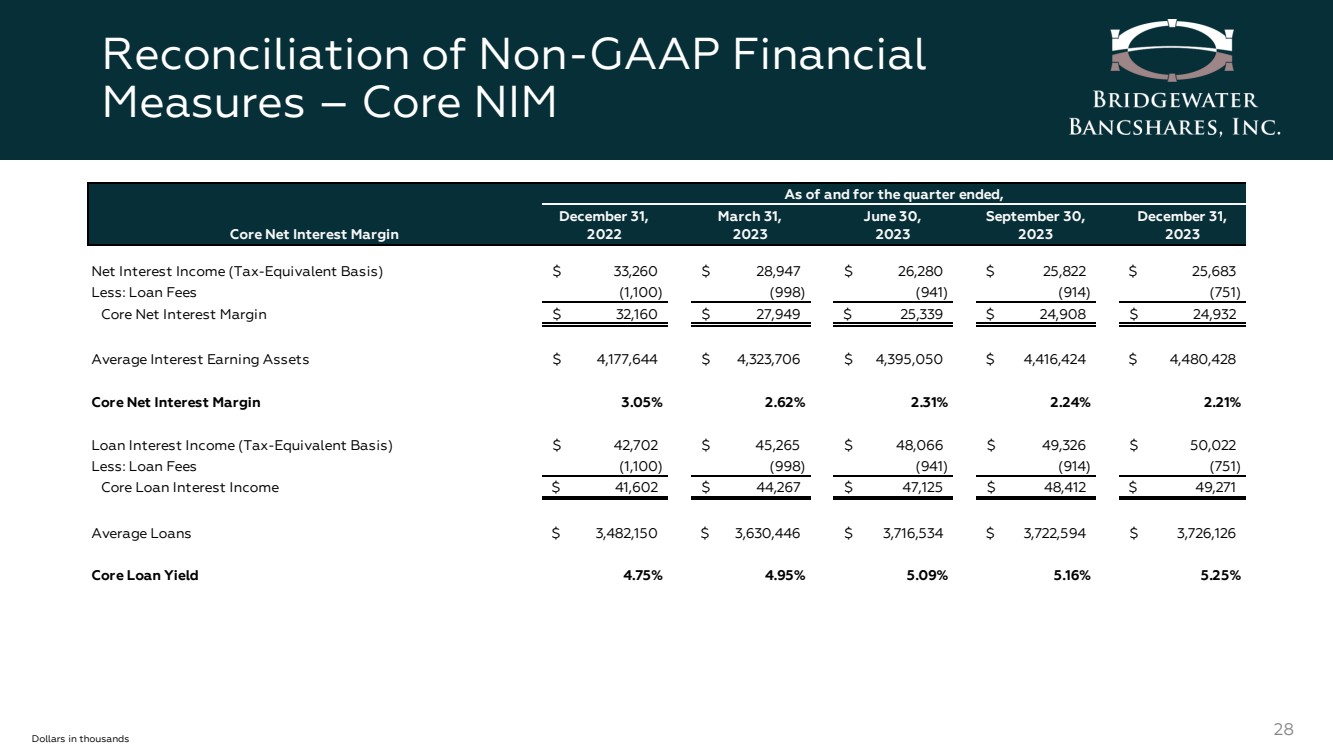

Net interest margin (on a fully tax-equivalent basis) for the fourth quarter of 2023 was 2.27%, a five basis point decline from 2.32% in the third quarter of 2023 and an 89 basis point decline from 3.16% in the fourth quarter of 2022. Core net interest margin (on a fully tax-equivalent basis), a non-GAAP financial measure which excludes the impact of loan fees, and prior to 2023, PPP balances, interest, and fees, was 2.21% for the fourth quarter of 2023, a three basis point decline from 2.24% in the third quarter of 2023, and an 84 basis point decline from 3.05% in the fourth quarter of 2022.

| ● | The linked-quarter and year-over-year declines in the margin were primarily due to higher funding costs, offset partially by higher earning asset yields. |

Net interest income was $25.3 million for the fourth quarter of 2023, a decrease of $107,000 from $25.4 million in the third quarter of 2023, and a decrease of $7.6 million from $32.9 million in the fourth quarter of 2022.

| ● | The linked-quarter and year-over year decreases in net interest income were primarily due to higher rates paid on deposits in the rising interest rate environment. |

| ● | Average interest earning assets were $4.48 billion for the fourth quarter of 2023, an increase of $64.0 million, or 1.4%, from $4.42 billion for the third quarter of 2023, and an increase of $302.8 million, or 7.2%, from $4.18 billion for the fourth quarter of 2022. The linked-quarter increase in average interest earning assets was primarily due to an increase in cash and purchases of investment securities. The year-over-year increase in average interest earning assets was primarily due to growth in the loan portfolio, purchases of investment securities, and an increase in cash. |

Interest income was $58.6 million for the fourth quarter of 2023, an increase of $1.7 million from $56.8 million in the third quarter of 2023, and an increase of $9.7 million from $48.9 million in the fourth quarter of 2022.

| ● | The yield on interest earning assets (on a fully tax-equivalent basis) was 5.22% in the fourth quarter of 2023, compared to 5.14% in the third quarter of 2023 and 4.67% in the fourth quarter of 2022. |

| ● | The linked-quarter increase in the yield on interest earning assets was primarily due to the purchase of higher yielding securities and loans repricing at yields accretive to the existing portfolio. |

| ● | The year-over-year increase in the yield on interest earning assets was primarily due to growth and repricing of the loan and securities portfolios in the rising interest rate environment. |

| ● | Loan interest income and loan fees remain the primary contributing factors to the changes in the yield on interest earning assets. The aggregate loan yield increased to 5.33% in the fourth quarter of 2023, which was seven basis points higher than 5.26% in the third quarter of 2023, and 46 basis points higher than 4.87% in the fourth quarter of 2022. |

| ● | While loan fees have historically maintained a relatively stable contribution to the aggregate loan yield, the recent periods saw fewer loan prepayments, which historically has accelerated the recognition of loan fees. Despite the overall decrease in fee recognition, the Company is encouraged that the core loan yield continues to rise as new loan originations and the existing portfolio reprice in the higher rate environment. |

A summary of interest and fees recognized on loans for the periods indicated is as follows:

|

|

Three Months Ended |

||||||||||||||

|

|

December 31, 2023 |

|

|

September 30, 2023 |

|

|

June 30, 2023 |

|

|

March 31, 2023 |

|

|

December 31, 2022 |

|

|

Interest |

|

5.25 |

% |

|

5.16 |

% |

|

5.09 |

% |

|

4.95 |

% |

|

4.75 |

% |

|

Fees |

|

0.08 |

|

|

0.10 |

|

|

0.10 |

|

|

0.11 |

|

|

0.12 |

|

|

Yield on Loans |

|

5.33 |

% |

|

5.26 |

% |

|

5.19 |

% |

|

5.06 |

% |

|

4.87 |

% |

|

Interest expense was $33.2 million for the fourth quarter of 2023, an increase of $1.9 million from $31.4 million in the third quarter of 2023, and an increase of $17.3 million from $16.0 million in the fourth quarter of 2022.

| ● | The cost of interest bearing liabilities was 3.97% in the fourth quarter of 2023, compared to 3.81% in the third quarter of 2023 and 2.22% in the fourth quarter of 2022. |

| ● | The linked-quarter increase in the cost of interest bearing liabilities was primarily due to higher rates paid on deposits in the rising interest rate environment. |

| ● | The year-over-year increase in the cost of interest bearing liabilities was primarily due to the rapid increase in market interest rates that occurred between the periods, which impacted all funding sources. |

Interest expense on deposits was $29.4 million for the fourth quarter of 2023, an increase of $2.2 million from $27.2 million in the third quarter of 2023, and an increase of $18.7 million from $10.8 million in the fourth quarter of 2022.

Page 3 of 17

| ● | The cost of total deposits was 3.19% in the fourth quarter of 2023, compared to 2.99% in the third quarter of 2023 and 1.31% in the fourth quarter of 2022. |

| ● | The linked-quarter increase in the cost of total deposits was primarily due to client demands for higher interest rates and increased competition for deposits. |

| ● | The year-over-year increase in the cost of total deposits was primarily due to upward repricing of the deposit portfolio in the higher interest rate environment. |

Provision for Credit Losses

The provision for credit losses on loans was $0 for both the fourth quarter of 2023 and the third quarter of 2023, compared to $1.5 million for the fourth quarter of 2022.

| ● | No provision for credit losses on loans was recorded in the fourth quarter of 2023 due to a more managed pace of loan growth. |

| ● | The allowance for credit losses on loans to total loans was 1.36% at both December 31, 2023 and September 30, 2023, compared to 1.34% at December 31, 2022. |

The provision for credit losses for off-balance sheet credit exposures was a negative provision of $250,000 for the fourth quarter of 2023, compared to a negative provision of $600,000 for the third quarter of 2023 and zero for the fourth quarter of 2022.

| ● | The negative provision during the quarter was due to a reduction in outstanding unfunded commitments primarily attributable to the migration to funded loans, as well as a moderation in volume of newly originated projects with unfunded commitments. |

Noninterest Income

Noninterest income was $1.4 million for the fourth quarter of 2023, a decrease of $317,000 from $1.7 million for the third quarter of 2023 and a decrease of $329,000 from $1.7 million for the fourth quarter of 2022.

| ● | The linked-quarter decrease was primarily due to $493,000 of FHLB prepayment income recognized in the previous quarter which did not reoccur, offset partially by higher letter of credit fees and other income. |

| ● | The year-over-year decrease was primarily due to lower other income. |

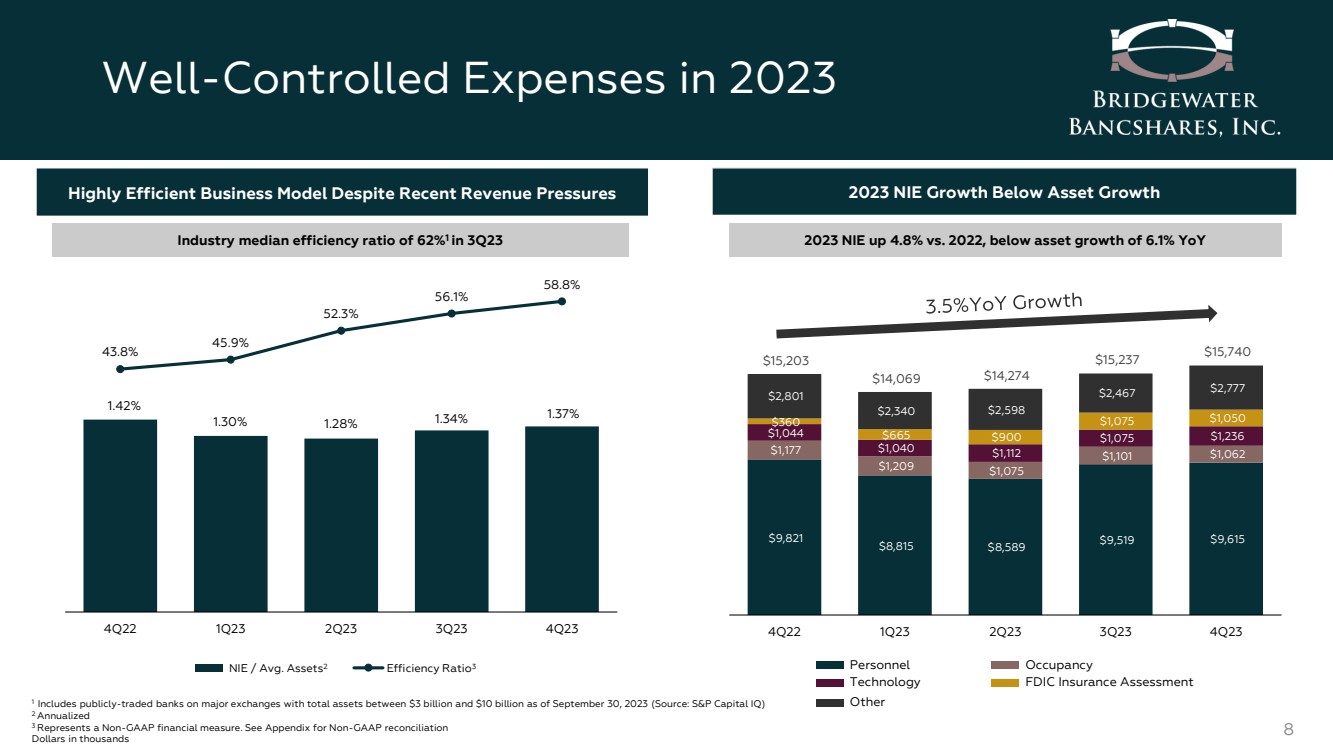

Noninterest Expense

Noninterest expense was $15.7 million for the fourth quarter of 2023, an increase of $503,000 from $15.2 million for the third quarter of 2023 and an increase of $537,000 from $15.2 million for the fourth quarter of 2022.

| ● | The linked-quarter increase was primarily due to increases in salaries and employee benefits, information technology and telecommunications, and marketing and advertising. |

| ● | The year-over-year increase was primarily attributable to industry-wide increases in the FDIC insurance assessment, higher professional and consulting fees and information technology and telecommunications, offset partially by decreases in salaries and employee benefits and occupancy and equipment. |

| ● | The efficiency ratio, a non-GAAP financial measure, was 58.8% for the fourth quarter of 2023, compared to 56.1% for the third quarter of 2023, and 43.8% for the fourth quarter of 2022. |

| ● | The Company had 255 full-time equivalent employees at both December 31, 2023 and September 30, 2023, compared to 246 employees at December 31, 2022. |

Income Taxes

The effective combined federal and state income tax rate for the fourth quarter of 2023 was 21.0%, a decrease from 23.0% for the third quarter of 2023 and 23.4% for the fourth quarter of 2022. The effective combined federal and state rate for the years ended December 31, 2023 and 2022 was 23.9% and 25.5%, respectively.

| ● | The linked-quarter decrease in the effective tax rate was primarily due to the delivery of two tax credits that occurred within the fourth quarter. |

| ● | The Company early adopted ASU 2023-02 applying the modified retrospective method which reclassified noninterest expense to income tax expense effective January 1, 2023. |

Page 4 of 17

Balance Sheet

Loans

(dollars in thousands) |

|

December 31, 2023 |

|

September 30, 2023 |

|

June 30, 2023 |

|

March 31, 2023 |

|

December 31, 2022 |

|

|||||

Commercial |

|

$ |

464,061 |

|

$ |

459,854 |

|

$ |

460,061 |

|

$ |

455,156 |

|

$ |

436,393 |

|

Construction and Land Development |

|

|

232,804 |

|

|

294,818 |

|

|

351,069 |

|

|

312,277 |

|

|

295,554 |

|

1 - 4 Family Construction |

|

|

65,087 |

|

|

64,463 |

|

|

69,648 |

|

|

85,797 |

|

|

70,242 |

|

Real Estate Mortgage: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 - 4 Family Mortgage |

|

|

402,396 |

|

|

404,716 |

|

|

400,708 |

|

|

380,210 |

|

|

355,474 |

|

Multifamily |

|

|

1,388,541 |

|

|

1,378,669 |

|

|

1,314,524 |

|

|

1,320,081 |

|

|

1,306,738 |

|

CRE Owner Occupied |

|

|

175,783 |

|

|

159,485 |

|

|

159,088 |

|

|

158,650 |

|

|

149,905 |

|

CRE Nonowner Occupied |

|

|

987,306 |

|

|

951,263 |

|

|

971,532 |

|

|

962,671 |

|

|

947,008 |

|

Total Real Estate Mortgage Loans |

|

|

2,954,026 |

|

|

2,894,133 |

|

|

2,845,852 |

|

|

2,821,612 |

|

|

2,759,125 |

|

Consumer and Other |

|

|

8,304 |

|

|

9,003 |

|

|

9,581 |

|

|

9,518 |

|

|

8,132 |

|

Total Loans, Gross |

|

|

3,724,282 |

|

|

3,722,271 |

|

|

3,736,211 |

|

|

3,684,360 |

|

|

3,569,446 |

|

Allowance for Credit Losses on Loans |

|

|

(50,494) |

|

|

(50,585) |

|

|

(50,701) |

|

|

(50,148) |

|

|

(47,996) |

|

Net Deferred Loan Fees |

|

|

(6,573) |

|

|

(7,222) |

|

|

(7,718) |

|

|

(8,735) |

|

|

(9,293) |

|

Total Loans, Net |

|

$ |

3,667,215 |

|

$ |

3,664,464 |

|

$ |

3,677,792 |

|

$ |

3,625,477 |

|

$ |

3,512,157 |

|

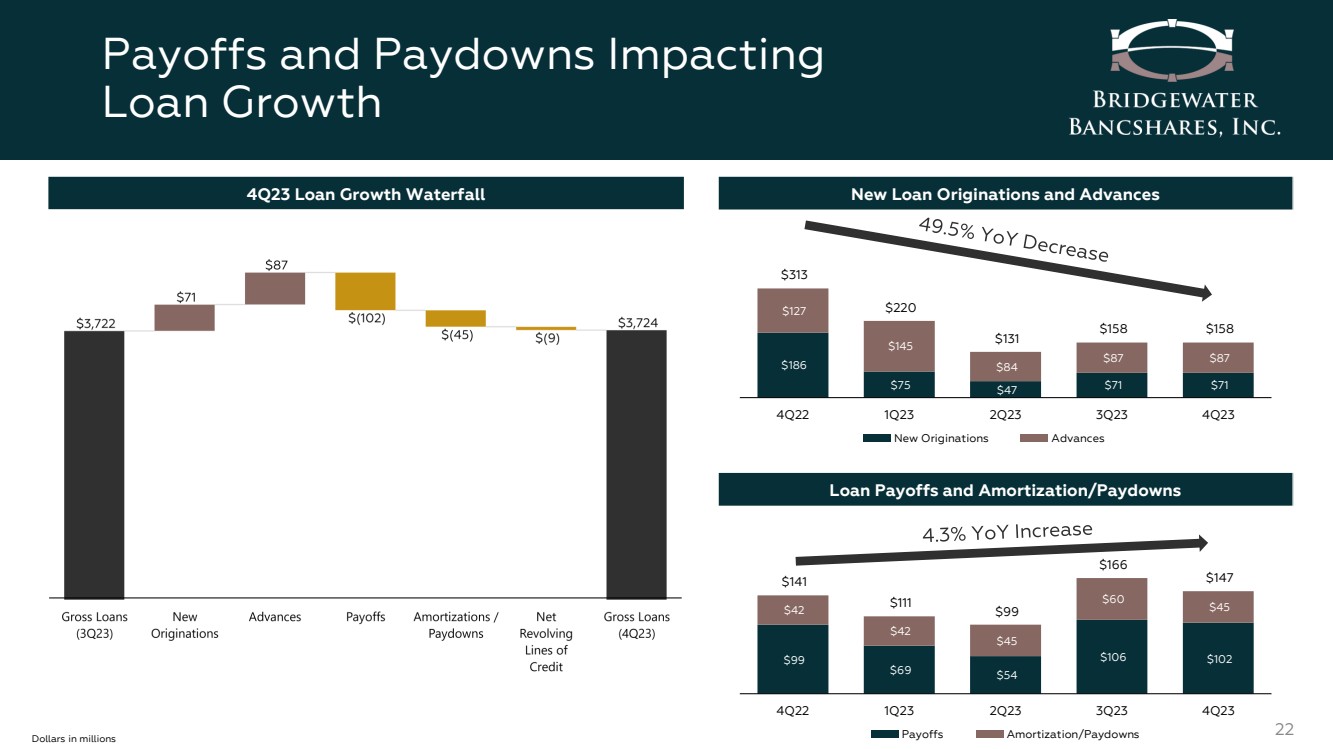

Total gross loans at December 31, 2023 were $3.72 billion, a slight increase of $2.0 million, or 0.2% annualized, over total gross loans of $3.72 billion at September 30, 2023, and an increase of $154.8 million, or 4.3%, over total gross loans of $3.57 billion at December 31, 2022.

| ● | The slower loan growth in the loan portfolio during the fourth quarter of 2023 was primarily due to moderating loan originations and decreased demand in the higher interest rate environment. |

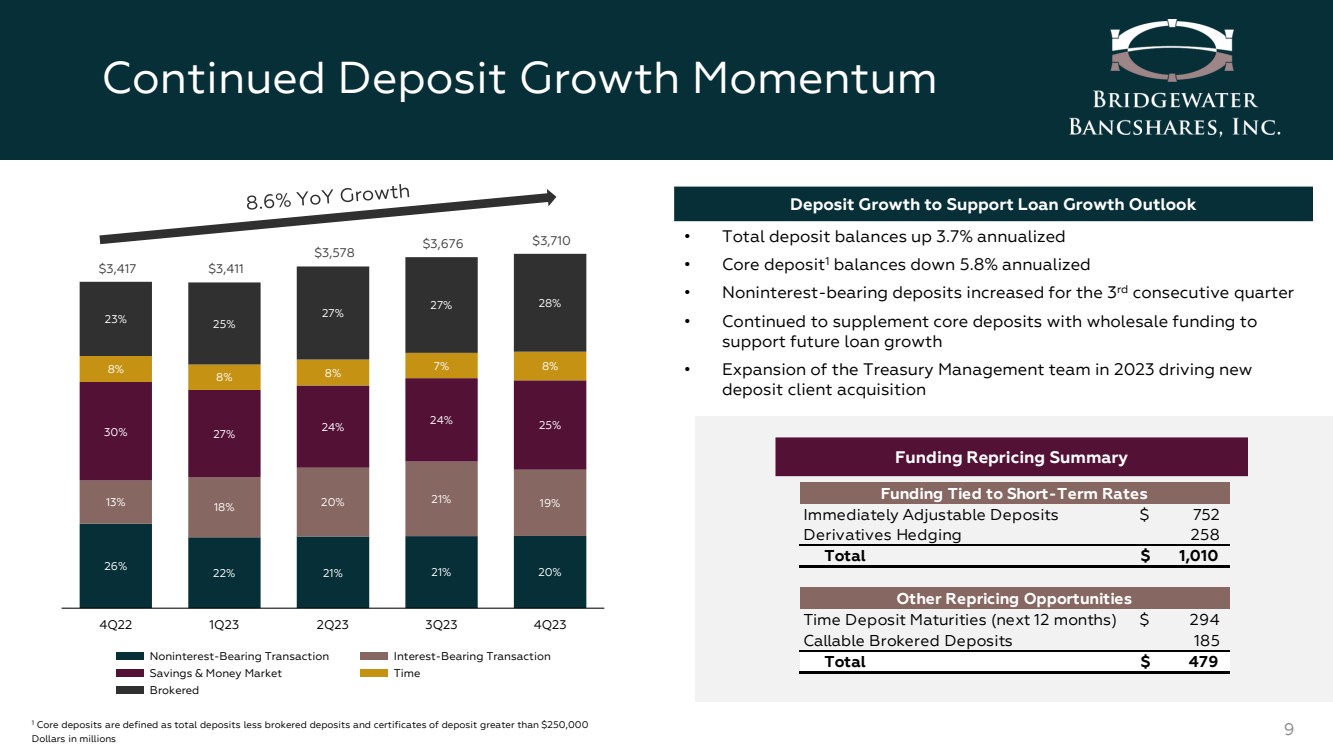

Deposits

(dollars in thousands) |

|

December 31, 2023 |

|

September 30, 2023 |

|

June 30, 2023 |

|

March 31, 2023 |

|

December 31, 2022 |

|

|||||

Noninterest Bearing Transaction Deposits |

|

$ |

756,964 |

|

$ |

754,297 |

|

$ |

751,217 |

|

$ |

742,198 |

|

$ |

884,272 |

|

Interest Bearing Transaction Deposits |

|

|

692,801 |

|

|

780,863 |

|

|

719,488 |

|

|

630,037 |

|

|

451,992 |

|

Savings and Money Market Deposits |

|

|

935,091 |

|

|

872,534 |

|

|

860,613 |

|

|

913,013 |

|

|

1,031,873 |

|

Time Deposits |

|

|

300,651 |

|

|

265,737 |

|

|

271,783 |

|

|

266,213 |

|

|

272,253 |

|

Brokered Deposits |

|

|

1,024,441 |

|

|

1,002,078 |

|

|

974,831 |

|

|

859,662 |

|

|

776,153 |

|

Total Deposits |

|

$ |

3,709,948 |

|

$ |

3,675,509 |

|

$ |

3,577,932 |

|

$ |

3,411,123 |

|

$ |

3,416,543 |

|

Total deposits at December 31, 2023 were $3.71 billion, an increase of $34.4 million, or 3.7% annualized, over total deposits of $3.68 billion at September 30, 2023, and an increase of $293.4 million, or 8.6%, over total deposits of $3.42 billion at December 31, 2022.

| ● | Core deposits, defined as total deposits excluding brokered deposits and time deposits greater than $250,000, remained stable year over year, despite industry and market turmoil. |

| ● | Brokered deposits continue to be used as a supplemental funding source, as needed. |

| ● | Uninsured deposits were 24% of total deposits as of December 31, 2023 and 22% of total deposits as of September 30, 2023. |

Page 5 of 17

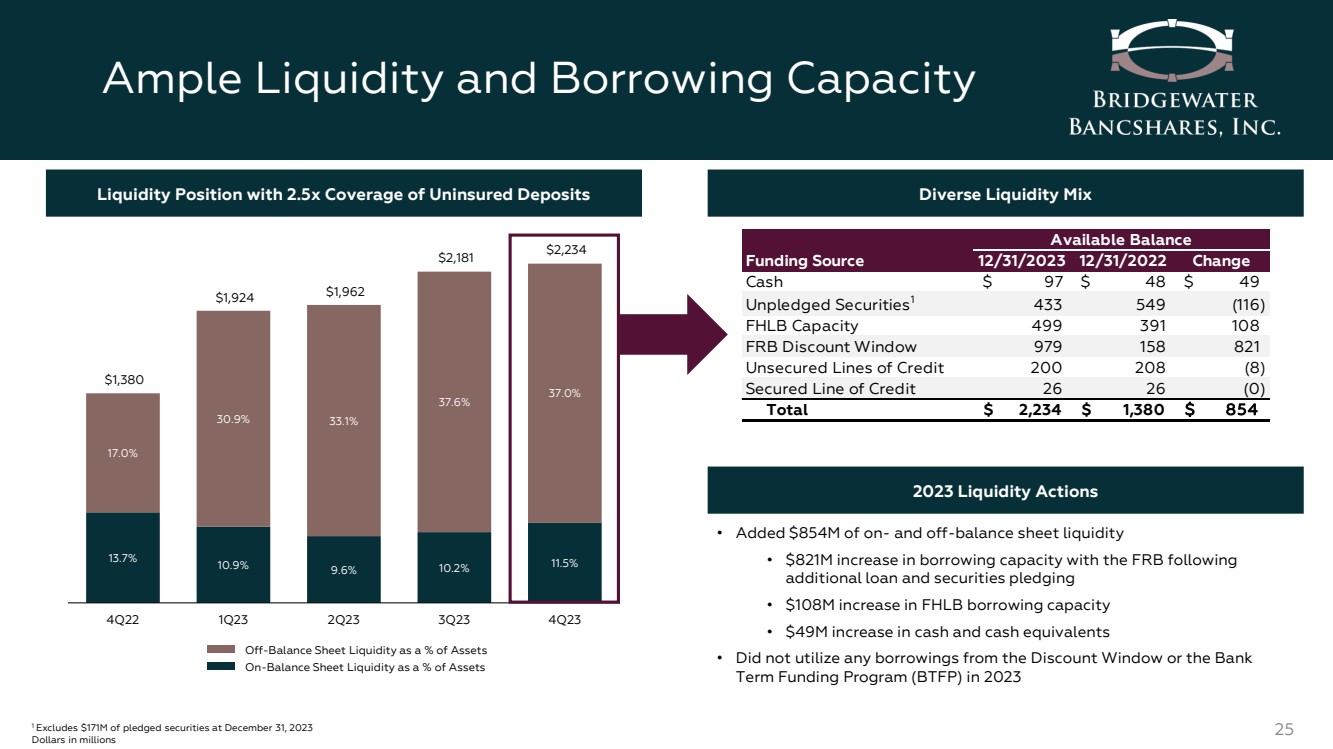

Liquidity

Total on- and off-balance sheet liquidity was $2.23 billion as of December 31, 2023, compared to $2.18 billion at September 30, 2023 and $1.38 billion at December 31, 2022. The Company did not utilize the Bank Term Funding Program (BTFP) or Federal Reserve Discount Window during the fourth quarter of 2023.

Primary Liquidity—On-Balance Sheet |

|

December 31, 2023 |

|

September 30, 2023 |

|

June 30, 2023 |

|

March 31, 2023 |

|

December 31, 2022 |

|

|||||

(dollars in thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and Cash Equivalents |

|

$ |

96,594 |

|

$ |

77,617 |

|

$ |

138,618 |

|

$ |

177,116 |

|

$ |

48,090 |

|

Securities Available for Sale |

|

|

604,104 |

|

|

553,076 |

|

|

538,220 |

|

|

559,430 |

|

|

548,613 |

|

Less: Pledged Securities |

|

|

(170,727) |

|

|

(164,277) |

|

|

(236,206) |

|

|

(234,452) |

|

|

— |

|

Total Primary Liquidity |

|

$ |

529,971 |

|

$ |

466,416 |

|

$ |

440,632 |

|

$ |

502,094 |

|

$ |

596,703 |

|

Ratio of Primary Liquidity to Total Deposits |

|

|

14.3 |

% |

|

12.7 |

% |

|

12.3 |

% |

|

14.7 |

% |

|

17.5 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Secondary Liquidity—Off-Balance Sheet Borrowing Capacity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Secured Borrowing Capacity with the FHLB |

|

$ |

498,736 |

|

$ |

516,501 |

|

$ |

400,792 |

|

$ |

246,795 |

|

$ |

390,898 |

|

Net Secured Borrowing Capacity with the Federal Reserve Bank |

|

|

979,448 |

|

|

1,022,128 |

|

|

986,644 |

|

|

990,685 |

|

|

157,827 |

|

Unsecured Borrowing Capacity with Correspondent Lenders |

|

|

200,000 |

|

|

150,000 |

|

|

108,000 |

|

|

158,000 |

|

|

208,000 |

|

Secured Borrowing Capacity with Correspondent Lender |

|

|

26,250 |

|

|

26,250 |

|

|

26,250 |

|

|

26,250 |

|

|

26,250 |

|

Total Secondary Liquidity |

|

$ |

1,704,434 |

|

$ |

1,714,879 |

|

$ |

1,521,686 |

|

$ |

1,421,730 |

|

$ |

782,975 |

|

Total Primary and Secondary Liquidity |

|

$ |

2,234,405 |

|

$ |

2,181,295 |

|

$ |

1,962,318 |

|

$ |

1,923,824 |

|

$ |

1,379,678 |

|

Ratio of Primary and Secondary Liquidity to Total Deposits |

|

|

60.2 |

% |

|

59.3 |

% |

|

54.8 |

% |

|

56.4 |

% |

|

40.4 |

% |

Asset Quality

Overall asset quality remained superb due to the Company’s measured risk selection, consistent underwriting standards, active credit oversight, and experienced lending and credit teams.

| ● | Annualized net charge-offs as a percentage of average loans were 0.01% for both the fourth quarter of 2023 and the third quarter of 2023, and 0.00% for the fourth quarter of 2022. |

| ● | At December 31, 2023, the Company’s nonperforming assets, which include nonaccrual loans, loans past due 90 days and still accruing, and foreclosed assets, were $919,000, or 0.02% of total assets, as compared to $749,000, or 0.02%, of total assets at September 30, 2023, and $639,000, or 0.01% of total assets at December 31, 2022. |

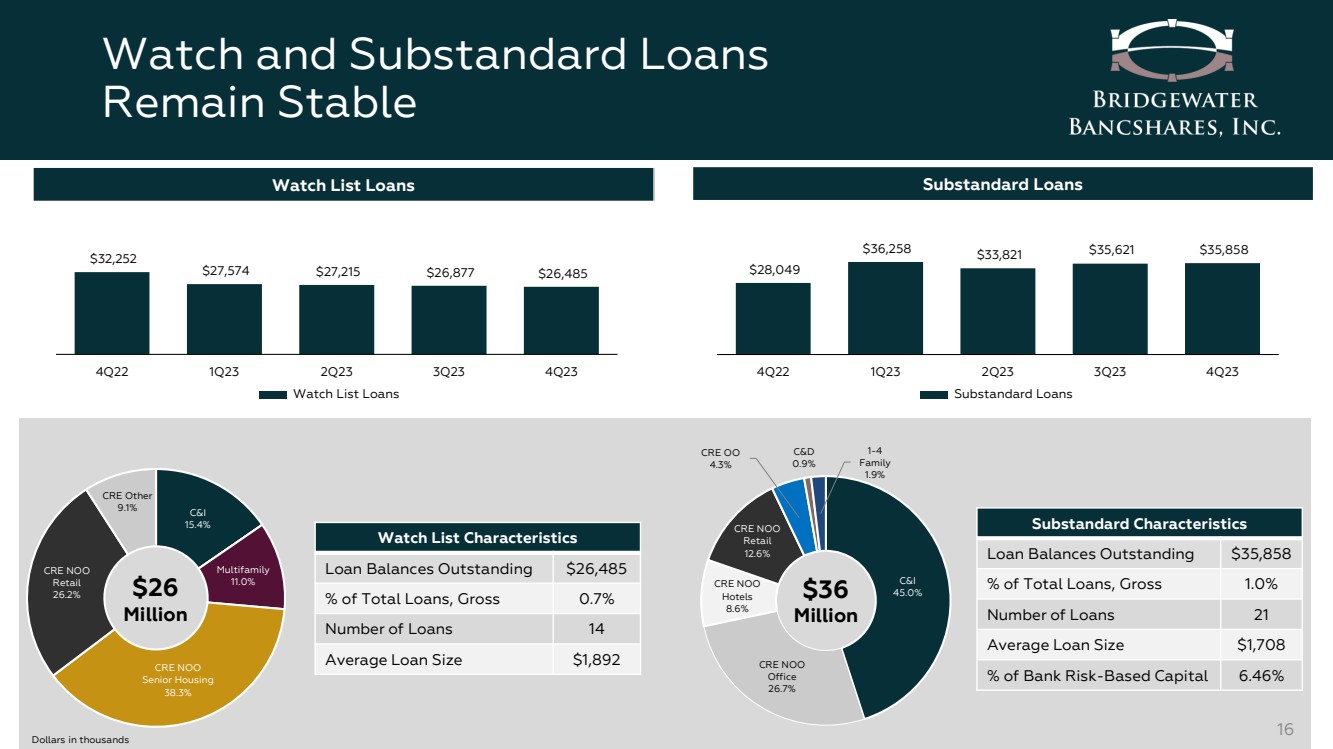

| ● | Loans with potential weaknesses that warrant a watchlist risk rating at December 31, 2023 totaled $26.5 million, compared to $26.9 million at September 30, 2023, and $32.3 million at December 31, 2022. |

| ● | Loans that warranted a substandard risk rating at December 31, 2023 totaled $35.9 million, compared to $35.6 million at September 30, 2023, and $28.0 million at December 31, 2022. |

| ● | Loans past due 30-89 days increased quarter over quarter due to the timing of closing on one matured loan. The closing occurred subsequent to year-end and the loan continues to perform as a pass-rated credit. |

Capital

Total shareholders’ equity at December 31, 2023 was $425.5 million, an increase of $9.6 million, or 2.3%, compared to total shareholders’ equity of $416.0 million at September 30, 2023, and an increase of $31.5 million, or 8.0%, over total shareholders’ equity of $394.1 million at December 31, 2022.

| ● | The linked-quarter increase was due to net income retained and a decrease in unrealized losses in the securities portfolio, offset partially by a decrease in unrealized gains in the derivatives portfolio, preferred stock dividends, and stock repurchases. |

| ● | The year-over-year increase was due to net income retained and a decrease in unrealized losses in the securities portfolio, offset partially by a decrease in unrealized gains in the derivatives portfolio, the adoption of the Current Expected Credit Losses (CECL) accounting methodology, preferred stock dividends, and stock repurchases. |

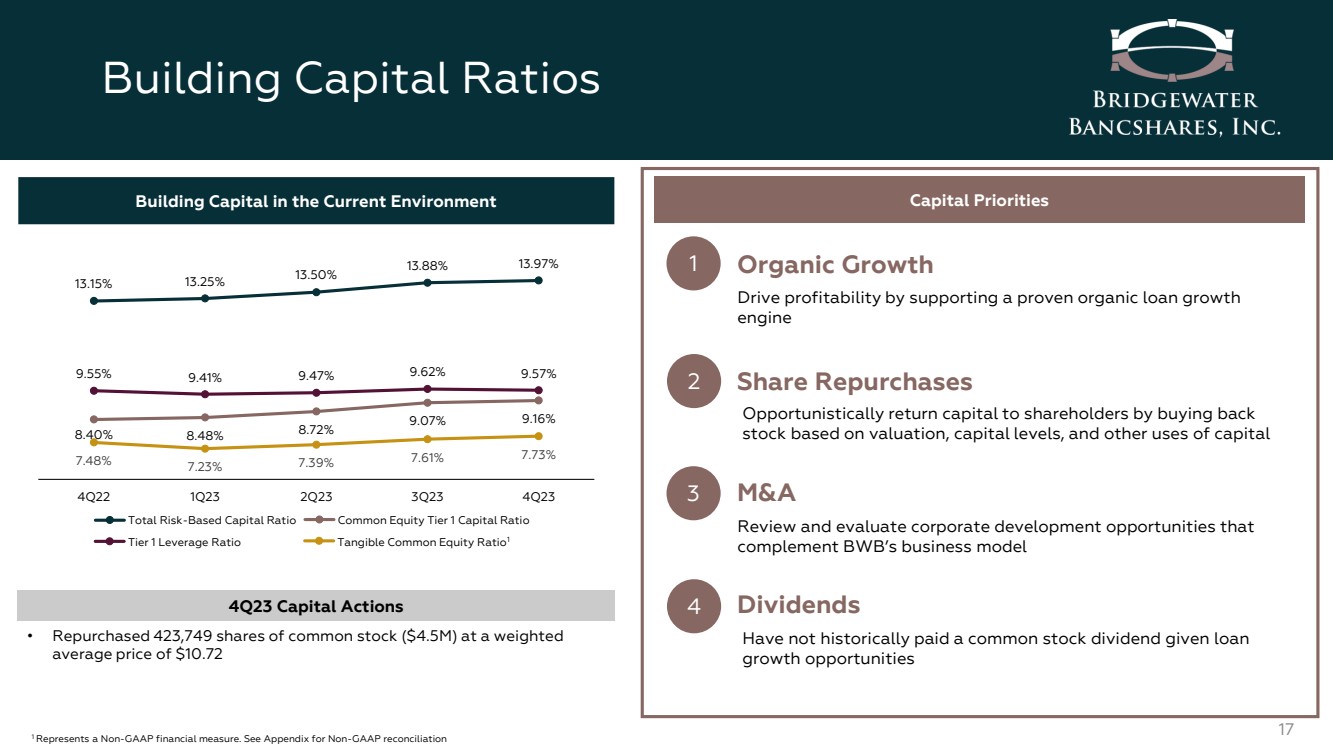

| ● | The Common Equity Tier 1 Risk-Based Capital Ratio was 9.16% at December 31, 2023, compared to 9.07% at September 30, 2023 and 8.40% at December 31, 2022. |

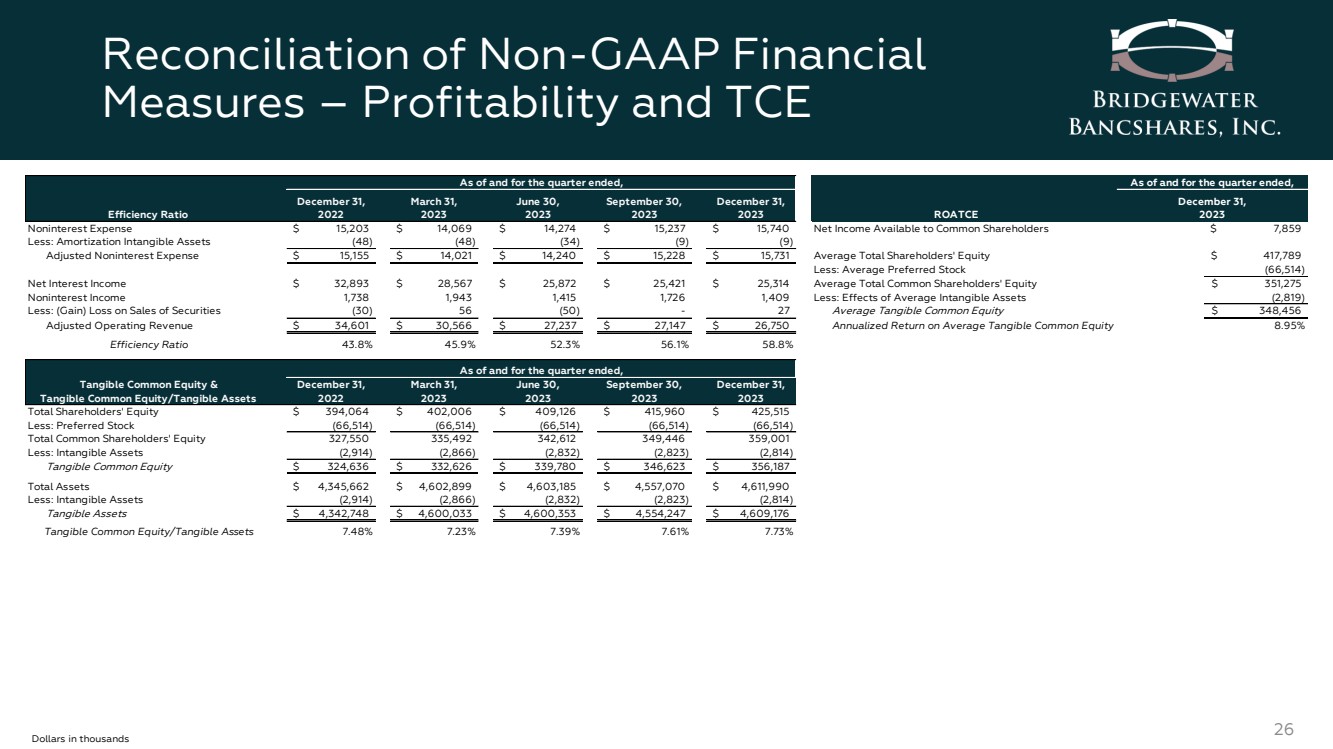

| ● | Tangible common equity as a percentage of tangible assets, a non-GAAP financial measure, was 7.73% at December 31, 2023, compared to 7.61% at September 30, 2023, and 7.48% at December 31, 2022. |

Tangible book value per share, a non-GAAP financial measure, was $12.84 as of December 31, 2023, an increase of 3.7% from $12.37 as of September 30, 2023, and an increase of 9.8% from $11.69 as of December 31, 2022.

| ● | The Company has increased tangible book value per share each of the past 28 quarters. |

During the fourth quarter of 2023, the company repurchased 423,749 shares of its common stock. Shares were repurchased at a weighted average price of $10.72 per share for a total of $4.5 million.

Page 6 of 17

| ● | The Company has $20.5 million remaining under its current share repurchase authorization. |

Today, the Company also announced that its Board of Directors has declared a quarterly cash dividend on its 5.875% Non-Cumulative Perpetual Preferred Stock, Series A (Series A Preferred Stock). The quarterly cash dividend of $36.72 per share, equivalent to $0.3672 per depositary share, each representing a 1/100th interest in a share of the Series A Preferred Stock (Nasdaq: BWBBP), is payable on March 1, 2024 to shareholders of record of the Series A Preferred Stock at the close of business on February 15, 2024.

Conference Call and Webcast

The Company will host a conference call to discuss its fourth quarter 2023 financial results on Thursday, January 25, 2024 at 8:00 a.m. Central Time. The conference call can be accessed by dialing 844-481-2913 and requesting to join the Bridgewater Bancshares earnings call. To listen to a replay of the conference call via phone, please dial 877-344-7529 and enter access code 4855149. The replay will be available through February 1, 2024. The conference call will also be available via a live webcast on the Investor Relations section of the Company’s website, investors.bridgewaterbankmn.com, and archived for replay.

About the Company

Bridgewater Bancshares, Inc. (Nasdaq: BWB) is a St. Louis Park, Minnesota-based financial holding company. Bridgewater's banking subsidiary, Bridgewater Bank, is a premier, full-service Twin Cities bank dedicated to serving the diverse needs of commercial real estate investors, entrepreneurs, business clients and successful individuals. By pairing a range of deposit, lending, and business services solutions with a responsive service model, Bridgewater has seen continuous growth and profitability. With total assets of $4.6 billion and seven branches as of December 31, 2023, Bridgewater is considered one of the largest locally led banks in the State of Minnesota, and has received numerous awards for its growth, banking services, and esteemed corporate culture.

Use of Non-GAAP financial measures

In addition to the results presented in accordance with U.S. Generally Accepted Accounting Principles (GAAP), the Company routinely supplements its evaluation with an analysis of certain non-GAAP financial measures. The Company believes these non-GAAP financial measures, in addition to the related GAAP measures, provide meaningful information to investors to help them understand the Company’s operating performance and trends, and to facilitate comparisons with the performance of peers. These disclosures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. Reconciliations of non-GAAP disclosures used in this earnings release to the comparable GAAP measures are provided in the accompanying tables.

Forward-Looking Statements

This earnings release contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements include, without limitation, statements concerning plans, estimates, calculations, forecasts and projections with respect to the anticipated future performance of the Company. These statements are often, but not always, identified by words such as “may”, “might”, “should”, “could”, “predict”, “potential”, “believe”, “expect”, “continue”, “will”, “anticipate”, “seek”, “estimate”, “intend”, “plan”, “projection”, “would”, “annualized”, “target” and “outlook”, or the negative version of those words or other comparable words of a future or forward-looking nature.

Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in the forward-looking statements. Therefore, you should not rely on any of these forward-looking statements.

Page 7 of 17

Important factors that could cause our actual results and financial condition to differ materially from those indicated in the forward-looking statements include, among others, the following: interest rate risk, including the effects of recent and potential additional rate increases by the Federal Reserve; fluctuations in the values of the securities held in our securities portfolio, including as the result of changes in interest rates; business and economic conditions generally and in the financial services industry, nationally and within our market area, including rising rates of inflation and possible recession; the effects of developments and events in the financial services industry, including the large-scale deposit withdrawals over a short period of time at Silicon Valley Bank, Signature Bank and First Republic Bank that resulted in the failure of those institutions; loan concentrations in our portfolio; the overall health of the local and national real estate market; our ability to successfully manage credit risk; our ability to maintain an adequate level of allowance for credit losses on loans; new or revised accounting standards; the concentration of large loans to certain borrowers; the concentration of large deposits from certain clients, who have balances above current FDIC insurance limits; our ability to successfully manage liquidity risk, which may increase our dependence on non-core funding sources such as brokered deposits, and negatively impact our cost of funds; our ability to raise additional capital to implement our business plan; our ability to implement our growth strategy and manage costs effectively; the composition of our senior leadership team and our ability to attract and retain key personnel; talent and labor shortages and high rates of employee turnover; the occurrence of fraudulent activity, breaches or failures of our or our third-party vendors’ information security controls or cybersecurity-related incidents, including as a result of sophisticated attacks using artificial intelligence and similar tools; interruptions involving our information technology and telecommunications systems or third-party servicers; competition in the financial services industry, including from nonbank competitors such as credit unions and “fintech” companies; the effectiveness of our risk management framework; the commencement and outcome of litigation and other legal proceedings and regulatory actions against us; the impact of recent and future legislative and regulatory changes, including in response to the failures of Silicon Valley Bank, Signature Bank and First Republic Bank in 2023; risks related to climate change and the negative impact it may have on our customers and their businesses; the imposition of other governmental policies impacting the value of products produced by our commercial borrowers; severe weather, natural disasters, wide spread disease or pandemics, acts of war or terrorism or other adverse external events, including the Israeli-Palestinian conflict and the Russian invasion of Ukraine; potential impairment to the goodwill the Company recorded in connection with our past acquisition; changes to U.S. or state tax laws, regulations and guidance, including the new 1% excise tax on stock buybacks by publicly traded companies; potential changes in federal policy and at regulatory agencies as a result of the upcoming 2024 presidential election; and any other risks described in the “Risk Factors” sections of reports filed by the Company with the Securities and Exchange Commission.

Any forward-looking statement made by us in this press release is based only on information currently available to us and speaks only as of the date on which it is made. The Company undertakes no obligation to publicly update any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future developments or otherwise.

Page 8 of 17

Bridgewater Bancshares, Inc. and Subsidiaries

Financial Highlights

(dollars in thousands, except share data)

|

|

As of and for the Three Months Ended |

|

|||||||||||||

|

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|

December 31, |

|

|||||

(dollars in thousands) |

|

2023 |

|

2023 |

|

2023 |

|

2023 |

|

2022 |

|

|||||

Income Statement |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Interest Income |

|

$ |

25,314 |

|

$ |

25,421 |

|

$ |

25,872 |

|

$ |

28,567 |

|

$ |

32,893 |

|

Provision for (Recovery of) Credit Losses |

|

|

(250) |

|

|

(600) |

|

|

50 |

|

|

625 |

|

|

1,500 |

|

Noninterest Income |

|

|

1,409 |

|

|

1,726 |

|

|

1,415 |

|

|

1,943 |

|

|

1,738 |

|

Noninterest Expense |

|

|

15,740 |

|

|

15,237 |

|

|

14,274 |

|

|

14,069 |

|

|

15,203 |

|

Net Income |

|

|

8,873 |

|

|

9,629 |

|

|

9,816 |

|

|

11,642 |

|

|

13,735 |

|

Net Income Available to Common Shareholders |

|

|

7,859 |

|

|

8,616 |

|

|

8,802 |

|

|

10,629 |

|

|

12,721 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Per Common Share Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic Earnings Per Share |

|

$ |

0.28 |

|

$ |

0.31 |

|

$ |

0.32 |

|

$ |

0.38 |

|

$ |

0.46 |

|

Diluted Earnings Per Share |

|

|

0.28 |

|

|

0.30 |

|

|

0.31 |

|

|

0.37 |

|

|

0.45 |

|

Book Value Per Share |

|

|

12.94 |

|

|

12.47 |

|

|

12.25 |

|

|

12.05 |

|

|

11.80 |

|

Tangible Book Value Per Share (1) |

|

|

12.84 |

|

|

12.37 |

|

|

12.15 |

|

|

11.95 |

|

|

11.69 |

|

Basic Weighted Average Shares Outstanding |

|

|

27,870,430 |

|

|

27,943,409 |

|

|

27,886,425 |

|

|

27,726,894 |

|

|

27,558,983 |

|

Diluted Weighted Average Shares Outstanding |

|

|

28,238,056 |

|

|

28,311,778 |

|

|

28,198,739 |

|

|

28,490,046 |

|

|

28,527,306 |

|

Shares Outstanding at Period End |

|

|

27,748,965 |

|

|

28,015,505 |

|

|

27,973,995 |

|

|

27,845,244 |

|

|

27,751,950 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Financial Ratios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on Average Assets (2) |

|

|

0.77 |

% |

|

0.85 |

% |

|

0.88 |

% |

|

1.07 |

% |

|

1.28 |

% |

Pre-Provision Net Revenue Return on Average Assets (1)(2) |

|

|

0.96 |

|

|

1.01 |

|

|

1.16 |

|

|

1.49 |

|

|

1.82 |

|

Return on Average Shareholders' Equity (2) |

|

|

8.43 |

|

|

9.23 |

|

|

9.69 |

|

|

11.70 |

|

|

14.06 |

|

Return on Average Tangible Common Equity (1)(2) |

|

|

8.95 |

|

|

9.92 |

|

|

10.48 |

|

|

12.90 |

|

|

15.86 |

|

Net Interest Margin (3) |

|

|

2.27 |

|

|

2.32 |

|

|

2.40 |

|

|

2.72 |

|

|

3.16 |

|

Core Net Interest Margin (1)(3) |

|

|

2.21 |

|

|

2.24 |

|

|

2.31 |

|

|

2.62 |

|

|

3.05 |

|

Cost of Total Deposits |

|

|

3.19 |

|

|

2.99 |

|

|

2.66 |

|

|

2.01 |

|

|

1.31 |

|

Cost of Funds |

|

|

3.23 |

|

|

3.10 |

|

|

2.91 |

|

|

2.41 |

|

|

1.67 |

|

Efficiency Ratio (1) |

|

|

58.8 |

|

|

56.1 |

|

|

52.3 |

|

|

45.9 |

|

|

43.8 |

|

Noninterest Expense to Average Assets (2) |

|

|

1.37 |

|

|

1.34 |

|

|

1.28 |

|

|

1.30 |

|

|

1.42 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance Sheet |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Assets |

|

$ |

4,611,990 |

|

$ |

4,557,070 |

|

$ |

4,603,185 |

|

$ |

4,602,899 |

|

$ |

4,345,662 |

|

Total Loans, Gross |

|

|

3,724,282 |

|

|

3,722,271 |

|

|

3,736,211 |

|

|

3,684,360 |

|

|

3,569,446 |

|

Deposits |

|

|

3,709,948 |

|

|

3,675,509 |

|

|

3,577,932 |

|

|

3,411,123 |

|

|

3,416,543 |

|

Total Shareholders' Equity |

|

|

425,515 |

|

|

415,960 |

|

|

409,126 |

|

|

402,006 |

|

|

394,064 |

|

Loan to Deposit Ratio |

|

|

100.4 |

% |

|

101.3 |

% |

|

104.4 |

% |

|

108.0 |

% |

|

104.5 |

% |

Core Deposits to Total Deposits (4) |

|

|

68.7 |

|

|

70.3 |

|

|

70.3 |

|

|

72.4 |

|

|

74.6 |

|

Uninsured Deposits to Total Deposits |

|

|

24.3 |

|

|

22.2 |

|

|

22.1 |

|

|

24.0 |

|

|

38.5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Asset Quality |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Loan Charge-Offs to Average Loans (2) |

|

|

0.01 |

% |

|

0.01 |

% |

|

0.00 |

% |

|

0.00 |

% |

|

0.00 |

% |

Nonperforming Assets to Total Assets (5) |

|

|

0.02 |

|

|

0.02 |

|

|

0.02 |

|

|

0.02 |

|

|

0.01 |

|

Allowance for Credit Losses to Total Loans |

|

|

1.36 |

|

|

1.36 |

|

|

1.36 |

|

|

1.36 |

|

|

1.34 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Capital Ratios (Consolidated) (6) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tier 1 Leverage Ratio |

|

|

9.57 |

% |

|

9.62 |

% |

|

9.47 |

% |

|

9.41 |

% |

|

9.55 |

% |

Common Equity Tier 1 Risk-based Capital Ratio |

|

|

9.16 |

|

|

9.07 |

|

|

8.72 |

|

|

8.48 |

|

|

8.40 |

|

Tier 1 Risk-based Capital Ratio |

|

|

10.79 |

|

|

10.69 |

|

|

10.33 |

|

|

10.08 |

|

|

10.03 |

|

Total Risk-based Capital Ratio |

|

|

13.97 |

|

|

13.88 |

|

|

13.50 |

|

|

13.25 |

|

|

13.15 |

|

Tangible Common Equity to Tangible Assets (1) |

|

|

7.73 |

|

|

7.61 |

|

|

7.39 |

|

|

7.23 |

|

|

7.48 |

|

| (1) | Represents a non-GAAP financial measure. See "Non-GAAP Financial Measures" for further details. |

| (2) | Annualized. |

| (3) | Amounts calculated on a tax-equivalent basis using the statutory federal tax rate of 21%. |

Page 9 of 17

| (4) | Core deposits are defined as total deposits less brokered deposits and certificates of deposit greater than $250,000. |

| (5) | Nonperforming assets are defined as nonaccrual loans plus 90 days past due and still accruing plus foreclosed assets. |

| (6) | Preliminary data. Current period subject to change prior to filings with applicable regulatory agencies. |

Page 10 of 17

Bridgewater Bancshares, Inc. and Subsidiaries

Consolidated Balance Sheets

(dollars in thousands, except share data)

|

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|

December 31, |

|||||

|

|

2023 |

|

2023 |

|

2023 |

|

2023 |

|

2022 |

|||||

|

|

(Unaudited) |

|

(Unaudited) |

|

(Unaudited) |

|

(Unaudited) |

|

|

|||||

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and Cash Equivalents |

|

$ |

128,562 |

|

$ |

124,358 |

|

$ |

177,101 |

|

$ |

209,192 |

|

$ |

87,043 |

Bank-Owned Certificates of Deposit |

|

|

— |

|

|

1,225 |

|

|

1,225 |

|

|

1,225 |

|

|

1,181 |

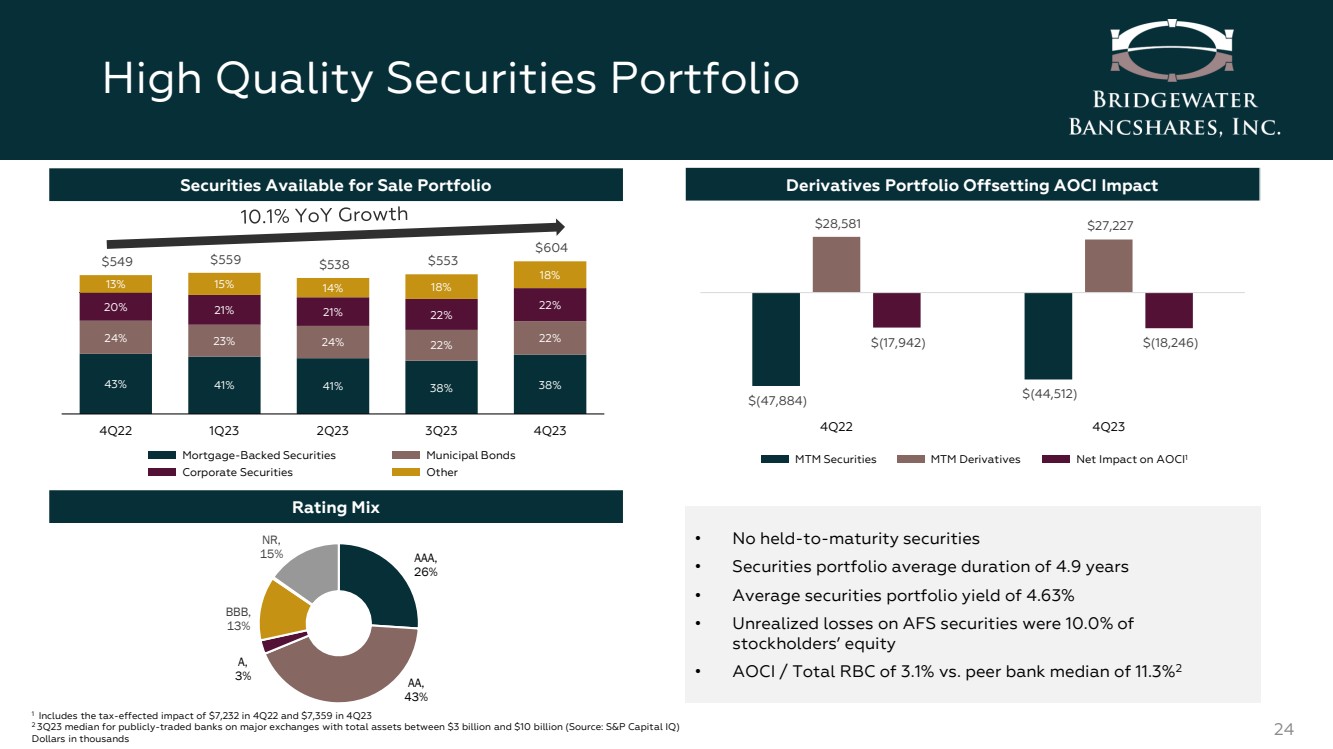

Securities Available for Sale, at Fair Value |

|

|

604,104 |

|

|

553,076 |

|

|

538,220 |

|

|

559,430 |

|

|

548,613 |

Loans, Net of Allowance for Credit Losses |

|

|

3,667,215 |

|

|

3,664,464 |

|

|

3,677,792 |

|

|

3,625,477 |

|

|

3,512,157 |

Federal Home Loan Bank (FHLB) Stock, at Cost |

|

|

17,097 |

|

|

17,056 |

|

|

21,557 |

|

|

28,632 |

|

|

19,606 |

Premises and Equipment, Net |

|

|

48,886 |

|

|

49,331 |

|

|

49,710 |

|

|

47,801 |

|

|

48,445 |

Foreclosed Assets |

|

|

— |

|

|

— |

|

|

116 |

|

|

116 |

|

|

— |

Accrued Interest |

|

|

16,697 |

|

|

15,182 |

|

|

13,822 |

|

|

13,377 |

|

|

13,479 |

Goodwill |

|

|

2,626 |

|

|

2,626 |

|

|

2,626 |

|

|

2,626 |

|

|

2,626 |

Other Intangible Assets, Net |

|

|

188 |

|

|

197 |

|

|

206 |

|

|

240 |

|

|

288 |

Bank-Owned Life Insurance |

|

|

34,477 |

|

|

34,209 |

|

|

33,958 |

|

|

33,719 |

|

|

33,485 |

Other Assets |

|

|

92,138 |

|

|

95,346 |

|

|

86,852 |

|

|

81,064 |

|

|

78,739 |

Total Assets |

|

$ |

4,611,990 |

|

$ |

4,557,070 |

|

$ |

4,603,185 |

|

$ |

4,602,899 |

|

$ |

4,345,662 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Liabilities and Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deposits: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest Bearing |

|

$ |

756,964 |

|

$ |

754,297 |

|

$ |

751,217 |

|

$ |

742,198 |

|

$ |

884,272 |

Interest Bearing |

|

|

2,952,984 |

|

|

2,921,212 |

|

|

2,826,715 |

|

|

2,668,925 |

|

|

2,532,271 |

Total Deposits |

|

|

3,709,948 |

|

|

3,675,509 |

|

|

3,577,932 |

|

|

3,411,123 |

|

|

3,416,543 |

Federal Funds Purchased |

|

|

— |

|

|

— |

|

|

195,000 |

|

|

437,000 |

|

|

287,000 |

Notes Payable |

|

|

13,750 |

|

|

13,750 |

|

|

13,750 |

|

|

13,750 |

|

|

13,750 |

FHLB Advances |

|

|

319,500 |

|

|

294,500 |

|

|

262,000 |

|

|

197,000 |

|

|

97,000 |

Subordinated Debentures, Net of Issuance Costs |

|

|

79,288 |

|

|

79,192 |

|

|

79,096 |

|

|

79,001 |

|

|

78,905 |

Accrued Interest Payable |

|

|

5,282 |

|

|

3,816 |

|

|

2,974 |

|

|

3,257 |

|

|

2,831 |

Other Liabilities |

|

|

58,707 |

|

|

74,343 |

|

|

63,307 |

|

|

59,762 |

|

|

55,569 |

Total Liabilities |

|

|

4,186,475 |

|

|

4,141,110 |

|

|

4,194,059 |

|

|

4,200,893 |

|

|

3,951,598 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SHAREHOLDERS' EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preferred Stock- $0.01 par value; Authorized 10,000,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preferred Stock - Issued and Outstanding 27,600 Series A shares ($2,500 liquidation preference) at December 31, 2023 (unaudited), September 30, 2023 (unaudited), June 30, 2023 (unaudited), March 31, 2023 (unaudited), and December 31, 2022 |

|

|

66,514 |

|

|

66,514 |

|

|

66,514 |

|

|

66,514 |

|

|

66,514 |

Common Stock- $0.01 par value; Authorized 75,000,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common Stock - Issued and Outstanding 27,748,965 at December 31, 2023 (unaudited), 28,015,505 at September 30, 2023 (unaudited), 27,973,995 at June 30, 2023 (unaudited), 27,845,244 at March 31, 2023 (unaudited), and 27,751,950 at December 31, 2022 |

|

|

277 |

|

|

280 |

|

|

280 |

|

|

278 |

|

|

278 |

Additional Paid-In Capital |

|

|

96,320 |

|

|

100,120 |

|

|

99,044 |

|

|

97,716 |

|

|

96,529 |

Retained Earnings |

|

|

280,650 |

|

|

272,812 |

|

|

264,196 |

|

|

255,394 |

|

|

248,685 |

Accumulated Other Comprehensive Loss |

|

|

(18,246) |

|

|

(23,766) |

|

|

(20,908) |

|

|

(17,896) |

|

|

(17,942) |

Total Shareholders' Equity |

|

|

425,515 |

|

|

415,960 |

|

|

409,126 |

|

|

402,006 |

|

|

394,064 |

Total Liabilities and Equity |

|

$ |

4,611,990 |

|

$ |

4,557,070 |

|

$ |

4,603,185 |

|

$ |

4,602,899 |

|

$ |

4,345,662 |

Page 11 of 17

Bridgewater Bancshares, Inc. and Subsidiaries

Consolidated Statements of Income

(dollars in thousands, except per share data)

(Unaudited)

|

|

Three Months Ended |

|

Year Ended |

|||||||||||||||||

|

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|

December 31, |

|

December 31, |

|

December 31, |

|||||||

(dollars in thousands) |

|

2023 |

|

2023 |

|

2023 |

|

2023 |

|

2022 |

|

2023 |

|

2022 |

|||||||

Interest Income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, Including Fees |

|

$ |

49,727 |

|

$ |

48,999 |

|

$ |

47,721 |

|

$ |

44,955 |

|

$ |

42,488 |

|

$ |

191,402 |

|

$ |

146,256 |

Investment Securities |

|

|

7,283 |

|

|

6,507 |

|

|

6,237 |

|

|

6,218 |

|

|

5,843 |

|

|

26,245 |

|

|

16,410 |

Other |

|

|

1,543 |

|

|

1,303 |

|

|

1,043 |

|

|

819 |

|

|

529 |

|

|

4,708 |

|

|

1,029 |

Total Interest Income |

|

|

58,553 |

|

|

56,809 |

|

|

55,001 |

|

|

51,992 |

|

|

48,860 |

|

|

222,355 |

|

|

163,695 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest Expense |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deposits |

|

|

29,448 |

|

|

27,225 |

|

|

22,998 |

|

|

16,374 |

|

|

10,781 |

|

|

96,045 |

|

|

23,379 |

Federal Funds Purchased |

|

|

268 |

|

|

548 |

|

|

2,761 |

|

|

4,944 |

|

|

3,379 |

|

|

8,521 |

|

|

4,507 |

Notes Payable |

|

|

299 |

|

|

296 |

|

|

285 |

|

|

263 |

|

|

202 |

|

|

1,143 |

|

|

202 |

FHLB Advances |

|

|

2,220 |

|

|

2,316 |

|

|

2,092 |

|

|

861 |

|

|

575 |

|

|

7,489 |

|

|

1,221 |

Subordinated Debentures |

|

|

1,004 |

|

|

1,003 |

|

|

993 |

|

|

983 |

|

|

1,030 |

|

|

3,983 |

|

|

4,688 |

Total Interest Expense |

|

|

33,239 |

|

|

31,388 |

|

|

29,129 |

|

|

23,425 |

|

|

15,967 |

|

|

117,181 |

|

|

33,997 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Interest Income |

|

|

25,314 |

|

|

25,421 |

|

|

25,872 |

|

|

28,567 |

|

|

32,893 |

|

|

105,174 |

|

|

129,698 |

Provision for (Recovery of) Credit Losses |

|

|

(250) |

|

|

(600) |

|

|

50 |

|

|

625 |

|

|

1,500 |

|

|

(175) |

|

|

7,700 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Interest Income After Provision for Credit Losses |

|

|

25,564 |

|

|

26,021 |

|

|

25,822 |

|

|

27,942 |

|

|

31,393 |

|

|

105,349 |

|

|

121,998 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest Income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Customer Service Fees |

|

|

359 |

|

|

379 |

|

|

368 |

|

|

349 |

|

|

344 |

|

|

1,455 |

|

|

1,236 |

Net Gain (Loss) on Sales of Securities |

|

|

(27) |

|

|

— |

|

|

50 |

|

|

(56) |

|

|

30 |

|

|

(33) |

|

|

82 |

Letter of Credit Fees |

|

|

418 |

|

|

315 |

|

|

379 |

|

|

634 |

|

|

358 |

|

|

1,746 |

|

|

1,592 |

Debit Card Interchange Fees |

|

|

152 |

|

|

150 |

|

|

155 |

|

|

138 |

|

|

148 |

|

|

595 |

|

|

586 |

Swap Fees |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

557 |

Bank-Owned Life Insurance |

|

|

268 |

|

|

252 |

|

|

238 |

|

|

234 |

|

|

238 |

|

|

992 |

|

|

762 |

FHLB Prepayment Income |

|

|

— |

|

|

493 |

|

|

— |

|

|

299 |

|

|

— |

|

|

792 |

|

|

— |

Other Income |

|

|

239 |

|

|

137 |

|

|

225 |

|

|

345 |

|

|

620 |

|

|

946 |

|

|

1,517 |

Total Noninterest Income |

|

|

1,409 |

|

|

1,726 |

|

|

1,415 |

|

|

1,943 |

|

|

1,738 |

|

|

6,493 |

|

|

6,332 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest Expense |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Salaries and Employee Benefits |

|

|

9,615 |

|

|

9,519 |

|

|

8,589 |

|

|

8,815 |

|

|

9,821 |

|

|

36,538 |

|

|

36,941 |

Occupancy and Equipment |

|

|

1,062 |

|

|

1,101 |

|

|

1,075 |

|

|

1,209 |

|

|

1,177 |

|

|

4,447 |

|

|

4,390 |

FDIC Insurance Assessment |

|

|

1,050 |

|

|

1,075 |

|

|

900 |

|

|

665 |

|

|

360 |

|

|

3,690 |

|

|

1,365 |

Data Processing |

|

|

424 |

|

|

392 |

|

|

401 |

|

|

357 |

|

|

371 |

|

|

1,574 |

|

|

1,396 |

Professional and Consulting Fees |

|

|

782 |

|

|

715 |

|

|

829 |

|

|

755 |

|

|

635 |

|

|

3,081 |

|

|

2,664 |

Derivative Collateral Fees |

|

|

573 |

|

|

543 |

|

|

404 |

|

|

380 |

|

|

535 |

|

|

1,900 |

|

|

687 |

Information Technology and Telecommunications |

|

|

812 |

|

|

683 |

|

|

711 |

|

|

683 |

|

|

673 |

|

|

2,889 |

|

|

2,495 |

Marketing and Advertising |

|

|

324 |

|

|

222 |

|

|

321 |

|

|

262 |

|

|

403 |

|

|

1,129 |

|

|

2,032 |

Intangible Asset Amortization |

|

|

9 |

|

|

9 |

|

|

34 |

|

|

48 |

|

|

48 |

|

|

100 |

|

|

191 |

Amortization of Tax Credit Investments |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

114 |

|

|

— |

|

|

408 |

Other Expense |

|

|

1,089 |

|

|

978 |

|

|

1,010 |

|

|

895 |

|

|

1,066 |

|

|

3,972 |

|

|

4,051 |

Total Noninterest Expense |

|

|

15,740 |

|

|

15,237 |

|

|

14,274 |

|

|

14,069 |

|

|

15,203 |

|

|

59,320 |

|

|

56,620 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income Before Income Taxes |

|

|

11,233 |

|

|

12,510 |

|

|

12,963 |

|

|

15,816 |

|

|

17,928 |

|

|

52,522 |

|

|

71,710 |

Provision for Income Taxes |

|

|

2,360 |

|

|

2,881 |

|

|

3,147 |

|

|

4,174 |

|

|

4,193 |

|

|

12,562 |

|

|

18,318 |

Net Income |

|

|

8,873 |

|

|

9,629 |

|

|

9,816 |

|

|

11,642 |

|

|

13,735 |

|

|

39,960 |

|

|

53,392 |

Preferred Stock Dividends |

|

|

(1,014) |

|

|

(1,013) |

|

|

(1,014) |

|

|

(1,013) |

|

|

(1,014) |

|

|

(4,054) |

|

|

(4,054) |

Net Income Available to Common Shareholders |

|

$ |

7,859 |

|

$ |

8,616 |

|

$ |

8,802 |

|

$ |

10,629 |

|

$ |

12,721 |

|

$ |

35,906 |

|

$ |

49,338 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|