UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d)

of The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): July 27, 2023

DIGITAL REALTY TRUST, INC.

(Exact name of registrant as specified in its charter)

|

|

|

Maryland |

001-32336 |

26-0081711 |

(State or other jurisdiction |

(Commission |

(IRS Employer |

|

|

5707 Southwest Parkway, Building 1, Suite 275 |

78735 |

(Address of principal executive offices) |

(Zip Code) |

(737) 281-0101

(Registrant’s telephone number, including area code)

N/A

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

Title of each class |

Trading |

Name of each exchange on |

Common Stock |

DLR |

New York Stock Exchange |

Series J Cumulative Redeemable Preferred Stock |

DLR Pr J |

New York Stock Exchange |

Series K Cumulative Redeemable Preferred Stock |

DLR Pr K |

New York Stock Exchange |

Series L Cumulative Redeemable Preferred Stock |

DLR Pr L |

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

|

Emerging growth company ☐ |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ◻ The information in this Item 2.02 of this Current Report on Form 8-K is also being furnished under Item 7.01 “Regulation FD Disclosure” of Form 8-K.

Item 2.02 Results of Operations and Financial Condition.

Such information, including the exhibits attached hereto, is furnished pursuant to Item 2.02 and shall not be deemed “filed” for any purpose, including for the purposes of Section 18 of the Securities Exchange Act of 1934, as amended (Exchange Act), or otherwise subject to the liabilities of that Section. The information in this Current Report on Form 8-K shall not be deemed incorporated by reference into any filing under the Securities Act of 1933, as amended (Securities Act), or the Exchange Act regardless of any general incorporation language in such filing.

On July 27, 2023, we issued a press release announcing our financial results for the quarter ended June 30, 2023. The press release referred to certain supplemental information that is available on the Company’s website at www.digitalrealty.com. A copy of the press release and supplemental information is attached hereto as Exhibit 99.1 and incorporated by reference herein.

On July 27, 2023, we also posted presentation materials to our website at www.digitalrealty.com. The presentation materials are attached hereto as Exhibit 99.2 and incorporated by reference herein.

Item 7.01 Regulation FD Disclosure.

The information in this Item 7.01 of this Current Report on Form 8-K is also being furnished under Item 2.02 “Results of Operations and Financial Condition” of Form 8-K. Such information, including the exhibits attached hereto, is furnished pursuant to Item 7.01 and shall not be deemed “filed” for any purpose, including for the purposes of Section 18 of the Exchange Act, or otherwise subject to the liabilities of that Section. The information in this Current Report on Form 8-K shall not be deemed incorporated by reference into any filing under the Securities Act or the Exchange Act regardless of any general incorporation language in such filing.

On July 27, 2023, we issued a press release announcing our financial results for the quarter ended June 30, 2023. The press release referred to certain supplemental information that is available on the Company’s website at www.digitalrealty.com. A copy of the press release and supplemental information is attached hereto as Exhibit 99.1 and incorporated by reference herein.

On July 27, 2023, we also posted presentation materials to our website at www.digitalrealty.com. The presentation materials are attached hereto as Exhibit 99.2 and incorporated by reference herein.

Item 9.01 Financial Statements and Exhibits.

(d) Exhibits.

|

|

|

Exhibit No. |

|

Description |

|

|

|

99.1 |

|

Earnings Press Release and Supplemental Information for the Quarter Ended June 30, 2023. |

99.2 |

|

|

104 |

|

Cover Page Interactive Data File (embedded within the Inline XBRL document) |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

|

Digital Realty Trust, Inc. |

|

By: |

/s/ JEANNIE LEE |

|

|

Jeannie Lee |

|

|

Executive Vice President, General Counsel and Secretary |

Date: July 27, 2023

Overview |

PAGE |

|

|

3 |

|

|

|

5 |

|

|

|

Consolidated Statements of Operations |

|

|

|

7 |

|

|

|

10 |

|

|

|

12 |

|

|

|

13 |

|

|

|

14 |

|

|

|

Balance Sheet Information |

|

|

|

15 |

|

|

|

16 |

|

|

|

17 |

|

|

|

18 |

|

|

|

Internal Growth |

|

|

|

19 |

|

|

|

20 |

|

|

|

21 |

|

|

|

22 |

|

|

|

23 |

|

|

|

24 |

|

|

|

External Growth |

|

|

|

25 |

|

|

|

26 |

|

|

|

Historical Capital Expenditures and Investments in Real Estate |

27 |

|

|

28 |

|

|

|

29 |

|

|

|

30 |

|

|

|

Additional Information |

|

|

|

Reconciliation of Earnings Before Interest, Taxes, Depreciation & Amortization and Financial Ratios |

31 |

|

|

32 |

|

|

|

34 |

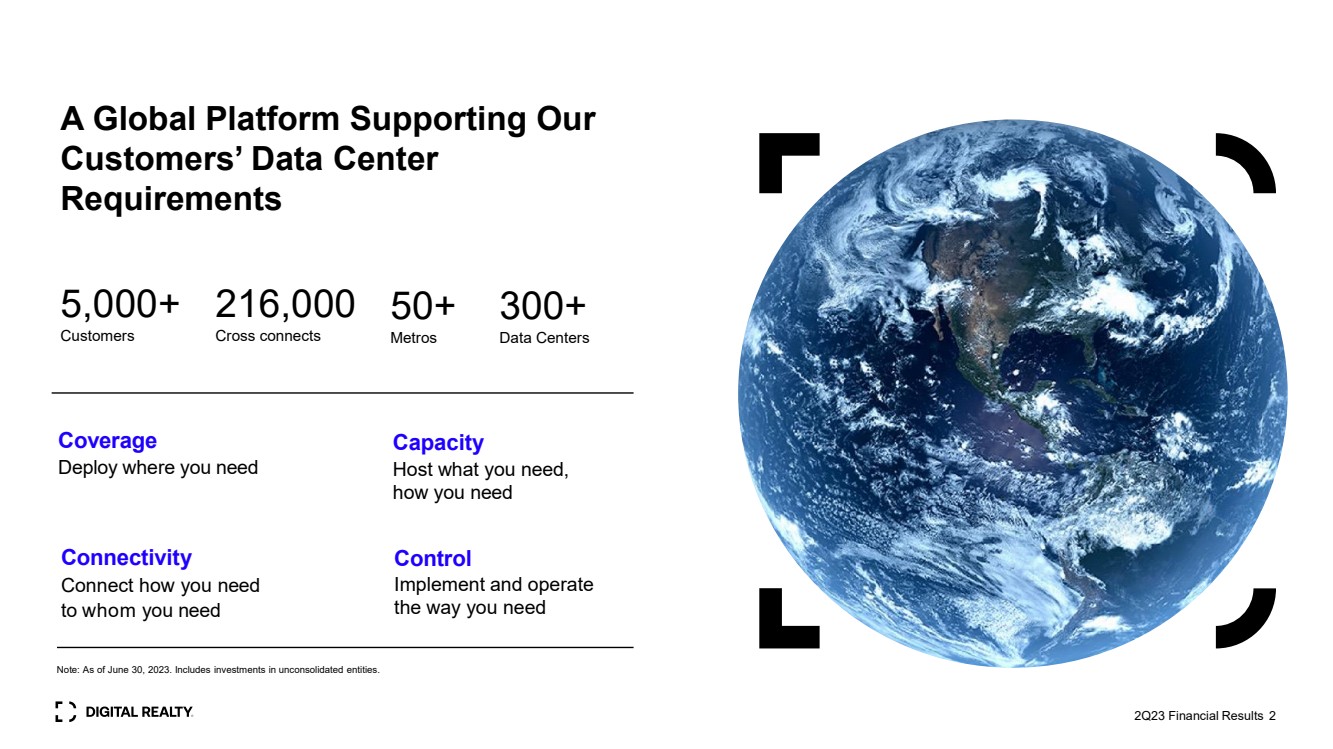

Corporate Profile

Digital Realty Trust, Inc. (“Digital Realty” or the “company”) owns, acquires, develops, and operates data centers through its operating partnership subsidiary, Digital Realty Trust, L.P. (the “operating partnership”). The company is focused on providing data center, colocation and interconnection solutions for domestic and international customers across a variety of industry verticals ranging from cloud and information technology services, communications and social networking to financial services, manufacturing, energy, healthcare, and consumer products. As of June 30, 2023, the company’s 316 data centers, including 61 data centers held as investments in unconsolidated joint ventures, contain applications and operations critical to the day-to-day operations of technology industry and corporate enterprise data center customers. Digital Realty’s portfolio is comprised of approximately 39.3 million square feet, excluding approximately 8.8 million square feet of space under active development and 3.9 million square feet of space held for future development, located throughout North America, Europe, South America, Asia, Australia, and Africa. For additional information, please visit the company’s website at https://www.digitalrealty.com/.

Corporate Headquarters

5707 Southwest Parkway, Building 1, Suite 275

Austin, TX 78735

Telephone: (737) 281-0101

Website: https://www.digitalrealty.com/

Senior Management

President & Chief Executive Officer: Andrew P. Power

Chief Financial Officer: Matthew R. Mercier

Chief Investment Officer: Gregory S. Wright

Chief Technology Officer: Christopher L. Sharp

Chief Revenue Officer: Colin M. McLean

Investor Relations

To request more information or to be added to our e-mail distribution list, please visit the Investor Relations section of our website at https://investor.digitalrealty.com/

Analyst Coverage

|

Bank of America |

|

BMO Capital |

BNP Paribas |

|

|||||||

Argus Research |

|

Merrill Lynch |

|

Barclays |

|

Markets |

|

Exane |

|

Citigroup |

|

Deutsche Bank |

Marie Ferguson |

|

David Barden |

|

Brendan Lynch |

|

Ari Klein |

|

Nate Crossett |

|

Michael Rollins |

|

Matthew Niknam |

(212) 425-7500 |

|

(646) 855-1320 |

|

(212) 526-9428 |

|

(212) 885-4103 |

|

(646) 725-3716 |

|

(212) 816-1116 |

|

(212) 250-4711 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Edward Jones |

|

Evercore ISI |

|

Green Street Advisors |

|

J.P. Morgan |

|

Jefferies |

|

MoffettNathanson |

|

Morgan Stanley |

Kyle Sanders |

|

Irvin Liu |

|

David Guarino |

|

Richard Choe |

|

Jonathan Petersen |

|

Nick Del Deo |

|

Simon Flannery |

(314) 515-0198 |

|

(415) 800-0183 |

|

(949) 640-8780 |

|

(212) 662-6708 |

|

(212) 284-1705 |

|

(212) 519-0025 |

|

(212) 761-6432 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Morningstar |

|

Raymond James |

|

RBC Capital Markets |

|

Stifel |

|

TD Cowen |

|

Truist Securities |

|

UBS |

Matthew Dolgin |

|

Frank Louthan |

|

Jonathan Atkin |

|

Erik Rasmussen |

|

Michael Elias |

|

Anthony Hau |

|

John Hodulik |

(312) 696-6783 |

|

(404) 442-5867 |

|

(415) 633-8589 |

|

(212) 271-3461 |

|

(646) 562-1358 |

|

(212) 303-4176 |

|

(212) 713- 4226 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Wells Fargo |

|

Wolfe Research |

|

|

|

|

|

|

|

|

||

Eric Luebchow |

|

Andrew Rosivach |

|

|

|

|

|

|

|

|

||

(312) 630-2386 |

|

(646) 582-9250 |

|

|

|

|

|

|

|

|

This Earnings Press Release and Supplemental Information package supplements the information provided in our quarterly and annual reports filed with the U.S. Securities and Exchange Commission. Additional information about Digital Realty and our business is also available on our website at www.digitalrealty.com.

3

Stock Listing Information

The stock of Digital Realty Trust, Inc. is traded primarily on the New York Stock Exchange under the following symbols:

Common Stock: |

|

DLR |

Series J Preferred Stock: |

|

DLRPRJ |

Series K Preferred Stock: |

|

DLRPRK |

Series L Preferred Stock: |

|

DLRPRL |

Symbols may vary by stock quote provider.

Credit Ratings

Standard & Poor’s |

|

|

|

Corporate Credit Rating: |

|

BBB |

(Negative Outlook) |

Preferred Stock: |

|

BB+ |

|

|

|

|

|

Moody’s |

|

|

|

Issuer Rating: |

|

Baa2 |

(Stable Outlook) |

Preferred Stock: |

|

Baa3 |

|

|

|

|

|

Fitch |

|

|

|

Issuer Default Rating: |

|

BBB |

(Stable Outlook) |

Preferred Stock: |

|

BB+ |

|

These credit ratings may not reflect the potential impact of risks relating to the structure or trading of the company’s securities and are provided solely for informational purposes. Credit ratings are not recommendations to buy, hold or sell any security, and may be revised or withdrawn at any time by the issuing rating agency at its sole discretion. The company does not undertake any obligation to maintain the ratings or to advise of any change in ratings. Each agency’s rating should be evaluated independently of any other agency’s rating. An explanation of the significance of the ratings may be obtained from each of the rating agencies.

Common Stock Price Performance

The following summarizes recent activity of Digital Realty’s common stock (DLR):

|

|

Three Months Ended |

|

|||||||||||||

|

|

30-Jun-23 |

|

31-Mar-23 |

|

31-Dec-22 |

|

30-Sep-22 |

|

30-Jun-22 |

|

|||||

High price |

|

|

$114.43 |

|

|

$122.43 |

|

|

$114.86 |

|

|

$138.09 |

|

|

$153.50 |

|

Low price |

|

|

$86.33 |

|

|

$90.72 |

|

|

$85.76 |

|

|

$96.08 |

|

|

$124.00 |

|

Closing price, end of quarter |

|

|

$113.87 |

|

|

$98.31 |

|

|

$100.27 |

|

|

$99.18 |

|

|

$129.83 |

|

Average daily trading volume |

|

|

3,112,901 |

|

|

2,232,417 |

|

|

2,168,114 |

|

|

1,608,999 |

|

|

1,580,520 |

|

Indicated dividend per common share (1) |

|

|

$4.88 |

|

|

$4.88 |

|

|

$4.88 |

|

|

$4.88 |

|

|

$4.88 |

|

Closing annual dividend yield, end of quarter |

|

|

4.3% |

|

|

5.0% |

|

|

4.9% |

|

|

4.9% |

|

|

3.8% |

|

Shares and units outstanding, end of quarter (2) |

|

|

305,723,430 |

|

|

297,760,767 |

|

|

297,436,891 |

|

|

293,803,727 |

|

|

291,033,400 |

|

Closing market value of shares and units outstanding (3) |

|

|

$34,812,727 |

|

|

$29,272,861 |

|

|

$29,823,997 |

|

|

$29,139,454 |

|

|

$37,784,866 |

|

| (1) | On an annualized basis. |

| (2) | As of June 30, 2023, the total number of shares and units includes 299,240,366 shares of common stock, 4,343,275 common units held by third parties and 2,139,789 common units and vested and unvested long-term incentive units held by directors, officers and others and excludes all shares of common stock potentially issuable upon conversion of our series J, series K and series L cumulative redeemable preferred stock upon certain change of control transactions. |

| (3) | Dollars in thousands as of the end of the quarter. |

This Earnings Press Release and Supplemental Information package supplements the information provided in our quarterly and annual reports filed with the U.S. Securities and Exchange Commission. Additional information about us and our data centers is also available on our website at www.digitalrealty.com.

4

Key Quarterly Financial Data |

|

Financial Supplement |

|---|---|---|

Unaudited, Dollars (except per share data) and Square Feet in Thousands |

Second Quarter 2023 |

Shares and Units at End of Quarter |

|

30-Jun-23 |

|

31-Mar-23 |

|

31-Dec-22 |

|

30-Sep-22 |

|

30-Jun-22 |

|||||

Common shares outstanding |

|

|

299,240,366 |

|

|

291,298,610 |

|

|

291,148,222 |

|

|

287,509,059 |

|

|

284,733,922 |

Common partnership units outstanding |

|

|

6,483,064 |

|

|

6,462,157 |

|

|

6,288,669 |

|

|

6,294,668 |

|

|

6,299,478 |

Total Shares and Units |

|

|

305,723,430 |

|

|

297,760,767 |

|

|

297,436,891 |

|

|

293,803,727 |

|

|

291,033,400 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enterprise Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Market value of common equity (1) |

|

|

$34,812,727 |

|

|

$29,272,861 |

|

|

$29,823,997 |

|

|

$29,139,454 |

|

|

$37,784,866 |

Liquidation value of preferred equity |

|

|

755,000 |

|

|

755,000 |

|

|

755,000 |

|

|

755,000 |

|

|

755,000 |

Total debt at balance sheet carrying value |

|

|

17,729,452 |

|

|

17,875,511 |

|

|

16,596,803 |

|

|

15,758,509 |

|

|

14,294,307 |

Total Enterprise Value |

|

|

$53,297,179 |

|

|

$47,903,372 |

|

|

$47,175,800 |

|

|

$45,652,963 |

|

|

$52,834,174 |

Total debt / total enterprise value |

|

|

33.3% |

|

|

37.3% |

|

|

35.2% |

|

|

34.5% |

|

|

27.1% |

Debt-plus-preferred-to-total-enterprise-value |

|

|

34.7% |

|

|

38.9% |

|

|

36.8% |

|

|

36.2% |

|

|

28.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Balance Sheet Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investments in real estate (before depreciation) |

|

|

$33,958,096 |

|

|

$33,805,740 |

|

|

$33,035,069 |

|

|

$31,046,413 |

|

|

$29,408,055 |

Total Assets |

|

|

42,388,735 |

|

|

41,953,068 |

|

|

41,484,998 |

|

|

39,215,217 |

|

|

35,956,057 |

Total Liabilities |

|

|

22,916,155 |

|

|

22,799,620 |

|

|

21,862,853 |

|

|

20,230,276 |

|

|

18,284,791 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Operating Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total operating revenues |

|

|

$1,366,267 |

|

|

$1,338,724 |

|

|

$1,233,108 |

|

|

$1,192,082 |

|

|

$1,139,321 |

Total operating expenses |

|

|

1,211,407 |

|

|

1,161,388 |

|

|

1,112,127 |

|

|

1,034,701 |

|

|

968,950 |

Net income |

|

|

115,647 |

|

|

68,839 |

|

|

763 |

|

|

238,791 |

|

|

63,862 |

Net income / (loss) available to common stockholders |

|

|

108,003 |

|

|

58,547 |

|

|

(6,093) |

|

|

226,894 |

|

|

53,245 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Financial Ratios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EBITDA (2) |

|

|

$667,866 |

|

|

$603,419 |

|

|

$493,244 |

|

|

$711,676 |

|

|

$515,642 |

Adjusted EBITDA (3) |

|

|

696,604 |

|

|

667,804 |

|

|

638,969 |

|

|

619,786 |

|

|

610,994 |

Net Debt to Adjusted EBITDA (4) |

|

|

6.8x |

|

|

7.1x |

|

|

6.9x |

|

|

6.7x |

|

|

6.2x |

Interest expense |

|

|

111,116 |

|

|

102,220 |

|

|

86,882 |

|

|

76,502 |

|

|

69,023 |

Fixed charges (5) |

|

|

149,181 |

|

|

139,172 |

|

|

121,644 |

|

|

103,987 |

|

|

93,335 |

Interest coverage ratio (6) |

|

|

4.5x |

|

|

4.7x |

|

|

5.3x |

|

|

6.1x |

|

|

6.6x |

Fixed charge coverage ratio (7) |

|

|

4.2x |

|

|

4.4x |

|

|

4.9x |

|

|

5.5x |

|

|

6.0x |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Profitability Measures |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income / (loss) per common share - basic |

|

|

$0.37 |

|

|

$0.20 |

|

|

($0.02) |

|

|

$0.79 |

|

|

$0.19 |

Net income / (loss) per common share - diluted |

|

|

$0.37 |

|

|

$0.19 |

|

|

($0.02) |

|

|

$0.75 |

|

|

$0.19 |

Funds from operations (FFO) / diluted share and unit (8) |

|

|

$1.52 |

|

|

$1.60 |

|

|

$1.45 |

|

|

$1.55 |

|

|

$1.55 |

Core funds from operations (Core FFO) / diluted share and unit (8) |

|

|

$1.68 |

|

|

$1.66 |

|

|

$1.65 |

|

|

$1.67 |

|

|

$1.72 |

Adjusted funds from operations (AFFO) / diluted share and unit (9) |

|

|

$1.59 |

|

|

$1.56 |

|

|

$1.29 |

|

|

$1.50 |

|

|

$1.63 |

Dividends per share and common unit |

|

|

$1.22 |

|

|

$1.22 |

|

|

$1.22 |

|

|

$1.22 |

|

|

$1.22 |

Diluted FFO payout ratio (8) (10) |

|

|

80.3% |

|

|

76.0% |

|

|

83.9% |

|

|

79.0% |

|

|

78.7% |

Diluted Core FFO payout ratio (8) (11) |

|

|

72.6% |

|

|

73.5% |

|

|

73.9% |

|

|

73.2% |

|

|

71.1% |

Diluted AFFO payout ratio (9) (12) |

|

|

76.7% |

|

|

78.2% |

|

|

94.8% |

|

|

81.5% |

|

|

75.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Portfolio Statistics |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Buildings (13) |

|

|

330 |

|

|

328 |

|

|

329 |

|

|

316 |

|

|

309 |

Data Centers (13) |

|

|

316 |

|

|

314 |

|

|

316 |

|

|

304 |

|

|

297 |

Cross-connects (13)(14) |

|

|

216,000 |

|

|

214,000 |

|

|

211,000 |

|

|

188,000 |

|

|

185,000 |

Net rentable square feet, excluding development space (13) |

|

|

39,310 |

|

|

38,804 |

|

|

38,156 |

|

|

36,699 |

|

|

36,803 |

Occupancy at end of quarter (15) |

|

|

82.9% |

|

|

83.5% |

|

|

84.7% |

|

|

84.7% |

|

|

83.9% |

Occupied square footage (13) |

|

|

32,603 |

|

|

32,394 |

|

|

32,327 |

|

|

31,077 |

|

|

30,866 |

Space under active development (16) |

|

|

8,841 |

|

|

9,243 |

|

|

9,245 |

|

|

8,878 |

|

|

8,289 |

Space held for development (17) |

|

|

3,941 |

|

|

3,742 |

|

|

3,351 |

|

|

2,896 |

|

|

2,661 |

Weighted average remaining lease term (years) (18) |

|

|

4.9 |

|

|

4.8 |

|

|

4.7 |

|

|

4.7 |

|

|

4.8 |

Same-capital occupancy at end of quarter (15) (19) |

|

|

83.3% |

|

|

83.3% |

|

|

83.8% |

|

|

83.1% |

|

|

82.6% |

5

Key Quarterly Financial Data |

|

Financial Supplement |

|---|---|---|

Unaudited, Dollars (except per share data) and Square Feet in Thousands |

Second Quarter 2023 |

| (1) | The market value of common equity is based on the closing stock price at the end of the quarter and assumes 100% redemption of the limited partnership units in our operating partnership, including common units and vested and unvested long-term incentive units, for shares of our common stock on a one-for-one basis. Excludes shares of common stock potentially issuable upon conversion of our series J, series K and series L cumulative redeemable preferred stock upon certain change of control transactions, as applicable. |

| (2) | EBITDA is calculated as earnings before interest expense, loss from early extinguishment of debt, tax expense, and depreciation and amortization. For a discussion of EBITDA, see page 32. For a reconciliation of net income available to common stockholders to EBITDA, see page 31. |

| (3) | Adjusted EBITDA is EBITDA excluding unconsolidated joint venture real estate related depreciation & amortization, unconsolidated joint venture interest and tax expense, severance, equity acceleration, and legal expenses, transaction and integration expenses, gain on sale / deconsolidation, impairment of investments in real estate, other non-core adjustments, net, non-controlling interests, preferred stock dividends, including undeclared dividends, and issuance costs associated with redeemed preferred stock. For a discussion of Adjusted EBITDA, see page 32. For a reconciliation of net income available to common stockholders to Adjusted EBITDA, see page 31. |

| (4) | Net Debt to Adjusted EBITDA is calculated as total debt at balance sheet carrying value (see page 5), plus capital lease obligations, plus our share of joint venture debt at carrying value, less cash and cash equivalents (including our share of joint venture cash), divided by the product of Adjusted EBITDA (including our share of joint venture EBITDA), multiplied by four. |

| (5) | Fixed charges consist of GAAP interest expense, capitalized interest, scheduled debt principal payments and preferred dividends. |

| (6) | Interest coverage ratio is Adjusted EBITDA divided by GAAP interest expense plus capitalized interest (including our share of unconsolidated joint venture interest expense). |

| (7) | Fixed charge coverage ratio is Adjusted EBITDA divided by fixed charges (including our share of unconsolidated joint venture fixed charges). |

| (8) | For definitions and discussion of FFO and Core FFO, see page 32. For reconciliations of net income available to common stockholders to FFO and Core FFO, see page 13. |

| (9) | For a definition and discussion of AFFO, see page 32. For a reconciliation of Core FFO to AFFO, see page 14. |

| (10) | Diluted FFO payout ratio is dividends declared per common share and unit divided by diluted FFO per share and unit. |

| (11) | Diluted Core FFO payout ratio is dividends declared per common share and unit divided by diluted Core FFO per share and unit. |

| (12) | Diluted AFFO payout ratio is dividends declared per common share and unit divided by diluted AFFO per share and unit. |

| (13) | Includes buildings held as investments in unconsolidated entities. Excludes buildings held-for-sale. |

| (14) | Represents approximate amounts. |

| (15) | Occupancy and same-capital occupancy exclude space under active development and space held for development. Occupancy represents our consolidated portfolio in addition to our managed portfolio of unconsolidated joint ventures and non-managed unconsolidated joint ventures. For some of our buildings, we calculate occupancy based on factors in addition to contractually leased square feet, including available power, required support space and common area. Excludes buildings held-for-sale. |

| (16) | Space under active development includes current Base Building and Data Centers projects in progress (see page 25). Excludes buildings held-for-sale. |

| (17) | Space held for development includes space held for future Data Center development and excludes space under active development (see page 28). Excludes buildings held-for-sale. |

| (18) | Weighted average remaining lease term excludes renewal options and is weighted by net rentable square feet. |

| (19) | Represents buildings owned as of December 31, 2021, with less than 5% of total rentable square feet under development. Excludes buildings that were undergoing, or were expected to undergo, development activities in 2022-2023, buildings classified as held-for-sale, and buildings sold or contributed to joint ventures for all periods presented. Prior period results have been adjusted to reflect current same-capital pool. |

6

Digital Realty Reports Second Quarter 2023 Results

Austin, TX — July 27, 2023 — Digital Realty (NYSE: DLR), the largest global provider of cloud- and carrier-neutral data center, colocation and interconnection solutions, announced today financial results for the second quarter of 2023. All per share results are presented on a fully diluted basis.

Highlights

| ◾ | Reported net income available to common stockholders of $0.37 per share in 2Q23, compared to $0.19 in 2Q22 |

| ◾ | Reported FFO per share of $1.52 in 2Q23, compared to $1.55 in 2Q22 |

| ◾ | Reported Core FFO per share of $1.68 in 2Q23, compared to $1.72 in 2Q22 |

| ◾ | Reported Constant-Currency Core FFO per share of $1.69 in 2Q23 and $3.38 per share for the six months ended June 30, 2023 |

| ◾ | Reported “Same-Capital” cash NOI growth of 5.6% in 2Q23 |

| ◾ | Reported rental rate increases on renewal leases of 6.9% on a cash basis in 2Q23 |

| ◾ | Signed total bookings during 2Q23 that are expected to generate $114 million of annualized GAAP rental revenue, including a $37 million contribution from the 0–1 megawatt category and a $13 million contribution from interconnection |

| ◾ | Adjusted 2023 Core FFO per share outlook to $6.55 - $6.65 |

Financial Results

Digital Realty reported revenues for the second quarter of 2023 of $1.4 billion, a 2% increase from the previous quarter and a 20% increase from the same quarter last year.

The company delivered second quarter of 2023 net income of $116 million, and net income available to common stockholders of $108 million, or $0.37 per diluted share, compared to $0.19 per diluted share in the previous quarter and $0.19 per diluted share in the same quarter last year.

Digital Realty generated second quarter of 2023 Adjusted EBITDA of $697 million, a 4% increase from the previous quarter and a 14% increase over the same quarter last year.

The company reported second quarter of 2023 funds from operations (FFO) of $466 million, or $1.52 per share, compared to $1.60 per share in the previous quarter and $1.55 per share in the same quarter last year.

Excluding certain items that do not represent core expenses or revenue streams, Digital Realty delivered second quarter of 2023 Core FFO per share of $1.68, compared to $1.66 per share in the previous quarter and $1.72 per share in the same quarter last year. Digital Realty delivered Constant-Currency Core FFO per share of $1.69 for the second quarter of 2023 and $3.38 per share for the six-month period ended June 30, 2023.

“Digital Realty’s second-quarter results demonstrate the positive momentum in our operating business, with improving fundamentals highlighted by strong enterprise leasing activity along with robust renewal spreads and healthy organic growth,” said Digital Realty President & Chief Executive Officer Andy Power. “We advanced our funding plan by completing two capital recycling transactions that generated more than $2 billion in gross proceeds, helping to position Digital Realty for the opportunity that lies ahead.”

Leasing Activity

In the second quarter, Digital Realty signed total bookings that are expected to generate $114 million of annualized GAAP rental revenue, including a $37 million contribution from the 0–1 megawatt category and a $13 million contribution from interconnection.

The weighted-average lag between new leases signed during the second quarter of 2023 and the contractual commencement date was eleven months.

In addition to new leases signed, Digital Realty also signed renewal leases representing $211 million of annualized GAAP rental revenue during the quarter. Rental rates on renewal leases signed during the second quarter of 2023 rolled up 6.9% on a cash basis and up 14.6% on a GAAP basis.

7

New leases signed during the second quarter of 2023 are summarized by region as follows:

|

|

Annualized GAAP |

|

|

|

|

|

|

|

|

|

|

|

|

|

Base Rent |

|

Square Feet |

|

GAAP Base Rent |

|

|

|

GAAP Base Rent |

|||

The Americas |

|

(in thousands) |

|

(in thousands) |

|

per Square Foot |

|

Megawatts |

|

per Kilowatt |

|||

0-1 MW |

|

|

$15,019 |

|

65 |

|

|

$232 |

|

5.6 |

|

|

$225 |

> 1 MW (1) |

|

|

11,506 |

|

30 |

|

|

387 |

|

3.2 |

|

|

300 |

Other (2) |

|

|

2,915 |

|

41 |

|

|

71 |

|

— |

|

|

— |

Total |

|

|

$29,441 |

|

136 |

|

|

$217 |

|

8.8 |

|

|

$252 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EMEA (3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

0-1 MW |

|

|

$15,427 |

|

60 |

|

|

$259 |

|

4.0 |

|

|

$319 |

> 1 MW |

|

|

47,329 |

|

477 |

|

|

99 |

|

31.7 |

|

|

124 |

Other (2) |

|

|

18 |

|

1 |

|

|

27 |

|

— |

|

|

— |

Total |

|

|

$62,774 |

|

537 |

|

|

$117 |

|

35.8 |

|

|

$146 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Asia Pacific (3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

0-1 MW |

|

|

$6,235 |

|

15 |

|

|

$404 |

|

1.4 |

|

|

$377 |

> 1 MW |

|

|

2,640 |

|

12 |

|

|

217 |

|

1.5 |

|

|

149 |

Other (2) |

|

|

87 |

|

1 |

|

|

96 |

|

— |

|

|

— |

Total |

|

|

$8,962 |

|

29 |

|

|

$314 |

|

2.9 |

|

|

$259 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All Regions (3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

0-1 MW |

|

|

$36,682 |

|

140 |

|

|

$263 |

|

11.0 |

|

|

$278 |

> 1 MW |

|

|

61,475 |

|

519 |

|

|

118 |

|

36.4 |

|

|

141 |

Other (2) |

|

|

3,020 |

|

43 |

|

|

70 |

|

— |

|

|

— |

Total |

|

|

$101,177 |

|

701 |

|

|

$144 |

|

47.4 |

|

|

$173 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interconnection |

|

|

$12,653 |

|

N/A |

|

|

N/A |

|

N/A |

|

|

N/A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Grand Total |

|

|

$113,830 |

|

701 |

|

|

$144 |

|

47.4 |

|

|

$173 |

Note: Totals may not foot due to rounding differences.

| (1) | >1 MW Base Rent includes the net uplift related to an eight-megawatt lease replacement which resulted in an increased rate for the same capacity. GAAP Base Rent per Square Foot and per Kilowatt metrics reflect the incremental additional Base Rent with no incremental capacity added. |

| (2) | Other includes Powered Base Building® shell capacity as well as storage and office space within fully improved data center facilities. |

| (3) | Based on quarterly average exchange rates during the three months ended June 30, 2023. |

Investment Activity

During the second quarter, Digital Realty sold a non‐core data center in Texas realizing approximately $150 million of net proceeds. The property was sold at a 4.4% cap rate, based on in-place net operating income (NOI), and generated a capital gain of approximately $88 million.

In Amsterdam during the second quarter, Digital Realty acquired the land and building shell of a previously leased 15 megawatts data center (AMS7) for €17 million or $18 million. This was a contractual purchase obligation which was a part of the Interxion transaction, and the asset was acquired at an 8.3% cap rate.

Digital Realty also acquired a nine‐acre land parcel located nearby AMS7 on its existing Amsterdam Schiphol campus for €26 million or $28 million. The Schiphol campus is one of the most highly connected data center campuses in the Netherlands. The parcel has the capacity to support a data center with a total IT load in excess of 40 megawatts and will be interconnected with Digital Realty’s existing Schiphol data centers.

After the close of the second quarter, Digital Realty partnered with GI Partners to establish a joint venture for the sale of a 65% interest in two stabilized hyperscale data center buildings in the Chicago metropolitan area. Digital received approximately $743 million of gross proceeds related to the joint venture and the associated financing and maintains a 35% interest in the joint venture while continuing to manage the day‐to‐day operations of the assets. Based on annualized in‐place cash NOI at June 30, 2023 and the benefit of leases signed but not yet commenced, the transaction values the two facilities at approximately a 6.5% cap rate. Digital Realty also granted GI Partners an option to purchase an interest in the third facility on the same data center campus.

In July, Digital Realty partnered with TPG Real Estate to establish a joint venture for the sale of an 80% interest in three stabilized hyperscale data center buildings in Northern Virginia. Digital Realty will receive approximately $1.3 billion of gross proceeds related to the joint venture and the associated financing and will maintain a 20% interest in the joint venture while continuing to manage the day‐to‐day operations of the assets. Based on annualized in‐place cash NOI on June 30, 2023, net of signed leases and known move-out, the transaction values the three facilities at approximately a 6.0% cap rate.

Also in July, Digital Realty announced the expansion of its joint venture in India with Brookfield Infrastructure through the addition of Jio, a Reliance Industries, Ltd. company. The new joint venture, ‘Digital Connexion: A Brookfield, Jio and Digital Realty Company’, succeeds BAM Digital Realty.

8

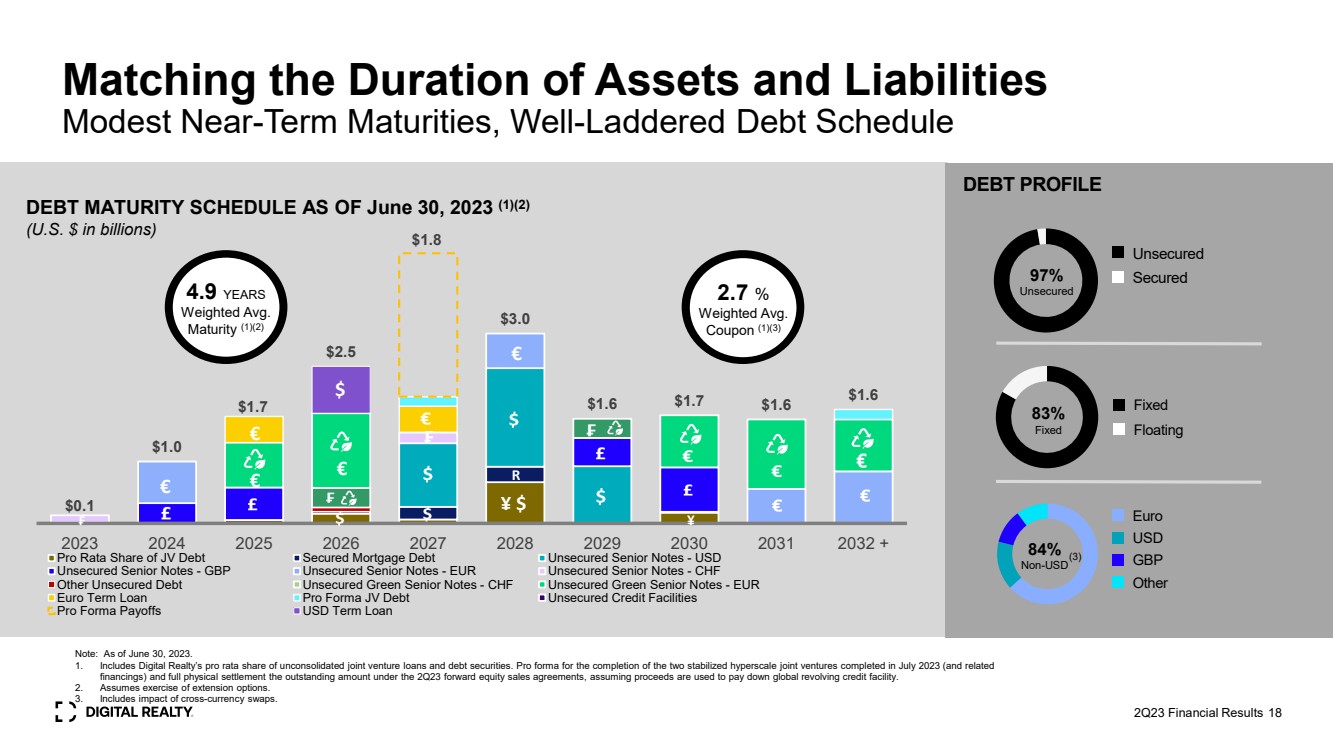

Balance Sheet

Digital Realty had approximately $17.7 billion of total debt outstanding as of June 30, 2023, comprised of $17.2 billion of unsecured debt and approximately $0.5 billion of secured debt and other. At the end of the second quarter of 2023, net debt-to-Adjusted EBITDA was 6.8x, debt-plus-preferred-to-total enterprise value was 34.7% and fixed charge coverage was 4.2x. Pro forma for the completion of the two stabilized hyperscale joint ventures completed in July 2023 and full physical settlement of the outstanding amount under the 2Q23 forward equity sales agreements, net debt-to-adjusted EBITDA was 6.3x and fixed charge coverage ratio was 4.6x.

During the second quarter, Digital Realty sold 7.8 million shares of its common stock at a weighted average price of $95.96 per share through its ATM program, realizing approximately $743 million of net proceeds. In addition, the company entered into forward sale agreements under its ATM program with respect to 3.5 million shares of its common stock at approximately $97.68 per share. Subsequent to quarter end, the company settled the outstanding forward sales for net proceeds of approximately $336 million.

9

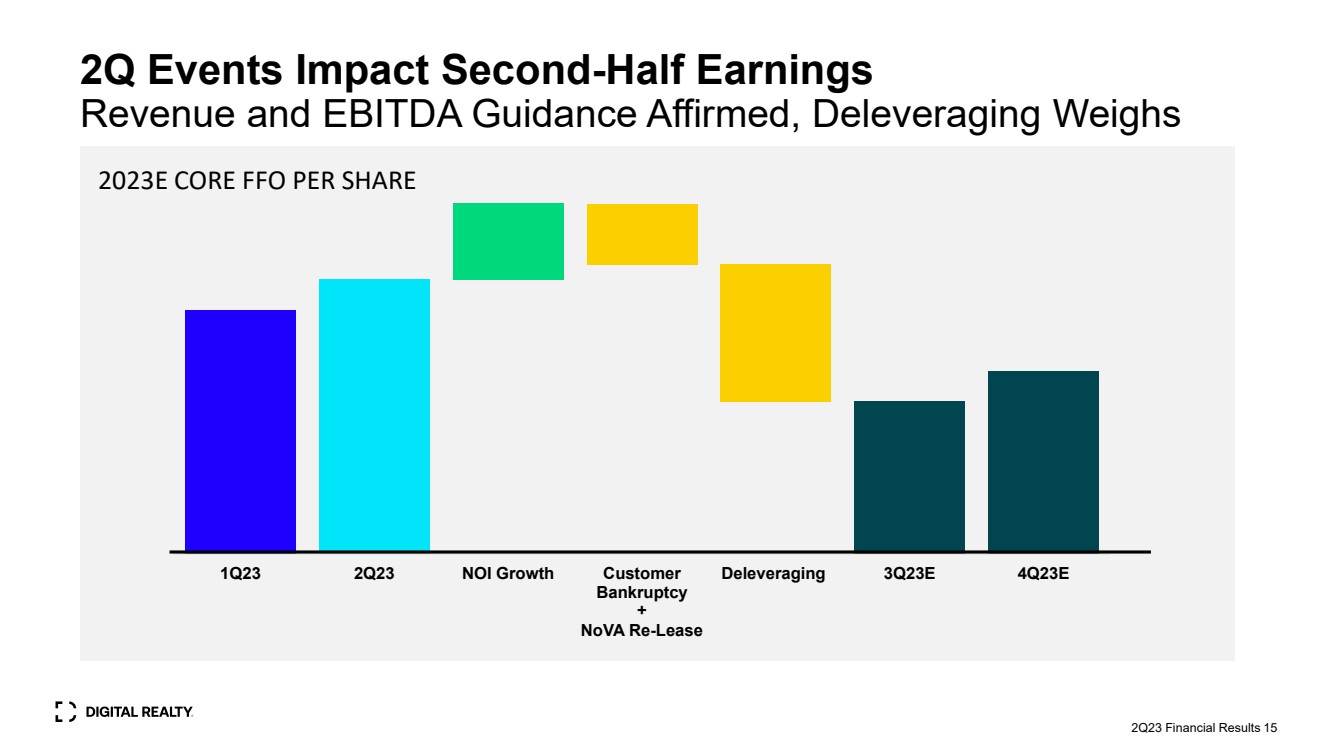

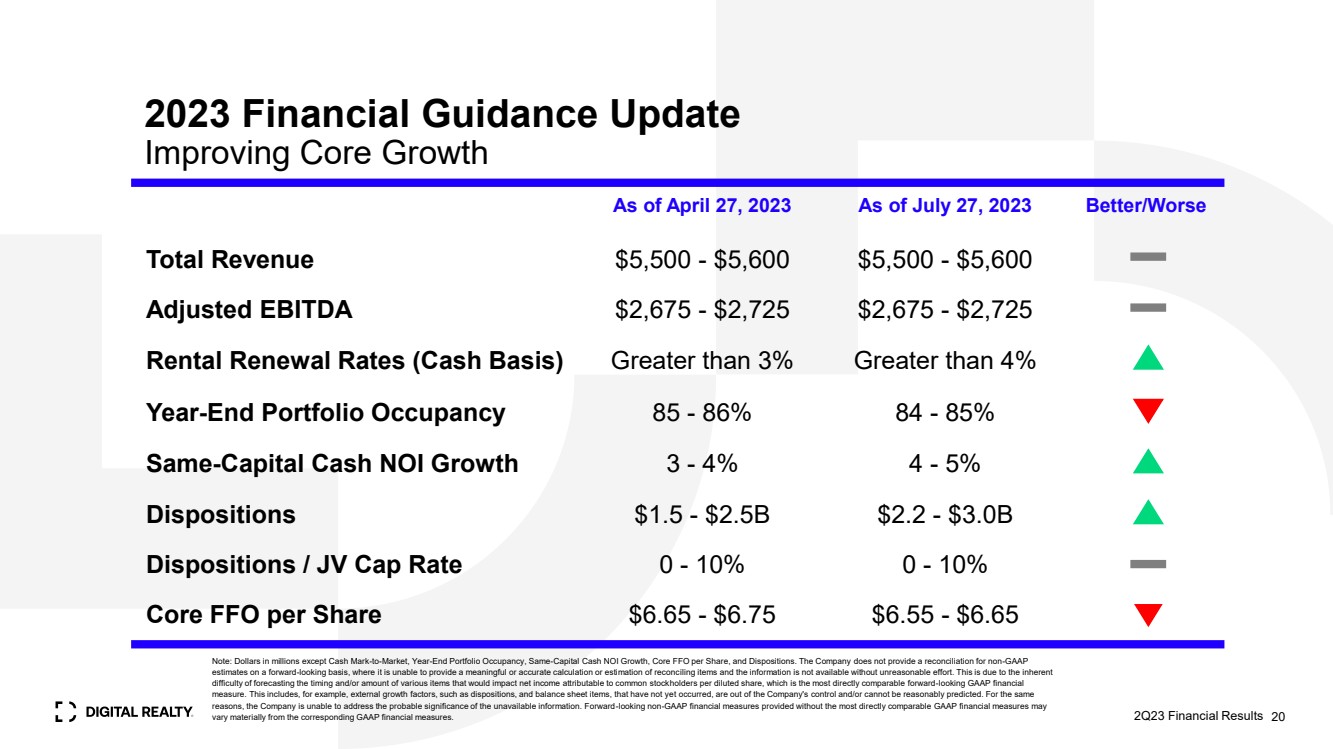

Digital Realty adjusted its 2023 Core FFO per share and constant-currency Core FFO per share outlook to $6.55 - $6.65. The assumptions underlying the outlook are summarized in the following table.

|

|

As of |

|

As of |

|

As of |

Top-Line and Cost Structure |

|

February 16, 2023 |

|

April 27, 2023 |

|

July 27, 2023 |

Total revenue |

|

$5.700 - $5.800 billion |

|

$5.500 - $5.600 billion |

|

$5.500 - $5.600 billion |

Net non-cash rent adjustments (1) |

|

($55 - $60 million) |

|

($55 - $60 million) |

|

($55 - $60 million) |

Adjusted EBITDA |

|

$2.675 - $2.725 billion |

|

$2.675 - $2.725 billion |

|

$2.675 - $2.725 billion |

G&A |

|

$425 - $435 million |

|

$425 - $435 million |

|

$425 - $435 million |

|

|

|

|

|

|

|

Internal Growth |

|

|

|

|

|

|

Rental rates on renewal leases |

|

|

|

|

|

|

Cash basis |

|

Greater than 3.0% |

|

Greater than 3.0% |

|

Greater than 4.0% |

GAAP basis |

|

Greater than 3.0% |

|

Greater than 3.0% |

|

Greater than 8.0% |

Year-end portfolio occupancy |

|

85.0% - 86.0% |

|

85.0% - 86.0% |

|

84.0% - 85.0% |

"Same-capital" cash NOI growth (2) |

|

3.0% - 4.0% |

|

3.0% - 4.0% |

|

4.0% - 5.0% |

|

|

|

|

|

|

|

Foreign Exchange Rates |

|

|

|

|

|

|

U.S. Dollar / Pound Sterling |

|

$1.20 - $1.25 |

|

$1.20 - $1.25 |

|

$1.20 - $1.25 |

U.S. Dollar / Euro |

|

$1.00 - $1.05 |

|

$1.05 - $1.10 |

|

$1.05 - $1.10 |

|

|

|

|

|

|

|

External Growth |

|

|

|

|

|

|

Dispositions / Joint Venture Capital |

|

|

|

|

|

|

Dollar volume |

|

$1.5 - $2.5 billion |

|

$1.5 - $2.5 billion |

|

$2.2 - $3.0 billion |

Cap rate |

|

0.0% - 10.0% |

|

0.0% - 10.0% |

|

0.0% - 10.0% |

Development |

|

|

|

|

|

|

CapEx (3) |

|

$2.3 - $2.5 billion |

|

$2.3 - $2.5 billion |

|

$2.3 - $2.5 billion |

Average stabilized yields |

|

9.0% - 15.0% |

|

9.0% - 15.0% |

|

9.0% - 15.0% |

Enhancements and other non-recurring CapEx (4) |

|

$15 - $20 million |

|

$15 - $20 million |

|

$15 - $20 million |

Recurring CapEx + capitalized leasing costs (5) |

|

$230 - $240 million |

|

$230 - $240 million |

|

$230 - $240 million |

|

|

|

|

|

|

|

Balance Sheet |

|

|

|

|

|

|

Long-term debt issuance |

|

|

|

|

|

|

Dollar amount |

|

$1.0 - $1.5 billion |

|

$1.0 - $1.5 billion |

|

$740 million |

Pricing |

|

4.5% - 5.5% |

|

5.5% - 6.0% |

|

5.5% |

Timing |

|

First Half 2023 |

|

First Half 2023 |

|

Completed |

|

|

|

|

|

|

|

Net income per diluted share |

|

$1.15 - $1.25 |

|

$1.15 - $1.25 |

|

$1.05 - $1.15 |

Real estate depreciation and (gain) / loss on sale |

|

$5.25 - $5.25 |

|

$5.25 - $5.25 |

|

$5.25 - $5.25 |

Funds From Operations / share (NAREIT-Defined) |

|

$6.40 - $6.50 |

|

$6.40 - $6.50 |

|

$6.30 - $6.40 |

Non-core expenses and revenue streams |

|

$0.25 - $0.25 |

|

$0.25 - $0.25 |

|

$0.25 - $0.25 |

Core Funds From Operations / share |

|

$6.65 - $6.75 |

|

$6.65 - $6.75 |

|

$6.55 - $6.65 |

Foreign currency translation adjustments |

|

$0.00 - $0.00 |

|

$0.00 - $0.00 |

|

$0.00 - $0.00 |

Constant-Currency Core Funds From Operations / share |

|

$6.65 - $6.75 |

|

$6.65 - $6.75 |

|

$6.55 - $6.65 |

| (1) | Net non-cash rent adjustments represent the sum of straight-line rental revenue and straight-line rental expense, as well as the amortization of above- and below-market leases (i.e., ASC 805 adjustments). |

| (2) | The “same-capital” pool includes properties owned as of December 31, 2021 with less than 5% of total rentable square feet under development. It excludes properties that were undergoing, or were expected to undergo, development activities in 2022-2023, properties classified as held for sale, and properties sold or contributed to joint ventures for all periods presented. |

| (3) | Includes land acquisitions. |

| (4) | Other non-recurring CapEx represents costs incurred to enhance the capacity or marketability of operating properties, such as network fiber initiatives and software development costs. |

| (5) | Recurring CapEx represents non-incremental improvements required to maintain current revenues, including second-generation tenant improvements and leasing commissions. |

Note: The Company does not provide a reconciliation for non-GAAP estimates on a forward-looking basis, where it is unable to provide a meaningful or accurate calculation or estimation of reconciling items and the information is not available without unreasonable effort. Please see Non-GAAP Financial Measures in this document for further discussion.

10

Non-GAAP Financial Measures

This document contains non-GAAP financial measures, including FFO, Core FFO, Adjusted FFO, Net Operating Income (NOI), “Same-Capital” Cash NOI and Adjusted EBITDA. A reconciliation from U.S. GAAP net income available to common stockholders to FFO, a reconciliation from FFO to Core FFO, a reconciliation from Core FFO to Adjusted FFO, reconciliation from NOI to Cash NOI, and definitions of FFO, Core FFO, Adjusted FFO, NOI and “Same-Capital” Cash NOI are included as an attachment to this document. A reconciliation from U.S. GAAP net income available to common stockholders to Adjusted EBITDA, a definition of Adjusted EBITDA and definitions of net debt-to-Adjusted EBITDA, debt-plus-preferred-to-total enterprise value, cash NOI, and fixed charge coverage ratio are included as an attachment to this document.

The Company does not provide a reconciliation for non-GAAP estimates on a forward-looking basis, where it is unable to provide a meaningful or accurate calculation or estimation of reconciling items and the information is not available without unreasonable effort. This is due to the inherent difficulty of forecasting the timing and/or amount of various items that would impact net income attributable to common stockholders per diluted share, which is the most directly comparable forward-looking GAAP financial measure. This includes, for example, external growth factors, such as dispositions, and balance sheet items, that have not yet occurred, are out of the Company's control and/or cannot be reasonably predicted. For the same reasons, the Company is unable to address the probable significance of the unavailable information. Forward-looking non-GAAP financial measures provided without the most directly comparable GAAP financial measures may vary materially from the corresponding GAAP financial measures.

Investor Conference Call

Prior to Digital Realty’s investor conference call at 5:00 p.m. ET / 4:00 p.m. CT on July 27, 2023, a presentation will be posted to the Investors section of the company’s website at https://investor.digitalrealty.com/. The presentation is designed to accompany the discussion of the company’s second quarter 2023 financial results and operating performance. The conference call will feature President & Chief Executive Officer Andy Power and Chief Financial Officer Matt Mercier.

To participate in the live call, investors are invited to dial +1 (888) 317-6003 (for domestic callers) or +1 (412) 317-6061 (for international callers) and reference the conference ID# 5098292 at least five minutes prior to start time. A live webcast of the call will be available via the Investors section of Digital Realty’s website at https://investor.digitalrealty.com/.

Telephone and webcast replays will be available after the call until August 27, 2023. The telephone replay can be accessed by dialing +1 (877) 344-7529 (for domestic callers) or +1 (412) 317-0088 (for international callers) and providing the conference ID# 3348387. The webcast replay can be accessed on Digital Realty’s website.

About Digital Realty

Digital Realty brings companies and data together by delivering the full spectrum of data center, colocation, and interconnection solutions. PlatformDIGITAL®, the company’s global data center platform, provides customers with a secure data “meeting place” and a proven Pervasive Datacenter Architecture (PDx®) solution methodology for powering innovation and efficiently managing Data Gravity challenges. Digital Realty gives its customers access to the connected communities that matter to them with a global data center footprint of 300+ facilities in 50+ metros across 27 countries on six continents. To learn more about Digital Realty, please visit digitalrealty.com or follow us on LinkedIn and Twitter.

Contact Information

Matt Mercier

Chief Financial Officer

Digital Realty

(737) 281-0101

Jordan Sadler / Jim Huseby

Investor Relations

Digital Realty

(737) 281-0101

11

Consolidated Quarterly Statements of Operations |

|

Financial Supplement |

|---|---|---|

Unaudited and Dollars in Thousands, Except Per Share Data |

Second Quarter 2023 |

|

|

|

Three Months Ended |

|

|

Six Months Ended |

||||||||||||||||

|

|

|

30-Jun-23 |

|

|

31-Mar-23 |

|

|

31-Dec-22 |

|

|

30-Sep-22 |

|

|

30-Jun-22 |

|

|

|

30-Jun-23 |

|

|

30-Jun-22 |

Rental revenues |

|

|

$869,298 |

|

|

$870,975 |

|

|

$834,374 |

|

|

$787,839 |

|

|

$767,313 |

|

|

|

$1,740,273 |

|

|

$1,519,275 |

Tenant reimbursements - Utilities |

|

|

330,416 |

|

|

317,148 |

|

|

247,725 |

|

|

251,420 |

|

|

218,198 |

|

|

|

647,565 |

|

|

442,745 |

Tenant reimbursements - Other |

|

|

46,192 |

|

|

40,150 |

|

|

46,045 |

|

|

49,419 |

|

|

52,688 |

|

|

|

86,342 |

|

|

104,198 |

Interconnection & other |

|

|

104,521 |

|

|

101,695 |

|

|

97,286 |

|

|

95,486 |

|

|

93,338 |

|

|

|

206,216 |

|

|

186,868 |

Fee income |

|

|

14,908 |

|

|

7,868 |

|

|

7,508 |

|

|

6,169 |

|

|

5,072 |

|

|

|

22,777 |

|

|

10,829 |

Other |

|

|

932 |

|

|

887 |

|

|

168 |

|

|

1,749 |

|

|

2,713 |

|

|

|

1,819 |

|

|

2,728 |

Total Operating Revenues |

|

|

$1,366,267 |

|

|

$1,338,724 |

|

|

$1,233,108 |

|

|

$1,192,082 |

|

|

$1,139,321 |

|

|

|

$2,704,991 |

|

|

$2,266,644 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Utilities |

|

|

$374,934 |

|

|

$346,364 |

|

|

$268,561 |

|

|

$271,844 |

|

|

$223,426 |

|

|

|

$721,298 |

|

|

$464,665 |

Rental property operating |

|

|

224,762 |

|

|

224,861 |

|

|

222,430 |

|

|

205,886 |

|

|

198,076 |

|

|

|

449,623 |

|

|

392,430 |

Property taxes |

|

|

46,718 |

|

|

40,424 |

|

|

42,032 |

|

|

39,860 |

|

|

47,213 |

|

|

|

87,141 |

|

|

93,738 |

Insurance |

|

|

4,385 |

|

|

4,355 |

|

|

4,578 |

|

|

4,002 |

|

|

3,836 |

|

|

|

8,739 |

|

|

7,534 |

Depreciation & amortization |

|

|

432,573 |

|

|

421,198 |

|

|

430,130 |

|

|

388,704 |

|

|

376,967 |

|

|

|

853,771 |

|

|

759,099 |

General & administration |

|

|

105,964 |

|

|

107,766 |

|

|

104,452 |

|

|

95,792 |

|

|

101,991 |

|

|

|

213,730 |

|

|

198,426 |

Severance, equity acceleration, and legal expenses |

|

|

3,652 |

|

|

4,155 |

|

|

15,980 |

|

|

1,655 |

|

|

3,786 |

|

|

|

7,807 |

|

|

5,863 |

Transaction and integration expenses |

|

|

17,764 |

|

|

12,267 |

|

|

17,350 |

|

|

25,862 |

|

|

13,586 |

|

|

|

30,031 |

|

|

25,554 |

Impairment of investments in real estate |

|

|

— |

|

|

— |

|

|

3,000 |

|

|

— |

|

|

— |

|

|

|

— |

|

|

— |

Other expenses |

|

|

655 |

|

|

— |

|

|

3,615 |

|

|

1,096 |

|

|

70 |

|

|

|

655 |

|

|

7,727 |

Total Operating Expenses |

|

|

$1,211,407 |

|

|

$1,161,388 |

|

|

$1,112,127 |

|

|

$1,034,701 |

|

|

$968,950 |

|

|

|

$2,372,795 |

|

|

$1,955,037 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income |

|

|

$154,860 |

|

|

$177,335 |

|

|

$120,981 |

|

|

$157,381 |

|

|

$170,371 |

|

|

|

$332,196 |

|

|

$311,607 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equity in earnings / (loss) of unconsolidated joint ventures |

|

|

5,059 |

|

|

14,897 |

|

|

(28,112) |

|

|

(12,254) |

|

|

(34,088) |

|

|

|

19,957 |

|

|

26,870 |

Gain / (loss) on sale of investments |

|

|

89,946 |

|

|

— |

|

|

(6) |

|

|

173,990 |

|

|

— |

|

|

|

89,946 |

|

|

2,770 |

Interest and other income / (expense), net |

|

|

(6,930) |

|

|

280 |

|

|

(22,894) |

|

|

15,752 |

|

|

13,008 |

|

|

|

(6,650) |

|

|

16,059 |

Interest (expense) |

|

|

(111,116) |

|

|

(102,220) |

|

|

(86,882) |

|

|

(76,502) |

|

|

(69,023) |

|

|

|

(213,336) |

|

|

(135,748) |

Income tax benefit / (expense) |

|

|

(16,173) |

|

|

(21,454) |

|

|

17,676 |

|

|

(19,576) |

|

|

(16,406) |

|

|

|

(37,627) |

|

|

(29,650) |

Loss from early extinguishment of debt |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

|

— |

|

|

(51,135) |

Net Income |

|

|

$115,647 |

|

|

$68,839 |

|

|

$763 |

|

|

$238,791 |

|

|

$63,862 |

|

|

|

$184,486 |

|

|

$140,773 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income / (loss) attributable to noncontrolling interests |

|

|

2,538 |

|

|

(111) |

|

|

3,326 |

|

|

(1,716) |

|

|

(436) |

|

|

|

2,427 |

|

|

(4,065) |

Net Income Attributable to Digital Realty Trust, Inc. |

|

|

$118,185 |

|

|

$68,728 |

|

|

$4,089 |

|

|

$237,075 |

|

|

$63,426 |

|

|

|

$186,913 |

|

|

$136,708 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preferred stock dividends, including undeclared dividends |

|

|

(10,181) |

|

|

(10,181) |

|

|

(10,181) |

|

|

(10,181) |

|

|

(10,181) |

|

|

|

(20,363) |

|

|

(20,363) |

Net Income / (Loss) Available to Common Stockholders |

|

|

$108,003 |

|

|

$58,547 |

|

|

($6,093) |

|

|

$226,894 |

|

|

$53,245 |

|

|

|

$166,550 |

|

|

$116,346 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted-average shares outstanding - basic |

|

|

295,390,446 |

|

|

291,218,549 |

|

|

289,364,739 |

|

|

286,693,071 |

|

|

284,694,064 |

|

|

|

293,316,022 |

|

|

284,610,492 |

Weighted-average shares outstanding - diluted |

|

|

306,818,538 |

|

|

303,064,832 |

|

|

301,712,082 |

|

|

296,414,726 |

|

|

285,109,903 |

|

|

|

304,453,040 |

|

|

284,979,709 |

Weighted-average fully diluted shares and units |

|

|

313,020,947 |

|

|

309,026,076 |

|

|

307,546,353 |

|

|

302,257,518 |

|

|

290,944,163 |

|

|

|

310,589,141 |

|

|

290,716,197 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income / (loss) per share - basic |

|

|

$0.37 |

|

|

$0.20 |

|

|

($0.02) |

|

|

$0.79 |

|

|

$0.19 |

|

|

|

$0.57 |

|

|

$0.41 |

Net income / (loss) per share - diluted |

|

|

$0.37 |

|

|

$0.19 |

|

|

($0.02) |

|

|

$0.75 |

|

|

$0.19 |

|

|

|

$0.57 |

|

|

$0.41 |

12

Funds From Operations and Core Funds From Operations |

|

Financial Supplement |

|---|---|---|

Unaudited and in Thousands, Except Per Share Data |

Second Quarter 2023 |

|

|

Three Months Ended |

|

|

Six Months Ended |

|||||||||||||||||

Reconciliation of Net Income to Funds From Operations (FFO) |

|

|

30-Jun-23 |

|

|

31-Mar-23 |

|

|

31-Dec-22 |

|

|

30-Sep-22 |

|

|

30-Jun-22 |

|

|

|

30-Jun-23 |

|

|

30-Jun-22 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income / (Loss) Available to Common Stockholders |

|

|

$108,003 |

|

|

$58,547 |

|

|

($6,093) |

|

|

$226,894 |

|

|

$53,245 |

|

|

|

$166,550 |

|

|

$116,346 |

Adjustments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-controlling interest in operating partnership |

|

|

2,500 |

|

|

1,500 |

|

|

(586) |

|

|

5,400 |

|

|

1,500 |

|

|

|

4,000 |

|

|

3,100 |

Real estate related depreciation & amortization (1) |

|

|

424,044 |

|

|

412,192 |

|

|

422,951 |

|

|

381,425 |

|

|

369,327 |

|

|

|

836,236 |

|

|

743,489 |

Depreciation related to non-controlling interests |

|

|

(14,144) |

|

|

(13,388) |

|

|

(13,856) |

|

|

(8,254) |

|

|

- |

|

|

|

(27,532) |

|

|

- |

Unconsolidated JV real estate related depreciation & amortization |

|

|

35,386 |

|

|

33,719 |

|

|

33,927 |

|

|

30,831 |

|

|

29,022 |

|

|

|

69,105 |

|

|

58,341 |

(Gain) / loss on real estate transactions |

|

|

(89,946) |

|

|

(7,825) |

|

|

572 |

|

|

(173,990) |

|

|

(1,144) |

|

|

|

(97,771) |

|

|

(3,914) |

Impairment of investments in real estate |

|

|

- |

|

|

- |

|

|

3,000 |

|

|

- |

|

|

- |

|

|

|

- |

|

|

- |

Funds From Operations - diluted |

|

|

$465,844 |

|

|

$484,745 |

|

|

$439,915 |

|

|

$462,306 |

|

|

$451,949 |

|

|

|

$950,589 |

|

|

$917,362 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted-average shares and units outstanding - basic |

|

|

301,593 |

|

|

297,180 |

|

|

295,199 |

|

|

292,536 |

|

|

290,528 |

|

|

|

299,452 |

|

|

290,346 |

Weighted-average shares and units outstanding - diluted (2)(3) |

|

|

313,021 |

|

|

309,026 |

|

|

307,546 |

|

|

302,258 |

|

|

290,944 |

|

|

|

310,589 |

|

|

290,716 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Funds From Operations per share - basic |

|

|

$1.54 |

|

|

$1.63 |

|

|

$1.49 |

|

|

$1.58 |

|

|

$1.56 |

|

|

|

$3.17 |

|

|

$3.16 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Funds From Operations per share - diluted (2)(3) |

|

|

$1.52 |

|

|

$1.60 |

|

|

$1.45 |

|

|

$1.55 |

|

|

$1.55 |

|

|

|

$3.13 |

|

|

$3.16 |

|

|

Three Months Ended |

|

|

Six Months Ended |

|||||||||||||||||

Reconciliation of FFO to Core FFO |

|

|

30-Jun-23 |

|

|

31-Mar-23 |

|

|

31-Dec-22 |

|

|

30-Sep-22 |

|

|

30-Jun-22 |

|

|

|

30-Jun-23 |

|

|

30-Jun-22 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Funds From Operations - diluted |

|

|

$465,844 |

|

|

$484,745 |

|

|

$439,915 |

|

|

$462,306 |

|

|

$451,949 |

|

|

|

$950,589 |

|

|

$917,362 |

Other non-core revenue adjustments |

|

|

27,454 |

|

|

(887) |

|

|

(3,786) |

|

|

(1,818) |

|

|

456 |

|

|

|

26,566 |

|

|

14,372 |

Transaction and integration expenses |

|

|

17,764 |

|

|

12,267 |

|

|

17,350 |

|

|

25,862 |

|

|

13,586 |

|

|

|

30,031 |

|

|

25,554 |

Loss from early extinguishment of debt |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

|

- |

|

|

51,135 |

Severance, equity acceleration, and legal expenses (4) |

|

|

3,652 |

|

|

4,155 |

|

|

15,980 |

|

|

1,655 |

|

|

3,786 |

|

|

|

7,807 |

|

|

5,863 |

(Gain) / Loss on FX revaluation |

|

|

(7,868) |

|

|

(6,778) |

|

|

14,564 |

|

|

(1,120) |

|

|

29,539 |

|

|

|

(14,647) |

|

|

(38,137) |

Other non-core expense adjustments |

|

|

655 |

|

|

- |

|

|

3,615 |

|

|

1,046 |

|

|

70 |

|

|

|

655 |

|

|

7,727 |

Core Funds From Operations - diluted |

|

|

$507,501 |

|

|

$493,500 |

|

|

$487,638 |

|

|

$487,931 |

|

|

$499,386 |

|

|

|

$1,001,001 |

|

|

$983,875 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted-average shares and units outstanding - diluted (2)(3) |

|

|

301,806 |

|

|

297,382 |

|

|

295,519 |

|

|

292,830 |

|

|

290,944 |

|

|

|

299,730 |

|

|

290,716 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Core Funds From Operations per share - diluted (2) |

|

|

$1.68 |

|

|

$1.66 |

|

|

$1.65 |

|

|

$1.67 |

|

|

$1.72 |

|

|

|

$3.34 |

|

|

$3.38 |

(1) Real Estate Related Depreciation & Amortization |

|

Three Months Ended |

|

|

Six Months Ended |

|||||||||||||||||

|

|

|

30-Jun-23 |

|

|

31-Mar-23 |

|

|

31-Dec-22 |

|

|

30-Sep-22 |

|

|

30-Jun-22 |

|

|

|

30-Jun-23 |

|

|

30-Jun-22 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation & amortization per income statement |

|

|

$432,573 |

|

|

$421,198 |

|

|

$430,130 |

|

|

$388,704 |

|

|

$376,967 |

|

|

|

$853,771 |

|

|

$759,099 |

Non-real estate depreciation |

|

|

(8,529) |

|

|

(9,006) |

|

|

(7,179) |

|

|

(7,279) |

|

|

(7,640) |

|

|

|

(17,535) |

|

|

(15,610) |

Real Estate Related Depreciation & Amortization |

|

|

$424,044 |

|

|

$412,192 |

|

|

$422,951 |

|

|

$381,425 |

|

|

$369,327 |

|

|

|

$836,236 |

|

|

$743,489 |