UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 8-K

CURRENT REPORTPURSUANT TO

SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of report (Date of earliest event reported): April 26, 2023

Alerus Financial Corporation

(Exact Name of Registrant as Specified in Charter)

Delaware |

001-39036 |

45-0375407 |

(State or Other Jurisdiction of Incorporation) |

(Commission File Number) |

(IRS Employer Identification No.) |

401 Demers Avenue

Grand Forks, North Dakota 58201

(Address of Principal Executive Offices) (Zip Code)

Registrant's telephone number, including area code: (701) 795-3200

N/A

(Former Name or Former Address, if Changed Since Last Report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

☐Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

☐Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

☐Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange

Act (17 CFR 240.14d-2(b))

☐Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange

Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading symbol |

|

Name of each exchange on which registered |

Common Stock, $1.00 par value per share |

|

ALRS |

|

The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§ 230.405 of this chapter) or Rule 12b–2 of the Securities Exchange Act of 1934 (§ 240.12b–2 of this chapter).

Emerging growth company ☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 2.02. Results of Operations and Financial Condition.

On April 26, 2023, Alerus Financial Corporation (the “Company”) issued a press release announcing its financial results for the three months ended March 31, 2023. A copy of the press release is attached as Exhibit 99.1 to this Form 8-K and is incorporated herein by reference.

The information in Item 2.02 of this Current Report on Form 8-K, and the related Exhibit 99.1, attached hereto is being “furnished” and will not, except to the extent required by applicable law or regulation, be deemed “filed” by the Company for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that section, nor will any of such information or exhibits be deemed incorporated by reference to any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as may be expressly set forth by specific reference in such filing.

Item 7.01. Regulation FD Disclosure.

On April 26, 2023, the Company posted a presentation to the Company’s investor relations website, located at investors.alerus.com. The presentation is also attached hereto as Exhibit 99.2.

The information in Item 7.01 of this Current Report on Form 8-K, and the related Exhibit 99.2, attached hereto is being “furnished” and will not, except to the extent required by applicable law or regulation, be deemed “filed” by the Company for purposes of Section 18 of the Exchange Act, or otherwise subject to the liabilities of that section, nor will any of such information or exhibits be deemed incorporated by reference to any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as may be expressly set forth by specific reference in such filing.

Item 9.01. Financial Statements and Exhibits.

(d) Exhibits

Exhibit No. |

|

Description |

99.1 |

|

Press Release of Alerus Financial Corporation, dated April 26, 2023 |

|

99.2 104 |

|

Investor Presentation of Alerus Financial Corporation Cover Page Interactive Data File (embedded within the Inline XBRL document) |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

Date: April 26, 2023 |

Alerus Financial Corporation |

|

|

|

|

|

|

|

|

By: |

/s/ Katie A. Lorenson |

|

Name: |

Katie A. Lorenson |

|

Title: |

President and Chief Executive Officer |

|

|

|

Exhibit 99.1

|

FOR RELEASE (04.26.2023) |

Alan A. Villalon, Chief Financial Officer 952.417.3733 (Office) |

ALERUS FINANCIAL CORPORATION REPORTS

FIRST QUARTER 2023 NET INCOME OF $8.2 MILLION

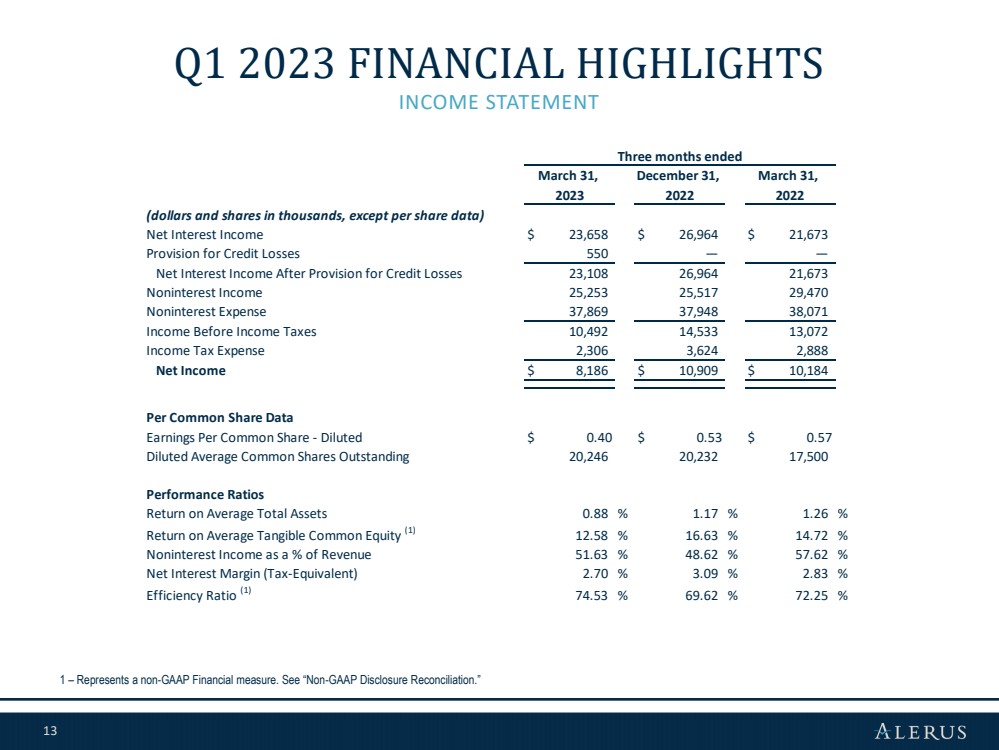

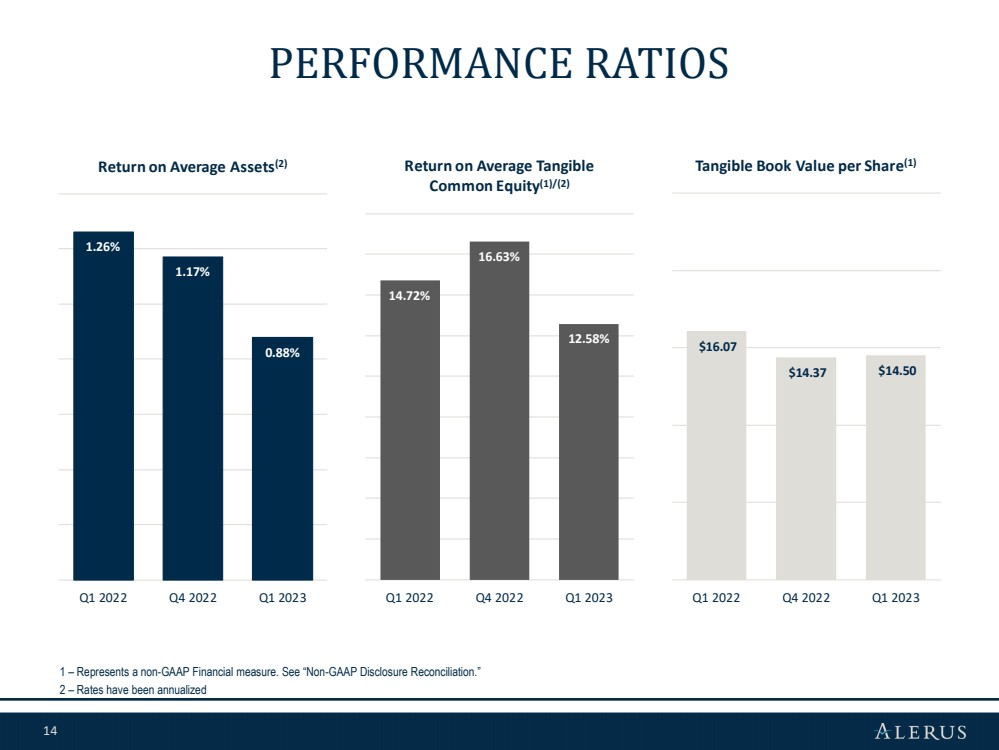

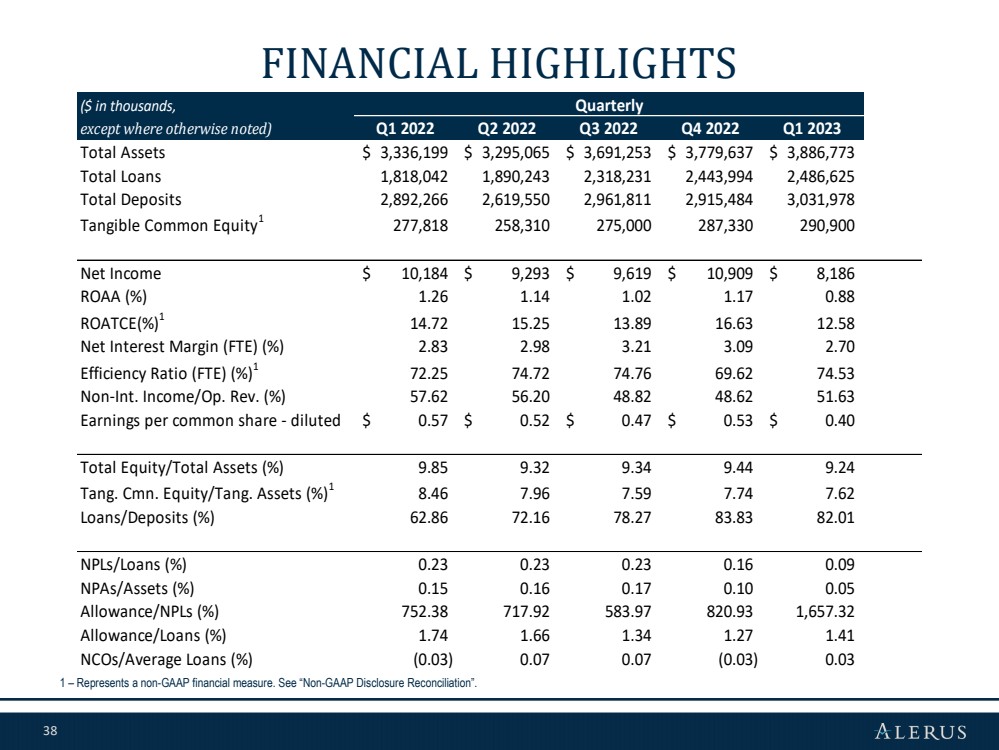

MINNEAPOLIS, MN (April 26, 2023) – Alerus Financial Corporation (Nasdaq: ALRS), or the Company, reported net income of $8.2 million for the first quarter of 2023, or $0.40 per diluted common share, compared to net income of $10.9 million, or $0.53 per diluted common share, for the fourth quarter of 2022, and net income of $10.2 million, or $0.57 per diluted common share, for the first quarter of 2022.

CEO Comments

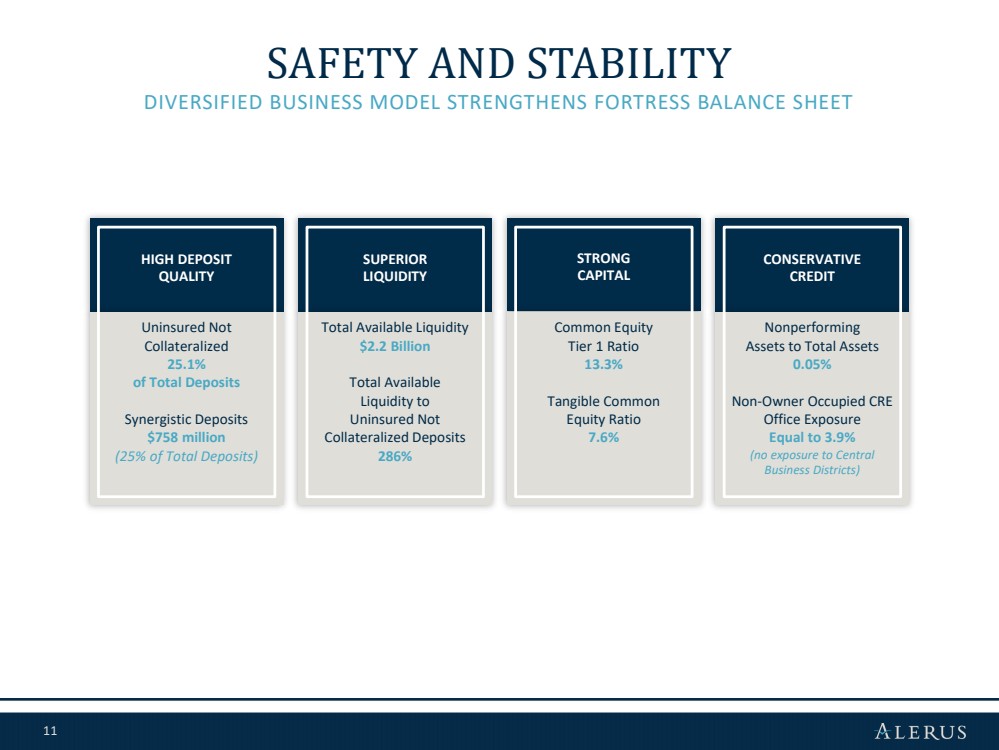

President and Chief Executive Officer Katie Lorenson said, “Alerus’ highly diversified business model is a unique differentiator in this challenging economic environment with fee income making up over 50.0% of total revenues, our banking franchise is anchored by a strong foundation of capital, risk management, and diversification. Our common equity tier 1 capital ratio at the end of the first quarter was 13.3% and our nearly all-core granular deposit based increased balances by 4.0% during the quarter. Our liquidity position is strong, with total available liquidity to uninsured and not collateralized deposits of 286%. The Company’s loan portfolio remains well diversified by sector and geography, with limited exposure to commercial office borrowers at 3.9% of total loans. The allowance for credit losses to was 1.4% to total loans and 1,675% of non-performing loans. Credit quality remains pristine with net charge-offs of 3 basis points, below the Company’s historical net charge-off rates of 0.27%.

Financial results for the first quarter were impacted by continuing margin pressure and headwinds in the mortgage sector. We are focused on improving long-term profitability and shareholder returns through ongoing restructuring and efficiency enhancing opportunities. We continue to have success in the transformation of our organic growth model and synergistic expansion as we added core holistic relationships in banking and wealth management. Our momentum in talent acquisition continued in the first quarter with key talent adds to the banking and treasury management teams. Thank you to our Alerus employees for your dedication and constant focus on building relationships with clients by bringing value to every interaction and together taking Alerus to new heights.”

Quarterly Highlights

| ◾ | Total deposits were $3.0 billion as of March 31, 2023, an increase of $116.5 million, or 4.0%, from December 31, 2022 |

| ◾ | Loan to deposit ratio as of March 31, 2023 was 82.0%, compared to 83.8% as of December 31, 2022 |

| ◾ | Common equity tier 1 capital to risk weighted assets as of March 31, 2023 was 13.30%, compared to 13.39% as of December 31, 2022 |

| ◾ | Return on average total assets of 0.88%, compared to 1.17% for the fourth quarter of 2022 |

| ◾ | Return on average common equity of 9.17%, compared to 12.37% for the fourth quarter of 2022 |

| ◾ | Return on average tangible common equity(1) of 12.58%, compared to 16.63% for the fourth quarter of 2022 |

| ◾ | Net interest margin (tax-equivalent) was 2.70%, compared to 3.09% for the fourth quarter of 2022 |

| ◾ | Noninterest expense was $37.9 million, no change compared to $37.9 million for the fourth quarter of 2022 |

| ◾ | Noninterest income was 51.63% of total revenue, compared to 48.62 for the fourth quarter of 2022 |

| ◾ | Allowance for credit losses to total loans was 1.41% compared to 1.27% as of December 31, 2022 |

| ◾ | Expanded the Company’s commercial banking team with the addition of four highly experienced mid-market and treasury management professionals |

| ◾ | The Board of Directors previously declared a regular quarterly cash dividend of $0.18 per share, which was paid on April 14, 2023 to shareholders of record as of March 15, 2023. As previously reported, this dividend represents a 12.5% increase over the dividend declared during the first quarter 2022. |

| (1) | Represents a non-GAAP financial measure. See “Non-GAAP to GAAP Reconciliations and Calculation of Non-GAAP Financial Measures.” |

Selected Financial Data (unaudited)

|

|

As of and for the |

|

|||||||

|

|

Three months ended |

|

|||||||

|

|

March 31, |

|

December 31, |

|

March 31, |

|

|||

(dollars and shares in thousands, except per share data) |

|

2023 |

|

2022 |

|

2022 |

|

|||

Performance Ratios |

|

|

|

|

|

|

|

|

|

|

Return on average total assets |

|

|

0.88 |

% |

|

1.17 |

% |

|

1.26 |

% |

Return on average common equity |

|

|

9.17 |

% |

|

12.37 |

% |

|

11.78 |

% |

Return on average tangible common equity (1) |

|

|

12.58 |

% |

|

16.63 |

% |

|

14.72 |

% |

Noninterest income as a % of revenue |

|

|

51.63 |

% |

|

48.62 |

% |

|

57.62 |

% |

Net interest margin (tax-equivalent) |

|

|

2.70 |

% |

|

3.09 |

% |

|

2.83 |

% |

Efficiency ratio (1) |

|

|

74.53 |

% |

|

69.62 |

% |

|

72.25 |

% |

Net charge-offs/(recoveries) to average loans |

|

|

0.03 |

% |

|

(0.03) |

% |

|

(0.03) |

% |

Dividend payout ratio |

|

|

45.00 |

% |

|

33.96 |

% |

|

28.07 |

% |

Per Common Share |

|

|

|

|

|

|

|

|

|

|

Earnings per common share - basic |

|

$ |

0.41 |

|

$ |

0.54 |

|

$ |

0.58 |

|

Earnings per common share - diluted |

|

$ |

0.40 |

|

$ |

0.53 |

|

$ |

0.57 |

|

Dividends declared per common share |

|

$ |

0.18 |

|

$ |

0.18 |

|

$ |

0.16 |

|

Book value per common share |

|

$ |

17.90 |

|

$ |

17.85 |

|

$ |

19.00 |

|

Tangible book value per common share (1) |

|

$ |

14.50 |

|

$ |

14.37 |

|

$ |

16.07 |

|

Average common shares outstanding - basic |

|

|

20,028 |

|

|

19,988 |

|

|

17,244 |

|

Average common shares outstanding - diluted |

|

|

20,246 |

|

|

20,232 |

|

|

17,500 |

|

Other Data |

|

|

|

|

|

|

|

|

|

|

Retirement and benefit services assets under administration/management |

|

$ |

33,404,342 |

|

$ |

32,122,520 |

|

$ |

35,333,131 |

|

Wealth management assets under administration/management |

|

$ |

3,675,684 |

|

$ |

3,582,648 |

|

$ |

4,584,856 |

|

Mortgage originations |

|

$ |

77,728 |

|

$ |

126,254 |

|

$ |

186,762 |

|

Results of Operations

Net Interest Income

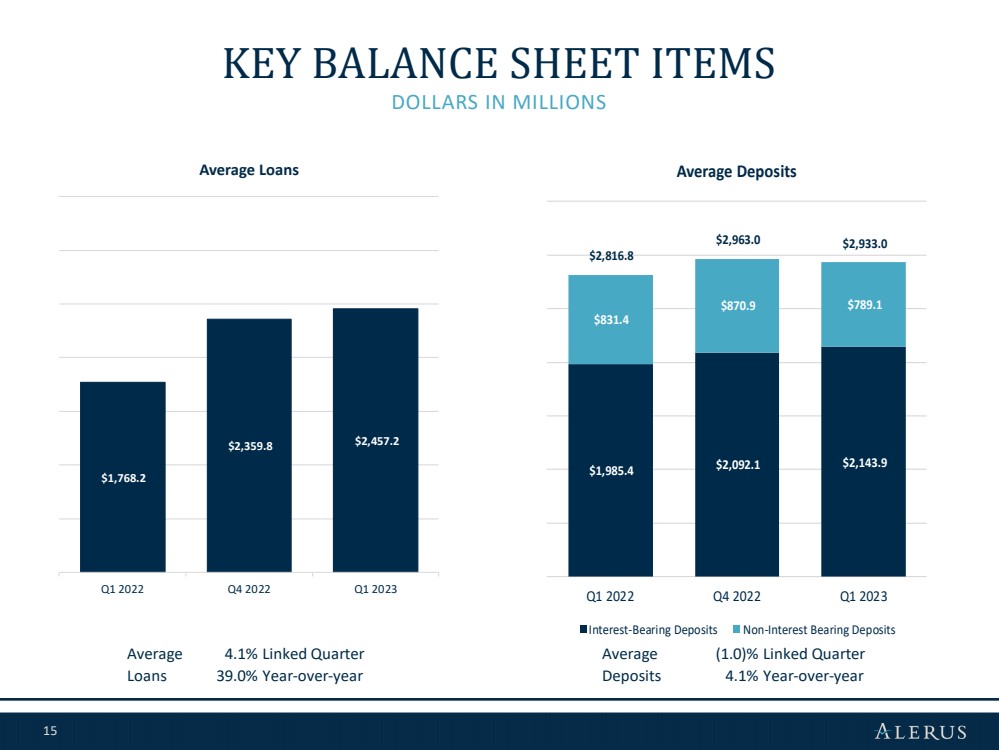

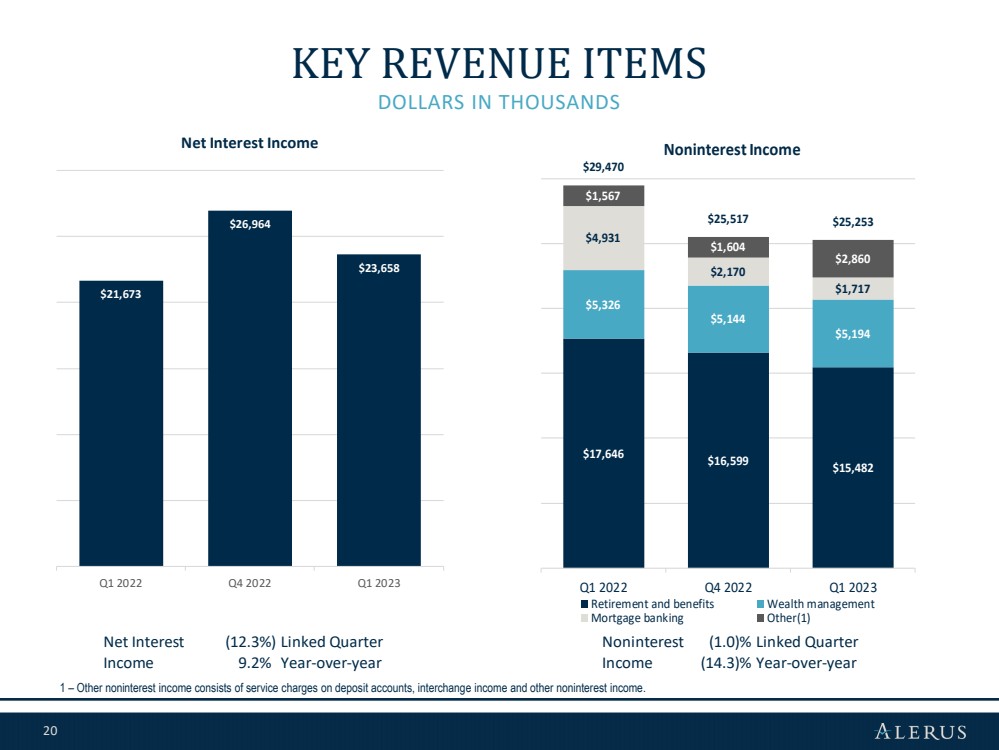

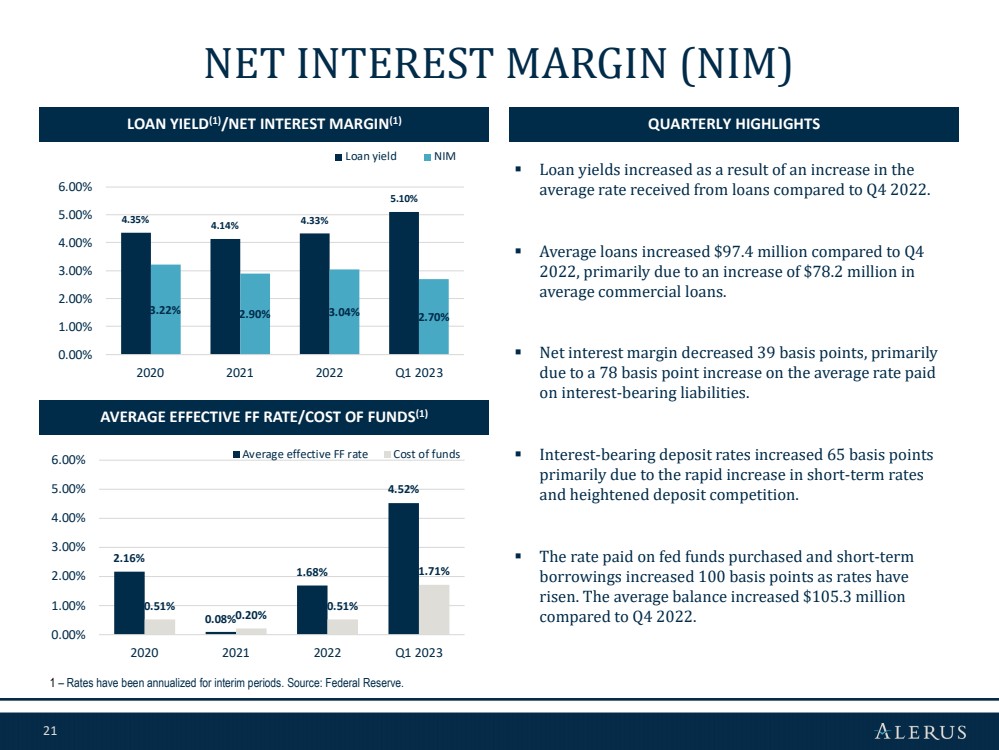

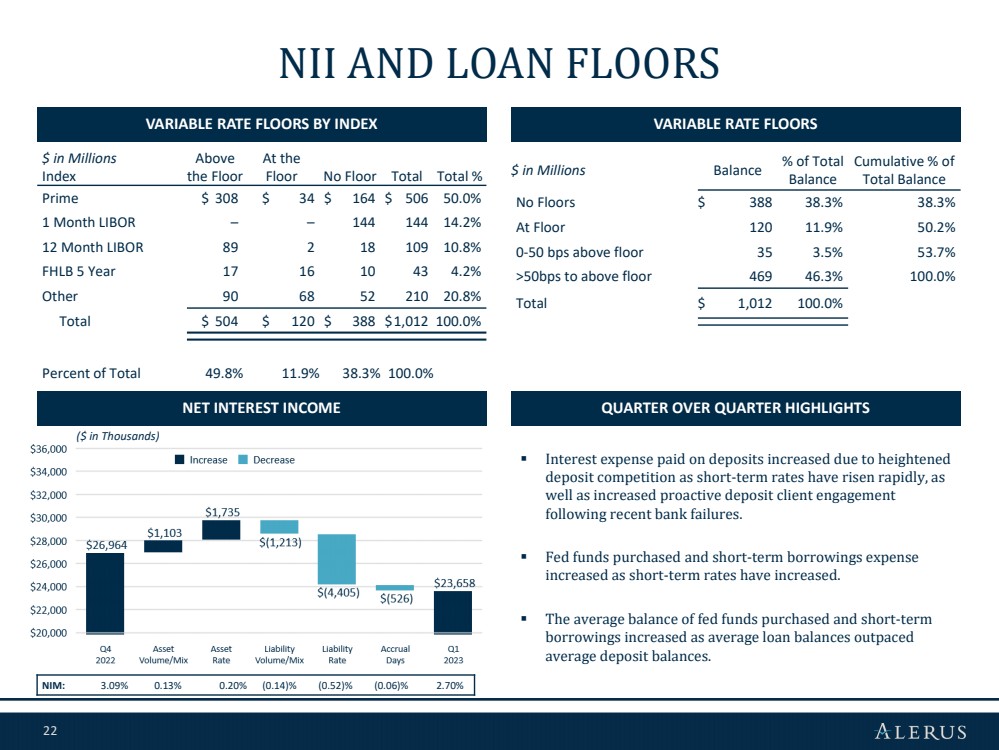

Net interest income for the first quarter of 2023 was $23.7 million, a $3.3 million, or 12.3%, decrease from the fourth quarter of 2022. Net interest income increased $2.0 million, or 9.2%, from $21.7 million for the first quarter of 2022. The linked quarter decrease in net interest income was primarily driven by a $5.3 million, or 59.9%, increase in interest expense, partially offset by a $2.0 million, or 5.6%, increase in interest income. The increase in interest expense was primarily driven by a $3.4 million increase in interest expense paid on deposits and $1.8 million in interest expense paid on short-term borrowings. The increase in interest expense paid on deposits was primarily due to the rapid increase in short-term rates and heightened deposit competition. Short-term borrowings expense increased as interest rates have increased and the average balance of fed funds purchased and short-term borrowings increased $105.3 million as compared to the fourth quarter of 2022. This increase was primarily driven by a $97.4 million increase in average loan balances, and a $29.9 million decline in average deposit balances, partially offset by a $12.2 million decline in average investment securities balance.

Net interest margin (tax-equivalent), was 2.70% for the first quarter of 2023, a 39 basis point decrease from 3.09% for the fourth quarter of 2022, and a 13 basis point decrease from 2.83% in the first quarter of 2022. The linked quarter decrease was primarily driven by a 78 basis point increase in the average rate paid on interest-bearing liabilities, partially offset by a 21 basis point increase in interest earning asset yields. The increase in the average rate paid on interest-bearing liabilities was the result of a 100 basis point increase in the average rate paid on fed funds purchased and short-term borrowings as well as a 65 basis point increase in the rate paid on interest-bearing deposits.

Noninterest Income

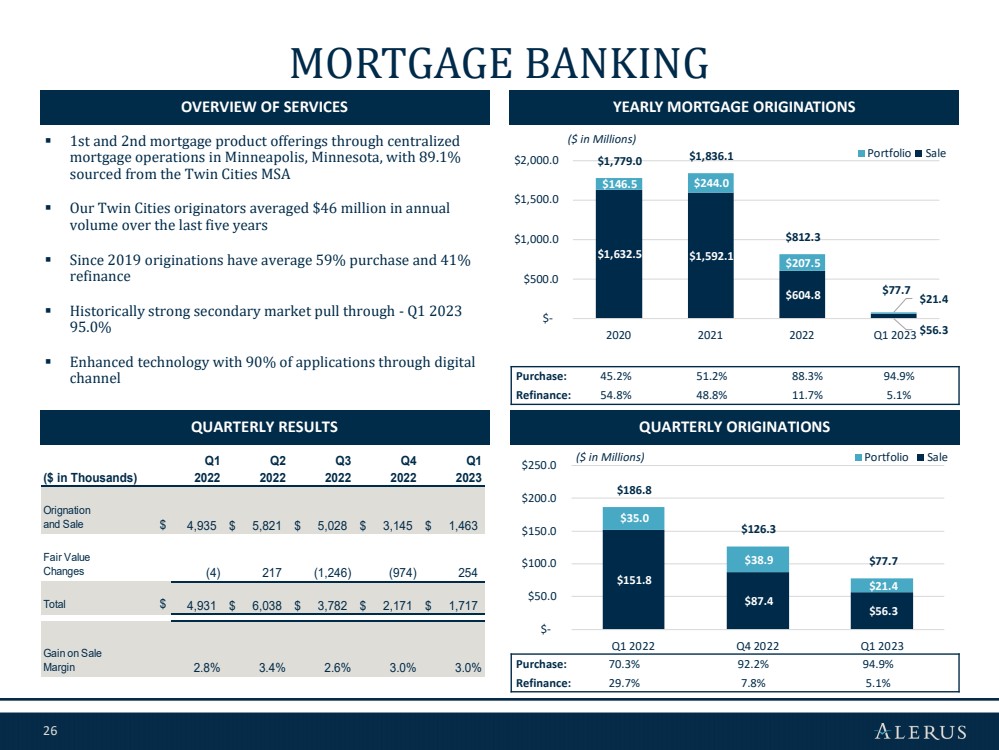

Noninterest income for the first quarter of 2023 was $25.3 million, a $264 thousand, or 1.0%, decrease from the fourth quarter of 2022. The quarter over quarter decrease was primarily driven by decreases of $1.1 million in retirement and benefit services revenue and $453 thousand in mortgage banking revenue, partially offset by a $1.2 million increase in other noninterest income. The decrease in retirement and benefit services revenue was primarily the result of seasonal decreases in administration fees, ESOP transaction fees and loan and distribution fees. Mortgage banking revenue decreased primarily due to a $48.5 million, or 38.4%, decrease in mortgage originations due to the rising interest rate environment and seasonality. Other noninterest income increased primarily due to a $1.2 million increase in proceeds received on a bank-owned life insurance claim.

2

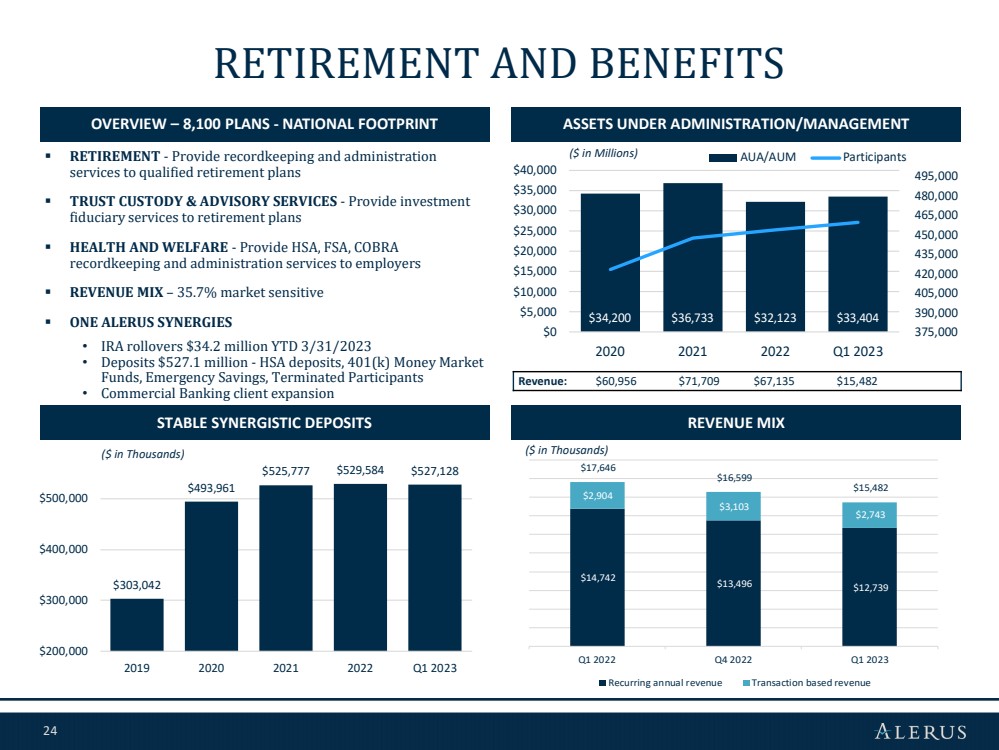

Noninterest income for the first quarter of 2023 decreased $4.2 million, or 14.3%, from $29.5 million in the first quarter of 2022. The decrease in noninterest income was primarily due to a $3.2 million decrease in mortgage banking revenue and a $2.2 million decrease in retirement and benefit services revenue, partially offset by a $1.4 million increase in other noninterest income. Mortgage banking revenue decreased primarily due to a $109.0 million, or 58.4% decrease in mortgage originations, driven by the rising interest rate environment and a reduction in mortgage personnel. Retirement and benefit services revenue decreased primarily due to a decrease in asset based fees as assets under administration/management decreased $1.9 billion, or 5.5%. Additionally, retirement and benefit services revenue experienced decreases of $528 thousand in payroll service fees resulting from the exit of payroll services and $310 thousand in plan document restatement fees. Other noninterest income increased for reasons previously stated.

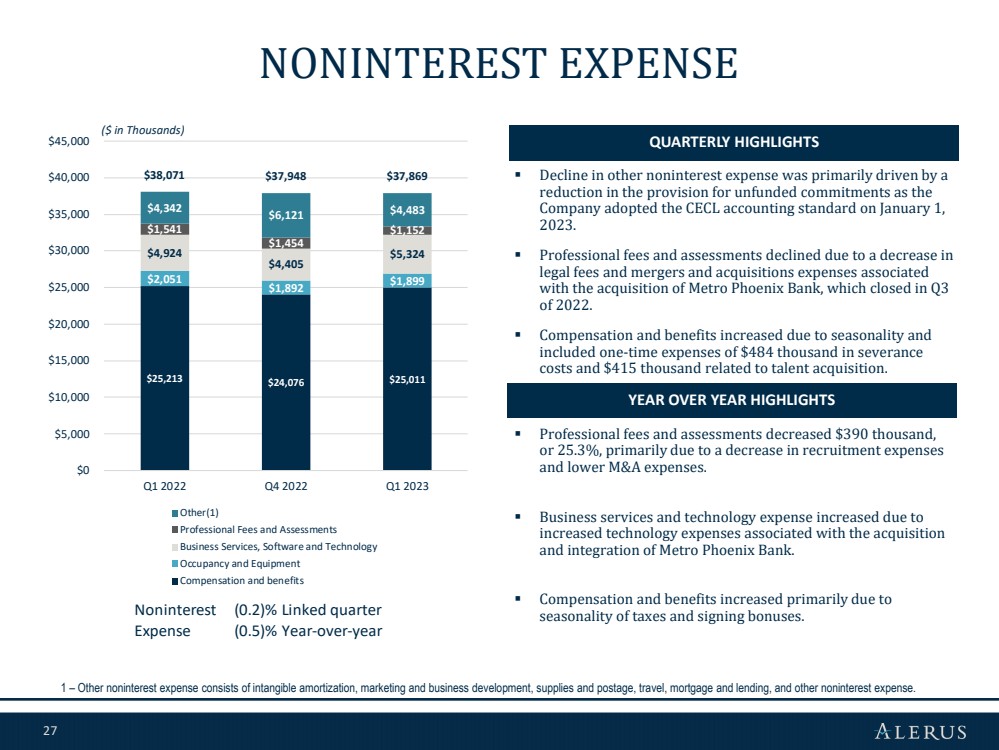

Noninterest Expense

Noninterest expense for both the first quarter of 2023 and the fourth quarter of 2022 was $37.9 million. The minor linked quarter changes in noninterest expense included a $983 thousand decrease in other noninterest expense and a $302 thousand decrease in professional fees and assessments, partially offset by an increase of $966 thousand in employee taxes and benefits, $919 thousand increase in business services, software and technology. Compensation expense remained flat quarter over quarter, despite the first quarter including one-time expenses of $484 thousand in severance costs and $415 thousand related to talent acquisition. The decrease in other noninterest expense was primarily driven by a reduction of the provision for unfunded commitments which is now being reported within the provision for credit losses, as the Company adopted the new Current Expected Credit Loss, or CECL, accounting standard on January 1, 2023. Professional fees and assessments declined, primarily due to a decrease in the legal fees and mergers and acquisition expenses associated with the acquisition of Metro Phoenix Bank, which was completed in the third quarter of 2022. Employee taxes and benefits increased primarily due to seasonality. Business services, software and technology expense increased primarily due to the recognition of the benefits of renegotiated contracts at lower rates in the fourth quarter.

Noninterest expense for the first quarter of 2023 decreased $202 thousand, or 0.5%, from $38.1 million in the first quarter of 2022. The year over year decrease in noninterest expense was primarily driven by a $389 thousand decrease in professional fees and assessments, partially offset by a $400 thousand increase in business services, software and technology expense. Professional fees and assessments decreased primarily due to a $284 thousand decrease in recruitment expenses. Business services, software and technology expense increased primarily due to increased technology expenses associated with the acquisition and integration of Metro Phoenix Bank.

Financial Condition

Total assets were $3.9 billion as of March 31, 2023, an increase of $107.1 million, or 2.8%, from December 31, 2022. The increase in assets included increases of $86.9 million in cash and cash equivalents, $42.6 million in loans held for investment, partially offset by a $19.8 million decrease in investment securities from December 31, 2022.

Loans

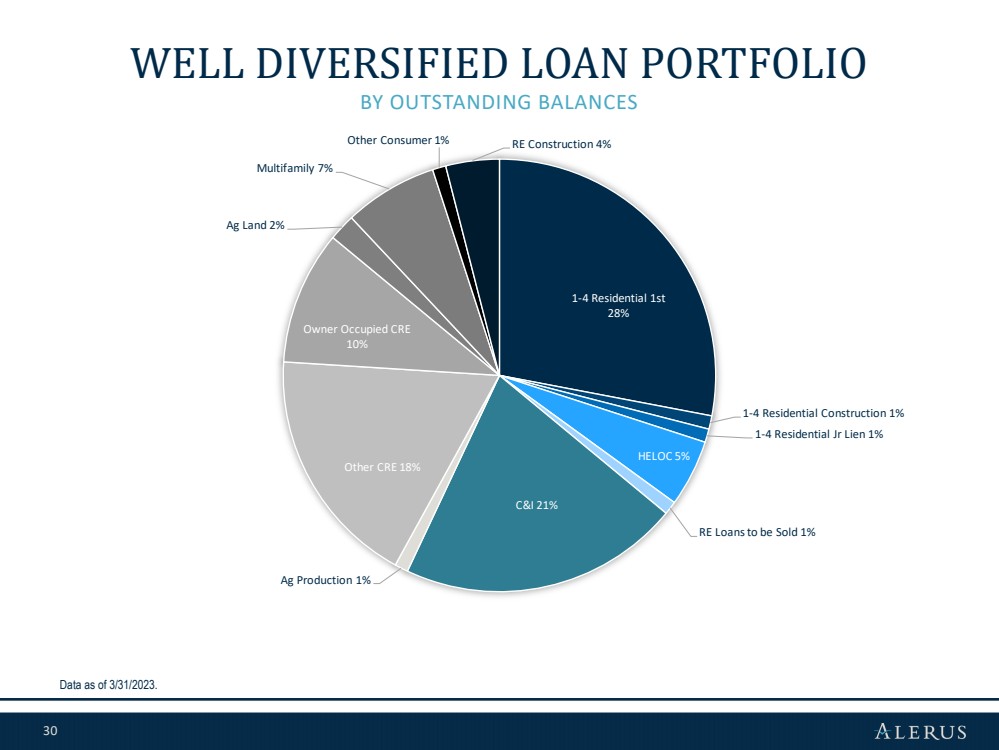

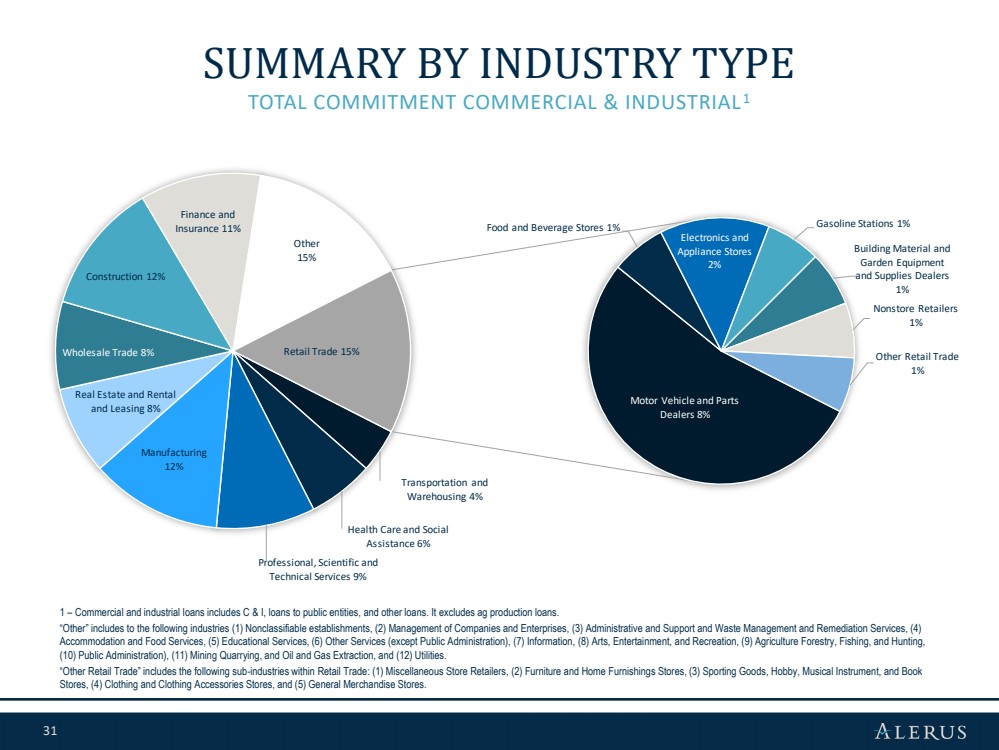

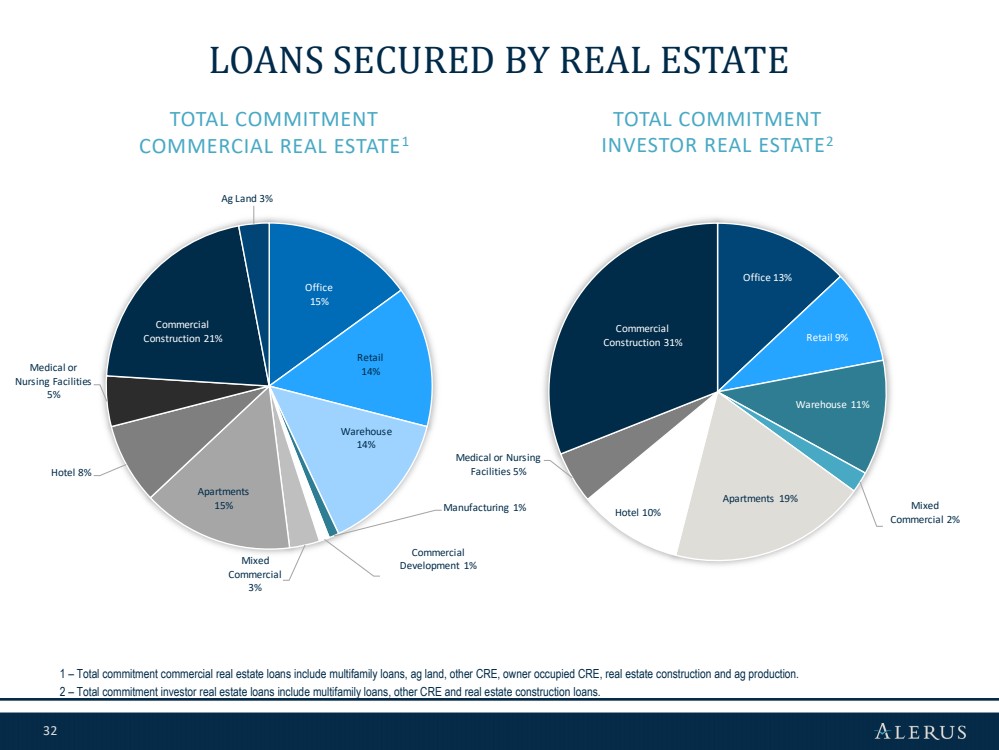

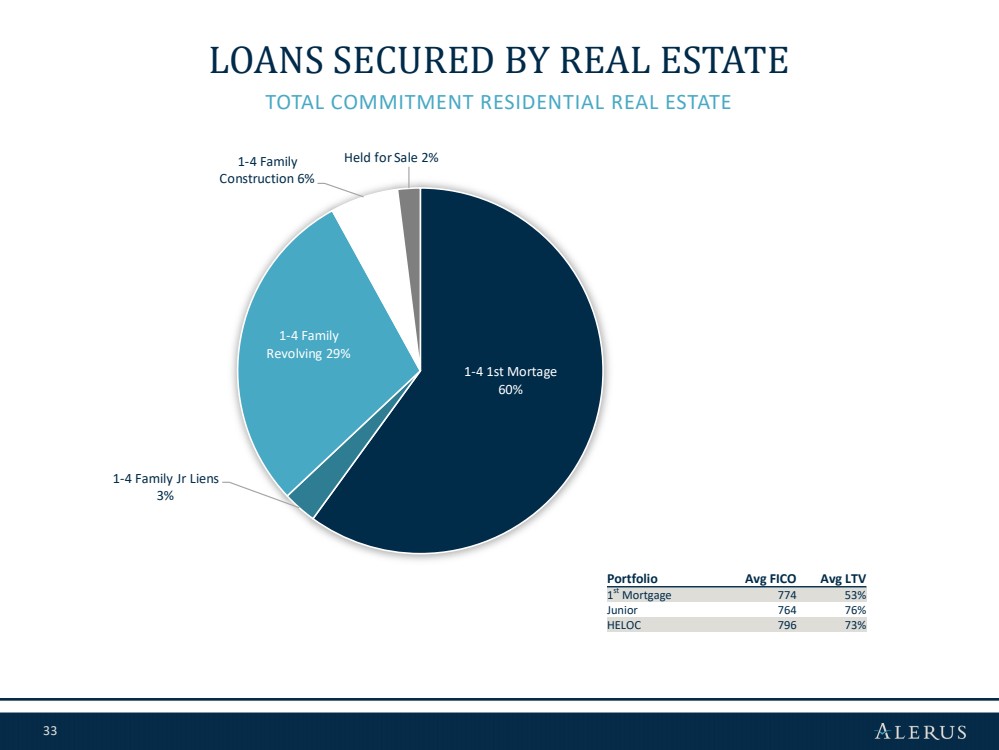

Total loans were $2.5 billion as of March 31, 2023, an increase of $42.6 million, or 1.7%, from December 31, 2022. The increase in total loans was primarily due to increases of $52.7 million in commercial real estate loans, $11.0 million in real estate construction loans and $20.3 million in residential real estate loans, partially offset by a $30.3 million decrease in commercial and industrial loans.

3

The following table presents the composition of our loan portfolio as of the dates indicated:

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|||||

(dollars in thousands) |

|

2023 |

|

2022 |

|

2022 |

|

2022 |

|

2022 |

|||||

Commercial |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial and industrial |

|

$ |

553,578 |

|

$ |

583,876 |

|

$ |

564,655 |

|

$ |

484,426 |

|

$ |

467,449 |

Real estate construction |

|

|

108,776 |

|

|

97,810 |

|

|

89,215 |

|

|

48,870 |

|

|

41,604 |

Commercial real estate |

|

|

934,324 |

|

|

881,670 |

|

|

819,068 |

|

|

599,737 |

|

|

602,158 |

Total commercial |

|

|

1,596,678 |

|

|

1,563,356 |

|

|

1,472,938 |

|

|

1,133,033 |

|

|

1,111,211 |

Consumer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Residential real estate first mortgage |

|

|

698,002 |

|

|

679,551 |

|

|

649,818 |

|

|

568,571 |

|

|

522,489 |

Residential real estate junior lien |

|

|

152,281 |

|

|

150,479 |

|

|

143,681 |

|

|

135,255 |

|

|

130,604 |

Other revolving and installment |

|

|

39,664 |

|

|

50,608 |

|

|

51,794 |

|

|

53,384 |

|

|

53,738 |

Total consumer |

|

|

889,947 |

|

|

880,638 |

|

|

845,293 |

|

|

757,210 |

|

|

706,831 |

Total loans |

|

$ |

2,486,625 |

|

$ |

2,443,994 |

|

$ |

2,318,231 |

|

$ |

1,890,243 |

|

$ |

1,818,042 |

Deposits

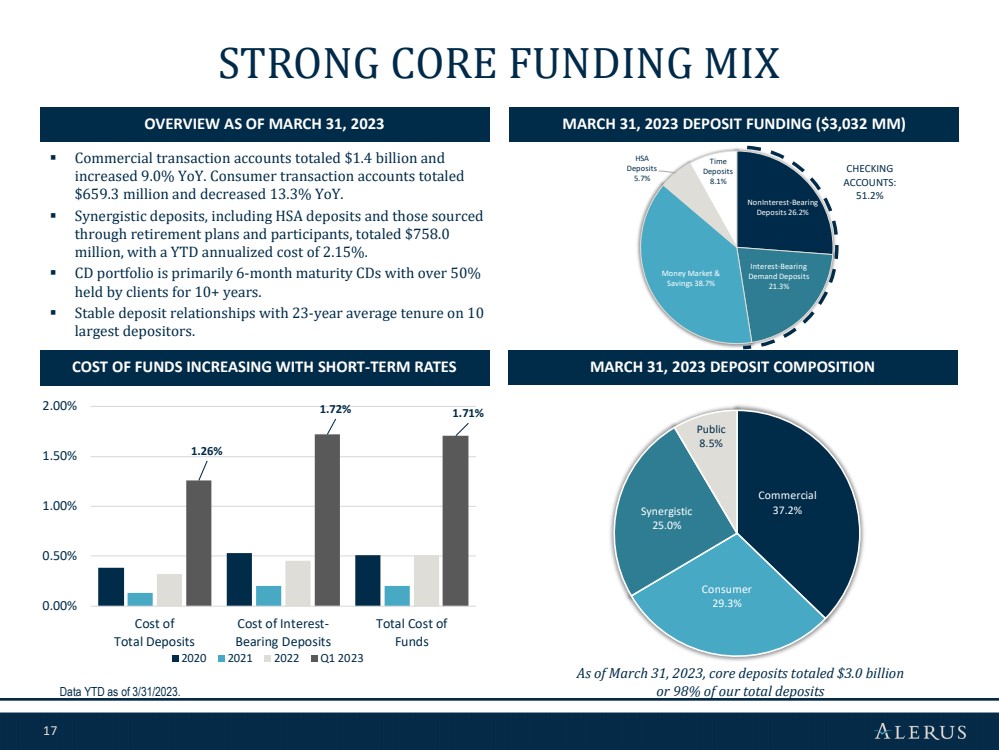

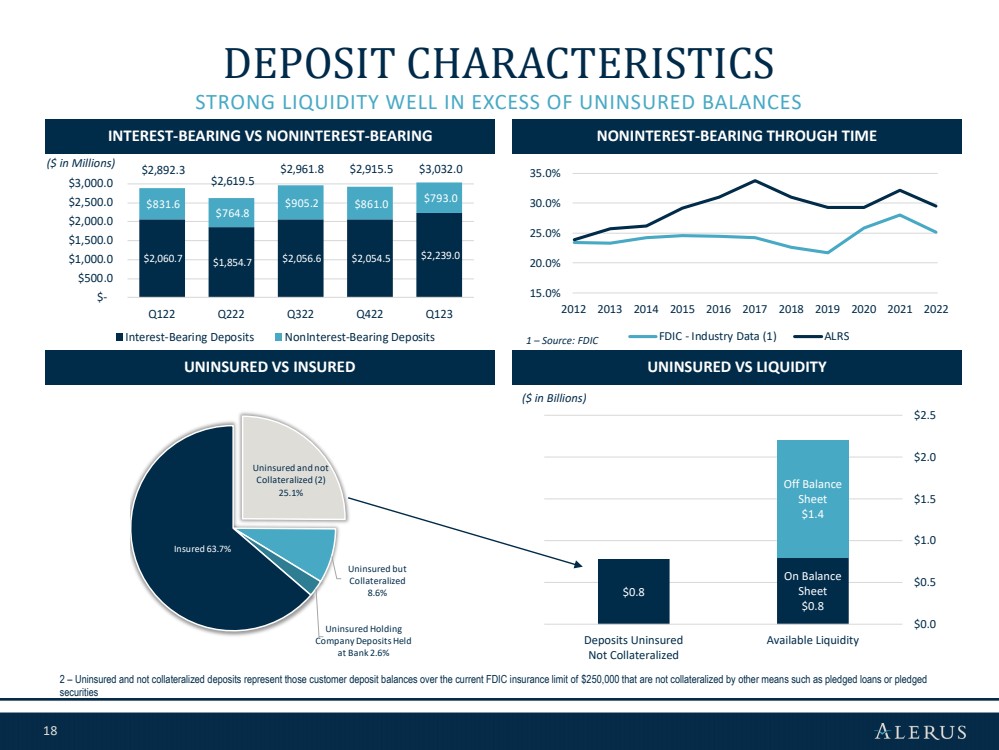

Total deposits were $3.0 billion as of March 31, 2023, an increase of $116.5 million, or 4.0%, from December 31, 2022. Interest-bearing deposits increased $184.5 million, while noninterest-bearing deposits decreased $68.0 million in the first quarter of 2023. The increase in interest-bearing deposits included increases of $111.4 million in interest-bearing demand deposits, $40.2 million in money market savings accounts and $33.1 million in time deposits. Interest-bearing deposits increased primarily due to an increase in our synergistic, commercial and public funds deposits. Synergistic deposits, which include deposits from our retirement and benefit services and wealth management segments including HSA deposits, increased $66.4 million. Excluding synergistic deposits, commercial transaction deposits including public funds increased $65.0 million, while consumer transaction deposits decreased $48.8 million in the first quarter of 2023. Noninterest bearing deposits as a percentage of total deposits was 26.2% as of March 31, 2023, compared to 29.5% as of December 31, 2022.

The following table presents the composition of our deposit portfolio as of the dates indicated:

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|||||

(dollars in thousands) |

|

2023 |

|

2022 |

|

2022 |

|

2022 |

|

2022 |

|||||

Noninterest-bearing demand |

|

$ |

792,977 |

|

$ |

860,987 |

|

$ |

905,228 |

|

$ |

764,808 |

|

$ |

831,558 |

Interest-bearing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing demand |

|

|

817,675 |

|

|

706,275 |

|

|

653,216 |

|

|

642,641 |

|

|

760,321 |

Savings accounts |

|

|

99,742 |

|

|

99,882 |

|

|

101,820 |

|

|

97,227 |

|

|

99,299 |

Money market savings |

|

|

1,076,166 |

|

|

1,035,981 |

|

|

1,079,520 |

|

|

914,423 |

|

|

976,905 |

Time deposits |

|

|

245,418 |

|

|

212,359 |

|

|

222,027 |

|

|

200,451 |

|

|

224,184 |

Total interest-bearing |

|

|

2,239,001 |

|

|

2,054,497 |

|

|

2,056,583 |

|

|

1,854,742 |

|

|

2,060,709 |

Total deposits |

|

$ |

3,031,978 |

|

$ |

2,915,484 |

|

$ |

2,961,811 |

|

$ |

2,619,550 |

|

$ |

2,892,267 |

Asset Quality

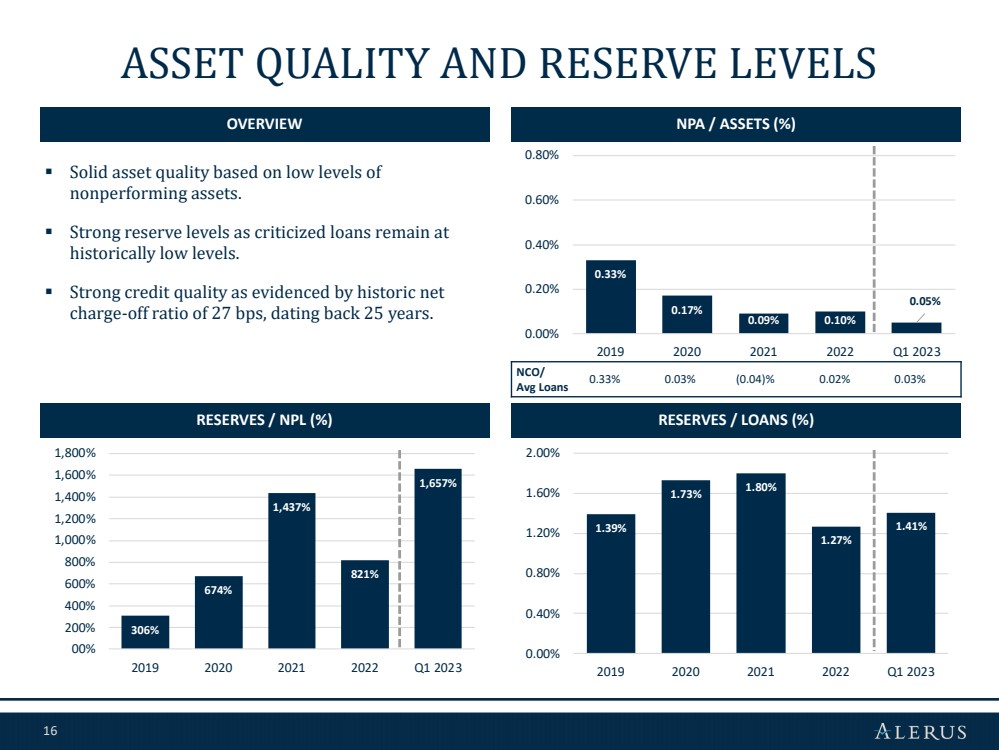

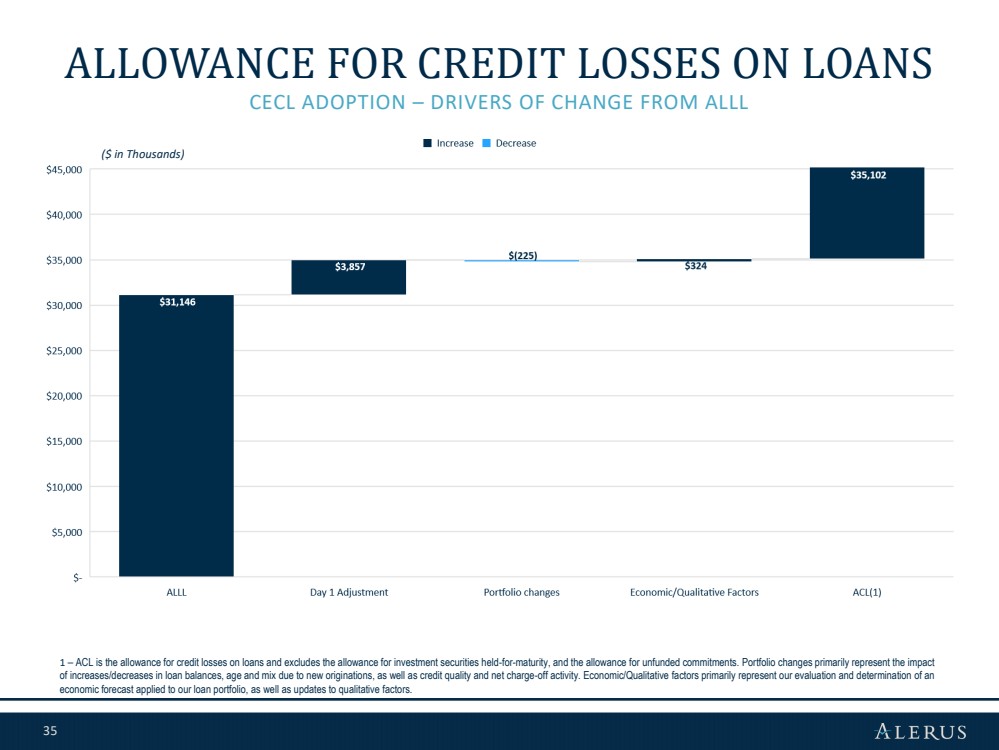

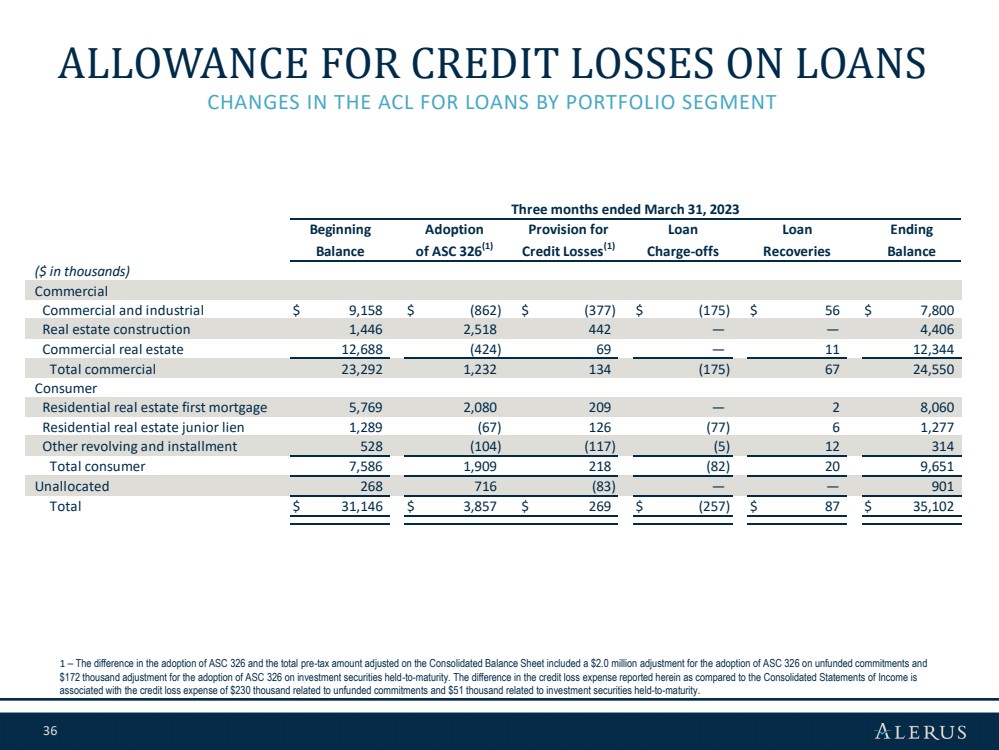

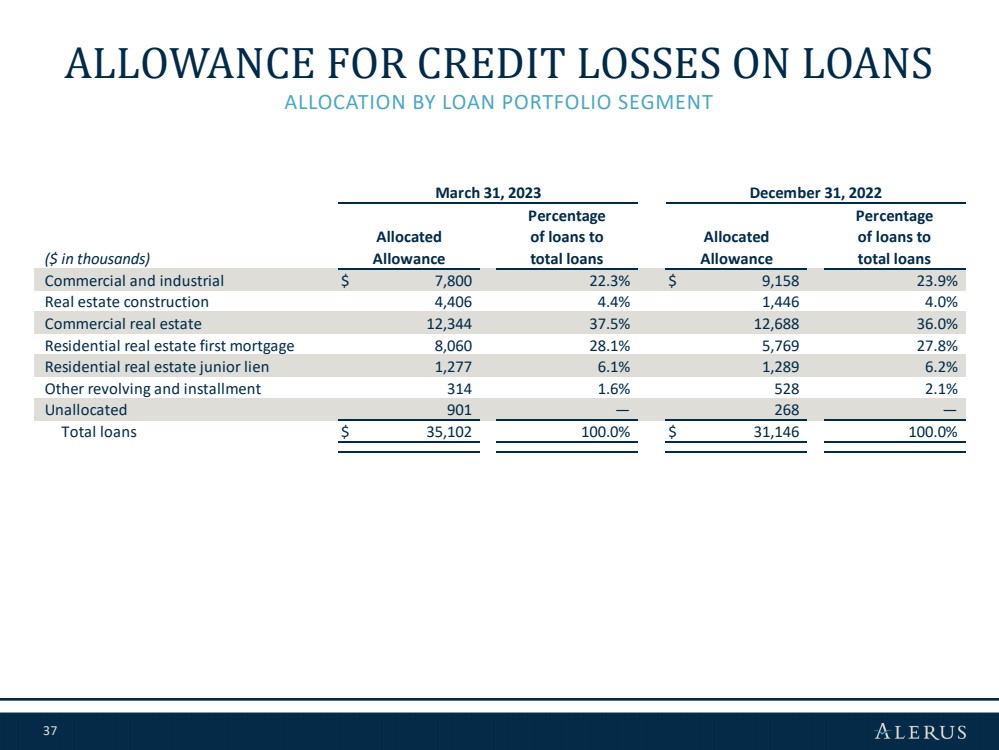

Effective January 1, 2023, the Company adopted the new CECL accounting standard. The adoption of CECL resulted in the Company’s allowance for credit losses increasing by approximately $5.9 million relative to the allowance held as of December 31, 2022. The adoption of CECL resulted in additional allowance of $3.9 million in the allowance for credit losses on loans and $1.9 million in additional allowance for credit losses on unfunded commitments. Total nonperforming assets were $2.1 million as of March 31, 2023, a decrease of $1.7 million, or 44.6%, from December 31, 2022. As of March 31, 2023, the allowance for credit losses on loans was $35.1 million, or 1.41% of total loans, compared to $31.1 million, or 1.27% of total loans, as of December 31, 2022. In addition, the fair value mark on the acquired Metro Phoenix Bank loan portfolio was $6.9 million and $7.1 million, as of March 31, 2023 and December 31, 2022, respectively.

4

The following table presents selected asset quality data as of and for the periods indicated:

|

|

As of and for the three months ended |

|

|||||||||||||

|

|

March 31, |

|

December 31, |

|

September 30, |

|

June 30, |

|

March 31, |

|

|||||

(dollars in thousands) |

|

2023 |

|

2022 |

|

2022 |

|

2022 |

|

2022 |

|

|||||

Nonaccrual loans |

|

$ |

2,118 |

|

$ |

3,794 |

|

$ |

4,303 |

|

$ |

4,370 |

|

$ |

4,069 |

|

Accruing loans 90+ days past due |

|

|

— |

|

|

— |

|

|

1,000 |

|

|

— |

|

|

146 |

|

Total nonperforming loans |

|

|

2,118 |

|

|

3,794 |

|

|

5,303 |

|

|

4,370 |

|

|

4,215 |

|

OREO and repossessed assets |

|

|

— |

|

|

30 |

|

|

904 |

|

|

860 |

|

|

865 |

|

Total nonperforming assets |

|

$ |

2,118 |

|

$ |

3,824 |

|

$ |

6,207 |

|

$ |

5,230 |

|

$ |

5,080 |

|

Net charge-offs/(recoveries) |

|

|

170 |

|

|

(178) |

|

|

405 |

|

|

340 |

|

|

(141) |

|

Net charge-offs/(recoveries) to average loans |

|

|

0.03 |

% |

|

(0.03) |

% |

|

0.07 |

% |

|

0.07 |

% |

|

(0.03) |

% |

Nonperforming loans to total loans |

|

|

0.09 |

% |

|

0.16 |

% |

|

0.23 |

% |

|

0.23 |

% |

|

0.23 |

% |

Nonperforming assets to total assets |

|

|

0.05 |

% |

|

0.10 |

% |

|

0.17 |

% |

|

0.16 |

% |

|

0.15 |

% |

Allowance for credit losses on loans to total loans |

|

|

1.41 |

% |

|

1.27 |

% |

|

1.34 |

% |

|

1.66 |

% |

|

1.74 |

% |

Allowance for credit losses on loans to nonperforming loans |

|

|

1,657 |

% |

|

821 |

% |

|

584 |

% |

|

718 |

% |

|

752 |

% |

For the first quarter of 2023, the Company had net charge-offs of $170 thousand compared to net recoveries of $178 thousand for the fourth quarter of 2022 and $141 thousand of net recoveries for the first quarter of 2022.

The Company recorded a provision for credit losses expense of $550 thousand in the three months ended March 31, 2023, a $550 thousand increase compared to both the three months ended December 31, 2022, and March 31, 2022. The provision for credit losses expense for the three months ended March 31, 2023, included $269 thousand in provision for credit losses on loans and $230 thousand in provision for credit losses on unfunded commitments. The increase in provision for credit losses was primarily a result of a change in forecasting assumptions in the new methodology with the adoption of CECL.

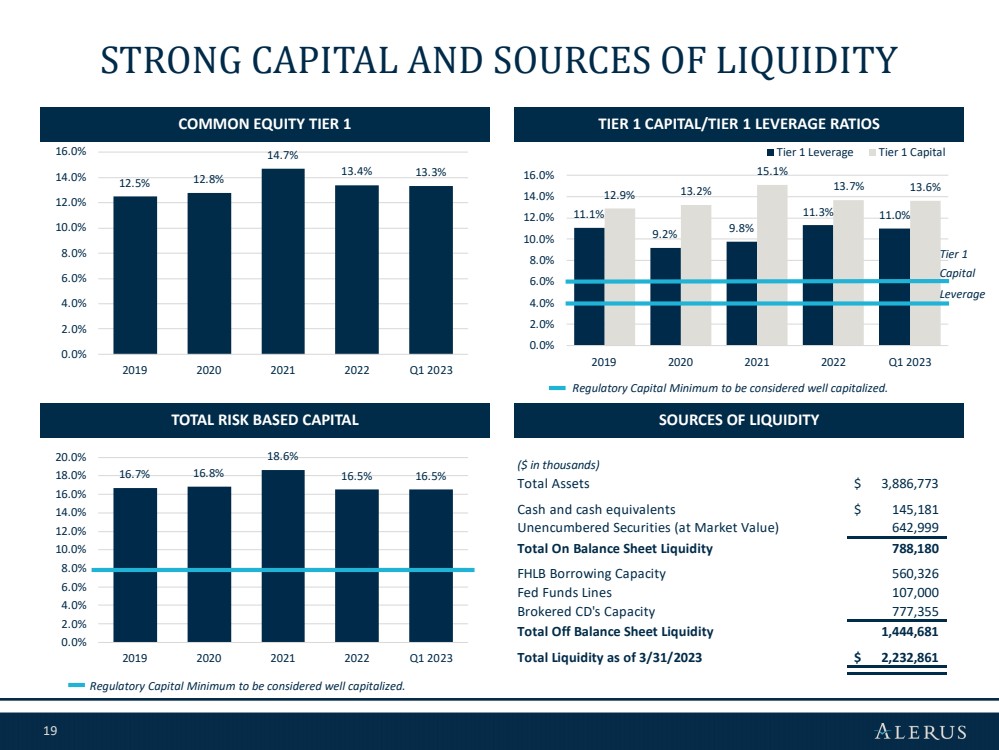

Capital

Total stockholders’ equity was $359.1 million as of March 31, 2023, an increase of $2.2 million, or 0.6%, from December 31, 2022. While stockholders’ equity remained relatively flat, the Company saw decreases of $4.5 million in retained earnings as a result of the adoption of CECL, partially offset by a $2.3 million decrease in the amount of other comprehensive loss. Tangible book value per common share, a non-GAAP financial measure, increased to $14.50 as of March 31, 2023, from $14.37 as of December 31, 2022. Tangible common equity to tangible assets, a non-GAAP financial measure, decreased to 7.62% as of March 31, 2023, from 7.74% as of December 31, 2022. Common equity tier 1 capital to risk weighted assets decreased to 13.30% as of March 31, 2023, from 13.39% as of December 31, 2022.

5

The following table presents our capital ratios as of the dates indicated:

|

|

March 31, |

|

December 31, |

|

March 31, |

|

|||

|

|

2023 |

|

2022 |

|

2022 |

|

|||

Capital Ratios(1) |

|

|

|

|

|

|

|

|

|

|

Alerus Financial Corporation Consolidated |

|

|

|

|

|

|

|

|

|

|

Common equity tier 1 capital to risk weighted assets |

|

|

13.30 |

% |

|

13.39 |

% |

|

14.27 |

% |

Tier 1 capital to risk weighted assets |

|

|

13.60 |

% |

|

13.69 |

% |

|

14.66 |

% |

Total capital to risk weighted assets |

|

|

16.51 |

% |

|

16.48 |

% |

|

18.12 |

% |

Tier 1 capital to average assets |

|

|

11.00 |

% |

|

11.25 |

% |

|

10.30 |

% |

Tangible common equity / tangible assets (2) |

|

|

7.62 |

% |

|

7.74 |

% |

|

8.46 |

% |

|

|

|

|

|

|

|

|

|

|

|

Alerus Financial, N.A. |

|

|

|

|

|

|

|

|

|

|

Common equity tier 1 capital to risk weighted assets |

|

|

12.67 |

% |

|

12.76 |

% |

|

13.52 |

% |

Tier 1 capital to risk weighted assets |

|

|

12.67 |

% |

|

12.76 |

% |

|

13.52 |

% |

Total capital to risk weighted assets |

|

|

13.87 |

% |

|

13.83 |

% |

|

14.77 |

% |

Tier 1 capital to average assets |

|

|

10.24 |

% |

|

10.48 |

% |

|

9.50 |

% |

| (1) | Capital ratios for the current quarter are to be considered preliminary until the Call Report for Alerus Financial, N.A. is filed. |

| (2) | Represents a non-GAAP financial measure. See “Non-GAAP to GAAP Reconciliations and Calculation of Non-GAAP Financial Measures.” |

Conference Call

The Company will host a conference call at 11:00 a.m. Central Time on Thursday, April 27, 2023, to discuss its financial results. The call can be accessed via telephone at (844) 200-6205, using access code 057461. A recording of the call and transcript will be available on the Company’s investor relations website at investors.alerus.com following the call.

About Alerus Financial Corporation

Alerus Financial Corporation is a diversified financial services company with corporate offices in Grand Forks, North Dakota, and the Minneapolis-St. Paul, Minnesota metropolitan area. Through its subsidiary, Alerus Financial, N.A., the Company provides innovative and comprehensive financial solutions to business and consumer clients through four distinct business segments—banking, retirement and benefit services, wealth management, and mortgage. The Company provides clients with a primary point of contact to help fully understand the unique needs and delivery channel preferences of each client. Clients are provided with competitive products, valuable insight and sound advice supported by digital solutions designed to meet the clients’ needs. The Company has banking, mortgage, and wealth management offices in Grand Forks and Fargo, North Dakota, the Minneapolis-St. Paul, Minnesota metropolitan area, and Phoenix, Scottsdale, and Mesa Arizona. Alerus Retirement and Benefits plan administration hubs are located in Minnesota, Michigan, and Colorado.

Non-GAAP Financial Measures

Some of the financial measures included in this press release are not measures of financial performance recognized by U.S. Generally Accepted Accounting Principles, or GAAP. These non-GAAP financial measures include the ratio of tangible common equity to tangible assets, tangible common equity per share, return on average tangible common equity, net interest margin (tax-equivalent), and the efficiency ratio. Management uses these non-GAAP financial measures in its analysis of its performance, and believes financial analysts and investors frequently use these measures, and other similar measures, to evaluate capital adequacy and financial performance. Reconciliations of non-GAAP disclosures used in this press release to the comparable GAAP measures are provided in the accompanying tables. Management, banking regulators, many financial analysts and other investors use these measures in conjunction with more traditional bank capital ratios to compare the capital adequacy of banking organizations with significant amounts of goodwill or other intangible assets, which typically stem from the use of the purchase accounting method of accounting for mergers and acquisitions.

These non-GAAP financial measures should not be considered in isolation or as a substitute for total stockholders’ equity, total assets, book value per share, return on average assets, return on average equity, or any other measure calculated in accordance with GAAP. Moreover, the manner in which the Company calculates these non-GAAP financial measures may differ from that of other companies reporting measures with similar names.

6

Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements include, without limitation, statements concerning plans, estimates, calculations, forecasts and projections with respect to the anticipated future performance of Alerus Financial Corporation. These statements are often, but not always, identified by words such as “may”, “might”, “should”, “could”, “predict”, “potential”, “believe”, “expect”, “continue”, “will”, “anticipate”, “seek”, “estimate”, “intend”, “plan”, “projection”, “would”, “annualized”, “target” and “outlook”, or the negative version of those words or other comparable words of a future or forward-looking nature. Examples of forward-looking statements include, among others, statements we make regarding our projected growth, anticipated future financial performance, financial condition, credit quality, management’s long-term performance goals and the future plans and prospects of Alerus Financial Corporation.

Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding the future of our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in forward-looking statements. Therefore, you should not rely on any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those indicated in forward-looking statements include, among others, the following: interest rate risks associated with our business, including the effects of recent and anticipated rate increases by the Federal Reserve; our ability to successfully manage credit risk and maintain an adequate level of allowance for credit losses; new or revised accounting standards, including as a result of the implementation of the new Current Expected Credit Loss Standard; business and economic conditions generally and in the financial services industry, nationally and within our market areas, including continued rising rates of inflation; the effects of recent developments and events in the financial services industry, including the large-scale deposit withdrawals over a short-period of time at Silicon Valley Bank and Signature Bank that resulted in the failure of those institutions; the overall health of the local and national real estate market; concentrations within our loan portfolio; the level of nonperforming assets on our balance sheet; our ability to implement our organic and acquisition growth strategies, including the integration of Metro Phoenix Bank which we acquired in 2022; the impact of economic or market conditions on our fee-based services; our ability to continue to grow our retirement and benefit services business; our ability to continue to originate a sufficient volume of residential mortgages; the occurrence of fraudulent activity, breaches or failures of our information security controls or cybersecurity-related incidents; interruptions involving our information technology and telecommunications systems or third-party servicers; potential losses incurred in connection with mortgage loan repurchases; the composition of our executive management team and our ability to attract and retain key personnel; rapid technological change in the financial services industry; increased competition in the financial services industry from non-banks such as credit unions and Fintech companies, including digital asset service providers; our ability to successfully manage liquidity risk, including our need to access higher cost sources of funds such as fed funds purchased and short-term borrowings; the concentration of large deposits from certain clients, who have balances above current FDIC insurance limits and may withdraw deposits to diversify their exposure; the effectiveness of our risk management framework; the commencement and outcome of litigation and other legal proceedings and regulatory actions against us or to which we may become subject; potential impairment to the goodwill we recorded in connection with our past acquisitions, including the acquisition of Metro Phoenix Bank; the extensive regulatory framework that applies to us; the impact of recent and future legislative and regulatory changes, including in response to the recent failures of Silicon Valley Bank and Signature Bank; fluctuations in the values of the securities held in our securities portfolio, including as a result of rising interest rates, which has resulted in unrealized losses in our portfolio; governmental monetary, trade and fiscal policies; risks related to climate change and the negative impact it may have on our customers and their businesses; severe weather, natural disasters, widespread disease or pandemics, such as the COVID-19 global pandemic; acts of war or terrorism, including the Russian invasion of Ukraine, or other adverse external events; any material weaknesses in our internal control over financial reporting; developments and uncertainty related to the future use and availability of some reference rates, such as the expected discontinuation of the London Interbank Offered Rate, as well as the development and implementation of other alternative reference rates; changes to U.S. or state tax laws, regulations and guidance, including the new 1.0% excise tax on stock buybacks by publicly traded companies; talent and labor shortages and employee turnover; our success at managing the risks involved in the foregoing items; and any other risks described in the “Risk Factors” sections of the reports filed by Alerus Financial Corporation with the Securities and Exchange Commission.

Any forward-looking statement made by us in this press release is based only on information currently available to us and speaks only as of the date on which it is made. We undertake no obligation to publicly update any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future developments or otherwise.

7

Alerus Financial Corporation and Subsidiaries

Consolidated Balance Sheets

(dollars in thousands, except share and per share data)

|

|

March 31, |

|

December 31, |

||

|

|

2023 |

|

2022 |

||

Assets |

|

(Unaudited) |

|

(Audited) |

||

Cash and cash equivalents |

|

$ |

145,181 |

|

$ |

58,242 |

Investment securities |

|

|

|

|

|

|

Available-for-sale, at fair value |

|

|

705,825 |

|

|

717,324 |

Held-to-maturity, at carrying value (allowance for credit losses of $223 at March 31, 2023) |

|

|

313,648 |

|

|

321,902 |

Loans held for sale |

|

|

16,900 |

|

|

9,488 |

Loans |

|

|

2,486,625 |

|

|

2,443,994 |

Allowance for credit losses on loans |

|

|

(35,102) |

|

|

(31,146) |

Net loans |

|

|

2,451,523 |

|

|

2,412,848 |

Land, premises and equipment, net |

|

|

17,631 |

|

|

17,288 |

Operating lease right-of-use assets |

|

|

5,122 |

|

|

5,419 |

Accrued interest receivable |

|

|

12,983 |

|

|

12,869 |

Bank-owned life insurance |

|

|

32,583 |

|

|

33,991 |

Goodwill |

|

|

47,087 |

|

|

47,087 |

Other intangible assets |

|

|

21,131 |

|

|

22,455 |

Servicing rights |

|

|

2,421 |

|

|

2,643 |

Deferred income taxes, net |

|

|

41,620 |

|

|

42,369 |

Other assets |

|

|

73,118 |

|

|

75,712 |

Total assets |

|

$ |

3,886,773 |

|

$ |

3,779,637 |

Liabilities and Stockholders’ Equity |

|

|

|

|

|

|

Deposits |

|

|

|

|

|

|

Noninterest-bearing |

|

$ |

792,977 |

|

$ |

860,987 |

Interest-bearing |

|

|

2,239,001 |

|

|

2,054,497 |

Total deposits |

|

|

3,031,978 |

|

|

2,915,484 |

Short-term borrowings |

|

|

372,145 |

|

|

378,080 |

Long-term debt |

|

|

58,872 |

|

|

58,843 |

Operating lease liabilities |

|

|

5,545 |

|

|

5,902 |

Accrued expenses and other liabilities |

|

|

59,115 |

|

|

64,456 |

Total liabilities |

|

|

3,527,655 |

|

|

3,422,765 |

Stockholders’ equity |

|

|

|

|

|

|

Preferred stock, $1 par value, 2,000,000 shares authorized: 0 issued and outstanding |

|

|

— |

|

|

— |

Common stock, $1 par value, 30,000,000 shares authorized: 20,066,807 and 19,991,681 issued and outstanding |

|

|

20,067 |

|

|

19,992 |

Additional paid-in capital |

|

|

154,818 |

|

|

155,095 |

Retained earnings |

|

|

280,540 |

|

|

280,426 |

Accumulated other comprehensive income (loss) |

|

|

(96,307) |

|

|

(98,641) |

Total stockholders’ equity |

|

|

359,118 |

|

|

356,872 |

Total liabilities and stockholders’ equity |

|

$ |

3,886,773 |

|

$ |

3,779,637 |

8

Alerus Financial Corporation and Subsidiaries

Consolidated Statements of Income

(dollars and shares in thousands, except per share data)

|

|

Three months ended |

|||||||

|

|

March 31, |

|

December 31, |

|

March 31, |

|||

|

|

2023 |

|

2022 |

|

2022 |

|||

Interest Income |

|

(Unaudited) |

|

(Unaudited) |

|

(Unaudited) |

|||

Loans, including fees |

|

$ |

30,933 |

|

$ |

29,248 |

|

$ |

17,292 |

Investment securities |

|

|

|

|

|

|

|

|

|

Taxable |

|

|

5,951 |

|

|

5,813 |

|

|

5,440 |

Exempt from federal income taxes |

|

|

190 |

|

|

210 |

|

|

216 |

Other |

|

|

735 |

|

|

541 |

|

|

116 |

Total interest income |

|

|

37,809 |

|

|

35,812 |

|

|

23,064 |

Interest Expense |

|

|

|

|

|

|

|

|

|

Deposits |

|

|

9,104 |

|

|

5,675 |

|

|

829 |

Short-term borrowings |

|

|

4,393 |

|

|

2,545 |

|

|

— |

Long-term debt |

|

|

654 |

|

|

628 |

|

|

562 |

Total interest expense |

|

|

14,151 |

|

|

8,848 |

|

|

1,391 |

Net interest income |

|

|

23,658 |

|

|

26,964 |

|

|

21,673 |

Provision for credit losses |

|

|

550 |

|

|

— |

|

|

— |

Net interest income after provision for credit losses |

|

|

23,108 |

|

|

26,964 |

|

|

21,673 |

Noninterest Income |

|

|

|

|

|

|

|

|

|

Retirement and benefit services |

|

|

15,482 |

|

|

16,599 |

|

|

17,646 |

Wealth management |

|

|

5,194 |

|

|

5,144 |

|

|

5,326 |

Mortgage banking |

|

|

1,717 |

|

|

2,170 |

|

|

4,931 |

Service charges on deposit accounts |

|

|

301 |

|

|

282 |

|

|

363 |

Other |

|

|

2,559 |

|

|

1,322 |

|

|

1,204 |

Total noninterest income |

|

|

25,253 |

|

|

25,517 |

|

|

29,470 |

Noninterest Expense |

|

|

|

|

|

|

|

|

|

Compensation |

|

|

19,158 |

|

|

19,189 |

|

|

19,051 |

Employee taxes and benefits |

|

|

5,853 |

|

|

4,887 |

|

|

6,162 |

Occupancy and equipment expense |

|

|

1,899 |

|

|

1,892 |

|

|

2,051 |

Business services, software and technology expense |

|

|

5,324 |

|

|

4,405 |

|

|

4,924 |

Intangible amortization expense |

|

|

1,324 |

|

|

1,324 |

|

|

1,053 |

Professional fees and assessments |

|

|

1,152 |

|

|

1,454 |

|

|

1,541 |

Marketing and business development |

|

|

686 |

|

|

950 |

|

|

600 |

Supplies and postage |

|

|

460 |

|

|

634 |

|

|

646 |

Travel |

|

|

248 |

|

|

356 |

|

|

179 |

Mortgage and lending expenses |

|

|

497 |

|

|

606 |

|

|

686 |

Other |

|

|

1,268 |

|

|

2,251 |

|

|

1,178 |

Total noninterest expense |

|

|

37,869 |

|

|

37,948 |

|

|

38,071 |

Income before income taxes |

|

|

10,492 |

|

|

14,533 |

|

|

13,072 |

Income tax expense |

|

|

2,306 |

|

|

3,624 |

|

|

2,888 |

Net income |

|

$ |

8,186 |

|

$ |

10,909 |

|

$ |

10,184 |

Per Common Share Data |

|

|

|

|

|

|

|

|

|

Earnings per common share |

|

$ |

0.41 |

|

$ |

0.54 |

|

$ |

0.58 |

Diluted earnings per common share |

|

$ |

0.40 |

|

$ |

0.53 |

|

$ |

0.57 |

Dividends declared per common share |

|

$ |

0.18 |

|

$ |

0.18 |

|

$ |

0.16 |

Average common shares outstanding |

|

|

20,028 |

|

|

19,988 |

|

|

17,244 |

Diluted average common shares outstanding |

|

|

20,246 |

|

|

20,232 |

|

|

17,500 |

9

Alerus Financial Corporation and Subsidiaries

Non-GAAP to GAAP Reconciliations and Calculation of Non-GAAP Financial Measures (unaudited)

(dollars and shares in thousands, except per share data)

|

|

March 31, |

|

December 31, |

|

March 31, |

|

|||

|

|

2023 |

|

2022 |

|

2022 |

|

|||

Tangible Common Equity to Tangible Assets |

|

|

|

|

|

|

|

|

|

|

Total common stockholders’ equity |

|

$ |

359,118 |

|

$ |

356,872 |

|

$ |

328,505 |

|

Less: Goodwill |

|

|

47,087 |

|

|

47,087 |

|

|

31,490 |

|

Less: Other intangible assets |

|

|

21,131 |

|

|

22,455 |

|

|

19,197 |

|

Tangible common equity (a) |

|

|

290,900 |

|

|

287,330 |

|

|

277,818 |

|

Total assets |

|

|

3,886,773 |

|

|

3,779,637 |

|

|

3,336,199 |

|

Less: Goodwill |

|

|

47,087 |

|

|

47,087 |

|

|

31,490 |

|

Less: Other intangible assets |

|

|

21,131 |

|

|

22,455 |

|

|

19,197 |

|

Tangible assets (b) |

|

|

3,818,555 |

|

|

3,710,095 |

|

|

3,285,512 |

|

Tangible common equity to tangible assets (a)/(b) |

|

|

7.62 |

% |

|

7.74 |

% |

|

8.46 |

% |

Tangible Book Value Per Common Share |

|

|

|

|

|

|

|

|

|

|

Total common stockholders’ equity |

|

$ |

359,118 |

|

$ |

356,872 |

|

$ |

328,505 |

|

Less: Goodwill |

|

|

47,087 |

|

|

47,087 |

|

|

31,490 |

|

Less: Other intangible assets |

|

|

21,131 |

|

|

22,455 |

|

|

19,197 |

|

Tangible common equity (c) |

|

|

290,900 |

|

|

287,330 |

|

|

277,818 |

|

Total common shares issued and outstanding (d) |

|

|

20,067 |

|

|

19,992 |

|

|

17,289 |

|

Tangible book value per common share (c)/(d) |

|

$ |

14.50 |

|

$ |

14.37 |

|

$ |

16.07 |

|

|

|

Three months ended |

|

|||||||

|

|

March 31, |

|

December 31, |

|

March 31, |

|

|||

|

|

2023 |

|

2022 |

|

2022 |

|

|||

Return on Average Tangible Common Equity |

|

|

|

|

|

|

|

|

|

|

Net income |

|

$ |

8,186 |

|

$ |

10,909 |

|

$ |

10,184 |

|

Add: Intangible amortization expense (net of tax) |

|

|

1,046 |

|

|

1,046 |

|

|

832 |

|

Net income, excluding intangible amortization (e) |

|

|

9,232 |

|

|

11,955 |

|

|

11,016 |

|

Average total equity |

|

|

361,857 |

|

|

349,812 |

|

|

350,545 |

|

Less: Average goodwill |

|

|

47,087 |

|

|

46,283 |

|

|

31,490 |

|

Less: Average other intangible assets (net of tax) |

|

|

17,209 |

|

|

18,243 |

|

|

15,569 |

|

Average tangible common equity (f) |

|

|

297,561 |

|

|

285,286 |

|

|

303,486 |

|

Return on average tangible common equity (e)/(f) |

|

|

12.58 |

% |

|

16.63 |

% |

|

14.72 |

% |

Efficiency Ratio |

|

|

|

|

|

|

|

|

|

|

Noninterest expense |

|

$ |

37,869 |

|

$ |

37,948 |

|

$ |

38,071 |

|

Less: Intangible amortization expense |

|

|

1,324 |

|

|

1,324 |

|

|

1,053 |

|

Adjusted noninterest expense (g) |

|

|

36,545 |

|

|

36,624 |

|

|

37,018 |

|

Net interest income |

|

|

23,658 |

|

|

26,964 |

|

|

21,673 |

|

Noninterest income |

|

|

25,253 |

|

|

25,517 |

|

|

29,470 |

|

Tax-equivalent adjustment |

|

|

124 |

|

|

124 |

|

|

94 |

|

Total tax-equivalent revenue (h) |

|

|

49,035 |

|

|

52,605 |

|

|

51,237 |

|

Efficiency ratio (g)/(h) |

|

|

74.53 |

% |

|

69.62 |

% |

|

72.25 |

% |

10

Alerus Financial Corporation and Subsidiaries

Analysis of Average Balances, Yields, and Rates (unaudited)

(dollars in thousands)

|

|

Three months ended |

||||||||||||||||

|

|

March 31, 2023 |

|

December 31, 2022 |

|

March 31, 2022 |

||||||||||||

|

|

|

|

|

Average |

|

|

|

|

Average |

|

|

|

|

Average |

|||

|

|

Average |

|

Yield/ |

|

Average |

|

Yield/ |

|

Average |

|

Yield/ |

||||||

|

|

Balance |

|

Rate |

|

Balance |

|

Rate |

|

Balance |

|

Rate |

||||||

Interest Earning Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing deposits with banks |

|

$ |

41,947 |

|

3.23 |

% |

|

$ |

26,510 |

|

2.16 |

% |

|

$ |

105,726 |

|

0.18 |

% |

Investment securities (1) |

|

|

1,034,288 |

|

2.43 |

% |

|

|

1,046,441 |

|

2.30 |

% |

|

|

1,216,256 |

|

1.90 |

% |

Fed funds sold |

|

|

— |

|

— |

% |

|

|

7,119 |

|

3.40 |

% |

|

|

— |

|

— |

% |

Loans held for sale |

|

|

10,345 |

|

4.98 |

% |

|

|

14,505 |

|

4.54 |

% |

|

|

24,656 |

|

2.57 |

% |

Loans |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial and industrial |

|

|

559,416 |

|

6.09 |

% |

|

|

561,252 |

|

5.80 |

% |

|

|

434,656 |

|

4.68 |

% |

Real estate construction |

|

|

103,099 |

|

6.56 |

% |

|

|

96,189 |

|

6.02 |

% |

|

|

41,139 |

|

3.89 |

% |

Commercial real estate |

|

|

911,634 |

|

4.95 |

% |

|

|

838,466 |

|

4.85 |

% |

|

|

601,024 |

|

3.64 |

% |

Total commercial |

|

|

1,574,149 |

|

5.46 |

% |

|

|

1,495,907 |

|

5.28 |

% |

|

|

1,076,819 |

|

4.07 |

% |

Consumer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Residential real estate first mortgage |

|

|

688,754 |

|

3.76 |

% |

|

|

665,135 |

|

3.64 |

% |

|

|

514,724 |

|

3.49 |

% |

Residential real estate junior lien |

|

|

149,720 |

|

7.21 |

% |

|

|

146,912 |

|

6.46 |

% |

|

|

125,997 |

|

4.45 |

% |

Other revolving and installment |

|

|

44,531 |

|

5.86 |

% |

|

|

51,836 |

|

5.62 |

% |

|

|

50,686 |

|

4.38 |

% |

Total consumer |

|

|

883,005 |

|

4.45 |

% |

|

|

863,883 |

|

4.24 |

% |

|

|

691,407 |

|

3.73 |

% |

Total loans (1) |

|

|

2,457,154 |

|

5.10 |

% |

|

|

2,359,790 |

|

4.90 |

% |

|

|

1,768,226 |

|

3.94 |

% |

Federal Reserve/FHLB stock |

|

|

23,668 |

|

6.87 |

% |

|

|

19,603 |

|

6.80 |

% |

|

|

6,486 |

|

4.38 |

% |

Total interest earning assets |

|

|

3,567,402 |

|

4.31 |

% |

|

|

3,473,968 |

|

4.10 |

% |

|

|

3,121,350 |

|

3.01 |

% |

Noninterest earning assets |

|

|

224,134 |

|

|

|

|

|

232,754 |

|

|

|

|

|

165,459 |

|

|

|

Total assets |

|

$ |

3,791,536 |

|

|

|

|

$ |

3,706,722 |

|

|

|

|

$ |

3,286,809 |

|

|

|

Interest-Bearing Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing demand deposits |

|

$ |

746,660 |

|

0.87 |

% |

|

$ |

692,217 |

|

0.50 |

% |

|

$ |

714,472 |

|

0.12 |

% |

Money market and savings deposits |

|

|

1,165,269 |

|

2.17 |

% |

|

|

1,185,502 |

|

1.39 |

% |

|

|

1,043,430 |

|

0.14 |

% |

Time deposits |

|

|

231,959 |

|

2.23 |

% |

|

|

214,264 |

|

1.20 |

% |

|

|

227,485 |

|

0.44 |

% |

Fed funds purchased |

|

|

290,187 |

|

4.85 |

% |

|

|

86,350 |

|

3.78 |

% |

|

|

— |

|

— |

% |

Short-term borrowings |

|

|

80,000 |

|

4.69 |

% |

|

|

178,533 |

|

3.82 |

% |

|

|

— |

|

— |

% |

Long-term debt |

|

|

58,858 |

|

4.51 |

% |

|

|

58,830 |

|

4.24 |

% |

|

|

58,908 |

|

3.87 |

% |

Total interest-bearing liabilities |

|

|

2,572,933 |

|

2.23 |

% |

|

|

2,415,696 |

|

1.45 |

% |

|

|

2,044,295 |

|

0.28 |

% |

Noninterest-Bearing Liabilities and Stockholders' Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest-bearing deposits |

|

|

789,134 |

|

|

|

|

|

870,948 |

|

|

|

|

|

831,441 |

|

|

|

Other noninterest-bearing liabilities |

|

|

67,612 |

|

|

|

|

|

70,266 |

|

|

|

|

|

60,528 |

|

|

|

Stockholders’ equity |

|

|

361,857 |

|

|

|

|

|

349,812 |

|

|

|

|

|

350,545 |

|

|

|

Total liabilities and stockholders’ equity |

|

$ |

3,791,536 |

|

|

|

|

$ |

3,706,722 |

|

|

|

|

$ |

3,286,809 |

|

|

|

Net interest income (1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest rate spread |

|

|

|

|

2.08 |

% |

|

|

|

|

2.65 |

% |

|

|

|

|

2.73 |

% |

Net interest margin, tax-equivalent (1) |

|

|

|

|

2.70 |

% |

|

|

|

|

3.09 |

% |

|

|

|

|

2.83 |

% |

| (1) | Taxable-equivalent adjustment was calculated utilizing a marginal income tax rate of 21.0%. |

11

|

EARNINGS PRESENTATION Q1 2023 NASDAQ: ALRS Alerus |

|

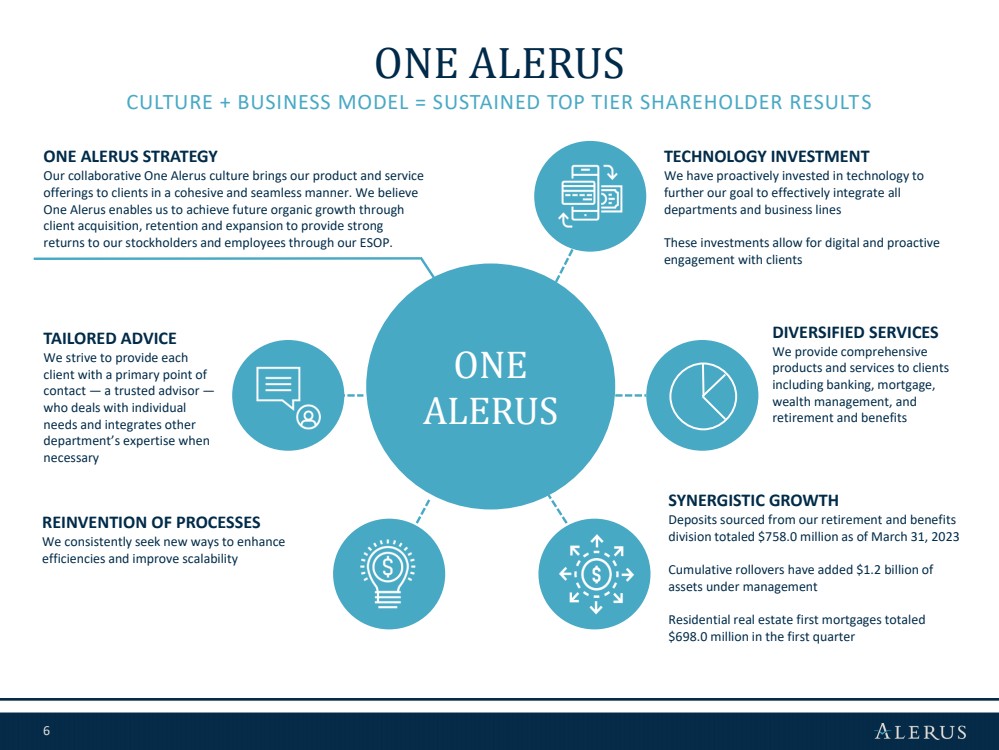

1 Forward-Looking Statements This presentation contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements include, without limitation, statements concerning plans, estimates, calculations, forecasts and projections with respect to the anticipated future performance of Alerus Financial Corporation. These statements are often, but not always, identified by words such as “may”, “might”, “should”, “could”, “predict”, “potential”, “believe”, “expect”, “continue”, “will”, “anticipate”, “seek”, “estimate”, “intend”, “plan”, “projection”, “would”, “annualized”, “target” and “outlook”, or the negative version of those words or other comparable words of a future or forward-looking nature. Examples of forward-looking statements include, among others, statements we make regarding our projected growth, anticipated future financial performance, financial condition, credit quality, management’s long-term performance goals and the future plans and prospects of Alerus Financial Corporation. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding the future of our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in forward-looking statements. Therefore, you should not rely on any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those indicated in forward-looking statements include, among others, the following: interest rate risks associated with our business, including the effects of recent and anticipated rate increases by the Federal Reserve; our ability to successfully manage credit risk and maintain an adequate level of allowance for credit losses on loans; new or revised accounting standards, including as a result of the implementation of the new Current Expected Credit Loss Standard; business and economic conditions generally and in the financial services industry, nationally and within our market areas, including continued rising rates of inflation; the effects of recent developments and events in the financial services industry, including the large-scale deposit withdrawals over a short period of time at Silicon Valley Bank and Signature Bank that resulted in the failure of those institutions; the overall health of the local and national real estate market; concentrations within our loan portfolio; the level of nonperforming assets on our balance sheet; our ability to implement our organic and acquisition growth strategies, including the integration of Metro Phoenix Bank which we acquired in 2022; the impact of economic or market conditions on our fee-based services; our ability to continue to grow our retirement and benefit services business; our ability to continue to originate a sufficient volume of residential mortgages; the occurrence of fraudulent activity, breaches or failures of our information security controls or cybersecurity-related incidents; interruptions involving our information technology and telecommunications systems or third-party servicers; potential losses incurred in connection with mortgage loan repurchases; the composition of our executive management team and our ability to attract and retain key personnel; rapid technological change in the financial services industry; increased competition in the financial services industry from non-banks such as credit unions and Fintech companies, including digital asset service providers; our ability to successfully manage liquidity risk, including our need to access higher cost sources of funds such as fed funds purchased and short-term borrowings; the concentration of large deposits from certain clients, who have balances above current FDIC insurance limits and may withdraw deposits to diversify their exposure; the effectiveness of our risk management framework; the commencement and outcome of litigation and other legal proceedings and regulatory actions against us or to which we may become subject; potential impairment to the goodwill we recorded in connection with our past acquisitions, including the acquisition of Metro Phoenix Bank; the extensive regulatory framework that applies to us; the impact of recent and future legislative and regulatory changes, including in response to the recent failures of Silicon Valley Bank and Signature Bank; fluctuations in the values of the securities held in our securities portfolio, including as a result of rising interest rates, which has resulted in unrealized losses in our portfolio; governmental monetary, trade and fiscal policies; risks related to climate change and the negative impact it may have on our customers and their businesses; severe weather, natural disasters, widespread disease or pandemics, such as the COVID-19 global pandemic; acts of war or terrorism, including the Russian invasion of Ukraine, or other adverse external events; any material weaknesses in our internal control over financial reporting; developments and uncertainty related to the future use and availability of some reference rates, such as the expected discontinuation of the London Interbank Offered Rate, as well as the development and implementation of other alternative reference rates; changes to U.S. or state tax laws, regulations and guidance, including the new 1.0% excise tax on stock buybacks by publicly traded companies; talent and labor shortages and employee turnover; our success at managing the risks involved in the foregoing items; and any other risks described in the “Risk Factors” sections of the reports filed by Alerus Financial Corporation with the Securities and Exchange Commission. Any forward-looking statement made by us in this presentation is based only on information currently available to us and speaks only as of the date on which it is made. We undertake no obligation to publicly update any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future developments or otherwise. Non-GAAP Financial Measures This presentation includes certain ratios and amounts that do not conform to U.S. Generally Accepted Accounting Principles, or GAAP. Management uses certain non-GAAP financial measures to evaluate financial performance and business trends from period to period and believes that disclosure of these non-GAAP financial measures will help investors, rating agencies and analysts evaluate the financial performance and condition of Alerus Financial Corporation. This presentation includes a reconciliation of each non-GAAP financial measure to the most comparable GAAP equivalent. Miscellaneous Except as otherwise indicated, this presentation speaks as of the date hereof. The delivery of this presentation shall not, under any circumstances, create any implication that there has been no change in the affairs of Alerus Financial Corporation after the date hereof. Certain of the information contained herein may be derived from information provided by industry sources. We believe that such information is accurate and that the sources from which it has been obtained are reliable. We cannot guarantee the accuracy of such information, however, and we have not independently verified such information. DISCLAIMERS |

|

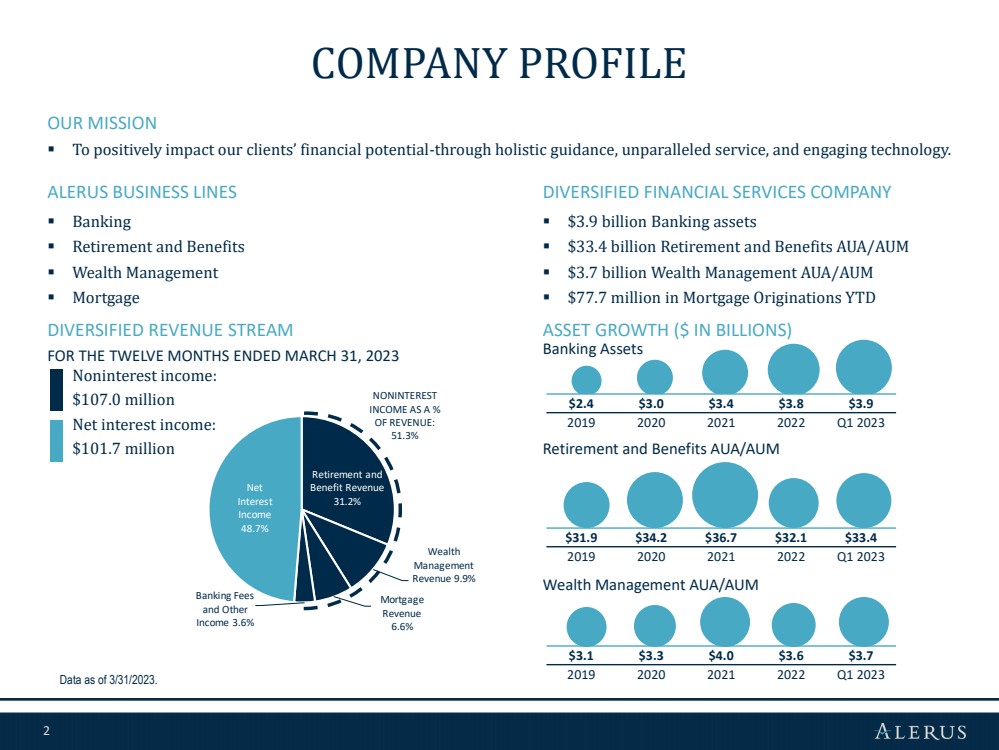

2 Retirement and Benefit Revenue 31.2% Wealth Management Revenue 9.9% Mortgage Revenue 6.6% Banking Fees and Other Income 3.6% Net Interest Income 48.7% FOR THE TWELVE MONTHS ENDED MARCH 31, 2023 Noninterest income: $107.0 million Net interest income: $101.7 million $31.9 $34.2 $36.7 $32.1 $33.4 2019 2020 2021 2022 Q1 2023 OUR MISSION ▪ To positively impact our clients’ financial potential-through holistic guidance, unparalleled service, and engaging technology. COMPANY PROFILE Data as of 3/31/2023. DIVERSIFIED REVENUE STREAM ASSET GROWTH ($ IN BILLIONS) Banking Assets Retirement and Benefits AUA/AUM Wealth Management AUA/AUM $3.1 $3.3 $4.0 $3.6 $3.7 2019 2020 2021 2022 Q1 2023 NONINTEREST INCOME AS A % OF REVENUE: 51.3% DIVERSIFIED FINANCIAL SERVICES COMPANY ▪ $3.9 billion Banking assets ▪ $33.4 billion Retirement and Benefits AUA/AUM ▪ $3.7 billion Wealth Management AUA/AUM ▪ $77.7 million in Mortgage Originations YTD ALERUS BUSINESS LINES ▪ Banking ▪ Retirement and Benefits ▪ Wealth Management ▪ Mortgage $2.4 $3.0 $3.4 $3.8 $3.9 2019 2020 2021 2022 Q1 2023 |

|

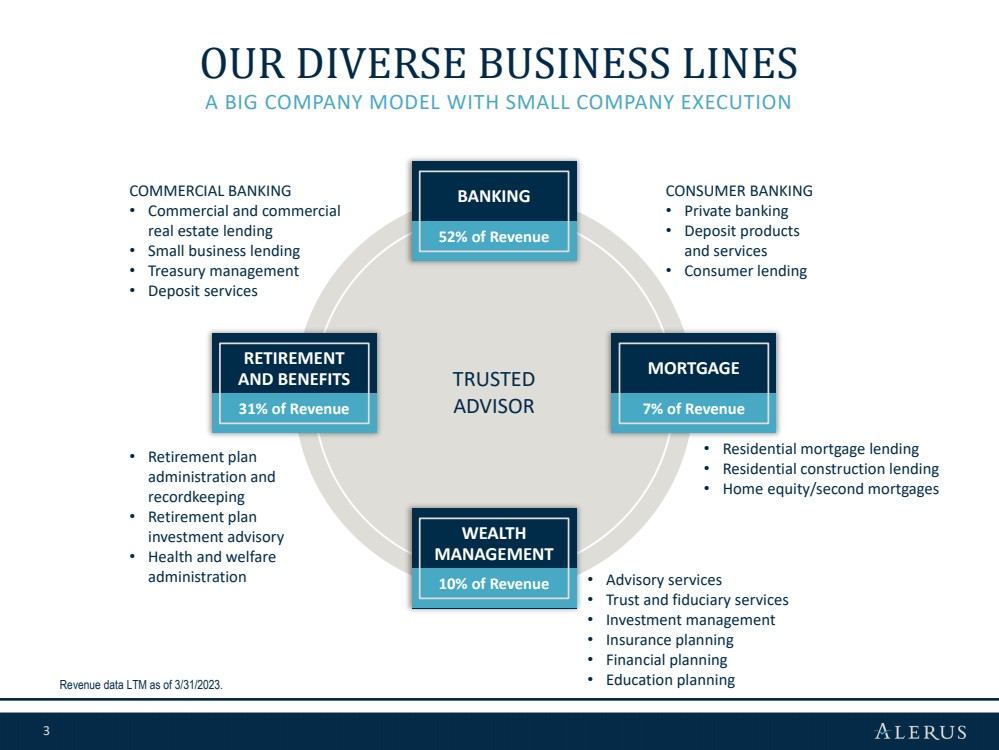

3 A BIG COMPANY MODEL WITH SMALL COMPANY EXECUTION OUR DIVERSE BUSINESS LINES Revenue data LTM as of 3/31/2023. TRUSTED ADVISOR BANKING WEALTH MANAGEMENT • Residential mortgage lending • Residential construction lending • Home equity/second mortgages • Advisory services • Trust and fiduciary services • Investment management • Insurance planning • Financial planning • Education planning • Retirement plan administration and recordkeeping • Retirement plan investment advisory • Health and welfare administration COMMERCIAL BANKING • Commercial and commercial real estate lending • Small business lending • Treasury management • Deposit services CONSUMER BANKING • Private banking • Deposit products and services • Consumer lending MORTGAGE RETIREMENT AND BENEFITS 31% of Revenue 7% of Revenue 10% of Revenue 52% of Revenue |

|

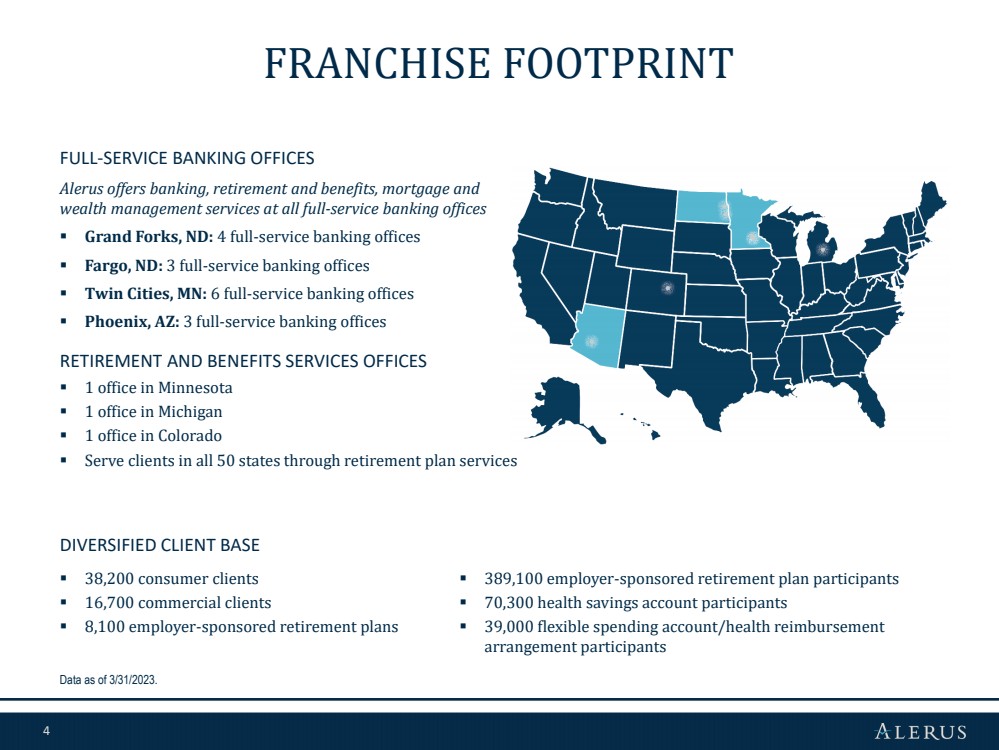

4 FRANCHISE FOOTPRINT FULL-SERVICE BANKING OFFICES Alerus offers banking, retirement and benefits, mortgage and wealth management services at all full-service banking offices ▪ Grand Forks, ND: 4 full-service banking offices ▪ Fargo, ND: 3 full-service banking offices ▪ Twin Cities, MN: 6 full-service banking offices ▪ Phoenix, AZ: 3 full-service banking offices RETIREMENT AND BENEFITS SERVICES OFFICES ▪ 1 office in Minnesota ▪ 1 office in Michigan ▪ 1 office in Colorado ▪ Serve clients in all 50 states through retirement plan services DIVERSIFIED CLIENT BASE ▪ 38,200 consumer clients ▪ 16,700 commercial clients ▪ 8,100 employer-sponsored retirement plans Data as of 3/31/2023. ▪ 389,100 employer-sponsored retirement plan participants ▪ 70,300 health savings account participants ▪ 39,000 flexible spending account/health reimbursement arrangement participants |

|

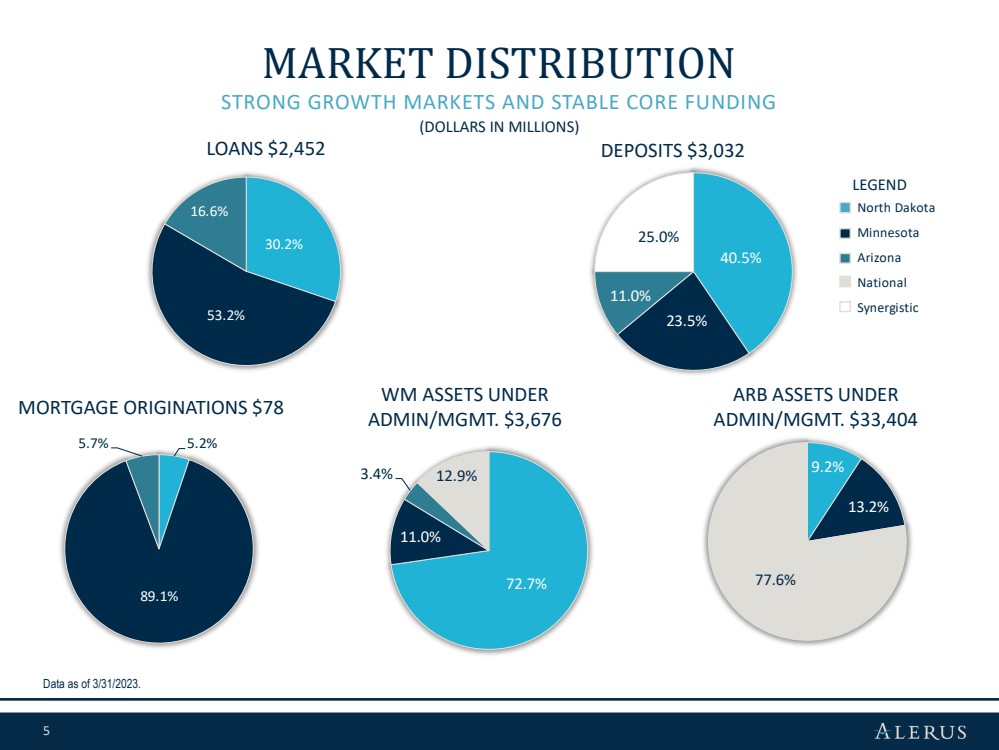

5 STRONG GROWTH MARKETS AND STABLE CORE FUNDING MARKET DISTRIBUTION LOANS $2,452 DEPOSITS $3,032 ARB ASSETS UNDER ADMIN/MGMT. $33,404 WM ASSETS UNDER ADMIN/MGMT. $3,676 MORTGAGE ORIGINATIONS $78 (DOLLARS IN MILLIONS) Data as of 3/31/2023. LEGEND 30.2% 53.2% 16.6% 40.5% 23.5% 11.0% 25.0% 5.2% 89.1% 5.7% 72.7% 11.0% 3.4% 12.9% 9.2% 13.2% 77.6% North Dakota Minnesota Arizona National Synergistic |

|