UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): February 17, 2022 (February 17, 2022)

Matson, Inc.

(Exact Name of Registrant as Specified in its Charter)

_____________________

Hawaii |

|

001-34187 |

|

99-0032630 |

(State or Other Jurisdiction of |

|

(Commission File Number) |

|

(I.R.S. Employer Identification |

1411 Sand Island Parkway |

|

|

Honolulu, Hawaii |

|

96819 |

(Address of principal executive offices) |

|

(zip code) |

Registrant’s telephone number, including area code: (808) 848-1211

(Former Name or former address, if changed since last report)

_____________________

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

Common Stock, without par value |

MATX |

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 2.02.Results of Operations and Financial Condition.

On February 17, 2022, Matson, Inc. (the “Company”) issued a press release announcing the Company’s earnings for the quarter and fiscal year ended December 31, 2021. A copy of the press release is attached hereto as Exhibit 99.1. In addition, the Company posted an investor presentation to its website. A copy of the investor presentation is attached hereto as Exhibit 99.2.

The information in this report (including Exhibits 99.1 and 99.2) is being furnished pursuant to Item 2.02 and shall not be deemed to be “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended.

Item 9.01.Financial Statements and Exhibits.

(a) - (c) Not applicable.

(d) Exhibits.

The exhibit listed below is being furnished with this Form 8-K.

99.1 |

Press Release issued by Matson, Inc., dated February 17, 2022 |

|

|

99.2 |

|

|

|

104 |

Cover Page Interactive Data File (formatted in Inline XBRL and included as Exhibit 101). |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

MATSON, INC. |

|

|

|

|

|

/s/ Joel M. Wine |

|

Joel M. Wine |

|

Executive Vice President and Chief Financial Officer |

|

|

|

|

Dated: February 17, 2022 |

|

Exhibit 99.1

Investor Relations inquiries: |

News Media inquiries: |

Lee Fishman |

Keoni Wagner |

Matson, Inc. |

Matson, Inc. |

510.628.4227 |

510.628.4534 |

lfishman@matson.com |

kwagner@matson.com |

FOR IMMEDIATE RELEASE

MATSON, INC. ANNOUNCES FOURTH QUARTER AND FULL YEAR 2021 RESULTS

| ● | 4Q21 EPS of $9.39 |

| ● | Full Year 2021 EPS of $21.47 |

| ● | Full Year 2021 Net Income and EBITDA of $927.4 million and $1,350.3 million, respectively |

| ● | Year-over-year increase in 4Q21 and consolidated operating income driven primarily by China service strength |

| ● | Repurchased approximately 1.0 million and 2.5 million shares in 4Q21 and full year 2021, respectively |

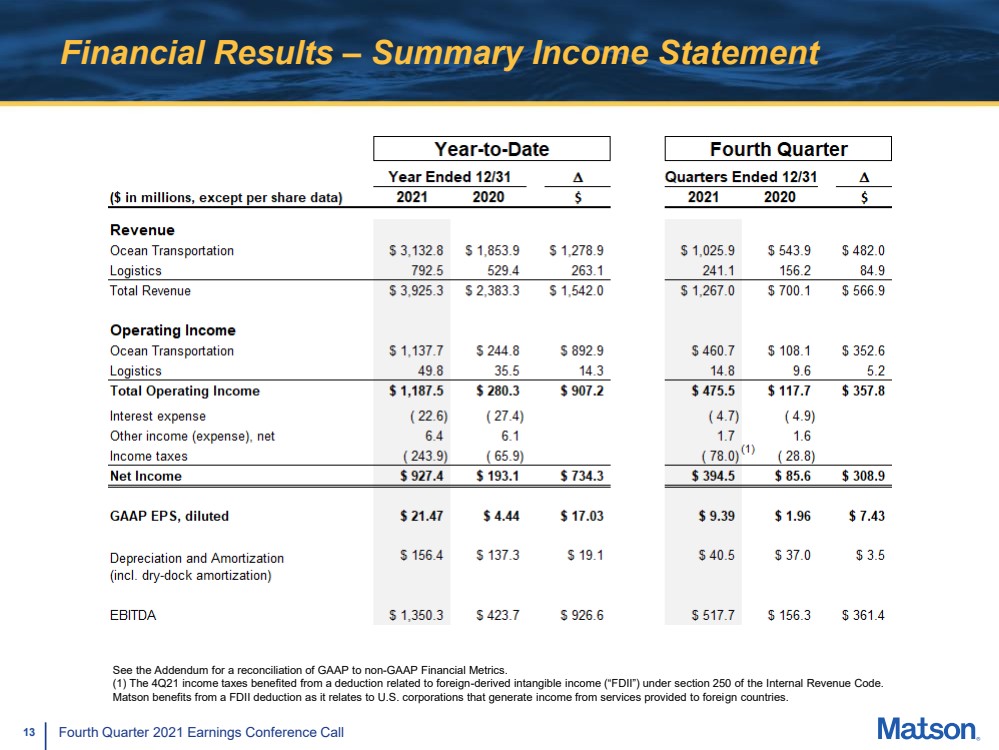

HONOLULU, Hawaii (February 17, 2022) – Matson, Inc. (“Matson” or the “Company”) (NYSE: MATX), a leading U.S. carrier in the Pacific, today reported net income of $394.5 million, or $9.39 per diluted share, for the quarter ended December 31, 2021. Net income for the quarter ended December 31, 2020 was $85.6 million, or $1.96 per diluted share. Consolidated revenue for the fourth quarter 2021 was $1,267.0 million compared with $700.1 million for the fourth quarter 2020.

For the twelve months ended December 31, 2021, Matson reported net income of $927.4 million, or $21.47 per diluted share compared with $193.1 million, or $4.44 per diluted share in 2020. Consolidated revenue for the twelve month period ended December 31, 2021 was $3,925.3 million, compared with $2,383.3 million in 2020.

“Matson finished off a strong year with continued improvement in economic and business trends in our markets driving solid performance in both Ocean Transportation and Logistics,” said Chairman and Chief Executive Officer Matt Cox. “Within Ocean Transportation, our China service continued to see significant demand for its expedited ocean services as volume for e-commerce, garments and other goods remained elevated. Continued strong demand for the China service was the primary driver of the increase in consolidated operating income year-over-year. Supply chain congestion remains the current issue in the Transpacific tradelane due to ongoing elevated consumption trends, U.S. domestic supply chain constraints, and inventory restocking. For 2022, we expect these conditions to remain largely in place through at least the October peak season and expect elevated demand for our China service for most of the year.”

Mr. Cox added, “In our domestic ocean tradelanes, we continued to see strong demand with higher year-over-year volumes, including the benefit of an extra week, compared to the largely pandemic-reduced volumes in the year ago period. In Hawaii, we experienced elevated westbound freight demand as the state’s tourism and economy continued to rebound from the pandemic lows and the slowdown in tourism at the beginning of the quarter as a result of the state’s efforts to address the spread of the COVID-19 Delta variant. In Logistics, operating income increased year-over-year compared to the operating income achieved in the year ago period as we continued to see elevated goods consumption, inventory restocking and favorable supply and demand fundamentals in our core markets.”

Fourth Quarter 2021 Discussion and Update on Business Conditions

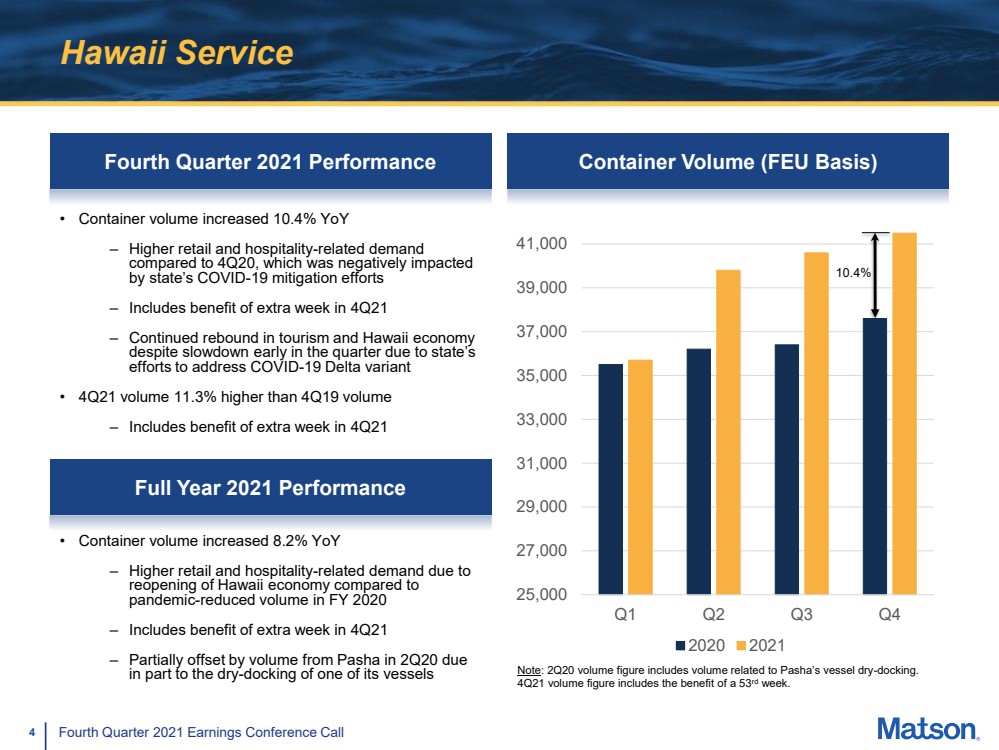

Ocean Transportation: The Company’s container volume in the Hawaii service in the fourth quarter 2021 was 10.4 percent higher year-over-year. The increase was primarily due to (i) higher retail- and hospitality-related demand due to the continued rebound in tourism and the Hawaii economy and (ii) the benefit of an extra week, compared to the pandemic-reduced volume in the year ago period.

1

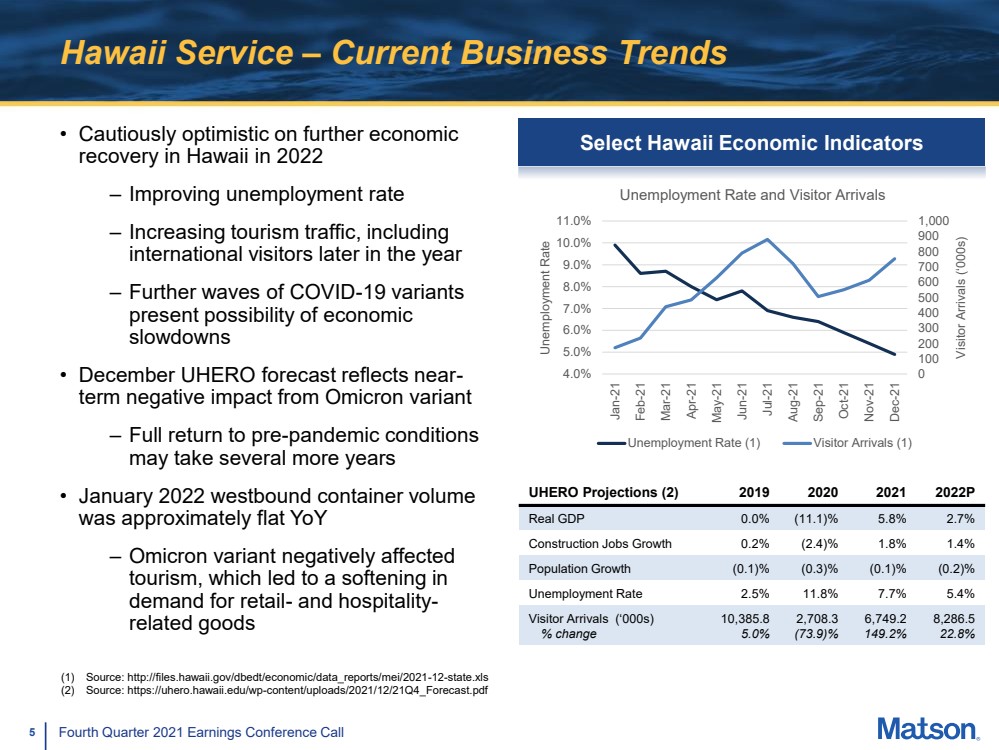

Volume in the fourth quarter 2020 was negatively impacted by the state’s COVID-19 mitigation efforts, including restrictions on tourism. Tourism and the Hawaii economy continued to rebound in the fourth quarter 2021 despite a softening in airline passenger traffic early in the quarter due to the state’s efforts to address the spread of the COVID-19 Delta variant. In the near-term, we are cautiously optimistic on further economic recovery in Hawaii primarily due to improvement in the unemployment rate and increasing tourism traffic, including international visitors later in the year, but incremental waves of COVID-19 variants present the possibility of further economic slowdowns.

In China, the Company’s container volume in the fourth quarter 2021 increased 32.7 percent year-over-year. The increase was primarily due to volume from the China-California Express (“CCX”) service and the benefit of an extra week. The total number of eastbound voyages in the China service, including the impact of an extra week, increased by nine year-over-year, of which eight were CCX voyages and one was a CLX voyage. Volume demand in the quarter was driven by e-commerce, garments and other goods. Matson continued to realize a significant rate premium over the Shanghai Containerized Freight Index in the fourth quarter 2021 and achieved average freight rates that were considerably higher than in the year ago period. Supply chain congestion remains the current issue in the Transpacific tradelane due to ongoing elevated consumption trends, U.S. domestic supply chain constraints, and inventory restocking. For 2022, we expect these conditions to remain largely in place through at least the October peak season and expect elevated demand for our China service for most of the year.

In Guam, the Company’s container volume in the fourth quarter 2021 increased 14.0 percent year-over-year primarily due to higher retail-related demand compared to the pandemic-reduced volume in the year ago period. In the near-term, we are cautiously optimistic on further economic growth in Guam as tourism traffic improves as the year progresses.

In Alaska, the Company’s container volume for the fourth quarter 2021 increased 10.2 percent year-over-year primarily due to (i) the increase in volume from the Alaska-Asia Express (“AAX”), (ii) the benefit of an extra week, and (iii) higher southbound volume. In the near-term, we expect improving economic trends in Alaska, but the recovery’s trajectory continues to remain uncertain.

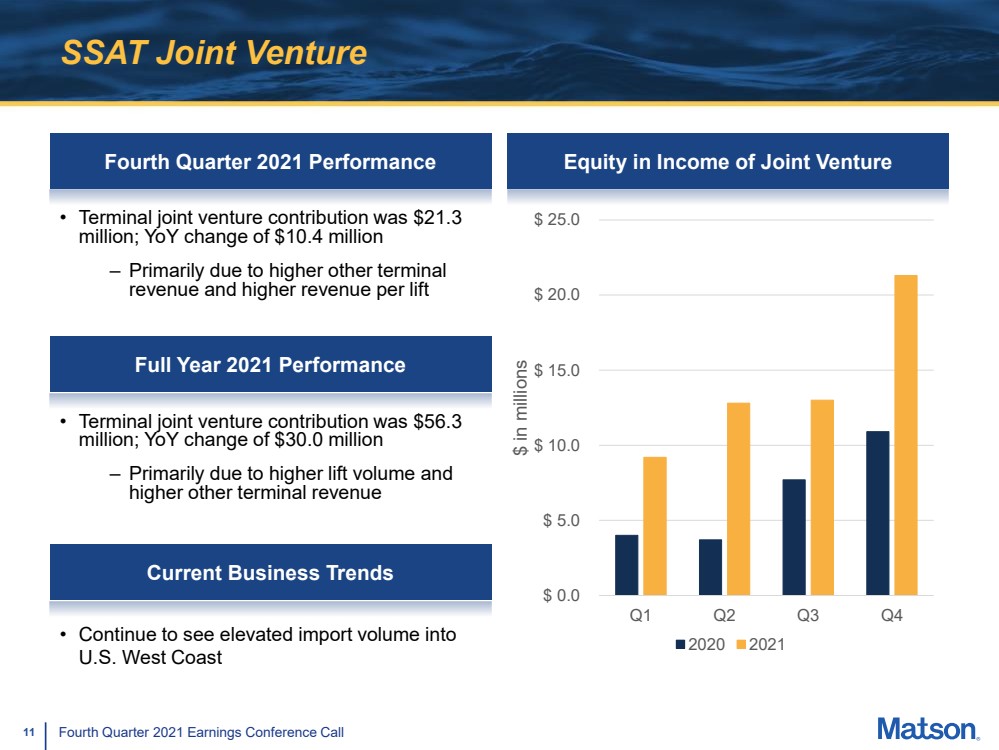

The contribution in the fourth quarter 2021 from the Company’s SSAT joint venture investment was $21.3 million, or $10.4 million higher than the fourth quarter 2020. The increase was primarily driven by higher other terminal revenue and higher revenue per lift.

Logistics: In the fourth quarter 2021, operating income for the Company’s Logistics segment was $14.8 million, or $5.2 million higher compared to the level achieved in the fourth quarter 2020. The increase was due primarily to higher contributions from supply chain management and transportation brokerage as a result of elevated goods consumption, inventory restocking and favorable supply and demand fundamentals in our core markets.

2

Results By Segment

Ocean Transportation — Three months ended December 31, 2021 compared with 2020

|

|

Three Months Ended December 31, |

|

|||||||||

(Dollars in millions) |

|

2021 |

|

2020 |

|

Change |

|

|||||

Ocean Transportation revenue |

|

$ |

1,025.9 |

|

$ |

543.9 |

|

$ |

482.0 |

|

88.6 |

% |

Operating costs and expenses |

|

|

(565.2) |

|

|

(435.8) |

|

|

(129.4) |

|

29.7 |

% |

Operating income |

|

$ |

460.7 |

|

$ |

108.1 |

|

$ |

352.6 |

|

326.2 |

% |

Operating income margin |

|

|

44.9 |

% |

|

19.9 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Volume (Forty-foot equivalent units (FEU), except for automobiles) (1) |

|

|

|

|

|

|

|

|

|

|

|

|

Hawaii containers |

|

|

41,500 |

|

|

37,600 |

|

|

3,900 |

|

10.4 |

% |

Hawaii automobiles |

|

|

10,600 |

|

|

12,200 |

|

|

(1,600) |

|

(13.1) |

% |

Alaska containers |

|

|

19,400 |

|

|

17,600 |

|

|

1,800 |

|

10.2 |

% |

China containers |

|

|

53,600 |

|

|

40,400 |

|

|

13,200 |

|

32.7 |

% |

Guam containers |

|

|

5,700 |

|

|

5,000 |

|

|

700 |

|

14.0 |

% |

Other containers (2) |

|

|

5,600 |

|

|

4,900 |

|

|

700 |

|

14.3 |

% |

| (1) | Approximate volumes included for the period are based on the voyage departure date, but revenue and operating income are adjusted to reflect the percentage of revenue and operating income earned during the reporting period for voyages in transit at the end of each reporting period. |

| (2) | Includes containers from services in various islands in Micronesia and the South Pacific, and Okinawa, Japan. |

Ocean Transportation revenue increased $482.0 million, or 88.6 percent, during the three months ended December 31, 2021, compared with the three months ended December 31, 2020. The increase was primarily due to higher revenue in China, higher fuel-related surcharge revenue, and higher revenue in Hawaii and Alaska. The higher revenue in China was primarily due to considerably higher average freight rates and higher volume. The higher revenue in Hawaii and Alaska was primarily the result of higher volume.

On a year-over-year FEU basis, Hawaii container volume increased 10.4 percent primarily due to (i) higher retail and hospitality-related demand due to the continued rebound in tourism and the Hawaii economy and (ii) the benefit of an extra week, compared to the volume in the year ago period, which was negatively impacted by the state’s COVID-19 mitigation efforts, including restrictions on tourism; Alaska volume increased 10.2 percent primarily due to the increase in volume from the AAX, the benefit of an extra week, and higher southbound volume; China volume was 32.7 percent higher primarily due to CCX volume and the benefit of an extra week; Guam volume was 14.0 percent higher primarily due to higher retail-related demand compared to the pandemic-reduced volume in the year ago period; and Other containers volume increased 14.3 percent primarily due to the addition of China-Auckland Express volume in the South Pacific.

Ocean Transportation operating income increased $352.6 million during the three months ended December 31, 2021, compared with the three months ended December 31, 2020. The increase was primarily due to considerably higher average freight rates and higher volume in China, partially offset by higher operating costs and expenses primarily due to the CCX service and higher incremental costs associated with the CLX+ service.

The Company’s SSAT terminal joint venture investment contributed $21.3 million during the three months ended December 31, 2021, compared to a contribution of $10.9 million during the three months ended December 31, 2020. The increase was primarily driven by higher other terminal revenue and higher revenue per lift.

3

Ocean Transportation — Year ended December 31, 2021 compared with 2020

|

|

Years Ended December 31, |

|

|||||||||

(Dollars in millions) |

|

2021 |

|

2020 |

|

Change |

|

|||||

Ocean Transportation revenue |

|

$ |

3,132.8 |

|

$ |

1,853.9 |

|

$ |

1,278.9 |

|

69.0 |

% |

Operating costs and expenses |

|

|

(1,995.1) |

|

|

(1,609.1) |

|

|

(386.0) |

|

24.0 |

% |

Operating income |

|

$ |

1,137.7 |

|

$ |

244.8 |

|

$ |

892.9 |

|

364.7 |

% |

Operating income margin |

|

|

36.3 |

% |

|

13.2 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Volume (Forty-foot equivalent units (FEU), except for automobiles) (1) |

|

|

|

|

|

|

|

|

|

|

|

|

Hawaii containers |

|

|

157,600 |

|

|

145,700 |

|

|

11,900 |

|

8.2 |

% |

Hawaii automobiles |

|

|

46,600 |

|

|

46,600 |

|

|

— |

|

0.0 |

% |

Alaska containers |

|

|

78,200 |

|

|

72,600 |

|

|

5,600 |

|

7.7 |

% |

China containers |

|

|

184,800 |

|

|

118,900 |

|

|

65,900 |

|

55.4 |

% |

Guam containers |

|

|

21,900 |

|

|

18,900 |

|

|

3,000 |

|

15.9 |

% |

Other containers (2) |

|

|

20,200 |

|

|

17,500 |

|

|

2,700 |

|

15.4 |

% |

| (1) | Approximate volumes included for the period are based on the voyage departure date, but revenue and operating income are adjusted to reflect the percentage of revenue and operating income earned during the reporting period for voyages in transit at the end of each reporting period. |

| (2) | Includes containers from services in various islands in Micronesia and the South Pacific, and Okinawa, Japan. |

Ocean Transportation revenue increased $1,278.9 million, or 69.0 percent, during the year ended December 31, 2021, compared with the year ended December 31, 2020. The increase was primarily due to higher revenue in China and Hawaii, higher fuel-related surcharge revenue, and higher revenue in Alaska. The higher revenue in China was primarily due to considerably higher average freight rates and higher volume. The higher revenue in Hawaii and Alaska was primarily the result of higher volume.

On a year-over-year FEU basis, Hawaii container volume increased 8.2 percent primarily due to (a) higher retail and hospitality-related demand due to the reopening of the Hawaii economy compared to the negatively impacted volume in the year ago period as a result of the pandemic and the state’s COVID-19 mitigation efforts and (b) the benefit of an extra week, partially offset by volume associated with the dry-docking of a competitor’s vessel in the second quarter of last year; Alaska volume increased by 7.7 percent due to (i) the increase in volume from the AAX, (ii) higher northbound volume primarily due to higher retail-related demand compared to the negatively impacted volume in the year ago period as a result of the pandemic and the state’s COVID-19 mitigation efforts, (iii) higher southbound volume, and (iv) the benefit of an extra week; China volume was 55.4 percent higher primarily due to (A) incremental volume from the CLX+ service, (B) the addition of volume from the CCX service, (C) higher volume on the CLX service as a result of increased capacity in the tradelane, and (D) the benefit of an extra week; Guam volume was 15.9 percent higher primarily due to higher retail-related demand compared to the negatively impacted volume in the year ago period as a result of the pandemic and the island’s COVID-19 mitigation measures; and Other container volume increased 15.4 percent primarily due to higher volume in Okinawa and the addition of China-Auckland Express volume in the South Pacific.

Ocean Transportation operating income increased $892.9 million during the year ended December 31, 2021, compared with the year ended December 31, 2020. The increase was primarily due to considerably higher average freight rates and higher volume in China, partially offset by higher operating costs and expenses primarily due to the CLX+ and CCX services.

The Company’s SSAT terminal joint venture investment contributed $56.3 million during the year ended December 31, 2021, compared to a contribution of $26.3 million during the year ended December 31, 2020. The increase was primarily driven by higher lift volume and higher other terminal revenue.

4

Logistics — Three months ended December 31, 2021 compared with 2020

|

|

Three Months Ended December 31, |

|

|||||||||

(Dollars in millions) |

|

2021 |

|

2020 |

|

Change |

|

|||||

Logistics revenue |

|

$ |

241.1 |

|

$ |

156.2 |

|

$ |

84.9 |

|

54.4 |

% |

Operating costs and expenses |

|

|

(226.3) |

|

|

(146.6) |

|

|

(79.7) |

|

54.4 |

% |

Operating income |

|

$ |

14.8 |

|

$ |

9.6 |

|

$ |

5.2 |

|

54.2 |

% |

Operating income margin |

|

|

6.1 |

% |

|

6.1 |

% |

|

|

|

|

|

Logistics revenue increased $84.9 million, or 54.4 percent, during the three months ended December 31, 2021, compared with the three months ended December 31, 2020. The increase was primarily due to higher transportation brokerage and supply chain management revenue.

Logistics operating income increased $5.2 million, or 54.2 percent, for the three months ended December 31, 2021, compared with the three months ended December 31, 2020. The increase was primarily due to higher contributions from supply chain management and transportation brokerage.

Logistics — Year ended December 31, 2021 compared with 2020

|

|

Years Ended December 31, |

|

|||||||||

(Dollars in millions) |

|

2021 |

|

2020 |

|

Change |

|

|||||

Logistics revenue |

|

$ |

792.5 |

|

$ |

529.4 |

|

$ |

263.1 |

|

49.7 |

% |

Operating costs and expenses |

|

|

(742.7) |

|

|

(493.9) |

|

|

(248.8) |

|

50.4 |

% |

Operating income |

|

$ |

49.8 |

|

$ |

35.5 |

|

$ |

14.3 |

|

40.3 |

% |

Operating income margin |

|

|

6.3 |

% |

|

6.7 |

% |

|

|

|

|

|

Logistics revenue increased $263.1 million, or 49.7 percent, during the year ended December 31, 2021, compared with the year ended December 31, 2020. The increase was primarily due to higher transportation brokerage and supply chain management revenue.

Logistics operating income increased $14.3 million, or 40.3 percent, for the year ended December 31, 2021, compared with the year ended December 31, 2020. The increase was due primarily to higher contributions from supply chain management, transportation brokerage and freight forwarding.

Liquidity, Cash Flows and Capital Allocation

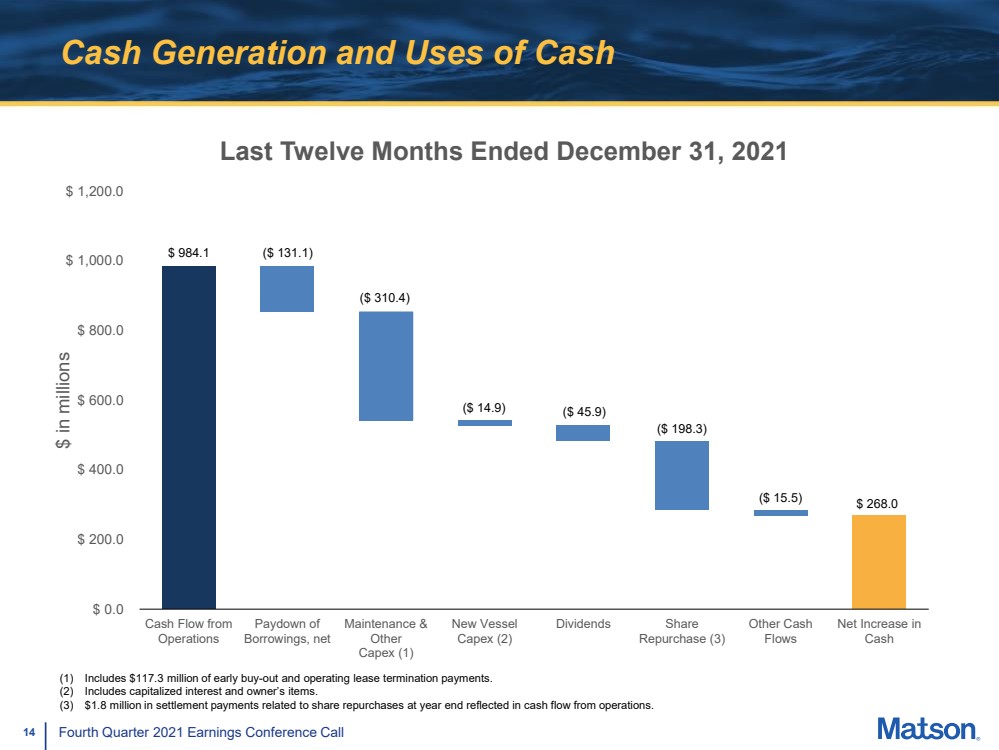

Matson’s Cash and Cash Equivalents increased by $268.0 million from $14.4 million at December 31, 2020 to $282.4 million at December 31, 2021. Matson generated net cash from operating activities of $984.1 million during the year ended December 31, 2021, compared to $429.8 million during the year ended December 31, 2020. Capital expenditures totaled $325.3 million for the year ended December 31, 2021, compared with $192.3 million for the year ended December 31, 2020. The increase in capital expenditures was primarily due to the lease termination payment of $95.8 million for Maunalei and the purchase of equipment to support our new China tradelane services. Total debt decreased by $131.1 million during the year to $629.0 million as of December 31, 2021, of which $564.0 million was classified as long-term debt. As of December 31, 2021 Matson had available borrowings under its revolving credit facility of $642.0 million and a leverage ratio per the amended debt agreements of approximately 0.5x.

During the fourth quarter and full year 2021, Matson repurchased approximately 1.0 million shares and 2.5 million shares for a total cost of $84.5 million and $200.1 million, respectively. From January 3, 2022 through February 16, 2022, Matson repurchased an additional approximately 0.3 million shares for a total cost of $30.5 million. On January 27, 2022 the Company announced an increase of three million shares in its existing share repurchase program.

As previously announced, Matson’s Board of Directors declared a cash dividend of $0.30 per share payable on March 3, 2022 to all shareholders of record as of the close of business on February 10, 2022.

5

Teleconference and Webcast

A conference call is scheduled on February 17, 2022 at 4:30 p.m. ET when Matt Cox, Chairman and Chief Executive Officer, and Joel Wine, Executive Vice President and Chief Financial Officer, will discuss Matson’s fourth quarter results.

Date of Conference Call: |

Thursday, February 17, 2022 |

Scheduled Time: |

4:30 p.m. ET / 1:30 p.m. PT / 11:30 a.m. HT |

Participant Toll Free Dial-In #: |

1-877-312-5524 |

International Dial-In #: |

1-253-237-1144 |

The conference call will be broadcast live along with an additional slide presentation on the Company’s website at www.matson.com, under Investors. A replay of the conference call will be available approximately two hours after the call through February 24, 2022 by dialing 1-855-859-2056 or 1-404-537-3406 and using the conference number 3023619. The slides and audio webcast of the conference call will be archived for one full quarter on the Company's website at www.matson.com, under Investors.

About the Company

Founded in 1882, Matson (NYSE: MATX) is a leading provider of ocean transportation and logistics services. Matson provides a vital lifeline to the domestic non-contiguous economies of Hawaii, Alaska, and Guam, and to other island economies in Micronesia. Matson also operates premium, expedited services from China to Long Beach, California, provides service to Okinawa, Japan and various islands in the South Pacific, and operates an international export service from Dutch Harbor to Asia. The Company's fleet of owned and chartered vessels includes containerships, combination container and roll-on/roll-off ships and custom-designed barges. Matson Logistics, established in 1987, extends the geographic reach of Matson’s transportation network throughout North America. Its integrated, asset-light logistics services include rail intermodal, highway brokerage, warehousing, freight consolidation, Asia supply chain services, and forwarding to Alaska. Additional information about the Company is available at www.matson.com.

GAAP to Non-GAAP Reconciliation

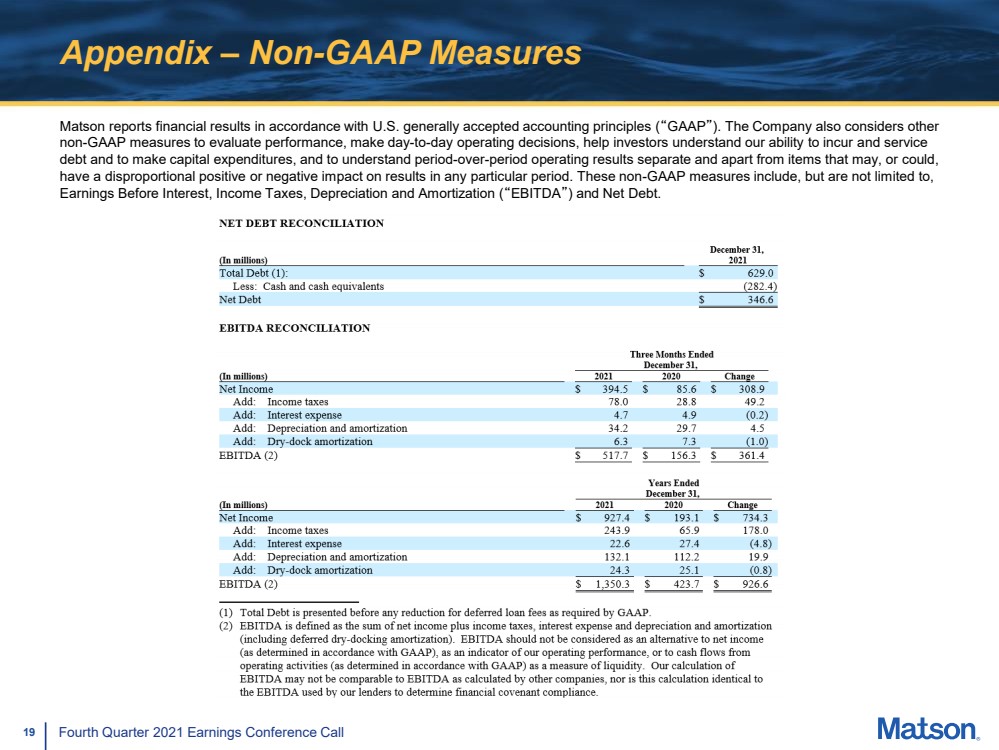

This press release, the Form 8-K and the information to be discussed in the conference call include non-GAAP measures. While Matson reports financial results in accordance with U.S. generally accepted accounting principles (“GAAP”), the Company also considers other non-GAAP measures to evaluate performance, make day-to-day operating decisions, help investors understand our ability to incur and service debt and to make capital expenditures, and to understand period-over-period operating results separate and apart from items that may, or could, have a disproportional positive or negative impact on results in any particular period. These non-GAAP measures include, but are not limited to, Earnings Before Interest, Income Taxes, Depreciation and Amortization (“EBITDA”) and Net Debt.

6

Forward-Looking Statements

Statements in this news release that are not historical facts are “forward-looking statements,” within the meaning of the Private Securities Litigation Reform Act of 1995, including without limitation those statements regarding performance and financial results; capital expenditures; vessel transit times; demand for our China services; duration of the CCX service; supply chain congestion; supply chain constraints; consumption trends; retail and e-commerce demand; inventory restocking conditions; timing and level of industry normalization; tourism and visitor levels; unemployment trends; economic recovery and drivers in Hawaii, Alaska and Guam; volume trends; impact of COVID-19 and its variants; lift activity at SSAT; import volume into U.S. West Coast; the costs and timing of liquefied natural gas installations on certain vessels; refleeting initiatives; cash flow expectations and uses of cash and cash flows; debt reduction; return of capital; capital allocation plans; payback on new equipment purchases; and tax deductions and effective tax rate. These statements involve a number of risks and uncertainties that could cause actual results to differ materially from those contemplated by the relevant forward-looking statement, including but not limited to risks and uncertainties relating to repeal, substantial amendment or waiver of the Jones Act or its application, or our failure to maintain our status as a United States citizen under the Jones Act; regional, national and international economic conditions; new or increased competition or improvements in competitors’ service levels; fuel prices, the availability of required fuels, and our ability to collect fuel-related surcharges; our relationship with vendors, customers and partners and changes in related agreements; the actions of our competitors; our ability to offer a differentiated service in China for which customers are willing to pay a significant premium; the imposition of tariffs or a change in international trade policies; the magnitude and timing of the impact of public health crises, including COVID-19; any unanticipated dry-dock or repair expenses; any delays or cost overruns related to the modernization of terminals; consummating and integrating acquisitions; changes in general economic and/or industry-specific conditions; competition and growth rates within the logistics industry; freight levels and increasing costs and availability of truck capacity or alternative means of transporting freight; changes in relationships with existing truck, rail, ocean and air carriers; changes in customer base due to possible consolidation among customers; conditions in the financial markets; changes in our credit profile and our future financial performance; our ability to obtain future debt financings; continuation of the Title XI and CCF programs; the impact of future and pending legislation and regulations, including regulations related to greenhouse gas emissions and other environmental laws and regulations; government regulations and investigations; relations with our unions; satisfactory negotiation and renewal of expired collective bargaining agreements without significant disruption to Matson’s operations; war, terrorist attacks or other acts of violence; the use of our information technology and communication systems and cybersecurity attacks; and the occurrence of marine accidents, poor weather or natural disasters. These forward-looking statements are not guarantees of future performance. This release should be read in conjunction with our Annual Report on Form 10-K for the year ended December 31, 2020 and our other filings with the SEC through the date of this release, which identify important factors that could affect the forward-looking statements in this release. We do not undertake any obligation to update our forward-looking statements.

7

MATSON, INC. AND SUBSIDIARIES

Condensed Consolidated Statements of Income

(Unaudited)

|

|

Three Months Ended |

|

Years Ended |

||||||||

|

|

December 31, |

|

December 31, |

||||||||

(In millions, except per share amounts) |

|

2021 |

|

2020 |

|

2021 |

|

2020 |

||||

Operating Revenue: |

|

|

|

|

|

|

|

|

|

|

|

|

Ocean Transportation |

|

$ |

1,025.9 |

|

$ |

543.9 |

|

$ |

3,132.8 |

|

$ |

1,853.9 |

Logistics |

|

|

241.1 |

|

|

156.2 |

|

|

792.5 |

|

|

529.4 |

Total Operating Revenue |

|

|

1,267.0 |

|

|

700.1 |

|

|

3,925.3 |

|

|

2,383.3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Costs and Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

Operating costs |

|

|

(748.0) |

|

|

(533.9) |

|

|

(2,557.6) |

|

|

(1,904.3) |

Income from SSAT |

|

|

21.3 |

|

|

10.9 |

|

|

56.3 |

|

|

26.3 |

Selling, general and administrative |

|

|

(64.8) |

|

|

(59.4) |

|

|

(236.5) |

|

|

(225.0) |

Total Costs and Expenses |

|

|

(791.5) |

|

|

(582.4) |

|

|

(2,737.8) |

|

|

(2,103.0) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income |

|

|

475.5 |

|

|

117.7 |

|

|

1,187.5 |

|

|

280.3 |

Interest expense |

|

|

(4.7) |

|

|

(4.9) |

|

|

(22.6) |

|

|

(27.4) |

Other income (expense), net |

|

|

1.7 |

|

|

1.6 |

|

|

6.4 |

|

|

6.1 |

Income before Income Taxes |

|

|

472.5 |

|

|

114.4 |

|

|

1,171.3 |

|

|

259.0 |

Income taxes |

|

|

(78.0) |

|

|

(28.8) |

|

|

(243.9) |

|

|

(65.9) |

Net Income |

|

$ |

394.5 |

|

$ |

85.6 |

|

$ |

927.4 |

|

$ |

193.1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic Earnings Per Share |

|

$ |

9.51 |

|

$ |

1.99 |

|

$ |

21.67 |

|

$ |

4.48 |

Diluted Earnings Per Share |

|

$ |

9.39 |

|

$ |

1.96 |

|

$ |

21.47 |

|

$ |

4.44 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted Average Number of Shares Outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

|

41.5 |

|

|

43.1 |

|

|

42.8 |

|

|

43.1 |

Diluted |

|

|

42.0 |

|

|

43.7 |

|

|

43.2 |

|

|

43.5 |

8

MATSON, INC. AND SUBSIDIARIES

Condensed Consolidated Balance Sheets

(Unaudited)

|

|

December 31, |

|

December 31, |

||

(In millions) |

|

2021 |

|

2020 |

||

ASSETS |

|

|

|

|

|

|

Current Assets: |

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

282.4 |

|

$ |

14.4 |

Other current assets |

|

|

422.1 |

|

|

291.5 |

Total current assets |

|

|

704.5 |

|

|

305.9 |

Long-term Assets: |

|

|

|

|

|

|

Investment in SSAT |

|

|

58.7 |

|

|

48.7 |

Property and equipment, net |

|

|

1,878.3 |

|

|

1,689.9 |

Goodwill |

|

|

327.8 |

|

|

327.8 |

Intangible assets, net |

|

|

181.1 |

|

|

192.0 |

Other long-term assets |

|

|

542.7 |

|

|

336.3 |

Total long-term assets |

|

|

2,988.6 |

|

|

2,594.7 |

Total assets |

|

$ |

3,693.1 |

|

$ |

2,900.6 |

|

|

|

|

|

|

|

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

Current Liabilities: |

|

|

|

|

|

|

Current portion of debt |

|

$ |

65.0 |

|

$ |

59.2 |

Other current liabilities |

|

|

547.4 |

|

|

452.3 |

Total current liabilities |

|

|

612.4 |

|

|

511.5 |

Long-term Liabilities: |

|

|

|

|

|

|

Long-term debt, net of deferred loan fees |

|

|

549.7 |

|

|

685.6 |

Deferred income taxes |

|

|

425.2 |

|

|

389.6 |

Other long-term liabilities |

|

|

438.4 |

|

|

352.7 |

Total long-term liabilities |

|

|

1,413.3 |

|

|

1,427.9 |

|

|

|

|

|

|

|

Total shareholders’ equity |

|

|

1,667.4 |

|

|

961.2 |

Total liabilities and shareholders’ equity |

|

$ |

3,693.1 |

|

$ |

2,900.6 |

9

MATSON, INC. AND SUBSIDIARIES

Condensed Consolidated Statements of Cash Flows

(Unaudited)

|

|

Years Ended December 31, |

|

|||||||

(In millions) |

|

2021 |

|

2020 |

|

2019 |

|

|||

Cash Flows From Operating Activities: |

|

|

|

|

|

|

|

|

|

|

Net income |

|

$ |

927.4 |

|

$ |

193.1 |

|

$ |

82.7 |

|

Reconciling adjustments: |

|

|

|

|

|

|

|

|

|

|

Depreciation and amortization |

|

|

135.9 |

|

|

114.9 |

|

|

100.4 |

|

Amortization of operating lease right of use assets |

|

|

103.3 |

|

|

74.8 |

|

|

60.7 |

|

Deferred income taxes |

|

|

33.2 |

|

|

52.1 |

|

|

23.6 |

|

(Gain) Loss on disposal of property and equipment |

|

|

(0.8) |

|

|

2.8 |

|

|

(1.4) |

|

Share-based compensation expense |

|

|

19.3 |

|

|

18.8 |

|

|

11.3 |

|

Income from SSAT |

|

|

(56.3) |

|

|

(26.3) |

|

|

(20.8) |

|

Distributions from SSAT |

|

|

46.9 |

|

|

55.4 |

|

|

25.2 |

|

Changes in assets and liabilities: |

|

|

|

|

|

|

|

|

|

|

Accounts receivable, net |

|

|

(90.3) |

|

|

(48.0) |

|

|

17.8 |

|

Deferred dry-docking payments |

|

|

(36.3) |

|

|

(16.8) |

|

|

(25.9) |

|

Deferred dry-docking amortization |

|

|

24.3 |

|

|

25.1 |

|

|

34.3 |

|

Prepaid expenses and other assets |

|

|

(48.1) |

|

|

21.9 |

|

|

24.5 |

|

Accounts payable, accruals and other liabilities |

|

|

39.6 |

|

|

44.8 |

|

|

(13.9) |

|

Operating lease liabilities |

|

|

(99.7) |

|

|

(75.9) |

|

|

(59.9) |

|

Other long-term liabilities |

|

|

(14.3) |

|

|

(6.9) |

|

|

(9.8) |

|

Net cash provided by operating activities |

|

|

984.1 |

|

|

429.8 |

|

|

248.8 |

|

|

|

|

|

|

|

|

|

|

|

|

Cash Flows From Investing Activities: |

|

|

|

|

|

|

|

|

|

|

Capitalized vessel construction expenditures |

|

|

(14.9) |

|

|

(87.8) |

|

|

(219.1) |

|

Other capital expenditures |

|

|

(310.4) |

|

|

(104.5) |

|

|

(91.2) |

|

Proceeds from disposal of property and equipment |

|

|

1.9 |

|

|

15.3 |

|

|

3.4 |

|

Cash deposits into Capital Construction Fund |

|

|

(31.2) |

|

|

(132.4) |

|

|

(96.2) |

|

Withdrawals from Capital Construction Fund |

|

|

31.2 |

|

|

132.4 |

|

|

96.2 |

|

Net cash used in investing activities |

|

|

(323.4) |

|

|

(177.0) |

|

|

(306.9) |

|

|

|

|

|

|

|

|

|

|

|

|

Cash Flows From Financing Activities: |

|

|

|

|

|

|

|

|

|

|

Proceeds from issuance of debt |

|

|

— |

|

|

325.5 |

|

|

— |

|

Repayments of debt |

|

|

(59.3) |

|

|

(216.5) |

|

|

(42.1) |

|

Proceeds from revolving credit facility |

|

|

304.3 |

|

|

648.0 |

|

|

622.1 |

|

Repayments of revolving credit facility |

|

|

(376.1) |

|

|

(955.3) |

|

|

(478.0) |

|

Payment of financing costs |

|

|

(3.0) |

|

|

(18.5) |

|

|

— |

|

Proceeds from issuance of common stock |

|

|

— |

|

|

0.1 |

|

|

0.3 |

|

Dividends paid |

|

|

(45.9) |

|

|

(39.2) |

|

|

(37.2) |

|

Repurchase of Matson common stock |

|

|

(198.3) |

|

|

— |

|

|

— |

|

Tax withholding related to net share settlements of restricted stock units |

|

|

(14.4) |

|

|

(5.6) |

|

|

(3.1) |

|

Net cash (used in) provided by financing activities |

|

|

(392.7) |

|

|

(261.5) |

|

|

62.0 |

|

|

|

|

|

|

|

|

|

|

|

|

Net Increase (Decrease) in Cash, Cash Equivalents and Restricted Cash |

|

|

268.0 |

|

|

(8.7) |

|

|

3.9 |

|

Cash, Cash Equivalents and Restricted Cash, Beginning of the Year |

|

|

19.7 |

|

|

28.4 |

|

|

24.5 |

|

Cash, Cash Equivalents and Restricted Cash, End of the Year |

|

$ |

287.7 |

|

$ |

19.7 |

|

$ |

28.4 |

|

|

|

|

|

|

|

|

|

|

|

|

Reconciliation of Cash, Cash Equivalents, and Restricted Cash, at End of the Year: |

|

|

|

|

|

|

|

|

|

|

Cash and Cash Equivalents |

|

$ |

282.4 |

|

$ |

14.4 |

|

$ |

21.2 |

|

Restricted Cash |

|

|

5.3 |

|

|

5.3 |

|

|

7.2 |

|

Total Cash, Cash Equivalents and Restricted Cash, End of the Year |

|

$ |

287.7 |

|

$ |

19.7 |

|

$ |

28.4 |

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Cash Flow Information: |

|

|

|

|

|

|

|

|

|

|

Interest paid, net of capitalized interest |

|

$ |

19.3 |

|

$ |

26.2 |

|

$ |

22.0 |

|

Income tax paid, net of income tax refunds |

|

$ |

241.6 |

|

$ |

(16.1) |

|

$ |

(24.2) |

|

|

|

|

|

|

|

|

|

|

|

|

Non-cash Information: |

|

|

|

|

|

|

|

|

|

|

Capital expenditures included in accounts payable, accruals and other liabilities |

|

$ |

6.4 |

|

$ |

24.7 |

|

$ |

8.5 |

|

10

MATSON, INC. AND SUBSIDIARIES

Total Debt to Net Debt and Net Income to EBITDA Reconciliations

(Unaudited)

NET DEBT RECONCILIATION

|

|

December 31, |

|

(In millions) |

|

2021 |

|

Total Debt (1): |

|

$ |

629.0 |

Less: Cash and cash equivalents |

|

|

(282.4) |

Net Debt |

|

$ |

346.6 |

EBITDA RECONCILIATION

|

|

Three Months Ended |

|

|||||||

|

|

December 31, |

|

|||||||

(In millions) |

|

2021 |

|

2020 |

|

Change |

|

|||

Net Income |

|

$ |

394.5 |

|

$ |

85.6 |

|

$ |

308.9 |

|

Add: Income taxes |

|

|

78.0 |

|

|

28.8 |

|

|

49.2 |

|

Add: Interest expense |

|

|

4.7 |

|

|

4.9 |

|

|

(0.2) |

|

Add: Depreciation and amortization |

|

|

34.2 |

|

|

29.7 |

|

|

4.5 |

|

Add: Dry-dock amortization |

|

|

6.3 |

|

|

7.3 |

|

|

(1.0) |

|

EBITDA (2) |

|

$ |

517.7 |

|

$ |

156.3 |

|

$ |

361.4 |

|

|

|

Years Ended |

|

|||||||

|

|

December 31, |

|

|||||||

(In millions) |

|

2021 |

|

2020 |

|

Change |

|

|||

Net Income |

|

$ |

927.4 |

|

$ |

193.1 |

|

$ |

734.3 |

|

Add: Income taxes |

|

|

243.9 |

|

|

65.9 |

|

|

178.0 |

|

Add: Interest expense |

|

|

22.6 |

|

|

27.4 |

|

|

(4.8) |

|

Add: Depreciation and amortization |

|

|

132.1 |

|

|

112.2 |

|

|

19.9 |

|

Add: Dry-dock amortization |

|

|

24.3 |

|

|

25.1 |

|

|

(0.8) |

|

EBITDA (2) |

|

$ |

1,350.3 |

|

$ |

423.7 |

|

$ |

926.6 |

|

| (1) | Total Debt is presented before any reduction for deferred loan fees as required by GAAP. |

| (2) | EBITDA is defined as the sum of net income plus income taxes, interest expense and depreciation and amortization (including deferred dry-docking amortization). EBITDA should not be considered as an alternative to net income (as determined in accordance with GAAP), as an indicator of our operating performance, or to cash flows from operating activities (as determined in accordance with GAAP) as a measure of liquidity. Our calculation of EBITDA may not be comparable to EBITDA as calculated by other companies, nor is this calculation identical to the EBITDA used by our lenders to determine financial covenant compliance. |

11

Exhibit 99.2

|

1 Fourth Quarter 2021 Earnings Conference Call Fourth Quarter 2021 Earnings Conference Call February 17, 2022 |

|

2 Fourth Quarter 2021 Earnings Conference Call Forward - Looking Statements Statements made during this presentation that set forth expectations, predictions, projections or are about future events are based on facts and situations that are known to us as of February 17, 2022. We believe that our expectations and assumptions are reasonable. Actual results may differ materially, due to risks and uncertainties, such as those described on pages 12 - 21 of our Form 10 - K filed on February 26, 2021 and other subsequent filings by Matson with the SEC. Statements made during this presentation are not guarantees of future performance. We do not undertake any obligation to update our forward - looking statements. |

|

3 Fourth Quarter 2021 Earnings Conference Call Opening Remarks • Recap of Matson’s 4Q21 results: – Matson finished off a strong year with continued improvement in economic and business trends in our markets driving solid performance in both Ocean Transportation and Logistics – Ocean Transportation: • China strength – continued strong demand for our expedited ocean services • In Hawaii, Alaska and Guam, continued to see strong demand with higher year - over - year volumes, including the benefit of a 53 rd week, compared to the largely pandemic - reduced volumes in 4Q20 – Logistics: • Continued to see elevated goods consumption, inventory restocking and favorable supply and demand fundamentals in our core markets • Matson is focused on reliable services and helping customers during this difficult period of supply chain congestion |

|

4 Fourth Quarter 2021 Earnings Conference Call Hawaii Service Fourth Quarter 2021 Performance • Container volume increased 10.4% YoY – Higher retail and hospitality - related demand compared to 4Q20, which was negatively impacted by state’s COVID - 19 mitigation efforts – Includes benefit of extra week in 4Q21 – Continued rebound in tourism and Hawaii economy despite slowdown early in the quarter due to state’s efforts to address COVID - 19 Delta variant • 4Q21 volume 11.3% higher than 4Q19 volume – Includes benefit of extra week in 4Q21 Container Volume (FEU Basis) 25,000 27,000 29,000 31,000 33,000 35,000 37,000 39,000 41,000 Q1 Q2 Q3 Q4 2020 2021 Note : 2Q20 volume figure includes volume related to Pasha’s vessel dry - docking. 4Q21 volume figure includes the benefit of a 53 rd week. 10.4% Full Year 2021 Performance • Container volume increased 8.2% YoY – Higher retail and hospitality - related demand due to reopening of Hawaii economy compared to pandemic - reduced volume in FY 2020 – Includes benefit of extra week in 4Q21 – Partially offset by volume from Pasha in 2Q20 due in part to the dry - docking of one of its vessels |

|

5 Fourth Quarter 2021 Earnings Conference Call Hawaii Service – Current Business Trends Select Hawaii Economic Indicators (1) Source: http://files.hawaii.gov/dbedt/economic/data_reports/mei/2021 - 12 - state.xls (2) Source: https://uhero.hawaii.edu/wp - content/uploads/2021/12/21Q4_Forecast.pdf UHERO Projections (2) 2019 2020 2021 2022P Real GDP 0.0% (11.1)% 5.8% 2.7% Construction Jobs Growth 0.2% (2.4)% 1.8% 1.4% Population Growth (0.1)% (0.3)% (0.1)% (0.2)% Unemployment Rate 2.5% 11.8% 7.7% 5.4% Visitor Arrivals (‘000s) % change 10,385.8 5.0% 2,708.3 (73.9)% 6,749.2 149.2% 8,286.5 22.8% • Cautiously optimistic on further economic recovery in Hawaii in 2022 – Improving unemployment rate – Increasing tourism traffic, including international visitors later in the year – Further waves of COVID - 19 variants present possibility of economic slowdowns • December UHERO forecast reflects near - term negative impact from Omicron variant – Full return to pre - pandemic conditions may take several more years • January 2022 westbound container volume was approximately flat YoY – Omicron variant negatively affected tourism, which led to a softening in demand for retail - and hospitality - related goods 0 100 200 300 400 500 600 700 800 900 1,000 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0% 11.0% Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Visitor Arrivals (‘000s) Unemployment Rate Unemployment Rate and Visitor Arrivals Unemployment Rate (1) Visitor Arrivals (1) |

|

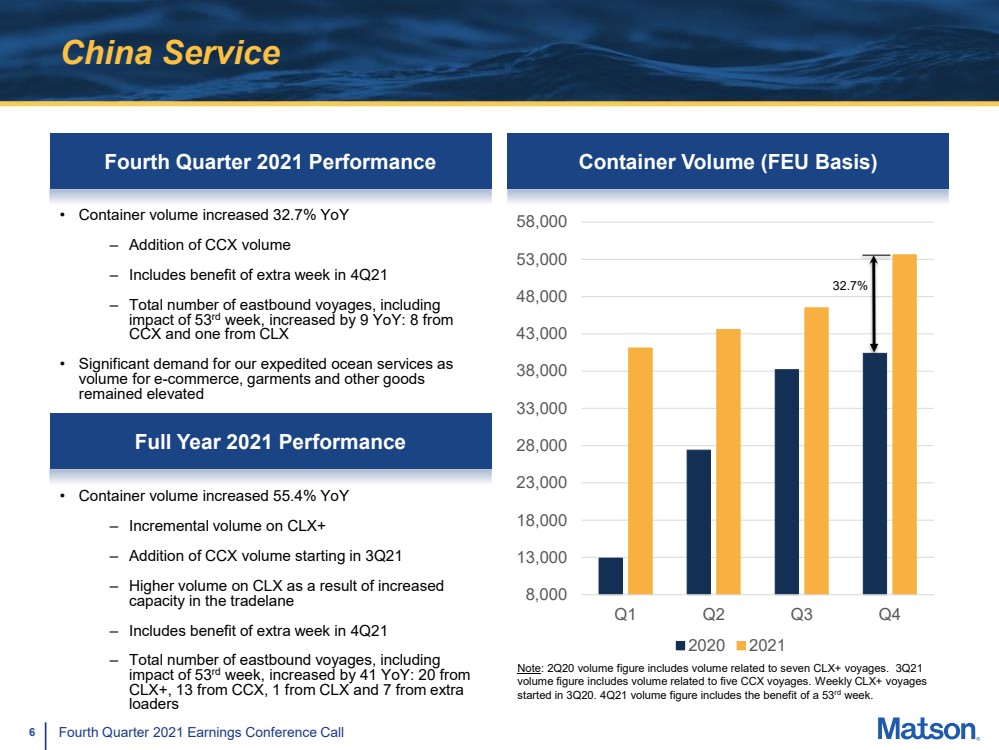

6 Fourth Quarter 2021 Earnings Conference Call China Service Fourth Quarter 2021 Performance Container Volume (FEU Basis) 8,000 13,000 18,000 23,000 28,000 33,000 38,000 43,000 48,000 53,000 58,000 Q1 Q2 Q3 Q4 2020 2021 Note : 2Q20 volume figure includes volume related to seven CLX+ voyages. 3Q21 volume figure includes volume related to five CCX voyages. Weekly CLX+ voyages started in 3Q20. 4Q21 volume figure includes the benefit of a 53 rd week. 32.7% • Container volume increased 32.7% YoY – Addition of CCX volume – Includes benefit of extra week in 4Q21 – Total number of eastbound voyages, including impact of 53 rd week, increased by 9 YoY: 8 from CCX and one from CLX • Significant demand for our expedited ocean services as volume for e - commerce, garments and other goods remained elevated Full Year 2021 Performance • Container volume increased 55.4% YoY – Incremental volume on CLX+ – Addition of CCX volume starting in 3Q21 – Higher volume on CLX as a result of increased capacity in the tradelane – Includes benefit of extra week in 4Q21 – Total number of eastbound voyages, including impact of 53 rd week, increased by 41 YoY: 20 from CLX+, 13 from CCX, 1 from CLX and 7 from extra loaders |

|

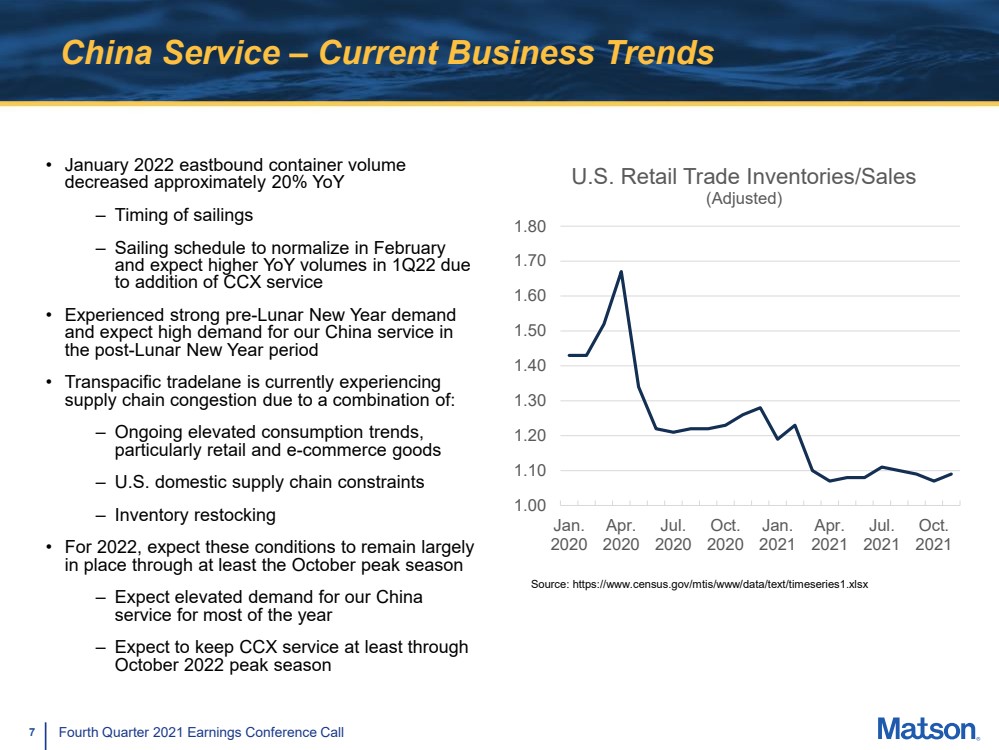

7 Fourth Quarter 2021 Earnings Conference Call China Service – Current Business Trends 1.00 1.10 1.20 1.30 1.40 1.50 1.60 1.70 1.80 Jan. 2020 Apr. 2020 Jul. 2020 Oct. 2020 Jan. 2021 Apr. 2021 Jul. 2021 Oct. 2021 U.S. Retail Trade Inventories/Sales (Adjusted) Source: https://www.census.gov/mtis/www/data/text/timeseries1.xlsx • January 2022 eastbound container volume decreased approximately 20% YoY – Timing of sailings – Sailing schedule to normalize in February and expect higher YoY volumes in 1Q22 due to addition of CCX service • Experienced strong pre - Lunar New Year demand and expect high demand for our China service in the post - Lunar New Year period • Transpacific tradelane is currently experiencing supply chain congestion due to a combination of: – Ongoing elevated consumption trends, particularly retail and e - commerce goods – U.S. domestic supply chain constraints – Inventory restocking • For 2022, expect these conditions to remain largely in place through at least the October peak season – Expect elevated demand for our China service for most of the year – Expect to keep CCX service at least through October 2022 peak season |

|

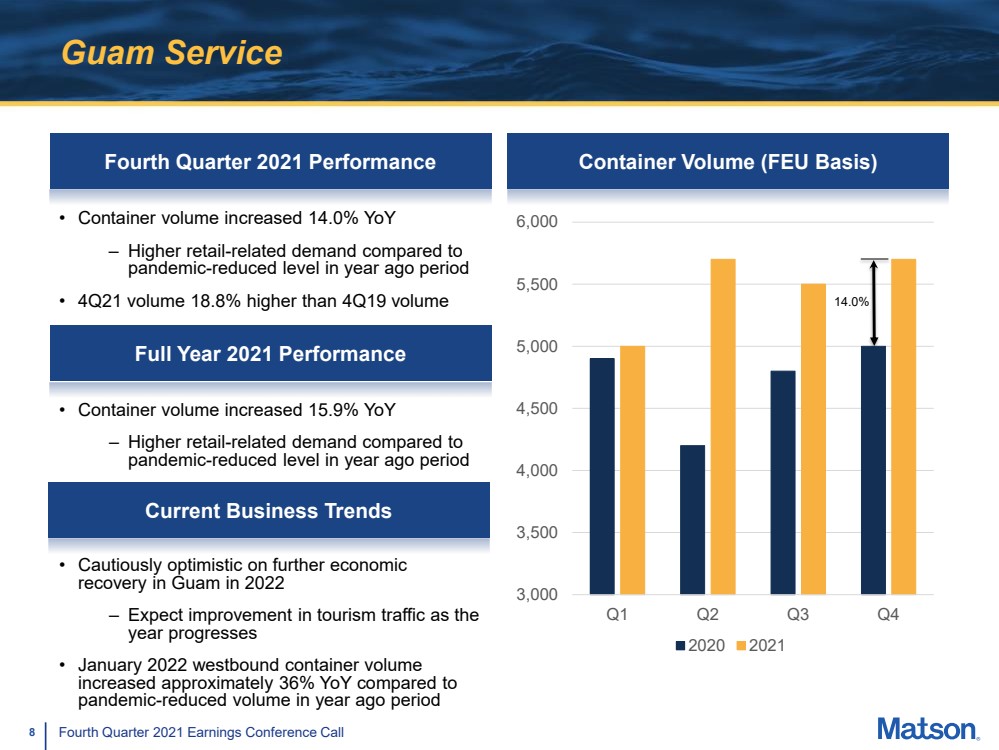

8 Fourth Quarter 2021 Earnings Conference Call Guam Service Fourth Quarter 2021 Performance Container Volume (FEU Basis) 3,000 3,500 4,000 4,500 5,000 5,500 6,000 Q1 Q2 Q3 Q4 2020 2021 14.0% • Container volume increased 14.0% YoY – Higher retail - related demand compared to pandemic - reduced level in year ago period • 4Q21 volume 18.8% higher than 4Q19 volume Current Business Trends • Cautiously optimistic on further economic recovery in Guam in 2022 – Expect improvement in tourism traffic as the year progresses • January 2022 westbound container volume increased approximately 36% YoY compared to pandemic - reduced volume in year ago period Full Year 2021 Performance • Container volume increased 15.9% YoY – Higher retail - related demand compared to pandemic - reduced level in year ago period |

|

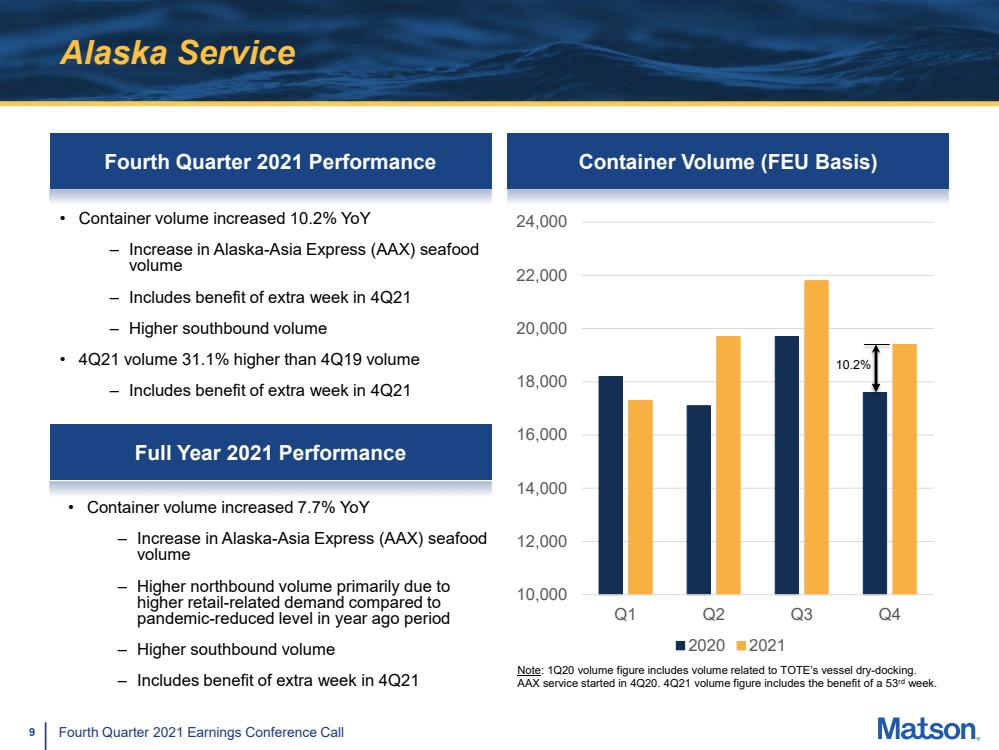

9 Fourth Quarter 2021 Earnings Conference Call Alaska Service Fourth Quarter 2021 Performance • Container volume increased 10.2% YoY – Increase in Alaska - Asia Express (AAX) seafood volume – Includes benefit of extra week in 4Q21 – Higher southbound volume • 4Q21 volume 31.1% higher than 4Q19 volume – Includes benefit of extra week in 4Q21 Container Volume (FEU Basis) 10,000 12,000 14,000 16,000 18,000 20,000 22,000 24,000 Q1 Q2 Q3 Q4 2020 2021 10.2% Note : 1Q20 volume figure includes volume related to TOTE’s vessel dry - docking. AAX service started in 4Q20. 4Q21 volume figure includes the benefit of a 53 rd week. Full Year 2021 Performance • Container volume increased 7.7% YoY – Increase in Alaska - Asia Express (AAX) seafood volume – Higher northbound volume primarily due to higher retail - related demand compared to pandemic - reduced level in year ago period – Higher southbound volume – Includes benefit of extra week in 4Q21 |

|

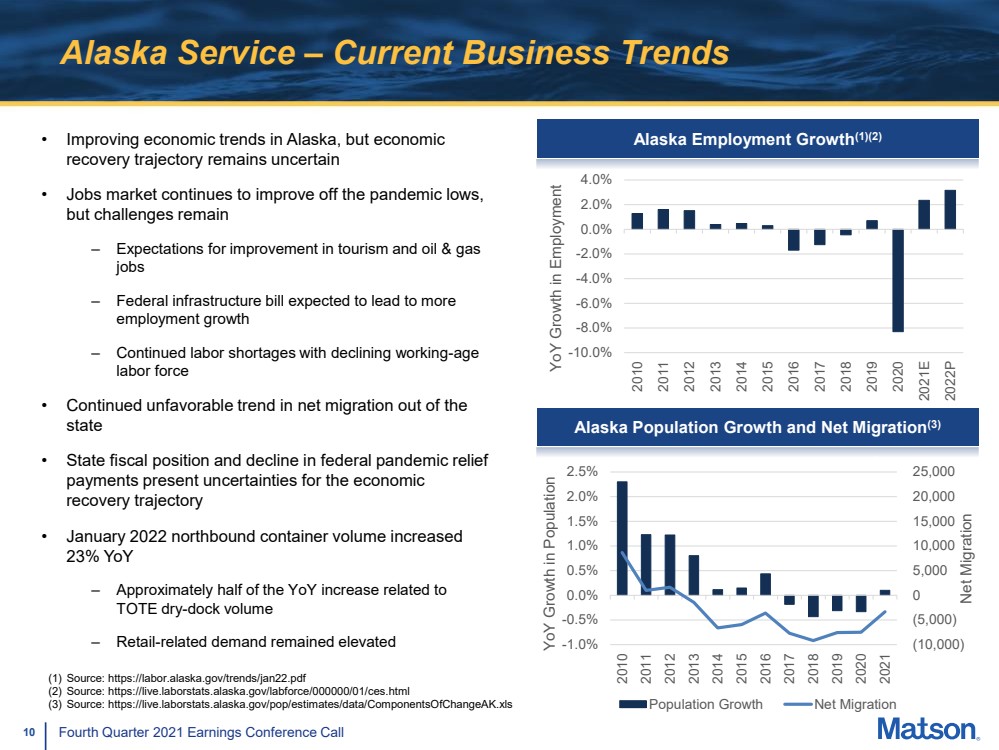

10 Fourth Quarter 2021 Earnings Conference Call Alaska Service – Current Business Trends • Improving economic trends in Alaska, but economic recovery trajectory remains uncertain • Jobs market continues to improve off the pandemic lows, but challenges remain – Expectations for improvement in tourism and oil & gas jobs – Federal infrastructure bill expected to lead to more employment growth – Continued labor shortages with declining working - age labor force • Continued unfavorable trend in net migration out of the state • State fiscal position and decline in federal pandemic relief payments present uncertainties for the economic recovery trajectory • January 2022 northbound container volume increased 23% YoY – Approximately half of the YoY increase related to TOTE dry - dock volume – Retail - related demand remained elevated -10.0% -8.0% -6.0% -4.0% -2.0% 0.0% 2.0% 4.0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021E 2022P YoY Growth in Employment Alaska Employment Growth (1)(2) (1) Source: https://labor.alaska.gov/trends/jan22.pdf (2) Source: https://live.laborstats.alaska.gov/labforce/000000/01/ces.html (3) Source: https://live.laborstats.alaska.gov/pop/estimates/data/ComponentsOfChangeAK.xls Alaska Population Growth and Net Migration (3) (10,000) (5,000) 0 5,000 10,000 15,000 20,000 25,000 -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Net Migration YoY Growth in Population Population Growth Net Migration |

|

11 Fourth Quarter 2021 Earnings Conference Call SSAT Joint Venture Fourth Quarter 2021 Performance Equity in Income of Joint Venture $ 0.0 $ 5.0 $ 10.0 $ 15.0 $ 20.0 $ 25.0 Q1 Q2 Q3 Q4 $ in millions 2020 2021 Current Business Trends • Terminal joint venture contribution was $21.3 million; YoY change of $10.4 million – Primarily due to higher other terminal revenue and higher revenue per lift • Continue to see elevated import volume into U.S. West Coast Full Year 2021 Performance • Terminal joint venture contribution was $56.3 million; YoY change of $30.0 million – Primarily due to higher lift volume and higher other terminal revenue |

|

12 Fourth Quarter 2021 Earnings Conference Call Matson Logistics Fourth Quarter 2021 Performance Operating Income $ 0.0 $ 2.0 $ 4.0 $ 6.0 $ 8.0 $ 10.0 $ 12.0 $ 14.0 $ 16.0 $ 18.0 Q1 Q2 Q3 Q4 $ in millions 2020 2021 • Operating income of $49.8 million; YoY change of $14.3 million – Higher contributions from supply chain management, transportation brokerage and freight forwarding Current Business Trends • Some business lines continue to benefit from elevated container volumes into Southern California Full Year 2021 Performance • Operating income of $14.8 million; YoY change of $5.2 million – Higher contributions from supply chain management and transportation brokerage • Benefitted from elevated goods consumption and inventory restocking and favorable supply and demand fundamentals in core markets |

|

13 Fourth Quarter 2021 Earnings Conference Call Financial Results – Summary Income Statement See the Addendum for a reconciliation of GAAP to non - GAAP Financial Metrics. (1) The 4Q21 income taxes benefited from a deduction related to foreign - derived intangible income (“FDII”) under section 250 of the Internal Revenue Code. Matson benefits from a FDII deduction as it relates to U.S. corporations that generate income from services provided to forei gn countries. |

|

14 Fourth Quarter 2021 Earnings Conference Call Cash Generation and Uses of Cash $ 0.0 $ 200.0 $ 400.0 $ 600.0 $ 800.0 $ 1,000.0 $ 1,200.0 Cash Flow from Operations Paydown of Borrowings, net Maintenance & Other Capex (1) New Vessel Capex (2) Dividends Share Repurchase (3) Other Cash Flows Net Increase in Cash $ in millions Last Twelve Months Ended December 31, 2021 $ 984.1 ($ 131.1) ($ 310.4) ($ 14.9) ($ 45.9) $ 268.0 ($ 15.5) (1) Includes $117.3 million of early buy - out and operating lease termination payments. (2) Includes capitalized interest and owner’s items. (3) $1.8 million in settlement payments related to share repurchases at year end reflected in cash flow from operations. ($ 198.3) |

|

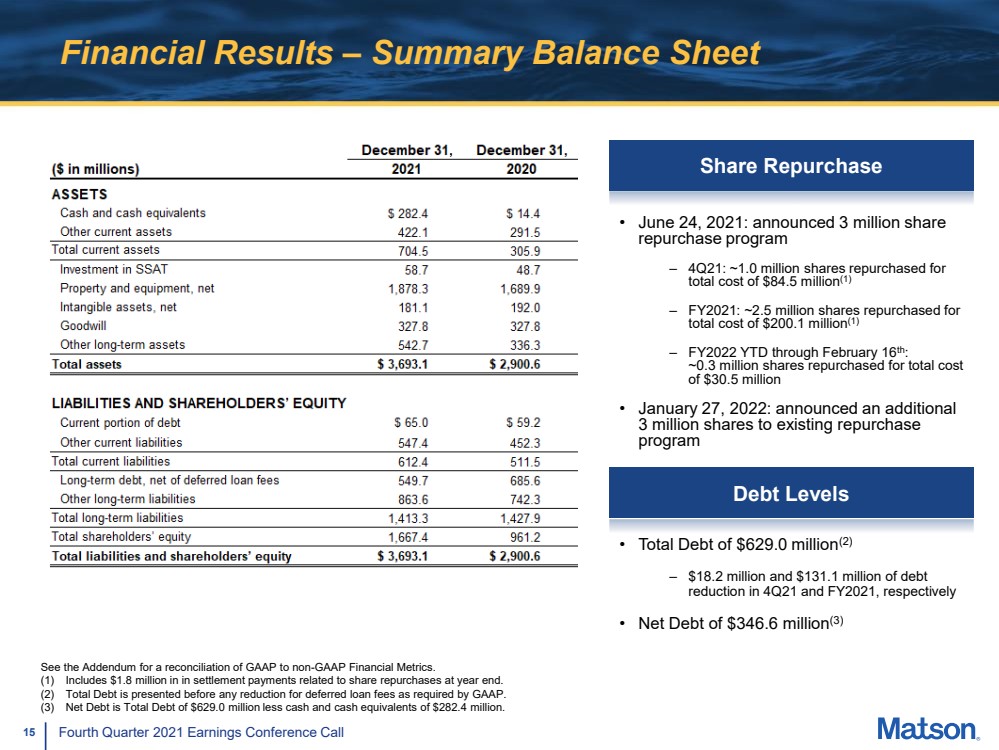

15 Fourth Quarter 2021 Earnings Conference Call Financial Results – Summary Balance Sheet • Total Debt of $629.0 million (2) – $18.2 million and $131.1 million of debt reduction in 4Q21 and FY2021, respectively • Net Debt of $346.6 million (3) See the Addendum for a reconciliation of GAAP to non - GAAP Financial Metrics. (1) Includes $1.8 million in in settlement payments related to share repurchases at year end. (2) Total Debt is presented before any reduction for deferred loan fees as required by GAAP. (3) Net Debt is Total Debt of $629.0 million less cash and cash equivalents of $282.4 million. Debt Levels Share Repurchase • June 24, 2021: announced 3 million share repurchase program – 4Q21: ~1.0 million shares repurchased for total cost of $84.5 million (1) – FY2021: ~2.5 million shares repurchased for total cost of $200.1 million (1) – FY2022 YTD through February 16 th : ~0.3 million shares repurchased for total cost of $30.5 million • January 27, 2022: announced an additional 3 million shares to existing repurchase program |

|

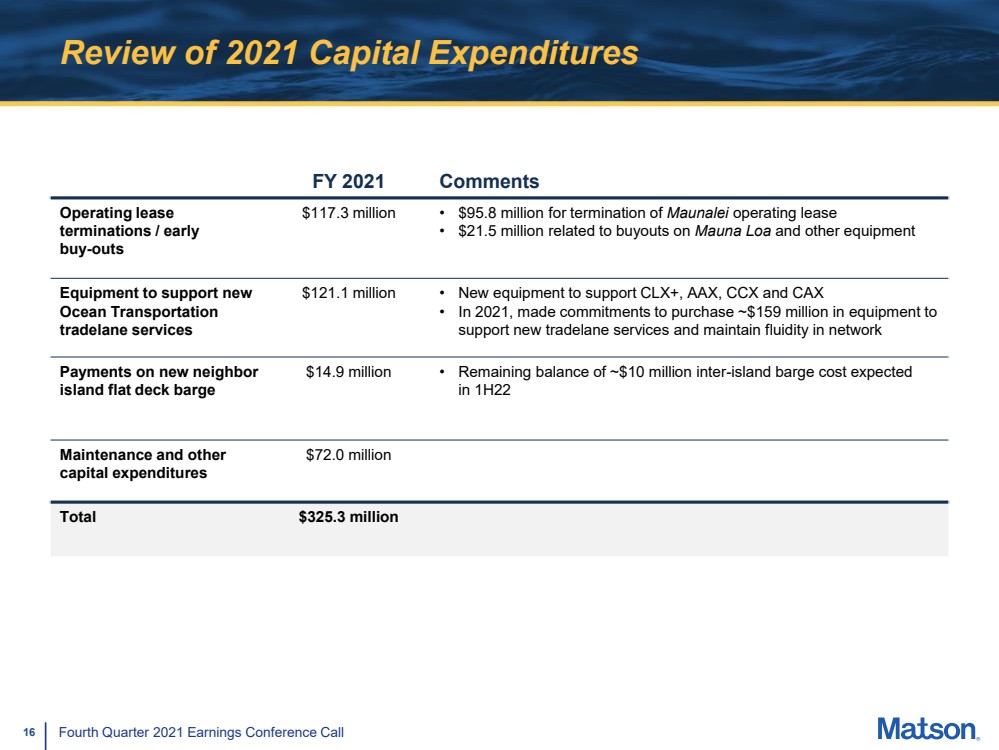

16 Fourth Quarter 2021 Earnings Conference Call Review of 2021 Capital Expenditures FY 2021 Comments Operating lease terminations / early buy - outs $117.3 million • $95.8 million for termination of Maunalei operating l ease • $21.5 million related to buyouts on Mauna Loa and other equipment Equipment to support new Ocean Transportation tradelane services $121.1 million • New equipment to support CLX+, AAX, CCX and CAX • In 2021, made commitments to purchase ~$159 million in equipment to support new tradelane services and maintain fluidity in network Payments on new neighbor island flat deck barge $14.9 million • Remaining balance of ~$10 million inter - island barge cost expected in 1H22 Maintenance and other capital expenditures $72.0 million Total $325.3 million |

|

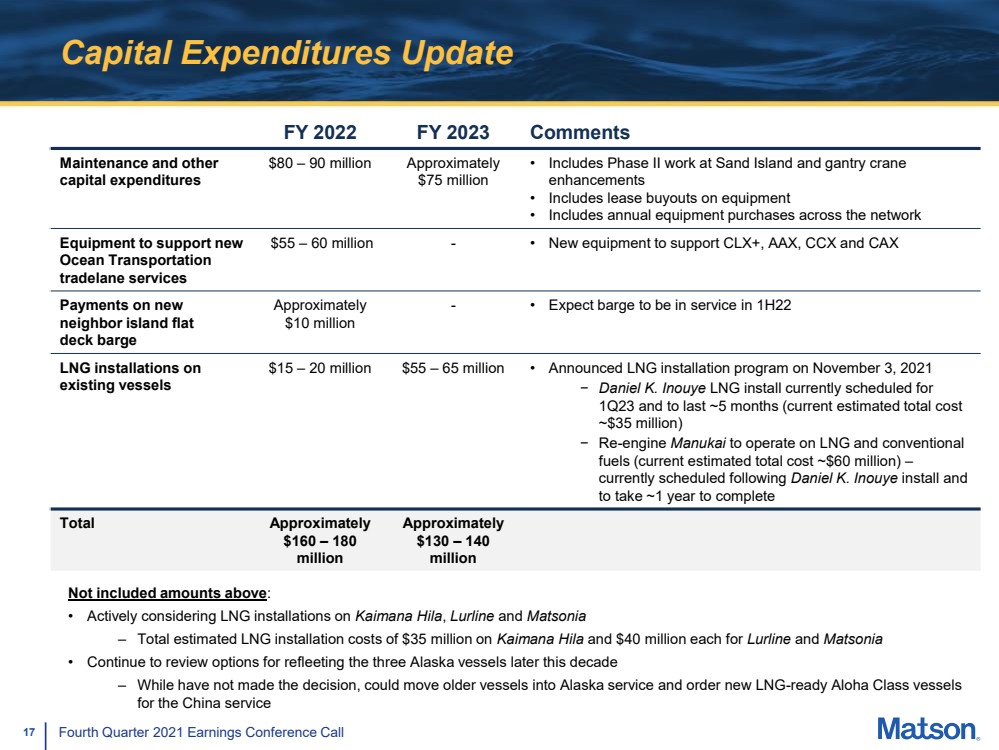

17 Fourth Quarter 2021 Earnings Conference Call Capital Expenditures Update FY 2022 FY 2023 Comments Maintenance and other capital expenditures $80 – 90 million Approximately $75 million • Includes Phase II work at Sand Island and gantry crane enhancements • Includes lease buyouts on equipment • Includes annual equipment purchases across the network Equipment to support new Ocean Transportation tradelane services $55 – 60 million - • New equipment to support CLX+, AAX, CCX and CAX Payments on new neighbor island flat deck barge Approximately $10 million - • Expect barge to be in service in 1H22 LNG installations on existing vessels $15 – 20 million $55 – 65 million • Announced LNG installation program on November 3, 2021 − Daniel K. Inouye LNG install currently scheduled for 1Q23 and to last ~5 months (current estimated total cost ~$35 million) − Re - engine Manukai to operate on LNG and conventional fuels (current estimated total cost ~$60 million) – currently scheduled following Daniel K. Inouye install and to take ~1 year to complete Total Approximately $160 – 180 million Approximately $130 – 140 million Not included amounts above : • Actively considering LNG installations on Kaimana Hila , Lurline and Matsonia – Total estimated LNG installation costs of $35 million on Kaimana Hila and $40 million each for Lurline and Matsonia • Continue to review options for refleeting the three Alaska vessels later this decade – While have not made the decision, could move older vessels into Alaska service and order new LNG - ready Aloha Class vessels for the China service |

|

18 Fourth Quarter 2021 Earnings Conference Call Appendix |

|

19 Fourth Quarter 2021 Earnings Conference Call Appendix – Non - GAAP Measures Matson reports financial results in accordance with U.S. generally accepted accounting principles ( “ GAAP ” ). The Company also considers other non - GAAP measures to evaluate performance, make day - to - day operating decisions, help investors understand our ability to incur a nd service debt and to make capital expenditures, and to understand period - over - period operating results separate and apart from items that may, or could, have a disproportional positive or negative impact on results in any particular period. These non - GAAP measures include, but are not limited to, Earnings Before Interest, Income Taxes, Depreciation and Amortization ( “ EBITDA ” ) and Net Debt. |