UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 Or 15d-16 Of

The Securities Exchange Act Of 1934

For the month of February 2024

Commission File Number: 001-14950

ULTRAPAR HOLDINGS INC.

(Translation of Registrant’s Name into English)

Brigadeiro Luis Antonio Avenue, 1343, 9th Floor

São Paulo, SP, Brazil 01317-910

(Address of Principal Executive Offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ____X____ Form 40-F ________

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ________ No ____X____

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ________ No ____X____

| 1 |

ULTRAPAR HOLDINGS INC.

TABLE OF CONTENTS

ITEM

| 2 |

| Ultrapar Participações S.A. and Subsidiaries |  |

| 4 |

(Convenience Translation into English from the Original Previously Issued in Portuguese)

Ultrapar Participações S.A.

Individual and Consolidated Financial Statements

for the Year Ended December 31, 2023

and Independent Auditor’s Report

Deloitte Touche Tohmatsu Auditores Independentes Ltda.

|

Deloitte Touche Tohmatsu Dr. Chucri Zaidan Avenue, 1.240 - 4th to 12th floors - Golden Tower 04711-130 - São Paulo - SP Brazil

Tel.: + 55 (11) 5186-1000 Fax: + 55 (11) 5181-2911 www.deloitte.com.br |

(Convenience Translation into English from the Original Previously Issued in Portuguese)

INDEPENDENT AUDITOR’S REPORT ON THE INDIVIDUAL AND CONSOLIDATED FINANCIAL STATEMENTS

To the Shareholders, Directors and Management of

Ultrapar Participações S.A.

Opinion

We have audited the accompanying individual and consolidated financial statements of Ultrapar Participações S.A. (“Company”), identified as Parent and Consolidated, respectively, which comprise the individual and consolidated statements of financial position as at December 31, 2023, and the related individual and consolidated statements of income, of comprehensive income, of changes in equity and of cash flows for the year then ended, and notes to the financial statements, including material accounting policies.

In our opinion, the individual and consolidated financial statements referred to above present fairly, in all material respects, the individual and consolidated financial position of Ultrapar Participações S.A. as at December 31, 2023, and its individual and consolidated financial performance and its individual and consolidated cash flows for the year then ended in accordance with accounting practices adopted in Brazil and International Financial Reporting Standards (“IFRSs”) issued by the International Accounting Standards Board (“IASB”).

Basis for opinion

We conducted our audit in accordance with Brazilian and International Standards on Auditing. Our responsibilities under those standards are further described in the “Auditor’s responsibilities for the audit of the individual and consolidated financial statements” section of our report. We are independent of the Company and its subsidiaries in accordance with the relevant ethical requirements set out in the Code of Ethics for Professional Accountants and the professional standards issued by the Brazilian Federal Accounting Council (“CFC”), and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Key audit matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the individual and consolidated financial statements of the current year. These matters were addressed in the context of our audit of the individual and consolidated financial statements as a whole, and in forming our opinion thereon, and, therefore, we do not provide a separate opinion on these matters.

|

|

|

Recoverability of tax credits (PIS and COFINS)

Critical Audit Matter Description

As disclosed in the footnote nº 7.a.2, as of December 31, 2023, the Company carries tax credits related to PIS and COFINS (Federal Value Added Taxes) at R$ 2,761,262. These tax credits may be utilized for offset against other federal taxes or may be refunded by the Federal Revenue Service through requests if they are filed within the applicable regulatory period.

The recognition and measurement of PIS and COFINS credits for the Company’s subsidiary Ipiranga Produtos de Petróleo S.A. require a high degree of judgment by Management, given the complexity underlying the interpretations of the applicable tax laws, as well as the uncertainties involving the expected realization of amounts and considerable efforts made by Management in preparing the calculations used to measure and to recognize those tax credits.

Such matter was considered a critical audit matter due to (i) the significance of the amounts involved, and (ii) the complexity and high degree of judgment involved in assessing and challenging Management’s assumptions and judgments regarding the realizability of tax credits.

How the Critical Audit Matter Was Addressed in the Audit

Our audit procedures related to the recoverability of tax credits included the following, among others: (i) we evaluated and tested the design and implementation of internal controls over the method, assumptions and data used in the projections to support the realization of the tax credits; (ii) the analysis, challenges and tests on the methodology and assumptions used for the projections that support the realization of the credits, including inquiries to the business, treasury and controllership areas about the assumptions and projections that support the projected results and historical performance, retrospective analysis of results, history of offsets and tax refunds, including the evaluation of contradictory evidence; (iii) inquiries to the Management; and (vi) the analysis and evaluation of the disclosures made in the individual and consolidated financial statements.

Based on the evidence obtained from performing our procedures described above, we consider that the accounting treatment applied to the aforesaid transaction and related disclosures made in the notes are acceptable in the context of the individual and consolidated financial statements taken as a whole.

Other matters

Statements of value added

The individual and consolidated statements of value added (“DVA”) for the year ended December 31, 2023, prepared under the responsibility of the Company’s Management and disclosed as supplemental information for purposes of the IFRSs, were subject to audit procedures performed together with the audit of the Company’s financial statements. In forming our opinion, we assess whether these individual and consolidated statements of value added are reconciled with the financial statements and accounting records, as applicable, and whether their form and content are in accordance with the criteria set out in technical pronouncement CPC 09 - Statement of Value Added. In our opinion, these statements of value added were appropriately prepared, in all material respects, in accordance with the criteria set out in such technical pronouncement and are consistent in relation to the individual and consolidated financial statements taken as a whole.

Other information accompanying the individual and consolidated financial statements and the independent auditor’s report

Management is responsible for the other information. The other information comprises the Management Report.

Our opinion on the individual and consolidated financial statements does not cover the Management Report and we do not express any form of audit conclusion thereon.

In connection with our audit of the individual and consolidated financial statements, our responsibility is to read the Management Report and, in doing so, consider whether this report is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement in the Management Report, we are required to report that fact. We have nothing to report in this regard.

|

|

|

Responsibilities of Management and those charged with governance for the individual and consolidated financial statements

Management is responsible for the preparation and fair presentation of the individual and consolidated financial statements in accordance with accounting practices adopted in Brazil and International Financial Reporting Standards (“IFRSs”), issued by the IASB, and for such internal control as Management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the individual and consolidated financial statements, Management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless Management either intends to liquidate the Company and its subsidiaries or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s and its subsidiaries’ financial reporting process.

Auditor’s responsibilities for the audit of the individual and consolidated financial statements

Our objectives are to obtain reasonable assurance about whether the individual and consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Brazilian and International Standards on Auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with Brazilian and International Standards on Auditing, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

|

|

|

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide those charged with governance with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and matters that may reasonably be thought to bear on our independence, and, when applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

The accompanying individual and consolidated financial statements have been translated into English for the convenience of readers outside Brazil.

São Paulo, February 28, 2024

| DELOITTE TOUCHE TOHMATSU | Daniel Corrêa de Sá |

| Auditores Independentes Ltda. | Engagement Partner |

| Ultrapar Participações S.A. and Subsidiaries | |

| Statements of financial position | |

| As of December 31, 2023 and 2022 | |

| (In thousands of Brazilian Reais) |

|

|

|

Parent |

|

Consolidated |

||||

|

|

Note |

12/31/2023 |

|

12/31/2022 |

|

12/31/2023 |

|

12/31/2022 |

|

Assets |

|

|

|

|

|

|

|

|

|

Current assets |

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

4.a |

412,840 |

|

605,461 |

|

5,925,688 |

|

5,621,769 |

|

Financial investments and derivative financial instruments |

4.b |

‐ |

|

‐ |

|

292,934 |

|

520,352 |

|

Trade receivables |

5.a |

‐ |

|

‐ |

|

3,921,790 |

|

4,149,111 |

|

Reseller financing |

5.b |

‐ |

|

‐ |

|

504,862 |

|

559,825 |

|

Trade receivables - sale of subsidiaries |

5.c |

208,487 |

|

184,754 |

|

924,364 |

|

184,754 |

|

Inventories |

6 |

‐ |

|

‐ |

|

4,291,431 |

|

4,906,083 |

|

Recoverable taxes |

7.a |

1,050 |

|

2,012 |

|

1,462,269 |

|

1,610,312 |

|

Recoverable income and social contribution taxes |

7.b |

25,006 |

|

43,080 |

|

171,051 |

|

96,134 |

|

Dividends receivable |

- |

414,973 |

|

147,299 |

|

3,572 |

|

4,296 |

|

Other receivables |

- |

105,229 |

|

101,955 |

|

263,806 |

|

174,153 |

|

Prepaid expenses |

- |

4,617 |

|

5,969 |

|

99,922 |

|

123,699 |

|

Contractual assets with customers - exclusivity rights |

10 |

‐ |

|

‐ |

|

787,206 |

|

614,112 |

|

Total current assets |

|

1,172,202 |

|

1,090,530 |

|

18,648,895 |

|

18,564,600 |

|

|

|

|

|

|

|

|

|

|

|

Non-current assets |

|

|

|

|

|

|

|

|

|

Financial investments and derivative financial instruments |

4.b |

295,637 |

|

‐ |

|

951,941 |

|

442,841 |

|

Trade receivables |

5.a |

‐ |

|

‐ |

|

13,216 |

|

61,463 |

|

Reseller financing |

5.b |

‐ |

|

‐ |

|

550,641 |

|

501,522 |

|

Trade receivables - sale of subsidiaries |

5.c |

‐ |

|

184,754 |

|

‐ |

|

911,811 |

|

Related parties |

8.a |

6,677 |

|

‐ |

|

31,892 |

|

‐ |

|

Deferred income and social contribution taxes |

9.a |

164,267 |

|

150,451 |

|

1,255,134 |

|

898,235 |

|

Recoverable taxes |

7.a |

75 |

|

74 |

|

2,741,370 |

|

2,172,959 |

|

Recoverable income and social contribution taxes |

7.b |

8,065 |

|

4,321 |

|

225,354 |

|

403,383 |

|

Escrow deposits |

18.a |

18 |

|

18 |

|

1,032,717 |

|

946,383 |

|

Indemnification asset - business combination |

18.c |

‐ |

|

‐ |

|

124,927 |

|

126,558 |

|

Other receivables and other assets |

- |

‐ |

|

‐ |

|

155,818 |

|

61,433 |

|

Prepaid expenses |

- |

13,752 |

|

13,047 |

|

73,387 |

|

74,813 |

|

Contractual assets with customers - exclusivity rights |

10 |

‐ |

|

‐ |

|

1,475,302 |

|

1,591,479 |

|

|

|

|

|

|

|

|

|

|

|

Investments in subsidiaries, joint ventures and associates |

11 |

12,322,055 |

|

12,247,087 |

|

318,356 |

|

111,384 |

|

Right-of-use assets, net |

12 |

7,527 |

|

6,943 |

|

1,711,526 |

|

1,791,377 |

|

Property, plant and equipment, net |

13 |

5,791 |

|

8,373 |

|

6,387,581 |

|

5,862,413 |

|

Intangible assets, net |

14 |

270,658 |

|

253,840 |

|

2,553,917 |

|

1,918,349 |

|

Total non-current assets |

|

13,094,522 |

|

12,868,908 |

|

19,603,079 |

|

17,876,403 |

|

Total assets |

|

14,266,724 |

|

13,959,438 |

|

38,251,974 |

|

36,441,003 |

The accompanying notes are an integral part of the financial statements.

| Ultrapar Participações S.A. and Subsidiaries | |

| Statements of financial position | |

| As of December 31, 2023 and 2022 | |

| (In thousands of Brazilian Reais) |

|

|

|

Parent |

|

Consolidated |

||||

|

|

Note |

12/31/2023 |

|

12/31/2022 |

|

12/31/2023 |

|

12/31/2022 |

|

Liabilities |

|

|

|

|

|

|

|

|

|

Current liabilities |

|

|

|

|

|

|

|

|

|

Trade payables |

16.a |

26,772 |

|

46,535 |

|

4,682,671 |

|

4,710,952 |

|

Trade payables - reverse factoring |

16.b |

‐ |

|

‐ |

|

1,039,366 |

|

2,666,894 |

|

Loans, financing and derivative financial instruments |

15 |

‐ |

|

‐ |

|

1,075,672 |

|

869,067 |

|

Debentures |

15 |

‐ |

|

1,800,213 |

|

917,582 |

|

2,491,610 |

|

Salaries and related charges |

- |

51,148 |

|

76,357 |

|

494,771 |

|

460,906 |

|

Taxes payable |

- |

1,457 |

|

1,444 |

|

168,730 |

|

192,430 |

|

Dividends payable |

- |

314,418 |

|

38,936 |

|

334,641 |

|

48,525 |

|

Income and social contribution taxes payable |

- |

‐ |

|

‐ |

|

551,792 |

|

315,053 |

|

Post-employment benefits |

17.b |

‐ |

|

1,396 |

|

23,612 |

|

21,809 |

|

Provision for decarbonization credit |

14.b |

‐ |

|

‐ |

|

741,982 |

|

272,969 |

|

Provisions for tax, civil and labor risks |

18.a |

907 |

|

‐ |

|

45,828 |

|

22,837 |

|

Leases payable |

12.b |

2,389 |

|

1,839 |

|

311,426 |

|

225,034 |

|

Financial liabilities of customers |

- |

‐ |

|

‐ |

|

157,615 |

|

154,405 |

|

Other payables |

- |

5,260 |

|

274 |

|

683,970 |

|

313,761 |

|

Total current liabilities |

|

402,351 |

|

1,966,994 |

|

11,229,658 |

|

12,766,252 |

|

|

|

|

|

|

|

|

|

|

|

Non-current liabilities |

|

|

|

|

|

|

|

|

|

Loans, financing and derivative financial instruments |

15 |

‐ |

|

‐ |

|

5,585,372 |

|

4,845,393 |

|

Debentures |

15 |

‐ |

|

‐ |

|

4,189,391 |

|

3,544,291 |

|

Related parties |

8.a |

2,875 |

|

2,875 |

|

3,118 |

|

3,492 |

|

Deferred income and social contribution taxes |

9.a |

‐ |

|

‐ |

|

206 |

|

299 |

|

Post-employment benefits |

17.b |

1,506 |

|

1,283 |

|

241,211 |

|

193,747 |

|

Provisions for tax, civil and labor risks |

18.a; 18.c |

188,757 |

|

142,283 |

|

1,258,302 |

|

1,017,335 |

|

Leases payable |

12.b |

6,197 |

|

6,035 |

|

1,212,508 |

|

1,298,735 |

|

Financial liabilities of customers |

- |

‐ |

|

‐ |

|

151,319 |

|

296,181 |

|

Subscription warrants - indemnification |

19 |

87,299 |

|

42,776 |

|

87,299 |

|

42,776 |

|

Provision for unsecured liabilities of subsidiaries, joint ventures and associates |

11 |

55,712 |

|

76,646 |

|

256 |

|

157 |

|

Other payables |

‐ |

15,532 |

|

11,805 |

|

263,508 |

|

257,377 |

|

Total non-current liabilities |

|

357,878 |

|

283,703 |

|

12,992,490 |

|

11,499,783 |

|

|

|

|

|

|

|

|

|

|

|

Equity |

|

|

|

|

|

|

|

|

|

Share capital |

20.a |

6,621,752 |

|

5,171,752 |

|

6,621,752 |

|

5,171,752 |

|

Equity instrument granted |

20.b |

75,925 |

|

43,987 |

|

75,925 |

|

43,987 |

|

Capital reserve |

20.g |

597,828 |

|

599,461 |

|

597,828 |

|

599,461 |

|

Treasury shares |

20.c |

(470,510) |

|

(479,674) |

|

(470,510) |

|

(479,674) |

|

Revaluation reserve of subsidiaries |

20.d |

3,802 |

|

3,975 |

|

3,802 |

|

3,975 |

|

Profit reserves |

20.e |

6,389,559 |

|

6,111,136 |

|

6,389,559 |

|

6,111,136 |

|

Accumulated other comprehensive income |

20.f |

154,108 |

|

179,974 |

|

154,108 |

|

179,974 |

|

Additional dividends to the minimum mandatory dividends |

22.h |

134,031 |

|

78,130 |

|

134,031 |

|

78,130 |

|

Equity attributable to: |

|

|

|

|

|

|

|

|

|

Shareholders of Ultrapar |

‐ |

13,506,495 |

|

11,708,741 |

|

13,506,495 |

|

11,708,741 |

|

Non-controlling interests in subsidiaries |

11 |

‐ |

|

‐ |

|

523,331 |

|

466,227 |

|

Total equity |

|

13,506,495 |

|

11,708,741 |

|

14,029,826 |

|

12,174,968 |

|

Total liabilities and equity |

|

14,266,724 |

|

13,959,438 |

|

38,251,974 |

|

36,441,003 |

| Ultrapar Participações S.A. and Subsidiaries | |

|

For the years ended December 31, 2023 and 2022 |

|

|

(In thousands of Brazilian Reais, except earnings per thousand shares) |

|

Parent |

|

Consolidated |

|||||||

|

Note |

12/31/2023 |

12/31/2022 |

12/31/2023 |

12/31/2022 |

|||||

|

Continuing operations |

|||||||||

|

Net revenue from sales and services |

21 |

‐ |

‐ |

126,048,701 |

143,634,708 |

||||

|

Cost of products and services sold |

22 |

‐ |

‐ |

(116,730,469) |

(136,276,257) |

||||

|

Gross profit |

‐ |

‐ |

9,318,232 |

7,358,451 |

|||||

|

Operating revenues (expenses) |

|||||||||

|

Selling and marketing |

22 |

‐ |

‐ |

(2,253,226) |

(2,141,985) |

||||

|

General and administrative |

22 |

(65,850) |

(35,817) |

(2,018,159) |

(1,534,481) |

||||

|

Results from disposal of property, plant and equipment and intangible assets |

23 |

5 |

2,798 |

121,935 |

169,289 |

||||

|

Other operating income (expenses), net |

22 |

46,776 |

(99) |

(602,865) |

(514,522) |

||||

|

Operating income (loss) before financial result and share of profit of subsidiaries, joint ventures and associates and income and social contribution taxes |

(19,069) |

(33,118) |

4,565,917 |

3,336,752 |

|||||

|

Share of profit of subsidiaries, joint ventures and associates |

11 |

2,490,504 |

1,312,346 |

11,908 |

12,181 |

||||

|

Income before financial result and income and social contribution taxes |

2,471,435 |

1,279,228 |

4,577,825 |

3,348,933 |

|||||

|

Financial income |

24 |

96,949 |

218,440 |

880,884 |

706,689 |

||||

|

Financial expenses |

24 |

(115,732) |

(181,869) |

(1,880,014) |

(2,175,897) |

||||

|

Financial result, net |

24 |

(18,783) |

36,571 |

(999,130) |

(1,469,208) |

||||

|

Income before income and social contribution taxes |

2,452,652 |

1,315,799 |

3,578,695 |

1,879,725 |

|||||

|

Income and social contribution taxes |

|||||||||

|

Current |

9.b; 9.c |

(26,641) |

151,630 |

(1,396,317) |

(637,973) |

||||

|

Deferred |

9.b |

13,784 |

31,552 |

335,375 |

296,459 |

||||

|

(12,857) |

183,182 |

(1,060,942) |

(341,514) |

||||||

|

Net income from continuing operations |

2,439,795 |

1,498,981 |

2,517,753 |

1,538,211 |

|||||

|

Discontinued operations |

30 |

‐ |

301,858 |

‐ |

301,858 |

||||

|

Net income for the year |

2,439,795 |

1,800,839 |

2,517,753 |

1,840,069 |

|||||

|

Income attributable to: |

|||||||||

|

Shareholders of Ultrapar |

2,439,795 |

1,800,839 |

2,439,795 |

1,800,839 |

|||||

|

Non-controlling interests in subsidiaries |

11 |

‐ |

‐ |

77,958 |

39,230 |

||||

|

Earnings per share from continuing operations (based on the weighted average number of shares outstanding) – R$ |

|||||||||

|

Basic |

25 |

2.2272 |

1.3727 |

2.2272 |

1.3727 |

||||

|

Diluted |

25 |

2.2081 |

1.3643 |

2.2081 |

1.3643 |

||||

|

Earnings per share from discontinued operations (based on the weighted average number of shares outstanding) – R$ |

|||||||||

|

Basic |

25 |

‐ |

0.2764 |

‐ |

0.2764 |

||||

|

Diluted |

25 |

‐ |

0.2747 |

‐ |

0.2747 |

||||

|

Total earnings per share (based on the weighted average number of shares outstanding) – R$ |

|||||||||

|

Basic |

25 |

2.2272 |

1.6491 |

2.2272 |

1.6491 |

||||

|

Diluted |

25 |

2.2081 |

1.6391 |

2.2081 |

1.6391 |

||||

The accompanying notes are an integral part of the financial statements.

| Ultrapar Participações S.A. and Subsidiaries | |

|

For the years ended December 31, 2023 and 2022 |

|

|

(In thousands of Brazilian Reais) |

|

Parent |

|

Consolidated |

||||||

|

Note |

12/31/2023 |

12/31/2022 |

12/31/2023 |

12/31/2022 |

||||

|

Net income for the year, attributable to shareholders of Ultrapar |

2,439,795 |

1,800,839 |

2,439,795 |

1,800,839 |

||||

|

Net income for the year, attributable to non-controlling interests in subsidiaries |

‐ |

‐ |

77,958 |

39,230 |

||||

|

Net income for the year |

2,439,795 |

1,800,839 |

2,517,753 |

1,840,069 |

||||

|

Items that will be subsequently reclassified to profit or loss: |

||||||||

|

Fair value adjustments of own financial instruments, net of income and social contribution taxes |

20.f.1 |

- |

27 |

- |

27 |

|||

|

Fair value adjustments of financial instruments of subsidiaries, joint ventures and associates, net of income and social contribution taxes |

20.f.1 |

(7,399) |

601,441 |

(7,399) |

601,470 |

|||

|

Other comprehensive income |

20.f.1 |

‐ |

983 |

‐ |

983 |

|||

|

Translation adjustments and hedge of net investments in foreign operations, net of income and social contribution taxes |

‐ |

(304,645) |

‐ |

(304,645) |

||||

|

Items that will not be subsequently reclassified to profit or loss: |

||||||||

|

Actuarial gains (losses) of post-employment benefits, net of income and social contribution taxes |

20.f.1 |

(18,467) |

(339) |

(32,971) |

(165) |

|||

|

Total comprehensive income for the year |

2,413,929 |

2,098,306 |

2,477,383 |

2,137,739 |

||||

|

Total comprehensive income for the year attributable to shareholders of Ultrapar |

2,413,929 |

2,098,306 |

2,413,929 |

2,098,306 |

||||

|

Total comprehensive income for the year attributable to non-controlling interests in subsidiaries |

‐ |

‐ |

63,454 |

39,433 |

||||

The accompanying notes are an integral part of the financial statements.

| Ultrapar Participações S.A. and Subsidiaries | |

|

For the years ended December 31, 2023 and 2022 |

|

|

(In thousands of Brazilian Reais, except earnings per thousand shares) |

|

Profit reserves |

Equity attributable to: |

|||||||||||||||||||||||||

|

Note |

Share capital |

Equity instrument granted |

Capital reserve |

Treasury shares |

Revaluation reserve of subsidiaries |

Legal reserve |

Investments statutory reserve |

Accumulated other comprehensive income |

Retained earnings |

Additional dividends to the minimum mandatory dividends |

Shareholders of Ultrapar |

Non-controlling interests (ii) |

Total equity |

|||||||||||||

|

Balance as of December 31, 2022 |

5,171,752 |

43,987 |

599,461 |

(479,674) |

3,975 |

882,575 |

5,228,561 |

179,974 |

‐ |

78,130 |

11,708,741 |

466,227 |

12,174,968 |

|||||||||||||

|

Net income for the year |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

2,439,795 |

‐ |

2,439,795 |

77,958 |

2,517,753 |

|||||||||||||

|

Other comprehensive income |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(25,866) |

‐ |

‐ |

(25,866) |

(14,504) |

(40,370) |

|||||||||||||

|

Total comprehensive income for the year |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(25,866) |

2,439,795 |

‐ |

2,413,929 |

63,454 |

2,477,383 |

|||||||||||||

|

Issuance of shares related to the subscription warrants - indemnification |

‐ |

‐ |

560 |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

560 |

‐ |

560 |

|||||||||||||

|

Equity instrument granted |

8.c; 20.b |

‐ |

31,938 |

(2,193) |

9,164 |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

38,909 |

‐ |

38,909 |

||||||||||||

|

Realization of revaluation reserve of subsidiaries |

‐ |

‐ |

‐ |

‐ |

‐ |

(173) |

‐ |

‐ |

‐ |

60 |

‐ |

(113) |

‐ |

(113) |

||||||||||||

|

Capital increase with reserves |

20.a |

1,450,000 |

‐ |

‐ |

‐ |

‐ |

(882,575) |

(567,425) |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

||||||||||||

|

Shareholder transaction - changes of ownership interest |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

2 |

‐ |

‐ |

‐ |

2 |

‐ |

2 |

||||||||||||

|

Loss due to change in ownership interest |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(45) |

(45) |

||||||||||||

|

Dividends prescribed |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

2,048 |

‐ |

2,048 |

‐ |

2,048 |

||||||||||||

|

Special reserve for mandatory dividend not distributed to non-controlling shareholders |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(11,145) |

(11,145) |

||||||||||||

|

Non-controlling interest in acquired subsidiary |

29.d |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

24,303 |

24,303 |

||||||||||||

|

Allocation of net income: |

||||||||||||||||||||||||||

|

Legal reserve |

20.h |

‐ |

‐ |

‐ |

‐ |

‐ |

121,990 |

- |

- |

(121,990) |

- |

- |

- |

- |

||||||||||||

|

Investments statutory reserve |

20.h |

- |

- |

- |

- |

- |

- |

1,606,431 |

- |

(1,606,431) |

- |

- |

- |

- |

||||||||||||

|

Additional minimum mandatory dividend (R$ 0.28 per share) |

20.h |

- |

- |

- |

- |

- |

- |

- |

- |

(305,653) |

- |

(305,653) |

- |

(305,653) |

||||||||||||

|

Additional dividends (R$ 0.12 per share) |

20.h |

- |

- |

- |

- |

- |

- |

- |

- |

(134.031) |

134.031 |

- |

- |

- |

||||||||||||

|

Dividends attributable to non-controlling interests |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(19,463) |

(19,463) |

||||||||||||

|

Approval of additional dividends by the Ordinary General Shareholders' Meeting |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(78,130) |

(78,130) |

‐ |

(78,130) |

||||||||||||

|

Interim dividends (R$ 0.25 per share) |

20.h |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(273,798) |

‐ |

(273,798) |

‐ |

(273,798) |

||||||||||||

|

Balance as of December 31, 2023 |

6,621,752 |

75,925 |

597,828 |

(470,510) |

3,802 |

121,990 |

6,267,569 |

154,108 |

- |

134.031 |

13,506,495 |

523,331 |

14,029,826 |

|||||||||||||

| Ultrapar Participações S.A. and Subsidiaries | |

|

Notes to the financial statements |

|

|

For the year ended December 31, 2023 |

|

Profit reserves |

Equity attributable to: |

|||||||||||||||||||||||||

|

Note |

Share capital |

Equity instrument granted |

Capital reserve |

Treasury shares |

Revaluation reserve of subsidiaries |

Legal reserve |

Investments statutory reserve |

Accumulated other comprehensive income (i) |

Retained earnings |

Additional dividends to the minimum mandatory dividends |

Shareholders of the Company |

Non-controlling interests (ii) |

Total equity |

|||||||||||||

|

Balance as of December 31, 2021 |

5,171,752 |

34,043 |

596,481 |

(488,425) |

4,154 |

792,533 |

4,073,876 |

(117,493) |

‐ |

‐ |

10,066,921 |

402,319 |

10,469,240 |

|||||||||||||

|

Net income for the year |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

1,800,839 |

‐ |

1,800,839 |

39,230 |

1,840,069 |

|||||||||||||

|

Other comprehensive income |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

297,467 |

‐ |

‐ |

297,467 |

203 |

297,670 |

|||||||||||||

|

Total comprehensive income for the year |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

297,467 |

1,800,839 |

‐ |

2,098,306 |

39,433 |

2,137,739 |

|||||||||||||

|

Issuance of shares related to the subscription warrants - indemnification |

‐ |

‐ |

941 |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

941 |

‐ |

941 |

|||||||||||||

|

Equity instrument granted |

8.c; 20.b |

‐ |

9,944 |

2,039 |

8,751 |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

20,734 |

‐ |

20,734 |

||||||||||||

|

Realization of revaluation reserve of subsidiaries |

‐ |

‐ |

‐ |

‐ |

(179) |

‐ |

‐ |

‐ |

179 |

‐ |

‐ |

‐ |

‐ |

|||||||||||||

|

Dividends prescribed |

‐ |

‐ |

‐ |

‐ |

- |

‐ |

‐ |

‐ |

2,948 |

‐ |

2,948 |

‐ |

2,948 |

|||||||||||||

|

Shareholder transaction - changes of ownership interest |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(6) |

‐ |

286 |

‐ |

280 |

(6,847) |

(6,567) |

|||||||||||||

|

Gain due to change in ownership interest |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(2,423) |

(2,423) |

|||||||||||||

|

Capital increase attributable to non-controlling interests |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

35,182 |

35,182 |

|||||||||||||

|

Allocation of net income: |

||||||||||||||||||||||||||

|

Legal reserve |

‐ |

‐ |

‐ |

‐ |

‐ |

90,042 |

‐ |

‐ |

(90,042) |

‐ |

‐ |

‐ |

‐ |

|||||||||||||

|

Investments statutory reserve |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

1,154,691 |

‐ |

(1,154,691) |

‐ |

‐ |

‐ |

‐ |

|||||||||||||

|

Additional minimum mandatory dividend (R$ 0.03 per share) |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(31,385) |

‐ |

(31,385) |

‐ |

(31,385) |

|||||||||||||

|

Additional dividends (R$ 0.07 per share) |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(78,130) |

78,130 |

‐ |

‐ |

‐ |

|||||||||||||

|

Interest on capital (R$ 0.41 per share) |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(450,004) |

‐ |

(450,004) |

‐ |

(450,004) |

|||||||||||||

|

Dividends attributable to non-controlling interests |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(1,437) |

(1,437) |

|||||||||||||

|

Balance as of December 31, 2022 |

5,171,752 |

43,987 |

599,461 |

(479,674) |

3,975 |

882,575 |

5,228,561 |

179,974 |

‐ |

78,130 |

11,708,741 |

466,227 |

12,174,968 |

|||||||||||||

| (i) | Cumulative translation adjustment from discontinued operations. The accumulated effects were reclassified to income as a result of the sale of Oxiteno. |

| (ii) | These amounts are substantially represented by non-controlling shareholders of Iconic. |

The accompanying notes are an integral part of the financial statements.

| 15 |

| Ultrapar Participações S.A. and Subsidiaries | |

| Statements of cash flows - indirect method | |

| For the years ended December 31, 2023 and 2022 | |

| (In thousands of Brazilian Reais) |

|

|

|

Parent |

|

Consolidated |

||||

|

|

Note |

12/31/2023 |

|

12/31/2022 |

|

12/31/2023 |

|

12/31/2022 |

|

Cash flows from operating activities |

|

|

|

|

|

|

|

|

|

Net income from continuing operations |

|

2,439,795 |

|

1,498,981 |

|

2,517,754 |

|

1,538,211 |

|

Adjustments to reconcile net income to cash provided (consumed by) operating activities |

|

|

|

|

|

|

|

|

|

Share of profit (loss) of subsidiaries, joint ventures and associates |

11 |

(2,490,504) |

|

(1,312,346) |

|

(11,908) |

|

(12,181) |

|

Amortization of contractual assets with customers - exclusivity rights |

10 |

‐ |

|

‐ |

|

607,446 |

|

504,907 |

|

Amortization of right-of-use assets |

12 |

2,291 |

|

11,444 |

|

305,900 |

|

288,419 |

|

Depreciation and amortization |

13; 14 |

10,216 |

|

1,608 |

|

848,894 |

|

738,904 |

|

Interest and foreign exchange rate variations |

|

23,336 |

|

104,377 |

|

1,349,953 |

|

1,625,987 |

|

Deferred income and social contribution taxes |

9.b |

(13,784) |

|

(31,552) |

|

(335,375) |

|

(296,459) |

|

Current income and social contribution taxes |

9.b |

26,641 |

|

(151,630) |

|

1,396,321 |

|

637,973 |

|

Gain (loss) on disposal or write-off of property, plant and equipment, intangible assets and other assets |

23 |

(33,983) |

|

(2,799) |

|

(192,744) |

|

(322,190) |

|

Reversal (loss) allowance for expected credit losses |

|

‐ |

|

‐ |

|

(27,190) |

|

(49,989) |

|

Provision (reversal) for losses with inventories |

|

‐ |

|

‐ |

|

(14,895) |

|

26,356 |

|

Provision for post-employment benefits |

|

(1,264) |

|

(292) |

|

(2,893) |

|

1,939 |

|

Equity instrument granted |

|

14,400 |

|

(5,126) |

|

38,909 |

|

9,944 |

|

Provision for decarbonization - CBIO |

22 |

‐ |

|

‐ |

|

740,298 |

|

638,542 |

|

Provisions for tax, civil and labor risks |

|

47,396 |

|

3,586 |

|

192,975 |

|

61,039 |

|

Other provisions and adjustments |

|

917 |

|

9,474 |

|

(202) |

|

5,448 |

|

|

|

25,457 |

|

125,725 |

|

7,413,243 |

|

5,396,850 |

|

(Increase) decrease in assets |

|

|

|

|

|

|

|

|

|

Trade receivables and reseller financing |

5 |

‐ |

|

‐ |

|

259,878 |

|

(779,239) |

|

Inventories |

6 |

‐ |

|

‐ |

|

645,301 |

|

(1,004,819) |

|

Recoverable taxes |

7 |

(11,226) |

|

(46,861) |

|

(1,201,440) |

|

(2,056,104) |

|

Dividends received from subsidiaries and joint ventures |

|

1,516,847 |

|

356,467 |

|

12,041 |

|

146 |

|

Other assets |

|

(24,909) |

|

(9,031) |

|

(87,797) |

|

(224,379) |

|

|

|

|

|

|

|

|

|

|

|

Increase (decrease) in liabilities |

|

|

|

|

|

|

|

|

|

Trade payables and trade payables - reverse factoring |

16 |

(19,763) |

|

19,654 |

|

(1,700,496) |

|

1,557,837 |

|

Salaries and related charges |

|

(25,209) |

|

20,879 |

|

30,965 |

|

130,586 |

|

Taxes payable |

|

13 |

|

348 |

|

(25,027) |

|

(9,442) |

|

Other liabilities |

|

54,656 |

|

(4,765) |

|

218,523 |

|

677,016 |

|

Acquisition of CBIO |

14 |

(389) |

|

‐ |

|

(778,885) |

|

(635,130) |

|

Payments of contractual assets with customers - exclusivity rights |

10 |

‐ |

|

‐ |

|

(597,798) |

|

(710,908) |

|

Payments of contingencies |

|

(15) |

|

‐ |

|

(70,128) |

|

(84,939) |

|

Income and social contribution taxes paid |

|

(123) |

|

(15,630) |

|

(268,558) |

|

(283,331) |

|

Net cash provided by operating activities from continuing operations |

|

1,515,339 |

|

446,786 |

|

3,849,822 |

|

1,974,144 |

|

Net cash provided by operating activities from discontinued operations |

|

‐ |

|

‐ |

|

‐ |

|

30,550 |

|

Net cash provided by operating activities |

|

1,515,339 |

|

446,786 |

|

3,849,822 |

|

2,004,694 |

|

|

|

|

|

|

|

|

|

|

|

Cash flows from investing activities |

|

|

|

|

|

|

|

|

|

Financial investments, net of redemptions |

4.b |

(272,011) |

|

625,420 |

|

73,973 |

|

1,567,962 |

|

Acquisition of property, plant and equipment |

13 |

(1,303) |

|

(26) |

|

(1,012,639) |

|

(929,236) |

|

Acquisition of intangible assets |

14 |

(23,266) |

|

(3,241) |

|

(274,691) |

|

(277,600) |

|

Receipt of intercompany loan owed by Oxiteno S.A. to Ultrapar International |

30.b |

‐ |

|

‐ |

|

‐ |

|

3,980,699 |

|

Cash provided by disposal of investments and property, plant and equipment |

|

231,979 |

|

2,503,875 |

|

512,827 |

|

2,839,676 |

|

Capital increase in subsidiaries, associates, and joint ventures |

11 |

(422,886) |

|

(345,956) |

|

- |

|

(28,000) |

|

Capital decrease in subsidiaries, associates, and joint ventures |

11 |

1,093,204 |

|

- |

|

3,100 |

|

- |

|

Net cash consumed by subsidiaries acquisition |

|

(60,930) |

|

(1,823,105) |

|

(265,479) |

|

(5,985) |

|

Transactions with discontinued operations |

|

‐ |

|

- |

|

- |

|

987,895 |

|

Investment purchase and sale transactions and other assets |

|

‐ |

|

‐ |

|

(38,143) |

|

- |

|

Initial direct costs of right-of-use assets |

|

‐ |

|

‐ |

|

(20,503) |

|

(12,120) |

|

Net cash provided (consumed) by investing activities from continuing operations |

|

544,787 |

|

956,967 |

|

(1,021,555) |

|

8,123,291 |

|

Net cash consumed by investing activities from discontinued operations |

|

‐ |

|

‐ |

|

‐ |

|

(220,190) |

|

Net cash provided (consumed) by investing activities |

|

544,787 |

|

956,967 |

|

(1,021,555) |

|

7,903,101 |

| Ultrapar Participações S.A. and Subsidiaries | |

| Statements of cash flows - indirect method | |

| For the years ended December 31, 2023 and 2022 | |

| (In thousands of Brazilian Reais) |

|

|

|

|

|

|

|

|

|

|

|

Cash flows from financing activities |

|

|

|

|

|

|

|

|

|

Loans, financing and debentures |

|

|

|

|

|

|

|

|

|

Proceeds |

15 |

‐ |

|

‐ |

|

2,903,031 |

|

1,519,580 |

|

Repayments |

15 |

(1,725,000) |

|

‐ |

|

(3,149,525) |

|

(5,848,611) |

|

Interest and derivatives paid |

|

(137,891) |

|

(182,552) |

|

(1,267,447) |

|

(1,398,229) |

|

Payments of lease |

|

|

|

|

|

|

|

|

|

Principal |

12.b |

(2,136) |

|

(4,371) |

|

(213,527) |

|

(351,011) |

|

Interest paid |

12.b |

(705) |

|

(52) |

|

(145,586) |

|

(6,868) |

|

Dividends paid |

|

(380,898) |

|

(635,725) |

|

(400,025) |

|

(638,280) |

|

Proceeds from financial liabilities of customers |

|

‐ |

|

‐ |

|

7,812 |

|

162,895 |

|

Payments of financial liabilities of customers |

|

‐ |

|

‐ |

|

(197,891) |

|

(173,948) |

|

Capital increase made by non-controlling interests and redemption of shares |

|

149 |

|

‐ |

|

‐ |

|

21,682 |

|

Related parties |

|

(6,266) |

|

2,875 |

|

(31,238) |

|

(18,926) |

|

Net cash consumed by financing activities from continuing operations |

|

(2,252,747) |

|

(819,825) |

|

(2,494,396) |

|

(6,731,716) |

|

Net cash consumed by financing activities from discontinued operations |

|

‐ |

|

‐ |

|

‐ |

|

(179,025) |

|

Net cash consumed by financing activities |

|

(2,252,747) |

|

(819,825) |

|

(2,494,396) |

|

(6,910,741) |

|

Effect of exchange rate changes on cash and cash equivalents in foreign currency - continuing operations |

|

- |

|

‐ |

|

(29,952) |

|

(24,025) |

|

Effect of exchange rate changes on cash and cash equivalents in foreign currency - discontinued operations |

|

‐ |

|

‐ |

|

‐ |

|

(19,316) |

|

Increase (decrease) in cash and cash equivalents - continuing operations |

|

(192,621) |

|

583,928 |

|

303,919 |

|

3,341,694 |

|

Decrease in cash and cash equivalents - discontinued operations |

|

‐ |

|

- |

|

‐ |

|

(387,981) |

|

Cash and cash equivalents at the beginning of the year - continuing operations |

4.a |

605,461 |

|

21,533 |

|

5,621,769 |

|

2,280,075 |

|

Cash and cash equivalents at the beginning of the year - discontinued operations |

|

‐ |

|

‐ |

|

‐ |

|

387,981 |

|

Cash and cash equivalents at the end of the year- continuing operations |

4.a |

412,840 |

|

605,461 |

|

5,925,688 |

|

5,621,769 |

|

Cash and cash equivalents at the end of the year - discontinued operations |

|

‐ |

|

‐ |

|

‐ |

|

‐ |

|

Non-cash transactions: |

|

|

|

|

|

|

|

|

|

Contingent consideration – acquisition of subsidiaries |

|

‐ |

|

‐ |

|

- |

|

89,640 |

|

Addition on right-of-use assets and leases payable |

|

‐ |

|

‐ |

|

257,201 |

|

482,439 |

|

Movement without cash effect of escrow deposits and provisions for tax, civil and labor risks |

|

‐ |

|

‐ |

|

- |

|

41,888 |

|

Addition on contractual assets with customers - exclusivity rights |

|

‐ |

|

‐ |

|

66,565 |

|

63,061 |

|

Capital increase made by non-controlling interests |

|

‐ |

|

- |

|

‐ |

|

13,519 |

|

Transfer between trade receivables and property, plant and equipment |

|

411 |

|

‐ |

|

25,646 |

|

- |

|

Issuance of shares related to the subscription warrants - indemnification - Extrafarma acquisition |

|

‐ |

|

942 |

|

411 |

|

942 |

|

Acquisition of property, plant and equipment and intangible assets without cash effect |

|

- |

|

- |

|

104,177 |

|

- |

The accompanying notes are an integral part of the financial statements.

| Ultrapar Participações S.A. and Subsidiaries | |

| Statements of value added | |

| For the years ended December 31, 2023 and 2022 | |

| (In thousands of Brazilian Reais) |

|

Parent |

Consolidated |

|||||||

|

Note |

12/31/2023 |

12/31/2022 |

12/31/2023 |

12/31/2022 |

||||

|

Revenues |

||||||||

|

Gross revenue from sales and services, except rents and royalties |

‐ |

‐ |

130,120,745 |

147,721,609 |

||||

|

Rebates, discounts and returns |

‐ |

‐ |

(1,031,600) |

(949,451) |

||||

|

Allowance for expected credit losses |

5 |

‐ |

‐ |

22,815 |

49,989 |

|||

|

Amortization of contractual assets with customers - exclusivity rights |

10 |

‐ |

‐ |

(607,447) |

(504,907) |

|||

|

Gain (loss) on disposal of assets and other operating income, net |

22; 23 |

46,781 |

2,699 |

(480,930) |

(345,233) |

|||

|

46,781 |

2,699 |

128,041,583 |

145,972,007 |

|||||

|

Materials purchased from third parties |

||||||||

|

Raw materials used |

‐ |

‐ |

(1,966,518) |

(5,772,808) |

||||

|

Cost of products and services sold |

‐ |

‐ |

(114,981,604) |

(130,740,502) |

||||

|

Materials, energy, third-party services and others |

175,338 |

189,923 |

(1,646,794) |

(2,279,098) |

||||

|

Provision for assets losses |

‐ |

‐ |

21,210 |

16,521 |

||||

|

175,338 |

189,923 |

(118,573,706) |

(138,775,887) |

|||||

|

Gross value added |

222,119 |

192,622 |

9,467,877 |

7,196,120 |

||||

|

Retentions |

||||||||

|

Depreciation and amortization of intangible assets and right-of-use assets |

12.a; 13; 14 |

(12,507) |

(13,052) |

(1,146,277) |

(1,020,660) |

|||

|

Net value added produced by the Company |

209,612 |

179,570 |

8,321,600 |

6,175,460 |

||||

|

Value added received in transfer |

||||||||

|

Share of profit (loss) of subsidiaries, joint ventures, and associates |

11 |

2,490,504 |

1,312,346 |

11,908 |

12,181 |

|||

|

Rents and royalties |

‐ |

‐ |

316,575 |

288,550 |

||||

|

Financial income |

24 |

96,949 |

218,440 |

880,884 |

706,689 |

|||

|

2,587,453 |

1,530,786 |

1,209,367 |

1,007,420 |

|||||

|

Value added from continuing operations available for distribution |

2,797,065 |

1,710,356 |

9,530,967 |

7,182,880 |

||||

|

Value added from discontinued operations available for distribution |

‐ |

106,516 |

‐ |

547,144 |

||||

|

Total value added available for distribution |

2,797,065 |

1,816,872 |

9,530,967 |

7,730,024 |

||||

|

Distribution of value added |

||||||||

|

Personnel and related charges |

||||||||

|

Salaries and wages |

159,812 |

140,753 |

1,448,728 |

1,021,980 |

||||

|

Benefits |

25,052 |

21,554 |

408,211 |

277,006 |

||||

|

Government Severance Indemnity Fund for Employees (FGTS) |

9,035 |

7,678 |

98,656 |

70,912 |

||||

|

Others |

7,219 |

7,592 |

120,234 |

88,631 |

||||

|

201,118 |

177,577 |

2,075,829 |

1,458,529 |

|||||

|

Taxes, fees, and contributions |

||||||||

|

Federal |

40,614 |

(144,949) |

2,452,578 |

1,459,408 |

||||

|

States |

‐ |

- |

411,320 |

418,464 |

||||

|

Municipal |

366 |

1,762 |

150,813 |

115,368 |

||||

|

40,980 |

(143,187) |

3,014,711 |

1,993,240 |

|||||

|

Financial expenses and rents |

||||||||

|

Interest, exchange variations and financial instruments |

44,586 |

235,095 |

1,625,188 |

1,713,156 |

||||

|

Rents |

4,905 |

8,643 |

96,012 |

23,256 |

||||

|

Others |

65,681 |

(66,753) |

201,474 |

456,488 |

||||

|

115,172 |

176,985 |

1,922,674 |

2,192,900 |

|||||

|

Remuneration of own capital |

||||||||

|

Dividends |

713,482 |

106,567 |

732,945 |

108,004 |

||||

|

Interest on capital |

‐ |

450,004 |

‐ |

450,004 |

||||

|

Retained earnings |

1,726,313 |

942,410 |

1,784,808 |

980,203 |

||||

|

2,439,795 |

1,498,981 |

2,517,753 |

1,538,211 |

|||||

|

Value added from continuing operations distributed |

2,797,065 |

1,710,356 |

9,530,967 |

7,182,880 |

||||

|

Value added from discontinued operations distributed |

‐ |

106,516 |

‐ |

547,144 |

||||

|

Value added distributed |

2,797,065 |

1,816,872 |

9,530,967 |

7,730,024 |

||||

The accompanying notes are an integral part of the financial statements.

| Ultrapar Participações S.A. and Subsidiaries | |

|

Notes to the financial statements |

|

|

For the year ended December 31, 2023 |

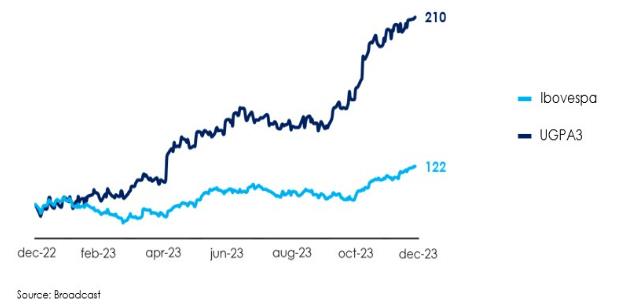

Ultrapar Participações S.A. (“Ultrapar” or “Company”) is a publicly-traded company headquartered at the Brigadeiro Luís Antônio Avenue, 1343 in the city of São Paulo – SP, Brazil, listed on B3 S.A. Brasil, Bolsa, Balcão (“B3”), in the Novo Mercado listing segment under the ticker “UGPA3” and on the New York Stock Exchange (“NYSE”) in the form of level III American Depositary Receipts (“ADRs”) under the ticker “UGP”.

The Company engages in the investment of its own capital in services, commercial and industrial activities, through the subscription or acquisition of shares of other companies. Through its subsidiaries, it operates on liquefied petroleum gas – LPG distribution (“Ultragaz”), fuel distribution and related businesses (“Ipiranga” or “IPP”) and storage services for liquid bulk (“Ultracargo”). The information on segments is disclosed in Note 26.a.

These financial statements were authorized for issuance by the Board of Directors on February 28, 2024.

a. Principles of consolidation and interest in subsidiaries

a.1 Principles of consolidation

In the preparation of the consolidated financial statements the investments of one company in another, balances of asset and liability accounts, revenues transactions, costs and expenses were eliminated, as well as the effects of transactions conducted between the companies. Non-controlling interests in subsidiaries are presented within consolidated equity and net income.

Consolidation of a subsidiary begins when the Company obtains direct or indirect control over an entity and ceases when the company loses control. Income and expenses of a subsidiary acquired are included in the consolidated statements of income and of comprehensive income from the date the Company gains the control. Income and expenses of a subsidiary, in which the Company loses control, are included in the consolidated statements of income and of comprehensive income until the date the Company loses control.

When necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies into line with the Company’s accounting policies.

| Ultrapar Participações S.A. and Subsidiaries | |

|

Notes to the financial statements |

|

|

For the year ended December 31, 2023 |

a.2. Interest in subsidiaries

The consolidated financial statements include the following direct and indirect subsidiaries:

|

% interest in the share capital |

|||||||||||

|

12/31/2023 |

12/31/2022 |

||||||||||

|

Control |

Control |

||||||||||

|

Location |

Segment |

Direct |

Indirect |

Direct |

Indirect |

||||||

|

Ipiranga Produtos de Petróleo S.A. |

Brazil |

Ipiranga |

100 |

- |

100 |

- |

|||||

|

am/pm Comestíveis Ltda. |

Brazil |

Ipiranga |

- |

100 |

- |

100 |

|||||

|

Icorban - Correspondente Bancário Ltda. |

Brazil |

Ipiranga |

- |

100 |

- |

100 |

|||||

|

Ipiranga Trading Limited |

British Virgin Islands |

Ipiranga |

- |

100 |

- |

100 |

|||||

|

Tropical Transportes Ipiranga Ltda. |

Brazil |

Ipiranga |

- |

100 |

- |

100 |

|||||

|

Ipiranga Imobiliária Ltda. |

Brazil |

Ipiranga |

- |

100 |

- |

100 |

|||||

|

Ipiranga Logística Ltda. |

Brazil |

Ipiranga |

- |

100 |

- |

100 |

|||||

|

Oil Trading Importadora e Exportadora Ltda. |

Brazil |

Ipiranga |

- |

100 |

- |

100 |

|||||

|

Iconic Lubrificantes S.A. |

Brazil |

Ipiranga |

- |

56 |

- |

56 |

|||||

|

Integra Frotas Ltda. |

Brazil |

Ipiranga |

- |

100 |

- |

100 |

|||||

|

Irupé Biocombustíveis Ltda.(13) |

Brazil |

Ipiranga |

- |

100 |

- |

- |

|||||

|

Imaven Imóveis Ltda.(10) |

Brazil |

Others |

- |

- |

- |

100 |

|||||

|

Ultragaz Participações Ltda. |

Brazil |

Ultragaz |

100 |

- |

100 |

- |

|||||

|

Ultragaz Energia Ltda. and subsidiaries(4) |

Brazil |

Ultragaz |

- |

100 |

- |

100 |

|||||

|

Companhia Ultragaz S.A.(3) |

Brazil |

Ultragaz |

- |

99 |

- |

99 |

|||||

|

Nova Paraná Distribuidora de Gás Ltda.(1) |

Brazil |

Ultragaz |

- |

100 |

- |

100 |

|||||

|

Utingás Armazenadora S.A. |

Brazil |

Ultragaz |

- |

57 |

- |

57 |

|||||

|

Bahiana Distribuidora de Gás Ltda. |

Brazil |

Ultragaz |

- |

100 |

- |

100 |

|||||

|

LPG International Inc. (14) |

Cayman Islands |

Ultragaz |

- |

- |

- |

100 |

|||||

|

NEOgás do Brasil Gas Natural Comprimido S.A. (5) |

Brazil |

Ultragaz |

- |

100 |

- |

- |

|||||

|

UVC Investimentos Ltda |

Brazil |

Others |

100 |

- |

100 |

- |

|||||

|

Centro de Conveniências Millennium Ltda. and subsidiaries (12) |

Brazil |

Others |

- |

- |

100 |

- |

|||||

|

Ultracargo - Operações Logísticas e Participações Ltda. |

Brazil |

Ultracargo |

100 |

- |

100 |

- |

|||||

|

Ultracargo Logística S.A. |

Brazil |

Ultracargo |

- |

99 |

- |

99 |

|||||

|

TEAS – Terminal Exportador de Álcool de Santos Ltda.(8) |

Brazil |

Ultracargo |

- |

- |

- |

100 |

|||||

|

Ultracargo Soluções Logísticas S.A.(2) |

Brazil |

Ultracargo |

- |

100 |

- |

100 |

|||||

|

Ultrapar International S.A. |

Luxembourg |

Others |

100 |

- |

100 |

- |

|||||

|

SERMA - Ass. dos usuários equip. proc. de dados |

Brazil |

Others |

- |

- |

- |

100 |

|||||

|

UVC - Fundo de investimento em participações multiestratégia investimento no exterior |

Brazil |

Others |

100 |

- |

100 |

- |

|||||

|

Imaven Imóveis Ltda.(10) |

Brazil |

Others |

100 |

- |

- |

- |

|||||

|

Eaí Clube Automobilista S.A. |

Brazil |

Others |

100 |

- |

100 |

- |

|||||

|

Abastece Aí Participações S.A.(9) |

Brazil |

Others |

- |

100 |

- |

- |

|||||

|

Abastece Aí Clube Automobilista Instituição de Pagamento Ltda(7) |

Brazil |

Others |

- |

100 |

- |

- |

|||||

|

Ultrapar Mobilidade Ltda.(6) |

Brazil |

Others |

100 |

- |

- |

- |

|||||

|

Serra Diesel Transportador Revendedor Retalhista Ltda.(11) |

Brazil |

Others |

- |

60 |

- |

- |

|||||

|

Centro de Conveniências Millennium Ltda. and subsidiaries(12) |

Brazil |

Others |

- |

100 |

- |

- |

|||||

The percentages in the table above are rounded.

| Ultrapar Participações S.A. and Subsidiaries | |

|

Notes to the financial statements |

|

|

For the year ended December 31, 2023 |

| (1) | Non-operating company in closing phase. |

| (2) | On June 16, 2023, the name of subsidiary Ultracargo Vila do Conde Logística Portuária S.A. was changed to Ultracargo Soluções Logísticas S.A. |

| (3) | On August 1, 2022, the subsidiary Companhia Ultragaz S.A. (“Ultragaz”) became directly controlled by Ultrapar. In November 2022, Ultragaz became an investee of Ultragaz Participações Ltda. |

| (4) | On November 18, 2022, the name of subsidiary Ultragaz Comercial Ltda. was changed to Ultragaz Energia Ltda. |

| (5) | On November 21, 2022, Ultrapar through its subsidiary Companhia Ultragaz S.A., signed an agreement for the acquisition of all shares of NEOgás do Brasil Gás Natural Comprimido S.A. The closing of the acquisition occurred on February 1, 2023. |

| (6) | Company established on February 28, 2023, with the purpose of holding interests in other companies. On October 2, 2023, the name of subsidiary Ultrapar Empreendimentos Ltda. was changed to Ultrapar Mobilidade Ltda. |

| (7) | On April 13, 2023, the company was acquired by Eaí Clube Automobilista S.A. The acquisition was made at book value. |

| (8) | On April 27, 2023, the Company was merged into Ultracargo Logística S.A. |

| (9) | Company established on June 1, 2023, with the purpose of holding interests in other companies. |

| (10) | On April 28, 2023, Imaven Imóveis Ltda. (“Imaven”), performed a partial spin-off of its assets, and the spin-off part was merged into the equity of the subsidiary Ipiranga Produtos de Petróleo S.A. On May 1, Imaven became directly controlled by Ultrapar. The entire transaction was carried out under common control. |

| (11) | On May 21, 2023, the Company, through its subsidiary Ultrapar Empreendimentos Ltda., signed an agreement for the acquisition of a 60% interest in Serra Diesel Transportador Revendedor Retalhista Ltda. The closing of the transaction occurred on September 1, 2023. |

| (12) | On October 2, 2023, Centro de Conveniências Millennium Ltda. and subsidiaries became directly controlled by Ultrapar Mobilidade Ltda. |

| (13) | Company established on October 2, 2023, engaged in the production, sale, import and export of biofuels, fertilizers and other agricultural inputs. |

| (14) | On June 30, 2023, the Company was dissolved. |

The main events occurred in the year are presented on Note 29.

| Ultrapar Participações S.A. and Subsidiaries | |

| Notes to the financial statements |

|

| For the year ended December 31, 2023 |

The individual and consolidated financial statements (“financial statements”) have been prepared in accordance with the International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”) and with the accounting practices adopted in Brazil.

The accounting practices adopted in Brazil include those in the Brazilian corporate law and in the Pronouncements, Guidance and Interpretations issued by the Accounting Pronouncements Committee (“CPC”), approved by the Brazilian Federal Accounting Council (“CFC”) and the Brazilian Securities and Exchange Commission (“CVM”).

All relevant specific information of the financial statements, and only this information, was presented and corresponds to that used by the Company’s and its subsidiaries’ Management.

The presentation currency of the Company’s financial statements is the Brazilian Real, which is the Company’s functional currency, unless otherwise stated.

The preparation of the financial statements requires management to make judgments, use estimates and adopt assumptions in the application of accounting policies that affect the presented amounts of income, expenses, assets and liabilities, including contingent liabilities. The uncertainty related to these judgments, assumptions and estimates could lead to results that require a significant adjustment to the carrying amount of certain assets and liabilities in future years.

The financial statements have been prepared on a historical cost basis, except for the following material items recognized in the statements of financial position:

(i) derivative and non-derivative financial instruments measured at fair value;

(ii) share-based payments and employee benefits measured at fair value;

(iii) deemed cost of property, plant and equipment.

The Company and its subsidiaries applied the material accounting policies described below in a consistent manner for all years presented in these financial statements.

| Ultrapar Participações S.A. and Subsidiaries | |

| Notes to the financial statements |

|

| For the year ended December 31, 2023 |

a. Revenue recognition

Revenues from sales and services rendered under contracts with customers are recognized on the accrual basis when, or as, performance obligations are satisfied by transferring the control of a promised good or service to a customer in such a way that the customer obtains substantially all rewards generated, according to incoterms of each transaction, and when it is highly probable that the Company and its subsidiaries will receive the consideration in exchange for the transferred goods or services.

The Company and its subsidiaries recognize revenue under the 5-step model, in accordance with IFRS 15/CPC 47: (1) identification of contracts with customers; (2) identification of the performance obligations; (3) determination of the transaction price; (4) allocation of the transaction price to performance obligations under the contracts, and (5) revenue recognition when (or as) the performance obligation is satisfied and the control of the goods and services is transferred to the customer.