000151029512-312023FYfalsehttp://fasb.org/us-gaap/2023#IncomeLossFromDiscontinuedOperationsNetOfTaxAttributableToReportingEntityhttp://fasb.org/us-gaap/2023#DepreciationDepletionAndAmortizationhttp://fasb.org/us-gaap/2023#CostOfGoodsAndServicesSoldhttp://fasb.org/us-gaap/2023#CostOfGoodsAndServicesSoldhttp://fasb.org/us-gaap/2023#CostOfGoodsAndServicesSoldhttp://fasb.org/us-gaap/2023#CostOfGoodsAndServicesSoldP1Yhttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsCurrenthttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsCurrenthttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationshttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationshttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligations http://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsCurrenthttp://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligations http://fasb.org/us-gaap/2023#LongTermDebtAndCapitalLeaseObligationsCurrenthttp://fasb.org/us-gaap/2023#RevenueFromContractWithCustomerExcludingAssessedTaxhttp://fasb.org/us-gaap/2023#RevenueFromContractWithCustomerExcludingAssessedTaxhttp://fasb.org/us-gaap/2023#RevenueFromContractWithCustomerExcludingAssessedTaxhttp://fasb.org/us-gaap/2023#DeferredCreditsAndOtherLiabilitiesNoncurrent http://fasb.org/us-gaap/2023#OtherLiabilitiesCurrenthttp://fasb.org/us-gaap/2023#DeferredCreditsAndOtherLiabilitiesNoncurrent http://fasb.org/us-gaap/2023#OtherLiabilitiesCurrent00015102952023-01-012023-12-3100015102952023-06-30iso4217:USD00015102952024-02-23xbrli:shares00015102952022-01-012022-12-3100015102952021-01-012021-12-31iso4217:USDxbrli:shares0001510295us-gaap:AccumulatedDefinedBenefitPlansAdjustmentNetUnamortizedGainLossMember2023-01-012023-12-310001510295us-gaap:AccumulatedDefinedBenefitPlansAdjustmentNetUnamortizedGainLossMember2022-01-012022-12-310001510295us-gaap:AccumulatedDefinedBenefitPlansAdjustmentNetUnamortizedGainLossMember2021-01-012021-12-310001510295us-gaap:AccumulatedDefinedBenefitPlansAdjustmentNetPriorServiceCostCreditMember2023-01-012023-12-310001510295us-gaap:AccumulatedDefinedBenefitPlansAdjustmentNetPriorServiceCostCreditMember2022-01-012022-12-310001510295us-gaap:AccumulatedDefinedBenefitPlansAdjustmentNetPriorServiceCostCreditMember2021-01-012021-12-310001510295mpc:AccumulatedGainLossOtherMember2023-01-012023-12-310001510295mpc:AccumulatedGainLossOtherMember2022-01-012022-12-310001510295mpc:AccumulatedGainLossOtherMember2021-01-012021-12-3100015102952023-12-3100015102952022-12-3100015102952021-12-3100015102952020-12-310001510295us-gaap:CommonStockMember2020-12-310001510295us-gaap:TreasuryStockCommonMember2020-12-310001510295us-gaap:AdditionalPaidInCapitalMember2020-12-310001510295us-gaap:RetainedEarningsMember2020-12-310001510295us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001510295us-gaap:NoncontrollingInterestMember2020-12-310001510295mpc:RedeemableNoncontrollingInterestMember2020-12-310001510295us-gaap:RetainedEarningsMember2021-01-012021-12-310001510295us-gaap:NoncontrollingInterestMember2021-01-012021-12-310001510295mpc:RedeemableNoncontrollingInterestMember2021-01-012021-12-310001510295us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001510295us-gaap:TreasuryStockCommonMember2021-01-012021-12-310001510295us-gaap:CommonStockMember2021-01-012021-12-310001510295us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001510295us-gaap:CommonStockMember2021-12-310001510295us-gaap:TreasuryStockCommonMember2021-12-310001510295us-gaap:AdditionalPaidInCapitalMember2021-12-310001510295us-gaap:RetainedEarningsMember2021-12-310001510295us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001510295us-gaap:NoncontrollingInterestMember2021-12-310001510295mpc:RedeemableNoncontrollingInterestMember2021-12-310001510295us-gaap:RetainedEarningsMember2022-01-012022-12-310001510295us-gaap:NoncontrollingInterestMember2022-01-012022-12-310001510295mpc:RedeemableNoncontrollingInterestMember2022-01-012022-12-310001510295us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001510295us-gaap:TreasuryStockCommonMember2022-01-012022-12-310001510295us-gaap:CommonStockMember2022-01-012022-12-310001510295us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001510295us-gaap:CommonStockMember2022-12-310001510295us-gaap:TreasuryStockCommonMember2022-12-310001510295us-gaap:AdditionalPaidInCapitalMember2022-12-310001510295us-gaap:RetainedEarningsMember2022-12-310001510295us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001510295us-gaap:NoncontrollingInterestMember2022-12-310001510295mpc:RedeemableNoncontrollingInterestMember2022-12-310001510295us-gaap:RetainedEarningsMember2023-01-012023-12-310001510295us-gaap:NoncontrollingInterestMember2023-01-012023-12-310001510295mpc:RedeemableNoncontrollingInterestMember2023-01-012023-12-310001510295us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001510295us-gaap:TreasuryStockCommonMember2023-01-012023-12-310001510295us-gaap:CommonStockMember2023-01-012023-12-310001510295us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001510295us-gaap:CommonStockMember2023-12-310001510295us-gaap:TreasuryStockCommonMember2023-12-310001510295us-gaap:AdditionalPaidInCapitalMember2023-12-310001510295us-gaap:RetainedEarningsMember2023-12-310001510295us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-310001510295us-gaap:NoncontrollingInterestMember2023-12-310001510295mpc:RedeemableNoncontrollingInterestMember2023-12-310001510295mpc:MarathonPetroleumCorporationMembermpc:MPLXLPMember2023-12-31xbrli:pure0001510295us-gaap:EnergyEquipmentMembersrt:MinimumMember2023-12-310001510295us-gaap:EnergyEquipmentMembersrt:MaximumMember2023-12-310001510295srt:OfficeBuildingMember2023-12-310001510295us-gaap:OtherCapitalizedPropertyPlantAndEquipmentMembersrt:MinimumMember2023-12-310001510295srt:MaximumMemberus-gaap:OtherCapitalizedPropertyPlantAndEquipmentMember2023-12-310001510295us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Member2023-12-310001510295us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CashAndCashEquivalentsMember2023-12-310001510295us-gaap:ShortTermInvestmentsMemberus-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Member2023-12-310001510295us-gaap:CertificatesOfDepositMemberus-gaap:FairValueInputsLevel2Member2023-12-310001510295us-gaap:CertificatesOfDepositMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CashAndCashEquivalentsMember2023-12-310001510295us-gaap:ShortTermInvestmentsMemberus-gaap:CertificatesOfDepositMemberus-gaap:FairValueInputsLevel2Member2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:USGovernmentDebtSecuritiesMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:USGovernmentDebtSecuritiesMemberus-gaap:CashAndCashEquivalentsMember2023-12-310001510295us-gaap:ShortTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:USGovernmentDebtSecuritiesMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:CorporateDebtSecuritiesMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:CorporateDebtSecuritiesMemberus-gaap:CashAndCashEquivalentsMember2023-12-310001510295us-gaap:ShortTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CorporateDebtSecuritiesMember2023-12-310001510295us-gaap:CashAndCashEquivalentsMember2023-12-310001510295us-gaap:ShortTermInvestmentsMember2023-12-310001510295us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Member2022-12-310001510295us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CashAndCashEquivalentsMember2022-12-310001510295us-gaap:ShortTermInvestmentsMemberus-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Member2022-12-310001510295us-gaap:CertificatesOfDepositMemberus-gaap:FairValueInputsLevel2Member2022-12-310001510295us-gaap:CertificatesOfDepositMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CashAndCashEquivalentsMember2022-12-310001510295us-gaap:ShortTermInvestmentsMemberus-gaap:CertificatesOfDepositMemberus-gaap:FairValueInputsLevel2Member2022-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:USGovernmentDebtSecuritiesMember2022-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:USGovernmentDebtSecuritiesMemberus-gaap:CashAndCashEquivalentsMember2022-12-310001510295us-gaap:ShortTermInvestmentsMemberus-gaap:FairValueInputsLevel1Memberus-gaap:USGovernmentDebtSecuritiesMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:CorporateDebtSecuritiesMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:CorporateDebtSecuritiesMemberus-gaap:CashAndCashEquivalentsMember2022-12-310001510295us-gaap:ShortTermInvestmentsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:CorporateDebtSecuritiesMember2022-12-310001510295us-gaap:CashAndCashEquivalentsMember2022-12-310001510295us-gaap:ShortTermInvestmentsMember2022-12-310001510295mpc:SpeedwayMemberus-gaap:DiscontinuedOperationsDisposedOfBySaleMember2021-05-142021-05-140001510295mpc:SpeedwayMemberus-gaap:DiscontinuedOperationsDisposedOfBySaleMember2022-01-012022-12-310001510295srt:SubsidiariesMembermpc:ShareRepurchaseAuthorizationNovember2020Member2020-11-020001510295srt:SubsidiariesMembermpc:ShareRepurchaseAuthorizationAugust2022Member2022-08-020001510295srt:SubsidiariesMember2023-01-012023-12-310001510295srt:SubsidiariesMember2022-01-012022-12-310001510295srt:SubsidiariesMember2021-01-012021-12-310001510295srt:SubsidiariesMember2023-12-310001510295us-gaap:SeriesBPreferredStockMembermpc:MPLXLPMember2023-02-150001510295us-gaap:SeriesBPreferredStockMembermpc:MPLXLPMember2023-02-152023-02-150001510295us-gaap:RetainedEarningsMemberus-gaap:SeriesBPreferredStockMembermpc:MPLXLPMember2023-02-152023-02-150001510295mpc:MPLXLPMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2023-12-310001510295mpc:MPLXLPMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001510295mpc:ArcherDanielsMidlandCompanyMembermpc:GreenBisonSoyProcessingLLCMember2023-12-310001510295mpc:MarathonPetroleumCorporationMembermpc:GreenBisonSoyProcessingLLCMember2023-12-310001510295mpc:LFBioenergyMember2023-03-080001510295us-gaap:RelatedPartyMember2023-01-012023-12-310001510295us-gaap:RelatedPartyMember2022-01-012022-12-310001510295us-gaap:RelatedPartyMember2021-01-012021-12-310001510295us-gaap:StockCompensationPlanMember2023-01-012023-12-310001510295us-gaap:StockCompensationPlanMember2022-01-012022-12-310001510295us-gaap:StockCompensationPlanMember2021-01-012021-12-310001510295mpc:ShareRepurchaseAuthorizationOctober2023Member2023-10-250001510295mpc:ShareRepurchaseAuthorizationMay2023Member2023-05-020001510295mpc:ShareRepurchaseAuthorizationJanuary2023Member2023-01-310001510295us-gaap:SubsequentEventMember2024-01-012024-01-31mpc:Segment0001510295mpc:RefiningAndMarketingMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310001510295mpc:RefiningAndMarketingMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310001510295mpc:RefiningAndMarketingMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310001510295mpc:MidstreamMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310001510295mpc:MidstreamMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310001510295mpc:MidstreamMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310001510295us-gaap:OperatingSegmentsMember2023-01-012023-12-310001510295us-gaap:OperatingSegmentsMember2022-01-012022-12-310001510295us-gaap:OperatingSegmentsMember2021-01-012021-12-310001510295us-gaap:CorporateNonSegmentMember2023-01-012023-12-310001510295us-gaap:CorporateNonSegmentMember2022-01-012022-12-310001510295us-gaap:CorporateNonSegmentMember2021-01-012021-12-310001510295mpc:MartinezRenewablesLLCMember2022-09-212022-09-210001510295mpc:RefiningAndMarketingMember2023-01-012023-12-310001510295mpc:RefiningAndMarketingMember2022-01-012022-12-310001510295mpc:RefiningAndMarketingMember2021-01-012021-12-310001510295mpc:RefiningAndMarketingMemberus-gaap:IntersegmentEliminationMember2023-01-012023-12-310001510295mpc:RefiningAndMarketingMemberus-gaap:IntersegmentEliminationMember2022-01-012022-12-310001510295mpc:RefiningAndMarketingMemberus-gaap:IntersegmentEliminationMember2021-01-012021-12-310001510295mpc:MidstreamMember2023-01-012023-12-310001510295mpc:MidstreamMember2022-01-012022-12-310001510295mpc:MidstreamMember2021-01-012021-12-310001510295mpc:MidstreamMemberus-gaap:IntersegmentEliminationMember2023-01-012023-12-310001510295mpc:MidstreamMemberus-gaap:IntersegmentEliminationMember2022-01-012022-12-310001510295mpc:MidstreamMemberus-gaap:IntersegmentEliminationMember2021-01-012021-12-310001510295us-gaap:IntersegmentEliminationMember2023-01-012023-12-310001510295us-gaap:IntersegmentEliminationMember2022-01-012022-12-310001510295us-gaap:IntersegmentEliminationMember2021-01-012021-12-310001510295mpc:DepreciationAndAmortizationMember2021-01-012021-12-310001510295us-gaap:CustomerConcentrationRiskMembermpc:A7ElevenMemberus-gaap:SalesRevenueNetMember2022-01-012022-12-310001510295us-gaap:CustomerConcentrationRiskMembermpc:Speedway7ElevenMemberus-gaap:SalesRevenueNetMember2021-01-012021-12-310001510295us-gaap:OtherNoncurrentAssetsMember2023-12-310001510295us-gaap:OtherNoncurrentAssetsMember2022-12-310001510295us-gaap:OtherNoncurrentLiabilitiesMember2023-12-310001510295us-gaap:OtherNoncurrentLiabilitiesMember2022-12-310001510295us-gaap:DomesticCountryMember2023-12-310001510295us-gaap:DomesticCountryMember2022-12-310001510295us-gaap:StateAndLocalJurisdictionMember2023-12-310001510295us-gaap:StateAndLocalJurisdictionMember2022-12-310001510295us-gaap:ForeignCountryMember2022-12-310001510295us-gaap:ForeignCountryMember2023-12-310001510295mpc:MarkwestTornadoGPLLCMember2023-12-152023-12-150001510295mpc:MarkwestTornadoGPLLCMember2023-12-150001510295mpc:SouthTexasGatewayTerminalMember2023-08-010001510295mpc:GibsonEnergyMembermpc:SouthTexasGatewayTerminalMember2023-08-012023-08-010001510295mpc:SouthTexasGatewayTerminalMember2023-08-012023-08-010001510295mpc:LFBioenergyMember2023-03-082023-03-080001510295mpc:CrowleyCoastalPartnersLLCMember2022-12-310001510295mpc:CrowleyOceanPartnersLLCMember2022-12-012022-12-010001510295mpc:CrowleyOceanPartnersLLCMember2022-12-310001510295mpc:NesteMembermpc:MartinezRenewablesLLCMember2022-09-212022-09-210001510295mpc:MartinezRenewablesLLCMember2022-09-300001510295mpc:WatsonCogenerationCompanyMember2022-06-010001510295mpc:WatsonCogenerationCompanyMember2022-06-012022-06-010001510295mpc:TheAndersonsMarathonHoldingsLLCMembermpc:RefiningAndMarketingMember2023-12-310001510295mpc:TheAndersonsMarathonHoldingsLLCMembermpc:RefiningAndMarketingMember2022-12-310001510295mpc:RefiningAndMarketingMembermpc:MartinezRenewablesLLCMember2023-12-310001510295mpc:RefiningAndMarketingMembermpc:MartinezRenewablesLLCMember2022-12-310001510295mpc:OtherEquityMethodInvesteesMembermpc:RefiningAndMarketingMember2023-12-310001510295mpc:OtherEquityMethodInvesteesMembermpc:RefiningAndMarketingMember2022-12-310001510295mpc:RefiningAndMarketingMember2023-12-310001510295mpc:RefiningAndMarketingMember2022-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:AndeavorLogisticsRioPipelineMember2023-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:AndeavorLogisticsRioPipelineMember2022-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:CentrahomaProcessingLLCMember2023-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:CentrahomaProcessingLLCMember2022-12-310001510295srt:SubsidiariesMembermpc:IllinoisExtensionPipelineCompanyLLCMembermpc:MidstreamMember2023-12-310001510295srt:SubsidiariesMembermpc:IllinoisExtensionPipelineCompanyLLCMembermpc:MidstreamMember2022-12-310001510295mpc:LoopLlcMembersrt:SubsidiariesMembermpc:MidstreamMember2023-12-310001510295mpc:LoopLlcMembersrt:SubsidiariesMembermpc:MidstreamMember2022-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:MarEnBakkenCompanyLLCMember2023-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:MarEnBakkenCompanyLLCMember2022-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:MarkWestEMGJeffersonDryGasGatheringCompanyL.L.C.Member2023-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:MarkWestEMGJeffersonDryGasGatheringCompanyL.L.C.Member2022-12-310001510295srt:SubsidiariesMembermpc:MarkwestTornadoGPLLCMembermpc:MidstreamMember2023-12-310001510295srt:SubsidiariesMembermpc:MarkwestTornadoGPLLCMembermpc:MidstreamMember2022-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:MarkWestUticaEMGMember2023-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:MarkWestUticaEMGMember2022-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:MinnesotaPipeLineCompanyLLCMember2023-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:MinnesotaPipeLineCompanyLLCMember2022-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:RendezvousGasServicesL.L.C.Member2023-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:RendezvousGasServicesL.L.C.Member2022-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:SherwoodMidstreamHoldingsMember2023-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:SherwoodMidstreamHoldingsMember2022-12-310001510295srt:SubsidiariesMembermpc:SherwoodMidstreamLLCMembermpc:MidstreamMember2023-12-310001510295srt:SubsidiariesMembermpc:SherwoodMidstreamLLCMembermpc:MidstreamMember2022-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:WhistlerPipelineLLCMember2023-12-310001510295srt:SubsidiariesMembermpc:MidstreamMembermpc:WhistlerPipelineLLCMember2022-12-310001510295mpc:OtherEquityMethodInvesteesMembersrt:SubsidiariesMembermpc:MidstreamMember2023-12-310001510295mpc:OtherEquityMethodInvesteesMembersrt:SubsidiariesMembermpc:MidstreamMember2022-12-310001510295srt:SubsidiariesMembermpc:MidstreamMember2023-12-310001510295srt:SubsidiariesMembermpc:MidstreamMember2022-12-310001510295srt:ParentCompanyMembermpc:MidstreamMembermpc:CaplinePipelineLLCMember2023-12-310001510295srt:ParentCompanyMembermpc:MidstreamMembermpc:CaplinePipelineLLCMember2022-12-310001510295srt:ParentCompanyMembermpc:MidstreamMembermpc:CrowleyCoastalPartnersLLCMember2023-12-310001510295srt:ParentCompanyMembermpc:MidstreamMembermpc:CrowleyCoastalPartnersLLCMember2022-12-310001510295srt:ParentCompanyMembermpc:MidstreamMembermpc:GrayOakPipelineLLCMember2023-12-310001510295srt:ParentCompanyMembermpc:MidstreamMembermpc:GrayOakPipelineLLCMember2022-12-310001510295mpc:LoopLlcMembersrt:ParentCompanyMembermpc:MidstreamMember2023-12-310001510295mpc:LoopLlcMembersrt:ParentCompanyMembermpc:MidstreamMember2022-12-310001510295srt:ParentCompanyMembermpc:MidstreamMembermpc:SouthTexasGatewayTerminalLLCMember2023-12-310001510295srt:ParentCompanyMembermpc:MidstreamMembermpc:SouthTexasGatewayTerminalLLCMember2022-12-310001510295mpc:OtherEquityMethodInvesteesMembersrt:ParentCompanyMembermpc:MidstreamMember2023-12-310001510295mpc:OtherEquityMethodInvesteesMembersrt:ParentCompanyMembermpc:MidstreamMember2022-12-310001510295srt:ParentCompanyMembermpc:MidstreamMember2023-12-310001510295srt:ParentCompanyMembermpc:MidstreamMember2022-12-310001510295mpc:MidstreamMember2023-12-310001510295mpc:MidstreamMember2022-12-310001510295us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOrGroupOfInvesteesMember2023-01-012023-12-310001510295us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOrGroupOfInvesteesMember2022-01-012022-12-310001510295us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOrGroupOfInvesteesMember2021-01-012021-12-310001510295us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOrGroupOfInvesteesMember2023-12-310001510295us-gaap:EquityMethodInvestmentNonconsolidatedInvesteeOrGroupOfInvesteesMember2022-12-310001510295mpc:RefiningAndMarketingMemberus-gaap:OperatingSegmentsMember2023-12-310001510295mpc:RefiningAndMarketingMemberus-gaap:OperatingSegmentsMember2022-12-310001510295mpc:MidstreamMemberus-gaap:OperatingSegmentsMember2023-12-310001510295mpc:MidstreamMemberus-gaap:OperatingSegmentsMember2022-12-310001510295us-gaap:CorporateNonSegmentMember2023-12-310001510295us-gaap:CorporateNonSegmentMember2022-12-310001510295us-gaap:ConstructionInProgressMember2023-12-310001510295us-gaap:ConstructionInProgressMember2022-12-310001510295mpc:RefiningAndMarketingMember2021-12-310001510295mpc:MidstreamMember2021-12-310001510295us-gaap:CustomerRelationshipsMember2023-12-310001510295us-gaap:CustomerRelationshipsMember2022-12-310001510295us-gaap:TrademarksAndTradeNamesMember2023-12-310001510295us-gaap:TrademarksAndTradeNamesMember2022-12-310001510295us-gaap:RoyaltyAgreementsMember2023-12-310001510295us-gaap:RoyaltyAgreementsMember2022-12-310001510295us-gaap:OtherIntangibleAssetsMember2023-12-310001510295us-gaap:OtherIntangibleAssetsMember2022-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001510295us-gaap:FairValueInputsLevel3Memberus-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001510295us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:EmbeddedDerivativeFinancialInstrumentsMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:EmbeddedDerivativeFinancialInstrumentsMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001510295us-gaap:EmbeddedDerivativeFinancialInstrumentsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001510295us-gaap:EmbeddedDerivativeFinancialInstrumentsMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001510295us-gaap:FairValueInputsLevel3Memberus-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001510295us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:EmbeddedDerivativeFinancialInstrumentsMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:EmbeddedDerivativeFinancialInstrumentsMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001510295us-gaap:EmbeddedDerivativeFinancialInstrumentsMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001510295us-gaap:EmbeddedDerivativeFinancialInstrumentsMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001510295us-gaap:FairValueInputsLevel3Membersrt:MinimumMember2023-12-310001510295srt:MaximumMemberus-gaap:FairValueInputsLevel3Member2023-12-310001510295us-gaap:FairValueInputsLevel3Member2023-12-31iso4217:USDutr:gal0001510295us-gaap:FairValueInputsLevel3Member2023-01-012023-12-310001510295us-gaap:CarryingReportedAmountFairValueDisclosureMember2023-12-310001510295us-gaap:EstimateOfFairValueFairValueDisclosureMember2023-12-310001510295us-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310001510295us-gaap:EstimateOfFairValueFairValueDisclosureMember2022-12-310001510295us-gaap:CommodityContractMemberus-gaap:OtherCurrentAssetsMember2023-12-310001510295us-gaap:CommodityContractMemberus-gaap:OtherCurrentAssetsMember2022-12-310001510295us-gaap:EmbeddedDerivativeFinancialInstrumentsMemberus-gaap:OtherCurrentLiabilitiesMember2023-12-310001510295us-gaap:EmbeddedDerivativeFinancialInstrumentsMemberus-gaap:OtherCurrentLiabilitiesMember2022-12-310001510295us-gaap:OtherNoncurrentLiabilitiesMemberus-gaap:EmbeddedDerivativeFinancialInstrumentsMember2023-12-310001510295us-gaap:OtherNoncurrentLiabilitiesMemberus-gaap:EmbeddedDerivativeFinancialInstrumentsMember2022-12-310001510295us-gaap:ExchangeTradedMembersrt:CrudeOilMember2023-01-012023-12-310001510295us-gaap:LongMemberus-gaap:ExchangeTradedMembersrt:CrudeOilMember2023-12-31utr:bbl0001510295us-gaap:ShortMemberus-gaap:ExchangeTradedMembersrt:CrudeOilMember2023-12-310001510295us-gaap:ExchangeTradedMembersrt:FuelMember2023-01-012023-12-310001510295us-gaap:LongMemberus-gaap:ExchangeTradedMembersrt:FuelMember2023-12-310001510295us-gaap:ShortMemberus-gaap:ExchangeTradedMembersrt:FuelMember2023-12-310001510295us-gaap:ExchangeTradedMembermpc:BlendingproductsMember2023-01-012023-12-310001510295us-gaap:LongMemberus-gaap:ExchangeTradedMembermpc:BlendingproductsMember2023-12-310001510295us-gaap:ShortMemberus-gaap:ExchangeTradedMembermpc:BlendingproductsMember2023-12-310001510295us-gaap:ExchangeTradedMembermpc:SoybeanOilMember2023-01-012023-12-310001510295us-gaap:LongMemberus-gaap:ExchangeTradedMembermpc:SoybeanOilMember2023-12-310001510295us-gaap:ShortMemberus-gaap:ExchangeTradedMembermpc:SoybeanOilMember2023-12-310001510295us-gaap:LongMemberus-gaap:OtherContractMemberus-gaap:ExchangeTradedMembersrt:CrudeOilMember2023-12-310001510295us-gaap:ShortMemberus-gaap:OtherContractMemberus-gaap:ExchangeTradedMembersrt:CrudeOilMember2023-12-310001510295us-gaap:LongMemberus-gaap:OtherContractMemberus-gaap:ExchangeTradedMembersrt:FuelMember2023-12-310001510295us-gaap:ShortMemberus-gaap:OtherContractMemberus-gaap:ExchangeTradedMembersrt:FuelMember2023-12-310001510295us-gaap:CommodityContractMemberus-gaap:SalesMember2023-01-012023-12-310001510295us-gaap:CommodityContractMemberus-gaap:SalesMember2022-01-012022-12-310001510295us-gaap:CommodityContractMemberus-gaap:SalesMember2021-01-012021-12-310001510295us-gaap:CostOfSalesMemberus-gaap:CommodityContractMember2023-01-012023-12-310001510295us-gaap:CostOfSalesMemberus-gaap:CommodityContractMember2022-01-012022-12-310001510295us-gaap:CostOfSalesMemberus-gaap:CommodityContractMember2021-01-012021-12-310001510295us-gaap:CommodityContractMemberus-gaap:OtherIncomeMember2023-01-012023-12-310001510295us-gaap:CommodityContractMemberus-gaap:OtherIncomeMember2022-01-012022-12-310001510295us-gaap:CommodityContractMemberus-gaap:OtherIncomeMember2021-01-012021-12-310001510295us-gaap:CommodityContractMember2023-01-012023-12-310001510295us-gaap:CommodityContractMember2022-01-012022-12-310001510295us-gaap:CommodityContractMember2021-01-012021-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMember2023-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMember2022-12-310001510295srt:ParentCompanyMember2023-12-310001510295srt:ParentCompanyMember2022-12-310001510295srt:ParentCompanyMembermpc:FinanceLeaseMember2023-12-310001510295srt:ParentCompanyMembermpc:FinanceLeaseMember2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMember2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMember2022-12-310001510295srt:SubsidiariesMembermpc:FinanceLeaseMember2023-12-310001510295srt:SubsidiariesMembermpc:FinanceLeaseMember2022-12-310001510295srt:SubsidiariesMember2022-12-310001510295us-gaap:CommercialPaperMember2016-02-260001510295us-gaap:CommercialPaperMember2016-02-262016-02-260001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMember2023-01-012023-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueSeptember2024Member2023-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueSeptember2024Member2022-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMay2025Member2023-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMay2025Member2022-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueDecember2026Member2023-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueDecember2026Member2022-12-310001510295srt:ParentCompanyMembermpc:SeniorNotesDueApril2028Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:ParentCompanyMembermpc:SeniorNotesDueApril2028Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2041Member2023-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2041Member2022-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueSeptember2044Member2023-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueSeptember2044Member2022-12-310001510295srt:ParentCompanyMembermpc:SeniorNotesDueDecember2045Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:ParentCompanyMembermpc:SeniorNotesDueDecember2045Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueApril2048Member2023-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueApril2048Member2022-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:AndeavorMembermpc:SeniorNotesDue20262048Member2023-12-310001510295srt:ParentCompanyMemberus-gaap:SeniorNotesMembermpc:AndeavorMembermpc:SeniorNotesDue20262048Member2022-12-310001510295srt:ParentCompanyMembermpc:SeniorNotesDueSeptember2054Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:ParentCompanyMembermpc:SeniorNotesDueSeptember2054Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMember2023-01-012023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueJuly2023Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueJuly2023Member2022-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueDecember2024Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueDecember2024Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueFebruary2025Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueFebruary2025Member2022-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueJune2025Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueJune2025Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:MarkWestMembermpc:SeniorNotesDue20232025Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:MarkWestMembermpc:SeniorNotesDue20232025Member2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2026Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2026Member2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2027Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2027Member2022-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueDecember2027Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueDecember2027Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueMarch2028Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueMarch2028Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueFebruary2029Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueFebruary2029Member2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueAugust2030Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueAugust2030Member2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueSeptember2032Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueSeptember2032Member2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2033Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2033Member2022-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueApril2038Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueApril2038Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2047Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2047Member2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueDecember2047Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueDecember2047Member2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDue20222047Membermpc:AndeavorLogisticsMember2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDue20222047Membermpc:AndeavorLogisticsMember2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueApril2048Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueApril2048Member2022-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueFebruary2049Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueFebruary2049Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueMarch2052Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueMarch2052Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2053Member2023-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2053Member2022-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueApril2058Memberus-gaap:SeniorNotesMember2023-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueApril2058Memberus-gaap:SeniorNotesMember2022-12-310001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMember2023-02-090001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2033Member2023-02-090001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueMarch2053Member2023-02-090001510295srt:SubsidiariesMemberus-gaap:SeriesBPreferredStockMembermpc:MPLXLPMember2023-02-152023-02-150001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueJuly2023Member2023-02-092023-03-310001510295us-gaap:SeniorNotesMembermpc:SeniorNotesDueJuly2023Member2023-01-012023-12-310001510295srt:SubsidiariesMembermpc:SeniorNotesDueMarch2052Memberus-gaap:SeniorNotesMember2022-03-140001510295srt:SubsidiariesMemberus-gaap:SeniorNotesMembermpc:SeniorNotesDueSeptember2032Member2022-08-110001510295srt:SubsidiariesMembermpc:SeniorNotesDueDecember2022Memberus-gaap:SeniorNotesMember2022-07-012022-09-300001510295srt:SubsidiariesMembermpc:SeniorNotesDueDecember2022Memberus-gaap:SeniorNotesMembermpc:ANDXMember2022-07-012022-09-300001510295srt:SubsidiariesMembermpc:SeniorNotesDueMarch2023Memberus-gaap:SeniorNotesMember2022-07-012022-09-300001510295mpc:MPCBankRevolvingCreditFacilityDueJuly2027Member2023-12-310001510295mpc:MPCTradeReceivablesSecuritizationDueSeptember2024Member2023-12-310001510295srt:SubsidiariesMembermpc:MPLXRevolvingCreditFacilityDueJuly2027Member2023-12-310001510295mpc:MPLXRevolvingCreditFacilityDueJuly2027Member2023-12-310001510295srt:ParentCompanyMembermpc:MPCRevolvingCreditFacilityDueOctober2023Member2022-07-070001510295srt:ParentCompanyMembermpc:MPCBankRevolvingCreditFacilityDueJuly2027Member2022-07-070001510295srt:ParentCompanyMemberus-gaap:LetterOfCreditMembermpc:MPCBankRevolvingCreditFacilityDueJuly2027Member2022-07-070001510295srt:ParentCompanyMembersrt:MaximumMembermpc:MPCBankRevolvingCreditFacilityDueJuly2027Member2022-07-07mpc:Period0001510295srt:ParentCompanyMembersrt:MaximumMemberus-gaap:BridgeLoanMembermpc:MPCBankRevolvingCreditFacilityDueJuly2027Member2022-07-070001510295srt:ParentCompanyMembersrt:MaximumMemberus-gaap:LetterOfCreditMembermpc:MPCBankRevolvingCreditFacilityDueJuly2027Member2022-07-070001510295srt:ParentCompanyMembermpc:MPCBankRevolvingCreditFacilityDueJuly2027Member2022-07-072022-07-070001510295mpc:MPCTradeReceivablesSecuritizationDueSeptember2024Member2022-07-310001510295mpc:MPLXRevolvingCreditFacilitydueJuly2024Membersrt:SubsidiariesMember2022-07-070001510295srt:SubsidiariesMembermpc:MPLXRevolvingCreditFacilityDueJuly2027Member2022-07-070001510295srt:SubsidiariesMembersrt:MaximumMemberus-gaap:LetterOfCreditMembermpc:MPLXRevolvingCreditFacilityDueJuly2027Member2022-07-070001510295srt:SubsidiariesMembersrt:MaximumMembermpc:MPLXRevolvingCreditFacilityDueJuly2027Member2022-07-070001510295srt:SubsidiariesMembermpc:MPLXRevolvingCreditFacilityDueJuly2027Member2022-07-072022-07-070001510295mpc:RefiningAndMarketingMembermpc:RefinedProductsMember2023-01-012023-12-310001510295mpc:RefiningAndMarketingMembermpc:RefinedProductsMember2022-01-012022-12-310001510295mpc:RefiningAndMarketingMembermpc:RefinedProductsMember2021-01-012021-12-310001510295srt:CrudeOilMembermpc:RefiningAndMarketingMember2023-01-012023-12-310001510295srt:CrudeOilMembermpc:RefiningAndMarketingMember2022-01-012022-12-310001510295srt:CrudeOilMembermpc:RefiningAndMarketingMember2021-01-012021-12-310001510295mpc:RefiningAndMarketingMembermpc:ServicesAndOtherMember2023-01-012023-12-310001510295mpc:RefiningAndMarketingMembermpc:ServicesAndOtherMember2022-01-012022-12-310001510295mpc:RefiningAndMarketingMembermpc:ServicesAndOtherMember2021-01-012021-12-310001510295mpc:MidstreamMembermpc:RefinedProductsMember2023-01-012023-12-310001510295mpc:MidstreamMembermpc:RefinedProductsMember2022-01-012022-12-310001510295mpc:MidstreamMembermpc:RefinedProductsMember2021-01-012021-12-310001510295mpc:MidstreamMembermpc:ServicesAndOtherMember2023-01-012023-12-310001510295mpc:MidstreamMembermpc:ServicesAndOtherMember2022-01-012022-12-310001510295mpc:MidstreamMembermpc:ServicesAndOtherMember2021-01-012021-12-310001510295us-gaap:PensionPlansDefinedBenefitMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-12-310001510295mpc:AccumulatedGainLossOtherMember2021-12-310001510295us-gaap:PensionPlansDefinedBenefitMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2022-01-012022-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2022-01-012022-12-310001510295us-gaap:PensionPlansDefinedBenefitMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2022-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2022-12-310001510295mpc:AccumulatedGainLossOtherMember2022-12-310001510295us-gaap:PensionPlansDefinedBenefitMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-01-012023-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-01-012023-12-310001510295us-gaap:PensionPlansDefinedBenefitMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMemberus-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-12-310001510295mpc:AccumulatedGainLossOtherMember2023-12-310001510295us-gaap:PensionPlansDefinedBenefitMember2022-12-310001510295us-gaap:PensionPlansDefinedBenefitMember2021-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2022-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2021-12-310001510295us-gaap:PensionPlansDefinedBenefitMember2023-01-012023-12-310001510295us-gaap:PensionPlansDefinedBenefitMember2022-01-012022-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2023-01-012023-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2022-01-012022-12-310001510295us-gaap:PensionPlansDefinedBenefitMember2023-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2023-12-310001510295us-gaap:PensionPlansDefinedBenefitMembermpc:PensionAnnuityLiftOutMember2022-01-012022-12-310001510295us-gaap:PensionPlansDefinedBenefitMembermpc:LoopLlcandExplorerPipelineMember2023-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMembermpc:LoopLlcandExplorerPipelineMember2023-12-310001510295us-gaap:PensionPlansDefinedBenefitMember2021-01-012021-12-310001510295us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2021-01-012021-12-310001510295mpc:MedicalBenefitsAgeLimitBelowSixtyFiveYearsMember2023-12-310001510295mpc:MedicalBenefitsAgeLimitBelowSixtyFiveYearsMember2022-12-310001510295mpc:MedicalBenefitsAgeLimitBelowSixtyFiveYearsMember2021-12-310001510295mpc:PrescriptionDrugsMember2023-12-310001510295mpc:PrescriptionDrugsMember2022-12-310001510295mpc:PrescriptionDrugsMember2021-12-310001510295mpc:MedicalBenefitsAgeLimitBelowSixtyFiveYearsMember2023-01-012023-12-310001510295mpc:MedicalBenefitsAgeLimitBelowSixtyFiveYearsMember2022-01-012022-12-310001510295mpc:MedicalBenefitsAgeLimitBelowSixtyFiveYearsMember2021-01-012021-12-310001510295mpc:PrescriptionDrugsMember2023-01-012023-12-310001510295mpc:PrescriptionDrugsMember2022-01-012022-12-310001510295mpc:PrescriptionDrugsMember2021-01-012021-12-310001510295us-gaap:EquitySecuritiesMember2023-12-310001510295us-gaap:FixedIncomeSecuritiesMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:CashAndCashEquivalentsMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:CashAndCashEquivalentsMember2023-12-310001510295us-gaap:CashAndCashEquivalentsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001510295us-gaap:CashAndCashEquivalentsMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:CashAndCashEquivalentsMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:CashAndCashEquivalentsMember2022-12-310001510295us-gaap:CashAndCashEquivalentsMemberus-gaap:FairValueInputsLevel3Member2022-12-310001510295us-gaap:CashAndCashEquivalentsMember2022-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:DefinedBenefitPlanEquitySecuritiesCommonStockMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:DefinedBenefitPlanEquitySecuritiesCommonStockMember2023-12-310001510295us-gaap:FairValueInputsLevel3Memberus-gaap:DefinedBenefitPlanEquitySecuritiesCommonStockMember2023-12-310001510295us-gaap:DefinedBenefitPlanEquitySecuritiesCommonStockMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:DefinedBenefitPlanEquitySecuritiesCommonStockMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:DefinedBenefitPlanEquitySecuritiesCommonStockMember2022-12-310001510295us-gaap:FairValueInputsLevel3Memberus-gaap:DefinedBenefitPlanEquitySecuritiesCommonStockMember2022-12-310001510295us-gaap:DefinedBenefitPlanEquitySecuritiesCommonStockMember2022-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:MutualFundMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:MutualFundMember2023-12-310001510295us-gaap:MutualFundMemberus-gaap:FairValueInputsLevel3Member2023-12-310001510295us-gaap:MutualFundMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:MutualFundMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:MutualFundMember2022-12-310001510295us-gaap:MutualFundMemberus-gaap:FairValueInputsLevel3Member2022-12-310001510295us-gaap:MutualFundMember2022-12-310001510295us-gaap:EquityFundsMemberus-gaap:FairValueInputsLevel1Member2023-12-310001510295us-gaap:EquityFundsMemberus-gaap:FairValueInputsLevel2Member2023-12-310001510295us-gaap:EquityFundsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001510295us-gaap:EquityFundsMember2023-12-310001510295us-gaap:EquityFundsMemberus-gaap:FairValueInputsLevel1Member2022-12-310001510295us-gaap:EquityFundsMemberus-gaap:FairValueInputsLevel2Member2022-12-310001510295us-gaap:EquityFundsMemberus-gaap:FairValueInputsLevel3Member2022-12-310001510295us-gaap:EquityFundsMember2022-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:CorporateDebtSecuritiesMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:CorporateDebtSecuritiesMember2023-12-310001510295us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001510295us-gaap:CorporateDebtSecuritiesMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:CorporateDebtSecuritiesMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:CorporateDebtSecuritiesMember2022-12-310001510295us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001510295us-gaap:CorporateDebtSecuritiesMember2022-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:USTreasuryAndGovernmentMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:USTreasuryAndGovernmentMember2023-12-310001510295us-gaap:USTreasuryAndGovernmentMemberus-gaap:FairValueInputsLevel3Member2023-12-310001510295us-gaap:USTreasuryAndGovernmentMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:USTreasuryAndGovernmentMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:USTreasuryAndGovernmentMember2022-12-310001510295us-gaap:USTreasuryAndGovernmentMemberus-gaap:FairValueInputsLevel3Member2022-12-310001510295us-gaap:USTreasuryAndGovernmentMember2022-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:FixedIncomeFundsMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:FixedIncomeFundsMember2023-12-310001510295us-gaap:FairValueInputsLevel3Memberus-gaap:FixedIncomeFundsMember2023-12-310001510295us-gaap:FixedIncomeFundsMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:FixedIncomeFundsMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:FixedIncomeFundsMember2022-12-310001510295us-gaap:FairValueInputsLevel3Memberus-gaap:FixedIncomeFundsMember2022-12-310001510295us-gaap:FixedIncomeFundsMember2022-12-310001510295us-gaap:PrivateEquityFundsMemberus-gaap:FairValueInputsLevel1Member2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:PrivateEquityFundsMember2023-12-310001510295us-gaap:PrivateEquityFundsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001510295us-gaap:PrivateEquityFundsMember2023-12-310001510295us-gaap:PrivateEquityFundsMemberus-gaap:FairValueInputsLevel1Member2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:PrivateEquityFundsMember2022-12-310001510295us-gaap:PrivateEquityFundsMemberus-gaap:FairValueInputsLevel3Member2022-12-310001510295us-gaap:PrivateEquityFundsMember2022-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:RealEstateMember2023-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:RealEstateMember2023-12-310001510295us-gaap:FairValueInputsLevel3Memberus-gaap:RealEstateMember2023-12-310001510295us-gaap:RealEstateMember2023-12-310001510295us-gaap:FairValueInputsLevel1Memberus-gaap:RealEstateMember2022-12-310001510295us-gaap:FairValueInputsLevel2Memberus-gaap:RealEstateMember2022-12-310001510295us-gaap:FairValueInputsLevel3Memberus-gaap:RealEstateMember2022-12-310001510295us-gaap:RealEstateMember2022-12-310001510295mpc:OtherPlanAssetsMemberus-gaap:FairValueInputsLevel1Member2023-12-310001510295mpc:OtherPlanAssetsMemberus-gaap:FairValueInputsLevel2Member2023-12-310001510295mpc:OtherPlanAssetsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001510295mpc:OtherPlanAssetsMember2023-12-310001510295mpc:OtherPlanAssetsMemberus-gaap:FairValueInputsLevel1Member2022-12-310001510295mpc:OtherPlanAssetsMemberus-gaap:FairValueInputsLevel2Member2022-12-310001510295mpc:OtherPlanAssetsMemberus-gaap:FairValueInputsLevel3Member2022-12-310001510295mpc:OtherPlanAssetsMember2022-12-310001510295us-gaap:FairValueInputsLevel1Member2023-12-310001510295us-gaap:FairValueInputsLevel2Member2023-12-310001510295us-gaap:FairValueInputsLevel1Member2022-12-310001510295us-gaap:FairValueInputsLevel2Member2022-12-310001510295us-gaap:FairValueInputsLevel3Member2022-12-310001510295us-gaap:OtherPensionPlansDefinedBenefitMember2023-12-310001510295us-gaap:PensionPlansDefinedBenefitMembermpc:CentralStatesSoutheastandSouthwestPensionPlanMember2023-01-012023-12-310001510295us-gaap:PensionPlansDefinedBenefitMembermpc:CentralStatesSoutheastandSouthwestPensionPlanMember2022-01-012022-12-310001510295us-gaap:PensionPlansDefinedBenefitMembermpc:CentralStatesSoutheastandSouthwestPensionPlanMember2021-01-012021-12-31mpc:employee0001510295mpc:MPC2021PlanMember2023-12-310001510295us-gaap:EmployeeStockOptionMember2023-01-012023-12-310001510295mpc:RestrictedStockandRestrictedStockUnitsMember2023-01-012023-12-310001510295mpc:MPC2021PlanMemberus-gaap:PerformanceSharesMember2023-01-012023-12-310001510295mpc:MPC2012PlanMemberus-gaap:PerformanceSharesMember2023-01-012023-12-310001510295us-gaap:PerformanceSharesMember2023-01-012023-12-310001510295us-gaap:EmployeeStockOptionMember2022-12-310001510295us-gaap:EmployeeStockOptionMember2023-12-310001510295us-gaap:EmployeeStockOptionMember2022-01-012022-12-310001510295us-gaap:EmployeeStockOptionMember2021-01-012021-12-310001510295us-gaap:RestrictedStockMember2022-12-310001510295us-gaap:RestrictedStockUnitsRSUMember2022-12-310001510295us-gaap:RestrictedStockMember2023-01-012023-12-310001510295us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001510295us-gaap:RestrictedStockMember2023-12-310001510295us-gaap:RestrictedStockUnitsRSUMember2023-12-310001510295us-gaap:RestrictedStockMember2022-01-012022-12-310001510295us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001510295us-gaap:RestrictedStockMember2021-01-012021-12-310001510295us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001510295us-gaap:PerformanceSharesMember2022-12-310001510295us-gaap:PerformanceSharesMember2023-12-310001510295mpc:PerformanceUnitsMember2023-01-012023-12-310001510295mpc:PerformanceUnitsMember2022-01-012022-12-310001510295mpc:PerformanceUnitsMember2021-01-012021-12-310001510295us-gaap:PerformanceSharesMember2022-01-012022-12-310001510295us-gaap:PerformanceSharesMember2021-01-012021-12-310001510295srt:MinimumMember2023-01-012023-12-310001510295srt:MaximumMember2023-01-012023-12-3100015102952022-07-3100015102952023-10-012023-12-310001510295us-gaap:AccountsReceivableMember2023-12-310001510295us-gaap:ReclassificationOtherMember2023-01-012023-12-310001510295mpc:GasGatheringAndTransmissionEquipmentAndFacilitiesMember2023-12-310001510295mpc:GasGatheringAndTransmissionEquipmentAndFacilitiesMember2022-12-310001510295mpc:ProcessingFractionationAndStorageFacilitiesMember2023-12-310001510295mpc:ProcessingFractionationAndStorageFacilitiesMember2022-12-310001510295us-gaap:PipelinesMember2023-12-310001510295us-gaap:PipelinesMember2022-12-310001510295mpc:TerminalsandrelatedassetsMember2023-12-310001510295mpc:TerminalsandrelatedassetsMember2022-12-310001510295mpc:LandBuildingOfficeEquipmentAndOtherMember2023-12-310001510295mpc:LandBuildingOfficeEquipmentAndOtherMember2022-12-310001510295us-gaap:PendingLitigationMember2023-01-012023-12-3100015102952020-07-012020-07-3100015102952020-10-012020-12-310001510295us-gaap:GuaranteeOfIndebtednessOfOthersMembermpc:LoopAndLocapLlcMemberus-gaap:FinancialGuaranteeMember2023-12-310001510295mpc:BakkenPipelineSystemMembermpc:IndirectMember2023-12-310001510295mpc:BakkenPipelineSystemMemberus-gaap:GuaranteeOfIndebtednessOfOthersMemberus-gaap:FinancialGuaranteeMember2023-12-310001510295mpc:CrowleyBlueWaterPartnersLLCMember2023-12-310001510295mpc:CrowleyBlueWaterPartnersLLCMemberus-gaap:GuaranteeOfIndebtednessOfOthersMemberus-gaap:FinancialGuaranteeMember2023-12-310001510295us-gaap:GuaranteeTypeOtherMember2023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

|

|

|

|

|

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2023

OR

|

|

|

|

|

|

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-35054

Marathon Petroleum Corporation

(Exact name of registrant as specified in its charter)

|

|

|

|

|

|

|

|

|

| Delaware |

|

27-1284632 |

| (State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

539 South Main Street, Findlay, OH 45840-3229

(Address of principal executive offices) (Zip code)

(419) 422-2121

(Registrant’s telephone number, including area code)

|

|

|

|

|

|

|

|

|

| Securities Registered pursuant to Section 12(b) of the Act |

| Title of each class |

Trading symbol(s) |

Name of each exchange on which registered |

| Common Stock, par value $.01 |

MPC |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer ☑ Accelerated filer ☐ Non-accelerated filer ☐ Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

The aggregate market value of common stock held by non-affiliates as of June 30, 2023 was approximately $47.2 billion. This amount is based on the closing price of the registrant’s common stock on the New York Stock Exchange on June 30, 2023. Shares of common stock held by executive officers and directors of the registrant are not included in the computation. The registrant, solely for the purpose of this required presentation, has deemed its directors and executive officers to be affiliates.

There were 361,358,732 shares of Marathon Petroleum Corporation common stock outstanding as of February 23, 2024.

Documents Incorporated By Reference

Portions of the registrant’s proxy statement relating to its 2024 Annual Meeting of Shareholders, to be filed with the Securities and Exchange Commission pursuant to Regulation 14A under the Securities Exchange Act of 1934, are incorporated by reference to the extent set forth in Part III, Items 10-14 of this Report.

Table of Contents

|

|

|

|

|

|

|

|

|

|

|

Page |

|

|

|

| Item 1. |

|

|

| Item 1A. |

|

|

| Item 1B. |

|

|

| Item 1C. |

|

|

| Item 2. |

|

|

| Item 3. |

|

|

| Item 4. |

|

|

|

|

|

|

|

|

| Item 5. |

|

|

| Item 7. |

|

|

| Item 7A. |

|

|

| Item 8. |

|

|

| Item 9. |

|

|

| Item 9A. |

|

|

| Item 9B. |

|

|

| Item 9C. |

|

|

|

|

|

|

|

|

| Item 10. |

|

|

| Item 11. |

|

|

| Item 12. |

|

|

| Item 13. |

|

|

| Item 14. |

|

|

|

|

|

|

|

|

| Item 15. |

|

|

|

|

|

Unless otherwise stated or the context otherwise indicates, all references in this Annual Report on Form 10-K to “MPC,” “us,” “our,” “we” or the “Company” mean Marathon Petroleum Corporation and its consolidated subsidiaries.

Glossary of Terms

Throughout this report, the following company or industry specific terms and abbreviations are used:

|

|

|

|

|

|

| ANS |

Alaska North Slope crude oil, an oil index benchmark price |

| ASC |

Accounting Standards Codification |

| ASU |

Accounting Standards Update |

| ATB |

Articulated tug barges |

| barrel |

One stock tank barrel, or 42 U.S. gallons liquid volume, used in reference to crude oil or other liquid hydrocarbons. |

| CARB |

California Air Resources Board |

| CARBOB |

California Reformulated Gasoline Blendstock for Oxygenate Blending |

| CBOB |

Conventional Gasoline Blendstock for Oxygenate Blending |

| EBITDA |

Earnings Before Interest, Tax, Depreciation and Amortization (a non-GAAP financial measure) |

| EPA |

U.S. Environmental Protection Agency |

| ESG |

Environmental, social and governance |

| FASB |

Financial Accounting Standards Board |

| GAAP |

Accounting principles generally accepted in the United States |

| GHG |

Greenhouse gas |

| LCFS |

Low Carbon Fuel Standard |

| LIFO |

Last in, first out |

| mbbls |

Thousands of barrels |

| mbpd |

Thousand barrels per day |

| mbpcd |

Thousand barrels per calendar day |

| MEH |

Magellan East Houston crude oil, an oil index benchmark price |

| MMcf/d |

One million cubic feet of natural gas per day |

| MMBtu |

One million British thermal units |

| NGL |

Natural gas liquids, such as ethane, propane, butanes and natural gasoline |

| NYMEX |

New York Mercantile Exchange |

| NYSE |

New York Stock Exchange |

| OSHA |

U.S. Occupational Safety and Health Administration |

| OTC |

Over-the-Counter |

| RFS2 |

Revised Renewable Fuel Standard program, as required by the Energy Independence and Security Act of 2007 |

| RIN |

Renewable Identification Number |

| SEC |

U.S. Securities and Exchange Commission |

| SOFR |

Secured overnight financing rate |

| STAR |

South Texas Asset Repositioning |

| ULSD |

Ultra-low sulfur diesel |

| USGC |

U.S. Gulf Coast |

| UST |

Underground storage tank |

| VIE |

Variable interest entity |

| VPP |

Voluntary Protection Program |

| WTI |

West Texas Intermediate crude oil, an oil index benchmark price |

Disclosures Regarding Forward-Looking Statements

This Annual Report on Form 10-K, particularly Item 1. Business, Item 1A. Risk Factors, Item 3. Legal Proceedings, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 7A. Quantitative and Qualitative Disclosures about Market Risk, includes forward-looking statements that are subject to risks, contingencies or uncertainties. You can identify forward-looking statements by words such as “anticipate,” “believe,” “commitment,” “could,” “design,” “estimate,” “expect,” “forecast,” “goal,” “guidance,” “intend,” “may,” “objective,” “opportunity,” “outlook,” “plan,” “policy,” “position,” “potential,” “predict,” “priority,” “project,” “prospective,” “pursue,” “seek,” “should,” “strategy,” “target,” “will,” “would” or other similar expressions that convey the uncertainty of future events or outcomes.

Forward-looking statements include, among other things, statements regarding:

•future financial and operating results;

•environmental, social and governance, which we refer to as “ESG”, plans and goals, including those related to greenhouse gas emissions and intensity, freshwater withdraw intensity, diversity and inclusion and ESG reporting;

•future levels of capital, environmental or maintenance expenditures, general and administrative and other expenses;

•the success or timing of completion of ongoing or anticipated capital or maintenance projects;

•business strategies, growth opportunities and expected investments, including plans to improve commercial performance, lower costs and optimize our asset portfolio;

•consumer demand for refined products, natural gas, renewables and natural gas liquids, such as ethane, propane, butanes and natural gasoline, which we refer to as “NGLs”;

•the timing, amount and form of any future capital return transactions, including dividends and share repurchases by MPC or distributions and unit repurchases by MPLX LP (“MPLX”); and

•the anticipated effects of actions of third parties such as competitors, activist investors, federal, foreign, state or local regulatory authorities, or plaintiffs in litigation.

Our forward-looking statements are not guarantees of future performance, and you should not rely unduly on them, as they involve risks, uncertainties and assumptions that we cannot predict. Forward-looking and other statements regarding our ESG plans and goals are not an indication that these statements are material to investors or required to be disclosed in our filings with the SEC. In addition, historical, current, and forward-looking ESG-related statements may be based on standards for measuring progress that are still developing, internal controls and processes that continue to evolve, and assumptions that are subject to change in the future. Material differences between actual results and any future performance suggested in our forward-looking statements could result from a variety of factors, including the following:

•general economic, political or regulatory developments, including inflation, interest rates, changes in governmental policies relating to refined petroleum products, crude oil, natural gas, NGLs or renewables, or taxation;

•the regional, national and worldwide availability and pricing of refined products, crude oil, natural gas, renewables, NGLs and other feedstocks;

•disruptions in credit markets or changes to credit ratings;

•the adequacy of capital resources and liquidity, including availability, timing and amounts of free cash flow necessary to execute business plans and to effect any share repurchases or to maintain or increase the dividend;

•the potential effects of judicial or other proceedings on our business, financial condition, results of operations and cash flows;

•the timing and extent of changes in commodity prices and demand for crude oil, refined products, feedstocks or other hydrocarbon-based products, or renewables;

•volatility in or degradation of general economic, market, industry or business conditions, including as a result of pandemics, other infectious disease outbreaks, natural hazards, extreme weather events, regional conflicts such as hostilities in the Middle East and in Ukraine, inflation or rising interest rates;

•our ability to comply with federal and state environmental, economic, health and safety, energy and other policies and regulations and enforcement actions initiated thereunder;

•adverse market conditions or other risks affecting MPLX;

•refining industry overcapacity or under capacity;

•foreign imports and exports of crude oil, refined products, natural gas and NGLs;

•changes in producer customers’ drilling plans or in volumes of throughput of crude oil, natural gas, NGLs, refined products, other hydrocarbon-based products or renewables;

•non-payment or non-performance by our customers;

•changes in the cost or availability of third-party vessels, pipelines, railcars and other means of transportation for crude oil, natural gas, NGLs, feedstocks, refined products and renewables;

•the price, availability and acceptance of alternative fuels and alternative-fuel vehicles and laws mandating such fuels or vehicles;

•political and economic conditions in nations that consume refined products, natural gas, renewables and NGLs, including the United States and Mexico, and in crude oil producing regions, including the Middle East, Russia, Africa, Canada and South America;

•actions taken by our competitors, including pricing adjustments, the expansion and retirement of refining capacity and the expansion and retirement of pipeline capacity, processing, fractionation and treating facilities in response to market conditions;

•completion of pipeline projects within the United States;

•changes in fuel and utility costs for our facilities;

•industrial incidents or other unscheduled shutdowns affecting our refineries, machinery, pipelines, processing, fractionation and treating facilities or equipment, means of transportation, or those of our suppliers or customers;

•acts of war, terrorism or civil unrest that could impair our ability to produce refined products, receive feedstocks or to gather, process, fractionate or transport crude oil, natural gas, NGLs, refined products or renewables;

•political pressure and influence of environmental groups and other stakeholders that are adverse to the production, gathering, refining, processing, fractionation, transportation and marketing of crude oil or other feedstocks, refined products, natural gas, NGLs, other hydrocarbon-based products or renewables;

•labor and material shortages;

•the timing and ability to obtain necessary regulatory approvals and permits and to satisfy other conditions necessary to complete planned projects or to consummate planned transactions within the expected timeframe, if at all;

•the availability of desirable strategic alternatives to optimize portfolio assets and the ability to obtain regulatory and other approvals with respect thereto;

•our ability to successfully implement our sustainable energy strategy and principles and achieve our ESG goals and targets within the expected timeframe, if at all;

•the costs, disruption and diversion of management’s attention associated with campaigns commenced by activist investors;

•personnel changes;

•the imposition of windfall profit taxes or maximum margin penalties on companies operating in the energy industry in California or other jurisdictions; and

•the other factors described in Item 1A. Risk Factors.

We undertake no obligation to update any forward-looking statements except to the extent required by applicable law.

PART I

Item 1. Business

OVERVIEW

MPC has more than 135 years of history in the energy business, and is a leading, integrated, downstream energy company. We operate one of the nation's largest refining systems with approximately 3.0 million barrels per day of crude oil refining capacity and believe we are one of the largest wholesale suppliers of gasoline and distillates to resellers in the United States. We distribute our refined products through one of the largest terminal operations in the United States and one of the largest private domestic fleets of inland petroleum product barges. In addition, our integrated midstream energy asset network links producers of natural gas and NGLs from some of the largest supply basins in the United States to domestic and international markets.

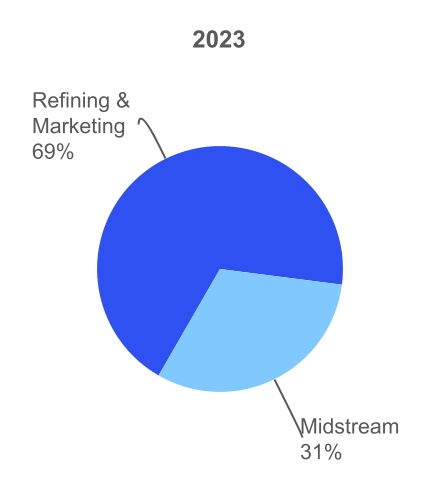

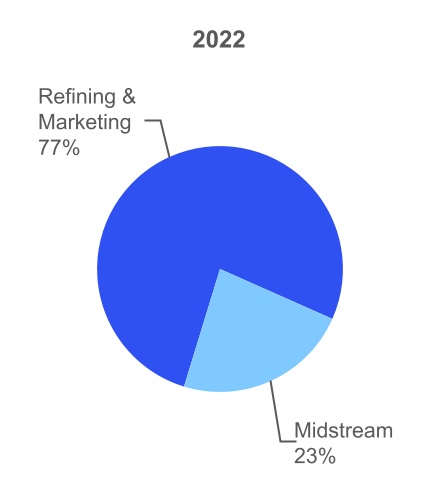

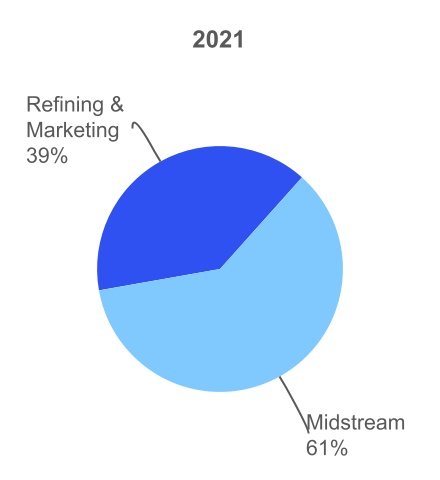

Our operations consist of two reportable operating segments: Refining & Marketing and Midstream. Each of these segments is organized and managed based upon the nature of the products and services it offers.

•Refining & Marketing – refines crude oil and other feedstocks, including renewable feedstocks, at our refineries in the Gulf Coast, Mid-Continent and West Coast regions of the United States, purchases refined products and ethanol for resale and distributes refined products, including renewable diesel, through transportation, storage, distribution and marketing services provided largely by our Midstream segment. We sell refined products to wholesale marketing customers domestically and internationally, to buyers on the spot market, to independent entrepreneurs who operate primarily Marathon® branded outlets and through long-term supply contracts with direct dealers who operate locations mainly under the ARCO® brand.

•Midstream – gathers, transports, stores and distributes crude oil, refined products, including renewable diesel, and other hydrocarbon-based products principally for the Refining & Marketing segment via refining logistics assets, pipelines, terminals, towboats and barges; gathers, processes and transports natural gas; and transports, fractionates, stores and markets NGLs. The Midstream segment primarily reflects the results of MPLX. MPLX is a diversified, large-cap master limited partnership (“MLP”) formed in 2012 that owns and operates midstream energy infrastructure and logistics assets and provides fuels distribution services. As of December 31, 2023, we owned the general partner of MPLX and approximately 65 percent of the outstanding MPLX common units.

Corporate History and Structure

MPC was incorporated in Delaware on November 9, 2009 in connection with an internal restructuring of Marathon Oil Corporation (“Marathon Oil”). On May 25, 2011, the Marathon Oil board of directors approved the spinoff of its Refining, Marketing & Transportation Business into an independent, publicly traded company, MPC, through the distribution of MPC common stock to the stockholders of Marathon Oil on June 30, 2011. Our common stock trades on the NYSE under the ticker symbol “MPC.”

On October 1, 2018, we acquired Andeavor. Andeavor shareholders received in the aggregate approximately 239.8 million shares of MPC common stock valued at $19.8 billion and $3.5 billion in cash. Andeavor was a highly integrated marketing, logistics and refining company operating primarily in the Western and Mid-Continent United States. Our acquisition of Andeavor in 2018 substantially increased our geographic diversification and the scale of our assets, which provides increased opportunities to optimize our system.

On May 14, 2021, we completed the sale of Speedway, LLC (“Speedway”), our company-owned and operated retail transportation fuel and convenience store business, to 7-Eleven, Inc. (“7-Eleven”) for cash proceeds of $21.38 billion ($17.22 billion after cash-tax payments). This transaction resulted in a pretax gain of $11.68 billion ($8.02 billion after income taxes), after deducting the book value of the net assets and certain other adjustments.

OUR OPERATIONS

Refining & Marketing

Refineries

We currently own and operate refineries in the Gulf Coast, Mid-Continent and West Coast regions of the United States with an aggregate crude oil refining capacity of 2,950 mbpcd. During 2023, our refineries processed 2,677 mbpd of crude oil and 237 mbpd of other charge and blendstocks. During 2022, our refineries processed 2,761 mbpd of crude oil and 190 mbpd of other charge and blendstocks.

Our refineries include crude oil atmospheric and vacuum distillation, fluid catalytic cracking, hydrocracking, catalytic reforming, coking, desulfurization and sulfur recovery units. The refineries process a wide variety of condensate and light and heavy crude oils purchased from various domestic and foreign suppliers. We produce numerous refined products, ranging from transportation fuels, such as reformulated gasolines, blend-grade gasolines intended for blending with ethanol and ULSD fuel, to heavy fuel oil and asphalt.

Additionally, we manufacture NGLs and petrochemicals and propane. See the Refined Product Sales section for further information about the products we produce.

Our refineries are largely integrated with each other via pipelines, terminals and barges to maximize operating efficiency. The transportation links that connect our refineries allow the movement of intermediate products between refineries to optimize operations, produce higher margin products and efficiently utilize our processing capacity. Also, shipping intermediate products between facilities during partial refinery shutdowns allows us to utilize processing capacity that is not directly affected by the shutdown work.

Following is a description of each of our refineries and their capacity by region.

Gulf Coast Region (1,228 mbpcd)

Galveston Bay, Texas City, Texas Refinery (631 mbpcd)

Our Galveston Bay refinery is a combination of our former Texas City refinery and Galveston Bay refinery. Following the completion of the STAR project in 2023, which added 40 mbpcd of capacity, it is now our largest refinery. The refinery is located on the Texas Gulf Coast southeast of Houston, Texas and can process a wide variety of crude oils into gasoline, distillates, NGLs and petrochemicals, heavy fuel oil and propane. The refinery has access to the export market and multiple options to sell refined products. Our cogeneration facility, which supplies the Galveston Bay refinery, currently has 1,055 megawatts of electrical production capacity and can produce 4.3 million pounds of steam per hour. Approximately 49 percent of the power generated in 2023 was used at the refinery, with the remaining electricity being sold into the electricity grid.

Garyville, Louisiana Refinery (597 mbpcd)

Our Garyville refinery is located along the Mississippi River in southeastern Louisiana between New Orleans, Louisiana and Baton Rouge, Louisiana. The Garyville refinery is configured to process a wide variety of crude oils into gasoline, distillates, NGLs and petrochemicals, propane, asphalt and heavy fuel oil. The refinery has access to the export market and multiple options to sell refined products. Our Garyville refinery has earned designation as an OSHA VPP Star site.

Mid-Continent Region (1,170 mbpcd)

Catlettsburg, Kentucky Refinery (300 mbpcd)

Our Catlettsburg refinery is located in northeastern Kentucky on the western bank of the Big Sandy River, near the confluence with the Ohio River. The Catlettsburg refinery processes sweet and sour crude oils, including production from the nearby Utica Shale, into gasoline, distillates, asphalt, NGLs and petrochemicals, propane and heavy fuel oil. Our Catlettsburg refinery has earned designation as an OSHA VPP Star site.

Robinson, Illinois Refinery (253 mbpcd)

Our Robinson refinery is located in southeastern Illinois. The Robinson refinery processes sweet and sour crude oils into gasoline, distillates, NGLs and petrochemicals, propane and heavy fuel oil. The Robinson refinery has earned designation as an OSHA VPP Star site.

Detroit, Michigan Refinery (140 mbpcd)

Our Detroit refinery is located in southwest Detroit. It is the only petroleum refinery currently operating in Michigan. The Detroit refinery processes sweet and heavy sour crude oils into gasoline, distillates, NGLs and petrochemicals, asphalt, propane and heavy fuel oil. Our Detroit refinery has earned designation as an OSHA VPP Star site.

El Paso, Texas Refinery (133 mbpcd)

Our El Paso refinery is located east of downtown El Paso. The El Paso refinery processes sweet and sour crude oils into gasoline, distillates, heavy fuel oil, asphalt, propane and NGLs and petrochemicals.

St. Paul Park, Minnesota Refinery (105 mbpcd)

Our St. Paul Park refinery is located along the Mississippi River southeast of St. Paul Park. The St. Paul Park refinery processes sweet and heavy sour crude oils into gasoline, distillates, asphalt, propane, NGLs and petrochemicals and heavy fuel oil.

Canton, Ohio Refinery (100 mbpcd)

Our Canton refinery is located south of Cleveland, Ohio. The Canton refinery processes sweet and sour crude oils, including production from the nearby Utica Shale, into gasoline, distillates, asphalt, propane, NGLs and petrochemicals and heavy fuel oil. The Canton refinery has earned designation as an OSHA VPP Star site.

Mandan, North Dakota Refinery (71 mbpcd)

Our Mandan refinery is located outside of Bismarck, North Dakota. The Mandan refinery processes primarily sweet domestic crude oil from North Dakota into gasoline, distillates, heavy fuel oil, propane and NGLs and petrochemicals.

Salt Lake City, Utah Refinery (68 mbpcd)

Our Salt Lake City refinery is the largest in Utah and is located north of downtown Salt Lake City. The Salt Lake City refinery processes crude oil from Utah, Colorado, Wyoming and Canada into gasoline, distillates, heavy fuel oil, propane and NGLs and petrochemicals.

West Coast Region (552 mbpcd)

Los Angeles, California Refinery (365 mbpcd)

Our Los Angeles refinery is located in Los Angeles County, near the Los Angeles Harbor. The Los Angeles refinery is the largest refinery on the West Coast and is a major producer of cleaner burning CARB fuels. The Los Angeles refinery processes heavy crude oil from California’s San Joaquin Valley and Los Angeles Basin, as well as crude oils from the Alaska North Slope, South America, West Africa and other international sources, into CARB gasoline and CARB diesel fuel, as well as conventional gasoline, distillates, NGLs and petrochemicals, heavy fuel oil and propane.

Anacortes, Washington Refinery (119 mbpcd)

Our Anacortes refinery is located north of Seattle on Puget Sound. The Anacortes refinery processes Canadian crude oil, domestic crude oil from North Dakota and the Alaska North Slope and international crude oils into gasoline, distillates, heavy fuel oil, propane and NGLs and petrochemicals.

Kenai, Alaska Refinery (68 mbpcd)