UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of September 2025

Commission File Number: 001-42445

Leishen Energy Holding Co., Ltd.

No. 528, 4th Avenue

103 Huizhong Li, B Building, Peking Times Square, Unit 15B10

Chaoyang District, Beijing, China

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Leishen Energy Holding Co., Ltd. | ||

| Date: September 30, 2025 | By: | /s/ Hongliang Li |

| Name: | Hongliang Li | |

| Title: | Chief Executive Officer | |

|

|

Exhibit Index

| Exhibit No. | Description | |

| 99.1 | Management’s Discussion and Analysis of Financial Condition and Results of Operations for the Six Months Ended March 31, 2025 | |

| 99.2 | Unaudited Interim Condensed Consolidated Financial Statements for the Six Months Ended March 31, 2025 | |

| 101. INS | Inline XBRL Instance Document. | |

| 101. SCH | Inline XBRL Taxonomy Extension Schema Document. | |

| 101. CAL | Inline XBRL Taxonomy Extension Calculation Linkbase Document. | |

| 101. DEF | Inline XBRL Taxonomy Extension Definition Linkbase Document. | |

| 101. LAB | Inline XBRL Taxonomy Extension Label Linkbase Document. | |

| 101. PRE | Inline XBRL Taxonomy Extension Presentation Linkbase Document. | |

| 104 | Cover Page Interactive Data File (formatted as Inline XBRL and contained in Exhibit 101). |

|

|

Exhibit 99.1

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our unaudited condensed consolidated financial statements (“CFS”) and related notes that appear in this interim report. In addition to historical consolidated financial information, the following discussion contains forward-looking statements that reflect our plans, estimates, and beliefs. Our actual results could differ materially from those discussed in the forward-looking statements.

Overview

Leishen Energy Holding Co., Ltd. (“Leishen Cayman”) was incorporated under the laws of Cayman Islands as an exempted company with limited liability on October 19, 2022. As a holding company with no material operations, Leishen Cayman conducts substantially all of its operations through its operating subsidiaries (collectively, the “Company”) in the PRC. The Company is a provider of clean-energy equipment and integrated solutions to the oil and gas industry, with a commitment to providing customers with high-performance, safe and cost-effective energy solutions. The Company’s major businesses segments include (i) clean-energy equipment; (ii) oil and gas engineering technical services; (iii) new energy production and operation; and (iv) digitalization and integration equipment. The Company’s business operations have expanded beyond the PRC to Central Asia, and Southeast Asia. At present, the Company holds 102 invention and utility model patent, 3 trademarks and 8 software copyrights.

On December 20, 2024, Leishen Cayman (Nasdaq: LSE) consummated its initial public offering (the “IPO”) of 1,375,000 ordinary shares, par value $0.001 at $4.00 per share (each, an “Ordinary Share”), with gross proceeds of $5.5 million. On January 8, 2025, Leishen Cayman issued and sold 150,000 additional Ordinary Shares at $4.00 per share, pursuant to the partial exercise of the Over-Allotment Option, resulting in additional gross proceeds of $600,000. As a result, Leishen Cayman raised aggregate gross proceeds of $6.1 million in the IPO. After deducting underwriting discounts and commissions, the Company received total net proceeds of $5.4 million.

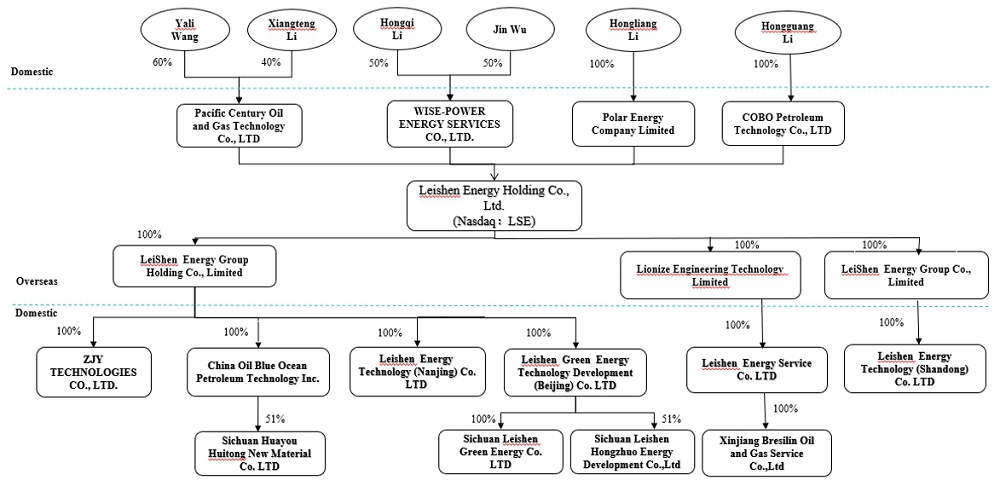

The Company’s corporate structure as of March 31, 2025 was as follows:

The Company’s principal subsidiaries are as follows:

| Legal Entity | Place of Incorporation | Date

of Incorporation |

Percentage of beneficial ownership | Principal activities |

||||

| Leishen Energy Holding Co., Ltd (“Leishen Cayman”) | Cayman Islands | October 19, 2022 | — | Holding company | ||||

| Leishen Energy Group Holding Co.,Ltd. (“Leishen (Holding) Hong Kong”) | Hongkong, China | November 25, 2022 | 100% | Holding company | ||||

| Leishen Energy Group Co., Ltd. (“Leishen Hong Kong”) | Hongkong, China | February 11, 2010 | 100% | Purchase and sale of oil and gas professional equipment and instruments | ||||

| ZJY Technologies Co., Ltd. (“ZJY Technologies”) | Beijing, China | March 2, 2007 | 100% | Design and sale of oil and gas professional equipment and after-sales support, and oilfield digitalization and integration service | ||||

| China Oil Blue Ocean Petroleum Technology Inc. (“China Oil Blue Ocean”) | Beijing, China | October 19, 2007 | 100% | Design and sale of oil and gas equipment and instruments, and engineering technology services | ||||

| Leishen Energy Technology (Nanjing) Co.,Ltd. (“Leishen Nanjing”) | Nanjing, China | September 27, 2022 | 100% | Purchase and sale of oil and gas professional equipment and instruments | ||||

| Leishen Green Energy Technology Development Co., Ltd. (“Beijing Leishen Green Energy”) | Beijing, China | January 29, 2018 | 100% | No business operations |

||||

| Leishen Energy Technology (Shandong) Co., Ltd. (“Leishen Shandong”) | Shandong, China | September 14, 2010 | 100% | Sales of oil and gas professional equipment and instruments | ||||

| Leishen Energy Services Co., Ltd. (“Leishen Services”) | Shandong, China | January 23, 2019 | 100% | No business operations |

||||

| Sichuan Leishen Green Energy Co., Ltd. (“Sichuan Leishen Green Energy”) | Chengdu, China | January 19, 2020 | 100% | Natural gas consultation service | ||||

| Sichuan Leishen Hongzhuo Energy Development Co., Ltd. (“Sichuan Leishen Hongzhuo”) | Chengdu, China | January 16, 2019 | 51% | Production, storage and transportation of natural gas (LNG/CNG) | ||||

| Sichuan Huayou Huitong New Material Co. Ltd. (“Huayou Huitong”) | Chengdu, China | May 29, 2020 | 51% | Production and sales of bonded composite pipes | ||||

| Xinjiang Breslin Oil and Gas Service Co., Ltd. (“Xinjiang Breslin”) | Xinjiang, China | August 22, 2024 | 100% | Purchase and sale of oil and gas professional equipment and instruments, and sales of oil and gas engineering technical service | ||||

| Lionize Engineering Technology Limited | Hongkong, China | February 21, 2025 | 100% | No business operations |

|

|

Results of Operations

Comparison of Results of Operations for the Six Months Ended March 31, 2025 and 2024

The following table summarizes our results of operations for the six months ended March 31, 2025 and 2024, and provides information regarding the dollar and percentage change during the six months.

| 2025 | 2024 | Variance | ||||||||||||||||||||||

| Amount | %

of revenue |

Amount | %

of revenue |

Amount | % | |||||||||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||||||||||

| Revenues | $ | 28,195,284 | 100 | % | $ | 39,883,516 | 100.0 | % | $ | (11,688,232 | ) | (29.3 | )% | |||||||||||

| Cost of revenues | (23,256,253 | ) | (82.5 | )% | (28,963,360 | ) | (72.6 | )% | 5,707,107 | (19.7 | )% | |||||||||||||

| Gross profit | 4,939,031 | 17.5 | % | 10,920,156 | 27.4 | % | (5,981,125 | ) | (54.8 | )% | ||||||||||||||

| Operating expenses: | ||||||||||||||||||||||||

| Selling and marketing | 635,306 | 2.3 | % | 959,481 | 2.4 | % | (324,175 | ) | (33.8 | )% | ||||||||||||||

| General and administrative | 6,362,965 | 22.6 | % | 3,700,169 | 9.3 | % | 2,662,796 | 72.0 | % | |||||||||||||||

| Research and development | 163,008 | 0.6 | % | 116,232 | 0.3 | % | 46,776 | 40.2 | % | |||||||||||||||

| Total operating expenses | 7,161,279 | 25.5 | % | 4,775,882 | 12.0 | % | 2,385,397 | 49.9 | % | |||||||||||||||

| (Loss) income from operations | (2,222,248 | ) | (8.0 | )% | 6,144,274 | 15.4 | % | (8,366,522 | ) | (136.2 | )% | |||||||||||||

| Other income (expense): | ||||||||||||||||||||||||

| Interest expense | (20,035 | ) | (0.1 | )% | (33,087 | ) | (0.1 | )% | 13,052 | (39.4 | )% | |||||||||||||

| Exchange gains | 45,795 | 0.2 | % | 3,651 | 0.0 | % | 42,144 | 1,154.3 | % | |||||||||||||||

| Income from equity investment | 171,368 | 0.6 | % | 65,043 | 0.2 | % | 106,325 | 163.5 | % | |||||||||||||||

| Net investment income (loss) | 826,153 | 2.9 | % | (116,219 | ) | (0.3 | )% | 942,372 | (810.9 | )% | ||||||||||||||

| Interest income from loans receivable | 50,805 | 0.2 | % | - | - | 50,805 | NA | |||||||||||||||||

| Gains from disposal of property and equipment | 116,311 | 0.4 | % | - | - | 116,311 | NA | |||||||||||||||||

| Other income (expenses), net | 77,831 | 0.3 | % | (10,935 | ) | 0.0 | % | 88,766 | (811.8 | )% | ||||||||||||||

| Total other income (expenses), net | 1,268,228 | 4.5 | % | (91,547 | ) | (0.2 | )% | 1,359,775 | (1,485.3 | )% | ||||||||||||||

| (Loss) income before income taxes | (954,020 | ) | (3.5 | )% | 6,052,727 | 15.2 | % | (7,006,747 | ) | (115.8 | )% | |||||||||||||

| Provision for income taxes | 14,635 | 0.1 | % | 879,909 | 2.2 | % | (865,274 | ) | (98.3 | )% | ||||||||||||||

| Net (loss) income | (968,655 | ) | (3.6 | )% | 5,172,818 | 13.0 | % | (6,141,473 | ) | (118.7 | )% | |||||||||||||

| Less: net loss attributable to non-controlling interests | (344,240 | ) | (1.2 | )% | (50,898 | ) | (0.1 | )% | (293,342 | ) | 576.3 | % | ||||||||||||

| Net (loss) income attributable to Leishen Energy Holding Co., Ltd. | $ | (624,415 | ) | (2.4 | )% | $ | 5,223,716 | 13.1 | % | $ | (5,848,131 | ) | (112.0 | )% | ||||||||||

|

|

Revenues

We have four revenue streams: clean-energy equipment sales, digitalization and integration equipment sales, new energy sales and delivery of oil and gas field engineering technical services. Revenues for the six months ended March 31, 2025 decreased by $11,688,232, or 29.3%, to $28,195,284 from $39,883,516 in 2024. The decrease in our revenues was primarily attributable to the decrease in revenue from sales of clean-energy equipment and new energy.

The following table sets forth the breakdown of our revenues for the six months ended March 31, 2025 and 2024:

| 2025 | 2024 | Variance | ||||||||||||||||||||||

| Amount | % | Amount | % | Amount | % | |||||||||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||||||||||

| Clean-energy equipment | $ | 13,196,043 | 46.8 | % | $ | 21,184,069 | 53.2 | % | $ | (7,988,026 | ) | (37.7 | )% | |||||||||||

| Digitalization and integration equipment | 2,629,399 | 9.3 | % | 1,694,214 | 4.2 | % | 935,185 | 55.2 | % | |||||||||||||||

| New energy sales | 10,337,148 | 36.7 | % | 14,000,065 | 35.1 | % | (3,662,917 | ) | (26.2 | )% | ||||||||||||||

| Oil and gas engineering technical services | 2,032,694 | 7.2 | % | 3,005,168 | 7.5 | % | (972,474 | ) | (32.4 | )% | ||||||||||||||

| Total | $ | 28,195,284 | 100.0 | % | $ | 39,883,516 | 100.0 | % | $ | (11,688,232 | ) | (29.3 | )% | |||||||||||

Revenues from clean-energy equipment sales. Revenues from clean-energy equipment sales accounted for 46.8% and 53.2% of our revenues for the six months ended March 31, 2025 and 2024, respectively. Revenue from clean-energy equipment sales decreased by $7,988,026 or 37.7% to $13,196,043 for the six months ended March 31, 2025 from $21,184,069 in 2024. The decrease was mainly due to the decrease in number of orders from a major customer. We expect this revenue stream will increase in the following six months to one year due to market development efforts to develop new customers and renew contractual relationships with existing customers.

Revenues from digitalization and integration equipment sales. Revenues from digitalization and integration equipment sales accounted for 9.3% and 4.2% of our revenues for the six months ended March 31, 2025 and 2024, respectively. Revenue from digitalization and integration equipment sales increased by $935,185 or 55.2% to $2,629,399 for the six months ended March 31, 2025 from $1,694,214 in 2024. The increase was mainly due to increase in orders from existing customers.

Revenues from new energy sales. Revenues from new energy sales accounted for 36.7% and 35.1% of our revenues for the six months ended March 31, 2025 and 2024, respectively. Revenue from new energy production and operation sales decreased by $3,662,917 or 26.2% to $10,337,148 for the six months ended March 31, 2025 from $14,000,065 in 2024. The decrease was mainly due to the decline in domestic demand for LNG and CNG, and fierce competition in the domestic gas trade market.

Revenues from oil and gas engineering technical services. Revenues from oil and gas engineering technical services accounted for 7.2% and 7.5% of our revenues for the six months ended March 31, 2025 and 2024, respectively. Revenues from oil and gas field engineering technical services decreased by $927,474 or 32.4% to $2,032,694 for the six months ended March 31, 2025 from $3,005,168 in 2024. The decrease was due mainly to the decrease in settlement price of our compressor rental service. The average daily settlement price dropped from RMB6,277($874) in 2024 to RMB5,784($806) in 2025.

|

|

Cost of Revenues

The following table sets forth the breakdown of our cost of revenue for the six months ended March 31, 2025 and 2024:

| 2025 | 2024 | Variance | ||||||||||||||||||||||

| Amount | % | Amount | % | Amount | % | |||||||||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||||||||||

| Clean-energy equipment | $ | 10,528,452 | 45.3 | % | $ | 13,025,854 | 45.0 | % | $ | (2,497,402 | ) | (19.2 | )% | |||||||||||

| Digitalization and integration equipment | 2,032,358 | 8.7 | % | 1,283,765 | 4.4 | % | 748,593 | 58.3 | % | |||||||||||||||

| New energy sales | 10,178,056 | 43.7 | % | 13,568,056 | 46.8 | % | (3,390,000 | ) | (25.0 | )% | ||||||||||||||

| Oil and gas engineering technical services | 517,387 | 2.3 | % | 1,085,685 | 3.8 | % | (568,298 | ) | (52.3 | )% | ||||||||||||||

| Total | $ | 23,256,253 | 100.0 | % | $ | 28,963,360 | 100.0 | % | $ | (5,707,107 | ) | (19.7 | )% | |||||||||||

Cost of clean-energy equipment sales decreased by $2,497,402, or 19.2%, to $10,528,452 for the six months ended March 31, 2025 from $13,025,854 in 2024, which was mainly due to the 37.7% decrease in related sales revenue.

Cost of digitalization and integration equipment sales increased by $748,593, or 58.3%, to $2,032,358 for the six months ended March 31, 2025 from $1,283,765 in 2024, which was mainly due to the increase in sales of digitalization and integration equipment.

Cost of new energy sales decreased by $3,390,000 or 25.0% to $10,178,056 for the six months ended March 31, 2025 from $13,568,056 in 2024, which was mainly due to the decrease of sales of new energy.

Cost of oil and gas engineering technical services decreased by $568,298 or 52.3% to $517,387 for the six months ended March 31, 2025 from $1,085,685 in 2024, which was mainly due to the decrease of oil and gas engineering technical services settlement price.

Gross Profit

Gross profit was $4,939,031 for the six months ended March 31, 2025, a decrease of $5,981,125 compared to $10,920,156 in 2024. Gross margin decreased to 17.5%, representing a 9.9% decline compared to 2024, mainly due to a decrease in gross margin on clean-energy equipment for the six months ended March 31, 2025 from 27.4% in 2024.

Our gross profit and gross margin by revenue types were as follows:

| Six Months Ended March 31, | ||||||||||||||||||||||||

| 2025 | 2024 | Variance | ||||||||||||||||||||||

| Gross Profit | Gross Margin % |

Gross Profit | Gross Margin % |

Gross Profit | Gross Margin % |

|||||||||||||||||||

| Clean-energy equipment | $ | 2,667,591 | 20.2 | % | $ | 8,158,215 | 38.5 | % | $ | (5,490,624 | ) | (18.3 | )% | |||||||||||

| Digitalization and integration equipment | 597,041 | 22.7 | % | 410,449 | 24.2 | % | 186,592 | (1.5 | )% | |||||||||||||||

| New energy sales | 159,092 | 1.5 | % | 432,009 | 3.1 | % | (272,917 | ) | (1.6 | )% | ||||||||||||||

| Oil and gas engineering technical services | 1,515,307 | 74.5 | % | 1,919,483 | 63.9 | % | (404,176 | ) | 10.6 | % | ||||||||||||||

| Total | $ | 4,939,031 | 17.5 | % | $ | 10,920,156 | 27.4 | % | $ | (5,981,125 | ) | (9.9 | )% | |||||||||||

|

|

Gross profit for clean-energy equipment sales decreased by $5,490,624 to $2,667,591 for the six months ended March 31, 2025, compared to $8,158,215 in 2024. The decrease in gross profit was due mainly to decrease of equipment sales. Gross margin decreased by 18.3% to 20.2%, primarily attributable to unfavorable product mix as we sold fewer high-margin products, such as compressors and expanders in the six months ended March 31, 2025 than in the comparable period of 2024.

Gross profit for digitalization and integration equipment sales increased by $186,592 to $597,041 for the six months ended March 31, 2025, compared to $410,449 in 2024. Gross margin decreased by 1.5%, to 22.7% for the six months ended March 31, 2025, from 24.2% in 2024. The decrease in gross margin was mainly attributable to higher production cost.

Gross profit for new energy sales decreased by $272,917 to $159,092 for the six months ended March 31, 2025, compared to $432,009 for the comparable period in 2024. The decrease in gross profit was mainly due to the decline in domestic demand for LNG and CNG, and fierce competition in the domestic gas trade market, which led to a reduction in overall sales prices and lower gross profit.

Gross profit for oil and gas engineering technical services decreased to $1,515,307 for the six months ended March 31, 2025 from $1,919,483 in 2024 due to the decrease of revenue. Gross margin increased by 10.6%, to 74.5% for the six months ended March 31, 2025, from 63.9% in 2024. The increase in gross margin was attributable to efforts to reduce our overall service costs.

Operating Expenses

Operating expenses were as following:

| Six Months Ended March 31, | ||||||||||||||||||||||||

| 2025 | 2024 | Variance | ||||||||||||||||||||||

| Amount | % | Amount | % | Amount | % | |||||||||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||||||||||

| Selling and marketing | $ | 635,306 | 8.9 | % | $ | 959,481 | 20.1 | % | $ | (324,175 | ) | (33.8 | )% | |||||||||||

| General and administrative | 6,362,965 | 88.8 | % | 3,700,169 | 77.5 | % | 2,662,796 | 72.0 | % | |||||||||||||||

| Research and development | 163,008 | 2.3 | % | 116,232 | 2.4 | % | 46,776 | 40.2 | % | |||||||||||||||

| Total operating expenses | $ | 7,161,279 | 100.0 | % | $ | 4,775,882 | 100.0 | % | $ | 2,385,397 | 49.9 | % | ||||||||||||

Selling and marketing Expenses

Selling and marketing expenses consist primarily of shipping and warehouse fees, consulting fees, bidding fees and payroll and benefits for employees involved in the sales and distribution functions. Selling and marketing expenses were $635,306 for the six months ended March 31, 2025, a decrease of $324,175, or 33.8%, from $959,481 in 2024. The decrease was due mainly to lower sales commissions resulting from reduced order volume, as well as decreases in shipping, warehousing and technical consulting fees. Selling and marketing expenses may increase as more production orders will lead to a higher commission fees and technical fees.

General and Administrative Expenses

General and administrative (“G&A”) expenses consist primarily of payroll and related costs for employees involved in general corporate functions, including accounting, finance, tax, legal and human resources, professional fees and other general corporate expenses as well as costs associated with the use by these functions of facilities and equipment, such as depreciation and rental expenses. Our G&A expenses were $6,362,965 for the six months ended March 31, 2025, an increase of $2,662,796, or 72.0%, from $3,700,169 in 2024. The increase was due mainly to (i) an increase of $988,000 in legal and auditing fees; and (ii) an increase of $1,942,900 of provision for expected credit losses in light of the slowdown of the PRC economy and difficult macroeconomic conditions. G&A expenses may continue to increase due to higher compliance and management requirements after the Company’s IPO.

|

|

Research and development expenses

R&D expenses consist primarily of payroll and related costs for employees involved in research functions and other general corporate expenses as well as costs associated with the use by these functions of facilities and equipment, such as depreciation and rental expenses. Our R&D expenses were $163,008 for the six months ended March 31, 2025, an increase of $46,776 from $116,232 in 2024 due to more materials used in R&D activities.

Other income (expenses), net

Other income (expenses) was as follows:

| Six Months Ended March 31, | ||||||||||||||||||||||||

| 2025 | 2024 | Variance | ||||||||||||||||||||||

| Amount | % | Amount | % | Amount | % | |||||||||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||||||||||

| Interest expense | $ | (20,035 | ) | (1.6 | )% | $ | (33,087 | ) | 36.1 | % | $ | 13,052 | (39.4 | )% | ||||||||||

| Exchange gains | 45,795 | 3.6 | % | 3,651 | (4.0 | )% | 42,144 | 1,154.3 | % | |||||||||||||||

| Income from equity investment | 171,368 | 13.5 | % | 65,043 | (71.0 | )% | 106,325 | 163.5 | % | |||||||||||||||

| Net investment income (loss) | 826,153 | 65.1 | % | (116,219 | ) | 127.0 | % | 942,372 | (810.9 | )% | ||||||||||||||

| Interest income from loans receivable | 50,805 | 4.0 | % | - | - | 50,805 | NA | |||||||||||||||||

| Gain from disposal of property and equipment | 116,311 | 9.3 | % | - | - | 116,311 | NA | |||||||||||||||||

| Other income (expenses), net | 77,831 | 6.1 | % | (10,935 | ) | 11.9 | % | 88,766 | (811.8 | )% | ||||||||||||||

| Total other income (expenses), net | $ | 1,268,228 | 100.0 | % | $ | (91,547 | ) | 100.0 | % | $ | 1,359,775 | (1,485.3 | )% | |||||||||||

Income from equity investment

Income from equity investment increased by $106,325, or 163.5%, to $171,368 for the six months ended March 31, 2025, from $65,043 for the six months ended March 31, 2024. The increase was mainly due to investee’s profitability during the six months ended March 31, 2025.

Net investment income (loss)

Net investment income increased by $942,372, or 810.9%, to $826,153 for the six months ended March 31, 2025, from net loss of $116,219 for the six months ended March 31, 2024. The increase was mainly due to the increase in the fair value of the trading securities.

Gain from disposal of property and equipment

For the six months ended March 31, 2025, The Company disposed of production equipment with net book value of RMB 4,846,387 ($676,199), received RMB 5,680,000 ($792,510) in cash, and recognized a gain on disposal of RMB 833,613 ($116,311).

Income Taxes

Our income tax was $14,635 for the six months ended March 31, 2025, a decrease of $865,274, or 98.3% from income tax of $879,909 in 2024.

Under the Enterprise Income Tax (“EIT”) Law of the PRC, domestic enterprises and Foreign Investment Enterprises (the “FIE”) are usually subject to a unified 25% EIT rate while preferential tax rates, tax holidays, and even tax exemptions may be granted on case-by-case basis. The PRC tax authorities grant preferential tax treatment to High and New Technology Enterprises (“HNTEs”). Under this preferential tax treatment, HNTEs are entitled to an income tax rate of 15%, subject to a requirement that they re-apply for HNTE status every three years. Since China Oil Blue Ocean was approved as an HNTE in December 2022, China Oil Blue Ocean is entitled to a reduced income tax rate of 15% beginning October 2022 and is able to enjoy the reduced income tax rate through October 2025. Since ZJY Technologies was approved as an HNTE in December 2022, ZJY Technologies is entitled to a reduced income tax rate of 15% beginning October 2022 and is able to enjoy the reduced income tax rate through October 2025. For the six months ended March 31, 2025 and 2024, our effective tax rates were -1.5% and 14.5%, respectively. The decrease in the effective tax rate was mainly due to the decrease in taxable income.

|

|

Net (loss) income

As a result of the foregoing, our net (loss) income for the six months ended March 31, 2025 and 2024 was loss of $968,655 and income of $5,172,818, respectively.

Net loss attributable to non-controlling interests

Non-controlling interests are recognized to reflect the portion of net income that is not attributable, directly or indirectly, to the Company as the controlling shareholder. For the Company’s consolidated subsidiaries, non-controlling interests are a minority shareholder’s 49% ownership interest in Sichuan Huayou Huitong New Material Co., Ltd and Sichuan Leishen Hongzhuo Energy Development Co., Ltd. Net loss attributable to non-controlling interest was $344,240 and $50,898 for the six months ended March 31, 2025 and 2024, respectively.

Net (loss) income attributable to Leishen Energy Holding Co., Ltd.

Net (loss) income attributable to Leishen Energy decreased by $5,848,131, or 112.0% from income of $5,223,716 for the six months ended March 31, 2024, to loss of $624,415 for the six months ended March 31, 2025.

Liquidity and Capital Resources

We are a holding company incorporated in the Cayman Islands. We conduct our operations primarily through our subsidiaries in China. As a result, our ability to pay dividends depends upon dividends paid by our subsidiaries in China. If our subsidiaries in China incur debt on their behalf, the instruments governing their debt may restrict their ability to pay dividends to us. In addition, our subsidiaries in China are permitted to pay dividends to us only out of its retained earnings, if any, as determined in accordance with PRC accounting standards and regulations. Under PRC law, our subsidiaries in China are required to set aside at least 10% of their after-tax profits each year, if any, to fund certain statutory reserve funds until such reserve funds reach 50% of their registered capital. Our subsidiaries in China may also allocate a portion of its after-tax profits based on PRC accounting standards to a discretionary surplus fund at its discretion. The statutory reserve funds and the discretionary funds are not distributable as cash dividends.

Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and trade and service-related foreign exchange transactions, can be made in foreign currencies without prior State Administration of Foreign Exchange of China (“SAFE”) approval as long as certain routine procedural requirements are fulfilled. However, capital account transactions, which include foreign direct investment and loans, must be approved by and/or registered with SAFE and its local branches.

As of March 31, 2025 and September 30, 2024, we had cash of $18,794,536 and $5,811,798, respectively. Our current assets were $63,613,523 and $61,747,189 as of March 31, 2025 and September 30, 2024, respectively. Our current liabilities were $28,388,726 and $27,140,909 as of March 31, 2025 and September 30, 2024, respectively. Our current ratios as of March 31, 2025 and September 30, 2024 were 224.1% and 227.5%, respectively. Total equity as of March 31, 2025 and September 30, 2024 was $43,358,819 and $40,455,513, respectively.

As of March 31, 2025, we had cash approximately $18.8 million and total working capital of approximately $35.2 million. As of September 30, 2024, we had cash approximately $5.8 million, restricted cash of $1.5 million and total working capital of approximately $34.6 million. Presently, our principal sources of liquidity are from our cash flows from operations, initial public offering and bank loans.

|

|

As of March 31, 2025, we had outstanding bank loans of approximately $3.9 million. We also entered into operating leases for our factory. The following table sets forth our contractual obligations as of March 31, 2025:

| Payment Due by Period | ||||||||||||||||||||

| Less than | More than | |||||||||||||||||||

| Contractual Obligations | Total | 1 year | 1 – 3 years | 3 – 5 years | 5 years | |||||||||||||||

| Operating lease obligations | $ | 719,162 | $ | 91,114 | $ | 179,442 | $ | 179,442 | $ | 269,164 | ||||||||||

| Loan Principal Obligations | 3,879,935 | 3,879,935 | - | - | - | |||||||||||||||

| Total | $ | 4,599,097 | $ | 3,971,049 | $ | 179,442 | $ | 179,442 | $ | 269,164 | ||||||||||

On December 20, 2024, we consummated our IPO and raised net proceeds of $5.4 million after deducting underwriting commission. We believe our current working capital is sufficient to support our operations for the next 12 months. We may, however, need additional cash in the future if we experience changes in business conditions or other developments. Our management believes it is necessary to enhance collection of outstanding accounts receivable and other receivables, and to be cautious on operational decisions and project selection. The Company reviews the accounts receivable on a periodic basis and makes general and specific allowances when there is doubt as to the collectability of individual balances. Our management is confident that the Company’s accounts receivable and other receivables are collectable.

Cash Flows Analysis

The following table sets forth a summary of our cash flows for the periods indicated:

Six Months Ended March 31, 2025 and 2024

| 2025 | 2024 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Net cash (used in) provided by operating activities | $ | (1,981,527 | ) | $ | 5,066,328 | |||

| Net cash provided by (used in) investing activities | 5,664,522 | (2,193,078 | ) | |||||

| Net cash provided by financing activities | 7,987,112 | 402,911 | ||||||

| Effect of foreign exchange rate on cash | (176,524 | ) | 16,239 | |||||

| Net increase in cash | 11,493,583 | 3,292,400 | ||||||

| Cash at the beginning of the period | 7,301,014 | 4,619,075 | ||||||

| Cash at the end of the period | $ | 18,794,597 | $ | 7,911,475 | ||||

Operating Activities

Net cash used in operating activities was $1,981,527 for the six months ended March 31, 2025, an increase of $7,047,855 from net cash provided by $5,066,328 for 2024. It was primarily due to the following: a) decrease of $5,253,314 in cash provided by accounts receivable and notes receivable, for reducing the use of notes and increase of the cash in payment; (b) an increase of $1,995,631 in cash used in advance payment to suppliers; (c) an increase of $1,766,789 in cash used in inventories for the fulfilment of new production orders; d) decrease of $365,346 in advance payment from customers due to fewer new orders in this period. These were partially offset by a decrease of $2,585,767 in cash used in accounts payable, for decreased orders in this period.

|

|

Investing Activities

Net cash provided by investing activities was $5,664,522 for the six months ended March 31, 2025, and net cash used in investing activities was $2,193,078 for the six months ended March 31, 2024. It was primarily due to: a) the purchase of property and equipment of $160,561 and $430,021 for the six months ended March 31, 2025 and 2024, respectively; b) purchase of short-term investments of $17,231,516 and $1,691,462 for the six months ended March 31, 2025 and 2024, respectively; c) maturities of short-term investments of $24,563,110 and nil for the six months ended March 31, 2025 and 2024, respectively; d) proceeds on disposal of property and equipment of $701,336 and nil for the six months ended March 31, 2025 and 2024, respectively; and e) loans to third parties of $2,299,751 and nil for the six months ended March 31, 2025 and 2024, respectively.

Financing Activities

Net cash provided by financing activities was $7,987,112 for the six months ended March 31, 2025. We obtained net borrowings of $2,733,921 via bank loans as working capital, and received approximately $5.4 million from IPO.

Net cash provided by financing activities was $402,911 for the six months ended March 31, 2024. We borrowed $113,759 via bank loans as working capital, and received $329,899 from non-controlling interests shareholders. And we paid $40,747 as offering cost.

Loan Facilities

(1) On April 18, 2023, the Company obtained a loan of RMB 670,000 ($93,317) from Shenzhen Qianhai Webank. From April 18, 2023 to March 31, 2025, the Company repaid RMB 638,095 ($88,893) in total. As of March 31, 2025, the balance of RMB 31,905 ($4,445) was outstanding. The amount was repaid on April 14, 2025.

(2) On April 18, 2023, the Company obtained a loan of RMB 400,000 ($55,711) from Shenzhen Qianhai Webank with. From April 18, 2023 to March 31, 2025, the Company repaid RMB 380,952 ($53,070) in total. As of March 31, 2025, the balance of RMB 19,048 ($2,654) was outstanding. The amount was repaid on April 14, 2025.

(3) On August 25, 2023, the Company obtained a loan of RMB 6 million ($835,864) from Bank of China Chengdu Hi-TechIndustrial Development Zone Sub-branch, which was due August 24, 2024. RMB 100,000 ($13,931) was repaid on July 25, 2024. On August 23, 2024, RMB 5,900,000 ($821,932) was refinanced and extended to August 23, 2025. The amount was repaid on August 23, 2025.

(4) On November 21, 2023, the Company obtained a loan of RMB 2 million ($278,559) from Bank of China Chengdu Hi-TechIndustrial Development Zone Sub-branch, which due November 20, 2024. RMB 100,000 ($13,931) was repaid in October, 2024. RMB 1,900,000 ($ 264,690) was refinanced and extended to October 15, 2025. RMB 100,000 ($13,931) was repaid on September 16, 2025.

(5) On March 18, 2025, the Company obtained a loan of RMB 10 million ($1,393,107) from Industrial and Commercial Bank of China Beijing Yayuncun Sub-branch, which is due March 17, 2026.

(6) On March 25, 2025, the Company obtained a loan of RMB 10 million ($1,393,107) from Industrial and Commercial Bank of China Beijing Yayuncun Sub-branch, which is due March 24, 2026.

Contingencies

From time to time, the Company may be subject to legal proceedings, claims and disputes that arise in the ordinary course of business. Amounts accrued, as well as the total amount of possible losses with respect to such matters, individually and in the aggregate, are not deemed to be material to the CFS.

Contractual Obligations

The Company leases certain office spaces and factories under operating lease agreements. Future minimum lease payments are $91,114 for the 12 months ending March 31, 2026.

|

|

Critical Accounting Estimates

Our CFS are prepared in accordance with accounting principles generally accepted in the U.S., which require us to make estimates and assumptions that affect the reported amounts of assets and liabilities. On an ongoing basis, we evaluate our estimates, including those estimates that may have a significant effect on our financial condition and results of operations. Our significant accounting policies are disclosed in Note 2 to our CFS. We base our estimates and judgment on historical experience and on various other factors that are believed to be reasonable under the circumstances. Actual results may differ from these estimates under different assumptions or conditions.

We consider an accounting estimate to be critical if:

| (a) | the nature of the estimate is material due to the levels of subjectivity and judgment necessary to account for highly uncertain matters or the susceptibility of such matters to change; and |

| (b) | the impact of the estimate on financial condition or operating performance is material. |

There are other items within our financial statements that require estimation but are not deemed critical, as defined above. Changes in estimates used in these and other items could have a material impact on our financial statements.

For a detailed description of our significant accounting policies and related judgments, please see Note 2. You should read the following description of critical accounting estimates in conjunction with our CFS and other disclosures included in our annual report for the year ended September 30, 2024.

Expected Credit Losses

Nature of estimate: Accounting Standards Update (ASU) No. 2016-13, “Financial Instruments – Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments,” requires us to record the full amount of expected credit losses for the life of a financial asset at the time it is originated or acquired, adjusted for subsequent changes in expected lifetime credit losses.

Assumptions: The Company assesses collectability by reviewing receivables on a collective basis where similar characteristics exist, primarily based on the size and nature of specific customers’ receivables. In determining the amount of the allowance for credit losses, the Company considers historical collectability based on past due status, the age of the receivable balances, credit quality of the Company’s customers based on ongoing credit evaluations, current economic conditions, reasonable and supportable forecasts of future economic conditions, and other factors that may affect the Company’s ability to collect from customers. Our allowance for expected credit losses is based on its assumptions regarding the probability of default. The expected probability of payment and time to default, which include assumptions about macroeconomic factors and customers’ performance. We recognized $3,317,683 and $1,374,786 expected credit losses of receivables and advances to suppliers for the six-months period ended March 31, 2025 and 2024, respectively.

Our estimate of the key assumptions did not change significantly throughout the periods presented.

|

|

Exhibit 99.2

LEISHEN ENERGY HOLDING CO., LTD. AND SUBSIDIARIES

INDEX TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| F- |

LEISHEN ENERGY HOLDING CO., LTD. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

| March 31, 2025 |

September 30, 2024 |

|||||||

| (Unaudited) | ||||||||

| ASSETS | ||||||||

| Current Assets: | ||||||||

| Cash | $ | 18,794,536 | $ | 5,811,798 | ||||

| Restricted cash | 61 | 1,489,216 | ||||||

| Short-term investments | 10,930,523 | 17,850,648 | ||||||

| Accounts receivable, net | 21,579,763 | 21,826,297 | ||||||

| Notes receivable | 406,787 | 1,054,528 | ||||||

| Advance to suppliers, net | 6,021,834 | 5,896,595 | ||||||

| Inventories | 3,661,309 | 5,396,634 | ||||||

| Due from related parties | 58,378 | 31,535 | ||||||

| Loan receivable - related party | 711,537 | 822,878 | ||||||

| Prepaid expenses and other current assets, net | 1,448,795 | 1,567,060 | ||||||

| Total current assets | 63,613,523 | 61,747,189 | ||||||

| Non-current assets: | ||||||||

| Long-term investments | 1,887,776 | 1,758,515 | ||||||

| Deferred offering costs | - | 437,653 | ||||||

| Property and equipment, net | 3,362,322 | 4,111,919 | ||||||

| Intangible assets | 128,638 | 140,070 | ||||||

| Operating lease right-of-use assets, net | 619,423 | 668,259 | ||||||

| Loans receivable, non-current | 3,004,626 | 725,699 | ||||||

| Other non-current assets | 39,341 | 44,746 | ||||||

| Total non-current assets | 9,042,126 | 7,886,861 | ||||||

| Total Assets | $ | 72,655,649 | $ | 69,634,050 | ||||

| LIABILITIES AND EQUITY | ||||||||

| Current Liabilities: | ||||||||

| Short-term loans | $ | 3,879,935 | $ | 50,899 | ||||

| Accounts payable | 8,061,974 | 10,731,238 | ||||||

| Advance from customers | 1,302,000 | 2,292,728 | ||||||

| Taxes payable | 3,108,801 | 3,418,725 | ||||||

| Due to related parties | 10,636,951 | 9,239,059 | ||||||

| Operating lease liabilities | 67,200 | 68,291 | ||||||

| Other payables and other current liabilities | 1,331,865 | 1,339,969 | ||||||

| Total current liabilities | 28,388,726 | 27,140,909 | ||||||

| Non-current Liabilities: | ||||||||

| Long-term loans | - |

1,127,380 | ||||||

| Deferred tax liabilities, net | 355,532 | 307,513 | ||||||

| Operating lease liabilities, non-current | 552,572 | 602,735 | ||||||

| Total non-current liabilities | 908,104 | 2,037,628 | ||||||

| Total Liabilities | 29,296,830 | 29,178,537 | ||||||

| Commitments and Contingencies | - | - | ||||||

| Equity: | ||||||||

| Ordinary shares (par value $0.001 per share, 50,000,000 shares authorized; 17,025,000 and 15,500,000 shares issued and outstanding as of March 31, 2025 and September 30, 2024, respectively) | 17,025 | 15,500 | ||||||

| Subscription receivable | (15,500 | ) | (15,500 | ) | ||||

| Additional paid-in capital | 6,431,979 | 1,617,966 | ||||||

| Statutory reserves | 1,737,024 | 1,690,994 | ||||||

| Retained earnings | 36,668,561 | 37,339,006 | ||||||

| Accumulated other comprehensive loss | (1,789,568 | ) | (861,374 | ) | ||||

| Total equity attributable to Leishen Energy Holding Co., Ltd | 43,049,521 | 39,786,592 | ||||||

| Non-controlling interests | 309,298 | 668,921 | ||||||

| Total Equity | 43,358,819 | 40,455,513 | ||||||

| Total Liabilities and Equity | $ | 72,655,649 | $ | 69,634,050 | ||||

| F- |

LEISHEN ENERGY HOLDING CO., LTD. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE (LOSS) INCOME

| Six Months Ended March 31, | ||||||||

| 2025 | 2024 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Revenues: | ||||||||

| Revenues - third parties | $ | 25,199,614 | $ | 37,249,302 | ||||

| Revenues - related parties | 2,995,670 | 2,634,214 | ||||||

| Total revenues | 28,195,284 | 39,883,516 | ||||||

| Cost of revenues | (23,256,253 | ) | (28,963,360 | ) | ||||

| Gross profit | 4,939,031 | 10,920,156 | ||||||

| Operating expenses: | ||||||||

| Selling and marketing | 635,306 | 959,481 | ||||||

| General and administrative | 6,362,965 | 3,700,169 | ||||||

| Research and development | 163,008 | 116,232 | ||||||

| Total operating expenses | 7,161,279 | 4,775,882 | ||||||

| (Loss) income from operations | (2,222,248 | ) | 6,144,274 | |||||

| Other income (expenses): | ||||||||

| Interest expense | (20,035 | ) | (33,087 | ) | ||||

| Exchange gains | 45,795 | 3,651 | ||||||

| Income from equity investment | 171,368 | 65,043 | ||||||

| Net investment income (loss) | 826,153 | (116,219 | ) | |||||

| Interest income from loans receivable | 50,805 | - | ||||||

| Gains from disposal of property and equipment | 116,311 | - | ||||||

| Other income (expenses), net | 77,831 | (10,935 | ) | |||||

| Total other income (expenses), net | 1,268,228 | (91,547 | ) | |||||

| (Loss) income before income taxes | (954,020 | ) | 6,052,727 | |||||

| Income taxes expense | 14,635 | 879,909 | ||||||

| Net (loss) income | (968,655 | ) | 5,172,818 | |||||

| Less: net loss attributable to non-controlling interests | (344,240 | ) | (50,898 | ) | ||||

| Net (loss) income attributable to Leishen Energy Holding Co., Ltd | $ | (624,415 | ) | $ | 5,223,716 | |||

| Comprehensive (loss) income | ||||||||

| Net (loss) income | $ | (968,655 | ) | $ | 5,172,818 | |||

| Foreign currency translation (loss) gain | (943,577 | ) | 400,578 | |||||

| Total comprehensive (loss) income | (1,912,232 | ) | 5,573,396 | |||||

| Less: comprehensive loss attributable to non-controlling interests | (359,623 | ) | (39,414 | ) | ||||

| Comprehensive (loss) income attributable to Leishen Energy Holding Co., Ltd | $ | (1,552,609 | ) | $ | 5,612,811 | |||

| (Loss) earnings per ordinary share | ||||||||

| – Basic and diluted | $ | (0.04 | ) | $ | 0.34 | |||

| Weighted average number of ordinary shares outstanding | ||||||||

| – Basic and diluted | 16,330,631 | 15,500,000 | ||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

| F- |

LEISHEN ENERGY HOLDING CO., LTD. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

SIX MONTHS ENDED MARCH 31, 2025 AND 2024

| Ordinary shares | Subscription |

Additional paid-in |

Statutory | Retained | Accumulated other comprehensive | Total equity attributable to Leishen Energy Holding | Non-controlling | Total | ||||||||||||||||||||||||||||||||

| Shares | Amount | receivable | capital | reserves | earnings | (loss) income | Co., Ltd | interests | equity | |||||||||||||||||||||||||||||||

| US$ | US$ | US$ | US$ | US$ | US$ | US$ | US$ | US$ | ||||||||||||||||||||||||||||||||

| Balance as of September 30, 2023 | 15,500,000 | $ | 15,500 | $ | (15,500 | ) | $ | 1,617,966 | $ | 1,565,649 | $ | 29,368,480 | $ | (1,746,809 | ) | $ | 30,805,286 | $ | 953,289 | $ | 31,758,575 | |||||||||||||||||||

| Contribution from non-controlling shareholders | - | - | - | - | - | - | - | - | 330,925 | 330,925 | ||||||||||||||||||||||||||||||

| Net income (loss) | - | - | - | - | - | 5,223,716 | - | 5,223,716 | (50,898 | ) | 5,172,818 | |||||||||||||||||||||||||||||

| Appropriation to statutory reserve | - | - | - | - | 426,125 | (426,125 | ) | - | - | - | - | |||||||||||||||||||||||||||||

| Foreign currency translation adjustment | - | - | - | - | - | - | 389,095 | 389,095 | 11,484 | 400,578 | ||||||||||||||||||||||||||||||

| Balance as of March 31, 2024 (Unaudited) | 15,500,000 | $ | 15,500 | $ | (15,500 | ) | $ | 1,617,966 | $ | 1,991,774 | $ | 34,166,071 | $ | (1,357,714 | ) | $ | 36,418,097 | $ | 1,244,800 | $ | 37,662,897 | |||||||||||||||||||

| Ordinary shares | Subscription |

Additional paid-in |

Statutory | Retained | Accumulated other comprehensive | Total equity attributable to Leishen Energy Holding | Non-controlling | Total | ||||||||||||||||||||||||||||||||

| Shares | Amount | receivable | capital | reserves | earnings | (loss) income | Co., Ltd | interests | equity | |||||||||||||||||||||||||||||||

| US$ | US$ | US$ | US$ | US$ | US$ | US$ | US$ | US$ | ||||||||||||||||||||||||||||||||

| Balance as of September 30, 2024 | 15,500,000 | $ | 15,500 | $ | (15,500 | ) | $ | 1,617,966 | $ | 1,690,994 | $ | 37,339,006 | $ | (861,374 | ) | $ | 39,786,592 | $ | 668,921 | $ | 40,455,513 | |||||||||||||||||||

| Shares issued in initial public offering | 1,525,000 | 1,525 | - | 4,814,013 | - | - | - | 4,815,538 | - | 4,815,538 | ||||||||||||||||||||||||||||||

| Net loss | - | - | - | - | - | (624,415 | ) | - | (624,415 | ) | (344,240 | ) | (968,655 | ) | ||||||||||||||||||||||||||

| Appropriation to statutory reserve | - | - | - | - | 46,030 | (46,030 | ) | - | - | - | - | |||||||||||||||||||||||||||||

| Foreign currency translation adjustment | - | - | - | - | - | - | (928,194 | ) | (928,194 | ) | (15,383 | ) | (943,577 | ) | ||||||||||||||||||||||||||

| Balance as of March 31, 2025(Unaudited) | 17,025,000 | $ | 17,025 | $ | (15,500 | ) | $ | 6,431,979 | $ | 1,737,024 | $ | 36,668,561 | $ | (1,789,568 | ) | $ | 43,049,521 | $ | 309,298 | $ | 43,358,819 | |||||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

| F- |

LEISHEN ENERGY HOLDING CO., LTD. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

| Six Months Ended March 31, | ||||||||

| 2025 | 2024 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Cash flows from operating activities: | ||||||||

| Net (loss) income | $ | (968,655 | ) | $ | 5,172,818 | |||

| Adjustments to reconcile net (loss) income to net cash (used in) provided by operating activities: | ||||||||

| Depreciation and amortization | 236,414 | 247,636 | ||||||

| (Gain) loss on disposal of property and equipment | (116,311 | ) | 1,966 | |||||

| Changes in fair value of short-term investments | (826,153 | ) | (177,275 | ) | ||||

| Provision for credit losses of receivables and advances to suppliers | 3,317,683 | 1,374,786 | ||||||

| Income from equity investment | (171,368 | ) | (49,600 | ) | ||||

| Non-cash lease expense | 28,670 | 33,612 | ||||||

| Deferred income tax | 55,422 | 112,095 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | (1,688,477 | ) | 3,814,706 | |||||

| Notes receivable | 623,613 | 163,897 | ||||||

| Advance to suppliers | (2,176,850 | ) | (181,200 | ) | ||||

| Inventories | 1,609,405 | 3,376,194 | ||||||

| Due from related parties | (27,636 | ) | - | |||||

| Prepaid expenses and other current assets | 93,910 | 415,253 | ||||||

| Accounts payable | (2,417,661 | ) | (5,003,428 | ) | ||||

| Advance from customers | (937,625 | ) | (572,279 | ) | ||||

| Taxes payable | (228,932 | ) | 1,090,704 | |||||

| Due to related parties | 1,620,234 | (4,907,100 | ) | |||||

| Other payables and other current liabilities | 23,817 | 186,248 | ||||||

| Lease liabilities | (31,027 | ) | (32,705 | ) | ||||

| Net cash (used in) provided by operating activities | (1,981,527 | ) | 5,066,328 | |||||

| Cash flows from investing activities: | ||||||||

| Purchase of property and equipment | (160,561 | ) | (430,021 | ) | ||||

| Proceeds from disposal of property and equipment | 701,336 | - | ||||||

| Repayment of loans from related party | 91,904 | - | ||||||

| Loans to third parties | (2,299,751 | ) | - | |||||

| Purchase of short-term investments | (17,231,516 | ) | (1,691,462 | ) | ||||

| Maturity of short-term investments | 24,563,110 | - | ||||||

| Purchase of long-term investments | - | (71,595 | ) | |||||

| Net cash provided by (used in) investing activities | 5,664,522 | (2,193,078 | ) | |||||

| Cash flows from financing activities: | ||||||||

| Proceeds from short-term loans | 3,055,629 | 113,759 | ||||||

| Repayments of short-term loans | (42,655 | ) | - | |||||

| Repayments of long-term loans | (279,053 | ) | - | |||||

| Net proceeds from initial public offering | 5,380,488 | - | ||||||

| Payment of offering expenses | (127,297 | ) | (40,747 | ) | ||||

| Capital contributions by noncontrolling interests | - | 329,899 | ||||||

| Net cash provided by financing activities | 7,987,112 | 402,911 | ||||||

| Effect of foreign exchange rate on cash | (176,524 | ) | 16,239 | |||||

| Net increase in cash | 11,493,583 | 3,292,400 | ||||||

| Cash at the beginning of the period | 7,301,014 | 4,619,075 | ||||||

| Cash at the end of the period | $ | 18,794,597 | $ | 7,911,475 | ||||

| Supplemental disclosures of cash flow information: | ||||||||

| Income taxes paid | $ | 153,192 | $ | 117,892 | ||||

| Interest paid | $ | 19,372 | $ | 33,087 | ||||

| Non-cash transactions: | ||||||||

| Operating right-of-use assets recognized for related operating lease liabilities | $ | (4,315 | ) | $ | 6,975 | |||

| Reclassification of deferred offering cost | $ | 437,653 | $ | - | ||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

| F- |

LEISHEN ENERGY HOLDING CO., LTD. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31, 2025 and September 30, 2024

NOTE 1 – ORGANIZATION AND BUSINESS DESCRIPTION

Leishen Energy Holding Co., Ltd. (“Leishen Cayman”) was incorporated under the laws of Cayman Islands as an exempted company with limited liability on October 19, 2022. As a holding company with no material operations, Leishen Cayman conducts substantially all of its operations through its operating subsidiaries (collectively, the “Company”) in the People’s Republic of China (“PRC” or “China”). The Company is a provider of clean-energy equipment and integrated solutions to the oil and gas industry, with a commitment to providing customers high-performance, safe and cost-effective energy solutions. The Company’s major businesses segments include (i) clean-energy equipment; (ii) oil and gas engineering technical services; (iii) new energy production and operation; and (iv) digitalization and integration equipment.

The Company’s corporate structure as of March 31, 2025 was as follows:

| F- |

The Company’s principal subsidiaries are as follows:

| Legal Entity | Place of Incorporation | Date

of Incorporation |

Percentage of beneficial ownership | Principal activities |

||||

| Leishen Energy Holding Co., Ltd (“Leishen Cayman”) | Cayman Islands | October 19, 2022 | — | Holding company | ||||

| Leishen Energy Group Holding Co.,Ltd. (“Leishen (Holding) Hong Kong”) | Hongkong, China | November 25, 2022 | 100% | Holding company | ||||

| Leishen Energy Group Co., Ltd. (“Leishen Hong Kong”) | Hongkong, China | February 11, 2010 | 100% | Purchase and sale of oil and gas professional equipment and instruments | ||||

| ZJY Technologies Co., Ltd. (“ZJY Technologies”) | Beijing, China | March 2, 2007 | 100% | Design and sale of oil and gas professional equipment and after-sales support, and oilfield digitalization and integration service | ||||

| China Oil Blue Ocean Petroleum Technology Inc. (“China Oil Blue Ocean”) | Beijing, China | October 19, 2007 | 100% | Design and sale of oil and gas equipment and instruments, and engineering technology services | ||||

| Leishen Energy Technology (Nanjing) Co.,Ltd. (“Leishen Nanjing”) | Nanjing, China | September 27, 2022 | 100% | Purchase and sale of oil and gas professional equipment and instruments | ||||

| Leishen Green Energy Technology Development Co., Ltd. (“Beijing Leishen Green Energy”) | Beijing, China | January 29, 2018 | 100% | No business operations | ||||

| Leishen Energy Technology (Shandong) Co., Ltd. (“Leishen Shandong”) | Shandong, China | September 14, 2010 | 100% | Sales of oil and gas professional equipment and instruments | ||||

| Leishen Energy Services Co., Ltd. (“Leishen Services”) | Shandong, China | January 23, 2019 | 100% | No business operations | ||||

| Sichuan Leishen Green Energy Co., Ltd. (“Sichuan Leishen Green Energy”) | Chengdu, China | January 19, 2020 | 100% | Natural gas consultation service | ||||

| Sichuan Leishen Hongzhuo Energy Development Co., Ltd. (“Sichuan Leishen Hongzhuo”) | Chengdu, China | January 16, 2019 | 51% | Production, storage and transportation of natural gas (LNG/CNG) | ||||

| Sichuan Huayou Huitong New Material Co. Ltd. (“Huayou Huitong”) | Chengdu, China | May 29, 2020 | 51% | Production and sales of bonded composite pipes | ||||

| Xinjiang Breslin Oil and Gas Service Co., Ltd. (“Xinjiang Breslin”) | Xinjiang, China | August 22, 2024 | 100% | Purchase and sale of oil and gas professional equipment and instruments, and sales of oil and gas engineering technical service | ||||

| Lionize Engineering Technology Limited | Hongkong, China | February 21, 2025 | 100% | No business operations |

Initial Public Offering (the “IPO”)

On December 20, 2024, Leishen Cayman (Nasdaq: LSE) consummated its initial public offering (the “IPO”) of 1,375,000 ordinary shares, par value $0.001 at $4.00 per share (each, an “Ordinary Share”), with gross proceeds of $5.5 million. On January 8, 2025, Leishen Cayman issued and sold 150,000 additional Ordinary Shares at $4.00 per share, pursuant to the partial exercise of the Over-Allotment Option, resulting in additional gross proceeds of $600,000. As a result, Leishen Cayman raised aggregate gross proceeds of $6.1 million in the IPO. After deducting the underwriting discounts and commissions, the Company received total net proceeds of $5.4 million.

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of presentation

The accompanying unaudited condensed consolidated financial statements (“CFS”) were prepared in accordance with accounting principles generally accepted in the U.S. of America (“U.S. GAAP”) and the rules and regulations of the Securities Exchange Commission (“SEC”). All adjustments necessary to present fairly in all material respects the financial position, results of operations and cash flows for all periods presented were made. While these CFS are prepared in accordance with US GAAP, they do not include all the information required for annual financial statements and should be read in conjunction with the audited CFS and accompanying notes included in the Company’s Form 20-F for the year ended September 30, 2024.

Principles of consolidation

The CFS include the financial statements of the Company and its majority-owned subsidiaries. All transactions and balances between the Company and its subsidiaries were eliminated upon consolidation.

| F- |

Non-controlling interests

Non-controlling interests are recognized to reflect the portion of subsidiary’s equity that is not attributable, directly or indirectly, to the Company as the controlling shareholder. For the Company’s consolidated subsidiaries, non-controlling interests are a minority shareholder’s 49% ownership interest in Huayou Huitong and Sichuan Leishen Hongzhuo.

Non-controlling interests were presented as a separate line item in the equity section of the Company’s consolidated balance sheets and were separately disclosed in the Company’s consolidated statements of operations and comprehensive (loss) income to distinguish the interests from that of the Company.

Use of estimates

In preparing the CFS in conformity with U.S. GAAP, management makes estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the dates of the CFS, as well as the reported amounts of revenue and expenses during the reporting periods. Significant items subject to such estimates and assumptions include, but are not limited to, the assessment of the allowance for credit losses, the valuation of inventories, useful lives of property and equipment and intangible assets, uncertain tax positions and realization of deferred tax assets. Actual results could differ from those estimates.

Foreign Currency Translation

The results of operations and the consolidated statements of cash flows are translated at the average rate of exchange during the reporting period. Assets and liabilities at the balance sheet date are translated at the applicable rates of exchange in effect at that date. The equity is translated at the historical rate of exchange at the time of capital contribution. Because cash flows are translated based on the average translation rate, amounts related to assets and liabilities reported on the consolidated statements of cash flows will not necessarily agree with changes in the corresponding balances on the consolidated balance sheets. Translation adjustments arising from the use of different exchange rates from period to period are included as a separate component of accumulated other comprehensive income (loss) included in consolidated statements of changes in equity. Gains and losses from foreign currency transactions are included in the Company’s consolidated statements of operations and comprehensive income.

The value of RMB against USD and other currencies fluctuates and is affected by, among other things, changes in the PRC’s political and economic conditions. Any significant revaluation of RMB may materially affect the Company’s financial condition in terms of USD reporting. The following table outlines the currency exchange rates used in preparing the CFS:

| March 31, | September 30, | Six Months Ended March 31, | ||||||||||||||

| 2025 | 2024 | 2025 | 2024 | |||||||||||||

| Foreign currency | Balance Sheet | Balance Sheet | Profits/Loss | Profits/Loss | ||||||||||||

| RMB:1USD | 7.1782 | 7.0074 | 7.1671 | 7.1234 | ||||||||||||

Cash

Cash includes cash on hand and demand deposits in accounts maintained with commercial banks. The Company maintains its bank accounts in mainland China and Hong Kong. In accordance with China’s Deposit Insurance Regulation that became effective in May 2015, pursuant to which banking financial institutions, such as commercial banks, established in the PRC are required to purchase deposit insurance for deposits in RMB and in foreign currency placed with them. The insurance limit is RMB 500,000 (approximately US$70,000) for each bank in China.

Restricted Cash

Cash that is legally restricted as to withdrawal or for use or pledged as security is reported separately on the face of the Company’s consolidated balance sheets. The Company’s restricted cash consisted of cash pledged as security for banker’s letter of guarantee. The Company follows Financial Accounting Standards Board (“FASB”) Accounting Standards Update (“ASU”) No. 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash and presented restricted cash within the ending cash and restricted cash balances on the Company’s consolidated statements of cash flows for the periods presented.

Short-term investments

Short-term investments consist of trading stock and debt securities, which include mutual funds and wealth management products issued by commercial banks. The Company accounts for its short-term investments in accordance with FASB ASC Topic 320 “Investments — Debt and Equity Securities.” Dividend and interest income, including amortization of the premium and discount arising at acquisition, for all categories of investments in securities is included in consolidated statements of operations. Net realized and unrealized holding gains and losses for short-term investments are included in net investment income (loss) in the consolidated statements of operations.

| F- |

If a security is acquired with the intent of selling it within hours or days, the security is classified as a trading security. The Company classifies investments in trading stock and mutual funds as trading securities. Unrealized holding gains and losses for trading securities are included in net investment income (loss).

If the Company has positive intent and ability to hold the investments to maturity, the security is classified as held-to-maturity security. The Company classifies investments in wealth management products issued by commercial banks as held-to-maturity securities as the Company intends to hold these investments in wealth management products until maturity and the maturity terms of these investments are within one year. Due to their short-term maturity, the investments in wealth management products are valued at carrying value, which approximates the amortized cost. For individual securities classified as held-to-maturity securities, the Company evaluates whether a decline in FV below the amortized cost basis is other-than-temporary, in accordance with ASC 320. Other-than-temporary impairment loss is recognized in earnings equal to the entire excess of the debt security’s amortized cost basis over its FV at the balance sheet date of the reporting period for which the assessment is made.

Accounts Receivable, net

Accounts receivable are presented net of an allowance for credit losses. On October 1, 2023, the Company adopted ASC 326, Credit Losses (“ASC 326”), which replaced previously issued guidance regarding the impairment of financial instruments with an expected loss methodology that will result in more timely recognition of credit losses. Upon adoption of ASC 326, the Company maintains an allowance for credit losses in accordance with ASC 326 and records the allowance for credit losses as an offset to assets such as accounts receivable, etc., and the estimated credit losses charged to the allowance are classified as general and administrative expenses in the consolidated statements of operations and comprehensive income (loss). The Company assesses collectability by reviewing receivables on a collective basis where similar characteristics exist. In determining the amount of the allowance for credit losses, the Company considers historical collectability based on past due status, the age of the receivable balances, credit quality of customers based on ongoing credit evaluations, current economic conditions, reasonable and supportable forecasts of future economic conditions, and other factors that may affect the Company’s ability to collect from customers. Bad debts are written off as incurred.

Notes Receivable

Notes receivable are trade accounts receivable due from various customers where the customers’ banks guaranteed the payments, which are non-interest bearing and generally range from three to six months from the date of issuance. The Company has the ability to submit request for payment to the customer’s bank earlier than the scheduled payment date but will incur an interest charge and a processing fee.

Advance to Suppliers, net

Advance to suppliers are balances paid to suppliers for inventories or services not provided or received. The Company reviews its advance to suppliers on a periodic basis and makes general and specific allowances when there is doubt as to the ability of a supplier to meet its contractual obligation or refund an advance.

Inventories

Inventories consist of raw materials, self-produced products, purchased products and compressed natural gas, and are stated at the lower of cost or net realizable value. Raw materials are primarily used to manufacture cleaning equipment which is the Company’s self-produced products, primarily including high-end cleaning equipment accessories. Cost is determined using the weighted average method. The Company periodically evaluates its inventories and will record an allowance for inventories that are either obsolete, slow-moving, may not be saleable or whose cost exceeds its net realizable value.

Loans receivable

Loans receivable consists of a loan to a related party and two loans to a third party. Loans receivables are stated at the historical carrying amount, net of allowance for credit losses.

| F- |

Property and Equipment, net

Property and equipment are carried at cost and are depreciated on the straight-line basis over the estimated useful lives of the underlying assets. The cost of repairs and maintenance is expensed as incurred; major replacements and improvements are capitalized. When assets are retired or disposed of, the cost and accumulated depreciation and amortization are removed from the accounts, and any resulting gains or losses are included in income in the year of disposition. The Company examines the possibility of decreases in the value of its property and equipment, when events or changes in circumstances reflect the fact that their recorded value may not be recoverable.

Estimated useful lives are as follows:

| Category | Estimated useful lives |

|

| Office equipment | 3-5 years | |

| Vehicle | 4 years | |

| Machine and equipment | 5-10 years |

Intangible Assets, net

Intangible assets consist primarily of accounting software that is carried at acquisition cost less accumulated amortization and impairment, if any. It is tested for impairment if triggering events occurred that could affect their carrying value. There were no asset impairment charges incurred during the six months ended March 31, 2025 and 2024. Amortization of intangible assets with finite lives is computed using the straight-line method over the estimated useful lives as below:

| Category | Estimated useful lives |

|

| Software | 10 years |

Fair value of financial instruments

FASB ASC 820, “Fair Value Measurement,” requires certain disclosures regarding the FV of financial instruments. FV is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. A three-level FV hierarchy prioritizes the inputs used to measure FV. The hierarchy requires entities to maximize the use of observable inputs and minimize the use of unobservable inputs. The three levels of inputs used to measure FV are as follows:

| ● | Level 1 - inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets. | |

| ● | Level 2 - inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, quoted market prices for identical or similar assets in markets that are not active, inputs other than quoted prices that are observable and inputs derived from or corroborated by observable market data. | |

| ● | Level 3 - inputs to the valuation methodology that are unobservable. |

Unless otherwise disclosed, the FV of the Company’s financial instruments including cash, short-term investments, accounts receivable, notes receivable, advance to suppliers, inventories, due from related parties, prepaid expenses and other current assets, short-term bank loans, long-term loans, accounts payable, advance from customers, taxes payable, due to related parties, and other payables and other current liabilities approximate their recorded values due to their short-term maturities. The FV of longer-term leases approximates their recorded values as their stated interest rates approximate the rates currently available.

The Company’s non-financial assets, such as property and equipment would be measured at FV only if they were determined to be impaired.

The Company’s investments are measured at FV. Short-term investment is wealth management products issued by commercial banks and stocks. The valuation for the Level 1 position is based on quoted prices in active markets. The following table presents information about our assets and liabilities that are measured at FV as of March 31, 2025 and September 30, 2024 and indicates the FV hierarchy of the valuation techniques we utilized to determine such FV. The valuation techniques are based on the FV measurement on a recurring basis of trading securities and held-to-maturity debt securities

| F- |

| Quoted | Significant | Significant | ||||||||||||||

| Prices in | Other | Other | ||||||||||||||

| As of | Active | Observable | Unobservable | |||||||||||||

| March 31 | Markets | Inputs | Inputs | |||||||||||||

| 2025 | (Level 1) | (Level 2) | (Level 3) | |||||||||||||

| (Unaudited) | ||||||||||||||||

| Trading securities | $ | 10,930,523 | $ | 10,930,523 | $ | - | $ | - | ||||||||

| Total | $ | 10,930,523 | $ | 10,930,523 | $ | - | $ | - | ||||||||

| Quoted | Significant | Significant | ||||||||||||||

| Prices in | Other | Other | ||||||||||||||

| As of | Active | Observable | Unobservable | |||||||||||||

| September 30 | Markets | Inputs | Inputs | |||||||||||||

| 2024 | (Level 1) | (Level 2) | (Level 3) | |||||||||||||

| Trading securities | $ | 17,850,648 | $ | 17,850,648 | $ | - | $ | - | ||||||||

| Total | $ | 17,850,648 | $ | 17,850,648 | $ | - | $ | - | ||||||||

Long-term Investments

Equity method investments are the Company’s investments in privately-held companies, over which it has significant influence but does not own a majority equity interest or otherwise control. The Company applies the equity method to account for an equity investment, in common stock or in-substance common stock, according to ASC 323 “Investment — Equity Method and Joint Ventures”.

An investment in in-substance common stock is an investment in an entity that has risk and reward characteristics that are substantially similar to that entity’s common stock. The Company considers subordination, risks and rewards of ownership and obligation to transfer value when determining whether an investment in an entity is substantially similar to an investment in that entity’s common stock.

Under the equity method, the Company’s share of the post-acquisition profits or losses of the equity investee is recognized in the consolidated income statements and its share of post-acquisition movements in accumulated other comprehensive income is recognized in shareholders’ equity. When the Company’s share of losses in the equity investee equals or exceeds its interest in the equity investee, the Company does not recognize further losses, unless the Company has incurred obligations or made payments or guarantees on behalf of the equity investee.

The Company continually reviews its investment in equity investees under equity method to determine whether a decline in FV to below the carrying value is other-than-temporary. The primary factors the Company considers in its determination are the duration and severity of the decline in FV, the financial condition, operating performance and the prospects of the equity investee, and other company specific information such as recent financing rounds. If the decline in FV is deemed to be other-than-temporary, the carrying value of the equity investee is written down to FV. There was no impairment during the six months ended March 31, 2025 and 2024.

Lease

ASC 842 requires lessees to recognize a right-of-use (“ROU”) asset and corresponding lease liability on the Consolidated Balance Sheets for all leases. The Company determines if an arrangement is a lease at inception of the arrangement and if such lease will be classified as an operating lease or a finance lease. As of March 31, 2025 and September 30, 2024, all of the Company’s leases are accounted for as operating leases.

ROU assets are the Company’s right to use an underlying asset for the lease term and lease liabilities are the Company’s obligation to make lease payments arising from the leases. ROU assets and lease liabilities are recognized at the lease commencement date based on the present value of lease payments over the lease term. Most leases do not provide an implicit interest rate; therefore, the Company used its incremental borrowing rate based on the information available at the inception date to determine the present value of the lease payments. Lease terms include options to extend the lease when it is reasonably certain that the Company will exercise that option. Lease cost for lease payments is recognized on a straight-line basis over the lease term. All ROU assets are reviewed for impairment annually. There was no impairment of the Company’s ROU assets as of March 31, 2025 and September 30, 2024.

Restricted net assets

Foreign exchange and other regulations in the PRC may further restrict the Company’s subsidiaries from transferring funds to the Company in the form of dividends, loans and advances. Amounts restricted include paid-in capital and statutory reserves of the Company’s PRC subsidiaries as determined pursuant to PRC generally accepted accounting principles.

| F- |

Revenue recognition

In accordance with FASB ASC 606, Revenue from Contracts with Customers, the Company recognizes revenue for the transfer of products or services to customers in an amount that reflects the consideration to which the Company expects to be entitled in such exchange. This requires the Company identify contractual performance obligations and determine whether revenue should be recognized at a point in time or over time, based on when control of the product or the benefit of the services transfers to the customer. Under the guidance of ASC 606, the Company is required to (a) identify the contract with a customer, (b) identify the performance obligations in the contract, (c) determine the transaction price, (d) allocate the transaction price to the performance obligations in the contract and (e) recognize revenue when (or as) the Company satisfies its performance obligations.

In accordance with ASC 606-10-55-89 through 55-91, the Company selected the type of good or service for presentation of disaggregated revenue. The Company’s presentation of its disaggregated revenues is aligned with information that can be reviewed by the Company’s chief operating decision maker for evaluating the financial performance of operating segments. The Company derives its revenues mainly from: sales of clean-energy equipment, sales of digitalization and integration equipment, sales of new energy and delivery of oil and gas engineering technical services. Revenues are the amount of consideration the Company is entitled to in exchange for the transfer of promised goods or services in the ordinary course of the Company’s activities and is recorded net of value-added tax (“VAT”). Consistent with the criteria of ASC 606, the Company recognizes revenue when the performance obligation in a contract is satisfied by transferring the control of promised goods or services to the customer. The Company also evaluates whether it is appropriate to record the gross amount of goods and services sold and the related costs.

The following table sets forth the breakdown of our revenues for the six months ended March 31, 2025 and 2024:

| 2025 | 2024 | |||||||||||||||

| Amount | % | Amount | % | |||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||

| Sales of clean-energy equipment | $ | 13,196,043 | 46.8 | $ | 21,184,069 | 53.2 | ||||||||||

| Sales of digitalization and integration equipment | 2,629,399 | 9.3 | 1,694,214 | 4.2 | ||||||||||||

| Sales of new energy | 10,337,148 | 36.7 | 14,000,065 | 35.1 | ||||||||||||

| Delivery of oil and gas engineering technical services | 2,032,694 | 7.2 | 3,005,168 | 7.5 | ||||||||||||

| Total | $ | 28,195,284 | 100.0 | $ | 39,883,516 | 100.0 | ||||||||||

Sale of clean-energy equipment