UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended April 30, 2025

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to _________.

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report:

Commission file number: 333-284137

Phaos Technology Holdings (Cayman) Limited

Phaos Technology (Cayman) Holdings Ltd

(Exact name of Registrant as Specified in its Charter)

Cayman Islands

(Jurisdiction of Incorporation or Organization)

83 Science Park Drive,

#04-01A/B The Curie, Singapore Science Park 1

Singapore 118258

+65 6250 3877

(Address of Principal Executive Offices)

Gan Hong Loon, Chief Financial Officer

+65 6250 3877

83 Science Park Drive,

#04-01A/B The Curie, Singapore Science Park 1

Singapore 118258

(Name, Telephone, E-mail and/or Facsimile Number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name of Each Exchange On Which Registered | ||

| Ordinary shares, par value US$0.0001 per share | POAS | NYSE American |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 10,601,750 Class A Ordinary Shares and 15,125,251 Class B Ordinary Shares , par value $0.001 per share, issued and outstanding as of April 30, 2025.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | Accelerated filer ☐ | Non-accelerated filer ☒ | Emerging growth company ☒ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☒ | U.S. GAAP | ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board | ☐ | Other |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s of assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262 (b)) by the registered public accounting firm that prepared or issued its audit report.

Yes ☐ No ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow: Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15 (d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court:

Yes ☐ No ☐

EXPLANATORY NOTE

On July 31, 2025, the Securities and Exchange Commission (the “SEC”) declared effective the Registration Statement on Form F-1 (Commission File No. 333-284137) (“Form F-1 Registration Statement”) of Phaos Technology Holdings (Cayman) Limited, a limited liability company organized under the law of Cayman Islands.

Rule 15d-2 (“Rule 15d-2”) under the Securities Exchange Act of 1934, as amended, provides generally that if a company’s registration statement under the Securities Act of 1933, as amended, does not contain certified financial statements for the company’s last full fiscal year preceding the year in which the registration statement becomes effective then the company must, within the later of 90 days after the effective date of the registration statement or four months following the end of the registrant’s latest full fiscal year, file a special financial report furnishing certified financial statements for the last full fiscal year, meeting the requirements of the form appropriate for annual reports of that company. Rule 15d-2 further provides that the special financial report is to be filed under cover of the facing sheet of the form appropriate for annual reports of the company.

The Form F-1 Registration Statement did not contain the certified financial statements of Phaos Technology Holdings (Cayman) Limited for the last fiscal year ended April 30, 2025; therefore, as required by Rule 15d-2, Phaos Technology Holdings (Cayman) Limited is hereby filing the certified financial statements of Phaos Technology Holdings (Cayman) Limited with the SEC under cover of the facing page of an annual report on Form 20-F.

|

|

|

|

Report of Independent Registered Public Accounting Firm

Board of Directors and Shareholders

Phaos Technology Holdings (Cayman) Limited

Opinion on the Financial Statements

We have audited the accompanying consolidated balance sheets of Phaos Technology Holdings (Cayman) Limited as of April 30, 2025 and 2024, and the related consolidated statements of operations and comprehensive loss, change in shareholders’ deficit, and cash flows for each of the two years in the period ended April 30, 2025, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of Phaos Technology Holdings (Cayman) Limited as of April 30, 2025 and 2024, and the results of its operations and its cash flows for each of the two years in the period ended April 30, 2025, in conformity with accounting principles generally accepted in the United States of America.

Going Concern

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 2 to the financial statements, the Company has incurred recurring losses from operations and has an accumulated deficit that raises substantial doubt about its ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 2. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion

These financial statements are the responsibility of the entity’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to Phaos Technology Holdings (Cayman) Limited in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. Phaos Technology Holdings (Cayman) Limited is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

/s/ Kreit & Chiu CPA LLP

We have served as Phaos Technology Holdings (Cayman) Limited’s auditor since 2023.

Los Angeles, California

September 18, 2025

| F- |

PHAOS TECHNOLOGY HOLDINGS (CAYMAN) LIMITED

CONSOLIDATED BALANCE SHEETS

| As of April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| ASSETS | ||||||||||||

| Current assets | ||||||||||||

| Cash and cash equivalents | 2,312,107 | 129,552 | 99,237 | |||||||||

| Accounts receivable, net | 412,589 | 38,384 | 29,402 | |||||||||

| Inventories | 187,584 | 310,007 | 237,465 | |||||||||

| Loan to third parties | 1,530,982 | 400,000 | 306,400 | |||||||||

| Deferred offering costs | 224,694 | 497,302 | 380,933 | |||||||||

| Other current assets | 65,156 | 140,400 | 107,546 | |||||||||

| Total current assets | 4,733,112 | 1,515,645 | 1,160,983 | |||||||||

| Non-current assets | ||||||||||||

| Property and equipment, net | 233,309 | 286,558 | 219,503 | |||||||||

| Right-of-use assets | 218,146 | 131,845 | 100,993 | |||||||||

| Total non-current assets | 451,455 | 418,403 | 320,496 | |||||||||

| TOTAL ASSETS | 5,184,567 | 1,934,048 | 1,481,479 | |||||||||

| LIABILITIES | ||||||||||||

| Current liabilities | ||||||||||||

| Accounts payable | 293,908 | 93,931 | 71,951 | |||||||||

| Accruals and other payables | 445,122 | 541,678 | 414,924 | |||||||||

| Amount due to major shareholders | 732,753 | 2,995,423 | 2,294,494 | |||||||||

| Bank loans, current | 440,455 | 55,613 | 42,600 | |||||||||

| Operating lease liabilities, current | 132,786 | 109,142 | 83,603 | |||||||||

| Total current liabilities | 2,045,024 | 3,795,787 | 2,907,572 | |||||||||

| Non-current liabilities | ||||||||||||

| Bank loans, non-current | 133,979 | 78,366 | 60,028 | |||||||||

| Operating lease liabilities, non-current | 85,360 | 22,703 | 17,390 | |||||||||

| Total non-current liabilities | 219,339 | 101,069 | 77,418 | |||||||||

| TOTAL LIABILITIES | 2,264,363 | 3,896,856 | 2,984,990 | |||||||||

| COMMITMENTS AND CONTINGENCIES | - | - | - | |||||||||

| SHAREHOLDERS’ (DEFICIT) / EQUITY | ||||||||||||

| Ordinary shares, Class A, USD 0.0001 par value and 10,601,750 outstanding at April 30 2025; Ordinary shares, Class A, USD 0.0001 par value and 10,473,625 outstanding at April 30 2024 | 1,428 | 1,445 | 1,107 | |||||||||

| Ordinary shares, Class B, USD 0.0001 par value and 15,125,251 shares outstanding at April 30, 2025; Ordinary shares, Class B, USD 0.0001 par value and 15,125,251 shares outstanding at April 30, 2024 | 2,063 | 2,063 | 1,580 | |||||||||

| Additional paid-in capital | 9,984,030 | 10,239,208 | 7,843,234 | |||||||||

| Subscription receivable | (37,251 | ) | (37,251 | ) | (28,534 | ) | ||||||

| Accumulated other comprehensive loss | - | (1,143 | ) | (876 | ) | |||||||

| Accumulated deficit | (7,030,066 | ) | (12,167,130 | ) | (9,320,022 | ) | ||||||

| Total shareholders’ (deficit) / equity | 2,920,204 | (1,962,808 | ) | (1,503,511 | ) | |||||||

| TOTAL LIABILITIES AND EQUITY | 5,184,567 | 1,934,048 | 1,481,479 | |||||||||

The accompanying notes are an integral part of these consolidated financial statements.

| F- |

PHAOS TECHNOLOGY HOLDINGS (CAYMAN) LIMITED

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

| For the years ended, April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Revenue | 1,882,803 | 167,707 | 128,464 | |||||||||

| Cost of Goods sold (excluding depreciation shown separately below) | (985,099 | ) | (130,641 | ) | (100,072 | ) | ||||||

| Employee benefits expenses | (1,851,971 | ) | (2,462,326 | ) | (1,886,142 | ) | ||||||

| Depreciation expenses | (176,713 | ) | (186,963 | ) | (143,214 | ) | ||||||

| Operating lease expense | (136,781 | ) | (142,670 | ) | (109,286 | ) | ||||||

| Research and Development Expenses | (90,566 | ) | (139,720 | ) | (107,026 | ) | ||||||

| Other operating expenses | (1,144,802 | ) | (1,161,663 | ) | (889,834 | ) | ||||||

| Impairment of loan to third parties | - | (1,223,608 | ) | (937,284 | ) | |||||||

| Loss from operations | (2,503,129 | ) | (5,279,884 | ) | (4,044,394 | ) | ||||||

| Non-operating income : | ||||||||||||

| Other income | 186,828 | 151,283 | 115,883 | |||||||||

| Interest expense | (43,543 | ) | (8,463 | ) | (6,483 | ) | ||||||

| Total non-operating income, net | 143,285 | 142,820 | 109,400 | |||||||||

| Loss before income taxes | (2,359,844 | ) | (5,137,064 | ) | (3,934,994 | ) | ||||||

| Income tax expense | - | - | - | |||||||||

| Net loss | (2,359,844 | ) | (5,137,064 | ) | (3,934,994 | ) | ||||||

| Weighted average number of outstanding ordinary shares* | ||||||||||||

| Basic and diluted | 23,540,241 | 25,662,939 | 25,662,939 | |||||||||

| Net loss per share attributable to ordinary shareholders | ||||||||||||

| Basic and diluted | (0.10 | ) | (0.20 | ) | (0.15 | ) | ||||||

| * | Give retroactive effect to reflect the reorganization on November 2024. See Note 1. |

The accompanying notes are an integral part of these consolidated financial statements.

| F- |

PHAOS TECHNOLOGY HOLDINGS (CAYMAN) LIMITED

CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ DEFICIT

| Ordinary shares (Class A and Class B) | ||||||||||||||||||||||||||||

| Shares Outstanding* | Par value** | Additional paid-in capital | Subscription Receivables | Accumulated other comprehensive loss | Accumulated deficit |

Total shareholders’ (deficit)/ equity |

||||||||||||||||||||||

| S$ | S$ | S$ | S$ | S$ | S$ | |||||||||||||||||||||||

| Balance as of April 30, 2024 | 25,598,876 | 3,491 | 9,984,030 | (37,251 | ) | - | (7,030,066 | ) | 2,920,204 | |||||||||||||||||||

| Net loss | - | (5,137,064 | ) | (5,137,064 | ) | |||||||||||||||||||||||

| Translation Gain/(Loss) | (1,143 | ) | (1,143 | ) | ||||||||||||||||||||||||

| Shares issued during the year | 128,125 | 17 | 255,178 | - | - | 255,195 | ||||||||||||||||||||||

| Balance as of April 30, 2025 | 25,727,001 | 3,508 | 10,239,208 | (37,251 | ) | (1,143 | ) | (12,167,130 | ) | (1,962,808 | ) | |||||||||||||||||

| US$ | US$ | US$ | US$ | US$ | US$ | |||||||||||||||||||||||

| Balance as of April 30, 2025 | 25,727,001 | 2,687 | 7,843,234 | (28,534 | ) | (876 | ) | (9,320,022 | ) | (1,503,511 | ) | |||||||||||||||||

| Ordinary shares (Class A and Class B) | ||||||||||||||||||||||||

|

Shares Outstanding |

Par value |

Additional paid-in capital |

Subscription Receivables |

Accumulated deficit |

Total shareholders’ (deficit) / equity |

|||||||||||||||||||

| Balance as of April 30, 2023 | 19,912,375 | 2,654 | 1,650,415 | 0 | (4,670,222 | ) | (3,017,153 | ) | ||||||||||||||||

| Net loss | - | - | - | - | (2,359,844 | ) | (2,359,844 | ) | ||||||||||||||||

| Proceeds from Investors | 5,686,501 | 837 | 8,333,615 | (37,251 | ) | - | 8,297,201 | |||||||||||||||||

| Balance as of April 30, 2024 | 25,598,876 | 3,491 | 9,984,030 | (37,251 | ) | (7,030,066 | ) | 2,920,204 | ||||||||||||||||

| US$ | US$ | US$ | US$ | US$ | ||||||||||||||||||||

| Balance as of April 30, 2024 | 25,598,876 | 2,560 | 7,322,288 | (27,320 | ) | (5,155,849 | ) | 2,141,679 | ||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

| F- |

PHAOS

TECHNOLOGY HOLDINGS (CAYMAN) LIMITED

CONSOLIDATED STATEMENTS OF CASH FLOWS

| For the years ended April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||||||

| Net loss | (2,359,844 | ) | (5,137,064 | ) | (3,934,994 | ) | ||||||

| Adjustments to reconcile net loss to net cash (used in) operating activities: | ||||||||||||

| Impairment of loan receivables | - | 1,223,608 | 937,284 | |||||||||

| Fixed assets written off | 16,929 | - | - | |||||||||

| Depreciation | 176,713 | 186,963 | 143,214 | |||||||||

| Operating lease expenses | 136,781 | 142,670 | 109,286 | |||||||||

| Change in operating assets and liabilities: | ||||||||||||

| Account receivables | 135,614 | 374,205 | 286,642 | |||||||||

| Contract assets | 18,827 | - | - | |||||||||

| Other current assets | 71,491 | (75,244 | ) | (57,637 | ) | |||||||

| Inventories | (36,061 | ) | (122,423 | ) | (93,777 | ) | ||||||

| Account payables | 202,814 | (199,977 | ) | (153,183 | ) | |||||||

| Accruals and other payables | 198,001 | 96,556 | 73,962 | |||||||||

| Contract liabilities | (33,951 | ) | - | - | ||||||||

| Operating lease obligations | (136,781 | ) | (142,670 | ) | (109,286 | ) | ||||||

| Net cash used in operating activities | (1,609,467 | ) | (3,653,376 | ) | (2,798,489 | ) | ||||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||||||

| Purchase of equipment | (121,318 | ) | (240,212 | ) | (184,003 | ) | ||||||

| Loan to third party | (1,530,982 | ) | (153,306 | ) | (117,432 | ) | ||||||

| Receipt from loan to third party | - | 60,680 | 46,480 | |||||||||

| Net cash used in investing activities | (1,652,300 | ) | (332,838 | ) | (254,955 | ) | ||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||||||

| Repayment of bank loans | (143,483 | ) | (440,455 | ) | (337,384 | ) | ||||||

| Proceeds from share issuance | 8,117,201 | 255,195 | 195,480 | |||||||||

| Loan from major shareholder | 636,127 | 2,600,000 | 1,991,600 | |||||||||

| Repayment to major shareholder | (2,865,374 | ) | (337,330 | ) | (258,395 | ) | ||||||

| Deferred offering cost | (224,694 | ) | (272,608 | ) | (208,818 | ) | ||||||

| Net cash provided by financing activities | 5,519,777 | 1,804,802 | 1,382,483 | |||||||||

| Translation loss | - | (1,143 | ) | (876 | ) | |||||||

| Net change in cash and cash equivalents | 2,258,010 | (2,182,555 | ) | (1,671,837 | ) | |||||||

| Cash and cash equivalents - beginning of year | 54,097 | 2,312,107 | 1,771,074 | |||||||||

| Cash and cash equivalents - end of year | 2,312,107 | 129,552 | 99,237 | |||||||||

| SUPPLEMENTAL CASH FLOW INFORMATION: | ||||||||||||

| Cash paid for interest | 43,543 | 8,463 | 6,483 | |||||||||

| New shares issued with consideration receivable | 37,251 | 37,251 | 28,534 | |||||||||

The accompanying notes form an integral part of these consolidated financial statements.

| F- |

PHAOS

TECHNOLOGY HOLDINGS (CAYMAN) LIMITED

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1 Organization and business overview

Phaos Technology Holdings (Cayman) Limited or the Company is an investment holding company incorporated on March 7, 2024 under the laws of the Cayman Islands. The Company, through its subsidiaries provides research and development, as well as the manufacturing and commercialization of advanced optical related technologies and products. Using its patented microsphere technology, the Company can significantly increase the magnification of existing traditional optical microscope by up to 4 times compared to its competitors, thereby allowing the Company’s client to see beyond the optical limit of 200nm in a cost effective manner. Currently, it is the only commercially available advanced optical microscope that can see below the 200nm optical limit with a commercially viable working distance.

In addition to selling optical and microscopy equipment, the Company develops software solution that is complimentary to the hardware equipment in order to provide partners and clients with a fully integrated hardware and software microscopy solution. The software is augmented by algorithms around Artificial Intelligence to allow for use cases in pathology and metrology, whereby partners and clients can use the software to further analyze what they see through the hardware equipment.

The Company and its subsidiaries are collectively referred to as the “Company”. The Company is headquartered in Singapore.

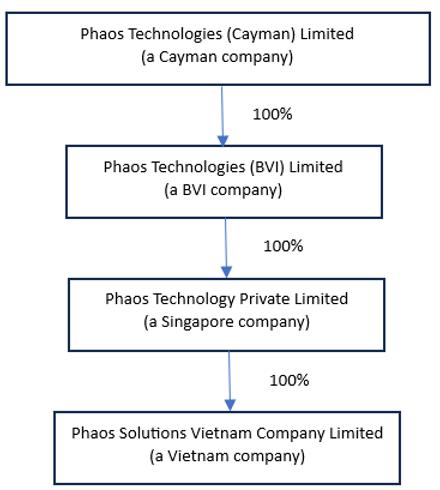

On November 29, 2024, the Company proceeded with an internal reorganization whereby Phaos Technology Private Limited (PTPL)became our indirect wholly-owned subsidiary through a share swap. Subject to completion of the restructuring, both the ordinary and preferential shares of PTPL were swapped on a 1:125 basis to Phaos Technology Holdings (BVI) Limited. Subsequently, the shares of Phaos Technology Holdings (BVI) Limited were swapped 1:1 to Phaos Technology (Cayman) Limited, where the holders of the ordinary shares of PTPL eventually being swapped to Class A Ordinary Shares, and the holders of preferential shares of PTPL being swapped to Class B Ordinary Shares.

The Reorganization has been accounted for as a recapitalization among entities under common control since the same controlling shareholders controlled all these entities before and after the Reorganization. The consolidation of the Company and its subsidiaries has been accounted for at historical cost and prepared on the basis as if the aforementioned transactions had become effective as of the beginning of the first period presented in the accompanying consolidated financial statements. Results of operations for the periods presented comprise those of the previously separate entities combined from the beginning of the period to the end of the period eliminating the effects of intra-entity transactions.

The consolidated financial statements of the Company include the following entities:

Schedule of company and subsidiaries

| Name |

Date of incorporation |

Percentage of direct or indirect interests |

Place of incorporation | Principal activities | ||||

| Phaos Technology Holdings (Cayman) Limited | March 7, 2024 | Parent Company | Cayman Island | Investment holding | ||||

| Phaos Technology Holdings (BVI) Limited | March 7, 2024 | Parent Company | British Virgin Islands | Investment holding | ||||

| Phaos Technology Pte. Ltd. | August 28, 2017 | 100% | Singapore | Research and development and commercialization of advanced microscopy-related solutions, technologies and products. | ||||

| Phaos Solutions Vietnam Co., Ltd | February 7, 2025 | 100% | Vietnam | Research and development and commercialization of advanced microscopy-related solutions, technologies and products. |

| F- |

| 2 | Summary of significant accounting policies |

Basis of presentation

This summary of significant accounting policies is presented to assist in understanding the Company’s consolidated financial statements and have been consistently applied in the preparation of the financial statements. The accompanying consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“US GAAP”) and pursuant to the rules and regulations of the U.S. Securities and Exchange Commission (“SEC”).

Consolidation

The accompanying consolidated financial statements include the accounts of the Company, its wholly owned subsidiaries. Significant inter-company balances, investment and capital, if any, have been eliminated upon consolidation.

Use of estimates

The preparation of consolidated financial statements in conformity with US GAAP requires management to make judgements, estimates and assumptions that affect the application of policies and reported amounts of assets, liabilities, income and expenses. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making the judgements about carrying values of assets and liabilities that are not readily apparent from other sources. Significant accounting estimates reflected in the Company’s consolidated financial statements include, but are not limited to the useful lives and impairment of long-lived assets, and collectability of accounts receivable and other current assets. Actual results may differ from these estimates.

Cash and cash equivalents

Cash and cash equivalents primarily consist of bank deposits with original maturities of three months or less, which are unrestricted as to withdrawal and use.

Accounts receivable, net

Accounts receivable mainly represent amounts due from customers that meet the revenue recognition criteria. These accounts receivables are recorded net of any allowance for credit losses and specific customer credit allowances. The Company maintains an allowance for estimated credit losses inherent in its accounts receivable portfolio. In establishing the required allowance, management considers historical losses adjusted to take into account current market conditions and the Company’s customers’ financial condition, the receivable amount in dispute, and the current receivables aging and current payment patterns, over the contractual life of the receivable. The Company writes off the receivable when it is determined to be uncollectible.

Other current assets

Other current assets primarily consists of deposits, prepayments made to vendors or services providers for future services that have not been provided, and other receivables from third parties. These advances are reviewed periodically to determine whether their carrying value has become impaired. As of April 30, 2024, management believes that the Company’s other current assets are not impaired. As of April 30, 2025, there was an impairment to loan to third parties of S$1,223,608 (US$937,284).

Inventories

Inventories are measured at the lower of cost or net realizable value. The cost of inventories is based on the first-in, first-out principle. Due to the minimal amount of inventory, the Company does not operate a batch program that aggregates the number of units of similar inventory.

The cost of inventories include expenditure incurred in acquiring the inventories and other costs incurred in bringing them to their existing location and condition. General and administrative costs are not charged to inventory as they are not considered direct costs towards production.

The Company does not mortgage, pledge or subject any inventory to lien. Inventories by the Company is not collateralized in any form.

Deferred offering costs

Pursuant to ASC 340-10-S99-1, offering costs directly attributable to an offering of equity securities are deferred and would be charged against the gross proceeds of the offering as a reduction of additional paid-in capital. These costs include legal fees related to the registration drafting and counsel, consulting fees related to the registration preparation, the SEC filing and print related costs. As of April 30, 2025, the Company had not concluded its IPO hence professional fees are recorded as deferred offering costs. As of April 30, 2025, the accumulated deferred offering cost was S$497,302 (US$380,933).

Property and equipment, net

Property and equipment are stated at cost less accumulated depreciation and impairment if applicable. The Company computes depreciation using the straight-line method over the estimated useful lives of the assets as follows:

Schedule of estimated useful lives

| Property and equipment | lesser of lease term or expected useful life | |

| Computers | 3 years | |

| Furniture and fittings | 5 years | |

| Office and production equipment | 3 to 5 years | |

| Renovation | 3 years |

| F- |

| 2 | Summary of significant accounting policies (cont’d) |

The cost and related accumulated depreciation of assets sold or otherwise retired are eliminated from the accounts and any gain or loss is included in the consolidated statement of income. Expenditures for maintenance and repairs are charged to expense as incurred, while additions renewals and betterments, which are expected to extend the useful life of assets, are capitalized. The Company also re-evaluates the periods of depreciation to determine whether subsequent events and circumstances warrant revised estimates of useful lives.

Impairment of long-lived assets

The Company evaluates the recoverability of its long-lived assets (asset groups), including property and equipment and operating lease right-of-use assets, for impairment whenever events or changes in circumstances indicate that the carrying amount of its asset (asset group) may not be fully recoverable. When these events occur, the Company measures impairment by comparing the carrying amount of the assets to the estimated undiscounted future cash flows expected to result from the use of the asset (asset group) and their eventual disposition. If the sum of the expected undiscounted cash flows is less than the carrying amount of the asset (asset group), the Company recognizes an impairment loss based on the excess of the carrying amount of the asset (asset group) over their fair value. Fair value is generally determined by discounting the cash flows expected to be generated by the asset (asset group), when the market prices are not readily available. The adjusted carrying amount of the asset is the new cost basis and is depreciated over the asset’s remaining useful life. Long-lived assets are grouped with other assets and liabilities at the lowest level for which identifiable cash flows are largely independent of the cash flows of other assets and liabilities. For the years ended April 30, 2024 and 2025, no impairment of long-lived assets was observed and recognized.

Fair value measurements

ASC 820 defines fair value as the price that would be received from selling an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. When determining the fair value measurements for assets and liabilities required or permitted to be recorded at fair value, the Company considers the principal or most advantageous market in pricing the asset or liability. ASC 820 establishes a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value as follows:

| Level 1 | - | observable inputs that reflect quoted prices (unadjusted) for identical assets or liabilities in active markets. | |

| Level 2 | - | other inputs that are directly or indirectly observable in the marketplace. | |

| Level 3 | - | unobservable inputs which are supported by little or no market activity. |

The carrying amounts of cash and cash equivalents, accounts receivable, other current assets, inventories and liabilities, accounts payable, and accruals and other payables approximate their fair values because of their generally short maturities.

Revenue recognition

The Company follows the revenue requirements of Accounting Standards Update (“ASU”) No. 2014-09, Revenue from Contracts with Customers (Topic 606) (“Accounting Standards Codification (“ASC”) 606”). The core principle underlying the revenue recognition of this ASC allows the Company to recognize revenue that represents the transfer of goods and services to customers in an amount that reflects the consideration to which the Company expect to be entitled in such exchange. This will require the Company to identify contractual performance obligations and determine whether revenue should be recognized at a point in time or over time, based on when control of goods and services transfers to a customer.

To achieve that core principle, the Company applies five-step model to recognize revenue from customer contracts. The five-step model requires that the Company (i) identify the contract with the customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction price, including variable consideration to the extent that it is probable that a significant future reversal will not occur, (iv) allocate the transaction price to the respective performance obligations in the contract, and (v) recognize revenue when (or as) the Company satisfies the performance obligation.

Revenues are generally recognized upon the transfer of control via acceptance of promised products provided to our customers, reflecting the amount of consideration we expect to receive for those products or services.

Adjustments to comparative figures – correction of errors

For the year ended April 30, 2024, the Company has identified a misstatement in the classification of a loan to 3rd party which was booked under “Cash Flows from Operating Activities” to the amount of S$1,539,982 (approximately US$1,122,822). This was adjusted to “Cash Flows from Investing Activities” for the year ended April 30, 2024.

There is no impact on net cash flow, total assets, opening cash balances and ending cash balances from this adjustment.

| F- |

| 2 | Summary of significant accounting policies (cont’d) |

The Company generates revenue from the following streams:

Sales of microscopes and parts

The Company sells microscopes and parts. Revenue is recognized when the goods are delivered to the customer and all criteria for acceptance have been satisfied. The goods are often sold with a right of return when goods are defective. Up till April 30, 2025, there has been no returns from customers.

The amount of revenue recognized is based on the transaction price, which comprises the contractual price. Based on the Company’s experience with similar types of contracts, variable consideration is typically constrained and is included in the transaction only to the extent that it is a highly probable that a significant reversal in the amount of cumulative revenue recognized will not occur when the uncertainty associated with the variable consideration is subsequently resolved.

The Company has elected to apply the practical expedient to recognize the incremental costs of obtaining a contract as an expense when incurred where the amortization period of the asset that would otherwise be recognized is one year or less.

Contract Assets and contract liabilities

The contract assets primarily relate to the Company’s rights to bill for work completed but not billed at the reporting date. The contract assets are transferred to receivables until the subsequent billing phase. The contract liabilities primarily relate to advance billing to customers based on the contract, for which project task has not yet been completed.

Segments

ASC 280, “Segment Reporting”, establishes standards for reporting information about operating segments on a basis consistent with the Company’s internal organizational structure as well as information about geographical areas, business segments and major clients in financial statements for detailing the Company’s business segments. Based on the criteria established by ASC 280, the Company’s chief operating decision maker (“CODM”) has been identified as the Chief Executive Officer, who reviews consolidated results when making decisions about allocating resources and assessing performance of the Company. As a whole and hence, the Company has only one reportable segment. The Company does not distinguish between markets or segments for the purpose of internal reporting.

Concentrations and credit risk

The Company maintains cash with banks in Singapore (“SGN”). Should any bank holding cash become insolvent, or if the Company is otherwise unable to withdraw funds, the Company would lose the cash with that bank; however, the Company has not experienced any losses in such accounts and believes it is not exposed to any significant risks on its cash in bank accounts. In Singapore, a depositor has up to S$100,000 insured by Singapore Deposit Insurance Corporation (“SDIC”).

Financial instruments that potentially expose the Company to the concentration of credit risk consist primarily of cash and cash equivalents and accounts receivable. The Company has designed their credit policies with an objective to minimize their exposure to credit risk. The Company’s accounts receivable are short term in nature and the associated risk is minimal. The Company conducts credit evaluations on its clients and generally does not require collateral or other security. The Company periodically evaluates the creditworthiness of the existing clients in determining the allowance for doubtful accounts primarily based upon the age of the receivables and factors surrounding the credit risk of specific clients.

As of April 30, 2024 and 2025, the Company’s assets were located in Singapore and the Company’s revenue was derived from the operation in Singapore.

For the financial years ended April 30, 2024 and 2025, top 5 customers accounted for 91% and 85% of total revenue, respectively. The top 5 suppliers accounted for 87% and 85% of our total cost of goods sold, respectively.

For the financial year ended April 30, 2024, customer A, customer B, customer C and customer D accounted for 73%, 6%, 5% and 4% of the Company’s total revenue and 45% customer A of the total accounts receivable as of April 30, 2024; whereas customers B, C and D have no outstanding as of April 30, 2024. For the financial year ended April 30, 2025, customer A, customer B, customer C, customer D and customer E accounted for 23%, 21%, 18%, 13% and 10% of the Company’s total revenue and customer A, customer D and customer E accounted for 13%, 30% and 46% of the total accounts receivable as of April 30, 2025; whereas customer B and customer C have no outstanding as of April 30, 2025.

For the financial year ended April 30, 2024, vendor A, vendor B, vendor C and vendor D accounted for 39%, 30%, 13% and 3% of the Company’s total purchases and 57% vendor B and 41% vendor C of the total accounts payable as of April 30, 2024; whereas vendors A and D have no outstanding as of April 30, 2024. For the financial year ended April 30, 2025, vendor A, vendor B, vendor C, vendor D and vendor E accounted for 30%, 28%, 18%, 6% and 3% of the Company’s total purchases and vendor A, vendor B and vendor E accounted for 34%, 57% and 8% of the total accounts payable as of April 30, 2025; whereas vendors C and D have no outstanding as of April 30, 2025.

Government grants

Government grants are recognized when there is reasonable assurance that the grant will be received, and all attaching conditions will be complied with. Government grant is recognized as ‘Other income’ in Consolidated statement of operations and comprehensive loss.

| F- |

| 2 | Summary of significant accounting policies (cont’d) |

Commitments and contingencies

In the normal course of business, the Company is subject to contingencies, including legal proceedings and claims arising out of the business that relate to a wide range of matters, such as government investigations and tax matters. The Company recognizes a liability for such contingency if it determines it is probable that a loss has occurred and a reasonable estimate of the loss can be made. The Company may consider many factors in making these assessments including historical and the specific facts and circumstances of each matter.

Employee benefits

Employee benefits are recognized as an expense, unless the cost qualifies to be capitalized as an asset.

| i) | Defined contribution plans |

Defined contribution plans are post-employment benefit plans under which the Company pays fixed contributions into separate entities such as the Central Provident Fund on a mandatory, contractual or voluntary basis. The Company has no further payment obligations once the contributions have been paid. Contributions to defined contribution pension schemes are recognized as an expense in the period in which the related service is performed.

| ii) | Short-term compensated absences |

Employee entitlements to annual leave are recognized when they accrue to employees. A provision is made for the estimated liability for annual leave as a result of services rendered by employees up to the balance sheet date.

Related parties

Parties are considered to be related if one party has the ability, directly or indirectly, to control the other party or exercise significant influence over the other party in making financial and operating decisions. Parties are also considered to be related if they are subject to common control or significant influence of the same party, such as a family member or relative, shareholder, or a related corporation.

The Company follows ASC 850 Related Party Disclosures for the identification of related parties and disclosure of related party transactions.

Foreign currency and foreign currency translation

The accompanying consolidated financial statements are presented in Singapore Dollars (“S$”), which is the reporting currency of the Company. The functional currency of the Company and its subsidiary in the British Virgin Island is United States Dollar (“US$”).

Convenience translation

Translations of the consolidated balance sheet, consolidated statement of operations and comprehensive loss, statement of shareholders deficit and consolidated statement of cash flows from S$ into US$ as of and for the year ended April 30, 2025 are solely for the convenience of the reader and were calculated at the rate of US$0.7660 = S$1 as set forth in the statistical release of the Federal Reserve System on April 30, 2025. No representation is made that the SGD amounts could have been, or could be, converted, realized or settled into US$ at that rate on April 30, 2025, or at any other rate., or at any other rate.

Income taxes

The Company accounts for income taxes under FASB ASC 740. Deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the consolidated financial statements carrying amounts of existing assets and liabilities and their respective tax bases. Deferred tax assets are also provided for net operating loss carry forward that can be utilized to offset future taxable income.

Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the period including the enactment date. A valuation allowance is established, when necessary, to reduce net deferred tax assets to the amount expected to be realized. Current income taxes are provided for in accordance with the laws of the relevant taxing authorities.

The provisions of FASB ASC 740-10-25, “Accounting for Uncertainty in Income Taxes,” prescribe a more-likely-than-not threshold for consolidated financial statement recognition and measurement of a tax position taken (or expected to be taken) in a tax return. This interpretation also provides guidance on the recognition of income tax assets and liabilities, classification of current and deferred income tax assets and liabilities, accounting for interest and penalties associated with tax positions, and related disclosures.

The Company did not accrue any liability, interest or penalties related to uncertain tax positions in its provision for income taxes for the years ended April 30, 2024 and 2025. The Company does not expect that its assessment regarding unrecognized tax positions will materially change over the next 12 months.

| F- |

| 2 | Summary of significant accounting policies (cont’d) |

Leases

The Company adopted ASC 842 on January 1, 2019. The Company is a lessee of non-cancellable operating leases for its corporate office premises. The Company determines if an arrangement is a lease at inception. Lease assets and liabilities are recognized at the present value of the future lease payments at the lease commencement date. The interest rate used to determine the present value of the future lease payments is the Company’s incremental borrowing rate based on the information available at the lease commencement date. The Company generally uses the base, non-cancellable lease term in calculating the right-of-use assets and liabilities.

The Company has elected not to recognize ROU assets and lease liabilities for short-term leases that have a lease term of 12 months or less. The Company recognizes the lease payments associated with its short-term leases as an expense on a straight-line basis over the lease term.

The Company evaluates the impairment of its right-of-use assets consistent with the approach applied for its other long-lived assets. The assessment of possible impairment is based on its ability to recover the carrying value of the asset from the expected undiscounted future pre-tax cash flows of the related operations. The Company has elected to include the carrying amount of finance and operating lease liabilities in any tested asset group and include the associated lease payments in the undiscounted future pre-tax cash flows. For the years ended April 30, 2024 and 2025, the Company did not have any impairment loss against its operating lease right-of-use assets.

The Company’s operating lease liabilities and right-of-use assets are disclosed in Note 8.

Basic earnings (loss) per share is computed by dividing net earnings (loss) attributable to ordinary shareholders by the weighted average number of ordinary shares outstanding during the year. Diluted earnings per share reflect the potential dilution that could occur if outstanding stock options, warrants and convertible debt were exercised or converted into ordinary shares. When the Company incurs a loss, diluted shares are not included, as their inclusion would have an anti-dilutive effect. The Company did not have any dilutive securities or debt for each of the years ended April 30, 2024 and 2025.

Going Concern

The accompanying audited condensed consolidated financial statements have been prepared assuming the Company will continue as a going concern. As of the year ending April 30, 2025, the Group had a net loss of S$5,137,064 (approximately US$3,934,994) and incurred a negative cashflow from operations of S$3,653,376 (approximately US$2,798,489), against a cash balance of S$129,552 (approximately US$99,237). This raises substantial doubt about our ability as a going concern.

To sustain it’s ability to support the Company’s operating activities, the Company considered supplementing its sources of funding through the following:

| - | Continuous support from major shareholders, such as TongHuai Enterprise which has provided for the shareholders loan. | |

| - | Repayment of loan to PT Neura from August 2025 onwards |

Management has commenced a strategy to raise debt and equity. However, there can be no certainty that these additional financings will be available on acceptable terms or at all. If management is unable to execute this plan, there will likely be a material adverse effect on the Company’s business. All these factors raise substantial doubt about the ability of the Company to continue as a going concern.

There is no immediate liquidation concern for the Company; however, there is substantial doubt on the Company being a going concern but the management has positive mitigation plan to handle going concern issue.

The audited consolidated financial statements do not include any adjustments that might be necessary if the Group is unable to continue as a going concern.

Recent Accounting Pronouncements

The Company is an “emerging growth company” (“EGC”) as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). Under the JOBS Act, EGC can delay adopting new or revised accounting standards issued subsequent to the enactment of the JOBS Act until such time as those standards apply to private companies. The Company made the election to delay the adoption of new or revised accounting standards.

In July 2023, the FASB issued ASU Update No. 2023-03, Presentation of Financial Statements (Topic 205), Income Statement—Reporting Comprehensive Income (Topic 220), Distinguishing Liabilities from Equity (Topic 480), Equity (505), and Compensation—Stock Compensation (Topic 718). This guidance amends, and addresses several topics pursuant to SEC Staff Accounting Bulletin No. 120, SEC Staff Announcement at the March 24, 2022 EITF Meeting, and Staff Accounting Bulletin Topic 6.B, Accounting Series Release 280—General Revision of Regulation S-X: Income or Loss Applicable to Common Stock. The effect of the amendments was not material to the Company’s consolidated financial statements.

In October 2023, the FASB issued ASU Update No. 2023-06 to incorporate into the Codification 14 of the 27 disclosures referred by the SEC in its Release No. 33-10532. This guidance amends 12 Codification Subtopics, to which the Company has identified several to further analyze the effect of the amendments to the Company’s consolidated financial statements. These amendments are to 1) 250-10 Accounting Changes and Error Corrections and 2) 270-10 Interim Reporting – Overall. The effect of the amendments was not material to the Company’s consolidated financial statements.

Except as mentioned above, the Group does not believe other recently issued but not yet effective accounting standards, if currently adopted, would have a material effect on the Company’s consolidated balance sheets, statements of operations and cash flows.

| F- |

| 3 | Account receivable, net |

Schedule of account receivable

| As of April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Accounts receivable | 436,196 | 38,384 | 29,402 | |||||||||

| Less: allowance for credit losses | (23,607 | ) | - | - | ||||||||

| Total accounts receivable | 412,589 | 38,384 | 29,402 | |||||||||

Movement of allowance for credit losses are as follows:

Schedule of allowance doubtful accounts

| As of April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Allowance for credit losses, beginning balance | 21,032 | 23,607 | 18,083 | |||||||||

| Addition | 2,575 | 19,217 | 14,720 | |||||||||

| Write off | - | (42,824 | ) | (32,803 | ) | |||||||

| Allowance for credit losses, ending balance | 23,607 | - | - | |||||||||

| 4 | Other current assets |

Schedule of other current assets

| As of April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Deposit | 43,250 | 48,108 | 36,851 | |||||||||

| Prepayment | 20,898 | 44,042 | 33,736 | |||||||||

| Other current assets | 1,008 | 48,250 | 36,959 | |||||||||

| Total other current assets | 65,156 | 140,400 | 107,546 | |||||||||

| 5 | Loan to third parties |

Schedule of loan to third parties

| As of April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Loan to third parties | 1,530,982 | 1,623,608 | 1,243,684 | |||||||||

| Allowance for impairment of loan | - | (1,223,608 | ) | (937,284 | ) | |||||||

| Loan to third parties, net | 1,530,982 | 400,000 | 306,400 | |||||||||

On 19th January 2024, the Company provided a loan to PT Neura Integrasi Solusi, a technology company providing pathology related software solutions. The loan bears an interest at a rate of 1% per annum, with a maturity date of 36 months and is due on demand. The purpose of the loan was to provide working capital for our Indonesian partner in the expansion of our business. For the year ending April 30, 2025, the Company loaned a total of S$153,305 (US$114,000) to PT Neura Integrasi Solusi while repayment made by PT Neura Integrasi Solusi was S$60,680 (US$45,000), giving rise to a balance of S$1,623,608 (US$1,243,684) as at April 30, 2025.

The carrying amount of the loan as of April 30, 2025 has been partially impaired by S$1,223,608 (US$937,284), with S$400,000 (US$306,400) as the carrying amount after impairment. As of August 2025, the Company has reached an agreement with PT Neura Integrasi Solusi where the first repayment of S$400,000 will happen in September 2025, expecting to make a total repayment of S$1,000,000 by December 31, 2025. The borrower of the loan, PT Neura Integrasi Solusi is neither affiliated with the Company nor the shareholders of the Company.

| F- |

| 6 | Property and equipment, net |

Schedule of property and equipment

| As of April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Production Equipment | 571,691 | 742,860 | 569,030 | |||||||||

| Computer and Software | 68,674 | 94,238 | 72,186 | |||||||||

| Furniture and Fittings | 4,046 | 9,070 | 6,948 | |||||||||

| Office Equipment | 6,688 | 6,689 | 5,124 | |||||||||

| Renovation | 111,633 | 117,803 | 90,237 | |||||||||

| Construction in Progress | - | 868 | 665 | |||||||||

| Total | 762,732 | 971,528 | 744,190 | |||||||||

| Less: accumulated depreciation | (529,423 | ) | (684,970 | ) | (524,687 | ) | ||||||

| Net book value | 233,309 | 286,558 | 219,503 | |||||||||

Depreciation expense for the years ended April 30, 2024 and 2025 was S$176,713 and S$186,963 (US$143,214), respectively.

| 7 | Inventories |

Schedule of inventories

| As of April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Parts | 23,978 | 53,021 | 40,614 | |||||||||

| Partial finished goods | 82,527 | 94,391 | 72,304 | |||||||||

| Finished goods | 81,079 | 162,595 | 124,547 | |||||||||

| Total inventories | 187,584 | 310,007 | 237,465 | |||||||||

| 8 | Leases |

The Company determines if a contract contains a lease at inception. US GAAP requires that the Company’s leases be evaluated and classified as operating or finance leases for financial reporting purposes. The classification evaluation begins at the commencement date and the lease term used in the evaluation includes the non-cancellable period for which the Company has the right to use the underlying asset, together with renewal option periods when the exercise of the renewal option is reasonably certain and failure to exercise such option which results in an economic penalty.

The Company has four office premises operating lease agreements with lease terms ranging from 2 two to 3 three years, respectively. The Company’s lease agreements do not contain any material residual value guarantees or material restrictive covenants. Upon adoption of ASU 2016-02, no right-of-use (“ROU”) assets nor lease liability was recorded for the lease with a lease term of one year.

| F- |

| 8 | Leases (cont’d) |

As of April 30, 2025, the Company had the following non-cancellable operating lease contracts:

Schedule of non-cancellable operating lease contracts

| Description of lease | Lease term | |

| Office premises | 2 to 3 years |

| (a) | Amount recognized in the consolidated balance sheets: |

Schedule of amount recognized in the consolidated balance sheets

| As of April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Right-of-use assets | 218,146 | 131,845 | 100,993 | |||||||||

| Operating lease liabilities | ||||||||||||

| Current | 132,786 | 109,142 | 83,603 | |||||||||

| Non-current | 85,360 | 22,703 | 17,390 | |||||||||

| Total operating lease liabilities | 218,146 | 131,845 | 100,993 | |||||||||

| (b) | A summary of lease cost recognized in the Group’s consolidated statements of operations is as follows: |

Schedule of lease cost

| Years Ended April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Operating lease expense | 136,781 | 142,670 | 109,285 | |||||||||

Lease Commitment

Future minimum lease payments under non-cancellable operating lease agreements as of April 30, 2025 were as follows:

Schedule of future minimum lease payments under non-cancellable operating lease agreements

| Minimum lease payment | ||||||||

| S$ | US$ | |||||||

| Years ending April 30, | ||||||||

| 2026 | 112,144 | 85,902 | ||||||

| 2027 | 23,189 | 17,763 | ||||||

| Total future minimum lease payments | 135,333 | 103,665 | ||||||

| Less imputed interest | (3,488 | ) | (2,672 | ) | ||||

| Present value of operating lease liabilities | 131,845 | 100,993 | ||||||

| Less: current portion | (109,142 | ) | (83,603 | ) | ||||

| Long-term portion | 22,703 | 17,390 | ||||||

The following summarizes other supplemental information about the Company’s lease as of April 30:

Schedule of other supplemental information about lease

| As of April 30, | ||||||||

| 2024 | 2025 | |||||||

| Weighted average discount rate | 5.00 | % | 4.75 | % | ||||

| Weighted average remaining lease term | 20 months | 13 months | ||||||

| F- |

| 9 | Bank loans |

On August 11, 2022, the Company has acquired a 5-year S$270,000 temporary bridging loan which expires in July 2027. The bank loan which carries interest of 4.75% per annum is secured by joint and several guarantee by Andrew Yeo Eng Sian (Chief Executive Officer) and Beh Hook Seng (Executive Chairman). As of April 30, 2024 and 2025, the carrying amount of the bank loan was S$187,017 and S$133,979 (US$102,628), respectively.

On November 1, 2022, the Company has acquired another 5-year S$500,000 secured fixed rate bank loan which expires in November 2027. The bank loan which carries interest of 7.75% per annum is secured by joint and several guarantee by Beh Hook Seng, Andrew Yeo Eng Sian, Wong Teck Far and Chua Jun Hao, David. As of April 30, 2025, the bank loan has been fully paid.

Interest expenses for the years ended April 30, 2024 and 2025 are S$43,543 and S$8,463 (US$6,483), respectively.

The maturities schedule is as follows:

Schedule of maturities

| Amount | Amount | |||||||

| S$ | US$ | |||||||

| Year ending April 30, | ||||||||

| 2026 | 55,613 | 42,600 | ||||||

| 2027 | 58,313 | 44,667 | ||||||

| 2028 | 20,053 | 15,361 | ||||||

| Total | 133,979 | 102,628 | ||||||

| Less: current portion | (55,613 | ) | (42,600 | ) | ||||

| Long-term portion | 78,366 | 60,028 | ||||||

| 10 | Accruals and other current liabilities |

Schedule of accruals and other current liabilities

| As of April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Accruals | 71,023 | 99,429 | 76,163 | |||||||||

| Goods and Services Tax payables | 26,161 | - | - | |||||||||

| Provision for reinstatement | 32,000 | 32,000 | 24,512 | |||||||||

| Other payables | 61,444 | 51,421 | 39,388 | |||||||||

| Non-trade creditors | 254,494 | 358,828 | 274,861 | |||||||||

| Total | 445,122 | 541,678 | 414,924 | |||||||||

| 11 | Equity |

Ordinary and Preference shares

The Company was incorporated under the laws of the Cayman Islands on March 7, 2024. The original authorized share capital of the Company was US$100,000 divided into 950,000,000 Class A Ordinary Shares and 50,000,000 Class B Ordinary Shares, par value US$0.0001 per share. Holders of Class A Ordinary Shares and Class B Ordinary Shares have the same rights except for voting rights. Each holder of our Class A Ordinary Share is entitled to one (1) vote per share. Each holder of our Class B Ordinary Share is entitled to twenty (20) votes per share.

The Company issued 25,598,876 Class A and Class B Ordinary Shares as of April 30, 2024 and 25,727,001 Class A and Class B Ordinary Shares as of April 30, 2025, where the Company received S$255,195 (US$193,000) from investors for the issuance of 128,125 shares for the year ended April 30, 2025.

Post restructuring, for April 30, 2024, the Company had received a total of S$8,297,201 (US$6,085,167) in share application monies, and S$37,251 (US$27,320) in monies to be received from investors, in relation to the planned issuance of 5,686,501 shares at an average issue price of S$1.46 per share.

The Company has completed the restructuring process on November 29, 2024.

| F- |

| 12 | Related party transactions and balances |

The table below sets forth the major related parties and their relationships with the Company as of April 30, 2024 and 2025:

Schedule of major related parties and their relationships with the company

| Name of related parties | Relationship with the Company | |

| Tonghuai SG Enterprise Pte. Ltd. | Major shareholder | |

| Singlight Technology Holdings Pte. Ltd. | Shareholder of the Company |

Amount due to major shareholder

The Company received advances from major shareholder, Tonghuai SG Enterprise Pte. Ltd. for business working purposes. The payable balance due to Tonghuai SG Enterprise Pte. Ltd. was S$732,753 and S$2,995,423 (US$2,294,494) as of April 30, 2024 and 2025. In the year ended April 30, 2025, loan from Tonghuai SG Entreprise Pte. Ltd. was S$2,600,000 (US$1,991,600) and repayment was S$337,330 (US250,000). Such balance is interest free, unsecured, and due on demand without an agreement. Due to the due in demand nature of the advance, we reclassified the “Amount due to major shareholder” from non-current liabilities to current liabilities. In accordance with Staff Accounting Bulletin (“SAB”) 99, Materiality, we evaluated the materiality of the error from qualitative and quantitative perspectives, and concluded that the error was immaterial to the Balance Sheet as of 30th April 2023 and 30th April 2024. We have corrected this error by making an adjustment for both periods ending 30th April 2023 and 30th April 2024, reducing Balance Sheet amounts for “Non-current liabilities” and increasing the Balance Sheet amounts for “Current liabilities”.

Tonghuai SG Enterprise Pte. Ltd will continue to provide cash injections to the Company based on agreement as and when signed.

| 13 | Income taxes |

Caymans and BVIs

The Company and its subsidiaries are domiciled in the Cayman Island and British Virgin Islands. The locality currently enjoys permanent income tax holidays; accordingly, the Company does not accrue for income taxes.

Singapore

Phaos Technology Pte. Ltd. is incorporated in Singapore and are subject to Singapore Corporate Tax on the taxable income as reported in its statutory financial statements adjusted in accordance with relevant Singapore tax laws. The applicable tax rate is 17% in Singapore, with 75% of the first S$10,000 taxable income and 50% of the next S$190,000 taxable income exempted from income tax.

Vietnam

Phaos Solutions Vietnam Company Limited is incorporated in Vietnam and are subject to Vietnam Corporate Tax on the taxable income as reported in its statutory financial statements adjusted in accordance with relevant Vietnam tax laws. The applicable tax rate is 20% in Vietnam, but from October 1, 2025 onwards, applicable rate will be 15% if the annual turnover is no more than VND 3 billion.

A reconciliation between of the statutory tax rate to the effective tax rate are as follows:

Schedule of reconciliation between of the statutory tax rate to the effective tax rate

| Years Ended April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Loss before tax | (2,359,844 | ) | (5,137,064 | ) | (3,934,994 | ) | ||||||

| Singapore income tax rate | (17.0 | )% | (17.0 | )% | (17.0 | )% | ||||||

| Reconciling items: | ||||||||||||

| Non-deductible expenses | 1.4 | % | 4.7 | % | 4.7 | % | ||||||

| Income not subject to tax | - | - | - | |||||||||

| Singapore Statutory stepped income exemption (Deductions under Section 14) | - | - | - | |||||||||

| Valuation allowance | 15.6 | % | 12.3 | % | 12.3 | % | ||||||

| Effective tax rate | - | - | - | |||||||||

| F- |

| 13 | Income taxes (cont’d) |

Deferred tax

Significant components of deferred tax were as follows:

Schedule of deferred tax

| Years Ended April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Net operating loss carried forward | 6,537,161 | 10,094,281 | 7,732,219 | |||||||||

| Deferred tax assets, gross | 1,111,317 | 1,716,028 | 1,314,477 | |||||||||

| Valuation allowance | (1,111,317 | ) | (1,716,028 | ) | (1,314,477 | ) | ||||||

| Deferred tax assets, net of valuation allowance | - | - | - | |||||||||

Deferred tax assets are recognized in the consolidated financial statements only to the extent that it is probable that future taxable income will be available against which the Company can utilize the benefits. The use of these tax losses is subject to the agreement of the tax authorities and compliance with certain provisions of the tax legislations of the respective countries in which the group companies operate.

The deferred tax assets not recognized as of April 30, 2024 and 2025 was S$1,111,317 and S$1,716,028 (US$1,314,477) respectively. The deferred tax assets not recognized was primarily related to the Company’s net loss (tax losses) carry forwards, in the judgment of management, are not more likely than not to be realized. In assessing the realizability of deferred tax assets, management considers whether it is more likely than not that all or some portion of the deferred tax assets will not be realized. The ultimate realization of deferred tax assets is dependent upon the generation of future taxable income during the periods in which those temporary differences become deductible. Tax losses on Net Operating Losses can be carried forward indefinitely unless there’s a major change in shareholding.

| 14 | Other operating expenses |

Schedule of Other operating expenses

| Years Ended April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Consumable expenses | 86,532 | - | - | |||||||||

| Marketing expenses | 87,008 | 58,008 | 44,434 | |||||||||

| Professional fees | 691,464 | 620,014 | 474,931 | |||||||||

| Travelling expenses | 136,651 | 165,435 | 126,723 | |||||||||

| Other expenses | 143,147 | 318,206 | 243,746 | |||||||||

| 1,144,802 | 1,161,663 | 889,834 | ||||||||||

| F- |

| 15 | Other income |

Schedule of other income

| Years Ended April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Interest income | 2 | 5,832 | 4,467 | |||||||||

| Government grants | 116,542 | 62,644 | 47,986 | |||||||||

| Gain on disposal of property and equipment | - | - | - | |||||||||

| Other | 70,284 | 82,807 | 63,430 | |||||||||

| 186,828 | 151,283 | 115,883 | ||||||||||

| 16 | Loss per share |

Basic loss per share is the amount of losses available to each ordinary share outstanding during the reporting period. Diluted loss per share is the amount of losses available to each ordinary share outstanding during the financial year April 30,2025.

Schedule of calculation of basic and diluted net income per share

| Years Ended April 30, | ||||||||||||

| 2024 | 2025 | 2025 | ||||||||||

| S$ | S$ | US$ | ||||||||||

| Numerator: | ||||||||||||

| Net loss available to ordinary shareholders | (2,359,844 | ) | (5,137,064 | ) | (3,934,994 | ) | ||||||

| Denominator: | ||||||||||||

| Weighted average ordinary Class A and Class B shares outstanding – basic and diluted | 23,540,241 | 25,662,939 | 25,662,939 | |||||||||

| Loss per ordinary share: | ||||||||||||

| Basic and diluted | (0.10 | ) | (0.20 | ) | (0.15 | ) | ||||||

| 17 | Commitment and Contingencies |

For the details on future minimum lease payment under the non-cancellable operating leases as of April 30, 2025, please refer to Note 8 set forth in the Notes to the Consolidated Financial Statements.

As of April 30, 2024 and 2025, the Company did not have any capital commitments and contingencies.

| 18 | Subsequent events |

The Company has assessed all subsequent events through the date that the consolidated financial statements were issued and other than the following, there are no further material subsequent events that require disclosure in these consolidated financial statements.

On July 31, 2025, the Company’s registration statement on Form F-1 was declared effective by the U.S. Securities and Exchange Commission. The Company expects to complete its initial public offering of 2,700,000 ordinary shares. In addition, shareholders namely Chua Jun Hao, David, ICHAM Master Fund VCC, Liew Ah Choy, Tan Chiew Hiah and Chua Kheng Choon are offering an aggregate of 900,900 shares at a price range of $4.00 to $5.00 per share by 31st October 2025. The offering is expected to generate gross proceeds of approximately $12,150,000 before underwriting discounts, commissions and offering expenses. The completion of the IPO will occur subsequent to the issuance of these consolidated financial statements; accordingly, no adjustments have been recorded in the accompanying financial statements related to this event.

| F- |

EXHIBIT INDEX

|

|

SIGNATURES

The registrant hereby certifies that it meets all of the requirements for filing on Form 20-F and that it has duly caused and authorized the undersigned to sign this annual report on its behalf.

| Phaos Technology Holdings (Cayman) Limited | ||

| By: | /s/ Andrew Yeo | |

| Name: | Andrew Yeo | |

| Title: | Chief Executive Officer | |

| By: | /s/ Gan Hong Loon | |

| Name: | Gan Hong Loon | |

| Title: | Chief Financial Officer | |

| Dated: | September 18, 2025 | |

|

|

Exhibit 12.1

CERTIFICATION OF PRINCIPAL EXECUTIVE OFFICER

PURSUANT TO EXCHANGE ACT RULE 13A-14(A)/15D-14(A) AS ADOPTED PURSUANT TO SECTION 302

OF THE SARBANES-OXLEY ACT OF 2002

I, Andrew Yeo, certify that:

| 1. | I have reviewed this annual report on Form 20-F of Phaos Technology Holdings (Cayman) Limited (the “Company”); |

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the Company as of, and for, the periods presented in this report; |

| 4. | The Company’s other certifying officer and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal control over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15(f)) for the Company and have: |

| (a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the Company, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; |

| (b) | Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; |

| (c) | Evaluated the effectiveness of the Company’s disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; and |

| (d) | Disclosed in this report any change in the Company’s internal control over financial reporting that occurred during the period covered by the annual report that has materially affected, or is reasonably likely to materially affect, the Company’s internal control over financial reporting; and |

| 5. | The Company’s other certifying officer and I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the Company’s auditors and the audit committee of the Company’s board of directors: |

| (a) | All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the Company’s ability to record, process, summarize and report financial information; and |

| (b) | Any fraud, whether or not material, that involves management or other employees who have a significant role in the Company’s internal control over financial reporting. |

| Date: September 18, 2025 | /s/ Andrew Yeo |

| Andrew Yeo | |

| Chief Executive Officer | |

| (Principal Executive Officer) |

Exhibit 12.2

CERTIFICATION OF PRINCIPAL FINANCIAL OFFICER

PURSUANT TO EXCHANGE ACT RULE 13A-14(A)/15D-14(A) AS ADOPTED PURSUANT TO SECTION 302

OF THE SARBANES-OXLEY ACT OF 2002

I, Gan Hong Loon, certify that:

| 1. | I have reviewed this annual report on Form 20-F of Phaos Technology Holdings (Cayman) Limited (the “Company”); |

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the Company as of, and for, the periods presented in this report; |

| 4. | The Company’s other certifying officer and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal control over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15(f)) for the Company and have: |

| (a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the Company, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; |

| (b) | Designed such internal control over financial reporting, or caused such internal control over financial re- porting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; |

| (c) | Evaluated the effectiveness of the Company’s disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; and |