UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 40-F

☐ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2023 |

Commission File Number 001-35254 |

Avino Silver & Gold Mines Ltd. |

(Exact name of Registrant as specified in its charter) |

British Columbia, Canada

(Jurisdiction of Incorporation or Organization)

1041

Primary Standard Industrial Classification Code Number

N/A

I.R.S. Employer Identification Number

Suite 900, 570 Granville Street, Vancouver

British Columbia, V6C 3P1, Canada

604-682-3701

(Address and telephone number of Registrant’s principal executive offices)

National Registered Agents, Inc.

1015 15th Street, N.W., Suite 1000

Washington, DC 20005 (202) 572-3133

(Name, address (including zip code) and telephone number (including area code)

of agent for service in the United States)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

Common Shares, without Par Value |

|

ASM |

|

NYSE American, LLC |

Securities registered or to be registered pursuant to Section 12(g) of the Act: N/A

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: N/A

For annual reports, indicate by check mark the information file with this Form:

|

☒ Annual information form |

☒ Audited annual financial statements |

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

There were 128,728,248 common shares, without par value, issued and outstanding as of December 31, 2023.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 2.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 12b-2 of the Exchange Act.

Emerging Growth Company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

EXPLANATORY NOTE

Avino Silver & Gold Mines Ltd. (“we”, “us”, “our”, or the “Company”) is a British Columbia company that is permitted, under a multijurisdictional disclosure system adopted by the United States, to prepare this annual report on Form 40-F (“Annual Report”) pursuant to Section 13 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), in accordance with disclosure requirements in effect in Canada, which are different from those of the United States.

FORWARD LOOKING STATEMENTS

This Annual Report, including the exhibits incorporated by reference therein, contains “forward-looking information” and “forward-looking statements” within the meaning of applicable Canadian and U.S. securities legislation. These forward-looking statements reflect our current view about future plans, intentions or expectations and include, in particular, statements about our plans, strategies and prospects and may be identified by terminology such as “may,” “will,” “should,” “expect,” “scheduled,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “aim,” “potential,” or “continue” or the negative of those terms or other comparable terminology. These forward-looking statements are subject to risks, uncertainties and assumptions about us. Although we believe that our plans, intentions and expectations are reasonable, we may not achieve our plans, intentions or expectations.

Important factors that could cause actual results to differ materially from the forward-looking statements we make in this Annual Report set forth under the caption “Risk Factors” contain in our Annual Information Form (“AIF”) filed as Exhibit 99.1. We undertake no obligation to update any of the forward-looking statements after the date of this Annual Report to conform those statements to reflect the occurrence of unanticipated events, except as required by applicable law. You should read this Annual Report with the understanding that our actual future results, levels of activity, performance and achievements may be materially different from what we expect. We qualify all our forward-looking statements by these cautionary statements.

DIFFERENCES IN UNITED STATES AND CANADIAN REPORTING PRACTICES

The Company is permitted, under a multijurisdictional disclosure system adopted by the United States, to prepare this Annual Report in accordance with Canadian disclosure requirements, which are different from those of the United States. The Company prepares its financial statements, which are filed with this Annual Report in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board. Therefore, they are not comparable in all respects to financial statements of United States companies that are prepared in accordance with United States generally accepted accounting principles.

MINERAL RESOURCE AND MINERAL RESERVE ESTIMATES

The Company's AIF filed as Exhibit 99.1 to this annual report on Form 40-F and management's discussion and analysis for the fiscal year ended December 31,2023 filed as Exhibit 99.3 have been prepared in accordance with the requirements of Canadian provincial securities laws, which differ from the requirements of United States securities laws.

As a result, the Company reports the mineral reserves and resources of the projects it has an interest in according to Canadian standards. Canadian reporting requirements for disclosure of mineral properties are governed by National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”). NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. These standards differ from the requirements of the SEC that are applicable to domestic United States reporting companies under subpart 1300 of Regulation S-K (“S-K 1300”) under the Exchange Act. As an issuer that prepares and files its reports with the SEC pursuant to the MJDS, the Company is not subject to the requirements of S-K 1300. Any mineral reserves and mineral resources reported by the Company in accordance with NI 43-101 may not qualify as such under or differ from those prepared in accordance with S-K 1300.

Accordingly, information included or incorporated by reference in the Company's AIF filed as Exhibit 99.1 to this annual report on Form 40-F and management's discussion and analysis for the fiscal year ended December 31, 2023 filed as Exhibit 99.3 concerning descriptions of mineralization and estimates of mineral reserves and resources under Canadian standards may not be comparable to similar information made public by United States companies subject to the reporting and disclosure requirements of S-K 1300.

| 2 |

PRINCIPAL DOCUMENTS

The following documents are part of, and are hereby incorporated by reference in, this Annual Report on Form 40-F:

A. Annual Information Form

Annual Information Form for the fiscal year ended December 31, 2023. See Exhibit 99.1 to this Annual Report.

B. Audited Annual Financial Statements

Audited Consolidated Financial Statements for the fiscal years ended December 31, 2023 and 2022, and notes thereto, together with the reports of the independent registered public accounting firm thereon. See Exhibit 99.2 of this Annual Report.

C. Management's Discussion and Analysis

Management's Discussion and Analysis of Financial Condition and Results of Operations for the fiscal year ended December 31, 2023. See Exhibit 99.3 of this Annual Report; and

| 3 |

D. Technical Report

Oxide Tailings Project Prefeasibility Study for the Avino Property, Durango, Mexico, NI 43-101 Technical Report dated February 5, 2024. See Exhibit 99.4 of this Annual Report.

E. Controls and Procedures

a. Certifications.

The required certifications for the Principal Executive Officer and Principal Financial Officer are attached as Exhibits 99.5, 99.6, 99.7 and 99.8 to this Annual Report.

b. Disclosure Controls and Procedures.

As required by paragraph (b) of Rules 13a-15 or 15d-15 under the Exchange Act, our principal executive officer and principal financial officer evaluated our Company’s disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) of the Exchange Act) as of the end of the period covered by this Annual Report. Based on the evaluation, these officers concluded that as of the end of the period covered by this Annual Report, our disclosure controls and procedures were effective to ensure that the information required to be disclosed by our Company in reports it files or submits under the Exchange Act is recorded, processed, summarized and reported within the time period specified in the rules and forms of the SEC. These disclosure controls and procedures include controls and procedures designed to ensure that such information is accumulated and communicated to our Company’s management, including our Company’s principal executive officer and principal financial officer, to allow timely decisions regarding required disclosure.

Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues, if any, within our company have been detected.

c. Management's Annual Report on Internal Control Over Financial Reporting.

Management is responsible for establishing and maintaining adequate internal control over financial reporting (as defined in Rules 13a-15(f) and 15d-15(f) of the Exchange Act) for our Company. Our Company’s internal control over financial reporting is designed to provide reasonable assurance, not absolute assurance, regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with International Financial Reporting Standards. Internal control over financial reporting includes those policies and procedures that: (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of our Company’s assets; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with International Financial Reporting Standards, and that our Company’s receipts and expenditures are being made only in accordance with authorizations of our management and directors; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use or disposition of assets that could have a material effect on our financial statements.

For the purposes of Exchange Act Rules 13a-15(f) and 15d-15(f), management, including our principal executive officer and principal financial officer, conducted an evaluation of the design and operation of our internal controls over financial reporting as of December 31, 2023, based on the criteria set forth in Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission. This evaluation included review of the documentation of controls, evaluation of the design effectiveness of controls, testing of the operating effectiveness of controls and a conclusion on this evaluation. Based on this evaluation, our management concluded our internal controls over financial reporting were effective as at December 31, 2023.

Deloitte LLP, the Company’s independent registered public accounting firm, who audited and reported on our consolidated financial statements, has issued an attestation report on the effectiveness of our internal control over financial reporting as of December 31, 2023. The attestation report is included within the consolidated financial statements in this Annual Report on Form 40-F.

| 4 |

Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues, if any, within our company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty and that breakdowns can occur because of simple error or mistake.

d. Attestation Report of the Independent Registered Public Accounting Firm.

See Exhibit 99.2 of this Annual Report.

e. Changes in Internal Control Over Financial Reporting.

During the year ended December 31, 2023, there were no changes in the Company’s internal control over financial reporting that have materially affected, or are reasonable likely to materially affect, its internal control over financial reporting.

F. Notices Pursuant To Regulation BTR

The Company was not required by Rule 104 of Regulation BTR to send any notices to any of its directors or executive officers during the fiscal year ended December 31, 2023.

G. Audit Committee Financial Expert

The following are the members of the Audit Committee:

Peter Bojtos (Chair) |

|

Independent |

Financially literate |

|

|

Jasman Yee |

|

Independent |

|

Financially literate |

|

Ronald Andrews |

|

Independent |

|

Financially literate |

|

The Company’s Board of Directors has determined that Mr. Peter Bojtos, Jasman Yee and Ronald Andrews are each qualified as an Audit Committee Financial Expert. Also, Mr. Peter Bojtos, Mr. Jasman Yee, and Mr. Ronald Andrews are each independent as determined by the NYSE American rules.

An Audit Committee Financial Expert must possess five attributes: (i) an understanding of IFRS and financial statements; (ii) the ability to assess the general application of such principles in connection with the accounting for estimates, accruals and reserves; (iii) experience preparing auditing, analyzing or evaluating financial statements that present a breadth and level of complexity of accounting issues that are generally comparable to the breadth and complexity of issues that can reasonably be expected to be raised by the registrant’s financial statements, or experience actively supervising one or more persons engaged in such activities; (iv) an understanding of internal controls and procedures for financial reporting; and (v) an understanding of audit committee functions.

Mr. Bojtos is a professional engineer with over 50 years of worldwide experience in the mining industry. He has an extensive background in corporate management as well as in all facets of the industry from exploration through the feasibility study stage to mine construction, operations and decommissioning. Mr. Bojtos graduated from the University of Leicester, England in 1972, following which he worked at open-pit iron-ore and underground base-metal and uranium mines in West Africa, the United States and Canada. Following that for 12 years, he worked in Toronto for Kerr Addison Mines Ltd., a Noranda Group company, in increasingly senior management and officer positions. From 1990 to 1992 he was the President & CEO of RFC Resource Finance Corp. developing a zinc mine in Washington State. From 1992 to 1993 Mr. Bojtos was the President & CEO of Consolidated Nevada Goldfields Corp. which operated precious metal mines in the United States. From 1993 to 1995 he was Chairman & CEO of Greenstone Resources Ltd, constructing and operating several gold mines in Central America. From 2017 to 2019 he was president of Pembridge Resources plc. For the past 30 years, he has been self-employed and he has served on over two dozen public company boards from 1996 to present. The Company believes that Mr. Bojtos is qualified as an Audit Committee Financial Expert based on his prior experiences as serving audit committee chair with another company.

| 5 |

Mr. Yee is a BASc, P.Eng (BC) 1970 graduate of the University of British Columbia with a degree in chemical engineering, a 1974 graduate of Toronto’s Ryerson Polytechnical Institute with a degree in economics, and holds a certificate for completing the Canadian Securities Course. The Company believes that Mr. Yee is qualified as an Audit Committee Financial Expert based on his prior accounting experience with other companies.

Mr. Andrews has a Bachelor of Science degree in horticulture from Washington State University and a Master’s degree in Political Science. Mr. Andrews is the owner and operator of Andrews Orchards and sells and distributes agricultural chemicals and fertilizers. The Company believes that Mr. Andrews is qualified as an Audit Committee Financial Expert because he has acted as director and chairman of the audit committee of several public mining companies.

H. Code of Ethics

The Company has adopted a Code of Ethics that applies to all directors, officers, consultants and employees of the Company.

The Code of Ethics covers a wide range of financial and non-financial business practices and procedures. This Code of Ethics does not cover every issue that may arise, but it sets out basic principles to guide all executive and staff of the Company. If a law or regulation conflicts with a policy in this Code of Ethics, then personnel must comply with such law or regulation. If any person has any questions about this Code of Ethics or potential conflicts with a law or regulation, they should refer to the Company’s Whistleblower Policy.

All executive and staff should recognize that they hold an important role in the overall corporate governance and ethical standards of the Company. Each person is capable and empowered to ensure that the Company’s, its shareholders’ and other stakeholders’ interests are appropriately balanced, protected and preserved. Accordingly, the Code of Ethics provides principles to which all personnel are expected to adhere and advocate. The Code of Ethics embodies rules regarding individual and peer responsibilities, as well as responsibilities to the Company, the shareholders, other stakeholders, and the public generally.

A copy of the Code of Ethics and Whistleblower Policy previously has been filed as an exhibit with the SEC and is available at the Company’s website at www.avino.com. You may obtain a copy of the Code of Ethics and Whistleblower Policy upon request by contacting the Company’s Corporate Secretary at Suite 900, 570 Granville Street, Vancouver, British Columbia V6C 3P1, Canada.

I. Principal Accountant Fees and Services

The Company’s independent auditor for the fiscal years ended December 31, 2023 and 2022, was Deloitte LLP.(PCAOB ID No. 1208).

The following summarizes the significant professional services rendered by Deloitte LLP for the years ended December 31, 2023, and 2022.

Financial Year Ending |

|

|

|

|

|

|

|

|

December 31 |

Audit Fees1 |

|

Audit Related Fees2 |

Tax Fees3 |

|

All Other Fees4 |

||

2023 |

|

C$1,235,025 |

|

C$29,631 |

|

C$34,035 |

|

Nil |

2022 |

|

C$543,560 |

|

C$25,923 |

|

Nil |

|

Nil |

____________

1 “Audit Fees” include fees necessary to perform the audit of the Company’s consolidated financial statements. Audit Fees include quarterly reviews, fees for review of tax provisions and for accounting consultations on matters reflected in the financial statements. Audit Fees also include audit or other attest services required by legislation or regulation, such as comfort letters, consents, reviews of securities filings and statutory audits.

2 “Audit-Related Fees” include services that are traditionally performed by the auditor. These audit-related services include audit or attest services not required by legislation or regulation.

3 “Tax Fees” include fees for all tax services other than those included in “Audit Fees” and “Audit- Related Fees”.

4 “All Other Fees” include fees relating to the aggregate fees billed in each of the last two fiscal years for products and services provided by the Company’s external auditor, other than the services reported under footnotes 1 to 3 above.

The Audit Committee will pre-approve all audit and non-audit services not prohibited by law to be provided by the independent auditors of the Company. These services may include audit services, audit-related services, tax services and other services. All services and fees described above were reviewed and pre-approved by the Audit Committee.

J. Off Balance Arrangements

The Company has no off-balance sheet arrangements. See Management's Discussion and Analysis of Financial Condition and Results of Operations for the fiscal year ended December 31, 2023, for an analysis of material cash requirements from known contractual and other obligations.

| 6 |

K. Audit Committee

The Company has a separately-designated standing Audit Committee established in accordance with Section 3(a)(58)(A) of the Exchange Act. The Audit Committee members consist of Mr. Peter Bojtos (Chair), Jasman Yee and Ronald Andrews.

L. Mine Safety Disclosure

The Company does not operate any mine in the United States and has no mine safety incidents to report for the year ended December 31, 2023.

M. Disclosure Regarding Foreign Jurisdictions That Prevent Inspections

None.

N. Recovery of erroneously awarded compensation

None.

O. Consent to Service of Process

The Company has previously filed with the SEC an Appointment of Agent for Service of Process and Undertaking on Form F-X with respect to the class of securities in relation to which the obligation to file this Form 40-F arises. Any change to the name or address of the Company's agent for service shall be communicated promptly to the SEC by amendment to the Form F-X referencing the file number of the Company.

| 7 |

EXHIBITS

| 8 |

SIGNATURE

Pursuant to the requirements of the Exchange Act, the registrant hereby certifies that it meets all of the requirements for filing this Form 40-F and has duly caused this annual report to be signed on its behalf by the undersigned, thereto duly authorized.

|

Avino Silver & Gold Mines, Ltd. |

|

|

|

|

|

|

Date: March 28, 2024 |

By: |

/s/ David Wolfin |

|

|

|

David Wolfin, President, and Chief Executive Officer |

|

| 9 |

EXHIBIT 97.1

Avino Silver & Gold Mines Ltd.

Clawback Policy

Introduction

The Board of Directors (the “Board”) of the Avino Silver & Gold Mines Ltd. (the “Company”), acting in the best interest of the Company and its shareholders, has therefore adopted this policy which provides for the recoupment of certain executive compensation in the event of an accounting restatement resulting from material noncompliance with financial reporting requirements under the federal securities laws (the “Policy”). This Policy is designed to comply with Section 10D of the Securities Exchange Act of 1934 (the “Exchange Act”) and Rule 811 of the NYSE American Company Guide (the “Rule 811”).

Administration

This Policy shall be administered by the Board or, if so designated by the Board, the Compensation Committee, in which case references herein to the Board shall be deemed references to the Compensation Committee. Any determinations made by the Board shall be final and binding on all affected individuals.

Covered Executives

This Policy applies to the Company’s current and former executive officers, including but not limited to the Company’s Principal Executive Officer and Principal Financial and Accounting Officer, as determined by the Board in accordance with the definition in Section 10D of the Exchange Act and Rule 811, and such other senior executives/employees who may from time to time be deemed subject to the Policy by the Board (“Covered Executives”).

Recoupment; Accounting Restatement

In the event the Company is required to prepare an accounting restatement of its financial statements due to the Company’s material noncompliance with any financial reporting requirement under the securities laws, including any required accounting restatement to correct an error in previously issued financial statements that is material to the previously issued financial statements or that would result in a material misstatement if the error were corrected in the current period or left uncorrected in the current period, the Board will require reimbursement or forfeiture of any excess Incentive Compensation received by any Covered Executive during the three completed fiscal years immediately preceding the date on which the Company is required to prepare an accounting restatement.

Incentive Compensation

Incentive Compensation means all incentive-based compensation received by a Covered Executive (i) on or after the Effective Date, regardless of if the incentive-based compensation results from a compensation contract or arrangement existing prior to the Effective Date, (ii) after beginning service as a Covered Executive, (iii) who served as a Covered Executive at any time during the applicable performance period for that incentive-based compensation, (iv) while the Company has a class of securities listed on a national securities exchange or a national securities association, and (v) during the three completed fiscal years immediately preceding the date that the Company is required to prepare an accounting restatement as defined above.

| 1 |

For purposes of this Policy, Incentive Compensation may include, but not limited to, any of the following; provided that, such compensation is granted, earned, or vested based wholly or in part on the attainment of a financial reporting measure: annual bonuses and other short- and long-term cash incentives, stock options, stock appreciation rights, restricted stock, restricted stock units, performance shares, or performance units.

For purpose of this Policy, financial reporting measures may include, but not limited to, any of the following: company stock price, revenues, or net income.

Excess Incentive Compensation: Amount Subject to Recovery

The amount to be recovered will be the excess of the Incentive Compensation paid to the Covered Executive based on the erroneous data over the Incentive Compensation that would have been paid to the Covered Executive had it been based on the restated results, as determined by the Board, without regard to any taxes paid by the Covered Executive in respect of the Incentive Compensation paid based on the erroneous data.

If the Board cannot determine the amount of excess Incentive Compensation received by the Covered Executive directly from the information in the accounting restatement, then it will make its determination based on a reasonable estimate of the effect of the accounting restatement.

Method of Recoupment

The Board will determine, in its sole discretion, the method for recouping Incentive Compensation hereunder which may include, without limitation:

|

| (a) | requiring reimbursement of cash Incentive Compensation previously paid; |

|

|

|

|

|

| (b) | seeking recovery of any gain realized on the vesting, exercise, settlement, sale, transfer, or other disposition of any equity-based awards; |

|

|

|

|

|

| (c) | offsetting the recouped amount from any compensation otherwise owed by the Company to the Covered Executive; |

|

|

|

|

|

| (d) | cancelling outstanding vested or unvested equity awards; and/or |

|

|

|

|

|

| (e) | taking any other remedial and recovery action permitted by law, as determined by the Board. |

| 2 |

No Indemnification

The Company shall not indemnify any Covered Executives against the loss of any incorrectly awarded Incentive Compensation.

Interpretation

The Board is authorized to interpret and construe this Policy and to make all determinations necessary, appropriate, or advisable for the administration of this Policy. It is intended that this Policy be interpreted in a manner that is consistent with the requirements of Section 10D of the Exchange Act, any applicable rules or standards adopted by the Securities and Exchange Commission, and Rule 811.

Effective Date

This Policy shall be effective as of November [*], 2023 (the “Effective Date”) and shall apply to Incentive Compensation that is received by Covered Executives on or after the Effective Date, even if such Incentive Compensation was approved, awarded, or granted to Covered Executives prior to the Effective Date.

Amendment; Termination

The Board has full discretion to amend, modify, supplement, rescind or replace all or any portion of this Policy at any time, except that no amendment or termination of this Policy shall be effective if such amendment or termination would cause the Company to violate any federal securities laws, SEC rule or NYSE American rule.

The Board may amend this Policy from time to time in its discretion and shall amend this Policy as it deems necessary to comply with the definitions and obligations set forth under the Rule 811, Section 10D, Rule 10D-1 and any other applicable law, regulation, rule or interpretation of the SEC or NYSE American promulgated or issued in connection therewith as of the Effective Date. This Policy shall be deemed to automatically update to conform to any amendment to the definitions and obligations set forth under the Rule 811, Section 10D, Rule 10D-1 and any other applicable law, regulation, rule or interpretation of the SEC or NYSE American promulgated or issued in connection therewith that are effective as of a date that is after the Effective Date.

Other Recoupment Rights

Any right of recoupment under this Policy is in addition to, and not in lieu of, any other remedies or rights of recoupment that may be available to the Company pursuant to the terms of any similar policy in any employment agreement, equity award agreement, or similar agreement and any other legal remedies available to the Company.

| 3 |

Relationship to Other Plans and Agreements

The Board intends that this Policy will be applied to the fullest extent of the law. Any employment agreement, equity award agreement, or similar agreement entered into on or after the Effective Date shall, as a condition to the grant of any benefit thereunder, be construed to incorporate an agreement by the Covered Executive to abide by the terms of this Policy. In the event of any inconsistency between the terms of the Policy and the terms of any employment agreement, equity award agreement, or similar agreement under which Incentive Compensation has been granted, awarded, earned or paid to a Covered Executive, whether or not deferred, the terms of the Policy shall govern.

Acknowledgment

The Covered Executives shall sign an acknowledgment form in the form attached hereto as Exhibit A in which they acknowledge that they have read and understand the terms of the Policy and are bound by the Policy.

Impracticability

The Board shall recover any excess Incentive Compensation in accordance with this Policy unless such recovery would be impracticable, as determined by the Board in accordance with Rule 10D-1 of the Exchange Act and Rule 811.

Successors

This Policy shall be binding and enforceable against all Covered Executives and their beneficiaries, heirs, executors, administrators or other legal representatives.

| 4 |

Exhibit A

ATTESTATION AND ACKNOWLEDGEMENT OF

CLAWBACK POLICY

I, the undersigned, affirm and acknowledge that I am fully bound by, and subject to, all of the terms and conditions of Avino Silver & Gold Mines Ltd.’s Clawback Policy, as may be amended, restated, supplemented or otherwise modified from time to time, (the “Policy”). In the event of any inconsistency between the Policy and the terms of any employment agreement to which I am a party, or the terms of any compensation plan, program or agreement under which any compensation has been granted, awarded, earned or paid, the terms of the Policy shall govern. In the event the Compensation Committee and/or Board determines that any amounts granted, awarded, earned or paid to me must be forfeited or reimbursed to the Company, I will promptly take any action necessary to effectuate such forfeiture and/or reimbursement. Any capitalized terms used in this Acknowledgment without definition shall have the meaning set forth in the Policy.

| By: |

|

| Date: |

|

|

|

|

|

|

|

| Name: |

|

|

|

|

|

|

|

|

|

|

| Title: |

|

|

|

|

| 5 |

EXHIBIT 99.1

ANNUAL INFORMATION FORM

FOR THE FINANCIAL YEAR ENDED DECEMBER 31, 2023

DATED MARCH 28, 2024

ANNUAL INFORMATION FORM

FOR THE FINANCIAL YEAR ENDED DECEMBER 31, 2023

TABLE OF CONTENTS

| PRELIMINARY NOTES | 3 |

| CORPORATE STRUCTURE | 6 |

| GENERAL DEVELOPMENT OF THE BUSINESS | 7 |

| DESCRIPTION OF THE BUSINESS | 11 |

| MINERAL RESOURCE ESTIMATES | 20 |

| MATERIAL MINERAL PROJECTS | 20 |

| RISK FACTORS | 21 |

| DIVIDENDS | 32 |

| GENERAL DESCRIPTION OF CAPITAL STRUCTURE | 33 |

| MARKET FOR SECURITIES | 33 |

| DIRECTORS AND OFFICERS | 34 |

| CEASE TRADE ORDERS, BANKRUPTCIES, PENALTIES OR SANCTIONS | 36 |

| CONFLICTS OF INTEREST | 37 |

| PROMOTERS | 37 |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | 37 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 38 |

| TRANSFER AGENT AND REGISTRAR | 38 |

| MATERIAL CONTRACTS | 38 |

| NAMES AND INTERESTS OF EXPERTS | 38 |

| AUDIT COMMITTEE INFORMATION | 39 |

| ADDITIONAL INFORMATION | 40 |

|

|

|

| APPENDIX “A” - DEFINITIONS, TECHNICAL TERMS, ABBREVIATIONS | A1 |

| APPENDIX “B” - AUDIT COMMITTEE CHARTER | B1 |

| APPENDIX “C” - MATERIAL MINERAL PROJECTS | C1 |

| - 2 - |

PRELIMINARY NOTES

Effective Date of Information

All information in this annual information form (this “AIF”) of Avino Silver & Gold Mines Ltd. (“Avino” or the “Company”) is as at December 31, 2023, unless otherwise indicated. This AIF is dated March 28, 2024.

Additional Information

Additional information is provided in the Company’s audited consolidated financial statements for the years ended December 31, 2023 and 2022 (the “2023 Annual Financial Statements”) and Management’s Discussion and Analysis dated March 20, 2024 for the year ended December 31, 2023 (the “2023 Annual MD&A”), each of which has been filed on the Company’s profile on the System for Electronic Document Analysis and Retrieval Plus (“SEDAR+”) (www.sedarplus.ca). Additional information, including directors’ and officers’ remuneration and indebtedness and information concerning the principal holders of the Company’s securities, and securities authorized for issuance under equity compensation plans, where applicable, will be contained in the Company’s Management Information Circular to be filed in connection with its upcoming annual meeting of shareholders for 2024 (the “2024 Circular”). This information, including the 2023 Annual MD&A and the 2023 Annual Financial Statements, and other additional information relating to the Company may be found in the Company's public filings with provincial securities regulatory authorities which can be found on the Company's profile on the SEDAR+ website at www.sedarplus.ca and with the U.S. Securities and Exchange Commission (the "SEC") on the Electronic Data-Gathering, Analysis and Retrieval ("EDGAR") website at www.sec.gov/edgar.html or, in the case of the 2024 Circular, will be made available in accordance with the time requirements of Canadian and U.S. securities laws.

Non-IFRS Measures

The Company has included certain non-IFRS and other financial measures, which the Company believes, that together with measures determined in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”), provide investors with an improved ability to evaluate the underlying performance of the Company. Non-IFRS financial measures do not have any standardized meaning prescribed under IFRS, and therefore they may not be comparable to similar non-IFRS and other financial performance measures employed by other companies. The data is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

Reconciliations and descriptions can be found under the heading, “Non-IFRS Measures” of the 2023 MD&A, which section is incorporated by reference herein and is available on SEDAR+ at www.sedarplus.ca.

Interpretation and Definitions

A glossary of certain technical terms, abbreviations and measurement conversions is set forth in Appendix “A”.

***

| - 3 - |

Currency and Exchange Rate

Unless otherwise indicated, in this AIF all references to “dollar” or the use of the symbol “$” are to the United States dollar and all references to “C$” are to the Canadian dollar. The daily average exchange rate for Canadian dollars in terms of the United States dollar on December 31, 2023 and March 27, 2024 as reported by the Bank of Canada was 1.3544 and 1.3587, respectively.

| United States Dollars into Canadian Dollars | 2023 | 2022 | 2021 |

| Closing | 1.3226 | 1.3544 | 1.2678 |

| Average | 1.3495 | 1.3017 | 1.2537 |

| High | 1.3875 | 1.3856 | 1.2942 |

| Low | 1.3215 | 1.2451 | 1.2040 |

Forward‐Looking Statements

Statements contained in this AIF that are not current or historical factual statements may constitute “forward-looking information” or ‘”forward-looking statements” within the meaning of applicable Canadian and United States securities laws (“forward-looking statements”). These forward-looking statements are presented for the purpose of assisting the Companys securityholders and prospective investors in understanding management's views regarding those future outcomes and may not be appropriate for other purposes. When used in this AIF, the words “may”, “would”, “could”, “will”, intend, “plan”, “anticipate”, “believe”, “seek”, “propose”, “estimate”, “expect”, and similar expressions, as they relate to the Company, are intended to identify forward-looking statements. All such forward-looking statements are subject to important risks, uncertainties and assumptions. These statements are forward-looking because they are based on current expectations, estimates and assumptions. It is important to know that: (i) unless otherwise indicated, forward-looking statements in this AlF and its appendices describe expectations as at the date hereof; and (ii) actual results and events could differ materially from those expressed or implied. Capitalized terms used but not defined in this “Forward-Looking Statements”section of the AIF shall have the meaning ascribed to such term elsewhere in the AIF.

Specific forward-looking statements in this AIF include, but are not limited to: any objectives, expectations, intentions, plans, results, levels of activity, goals or achievements; estimates of mineral resources; the realization of mineral resource estimates; the impairment of mineral properties and non-producing properties; the timing and amount of estimated future production, production guidance, costs of production, capital expenditures, costs and timing of development; the success of exploration and development activities.

With respect to underground development improvements, equipment procurement and the drilling program and expected results thereof; material uncertainties that may impact the Company’s liquidity in the short term; the effects of COVID-19; changes in accounting policies not yet in effect; permitting timelines; government regulation of mining operations; environmental risks; labour relations, employee recruitment and retention; the timing and possible outcomes of pending disputes or litigation; negotiations or regulatory investigations; exchange rate fluctuations; cyclical or seasonal aspects of our business; our dividend policy; capital expenditures; the Company’s ability to operate mine; statements relating to the future financial condition, assets, liabilities (contingent or otherwise), business, operations or prospects of the Company; the suspension of certain operating metrics such as cash costs and all-in sustaining costs; the liquidity of the Common Shares; and other events or conditions that may occur in the future.

Inherent in the forward-looking statements are known and unknown risks, uncertainties and other factors beyond the Company’s ability to control or predict that may cause the actual results, performance or achievements of the Company, or developments in the Company’s business or in its industry, to differ materially from the anticipated results, performance, achievements or developments expressed or implied by such forward-looking statements.

| - 4 - |

Some of the risks and other factors (some of which are beyond the Company’s control) that could cause results to differ materially from those expressed in the forward-looking statements and information contained in this AIF include, but are not limited to: risks associated with market fluctuations in commodity prices; risks related to changing global economic conditions, which may affect the Company's results of operations and financial condition including risks related to mineral resources, development and production and the Company's ability to sustain or increase present production; risks related to global financial and economic conditions; risks related to government regulation and environmental compliance; risks related to mining property claims and titles, and surface rights and access; risks related to labour relations, disputes and/or disruptions, employee recruitment and retention; the Company's material properties are located in Mexico and are subject to changes in political and economic conditions and regulations in that country; risks related to the Company’s relationship with the communities where it operates; risks related to actions by certain non-governmental organizations; substantially all of the Company's assets are located outside of Canada, which could impact the enforcement of civil liabilities obtained in Canadian and U.S. courts; risks related to currency fluctuations that may adversely affect the financial condition of the Company; the Company may need additional capital in the future and may be unable to obtain it or to obtain it on favourable terms; risks associated with the Company's outstanding debt and its ability to make scheduled payments of interest and principal thereon; the Company may engage in hedging activities; risks associated with the Company's business objectives; risks relating to mining and exploration activities and future mining operations; operational risks and hazards inherent in the mining industry; risks related to competition in the mining industry; risks relating to negative operating cash flows; risks relating to the possibility that the Company’s working capital requirements may be higher than anticipated and/or its revenue may be lower than anticipated over relevant periods; and risks relating to climate change and the legislation governing it.

The list above is not exhaustive of the factors that may affect any of the Company's forward-looking statements. Investors and others should carefully consider these and other factors and not place undue reliance on the forward-looking statements. The forward-looking statements contained in this AIF represent the Company’s views only as of the date such statements were made. Forward-looking statements contained in this AIF are based on management’s plans, estimates, projections, beliefs and opinions as at the time such statements were made and the assumptions related to these plans, estimates, projections, beliefs and opinions may change. Although forward-looking statements contained in this AIF are based on what management considers to be reasonable assumptions based on information currently available to it, there can be no assurances that actual events, performance or results will be consistent with these forward- looking statements, and management's assumptions may prove to be incorrect. Some of the important risks and uncertainties that could affect forward-looking statements are described further in the AIF. The Company cannot guarantee future results, levels of activity, performance or achievements, should one or more of these risks and uncertainties materialize, or should underlying assumptions prove incorrect, the actual results or developments may differ materially from those contemplated by the forward-looking statements. The Company does not undertake to update any forward-looking statements, even if new information becomes available, as a result of future events or for any other reason, except to the extent required by applicable securities laws.

| - 5 - |

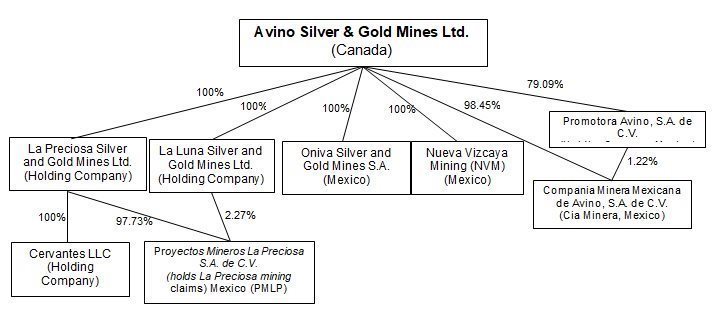

CORPORATE STRUCTURE

Name, Address and Incorporation

The Company was incorporated by Memorandum of Association under the laws of the Province of British Columbia on May 15, 1968, and on August 22, 1969, by virtue of an amalgamation with Ace Mining Company Ltd., became a public company whose common shares are registered under the Exchange Act, changing its name to Avino Mines & Resources Limited. On April 12, 1995, the Company changed its corporate name to International Avino Mines Ltd., and on August 29, 1997, the Company changed its corporate name to Avino Silver & Gold Mines Ltd., its current name, to better reflect the business of the Company of exploring for and mining silver and gold.

The Company is a reporting issuer in all Provinces of Canada, except for Quebec, a foreign private issuer in the United States, and is listed on the Toronto Stock Exchange, under the symbol “ASM”, on the NYSE-American under the symbol “ASM”, and on the Berlin and Frankfurt Stock Exchanges under the symbol “GV6”. The principal executive office of the Company is located at Suite 900, 570 Granville Street, Vancouver, British Columbia V6C 3P1, and its telephone number is 604-682-3701.

The Company is a natural resource company primarily engaged in the extracting and processing of silver and to a lesser extent, gold and copper and the acquisition and exploration of natural resource properties. The Company’s principal business activities have been the exploration for and extracting and processing of silver, gold and copper at mineral properties located in the State of Durango, Mexico. To a lesser extent, the Company also owns other exploration and evaluation assets in British Columbia, Canada.

Our Common Shares are listed on the Toronto Stock Exchange (the “TSX”) under the symbol “ASM.TO”, on the NYSE American under the symbol “ASM”, and on the Berlin and Frankfurt Stock Exchanges under the symbol “GV6”.

Inter-Corporate Relationships

The organizational chart below indicates the inter-corporate relationships between the Company and its material subsidiaries (and includes their jurisdiction of organization) as of the date hereof. Unless otherwise indicated, all such subsidiaries are wholly owned.

| - 6 - |

GENERAL DEVELOPMENT OF THE BUSINESS

Overview

Avino Silver & Gold Mines Ltd. (the “Company” or “Avino”) was incorporated in 1968 under the laws of the Province of British Columbia, Canada. The Company is engaged in the production and sale of silver, gold, and copper and the acquisition, exploration, and advancement of mineral properties.

The Company’s head office and principal place of business is Suite 900, 570 Granville Street, Vancouver, BC, Canada. The Company is a reporting issuer in Canada and the United States, and trades on the Toronto Stock Exchange (“TSX”), the NYSE American, and the Frankfurt and Berlin Stock Exchanges.

In Durango, Mexico, the Company operates the Avino Mine which produces copper, silver and gold at the historic Avino property in the state of Durango, Mexico (the “Avino Property”), after declaring commercial production effective July 1, 2015. As of today, the Company continues to produce from the Avino Mine. Also in Durango, the Company also holds 100% interest in Proyectos Mineros La Preciosa S.A. de C.V . (“La Preciosa”), a Mexican corporation which owns the La Preciosa property in Durango, Mexico (the “La Preciosa Property”), located approximately 20 kms southwest of the Avino Property.

Avino’s remaining Mexican properties, as well as its Canadian properties, are all in the exploration stage. In order to determine if a commercially viable mineral deposit exists in any of these properties, further geological work will need to be done, and based upon the results of that work a final evaluation will need to be made to conclude on economic and legal feasibility. The Company is currently focusing on extracting and processing resources at the Avino Property and continuing to advance the La Preciosa Property. The Company’s other Canadian properties are not deemed to be material and have been optioned to Endurance Gold Corporation, or have been sold. (see: Three Year History- Fiscal 2022 and Fiscal 2023 below for further details).

Three Year History

Fiscal 2021

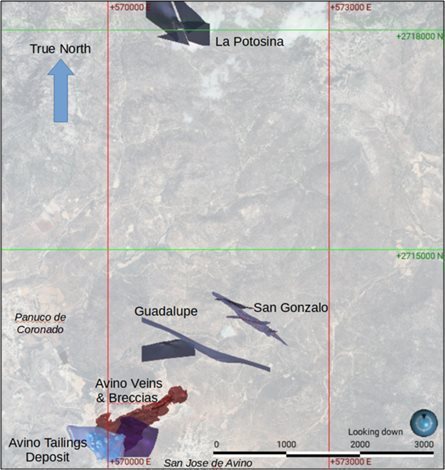

On January 13, 2021, the Company announced an updated mineral resource estimate for the Company’s Avino Property located near Durango in west-central Mexico. The updated estimate includes the Avino Property’s Avino Mine (Elena Tolosa – “ET”) vein systems, the San Gonzalo Mine, and the Avino Property’s Oxide Tailings.

On January 29, 2021, the Company announced that it had entered into a sales agreement with Cantor Fitzgerald & Co. (the “Designated Agent”), H.C. Wainwright & Co., LLC, Roth Capital Partners, LLC, and A.G.P./Alliance Global Partners (collectively, with the Designated Agent, the “Agents”), as agents or as principals, for the distribution of the Offered Shares in the United States up to the aggregate sales amount of $25.0 million (the “Maximum Amount”), in accordance with the terms of the Sales Agreement (the “Offering” or the “ATM”). Pursuant to the Offering, during fiscal 2021, the Company sold, through the Designated Agent, approximately 10.3 million common shares at average price per share of $1.87 for gross proceeds of approximately $19.2 million.

On August 3, 2021, the Company announced that mining operations had restarted at its Avino Mine.

On October 27, 2021, the Company announced that it has entered into a share purchase agreement (the “La Preciosa Transaction”) with Coeur Mining Inc. (“Coeur”) to acquire through the purchase of shares of certain holding companies, the La Preciosa Property. The La Preciosa Property is located adjacent to the Avino Mine in the state of Durango, Mexico. The La Preciosa Transaction closed on March 21, 2022.

The Company acquired the La Preciosa property for consideration of $20,000,000, of which $15,000,000 was paid at the closing of the La Preciosa Transaction and the remaining $5,000,000 was payable pursuant to a non-interest bearing promissory note, which was paid before the first anniversary of the closing date.

| - 7 - |

Avino also issued to Coeur 14,000,000 common shares and share purchase warrants which were exercisable to acquire up to 7,000,000 common shares at $1.09 per share until September 23, 2023.

Additional cash consideration of $8.75 million will be payable by the Company to Coeur within 12 months of initial production of the La Preciosa Property. Avino may elect to pay up to half of the contingent cash consideration in Avino shares, subject to certain limitations. Coeur will retain ownership of a 1.25% net smelter royalty on the Gloria and Abundancia areas of the La Preciosa Property, and a 2.00% gross value royalty on all areas of the La Preciosa Property, other than the Gloria and Abundancia areas. The Company has also agreed to pay Coeur $0.25 per silver equivalent ounce (subject to inflationary adjustment) of new mineral reserves (as defined by NI 43-101) discovered and declared outside of the current mineral resource area at the La Preciosa Property, subject to a cap of $50 million, and any such payments will be credited against any existing or future payments owing on the gross value royalty.

The completion of the La Preciosa Transaction was subject to a number of customary conditions precedent, as well as, the authorization of the Mexican Federal Economic Commission. The Toronto Stock Exchange provided approval of the project and the NYSE American approved the listing of the common shares and warrants to be issued in the La Preciosa Transaction.

Fiscal 2022

On March 21, 2022, the Company announced the closing of the La Preciosa Transaction. The La Preciosa Property hosts of one of the largest undeveloped primary silver resources in Mexico and is located adjacent to Avino’s existing operations at the Avino Property. Avino believes that the La Preciosa Transaction has a strong rationale given the close proximity of the La Preciosa Property to Avino’s existing mine and infrastructure which could yield numerous financial and operational synergies, including reducing the environmental footprint associated with the development of a stand alone La Preciosa operation.

On April 7, 2022, the Company announced the results from the Oxide Tailings Project that sits within our tailings storage facility #1 (“TSF#1”) on the Avino Property. The 2021 drill program included 110 drill holes for a total of 3,645 metres of drilling. The drilling follows up the 2015/2016 campaign for which the 2016 NI 43-101 Preliminary Economic Assessment (“PEA”) was based on, which can be found on Avino’s SEDAR profile. The drill density of the current program should be sufficient to upgrade most of the existing inferred mineral resources to the measured and indicated categories, and to potentially expand the resources. Furthermore, a comprehensive sampling program is underway for an upcoming metallurgical testing program. Once completed and assuming results are conclusive, the existing PEA will be used as the framework for an updated study with the intention of increasing confidence to the Pre-Feasibility Study level.

By an option agreement dated May 2, 2022, the Company granted Endurance Gold Corporation (“Endurance”) the right to acquire an option to earn 100% ownership of the former Minto Gold Mine, Olympic and Kelvin gold prospects contained within a parcel of crown grants and mineral claims in British Columbia, Canada (the “Olympic Claims”). The Olympic Claims are owned by Avino and are located on the north and south shores of British Columbia’s Hydro’s Carpenter Lake Reservoir in the Bridge River Valley, east of the Royal Shear trend.

Under the terms of the option agreement, Endurance can earn a 100% interest in the Olympic Claims if they pay Avino a total cash consideration in the aggregate amount of C$100,000(of which $55,000 has been paid), issue up to a total of 1,500,000 common shares (of which 600,000 have been issued) of Endurance (the “Endurance Shares”) and incur exploration expenditures in the aggregate amount of C$300,000; all of which is to be incurred by December 31, 2024.

| - 8 - |

In the event that Endurance earns the 100% interest, the Olympic Claims will be subject to a 2% net smelter return royalty (“NSR”), of which 1% NSR can be purchased by Endurance for C$750,000 and the remaining balance of the NSR can be purchased for C$1,000,000.

As part of the final requirement to earn its interest, Endurance agreed to grant to Avino 750,000 share purchase warrants of Endurance (“the Endurance Warrants”) by December 31, 2024, that offer Avino the option to purchase Endurance Shares for a period of three years from the date of issuance. The exercise price of the Endurance Warrants will be set at a 25% premium to the 20-day VWAP share price at the issuance date. During the option period, if Endurance is successful in defining a compliant mineral resource of at least 500,000 gold-equivalent ounces on the Olympic Claims then Endurance will be obliged to pay Avino a C$1,000,000 discovery bonus.

Any Endurance Shares or Endurance Warrants issued under the option agreement will be subject to a four-month and a day hold period on issuance in accordance with applicable securities legislation.

Fiscal 2023

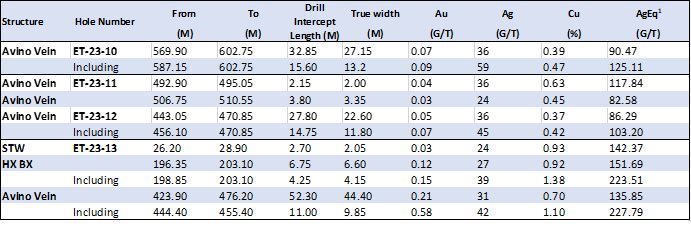

On July 5, 2023, the Company released the results of three holes from below Level 17, the current deepest workings at the ET area of the Avino system. Drill Hole ET-23-13 showed 44.40 metres true width of mineralization and is a step-out 50 metres to the west of Avino’s most westerly drill hole at 200 metres downdip below Level 17. This mineralized intercept is exceptionally wide and has very high silver, gold and copper grades. The vein system continues to be open along strike and at depth.

On September 14, 2023, the Company released the results of four additional holes from below Level 17, the current deepest workings at the Elena Tolosa (“ET”) area of the Avino system. These latest deep step-out holes test the SW extent of the robust Avino vein, and one infill hole was drilled to confirm local continuity. This drilling follows the continuity of the steeply dipping mineralization and aids in understanding the deep source of the mineralization. The Company is looking at the potential geometry and controls of the mineralization to come up with a model. Avino has completed its planned and budgeted drilling program for the year by drilling 7,545 metres in 13 drill holes. Our geologists on site are working through the recommendations made by our consulting geologists to study the potential of the entire ore body. The 2023 results will be reviewed to determine exploration plans and budget for 2024. The drill holes hits substantial widths at grades well above our current cut-off grades for mining.

The dry stack tailings facility has been fully operational for a year. The conveyor system is installed and is currently transporting the pressed dry residues to the disused Avino open pit area. A tab is now available on our website that provides further information on our tailings management system, along with a video (in Spanish) from the minesite that can be viewed. In addition, a selection of short videos of the facility in operation can be viewed under Videos and Media.

During the year ended December 31, 2023, the Company sold its 100% interest in 14 quartz leases located in the Mayo Mining Division of Yukon, Canada, which collectively comprise the Eagle Property, to a subsidiary of Hecla Mining Company, for cash consideration of C$250,000.

Corporate Social Responsibility (CSR) Award

In August 2023, the Company announce that it has received for the first time, the ESR “Empresa Socialmente Responsible ESR 2022” Award granted by the Mexican Center for Philanthropy (El Centro Mexicano para la Filantropia or Cemefi, and the Alliance for Corporate Social Responsibility (Alizanza por la Responsabilidad Social Empresarial or (AliaRSE)).

The ESR® Award is obtained through a diagnostic process based on indicators reviewed and endorsed annually by a committee of experts in the various CSR areas, supported with documentary evidence, an assessment differentiated by company size and by maturity levels, and an external verification process.

| - 9 - |

Recent Developments

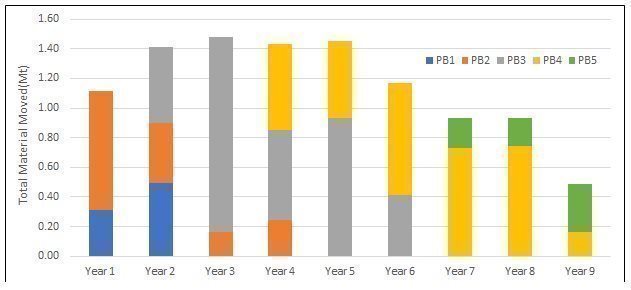

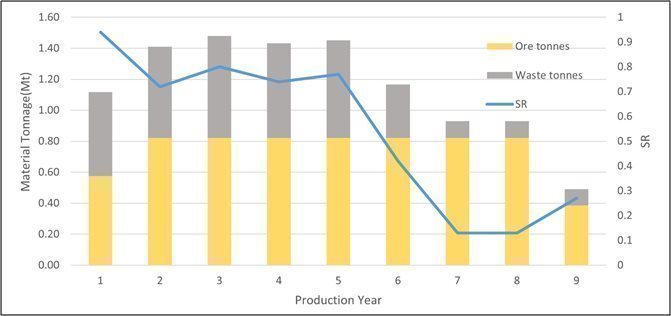

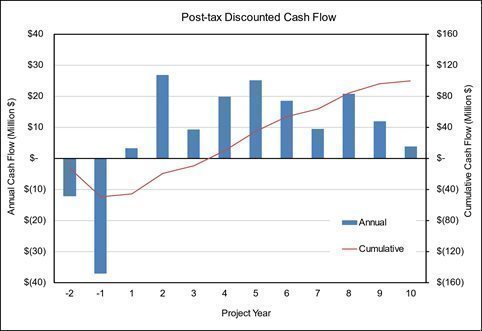

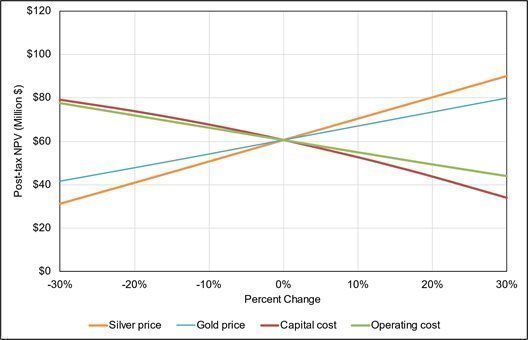

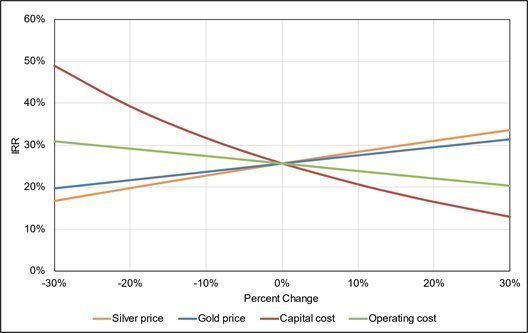

On February 5, 2024, the Company released the results of the Oxide Tailings Project Prefeasibility Study for the Avino Property, Durango Mexico (the “Report”) prepared in accordance with National Instrument 43-101 – Standard for Disclosure for Mineral Projects with a NPV US$98 million (pre-tax) and US$61 million (post-tax) at a 5% discount rate, IRR 35% (pre-tax) and 26% (post-tax), proven and probable mineral reserves of 6.70 million tonnes at a silver and gold grade of 55 g/t and 0.47 g/t respectively, over a 9-year LOM in respect of the existing oxide tailings. The completion of the Report is a milestone in our 5-year growth plan to become an intermediate silver producer in Mexico.

On January 9, 2024, the Company announced that it had signed a long-term land-use agreement with a local community for the development of La Preciosa in Durango, Mexico. La Preciosa hosts one of the largest undeveloped primary silver resources in Mexico and is located approximately 19 kilometres from the current Avino Mine production operations. With this long-term land-use agreement in place, the Company will start planning to commence hauling of old surface stockpiles of material to our mill at the Avino Mine for processing. In addition, the Company will now begin the filing of the environmental permit for underground extraction. The La Preciosa mine represents a key pillar in Avino’s transformational growth strategy.

DESCRIPTION OF THE BUSINESS

Summary

The Company is engaged in the evaluation, acquisition, exploration, development and operation of precious metals and polymetallic mineral properties, primarily those already producing or with the potential for near- term production. The Company’s geographic focus is Mexico. The Company owns and operates the Avino Mine on the Avino Property in Durango, Mexico and owns the La Preciosa Property in Durango, Mexico.

Principal Product

The Company produces copper concentrates containing silver, gold and copper. The Company believes that because of the availability of alternate processing and commercialization options for its concentrates, it is not dependent on a particular purchaser with regard to the sale of its products. However, the company has entered into a long-term concentrate sales agreement with Samsung C&T U.K Limited for the sale of Avino’s concentrates at the Avino Mine.

Production

The Company operates the 100% owned Avino Mine on the Avino Property located near in the State of Durango, Mexico. The Company previously produced a silver-gold concentrate from the San Gonzalo Mine on the same property; however, in 2019, the Company ceased production operations at San Gonzalo to focus on the Avino Mine.

The Avino Mine produces a copper concentrate containing copper, silver and gold. Ore mined at the Avino Mine is milled on the Avino Property.

| - 10 - |

Consolidated Results and Developments

Financial Results – in 000s

|

|

| 2023 |

|

| 2022 |

|

| 2021 |

|

|||

| Revenue from mining operations |

|

| 43,889 |

|

| $ | 44,187 |

|

| $ | 11,228 |

|

| Cost of sales |

|

| 36,070 |

|

|

| 29,125 |

|

|

| 7,681 |

|

| Mine operating income |

|

| 7,819 |

|

|

| 15,062 |

|

|

| 3,547 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

| General and administrative expenses |

|

| 5,620 |

|

|

| 5,156 |

|

|

| 3,566 |

|

| Share-based payments |

|

| 2,269 |

|

|

| 2,024 |

|

|

| 1,469 |

|

| Income (loss) before other items |

|

| (70 | ) |

|

| 7,882 |

|

|

| (1,488 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Other items |

|

|

|

|

|

|

|

|

|

|

|

|

| Interest and other income |

|

| 414 |

|

|

| 20 |

|

|

| 178 |

|

| Unrealized gain (loss) on long-term investments |

|

| (931 | ) |

|

| (2,103 | ) |

|

| (423 | ) |

| Fair value adjustment on warrant liability |

|

| 478 |

|

|

| 2,395 |

|

|

| 1,581 |

|

| Realized loss on warrants exercised |

|

| - |

|

|

| - |

|

|

| (1,106 | ) |

| Unrealized Foreign exchange gain (loss) |

|

| 110 |

|

|

| (17 | ) |

|

| (61 | ) |

| Project evaluation expenses |

|

| - |

|

|

| (81 | ) |

|

| (176 | ) |

| Finance cost |

|

| (81 | ) |

|

| (273 | ) |

|

| (52 | ) |

| Accretion of reclamation provision |

|

| (49 | ) |

|

| (44 | ) |

|

| (47 | ) |

| Interest expense |

|

| (381 | ) |

|

| (99 | ) |

|

| (24 | ) |

| Income (loss) from continuing operations before income taxes |

|

| (510 | ) |

|

| 7,680 |

|

|

| (1,618 | ) |

| Income taxes: |

|

|

|

|

|

|

|

|

|

|

|

|

| Current income tax expense |

|

| 527 |

|

|

| (1,144 | ) |

|

| (27 | ) |

| Deferred income tax (expense) recovery |

|

| 525 |

|

|

| (3,440 | ) |

|

| (412 | ) |

| Income tax (expense) recovery |

|

| 1,052 |

|

|

| (4,584 | ) |

|

| (439 | ) |

| Net income (loss) |

|

| 542 |

|

|

| 3,096 |

|

|

| (2,057 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Other comprehensive income (loss) |

|

|

|

|

|

|

|

|

|

|

|

|

| Currency translation differences |

|

| 15 |

|

|

| (254 | ) |

|

| (159 | ) |

| Total comprehensive income (loss) |

|

| 557 |

|

| $ | 2,842 |

|

| $ | (2,216 | ) |

| Earnings (loss) per share from continuing operations |

|

|

|

|

|

|

|

|

|

|

|

|

| Basic & Diluted |

| $ | 0.00 |

|

| $ | 0.03 |

|

| $ | (0.02 | ) |

| Earnings (loss) per share |

|

|

|

|

|

|

|

|

|

|

|

|

| Basic & Diluted |

| $ | 0.00 |

|

| $ | 0.03 |

|

| $ | (0.02 | ) |

| Weighted average number of common shares outstanding |

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

| 121,261,696 |

|

|

| 114,372,371 |

|

|

| 100,161,357 |

|

| Diluted |

|

| 125,346,674 |

|

|

| 117,615,898 |

|

|

| 100,161,357 |

|

| - 11 - |

Financial Results – Year ended December 31, 2023, compared to year ended December 31, 2022

Revenues

The Company recognized revenues net of penalties, treatment costs and refining charges, of $43.9 million on the sale of Avino Mine bulk copper/silver/gold concentrate, compared to $44.2 million revenues for year ended December 31, 2022, a decrease of $0.3 million. The sales are in line with prior year as a result of higher realized metal prices in 2023, primarily for gold and silver, partially offset by lower payable silver equivalent ounces sold in the current period of 2.08 million, compared to 2.45 million in 2022. This was a result of mine production in areas of lower feed grade, resulting in lower recoveries and fewer ounces produced in the current year compared to 2022. The decrease was partially offset by higher realized metal prices for silver and gold in the current year.

Metal prices for revenues recognized during the period were $23.46 per ounce of silver, $1,953 per ounce of gold, and $8,439 per tonne of copper, compared to $21.51, $1,788, and $8,552, respectively, for the same period in 2022.

Cost of Sales & Mine Operating Income

Cost of sales was $36.1 million, compared to $29.1 million in 2022, an increase of $7.0 million. The increase in cost of sales is partially attributable to 14% higher milled tonnes during 2023 compared to 2022, as well as 24% higher mined tonnes in the same period, which resulted in higher overall overhead costs despite lower ounces sold in the current year when compared to 2022. The increase is also attributable to a stronger Mexican peso during the period, which directly impacted labour and contractor costs. The Company prides itself in operating primarily with local workers and contractors for its mining operations.

Mine operating income, after depreciation and depletion, was $7.8 million, compared to $15.1 million in 2022. The decrease in mine operating income is a result of the increased cost of sales noted above. Further, unit costs were directly impacted due to a stronger Mexican Peso, especially labour and contractor costs. These increases were partially offset by higher realized metal prices during 2023 compared to 2022, as noted above.

General and Administrative Expenses & Share-Based Payments

General and administrative expenses was $5.6 million, compared to $5.2 million during the corresponding period in 2022, with the increases primarily due to additional professional fees incurred following the inclusion of La Preciosa into ongoing operations.

Share-based payments was $2.3 million, compared to $2.0 million for the same period in 2022, an increase of $0.3 million. The increase is a direct result of the timing of option and RSU grants, and fluctuations in share price on the date of issuance.

Other Items

Other Items totaled loss of $0.4 million for the period, a change of $0.2 million compared to $0.2 million in 2022.

Unrealized loss on long-term investments was $0.9 million, a positive movement of $1.2 million compared to a loss of $2.1 million in 2022. This is a direct result of fluctuations in the Company’s investment in shares of Talisker Resources , and to a less extent, the Company’s investment in shares of Silver Wolf Exploration and Endurance Gold Corp.

| - 12 - |

Fair value adjustment on warrant liability was a gain of $0.5 million, a decrease to income of $1.9 million compared to a gain of $2.4 million in 2022. The fair value adjustment on the Company’s warrant liability relates to the issuance of US dollar-denominated warrants, which are re-valued each reporting period, and the value fluctuates with changes in the US-Canadian dollar exchange rate, and in the variables used in the valuation model, such as the Company’s US share price, and expected share price volatility. All US dollar-denominated warrants expired in September 2023.

Interest expense for the period was $0.4 million, a change of $0.3 million compared to an expense of $0.1 million in the comparable period of 2022. The increase in interest expense is mainly attributable to new mining equipment acquired under leases during 2023.

Foreign exchange gain for the period was $0.1 million, a change of $0.1 million compared to a loss of Nil in the comparable period of 2022. Foreign exchange gains or losses result from transactions in currencies other than the Canadian dollar functional currency. During both periods, the Canadian dollar and the US dollar depreciated in relation to the Mexican peso, resulting in a foreign exchange loss.

The remaining Other Items resulting in a gain of $0.3 million for the year ended December 31, 2023 and a loss of $0.2 million for the year ended December 31, 2022.

Current and Deferred Income Taxes

Current income tax recovery was $0.5 million in 2023, a change of $1.6 million compared to $1.1 in income tax expense for the comparable period of 2022. The movements are a result of higher profits generated in 2022, resulting in increased income tax expense, whereas in 2023, the Company was in a recovery position as a result of less profitable mining operations in the early part of the year.

Deferred income tax recovery was $0.5 million, a change of $3.9 million compared to a tax expense of $3.4 million in 2022. Deferred income tax fluctuates due to movements in taxable and deductible temporary differences related to the special mining duty in Mexico and to changes in inventory, plant, equipment and mining properties, and exploration and evaluation assets, amongst other factors. The changes in current income taxes and deferred income taxes during the current and comparable periods primarily relate to movements in the tax bases and mining profits and/or losses in Mexico.

Net Income/Loss

Net income was $0.5 million for the period, or $0.00 per share, compared to income of $3.1 million, or $0.03 per share during comparable period of 2022. The changes are a result of the items noted above, which are primarily increases in cost of sales resulting in a decrease of mine operating income, slight increases in general and administrative expenses and share-based payments. Net income was further impacted by movements in unrealized foreign exchange, fair value adjustments on the warrant liability, and a decreased unrealized loss on investments, as noted above.

Financial Results – Year ended December 31, 2022, compared to year ended December 31, 2021

Revenues

The Company recognized revenues net of penalties, treatment costs and refining charges, of $44.2 million on the sale of Avino Mine bulk copper/silver/gold concentrate, compared to revenues of $11.2 million for year ended December 31, 2021, an increase of $33.0 million, or 294%. The increase is a direct result of a full year of revenues during 2022 compared to only 4 months of revenues in 2021, following the restart of mining operations in August 2021. The Company sold 2.45 million silver equivalent payable ounces in 2022, compared to 525 thousand silver equivalent payable ounces in 2021, representing an increase of 367%.

The increase in revenues were partially offset by lower metal prices in 2022 compared to 2021. Metal prices for revenues recognized during the period were $21.51 per ounce of silver, $1,788 per ounce of gold, and $8,552 per tonne of copper, in the prior year quarter, compared to $23.18, $1,802, and $9,524, respectively, for the same period in 2021.

| - 13 - |

Cost of Sales & Mine Operating Income

Cost of sales was $29.1 million, compared to $7.7 million in 2021, an increase of $21.4 million, or 278%. The increase in cost of sales is inline with the increase in ounces sold and revenues noted above and is directly attributable to mining operations being active during the full year ended December 31, 2022.

In 2022, tonnes milled increased by 228%, and total silver equivalent ounces produced increased by 215%, when compared to 2021. This is a direct result of full mining operations for the twelve-month period in 2022 when compared to four months of production mining operations in 2021. Further, a write down of equipment was recorded for the period totaling $0.3 million, compared with $Nil in prior year.

Mine operating income was $15.1 million, compared to mine operating income of $3.5 million, an increase of $11.6 million. This is a direct result of the items noted above.

General and Administrative Expenses & Share-Based Payments

General and administrative expenses was $5.1 million, compared to $3.6 million in 2021, with the increases coming from the increased corporate activity surrounding ramp up procedures and the acquisition of La Preciosa.

Share-based payments was $2.0 million, compared to $1.5 million in 2021, an increase of $0.5 million. Movements in share-based payments are a direct result of the 2022 option and RSU grants carrying a higher expense when compared to the vesting of option and RSU issuances from 2020 and prior years, as well as the fact that there were no grants in 2021.

Other Items

Other Items totaled $0.2 million in losses for the period, an increase of $0.1 million compared to a loss of $0.1 million related to other items in the comparable period in 2021.