UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ☒ |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2024 | ||

| or | ||

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the transition period from ___________ to ___________ | ||

Commission File Number: 001-38873

Palomar Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Delaware |

|

83-3972551 |

| (State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

| |

|

|

| 7979 Ivanhoe Avenue, Suite 500 La Jolla, California |

|

92037 |

| (Address of principal executive offices) |

|

(Zip Code) |

(619) 567-5290

Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

| Common Stock, par value $0.0001 per share |

PLMR |

The Nasdaq Stock Market LLC |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☒ |

Accelerated filer ☐ |

| Non-accelerated filer ☐ |

Smaller reporting company ☐ |

| Emerging growth company ☐ |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

Aggregate market value of shares of the registrant’s common stock held by non-affiliates as of June 30, 2024 was approximately $1,977,345,127

Number of shares of the registrant’s common shares outstanding at February 22, 2025: 26,677,622

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the registrant’s definitive proxy statement relating to its 2025 annual meeting of stockholders (the "2025 Proxy Statement") are incorporated by reference into Part III of this Annual Report on Form 10-K. The 2025 Proxy Statement will be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year covered by this Annual Report on Form 10-K.

| |

|

Page |

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| Item 1C. | Cybersecurity | 51 |

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

||

| |

|

|

| |

|

|

| |

|

|

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

||

| |

|

|

| |

|

|

| |

|

|

| Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

||

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

||

| |

|

|

| Certain Relationships and Related Transactions, and Director Independence |

||

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

Who We Are

We are a specialty insurance company that provides property and casualty insurance products to individuals and businesses. We use our underwriting and analytical expertise to provide innovative insurance products serving five categories: Earthquake, Inland Marine and Other Property, Casualty, Fronting, and Crop. We use proprietary data analytics and a modern technology platform to offer our customers flexible products with customized and granular pricing for both the admitted and excess and surplus lines (“E&S”) markets. Our insurance company subsidiaries, Palomar Specialty Insurance Company (“PSIC”) and Palomar Excess and Surplus Insurance Company (“PESIC”) carry an “A” rating from A.M. Best Company (“A.M. Best”), a leading rating agency for the insurance industry.

We distribute our products through multiple channels, including retail agents, program administrators, wholesale brokers, and partnerships with other insurance companies. Our business strategy is supported by a comprehensive risk transfer program with reinsurance coverage that we believe reduces earnings volatility and provides appropriate levels of protection from catastrophic events. Our management team combines decades of insurance industry experience across specialty underwriting, reinsurance, program administration, distribution, and analytics.

Founded in 2014, we have significantly grown our business and have generated attractive returns. We have organically increased gross written premiums from $16.6 million in our first year of operations to $1.5 billion for the year ended December 31, 2024, which reflects a compound annual growth rate of approximately 57%. We have also been profitable since 2016 and our net income growth since 2016 reflects a compound annual growth rate of 43%.

We seek to continuously grow our income by developing products in lines of business that harness our core competencies and where we believe we can generate attractive risk adjusted returns. In recent years, we have introduced several new products including Crop, Environmental Liability, and E&S Casualty. In January 2025, we completed the acquisition of First Indemnity of America ("FIA"), a New Jersey domiciled insurance carrier specializing in surety bonds for small to medium sized contractors primarily in the Northeast United States. These new products diversify our book of business and broaden our product portfolio. We believe that our market opportunity, distinctive products, and differentiated business model position us to grow our business profitably.

Our Business

Our management team founded our company to address unmet needs that we perceived to exist in certain specialty insurance markets. These markets have primarily been served by either large generalist insurance companies and state-managed entities applying “one-size-fits-all” pricing and policy forms across broad geographies. Our admitted products feature rates and policy forms approved by state insurance departments and are backed by state guaranty funds, providing a further level of security to policyholders. We believe that for our personal lines products, both our customers and distribution partners prefer the ease of use and security of admitted products with flexible coverages. We write surplus lines policies primarily for our commercial business. As the E&S market does not involve the same level of regulation and required approvals as the admitted market, our surplus lines products enable us to react quickly to changing market conditions.

We believe that we can generate superior risk-adjusted returns through the use of underwriting methods that apply a more granular approach to pricing than what is typically offered by standard carriers and that better reflect our customers' underlying risk. We believe this market acceptance and return potential is evidenced by the fact that we have quickly and profitably grown to become the 2nd largest earthquake insurer in the state of California and the 3rd largest earthquake insurer in the United States. We also continue to experience growth and profitability across our other lines of business.

Our five product lines include: Earthquake, Inland Marine and Other Property, Casualty, Fronting, and Crop. We seek to write a diverse mix of business by loss exposure, customer type and geography to capitalize on market opportunities, mitigate the potential impact of any single catastrophe event or shock loss, and reduce our cost of reinsurance.

We continue to develop new product offerings for lines of business that harness our core competencies and where we believe we can generate attractive risk-adjusted returns. Recent examples of our commitment to developing new products include the expansion of our Casualty and Crop insurance offerings. In January 2025, we completed the acquisition of FIA, a New Jersey domiciled insurance carrier specializing in surety bonds for small to medium sized contractors primarily in the Northeast United States. We believe these markets complement our existing product offerings and offer significant growth opportunities across both the admitted and E&S markets.

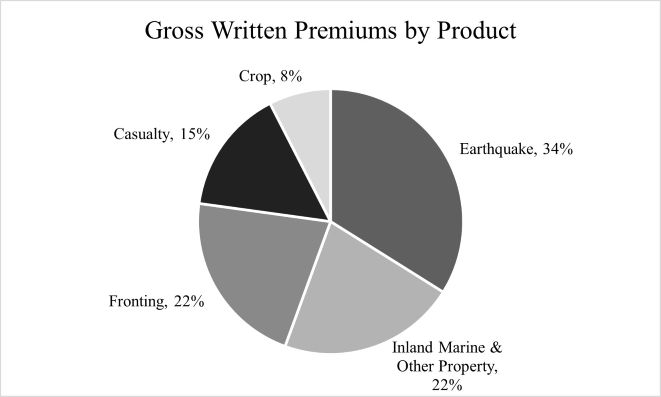

We seek to have a diversified business mix, anchored by our core earthquake offerings and we have made substantial progress diversifying our business by product, market, and geography. In 2014, our first year of operations, all our premiums were related to earthquake insurance. For the year ended December 31, 2024, 34% of our gross written premiums were related to earthquake insurance and non-earthquake related premiums grew 45% while earthquake related premiums grew 20% versus the prior year.

Our admitted insurance subsidiary, PSIC, is licensed in 44 states and we have the flexibility to write nationally through our surplus lines subsidiary, PESIC. California represents our largest current exposure with 43% of our gross written premiums for the year ended December 31, 2024. Our business strategy involves continuing to grow our core earthquake insurance business, extending the reach of Inland Marine and Other Property Products, and diversifying our book of business into uncorrelated products such as Casualty, Fronting and Crop. The following charts illustrate our business mix by product, state, and entity for the year ended December 31, 2024:

We employ a highly granular and analytical underwriting process to assess each insurance policy that we write, and we ensure that the risk characteristics of business assumed through our channel partnerships or written by program administrator partners are consistent with our underwriting of direct business. Our systems enable us to underwrite our personal lines business automatically within minutes by leveraging our proprietary modeling techniques to analyze data at the geocode or ZIP code level. With our commercial products, we balance automation with human expertise and controls to underwrite more complex risks. Because the data we collect through our underwriting process is highly granular, we can utilize detailed portfolio analytics to actively manage aggregation of policies and to ensure an appropriate dispersion of risks across our full portfolio. Similarly, our Casualty products are subject to extensive risk analysis, including review by experienced underwriters, thorough actuarial review, fostering broker relationships to obtain complete underwriting information, and accurately assessing and quantifying loss exposures to inform pricing, terms and conditions, limits, and attachment points.

Our Competitive Strengths

We believe that our competitive strengths include:

Focus on capturing market share and expanding underserved markets. We focus on specialty insurance markets that we believe are underserved, and where we believe we can capture market share and expand the market to new customers. In our target markets, there are few direct competitors who focus exclusively on specialty risks. With our specialized knowledge of these risks and our customized products, pricing and risk management, we believe we can serve these markets better than our competitors. Furthermore, we can expand our markets by creating products that attract insureds who previously had not obtained coverage. Our focus and expertise have enabled us to rapidly increase our market share; for example, we have grown to become the 2nd largest earthquake insurer in California and the 3rd largest earthquake insurer in the United States. In markets with similar characteristics, we are experiencing growth and profitability across our other lines of business. We believe that our focus on addressing the needs of underserved specialty markets provides us with a competitive advantage.

Differentiated products built with the customer in mind. We have invested significant time and resources into developing what we believe are innovative and unique product offerings to address customer needs within our target markets. Our products generally offer our customers flexible features that are not typical of standard products in our markets. By offering our customers the ability to manage pricing, coverage options, and deductibles, we believe we have created products that are attractive both to those who have existing coverages with our competitors, and to those who have not historically bought insurance in our target markets. Furthermore, since our admitted products have been approved by individual state regulators and are supported by proprietary pricing models, we believe that these products are not easily replicable, particularly by existing carriers who would face the burden of gathering data, building new models, and revising existing rates and policy forms with regulators.

Product offerings in both the admitted and E&S markets. We believe that our core capabilities can be applied to both the admitted as well as the E&S insurance markets. Admitted products are backed by state guarantee funds and, as a result, are subject to more regulation, as admitted insurance companies must receive approval for rates and policy forms from individual state regulators. Our admitted insurance company subsidiary, PSIC, is licensed to write business in 44 states. We primarily serve the personal lines insurance market through the sale of admitted insurance products as those risks tend to be more homogenous in nature and retail agents prefer the sale of admitted products. We offer E&S insurance products through our surplus lines insurance company subsidiary, PESIC, which is licensed to do business on a national basis. We primarily serve the commercial lines insurance market through the sale of E&S insurance products as those markets are better suited to the flexibility of rate and form available to E&S carriers. Having E&S offerings allows us to react quickly to changing market conditions and to accelerate the expansion of our business nationally as we do not have to go through the process of receiving required approvals from individual state regulators.

Analytically driven, disciplined and scalable underwriting. Our underwriting approach combines decades of specialized underwriting experience of our management team with sophisticated, customized modeling tools we have developed that utilize extensive geospatial and actuarial data across all our lines of business. Our proprietary models enable automated pricing of risks at the geocode or ZIP code level, in contrast to our competitors who we believe use less granular analytics and more manual underwriting processes. For example, our Residential Flood products underwrite risks at the distinct address level compared to broader pricing zones employed by alternative product offerings in the market. Our analytical pricing framework is embedded in all facets of our business and is incorporated into our filings, pricing, underwriting and risk management. We believe that our analytically-driven underwriting approach has been the foundation of our ability to generate attractive risk-adjusted underwriting margins.

Multi-channel distribution model. Our open architecture distribution framework allows us to attract and underwrite business from multiple channels. We work with a wide variety of retail agents, program administrators, and wholesale brokers. We serve over 25 insurance companies as a specialty partner either by issuing companion policies or providing reinsurance for in-force risks that fit our strict underwriting parameters. The breadth and flexibility of our distribution model allows us to generate premium from many different parts of the insurance ecosystem and to rapidly take advantage of changing market conditions.

Sophisticated and conservative risk transfer program. Our risk transfer program utilizes excess of loss, quota share and property per risk coverages for both our property and casualty products. We manage our exposure to catastrophe events through several risk mitigation strategies, including the purchase of reinsurance. We believe that our reinsurance program provides appropriate levels of protection and improves visibility into our earnings. Our current reinsurance program is designed to limit our net loss before tax from a single event to $20 million, equivalent to approximately 2.7% of our total stockholders’ equity as of December 31, 2024. At each reinsurance treaty renewal, we consider any plans to change the underlying insurance coverage we offer, our current capital, our risk appetite, and the cost and availability of reinsurance coverage, which may vary from time to time. Further, we buy program specific quota share reinsurance coverage for certain lines of business to mitigate the impact of attritional losses on underwriting results. In our quota share agreements, we cede a portion of our premiums to reinsurers and, in return, we also cede a proportionate amount of losses and receive ceding commissions from the reinsurers.

Emphasis on the use of technology and analytics across our business. We have built a proprietary operating platform that employs best practices derived from our management team’s extensive prior experience. Our technology platform is not burdened by outdated technology and processes which may be utilized by older insurance companies. In building our platform, we have emphasized automated processes that use granular data and analytics consistently across all aspects of our business. Our internally developed Palomar Automated Submission System (“PASS”) acts as our interface with retail agents and wholesale brokers. PASS serves as the conduit to our policy administration system that integrates policy issuance, underwriting, billing and portfolio analytics. Our platform enables us to rapidly quote and bind policies via automated processing, and to run detailed risk-management analytics for internal and external constituents including distribution partners, carrier partners and reinsurers. We believe that this real-time access to data and analytics provides us with an advantage in distributing our products, managing our risk, and purchasing reinsurance.

Highly experienced management team and board. Our management team is highly qualified, with an average of more than twenty years of relevant experience in insurance, reinsurance and capital markets. We are led by our Chairman and Chief Executive Officer, Mac Armstrong, who prior to founding Palomar was President of Arrowhead General Insurance Agency (“Arrowhead”). Many of our key management team members such as Mr. Armstrong, Jon Christianson, our President, Jon Knutzen, our Chief Risk Officer, and Chris Uchida, our Chief Financial Officer, have served in their roles for over five years and worked together prior to Palomar. We have also recently made key management hires in operations, technology, claims, people and talent, E&S Casualty, and Crop. These new management hires are insurance industry veterans with proven track records and deep industry knowledge. We believe their skills and experience will assist Palomar during our next phase of growth and expansion. In addition, our Board of Directors is comprised of accomplished industry veterans who bring decades of experience from prior roles with insurance and other companies.

Our Strategy

We believe that our approach will allow us to achieve our goals of both growing our business and generating attractive returns. Our strategy involves:

Expand our presence in existing markets. We compete in the United States property and casualty market that represented over $965 billion in total written premiums during 2023. By comparison, we generated $1.5 billion of gross written premiums for the year ended December 31, 2024. We believe that our differentiated product offerings will enable us to continue growing in our existing markets by (i) gaining market share from competitors who have less flexible product offerings; (ii) continuing to expand our strong distribution network; and (iii) increasing the total addressable market by providing attractive products to customers who previously elected not to purchase coverage. We continue to evaluate additional geographic markets and lines of business where we believe we can generate attractive risk-adjusted returns by harnessing our core competencies.

Maintain our distinctive combination of profitability and growth. Our analytically informed risk selection and disciplined underwriting guidelines enable us to identify segments of the market that are both underserved and mispriced. As a result, we are able to generate an attractive underwriting profit by expanding the addressable market and winning market share with our distinctive products. For the years ended December 31, 2024 and 2023, our return on equity (“ROE”) was 19.6% and 18.5%, and our adjusted ROE was 22.2% and 21.9%, respectively. As we seek premium growth, we intend to remain disciplined in our pricing, underwriting, and risk management processes, including closely managing our net probable maximum loss (“PML”), average annual loss (“AAL”), and spread of risk. We will remain focused on lines of business with attractive pricing dynamics and a favorable risk / return profile, and we will not participate in markets where we believe our business model cannot add incremental value.

Maintain a diversified book of business. We currently write a book of specialty insurance that is diversified by underlying loss exposure, customer type and geography. Our major product lines and exposures are uncorrelated, such that events contributing to a loss in one product line are unlikely to generate material losses in our other product lines. Furthermore, our Crop products are uncorrelated with the traditional P&C cycle, enhancing the diversification of our specialty product portfolio. The diversification of our book of business improves our risk-adjusted returns, insulates us from swings in any single insurance or reinsurance market, and allows us to capitalize on market shifts opportunistically. As we grow, we intend to maintain a diversified book of business and continually capitalize on these advantages.

Leverage our underwriting, analytics, and risk transfer acumen to generate fee income. We generate fee income through the use of quota share reinsurance treaties whereby third-party reinsurers pay us a ceding commission in order to access attractive pools of risk. Our Fronting and Crop products offer additional sources of fee income that we earn from program administrators and reinsurers seeking to access our licensed insurance companies. Our multi-channel distribution model produces attractive business that we aim to translate into a balanced mix of underwriting and fee income. As a result, we have an increasing number of partnerships where we write policies on behalf of other insurance and reinsurance companies who pay us a ceding commission to access the business. We believe these partnerships are an important validation of the intellectual property and expertise we have developed, and that this strategy enables us to scale our business more quickly and profitably and provides a growing and valuable fee stream to complement our profitable underwriting operations.

Continue to purchase conservative reinsurance coverage, while optimizing for risk-adjusted returns. We believe that protecting our earnings and balance sheet through the use of reinsurance is critical to our business and supports our ability to meet obligations to our policyholders and other constituents, and generate strong returns for our stockholders. We plan to maintain a conservative, robust reinsurance program to provide protection against severe or frequent losses. Our goal is to protect our earnings by constructing a reinsurance program that mitigates losses and ensures profitability in spite of potential shock losses or catastrophic activity. As we grow, we expect that we will benefit from increased scale and diversification of risk in our business, and we plan to optimize our reinsurance program continuously by adjusting terms, structure, pricing, and participants to maximize our risk-adjusted returns.

Continue to invest in proprietary technology assets that deepen our competitive advantage. We believe that the success of our business is centered upon our relentless commitment to using technology to improve our business. For example, we have dedicated software developers focused on building application programming interfaces (“APIs”), which enable seamless integration into the point-of-sale systems of our partner carriers and distribution partners. This integration increases the ease of use for our partners, embeds us within their systems, and facilitates real-time sharing of information between our distribution, underwriting, and risk management functions. We will continue to evaluate and invest in proprietary and third-party technology assets, which deepen our competitive advantage, strengthen our operations, and improve our returns.

History

We are an insurance holding company that was originally incorporated under the laws of the Cayman Islands in October 2013. In March 2019, we implemented a domestication pursuant to Section 388 of the Delaware General Corporation Law and became a Delaware corporation.

Our primary operating subsidiary, PSIC, is an insurance company domiciled in the state of Oregon and is an admitted insurer licensed to write business in 44 states as of December 31, 2024. PSIC was formed in February 2014. In August 2014, we incorporated Palomar Specialty Reinsurance Company Bermuda Ltd.(“PSRE”), a Bermuda-based reinsurance subsidiary that provides reinsurance support exclusively to PSIC and PESIC. In August 2015, we incorporated Prospect General Insurance Agency, Inc., now known as Palomar Insurance Agency, Inc., (“PIA”), to underwrite specialty insurance products on behalf of third-party insurance companies. During 2020, we received regulatory approval for and capitalized PESIC. PESIC is domiciled in the State of Arizona and licensed in Arizona to write surplus lines business on a nationwide basis across all our existing lines of business. During 2023, we formed Palomar Underwriters Exchange Organization, Inc. ("PUEO"), a Delaware incorporated management company that provides services by serving as the attorney-in-fact to Laulima Exchange (“Laulima”), a Hawaii domiciled reciprocal exchange.

Our Products

We provide personal and commercial specialty insurance products in our target markets. With the goal of giving customers better options, we designed an analytical framework to create flexible products with innovative coverages and pricing that we believe better reflects the underlying risk. Using this framework, we initially introduced Residential and Commercial Earthquake products in 2014 and have subsequently expanded our product portfolio to cover multiple specialty risks in the United States. We have grown our business by entering markets that demonstrated one or more of the following attributes: (i) have loss characteristics, including limited attritional losses, similar to our initial earthquake product, (ii) can benefit from our technology platform, data analytics and customer centric products, and/or (iii) allow us to leverage our existing underwriting talent, reinsurance expertise and/or distribution relationships.

Our lines of business include: Earthquake, Inland Marine and Other Property, Casualty, Fronting, and Crop. We aim to develop a diversified portfolio with exposure spread across geographic regions with limited correlation. Although our largest exposure is in the state of California, we write business across the United States. We tailor our risk participation to optimize our returns depending on the conditions of specific markets. In total, we are licensed as an admitted insurer in 44 total states. The following tables show gross written premiums (“GWP”) by state and product for the years ended December 31, 2024, 2023 and 2022.

| Year Ended December 31, |

||||||||||||||||||||||||

| 2024 |

2023 |

2022 |

||||||||||||||||||||||

| ($ in thousands) |

||||||||||||||||||||||||

| % of |

% of |

% of |

||||||||||||||||||||||

| Amount |

GWP |

Amount |

GWP |

Amount |

GWP |

|||||||||||||||||||

| State |

||||||||||||||||||||||||

| California |

$ | 668,635 | 43.4 | % | $ | 600,791 | 52.6 | % | $ | 418,809 | 47.5 | % | ||||||||||||

| Texas |

124,416 | 8.1 | % | 95,517 | 8.4 | % | 90,459 | 10.3 | % | |||||||||||||||

| Hawaii |

72,558 | 4.7 | % | 47,388 | 4.2 | % | 40,157 | 4.5 | % | |||||||||||||||

| Florida |

67,008 | 4.3 | % | 47,595 | 4.2 | % | 38,715 | 4.4 | % | |||||||||||||||

| Washington |

57,900 | 3.8 | % | 49,494 | 4.3 | % | 41,827 | 4.7 | % | |||||||||||||||

| New York |

38,919 | 2.5 | % | 18,424 | 1.6 | % | 12,510 | 1.5 | % | |||||||||||||||

| Oregon |

29,550 | 1.9 | % | 23,220 | 2.0 | % | 24,108 | 2.7 | % | |||||||||||||||

| Illinois |

20,901 | 1.4 | % | 22,340 | 2.0 | % | 17,368 | 2.0 | % | |||||||||||||||

| Other |

462,075 | 30.0 | % | 236,789 | 20.7 | % | 197,915 | 22.4 | % | |||||||||||||||

| Total Gross Written Premiums |

$ | 1,541,962 | 100.0 | % | $ | 1,141,558 | 100.0 | % | $ | 881,868 | 100.0 | % | ||||||||||||

| Year Ended December 31, |

||||||||||||||||||||||||

| 2024 |

2023 |

2022 |

||||||||||||||||||||||

| ($ in thousands) |

||||||||||||||||||||||||

| % of |

% of |

% of |

||||||||||||||||||||||

| Amount |

GWP |

Amount |

GWP |

Amount |

GWP |

|||||||||||||||||||

| Product (1) |

||||||||||||||||||||||||

| Earthquake |

$ | 522,864 | 33.9 | % | $ | 436,897 | 38.3 | % | $ | 345,480 | 39.2 | % | ||||||||||||

| Inland Marine and Other Property |

334,079 | 21.7 | % | 250,022 | 21.9 | % | 232,918 | 26.4 | % | |||||||||||||||

| Fronting |

333,188 | 21.6 | % | 352,141 | 30.8 | % | 223,249 | 25.3 | % | |||||||||||||||

| Casualty |

235,592 | 15.3 | % | 90,388 | 7.9 | % | 80,221 | 9.1 | % | |||||||||||||||

| Crop |

116,239 | 7.5 | % | 12,110 | 1.1 | % | — | — | % | |||||||||||||||

| Total Gross Written Premiums |

$ | 1,541,962 | 100.0 | % | $ | 1,141,558 | 100.0 | % | $ | 881,868 | 100.0 | % | ||||||||||||

(1) - Beginning in 2024, the Company has updated the categorization of its products to align with management's current strategy and view of the business. Prior year amounts have been reclassified for comparability purposes. The recategorization is for presentation purposes only and does not impact overall gross written premiums.

Our five product lines are summarized as follows:

Earthquake

We offer Residential and Commercial Earthquake products on both admitted and E&S basis. Our Residential Earthquake products insure against home damage, contents, appurtenant structures, and temporary housing costs following an earthquake. Our products are designed with flexibility, offering a variety of deductible options and customizable coverage limits. We aim to attract customers who haven't previously purchased earthquake insurance. Our pricing model, based on data from top catastrophe models, allows us to accurately assess and price risks at the ZIP code or geocode level. Unlike competitors who use broad pricing zones, we factor in regional differences like soil types, liquefaction risk, and proximity to fault lines. This approach helps us offer more precise rates and often provides rate relief, especially in low-risk areas with historically low earthquake insurance uptake. Our Commercial Earthquake products focus on providing coverage for benign commercial risks where the business interruption exposure is typically less than 15% of the total insured value (“TIV”). We attempt to avoid risks where the contents are hard to value or represent a disproportionate percentage of the value.

Inland Marine and Other Property

Our Inland Marine and Other Property products include Inland Marine, Hawaii Hurricane, Commercial All Risk, Excess National Property, Residential Flood, and other miscellaneous property products. These products are written on an admitted and on an E&S basis directly and through program administrators. Policy limits vary by product; however, our E&S offerings are designed to target larger limit business and do not directly compete with our admitted offerings. We believe the flexibility of these products enables us to compete in select market segments and price risk appropriately.

Casualty

We provide Casualty products on an admitted and E&S basis. We primarily focus on niche segments of the Casualty market including Real Estate Agent Errors and Omissions, Excess Liability, and Environmental Liability coverages written directly and through program administrators. We utilize experienced underwriters and thorough actuarial review to optimize our pricing, terms and conditions, limits, and attachment points.

In addition to our existing Casualty product offerings, we announced the launch of our E&S Casualty product at the end of 2024. The new product will focus on Primary & Excess Construction and Excess Liability lines of business. This new line of business further demonstrates our commitment to providing comprehensive insurance solutions that address evolving market needs. On January 1, 2025 we completed the acquisition of FIA, a New Jersey domiciled insurance carrier specializing in surety bonds for small to medium sized contractors primarily in the Northeast United States.

Fronting

Our Fronting products offer reinsurers, insurance carriers and managing general agents the ability to utilize our licensed admitted and E&S insurance companies to design and operate customized insurance programs. We issue insurance policies for other insurance companies that may not have the licensure, product suite or rating to serve their desired markets, or for programs supported by reinsurance or alternative capital providers. In addition, we enter fronting arrangements with program administrators that require a broadly licensed, highly rated carrier to conduct business in certain states.

Crop

Our Crop insurance products are comprised primarily of multi-peril crop insurance offered in connection with the U.S. Department of Agriculture's Risk Management Agency and designed to cover revenue shortfalls or production losses due to natural causes such as drought, hail, and wind. We currently write Crop insurance with the goal of minimizing exposure to any single region. We also offer Livestock and Private Product Crop solutions.

Marketing and Distribution

We market and distribute our products through a multi-channel, open architecture distribution model which includes retail agents, wholesale brokers, program administrators and carrier partnerships. We have well-defined underwriting criteria and have designed our distribution model to access our targeted risks through what we believe to be the most efficient channels.

Retail Agents: We primarily distribute our personal lines products through retail agents. We believe that retail agents are an important pillar of our distribution model due to the high retention rates and rate stability that we are able to achieve with policies sold through this channel. We provide agents with flexible products that are preferred by end consumers and are easier for agents to sell. In many cases, we provide agents with direct access to our policy management system that enables them to quote, bind and issue policies in a matter of minutes. We believe this ease of use and quick speed-to-quote serves as a competitive advantage.

Wholesale Brokers: We distribute our commercial lines products primarily through wholesale brokers. Wholesale brokers are an important channel for commercial insurance products as they control much of the premium in these segments. We target brokers with experience serving our target markets and with business plans consistent with our strategy and underwriting objectives. Brokers must demonstrate an ability to produce both the quality and quantity of business that we seek. To assist with this goal, our underwriters regularly visit with brokers to market and discuss the products we offer.

Program Administrators: Within select lines of business, we partner with program administrators to harness the efficiency and scale of their existing marketing and distribution infrastructures. In some cases, policies bound by our program administrators are pre-underwritten using pricing models that we have developed and are programmed into the policy administration system of those partners. For business that is not automatically underwritten, we set strict underwriting guidelines to which our partners must adhere. We audit the underwriting, systems, financial strength and reporting capabilities of all of our program administrators on a regular basis.

Carrier Partnerships: Given our unique specialty focus and underwriting expertise, we are a carrier of choice for other insurance companies seeking a specialty insurance partner to act as a fronting carrier, transfer certain classes of risk, satisfy insurance department mandatory offer requirements or provide a more comprehensive risk solution to their customers. As of December 31, 2024, we had partnerships with over 25 insurance companies. Several carriers invite us to provide a companion offer for residential earthquake insurance alongside their homeowners’ insurance policy offerings. Other carriers will direct their captive agents to our online system so that they may quote, bind and issue policies directly. Finally, we offer assumed reinsurance arrangements to carriers whereby we assume up to 100% of the underlying risk for specific classes of business in exchange for a ceding commission. Our assumed reinsurance treaties represent risks that we would ordinarily underwrite on a primary basis and/or that fit well within our risk tolerance, however, the cedant either (i) has already written these policies or (ii) the cedant wants to issue the policies on its paper but not retain any of the risk and as such prefers an assumed reinsurance partnership. We believe that our carrier partnerships with sophisticated industry participants speak to the value and quality of our products, service offering and systems. Furthermore, carrier partnerships are a highly scalable distribution model as they enable us to tap into a sizable customer base and to quickly build scale in new markets. With all partnerships, we review pricing at the policy level to ensure that the risk characteristics of both new and assumed business are consistent with our underwriting of direct business.

Underwriting

Our underwriting team combines comprehensive data analysis with experienced underwriting techniques to build a profitable, stable and diversified book of business. Our underwriting process involves securing an adequate level of underwriting information, classifying and evaluating each individual risk exposure, assessing the impact of the risk upon our existing portfolio, and pricing the risk accordingly. Our overarching underwriting philosophy is ‘to write what we know’ a straightforward approach that allows our underwriters to focus on business they understand and can process quickly without sacrificing diligence and attention to detail.

We develop our underwriting guidelines and pricing models for our property and casualty products through traditional underwriting metrics, management experience, and advanced data analytics. Our underwriters actively collaborate with our actuarial team to determine pricing and risk exposure. This analytical and underwriting expertise framework enables us to offer rate relief in low risk areas and to accurately price risks that are at higher risk.

Personal lines policies are issued via automated underwriting. Using our predefined underwriting guidelines, distribution partners can rapidly quote and bind accounts lower in limit via automated processing. We believe that automated underwriting of personal lines policies improves efficiency, reduces errors, and enhances the customer experience.

Since commercial lines risks involve additional complexity and do not lend themselves to highly automated underwriting, we combine robust risk analysis and data collection with underwriter expertise to evaluate individual risks and to quote business efficiently. We regularly audit data gathered during our underwriting process to determine the accuracy of rating information and risk pricing. For example, we often inspect properties as part of our underwriting process to discover any unrepaired damage and identify any other conditions that affect the insurability of the property. Similarly, our casualty products are subject to extensive risk analysis, including review by experienced underwriters, thorough actuarial review, fostering broker relationships to obtain complete underwriting information, and accurately assessing and quantifying loss exposures to inform pricing, terms and conditions, limits, and attachment points. Our underwriters bring specific line of business experience including underwriting expertise, distribution relationships and support from the reinsurance community while collaborating closely with our actuarial team on pricing. In addition, we continue to pursue the use of technology to streamline inspections and other components of the underwriting process.

We apply disciplined underwriting principles when selecting program administrator partners. We proactively engage with our program managers to create specific underwriting guidelines and techniques. We regularly conduct underwriting, claims and financial audits to ensure consistent execution upon underwriting guidelines, claims processing and compliance with regulatory requirements.

Ongoing risk management of our portfolio in aggregate is a critical component of our underwriting process. We use third-party catastrophe modeling software to evaluate our ongoing risk exposure. We regularly review the output of these models to evaluate the geographic spread of our risk, including the evaluation of AAL and PML by line of business and for the portfolio as a whole. This review enables us to monitor our exposure to correlated risks and optimize the design and pricing of our reinsurance program including the purchase of appropriate reinsurance coverage.

Claims Management

Claims are overseen by our in-house claims team, led by our Chief Claims Officer. To supplement our in-house team, we outsource part of our claims handling infrastructure to third-party administrators (“TPAs”). We currently contract with multiple TPAs to reduce our reliance on any single TPA, as well as to benefit from expertise of individual vendors in specific lines of business. Our Chief Claims Officer is responsible for overseeing our TPAs, including the management of catastrophe event preparation, loss reserves, claim evaluation, arbitration, mediation, and settlement. Claims are reported directly to us and the applicable TPA, which adheres to agreed upon service level standards.

In the case of a catastrophe event, our technology infrastructure and data analytics enable us to identify potentially affected policies immediately and begin assisting our customers by notifying our TPAs, our reinsurance partners and other potentially impacted parties. Contracting with a network of TPAs improves our ability to mobilize claims adjusters immediately to the areas where our customers are most affected and helps insulate us from the “demand surge” following a catastrophe event. To prepare for a potential catastrophe event, we run simulations and work closely with our TPAs to ensure there are dedicated desk and field adjusters to handle the volume of claims that would be expected in each loss scenario. Using each earthquake and hurricane scenario, we project losses and identify an individualized and optimal catastrophe response plan for each event.

We review claims files and claims reports from our TPAs for accuracy and reasonableness on an ongoing basis. We review all claims received from our TPAs to validate coverage, limits, and deductibles prior to making payment. In addition, we have certain managerial requirements of our TPAs around notification, reserve approval, payment management, correspondence with insureds, timeliness, regulatory compliance, and reports for all claims in excess of the claims analyst’s authority. We also monitor possible litigation and litigation trends associated with our claims.

Reinsurance

We purchase a significant amount of reinsurance from third parties that we believe enhances our business by reducing our exposure to potential catastrophe and attritional losses, limiting volatility in our underwriting performance, and providing us with greater visibility into our future earnings. Reinsurance involves transferring, or ceding, a portion of our risk exposure on policies that we write to another insurer, the reinsurer, in exchange for a premium.

We purchase several types of reinsurance, including catastrophe excess of loss (“XOL”), in which the reinsurer(s) agree to assume all or a portion of losses relating to a group of policies occurring in relation to specified events, subject to customary exclusions, in excess of a specified amount. In addition, we buy reinsurance coverage for specific lines of business on a quota share, property per risk, or a facultative basis. In quota share reinsurance, the reinsurer agrees to assume a specified percentage of the ceding company’s losses arising out of a defined class of business in exchange for a corresponding percentage of premiums, net of a ceding commission. Property per risk coverage is similar to catastrophe excess of loss except that the treaty applies in individual property losses rather than in the aggregate for all claims associated with a single catastrophic loss occurrence. Facultative coverage refers to a reinsurance contract on individual risks as opposed to a group or class of business. We use facultative reinsurance selectively to supplement limits or to cover risks or perils excluded from other reinsurance contracts.

We have a robust program utilizing a mix of traditional reinsurers and insurance linked securities. We currently purchase reinsurance from over 100 reinsurers, who either have an “A−” (Excellent) (Outlook Stable) or better financial strength rating by A.M. Best or post collateral. Our reinsurance contracts include special termination provisions that allow us to cancel and replace any participating reinsurer that is downgraded below a rating of “A−” (Excellent) (Outlook Stable) from A.M. Best, or whose surplus drops by more than 20%.

In addition to reinsurance from traditional reinsurers, we utilize collateralized protection via catastrophe bonds. We currently have $895 million of multi-year indemnity-based reinsurance coverage for earthquake events, all issued through Torrey Pines Re Ltd, a Bermuda-domiciled special purpose insurer. Our latest bond, a $420 million 144A issuance, became effective on June 1, 2024.

Our largest single XOL reinsurer, excluding Torrey Pines Re, comprises 9.14% of the total catastrophe XOL reinsurance limit we have in effect. The table below reflects the ratings of our largest individual reinsurers.

| Reinsurer Ratings |

A.M Best |

S&P |

||

| Torrey Pines Re, LTD |

Collateralized |

Collateralized |

||

| Ariel Re BDA, Ltd obo Lloyds Syndicate 1910 |

A+ |

AA- |

||

| Houston Casualty Company |

A++ |

A+ |

||

| Fidelis Insurance Bermuda |

A |

A- |

||

| Arch Reinsurance, Ltd. |

A+ |

A+ |

||

| Hannover Ruck |

A+ |

AA- |

||

| Swiss Reinsurance America |

A+ |

AA- |

||

| MS Amlin AG Bermuda |

A+ |

A+ |

||

| Lloyds Syndicate 1301 - Inigo | A+ | AA- | ||

| Lloyds Syndicate 1084 - Chaucer | A+ | AA- |

Catastrophe XOL Reinsurance Coverage

Our catastrophe event retention before any tax effect is currently $20 million for earthquake events and $15.5 million for hurricane events and all other perils. Our reinsurance coverage exhausts at $3.08 billion for earthquake events, $735 million for Hawaii hurricane events, and $117.5 million for continental U.S. hurricane events, providing coverage in excess of our 1:250 year peak zone PML and in excess of our A.M. Best threshold. In addition, we maintain reinsurance coverage equivalent to or better than the 1 in 250 year PML for our other lines. As of December 31, 2024, our first event retention represented approximately 2.7% of our stockholders’ equity.

In the event that multiple catastrophe events occur during a treaty period, many of our contracts include the right to reinstate reinsurance limits for potential future recoveries during the same contract year and preserve our limit for subsequent events. This feature for subsequent event coverage is known as a “reinstatement.”

To assess the sufficiency of our catastrophe XOL reinsurance coverage, we continuously quantify our exposure to catastrophes including earthquakes, hurricanes, tornadoes, and hailstorms. We evaluate and monitor the total policy limit insured for each peril and in each geographic region, and we use third-party catastrophe models to evaluate the AAL as well as the estimated PML at various intervals. Our PML modeling is consistent with standards established by A.M. Best and includes “demand surge,” and loss amplification. To protect against model bias, we perform probabilistic modeling as well as deterministic modeling using a variety of industry models including AIR Touchstone and RMS RiskLink for all perils and regions.

We believe our current reinsurance program provides coverage well in excess of our theoretical losses from any recorded historical event. The below table shows the PML from selected historical catastrophe events, all of which are less than the amount covered by our current catastrophe reinsurance program. Should an event equivalent to one of these historical events recur, our hypothetical net loss before any tax effect would be capped at our current net retention of $20.0 million for earthquake events or $15.5 million for hurricane events and all other perils.

| |

12/31/2024 |

|||

| Historical Event |

modeled PML |

|||

| |

($ millions) |

|||

| CA 1906 San Francisco M7.8 |

$2,177 | |||

| CA 1994 Northridge M6.7 |

1,624 | |||

| CA 1971 San Fernando M6.7 |

817 | |||

| CA 1868 Hayward M7.0 |

773 | |||

| NM 1811‑12 sequence M7.8 |

680 | |||

| HI 1992 Hurricane Iniki |

673 | |||

| NW 1949 Puget Sound M7.1 |

518 | |||

| CA 1857 Fort Tejon M7.9 |

465 | |||

| CA 1933 Long Beach M6.4 |

437 | |||

| NW 1965 Puget Sound M6.5 |

225 | |||

While we only select reinsurers whom we believe to have acceptable credit or a minimum A.M. Best rating of “A−”, if our reinsurers are unable to pay the claims for which they are responsible, we ultimately retain primary liability to our policyholders. In addition, at each reinsurance treaty renewal, we consider any plans to change the underlying insurance coverage we offer, our current capital, our risk appetite, and the cost and availability of reinsurance coverage, which may vary from time to time.

Program Specific Reinsurance Coverage

In addition to our catastrophe XOL coverage, we purchase reinsurance for specific programs in order to control our net exposure for any single risk, manage our exposure to attritional losses and improve our economics through ceding a portion of the risk to reinsurers in exchange for a ceding commission which generates fee income. We purchase program specific reinsurance, consisting primarily of quota share coverage, for certain lines of business with an attritional loss component such as Inland Marine and Casualty. We also utilize a combination of XOL and quota share reinsurance to provide coverage for our Flood, Inland Marine, and Crop products. Specific to our Crop portfolio, we purchase private reinsurance coverage which is applied to premiums and liabilities net of the inuring protection afforded by the Standard Reinsurance Agreement provided via the Federal Crop Insurance Corporation.

Technology

Our integrated technology systems form the backbone of our business as they enable us to offer quality and timely service to our policyholders and producers, communicate seamlessly with reinsurers and partner carriers, and run our business more efficiently and cost effectively. Our systems offer greater ease of use to distribution partners and provide seamless integration between our pricing models, quoting tools, policy administration systems and portfolio analytics databases. Our proprietary operating platform is based on applications licensed from multiple third-party software vendors. We have invested significantly in customizing, building on top of and extending these applications to increase automation and enhance efficiency. We have dedicated in-house software developers as well as external resources. Our internally developed PASS provides producers direct access to our retail and wholesale distributed products including Residential Earthquake, Hawaii Hurricane, and Residential Flood. PASS also serves as the administration system for select policy data and the access point for business written through direct personal lines partnerships. PASS enables the effective use of predefined underwriting, providing efficiency and optimization to our production partners and real-time transparency in underwriting and aggregate management. Our software development team develops programing interfaces where applicable so that partner carriers and distribution partners can seamlessly access our system.

Our pricing models are based on the most recent versions of catastrophe models from industry leading vendors and our internal expertise. For certain products where limited models are available, we have worked directly with the vendors to develop proprietary models. We update our pricing models as new versions are released, which mitigates our exposure to changes in our business following industry-wide model changes. For personal lines products issued through automated underwriting, our pricing models integrate directly into our policy administration system as well as the systems of program administrator partners. Since our commercial lines products do not lend themselves to highly automated underwriting, we have built a customized operating platform that our underwriters use to evaluate risk and to efficiently quote business. Our custom application platform seamlessly integrates policy administration, billing, and maintenance.

We emphasize the use of technology in our analytics and enterprise risk management (“ERM”) operations. Our data and analytics team, which reports to our Chief Technology Officer, uses multiple catastrophe modeling software applications to evaluate our ongoing risk exposure. Our data analytics enable us to provide timely reporting of our in-force portfolio to our reinsurers, TPAs and distribution partners on a regular basis and during severe weather events. This reporting combines content from the catastrophe models that we license with internally developed content. Event reporting is an element of our overall ERM framework which monitors our risks and ensures that we have appropriate controls and preparations are in place. Our technology infrastructure is designed to function through any major disruption, with all data stored offsite and employees provided with the resources to work remotely.

Reserves

When a claim is reported to us or when an event occurs, we establish loss reserves to cover our estimated ultimate losses under all insurance policies that we underwrite, and loss adjustment expenses relating to the investigation and settlement of policy claims. These reserves include estimates of the cost of the claims reported to us (case reserves) and estimates of the cost of claims that have been incurred but not yet reported (“IBNR”) and are net of estimated related salvage, subrogation recoverables and reinsurance recoverables. Reserves are estimates involving actuarial projections of the expected ultimate cost to settle and administer claims at a given time, but are not expected to represent precisely the ultimate liability. Estimates are based upon past loss experience modified for current trends as well as prevailing economic, legal and social conditions. Such estimates will also be based on facts and circumstances then known, but are subject to significant uncertainty based on the outcome of various factors, such as future events, future trends in claim severity, inflation and changes in the judicial interpretation of policy provisions relating to the determination of coverage.

When a claim is reported and investigated by a claims adjuster, we establish a case reserve for the estimated amount of the ultimate payment after an appropriate assessment of coverage, damages and other information as applicable. The estimate is based on general insurance reserving practices and on the claim adjuster’s experience and knowledge of the nature and value of the specific type of claim. Case reserves are revised periodically based on subsequent developments associated with each claim.

We establish IBNR reserves in accordance with industry practice to provide for (i) the estimated amount of future loss payments on incurred claims not yet reported, and (ii) potential development on reported claims. IBNR reserves are estimated based on generally accepted actuarial reserving techniques that consider quantitative loss experience data and, where appropriate, qualitative factors.

We regularly review our loss reserves using a variety of actuarial techniques. We also update the reserve estimates as historical loss experience develops, additional claims are reported and/or settled and new information becomes available. A reserve can be increased or decreased over time as claims move towards settlement, which can impact earnings in the form of either adverse development or reserve releases.

The following tables present the development of our loss reserves by accident year on a gross basis and net of reinsurance recoveries during each of the below calendar years:

| Gross Ultimate Loss and LAE |

||||||||||||||||||||||||||||

| Development- (Favorable) Unfavorable |

||||||||||||||||||||||||||||

| Calendar Year |

2021 to |

2022 to |

2023 to |

|||||||||||||||||||||||||

| Accident Year |

2021 |

2022 |

2023 |

2024 |

2022 |

2023 |

2024 |

|||||||||||||||||||||

| (in thousands) |

||||||||||||||||||||||||||||

| Prior |

$ | 450,570 | $ | 450,904 | $ | 417,234 | $ | 416,443 | $ | 334 | $ | (33,670 | ) | $ | (791 | ) | ||||||||||||

| 2022 |

200,765 | 198,635 | 182,660 | — | (2,130 | ) | (15,975 | ) | ||||||||||||||||||||

| 2023 |

334,520 | 308,049 | — | — | (26,471 | ) | ||||||||||||||||||||||

| 2024 |

537,646 | — | — | — | ||||||||||||||||||||||||

| $ | 334 | $ | (35,800 | ) | $ | (43,237 | ) | |||||||||||||||||||||

| Net Ultimate Loss and LAE |

||||||||||||||||||||||||||||

| Development- (Favorable) Unfavorable |

||||||||||||||||||||||||||||

| |

Calendar Year |

2021 to |

2022 to |

2023 to |

||||||||||||||||||||||||

| Accident Year |

2021 |

2022 |

2023 |

2024 |

2022 |

2023 |

2024 |

|||||||||||||||||||||

| (in thousands) |

||||||||||||||||||||||||||||

| Prior |

$ | 139,530 | $ | 141,913 | $ | 137,405 | $ | 139,173 | $ | 2,383 | $ | (4,508) | $ | 1,768 | ||||||||||||||

| 2022 |

76,289 | 83,026 | 80,551 | — | 6,737 | (2,475 | ) | |||||||||||||||||||||

| 2023 |

70,346 | 68,015 | — | — | (2,331 | ) | ||||||||||||||||||||||

| 2024 |

137,788 | — | — | — | ||||||||||||||||||||||||

| $ | 2,383 | $ | 2,229 | $ | (3,038 | ) | ||||||||||||||||||||||

Investments

Investment income is an important component of our earnings. We collect premiums and are required to hold a portion of these funds in reserves until claims are paid. We invest these reserves, primarily in fixed maturity investments. Our fixed maturity investment portfolio is primarily managed by an external investment advisory firm that is an experienced manager of insurance company assets, and operates under guidelines approved by our Board of Directors. We believe our investment strategy allows us to eliminate the expense of a treasury department while allowing our management to maintain oversight over the investment portfolio.

Our cash and invested assets consist of fixed maturity securities, short-term investments, cash and cash equivalents, mutual funds, exchange traded funds and equity securities. We also have one equity method investment and a small portion of our portfolio invested in limited partnerships, which are classified as other investments on our consolidated balance sheet. Our fixed maturity securities are classified as “available-for-sale” and are carried at fair value with unrealized gains and losses on these securities reported, net of tax, as a separate component of accumulated other comprehensive income (loss). Our equity investments are measured at fair value with changes in fair value recognized in net income. Fair value generally represents quoted market value prices for securities traded in the public market or prices analytically determined using bid or closing prices for securities not traded in the public marketplace. Our equity method investment is measured following the consolidation model, by increasing or decreasing the carrying amount of the investment to reflect our share of contributions, distributions, earnings, or losses. Our other investments are measured at estimated fair value utilizing a net asset value per share (or its equivalent) as a practical expedient. Short-term investments are reported at cost and include investments that are both readily convertible to known amounts of cash and have maturities of 12 months or less upon acquisition by us.

Our investment securities available totaled $987.7 million and $689.6 million at December 31, 2024 and 2023 respectively, and are summarized as follows:

| |

Fair |

% of Total |

||||||

| December 31, 2024 |

Value |

Fair Value |

||||||

| Fixed maturities: |

|

|

||||||

| U.S. Governments |

$ | 32,806 | 3.3 | % | ||||

| U.S. States, Territories, and Political Subdivisions |

9,778 | 1.0 | % | |||||

| Special revenue excluding mortgage/asset‑backed securities |

26,634 | 2.7 | % | |||||

| Corporate and other |

475,491 | 48.2 | % | |||||

| Mortgage/asset‑backed securities |

394,337 | 39.9 | % | |||||

| Total fixed maturities |

$ | 939,046 | 95.1 | % | ||||

| Equity securities |

40,529 | 4.1 | % | |||||

| Equity method investment |

2,277 | 0.2 | % | |||||

| Other investments |

5,863 | 0.6 | % | |||||

| Total investments |

$ | 987,715 | 100.0 | % | ||||

| |

Fair |

% of Total |

||||||

| December 31, 2023 |

Value |

Fair Value |

||||||

| Fixed maturities: |

|

|

||||||

| U.S. Governments |

$ | 39,420 | 5.7 | % | ||||

| U.S. States, Territories, and Political Subdivisions |

9,902 | 1.4 | % | |||||

| Special revenue excluding mortgage/asset‑backed securities |

29,511 | 4.3 | % | |||||

| Corporate and other |

300,239 | 43.5 | % | |||||

| Mortgage/asset‑backed securities |

264,727 | 38.4 | % | |||||

| Total fixed maturities |

$ | 643,799 | 93.3 | % | ||||

| Equity securities |

43,160 | 6.3 | % | |||||

| Equity method investment |

2,617 | 0.4 | % | |||||

| Total investments |

$ | 689,576 | 100.0 | % | ||||

Our primary investment focus is to preserve capital to support our insurance operations through investing primarily in high quality fixed maturity securities with a secondary focus on maximizing our risk-adjusted investment returns. Our investment policy is set by our Board of Directors, subject to the limits of applicable regulations.

Our investment policy imposes strict requirements for credit quality, with a minimum average credit quality of the portfolio being rated “A” or higher by Standard & Poor’s or the equivalent rating from another nationally recognized rating agency. Our investment policy also imposes restrictions on concentrations of securities by class and issuer and any new asset class must be approved by management and our Board of Directors. Given our existing exposure to property values, notably in the state of California, we have imposed restrictions on municipal obligations in the state of California and CMBS single issuers concentrated in the state of California. In addition, we allocate at least 2% of our investment portfolio to investments in green bonds- or fixed income investments tailored towards environmental solutions such as renewable energy, clean transportation, green building, and wastewater treatment – a commitment that is consistent with both our investment objectives and our company values.

Enterprise Risk Management (“ERM”)

We maintain a dedicated ERM function that is responsible for analyzing and reporting our risks, monitoring that risks remain within established tolerances, and monitoring, on an ongoing basis, that our ERM objectives are met. These objectives include ensuring proper risk controls are in place, risks are effectively identified, assessed, and managed, and key risks to which we are exposed are appropriately disclosed. Our ERM framework plays an important role in fostering our risk management culture and practices. We continue to enhance our ERM framework, which is guided by the Own Risk and Solvency Assessment (“ORSA”) model developed by the National Association of Insurance Commissioners (“NAIC”) and the National Institute of Standards and Technology (“NIST”) cybersecurity framework. These ongoing enhancements include the creation of an ERM Committee of the Board of Directors which is comprised of select board members and select members of executive management, creation and maintenance of a risk register, and regular reporting on risk management.

An additional important part of our ERM is business continuity, including in the circumstances of a catastrophe event. We have established a business continuity team made up of executive management with predefined roles and responsibilities in the event of an emergency response situation and a business continuity communication site where employees are directed to receive instructions that are tailored to various scenarios. We store all data offsite and ensure it is accessible remotely. Our communications, virtual file servers, underwriting and distribution systems, and claims portal are hosted in geographically diverse data centers domestically and globally. We maintain an additional office in Edina, Minnesota and purchase business continuity services to support our offices in the event of a disruptive event. The majority of our workforce is also equipped to work remotely should they be unable to access our offices.

Sustainability Matters

Our Board of Directors has established a Sustainability Committee which is comprised of various members of our Board. The Sustainability Committee oversees and provides guidance on the company’s strategies related to several factors, including community resiliency, health and safety, corporate social responsibility, governance, partner diversity, and public policy matters relevant to our business.

Specific duties of the Sustainability Committee include:

• Assisting the management team in setting general strategy relating to sustainability matters;

• Developing, implementing and monitoring initiatives and policies based on that strategy; and

• Overseeing communications with employees, investors and shareholders with respect to sustainability matters.

The Sustainability Committee meets on a quarterly basis to assess progress on sustainability matters and will continue to look for opportunities to integrate sustainability concerns in our strategy.

Environmental and Climate Change

Our economic model is closely tied to our coverages for natural disasters and catastrophes. We believe the existing scientific consensus that man-made changes to climate conditions are leading to increases in sea levels and global temperatures, and that the severity and frequency of weather-related natural disasters may increase relative to historical experience. We believe that this increase in severe weather, coupled with currently projected demographic trends in catastrophe-exposed regions, contributes to factors that will increase the average economic value of expected losses, increase the number of people exposed per year to natural disasters and in general exacerbate disaster risk, including risks to infrastructure, global supply chains and agricultural production. In addition to the impacts that environmental incidents have on our business, changes to law and regulation related to climate change could also directly affect our business, including state insurance regulations that could impact the Company’s ability to manage property exposures in areas vulnerable to significant climate driven losses, and possible new requirements that insurers integrate the financial risk of climate change into business operations and governance.

From an underwriting standpoint, we carefully consider the development and deployment of insurance products in coastal areas that may be impacted by rising sea levels, and we incorporate scenarios into our catastrophe modeling that involve elevated sea surface temperatures and other relevant data. Evidence of the Company’s commitment to the environment and combating climate change can be found in the Sustainability and Citizenship report available on our corporate website.

The company considers sustainability factors as part of its investment strategy and reviews individual investments to ensure congruence with company goals in this area. We have also made commitments to automate manual or paper-intensive processes and promote the paperless delivery of documents to our policyholders and producers. We will remain proactive in our efforts to evolve our business in response to our changing natural environment.

Competition

The specialty insurance industry is highly competitive. While we currently target specialty markets, some of our competitors have greater resources than we do. Our primary competitors include national specialty insurance companies, including Kinsale Capital Group, Inc., RLI Corp., Skyward Specialty Insurance Group, Inc. and W.R. Berkley. We also compete with Lloyd’s of London in some of our lines. In addition, we compete against state or other publicly managed enterprises including the California Earthquake Authority and the National Flood Insurance Program. We may also compete with new market entrants in the future. Competition is based on many factors, including the reputation and experience of the insurer, coverages offered, pricing and other terms and conditions, customer service, relationships with brokers and agents (including ease of doing business, service provided and commission rates paid), size and financial strength ratings, among other considerations.

Ratings

Our insurance company subsidiaries, PSIC and PESIC each has a rating of “A” (Excellent) (Outlook Stable) from A.M. Best, which rates insurance companies based on factors of concern to policyholders. A.M. Best currently assigns 16 ratings to insurance companies, which currently range from “A++” (Superior) to “F” for insurance companies that have been publicly placed in liquidation. “A” (Excellent) (Outlook Stable) is the third highest rating. In evaluating a company’s financial and operating performance, A.M. Best reviews the company’s profitability, leverage and liquidity, as well as its book of business, the adequacy and soundness of its reinsurance, the quality and estimated market value of its assets, the adequacy of its loss and loss expense reserves, the adequacy of its surplus, its capital structure, the experience and competence of its management and its market presence. A.M. Best’s ratings reflect its opinion of an insurance company’s financial strength, operating performance and ability to meet its obligations to policyholders. These evaluations are not directed to purchasers of an insurance company’s securities.

Laulima has a rating of "A" (Exceptional) from Demotech, which rates insurance companies on their financial stability.

Intellectual Property

We have registered our logo as a trademark in the United States. We will pursue additional trademark registrations and other intellectual property protection to the extent we believe it would be beneficial and cost effective.

Regulation

Insurance Regulation

We are regulated by insurance regulatory authorities in the states in which we operate. State insurance laws and regulations generally are designed to protect the interests of policyholders, consumers and claimants rather than stockholders or other investors. The nature and extent of state regulation varies by jurisdiction, and state insurance regulators generally have broad administrative power relating to, among other matters, setting capital and surplus requirements, licensing of insurers and insurance producers, review and approval of product forms and rates, establishing standards for reserve adequacy, prescribing statutory accounting methods and the form and content of statutory financial reports, regulating certain transactions with affiliates and prescribing types and amounts of investments.

Regulation of insurance companies constantly changes as governmental agencies and legislatures react to real or perceived issues. In recent years, the state insurance regulatory framework has come under increased federal scrutiny, and some state legislatures have considered or enacted laws that alter and, in many cases, increase, state authority to regulate insurance companies and insurance holding company systems. Further, the NAIC and some state insurance regulators are re-examining existing laws and regulations specifically focusing on issues relating to the solvency of insurance companies, interpretations of existing laws and the development of new laws. Although the federal government does not directly regulate the business of insurance, federal initiatives often affect the insurance industry in a variety of ways. In addition, the Federal Insurance Office (the "FIO") was established within the U.S. Department of the Treasury by the Dodd-Frank Wall Street Reform and Consumer Protection Act (the "Dodd-Frank Act") in July 2010 to monitor all aspects of the insurance industry, although FIO has no express regulatory authority over insurance companies or other insurance industry participants.

Insurance Holding Company Regulation