UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

☐ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

☐ |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-38354

CORPORACIÓN AMÉRICA AIRPORTS S.A. |

(Exact name of registrant as specified in its charter) |

|

Not Applicable |

(Translation of registrant’s name into English) |

|

Grand Duchy of Luxembourg |

(Jurisdiction of incorporation or organization) |

|

Jorge Arruda Filho, Chief Financial Officer |

(Name, Telephone, E-mail and or Facsimile number and Address Company Contact Person)) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol |

|

Name of each exchange in which registered |

Common Shares, U.S.$1.00 nominal value per share |

|

CAAP |

|

New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report

163,222,707 Common Shares, as of December 31, 2023

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b2 of the Exchange Act.

Large accelerated filer |

☐ |

Accelerated filer |

☒ |

Non-Accelerated filer |

☐ |

Emerging growth company |

☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ |

International Financial Reporting Standards as issued |

Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act)

Yes ☐ No ☒

TABLE OF CONTENTS

|

|

Page |

|

|

|

CAUTIONARY STATEMENT WITH RESPECT TO FORWARD-LOOKING STATEMENTS |

2 |

|

|

|

|

3 |

||

|

|

|

4 |

||

|

|

|

6 |

||

|

|

|

6 |

||

|

|

|

6 |

||

|

|

|

6 |

||

|

|

|

37 |

||

|

|

|

133 |

||

|

|

|

133 |

||

|

|

|

181 |

||

|

|

|

188 |

||

|

|

|

191 |

||

|

|

|

199 |

||

|

|

|

199 |

||

|

|

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES REGARDING MARKET RISK |

213 |

|

|

|

|

213 |

||

|

|

|

214 |

||

|

|

|

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

214 |

|

|

|

|

214 |

||

|

|

|

215 |

||

|

|

|

215 |

||

|

|

|

215 |

||

|

|

|

215 |

||

|

|

|

216 |

||

|

|

|

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

216 |

|

|

|

|

216 |

||

|

|

|

216 |

||

|

|

|

218 |

||

|

|

|

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS |

218 |

|

|

|

|

218 |

||

|

|

|

218 |

||

|

|

|

220 |

||

|

|

|

221 |

||

|

|

|

222 |

||

|

|

|

|

223 |

|

i

CAUTIONARY STATEMENT WITH RESPECT TO FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements about our expectations, beliefs and intentions regarding, among other things, our products and services, development efforts, business, financial condition, results of operations, strategies, plans and prospects. Forward-looking statements can be identified by the use of forward-looking words such as “believe,” “expect,” “intend,” “plan,” “may,” “should,” “could,” “might,” “seek,” “target,” “will,” “project,” “forecast,” “continue” or “anticipate” or their negatives or variations of these words or other comparable words or by the fact that these statements do not relate strictly to historical matters. Forward-looking statements relate to anticipated or expected events, activities, trends or results as of the date they are made. Because forward-looking statements relate to matters that have not yet occurred, these statements are inherently subject to risks and uncertainties that could cause our actual results to differ materially from any future results expressed or implied by the forward-looking statements. Many factors could cause our actual activities or results to differ materially from the activities and results anticipated in forward-looking statements, including, but not limited to, the factors listed below:

| ● | our business strengths and future results of operation; |

| ● | delays or unexpected casualties related to construction under our investment plans and master plans; |

| ● | our ability to generate or obtain the required capital to fully develop and operate our airports; |

| ● | impact of epidemics, pandemics, and public health crises; |

| ● | general economic, political, demographic and business conditions in the geographic markets we serve; |

| ● | decreases in passenger traffic; |

| ● | changes in the fees we may charge under our concession agreements; |

| ● | inflation and hyperinflation, depreciation, and devaluation of the AR$, EUR, BRL, UYU or AMD, against the U.S. dollar; |

| ● | the early termination, revocation, or failure to renew or extend any of our concession agreements; |

| ● | the right of the Argentine Government to buy out the AA2000 Concession Agreement (as defined herein); |

| ● | changes in our investment commitments or our ability to meet our obligations thereunder; |

| ● | existing and future governmental regulations; |

| ● | natural disaster-related losses which may not be fully insurable; |

| ● | the ongoing war events; and |

| ● | cyberterrorism in the international markets we serve. |

We believe these forward-looking statements are reasonable; however, these statements speak only as of the date of this annual report and are subject to known and unknown risks, uncertainties and other factors that may cause our or our industry’s actual results, levels of activity, performance, or achievements to be materially different from those anticipated by the forward-looking statements. We discuss these risks in this annual report in greater detail under the heading “Risk Factors.” Given these uncertainties, you should not rely upon forward-looking statements as predictions of future events.

Unless required by law, we undertake no obligation to update or revise any forward-looking statement, whether as a result of new information, future events, or developments or otherwise.

2

CERTAIN CONVENTIONS

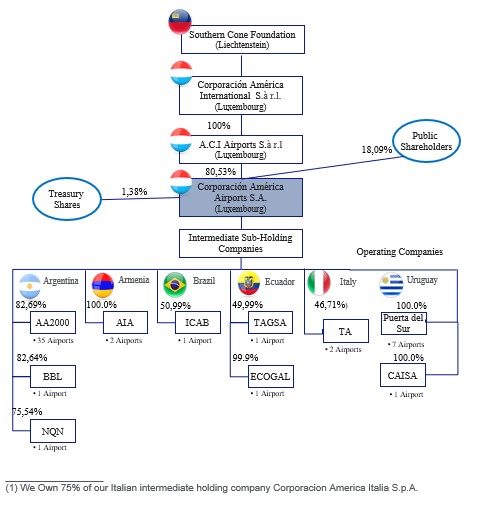

Corporación América Airports S.A. (“CAAP”) was incorporated under the laws of the Grand Duchy of Luxembourg (“Luxembourg”) on December 14, 2012. The Company owns no material assets other than its direct and indirect ownership of the issued share capital of other intermediate holding companies for all our operating subsidiaries. Except where the context otherwise requires or where otherwise indicated, all references to the “Company,” “CAAP,” “we,” “us” and “our” refer to Corporación América Airports S.A. and its consolidated subsidiaries, as well as those businesses we account for using the equity method.

In this annual report, unless otherwise specified or the context otherwise requires:

| ● | “U.S.$” and “U.S. dollar” each refers to the United States dollar; |

| ● | “AR$” refers to the Argentine peso; |

| ● | “€,” “EUR” or “euro” each refers to the euro, the single currency established for members of the European Economic and Monetary Union since January 1, 1999; |

| ● | “R$” or “BRL” each refers to the Brazilian real; |

| ● | “$U” or “UYU” each refers to the Uruguayan peso; and |

| ● | “AMD” refers to the Armenian dram. |

We have translated some of the local currency amounts contained in this annual report into U.S. dollars for convenience purposes only. The U.S. dollar-equivalent information presented in this annual report is provided solely for convenience and should not be construed as implying that the amounts represent, or could have been or could be converted into, U.S. dollars at such rates or at any other rate. See “Item 3. Key Information— Risk Factors— Depreciation or fluctuation of the currencies of the countries where we operate could adversely affect our results of operations and financial condition.”

Certain numbers and percentages included in this annual report have been subject to rounding adjustments. Accordingly, figures shown for the same category presented in various tables or other sections of this annual report may vary slightly, and figures shown as totals in certain tables may not be the arithmetic aggregation of the figures that precede them.

3

PRESENTATION OF FINANCIAL INFORMATION

This annual report contains our audited consolidated financial statements as of December 31, 2023 and 2022 and for our fiscal years ended December 31, 2023, 2022 and 2021 (our “Audited Consolidated Financial Statements”).

We prepare our Audited Consolidated Financial Statements in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”). We have applied all IFRS Accounting Standards adopted by the International Accounting Standards Board (IASB) effective at the time of preparing our Audited Consolidated Financial Statements. Our Audited Consolidated Financial Statements have been audited by Price Waterhouse & Co. S.R.L. (“PwC”), a member firm of the PricewaterhouseCoopers global network, and an independent registered public accounting firm, whose report dated March 20, 2024, is also included in this annual report.

Our Audited Consolidated Financial Statements are presented in U.S. dollars. Our fiscal year ends on December 31 of each year. Accordingly, all references to a particular year are to the year ended December 31 of that year.

Our Segments

As of and for the fiscal year ended December 31, 2023, we have identified six reportable segments: Argentina, Italy, Brazil, Uruguay, Ecuador and Armenia. See Note 4 to our Audited Consolidated Financial Statements and “Adjusted Segment EBITDA and Adjusted Segment EBITDA excluding Construction Services.”

In December 2021, we transferred our 50% ownership interest in Aeropuertos Andinos del Perú S.A. (“AAP”) to Andino Investment Holding S.A. See “Business Overview—Our Airports by Country in Which We Operate—Peru.” The elimination of any intersegment revenues and other significant intercompany operations are included in the “Intrasegment Adjustments” column. AAP was not previously classified as an asset held for sale or as a discontinued operation. All the financial and operational information provided for our Peruvian segment for the year ended December 31, 2021 includes our financial information and results of operation until December 16, 2021, date on which the transfer of our interest in AAP was completed.

Factors Affecting Comparability of Prior Periods

During 2020 and 2021, the Company’s operations were significantly affected due to the impact of the COVID-19 pandemic and the related measures that affected passenger traffic. The significant decrease in our results of operations due to the COVID-19 pandemic and the subsequent rebound in our results of operations after the termination of measures affecting passenger traffic, affected the comparability of the figures reported for the years ended December 31, 2023 and 2022 with the corresponding period in 2021.

Adjusted Segment EBITDA and Adjusted Segment EBITDA excluding Construction Services

“Adjusted Segment EBITDA” is defined, with respect to each segment, as income/(loss) from continuing operations before financial income, financial loss, income tax expense, depreciation, and amortization for such segment. Adjusted Segment EBITDA excludes certain items that are not considered part of our core operating results. Specifically, we do not allocate financial income, financial loss, income tax expense, depreciation, and amortization to our reportable segments. Our management also reviews a metric of performance, denominated “Adjusted Segment EBITDA excluding Construction Services,” which only differs with the Adjusted Segment EBITDA measure by excluding the Construction Services margin.

Although Adjusted EBITDA, and consequently, Adjusted EBITDA excluding Construction Services, are commonly viewed as non-IFRS measures in other contexts, pursuant to IFRS 8, “Segment Information,” these are treated as IFRS measures in the manner in which we utilize them. We use Adjusted EBITDA and Adjusted EBITDA excluding Construction Services for purposes of making decisions about allocating resources to our segments and to internally evaluate their financial performance because we believe they reflect current core operating performance and provide an indicator of the segment’s ability to generate cash.

Non-IFRS Information

Adjusted EBITDA and Adjusted EBITDA excluding Construction Services

“Adjusted EBITDA” is a non-IFRS financial measure defined as net income/(loss) from continuing operations before financial income, financial loss, income tax expense, depreciation, and amortization. “Adjusted EBITDA excluding Construction Services” only differs with the previously mentioned measure by excluding Construction Services margin.

4

Adjusted EBITDA and Adjusted EBITDA excluding Construction Services are not defined under IFRS and have important limitations as analytical tools. You should not consider them in isolation or as a substitute for analysis of our results as reported under IFRS. For example, Adjusted EBITDA and Adjusted EBITDA excluding Construction Services have the following limitations:

| ● | exclude certain tax payments that may represent a reduction in cash available to us; |

| ● | do not reflect any cash capital expenditure requirements for the assets being depreciated and amortized that may have to be replaced in the future; |

| ● | do not reflect changes in, or cash requirements for, our working capital needs; and |

| ● | do not reflect the significant interest expense, or the cash requirements, necessary to service our debt. |

We believe that the presentation of Adjusted EBITDA and Adjusted EBITDA excluding Construction Services enhances investors’ understanding of our performance. We believe these measures are useful metrics for investors to assess our operating performance from period to period by excluding certain items that we believe are not representative of our core business. We present Adjusted EBITDA and Adjusted EBITDA excluding Construction Services to provide supplemental information that we consider relevant for the readers of our Audited Consolidated Financial Statements included elsewhere in this annual report, and such information is not meant to replace or supersede IFRS measures.

In addition, our management believes Adjusted EBITDA and Adjusted EBITDA excluding Construction Services are useful because they allow us to evaluate our operating performance and compare the results of our operations from period to period without regard to our financing methods, capital structure or income taxes more effectively. We exclude the items listed above from income for the year in arriving at Adjusted EBITDA and Adjusted EBITDA excluding Construction Services because these amounts can vary substantially from company to company within our industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired.

Adjusted EBITDA and Adjusted EBITDA excluding Construction Services should not be considered as alternatives to, or more meaningful than, consolidated net income for the year as determined in accordance with IFRS or as indicators of our operating performance from continuing operations.

Adjusted EBITDA and Adjusted EBITDA excluding Construction Services may not be the same as similarly titled measures used by other companies.

We have included the reconciliation of Adjusted EBITDA and Adjusted EBITDA excluding Construction Services to consolidated net income from continuing operations for all the periods presented. See “Operating and Financial Review and Prospects—Operating Results—Adjusted EBITDA Reconciliation to Net Income/(Loss) from Continuing Operations.”

Capital Increase

As part of the management share compensation plan (see “Item 6. Directors, Senior Management and Employees—Compensation—Management Compensation Plan”), on October 9, 2020, the board of directors of the Company increased the Company’s share capital by the amount of U.S.$3,200,445 through the issuance of 3,200,445 new shares having a nominal value of U.S.$1.00 each. As a result of the issuance of these new shares, which were subscribed by A.C.I. Airports S.à r.l., the Company’s controlling shareholder, the outstanding share capital of the Company as of December 31, 2023 is 163,222,707 shares. The shares were subscribed for a total subscription price of U.S.$6,144,854.40 (i.e., a subscription price of U.S.$1.92 per new share, being the market price per share as of October 8, 2020), and paid for through the incorporation of the corresponding amount which was allocated to the Company’s free distributable reserves. The new shares were, subsequently and on the same date, transferred by the controlling shareholder to the Company to be held in treasury until their allocation to key employees in accordance with the management share compensation plan. As of the date of this annual report, 949,322 shares have been delivered to key employees under the management share compensation plan and the remaining outstanding 2,251,123 shares are still held in treasury.

5

PRESENTATION OF INDUSTRY AND MARKET DATA

In this annual report, we rely on, and refer to, information regarding our business and the markets in which we operate and compete. The market data and certain economic and industry data and forecasts used in this annual report were obtained from internal surveys, market research, governmental and other publicly available information, and independent industry publications. Industry publications, surveys, and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. We believe that these industry publications, surveys, and forecasts are reliable, but we have not independently verified them and cannot guarantee their accuracy or completeness.

Certain market share information and other statements presented herein regarding our position relative to our competitors are not based on published statistical data or information obtained from independent third parties but reflect our best estimates. We have based these estimates upon information obtained from publicly available information from our competitors in the industry in which we operate.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A.Reserved

B.CAPITALIZATION AND INDEBTEDNESS

Not applicable.

C.REASONS FOR THE OFFER AND USE OF PROCEEDS

Not applicable.

D.RISK FACTORS

You should carefully consider the risks and uncertainties described below, together with the other information contained in this annual report, before making any investment decision. Any of the following risks and uncertainties could have a material adverse effect on our business, prospects, results of operations and financial condition. The market price of our common shares could decline due to any of these risks and uncertainties, and you could lose all or part of your investment. The risks described below are those that we currently believe may materially affect us.

Summary of Risk Factors

The following is a series of concise statements highlighting the principal, but not all, risk factors that we face. The list is followed by a discussion of the Company’s risk factors, including those highlighted below.

Risks Related to Our Business and Industry

| ● | Our concessions may be terminated under various circumstances, some of which are beyond our control. |

| ● | We may be subject to monetary penalties or early termination if we fail to comply with the terms of our concession agreements. |

| ● | Our revenue is highly dependent on levels of air traffic, which depend in part on factors beyond our control, including economic and political conditions in the countries where we operate our airports. |

6

| ● | Outbreaks of diseases as well as any other public health crises that may arise in the future, have had, and may continue to have a negative impact on passenger traffic levels, air traffic operations and in our results of operations, financial position, and cash flows. |

| ● | Geopolitical uncertainties and an increase of trade protectionism could have a material adverse effect on our business, results of operation and financial condition. |

| ● | We are dependent on information and communication technologies, and our systems and infrastructures face certain risks, including cybersecurity risks. |

Risks Related to Argentina and the AA2000 Concession Agreement

| ● | The Argentine Government extended the term of the AA2000 Concession Agreement until 2038 subject to our compliance with certain commitments, which if we fail to comply with, could result in the imposition of fines or the termination or revocation of the AA2000 Concession Agreement. |

| ● | Pursuant to the AA2000 Concession Agreement, since February 2018, the Argentine Government may buy out our concession, which would materially affect our revenues and operations. |

| ● | The Organismo Regulador del Sistema Nacional de Aeropuertos (“ORSNA”) may adjust the fees we charge for aeronautical services, the payments we are required to make to the Argentine Government and our investment plan in a way that is detrimental to us or fail to adjust them to restore the AA2000 Concession Agreement’s economic equilibrium. |

| ● | If the ORSNA does not approve the capital expenditures already made under the AA2000 Concession Agreement, we could be required to make additional capital expenditures, which may affect our cash flows and financial condition. |

Risks Related to Our Other Principal Operations and Other Principal Markets in Which We Operate

| ● | Italy. If the approval process from local and national authorities of the master plan for the Florence Airport is further delayed, our financial results from the operation of such airport will be negatively impacted. |

| ● | Uruguay. A deterioration in the economic conditions of our neighboring markets, particularly Argentina has the potential to affect the number of passengers at our Uruguayan airports mainly Punta del Este airport. |

| ● | Armenia. The ongoing war between Russia and Ukraine has and will likely continue to disrupt or impact the connecting flights between our Armenian Airports and Russia, which could affect our results of operation. |

Risks Related to Our Common Shares

| ● | We issued, and may further issue, options, restricted shares, and other forms of share-based compensation, which have the potential to dilute shareholder value and cause the price of our common shares to decline. |

| ● | A significant portion of our common shares may be sold into the public market, which could cause the market price of our common stock to drop significantly, even if our business is doing well. |

Risks Related to Our Business and Industry

Our concessions may be terminated under various circumstances, some of which are beyond our control.

Our business consists of acquiring, developing and operating airport concessions. These concessions are granted by governmental authorities for a limited period of time and subject to several conditions and obligations.

7

Our concessions may be terminated under various circumstances, some of which are beyond our control. In general, our concession agreements may be terminated at any time by the relevant governments or agencies for public interest reasons. Concession agreements may also be terminated due to our material and repeated breach of the concession terms. The termination of one or more of our concessions could have a material adverse effect on our business, financial condition, and results of operations.

If an applicable governmental authority terminates any of our concessions, with or without cause, we may be entitled to seek claims for compensation from such terminating governmental authority. Although termination payments vary by concession, they usually include a claim for indemnification equal to the value of the non-amortized investments made by us for purposes of operating the airports and rendering the services agreed under the concession agreements. If the applicable governmental authority terminates one of our concessions due to our material and repeated breach or failure to make the committed investments, we may assert claims for indemnification equal to those non-amortized investments we made for purposes of operating the relevant airports and rendering of the services agreed under the relevant concession agreements. If the concession is terminated by the relevant government or agency for public interest reasons or without cause, we may assert claims for indemnification equal to the non-amortized investments plus loss of profits. Collecting on such claims may be difficult and time-consuming, and any amounts collected in respect of such claims may not provide us with the expected level of returns, which could have a material adverse effect on our business, financial condition, and results of operations.

In the AA2000 Concession Agreement, our largest concession operations, the Argentine Government has the right to buy out the concession agreement upon prior notification to us and indemnify us for certain investments we incurred for purposes of operating the airports and rendering the services agreed thereunder. See “Item 3. Key Information—Risk Factors—Risks Related to Argentina and the AA2000 Concession Agreement—Pursuant to the AA2000 Concession Agreement, since February 2018, the Argentine Government may buy out our concession, which would materially affect our revenues and operations.”

We may be subject to monetary penalties or early termination if we fail to comply with the terms of our concession agreements.

We may be subject to monetary penalties if we violate or otherwise fail to comply with the terms of our concessions. Some violations of a concession agreement may provide for cure periods or other remedial action, while other violations, whenever they are substantial and repeated, can result in the immediate termination of the relevant concession. If we experience difficulties, we may encounter problems in satisfying our obligations under our concession agreements and the relevant governmental authorities may impose sanctions on us. For a description of the consequences that may result from the violation of various terms of our concessions, or local laws and regulations related to such concessions, see “Item 4. Company Information—Business Overview—Regulatory and Concessions Framework.” Monetary penalties could negatively affect our results of operations.

In addition, under all our concession agreements, we are required to establish and comply with an investment plan for the airports covered under such concession agreements. If we do not fulfill our investment commitments on a timely basis or obtain necessary financing to complete the projects, such failures could lead to a breach of the relevant concession agreement, which may subject us to monetary fines or the early termination of our concession agreements.

Our revenue and profitability may be affected if we fail to win new concession agreements, acquire companies with existing concession agreements, or otherwise improve or expand our current operations.

Our growth strategy relies upon identifying and winning new concession agreements, acquiring companies with existing concession agreements, or improving and expanding our current operations. Our future growth may also depend on new (greenfield) development projects, which may require significant time and upfront financial commitments for construction and development. While we anticipate having opportunities to bid for concession agreements or purchase existing concessionaires in the future, we cannot predict the frequency or accuracy of such opportunities. We must also strategically identify which concession agreements and existing concessionaires to target based on numerous factors such as number of passengers, size of the relevant airport(s), type, location, and quality of the available airports and subconcession space, rental structure, financial return, regulatory requirements, and the competitive landscape within such market. We may not be able to successfully expand, as we may not correctly analyze the suitability of airport locations, anticipate all the challenges imposed by expanding our operations or succeed in executing our growth plan efficiently. We also may fail to expand within budget, on a timely basis or expand at all. In addition, to win a particular concession contract, we may be required to make investments or incur other expenses that would render such concession less economically attractive.

Our growth strategy and the substantial investment associated with the acquisition of each new concession agreement, existing concessions or expansion of existing concessions may cause our operating results to fluctuate and be unpredictable.

8

Outbreaks of diseases as well as any other public health crises that may arise in the future, have had, and may continue to have a negative impact on passenger traffic levels, air traffic operations and in our results of operations, financial position, and cash flows.

Future outbreaks of existing or future diseases as well as any other public health crises, or the fear of such events and governmental responses to such events, especially after the COVID-19 pandemic, could provoke responses that negatively affect passenger air traffic. The COVID-19 pandemic that resulted in several cities being placed under quarantine, increased travel restrictions from and to several countries, and extended shutdowns of certain businesses in certain regions, also forced airlines to cancel flights and disrupted the frequency and pattern of air travel worldwide. New strains of the COVID-19 virus, as well as, future public health crises similar to the outbreak of the Severe Acute Respiratory Syndrome (known as SARS) between 2002 and 2003, the outbreak of the A/H1N1 virus in 2009, the Ebola outbreak in 2014 and 2015 and the outbreak of the Zika virus in 2018 and 2019, could have a negative impact on our business and our revenue which is largely dependent on the level of passenger traffic in our airports. Any outbreaks of health epidemics could result in decreased passenger traffic and increased costs for the air travel industry and, as a result, could have a material adverse effect on our business revenues and results of operations.

Our business, operating results and growth rates may be adversely affected by current or future unfavorable economic and market conditions and adverse developments in the global economy.

Our business depends on the economic health of the global economy. If the conditions of the global economy remain uncertain or continue to be volatile, or if they deteriorate, including as a result of the impact of military conflict, such as the war between Russia and Ukraine and the conflict between Israel and Hamas, terrorism or other geopolitical events, our business, our operating results and our financial condition may be materially adversely affected.

In the aftermath of the COVID-19 pandemic, the United States and global markets have encountered a material increase in the level of inflation. Increases in inflation rates raise our costs for commodities, labor, materials and services and other costs required to grow and operate our business, and failure to secure these on reasonable terms may adversely impact on our financial condition. Additionally, increases in inflation rates have caused, and may cause in the future, global economic uncertainty and uncertainty about the interest rate environment, which may make it more difficult, costly or dilutive for us to secure additional financing. A failure to adequately respond to these risks could have a material adverse impact on our financial condition, results of operations or cash flows.

There can be no assurance that future credit and financial market instability and a deterioration in confidence in global economic conditions will not occur. Our general business strategy may be adversely affected by any such economic downturn, liquidity shortages, volatile business environment or continued unpredictable and unstable market conditions. If the current equity and credit markets deteriorate, or if adverse developments are experienced by financial institutions, it may cause short-term liquidity risk and also make any necessary debt or equity financing more difficult, more costly, more onerous with respect to financial and operating covenants and more dilutive. Failure to secure any necessary financing in a timely manner and on favorable terms could have a material adverse effect on our growth strategy, financial performance and stock price and could require us to alter our operating plans. In addition, there is a risk that one or more of our service providers, financial institutions, manufacturers, suppliers and other partners may be adversely affected by the foregoing risks, which could directly affect our ability to attain our operating goals on schedule and on budget.

Geopolitical uncertainties and an increase of trade protectionism could have a material adverse effect on our business, results of operation and financial condition.

Russia’s war against neighboring Ukraine continues to disrupt international travel from and to Russia and Ukraine and other destinations. Additionally, as a response to the ban of flights to Russia by Western countries and the European Union, Russia has closed its skies for carriers registered in Western countries and carriers also avoid overflying the war zone, disrupting global supply chains (including aircraft components), and adversely affecting air travel (including air travel routs and accessibility to airports).

In addition to travel restrictions, in response to Russia’s invasion of Ukraine, the European Union, the U.K. and the U.S. introduced extensive sanctions on Russia (as well as Belarus for its role in Russia’s invasion) comprised of targeted, restrictive measures on certain individuals and entities, export controls, restrictions on economic relations, trade and other financial transactions. These sanctions have had, and are expected to continue to have, a significant disruptive effect on global markets, including oil and gas markets. Geopolitical events may lead to further instability across Europe and worldwide.

9

The imposition of tariffs on certain imported products by the U.S. has triggered retaliatory actions from certain foreign governments and may trigger retaliatory actions by other foreign governments, potentially resulting in a “trade war”. Certain foreign governments have instituted or are considering imposing trade sanctions on certain U.S. goods. Others are considering the imposition of sanctions that will deny U.S. companies access to critical raw materials.

Relatedly, global markets and supply chains have been further disrupted by Hamas attack on October 7, 2023. Hamas, an organization designated by the U.S. as a terrorist organization, launched a series of coordinated attacks from the Gaza Strip onto Israel. On October 8, 2023, Israel formally declared war on Hamas, and the armed conflict is ongoing as of the date of this filing. Hostilities between Israel and Hamas could escalate and involve surrounding countries in the Middle East. To date, we have not experienced any material disruptions and interruptions in our infrastructure, supplies, technology systems, or networks needed to support our operations as a result of the conflict between Israel and Hamas, but cannot discard the possibility of future disruptions and interruptions as a result of this conflict.

We cannot predict the progress, outcome or consequences of the conflicts between Russia and Ukraine, or Israel and Hamas, or their impacts in Ukraine, Russia, Belarus, Europe, the U.S., or the Middle East. The length, impact, and outcome of ongoing military conflicts is highly unpredictable and could lead to significant market and other disruptions, including significant volatility in commodity prices and supply of energy resources, instability in financial markets, supply chain disruptions, political and social instability, trade disputes or trade barriers, changes in consumer or purchaser preferences, as well as an increase in cyberattacks and espionage. The above geopolitical and trade uncertainty and tensions have resulted in fuel price increases, and have affected, and may continue to affect, our profitability. Sanctions, trade wars between certain countries or blocks of countries, or other governmental action related to tariffs or international trade agreements, could have a material adverse effect on passenger traffic on our airports as well as on our services, costs and suppliers or world economy or certain sectors thereof and, consequently, on our business and financial results.

We could be subject to acts of terrorism or war, which could have a negative impact on air travel and result in increased security requirements.

Our airports operate within a stringent and complex security regime, as required by the relevant governmental authorities, which may impose additional security measures from time to time. The consequences of the Russian and Ukraine war, the Israel and Hamas conflict, as well as any future terrorist action, threat or war may include the cancellation or delay of flights, fewer airlines and passengers using our airports, liability for damage or loss and the costs of repairing damage. If as a consequence of conflict or terrorist attack one of the airports we operate is affected, the airport in question could be closed, in whole or in part, for the time needed to care for victims, investigate the circumstances of the attack, rebuild any damaged areas or otherwise, with a subsequent decrease in the revenue and increase in costs for the reconstruction of the affected areas (to the extent these are not covered by insurance policies).

Moreover, if an accident, act of terrorism or threat affects the safety standard perception on customers thereof or were to occur in a country in which we operate, even if not at our airports, the perception of safety by airport users could decrease, and, consequently, there could be a reduction in passenger air traffic for an indefinite period of time, which could adversely affect our business, financial condition, and results of operations.

Furthermore, the implementation of additional security measures at our airports in the future could lead to additional limitations on airport capacity or retail space, overcrowding, increases in operating costs and delays to passenger movement through the airport, any of which could have a material adverse effect on our business, financial condition, and results of operations.

Our business may also be affected by the outbreak of wars or armed conflicts in any region of the world, including, for example, the Russian and Ukraine war, and the Israel and Hamas conflict. Among other things, wars can lead to increased prices of fuel, supplies, and interest rates for aircraft leases, which could, in turn, lead to increased prices of airline tickets and a decline in demand for air transportation in general. Likewise, the occurrence of armed conflicts could result in increased security measures, thereby increasing security costs.

10

We are dependent on information and communication technologies, and our systems and infrastructures face certain risks, including cybersecurity risks.

The operation of complex infrastructures, such as airports, and the coordination of the many actors involved in its operation require the use of several highly specialized information systems, including both our own information technology systems and those of third-party service providers, such as systems that monitor our operations or the status of our facilities, communication systems to inform the public, access control systems and closed circuit television security systems, infrastructure monitoring systems, passenger ticketing and boarding, automated baggage handling, points of sale, terminals and radio and voice communication systems used by our personnel. In addition, our accounting and fixed assets, payroll, budgeting, human resources, supplier and commercial, hiring, payments and billing systems and our websites are key to the functioning of our airports. The proper functioning of these systems is critical to our operations and business management. These systems may, from time to time, require modifications or improvements as a result of changes in technology, the growth of our business and the functioning of each of these systems.

Attempts to gain unauthorized access to our information technology systems have become more sophisticated over time. The risk of cyber - crime has been increasing, especially as infiltrating technology continues to become increasingly sophisticated. We and certain of our service providers may from time to time be subject to cyberattacks and security incidents. While we have not experienced any significant system failure, accident or security breach to date, if such an event were to occur and cause interruptions in our and our critical third parties’ operations, it could result in material disruptions to our programs, our operations, and ultimately, our financial results. In particular, if we are unable to contain or minimize the effects of a significant cyber - attack, such attack could materially affect the number of passengers at our airports, cause the loss or exposure of information, damage our reputation and lead to regulatory penalties and financial losses. Any security compromise affecting us, our service providers, strategic partners, other contractors, consultants, or our industry, whether real or perceived, could harm our reputation, erode confidence in the effectiveness of our security measures and lead to regulatory scrutiny. To the extent that any disruption or security breach were to result in a loss of, or damage to, our data or systems, or inappropriate disclosure of confidential or proprietary or personal information, we could incur liability, including litigation exposure, penalties and fines, we could become the subject of regulatory action or investigation, our competitive position could be harmed and the further development and commercialization of our products and services could be delayed. If such an event were to occur and cause interruptions in our operations, it could result in a material disruption of our business.

In order to face these issues, we created a global information security department which reports to the Executive Committee. We also hired a global information security manager and reinforced the global information security department with multicultural security specialists in different locations. This new area focuses on cybersecurity, contingency procedures, security governance, access and identity management, infrastructure protection and monitoring, researching and deploying new technology to improve protection of information and communication systems.

Additionally, we are implementing a global security monitoring service (SOC) including a new incident response and threat intelligence service. This service allows us to respond more quickly and efficiently to any potential security breach. On the other hand, we are implementing and strengthening security measures to maintain and improve protection of information, increasing endpoint and perimeter protection, vulnerability management processes in order to improve the global posture of the company in terms of information security. However, these information technology systems cannot be completely protected against certain events such as natural disasters, fraud, computer viruses, hacking, communication failures, equipment breakdown, software errors and other technical problems. The occurrence of any of these events could disrupt our operations, result in an increase in costs and a decrease in revenue and damage our public image and our business in general.

The loss or impairment of our relationship with governments and their agencies in the markets in which we operate could adversely affect our business, future revenues, and growth prospects.

Our principal assets are concession rights granted by governments in the countries in which we operate. Our business depends to a large extent on our ability to manage relationships with the relevant governments and their agencies. During the term of our concessions, we are in continuous communications with the relevant governments and their agencies regarding, among other things, the terms and conditions of the concession, compliance with the concession agreement, the applicable master plan and works to be performed at the airports, including works not specifically required by the terms of the relevant concession, and the establishment of tariffs. Our business, prospects, financial condition, or operating results could be materially harmed if we were suspended or debarred from contracting with any such government or government agency or if our reputation or relationship with any such government or agency is impaired.

11

Our revenue is highly dependent on levels of air traffic, which depend in part on factors beyond our control, including economic and political conditions in the countries where we operate our airports.

Our revenue is closely linked to passenger and cargo traffic volumes and the number of air traffic movements at our airports. These factors directly determine our aeronautical revenue and indirectly determine our commercial revenue. Passenger and cargo traffic volumes and air traffic movements depend, in part, on many factors beyond our control. Such factors include economic conditions and the political situation in the countries where we operate our airports, epidemics, pandemics and other public health crises, terrorism, fluctuations in petroleum prices (which can have a negative impact on traffic as a result of fuel surcharges or other measures adopted by airlines in response to increased fuel costs), currency exchange rate fluctuations, hyperinflation, geopolitical considerations and changes in regulatory policies applicable to the aviation industry. The occurrence of any of these risks may result in a reduction of passenger air traffic levels and air traffic movements globally and in the regions in which we operate. A significant decline in passenger and cargo traffic volumes and the number of air traffic movements at our airports could have a material adverse effect on our business, financial condition, and results of operations.

We face risks related to our dependence on the revenue from Ezeiza Airport.

During the years ended December 31, 2023, 2022 and 2021, the Ministro Pistarini International Airport (“Ezeiza Airport”) generated U.S.$253.7 million or 18.2% of our consolidated revenue, U.S.$278.1 million or 20.2 % of our consolidated revenue, and U.S.$123.3 million or 17.4% of our consolidated revenue, respectively, for each of such periods. As a result of the substantial contribution to our revenue from the Ezeiza Airport, any event or condition affecting this airport (in addition to any potential termination or buyout of the AA2000 Concession Agreement) could materially adversely affect our business, financial condition, and results of operations. For example, an economic recession in Argentina, a reduction in the operations of Ezeiza Airport, competition from other airports or a decrease in the number of passengers traveling to Buenos Aires as tourists could cause a decrease in our revenue from this airport which, in turn, could materially adversely affect our business, financial condition and results of operations.

Increases in international fuel prices could reduce demand for air travel.

The price of fuel may be subject to fluctuations resulting from a reduction or increase in output of petroleum, voluntary or otherwise, by oil producing countries, other market forces, any future terrorist attacks, a general increase in international hostilities, including, for example, the Russian and Ukraine war, and the Israel and Hamas conflict. In the past, increased fuel costs were among the factors leading to cancellations of routes, decreases in frequencies of flights and, in some cases, even contributed to filings for bankruptcy by some airlines. Although fuel is a widely traded global commodity, in the event of a significant increase in fuel prices in one or more of the countries in which we operate, or in one or more countries that provide significant numbers of international air passengers to the countries in which we operate, the effects of a localized price increase may be more significant than a general, worldwide increase in fuel prices. Significant fluctuations may result in higher airline ticket prices and in a decrease in demand for air travel generally, both of which could have an adverse effect on our revenues and results of operations.

Extended interruptions or disruptions at the airports where we operate due to natural disasters, prolonged weather conditions and other adverse incidents could affect our business and results of operations.

A significant extended interruption or disruption in service at the airports where we operate could have a material adverse impact on our business, financial condition, and results of operations. Our operations could be impacted by flight cancellations and airport closures caused by weather and natural disasters. Severe weather conditions, particularly heavy snowfall, increases in the frequency, severity, and duration of natural disasters such as hurricanes, tornadoes, volcanic activity, earthquakes, and tsunamis, can significantly disrupt service, cause cancellation of flights and negatively affect passenger traffic at airports, which may result in decreased revenues and increased costs. The disaster recovery and business continuity plans we have in place may prove inadequate in the event of a serious disaster or similar event. We may incur substantial expenses as a result of the limited nature of our disaster recovery and business continuity plans, which could have a material adverse effect on our business.

Competition from other destinations could adversely affect our business.

The principal factor affecting our business is the number of passengers that use our airports. Our passenger traffic volume may be adversely affected by the attractiveness, affordability, and accessibility of competing destinations. In addition, our passenger traffic volume may be adversely affected by the level of business activity in each destination or the likelihood of airlines using any of those destinations as a hub or base for their operations. If business activity and tourism levels and, therefore, the number of passengers using our airports, is negatively impacted by competing airports and hubs in the geographic regions in which we operate, such development could have an adverse effect on our business, financial condition, or results of operations.

12

We are subject to the risk of union disputes and work stoppages at our locations, which could have a material adverse effect on our business.

Some of our employees are members of labor unions. For example, as of December 31, 2023, approximately 63% and 32.7% (64.8% and 48.9 %, as of December 31, 2022) of our employees in Argentina and Italy, respectively, were members of labor unions. Negotiating labor contracts, either for new locations or to replace expiring contracts, is time consuming or may not be accomplished on a timely basis. In addition, we negotiate some of our collective bargaining agreements on an annual basis. If we are unable to satisfactorily negotiate those labor contracts with the labor unions on terms acceptable to us or without a strike or work stoppage, the effects on our business could be materially adverse. Any strike or work stoppage could disrupt our business, adversely affecting our results of operations and our public image could be materially adversely affected by such labor disputes. In addition, existing labor contracts may not prevent a strike or work stoppage, and any such work stoppage could have a material adverse effect on our business.

The operations of our airports may be adversely affected by actions or inactions of third parties that are beyond our control.

In most of our airports, our operations are largely dependent on the services provided by governments and other third parties who render services to passengers and airlines, such as meteorology, air traffic control, security, electricity, and immigration and customs services. In addition, in some of our airports we are dependent on third-party providers of certain complementary services such as baggage handling, fuel services, catering and aircraft maintenance and repair. While we are responsible for adopting security measures at some of our airports, we do not control the management or operation of security, which is controlled by government agencies or third parties. We are not responsible for, and cannot control, any of these services. Any disruption in, or other adverse situation related to, such services, including work strikes or other similar events, could cause the cancellation of flights and negatively affect passenger traffic at our airports, which may ultimately result in decreased revenues and have an adverse effect on our business, financial condition, or results of operations.

The loss of one or more of our aeronautical customers or the interruption of their operations could result in a loss of a significant amount of our passenger traffic.

None of our agreements with our aeronautical customers obligate them to provide service at or to our airports. If any of our aeronautical customers were to reduce their use of our airports or cease to operate at them for any reason, including merger, bankruptcy, or due to regulatory restrictions or the impact of any disease outbreak, or impacts of the Russia and Ukraine war or the Israel and Hamas conflict, among other factors, the remaining airlines may not increase their flight frequency to replace the flights that our aeronautical customers could no longer operate. Our business and revenue, and our ability to recover receivables, could be adversely affected if we are unable to replace the business of our main aeronautical customers.

Our main aeronautical customers are Aerolíneas Argentinas Group and LATAM Group. For the year ended December 31, 2023, Aerolíneas Argentinas Group and LATAM Group accounted for 11.1% and 13.1% of our consolidated aeronautical revenue, respectively. For the year ended December 31, 2022, Aerolíneas Argentinas Group and LATAM Group accounted for 15.8% and 10.8% of our consolidated aeronautical revenue, respectively. For the year ended December 31, 2021, Aerolíneas Argentinas Group and LATAM Group accounted for 8.7% and 10.1% of our consolidated aeronautical revenue, respectively.

Consequently, we have a significant concentration of aeronautical customers, which may expose us to a material adverse effect if one or more of our large aeronautical customers were to significantly suspend or interrupt payments to us for any reason. Furthermore, a delay in payment or non-payment by a major aeronautical customer could materially and adversely affect the results of our operations.

An aircraft accident or other material factors beyond our control, such as disasters, climate - related catastrophes, among others, may affect the operation of our runways.

Our runways may require unscheduled repair, renovation or reconstruction due to natural disasters, climate - related catastrophes, aircraft accidents and other factors beyond our control. The closure of any runway for a significant period of time could have a material adverse effect on the number of passengers that use our airports, and therefore, a material adverse effect on our operations and financial results.

13

Ongoing and proposed construction, renovation or repair work at our airports could have a negative impact on our revenues.

At any time, we may be in the process of constructing, renovating and/or repairing a number of our airports. These works may sometimes affect the passenger experience, which may ultimately adversely affect our commercial revenue. The operations of our other airports may decrease or be adversely affected by future construction, renovations, or repairs, and this could have an adverse effect on our business, financial condition or results of operations.

We are exposed to certain risks in connection with the use of certain spaces by subconcessionaires at our airports.

We are exposed to risks related to the spaces subconcessioned to third parties, such as non-payment by subconcessionaires of certain fees and other lease arrangements or a weakening demand for the use of the spaces allocated to subconcessionaires. For example, many of our subconcessionaires’ locations are situated beyond the security checkpoints at airports, and they rely heavily on their customers spending a significant amount of time in the terminal and waiting areas of the airport terminals in which they have subconcessioned space. Changes in customers’ travel habits prior to departure, including an increase in the availability or popularity of airline business and first-class lounges, or an increase in the efficiency of ticketing, transportation safety procedures and air traffic control systems could reduce the amount of time that customers spend at such subconcessioned locations, which could materially reduce the revenue they are able to generate and which, in turn, could reduce the amount of fees and rent we can collect from our subconcessionaires. Any material reduction in the fees and lease payments that we are able to charge to our subconcessionaires could adversely affect our business, results of operations and financial condition.

Our insurance policies may not provide sufficient coverage against all liabilities.

We are required to maintain insurance under all our concession agreements, and we seek to ensure all risks for which insurance coverage is available on commercially reasonable terms. We can offer no assurance that our insurance policies will cover all our liabilities in the event of an accident, natural disaster, terrorist attack or other incident. The insurance market for airport liability coverage generally, and for airport construction in particular, is limited and a change in the coverage policy by the insurance companies involved could reduce our ability to obtain and maintain adequate or cost-effective coverage. For example, insurance alternatives in Armenia are limited, therefore, we could incur in higher costs in obtaining insurance policies as required under the concession.

Similarly, for some of our airports, we do not currently carry business interruption insurance or property insurance against terrorism and related risks. Consequently, any substantial interruption of our business or terrorist attacks could have a material adverse effect in our results of operations and our financial condition.

We are exposed to liability to third parties for injuries or damages.

We are obligated to protect the public and to reduce the risk of accidents at our airports. As with any company dealing with the security of individuals, we must implement measures for the protection of the public, such as hiring private security services, maintaining our airports’ infrastructure and fire safety in public spaces, and providing emergency medical services. These obligations could expose us to liability to third parties for personal injury or property damage and, to the extent not adequately covered by insurance, could adversely affect our financial condition and results of operations.

Most of our operations are in emerging markets.

Our existing concessions are mostly in countries with emerging economies and investing in developing economies generally involves risks. These risks include political, social, and economic events, any of which could impact our operations or the market value of our common shares and have a material adverse effect on our business, financial condition, and results of operations. These risks and instability are caused by many different factors, including the following:

| ● | adverse external economic factors; |

| ● | inconsistent fiscal and monetary policies (including currency devaluation); |

| ● | dependence on external financing; |

| ● | changes in governmental economic and tax policies and regulations; |

| ● | high levels of inflation; |

14

| ● | fluctuations in currency values; |

| ● | high interest rates; |

| ● | wage increases and price controls; |

| ● | limitation on imports; |

| ● | exchange rates and capital controls; |

| ● | political and social tensions; |

| ● | fluctuations in central bank reserves; and |

| ● | trade barriers. |

Emerging markets have historically experienced uneven periods of economic growth, as well as recession, periods of high inflation and economic instability. Adverse economic conditions in any of these countries could have a material adverse effect on our business, financial condition, and results of operations.

Some of the countries in which we operate have experienced, or are currently experiencing, high rates of inflation. In an effort to control inflation, governments of these countries often maintain a tight monetary policy with high interest rates, thereby restricting the availability of credit and retarding economic growth. Inflation, measures to combat inflation and public speculation about possible additional actions have also contributed significantly to economic uncertainty in many of these countries and to heightened volatility in their securities markets. Periods of higher inflation may also slow the growth rate of local economies. Inflation is also likely to increase some of our costs and expenses, which we may not be able to fully transfer to our clients, which could adversely affect our operating margins and operating income in some of the emerging markets in which we operate.

Depreciation or fluctuation of the currencies of the countries where we operate could adversely affect our results of operations and financial condition.

Many of the countries where we operate have experienced volatility in the exchange rate of their currency against the U.S. dollar. Because we present our financial statements in U.S. dollars, this volatility may reduce the revenues we report or increase the expenses we report in any given period. These effects may in turn have an adverse effect on the market of our common shares. In addition, because we have a substantial amount of dollar-denominated indebtedness, exchange rate volatility may result in increased debt service costs. Finally, in some instances we receive revenues in a currency different from that in which we pay expenses, in which case currency volatility can affect the profitability of our operations.

We are subject to various environmental laws, regulations and authorizations that affect our operations and may expose us to significant costs, liabilities, obligations, or restrictions.

We, our subconcessionaires and our aeronautical customers are subject to various environmental laws, regulations and authorizations governing, among other things, the generation, use, transportation, management and disposal of hazardous materials, the emission and discharge of hazardous materials into the ground, air or water, and human health and safety. Failure to comply with these environmental requirements, including the terms of our concession agreements, could result in our being subject to litigation, fines, or other sanctions. We could also incur significant capital or other compliance costs relating to such requirements. We could also be held responsible for contamination, human exposure to hazardous materials or other environmental damage at our airports or otherwise related to our operations. Environmental claims have been asserted against us, and additional claims may be asserted against us in the future. See “Item 8. Financial Information—Consolidated Statements and Other Financial Information—Legal Proceedings—Argentine Proceedings—Environmental Proceedings.” We are unable to determine our potential liability under these pending or possible future claims. We only have environmental insurance coverage for environmental damages at a limited number of our airports.

These environmental requirements, and the enforcement and interpretation thereof, change frequently and have tended to become more stringent over time. Future environmental laws, regulations and authorizations may require us to incur additional costs in order to bring our airports into, and maintain, compliance. Our costs, liabilities, obligations, and restrictions relating to environmental matters could have a material adverse effect on our business, results of operations and financial condition.

15

We are subject to review by taxing authorities, and an incorrect interpretation by us of tax laws and regulations may have a material adverse effect on us.

Taxes payable by companies in many of the countries in which we operate are substantial and include value-added tax, excise duties, profit taxes, payroll related taxes, property taxes, and other taxes. In certain countries in which we operate, such as Brazil or Argentina, the tax system is highly complex and the interpretation of the tax laws and regulations is commonly controversial, leading to disputes which are sometimes subject to prolonged evaluation periods until a final resolution is reached. In addition, there may be changes that result from enactment of additional tax reforms or changes to the manner in which current tax laws are applied that cannot be quantified and there can be no assurance that any such reforms or changes would not have an adverse effect upon our revenues. For instance, most jurisdictions in which we operate have recently adopted new transfer pricing measures. If tax authorities impose significant additional tax liabilities as a result of transfer pricing adjustments, it could have an adverse effect on us.

Over the past few years, tax administrations around the world have put in place a number of initiatives to facilitate communication and information exchange among each other, have become more rigid in exercising any discretion they may have, and have increased their scrutiny of company tax filings. In this regard, the G20 / OECD Inclusive Framework has been working on addressing a number of tax challenges such as transparency, exchange of information, coherence, and substance, and to this end has proposed numerous tax law changes under its Base Erosion and Profit Shifting (BEPS) Action Plans. Particularly, in December 2021, the OECD released the Pillar Two model rules (the Global Anti-Base Erosion Proposal, or ‘GloBE’ rules) for a new global minimum tax framework introducing a minimum tax regime for multinationals. At the EU level, the European Council formally adopted the directive implementing Pillar Two and Member States were obliged to transpose the directive into national laws before 31 December 2023 (the five Member States that have not done it within the deadline are now expected to do so soon, as penalties from the CJEU can be imposed). The EU has also adopted a number of Directives (namely, the Anti-Tax Avoidance Directives, or ATAD), which seek to prevent tax avoidance by companies and to ensure that companies pay appropriate taxes in the markets where profits are effectively made, and business is effectively performed.

In establishing a provision for income tax expense and filing returns, we must make judgments and interpretations about the application of these inherently complex tax laws that may be interpreted differently by the competent tax authorities and courts. For example, applying the GloBE rules and determining the impact are likely to be very complex and pose a number of practical challenges. While disclosing quantitatively the full effect of these laws is realistically not possible at this stage, we believe that they could have an adverse effect on us, as the new rules could result in new taxes and/or additional costs for the Company when complying with the new reporting obligations.

In addition, in some jurisdictions where we operate, the interpretations of tax laws by the taxing authorities are sometimes unpredictable and frequently involve litigation, introducing further uncertainty and risk to our tax liability. It is also possible that tax authorities in the countries in which we operate will introduce additional revenue raising measures. If the judgment, estimates and assumptions we use in preparing our tax returns are subsequently determined to be incorrect, there could be a material adverse effect on us, which may ultimately affect our revenues. See “Item 8. Financial Information—Consolidated Statements and Other Financial Information—Legal Proceedings” and “Item 8. Financial Information—Consolidated Statements and Other Financial Information—Legal Proceedings—Argentine Proceedings— Tax Proceedings Related to Technical Assistance Agreements.”

Any of these events occurring, alone or jointly, could lead to an increase of our tax burden and have a material adverse effect on our business, financial condition, results of operations and prospects.

Our acquisition strategy could involve additional risks to us, many of which could have an adverse effect on our business, financial condition, and results of operations.

We continue to examine opportunities to acquire or invest in existing or new concessions that complement or expand our business. These opportunities may involve government-owned entities as well as private sector companies. Any future acquisitions may result in a dilutive issuance of equity securities, incurrence of additional debt, reduction of existing cash balances, amortization of expenses related to goodwill and other intangible assets or other charges to operations. Additional leverage could require us to dedicate cash flow to fund debt service requirements, thus decreasing the funds available to us to finance working capital and business operations generally. All of the foregoing factors could have an adverse effect on our business, financial condition, results of operations or prospects.

16

Future concession or acquisitions could involve numerous risks, including that we may recognize lower relative operating margins associated with such acquisitions, and we may recognize impairment charges with respect to future acquired assets due to the performance of such assets. Our results of operations may also be affected by the timing of acquisitions, the timing and amount of integration costs related to such acquisitions and the degree to and the rate at which the economic benefits of integration are realized.

Future growth may also place additional demands on our personnel and other resources, including an increased level of responsibility for management. Our ability to manage growth effectively will require us to continue to improve our operational, management and financial systems and controls and to successfully train, motivate and manage our employees. If our management is unable to manage growth effectively, our business could be adversely affected.

Our inability to raise additional financing may limit our operations.

We may have limited ability to incur additional financing for some of our concession agreements, which may entail important consequences for investors, among them (i) limiting our capacity to satisfy our future investment obligations with respect to the airports we operate pursuant to the terms and conditions of our concession agreements, or other capital expenditures required for the operation of such airports; and (ii) limiting our flexibility to take advantage of opportunities for new business within the markets we operate or potential new markets. Any of these situations may ultimately affect our operations and financial results.

Many of our most significant subsidiaries have substantial non - controlling interests owned by third-parties, and any substantial conflict with minority shareholders may have an adverse effect on our business.

We indirectly own 82.7%, and 51.0% of our principal Argentina and Brazil operating subsidiaries, respectively, which are namely Aeropuertos Argentina 2000 S.A. (“AA2000”) and ICAB. Likewise, we indirectly own 75.0% of Corporación América Italia S.p.A. (“CA Italy”) who owns 62.3% of our principal Italian operating subsidiary, Toscana Aeroporti S.p.A. (“TA”). Because we control these entities, we record all their revenues and expenses and then allocate net income between controlling and non-controlling interest. The other shareholders of these entities, including, in the case of Italy, public shareholders, may have interests different from ours, and any substantial conflict with minority shareholders may have an adverse effect on our business, financial condition or results of operations.

We may have conflicts of interest with ACI Airports S.à r.l., our majority shareholder, and we may not be able to resolve such conflicts on terms favorable to us.