FALSEFY20230001401521December 3189,760,000200,951237,73516,1183,072—0.00011,000,000.00001,000,000.0000——————100,000,000100,000,00046,989,08943,492,25646,777,00643,280,173212,083212,08351,00032,0000097333P7Y—82P3Y4MP0Y4MP4Y4MP1Y4Mhttp://fasb.org/us-gaap/2023#OtherAssetshttp://fasb.org/us-gaap/2023#OtherAssetshttp://fasb.org/us-gaap/2023#PropertyPlantAndEquipmentNethttp://fasb.org/us-gaap/2023#OtherLiabilitiesP1Y5MP0Y0MP2Y1MP0Y9MRELATED PARTY TRANSACTIONSP7Y8MP7Y10MP7Y6MP7Y6M27,48927,43226,33623,8655,6455,13470,19761,84953,61946,31017,66516,113370,22175,15512,29475,20510,57425,041247,312281,884293,05700014015212023-01-012023-12-3100014015212023-06-30iso4217:USD00014015212024-03-04xbrli:shares0001401521uihc:CommercialLinesReportingSegmentMember2023-01-012023-12-310001401521uihc:PersonalLinesReportingSegmentMember2023-01-012023-12-310001401521us-gaap:FixedMaturitiesMember2023-12-310001401521us-gaap:FixedMaturitiesMember2022-12-310001401521us-gaap:SegmentContinuingOperationsMember2023-12-310001401521us-gaap:SegmentContinuingOperationsMember2022-12-3100014015212023-12-3100014015212022-12-31iso4217:USDxbrli:shares00014015212022-01-012022-12-3100014015212021-01-012021-12-310001401521us-gaap:CommonStockMember2020-12-310001401521us-gaap:AdditionalPaidInCapitalMember2020-12-310001401521us-gaap:TreasuryStockCommonMember2020-12-310001401521us-gaap:ComprehensiveIncomeMember2020-12-310001401521us-gaap:RetainedEarningsMember2020-12-310001401521us-gaap:ParentMember2020-12-310001401521us-gaap:NoncontrollingInterestMember2020-12-3100014015212020-12-310001401521us-gaap:RetainedEarningsMember2021-01-012021-12-310001401521us-gaap:ParentMember2021-01-012021-12-310001401521us-gaap:NoncontrollingInterestMember2021-01-012021-12-310001401521us-gaap:ComprehensiveIncomeMember2021-01-012021-12-310001401521us-gaap:CommonStockMember2021-01-012021-12-310001401521us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001401521us-gaap:CommonStockMember2021-12-310001401521us-gaap:AdditionalPaidInCapitalMember2021-12-310001401521us-gaap:TreasuryStockCommonMember2021-12-310001401521us-gaap:ComprehensiveIncomeMember2021-12-310001401521us-gaap:RetainedEarningsMember2021-12-310001401521us-gaap:ParentMember2021-12-310001401521us-gaap:NoncontrollingInterestMember2021-12-3100014015212021-12-310001401521us-gaap:RetainedEarningsMember2022-01-012022-12-310001401521us-gaap:ParentMember2022-01-012022-12-310001401521us-gaap:NoncontrollingInterestMember2022-01-012022-12-310001401521us-gaap:ComprehensiveIncomeMember2022-01-012022-12-310001401521us-gaap:CommonStockMember2022-01-012022-12-310001401521us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001401521us-gaap:CommonStockMember2022-12-310001401521us-gaap:AdditionalPaidInCapitalMember2022-12-310001401521us-gaap:TreasuryStockCommonMember2022-12-310001401521us-gaap:ComprehensiveIncomeMember2022-12-310001401521us-gaap:RetainedEarningsMember2022-12-310001401521us-gaap:ParentMember2022-12-310001401521us-gaap:RetainedEarningsMember2023-01-012023-12-310001401521us-gaap:ParentMember2023-01-012023-12-310001401521us-gaap:ComprehensiveIncomeMember2023-01-012023-12-310001401521us-gaap:CommonStockMember2023-01-012023-12-310001401521us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001401521us-gaap:CommonStockMember2023-12-310001401521us-gaap:AdditionalPaidInCapitalMember2023-12-310001401521us-gaap:TreasuryStockCommonMember2023-12-310001401521us-gaap:ComprehensiveIncomeMember2023-12-310001401521us-gaap:RetainedEarningsMember2023-12-310001401521us-gaap:ParentMember2023-12-310001401521us-gaap:SegmentDiscontinuedOperationsMember2022-01-012022-12-310001401521us-gaap:SegmentDiscontinuedOperationsMember2023-01-012023-12-310001401521us-gaap:SegmentDiscontinuedOperationsMember2021-01-012021-12-310001401521uihc:UPCInsuranceMemberus-gaap:SegmentDiscontinuedOperationsMember2023-02-270001401521uihc:UPCInsuranceMemberus-gaap:SegmentDiscontinuedOperationsMember2022-12-310001401521uihc:ServiceEntitiesMemberus-gaap:SegmentDiscontinuedOperationsMember2023-12-310001401521uihc:ServiceEntitiesMemberus-gaap:SegmentDiscontinuedOperationsMember2022-12-310001401521uihc:AdjustmentsAndReconcilingItemsMember2023-01-012023-12-310001401521us-gaap:SegmentContinuingOperationsMember2023-01-012023-12-31xbrli:pure0001401521uihc:CommercialLinesReportingSegmentMember2022-01-012022-12-310001401521uihc:PersonalLinesReportingSegmentMember2022-01-012022-12-310001401521uihc:AdjustmentsAndReconcilingItemsMember2022-01-012022-12-310001401521us-gaap:SegmentContinuingOperationsMember2022-01-012022-12-310001401521uihc:CommercialLinesReportingSegmentMember2021-01-012021-12-310001401521uihc:PersonalLinesReportingSegmentMember2021-01-012021-12-310001401521uihc:AdjustmentsAndReconcilingItemsMember2021-01-012021-12-310001401521us-gaap:SegmentContinuingOperationsMember2021-01-012021-12-310001401521uihc:PersonalLinesReportingSegmentMemberus-gaap:SegmentContinuingOperationsMember2022-01-012022-12-310001401521uihc:CommercialLinesReportingSegmentMember2023-12-310001401521uihc:PersonalLinesReportingSegmentMember2023-12-310001401521uihc:AdjustmentsAndReconcilingItemsMember2023-12-310001401521us-gaap:IntersegmentEliminationMemberuihc:CommercialLinesReportingSegmentMember2023-12-310001401521uihc:PersonalLinesReportingSegmentMemberus-gaap:IntersegmentEliminationMember2023-12-310001401521us-gaap:IntersegmentEliminationMemberuihc:AdjustmentsAndReconcilingItemsMember2023-12-310001401521uihc:CommercialLinesReportingSegmentMember2022-12-310001401521uihc:PersonalLinesReportingSegmentMember2022-12-310001401521uihc:AdjustmentsAndReconcilingItemsMember2022-12-310001401521us-gaap:IntersegmentEliminationMemberuihc:CommercialLinesReportingSegmentMember2022-12-310001401521uihc:PersonalLinesReportingSegmentMemberus-gaap:IntersegmentEliminationMember2022-12-310001401521us-gaap:IntersegmentEliminationMemberuihc:AdjustmentsAndReconcilingItemsMember2022-12-310001401521us-gaap:USTreasuryAndGovernmentMember2023-12-310001401521us-gaap:USStatesAndPoliticalSubdivisionsMember2023-12-310001401521us-gaap:PublicUtilityBondsMember2023-12-310001401521us-gaap:AllOtherCorporateBondsMember2023-12-310001401521us-gaap:MortgageBackedSecuritiesMember2023-12-310001401521us-gaap:AssetBackedSecuritiesMember2023-12-310001401521us-gaap:USTreasuryAndGovernmentMember2022-12-310001401521us-gaap:ForeignGovernmentDebtSecuritiesMember2022-12-310001401521us-gaap:USStatesAndPoliticalSubdivisionsMember2022-12-310001401521us-gaap:PublicUtilityBondsMember2022-12-310001401521us-gaap:AllOtherCorporateBondsMember2022-12-310001401521us-gaap:MortgageBackedSecuritiesMember2022-12-310001401521us-gaap:AssetBackedSecuritiesMember2022-12-310001401521us-gaap:MutualFundMember2023-12-310001401521us-gaap:MutualFundMember2022-12-310001401521us-gaap:FixedMaturitiesMember2023-01-012023-12-310001401521us-gaap:FixedMaturitiesMember2022-01-012022-12-310001401521us-gaap:FixedMaturitiesMember2021-01-012021-12-310001401521us-gaap:EquitySecuritiesMember2023-01-012023-12-310001401521us-gaap:EquitySecuritiesMember2022-01-012022-12-310001401521us-gaap:EquitySecuritiesMember2021-01-012021-12-310001401521us-gaap:ShortTermInvestmentsMember2023-01-012023-12-310001401521us-gaap:ShortTermInvestmentsMember2022-01-012022-12-310001401521us-gaap:ShortTermInvestmentsMember2021-01-012021-12-310001401521srt:PartnershipInterestMember2023-01-012023-12-310001401521us-gaap:DebtSecuritiesMember2023-01-012023-12-310001401521us-gaap:DebtSecuritiesMember2022-01-012022-12-310001401521us-gaap:DebtSecuritiesMember2021-01-012021-12-310001401521us-gaap:EquitySecuritiesMember2023-01-012023-12-310001401521us-gaap:EquitySecuritiesMember2022-01-012022-12-310001401521us-gaap:EquitySecuritiesMember2021-01-012021-12-310001401521uihc:CashCashEquivalentsAndShortTermInvestmentsMember2023-01-012023-12-310001401521uihc:CashCashEquivalentsAndShortTermInvestmentsMember2022-01-012022-12-310001401521uihc:CashCashEquivalentsAndShortTermInvestmentsMember2021-01-012021-12-310001401521srt:PartnershipInterestMember2023-01-012023-12-310001401521srt:PartnershipInterestMember2022-01-012022-12-310001401521srt:PartnershipInterestMember2021-01-012021-12-31uihc:security0001401521us-gaap:CorporateDebtSecuritiesMember2023-12-310001401521us-gaap:CorporateDebtSecuritiesMember2022-12-310001401521us-gaap:FairValueInputsLevel1Memberus-gaap:USTreasuryAndGovernmentMember2023-12-310001401521us-gaap:USTreasuryAndGovernmentMemberus-gaap:FairValueInputsLevel2Member2023-12-310001401521us-gaap:USTreasuryAndGovernmentMemberus-gaap:FairValueInputsLevel3Member2023-12-310001401521us-gaap:FairValueInputsLevel1Memberus-gaap:USStatesAndPoliticalSubdivisionsMember2023-12-310001401521us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueInputsLevel2Member2023-12-310001401521us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001401521us-gaap:PublicUtilityBondsMemberus-gaap:FairValueInputsLevel1Member2023-12-310001401521us-gaap:PublicUtilityBondsMemberus-gaap:FairValueInputsLevel2Member2023-12-310001401521us-gaap:PublicUtilityBondsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001401521us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2023-12-310001401521us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2023-12-310001401521us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001401521us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueInputsLevel1Member2023-12-310001401521us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueInputsLevel2Member2023-12-310001401521us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001401521us-gaap:FairValueInputsLevel1Memberus-gaap:AssetBackedSecuritiesMember2023-12-310001401521us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel2Member2023-12-310001401521us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001401521us-gaap:FixedMaturitiesMemberus-gaap:FairValueInputsLevel1Member2023-12-310001401521us-gaap:FixedMaturitiesMemberus-gaap:FairValueInputsLevel2Member2023-12-310001401521us-gaap:FixedMaturitiesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001401521us-gaap:OtherLongTermInvestmentsMember2023-12-310001401521us-gaap:FairValueInputsLevel1Memberus-gaap:OtherLongTermInvestmentsMember2023-12-310001401521us-gaap:OtherLongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Member2023-12-310001401521us-gaap:OtherLongTermInvestmentsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001401521us-gaap:FairValueInputsLevel1Member2023-12-310001401521us-gaap:FairValueInputsLevel2Member2023-12-310001401521us-gaap:FairValueInputsLevel3Member2023-12-310001401521us-gaap:FairValueInputsLevel1Memberus-gaap:USTreasuryAndGovernmentMember2022-12-310001401521us-gaap:USTreasuryAndGovernmentMemberus-gaap:FairValueInputsLevel2Member2022-12-310001401521us-gaap:USTreasuryAndGovernmentMemberus-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:FairValueInputsLevel1Memberus-gaap:ForeignGovernmentDebtSecuritiesMember2022-12-310001401521us-gaap:FairValueInputsLevel2Memberus-gaap:ForeignGovernmentDebtSecuritiesMember2022-12-310001401521us-gaap:FairValueInputsLevel3Memberus-gaap:ForeignGovernmentDebtSecuritiesMember2022-12-310001401521us-gaap:FairValueInputsLevel1Memberus-gaap:USStatesAndPoliticalSubdivisionsMember2022-12-310001401521us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueInputsLevel2Member2022-12-310001401521us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:PublicUtilityBondsMemberus-gaap:FairValueInputsLevel1Member2022-12-310001401521us-gaap:PublicUtilityBondsMemberus-gaap:FairValueInputsLevel2Member2022-12-310001401521us-gaap:PublicUtilityBondsMemberus-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2022-12-310001401521us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2022-12-310001401521us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueInputsLevel1Member2022-12-310001401521us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueInputsLevel2Member2022-12-310001401521us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:FairValueInputsLevel1Memberus-gaap:AssetBackedSecuritiesMember2022-12-310001401521us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel2Member2022-12-310001401521us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:FixedMaturitiesMemberus-gaap:FairValueInputsLevel1Member2022-12-310001401521us-gaap:FixedMaturitiesMemberus-gaap:FairValueInputsLevel2Member2022-12-310001401521us-gaap:FixedMaturitiesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:MutualFundMemberus-gaap:FairValueInputsLevel1Member2022-12-310001401521us-gaap:MutualFundMemberus-gaap:FairValueInputsLevel2Member2022-12-310001401521us-gaap:MutualFundMemberus-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:EquitySecuritiesMember2022-12-310001401521us-gaap:FairValueInputsLevel1Memberus-gaap:EquitySecuritiesMember2022-12-310001401521us-gaap:FairValueInputsLevel2Memberus-gaap:EquitySecuritiesMember2022-12-310001401521us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:OtherLongTermInvestmentsMember2022-12-310001401521us-gaap:FairValueInputsLevel1Memberus-gaap:OtherLongTermInvestmentsMember2022-12-310001401521us-gaap:OtherLongTermInvestmentsMemberus-gaap:FairValueInputsLevel2Member2022-12-310001401521us-gaap:OtherLongTermInvestmentsMemberus-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:FairValueInputsLevel1Member2022-12-310001401521us-gaap:FairValueInputsLevel2Member2022-12-310001401521us-gaap:FairValueInputsLevel3Member2022-12-310001401521us-gaap:LimitedPartnerMember2023-12-310001401521us-gaap:ShortTermInvestmentsMember2023-12-310001401521uihc:UsGaap_OtherLongTermInvestmentsMemberMember2023-12-310001401521us-gaap:LimitedPartnerMember2022-12-310001401521us-gaap:ShortTermInvestmentsMember2022-12-310001401521uihc:UsGaap_OtherLongTermInvestmentsMemberMember2022-12-310001401521us-gaap:ComputerEquipmentMember2023-12-310001401521us-gaap:ComputerEquipmentMember2022-12-310001401521us-gaap:OfficeEquipmentMember2023-12-310001401521us-gaap:OfficeEquipmentMember2022-12-310001401521us-gaap:LeaseholdImprovementsMember2023-12-310001401521us-gaap:LeaseholdImprovementsMember2022-12-310001401521us-gaap:VehiclesMember2023-12-310001401521us-gaap:VehiclesMember2022-12-310001401521us-gaap:IntangibleAssetsArisingFromInsuranceContractsAcquiredInBusinessCombinationMember2023-12-310001401521us-gaap:CustomerRelationshipsMember2023-12-310001401521us-gaap:TradeNamesMember2023-12-310001401521us-gaap:IntangibleAssetsArisingFromInsuranceContractsAcquiredInBusinessCombinationMember2022-12-310001401521us-gaap:CustomerRelationshipsMember2022-12-310001401521us-gaap:TradeNamesMember2022-12-310001401521uihc:AmericanCoastalInsuranceCompanyMemberuihc:CatastropheExcessOfLossMember2023-01-012023-12-310001401521uihc:AmericanCoastalInsuranceCompanyMember2023-01-012023-12-310001401521uihc:UPCReMember2023-01-012023-12-310001401521uihc:AmericanCoastalInsuranceCompanyMemberuihc:AllOtherPerilsCatastropheExcessOfLossMember2023-01-012023-12-310001401521uihc:CatastropheExcessOfLossMemberuihc:InterboroInsuranceCompanyMember2023-01-012023-12-310001401521uihc:InterboroInsuranceCompanyMember2023-01-012023-12-310001401521XOL Commutation2023-01-012023-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2014-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2015-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2016-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2017-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2018-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2019-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2020-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2021-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2022-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2023-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2013Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2015-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2013Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2016-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2013Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2017-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2013Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2018-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2013Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2019-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2013Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2020-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2013Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2021-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2013Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2022-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2013Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2023-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2014Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2016-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2014Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2017-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2014Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2018-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2014Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2019-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2014Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2020-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2014Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2021-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2014Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2022-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2014Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2023-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2015Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2017-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2015Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2018-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2015Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2019-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2015Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2020-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2015Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2021-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2015Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2022-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2015Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2023-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2018-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2019-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2020-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2021-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2022-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2023-12-310001401521us-gaap:ShortDurationInsuranceContractsAccidentYear2017Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2019-12-310001401521us-gaap:ShortDurationInsuranceContractsAccidentYear2017Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2020-12-310001401521us-gaap:ShortDurationInsuranceContractsAccidentYear2017Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2021-12-310001401521us-gaap:ShortDurationInsuranceContractsAccidentYear2017Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2022-12-310001401521us-gaap:ShortDurationInsuranceContractsAccidentYear2017Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2023-12-310001401521us-gaap:ShortDurationInsuranceContractsAccidentYear2018Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2020-12-310001401521us-gaap:ShortDurationInsuranceContractsAccidentYear2018Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2021-12-310001401521us-gaap:ShortDurationInsuranceContractsAccidentYear2018Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2022-12-310001401521us-gaap:ShortDurationInsuranceContractsAccidentYear2018Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2023-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2021-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2022-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2023-12-310001401521us-gaap:ShortDurationInsuranceContractAccidentYear2020Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2022-12-310001401521us-gaap:ShortDurationInsuranceContractAccidentYear2020Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2023-12-310001401521us-gaap:ShortDurationInsuranceContractAccidentYear2021Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2023-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2023-12-310001401521us-gaap:ShortdurationInsuranceContractsAccidentYear2011Memberus-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2014-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2015-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2016-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2017-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2018-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2019-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2020-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2021-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2022-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2012Member2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2013Member2015-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2013Member2016-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2013Member2017-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2013Member2018-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2013Member2019-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2013Member2020-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2013Member2021-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2013Member2022-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2013Member2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2014Member2016-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2014Member2017-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2014Member2018-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2014Member2019-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2014Member2020-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2014Member2021-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2014Member2022-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2014Member2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2015Member2017-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2015Member2018-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2015Member2019-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2015Member2020-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2015Member2021-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2015Member2022-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2015Member2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2018-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2019-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2020-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2021-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2022-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2016Member2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2019-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2020-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2021-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2022-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2017Member2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2020-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2021-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2022-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractsAccidentYear2018Member2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2021-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2022-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2019Member2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2022-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2023-12-310001401521us-gaap:ShortDurationInsuranceContractAccidentYear2021Memberus-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMember2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMember2023-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMemberus-gaap:ShortdurationInsuranceContractsAccidentYear2011Member2023-12-310001401521us-gaap:PropertyAndCasualtyPersonalInsuranceProductLineMember2022-12-310001401521us-gaap:PropertyAndCasualtyCommercialInsuranceProductLineMember2022-12-310001401521uihc:A150MSeniorNotesMember2023-01-012023-12-310001401521uihc:A150MSeniorNotesMember2023-12-31utr:Rate0001401521uihc:A150MSeniorNotesMember2022-12-310001401521us-gaap:NotesPayableOtherPayablesMember2023-01-012023-12-310001401521us-gaap:NotesPayableOtherPayablesMember2023-12-310001401521us-gaap:NotesPayableOtherPayablesMember2022-12-310001401521uihc:BBTTermNotePayableMember2023-01-012023-12-310001401521uihc:BBTTermNotePayableMember2023-12-310001401521uihc:BBTTermNotePayableMember2022-12-310001401521us-gaap:NotesPayableOtherPayablesMember2006-09-220001401521uihc:BBTTermNotePayableMember2016-05-2600014015212020-01-010001401521us-gaap:SegmentDiscontinuedOperationsMember2022-12-310001401521uihc:AmericanCoastalInsuranceCompanyMember2023-12-310001401521uihc:AmericanCoastalInsuranceCompanyMember2022-12-310001401521uihc:InterboroInsuranceMember2023-12-310001401521uihc:InterboroInsuranceMember2022-12-310001401521uihc:AmericanCoastalInsuranceCompanyMember2023-12-310001401521uihc:InterboroInsuranceCompanyMember2023-12-310001401521uihc:AmericanCoastalInsuranceCompanyMember2022-01-012022-12-310001401521uihc:AmericanCoastalInsuranceCompanyMember2021-01-012021-12-310001401521uihc:InterboroInsuranceMember2023-01-012023-12-310001401521uihc:InterboroInsuranceMember2022-01-012022-12-310001401521uihc:InterboroInsuranceMember2021-01-012021-12-310001401521uihc:ConsolidatedEntityExcludingNoncontrollingInterestsMember2021-01-012021-12-310001401521uihc:ConsolidatedEntityExcludingNoncontrollingInterestsMember2022-01-012022-12-310001401521uihc:ConsolidatedEntityExcludingNoncontrollingInterestsMember2023-01-012023-12-3100014015212023-01-012023-03-3100014015212022-01-012022-03-3100014015212021-01-012021-03-3100014015212023-04-012023-06-3000014015212022-04-012022-06-3000014015212021-04-012021-06-3000014015212023-07-012023-09-3000014015212022-07-012022-09-3000014015212021-07-012021-09-3000014015212023-10-012023-12-3100014015212022-10-012022-12-3100014015212021-10-012021-12-310001401521uihc:EmployeeMember2023-01-012023-12-310001401521uihc:EmployeeMember2022-01-012022-12-310001401521uihc:EmployeeMember2021-01-012021-12-310001401521srt:DirectorMember2023-01-012023-12-310001401521srt:DirectorMember2022-01-012022-12-310001401521srt:DirectorMember2021-01-012021-12-310001401521uihc:EmployeeMember2023-12-310001401521srt:DirectorMember2023-12-310001401521us-gaap:RestrictedStockMember2023-01-012023-12-310001401521us-gaap:RestrictedStockMember2022-01-012022-12-310001401521us-gaap:RestrictedStockMember2021-01-012021-12-310001401521us-gaap:RestrictedStockMember2020-12-310001401521us-gaap:RestrictedStockMember2021-12-310001401521us-gaap:RestrictedStockMember2022-12-310001401521us-gaap:RestrictedStockMember2023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________________

FORM 10-K

___________________________________

☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period _____ to _____

Commission File Number 001-35761

American Coastal Insurance Corporation

(Exact Name of Registrant as Specified in Its Charter)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Delaware |

|

75-3241967 |

|

|

(State or Other Jurisdiction of

Incorporation or Organization) |

|

(IRS Employer Identification Number) |

|

|

|

|

|

|

|

|

800 2nd Avenue S. |

|

33701 |

|

|

St. Petersburg, |

Florida |

|

(Zip Code)

|

|

|

(Address of Principal Executive Offices)

|

|

|

|

727-633-0851

(Telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

|

|

|

|

| Title of Each Class |

Trading Symbol(s) |

Name of Each Exchange on Which Registered |

| Common Stock, $0.0001 par value per share |

ACIC |

Nasdaq Stock Market LLC |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No R

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No R

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No £

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes R No £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Large accelerated filer |

£ |

|

Accelerated filer |

þ |

| Non-accelerated filer |

£ |

|

Smaller reporting company |

☑ |

|

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. £

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No R

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). £

The aggregate market value of shares of the registrant’s common stock held by non–affiliates of the registrant was approximately $89,760,000 as of June 30, 2023, calculated using the closing sales price reported for such date on the Nasdaq Stock Market. For purposes of this disclosure, shares of common stock held by persons who hold more than 10% of the outstanding shares of common stock and shares held by executive officers and directors of the registrant have been excluded because such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of March 4, 2024, 47,799,465 shares of the registrant’s common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Form 10-K incorporates by reference certain information from the Proxy Statement for the 2024 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission within 120 days after the end of our fiscal year ended December 31, 2023.

AMERICAN COASTAL INSURANCE CORPORATION

|

|

|

|

|

|

|

|

|

| Forward-Looking Statements |

|

|

|

|

|

|

|

Item 1A. Risk Factors |

|

|

Item 1B. Unresolved Staff Comments |

|

|

Item 1C. Cybersecurity |

|

|

Item 2. Properties |

|

|

Item 3. Legal Proceedings |

|

|

Item 4. Mine Safety Disclosures |

|

| Part II. |

|

|

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

|

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

|

Item 7A. Quantitative and Qualitative Disclosures about Market Risk |

|

|

Item 8. Financial Statements and Supplementary Data |

|

|

Auditor’s Report (PCAOB ID 34) |

|

|

Consolidated Balance Sheets |

|

|

Consolidated Statements of Comprehensive Income (Loss) |

|

|

Consolidated Statements of Stockholders’ Equity (Deficit) |

|

|

Consolidated Statements of Cash Flows |

|

|

Notes to Consolidated Financial Statements |

|

|

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

|

Item 9A. Controls and Procedures |

|

|

Item 9B. Other Information |

|

|

Item 9C. Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

|

| Part III. |

|

|

Item 10. Directors, Executive Officers and Corporate Governance |

|

|

Item 11. Executive Compensation |

|

|

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

|

Item 13. Certain Relationships and Related Transactions, and Director Independence |

|

|

Item 14. Principal Accountant Fees and Services |

|

| Part IV. |

|

|

Item 15. Exhibits and Financial Statement Schedules |

|

|

Exhibit Index |

|

|

Item 16. Form 10-K Summary |

|

| Signatures |

|

Throughout this Annual Report on Form 10-K (Form 10-K), we present amounts in all tables in thousands, except for share amounts, per share amounts, policy and claim counts or where more specific language or context indicates a different presentation. In the narrative sections of this Form 10-K, we show full values rounded to the nearest thousand.

AMERICAN COASTAL INSURANCE CORPORATION

FORWARD-LOOKING STATEMENTS

Statements in this Form 10-K or in documents incorporated by reference contain or may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements include statements about anticipated growth in revenues, gross written premium, earnings per share, estimated unpaid losses on insurance policies, investment returns, and diversification and expectations about our liquidity, our ability to meet our investment objectives and our ability to manage and mitigate market risk with respect to our investments. Without limiting the generality of the foregoing, words such as “may,” “will,” “expect,” “endeavor,” “project,” “believe,” “plan,” “anticipate,” “intend,” “could,” “would,” “estimate,” or “continue” or the negative variations thereof or comparable terminology are intended to identify forward-looking statements. These statements are based on current expectations, estimates and projections about the industry and market in which we operate, and management’s beliefs and assumptions. Forward-looking statements are not guarantees of future performance and involve certain known and unknown risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements. The risks and uncertainties include, without limitation:

•our exposure to catastrophic events and severe weather conditions;

•the regulatory, economic and weather conditions present in Florida and New York, the states in which we are most concentrated;

•our ability to cultivate and maintain agent relationships, particularly our relationship with AmRisc, LLC (AmRisc);

•the possibility that actual claims incurred may exceed our loss reserves for claims;

•assessments charged by various governmental agencies;

•our ability to implement and maintain adequate internal controls over financial reporting, including our ability to remediate any existing material weakness in our internal controls over financial reporting and the timing of any such remediation, as well as to reestablish effective internal controls over financial reporting and disclosure controls and procedures;

•our ability to maintain information technology and data security systems, and to outsource relationships;

•our reliance on key vendor relationships, and the ability of our vendors to protect the personally identifiable information of our customers, claimants or employees;

•our ability to attract and retain the services of senior management;

•risks and uncertainties relating to our mergers, dispositions and other strategic transactions;

•risks associated with investments in which we share ownership or management with third parties;

•our ability to generate sufficient cash to service all of our indebtedness and comply with covenants and other requirements related to our indebtedness;

•our ability to maintain our market share;

•changes in the regulatory environment present in the states in which we operate;

•the impact of new federal or state regulations that affect the insurance industry;

•the cost, viability and availability of reinsurance;

•our ability to collect from our reinsurers on our reinsurance claims;

•dependence on investment income and the composition of our investment portfolio and related market risks;

•the possibility of the pricing and terms for our products to decline due to the historically cyclical nature of the property and casualty insurance and reinsurance industry;

•the outcome of litigation pending against us, including the terms of any settlements;

•downgrades in our financial strength or stability ratings;

•the impact of future transactions of substantial amounts of our common stock by us or our significant stockholders on our stock price;

•our ability to meet the standards for continued listing on Nasdaq;

•our ability to pay dividends in the future, which may be constrained by our holding company structure;

•the ability of our subsidiaries to pay dividends in the future, which may affect our liquidity and our ability to meet our

obligations;

•the ability of R. Daniel Peed and his affiliates to exert significant control over us due to substantial ownership of our common stock, subject to certain restrictive covenants that may restrict our ability to pursue certain opportunities;

•the impact of transactions by R. Daniel Peed and his affiliates on the price of our common stock;

•provisions in our charter documents that may make it harder for others to obtain control of us; and

•other risks and uncertainties described in this report, including under “Risk Factors” in Part I, Item 1A.

We caution you to not place reliance on these forward-looking statements, which are valid only as of the date they were made. Except as may be required by applicable law, we undertake no obligation to update or revise any forward-looking statements to reflect new information, the occurrence of unanticipated events or otherwise.

AMERICAN COASTAL INSURANCE CORPORATION

PART I

Item 1. Business

INTRODUCTION

Company Overview

American Coastal Insurance Corporation (referred to in this Form 10-K as we, our, us, the Company or ACIC) is a holding company primarily engaged in the commercial and personal property and casualty insurance business with investments in the United States. On July 10, 2023, we changed our corporate name from United Insurance Holdings Corp. to American Coastal Insurance Corporation. We conduct our business principally through our two wholly-owned insurance subsidiaries: American Coastal Insurance Company (AmCoastal); and Interboro Insurance Company (IIC). Collectively, we refer to the holding company and all our subsidiaries, including non-insurance subsidiaries, as “American Coastal Insurance Corporation,” which is the preferred brand identification for our Company.

Our Company’s primary source of revenue is generated from writing insurance in Florida and New York. Our target market in such areas consists of states where the perceived threat of natural catastrophe has caused large national insurance carriers to reduce their concentration of policies. We believe an opportunity exists for ACIC to write profitable business in such areas. During 2022, we also wrote commercial residential insurance in South Carolina and Texas, however, effective May 1, 2022, we no longer write in these states. In addition, during 2022 we wrote personal residential business in six other states, however on February 27, 2023, our former insurance subsidiary, United Property & Casualty Insurance Company (UPC) was placed into receivership with the Florida Department of Financial Services (the "DFS"), which divested our ownership of UPC. The events leading to receivership and results of this subsidiary for periods prior to receivership, now included within discontinued operations, can be seen in

Note 3 of the Notes to Consolidated Financial Statements below.

We have historically grown our business through strong organic growth, complemented by strategic acquisitions and partnerships, including our acquisitions of AmCo Holding Company, LLC (AmCo) and its subsidiaries, including AmCoastal, in April 2017, IIC in April 2016, and Family Security Holdings, LLC (FSH), including its subsidiary Family Security Insurance Company, Inc. (FSIC), in February 2015, and our strategic partnership with a subsidiary of Tokio Marine Kiln Group Limited (Tokio Marine), which formed Journey Insurance Company (JIC) in August 2018. Effective June 1, 2022, we merged JIC into AmCoastal, with AmCoastal being the surviving entity. Effective May 31, 2022, we merged FSIC into our former subsidiary, UPC, with UPC being the surviving entity.

As of October 6, 2023 we were seeking a buyer for IIC to complete our exit from the personal lines business and expect the sale price to be the book value of the entity. The Company entered into a non-binding term sheet on October 6, 2023 for the sale of IIC whereby the buyer will acquire 100% of the issued and outstanding common stock of IIC in exchange for a cash purchase price equal to the GAAP book value of IIC at the time of closing, subject to negotiating and entering into definitive documents containing customary terms and conditions and obtaining regulatory approval(s).

Financial strength or stability ratings are important to insurance companies in establishing their competitive position and may impact an insurance company’s ability to write policies. We are rated by Demotech and Kroll Bond Rating Agency (Kroll). Demotech maintains a letter-scale financial stability rating system ranging from A’’ (A double prime) to L (licensed by insurance regulatory authorities). Kroll maintains a letter-scale financial strength rating system for insurance companies ranging from AAA (extremely strong operations and no risk) to R (operating under regulatory supervision). The financial strength or stability ratings of our insurance company subsidiaries as of December 31, 2023 are listed below. With these ratings, we expect our property insurance policies will be acceptable to the secondary mortgage marketplace and mortgage lenders.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Subsidiary |

|

Demotech Rating |

|

Kroll Rating |

| AmCoastal |

|

A |

|

A- |

| IIC |

|

A |

|

A- |

| ACIC |

|

|

|

BB+ |

AMERICAN COASTAL INSURANCE CORPORATION

Our Strategy

Our vision is to be a top-quartile underwriter of catastrophe exposed property insurance. Our plan is to focus primarily on low-rise commercial property insurance in Florida, through our exclusive managing general agency agreement and long-term partnership with AmRisc, LLC. The Company’s continuous portfolio optimization process strives to balance our risk appetite and underwriting profit opportunities with our available capital and reinsurance capacity to achieve consistent and sustainable underwriting profitability for the Company and its reinsurers over time.

We desire to have the right combination of price, underwriting rules, deductibles and coverages to earn a return on capital that exceeds our cost of capital throughout the insurance market cycle. The Company also seeks to have risks maintain an appropriate insurance to value through annual re-underwriting and inspection of each property to ensure it meets or exceeds our underwriting guidelines with verified data quality and integrity regarding the key risk characteristics of our covered properties.

With UPC in receivership, the Company’s personal lines business is limited to IIC in New York and activities supporting the run-off and liquidation of UPC. As a result of our desire to focus on commercial lines, we expect to divest IIC, which would result in ACIC being our only operating insurance subsidiary at some point in the future.

Our commercial lines portfolio is concentrated in Florida and personal lines portfolio is concentrated in New York with an ongoing threat of natural catastrophes which exposes the Company to risk and volatility.

PRODUCTS AND DISTRIBUTION

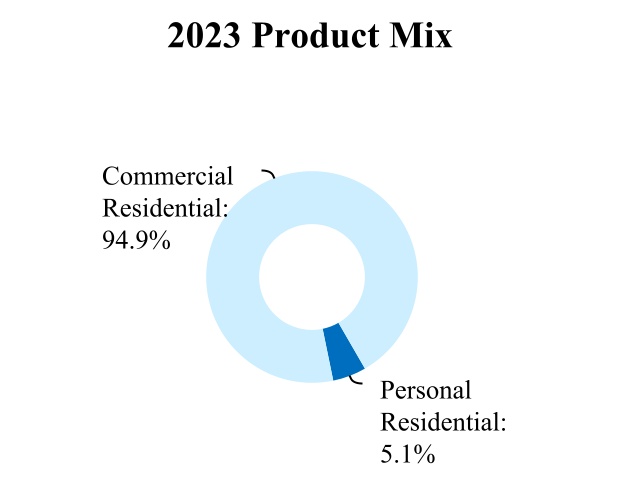

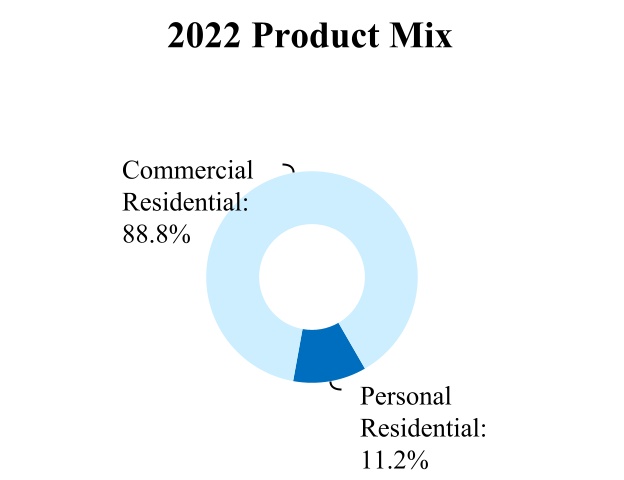

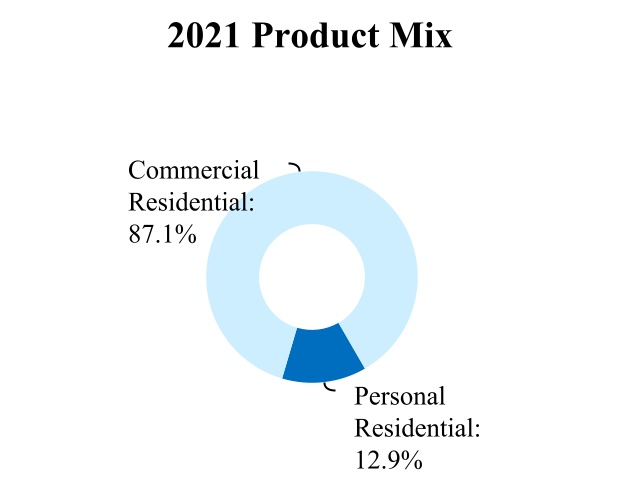

In July of 2020, we implemented a strategy to de-risk the Company by reducing premiums and exposure from our personal lines segment that was offset with growth in our commercial lines segment. The graphs below show our product mix distribution based on gross written premium, excluding our premiums attributable to discontinued operations.

AMERICAN COASTAL INSURANCE CORPORATION

Personal Residential Products

Policies we issue under our homeowners’ program provide structure, content and liability coverage for standard single-family homeowners, renters and condominium unit owners through our subsidiary IIC. Personal residential products are offered New York. We include coverage to policyholders for loss or damage to dwellings, detached structures or equipment caused by covered causes of loss such as fire, wind, hail, water, theft and vandalism.

In 2023, personal residential property policies (by which we mean both standard homeowners’, dwelling fire, renters and condo owners’ policies) produced written premium of $34,334,000 and accounted for 5.1% of our total gross written premium. All of the personal residential gross written premium was written in New York.

Loss and loss adjustment expenses related to our personal residential products tend to be higher during periods of severe or inclement weather, which varies from state to state.

We are actively working to divest of IIC and its exposure to complete our exit from personal lines.

Commercial Residential Products

We primarily provide commercial multi-peril property insurance for residential condominium associations and apartments in Florida. In 2020, we began writing commercial policies in Texas and South Carolina. Effective May 31, 2022, we no longer write commercial policies in Texas and South Carolina. We include coverage to policyholders for loss or damage to buildings, inventory or equipment caused by covered causes of loss such as fire, wind, hail, water, theft and vandalism.

In 2023, commercial policies produced written premium of $635,709,000 and accounted for 94.9% of our total gross written premium.

Not-At-Risk Offerings

On our equipment breakdown, identity theft, and cyber security policies we earn a commission while retaining no risk of loss, since all such risk is ceded to other private companies (other risks). Previously, we offered flood policies that were ceded to the federal government via the National Flood Insurance Program (NFIP). However, on June 9, 2022, we entered into a renewal rights agreement with Wright National Flood Insurance Company to sell our entire NFIP Write Your Own flood insurance business and are no longer offering flood policies.

Underwriting

We price our products at levels that we project will generate an acceptable underwriting profit. We aim to accurately underwrite the risk and profitability of each potential policy. The Company uses pricing algorithms, judgement-based rating and consent to rate methodologies that consider historical attritional loss costs for the rating territory in which the risk resides, as well as modeled expected losses for catastrophes and projected reinsurance costs based on the specific geographic and structural characteristics of the property. We seek to optimize our portfolio by managing our probable maximum loss, total insured value and average annual loss. As part of this optimization process, we use the output from third-party modeling software to analyze our risk exposures, including wind exposures, by zip code or street address.

We measure our underwriting profitability by the combined ratio, which is a sum of the ratios of losses, loss adjustment expenses, and underwriting expenses to either gross or net earned premiums. A combined ratio under 100% indicates an underwriting profit. Refer to Management’s Discussion and Analysis of Financial Condition and Results of Operations in Part II, Item 7 of this report for further details on our combined ratio.

Distribution Channels

Our commercial lines policies are marketed and distributed to condominium associations by AmRisc, LLC through a network of independent agencies managed by AmRisc, LLC that specialize in commercial residential insurance. AmRisc, LLC is an unaffiliated third-party and represents 100% of our commercial lines revenue based on our exclusive agreement in Florida.

As of December 31, 2023, we marketed and distributed our personal lines policies to consumers through approximately 400 independent agencies.

AMERICAN COASTAL INSURANCE CORPORATION

The Company focused on the independent agency distribution channel since its inception, and we believe independent agents and agencies build relationships in their communities that can lead to profitable business and policyholder satisfaction. We believe we have built significant credibility and loyalty with the independent agent communities in the states in which we operate through (i) our extensive training for full-service insurance agencies that distribute our products and (ii) periodic business reviews using established benchmarks and goals for premium volume and profitability.

Typically, a full-service agency is small to medium in size and represents several insurance companies for both personal and commercial product lines. We depend on our independent agents to produce new business for us. We compensate our independent agents primarily with fixed-rate commissions that we believe are consistent with those generally prevailing in the market.

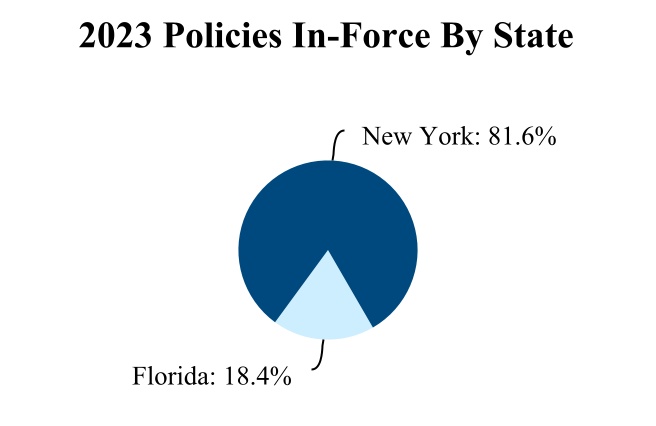

GEOGRAPHIC MARKETS

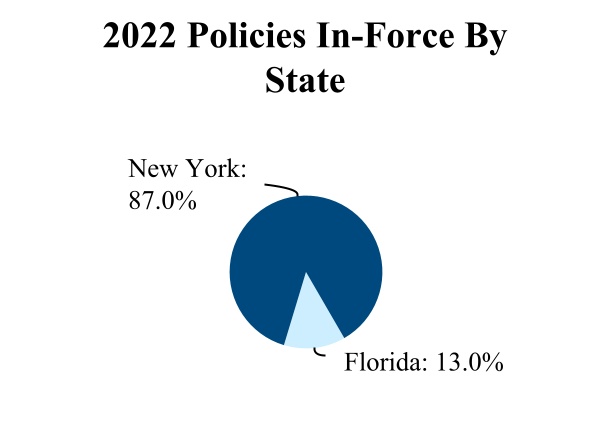

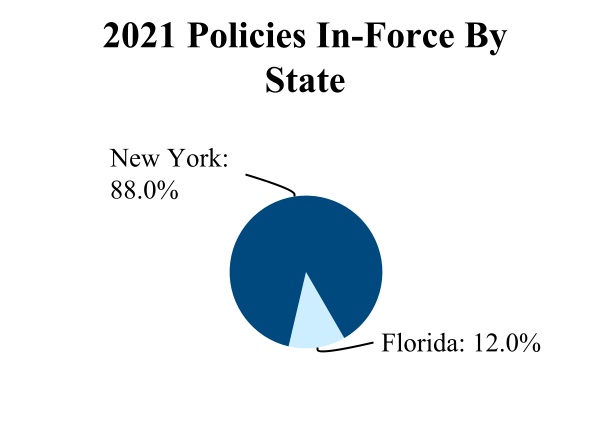

The table below shows the geographic distribution of our policies in-force as of December 31, 2023, 2022 and 2021, excluding our policies attributable to discontinued operations. The graphs below exclude states with policies that are less than 0.2% of our total policies in-force.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Policies In-Force By State (1) |

|

2023 |

|

2022 |

|

2021 |

| New York |

|

18,640 |

|

|

35,868 |

|

|

43,529 |

|

| Florida |

|

4,208 |

|

|

5,348 |

|

|

5,909 |

|

| Texas |

|

— |

|

|

26 |

|

|

88 |

|

| South Carolina |

|

— |

|

|

— |

|

|

28 |

|

| Total |

|

22,848 |

|

|

41,242 |

|

|

49,554 |

|

(1) We are no longer writing in Texas or South Carolina as of May 31, 2022.

AMERICAN COASTAL INSURANCE CORPORATION

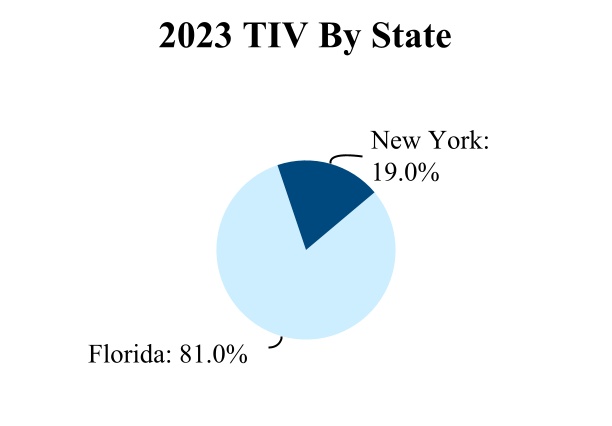

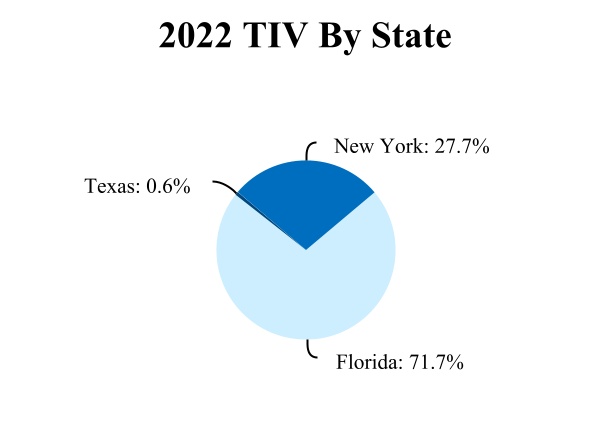

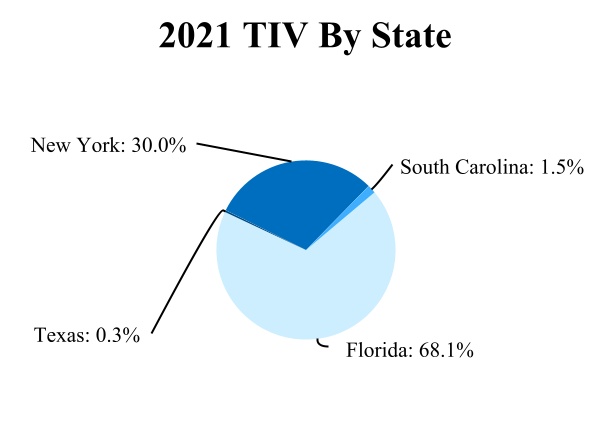

The table below shows the geographic distribution of our total insured value (TIV) of all polices in-force as of December 31, 2023, 2022 and 2021, excluding our policies attributable to discontinued operations.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TIV By State(1) |

|

2023 |

|

2022 |

|

2021 |

| Florida |

|

$ |

56,340,145 |

|

|

$ |

68,961,070 |

|

|

$ |

72,638,543 |

|

| New York |

|

13,255,735 |

|

|

26,697,590 |

|

|

32,012,956 |

|

| Texas |

|

— |

|

|

615,670 |

|

|

372,633 |

|

| South Carolina |

|

— |

|

|

— |

|

|

1,650,412 |

|

| Total |

|

$ |

69,595,880 |

|

|

$ |

96,274,330 |

|

|

$ |

106,674,544 |

|

(1) We are no longer writing in Texas or South Carolina as of May 31, 2022.

COMPETITION

The property and casualty insurance market in the United States is highly competitive and rapidly changing. Our primary competitors range from large national property and casualty insurance companies that write most classes of business using traditional products and pricing to small and mid-size regional insurance companies that provide specialty coverages.

We compete primarily on the basis of policy features, the strength of our distribution network and the quality of our services to our agents and policyholders. Our track record writing homeowners’ insurance in catastrophe-exposed areas has enabled us to develop sophisticated pricing techniques that endeavor to accurately reflect the risk of loss while allowing us to be competitive in our target markets. This pricing segmentation approach allows us to offer products in areas that have a high demand for property insurance yet are under-served by the national carriers. However, we face the risk that policyholders may be able to obtain more favorable terms from competitors rather than renewing coverage with us.

Our ability to compete is dependent on a number of factors. One factor is the financial strength or stability ratings assigned to our insurance subsidiaries by independent rating agencies. A downgrade in these ratings could negatively impact our position in the market. Another, is that we must attract and retain key employees and highly skilled people in order to be successful in the market.

AMERICAN COASTAL INSURANCE CORPORATION

There is intense competition in our industry which could lead to higher than expected employee turnover or difficulty attracting new employees. Finally, technological advancements and innovation in the insurance industry provide opportunities for a competitive advantage. Advancements and innovation are being used in all aspects of the industry including digital-based distribution methods, underwriting and claims handling. We continue to leverage the technology that we have and have made substantial investments into new technology in an effort to gain an advantage over our competitors.

REGULATION

We are subject to extensive regulation in the jurisdictions in which our insurance company subsidiaries are domiciled and licensed to transact business, primarily at the state level. AmCoastal is domiciled in Florida and IIC is domiciled in New York. In general, these regulations are designed to protect the interests of insurance policyholders.

Such regulations have a substantial effect on certain areas of our business, including:

•insurer solvency,

•reserve adequacy,

•insurance company licensing and examination,

•agent and adjuster licensing,

•rate setting, underwriting rules and coverage forms,

•investments,

•assessments or other surcharges for guaranty funds,

•transactions with affiliates,

•the payment of dividends,

•reinsurance,

•protection of personally identifiable information,

•risk solvency assessment and enterprise risk management,

•cybersecurity,

•statutory accounting methods, and

•numerous requirements relating to other areas of insurance operations, including policy forms, underwriting standards and claims practices.

Our insurance subsidiaries provide audited statutory financial statements to the various insurance regulatory authorities. With regard to periodic examinations of an insurance company’s affairs, insurance regulatory authorities, in general, defer to the insurance regulatory authority in the state in which an insurer is domiciled; however, insurance regulatory authorities from any state in which we operate may conduct examinations at their discretion.

In 2021, the Florida Office of Insurance Regulation (FLOIR) began a statutory examination of JIC for the year ended December 31, 2020. This examination concluded in 2022, with no significant findings. In 2023, the FLOIR notified the Company of a statutory financial examination of AmCoastal as of December 31, 2023, to commence in 2024.

For a discussion of statutory financial information and regulatory contingencies, see

Note 16 to our Notes to Consolidated Financial Statements in Part II, Item 8 of this report.

Risk-Based Capital Requirements

To enhance the regulation of insurer solvency, the NAIC has published risk-based capital (RBC) guidelines for insurance companies designed to assess capital adequacy and to raise the level of protection statutory surplus provides for policyholders. The guidelines measure three major areas of risk facing property and casualty insurers: (i) underwriting risks, which encompass the risk of adverse loss developments and inadequate pricing; (ii) declines in asset values arising from credit risk; and (iii) other business risks. Most states, including Florida and New York, have enacted the NAIC guidelines as statutory requirements, and insurers having less statutory surplus than required will be subject to varying degrees of regulatory action, depending on the level of capital inadequacy.

AMERICAN COASTAL INSURANCE CORPORATION

The level of required risk-based capital is calculated and reported annually. The table below outlines each of our subsidiary’s RBC ratios, all of which were in excess of minimum requirements, as of December 31, 2023.

|

|

|

|

|

|

|

|

|

| Subsidiary |

|

RBC Ratio |

| ACIC |

|

979 |

% |

| IIC |

|

477 |

% |

Underwriting and Marketing Restrictions

During the past several years, various regulatory and legislative bodies have adopted or proposed new laws or regulations to address the cyclical nature of the insurance industry, catastrophic events and insurance capacity and pricing. These regulations: (i) created “market assistance plans” under which insurers are induced to provide certain coverage; (ii) restrict the ability of insurers to reject insurance coverage applications, to rescind or otherwise cancel certain policies in mid-term, and to terminate agents; (iii) restrict certain policy non-renewals and require advance notice on certain policy non-renewals; and (iv) limit rate increases or decrease rates permitted to be charged.

Most states also have insurance laws requiring that rate schedules and other information be filed with the insurance regulatory authority, either directly or through a rating organization with which the insurer is affiliated. The insurance regulatory authority may disapprove a rate filing if it finds that the rates are inadequate, excessive or unfairly discriminatory.

Most states require licensure or insurance regulatory authority approval prior to the marketing of new insurance products. Typically, licensure review is comprehensive and includes a review of a company’s business plan, solvency, reinsurance, rates, forms and other financial and non-financial aspects of a company, such as the character of its officers and directors. The insurance regulatory authorities may prohibit entry into a new market by not granting a license or by withholding approval.

Limitations on Dividends by Insurance Subsidiaries

As a holding company with no significant business operations of our own, we rely on payments from our insurance subsidiaries as one of the principal sources of cash to pay dividends and meet our obligations. Our insurance affiliates are regulated as property and casualty insurance companies and their ability to pay dividends is restricted by Florida and New York law.

The state laws of Florida and New York permit an insurer to pay dividends or make distributions out of that part of statutory surplus derived from net operating profit and net realized capital gains or adjusted net investment income. The state laws further provide calculations to determine the amount of dividends or distributions that can be made without the prior approval of the insurance regulatory authorities and the amount of dividends or distributions that would require prior approval of the insurance regulatory authorities in those states. Statutory risk-based capital requirements may further restrict our insurance subsidiaries’ ability to pay dividends or make distributions if the amount of the intended dividend or distribution would cause statutory surplus to fall below minimum risk-based capital requirements.

In addition, in connection with the filed plan of withdrawal in New York for our former insurance subsidiary, UPC, our subsidiary, IIC, has agreed not to pay ordinary dividends until January 1, 2025, without the prior approval of the New York Department of Financial Services.

Insurance Holding Company Regulation

As a holding company of insurance subsidiaries, we are subject to laws governing insurance holding companies in Florida and New York. These laws, among other things: (i) require us to file periodic information with the insurance regulatory authority, including information concerning our capital structure, ownership, financial condition and general business operations; (ii) regulate certain transactions between our affiliates and us, including the amount of dividends and other distributions and the terms of surplus notes: and (iii) restrict the ability of any one person to acquire certain levels of our voting securities without prior regulatory approval. Any purchaser of 5% or more of the outstanding shares of our common stock could be presumed to have acquired control of us unless the insurance regulatory authority, upon application, determines otherwise.

AMERICAN COASTAL INSURANCE CORPORATION

Insurance holding company regulations also govern the amount any affiliate of the holding company may charge our insurance affiliates for services (i.e., management fees and commissions). The Company allocates a portion of relevant expenses to AmCoastal for statutory accounting purposes at cost.

AmRisc, a managing general underwriter, handles the underwriting, claims processing and premium collection for our AmCoastal commercial business written in Florida. In return, AmRisc is reimbursed through monthly management fees.

The Company does not utilize a managing general agent structure in New York. Instead, ACIC allocates a portion of relevant expenses to IIC for statutory accounting purposes at cost.

CORPORATE RESPONSIBILITY AND SUSTAINABILITY

As a company with more than 20 years of history and experience, we strive to create and maintain a culture within our business where people are empowered to address risks as they emerge, and where we expect all associates to hold themselves and their teammates accountable for personal integrity and professionalism. To demonstrate this culture our leaders must lead by example and clear standards of behavior should be well understood by the entire company. We maintain five core values; collaboration, communication, loyalty, resiliency, and integrity, to accomplish this goal.

In addition to our cultural goals, we are committed to conducting business in a manner that supports environmental, social, and governance (ESG) matters. ACIC believes that an effective ESG strategy leads to improved decision making, associate engagement, and financial results over time.

To show our commitment to conducting business that supports ESG matters, in the second quarter of 2021 we published our Sustainability & Responsibility report, which outlines our ESG practices and goals. Highlights from the report can be seen below, and the full report is available on our company website under Environmental, Social and Governance.

Environmental Matters

As a data driven organization some of the facts surrounding climate change have our attention. Several factors, including the rise in carbon dioxide concentration levels in the atmosphere, higher global mean air and water temperatures, and sea and Arctic ice levels have been identified as potential culprits of the higher frequency and severity of catastrophe losses we have incurred over the past five years.

There is a growing consensus today that the frequency and severity of catastrophic events or severe weather conditions is increasing as a result of climate change. We recognize current trends and potential financial impact are not sustainable. As a result, we have taken the following steps to improve our environmental footprint and reduce our contribution to climate change:

•Reducing waste: paperless policy document delivery option and investment in paperless technologies;

•Eco-friendly disposal of retired equipment and electronics;

•Installed filtered water dispensers to promote re-usable bottles over disposables;

•Utilization of recycling bins throughout our offices;

•Implemented a remote work environment to both enhance productivity and curb the impact of daily commuting; and

•Use of energy efficient LED lighting, motion-activated lighting, and programmable thermostats to reduce energy use.

ACIC continuously monitors our environmental footprint and will continue to make steps to reduce this footprint where possible. We have committed to achieve net-zero carbon emissions in our operations and through our value chain by no later than 2030.

Social Responsibility

We understand that research shows diverse teams perform better, innovate more, and are more effective at managing risks. As a result, our organization has a vested interest in hiring associates and building teams that reflect the diversity of society and the communities that we seek to serve. Details of our accomplishments creating a diverse and inclusive workplace can be seen in Part I, Item 1., “Human Capital Management”.

In addition to our social responsibility as an employer within the community, ACIC also seeks to support our community through various initiatives intended to give back and promote goodwill. Over the past several years we have provided support to numerous non-for-profit organizations. Some of the causes we have provided support to include, but are not limited to, youth education, work force development, medical care and research, domestic violence shelters and prevention, and child-care services.

AMERICAN COASTAL INSURANCE CORPORATION

We are committed to giving back and investing in the communities we serve.

Governance Matters

Our Board of Directors oversee and monitor our management in the interest and for the benefit of our stockholders. Our Board is currently comprised of nine directors, divided into two classes. Each class of directors is elected for a two-year term, in accordance with our Certificate of Incorporation. Eight of our Directors, or 88.9%, are considered to be independent.

Our Board of Directors has several committees, including an Audit Committee, a Compensation and Benefits Committee, a Nominating and Corporate Governance Committee, and an Investment Committee. All members of these committees qualify as independent directors under SEC and Nasdaq standards as well as under the independence standards specific to their committees. ACIC has also committed to adding at least two new Directors to our Board of Directors to improve overall diversity at the highest level of corporate governance.

HUMAN CAPITAL MANAGEMENT

Diversity and Employment Statistics

As of December 31, 2023, we had 71 employees, of which 17 worked in Claims, and eight worked in Sales and Underwriting, respectively. These employees have regular direct contact with our vendors, agencies, or customers. We are not party to any collective bargaining agreements and we have not experienced any work stoppages or strikes as a result of labor disputes.

The following table shows the diversity in our workforce population at December 31, 2023 and how this diversity has changed from December 31, 2022.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gender (1) |

|

Change from

December 31, 2022

|

|

Race (1) |

|

Change from

December 31, 2022

|

| Executive Officers |

|

20.0% |

|

0 points |

|

40.0% |

|

0 points |

Management Team (2) |

|

44.7% |

|

5.7 points |

|

14.9% |

|

(11.9) points |

| All Other Employees |

|

42.1% |

|

(2.8) points |

|

15.8% |

|

(18.5) points |

(1) Information regarding gender and race is based on information provided by employees.

(2) Our management team is comprised of employees in supervisory roles at the manager and director level or above.