FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of May 2026

Commission File Number: 001-12568

BBVA Argentina Bank S.A.

(Translation of registrant’s name into English)

111 Córdoba Av, C1054AAA

Buenos Aires, Argentina

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

| Form 20-F |

X |

Form 40-F |

|

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

| Yes |

|

No |

X |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

| Yes |

|

No |

X |

Indicate by check mark whether by furnishing the information contained in this Form, the Registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934:

| Yes |

|

No |

X |

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): N/A

Banco BBVA Argentina S.A.

TABLE OF CONTENTS

|

Item |

|

| 1. | Banco BBVA Argentina S.A. reports consolidated first quarter earnings for fiscal year 2026. |

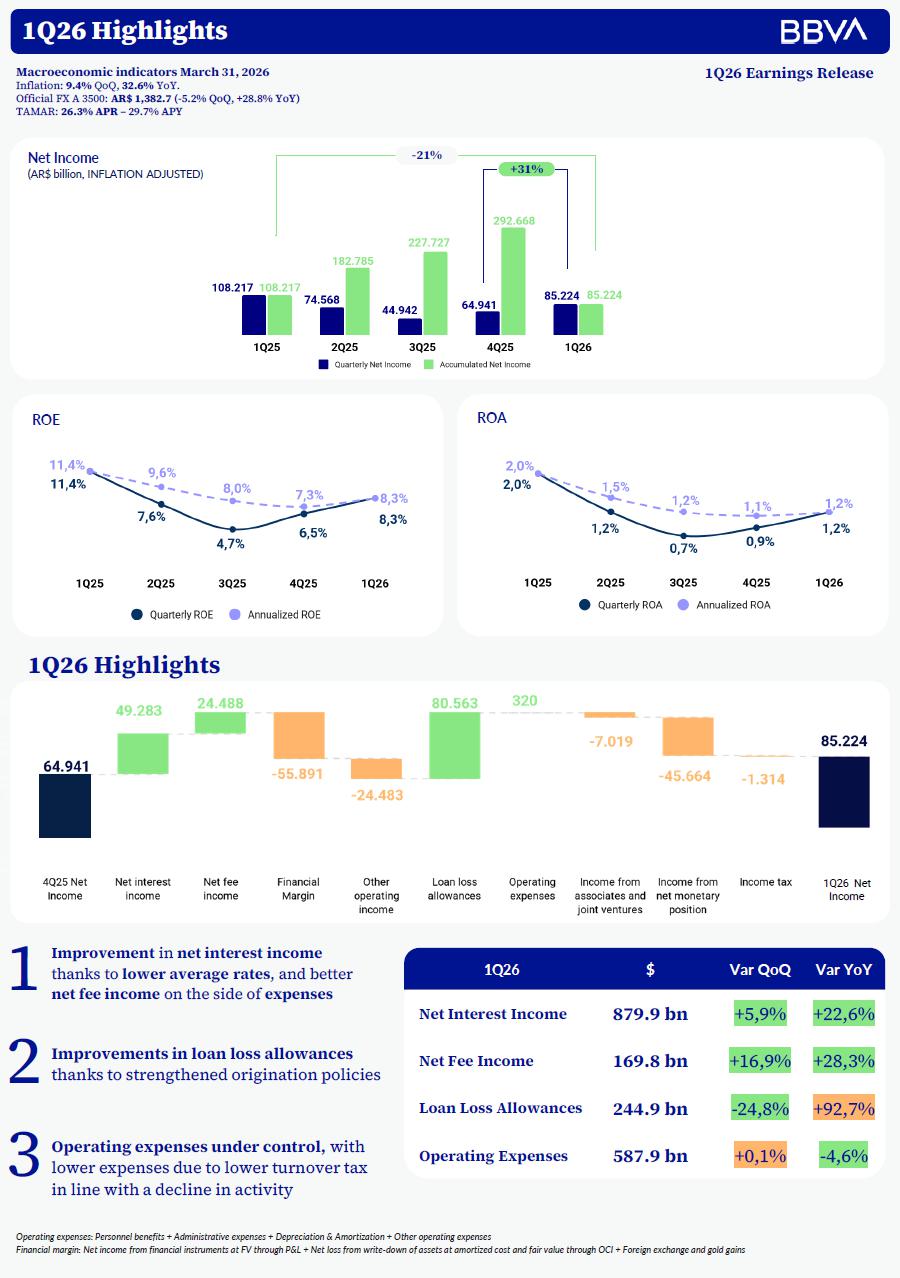

1Q26 Conference Call Wednesday, May 27, 2026 12:00 p.m. Buenos Aires time ––(11:00 a.m. To participate click here to register BBVA Argentina May 26th, 2026 Buenos Aires, Argentina 1Q26 Earnings Release Improvement Improvement in in net interest income net interest income thanks to thanks to lower average rateslower average rates, and better , and better net fee income net fee income on the side of on the side of expensesexpenses Operating expenses under control, Operating expenses under control,with with lower expenses due to lower turnover tax lower expenses due to lower turnover tax in line with a decline in activityin line with a decline in activity Improvements in loan loss allowances Improvements in loan loss allowances thanks to strengthened origination policiesthanks to strengthened origination policies 1 1 3 3 2 2 Highlights Highlights 1Q26 Earnings Release 1Q26 Earnings Release Operating expenses: Personnel benefits + Administrative expenses + Depreciation & Amortization + Other operating expenses Operating expenses: Personnel benefits + Administrative expenses + Depreciation & Amortization + Other operating expenses Financial margin: Net income from financial instruments at FV through P&L + Net loss from write Financial margin: Net income from financial instruments at FV through P&L + Net loss from write--down of assets at amortized costdown of assets at amortized costand fair value through OCI + Foreign exchange and gold gainsand fair value through OCI + Foreign exchange and gold gains 1Q26 Net 1Q26 Net IncomeIncome 1Q26 Highlights 1Q26 Highlights 1Q26 1Q26HighlightsHighlights Net Income Net Income ( (AR$ billionAR$ billion, , INFLATION ADJUSTED)INFLATION ADJUSTED) Macroeconomic MacroeconomicindicatorsindicatorsMarch March 31, 31, 20262026 Inflation Inflation: : 9.4%9.4%QoQQoQ, , 32.6%32.6%YoYYoY.. Official OfficialFX A 3500: FX A 3500: AR$ 1,382.7AR$ 1,382.7((--5.2% 5.2% QoQQoQ, +28.8% , +28.8% YoYYoY)) TAMAR: TAMAR: 26.3% APR26.3% APR––29.7% APY29.7% APY +31% +31% - -21%21% 1Q26 1Q26 $ $ Var Var QoQQoQ Var Var YoYYoY Net Interest Income Net Interest Income 879.9 bn 879.9 bn +5,9% +5,9% +22,6% +22,6% Net Fee Income Net Fee Income 169.8 bn 169.8 bn +16,9% +16,9% +28,3% +28,3% Loan Loss Allowances Loan Loss Allowances 244.9 bn 244.9 bn - -24,8%24,8% +92,7% +92,7% Operating Expenses Operating Expenses 587.9 bn 587.9 bn +0,1% +0,1% - -4,6%4,6% ROA ROA ROE ROE **Adjusted NIM: (Quarterly Net Interest Income **Adjusted NIM: (Quarterly Net Interest Income --Net Monetary Position Results) / Average quarterly interest earning assets.Net Monetary Position Results) / Average quarterly interest earning assets. Fees Fees--toto--expenses ratios = (Net fee Income + Rental of safe deposit boxes) / (Personnel benefits + Administrative expenses + Deprexpenses ratios = (Net fee Income + Rental of safe deposit boxes) / (Personnel benefits + Administrative expenses + Depreciation and amortization)eciation and amortization) Highlights Highlights 1Q26 Earnings Release 1Q26 Earnings Release 1Q26 Highlights 1Q26 Highlights Macroeconomic MacroeconomicindicatorsindicatorsMarch March 31, 31, 20262026 Inflation Inflation: : 9.4%9.4%QoQQoQ, , 32.6%32.6%YoYYoY.. Official OfficialFX A 3500: FX A 3500: AR$ 1,382.7AR$ 1,382.7((--5.2% 5.2% QoQQoQ, +28.8% , +28.8% YoYYoY)) TAMAR: TAMAR: 26.3% APR26.3% APR––29.7% APY29.7% APY Quarterly efficiency Ratio Quarterly efficiency Ratio (%, INFLATION ADJUSTED) (%, INFLATION ADJUSTED) Net Interest Income Net Interest Income (net of monetary position result)(net of monetary position result)& Adjusted & Adjusted NIM**NIM** (AR$ billion, INFLATION ADJUSTED) (AR$ billion, INFLATION ADJUSTED) Fees Fees--toto--Expenses Ratio Expenses Ratio (Fees / Expenses)(Fees / Expenses) (%, INFLATION ADJUSTED) (%, INFLATION ADJUSTED) Cost of Risk Cost of Risk (%, INFLATION ADJUSTED) (%, INFLATION ADJUSTED) NPL & COVERAGE NPL & COVERAGE PRIVATE LOANS PRIVATE LOANS PRIVATE DEPOSITS PRIVATE DEPOSITS PRIVATE DEPOSITS MARKET SHARE* PRIVATE DEPOSITS MARKET SHARE* **Other includes special saving accounts and Checking accounts include interest **Other includes special saving accounts and Checking accounts include interest--bearing checking bearing checking accounts.accounts. (AR$ BILLION, INFLATION ADJUSTED) (AR$ BILLION, INFLATION ADJUSTED) Lower quarterly activity with higher market share Lower quarterly activity with higher market share (%, CONSOLIDATED, (%, CONSOLIDATED, INFLATION ADJUSTEDINFLATION ADJUSTED)) C Cost of Risk: Current period loan loss allowances / Total average loans. ost of Risk: Current period loan loss allowances / Total average loans. Total average loans calculated as the average between loans at prior period end, and total loans in Total average loans calculated as the average between loans at prior period end, and total loans in the current period.the current period. *Source: Informe sobre bancos, BCRA, March 2026. *Source: Informe sobre bancos, BCRA, March 2026. Quarterly decline with higher weight of time deposits Quarterly decline with higher weight of time deposits PRIVATE LOAN AND DEPOSITS MARKET SHARE % PRIVATE LOAN AND DEPOSITS MARKET SHARE % vs 2020 vs 2020 TOTAL GROSS LOANS / TOTAL DEPOSITS TOTAL GROSS LOANS / TOTAL DEPOSITS * RPC includes 100% of quarterly results * RPC includes 100% of quarterly results CAPITAL RATIO % CAPITAL RATIO % (AR$ BILLION, INFLATION ADJUSTED) (AR$ BILLION, INFLATION ADJUSTED) *Based on daily information from BCRA. Capital balance as of last day of every quarter. Consolidates PSA, *Based on daily information from BCRA. Capital balance as of last day of every quarter. Consolidates PSA, VWFS, Rombo & FCA. 1Q25 does not include FCA.VWFS, Rombo & FCA. 1Q25 does not include FCA. Retail: consumer, mortgages, credit cards, pledge and loans to personnel. Retail: consumer, mortgages, credit cards, pledge and loans to personnel. Commercial: discounted instruments, overdrafts, financial leases, financing and prefinancing of exports, other Commercial: discounted instruments, overdrafts, financial leases, financing and prefinancing of exports, other loans.loans. BBVA loans BBVA loans BBVA deposits BBVA deposits 1Q26 Highlights 1Q26 Highlights 81% 81%82% 85%82% 85% 9,15% 10,01% 9,93% 9,15% 10,01% 9,93% 48% 44% 48% 44%45%45% TOTAL LIQUID ASSETS/ TOTAL DEPOSITS TOTAL LIQUID ASSETS/ TOTAL DEPOSITS 11,25% 12,04% 11,25% 12,04%12,15%12,15% PRIVATE LOANS MARKET SHARE* PRIVATE LOANS MARKET SHARE* +28% +28% - -3%3% +16% +16% - -9%9% +366 b +366 bpsps +280 +280 bpsbps BBVA loans BBVA loans BBVA deposits BBVA deposits 11.5% 11.5% 8% 8% System NPL* System NPL* 6.67% 6.67% Mar’26Mar’26 Buenos Aires, May 26, 2025 – Banco BBVA Argentina S.A (NYSE; BYMA; MAE: BBAR; LATIBEX: XBBAR) (“BBVA Argentina” or “BBVA” or “the Bank”) announced today its consolidated results for the first quarter (1Q26), ended on March 31, 2026.

Banco BBVA Argentina S.A. announces First Quarter 2025

As of January 1, 2020, the Bank started to inform its inflation adjusted results pursuant to IAS 29 reporting. To facilitate comparison, figures of comparable quarters of 2025 and 2026 have been updated according to IAS 29 reporting to reflect the accumulated effect of inflation adjustment for each period up to March 31, 2025.

1Q26 Highlights

| ● | BBVA Argentina's inflation-adjusted net income in 1Q26 was $85.2 billion, 31.2% higher than the one recorded in the fourth quarter of 2025 (4Q25), and 21.2% lower than the result reported in the first quarter of 2025 (1Q25). |

| ● | In 1Q26, BBVA Argentina posted an inflation adjusted average return on equity (ROAE) of 8.3% versus 6.5% the prior quarter, and an inflation adjusted average return on assets (ROAA) of 1.2% versus 0.9% the prior quarter. |

| ● | The 1Q26 total NIM was 18.6% versus 17.5% in 4Q25. NIM in local currency was 22.3% and NIM in USD was 4.1%. |

| ● | In terms of activity, total consolidated financing to the private sector in 1Q26 totaled $15.7 trillion, decreasing 3.5% in real terms compared to 4Q25, and increasing 28.1% compared to 1Q25, both in real terms. BBVA’s market share was 12.15% in 1Q26, increasing 11 bps Quarter-over-Quarter (QoQ) and 95 bps Year-over-Year (YoY). |

| ● | Total consolidated deposits in 1Q26 totaled $17.5 trillion, decreasing 7.3% in real terms during the quarter, and increasing 20.0% YoY. The Bank’s consolidated market share of private deposits reached 9.93% as of 1Q26, falling 8 bps QoQ and increasing 78 bps YoY. |

| ● | As of 1Q26, the non-performing loan ratio (NPL) reached 5.60%, with an 88.41% coverage ratio. |

| ● | The quarterly efficiency ratio in 1Q26 was 51,4%. |

| ● | As of 1Q26, BBVA Argentina reached a regulatory capital ratio of 18.8% (Tier 1: 18.8%), entailing a 128.7% excess over minimum regulatory requirement. |

| ● | Total liquid assets represented 45,5% of the Bank’s total deposits as of 1Q26, above the 44,2% reported in 4Q25 and below the 47.6% reported in 1Q25. |

|

1Q26 Earnings Release | p. |

Message from the CFO

“During the first quarter of the year, BBVA Argentina’s business model demonstrated resilience in an operating environment that continues to be challenging. The Bank recorded a net income of $85.2 billion, representing a 31.2% increase compared to the previous quarter and an 8.3% quarterly ROE, reflecting the institution’s ability to generate value in transitional contexts.

In a quarter in which commercial activity within the financial system declined slightly, in line with market trends and the seasonality of the quarter, BBVA Argentina managed to maintain its market share gain trend up to 12.15%, even after a very strong end to 2025, mainly driven by demand for commercial loans.

This progress is consistent with our strategic determination to play a leading role in the Argentine financial system and to lead credit supply as the cycle normalizes.

During the quarter, volatility in interest rates declined, while rates maintained the downward trend that began following the midterm elections. The Central Bank continued unraveling the prudential measures implemented in the third quarter of last year and began successfully executing the reserve purchase plan announced last December.

Likewise, the government continued advancing its structural economic reform plan, managing to approve important initiatives such as the Labor Reform, the amendment to the Glacier Law, and the 2026 Budget. The Incentive Regime for Large Investments (RIGI) continued attracting investment projects, and a second phase has recently been announced focusing on productive sectors with little or no presence in the country.

The trade balance for the first quarter reached USD 5.5 billion, multiplying by five the balance from the previous year, with record exports in the energy sector. At the same time, Argentine companies and provinces have secured financing in international capital markets exceeding USD 10 billion in recent months. Fitch recently announced an upgrade to the country’s sovereign rating. All of this has occurred in a context of fiscal and monetary discipline, while April inflation data once again showed signs of deceleration.

This evolution allows us to remain optimistic regarding the potential path of credit recovery in the coming quarters and a reversal in the trend of credit quality indicators that have affected both the Bank and the financial system during recent quarters.

The positive evolution of the Bank’s results, even in a quarter in which inflation was higher, responds both to the strong performance of revenues and to the control of recurring expenses and improved cost of risk performance, which, although still at elevated levels, reflects a reduction compared to the previous quarter.

Net interest income increased by 5.9%, supported by the faster decline in funding costs in a context of falling interest rates and by efficient management of origination pricing. Fees maintained positive performance even in a quarter of lower activity, while expenses, net of non-recurring impacts, declined slightly during the period.

Regarding asset quality, although BBVA's non-performing loan ratio continued to rise to 5.6%, this growth was lower than what occurred at the systemic level, and this value remains among the lowest in the financial system. In this regard, we understand that the precautionary measures and strict origination criteria implemented by the Bank would allow for a normalization trend to begin in the coming quarters.

BBVA Argentina currently has the necessary tools to lead the market, supported by robust liquidity and capital levels. The Common Equity Tier 1 capital ratio stands at 18.8%, placing it at appropriate levels to sustain our growth strategy. Within this framework of strength, the Shareholders’ Meeting approved a dividend distribution of $63,057 million (at December 2025 values), which would become effective starting in June.

Within this framework of strength, BBVA Argentina has all the necessary tools to lead the market. In light of the context of fiscal and monetary discipline and the potential path of credit recovery in the coming quarters, we move forward with optimism and determination to consolidate our role and lead credit supply in the Argentine financial system ”

Carmen Morillo Arroyo, CFO at BBVA Argentina

|

|

1Q26 Earnings Release | p. |

Safe Harbor Statement

This press release contains certain forward-looking statements that reflect the current views and/or expectations of Banco BBVA Argentina and its management with respect to its performance, business and future events. We use words such as “believe,” “anticipate,” “plan,” “expect,” “intend,” “target,” “estimate,” “project,” “predict,” “forecast,” “guideline,” “seek,” “future,” “should” and other similar expressions to identify forward-looking statements, but they are not the only way we identify such statements. Such statements are subject to a number of risks, uncertainties and assumptions. We caution you that a number of important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in this release. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (i) changes in general economic, financial, business, political, legal, social or other conditions in Argentina or elsewhere in Latin America or changes in either developed or emerging markets, (ii) changes in regional, national and international business and economic conditions, including inflation, (iii) changes in interest rates and the cost of deposits, which may, among other things, affect margins, (iv) unanticipated increases in financing or other costs or the inability to obtain additional debt or equity financing on attractive terms, which may limit our ability to fund existing operations and to finance new activities, (v) changes in government regulation, including tax and banking regulations, (vi) changes in the policies of Argentine authorities, (vii) adverse legal or regulatory disputes or proceedings, (viii) competition in banking and financial services, (ix) changes in the financial condition, creditworthiness or solvency of the customers, debtors or counterparties of Banco BBVA Argentina, (x) increase in the allowances for loan losses, (xi) technological changes or an inability to implement new technologies, (xii) changes in consumer spending and saving habits, (xiii) the ability to implement our business strategy and (xiv) fluctuations in the exchange rate of the Peso. The matters discussed herein may also be affected by risks and uncertainties described from time to time in Banco BBVA Argentina’s filings with the U.S. Securities and Exchange Commission (SEC) and Comisión Nacional de Valores (CNV). Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as the date of this document. Banco BBVA Argentina is under no obligation and expressly disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Information

This earnings release has been prepared in accordance with the accounting framework established by the Central Bank of Argentina (“BCRA”), based on International Financial Reporting Standards (“I.F.R.S.”) and the resolutions adopted by the International Accounting Standards Board (“I.A.S.B”) and by the Federación Argentina de Consejos Profesionales de Ciencias Económicas (“F.A.C.P.E.”), and with the the exclusion of the application of the IFRS 9 impairment model for non-financial public sector debt instruments.

The information in this press release contains unaudited financial information that consolidates, line item by line item, all of the banking activities of BBVA Argentina, including: BBVA Asset Management Argentina S.A.U. Sociedad Gerente de Fondos Comunes de Inversión y Agente de Liquidación y Compensación Integral, Consolidar AFJP-undergoing liquidation proceeding, PSA Finance Argentina Compañía Financiera S.A. (“PSA”) , Volkswagen Financial Services Compañía Financiera S.A (“VWFS”) and FCA Compañía Financiera S.A. ("FCA").

BBVA Seguros Argentina S.A. is disclosed on a consolidated basis recorded as Investments in associates (reported under the proportional consolidation method), and the corresponding results are reported as “Income from associates”), same as Rombo Compañía Financiera S.A. (“Rombo”), Play Digital S.A. (“MODO”), Openpay Argentina S.A. and Interbanking S.A.

Financial statements of subsidiaries have been elaborated as of the same dates and periods as Banco BBVA Argentina S.A.’s. In the case of consolidated companies PSA, VWFS and FCA, financial statements were prepared considering the B.C.R.A. accounting framework for institutions belonging to “Group C”, considering the model established by the IFRS 9 5.5. “Impairment” section for periods starting as of January 1, 2022, excluding debt instruments from the non-financial public sector.

The information published by the BBVA Group for Argentina is prepared according to IFRS, without considering the temporary exceptions established by BCRA.

|

|

1Q26 Earnings Release | p. |

Quarterly Results

| INCOME STATEMENT | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Net Interest Income | 879,880 | 830,597 | 717,834 | 5.9% | 22.6% |

| Net Fee Income | 169,784 | 145,296 | 132,330 | 16.9% | 28.3% |

| Net income from measurement of financial instruments at fair value through P&L | 21,210 | 8,987 | 42,701 | 136.0% | (50.3%) |

| Net income from write-down of assets at amortized cost and at fair value through OCI | (2,759) | 57,561 | 106,274 | (104.8%) | (102.6%) |

| Foreign exchange and gold gains | 53,327 | 61,121 | 10,786 | (12.8%) | 394.4% |

| Other operating income | 65,591 | 90,074 | 51,463 | (27.2%) | 27.5% |

| Loan loss allowances | (244,848) | (325,411) | (127,077) | 24.8% | (92.7%) |

| Net operating income | 942,185 | 868,225 | 934,311 | 8.5% | 0.8% |

| Personnel benefits | (186,502) | (149,109) | (160,702) | (25.1%) | (16.1%) |

| Adminsitrative expenses | (166,318) | (158,791) | (194,064) | (4.7%) | 14.3% |

| Depreciation and amortization | (32,151) | (35,281) | (27,593) | 8.9% | (16.5%) |

| Other operating expenses | (202,955) | (245,065) | (179,663) | 17.2% | (13.0%) |

| Operarting expenses | (587,926) | (588,246) | (562,022) | 0.1% | (4.6%) |

| Operating income | 354,259 | 279,979 | 372,289 | 26.5% | (4.8%) |

| Income from associates | (3,754) | 3,265 | 981 | (215.0%) | (482.7%) |

| Income from net monetary position | (218,530) | (172,866) | (198,437) | (26.4%) | (10.1%) |

| Net income before income tax | 131,975 | 110,378 | 174,833 | 19.6% | (24.5%) |

| Income tax | (46,751) | (45,437) | (66,616) | (2.9%) | 29.8% |

| Net income for the period | 85,224 | 64,941 | 108,217 | 31.2% | (21.2%) |

| Owners of the parent | 78,421 | 58,932 | 104,006 | 33.1% | (24.6%) |

| Non-controlling interests | 6,803 | 6,009 | 4,211 | 13.2% | 61.6% |

| Other comprehensive Income (OCI) (1) | 59,916 | 250,819 | (145,660) | (76.1%) | 141.1% |

| Total comprehensive income | 145,140 | 315,760 | (37,443) | (54.0%) | 487.6% |

| (1) Net of Income Tax. | |||||

As of 1Q26, BBVA Argentina achieved a net income of $85.2 billion, representing an increase of 31.2% for the quarter and a decrease of 21.2% versus 1Q25. The ROE for the quarter reached 8.3%, and the ROA 1.2%.

The 31.2% increase in the quarter's results is mainly explained by higher operating income, with expenses remaining stable overall. The increase in income is explained by (i) lower loan loss allowances, (ii) better net interest income, and (iii) improvements in fee income.

While net interest income benefited from the lower rate environment, with deposits renewing at higher rates faster than assets; fees continued the positive trend started several quarters ago.

The reduction in loan loss allowances is explained both by (i) the strengthening of origination and restructuring policies that have allowed the reinforcement of customers' credit profiles, and (ii) by improvements in the ratings of certain commercial groups.

Although personnel expenses increased 25.1% in the quarter, excluding non-recurring factors, they would have fallen slightly in the period of analysis. The item of Other operating expenses fell by 17.2%, mainly reflecting the lower impact of the turnover tax, due to lower activity and lower rates. Lower charges from results from initial loss of loans below market rate were also observed there, as a result of the lower seasonality of credit card promotions in the first quarter, compared to the fourth quarter of each year.

Net income from the net monetary position was 26.8% higher QoQ, in a context of increasing inflation (9.44% versus 7.86% in 4Q251).

1 Source: Instituto Nacional de Estadística y Censos (INDEC)

|

|

1Q26 Earnings Release | p. |

It is important to mention that the incorporation of FCA Compañía Financiera was made at a balance sheet level on December 31, 2025, but not in the income statement. As of January 2026, FCA consolidates line by line, the same way as VWFS and PSA do.

| OTHER COMPREHENSIVE INCOME | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Net income for the period | 85,224 | 64,941 | 108,217 | 31.2% | (21.2%) |

| Other comprehensive income components to be reclassified to income/(loss) for the period | |||||

| Profit or losses from hedge instruments - Cashflow hedge | 76 | - | - | N/A | N/A |

| Profit or losses from hedge instruments | 117 | - | - | N/A | N/A |

| Income tax | (41) | - | - | N/A | N/A |

| Profit or losses from financial isntruments at fair value through OCI | 60,431 | 250,000 | (147,831) | (75.8%) | 140.9% |

| Profit or losses from financial instruments at fair value through OCI | 90,155 | 442,177 | (121,158) | (79.6%) | 174.4% |

| Reclassification adjustment for the period | 2,816 | (57,561) | (106,274) | 104.9% | 102.6% |

| Income tax | (32,540) | (134,616) | 79,601 | 75.8% | (140.9%) |

| Other comprehensive income coponents not to be reclassified to income/(loss) for the period | |||||

| Income or loss on equity instruments at fair value through OCI | (591) | 819 | 2,171 | (172.2%) | (127.2%) |

| Resultado por instrumentos de patrimonio a VR con cambios en ORI | (591) | 819 | 2,171 | (172.2%) | (127.2%) |

| Total Other Comprehensive Income/(loss) for the period | 59,916 | 250,819 | (145,660) | (76.1%) | 141.1% |

| Total Comprehensive Income | 145,140 | 315,760 | (37,443) | (54.0%) | 487.6% |

| Attributable to owners of the Parent | 138,295 | 309,751 | (41,655) | (55.4%) | 432.0% |

| Attributable to non-controlling interests | 6,845 | 6,009 | 4,212 | 13.9% | 62.5% |

The Other Comprehensive Income (OCI) line totaled a gain of $59.9 billion in 1Q26, resulting from the improvement in the valuation of financial instruments at fair value (FV) with changes in OCI.

| EARNINGS PER SHARE | BBVA ARGENTINA CONSOLIDATED | ||||

| ∆ % | |||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Financial Statement information | |||||

| Net income for the period attributable to owners of the parent (in AR$ millions, inflation adjusted) | 78,421 | 53,848 | 78,432 | 45.6% | (0.0%) |

| Total shares outstanding (1) | 612,710,079 | 612,710,079 | 612,710,079 | - | - |

| Market information | |||||

| Closing price of ordinary share at BYMA (in AR$) | 7,940.00 | 9,140.00 | 7,750.00 | (13.1%) | 2.5% |

| Closing price of ADS at NYSE (in USD) | 16.10 | 18.10 | 18.10 | (11.1%) | (11.4%) |

| Book value per share (in AR$) | 6,357 | 5,603 | 4,518 | 13.5% | 40.7% |

| Price-to-book ratio (BYMA price) (%) | 1.25 | 1.63 | 1.72 | (23.4%) | (27.2%) |

| Earnings per share (in AR$) | 128 | 88 | 128 | 45.6% | - |

| Earnings per ADS (1) in ARS | 384 | 264 | 384 | 45.6% | - |

| Market Cap (USD millions) | 3,280 | 3,691 | 3,701 | (11.1%) | (11.4%) |

| (1) Each ADS accounts for 3 ordinary shares | |||||

| Book value, Equity and Results not adjusted by inflation | |||||

|

|

1Q26 Earnings Release | p. |

Net Interest Income

| NET INTEREST INCOME | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Net Interest Income | 879,880 | 830,597 | 717,834 | 5.9% | 22.6% |

| Interest Income | 1,528,705 | 1,716,416 | 1,217,424 | (10.9%) | 25.6% |

| From government securities | 237,772 | 290,689 | 224,307 | (18.2%) | 6.0% |

| From private securities | 925 | 1,417 | 952 | (34.7%) | (2.8%) |

| Interest from loans and other financing | 1,088,733 | 1,246,179 | 846,256 | (12.6%) | 28.7% |

| Financial Sector | 19,013 | 31,955 | 8,684 | (40.5%) | 118.9% |

| Overdrafts | 100,788 | 147,950 | 79,357 | (31.9%) | 27.0% |

| Discounted Instruments | 274,922 | 316,855 | 220,523 | (13.2%) | 24.7% |

| Mortgage loans | 13,648 | 12,909 | 6,915 | 5.7% | 97.4% |

| Pledge loans | 57,639 | 49,899 | 31,305 | 15.5% | 84.1% |

| Consumer Loans | 192,921 | 213,987 | 182,686 | (9.8%) | 5.6% |

| Credit Cards | 216,924 | 250,484 | 190,336 | (13.4%) | 14.0% |

| Financial leases | 4,552 | 5,154 | 4,348 | (11.7%) | 4.7% |

| Loans for the prefinancing and financing of exports | 36,890 | 42,250 | 15,149 | (12.7%) | 143.5% |

| Other loans | 171,436 | 174,736 | 106,953 | (1.9%) | 60.3% |

| Premiums on reverse REPO transactions | 270 | 35 | - | n.m | N/A |

| CER/UVA clause adjustment | 183,868 | 156,455 | 141,707 | 17.5% | 29.8% |

| Other interest income | 17,137 | 21,641 | 4,202 | (20.8%) | 307.8% |

| Interest expenses | 648,825 | 885,819 | 499,590 | (26.8%) | 29.9% |

| Deposits | 541,367 | 763,461 | 443,873 | (29.1%) | 22.0% |

| Checking accounts* | 65,493 | 101,043 | 69,859 | (35.2%) | (6.2%) |

| Savings accounts | 2,513 | 2,015 | 2,383 | 24.7% | 5.5% |

| Time deposits | 473,060 | 660,098 | 294,404 | (28.3%) | 60.7% |

| Investment accounts | 301 | 305 | 77,227 | (1.3%) | (99.6%) |

| Other liabilities from financial transactions | 49,321 | 46,494 | 24,237 | 6.1% | 103.5% |

| Interfinancial loans received | 37,345 | 46,532 | 22,564 | (19.7%) | 65.5% |

| Premiums on REPO transactions | 12,998 | 21,187 | 2,018 | (38.7%) | n.m |

| Guaranteed securities loans | 4,071 | 6,670 | 1,065 | (39.0%) | 282.3% |

| CER/UVA clause adjustment | 3,723 | 1,475 | 5,833 | 152.4% | (36.2%) |

| Other interest expense | - | - | - | N/A | N/A |

| *Includes interest-bearing checking accounts | |||||

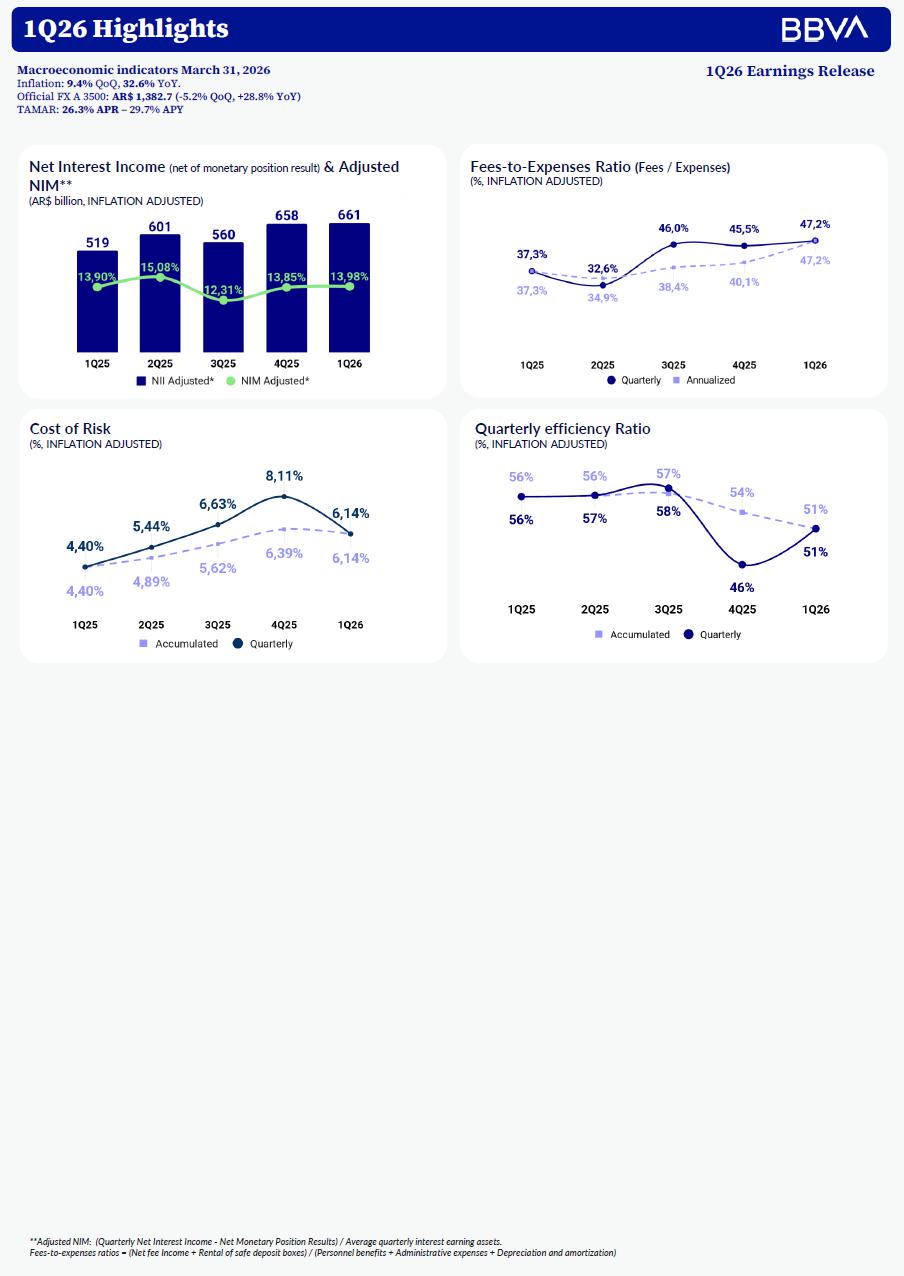

Net interest income for 1Q26 amounted to $879.9 billion, an increase of 5.9% compared to 4Q25 and 22.6% compared to 1Q25. In 1Q26, interest income decreased to a lesser extent than expenses, in monetary and percentage terms.

The downward trend in interest rates (the average TAMAR rate recorded a 640 bps decrease compared to 4Q25, reaching 31.9%) allowed interest expenses to continue decreasing at a faster pace than income, due to the shorter average life of liabilities.

On the other hand, income with UVA adjustment began to reflect the increase in higher inflation rates in recent months, growing 17.5% in the period. The CER index accrued by products with this adjustment is recorded with a certain lag. 52% of interest income from CER/UVA adjustments is explained by the interest generated by CPI-linked securities, while 48% is explained by loans.

Interest income from loans decreased by 12.6% QoQ to $1.1trillion, affected by the drop in the average TAMAR rate, impacting short-term products.

Income from government securities fell 18.2% in 1Q26, with 96% of income coming from fair value through OCI (Other Comprehensive Income) securities.

|

|

1Q26 Earnings Release | p. |

Interest expenses totaled $648.8 billion, falling 26.8% in 1Q26 (due to lower expenses from time deposits and current accounts). Interest on time deposits (73.0% of total expenses) fell 28.3%.

NIM

In 1Q26, the total net interest margin (NIM) was 18.6%, higher than the 17.5% of 4Q25 and below the 19.2% of 1Q25. While the NIM in pesos increased 210 bps to 22.3% due to a higher speed in the reduction of passive rates, the NIM in dollars fell 110 bps to 4.1% due to increased competition for loans in foreign currency.

The quarter again showed a greater weight of dollar-earning assets in the mix.

As highlighted in the graphs accompanying the first section of this document, the NIM net of the net result from the monetary position has remained relatively stable over the last quarters.

| ASSETS & LIABILITIES PERFORMANCE - TOTAL | BBVA ARGENTINA CONSOLIDATED | ||||||||

| In millions of AR$. Rates and spreads in annualized % | |||||||||

| 1Q26 | 4Q25 | 1Q25 | |||||||

| Average Balance | Interest Earned/Paid | Average Real Rate | Average Balance | Interest Earned/Paid | Average Real Rate | Average Balance | Interest Earned/Paid | Average Real Rate | |

| Total interest-earning assets | 19,155,715 | 1,527,638 | 32.3% | 18,726,359 | 1,712,360 | 36.3% | 15,153,977 | 1,217,424 | 32.6% |

| Debt securities | 3,752,653 | 333,337 | 36.0% | 3,789,751 | 383,816 | 40.2% | 3,684,374 | 330,013 | 36.3% |

| Loans to customers/financial institutions | 15,254,892 | 1,193,967 | 31.7% | 14,697,196 | 1,328,480 | 35.9% | 11,264,783 | 887,411 | 31.9% |

| Loans to the BCRA | 795 | 85 | 43.4% | 667 | 50 | 29.7% | 750 | - | - |

| Other assets | 147,375 | 249 | 0.7% | 238,745 | 14 | 0.0% | 204,070 | - | - |

| Total non interest-earning assets | 6,647,147 | 1,067 | 0.1% | 7,404,044 | 4,056 | 0.2% | 6,607,712 | - | - |

| Total Assets | 25,802,862 | 1,528,705 | 24.0% | 26,130,403 | 1,716,416 | 26.1% | 21,761,689 | 1,217,424 | 22.7% |

| Total interest-bearing liabilities | 16,435,112 | 648,825 | 16.0% | 16,866,051 | 885,819 | 20.8% | 12,481,285 | 499,590 | 16.2% |

| Savings accounts | 5,892,716 | 4,232 | 0.3% | 5,973,871 | 3,141 | 0.2% | 5,300,850 | 2,396 | 0.2% |

| Time deposits and investment accounts | 7,297,191 | 477,082 | 26.5% | 7,376,866 | 661,880 | 35.6% | 5,240,983 | 377,463 | 29.2% |

| Debt securities issued | 632,047 | 20,475 | 13.1% | 511,247 | 14,610 | 11.3% | 219,049 | 12,872 | 23.8% |

| Other liabilities | 2,613,158 | 147,036 | 22.8% | 3,004,067 | 206,188 | 27.2% | 1,720,403 | 106,859 | 25.2% |

| Total non-interest-bearing liabilities | 9,367,750 | - | - | 9,264,352 | - | - | 9,280,404 | - | - |

| Total liabilities and equity | 25,802,862 | 648,825 | 10.2% | 26,130,403 | 885,819 | 13.4% | 21,761,689 | 499,590 | 9.3% |

| NIM - Total | 18.6% | 17.5% | 19.2% | ||||||

| Spread - Total | 16.3% | 15.4% | 16.3% | ||||||

| Nominal rates are calculated over a 365-day year | |||||||||

| Does not include Net income from measurement of financial instruments at fair value through P&L nor Net income from write-down of assets at amortized cost and at fair value through OCI | |||||||||

| Interest-bearing checking accounts included in other interest-bearing liabilities. Non interest-bearing accounts are included in non-interest-bearing liabilities. | |||||||||

| Non.interest earning assets include all assets that do not have an impact in the interest margin. | |||||||||

| ASSETS & LIABILITIES PERFORMANCE - ARS | BBVA ARGENTINA CONSOLIDATED | ||||||||

| In millions of AR$. Rates and spreads in annualized % | |||||||||

| 1Q26 | 4Q25 | 1Q25 | |||||||

| Average Balance | Interest Earned/Paid | Average Real Rate | Average Balance | Interest Earned/Paid | Average Real Rate | Average Balance | Interest Earned/Paid | Average Real Rate | |

| Total interest-earning assets | 15,250,336 | 1,470,270 | 39.1% | 15,448,017 | 1,653,486 | 42.5% | 12,922,925 | 1,192,952 | 37.4% |

| Debt securities | 3,693,493 | 332,952 | 36.6% | 3,752,726 | 383,224 | 40.5% | 3,581,340 | 329,327 | 37.3% |

| Loans to customers/financial institutions | 11,490,298 | 1,136,991 | 40.1% | 11,495,293 | 1,270,212 | 43.8% | 9,136,841 | 863,625 | 38.3% |

| Loans to the BCRA | 765 | 85 | 45.1% | 659 | 50 | 30.1% | 747 | - | - |

| Other assets | 65,780 | 242 | 1.5% | 199,339 | - | - | 203,997 | - | - |

| Total non interest-earning assets | 3,063,643 | - | - | 3,213,225 | - | - | 3,488,873 | - | - |

| Total Assets | 18,313,979 | 1,470,270 | 32.6% | 18,661,242 | 1,653,486 | 35.2% | 16,411,798 | 1,192,952 | 29.5% |

| Total interest-bearing liabilities | 10,077,146 | 631,091 | 25.4% | 10,587,333 | 866,754 | 32.5% | 8,294,832 | 496,825 | 24.3% |

| Savings accounts | 1,389,130 | 2,440 | 0.7% | 1,441,889 | 1,935 | 0.5% | 1,531,462 | 2,323 | 0.6% |

| Time deposits and investment accounts | 5,962,328 | 469,034 | 31.9% | 6,187,537 | 653,518 | 41.9% | 4,913,102 | 376,704 | 31.1% |

| Debt securities issued | 369,838 | 20,475 | 22.5% | 290,735 | 14,610 | 19.9% | 200,304 | 12,872 | 26.1% |

| Other liabilities | 2,355,850 | 139,142 | 24.0% | 2,667,172 | 196,691 | 29.3% | 1,649,964 | 104,926 | 25.8% |

| Total non-interest-bearing liabilities | 8,178,144 | - | - | 8,084,003 | - | - | 8,003,359 | - | - |

| Total liabilities and equity | 18,255,290 | 631,091 | 14.0% | 18,671,336 | 866,754 | 18.4% | 16,298,191 | 496,825 | 12.4% |

| NIM - Total | 22.3% | 20.2% | 21.8% | ||||||

| Spread - Total | 13.7% | 10.0% | 13.1% | ||||||

| Nominal rates are calculated over a 365-day year | |||||||||

| Does not include Net income from measurement of financial instruments at fair value through P&L nor Net income from write-down of assets at amortized cost and at fair value through OCI | |||||||||

| Interest-bearing checking accounts included in other interest-bearing liabilities. Non interest-bearing accounts are included in non-interest-bearing liabilities. | |||||||||

| Non.interest earning assets include all assets that do not have an impact in the interest margin. | |||||||||

|

|

1Q26 Earnings Release | p. |

| ASSETS & LIABILITIES PERFORMANCE - USD | BBVA ARGENTINA CONSOLIDATED | ||||||||

| In millions of AR$. Rates and spreads in annualized % | |||||||||

| 1Q26 | 4Q25 | 1Q25 | |||||||

| Average Balance | Interest Earned/Paid | Average Real Rate | Average Balance | Interest Earned/Paid | Average Real Rate | Average Balance | Interest Earned/Paid | Average Real Rate | |

| Total interest-earning assets | 3,905,379 | 57,368 | 6.0% | 3,278,342 | 58,874 | 7.1% | 2,231,052 | 24,472 | 4.4% |

| Debt securities | 59,160 | 385 | 2.6% | 37,025 | 592 | 6.3% | 103,034 | 686 | 2.7% |

| Loans to customers/financial institutions | 3,764,594 | 56,976 | 6.1% | 3,201,903 | 58,268 | 7.2% | 2,127,942 | 23,786 | 4.5% |

| Loans to the BCRA | 30 | - | - | 8 | - | - | 3 | - | - |

| Other assets | 81,595 | 7 | 0.0% | 39,406 | 14 | 0.1% | 73 | - | - |

| Total non interest-earning assets | 3,583,504 | 1,067 | - | 4,190,819 | 4,056 | 0.4% | 3,118,839 | - | - |

| Total Assets | 7,488,883 | 58,435 | 3.2% | 7,469,161 | 62,930 | 3.3% | 5,349,891 | 24,472 | 1.9% |

| Total interest-bearing liabilities | 6,357,966 | 17,734 | 1.1% | 6,278,718 | 19,065 | 1.2% | 4,186,453 | 2,765 | 0.3% |

| Savings accounts | 4,503,586 | 1,792 | 0.2% | 4,531,982 | 1,206 | 0.1% | 3,769,388 | 73 | 0.0% |

| Time deposits and investment accounts | 1,334,863 | 8,048 | 2.4% | 1,189,329 | 8,362 | 2.8% | 327,881 | 759 | 0.9% |

| Debt securities issued | 262,209 | - | - | 220,512 | - | - | 18,745 | - | - |

| Other liabilities | 257,308 | 7,894 | 12.4% | 336,895 | 9,497 | 11.2% | 70,439 | 1,933 | 11.1% |

| Total non-interest-bearing liabilities | 1,189,606 | - | - | 1,180,349 | - | - | 1,277,045 | - | - |

| Total liabilities and equity | 7,547,572 | 17,734 | 1.0% | 7,459,067 | 19,065 | 1.0% | 5,463,498 | 2,765 | 0.2% |

| NIM - Total | 4.1% | 4.8% | 3.9% | ||||||

| Spread - Total | 4.8% | 5.9% | 4.2% | ||||||

| Nominal rates are calculated over a 365-day year | |||||||||

| Does not include Net income from measurement of financial instruments at fair value through P&L nor Net income from write-down of assets at amortized cost and at fair value through OCI | |||||||||

| Interest-bearing checking accounts included in other interest-bearing liabilities. Non interest-bearing accounts are included in non-interest-bearing liabilities. | |||||||||

| Non.interest earning assets include all assets that do not have an impact in the interest margin. | |||||||||

|

|

1Q26 Earnings Release | p. |

Net Fee Income

| NET FEE INCOME | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Net Fee Income | 169,784 | 145,296 | 132,330 | 16.9% | 28.3% |

| Fee Income | 247,812 | 250,350 | 239,521 | (1.0%) | 3.5% |

| Linked to liabilities | 60,006 | 58,098 | 63,830 | 3.3% | (6.0%) |

| From credit cards (1) | 140,270 | 144,856 | 123,072 | (3.2%) | 14.0% |

| Linked to loans | 25,187 | 23,951 | 25,773 | 5.2% | (2.3%) |

| From insurance | 8,389 | 8,437 | 8,588 | (0.6%) | (2.3%) |

| From foreign trade and foreign currency transactions | 10,213 | 10,149 | 8,029 | 0.6% | 27.2% |

| Linked to loan commitments | - | 53 | 1,774 | (100.0%) | (100.0%) |

| From guarantees granted | 157 | 131 | 95 | 19.8% | 65.3% |

| Linked to securities | 3,590 | 4,675 | 8,360 | (23.2%) | (57.1%) |

| Fee expenses | 78,028 | 105,054 | 107,191 | (25.7%) | (27.2%) |

| (1) Includes results from Puntos BBVA royalty program pursuant to IFRS 15 regulation. | |||||

Net fee income in 1Q26 totaled $169.8 billion, an increase of 16.9% compared to 4Q25 and 28.3% compared to 1Q25. Although this figure includes some positive one-off impacts in the quarter, it is important to note that, even without these effects, the evolution would have been slightly positive. This, in a quarter with low seasonality due to lower commercial activity, reinforces the growth process that the entity has been showing in this line item for several quarters.

Net Income from Measurement of Financial Instruments at Fair Value and Foreign Exchange and Gold Gains/Losses

| NET INCOME FROM FINANCIAL INSTRUMENTS AT FAIR VALUE (FV) THROUGH P&L | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Net Income from financial instruments at FV through P&L | 21,210 | 8,987 | 42,701 | 136.0% | (50.3%) |

| Income from government securities | 22,229 | 4,168 | 40,566 | 433.3% | (45.2%) |

| Income from private securities | 6,022 | 8,964 | 1,271 | (32.8%) | 373.8% |

| Interest rate swaps | (1) | 1,904 | (491) | (100.1%) | 99.8% |

| Income from foreign currency forward transactions | (7,099) | (6,320) | 1,355 | (12.3%) | n.m |

| Income from corporate bonds | 26 | 28 | - | (7.1%) | N/A |

| Other | 33 | 243 | - | (86.4%) | N/A |

In 1Q26, the net income from the measurement of financial instruments valued at fair value with changes in results was $21.2 billion, increasing 136.0% mainly due to larger trading positions and the positive evolution of sovereign bond prices.

| DIFFERENCES IN QUOTED PRICES OF GOLD AND FOREIGN FOREIGN CURRENCY | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Foreign exchange and gold gains/(losses) (1) | 53,327 | 61,121 | 10,786 | (12.8%) | 394.4% |

| From foreign exchange position | (2,274) | (9,563) | (14,539) | 76.2% | 84.4% |

| Income from purchase-sale of foreign currency | 55,601 | 70,684 | 25,325 | (21.3%) | 119.5% |

| Net income from financial instruments at FV through P&L (2) | (7,099) | (6,320) | 1,355 | (12.3%) | n.m |

| Income from foreign currency forward transactions | (7,099) | (6,320) | 1,355 | (12.3%) | n.m |

| Total differences in quoted prices of gold & foreign currency (1) + (2) | 46,228 | 54,801 | 12,141 | (15.6%) | 280.8% |

The total result of foreign currency exchange difference generated a gain of $53.3 billion in 1Q26, decreasing by 12.8% in the quarter.

|

|

1Q26 Earnings Release | p. |

The quarterly drop in exchange difference is mainly explained by a lower volume of buying and selling activity, compared to a fourth quarter with greater hedging activity prior to the mid-term elections, and also partly, by the 5.5% appreciation of the Argentine peso.

Other Operating Income

| OTHER OPERATING INCOME | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Operating Income | 65,591 | 90,074 | 51,463 | (27.2%) | 27.5% |

| Rental of safe deposit boxes (1) | 12,009 | 10,922 | 10,192 | 10.0% | 17.8% |

| Adjustments and interest on miscellaneous receivables (1) | 9,470 | 15,519 | 12,183 | (39.0%) | (22.3%) |

| Punitive interest (1) | 10,462 | 10,235 | 4,773 | 2.2% | 119.2% |

| Loans recovered | 3,803 | 19,820 | 4,089 | (80.8%) | (7.0%) |

| Fee income from credit and debit cards (1) | 9,284 | 8,703 | 8,444 | 6.7% | 9.9% |

| Fee expenses recovery | 2,151 | 2,252 | 2,017 | (4.5%) | 6.6% |

| Rents | 2,411 | 2,684 | 2,385 | (10.2%) | 1.1% |

| Sindicated transaction fees | 1,305 | 812 | 515 | 60.7% | 153.4% |

| Disaffected provisions | 123 | 22 | 2,246 | 459.1% | (94.5%) |

| Recovery of impairment loss | - | 10,674 | - | (100.0%) | N/A |

| Other Operating Income(2) | 14,573 | 8,431 | 4,619 | 72.9% | 215.5% |

| (1) Included in the efficiency ratio calculation | |||||

| (2) Includes some of the concepts used in the efficiency ratio calculation | |||||

In 1Q26, the other operating income line totaled $65.6 billion, falling 27.2% QoQ, and increasing 27.5% YoY. The lower result in recovered loans is explained by higher income in 4Q25, related to a significant recovery with a commercial portfolio client.

|

|

1Q26 Earnings Release | p. |

Operating Expenses

Personnel Benefits & Administrative Expenses

| PERSONNEL BENEFITS & ADMINISTRATIVE EXPENSES | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Total Personnel Benefits and Adminsitrative Expenses | 352,820 | 307,900 | 354,766 | 14.6% | (0.5%) |

| Personnel Benefits (1) | 186,502 | 149,109 | 160,702 | 25.1% | 16.1% |

| Administrative expenses (1) | 166,318 | 158,791 | 194,064 | 4.7% | (14.3%) |

| Travel expenses | 1,359 | 2,271 | 1,354 | (40.2%) | 0.4% |

| Outsourced administrative expenses | 23,015 | 22,550 | 35,939 | 2.1% | (36.0%) |

| Security services | 4,116 | 6,298 | 8,324 | (34.6%) | (50.6%) |

| Fees to Bank Directors and Supervisory Committee | 239 | 380 | 236 | (37.1%) | 1.3% |

| Other fees | 8,675 | 8,363 | 6,647 | 3.7% | 30.5% |

| Insurance | 1,746 | 1,453 | 1,797 | 20.2% | (2.8%) |

| Rent | 24,170 | 19,025 | 19,009 | 27.0% | 27.2% |

| Stationery and supplies | 188 | 566 | 257 | (66.8%) | (26.8%) |

| Electricity and communications | 7,353 | 8,132 | 6,918 | (9.6%) | 6.3% |

| Advertising | 11,733 | 11,013 | 17,872 | 6.5% | (34.3%) |

| Taxes | 20,994 | 21,654 | 23,576 | (3.0%) | (11.0%) |

| Maintenance costs | 16,939 | 17,490 | 15,917 | (3.2%) | 6.4% |

| Armored transportation services | 13,718 | 13,641 | 27,281 | 0.6% | (49.7%) |

| Software | 13,525 | 9,127 | 5,754 | 48.2% | 135.1% |

| Document distribution | 4,510 | 6,376 | 7,536 | (29.3%) | (40.2%) |

| Commercial reports | 4,791 | 1,019 | 7,032 | 370.2% | (31.9%) |

| Other administrative expenses | 9,247 | 9,433 | 8,615 | (2.0%) | 7.3% |

| Headcount* | |||||

| BBVA (Bank) | 6,408 | 6,583 | 6,301 | (175) | 107 |

| Subsidiaries (2) | 147 | 104 | 100 | 43 | 47 |

| Total employees* | 6,555 | 6,687 | 6,401 | (132) | 154 |

| Number of branches*** | 234 | 234 | 235 | - | (1) |

| Own | 120 | 120 | 118 | - | 2 |

| Rented | 114 | 114 | 117 | - | (3) |

| Efficiency Ratio | |||||

| Efficiency Ratio | 51.4% | 45.9% | 56.3% | 545 pbs | (496)pbs |

| Accumulated Efficiency Ratio | 51.4% | 53.9% | 56.3% | (250)pbs | (490)pbs |

| (1) Concept included in the efficiency ratio calculation | |||||

| (2) Includes BBVA Asset Management, PSA & VWFS. Employees included in Main Office. | |||||

| *Total effective employees, net of temporary contract employees. Expatriates excluded. | |||||

| **Branch employees + Business Center managers | |||||

| ***Excludes administrative branches | |||||

In 1Q26, personnel benefits and administrative expenses totaled $352.8 billion, increasing 14.6% QoQ, and falling slightly 0.5% YoY in real terms.

Regarding personnel benefits, although an increase of 25.1% is observed, this figure incorporates non-recurring expenses for severance payments. Excluding these expenses, and neutralizing other specific and seasonal effects of the fourth quarter, expenses would have experienced a slight decrease in real terms.

Administrative expenses rose 4.7% in 1Q26, mainly in the lines of rent, software, and commercial reports, the first two associated with expenses related to the parent company, which had a greater seasonal impact in the first quarter. This was offset by a decrease in the document distribution line. In general terms, expenses are expected to reflect a favorable behavior throughout the year, associated with the efficiency and expense control measures that the Bank is implementing The quarterly efficiency ratio for 1Q26 was 51.4%, above the 45.9% of 4Q25 and below the 56.3% registered in 1Q25.

|

|

1Q26 Earnings Release | p. |

The quarterly deterioration is explained both by the aforementioned increase in expenses and the greater loss from the net monetary position in the quarter.

Other Operating Expenses

| OTHER OPERATING EXPENSES | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Other Operating Expenses | 202,955 | 245,065 | 179,663 | (17.2%) | 13.0% |

| Turnover tax (1) | 147,739 | 165,800 | 117,677 | (10.9%) | 25.5% |

| Initial loss of loans below market rate (1) | 24,610 | 36,709 | 28,929 | (33.0%) | (14.9%) |

| Contribution to the Deposit Guarantee Fund (SEDESA) (1) | 7,364 | 7,301 | 5,929 | 0.9% | 24.2% |

| Interest on liabilities from financial lease | 1,412 | 1,501 | 1,354 | (5.9%) | 4.3% |

| Other allowances | 2,272 | 1,497 | 9,059 | 51.8% | (74.9%) |

| Loss for sale or devaluation of investment properties and other non-financial assets | - | 1,119 | - | (100.0%) | N/A |

| Adjustments for currency homogeneity on dividends | 362 | 1,266 | - | (71.4%) | N/A |

| Claims | 1,877 | 1,889 | 2,714 | (0.6%) | (30.8%) |

| Other operating expenses (2) | 17,319 | 27,983 | 14,001 | (38.1%) | 23.7% |

| (1) Concept included for the calculation of the efficiency ratio | |||||

| (2) Considers some concepts included for the acalculation of the efficiency ratio | |||||

In 1Q26, other operating expenses totaled $202.9 billion, decreasing 17.2% QoQ, and increasing 13.0% versus 1Q25.

The quarter was marked by a decrease in (i) turnover tax, followed by (ii) result from initial loss of loans below market rate, and (iii) other operating expenses. In the case of turnover tax, the drop is explained by lower interest rates and credit activity, while the result from initial loss of loans below market rate is linked to a more restrictive origination policy regarding installment promotions, in part with a certain seasonal component. With respect to other operating expenses, this line includes provisions made for uncollectible package fees, which decreased during the quarter.

Income from Associates

The income from associates line item shows the results of unconsolidated companies. During 1Q26, a loss of 3.8 billion was recorded, mainly due to the Bank's shareholding in BBVA Seguros Argentina S.A., Rombo Compañía Financiera S.A., Interbanking S.A., Play Digital S.A., and Openpay Argentina S.A.

Income Tax

The accumulated income tax of three months of 2026 showed a loss of $48.3 billion.

The accumulated effective tax rate of three months of 2026 was 35%2, while in 2025 it was 38% .

2 Income tax, in accordance with IAS No. 34, is recognized in interim periods based on the best estimate of the weighted average tax rate that the Entity expects for the year.

|

|

1Q26 Earnings Release | p. |

Balance Sheet and Activity

Loans and other financing

| LOANS AND OTHER FINANCING | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| To the public sector | 5,560 | 3,450 | 4,357 | 61.2% | 27.6% |

| To the financial sector | 196,002 | 254,954 | 95,661 | (23.1%) | 104.9% |

| Non-financial private sector and residents abroad | 15,664,290 | 16,229,463 | 12,223,545 | (3.5%) | 28.1% |

| Non-financial private sector and residents abroad - AR$ | 11,715,102 | 12,530,589 | 9,880,304 | (6.5%) | 18.6% |

| Overdrafts | 1,243,397 | 1,299,234 | 1,096,014 | (4.3%) | 13.4% |

| Discounted instruments | 2,674,071 | 2,945,183 | 2,564,613 | (9.2%) | 4.3% |

| Mortgage loans | 731,881 | 682,095 | 414,960 | 7.3% | 76.4% |

| Pledge loans | 1,027,927 | 832,774 | 299,211 | 23.4% | 243.5% |

| Consumer loans | 1,531,314 | 1,571,386 | 1,440,012 | (2.6%) | 6.3% |

| Credit cards | 3,245,733 | 3,442,267 | 2,895,055 | (5.7%) | 12.1% |

| Receivables from financial leases | 42,063 | 39,174 | 34,013 | 7.4% | 23.7% |

| Loans to personnel | 148,901 | 144,886 | 81,773 | 2.8% | 82.1% |

| Other loans | 1,069,815 | 1,573,590 | 1,054,653 | (32.0%) | 1.4% |

| Non-financial private sector and residents abroad - Foreign Currency | 3,949,188 | 3,698,874 | 2,343,241 | 6.8% | 68.5% |

| Overdrafts | 22 | 23 | 33 | (4.3%) | (33.3%) |

| Discounted instruments | 341,209 | 372,785 | 76,589 | (8.5%) | 345.5% |

| Credit cards | 144,014 | 191,015 | 110,233 | (24.6%) | 30.6% |

| Receivables from financial leases | 4,184 | 4,502 | 2,368 | (7.1%) | 76.7% |

| Loans for the prefinancing and financing of exports | 2,819,925 | 2,539,520 | 1,755,068 | 11.0% | 60.7% |

| Other loans | 639,834 | 591,029 | 398,950 | 8.3% | 60.4% |

| % of total loans to Private sector in AR$ | 74.8% | 77.2% | 80.8% | (242)pbs | (604)pbs |

| % of total loans to Private sector in Foreign Currency | 25.2% | 22.8% | 19.2% | 242 pbs | 604 pbs |

| % of mortgage loans with UVA adjustments / Total mortgage loans (1) | 98.9% | 98.8% | 97.7% | 8 pbs | 116 pbs |

| % of pledge loans with UVA adjustments / Total pledge loans (1) | 16.1% | 22.0% | 13.3% | (590)pbs | 279 pbs |

| % of consumer loans with UVA adjustments / Total consumer loans (1) | 0.0% | 0.0% | 0.0% | (0)pbs | (0)pbs |

| % of loans with UVA adjustments / Total loans and other financing(1) | 5.0% | 4.6% | 2.0% | 35 pbs | 298 pbs |

| Total loans and other financing | 15,865,852 | 16,487,867 | 12,323,563 | (3.8%) | 28.7% |

| Allowances | (798,266) | (675,423) | (284,572) | (18.2%) | (180.5%) |

| Total net loans and other financing | 15,067,586 | 15,812,444 | 12,038,991 | (4.7%) | 25.2% |

| (1) Excludes effect of accrued interests adjustments. | |||||

| Total loans / Total Deposits | 85.3% | 82.0% | 80.8% | 328 pbs | 445 pbs |

| Private Loans/Private Deposits ARS | 98.4% | 97.5% | 93.9% | 94 pbs | 447 pbs |

| Private Loans/Private Deposits USD | 64.8% | 53.9% | 50.7% | 1,087 pbs | 1,407 pbs |

| LOANS AND OTHER FINANCING TO NON-FINANCIAL PRIVATE SECTOR AND RESIDENTS ABROAD IN FOREIGN CURRENCY | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of USD | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| FX rate* | 1,382.76 | 1,459.42 | 1,073.88 | (5.3%) | 28.8% |

| Non-financial private sector and residents abroad - Foreign Currency (USD) | 2,856 | 2,316 | 1,646 | 23.3% | 73.6% |

| *Wholesale U.S. dollar foreign exchange rates on BCRA’s Communication “A” 3500, as of the end of period. | |||||

As of 1Q26, the private loan portfolio totaled $11.7 trillion, a decrease of 3.5% in the quarter, and an increase of 18.6% versus 4Q25. It is worth mentioning that the consolidation with FCA is not incorporated in 1Q25.

|

|

1Q26 Earnings Release | p. |

In a quarter marked by low seasonality, the drop in private loans is generated primarily in short-term commercial loans in pesos, such as (i) documents, (ii) overdrafts, and (iii) other loans (financial and floorplan).

As a consequence of the context, individual portfolios in consumer products (credit cards and personal loans) also did not gain traction. We highlight the continuous momentum of pledge and mortgage loans, which continue to gain ground within the retail portfolio, as a consequence of the financial stability and good credit performance that these products have been demonstrating. This creates better conditions for our customers to make long-term investment decisions.

In summary, the local currency private loan portfolio fell 6.5% in the quarter, partially offset by a 6.8% rise in foreign currency private loans. It is noteworthy that the latter denominated in U.S. dollars, mainly commercial, grew 23.3% in the period and 73.6% in the last 12 months.

| LOANS AND OTHER FINANCING | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Non-financial private sector and residents abroad - Retail | 6,829,770 | 6,864,423 | 5,241,244 | (0.5%) | 30.3% |

| Mortgage loans | 731,881 | 682,095 | 414,960 | 7.3% | 76.4% |

| Pledge loans | 1,027,927 | 832,774 | 299,211 | 23.4% | 243.5% |

| Consumer loans | 1,531,314 | 1,571,386 | 1,440,012 | (2.6%) | 6.3% |

| Credit cards | 3,389,747 | 3,633,282 | 3,005,288 | (6.7%) | 12.8% |

| Loans to personnel | 148,901 | 144,886 | 81,773 | 2.8% | 82.1% |

| Non-financial private sector and residents abroad - Commercial | 8,834,520 | 9,365,040 | 6,982,301 | (5.7%) | 26.5% |

| Overdrafts | 1,243,419 | 1,299,257 | 1,096,047 | (4.3%) | 13.4% |

| Discounted instruments | 3,015,280 | 3,317,968 | 2,641,202 | (9.1%) | 14.2% |

| Receivables from financial leases | 46,247 | 43,676 | 36,381 | 5.9% | 27.1% |

| Loans for the prefinancing and financing of exports | 2,819,925 | 2,539,520 | 1,755,068 | 11.0% | 60.7% |

| Other loans | 1,709,649 | 2,164,619 | 1,453,603 | (21.0%) | 17.6% |

| % of total loans to Retail sector | 43.6% | 42.3% | 42.9% | 130 pbs | 72 pbs |

| % of total loans to Commercial sector | 56.4% | 57.7% | 57.1% | (130)pbs | (72)pbs |

| LOANS AND OTHER FINANCING - NON RESTATED FIGURES | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Non-financial private sector and residents abroad - Retail | 6,829,770 | 6,257,927 | 3,952,492 | 9.1% | 72.8% |

| Non-financial private sector and residents abroad - Commercial | 8,834,520 | 8,571,325 | 5,265,444 | 3.1% | 67.8% |

| Total loans and other financing (1) | 15,865,852 | 15,065,363 | 9,293,361 | 5.3% | 70.7% |

| (1) Does not include allowances | |||||

In nominal terms, BBVA Argentina's retail, commercial, and total loan portfolios increased by 9.1%, 3.1%, and 5.3% respectively during the quarter, below the inflation level in all cases.

La participación de préstamos totales sobre activo es de 59%, versus 57% en el 4T25 y 56% en el 1T25.

| MARKET SHARE - PRIVATE SECTOR LOANS | BBVA ARGENTINA CONSOLIDATED | ||||

| In % | ∆ bps | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Private sector loans - Bank | 10.77% | 10.70% | 10.30% | 7 pbs | 47 pbs |

| Private sector loans - Consolidated* | 12.15% | 12.04% | 11.20% | 11 pbs | 95 pbs |

| Based on daily BCRA information. Capital balance as of the last day of each quarter. There may be differences generated by the gap between the siscen BCRA information and published financial statements | |||||

| * Consolidates PSA, VWFS & Rombo | |||||

|

|

1Q26 Earnings Release | p. |

Asset Quality

| ASSET QUALITY | BBVA ARGENTINA CONSOLIDATED | |||||

| In millions of AR$ - Inflation adjusted | ∆ % | |||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | ||

| Commercial non-performing portfolio (1) | 36,404 | 25,714 | 8,248 | 41.6% | 341.4% | |

| Total commercial portfolio | 7,220,023 | 7,130,943 | 5,804,859 | 1.2% | 24.4% | |

| Commercial non-performing portfolio / Total commercial portfolio | 0.50% | 0.36% | 0.14% | 14 pbs | 36 pbs | |

| Retail non-performing portfolio (1) | 866,471 | 675,186 | 164,937 | 28.3% | 425.3% | |

| Total retail portfolio | 8,889,497 | 9,617,227 | 6,779,749 | (7.6%) | 31.1% | |

| Retail non-performing portfolio / Total retail portfolio | 9.75% | 7.02% | 2.43% | 273 pbs | 731 pbs | |

| Total non-performing portfolio (1) | 902,875 | 700,900 | 173,185 | 28.8% | 421.3% | |

| Total portfolio | 16,109,520 | 16,748,170 | 12,584,608 | (3.8%) | 28.0% | |

| Total non-performing portfolio / Total portfolio | 5.60% | 4.18% | 1.38% | 142 pbs | 423 pbs | |

| Allowances | 798,266 | 675,423 | 284,572 | 18.2% | 180.5% | |

| Allowances /Total non-performing portfolio | 88.41% | 96.37% | 164.32% | (795)pbs | (7,590)pbs | |

| Quarterly change in Write-offs | 76,048 | 105,817 | 42,785 | (28.1%) | 77.7% | |

| Write offs / Total portfolio | 0.47% | 0.63% | 0.34% | (16)pbs | 13 pbs | |

| Cost of Risk (CoR) - Quarterly | 6.14% | 8.11% | 4.40% | (197)pbs | 173 pbs | |

| Cost of Risk (CoR)- Accumulated | 6.14% | 6.39% | 4.40% | (25)pbs | 173 pbs | |

| (1) Non-performing loans include: all loans to borrowers classified as "Deficient Servicing (Stage 3)", "High Insolvency Risk (Stage 4)", "Irrecoverable" and/or "Irrecoverable for Technical Decision" (Stage 5) according to BCRA debtor classification system | ||||||

In 1Q26, the NPL ratio (non-performing loans / total loans) increased from 4.18% to 5.60%, mainly focused on the retail non-performing loan portfolio in credit cards and personal loans, in line with the systemic context. Commercial delinquency maintained a good performance, with a slight increase of 14 bps mainly due to small companies.

The coverage ratio (provisions / non-performing loans) reached 88.41% in 1T26. Despite the increase in non-performing loans, the bank continues to show an adequate level of provisions to cope with insolvencies.

The quarterly cost of risk (loan loss allowances / average total loans) reached 6.14% in 1Q26, compared to 8.11% in 4Q25. The drop is related to (i) lower origination, (ii) strengthened origination and restructuring policies that have allowed the credit profile of customers to improve, and (iii) an improvement in the ratings of certain aforementioned commercial groups.

In annual accumulated terms, the cost of risk of 6.14% in 1Q26 compares to 4.40% in 1Q25.

| ANALYSIS FOR THE ALLOWANCE OF LOAN LOSSES | BBVA ARGENTINA CONSOLIDATED | |||||

| In millions of AR$ | ||||||

| Balance at 12/31/2025 | Stage 1 | Stage 2 | Stage 3 | Monetary result generated by allowances | Balance at 03/31/2026 | |

| Other financial assets | 2,979 | - | - | 100 | (257) | 2822 |

| Loans and other financing | 675,425 | (1,690) | (1,207) | 195,421 | (69,683) | 798266 |

| Other debt securities | 144 | (71) | - | - | (10) | 63 |

| Eventual commitments | 23,906 | (985) | (1,147) | 104 | (1,958) | 19920 |

| Total allowances | 702,454 | (2,746) | (2,354) | 195,625 | (71,908) | 821,071 |

| Note: to be consistent with Financial Statements, it must be recorded from the beginning of the year instead of the quarter | ||||||

Allowances for the Bank in 1Q26 reflect expected losses driven by the adoption of the IFRS 9 standards as of January 1, 2020, except for debt instruments issued by the nonfinancial government sector which were excluded from the scope of such standard.

|

|

1Q26 Earnings Release | p. |

Public Sector Exposure

| NET PUBLIC DEBT EXPOSURE* | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Treasury and National Government | 554,254 | 378,411 | 555,495 | 46.5% | (0.2%) |

| National Treasury Public Debt in AR$ | 256,694 | 239,179 | 429,967 | 7.3% | (40.3%) |

| National Treasury Public Debt CPI-linked | 279,314 | 119,430 | 125,445 | 133.9% | 122.7% |

| National Treasury Public Debt in USD** | 3,108 | 3,870 | 83 | (19.7%) | n.m |

| National Treasury Public Debt in ARS, USD-linked | 15,138 | 15,932 | - | (5.0%) | N/A |

| BCRA | 121 | - | - | N/A | N/A |

| BOPREAL | 121 | - | - | N/A | N/A |

| Public securities at FV through P&L | 554,375 | 378,411 | 555,495 | 46.5% | (0.2%) |

| Treasury and National Government | 24,190 | 639,119 | 167,423 | (96.2%) | (85.6%) |

| National Treasury Public Debt in AR$ | 6,890 | 631,580 | 13,695 | (98.9%) | (49.7%) |

| National Treasury Public Debt CPI-linked | 17,300 | 7,539 | 153,728 | 129.5% | (88.7%) |

| Public securities at Amortized Cost | 24,190 | 639,119 | 167,423 | (96.2%) | (85.6%) |

| Treasury and National Government | 3,569,398 | 3,289,640 | 2,956,052 | 8.5% | 20.7% |

| National Treasury Public Debt in AR$ | 2,389,750 | 2,075,298 | 1,559,623 | 15.2% | 53.2% |

| National Treasury Public Debt CPI-linked | 1,076,280 | 1,208,986 | 1,266,240 | (11.0%) | (15.0%) |

| National Treasury Public Debt in USD** | 103,368 | - | - | N/A | N/A |

| National Treasury Public Debt in ARS, USD-linked | - | 5,356 | 130,189 | (100.0%) | (100.0%) |

| BCRA | 35,048 | 38,604 | 56,705 | (9.2%) | (38.2%) |

| BOPREAL | 35,048 | 38,604 | 56,705 | (9.2%) | (38.2%) |

| Public securities at FV through OCI | 3,604,446 | 3,328,244 | 3,012,757 | 8.3% | 19.6% |

| Total Public securities | 4,183,011 | 4,345,774 | 3,735,675 | (3.7%) | 12.0% |

| Loans to the non-financial public sector | 5,560 | 3,450 | 4,357 | 61.2% | 27.6% |

| Loans to the Central Bank | - | - | - | - | - |

| Total loans to the public sector | 5,560 | 3,450 | 4,357 | 61.2% | 27.6% |

| Total public sector exposure | 4,188,571 | 4,349,224 | 3,740,032 | (3.7%) | 12.0% |

| Public sector exposure (Excl. BCRA) | 4,153,402 | 4,310,620 | 3,683,327 | (3.6%) | 12.8% |

| % Public sector exposure (Excl. BCRA) / Assets | 16.2% | 15.5% | 17.1% | 65 pbs | (90)pbs |

| *Deposits at the Central Bank used to comply with reserve requirements not included. Includes assets used as collateral. | |||||

| **Securities denominated in foreign currency | |||||

In 1T26, total public sector exposure, excluding exposure to the BCRA, totaled $4.2 trillion, falling 3.6% QoQ and increasing 12.8% YoY, with no relevant changes in the portfolio composition in the last three months.

Exposure to the public sector, excluding exposure to the BCRA (Central Bank of Argentina), represents 16.2% of total assets, above the 15.5% of 4Q25 and below the 17.1% of 1Q25.

|

|

1Q26 Earnings Release | p. |

Deposits

| TOTAL DEPOSITS | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Total deposits | 17,460,551 | 18,829,618 | 14,553,136 | (7.3%) | 20.0% |

| Non-financial Public Sector | 795,738 | 513,623 | 148,977 | 54.9% | 434.1% |

| Financial Sector | 9,639 | 8,529 | 9,341 | 13.0% | 3.2% |

| Non-financial private sector and residents abroad | 16,655,174 | 18,307,466 | 14,394,818 | (9.0%) | 15.7% |

| Non-financial private sector and residents abroad - AR$ | 10,560,907 | 11,448,877 | 9,775,508 | (7.8%) | 8.0% |

| Checking accounts | 1,521,196 | 1,664,466 | 1,587,356 | (8.6%) | (4.2%) |

| Savings accounts | 1,493,598 | 1,795,473 | 1,649,730 | (16.8%) | (9.5%) |

| Time deposits | 5,878,980 | 6,303,469 | 4,130,950 | (6.7%) | 42.3% |

| Investment accounts ** | 15,095 | 14,155 | 1,150,639 | 6.6% | (98.7%) |

| Other* | 1,652,038 | 1,671,314 | 1,256,833 | (1.2%) | 31.4% |

| Non-financial private sector and res. abroad - Foreign Currency | 6,094,267 | 6,858,589 | 4,619,310 | (11.1%) | 31.9% |

| Checking accounts | 417 | 1,380 | 772 | (69.8%) | (46.0%) |

| Savings accounts | 4,267,753 | 5,116,767 | 4,258,491 | (16.6%) | 0.2% |

| Time deposits | 1,341,192 | 1,291,929 | 316,619 | 3.8% | 323.6% |

| Other* | 484,905 | 448,513 | 43,428 | 8.1% | n.m |

| % of total portfolio in the private sector in AR$ | 63.4% | 62.5% | 67.9% | 87 pbs | (450)pbs |

| % of total portfolio in the private sector in Foregin Currency | 36.6% | 37.5% | 32.1% | (87)pbs | 450 pbs |

| % of UVA Time deposits & Investment accounts / Total AR$ Time deposits & Investment accounts | 0.7% | 0.4% | 1.3% | 34 pbs | (56)pbs |

| *Includes interest-bearing checking accounts and special checking accounts | |||||

| **Refers to callable time deposits | |||||

| DEPOSITS TO THE NON-FINANCIAL PRIVATE SECTOR AND RES. ABROAD IN FOREIGN CURRENCY | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of USD | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| FX rate* | 1,382.76 | 1,459.42 | 1,073.88 | (5.3%) | 28.8% |

| Non-financial private sector and residents abroad - Foreign Currency (USD) | 4,407 | 4,294 | 3,244 | 2.6% | 35.9% |

| *Wholesale U.S. dollar foreign exchange rates on BCRA’s Communication “A” 3500, as of the end of period. | |||||

During 1Q26, total deposits reached $17.5 trillion, a drop of 7.3% during the quarter, and an increase of 20.0% versus 1Q25.

Total deposits from the private sector in 1Q26 reached $16.7 trillion, showing a drop of 9.0% QoQ, and an increase of 15.7% YoY.

Los depósitos al sector privado no financiero en moneda extranjera expresados en pesos totalizaron $6.094.267 millones, cayendo 11,1% en el trimestre y aumentando 31,9% versus el 1T25. Esto se debe principalmente por una caída de caja de ahorro de 16,6%. Se destaca que los depósitos en moneda extranjera expresados en USD aumentaron 2,6% en el trimestre, denotando un efecto de la apreciación del peso argentino en las caídas mencionadas anteriormente.

Deposits from the non-financial private sector in pesos totaled $10.6 trillion, decreasing 7.8% QoQ and increasing 8.0% YoY. The quarterly variation is explained by (i) a decrease in time deposits of 6.7%, followed by (ii) a decrease of 16.8% in savings accounts, and (iii) a decrease of 8.6% in current accounts.

Deposits from the non-financial private sector in foreign currency, expressed in pesos, totaled $6.1 trillion, falling 11.1% QoQ and increasing 31.9% YoY. This is mainly due to a 16.6% drop in savings accounts. It is noteworthy that deposits in foreign currency expressed in U.S dollars increased 2.6% in the quarter, denoting an effect of the appreciation of the Argentine peso on the aforementioned decreases.

|

|

1Q26 Earnings Release | p. |

| PRIVATE DEPOSITS | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Non-financial private sector and residents abroad | 16,655,174 | 18,307,466 | 14,394,818 | (9.0%) | 15.7% |

| Sight deposits | 9,419,907 | 10,697,913 | 8,796,610 | (11.9%) | 7.1% |

| Checking accounts | 1,521,613 | 1,665,846 | 1,588,128 | (8.7%) | (4.2%) |

| Savings accounts | 5,761,351 | 6,912,240 | 5,908,221 | (16.7%) | (2.5%) |

| Other* | 2,136,943 | 2,119,827 | 1,300,261 | 0.8% | 64.3% |

| Time deposits | 7,235,267 | 7,609,553 | 5,598,208 | (4.9%) | 29.2% |

| Time deposits | 7,220,172 | 7,595,398 | 4,447,569 | (4.9%) | 62.3% |

| Investment accounts** | 15,095 | 14,155 | 1,150,639 | 6.6% | (98.7%) |

| % of sight deposits over total private deposits | 58.6% | 59.6% | 61.5% | (103)pbs | (297)pbs |

| % of time deposits over total private deposits | 41.4% | 40.4% | 38.5% | 103 pbs | 297 pbs |

| *Includes interest-bearing checking accounts and special checking accounts | |||||

| **Refers to callable time deposits | |||||

| PRIVATE DEPOSITS - NON RESTATED FIGURES | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Sight deposits | 9,419,907 | 9,774,941 | 6,633,637 | (3.6%) | 42.0% |

| Time deposits | 7,235,267 | 6,953,032 | 4,221,684 | 4.1% | 71.4% |

| Total deposits | 16,655,174 | 16,727,973 | 10,855,321 | (0.4%) | 53.4% |

In nominal terms, sight deposits fell 3.6%, time deposits rose 4.1%, and total deposits decreased 0.4%, not exceeding the period's inflation in any case.

As of 1Q26, the Bank's transactional deposits (current accounts and savings accounts) represented 41.7% of total private non-financial deposits, versus 45.6% in 4Q25 and 51.5% in 1Q25.

| MARKET SHARE - PRIVATE SECTOR DEPOSITS | BBVA ARGENTINA CONSOLIDATED | ||||

| In % | ∆ bps | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Private sector Deposits - Consolidated* | 9.93% | 10.01% | 9.15% | (8)pbs | 78 pbs |

| Based on daily BCRA information. Capital balance as of the last day of each quarter. There may be differences generated by the gap between the siscen BCRA information and published financial statements | |||||

In 1Q26, the market share of private deposits had a slight decline of 8 bps, while growing 78 bps compared to 1Q25.

Other Source of Funds

| OTHER SOURCES OF FUNDS | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Other sources of funds | 5,335,164 | 5,969,033 | 4,453,292 | (10.6%) | 19.8% |

| Central Bank | 557 | 1,885 | 368 | (70.5%) | 51.4% |

| Banks and international organizations | 172,433 | 288,700 | 62,705 | (40.3%) | 175.0% |

| Financing received from local financial institutions | 403,107 | 614,134 | 313,252 | (34.4%) | 28.7% |

| REPOs | 66,898 | 512,439 | - | (86.9%) | N/A |

| Corporate bonds | 668,576 | 673,421 | 341,076 | (0.7%) | 96.0% |

| Equity | 4,023,593 | 3,878,454 | 3,735,891 | 3.7% | 7.7% |

In 1Q26, the total amount of other source of funds was $5.3 trillion, decreasing 10.6% QoQ, and increasing 19.8% YoY.

The QoQ variation is mainly explained by the decrease in repo and reverse repo operations of 86.9%, followed by a drop in financing received from local financial institutions of 34.4%. On the other hand, equity positively offsets with an increase of 3.7%.

|

|

1Q26 Earnings Release | p. |

Liquid Assets

| TOTAL LIQUID ASSETS | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Total liquid assets | 7,947,387 | 8,317,584 | 6,924,362 | (4.5%) | 14.8% |

| Cash and deposits in banks | 4,005,427 | 5,201,053 | 3,250,050 | (23.0%) | 23.2% |

| Debt securities at fair value through P&L | 475,604 | 344,717 | 563,552 | 38.0% | (15.6%) |

| Government securities | 475,483 | 344,717 | 563,552 | 37.9% | (15.6%) |

| BCRA Instruments | 121 | - | - | N/A | N/A |

| Net REPO transactions | (66,898) | (512,439) | - | 86.9% | N/A |

| Other debt securities | 3,532,632 | 3,284,253 | 3,107,006 | 7.6% | 13.7% |

| Government securities | 3,532,632 | 3,284,253 | 3,050,301 | 7.6% | 15.8% |

| BCRA Instruments | - | - | 56,705 | N/A | (100.0%) |

| Overnight transactios in foreign banks | 622 | - | 3,754 | N/A | (83.4%) |

| Liquid assets / Total Deposits | 45.5% | 44.2% | 47.6% | 134 pbs | (206)pbs |

| Liquid assets / Total Deposits ARS | 43.4% | 37.7% | 43.8% | 570 pbs | (40)pbs |

| Liquid assets / Total Deposits USD | 48.9% | 55.2% | 55.4% | (625)pbs | (651)pbs |

In 1Q26, the Bank's liquid assets reached $7.9 trillion, decreasing 4.5% QoQ, and increasing 14.8% YoY.

In the quarter, the liquidity ratio (liquid assets / total deposits) reached a level of 45.5%. The liquidity ratio in local and foreign currency reached 43.4% and 48.9% respectively.

Solvency

| MINIMUM CAPITAL REQUIREMENT | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| Minimum capital requirement | 1,529,107 | 1,571,269 | 1,268,072 | (2.7%) | 20.6% |

| Credit risk | 1,441,565 | 1,504,677 | 1,240,323 | (4.2%) | 16.2% |

| Market risk | 7,868 | 5,574 | 7,155 | 41.2% | 10.0% |

| Operational risk | 79,674 | 61,017 | 20,594 | 30.6% | 286.9% |

| Integrated Capital - RPC (1)* | 3,497,604 | 3,487,354 | 3,313,941 | 0.3% | 5.5% |

| Ordinary Capital Level 1 ( COn1) | 3,953,814 | 3,915,326 | 3,696,733 | 1.0% | 7.0% |

| Deductible items COn1 | (456,210) | (427,973) | (382,793) | (6.6%) | (19.2%) |

| Excess Capital | |||||

| Integration excess | 1,968,497 | 1,916,085 | 2,045,868 | 2.7% | (3.8%) |

| Excess as % of minimum capital requirement | 128.7% | 121.9% | 161.3% | 679 pbs | (3,260)pbs |

| Risk-weighted assets (RWA, according to B.C.R.A. regulation) (2) | 18,588,992 | 19,093,036 | 15,399,328 | (2.6%) | 20.7% |

| Regulatory Capital Ratio (1)/(2) | 18.8% | 18.3% | 21.5% | 55 pbs | (270)pbs |

| TIER I Capital Ratio (Ordinary Capital Level 1/ RWA) | 18.8% | 18.3% | 21.5% | 55 pbs | (270)pbs |

| * RPC includes 100% of quarterly results | |||||

BBVA Argentina continues to show solid solvency indicators as of 1Q26. The capital ratio reached 18.8%, stable compared to 18.3% in 4Q25. The excess over the regulatory requirement reached $2.0 trillion or 128.7%.

The increase in the ratio in the quarter was due both to a slight increase in Common Equity Tier 1 (CET1) of 1.0%, and a 2.6% drop in risk-weighted assets.

BBVA Argentina Asset Management S.A.

|

|

1Q26 Earnings Release | p. |

| MUTUAL FUNDS ASSETS | BBVA ARGENTINA CONSOLIDATED | ||||

| In millions of AR$ - Inflation adjusted | ∆ % | ||||

| 1Q26 | 4Q25 | 1Q25 | QoQ | YoY | |

| FBA Renta Pesos | 3,523,376 | 3,535,248 | 4,081,735 | (0.3%) | (13.7%) |

| FBA Renta Fija Dólar I | 307,308 | 221,279 | 151,858 | 38.9% | 102.4% |

| FBA Ahorro Pesos | 160,283 | 132,863 | 204,208 | 20.6% | (21.5%) |

| FBA Money Market Dólar | 111,204 | 66,553 | - | 67.1% | N/A |

| FBA Bonos Argentina | 97,912 | 73,429 | 39,661 | 33.3% | 146.9% |

| FBA Horizonte | 90,807 | 83,639 | 46,518 | 8.6% | 95.2% |

| FBA Acciones Argentinas | 87,585 | 99,789 | 142,479 | (12.2%) | (38.5%) |

| FBA Gestión I | 56,229 | - | - | N/A | N/A |

| FBA Renta Fija Plus | 45,953 | 31,452 | 39,132 | 46.1% | 17.4% |

| FBA Renta Fija Dólar Plus I | 34,204 | 23,695 | 1,053 | 44.4% | n.m |

| FBA Renta Pública I | 22,834 | 11,600 | 9,497 | 96.8% | 140.4% |

| FBA Acciones Latinoamericanas | 17,563 | 14,171 | 13,062 | 23.9% | 34.5% |

| FBA Renta Mixta | 14,311 | 15,722 | 20,478 | (9.0%) | (30.1%) |

| FBA Renta Fija Dólar Latam I | 138 | 159 | - | (13.2%) | N/A |