Mar UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________

FORM 40-F

__________________

| ☐ | Registration Statement pursuant to Section 12 of the Securities Exchange Act of 1934 |

or

| ☒ | Annual Report pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2025

Commission File Number: 001-40786

__________________

SIGMA LITHIUM CORPORATION

(Exact name of Registrant as specified in its charter)

__________________

| Canada | 1000 | Not Applicable | ||

| (Province or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

181, Bay Street, Suite 4400, Toronto, Ontario

M5J 2T3, Canada

Tel: +55 11-2985-0089

(Address and telephone number of Registrant’s principal executive offices)

C T Corporation System

28 Liberty Street

New York, New York 10005

Telephone: (212) 894-8940

(Name, address (including zip code) and telephone number (including area code) of agent for

service in the United States)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

| Common Shares, no par value | SGML | The Nasdaq Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

For annual reports, indicate by check mark the information filed with this Form:

| ☒ Annual Information Form | ☒ Audited Annual Financial Statements |

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

111,402,979 Common Shares outstanding as of December 31, 2025

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the Registrant is an emerging growth company as defined in Rule 12b-2 of the Exchange Act.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the Registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the Registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the Registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

INTERNAL CONTROL OVER FINANCIAL REPORTING AND DISCLOSURE CONTROLS AND PROCEDURES

The Internal Control over Financial Reporting is filed in Exhibit 99.2 hereto which contains the link to the Management’s Discussion and Analysis for the year ended December 31, 2025, incorporated herein by reference.

MANAGEMENT’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND DISCLOSURE CONTROLS AND PROCEDURES

The Internal Control over Financial Reporting is filed in Exhibit 99.2 hereto which contains the link to the Management’s Discussion and Analysis for the year ended December 31, 2025, incorporated herein by reference.

AUDIT COMMITTEE FINANCIAL EXPERT

The Company’s Board of Directors has determined that it has at least one audit committee financial expert serving on its Audit Committee. The Board has determined that Junaid Jafar is an audit committee financial expert and is independent, as that term is defined by the Exchange Act and the Nasdaq corporate governance standards applicable to the Company.

The Audit Committee has indicated that the designation of a person as an audit committee financial expert does not make such person an “expert” for any purpose, impose on such person any duties, obligations or liability that are greater than those imposed on such person as a member of the Audit Committee and the Board in the absence of such designation and does not affect the duties, obligations or liability of any other member of the Audit Committee or Board.

CODE OF ETHICS

The Board has adopted a written code of business conduct and ethics (the “Code”), which applies to the Board and all officers and employees of the Company, including the Company’s principal executive officer, principal financial officer and principal accounting officer or controller. There were no waivers granted in respect of the Code during the fiscal year ended December 31, 2025. The Code is posted on the Company’s website at www.sigmalithiumresources.com. If there is an amendment to the Code, or if a waiver of the Code is granted to any of Company’s principal executive officers, principal financial officer, principal accounting officer or controller, the Company intends to disclose any such amendment or waiver by posting such information on the Company’s website. Unless and to the extent specifically referred to herein, the information on the Company’s website shall not be deemed to be incorporated by reference in this Annual Report.

PRINCIPAL ACCOUNTANT FEES AND SERVICES

Grant Thornton Auditores Independentes Ltda., São Paulo, Brazil, Audit Firm ID: 5270, acted as the Company’s independent registered public accounting firm for the fiscal year ended December 31, 2025 and 2024. See page 75 of the Company’s Annual Information Form, which is attached hereto as Exhibit 99.1, for the total amount billed to the Company by Grant Thornton Auditores Independentes Ltda. for services performed in the last two fiscal years by category of service (for audit fees, audit-related fees, tax fees and all other fees).

AUDIT COMMITTEE PRE-APPROVAL POLICIES AND PROCEDURES

See page 75 of the Company’s Annual Information Form, which is attached hereto as Exhibit 99.1. No audit-related fees, tax fees or other non-audit fees were approved by the Audit Committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

OFF-BALANCE SHEET ARRANGEMENTS

The information included in “Financial risk factors—Market Risk” attached hereto as Exhibit 99.2 which contains the link to the Management’s Discussion and Analysis for the year ended December 31, 2025, incorporated herein by reference.

IDENTIFICATION OF THE AUDIT COMMITTEE

The Board has a separately designated standing Audit Committee established in accordance with section 3(a)(58)(A) of the Exchange Act and satisfies the requirements of Exchange Act Rule 10A-3. The Company’s Audit Committee is comprised of Junaid Jafar, Alexandre Rodrigues Cabral and Kátia Abreu, all of whom, in the opinion of the Company’s Board of Directors, are independent (as determined under Rule 10A-3 of the Exchange Act and the Nasdaq Rules) and all of whom are financially literate.

CORPORATE GOVERNANCE PRACTICES

There are certain differences between the corporate governance practices applicable to the Company and those applicable to U.S. companies under the Nasdaq Corporate Governance Requirements. A summary of the significant differences can be found on the Company’s website at www.sigmalithiumresources.com. Information contained in or otherwise accessible through the Company’s website does not form part of this Annual Report and is not incorporated into this Annual Report by reference.

MINE SAFETY DISCLOSURE

Pursuant to Section 1503(a) of the Dodd-Frank Act, issuers that are operators, or that have a subsidiary that is an operator, of a coal or other mine in the United States are required to disclose specified information about mine health and safety in their periodic reports. These reporting requirements are based on the safety and health requirements applicable to mines under the Federal Mine Safety and Health Act of 1977 (the “Mine Act”) which is administered by the U.S. Department of Labor’s Mine Safety and Health Administration (“MSHA”). During the fiscal year ended December 31, 2025, the Company and its subsidiaries were not subject to regulation by MSHA under the Mine Act and thus no disclosure is required under Section 1503(a) of the Dodd-Frank Act.

DIFFERENCES IN UNITED STATES AND CANADIAN REPORTING PRACTICES

The Company is permitted, under a multijurisdictional disclosure system adopted by the United States, to prepare this report in accordance with Canadian disclosure requirements, which are different from those of the United States. The Company prepares its financial statements, which are filed with this Annual Report in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board, and the audit is subject to Canadian auditing and auditor independence standards.

Disclosure regarding the Company’s mineral properties, including with respect to mineral reserve and mineral resource estimates included in this Annual Report, was prepared in accordance with NI 43-101. NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. NI 43-101 differs significantly from the disclosure requirements of the SEC generally applicable to U.S. companies. Accordingly, information contained in this Annual Report is not comparable to similar information made public by U.S. companies reporting pursuant to SEC disclosure requirements.

INCORPORATED DOCUMENTS

Annual Information Form

The Company’s AIF is filed as Exhibit 99.1 to this Annual Report.

Management’s Discussion and Analysis

The Company’s management’s discussion and analysis (“MD&A”) is filed as Exhibit 99.2 to this Annual Report.

Audited Annual Financial Statements

The Company’s consolidated financial statements and auditor’s reports thereon are filed as Exhibit 99.3 to this Annual Report.

UNDERTAKING AND CONSENT TO SERVICE OF PROCESS

A. Undertaking

The Company undertakes to make available, in person or by telephone, representatives to respond to inquiries made by the Commission staff, and to furnish promptly, when requested to do so by the Commission staff, information relating to: the securities in relation to which the obligation to file an annual report on Form 40-F arises; or transactions in said securities.

B. Consent to Service of Process

The Company has filed an Appointment of Agent for Service of Process and Undertaking on Form F-X with respect to the class of securities in relation to which the obligation to file this Annual Report arises.

EXHIBIT INDEX

SIGNATURE

Pursuant to the requirements of the Exchange Act, Sigma Lithium Corporation certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this annual report to be signed on its behalf by the undersigned, thereto duly authorized.

Dated: March 30, 2026

| SIGMA LITHIUM CORPORATION | |||

| By: | /s/ | ||

| Name: | Ana Cristina Cabral | ||

| Title: | Chief Executive Officer | ||

SIGMA LITHIUM CORPORATION

CLAWBACK POLICY

The Board of Directors (“Board”) of Sigma Lithium Corporation (the “Company”) has adopted this Policy in accordance with Nasdaq listing requirements.

A. Application of Policy

This Policy applies in the event of any restatement (“Restatement”) of the Company’s financial results due to its material non-compliance with financial reporting requirements under the securities laws.1 This Policy does not apply to restatements that are not caused by non-compliance with financial reporting requirements, such as, but not limited to, a retrospective: (1) application of a change in accounting principles; (2) revision to reportable segment information due to a change in the structure of the Company’s internal organization; (3) reclassification due to a discontinued operation; (4) application of a change in reporting entity, such as from a reorganization of entities under common control; (5) adjustment to provision amounts in connection with a prior business combination; and (6) revision for stock splits, reverse stock splits, dividends or other changes in capital structure (collectively the “Restatement Exclusions”).

B. Executive Officers Subject to the Policy

The “executive officers” of the Company are covered by this Policy. This includes the Company’s current or former Chief Executive Officer, Chief Financial Officer, any Vice-President of the Company in charge of a principal business unit, division or function, and any other current or former officer or person who performs a significant policy-making function for the Company, including executive officers of Company subsidiaries (the “Executive Officers”). All of these Executive Officers are subject to this Policy, even if an Executive Officer had no responsibility for the financial statement errors which required restatement.

C. Compensation Subject to the Policy

This Policy applies to any incentive-based compensation received by an Executive Officer during the period (the “Clawback Period”) consisting of any of the three fiscal completed years immediately preceding:

| · | the date that the Company’s Board (or Audit Committee) concludes, or reasonably should have concluded, that the Company is required to prepare a Restatement, or |

| 1 | Please note that this includes both big “R” restatement (to correct a material error to previously issued financial statements) and little “r” restatements (to correct errors that are not material to previously issued financial statements but would result in a material misstatement if (a) the errors were left uncorrected in the current report or (b) the error correction was recognized in the current period). |

|

|

| · | the date that a court, regulator, or other legally authorized body directs the Company to prepare a Restatement. |

This Policy covers all incentive-based compensation (including any cash or equity compensation) that is granted, earned or vested based wholly or in part upon the attainment of any “financial reporting measure”. Financial reporting measures are those that are determined and presented in accordance with the accounting principles used in preparing the Company’s financial statements and any measures derived wholly or in part from such financial information (including non-GAAP measures, stock price and total shareholder return). Incentive-based compensation is deemed “received” in the fiscal period during which the applicable financial reporting measure (as specified in the terms of the award) is attained, even if the payment or grant occurs after the end of that fiscal period.

Incentive-based compensation does not include base annual salary, compensation which is awarded based solely on service to the Company (e.g. a time-vested award, including time-vesting stock options or restricted share units), nor does it include compensation which is awarded based on subjective standards, strategic measures (e.g. completion of a merger) or operational measures (e.g. attainment of a certain market share).

D. Amount Required to be Repaid Pursuant to this Policy

The amount of incentive-based compensation that must be repaid (subject to the few limitations discussed below) is the amount of incentive-based compensation received by the Executive Officer that exceeds the amount of incentive-based compensation that otherwise would have been received had it been determined based on the Restatement (the “Recoverable Amount”). Applying this definition, after a Restatement, the Company will recalculate the applicable financial reporting measure and the Recoverable Amount in accordance with SEC and exchange rules. The Company will determine whether, based on that financial reporting measure as calculated relying on the original financial statements, an Executive Officer received a greater amount of incentive-based compensation than would have been received applying the recalculated financial measure. Where incentive-based compensation is based only in part on the achievement of a financial reporting measure performance goal, the Company will determine the portion of the original incentive-based compensation based on or derived from the financial reporting measure which was restated and will recalculate the affected portion based on the financial reporting measure as restated to determine the difference between the greater amount based on the original financial statements and the lesser amount that would have been received based on the Restatement. The Recoverable Amounts will be calculated on a pre-tax basis to ensure that the Company recovers the full amount of incentive-based compensation that was erroneously awarded.

In no event shall the Company be required to award Executive Officers an additional payment if the restated or accurate financial results would have resulted in a higher incentive compensation payment.

|

|

If equity compensation is recoverable due to being granted to the Executive Officer (when the accounting results were the reason the equity compensation was granted) or vested by the Executive Officer (when the accounting results were the reason the equity compensation was vested), in each case in the Clawback Period, the Company will recover the excess portion of the equity award that would not have been granted or vested based on the Restatement, as follows:

| · | if the equity award is still outstanding, the Executive Officer will forfeit the excess portion of the award; |

| · | if the equity award has been exercised or settled into shares (the “Underlying Shares”), and the Executive Officer still holds the Underlying Shares, the Company will recover the number of Underlying Shares relating to the excess portion of the award (less any exercise price paid for the Underlying Shares); and |

| · | if the Underlying Shares have been sold by the Executive Officer, the Company will recover the proceeds received by the Executive Officer from the sale of the Underlying Shares relating to the excess portion of the award (less any exercise price paid for the Underlying Shares). |

The Board will take such action as it deems appropriate, in its sole and absolute discretion, reasonably promptly to recover the Recoverable Amount, unless all of the independent directors of the Board determine that it would be impracticable to recover such amount because (1) the direct costs of enforcing recovery would exceed the Recoverable Amount,2 or (2) recovery would likely cause an otherwise tax-qualified retirement plan, under which benefits are broadly available to employees of the Company, to fail to meet the requirements of 26 U.S.C. 401(a)(13) or 26 U.S.C. 411(a) and regulations thereunder3, or (3) if the recovery of the incentive-based compensation would violate the home-country laws of the Company.

E. Additional Clawback Required by Section 304 of the Sarbanes-Oxley Act of 2002

In addition to the provisions described above, if the Company is required to prepare an accounting restatement due to the material noncompliance of the Company, as a result of misconduct, with any financial reporting requirement under the securities laws, then, in accordance with Section 304 of the Sarbanes-Oxley Act of 2002, the Chief Executive Officer and Chief Financial Officer (at the time the financial document embodying such financial reporting requirement was originally issued) shall reimburse the Company for:

| · | any bonus or other incentive-based or equity-based compensation received from the Company during the 12-month period following the first public issuance or filing with the Commission (whichever first occurs) of such financial document; and |

| 2 | To reach this determination, the Company must have first made a reasonable and documented attempt at recovery. |

| 3 | To reach this determination, the Company must obtain an opinion of counsel. |

|

|

| · | any profits realized from the sale of securities of the Company during that 12-month period. |

F. Crediting of Recovery Amounts

To the extent that subsections A, B, C and D of this policy (the “Rule 10D-1 Clawback Requirements”) would provide for recovery of incentive-based compensation recoverable by the Company pursuant to Section 304 of the Sarbanes-Oxley Act, in accordance with subsection E of this policy (the “Sarbanes-Oxley Clawback Requirements”), and/or any other recovery obligations (including pursuant to employment agreements, or plan awards), the amount such Executive Officer has already reimbursed the Company shall be credited to the required recovery under the Rule 10D-1 Clawback Requirements. Recovery pursuant to the Rule 10D-1 Clawback Requirements does not preclude recovery under the Sarbanes-Oxley Clawback Requirements, to the extent any applicable amounts have not been reimbursed to the Company.

G. General Provisions

This Policy may be amended by the Board from time to time. Changes to this Policy will be communicated to all persons to whom this Policy applies.

The Company will not indemnify or provide insurance to cover any repayment of incentive-based compensation in accordance with this Policy.

The provisions of this Policy apply to the fullest extent of the law; provided however, to the extent that any provisions of this Policy are found to be unenforceable or invalid under any applicable law, such provision will be applied to the maximum extent permitted, and shall automatically be deemed amended in a manner consistent with its objectives to the extent necessary to conform to any limitations required under applicable law.

This Policy is in addition to (and not in lieu of) any right of repayment, forfeiture or right of offset against any Executive Officer that is required pursuant to any other statutory repayment requirement (regardless of whether implemented at any time prior to or following the adoption of this Policy). Nothing in this Policy in any way detracts from or limits any obligation that those subject to it have in law or pursuant to a management, employment, consulting or other agreement with the Company or any of its subsidiaries.

All determinations and decisions made by the Board (or any committee thereof) pursuant to the provisions of this Policy shall be final, conclusive and binding on the Company, its subsidiaries and the persons to whom this Policy applies. Executive Officers (as defined above) are required to acknowledge that they have read this Policy annually. If you have questions about the interpretation of this Policy, please contact the Chief Legal Officer of the Company.

|

|

| |

Definitions

For a description of defined terms and other reference information used in this Annual Information Form (this “AIF”), please refer to Schedule “B”.

CIM Definition Standards

The disclosure included in this AIF uses mineral resource and mineral reserve classification terms that comply with reporting standards in Canada. All mineral resource and mineral reserve estimates are made in accordance with the CIM Definition Standards and National Instrument 43-101 (“NI 43-101”), which is a set of rules developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects and operations. The following definitions are reproduced from the CIM Definition Standards:

A “mineral resource” is a concentration or occurrence of solid material of economic interest in or on the Earth’s crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other geological characteristics of a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling. Mineral resources are sub-divided, in order of increasing geological confidence, into inferred, indicated and measured categories, which are defined as follows:

| · | An “inferred mineral resource” is that part of a mineral resource for which quantity, grade or quality are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade or quality continuity. An inferred mineral resource has a lower level of confidence than that applying to an indicated mineral resource and must not be converted to a mineral reserve. It is reasonably expected that the majority of inferred mineral resources could be upgraded to indicated mineral resources with continued exploration. |

| · | An “indicated mineral resource” is that part of a mineral resource for which quantity, grade or quality, densities, shape and physical characteristics are estimated with sufficient confidence to allow the application of modifying factors (as defined below) in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation. An indicated mineral resource has a lower level of confidence than that applying to a measured mineral resource and may only be converted to a probable mineral reserve. |

| · | A “measured mineral resource” is that part of a mineral resource for which quantity, grade or quality, densities, shape, and physical characteristics are estimated with confidence sufficient to allow the application of modifying factors to support detailed mine planning and final evaluation of the economic viability of the deposit. Geological evidence is derived from detailed and reliable exploration, sampling and testing, and is sufficient to confirm geological and grade or quality continuity between points of observation. A measured mineral resource has a higher level of confidence than that applying to either an indicated mineral resource or an inferred mineral resource. It may be converted to a proven mineral reserve or to a probable mineral reserve. |

“Modifying factors” are considerations used to convert mineral resources to mineral reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social and governmental factors.

A “mineral reserve” is the economically mineable part of a measured and/or indicated mineral resource. It includes diluting materials and allowances for losses which may occur when the material is mined or extracted and is defined by studies at pre-feasibility or feasibility level as appropriate that include application of modifying factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified. Mineral reserves are sub-divided, in order of increasing geological confidence, into probable and proven categories, which are defined as follows:

| |

| · | A “probable mineral reserve” is the economically mineable part of an indicated, and in some circumstances, a measured mineral resource. The confidence in the modifying factors applying to a probable mineral reserve is lower than that applying to a proven mineral reserve. |

| · | A “proven mineral reserve” is the economically mineable part of a measured mineral resource. A proven mineral reserve implies a high degree of confidence in the modifying factors. |

CAUTIONARY NOTE REGARDING FORWARD LOOKING INFORMATION

Certain information and statements in the MD&A included herein and in this AIF may constitute “forward-looking information” within the meaning of Canadian securities legislation and “forward-looking statements” within the meaning of U.S. securities legislation (collectively, “Forward-Looking Information”), which involve known and unknown risks, uncertainties, and other factors which may cause the actual results, performance or achievements of the Company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such Forward-Looking Information. All statements, other than statements of historical fact, may be Forward-Looking Information, including, but not limited to, mineral resource or mineral reserve estimates (which reflect a prediction of the mineralization that would be realized by development). When used in this AIF, such statements generally use words such as “may”, “would”, “could”, “will”, “intend”, “expect”, “believe”, “plan”, “anticipate”, “estimate” and other similar terminology. These statements reflect management’s current expectations regarding future events and operating performance and speak only as of the date of this AIF. Forward Looking Information involves significant risks and uncertainties, should not be read as guarantees of future performance or results, and does not necessarily provide accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from the results discussed in the Forward Looking Information, which is based upon what management believes are reasonable assumptions, and there can be no assurance that actual results will be consistent with the Forward Looking Information.

In particular (but without limitation), this AIF contains Forward Looking Information with respect to the following matters: statements regarding anticipated decision making with respect to the Company; capital expenditure programs; estimates of mineral resources and mineral reserves; development of mineral resources and mineral reserves; government regulation of mining operations and treatment under governmental and taxation regimes; the future price of commodities, including lithium; the realization of mineral resource and mineral reserve estimates, including whether mineral resources will ever be developed into mineral reserves; the timing and amount of future production; currency exchange and interest rates; expected outcome and timing of environmental surveys and permit applications and other environmental matters; potential positive or negative implications of change in government; the Company’s ability to raise capital and obtain project financing; expected expenditures to be made by the Company on its properties; successful operations and the timing, cost, quantity, capacity and quality of production; capital costs, operating costs and sustaining capital requirements, including the cost of construction of the processing plant; and competitive conditions and the ongoing uncertainties and effects in respect of the military and global conflicts.

Forward-Looking Information does not take into account the effect of transactions or other items announced or occurring after the statements are made. Forward-Looking Information is based upon a number of expectations and assumptions and is subject to several risks and uncertainties, many of which are beyond the Company’s control, that could cause actual results to differ materially from those disclosed in or implied by such Forward-Looking Information. With respect to the Forward-Looking Information, the Company has made assumptions regarding, among other things:

| · | General economic and political conditions (including but not limited to the impact of the continuance or escalation of the military conflict between Russia and Ukraine, the military conflict in Middle East, and other military and global conflicts, and the multinational economic sanctions in relation to such conflicts). |

| |

| · | Stable and supportive legislative, regulatory and community environment in the jurisdictions where the Company operates. |

| · | Stability and inflation of the Brazilian Real, including any foreign exchange or capital controls which may be enacted in respect thereof, and the effect of current or any additional regulations on the Company’s operations. |

| · | Demand for lithium, including that such demand is supported by growth in the EV market. |

| · | Estimates of, and changes to, the market prices for lithium. |

| · | The impact of increasing competition in the lithium business and the Company’s competitive position in the industry. |

| · | The Company’s market position and financial and operating performance. |

| · | The Company’s estimates of mineral resources and mineral reserves, including whether mineral resources will ever be developed into mineral reserves. |

| · | Anticipated timing and results of exploration, development and construction activities. |

| · | Reliability of technical data. |

| · | The Company’s ability to maintain full capacity commercial production, including that the Company will not experience any materials or equipment shortages, any labor or service provider outages or delays or any technical issues. |

| · | The Company’s ability to obtain financing on satisfactory terms to develop its projects, if required. |

| · | The Company’s ability to obtain and maintain mining, exploration, environmental and other permits, authorizations and approvals. |

| · | The timing and outcome of regulatory and permitting matters. |

| · | The exploration, development, construction and operational costs. |

| · | The accuracy of budget, construction and operations estimates for the Company. |

| · | Successful negotiation of definitive commercial agreements. |

| · | The Company’s ability to operate in a safe and effective manner. |

Although management believes that the assumptions and expectations reflected in such Forward-Looking Information are reasonable, there can be no assurance that these assumptions and expectations will prove to be correct. Since Forward-Looking Information inherently involves risks and uncertainties, undue reliance should not be placed on such information.

In addition, Forward Looking Information with respect to the potential outlook and future financial results contained in this AIF is based on assumptions noted above and about future events, including economic conditions and proposed courses of action, based on management's assessment of the relevant information available as at the date of such information. Readers are cautioned that any such information should not be used for purposes other than for which it is disclosed.

The Company’s actual results could differ materially from those anticipated in any Forward-Looking Information as a result of various known and unknown risk factors, including (but not limited to) the risk factors referred to under the heading “Risk Factors” in this AIF. Such risks relate to, but are not limited to, the following:

| · | The Company’s mineral resource and mineral reserve estimates are estimates only and no assurance can be given that any particular level of recovery of minerals will in fact be realized or that identified mineral resources or mineral reserves will ever qualify as a commercially mineable (or viable) deposit. |

| · | The Company’s future production estimates are based on existing mine plans and other assumptions which change from time to time. No assurance can be given that such estimates will be achieved. |

| · | The Company’s capital and operating cost estimates may vary from actual costs and revenues for reasons outside of the Company’s control. |

| · | The Company's operations are subject to the high degree of risk normally incidental to the exploration for, and the development and operation of, mineral properties. |

| |

| · | Insurance may not be available to insure against all such risks, or the costs of such insurance may be uneconomic. Losses from uninsured and underinsured losses have the potential to materially affect the Company’s financial position and prospects. |

| · | The Company is subject to risks associated with securing title, property interests and exploration and exploitation rights. |

| · | The Company is subject to strong competition in Brazil and in the global mining industry. |

| · | There can be no assurance that market prices for lithium will remain at current levels or that such prices will improve. |

| · | The market for EVs and other large format batteries remains an emerging technology in several markets. No assurances can be given for the rate at which this market will develop, if at all, which could affect the success of the Company and its ability to expand lithium operations. |

| · | Changes in technology or other developments could result in preferences for substitute products. |

| · | The imbalance in the lithium market due to an excess of supply from new or existing competitors could adversely affect prices. |

| · | The Company’s financial condition, operations and results of operations are subject to political, economic, social, regulatory and geographic risks of doing business in Brazil. |

| · | Inflation in Brazil, along with Brazilian governmental measures to combat inflation, may have a significant negative effect on the Brazilian economy and, as a result, on the Company’s financial condition and results of operations. |

| · | Violations of anti-corruption, anti-bribery, anti-money laundering and economic sanctions laws and regulations could materially adversely affect the Company’s business, reputation, results of operations and financial condition. |

| · | Corruption and fraud in Brazil relating to ownership of real estate could materially adversely affect the Company’s business, reputation, results of operations and financial condition. |

| · | The Company is subject to regulatory frameworks applicable to the Brazilian mining industry which could be subject to further change, as well as government approval and permitting requirements, which may result in limitations on the Company’s business and activities. |

| · | The Company is subject to currency fluctuation risks. |

| · | The Company is subject to interest rates fluctuation. |

| · | The Company may face challenges in accessing global capital markets. |

| · | The Company is exposed to risks associated with doing business with counterparties, which may impact the Company’s operations and financial condition. |

| · | The Company may not be able to secure the supply of key raw material. |

| · | The Company may not be able to meet the quality requirements of its customers. |

| · | Any limitation on the transfer of cash or other assets between the Company and the Company’s subsidiaries, or among such entities, could restrict the Company’s ability to fund its operations efficiently or the ability of its subsidiaries to distribute cash otherwise available for distributions. |

| · | The Company is subject to risks associated with its reliance on consultants and others for mineral exploration and exploitation expertise. |

| · | Operating cash flow may be insufficient for future needs. |

| · | The Company may be unable to achieve cash flow from operating activities sufficient to permit it to pay the principal, premium, if any, and interest on the Company’s indebtedness, or maintain its debt covenants. |

| · | The Company may not be able to obtain sufficient financing in the future on acceptable terms, which could have a material adverse effect on the Company’s business, results of operations and financial condition. In order to obtain additional financing, the Company may conduct additional (and possibly dilutive) equity offerings or debt issuances in the future. |

| · | From time to time, the Company may become involved in litigation, which may have a material adverse effect on its business, financial condition and prospects. |

| |

| · | Failure to retain key officers, consultants and employees or to attract and retain additional key individuals with necessary skills could have a materially adverse impact upon the Company’s success. |

| · | The Company’s business depends on strong labor and employment relations. |

| · | Failure in the infrastructure that the Company relies upon could have an adverse effect on its operations. |

| · | The Company’s operations are subject to numerous environmental laws and regulations and expose the Company to environmental compliance risks, which may result in significant costs and have the potential to reduce the profitability of operations. |

| · | Physical climate change events and the trend toward more stringent regulations aimed at reducing the effects of climate change could have an adverse effect on the Company’s business and operations. |

| · | The Company may become subject to government orders, investigations, inquiries or other proceedings (including civil claims) relating to securities, labor, environmental and health and safety matters, which could result in consequences material to its business and operations. |

| · | The Company’s operations and the development of Sigma Lithium’s properties may be adversely affected if it is unable to maintain positive community relations. |

| · | Actions taken by foreign governments regarding critical minerals may affect the Company’s business. |

| · | The Company’s operations may be adversely affected if its licenses and permits are challenged, revoked, amended, not issued or not renewed. |

| · | The Company may be subject to sudden tax changes, which can have a material adverse effect on profitability. |

| · | The Company has not declared or paid dividends in the past and may not declare or pay dividends in the future. |

| · | The market price for the Company’s Common Shares may be volatile and subject to wide fluctuations in response to numerous factors beyond its control, and the Company may be subject to securities litigation as a result. |

| · | If securities analysts, industry analysts or activist short sellers publish research or other reports about the Company’s business, prospects or value, which questions or downgrades the value of the Company, the price of the Common Shares could decline. |

| · | The Company will have broad discretion over the use of the net proceeds from offerings of its securities. |

| · | There is no guarantee that the Common Shares will earn any positive return in the short term or long term. |

| · | The Company has increased costs as a result of being a public company both in Canada listed on the TSXV and in the United States listed on the Nasdaq, and its management is required to devote further substantial time to United States public company compliance efforts. |

| · | If the Company does not implement and maintain adequate and appropriate internal controls over financial reporting as outlined in accordance with NI 52109 or the Rules and Regulations of the SEC, inappropriately designed or ineffective controls could result in inaccurate financial reporting. |

| · | As a foreign private issuer, the Company is subject to different U.S. securities laws and rules than a domestic U.S. issuer, which may limit the information publicly available to its shareholders. |

| · | The Company may be a Passive Foreign Investment Company, which may result in adverse U.S. federal income tax consequences for U.S. holders of Common Shares. |

| · | The current military conflict in Ukraine and the Middle East and the economic or other sanctions imposed in response to such military conflicts and other global conflicts may impact global markets in such a manner as to have a material adverse effect on the Company’s business, operations, financial condition and stock price. |

| · | Certain directors and officers of the Company are, or may become, associated with other natural resource companies which may give rise to conflicts of interest. |

| · | The Company has a major shareholder which owns 42.77% of the outstanding Common Shares and, as such, for as long as such shareholder directly or indirectly maintains a significant interest in the Company, it may be in a position to affect the Company’s governance, operations and the market price of the Common Shares. |

| |

| · | As the Company is a Canadian corporation but many of its directors and officers are not citizens or residents of Canada or the U.S., it may be difficult or impossible for an investor to enforce judgements against the Company and its directors and officers outside of Canada and the U.S. which may have been obtained in Canadian or U.S. courts or initiate court action outside Canada or the U.S. against the Company and its directors and officers in respect of an alleged breach of securities laws or otherwise. Similarly, it may be difficult for U.S. shareholders to effect service on the Company to realize on judgments obtained in the United States. |

| · | The Company is governed by the Ontario Business Corporations Act and by the securities laws of the province of Ontario, which in some cases have a different effect on shareholders than U.S. corporate laws and U.S. securities laws. |

| · | The Company is subject to risks associated with its information technology systems and cyber-security. |

Readers are cautioned that the foregoing lists of assumptions and risks is not exhaustive. The Forward-Looking Information contained in this AIF is expressly qualified by these cautionary statements. All Forward Looking Information in this AIF speaks as of the date of this AIF. The Company does not undertake any obligation to update or revise any Forward-Looking Information, whether as a result of new information, future events or otherwise, except as required by applicable securities law. Additional information about these assumptions, risks and uncertainties is contained in the Company’s filings with securities regulators, including the Company’s most recent annual MD&A, which are available on SEDAR+ at www.sedarplus.ca and on EDGAR at www.sec.gov.

CAUTIONARY NOTE REGARDING MINERAL RESOURCE AND MINERAL RESERVE ESTIMATES

Technical disclosure included in this AIF regarding the Company’s properties, and in the documents incorporated herein by reference, has not been prepared in accordance with the requirements of U.S. securities laws. Without limiting the foregoing, such technical disclosure uses terms that comply with reporting standards in Canada and estimates are made in accordance with NI 43-101. Unless otherwise indicated, all mineral reserve and mineral resource estimates contained in the technical disclosure have been prepared in accordance with NI 43-101 and the CIM Definition Standards.

NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. NI 43-101 differs significantly from the disclosure requirements of the SEC generally applicable to U.S. companies. Accordingly, information contained in this AIF is not comparable to similar information made public by U.S. companies reporting pursuant to SEC disclosure requirements.

Currency and Functional Currency

The Company's functional currency is the currency of the primary economic environment in which it operates and that best reflects its business and operations. The Company’s operations are held by the Brazilian subsidiary, Sigma Mineração S.A., which provides the entirety of the inflows and outflows of the Company, including any dividends to be remitted. The Parent Company in Canada is a pure holding company with no operations and depends on the Brazilian subsidiary to provide its cash flow. The prices of the lithium commodity are globally referenced in U.S. dollars to provide reference for market players located in different countries and different currencies. Consequently, the Company’s revenues are translated into the Brazilian Real, which is the currency that most of the costs for supplying products or services are incurred and which the costs are normally expressed and settled. Accordingly, the Company’s functional currency is the Brazilian Real ("R$").

| |

This AIF contains references to United States dollars, Canadian dollars and Brazilian Reais. All dollar amounts referenced, unless otherwise indicated, are expressed in United States dollars, referred to herein as “US$”. Canadian dollars are referred to herein as “CAD”. Brazilian Reais are referred to herein as “R$”.

The following table sets forth the high and low, average and period-end exchange rates for one US dollar expressed in Canadian dollars and Brazilian Reais for each period indicated, based upon the daily exchange rates provided by Central Bank of Brazil (“Banco Central do Brasil”) and Bank of Canada:

| 2025 | 2024 | |

| High | CAD1.46/R$6.21 | CAD1.44/R$6.20 |

| Low | CAD1.36/R$5.27 | CAD1.33/R$4.85 |

| Rate as of December 31 | CAD1.37/R$5.50 | CAD1.44/R$6.19 |

| Average rate for period (full year) | CAD1.40/R$5.59 | CAD1.37/R$5.39 |

Presentation currency of the financial statements

On January 1, 2025, the Company elected to change its presentation currency from Canadian Dollars (“CAD”) to United States Dollars (“US$”). This change was made to better reflect the Company’s business operations and to enhance the comparability of its financial results with those of other publicly traded companies in the mining industry. The change in presentation currency has been applied retrospectively, and comparative financial information has been restated as though US$ had always been the Company’s presentation currency, in accordance with IAS 21 and IAS 8 - Accounting Policies, Changes in Accounting Estimates and Errors.

For reporting periods prior to January 1, 2025, the statements of financial position have been translated from the functional currency (R$) to the new presentation currency (US$) using the exchange rates prevailing at each respective reporting date. Equity items, however, have been translated using historical accumulated rates dating back to the Company’s incorporation in 2018. The statements of income / (loss) and comprehensive income / (loss) were translated at average exchange rates for each reporting period, or at the rate prevailing on the date of the transaction. Exchange differences arising from the translation of 2024 financial information from R$ (functional currency) to US$ (presentation currency) have been recognized in other comprehensive income / (loss) and accumulated in a separate component of equity.

In compliance with IFRS Accounting Standards, the Company also presented a third statement of financial position as of January 1, 2024. Equity balances were restated using historical average exchange rates, except for significant transactions, which were translated using the actual historical rates. Any resulting differences were recorded as adjustments to the foreign currency translation reserve.

Third Party Information

This AIF includes market, industry and economic data and projections obtained from various publicly available sources and other sources believed by the Company to be true. Although the Company believes these to be reliable, it has not independently verified the information from third party sources, or analyzed or verified the underlying reports relied upon or referred to by the third parties or ascertained the underlying economic and other assumptions relied upon by the third parties. The Company believes that the market, industry and economic data and projections are accurate and that the estimates and assumptions are reasonable, but there can be no assurance as to their accuracy or completeness. The accuracy and completeness of the market, industry and economic data and projections in this AIF are not guaranteed and the Company does not make any representation as to the accuracy or completeness of such information.

Non-GAAP Measures

This AIF and the 2025 Technical Report incorporated by reference herein contain certain non-GAAP measures. The non-GAAP measures do not have any standardized meaning within IFRS Accounting Standards, and therefore may not be comparable to similar measures presented by other companies. These measures provide information that is customary in the mining industry and that is useful in evaluating Sigma Lithium’s business.

| |

This data should not be considered as a substitute for measures of performance prepared in accordance with IFRS Accounting Standards.

Qualified Person

Mr. Marc-Antoine Laporte, P.Geo, William van Breugel, P. Eng., Johnny Canosa, P. Eng., and Joseph Keane, P. Eng., are the “qualified persons” under NI 43-101, who reviewed and approved the technical information disclosed in this AIF and the documents incorporated by reference herein.

Date of Information

Except as otherwise indicated, all information disclosed in this AIF is as of March 30, 2026.

Name, Address and Incorporation

Sigma Lithium Corporation (the “Company”, “Sigma Lithium” or “Sigma”) is domiciled in Canada and was incorporated under the Canada Business Corporations Act (“CBCA”) on June 8, 2011 originally under the name Margaux Red Capital Inc. The current business of Sigma Lithium was acquired through a reverse take-over transaction on April 30, 2018 pursuant to which the Company acquired Sigma Lithium Holdings Inc. (“Sigma Holdings”) which held the Grota do Cirilo Project, located in the state of Minas Gerais in Brazil (the “Project”), which was since developed into an industrial mining complex (“Mining Operations”), through a Brazilian wholly-owned subsidiary, Sigma Mineração S.A. (“Sigma Brazil”). On completion of the reverse take-over transaction, the Company implemented a share consolidation and changed its name to “Sigma Lithium Resources Corporation”. On July 5, 2021, the Company changed its name to “Sigma Lithium Corporation”. On October 15, 2024 the Company received a Certificate of Continuance under the Business Corporations Act (Ontario) (“OBCA”), officially completing its transition from the CBCA. The Company is now governed by the OBCA.

The registered office of the Company is at 181, Bay Street, Suite 4400, Toronto, Ontario, M5J 2T3, Canada. The Company’s web site is https://sigmalithiumcorp.com/.

Intercorporate Relationships

The corporate structure of the Company and its subsidiaries (each of which is wholly owned), and their relative jurisdictions of incorporation are set out in the following chart:

| |

GENERAL DEVELOPMENT OF THE BUSINESS

Overview

Sigma Lithium (NASDAQ: SGML, TSXV: SGML, BVMF: S2GM34) is the largest producer of lithium oxide concentrate in the Americas and dedicated to industrializing socially and environmentally sustainable lithium materials to supply global producers of batteries for energy security.

The Company operates one of the world’s largest lithium production sites at its Grota do Cirilo operation in Brazil. Sigma Lithium is at the forefront of environmental and social sustainability in the electric battery materials supply chain. The Company’s Greentech Industrial Plant combines dry stacking, the reuse of 100% of water, zero use of toxic chemicals and the use of 100% renewable electricity. For more than two years Sigma Lithium has not experienced an accident with lost time.

Sigma Lithium currently has a nameplate capacity to produce 270,000 tonnes of lithium oxide concentrate on an annualized basis (approximately 38,000–40,000 tonnes of LCE) at its Xuxa mine (“Mine 1”) and state-of-the-art Greentech Industrial Plant. The Company has initiated investing in a Phase 2 expansion that is planned to close to double production capacity.

For further information on the business of the Company, please refer to “Description of the Business”.

| |

Three Year History

The following is a summary of the key developments that have generally influenced the development of the Company’s business and projects over the last three fiscal years (and its current fiscal year to date).

2026 and Next Steps

In 2026, the focus of the Company will be on executing its Phase 2 expansion, including increasing the capacity of Mine 1 and building the Phase 2 Industrial Greentech Plant.

2025

In 2025, Sigma Lithium operated its Phase 1 mining operations throughout the year, with the exception of a pause for a restructuring in the fourth quarter, and its Phase 1 Industrial Greentech Plant. Lithium oxide concentrate production totaled 183,700 tonnes and net sales revenue was US$110.0 million. The Company advanced its planned Phase 2 expansion throughout the year, with focus on Mine 1 preparation.

On December 1, 2025, Sigma Lithium participated in high-level policy, climate, and industry discussions at COP30 in Belém, Brazil. Senior executives, including Co-Chair and CEO Ana Cabral, VP of Sustainability Lígia Pinto, and VP of Business Development and International Affairs Daniel Abdo, engaged across multiple official panels, ministerial dialogues, and academic forums, reinforcing Brazil's potential to lead the global sustainable lithium market and positioning Sigma Lithium as an international benchmark for responsible mineral supply chains ahead of Brazil's COP30 presidency.

On October 17, 2025, Sigma Lithium announced that its US-listed shares (NASDAQ: SGML) had been added to the Morgan Stanley National Security Stock Index, a thematic equity index tracking publicly listed companies whose operations, products, or technologies contribute to national security, supply chain resilience, and strategic infrastructure. The inclusion reflects Sigma Lithium's recognized role as a critical supplier of battery materials within global supply chains, alongside other leading producers of strategic materials.

On October 6, 2025, as part of the implementation of the management’s business plan, the Company announced a restructuring of its mining operations to increase capacity and improve efficiency by bringing mining operations in-house instead of using a mining contractor and using larger equipment, such as trucks and excavators. With the upgrade, management anticipates being able to markedly improve the Company’s operating margins. The increase in capacity was required for debottlenecking so that Sigma Lithium’s Mine 1 would be able to deliver a greater volume of ore and at a more constant pace to optimize recoveries at the Company’s Greentech Industrial Plant, which had undergone substantial improvements. These improvements, over time, had substantially increased the plant’s processing capacity, from 240,000 tonnes per year to 300,000 tonnes per year. Another reason for the restructuring was to prepare Mine 1 for the planned Phase 2 capacity expansion. Sigma Lithium plans to use the ore from Mine 1 to continue to feed both the existing Greentech Industrial Plant and the planned Greentech Industrial Plant 2 during ramp-up. To implement mine operations restructuring, Sigma Lithium’s Mine 1 underwent a demobilization started at the beginning of October 2025 and a remobilization that began at the end of January 2026. During the time the mine was demobilized, the Company’s Greentech Industrial Plant 1 continued to operate, reprocessing tailings.

On August 8, 2025, Felipe Peres was appointed Chief Financial Officer of the Company, consolidating the entire finance team under his leadership. Mr. Peres joined the Company in 2020 and previously served as CFO from 2020 to 2023, leading Sigma Lithium's Nasdaq listing in 2021. He subsequently served as deputy to the CEO on the Sigma Brazil site, overseeing contracts, procurement, cost controls, and capital investments for the Industrial Greentech Plant expansion. Mr. Peres has over 30 years of executive experience in large multinational natural resource companies, including prior roles at Vale International, Shell, and CSN.

Also on August 8, 2025, Sigma Lithium announced the results of its annual general meeting of shareholders held on June 30, 2025. All five director nominees were elected with an average of 93% of votes cast, to hold office until the next annual meeting of shareholders on June 30, 2026.

On March 13, 2025, the Company appointed Junaid Jafar as a new independent member of the Board of Directors. Mr. Jafar holds the role of Chief Investment Officer at Al Muhaidib Investment Office, the family office of Al Muhaidib Group, one of the largest private conglomerates in the Middle East, headquartered in Dammam, Saudi Arabia. Mr. Jafar has nearly 30 years of investment management experience across private equity, private credit, infrastructure, and venture capital, having previously worked at J.P. Morgan, Fitch Ratings, and Janus Henderson, among others. He joined the Board in place of Mr. Bechara Azar, who stepped down for personal reasons.

| |

On January 1, 2025, the Company elected to change its presentation currency from Canadian dollars to United States dollars, effective for all financial reporting from that date, to better reflect its business operations and enhance comparability with other publicly traded mining companies. The change was applied retrospectively in accordance with IAS 21 and IAS 8.

2024

In 2024, Sigma Lithium continued to operate its Phase 1 Mine and Phase 1 Industrial Greentech Plant. During this year, total lithium concentrate production totaled 240,800 tonnes.

The Company also advanced with its Phase 2 expansion with the final investment decision made on March 22, 2024. Phase 2 is to increase production capacity by 250,000 tonnes per year of spodumene concentrate from Sigma Lithium's Grota do Cirilo Project operations. Once operational, the new production line is expected to increase Sigma Lithium's total nameplate capacity to 520,000 tonnes.

On December 21, 2024, the Company received a Triple Environmental License (Licença Operacional (LO), Licença Prévia (LP), and Licença de Instalação (LI)) for its Phase 2 mine (“Mine 2”), also known as Barreiro mine. Barreiro is the second mine site within the Grota do Cirilo Project, planned for sequential integration into Sigma Lithium’s Mining Operations in the coming years.

On September 24, 2024, the Company hosted its Investor Day at Nasdaq, marking its first full year of production and the record-setting ramp up of its Phase 1 Industrial Greentech Plant. The Company outlined its capital-efficient plans to increase its industrial capacity. Following adjustments to the current flowsheet of the Phase 1 Industrial Greentech Plant, the growth plans now include two additional production lines, each with a capacity of approximately 40,000 tonnes of LCE. These growth projects will follow nearly identical processing flowsheets as the existing plant and will leverage its established infrastructure.

On September 16, 2024, Rogério Marchini Santos was promoted to the role of CFO. Mr. Marchini joined Sigma Lithium with a deep experience of more than 24 years in finance. He was the CFO of Origo, a private equity portfolio company of TPG International in the energy transition space, leading a 40-person team through business transformation from start-up to final monetization. Mr. Marchini also served as Director of Finance at Embraer (one of the top global aircraft manufacturers), where he worked for 13 years.

On May 8, 2024, Sigma Lithium announced an increase of its proven and probable mining reserves at the Company’s Mining Operations of 40%, equivalent to 22.2 million tonnes. Sigma Lithium increased its consolidated proven and probable reserve balance to 77.0 million tonnes at 1.40% lithium oxide (Li2O) from 54.8 million tonnes at 1.44% previously. The increase resulted in a lengthening of the duration of the Company’s Mining Operations to an estimated 25 years at two lines of processing capacity totaling 520,000 tonnes per annum.

On February 12, 2024, the Company received a Letter of Intent from the Brazilian Development Bank (“BNDES”) to fund construction of its Phase 2 expansion. The Letter of Intent was followed by a binding commitment letter from the BNDES received on August 27, 2024 with the final approval for a R$486.8 million development loan, which represents almost 99% of the R$492 million capex budget submitted to the BNDES (the “Development Loan”). The Development Loan provides the Company with a 16-year repayment period at the low interest rate of 7.45% per year. The closing of the Development Loan remains subject to the Company's submission of satisfactory letters of credit ("Carta de Fiança Bancária") issued by a Brazilian banking institution accredited by the BNDES, as well as the customary closing conditions for a development loan of this nature, including the Company's constant adherence to the operating policies of the BNDES.

On January 31, 2024, Sigma Lithium published its updated resource estimate following its 2023 drill campaign. The aggregate measured, indicated and inferred estimate increased to 108.9 million tonnes at an average grading of 1.40% lithium oxide. This was an increase of 27% over the prior estimate of 85.6 million tonnes and a slight decrease in the average grading of lithium oxide at 1.43%. The majority of the revisions were made to the Phase 3 (Nezinho do Chicão) and Phase 4 (Murial) deposits, but the Company also announced a maiden resource estimate of 2.1 million tonnes inferred for its Phase 5, Elvira, prospect.

| |

On January 31, 2024, Sigma Lithium was awarded a concurrent LP, LI, LO environmental license to install and operate ("Full Environmental License") the Phase 2 Industrial Greentech Plant by the State of Minas Gerais. The Full Environmental License allows the Company to further expand its industrial beneficiation and processing capacity of lithium minerals to up to a total of 3.7 million tonnes per year.

2023

In 2023, Sigma Lithium successfully commissioned and began commercial operations at its Phase 1 Industrial Greentech Plant and mine. During the year, total lithium concentrate production exceeded 105,000 tonnes, with operations sustaining annualized nameplate capacity utilization rates of 270,000 tonnes for the month of December.

The Company also advanced its plans to triple its lithium oxide concentrate production capacity. This included completing engineering to FEL-3 stage precision of its Phase 2 and 3 Industrial Greentech Plants. Said plants are to source feedstock ore from the Barreiro and Nezinho do Chicão deposits, which were investigated in the preliminary feasibility study (“Phase 2 & Phase 3 PFS”) included in the Restated Technical Report filed on June 12, 2023.

Congruent with Sigma Lithium’s efforts to expand its production footprint, were initiatives to build upon the Company’s existing resource estimate. In 2023, Sigma Lithium completed a 30,000-meter drill campaign, which resulted in an increase to its overall, pit constrained, measured, indicated and inferred resource estimate, as published on January 31, 2024.

In November 2023, the Company actively participated in COP-28, where multiple members of the senior management team hosted workshops on “Impact Investing in Mining.” Sigma Lithium’s CEO and Co-Chairperson Ana Cabral was featured as a keynote speaker.

On October 6, 2023, Sigma Lithium announced the promotion of Reinaldo Brandão, Keith Prentice and Iran Zan to the positions of Co-General Managers of Mining, Processing and Geology, respectively. The leaders were promoted following the successful commissioning and ramp of the Company’s Phase 1 Industrial Greentech Plant and the departure of the Company’s COO, Brian Talbott, for health reasons.

In September 2023, Sigma Lithium was a participant in the “Combining Environmental and Social Agendas” panel at the Brazil Climate Summit at Columbia Business School.

On August 11, 2023, Caio Araujo was appointed as Chief Financial Officer of Sigma Lithium following the tenure of interim CFO Rodrigo Menck. Mr. Araujo joined Sigma Lithium in June 2023 with 33 years of experience in finance and controlling, having started his career at PWC. Previously, he was CFO at a portfolio company of BTG. Mr. Araujo most recently headed the finance department at CSN, one of the first Brazilian metals and mining companies to register an ADR level on the NYSE, where he implemented the SEC reporting/SOX compliance.

On June 12, 2023, the Company’s Restated Technical Report was filed on SEDAR+ and EDGAR, including all of the study results and resource and reserve estimates that were included in the Updated Technical Report with updated information on the licensing and regulatory approval status of the Grota do Cirilo Project and the Murial drilling programs. The Restated Technical Report was prepared by independent mining consultancies, with the professional services firms Primero Group Ltd (“Primero”), SGS Canada Inc. (“SGS”), and GE21 Consultoria Mineral (“GE21”). Please refer to “Description of the Business – Current Status of the Project”.

On April 17, 2023, the Company announced that it had initiated production of spodumene concentrate at its Mining Operations. Production followed the successful commissioning of the Industrial Greentech Plant 1’s dense media separation line, after having completed construction and commissioning of the crushing circuit earlier in the year.

| |

Overview

Sigma Lithium is the largest producer of mineral lithium oxide concentrate in the Americas and is dedicated to industrializing socially and environmentally sustainable lithium materials to supply global producers of batteries for energy security. The Company operates one of the world’s largest lithium production sites at its Grota do Cirilo operation in Brazil. Sigma Lithium is at the forefront of environmental and social sustainability in the electric battery materials supply chain. The Company’s Industrial Greentech Plant 1 combines dry stacking, the reuse of 100% of water, zero use of toxic chemicals, and the use of 100% renewable electricity. For more than two years Sigma Lithium has not experienced an accident with lost time. Sigma Lithium currently has a nameplate capacity to produce 270,000 tonnes of lithium oxide concentrate on an annualized basis (approximately 38,000–40,000 tonnes of LCE) at its mine and state-of-the-art Industrial Greentech Plant. The Company has initiated a Phase 2 expansion that is planned to close to double production capacity.

Distribution

The Company sells its products to a diversified and solid base of international customers across key lithium markets. Sigma Lithium’s commercial team maintains a continuous engagement with this global customer base, supporting long-term commercial relationships and ensuring alignment with evolving market dynamics and customer needs. Representatives of the Company participate in major industry conferences and events, which provide important opportunities to strengthen relationships with existing customers, engage with potential new customers, and monitor developments in the lithium and battery materials markets. Products are exported through an efficient logistics structure and transported by sea freight via international shipping routes to delivery locations designated by customers.

Sales revenues

The revenues for each category of products for the two most complete financial years are presented in the following table.

| Net Sales Revenue (US$’000) | 12/31/2025 | 12/31/2024 (1) | ||

| Gross sales revenue – lithium concentrate | 96,101 | 193,229 | ||

| Provisional price adjustment | 4,167 | (46,839) | ||

| Shipping services | 9,744 | 4,962 | ||

| Total net sales revenue | 110,012 | 151,352 |

| (1) | On January 1, 2025, the Company began to present its financial statements in United States dollars. |

Gross sales revenue from lithium concentrate totaled $96.1 million for the year ended December 31, 2025, compared to $193.2 million in the prior year. The decrease reflects lower sales volumes (150.5 kt versus 236.9 kt) that resulted from the abovementioned restructuring of mining operations, combined with a decline in the average realized price to approximately $661 per tonne, compared to $850 per tonne in the same period of 2024.

Additionally, provisional price adjustments were a positive $4.2 million, compared to a negative $46.8 million for the year ended December 31, 2024, resulting in a smaller adverse impact on revenue relative to the prior period.

Shipping services revenue totaled $9.7 million, compared to $5.0 million in the prior year period.

Lithium Properties

The Company’s Lithium Properties are located in the municipalities of Araçuaí and Itinga in the northeastern part of the state of Minas Gerais, Brazil, approximately 25 km east of the town of Araçuaí́ and 600 km northeast of Belo Horizonte, the state capital, and about 700 km from the Port of Vitoria, from where the Company ships to global markets.

Sigma Lithium owns 100% of the Company’s operating assets indirectly through its wholly owned subsidiary, Sigma Brazil, including the Lithium Properties. The leasehold area is comprised of 29 mineral rights (which include mining concessions, applications for mining concessions, exploration authorizations, applications for mineral exploration authorizations) spread over 185 km2, located within the broader 19,000-hectare land package held by Sigma Brazil (“Lithium Properties”).

Sigma Lithium’s mining concessions comprise four properties: Grota do Cirilo (the area where Phase 1, 2 and 3 are located), and the Sao Jose, Genipapo and Santa Clara properties.

| |

Operations

Sigma Lithium’s Mining Operations are vertically integrated, with the Company’s mine supplying spodumene bearing material to its lithium production and processing plant (the “Industrial Greentech Plant”, “Industrial Greentech Plant 1” or “Plant 1”). The Industrial Greentech Plant is designed and operated to produce a high purity lithium oxide concentrate in an environmentally friendly way through a fully automated and digital dense medium separation (“DMS”) technology process, engineered to the specifications of the Company’s customers in the rapidly expanding lithium-ion battery supply chain for electric vehicles (“EVs”) and battery energy storage systems (“BESS”).

Sigma Lithium is taking a phased approach to a planned expansion of its operations. Phase 1 production at its Mine 1 and Industrial Greentech Plant 1 commenced in April 2023. At a production capacity of 270,000 tonnes per annum of 5% lithium oxide concentrate, Phase 1 has positioned the Company as a globally relevant, Tier-1 lithium oxide concentrate producer. Sigma Lithium issued a Final Investment Decision (“FID”) on its Phase 2 on March 22, 2024. Phase 2 would take consolidated capacity to 520,000 tonnes per annum of 5% lithium oxide concentrate. The existing infrastructure built with the Phase 1 mine and Industrial Greentech Plant is expected to support two additional production lines, with each of the two planned phases of expansion designed to follow a similar flowsheet as demonstrated in Phase 1.

The Sigma Lithium Industrial Greentech Plant also produces tailings that consist of a low-grade, high-purity, zero-chemical, hyperfine by-product (“Green By-Products”) with approximately 1.0% lithium oxide (“Li2O”) content. Provided lithium market conditions are favorable, these Green By-Products can be sold either as high purity lithium fines or as an input for different industries. In addition, from time to time, the Company may commercialize intermediate lithium oxide concentrate products with lithium oxide content between 1% and 5%. The sales strengthen Sigma Lithium’s ESG-centric approach, as they result in a “zero tailings” environmental sustainability strategy, minimizing the environmental footprint of tailings storage with a positive ecosystem impact, while also generating an additional revenue stream for the Company.

Since its inception in 2012, Sigma Lithium’s mission has emphasized environmental, social, and governance (“ESG”) practices to support sustainable development. The Company is actively engaged in social programs that promote sustainable development and inclusion.

Sigma Lithium is committed to leading the way in socially and environmentally sustainable lithium. The Company’s approach to sustainability reflects not only the Company´s regulatory obligations, but also the evolving expectations of the Sigma Lithium’s stakeholders, including customers, investors, local communities, employees, and public institutions.

| |

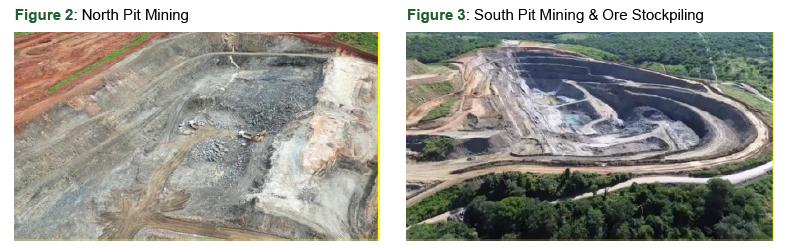

Figure 1: Overhead view of Phase 1 Industrial Greentech Plant, with DMS circuit in foreground and crushing circuit in the background

Mining Operations Update

As of the date of this AIF, the Company reports the following highlights and advancements in its mining activities:

| § | In 2025, a decision was taken to restructure mining operations to increase capacity and improve efficiency by moving to using larger equipment, such as trucks and excavators, and bringing mining operations in-house instead of using a mining contractor. |

| |

| § | The restructuring required a pause in mining operations. In the three months ending December 31, 2025, no Run of Mine (“ROM”) ore was delivered to the Greentech Industrial Plant. Mine operations underwent a demobilization started at the beginning of October 2025 and a remobilization begun at the end of January 2026. |