UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 40-F

☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13(a) OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2025

Commission file number: 001-32135

Seabridge Gold Inc.

(Exact name of Registrant as specified in its charter)

| Canada | 1040 | Not Applicable | ||

| (Province

or other jurisdiction of incorporation or organization) |

(Primary

Standard Industrial Classification Code Number) |

(I.R.S.

Employer Identification No.) |

106 Front Street East, Suite 400

Toronto, Ontario Canada M5A 1E1

(416) 367-9292

(Address and telephone number of Registrant’s principal executive offices)

Corporation Service Company

1180 Sixth Avenue

New York, New York 10036

(212) 299-5656

(Name, address and telephone number of agent for service in the United States)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common Shares | SA | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

For annual reports, indicate by check mark the information filed with this form:

| ☒ Annual Information Form | ☒ Audited Annual Financial Statements |

Indicate the number of outstanding shares of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 91,912,919 Common Shares (as at December 31, 2025).

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 12b-2 of the Exchange Act.

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

The annual report on Form 40-F shall be incorporated by reference into or as an exhibit to, as applicable, the Registrant’s Registration Statements under the Securities Act of 1933, as amended: Form F-10 (File No. 333-283616) and Form S-8 (File No. 333-211331).

EXPLANATORY NOTE

Seabridge Gold Inc. (the “Registrant” or “we” or “us”) is a Canadian issuer eligible to file its annual report pursuant to Section 13 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), on Form 40-F (“Form 40-F”) pursuant to the multi-jurisdictional disclosure system of the Exchange Act. We are a “foreign private issuer” as defined in Rule 3b-4 under the Exchange Act. Accordingly, our equity securities are exempt from Sections 14(a), 14(b), 14(c), 14(f) and 16 of the Exchange Act pursuant to Rule 3a12-3.

PRINCIPAL DOCUMENTS

The following documents have been filed as part of this Annual Report on Form 40-F and incorporated by reference herein:

A. Annual Information Form

For our Annual Information Form (the “AIF”) for the year ended December 31, 2025, see Exhibit 99.1 of this Annual Report on Form 40-F.

B. Audited Annual Financial Statements

For our audited annual financial statements (“Audited Financial Statements”), for the years ended December 31, 2025 and December 31, 2024, including the Report of Independent Registered Public Accounting Firm, see Exhibit 99.2 of this Form 40-F. The Audited Financial Statements are stated in Canadian Dollars (Cdn$) and are prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

C. Management’s Discussion and Analysis

For our management’s discussion and analysis (the “MD&A”) for the year ended December 31, 2025, see Exhibit 99.3 of this Form 40-F.

FORWARD-LOOKING STATEMENTS

This Form 40-F and the exhibits attached hereto contain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Exchange Act, and forward-looking information within the meaning of Canadian securities laws concerning our projects, business approach and plans, including estimated production, capital, operating and cash flow estimates and other matters at our projects. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects”, “anticipates”, “plans”, “projects”, “estimates”, “assumes”, “intends”, “strategy”, “goals”, “objectives” or variations thereof or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements and forward-looking information (collectively referred to in the following information simply as “forward-looking statements”). In addition, statements concerning mineral reserve and mineral resource estimates constitute forward-looking statements to the extent that they involve estimates of the mineralization expected to be encountered if a mineral property is developed and the economics of developing a property and producing minerals.

Forward-looking statements are necessarily based on estimates and assumptions made by us in light of our experience and perception of historical trends, current conditions and expected future developments. In making the forward-looking statements in this Form 40-F and the exhibits attached hereto, we have applied several material assumptions including, but not limited to, the assumption that: (i) any additional financing needed will be available on reasonable terms; (ii) the potential for production at our mineral projects will continue operationally, legally, economically and socially; (iii) market fundamentals will result in sustained demand and prices for gold and copper, and to a much lesser degree, silver and molybdenum; (iv) estimated resources at our projects have merit and there is continuity of mineralization as reflected in such estimates and (v) we will receive and maintain all required regulatory approvals required in respect of our projects.

Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual events or results to differ from those expressed or implied by the forward-looking statements, including, without limitation:

| ● | the Issuer’s history of net losses and negative cash flows from operations and expectation of future losses and negative cash flows from operations; |

| ● | although the Issuer has identified a preferred potential partnership candidate for the KSM Project, there is no assurance that terms of a partnership for advancing the KSM Project will be agreed; |

| ● | risks related to the Issuer’s ability to continue its exploration activities and future advancement activities, and to continue to maintain corporate office support of these activities, which are dependent on the Issuer’s ability to obtain suitable financing, enter into joint ventures, to sell property interests; |

| ● | the Issuer’s indebtedness requires quarterly interest payments and may require repayment in full, which may adversely affect its cash flow and ability to advance its business and necessitate dilutive financing or asset sales; |

| ● | risks related to fluctuations in the market price of gold, copper and other metals; |

| ● | uncertainty whether the reserves estimated on the Issuer’s mineral properties will be brought into production; |

| ● | risks related to unsettled First Nations rights and title and settled Treaty Nations’ rights and uncertainties relating to the process of making Canadian laws consistent with the United Nations Declaration on the Rights of Indigenous Peoples; |

| ● | risks related to obtaining and maintaining all necessary permits and governmental approvals, or extensions or renewals thereof, for exploration and advancement activities, including in respect of environmental regulation and the KSM Project’s environmental assessment certificate; |

| ● | risks associated with the use of information technology systems and cybersecurity; |

| ● | the Issuer is subject to substantial government regulatory and environmental requirements which could cause delays in advancing its projects or could result in a restriction or suspension of its operations;; |

| ● | the risk of having the “substantially started” determination for the KSM Project quashed and, if quashed, such determination not reconfirmed and the ultimate loss of the KSM Project environmental assessment certificate; | |

| ● | risks relating to the Issuer’s internal control over financial reporting being ineffective; |

| ● | uncertainties relating to the assumptions underlying the Issuer’s reserve and resource estimates; |

| ● | uncertainty of estimates of capital costs, operating costs, production and economic returns; |

| ● | risks relating to the commencement of site access and early site preparation construction activities at the KSM Project; |

| ● | risks related to commercially producing precious metals and copper from the Issuer’s mineral properties; |

| ● | risks related to fluctuations in foreign exchange rates; |

| ● | mining, exploration and advancement risks that could result in damage to mineral properties, plant and equipment, personal injury, environmental damage and delays in mining, which may be uninsurable or not insurable in adequate amounts; |

| ● |

risks related to the possibility of unregistered agreements, transfers, claims or other defects impacting title to the Issuer’s mineral properties; |

| ● | risks related to increases in demand for exploration, advancement and construction services and equipment, and related cost increases following metals price increases; |

| ● | successful completion of the proposed spin-out of the Courageous Lake Project on the terms proposed or not at all; |

| ● | increased competition in the mining industry; |

| ● | risks related to international trade disputes and the imposition of tariffs and the potential impacts it may have on the Company’s ability to raise funds and obtain supplies needed for work programs; |

| ● | regulatory initiatives and ongoing concerns regarding carbon emissions and the impacts of measures taken to induce or mandate lower carbon emissions on the ability to secure permits, finance projects and realize profitability at a project; |

| ● | the Issuer’s current and proposed operations are subject to risks relating to climate and climate change that may adversely impact its ability to conduct operations and raise capital, increase operating costs, interfere with materials and equipment supply, delay execution or reduce the profitability of a future mining operation; |

| ● | risks that regulatory measures directed at climate change issues adversely affect the Issuer’s business; |

| ● | the Issuer’s reliance on key personnel and the need to retain key executives and attract qualified personnel; |

| ● | the public’s views of the mining industry can present increased risks for permitting, financing and staffing; |

| ● | risks related to some of the Issuer’s directors’ and officers’ involvement with other natural resource companies; |

| ● | uncertainty surrounding an audit by the Canada Revenue Agency (“CRA”) of Canadian exploration expenses incurred by the Issuer during the 2014, 2015 and 2016 financial years which the Issuer has renounced to subscribers of flow-through share offerings and the CRA’s decision to reassess such subscribers; |

| ● | the risk of the CRA appealing the Issuer’s successful challenge to the reassessment by the CRA of the Issuer’s refund claim for the 2010 and 2011 financial years in respect of the British Columbia Mining Exploration Tax Credit and the decision being overturned; |

| ● | the risks associated with the volatility of the trading volume and price of the Issuer’s Common shares; |

| ● |

the return on an investment in the Issuer’s Common shares is limited to capital gains or losses since the Issuer does not pay dividends; |

| ● | the Issuer’s classification as a “passive foreign investment company” under the United States tax code; |

| ● | risks related to the pro-environmental groups anti-mining efforts, and sometimes focused efforts on specific projects impacting the Company’s share price. |

This list is not exhaustive of the factors that may affect any of our forward-looking statements. Forward-looking statements are statements about the future and are inherently uncertain, and actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those referred to in our AIF attached hereto as Exhibit 99.1 under the heading “Risk Factors” and elsewhere in the AIF, and in the documents incorporated by reference in this Form 40-F and the AIF. In addition, although we have attempted to identify important factors that could cause actual achievements, events or conditions to differ materially from those identified in the forward-looking statements, there may be other factors that cause achievements, events or conditions not to be as anticipated, estimated or intended. It is also noted that while we engage in exploration and development of our properties, we will not undertake production activities by ourselves.

These forward-looking statements are based on the beliefs, expectations and opinions of management on the date the statements are made and we do not assume any obligation to update forward-looking statements, except as required by applicable securities laws, if circumstances or management’s beliefs, expectations or opinions should change. For the reasons set forth above, persons should not place undue reliance on forward-looking statements.

CURRENCY

Unless otherwise indicated, all dollar amounts in this Form 40-F are in Canadian dollars.

NOTE TO UNITED STATES READERS - DIFFERENCES IN UNITED STATES AND CANADIAN REPORTING PRACTICES

We are permitted under the multi-jurisdictional disclosure system adopted by the United States Securities and Exchange Commission (the “SEC”), to prepare this Form 40-F in accordance with Canadian disclosure requirements, which differ from those of the SEC. We have prepared our financial statements, which are filed as Exhibit 99.2 to this Form 40-F, in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board, and they are not comparable with financial statements of U.S. and other companies prepared in accordance with U.S. generally accepted accounting principles.

RESOURCE AND RESERVE ESTIMATES

The Registrant’s AIF, attached as Exhibit 99.1 to this annual report on Form 40-F, and the MD&A, attached as Exhibit 99.3 to this annual report on Form 40-F, have been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of United States securities laws. Mineral resource estimates included in this annual report on Form 40-F and in any document incorporated by reference herein or therein have been prepared in accordance with, and use terms that comply with, the reporting standards in accordance with Canadian National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”). NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. In accordance with NI 43-101, the Registrant uses the terms mineral reserves and resources as they are defined in accordance with the CIM Definition Standards on mineral reserves and resources (the “CIM Definition Standards”) adopted by the Canadian Institute of Mining, Metallurgy and Petroleum.

For United States reporting purposes, the SEC has adopted amendments to its disclosure rules (the “SEC Modernization Rules”) to modernize the mining property disclosure requirements for issuers whose securities are registered with the SEC under the U.S. Securities Exchange Act of 1934, as amended (the “U.S. Exchange Act”). The SEC Modernization Rules more closely align the SEC’s disclosure requirements and policies for mining properties with current industry and global regulatory practices and standards, including NI 43-101, and replace the historical property disclosure requirements for mining registrants that were included in Industry Guide 7 under the U.S. Securities Act. As a foreign private issuer that is eligible to file reports with the SEC pursuant to the MJDS, the Registrant is not required to provide disclosure on its mineral properties under the SEC Modernization Rules and provides disclosure under NI 43-101 and the CIM Definition Standards. Accordingly, mineral reserve and mineral resource information contained or incorporated by reference herein may not be comparable to similar information disclosed by United States companies.

As a result of the adoption of the SEC Modernization Rules, the SEC recognizes estimates of “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources.” In addition, the SEC has amended its definitions of “proven mineral reserves” and “probable mineral reserves” to be “substantially similar” to the corresponding CIM Definition Standards that are required under NI 43-101. While the above terms are “substantially similar” to CIM Definitions, there are differences in the definitions under the SEC Modernization Rules and the CIM Definition Standards. There is no assurance any mineral reserves or mineral resources that the Registrant may report as “proven mineral reserves”, “probable mineral reserves”, “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources” under NI 43-101 would be the same had the Registrant prepared the reserve or resource estimates under the standards adopted under the SEC Modernization Rules.

Accordingly, information contained in this annual report on Form 40-F and the portions of documents incorporated by reference herein contain descriptions of the Registrant’s mineral deposits that may not be comparable to similar information made public by U.S. companies who prepare their disclosure in accordance with U.S. federal securities laws and the rules and regulations thereunder.

DISCLOSURE CONTROLS AND PROCEDURES

Evaluation of Disclosure Controls and Procedures

At the end of the period covered by this annual report on Form 40-F, an evaluation was carried out under the supervision of, and with the participation of our management, including the Chief Executive Officer (“CEO”) and the Chief Financial Officer (“CFO”), of the effectiveness of the design and operation of our disclosure controls and procedures (as defined in Rule 13a-15(e) and Rule 15d-15(e) under the Exchange Act). Based on that evaluation, the CEO and the CFO have concluded that as of the end of the period covered by this annual report, our disclosure controls and procedures were adequately designed and effective in ensuring that: (i) information required to be disclosed by us in reports that we file or submit to the SEC under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in applicable SEC rules and forms and (ii) material information required to be disclosed in our reports filed under the Exchange Act is accumulated and communicated to our management, including the CEO and the CFO, as appropriate, to allow for accurate and timely decisions regarding required disclosure.

Management’s Annual Report on Internal Control over Financial Reporting

For management’s report on internal control over financial reporting, see “Internal Controls over Financial Reporting” in our MD&A attached as Exhibit 99.3 to this annual report on Form 40-F and incorporated by reference herein.

Attestation Report of the Independent Registered Public Accounting Firm

Our independent registered public accounting firm has issued an attestation report on our internal control over financial reporting as of December 31, 2025, which immediately precedes the audited consolidated financial statements included as part of Exhibit 99.2 to this annual report on Form 40-F and incorporated by reference herein.

Changes in Internal Controls over Financial Reporting

During the fiscal year ended December 31, 2025, no changes occurred in our internal control over financial reporting that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

Certifications

See Exhibits 31.1, 31.2, 32.1 and 32.2 to this Form 40-F.

CORPORATE GOVERNANCE

We are subject to a variety of corporate governance guidelines and requirements of the Toronto Stock Exchange, the New York Stock Exchange (the “NYSE”), the Canadian Securities Administrators and the SEC. We believe that we meet or exceed the applicable corporate governance requirements. According to the NYSE Rules, a listed company must adopt and disclose a set of corporate governance guidelines with respect to specified topics. Such guidelines are required to be posted on the registrant’s website. Although we are listed on the NYSE, we are not required to comply with all of that exchange’s corporate governance rules which are applicable to U.S. corporations. The significant ways in which the NYSE governance rules differ for us, as a foreign company, are a reduced quorum requirement for shareholder meetings, shareholder approval for issuance of common shares that could result in a 20% increase in the number of outstanding common shares and shareholder approval of certain compensation plans. The guidelines are available for viewing on our website at http://www.seabridgegold.com/company/governance and are available without charge in print to any shareholder who requests them. Requests for copies of the guidelines should be made to the Secretary of our company at 106 Front Street East, Suite 400, Toronto, Ontario, Canada M5A 1E1, Telephone (416) 367-9292.

We review our governance practices and monitor developments in Canada and the United States on an on-going basis to ensure we remain in compliance with applicable rules and standards. The Board is committed to sound corporate governance practices which are both in the interest of our shareholders and contribute to effective and efficient decision making.

AUDIT COMMITTEE

Audit Committee

The Board has a separately designated standing Audit Committee established in accordance with Section 3(a)(58)(A) of the Exchange Act. The members of our Audit Committee are identified under the heading “Audit Committee Information” in the AIF which is attached as Exhibit 99.1 to this annual report on Form 40-F and incorporated by reference herein. In the opinion of the Board, all members of the Audit Committee are financially literate and independent, as such terms are defined by the NYSE’s corporate governance listing standards applicable to us and as determined by Rule 10A-3 under the Exchange Act.

Audit Committee Financial Expert

The Board has determined that Ms. Julie Robertson, the Audit Committee Chair, and Ms. Carol Willson, another member of the Audit Committee, have the necessary qualifications to be designated as an “audit committee financial expert” within the meaning of applicable SEC Rules and each is an “independent director”, as defined pursuant to Item 407(d)(5) of SEC Regulation S-K and Section 303A.02 of the New York Stock Exchange Listed Company Manual.

Ms. Julie Robertson is a Chartered Public Accountant and brings extensive experience in various finance roles, including the development of capital projects finance framework. She has expertise in the areas of International Financial Reporting Standards, US Generally Accepted Accounting Principles, external reporting, internal control optimization and compliance, including SOX, risk assessment processes, capital project management, ESG reporting and cybersecurity. She is currently the Senior Vice President Finance of Kinross Gold Corporation, and was the former Chief Financial Officer of Marathon Gold Corp.

Ms. Carol Willson retired from EY in 2021 after a 28-year career where she was engagement partner for Internal Audit of clients which included multi-year internal audit outsourced projects and related internal audit transformations and reviews, fraud investigations, and in various assurance and advisory capacities including capital projects, ESG, finance function-related improvements, and cybersecurity. During Ms. Willson’s career as an experienced internal audit and risk professional, she was retained to lead risk, internal audit and SOX functions for a variety of public corporations including several major mining companies. She served for three years as the global head of internal audit and SOX for a large Canadian gold producer where her key audit areas included: supply chain, capital projects, procure to pay, ERP/cybersecurity, sustainability, budgeting & forecasting, fixed assets, and treasury. Ms. Willson had her own consulting business where she served as a senior risk advisor for clients from 2021 to 2024. She holds a Bachelor of Arts degree from the University of Western Ontario and an MBA-Accounting degree from the University of Toronto.

The SEC has indicated that the designation of an audit committee financial expert does not make that person an “expert” for any purpose, impose any duties, obligations, or liability on that person that are greater than those imposed on members of the audit committee and board of directors who do not carry this designation, or affect the duties, obligations, or liabilities of any other member of the audit committee or board of directors.

Audit Committee Charter

Our Audit Committee Charter is available on our website at www.seabridgegold.com, and is provided in Schedule A to the AIF, which is attached as Exhibit 99.1 to this annual report on Form 40-F and incorporated by reference herein. The Charter also is available in print to any shareholder that provides us with a written request. Requests for copies should be made to the Secretary of our company at 106 Front Street East, Suite 400, Toronto, Ontario, Canada M5A 1E1, Telephone (416) 367-9292.

PRINCIPAL

ACCOUNTING FEES AND SERVICES - INDEPENDENT REGISTERED PUBLIC

ACCOUNTING FIRM

Our independent registered public accounting firm is KPMG LLP, Toronto, ON, Canada, Auditor Firm ID: 85.

KPMG LLP acted as our independent registered public accounting firm for the fiscal years ended December 31, 2025 and 2024. For a description of the total amount billed by KPMG LLP to us for services performed in the last two fiscal years by category of service (audit fees, audit-related fees, tax fees and all other fees), see Item 9 “Audit Committee Information - External Auditor Service Fees (by Category)” in the AIF, which is attached as Exhibit 99.1 to this Form 40-F and incorporated by reference herein.

AUDIT COMMITTEE PRE-APPROVAL POLICIES AND PROCEDURES

For a description of our pre-approval policies and procedures related to the provision of non-audit services, see Item 9 “Audit Committee Information- Pre-Approval of Audit and Non-Audit Services Provided by Independent Auditors” in the AIF, which is attached as Exhibit 99.1 to this Form 40-F and incorporated by reference herein.

RECOVERY OF ERRONEOUSLY AWARDED COMPENSATION

The Registrant has adopted a compensation recovery policy (referred to as the “Incentive Compensation Clawback Policy”) as required by NYSE listing standards and pursuant to Rule 10D-1 of the Exchange Act. The Executive Compensation Clawback Policy is incorporated by reference as Exhibit 97.1 to this Form 40-F. At no time during or after the fiscal year ended December 31, 2025 (as of the date of this Annual Report), was the Registrant required to prepare an accounting restatement that required recovery of erroneously awarded compensation pursuant to the Incentive Compensation Clawback Policy and, as of December 31, 2025, there was no outstanding balance of erroneously awarded compensation to be recovered from the application of the Incentive Compensation Clawback Policy to a prior restatement.

OFF-BALANCE SHEET ARRANGEMENTS

The Registrant does not have any commitments or obligations, including contingent obligations, arising from arrangements with unconsolidated entities or persons (which are not otherwise discussed in the Registrant’s Management’s Discussion and Analysis for the fiscal year ended December 31, 2025, filed as Exhibit 99.3 to this annual report on Form 40-F), that have or are reasonably likely to have a material current or future effect on its financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, cash requirements or capital resources.

CODE OF BUSINESS CONDUCT AND ETHICS

We have adopted a Code of Business Conduct and Ethics (the “Code”) covering our executive officers and directors. The Code is available on our website at http://www.seabridgegold.com/company/governance and from our office at the address listed on the cover of this Form 40-F.

All amendments and all waivers of the Code to the officers covered by it will be posted on our website, furnished to the SEC as required, and provided to any shareholder who requests them. During the fiscal year ended December 31, 2025, we did not grant any waiver, including an implicit waiver, from a provision of the Code to any executive officer or director.

CONTRACTUAL OBLIGATIONS

The disclosure is included under the heading “Contractual Obligations” in our MD&A attached as Exhibit 99.3 to this annual report on Form 40-F and incorporated by reference herein. Amounts shown for mining leases include estimates of option payments, mineral lease payments, work commitments and tax levies that are required to maintain our interest in the mineral projects.

MINE SAFETY DISCLOSURE

Pursuant to Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, issuers that are operators, or that have a subsidiary that is an operator, of a coal or other mine in the United States are required to disclose in their periodic reports filed with the SEC information regarding specified health and safety violations, orders and citations, related assessments and legal actions, and mining-related fatalities under the regulation of the Federal Mine safety and Health Administration under the Federal Mine Safety and Health Act of 1977. During the fiscal year ended December 31, 2025, we were not an operator, of a coal or other mine in the United States.

TAX MATTERS

Purchasing, holding or disposing of securities of the Registrant may have tax consequences under the laws of the United States and Canada that are not described in this Annual Report on Form 40-F.

NOTICES PURSUANT TO REGULATION BTR

We did not send any notices required by Rule 104 of Regulation BTR during the fiscal year ended December 31, 2025 concerning any equity security subject to a blackout period under Rule 101 of Regulation BTR.

ADDITIONAL INFORMATION

Additional information relating to us, including the Audited Financial Statements, the MD&A and the AIF, can be found on SEDAR+ www.sedarplus.ca, on the SEC website at www.sec.gov, or on our website at www.seabridgegold.com. Shareholders may also contact the Assistant Corporate Secretary of our company by phone at (416) 367-9292 or by e-mail at info@seabridgegold.com to request copies of these documents and this annual report on Form 40-F.

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS

Not applicable.

DISCLOSURE PURSUANT TO SECTION 13(r) OF THE EXCHANGE ACT

In accordance with Section 13(r) of the Exchange Act, the Registrant is required to include certain disclosures in its periodic reports if it or any of its affiliates knowingly engaged in certain specified activities during the period covered by the report. Neither the Registrant nor its affiliates have knowingly engaged in any transaction or dealing reportable under Section 13(r) of the Exchange Act during the year ended December 31, 2025.

UNDERTAKING AND CONSENT TO SERVICE OF PROCESS

A. Undertaking

We undertake to make available, in person or by telephone, representatives to respond to inquiries made by the SEC staff, and to furnish promptly, when requested to do so by the SEC staff, information relating to: the securities registered pursuant to Form 40-F; the securities in relation to which the obligation to file an annual report on Form 40-F arises; or transactions in said securities.

B. Consent to Service of Process

We have previously filed with the SEC a written consent to service of process and power of attorney on Form F-X. Any change to the name or address of our agent for service shall be communicated promptly to the SEC by amendment to the Form F-X referencing our file number.

SIGNATURES

Pursuant to the requirements of the Exchange Act, the Registrant certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this annual report to be signed on its behalf by the undersigned, thereto duly authorized.

| Seabridge Gold Inc. | ||

| By: | /s/ Rudi P. Fronk | |

| Rudi P. Fronk | ||

| Chairman and Chief Executive Officer | ||

Date: March 26, 2026

EXHIBITS

| Annual Information | ||

| 99.1 | Annual Information Form for the year ended December 31, 2025 | |

| 99.2 | Audited Financial Statements for the year ended December 31, 2025 | |

| 99.3 | Management’s Discussion and Analysis for the year ended December 31, 2025 | |

| 101 | Interactive Data File | |

| 104 | Cover Page Interactive Data File (formatted as Inline XBRL and contained in Exhibit 101). | |

| * | Previously Filed |

Exhibit 23.1

|

KPMG LLP Bay Adelaide Centre 333 Bay Street Suite 4600 Toronto ON M5H 2S5 Canada |

Telephone (416) 777-8500 Fax (416) 777-8818 Internet www.kpmg.ca |

Consent of Independent Registered Public Accounting Firm

The Board of Directors of Seabridge Gold Inc.

We consent to the use of:

| ● | our report dated March 26, 2026 on the consolidated financial statements of Seabridge Gold Inc. (the “Entity”) which comprise the consolidated statements of financial position as of December 31, 2025 and 2024, the related consolidated statements of operations and comprehensive income (loss), changes in shareholders’ equity and cash flows for each of the years then ended, and the related notes (collectively the “consolidated financial statements”); and |

| ● | our report dated March 26, 2026 on the effectiveness of the Entity’s internal control over financial reporting as of December 31, 2025, |

each of which is included in the Annual Report on Form 40-F of the Entity for the fiscal year ended December 31, 2025.

We also consent to the incorporation by reference of such reports in the Registration Statement (No. 333-283616) on Form F-10, and the Registration Statement (No. 333-211331) on Form S-8 of the Entity.

/s/ KPMG LLP

Chartered Professional Accountants, Licensed Public Accountants

March 26, 2026

Toronto, Canada

Exhibit 23.2

Tetra Tech Canada Inc.

March 26, 2026

| To: | Seabridge Gold Inc. |

United States Securities and Exchange Commission

| Re: | Seabridge Gold Inc. (the “Company”) |

Consent of Expert

Ladies and Gentlemen:

Reference is made to the technical report titled “KSM (Kerr-Sulphurets-Mitchell) Prefeasibility Study and Preliminary Economic Assessment, NI 43-101 Technical Report” dated August 8, 2022 (the “Technical Report”) prepared for the Company.

In connection with the Company’s Annual Report on Form 40-F (the “40-F”) in respect of the financial year ended December 31, 2025, to be filed with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Securities Exchange Act of 1934, as amended, I, Hassan Ghaffari, P. Eng., on behalf of Tetra Tech Canada Inc. hereby:

| 1. | consent to the public filing of the Technical Report and the use of any extracts from or a summary of the Technical Report in the 40-F; |

| 2. | consent to the use of Tetra Tech Canada Inc.’s name and references to the Technical Report, or portions thereof, in the 40-F and to the inclusion or incorporation by reference of information derived from the Technical Report in the 40-F; |

| 3. | confirm that I have read the 40-F and that it fairly and accurately represents the information in the sections of the Technical Report for which I am responsible; and |

| 4. | confirm that I have read the 40-F and have no reason to believe that there are any misrepresentations in the information contained therein that are derived from the Technical Report or that are within my knowledge as a result of the services performed by Tetra Tech Canada Inc. in connection with the Technical Report. |

| Yours Truly, | |

| /s/ Hassan Ghaffari, P. Eng. | |

| Hassan Ghaffari, P. Eng. | |

| Director of Metallurgy | |

| Tetra Tech Canada Inc. |

Exhibit 23.3

Tetra Tech Inc.

March 26, 2026

| To: | Seabridge Gold Inc. |

United States Securities and Exchange Commission

| Re: | Seabridge Gold Inc. (the “Company”) |

Consent of Expert

Ladies and Gentlemen:

Reference is made to the technical report titled “KSM (Kerr-Sulphurets-Mitchell) Prefeasibility Study and Preliminary Economic Assessment, NI 43-101 Technical Report” dated August 8, 2022 (the “Technical Report”) prepared for the Company.

In connection with the Company’s Annual Report on Form 40-F (the “40-F”) in respect of the year ended December 31, 2025, to be filed with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Securities Exchange Act of 1934, as amended, I, Dr. Jianhui Huang P. Eng., on behalf of Tetra Tech Inc. hereby:

| 1. | consent to the public filing of the Technical Report and the use of any extracts from or a summary of the Technical Report in the 40-F; |

| 2. | consent to the use of Tetra Tech Inc.’s name and references to the Technical Report, or portions thereof, in the 40-F and to the inclusion or incorporation by reference of information derived from the Technical Report in the 40-F; |

| 3. | confirm that I have read the 40-F and that it fairly and accurately represents the information in the sections of the Technical Report for which I am responsible; and |

| 4. | confirm that I have read the 40-F and have no reason to believe that there are any misrepresentations in the information contained therein that are derived from the Technical Report or that are within my knowledge as a result of the services performed by Tetra Tech Inc. in connection with the Technical Report. |

| Yours Truly, | |

| /s/ Dr. Jianhui (John) Huang, P. Eng. | |

| Dr. Jianhui (John) Huang, P. Eng. | |

| Senior Metallurgist | |

| Tetra Tech Inc. |

Exhibit 23.4

March 26, 2026

| TO: | Seabridge Gold Inc. |

| United States Securities and Exchange Commission |

| Re: | Seabridge Gold Inc. (the “Company”) |

Consent of Expert

Ladies and Gentlemen:

Reference is made to:

| ● | the technical report titled “KSM (Kerr-Sulphurets-Mitchell) Prefeasibility Study and Preliminary Economic Assessment, NI 43-101 Technical Report” dated August 8, 2022 (the “Technical Report”) prepared for the Company; and |

| ● | the 2024 updated resource estimates for the Iron Cap and Kerr deposits at the KSM Project, effective January 10, 2024 (such disclosure collectively, the “Estimates”). |

In connection with the Company’s Annual Report on Form 40-F (the “40-F”) in respect of the financial year ended December 31, 2025, to be filed with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Securities Exchange Act of 1934, as amended, the undersigned hereby:

| 1. | consents to being named directly or indirectly in the Form 40-F; and |

| 2. | consents to: |

| (a) | the use of the content in the Technical Report that I am responsible for preparing; and |

| (b) | the inclusion of the Estimates in the 40-F; |

| Yours Truly, | |

| /s/ Henry Kim, P. Geo. | |

| Henry Kim, P. Geo. | |

| Principal Resource Geologist Wood Canada Limited |

Exhibit 23.5

March 26, 2026

| TO: | Seabridge Gold Inc. |

| United States Securities and Exchange Commission |

| Re: |

Seabridge Gold Inc. (the “Company”) Consent of Expert |

Ladies and Gentlemen:

Reference is made to the technical report titled “KSM (Kerr-Sulphurets-Mitchell) Prefeasibility Study and Preliminary Economic Assessment, NI 43-101 Technical Report” dated August 8, 2022 (the “Technical Report”) prepared for the Company.

In connection with the Company’s Annual Report on Form 40-F (the “40-F”) in respect of the financial year ended December 31, 2025, to be filed with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Securities Exchange Act of 1934, as amended, I, James H. Gray, P.Eng., on behalf of myself and Moose Mountain Technical Services, hereby:

| 1. | consent to the public filing of the Technical Report and the use of any extracts from or a summary of the Technical Report in the 40-F; |

| 2. | consent to the use of my name and Moose Mountain Technical Services’s name and references to the Technical Report, or portions thereof, in the 40-F and to the inclusion or incorporation by reference of information derived from the Technical Report in the 40-F; |

| 3. | confirm that I have read the 40-F and that it fairly and accurately represents the information in the sections of the Technical Report for which I am responsible; and |

| 4. | confirm that I have read the 40-F and have no reason to believe that there are any misrepresentations in the information contained therein that are derived from the Technical Report or that are within my knowledge as a result of the services performed by me in connection with the Technical Report. |

| Yours Truly | |

| /s/ James H. Gray, P. Eng. | |

| James H. Gray, P. Eng. | |

| Principal Mining Engineer | |

| Moose Mountain Technical Services |

Exhibit 23.6

March 26, 2026

| TO: | Seabridge Gold Inc. |

| United States Securities and Exchange Commission |

| Re: | Seabridge Gold Inc. (the “Company”) |

Ladies and Gentlemen:

Reference is made to the technical report titled “KSM (Kerr-Sulphurets-Mitchell) Prefeasibility Study and Preliminary Economic Assessment, NI 43-101 Technical Report” dated August 8, 2022 (the “Technical Report”) prepared for the Company.

In connection with the Company’s Annual Report on Form 40-F (the “40-F”) in respect of the financial year ended December 31, 2025, to be filed with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Securities Exchange Act of 1934, as amended, I, Neil Brazier, P.Eng., on behalf of myself and W.N. Brazier Associates Inc., hereby:

| 1. | consent to the public filing of the Technical Report and the use of any extracts from or a summary of the Technical Report in the 40-F; |

| 2. | consent to the use of my name and W.N. Brazier Associates lnc.’s name and references to the Technical Report, or portions thereof, in the 40-F and to the inclusion or incorporation by reference of information derived from the Technical Report in the 40-F; |

| 3. | confirm that I have read the 40-F and that it fairly and accurately represents the information in the sections of the Technical Report for which I am responsible; and |

| 4. | confirm that I have read the 40-F and have no reason to believe that there are any misrepresentations in the information contained therein that are derived from the Technical Report or that are within my knowledge as a result of the services performed by me in connection with the Technical Report. |

| Yours Truly, | |

| /s/ Neil Brazier, P. Eng. | |

| Neil Brazier, P. Eng. | |

| Principal | |

| W.N. Brazier Associates Inc. |

Exhibit 23.7

March 26, 2026

| TO: | Seabridge Gold Inc. |

United States Securities and Exchange Commission

| Re: | Seabridge Gold Inc. (the “Company”) |

Consent of Expert

Ladies and Gentlemen:

Reference is made to the technical report titled “KSM (Kerr-Sulphurets-Mitchell) Prefeasibility Study and Preliminary Economic Assessment, NI 43-101 Technical Report” dated August 8, 2022 (the “Technical Report”) prepared for the Company.

In connection with the Company’s Annual Report on Form 40-F (the “40-F”) in respect of the financial year ended December 31, 2025, to be filed with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Securities Exchange Act of 1934, as amended, I, Rolf Schmitt, M.Sc., P.Geo., on behalf of ERM Consultants Canada Ltd., hereby:

| 1. | consent to the public filing of the Report and the use of any extracts from or a summary of the Technical Report in the 40-F; |

| 2. | consent to the use of ERM Consultants Canada Ltd.’s name and references to the Technical Report, or portions thereof, in the 40-F and to the inclusion or incorporation by reference of information derived from the Technical Report in the 40-F; |

| 3. | confirm that I have read the 40-F and that it fairly and accurately represents the information in the sections of the Report for which I am responsible; and |

| 4. | confirm that I have read the 40-F and have no reason to believe that there are any misrepresentations in the information contained therein that are derived from the Technical Report or that are within my knowledge as a result of the services performed by ERM Consultants Canada Ltd. in connection with the Technical Report. |

| Yours Truly, | |

| /s/ Rolf Schmitt, P. Geo. | |

| Rolf Schmitt, P. Geo. | |

| Technical Director – Permitting | |

| ERM Consultants Canada Ltd. |

Exhibit 23.8

March 26, 2026

| TO: | Seabridge Gold Inc. |

| United States Securities and Exchange Commission |

| Re: | Seabridge Gold Inc. (the “Company”) |

| Consent of Expert |

Ladies and Gentlemen:

Reference is made to the technical report titled “KSM (Kerr-Sulphurets-Mitchell) Prefeasibility Study and Preliminary Economic Assessment, NI 43-101 Technical Report” dated August 8, 2022 (the “Technical Report”) prepared for the Company.

In connection with the Company’s Annual Report on Form 40-F (the “40-F”) in respect of the financial year ended December 31, 2025, to be filed with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Securities Exchange Act of 1934, as amended, I, David Willms, P. Eng., hereby:

| 1. | consent to the public filing of the Technical Report and the use of any extracts from or a summary of the Technical Report in the 40-F; |

| 2. | consent to the use of Klohn Crippen Berger Ltd.’s name and references to the Technical Report, or portions thereof, in the 40-F and to the inclusion or incorporation by reference of information derived from the Technical Report in the 40-F; |

| 3. | confirm that I have read the 40-F and that it fairly and accurately represents the information in the sections of the Technical Report for which I am responsible; and |

| 4. | confirm that I have read the 40-F and have no reason to believe that there are any misrepresentations in the information contained therein that are derived from the Technical Report or that are within my knowledge as a result of the services performed by Klohn Crippen Berger Ltd. in connection with the Technical Report. |

| Yours Truly, | |

| /s/ David Willms, P. Eng. | |

| David Willms, P. Eng. | |

| Senior Geotechnical Engineer | |

| Klohn Crippen Berger Ltd. |

Exhibit 23.9

BGC Engineering Inc.

March 26, 2026

| To: | Seabridge Gold Inc. |

| United States Securities and Exchange Commission |

| Re: | Seabridge Gold Inc. (the “Company”) |

| Consent of Expert |

Ladies and Gentlemen:

Reference is made to the technical report titled “KSM (Kerr-Sulphurets-Mitchell) Prefeasibility Study and Preliminary Economic Assessment, NI 43-101 Technical Report” dated August 8, 2022 (the “Technical Report”) prepared for the Company.

In connection with the Company’s Annual Report on Form 40-F (the “40-F”) in respect of the financial year ended December 31, 2025, to be filed with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Securities Exchange Act of 1934, as amended, I, Derek Kinakin, M.Sc., P.Geo., P.G., on behalf of myself and BGC Engineering Inc., hereby:

| 1. | consent to the public filing of the Technical Report and the use of any extracts from or a summary of the Technical Report in the 40-F; |

| 2. | consent to the use of my name and BGC Engineering Inc.’s name and references to the Technical Report, or portions thereof, in the 40-F and to the inclusion or incorporation by reference of information derived from the Technical Report in the 40-F; |

| 3. | confirm that I have read the 40-F and that it fairly and accurately represents the information in the sections of the Technical Report for which I am responsible; and |

| 4. | confirm that I have read the 40-F and have no reason to believe that there are any misrepresentations in the information contained therein that are derived from the Technical Report or that are within my knowledge as a result of the services performed by me in connection with the Technical Report. |

| Yours Truly, | |

| /s/ Derek Kinakin, M.Sc., P.Geo., P.G. | |

| Derek Kinakin, M.Sc., P.Geo., P.G. |

Exhibit 23.10

Consent of Ross D. Hammett

WSP Canada Inc.

Annual Report on Form 40-F

March 26, 2026

| To: | Seabridge Gold Inc. |

| United States Securities and Exchange Commission |

| Re: | Seabridge Gold Inc. (the “Company”) |

| Consent of Expert |

Reference is made to the technical report titled “KSM (Kerr-Sulphurets-Mitchell) Prefeasibility Study and Preliminary Economic Assessment, NI 43-101 Technical Report” dated August 8, 2022 (the “Technical Report”) prepared for the Company.

In connection with the Company’s Annual Report on Form 40-F (the “40-F”) in respect of the financial year ended December 31, 2025, to be filed with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Securities Exchange Act of 1934, as amended, I, Ross D. Hammett, Ph.D., P.Eng., hereby:

| 1. | consent to the quotation, inclusion or summary of those portions of the Technical Report prepared by me in the 40-F; |

| 2. | consent to the use of my name and references to my name in the 40-F, where used or referenced in the 40-F. |

in each case above, where used or incorporated by reference into the 40-F.

| Yours truly, | |

| /s/ Ross D. Hammett, Ph.D., P.Eng. | |

| Ross D. Hammett, Ph.D., P.Eng. | |

| WSP Canada Inc. |

Exhibit 31.1

CERTIFICATIONS PURSUANT TO SECTION 302

OF

THE SARBANES-OXLEY ACT OF 2002

I, Rudi P. Fronk, Chairman and CEO, certify that:

| 1. | I have reviewed this Annual Report on Form 40-F of Seabridge Gold Inc. (the “Issuer”): |

| 2. | Based on my knowledge, this annual report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this annual report, fairly present in all material respects the financial condition, results of operations and cash flows of the Issuer as of, and for, the periods presented in this report; |

| 4. | The Issuer’s other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal control over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15(f)) for the Issuer and have: |

| a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the Issuer, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this annual report is being prepared; |

| b) | Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; |

| c) | Evaluated the effectiveness of the Issuer’s disclosure controls and procedures and presented in this annual report our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this annual report based on such evaluation; and |

| d) | Disclosed in this annual report any change in the Issuer’s internal control over financial reporting that occurred during the period covered by the annual report that has materially affected, or is reasonably likely to materially affect, the Issuer’s internal control over financial reporting; and |

| 5. | The Issuer’s other certifying officer(s) and I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the Issuer’s auditors and the audit committee of the Issuer’s board of directors (or persons performing the equivalent functions): |

| a) | All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the Issuer’s ability to record, process, summarize and report financial information; and |

| b) | Any fraud, whether or not material, that involves management or other employees who have a significant role in the Issuer’s internal control over financial reporting. |

| Date: March 26, 2026 | By: | /s/ Rudi P. Fronk |

| Rudi P. Fronk | ||

| Chairman and CEO |

Exhibit 31.2

CERTIFICATIONS PURSUANT TO SECTION 302

OF

THE SARBANES-OXLEY ACT OF 2002

I, Christopher J. Reynolds, VP Finance and CFO, certify that:

| 1. | I have reviewed this Annual Report on Form 40-F of Seabridge Gold Inc. (the “Issuer”): |

| 2. | Based on my knowledge, this annual report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this annual report, fairly present in all material respects the financial condition, results of operations and cash flows of the Issuer as of, and for, the periods presented in this report; |

| 4. | The Issuer’s other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal control over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15(f)) for the Issuer and have: |

| a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the Issuer, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this annual report is being prepared; |

| b) | Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; |

| c) | Evaluated the effectiveness of the Issuer’s disclosure controls and procedures and presented in this annual report our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this annual report based on such evaluation; and |

| d) | Disclosed in this annual report any change in the Issuer’s internal control over financial reporting that occurred during the period covered by the annual report that has materially affected, or is reasonably likely to materially affect, the Issuer’s internal control over financial reporting; and |

| 5. | The Issuer’s other certifying officer(s) and I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the Issuer’s auditors and the audit committee of the Issuer’s board of directors (or persons performing the equivalent functions): |

| a) | All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the Issuer’s ability to record, process, summarize and report financial information; and |

| b) | Any fraud, whether or not material, that involves management or other employees who have a significant role in the Issuer’s internal control over financial reporting. |

| Date: March 26, 2026 | By: | /s/ Christopher J. Reynolds |

| Christopher J. Reynolds | ||

| VP Finance and CFO |

Exhibit 32.1

CERTIFICATION PURSUANT TO 18 U.S.C. §1350, AS ADOPTED PURSUANT TO

SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

In connection with this Annual Report of Seabridge Gold Inc. (the “Company”) on Form 40-F for the period ended December 31, 2025, as filed with the Securities and Exchange Commission on the date hereof (the “Annual Report”), I, Rudi P. Fronk, Chief Executive Officer of the Company, certify, pursuant to U.S.C. §1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, that:

| (1) | The Annual Report fully complies with the requirements of Section 13(a) or 15(d) of the Securities Exchange Act of 1934; and |

| (2) | The information contained in this Annual Report fairly presents, in all material respects, the financial condition and results of operations of the Company. |

| Date: March 26, 2026 | By: | /s/ Rudi P. Fronk |

| Rudi P. Fronk | ||

| Chief Executive Officer |

This certification accompanies the Annual Report pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and may not be used or relied upon for any other purpose including Section 18 of the Securities Exchange Act of 1934. A signed original of this written statement required by Section 906 has been provided to the Company and will be retained by the Company and furnished to the Securities and Exchange Commission or its staff upon request.

Exhibit 32.2

CERTIFICATION PURSUANT TO 18 U.S.C. §1350, AS ADOPTED PURSUANT TO

SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

In connection with this Annual Report of Seabridge Gold Inc. (the “Company”) on Form 40-F for the period ended December 31, 2025, as filed with the Securities and Exchange Commission on the date hereof (the “Annual Report”), I, Christopher J. Reynolds, Vice President Finance and Chief Financial Officer of the Company, certify, pursuant to U.S.C. §1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, that:

| (1) | The Annual Report fully complies with the requirements of Section 13(a) or 15(d) of the Securities Exchange Act of 1934; and |

| (2) | The information contained in this Annual Report fairly presents, in all material respects, the financial condition and results of operations of the Company. |

| Date: March 26, 2026 | By: | /s/ Christopher J. Reynolds |

| Christopher J. Reynolds | ||

| Vice President Finance and CFO |

This certification accompanies the Annual Report pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and may not be used or relied upon for any other purpose including Section 18 of the Securities Exchange Act of 1934. A signed original of this written statement required by Section 906 has been provided to the Company and will be retained by the Company and furnished to the Securities and Exchange Commission or its staff upon request.

Exhibit 99.1

ANNUAL

INFORMATION

FORM

FOR THE YEAR ENDED

DECEMBER 31, 2025

DATED: MARCH 26, 2026

TABLE OF CONTENTS

Contents

The information in this Annual Information Form (“AIF”) is presented as of December 31, 2025 unless specified otherwise.

All dollar amounts are expressed in Canadian dollars unless otherwise indicated. The Issuer’s quarterly and annual financial statements are presented in Canadian dollars.

In this AIF a combination of Imperial and metric measures are used with respect to the Issuer’s mineral properties. Conversion rates from Imperial measure to metric and from metric to Imperial are provided below:

| Imperial Measure = Metric Unit | Metric Measure = Imperial Unit | ||

| 2.47 acres | 1 hectare (h) | 0.4047 hectares | 1 acre |

| 3.28 feet | 1 meter (m) | 0.3048 meters | 1 foot |

| 0.62 miles | 1 kilometer (km) | 1.609 kilometers | 1 mile |

| 0.032 ounces (troy) (oz) | 1 gram (g) | 31.1035 grams | 1 ounce (troy) |

| 1.102 tons (short) | 1 tonne (t) | 0.907 tonnes | 1 ton |

| 0.029 ounces (troy)/ton | 1 gram/tonne (g/t) | 34.28 grams/tonne | 1 ounce (troy/ton) |

Abbreviations of unit measures are used in this AIF in addition to those in brackets in the table above as follows:

| Bt - Billion tonnes | Ga - Giga-annum | kWh - Kilowatt hours | Mlb - Million pounds |

| Mm³ - Million cubic meters | Moz - Million ounces | m/s - Meters per second | Mt - Million tonnes |

| MWh - Megawatt hours | ppm - Parts per million | tpd - tonnes per day | W/m²- Watt per square meter |

See “Glossary of Technical Terms” for a description of some important technical terms used in this AIF.

Cautionary Note Regarding Forward-Looking Statements

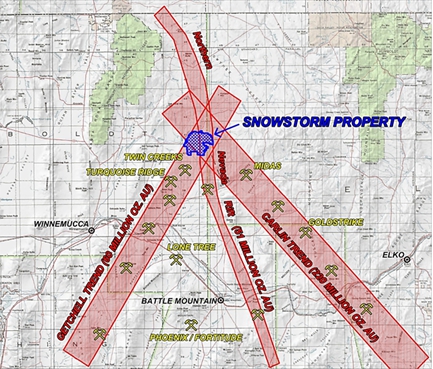

This AIF contains forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 and forward-looking information within the meaning of Canadian securities laws concerning future events or future performance with respect to the Issuer’s projects, business approach and plans, including production, capital, operating and cash flow estimates; business transactions such as the potential joint venture of the Issuer’s KSM Project or the spin-out of the Courageous Lake Project (each as defined herein) and the acquisition or disposition of interests in other mineral properties; requirements for additional capital; the estimation of mineral resources and reserves; and the timing of completion and success of exploration and advancement activities, community relations, required regulatory and third party consents, litigation, permitting and related programs in relation to the KSM Project, Iskut Project, Courageous Lake Project, Snowstorm Project or 3 Aces Project. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives or future events or performance (often, but not always, using words or phrases such as “expects”, “anticipates”, “believes”, “plans”, “projects”, “estimates”, “intends”, “strategy”, “goals”, “objectives” or variations thereof or stating that certain actions, events or results “may”, “could”, “would”, “might”, or “will” be taken, occur or be achieved, or statements of “potential” or something “possible”, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements and forward-looking information (collectively referred to in the following information simply as “forward-looking statements”). In addition, statements concerning mineral reserve and mineral resource estimates constitute forward-looking statements to the extent that they involve estimates of the mineralization expected to be encountered if a mineral property is developed and, in the case of reserves, the economics of a proposed mining operation.

Forward-looking statements are necessarily based on estimates and assumptions made by the Issuer in light of its experience and perception of historical trends, current conditions and expected future developments. In making the forward-looking statements in this AIF the Issuer has applied several material assumptions including, but not limited to, the assumption that: (1) market fundamentals will result in sustained demand and prices for gold and copper, and to a much lesser degree, silver and molybdenum; (2) the potential for production at its advanced mineral projects will continue operationally, legally and economically; (3) any additional financing needed will be available on reasonable terms; (4) estimated mineral reserves and mineral resources at the Issuer’s projects have merit and there is continuity of mineralization as reflected in such estimates; (5) the Issuer will receive and maintain all required regulatory approvals required in respect of its projects.

Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual events or results to differ from those expressed or implied by the forward-looking statements, including, without limitation:

| ● | the Issuer’s history of net losses and negative cash flows from operations and expectation of future losses and negative cash flows from operations; |

| ● | although the Issuer has identified a preferred potential partnership candidate for the KSM Project, there is no assurance that terms of a partnership for advancing the KSM Project will be agreed; |

| ● | risks related to the Issuer’s ability to continue its exploration activities and future advancement activities, and to continue to maintain corporate office support of these activities, which are dependent on the Issuer’s ability to obtain suitable financing, enter into joint ventures or sell property interests |

| ● | the Issuer’s indebtedness requires quarterly interest payments and may require repayment of the principal in full and a repayment premium, which may adversely affect its cash flow and ability to advance its business and necessitate dilutive financing or asset sales; |

| ● | changes in the market price of gold, copper and other metals, which in the past have fluctuated widely, affect the Issuer’s ability to finance its operations and the potential profitability of the Issuer’s projects; |

| ● | uncertainty whether the reserves at its projects can be brought into production; |

| ● | the uncertainty related to unsettled rights and title of Indigenous groups, as well as settled Treaty Nation’s rights, in British Columbia, the Yukon Territory and the Northwest Territories and uncertainties relating to the process of making Canadian laws consistent with the United Nations Declaration on the Rights of Indigenous Peoples |

| ● | risks related to obtaining and maintaining all necessary permits and governmental approvals, or extensions, amendments or renewals thereof, for exploration and advancement activities, including in respect of environmental regulation and the KSM Project’s environmental assessment certificate; |

| ● | risks associated with the use of information technology systems and cybersecurity; |

| ● | the Issuer is subject to substantial government regulatory and environmental requirements which could cause delays in advancing its projects or could result in a restriction or suspension of its operations; |

| ● | risks related to court challenges to the “substantially started” determination for the KSM Project; |

| ● | risks relating to the Issuer’s internal control over financial reporting being ineffective; |

| ● | figures for the Issuer’s resources, reserves and recoveries are estimates only and the Issuer’s properties may yield less mineral production or less profit than currently estimated; |

| ● | uncertainty of estimates of capital costs, operating costs, production and economic returns; |

| ● | risks relating to the construction and maintenance of initial infrastructure at the KSM Project by the Issuer; |

| ● | risks related to commercially producing precious metals and base metals from the Issuer’s mineral properties; |

| ● | risks related to fluctuations in foreign exchange rates; |

| ● | mining, exploration and advancement risks that could result in damage to mineral properties, plant and equipment, personal injury, environmental damage and delays in mining, which may be uninsurable or not insurable in adequate amounts; |

| ● | risks related to the possibility of unregistered agreements, transfers, claims or other defects impacting title to the Issuer’s mineral properties; |

| ● | risks related to increases in demand for exploration, advancement and construction services and equipment, and related cost increases following metals price increases; |

| ● | risks related to the successful completion of the proposed spin-out of the Courageous Lake Project on the terms proposed or not at all; |

| ● | increased competition in the mining industry; |

| ● | risks related to international trade disputes and the imposition of tariffs and the potential impacts it may have on the Issuer’s ability to raise funds and obtain supplies or, if available, the cost of supplies, needed for work programs; |

| ● | regulatory initiatives and ongoing concerns regarding carbon emissions and the impacts of measures taken to induce or mandate lower carbon emissions on the ability to secure permits, finance projects and realize profitability at a project; |

| ● | the Issuer’s current and proposed operations are subject to risks relating to climate change and nature loss that may adversely impact its ability to conduct operations increase its operating costs, interfere with materials and equipment supply, delay execution or reduce the profitability of a future mining operation; |

| ● | risks that changes to climate change or nature related regulatory regimes could adversely affect the Issuer’s business; |

| ● | the Issuer’s reliance on key personnel and the need to retain key executives and attract qualified personnel; |

| ● | the public’s views of the mining industry can present increased risks for permitting, financing and staffing; |

| ● | risks related to some of the Issuer’s directors’ and officers’ involvement with other natural resource companies; |

| ● | uncertainty surrounding an audit by the Canada Revenue Agency (“CRA”) of Canadian exploration expenses incurred by the Issuer during the 2014, 2015 and 2016 financial years which the Issuer has renounced to subscribers of flow-through share offerings and the CRA’s decision to reassess such subscribers; |

| ● | the risks associated with the volatility of the trading volume and price of the Issuer’s Common shares; |

| ● | the return on an investment in the Issuer’s Common shares is limited to capital gains or losses since the Issuer does not pay dividends; |

| ● | the Issuer’s reliance on equity financing creates the potential for dilution of the Issuer’s Common shares; |

| ● | the Issuer’s classification as a “passive foreign investment company” under the United States tax code; and |

| ● | risks related to the pro-environmental groups anti-mining efforts, and sometimes focused efforts on specific projects impacting the Issuer’s share price. |

This list is not exhaustive of the factors that may affect any of the Issuer’s forward-looking statements. Forward-looking statements are statements about the future and are inherently uncertain, and actual achievements of the Issuer or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those referred to in this AIF under the heading “Risk Factors” and elsewhere in this AIF. In addition, although the Issuer has attempted to identify important factors that could cause actual achievements, events or conditions to differ materially from those identified in the forward-looking statements, there may be other factors that cause achievements, events or conditions not to be as anticipated, estimated or intended. Many of the foregoing factors are beyond the Issuer’s ability to control or predict. It is also noted that while Seabridge engages in exploration and advancement of its properties, including data collection and site work in preparation for feasibility study work or early construction work, it will not undertake production activities by itself.

These forward-looking statements are based on the beliefs, expectations and opinions of management on the date the statements are made and the Issuer does not assume any obligation to update forward-looking statements, except as required by applicable securities laws, if circumstances or management’s beliefs, expectations or opinions should change. For the reasons set forth above, investors should not place undue reliance on forward-looking statements.

Cautionary Note to United States Investors Regarding Resource Estimates

This AIF has been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of United States securities laws. Mineral resource estimates included in this AIF and in any document incorporated by reference herein or therein have been prepared in accordance with, and use terms that comply with, the reporting standards in accordance with Canadian National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”). NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. In accordance with NI 43-101, the Issuer uses the terms mineral reserves and resources as they are defined in accordance with the CIM Definition Standards on mineral reserves and resources (the “CIM Definition Standards”) adopted by the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”).

The U.S. Securities and Exchange Commission (the “SEC”) has adopted amendments to its disclosure rules to modernize the mineral property disclosure requirements for issuers whose securities are registered with the SEC under the Exchange Act. These amendments became effective February 25, 2019 (the “SEC Modernization Rules”) and have replaced the historical property disclosure requirements for mining registrants that were included in SEC Industry Guide 7. As a foreign private issuer that files its annual report on Form 40-F with the SEC pursuant to the multi-jurisdictional disclosure system (“MJDS”), the Issuer is not required to provide disclosure on its mineral properties under the SEC Modernization Rules and will continue to provide disclosure under NI 43-101 and the CIM Definition Standards. However, if the Issuer either ceases to be a “foreign private issuer” or ceases to be entitled to file reports under the MJDS, then the Issuer will be required to provide disclosure on its mineral properties under the SEC Modernization Rules.