UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the Month of January 2026

Commission File Number 001-35948

Kamada Ltd.

(Translation of registrant’s name into English)

2 Holzman Street

Science Park, P.O. Box 4081

Rehovot 7670402

Israel

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

This Form 6-K is being incorporated by reference into the Registrant’s Form S-8 Registration Statements, File Nos. 333-192720, 333-207933, 333-215983, 333-222891, 333-233267 and 333-265866.

The following exhibit is attached:

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Date: January 7, 2026 | KAMADA LTD. | |

| By: | /s/ Nir Livneh | |

|

Nir Livneh Vice President General Counsel and |

||

EXHIBIT INDEX

3

Exhibit 99.1

Kamada Provides 2026 Annual Guidance of $200

- $205 Million in Revenues and $50 - $53 Million of

Adjusted EBITDA, Representing Double-Digit Growth and Affirms 2025

Financial Guidance

| ● | 2026 Guidance Represents Year-Over-Year Increase of 13% in Revenues and 23% in Adjusted EBITDA Based on Mid-Point of 2025 Annual Guidance |

| ● | 2026 Annual Guidance is Based Solely on Continued Organic Growth |

| ● | Company Continues to Focus on Securing New Business Development and M&A Transactions to Accelerate Long-Term Profitable Growth |

| ● | Kamada Affirms 2025 Guidance of $178 Million - $182 Million in Revenues and $40 Million - $44 Million of Adjusted EBITDA |

| ● | 2025 Year-End Cash of Approximately $75 Million |

REHOVOT, Israel, and HOBOKEN, NJ – January 7, 2026 -- Kamada Ltd. (NASDAQ: KMDA; TASE: KMDA.TA), a global biopharmaceutical company with a portfolio of marketed products indicated for rare and serious conditions and a leader in the specialty plasma-derived field, today announced that, based on its positive outlook for 2026, it is forecasting continued double-digit profitable growth with 2026 annual guidance of $200 million - $205 million in revenues and $50 million - $53 million of adjusted EBITDA. Importantly, the projected 2026 growth is based solely on continued organic growth of the Company’s diverse commercial products portfolio in multiple markets in both its Proprietary segment which covers the specialty plasma therapies and the Distribution segment which covers commercialization of in-licensing third parties biopharmaceutical products. The 2026 midpoint guidance range represents a year-over-year increase of 13% in revenues and 23% in adjusted EBITDA, based on the mid-points of Kamada’s 2025 guidance. The Company further announced that it expects to achieve its 2025 financial guidance of $178 million - $182 million in revenues and $40 million - $44 million of adjusted EBITDA, with 2025 year-end cash of approximately $75 million. Kamada intends to publish its 2025 financial results during the first half of March 2026.

“We enter 2026 from a position of significant commercial and financial strength and are excited about the progress we have made over the past year,” said Amir London, Kamada’s Chief Executive Officer. “We look forward to achieving our value generating objectives for 2026, driven by continued organic growth of our diverse commercial product portfolio marketed in over 30 countries. We are also pleased with our ability to consistently convert adjusted EBITDA into operational cash.”

“Our projected growth in 2026 is expected to be driven by continued expansion of our entire commercial product portfolio, including growth in our U.S. sales, and continued increase in sales of KAMRAB®, GLASSIA®, HEPAGAM® and VARIZIG® in ex-U.S. markets. We also anticipate continued growth of our Distribution segment through the launch of additional biosimilar products in the Israeli market, as well as the expansion of the Distribution business to the MENA region, and initial sales of normal source plasma collected in our multiple centers in Texas. The overall profitable growth is achievable even after accounting for a reduction of the GLASSIA royalty payments rate received from TAKEDA, which became effective in August 2025 and will have its first full-year impact in 2026, further solidifying the strength of our diverse commercial infrastructure,” continued Mr. London.

“We also continue to focus on identifying and securing compelling new business development and M&A transactions. We expect that these initiatives will enrich our current portfolio of marketed products and generate synergies with our existing commercial operations. In addition, we expect to continue increasing the plasma collection in our three plasma centers aiming to strengthen our vertical integration, reduce specialty plasma costs and support continued growth through sales of normal source plasma,” concluded Mr. London.

Non-IFRS financial measures

We present EBITDA and Adjusted EBITDA because we use these non-IFRS financial measures to assess our operational performance, for financial and operational decision-making, and as a means to evaluate period-to-period comparisons on a consistent basis. Management believes these non-IFRS financial measures are useful to investors because: (1) they allow for greater transparency with respect to key metrics used by management in its financial and operational decision-making and provide investors with a meaningful perspective on the current underlying performance of the Company’s core ongoing operations; and (2) they exclude the impact of certain items that are not directly attributable to our core operating performance and that may obscure trends in the core operating performance of the business. Non-IFRS financial measures have limitations as an analytical tool and should not be considered in isolation from, or as a substitute for, our IFRS results. We expect to continue reporting non-IFRS financial measures, adjusting for the items described below, and we expect to continue to incur expenses similar to certain of the non-cash, non-IFRS adjustments described below. Accordingly, unless otherwise stated, the exclusion of these and other similar items in the presentation of non-IFRS financial measures should not be construed as an inference that these items are unusual, infrequent or non-recurring. EBITDA and Adjusted EBITDA are not recognized terms under IFRS and do not purport to be an alternative to IFRS terms as an indicator of operating performance or any other IFRS measure. Moreover, because not all companies use identical measures and calculations, the presentation of EBITDA and Adjusted EBITDA may not be comparable to other similarly titled measures of other companies. EBITDA is defined as net income (loss), plus income tax expense, plus or minus financial income or expenses, net, plus or minus income or expense in respect of securities measured at fair value, net, plus or minus income or expenses in respect of currency exchange differences and derivatives instruments, net, plus depreciation and amortization expense. Adjusted EBITDA is EBITDA plus non-cash share-based compensation expenses and certain other costs.

For the projected 2026 and 2025 adjusted EBITDA information presented herein, the Company is unable to provide a reconciliation of this forward measure to the most comparable IFRS financial measure because the information for these measures is dependent on future events, many of which are outside of the Company’s control. Additionally, estimating such forward-looking measures and providing a meaningful reconciliation consistent with the Company’s accounting policies for future periods is meaningfully difficult and requires a level of precision that is unavailable for these future periods and cannot be accomplished without unreasonable effort. Forward-looking non-IFRS measures are estimated in a manner consistent with the relevant definitions and assumptions noted in the Company’s adjusted EBITDA for historical periods.

About Kamada

Kamada Ltd. (the “Company”) is a global biopharmaceutical company with a portfolio of marketed products indicated for rare and serious conditions and a leader in the specialty plasma-derived therapies field. FIMI Opportunity Funds, the leading private equity firm in Israel, is the Company’s controlling shareholder, beneficially owning approximately 38% of the outstanding ordinary shares. The Company’s strategy is focused on driving profitable growth through four primary growth pillars: First, organic growth of its specialty plasma therapies products portfolio, including continued investment in the commercialization and life cycle management of its proprietary products, including six FDA-approved specialty plasma-derived products: KEDRAB®, GLASSIA®, CYTOGAM®, VARIZIG®, WINRHO SDF® and HEPAGAM B®, as well as KAMRAB®, and two types of equine-based anti-snake venom products. Second, distribution of third parties’ pharmaceutical products in Israel & MENA through in-licensing partnerships, mainly through the launch of several biosimilar products in Israel. Third, the Company is expanding its plasma collection operations to support revenue growth through the sale of normal source plasma to other plasma-derived manufacturers, and to support its increasing demand for hyper-immune plasma. The Company currently owns three operating plasma collection centers in the United States, in Beaumont Texas, Houston Texas, and San Antonio, Texas. Forth, the Company aims to secure new mergers and acquisitions, business development, in-licensing and/or collaboration opportunities, which are anticipated to enhance the Company’s marketed products portfolio and leverage its financial strength and existing commercial infrastructure to drive long-term profitable growth. The Company is leveraging its manufacturing, research and development expertise to advance the development and commercialization of additional product candidates, targeting areas of significant unmet medical need.

Cautionary Note Regarding Forward-Looking Statements

This release includes forward-looking statements within the meaning of Section 21E of the U.S. Securities Exchange Act of 1934, as amended, and the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements are statements that are not historical facts, including (among others) statements regarding: 1) positive outlook for 2026, including double-digit profitable growth, annual guidance of $200-$205 million in revenues and $50-$53 million of adjusted EBITDA based solely on continued organic growth; 2) achieving 2025 full-year revenue guidance of $178-$182 million and adjusted EBITDA of $40-$44 million; 3) 2025 year-end cash of approximately $75 million; 4) 2026 growth driven by expansion of the entire commercial product portfolio; 5) launch of additional biosimilar products in the Israeli market; 6) expansion of the Distribution business to the MENA region; 7) intentions to focus on identifying and securing compelling new business development and M&A transactions, and expecting that these initiatives will enrich the Company’s current portfolio of marketed products and generate synergies with its existing commercial operations accelerating long-term profitable growth, and 8) expectation to continue increasing the plasma collection aiming to strengthen the Company’s vertical integration, reduce specialty plasma costs and support continued growth through sales of normal source plasma, including initial sales in 2026 of normal source plasma. Forward-looking statements are based on Kamada’s current knowledge and its present beliefs and expectations regarding possible future events and are subject to risks, uncertainties and assumptions. Actual results and the timing of events could differ materially from those anticipated in these forward-looking statements as a result of several factors including, but not limited to the evolving nature of the conflicts in the Middle East and the impact of such conflicts in Israel, the Middle East and the rest of the world, the impact of these conflicts on market conditions and the general economic, industry and political conditions in Israel, the U.S. and globally, effect of potential imposed tariff on overall international trade and specifically on Kamada’s ability to continue maintaining expected sales and profit levels in light of such potential tariff, the effect on establishment and timing of business initiatives, the ability to acquire strategic business opportunities and successfully integrating them into existing businesses, operational capabilities of Kamada’s plasma centers, regulatory approvals and regulatory delays and other risks detailed in Kamada’s filings with the U.S. Securities and Exchange Commission (the “SEC”) including those discussed in its most recent Annual Report on Form 20-F and in any subsequent reports on Form 6-K, each of which is on file or furnished with the SEC and available at the SEC’s website at www.sec.gov. The forward-looking statements made herein speak only as of the date of this announcement and Kamada undertakes no obligation to update publicly such forward-looking statements to reflect subsequent events or circumstances, except as otherwise required by law.

CONTACTS:

Chaime Orlev

Chief Financial Officer

IR@kamada.com

Brian Ritchie

LifeSci Advisors, LLC

212-915-2578

britchie@LifeSciAdvisors.com

Exhibit 99.2

Corporate Presentation January 2026 TURNING STRATEGIC DRIVERS INTO PROFITABLE GROWTH NASDAQ: KMDA; TASE: KMDA.TA 2 FORWARD - LOOKING STATEMENT This presentation is not intended to provide investment or medical advice . This presentation contains forward - looking statements, which express the current beliefs and expectations of Kamada’s management . Such statements include 2025 and 2026 financial guidance ; growth strategy and plans for double digit growth ; growth prospects related to KEDRAB®, GLASSIA®, CYTOGAM®, and the Israeli, MENA and LATAM distribution operations ; advancement and future expected revenues driven by our plasma collection operation ; and success in identifying and integrating M&A targets for growth . These statements involve a number of known and unknown risks and uncertainties that could cause Kamada's future results, performance or achievements to differ significantly from the projected results, performances or achievements expressed or implied by such forward - looking statements . Important factors that could cause or contribute to such differences include, but are not limited to, risks relating to Kamada's ability to successfully develop and commercialize its products and product candidates, progress and results of any clinical trials, introduction of competing products, continued market acceptance of Kamada’s commercial products portfolio, impact of geo - political environment in the middle east, impact of any changes in regulation and legislation that could affect the pharmaceutical industry, difficulty in predicting, obtaining or maintaining U . S . Food and Drug Administration, European Medicines Agency and other regulatory authority approvals, restrains related to third parties’ IP rights and changes in the health policies and structures of various countries, success of M&A strategies, environmental risks, changes in the worldwide pharmaceutical industry and other factors that are discussed under the heading “Risk Factors” of Kamada’s 2024 Annual Report on Form 20 - F (filed on March 5 , 2025 ), as well as in Kamada’s recent Forms 6 - K filed with the U . S . Securities and Exchange Commission . This presentation includes certain non - IFRS financial information, which is not intended to be considered in isolation or as a substitute for, or superior to, the financial information prepared and presented in accordance with IFRS . The non - IFRS financial measures may be calculated differently from, and therefore may not be comparable to, similarly titled measures used by other companies . In accordance with the requirement of the SEC regulations a reconciliation of these non - IFRS financial measures to the comparable IFRS measures is included in an appendix to this presentation . Management uses these non - IFRS financial measures for financial and operational decision - making and as a means to evaluate period - to - period comparisons . Management believes that these non - IFRS financial measures provide meaningful supplemental information regarding Kamada’s performance and liquidity . Forward - looking statements speak only as of the date they are made, and Kamada undertakes no obligation to update any forward - looking statement to reflect the impact of circumstances or events that arise after the date the forward - looking statement was made, except as required by applicable law .

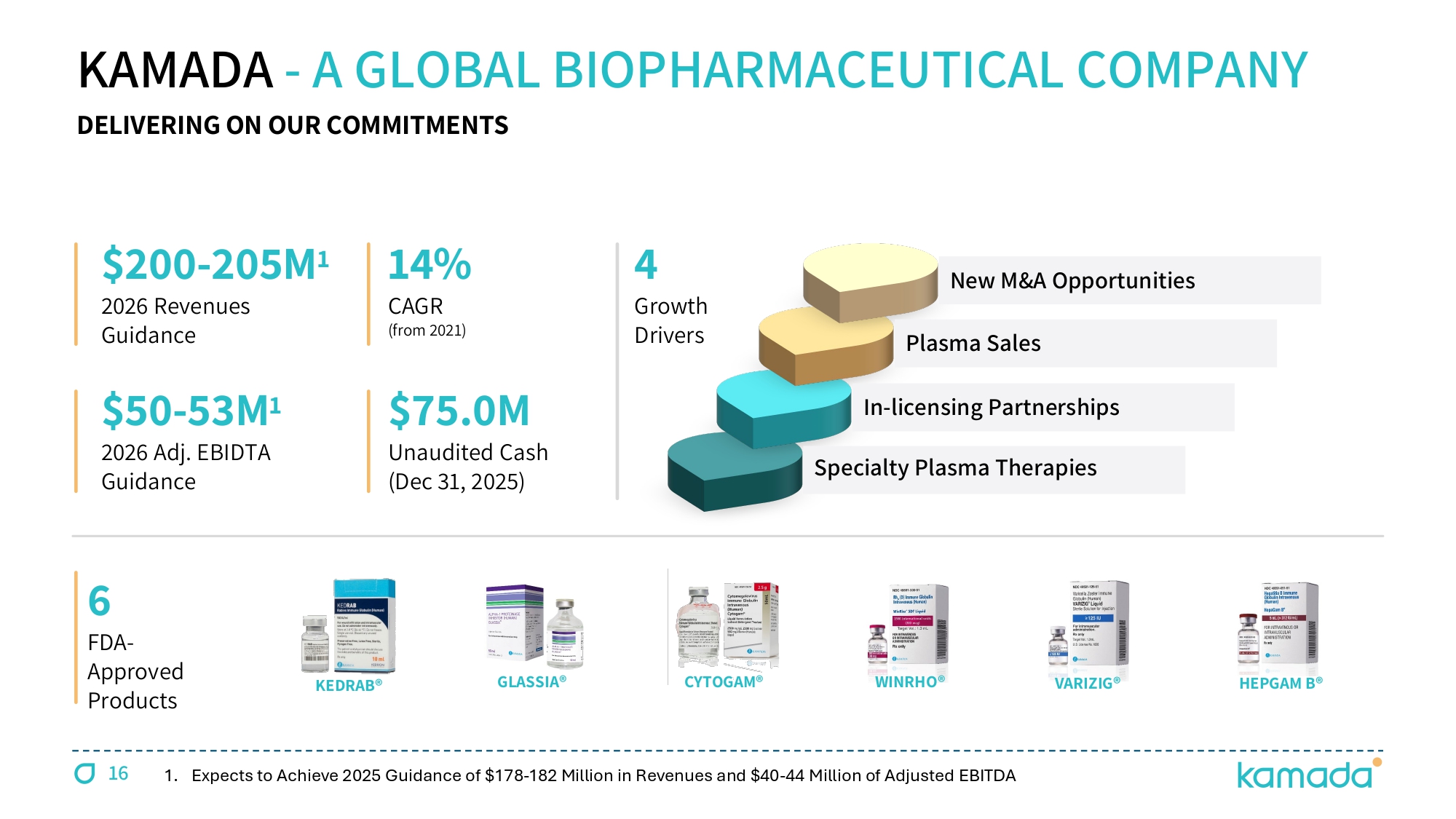

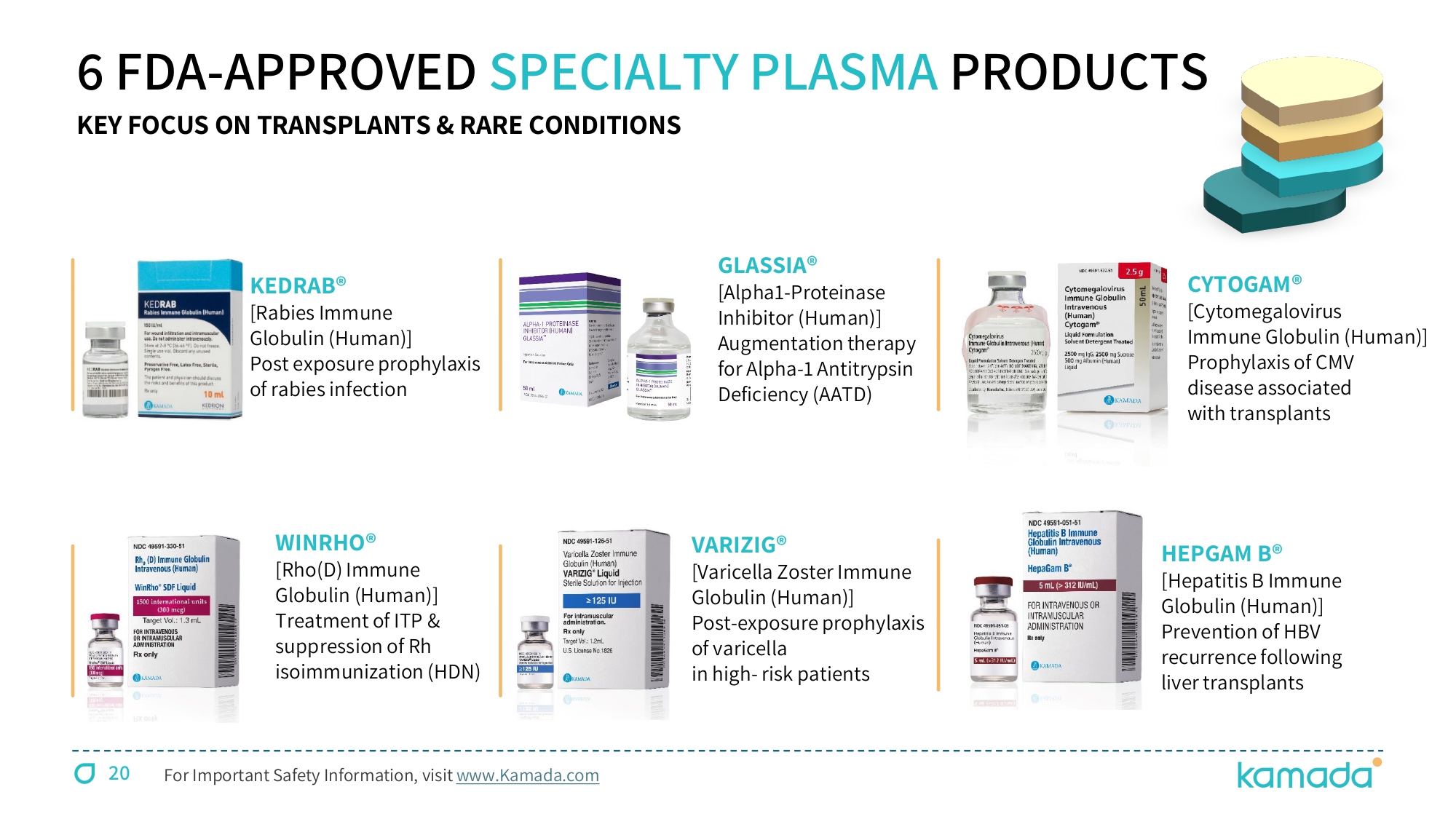

KEDRAB® CYTOGAM® HEPGAM B® VARIZIG® WINRHO® GLASSIA® KAMADA - A GLOBAL BIOPHARMACEUTICAL COMPANY 6 FDA - Approved Products 14 % CAGR (from 2021) $ 200 - 205M 1 2026 Revenues Guidance $ 50 - 53M 1 2026 Adj. EBIDTA Guidance 4 Growth Drivers A LEADER IN SPECIALTY PLASMA THERAPIES, WITH A PORTFOLIO OF MARKETED PRODUCTS INDICATED FOR RARE AND SERIOUS CONDITIONS $ 7 đ .0 M Unaudited Cash (Dec 31 , 2025 ) 3 1.

Expects to Achieve 2025 Guidance of $178 - 182 Million in Revenues and $40 - 44 Million of Adjusted EBITDA New M&A Opportunities Plasma Sales In - licensing Partnerships Specialty Plasma Therapies GLOBAL COMMERCIAL FOOTPRINT United States Israel UAE Focused on lifecycle management and expansion to new markets, mainly in the MENA and LATAM regions Commercial operations in the US with seasoned staff, experienced in specialty plasma products Corporate offices in Israel , US and UAE; key markets are the US, Israel, Canada, LATAM, MENA and CIS Regions STRONG DISTRIBUTION NETWORK IN OVER 30 COUNTRIES 4 5 EXPERIENCED LEADERSHIP Amir London CEO Hanni Neheman VP Marketing & Sales Liron Reshef VP Human Resources Shavit Beladev VP Kamada Ɗ Plasma Chaime Orlev CFO Jon Knight VP U.S Commercial Yael Brenner VP Quality Boris Gorelik VP Business Development & Strategic Programs Nir Livneh VP Legal, General Counsel & Corporate Secretary Eran Nir COO Orit Pinchuk VP Regulatory Affairs & PVG WITH PROVEN TRACK RECORD

DELIVERING ON OUR COMMITMENTS 6

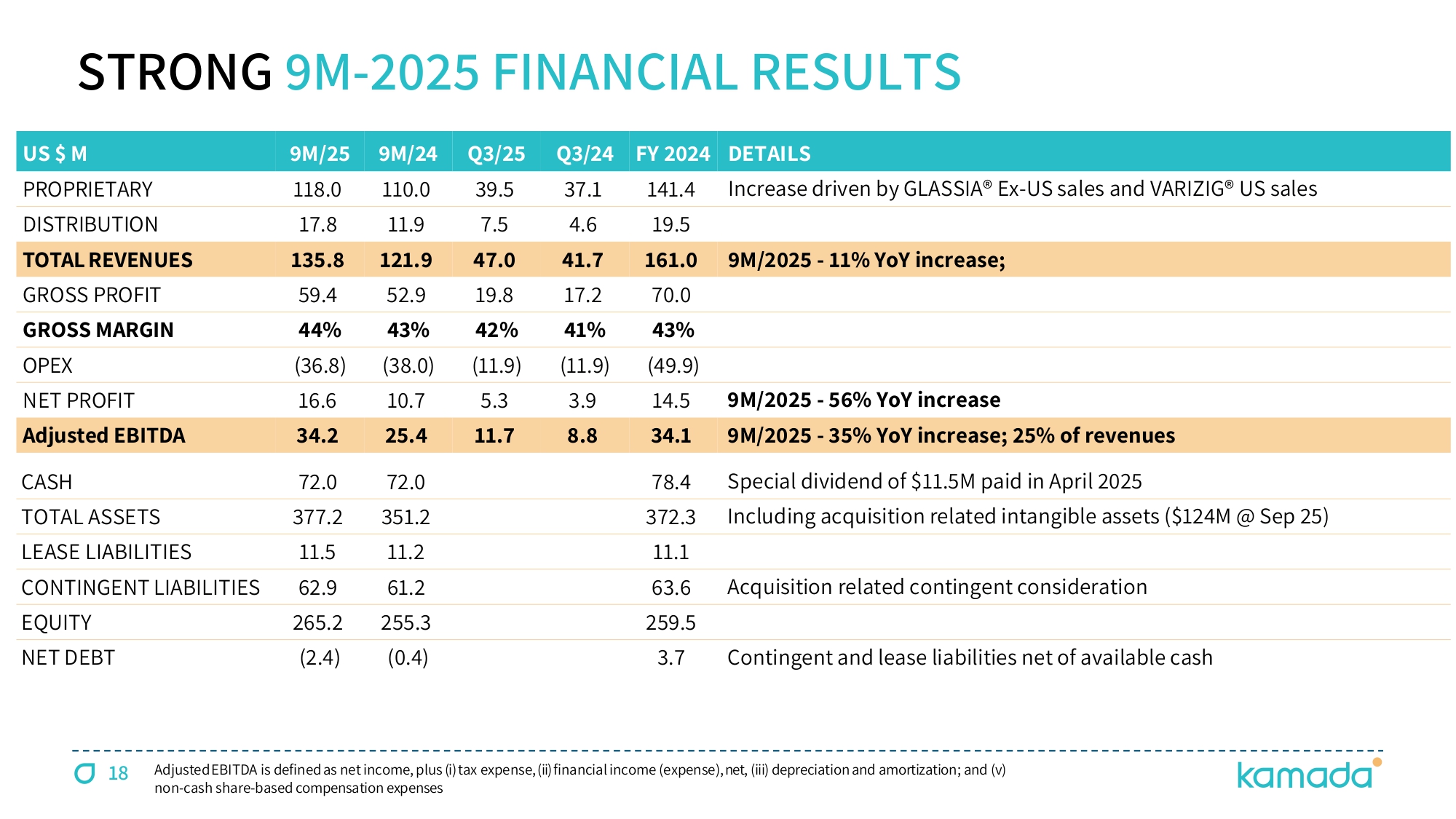

7 ANNUAL DOUBLE - DIGIT GROWTH TRAJECTORY 6 18 24 34 40 - 44 50 - 53 2021 2022 2023 2024 2025 2026 104 129 142 161 178 - 182 200 - 205 2021 2022 2023 2024 2025 2026 ADJUSTED EBITDA US$M 53 % CAGR 2025 and 2026 represents annual guidance 2025 and 2026 represents annual guidance REVENUES US$M 14 % CAGR 9 M $ 136 M ( 75 %) 9 M $ 34 M ( 81 %) 2026 annual guidance is based solely on organic growth 8 9 M - 2025 CONTINUING THE GROWTH YoY DOUBLE DIGIT REVENUE AND PROFITABILITY INCREASE Paid special cash dividend of $ 0.20 per share (totaling approximately $ 11.5 M) on April 7 , 2025 GROSS PROFIT REVENUE 12% 2024 $52.9 2025 $ 59.4 11% 2024 $121.9 2025 $ 135.8 Adj.

EBITDA EPS 35% 2024 $25.4 2025 $ 34.2 61% 2024 $0.18 2025 $0.29

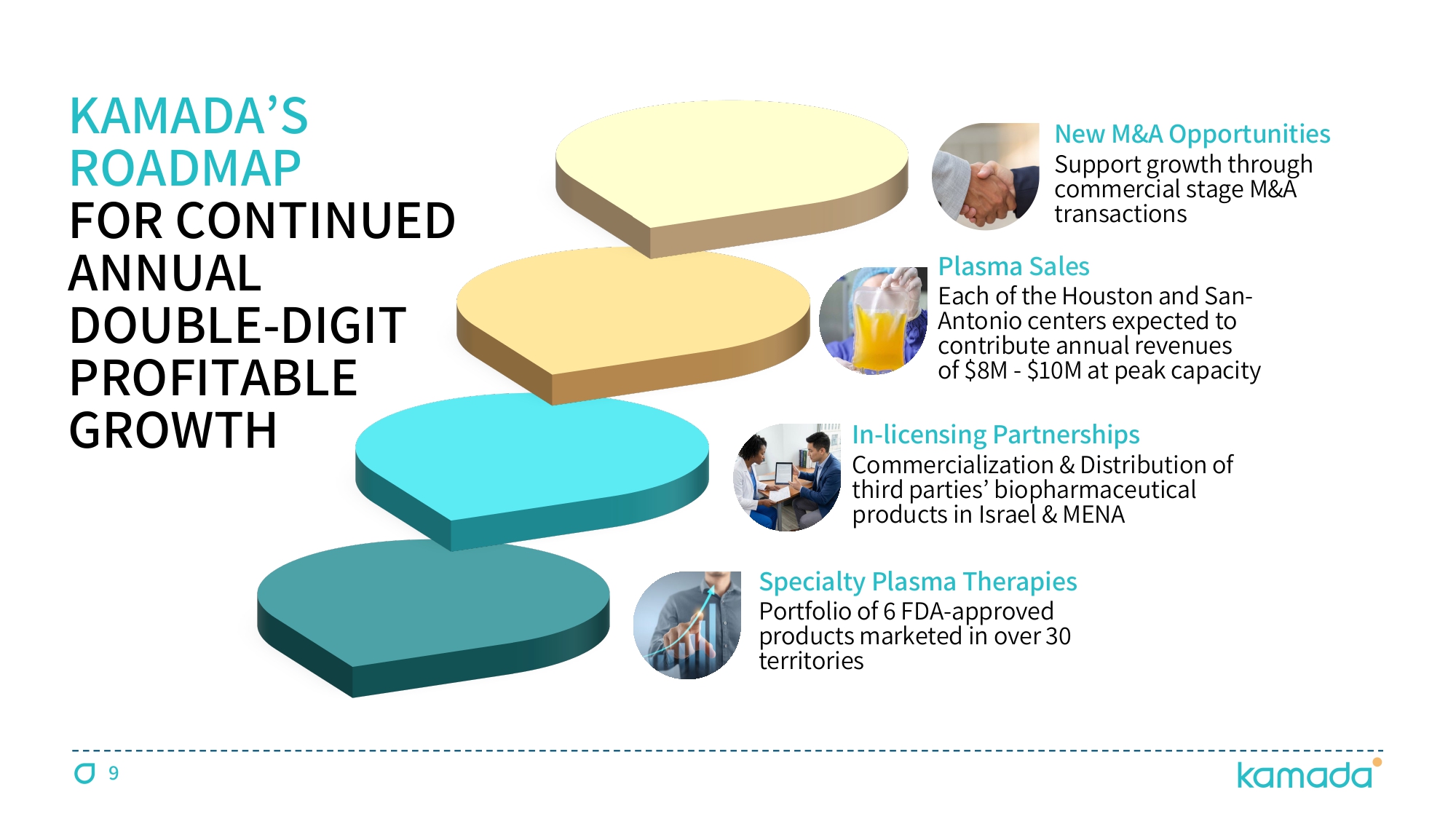

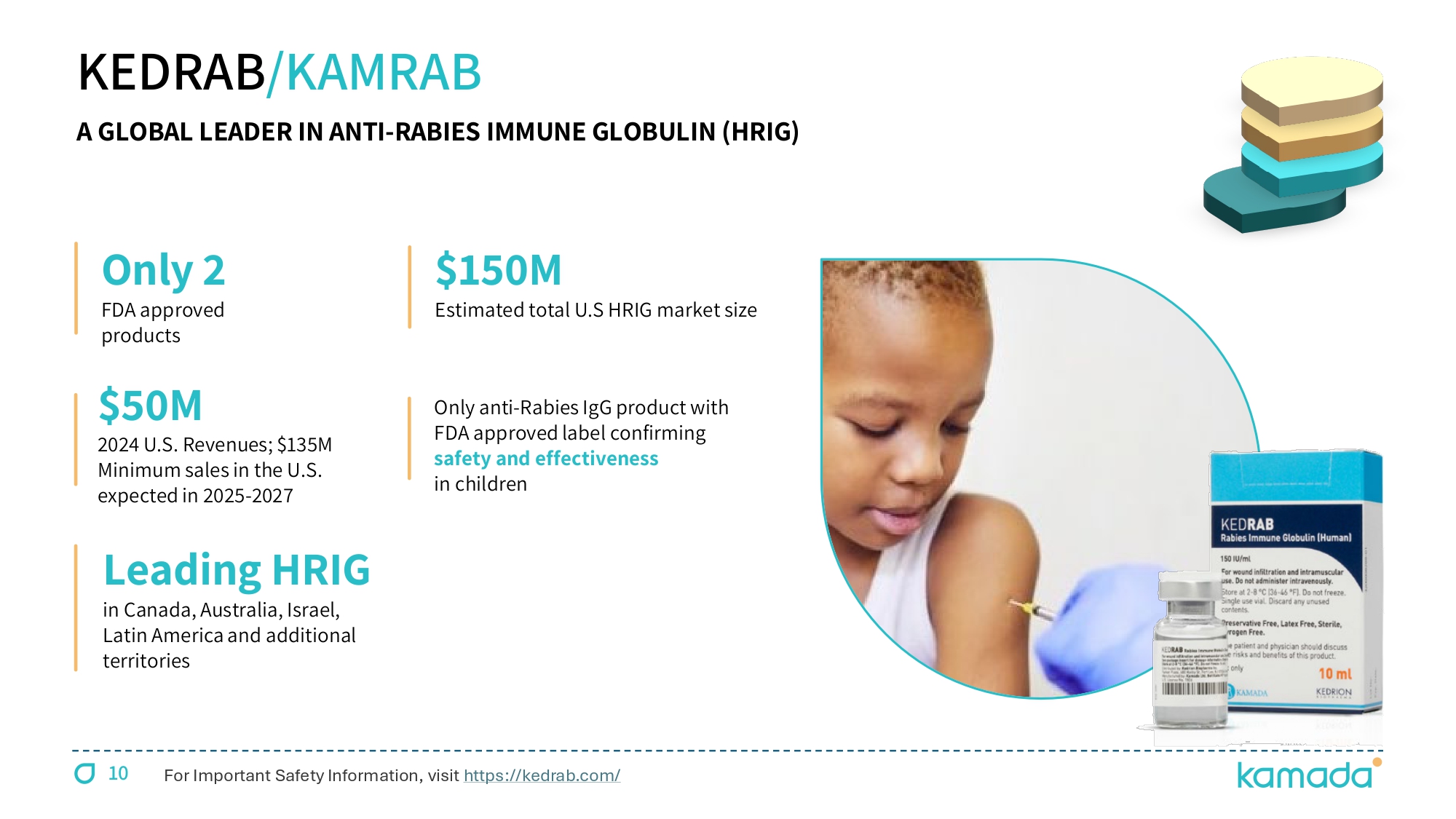

9 KAMADA ’ S ROADMAP FOR CONTINUED ANNUAL DOUBLE - DIGIT PROFITABLE GROWTH Specialty Plasma Therapies Portfolio of 6 FDA - approved products marketed in over 30 territories In - licensing Partnerships Commercialization & Distribution of third parties ’ biopharmaceutical products in Israel & MENA Plasma Sales Each of the Houston and San - Antonio centers expected to contribute annual revenues of $8M - $10M at peak capacity New M&A Opportunities Support growth through commercial stage M&A transactions $ 150 M Estimated total U.S HRIG market size Only anti - Rabies IgG product with FDA approved label confirming safety and effectiveness in children KEDRAB /KAMRAB $ 50 M 2024 U.S. Revenues; $ 135 M Minimum sales in the U.S. expected in 2025 - 2027 Only 2 FDA approved products Leading HRIG in Canada, Australia, Israel, Latin America and additional territories A GLOBAL LEADER IN ANTI - RABIES IMMUNE GLOBULIN (HRIG) For Important Safety Information, visit https://kedrab.com/ 10

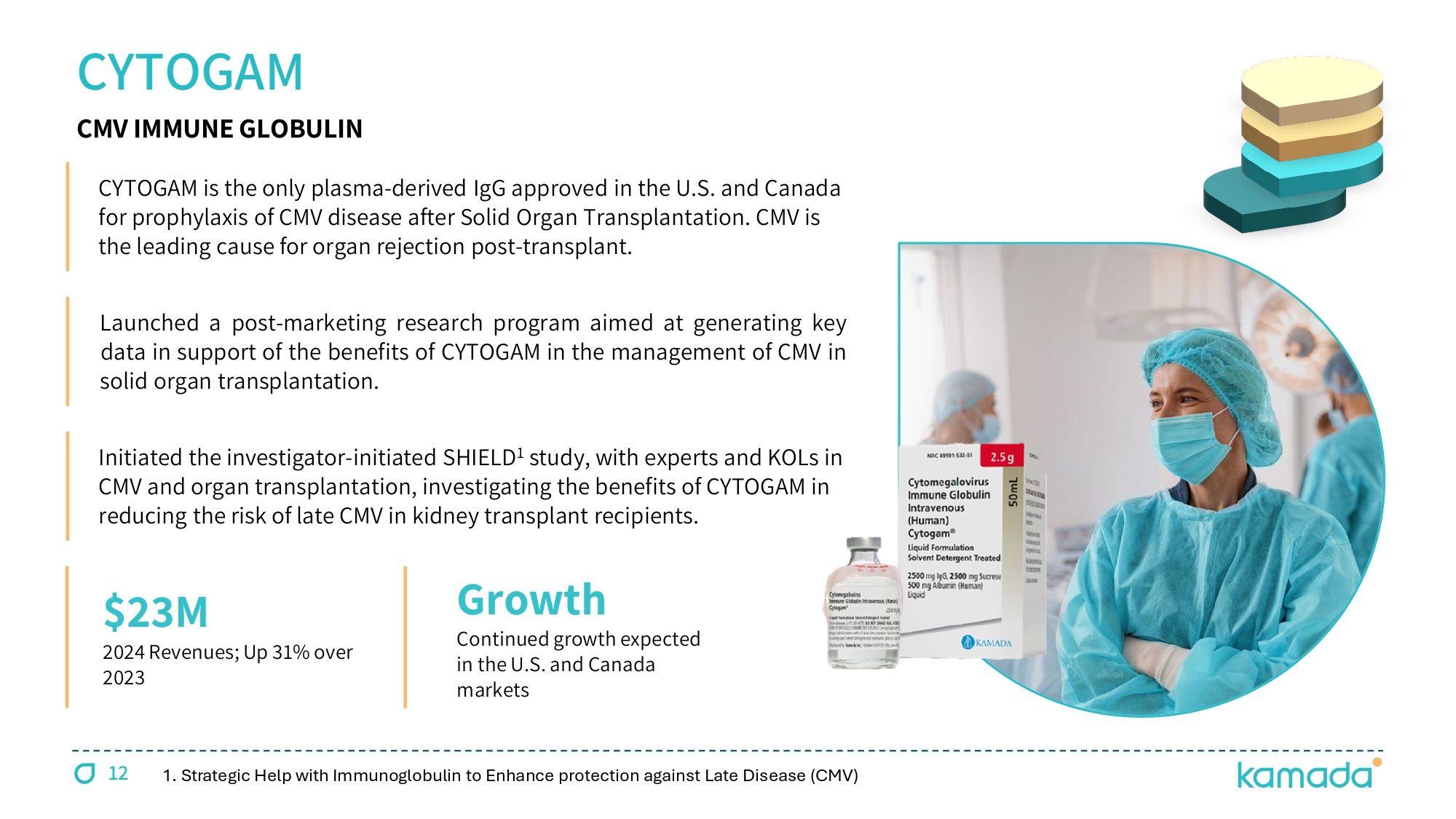

11 GLASSIA LIQUID AAT FOR THE TREATMENT OF AAT DEFICIENCY (AATD) Out - licensed to Takeda for distribution in the USA, Canada, Australia and New Zealand ; Royalties income from Takeda at a rate of 6 % ; 2026 royalties' income expected at approximately $ 10 M ; growing 5 % - 8 % per year thereafter through 2040 GLASSIA is marketed by Kamada directly, and through a network of partners & distributors outside the Takeda territories with key markets including Argentina , Russia, Israel, Switzerland and other LATAM markets . Continued investment in disease awareness and patients ’ diagnosis expected to support ongoing growth $ 15 M 2024 Glassia sales by Kamada; 2 X over 2023 sales $ 17 M 2024 Royality Income; Up 5 % over 2023 12 CYTOGAM CMV IMMUNE GLOBULIN 1.

Strategic Help with Immunoglobulin to Enhance protection against Late Disease (CMV) CYTOGAM is the only plasma - derived IgG approved in the U.S. and Canada for prophylaxis of CMV disease after Solid Organ Transplantation. CMV is the leading cause for organ rejection post - transplant. Launched a post - marketing research program aimed at generating key data in support of the benefits of CYTOGAM in the management of CMV in solid organ transplantation . Initiated the investigator - initiated SHIELD 1 study, with experts and KOLs in CMV and organ transplantation, investigating the benefits of CYTOGAM in reducing the risk of late CMV in kidney transplant recipients. Growth Continued growth expected in the U.S.

and Canada markets $ 23 M 2024 Revenues; Up 31 % over 2023 13 IN LICENSING PRODUCTS GROWTH More than 25 products exclusively licensed from leading international pharmaceutical companies, marketed in the Israeli market EXCLUSIVE DISTRIBUTOR IN ISRAEL FOR LEADING BIOPHARMACEUTICAL COMPANIES EXPANDING THE DISTRIBUTION BUSINESS TO THE MENA REGION Key areas : plasma - derived, respiratory, rare diseases, infectious diseases, biosimilar portfolio of several product candidates, mainly from Alvotech Two biosimilars launched and two additional expected to be launched in Israel in the coming months Additional biosimilar products are expected to be launched in Israel over the coming years, at a rate of 1 - 3 products per year Biosimilar portfolio expected to generate annual sales of $15 - 20M within the next four to five years 14 PLASMA SALES EXPANDING VERTICAL INTEGRATION & REVENUE GROWTH Collecting hyper - immune plasma for our specialty IgG products and normal source plasma (NSP) to support revenue growth Operating three plasma collection centers in Texas; Houston, San Antonio and Beaumont Houston center approved by the FDA in 2025, and San Antonio is expected to be approved during 2026 At full collection capacity, each of the Houston and San Antonio centers is expected to generate annual revenues of $8M to $10M from sales of NSP

15 NEW M&A OPPORTUNITIES EXPECT TO SECURE NEW M&A TRANSACTIONS IN 2026; LEVERAGING OVERALL FINANCIAL STRENGTH AND COMMERCIAL INFRASTRUCTURE Screening strategic business development opportunities to identify potential acquisition to accelerate long - term growth Focusing on products synergistic to our existing commercial and/or production activities as well as marketing infrastructure Strong financial position, commercial infrastructure and proven successful M&A capabilities KEDRAB® CYTOGAM® HEPGAM B® VARIZIG® WINRHO® GLASSIA® KAMADA - A GLOBAL BIOPHARMACEUTICAL COMPANY 6 FDA - Approved Products 14 % CAGR (from 2021) $ 200 - 205M 1 2026 Revenues Guidance $ 50 - 53M 1 2026 Adj.

EBIDTA Guidance 4 Growth Drivers DELIVERING ON OUR COMMITMENTS $ 7 đ .0 M Unaudited Cash (Dec 31 , 2025 ) 16 1. Expects to Achieve 2025 Guidance of $178 - 182 Million in Revenues and $40 - 44 Million of Adjusted EBITDA New M&A Opportunities Plasma Sales In - licensing Partnerships Specialty Plasma Therapies THANK YOU www.kamada.com NASDAQ: KMDA; TASE: KMDA.TA

18 Adjusted EBITDA is defined as net income, plus ( i ) tax expense, (ii) financial income (expense), net, (iii) depreciation and amortization ; and (v) non - cash share - based compensation expenses STRONG 9 M - 2025 FINANCIAL RESULTS DETAILS FY 2024 Q3/24 Q3/25 9M/24 9 M/ 25 US $ M Increase driven by GLASSIA® Ex - US sales and VARIZIG® US sales 141.4 37.1 39.5 110.0 118.0 PROPRIETARY 19.5 4.6 7.5 11.9 17.8 DISTRIBUTION 9M/2025 - 11% YoY increase; 161.0 41.7 47.0 121.9 135.8 TOTAL REVENUES 70.0 17.2 19.8 52.9 59.4 GROSS PROFIT 43 % 41 % 42 % 43 % 44 % GROSS MARGIN ( 49.9 ) ( 11.9 ) ( 11.9 ) ( 38.0 ) ( 36.8 ) OPEX 9M/2025 - 56% YoY increase 14.5 3.9 5.3 10.7 16.6 NET PROFIT 9M/2025 - 35% YoY increase; 25% of revenues 34.1 8.8 11.7 25.4 34.2 Adjusted EBITDA Special dividend of $11.5M paid in April 2025 78.4 72.0 72.0 CASH Including acquisition related intangible assets ($124M @ Sep 25) 372.3 351.2 377.2 TOTAL ASSETS 11.1 11.2 11.5 LEASE LIABILITIES Acquisition related contingent consideration 63.6 61.2 62.9 CONTINGENT LIABILITIES 259.5 255.3 265.2 EQUITY Contingent and lease liabilities net of available cash 3.7 ( 0.4 ) ( 2.4 ) NET DEBT 19 NON - IFRS MEASURES – ADJUSTED EBITDA Adjusted EBITDA is defined as net income, plus ( i ) tax expense, (ii) financial income (expense), net, (iii) depreciation and amortization ; and (v) non - cash share - based compensation expenses FY 2024 Q 3 / 24 Q 3 / 25 9 M/ 24 9 M/ 25 US $ M 14.5 3.9 5.3 10.7 16.6 NET PROFIT (1.1) 0.1 1.1 0.2 2.1 TAXES ON INCOME 8.1 1.8 1.7 5.3 4.1 REVALUATION OF ACQUISITION RELATED CONTINGENT CONSIDERATION (1.4) ( 0.4 ) ( 0.2 ) ( 1.2 ) ( 0.1 ) OTHER FINANCIAL EXPENSE, NET 7.1 1.8 1.8 5.3 5.3 AMORTIZATION OF ACQUISITION RELATED INTANGIBLE ASSETS 6.2 1.5 2.0 4.4 5.8 OTHER DEPRECIATION AND AMORTIZATION EXPENSES 0.9 0.2 0.1 0.7 0.4 NON - CASH SHARE - BASED COMPENSATION EXPENSES 34.1 8.8 11.7 25.4 34.2 ADJUSTED EBITDA

20 6 FDA - APPROVED SPECIALTY PLASMA PRODUCTS KEDRAB® [Rabies Immune Globulin (Human)] Post exposure prophylaxis of rabies infection CYTOGAM® [Cytomegalovirus Immune Globulin (Human)] Prophylaxis of CMV disease associated with transplants HEPGAM B® [Hepatitis B Immune Globulin (Human)] Prevention of HBV recurrence following liver transplants VARIZIG® [Varicella Zoster Immune Globulin (Human)] Post - exposure prophylaxis of varicella in high - risk patients WINRHO® [Rho(D) Immune Globulin (Human)] Treatment of ITP & suppression of Rh isoimmunization (HDN) KEY FOCUS ON TRANSPLANTS & RARE CONDITIONS For Important Safety Information, visit www.Kamada.com GLASSIA® [Alpha 1 - Proteinase Inhibitor (Human)] Augmentation therapy for Alpha - 1 Antitrypsin Deficiency (AATD)

21 IMMUNE GLOBULIN (IgG) MANUFACTURING Some of the photos by Unknown Author are licensed under CC BY - NC - ND 02 Plasma Screening: High Titer Antibodies 03 Plasma Fractionation Purification process 01 Plasma Collection in the United States 04 Viral Inactivation and Reduction 05 Formulation and Final Filling