UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 or 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of June, 2026

Commission File Number: 001-14946

Cemex, S.A.B. de C.V.

(Translation of Registrant’s name into English)

Avenida Ricardo Margáin Zozaya #325, Colonia Valle del Campestre

San Pedro Garza García, Nuevo León, 66265, Mexico

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ☐

We may disclose to prospective investors certain information that has not been previously publicly reported. This report and the information, statements, and opinions contained in this report do not constitute a public offer under any applicable legislation, an offer to sell, or solicitation of any offer to buy any securities or financial instruments, or any advice or recommendation with respect to such securities or other financial instruments. We have elected to provide the information in this report for informational purposes.

Cautionary Statement Regarding Forward-Looking Statements

This report contains, and the reports we will file or furnish in the future may contain, forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We intend these forward-looking statements to be covered by the “safe harbor” provisions for forward-looking statements within the meaning of applicable securities laws and regulations in all jurisdictions where such provisions exist, including but not limited to the United States Private Securities Litigation Reform Act of 1995. In some cases, these statements can be identified by the use of forward-looking words such as, but not limited to, “will,” “may,” “assume,” “might,” “should,” “could,” “continue,” “would,” “can,” “consider,” “anticipate,” “estimate,” “expect,” “envision,” “plan,” “believe,” “foresee,” “predict,” “potential,” “target,” “goal,” “strategy,” “intend,” “aimed,” or other forward-looking words. Unless otherwise indicated, these forward-looking statements reflect our current expectations and projections about the future, which are based on certain assumptions and on our knowledge of facts and circumstances as of the date such forward-looking statements are made. These forward-looking statements and information necessarily involve risks, uncertainties and assumptions, including, but not limited to, statements related to our plans, objectives, goals, targets and expectations (operative, financial or otherwise) and other important factors that could cause results and any estimate, projection and/or guidance presented in this report to differ materially from historical results, performance and/or achievements or those anticipated by forward-looking statements. Although we believe that our expectations are reasonable, we can give no assurance that these expectations will prove to be correct, and actual results, performance and/or achievements may vary, including materially, from historical results, performance and/or achievements or those anticipated by forward-looking statements due to various factors. Among others, such risks, uncertainties, assumptions, and other important factors that could cause results and any estimate, projection and/or guidance presented in this report to differ or fail to materialize, or that otherwise could have an impact on us include those discussed in this report and those detailed from time to time in our other filings with the U.S. Securities and Exchange Commission (the “SEC”), the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores) (the “CNBV”) and the Mexican Stock Exchange (Bolsa Mexicana de Valores) (the “MSE”), including, but not limited to:

| • | changes in general economic, political and social conditions, including government shutdowns, new governments or regimes and decisions implemented by such new governments or regimes, changes in laws or regulations in the countries in which we do business, elections, changes in inflation, interest and foreign exchange rates, employment levels, population growth, any slowdown in the flow of remittances into countries where we operate, consumer confidence, and the liquidity of the financial and capital markets in Mexico, the United States, the European Union (the “EU”), the United Kingdom or other countries in which we operate; |

| • | the cyclical activity of the construction sector and reduced construction activity in our end markets or reduced use in our end markets for our products; |

| • | our exposure to sectors that impact our and our clients’ businesses, particularly those operating in the commercial and residential construction sectors, and the public and private infrastructure and energy sectors; |

| • | volatility in pension plan asset values and liabilities, which may require cash or other contributions to the pension plans; |

| • | changes in spending levels for residential and commercial construction and general infrastructure projects; |

| • | the availability of short-term credit lines or working capital facilities, which can assist us in connection with market cycles; |

| • | any impact of not maintaining investment grade debt rating or not obtaining investment grade debt ratings from additional rating agencies on our cost of capital and on the cost of the products and services we purchase; |

| • | availability of raw materials and related fluctuating prices of raw materials, as well as of general goods and services, in particular increases in prices of raw materials, goods and services, as a result of inflation, trade barriers, measures imposed by governments or as a result of conflicts between countries that disrupt supply chains; |

| • | our ability to maintain and expand our distribution network and maintain favorable relationships with third parties who supply us with equipment, services and essential supplies; |

| • | competition in the markets in which we offer our products and services; |

| • | the impact of environmental cleanup costs and other remedial actions, and other environmental, climate and related liabilities relating to existing and/or divested businesses, assets and/or operations; |

| • | our ability to secure and permit aggregates reserves in strategically located areas in amounts that our operations require to operate or operate in a cost-efficient manner; |

| • | the timing and amount of federal, state, and local funding for infrastructure; |

| • | changes in our effective tax rate; |

| • | our ability to comply with regulations and implement technologies and other initiatives that aim to reduce and/or capture CO2 emissions and comply with related carbon emissions regulations in place in the jurisdictions where we have operations; |

| • | the legal and regulatory environment, including environmental, climate, trade, energy, tax, antitrust, sanctions, import and export controls, construction, human rights, and labor welfare, and acquisition-related rules and regulations in the countries and regions in which we have operations; |

| • | the effects of currency fluctuations on our results of operations and financial condition; |

| • | our ability to satisfy our obligations under our debt agreements, the indentures that govern our outstanding 5.450% Dollar denominated notes due 2029, 5.200% Dollar denominated notes due 2030, 3.875% Dollar denominated notes due 2031, and the Long-Term Notes 1, Long-Term Notes 2 and Long-Term Notes 3 in the Mexican market and our other debt instruments and financial obligations, and also regarding our subordinated notes with no fixed maturity and other financial obligations; |

| • | adverse legal or regulatory proceedings or disputes, such as class actions or enforcement or other proceedings brought by third parties, government and regulatory agencies, including antitrust investigations and claims; |

| • | our ability to protect our reputation and intellectual property; |

| • | our ability to consummate asset sales or consummate asset sales in terms favorable to us, fully integrate newly acquired businesses, achieve cost-savings from our cost-reduction initiatives, implement our pricing and commercial initiatives for our products and services, and generally meet our business strategy’s goals; |

| • | the increasing reliance on information technology infrastructure for our sales, invoicing, procurement, financial statements, and other processes that can adversely affect our sales and operations in the event that the infrastructure does not work as intended, experiences technical difficulties, or is subjected to invasion, disruption, or damage caused by circumstances beyond our control, including cyber-attacks, catastrophic events, power outages, natural disasters, computer system or network failures, or other security breaches; |

| • | the effects of climate change, in particular reflected in weather conditions, including, but not limited to, excessive rain and snow, shortage of usable water, wildfires and natural disasters, such as earthquakes, hurricanes, tornadoes and floods, that could affect our facilities or the markets in which we offer our products and services or from where we source our raw materials; |

| • | trade barriers, including, but not limited to, tariffs or import taxes, including those imposed by the United States to key markets in which we operate, in particular, Mexico, China and the EU, and changes in existing trade policies or changes to, or withdrawals from, free trade agreements, including the United States-Mexico-Canada Agreement, and the overall impact that the imposition or threat of trade barriers may cause on the overall economy of the countries in which we do business or that are part of our global supply chain; |

| • | availability and cost of trucks, railcars, barges, and ships, terminals, warehouses, as well as their licensed operators, drivers, staff and workers, for transport, loading and unloading of our materials or that are otherwise a part of our supply chain; |

| • | labor shortages and constraints; |

| • | our ability to hire, effectively compensate and retain our key personnel and maintain satisfactory labor relations; |

| • | our ability to detect and prevent money laundering, terrorism financing and corruption, as well as other illegal activities and how any measures implemented by governments to detect and prevent money laundering, terrorism financing and corruption, and other illegal activities, affect our customers, suppliers and countries in which we do business; |

| • | defaults, losses or disruptions in agreements, financial transactions or operations resulting from sanctions or restrictions imposed on any financial institution, including, but not limited to, banks, common representatives, trustees, payment processors, paying agents or other financial intermediaries, or any related parties; |

| • | terrorist and organized criminal activities, social unrest, as well as geopolitical events, such as global, regional or national instability, hostilities, war, and armed conflicts, including the current war between Russia and Ukraine, the ongoing war among Israel, the United States and the Islamic Republic of Iran, conflicts in the Middle East and any insecurity and hostilities in Mexico related to illegal activities or organized crime and any actions any government takes to prevent these illegal activities and organized crime; |

| • | the impact of pandemics, epidemics, or outbreaks of infectious diseases and the response of governments and other third parties, which could adversely affect, among other matters, the ability of our operating facilities to operate at full or any capacity, supply chains, international operations, availability of liquidity, investor confidence and consumer spending, as well as the availability of, and demand for, our products and services; |

| • | changes in the economy that affect demand for consumer goods, consequently affecting demand for our products and services; |

| • | the depth and duration of an economic slowdown or recession, instability in the business landscape and lack of availability of credit; |

| • | declarations of insolvency or bankruptcy, or becoming subject to similar proceedings; |

| • | natural disasters and other unforeseen events (including global health hazards such as COVID-19); |

| • | our ability to implement our climate action program in effect at any given time, if any, including our current “Future in Action” climate action and nature program, and to achieve our sustainability goals and objectives in effect at any given time, if any, including under our current “Future in Action” climate action and nature program; and |

| • | the other risks and uncertainties described under “Item 3. Key Information—Risk Factors” and elsewhere in our Annual Report on Form 20-F for the year ended December 31, 2025. |

Many factors could cause our expectations, expected results, and/or projections expressed in this report not being reached and/or not producing the expected benefits and/or results, as any such benefits or results are subject to uncertainties, costs, performance, and rate of success and/or implementation of technologies, some of which are not yet proven, among other factors. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results, performance and/or achievements may vary materially from historical results, performance, and/or achievements and/or results, performance, or achievements expressly or implicitly anticipated by the forward-looking statements, or otherwise could have an impact on us. Forward-looking statements should not be considered guarantees of future performance, and past results or developments are not indicative of results or developments in subsequent periods. Actual results, performance and/or achievements of our operations and the development of market conditions in which we operate, or other circumstances that may materialize, may differ materially from those described in, or suggested by, the forward-looking statements contained herein, and events referenced therein. Any or all of our forward-looking statements may turn out to be inaccurate and the factors identified above are not exhaustive. Accordingly, readers should not place undue reliance on forward-looking statements, as such forward-looking statements speak only as of the date on which they are made. The forward-looking statements and the information disclosed in this report are made as of the dates specified in this report and are subject to change without notice; and, except to the extent legally required, we expressly disclaim any obligation or undertaking to update or correct the information contained in this report, or revise any forward-looking statements in this report, whether to reflect new information, the occurrence of anticipated or unanticipated future events or circumstances, any change in our expectations regarding those forward-looking statements, any change in events, conditions, or circumstances on which any such statement is based, or otherwise. Readers should review future reports filed or furnished by us with the SEC, the CNBV and the MSE.

This report contains statistical data regarding, but not limited to, the production, distribution, marketing, and sale of cement, ready-mix concrete, clinker, aggregates, and Urbanization Solutions. We generated some of this data internally, and some was obtained from independent industry publications and reports, available as of the date of this report, that we believe to be reliable sources. We have not independently verified this data nor sought the consent of any organizations to refer to their reports in this report.

We act in strict compliance with antitrust laws and as such, among other measures, maintain an independent pricing policy that has been independently developed. Our policy’s core element is to price our products and services based on their quality and characteristics as well as their value to our customers. We do not accept any communications or agreements of any type with competitors regarding the determination of our prices for our products and services. Unless the context indicates otherwise, all references to pricing initiatives, price increases or price decreases, refer to our prices for our products.

This report includes certain financial measures that differ from financial information presented by Cemex in accordance with IFRS Accounting Standards (“IFRS”) in its financial statements and reports containing financial information. These aforementioned non-IFRS financial measures include “Operating EBITDA” (operating earnings before other expenses, net plus depreciation and amortization) and “Operating EBITDA Margin.” The closest financial measure to Operating EBITDA in our financial statements under IFRS is the line item of “Operating earnings before other expenses, net,” as Operating EBITDA adds depreciation and amortization to this line item. Our Operating EBITDA Margin is calculated by dividing our Operating EBITDA for the period by our revenues as reported in our financial statements for the same period. We believe there is no close IFRS financial measure to compare Operating EBITDA Margin. These non-IFRS financial measures are designed to complement and should not be considered superior to financial measures calculated in accordance with IFRS. Although Operating EBITDA and Operating EBITDA Margin are not measures of operating performance, an alternative to cash flows or a measure of financial position under IFRS, Operating EBITDA is the financial measure used by our management to review operating performance and profitability, for decision-making purposes and to allocate resources. Moreover, our Operating EBITDA is a measure used by our creditors to review our ability to internally fund capital expenditures, to service or incur debt and to comply with financial covenants under our financing agreements. Furthermore, our management regularly reviews our Operating EBITDA Margin by reportable segment and on a consolidated basis as a measure of performance and profitability. These non-IFRS financial measures do not have any standardized meaning and are therefore unlikely to be comparable to similarly titled measures presented by other companies. Non-IFRS financial measures presented in this report are being provided for informative purposes only and shall not be construed as investment, financial, or other advice.

The information, statements, and opinions contained in this report are for informational purposes and do not constitute a public offer under any applicable legislation, an offer to sell, or solicitation of any offer to buy any securities or financial instruments, or any advice or recommendation with respect to such securities or other financial instruments. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. We are not responsible for any third-party information referenced in this report.

Cautionary Statement Regarding Environmental, Social, and Governance (“ESG”) and Sustainability-Related Data, Metrics, and Methodologies

This report includes non-financial metrics, estimates, or other information related to ESG and sustainability matters that are subject to significant uncertainties, which may include the methodology, collection, and verification of data, various estimates, and assumptions, and/or underlying data that is obtained from third parties, some of which cannot be independently verified.

The preparation of certain information on ESG and sustainability matters contained in this report requires the application of a number of key judgments, assumptions, and estimates. The reported measures in this report reflect good faith estimates, assumptions, and judgments at the given point in time. There is a risk that these judgments, estimates, or assumptions may subsequently prove to be incorrect and/or, to the extent legally required, may need to be restated or changed. The disclosure of information on sustainability-related matters is not yet subject to the same recognized or accepted reporting or accounting principles and rules as traditional financial information. Consequently, there are no commonly accepted reporting practices for us to follow, and ESG metrics among organizations in our industry may not be comparable. In addition, the underlying data, systems, and controls that support non-financial reporting are generally considerably less sophisticated than the systems and internal control for financial reporting and rely on manual processes. This may result in non-comparable information between organizations and/or between reporting periods within organizations as methodologies continue to develop and/or be socialized. The further development of or changes to accounting and/or reporting standards could materially impact the performance metrics, data points, and targets contained in this report, and the reader may not be able to compare non-financial information performance metrics, data points, or targets between reporting periods on a direct like-for-like basis.

Additionally, the information disclosed in this report contains references to “green,” “social,” “sustainable,” or equivalent-labelled activities, products, assets, or projects. There is currently no single globally recognized or accepted, consistent and comparable set of definitions or standards (legal, regulatory, or otherwise) of, nor widespread cross-market consensus (i) as to what constitutes, a “green,” “social,” “sustainable,” or having equivalent-labelled activity, product, or asset; (ii) as to what precise attributes are required for a particular activity, product, or asset to be defined as “green,” “social,” “sustainable” or such other equivalent label; or (iii) as to climate and sustainable funding and financing activities and their classification and reporting.

Therefore, there is little certainty, and no assurance or representation is given, that such activities, products, assets, or projects and/or reporting of such activities, products, assets or projects will meet any present or future expectations or requirements for describing or classifying such activities, products, assets or projects as “green,” “social,” “sustainable,” or attributing similar labels. We expect policies, regulatory requirements, standards, and definitions to be developed and continuously evolve over time.

Cautionary Statement Regarding Forward-Looking ESG or Sustainability Statements

Certain sections in this report contain ESG- or sustainability-related forward-looking statements, such as aims, ambitions, estimates, forecasts, plans, projections, targets, goals and other metrics, including but not limited to: climate and emissions, business and human rights, corporate governance, research and development and partnerships, development of products and services that intend to address sustainability-related concerns and sustainability related targets/ ambitions when finalized, including the implementation of technologies and other initiatives that aim to reduce and/or capture CO2 emissions.

These forward-looking statements also include references to specific programs, such as our current “Future in Action” climate action and nature program, as well as various ESG-related indicators, objectives or metrics disclosed previously or that may be disclosed in the future, none of which are guarantees and any and all of which may ultimately not be achieved or may be abandoned at any time, whether in part, in full, or within any specific timeframe. There are many significant uncertainties, assumptions, judgements, opinions, estimates, forecasts and statements made of future expectations underlying these forward-looking statements which could cause actual results, performance, outcomes or events to differ materially from those expressed or implied in these forward-looking statements, which include, but are not limited to:

| • | the extent and pace of climate change, including the timing and manifestation of physical and transition risks; |

| • | the macroeconomic environment; |

| • | uncertainty around future climate-related policy and regulations, including the timely implementation and integration of adequate government policies; |

| • | the effectiveness of actions of governments, legislators, regulators, businesses, investors, customers, and other stakeholders to mitigate the impact of climate and sustainability-related risks; |

| • | changes in customer behavior and demand, changes in the available technology for mitigation and the effectiveness of any such technologies, as some of these new technologies may be unproven; |

| • | excessive costs and expenses related to acquire and/or develop technology for mitigation; |

| • | the roll-out of low carbon infrastructure; |

| • | the availability and adoption of renewable energy in our value chain; |

| • | the development of carbon capture, circular utilization, and sequestration technologies, including the adoption of cost-effective carbon-related technologies such as carbon capture, utilization, and storage; |

| • | the availability of accurate, verifiable, reliable, consistent, and comparable climate-related data; |

| • | lack of transparency and comparability of climate-related forward-looking methodologies; |

| • | variation in approaches and outcomes, as variations in methodologies may lead to under or overestimates and consequently present exaggerated indication of climate-related risk; and |

| • | reliance on assumptions and future uncertainty (calculations of forward-looking metrics are complex and require many methodological choices and assumptions). |

Accordingly, undue reliance should not be placed on these forward-looking statements. Furthermore, changing national and international standards, industry and scientific practices, regulatory requirements, and market expectations regarding climate change, which remain under continuous development, are subject to different interpretations.

There can be no assurance that these standards, practices, requirements, and expectations will not be interpreted differently than our understanding when defining sustainability-related ambitions and targets or change in a manner that substantially increases the cost or effort for us to achieve such ambitions and targets.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, Cemex, S.A.B. de C.V. has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Cemex, S.A.B. de C.V. |

||||||

| (Registrant) | ||||||

| Date: June 1, 2026 | ||||||

| By: | /s/ Jaime Martínez Merla |

|||||

| Name: Jaime Martínez Merla | ||||||

| Title: Chief Comptroller | ||||||

EXHIBIT INDEX

| EXHIBIT NO. | DESCRIPTION |

|

| 1 | Certain information with respect to Cemex, S.A.B. de C.V. (NYSE: CX) and its direct and indirect subsidiaries. | |

Exhibit 1

The following summarizes certain information, including financial information, that we may disclose to prospective investors. The information set forth below updates the information contained in our annual report on Form 20-F for the year ended December 31, 2025 (the “2025 Annual Report”), filed with the U.S. Securities and Exchange Commission (the “SEC”) on April 24, 2026 and any other documents that we have filed or furnished with the SEC and should be read in conjunction therewith. Except as the context otherwise may require, references in this report to “Cemex,” the “Company,” “we,” “us” or “our” refer to Cemex, S.A.B. de C.V. and its consolidated entities. See note 3 to our audited consolidated financial statements included in the 2025 Annual Report for a description of our material accounting policies including our principles of consolidation.

Unless otherwise indicated, references in this report to “$” and “Dollars” are to United States Dollars, references to “€” are to Euros, references to “£,” “Pounds Sterling” and “Pounds” are to British Pounds, and references to “Ps,” “Mexican Pesos” and “Pesos” are to Mexican Pesos. References to “billion” mean one thousand million. References in this report to “CPOs” are to Cemex, S.A.B. de C.V.’s Ordinary Participation Certificates (Certificados de Participación Ordinarios), each CPO represents two Series A shares (as defined below) and one Series B share (as defined below) of Cemex, S.A.B. de C.V. References to “ADSs” are to American Depositary Shares of Cemex, S.A.B. de C.V., each ADS represents 10 CPOs.

Unless otherwise indicated, all information in this report excludes our operations in the Dominican Republic and Panama, which we disposed of in January 2025 and October 2025, respectively. For the period from January 1 to January 30, 2025, our operations in the Dominican Republic are reported in the income statements, net of income tax, in the single line item “Discontinued operations.” For the three-month period ended March 31, 2025, our operations in Panama are reported in the income statements, net of income tax, in the single line item “Discontinued operations.” See note 5.2 to Cemex, S.A.B. de C.V.’s 2025 audited consolidated financial statements included in the 2025 Annual Report for more information.

See notes 3.4, 18.1 and 18.2 to Cemex, S.A.B. de C.V.’s 2025 audited consolidated financial statements included in the 2025 Annual Report for a detailed description of our debt and other financial obligations. Total debt plus other financial obligations differs from the calculation of debt under our main credit agreements, being the Credit Agreement, dated as of October 29, 2021 (as last amended on October 30, 2023 and as further amended and/or restated from time to time, the “2023 Credit Agreement”), the Credit Agreement dated as of October 7, 2022 (as last amended on April 11, 2024 and as further amended and/or restated from time to time, the “Euro Credit Agreement”) and the Credit Agreement dated as of December 20, 2021, entered into with Banco Mercantil del Norte, S.A., Institución de Banca Múltiple, Grupo Financiero Banorte (as last amended on December 6, 2023 and as further amended and/or restated from time to time, the “Peso Bilateral Term Loan”) (collectively, the “Credit Agreements”). See “Management’s Discussion and Analysis of Financial Results of Operations—Liquidity and Capital Resources—Our Indebtedness” for more information.

Under IAS 32, Financial Instruments: Presentation (“IAS 32”), we concluded that our outstanding 5.125% Subordinated Notes and our 7.200% Subordinated Notes (together, the “Subordinated Notes”) do not meet the definition of financial liability, and consequently are classified in controlling interest stockholders’ equity within Other equity reserves. See note 22.2 to Cemex, S.A.B. de C.V.’s 2025 audited consolidated financial statements included in the 2025 Annual Report for a detailed description of the Subordinated Notes.

We also refer in various places within this report to non-IFRS measures, including “Operating EBITDA.” Operating EBITDA equals operating earnings before other expenses, net, plus depreciation and amortization expenses, as more fully explained in “Selected Consolidated Financial Information.” Additionally, we refer to “Operating EBITDA Margin,” which is calculated by dividing our Operating EBITDA by our revenues. The presentation of these non-IFRS measures is not meant to be considered in isolation or as a substitute for Cemex, S.A.B. de C.V.’s 2025 audited consolidated financial results prepared in accordance with IFRS as issued by the IASB.

We have approximated certain numbers in this report to their closest round numbers or a given number of decimal places. Due to rounding, figures shown as totals in tables may not be arithmetic aggregations of the figures preceding them.

1

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report contains, and the reports we will file or furnish in the future may contain, forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended. We intend these forward-looking statements to be covered by the “safe harbor” provisions for forward-looking statements within the meaning of applicable securities laws and regulations in all jurisdictions where such provisions exist, including but not limited to the United States Private Securities Litigation Reform Act of 1995. In some cases, these statements can be identified by the use of forward-looking words such as, but not limited to, “will,” “may,” “assume,” “might,” “should,” “could,” “continue,” “would,” “can,” “consider,” “anticipate,” “estimate,” “expect,” “envision,” “plan,” “believe,” “foresee,” “predict,” “potential,” “target,” “goal,” “strategy,” “intend,” “aimed,” or other forward-looking words. Unless otherwise indicated, these forward-looking statements reflect our current expectations and projections about the future, which are based on certain assumptions and on our knowledge of facts and circumstances as of the date such forward-looking statements are made. These forward-looking statements and information necessarily involve risks, uncertainties and assumptions, including, but not limited to, statements related to our plans, objectives, goals, targets and expectations (operative, financial or otherwise) and other important factors that could cause results and any estimate, projection and/or guidance presented in this report to differ materially from historical results, performance and/or achievements or those anticipated by forward-looking statements. Although we believe that our expectations are reasonable, we can give no assurance that these expectations will prove to be correct, and actual results, performance and/or achievements may vary, including materially, from historical results, performance and/or achievements or those anticipated by forward-looking statements due to various factors. Among others, such risks, uncertainties, assumptions, and other important factors that could cause results and any estimate, projection and/or guidance presented in this report to differ or fail to materialize, or that otherwise could have an impact on us include those discussed in this report and those detailed from time to time in our other filings with the SEC, the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores) (the “CNBV”) and the Mexican Stock Exchange (Bolsa Mexicana de Valores) (the “MSE”), including, but not limited to:

| • | changes in general economic, political and social conditions, including government shutdowns, new governments or regimes and decisions implemented by such new governments or regimes, changes in laws or regulations in the countries in which we do business, elections, changes in inflation, interest and foreign exchange rates, employment levels, population growth, any slowdown in the flow of remittances into countries where we operate, consumer confidence, and the liquidity of the financial and capital markets in Mexico, the United States, the European Union (the “EU”), the United Kingdom or other countries in which we operate; |

| • | the cyclical activity of the construction sector and reduced construction activity in our end markets or reduced use in our end markets for our products; |

| • | our exposure to sectors that impact our and our clients’ businesses, particularly those operating in the commercial and residential construction sectors, and the public and private infrastructure and energy sectors; |

| • | volatility in pension plan asset values and liabilities, which may require cash or other contributions to the pension plans; |

| • | changes in spending levels for residential and commercial construction and general infrastructure projects; |

| • | the availability of short-term credit lines or working capital facilities, which can assist us in connection with market cycles; |

| • | any impact of not maintaining investment grade debt rating or not obtaining investment grade debt ratings from additional rating agencies on our cost of capital and on the cost of the products and services we purchase; |

| • | availability of raw materials and related fluctuating prices of raw materials, as well as of general goods and services, in particular increases in prices of raw materials, goods and services, as a result of inflation, trade barriers, measures imposed by governments or as a result of conflicts between countries that disrupt supply chains; |

2

| • | our ability to maintain and expand our distribution network and maintain favorable relationships with third parties who supply us with equipment, services and essential supplies; |

| • | competition in the markets in which we offer our products and services; |

| • | the impact of environmental cleanup costs and other remedial actions, and other environmental, climate and related liabilities relating to existing and/or divested businesses, assets and/or operations; |

| • | our ability to secure and permit aggregates reserves in strategically located areas in amounts that our operations require to operate or operate in a cost-efficient manner; |

| • | the timing and amount of federal, state, and local funding for infrastructure; |

| • | changes in our effective tax rate; |

| • | our ability to comply with regulations and implement technologies and other initiatives that aim to reduce and/or capture CO2 emissions and comply with related carbon emissions regulations in place in the jurisdictions where we have operations; |

| • | the legal and regulatory environment, including environmental, climate, trade, energy, tax, antitrust, sanctions, import and export controls, construction, human rights, and labor welfare, and acquisition-related rules and regulations in the countries and regions in which we have operations; |

| • | the effects of currency fluctuations on our results of operations and financial condition; |

| • | our ability to satisfy our obligations under our debt agreements, the indentures that govern our outstanding Notes (as defined herein) and our other debt instruments and financial obligations, and also regarding the Subordinated Notes with no fixed maturity and other financial obligations; |

| • | adverse legal or regulatory proceedings or disputes, such as class actions or enforcement or other proceedings brought by third parties, government and regulatory agencies, including antitrust investigations and claims; |

| • | our ability to protect our reputation and intellectual property; |

| • | our ability to consummate asset sales or consummate asset sales in terms favorable to us, fully integrate newly acquired businesses, achieve cost-savings from our cost-reduction initiatives, implement our pricing and commercial initiatives for our products and services, and generally meet our business strategy’s goals; |

| • | the increasing reliance on information technology infrastructure for our sales, invoicing, procurement, financial statements, and other processes that can adversely affect our sales and operations in the event that the infrastructure does not work as intended, experiences technical difficulties, or is subjected to invasion, disruption, or damage caused by circumstances beyond our control, including cyber-attacks, catastrophic events, power outages, natural disasters, computer system or network failures, or other security breaches; |

| • | the effects of climate change, in particular reflected in weather conditions, including, but not limited to, excessive rain and snow, shortage of usable water, wildfires and natural disasters, such as earthquakes, hurricanes, tornadoes and floods, that could affect our facilities or the markets in which we offer our products and services or from where we source our raw materials; |

| • | trade barriers, including, but not limited to, tariffs or import taxes, including those imposed by the United States to key markets in which we operate, in particular, Mexico, China and the EU, and changes in existing trade policies or changes to, or withdrawals from, free trade agreements, including the United States-Mexico-Canada Agreement (the “USMCA”), and the overall impact that the imposition or threat of trade barriers may cause on the overall economy of the countries in which we do business or that are part of our global supply chain; |

3

| • | availability and cost of trucks, railcars, barges, and ships, terminals, warehouses, as well as their licensed operators, drivers, staff and workers, for transport, loading and unloading of our materials or that are otherwise a part of our supply chain; |

| • | labor shortages and constraints; |

| • | our ability to hire, effectively compensate and retain our key personnel and maintain satisfactory labor relations; |

| • | our ability to detect and prevent money laundering, terrorism financing and corruption, as well as other illegal activities and how any measures implemented by governments to detect and prevent money laundering, terrorism financing and corruption, and other illegal activities, affect our customers, suppliers and countries in which we do business; |

| • | defaults, losses or disruptions in agreements, financial transactions or operations resulting from sanctions or restrictions imposed on any financial institution, including, but not limited to, banks, common representatives, trustees, payment processors, paying agents or other financial intermediaries, or any related parties; |

| • | terrorist and organized criminal activities, social unrest, as well as geopolitical events, such as global, regional or national instability, hostilities, war, and armed conflicts, including the current war between Russia and Ukraine, the ongoing war among Israel, the United States and the Islamic Republic of Iran, conflicts in the Middle East and any insecurity and hostilities in Mexico related to illegal activities or organized crime and any actions any government takes to prevent these illegal activities and organized crime; |

| • | the impact of pandemics, epidemics, or outbreaks of infectious diseases and the response of governments and other third parties, which could adversely affect, among other matters, the ability of our operating facilities to operate at full or any capacity, supply chains, international operations, availability of liquidity, investor confidence and consumer spending, as well as the availability of, and demand for, our products and services; |

| • | changes in the economy that affect demand for consumer goods, consequently affecting demand for our products and services; |

| • | the depth and duration of an economic slowdown or recession, instability in the business landscape and lack of availability of credit; |

| • | declarations of insolvency or bankruptcy, or becoming subject to similar proceedings; |

| • | natural disasters and other unforeseen events (including global health hazards such as COVID-19); |

| • | our ability to implement our climate action program in effect at any given time, if any, including our current “Future in Action” climate action and nature program, and to achieve our sustainability goals and objectives in effect at any given time, if any, including under our current “Future in Action” climate action and nature program; and |

| • | the other risks and uncertainties described under “Item 3. Key Information—Risk Factors” and elsewhere in the 2025 Annual Report. |

Many factors could cause our expectations, expected results, and/or projections expressed in this report not being reached and/or not producing the expected benefits and/or results, as any such benefits or results are subject to uncertainties, costs, performance, and rate of success and/or implementation of technologies, some of which are not yet proven, among other factors.

4

Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results, performance and/or achievements may vary materially from historical results, performance, and/or achievements and/or results, performance, or achievements expressly or implicitly anticipated by the forward-looking statements, or otherwise could have an impact on us. Forward-looking statements should not be considered guarantees of future performance, and past results or developments are not indicative of results or developments in subsequent periods. Actual results, performance and/or achievements of our operations and the development of market conditions in which we operate, or other circumstances that may materialize, may differ materially from those described in, or suggested by, the forward-looking statements contained herein, and events referenced therein. Any or all of our forward-looking statements may turn out to be inaccurate and the factors identified above are not exhaustive. Accordingly, readers should not place undue reliance on forward-looking statements, as such forward-looking statements speak only as of the date on which they are made. The forward-looking statements and the information disclosed in this report are made as of the dates specified in this report and are subject to change without notice; and, except to the extent legally required, we expressly disclaim any obligation or undertaking to update or correct the information contained in this report, or revise any forward-looking statements in this report, whether to reflect new information, the occurrence of anticipated or unanticipated future events or circumstances, any change in our expectations regarding those forward-looking statements, any change in events, conditions, or circumstances on which any such statement is based, or otherwise. Readers should review future reports filed or furnished by us with the SEC, the CNBV and the MSE.

This report contains statistical data regarding, but not limited to, the production, distribution, marketing, and sale of cement, ready-mix concrete, clinker, aggregates, and Urbanization Solutions. We generated some of this data internally, and some was obtained from independent industry publications and reports, available as of the date of this report, that we believe to be reliable sources. We have not independently verified this data nor sought the consent of any organizations to refer to their reports in this report.

We act in strict compliance with antitrust laws and as such, among other measures, maintain an independent pricing policy that has been independently developed. Our policy’s core element is to price our products and services based on their quality and characteristics as well as their value to our customers. We do not accept any communications or agreements of any type with competitors regarding the determination of our prices for our products and services. Unless the context indicates otherwise, all references to pricing initiatives, price increases or price decreases, refer to our prices for our products.

This report includes certain non-IFRS financial measures that differ from financial information presented by Cemex in accordance with IFRS in its financial statements and reports containing financial information. These aforementioned non-IFRS financial measures include “Operating EBITDA” (operating earnings before other expenses, net plus depreciation and amortization) and “Operating EBITDA Margin.” The closest financial measure to Operating EBITDA in our financial statements under IFRS is the line item of “Operating earnings before other expenses, net,” as Operating EBITDA adds depreciation and amortization to this line item. Our Operating EBITDA Margin is calculated by dividing our Operating EBITDA for the period by our revenues as reported in our financial statements for the same period. We believe there is no close IFRS financial measure to compare Operating EBITDA Margin. These non-IFRS financial measures are designed to complement and should not be considered superior to financial measures calculated in accordance with IFRS. Although Operating EBITDA and Operating EBITDA Margin are not measures of operating performance, an alternative to cash flows or a measure of financial position under IFRS, Operating EBITDA is the financial measure used by our management to review operating performance and profitability, for decision-making purposes and to allocate resources. Moreover, our Operating EBITDA is a measure used by our creditors to review our ability to internally fund capital expenditures, to service or incur debt and to comply with financial covenants under our financing agreements. Furthermore, our management regularly reviews our Operating EBITDA Margin by reportable segment and on a consolidated basis as a measure of performance and profitability. These non-IFRS financial measures do not have any standardized meaning and are therefore unlikely to be comparable to similarly titled measures presented by other companies. Non-IFRS financial measures presented in this report are being provided for informative purposes only and shall not be construed as investment, financial, or other advice.

The information, statements, and opinions contained in this report are for informational purposes and do not constitute a public offer under any applicable legislation, an offer to sell, or solicitation of any offer to buy any securities or financial instruments, or any advice or recommendation with respect to such securities or other financial instruments. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. We are not responsible for any third-party information referenced in this report.

5

CAUTIONARY STATEMENT REGARDING ENVIRONMENTAL, SOCIAL, AND GOVERNANCE

(“ESG”) AND SUSTAINABILITY-RELATED DATA, METRICS, AND METHODOLOGIES

This report includes non-financial metrics, estimates, or other information related to ESG and sustainability matters that are subject to significant uncertainties, which may include the methodology, collection, and verification of data, various estimates, and assumptions, and/or underlying data that is obtained from third parties, some of which cannot be independently verified.

The preparation of certain information on ESG and sustainability matters contained in this report requires the application of a number of key judgments, assumptions, and estimates. The reported measures in this report reflect good faith estimates, assumptions, and judgments at the given point in time. There is a risk that these judgments, estimates, or assumptions may subsequently prove to be incorrect and/or, to the extent legally required, may need to be restated or changed. The disclosure of information on sustainability-related matters is not yet subject to the same recognized or accepted reporting or accounting principles and rules as traditional financial information. Consequently, there are no commonly accepted reporting practices for us to follow, and ESG metrics among organizations in our industry may not be comparable. In addition, the underlying data, systems, and controls that support non-financial reporting are generally considerably less sophisticated than the systems and internal control for financial reporting and rely on manual processes. This may result in non-comparable information between organizations and/or between reporting periods within organizations as methodologies continue to develop and/or be socialized. The further development of or changes to accounting and/or reporting standards could materially impact the performance metrics, data points, and targets contained in this report, and the reader may not be able to compare non-financial information performance metrics, data points, or targets between reporting periods on a direct like-for-like basis.

Additionally, the information disclosed in this report contains references to “green,” “social,” “sustainable,” or equivalent-labelled activities, products, assets, or projects. There is currently no single globally recognized or accepted, consistent and comparable set of definitions or standards (legal, regulatory, or otherwise) of, nor widespread cross-market consensus (i) as to what constitutes, a “green,” “social,” “sustainable,” or having equivalent-labelled activity, product, or asset; (ii) as to what precise attributes are required for a particular activity, product, or asset to be defined as “green,” “social,” “sustainable” or such other equivalent label; or (iii) as to climate and sustainable funding and financing activities and their classification and reporting.

Therefore, there is little certainty, and no assurance or representation is given, that such activities, products, assets, or projects and/or reporting of such activities, products, assets or projects will meet any present or future expectations or requirements for describing or classifying such activities, products, assets or projects as “green,” “social,” “sustainable,” or attributing similar labels. We expect policies, regulatory requirements, standards, and definitions to be developed and continuously evolve over time.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING ESG OR SUSTAINABILITY STATEMENTS

Certain sections in this report contain ESG- or sustainability-related forward-looking statements, such as aims, ambitions, estimates, forecasts, plans, projections, targets, goals and other metrics, including but not limited to: climate and emissions, business and human rights, corporate governance, research and development and partnerships, development of products and services that intend to address sustainability-related concerns and sustainability related targets/ ambitions when finalized, including the implementation of technologies and other initiatives that aim to reduce and/or capture CO2 emissions. These forward-looking statements also include references to specific programs, such as our current “Future in Action” climate action and nature program, as well as various ESG-related indicators, objectives or metrics disclosed previously or that may be disclosed in the future, none of which are guarantees and any and all of which may ultimately not be achieved or may be abandoned at any time, whether in part, in full, or within any specific timeframe. There are many significant uncertainties, assumptions, judgements, opinions, estimates, forecasts and statements made of future expectations underlying these forward-looking statements which could cause actual results, performance, outcomes or events to differ materially from those expressed or implied in these forward-looking statements, which include, but are not limited to:

| • | the extent and pace of climate change, including the timing and manifestation of physical and transition risks; |

6

| • | the macroeconomic environment; |

| • | uncertainty around future climate-related policy and regulations, including the timely implementation and integration of adequate government policies; |

| • | the effectiveness of actions of governments, legislators, regulators, businesses, investors, customers, and other stakeholders to mitigate the impact of climate and sustainability-related risks; |

| • | changes in customer behavior and demand, changes in the available technology for mitigation and the effectiveness of any such technologies, as some of these new technologies may be unproven; |

| • | excessive costs and expenses related to acquire and/or develop technology for mitigation; |

| • | the roll-out of low carbon infrastructure; |

| • | the availability and adoption of renewable energy in our value chain; |

| • | the development of carbon capture, circular utilization, and sequestration technologies, including the adoption of cost-effective carbon-related technologies such as carbon capture, utilization, and storage; |

| • | the availability of accurate, verifiable, reliable, consistent, and comparable climate-related data; |

| • | lack of transparency and comparability of climate-related forward-looking methodologies; |

| • | variation in approaches and outcomes, as variations in methodologies may lead to under or overestimates and consequently present exaggerated indication of climate-related risk; and |

| • | reliance on assumptions and future uncertainty (calculations of forward-looking metrics are complex and require many methodological choices and assumptions). |

Accordingly, undue reliance should not be placed on these forward-looking statements. Furthermore, changing national and international standards, industry and scientific practices, regulatory requirements, and market expectations regarding climate change, which remain under continuous development, are subject to different interpretations.

There can be no assurance that these standards, practices, requirements, and expectations will not be interpreted differently than our understanding when defining sustainability-related ambitions and targets or change in a manner that substantially increases the cost or effort for us to achieve such ambitions and targets.

7

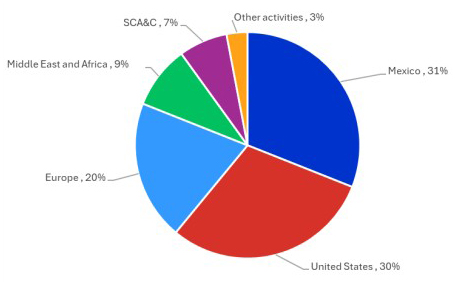

BREAKDOWN OF EXTERNAL REVENUES BY REPORTABLE SEGMENT FOR THE THREE-MONTH

PERIOD ENDED MARCH 31, 2026

The following chart indicates the geographic breakdown of our external revenues by reportable segment, for the three-month period ended March 31, 2026:

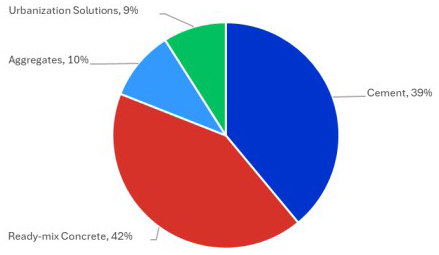

BREAKDOWN OF EXTERNAL REVENUES BY LINE OF BUSINESS FOR THE THREE-MONTH

PERIOD ENDED MARCH 31, 2026

The following chart indicates the breakdown of our external revenues by line of business for the three-month period ended March 31, 2026:

8

RECENT DEVELOPMENTS

Recent Developments Relating to Our Financial Obligations

2026 Credit Agreement

On May 28, 2026, Cemex, S.A.B. de C.V. signed a 5-year committed Dollar-denominated $3,000 million syndicated sustainability-linked revolving credit agreement (the “2026 Credit Agreement”), which proceeds will be used for general corporate purposes (including refinancing financial obligations of Cemex and its affiliates). The 2026 Credit Agreement, denominated exclusively in Dollars, maintains interest rate margin and financial covenants, consistent with an investment-grade capital structure, which provide for a maximum ratio of Consolidated Net Debt (as defined below) to Consolidated Operating EBITDA (as defined below) (“Consolidated Leverage Ratio”) of 3.75 times throughout the life of the loan and a minimum ratio of Consolidated Operating EBITDA to interest expense (“Consolidated Coverage Ratio”) of 2.75 times. All tranches under the 2026 Credit Agreement include a margin over the Secured Overnight Financing Rate (“SOFR”) from 85 basis points to 137.5 basis points, depending on the credit rating ranging from BBB+/Baa1 or higher in the lower end to BB+/Ba1 or lower in the higher end.

The 2026 Credit Agreement is guaranteed by Cemex Corp. Cemex will not be able to borrow under the 2026 Credit Agreement until certain conditions are satisfied, which Cemex currently expects to be satisfied in the short-term (possibly prior to June 30, 2026).

The 2026 Credit Agreement contains ongoing representations, warranties, affirmative and negative covenants, including financial covenants. Under the 2026 Credit Agreement, at the end of each quarter for each period of four consecutive quarters, Cemex must comply with a maximum Consolidated Leverage Ratio of 3.75 times and a minimum Consolidated Coverage Ratio of 2.75 times throughout the life of the credit agreement. These financial ratios are calculated using the consolidated amounts under IFRS. Under the 2026 Credit Agreement, (i) the Consolidated Leverage Ratio is calculated by dividing “Consolidated Net Debt” by “Consolidated Operating EBITDA” for the last 12 months as of the calculation date. Consolidated Net Debt equals debt, as reported in the statement of financial position, net of cash and cash equivalents, excluding any existing or future obligations under any securitization program and any subordinated notes of Cemex adjusted for net mark-to-market of all derivative instruments, as applicable, among other adjustments including in relation for business acquisitions or disposals; (ii) Consolidated Operating EBITDA, represents Operating EBITDA for the last 12 months as of the calculation date, as adjusted for any Operating EBITDA attributable to discontinued operations, and solely for the purpose of calculating the Consolidated Leverage Ratio on a pro forma basis for any material disposition and/or material acquisition; and (iii) Consolidated Coverage Ratio is calculated by dividing Consolidated Operating EBITDA by Consolidated Interest Expense for the last 12 months as of the calculation date. Cemex’s ability to comply with these ratios may be affected by economic conditions, volatility in foreign exchange rates, as well as by overall conditions in the financial and capital markets or other factors.

9

Accounts Receivables Securitization Program

On May 29, 2026, our accounts receivables securitization program in Mexico was fully repaid and terminated for an aggregate amount of Ps. 1,800 million.

EUAs Forward Program

As of the date of this report, the EUAs Forward Program (as defined herein) is comprised of 3 million EUAs for the years 2029 to 2035 for an aggregate amount of $344 million.

Recent Developments Relating to our Regulatory Matters and Legal Proceedings

Maceo, Colombia—Legal Proceedings in Colombia

In May 2026, the free trade zone benefits related to the Maceo Project expired. As of the date of this report, we do not expect this to have a material adverse effect on our results of operations, liquidity, or financial condition.

10

Imposition of Tariffs by the United States

On May 7, 2026, the U.S. Court of International Trade ruled that the 10% ad valorem tariff imposed by the United States in February 2026 on imports from substantially all trading partners under Section 122 of the Trade Act of 1974 (“Section 122 Tariffs”) are unlawful. The court’s ruling was limited to the successful plaintiffs and did not apply universally. The United States government appealed to the U.S. Court of Appeals for the Federal Circuit, which entered an administrative stay suspending the lower court’s order while it considers the appeal. As of the date of this report, the Section 122 Tariffs remain in effect until their statutory expiration on July 24, 2026 for most importers pending the outcome of the appeal. As of the date of this report, goods that comply with rules of origin established under the United States-Mexico-Canada Agreement (“USMCA”) remain exempt from Section 122 Tariffs.

The public comment periods for the two Section 301 investigations initiated by the United States Trade Representative in March 2026 have closed, and public hearings were held in late April and early May 2026. These investigations are expected to conclude and potentially result in the imposition of tariffs by July 24, 2026, concurrent with the expiration of the Section 122 Tariffs. The tariff rates applied pursuant to these Section 301 investigations could be equivalent to or exceed the country-specific reciprocal tariffs imposed by the United States in 2025 and invalidated by the U.S. Supreme Court in February 2026. The cement sector is among those specifically identified in the Section 301 investigation regarding structural excess capacity and overproduction in manufacturing sectors as unreasonable or discriminatory and burdensome or restrictive on U.S. commerce.

The USMCA is subject to a mandatory joint review, with the Free Trade Commission required to convene on July 1, 2026. At that review, each party must confirm in writing whether it wishes to extend the agreement for an additional 16-year term. If any party declines to confirm extension, the agreement shifts to annual reviews and would expire on July 1, 2036, unless the parties later reach a consensus on extension. Changes to the USMCA’s preferential treatment regime, including rules of origin, could affect the tariff treatment of products we import into the United States from Mexico and Canada.

As of the date of this report, according to our interpretation of applicable laws and regulations and the various court rulings, imports of our products from the main countries in which we have operations into the United States and/or from which we generally source products we import into the United States and/or from which products imported into the United States in our industry are generally sourced, are subject to the following tariffs on a country-by-country basis: (i) Mexico and Canada: 0% on USMCA-compliant products; 10% on non-USMCA-compliant products (subject to the ongoing judicial challenge to the Section 122 Tariffs); and for steel and aluminum products, tiered rates of 50%, 25%, 15%, 10%, or 0% depending on product category and country of origin; (ii) China: approximately 35%, considering estimates of the blended effective rate for Chinese goods; and (iii) other countries: 10% (subject to the ongoing judicial challenge to the Section 122 Tariffs), and for steel and aluminum products, tiered rates of 50%, 25%, 15%, 10%, or 0% depending on product category and country of origin. As of the date of this report, we believe that substantially all products we import into the United States from Mexico and Canada as part of our business are compliant with the USMCA.

SELECTED CONSOLIDATED FINANCIAL INFORMATION

The financial data set forth below for the three-month periods ended March 31, 2025 and 2026 have been derived from, and should be read in conjunction with, and are qualified in their entirety by reference to, Cemex, S.A.B. de C.V.’s unaudited condensed consolidated financial statements as of December 31, 2025 and March 31, 2026 and for the three-month periods ended March 31, 2025 and 2026 and the notes thereto included herein. In the opinion of management, the unaudited condensed consolidated financial statements reflect all adjustments (consisting of normal recurring items) that are necessary to properly present, in all material respects, the results for the interim periods. The interim results of operations for the three-month period ended March 31, 2026 are not indicative of operating results to be expected for the entire year.

Our audited consolidated financial statements included in the 2025 Annual Report were prepared in accordance with IFRS, which differ in significant respects from U.S. generally accepted accounting principles (“GAAP”). The regulations of the SEC do not require foreign private issuers that prepare their financial statements on the basis of IFRS (as published by the IASB) to reconcile such financial statements to U.S. GAAP. Accordingly, we do not reconcile our financial information to U.S. GAAP.

11

Cemex, S.A.B. de C.V.’s unaudited condensed consolidated financial statements as of December 31, 2025 and March 31, 2026 and for the three-month periods ended March 31, 2025 and 2026 included herein are prepared in accordance with International Accounting Standard 34 Interim Financial Reporting (“IAS 34”) as issued by the International Accounting Standards Board (“IASB”), on a basis consistent with the accounting policies used in the preparation and presentation of our audited consolidated financial statements included in the 2025 Annual Report.

CEMEX, S.A.B. DE C.V. AND SUBSIDIARIES

Selected Consolidated Financial Information

| For the Three- Month Period Ended March 31, |

||||||||

| 2025 | 2026 | |||||||

| (in millions of Dollars, except ratios and share and per share amounts) |

||||||||

| Statement of Income Information: |

||||||||

| Revenues |

$ | 3,614 | $ | 4,019 | ||||

| Cost of sales(1) |

(2,490 | ) | (2,699 | ) | ||||

| Gross profit |

1,124 | 1,320 | ||||||

| Operating expenses |

(834 | ) | (867 | ) | ||||

| Operating earnings before other expenses, net(2) |

290 | 453 | ||||||

| Other expenses, net |

(44 | ) | (43 | ) | ||||

| Operating earnings(2) |

246 | 410 | ||||||

| Financial items(3) |

(75 | ) | (92 | ) | ||||

| Share of profit of equity accounted investees |

5 | 7 | ||||||

| Earnings before income tax |

176 | 325 | ||||||

| Income tax |

(52 | ) | (94 | ) | ||||

| Discontinued operations(4) |

618 | 3 | ||||||

| Non-controlling interest net income |

8 | 6 | ||||||

| Controlling interest net income |

734 | 228 | ||||||

| Basic earnings per share(5)(6) |

0.0169 | 0.0054 | ||||||

| Diluted earnings per share(5)(6) |

0.0166 | 0.0052 | ||||||

| Basic earnings per share from continuing operations(5)(6) |

0.0027 | 0.0053 | ||||||

| Diluted earnings per share from continuing operations(5)(6) |

0.0026 | 0.0051 | ||||||

| Weighted-average number of shares outstanding - basic(5)(7) |

43,463 | 43,354 | ||||||

| Weighted-average number of shares outstanding - diluted(5)(7) |

44,122 | 43,895 | ||||||

| As of | ||||||||

| December 31, 2025 | March 31, 2026 | |||||||

| (in millions of Dollars) | ||||||||

| Statement of Financial Position Information: |

||||||||

| Cash and cash equivalents |

$ | 1,822 | $ | 687 | ||||

| Assets held for sale and other current assets(8) |

144 | 550 | ||||||

| Property, machinery and equipment, net and assets for the right-of-use, net(11) |

12,168 | 11,927 | ||||||

| Other assets |

14,811 | 14,936 | ||||||

| Total assets |

28,945 | 28,100 | ||||||

12

| As of | ||||||||

| December 31, 2025 | March 31, 2026 | |||||||

| (in millions of Dollars) | ||||||||

| Current debt |

1,187 | 397 | ||||||

| Other current liabilities |

6,160 | 6,122 | ||||||

| Non-current debt |

4,457 | 4,758 | ||||||

| Other non-current liabilities |

3,503 | 3,380 | ||||||

| Total liabilities |

15,307 | 14,657 | ||||||

| Non-controlling interest |

308 | 306 | ||||||

| Total controlling interest |

13,330 | 13,137 | ||||||

| For the Three-Month Period Ended March 31, |

||||||||

| 2025 | 2026 | |||||||

| (in millions of Dollars, except ratios and share and per share amounts) |

||||||||

| Other Financial Information: |

||||||||

| Book value per share(5)(9) |

$ | 0.3024 | $ | 0.2993 | ||||

| Operating EBITDA(10) |

595 | 794 | ||||||

| Capital expenditures |

249 | 156 | ||||||

| Depreciation and amortization of assets |

305 | 341 | ||||||

| Cash flows provided by operating activities from continuing operations |

37 | 310 | ||||||

| Basic earnings per CPO from continuing operations(5)(6) |

0.0081 | 0.0159 | ||||||

| Basic earnings per CPO(5)(6) |

0.0507 | 0.0162 | ||||||

| Total debt plus other financial obligations(11) |

7,460 | 6,859 | ||||||

| (1) | Cost of sales represents the production cost of inventories at the moment of sale and includes depreciation, amortization and depletion of assets involved in production, expenses related to storage in production plants, freight expenses of raw materials in plants and delivery expenses of our ready-mix concrete business. Our cost of sales excludes (i) expenses related to personnel and equipment comprising our selling network and those expenses related to warehousing at the points of sale and (ii) freight expenses of finished products from our producing plants to our points of sale and from our points of sale to our customers’ locations, which are all included as part of the line item titled “Operating expenses.” |

| (2) | In the income statements, we include the line item titled “Operating earnings before other expenses, net” considering that it is a subtotal relevant for the determination of our “Operating EBITDA” as explained in note 2 to Cemex, S.A.B. de C.V.’s 2025 audited consolidated financial statements included in the 2025 Annual Report. The line item of “Operating earnings before other expenses, net” allows for easy reconciliation of the amount in these financial statements under IFRS to the non-IFRS measure of Operating EBITDA by adding back depreciation and amortization. Under current IFRS, the inclusion of certain subtotals such as “Operating earnings before other expenses, net” and the display of the income statements varies significantly by industry and company according to specific needs. |

| (3) | Financial items include our financial expense and our financial income and other items, net, which includes net interest cost of pension liabilities, financial income, results from financial instruments, net (derivatives, fixed-income investments and other securities), foreign exchange results, effects of amortized cost on assets and liabilities and others, net. See notes 6 and 7 to Cemex, S.A.B. de C.V.’s unaudited condensed consolidated financial statements as of December 31, 2025 and March 31, 2026 and for the three-month periods ended March 31, 2025 and 2026 included herein. |

| (4) | Considering any component that has been disposed of or classified as held for sale and represents a separate major line of business, geographical area, or is part of a single disposal plan, our income statements present as part of the single line item of “Discontinued operations,” net of income tax, the results of: (a) Dominican Republic operations for the period from January 1 to January 30, 2025 and (b) Panama for the three-month period ended March 31, 2025. There were no discontinued operations for the three-month period ended March 31, 2026. See note 4.1 to Cemex, S.A.B. de C.V.’s unaudited condensed consolidated financial statements as of December 31, 2025 and March 31, 2026 and for the three-month periods ended March 31, 2025 and 2026 included herein. |

| (5) | Cemex, S.A.B. de C.V.’s capital stock consists of Series A shares and Series B shares. Each CPO represents two Series A shares and one Series B share. As of March 31, 2026, 99.99% of Cemex, S.A.B. de C.V.’s outstanding share capital was represented by CPOs, with each ADS representing 10 CPOs. No CPOs were repurchased in the three-month period ended March 31, 2025. During the three-month period ended March 31, 2026, 78,803,711 CPOs were repurchased under Cemex, S.A.B. de C.V.’s authorized repurchase programs, which |

13

| represented 0.543% of Cemex, S.A.B. de C.V.’s outstanding share capital as of December 31, 2025, at a weighted-average price in Mexican Pesos equivalent to $1.2678 (based on an exchange rate of Ps 17.2013 to $1.00 as of March 31, 2026) per CPO, which was equivalent to an amount of $99.9 million (based on an exchange rate of Ps 17.2013 to $1.00 as of March 31, 2026), excluding fees and value-added tax. |

| (6) | Earnings per share is calculated based upon the weighted-average number of shares outstanding during the year. Basic earnings per CPO is determined by multiplying the basic earnings per share for each period by three (the number of shares underlying each CPO). Basic earnings per CPO is presented solely for the convenience of the reader and does not represent a measure under IFRS. As shown in note 4.1 to Cemex, S.A.B. de C.V.’s unaudited condensed consolidated financial statements as of December 31, 2025 and March 31, 2026 and for the three-month periods ended March 31, 2025 and 2026 included herein, and in connection with our discontinued operations mentioned above, for the three-month period ended March 31, 2025, “Basic earnings per share” and “Diluted earnings per share” include $0.0027 and $0.0026, respectively, from “Continuing operations” and for the three-month period ended March 31, 2026, “Basic earnings per share” and “Diluted earnings per share” include $0.0053 and $0.0051, respectively. In addition, for the three-month period ended March 31, 2025, “Basic earnings per share” and “Diluted earnings per share” include $0.0142 and $0.0140, respectively, from “Discontinued operations” and for the three-month period ended March 31, 2026, “Basic earnings per share” and “Diluted earnings per share” include $0.0001 and $0.0001, respectively, from “Discontinued operations.” |

| (7) | Pursuant to the resolutions adopted at Cemex, S.A.B. de C.V.’s ordinary general shareholders’ meeting held on March 22, 2024, Cemex, S.A.B. de C.V. approved the payment of a $120 million dividend, payable in four equal installments. Cemex, S.A.B. de C.V. paid the fourth and last installment of a cash dividend to shareholders during the three-month period ended March 31, 2025 in the amounts of $0.013974 Mexican Pesos per share (equivalent to $0.000689 per share). No recapitalization of retained earnings was proposed at Cemex, S.A.B. de C.V.’s ordinary general shareholders’ meeting held on March 25, 2025. Pursuant to the resolutions adopted at Cemex, S.A.B. de C.V.’s ordinary general shareholders’ meeting held on March 25, 2025, Cemex, S.A.B. de C.V. approved the payment of a $130 million dividend, payable in four equal installments. Cemex, S.A.B. de C.V. paid the fourth and last installment of a cash dividend to shareholders during the three-month period ended March 31, 2026 in the amounts of $0.013127 Mexican Pesos per share (equivalent to $0.000750 per share). No recapitalization of retained earnings was proposed at Cemex, S.A.B. de C.V.’s ordinary general shareholders’ meeting held on March 26, 2026. Pursuant to the resolutions adopted at Cemex, S.A.B. de C.V.’s ordinary general shareholders’ meeting held on March 26, 2026, Cemex, S.A.B. de C.V. approved the payment of a $180 million dividend, payable in four equal installments. |

| (8) | As of December 31, 2025 and March 31, 2026 included assets held for sale for $42 million and $436 million, respectively. |

| (9) | Book value per share is calculated by dividing the total controlling interest by the number of shares outstanding. |