UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): October 23, 2025

POPULAR, INC.

(Exact name of registrant as specified in its charter)

| Puerto Rico | 001-34084 | 66-0667416 | ||

| (State or other jurisdiction of incorporation or organization) |

(Commission File Number) |

(IRS Employer Identification Number) |

| 209 Muñoz Rivera Avenue | ||

| Hato Rey, Puerto Rico | 00918 | |

| (Address of principal executive offices) | (Zip code) |

(787) 765-9800

(Registrant’s telephone number, including area code)

NOT APPLICABLE

(Former name, former address and former fiscal year, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

| ☐ | Written communication pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ | Pre-commencement communication pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ | Pre-commencement communication pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading |

Name of each exchange |

||

| Common Stock ($0.01 par value) | BPOP | The NASDAQ Stock Market | ||

| 6.125% Cumulative Monthly Income Trust Preferred Securities | BPOPM | The NASDAQ Stock Market |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

| Item 2.02. | Results of Operations and Financial Condition. |

On October 23, 2025, Popular, Inc. (the “Corporation”) issued a press release announcing its unaudited financial results for the quarter ended September 30, 2025, a copy of which is attached as Exhibit 99.1 to this Current Report on Form 8-K.

The information furnished pursuant to this Item 2.02 of this Current Report on Form 8-K, including Exhibit 99.1, shall not be deemed “filed” for purposes of the Securities Exchange Act of 1934, as amended, nor shall it be incorporated by reference into any of the Corporation’s filings under the Securities Act of 1933, as amended, unless otherwise expressly stated in such filing.

| Item 7.01. | Regulation FD Disclosure. |

The Corporation is furnishing information regarding its conference call to discuss its financial results for the quarter ended September 30, 2025. A copy of the presentation to be used by the Corporation on the conference call is attached hereto as Exhibit 99.2.

The information furnished pursuant to this Item 7.01 of this Current Report on Form 8-K, including Exhibit 99.2, shall not be deemed “filed” for purposes of the Securities Exchange Act of 1934, as amended, nor shall it be incorporated by reference into any of the Corporation’s filings under the Securities Act of 1933, as amended, unless otherwise expressly stated in such filing.

| Item 9.01. | Financial Statements and Exhibits. |

Exhibits 99.1 and 99.2 shall not be deemed to be “filed” for purposes of the Securities Exchange Act of 1934, as amended.

| 99.1 | Press Release dated October 23, 2025 – Third Quarter 2025 Financial Results. | |

| 99.2 | Popular, Inc. Conference Call Presentation – Third Quarter 2025 Financial Results. | |

| 101 | Pursuant to Rule 406 of Regulation S-T, the cover page is formatted in Inline XBRL (Inline eXtensible Business Reporting Language). | |

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document and included in Exhibit 101). | |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| POPULAR, INC. (Registrant) |

||||||

| Date: October 23, 2025 | By: | /s/ Denissa M. Rodríguez |

||||

| Denissa M. Rodríguez | ||||||

| Senior Vice President and Corporate Comptroller | ||||||

Exhibit 99.1

Popular, Inc. Announces Third Quarter 2025 Financial Results

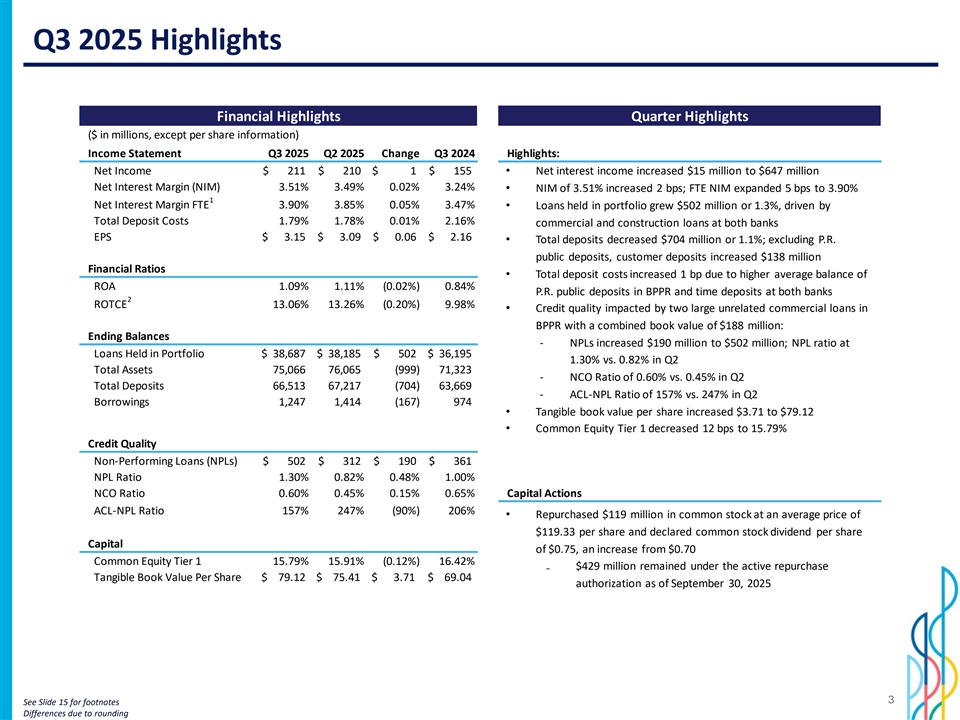

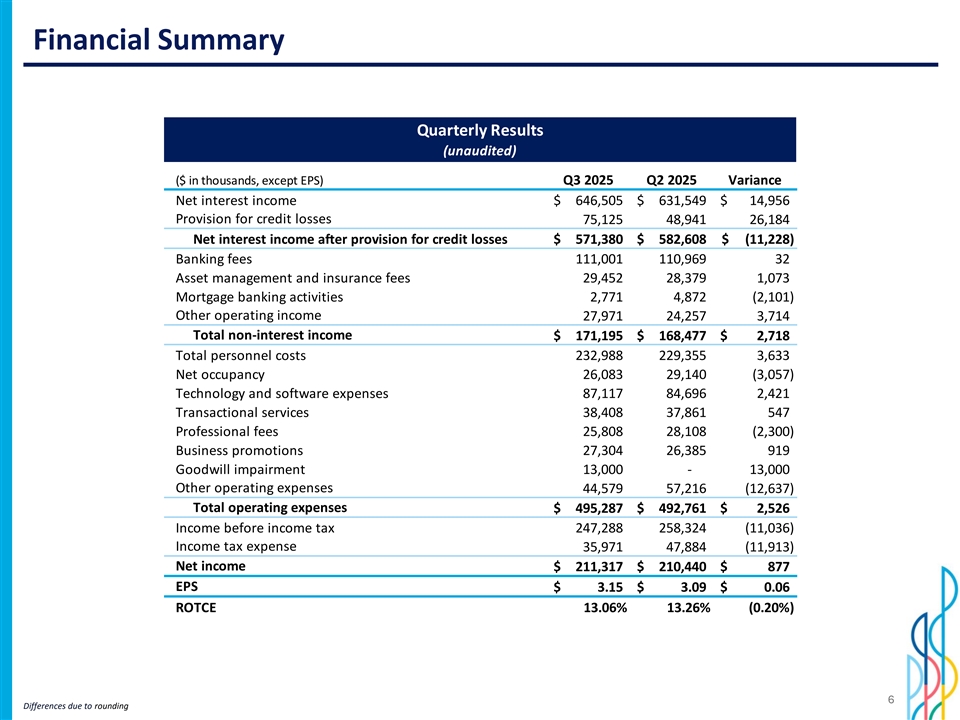

| • | Net income of $211.3 million in Q3 2025, compared to net income of $210.4 million in Q2 2025. |

| • | Earnings per share (“EPS”) of $3.15 in Q3 2025 vs. $3.09 in Q2 2025. |

| • | Net interest income of $646.5 million in Q3 2025, an increase of $15.0 million compared to Q2 2025: |

| • | Net interest margin of 3.51% in Q3 2025, compared to 3.49% in Q2 2025; net interest margin on a taxable equivalent basis of 3.90% in Q3 2025, compared to 3.85% in Q2 2025. |

| • | Non-interest income of $171.2 million in Q3 2025, compared to $168.5 million in Q2 2025. |

| • | Operating expenses amounted to $495.3 million, compared to $492.8 million in Q2 2025. |

| • | Credit quality metrics: |

| • | Non-performing loans held-in-portfolio (“NPLs”) increased by $190.6 million from Q2 2025, primarily due to two unrelated large commercial loans with book values of $158.3 million and $30.1 million; the NPLs to loans ratio increased to 1.30% from 0.82% in Q2 2025. |

| • | Net charge-offs (“NCOs”) increased by $15.6 million from Q2 2025, mainly due to a $13.5 million commercial loan charge-off on the $30.1 million commercial NPL inflow; annualized NCOs to average loans held-in-portfolio at 0.60% vs. 0.45% in Q2 2025. |

| • | Allowance for credit losses (“ACL”) to loans held-in-portfolio at 2.03% vs. 2.02% in Q2 2025; and |

| • | ACL to NPLs at 156.6% vs. 246.9% in Q2 2025. |

| • | Loans held-in-portfolio, excluding loans held-for-sale, amounted to $38.7 billion, an increase of $502.0 million from Q2 2025; average quarterly loan balances higher by $859.2 million. |

| • | Money market and investment securities decreased by $1.5 billion from Q2 2025; average quarterly balances decreased by $111.6 million. |

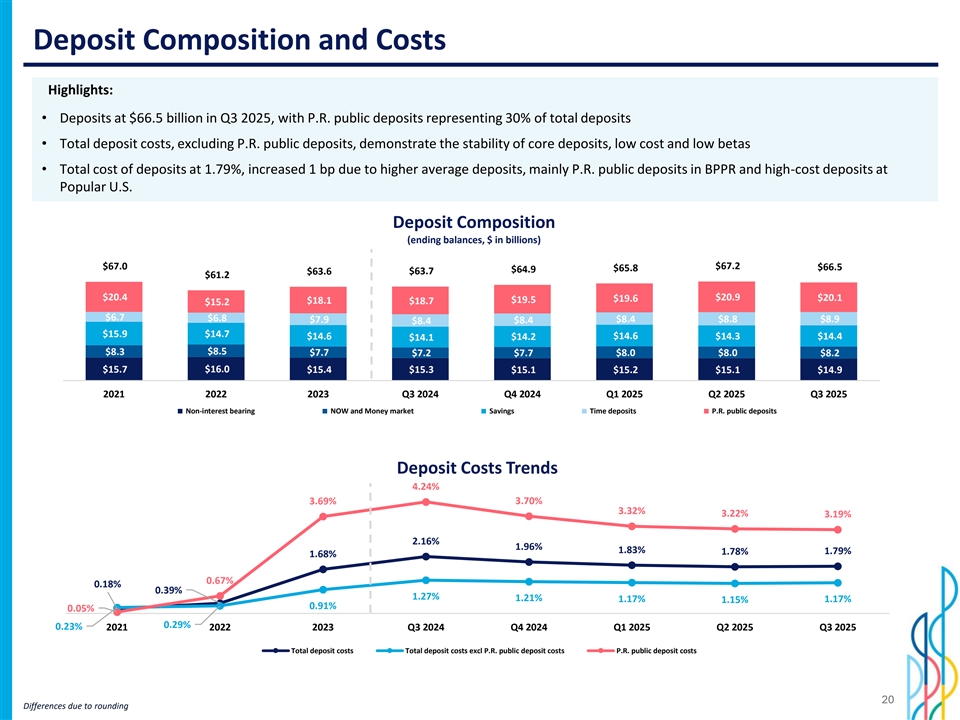

| • | Deposits at $66.5 billion, decreased $704.1 million from Q2 2025, including a decrease of $841.9 million in P.R. public deposits; average quarterly deposits higher by $793.2 million, including an increase of $433.2 million in P.R. public deposits. |

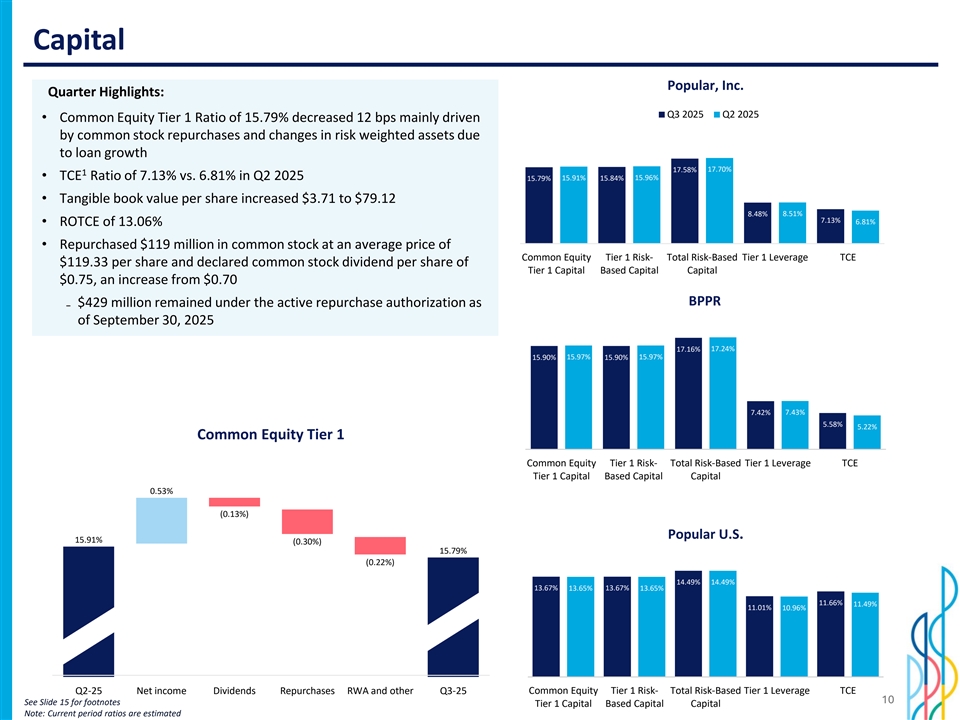

| • | Common Equity Tier 1 ratio of 15.79%, Common Equity per share of $91.00 and Tangible Book Value per share increased $3.71 to $79.12. |

| • | Capital actions for the third quarter of 2025 included the repurchase of 1,000,862 shares of common stock for $119.4 million, at an average price of $119.33 per share and the declaration of a common stock dividend of $0.75 per share, an increase from $0.70 per share. As of September 30, 2025, a total of $429.0 million remained available for stock repurchases under the active repurchase authorization. |

1

SAN JUAN, Puerto Rico – (BUSINESS WIRE) – Popular, Inc. (the “Corporation,” “Popular,” “we,” “us,” “our”) (NASDAQ:BPOP) reported net income of $211.3 million for the quarter ended September 30, 2025, compared to net income of $210.4 million for the quarter ended June 30, 2025.

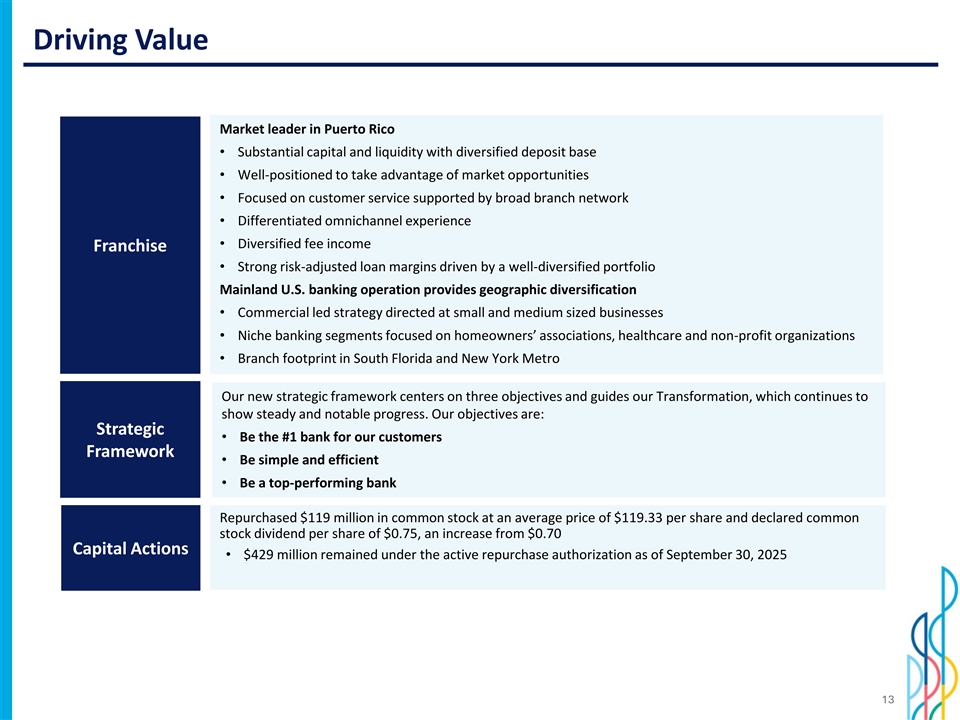

“We are very pleased with our strong results in the third quarter, which were driven by higher revenues, continued expansion of our net interest margin, and discipline in expense management,” said Javier D. Ferrer, President and Chief Executive Officer of Popular, Inc. “We are also encouraged by strong loan growth in both markets, stable customer deposit balances, and solid performance across most fee-generating segments, including robust transaction activity supported by continued customer growth.

We are focused on executing on our new strategic framework, which has three objectives: be the #1 bank for our customers, be simple and efficient, and be a top-performing bank with first-rate talent and which delivers sustainable returns to our shareholders. This framework guides our Transformation, which continues to show steady and notable progress.

Our team is clear about our priorities and energized about the opportunities that lie ahead. I want to thank all our colleagues for their dedication and outstanding work—their commitment continues to drive our success.”

2

Earnings Highlights

| (Unaudited) |

Quarters ended | Nine months ended | ||||||||||||||||||

| (Dollars in thousands, except per share information) |

30-Sep-25 | 30-Jun-25 | 30-Sep-24 | 30-Sep-25 | 30-Sep-24 | |||||||||||||||

| Net interest income |

$ | 646,505 | $ | 631,549 | $ | 572,473 | $ | 1,883,651 | $ | 1,691,529 | ||||||||||

| Provision for credit losses |

75,125 | 48,941 | 71,448 | 188,147 | 190,840 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income after provision for credit losses |

571,380 | 582,608 | 501,025 | 1,695,504 | 1,500,689 | |||||||||||||||

| Other non-interest income |

171,195 | 168,477 | 164,082 | 491,733 | 494,206 | |||||||||||||||

| Operating expenses |

495,287 | 492,761 | 467,321 | 1,459,060 | 1,420,010 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income tax |

247,288 | 258,324 | 197,786 | 728,177 | 574,885 | |||||||||||||||

| Income tax expense |

35,971 | 47,884 | 42,463 | 128,918 | 138,490 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 211,317 | $ | 210,440 | $ | 155,323 | $ | 599,259 | $ | 436,395 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income applicable to common stock |

$ | 210,964 | $ | 210,087 | $ | 154,970 | $ | 598,200 | $ | 435,336 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income per common share-basic |

$ | 3.15 | $ | 3.09 | $ | 2.16 | $ | 8.78 | $ | 6.06 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income per common share-diluted |

$ | 3.14 | $ | 3.09 | $ | 2.16 | $ | 8.78 | $ | 6.05 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

3

Non-GAAP Financial Measures

This press release contains financial information prepared under accounting principles generally accepted in the United States (“U.S. GAAP”) and non-GAAP financial measures. Management uses non-GAAP financial measures when it determines that these measures provide more meaningful information of the underlying performance of the ongoing operations. Non-GAAP financial measures used by the Corporation may not be comparable to similarly named non-GAAP financial measures used by other companies.

Net interest income on a taxable equivalent basis

Net interest income, on a taxable equivalent basis, is presented with its different components in Tables D, E and F for the quarter ended September 30, 2025. Net interest income, on a taxable equivalent basis, is a non-GAAP financial measure. Management believes that this presentation provides meaningful information since it facilitates the comparison of revenues arising from taxable and tax-exempt sources.

Tangible Common Equity

Tangible common equity, the tangible common equity ratio, tangible assets and tangible book value per common share are non-GAAP financial measures. The tangible common equity ratio and tangible book value per common share are commonly used by banks and analysts in conjunction with more traditional bank capital ratios to compare the capital adequacy of banking organizations with significant amounts of goodwill or other intangible assets, typically stemming from the use of the purchase accounting method for mergers and acquisitions. Neither tangible common equity nor tangible assets or related measures should be used in isolation or as a substitute for stockholders’ equity, total assets or any other measure calculated in accordance with GAAP.

Refer to Table R for a reconciliation of total stockholders’ equity to tangible common equity and total assets to tangible assets.

Net Interest Income and Net Interest Margin

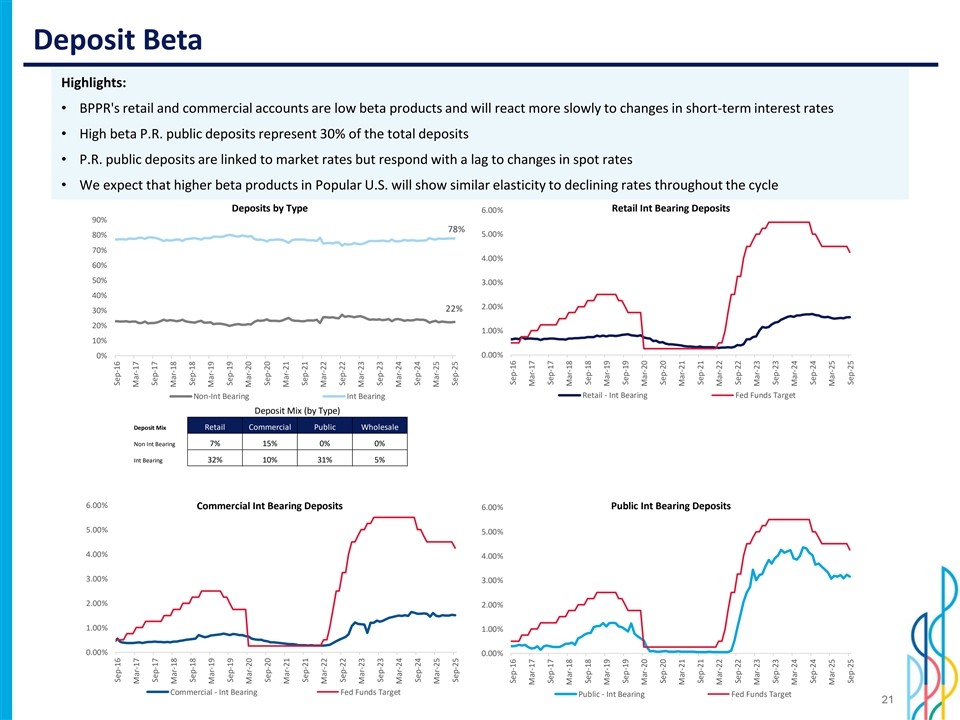

Net interest income (“NII”) for the third quarter of 2025 of $646.5 million, an increase of $15.0 million when compared to the previous quarter. These results continue to reflect the favorable impact of asset repricing, and the Corporation’s focus on deposit retention. During the period, the investments in U.S. Treasury securities with higher yields contributed positively to the period’s net interest income, supported by an increase of $793.2 million in average deposits compared to the second quarter of 2025, primarily in P.R. public deposits and high-cost deposits in our U.S. operations, offset in part by a reduction in overnight Fed funds balances. Conversely, total interest expense on deposits increased by $8.4 million when compared with the second quarter of 2025, driven by higher average deposits during the quarter. The additional day in the quarter, when compared to the previous quarter, resulted in higher NII by $5.1 million.

Net interest margin (“NIM”) for the quarter was 3.51%, compared to 3.49% in the second quarter of 2025, an increase of two basis points. NIM expansion for the period was driven by earning assets mix, including higher yielding U.S. Treasury securities by approximately 10 basis points, partially offset by changes in the loan portfolios composition, which resulted in lower loan yields by four basis points. Total deposit costs of 1.79% increased by one basis point when compared to the second quarter of 2025. P.R. public deposit costs, which are market-linked, decreased by three basis points to 3.19%. Excluding P.R. public deposits, average deposits increased by $359.9 million and total deposit costs increased two basis points to 1.17% when compared to the second quarter of 2025.

Net Interest Income and Net Interest Margin Taxable Equivalent (Non-GAAP)

Net interest income on a taxable equivalent basis for the third quarter of 2025 was $720.8 million, an increase of $23.6 million. Net interest margin on a taxable equivalent basis for the third quarter of 2025 was 3.90%, an increase of five basis points.

4

The main drivers of net interest income on a taxable equivalent basis were:

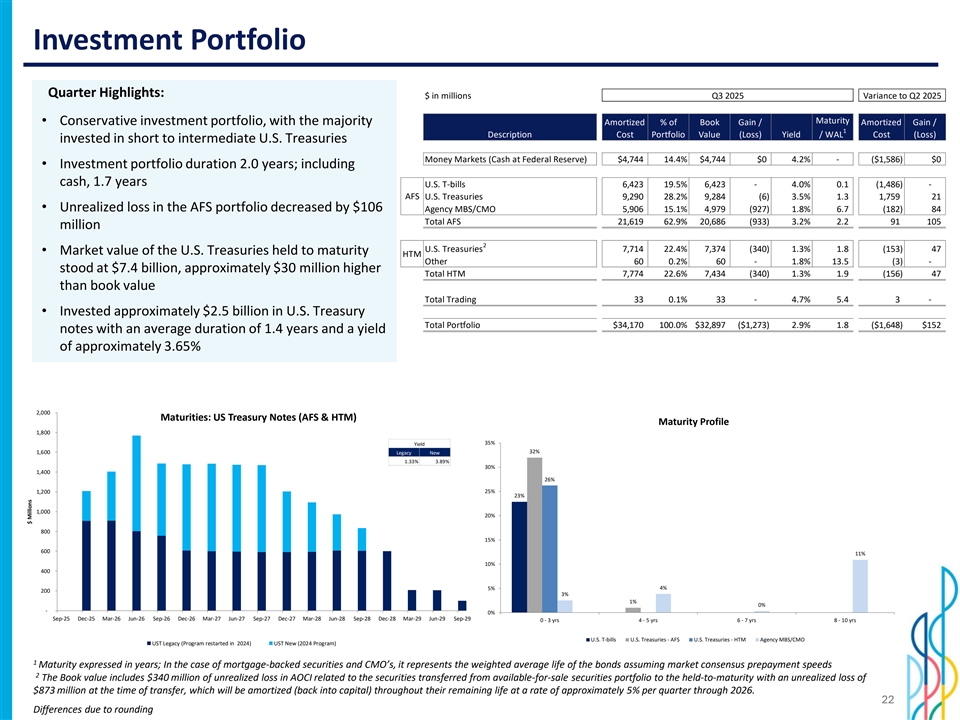

| • | higher income from investment securities by $12.7 million or 13 basis points, due to higher investments in U.S. Treasury securities, which are tax-exempt in Puerto Rico, by $290.4 million and higher yields by 17 basis points. During the quarter we purchased approximately $2.5 billion of U.S. Treasury notes with an average duration of 1.4 years and a yield of approximately 3.65%, through a combination of approximately $1.0 billion in maturing U.S. Treasuries and a reduction of approximately $1.5 billion in overnight Fed funds. This further supports a reduction in the portfolio’s sensitivity to future rate decreases; and |

| • | higher interest income from loans by $21.4 million, primarily as a result of higher average loan balances by $859.7 million due to growth in the loan portfolios, most notably in the commercial and mortgage loan portfolios which in Banco Popular de Puerto Rico (“BPPR”) include certain loans that are tax- exempt; |

partially offset by:

| • | higher interest expense on deposits by $8.4 million or one basis point, primarily as result of higher average balance of P.R. public deposits, which increased by $433.2 million, and high-cost deposits in Popular Bank (“PB” or “Popular U.S.”), partially offset by the lower repricing of market linked P.R. public deposits; and |

| • | lower income from money market investments by $2.7 million mainly due to the use of funds to support loan growth and U.S. Treasury securities purchases, as previously noted. |

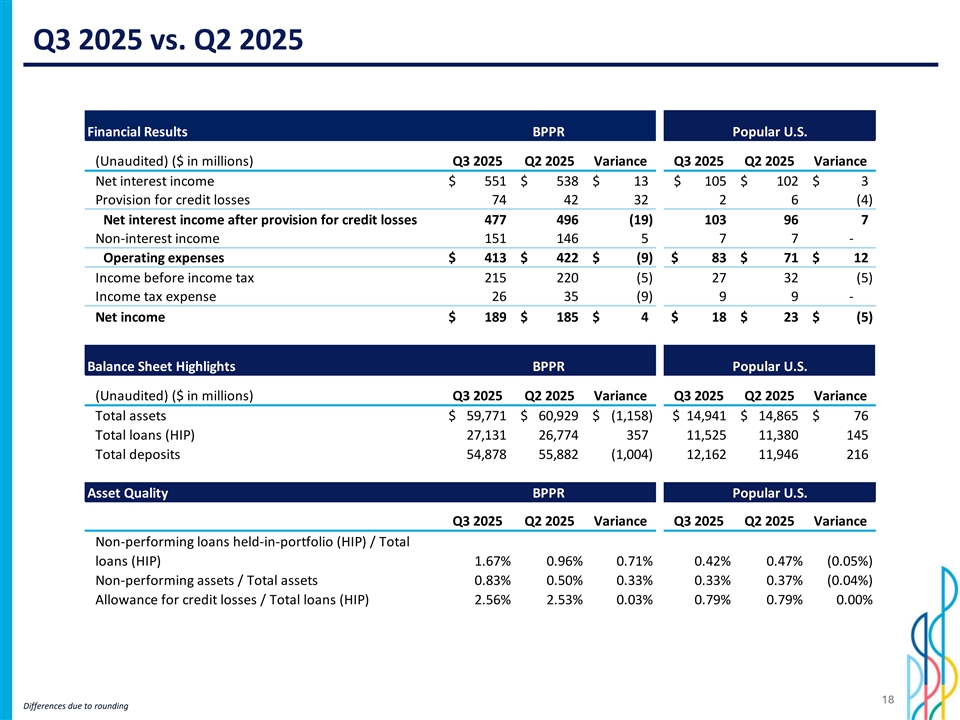

Net Interest Income and Net Interest Margin (Banco Popular de Puerto Rico Segment)

For the BPPR segment, net interest income for the third quarter of 2025 was $550.7 million, an increase of $12.2 million over the previous quarter. Net interest margin increased by three basis points to 3.71%. Total deposits cost in BPPR increased by one basis point to 1.53%.

The main drivers of higher net interest income for the BPPR segment include:

| • | higher income from investment securities by $8.0 million, or an eight basis points increase, driven by higher yields by 10 basis points and higher average balances of U.S. Treasury securities by $255.0 million, driven by higher average deposits and a reduction in overnight Fed funds; and |

| • | higher income from loans by $11.8 million primarily attributable to growth in all portfolios, mainly in the commercial and mortgage portfolios which on average grew balances by $382.4 million and $144.8 million, respectively, partially offset by lower yields in commercial loan portfolio by 15 basis points, driven by the impact of certain large commercial loan originations at lower yields that have occurred during the second and third quarter of 2025 and the impact of 6 basis points due to the reversal of accrued interest income receivable on a large commercial loan classified as non-accrual during the period; |

partially offset by:

| • | higher average deposits by $389.2 million, driven by higher P.R. public deposits by $433.2 million, resulting in higher interest expense by $3.7 million; and |

| • | lower income from money market investments by $3.3 million mainly due to the use of funds to support loan growth and U.S. Treasury securities purchases. |

5

Net Interest Income and Net Interest Margin (Popular Bank Segment)

In the Popular Bank segment, net interest income was $105.2 million, $3.0 million higher when compared to the previous quarter. Net interest margin in the PB segment increased by one basis point to 2.94%. Total cost of deposits increased by one basis point during the quarter to 2.96%.

The main drivers for the higher net interest income for the Popular Bank segment include:

| • | an increase in interest income on loan portfolios by $5.7 million, or two basis points, compared to the previous quarter, driven by growth in the commercial and construction loan portfolios; and |

partially offset by:

| • | higher interest expense on deposits by $3.2 million, or one basis point, attributed to higher average deposits, mainly in high-cost deposits including online deposits and time deposits. |

Refer to tables D and E for more details on the components of net interest income and net interest margin on a taxable equivalent basis.

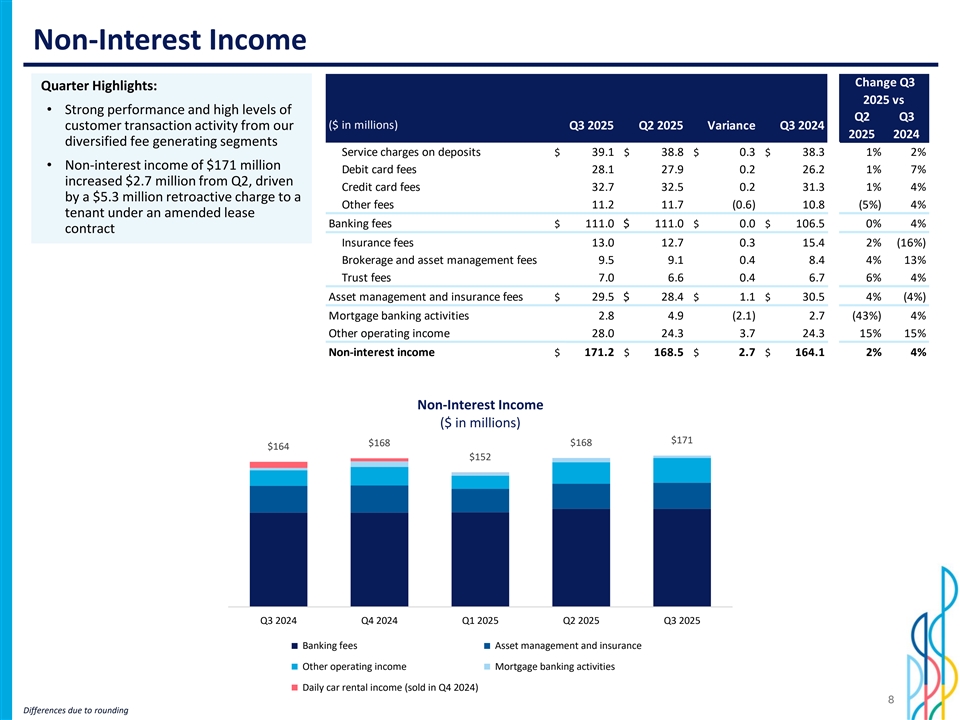

Non-interest income

Non-interest income amounted to $171.2 million for the quarter ended September 30, 2025, an increase of $2.7 million when compared to $168.5 million for the previous quarter. Our diverse fee-generating segments, together with robust customer transaction activity, have contributed to solid performance in the third quarter of 2025.

The main variances in non-interest income include:

| • | higher other operating income by $3.6 million mainly due to income of $5.3 million related to a retroactive charge billed to a tenant for energy supplied in prior years and higher income from investments accounted under the equity method by $2.7 million, partially offset by the impact of $3.5 million related to certain transactions recognized during the second quarter of 2025 which included income on a tax-related reimbursement and a cash distribution from a legacy equity investment; |

partially offset by:

| • | lower income from mortgage banking activities by $2.1, million mainly due to an unfavorable variance in the fair value adjustment of Mortgage Servicing Rights (“MSRs”) driven by a reduction in market rates that impacted interest earned on escrowed accounts and net portfolio runoff. |

Refer to Table B for further details.

6

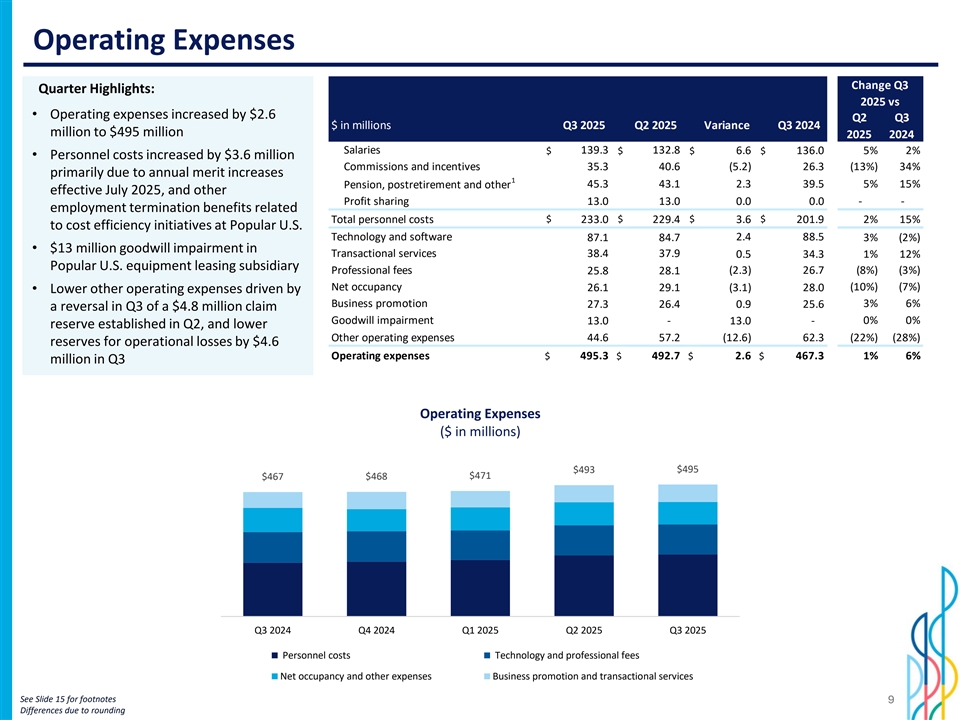

Operating expenses

Operating expenses for the third quarter of 2025 totaled $495.3 million, an increase of $2.5 million when compared to the second quarter of 2025. The variance in operating expenses was driven primarily by:

| • | a non-cash goodwill impairment of $13.0 million in our U.S. based equipment leasing subsidiary due to lower projected earnings for the forecasted period, driven by lower lending activity; |

| • | higher personnel costs by $3.6 million mainly as a result of higher salary expense by $6.6 million due in part to annual salary and merit increases effective in the third quarter of 2025, and the impact of an additional day in the quarter, and higher other personnel costs by $2.0 million, driven by employee termination benefits resulting from ongoing efforts to improve our profitability, including the decision to exit the U.S. Residential Mortgage origination business and close four underperforming branches in the New York metro area at Popular U.S.; partially offset by lower incentive expenses by $6.5 million related to restricted stock grants and performance shares awarded in the second quarter of 2025; |

| • | higher technology and software expenses by $2.4 million, including software cost amortization, related to investments in the Corporation’s cloud infrastructure, among other continuing investments in technology and transformation initiatives, partially offset by a decrease in network management services expenses; and |

| • | higher FDIC deposit insurance expense by $1.5 million, mainly driven by Popular U.S., due to changes in the assessment impacted by its wholesale funding composition and an increase in construction loans; |

partially offset by:

| • | lower other operating expenses by $13.5 million, driven by a reversal in the third quarter of a $4.8 million claim reserve established during the second quarter of 2025 and the release of several sundry loss reserves by $4.6 million mainly related to the mortgage servicing business; |

| • | lower net occupancy expenses by $3.1 million, driven by a favorable reassessment of the real property tax estimate for certain properties in Puerto Rico by $3.0 million; and |

| • | lower professional fees by $2.3 million, mainly due to lower costs associated with regulatory compliance activities. |

Full-time equivalent employees were 9,263 as of September 30, 2025, compared to 9,303 as of June 30, 2025.

For a breakdown of operating expenses by category refer to Table B.

Income taxes

For the third quarter of 2025, the Corporation recorded an income tax expense of $36.0 million, compared to an income tax expense of $47.9 million for the previous quarter. The lower income tax expense of $11.9 million is mainly driven by lower income before tax and higher income that is exempt or subject to a preferential tax rate.

The effective tax rate (“ETR”) for the third quarter of 2025 was 14.5%, compared to 18.5% for the previous quarter. The ETR of the Corporation is impacted by the composition source of its taxable income and tax credit activities.

Upon an amendment to the Puerto Rico internal revenue code during the third quarter of 2025, the Corporation elected to treat certain single members LLCs as disregarded entities, as allowed by this amendment, on its 2024 corporate income tax return filed subsequent to the quarter end in October. It is expected that this election will lower our income tax expense by approximately $7.7 million during the fourth quarter of 2025, essentially reversing the year’s income tax expense related to this matter. We expect the ETR for the fourth quarter of 2025 to be within a range of 14% - 16% and within a range from 16% - 18% for the year 2025.

7

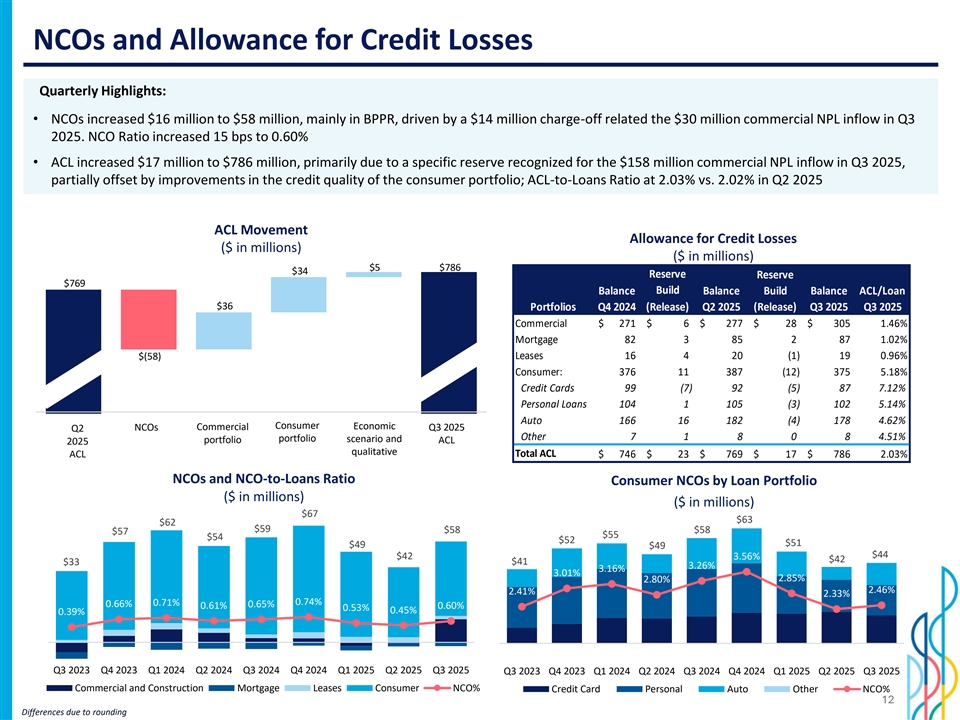

Credit Quality

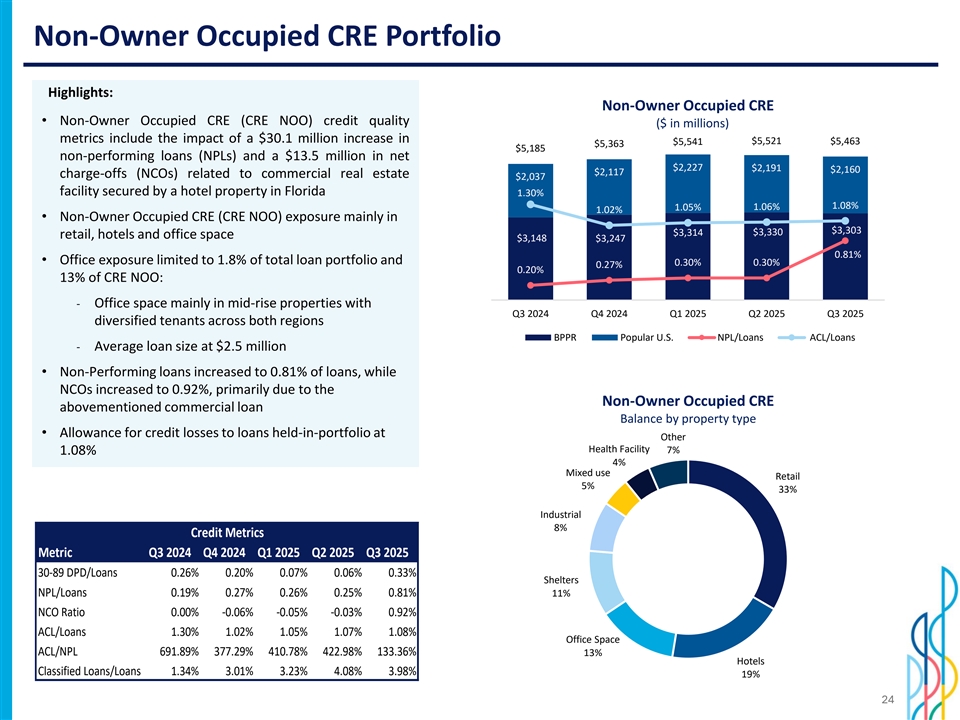

During the third quarter of 2025, the Corporation’s credit quality metrics were affected by two significant unrelated commercial exposures, resulting in a $188.4 million increase in NPLs and $13.5 million in NCOs tied to these borrowers. These impacts stemmed from issues specific to the individual borrowers and are not indicative of a broader decline in portfolio credit quality.

The first loan classified as NPL is a $158.3 million commercial and industrial facility issued to a telecommunications company in Puerto Rico experiencing reduced revenue due to operational challenges following a business acquisition and client attrition. The second loan classified as NPL is a $30.1 million commercial real estate facility, following a $13.5 million charge-off during the quarter, and is secured by a hotel property in Florida.

Excluding these cases, credit quality metrics were stable. The Corporation continues to closely monitor the economic landscape and borrower performance, as economic uncertainty remains a key consideration. Management believes that the improvements in risk management practices over recent years and the overall credit risk profile of the loan portfolio position the Corporation to continue to operate successfully in the current environment.

The following presents credit quality results for the third quarter of 2025:

Non-Performing Loans and Net Charge Offs

Total NPLs increased by $190.6 million to $502.2 million compared to the previous quarter. Excluding consumer loans, inflows of NPLs held-in-portfolio increased by $205.4 million in the third quarter of 2025. The ratio of NPLs to total loans held in the portfolio was 1.30% for the third quarter of 2025, compared to 0.82% for the previous quarter. NPLs variances per reporting segment include:

| • | In the BPPR segment, NPLs increased by $195.7 million, primarily due to the classification of two significant commercial exposures with book values of $158.3 million and $30.1 million as NPLs. These classifications are attributable to borrower specific circumstances and management believes they are not a reflection of the broader credit quality within the portfolio. Excluding consumer loans, inflows to NPLs in the BPPR segment increased by $209.5 million compared to the previous quarter, largely driven by the previously mentioned commercial exposures. |

| • | In the PB segment, NPLs decreased by $5.1 million driven by lower commercial NPLs by $4.9 million. Inflows to NPLs, excluding consumer loans, decreased by $4.1 million quarter-over-quarter, mainly related to commercial loans. |

Total NCOs of $57.8 million increased by $15.6 million when compared to the second quarter of 2025. The Corporation’s ratio of annualized NCOs to average loans held-in-portfolio for the third quarter was 0.60%, compared to 0.45% in the second quarter of 2025.

NCOs variances per reporting segment include:

| • | In the BPPR segment, NCOs increased by $16.4 million, mostly due to a $13.5 million charge-off related to the $30.1 million commercial NPL inflow referenced above. Consumer NCOs increased by $3.7 million, mostly due to higher auto loans NCOs by $5.5 million, while the credit cards NCOs decreased by $2.0 million. |

| • | In the PB segment, NCOs decreased by $0.8 million, mostly due to lower consumer NCOs. |

Including other real estate owned (“OREO”) assets of $43.0 million, non-performing assets (“NPAs”) for the Corporation amounted to $545.2 million, an increase of $187.4 million during the period, driven by the increase in NPLs, as previously discussed, partially offset by a net reduction of $3.2 million in OREO assets, mainly due to the sale of residential properties at the BPPR segment, at a net gain.

8

Allowance for Credit Losses and Provision for Credit Losses

The ACL as of September 30, 2025 amounted to $786.2 million, an increase of $16.7 million when compared to the second quarter of 2025. The increase in ACL was primarily due to a specific reserve recognized for the $158.3 million commercial NPL inflow, partially offset by improvements in the credit quality of the consumer portfolio, as further described below.

In the BPPR segment, the ACL increased by $16.1 million when compared to the previous quarter, mostly due to a $25.6 million increase in the reserves for commercial loans driven by the aforementioned NPL inflow, higher loan balances, and changes in macroeconomic scenarios. The ACL for mortgage loans increased by $2.6 million mostly due to changes in the macroeconomic scenarios. These increases were partially offset by a $11.6 million reduction in the reserves for consumer loans, mainly in the auto loans and credit card portfolios, reflecting improvements in credit quality. In the Popular U.S. segment, the ACL remained stable, increasing by $0.6 million from the previous quarter.

The Corporation’s ratio of the ACL to loans held-in-portfolio was 2.03% in the third quarter of 2025, compared to 2.02% in the previous quarter. The ratio of the ACL to NPLs held-in-portfolio decreased to 156.6%, from 246.9% in the previous quarter, mainly due to the impact of the two commercial exposures previously mentioned.

The provision for loan losses for the loan and lease portfolios for the third quarter of 2025 was $74.5 million, an increase of $25.0 million when compared to $49.5 million in the previous quarter. The provision for loan losses for the BPPR segment amounted to $72.6 million, compared to $43.2 million in the previous quarter. This increase was mainly driven by higher provision expenses for commercial loans, due to the impact of the above-mentioned large commercial exposures entering NPL status, partially offset by a lower provision for the consumer loan portfolio. The provision for loan losses for the PB segment amounted to $1.9 million, compared to $6.4 million in the prior quarter. The reduction in provision expense occurred mainly within the commercial loan portfolio.

The provision for credit losses for the third quarter of $75.1 million includes the provision for loan and lease losses, along with the $0.8 million reserve related to unfunded loan commitments and the $0.2 million reserve release for the Corporation’s investment portfolio.

Refer to Table L for breakdown of non-performing assets and related ratios and to Table N for allowance for credit losses, net charge-offs and related ratios.

9

Non-Performing Assets

| (Unaudited) |

||||||||||||

| (In thousands) |

30-Sep-25 | 30-Jun-25 | 30-Sep-24 | |||||||||

| Non-performing loans held-in-portfolio |

$ | 502,202 | $ | 311,625 | $ | 361,398 | ||||||

| Other real estate owned |

42,950 | 46,126 | 63,028 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total non-performing assets |

$ | 545,152 | $ | 357,751 | $ | 424,426 | ||||||

|

|

|

|

|

|

|

|||||||

| Net charge-offs for the quarter |

$ | 57,788 | $ | 42,202 | $ | 58,529 | ||||||

|

|

|

|

|

|

|

|||||||

| Ratios: |

||||||||||||

| Loans held-in-portfolio |

$ | 38,687,158 | $ | 38,185,178 | $ | 36,194,967 | ||||||

| Non-performing loans held-in-portfolio to loans held-in-portfolio |

1.30 | % | 0.82 | % | 1.00 | % | ||||||

| Allowance for credit losses to loans held-in-portfolio |

2.03 | 2.02 | 2.06 | |||||||||

| Allowance for credit losses to non-performing loans, excluding loans held-for-sale |

156.55 | 246.93 | 205.96 | |||||||||

Refer to Table L for additional information.

Provision for Credit Losses (Benefit)- Loan Portfolios

| (Unaudited) |

Quarters ended | Nine months ended | ||||||||||||||||||

| (In thousands) |

30-Sep-25 | 30-Jun-25 | 30-Sep-24 | 30-Sep-25 | 30-Sep-24 | |||||||||||||||

| Provision for credit losses (benefit) - loan portfolios: |

||||||||||||||||||||

| BPPR |

$ | 72,639 | $ | 43,150 | $ | 77,147 | $ | 168,479 | $ | 186,740 | ||||||||||

| Popular U.S. |

1,878 | 6,389 | (4,378 | ) | 20,795 | 2,572 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total provision for credit losses (benefit) - loan portfolios |

$ | 74,517 | $ | 49,539 | $ | 72,769 | $ | 189,274 | $ | 189,312 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Credit Quality by Segment

| (Unaudited) | ||||||||||||

| (Dollars in thousands) |

Quarters ended | |||||||||||

| BPPR |

30-Sep-25 | 30-Jun-25 | 30-Sep-24 | |||||||||

| Provision for credit losses - loan portfolios |

$ | 72,639 | $ | 43,150 | $ | 77,147 | ||||||

| Net charge-offs |

56,539 | 40,164 | 54,581 | |||||||||

| Total non-performing loans held-in-portfolio |

453,369 | 257,648 | 288,815 | |||||||||

| Annualized net charge-offs to average loans held-in-portfolio |

0.84 | % | 0.61 | % | 0.86 | % | ||||||

| Allowance / loans held-in-portfolio |

2.56 | % | 2.53 | % | 2.59 | % | ||||||

| Allowance / non-performing loans held-in-portfolio |

153.38 | % | 263.63 | % | 230.66 | % | ||||||

| Quarters ended | ||||||||||||

| Popular U.S. |

30-Sep-25 | 30-Jun-25 | 30-Sep-24 | |||||||||

| Provision for credit losses (benefit) - loan portfolios |

$ | 1,878 | $ | 6,389 | $ | (4,378 | ) | |||||

| Net charge-offs |

1,249 | 2,038 | 3,948 | |||||||||

| Total non-performing loans held-in-portfolio |

48,833 | 53,977 | 72,583 | |||||||||

| Annualized net charge-offs to average loans held-in-portfolio |

0.04 | % | 0.07 | % | 0.15 | % | ||||||

| Allowance / loans held-in-portfolio |

0.79 | % | 0.79 | % | 0.75 | % | ||||||

| Allowance / non-performing loans held-in-portfolio |

186.07 | % | 167.17 | % | 107.66 | % | ||||||

10

Financial Condition Highlights

| (Unaudited) |

||||||||||||

| (In thousands) |

30-Sep-25 | 30-Jun-25 | 30-Sep-24 | |||||||||

| Cash and money market investments |

$ | 5,131,470 | $ | 6,741,417 | $ | 6,958,382 | ||||||

| Investment securities |

28,371,673 | 28,283,970 | 25,280,451 | |||||||||

| Loans |

38,687,158 | 38,185,178 | 36,194,967 | |||||||||

| Total assets |

75,065,798 | 76,065,090 | 71,323,074 | |||||||||

| Deposits |

66,513,404 | 67,217,491 | 63,668,501 | |||||||||

| Borrowings |

1,246,807 | 1,414,494 | 973,736 | |||||||||

| Total liabilities |

68,950,126 | 70,111,072 | 65,532,560 | |||||||||

| Stockholders’ equity |

6,115,672 | 5,954,018 | 5,790,514 | |||||||||

11

Total assets amounted to $75.1 billion at September 30, 2025, a decrease of $1.0 billion from the second quarter of 2025, driven by:

| • | a decrease in money market investments of $1.6 billion, mainly driven by lower deposits, loan origination activity and the purchase of investments in U.S. Treasury securities; and |

| • | a decrease in securities held-to-maturity (“HTM”) of $108.6 million, driven by maturities and principal paydowns, partially offset by the amortization of $47.2 million of the discount related to U.S. Treasury securities previously reclassified from available-for-sale (“AFS”) to HTM; |

partially offset by:

| • | an increase in loans held-in-portfolio by $502.0 million, driven by an increase of $356.8 million in the BPPR segment across most portfolios, particularly commercial, and mortgage loans, coupled with an increase of $145.2 million in the PB segment, mainly due to commercial and construction loans; and |

| • | an increase in AFS securities of $196.2 million, driven by an increase in investments in U.S. Treasury securities and a decrease in the unrealized losses of $105.9 million, partially offset by maturities and principal paydowns, mainly in mortgage-backed securities. |

Total liabilities decreased by $1.2 billion from the second quarter of 2025, driven by:

| • | a decrease of $704.1 million in deposits, primarily driven by a decrease in P.R. public deposits of approximately $841.9 million, mainly due to annual contributions to the government’s pension reserve and debt service payments, and lower demand deposits by $240.6 million, mainly commercial deposits, partially offset by an increase in retail deposits of $185.4 million, primarily at BPPR, and an increase in high-cost deposits of $193.0 million, mainly at PB; P.R. public deposits totaled $20.1 billion and represented 30% of the Corporation’s total deposit portfolio at September 30, 2025; |

| • | a decrease in other liabilities of $289.2 million, mainly due to lower unsettled U.S. Treasury securities purchases; and |

| • | a decrease in other short-term borrowings of $150.0 million due to lower FHLB advances in PB. |

Stockholders’ equity increased by $161.7 million when compared to the second quarter of 2025 mainly due to the quarter’s net income of $211.3 million, a decrease in net unrealized losses in the portfolio of AFS securities of $94.7 million and the amortization of unrealized losses from securities previously reclassified to HTM of $37.8 million, net of tax, partially offset by an increase in Treasury Stock of $119.1 million, mainly due to common stock repurchases during the quarter, common and preferred dividends declared during the quarter of $50.7 million, and an unfavorable variance in foreign currency translation adjustments of $14.5 million from investments accounted for under the equity method.

During the quarter and nine months ended September 30, 2025, Popular repurchased 1,000,862 shares of common stock for $119.4 million at an average price of $119.33, per share, and 3,407,821 shares of common stock for $353.7 million at an average price of $103.78, per share, respectively, as part of the 2024 and 2025 common stock repurchase programs previously announced. As of September 30, 2025, $429.0 million remained available for stock repurchase under the active repurchase authorization.

The Corporation is in the process of completing its annual goodwill impairment test, using July 31, 2025, as the evaluation date. During the third quarter of 2025, an impairment charge of $13.0 million related to our U.S. based equipment leasing subsidiary was recognized. The Corporation expects to finalize its goodwill evaluation prior to the filing of its Form 10-Q for the quarter ended September 30, 2025, with the Securities and Exchange Commission. Any further impairment of goodwill would result in a non-cash expense, net of tax impact. A charge to earnings related to goodwill impairment would not materially impact regulatory capital and tangible capital calculations.

12

Common Equity Tier 1 ratio (“CET1”), common equity per share and tangible book value per share were 15.79%, $91.00 and $79.12, respectively, at September 30, 2025, compared to 15.91%, $87.31 and $75.41, respectively, at June 30, 2025.

Refer to Table A for capital ratios.

Cautionary Note Regarding Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995, including without limitation those regarding Popular’s business, financial condition, results of operations, plans, objectives and future performance. These statements are not guarantees of future performance, are based on management’s current expectations and, by their nature, involve risks, uncertainties, estimates and assumptions. Potential factors, some of which are beyond the Corporation’s control, could cause actual results to differ materially from those expressed in, or implied by, such forward-looking statements. Risks and uncertainties include, without limitation, the effect of competitive and economic factors, and our reaction to those factors, the adequacy of the allowance for loan losses, delinquency trends, market risk and the impact of interest rate changes (including on our cost of deposits), our ability to attract deposits and grow our loan portfolio, capital market conditions, capital adequacy and liquidity, the effect of legal and regulatory proceedings, new regulatory requirements or accounting standards on the Corporation’s financial condition and results of operations, the occurrence of unforeseen or catastrophic events, such as extreme weather events, pandemics, man-made disasters or acts of violence or war, as well as actions taken by governmental authorities in response thereto, and the direct and indirect impact of such events on Popular, our customers, service providers and third parties. Other potential factors include Popular’s ability to successfully execute its transformation initiative, including, but not limited to, achieving projected earnings, efficiencies and return on tangible common equity and accurately anticipating costs and expenses associated therewith, imposition of additional or special FDIC assessments, or increases thereto, changes to regulatory capital, liquidity and resolution-related requirements applicable to financial institutions in response to recent developments affecting the banking sector, the impact of bank failures or adverse developments at other banks and related negative media coverage of the banking industry in general on investor and depositor sentiment regarding the stability and liquidity of banks, the impact of the current or any future U.S. government shutdown and changes in and uncertainty regarding federal funding, tax and trade policies, and rulemaking, supervision, examination and enforcement priorities of the federal administration. All statements contained herein that are not clearly historical in nature, are forward-looking, and the words “anticipate,” “believe,” “continues,” “expect,” “estimate,” “intend,” “project” and similar expressions, and future or conditional verbs such as “will,” “would,” “should,” “could,” “might,” “can,” “may” or similar expressions, are generally intended to identify forward-looking statements.

More information on the risks and important factors that could affect the Corporation’s future results and financial condition is included in our Form 10-K for the year ended December 31, 2024, our Form 10-Q for the quarters ended March 31, 2025 and June 30, 2025, and our Form 10-Q for the quarter ended September 30, 2025 to be filed with the Securities and Exchange Commission. Our filings are available on the Corporation’s website (www.popular.com) and on the Securities and Exchange Commission website (www.sec.gov). The Corporation assumes no obligation to update or revise any forward-looking statements or information which speak as of their respective dates.

About Popular, Inc.

Popular, Inc. (NASDAQ: BPOP) is the leading financial institution in Puerto Rico, by both assets and deposits, and ranks among the top 50 U.S. bank holding companies by assets. Founded in 1893, Banco Popular de Puerto Rico, Popular’s principal subsidiary, provides retail, mortgage and commercial banking services in Puerto Rico and the U.S. and British Virgin Islands, as well as auto and equipment leasing and financing in Puerto Rico. Popular also offers broker-dealer and insurance services in Puerto Rico through specialized subsidiaries. In the mainland United States, Popular provides retail, mortgage and commercial banking services through its New York-chartered banking subsidiary, Popular Bank, which has branches located in New York, New Jersey and Florida.

13

Conference Call

Popular will hold a conference call to discuss its financial results today, Thursday, October 23, 2025 at 11:00 a.m. Eastern Time. The call will be broadcast live over the Internet and can be accessed through the Investor Relations section of the Corporation’s website: www.popular.com.

Listeners are recommended to go to the website at least 15 minutes prior to the call to download and install any necessary audio software. The call may also be accessed through a dial-in telephone number 1-833-470-1428 (Toll Free) or 1-646-844-6383 (Local). The dial-in access code is 828640.

A replay of the webcast will be archived in Popular’s website. A telephone replay will be available one hour after the end of the conference call through Saturday, November 22, 2025, 11:59 p.m. Eastern Time. The replay dial in is: 1-866-813-9403 or 1-929-458-6194. The replay passcode is 785813.

An electronic version of this press release can be found at the Corporation’s website: www.popular.com.

14

Popular, Inc.

Financial Supplement to Third Quarter 2025 Earnings Release

Table A - Selected Ratios and Other Information

Table B - Consolidated Statement of Operations

Table C - Consolidated Statement of Financial Condition

Table D - Analysis of Levels and Yields on a Taxable Equivalent Basis (Non-GAAP) - QUARTER

Table E - Analysis of Levels and Yields on a Taxable Equivalent Basis (Non-GAAP) - QUARTER

Table F - Analysis of Levels and Yields on a Taxable Equivalent Basis (Non-GAAP) - YEAR-TO-DATE

Table G - Mortgage Banking Activities and Other Service Fees

Table H - Consolidated Loans and Deposits

Table I - Loan Delinquency - BPPR Operations

Table J - Loan Delinquency - Popular U.S. Operations

Table K - Loan Delinquency - Consolidated

Table L - Non-Performing Assets

Table M - Activity in Non-Performing Loans

Table N - Allowance for Credit Losses, Net Charge-offs and Related Ratios

Table O - Allowance for Credit Losses “ACL” - Loan Portfolios - BPPR Operations

Table P - Allowance for Credit Losses “ACL” - Loan Portfolios - Popular U.S. Operations

Table Q - Allowance for Credit Losses “ACL” - Loan Portfolios - Consolidated

Table R - Reconciliation to GAAP Financial Measures

15

POPULAR, INC.

Financial Supplement to Third Quarter 2025 Earnings Release

Table A - Selected Ratios and Other Information

(Unaudited)

| Quarters ended | Nine months ended | |||||||||||||||||||

| 30-Sep-25 | 30-Jun-25 | 30-Sep-24 | 30-Sep-25 | 30-Sep-24 | ||||||||||||||||

| Basic EPS |

$ | 3.15 | $ | 3.09 | $ | 2.16 | $ | 8.78 | $ | 6.06 | ||||||||||

| Diluted EPS |

$ | 3.14 | $ | 3.09 | $ | 2.16 | $ | 8.78 | $ | 6.05 | ||||||||||

| Average common shares outstanding |

67,058,260 | 68,050,361 | 71,807,136 | 68,121,447 | 71,882,273 | |||||||||||||||

| Average common shares outstanding - assuming dilution |

67,095,421 | 68,079,649 | 71,828,402 | 68,143,888 | 71,912,153 | |||||||||||||||

| Common shares outstanding at end of period |

66,959,866 | 67,937,468 | 71,787,349 | 66,959,866 | 71,787,349 | |||||||||||||||

| Market value per common share |

$ | 129.10 | $ | 110.21 | $ | 100.27 | $ | 129.10 | $ | 100.27 | ||||||||||

| Market capitalization - (In millions) |

$ | 8,645 | $ | 7,487 | $ | 7,198 | $ | 8,645 | $ | 7,198 | ||||||||||

| Return on average assets |

1.09 | % | 1.11 | % | 0.84 | % | 1.06 | % | 0.79 | % | ||||||||||

| Return on average common equity |

11.60 | % | 11.77 | % | 8.82 | % | 11.15 | % | 8.43 | % | ||||||||||

| Net interest margin (non-taxable equivalent basis) |

3.51 | % | 3.49 | % | 3.24 | % | 3.46 | % | 3.20 | % | ||||||||||

| Net interest margin (taxable equivalent basis) -non-GAAP |

3.90 | % | 3.85 | % | 3.47 | % | 3.83 | % | 3.44 | % | ||||||||||

| Common equity per share |

$ | 91.00 | $ | 87.31 | $ | 80.35 | $ | 91.00 | $ | 80.35 | ||||||||||

| Tangible common book value per common share (non-GAAP) [1] |

$ | 79.12 | $ | 75.41 | $ | 69.04 | $ | 79.12 | $ | 69.04 | ||||||||||

| Tangible common equity to tangible assets (non-GAAP) [1] |

7.13 | % | 6.81 | % | 7.03 | % | 7.13 | % | 7.03 | % | ||||||||||

| Return on average tangible common equity [1] |

13.06 | % | 13.26 | % | 9.98 | % | 12.57 | % | 9.56 | % | ||||||||||

| Tier 1 capital |

15.84 | % | 15.96 | % | 16.48 | % | 15.84 | % | 16.48 | % | ||||||||||

| Total capital |

17.58 | % | 17.70 | % | 18.24 | % | 17.58 | % | 18.24 | % | ||||||||||

| Tier 1 leverage |

8.48 | % | 8.51 | % | 8.67 | % | 8.48 | % | 8.67 | % | ||||||||||

| Common Equity Tier 1 capital |

15.79 | % | 15.91 | % | 16.42 | % | 15.79 | % | 16.42 | % | ||||||||||

| [1] | Refer to Table R for reconciliation to GAAP financial measures. |

16

POPULAR, INC.

Financial Supplement to Third Quarter 2025 Earnings Release

Table B - Consolidated Statement of Operations

(Unaudited)

| Quarters ended | Variance | Quarter ended | Variance | Nine months ended | ||||||||||||||||||||||||

| Q3 2025 | Q3 2025 | |||||||||||||||||||||||||||

| (In thousands, except per share information) |

30-Sep-25 | 30-Jun-25 | vs. Q2 2025 | 30-Sep-24 | vs. Q3 2024 | 30-Sep-25 | 30-Sep-24 | |||||||||||||||||||||

| Interest income: |

||||||||||||||||||||||||||||

| Loans |

$ | 702,039 | $ | 684,587 | $ | 17,452 | $ | 664,731 | $ | 37,308 | $ | 2,053,299 | $ | 1,952,200 | ||||||||||||||

| Money market investments |

66,867 | 69,532 | (2,665 | ) | 96,061 | (29,194 | ) | 206,565 | 272,893 | |||||||||||||||||||

| Investment securities |

197,743 | 189,753 | 7,990 | 176,656 | 21,087 | 567,655 | 528,403 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total interest income |

966,649 | 943,872 | 22,777 | 937,448 | 29,201 | 2,827,519 | 2,753,496 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Interest expense: |

||||||||||||||||||||||||||||

| Deposits |

303,432 | 295,058 | 8,374 | 350,985 | (47,553 | ) | 896,353 | 1,020,420 | ||||||||||||||||||||

| Short-term borrowings |

4,616 | 5,300 | (684 | ) | 1,430 | 3,186 | 11,342 | 3,748 | ||||||||||||||||||||

| Long-term debt |

12,096 | 11,965 | 131 | 12,560 | (464 | ) | 36,173 | 37,799 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total interest expense |

320,144 | 312,323 | 7,821 | 364,975 | (44,831 | ) | 943,868 | 1,061,967 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net interest income |

646,505 | 631,549 | 14,956 | 572,473 | 74,032 | 1,883,651 | 1,691,529 | |||||||||||||||||||||

| Provision for credit losses |

75,125 | 48,941 | 26,184 | 71,448 | 3,677 | 188,147 | 190,840 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net interest income after provision for credit losses |

571,380 | 582,608 | (11,228 | ) | 501,025 | 70,355 | 1,695,504 | 1,500,689 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Service charges on deposit accounts |

39,077 | 38,826 | 251 | 38,315 | 762 | 116,957 | 113,283 | |||||||||||||||||||||

| Other service fees |

101,376 | 100,522 | 854 | 98,748 | 2,628 | 296,406 | 289,883 | |||||||||||||||||||||

| Mortgage banking activities |

2,771 | 4,872 | (2,101 | ) | 2,670 | 101 | 11,332 | 12,753 | ||||||||||||||||||||

| Net gain (loss), including impairment, on equity securities |

2,197 | 1,862 | 335 | (546 | ) | 2,743 | 3,645 | 876 | ||||||||||||||||||||

| Net gain on trading account debt securities |

398 | 538 | (140 | ) | 817 | (419 | ) | 1,456 | 1,455 | |||||||||||||||||||

| Adjustments to indemnity reserves on loans sold |

36 | 120 | (84 | ) | 808 | (772 | ) | 329 | 783 | |||||||||||||||||||

| Other operating income |

25,340 | 21,737 | 3,603 | 23,270 | 2,070 | 61,608 | 75,173 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total non-interest income |

171,195 | 168,477 | 2,718 | 164,082 | 7,113 | 491,733 | 494,206 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Operating expenses: |

||||||||||||||||||||||||||||

| Personnel costs |

||||||||||||||||||||||||||||

| Salaries |

139,350 | 132,752 | 6,598 | 135,983 | 3,367 | 403,052 | 394,001 | |||||||||||||||||||||

| Commissions, incentives and other bonuses |

35,309 | 40,551 | (5,242 | ) | 26,350 | 8,959 | 113,846 | 95,587 | ||||||||||||||||||||

| Profit sharing |

13,000 | 13,000 | — | — | 13,000 | 26,000 | — | |||||||||||||||||||||

| Pension, postretirement and medical insurance |

18,749 | 18,458 | 291 | 16,387 | 2,362 | 51,773 | 50,391 | |||||||||||||||||||||

| Other personnel costs, including payroll taxes |

26,580 | 24,594 | 1,986 | 23,136 | 3,444 | 80,385 | 74,678 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total personnel costs |

232,988 | 229,355 | 3,633 | 201,856 | 31,132 | 675,056 | 614,657 | |||||||||||||||||||||

| Net occupancy expenses |

26,083 | 29,140 | (3,057 | ) | 28,031 | (1,948 | ) | 82,441 | 83,764 | |||||||||||||||||||

| Equipment expenses |

5,313 | 5,789 | (476 | ) | 9,349 | (4,036 | ) | 16,404 | 28,578 | |||||||||||||||||||

| Other taxes |

17,967 | 18,632 | (665 | ) | 17,757 | 210 | 55,324 | 47,465 | ||||||||||||||||||||

| Professional fees |

25,808 | 28,108 | (2,300 | ) | 26,708 | (900 | ) | 80,741 | 93,370 | |||||||||||||||||||

| Technology and software expenses |

87,117 | 84,696 | 2,421 | 88,452 | (1,335 | ) | 255,481 | 247,666 | ||||||||||||||||||||

| Processing and transactional services |

||||||||||||||||||||||||||||

| Credit and debit cards |

14,728 | 13,044 | 1,684 | 11,761 | 2,967 | 40,698 | 37,644 | |||||||||||||||||||||

| Other processing and transactional services |

23,680 | 24,817 | (1,137 | ) | 22,559 | 1,121 | 73,352 | 69,966 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total processing and transactional services |

38,408 | 37,861 | 547 | 34,320 | 4,088 | 114,050 | 107,610 | |||||||||||||||||||||

| Communications |

4,836 | 5,010 | (174 | ) | 5,229 | (393 | ) | 14,750 | 14,143 | |||||||||||||||||||

| Business promotion |

||||||||||||||||||||||||||||

| Rewards and customer loyalty programs |

17,656 | 18,047 | (391 | ) | 16,533 | 1,123 | 52,068 | 46,995 | ||||||||||||||||||||

| Other business promotion |

9,648 | 8,338 | 1,310 | 9,104 | 544 | 25,296 | 25,080 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total business promotion |

27,304 | 26,385 | 919 | 25,637 | 1,667 | 77,364 | 72,075 | |||||||||||||||||||||

| Deposit insurance |

10,873 | 9,407 | 1,466 | 10,433 | 440 | 30,315 | 44,901 | |||||||||||||||||||||

| Other real estate owned (OREO) expense (income) |

(3,408 | ) | (4,124 | ) | 716 | (2,674 | ) | (734 | ) | (10,862 | ) | (13,745 | ) | |||||||||||||||

| Other operating expenses |

||||||||||||||||||||||||||||

| Operational losses |

1,634 | 6,185 | (4,551 | ) | 5,769 | (4,135 | ) | 13,957 | 21,153 | |||||||||||||||||||

| All other |

6,980 | 15,932 | (8,952 | ) | 15,750 | (8,770 | ) | 39,673 | 56,140 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total other operating expenses |

8,614 | 22,117 | (13,503 | ) | 21,519 | (12,905 | ) | 53,630 | 77,293 | |||||||||||||||||||

| Amortization of intangibles |

384 | 385 | (1 | ) | 704 | (320 | ) | 1,366 | 2,233 | |||||||||||||||||||

| Goodwill impairment |

13,000 | — | 13,000 | — | 13,000 | 13,000 | — | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total operating expenses |

495,287 | 492,761 | 2,526 | 467,321 | 27,966 | 1,459,060 | 1,420,010 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income before income tax |

247,288 | 258,324 | (11,036 | ) | 197,786 | 49,502 | 728,177 | 574,885 | ||||||||||||||||||||

| Income tax expense |

35,971 | 47,884 | (11,913 | ) | 42,463 | (6,492 | ) | 128,918 | 138,490 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income |

$ | 211,317 | $ | 210,440 | $ | 877 | $ | 155,323 | $ | 55,994 | $ | 599,259 | $ | 436,395 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income applicable to common stock |

$ | 210,964 | $ | 210,087 | $ | 877 | $ | 154,970 | $ | 55,994 | $ | 598,200 | $ | 435,336 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income per common share - basic |

$ | 3.15 | $ | 3.09 | $ | 0.06 | $ | 2.16 | $ | 0.99 | $ | 8.78 | $ | 6.06 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income per common share - diluted |

$ | 3.14 | $ | 3.09 | $ | 0.05 | $ | 2.16 | $ | 0.98 | $ | 8.78 | $ | 6.05 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Dividends Declared per Common Share |

$ | 0.75 | $ | 0.70 | $ | 0.05 | $ | 0.62 | $ | 0.13 | $ | 2.15 | $ | 1.86 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

17

Popular, Inc.

Financial Supplement to Third Quarter 2025 Earnings Release

Table C - Consolidated Statement of Financial Condition

(Unaudited)

| Variance | ||||||||||||||||

| Q3 2025 vs. | ||||||||||||||||

| (In thousands) |

30-Sep-25 | 30-Jun-25 | 30-Sep-24 | Q2 2025 | ||||||||||||

| Assets: |

||||||||||||||||

| Cash and due from banks |

$ | 377,079 | $ | 400,631 | $ | 427,594 | $ | (23,552 | ) | |||||||

| Money market investments |

4,754,391 | 6,340,786 | 6,530,788 | (1,586,395 | ) | |||||||||||

| Trading account debt securities, at fair value |

33,122 | 29,643 | 30,843 | 3,479 | ||||||||||||

| Debt securities available-for-sale, at fair value |

20,686,423 | 20,490,212 | 17,186,123 | 196,211 | ||||||||||||

| Debt securities held-to-maturity, at amortized cost |

7,433,135 | 7,541,724 | 7,865,294 | (108,589 | ) | |||||||||||

| Less: Allowance for credit losses |

5,837 | 5,999 | 5,430 | (162 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Debt securities held-to-maturity, net |

7,427,298 | 7,535,725 | 7,859,864 | (108,427 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Equity securities |

218,993 | 222,391 | 198,191 | (3,398 | ) | |||||||||||

| Loans held-for-sale, at lower of cost or fair value |

7,783 | 2,898 | 5,509 | 4,885 | ||||||||||||

| Loans held-in-portfolio |

39,111,956 | 38,611,834 | 36,599,612 | 500,122 | ||||||||||||

| Less: Unearned income |

424,798 | 426,656 | 404,645 | (1,858 | ) | |||||||||||

| Allowance for credit losses |

786,220 | 769,485 | 744,320 | 16,735 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total loans held-in-portfolio, net |

37,900,938 | 37,415,693 | 35,450,647 | 485,245 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Premises and equipment, net |

679,651 | 649,191 | 624,376 | 30,460 | ||||||||||||

| Other real estate |

42,950 | 46,126 | 63,028 | (3,176 | ) | |||||||||||

| Accrued income receivable |

297,347 | 274,867 | 257,406 | 22,480 | ||||||||||||

| Mortgage servicing rights, at fair value |

99,523 | 103,077 | 108,827 | (3,554 | ) | |||||||||||

| Other assets |

1,744,886 | 1,745,052 | 1,767,919 | (166 | ) | |||||||||||

| Goodwill |

789,954 | 802,954 | 804,428 | (13,000 | ) | |||||||||||

| Other intangible assets |

5,460 | 5,844 | 7,531 | (384 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total assets |

$ | 75,065,798 | $ | 76,065,090 | $ | 71,323,074 | $ | (999,292 | ) | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Liabilities and Stockholders’ Equity: |

||||||||||||||||

| Liabilities: |

||||||||||||||||

| Deposits: |

||||||||||||||||

| Non-interest bearing |

$ | 14,874,026 | $ | 15,114,614 | $ | 15,276,071 | $ | (240,588 | ) | |||||||

| Interest bearing |

51,639,378 | 52,102,877 | 48,392,430 | (463,499 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total deposits |

66,513,404 | 67,217,491 | 63,668,501 | (704,087 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Assets sold under agreements to repurchase |

56,853 | 56,043 | 55,360 | 810 | ||||||||||||

| Other short-term borrowings |

400,000 | 550,000 | — | (150,000 | ) | |||||||||||

| Notes payable |

789,954 | 808,451 | 918,376 | (18,497 | ) | |||||||||||

| Other liabilities |

1,189,915 | 1,479,087 | 890,323 | (289,172 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total liabilities |

68,950,126 | 70,111,072 | 65,532,560 | (1,160,946 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Stockholders’ equity: |

||||||||||||||||

| Preferred stock |

22,143 | 22,143 | 22,143 | — | ||||||||||||

| Common stock |

1,049 | 1,049 | 1,048 | — | ||||||||||||

| Surplus |

4,920,767 | 4,919,950 | 4,853,869 | 817 | ||||||||||||

| Retained earnings |

5,022,546 | 4,861,958 | 4,495,878 | 160,588 | ||||||||||||

| Treasury stock |

(2,574,573 | ) | (2,455,425 | ) | (2,069,430 | ) | (119,148 | ) | ||||||||

| Accumulated other comprehensive loss, net of tax |

(1,276,260 | ) | (1,395,657 | ) | (1,512,994 | ) | 119,397 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total stockholders’ equity |

6,115,672 | 5,954,018 | 5,790,514 | 161,654 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total liabilities and stockholders’ equity |

$ | 75,065,798 | $ | 76,065,090 | $ | 71,323,074 | $ | (999,292 | ) | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

18

Popular, Inc.

Financial Supplement to Third Quarter 2025 Earnings Release

Table D - Analysis of Levels and Yields on a Taxable Equivalent Basis (Non-GAAP)

For the quarters ended September 30, 2025 and June 30, 2025

(Unaudited)

| Variance | ||||||||||||||||||||||||||||||||||||||||||||

| Average Volume | Average Yields / Costs | Interest | Attributable to | |||||||||||||||||||||||||||||||||||||||||

| 30-Sep-25 |

30-Jun-25 | Variance | 30-Sep-25 | 30-Jun-25 | Variance | 30-Sep-25 | 30-Jun-25 | Variance | Rate | Volume | ||||||||||||||||||||||||||||||||||

| (In millions) | (In thousands) | |||||||||||||||||||||||||||||||||||||||||||

| $ | 5,990 | $ | 6,251 | $ | (261 | ) | 4.43 | % | 4.46 | % | (0.03 | )% | Money market investments |

$ | 66,867 | $ | 69,532 | $ | (2,665 | ) | $ | 246 | $ | (2,911 | ) | |||||||||||||||||||

| 28,957 | 28,809 | 148 | 3.42 | 3.29 | 0.13 | Investment securities [1] |

249,071 | 236,372 | 12,699 | 10,895 | 1,804 | |||||||||||||||||||||||||||||||||

| 28 | 27 | 1 | 5.43 | 5.99 | (0.56 | ) | Trading securities |

391 | 407 | (16 | ) | (35 | ) | 19 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| 34,975 | 35,087 | (112 | ) | 3.59 | 3.50 | 0.09 | Total money market, investment and trading securities |

316,329 | 306,311 | 10,018 | 11,106 | (1,088 | ) | |||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Loans: |

||||||||||||||||||||||||||||||||||||||||||||

| 19,229 | 18,676 | 553 | 6.72 | 6.73 | (0.01 | ) | Commercial |

325,869 | 313,493 | 12,376 | 3,031 | 9,345 | ||||||||||||||||||||||||||||||||

| 1,549 | 1,459 | 90 | 8.24 | 8.19 | 0.05 | Construction |

32,184 | 29,806 | 2,378 | 526 | 1,852 | |||||||||||||||||||||||||||||||||

| 1,981 | 1,963 | 18 | 7.26 | 7.18 | 0.08 | Leasing |

35,957 | 35,249 | 708 | 378 | 330 | |||||||||||||||||||||||||||||||||

| 8,484 | 8,339 | 145 | 5.96 | 5.89 | 0.07 | Mortgage |

126,352 | 122,873 | 3,479 | 1,324 | 2,155 | |||||||||||||||||||||||||||||||||

| 3,257 | 3,211 | 46 | 13.80 | 14.00 | (0.20 | ) | Consumer |

113,280 | 112,083 | 1,197 | (476 | ) | 1,673 | |||||||||||||||||||||||||||||||

| 3,945 | 3,937 | 8 | 9.15 | 9.14 | 0.01 | Auto |

91,006 | 89,706 | 1,300 | 1,138 | 162 | |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| 38,445 | 37,585 | 860 | 7.49 | 7.50 | (0.01 | ) | Total loans |

724,648 | 703,210 | 21,438 | 5,921 | 15,517 | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| $ | 73,420 | $ | 72,672 | $ | 748 | 5.63 | % | 5.57 | % | 0.06 | % | Total earning assets |

$ | 1,040,977 | $ | 1,009,521 | $ | 31,456 | $ | 17,027 | $ | 14,429 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Interest bearing deposits: |

||||||||||||||||||||||||||||||||||||||||||||

| $ | 8,184 | $ | 8,062 | $ | 122 | 1.77 | % | 1.71 | % | 0.06 | % | NOW and money market |

$ | 36,421 | $ | 34,288 | $ | 2,133 | $ | 967 | $ | 1,166 | ||||||||||||||||||||||

| 14,529 | 14,605 | (76 | ) | 0.81 | 0.83 | (0.02 | ) | Savings |

29,772 | 30,378 | (606 | ) | (351 | ) | (255 | ) | ||||||||||||||||||||||||||||

| 8,825 | 8,532 | 293 | 3.16 | 3.15 | 0.01 | Time deposits |

70,196 | 67,032 | 3,164 | 728 | 2,436 | |||||||||||||||||||||||||||||||||

| 20,766 | 20,333 | 433 | 3.19 | 3.22 | (0.03 | ) | P.R. public deposits |

167,043 | 163,360 | 3,683 | 139 | 3,544 | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| 52,304 | 51,532 | 772 | 2.30 | 2.29 | 0.01 | Total interest bearing deposits |

303,432 | 295,058 | 8,374 | 1,483 | 6,891 | |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| 14,846 | 14,825 | 21 | Non-interest bearing demand deposits |

|||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

| 67,150 | 66,357 | 793 | 1.79 | 1.78 | 0.01 | Total deposits |

303,432 | 295,058 | 8,374 | 1,483 | 6,891 | |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| 405 | 470 | (65 | ) | 4.52 | 4.52 | — | Short-term borrowings |

4,616 | 5,300 | (684 | ) | 62 | (746 | ) | ||||||||||||||||||||||||||||||

| 812 | 832 | (20 | ) | 5.98 | 5.79 | 0.19 | Other medium and long-term debt |

12,096 | 11,965 | 131 | 198 | (67 | ) | |||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| 53,521 | 52,834 | 687 | 2.37 | 2.36 | 0.01 | Total interest bearing liabilities (excluding demand deposits) |

320,144 | 312,323 | 7,821 | 1,743 | 6,078 | |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| 5,053 | 5,013 | 40 | Other sources of funds |

|||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

| $ | 73,420 | $ | 72,672 | $ | 748 | 1.73 | % | 1.72 | % | 0.01 | % | Total source of funds |

320,144 | 312,323 | 7,821 | 1,743 | 6,078 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

| 3.90 | % | 3.85 | % | 0.05 | % | Net interest margin/income on a taxable equivalent basis (Non-GAAP) |

720,833 | 697,198 | 23,635 | $ | 15,284 | $ | 8,351 | |||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

| 3.26 | % | 3.21 | % | 0.05 | % | Net interest spread |

||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

| Taxable equivalent adjustment |

74,328 | 65,649 | 8,679 | |||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

| 3.51 | % | 3.49 | % | 0.02 | % | Net interest margin/income non-taxable equivalent basis (GAAP) |

$ | 646,505 | $ | 631,549 | $ | 14,956 | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

Note: The changes that are not due solely to volume or rate are allocated to volume and rate based on the proportion of the change in each category.

| [1] | Average balances exclude unrealized gains or losses on debt securities available-for-sale and the unrealized loss related to certain securities transferred from available-for-sale to held-to-maturity. |

19

Popular, Inc.

Financial Supplement to Third Quarter 2025 Earnings Release

Table E - Analysis of Levels and Yields on a Taxable Equivalent Basis (Non-GAAP)

For the quarters ended September 30, 2025 and September 30, 2024

(Unaudited)

| Variance | ||||||||||||||||||||||||||||||||||||||||||||

| Average Volume | Average Yields / Costs | Interest | Attributable to | |||||||||||||||||||||||||||||||||||||||||

| 30-Sep-25 |

30-Sep-24 | Variance | 30-Sep-25 | 30-Sep-24 | Variance | 30-Sep-25 | 30-Sep-24 | Variance | Rate | Volume | ||||||||||||||||||||||||||||||||||

| (In millions) | (In thousands) | |||||||||||||||||||||||||||||||||||||||||||

| $ | 5,990 | $ | 7,033 | $ | (1,043 | ) | 4.43 | % | 5.43 | % | (1.00 | )% | Money market investments |

$ | 66,867 | $ | 96,061 | $ | (29,194 | ) | $ | (16,107 | ) | $ | (13,087 | ) | ||||||||||||||||||

| 28,957 | 27,569 | 1,388 | 3.42 | 2.92 | 0.50 | Investment securities [1] |

249,071 | 202,317 | 46,754 | 32,970 | 13,784 | |||||||||||||||||||||||||||||||||

| 28 | 30 | (2 | ) | 5.43 | 5.87 | (0.44 | ) | Trading securities |

391 | 436 | (45 | ) | (31 | ) | (14 | ) | ||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| 34,975 | 34,632 | 343 | 3.59 | 3.43 | 0.16 | Total money market, investment and trading securities |

316,329 | 298,814 | 17,515 | 16,832 | 683 | |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Loans: |

||||||||||||||||||||||||||||||||||||||||||||

| 19,229 | 17,798 | 1,431 | 6.72 | 6.90 | (0.18 | ) | Commercial |

325,869 | 308,734 | 17,135 | (7,239 | ) | 24,374 | |||||||||||||||||||||||||||||||

| 1,549 | 1,129 | 420 | 8.24 | 8.85 | (0.61 | ) | Construction |

32,184 | 25,102 | 7,082 | (1,732 | ) | 8,814 | |||||||||||||||||||||||||||||||

| 1,981 | 1,851 | 130 | 7.26 | 6.97 | 0.29 | Leasing |

35,957 | 32,241 | 3,716 | 1,378 | 2,338 | |||||||||||||||||||||||||||||||||

| 8,484 | 7,911 | 573 | 5.96 | 5.73 | 0.23 | Mortgage |

126,352 | 113,409 | 12,943 | 4,523 | 8,420 | |||||||||||||||||||||||||||||||||

| 3,257 | 3,211 | 46 | 13.80 | 14.08 | (0.28 | ) | Consumer |

113,280 | 112,423 | 857 | (787 | ) | 1,644 | |||||||||||||||||||||||||||||||

| 3,945 | 3,879 | 66 | 9.15 | 8.94 | 0.21 | Auto |

91,006 | 87,189 | 3,817 | 2,338 | 1,479 | |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| 38,445 | 35,779 | 2,666 | 7.49 | 7.56 | (0.07 | ) | Total loans |

724,648 | 679,098 | 45,550 | (1,519 | ) | 47,069 | |||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| $ | 73,420 | $ | 70,411 | $ | 3,009 | 5.63 | % | 5.53 | % | 0.10 | % | Total earning assets |

$ | 1,040,977 | $ | 977,912 | $ | 63,065 | $ | 15,313 | $ | 47,752 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Interest bearing deposits: |

||||||||||||||||||||||||||||||||||||||||||||

| $ | 8,184 | $ | 7,387 | $ | 797 | 1.77 | % | 2.04 | % | (0.27 | )% | NOW and money market |

$ | 36,421 | $ | 37,857 | $ | (1,436 | ) | $ | (4,891 | ) | $ | 3,455 | ||||||||||||||||||||

| 14,529 | 14,318 | 211 | 0.81 | 0.92 | (0.11 | ) | Savings |

29,772 | 33,134 | (3,362 | ) | (3,981 | ) | 619 | ||||||||||||||||||||||||||||||

| 8,825 | 8,366 | 459 | 3.16 | 3.45 | (0.29 | ) | Time deposits |

70,196 | 72,503 | (2,307 | ) | (6,096 | ) | 3,789 | ||||||||||||||||||||||||||||||

| 20,766 | 19,468 | 1,298 | 3.19 | 4.24 | (1.05 | ) | P.R. public deposits |

167,043 | 207,491 | (40,448 | ) | (52,899 | ) | 12,451 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|