| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Title of each class |

Trading symbol |

Name of each exchange on which registered | ||

American Depositary Shares |

WDS |

New York Stock Exchange | ||

Ordinary Shares, no par value per share* |

New York Stock Exchange |

| Large accelerated filer ☒ | Accelerated filer ☐ |

Non-accelerated

|

Emerging growth company ☐ |

| U.S. GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ |

Other ☐ |

TABLE OF CONTENTS

| INTRODUCTION | 3 | |||||

| FORWARD-LOOKING STATEMENTS, INDUSTRY AND MARKET DATA AND CLIMATE STRATEGY AND EMISSIONS DATA | 4-5 | |||||

| USE AND RECONCILIATION OF NON-IFRS FINANCIAL MEASURES | 6 | |||||

| PART I | 7 | |||||

| ITEM 1. | 7 | |||||

| A. |

7 | |||||

| B. |

7 | |||||

| C. |

7 | |||||

| ITEM 2. | 7 | |||||

| A. |

7 | |||||

| B. |

7 | |||||

| ITEM 3. | 7 | |||||

| A. |

7 | |||||

| B. |

7 | |||||

| C. |

7 | |||||

| D. |

8 | |||||

| ITEM 4. | 16 | |||||

| A. |

16 | |||||

| B. |

17 | |||||

| C. |

30 | |||||

| D. |

30 | |||||

| ITEM 4A. | 30 | |||||

| ITEM 5. | 30 | |||||

| A. |

30 | |||||

| B. |

36 | |||||

| C. |

36 | |||||

| D. |

37 | |||||

| E. |

37 | |||||

| ITEM 6. | 37 | |||||

| A. |

37 | |||||

| B. |

37 | |||||

| C. |

37 | |||||

| D. |

37 | |||||

| E. |

37 | |||||

| F. |

Disclosure of a registrant’s action to recover erroneously awarded compensation. |

37 | ||||

| ITEM 7. | 37 | |||||

| A. |

37 | |||||

| B. |

38 | |||||

| C. |

38 | |||||

| ITEM 8. | 38 | |||||

| A. |

38 | |||||

| B. |

38 | |||||

| ITEM 9. | 38 | |||||

| A. |

38 | |||||

| B. |

38 | |||||

| C. |

38 | |||||

| D. |

38 | |||||

| E. |

38 | |||||

| F. |

39 | |||||

| ITEM 10. | 39 | |||||

| A. |

39 | |||||

| B. |

39 | |||||

| C. |

39 | |||||

| D. |

39 | |||||

1

| E. |

39 | |||||

| F. |

42 | |||||

| G. |

42 | |||||

| H. |

42 | |||||

| I. |

42 | |||||

| J. |

43 | |||||

| ITEM 11. | 43 | |||||

| ITEM 12. | 43 | |||||

| A. |

43 | |||||

| B. |

43 | |||||

| C. |

43 | |||||

| D. |

43 | |||||

| PART II | ||||||

| ITEM 13. | 43 | |||||

| ITEM 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

43 | ||||

| ITEM 15. | 43 | |||||

| ITEM 16. | 44 | |||||

| ITEM 16A. | 44 | |||||

| ITEM 16B. | 44 | |||||

| ITEM 16C. | 44 | |||||

| ITEM 16D. | 44 | |||||

| ITEM 16E. | PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

44 | ||||

| ITEM 16F. | 45 | |||||

| ITEM 16G. | 45 | |||||

| ITEM 16H. | 45 | |||||

| ITEM 16I. | DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS |

45 | ||||

| ITEM 16J. | 46 | |||||

| ITEM 16K. | 46 | |||||

| PART III | ||||||

| ITEM 17. | 47 | |||||

| ITEM 18. | 47 | |||||

| ITEM 19. | ||||||

| CONSOLIDATED FINANCIAL STATEMENTS | F-1 | |||||

2

INTRODUCTION

Unless otherwise indicated, all references herein to “we”, “our”, the “company”, the “group” or “Woodside” are references to Woodside Energy Group Ltd and its consolidated subsidiaries.

This document is our annual report on Form 20-F for the year ended 31 December 2024 (“2024 Form 20-F”). Reference is made to our 2024 Annual Report, portions of which are attached hereto as Exhibit 15.2 (the “2024 Annual Report”). Only (i) the information included in this 2024 Form 20-F, (ii) the information in the 2024 Annual Report that is incorporated by reference in this 2024 Form 20-F (excluding any information that is identified as intentionally omitted in Exhibit 15.2 hereto and any page references incorporated in the incorporated material unless specifically noted otherwise), and (iii) the other exhibits to this 2024 Form 20-F shall be deemed to be filed with the Securities and Exchange Commission (“SEC”) for any purpose, including incorporation by reference into the Registration Statement on Form F-3 filed on 29 February 2024 (File No. 333-277499), Form S-8 filed on 1 March 2024 (File No. 333-277568 ), Form S-8 filed on 1 September 2023 (File No. 333-274296), Form S-8 filed on 28 February 2023 (File No. 333-270076) and Form S-8 filed on 15 September 2022 (File No. 333-267432) and any other documents filed by us pursuant to the Securities Act of 1933, as amended, which purport to incorporate by reference the 2024 Form 20-F. The full 2024 Annual Report, inclusive of our sustainability report and other information omitted from, or otherwise not incorporated by reference into, this 2024 Form 20-F, has been furnished to the SEC on a Report on Form 6-K.

Unless otherwise indicated, references to major headings include all information under such major headings, including subheadings, unless such reference is a reference to a subheading, in which case such reference includes only the information contained under such subheading. Any other information shall not be deemed to be so incorporated by reference.

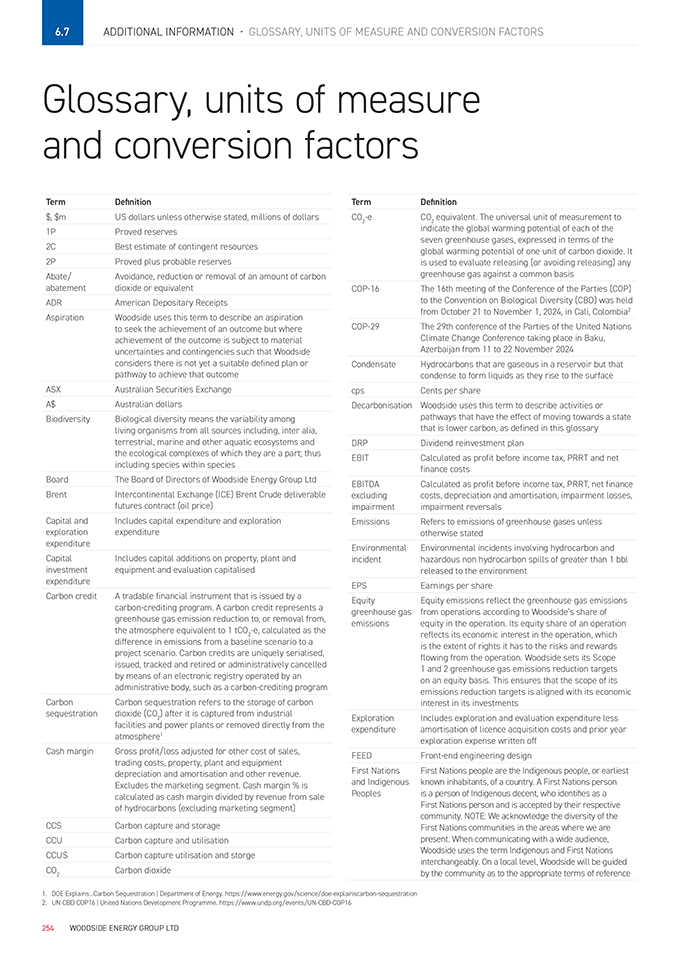

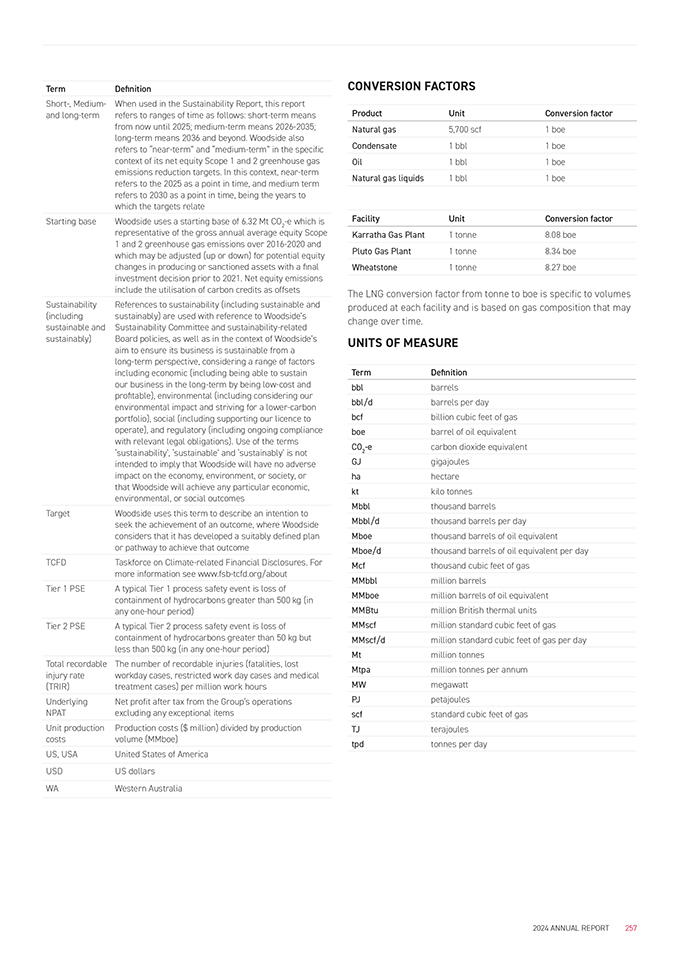

In addition to the information set out below, the information set forth under the heading “Glossary, units of measure and conversion factors” in Section 6.7 on pages 254-257 of the 2024 Annual Report is incorporated herein by reference.

The 2024 Form 20-F contains references to our website (https://www.woodside.com). Information on our website or any other website referenced in the 2024 Form 20-F is not incorporated into this document and should not be considered part of this document. All references to websites in this 2024 Form 20-F are intended to be inactive textual references for information only and any information contained in or accessible through any such website does not form a part of this 2024 Form 20-F.

The SEC maintains an Internet website that contains reports and other information regarding issuers that file electronically with the SEC. Our filings with the SEC are available to the public through the SEC’s website at http://www.sec.gov.

In this report, references to a year are to the calendar and financial year ended 31 December 2024 unless otherwise stated. All references to dollars, cents or $ in this report are references to US currency and are stated in Woodside share, unless otherwise stated.

Unless otherwise stated, all Woodside results set out in this 2024 Form 20-F include the performance of the interests acquired as part of the merger with BHP’s petroleum business from 1 June 2022.

3

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements with respect to Woodside’s business and operations, market conditions, results of operations and financial condition, including, for example, but not limited to, outcomes of transactions, statements regarding long-term demand for Woodside’s products, development, completion and execution of Woodside’s projects, expectations regarding future capital expenditures, the payment of future dividends and the amount thereof, future results of projects, operating activities and new energy products, expectations and plans for renewables production capacity and investments in, and development of, renewables projects, expectations and guidance with respect to production, capital and exploration expenditure and gas hub exposure, and expectations regarding the achievement of Woodside’s net equity Scope 1 and 2 greenhouse gas emissions reduction and new energy investment targets and other climate and sustainability goals. All statements, other than statements of historical or present facts, are forward-looking statements and generally may be identified by the use of forward-looking words such as ‘guidance’, ‘foresee’, ‘likely’, ‘potential’, ‘anticipate’, ‘believe’, ‘aim’, ‘aspire’, ‘estimate’, ‘expect’, ‘intend’, ‘may’, ‘target’, ‘plan’, ‘strategy’, ‘forecast’, ‘outlook’, ‘project’, ‘schedule’, ‘will’, ‘should’, ‘seek’ and other similar words or expressions. Similarly, statements that describe the objectives, plans, goals or expectations of Woodside are forward-looking statements. Forward-looking statements in this report are not guidance, forecasts, guarantees or predictions of future events or performance, but are in the nature of future expectations that are based on management’s current expectations and assumptions.

Those statements and any assumptions on which they are based are subject to change without notice and are subject to inherent known and unknown risks, uncertainties, contingencies and other factors, many of which are beyond the control of Woodside, its related bodies corporate and their respective officers, directors, employees, advisers or representatives.

Important factors that could cause actual results to differ materially from those in the forward-looking statements and assumptions on which they are based include, but are not limited to, fluctuations in commodity prices, actual demand for Woodside products, currency fluctuations, geotechnical factors, drilling and production results, gas commercialisation, development progress, operating results, engineering estimates, reserve and resource estimates, loss of market, industry competition, sustainability and environmental risks, climate related transition and physical risks, safety and personnel risks, changes in accounting standards, economic and financial markets conditions in various countries and regions the actions of third parties, project delay or advancement, regulatory approvals, political risks and the impact of armed conflict and political instability (such as the ongoing conflict in Ukraine) on economic activity and oil and gas supply and demand, cost estimates, legislative, fiscal and regulatory developments and the effect of future regulatory or legislative actions on Woodside or the industries in which it operates, including potential changes to tax laws, the impact of general economic conditions, inflationary conditions, prevailing exchange rates and interest rates and conditions in financial markets, and risks associated with acquisitions, mergers and joint ventures, including difficulties integrating or separating businesses, uncertainty associated with financial projections, restructuring, increased costs and adverse tax consequences, and uncertainties and liabilities associated with acquired and divested properties and businesses.

A more detailed summary of the key risks relating to Woodside and its business can be found in Item 3.D. Risk Factors. You should review and have regard to these risks when considering the information contained in this report. If any of the assumptions on which a forward-looking statement is based were to change or be found to be incorrect, this would likely cause outcomes to differ from the statements made in this report.

Investors are strongly cautioned not to place undue reliance on any forward-looking statements. Actual results or performance may vary materially from those expressed in, or implied by, any forward-looking statements. None of Woodside nor any of its related bodies corporate, nor any of their respective officers, directors, employees, advisers or representatives, nor any person named in this report or involved in the preparation of the information in this report, makes any representation, assurance, guarantee or warranty (either express or implied) as to the accuracy or likelihood of fulfilment of any forward-looking statement, or any outcomes, events or results expressed or implied in any forward-looking statement in this report. All forward-looking statements contained in this report reflect Woodside’s views held as at the date of this report and, except as required by applicable law, neither Woodside, its related bodies corporate, nor any of their respective officers, directors, employees, advisers or representatives nor any person named in this report or involved in the preparation of the information in this report intends to, undertakes to, or assumes any obligation to, provide any additional information or update or revise any of these statements after the date of this report, either to make them conform to actual results or as a result of new information, future events or results, changes in Woodside’s expectations or otherwise.

Past performance (including historical financial and operational information) is given for illustrative purposes only. It should not be relied on as, and is not necessarily, a reliable indicator of future performance, including future security prices.

INDUSTRY AND MARKET DATA

This report contains industry, market and competitive position data based on industry publications and studies conducted by third parties, as well as Woodside’s internal estimates and research. These industry publications and third-party studies generally state that the information they contain has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While Woodside believes that each of these publications and third-party studies is reliable and has been prepared by a reputable source, Woodside has not independently verified the market and industry data obtained from these third-party sources and cannot guarantee the accuracy or completeness of such data. Accordingly, undue reliance should not be placed on any of the industry, market and competitive position data contained in this report.

4

Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements contained in this report and may differ among third-party sources. These forecasts and forward-looking information are subject to uncertainty and risk due to a variety of factors, including those described in the sections captioned “Risk Factors” and “Forward-Looking Statements” elsewhere in this report. These and other factors could cause results to differ materially from those expressed in Woodside’s forecasts or estimates or those of independent third parties. While Woodside believes its internal research is reliable and its selection of industry publications and third-party studies and the description of its market and industry are appropriate, neither such research nor these descriptions have been verified by any independent source.

CLIMATE STRATEGY AND EMISSIONS DATA

All greenhouse gas emissions data in, or incorporated by reference into, this report are estimates, due to the inherent uncertainty and limitations in measuring or quantifying greenhouse gas emissions, and our methodologies for measuring or quantifying greenhouse gas emissions may evolve as best practices continue to develop and data quality and quantity continue to improve.

Woodside “greenhouse gas” or “emissions” information reported are net equity Scope 1 greenhouse gas emissions, Scope 2 greenhouse gas emissions, and/or Scope 3 greenhouse gas emissions, as the context requires.

Actual performance against Woodside’s targets (including items that are described as a target) and aspirations or goals may be affected by various risks associated with the Woodside business, the uncertainty as to how the global energy transition to a lower carbon economy will evolve, and physical risks associated with climate change, many of which are beyond Woodside’s control.

The glossary and footnotes included, or incorporated by reference, into this 2024 Form 20-F provide further clarification of “lower carbon” where applicable. Woodside uses the term “lower-carbon services” to describe technologies, such as carbon capture utilization and storage, or “CCUS”, or offsets, that may be capable of reducing the net greenhouse gas emissions of our customers.

Additionally, the developments of environmental and climate change-related issues discussed in this report or the information incorporated by reference herein are based on various frameworks and the interests of various stakeholders that are subject to evolve independently of our will. Moreover, materiality, as used in the context of climate and sustainability-related disclosures, may differ from the materiality standards applied by other reporting regimes, including as defined for SEC reporting purposes. Our disclosures on such issues, including climate-related disclosures that are identified as material for purposes of sustainability in this report, may include information that is not necessarily “material” under US securities laws for SEC reporting purposes or under applicable securities law.

Scope 3 targets are subject to commercial arrangements, commercial feasibility, regulatory and joint venture approvals, and third party activities (which may or may not proceed). Individual investment decisions are subject to Woodside’s investment targets. Such targets are not guidance. Scope 3 targets potentially include both organic and inorganic investment.

5

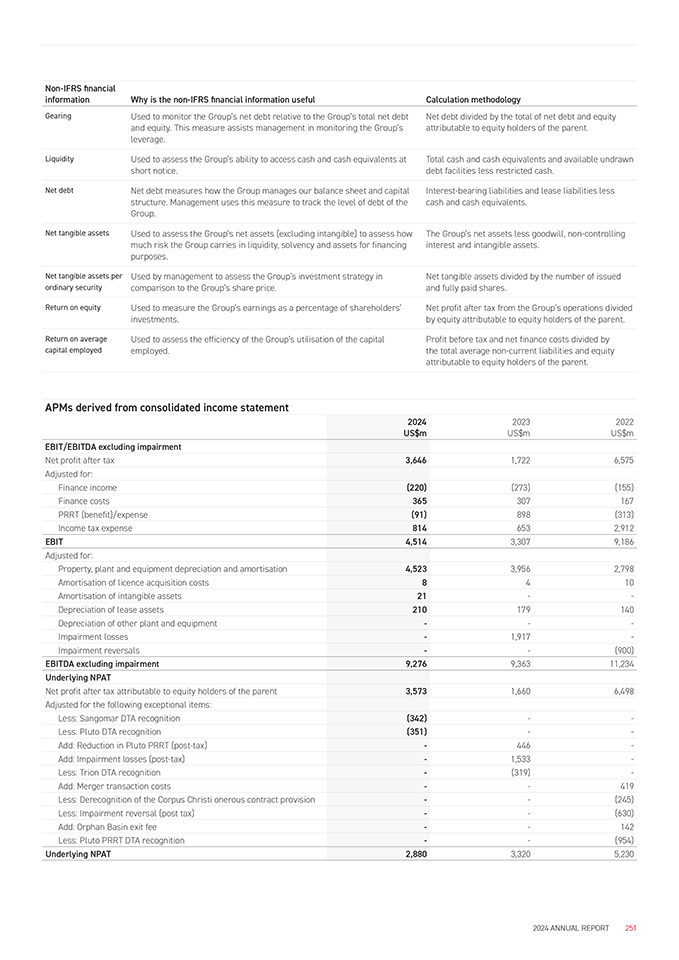

USE AND RECONCILIATION OF NON-IFRS FINANCIAL MEASURES

Woodside’s financial statements are prepared in accordance with the Australian Accounting Standards and other authoritative pronouncements of the Australian Accounting Standards Board (AASB) and comply with the International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

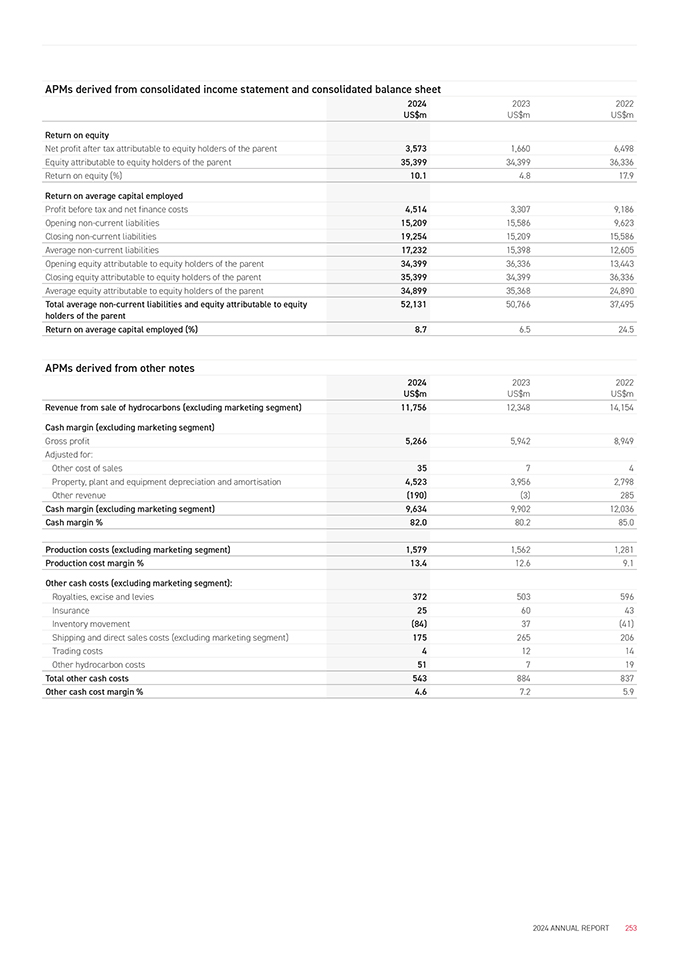

Certain parts of this report contain financial measures that are not defined in, and have not been prepared in accordance with, IFRS and are not recognised measures of financial performance or liquidity under IFRS. In addition to the financial information contained in this report presented in accordance with IFRS, certain “non-GAAP financial measures” (as defined in Item 10(e) of Regulation S-K under the US Securities Act of 1933, as amended) have been included in this report. These measures include: EBIT, EBITDA, EBITDA excluding impairment, Gearing, Underlying NPAT, Net debt, Free cash flow, Operating cash flow, Cash margin, Capital expenditure, Exploration expenditure, Net tangible assets, and Net tangible asset per ordinary security.

For further details and a reconciliation of these measures to the most directly comparable IFRS measure presented in Woodside’s financial statements, refer to the information set forth under the heading “Alternative performance measures” in Section 6.6 on pages 250-253 of the 2024 Annual Report is incorporated herein by reference. These non-IFRS financial measures are defined in under the heading “Glossary, units of measure and conversion factors” in Section 6.7 on pages 254-257 of the 2024 Annual Report.

6

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

| A. | Directors and Senior Management |

Not applicable.

| B. | Advisers |

Not applicable.

| C. | Auditors |

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

| A. | Offer statistics |

Not applicable.

| B. | Method and Expected Timetable |

Not applicable.

ITEM 3. KEY INFORMATION

| A. | [Reserved] |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reason for the Offer and Use of Proceeds |

Not applicable.

7

| D. | Risk Factors |

Woodside recognises that taking risk is necessary for our business and that effective risk management is vital to meeting our objectives. We are committed to managing risks in a proactive, informed and effective manner as a source of competitive advantage.

Our approach is intended to enable risk-informed decision making, which protects us against potential negative impacts and enable us to seek the right opportunities. The objective of our risk management framework is to provide a consolidated view of risks across the company to understand our full risk exposure and prioritise risk management and governance.

Woodside’s Risk Appetite Statement is a vital element of our risk framework. It sets out the Board’s appetite to take risk in pursuit of our strategic objectives. It provides guidance to the executive and senior management teams on the type and amount of risk that is acceptable when making decisions, consistent with other company policies.

Woodside’s risk management process is designed to identify, assess and control risks across the organisation. Company-wide risk management activities occur throughout the year and are reported to the Audit & Risk Committee and executive twice annually, in addition to deep dives on particular risk areas that occur throughout the year.

We categorise risks in three different ways:

1. Strategic risks

These are risks within Woodside’s sphere of influence that could affect our ability to achieve our strategic objectives. Management and the Board consider a range of risks and opportunities that have the potential to deliver or erode value for our organisation in both the near and longer term. We factor these risks into our strategic decision making, as the decisions we make can create, amplify, reduce, or remove current risks and improve our resilience to emerging risks.

Examples of strategic risks and opportunities relevant to Woodside include delivering growth and long-term value through acquisitions and divestments, and the competitiveness of our portfolio mix under a range of scenarios.

2. Emerging risks

These risks capture external threats or factors that have a high degree of uncertainty, are not readily controlled by Woodside and may be unpredictable or rapidly changing. They have the potential to materially affect the achievement of our strategic objectives. Examples include a shifting geopolitical landscape or rapid technological change.

3. Current risks

These quantifiable risks could affect Woodside’s ability to deliver our objectives and require appropriate control and management.

Informed by the International Standard ISO31000 for Risk Management, our risk management process involves these features:

| • | Communicating and consulting |

| • | Defining risk scope, context and criteria |

| • | Assessing risk |

| • | Treating risk |

| • | Monitoring and review |

| • | Recording and reporting risks. |

The risk management process provides a consistent way of identifying, managing and reporting risks that have the potential to materially affect the achievement of Woodside’s objectives. Potential impacts of these risks, were they to eventuate, include those related to health and safety, the environment, the community and culture, our reputation and brand, legal and compliance, and financial. These impacts may lead to a loss in shareholder value, loss of market share to competitors, decreases in the value of assets, delays or stoppages in our operations, loss of revenue, increased expenses, infringements on our ability to execute and complete transactions, reduced capacity to fund capital projects, delayed or suspended regulatory approvals, legal liabilities and adverse impacts on Woodside’s reputation, social licence to operate and on the delivery of our strategy.

8

Woodside prioritises risk management actions and governance through use of a risk register. The functionality within the register provides transparency and enhances the ability of senior leaders to effectively manage and govern risks, including checking that identified actions to address, manage or remove risk have been closed out.

Woodside’s Risk Management Process

The Audit & Risk Committee plays a crucial role in enabling the Board to meet its oversight responsibility in relation to Woodside’s risk management. The Sustainability Committee also focuses on sustainability-related risk management.

Overview of our risk factors

HEALTH & SAFETY

Our business is subject to risks related to safety or major hazard events associated with our activities or facilities. These may include unanticipated or unforeseeable adverse events that affect our ability to respond, manage and recover from such events.

How is this factor relevant to Woodside?

At Woodside, we believe that our ability to operate safely is critical to our competitiveness. Failure to continue to do so could result in potential impacts on people, as well as reputational damage with customers, employees, commercial partners and other stakeholders, and sustained production interruptions leading to an inability to meet production forecasts.

Examples of how this factor may affect Woodside

| • | A loss of containment event or other operational incident on or related to our property or operations could occur, which could have significant impacts including to human health and safety, from personal health, safety and wellbeing through to fatalities. This could result in financial, legal and reputational impacts. |

| • | Natural disasters and severe weather events, such as cyclones, floods, freezes and heatwaves, droughts, earthquakes or other acts of nature, social unrest, pandemic diseases, and criminal actions by external parties could result in injuries, loss of life, disruption of our operations or the loss or suspension of permits or other approvals. Coastal operations may be particularly susceptible to disruption from severe weather events. |

| • | Woodside’s operations are subject to numerous laws and regulations relating to public and occupational health and safety. The requirements of these laws and regulations are becoming increasingly complex, stringent and expensive to implement and comply with. |

ENVIRONMENT

Risks associated with major environmental incidents in connection with our activities or facilities include potential incidents resulting in significant loss of hydrocarbon. We are also subject to risks associated with biodiversity and failure to deliver emission reductions in a timely manner, consistent with regulatory and stakeholder expectations.

How is this factor relevant to Woodside?

Woodside’s operations are subject to environmental impacts or risks that can arise as a result of the nature of our operations.

Examples of how this factor may affect Woodside

| • | An incident may result in a significant loss of hydrocarbon to the environment, including when caused by factors that are outside Woodside’s direct control. These factors include natural disasters and severe weather events, such as cyclones, floods, freezes and heatwaves, droughts, earthquakes or other acts of nature, pandemics, well blowouts, fires, explosions, pipeline ruptures, chemical releases, oil releases including maritime releases, releases into navigable waters and groundwater contamination, material or mechanical failure, power outages, industrial accidents, physical or cyber attacks, abnormally pressured or structured formations and other events that cause operations to cease or be curtailed. This may negatively affect Woodside’s businesses and the communities in which we operate. |

| • | Woodside’s operations are subject to numerous laws and regulations relating to environmental protection. The requirements of these laws and regulations are becoming increasingly complex, stringent and expensive to implement. Costs of compliance with these laws and regulations are significant and can be unpredictable. |

| • | Applicable laws and regulations may obligate Woodside to adjust our various operational practices, plans or strategies, which in turn could cause uncertainty and delay, materially adversely affect our business, financial condition or results of operations. We may also be required to maintain financial assurance through bonds or insurance. |

| • | Third-party insurance may not provide adequate coverage or Woodside may be self-insured with respect to the related losses. |

9

CLIMATE

The global response to climate change is changing the way the world produces and consumes energy. Our strategy requires us to make risk-based decisions and seek opportunities to deliver energy solutions. The complex and pervasive nature of climate change means transition risks are interconnected with, and may amplify, other risks. Additionally, the inherent uncertainty of potential societal responses to climate change may create a systemic risk to the global economy. Continuing political, social and industry attention to climate change has resulted in both existing and pending international agreements and national, regional and local legislation and regulatory programs to reduce emissions. These and other government actions could require Woodside to increase operating and maintenance costs and may result in reduced demand for oil and gas. Climate change may also create significant physical risks, such as increased frequency and severity of storms, wildfires, floods and other climatic events, as well as chronic shifts in temperature and precipitation patterns.

How is this factor relevant to Woodside?

Woodside’s risks associated with climate change and the transition to a lower-carbon economy include possible impacts to demand (and pricing) for oil, gas and their substitutes, the policy and legal environment for its exploration, development and production, and Woodside’s reputation and operating environment. We may also face risks related to climate change’s potential to cause physical damage or disruptions to our assets or our value chains.

Examples of how this factor may affect Woodside

| • | Physical impacts on our assets or those of our suppliers, customers or communities caused by increased frequency or intensity of natural disasters and severe weather events. |

| • | Over- and under- investing in oil and gas reserves leading to an imbalance between our supply and global demand. |

| • | Failure to transition to new energy at a pace that serves the global demand, or stakeholder sentiments, or to develop and implement lower-carbon technologies on which Woodside’s strategy may depend. |

| • | Some of Woodside’s goals are dependent upon the successful implementation of new and existing technologies on an industrial scale. These technologies are in various stages of development or implementation and may require more capital, or take longer to develop, than currently expected. |

| • | Climate-driven changes to legislation, regulation and policy or climate-related litigation resulting in additional costs, preventing or restricting Woodside from conducting activities and having adverse impacts on Woodside’s reputation. |

| • | Failure of other organisations to meet emissions targets across the broader oil and gas industry and the reputational impacts for the industry as a whole. |

PRODUCTION AND OPERATIONS

We manage a range of risks within our operations, including commercial risks relating to third-party relationships such as joint venture partners, contract counterparties and our supply chain. Woodside is subject to extensive governmental oversight and regulation in the jurisdictions in which we operate, and such regulations may change in ways that adversely affect our business, results of operations and financial condition. In addition, we are required to comply with securities regulations in Australia, the United States and elsewhere.

We manage the estimation of proved oil and gas reserves by using judgement and the application of complex rules, and subsequent downward adjustments of Woodside’s reported reserves estimates are possible.

How is this factor relevant to Woodside?

Our operating assets are subject to a range of operating risks associated with process safety incidents, breaches of cybersecurity, extreme weather events and supply chain disruptions. Disruptions to our supply chain or failure of our contractual counterparties to fulfil their obligations could adversely affect our production, operations and our financial performance, result in litigation or class actions and cause long-term damage to our reputation.

The majority of our major projects and operations are conducted in joint ventures, which may limit our control over, and our ability to effectively manage risks associated with, such projects. For projects in which we are not the operator, we may be unable to directly control the behaviour, performance and cost of operations.

Our operations are subject to various national and local laws, regulations and approvals relating to the exploration, development, production, marketing, pricing, transportation and storage of our products, as well as the management, decommissioning, clean-up and restoration of our properties, and management and disclosure of our operations and impacts.

These laws or regulations could change, and any such changes could have a material adverse effect on our business and financial condition. As such laws and regulations are subject to amendment and reinterpretation over time, we are unable to predict the future cost or impact of complying with such laws. We have incurred and will continue to incur operating and capital expenditures, some of which may be material, to comply with applicable laws, regulations and approvals. The adoption and implementation of new or more stringent legislation, regulations or other regulatory initiatives that result in the imposition of more stringent standards for greenhouse gas emissions from the oil and gas industry could restrict the areas in which this sector may operate and could result in increased compliance costs and changes in product pricing, which could affect consumer demand for our products.

10

Additionally, the conduct of Woodside, our employees and our third-party partners could result in actual or alleged breaches of laws, regulations and approvals, including fraud, corruption, anti-competitive behaviour, money laundering, breaching trade or financial sanctions, market manipulation, privacy breaches, ethical misconduct and wider organisational cultural failings.

Estimating proved oil and gas reserves involves subjective judgements and determinations based on available geological, technical, contractual and economic information. New information from production or drilling activities, changes in economic factors, such as oil and gas prices, alterations in the regulatory policies of host governments in the jurisdictions in which we operate, or other events may cause estimates to change over time. Additionally, estimates may change to reflect acquisitions, divestments, new discoveries, extensions of existing fields and improved recovery techniques.

Examples of how this factor may affect Woodside

| • | Certain activities are undertaken in deep waters where operations, support services and decommissioning activities are more difficult and costly than in shallower waters. Deepwater locations lack the physical and oilfield service infrastructure present in shallower waters. As a result, these operations may have additional risks and require significant time between a discovery and the time that Woodside can market its production. |

| • | Our joint venture participants (JVPs) may have the ability to exercise veto rights to block certain key decisions or actions that we believe are in our or the joint venture’s best interests or approve those matters without our support. |

| • | Our JVPs and contractual counterparties may not be able to meet their financial or other obligations to the projects. In addition, the actions of our partners, contractors and subcontractors could result in legal liability and financial loss for Woodside. |

| • | A failure to comply with applicable laws, regulations and approvals relating to our operations may result in the assessment of sanctions, including administrative, civil, and criminal penalties, the imposition of investigatory, remedial, and corrective action obligations or the incurrence of capital expenditures and demand for reimbursement for government or regulatory actions, the occurrence of restrictions, delays or cancellations in the permitting, development or expansion of current or proposed projects including via government orders, suspension or revocation of licences, permits, government contracts or approvals, and issuance of injunctions restricting or prohibiting some or all of our activities in a particular area. |

| • | Supply chain disruptions such as extended lead times for critical spares or imposition of trade sanctions or export controls on key suppliers, may cause outages at our operations, increased costs or delays on our projects. |

| • | Joint venture participants or contractual counterparties may be primarily responsible for the adequacy of the human or technical competencies and capabilities which they bring to bear on the joint project, which may not be adequate. |

| • | The suspension, revocation, failure to renew or alteration of, or challenges to, the terms of the licences, permits, government contracts or approvals required for our operations. |

| • | Government policy objectives in the countries in which we do business, now or in the future, could take the form of increased governmental regulations (including in respect of restoration, protection of the environment, levels of greenhouse gas emissions, protection of natural resources, and worker health and safety), redirection of product distribution (such as domestic gas reservation policies), changes in taxation regulation or enforcement (including, for example, changes in tax rates or increased focus on audits), taxation subsidies or royalties, nationalisation of resource assets or restrictions or moratoriums on our operations on government leases, limitations on periods of lease retention, interference with the confidentiality and availability of information, forced renegotiation of contracts, changes in laws and policies governing operations of foreign-based companies, trade sanctions, currency restrictions and exchange rate fluctuations and other governmental steps. |

| • | Actual or alleged violations of the securities laws that we are subject to could result in private or governmental litigation, civil penalties, regulatory action and shareholder class actions. |

| • | The process of estimating oil and natural gas reserves is complex and requires significant decisions and assumptions in the evaluation of available geological, geophysical, engineering and economic data for each reservoir and is therefore inherently uncertain. Actual production, revenues, expenditures, prices of hydrocarbons and taxes with respect to Woodside’s reserves may vary from estimates and the variance may be material. Woodside has in the past and may in the future record impairments resulting from declines in oil and gas prices or other factors. Downward adjustments of our reported reserves estimates could indicate lower future production volumes or the impairment of assets. |

11

GROWTH

Growth risks associated with delivery of both major and complex multi-year execution project activities and transactions (including acquisitions and divestments) across multiple locations around the world, including a reliance on third parties for materials, products and services.

How is this factor relevant to Woodside?

Oil and gas

In order to maintain our production levels and deliver shareholder value, Woodside must continue to identify growth opportunities, organic and inorganic, and commercialise them. To maintain a stable pipeline of future projects and realise the full value of growth opportunities, Woodside competes with a wide range of multinational and nationalised oil and gas companies, in addition to individual producers and new energy companies. Failure to effectively compete with these companies may result in the inability to continue to expand Woodside’s current operations and meet our objectives.

Woodside must continue to effectively manage relationships with industry partners. For example, at times we enter joint ventures with organisations that may also be competing oil and gas suppliers. It is essential that our voice is heard both within our industry and more broadly. In order for us to effectively communicate, we may at times align with industry bodies to advocate what we believe is in the best interests of our stakeholders. In addition, our current and planned projects involve uncertainties and operating risks that could prevent us from realising profits or result in the total or partial loss of our investment.

New energy

We have set targets for our new energy products and lower-carbon services.1 There is uncertainty around the pace of required technological innovation and the reliability of technologies that will be needed to transition to a lower-carbon economy. In addition, new sources of energy, such as hydrogen or ammonia, may be more difficult to commercialise than expected or may not be able to be commercialised safely or as efficiently as expected at scale. Woodside may also face unforeseen obstacles in the commercialisation of a future carbon capture business and in the implementation of other lower-carbon services and emission reduction efforts.

Examples of how this factor may affect Woodside

| • | An unbalanced portfolio of oil and gas and new energy, which may not meet the market’s needs. |

| • | Limited or reduced market share resulting in a loss of shareholder value. |

| • | Our competitors may be able to pay more for exploratory prospects and productive oil and natural gas properties or may be able to define, evaluate, bid for and purchase a greater number of properties and prospects, including operatorships and licences, than our financial or human resources permit. |

| • | Our projects could experience slippage in implementing schedules, permitting delays, shortages of or delays in the delivery of equipment or purpose-built components from suppliers, escalation in capital cost estimates, possible shortages of construction or other personnel, other labour shortages, environmental occurrences during construction that result in a failure to comply with environmental regulations or conditions on development, or delays and higher-than-expected costs due to the remote location of the projects, the impact of global conflicts on the relevant workforce or supply chain, other unanticipated supply chain disruptions, natural disasters, accidents, miscalculations, political or other opposition, litigation, acts of terrorism, operational difficulties, climate change-related risks or other events associated with that construction that may result in the delay, suspension or termination of our projects. |

| • | An inability to obtain financing at acceptable costs, or at all, for the development of new projects. |

| • | Failure to implement our new energy plans within our anticipated timeframe and in line with global demands. |

| 1. | Scope 3 targets are subject to commercial arrangements, commercial feasibility, regulatory and joint venture approvals, and third-party activities (which may or may not proceed). Individual investment decisions are subject to Woodside’s investment targets. Not guidance. Potentially includes both organic and inorganic investment. |

12

| • | Failure to identify, execute or implement strategic transactions, including acquisitions and divestments, or to achieve the full benefits of those transactions. In particular, difficulties in integrating and developing acquired assets may result in operational and other challenges, including the diversion of management’s attention from ongoing business concerns. The integration and development process may be subject to delays or changed circumstances, and we can give no assurance that the acquired assets will perform in accordance with our expectations or that our expectations with respect to the opportunities from any acquisitions will materialise. |

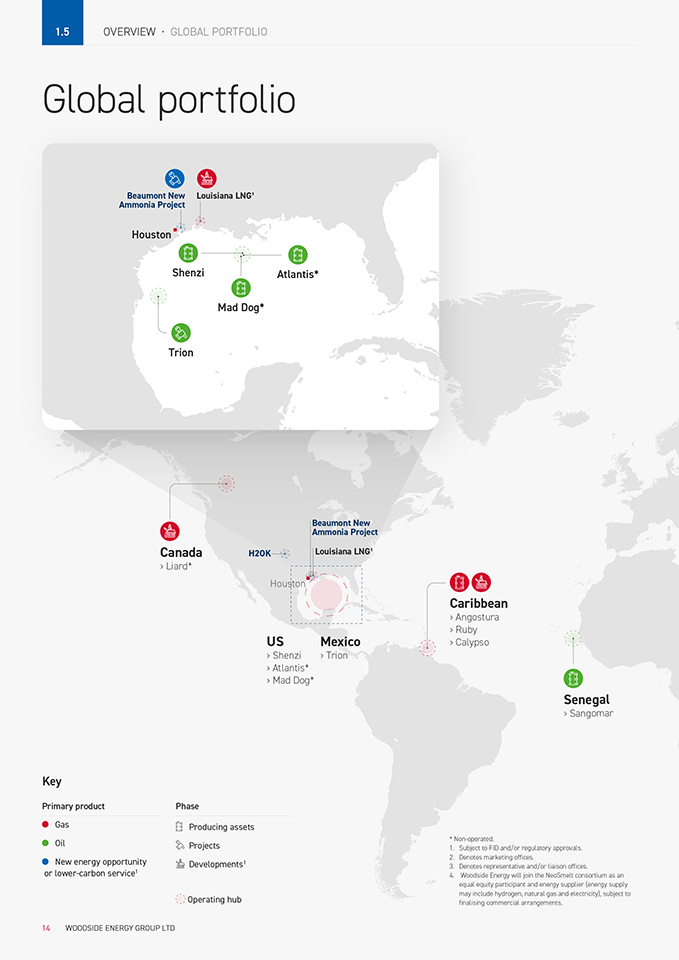

| • | The development of acquired assets may lead to the incurrence of significant capital and operating expenses, in addition to potential capital expenditures that may occur as a result of executing our previously disclosed strategy in relation to our new energy investment target and other potential growth projects. For instance, in 2024, we completed two significant transactions involving major energy projects in the US Gulf Coast – Louisiana LNG and the Beaumont New Ammonia Project. The complexity and magnitude of the development effort associated with the acquired assets, particularly in relation to Louisiana LNG, may require significant capital and operating expenses to support the development of those operations. |

| • | A significant increase in capital expenditures could have adverse consequences on our business, financial conditions and future prospects, including that we may be required to incur additional debt and we may not be able to obtain financing in the future on acceptable terms or at all for working capital, capital expenditures, acquisitions, debt service requirements or other purposes. |

| • | Credit rating agencies could downgrade our credit ratings below currently expected levels, and we may be less able to take advantage of significant business opportunities and to react to changes in market or industry conditions. |

| • | Failure to remain commercially and technologically competitive to efficiently develop and operate an attractive portfolio of assets, to obtain access to new opportunities and to keep pace with deployment of new technologies and products. |

| • | Woodside operates in highly competitive markets. A number of competitors are larger and have greater resources than Woodside. There may be greater-than-expected competition in the markets in which Woodside competes, including those for new energy products and lower-carbon services. |

| • | Failure to generate returns in line with our capital allocation framework. |

SOCIAL LICENCE

Social licence risks are associated with actual or perceived deviation from social or business expectations of ethical behaviour (including breaches of laws or regulations) and social responsibility (including environmental impact and community contribution), particularly as these expectations evolve and as Woodside expands its operations around the world.

How is this factor relevant to Woodside?

Traditional Owners and Custodians, government authorities, investors and other groups form significant relationships with our organisation. These relationships are built on the trust that Woodside will meet our stakeholders’ expectations. We must also consider the role our commercial agreements play in relation to human rights around the world, as we have a responsibility to ensure the rights of all humans are not negatively affected by our organisation.

These are some of the most significant risks to our relationships with stakeholders:

| • | Engaging in activities that have real or perceived adverse impacts on the environment, climate, biodiversity, human rights or cultural heritage. |

| • | Failing to meet our net equity Scope 1 and 2 emissions reduction targets. or investment targets in new energy products and lower carbon services.1,2 |

| • | Inadequately responding to quickly evolving expectations of Woodside (including expectations that may significantly differ in the various jurisdictions in which we operate). |

Additionally, third-party risks that are outside of our control could negatively affect our reputation and licence to operate, such as oil spills or other disasters, or crisis scenarios that cause collateral damage to Woodside’s licence to operate via reputational damage to the oil and gas industry at large.

| 1. | Targets and aspiration are for net equity Scope 1 and 2 greenhouse gas emissions relative to a starting base of 6.32 Mt CO2-e which is representative of the gross annual average equity Scope 1 and 2 greenhouse gas emissions over 2016-2020 and which may be adjusted (up or down) for potential equity changes in producing or sanctioned assets with a FID prior to 2021. Net equity emissions include the utilisation of carbon credits as offsets. |

| 2. | Scope 3 targets are subject to commercial arrangements, commercial feasibility, regulatory and joint venture approvals, and third-party activities (which may or may not proceed). Individual investment decisions are subject to Woodside’s investment targets. Not guidance. Potentially includes both organic and inorganic investment. |

13

Examples of how this factor may affect Woodside

| • | Lost or limited stakeholder support for our current business and future opportunities, including the refusal of, or delay in, the extension or grant of exploration, development or production contracts or leases, and development delays and cost overruns due to approval delays for, or denial of, drilling, construction, environmental and other regulatory approvals, permits and authorisations. |

| • | Woodside is a global company, operating in a number of jurisdictions. Stakeholders and regulators in the areas in which we operate have increasingly expressed or pursued divergent views, legislation and investment expectations with respect to sustainability matters, which may increase the social licence risks in those areas. |

| • | New or amended laws and regulations, or new or different applications or interpretations of existing laws and regulations, |

| • | Risks related to the violation of certain laws and regulations, including class action lawsuits, litigation and activism, allegations of legal compliance failures and greenwashing. |

| • | Reductions in the availability of, or less favourable terms for, financing and other forms of capital. |

| • | Decreased ability to attract and retain a talented workforce, and other operational concerns. |

PEOPLE & CULTURE

These risks are associated with the ability to attract, retain, develop and motivate key employees to succeed and safeguard both current and future performance and growth.

How is this factor relevant to Woodside?

People are key to the success of Woodside. We must build and maintain a capable workforce if we are to achieve our objectives. An effective operating model with a balanced organisational structure will allow us to conduct our operations and pursue new opportunities. For Woodside to remain an employer of choice, our culture must support our current employees and attract the best new candidates. The conduct of Woodside, our employees and our third-party partners could result in actual or alleged breaches of laws, regulations and approvals, including fraud, corruption, anti-competitive behaviour, money laundering, breaching trade or financial sanctions, market manipulation, privacy breaches, ethical misconduct and wider organisational cultural failings.

Examples of how this factor may affect Woodside

| • | During periods of high demand for skilled resources, Woodside may be unable to fill critical roles at acceptable costs or at all, leading to operational impacts. |

| • | A limited ability to operate due to our people leaving critical roles. |

| • | An inability to pursue innovation opportunities due to a skills shortage. |

| • | Loss of key personnel or expert knowledge. |

| • | An inability to reach timely agreements with employees including where representation by third parties may result in industrial action. |

| • | Actual or alleged misconduct, including fraud and corruption. |

FINANCIAL MANAGEMENT

These risks are those associated with interest rates, inflation, and fluctuations in commodity price and foreign exchange.

How is this factor relevant to Woodside?

Woodside must be financially well positioned in order to pursue our strategic objectives and remain resilient during times of economic challenge. Several factors can affect our position.

Capital management

For Woodside to operate sustainably we must make risk-informed decisions related to allocation of capital. We seek to apply a disciplined and balanced approach to capital management through the commodity price cycle.

From time to time, Woodside has relied on access to capital markets for funding. Our ability to obtain additional financing or refinancing will be subject to a number of factors, including general economic and market conditions such as rising interest rates, inflation or unstable or illiquid market conditions.

14

Foreign exchange risk:

Woodside is exposed to foreign currency risk from future commitments, financial assets and financial liabilities that are not denominated in US dollars. See section A in Notes to the financial Statements in “Item 18. Financial Statements” in this 2024 Form 20-F for further information.

Interest rate risk:

This is the risk that Woodside’s financial position will fluctuate due to changes in market interest rates. Woodside’s risk relates primarily to financial instruments with floating interest rates including long-term debt obligations, cash and short-term deposits. See section C in Notes to the financial Statements in “Item 18. Financial Statements” in this 2024 Form 20-F for further information.

Examples of how this factor may affect Woodside

| • | A reduced ability to fund our strategy including our projects. |

| • | Impairments of assets, goodwill or other intangible assets, or a significant increase in capital and operational expenditure as a result of acquisitions, could have a significant negative effect on our reported net income and our ability to pay dividends in one or more accounting periods if the level of impairment were to exceed profits available for distribution. |

COMMERCIAL AND MARKET

Commercial and market risks are associated with the ability to capture value whether markets are stable or volatile. Generally, Woodside does not have control over the factors that affect market development and prices.

How is this factor relevant to Woodside?

Woodside’s revenues are primarily derived from the sale of oil and gas. The prices Woodside receives for these products are variable and are affected by global economic factors beyond Woodside’s control. We seek to forecast changes in the economic factors to enable us to maintain a strong market position during challenging economic times. See “Item 11. Quantitative and qualitative disclosures about market risk” of this 2024 Form 20-F.

Examples of how this factor may affect Woodside

| • | Significant volatility in energy prices, such as the volatility experienced in recent years, may increase the challenges associated with future revenue and delivery of our strategy |

| • | An imbalance in supply and demand can affect commodity prices and our ability to forecast market conditions determines whether we are affected positively or negatively. |

| • | The exploration and production of hydrocarbons is a highly competitive business. Woodside has many competitors (including national oil companies), some of which are larger and better funded; may be willing to accept greater risks; have greater access to capital; have substantially larger staffs; or have special competencies. |

| • | Woodside may become a less attractive joint venture participant. |

| • | Shareholder returns are reduced due to lower commodity prices. |

| • | Woodside’s acquisition activities carry risks that it may not fully realise anticipated benefits due to less-than-expected reserves or production or changed circumstances, such as declines in prices of hydrocarbons or an inability to capture market optimisation opportunities; bear unexpected integration costs or experience other integration difficulties; experience share price declines based on the market’s evaluation of the activity; or be subject to costs or liabilities that are greater than anticipated. |

| • | If we inaccurately forecast the global demand for our LNG products we may face difficulties obtaining longer-term sales contracts with desirable commercial terms. |

| • | If counterparties to our derivative instruments are unable to fulfil their obligations, a larger percentage of our future oil and gas production could be subject to price changes. |

DIGITAL AND CYBERSECURITY

These risks are associated with adopting and implementing new technologies, while safeguarding our digital information and landscape (including from cyber threats) across our value chain.

15

How is this factor relevant to Woodside?

Woodside must relentlessly protect the confidentiality, integrity and availability of digital information and operational technologies. Woodside’s technology systems including artificial intelligence and machine learning technologies may be targeted by an internal or external malicious act or our systems may be disrupted unintentionally. Additionally, the cost of implementing and maintaining effective technology systems may be higher than anticipated. While our technology controls are designed to protect against all causes of disruption, we cannot be certain that they will protect our systems in all cases.

Examples of how this factor may affect Woodside

| • | In the event of a cyber attack, Woodside’s confidential or sensitive information may be made public or held for ransom. |

| • | Our operations may be disrupted if unauthorised access to our process control systems, or the systems of vendors on which we rely, occurs. |

| • | Litigation and governmental investigations may arise from the occurrence of a cyber attack. |

| • | There may be potential adverse impacts on our reputation, the safety and privacy of our employees and the communities in which we operate. |

ITEM 4. INFORMATION ON THE COMPANY

| A. | History and Development of the Company |

Woodside was registered under Australian corporate law in 1971 and listed on the Australian Securities Exchange (the ASX) on 18 November 1971. Woodside’s shares are currently listed on the ASX under the ticker symbol ‘WDS’ and its American Depositary Shares (ADS) are listed on the NYSE under the symbol ‘WDS’. Following the approval of Woodside shareholders at Woodside’s Annual General Meeting on 19 May 2022, Woodside changed its name from ‘Woodside Petroleum Ltd.’ to ‘Woodside Energy Group Ltd’ effective 20 May 2022. Woodside’s registered office is Mia Yellagonga, 11 Mount Street, Perth, Western Australia 6000, Australia, telephone +61 8 9348 4000.

The information set forth under the following headings of the 2024 Annual Report is incorporated herein by reference:

| • | Section 1: Overview from pages 6-15 |

| • | Section 3: Our Business from pages 26-42 |

| • | Documents on display in Section 6.4: Shareholder statistics on page 240. |

See Three-Year Financial Analysis in “Item 5.A Operating Results” of this 2024 Form 20-F.

16

| B. | Business Overview |

The information set forth under the following headings of the 2024 Annual Report is incorporated herein by reference:

| • | Section 1: Overview from pages 6-15 |

| • | Section 2: Strategy and Financial Performance from pages 16-25 |

| • | Section 3: Our Business from pages 26-42 |

| • | Section 6.3: Additional disclosures from pages 225-237. |

See Three-Year Financial Analysis in “Item 5.A Operating Results” of this 2024 Form 20-F.

Applicable laws and regulations

The information set forth under the following headings of the 2024 Annual Report is incorporated herein by reference:

| • | Government regulations in Section 6.3: Additional disclosures from pages 230-236 |

| • | Material limitations in Section 6.3: Additional disclosures on page 236 |

| • | Summary of material legal proceedings in Section 6.3: Additional disclosures on page 236-237. |

Disclosures regarding oil and gas operations

The information set forth under the following headings of the 2024 Annual Report is incorporated herein by reference:

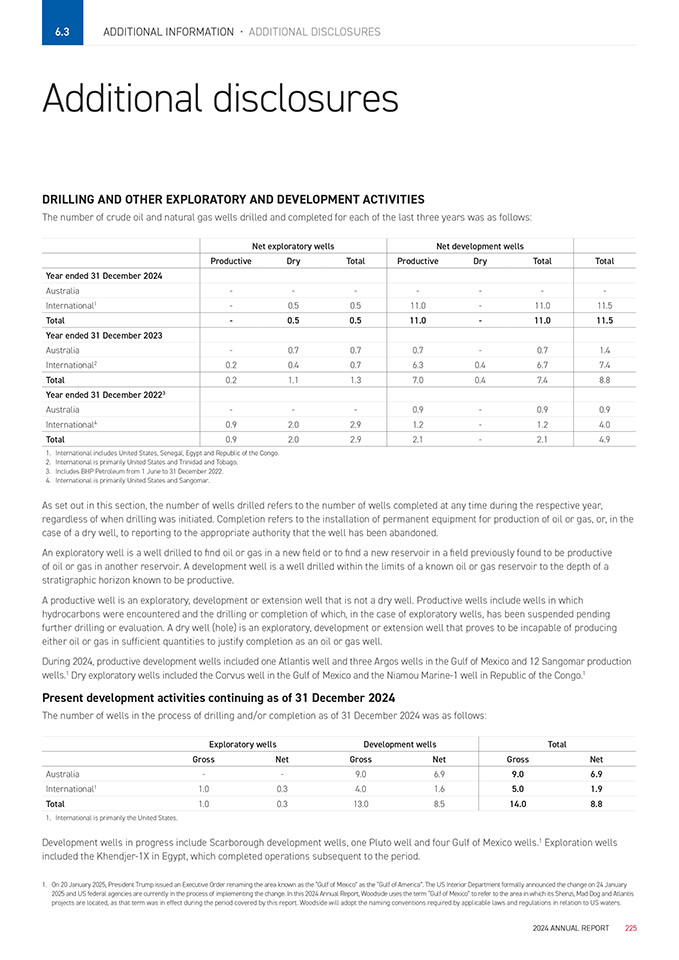

| • | Drilling and other exploratory and development activities in Section 6.3: Additional disclosures on page 225 |

| • | Present development activities continuing as of 31 December 2024 in Section 6.3: Additional disclosures on page 225 |

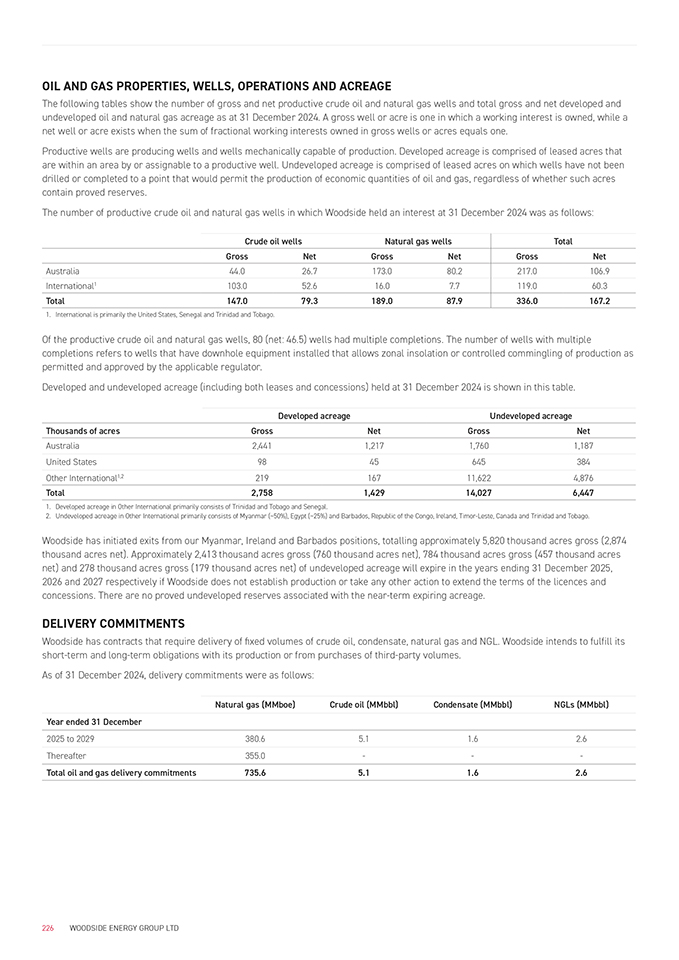

| • | Oil and gas properties, wells, operations and acreage in Section 6.3: Additional disclosures on pages 226 |

| • | Delivery commitments in Section 6.3: Additional disclosures on page 226 |

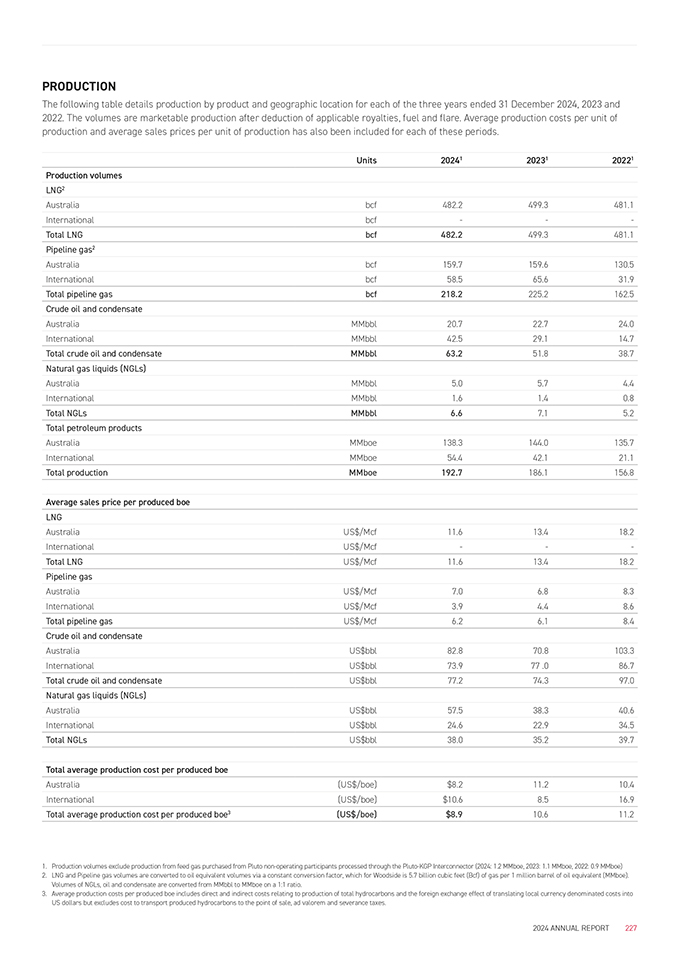

| • | Production in Section 6.3: Additional disclosures on page 227. |

RESERVES STATEMENT

About the Reserves Statement

This Reserves Statement presents Woodside’s proved oil and gas reserves, as of 31 December 2024, in accordance with the regulations of the United States Securities and Exchange Commission (SEC).1

Unless stated otherwise, the following apply to this Reserves Statement: The effective date for reserves estimates is 31 December 2024. Estimates have been prepared in accordance with the reserves definitions of Rules 4-10(a) of SEC Regulations S-X and are calculated using SEC-compliant economic assumptions and pricing. Production is reported for the period from 1 January 2024 to 31 December 2024. Reserves and production stated are Woodside’s net share and inclusive of fuel consumed in operations. See “Methodology” below.

All numbers are internal estimates produced by Woodside. Estimates of reserves should be regarded only as estimates that may change over time as additional information and production history becomes available. See “Forward-Looking Statements”.

2024 proved reserves

Woodside produced a total of 206.3 MMboe in 2024, including 192.7 MMboe produced for sale and 13.6 MMboe of production consumed primarily as fuel in operations.2 At 31 December 2024, Woodside’s remaining proved (1P) reserves were 1,975.7 MMboe (Table 1, 2).

As a result of completion of the sale of 10.0% and 15.1% non-operating participating interest in the Scarborough Joint Venture in Australia, Woodside’s proved undeveloped reserves decreased by 323.0 MMboe (shown as acquisitions and divestments in Table 2, 3).

17

In 2024, revisions of previous estimates and extensions resulted in proved reserves increases of 54.9 MMboe. Key drivers for these changes include:

| • | post start-up field performance at Sangomar in Senegal contributed to a proved reserves increase of 16.2 MMboe |

| • | performance based revisions, technical updates, and the final investment decision on a development opportunity in North West Shelf in Australia contributed to a proved reserves increase of 13.4 MMboe3 |

| • | performance and technical updates at Bass Strait and multiple Exmouth fields in Australia contributed to a proved reserves increase of 20.5 MMboe |

| • | final investment decision on Xena-3 in Greater Pluto in Australia resulted in extensions of proved reserves of 7.1 MMboe |

| • | initial field performance and technical updates at Mad Dog Phase 2 in the United States contributed to a proved reserves decrease of 8.1 MMboe |

The transfers of undeveloped to developed reserves associated with successful start-up of Sangomar, start-up of development wells in the United States and start-up of two compression projects in Australia are discussed in the 2024 proved undeveloped reserves section of this Reserves Statement.

Table 1: Woodside’s proved reserves4,5,6 overview (net Woodside share, as at 31 December 2024)

| Natural gas7 Bcf10 |

NGLs8 MMbbl11 |

Oil & condensate MMbbl |

Total9 MMboe12 |

Fuel included in total |

||||||||||||||||

| Proved13 developed14 and undeveloped15 |

8,049.9 | 18.9 | 544.6 | 1,975.7 | 178.2 | |||||||||||||||

| Proved developed |

1,995.0 | 17.4 | 339.4 | 706.8 | 59.3 | |||||||||||||||

| Proved undeveloped |

6,054.9 | 1.5 | 205.2 | 1,268.9 | 119.0 | |||||||||||||||

Small differences due to rounding

2023 proved reserves

Woodside produced a total of 201.0 MMboe in 2023, including 186.1 MMboe produced for sale and 15.0 MMboe of production consumed primarily as fuel in operations.2 At 31 December 2023, Woodside’s remaining proved reserves were 2,450.1 MMboe (Table 2).

The first-time booking of reserves at Trion in Mexico and Mad Dog Southwest in the United States increased proved reserves by 204.1 MMboe (shown as extensions and discoveries in Table 2), of which:

| • | final investment decision and regulatory approval of the field development plan at Trion in August 2023 increased proved reserves by 194.8 MMboe16; and |

| • | approval of the Mad Dog Southwest Extension project increased proved reserves by 9.3 MMboe. |

Revisions of previous estimates in 2023 resulted in a net increase of 61.8 MMboe for proved reserves. Key drivers for these revisions include:

| • | asset optimisation, including injector to producer conversions, and field performance at Angostura and Ruby in Trinidad and Tobago contributed to a proved reserves increase of 13.0 MMboe |

| • | improved overall field performance and technical updates in North West Shelf increased proved reserves by 49.7 MMboe |

| • | performance based revisions at Shenzi decreased proved reserves by 13.4 MMboe. |

The transfers of undeveloped reserves to developed reserves are discussed in the 2023 proved undeveloped reserves section of this Reserves Statement.

2022 proved reserves

Woodside produced 156.8 MMboe for sale in 2022, including 61.4 MMboe produced from 1 June 2022 from interests acquired as part of the merger with the BHP Petroleum business on 1 June 2022 (Acquired Assets). An additional 14.9 MMboe of production was consumed primarily as fuel in operations in the year ended 31 December 2022 resulting in a total production of 171.7 MMboe for 2022.2 At 31 December 2022, Woodside’s remaining proved reserves were 2,385.2 MMboe (Table 2).

18

The acquisition of the Acquired Assets on 1 June 2022 increased Woodside’s proved reserves as at 1 June 2022 by 922.8 MMboe to 2,339.6 MMboe. These changes are further described below.

2022 included revisions of previous estimates of 202.5 MMboe for proved reserves. Key drivers for the revisions include:

| • | completion of an Atlantis full field integrated subsurface study that resulted in a 46.3 MMboe increase in proved reserves |

| • | inclusion of offshore fuel gas reserves and favourable commodity prices resulting in a net increase of 51.7 MMboe to proved undeveloped reserves at Scarborough |

| • | inclusion of fuel gas reserves and incorporation of drilling results at Sangomar resulting in a proved undeveloped reserves increase of 24.7 MMboe |

| • | improved overall field performance at Pluto, North West Shelf, and Julimar-Brunello led to proved reserves increases of 31.7 MMboe, 17.6 MMboe, and 25.7 MMboe, respectively. |

The transfers of undeveloped reserves to developed reserves are discussed in the 2022 proved undeveloped reserves section of this Reserves Statement.

Methodology

Reserves estimates have not been adjusted for risk. Proved reserves are estimated and reported on a net interest basis, excluding royalties owned by others, in accordance with the SEC regulations and have been determined in accordance with SEC Rule 4-10(a) of Regulation S-X. As defined by the SEC, proved reserves are those quantities of crude oil, natural gas, and natural gas liquids that, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible from a given date forward from known reservoirs and under existing economic conditions, operating methods, operating contracts, and government regulations. Unless evidence indicates that renewal of existing operating contracts is reasonably certain, estimates of economically producible reserves reflect only the period before the contracts expire. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence within a reasonable time.

Proved reserves are estimated by reference to available well and reservoir information, including but not limited to well logs, well test data, core data, production and pressure data, geologic data, seismic data and, in some cases, similar data from analogous, producing reservoirs. A wide range of engineering and geoscience methods, including performance analysis, numerical simulation, well analogues and geologic studies, have been used to develop high confidence in estimated quantities.

Governance and assurance

Woodside has several processes designed to provide assurance for reserves reporting, including its Reserves and Resources Policy and Standards, reserves estimation guidance, annual staff training and minimum experience levels. In addition, Woodside has a dedicated and independent Corporate Reserves Team (CRT) that provides oversight and assurance of the reserves assessments and reporting processes. Reserves are estimated by staff in teams directly responsible for development and production activities. These individuals are trained in the fundamentals of reserves reporting and are approved by the CRT on an annual basis. Reserves estimates are reviewed annually by the CRT to ensure technical quality, adherence to Woodside’s Reserves and Resources Policy and Standards and compliance with SEC reporting requirements. All reserves are reviewed and approved by Woodside’s Qualified Petroleum Reserves Evaluator and approved by senior management and Woodside’s Board prior to public reporting.

Qualified Petroleum Reserves Evaluator statement

The estimates of petroleum reserves are based on and fairly represent information and supporting documentation prepared by, or under the supervision of Mr. Benjamin Ziker, Woodside’s Vice President Reserves and Subsurface, who is a full-time employee of the company and a member of the Society of Petroleum Engineers. The Reserves Statement as a whole has been approved by Mr. Ziker. Mr. Ziker’s qualifications include a Bachelor of Science (Chemical Engineering) from Rice University (Houston, Texas, USA), and 26 years of relevant experience.

19

Table 2: Proved developed and undeveloped reserves reconciliation (net Woodside share, three years ending 31 December 2024)

| Australia | International17 | Total | ||||||||||||||||||||||||||||||||||||||||||||||

| Natural gas |

NGLs |

Oil & |

Total | Natural |

NGLs |

Oil & |

Total |

Natural |

NGLs |

Oil & |

Total |

|||||||||||||||||||||||||||||||||||||

| Bcf | MMbbl | MMbbl | MMboe | Bcf | MMbbl | MMbbl | MMboe | Bcf | MMbbl | MMbbl | MMboe | |||||||||||||||||||||||||||||||||||||

| Reserves as at 31 December 2021 |

7,370.0 | 0.0 | 57.5 | 1,350.5 | 0.0 | 0.0 | 81.2 | 81.2 | 7,370.0 | 0.0 | 138.7 | 1,431.6 | ||||||||||||||||||||||||||||||||||||

| Acquisitions and divestments18 |

3,096.1 | 18.3 | 34.0 | 595.4 | 251.2 | 7.7 | 275.6 | 327.4 | 3,347.4 | 26.0 | 309.6 | 922.8 | ||||||||||||||||||||||||||||||||||||

| Extensions and discoveries19 |

0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||||||||||||||||||||||

| Revision of previous estimates20 |

682.3 | 3.6 | 12.3 | 135.6 | 112.0 | 2.1 | 45.2 | 66.9 | 794.3 | 5.7 | 57.5 | 202.5 | ||||||||||||||||||||||||||||||||||||

| Production |

-692.5 | -4.5 | -24.0 | -150.0 | -35.4 | -0.8 | -14.7 | -21.7 | -728.0 | -5.3 | -38.7 | -171.7 | ||||||||||||||||||||||||||||||||||||

| Reserves as at 31 December 2022 |

10,455.8 | 17.3 | 79.7 | 1,931.4 | 327.8 | 9.0 | 387.3 | 453.8 | 10,783.6 | 26.3 | 467.0 | 2,385.2 | ||||||||||||||||||||||||||||||||||||

| Acquisitions and divestments |

0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||||||||||||||||||||||||||||||

| Extensions and discoveries |

0.0 | 0.0 | 0.0 | 0.0 | 177.9 | 0.4 | 172.5 | 204.1 | 177.9 | 0.4 | 172.5 | 204.1 | ||||||||||||||||||||||||||||||||||||

| Revision of previous estimates |

308.6 | 2.2 | 15.4 | 71.8 | 35.6 | -0.6 | -15.6 | -9.9 | 344.3 | 1.6 | -0.2 | 61.8 | ||||||||||||||||||||||||||||||||||||

| Production |

-738.4 | -5.9 | -22.7 | -158.1 | -70.6 | -1.4 | -29.2 | -43.0 | -809.0 | -7.3 | -51.8 | -201.0 | ||||||||||||||||||||||||||||||||||||

| Reserves as at 31 December 2023 |

10,026.1 | 13.6 | 72.5 | 1,845.1 | 470.7 | 7.4 | 515.0 | 605.0 | 10,496.9 | 21.0 | 587.5 | 2,450.1 | ||||||||||||||||||||||||||||||||||||

| Acquisitions and divestments |

-1,841.3 | 0.0 | 0.0 | -323.0 | 0.0 | 0.0 | 0.0 | 0.0 | -1,841.3 | 0.0 | 0.0 | -323.0 | ||||||||||||||||||||||||||||||||||||

| Extensions and discoveries |

37.7 | 0.0 | 0.5 | 7.1 | 0.0 | 0.0 | 0.0 | 0.0 | 37.7 | 0.0 | 0.5 | 7.1 | ||||||||||||||||||||||||||||||||||||

| Revision of previous estimates |

108.6 | 4.3 | 11.1 | 34.4 | 25.8 | 0.2 | 8.6 | 13.4 | 134.4 | 4.5 | 19.8 | 47.9 | ||||||||||||||||||||||||||||||||||||

| Production |

-714.2 | -5.1 | -20.7 | -151.1 | -63.5 | -1.6 | -42.5 | -55.2 | -777.8 | -6.7 | -63.2 | -206.3 | ||||||||||||||||||||||||||||||||||||

| Reserves as at 31 December 202421 |

7,616.9 | 12.8 | 63.4 | 1,412.5 | 433.0 | 6.0 | 481.2 | 563.2 | 8,049.9 | 18.9 | 544.6 | 1,975.7 | ||||||||||||||||||||||||||||||||||||

| Fuel included in 31 December 2024 reserves | 859.7 | 0.8 | 0.0 | 151.7 | 151.5 | 0.0 | 0.0 | 26.6 | 1,011.2 | 0.8 | 0.0 | 178.2 | ||||||||||||||||||||||||||||||||||||

| Proved developed and undeveloped reserves |

|

|||||||||||||||||||||||||||||||||||||||||||||||

| Proved developed reserves |

||||||||||||||||||||||||||||||||||||||||||||||||

| as at 31 December 2021 |

1,744.5 | 0.0 | 50.2 | 356.3 | 0.0 | 0.0 | 0.0 | 0.0 | 1,744.5 | 0.0 | 50.2 | 356.3 | ||||||||||||||||||||||||||||||||||||

| as at 31 December 2022 |

2,722.6 | 16.7 | 73.3 | 567.6 | 202.5 | 5.9 | 161.0 | 202.4 | 2,925.1 | 22.5 | 234.3 | 770.0 | ||||||||||||||||||||||||||||||||||||

| as at 31 December 2023 |

2,361.3 | 12.6 | 67.9 | 494.8 | 220.8 | 6.1 | 198.0 | 242.8 | 2,582.1 | 18.7 | 266.0 | 737.7 | ||||||||||||||||||||||||||||||||||||

| as at 31 December 2024 |

1,748.5 | 12.4 | 58.4 | 377.6 | 246.5 | 5.0 | 281.0 | 329.2 | 1,995.0 | 17.4 | 339.4 | 706.8 | ||||||||||||||||||||||||||||||||||||

| Proved undeveloped reserves |

||||||||||||||||||||||||||||||||||||||||||||||||

| as at 31 December 2021 |

5,625.5 | 0.0 | 7.2 | 994.2 | 0.0 | 0.0 | 81.2 | 81.2 | 5,625.5 | 0.0 | 88.4 | 1,075.3 | ||||||||||||||||||||||||||||||||||||

| as at 31 December 2022 |

7,733.2 | 0.7 | 6.4 | 1,363.8 | 125.2 | 3.1 | 226.3 | 251.4 | 7,858.5 | 3.8 | 232.8 | 1,615.2 | ||||||||||||||||||||||||||||||||||||

| as at 31 December 2023 |

7,664.9 | 1.0 | 4.6 | 1,350.3 | 249.9 | 1.3 | 317.0 | 362.2 | 7,914.7 | 2.3 | 321.6 | 1,712.5 | ||||||||||||||||||||||||||||||||||||

| as at 31 December 2024 |

5,868.4 | 0.4 | 5.0 | 1,034.9 | 186.5 | 1.1 | 200.2 | 234.0 | 6,054.9 | 1.5 | 205.2 | 1,268.9 | ||||||||||||||||||||||||||||||||||||

Small differences due to rounding

2024 proved undeveloped reserves

At 31 December 2024, Woodside’s remaining proved undeveloped reserves were 1,268.9 MMboe, representing a decrease of 443.6 MMboe from the 1,712.5 MMboe as at 31 December 2023 (Table 3).

Following completion of the sales of 10.0% and 15.1% non-operating participating interest in the Scarborough Joint Venture in March 2024 and October 2024, respectively, Woodside’s proved undeveloped reserves decreased by 323.0 MMboe.

In 2024, 132.6 MMboe of proved undeveloped reserves were transferred to proved developed reserves with start-up of development wells in Sangomar (94.5 MMboe), Mad Dog and Atlantis (24.0 MMboe), and compression projects at Bass Strait (9.3 MMboe) and Macedon (4.9 MMboe).

20

Revisions of previous estimates resulted in proved undeveloped reserves increases of 5.0 MMboe. Technical updates at Greater Pluto resulted in proved undeveloped reserves increases of 20.7 MMboe, primarily due to production acceleration and onshore facility limits. Initial field performance and technical updates at Mad Dog and strong base performance at Julimar-Brunello in Australia contributed to proved undeveloped reserves decreases of 12.4 MMboe and 7.4 MMboe, respectively. The final investment decision and approval of multiple development opportunities in the United States and Australia, and minor development plan changes in the United States, resulted in proved undeveloped reserves increases of 5.2 MMboe.

The final investment decision on a single well development in Greater Pluto (Xena-3) resulted in extensions of proved undeveloped reserves of 7.1 MMboe.

Only undeveloped reserves in Julimar-Brunello have remained undeveloped for longer than five years from the dates they were initially reported and are expected to be developed in a phased manner to meet long-term contractual commitments. The project is included in the company business plan, demonstrating the intent to proceed with the development.

As of 31 December 2024, approximately 88% of Woodside’s proved undeveloped reserves are scheduled to be developed within five years of initial disclosure. The remaining proved undeveloped reserves (approximately 12%) are associated with large and complex capital investment projects, which are scheduled to be developed beyond five years from initial disclosure primarily due to facility ullage constraints and scheduled offshore drilling campaigns. Woodside is committed to these projects and continues to actively progress the development of these volumes.

During 2024, Woodside incurred approximately US$4.0 billion progressing the transfer of proved undeveloped reserves for projects where development status was achieved in 2024 or is expected to be achieved when development is completed in the future.

2023 proved undeveloped reserves

At 31 December 2023, Woodside’s remaining proved undeveloped reserves were 1,712.5 MMboe, representing an increase of 97.2 MMboe from the 1,615.2 MMboe as at 31 December 2022 (Table 3).