UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): 4/29/2024

UMB FINANCIAL CORPORATION

(Exact name of registrant as specified in its charter)

Commission File Number: 001-38481

| Missouri | 43-0903811 | |

| (State or other jurisdiction of incorporation) |

(IRS Employer Identification No.) |

1010 Grand Blvd., Kansas City, MO 64106

(Address of principal executive offices, including zip code)

(816) 860-7000

(Registrant’s telephone number, including area code)

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ☐ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ | Pre-commencement communications pursuant to Rule 13c-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of each class |

Trading |

Name of each exchange on which registered |

||

| Common Stock, $1.00 Par Value | UMBF | The NASDAQ Global Select Market |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

| Item 2.02 | Results of Operations and Financial Condition |

On April 29, 2024, UMB Financial Corporation (the “Company”) issued a press release announcing the financial results for the Company for the quarter ended March 31, 2024. A copy of the press release is attached as Exhibit 99.1 and the information is hereby incorporated by reference herein. The Company does not incorporate by reference information presented at any website referenced in the press release.

The information contained in Item 2.02 of this Current Report on Form 8-K, including Exhibit 99.1 hereto, is being furnished and shall not be deemed to be “filed” with the Securities and Exchange Commission (“SEC”) for the purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise subject to the liabilities of that section and is not incorporated by reference into any filing of the Company under the Securities Act of 1933, as amended (the “Securities Act”), or the Exchange Act, whether made before or after the date hereof, except as shall be expressly set forth by specific reference to this Current Report on Form 8-K in such a filing.

| Item 7.01 | Regulation FD Disclosure |

On April 29, 2024, the Company announced in the same press release that the Board of Directors of the Company had declared a quarterly dividend of $0.39 per share that is payable on July 1, 2024 to shareholders of record of the Company as of the close of business on June 10, 2024.

The April 29, 2024 press release that is attached as Exhibit 99.1 also announced that the Board has authorized the repurchase of up to one million shares of the Company’s common stock from time to time until the meeting of the Board that immediately follows the 2025 annual meeting of the Company’s shareholders.

The Company is furnishing a copy of the investor presentation materials dated April 30, 2024, addressing the Company’s first quarter earnings. A copy of the materials is attached as Exhibit 99.2 and will be available on the Company’s website at www.umb.comThe Company disclaims any obligation to correct or update any of the materials in the future.

The information provided under Item 7.01 of this Current Report on Form 8-K, including Exhibits 99.1 and 99.2 hereto, is being furnished and is not deemed to be “filed” with the SEC for the purposes of Section 18 of the Exchange Act or otherwise subject to the liabilities of that section and is not incorporated by reference into any filing of the Company under the Securities Act or the Exchange Act, whether made before or after the date hereof, except as shall be expressly set forth by specific reference to this Current Report on Form 8-K in such a filing. The Company does not incorporate by reference to this Current Report on Form 8-K information presented at any website referenced in this report or in any of the Exhibits attached hereto.

| Item 9.01 | Financial Statements and Exhibits |

| 99.1 | Press Release announcing financial results for quarter ended March 31, 2024, and announcing dividend declaration and share repurchase. | |

| 99.2 | Investor Presentation Materials, dated April 29, 2024. | |

| 104 | The cover page from this Current Report on Form 8-K, formatted in Inline XBRL. | |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| UMB FINANCIAL CORPORATION | ||

| By: | /s/ Ram Shankar |

|

| Ram Shankar | ||

| Chief Financial Officer | ||

Date: April 29, 2024

Exhibit 99.1

| UMB Financial Corporation 1010 Grand Boulevard Kansas City, MO 64106 816.860.7000 umb.com |

News Release |

//FOR IMMEDIATE RELEASE//

Media Contact: Stephanie Hague: 816.729.1027

Investor Relations Contact: Kay Gregory: 816.860.7106

UMB Financial Corporation Reports First Quarter 2024 Net Income of $110.3 Million and Net Operating Income(i) of $120.7 Million.

UMB investment community call today, Monday, April 29, at 7:30 a.m. (CT) / 8:30 a.m. (ET)

First Quarter 2024 Financial Highlights

| • | GAAP net income of $110.3 million, or $2.25 per diluted share. |

| • | Net operating income(i) of $120.7 million, or $2.47 per diluted share. |

| • | Average loans increased 4.2% on a linked-quarter, annualized basis, to $23.4 billion. |

| • | Average loans increased $2.1 billion, or 9.8%, as compared to the first quarter of 2023. |

| • | Average deposits increased 10.4% on a linked-quarter, annualized basis, to $33.5 billion. |

| • | Net interest income increased 3.9% from the linked quarter. |

| • | Net interest margin was 2.48%, an increase of two basis points from the linked quarter. |

| • | Noninterest income increased 22.3% from the first quarter of 2023, equal to 39.9% of total revenue. |

| • | Credit quality remained strong, with net charge-offs of just 0.05% of average loans. |

KANSAS CITY, Mo. (April 29, 2024) – UMB Financial Corporation (Nasdaq: UMBF), a financial services company, announced net income for the first quarter of 2024 of $110.3 million, or $2.25 per diluted share, compared to $70.9 million, or $1.45 per diluted share, in the fourth quarter of 2023 (linked quarter) and $92.4 million, or $1.90 per diluted share, in the first quarter of 2023. The results for the first quarter of 2024 and the fourth quarter of 2023 include pre-tax expense of $13.0 million and $52.8 million, respectively, for the industry-wide FDIC special assessment.

Net operating income, a non-GAAP financial measure reconciled later in this release to net income, the nearest comparable GAAP measure, was $120.7 million, or $2.47 per diluted share, for the first quarter of 2024, compared to $112.0 million, or $2.29 per diluted share, for the linked quarter and $92.8 million, or $1.91 per diluted share, for the first quarter of 2023. Operating pre-tax, pre-provision income (operating PTPP), a non-GAAP measure reconciled later in this release to the components of net income before taxes, the nearest comparable GAAP measure, was $157.5 million, or $3.22 per diluted share, for the first quarter of 2024, compared to $134.9 million, or $2.76 per diluted share, for the linked quarter, and $135.4 million, or $2.78 per diluted share, for the first quarter of 2023. These operating PTPP results represent increases of 16.7% on a linked-quarter basis and 16.3% compared to the first quarter of 2023.

“Our 2024 is off to a great start, with strong first quarter financial results driven by balance sheet and net interest income growth, net interest margin expansion, double-digit growth in our fee income revenue, and stable credit metrics,” said Mariner Kemper, UMB Financial Corporation chairman and chief executive officer.

“Our performance validates the perspective I shared earlier this year that the dramatized and highly exaggerated regional bank crisis from a year ago—and similar frenzy over idiosyncratic commercial real estate headlines earlier this year—do not apply to the whole regional banking industry, which remains on strong footing. As students of history, we believe in gravity and that what goes up will eventually come down. We run the company based on this expectation.

While indications suggest the economy is on reasonably stable footing, persistently high inflation, an upcoming presidential election cycle, and a potential ‘No Landing’ scenario may dictate a constrictive Federal Reserve monetary policy that could pose economic challenges.

In the first quarter of 2024, average loans increased 9.8% to $23.4 billion, while average deposits increased $2.0 billion or 6.2%, from one year ago. Our financial metrics demonstrate our borrowers and depository clients remain cautiously optimistic and selective with their investments. The overall loan portfolio remains healthy as exemplified by net charge-offs averaging less than 10 basis points in each of the past seven quarters, and non-performing loans at a meager eight basis points of total loans. Also of note for the quarter is that we closed on the purchase of a co-branded credit card portfolio partnership with Rural King, a preeminent, family-owned general merchandise store with more than 130 locations in a 13-state footprint.”

(i) A non-GAAP financial measure reconciled later in this release to net income, the nearest comparable GAAP measure.

First Quarter 2024 earnings discussion

| Summary of quarterly financial results |

UMB Financial Corporation | |||||||||||

| (unaudited, dollars in thousands, except per share data) | ||||||||||||

| Q1 2024 |

Q4 2023 |

Q1 2023 |

||||||||||

| Net income (GAAP) |

$ | 110,258 | $ | 70,923 | $ | 92,437 | ||||||

| Earnings per share - diluted (GAAP) |

2.25 | 1.45 | 1.90 | |||||||||

| Operating pre-tax, pre-provision income (Non-GAAP)(i) |

157,451 | 134,901 | 135,369 | |||||||||

| Operating pre-tax, pre-provision earnings per share - diluted (Non-GAAP)(i) |

3.22 | 2.76 | 2.78 | |||||||||

| Operating pre-tax, pre-provision income - FTE (Non-GAAP)(i) |

163,967 | 141,571 | 141,924 | |||||||||

| Operating pre-tax, pre-provision earnings per share - FTE - diluted (Non-GAAP)(i) |

3.35 | 2.90 | 2.91 | |||||||||

| Net operating income (Non-GAAP)(i) |

120,712 | 112,038 | 92,836 | |||||||||

| Operating earnings per share - diluted (Non-GAAP)(i) |

2.47 | 2.29 | 1.91 | |||||||||

| GAAP |

||||||||||||

| Return on average assets |

1.06 | % | 0.69 | % | 0.97 | % | ||||||

| Return on average equity |

14.11 | 9.52 | 13.76 | |||||||||

| Efficiency ratio |

63.44 | 77.65 | 63.12 | |||||||||

| Non-GAAP(i) |

||||||||||||

| Operating return on average assets |

1.16 | % | 1.10 | % | 0.98 | % | ||||||

| Operating return on average equity |

15.44 | 15.04 | 13.82 | |||||||||

| Operating efficiency ratio |

60.04 | 63.06 | 62.98 | |||||||||

| (i) | See reconciliation of Non-GAAP measures to their nearest comparable GAAP measures later in this release. |

| Summary of revenue |

UMB Financial Corporation | |||||||||||||||||||

| (unaudited, dollars in thousands) | ||||||||||||||||||||

| Q1 | Q4 | Q1 | CQ vs. | CQ vs. | ||||||||||||||||

| 2024 | 2023 | 2023 | LQ | PY | ||||||||||||||||

| Net interest income |

$ | 239,434 | $ | 230,522 | $ | 241,696 | $ | 8,912 | $ | (2,262 | ) | |||||||||

| Noninterest income: |

||||||||||||||||||||

| Trust and securities processing |

69,478 | 66,584 | 62,359 | 2,894 | 7,119 | |||||||||||||||

| Trading and investment banking |

5,462 | 5,751 | 5,308 | (289 | ) | 154 | ||||||||||||||

| Service charges on deposit accounts |

20,757 | 21,330 | 21,159 | (573 | ) | (402 | ) | |||||||||||||

| Insurance fees and commissions |

283 | 238 | 274 | 45 | 9 | |||||||||||||||

| Brokerage fees |

13,160 | 13,439 | 13,676 | (279 | ) | (516 | ) | |||||||||||||

| Bankcard fees |

21,968 | 18,672 | 18,172 | 3,296 | 3,796 | |||||||||||||||

| Investment securities gains (losses), net |

9,371 | 1,014 | (5,324 | ) | 8,357 | 14,695 | ||||||||||||||

| Other |

18,765 | 13,226 | 14,576 | 5,539 | 4,189 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total noninterest income |

$ | 159,244 | $ | 140,254 | $ | 130,200 | $ | 18,990 | $ | 29,044 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total revenue |

$ | 398,678 | $ | 370,776 | $ | 371,896 | $ | 27,902 | $ | 26,782 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income (FTE) |

$ | 245,950 | $ | 237,192 | $ | 248,251 | ||||||||||||||

| Net interest margin (FTE) |

2.48 | % | 2.46 | % | 2.76 | % | ||||||||||||||

| Total noninterest income as a % of total revenue |

39.9 | 37.8 | 35.0 | |||||||||||||||||

Net interest income

| • | First quarter 2024 net interest income totaled $239.4 million, an increase of $8.9 million, or 3.9%, from the linked quarter, driven primarily by continued growth in average loans and higher levels of liquidity, $1.4 million in municipal bond hedge gain amortization, partially offset by higher interest expense. |

| • | Average earning assets increased $1.6 billion, or 4.1%, from the linked quarter, largely driven by an increase of $931.4 million in interest-bearing due from banks, an increase of $428.4 million in average securities, and an increase of $245.0 million in average loans. |

| • | Average interest-bearing liabilities increased $1.3 billion, or 4.9%, from the linked quarter, primarily driven by increases of $903.2 million in interest-bearing deposits and $501.4 million in federal funds and repurchase agreements, partially offset by a decrease of $102.8 million in borrowed funds. Average noninterest-bearing demand deposits decreased $52.3 million, or 0.5%, as compared to the linked quarter. |

| • | Net interest margin for the first quarter was 2.48%, an increase of two basis points from the linked quarter, driven by increased loan yields, the benefit of free funds, favorable impact of bond hedge gain amortization, and earning asset mix changes, partially offset by the increased cost of interest-bearing liabilities. The cost of interest-bearing liabilities increased eight basis points to 4.03%. Total cost of funds increased nine basis points from the linked quarter to 2.96%. Both average loan yields and earning asset yields increased 10 basis points from the linked quarter. |

| • | On a year-over-year basis, net interest income decreased $2.3 million, or 0.9%, driven by higher interest expense, primarily due to an unfavorable mix shift in the composition of liabilities and new deposit client acquisitions at prevailing market rates. This decrease was partially offset by a $2.1 billion, or 9.8%, increase in average loans as well as the benefit from higher short-term interest rates on loan pricing and yields. |

| • | Compared to the first quarter of 2023, average earning assets increased $3.4 billion, or 9.4%, largely driven by the increase in average loans noted above and an increase of $1.8 billion in interest-bearing due from banks, partially offset by a decrease of $244.7 million in federal funds sold and resell agreements. |

| • | Average deposits increased 6.2% compared to the first quarter of 2023. Average noninterest-bearing demand deposit balances decreased 15.5% compared to the first quarter of 2023, driven by migration to rate-bearing deposit categories, as expected in a higher interest rate environment. Average demand deposit balances comprised 30.0% of total deposits, compared to 31.0% in the linked quarter and 37.8% in the first quarter of 2023. |

| • | Average borrowed funds decreased $102.8 million as compared to the linked quarter and increased $983.1 million as compared to the first quarter of 2023, driven by short-term borrowings with the Federal Home Loan Bank and the Federal Reserve. |

Noninterest income

| • | First quarter 2024 noninterest income increased $19.0 million, or 13.5%, on a linked-quarter basis, largely due to: |

| • | $8.4 million in higher investment securities gains, primarily driven by a net $8.6 million gain on disposition of two of the company’s non-marketable securities. The company recognized a gain of $10.7 million and a loss of $2.1 million, respectively, on these two securities. |

| • | An increase of $5.8 million in other miscellaneous income, recorded in other income, related to a $4.0 million legal settlement and a $1.8 million gain on sale of land, both recorded during the first quarter of 2024. |

| • | An increase of $3.3 million in bankcard income primarily driven by higher interchange revenue and lower rebates and rewards expense as compared to the linked quarter. |

| • | Increases of $1.1 million in trust income, $1.0 million in fund services income, and $0.8 million in corporate trust income, all recorded in trust and securities processing. |

| • | These increases were partially offset by decreases of $0.8 million in derivative income, recorded in other income, and $0.6 million in service charges on deposits. |

| • | Compared to the prior year, noninterest income in the first quarter of 2024 increased $29.0 million, or 22.3%, primarily driven by: |

| • | An increase of $14.7 million in investment securities gains, primarily driven by a $10.7 million gain on disposition of one of the company’s non-marketable securities during the first quarter of 2024, coupled with the impairment loss on an available-for-sale subordinated debt security recorded in the prior year. |

| • | An increase of $5.7 million in other miscellaneous income, recorded in other income, related to a $4.0 million legal settlement and a $1.8 million gain on sale of land, both recorded during the first quarter of 2024. |

| • | Increases of $5.0 million in fund services income, $1.1 million in trust income, and $1.0 million in corporate trust income, all recorded in trust and securities processing. |

| • | An increase of $3.8 million in bankcard income primarily driven by higher interchange revenue and lower rebates and rewards expense as compared to the prior year. |

| • | These increases were partially offset by a decrease of $2.4 million in derivative income, recorded in other income. |

Noninterest expense

| Summary of noninterest expense |

UMB Financial Corporation | |||||||||||||||||||

| (unaudited, dollars in thousands) | ||||||||||||||||||||

| Q1 | Q4 | Q1 | CQ vs. | CQ vs. | ||||||||||||||||

| 2024 | 2023 | 2023 | LQ | PY | ||||||||||||||||

| Salaries and employee benefits |

$ | 143,006 | $ | 134,231 | $ | 142,498 | $ | 8,775 | $ | 508 | ||||||||||

| Occupancy, net |

12,270 | 12,296 | 12,177 | (26 | ) | 93 | ||||||||||||||

| Equipment |

16,503 | 16,579 | 17,849 | (76 | ) | (1,346 | ) | |||||||||||||

| Supplies and services |

3,301 | 5,546 | 3,875 | (2,245 | ) | (574 | ) | |||||||||||||

| Marketing and business development |

6,025 | 6,659 | 5,335 | (634 | ) | 690 | ||||||||||||||

| Processing fees |

27,936 | 27,271 | 23,240 | 665 | 4,696 | |||||||||||||||

| Legal and consulting |

7,894 | 8,424 | 7,285 | (530 | ) | 609 | ||||||||||||||

| Bankcard |

10,567 | 8,677 | 7,133 | 1,890 | 3,434 | |||||||||||||||

| Amortization of other intangible assets |

1,960 | 2,048 | 2,298 | (88 | ) | (338 | ) | |||||||||||||

| Regulatory fees |

19,395 | 59,183 | 5,551 | (39,788 | ) | 13,844 | ||||||||||||||

| Other |

5,947 | 9,060 | 9,811 | (3,113 | ) | (3,864 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total noninterest expense |

$ | 254,804 | $ | 289,974 | $ | 237,052 | $ | (35,170 | ) | $ | 17,752 | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| • | GAAP noninterest expense for the first quarter of 2024 was $254.8 million, a decrease of $35.2 million, or 12.1%, from the linked quarter and an increase of $17.8 million, or 7.5% from the first quarter of 2023. Operating noninterest expense, a non-GAAP financial measure reconciled later in this release to noninterest expense, the nearest comparable GAAP measure, was $241.2 million for the first quarter of 2024, an increase of $5.4 million, or 2.3%, from the linked quarter and an increase of $4.7 million, or 2.0%, from the first quarter of 2023. |

| • | The linked-quarter decrease in GAAP noninterest expense was driven by: |

| • | A decrease of $39.8 million in regulatory fees expense, driven by the lower FDIC special assessment levied on banks to recoup the losses related to two of the bank failures in March 2023. The results for the first quarter of 2024 and the fourth quarter of 2023 include pre-tax expense of $13.0 million and $52.8 million, respectively, for the industry-wide FDIC special assessment. |

| • | A decrease of $2.2 million in supplies driven by purchases of computers during the linked quarter. |

| • | Decreases of $1.5 million in operational losses and $1.3 million in charitable contribution expense, both recorded in other expense. |

| • | These decreases were partially offset by a seasonal increase of $9.1 million in payroll taxes, insurance, and 401(k) expense recognized in the first quarter. |

| • | The year-over-year increase in GAAP noninterest expense was driven by: |

| • | An increase of $13.8 million in regulatory fees, primarily driven by the aforementioned $13.0 million FDIC special assessment recorded in the first quarter of 2024. |

| • | An increase of $4.7 million in processing fees expense due to the ongoing modernization of the company’s core systems and the timing of multiple software projects. |

| • | An increase of $3.4 million in bankcard expense driven by higher administrative expenses and fraud losses. |

| • | These increases were partially offset by decreases of $3.5 million in operational losses, recorded in other expense, and $1.3 million in equipment expense, driven by reduced software expense. |

Income taxes

| • | The company’s effective tax rate was 17.6% for the three months ended March 31, 2024, compared to 17.2% for the same period in 2023. |

Balance sheet

| • | Average total assets for the first quarter of 2024 were $42.0 billion compared to $40.5 billion for the linked quarter and $38.5 billion for the same period in 2023. |

| Summary of average loans and leases - QTD Average |

UMB Financial Corporation | |||||||||||||||||||

| (unaudited, dollars in thousands) | ||||||||||||||||||||

| Q1 | Q4 | Q1 | CQ vs. | CQ vs. | ||||||||||||||||

| 2024 | 2023 | 2023 | LQ | PY | ||||||||||||||||

| Commercial and industrial |

$ | 9,942,457 | $ | 9,825,043 | $ | 9,287,319 | $ | 117,414 | $ | 655,138 | ||||||||||

| Specialty lending |

485,989 | 496,816 | 564,633 | (10,827 | ) | (78,644 | ) | |||||||||||||

| Commercial real estate |

9,026,511 | 8,890,057 | 7,812,140 | 136,454 | 1,214,371 | |||||||||||||||

| Consumer real estate |

2,968,320 | 2,945,114 | 2,738,184 | 23,206 | 230,136 | |||||||||||||||

| Consumer |

154,062 | 153,791 | 136,571 | 271 | 17,491 | |||||||||||||||

| Credit cards |

489,546 | 495,502 | 453,704 | (5,956 | ) | 35,842 | ||||||||||||||

| Leases and other |

287,158 | 302,740 | 279,049 | (15,582 | ) | 8,109 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total loans |

$ | 23,354,043 | $ | 23,109,063 | $ | 21,271,600 | $ | 244,980 | $ | 2,082,443 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| • | Average loans for the first quarter of 2024 increased $245.0 million, or 1.1%, on a linked-quarter basis and $2.1 billion, or 9.8%, compared to the first quarter of 2023. |

| Summary of average securities - QTD Average |

UMB Financial Corporation | |||||||||||||||||||

| (unaudited, dollars in thousands) | ||||||||||||||||||||

| Q1 | Q4 | Q1 | CQ vs. | CQ vs. | ||||||||||||||||

| 2024 | 2023 | 2023 | LQ | PY | ||||||||||||||||

| Securities available for sale: |

||||||||||||||||||||

| U.S. Treasury |

$ | 1,127,611 | $ | 859,114 | $ | 783,170 | $ | 268,497 | $ | 344,441 | ||||||||||

| U.S. Agencies |

199,719 | 169,723 | 171,825 | 29,996 | 27,894 | |||||||||||||||

| Mortgage-backed |

3,595,619 | 3,466,152 | 3,938,137 | 129,467 | (342,518 | ) | ||||||||||||||

| State and political subdivisions |

1,254,148 | 1,218,176 | 1,356,785 | 35,972 | (102,637 | ) | ||||||||||||||

| Corporates |

341,142 | 345,634 | 364,854 | (4,492 | ) | (23,712 | ) | |||||||||||||

| Collateralized loan obligations |

347,063 | 349,149 | 348,477 | (2,086 | ) | (1,414 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total securities available for sale |

$ | 6,865,302 | $ | 6,407,948 | $ | 6,963,248 | $ | 457,354 | $ | (97,946 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Securities held to maturity: |

||||||||||||||||||||

| U.S. Agencies |

$ | 123,225 | $ | 123,195 | $ | 123,106 | $ | 30 | $ | 119 | ||||||||||

| Mortgage-backed |

2,707,780 | 2,756,528 | 2,934,113 | (48,748 | ) | (226,333 | ) | |||||||||||||

| State and political subdivisions |

2,821,799 | 2,825,138 | 2,814,912 | (3,339 | ) | 6,887 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total securities held to maturity |

$ | 5,652,804 | $ | 5,704,861 | $ | 5,872,131 | $ | (52,057 | ) | $ | (219,327 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Trading securities |

$ | 17,893 | $ | 16,880 | $ | 9,258 | $ | 1,013 | $ | 8,635 | ||||||||||

| Other securities |

478,805 | 456,758 | 359,238 | 22,047 | 119,567 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total securities |

$ | 13,014,804 | $ | 12,586,447 | $ | 13,203,875 | $ | 428,357 | $ | (189,071 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| • | Average total securities increased 3.4% on a linked-quarter basis and decreased 1.4% compared to the first quarter of 2023. |

| • | At March 31, 2024, the unrealized pre-tax net loss on the available-for-sale securities portfolio was $665.9 million, or 9.2% of the $7.2 billion amortized cost balance. At March 31, 2024, the unrealized pre-tax net loss on the securities designated as held to maturity was $601.3 million, or 10.7% of the $5.6 billion amortized cost value. |

| Summary of average deposits - QTD Average |

UMB Financial Corporation | |||||||||||||||||||

| (unaudited, dollars in thousands) | ||||||||||||||||||||

| Q1 | Q4 | Q1 | CQ vs. | CQ vs. | ||||||||||||||||

| 2024 | 2023 | 2023 | LQ | PY | ||||||||||||||||

| Deposits: |

||||||||||||||||||||

| Noninterest-bearing demand |

$ | 10,066,409 | $ | 10,118,748 | $ | 11,919,277 | $ | (52,339 | ) | $ | (1,852,868 | ) | ||||||||

| Interest-bearing demand and savings |

20,701,659 | 19,457,878 | 18,427,662 | 1,243,781 | 2,273,997 | |||||||||||||||

| Time deposits |

2,758,064 | 3,098,636 | 1,215,506 | (340,572 | ) | 1,542,558 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total deposits |

$ | 33,526,132 | $ | 32,675,262 | $ | 31,562,445 | $ | 850,870 | $ | 1,963,687 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Noninterest bearing deposits as % of total |

30.0 | % | 31.0 | % | 37.8 | % | ||||||||||||||

| • | Average deposits increased 2.6% on a linked-quarter basis and 6.2% compared to the first quarter of 2023. |

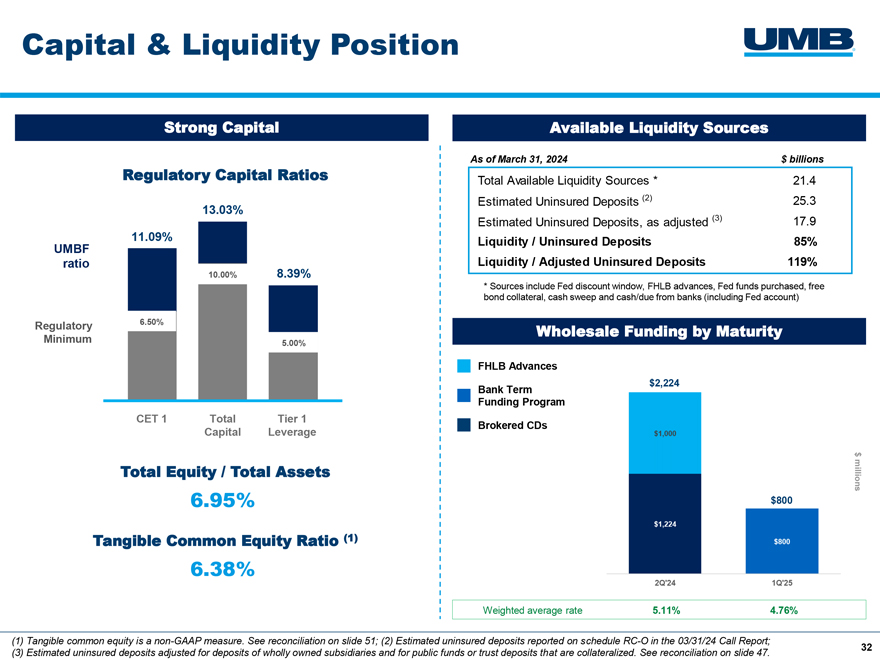

| • | As of March 31, 2024, total estimated uninsured deposits were $25.3 billion, or approximately 68.4% of total deposits. Estimated uninsured deposits, when adjusted to exclude affiliate (company-owned) and collateralized deposits, were $17.9 billion, and represented approximately 48.6% of total deposits. During the quarter, estimated adjusted uninsured deposits averaged $14.4 billion, or approximately 43.0% of total average deposits. |

Capital

| Capital information |

UMB Financial Corporation | |||||||||||

| (unaudited, dollars in thousands, except per share data) | ||||||||||||

| March 31, 2024 |

December 31, 2023 |

March 31, 2023 |

||||||||||

| Total equity |

$ | 3,152,816 | $ | 3,100,419 | $ | 2,814,659 | ||||||

| Accumulated other comprehensive loss, net |

(594,538 | ) | (556,935 | ) | (626,776 | ) | ||||||

| Book value per common share |

64.68 | 63.85 | 58.03 | |||||||||

| Tangible book value per common share (Non-GAAP)(i) |

59.01 | 58.12 | 52.17 | |||||||||

| Regulatory capital: |

||||||||||||

| Common equity Tier 1 capital |

$ | 3,503,837 | $ | 3,418,676 | $ | 3,196,111 | ||||||

| Tier 1 capital |

3,503,837 | 3,418,676 | 3,196,111 | |||||||||

| Total capital |

4,115,097 | 4,014,910 | 3,776,407 | |||||||||

| Regulatory capital ratios: |

||||||||||||

| Common equity Tier 1 capital ratio |

11.09 | % | 10.94 | % | 10.57 | % | ||||||

| Tier 1 risk-based capital ratio |

11.09 | 10.94 | 10.57 | |||||||||

| Total risk-based capital ratio |

13.03 | 12.85 | 12.49 | |||||||||

| Tier 1 leverage ratio |

8.39 | 8.49 | 8.35 | |||||||||

| (i) | See reconciliation of Non-GAAP measures to their nearest comparable GAAP measures later in this release. |

| • | At March 31, 2024, the regulatory capital ratios presented in the foregoing table exceeded all “well-capitalized” regulatory thresholds. |

Asset Quality

| Credit quality |

UMB Financial Corporation | |||||||||||||||||||

| (unaudited, dollars in thousands) | ||||||||||||||||||||

| Q1 | Q4 | Q3 | Q2 | Q1 | ||||||||||||||||

| 2024 | 2023 | 2023 | 2023 | 2023 | ||||||||||||||||

| Net charge-offs (recoveries) - total loans |

$ | 3,017 | $ | 1,352 | $ | 4,618 | $ | (139 | ) | $ | 4,643 | |||||||||

| Net loan charge-offs (recoveries) as a % of total average loans |

0.05 | % | 0.02 | % | 0.08 | % | (0.00 | )% | 0.09 | % | ||||||||||

| Loans over 90 days past due |

$ | 3,076 | $ | 3,111 | $ | 3,044 | $ | 10,675 | $ | 1,723 | ||||||||||

| Loans over 90 days past due as a % of total loans |

0.01 | % | 0.01 | % | 0.01 | % | 0.05 | % | 0.01 | % | ||||||||||

| Nonaccrual and restructured loans |

$ | 17,756 | $ | 13,212 | $ | 17,042 | $ | 19,347 | $ | 15,480 | ||||||||||

| Nonaccrual and restructured loans as a % of total loans |

0.08 | % | 0.06 | % | 0.07 | % | 0.09 | % | 0.07 | % | ||||||||||

| Provision for credit losses |

$ | 10,000 | $ | — | $ | 4,977 | $ | 13,000 | $ | 23,250 | ||||||||||

| • | Provision for credit losses for the first quarter increased $10.0 million from the linked quarter and decreased $13.3 million from the first quarter of 2023. This quarter’s provision included approximately $6.7 million related to the purchase of $109.4 million in co-branded credit card receivables. Excluding this, the variances in provision expense were driven largely by changes in macro-economic variables and credit metrics in the current period as compared to the prior periods. |

| • | Net charge-offs for the first quarter totaled $3.0 million, or 0.05% of average loans, compared to $1.4 million, or 0.02% of average loans in the linked quarter, and $4.6 million, or 0.09% of average loans for the first quarter of 2023. |

Dividend Declaration and Share Repurchase Authorization

At the company’s quarterly board meeting, the Board of Directors declared a $0.39 per share quarterly cash dividend, payable on July 1, 2024, to shareholders of record at the close of business on June 10, 2024.

The Board also approved the repurchase of up to 1,000,000 shares of the company’s common stock. Share repurchases may occur from time to time at any point until the regular meeting of the Board that immediately follows the 2025 annual meeting of the company’s shareholders. Shares acquired under the repurchase program may be available for reissuance or resale, including in connection with the company’s compensation plans and dividend reinvestment plan. Under the repurchase program, the company may acquire the shares from time to time in open market or privately negotiated transactions, at the discretion of management.

Conference Call

The company will host a call for the investment community on Monday, April 29, 2024, at 7:30 a.m. (CT). This call has been rescheduled from the previously announced date and time.

Interested parties may access the call by dialing (toll-free) 833-470-1428 or (international) 404-975-4839 and requesting to join the UMB Financial call with access code 397231. The live call may also be accessed by visiting investorrelations.umb.com or by using the following link:

UMB Financial Conference Call

A replay of the conference call may be heard through May 13, 2024, by calling (toll-free) 866-813-9403 or (international) 929-458-6194. The replay access code required for playback is 182605. The call replay may also be accessed at investorrelations.umb.com.

Non-GAAP Financial Information

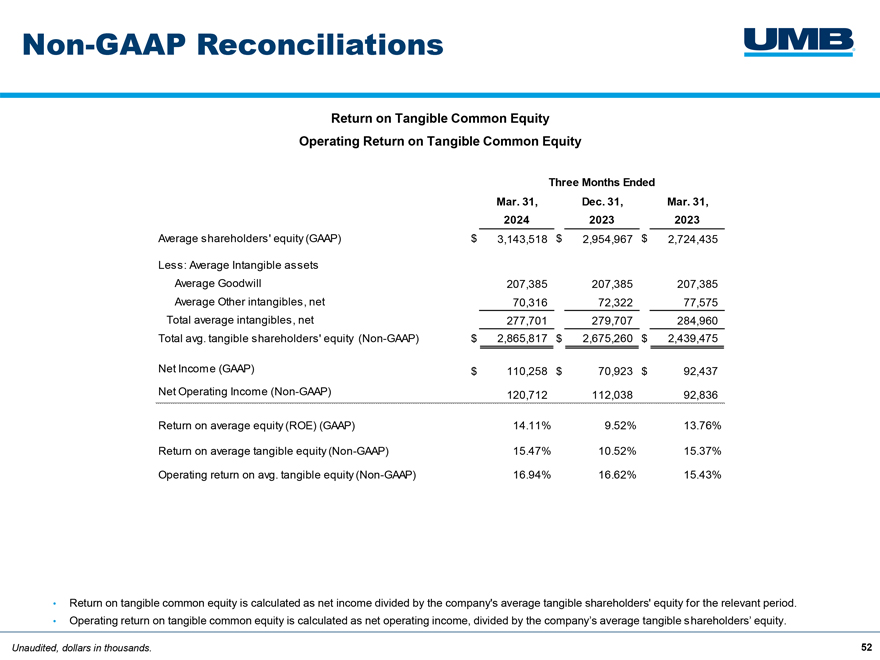

In this release, we provide information about net operating income, operating earnings per share – diluted (operating EPS), operating return on average equity (operating ROE), operating return on average assets (operating ROA), operating noninterest expense, operating efficiency ratio, operating pre-tax, pre-provision income (operating PTPP), operating pre-tax, pre-provision earnings per share – diluted (operating PTPP EPS), operating pre-tax, pre-provision income on a fully tax equivalent basis (operating PTPP-FTE), operating pre-tax, pre-provision FTE earnings per share – diluted (operating PTPP-FTE EPS), tangible shareholders’ equity, and tangible book value per share, all of which are non-GAAP financial measures. This information supplements the results that are reported according to generally accepted accounting principles in the United States (GAAP) and should not be viewed in isolation from, or as a substitute for, GAAP results. The differences between the non-GAAP financial measures – net operating income, operating EPS, operating ROE, operating ROA, operating noninterest expense, operating efficiency ratio, operating PTPP, operating PTPP EPS, operating PTPP-FTE, operating PTPP-FTE EPS, tangible shareholders’ equity, and tangible book value per share – and the nearest comparable GAAP financial measures are reconciled later in this release. The company believes that these non-GAAP financial measures and the reconciliations may be useful to investors because they adjust for acquisition-and severance-related items, and the FDIC special assessment that management does not believe reflect the company’s fundamental operating performance.

Net operating income for the relevant period is defined as GAAP net income, adjusted to reflect the impact of excluding expenses related to acquisitions, severance expense, the FDIC special assessment, and the cumulative tax impact of these adjustments.

Operating EPS (diluted) is calculated as earnings per share as reported, adjusted to reflect, on a per share basis, the impact of excluding the non-GAAP adjustments described above for the relevant period. Operating ROE is calculated as net operating income, divided by the company’s average total shareholders’ equity for the relevant period. Operating ROA is calculated as net operating income, divided by the company’s average assets for the relevant period. Operating noninterest expense for the relevant period is defined as GAAP noninterest expense, adjusted to reflect the pre-tax impact of non-GAAP adjustments described above. Operating efficiency ratio is calculated as the company’s operating noninterest expense, net of amortization of other intangibles, divided by the company’s total non-GAAP revenue (calculated as net interest income plus noninterest income, less gains on sales of securities available for sale, net).

Operating PTPP income for the relevant period is defined as GAAP net interest income plus GAAP noninterest income, less noninterest expense, adjusted to reflect the impact of excluding expenses related to acquisitions and severance, and the FDIC special assessment.

Operating PTPP-FTE for the relevant period is defined as GAAP net interest income on a fully tax equivalent basis plus GAAP noninterest income, less noninterest expense, adjusted to reflect the impact of excluding expenses related to acquisitions and severance, and the FDIC special assessment.

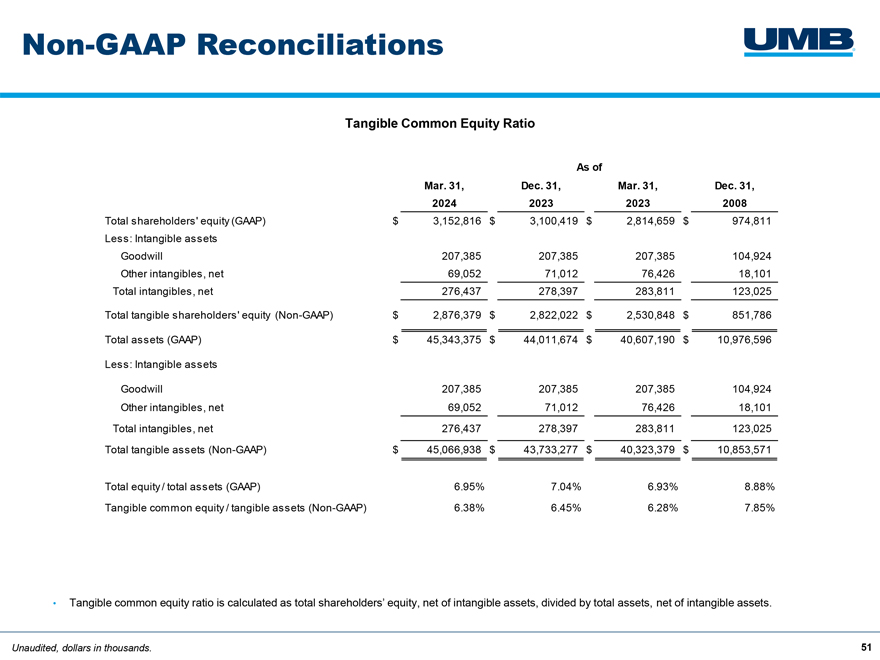

Tangible shareholders’ equity for the relevant period is defined as GAAP shareholders’ equity, net of intangible assets. Tangible book value per share is defined as tangible shareholders’ equity divided by the Company’s total shares outstanding.

Forward-Looking Statements:

This press release contains, and our other communications may contain, forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements can be identified by the fact that they do not relate strictly to historical or current facts. Forward-looking statements often use words such as “believe,” “expect,” “anticipate,” “intend,” “estimate,” “project,” “outlook,” “forecast,” “target,” “trend,” “plan,” “goal,” or other words of comparable meaning or future-tense or conditional verbs such as “may,” “will,” “should,” “would,” or “could.” Forward-looking statements convey our expectations, intentions, or forecasts about future events, circumstances, results, or aspirations. All forward-looking statements are subject to assumptions, risks, and uncertainties, which may change over time and many of which are beyond our control. You should not rely on any forward-looking statement as a prediction or guarantee about the future. Our actual future objectives, strategies, plans, prospects, performance, condition, or results may differ materially from those set forth in any forward-looking statement.

Some of the factors that may cause actual results or other future events, circumstances, or aspirations to differ from those in forward-looking statements are described in our Annual Report on Form 10-K for the year ended December 31, 2023, our subsequent Quarterly Reports on Form 10-Q or Current Reports on Form 8-K, or other applicable documents that are filed or furnished with the U.S. Securities and Exchange Commission (SEC). In addition to such factors that have been disclosed previously: macroeconomic and adverse developments and uncertainties related to the collateral effects of the collapse of, and challenges for, domestic and international banks, including the impacts to the U.S. and global economies; sustained levels of high inflation and the potential for an economic recession on the heels of aggressive quantitative tightening by the Federal Reserve; and impacts related to or resulting from instability in the Middle East and Russia’s military action in Ukraine, such as the broader impacts to financial markets and the global macroeconomic and geopolitical environments, may also cause actual results or other future events, circumstances, or aspirations to differ from our forward-looking statements. Any forward-looking statement made by us or on our behalf speaks only as of the date that it was made. We do not undertake to update any forward-looking statement to reflect the impact of events, circumstances, or results that arise after the date that the statement was made, except to the extent required by applicable securities laws. You, however, should consult further disclosures (including disclosures of a forward-looking nature) that we may make in any subsequent Annual Report on Form 10-K, Quarterly Report on Form 10-Q, Current Report on Form 8-K, or other applicable document that is filed or furnished with the SEC.

About UMB:

UMB Financial Corporation (Nasdaq: UMBF) is a financial services company headquartered in Kansas City, Missouri. UMB offers commercial banking, which includes comprehensive deposit, lending and investment services, personal banking, which includes wealth management and financial planning services, and institutional banking, which includes asset servicing, corporate trust solutions, investment banking, and healthcare services. UMB operates branches throughout Missouri, Illinois, Colorado, Kansas, Oklahoma, Nebraska, Arizona and Texas. As the company’s reach continues to grow, it also serves business clients nationwide and institutional clients in several countries. For more information, visit UMB.com, UMB Blog, UMB Facebook and UMB LinkedIn.

| Consolidated Balance Sheets |

UMB Financial Corporation | |||||||

| (unaudited, dollars in thousands) | ||||||||

| March 31, | ||||||||

| 2024 | 2023 | |||||||

| ASSETS |

||||||||

| Loans |

$ | 23,637,649 | $ | 21,812,972 | ||||

| Allowance for credit losses on loans |

(226,159 | ) | (210,509 | ) | ||||

|

|

|

|

|

|||||

| Net loans |

23,411,490 | 21,602,463 | ||||||

| Loans held for sale |

4,415 | 1,422 | ||||||

| Securities: |

||||||||

| Available for sale |

6,541,391 | 6,907,897 | ||||||

| Held to maturity, net of allowance for credit losses |

5,622,617 | 5,859,323 | ||||||

| Trading securities |

40,187 | 19,823 | ||||||

| Other securities |

473,434 | 416,337 | ||||||

|

|

|

|

|

|||||

| Total securities |

12,677,629 | 13,203,380 | ||||||

| Federal funds sold and resell agreements |

180,275 | 368,158 | ||||||

| Interest-bearing due from banks |

6,673,104 | 3,121,323 | ||||||

| Cash and due from banks |

356,963 | 472,248 | ||||||

| Premises and equipment, net |

231,918 | 260,623 | ||||||

| Accrued income |

221,447 | 181,586 | ||||||

| Goodwill |

207,385 | 207,385 | ||||||

| Other intangibles, net |

69,052 | 76,426 | ||||||

| Other assets |

1,309,697 | 1,112,176 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 45,343,375 | $ | 40,607,190 | ||||

|

|

|

|

|

|||||

| LIABILITIES |

||||||||

| Deposits: |

||||||||

| Noninterest-bearing demand |

$ | 13,251,090 | $ | 12,488,803 | ||||

| Interest-bearing demand and savings |

21,018,911 | 16,760,603 | ||||||

| Time deposits under $250,000 |

2,044,280 | 456,129 | ||||||

| Time deposits of $250,000 or more |

599,329 | 2,226,369 | ||||||

|

|

|

|

|

|||||

| Total deposits |

36,913,610 | 31,931,904 | ||||||

| Federal funds purchased and repurchase agreements |

2,225,474 | 2,160,808 | ||||||

| Short-term debt |

1,800,000 | 2,800,000 | ||||||

| Long-term debt |

383,742 | 381,796 | ||||||

| Accrued expenses and taxes |

374,888 | 207,633 | ||||||

| Other liabilities |

492,845 | 310,390 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

42,190,559 | 37,792,531 | ||||||

|

|

|

|

|

|||||

| SHAREHOLDERS’ EQUITY |

||||||||

| Common stock |

55,057 | 55,057 | ||||||

| Capital surplus |

1,127,806 | 1,120,877 | ||||||

| Retained earnings |

2,903,106 | 2,609,928 | ||||||

| Accumulated other comprehensive loss, net |

(594,538 | ) | (626,776 | ) | ||||

| Treasury stock |

(338,615 | ) | (344,427 | ) | ||||

|

|

|

|

|

|||||

| Total shareholders’ equity |

3,152,816 | 2,814,659 | ||||||

|

|

|

|

|

|||||

| Total liabilities and shareholders’ equity |

$ | 45,343,375 | $ | 40,607,190 | ||||

|

|

|

|

|

|||||

| Consolidated Statements of Income |

UMB Financial Corporation | |||||||

| (unaudited, dollars in thousands except share and per share data) | ||||||||

| Three Months Ended March 31, |

||||||||

| 2024 | 2023 | |||||||

| INTEREST INCOME |

||||||||

| Loans |

$ | 385,566 | $ | 308,441 | ||||

| Securities: |

||||||||

| Taxable interest |

61,111 | 53,049 | ||||||

| Tax-exempt interest |

25,333 | 25,306 | ||||||

|

|

|

|

|

|||||

| Total securities income |

86,444 | 78,355 | ||||||

| Federal funds and resell agreements |

3,062 | 5,651 | ||||||

| Interest-bearing due from banks |

44,688 | 16,166 | ||||||

| Trading securities |

305 | 134 | ||||||

|

|

|

|

|

|||||

| Total interest income |

520,065 | 408,747 | ||||||

|

|

|

|

|

|||||

| INTEREST EXPENSE |

||||||||

| Deposits |

223,875 | 127,899 | ||||||

| Federal funds and repurchase agreements |

27,662 | 23,302 | ||||||

| Other |

29,094 | 15,850 | ||||||

|

|

|

|

|

|||||

| Total interest expense |

280,631 | 167,051 | ||||||

|

|

|

|

|

|||||

| Net interest income |

239,434 | 241,696 | ||||||

| Provision for credit losses |

10,000 | 23,250 | ||||||

|

|

|

|

|

|||||

| Net interest income after provision for credit losses |

229,434 | 218,446 | ||||||

|

|

|

|

|

|||||

| NONINTEREST INCOME |

||||||||

| Trust and securities processing |

69,478 | 62,359 | ||||||

| Trading and investment banking |

5,462 | 5,308 | ||||||

| Service charges on deposit accounts |

20,757 | 21,159 | ||||||

| Insurance fees and commissions |

283 | 274 | ||||||

| Brokerage fees |

13,160 | 13,676 | ||||||

| Bankcard fees |

21,968 | 18,172 | ||||||

| Investment securities gains (losses), net |

9,371 | (5,324 | ) | |||||

| Other |

18,765 | 14,576 | ||||||

|

|

|

|

|

|||||

| Total noninterest income |

159,244 | 130,200 | ||||||

|

|

|

|

|

|||||

| NONINTEREST EXPENSE |

||||||||

| Salaries and employee benefits |

143,006 | 142,498 | ||||||

| Occupancy, net |

12,270 | 12,177 | ||||||

| Equipment |

16,503 | 17,849 | ||||||

| Supplies and services |

3,301 | 3,875 | ||||||

| Marketing and business development |

6,025 | 5,335 | ||||||

| Processing fees |

27,936 | 23,240 | ||||||

| Legal and consulting |

7,894 | 7,285 | ||||||

| Bankcard |

10,567 | 7,133 | ||||||

| Amortization of other intangible assets |

1,960 | 2,298 | ||||||

| Regulatory fees |

19,395 | 5,551 | ||||||

| Other |

5,947 | 9,811 | ||||||

|

|

|

|

|

|||||

| Total noninterest expense |

254,804 | 237,052 | ||||||

|

|

|

|

|

|||||

| Income before income taxes |

133,874 | 111,594 | ||||||

| Income tax expense |

23,616 | 19,157 | ||||||

|

|

|

|

|

|||||

| NET INCOME |

$ | 110,258 | $ | 92,437 | ||||

|

|

|

|

|

|||||

| PER SHARE DATA |

||||||||

| Net income – basic |

$ | 2.27 | $ | 1.91 | ||||

| Net income – diluted |

2.25 | 1.90 | ||||||

| Dividends |

0.39 | 0.38 | ||||||

| Weighted average shares outstanding – basic |

48,663,515 | 48,435,016 | ||||||

| Weighted average shares outstanding – diluted |

48,920,863 | 48,746,562 | ||||||

| Consolidated Statements of Comprehensive Income |

UMB Financial Corporation | |||||||

| (unaudited, dollars in thousands) | ||||||||

| Three Months Ended March 31, |

||||||||

| 2024 | 2023 | |||||||

| Net income |

$ | 110,258 | $ | 92,437 | ||||

| Other comprehensive (loss) income, before tax: |

||||||||

| Unrealized gains and losses on debt securities: |

||||||||

| Change in unrealized holding gains and losses, net |

(41,553 | ) | 93,657 | |||||

| Less: Reclassification adjustment for net (gains) losses included in net income |

(139 | ) | 433 | |||||

| Amortization of net unrealized loss on securities transferred from available-for-sale to held-to-maturity |

8,789 | 9,983 | ||||||

|

|

|

|

|

|||||

| Change in unrealized gains and losses on debt securities |

(32,903 | ) | 104,073 | |||||

| Unrealized gains and losses on derivative hedges: |

||||||||

| Change in unrealized gains and losses on derivative hedges, net |

(13,658 | ) | (1,527 | ) | ||||

| Less: Reclassification adjustment for net gains included in net income |

(3,660 | ) | (2,561 | ) | ||||

|

|

|

|

|

|||||

| Change in unrealized gains and losses on derivative hedges |

(17,318 | ) | (4,088 | ) | ||||

| Other comprehensive (loss) income, before tax |

(50,221 | ) | 99,985 | |||||

| Income tax benefit (expense) |

12,618 | (24,026 | ) | |||||

|

|

|

|

|

|||||

| Other comprehensive (loss) income |

(37,603 | ) | 75,959 | |||||

|

|

|

|

|

|||||

| Comprehensive income |

$ | 72,655 | $ | 168,396 | ||||

|

|

|

|

|

|||||

| Consolidated Statements of Shareholders’ Equity |

UMB Financial Corporation | |||

| (unaudited, dollars in thousands except per share data) | ||||

| Common Stock |

Capital Surplus |

Retained Earnings |

Accumulated Other Comprehensive (Loss) Income |

Treasury Stock |

Total | |||||||||||||||||||

| Balance - January 1, 2023 |

$ | 55,057 | $ | 1,125,949 | $ | 2,536,086 | $ | (702,735 | ) | $ | (347,264 | ) | $ | 2,667,093 | ||||||||||

| Total comprehensive income |

— | — | 92,437 | 75,959 | — | 168,396 | ||||||||||||||||||

| Dividends ($0.38 per share) |

— | — | (18,595 | ) | — | — | (18,595 | ) | ||||||||||||||||

| Purchase of treasury stock |

— | — | — | — | (7,902 | ) | (7,902 | ) | ||||||||||||||||

| Issuances of equity awards, net of forfeitures |

— | (9,764 | ) | — | — | 10,483 | 719 | |||||||||||||||||

| Recognition of equity-based compensation |

— | 4,516 | — | — | — | 4,516 | ||||||||||||||||||

| Sale of treasury stock |

— | 71 | — | — | 56 | 127 | ||||||||||||||||||

| Exercise of stock options |

— | 105 | — | — | 200 | 305 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Balance - March 31, 2023 |

$ | 55,057 | $ | 1,120,877 | $ | 2,609,928 | $ | (626,776 | ) | $ | (344,427 | ) | $ | 2,814,659 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Balance - January 1, 2024 |

$ | 55,057 | $ | 1,134,363 | $ | 2,810,824 | $ | (556,935 | ) | $ | (342,890 | ) | $ | 3,100,419 | ||||||||||

| Total comprehensive income (loss) |

— | — | 110,258 | (37,603 | ) | — | 72,655 | |||||||||||||||||

| Dividends ($0.39 per share) |

— | — | (17,976 | ) | — | — | (17,976 | ) | ||||||||||||||||

| Purchase of treasury stock |

— | — | — | — | (7,537 | ) | (7,537 | ) | ||||||||||||||||

| Issuances of equity awards, net of forfeitures |

— | (10,964 | ) | — | — | 11,667 | 703 | |||||||||||||||||

| Recognition of equity-based compensation |

— | 4,271 | — | — | — | 4,271 | ||||||||||||||||||

| Sale of treasury stock |

— | 70 | — | — | 60 | 130 | ||||||||||||||||||

| Exercise of stock options |

— | 66 | — | — | 85 | 151 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Balance - March 31, 2024 |

$ | 55,057 | $ | 1,127,806 | $ | 2,903,106 | $ | (594,538 | ) | $ | (338,615 | ) | $ | 3,152,816 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Average Balances / Yields and Rates |

UMB Financial Corporation | |||

| (tax - equivalent basis) (unaudited, dollars in thousands) |

||||

| Three Months Ended March 31, | ||||||||||||||||

| 2024 | 2023 | |||||||||||||||

| Average Balance |

Average Yield/Rate |

Average Balance |

Average Yield/Rate |

|||||||||||||

| Assets |

||||||||||||||||

| Loans, net of unearned interest |

$ | 23,354,043 | 6.64 | % | $ | 21,271,600 | 5.88 | % | ||||||||

| Securities: |

||||||||||||||||

| Taxable |

9,264,789 | 2.65 | 9,349,351 | 2.30 | ||||||||||||

| Tax-exempt |

3,732,122 | 3.42 | 3,845,266 | 3.35 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total securities |

12,996,911 | 2.87 | 13,194,617 | 2.61 | ||||||||||||

| Federal funds and resell agreements |

206,443 | 5.97 | 451,188 | 5.08 | ||||||||||||

| Interest bearing due from banks |

3,304,142 | 5.44 | 1,533,704 | 4.27 | ||||||||||||

| Trading securities |

17,893 | 7.33 | 9,258 | 6.31 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total earning assets |

39,879,432 | 5.31 | 36,460,367 | 4.62 | ||||||||||||

| Allowance for credit losses |

(222,116 | ) | (196,128 | ) | ||||||||||||

| Other assets |

2,360,092 | 2,239,140 | ||||||||||||||

|

|

|

|

|

|||||||||||||

| Total assets |

$ | 42,017,408 | $ | 38,503,379 | ||||||||||||

|

|

|

|

|

|||||||||||||

| Liabilities and Shareholders’ Equity |

||||||||||||||||

| Interest-bearing deposits |

$ | 23,459,723 | 3.84 | % | $ | 19,643,168 | 2.64 | % | ||||||||

| Federal funds and repurchase agreements |

2,384,754 | 4.67 | 2,461,942 | 3.84 | ||||||||||||

| Borrowed funds |

2,183,494 | 5.36 | 1,200,346 | 5.36 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total interest-bearing liabilities |

28,027,971 | 4.03 | 23,305,456 | 2.91 | ||||||||||||

| Noninterest-bearing demand deposits |

10,066,409 | 11,919,277 | ||||||||||||||

| Other liabilities |

779,510 | 554,211 | ||||||||||||||

| Shareholders’ equity |

3,143,518 | 2,724,435 | ||||||||||||||

|

|

|

|

|

|||||||||||||

| Total liabilities and shareholders’ equity |

$ | 42,017,408 | $ | 38,503,379 | ||||||||||||

|

|

|

|

|

|||||||||||||

| Net interest spread |

1.28 | % | 1.71 | % | ||||||||||||

| Net interest margin |

2.48 | 2.76 | ||||||||||||||

| Business Segment Information |

UMB Financial Corporation | |||

| (unaudited, dollars in thousands) | ||||

| Three Months Ended March 31, 2024 | ||||||||||||||||

| Commercial Banking |

Institutional Banking |

Personal Banking |

Total | |||||||||||||

| Net interest income |

$ | 157,247 | $ | 49,860 | $ | 32,327 | $ | 239,434 | ||||||||

| Provision for credit losses |

7,520 | 479 | 2,001 | 10,000 | ||||||||||||

| Noninterest income |

42,966 | 92,716 | 23,562 | 159,244 | ||||||||||||

| Noninterest expense |

92,420 | 100,376 | 62,008 | 254,804 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) before taxes |

100,273 | 41,721 | (8,120 | ) | 133,874 | |||||||||||

| Income tax expense (benefit) |

17,223 | 7,656 | (1,263 | ) | 23,616 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

$ | 83,050 | $ | 34,065 | $ | (6,857 | ) | $ | 110,258 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Three Months Ended March 31, 2023 | ||||||||||||||||

| Commercial Banking |

Institutional Banking |

Personal Banking |

Total | |||||||||||||

| Net interest income |

$ | 151,027 | $ | 55,085 | 35,584 | $ | 241,696 | |||||||||

| Provision for credit losses |

21,045 | 96 | 2,109 | 23,250 | ||||||||||||

| Noninterest income |

22,902 | 84,238 | 23,060 | 130,200 | ||||||||||||

| Noninterest expense |

84,002 | 89,372 | 63,678 | 237,052 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) before taxes |

68,882 | 49,855 | (7,143 | ) | 111,594 | |||||||||||

| Income tax expense (benefit) |

11,646 | 8,504 | (993 | ) | 19,157 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

$ | 57,236 | $ | 41,351 | $ | (6,150 | ) | $ | 92,437 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

The company has strategically aligned its operations into the following three reportable segments: Commercial Banking, Institutional Banking, and Personal Banking. Senior executive officers regularly evaluate business segment financial results produced by the company’s internal reporting system in deciding how to allocate resources and assess performance for individual business segments. The company’s reportable segments include certain corporate overhead, technology and service costs that are allocated based on methodologies that are applied consistently between periods. For comparability purposes, amounts in all periods are based on methodologies in effect at March 31, 2024.

Non-GAAP Financial Measures

| Net operating income Non-GAAP reconciliations: |

UMB Financial Corporation | |||

| (unaudited, dollars in thousands except per share data) | ||||

| Three Months Ended March 31, |

||||||||

| 2024 | 2023 | |||||||

| Net income (GAAP) |

$ | 110,258 | $ | 92,437 | ||||

| Adjustments: |

||||||||

| Acquisition expense |

431 | 39 | ||||||

| Severance expense |

146 | 486 | ||||||

| FDIC special assessment |

13,000 | — | ||||||

| Tax-impact of adjustments (i) |

(3,123 | ) | (126 | ) | ||||

|

|

|

|

|

|||||

| Total Non-GAAP adjustments (net of tax) |

10,454 | 399 | ||||||

|

|

|

|

|

|||||

| Net operating income (Non-GAAP) |

$ | 120,712 | $ | 92,836 | ||||

|

|

|

|

|

|||||

| Earnings per share - diluted (GAAP) |

$ | 2.25 | $ | 1.90 | ||||

| Acquisition expense |

0.01 | — | ||||||

| Severance expense |

— | 0.01 | ||||||

| FDIC special assessment |

0.27 | — | ||||||

| Tax-impact of adjustments (i) |

(0.06 | ) | — | |||||

|

|

|

|

|

|||||

| Operating earnings per share - diluted (Non-GAAP) |

$ | 2.47 | $ | 1.91 | ||||

|

|

|

|

|

|||||

| GAAP |

||||||||

| Return on average assets |

1.06 | % | 0.97 | % | ||||

| Return on average equity |

14.11 | 13.76 | ||||||

| Non-GAAP |

||||||||

| Operating return on average assets |

1.16 | % | 0.98 | % | ||||

| Operating return on average equity |

15.44 | 13.82 | ||||||

(i) Calculated using the company’s marginal tax rate of 23.0% for 2024 and 24.0% for 2023.

| Operating noninterest expense and operating efficiency ratio Non-GAAP reconciliations: |

UMB Financial Corporation | |||

| (unaudited, dollars in thousands) | ||||

| Three Months Ended March 31, |

||||||||

| 2024 | 2023 | |||||||

| Noninterest expense |

$ | 254,804 | $ | 237,052 | ||||

| Adjustments to arrive at operating noninterest expense (pre-tax): |

||||||||

| Acquisition expense |

431 | 39 | ||||||

| Severance expense |

146 | 486 | ||||||

| FDIC special assessment |

13,000 | — | ||||||

|

|

|

|

|

|||||

| Total Non-GAAP adjustments (pre-tax) |

13,577 | 525 | ||||||

|

|

|

|

|

|||||

| Operating noninterest expense (Non-GAAP) |

$ | 241,227 | $ | 236,527 | ||||

|

|

|

|

|

|||||

| Noninterest expense |

$ | 254,804 | $ | 237,052 | ||||

| Less: Amortization of other intangibles |

1,960 | 2,298 | ||||||

|

|

|

|

|

|||||

| Noninterest expense, net of amortization of other intangibles (Non-GAAP) (numerator A) |

$ | 252,844 | $ | 234,754 | ||||

|

|

|

|

|

|||||

| Operating noninterest expense |

$ | 241,227 | $ | 236,527 | ||||

| Less: Amortization of other intangibles |

1,960 | 2,298 | ||||||

|

|

|

|

|

|||||

| Operating expense, net of amortization of other intangibles (Non-GAAP) (numerator B) |

$ | 239,267 | $ | 234,229 | ||||

|

|

|

|

|

|||||

| Net interest income |

$ | 239,434 | $ | 241,696 | ||||

| Noninterest income |

159,244 | 130,200 | ||||||

| Less: Gains (losses) on sales of securities available for sale, net |

139 | (2 | ) | |||||

|

|

|

|

|

|||||

| Total Non-GAAP Revenue (denominator A) |

$ | 398,539 | $ | 371,898 | ||||

|

|

|

|

|

|||||

| Efficiency ratio (numerator A/denominator A) |

63.44 | % | 63.12 | % | ||||

| Operating efficiency ratio (Non-GAAP) (numerator B/denominator A) |

60.04 | 62.98 | ||||||

| Operating pre-tax, pre-provision income non-GAAP reconciliations: |

UMB Financial Corporation | |||

| (unaudited, dollars in thousands except per share data) | ||||

| Three Months Ended March 31, |

||||||||

| 2024 | 2023 | |||||||

| Net interest income (GAAP) |

$ | 239,434 | $ | 241,696 | ||||

| Noninterest income (GAAP) |

159,244 | 130,200 | ||||||

| Noninterest expense (GAAP) |

254,804 | 237,052 | ||||||

| Adjustments to arrive at operating noninterest expense: |

||||||||

| Acquisition expense |

431 | 39 | ||||||

| Severance expense |

146 | 486 | ||||||

| FDIC special assessment |

13,000 | — | ||||||

|

|

|

|

|

|||||

| Total Non-GAAP adjustments |

13,577 | 525 | ||||||

|

|

|

|

|

|||||

| Operating noninterest expense (Non-GAAP) |

241,227 | 236,527 | ||||||

|

|

|

|

|

|||||

| Operating pre-tax, pre-provision income (Non-GAAP) |

$ | 157,451 | $ | 135,369 | ||||

|

|

|

|

|

|||||

| Net interest income earnings per share - diluted (GAAP) |

$ | 4.89 | $ | 4.96 | ||||

| Noninterest income (GAAP) |

3.26 | 2.67 | ||||||

| Noninterest expense (GAAP) |

5.21 | 4.86 | ||||||

| Acquisition expense |

0.01 | — | ||||||

| Severance expense |

— | 0.01 | ||||||

| FDIC special assessment |

0.27 | — | ||||||

|

|

|

|

|

|||||

| Operating pre-tax, pre-provision earnings per share - diluted (Non-GAAP) |

$ | 3.22 | $ | 2.78 | ||||

|

|

|

|

|

|||||

| Operating pre-tax, pre-provision income - FTE Non-GAAP reconciliations: |

UMB Financial Corporation | |||

| (unaudited, dollars in thousands except per share data) | ||||

| Three Months Ended March 31, |

||||||||

| 2024 | 2023 | |||||||

| Net interest income (GAAP) |

$ | 239,434 | $ | 241,696 | ||||

| Adjustments to arrive at net interest income - FTE: |

||||||||

| Tax equivalent interest |

6,516 | 6,555 | ||||||

|

|

|

|

|

|||||

| Net interest income - FTE (Non-GAAP) |

245,950 | 248,251 | ||||||

|

|

|

|

|

|||||

| Noninterest income (GAAP) |

159,244 | 130,200 | ||||||

| Noninterest expense (GAAP) |

254,804 | 237,052 | ||||||

| Adjustments to arrive at operating noninterest expense: |

||||||||

| Acquisition expense |

431 | 39 | ||||||

| Severance expense |

146 | 486 | ||||||

| FDIC special assessment |

13,000 | — | ||||||

|

|

|

|

|

|||||

| Total Non-GAAP adjustments |

13,577 | 525 | ||||||

|

|

|

|

|

|||||

| Operating noninterest expense (Non-GAAP) |

241,227 | 236,527 | ||||||

|

|

|

|

|

|||||

| Operating pre-tax, pre-provision income - FTE (Non-GAAP) |

$ | 163,967 | $ | 141,924 | ||||

|

|

|

|

|

|||||

| Net interest income earnings per share - diluted (GAAP) |

$ | 4.89 | $ | 4.96 | ||||

| Tax equivalent interest |

0.13 | 0.13 | ||||||

|

|

|

|

|

|||||

| Net interest income - FTE (Non-GAAP) |

5.02 | 5.09 | ||||||

|

|

|

|

|

|||||

| Noninterest income (GAAP) |

3.26 | 2.67 | ||||||

| Noninterest expense (GAAP) |

5.21 | 4.86 | ||||||

| Acquisition expense |

0.01 | — | ||||||

| Severance expense |

— | 0.01 | ||||||

| FDIC special assessment |

0.27 | — | ||||||

|

|

|

|

|

|||||

| Operating pre-tax, pre-provision income - FTE earnings per share - diluted (Non-GAAP) |

$ | 3.35 | $ | 2.91 | ||||

|

|

|

|

|

|||||

| Tangible book value non-GAAP reconciliations: |

UMB Financial Corporation | |||

| (unaudited, dollars in thousands except share and per share data) | ||||

| As of March 31, | ||||||||

| 2024 | 2023 | |||||||

| Total shareholders’ equity (GAAP) |

$ | 3,152,816 | $ | 2,814,659 | ||||

| Less: Intangible assets |

||||||||

| Goodwill |

207,385 | 207,385 | ||||||

| Other intangibles, net |

69,052 | 76,426 | ||||||

|

|

|

|

|

|||||

| Total intangibles, net |

276,437 | 283,811 | ||||||

|

|

|

|

|

|||||

| Total tangible shareholders’ equity (Non-GAAP) |

$ | 2,876,379 | $ | 2,530,848 | ||||

|

|

|

|

|

|||||

| Total shares outstanding |

48,743,348 | 48,507,116 | ||||||

| Ratio of total shareholders’ equity (book value) per share |

$ | 64.68 | $ | 58.03 | ||||

| Ratio of total tangible shareholders’ equity (tangible book value) per share (Non-GAAP) |

59.01 | 52.17 | ||||||

Exhibit 99.2

Quarter 2024 Update Kansas City, MO April 29, 2024

Presentation Index Corporate Overview 3 Opportunity – Our Investment Thesis 8 1st Quarter 2024 Results 17 Line of Business Updates 33 Appendix 44 Board of Directors Peer Group Forward-Looking Statements Non-GAAP Reconciliations Please refer to the Forward-Looking Statements on slide 46 for important disclosures about information contained in this presentation. 2

Corporate Overview Highlights Founded 1913 Ticker UMBF—Nasdaq Market Cap $4.2 B Total Assets $45.3 B Gross Loans $23.6 B Total Deposits $36.9 B Private Wealth Customer Assets (1) $16.2 B Institutional Assets Under Administration (AUA) (2) $483.4 B UMB Financial Corporation Headquarters Common Equity Tier 1 Capital Ratio 11.09% Total Risk Based Capital Ratio 13.03% UMB Bank Presence & Expansion • 90 banking centers • 237 ATMs Return on Equity 14.11% Operating ROTCE (3) 16.94% National Presence • Asset-based lending • Specialized Lending Verticals Net Charge-offs / Average Loans 0.05% • Healthcare Services • Corporate Trust • Private Wealth Management • Capital Markets (4) NPLs / Total Loans 0.08% & Personal Trust • Fund Services ACL / Total Loans 0.96% International Presence Fee Income / Revenue 39.9% • UMBF Trust & Agency Services – Dublin, Ireland At, or for, 3 months ended 03/31/24. (1) Includes $13.0B in managed assets & $3.2B in Assets Under Administration for Private Wealth customers; (2) Includes AUA in Fund Services/custody, 3 corporate trust and Healthcare Services; (3) Operating ROTCE is a non-GAAP measure. See reconciliation on slide 52; (4) UMB Bank, n.a. Capital Markets Div.

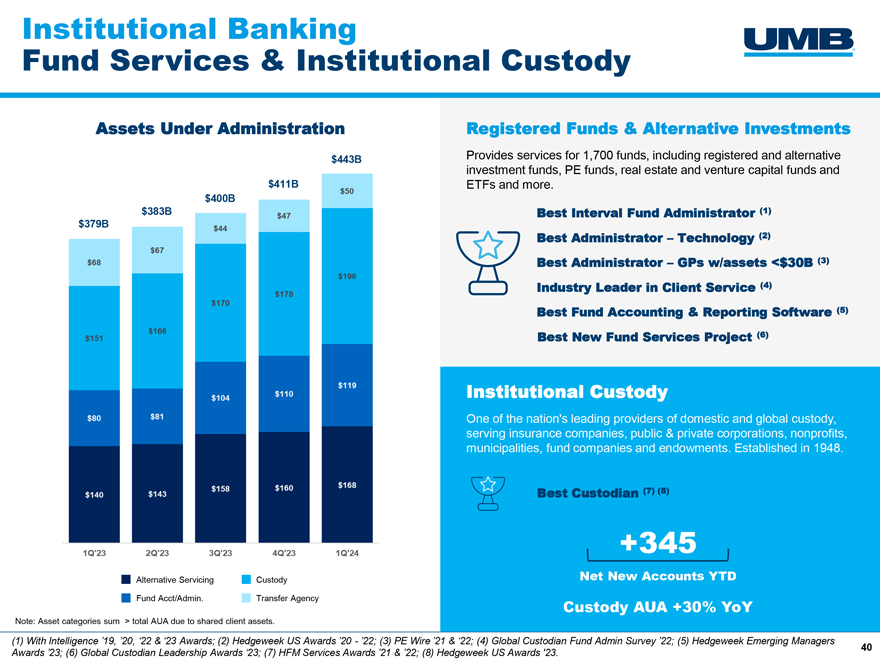

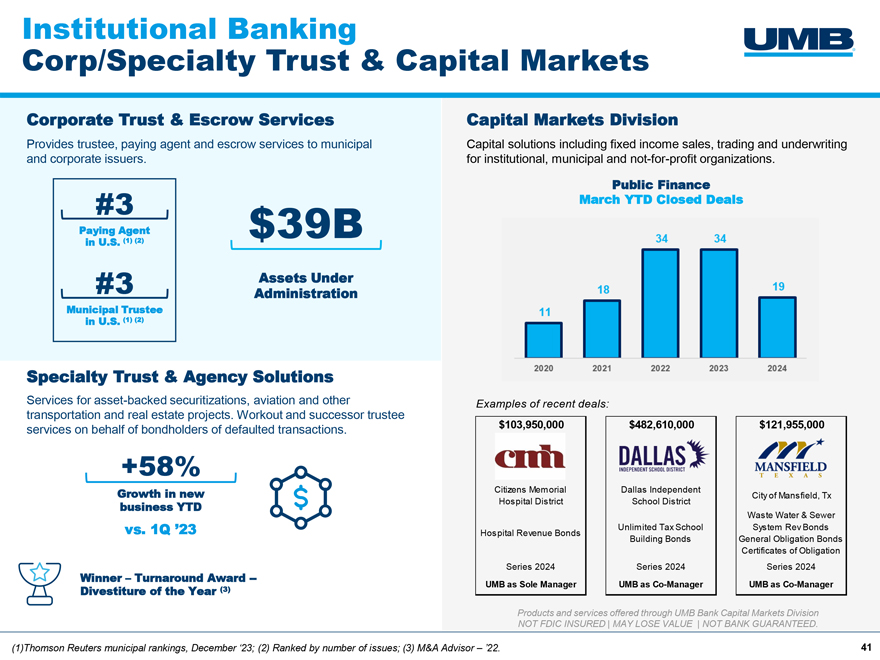

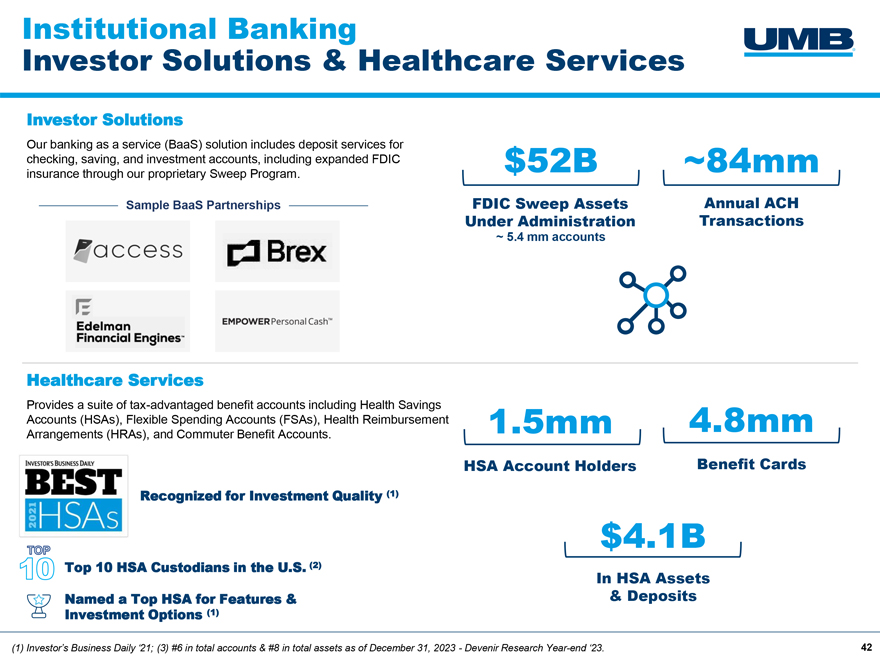

Business Model Our Diverse Foundation Commercial & Personal Banking Services 1Q’24 Revenue: $256.1 million. 1Q’24 Average Deposits: $19.8 billion (1) Commercial Consumer Private Wealth Average loans: $19.7B (2) Average loans: $3.1B (2) (3) AUM = $13.0B Average deposits: $13.3B Average deposits: $6.5B AUA = $3.2B C&I lending Treasury management Retail deposit & lending services Financial planning Small business lending Merchant payments through 90 branches and online Investment management CRE & Construction lending Private banking services Wealth solutions Consumer mortgage Business succession and exit planning Specialized Expertise: – Agribusiness – Aviation Trust & custody – Energy – Asset-based lending Estate planning – Practice finance – Beverage Direct private equity investment access – Mezzanine debt & equity investments Institutional Banking Services 1Q’24 Revenue: $142.6 million. 1Q’24 Average Deposits: $12.4 billion (1) Institutional Banking provides solutions for the entire marketplace; $483.4 billion in AUA (4) Corporate Trust Specialty Trust & Agency Solutions Investor Solutions Bond trustee, paying agent & escrow services Default workout & successor trustee services Banking, cash management & specialty Aviation, ABS & loan agency services services for financial firms Institutional Custody Capital Markets Division (5) Healthcare Services Domestic & international custody services Fixed income sales & trading Health savings & benefit spending accounts Fund Services Public finance Healthcare payment solutions Fund accounting, fund administration & Asset / liability management services transfer agency Alternative investment servicing Balances at, or for quarter ended, 03/31/24 (1) Excludes brokered deposits issued by Corp. Treasury; (2) Excludes credit card; (3) Includes consumer plus residential real estate loans; (4) Includes AUA in 4 Fund Services/custody, corporate trust & Healthcare Services; (5) Products offered through UMB Bank Capital Markets Div.: NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARANTEED.

Beyond Financials Our Culture Our Vision Customers First the We do the unparalleled to create an environment that unparalleled consistently exceeds the expectations of our customers. customer experience Integrity & Trust We demonstrate our uncompromising honesty and integrity to earn the trust of everyone we serve. Performance & Strength We achieve sustainable greatness by delivering on our Our Commitment promise, remaining independent and maintaining financial soundness. Associate Spirit We rely upon our people and their collective attitude and skills to differentiate us from our competitors. An unwavering commitment to doing more for our customers Inclusion & Diversity . We believe an inclusive and diverse culture energizes the workplace and ignites innovation. 5

Beyond Financials Our Culture Creating an unparalleled customer experience requires a culture where our people feel part of something more, something bigger. We foster this experience through our policies, our business decisions and our expectations of each associate. MORE MORE MORE HEART TRUST OPPORTUNITY Whether it’s having a Our associates have Our goal is to grow the heart for each other, our confidence they will be existing strengths and customers or our encouraged and expected build new skills. We’re unparalleled communities, we support to do the right thing at all committed to empowering customer work through inclusive times — no matter what. our workforce to make an policies and empowering We’re focused on setting impact and achieve their experience people to create fulfilling clear expectations and a goals through open lives in and out of the leadership team who is conversations and workplace. accessible and providing the tools to transparent. develop potential. 6