UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 6-K

REPORT OF FOREIGN ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of April, 2024

Commission file number: 1-10110

BANCO BILBAO VIZCAYA ARGENTARIA, S.A.

(Exact name of Registrant as specified in its charter)

BANK BILBAO VIZCAYA ARGENTARIA, S.A.

(Translation of Registrant’s name into English)

Calle Azul 4,

28050 Madrid

Spain

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ☐ No ☒

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ☐ No ☒

|

|

Main data

| BBVA GROUP MAIN DATA (CONSOLIDATED FIGURES) |

||||||||||||||||

| 31-03-24 | Δ % | 31-03-23 | 31-12-23 | |||||||||||||

| Balance sheet (millions of euros) |

||||||||||||||||

| Total assets |

801,690 | 8.4 | 739,564 | 775,558 | ||||||||||||

| Loans and advances to customers (gross) |

400,457 | 7.2 | 373,481 | 388,912 | ||||||||||||

| Deposits from customers |

436,763 | 10.3 | 395,880 | 413,487 | ||||||||||||

| Total customer funds |

615,076 | 10.5 | 556,839 | 577,853 | ||||||||||||

| Total equity |

55,778 | 8.4 | 51,471 | 55,265 | ||||||||||||

| Income statement (millions of euros) |

||||||||||||||||

| Net interest income |

6,512 | 15.4 | 5,642 | 23,089 | ||||||||||||

| Gross income |

8,218 | 18.1 | 6,958 | 29,542 | ||||||||||||

| Operating income |

4,835 | 22.7 | 3,942 | 17,233 | ||||||||||||

| Net attributable profit (loss) |

2,200 | 19.1 | 1,846 | 8,019 | ||||||||||||

| The BBVA share and share performance ratios |

||||||||||||||||

| Number of shares outstanding (million) |

5,838 | (3.2) | 6,030 | 5,838 | ||||||||||||

| Share price (euros) |

11.04 | 68.0 | 6.57 | 8.23 | ||||||||||||

| Adjusted earning (loss) per share (euros) (1) |

0.37 | 20.9 | 0.30 | 1.32 | ||||||||||||

| Earning (loss) per share (euros) (1) |

0.36 | 23.4 | 0.29 | 1.29 | ||||||||||||

| Book value per share (euros) (1) |

9.04 | 12.7 | 8.02 | 8.86 | ||||||||||||

| Tangible book value per share (euros) (1) |

8.62 | 12.7 | 7.65 | 8.46 | ||||||||||||

| Market capitalization (millions of euros) |

64,451 | 62.7 | 39,624 | 48,023 | ||||||||||||

| Significant ratios (%) |

||||||||||||||||

| ROE (net attributable profit (loss)/average shareholders’ funds +/- average accumulated other comprehensive income) (1) |

16.9 | 15.5 | 16.2 | |||||||||||||

| ROTE (net attributable profit (loss)/average shareholders’ funds excluding average intangible assets +/- average accumulated other comprehensive income) (1) |

17.7 | 16.3 | 17.0 | |||||||||||||

| ROA (profit (loss) for the period / average total assets-ATA) (1) |

1.19 | 1.11 | 1.12 | |||||||||||||

| RORWA (profit (loss) for the period / average risk-weighted assets - RWA) (1) |

2.50 | 2.36 | 2.38 | |||||||||||||

| Efficiency ratio (1) |

41.2 | 43.3 | 41.7 | |||||||||||||

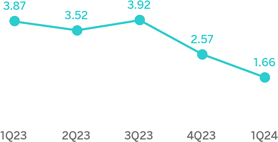

| Cost of risk (1) |

1.39 | 1.05 | 1.15 | |||||||||||||

| NPL ratio (1) |

3.4 | 3.3 | 3.4 | |||||||||||||

| NPL coverage ratio (1) |

76 | 82 | 77 | |||||||||||||

| Capital adequacy ratios (%) |

||||||||||||||||

| CET1 fully-loaded |

12.82 | 13.13 | 12.67 | |||||||||||||

| CET1 phased-in (2) |

12.82 | 13.13 | 12.67 | |||||||||||||

| Total ratio phased-in (2) |

16.66 | 16.30 | 16.58 | |||||||||||||

| Other information |

||||||||||||||||

| Number of active customers (million) (3) |

74.1 | 6.6 | 69.4 | 73.0 | ||||||||||||

| Number of shareholders (4) |

726,100 | (7.6) | 786,031 | 742,194 | ||||||||||||

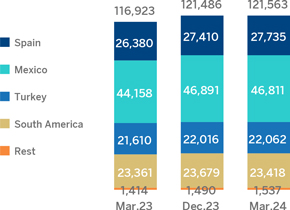

| Number of employees |

121,563 | 4.0 | 116,923 | 121,486 | ||||||||||||

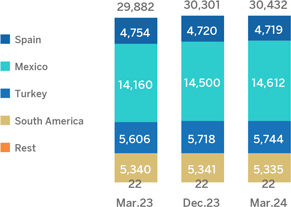

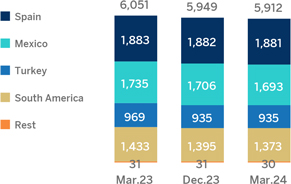

| Number of branches |

5,912 | (2.3) | 6,051 | 5,949 | ||||||||||||

| Number of ATMs |

30,432 | 1.8 | 29,882 | 30,301 | ||||||||||||

(1) For more information, see Alternative Performance Measures at the end of this report.

(2) Phased-in ratios include the temporary treatment on the impact of IFRS 9, calculated in accordance with Article 473 bis amendments of the Capital Requirements Regulation (CRR), introduced by the Regulation (EU) 2020/873. For the periods shown in this table, there are no differences between phased-in and fully-loaded ratios due to the aforementioned temporary treatment.

(3) Reported figures include clients from Italy, as well as an adjustment for homogenization of criteria in Peru with the rest of the countries.

(4) See footnote to table of structural distribution of shareholders in the Capital and shareholders chapter of this report.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

| 4 | ||||

| 8 | ||||

| 9 | ||||

| 9 | ||||

| 14 | ||||

| 16 | ||||

| 19 | ||||

| 25 | ||||

| 28 | ||||

| 31 | ||||

| 34 | ||||

| 38 | ||||

| 43 | ||||

| 46 | ||||

| 48 | ||||

| 51 | ||||

| 57 | ||||

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

4 |

Results and business activity

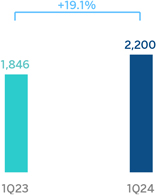

The BBVA Group generated a net attributable profit of €2,200m between January and March of 2024, driven by the performance of recurring revenues of the banking business. Thus, the net interest income grew at a year-on-year rate of 15.4% and net fees and commissions by 31.1%. This result represents an increase of 19.1% compared to the same period of the previous year, 38.1% excluding the impact of the evolution of currencies.

These results include the recording of the total estimated annual amount of the temporary tax on credit institutions and financial credit institutions for €285m, included in the other operating income and expenses line of the income statement.

Operating expenses increased by 19.5% at Group level at constant exchange rates, affected by the inflation rates observed in the countries in which the Group operates. Thanks to the remarkable growth in gross income (+31.0%), greater than the growth in operating expenses, the efficiency ratio stood at 41.2% as of March 31, 2024, with an improvement of 398 basis points, in constant terms, compared to the ratio recorded 12 months earlier.

The provisions for impairment on financial assets increased (+40.7% in year-on-year terms and at constant exchange rates), with higher requirements linked to the growth in the most profitable segments, in line with the Group´s strategy.

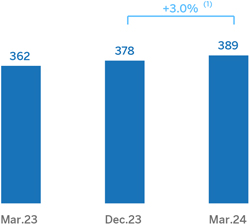

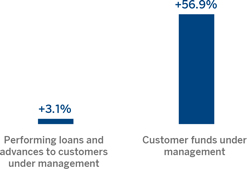

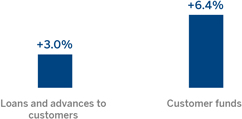

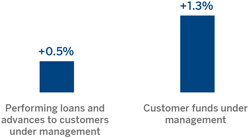

Loans and advances to customers recorded an increase of 3.0% compared to the end of December 2023, particularly driven by the evolution of corporate loans (+3.2% at Group level), and by the positive performance of loans of all segments to individuals.

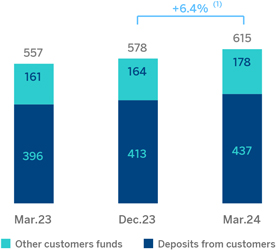

Customer funds increased by 6.4% compared to the end of the previous year, thanks to both the growth in deposits from customers, which increased by 5.6%, and to the increase in off-balance sheet funds, which grew by 8.5%.

| LOANS AND ADVANCES TO CUSTOMERS AND TOTAL CUSTOMER FUNDS (VARIATION COMPARED TO 31-12-2023) |

Business areas

As for the business areas evolution, excluding the effect of currency fluctuation in those areas where it has an impact, in each of them it is worth mentioning:

| – | Spain generated a net attributable profit of €725m in the first quarter of 2024, 36.5% higher than in the same period of the previous year, mainly supported by the favorable evolution of the net interest income. These solid results include the negative impact of €285m caused by the recording of the temporary tax on credit institutions and financial credit institutions. |

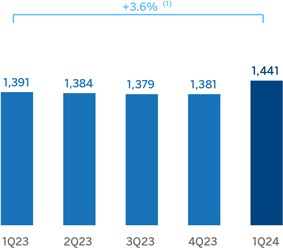

| – | In Mexico, BBVA achieved a cumulative net attributable profit of €1,441m by the end of March 2024, representing an increase of 3.6% compared to the same period of the previous year, mainly as a result of the strength of the recurring income from the banking business. |

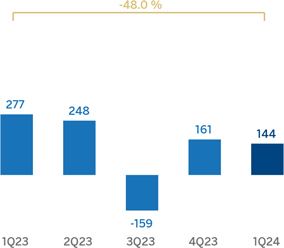

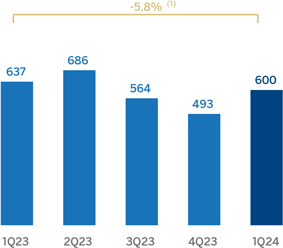

| – | Turkey generated a net attributable profit of €144m during the first quarter of 2024, which compares positively with the accumulated result reached at the end of March 2023 at constant exchange rate, both periods reflecting the impact of the application of hyperinflation accounting. |

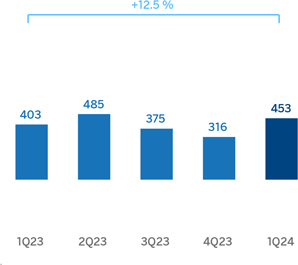

| – | South America generated a cumulative net attributable profit of €119m at the end of the first quarter of 2024, which represents a year-on-year increase of +54.6%, driven by the good performance of recurring income (84.1%) and the area’s NTI (net trading income). |

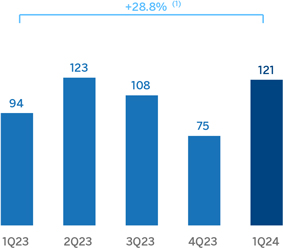

| – | Rest of Business achieved an accumulated net attributable profit of €121m during the first quarter of 2024, 28.8% higher than in the same period of the previous year, favored by the performance of the net interest income and the NTI. |

The Corporate Center recorded a net attributable loss of €-350m between January and March of 2024, which is an improvement compared with the €-515m recorded in the same period of the previous year.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

5 |

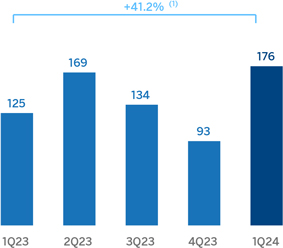

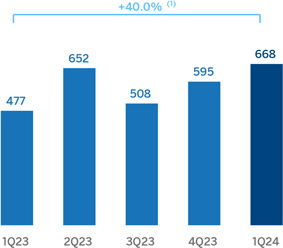

Lastly, and for a broader understanding of the Group’s activity and results, supplementary information is provided below for the wholesale business, Corporate & Investment Banking (CIB), carried out by BBVA in the countries where it operates. CIB generated a net attributable profit of €668m between January and March of 2024. These results represent an increase of 40.0% on a year-on-year basis and reflect the contribution of the diversification of products and geographical areas, as well as the progress of the Group’s wholesale businesses in its strategy, leveraged on globality and sustainability, with the purpose of being relevant to its clients.

|

NET ATTRIBUTABLE PROFIT (LOSS) (MILLIONS OF EUROS) |

NET ATTRIBUTABLE PROFIT BREAKDOWN (1) (PERCENTAGE. 1Q24) |

|||

|

|

|||

Solvency

The Group’s CET1 fully-loaded ratio stood at 12.82% as of March 31, 2024, which allows to keep maintaining a large management buffer over the Group’s CET1 requirement (9.10%)1 and above the Group’s established target management range of 11.5-12.0% of CET1.

Shareholder remuneration

Regarding shareholder remuneration, as approved by the General Shareholders´ Meeting on March 15, 2024, in its first item on the agenda, on April 10, 2024, a cash payment of €0.39 gross per each outstanding BBVA share entitled to receive such amount was made against the 2023 results, as an additional shareholder remuneration for the financial year 2023. Thus, the total amount of cash distributions for 2023, taking into account the €0.16 gross per share that was distributed in October 2023, amounted to €0.55 gross per share.

Total shareholder remuneration includes, in addition to the cash payments mentioned above, the remuneration resulting from the BBVA’s buyback program for the repurchase of own shares announced on January 30, 2024 for a maximum amount of €781m, and which started being executed on March 1, 2024. By means of an Other Relevant Information notice dated April 9, 2024, BBVA announced the completion of the share buyback program upon reaching the maximum monetary amount, having acquired 74,654,915 own shares, between March 4 and April 9, 2024, representing, approximately, 1.28% of BBVA’s share capital as of such date. The redemption of such shares is pending execution.

1 This includes the update of the countercyclical capital buffer calculated on the basis of exposure at end December 2023.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

6 |

Sustainability

Channeling sustainable business

| SUSTAINABLE BUSINESS BREAKDOWN (PERCENTAGE. TOTAL AMOUNT CHANNELED 2018-MARCH 2024) |

(1) In those cases where it is not feasible or sufficient information is not available to allow an exact distribution between the categories of climate change and inclusive growth, internal estimates are made based on the available information.

(2) It fundamentally includes products whose funds are allocated to activities considered sustainable (in accordance with both internal and market standards, existing regulations and best practices), as well as products linked to sustainability (in accordance with both internal and market and best practices), such as those linked to environmental and/or social indicators.

(3) Bonds in which BBVA acts as bookrunner.

(4) Investment products art.8 or 9 under SFDR or similar criteria outside the EU managed, intermediated or marketed by BBVA. “Other” includes deposits under the Sustainable Transaction Banking Framework until its replacement by the CIB Sustainable Products Framework (both Frameworks published on the bank’s website), insurance policies related to energy efficiency and inclusive growth and electric vehicle autorenting, mainly.

(5) Includes the activity of the BBVA Microfinance Foundation (BBVAMF), which is not part of the consolidated Group and which has channeled around €8 billion in the period from 2018 to March 2024 to support vulnerable entrepreneurs with microcredits.

Regarding the objective of channeling €300 billion between 2018 and 20252 as part of the sustainability strategy, the BBVA Group has mobilized an approximate total of €226 billion in sustainable business between 2018 and March 2024, of which approximately 77% corresponds to the area of promoting the fight against climate change and the remaining 23% to promote inclusive growth. The amount channeled includes financing, intermediation, investment, off-balance sheet and insurance transactions. These operations have contractual maturity or amortization dates, so the above mentioned accumulated figure does not represent the amount reflected on the balance sheet.

During the first quarter of 2024, approximately €20 billion were mobilized (+41% compared with the same period of the previous year).

In this first quarter, retail business has been mobilized for an amount of around €2.6 billion. During this quarter, BBVA has continued to promote customized digital solutions aimed at the mass consumer market, offering retail customers a vision of the potential savings they can obtain by adopting energy-saving measures in their homes and transportation. It is worth highlighting the good performance of the channeling related to the acquisition of hybrid or electric vehicles with €124 million, which represents a growth of 136% compared to the same period of the previous year.

Between January and March 2024, the commercial business (enterprises) mobilized around €7 billion. This quarter, the unit continued to advise corporate clients on sustainable solutions that enable economic savings by focusing on cross-cutting issues such as energy efficiency, car fleet renewal and water. In this regard, it is worth highlighting the financing allocated to agribusiness, water and circular economy with €700m, representing an increase of 258% year-on-year. In this area, Mexico’s contribution is fundamental, as it accounts for about half of this channeling.

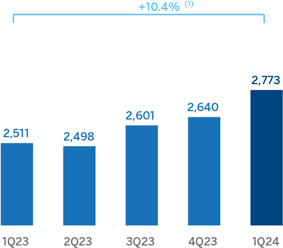

CIB has channeled around €10.4 billion during the first quarter of 2024, with a positive performance in all products, both long and short-term financing and the intermediation of green, social, sustainable and environmental and/or social indicators-linked bonds in which BBVA acts as bookrunner. During the quarter, BBVA has continued to promote in the wholesale segment the financing of clean technologies and of renewable energy projects as well as confirming linked to sustainability, among other strategic lines. In terms of channeling, the financing of renewable energy projects stands out, contributing around €800m during this quarter and more than doubling compared to the same period of the previous year.

2 For the purposes of the 2025 goal, channeling is considered as any mobilization of financial flows, on a cumulative basis, in relation to activities, customers or products considered sustainable or that promote sustainability primarily in accordance with internal standards inspired by existing regulations, market standards such as the Green Bond Principles, the Social Bond Principles and the Sustainability Linked Bond Principles of the International Capital Markets Association, as well as the Green Loan Principles, Social Loan Principles and Sustainability Linked Loan Principles of the Loan Market Association, existing regulations and best market practices. The foregoing is without prejudice to the fact that such mobilization, both initially and at a later time, may not be recorded in the balance sheet. To determine the amount of sustainable business channeled, internal criteria are used based on both internal and external information, whether public, provided by customers or by a third party (mainly data providers and independent experts).

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

7 |

Relevant advances in the field of sustainability

| • | TCFD |

In March 2024, BBVA published its fifth TCFD (Task Force on Climate-Related Financial Disclosure) report, which summarizes its strategy to manage the risks and opportunities related to climate change, as well as the measures it is taking in this regard. The Group has continued to incorporate the elements of a Transition Plan, applying the guides and recommendations for financial institutions published by Glasgow Financial Alliance for Net Zero (GFANZ) in November 2022.

| • | Target presence of women in management positions by 2026 |

To promote gender equality, in 2022 BBVA set a target of 35% women in management positions by 2024. After achieving an indicator of 34.7% in 2023, in February 2024 a new target was announced for the next 2 years, so that BBVA aims to have 36.8% of women in management positions by the end of 2026.

This indicator, which measures the evolution of the representation of women in management positions in the Group, is included in the long-term variable incentives for executive directors and senior management.

| • | Issuance of a green bond |

In March 2024, BBVA issued a senior preferred green bond in the amount of €1,000m, maturing in 7 years and at a price set at mid swap plus 90 basis points. For this new issue, projects financed during the 6 months prior to the bond issue have been identified and divided into two eligible categories according to BBVA’s Sustainable Debt Financing Framework: renewable energy and clean transportation.

| • | Sustainability forums |

On February 29, 2024, the third edition of the BBVA Sustainability Forum was held in BBVA City. The event, which welcomed more than 400 attendees including representatives of the Public Administration, personalities and global companies and institutions very active in the fight against climate change and the promotion of inclusive growth, has become a reference event for the high-level dialogue on the economic and social challenges of sustainability.

On March 20, 2024, the first edition of the BBVA Sustainability Summit in Peru took place in Lima. A space that brought together more than 500 attendees including clients, businessmen, representatives of institutions and important local and international personalities from the world of sustainability at the bank’s headquarters. At the meeting, experiences, strategies and sustainable practices were shared with the aim of informing, raising awareness and mobilizing about the challenges and opportunities that sustainability represents for the private sector.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

8 |

The high inflation, the tightening of monetary conditions and the gradual fading of the positive effects linked to the reopening after the COVID-19 pandemic have contributed to a slowdown in economic activity in recent quarters. However, the slowdown has been, in general, less abrupt than expected, and economic activity remains relatively dynamic, particularly in the United States and in the services sector, thanks to the dynamism of the labor markets, expansionary fiscal policies and the gradual fading of supply shocks triggered by the pandemic and the war in Ukraine.

The resilience of aggregate demand has contributed to inflation remaining relatively high in the first months of 2024 (3.5% in the United States and 2.4% in the Eurozone in March 2024), after decreasing significantly since mid-2022.

According to BBVA Research, it is most likely that inflation will moderate in the next months, enabling the start of a gradual process of relaxation of monetary conditions around mid-2024, which would take monetary policy interest rates to around 4.75% in the United States and 3.25% (in the case of the deposit facility interest rate) in the Eurozone by the end of 2024.

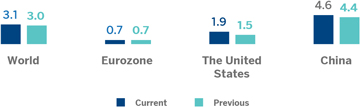

BBVA Research forecasts that global growth will be approximately 3.1% in 2024, close to the estimated GDP growth for 2023 and slightly over the previous forecast (3.0%). In the United States, the strong domestic demand has supported a GDP growth of 2.5% in 2023 and a revision of growth forecasts for 2024 to 1.9% (40 basis points above the previous forecast). In China, structural challenges to avoid a fast economic deceleration remain, but a series of stimulus measures have enabled a greater than expected dynamism of activity in the past few months and a 5.2% GDP growth in 2023. The GDP growth forecast for 2024 has been adjusted somewhat upwards to 4.6% (20 basis points above the previous forecast). In the Eurozone, economic activity came to a standstill in the last months, reinforcing the low growth prospects. After expanding by around 0.5% in 2023, the forecast of the GDP expansion is expected to grow 0.7% for 2024 (with no change compared to the previous forecast).

Although it is expected that inflation will gradually moderate both in United States and Eurozone, and it is likely to remain low in China, it is most likely that inflationary pressures -and, therefore, interest rates- will continue to be above the levels observed before the COVID-19 pandemic due to the geopolitical factors, such as the war in Ukraine and the armed conflict in Middle East, and to other factors like protectionist policies, an expansionary fiscal stance and climatic shocks. Indeed, these factors increase the uncertainty about the evolution of the global economy and the risk of having a higher inflation and interest rates than currently expected.

| GDP GROWTH ESTIMATES IN 2024 (PERCENTAGE. YEAR-ON-YEAR |

Source: BBVA Research estimates.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

9 |

The BBVA Group generated a net attributable profit of €2,200m between January and March of 2024, driven by the performance of recurring revenues of the banking business. Thus, the net interest income grew at a year-on-year rate of 15.4% and net fees and commissions by 31.1%. This result represents an increase of 19.1% compared to the same period of the previous year.

It should to be noted that the results of the first quarter of 2024 include the recording for the total annual amount paid for the temporary tax on credit institutions and financial credit institutions for €285m, included in the other operating income and expenses line of the income statement. This amount is higher than the recorded in the same line in the same period of the previous year.

| CONSOLIDATED INCOME STATEMENT (MILLIONS OF EUROS) |

||||||||||||||||

| 1Q24 | Δ % | Δ % at constant exchange rates |

1Q23 | |||||||||||||

| Net interest income |

6,512 | 15.4 | 24.5 | 5,642 | ||||||||||||

| Net fees and commissions |

1,887 | 31.1 | 36.5 | 1,439 | ||||||||||||

| Net trading income |

772 | 76.2 | 123.9 | 438 | ||||||||||||

| Other operating income and expenses |

(952) | 69.7 | 39.5 | (561) | ||||||||||||

| Gross income |

8,218 | 18.1 | 31.0 | 6,958 | ||||||||||||

| Operating expenses |

(3,383) | 12.2 | 19.5 | (3,016) | ||||||||||||

| Personnel expenses |

(1,778) | 14.7 | 22.9 | (1,551) | ||||||||||||

| Other administrative expenses |

(1,229) | 9.1 | 17.4 | (1,127) | ||||||||||||

| Depreciation |

(375) | 10.9 | 11.2 | (339) | ||||||||||||

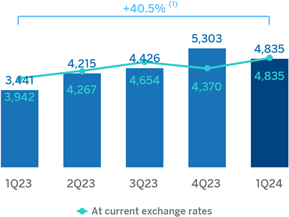

| Operating income |

4,835 | 22.7 | 40.5 | 3,942 | ||||||||||||

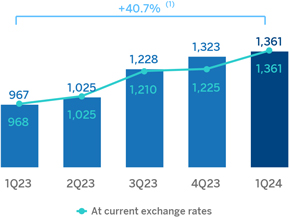

| Impairment on financial assets not measured at fair value through profit or loss |

(1,361) | 40.5 | 40.7 | (968) | ||||||||||||

| Provisions or reversal of provisions |

(57) | n.s. | n.s. | (14) | ||||||||||||

| Other gains (losses) |

40 | n.s. | n.s. | (16) | ||||||||||||

| Profit (loss) before tax |

3,458 | 17.4 | 41.2 | 2,944 | ||||||||||||

| Income tax |

(1,151) | 21.2 | 43.0 | (950) | ||||||||||||

| Profit (loss) for the period |

2,307 | 15.7 | 40.4 | 1,994 | ||||||||||||

| Non-controlling interests |

(107) | (27.9) | 111.1 | (148) | ||||||||||||

| Net attributable profit (loss) |

2,200 | 19.1 | 38.1 | 1,846 | ||||||||||||

| Adjusted earning (loss) per share (euros) (1) |

0.37 | 0.30 | ||||||||||||||

| Earning (loss) per share (euros) (1) |

0.36 | 0.29 | ||||||||||||||

(1) Adjusted by additional Tier 1 instrument remuneration. For more information, see Alternative Performance Measures at the end of this report.

Unless expressly indicated otherwise, for a better understanding of the changes under the main headings of the Group’s income statement, the rates of change provided below refer to constant exchange rates. When comparing two dates or periods in this report, the impact of changes in the exchange rates against the euro of the currencies of the countries in which BBVA operates is sometimes excluded, assuming that exchange rates remain constant. For this purpose, the average exchange rate of the currency of each geographical area of the most recent period is used for both periods, except for those countries whose economies have been considered hyperinflationary, for which the closing exchange rate of the most recent period is used.

3 In compliance with Law 38/2022, of December 27, which establishes the obligation to pay a patrimonial benefit of a public and non-taxable nature during the years 2023 and 2024 for credit institutions that operate in Spanish territory whose sum of total interest income and fee and commission income corresponding to the year 2019 is equal to or greater than €800m.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

10 |

| CONSOLIDATED INCOME STATEMENT: QUARTERLY EVOLUTION (MILLIONS OF EUROS) |

||||||||||||||||||||

| 2024 | 2023 | |||||||||||||||||||

| 1Q | 4Q | 3Q | 2Q | 1Q | ||||||||||||||||

| Net interest income |

6,512 | 5,246 | 6,434 | 5,768 | 5,642 | |||||||||||||||

| Net fees and commissions |

1,887 | 1,694 | 1,685 | 1,470 | 1,439 | |||||||||||||||

| Net trading income |

772 | 753 | 658 | 334 | 438 | |||||||||||||||

| Other operating income and expenses |

(952) | (255) | (820) | (383) | (561) | |||||||||||||||

| Gross income |

8,218 | 7,438 | 7,956 | 7,189 | 6,958 | |||||||||||||||

| Operating expenses |

(3,383) | (3,068) | (3,303) | (2,922) | (3,016) | |||||||||||||||

| Personnel expenses |

(1,778) | (1,693) | (1,756) | (1,530) | (1,551) | |||||||||||||||

| Other administrative expenses |

(1,229) | (1,025) | (1,169) | (1,054) | (1,127) | |||||||||||||||

| Depreciation |

(375) | (349) | (378) | (337) | (339) | |||||||||||||||

| Operating income |

4,835 | 4,370 | 4,654 | 4,267 | 3,942 | |||||||||||||||

| Impairment on financial assets not measured at fair value through profit or loss |

(1,361) | (1,225) | (1,210) | (1,025) | (968) | |||||||||||||||

| Provisions or reversal of provisions |

(57) | (163) | (81) | (115) | (14) | |||||||||||||||

| Other gains (losses) |

40 | (49) | 2 | 50 | (16) | |||||||||||||||

| Profit (loss) before tax |

3,458 | 2,932 | 3,365 | 3,178 | 2,944 | |||||||||||||||

| Income tax |

(1,151) | (799) | (1,226) | (1,028) | (950) | |||||||||||||||

| Profit (loss) for the period |

2,307 | 2,133 | 2,139 | 2,150 | 1,994 | |||||||||||||||

| Non-controlling interests |

(107) | (75) | (56) | (118) | (148) | |||||||||||||||

| Net attributable profit (loss) |

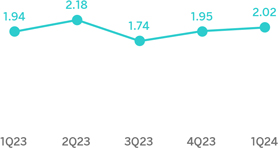

2,200 | 2,058 | 2,083 | 2,032 | 1,846 | |||||||||||||||

| Adjusted earning (loss) per share (euros) (1) |

0.37 | 0.34 | 0.34 | 0.34 | 0.30 | |||||||||||||||

| Earning (loss) per share (euros) (1) |

0.36 | 0.33 | 0.33 | 0.33 | 0.29 | |||||||||||||||

(1) Adjusted by additional Tier 1 instrument remuneration. For more information, see Alternative Performance Measures at the end of this report.

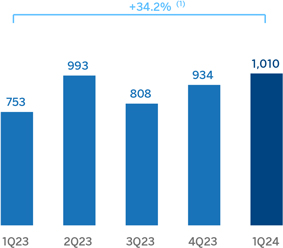

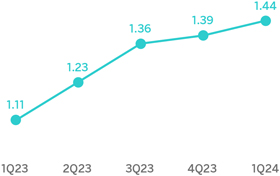

The accumulated net interest income as of March 31, 2024 was higher than in the same period of the previous year (+24.5%), with increases in all business areas except for Turkey, as a result of greater volumes of performing loan. The good evolution in South America and Spain is noteworthy.

Positive evolution in the net fees and commissions line, which increased by 36.5% year-on-year due to the favorable performance in payment systems and, to a lesser extent, asset management. By business areas, Turkey´s and Mexico´s contribution stood out.

| NET INTEREST INCOME / AVERAGE TOTAL ASSETS (PERCENTAGE AT CONSTANT EXCHANGE RATES) |

|

NET INTEREST INCOME PLUS NET FEES AND COMMISSIONS (MILLIONS OF EUROS AT CONSTANT EXCHANGE RATES) |

||

|

|

|

|||

At the end of March 2024, NTI grew by 123.9%, with a positive performance of this line in all business areas, favored by the results of the Global Markets unit, which offset comfortably the negative results recorded in the Corporate Center.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

11 |

The other operating income and expenses line accumulated as of March 31, 2024 a result that compares negatively with the same date of the same period of last year, mainly due to the recording in the line of a more negative adjustment for hyperinflation in Argentina. This line also reflects the total estimated amount of the temporary tax on credit institutions and financial credit establishments for year 2024 registered in the first quarter of 2024 and 60 million higher than the annual amount estimated for year 2023, registered in the first quarter of that year.

|

GROSS INCOME (MILLIONS OF EUROS AT CONSTANT EXCHANGE RATES) |

||||

|

(1) At current exchange rates: +18.1%. |

||||

On a year-on-year basis, operating expenses increased by 19.5% at the Group level, a rate that is below the inflation rates observed in the countries in which the Group operates (an average of 19,7% in the last 12 months).

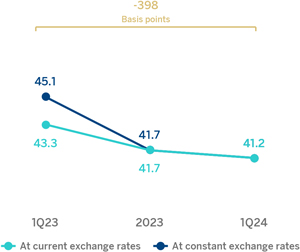

Thanks to the remarkable growth in gross income (+31.0%), the efficiency ratio stood at 41.2% as of March 31, 2024, with an improvement of 398 basis points compared to the ratio recorded 12 months earlier.

| OPERATING EXPENSES (MILLIONS OF EUROS AT CONSTANT EXCHANGE RATES) |

|

EFFICIENCY RATIO (PERCENTAGE) | ||

|

(1) At current exchange rates: +12.2%. |

|

|||

The impairment on financial assets not measured at fair value through profit or loss (impairment on financial assets) at the end of March 2024 was 40.7% higher than in the same period of the previous year, with higher requirements linked to the growth in the most profitable segments, in line with the Group´s strategy.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

12 |

| OPERATING INCOME (MILLIONS OF EUROS AT CONSTANT EXCHANGE RATES) |

|

IMPAIRMENT ON FINANCIAL ASSETS (MILLIONS OF EUROS AT CONSTANT EXCHANGE RATES) |

||

|

(1) At current exchange rates: +22.7%. |

(1) At current exchange rates: +40.5%. |

|||

The provisions or reversal of provisions line (hereinafter, provisions) registered at the end of March 2024 higher provisions compared to the same period of the previous year, mainly originated in Spain and South America.

On the other hand, the other gains (losses) line ended March 2024 with a balance of €40m, which compares favorably with the result of the previous year and reflects the positive impact of the reversal of impairments for investments on associated companies.

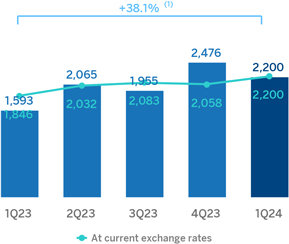

As a result of the above, the BBVA Group generated a net attributable profit of €2,200m between January and March of the year 2024, which compares very positively with the result of the same period of the previous year. These solid results are supported by the favorable evolution of the banking business recurring income, which offsets the higher operating expenses and the increase in provisions for impairment losses on financial assets.

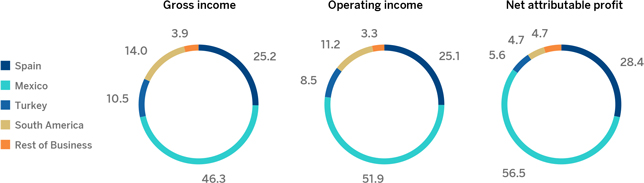

The cumulative net attributable profits, in millions of euros, at the end of March 2024 for the business areas that compose the Group were as follows: €725m in Spain, €1,441m in Mexico, €144m in Turkey, €119m in South America and €121m in Rest of Business.

|

NET ATTRIBUTABLE PROFIT (LOSS) (MILLIONS OF EUROS AT CONSTANT EXCHANGE RATES) |

||||

|

(1) At current exchange rates: +19.1% |

||||

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

13 |

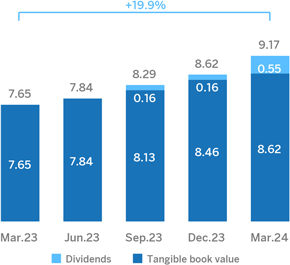

The Group’s excellent performance has also allowed to accelerate value creation, as reflected in the growth of the tangible book value per share and dividends, which as of the end of March 2024 was 19.9% higher than in the same period of the previous year.

| TANGIBLE BOOK VALUE PER SHARE AND DIVIDENDS (EUROS) |

|

EARNING (LOSS) PER SHARE (EUROS) | ||

|

|

|

|||

|

General note: replenishing dividends paid in the period. For more information, see Alternative Performance Measures at the end of this report. |

General note; adjusted by additional Tier 1 instrument remuneration. For more information, see Alternative Performance Measures at the end of this report. |

|||

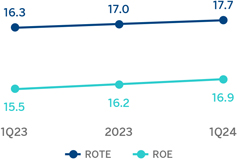

Lastly, the Group’s profitability indicators improved in year-on-year terms supported by the favorable performance of results.

| ROE AND ROTE (PERCENTAGE) |

|

ROA AND RORWA (PERCENTAGE) |

||

|

|

|

|||

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

14 |

Balance sheet and business activity

The most relevant aspects related to the evolution of the Group’s balance sheet and business activity as of March 31, 2024 are summarized below:

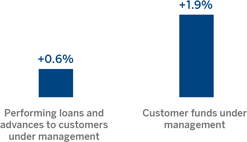

| – | Loans and advances to customers recorded an increase of 3.0% compared to the end of December 2023, particularly driven by the evolution of corporate loans (+3.2% at Group level), and by the positive performance of loans of all segments to individuals, especially consumer loans (+3.5%). |

| – | Customer funds increased by 6.4% compared to the end of 2023, thanks to both the growth in deposits from customers, which increased by 5.6% due to the positive evolution of time deposits in all business areas, especially Spain and Rest of Business, and to the increase in off-balance sheet funds, which grew by 8.5%, favored by the evolution of mutual funds and customer portfolios, with the good performance in Mexico and Spain. |

|

CONSOLIDATED BALANCE SHEET (MILLIONS OF EUROS)

|

||||||||||||||||

| 31-03-24 | Δ % | 31-12-23 | 31-03-23 | |||||||||||||

| Cash, cash balances at central banks and other demand deposits |

76,524 | 1.5 | 75,416 | 83,267 | ||||||||||||

| Financial assets held for trading |

144,253 | 2.3 | 141,042 | 119,877 | ||||||||||||

| Non-trading financial assets mandatorily at fair value through profit or loss |

9,384 | 7.4 | 8,737 | 7,227 | ||||||||||||

| Financial assets designated at fair value through profit or loss |

840 | (12.1) | 955 | 997 | ||||||||||||

| Financial assets at fair value through accumulated other comprehensive income |

62,884 | 1.1 | 62,205 | 66,277 | ||||||||||||

| Financial assets at amortized cost |

470,380 | 4.1 | 451,732 | 427,259 | ||||||||||||

| Loans and advances to central banks and credit institutions |

28,975 | 17.7 | 24,627 | 22,256 | ||||||||||||

| Loans and advances to customers |

388,949 | 3.0 | 377,643 | 362,317 | ||||||||||||

| Debt securities |

52,456 | 6.1 | 49,462 | 42,686 | ||||||||||||

| Investments in joint ventures and associates |

996 | 2.0 | 976 | 920 | ||||||||||||

| Tangible assets |

9,660 | 4.4 | 9,253 | 8,945 | ||||||||||||

| Intangible assets |

2,407 | 1.9 | 2,363 | 2,209 | ||||||||||||

| Other assets |

24,362 | 6.5 | 22,878 | 22,586 | ||||||||||||

| Total assets |

801,690 | 3.4 | 775,558 | 739,564 | ||||||||||||

| Financial liabilities held for trading |

118,731 | (2.5) | 121,715 | 107,185 | ||||||||||||

| Other financial liabilities designated at fair value through profit or loss |

14,544 | 9.4 | 13,299 | 11,309 | ||||||||||||

| Financial liabilities at amortized cost |

584,698 | 4.9 | 557,589 | 542,326 | ||||||||||||

| Deposits from central banks and credit institutions |

53,824 | (10.8) | 60,349 | 75,109 | ||||||||||||

| Deposits from customers |

436,763 | 5.6 | 413,487 | 395,880 | ||||||||||||

| Debt certificates |

73,627 | 7.2 | 68,707 | 54,586 | ||||||||||||

| Other financial liabilities |

20,484 | 36.1 | 15,046 | 16,751 | ||||||||||||

| Liabilities under insurance and reinsurance contracts |

12,241 | 1.1 | 12,110 | 11,010 | ||||||||||||

| Other liabilities |

15,697 | 0.8 | 15,580 | 16,263 | ||||||||||||

| Total liabilities |

745,912 | 3.6 | 720,293 | 688,093 | ||||||||||||

| Non-controlling interests |

3,775 | 5.9 | 3,564 | 3,680 | ||||||||||||

| Accumulated other comprehensive income |

(14,944) | (8.1) | (16,254) | (16,195) | ||||||||||||

| Shareholders’ funds |

66,947 | (1.5) | 67,955 | 63,986 | ||||||||||||

| Total equity |

55,778 | 0.9 | 55,265 | 51,471 | ||||||||||||

| Total liabilities and equity |

801,690 | 3.4 | 775,558 | 739,564 | ||||||||||||

| Memorandum item: |

||||||||||||||||

| Guarantees given |

62,077 | 3.4 | 60,019 | 55,042 | ||||||||||||

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

15 |

|

LOANS AND ADVANCES TO CUSTOMERS (MILLIONS OF EUROS)

|

|

|||||||||||||||||||||||||||

| 31-03-24 | Δ % | 31-12-23 | 31-03-23 | |||||||||||||||||||||||||

| Public sector | 24,012 | 3.2 | 23,269 | 21,752 | ||||||||||||||||||||||||

| Individuals | 172,604 | 2.7 | 168,123 | 161,346 | ||||||||||||||||||||||||

| Mortgages |

94,887 | 1.6 | 93,358 | 91,999 | ||||||||||||||||||||||||

| Consumer |

44,175 | 3.5 | 42,695 | 40,147 | ||||||||||||||||||||||||

| Credit cards |

22,816 | 5.6 | 21,609 | 18,997 | ||||||||||||||||||||||||

| Other loans |

10,725 | 2.5 | 10,461 | 10,203 | ||||||||||||||||||||||||

| Business | 188,902 | 3.2 | 183,076 | 177,168 | ||||||||||||||||||||||||

| Non-performing loans | 14,938 | 3.4 | 14,444 | 13,215 | ||||||||||||||||||||||||

| Loans and advances to customers (gross) |

400,457 | 3.0 | 388,912 | 373,481 | ||||||||||||||||||||||||

| Allowances (1) |

(11,508) | 2.1 | (11,269) | (11,164) | ||||||||||||||||||||||||

| Loans and advances to customers |

388,949 | 3.0 | 377,643 | 362,317 | ||||||||||||||||||||||||

(1) Allowances include valuation adjustments for credit risk throughout the expected residual life in those financial instruments that have been acquired (mainly originating from the acquisition of Catalunya Banc, S.A.). As of March 31, 2024, December 31, 2023 and March 31, 2023 the remaining amount was €134m, €142m and €173m respectively.

| LOANS AND ADVANCES TO CUSTOMERS (BILLIONS OF EUROS) |

CUSTOMER FUNDS (BILLIONS OF EUROS) | |||

|

(1) At constant exchange rates: +2.4%. |

|

|||

| (1) At constant exchange rates: +6.0%. |

||||

|

CUSTOMER FUNDS (MILLIONS OF EUROS)

|

|

|||||||||||||||||||||||||||

| 31-03-24 | Δ % | 31-12-23 | 31-03-23 | |||||||||||||||||||||||||

| Deposits from customers | 436,763 | 5.6 | 413,487 | 395,880 | ||||||||||||||||||||||||

| Current accounts |

318,367 | 0.3 | 317,543 | 308,918 | ||||||||||||||||||||||||

| Time deposits |

103,807 | 13.4 | 91,524 | 83,516 | ||||||||||||||||||||||||

| Other deposits |

14,589 | 230.1 | 4,420 | 3,446 | ||||||||||||||||||||||||

| Other customer funds | 178,313 | 8.5 | 164,367 | 160,959 | ||||||||||||||||||||||||

| Mutual funds and investment companies and customer portfolios (1) |

143,345 | 8.7 | 131,849 | 118,640 | ||||||||||||||||||||||||

| Pension funds |

29,286 | 3.4 | 28,326 | 38,901 | ||||||||||||||||||||||||

| Other off-balance sheet funds |

5,682 | 35.5 | 4,192 | 3,418 | ||||||||||||||||||||||||

| Total customer funds |

615,076 | 6.4 | 577,853 | 556,839 | ||||||||||||||||||||||||

(1) Includes the customer portfolios in Spain, Mexico, Colombia (preliminary data) and Peru.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

16 |

Capital base

The BBVA Group’s strong results during the quarter, which are in line with those of the fourth quarter of 2023, contributed to the consolidated CET1 fully-loaded ratio to reach 12.82% as of March 31, 2024, which allows to keep maintaining a large management buffer over the Group’s CET1 requirement (9.10%)4 and above the Group’s established target management range of 11.5-12.0% of CET1.

During the first quarter of the year, the CET1 ratio increased by 15 basis points. The strong generation of profit, net of dividends and remuneration of capital instruments, generated a contribution of 27 basis points in the CET1 ratio, which, together with the compensation in equity of the negative effect on results due to the monetary loss given by the net monetary position in hyperinflationary economies allowed it to absorb the growth of risk-weighted assets (RWA) derived from the increase in activity in the quarter (consumption of -43 basis points), in line with the Group’s strategy of promoting profitable growth. On the other hand, among the other impacts, it is worth highlighting those associated with market variables, where the negative evolution of some currencies in the quarter stands out (mainly the impact of the Turkish lira and the US dollar), and in a lesser extent, the evolution of the fixed income portfolios valuation, partially offset by the positive evolution of the investments in equity portfolio.

| Quarterly evolution of the CET1 fully-loaded ratio |

|

(1) Includes, among others, Held to collect and sale (HTC&S) currencies and portfolios, non-controlling interests and a positive increase of “Accumulated other comprehensive income”, which offsets the negative impact on the income statement of the value loss of the net monetary position in hyperinflationary economies.

The consolidated fully-loaded additional Tier 1 capital (AT1) stood at 1.35% as of March 31, 2024, resulting a decrease of -31 basis points from the previous quarter, mainly due to the early redemption of a contingent convertible issuance valued at €1 billion.

On the other hand, the consolidated fully-loaded Tier 2 ratio at the end of March 2024 stood at 2.49%, with an increase of 24 basis points in the quarter, mainly due to the issuance of a subordinated bond in Spain for € 1,250m and, to a lesser extent, to the issuance in Mexico, Turkey and Peru of subordinated debt valued at 900, 500 and 300 million dollars, respectively. On the contrary, a subordinated issuance valued at €750 million has been redeemed in Spain Thus, the total fully-loaded capital ratio stood at 16.66%.

Following the latest SREP (Supervisory Review and Evaluation Process) decision, the ECB has informed to the Group that, with effect from January 1, 2024, it will have to maintain a total capital ratio of 13.25% and a CET1 capital ratio of 9.09% at the consolidated level (9.10% with the countercyclical buffer update calculated as of December 31, 2023), which includes the consolidated Pillar 2 requirement of 1.68% (of which at least 1.02% shall be met with CET1), of which 0.18% is determined on the basis of the ECB’s prudential provisioning expectation and shall be met with CET1.

It is worth mentioning that, with effect from January 1, 2023, the application of part of the transitional effects applied by the Group in the determination of the phased-in ratio has ended, so that as of March 31, 2024, this ratio coincides with the fully-loaded ratio.

4 This includes the update of the countercyclical capital buffer calculated on the basis of exposure at end December 2023.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

17 |

| FULLY-LOADED CAPITAL RATIOS (PERCENTAGE) |

|

|

CAPITAL BASE (MILLIONS OF EUROS)

|

|

|||||||||||||||||||||||

| Phased-in (1) | Fully-loaded (1) | |||||||||||||||||||||||

| 31-03-24 (2) | 31-12-23 | 31-03-23 | 31-03-24 (2) | 31-12-23 | 31-03-23 | |||||||||||||||||||

| Common Equity Tier 1 (CET1) |

48,739 | 46,116 | 45,761 | 48,739 | 46,116 | 45,761 | ||||||||||||||||||

| Tier 1 |

53,868 | 52,150 | 50,948 | 53,868 | 52,150 | 50,948 | ||||||||||||||||||

| Tier 2 |

9,450 | 8,182 | 5,865 | 9,450 | 8,182 | 5,865 | ||||||||||||||||||

| Total capital (Tier 1 + Tier 2) |

63,318 | 60,332 | 56,812 | 63,318 | 60,332 | 56,812 | ||||||||||||||||||

| Risk-weighted assets |

380,044 | 363,915 | 348,598 | 380,044 | 363,915 | 348,598 | ||||||||||||||||||

| CET1 (%) |

12.82 | 12.67 | 13.13 | 12.82 | 12.67 | 13.13 | ||||||||||||||||||

| Tier 1 (%) |

14.17 | 14.33 | 14.62 | 14.17 | 14.33 | 14.62 | ||||||||||||||||||

| Tier 2 (%) |

2.49 | 2.25 | 1.68 | 2.49 | 2.25 | 1.68 | ||||||||||||||||||

| Total capital ratio (%) |

16.66 | 16.58 | 16.30 | 16.66 | 16.58 | 16.30 | ||||||||||||||||||

(1) The difference between the phased-in and fully-loaded ratios arises from the temporary treatment of certain capital items, mainly of the impact of IFRS 9, to which the BBVA Group has adhered voluntarily (in accordance with article 473bis of the CRR and the subsequent amendments introduced by the Regulation (EU) 2020/873). For the periods shown in this table, there are no differences between phased-in and fully-loaded ratios due to the aforementioned temporary treatment.

(2) Preliminary data.

Regarding leverage ratio, as of March 31, 2024, the Group’s fully-loaded ratio stood at 6.5%5, -6 basis points less than in December 2023, mainly due to the increase of the exposure.

| LEVERAGE RATIO (FULLY-LOADED) | ||||||||||||

| 31-03-24 | 31-12-23 | 31-03-23 | ||||||||||

| Exposure to Leverage Ratio (fully-loaded) (million euros) |

830,725 | 797,888 | 773,495 | |||||||||

| Leverage ratio (fully-loaded) (%) |

6.5 | 6.5 | 6.6 | |||||||||

Lastly, with regard to MREL, the RWA and leverage ratios6 stand at 27.8% and 11.5%, respectively, reaching the subordinated ratios of 22.0% and 9.1%, respectively. A summarizing chart is shown below:

|

MREL

|

||||||||||||

| 31-03-24 | 31-12-23 | 31-03-23 | ||||||||||

| Total own funds and eligible liabilities (million euros) |

53,171 | 49,398 | 48,745 | |||||||||

| Total RWA of the resolution group (million euros) |

219,681 | 214,757 | 206,655 | |||||||||

| RWA ratio (%) |

27.8 | 26.4 | 26.9 | |||||||||

| Total exposure for the Leverage calculation (million euros) |

530,175 | 517,470 | 508,210 | |||||||||

| Leverage ratio (%) |

11.5 | 10.9 | 10.94 | |||||||||

5 The Group’s leverage ratio is provisional at the date of release of this report.

6 Calculated at consolidated level in accordance with the resolution strategy MPE (“Multiple Point of Entry”) of the BBVA Group, established by the SRB. The resolution group is made up of Banco Bilbao Vizcaya Argentaria, S.A. and subsidiaries that belong to the same European resolution group.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

18 |

In terms of requirements, on March 27, 2024 the Group disclosed the receipt of a new communication from the Bank of Spain regarding its MREL requirement, established by the Single Resolution Board (hereinafter “SRB”). In accordance with this communication, BBVA has to reach, from that day on, an MREL in RWA equal to 22.79%7, without taking into consideration the current combined capital requirement of 3.61%. Additionally, BBVA must reach, also by March 27, 2024, a volume of own funds and eligible liabilities in terms of total exposure considered for the purpose of the calculation of the leverage ratio of 8.48% (the “MREL in LR”)8. Given the own funds and eligible liabilities of the resolution group, as of March 31, 2024, the Group meets the requirements.

Likewise, with the aim of reinforcing compliance with these requirements, BBVA has made several debt issuances during the first quarter of 2024. For more information on made issues, see “Structural risks” section within the “Risk management” chapter.

Shareholder remuneration

Regarding shareholder remuneration, as approved by the General Shareholders´ Meeting on March 15, 2024, in its first item on the agenda, on April 10, 2024, a cash payment of €0.39 gross per each outstanding BBVA share entitled to receive such amount was made against the 2023 results, as an additional shareholder remuneration for the financial year 2023. Thus, the total amount of cash distributions for 2023, taking into account the €0.16 gross per share that was distributed in October 2023, amounted to €0.55 gross per share.

Total shareholder remuneration includes, in addition to the cash payments mentioned above, the remuneration resulting from the BBVA’s buyback program for the repurchase of own shares announced on January 30, 2024 for a maximum amount of €781m, and which started being executed on March 1, 2024. By means of an Other Relevant Information notice dated April 9, 2024, BBVA announced the completion of the share buyback program upon reaching the maximum monetary amount, having acquired 74,654,915 own shares, between March 4 and April 9, 2024, representing, approximately, 1.28% of BBVA’s share capital as of such date. The redemption of such shares is pending execution.

As of March 31, 2024 and December 31, 2023, BBVA’s share capital amounted to €2,860,590,786.20 divided into 5,837,940,380 shares.

| SHAREHOLDER STRUCTURE (31-03-24) | ||||||||||||||||

| Shareholders | Shares outstanding | |||||||||||||||

| Number of shares | Number | % | Number | % | ||||||||||||

| Up to 500 |

311,091 | 42.8 | 57,443,656 | 1.0 | ||||||||||||

| 501 to 5,000 |

325,542 | 44.8 | 576,148,338 | 9.9 | ||||||||||||

| 5,001 to 10,000 |

48,110 | 6.6 | 337,256,570 | 5.8 | ||||||||||||

| 10,001 to 50,000 |

37,273 | 5.1 | 711,737,987 | 12.2 | ||||||||||||

| 50,001 to 100,000 |

2,639 | 0.4 | 180,407,925 | 3.1 | ||||||||||||

| 100,001 to 500,000 |

1,187 | 0.2 | 210,691,513 | 3.6 | ||||||||||||

| More than 500,001 |

258 | 0.04 | 3,764,254,391 | 64.5 | ||||||||||||

|

Total |

726,100 | 100 | 5,837,940,380 | 100 | ||||||||||||

Note: in the case of shares kept by investors through a custodian placed outside Spain, only the custodian will be considered as a shareholder, which is who appears registered in the accounting record of book entries, so the number of shareholders stated does not consider those indirect holders.

Ratings

During the first quarter of 2024, BBVA’s rating has continued to demonstrate its strength and all agencies have maintained their rating in the A category. In March, Moody´s changed its long-term outlook on the senior preferred debt from stable to positive (maintaining its rating in A3) after a similar action on the Spanish Sovereign rating and reflecting the expectations of the agency that the profitability levels of the bank will continue being high and that the pressures on the quality of assets will remain contained. Additionally, in March too, DBRS communicated the result of its annual revision of BBVA confirming the rating in A (high) with a stable outlook. S&P and Fitch have maintained without changes in the quarter the BBVA rating in A and A-, respectively, both of them with a stable outlook. The following table shows the credit ratings and outlooks assigned by the agencies:

|

RATINGS

|

||||||||

| Rating agency | Long term (1) | Short term | Outlook | |||||

| DBRS |

A (high) | R-1 (middle) | Stable | |||||

| Fitch |

A- | F-2 | Stable | |||||

| Moody’s |

A3 | P-2 | Positive | |||||

| Standard & Poor’s |

A | A-1 | Stable | |||||

(1) Ratings assigned to long term senior preferred debt. Additionally, Moody’s and Fitch assign A2 and A- rating, respectively, to BBVA’s long term deposits.

7 The subordination requirement in RWA is 13.5%.

8 The subordination requirement in Leverage ratio is 5.78%.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

19 |

Credit risk

Uncertainty within the macroeconomic environment remains high, and the geopolitical turbulence at the time of preparation of this report could contribute to a new spike in energy prices, and therefore, increase the biases towards more negative scenarios, with higher than expected interest rates, and more persistent inflation, which can affect credit demand and hinder the payment capacity of families and business.

For the estimation of expected losses, the models include individual and collective estimates, taking into account the macroeconomic forecasts in accordance with IFRS 9. Thus, the estimate at the end of the year includes the effect on expected losses of updating macroeconomic forecasts, which take into account the current global environment. Additionally, the Group may complement the expected losses either by considering additional risk drivers, the incorporation of sectorial particularities or those that may affect a set of operations or borrowers, following a formal internal process established for the purpose.

By region, the evolution during the year has been uneven. In Spain, growth forecasts for 2024 have been revised upwards, and the household debt levels are far from the historical highs, whereas in Mexico, less dynamism in activity is observed while we await a gradual cycle of monetary policy normalization. The uncertainty in Turkey continues, although growth remains solid. Despite changes in economic policy, quality indicators for the system remain at low levels. Finally, in general, growth has been less dynamic in South America, in a context of high inflation and interest rates on a downward trend.

BBVA Group’s credit risk indicators

The evolution of the Group’s main credit risk indicators is summarized below:

| – | Credit risk increased in the first quarter of the year by 3.0% (+2.4% in constant terms), with generalized growth at constant exchange rates in all geographical areas. |

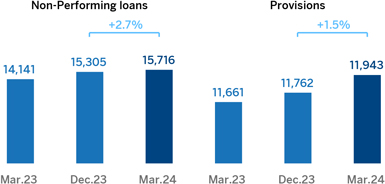

| – | Non-performing loans increased by 2.7% at the Group level between December 2023 and March 2024 (+2.1% in constant terms), with general increases in all geographical areas except of Turkey, which has been favored by the effect of exchange rates, sales of retail portfolios and positive dynamics in the recovery and repayments of the wholesale business. In general, the increases were concentrated in retail portfolios and, in the case of Rest of Business, in the entry into default of a single customer. |

|

NON-PERFORMING LOANS AND PROVISIONS (MILLIONS OF EUROS)

|

||||

| – | The NPL remained practically stable as of March 31, 2024, standing at 3.4%. |

| – | The NPL coverage ratio ended the quarter at 76%, steady compared to the previous quarter (86 basis points below the figure of the end of December), with stability in Spain and decreases in the rest of business areas, mainly in Mexico and Rest of Business. |

| – | The cumulative cost of risk as of March 31, 2024 stood at 1.39%, which is above the previous quarter, yet in line with the expectations, with lower requirements in Spain, more normalized levels in Turkey, South America continuing the trend observed in 2023 and Mexico affected by the requirements of the retail portfolio. |

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

20 |

|

NPL AND NPL COVERAGE RATIOS AND COST OF RISK (PERCENTAGE)

|

|

CREDIT RISK (1) (MILLIONS OF EUROS)

|

| 31-03-24 | 31-12-23 | 30-09-23 | 30-06-23 | 31-03-23 | ||||||||||||||||

| Credit risk |

462,457 | 448,840 | 444,984 | 436,174 | 428,423 | |||||||||||||||

| Stage 1 |

405,765 | 392,528 | 394,329 | 386,711 | 377,908 | |||||||||||||||

| Stage 2 |

40,975 | 41,006 | 35,791 | 34,772 | 36,373 | |||||||||||||||

| Stage 3 (non-performing loans) |

15,716 | 15,305 | 14,864 | 14,691 | 14,141 | |||||||||||||||

|

Provisions |

11,943 | 11,762 | 11,751 | 11,697 | 11,661 | |||||||||||||||

| Stage 1 |

2,198 | 2,142 | 2,143 | 2,107 | 2,062 | |||||||||||||||

| Stage 2 |

2,130 | 2,170 | 2,198 | 2,181 | 2,243 | |||||||||||||||

| Stage 3 (non-performing loans) |

7,615 | 7,450 | 7,410 | 7,409 | 7,357 | |||||||||||||||

| NPL ratio (%) |

3.4 | 3.4 | 3.3 | 3.4 | 3.3 | |||||||||||||||

| NPL coverage ratio (%) (2) |

76 | 77 | 79 | 80 | 82 | |||||||||||||||

(1) Includes gross loans and advances to customers plus guarantees given.

(2) The NPL coverage ratio includes the valuation adjustments for credit risk throughout the expected residual life in those financial instruments that have been acquired (mainly originating from the acquisition of Catalunya Banc, S.A.). If these valuation corrections had not been taken into account, the NPL coverage ratio would have stood at 76% as of March 31, 2024.

|

NON-PERFORMING LOANS EVOLUTION (MILLIONS OF EUROS)

|

| 1Q24 (1) | 4Q23 | 3Q23 | 2Q23 | 1Q23 | ||||||||||||||||||||||||||||||||

| Beginning balance |

15,305 | 14,864 | 14,691 | 14,141 | 14,463 | |||||||||||||||||||||||||||||||

| Entries |

3,243 | 3,038 | 2,898 | 2,875 | 2,256 | |||||||||||||||||||||||||||||||

| Recoveries |

(1,585) | (1,373) | (1,538) | (1,394) | (1,489) | |||||||||||||||||||||||||||||||

| Net variation |

1,661 | 1,665 | 1,360 | 1,481 | 767 | |||||||||||||||||||||||||||||||

| Write-offs |

(1,211) | (983) | (830) | (877) | (1,081) | |||||||||||||||||||||||||||||||

| Exchange rate differences and other |

(36) | (241) | (357) | (54) | (8) | |||||||||||||||||||||||||||||||

|

Period-end balance |

15,716 | 15,305 | 14,864 | 14,691 | 14,141 | |||||||||||||||||||||||||||||||

| Memorandum item: |

||||||||||||||||||||||||||||||||||||

| Non-performing loans |

14,938 | 14,444 | 13,947 | 13,787 | 13,215 | |||||||||||||||||||||||||||||||

| Non performing guarantees given |

778 | 862 | 918 | 905 | 926 | |||||||||||||||||||||||||||||||

(1) Preliminary data.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

21 |

Structural risks

Liquidity and funding

Liquidity and funding management at BBVA promotes the financing of the recurring growth of the banking business at suitable maturities and costs using a wide range of funding sources. BBVA’s business model, risk appetite framework and funding strategy are designed to reach a solid funding structure based on stable customer deposits, mainly retail (granular). As a result of this model, deposits have a high degree of assurance in each geographical area, close to 55% in Spain and Mexico. It is important to note that, given the nature of BBVA’s business, lending is mainly financed through stable customer funds.

One of the key elements in the BBVA Group’s liquidity and funding management is the maintenance of large high-quality liquidity buffers in all geographical areas. In this respect, the Group has maintained during the last 12 months an average volume of high quality liquid assets (HQLA) of €132.5 billion, of which 97% correspond to maximum quality assets (level 1 in the liquidity coverage ratio, LCR).

Due to its subsidiary-based management model, BBVA is one of the few major European banks that follows the Multiple Point of Entry (MPE) resolution strategy: the parent company sets the liquidity policies, but the subsidiaries are self-sufficient and responsible for managing their own liquidity and funding (taking deposits or accessing the market with their own rating). This strategy limits the spread of a liquidity crisis among the Group’s different areas and ensures the adequate transmission of the cost of liquidity and financing to the price formation process.

The BBVA Group maintains a solid liquidity position in every geographical area in which it operates, with ratios well above the minimum required:

| – | The LCR requires banks to maintain a volume of high-quality liquid assets sufficient to withstand liquidity stress for 30 days. BBVA Group’s consolidated LCR remained comfortably above 100% during the first quarter and stood at 151% as of March 31, 2024. It should be noted that, given the MPE nature of BBVA, this ratio limits the numerator of the LCR for subsidiaries other than BBVA S.A. to 100% of its net outflows. Therefore, the resulting ratio is below that of the individual units (the LCR of the main components reaches 179% in BBVA, S.A., 165% in Mexico and 193% in Turkey). Without considering this restriction, the Group’s LCR ratio reaches 186%. |

| – | The net stable funding ratio (NSFR) requires banks to maintain a stable funding profile in relation to the composition of their assets and off-balance sheet activities. The BBVA Group’s NSFR ratio stood at 132% as of March 31, 2024. |

The breakdown of these ratios in the main geographical areas in which the Group operates is shown below:

|

LCR AND NSFR RATIOS (PERCENTAGE. 31-03-24)

|

||||||||

| BBVA, S.A. | Mexico | Turkey | South America | |||||

|

LCR |

179% | 165% | 193% | All countries >100 | ||||

|

NSFR |

124% | 135% | 168% | All countries >100 | ||||

In addition to the above, the most relevant aspects related to the main geographical areas are the following:

| – | BBVA, S.A. has maintained a strong position with a large high-quality liquidity buffer, having repaid the entire TLTRO III program, maintaining at all times the regulatory liquidity metrics well above the set minimums. During the first quarter of 2024, commercial activity has provided liquidity to the balance sheet mainly due to the good evolution of customer deposits, with growth greater than that of lending activity. |

| – | BBVA Mexico shows a solid liquidity situation, even though the credit gap increased in the first quarter of the year as a consequence of the outflows of the end-year seasonal fund gathering. Despite that, the cost of funds has been efficiently managed. |

| – | In Turkey, in the first quarter of 2024, the lending gap in local currency increased, due to a greater growth in loans than in deposits, while the lending gap in foreign currency decreased due to higher demand for foreign currency deposits before the local elections. Garanti BBVA continues to maintain a stable liquidity position with comfortable ratios. On the other hand, the Central Bank of Turkey has continued updating the measures to continue with the dedollarization process of the economy and control the inflation. |

| – | In South America, the liquidity situation remains adequate throughout the region. In Argentina, liquidity in the system continues to increase, as well as in BBVA due to a higher growth in deposits than in loans in both local and foreign currency. In BBVA Colombia, the credit gap remains essentially unchanged in the first quarter, after a slight fall of the volume of credit investment, in line with the evolution of customer deposits. BBVA Peru maintains solid liquidity levels. |

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

22 |

The main wholesale financing transactions carried out by the BBVA Group during the first quarter of 2024 are listed below:

| Issuer |

Type of issue | Date of issue | Nominal (millions) |

Currency | Coupon | Early redemption |

Maturity date | |||||||||

| BBVA, S.A. | Senior preferred |

Jan-24 | 1,250 | EUR | 3.875 % | — | Jan-34 | |||||||||

|

|

||||||||||||||||

| Tier 2 | Feb-24 | 1,250 | EUR | 4.875 % | Feb-31 | Feb-36 | ||||||||||

|

|

||||||||||||||||

| Senior preferred |

Mar-24 | 1,000 | USD | 5.381 % | — | Mar-29 | ||||||||||

|

|

||||||||||||||||

| Senior non-preferred |

Mar-24 | 1,000 | USD | 6.033% | — | Mar-35 | ||||||||||

|

|

||||||||||||||||

|

|

Senior preferred (green bond) |

Mar-24 | 1,000 | EUR | 3.500 % | — | Mar-31 | |||||||||

Additionally, BBVA, S.A. redeemed two capital issuances in the first quarter: in February 2024, a Tier 2 issuance of subordinated bonds issued in February 2019, for an amount of €750m and, in March 2024, an AT1 issued in 2019 on its first date of optional redemption, for an amount of €1,000m.

BBVA Mexico issued in January Tier 2 bonds for USD 900m with a maturity of 15 years and early repayment option in 10 years with a coupon of 8.125%.

In Turkey, Garanti BBVA issued Tier 2 10-year bonds for an amount of USD 500m, with a coupon of 8.375% and a redemption option in 5 years.

For its part, BBVA Peru issued Tier 2 bonds in the international market for USD 300m, with a 6.20% coupon, a term of 10.25-year maturity and an early redemption option in year 5.

In conclusion, the first quarter of 2024 has turned into one of the historically more actives in terms of issuance of wholesale funding of BBVA, S.A., with €5,400m funded in 5 tranches. If we also consider the issuance activity of BBVA Mexico, BBVA Turkey and BBVA Peru, this access to international markets increases by USD 1,700m, which shows the strength of the Group´s access to wholesale markets from its main issuance units.

Additionally, on April 10th, BBVA Mexico issued senior bank bonds for 15,000m Mexican pesos, in two tranches. The first one was placed with a term of three and a half years, with a variable TIIE anchoring rate of one day plus 32 basis points, registering a total of 8,439m Mexican pesos. The second tranche was issued to seven years, with a fixed 10.35% rate, for a total of 6,561m Mexican pesos.

Foreign exchange

Foreign exchange risk management aims to reduce both the sensitivity of the capital ratios and the net attributable profit variability to currency fluctuations.

The performance of the Group’s main currencies during the first quarter of 2024 has been very uneven. Due to its relevance for the Group, it should be noted the strength of the Mexican peso, which has appreciated 4.5% against the euro. In the same way, the US dollar and the Peruvian sol registered an appreciation of 2.2% against the euro and, in the case of the Colombian peso, this appreciation was slightly smaller, of 1.7%. On the downside, the depreciation of the Chilean peso (-7.9%), of the Turkish lira (-6.6%) and, to a lesser extent, of the Argentinian peso (-3.7%) stand out.

|

EXCHANGE RATES (EXPRESSED IN CURRENCY/EURO)

|

||||||||||||||||

| Year-end exchange rates | Average exchange rates | |||||||||||||||||||

| Δ % on | Δ % on | Δ % on | ||||||||||||||||||

| 31-03-24 | 31-03-23 | 31-12-23 | 1Q24 | 1Q23 | ||||||||||||||||

| U.S. dollar |

1.0811 | 0.6 | 2.2 | 1.0857 | (1.2) | |||||||||||||||

| Mexican peso |

17.9179 | 9.6 | 4.5 | 18.4409 | 8.7 | |||||||||||||||

| Turkish lira (1) |

34.9487 | (40.3) | (6.6) | — | — | |||||||||||||||

| Peruvian sol |

4.0144 | 1.9 | 2.2 | 4.0789 | 0.3 | |||||||||||||||

| Argentine peso (1) |

926.95 | (75.5) | (3.7) | — | — | |||||||||||||||

| Chilean peso |

1,061.33 | (19.1) | (7.9) | 1,027.06 | (15.2) | |||||||||||||||

| Colombian peso |

4,153.91 | 21.1 | 1.7 | 4,253.73 | 20.1 | |||||||||||||||

(1) According to IAS 21 “The effects of changes in foreign exchange rates”, the year-end exchange rate is used for the conversion of the Turkey and Argentina income statement.

In relation to the hedging of the capital ratios, BBVA covers, in aggregate, 70% of its subsidiaries’ capital excess. The sensitivity of the Group’s CET1 fully-loaded ratio to 10% depreciations in major currencies is estimated at: +17 basis points for the U.S. dollar, -10 basis

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

23 |

points for the Mexican peso and -4 basis points for the Turkish lira9. With regard to the hedging of results, BBVA hedges between 40% and 50% of the aggregate net attributable profit it expects to generate in the next 12 months. For each currency, the final amount hedged depends on its expected future evolution, the costs and the relevance of the incomes related to the Group’s results as a whole.

Interest rate

Interest rate risk management seeks to limit the impact that BBVA may suffer, both in terms of net interest income (short-term) and economic value (long-term), from adverse movements in the interest rate curves in the various currencies in which the Group operates. BBVA carries out this work through an internal procedure, pursuant to the guidelines established by the European Banking Authority (EBA), with the aim of analyzing the potential impact that could derive from a range of scenarios on the Group’s different balance sheets.

The model is based on assumptions intended to realistically mimic the behavior of the balance sheet. The assumptions regarding the behavior of accounts with no explicit maturity and prepayment estimates are specially relevant. These assumptions are reviewed and adapted at least once a year according to the evolution in observed behaviors.

At the aggregate level, BBVA continues to have a positive sensitivity toward interest rate increases in the net interest income.

In the first quarter of 2024, inflation data were slightly surprisingly high. This has caused the market to anticipate smaller rate drops for the year in Europe and in the United States and to expect the first rate fall from the Fed by the end of the summer, which has triggered a rise in sovereign bond profitability and has led to a slightly negative performance in most debt portfolios of the Group. For their part, peripheral rate curve spreads remain well supported, even tightening in the quarter. In Mexico, the central bank cut for the first time in three years the official interest rate, in line with the monetary policy actions of most South American countries, where by end-2023 interest rate cuts had begun. In Turkey, the Central Bank of Turkey has continued the tightening of its monetary policy launched in June 2023.

By area, the main features are:

| – | Spain has a balance sheet characterized by a lending portfolio with high proportion of variable-rate loans (mortgages and corporate lending) and liabilities composed mainly by customer demand deposits. The ALCO portfolio acts as a management lever and hedge for the balance sheet, mitigating its sensitivity to interest rate fluctuations. In an environment of high rates, currently close to their market-predicted terminal rates, the interest rate risk profile of the balance sheet has been reduced in the last quarters. |

| On the other hand, the ECB left rates unchanged in the first quarter of the year, bringing the benchmark interest rate by the end of March to 4.5%, the marginal deposit facility rate at 4.0% and the marginal loan facility rate at 4.75%. Additionally, the ECB announced in March the changes on its operative framework, highlighting that, from September on, the spread between the benchmark interest rate and that of the deposit facility will be reduced to 15 basis points. Finally, the market expectations on the start of rate falls by mid-2024 has continued, which has led to the benchmark Euribor types to remain fundamentally stable during the first quarter. |

| – | Mexico continues to show a balance between fixed and variable interest rates balances, which results in a limited sensitivity to interest rates fluctuations. In terms of assets that are most sensitive to interest rate changes, the commercial portfolio stood out, while consumer loans and mortgages are mostly at a fixed rate. With regard to customer funds, the high proportion of non-interest bearing deposits, which are insensitive to interest rate movements, should be highlighted. The ALCO portfolio is invested primarily in fixed-rate sovereign bonds with limited maturities. The monetary policy rate stood at 11.00%, 25 basis points below the end-of-year level of 2023. |

| – | In Turkey, the sensitivity of deposits is offset by the ALCO portfolio and loans (fixed rate and relatively short-term). The sensitivity of the net interest income remains very limited thanks to the different efforts carried out by the Bank. The CBRT has recently increased monetary policy rates, taking interest rates from 8.5% by the end of March 2023 to 50% by the end of March 2024. Linked to regulatory measures, the central bank has also started to remunerate some reserves in Turkish lira. |

| – | In South America, the interest rate risk profile remains low as most countries in the area have a fixed/variable composition and maturities that are very similar for assets and liabilities, with limited net interest income sensitivity. In addition, the in balance sheets with several currencies, the interest rate risk is managed for each of the currencies, showing a very low level of exposure. Regarding benchmark rates, the cut cycle has begun in the region. In Peru it stood at 6.25% as of March 2024, 50 basis points below its 2023 closing level. In Colombia, the interest rate was placed by the end of March 2024 in 12.25%, 75 basis points below the end of 2023. In Argentina, the central bank unexpectedly cut in March the benchmark interest rate to 80%, making another cut of 10 basis points in April up to 70%, which is a decrease of 30 basis points from 100% as of December 2023. |

9 This sensitivity does not include the cost of capital hedges, which are currently estimated at 3 basis points per quarter for Mexican peso and 3 basis points per quarter for Turkish lira.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

24 |

|

INTEREST RATES (PERCENTAGE)

|

||||||||||||||||||||

| 31-03-24 | 31-12-23 | 30-09-23 | 30-06-23 | 31-03-23 | ||||||||||||||||

| Official ECB rate | 4.50 | 4.50 | 4.50 | 4.00 | 3.50 | |||||||||||||||

| Euribor 3 months (1) | 3.92 | 3.94 | 3.88 | 3.54 | 2.91 | |||||||||||||||

| Euribor 1 year (1) | 3.72 | 3.68 | 4.15 | 4.01 | 3.65 | |||||||||||||||

| USA Federal rates | 5.50 | 5.50 | 5.50 | 5.25 | 5.00 | |||||||||||||||

| TIIE (Mexico) | 11.00 | 11.25 | 11.25 | 11.25 | 11.25 | |||||||||||||||

| CBRT (Turkey) | 50.00 | 42.50 | 30.00 | 15.00 | 8.50 | |||||||||||||||

(1) Calculated as the month average.

Translation of this report originally issued in Spanish. In the event of a discrepancy, the Spanish-language version prevails.

|

|

25 |

This section presents the most relevant aspects of the Group’s different business areas. Specifically, for each one of them, it shows a summary of the income statements and balance sheets, the business activity figures and the most significant ratios.

The structure of the business areas reported by the BBVA Group as of March 31, 2024, is the same as the one presented at the end of 2023.