| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Title of each class |

Name of each exchange on which registered | |

American Depositary Shares, each representing the right to receive three ordinary shares, par value Ps.1.00 per share |

New York Stock Exchange | |

Ordinary shares, par value Ps.1.00 per share |

New York Stock Exchange* |

* |

The ordinary shares are not listed for trading,but are listed only in connection with the registration of the American Depositary Shares, pursuant to requirements of the New York Stock Exchange. |

| Title of class |

Number of shares outstanding | |

Ordinary Shares, par value Ps.1.00 per share |

612,710,079 |

| Large accelerated filer | ☐ | Accelerated filer | ☒ | |||

Non-accelerated filer |

☐ | Emerging growth company | ☐ | |||

| U.S. GAAP | ☐ | International Financial Reporting Standards by the International Accounting Standards Board as issued | ☒ | Other | ☐ |

| Auditor firm ID: | 1449 | Auditor name: | Pistrelli, Henry Martin y Asociados S.R.L. (Member of Ernst & Young Global Limited) | Auditor location: | Argentina | |||||

| Auditor firm ID: | 1410 | Auditor name: | KPMG | Auditor location: | Argentina |

TABLE OF CONTENTS

| Page | ||||||

| FORWARD-LOOKING STATEMENTS | 1 | |||||

| PRESENTATION OF FINANCIAL INFORMATION | 2 | |||||

| CERTAIN TERMS AND CONVENTIONS | 3 | |||||

| PART I | ||||||

| 4 | ||||||

| 4 | ||||||

| 4 | ||||||

| 30 | ||||||

| 109 | ||||||

| 109 | ||||||

| 136 | ||||||

| 151 | ||||||

| 154 | ||||||

| 155 | ||||||

| 159 | ||||||

| 171 | ||||||

| 180 | ||||||

| PART II | ||||||

| 182 | ||||||

| MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

182 | |||||

| 182 | ||||||

| 184 | ||||||

| 184 | ||||||

| 184 | ||||||

| 185 | ||||||

| PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

185 | |||||

| 185 | ||||||

| 185 | ||||||

| 188 | ||||||

| DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS |

188 | |||||

| 188 | ||||||

| 189 | ||||||

| PART III | ||||||

| 191 | ||||||

| 191 | ||||||

| 191 | ||||||

FORWARD-LOOKING STATEMENTS

This Form 20-F contains words, such as “believe”, “expect”, “estimate”, “intend”, “plan”, “may” and “anticipate” and similar expressions that identify forward-looking statements, which reflect our views about future events and financial performance. Actual results could differ materially as a result of factors beyond our control, including but not limited to:

| • | changes in general economic, business or political or other conditions in the Republic of Argentina (“Argentina” or “the Republic”) or changes in general economic or business conditions in worldwide; |

| • | governmental intervention and regulation (including banking and tax regulations); |

| • | developments in the global financial markets; |

| • | deterioration in the Argentine financial system or regional business and economic conditions; |

| • | inflation; |

| • | the outbreak and spread of a pandemic and other large-scale public health events; |

| • | changes in exchange rates or capital markets in general that may affect policies towards or lending to Argentina or Argentine companies; |

| • | changes in interest rates which may adversely affect our margins; |

| • | adverse legal or regulatory disputes or proceedings; |

| • | credit and other risks of lending, such as increases in defaults by borrowers and other delinquencies; |

| • | increase in the provisions for loan losses; |

| • | fluctuations and declines in the value of Argentine public debt; |

| • | decreases in deposits or in the number of our customers; |

| • | competition in the banking, financial services and related industries and the loss of market share; |

| • | unanticipated increases in financing and other costs or the inability to obtain additional debt, equity or wholesale financing on attractive terms or at all; and |

| • | the factors discussed under “Item 3. Key Information—D. Risk Factors”. |

Accordingly, readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Banco BBVA Argentina S.A. (“BBVA Argentina” or the “Bank”) undertakes no obligation to update or revise these forward-looking statements or to publicly release the results of any revisions to these forward-looking statements. The accompanying information in this annual report, including, without limitation, the information under “Item 4. Information on the Company”, “Item 5. Operating and Financial Review and Prospects” and “Item 11. Quantitative and Qualitative Disclosures About Market Risk” identifies important factors that could cause material differences between any forward-looking statements and actual results.

1

PRESENTATION OF FINANCIAL INFORMATION

General

The Bank’s audited consolidated financial statements as of December 31, 2023 and 2022 and for the years ended December 31, 2023, 2022 and 2021 included herein (the “Consolidated Financial Statements”) are prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS-IASB”).

All 2023, 2022 and 2021 data included in this report have been prepared in accordance with IFRS-IASB for the sole purpose of filing this annual report on Form 20-F with the U.S. Securities and Exchange Commission (“SEC”).

The statutory consolidated annual financial statements that the Bank prepares to comply with the requirements of the Argentine Central Bank (the “Central Bank” or “BCRA”) are prepared pursuant to the reporting framework established by the Central Bank requiring supervised entities to submit financial statements prepared pursuant to IFRS-IASB except for:

| (i) | the application of the expected credit loss model set forth under paragraph 5.5. of IFRS 9 for debt instruments issued by the public sector; |

| (ii) | for 2021, the accounting treatment applied to the investment held by the Bank in Prisma Medios de Pago S.A., which was made on the basis of the provisions of Memoranda No. 7/2019 and No. 8/2021 issued by the BCRA, each dated on April 29, 2019 and May 22, 2021, respectively. In March 2022, we transferred to a third party the shares we owned in Prisma Medios de Pago S.A and, as a result the income (loss) thereof was recorded in the three-month period ended March 31, 2022. If the fair value of our interest in Prisma Medios de Pago S.A. had been determined on the basis of IFRS-IASB, the income (loss) for previous years and for the year ended December 31, 2022 would have been different. This accounting treatment does not affect the shareholders’ equity value as of December 31, 2022; and |

| (iii) | the treatment to be applied to uncertain tax positions, which follows the guidance prescribed by Memorandum No. 6/2017 Financial Reporting Framework Established by the BCRA issued on May 29, 2017. As of December 31, 2021, such provision had been reversed in the statutory consolidated financial statements. |

Because of such differences, our statutory consolidated annual financial statements for the fiscal years ended December 31, 2023, 2022 and 2021 are not comparable with the Consolidated Financial Statements included herein. In addition, we will continue to have differences during 2024 between our statutory consolidated financial statements and the financial statements required by IFRS-IASB. We do not intend to report in accordance with IFRS-IASB on an interim basis during 2024. Consequently, our interim financial information for 2024 will not be comparable with the Consolidated Financial Statements and other information contained in this annual report on Form 20-F. We refer in this annual report on Form 20-F to IFRS-IASB as adjusted by the regulations of the BCRA as “IFRS-BCRA”.

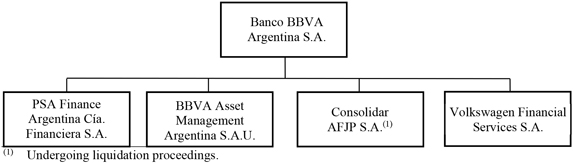

The Consolidated Financial Statements consolidate all the subsidiaries of the Bank in which the Bank holds direct or indirect control. See “Item 4. Information on the Company—C. Organizational Structure” for an organizational chart of BBVA Argentina and its subsidiaries.

In this annual report, references to “$”, “US$”, “U.S. dollars”, “US dollars” and “dollars” are to United States dollars and references to “Ps.”, “Pesos” and “pesos” are to Argentine pesos. Percentages and certain dollar and peso amounts have been rounded for ease of presentation. Unless otherwise stated, all market share and other industry information has been derived from information published by the Central Bank.

Unless otherwise indicated, financial information contained in this annual report reflects the consolidation of the following subsidiaries at the year end and for the fiscal years indicated below:

| As of and for the year ended December 31, |

||||||

| Entity |

2023 | 2022 | 2021 | |||

| Volkswagen Financial Services Compañía Financiera S.A. |

X | X | X | |||

| Consolidar AFJP S.A. (undergoing liquidation proceedings) |

X | X | X | |||

| BBVA Asset Management Argentina S.A.U. |

X | X | X | |||

| PSA Finance Argentina Compañía Financiera S.A. |

X | X | X | |||

2

IAS 29 Financial Reporting in Hyperinflationary Economies requires that an entity whose functional currency is the currency of a hyperinflationary economy must state its assets, liabilities, income and expenses in terms of the measuring unit current at the end of the reporting period (December 31, 2023). The Bank has applied IAS 29 as follows for purposes of the Consolidated Financial Statements:

| • | Restated the consolidated statement of profit or loss, the consolidated statement of comprehensive income, the consolidated statement of changes in equity and consolidated statements of cash flow for the years ended December 31, 2022 and 2021. |

| • | Restated the consolidated statement of financial position as of December 31, 2022. |

| • | Adjusted the consolidated statement of financial position as of December 31, 2023. |

| • | Adjusted the consolidated statement of profit or loss, the consolidated statement of comprehensive income, the consolidated statement of changes in equity and consolidated statements of cash flow for the year ended December 31, 2023, including the calculation and separate disclosure of the gain or loss on the net monetary position. |

For further information regarding the methodology and criteria applied see Note 2.1.5 to the Consolidated Financial Statements.

See “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Exchange Rates” for information regarding the evolution of rates of exchange since 2019.

All figures and percentages of variations in this annual report on Form 20-F, unless otherwise stated, are presented in the measuring unit current at December 31, 2023. All comparisons of the financial system contained in this annual report on Form 20-F are presented in nominal terms.

CERTAIN TERMS AND CONVENTIONS

The terms below are used as follows throughout this report:

| • | “BBVA Argentina”, the “Bank” or the “Company” and terms such as “we”, “us” and “our” mean Banco BBVA Argentina S.A. and its consolidated subsidiaries unless otherwise indicated or the context otherwise requires. |

| • | “BBVA” or the “BBVA Group” means Banco Bilbao Vizcaya Argentaria, S.A. and its consolidated subsidiaries unless otherwise indicated or the context otherwise requires. |

| • | “Consolidated Financial Statements” means our audited consolidated financial statements as of December 31, 2023 and 2022 and for the years ended December 31, 2023, 2022 and 2021, prepared in accordance with IFRS-IASB and included in this annual report on Form 20-F. |

3

- PART I -

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

| A. | Selected Financial Data |

Reserved.

| B. | Capitalization and indebtedness |

Not applicable.

| C. | Reasons for the offer and use of proceeds |

Not applicable.

| D. | Risk Factors |

The following summarizes some, but not all, of the risks provided below. Please carefully consider all of the information discussed in this Item 3.D. “Risk Factors” in this annual report for a more thorough description of these and other risks:

| • | Risks Relating to Argentina |

| • | economic and political instability in Argentina; |

| • | current levels of inflation; |

| • | high levels of public spending; |

| • | the Argentine economy could be adversely affected by economic events in other markets; |

| • | a decline in international prices for or in the amount of Argentina’s principal commodity exports; |

| • | exchange controls and restrictions on capital inflows and outflows; |

| • | the insufficiency of the measures adopted to resolve the crisis in the energy sector; |

| • | any failure to adequately address actual and perceived risks of institutional deterioration and corruption; |

| • | fluctuations in the value of the peso; |

| • | the inability of the Republic to obtain financing on satisfactory terms; |

| • | salary increases or additional employments benefits as a result of government measures or pressure from union sectors; |

| • | government intervention in the Argentine economy; |

| • | amendments to the Central Bank’s Charter and the Convertibility Law; and |

| • | the outbreak and spread of a pandemic and other large-scale public health events. |

| • | Risks Relating to the Argentine Financial System and to BBVA Argentina |

| • | the short-term structure of the deposit base of the Argentine financial system, including the deposit base of the Bank, could lead to a reduction in liquidity levels and limit the long-term expansion of financial intermediation; |

| • | reduced spreads between interest rates received on loans and those paid on deposits; |

| • | volatility in interest rates; |

| • | a mismatch between UVA (“Unidad de Valor Adquisitivo”, in Spanish) loans and UVA deposits; |

4

| • | the inaccuracy and/or insufficiency of our estimates and established reserves for credit risk and potential credit losses; |

| • | exposure to public sector debt; |

| • | increased competition in the banking industry; |

| • | activities across the BBVA Group could adversely affect us; |

| • | the dependency of our credit ratings on Argentine sovereign credit ratings; |

| • | the increasing dependency of the financial industry on information technology systems; |

| • | security risks; |

| • | an increase in fraud or transaction errors; |

| • | any insolvency proceeding against us that could subject us to the powers of, and intervention by, the Central Bank; |

| • | lawsuits brought against us outside Argentina; |

| • | class actions against financial institutions for an indeterminate amount; |

| • | the ability of BBVA, our controlling shareholder, to direct our business; |

| • | our ability to grow our business is dependent on our ability to manage our relationships with partners and grow our deposit base; |

| • | acquisitions that could adversely affect the value of the Bank; |

| • | any adverse consequences related to our calculation of income tax for the years ended December 31, 2018 and 2020; |

| • | the application of IAS 29 to our Consolidated Financial Statements; |

| • | restrictions on our ability to pay dividends; and |

| • | exposure to risks in connection with climate change. |

| • | Legal, Regulatory and Compliance Risks |

| • | material weaknesses in our internal control over financial reporting; |

| • | our operations are conducted in a highly regulated environment; |

| • | the instability of the regulatory framework, in particular the regulatory framework affecting financial institutions; |

| • | our exposure to multiple provincial and municipal legislation and regulations; |

| • | limitations arising from the Consumer Protection Law and the Credit Card Law; |

| • | compliance risks; |

| • | differences between U.S. and Argentine corporate disclosure, governance and accounting standards; and |

| • | special rules that govern the priority of different stakeholders of financial institutions in Argentina. |

Risks Relating to Argentina

Overview

We are an Argentine corporation (public limited company), and the vast majority of our operations, properties and customers are located in Argentina. Accordingly, the quality of our assets, our financial condition and our results of operations are significantly affected by macroeconomic and political conditions prevailing in Argentina.

Economic and political instability in Argentina may adversely and materially affect our business, results of operations and financial condition.

The Argentine economy has experienced significant volatility in recent decades, characterized by periods of low or negative growth, high levels of inflation and currency devaluation. As a consequence, our business and operations have been, and could in the future be, affected from time to time to varying degrees by economic and political developments and other material events affecting the Argentine economy, such as inflation, price controls, foreign exchange controls, fluctuations in foreign currency exchange rates and interest rates, governmental policies regarding spending and investment, national, provincial or municipal tax increases and other initiatives increasing government involvement in business activities, and civil unrest and local security concerns.

Between 2001 and 2015, the Argentine economy was very volatile combining periods of severe economic and political crisis resulting, among others, in restrictions on deposit withdrawals and the “pesification” of deposits (which were reclassified as peso denominated), with certain periods of recovery.

5

In 2015, Mr. Mauricio Macri was elected President of Argentina and his administration (the “Macri administration”) launched a wide array of measures intended to correct the longstanding fiscal and monetary policies that had resulted in recurrent public deficit, high inflation, pervasive foreign exchange controls and limited foreign investment.

However, in 2018, the worsening of economic and politic conditions worldwide and in Argentina particularly, resulted in significant capital outflows from Argentina, the closing of global credit markets for Argentine issuers and a strong devaluation of the Argentine peso. By the end of September 2018, a new monetary and foreign exchange scheme, highly influenced by the International Monetary Fund (“IMF”), was announced and while economic conditions stabilized, in October 2019, President Macri lost the elections to Alberto Fernandez, whose administration (the “Fernandez administration”) took office in December 2019. The Fernandez administration implemented a wide range of economic and political reforms, including a sovereign debt restructuring designed to make Argentina’s debt sustainable pursuant to which investors agreed to exchange their defaulted bonds by new bonds, and a restructuring of domestic debt.

The Argentine economy was adversely affected by the Covid-19 pandemic and partially recovered in 2021, as a result of eased mobility restrictions and a consequent increase in economic activity. In 2021, Argentina held mid-term elections, testing the Fernández Administration, which received only 33.5% of the votes (compared to 48% in the elections held in 2019), while the main opposition coalition obtained 41.9% of the votes.

Thereafter, the government presented to Congress a bill for a new agreement with the IMF to replace the stand-by agreement (“SBA”) signed in 2018. The bill was approved in March 2022 despite the lack of endorsement by the Kirchnerist wing of the ruling coalition. This program is an Extended Fund Facility (“EFF”), for a ten-year term, (with a grace period of 4 and a half years), and it does not require any structural reforms. Compliance with the EFF is reviewed on a quarterly basis and compliance of the economic targets is necessary to cover the maturities of the SBA. The EFF contains the minimum requirements for fiscal convergence, reserve accumulation and reduction of monetary issuance for a path towards fiscal balance in 2025, an accumulation of US$15 billion of net international reserves in the next three years, and a reduction of the Treasury’s monetary financing to zero in 2024. Any failure to meet such targets could result in the termination of the EFF program, which could bring political, financial and exchange rate instability due to the government’s inability to access external financing. The EFF program may be subject to adjustments, mainly in terms of disbursements and structural reforms, but it is expected to remain in effect.

In 2022 political and economic instability was high, including with regards to the economic cabinet, which had three Ministers of Economy during the year. In July, following a month of very high economic and financial tensions, the Minister of Economy Martín Guzmán unexpectedly resigned being replaced by Silvina Batakis. She was appointed without the support of the entire ruling coalition, and in the midst of a failed attempt to calm financial tensions, she was replaced by Sergio Massa (a lawyer by profession and one of the main partners of the ruling coalition) only 24 days after taking office. His appointment brought calm to the markets, and soon after his arrival he implemented a slow but consistent reduction of the fiscal deficit, focused on the revision of subsidies to public services tariffs, and an accumulation of international reserves centered on a multiple exchange rate scheme, benefitting soybean exporters.

Finally, direct transfers from the Central Bank to the Treasury, as promised by Minister Massa upon taking office, ceased.

In addition to the instability caused by the successive changes in the Ministry of Economy, Vice-President Cristina Kirchner was the victim of an assassination attempt in Buenos Aires. Although Argentina had not experienced similar events in the last decades, violent political events may occur and have adverse effects on the political and social stability.

Massa’s management as Minister of Economy was based on three pillars: (i) avoiding an abrupt devaluation of the official exchange rate, for which a multiple exchange rate scheme was generated that allowed exporters to settle at a higher differential exchange rate, or partially access the parallel exchange rate, which is always higher than the official exchange rate. This task became especially difficult in the context of the severe drought suffered for the last three years which adversely affected the agricultural sector, resulting in an estimated reduction in dollar inflows of approximately US$20 billion in 2023; (ii) the containment and reduction of inflation, by implementing a variety of measures, such as price controls (through agreements and sanctions) and raising the monetary policy rate (which was generally not positive in real terms, although it was close to the inflation rate); and (iii) the containment of the gap between the parallel and official exchange rates, for which the government intervened to accommodate prices and prevent the gap from widening. Another objective, less relevant for the government than the previous ones, was to moderate the deviations with respect to the targets set forth in the EFF. In order to help the Treasury achieve its issuance target, the government continued to resort to the methodology already applied by former Minister Guzmán, whereby the Central Bank participated in the secondary debt market of the Treasury, so that the latter could take a greater volume of debt to finance spending; for the fiscal target, Minister Massa undertook a partial price adjustment of utility tariffs, although this was set aside in the context of the Presidential elections.

6

The reserve accumulation target was reduced as a result of the difficulties posed by the severe drought suffered in 2023.

Although the results were not as expected: inflation went from 71% year-on-year in July 2022 to 114% year-on-year in May 2023, international reserves went from US$40 billion (monthly average) in July 2022 to US$26 billion (monthly average) in July 2023 and the exchange rate gap was still very high, the government chose Minister Massa as its candidate for President.

Primary elections took place on August 13, 2023. Javier Milei, candidate for La Libertad Avanza (LLA), was the most voted in the primary presidential elections with 30.0% of the total votes. The second most voted political party was Juntos por el Cambio, whose candidates achieved 28.3% of the votes, followed by the candidates of Unión por la Patria (Massa’s party) who achieved 27.3% of the votes. These results were surprising not only because of the parity between the main parties, but also because of the unexpected victory of Milei. The day after the elections, the government validated a 22% increase in the exchange rate and a 22 percentage points increase in the monetary policy rate. This devaluation jump was not accompanied by a stabilization plan, so the benefits of depreciating the real exchange rate were almost non-existent and monthly inflation accelerated to 12.4% and 12.7% in August and September 2023, respectively, the highest values (at that time) in more than 30 years.

After the primary elections, Minister Massa took a series of measures to improve the population’s income in the short term, including one-time bonuses and tax cuts. We estimate the fiscal impact of these measures at 1% of GDP. In the general elections, Sergio Massa obtained 36.7% of the votes, followed by Javier Milei who obtained 30.0% of the votes and Patricia Bullrich, a member of Mauricio Macri’s party, who obtained 23.8% of the votes. The new Congress is fragmented, which will force the new President to negotiate the approval of laws.

On November 19, 2023, Javier Milei was elected President of Argentina with 55.7% of the votes, and he took office on December 10, 2023 (the “Milei administration”). In the first months of the Milei administration, the Central Bank raised by 120% the value of the US$/Peso exchange rate, allowing for the acquisition of international reserves amounting to US$5,624 million from December 11, 2023 to February 15, 2024. At the same time, the Central Bank implemented a debt payment process with importers consisting of the subscription of US$-denominated bonds issued by the Central Bank but payable with Argentine peso, which allowed the Central Bank to withdraw pesos from the economy. Finally, the Central Bank also decided to lower the monetary policy rate -which was yielding 133% per annum- to 70% per annum, in order to reduce the interest payments that the Central Bank pays to banks for their interest-bearing liabilities. This measure is having a negative effect on the Bank as we are receiving lower remuneration on the money we lend to the Central Bank. On the political front, Milei’s government sent to Congress an extensive package of laws aimed at deregulating the economy, which was not approved given the insufficient support that the Milei administration has in Congress.

We cannot assure whether Milei will implement aggressive political and economic policies, such as the dollarization of our economy, or whether his government will take a more moderate path. The implementation of aggressive political and economic policies could result in further uncertainty and the instability of the Argentine economy, all of which could adversely result our results of operations. Additionally, the dollarization of the economy or other disruptive exchange rate measures could trigger hyperinflation and a banking crisis, damaging our balance sheet and potentially reducing our net income.

If current levels of inflation continue, the Argentine economy and the Bank’s business, results of operations and financial condition could be adversely affected.

Argentina has been facing high inflation levels since 2007. The INDEC reported an annual variation of the CPI of 50.9%, 94.8 % and 211.4 % in 2021, 2022 and 2023, respectively.

During the first half of 2022, and as in 2021, the government tried to contain the inflationary acceleration produced by the monetary overhang derived from the monetary issuance in 2020 and 2021, with an appreciation of the real exchange rate and a freeze in the price of utility tariffs. This strategy was inefficient to reduce inflation, which averaged 5.3% per month in the first half of 2022. In July 2022, after the sudden departure of Minister Martín Guzmán, parallel exchange rates rose 20% in one week and determined a successive remarking of prices that accelerated the already very high inflation, leading to a 6.8% monthly average in the third quarter of the year.

7

The arrival of Minister Massa resulted in a decrease of inflation values; however the adjustment of regulated prices (mainly utility rates) was one of the main inflationary drivers of the last months of 2022 and the beginning of 2023.

As a result of the strong drought suffered in Argentina for the last three years; inflation decelerated sharply in November and December 2022 and then accelerated until April 2023. After the primary elections the government adjusted the exchange rate and approved a 22% rise of the parity exchange rate between the U.S. dollar and the Argentine peso. As a result, monthly inflation started to increase at double-digit and year-on-year inflation at December 2023 reached 211%. At the same time, the official exchange rate was 27% more appreciated than the average of the last 20 years. President Milei has already announced that a price stabilization plan will be launched with the aim to reach fiscal equilibrium but, as of the date of this annual report on Form 20-F, there is no certainty as to how this plan will be implemented and the effects it will have on the exchange rate market and/or the fiscal deficit. The Bank’s balance sheet is exposed to the interest-bearing liabilities of the Central Bank (both LELIQ, which is a 28-day instrument, and 1-day REPO), and if the government implements measures aimed to reduce the Central Bank’s interest-bearing issuance, including a rate reduction or a plan to exchange these instruments, the Bank’s balance sheet and net income will be adversely affected.

After the increase in the parity exchange rate, inflation increased from 12.8% per month in November 2023 to 25.5% per month in December 2023, 20.6% per month in January 2024 and 13.2% per month in February 2024. At the same time, the new government announced the deregulation of a series of regulated prices (such as health insurance, transportation and utility rates) that could continue to drive inflation in the short term. We cannot predict whether any measures to be implemented by the Milei administration to control inflation will have the desired effect. Currently and in the past, inflation has adversely affected the Argentine economy and the government’s ability to create conditions leading to growth. An environment of high inflation rates also negatively affects Argentina’s international competitiveness, real wages, employment rates, the consumption rate, and interest rates. High levels of inflation and the high level of uncertainty regarding economic variables, have in the past, and may in the future, adversely affect economic activity, which could materially and adversely affect our business, results of operations and financial condition.

High levels of inflation adversely affect the financial sector’s ability to provide long-term loans because of the difficulty in establishing an appropriate interest rate, typically making lending more expensive for banks, including us.

A high level of public spending could negatively affect the Argentine economy and its access to financial markets.

While the Macri administration had managed to significantly reduce fiscal deficit by 2019, increased public spending and reduced revenue during 2020 as a result of the Covid-19 pandemic, significantly increased the fiscal deficit in 2020, which reached 6.4% of GDP. Although the Treasury showed signs of fiscal austerity by the end of 2020, the inaccessibility to debt markets forced the government to finance its fiscal needs almost exclusively with monetary issuance from the Central Bank. As of December 31, 2021, the fiscal deficit accounted for 2.1% of GDP (3.0% if IMF’s special drawing rights (“SDRs”) were not taken into account), which showed that, even though the fiscal balance was not moving towards an equilibrium as fast as the economy demanded, the fiscal gap was lower in 2021 than in 2020. The lower fiscal deficit in 2021 was not only explained by a deceleration in public spending compared to 2020 but also by a significant increase in economic activity, higher export duties and a one-off tax on large fortunes.

The government had proposed a fiscal deficit of 3.3% of GDP for 2022 at the beginning of the year through the presentation of the revenue and expenditure budget for the national public sector. However, this bill was not approved, and the government had to negotiate a fiscal deficit target with the IMF without the consensus of the political opposition. The government finally agreed to a target of 2.5% of GDP, which was complied with. The tariffs adjustment and the additional revenues received by the Treasury from taxes levied on soybean exporters who liquidated commodities at a higher exchange rate, allowed the Treasury to improve the fiscal balance. We believe that it will be critical for the government to keep reducing the fiscal deficit to ensure less reliance on debt issuance and monetary financing in order to reduce the very high levels of inflation.

The Fernandez administration had proposed a primary fiscal deficit target of 1.9% of GDP for 2023, however, fiscal deficit reached Ps.5.1 trillion (accounting for approximately 2.7% of GDP pending publication of public official figures). The impact of the fiscal measures that took place between the primary and general elections was close to 1% of GDP. Milei’s stabilization plan aims to reduce the fiscal deficit to zero by ceasing money issuances by the Central Bank to assist the Treasury. It is uncertain how this stabilization plan will be implemented, if at all, and the effects it could have on the fiscal deficit. The Treasury had already reached fiscal surplus in January 2024, primarily as a result of expenses growing below inflation levels and expense cuts.

8

The Treasury will face high debt maturities in the upcoming months and, any poor performance in the local debt market, with debt rollovers below 100%, could complicate the public sector’s sources of financing, increasing the possibility of requiring higher direct financing from the Central Bank, which would increase the already high level of inflation.

In addition, any deterioration in the government’s fiscal position negatively affects its ability to access debt markets in the future and could result in greater restrictions on accessing those markets by Argentine companies, including the Bank.

A weaker fiscal position could have a material adverse effect on the government’s ability to obtain long-term financing and adversely affect economic conditions in Argentina, which could adversely affect the business, results of operations and financial condition of the Bank.

The Argentine economy could be adversely affected by economic events in other markets.

Weak or no economic growth or recession or adverse situations that affect any of Argentina’s main trading partners could negatively affect the balance of payments and, therefore, the economic growth of Argentina. In recent years, several Argentine trading partners (such as Brazil, Europe and China) have experienced significant slowdowns or periods of recession in their economies. If these slowdowns or recessions were to occur again, this could impact the demand for products that come from Argentina and thus affect its economy.

Furthermore, the global economy faces significant challenges. There have been concerns about unrest and terrorist threats in the Middle East, Europe and Africa and conflicts involving Russia, Ukraine, Israel, Iran and Syria. Likewise, economic and social crises have emerged in several Latin American countries in recent years, including the recent crisis in Ecuador. There has also been concern about the relationship between China and other Asian countries, which can result in or intensify potential conflicts in relation to territorial disputes, and the possibility of a trade war between the United States and China. Russia’s invasion of Ukraine, the largest military attack on a European state since World War II, has led to significant disruption, instability and volatility in global markets, as well as higher inflation (including by contributing to further increases in the prices of energy, oil and other commodities and further disrupting supply chains) and lower growth. The EU, UK, U.S. and other governments have imposed significant sanctions and export controls against Russia and Russian interests and threatened additional sanctions and controls. While we have limited exposure to Ukraine and Russia, this or similar conflicts could significantly and adversely affect our business, financial condition and results of operations. The Covid-19 pandemic led to economic contractions in most of the world’s economies in 2020, both developed and emerging. This affected the Argentine economy mainly through trade since the demand for its exports (mainly from Brazil and Europe) dropped substantially. In 2021, most economies experienced significant growth compared to 2020, which together with higher commodity prices (mostly soybean) during the second quarter of 2021 led to higher exports for Argentina. As a result, in 2021, the Argentine economy accumulated a US$14,750 million surplus, representing a 17.7% increase compared to 2020.

Additionally, the inflationary acceleration that has taken place in the United States and Europe has led central banks to tighten monetary policy, resulting in significant interest rate hikes. This fact restricts market access to emerging markets, including Argentina, since investors tend to invest in more stable economies.

In addition, in early 2023, concerns have arisen with respect to the financial condition of a number of banking organizations in the United States and Europe, in particular those with exposure to certain types of depositors and large portfolios of investment securities. On March 10, 2023 Silicon Valley Bank was closed by the California Department of Financial Protection and Innovation and the Federal Deposit Insurance Corporation was appointed receiver of Silicon Valley Bank. On March 11, 2023, Signature Bank was similarly closed and placed into receivership and concurrently the Federal Reserve Board announced it would make available additional funding to eligible depository institutions to assist eligible banking organizations with potential liquidity needs. In Europe, on March 15, 2023 the National Swiss Bank announced several measures amounting to approximately 50 billion Swiss francs to provide Credit Suisse with liquidity and on March 20, 2023 UBS announced that it would acquire Credit Suisse for approximately US$3,250 million. While our business, balance sheet and depositor profile differ substantially from banking institutions such as Silicon Valley Bank and Signature Bank, the operating environment and public trading prices of financial services sector securities can be highly correlated, in particular in times of stress, which may adversely affect the trading price of our securities and potentially our results of operations.

9

If international and local economic conditions fail to improve or deteriorate even more, the Argentine economy could be negatively affected as a result of lower international demand and lower prices for its products and services, higher international interest rates, less capital inflow and greater aversion to risk. Any of the foregoing could also adversely affect the Bank’s business, results of operations and financial condition.

A decline in international prices for or in the amount of Argentina’s principal commodity exports could have a material adverse effect on Argentina’s economy and public finances, and, as a result, on our business.

Historically, the commodities market has been characterized by high volatility. Despite the volatility of prices of most of Argentina’s commodities exports, commodities significantly contributed to the government’s revenues during the 2000s due to the imposition of export duties on agricultural products in 2002. Although most duties were eliminated and the export tax on soy was reduced from 35% to 30% by the Macri administration in 2016, and was further reduced in 2018 by 0.5% per month, the Argentine economy is still relatively dependent on the price of its main agricultural exports, primarily soy. This dependence, in turn, renders the Argentine economy vulnerable to commodity prices fluctuations. International soybean prices decreased slightly during 2017 and further in 2018 due to growing trade tensions between the United States and China. During 2019, soybean prices reached their lowest prices over the prior five years, but recovered from US$305.5 per ton in May 2019 to US$335.0 per ton in December 2019. During the last months of 2020 soybean prices showed an upward trend (due to purchases from China, the monetary stimulus of the main central banks of the world and the promising news regarding the Covid-19 vaccine) that continued until the second quarter of 2022 when they reached US$621 per ton, the higher value in 10 years. However, soybean prices have declined after that, reaching US$507.0 per ton in October 2022. and have continued to decline since then, being close to US$455 per ton by the end of 2023, the lowest since December 2020.

The amount of agricultural products harvested in any given period may decrease due to adverse weather conditions. For example, as a result of the severe drought suffered during the last three years, Argentina experienced a significant water deficit, which resulted in soybean production being less than half as expected and in an estimated reduction in dollar inflows of approximately US$20 billion. This has been, together with the appreciation of the official exchange rate, one of the main causes of the drop in the Central Bank’s gross reserves from US$38 billion on November 30, 2022, to US$23.0 billion on December 31, 2023.

Declines in the prices or the amount of highly exported commodities may adversely affect the Argentine economy and the government’s fiscal revenues, which could in turn adversely impact the business, results of operations and financial condition of the Bank.

Exchange controls and restrictions on capital inflows and outflows could have a material adverse effect on Argentine public sector activity, and, as a result, on our business.

With the exception of some limited periods of time, since 2011, the different Argentine governments have implemented exchange controls and restrictions on the transfer and entry of foreign currency, significantly limiting the ability of companies to hold foreign currency in Argentina or make payments abroad.

During 2021, the government maintained the tightened restrictions on imports and financial transactions with bonds that had been implemented in previous years. In October 2021, the Central Bank reduced the minimum threshold above which imports required authorization (which resulted in less imports being automatically approved). Meanwhile, the monetary authority significantly reduced the allowed weekly trading amount for domestic-law bonds, resulting in blue chip swap transactions being required to be carried out with foreign-law bonds.

During 2022, the government not only maintained most of the restrictions imposed in 2020 and 2021, but also implemented an exchange rate regime with differential effective exchange rates for different sectors of the economy, which resulted in increased complexity. For instance, the government implemented the “soybean dollar”, a transitory exchange rate for exporters of the soybean sector, which was higher than the official exchange rate during the months of September and December, leading to higher dollar settlements related to the agricultural sector during those months and very low US$ settlements from the agricultural sector in the others. At the same time, through taxes or withholdings, new exchange rates were created: for tourism and international artists, among others. Finally, a new import monitoring system with additional supervision of payments was set up.

10

During 2023, new exchange rates continued to appear for certain sectors, similar to the soybean dollar in 2022 as the shortage of Central Bank reserves prevented the government’s ability to avoid a significant increase in the exchange rate between the U.S. dollar and the Argentine peso. In this sense, the Fernandez administration launched several campaigns allowing exporters to settle 30% of their exports through the parallel exchange rate market with the remaining 70% having to be liquidated at the official exchange rate. Initially, this campaign only applied to soybean exporters, but it was later extended to all types of exports. After the elections, and with an increased need to generate foreign currency inflows, the proportion of export dollars that could be liquidated at the parallel exchange rate was increased from 30% to 50%, which granted some short-term relief in the Central Bank’s stock of reserves. The Milei administration has modified these values and as of the date of this annual report, exporters are allowed to settle 20% of their exports in the parallel exchange rate market, while the remaining 80% needs to be settled in the official exchange rate market.

Milei has announced that all current exchange rate restrictions will be eliminated as soon as the fiscal deficit is reduced. There is no certainty as to the scope or timing for any of these measures and the effect they would have on the Bank. The lifting of these exchange rate restrictions could result in an acceleration of inflation, which could negatively affect our balance sheet and net income.

The establishment of new restrictions on foreign trade or related to the foreign exchange market, together with the application of new exchange rates, could require the Bank to allocate additional and unbudgeted resources to provide customers with the tools they require to carry out transactions under the new regulatory framework. Additionally, such tools may not be developed on a timely basis due to changing demands.

Any changes in the policies of the current government concerning economic, exchange and financial matters in order to preserve the balance of payments, the Central Bank’s reserves, a capital outflow or a significant depreciation of the Peso, such as the mandatory conversion into Pesos of obligations assumed by legal entities resident in Argentina in US dollars which could be due to a period of crisis and political, economic and social instability affecting Argentina, or otherwise, could have an adverse effect on Argentina’s economic activity and the Bank’s business, results of operations and financial condition.

The measures adopted to resolve the crisis in the energy sector may not be sufficient, which could affect the business, the results of operations and the financial condition of the Bank.

The economic policies applied since the Argentine crisis of 2001-2002 have had an adverse effect on the Argentine energy sector. The failure to reverse the freeze on electricity and natural gas rates imposed during the crisis became a barrier to investment in the energy sector. The government tried to encourage investment by subsidizing energy consumption but the policy proved ineffective and served to further discourage investment in the energy sector, causing oil and gas production and electricity generation, transmission and distribution to stagnate while consumption continued to rise. To address the power supply shortage that began in 2011, the government attempted to increase imports of electrical power, with adverse consequences for the trade balance and international reserves.

In response to the growing energy crisis, the Macri administration declared a state of emergency for the national electricity system, which ended on December 31, 2017. The state of emergency allowed the government to take measures to stabilize the supply of electricity to the country. In this context, subsidy policies were re-examined and new electricity rates were adopted.

However, utility rates were almost frozen from 2019 to 2022, which worsened the national energy situation by promoting higher demand and discouraging new investments from supplying companies, resulting in an energy deficit heightened by the lack of dollar inflows.

Although actions have been carried out to attempt to address the crisis in the energy sector, in 2023, the partial removal of subsidies to fund utilities (particularly with respect to high income families), the lack of a definitive resolution of the negative effects on the generation, transport and distribution of electricity in Argentina with respect to residential and industrial supply could undermine confidence and adversely affect Argentina’s economic and financial condition, resulting in political instability, and adversely affecting the Bank’s business and results of operations.

The Milei administration has continued to remove subsidies for utilities and public transportation and has decided to stop all public works until 2024. The elimination of subsidies and the progressive increase in prices could continue to generate social unrest and be challenged in local courts.

11

Additionally, the decision to stop all public works could result in the failure to progress on the construction of the gas pipeline that will take gas from Patagonia to Buenos Aires and generally result in lower investment and a lower need for funding to finance that investment, which would adversely affect the Bank. We can give no assurance that the measures adopted by the Milei administration to deal with the energy crisis will be sufficient to restore energy production in Argentina in the short or medium term.

The current lack of resolution on tariffs results in uncertainty regarding the future situation of the energy market in Argentina and constitutes a source of potential risk for the country’s economy and could lead to exchange rate volatility, either of which could adversely affect the Bank’s business, results of operations and financial condition.

Any failure to adequately address actual and perceived risks of institutional deterioration and corruption may adversely affect Argentina’s economy and financial condition.

The lack of a sound institutional framework and corruption have been identified as, and continue to be, critical problems for Argentina. Argentina ranked 98 out of 180 countries in the 2023 Corruption Perceptions Index published by Transparency International.

Failure to address these issues could increase the risk of political instability, distort decision-making processes and adversely affect Argentina’s international reputation and ability to attract foreign investment, and consequently, may negatively affect our business, financial condition and results of operations. Although the Argentine government has taken several measures aimed at strengthening Argentina’s institutions, these measures may be insufficient to ensure transparency and integrity in a highly polarized political context, which could have a material adverse effect on the business, the results of operations and the financial condition of the Bank.

Fluctuations in the value of the peso could adversely affect the Argentine economy and Argentine’s ability to service its debt obligations.

Fluctuations in the value of the peso may adversely affect the Argentine economy. A devaluation of the peso may adversely affect the government’s revenues (measured in U.S. dollars), fuel inflation and significantly reduce real wages.

The Central Bank has maintained the same exchange rate policy since December 2019, consisting of avoiding foreign exchange disruptions by applying more controls, selling foreign reserves and establishing multiple exchange rates. The Central Bank invested more than US$2.1 billion of reserves in the official exchange rate market from August 2021 to August 2022 to curb the depreciation of the Argentine peso. However, the Central Bank purchased US$5.8 billion of reserves in the official exchange rate market, between September 2022 and December 2022, for a transitory differential exchange rate regime that allowed soybean exporters to sell dollars to the Central Bank at a higher exchange rate during the months of September and December.

The government aimed to maintain the US$/Peso parity to prevent the undesired effect that a devaluation would have on inflation, and validated a real appreciation of the official exchange rate in 2022. The nominal exchange rate rose 72.4% in 2022, while accumulated inflation in the same period was 94.8%. The December 2022 real exchange rate was 24% lower than the real exchange rate in December 2019.

The exchange rate premium arising from exchange controls further complicates the foreign exchange market due to the coexistence of an appreciated real exchange rate, and a parallel exchange rate that increases devaluation expectations, discouraging exports and encouraging imports. In this regard, between January 2022 and August 2022, the Central Bank only bought the equivalent of 1% of the stock of dollars it bought in the same period of the previous year. This situation, which jeopardized compliance with the IMF’s third quarter reserves target, led the government to apply a differential exchange rate for soybean exporters, which was 40% higher than the official exchange rate. This exchange rate was in effect in September 2022 and allowed the Central Bank to buy US$4,966 million in the official exchange market. The application of differential exchange rates adversely impacted the Central Bank’s balance sheet due to the difference between the higher price at which it bought dollars and the lower price at which it sold dollars to importers.

12

Nevertheless, the Central Bank launched a differential dollar for soybean exports, 40% higher than the official exchange rate, effective from November 28 to December 31, 2022, in order to buy the necessary dollars to meet the fourth quarter target with the IMF.

The official exchange rate grew 356.4% between December 31, 2022 and December 31, 2023. However, in 2023, the real exchange rate experienced significant variations during the year, with the real exchange rate experiencing a 2% depreciation until the day of the primary elections. However, the government decided to freeze this exchange rate between August 14, 2023 and November 14, 2023, with monthly inflation during this period reaching 12.4%, 12.7%, 8.3% and 12.8%, respectively. As a result, the real exchange rate lost all the depreciation accumulated during the year and continued to appreciate until year end.

As the level of inflation remains high, a stronger nominal appreciation of the peso could lead to concerns regarding the appreciation of the peso against the U.S. dollar in real terms. Such appreciation may reduce the level of exports due to the loss of external competitiveness and a deterioration of the current account deficit. Any such appreciation could also have a negative effect on economic growth and employment, reduce tax revenues in real terms and raise concerns regarding the possibility and impact of a sudden stop in capital flows.

Political uncertainty or changes in liquidity in international markets are likely to lead to greater volatility, and a reduction in the reserves of the Central Bank as a result of intervention in the exchange market could adversely affect inflation expectations, economic performance and the ability of the Republic of Argentina to service its debt.

The lack of rainfalls, together with the high temperatures and the unexpected frosts had a negative impact on the country’s main exports (soybean, wheat and corn, among others) in 2023. Adverse weather conditions might increase pressure on exchange rates due to the reduction in dollar inflows.

Any of these factors could substantially and adversely affect the business, the results of operations and the financial condition of the Bank.

There can be no assurances that Argentina will be able to obtain financing on satisfactory terms in the future, which could have a material adverse effect on its ability to make payments on its outstanding public debt.

Argentina’s future tax revenue and fiscal results may be insufficient to meet its debt service obligations and Argentina may have to rely in part on additional financing from domestic and international capital markets in order to meet future debt service obligations. However, Argentina may not be able to access international or domestic capital markets at acceptable prices or at all, and, if that is the case, Argentina’s ability to service its outstanding public debt could be adversely affected, which could in turn adversely affect Argentina’s economy and financial condition and thereby have a material adverse effect on our business, results of operations and financial condition.

Measures taken by the government, as well as pressure from union sectors, could require salary increases or additional benefits, all of which could increase the Bank’s operating costs.

In the past, the government has passed laws and regulations requiring private companies to maintain certain salary levels and to provide additional benefits to their employees. Likewise, public sector and private sector employers have been subject to intense pressure from their workforce or the unions that represent them, to increase wages and provide certain benefits to workers, particularly due to high inflation rates.

Labor relations in Argentina are governed by specific laws such as the Labor Contract Law No. 20,744 and the Law of Collective Labor Agreements No. 14,250 which, among other things, establish how to carry out wage negotiations and other labor issues. Each industrial or commercial sector is regulated by a collective bargaining agreement that classifies companies by sector and by union. Although the bargaining process is standardized, each chamber of industry or commerce negotiates wage increases and employment benefits with the corresponding union in the relevant sector.

13

According to data published by INDEC, the wage index grew by 152.7% during 2023, as a result of a 165.8% increase in the private sector and 148.6% in the public sector. The registered wage index grew by 159.5% in 2023.

Existing employment laws have led to salary increases that have resulted in an increase in operating costs that has adversely affected the results of operations of Argentine companies. Additionally, the adoption of new measures providing for wage increases or additional benefits for workers due to inflation or additional pressure from workers and unions or otherwise, could result in a further increase in costs and a decrease in the results of operations of Argentine companies, including those of the Bank, which could adversely affect the business, the results of operations and the financial condition of the Bank.

Government intervention in the Argentine economy could adversely affect the business, results of operations and financial condition of the Bank.

During the Kirchner administration, the direct intervention of the government in the Argentine economy increased, including through the implementation of expropriation and nationalization measures, and price and exchange controls.

Since the beginning of the Fernández administration there has been a strong intervention in the foreign exchange and labor markets, as well as a hefty fiscal deficit. The debt restructuring process brought a sign of sustainability which was perceived by both the market and the main credit rating agencies. Sovereign country risk fell more than 1,000 basis points following the debt restructuring agreement. However, only a week after the long-awaited agreement, the aforementioned measures led to a sharp fall in sovereign bond prices as well as in the main Argentinian stocks in New York. All of this, together with foreign exchange restrictions, import controls and the delay in the negotiations with the IMF contributed to an increase in sovereign risk, which continued to increase after the debt restructuring process and reached 1,688 basis points as of December 31, 2021. The sovereign risk has remained high even after the announcement of the IMF agreement as a result of current macroeconomic imbalances.

In June 2022, the Central Bank actively participated in the secondary market of Treasury securities. The Central Bank injected more than 30% of the monetary base into the economy through its participation in the secondary market and through direct transfers to assist the Treasury. This intervention raised concerns in the market regarding the government’s fiscal path and its capacity to finance future deficits in the local debt market. In turn, the departure of the Minister of Economy Martin Guzmán at the beginning of July and the appointment of Silvina Batakis caused the country risk to increase from 1,912 basis points on June 1, 2022 to 2,913 basis points by mid July 2022. As of March 22, 2023 the country risk was 2,465 basis points.

In January 2023, the National Treasury carried out a voluntary debt exchange of Peso-denominated bonds maturing in the first quarter of 2023. Out of a total of Ps.4.3 billion, Ps.2.9 billion accepted the offer (67%), postponing payments mainly until the second quarter of the year. As approximately 55% of the total Peso-denominated bonds maturing in the first quarter of 2023 were held by public agencies (especially the Central Bank), the acceptance within the private sector was less than 30%. This fact, together with the difficulties that the Treasury had to issue debt maturing after October 2023, led the rating agency S&P to consider this transaction as “distressed” and consequently downgraded Argentina’s sovereign rating to “Selective Default” for four days. After the settlement of the debt exchange, S&P raised Argentina’s sovereign rating back to CCC-.

Historically, the actions carried out by the government in economic matters, including decisions regarding interest rates, taxes, price controls, wage increases, increased benefits for workers, exchange controls and potential changes in the market of currencies have had a substantial adverse effect on Argentina’s economic growth.

Expropriations, price controls and exchange controls and other direct government interventions in the economy have had a negative impact on the level of investment in Argentina, access to international capital markets by Argentine companies and Argentine trade and diplomatic relations with other countries. If the government decides to increase the level of intervention in the economy, in accordance with historic practice or otherwise, the Argentine economy and, in turn, the business, the results of operations and financial condition of the Bank could be adversely affected.

Amendments to the Central Bank’s Charter and the Convertibility Law may adversely affect the economy of Argentina.

In March 2012, Law No. 26,739 was passed amending both the Central Bank’s Charter and the Convertibility Law. This law amended the mission of the Central Bank (as established in its Charter (as defined herein)) and eliminated certain provisions previously in force. In accordance with the Central Bank’s Charter and the Convertibility Law, the Central Bank must promote monetary and financial stability, as well as promote development with social equity.

14

Furthermore, the concept of “freely available reserves” was eliminated, allowing the Argentine government to use additional reserves to cancel debts. Additionally, the Convertibility Law established that the Central Bank may set the interest rate and the terms of the loans granted by financial institutions. Additionally, any use of reserves by the government to repay public debt or finance public spending may result in an increase in inflation, which would hinder economic growth. Moreover, a decrease in the reserves of the Central Bank might adversely affect the ability of the Argentine financial system to resist and overcome the effects of an economic crisis (whether domestic or international), adversely affecting economic growth and therefore the business, results of operations and financial condition of the Bank.

The outbreak and spread of a pandemic and other large-scale public health events could have a material adverse effect on the Bank’s business, financial condition and results of operations

Economic conditions in Argentina and worldwide may be adversely affected by an outbreak of a contagious disease, such as COVID-19 (coronavirus), which develops into a regional or global pandemic and other large scale public health events. The measures taken by governments, regulators and businesses to respond to any such pandemic or event may lead to slower or negative economic growth, supply disruptions, inflationary pressures and significant increases in public debt, and may also adversely affect the Bank’s counterparties (including borrowers), which may lead to increased loan losses. Such measures could also impact the business and operations of third parties that provide critical services to the Bank.

During the outbreak of COVID-19, the Bank experienced a decline in activity, including as a result of branch closures and remote working requirements, and was affected by a number of regulatory measures.

If there were an outbreak of a new pandemic or another large-scale public health event occurs in the future, the Bank may experience an adverse impact, which may be material, on its business, financial condition and results of operations, including as a result of the exacerbation of any of the other risks described in this section.

Risks Relating to the Argentine Financial System and to BBVA Argentina

The short-term structure of the deposit base of the Argentine financial system, including the deposit base of the Bank, could lead to a reduction in liquidity levels and limit the long-term expansion of financial intermediation.

In recent years, the growth of the Argentine financial sector has been heavily dependent on deposit levels because of the relatively small size of the Argentine capital markets and the lack of access to foreign capital markets.

While banks’ liquidity in foreign currency is high, a significant share of it is deposited at the Central Bank, and as a result banks have to rely on the Central Bank in order to access those funds. Dollar deposits fell during 2020 by around 25% and remained mainly stable through 2021, 2022 and 2023.

Liquidity in local currency of the Argentine financial sector is currently high, with a high level of minimum cash requirements applicable to Argentine financial institutions, which the Central Bank has raised several times since 2018. Loan demand has recovered to some extent after the 2019 collapse, but still keeps lagging compared to inflation and the aggregated balance of the financial system is very low related to GDP in historical terms.

Notwithstanding the above, because most deposits are short-term deposits, a substantial part of loans must also have short-term maturities to match the terms of the deposits. The proportion of long-term credit lines, such as mortgages, is small, and long-term loan origination has fallen sharply since 2019 as a consequence of higher interest rates and inflation, and the difficult financial environment. As of the date of this annual report, the Bank is primarily exposed to the public sector, in particular, the Central Bank and Treasury, which is where it channels most of its customers’ deposits.

We have a continuous demand for liquidity to fund our business activities. Our profitability or solvency could be adversely affected if access to liquidity and funding is constrained or made more expensive for a prolonged period of time. Furthermore, withdrawals of deposits or other sources of liquidity may make it more difficult or costly for us to fund our business on favorable terms. Although we believe that deposit liquidity levels are currently reasonable, no assurance can be given that those levels will not be reduced due to future negative economic conditions or otherwise. If depositors lose confidence as a result of negative economic conditions or otherwise and withdraw significant funds from financial institutions, there will be a substantial negative impact on the manner in which financial institutions, including us, conduct their business and on their and our ability to operate as financial intermediaries.

15

If we are unable to access adequate sources of medium and long-term funding or if we are required to pay high costs in order to obtain the same and/or if we cannot generate profits and/or maintain our current volume and/or scale of our business, whether due to a decline in deposits or otherwise, our liquidity position and ability to honor our debts as they come due may be adversely affected, which could have a material adverse effect on our business, results of operations and financial condition.

Reduced spreads between interest rates received on loans and those paid on deposits could adversely affect our profitability.

The spread between the interest rates on loans and deposits could be affected as a result of increased competition in the banking sector and the government’s tightening or loosening of monetary policy in response to inflation concerns. During recent years, as a consequence of higher inflation, interest rates have significantly increased in Argentina.

After the Macri administration took office, expectations were of a decline in both inflation and interest rates and therefore banking spreads. However, since 2018 devaluation of the peso and higher inflation led the Central Bank to substantially raise interest rates, ending the margin contraction trend. During 2020 the Central Bank reduced interest rates, in part as a response to the Covid-19 crisis. In 2021 interest rates remained stable, most of them negative in real terms. At the same time, after an economic slowdown in 2020 resulting from the economic downturn caused by the Covid-19 pandemic, inflation increased in 2021 (51%) and adopted an upward trend that accelerated in 2022 (reaching an inflation level of almost 100%) and continued in 2023 (reaching an inflation level of 211%). Inflation evolution in Argentina is still uncertain, and from 2020 an increasing amount of our liabilities and assets interest rates have been regulated by the Central Bank. This situation could result in renewed pressure on banking spreads. Moreover, a change in the composition of the source of funding, which is currently heavily weighted to non-interest-bearing deposits, could also put downward pressure on margins. Also, a change in the composition of the source of funding arising from an eventual higher demand of credit and therefore a need to increase the amount of time deposits or other types of interest bearing-liabilities could result in lower spreads.

Another source of spread contraction could be an increase in the regulation of subsidized loans. In October 2020, the Central Bank re-introduced mandatory credit lines for SMEs, under which banks have to lend a portion of their deposits to small and mid-size companies at regulated rates. This regulation continued through 2021 and 2022 and has continued during 2023. An increase in the use of these measures by the Central Bank could further affect our margins.

Any reductions in spreads could have a material adverse effect on our business, results of operation and financial condition.

Our business is particularly vulnerable to volatility in interest rates.

Our results of operations are substantially dependent upon the level of our net interest income, which is the difference between interest income from interest-earning assets and interest expense on interest-bearing liabilities. Interest rates are highly sensitive to many factors beyond our control, including fiscal and monetary policies of governments and central banks, regulation of the financial sector in the market in which we operate, domestic and international economic and political conditions and other factors.

The Central Bank decreased interest rates in December, 2023 from a 133% annual rate to a 70% annual rate with the aim to improve the Central Bank’s balance sheet by lowering interest bearing liabilities, which could result in additional inflation in the short term. Additionally, the government could continue to enact regulation that could adversely affect our intermediation margins. Any of the foregoing could adversely affect our financial spread as a result of differential movements in interest rates for deposits, loans or other bank assets and liabilities. In addition, high interest rates could reduce the demand for credit and our ability to generate credit for our clients, as well as contribute to an increase in the credit default rate. As a result of these and the above factors, significant changes or volatility in interest rates could have a material adverse effect on our business, results of operations and financial condition.

Mismatch between UVA loans and UVA deposits could adversely affect our profitability.

During 2017, new UVA (inflation-adjusted) mortgages grew significantly. At the same time, the Bank launched UVA deposits, but such deposits grew at a slower pace, leading to a mismatch in this activity. During 2018, as a consequence of the peso devaluation, higher inflation and interest rates, growth in both UVA loans and liabilities slowed and since 2019 new origination has come to a halt which has extended until now.

16

As of December 2023, UVA loans exceed UVA deposits balances, so the Bank has a long position in inflation adjusted net assets that matches our current expectations of negative interest rates for at least part of 2024. This long UVA position is complemented by a portfolio of Argentina Treasury bonds that adjust by inflation.

Independent of how this activity may develop in the future and how we manage our bond portfolio, there will probably still be a mismatch among UVA loans and deposits, as loans are mainly mortgages with long maturities, and this mismatch could have a material adverse effect on our business, results of operations and financial condition, particularly in the event that interest rates turn positive in real terms and the Bank were not able to hedge with inflation adjusted liabilities.

Our estimates and established reserves for credit risk and potential credit losses may prove to be inaccurate and/or insufficient, which may materially and adversely affect our results of operations and financial condition.

A number of our products expose us to credit risk, including consumer loans, commercial loans and other receivables. Changes in the income levels of our borrowers, increases in the inflation rate or an increase in interest rates could have a negative effect on the quality of our loan portfolio, causing us to increase provisions for loan losses and resulting in reduced profits or in losses. Our non-performing loan portfolio amounted to Ps.35,207 million at December 31, 2023 compared to Ps.39,177 million at December 31, 2022. The non-performing loan ratio increased to 1.29% at December 31, 2023 from 1.13% at December 31, 2022.

We estimate and establish reserves for credit risk and expected credit losses. This process involves subjective and complex judgments, including projections of economic conditions and assumptions on the ability of our borrowers to repay their loans. We may not be able to timely detect these risks before they occur, which may increase our exposure to credit risk. Overall, if we are unable to effectively control the level of non-performing or poor credit quality loans in the future, or if our loan loss reserves are insufficient to cover future loan losses, this could have a material adverse effect on our business, results of operations and financial condition.

Argentine financial institutions (including BBVA Argentina) continue to have exposure to public sector debt (including securities issued by the BCRA) and its repayment capacity, which in periods of economic recession, may negatively affect their results of operations.

Argentine financial institutions continue to be exposed, to some extent, to public sector debt and the public sector’s repayment capacity. The Argentine government’s ability to honor its financial obligations is dependent on, among other things, its ability to establish economic policies that succeed in fostering sustainable growth and development in the long term, generating tax revenues and controlling public expenditures, which could, either partially or totally, fail to take place.

The Bank’s exposure to the public sector as of December 31, 2023 was Ps.2,308,820 million, representing approximately 38% of its total assets. Of this total, Ps.1,332,679 million were BCRA debt instruments and Ps.976,141 million corresponded to Argentine government securities. As a result, BBVA Argentina’s income-generating capacity may be materially impacted or may be particularly affected by the Argentine public sector’s repayment capacity and the performance of public sector bonds, which, in turn, is dependent on the factors referred to above.

Increased competition in the banking industry may adversely affect the Bank’s operations.