EXHIBIT 99.1

Cameco Corporation

2023 Annual Information Form

March 22, 2024

Cameco Corporation

2023 Annual information form

March 22, 2024

Contents

| Important information about this document |

1 | |||

| Our business |

6 | |||

| Our vision, values and strategy |

11 | |||

| Operations, projects and investments |

25 | |||

| Uranium – Tier-one operations |

26 | |||

| Uranium – Tier-two operations |

71 | |||

| Uranium – Advanced projects |

73 | |||

| Uranium – Exploration |

74 | |||

| Fuel services |

76 | |||

| Westinghouse Electric Company |

79 | |||

| Other nuclear fuel cycle investments |

86 | |||

| Mineral reserves and resources |

87 | |||

| Our ESG principles and practices |

92 | |||

| The regulatory environment |

96 | |||

| Risks that can affect our business |

107 | |||

| 1 – Operational risks |

107 | |||

| 2 – Financial risks |

114 | |||

| 3 – Governance and compliance risks |

121 | |||

| 4 – Social risks |

123 | |||

| 5 – Environmental risks |

124 | |||

| 6 – Strategic risks |

125 | |||

| Legal proceedings |

134 | |||

| Investor information |

134 | |||

| Governance |

139 | |||

| Appendix A |

144 | |||

Important information about this document

This annual information form (AIF) for the year ended December 31, 2023 provides important information about Cameco Corporation. It describes our history, our markets, our operations and projects, our mineral reserves and resources, our approach to environmental, social and governance matters (ESG), our regulatory environment, the risks we face in our business and the market for our shares, among other things.

It also incorporates by reference:

| • our management’s discussion and analysis for the year ended December 31, 2023 (2023 MD&A), which is available on SEDAR+ (sedarplus.com) and on EDGAR (sec.gov) as an exhibit to our Annual Report on Form 40-F; and

• our audited consolidated financial statements for the year ended December 31, 2023 (2023 financial statements), which are also available on SEDAR+ and on EDGAR as an exhibit to our Annual Report on Form 40-F. |

Throughout this document, the terms we, us, our, the company and Cameco mean Cameco Corporation and its subsidiaries. |

We have prepared this document to meet the requirements of Canadian securities laws, which are different from what United States (US) securities laws require.

The information contained in this AIF is presented as at December 31, 2023, the last day of our most recently completed financial year, and is based on what we knew as of March 15, 2024, except as otherwise stated.

Reporting currency and financial information

Unless we have specified otherwise, all dollar amounts are in Canadian dollars. Any references to $(US) mean US dollars.

The financial information in this AIF has been presented in accordance with International Financial Reporting Standards (IFRS).

Caution about forward-looking information

Our AIF and the documents incorporated by reference include statements and information about our expectations for the future. When we discuss our strategy, plans and future financial and operating performance, or other things that have not yet taken place, we are making statements considered to be forward-looking information or forward-looking statements under Canadian and US securities laws. We refer to them in this AIF as forward-looking information. In particular, the discussions under the headings Market overview and developments, Building a balanced portfolio, and Westinghouse Electric Company in this AIF contain forward-looking information.

Key things to understand about the forward-looking information in this AIF:

| • | It typically includes words and phrases about the future, such as anticipate, believe, estimate, expect, plan, will, intend, goal, target, forecast, project, strategy and outlook (see examples on page 2). |

| • | It represents our current views and can change significantly. |

| • | It is based on a number of material assumptions, including those we have listed below on pages 4 and 5, which may prove to be incorrect. |

| • | Actual results and events may be significantly different from what we currently expect, due to the risks associated with our business. We list a number of these material risks below. We recommend you also review other parts of this document, including Risks that can affect our business starting on page 107, and our 2023 MD&A, which includes a discussion of other material risks that could cause actual results to differ significantly from our current expectations. |

Forward-looking information is designed to help you understand management’s current views of our near- and longer-term prospects, and it may not be appropriate for other purposes. We will not necessarily update this information unless we are required to by Canadian or US securities laws.

| 2023 ANNUAL INFORMATION FORM | Page 1 |

Examples of forward-looking information in this AIF

| • | our view that we have the strengths to take advantage of the world’s rising demand for safe, reliable, affordable, and carbon-free energy, and our vision to energize a clean-air world |

| • | that we will continue to focus on delivering our products responsibly and addressing the environmental, social and governance (ESG) risks and opportunities that we believe will make our business sustainable and will build long-term value |

| • | our expectations for the future of the nuclear industry and the potential for new enrichment technology, including that nuclear power must be a central part of the solution to the world’s shift to a low-carbon climate-resilient economy and that our investment in enrichment technology, if successful, will allow us to participate in the entire nuclear fuel value chain |

| • | our expectations about 2024 and future global uranium supply, consumption, contracting, demand, geopolitical issues and the market, including the discussion under the headings Market overview and developments and Building a balanced portfolio |

| • | our expectations about 2024 and future consumption of conversion services |

| • | our expectations about 2024 and future global consumption, contracting, demand, geopolitical and market issues relating to Westinghouse Electric Company’s (Westinghouse): fuel fabrication for light water reactors; reactor maintenance and other services; design, engineering, and support for the development of new reactors; and nuclear sustainability services |

| • | our expectations about when future reactors will come online |

| • | our efforts to participate in the commercialization and deployment of small modular reactors (SMRs) and contribute to the mitigation of global climate change and help to provide energy security and affordability by exploring SMRs and other emerging opportunities within the fuel cycle |

| • | our expectations about future demand for SMRs |

| • | our expectation that the US Department of Energy (DOE) will make available a portion of its excess uranium inventory over the next two decades |

| • | the discussion under the heading Our ESG principles and practices, including our belief there is a significant opportunity for us to be part of the solution to combat climate change and that we are well positioned to deliver significant long-term business value |

| • | our ability to implement and execute our overarching low-carbon transition strategy |

| • | our expectations relating to care and maintenance costs |

| • | our expectations of executing major supply contracts |

| • | our ability to capitalize on the current backlog of long-term contracting as a proven and reliable supplier with tier-one productive capacity and a record of honouring supply commitments, and to increase value throughout these price cycles |

| • | future plans and expectations for our uranium properties, advanced projects, and fuel services operating sites, including production levels and the suspension of production at certain properties, pace of advancement and expansion capacity, and carbon reduction targets |

| • | estimates of operating and capital costs and mine life for our tier one uranium operations |

| • | our expectations regarding our licence for Crow Butte |

| • | our ability to successfully negotiate a new collective agreement for the unionized employees at McArthur River |

| • | estimated decommissioning and reclamation costs for uranium properties and fuel services operating sites |

| • | Kazatomprom’s planned production levels and timing for JV Inkai in 2024 |

| • | our mineral reserve and resource estimates |

| • | our expectations that the price of uranium, production costs, and recovery rates will allow us to operate or develop a particular site or sites |

| • | estimates of metallurgical recovery and other production parameters for each uranium property |

| • | production estimates at the McArthur River/Key Lake, Cigar Lake and Inkai operations, and the Port Hope UF6 conversion facility |

| • | our discussion of the ongoing conflict between Russia and Ukraine |

| • | our views on our ability to align our production with market opportunities and our contract portfolio |

| • | our expectation regarding opportunities to improve operational effectiveness and to reduce our impact on the environment, including through the use of digital and automation technologies |

| • | our expectations relating to our Canada Revenue Agency (CRA) transfer pricing dispute, including our confidence that the courts would reject any attempt by CRA to utilize the same or similar positions for other tax years currently in dispute and our belief that CRA should return the full amount of cash and security that has been paid or otherwise secured by us |

| • | our expectations regarding the amount of security we will need to provide to CRA in connection with the tax debts CRA considers us owing for 2017 |

| 2023 ANNUAL INFORMATION FORM | Page 2 |

| • | our investments allowing us to participate in the entire nuclear fuel value chain; fuel fabrication; reactor maintenance; development of new reactors; and nuclear sustainability services |

| • | the discussion of our expectations relating to our recent acquisition of a 49% interest in Westinghouse, including its future prospects, our belief that Westinghouse is well-positioned for long-term growth driven by the expected increase in global demand for nuclear power, our expectation that the acquisition will be transformative and accretive to Cameco, our expectation that the investment will augment the core of our business and offer more solutions to our customers across the nuclear fuel cycle various factors and drivers for Westinghouse’s business segments, our expectation that there will be new opportunities for Westinghouse to compete for and win new business and other matters discussed under the heading Westinghouse Electric Company |

Material risks

| • | actual sales volumes or market prices for any of our products or services are lower than we expect, or cost of sales is higher than we expect, for any reason, including changes in market prices, loss of market share to a competitor, trade restrictions, geopolitical issues or the impact of a pandemic |

| • | we are adversely affected by changes in currency exchange rates, royalty rates, tax rates or inflation |

| • | our production costs are higher than planned, or necessary supplies are not available or not available on commercially reasonable terms |

| • | our strategies may change, be unsuccessful or have unanticipated consequences, or we may not be able to achieve anticipated operational flexibility and efficiency |

| • | changing views of governments regarding the pursuit of carbon reduction strategies or our view may prove to be inaccurate on the role of nuclear power in pursuit of those strategies |

| • | our estimates and forecasts prove to be inaccurate, including production, purchases, deliveries, cash flow, revenue, costs, decommissioning, reclamation expenses, or receipt of future dividends from JV Inkai |

| • | that we may not realize the expected benefits from the Westinghouse acquisition |

| • | Westinghouse fails to generate sufficient cash flow to fund its approved annual operating budget or make quarterly distributions to the partners |

| • | we are unable to enforce our legal rights under our existing agreements, permits or licences |

| • | we are subject to litigation or arbitration that has an adverse outcome |

| • | that the courts may accept the same, similar or different positions and arguments advanced by CRA to reach decisions that are adverse to us for other tax years |

| • | the possibility of a materially different outcome in disputes with CRA for other tax years |

| • | our uranium suppliers or purchasers fail to fulfil their commitments |

| • | our McArthur River or Cigar Lake development, mining or production plans are delayed or do not succeed for any reason |

| • | our production plans for our Port Hope UF6 conversion facility do not succeed for any reason |

| • | McClean Lake’s mill production plan is delayed or does not succeed for any reason |

| • | water quality and environmental concerns could result in a potential deferral of production and additional capital and operating expenses required for the Cigar Lake and McArthur River/Key Lake operations |

| • | JV Inkai’s development, mining or production plans are delayed or do not succeed for any reason or JV Inkai is unable to transport and deliver its production |

| • | we may be unsuccessful in pursuing innovation or implementing advanced technologies, including the risk that the commercialization and deployment of SMRs or new enrichment technology may incur unanticipated delays or expenses, or ultimately prove to be unsuccessful |

| • | the risk that we may become unable to pay future dividends at the expected rate |

| • | our expectations relating to care and maintenance costs prove to be inaccurate |

| • | the risk that we may not be able to refinance our debenture on terms that are as favourable as we expect, or that we may not realize our expected cash flow, or meet our expectations in reducing total debt |

| • | we are affected by natural phenomena, including inclement weather, fire, flood and earthquakes |

| • | the risks that generally apply to all our operations and advanced uranium projects that are discussed under the heading Risks that can affect our business in this AIF and under the heading Managing the risks in our 2023 MD&A |

| 2023 ANNUAL INFORMATION FORM | Page 3 |

| • | that CRA does not agree that the court rulings for the years that have been resolved in Cameco’s favour should apply to subsequent tax years |

| • | that CRA will not return all or substantially all of the cash and security that has been paid or otherwise secured in a timely manner, or at all |

| • | there are defects in, or challenges to, title to our properties |

| • | our mineral reserve and resource estimates are not reliable, or there are unexpected or challenging geological, hydrological or mining conditions |

| • | we are affected by environmental, safety and regulatory risks |

| • | we are adversely affected by subsurface contamination from current or legacy operations |

| • | necessary permits or approvals from government authorities cannot be obtained or maintained |

| • | we are affected by political risks, including any potential future unrest in Kazakhstan |

| • | operations are disrupted due to problems with our own or our suppliers’ or customers’ facilities, the unavailability of reagents, equipment, operating parts and supplies critical to production, equipment failure, lack of tailings capacity, labour shortages, labour relations issues, strikes or lockouts, underground floods, cave-ins, ground movements, tailings dam failures, transportation disruptions or accidents, aging infrastructure, or other development and operating risks |

| • | we are affected by terrorism, sabotage, blockades, civil unrest, social or political activism, outbreak of illness (such as a pandemic), accident or a deterioration in political support for, or demand for, nuclear energy |

| • | a major accident at a nuclear power plant |

| • | we are impacted by changes in the regulation or public perception of the safety of nuclear power plants, which adversely affect the construction of new plants, the re-licensing of existing plants, and the demand for uranium |

| • | government laws, regulations, policies, or decisions that adversely affect us, including tax and trade laws and sanctions on nuclear fuel imports |

| • | the risk that Westinghouse may not be able to meet sales commitments for any reason |

| • | the risk that Westinghouse may not achieve the expected growth or success in its business |

| • | the risk to Westinghouse’s business associated with potential production disruptions, including those related to global supply chain disruptions, global economic uncertainty, political volatility, labour relations issues, and operating risks |

| • | the risk that Westinghouse’s strategies may change, be unsuccessful, or have unanticipated consequences |

| • | the risk that Westinghouse may fail to comply with nuclear licence and quality assurance requirements at its facilities |

| • | the risk that Westinghouse may be delayed in announcing its future financial results |

| • | the risk that Westinghouse may lose protections against liability for nuclear damage, including discontinuation of global nuclear liability regimes and indemnities |

| • | the risk that increased trade barriers may adversely impact Westinghouse’s business |

| • | the risk that Westinghouse may default under its credit facilities, impacting adversely Westinghouse’s ability to fund its ongoing operations and to make distributions |

| • | the risk that liabilities at Westinghouse may exceed our estimates and the discovery of unknown or undisclosed liabilities |

| • | the risk that occupational health and safety issues may arise at Westinghouse’s operations |

| • | the risk that there may be disputes between us and Brookfield regarding our strategic partnership |

| • | the risk that we may default under the governance agreement with Brookfield, including us losing some or all of our interest in Westinghouse |

Material assumptions

| • | our expectations regarding sales and purchase volumes and prices for uranium and fuel services, cost of sales, trade restrictions, inflation, and that counterparties to our sales and purchase agreements will honour their commitments |

| • | our expectations for the nuclear industry, including its growth profile, market conditions, geopolitical issues, and the demand for and supply of uranium |

| • | the continuing pursuit of carbon reduction strategies by governments and the role of nuclear in the pursuit of those strategies |

| • | that no major accident at a nuclear power plant will occur |

| • | the absence of new and adverse government regulations, policies or decisions |

| • | JV Inkai’s development, mining and production plans succeed, and that JV Inkai will be able to transport and deliver its production |

| • | the ability of JV Inkai to pay dividends |

| • | that care and maintenance costs will be as expected |

| 2023 ANNUAL INFORMATION FORM | Page 4 |

| • | our expectations regarding spot prices and realized prices for uranium |

| • | that the construction of new nuclear power plants and the re-licensing of existing nuclear power plants will not be more adversely affected than expected by changes in regulation or in the public perception of the safety of nuclear power plants |

| • | our ability to continue to supply our products and services in the expected quantities and at the expected times |

| • | our expected production levels for Cigar Lake, McArthur River/Key Lake, JV Inkai and our fuel services operating sites |

| • | our cost expectations, including production costs, operating costs, and capital costs |

| • | our expectations regarding tax payments, tax rates, royalty rates, currency exchange rates and interest rates |

| • | our entitlement to and ability to receive expected refunds and payments from CRA |

| • | in our dispute with CRA, that courts will reach consistent decisions for other tax years that are based upon similar positions and arguments |

| • | that CRA will not successfully advance different positions and arguments that may lead to different outcomes for other tax years |

| • | our expectation that we will recover all or substantially all of the amounts paid or secured in respect of the CRA dispute to date |

| • | our decommissioning and reclamation estimates, including the assumptions upon which they are based, are reliable |

| • | our mineral reserve and resource estimates, and the assumptions upon which they are based, are reliable |

| • | our understanding of the geological, hydrological and other conditions at our uranium properties |

| • | our Cigar Lake and McArthur River development, mining and production plans succeed |

| • | our Key Lake mill production plan succeeds |

| • | the McClean Lake mill is able to process Cigar Lake ore as expected |

| • | our production plans for our Port Hope UF6 conversion facility succeed |

| • | our operations are not significantly disrupted as a result of political instability, nationalization, terrorism, sabotage, blockades, civil unrest, breakdown, natural disasters, outbreak of illness (such as a pandemic), governmental or political actions, litigation or arbitration proceedings, cyber-attacks, the unavailability of reagents, equipment, operating parts and supplies critical to production, labour shortages, labour relations issues, strikes or lockouts, underground floods, cave-ins, ground movements, tailings dam failure, lack of tailings capacity, transportation disruptions or accidents, aging infrastructure or other development or operating risks |

| • | our and our contractors’ ability to comply with current and future environmental, safety and other regulatory requirements, and to obtain and maintain required regulatory approvals |

| • | that we will be successful in our efforts to renew our operating license for Crow Butte |

| • | nuclear power and uranium demand, supply, consumption, long-term contracting, growth in the demand for and global public acceptance of nuclear energy, and prices |

| • | Westinghouse’s ability to generate cash flow and fund its approved annual operating budget and make quarterly distributions to the partners |

| • | our ability to compete for additional business opportunities so as to generate additional revenue for us as a result of the Westinghouse acquisition |

| • | Westinghouse’s production, purchases, sales, deliveries, and costs |

| • | the market conditions and other factors upon which we have based Westinghouse’s future plans and forecasts |

| • | Westinghouse’s ability to mitigate adverse consequences of delays in production and construction |

| • | the success of Westinghouse’s plans and strategies |

| • | that there will not be any significant adverse consequences to Westinghouse’s business resulting from business disruptions, including those relating to supply disruptions, economic or political uncertainty and volatility, labour relation issues, and operating risks |

| • | Westinghouse’s ability to announce future financial results when expected |

| • | Westinghouse will comply with the covenants in its credit agreements |

| • | Westinghouse will comply with nuclear license and quality assurance requirements at its facilities |

| • | Westinghouse maintaining protections against liability for nuclear damage, including continuation of global nuclear liability regimes and indemnities |

| • | that known and unknown liabilities at Westinghouse will not materially exceed our estimates |

| • | the absence of disputes between us and Brookfield regarding our strategic partnership, and that we do not default under the governance agreement with Brookfield |

| • | that we will be able to refinance our senior unsecured debentures, and assumptions regarding our expected cash flow and our ability to reduce total debt |

| 2023 ANNUAL INFORMATION FORM | Page 5 |

Our business

| Our vision is to energize a clean-air world. We have a 35-year proven track record of providing secure and reliable nuclear fuel supplies to a global customer base to generate safe, reliable, and affordable baseload carbon-free energy. Nuclear energy plants around the world use our uranium and fuel services to generate one of the cleanest sources of electricity available today.

Our operations span the nuclear fuel cycle from exploration to fuel services, which include uranium production, refining, UO2 and UF6 conversion services and CANDU fuel manufacturing for heavy water reactors. We have also further enhanced our ability to meet our customers’ growing demand for reliable and secure nuclear fuel supplies, services and technologies by investing in Westinghouse. Westinghouse’s assets are expected to augment the core of our business, providing fuel fabrication for light water reactors; reactor maintenance and other services; the design engineering and support for the development of new reactors; and nuclear sustainability services. We also have made an investment in a third-generation enrichment technology, that if successful we expect will allow us to participate in the entire nuclear fuel value chain. |

Cameco Corporation 2121 – 11th Street West Saskatoon, Saskatchewan Canada S7M 1J3 Telephone: 306.956.6200

This is our head office, registered office and principal place of business.

We are publicly listed on the Toronto and New York stock exchanges, and had a total of 2,638 employees at December 31, 2023. |

With extraordinary assets, a proven operating track record, long-term contract portfolio, strong ESG commitment, employee expertise, comprehensive industry knowledge, and a strong balance sheet, the company is making investments that it expects will create a platform for strategic growth. We are confident in our ability to increase long-term growth by positioning the company as one of the global leaders in supporting the clean energy transition. And we are doing so at a time when the world’s prioritization of decarbonization and energy security is driving growth in demand and when geopolitics are creating concerns about the origin and security of supplies across the nuclear fuel cycle.

Business segments

URANIUM

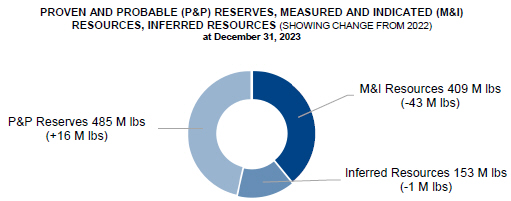

Our uranium production capacity is among the world’s largest. In 2023, we continued to ramp-up to our tier-one production run rate and accounted for 16% of world production. We have controlling ownership of the world’s largest high-grade mineral reserves.

Product

| • | uranium concentrates (U3O8) |

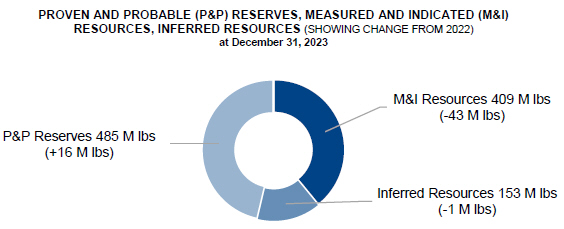

Mineral reserves and resources

Mineral reserves

| • | approximately 485 million pounds proven and probable |

Mineral resources

| • | approximately 409 million pounds measured and indicated |

| • | approximately 153 million pounds inferred |

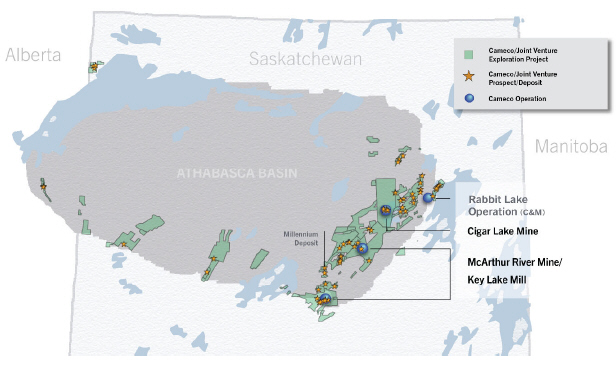

Tier-one operations

| • | McArthur River and Key Lake, Saskatchewan |

| • | Cigar Lake, Saskatchewan |

| • | Inkai, Kazakhstan |

Tier-two operations

| • | Rabbit Lake, Saskatchewan |

| • | Smith Ranch-Highland, Wyoming |

| • | Crow Butte, Nebraska |

Advanced projects

| • | Millennium, Saskatchewan |

| • | Yeelirrie, Australia |

| • | Kintyre, Australia |

Exploration

| • | focused on North America |

| • | approximately 0.74 million hectares of land |

| 2023 ANNUAL INFORMATION FORM | Page 6 |

FUEL SERVICES

We are an integrated uranium fuel supplier, offering refining, conversion, and fuel manufacturing services.

Products

| • | uranium trioxide (UO3) |

| • | uranium hexafluoride (UF6) for light-water reactors (we have about 21% of world primary conversion capacity) |

| • | uranium dioxide (UO2) for CANDU heavy-water reactors |

| • | fuel bundles, reactor components and monitoring equipment used by CANDU heavy-water reactors |

Operations

| • | Blind River refinery, Ontario (refines uranium concentrates to UO3) |

| • | Port Hope conversion facility, Ontario (converts UO3 to UF6 or UO2) |

| • | Cameco Fuel Manufacturing Inc. (CFM), Ontario (manufactures fuel bundles and reactor components for CANDU heavy-water reactors) |

WESTINGHOUSE ELECTRIC COMPANY (Westinghouse)

In 2023, we completed the acquisition of Westinghouse, in a strategic partnership with Brookfield. We own a 49% interest.

Products

| • | Operating plant services (core business) – Provides outage and maintenance services, engineering support, instrumentation and controls equipment, plant modifications, and components and parts to nuclear reactors |

| • | Nuclear fuel (core business) – designs and manufactures nuclear fuel supplies and services for light water reactors |

| • | New build – designs, develops and procures equipment for new nuclear plant projects |

Operations

| • | Columbia, South Carolina |

(fuel fabrication)

| • | Springfields, United Kingdom |

(fuel fabrication)

| • | Västerås, Sweden |

(fuel fabrication)

For information about the financial performance of our segments for the years ended December 31, 2023 and 2022, see our 2023 MD&A as follows:

| • | uranium – page 61 |

| • | fuel services – page 62 |

| • | Westinghouse – page 63 |

OTHER NUCLEAR FUEL CYCLE INVESTMENTS

Enrichment

We have a 49% interest in Global Laser Enrichment LLC (GLE) which is testing third-generation enrichment technology that, if successful, will use lasers to commercially enrich uranium. GLE is the exclusive licensee of the proprietary SILEX laser enrichment technology, that is in the development phase.

| 2023 ANNUAL INFORMATION FORM | Page 7 |

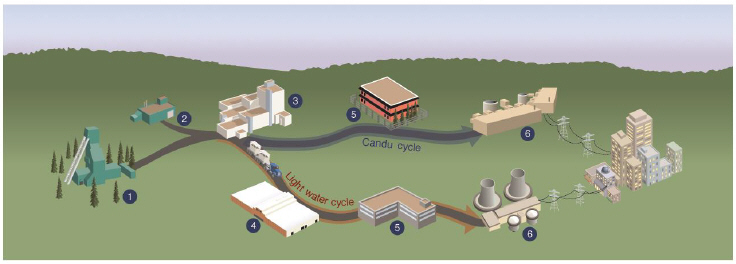

The nuclear fuel cycle

Our operations and investments span the nuclear fuel cycle, from exploration to fuel manufacturing.

|

|

Mining |

Once an orebody is discovered and defined by exploration, there are three common ways to mine uranium, depending on the depth of the orebody and the deposit’s geological characteristics:

| • | Open pit mining is used if the ore is near the surface. The ore is usually mined using drilling and blasting. |

| • | Underground mining is used if the ore is too deep to make open pit mining economical. Tunnels and shafts provide access to the ore. |

| • | In situ recovery (ISR) does not require large scale excavation. Instead, holes are drilled into the ore and a solution is used to dissolve the uranium. The solution is pumped to the surface where the uranium is recovered. |

|

|

Mining |

Ore from open pit and underground mines is processed to extract the uranium and package it as a powder typically referred to as uranium ore concentrates (UOC) or yellowcake (U3O8). The leftover processed rock and other solid waste (tailings) is placed in an engineered tailings facility.

|

|

Refining |

Refining removes the impurities from the uranium concentrate and changes its chemical form to uranium trioxide (UO3).

|

|

Conversion |

For light water reactors, the UO3 is converted to uranium hexafluoride (UF6) gas to prepare it for enrichment. For heavy water reactors like the CANDU reactor, the UO3 is converted into powdered uranium dioxide (UO2).

|

|

Enrichment |

Uranium is made up of two main isotopes: U-238 and U-235. Only U-235 atoms, which make up 0.7% of natural uranium, are involved in the nuclear reaction (fission). Most of the world’s commercial nuclear reactors require uranium that has an enriched level of U-235 atoms.

The enrichment process increases the concentration of U-235 to between 3% and 5% by separating U-235 atoms from the U-238. Enriched UF6 gas is then converted to powdered UO2.

|

|

Fuel manufacturing |

Natural or enriched UO2 is pressed into pellets, which are baked at a high temperature. These are packed into zircaloy or stainless steel tubes, sealed and then assembled into fuel bundles.

|

|

Generation |

Nuclear reactors are used to generate electricity. U-235 atoms in the reactor fuel fission, creating heat that generates steam to drive turbines. The fuel bundles in the reactor need to be replaced as the U-235 atoms are depleted, typically after one or two years depending upon the reactor type. The used – or spent – fuel is stored or reprocessed. Typical activities to ensure the safe and reliable operation of nuclear power plants include overhaul, repair and replacement of system components, testing and calibration of parts, and in-service inspections. Nuclear reactors are refueled every 18 to 24 months.

Spent fuel management

The majority of spent fuel is safely stored at the reactor site. A small amount of spent fuel is reprocessed. The reprocessed fuel is used in some European and Japanese reactors.

| 2023 ANNUAL INFORMATION FORM | Page 8 |

Major developments

| 2021 | 2022 | 2023 | ||

| January | January | March | ||

| • We announce the closing of the agreement between Cameco, Silex Systems Limited and GE-Hitachi Nuclear Energy, completing the ownership restructuring of GLE with Cameco’s interest in GLE increasing from 24% to 49%.

February

• We announce the Supreme Court of Canada dismissed CRA’s application for leave to appeal the June 26, 2020 decision of the Federal Court of Appeal with respect to the 2003, 2005 and 2006 tax years.

April

• We announce plans to restart production at the Cigar Lake mine.

October

• We file a notice of appeal with the Tax Court of Canada, asking it to order the reversal of CRA’s transfer pricing adjustment and the return of $777 million in cash and letters of credit we paid or secured for the tax years 2007 through 2013, with costs. |

• We announce plans to transition McArthur River and Key Lake from care and maintenance to planned production of 15 million pounds per year (100% basis) by 2024, 40% below its annual licensed capacity, and to reduce production at Cigar Lake in 2024 to 13.5 million pounds per year (100% basis), 25% below its annual licensed capacity starting in 2024.

May

• We acquire an additional 4.522% interest in Cigar Lake increasing our interest to 54.547%.

October

• We announce our plans to form a strategic partnership with Brookfield Renewable Partners L.P., together with its institutional partners (Brookfield Renewable), to acquire Westinghouse, a global provider of nuclear services, from Brookfield Renewable. Brookfield Renewable will own a 51% interest and we will own a 49% interest in Westinghouse. We are responsible to contribute approximately $2.2 billion (US) in respect of the acquisition.

• We issue 34,057,250 common shares at a price of $21.95 (US) per share for gross proceeds to us of approximately $747.6 million (US) pursuant to a bought deal. The net offering proceeds are intended to partially fund our share of the acquisition of Westinghouse.

November

• We announce that the first pounds of uranium ore from the McArthur River mine have now been milled and packaged at the Key Lake mill, marking the achievement of initial production as these facilities transition back to normal operations. |

• We sign a major supply contract to provide sufficient volumes of natural uranium hexafluoride, or UF6 (consisting of uranium and conversion services), to meet Ukraine’s full nuclear fuel needs through 2035.

• CRA has issued revised assessments for the 2007 through 2013 tax years, which resulted in a refund of $297 million, consisting of $86 million in cash and $211 million in letters of credit, which were returned in the second quarter. CRA continues to hold $483 million that we have remitted or secured based on prior reassessments CRA had issued in our longstanding tax dispute.

November

• We announce that the acquisition of Westinghouse in a strategic partnership with Brookfield Renewable closed on November 7, 2023. |

||

| 2023 ANNUAL INFORMATION FORM | Page 9 |

Updated 2024 production plan for McArthur Rive/Key Lake and Cigar Lake

In February 2024, we announced our plan for McArthur River/Key Lake to produce 18 million pounds per year (100% basis) starting in 2024 and to continue to operate Cigar Lake at its licensed capacity of 18 million pounds per year (100% basis) in 2024.

We also plan to begin the work necessary to extend the mine life at Cigar Lake to 2036. In addition, at McArthur River/Key Lake, we plan to undertake an evaluation of the work and investment necessary to expand production up to its annual licensed capacity of 25 million pounds (100% basis), which we expect will allow us to take advantage of this opportunity when the time is right.

Update for 2024 production at Inkai

Based on Kazatomprom (KAP)’s announcement on February 1, 2024, production in Kazakhstan is expected to remain approximately 20% below the level stipulated in subsoil use agreements, primarily due to the sulfuric acid shortage in the country and delays in development of new deposits.

Our current target for production at Inkai in 2024 is 8.3 million pounds of U3O8 (100% basis). However, this target is tentative and contingent upon receipt of sufficient quantities of sulfuric acid. In addition, the allocation of such production between JV Inkai participants is currently under discussion by Cameco and KAP.

How Cameco was formed

Cameco was incorporated under the Canada Business Corporations Act on June 19, 1987.

We were formed when two crown corporations were privatized and their assets merged:

| • | Saskatchewan Mining Development Corporation (SMDC) (uranium mining and milling operations); and |

| • | Eldorado Nuclear Limited (uranium mining, refining and conversion operations) (now Canada Eldor Inc.) |

There are constraints and restrictions on ownership of shares in the capital of Cameco (Cameco shares) set out in our company articles, and a related requirement to maintain offices in Saskatchewan. These are requirements of the Eldorado Nuclear Limited Reorganization and Divestiture Act (Canada), as amended, and The Saskatchewan Mining Development Corporation Reorganization Act, as amended, and are described on pages 135 and 136.

We have made the following amendments to our articles:

| 2002 | • increased the maximum share ownership for individual non-residents to 15% from 5%

• increased the limit on voting rights of non-residents to 25% from 20% |

|

| 2003 | • allowed the board to appoint new directors between shareholder meetings as permitted by the Canada Business Corporations Act, subject to certain limitations

• eliminated the requirement for the chair of the board to be ordinarily resident in the province of Saskatchewan |

|

We have one main subsidiary:

| • | Cameco Europe Ltd., a Swiss company that we have 100% ownership of through subsidiaries |

At January 1, 2024, we do not have any other subsidiary that is material, either individually or collectively.

For more information

You can find more information about Cameco on SEDAR+ (sedarplus.com), EDGAR (sec.gov) and on our website (cameco.com).

See our most recent management proxy circular for additional information, including how our directors and officers are compensated and any loans to them, principal holders of our securities, and securities authorized for issue under our equity compensation plans. We expect the circular for our May 9, 2024 annual meeting of shareholders to be available on April 5, 2024.

See our 2023 financial statements and 2023 MD&A for additional financial information.

| 2023 ANNUAL INFORMATION FORM | Page 10 |

Our vision, values and strategy

Our vision

Our vision – “Energizing a clean-air world” – recognizes that we have an important role to play in enabling the vast reductions in global greenhouse gas (GHG) emissions required to achieve a resilient net-zero carbon economy. We support climate action that is consistent with the ambition of the Paris Agreement and the Canadian government’s corresponding commitment to limit global temperature rise to less than 2°C. We believe that this means the world needs to reach net-zero emissions by 2050 or sooner. The uranium we produce is used around the world in the generation of safe, carbon-free, affordable, baseload nuclear power.

We believe we have the right strategy to achieve our vision and we will do so in a manner that reflects our values. For 35 years, we have been delivering our products responsibly. Building on that strong foundation, we remain committed to our efforts to reduce our own, already low, GHG footprint in our ambition to reach net-zero emissions, while identifying and addressing the ESG risks and opportunities that we believe may have a significant impact on our ability to add long-term value for our stakeholders.

Committed to our values

Our values are discussed below. They define who we are as a company, are at the core of everything we do and help to embed ESG principles and practices as we execute on our strategy in pursuit of our vision. They are:

| • | safety and environment |

| • | people |

| • | integrity |

| • | excellence |

Safety and Environment

The safety of people and protection of the environment are the foundations of our work. All of us share in the responsibility of continually improving the safety of our workplace and the quality of our environment.

We are committed to keeping people safe and conducting our business with respect and care for both the local and global environment.

People

We value the contribution of every employee and we treat people fairly by demonstrating our respect for individual dignity, creativity and cultural diversity. By being open and honest, we achieve the strong relationships we seek.

We are committed to developing and supporting a flexible, skilled, stable and diverse workforce, in an environment that:

| • | attracts and retains talented people and inspires them to be fully productive and engaged |

| • | encourages relationships that build the trust, credibility and support we need to grow our business |

Integrity

Through personal and professional integrity, we lead by example, earn trust, honour our commitments and conduct our business ethically.

We are committed to acting with integrity in every area of our business, wherever we operate.

Excellence

We pursue excellence in all that we do. Through leadership, collaboration and innovation, we strive to achieve our full potential and inspire others to reach theirs.

Our strategy

We are a pure-play investment in the growing demand for nuclear energy, focused on taking advantage of the near-, medium-, and long-term growth occurring in our industry. We provide nuclear fuel and nuclear power products, services, and technologies across the fuel cycle, augmented by our investment in Westinghouse, that support the generation of clean, reliable, secure, and affordable energy. Our strategy is set within the context of what we believe is a transitioning market

| 2023 ANNUAL INFORMATION FORM | Page 11 |

environment. Increasing populations, a growing focus on electrification and decarbonization, and concerns about energy security and affordability are driving a global focus on tripling nuclear power capacity by 2050, which is expected to durably strengthen the long-term fundamentals for our industry. Nuclear energy must be a central part of the solution to the world’s shift to a low-carbon, climate resilient economy. It is an option that can provide the power needed, not only reliably, but also safely and affordably, and in a way that will help avoid some of the worst consequences of climate change.

Our strategy is to capture full-cycle value by:

| • | remaining disciplined in our contracting activity, building a balanced portfolio in accordance with our contracting framework |

| • | profitably producing from our tier-one assets and aligning our production decisions in all segments of the fuel cycle with contracted demand and customer needs |

| • | being financially disciplined to allow us to: |

| • | execute our strategy |

| • | invest in new opportunities that are expected to add long-term value |

| • | self-manage risk |

| • | exploring other emerging opportunities within the nuclear power value chain, which align with our commitment to manage our business responsibly and sustainably, contribute to decarbonization, and help to provide secure and affordable energy |

We continually evaluate investment opportunities within the nuclear fuel value chain, which align well with our commitment to manage our business responsibly and sustainably, increase our contributions to decarbonization and help provide energy security. Expanding our participation in the fuel cycle is expected to complement our tier-one uranium and fuel services assets, creating new revenue opportunities, and it enhances our ability to meet the increasing needs of existing and new customers for secure, reliable nuclear fuel supplies, services and technologies.

We have signed a number of non-binding arrangements to explore several areas of cooperation to advance the commercialization and deployment of small modular reactors in Canada and around the world.

We will make an investment decision when an opportunity is available at the right time and the right price. We strive to pursue corporate development initiatives that will leave us and our stakeholders in a fundamentally stronger position. As such, an investment opportunity is never assessed in isolation. Investments must compete for investment capital with our own internal growth opportunities. They are subject to our capital allocation process described in our 2023 MD&A under Capital Allocation – Focus on Value, starting on page 30.

We expect our strategy will allow us to increase long-term value, and we will execute it with an emphasis on safety, people and the environment.

For more information on our strategy, see our 2023 MD&A under Our vision, value and strategy – Strategy, starting on page 23.

Market overview and developments

A market in transition

In 2023, geopolitical uncertainty and heightened concerns about energy security and climate change continued to improve the demand and supply fundamentals for the nuclear power industry and the fuel cycle that is required to support it. Increasingly, countries and companies around the globe are recognizing the critical role nuclear power must play in providing clean and secure baseload power. This growing support has led to a rise in demand as reactors are being saved from earlier retirement, 10- and 20-year life extensions are being sought and approved for existing reactor fleets in several countries, and numerous commitments and plans are being made for the construction of new nuclear generating capacity. In addition, there is increasing interest in small modular reactors (SMR), including smaller versions of existing technology and advanced technology designs, which are expected to add to demand in the decades to come, with several projects already underway.

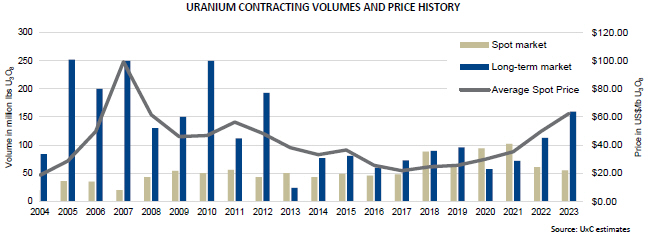

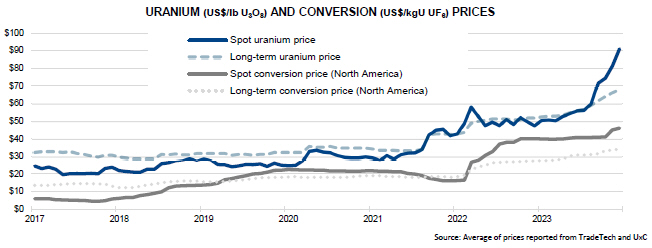

While demand continues to increase, future supply is not keeping pace. Heightened supply risk caused by growing geopolitical uncertainty, shrinking secondary supplies and a lack of investment in new capacity over the past decade has motivated utilities to evaluate their near-, mid-and long-term nuclear fuel supply chains. The uncertainty about where nuclear fuel supplies will come from to satisfy growing demand has led to increased long-term contracting activity and in 2023, about 160 million pounds of uranium was placed under long-term contracts by utilities. While it is the highest annual volume contracted since 2012, it remains below replacement rate and includes our contract with Ukraine, which alone accounted for about 30 million of those pounds. Prices across the nuclear fuel cycle continued to rise in 2023, with spot enrichment prices up 38%, conversion prices continuing to achieve record highs, uranium spot prices more than doubling from around $48 (US) per pound at the end

| 2023 ANNUAL INFORMATION FORM | Page 12 |

of 2022 to $100 (US) per pound at the end of January 2024, after peaking at $106 (US) per pound earlier in the month, and the long-term price for uranium increasing about 38% over the same period. We expect there will be continued competition to secure uranium, conversion services and enrichment services under long-term contracts with proven producers and suppliers who have a diversified portfolio of assets in geopolitically attractive jurisdictions, with strong environmental, social and governance (ESG) performance, and on terms that help ensure a reliable supply is available to satisfy demand.

Durable demand growth

The benefits of nuclear energy have come clearly into focus, supporting a level of durability of demand that, we believe, has not been previously seen. The durability is being driven not only by accountability for achieving the net-zero carbon targets set by countries and companies around the world, but also by a geopolitical realignment in energy markets that is causing countries to reexamine how they plan to address their energy needs. Net-zero carbon targets are turning global attention to a triple challenge. First, about one-third of the global population must be lifted out of energy poverty by improving access to clean and reliable baseload electricity. Second, approximately 80% of the current global electricity grids that run on carbon-emitting sources of thermal power must be replaced with a clean, reliable alternative. And finally, global power grids must grow by electrifying industries, such as private and commercial transportation, and home and industrial heating, which today are largely powered with carbon-emitting sources of thermal energy. Additionally, geopolitical uncertainty has deepened concerns about energy security, highlighting the role of energy policy in balancing three main objectives: providing a clean emissions profile; providing a reliable and secure baseload profile; and providing an affordable, levelized cost profile. There is increasing recognition that nuclear power meets these objectives and has a key role to play in achieving decarbonization and energy security goals. The growth in demand is not just long-term and in the form of new builds, but medium-term in the form of reactor life extensions, and near-term with early reactor retirement plans being deferred or cancelled and new markets continuing to emerge. And, we are seeing even more long-term momentum building with the development of SMRs, where the use case extends beyond just power generation and numerous companies and countries are pursuing projects.

Demand and energy policy highlights

| • | In September, the World Nuclear Association released its biennial Global Nuclear Fuel Report which provides scenarios for demand and supply availability across the fuel supply chain through 2040. This included a robust demand outlook showing global nuclear generating capacity increasing to 686 GWe by 2040 in the Reference Scenario, an average annual growth rate of 3.6%, compared to 2.6% in the 2021 report. This improvement was driven by improved government support, life extensions, new builds and importantly, that starting in the 2030s, the deployment of SMRs is forecasted to contribute to capacity growth. Additional key themes include assumed reductions to secondary supply and decreased availability of mobile inventories, along with the need for a growing volume of future uranium supply requiring higher incentive pricing to balance the market after 2030. |

| • | At the 28th annual Conference of Parties (COP28), the 2023 United Nations Climate Change Conference held in the United Arab Emirates, 22 countries (now 28) launched a declaration to triple nuclear energy capacity by 2050. For the first time at the conference, nuclear energy was recognized alongside other low-emissions technologies for the key role it must play in reaching global net-zero GHG emissions by 2050. In addition, the inaugural global stocktake was introduced at COP28, a process where countries and stakeholders can provide an update every five years to track the world’s progress toward the Paris Agreement targets. In 2023, the initiative concluded that more action is required, as emissions continue to rise and put 2030 targets at risk, reinforcing that in order to achieve net zero by 2050, the world needs “absolute economy-wide emission reduction targets”, which were estimated at a cost of “trillions of dollars”. |

| • | China Nuclear Energy Association published the “China Nuclear Energy Development Report 2023” in April, which highlighted China’s continuing growth. According to the report, the country is expected to lead the world in installed nuclear capacity with 110 GWe expected by 2030, rising to 150 GWe expected by 2035, and plans to build over 90% of their major nuclear power reactors domestically. Additionally, a proposal drafted by 15 Chinese national policy advisors was submitted to the government advocating for the development of new nuclear power plants at inland sites, which are now being considered following the end of a post-Fukushima moratorium on proposed inland nuclear power plants. |

| • | In Japan, Takahama unit 2 restarted in September, becoming the country’s 12th reactor to restart since Fukushima. Onagawa unit 2 and Shimane unit 2 are expected to restart in 2024. In November, the Nuclear Regulation Authority approved 20-year life extensions (beyond 40 years) for Sendai units 1 and 2; additionally, Takahama units 3 and 4 are expected to receive similar life extensions, pending generator work in 2026 and 2027. In addition, Japan enacted a bill in May allowing nuclear reactors to operate beyond the 60-year limit. |

| 2023 ANNUAL INFORMATION FORM | Page 13 |

| • | In South Korea, Korea Hydro and Nuclear Power (KHNP) announced in September that they successfully completed fuel loading at Shin Hanul unit 2, a new 1,400 MWe APR-1400 pressurized water reactor (PWR) unit. This followed an announcement from the Ministry of Industry and Energy that Shin Hanul units 3 and 4 would be completed by the end of 2024. Additionally, to help achieve the plans set out in their 10th Basic Plan for Electricity Supply and Demand 2030, which targets more than 30% of its power supply to come from nuclear, the Ministry confirmed a review of the need for new nuclear power plants was underway. |

| • | In India, the first domestically designed 700 MWe pressurized heavy water reactor, Kakrapar unit 3, reached full operating capacity in August. Three more units of the same design are expected to come online in the next few years. The country is targeting an expansion of nuclear generating capacity to 22.5 GWe by 2031. |

| • | In February, the European Nuclear Alliance was launched. Led by France, the initiative commits 11 European countries to cooperate across the nuclear fuel supply chain, and to promote new nuclear generation projects and technologies, including the advancement of SMRs. Throughout 2023, the alliance expanded and now includes a commitment from 16 European countries that will prepare a roadmap to develop an integrated European nuclear industry and target 150 GWe of nuclear power by 2050. |

| • | In France, plans were advanced to relaunch the country’s reactor construction program: the government committed to life extensions with a proposed “industrial build” program that initially includes six new European Pressurized Reactors (EPR), as well as eight additional EPRs in the future. Électricité de France filed an application to build the first pair of 1,650 MWe EPRs with construction scheduled to begin in 2028. |

| • | In January 2024, the United Kingdom (UK) announced that they are seeking to quadruple their nuclear power output by 2050. Under the “Civil Nuclear Roadmap”, the UK will invest into developing new advanced nuclear fuel, new regulations, and a new nuclear reactor. |

| • | In June, Sweden’s parliament adopted a new energy target, changing its focus to “100% fossil-free” electricity as opposed to the previously stated focus of “100% renewable”. In August, the government announced a target to further expand the role of nuclear power and in November, announced its intention to build up to 2,500 MWe of new nuclear power capacity by 2035, and up to 10 new reactors by 2045, backed by an offer of loan guarantees. |

| • | In Belgium, the government and nuclear operator ENGIE reached an agreement following prolonged negotiations to extend the lifespans of the Doel unit 4 and Tihange unit 3 reactors by 10 years, with each now expected to operate until 2035. |

| • | In Bulgaria, the government issued its 30-year energy strategy to 2053, which envisions the construction of four new nuclear reactor units. In December, parliament approved a government proposal to inject up to 1.5 billion levs ($(US) 838 million) into the state-owned Kozloduy Nuclear Power Plant to fund the planned construction of the first of two proposed reactors using Westinghouse’s AP1000® technology. |

| • | In Poland, the government adopted a resolution committing to finance the country’s first nuclear power plant. The funds will go to Polish utility Polskie Elektrownie Jadrowe, which signed a contract with Westinghouse for multiple AP1000 reactors in February of 2023. |

| • | In the US, Vogtle unit 3 entered commercial service on July 31, after becoming the first Westinghouse AP1000 reactor in the US to successfully connect to the electrical grid. Vogtle unit 4 is expected to begin operating in the second quarter of 2024. |

| • | Throughout 2023, many US states expressed local support for nuclear: Ohio, Virginia, Kentucky, and Tennessee all began creating state-level advisory authorities to promote, research and develop nuclear power technologies, and Michigan formed a new Nuclear Caucus to support the reopening of the Palisades nuclear power plant, and also approved extending operations at the Monticello nuclear power plant through 2040. |

| • | In Canada, provincial support for nuclear increased in 2023. New Brunswick Power signed a three-year contract with Ontario Power Generation (OPG) to enhance the operational performance of the Point Lepreau nuclear power plant. In Ontario, the Minister of Energy announced support to advance the long-term planning required to explore nuclear expansion options for Bruce Power, outlining the need for nearly 18 GWe in new nuclear capacity to help the province reach its electrification and net-zero goals. Additionally, in Saskatchewan, Crown Investments Corporation provided around $479,000 to help local firms build small, advanced, and micro reactors supply chain capacity, while the Alberta government announced plans to invest around $7 million to study SMRs. |

| • | In January 2024, OPG announced plans to proceed with the refurbishment of the Pickering Nuclear Generating Station’s “B” units (units 5, 6, 7 and 8). Once the project is completed in the mid-2030s, Pickering would produce a total of 2 GWe of electricity, to help meet increasing electricity demand and fuel the province’s economic growth. |

| 2023 ANNUAL INFORMATION FORM | Page 14 |

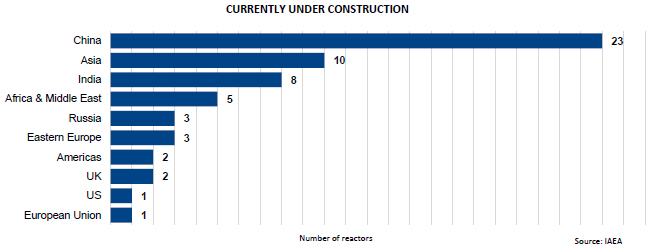

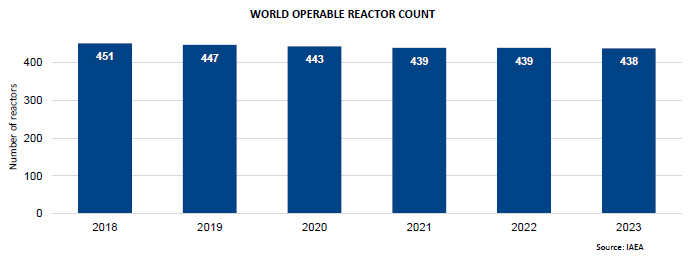

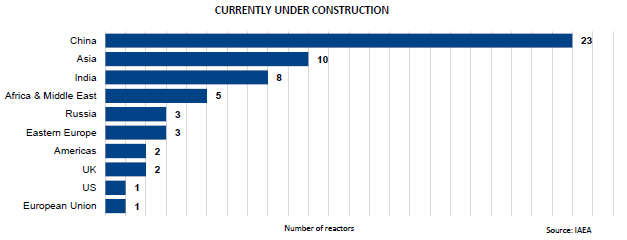

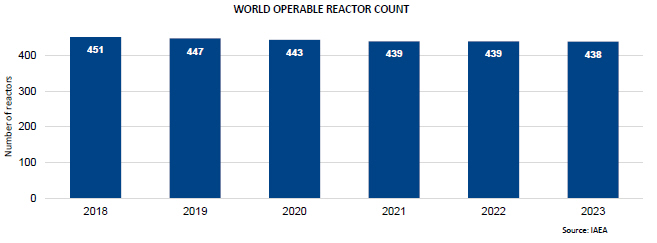

According to the International Atomic Energy Agency (IAEA), globally there are currently 438 operable reactors and 58 reactors under construction. Several nations are appreciating the clean energy and energy security benefits of nuclear power and have reaffirmed their commitment with plans underway to support existing reactor units and review policies to encourage more nuclear generation. Several other non-nuclear countries have emerged as candidates for new nuclear capacity. In the EU, specific nuclear energy projects have been identified for inclusion under its sustainable financing taxonomy and are therefore eligible for access to low-cost financing. In Canada, the government revised the Canada Green Bond Framework to include nuclear energy projects. In some countries where phase-out policies have been in place, policy reversals and decisions have been made to temporarily keep reactors running, with public opinion polls showing increasing support. With a number of reactor construction projects recently approved and many more planned, demand for uranium continues to improve. There is growing recognition of the role nuclear must play in providing safe, affordable, carbon-free baseload electricity to achieve a low-carbon economy, while being a reliable energy source that helps countries move away from Russian energy supply.

Supply uncertainty

Geopolitical uncertainty remained the most notable factor impacting security of supply in 2023. Driven by the Russian invasion of Ukraine, and more recently, the coup d’état in Niger, many governments and utilities are re-examining supply chains and procurement strategies that rely on nuclear fuel supplies from these jurisdictions. In addition, sanctions on Russia and Niger, government restrictions, and restrictions on and cancellations of some cargo insurance coverages continue to create transportation and supply chain risks for nuclear fuel supplies coming out of Central Asia. There are also transportation risks to material being shipped from Australia to Europe as a result of the conflict in the Middle East. Despite the recent increase in market prices, the deepening geopolitical uncertainty and years of underinvestment in new uranium and fuel cycle service capacities has shifted risk from producers to utilities.

| 2023 ANNUAL INFORMATION FORM | Page 15 |

Supply and trade policy highlights

| • | Sprott Physical Uranium Trust (SPUT) purchased about 4 million pounds U3O8 in 2023, bringing total purchases since inception to over 45 million pounds U3O8 and increasing the total net asset value to around $(US)7 billion. Volatility in equity markets has impacted SPUT’s valuation (discount or premium to its net asset value) and therefore its ability to raise funds to purchase uranium. |

| • | In June, KAP announced plans to start production at a new uranium deposit, Inkai 3 (100% owned by KAP). KAP expects approval of a Subsoil Use Agreement (SSUA) to produce 10.4 million pounds U3O8 annually for 25 years from Inkai 3’s uranium resources of about 216 million pounds U3O8. |

| • | In September, KAP had restated its plan to increase production in 2024 to 90% of SSUAs and announced a ramp up to 100% of SSUAs in 2025, though the company also warned that geopolitical uncertainty, global supply chain issues, and inflationary pressure could create challenges. On January 12, 2024, KAP announced that it had faced challenges in completing the development required to achieve the planned 2024 production increase, and that it expected to lower its 2024 uranium production guidance due to limited availability of sulfuric acid and delays in the construction and development of new assets, including Budenovskoye 6 and 7. On February 1, 2024, KAP rescinded its 2024 target due to the shortage of sulfuric acid and construction delays in 2023, and they now plan to remain about 20% below SSUAs, expecting to produce between 55 million and 59 million pounds U3O8 in 2024 (previously 65 million to 66 million pounds U3O8). KAP also warned that if the acid, supply chain and construction issues persist throughout 2024, the company’s 2025 plan to increase production to 100% of SSUAs (79 million to 82 million pounds U3O8) may also be affected. |

| • | In April, five of the G7 countries (Canada, France, Japan, UK, and US), entered into a civil nuclear fuel security agreement that attempts to reduce Russia’s influence in the global nuclear fuel supply chain. |

| • | In December, Urenco announced its decision to expand enrichment capacity at their facility in Almelo, Netherlands, increasing capacity by 15% or approximately 750,000 separative work units (SWU), by 2027. This followed a prior announcement of plans to expand enrichment capacity at its Urenco USA site, increasing capacity there by 15% or approximately 700,000 SWU, by 2025. |

| • | In October, Orano announced a planned enrichment capacity extension project at Georges Besse 2. The project, forecasted to cost €1.7 billion, seeks to increase capacity by over 30% or approximately 2.5 million SWU, beginning in 2028. |

| • | In July, ConverDyn announced the restart of Honeywell’s Metropolis uranium conversion facility. The restart plan had been delayed by a safety equipment failure in June, resulting in a special inspection by the US Nuclear Regulatory Commission (NRC). The facility restarted production in July 2023. |

| • | In July, a coup d’état in Niger resulted in a group of military officers removing President Mohamed Bazoum and seizing power. All exports of uranium and gold to France were suspended and in September, Orano stated that it had halted uranium processing operations at the company’s majority-owned SOMAIR (Arlit) project in Niger due to logistical complications caused by international sanctions. This resulted in 2023 production dropping to 3.9 million pounds U3O8, compared to around 5.2 million pounds U3O8 in 2022. |

| • | In December, the US House of Representatives passed the Prohibiting Russian Uranium Impacts Act. The act proposes to prohibit the import of Russian low-enriched uranium (LEU) into the US but includes waivers that allow the import of LEU from Russia if the US Energy Secretary determines no alternative source can be procured, or if the shipments are of national interest. The waivers would gradually reduce and eliminate Russian uranium imports by 2028. The bill is awaiting further action after it was blocked by the US Senate on grounds unrelated to the bill itself. Separately, the US Senate Energy and Natural Resources Committee passed the Nuclear Fuel Security Act of 2023, which directs the Department of Energy to create a “Nuclear Fuel Security Program” and strengthen the US nuclear fuel supply chain, including new LEU and high-assay low-enriched uranium (HALEU) capacity, though no new funding has yet been appropriated. Finally, a Supplemental Funding Bill is progressing through Congress and includes roughly $111 billion (US) for national security measures, including a provision for $2.72 billion (US) to be allocated to a new “American Energy Independence Fund”, which would acquire non-Russian LEU and HALEU, subject to the ban on Russian imports becoming law. |

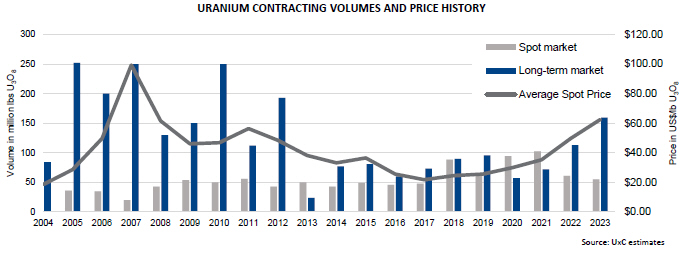

Long-term contracting creates full-cycle value for proven productive assets

Like other commodities, the demand for uranium is cyclical. However, unlike other commodities, uranium is not traded in meaningful quantities on a commodity exchange. The uranium market is principally based on bilaterally negotiated long-term contracts covering the annual run-rate requirements of nuclear power plants, with a small spot market to serve discretionary demand. History demonstrates that in general, when prices are rising and high, uranium is perceived as scarce, and more

| 2023 ANNUAL INFORMATION FORM | Page 16 |

contracting activity takes place with proven and reliable suppliers. The higher demand discovered during this contracting cycle drives investment in higher-cost sources of production, which due to lengthy development timelines, tend to miss the contracting cycle and ramp up after demand has already been won by proven producers. When prices are declining and low, there is no perceived urgency to contract, and contracting activity and investment in new supply dramatically decreases. After years of low prices, and a lack of investment in supply, and as the uncommitted material available in the spot market begins to thin, security-of-supply tends to overtake price concerns. Utilities typically re-enter the long-term contracting market to ensure they have a reliable future supply of uranium to run their reactors.

UxC reports that over the last five years approximately 510 million pounds U3O8 equivalent have been locked-up in the long-term market, while approximately 780 million pounds U3O8 equivalent have been consumed in reactors. We remain confident that utilities have a growing gap to fill.

We believe the current backlog of long-term contracting presents a substantial opportunity for proven and reliable suppliers with tier-one productive capacity and a record of honoring supply commitments. As a low-cost producer, we manage our operations to increase value throughout these price cycles.

In our industry, customers do not come to the market right before they need to load nuclear fuel into their reactors. To operate a reactor that could run for more than 60 years, natural uranium and the downstream services have to be purchased years in advance, allowing time for a number of processing steps before a finished fuel bundle arrives at the power plant. At present, we believe there is a significant amount of uranium that needs to be contracted to keep reactors running into the next decade.

| 2023 ANNUAL INFORMATION FORM | Page 17 |

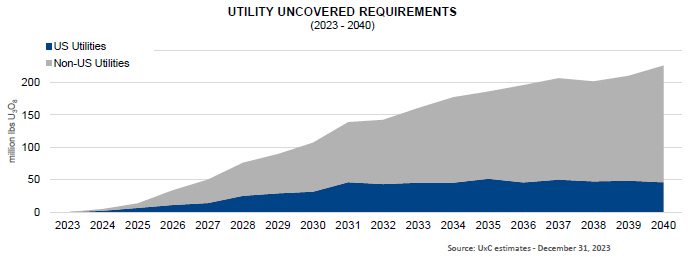

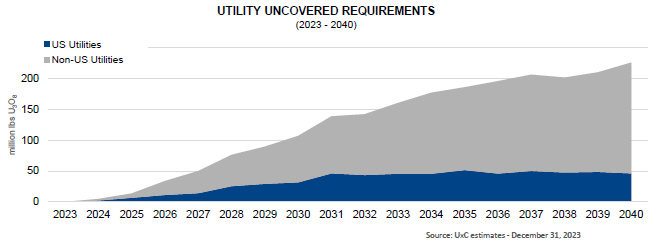

UxC estimates that cumulative uncovered requirements are about 2.2 billion pounds to the end of 2040. With the lack of investment over the past decade, there is growing uncertainty about where uranium will come from to satisfy growing demand, and utilities are becoming increasingly concerned about the availability of material to meet their long-term needs. In addition, secondary supplies have diminished, and the material available in the spot market has thinned as producers and financial funds continue to purchase material. Furthermore, geopolitical uncertainty is causing some utilities to seek nuclear fuel suppliers whose values are aligned with their own or whose origin of supply better protects them from potential interruptions, including from transportation challenges or the possible imposition of formal sanctions.

We will continue to take the actions we believe are necessary to position the company for long-term success. Therefore, we will continue to align our production decisions with our customers’ needs under our contract portfolio. We will undertake contracting activity which is intended to ensure we have adequate protection while maintaining exposure to the benefits that come from having uncommitted, low-cost supply to place into a strengthening market.

Building a balanced portfolio

The purpose of our contracting framework is to deliver value. Our approach is to secure a solid base of earnings and cash flow by maintaining a balanced contract portfolio that optimizes our realized price.

Contracting decisions in all segments of our business need to consider the nuclear fuel market structure, the nature of our competitors, and the current market environment. The vast majority of run-rate fuel requirements are procured under long-term contracts. The spot market is thinly-traded where utilities buy small, discretionary volumes. This market structure is reflective of the baseload nature of nuclear power and the relatively small proportion of the overall operating costs the fuel represents compared to other sources of baseload electricity. Additionally, about half of the fuel supply typically comes from diversified mining companies that produce uranium as a by-product, or by state-owned entities with production volume strategies or ambitions to serve state nuclear power ambitions with low-cost fuel supplies. We evaluate our strategy in the context of our market environment and continue to adjust our actions in accordance with our contracting framework:

| • | First, we build a long-term contract portfolio by layering in volumes over time. In addition to our committed sales, we will compete for customer demand in the market where we think we can obtain value and, in general, as part of longer-term contracts. We will take advantage of opportunities the market provides, where it makes sense from an economic, logistical, diversification and strategic point of view. Those opportunities may come in the form of spot, mid-term or long-term demand, and will be additive to our current committed sales. |

| • | As we build our portfolio of long-term contracts, we decide how to best source material to satisfy that demand, planning our production in accordance with our contract portfolio and other available sources of supply. We will not produce from our tier-one assets to sell into an oversupplied spot market. |

| • | We do not intend to build an inventory of excess uranium. Excess inventory serves to contribute to the sense that uranium is abundant and creates an overhang on the market, and it ties up working capital on our balance sheet. |

| • | Depending on the timing and volume of our production, purchase commitments, and our inventory volumes, we may be active buyers in the market in order to meet our annual delivery commitments. Historically, prior to the supply curtailments that we began in 2016, we have generally planned our annual delivery commitments to slightly exceed the annual supply we expect to come from our annual production and our long-term purchase commitments and have therefore relied on the spot market to meet a small portion of our delivery commitments. In general, if we choose to purchase material to meet demand, we expect the cost of that material will be more than offset by the volume of commitments in our sales portfolio that are exposed to market prices at the time of delivery over the long-term. |

In addition to this framework, our contracting decisions always factor in who the customer is, our desire for regional diversification, the product form, and logistical factors.

Ultimately, our goal is to protect and extend the value of our contract portfolio on terms that recognize the value of our assets, including future development projects, and pricing mechanisms that provide adequate protection when prices go down and exposure to rising prices. We believe using this framework will allow us to create long-term value. Our focus will continue to be on ensuring we have the financial capacity to execute on our strategy and self-manage risk.

| 2023 ANNUAL INFORMATION FORM | Page 18 |

Long-term contracting

Uranium is not traded in meaningful quantities on a commodity exchange. Utilities have historically bought the majority of their uranium and fuel services products under long-term contracts that are bilaterally negotiated with suppliers. The spot market is discretionary and typically used for one-time volumes, not to satisfy annual demand. We sell uranium and fuel products and services directly to nuclear utilities around the world as uranium concentrates, UO2 and UF6, conversion services, or fuel fabrication and reactor components for CANDU heavy water reactors. We have a solid portfolio of long-term sales contracts that reflect our reputation as a proven, reliable supplier of geographically stable supply, and the long-term relationships we have built with our customers.

In general, we are active in the market, buying and selling uranium when it is beneficial for us and in support of our long-term contract portfolio. We undertake activity in the spot and term markets prudently, looking at the prices and other business factors to decide whether it is appropriate to purchase or sell into the spot or term market. Not only is this activity a source of profit, but it also gives us insight into underlying market fundamentals.

We deliver the majority of our uranium under long-term contracts each year, some of which are tied to market-related pricing mechanisms quoted at time of delivery. Therefore, our net earnings and operating cash flows are generally affected by changes in the uranium price. Market prices are influenced by the fundamentals of supply and demand, market access and trade policy issues, geopolitical events, disruptions in planned supply and demand, and other market factors.

The objectives of our contracting strategy are to:

| • | optimize realized price by balancing exposure to future market prices while providing some certainty for our future earnings and cash flow |

| • | focus on meeting the nuclear industry’s growing annual uncovered requirements with our tier-one production |

| • | establish and grow market share with strategic and regionally diverse customers |

We have a portfolio of long-term contracts, each bilaterally negotiated with customers, that have a mix of base-escalated pricing and market-related pricing mechanisms, including provisions that provide exposure to rising market prices and also protect us when the market price is declining. This is a balanced and flexible approach that allows us to adapt to market conditions, put a floor on our average realized price and deliver the best value over the long term.

This approach has allowed our realized price to outperform the market during periods of weak uranium demand, and we expect it will enable us to realize increases linked to higher market prices in the future.

Base-escalated contracts for uranium: use a pricing mechanism based on a term-price indicator at the time the contract is accepted and escalated to time of each delivery over the term of the contract.

Market-related contracts for uranium: are different from base-escalated contracts in that the pricing mechanism may be based on either the spot price or the long-term price, and that price is generally set a month or more prior to delivery rather than at the time the contract is accepted. These contracts may provide for discounts, and typically include floor prices and/or ceiling prices, which are established at time of contract acceptance and usually escalate over the term of the contract.