UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): June 15, 2023

Patterson-UTI Energy, Inc.

(Exact name of Registrant as Specified in Its Charter)

| Delaware | 1-39270 | 75-2504748 | ||

| (State or Other Jurisdiction of Incorporation ) |

(Commission File Number) |

(IRS Employer Identification No.) |

| 10713 W. Sam Houston Pkwy N., Suite 800, Houston, Texas | 77064 | |||

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant’s Telephone Number, Including Area Code: 281-765-7100

Not Applicable

(Former Name or Former Address, if Changed Since Last Report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instructions A.2. below):

| ☒ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading |

Name of each exchange on which registered |

||

| Common Stock, $0.01 Par Value | PTEN | The Nasdaq Global Select Market |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 8.01 Other Events.

On June 15, 2023, Patterson-UTI Energy, Inc., a Delaware corporation (“Patterson-UTI”), released certain communications regarding a business combination transaction between Patterson-UTI and NexTier Oilfield Solutions Inc. (“NexTier”), which are filed as Exhibit 99.1, Exhibit 99.2, Exhibit 99.3, Exhibit 99.4 (revised) and Exhibit 99.5.

Important Information for Stockholders

In connection with the proposed transaction, Patterson-UTI intends to file with the SEC a registration statement on Form S-4 that will include a joint proxy statement of Patterson-UTI and NexTier that also constitutes a prospectus of Patterson-UTI. Each of Patterson-UTI and NexTier also plan to file other relevant documents with the SEC regarding the proposed transaction. No offering of securities shall be made, except by means of a prospectus meeting the requirements of Section 10 of the U.S. Securities Act of 1933, as amended. Any definitive joint proxy statement/prospectus (if and when available) will be mailed to shareholders of Patterson-UTI and NexTier. INVESTORS AND STOCKHOLDERS ARE URGED TO READ THE REGISTRATION STATEMENT, JOINT PROXY STATEMENT/PROSPECTUS AND OTHER DOCUMENTS THAT MAY BE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. Investors and shareholders will be able to obtain free copies of these documents (if and when available) and other documents containing important information about Patterson-UTI and NexTier once such documents are filed with the SEC through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by Patterson-UTI will be available free of charge on Patterson-UTI’s website at http://www.patenergy.com or by contacting Patterson-UTI’s Investor Relations Department by phone at (281) 765-7170. Copies of the documents filed with the SEC by NexTier will be available free of charge on NexTier’s website at https://nextierofs.com or by contacting NexTier’s Investor Relations Department by phone at (346) 242-0519.

Participants in the Solicitation

Patterson-UTI, NexTier and certain of their respective directors and executive officers may be deemed to be participants in the solicitation of proxies in respect of the proposed transaction. Information about the directors and executive officers of Patterson-UTI is set forth in its proxy statement for its 2023 annual meeting of shareholders, which was filed with the SEC on April 11, 2023, and Patterson-UTI’s Annual Report on Form 10-K for the fiscal year ended December 31, 2022, which was filed with the SEC on February 13, 2023. Information about the directors and executive officers of NexTier is set forth in its proxy statement for its 2023 annual meeting of shareholders, which was filed with the SEC on April 28, 2023, and NexTier’s Annual Report on Form 10-K for the fiscal year ended December 31, 2022, which was filed with the SEC on February 16, 2023. Other information regarding the participants in the proxy solicitations and a description of their direct and indirect interests, by security holdings or otherwise, will be contained in the joint proxy statement/prospectus and other relevant materials to be filed with the SEC regarding the proposed transaction when such materials become available. Investors should read the joint proxy statement/prospectus carefully when it becomes available before making any voting or investment decisions. You may obtain free copies of these documents from Patterson-UTI or NexTier using the sources indicated above.

No Offer or Solicitation

This communication is not intended to and does not constitute an offer to sell or the solicitation of an offer to subscribe for or buy or an invitation to purchase or subscribe for any securities or the solicitation of any vote in any jurisdiction pursuant to the proposed transaction or otherwise, nor shall there be any sale, issuance or transfer of securities in any jurisdiction in contravention of applicable law. Subject to certain exceptions to be approved by the relevant regulators or certain facts to be ascertained, the public offer will not be made directly or indirectly, in or into any jurisdiction where to do so would constitute a violation of the laws of such jurisdiction, or by use of the mails or by any means or instrumentality (including without limitation, facsimile transmission, telephone and the internet) of interstate or foreign commerce, or any facility of a national securities exchange, of any such jurisdiction.

Cautionary Statement Regarding Forward-Looking Statements

This communication contains forward-looking statements which are protected as forward-looking statements under the Private Securities Litigation Reform Act of 1995 that are not limited to historical facts, but reflect Patterson-UTI’s and NexTier’s current beliefs, expectations or intentions regarding future events. Words such as “anticipate,” “believe,” “budgeted,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “potential,” “project,” “pursue,” “should,” “strategy,” “target,” or “will,” and similar expressions are intended to identify such forward-looking statements. The statements in this communication that are not historical statements, including statements regarding Patterson-UT’‘s and NexTier’s future expectations, beliefs, plans, objectives, financial conditions, assumptions or future events or performance that are not historical facts, are forward-looking statements within the meaning of the federal securities laws. These statements are subject to numerous risks and uncertainties, many of which are beyond Patterson-UTI’s and NexTier’s control, which could cause actual results to differ materially from the results expressed or implied by the statements. The statements include, without limitation, projections as to the anticipated benefits of the proposed transaction, the impact of the proposed transaction on Patterson-UTI’s and NexTier’s business and future financial and operating results, the amount and timing of synergies from the proposed transaction, the combined company’s projected revenues, adjusted EBITDA and cash flow, accretion, business and employee opportunities, capital return policy, and the closing date for the proposed transaction, are based on management’s estimates, assumptions and projections, and are subject to significant uncertainties and other factors, many of which are beyond Patterson-UTI’s and NexTier’s control. These factors and risks include, but are not limited to, adverse oil and natural gas industry conditions; global economic conditions, including inflationary pressures and risks of economic downturns or recessions in the United States and elsewhere; volatility in customer spending and in oil and natural gas prices that could adversely affect demand for Patterson-UTI’s and NexTier’s services and their associated effect on rates; excess availability of land drilling rigs, pressure pumping and directional drilling equipment, including as a result of reactivation, improvement or construction; competition and demand for Patterson-UTI’s and NexTier’s services; the impact of the ongoing conflict in Ukraine; strength and financial resources of competitors; utilization, margins and planned capital expenditures; liabilities from operational risks for which Patterson-UTI or NexTier do not have and receive full indemnification or insurance; operating hazards attendant to the oil and natural gas business; failure by customers to pay or satisfy their contractual obligations (particularly with respect to fixed-term contracts); the ability to realize backlog; specialization of methods, equipment and services and new technologies, including the ability to develop and obtain satisfactory returns from new technology; the ability to retain management and field personnel; loss of key customers; shortages, delays in delivery, and interruptions in supply, of equipment and materials; cybersecurity events; synergies, costs and financial and operating impacts of acquisitions; difficulty in building and deploying new equipment; governmental regulation; climate legislation, regulation and other related risks; environmental, social and governance practices, including the perception thereof; environmental risks and ability to satisfy future environmental costs; technology-related disputes; legal proceedings and actions by governmental or other regulatory agencies; the ability to effectively identify and enter new markets; public health crises, pandemics and epidemics; weather; operating costs; expansion and development trends of the oil and natural gas industry; ability to obtain insurance coverage on commercially reasonable terms; financial flexibility; interest rate volatility; adverse credit and equity market conditions; availability of capital and the ability to repay indebtedness when due; our return of capital to stockholders; stock price volatility; and compliance with covenants under Patterson-UTI’s and NexTier’s debt agreements; and other risk factors and additional information. In addition, material risks that could cause actual results to differ from forward-looking statements include: the inherent uncertainty associated with financial or other projections; the prompt and effective integration of Patterson-UTI’s and NexTier’s businesses and the ability to achieve the anticipated synergies and value-creation contemplated by the proposed transaction; the risk associated with Patterson-UTI’s and NexTier’s ability to obtain the approval of the proposed transaction by their shareholders required to consummate the proposed transaction and the timing of the closing of the proposed transaction, including the risk that the conditions to the transaction are not satisfied on a timely basis or at all and the failure of the transaction to close for any other reason; the risk that a consent or authorization that may be required for the proposed transaction is not obtained or is obtained subject to conditions that are not anticipated; unanticipated difficulties or expenditures relating to the transaction, the response of business partners and retention as a result of the announcement and pendency of the transaction; and the diversion of management time on transaction-related issues.

Additional information concerning factors that could cause actual results to differ materially from those in the forward-looking statements is contained from time to time in Patterson-UTI’s or NexTier’s SEC filings, both of which are available through the Securities and Exchange Commission’s (the “SEC”) Electronic Data Gathering and Analysis Retrieval System (EDGAR) at http://www.sec.gov, or with respect to Patterson-UTI’s SEC filings, Patterson-UTI’s website at http://www.patenergy.com, or with respect to NexTier’s SEC filings, NexTier’s website at https://nextierofs.com. Patterson-UTI and NexTier undertake no obligation to publicly update or revise any forward-looking statement.

Item 9.01 Financial Statements and Exhibits.

(d) Exhibits:

| 99.1 | Transcript of Investor Call. | |

| 99.2 | Social Media Posts. | |

| 99.3 | Infographic. | |

| 99.4 | Employee Town Hall Presentation (revised). | |

| 99.5 | Transcript of Employee Town Hall Presentation. | |

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document). | |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

Date: June 15, 2023

| Patterson-UTI Energy, Inc. | ||||

| By: | /s/ C. Andrew Smith |

|||

| Name: | C. Andrew Smith | |||

| Title: | Executive Vice President and Chief Financial Officer | |||

Exhibit 99.1

REFINITIV STREETEVENTS | www.refinitiv.com | Contact Us

| ©2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. ‘Refinitiv’ and the Refinitiv logo are registered trademarks of Refinitiv and its affiliated companies. |

|

CORPORATE PARTICIPANTS

C. Andrew Smith Patterson-UTI Energy, Inc. - Executive VP & CFO

James Michael Drickamer Patterson-UTI Energy, Inc. - VP of IR

Kenneth H. Pucheu NexTier Oilfield Solutions Inc. - Executive VP & CFO

Robert Wayne Drummond NexTier Oilfield Solutions Inc. - President, CEO, & Director

William Andrew Hendricks Patterson-UTI Energy, Inc. - President, CEO & Director

CONFERENCE CALL PARTICIPANTS

Daniel Robert Kutz Morgan Stanley, Research Division - Research Associate

Derek John Podhaizer Barclays Bank PLC, Research Division - Equity Research Analyst

Donald Peter Crist Johnson Rice & Company, L.L.C., Research Division - Research Analyst

Douglas Lee Becker Capital One Securities, Inc., Research Division - Research Analyst

John Daniel

Keith MacKey RBC Capital Markets, Research Division - Analyst

Kurt Kevin Hallead The Benchmark Company, LLC, Research Division - Research Analyst

Marc Gregory Bianchi TD Cowen, Research Division - MD & Senior Energy Analyst

Saurabh Pant BofA Securities, Research Division - VP

Scott Andrew Gruber Citigroup Inc., Research Division - Director, Head of Americas Energy Sector & Senior Analyst

Stephen David Gengaro Stifel, Nicolaus & Company, Incorporated, Research Division - MD & Senior Analyst

PRESENTATION

Operator

Hello, and thank you for standing by. Welcome to today’s conference call to discuss the combination of Patterson -UTI Energy and NexTier Oilfield Solutions. (Operator Instructions) As a reminder, this conference call is being recorded, and the press release and slide presentation regarding the transaction are available at the Investor Relations section of each company’s website. The archived replay can be accessed there following the call.

I would now like to hand the conference over to Mike Drickamer, Vice President, Investor Relations at Patterson-UTI Energy. Mike?

James Michael Drickamer - Patterson-UTI Energy, Inc. - VP of IR

Thank you, Todd. Welcome everybody. This morning, we will discuss the combination of Patterson-UTI Energy and NexTier Oilfield Solutions. Our remarks that follow including answers to your questions, contain statements that we believe to be forward-looking statements within the meaning of the Private Securities Litigation Reform Act. These forward-looking statements are subject to risks and uncertainties that could cause actual results to be materially different from those expressed or implied by such forward-looking statements. These risks include, among others, matters that we described in our press release announcing this transaction in our SEC filings. We disclaim any obligation to update these forward-looking statements.

Our participants today include Patterson-UTI’s CEO, Andy Hendricks and CFO, Andy Smith; as well as NexTier’s CEO, Robert Drummond; and CFO, Kenny Pucheu. After our prepared remarks, we’ll open it up for Q&A.

Now let me turn it over to Andy Hendricks.

2

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

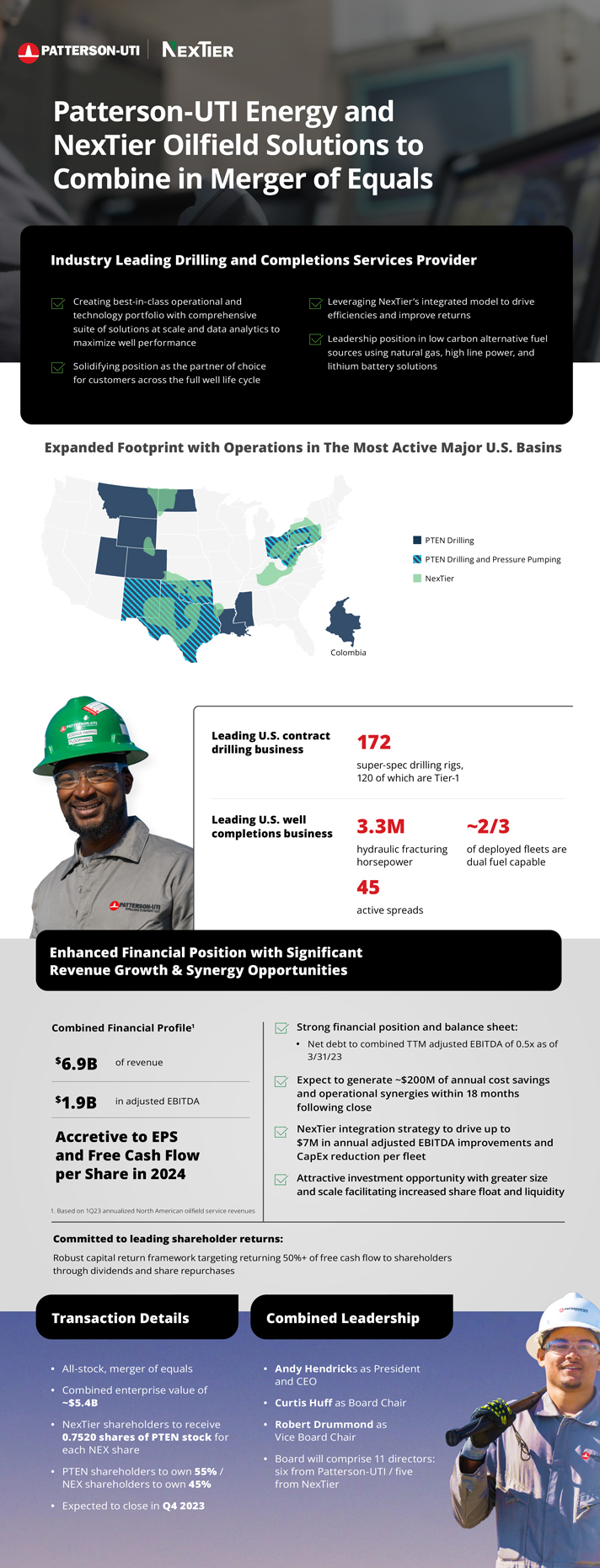

Thanks, Mike. Welcome, everyone, and thank you for joining us today. We’re excited to discuss the merger of Patterson-UTI and NexTier Oilfield Services. Robert and I will take you through the key highlights of this merger with equals, as well as the transaction terms and strategic benefits. Andy Smith will discuss the financials in a bit more detail. This merger will create a comprehensive drilling and completions franchise with leadership positions in contract drilling, pressure pumping and directional drilling. We believe our combined ability to serve our customers with a strong synergy potential for new transaction will create significant value for shareholders of both companies.

Additionally, we believe the combined company will be an attractive investment platform with greater size and scale, facilitating improved free cash flow, increased share and liquidity, making it more appealing to a larger number of long-term shareholders. Patterson-UTI and NexTier have each committed to target the return of 50% of free cash flow to shareholders and this will remain the case for the new company.

Moving on to the terms of the transaction. NexTier’s shareholders will receive 0.7520 shares of Patterson-UTI common stock for each share of NexTier common stock. The transaction has implied enterprise value on a combined basis of approximately $5.4 billion, and we expect the merger to be tax-free to shareholders of both companies. Upon closing, Patterson-UTI shareholders will own approximately 55% and NexTier shareholders will own approximately 45% of the combined company on a fully diluted basis.

As for leadership, post close, I will serve as President and CEO; Robert will become Vice Chair of the Board; Curtis Huff, Patterson-UTI’s current Chair, will continue to serve in that role. We’ll have an 11-director Board that will comprise 6 directors from Patterson-UTI and 5 from Nextier. We’ll be headquartered here in Houston and Patterson-UTI Energy will be the combined company name. Representing the strength of NexTier’s platform, our well completion segment will operate under the NexTier completions brand. Finally, we expect to close the transaction in the fourth quarter of this year subject to the receipt of Patterson-UTI and NexTier shareholder approvals, regulatory approvals and other customary closing conditions.

We believe this combination represents a unique opportunity for both companies to deliver value to shareholders, employees, customers and communities alike. Both companies have evolved over the last several years to meet the increasing challenges of drilling and completing more complex wells. Our customers’ technical and operational challenges continue to increase, continue to grow in both Patterson-UTI and NexTier have stayed ahead of the curve to ensure we are delivering solid execution and innovative solutions to our customers, while also providing improving financial returns for our shareholders.

Among the many important benefits, we expect to realize the combined company will have a diversified suite of offerings across the oilfield services value chain to better serve our customers with leading positions in contract drilling, pressure pumping and directional drilling. These offerings will be bolstered by best-in-class operational execution and a strong technology portfolio.

Let me turn it over to Andy Smith, Patterson-UTI’s CFO, to review the financial benefits of this merger.

C. Andrew Smith - Patterson-UTI Energy, Inc. - Executive VP & CFO

Thank you. Good morning. The transaction is expected to be accretive to both earnings and free cash flow per share in 2024. We will also have an outstanding balance sheet with trailing 12-month net debt to adjusted EBITDA of 0.5x. Together, we’ll be a financially stronger company positioned to deliver significant returns for our shareholders. We will maintain strong capital discipline with a focus on high free cash flow conversion and intend to continue the practices of both companies of distributing at least the 50% of free cash flow to shareholders.

The merged company will be one of the largest North American oilfield services provider in terms of revenue, having generated approximately $6.9 billion of combined annualized revenue in the first quarter of 2023. Both companies have strong track records of executing and realizing synergy opportunities with prior transactions, and we are confident in our ability to build on that. We expect to realize annual cost savings and operational synergies of approximately $200 million within 18 months following the close. Synergies will be achieved in 3 distinct areas.

3

First, we expect to benefit by utilizing NexTier’s integrated completions offering, including Wireline, Power Solutions in the NexHub Digital Center across the existing Patterson-UTI frac fleets. Our expectation is that we will see revenue uplift from the additional service offerings as well as a reduction in maintenance CapEx and a corresponding increase in equipment uptime based on NexTier’s digital equipment monitoring platform.

Second, by sharing best practices and preferred vendor arrangements, we expect to secure cost savings across our supply chain. With over $3.3 billion of non-payroll addressable spend, including CapEx, even small improvements in this area will result in meaningful dollar savings. Finally, with any merger, there will be some organizational overlap. While both companies have historically been pretty lean, we will see savings as we streamline the combined organization. Across these 3 areas, we believe $200 million in benefit is not only achievable, but over time, potentially beatable. Onetime costs expected to be incurred to achieve these synergies are approximately $80 million, of which about $65 million will be expensed and $15 million will be CapEx.

With that, I’ll turn the call back over to Andy Hendricks.

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

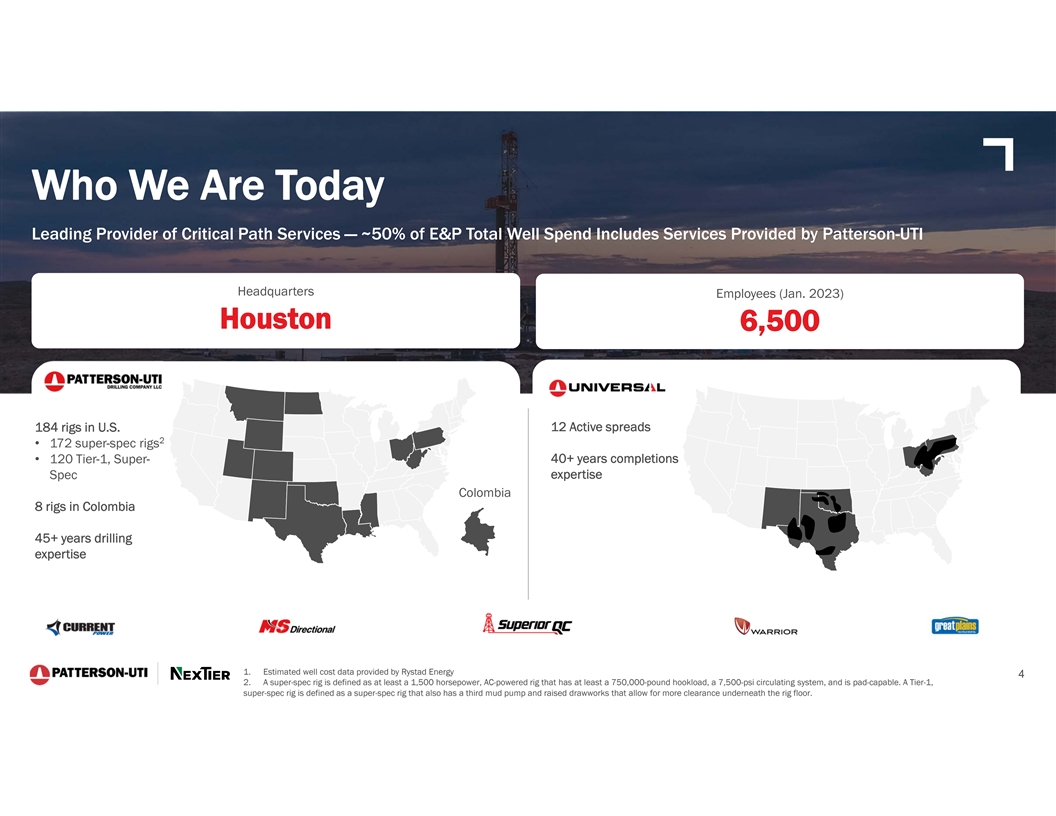

Thanks, Andy. The combined company will remain the drilling leader that Patterson-UTI is today. Our drilling business continues to outperform with 126 active rigs and is benefiting from the continued strong demand for Tier 1 super-spec rig. In total, we have 172 super-spec drilling rigs in our fleet, of which 120 are, what we refer to as a Tier 1 super-spec having all the capabilities that are most demanded by our customers.

In addition to contract drilling, the combined company will also be a leader in directional drilling with Patterson-UTI’s MS Directional business. MS Directional is differentiating itself in the directional drilling business through service quality and fleet of high-quality impact mud motors. This combination has made MS a leader in terms of drilling some of the most complex wells, including conventionally drilling horseshoe wells, which involves utilizing a high-performance mine motor to drill 10,000-foot laterals within a single 5,000-foot section.

Building upon the technology offered in our PTEN plus Performance Center, MS has been able to offer remote MWD operations taking a person off the rig and allowing a person to monitor multiple MWD jobs across several rigs from our GOTEC Center here in Houston. As the drilling and completion industries continue to generate more data, data analytics are becoming increasingly important. Patterson-UTI has a leading position with our superior QC division in using data analytics for wellbore placement, utilizing space like navigation algorithms to better understand where the business is located during drilling operations and what adjustments need to be made to keep the well on path. Better understanding the placement of well horse on a pad also helps to better design frac jobs.

And with that, I’ll hand it over to Robert Drummond.

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

Thank you, Andy. And I thank everyone for joining us today on this call. I echo Andy’s enthusiasm about this transaction and the excitement for the value we can unlock together. I want to use my time today to explain why we have such a strong conviction that this transaction is the right step forward for NexTier to build on our momentum in an evolving energy market.

NexTier has an extensive track record of participating in successful value creating M&A that has allowed us and our counterparties to capabilities, accelerate innovation, better serve customers and drive value for shareholders. This desire to grow and strengthen our leadership position is what brought C&J and Keane together back in 2019 and that’s what brings NexTier and Patterson-UTI together today.

As we consider the future of the North American energy market, we believe diversification will be a key competitive differentiator for our company. Combining with Patterson-UTI provides a unique opportunity to expand our capabilities while showing the excitement that we have for the future of the U.S. onshore market. Together, we will have a comprehensive portfolio of leading solutions across the well life cycle with an expanded footprint across most of the active U.S. basins. We believe the combination creates the new premier North American pure-play leader with potential to create significant value for our shareholders.

4

Andy provided an overview of the breadth of the completions portfolio we are creating. Our integrated platform is what will tie these capabilities together and unlock considerable value for our shareholders. At NexTier, we’ve worked diligently to develop a strategy that combines the complementary services around our frac fleet with each of these services having the potential to add value to the process either through cost reduction or efficiency gains. The focus is on helping our customers maximize their returns while also maximizing our own returns. By creating value for our customers, we create value for our shareholders. We call this our wellsite integration strategy, which differs from a bundling strategy of unaligned services.

This integration is enabled by our NexHub Digital Center that allows our Last-Mile Logistics, Power Solutions and Wireline Solutions to work seamlessly together. And by doing so, we drive significant efficiencies, lower total cost and reduce the carbon footprint of projects for our customers. As I said previously, this value-creating strategy has helped both NexTier and our customers grow their returns. A fully integrated frac completion fleet can drive an additional $7 million in annual cash value for us, while also improving our customers’ well economics. With Patterson-UTI, we’ll be able to amplify this model over a scaled fleet, driving cost savings and sustainability for our newly combined business.

We’re also excited about the potential of integrating the NexTier Wireline portfolio which plays an important role in raising frac efficiency. We’ve demonstrated this unique ability to integrate the Wireline operations into the frac workflow in a matter that delivers low nonproductive time for all of our assets.

Our Last Mile Logistics platform is another key element to our strategy. We’ve built a leading portfolio of Last Mile Logistics capabilities that is aligned with our frac efficiency objectives. And by impacting more of the frac supply chain, we can lower total cost and drive sustainability at the wellsite, optimizing the logistics of sand transportation around the completion wellsite where thousands of truckloads are delivered to each pad is a massive opportunity for value creation and key component of the NexTier wellsite integration strategy.

We believe that we’re creating the lowest cost and carbon footprint transportation system in this space and are excited to execute our strategy across a larger platform. One of the most exciting benefits of this merger is the increasing potential of our rapidly growing Power Solutions natural gas fueling division. The increased frac capacity created by this transaction will enable this organic growth to continue as we add capacity to service the combined fleet. Universal’s newly upgraded natural gas frac fleet provides additional runway for this growing division of the company.

The Power Solutions platform allows us to maximize the benefits of the fuel cost arbitrage between diesel and natural gas price. The value potential here can be more than $10 million per fleet per year and the fuel cost arbitrage increases as diesel displacement moves higher. NexTier’s frac fleet performance and this fuel cost saving arena has been excellent, thanks in part to the integration of Power Solutions with our natural gas capable frac fleets, which also raises the marketability of natural gas-powered assets.

For NexTier, our entire operational strategy is enabled by our NexHub Digital Center, which is the backbone of our organization and is critical to value creation through the process of efficiency and waste elimination. Directly, our digital equipment health management program has been responsible for reducing the maintenance CapEx burden by an estimated $1.5 million per year per fleet. Our robust asset tracking program has significantly lengthened the life cycle of major components through predictive analytics and reduced catastrophic failures with mounting evidence supporting the program’s success.

Additionally, the digital center unlocks the full capability of our website integration strategy. Process coordination is paramount to value creation across our suite of services with NexHub allowing us to realize the full potential from our investments. We’ve used our digital strategy to elevate the capital efficiency in our business, resulting in significant process improvement and cost reduction, maximizing our returns while delivering the highest level of service quality to our customers.

As the return on capital focus further entrenches itself in our industry, we strongly believe that asset efficiency will be key to win in the future. Our digital strategy will be front and center through the cycle. As we started this discussion on this merger, the complementary digital strategies were one of the most exciting aspects of the potential new company for me. We came away highly impressed by what Patterson is doing and we moved deeper into the process, we became even more excited about the upside potential as these 2 enterprises combine these complementary strategies to create a new best-in-class digital environment to drive further returns to our shareholders.

With that, I’m glad to turn it over to Andy.

5

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Thanks, Robert. Additionally, the technology that NexTier has developed with their NexHub Digital Center is very complementary to Patterson-UTI’s PTEN plus Performance Center, which allows for the real-time collection, aggregation, analysis and visualization of data from drilling rigs and frac spreads.

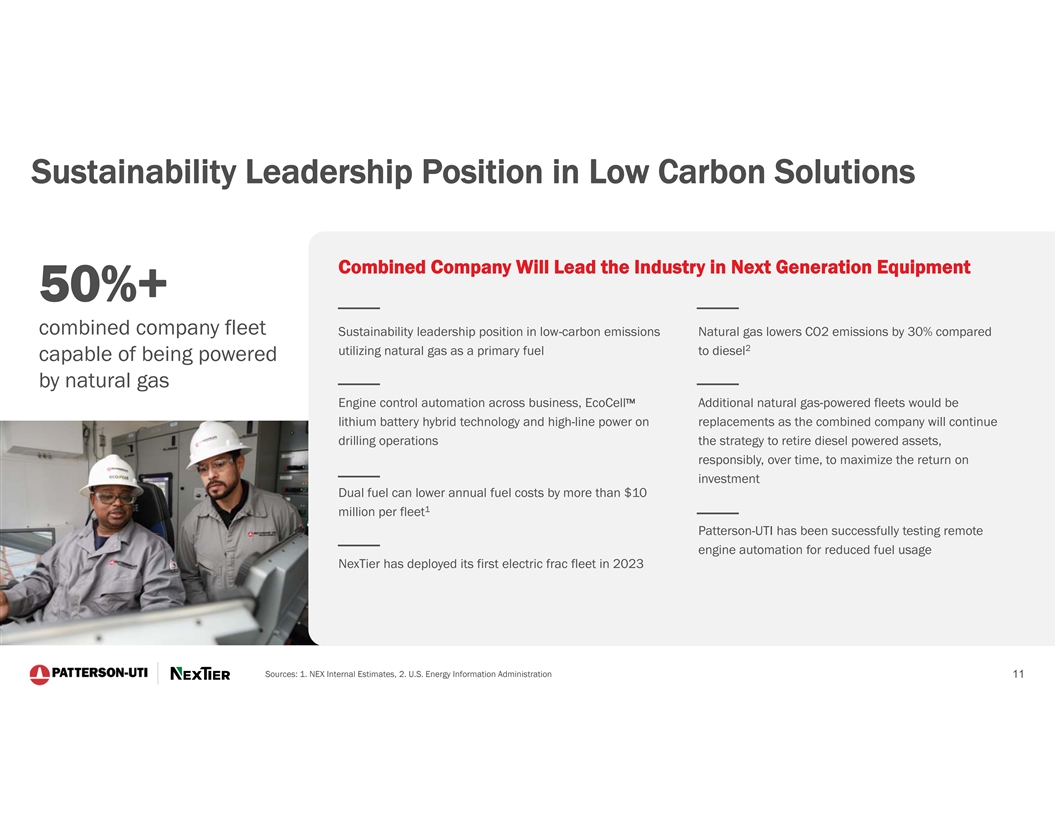

A critical piece of the innovation in both companies centers around sustainable operations. The combined company will have a leading position in low-carbon alternative fuel sources for wellsite drilling and completion operations, including 78 drilling rigs capable of using natural gas, high line power or our EcoCell lithium battery hybrid energy management system.

As our 2 teams held discussions leading to the merger, it was clear that we had a strong cultural alignment. One way that really stands out is around the talent of our teams and shared commitment to investing in and developing employees. Safety, leadership training, performance management, career development, diversity and inclusion and recruitment are all core to how the 2 companies operate, and they will be the key to how operate the go-forward company. As a result, we are confident that the combined company will be an employer of choice in the energy industry. We’re excited to bring our teams together to learn from one another and build on our collective strengths.

Before we begin the Q&A session, I want to highlight the key reasons to own the combined company and why we’re so excited about this merger. First, we’ll have a diversified offering across the drilling and well completion value chain to deliver for our customers. These offerings are backed by leading technology and innovation platforms. Second, we are well positioned to meet growing customer needs for low carbon fuel operations. Third, we have a track record delivering on synergies and a significant opportunity to further enhance the value of the merger. And finally, each of these benefits accelerates our opportunity to return free cash flow to shareholders. We couldn’t be more excited about what the future holds for both of us.

Todd, we can now begin the Q&A session.

QUESTIONS AND ANSWERS

Operator

(Operator Instructions) Our first question comes from Scott Gruber with Citigroup.

Scott Andrew Gruber - Citigroup Inc., Research Division - Director, Head of Americas Energy Sector & Senior Analyst

Congrats on the transaction. Andy, you’ve always been a bit different in operating both a rig fleet and the frac fleet and now you have much improved scale and integration capability on the completion side. Can you just speak a bit more to how you think about the operational advantage, having scale on both sides of the ledger? And obviously, how that compares to peers which tend to specialize in drilling more completion?

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

It’s Scott. Yes, we’re really excited about the potential of this combination in having such leading positions in both contract drilling and well completions and directional, et cetera, all the service lines that we do and the ability to do more process together. We have really strong relationships with a lot of customers in this industry. And these relationships prove beneficial, especially when you start to enhance what you can do across your portfolio.

6

And so really excited about the opportunities from that standpoint. I can’t say enough about what NexTier has done over the years. And I also want to thank our team at Universal and combining these 2 together, makes a solid force on the well completion site and we’re just excited about the potential here. Rob?

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

Yes, I could add, to. I think the digital programs that we both have the ability to utilize the analytics that are being created on both sides, I think we can get to the point where - how wells are drilled impacts how they’re fraced and how they ultimately produce. You will hear some of our big customers talking about that more and more focus, I think, is coming on ultimate well recovery. And I think having a company to have both of those and those digital capabilities bring all it together much more efficiently than could be done independently.

And I don’t think you can underestimate the benefits of the scale around the technology development that can occur. Patterson-UTI got a great engineering outfit, and I think that the benefits of being able to use that across the whole pure-play shale development is something that’s going to be differentiating for us.

Scott Andrew Gruber - Citigroup Inc., Research Division - Director, Head of Americas Energy Sector & Senior Analyst

That’s why I was going to follow up because one of the great differentiators of the companies with scale in the industry is that technology development. So is the kind of incremental focus in terms of R&D and technology development going to be on that digital side and drilling and completion optimization side? Or do you think it’s more on kind of next-gen equipment?

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

I think you’re going to see it across the board. We have this potential to pull together the data analytics systems in a way where they can share data better and not that they would necessarily merge, but the way it is in digital systems today, you can share across multiple platforms in ways you never could before. And it allowed us to enhance our operations, understand better what’s going on and not just what’s happening at surface, but also potentially subsurface and provide stronger value to our customers.

And so there’s lots of opportunity there on the digital side, as Robert said, when it comes to R&D and engineering, it’s early days in the discussions from that standpoint, but we both got strong track records in developing new technology and bringing it to the market. And over time, combining those elements and those skill sets and the brainpower we have and engineering of both companies has exciting potential.

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

Scott, I don’t think it could be underestimated from the investor perspective is having a pure-play investment in shale is not something that’s relatively available in the market today. It’s something that has a scale to be investable by big sizable investments.

Scott Andrew Gruber - Citigroup Inc., Research Division - Director, Head of Americas Energy Sector & Senior Analyst Understood. Appreciate it and looking forward to the outlook. Congrats again.

Operator

Our next question comes from Marc Bianchi with TD Cowen.

7

Marc Gregory Bianchi - TD Cowen, Research Division - MD & Senior Energy Analyst

I’m curious if you could talk a little bit about how you came to the respective valuations for the deal. It seems like mostly using sort of trailing figures. So could you comment on that first? And then second question is if you could offer any kind of a forward outlook that might help us think about the valuations as well?

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

I’ll go first, and then I’ll hand it over to our guys that understand the finances much better than I do. But as we looked at the deal, we certainly had to work up some potential projections between the 2 companies. But in explaining the deal, we thought it best to just anchor on data that’s already public. And that way, people can just judge for themselves based on what their outlook is, based on what your opinion is and what’s happening in the industry. So the numbers that we’re presenting today are anchored on - Q1 2023 annualized just because it’s an easy way to take public figures and look at the 2 companies together. Anybody else want to follow up on...

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

Yes, I’d just say, as a merger of equals, you can let the market be a guide on that a bit. And this is a trade right at the market currently.

C. Andrew Smith - Patterson-UTI Energy, Inc. - Executive VP & CFO

Yes. I mean, that’s exactly right. I mean, we’re for sale every day in the marketplace and you can look at the valuations over time and how they’ve compared. And while on a results basis, we might be pretty similar, the valuation of the market sort of spoke for itself, that’s where the ultimate trade came out.

Marc Gregory Bianchi - TD Cowen, Research Division - MD & Senior Energy Analyst

Yes. Makes sense. And maybe we’ve got you guys on a very public call here. I’d be curious if you could offer any commentary on the forward outlook.

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Yes. I’m just going to say one thing on the floor. This is just a softening in the market that we’re going through. OPEC out there is trying to keep the floor on oil prices. And if you look at natural gas, I just checked yesterday, it looked like the forward strip in December is at $3.40, some- odd. That’s very positive for our customers who are drilling for natural gas. So I’m really upbeat as we move toward the end of the year just based on that. And I just see this as a temporary softening where we are today in the year.

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

I echo that and also add that - I mean, I’m very bullish on U.S. shale. I mean, I have been for a while. I think that we have - technology is going to continue to make more and more wells economical and efficiencies that are coming to make more and more Tier 2, Tier 1 and so forth as we go forward. So that’s an oil price question and very difficult to answer all of them.

Operator

Our next question comes from Keith MacKey with RBC Capital Markets.

8

Keith MacKey - RBC Capital Markets, Research Division - Analyst

Maybe just wanted to start out with maybe a philosophical kind of question on valuation. I got the question already, who were the peers for this company? Admittedly, my mind went to the company that Patterson would have already been comped to. So what do you guys generally think is really the driver of valuation from here? Is it the increased scale? Is it fewer competitors in the pumping marketplace? Can you just help us investors think about that as clearly as we can?

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Keith, thanks for the question. I think the way you have to look at this is a company that’s focused primarily on U.S. conventionals and producing strong free cash flows. And who are the real peers that are producing similar free cash flow yields that this combination can produce. It’s not necessarily about what we do operationally, but what are we doing financially. This is a great combination of 2 companies that have a great track record of returning cash to shareholders and with a strong outlook on free cash flow. So we’re doing a number of different things across the value chain for the customers and unconventionals. And we’re staying focused on shareholders at the same time.

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

I would echo that. I mean, plus there’s $200 million in synergies supporting that deal and the scale of being able to invest in a $5 billion - $5.5 billion enterprise value company is something many of our investors have expressed an interest in.

Keith MacKey - RBC Capital Markets, Research Division - Analyst

I appreciate the color. And maybe in that free cash flow context, Andy, why is NexTier, do you think the right partner to do this transaction versus, say, a different pressure pumping focused company or trying to get larger in the drilling side?

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Well, we’ve done a number of Patterson-UTI, we’ve done a number of transactions mergers and acquisitions over the decade plus to grow into the drilling space. We’re a formidable force with a strong 45-year franchise in drilling. And our team in that area just does a fantastic job, hats off to what we’ve done in pressure pumping over the decades. We were the first at Universal to fracture the Marcellus horizontal and help bring that in, in the Northeast. We’ve got a great history there.

But as we watch NexTier and the companies that they put together and then the cultures that they combine, we think that it’s just very similar to how we’ve run our business and the philosophy we’ve had over the years. And we look at their performance and their free cash flow and how they’re returning cash to shareholders and how we’ve been doing it for over a decade, we just think it’s a great match.

Operator

Our next question comes from John Daniel with Daniel Energy Partners.

John Daniel

Echo my congratulations. I guess the impressive thing for me was just the magnitude of the synergies. And I mean, obviously, some of that is clearly going to be G&A. But could you bucket for us what some of the - what percent is not G&A and just some of the key things where you’re going to be laser-focused right out of the gates? John, this is Kenny.

9

Kenneth H. Pucheu - NexTier Oilfield Solutions Inc. - Executive VP & CFO

So look, before I jump into the synergy question, I just want to mention something I believe is important on the integration of the 2 companies. Both companies are executing at a very high level today on both the drilling and completion side of the business. So our focus will be to maintain that execution with 0 disruption as we go through our integration planning. But on your question, a little less than 2/3 of the synergies will come from the combination of the completions business. These 2 pillars are focused on operations integration.

And secondly, as Andy mentioned, supply chain management. I do want to highlight on the operations integration side, we will be focused on capturing the best from both companies and we will have further runway to further our current wellside integration strategy as (inaudible). And then finally, the remaining synergies will come from SG&A, it’s about 1/3 of that. So we have high conviction that these synergies are achievable and we’ll get started with our integration plan very soon.

John Daniel

Okay. And then just one for Robert, because you called out that the benefits that you’ve experienced with the fully integrated wireline frac package. As you look at the - integrating that with the Patterson fleet, do you have available capacity now to meet that? Do you buy new wireline units? Or how do you - how would that evolve?

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

I appreciate that question, John. When I think about the benefits, Universal has done a great job of investing in the fleet over the last few years, something we’ve been really watching as they’ve converted, I think, up to 3/4 of the fleet by this year to natural gas capabilities. The Power Solutions integration aspect is something that we believe has made a big difference for us and we think it can make a big difference as we add additional capacity. But the thing about Power Solutions is we’ve been able to sell it as fast as we’ve been building it, and we have been making multiple gains there. So that will require some additional investment to capture and that is already in the works.

From a wireline perspective, we have a big franchise in wireline that we picked up from (inaudible) Solutions through the C&J merger and a lot of capacity that we have there would be very low cost increase of capacity to take advantage of that. And I don’t want to underestimate the focus that we have on Last Mile Logistics. When you have as many trucks as you know that are moving around the location, being able to optimize that more and more is a big deal. And that focus of the strategy, I think, very easily bolts together with Universal’s excellent moves. So I think that, that - I’m glad you picked up on it is an opportunity for us to have upside to these numbers that Kenny referred to.

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Yes, I’d like to follow up on that. We believe that there are benefits to bringing in wireline and integrating into what we do in completion to the point where not many people know this, but our Universal team brought in expertise and actually acquired some assets in early ‘20 to start our own wireline operations. Now other things happened in 2020 to cause us to have to make some changes to those plans. But that’s how strongly we believe that wireline can successfully add value to these completions businesses.

The other part is NexTier’s power business. I think that’s just hugely underappreciated. And when you look at the expertise we have across all ourbusiness lines with Patterson-UTI and our understanding of how to use natural gas and 100% natural gas engines or dual fuel on rigs or dual fuel on frac spreads and you look at what NexTier’s has done in developing technology organically on their own and deploying that, that can combine both CNG and pipeline depths at the wellsite and be able to use that and capture some of that arbitrage, that’s just huge across the value chain and that plays into how Andy Smith and Kenny are looking at synergies and what the potential upside is as well.

Operator

Our next question comes from Kurt Hallead with Benchmark Company.

10

Kurt Kevin Hallead - The Benchmark Company, LLC, Research Division - Research Analyst

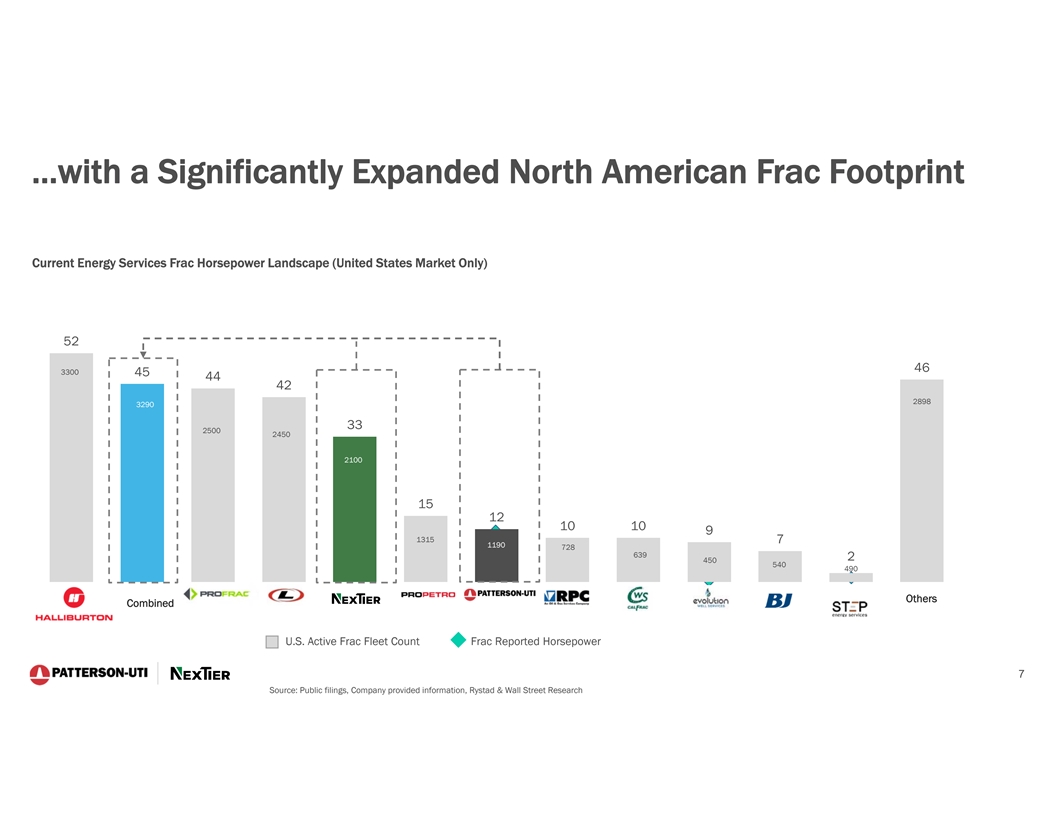

Congratulations. Well done, guys. So I guess, focus on my question here, like when we look at the combined operation, clearly, the biggest impact is on the U.S. frac-related business given that NexTier doesn’t have any land drilling operations, a little bit steady and be obvious on that. But from my dynamic, I’m kind of curious as that - with the combination, with the scale you’re going to get, how does this accelerate the scrapping of Tier 2 frac fleets?

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

Look, I think that when you look at the balance of supply and demand and frac capacity in the market and you look at the outlook that the E&Ps put out for future growth in the sector, we are in a space that’s been unique for a long time. The investment that goes into CapEx outside of maintenance and pure frac will be transitioning to equipment that uses natural gas in one shape or form all the way up and to - including electric.

So I think that, that process will continue and at the same time, because of the macro balance that the Tier 2 diesel equipment that uses the higher-cost fuel source will be retired. Some of the material that we put out before show that when you get to about the third rebuild cycle of a Tier 2 frac fleet, the return on investment becomes better to go to a new source and that’s where the market is kind of at. So that transition will continue.

I think the strength that the combined company’s balance sheet has here, the great options it will have for capital deployment between the speed of that transition and frac balance with all the speed of transition that Patterson has been doing with these great high-spec Tier 1 rigs is a good challenge to have, both of which will drive high return on capital.

Kurt Kevin Hallead - The Benchmark Company, LLC, Research Division - Research Analyst

So in the context, I know you guys have said independently that both of you have indicated that the frac fleet in total for the U.S. market will probably remain flat as you do get some scrapping of assets. So I guess, just by the answer to your question, you guys will kind of ease into this and then determine how you’re going to handle your Tier 2 assets from here. Is that fair?

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Well, right now, Patterson-UTI, we have almost all of our horsepower deployed. And through our maintenance CapEx program, we’ve been swapping out older Tier 2 engines for near Tier 4 engines, and that continues today. So the engine is just one component on the trailer, but as the engine days out, there’s a benefit to switch out to Tier 4 and go to Tier 4 dual fuel, where we get paid even more for that. And so even on the Patterson-UTI side, we’re going to continue that process.

Kurt Kevin Hallead - The Benchmark Company, LLC, Research Division - Research Analyst

Okay. That’s great. And then maybe my follow-up here would be kind of staying on the frac side of the business. Does this combination enabled the companies to accelerate the deployment of electric frac fleets or is the deployment of the electric frac fleets really just a function of the adaptation by the oil and gas companies in the market?

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

Look, the way that we’ve been doing it, and I think the way Andy does it is very similar when it comes to CapEx and return on focused investments. I think the transition to electric will be at a pace that is balanced with return on capital. And I think that we will have the capabilities to go faster if we wanted to. But we might not want to, depending on if the return on capital investment (inaudible) CapEx of a better path.

11

Look, many customers want to go electric, but most all customers want to go towards the best solution that moves toward natural gas as a fuel source. And this is an equation that’s still evolving. So I would just look well enough by saying the new co is a lot stronger than us independently gives us the ability to move at a pace that is suitable for a return on investment for our investors as well as addressing the needs of our customers.

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

While we both continue to operate independently until we get to close, there has been not a shared philosophy, but we have similar philosophies because - and that’s what makes the merger some interesting, but as Robert said, it’s all about capital discipline at the end of the day and we’re going to do what’s right in balancing customer needs and shareholder needs at the same time.

Operator

Our next question comes from Stephen Gengaro with Stifel.

Stephen David Gengaro - Stifel, Nicolaus & Company, Incorporated, Research Division - MD & Senior Analyst

Two from me. One, when you think about capital allocation, and maybe this is for - more from a Patterson perspective, but historically, how do you think about allocating capital between the frac side and the drilling side?

C. Andrew Smith - Patterson-UTI Energy, Inc. - Executive VP & CFO

Stephen, this is Andy Smith. Historically, again, as we looked at our business. Certainly, throughout the cycle, we always view drilling as being a little bit more stable, just kind of given the commercial nature of it. And so we tended to allocate more towards drilling. Now with this transaction, obviously, pressure pumping will be a much larger piece of our business. And so the allocation will balance somewhat. Again, I think that the combination of these 2 businesses provides for a through cycle more sustainable or durable maybe cash flow. And so I think that as we continue on with these 2 businesses, we’ll have plenty of capital to allocate to both to make sure that we keep and protect both franchises.

Stephen David Gengaro - Stifel, Nicolaus & Company, Incorporated, Research Division - MD & Senior Analyst

And I’m not sure if you can comment on this or not. Was there any thought in this process of simply selling frac assets, and that’s having 2 separate entities?

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Look, we’re really excited about the combination of the 2, the breadth of the offering that we can offer to the market and the potential for cash flow, we just think that this becomes a new leader in unconventionals in the market and an exciting opportunity for investors. We think that this combination just has a lot of potential in all those respect. So that’s the path we’re going down. We just have a firm belief in that, that this is going to be a great vehicle for investors when you’re looking at energy in the U.S. today.

Unidentified Company Representative

And Stephen, I would - going back to the original comment to Bob. The whole idea about taking technology to the next level and the next step in the shale evolution as far as making more and more wells economical, I don’t think another combination of 2 frac companies address that the way this combination can do it. That’s not to be - it’s not a light comment about being able to drill wells that are focused on higher production and how they’re fraced. I think that’s something that the operators are constantly kind of looking at, and we’ll be very well positioned combined to be able to do more in that arena, 2 frac companies...

12

Stephen David Gengaro - Stifel, Nicolaus & Company, Incorporated, Research Division - MD & Senior Analyst

I appreciate the color. Just one quick one. I know NEX’s approach has been balanced between dividends and buying back stock. Do you think the combined entity continues down that path where you’re returning free cash, which seems to be significant free cash to shareholders through both avenues?

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

Going forward, once we get to closing, we’ll work with the new combined Board to determine what’s the right answer for return to shareholders, but we will continue the same philosophy of returning at least 50% of our free cash flow to shareholders.

Stephen David Gengaro - Stifel, Nicolaus & Company, Incorporated, Research Division - MD & Senior Analyst Great. And again, congrats.

Operator

Our next question comes from Derek Podhaizer with Barclays.

Derek John Podhaizer - Barclays Bank PLC, Research Division - Equity Research Analyst

Andy and Robert, congrats on the deal again. I guess just going back to Kurt’s question around the Tier 2 diesel fleets and transitioning over to more of the next gens. I know you’re fully deployed, Andy, like you said, but investors will sell point to the stated horsepower you have and can make an assumption depending on the fleet size as we get 5, 6 or 7 fleets on the side like technically, even though you’re fully deployed.

But just how should we think about that? Should we expect some impairment to start coming through from the combined company to rationalize that horsepower? Or would this help beef up your maintenance swing program because I know fleets have been pretty thin in NexTier showing they’ve been able to (inaudible) fleets along different fleets. I just want some more help around the Tier 2 stuff at (inaudible) and just thinking about the rationalization of legacy Patterson fleets?

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

First off, I think there’s an underappreciation in the market for the size of frac spread on location today. In almost all of our cases, certainly for Patterson -UTI, the intensity of what we do, higher pressures, much increased flow rates, we just have a lot more pumps at the wellsite than we did in the past, say, 3 or 4 years ago. And so just about everything we have is deployed. So we certainly don’t have a frac spread on the sideline.

So between what is at the wellsite and what’s cycling through the maintenance systems, just about everything we have today is fully deployed. So we’re going to continue on our program to Patterson-UTI of swapping out the older Tier 2s for the new Tier 4 engines and dual fuel. But in terms of overall asset write-downs, I wouldn’t say anything imminent, and we won’t be able to investigate further and we get to close. But on our side, we’re just not fully utilized.

C. Andrew Smith - Patterson-UTI Energy, Inc. - Executive VP & CFO

Yes, Derek, this is Andy Smith. I would say that as we look at our equipment and especially the book values of our equipment, I would expect that you’ll see those values, I mean, again, over time. They’ll come down, but I think you’ll see all of that equipment reach the end of its useful life. I don’t think you’ll see any significant impairments down the road.

13

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

Look, I would just add that I don’t think it matters if we were to operate independently or together when it comes to that question. Fleet configuration that Andy pointed out is something that almost every fleet that’s out there, I believe, is probably running a little bit shorter than the kind of horsepower they’d like to have with that fleet. The fleets are running more harder than they have ever been run and that has attrition built into it. It’s just that you start to quit supporting maintenance CapEx and transition into a new bill, if that continues to occur.

At NEX, we have already committed taking 150,000 horsepower out and we’re on that path to do so. But that’s not just taking an operating fleet and shutting it down. It’s just a transition to Tier 4 dual fuel or electric that allows you to capture that return on investment I was referring to that’s better than continuing to support maintenance CapEx. I just - I would just say - that would be the way I would say.

Derek John Podhaizer - Barclays Bank PLC, Research Division - Equity Research Analyst

That’s very helpful. I appreciate the color. And just my next question. Just wondering if you can maybe expand on some of the cross-selling synergies you can see here with your customer base. Just how much you have an overlapping customer base, what could be new customer base as for the combined companies? Just thinking about existing competitors that are on both sides of the deal that you may be expanding that wallet or separately one customer that has maybe a Patterson drilling rig, but not NexTier completion and what it can mean. Just any comments on the value creation now on your bigger customer base and what that overlap looks like?

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Today, we’re still 2 separate companies, and we have to continue to operate that way. We’ll dig more into that when we get to closing. But we really can’t discuss customers and overlap at this point in this process. But I appreciate the question, but we do see a lot of - on each side separately, we see a lot of upside here on how we can combine some things, but we’re not at a point where we can really go into those discussions yet.

Operator

Our next question comes from Saurabh Pant with Bank of America.

Saurabh Pant - BofA Securities, Research Division - VP

I think I will go back to Scott’s question upfront, he asked about drilling and completion, right? So I just want to go back to that and think about the value in offering, right? Clearly, you’ve done this, Andy, for a long time. There was another competitor of yours on the drilling side that took that same approach and it tended to work out for them and the assets actually ended up in NexTier, right? So you’re getting some of it to you, right? I’m just trying to think how do you make it work? And what are the risks that the opportunities that you see might not be realized 3 or 5 years from now?

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Well, these are - I’ll start by saying these are well-established companies with great franchises and through their histories, lots of success. And so we’re bringing together 2 strong companies with strong balance sheet, strong cash flow and just really excited about the potential for the investment this year.

So there’s nonoperational concern to worry about. Our companies are both hitting it out of the park on all levels from an operations standpoint. I can’t say enough about the teams on each side, and I don’t get to see much about the NexTier team at this point, like certainly talk from the Patterson-UTI side and Universal Pressure Pumping side, how well the operations are running. So there’s no question in my mind that, that’s going to continue the way it is and I’m just - I’m excited about the potential for the combined entities, but more so just from the financial health and strength that this combination provides.

14

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

And I would add on the culture side, they had a lot to do with everything. And when we look at these 2 companies, this is the 2 companies coming together partners of choice. I mean, strong leadership is very attractive to NexTier to go and get involved, but we’re creating a great place to work. You’ve got a bunch of people who have more career opportunities they are never going to have before. And we’re building a company that’s big enough to create a lot of opportunities. So I think it’s a completely different equation than the one you referred to.

Saurabh Pant - BofA Securities, Research Division - VP

Okay. Okay. Really appreciate that. And a quick follow up. I know a couple of people asked on capital allocation, how do you think about that (inaudible) completion, right? But again just thinking about the completion side of things, Robert, I know on your side, you talked about CapEx being 8% to 9% of revenue going forward, right? That obviously, there has been a certain cadence of high grading, right? But now that you think about the combined company, how should we think about that upgrading, high-grading cadence and maybe CapEx requirements as a result of that?

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

I like that question because I think it goes that to what Andy said around both companies being committed to returning 50% of our free cash flow back to our shareholders. In that math, for the frac franchise, it has been that we can operate within 89% of revenue and continue to do that while also transitioning the fleet from diesel all the way to natural gas being the power source. So it fits very well. We described that numerous times in the NexTier portfolio. This is exactly the same math when you put the 2 together. So that’s what I like - that’s why we like this combination so much. It gives us even more sustainability to do that from a financial perspective.

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Yes, I would say that both companies have kind of been on a similar path on that front. And so if you look at the combined guidance that’s been put out around CapEx, I think you’ve got a pretty good idea of what it looks like going forward.

Operator

Our next question comes from Dan Kutz from Morgan Stanley.

Daniel Robert Kutz - Morgan Stanley, Research Division - Research Associate

Congratulations on the deal. I guess I just wanted to ask a question about capital structure. So it’s good to see that the way that the deal is structured kind of allows the combined line entity to maintain low leverage. I’m just wondering if there would be any appetite or if you guys would be looking at Patterson as a pretty long- duration maturity schedule, NexTier still has a couple of years before it has a major maturity. I’m just wondering if there would be consideration around any debt restructuring once the company is combined.

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

So yes, so I appreciate the question. I think - again, as we look at the cash flow characteristics of both companies, I don’t know there will necessarily be a requirement for a debt restructuring. Certainly, there’s no need with the Patterson debt that’s outstanding today. Again, we have a lot of liquidity available to us on our balance sheet. But as we go through the process between finding and closing, we’ll take a look at all of that and decide kind of what the best and most efficient way is to move forward. Potentially, there will be, I can’t say today, but I know exactly what that looks like.

15

Daniel Robert Kutz - Morgan Stanley, Research Division - Research Associate

Got it. That’s helpful. And then maybe just - so going back to Derek’s question about the size of the fleet. I think both NexTier and Patterson have done a good job of communicating that fleet sizes are getting bigger. I had also kind of ran into that, that maybe both companies were a little bit more involved in simul frac operations than maybe the broader industry. I wanted to see if that’s the case and see if you kind of view the knowledge sharing in that area of the market as a potential tailwind to the operations of the combined business.

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

Look, I like that question. I appreciate that you’ve been listening to us about the fleet configuration changes, definitely migrating larger. Simul-frac is a part of that. But in fact, the commercial model has been evolving more towards the economics being around the pump, the individual pump instead of the fleet. And because of that, when you configure into a larger fleet, you can make more profitability and more revenue per fleet. And that’s the way it should be. You deliver more, you get more.

So fleet configuration, how many fleets you have with the same amount of horsepower is going to always be in flux, I think. And simul-frac works in some cases where the well pads are establishing in the right way. But the commercial model in frac is evolved to make that work very well for us. We’ve had some of that transition that’s incurred lately that works better to be simul-frac and it used to be in the very beginning, and maybe that was the case. So probably getting smarter over time.

Daniel Robert Kutz - Morgan Stanley, Research Division - Research Associate Got it. That’s really helpful. And congrats again.

Operator

Our next question comes from Doug Becker with Capital One.

Douglas Lee Becker - Capital One Securities, Inc., Research Division - Research Analyst

That’s been touched on a couple of times, but one of the compelling aspects of this deal really seems to be that large size of synergies relative to the size of the combined company. How would you characterize how much of those are in the hands - the operational synergies are in the hands of the combined company versus relying on external factors like customer acceptance? Really just trying to get a sense that operational synergies are likely to materialize when something else that’s been - hasn’t worked, at least it’s tough to see from the outside looking in?

Robert Wayne Drummond - NexTier Oilfield Solutions Inc. - President, CEO, & Director

Look, I would say that we’re very confident about the number because both companies have a track record of doing integration and the track record includes capturing the guided synergies, that’s number one. Number two, I’d say, I couldn’t have any more confidence that, that process works under the leadership of Andy and Kenny and - both Andy’s and Kenny. So I think that doesn’t require - I mean, I think there’s upside to the synergies what I’m trying to say. I just think the 200 is a number that we’ve been carefully thinking through and does include components around supply chain, it doesn’t require a customer decision and some of them do. But we’ve been conservative about that.

16

Douglas Lee Becker - Capital One Securities, Inc., Research Division - Research Analyst

That makes sense. And then any skew to the timing? I know you’ve laid out an 18-month window, do we see more of the cost savings early in the process and maybe some of the completions integration benefits later in the period?

C. Andrew Smith - Patterson-UTI Energy, Inc. - Executive VP & CFO

Yes. I think you probably will see a majority of it kind of come through in the first 9 months of 2024. You’ll see a little bit maybe towards the end of this - depending on when we close, you’ll see a little towards the end of this year than the - probably in the first 9 months of 2024 and then rounding it out towards the end of ‘24 beginning at - even if it goes that long, beginning at ‘25.

Douglas Lee Becker - Capital One Securities, Inc., Research Division - Research Analyst Congratulations.

Operator

Our next question comes from Don Crist with Johnson Rice.

Donald Peter Crist - Johnson Rice & Company, L.L.C., Research Division - Research Analyst

Andy, I wanted to ask a more macro question since most of the details have already been asked. Over the years, there’s been a lot of discussion about the pricing model. And now that you’re creating a true company at scale that has the capabilities to both drill and frac a well, do you think it reopens those discussions with customers where you can more move away from the day rate pricing model towards more of a performance-based model and/or kind of turnkey pricing model for wells? Just any thoughts there because this is the first company that’s really had the capabilities to do all aspects of drilling and completing a well.

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

I’m going to start by saying that there may be some potential to do that in the future. But what we’re going to be focused is on value creation, returning cash to shareholders and that starts with how we work with our customers. What we don’t want to do is have to take more risk where we don’t need to take more risk operationally. We want to work to bring value to the customers, but at the same time, we want to manage the risk profile.

Drilling and completing horizontal wells is a complicated process. I realize thousands of them get done every week, but it is a complicated process. And today, a lot of the risk is still beared out by our customers. And so we have to be careful in how much of that risk we want to transfer over to our side and how we get compensated for that as we do. I would say that if you look at the track record, especially over the last few years, both companies have done a job in capturing value even with the business models that we work today. And we’ve been able to layer in strong returns to shareholders at the same time that we’re doing that.

There may be some potential down the road where we look at churning teams to drilling operations down to a certain point at the well, maybe the kickoff point, maybe the landing before we get into the horizontal. We’re not going to do things where we accept subsurface risk. There may be some opportunity down the road to combine some of the things we do, both on drilling and frac. But it’s not something we’re going to delve into right away. Like I said, our team is doing a great job today, doing what they’re doing, working with our customers, solving technical and operational challenges, creating value at the wellside and then that all flows through to the shareholders at the end of the day. So it has been mentioned on this call earlier, we’re not going to do anything that interrupts what these great operational teams are doing today.

17

Operator

This concludes question-and-answer session. I’ll turn it back to Mr. Hendricks for closing remarks.

William Andrew Hendricks - Patterson-UTI Energy, Inc. - President, CEO & Director

Thanks, Todd. Listen, as we close, let me just say that I want to thank everybody for participating on this call. This is a historic day for both companies, and we’re excited to create a new industry leader. So that concludes today’s call. Thank you.

Operator

Ladies and gentlemen, this does conclude today’s conference call. We thank you for your participation. You may disconnect at any time.

DISCLAIMER

Refinitiv reserves the right to make changes to documents, content, or other information on this web site without obligation to notify any person of such changes.

In the conference calls upon which Event Transcripts are based, companies may make projections or other forward-looking statements regarding a variety of items. Such forward-looking statements are based upon current expectations and involve risks and uncertainties. Actual results may differ materially from those stated in any forward-looking statement based on a number of important factors and risks, which are more specifically identified in the companies’ most recent SEC filings. Although the companies may indicate and believe that the assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove inaccurate or incorrect and, therefore, there can be no assurance that the results contemplated in the forward-looking statements will be realized.

THE INFORMATION CONTAINED IN EVENT TRANSCRIPTS IS A TEXTUAL REPRESENTATION OF THE APPLICABLE COMPANY’S CONFERENCE CALL AND WHILE EFFORTS ARE MADE TO PROVIDE AN ACCURATE TRANSCRIPTION, THERE MAY BE MATERIAL ERRORS, OMISSIONS, OR INACCURACIES IN THE REPORTING OF THE SUBSTANCE OF THE CONFERENCE CALLS. IN NO WAY DOES REFINITIV OR THE APPLICABLE COMPANY ASSUME ANY RESPONSIBILITY FOR ANY INVESTMENT OR OTHER DECISIONS MADE BASED UPON THE INFORMATION PROVIDED ON THIS WEB SITE OR IN ANY EVENT TRANSCRIPT. USERS ARE ADVISED TO REVIEW THE APPLICABLE COMPANY’S CONFERENCE CALL ITSELF AND THE APPLICABLE COMPANY’S SEC FILINGS BEFORE MAKING ANY INVESTMENT OR OTHER DECISIONS.

©2023, Refinitiv. All Rights Reserved.

18

Exhibit 99.2

Today we announced that Patterson-UTI will merge with NexTier Oilfield Solutions. This creates an industry leading drilling and completions services provider that will have leadership positions in contract drilling, pressure pumping and directional drilling. We’re excited to deliver superior value to customers, employees, communities and shareholders.

We invite you to join our investor conference call this morning at 7:30 a.m. CT: https://ow.ly/Pl0A50OP4hk

Learn more about today’s announcement here: https://ow.ly/kFns50OP4hf