Board of Directors of ZIM Integrated Shipping Services Files

Investor Presentation and Issues Letter to Shareholders

HAIFA, Israel, Dec. 9, 2025 – The independent Board of

Directors of ZIM Integrated Shipping Services Ltd. (NYSE: ZIM) (“ZIM” or the “Company”) today released a presentation and issued a letter to shareholders highlighting the Company’s strong performance, robust capital returns

and commitment to shareholder value and providing an update on ZIM’s ongoing strategic review process and the proxy fight led by Mor Gemel & Pension Ltd., Reading Capital Ltd., and Sparta 24 Ltd. The presentation and letter to shareholders

can be accessed on ZIM’s website here.

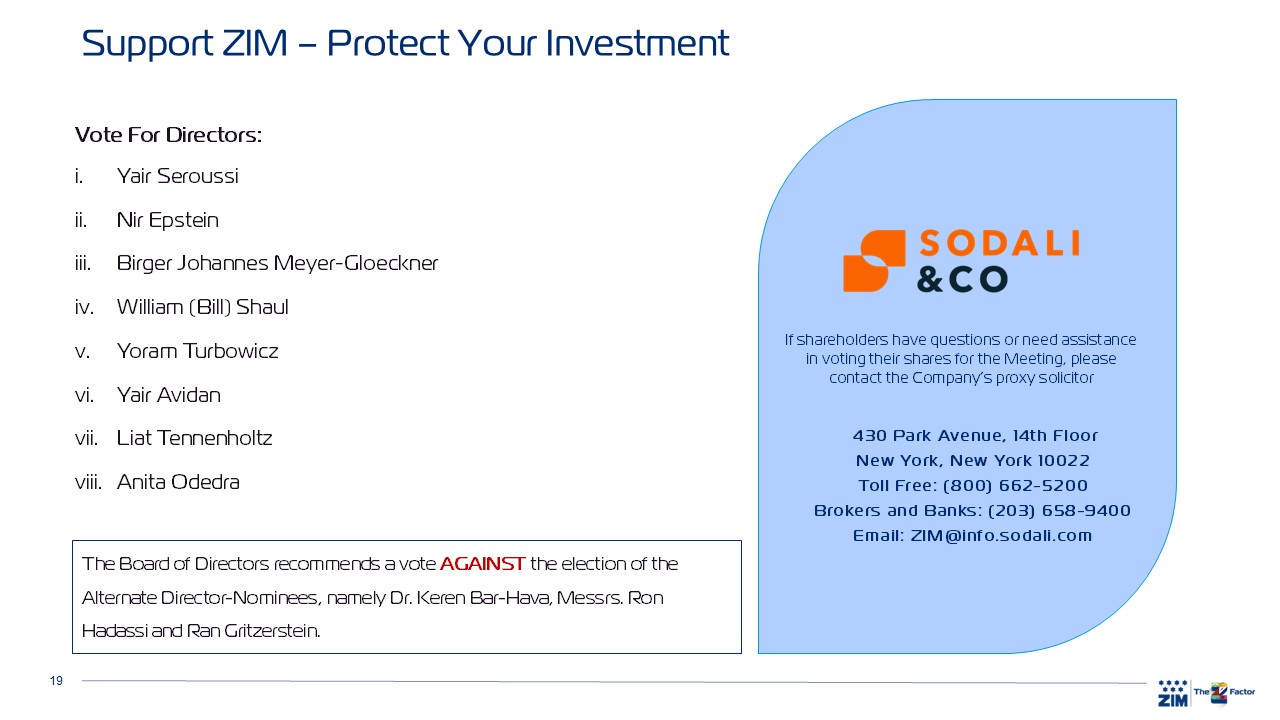

The Board urges shareholders to vote ONLY “FOR” all eight of ZIM’s director nominees and “AGAINST” the three director nominees proposed by the dissident shareholders in connection with the Company’s

Annual and Extraordinary General Meeting of Shareholders of ZIM on December 26, 2025.

The full text of the letter follows:

Letter to Shareholders

Dear Fellow Shareholders,

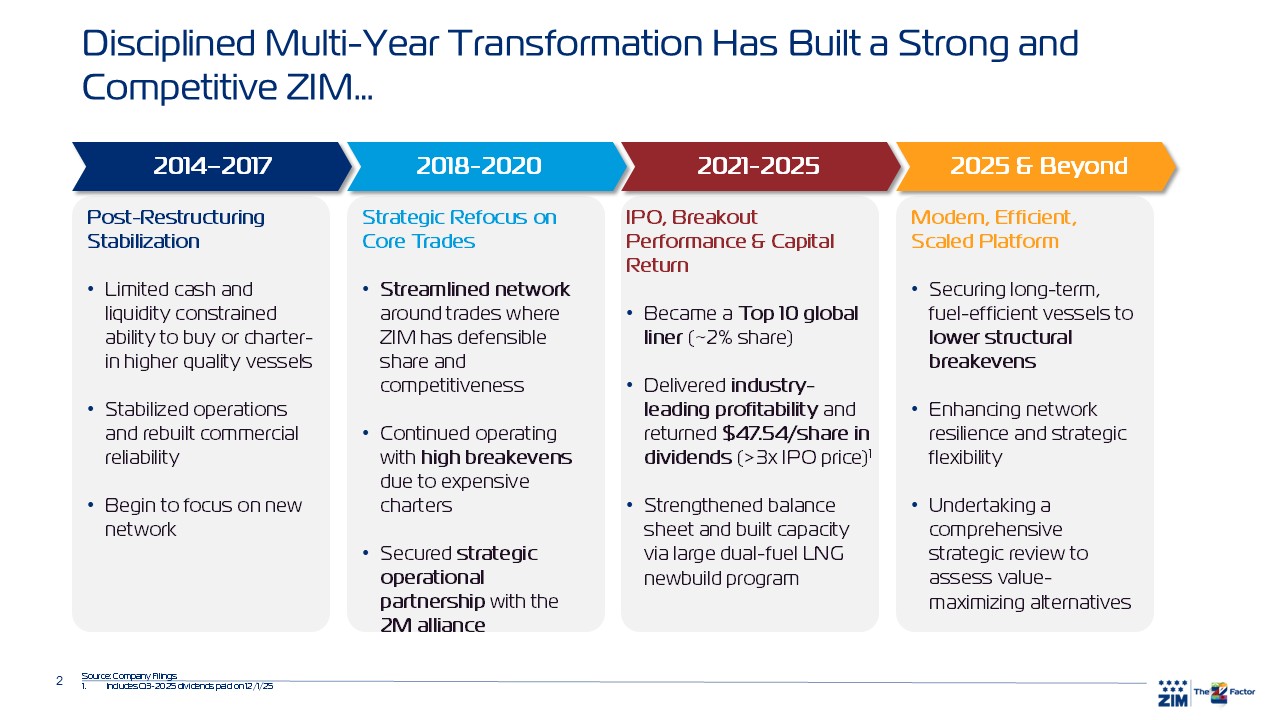

We want to begin by thanking you for your ongoing engagement with ZIM during this important period for the Company. Over the past several years, our Company has undergone a remarkable operational and financial

transformation. We have strengthened our operating platform, modernized our fleet, honed our commercial network, returned significant capital to shareholders, and built a governance framework centered on independence, expertise, and disciplined

oversight. These efforts have positioned ZIM as a strong Company that is highly competitive in an industry experiencing significant change.

As we approach our upcoming Annual General Meeting, it is important that we share with you – clearly and candidly – why ZIM is well-positioned for the future, why the Board is conducting a comprehensive strategic

review, and why your Board unanimously believes that supporting all eight of ZIM’s nominees is essential to protecting and maximizing the value of your investment.

ZIM Today: A Strong, Transformed, Highly Competitive Company

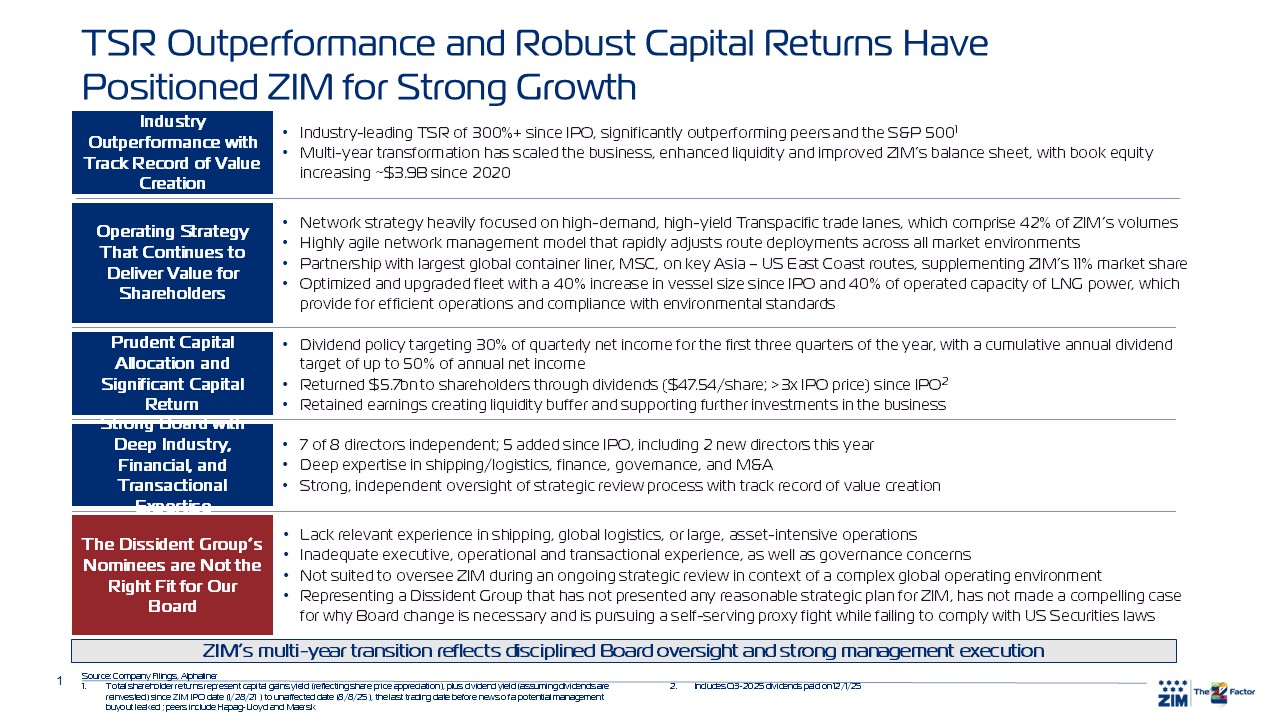

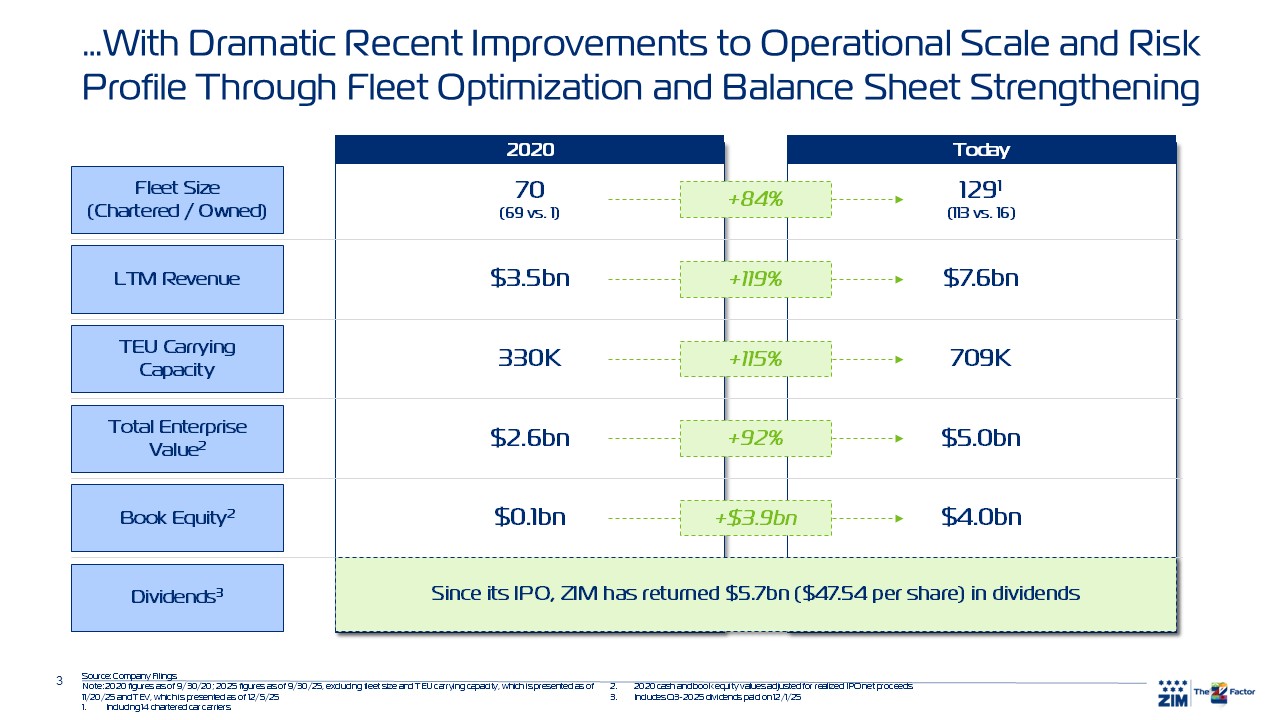

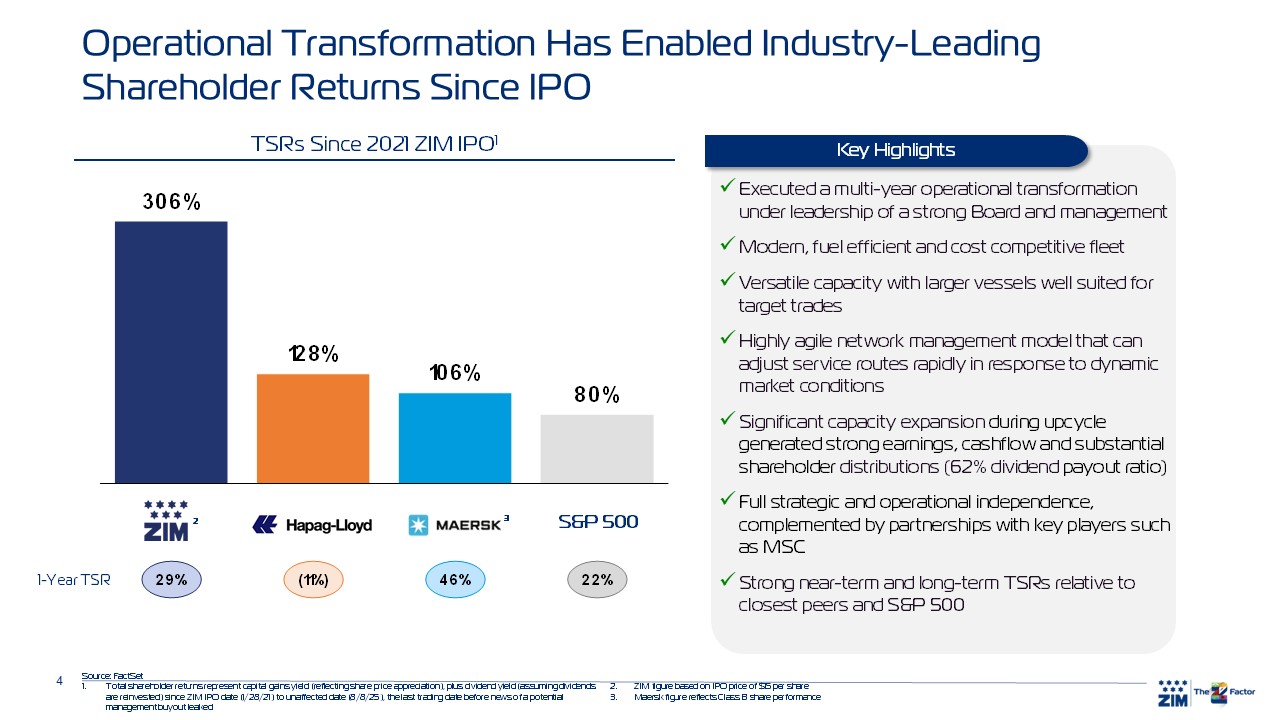

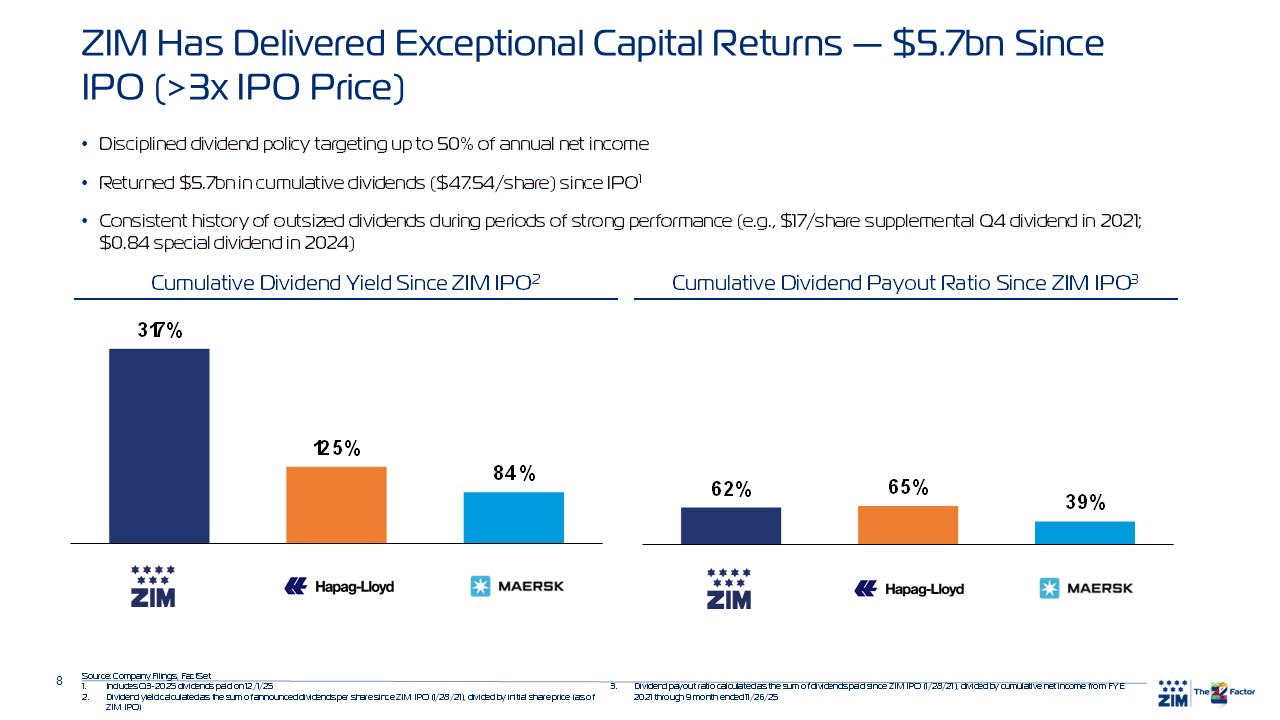

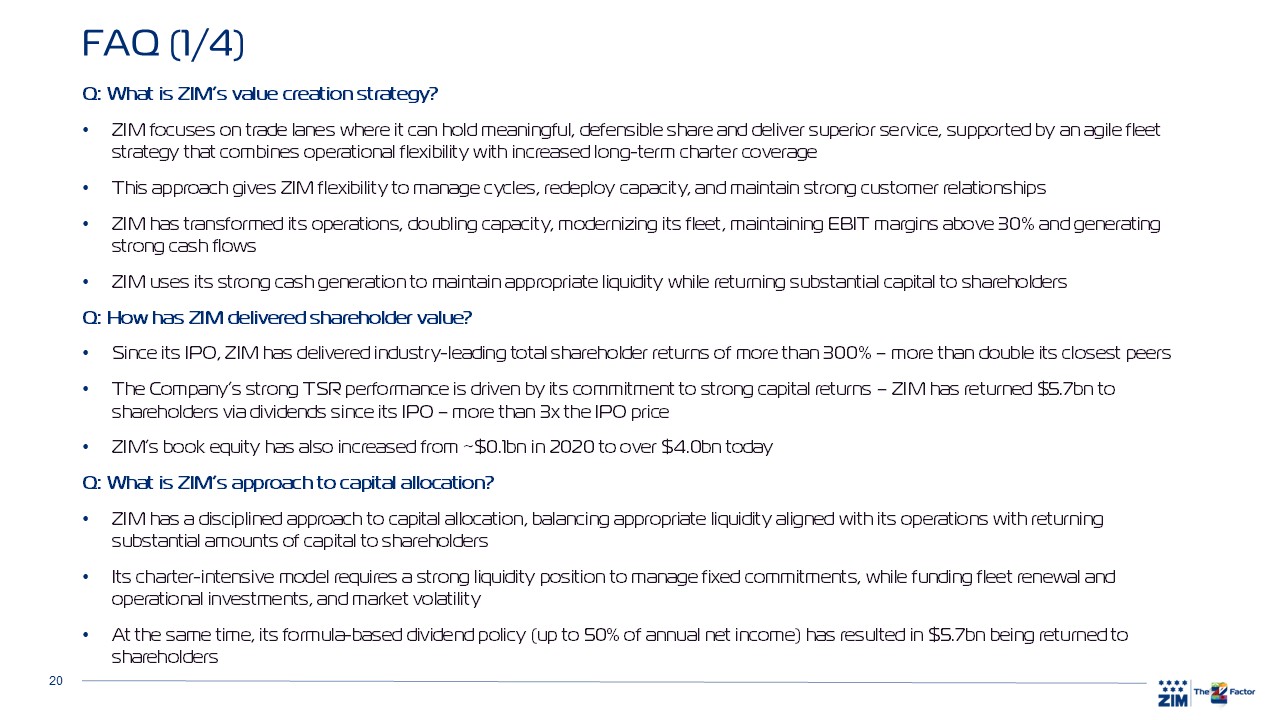

Since our IPO in 2021, ZIM has delivered peer-leading total shareholder returns of more than 300%, significantly outperforming larger global carriers and the S&P 5001. This outperformance is the result

of a multi-year transformation executed with discipline and guided by a Board committed to operational excellence and value creation.

Specifically, since 20202:

|

• |

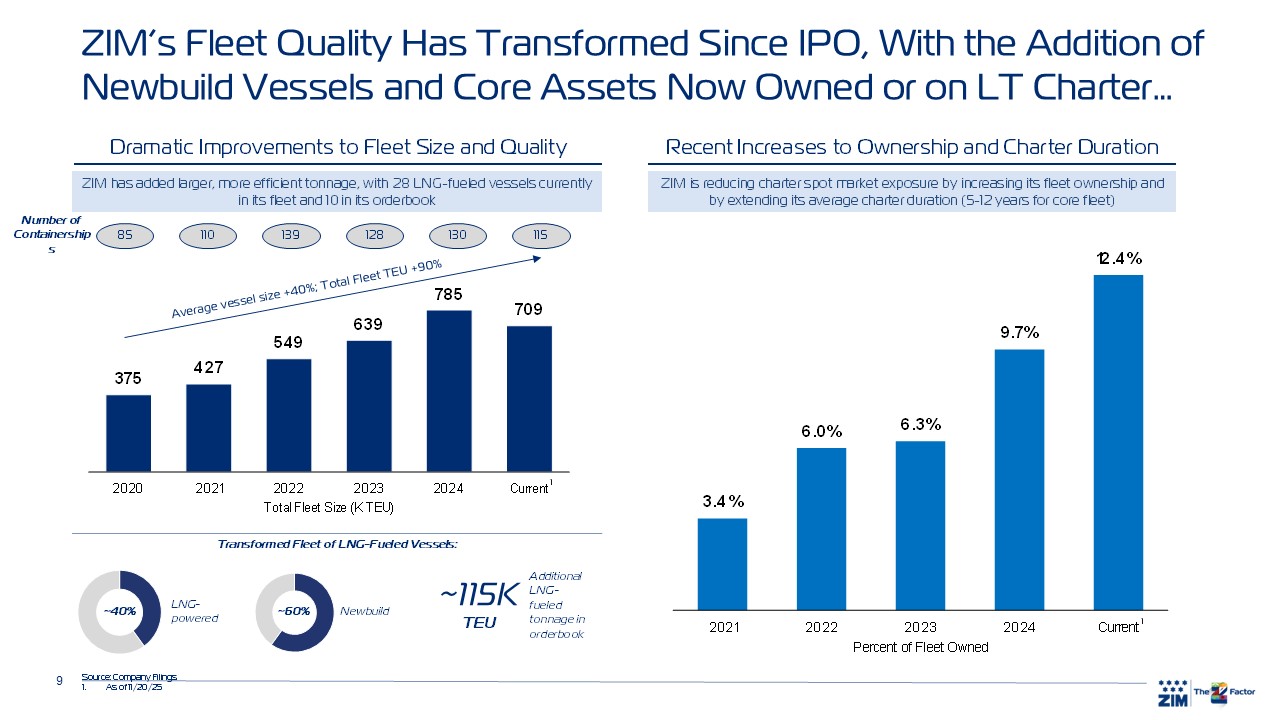

We have grown our fleet from ~70 to ~129 vessels and doubled our TEU carrying capacity.

|

|

• |

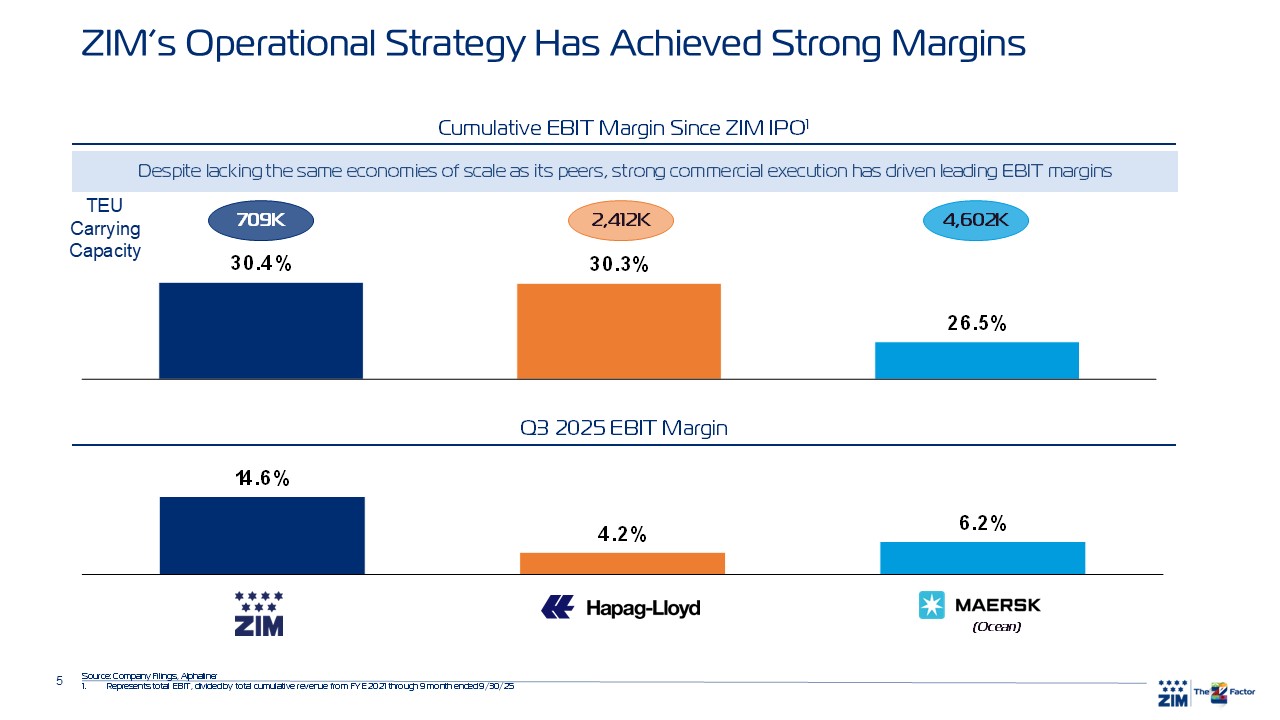

Our EBIT margins have averaged 30% since our IPO, superior or comparable to larger carriers with significant scale advantages.

|

|

• |

We have returned an extraordinary $5.7 billion in dividends since our IPO – over $47 a share or more than three times the IPO price – reflective of strong financial performance and a thoughtful capital return policy.

|

|

• |

Book equity has increased from ~$0.1 billion to approximately $4.0 billion, reflecting the significant earnings and strength of our balance sheet and operating model.

|

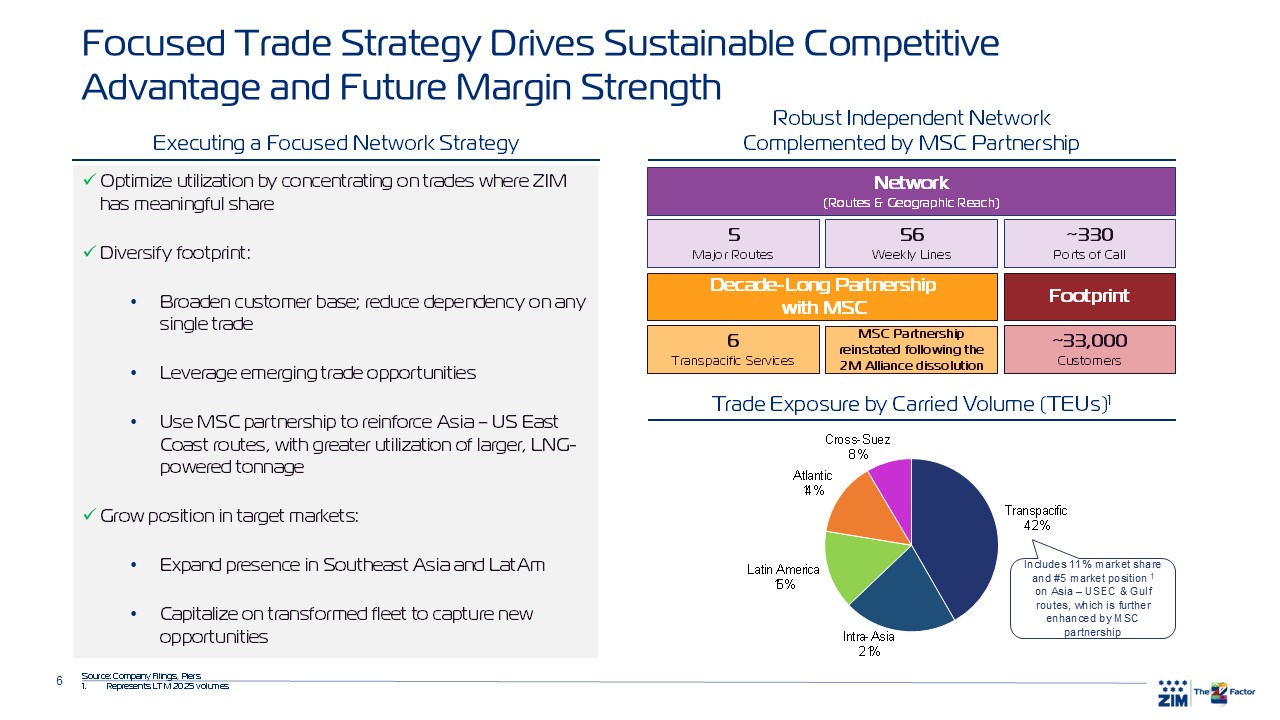

Underpinning these results is a clear operating strategy. ZIM focuses on trade lanes where it can hold meaningful, defensible share and deliver superior service. Our largest lane – the Transpacific – represents 42%

of volumes and continues to demonstrate strong demand and attractive rate dynamics. Our long-standing partnership with MSC further enhances scale and reliability on key routes.

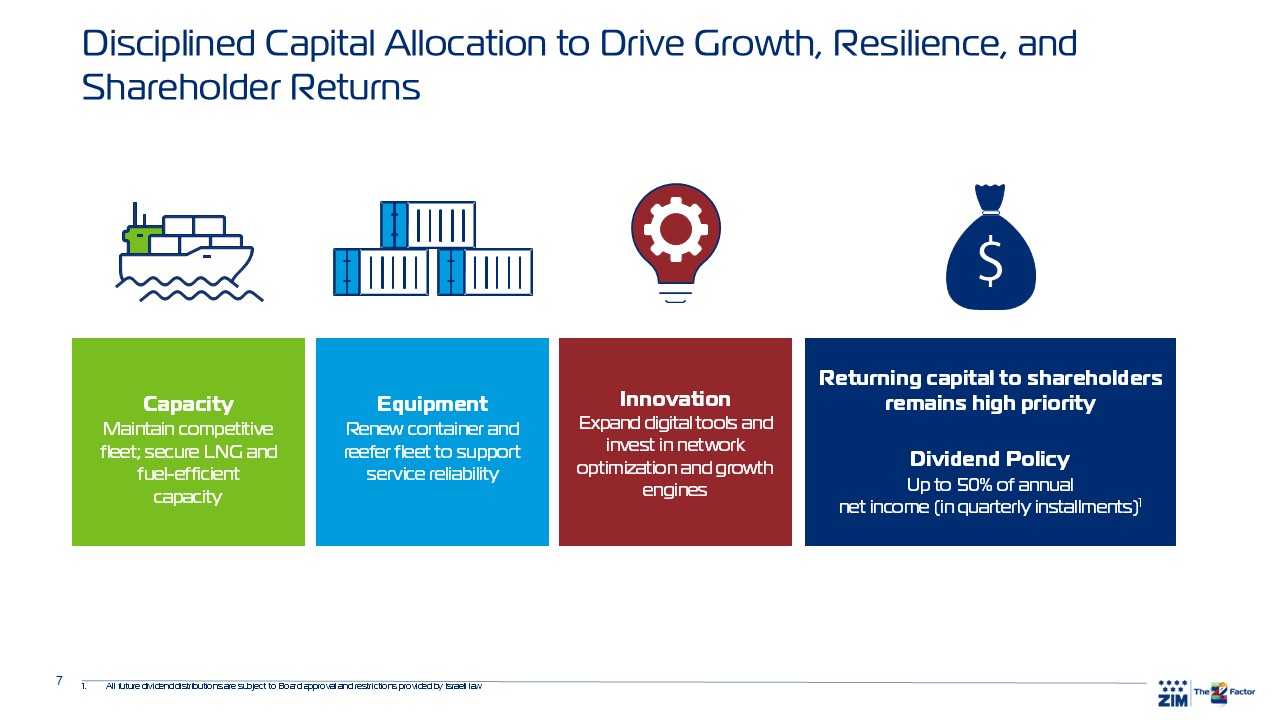

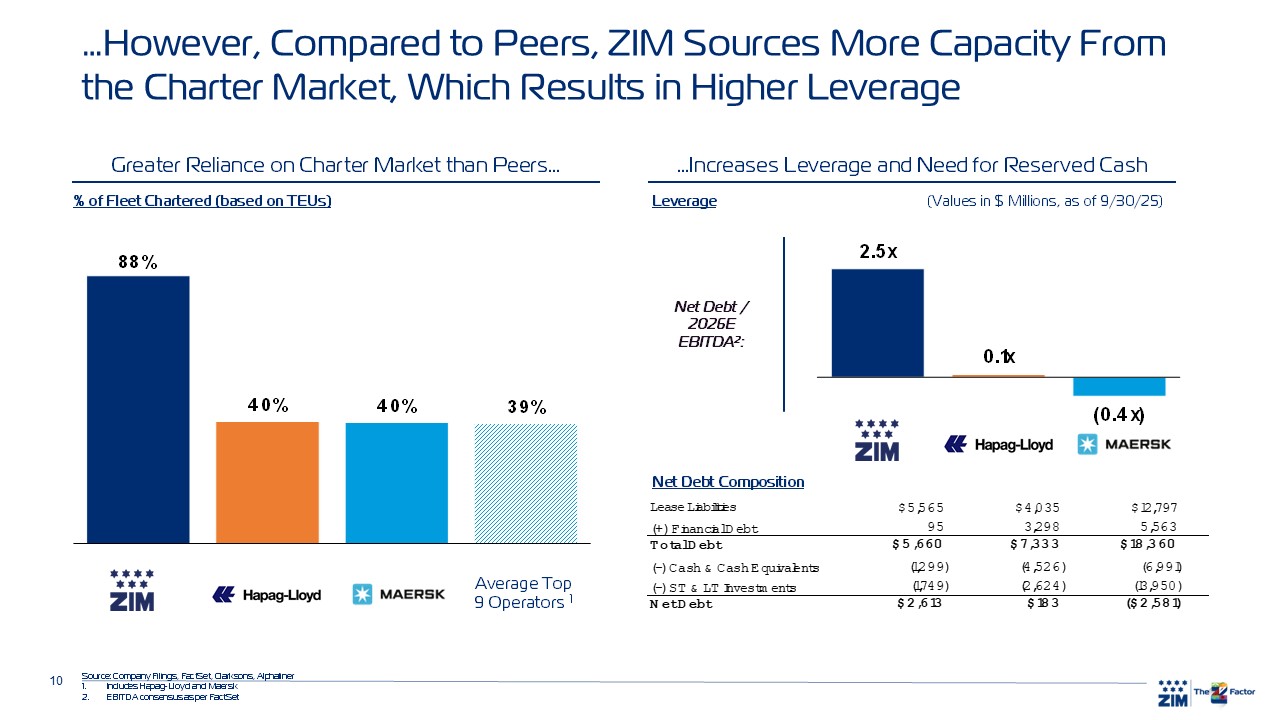

Just as importantly, ZIM operates with agility. Our charter-intensive fleet model gives us flexibility to adjust capacity as market conditions evolve. At the same time, the Company has steadily increased the

proportion of owned or long-term chartered vessels, improving fleet quality and reducing exposure to short-term charter volatility.

These strategic decisions have created a modern, efficient customer-focused platform capable of generating strong earnings across cycles – a testament to the disciplined execution of our management team and the

oversight of your Board.

Why the Board Is Conducting a Strategic Review

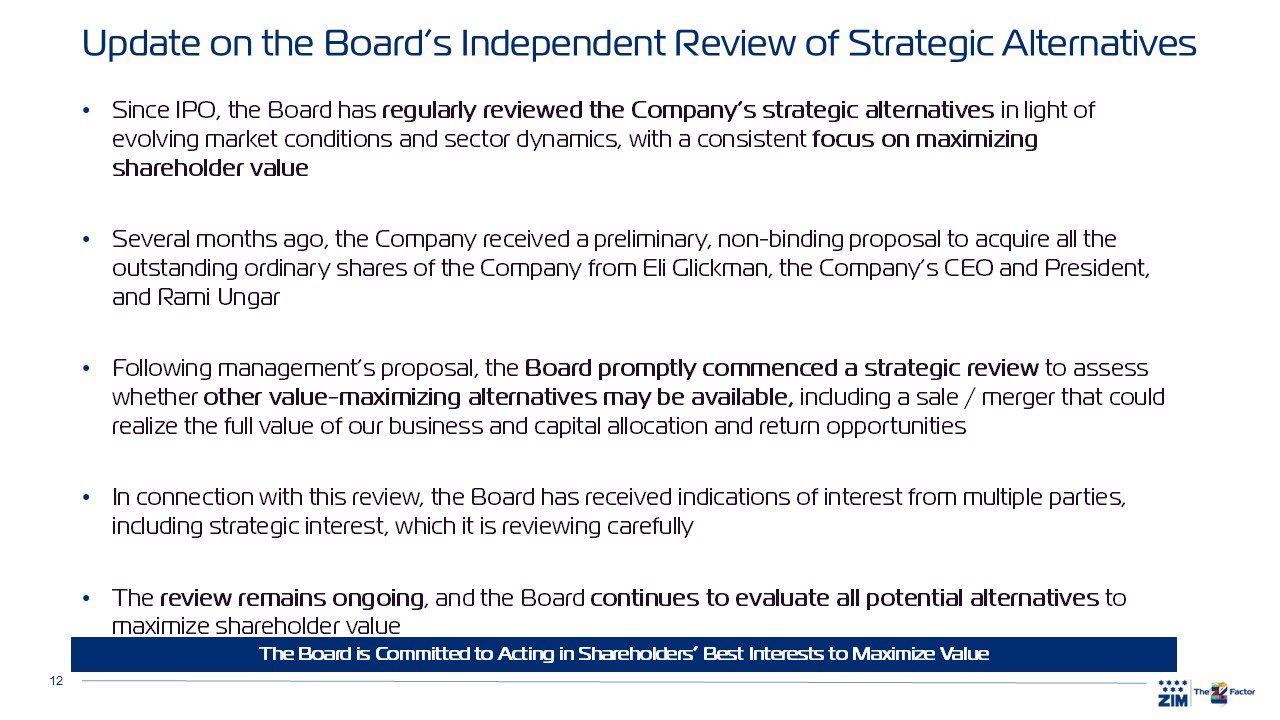

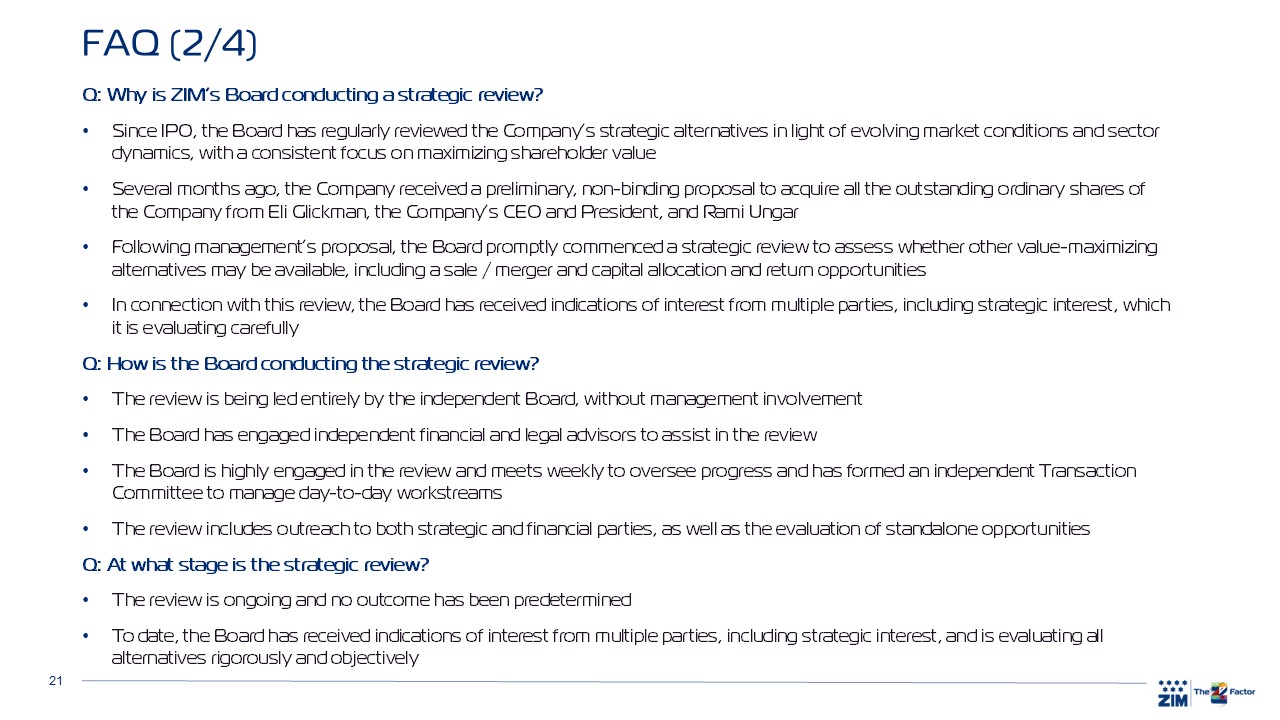

The Board’s mandate is to act in the best interests of all shareholders and to continually assess opportunities to enhance value. Since the IPO, the Board has consistently reviewed strategic alternatives in light of

evolving industry dynamics, competitive developments, and ZIM’s own scale and fleet profile.

Several months ago, the Board received an unsolicited preliminary, non-binding proposal from Eli Glickman, the Company’s CEO and

President, and Rami Ungar. In accordance with our governance framework, the independent Board, excluding management, evaluated the proposal and unanimously determined that it materially undervalued the Company.

1 Total shareholder returns represent capital gains yield (reflecting share price appreciation), plus dividend

yield (assuming dividends are reinvested) since ZIM IPO date (1/28/21) to unaffected date (8/8/25), the last trading date before news of a potential unsolicited management buyout leaked

2 2020 figures as of 9/30/20

Given this interest and taking into account ZIM’s trading levels and broader sector dynamics, the Board determined that it would be prudent and in the interests of all shareholders to assess whether other

value-maximizing opportunities might be available. As part of this process, the Board has:

|

• |

Initiated a comprehensive, independent review of potential alternatives;

|

|

• |

Engaged leading independent financial and legal advisors;

|

|

• |

Formed an independent Transaction Committee;

|

|

• |

Appointed two new independent directors who bring substantial financial and transactional expertise to bolster the review; and

|

|

• |

Conducted outreach to multiple strategic and financial parties.

|

The review is ongoing, rigorous, and objective and includes evaluation of potential alternatives, as well as enhancements to our standalone plan. Multiple indications of interest have been received, which the Board is

evaluating carefully. Our focus is singular: to identify the path that maximizes value for all shareholders. Management is not participating in the evaluation of alternatives and the review is being conducted solely by the independent Board.

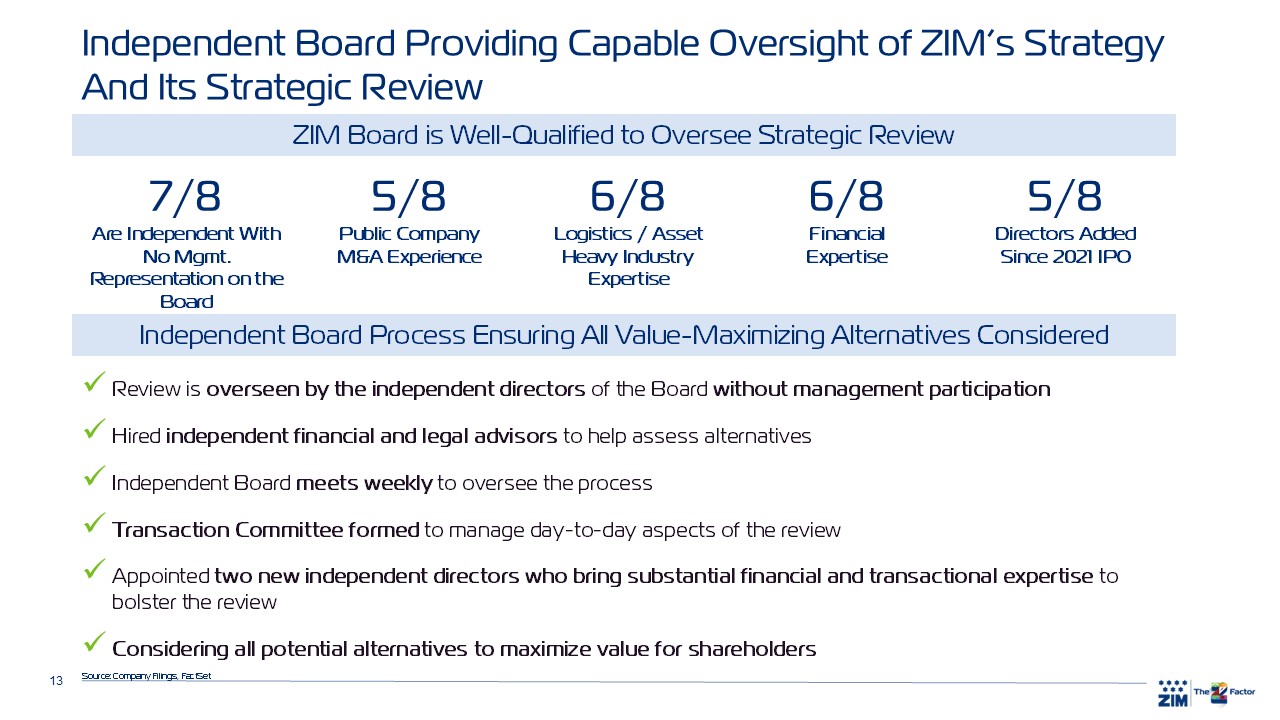

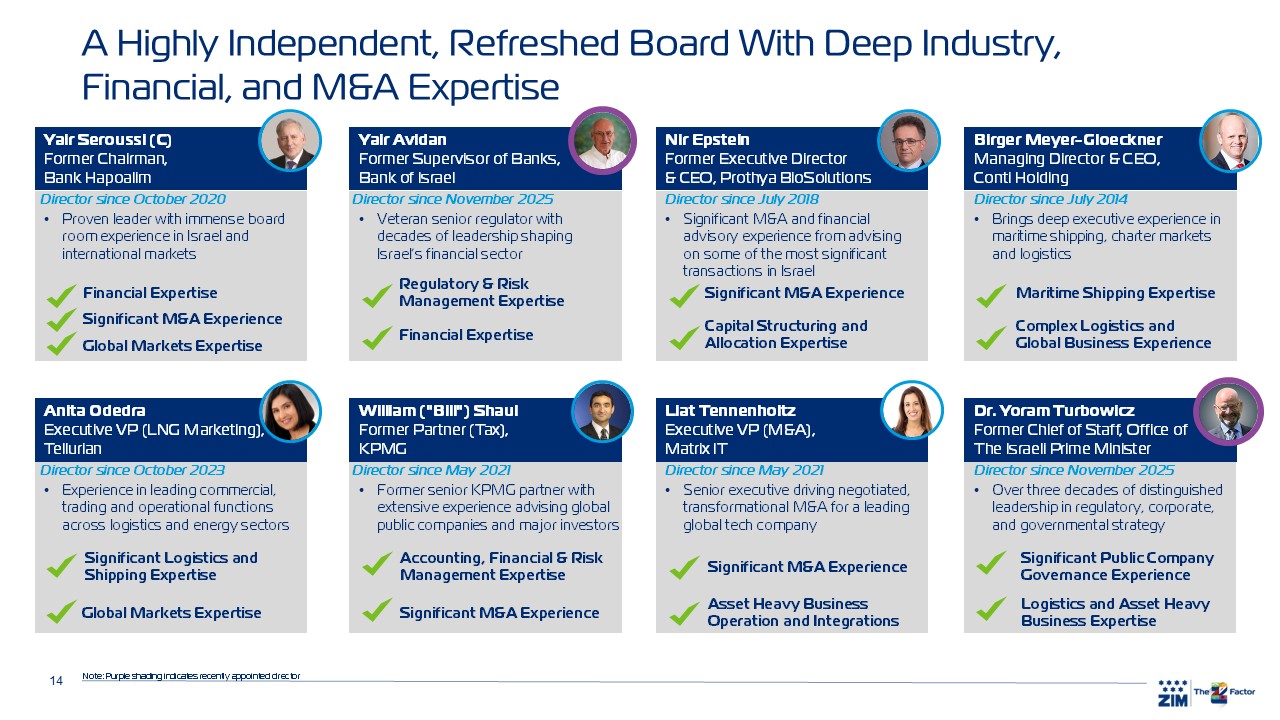

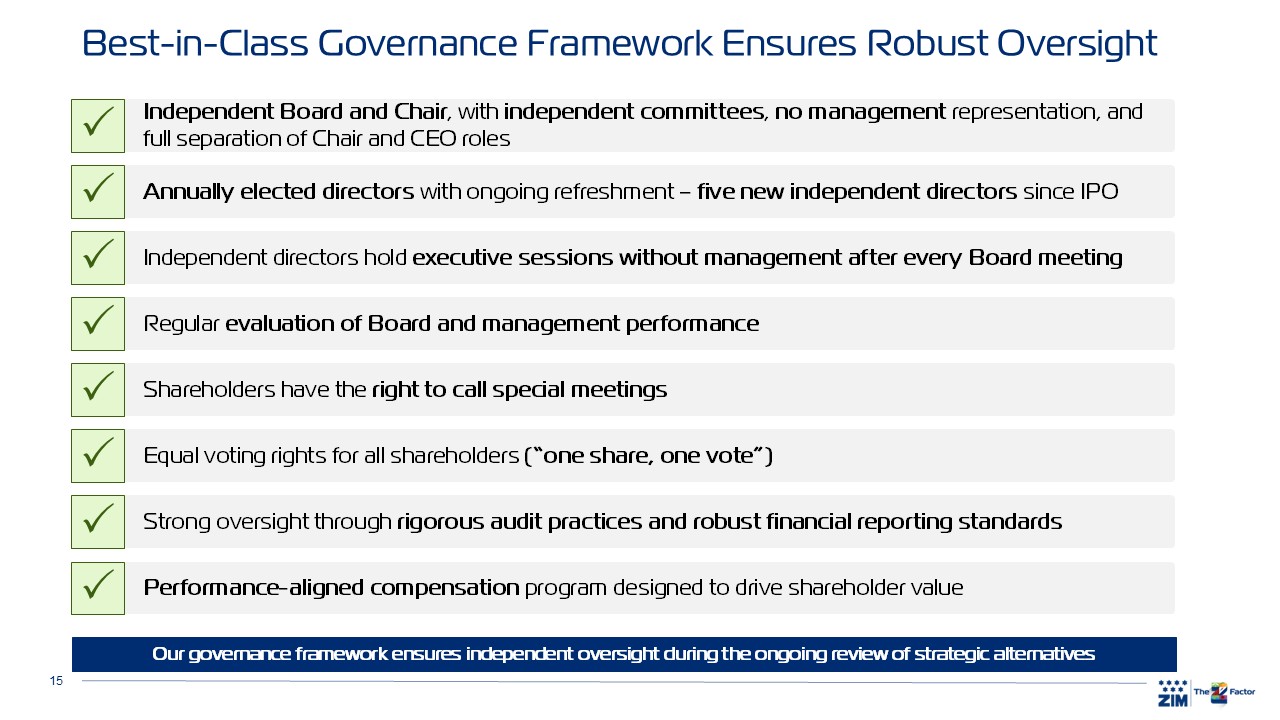

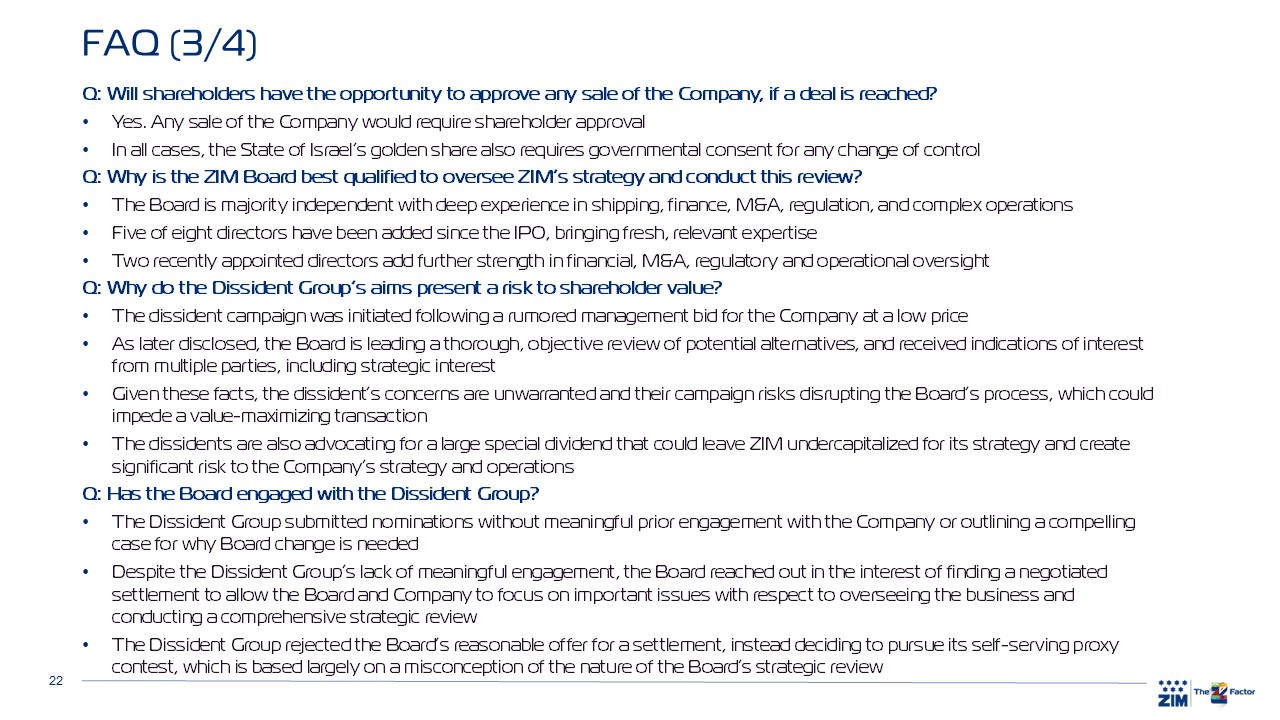

A Highly Qualified, Refreshed, Independent Board

ZIM benefits from an independent, significantly refreshed Board, with five of eight directors added since the IPO, including two newly appointed directors who bring substantial financial, M&A, regulatory, and

operational leadership experience.

Collectively, the Board has:

|

• |

Maritime, logistics, and industrial operating expertise;

|

|

• |

Significant M&A, financial, and capital allocation experience;

|

|

• |

Meaningful regulatory, governmental, and risk-oversight backgrounds; and

|

|

• |

Strong public company governance experience.

|

The independent Board meets weekly to oversee the strategic review process and each of our directors is highly engaged. This combination of independence, relevant expertise, and active oversight uniquely qualifies the

Board to guide ZIM through this evaluation.

Why the Dissident Group’s Campaign Is Misguided and Harmful

| 1. |

The Dissident Group’s Campaign Is Based on Misleading Assumptions Regarding the Strategic Review and ZIM’s Capital Allocation Strategy

|

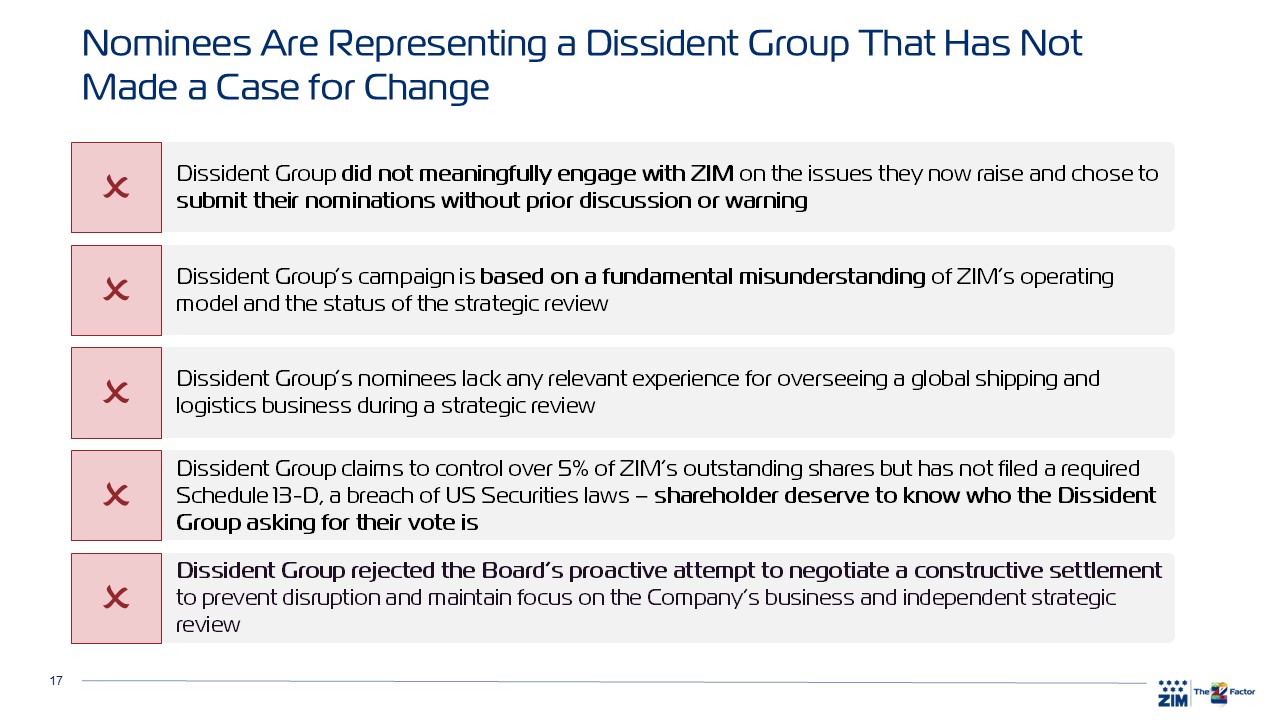

The dissident group did not meaningfully engage with us on the issues they now raise and chose to submit their nominations without prior discussion or warning. Their campaign appears to be rooted in the false

assumption that the Board is planning to sell the Company to the management group at an inadequate price.

They initiated their campaign following media speculation that the Board was open to considering an unsolicited management bid at a

price below ZIM’s cash balance, before the Company disclosed that the Board has initiated a strategic review. The rumor that the Board was willing to accept such an undervalued bid was clearly false. The Board had already evaluated the

management group’s proposal and rejected it as undervaluing the Company. As the Board has disclosed publicly, it is instead pursuing a broad process and has already received indications of interest from multiple parties, including strategic

interest.

Importantly, despite seeking to control almost half of the Board, the dissident group has not articulated any other ideas to improve ZIM’s operations, fleet strategy, capital allocation, or competitive positioning.

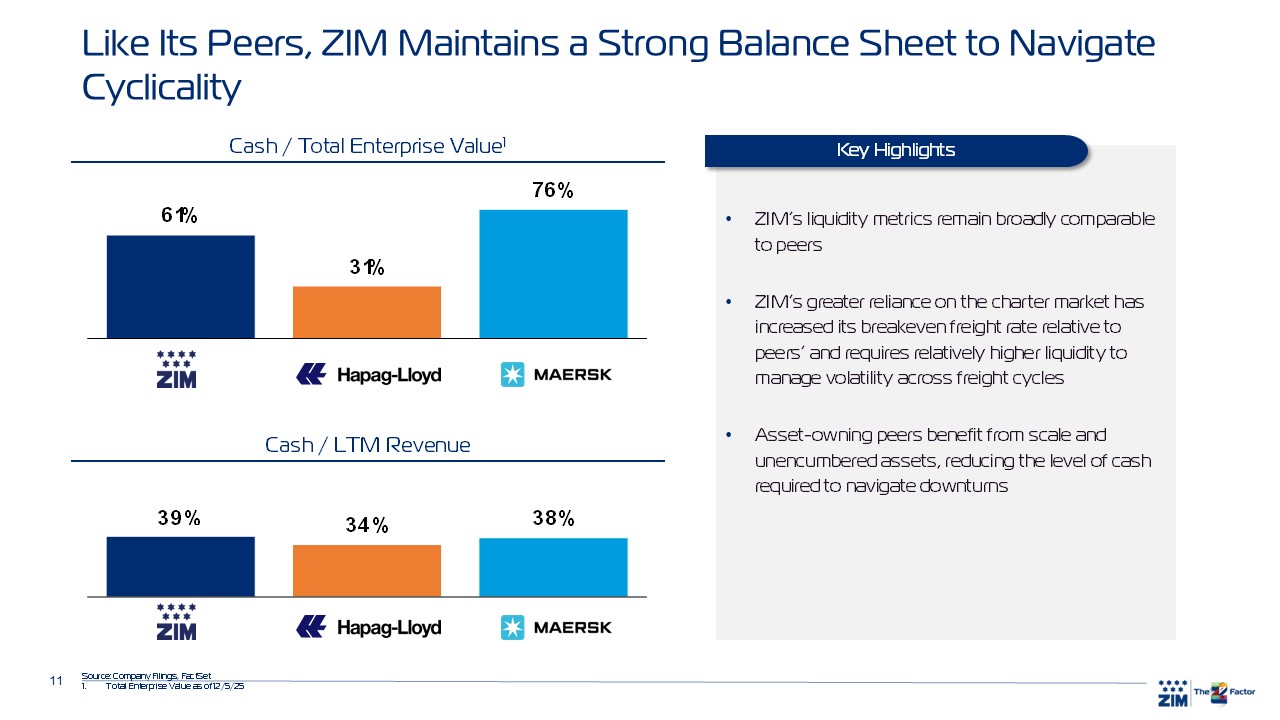

The only substantive proposal they have made relates to statements made to Israeli media regarding their desire for ZIM to issue a large special dividend that would undermine ZIM’s liquidity and create substantial risk to shareholder value given

our charter-intensive model, which requires adequate cash to navigate industry cycles.

On December 5, 2025, leading independent proxy advisory firm Institutional Shareholder Services (“ISS”) issued a report recommending that ZIM shareholders vote for all eight of ZIM’s director nominees and against the

three director nominees proposed by the dissident group. In coming to its conclusion, ISS noted that the dissident group “[had] made no attempt to work constructively with the board nor provided any suggestions for improving the company’s business

or any other insight into how to create long-term value for shareholders” and that they “[had] not provided a compelling or sufficient rationale to support the proposed candidates or to demonstrate that a change to the board is warranted.”

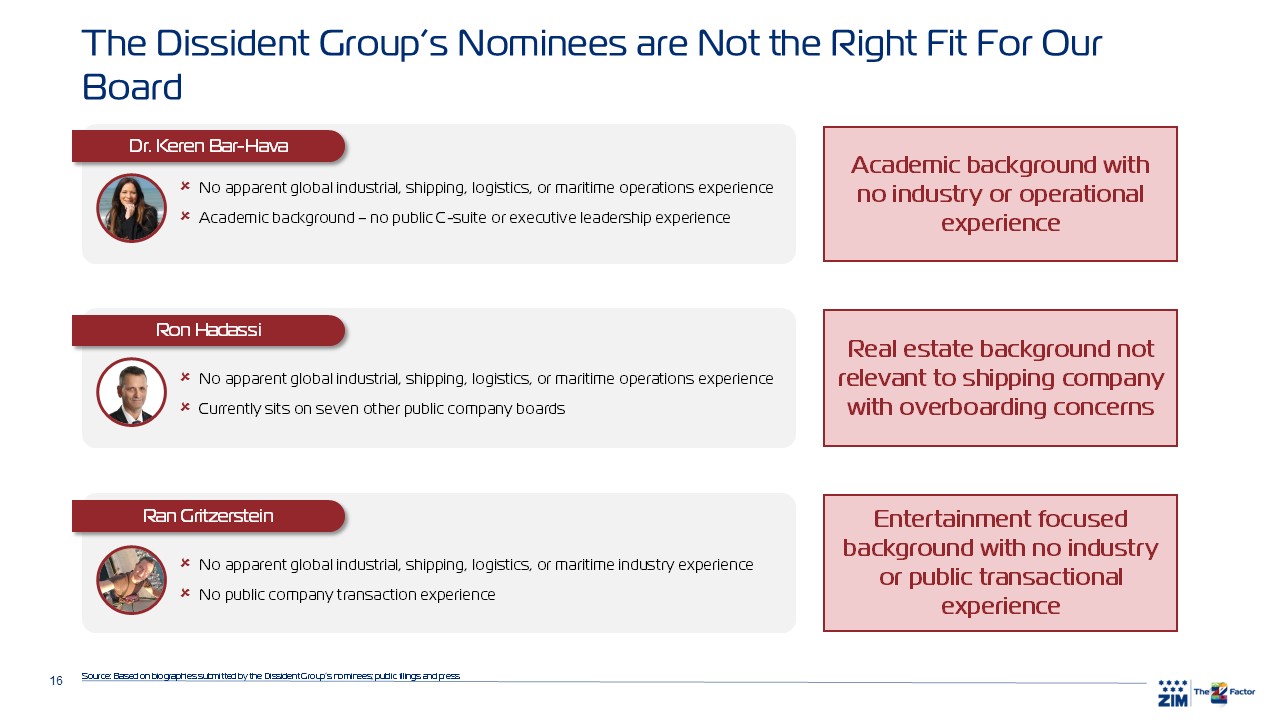

| 2. |

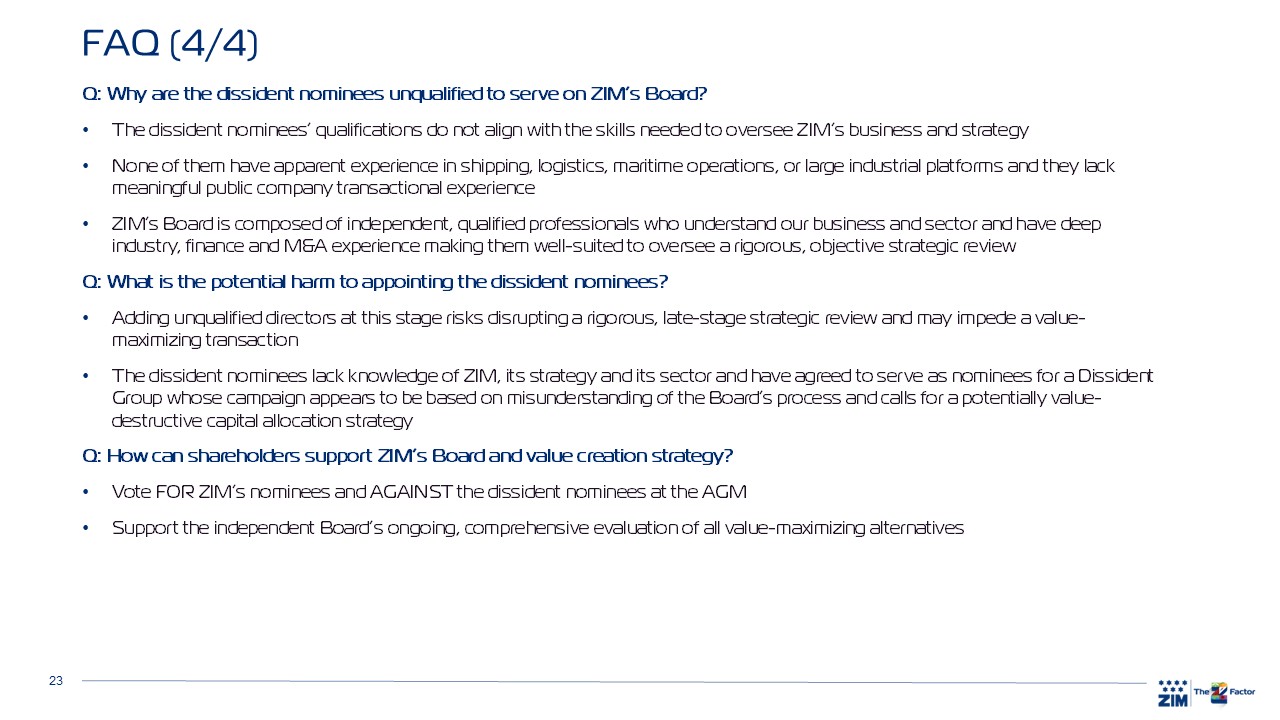

The Dissident Group Nominees Lack Relevant Experience

|

The dissident nominees have limited experience in shipping, logistics, maritime operations, or managing large industrial platforms, and lack meaningful public company transactional experience. This stands in stark

contrast to the capabilities required to oversee ZIM’s global footprint or the ongoing strategic review and the dissident group has not provided any reason why their hand-picked directors are qualified to oversee a global shipping company.

Replacing independent, experienced, qualified directors with nominees lacking relevant industry, transactional and governance expertise would risk disrupting the strategic review at a late stage and could impair the

Board’s ability to secure a value-maximizing outcome for shareholders.

| 3. |

The Dissident Group Has Failed to Provide Adequate Disclosures in Compliance With Securities Laws

|

In making their nominations, the dissident group has represented that they own over 5% of ZIM’s outstanding shares. This level of ownership, combined with their coordinated actions to replace almost half of ZIM’s

Board, requires the filing of a Schedule 13-D under the U.S. securities laws, which requires them to identify the members of the group and information regarding their ownership. To date, the dissident group has failed to provide these required

disclosures, raising serious questions about their transparency and intent.

As a ZIM shareholder, you deserve to know who is asking for your vote and why they have chosen not to comply with basic securities laws in conducting their campaign. It is the Board’s view that this basic lack of

transparency should be disqualifying for a group of shareholders who are seeking to substantially influence the future of ZIM, including the evaluation of potentially value-maximizing alternatives.

Your Board’s Commitment and a Call for Your Support

Your Board is fully capable and committed to acting in the best interests of all shareholders. We are overseeing the business to ensure that ZIM maintains the financial strength, operational flexibility, and

governance discipline needed to continue to deliver peer-leading shareholder returns in a dynamic global environment. We are also conducting a rigorous and objective review of strategic alternatives with the goal of maximizing value for

shareholders.

At this critical juncture, continuity of independent, qualified Board oversight is essential. Supporting the Company’s nominees and voting against the shareholder group’s nominees will help preserve the integrity of

our Board’s oversight of our business and strategy, as well as the strategic review, and protect the value of your investment.

For these reasons, we strongly urge you to vote FOR ALL eight of ZIM’s director nominees and AGAINST the dissident nominees at the upcoming Annual General Meeting.

We appreciate your consideration and engagement as you evaluate these important matters.

Sincerely,

The Board of Directors

ZIM Integrated Shipping Services Ltd.

Your Vote is Important

Consistent with ISS’s recommendation, the Board of Directors strongly urges all ZIM shareholders to protect the value of their investment by voting “FOR ALL” of the Company's nominees TODAY.

If shareholders have questions or require assistance in voting their shares for the Meeting, please contact the Company’s proxy solicitor, Sodali & Co, at the following contact information:

Sodali & Co

Toll Free: (800) 662-5200

Brokers and Banks: (203) 658-9400

Email: ZIM@info.sodali.com

About ZIM

Founded in Israel in 1945, ZIM is a leading global container liner shipping company with established operations in more than 90 countries serving approximately 33,000 customers in over 300 ports worldwide. ZIM

leverages digital strategies and a commitment to ESG values to provide customers with innovative seaborne transportation and logistics services and exceptional customer experience. ZIM’s differentiated global-niche strategy, based on agile fleet

management and deployment, covers major trade routes with a focus on select markets where the company holds competitive advantages. Additional information about ZIM is available at www.ZIM.com.

Forward-Looking Statements

This press release contains, or may be deemed to contain, forward-looking statements (as defined in the U.S. Private Securities Litigation Reform Act of 1995). In some cases, you can identify these statements by

forward-looking words such as “may,” “might,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “proposed,” potential” or “continue,” the negative of these terms and other comparable terminology. These statements

are only predictions based on the Company’s current expectations and projections about future events or results. There are important factors that could cause the Company’s actual results, level of activity, performance or achievements to differ

materially from the results, level of activity, performance or achievements expressed or implied by the forward-looking statements. Factors that could cause such differences include risks and uncertainties detailed from time to time in the

Company’s filings with the U.S. Securities and Exchange Commission (the “SEC”), including under the caption “Risk Factors” in its 2024 Annual Report filed with the SEC on March 12, 2025. Neither the Company nor any other person assumes

responsibility for the accuracy and completeness of any of these forward-looking statements. The Company assumes no duty to update any of these forward-looking statements after the date hereof to conform its prior statements to actual results or

revised expectations, except as otherwise required by law.

Investor Relations:

Sodali & Co