|

|

|

|

|

KENON HOLDINGS LTD.

|

|

|

|

|

|

|

Date: March 12, 2025

|

By:

|

/s/ Robert L. Rosen

|

|

|

Name:

|

Robert L. Rosen

|

|

|

Title:

|

Chief Executive Officer

|

| 1. |

Executive Summary1

|

|

For the

|

For the

|

||||||||||||||||||||||||

|

Year Ended

|

Three Months Ended

|

||||||||||||||||||||||||

|

December 31

|

December 31

|

||||||||||||||||||||||||

|

2024

|

2023

|

%

|

2024

|

2023

|

%

|

||||||||||||||||||||

|

Consolidated

|

EBITDA after proportionate consolidation

|

1,208

|

1,099

|

10

|

%

|

228

|

319

|

(29

|

)%

|

||||||||||||||||

|

|

Net income

|

197

|

169

|

17

|

%

|

123

|

29

|

324

|

%

|

||||||||||||||||

|

|

Adjusted net income (loss)

|

115

|

180

|

(64

|

)%

|

(47

|

)

|

43

|

(209

|

)%

|

|||||||||||||||

|

|

FFO |

726

|

648

|

12

|

%

|

154

|

4

|

3,750

|

%

|

||||||||||||||||

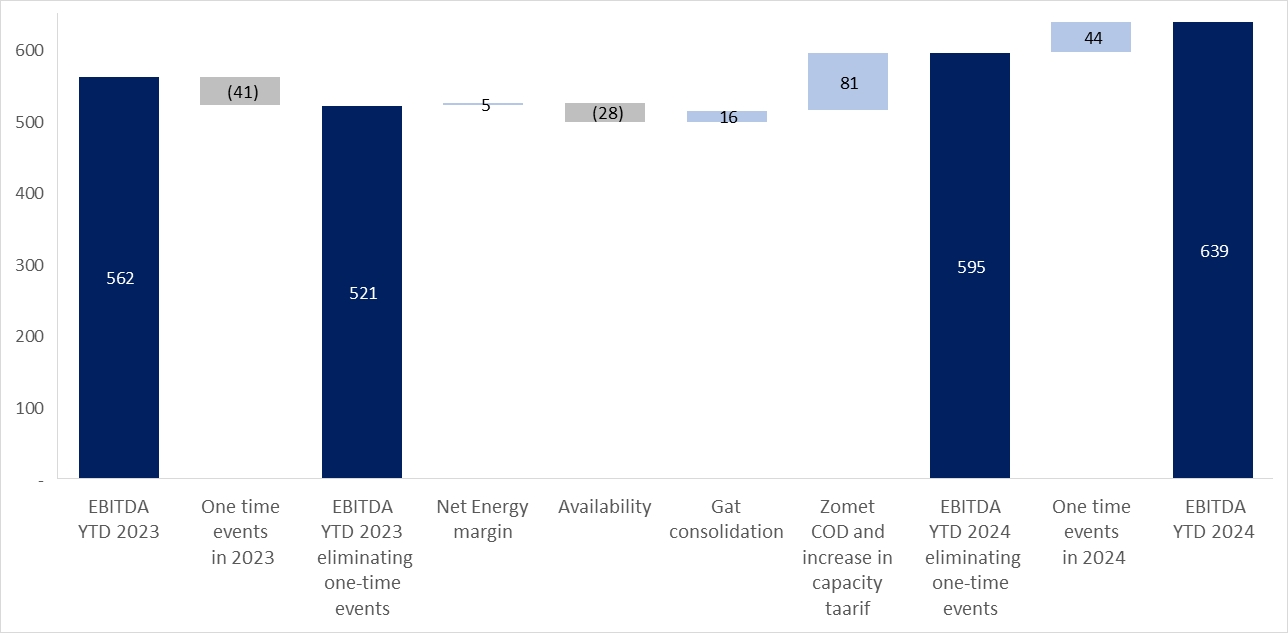

|

Israel

|

EBITDA

|

639

|

562

|

14

|

%

|

98

|

135

|

(27

|

)%

|

||||||||||||||||

|

|

FFO |

428

|

440

|

(3

|

)%

|

45

|

10

|

350

|

%

|

||||||||||||||||

|

U.S.

|

EBITDA after proportionate consolidation

|

589

|

564

|

4

|

%

|

137

|

191

|

(28

|

)%

|

||||||||||||||||

|

|

FFO |

339

|

264

|

28

|

%

|

111

|

(8

|

)

|

1,488

|

%

|

|||||||||||||||

|

|

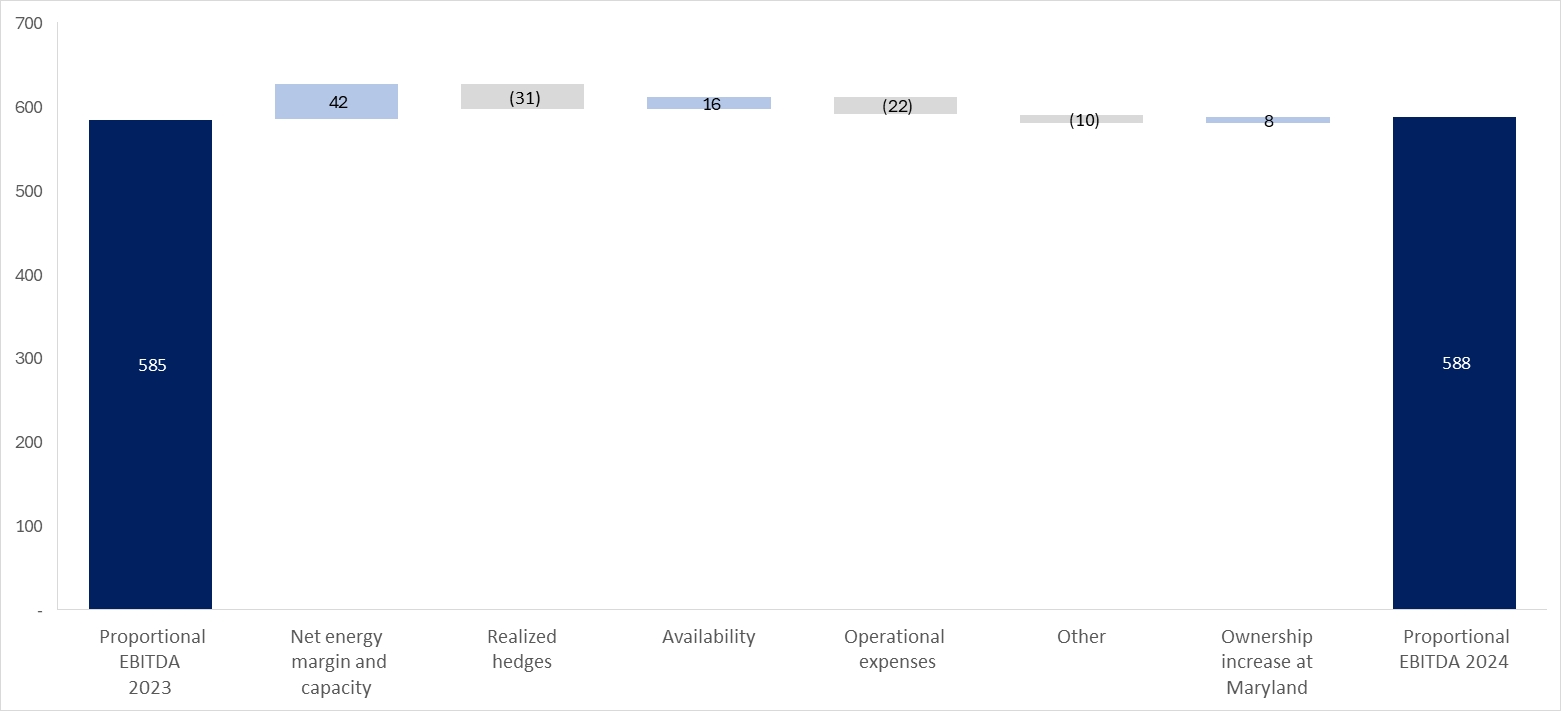

EBITDA after proportionate consolidation – energy transition

|

588

|

585

|

1

|

%

|

141

|

163

|

(13

|

)%

|

||||||||||||||||

|

|

EBITDA after proportionate consolidation – renewable energies

|

112

|

31

|

261

|

%

|

28

|

14

|

100

|

%

|

||||||||||||||||

|

|

* |

EBITDA, EBITDA after proportionate consolidation, adjusted net income and FFO are not recognized in accordance with IFRS – for definitions and the manner of their calculation – see Sections 4B and 4F below.

|

| 1 |

The Executive Summary below is presented solely for convenience and it is not a substitute for reading the full detail (including with reference to the matters referred to in the Summary) as stated in this

report with all its parts (including warnings relating to “forward‑looking” information as it is defined in the Securities Law, 1968 (“the Securities Law”) definitions or explanations with respect to the indices for measurement of the

results and including the information included by means of reference, as applicable). This Summary includes estimates, plans and assessment of the Company, which constitute “forward‑looking” information regarding which there is no certainty

it will materialize and the readers are directed to the detail presented in this report below.

|

| 1. |

Executive Summary (Cont.)

|

|

Israel

|

Ramat Beka project – the Company is continuing to advance a consolidated project for generation of electricity using photovoltaic technology with integrated

storage with a cumulative capacity of about 505 megawatts and about 2,760 megawatts per hour of storage. See also Section 6A(2) below. In September 2024, the Group made an initial payment to Israel Lands Authority (ILA) in respect of the

Ramat Beka 2 tender, in the amount of about NIS 178 million (the Company’s share – about NIS 142 million), constituting 20% of the aggregate consideration for the areas of the second tender. As at the approval date of the report, to the

best of the Company’s knowledge government was received for advancement of the plan to State’s National Infrastructures Board – for details see Section 7.3.13.1 of Part A of the Periodic Report.

|

|

Additional renewable energy projects – as part of its strategic entry into the renewable energies area in Israel, the

Company is developing additional projects using photovoltaic technology with integrated storage, with a cumulative capacity of about 215 megawatts and about 1,100 megawatt hours of storage. To the best of the Company’s knowledge,

government was received for advancement of the plan to State’s National Infrastructures Board – for details see Section 6A(2) below.

|

|

|

Memorandum of principles with Intel for construction of a power plant with a capacity of 450–650 megawatts – in March 2024, a non‑binding memorandum of

principles for supply of electricity to Intel’s facilities in Kiryat Gat was signed, including expansion of the currently‑existing facilities, for a period of 20 years from the date of commencement of operation. See also – Section 6A(1)

below.

|

|

|

Sale of electricity to consumers of Partner Communications Ltd. (“Partner”) that are household consumers and small businesses and a decision regarding smart meters

– in February 2024, an agreement was signed with Partner that will permit diversification of the mix of the Company’s customers. In April 2024, a decision of the Electricity Authority was received that will permit the Company to also sell

electricity to household consumers without a smart meter and assignment thereof to a private conventional supplier commencing from November 1, 2024.

|

|

|

Refinancing in Israel – in August 2024, OPC Holdings Israel signed two bank financing agreements, with an aggregate scope of NIS 1.65 billion, which were used

mainly for purposes of early repayment of the project financing of the Zomet and Gat power plants. In February 2025, OPC Israel signed an additional bank financing agreement in the aggregate amount of NIS 300 million under similar

conditions. See also Note 14B(1) to the Financial Statements.

|

|

|

Hadera 2 project – after the government’s rejection of the plan for construction of a power plant for generation of electricity using natural gas in April

2024, in June 2024 Hadera 2 submitted a petition to the High Court of Justice regarding cancellation of the said Government Decision and approval of the plan. In December 2024, a conditional order was issued by High Court of Justice

instructing the government to provide reasons why not to return of the plan for a rehearing by the National Infrastructures Board or, alternatively, to provide reasons why not to approve the plan. A hearing of the petition was scheduled

for April 2025. See also – Section 6A.

|

|

|

Public Announcement regarding a proposal for changes in the tariff structure (the generation component) – for details – see Section 3.2E below and

Section 7.2.3 to Part A of the Periodic Report.

|

| 1. |

Executive Summary (Cont.)

|

|

U.S.

|

Transactions for increase in the holdings in the Shore and Maryland power plants in the area of Energy Transition in the U.S. – in October 2024, acquisition of

25% of the Maryland power plant was completed and in December 2024 acquisition of an additional 25% of Maryland and 31% of Shore was completed. On the completion date of the transactions, consideration was paid in the aggregate amount of

about $188 million – see also Section 24C to the financial statements. Furthermore, in February 2025 the CPV Group signed an agreement, subject to preconditions that have not yet been actualized, for acquisition of an additional 20% of

the Shore power plant. As part of the aforesaid transactions, the total investment commitments were increased and provision of shareholders’ loans to the CPV Group, in the amount of about $220 million, such that subject to investment of

the full amount of the commitments, the Company’s holdings (indirectly) will be about 70.7%.

|

|

Entry of an investor into the area of renewable energy activities in the U.S. – in August 2024, the CPV Group signed binding investment agreements with

Harrison Street, in the aggregate amount of $300 million in CPV Renewable, in exchange for 33.3% of the ordinary rights in CPV’s renewable‑energy activities, based on a value “before the money” of $600 million. In November 2024, the

transaction was completed. See also – Section 23E to the financial statements.

|

|

|

Capacity auctions in the PJM market for the period June 2025 through May 2026 – in July 2024, the results of auctions for capacity prices in PJM were

published, with a significant increase in the prices to about $270 per megawatt per day. For details regarding the estimated addition to the Group’s revenues from capacity for the period of the auction and with respect to expected changes

in the methodology of the auctions on the capacity prices in PJM for 2026–2027, and particularly determination of minimum and maximum (collar) prices of 175–325 megawatts per day – see Section 3.3M below.

|

|

|

Basin Ranch project – the CPV Group is continuing to advance the Basin Ranch project, a natural gas project with future carbon capture potential located in the

western part of Texas, with a capacity of about 1.35 gigawatts, the construction cost of which is estimated at about $1.8 – $2 billion and commencement of its construction is expected by the end of 2025. The project was chosen by the TEF

to advance to the stage of due diligence examinations for receipt of a subsidized loan in the amount of about $1 billion. In addition, as at the approval date of the report, the CPV Group is working on a private fundraising process that

is required for construction of the project. For additional details – see Section 6B(2) below.

|

|

|

Refinancing in Towantic, Fairview, Shore and reductions of interest in Maryland and Fairview – during 2024 and in February 2025, undertakings for refinancing

in Towantic, Fairview and Shore were completed. In addition, in September 2024 and February 2025, the transactions for interest reductions (repricing) in Maryland and Fairview were completed. See also Section 9 below.

|

|

|

Start of construction of the Rogue’s Wind project (wind‑energy power plant with a capacity of 114 megawatts located in Pennsylvania) – in August 2024 a Work

Commencement Order was issued concurrent with completion of the receipt of financing for construction of the project. See also Section 6A(2) below.

|

| 1. |

Executive Summary (Cont.)

|

|

U.S. (Cont.)

|

Tax partner agreement in the Backbone project (solar technology‑based power plant with a capacity of 179 megawatts, in the state of Maryland) – in October

2024, a binding agreement was signed with a tax partner for investment of an aggregate amount of about $116 million. See also Section 6A(2) below.

|

|

Commercial operation of the Stagecoach project with a capacity of 102 megawatts – in May 2024, the project reached commercial operation and an agreement was

signed with a tax partner (PTC) in the aggregate amount of about $52 million.

|

|

|

Group headquarters

|

Raising of capital – in July 2024, the Company completed raising of capital, in the amount of about NIS 800 million.

|

|

Credit rating – in July 2024, S&P Maalot reconfirmed the credit rating of the Company and its debentures at the level of ilA– and updated the rating

outlook from negative to stable.

|

|

|

Issuance of a new series of debentures (Series D) – in January 2024, the debentures (Series D) were issued in the amount of NIS 200 million with a term of

about 6.4 years and bearing annual interest of 6.2%.

|

|

|

(1) |

Commencing from the fourth quarter of 2024, renewable energy projects are presented in accordance with the relative share of the CPV Group in this area of activities (about 66.7%). For details – see also Section 2(2), below.

|

|

|

(2) |

Natural gas projects are presented in accordance with the relative share of the CPV Group in each project. The above chart does not include the transaction for acquisition of additional holdings, at the rate of 20%, in the Shore power

plant, which as at the approval date of the report had not yet been completed.

|

| 1. |

Executive Summary (Cont.)

|

| (1) |

The above chart does not include the Hadera 2 project, with a capacity of 850 megawatts, in light of the Government’s decision to reject the plan. As at the approval date of the report, a petition is underway in the Supreme Court sitting

as the High Court of Justice regarding cancellation of the said Government decision. For details – see Section 6A(2) below and Section 7.3.13.4 of Part A to the Periodic Report.

|

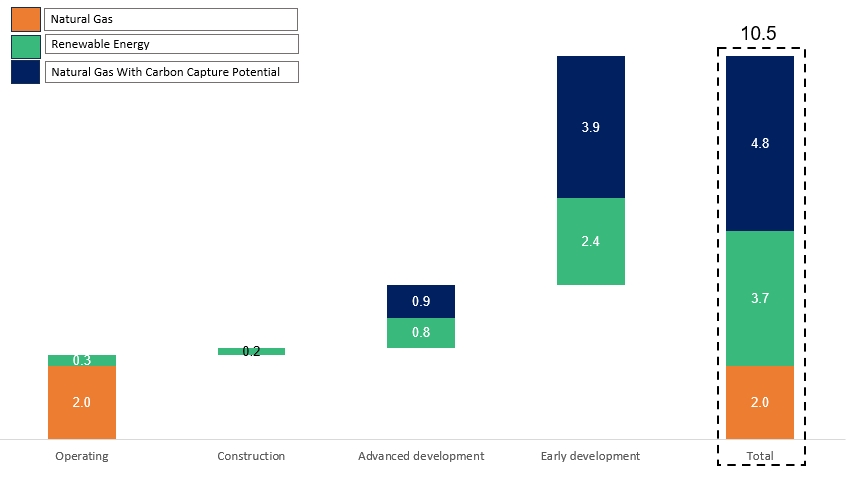

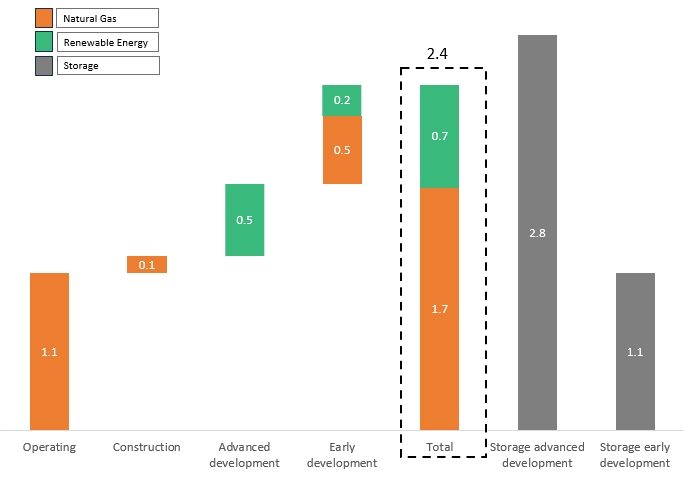

| 2. |

Brief description of the areas of activity

|

|

|

(1) |

Israel (by means of OPC Holdings Israel Ltd.2) – as part of this area of activities, the Group is engaged in generation and supply of electricity and energy, mainly to private customers and to Noga

Electricity System Management Ltd. (“the System Manager”), as well as in initiation, development, construction and operation of power plants and facilities for generation of energy by means of natural gas and renewable energy in Israel;

|

|

|

(2) |

Renewable Energy in the U.S. (by means of the CPV Group3) – as part of this area of activities, the Group is engaged in initiation, development and operation of power plants running on renewable energy in

the U.S. (solar and wind). For details regarding an investment transaction, in the aggregate amount of $300 million, in CPV Renewable in exchange for 33.3% of the ordinary rights in the renewable energy activities in the U.S, which was

completed in the fourth quarter of 2024 – see Note 23E to the financial statements. Accordingly, starting from the completion date of the transaction, the Company includes the renewable‑energy activities in the U.S. held by the CPV Group at

the rate of about 66.7% and that constitutes an associated company (that is not consolidated in the financial statements of the CPV Group and, in turn, the Company’s financial statements);

|

|

|

(3) |

Energy transition in the U.S. (by means of the CPV Group4) – as part of this area of activities, the Group is engaged in holding and operation of power plants running on conventional energy in the U.S.

(natural gas), which efficiently and dependably supply electricity. As at the date of the report, all the power plants operating in this area are held by associated companies at various different holding rates (that are not consolidated in

the financial statements of the CPV Group and, in turn, in the Company’s financial statements). For additional details regarding the acquisition of additional holdings in Shore and Maryland in the fourth quarter of 2024 and an agreement for

acquisition of additional holdings in the Shore power plant, which was signed after the date of the report – see Note 24C to the financial statements.

|

| 2 |

As at the date of the report, the Company holds directly 80% of the shares of OPC Israel while the other 20% is held by Veridis Power Plants Ltd. (“Veridis”).

|

| 3 |

As at the date of the report, the Company holds indirectly about 70.46% of the shares of CPV (for details regarding increase of the investment commitment in the fourth quarter of 2024 – see Note 23A(3) to the financial statements). The

balance of the rights in CPV is held, indirectly, by institutional financial investors from Israel.

|

| 4 |

It is noted that the carbon capture process constitutes an additional separate component of the natural gas projects under development, which are subject to separate uncertainty and risks and could be developed or executed (if ultimately

executed) according to a different timetable.

|

| 2. |

Brief description of the areas of activity (Cont.)

|

|

|

(1) |

Initiation and development of projects for generation of electricity (highly‑efficient power plants running on natural gas) with integration of future carbon‑capture potential4 (some of the projects in this area are being

developed by associated companies);

|

|

|

(2) |

Retail activities involving sale of electricity from renewable sources to commercial customers.

|

| 5 |

It is clarified that in some of the cases additional details are provided in order to present a comprehensive picture of the matter addressed or the relevant business environment. References to reports in this report include the

information provided in the said reports by means of the reference.

|

| 3. |

Main Developments in the Business Environment

|

|

|

3.1 |

General

|

|

|

A. |

Macro‑economic environment (particularly inflation and interest) – in 2024, in the U.S. and in Israel, there was a certain moderation in the inflation rates with an increase of 2.7% and 3.4%, respectively.

|

|

Dollar/shekel exchange rate*

|

2024

|

2023

|

Change

|

||||||

|

On December 31

|

3.647

|

3.627

|

0.6

|

%

|

|||||

|

On September 30

|

3.710

|

3.824

|

(3.0

|

)%

|

|||||

|

Average January– December

|

3.699

|

3.689

|

0.3

|

%

|

|||||

|

Average October– December

|

3.703

|

3.823

|

(3.1

|

)%

|

|

|

* |

The dollar/shekel exchange rate shortly before the approval date of the report (on March 6, 2025) is 3.615.

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.1 |

General (Cont.)

|

|

Bank of

|

|||||||

|

Israel

|

Federal

|

||||||

|

Israeli

|

U.S.

|

Interest

|

interest

|

||||

|

CPI

|

CPI

|

Rate

|

rate

|

||||

|

On March 6, 2025

|

115.4

|

317.6

|

4.5%

|

4.25%–4.50%

|

|||

|

On December 31, 2024

|

115.1

|

315.5

|

4.5%

|

4.25%–4.50%

|

|||

|

On September 30, 2024

|

115.2

|

314.8

|

4.5%

|

4.75%–5.00%

|

|||

|

On December 31, 2023

|

111.3

|

307.1

|

4.75%

|

5.25%–5.50%

|

|||

|

On September 30, 2023

|

111.2

|

307.0

|

4.75%

|

5.25%–5.50%

|

|||

|

On December 31, 2022

|

107.7

|

297.7

|

3.25%

|

4.25%–4.50%

|

|||

|

Change in 2024

|

3.4%

|

2.7%

|

(0.25)%

|

(1)%

|

|||

|

Change in 2023

|

3.3%

|

3.1%

|

1.5%

|

1%

|

|||

|

Change in the fourth quarter of 2024

|

(0.1)%

|

0.2%

|

0%

|

(0.50)%

|

|||

|

Change in the fourth quarter of 2023

|

0.1%

|

0.1%

|

0%

|

0.25%

|

|

|

B. |

Domestic and geopolitical instability in the defense (security) situation in Israel – 2023 was characterized by significant instability against the background of internal domestic events and geopolitical defense (security)

matters. On October 7, 2023, the “Iron Swords” war (“the War”) broke out in the Gaza Strip. Furthermore, during 2024 the War and the security tensions increased in additional areas, particularly in the northern part of the State, as well as

with Iran and the Houthis organization. The War and the security situation led to impacts and various restrictions for different time periods on the Israeli economy.

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

| 3.1 |

General (Cont.)

|

|

|

C. |

Change of the government in the U.S. – the recent policy changes stemming from entry into office of the new Trump government has created uncertainty along with opportunities in the energy sector in the U.S. Since his entry into

the position in January 2025, President Trump has issued executive orders promoting the production of fossil fuels, including with respect to natural gas and LNG and reduction of government support in the area of renewable energies relating

to, among other things, off‑shore wind. In addition, the Trump administration has suspended plans for Federal funding of clean energy and Federal licensing processes for wind projects. In the estimation of the CPV Group, as at the approval

date of the report, the said executive orders do not have a significant impact on the activities of the CPV Group in the renewable energy area, and they may have a favorable impact on the business environment and the overall sentiment in

the area of natural gas. Furthermore, President Trump has imposed tariffs or has announced the intention to impose tariffs on imports from certain countries, in such a manner that could impact equipment costs (both in the areas of

renewable‑energy projects and natural‑gas projects) and trigger disruptions in the supply chain and, ultimately, lead to an increase in the construction costs of projects6.

|

|

|

3.2 |

Activities in Israel

|

|

|

D. |

Update of the electricity tariffs – during 2023, there were a number of updates to the electricity tariffs such that the average generation component in 2023 was set at NIS 30.53 per kilowatt hour.

|

| 6 |

That stated in this Section above constitutes “forward‑looking” information, as it is defined in the Securities Law, which is based solely on the Company’s estimates as at the approval date of the report, which are subject to uncertainty

and changes that are not under the Company’s control.

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.2 |

Activities in Israel (Cont.)

|

|

|

D. |

(Cont.)

|

|

Period

|

2024

|

2023

|

Change

|

|||||||||

|

January–December average

|

30.10

|

30.53

|

(1.4

|

)%

|

||||||||

|

October–December average

|

30.07

|

30.39

|

(1.1

|

)%

|

||||||||

|

|

E. |

Public announcement regarding a proposal for changes in the tariff structure (the generation component) – for additional details – see Section 7.2.3 of Part A of the Periodic Report. It is clarified that the said proposal for

changes in the structure of the tariff for the generation component and the manner of its determination was published as part of a “Public Announcement” for receipt of in‑principle positions from the public prior to publication of a hearing

that will be subject to responses, changes and administrative processes and, therefore, at this early stage, there is no certainty regarding the final arrangements that will be stipulated in the decisions (if so stipulated) and the timing

thereof, which could be different – even significantly – than that stated in the “Public Announcement”. As at the approval date of the report, the Company had submitted a response as part of the “Public Announcement”, which includes a

professional opinion and comments with respect to the arrangements presented therein, and is continuing to study the proposed arrangements, their possible impacts on its activities (if they are ultimately stipulated in the decision), and

the manner of its response, and as at the present time it is not able to estimate the impact of the “Public Announcement”, if any, on its financial results. It is further clarified that changes in the generation component, including

following the Public Announcement, if approved, could have an unfavorable impact – even a significant one – on the results of the Company’s activities in Israel, as described further including in Section 19.2.1 of Part A of the Periodic

Report. In the Company’s estimation, in the present format of the generation component, in general, a change of 1 Agura in the generation component has an impact of about NIS 30 million on the segment’s EBITDA in Israel7.

|

|

|

F. |

Supplementary arrangements and granting of a supply license to Rotem – for details regarding provision of a supply license to Rotem and supplementary arrangements and imposition of certain covenants on Rotem commencing from

July 1, 2024 – see Section 7.3.7 of Part A of the Periodic Report.

|

| 7 |

That stated constitutes an indicative estimate of the impact of changes to the generation component on the Company, which is subject to changes in, among other things, as a result of the manner of determining the periodic generation

component and/or the manner of its application to the demand‑hours brackets, operating factors and/or occurrence of one or more of the risk factors to which the Company is exposed, as stated in Section 19.2 Section A of the Periodic

Report.

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.2 |

Activities in Israel (Cont.)

|

|

|

G. |

Decision regarding assignment of household consumers to – for details – see Section 7.2.2.3 of Part A of the Periodic Report. The decision permits the Company to expand the diversity of its customers by means of sale of

electricity, directly and/or indirectly to all household consumers.

|

|

|

H. |

Hearing regarding bilateral market regulation for generation facilities in the transmission network – for details – see Section 7.3.5 of Part A of the Periodic Report. It is noted that the Ramat Beka solar project that is being

developed by the Company, might operate under this regulation, to the extent it is actually advanced and subject to the final regulations that will be determined (if any).

|

|

|

I. |

Targets of the Israeli government regarding emission of greenhouse gases and amendment of the Excise Tax on Fuel Order – for details regarding the amendment to the Excise Order on Fuel (Imposition of Excise Tax), entered into

effect commencing from January 1, 2025, particularly relating to a gradual increase in the excise tax tariff on natural gas – see Section 7.2.8 of Part A of the Periodic Report. The increase in the Excise Tax on natural gas is expected to

raise the Group’s natural gas cost in Israel, where in the Company’s estimation part of this impact will be reduced by an increase in the Group’s revenues in Israel, if and to the extent there is an increase in the generation component and

subject to the expected impact of such an increase on the natural gas price, which is linked to the generation component. As noted above, the generation component has a material impact on both the Company’s revenues from sale of energy and

on its natural‑gas costs in Israel (for details – see Section 19.2.1 of Part A of the Periodic Report and Note 26C(5) to the Financial Statements). As at the approval date of the report, the Company is not able to estimate the full impact

of the amended Excise Tax Order on the Company’s results over time due to the uncertainty involved with the manner of determining the tariff, in general, and the generation component, in particular, and the manner in which the decision is

ultimately applied, as well as in light of possible impacts of conclusion of significant natural‑gas agreements in the economy. Regarding 2025, in the Company’s estimation the amended Excise Tax Order is not expected to have a material

impact on its results8.

|

|

|

J. |

Decision regarding methodology for determination of SMP tariff and decision with respect to determination of the maximum tariff for the supplementary tariffs – for details – see Sections 7.3.2 and 7.3.3 of Part A of the Periodic

Report.

|

| 8 |

The Company’s estimate regarding the impact of the decision with respect to the amendment to the Excise Order on the Company and the possibility of its reduction constitutes “forward‑looking” information as it

is defined in the Securities Law, regarding which there is no certainty it will be realized. Ultimately, the impacts of the amendment to the Excise Order might not be reduced and may not be expressed as a part of the generation component

due to the manner of determination of the generation component, which is not under the Company’s control.

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.3 |

Activities in the U.S.

|

|

|

K. |

Electricity and natural gas prices

|

|

For the

|

For the

|

|||||||||||||||||||||||

|

Year Ended

|

Three Months Ended

|

|||||||||||||||||||||||

|

Region

|

December 31

|

December 31

|

||||||||||||||||||||||

|

(Power Plant)

|

2024

|

2023

|

Change

|

2024

|

2023

|

Change

|

||||||||||||||||||

|

PJM West (Shore, Maryland)

|

33.83

|

33.06

|

2

|

%

|

34.71

|

36.31

|

(4

|

)%

|

||||||||||||||||

|

PJM AEP Dayton (Fairview)

|

30.73

|

30.81

|

0

|

%

|

32.48

|

31.30

|

4

|

%

|

||||||||||||||||

|

New York Zone G (Valley)

|

37.64

|

33.27

|

13

|

%

|

46.26

|

31.52

|

47

|

%

|

||||||||||||||||

|

Mass Hub (Towantic)

|

41.47

|

36.82

|

13

|

%

|

54.49

|

34.66

|

57

|

%

|

||||||||||||||||

|

PJM ComEd (Three Rivers)

|

25.55

|

26.68

|

(4

|

)%

|

24.58

|

26.31

|

(7

|

)%

|

||||||||||||||||

|

|

* |

Based on Day‑Ahead prices as published by the relevant ISO.

|

|

Power plant

|

For the year ended December 31

|

|||||||

|

2024

|

2023

|

|||||||

|

Shore

|

(6.25

|

)

|

(8.32

|

)

|

||||

|

Maryland

|

3.59

|

2.47

|

||||||

|

Fairview

|

(2.18

|

)

|

(1.90

|

)

|

||||

|

Valley

|

(1.00

|

)

|

(1.41

|

)

|

||||

|

Towantic

|

(2.77

|

)

|

(3.02

|

)

|

||||

|

Three Rivers

|

(1.01

|

)

|

(1.18

|

)

|

||||

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.3 |

Activities in the U.S. (Cont.)

|

|

|

K. |

Electricity and natural gas prices (Cont.)

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.3 |

Activities in the U.S. (Cont.)

|

|

|

K. |

Electricity and natural gas prices (Cont.)

|

|

For the Year Ended

|

For the Three Months Ended

|

|||||||||||||||||||||||

|

Region

|

December 31

|

December 31

|

||||||||||||||||||||||

|

(Power Plant)

|

2024

|

2023

|

Change

|

2024

|

2023

|

Change

|

||||||||||||||||||

|

Texas Eastern M‑3 (Shore, Valley – 70%)

|

2.07

|

1.90

|

9

|

%

|

2.37

|

1.78

|

33

|

%

|

||||||||||||||||

|

Transco Zone 5 North (Maryland)

|

2.51

|

2.74

|

(8

|

)%

|

2.38

|

2.77

|

(14

|

)%

|

||||||||||||||||

|

Texas Eastern M‑2 (Fairview)

|

1.71

|

1.63

|

5

|

%

|

1.99

|

1.61

|

24

|

%

|

||||||||||||||||

|

Dominion South Pt (Valley – 30%)

|

1.67

|

1.63

|

2

|

%

|

1.97

|

1.64

|

20

|

%

|

||||||||||||||||

|

Algonquin City Gate (Towantic)

|

3.03

|

2.94

|

3

|

%

|

4.42

|

2.69

|

64

|

%

|

||||||||||||||||

|

Chicago City Gate (Three Rivers)

|

2.12

|

2.30

|

(8

|

)%

|

2.21

|

2.28

|

(3

|

)%

|

||||||||||||||||

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.3 |

Activities in the U.S. (Cont.)

|

|

|

K. |

Electricity and natural gas prices (Cont.)

|

|

|

|

The Spark Spread is calculated based on the following formula:

|

|

For the

|

For the

|

|||||||||||||||||||||||

|

Year Ended

|

Three Months Ended

|

|||||||||||||||||||||||

|

December 31

|

December 31

|

|||||||||||||||||||||||

|

Power Plant9

|

2024

|

2023

|

Change

|

2024

|

2023

|

Change

|

||||||||||||||||||

|

Shore

|

19.55

|

19.95

|

(2

|

)%

|

18.36

|

24.03

|

(24

|

)%

|

||||||||||||||||

|

Maryland

|

16.51

|

14.15

|

17

|

%

|

18.29

|

17.20

|

6

|

%

|

||||||||||||||||

|

Valley

|

24.19

|

20.72

|

17

|

%

|

30.74

|

19.53

|

57

|

%

|

||||||||||||||||

|

Towantic

|

21.78

|

17.71

|

23

|

%

|

25.76

|

17.18

|

50

|

%

|

||||||||||||||||

|

Fairview

|

19.62

|

20.22

|

(3

|

)%

|

19.55

|

20.84

|

(6

|

)%

|

||||||||||||||||

|

Three Rivers

|

11.77

|

11.73

|

0

|

%

|

10.22

|

11.49

|

(11

|

)%

|

||||||||||||||||

|

|

* |

Based on electricity prices as shown in the above table, with a discount for the thermal conversion ratio (heat rate) of 6.9 MMBtu/MWh for Maryland, Shore and Valley, and a thermal conversion ratio of 6.5 MMBtu/MWh for Three Rivers,

Towantic and Fairview. It is clarified that the actual energy margins of the power plants of the CPV Group could be significantly different due to, among other things, the existence of Power Basis and a different breakdown in the scope of

the electricity sold in the peak and off‑peak hours in CPV’s power plants and that shown above (which was calculated based on the assumption of generation in all the hours of the 24‑hour period).

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.3 |

Activities in the U.S. (Cont.)

|

|

|

K. |

Electricity and natural gas prices (Cont.)

|

|

|

L. |

Tax on carbon emissions (RGGI)

|

|

Average for

|

Average for

|

|||||||||||||||||||||||

|

the year ended

|

the three months ended

|

|||||||||||||||||||||||

|

December 31

|

December 31

|

|||||||||||||||||||||||

|

2024

|

2023

|

Change

|

2024

|

2023

|

Change

|

|||||||||||||||||||

|

Price of carbon emission tax in the RGGI

|

||||||||||||||||||||||||

|

tenders ($ per short ton / 2,000 pounds)*

|

19.42

|

13.02

|

49

|

%

|

25.75

|

13.85

|

86

|

%

|

||||||||||||||||

|

Cost of the carbon emission tax (in terms

|

||||||||||||||||||||||||

|

of gas cost) ($ per MMBtu)**

|

1.16

|

0.77

|

49

|

%

|

1.53

|

0.82

|

86

|

%

|

||||||||||||||||

|

|

* |

The prices of the carbon emissions tax are presented on the assumption that the price of the tender that is held prior to a certain quarter represents the price of the carbon emissions tax. For example, the tender held in December 2024

will represent the price for the first quarter of 2025. It is noted that the actual price of the carbon emissions tax could be different than the tender prices as a result of transactions made in the secondary market.

|

|

|

** |

The cost of the carbon emissions tax (in terms of gas cost) is calculated under the assumption of emissions of carbon dioxide with a reference (ratio) of 119 lbs./MMBtu. It is noted that the actual carbon dioxide emissions ratio varies

between the different power plants, and in the estimation of the CPV Group a ratio of 119 lbs./MMBtu is a representative ratio for power plants running on natural gas.

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.3 |

Activities in the U.S. (Cont.)

|

|

|

M. |

Capacity revenues

|

|

Sub-Region

|

CPV Plants10

|

2025/2026

|

2024/2025

|

2023/2024

|

2022/2023

|

|

PJM RTO

|

269.92

|

28.92

|

34.13

|

50.00

|

|

|

PJM COMED

|

Three Rivers

|

269.92

|

28.92

|

34.13

|

–

|

|

PJM MAAC

|

Fairview, Maryland, Maple Hill

|

269.92

|

49.49

|

49.49

|

95.79

|

|

PJM EMAAC

|

Shore

|

269.92

|

54.95

|

49.49

|

97.86

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.3 |

Activities in the U.S. (Cont.)

|

|

|

M. |

Capacity revenues (Cont.)

|

| 11 |

That stated in this Section regarding the estimate of the CPV Group constitutes “forward‑looking” information as it is defined in the Securities Law, regarding which there is no certainty it will be

realized. Ultimately, the revenues of the CPV Group from capacity could be different (even significantly) as a result of, among other things, regulatory changes (including appeal processes or other processes in the PJM market or as part

of other municipal authorities), operating factors, changes in the business environment and/or the occurrence of one or more of the risk factors to which the CPV Group is exposed. In addition, as at the approval date of the report the

increase of the additional holdings in the Shore power plant had not yet been completed, the completion of which is subject to conditions that have not yet been fulfilled and there is no certainty regarding their fulfillment.

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.3 |

Activities in the U.S. (Cont.)

|

|

|

M. |

Capacity revenues (Cont.)

|

|

Sub-Area

|

CPV

Plants

|

Winter 2024/2025

|

Summer

2024

|

Winter 2023/2024

|

|

NYISO

Rest of the Market

|

–

|

66.30

|

168.91

|

127.25

|

|

Lower Hudson Valley

|

Valley

|

66.30

|

168.91

|

128.90

|

| 3. |

Main Developments in the Business Environment (Cont.)

|

|

|

3.3 |

Activities in the U.S. (Cont.)

|

|

|

M. |

Capacity revenues (Cont.)

|

|

Sub-Region

|

CPV Power Plants

|

2027/2028

|

2026/2027

|

2025/2026

|

|

ISO-NE

Rest of the Market

|

Towantic

|

117.70

|

85.15

|

85.15

|

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS)

|

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS) (Cont.)

|

|

|

A. |

Statement of income

|

|

For the Year Ended

|

||||||||

|

Section

|

December 31

|

|||||||

|

|

2024

|

2023

|

||||||

|

Revenues from sales and provision of services (1)

|

2,779

|

2,552

|

||||||

|

Cost of sales and provision of services (without depreciation and amortization) (2)

|

(1,931

|

)

|

(1,827

|

)

|

||||

|

Depreciation and amortization

|

(317

|

)

|

(288

|

)

|

||||

|

Gross profit

|

531

|

437

|

||||||

|

Administrative and general expenses

|

(263

|

)

|

(212

|

)

|

||||

|

Share in earnings of associated companies

|

166

|

242

|

||||||

|

Business development expenses

|

(45

|

)

|

(58

|

)

|

||||

|

Compensation for lost revenues

|

44

|

41

|

||||||

|

Other expenses, net

|

(56

|

)

|

(16

|

)

|

||||

|

Gain on loss of control in the renewable energies segment in the U.S.

|

259

|

–

|

||||||

|

Operating income

|

636

|

434

|

||||||

|

Financing expenses, net

|

(252

|

)

|

(197

|

)

|

||||

|

Loss from extinguishment of financial liabilities

|

(49

|

)

|

–

|

|||||

|

Income before taxes on income

|

335

|

237

|

||||||

|

Taxes on income expenses

|

(138

|

)

|

(68

|

)

|

||||

|

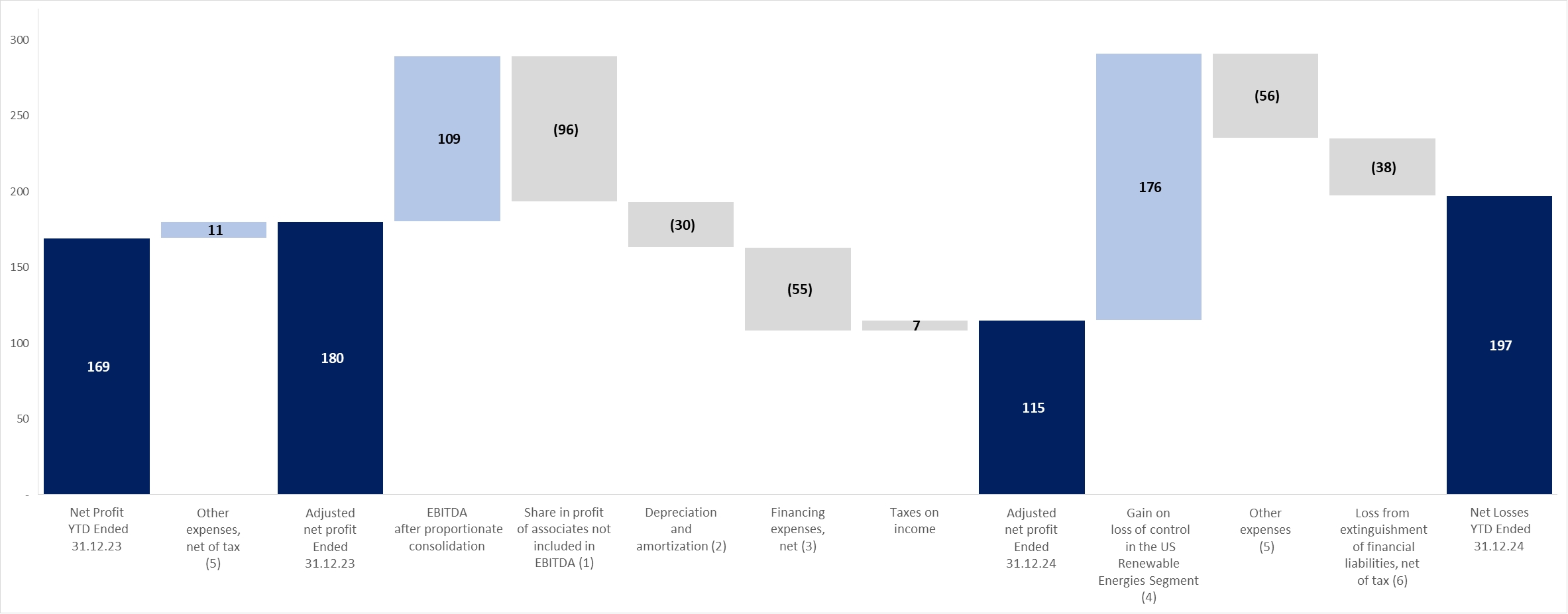

Net income for the year*

|

197

|

169

|

||||||

|

Attributable to:

|

||||||||

|

The Company’s shareholders

|

111

|

144

|

||||||

|

Holders of non‑controlling interests

|

86

|

25

|

||||||

|

|

* |

For an analysis of the change in the net income and a definition and analysis of the change in the adjusted net income – see Section 4G below.

|

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS) (Cont.)

|

|

|

A. |

Statement of income (Cont.)

|

|

Revenues

|

For the

|

Board’s Explanations

|

|||||||

|

Year Ended

|

|||||||||

|

December 31

|

|||||||||

|

2024

|

2023

|

||||||||

|

Revenues in Israel

|

|||||||||

|

Revenues from sale of energy to private customers

|

1,368

|

1,424

|

|||||||

|

Revenues from sale of energy to the System Operator and to other suppliers

|

165

|

120

|

Most of the increase, in the amount of about NIS 32 million, stems from the commercial operation of Zomet at the end of the second quarter of

2023.

|

||||||

|

Revenues in respect of capacity payments

|

171

|

59

|

Most of the increase stems from the commercial operation of Zomet at the end of the second quarter of 2023.

|

||||||

|

Revenues from sale of energy at cogeneration tariff

|

83

|

82

|

|||||||

|

Revenues from sale of steam

|

57

|

59

|

|||||||

|

Other revenues

|

23

|

59

|

Most of the decline derives from sales of electricity recognized in the corresponding period last year, in the amount of about NIS 26 million,

from the Zomet power plant prior to the commercial operation at the end of June 2023.

|

||||||

|

Total revenues from sale of energy and others in Israel (without infrastructure services)

|

1,867

|

1,803

|

|||||||

|

Revenues from private customers in respect of infrastructure services

|

445

|

480

|

|||||||

|

Total revenues in Israel

|

2,312

|

2,283

|

|||||||

|

Revenues in the U.S.

|

|||||||||

|

Revenues from sale of electricity from renewable energy

|

195

|

136

|

The increase derives mainly from the first‑time consolidation of the Mountain Wind project starting from the second quarter of 2023 and the

commercial operation of the Maple Hill and Stagecoach projects starting from the fourth quarter of 2023 and the second quarter of 2024, respectively. This increase was partly offset by discontinuance of consolidation of renewable energies

segment in November 2024, deriving from loss of control in CPV Renewable and as a result of transition to the equity method of accounting. For additional details – see Note 23E to the Financial Statements.

|

||||||

|

Revenues from sale of electricity (retail) activities and others

|

272

|

133

|

The increase stems mainly from an increase in the scope of the activities.

|

||||||

|

Total revenues in the U.S.

|

467

|

269

|

|||||||

|

Total revenues

|

2,779

|

2,552

|

|||||||

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS) (Cont.)

|

|

|

A. |

Statement of income (Cont.)

|

|

|

(2) |

Changes in the cost of sales and provision of services (not including depreciation and amortization):

|

|

Cost of Sales and

Provision of Services

|

For the

Year Ended

|

Board’s Explanations

|

|||||||

|

December 31

|

|||||||||

|

2024

|

2023

|

||||||||

|

Cost of sales in Israel

|

|||||||||

|

Natural gas and diesel oil

|

645

|

663

|

|||||||

|

Expenses in respect of acquisition of energy

|

320

|

303

|

Most of the increase stems mainly from the background of the maintenance work at the Rotem power plant in the first half of 2024 and the Gat power

plant in the second half of 2024.

|

||||||

|

Cost of transmission of gas

|

55

|

41

|

The increase stems mainly from the first‑time consolidation of Gat, starting from the second quarter of 2023 and the commercial operation of Zomet

starting from the end of the second quarter of 2023.

|

||||||

|

Salaries and related expenses

|

46

|

37

|

|||||||

|

Operating expenses

|

120

|

87

|

The increase stems mainly from the first‑time consolidation of Gat commencing from the second quarter of 2023 and the commercial operation of

Zomet starting from the end second quarter of 2023.

|

||||||

|

Other expenses

|

18

|

65

|

In 2023, includes mainly natural gas and other at the Zomet power plant prior to commercial operation at the end of June 2023.

|

||||||

|

Total cost of sales in Israel without infrastructure services

|

1,204

|

1,196

|

|||||||

|

Expenses in respect of infrastructure services

|

445

|

480

|

|||||||

|

Total cost of sales in Israel

|

1,649

|

1,676

|

|||||||

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS) (Cont.)

|

|

|

A. |

Statement of income (Cont.)

|

|

|

(2) |

Changes in the cost of sales and provision of services (not including depreciation and amortization): (Cont.)

|

|

Cost of sales and services in the U.S.

|

|||||||||

|

Cost of sales in respect of sale of electricity from renewable energy

|

60

|

49

|

The increase stems mainly from the first‑time consolidation of the Mountain Wind project, commencing from the second quarter of 2023 and

commercial operation of the Maple Hill and Stagecoach projects, starting from the fourth quarter of 2023 and the second quarter of 2024, respectively. This increase was partly offset by discontinuance of consolidation of renewable

energies segment in November 2024 deriving from loss of control in CPV Renewable and as a result of transition to the equity method of accounting. For additional details – see Note 23E to the Financial Statements.

|

||||||

|

Cost of sales in respect of sale of electricity (Retail) and others

|

222

|

102

|

The increase stems mainly from an increase in the scope of the activities.

|

||||||

|

Total cost of sales and provision of services in the U.S.

|

282

|

151

|

|||||||

|

Total cost of sales and provision of services

|

1,931

|

1,827

|

|||||||

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS) (Cont.)

|

|

|

B. |

EBITDA, FFO and net cash flows after debt service

|

|

|

1. |

EBITDA indices

|

|

|

2. |

“FFO” (funds from operations) – with respect to active projects – cash flows from current operating activities for the period (including changes in working capital) and less investments in property, plant and equipment and

periodic maintenance costs that are not included in the operating activities and less net interest payments. With respect to the rest of the Group’s activities – cash flows from current operating activities for the period (including

changes in working capital) and less net interest payments (to the extent they do not relate to projects under construction). It is clarified that investments in property, plant and equipment (under construction and/or in development)

including the net interest payments in respect thereof, are not included in FFO.

|

|

|

3. |

“Net cash flows after service of project debt” – the “FFO” less/plus payment of principal in respect of financial debt and/or taking out of project debt and non‑project debt (loans and/or debentures), and after adjustments for a

change in other credit from banks and a change in cash, including cash restricted for debt service and deposits (including to secure transactions hedging electricity margins).

|

| 12 |

It is clarified that income in respect of lost profits is included in EBITDA in the consolidated statements.

|

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS) (Cont.)

|

|

|

B. |

EBITDA, FFO and net cash flows after debt service (Cont.)

|

|

For the Year Ended

|

||||||||

|

December 31

|

||||||||

|

2024

|

2023

|

|||||||

|

Revenues from sales and provision of services

|

2,779

|

2,552

|

||||||

|

Cost of sales (without depreciation and amortization)

|

(1,931

|

)

|

(1,827

|

)

|

||||

|

Administrative and general expenses (without depreciation and amortization)

|

(247

|

)

|

(197

|

)

|

||||

|

Business development expenses

|

(45

|

)

|

(58

|

)

|

||||

|

Share in income of associated companies

|

166

|

242

|

||||||

|

Compensation for lost revenues

|

44

|

41

|

||||||

|

Consolidated EBITDA

|

766

|

753

|

||||||

|

Elimination of the share in income of associated companies

|

(166

|

)

|

(242

|

)

|

||||

|

Plus – Group’s share of the proportionate EBITDA of associated companies

|

||||||||

|

in the Energy Transition segment (1)

|

592

|

588

|

||||||

|

Plus – Group’s share of the proportionate EBITDA of activities in the

|

||||||||

|

renewable energies segment in the U.S. (2)

|

16

|

–

|

||||||

|

EBITDA after proportionate consolidation

|

1,208

|

1,099

|

||||||

| 13 |

It is noted that other companies might define EBITDA and FFO indices differently.

|

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS) (Cont.)

|

|

|

B. |

EBITDA, FFO and net cash flows after debt service (Cont.)

|

|

|

(1) |

Calculation of the Group’s share in the proportionate EBITDA, FFO and net cash flows after service of project debt of associated companies in the Energy Transition segment (in millions of NIS):

|

|

For the year ended

December 31, 2024

|

Fairview

|

Towantic

|

Maryland

|

(1)

Shore |

Valley

|

Three

Rivers

|

Total

|

|||||||||||||||||||||

|

Revenues from sales of energy

|

206

|

217

|

185

|

155

|

352

|

61

|

1,176

|

|||||||||||||||||||||

|

Cost of natural gas

|

91

|

98

|

73

|

73

|

127

|

36

|

498

|

|||||||||||||||||||||

|

Carbon emissions tax (RGGI)

|

–

|

41

|

33

|

47

|

80

|

–

|

201

|

|||||||||||||||||||||

|

Cost of sales – other expenses (without

|

||||||||||||||||||||||||||||

|

depreciation and amortization)

|

2

|

4

|

8

|

6

|

7

|

2

|

29

|

|||||||||||||||||||||

|

Gain (loss) on realization of transactions

|

||||||||||||||||||||||||||||

|

hedging the electricity margins

|

21

|

(12

|

)

|

(3

|

)

|

14

|

47

|

17

|

84

|

|||||||||||||||||||

|

Net energy margin

|

134

|

62

|

68

|

43

|

185

|

40

|

532

|

|||||||||||||||||||||

|

Revenues from capacity payments

|

18

|

122

|

16

|

19

|

58

|

4

|

237

|

|||||||||||||||||||||

|

Other income

|

4

|

6

|

9

|

6

|

3

|

2

|

30

|

|||||||||||||||||||||

|

Gross profit

|

156

|

190

|

93

|

68

|

246

|

46

|

799

|

|||||||||||||||||||||

|

Fixed costs (without depreciation and

|

||||||||||||||||||||||||||||

|

amortization)

|

14

|

21

|

28

|

28

|

76

|

13

|

180

|

|||||||||||||||||||||

|

Administrative and general expenses

|

||||||||||||||||||||||||||||

|

(without depreciation and amortization)

|

5

|

4

|

5

|

5

|

8

|

2

|

29

|

|||||||||||||||||||||

|

Gain (loss) from revaluation of unrealized

|

||||||||||||||||||||||||||||

|

hedging transactions

|

10

|

(1

|

)

|

(1

|

)

|

(6

|

)

|

–

|

–

|

2

|

||||||||||||||||||

|

Group’s share in proportionate

EBITDA in the Energy

|

||||||||||||||||||||||||||||

|

Transition segment (2)

|

147

|

164

|

59

|

29

|

162

|

31

|

592

|

|||||||||||||||||||||

|

Group’s share in FFO

|

106

|

157

|

21

|

18

|

68

|

15

|

385

|

|||||||||||||||||||||

|

Net cash flows after service of

project debt (3)

|

(4)289 |

|

65

|

8

|

17

|

(1

|

)

|

10

|

388

|

|||||||||||||||||||

| (1) |

At the Shore power plant – gas transmission costs (totaling in 2024 about NIS 22 million) are classified in accordance with IFRS 16 as depreciation expenses and, accordingly, are not included in the EBITDA.

|

| (2) |

It is noted that the increase in the holdings in the Shore and Maryland power plants in the fourth quarter of 2024, as detailed in Note 24C to the financial statements, did not have a significant impact on the results of the Energy

Transition segment in the U.S. in 2024.

|

| (3) |

It is pointed out that the financing agreements of the CPV Group include arrangements for mechanisms of the “cash sweep” type, in the framework of which all or part of the free cash flows of the projects is designated for repayment of

loan principal on a current basis along with a predetermined minimum repayment schedule relating to every long‑term loan. Accordingly, there could be an acceleration of execution of repayments upon occurrence of certain events and there

are also restrictions on distributions of dividends.

|

| (4) |

The net cash flows after debt service in Fairview include taking out of additional financing for the project as part of a refinancing made in the third quarter of 2024 (which was distributed as a dividend to the partners in the

project). For details – see Section 8.17.4 of Part A of the Periodic Report.

|

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS) (Cont.)

|

|

|

B. |

EBITDA, FFO and net cash flows after debt service (Cont.)

|

|

|

(1) |

Calculation of the Group’s share in the proportionate EBITDA, FFO and net cash flows after service of project debt of associated companies (in millions of NIS):

|

|

For the year ended

December 31, 2023

|

Fairview

|

Towantic

|

Maryland

|

(1)

Shore |

Valley

|

(2)

Three

Rivers

|

Total

|

|||||||||||||||||||||

|

Revenues from sales of energy

|

191

|

181

|

156

|

147

|

268

|

28

|

971

|

|||||||||||||||||||||

|

Cost of natural gas

|

81

|

90

|

77

|

71

|

107

|

17

|

443

|

|||||||||||||||||||||

|

Carbon emissions tax (RGGI)**

|

(1

|

)

|

27

|

20

|

29

|

43

|

–

|

118

|

||||||||||||||||||||

|

Cost of sales – other expenses (without

|

||||||||||||||||||||||||||||

|

depreciation and amortization)

|

2

|

3

|

7

|

6

|

6

|

–

|

24

|

|||||||||||||||||||||

|

Gain on realization of transactions hedging

|

||||||||||||||||||||||||||||

|

the electricity margins

|

32

|

(2

|

)

|

8

|

(1

|

)

|

77

|

–

|

114

|

|||||||||||||||||||

|

Net energy margin

|

141

|

59

|

60

|

40

|

189

|

11

|

500

|

|||||||||||||||||||||

|

Revenues from capacity payments

|

23

|

106

|

24

|

25

|

57

|

2

|

237

|

|||||||||||||||||||||

|

Other income

|

2

|

3

|

3

|

5

|

4

|

1

|

18

|

|||||||||||||||||||||

|

Gross profit

|

166

|

168

|

87

|

70

|

250

|

14

|

755

|

|||||||||||||||||||||

|

Fixed costs (without depreciation and

|

||||||||||||||||||||||||||||

|

amortization)

|

12

|

19

|

19

|

26

|

68

|

4

|

148

|

|||||||||||||||||||||

|

Administrative and general expenses

|

||||||||||||||||||||||||||||

|

(without depreciation and amortization)

|

4

|

5

|

4

|

5

|

8

|

1

|

27

|

|||||||||||||||||||||

|

Gain (loss) from revaluation of unrealized

|

||||||||||||||||||||||||||||

|

hedging transactions

|

(9

|

)

|

56

|

(1

|

)

|

(39

|

)

|

–

|

1

|

8

|

||||||||||||||||||

|

Group’s share in proportionate

EBITDA in the Energy

|

||||||||||||||||||||||||||||

|

Transition segment

|

141

|

200

|

63

|

–

|

174

|

10

|

588

|

|||||||||||||||||||||

|

Group’s share in FFO

|

124

|

103

|

(3)15 |

|

(4)5 |

|

75

|

–

|

322

|

|||||||||||||||||||

|

Net cash flows after service of project debt

|

11

|

(37

|

)

|

10

|

(8

|

)

|

11

|

–

|

(13

|

)

|

||||||||||||||||||

| (1) |

At the Shore power plant – gas transport costs (totaling in 2023 about NIS 22 million) are classified in accordance with IFRS 16 as depreciation expenses and, accordingly, are not included in the EBITDA.

|

| (2) |

The financial results of Three Rivers are included starting from the commercial operation date, which took place in the third quarter of 2023.

|

| (3) |

The FFO in 2023 includes a payment in respect of project for upgrading facilities in the Maryland power plant, in the amount of about NIS 8 million.

|

| (4) |

The FFO in 2023 includes a payment, in the amount of about NIS 9 million, in respect of significant maintenance work performed.

|

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS) (Cont.)

|

|

|

B. |

EBITDA, FFO and net cash flows after debt service (Cont.)

|

|

|

(2) |

Calculation of the Group’s share in EBITDA after proportionate consolidation of the renewable energies segment (in NIS millions):

|

|

January–

|

November–

|

Total

|

||||||||||||||

|

October

|

December

|

2024

|

Total

|

|||||||||||||

|

2024

|

2024

|

Proportionate

|

2023

|

|||||||||||||

|

Consolidated

|

Associated

|

Consolidation

|

Consolidated

|

|||||||||||||

|

Revenues

|

203

|

29

|

232

|

136

|

||||||||||||

|

Fixed costs (without depreciation and

|

||||||||||||||||

|

amortization)

|

(61

|

)

|

(5

|

)

|

(66

|

)

|

(41

|

)

|

||||||||

|

Administrative and general

|

(26

|

)

|

(4

|

)

|

(30

|

)

|

(23

|

)

|

||||||||

|

EBITDA from active projects

|

126

|

20

|

142

|

72

|

||||||||||||

|

Business development and other costs

|

(26

|

)

|

(4

|

)

|

(30

|

)

|

(41

|

)

|

||||||||

|

Share of the Group in EBITDA after

|

||||||||||||||||

|

proportionate consolidation in the renewable

|

||||||||||||||||

|

energies segment in the U.S.

|

96

|

16

|

112

|

31

|

||||||||||||

| 4. |

Analysis of the results of operations for the Year Ended December 31, 2024 (in millions of NIS) (Cont.)

|

|

|

B. |

EBITDA, FFO and net cash flows after debt service (Cont.)

|

|

|

(3) |

Set forth below is a breakdown of the EBITDA after proportionate consolidation data broken down by subsidiaries (on a consolidated basis) and the associated companies (on a proportionate basis, based on the rate of the holdings of the

CPV Group therein) as well as FFO and cash flows after service of project debt data (in NIS millions):

|

|

For the year ended

|

For the year ended

|

|||||||||||||||||||||||||||

|

Main projects in operation

|

Basis of

|

December 31, 2024

|

December 31, 2023

|

|||||||||||||||||||||||||

|

presentation

|

Net cash

|

Net cash

|

||||||||||||||||||||||||||

|

in the

|

EBITDA

|

flows

|

EBITDA

|

flows

|

||||||||||||||||||||||||

|

Company’s

|

after

|

after

|

after

|

after

|

||||||||||||||||||||||||

|

financial

|

proportionate

|

debt

|

proportionate

|

debt

|

||||||||||||||||||||||||

|

statements

|

consolidation

|

FFO

|

service

|

consolidation

|

FFO

|

service

|

||||||||||||||||||||||

|

Total operating projects in Israel and

|

||||||||||||||||||||||||||||

|

accompanying business activities (1)

|

Consolidated

|

670

|

498

|

(9)(8)361 |

|

602

|

483

|

412

|

||||||||||||||||||||

|

Business development costs,

|

||||||||||||||||||||||||||||

|

headquarters in Israel and other costs

|

Consolidated

|

(31

|

)

|

(70

|

)

|

(9)(8)59 |

|

(40

|

)

|

(43

|

)

|

(43

|

)

|

|||||||||||||||

|

Total Israel

|

639

|

428

|

420

|

562

|

440

|

369

|

||||||||||||||||||||||

|

Total operating projects (2)

|

Associated

|

592

|

385

|

388

|

589

|

322

|

(13

|

)

|

||||||||||||||||||||

|

Other costs

|

Consolidated

|

(4

|

)

|

(14

|

)

|

(14

|

)

|

(4

|

)

|

(4

|

)

|

(4

|

)

|

|||||||||||||||

|

Total energy transition in the U.S.

|

588

|

371

|

374

|

585

|

318

|

(17

|

)

|

|||||||||||||||||||||

|

Total operating projects (2) (3)

|

Associated

|

142

|

74

|

14

|

72

|

54

|

6

|

|||||||||||||||||||||

|

Business development and other costs

|

Associated

|

(30

|

)

|

(23

|

)

|

(23

|

)

|

(41

|

)

|

(41

|

)

|

(41

|

)

|

|||||||||||||||

|

Total renewable energy in the U.S.

|

|

|

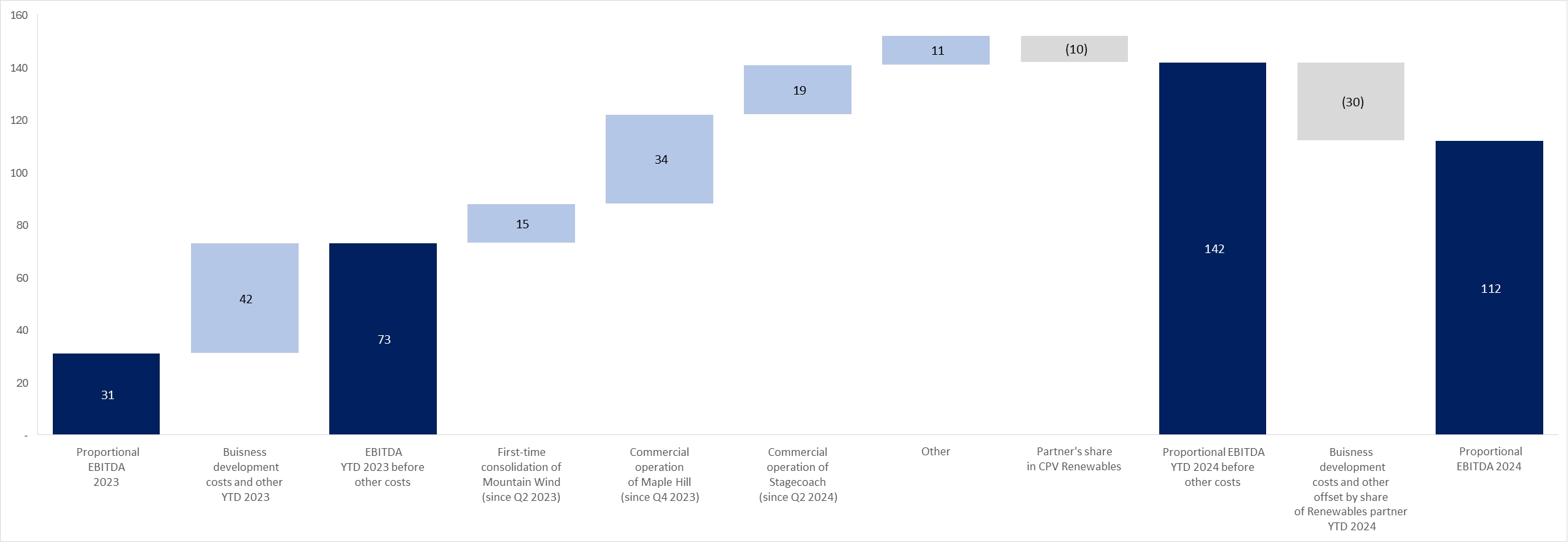

112

|

51

|

(9

|

)

|

31

|

13

|

(35

|

)

|

||||||||||||||||||

|

Total activities as part of the “others”

|

||||||||||||||||||||||||||||

|

segment (4)

|

Consolidated

|

(22

|

)

|

(22

|

)

|

(22

|

)

|

(26

|

)

|

(26

|

)

|

(26

|

)

|

|||||||||||||||

|

Headquarters in the United States (5) (6)

|

Consolidated

|

(89

|

)

|

(61

|

)

|

(61

|

)

|

(26

|

)

|

(41

|

)

|

(41

|

)

|

|||||||||||||||

|

Total United States

|

589

|

339

|

282

|

564

|

264

|

(119

|

)

|

|||||||||||||||||||||

|

Company headquarters (not allocated

|

||||||||||||||||||||||||||||

|

to the segments)

|

Consolidated

|

(20

|

)

|

(41

|

)

|

(37

|

)

|

(27

|

)

|

(56

|

)

|

(87

|

)

|

|||||||||||||||

|

Total consolidated (7)

|

1,208

|

726

|

665

|

1,099

|

648

|

163

|

||||||||||||||||||||||

| (1) |

The accompanying business activities in Israel include mainly virtual supply activities through OPC Israel, sale of electricity from facilities for generation of energy on the customer’s premises through a subsidiary (indirect) and

sale/purchase of natural gas, including with third parties through OPC Natural Gas.

|

| (2) |