SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

FOR ANNUAL AND TRANSITION REPORTS

PURSUANT TO SECTION 13 OR 15(d) THE SECURITIES EXCHANGE ACT OF 1934

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ___________

Commission File Number 0-4776

STURM, RUGER & COMPANY, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 06-0633559 |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

| 1 Lacey Place, Southport, Connecticut | 06890 |

| (Address of Principal Executive Offices) | (Zip Code) |

(203) 259-7843

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

| Common Stock, $1 par value | RGR | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☒ NO ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether registrant (1) has filed all reports required to be filed by Section 13 or Section 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or shorter such period of time that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). YES ☒ NO ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definition of “accelerated filer,” “large accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. Large accelerated filer ☒ Accelerated filer ☐ Non-accelerated filer ☐ Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. YES ☐ NO ☒

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of June 30, 2023:

Common Stock, $1 par value - $1,112,555,000

The number of shares outstanding of the registrant's common stock as of February 15, 2024: Common Stock, $1 par value –17,664,200 shares

DOCUMENTS INCORPORATED BY REFERENCE.

Portions of the registrant’s Proxy Statement relating to the 2024 Annual Meeting of Stockholders to be held May 30, 2024 are incorporated by reference into Part III (Items 10 through 14) of this Report.

TABLE OF CONTENTS

| PART IV | ||

| Item 15. | Exhibits and Financial Statement Schedules | 81 |

| Signatures | 84 | |

| Exhibit Index | 85 | |

| Financial Statement Schedule | 87 | |

| Exhibits | 89 | |

EXPLANATORY NOTE:

In this Annual Report on Form 10-K, Sturm, Ruger & Company, Inc. and Subsidiary (the “Company”) makes forward-looking statements and projections concerning future expectations. Such statements are based on current expectations and are subject to certain qualifying risks and uncertainties, such as market demand, sales levels of firearms, anticipated castings sales and earnings, the need for external financing for operations or capital expenditures, the results of pending litigation against the Company, the impact of future firearms control and environmental legislation, and accounting estimates, any one or more of which could cause actual results to differ materially from those projected. Words such as “expect,” “believe,” “anticipate,” “intend,” “estimate,” “will,” “should,” “could” and other words and terms of similar meaning, typically identify such forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date made. The Company undertakes no obligation to publish revised forward-looking statements to reflect events or circumstances after the date such forward-looking statements are made or to reflect the occurrence of subsequent unanticipated events.

PART I

ITEM 1—BUSINESS

Company Overview

Sturm, Ruger & Company, Inc. and Subsidiary (the “Company”) is principally engaged in the design, manufacture, and sale of firearms to domestic customers. Virtually all of the Company’s sales for the year ended December 31, 2023 were from the firearms segment, with less than 1% from the castings segment. Export sales represent approximately 6% of firearms sales. The Company’s design and manufacturing operations are located in the United States and almost all product content is domestic.

The Company has been in business since 1949 and was incorporated in its present form under the laws of Delaware in 1969. The Company primarily offers products in three industry product categories – rifles, pistols, and revolvers. The Company’s firearms are sold through independent wholesale distributors, principally to the commercial sporting market.

The Company manufactures and sells investment castings made from steel alloys and metal injection molding (“MIM”) parts for internal use in the firearms segment and has minimal sales to outside customers. The castings and MIM parts are sold to outside customers, either directly or through manufacturers’ representatives.

For the years ended December 31, 2023, 2022, and 2021, net sales attributable to the Company's firearms operations were $540.7 million, $593.3 million and $728.1 million. The balance of the Company's net sales for the aforementioned periods was attributable to its castings operations.

Firearms Products

The Company presently manufactures firearm products, under the “Ruger” name and trademark, in the following industry categories:

| Rifles | Revolvers | ||

| ● | Single-shot | ● | Single-action |

| ● | Autoloading | ● | Double-action |

| ● | Bolt-action | ||

| ● | Modern sporting | ||

| Pistols | |||

| ● | Rimfire autoloading | ||

| ● | Centerfire autoloading | ||

In addition, the Company manufactures lever-action rifles under the “Marlin” name and trademark.

Most firearms are available in several models based upon caliber, finish, barrel length, and other features.

Rifles

A rifle is a long gun with spiral grooves cut into the interior of the barrel to give the bullet a stabilizing spin after it leaves the barrel. Net sales of rifles by the Company accounted for $306.8 million, $305.4 million, and $317.5 million of total net sales for the years 2023, 2022, and 2021, respectively.

Pistols

A pistol is a handgun in which the ammunition chamber is an integral part of the barrel and which typically is fed ammunition from a magazine contained in the grip. Net sales of pistols by the Company accounted for $131.4 million, $184.7 million, and $278.4 million of revenues for the years 2023, 2022, and 2021, respectively.

Revolvers

A revolver is a handgun that has a cylinder that holds the ammunition in a series of chambers which are successively aligned with the barrel of the gun during each firing cycle. There are two general types of revolvers, single-action and double-action. To fire a single-action revolver, the hammer is pulled back to cock the gun and align the cylinder before the trigger is pulled. To fire a double-action revolver, a single trigger pull advances the cylinder and cocks and releases the hammer. Net sales of revolvers by the Company accounted for $72.5 million, $70.0 million, and $84.4 million of revenues for the years 2023, 2022, and 2021, respectively.

Accessories

The Company also manufactures and sells accessories and replacement parts for its firearms. These sales accounted for $30.0 million, $33.2 million, and $47.8 million of total net sales for the years 2023, 2022, and 2021, respectively.

Castings Products

Net sales attributable to the Company’s casting operations (excluding intercompany transactions) accounted for $3.0 million, $2.6 million, and $2.6 million, for 2023, 2022, and 2021, respectively. These sales represented less than 1% of total net sales in each of 2023, 2022, and 2021.

Manufacturing

Firearms

The Company produces some of its pistol models, most of its revolvers, and some of its rifle models at the Newport, New Hampshire facility. One model of revolver, one model of rifle, and most of the Company’s pistols are produced at the Prescott, Arizona facility. Some rifle models and pistol models are produced at the Mayodan, North Carolina facility.

Many of the basic metal component parts of the firearms manufactured by the Company are produced by the Company's castings segment through processes known as precision investment casting. The Company also uses many MIM parts in its firearms. See "Manufacturing- Investment Castings and Metal Injected Moldings" below for a description of these processes. The Company believes that investment castings and MIM parts provide greater design flexibility and result in component parts which are generally close to their ultimate shape and, therefore, require less machining than processes requiring machining a solid billet of metal to obtain a part. Through the use of investment castings and MIM parts, the Company endeavors to produce durable and less costly component parts for its firearms.

All assembly, inspection, and testing of firearms manufactured by the Company are performed at the Company's manufacturing facilities. Every firearm, including every chamber of every revolver manufactured by the Company, is test-fired prior to shipment.

Investment Castings and Metal Injection Moldings

To produce a product by the investment casting method, a wax model of the part is created and coated (“invested”) with several layers of ceramic material. The shell is then heated to melt the interior wax, which is poured off, leaving a hollow mold. To cast the desired part, molten metal is poured into the mold and allowed to cool and solidify. The mold is then broken off to reveal a near net shape cast metal part.

Metal injection molding is a three part powder metallurgy process by which a feedstock consisting of finely powdered metal and binders is processed through injection molding, debinding, and sintering equipment to produce steel, stainless steel, and alloy parts of complex shape and geometry. This process allows for high volume production while eliminating many of the wastes of traditional metal working methods, yielding net shape and near net shape parts.

Marketing and Distribution

Firearms

The Company's firearms are primarily marketed through a network of federally licensed, independent wholesale distributors who purchase the products directly from the Company. They resell to federally licensed, independent retail firearms dealers who in turn resell to legally authorized end users. All retail purchasers are subject to a point-of-sale background check by law enforcement. These end users include sportsmen, hunters, people interested in self-defense, law enforcement and other governmental organizations, and gun collectors. Each domestic distributor carries the entire line of firearms manufactured by the Company for the commercial market. Currently, 15 distributors service the domestic commercial market, with an additional 26 distributors servicing the domestic law enforcement market and 44 distributors servicing the export market.

In 2023, the Company’s largest customers and the percent of firearms sales they represented were as follows: Lipsey’s – 24%; Davidson’s - 19%; and Sports South - 15%.

In 2022, the Company’s largest customers and the percent of firearms sales they represented were as follows: Lipsey’s - 23%; Davidson’s - 23%; and Sports South - 21%.

In 2021, the Company’s largest customers and the percent of firearms sales they represented were as follows: Lipsey’s - 21%; Sports South - 19%; and Davidson’s - 19%.

The Company employs 18 employees who service these distributors and call on retailers and law enforcement agencies. Because the ultimate demand for the Company's firearms comes from end users rather than from the independent wholesale distributors, the Company believes that the loss of any distributor would not have a material, long-term adverse effect on the Company, but may have a material adverse effect on the Company’s financial results for a particular period.

The Company considers its relationships with its distributors to be satisfactory.

The Company also exports its firearms through a network of selected commercial distributors and directly to certain foreign customers, consisting primarily of law enforcement agencies and foreign governments. Foreign sales were 6% of the Company’s consolidated net sales for the year ended December 31, 2023, and 6% of the Company’s consolidated net sales for the year ended December 31, 2022, and 5% of the Company's consolidated net sales for year ended December 31, 2021.

The Company does not consider its overall firearms business to be predictably seasonal; however, orders of many models of firearms from the distributors tend to be stronger in the first quarter of the year and weaker in the third quarter of the year.

Investment Castings and Metal Injection Moldings

The castings segment provides castings and MIM parts for the Company’s firearms segment. In addition, the castings segment produces some products for a number of customers in a variety of industries.

Competition

Firearms

Competition in the firearms industry is intense and comes from both foreign and domestic manufacturers. While some of these competitors concentrate on a single industry product category such as rifles or pistols, several competitors manufacture products in all four industry categories (rifles, shotguns, pistols, and revolvers). The principal methods of competition in the industry are product innovation, quality, availability, brand, and price. The Company believes that it can compete effectively with all of its present competitors.

Investment Castings and Metal Injection Moldings

There are a large number of investment castings and MIM manufacturers, both domestic and foreign, with which the Company competes. Competition varies based on the type of investment castings products and the end use of the product. Companies offering alternative methods of manufacturing such as wire electric discharge machining (EDM) and advancements in computer numeric controlled (CNC) machining also compete with the Company’s castings segment. Many of these competitors are larger corporations than the Company with substantially greater financial resources than the Company, which could affect the Company’s ability to compete with these competitors. The principal methods of competition in the industry are quality, price, and production lead time.

Human Capital

The Company is an equal opportunity employer dedicated to the attraction, development, and retention of our employees by providing a preferred work environment that promotes and celebrates our core values of Integrity, Respect, Innovation and Teamwork. Our goal is to develop, motivate, retain and reward passionate and dedicated employees.

As of February 1, 2024, the Company employed approximately 1,820 full-time employees, approximately 32% of whom had at least ten years of service with the Company.

The Company attracts candidates and retains employees by offering competitive compensation packages, which include:

| ● | Base wages, |

| ● | Profit sharing, |

| ● | Medical and welfare benefits, |

| ● | Holidays and other paid time off, and |

| ● | 401(k) plan participation and matching program. |

The Company believes its compensation packages:

| ● | Provide a base level of compensation to reflect an individual’s role and responsibilities, |

| ● | Recognize and reward employees for the Company’s success, and |

| ● | Provide for the safety, security and well-being of employees. |

Our primary vehicle for human capital development is Ruger University, which has a mission to:

| ● | Enhance the understanding of our industry, Company and culture, |

| ● | Strengthen the technical, interpersonal and leadership skills of each employee, and |

| ● | Allow employees to positively change their own lives while creating value for all Ruger stakeholders. |

In addition to providing a competitive compensation package and emphasizing the development of employees, the Company retains its employees by maintaining a safe, responsible, and preferred workplace. The Company is committed to conducting business in conformance with the highest ethical standards and in compliance with all applicable legal and regulatory requirements. The “Code of Business Conduct and Ethics” and the “Corporate Compliance Program” are two active programs that guide the Company’s practices to achieve these goals.

In addition, since the beginning of the global outbreak of the Coronavirus disease 2019 (“COVID-19”) in March 2020, the Company continues to take multiple proactive steps to promote the health and safety of its employees and maintain a clean, safe, and preferred workplace.

To assess and improve employee retention and engagement, the Company surveys employees on an annual basis with the assistance of a third-party consultant, and takes actions to address areas of employee concern and build on the competencies that are important for our future success.

Research and Development

In 2023, 2022, and 2021, the Company spent approximately $9.8 million, $9.6 million, and $11.7 million, respectively, on research and development activities relating to new products and the improvement of existing products. Research and development expenses are included in costs of products sold. As of February 1, 2024, the Company had approximately 67 employees whose primary responsibilities were research and development activities.

Patents and Trademarks

The Company owns various United States and foreign patents and trademarks which have been secured over a period of years and which expire at various times. It is the policy of the Company to apply for patents and trademarks whenever new products or processes deemed commercially valuable are developed or marketed by the Company. The Company deems its patents and trademarks to be valuable and therefore works to police and protect them.

Environmental Matters

The Company is committed to achieving high standards of environmental quality and product safety, and strives to provide a safe and healthy workplace for its employees and others in the communities in which it operates. The Company has programs in place that monitor compliance with various environmental regulations. However, in the normal course of its manufacturing operations the Company is subject to governmental proceedings and orders pertaining to waste disposal, air emissions, and water discharges into the environment. These regulations are integrated into the Company’s manufacturing, assembly, and testing processes. The Company believes that it is generally in compliance with applicable environmental regulations and that the outcome of any environmental proceedings and orders will not have a material adverse effect on the financial position of the Company, but could have a material adverse effect on the financial results for a particular period.

Information about our Executive Officers

Set forth below are the names, ages, and positions of the executive officers of the Company. Officers serve at the discretion of the Board of Directors of the Company.

| Name | Age | Position With Company |

| Christopher J. Killoy | 65 | President and Chief Executive Officer |

| Thomas A. Dineen | 55 | Senior Vice President, Treasurer, and Chief Financial Officer |

| Kevin B. Reid, Sr. | 63 | Vice President, General Counsel, and Corporate Secretary |

| Shawn C. Leska | 52 | Vice President, Sales |

| Sarah F. Colbert | 43 | Vice President, Administration |

| Timothy M. Lowney | 60 | Vice President of Operations for Newport, Prescott and RPM Manufacturing |

| Michael W. Wilson | 47 | Vice President of Operations for New Product Development, Product Engineering and Mayodan Manufacturing |

| Robert J. Werkmeister, Jr. | 49 | Vice President of Marketing |

Christopher J. Killoy became President & Chief Executive Officer on May 9, 2017. Previously he served as President and Chief Operating Officer since January 1, 2014. Prior to that he served as Vice President of Sales and Marketing since November 27, 2006. Mr. Killoy originally joined the Company in 2003 as Executive Director of Sales and Marketing, and subsequently served as Vice President of Sales and Marketing from November 1, 2004 to January 25, 2005.

Thomas A. Dineen became Senior Vice President on July 10, 2017. Previously he served as Vice President since May 24, 2006. Prior to that he served as Treasurer and Chief Financial Officer since May 6, 2003 and had been Assistant Controller since 2001. Mr. Dineen joined the Company as Manager, Corporate Accounting in 1997.

Kevin B. Reid, Sr. became Vice President and General Counsel on April 23, 2008. Previously he served as the Company’s Director of Marketing from June 4, 2007. Mr. Reid joined the Company in July 2001 as an Assistant General Counsel.

Shawn C. Leska became Vice President, Sales on November 6, 2015. Mr. Leska joined the Company in 1989 and has served in a variety of positions in the sales department. Most recently, Mr. Leska served as Director of Sales since 2011.

Sarah F. Colbert became Vice President of Administration on June 1, 2017. Ms. Colbert has served the Company in various human resource and legal capacities since joining the Company in 2011.

Timothy M. Lowney became Vice President of Operations for Newport, Prescott and RPM Manufacturing on June 15, 2023. Previously, he served as the Company’s Vice President of Prescott Operations since April 1, 2019. Mr. Lowney joined the Company in January 2007.

Michael W. Wilson became Vice President of Operations for New Product Development, Product Engineering and Mayodan Manufacturing on June 15, 2023. Previously, he served as the Company’s Vice President of Mayodan Operations since June 1, 2017. Mr. Wilson joined the Company in July 2007.

Robert J. Werkmeister, Jr. became Vice President of Marketing upon joining the Company on June 1, 2017. Mr. Werkmeister has served as the Company’s Director of Marketing since January 2013 as President and founder of Symbolic, Inc., a full-service marketing agency. While with Symbolic, Rob began working with Ruger as a client in 2002 and has been the primary strategic marketing driver for the Ruger account since 2007.

Where You Can Find More Information

The Company is subject to the informational requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and accordingly, files its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Definitive Proxy Statements, Current Reports on Form 8-K, and other information with the Securities and Exchange Commission (the “SEC”). As an electronic filer, the Company's public filings are maintained on the SEC's Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The address of that website is http://www.sec.gov.

The Company makes its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Definitive Proxy Statements, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act accessible free of charge through the Company's Internet site after the Company has electronically filed such material with, or furnished it to, the SEC. The address of that website is http://www.ruger.com. However, such reports may not be accessible through the Company's website as promptly as they are accessible on the SEC’s website.

Additionally, the Company’s corporate governance materials, including its Corporate Governance Guidelines, the charters of the Audit, Compensation, Nominating and Corporate Governance, Risk Oversight and Capital Policy committees, and the Code of Business Conduct and Ethics may also be found under the “Investor Relations” subsection of the “Corporate” section of the Company’s Internet site at http://www.ruger.com/corporate. A copy of the foregoing corporate governance materials is available upon written request to the Corporate Secretary at Sturm, Ruger & Company, Inc., 1 Lacey Place, Southport, Connecticut 06890.

ITEM 1A—RISK FACTORS

The Company’s operations could be affected by various risks, many of which are beyond its control. Based on current information, the Company believes that the following identifies the most significant risk factors that could have a material, adverse effect on its business, operating results, and financial condition.

Past financial performance may not be a reliable indicator of future performance and historical trends should not be used to anticipate results or trends in future periods.

In evaluating the Company’s business, the following risk factors, as well as other information in this report, should be carefully considered.

Changes in government policies and firearms legislation could adversely affect the Company’s financial results.

The sale, purchase, ownership, and use of firearms are subject to thousands of federal, state and local governmental regulations. The basic federal laws are the National Firearms Act, the Federal Firearms Act, and the Gun Control Act of 1968. Federal law generally prohibits the private ownership of fully automatic weapons manufactured after 1986 and places certain restrictions on the interstate sale of firearms unless certain licenses are obtained. The Company does not manufacture fully automatic weapons and holds all necessary licenses under these federal laws. If the scope of the National Firearms Act is expanded to regulate firearms currently regulated by the Gun Control Act, it could make acquisition of commonly owned and used firearms more expensive and complicated for consumers, which could have a material adverse impact on demand for Company products. Several states currently have laws in effect similar to the aforementioned legislation.

In 2005, Congress enacted the Protection of Lawful Commerce in Arms Act (“PLCAA”). The PLCAA was enacted to address abuses by cities and agenda-driven individuals who wrongly sought to make firearms manufacturers liable for legally manufactured and lawfully sold products if those products were later used in criminal acts. The Company believes the PLCAA merely codifies common sense and long standing tort principles. If the PLCAA is repealed or efforts to circumvent it are successful and lawsuits similar to those filed by cities and agenda-driven individuals in the late 1990s and early 2000s are allowed to proceed, it could have a material adverse impact on the Company.

Currently, federal and several states’ legislatures are considering additional legislation relating to the regulation of firearms, and a number of new laws have been enacted at the federal, state, and local level. Enacted legislation and proposed bills are numerous and extremely varied, but many seek to limit magazine capacity, restrict or ban the sale and, in some cases, the ownership of various types of firearms, or ban commonly owned firearms with certain features. Other legislation seeks to require new technologies, such as microstamping and so-called “smart gun” technology, which are not proven, reliable or feasible.

The Company believes that the lawful private ownership of firearms is guaranteed by the Second Amendment to the United States Constitution and that the widespread private ownership of firearms in the United States will continue. However, there can be no assurance that the regulation of firearms will not become more restrictive in the future and that any such restriction would not have a material adverse effect on the business of the Company. Numerous bills regulating the ownership of firearms have been proposed at the state and federal levels, and these bills propose a wide variety of restrictions including, for example, limiting the number of firearms that may be purchased in a specified time, increasing the age for ownership, imposing additional licensing or registration requirements, creating additional restrictions on certain, common firearm features, and levying new taxes on firearms and/or ammunition.

The Company’s results of operations could be further adversely affected if legislation with diverse requirements is enacted.

With literally thousands of laws being proposed at the federal, state and local levels, if even a small percentage of these laws are enacted and they are incongruent, the Company could find it difficult, expensive or even practically impossible to comply with them, impeding new product development and distribution of existing products.

The Company’s results of operations could be adversely affected by litigation.

The Company faces risks arising from various asserted and unasserted litigation matters. These matters include, but are not limited to, assertions of allegedly defective product design or manufacture, alleged failure to warn, claimed unfair trade practices, purported class actions against firearms manufacturers, generally seeking relief such as medical expense reimbursement, property damages, and punitive damages arising from accidents involving firearms or the criminal misuse of firearms, and those lawsuits filed on behalf of municipalities alleging harm to the general public. Various factors or developments can lead to changes in current estimates of liabilities such as final adverse judgment, significant settlement or changes in applicable law. A future adverse outcome in any one or more of these matters could have a material adverse effect on the Company’s financial results. See Note 20 to the financial statements which are included in this Annual Report on Form 10-K.

The Company relies upon relationships with financial institutions.

The Company utilizes the services of numerous financial institutions, including banks, insurance carriers, transfer agents, and others. Anti-gun politicians, gun-control activists, and others may target these institutions and attempt to pressure them into ceasing to do business with the Company, or to use financial relationships to impose unacceptable and improper restrictions on the Company’s business, which could have a material adverse impact on the Company’s business, operating results, and financial condition.

The Company’s insurance may be insufficient to protect us from claims or losses.

The Company maintains insurance coverage with third-party insurers. However, not every risk or liability is or can be protected by insurance, and, for those risks it insures, the limits of coverage it purchases or that are reasonably obtainable in the market may not be sufficient to cover all actual losses or liabilities incurred. Moreover, there is a risk that commercially available liability insurance will not continue to be available to the Company at a reasonable cost, if at all. If liability claims or losses exceed the Company’s current or available insurance coverage, its business may be harmed.

The Company’s results of operations could be adversely affected by a decrease in demand for Company products.

If demand for the Company’s products decreases significantly, the Company would be unable to efficiently utilize its capacity, and profitability would suffer. Decreased demand could result from a macroeconomic downturn, or could be specific to the firearms industry as a result of social, political, or other factors.

If the decrease in demand occurs abruptly, the adverse impact would be even greater.

The financial health of the Company’s independent distributors is critical to its success.

Over 90% of the Company’s sales are made to 15 federally licensed, independent wholesale distributors. The Company reviews its distributors’ financial statements and has credit insurance for many of them. However, the Company’s credit evaluations of distributors and credit insurance may not be completely effective, especially if higher interest rates continue to exact a financial strain. If one or more independent distributors experience financial distress or liquidity issues, the Company’s sales could be adversely affected and the Company may not be able to collect its accounts receivable on a timely basis, which would have an adverse impact on its operating results and financial condition.

The Company must comply with various laws and regulations pertaining to workplace safety and environment, environmental matters, and firearms manufacturing.

In the normal course of its manufacturing operations, the Company is subject to numerous federal, state and local laws and governmental regulations, and governmental proceedings and orders. These laws and regulations pertain to matters like workplace safety and environment, firearms serial number tracking and control, waste disposal, air emissions and water discharges into the environment. Noncompliance with any one or more of these laws and regulations could have a material adverse impact on the Company.

Misconduct of the Company’s employees or contractors could cause the Company to lose customers and could have a significant adverse impact on its business and reputation.

Misconduct, fraud or other improper activities by the Company’s employees or contractors could have a material adverse impact on its business and reputation. Such misconduct could include the failure to comply with federal, state, local or foreign government procurement regulations, regulations regarding the protection of personal information, laws and regulations relating to antitrust and any other applicable laws or regulations.

Product quality and performance is important to the Company’s success.

The Company has a long history of producing rugged, reliable firearms for the commercial market. While the Company believes its record of designing, manufacturing, and selling high-quality products demonstrates its commitment to safety and quality, the Company has occasionally identified design and/or manufacturing issues with respect to some firearms and, as a result, issued a product safety bulletin or initiated a product recall. Depending upon the volume of products the Company has shipped into the market, any future recall or safety bulletin could harm its reputation, cause the Company to lose business, and cause the Company to incur significant support and repair costs.

Business disruptions at one of the Company’s manufacturing facilities could adversely affect the Company’s financial results.

The Newport, New Hampshire, Prescott, Arizona, Mayodan, North Carolina, and Earth City, Missouri facilities are critical to the Company’s success. These facilities house the Company’s principal production, research, development, engineering, design, and shipping operations. Any event that causes a disruption of the operation of any of these facilities for even a relatively short period of time could have a material adverse effect on the Company’s ability to produce and ship products and to provide service to its customers.

The Company relies on its information and communications systems in its operations. Security breaches and other disruptions could adversely affect its business and results of operations.

Cybersecurity threats are significant and evolving and include, among others, malicious software, attempts to gain unauthorized access to data, and other electronic security breaches that could lead to disruptions in mission critical systems, unauthorized release of confidential or otherwise protected information and corruption of data. In addition to security threats, the Company is also subject to other systems failures, including network, software or hardware failures, whether caused by the Company, third-party service providers, natural disasters, power shortages, terrorist attacks or other events. The unavailability of the Company’s information or communications systems, the failure of these systems to perform as anticipated or any significant breach of data security could cause loss of data, disrupt Company operations, lead to financial losses from remedial actions, require significant management attention and resources, and negatively impact the Company’s reputation among its customers and the public, which could have a negative impact on the Company’s financial condition, results of operations and liquidity.

The lack of available raw materials or component parts could disrupt or even cease the Company’s manufacturing operations. Even if manufacturing operations are not disrupted, increased costs of raw materials and component parts could adversely affect the Company’s financial results.

Third parties supply the Company with various raw materials for its firearms and castings, such as fabricated steel components, walnut, birch, beech, maple and laminated lumber for rifle stocks, wax, ceramic material, metal alloys, various synthetic products and other component parts. There is a limited supply of these materials in the marketplace at any given time, which can cause the purchase prices to vary based upon numerous market factors. If market conditions result in a significant prolonged inflation of certain prices or if adequate quantities of raw materials cannot be obtained, the Company’s manufacturing processes could be interrupted and the Company’s financial condition or results of operations could be materially adversely affected.

The Company relies primarily on third parties for transportation of the products it manufactures as well as delivery of its raw materials.

Any increase in the cost of the transportation of the Company’s raw materials or products, as a result of increases in fuel or labor costs, higher demand for logistics services, consolidation in the transportation industry or otherwise, increased restrictions on the transportation of firearms, may adversely affect its results of operations. If any of these providers were to fail to deliver raw materials to the Company in a timely manner, the Company may be unable to manufacture and deliver its products in a timely manner. In addition, if any of these third parties were to cease operations or cease doing business with the Company, the Company may be unable to replace them at a reasonable cost. And such failure of a third-party transportation provider could harm the Company’s reputation, negatively affect its customer relationships and have a material adverse effect on its financial position and results of operations.

Availability and retention of the Company’s labor force, especially its key management, is critical to the success of the Company.

The Company has observed an overall tightening and increasingly competitive labor market, which could inhibit its ability to recruit and retain the employees it requires and could lead to increased costs, such as additional overtime to meet demand and increased wage rates to attract and retain employees. The Company relies on the knowledge, experience, and leadership skills of its senior management team. The Company’s senior executives are not bound by employment agreements. The loss of the services of one or more of the Company’s senior executives or other key personnel could have a significant adverse impact on its business.

A pandemic, like the COVID-19 pandemic, could have a significant adverse impact on the Company’s operations, financial results, cash flow, and financial condition.

The COVID-19 pandemic created significant uncertainty and adversely impacted many industries throughout the global economy. Thus far, the Company has been able to mitigate the impact of COVID-19 through its proactive measures. The extent to which a future pandemic may impact the Company’s operations, financial results, cash flow, and financial condition is difficult to predict and dependent upon many factors over which the Company has no control. These factors include, but are not limited to, the duration and severity of the pandemic; government restrictions on businesses and individuals; potential significant adverse impacts on the Company’s employees, customers, suppliers, or service providers; the impact on U.S. and global economies and the timing and rate of economic recovery; and potential adverse effects on the financial markets, any of which could negatively impact the Company.

ITEM 1B—UNRESOLVED STAFF COMMENTS

None

ITEM 1C—CYBERSECURITY

Risk management and strategy

The Company has processes for assessing, identifying, and managing material risks from cybersecurity threats. These processes are integrated into the Company’s overall risk management systems, as overseen by the Company’s Board of Directors, primarily through its Risk Oversight Committee. These processes also include overseeing and identifying risks from cybersecurity threats associated with the use of third-party service providers. The Company conducts security assessments of certain third-party providers before engagement and has established monitoring procedures in its effort to mitigate risks related to data breaches or other security incidents originating from third parties. The Company from time to time engages third-party consultants, legal advisors, and audit firms in evaluating and testing the Company’s risk management systems and assessing and remediating certain potential cybersecurity incidents as appropriate.

The Company has an Information Security Program (“Program”) to protect personal and proprietary information in compliance with applicable federal and state requirements. The Program is designed to:

| ● | Ensure the security and confidentiality of employee and customer personal information and Company proprietary information; |

| ● | Protect against anticipated threats or hazards to the security or integrity of such information; and |

| ● | Protect against unauthorized access to, use of, or transfer of such information in a manner that could harm or inconvenience the Company, employees or customers. |

For more information about these risks, see the risk factor titled “The Company relies on its information and communications systems in its operations. Security breaches and other disruptions could adversely affect its business and results of operations” under Item 1A.

Governance

The Company’s Board of Directors has assigned oversight of cybersecurity risk management to the Risk Oversight Committee. The Risk Oversight Committee regularly receives reports from management, including senior information technology (“IT”) leadership, and third parties on cybersecurity matters. In addition, the Company’s full Board of Directors receives reports addressing cybersecurity as part of the Company’s overall enterprise risk management program and to the extent cybersecurity matters are addressed in regular business updates.

Senior IT leaders are responsible for developing appropriate cybersecurity programs, including as may be required by applicable law or regulation. These individuals’ expertise in IT and cybersecurity generally has been gained from a combination of education, including relevant degrees and/or certifications, and work experience. They are informed by their respective cybersecurity teams about, and monitor, the prevention, detection, mitigation and remediation of cybersecurity incidents as part of the cybersecurity programs described above.

Information regarding cybersecurity risks may be elevated by IT leadership through a variety of channels, including discussions between or among key leaders and Company management and reports to the Company’s Board of Directors and/or certain Board committees. As noted above, the Risk Oversight Committee regularly receives reports on cybersecurity matters from senior IT leadership.

ITEM 2—PROPERTIES

The Company’s manufacturing operations are carried out at four facilities. The following table sets forth certain information regarding each of these facilities:

| Approximate Aggregate Usable Square Feet |

Status | Segment | ||||

| Newport, New Hampshire | 350,000 | Owned | Firearms/Castings | |||

| Prescott, Arizona | 230,000 | Leased | Firearms | |||

| Mayodan, North Carolina | 220,000 | Owned | Firearms | |||

| Earth City, Missouri | 35,000 | Leased | Castings | |||

Each firearms facility contains enclosed ranges for testing firearms. The lease of the Prescott facility provides for rental payments which are approximately equivalent to estimated rates for real property taxes.

The Company has other facilities that were not used in its manufacturing operations in 2023:

| Approximate Aggregate Usable Square Feet |

Status | Segment | ||||

| Southport, Connecticut | 25,000 | Owned | Corporate | |||

| Newport, New Hampshire(Dorr Woolen Building) | 45,000 | Owned | Firearms | |||

| Enfield, Connecticut | 10,000 | Leased | Firearms | |||

| Fairport, New York | 3,700 | Leased | Corporate | |||

| Mayodan, North Carolina | 225,000 | Owned | Firearms |

There are no mortgages or any other major encumbrance on any of the real estate owned by the Company.

The Company’s principal executive offices are located in Southport, Connecticut.

ITEM 3—LEGAL PROCEEDINGS

The nature of the legal proceedings against the Company is discussed at Note 20 to the financial statements, which are included in this Form 10-K.

The Company has reported all cases instituted against it through September 30, 2023, and the results of those cases, where terminated, to the SEC on its previous Form 10-Q and 10-K reports, to which reference is hereby made.

There was one lawsuit formally instituted against the Company during the three months ending December 31, 2023, as follows: Jennifer Laws v. Sturm, Ruger & Co., filed in the U.S. District Court for the District of New Mexico on November 20, 2023.

ITEM 4—MINE SAFETY DISCLOSURES – NOT APPLICABLE

PART II

| ITEM 5— | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

The Company’s common stock is traded on the New York Stock Exchange under the symbol “RGR.” At February 5, 2024, the Company had 1,800 stockholders of record.

Issuer Repurchase of Equity Securities

In 2022 and 2023 the Company repurchased shares of its common stock. In 2021, the Company did not repurchase any shares of its common stock. Details of the purchases in 2022 and 2023 follow:

| Period | Total Number of Shares Purchased |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Program |

Maximum Dollar Value of Shares that May Yet Be Purchased Under the Program |

||||||||||||

| Third Quarter 2022 | ||||||||||||||||

| July 3 to July 30 | — | — | — | |||||||||||||

| July 31 to August 27 | — | — | — | |||||||||||||

| August 28 to October 1 | 2,136 | $ | 49.97 | 2,136 | ||||||||||||

| Fourth Quarter 2022 | ||||||||||||||||

| October 2 to October 29 | — | — | — | |||||||||||||

| October 30 to November 26 | 2,304 | $ | 49.77 | 2,304 | ||||||||||||

| November 27 to December 31 | — | — | — | |||||||||||||

| Fourth Quarter 2023 | — | — | ||||||||||||||

| October 1 to October 28 | — | |||||||||||||||

| October 29 to November 25 | 179,341 | $ | 45.20 | 179,341 | ||||||||||||

| November 26 to December 31 | 84,721 | $ | 43.67 | 84,721 | ||||||||||||

| Total | 268,502 | $ | 44.79 | 268,502 | $ | 74,680,000 | ||||||||||

All of these purchases were made with cash held by the Company and no debt was incurred.

At December 31, 2023 approximately $74.7 million remained authorized for share repurchases.

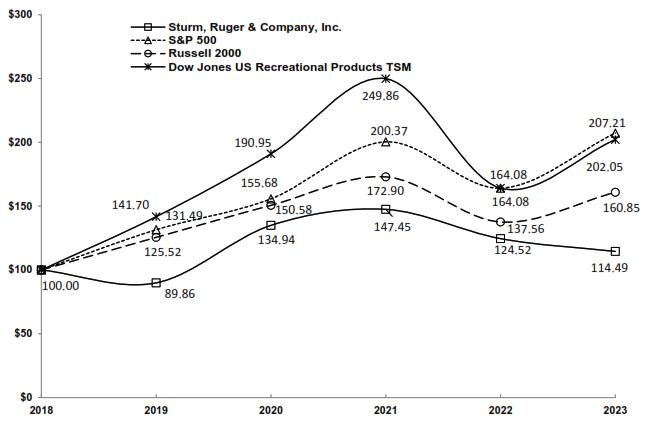

|

Comparison of Five-Year Cumulative Total Return* |

| Sturm, Ruger & Co., Inc., Standard & Poor’s 500, Dow Jones US Recreational Products TSM Index, and Russell 2000 Index |

| (Performance Results Through 12/31/23) |

*Assumes $100 invested on 12/31/18 in stock or index including reinvestment of dividends

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |||||||||||||||||||

| Sturm, Ruger & Company, Inc. | 100.00 | 89.86 | 134.94 | 147.45 | 124.52 | 114.49 | ||||||||||||||||||

| Standard & Poors 500 | 100.00 | 131.49 | 155.68 | 200.37 | 164.08 | 207.21 | ||||||||||||||||||

| Russell 2000 Index | 100.00 | 125.52 | 150.58 | 172.90 | 137.56 | 160.85 | ||||||||||||||||||

| Dow Jones US Recreational Products TSM | 100.00 | 141.70 | 190.95 | 249.86 | 164.08 | 202.05 |

For the year ended December 31, 2023, the Company has provided the five year cumulative total return results for the Dow Jones US Recreational Products Index, a widely-published index tracking companies that provide recreational products.

ITEM 6—[RESERVED]

| ITEM 7— | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Company Overview

Sturm, Ruger & Company, Inc. (the “Company”) is principally engaged in the design, manufacture, and sale of firearms to domestic customers. Approximately 99% of sales are from firearms. Export sales represent approximately 6% of total sales. The Company’s design and manufacturing operations are located in the United States and almost all product content is domestic. The Company’s firearms are sold through a select number of independent wholesale distributors, principally to the commercial sporting market.

The Company also manufactures investment castings made from steel alloys and metal injection molding (“MIM”) parts for internal use in its firearms and for sale to unaffiliated, third-party customers. Less than 1% of sales are from the castings segment.

Orders of many models of firearms from the independent distributors tend to be stronger in the first quarter of the year and weaker in the third quarter of the year.

Results of Operations - 2023

Product Demand

The estimated sell-through of the Company’s products from the independent distributors to retailers in 2023 decreased 7% from 2022. For the same period, adjusted NICS decreased 4%. The greater reduction in the sell-through of the Company’s products relative to adjusted NICS background checks may be attributable to aggressive promotions, discounts, rebates, and the extension of payment terms offered by the Company’s competitors.

Estimated sell-through from distributors to retailers and total adjusted NICS background checks:

| 2023 | 2022 | 2021 | ||||||||||

| Estimated Units Sold from Distributors to Retailers (1) | 1,406,600 | 1,506,800 | 2,017,800 | |||||||||

| Total Adjusted NICS Background Checks (2) | 15,848,000 | 16,425,000 | 18,515,000 | |||||||||

| (1) | The estimates for each period were calculated by taking the beginning inventory at the distributors, plus shipments from the Company to distributors during the period, less the ending inventory at distributors. These estimates are only a proxy for actual market demand as they: |

| ● | Rely on data provided by independent distributors that are not verified by the Company, |

| ● | Do not consider potential timing issues within the distribution channel, including goods-in-transit, and |

| ● | Do not consider fluctuations in inventory at retail. |

| (2) | NICS background checks are performed when the ownership of most firearms, either new or used, is transferred by a Federal Firearms Licensee. NICS background checks are also performed for permit applications, permit renewals, and other administrative reasons. |

The adjusted NICS data presented above was derived by the NSSF by subtracting NICS checks that are not directly related to the sale of a firearm, including checks used for concealed carry (“CCW”) permit application checks as well as checks on active CCW permit databases.

Adjusted NICS data can be impacted by changes in state laws and regulations and any directives and interpretations issued by governmental agencies.

Orders Received and Ending Backlog

The Company uses the estimated unit sell-through of its products from the independent distributors to retailers, along with inventory levels at the independent distributors and at the Company, as the key metrics for planning production levels.

The units ordered, value of orders received and ending backlog, net of Federal Excise Tax, for the trailing three years are as follows (dollars in millions, except average sales price):

| 2023 | 2022 | 2021 | ||||||||||

| Orders Received | $ | 433.8 | $ | 451.2 | $ | 606.5 | ||||||

| Average Sales Price of Orders Received | $ | 374 | $ | 416 | $ | 330 | ||||||

| Ending Backlog | $ | 229.0 | $ | 314.4 | $ | 429.7 | ||||||

| Average Sales Price of Ending Backlog | $ | 522 | $ | 486 | $ | 357 | ||||||

Production

The Company reviews the estimated sell-through from the independent distributors to retailers, as well as inventory levels at the independent distributors and at the Company, to plan production levels and manage inventories. These reviews resulted in a decrease in total unit production of 19% in 2023 compared to 2022.

Annual Summary Unit Data

Firearms unit data for orders, production, and shipments follows:

| 2023 | 2022 | 2021 | ||||||||||

| Units Ordered | 1,159,000 | 1,083,800 | 1,835,500 | |||||||||

| Units Produced | 1,398,200 | 1,733,200 | 2,154,600 | |||||||||

| Units Shipped | 1,367,500 | 1,641,000 | 2,142,900 | |||||||||

| Average Sales Price | $ | 395 | $ | 362 | $ | 340 | ||||||

| Units – Backlog | 438,800 | 647,300 | 1,204,500 | |||||||||

Inventories

The Company’s finished goods inventory increased by 30,700 units during 2023.

Distributor inventories of the Company’s products decreased by 39,100 units during 2023, and approximate a reasonable level to support rapid fulfillment of retailer demand for most product families.

Inventory data follows:

| 2023 | 2022 | 2021 | ||||||||||

| Units – Company Inventory | 143,500 | 112,800 | 20,600 | |||||||||

| Units – Distributor Inventory (3) | 259,300 | 298,400 | 164,200 | |||||||||

| Total inventory (4) | 402,800 | 411,200 | 184,800 |

| (3) | Distributor ending inventory as provided by the independent distributors of the Company’s products. These numbers do not include goods-in-transit inventory that has been shipped from the Company but not yet received by the distributors. |

| (4) | This total does not include inventory at retailers. The Company does not have access to data on retailer inventories. |

Year ended December 31, 2023, as compared to year ended December 31, 2022:

Net Sales, Cost of Products Sold, and Gross Profit

Net sales, cost of products sold, and gross profit data for the year ended (dollars in millions):

| December 31, 2023 |

December 31, 2022 |

Change | % Change | |||||||||||||

| Net firearms sales | $ | 540.7 | $ | 593.3 | $ | (52.6 | ) | (8.9 | )% | |||||||

| Net casting sales | 3.0 | 2.5 | 0.5 | 18.3% | ||||||||||||

| Total net sales | 543.7 | 595.8 | (52.1 | ) | (8.7 | )% | ||||||||||

| Cost of products sold | 410.1 | 415.7 | (5.6 | ) | (1.3 | )% | ||||||||||

| Gross profit | $ | 133.6 | $ | 180.1 | $ | (46.5 | ) | (25.8 | )% | |||||||

| Gross margin | 24.6% | 30.2% | (5.6 | )% | (18.5 | )% |

Firearms sales and unit shipments decreased 9% and 17%, respectively, in 2023. New products represented $121.7 million or 23% of firearms sales in 2023, an increase from $78.4 million or 14% of firearms sales in 2022. New product sales include only major new products that were introduced in the past two years. In 2023, new products included the MAX-9 pistol (during the first quarter only), Security-380 pistol, Super Wrangler revolver, LCP MAX pistol, Marlin lever-action rifles, LC Carbine, Small-Frame Autoloading Rifle, and American Centerfire Rifle Generation II.

The decreased gross profit for the year ended December 31, 2023 is attributable to the significant decrease in sales, as well as inflationary cost increases in materials, commodities, services, wages, energy, fuel and transportation, unfavorable deleveraging of fixed costs resulting from decreased production, a product mix shift toward products with relatively lower margins that remain in stronger demand, and increased promotional costs.

The decrease in gross margin for the year ended December 31, 2023 is attributable to the aforementioned factors, partially offset by increased pricing.

Selling, General and Administrative

Selling and general and administrative expenses data for the year ended (dollars in millions):

| December 31, 2023 |

December 31, 2022 |

Change | % Change | |||||||||||||

| Selling expenses | $ | 38.8 | $ | 36.1 | $ | 2.7 | 7.4% | |||||||||

| General and administrative expenses | 42.7 | 40.5 | 2.2 | 5.4% | ||||||||||||

| Total operating expenses | $ | 81.5 | $ | 76.6 | $ | 4.9 | 6.4% |

The increase in selling expenses for the year ended December 31, 2023 was primarily attributable to increased trade show costs, travel expenditures, and advertising, partially offset by decreased sales volume.

The increase in general, and administrative expenses for the year ended December 31, 2023 was primarily attributable to increased professional service costs.

Operating Income

Operating income was $52.1 million or 9.6% of sales in 2023. This is a decrease of $51.4 million from 2022 operating income of $103.5 million or 17.3% of sales.

Other Operating Income (Expense), Net

Other income data for the year ended (dollars in millions):

| December 31, 2023 |

December 31, 2022 |

Change | % Change | |||||||||||||

| Royalty income | $ | 0.6 | $ | 0.8 | (0.2 | ) | (21.4% | ) | ||||||||

| Interest income | 5.5 | 2.6 | 2.9 | 114.1% | ||||||||||||

| Interest expense | (0.2 | ) | (0.3 | ) | 0.1 | (19.9% | ) | |||||||||

| Other income, net | 0.8 | 1.7 | (0.9 | ) | (51.4% | ) | ||||||||||

| Other income | $ | 6.7 | $ | 4.8 | $ | 1.9 | 39.7% | |||||||||

The increase in other income for the year ended December 31, 2023 was the result of increases in interest income due to increased interest rates earned on short-term investments, partially offset by decreased royalty and other income.

Income Taxes and Net Income

The effective income tax rate was 18.0% in 2023 and 18.4% in 2022. The Company's 2023 and 2022 effective tax rate differs from the statutory federal tax rate due principally to the availability of research and development tax credits, state income taxes, and the nondeductibility of certain executive compensation. The impact related to research and development tax credits on the effective tax rate is expected to decline in future years.

As a result of the foregoing factors, consolidated net income was $48.2 million in 2023. This represents a decrease of $40.1 million from 2022 consolidated net income of $88.3 million.

Non-GAAP Financial Measure

In an effort to provide investors with additional information regarding its results, the Company refers to various United States generally accepted accounting principles (“GAAP”) financial measures and two non-GAAP financial measures, EBITDA and EBITDA margin, which management believes provides useful information to investors. These non-GAAP measures may not be comparable to similarly titled measures being disclosed by other companies. In addition, the Company believes that the non-GAAP financial measures should be considered in addition to, and not in lieu of, GAAP financial measures. The Company believes that EBITDA and EBITDA margin are useful to understanding its operating results and the ongoing performance of its underlying business, as EBITDA provides information on the Company’s ability to meet its capital expenditure and working capital requirements, and is also an indicator of profitability. The Company believes that this reporting provides better transparency and comparability to its operating results. The Company uses both GAAP and non-GAAP financial measures to evaluate its financial performance.

Non-GAAP Reconciliation – EBITDA

EBITDA

(Unaudited, dollars in thousands)

| Year ended December 31, | 2023 | 2022 | ||||||

| Net income | $ | 48,215 | $ | 88,332 | ||||

| Income tax expense | 10,609 | 19,947 | ||||||

| Depreciation and amortization expense | 22,383 | 25,789 | ||||||

| Interest expense | 205 | 256 | ||||||

| Interest income | (5,465 | ) | (2,552 | ) | ||||

| EBITDA | $ | 75,947 | $ | 131,772 | ||||

| EBITDA margin | 14.0% | 22.1% | ||||||

EBITDA is defined as earnings before interest, taxes, and depreciation and amortization. The Company calculates this by adding the amount of interest expense, income tax expense and depreciation and amortization expenses that have been deducted from net income back into net income, and subtracting the amount of interest income that was included in net income from net income to arrive at EBITDA. The Company’s EBITDA calculation also excludes any one-time non-cash, non-operating expense.

Quarterly Data

To supplement the summary annual unit data and discussion above, the same data for the last eight quarters follows:

| 2023 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Units Ordered | 316,600 | 176,300 | 258,100 | 408,000 | ||||||||||||

| Units Produced | 305,200 | 324,500 | 387,500 | 381,000 | ||||||||||||

| Units Shipped | 337,800 | 308,400 | 336,400 | 384,900 | ||||||||||||

| Estimated Units Sold from Distributors to Retailers | 384,700 | 307,400 | 323,000 | 391,500 | ||||||||||||

| Total Adjusted NICS Background Checks | 4,742,000 | 3,284,000 | 3,654,000 | 4,168,000 | ||||||||||||

| Average Unit Sales Price | $ | 383 | $ | 390 | $ | 422 | $ | 387 | ||||||||

| Units – Backlog | 438,800 | 460,000 | 592,100 | 670,400 | ||||||||||||

| Units – Company Inventory | 143,500 | 176,100 | 160,000 | 108,900 | ||||||||||||

| Units – Distributor Inventory (5) | 259,300 | 306,200 | 305,200 | 291,800 | ||||||||||||

| 2022 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Units Ordered | 156,000 | 295,600 | 250,600 | 381,600 | ||||||||||||

| Units Produced | 397,300 | 382,800 | 431,800 | 521,300 | ||||||||||||

| Units Shipped | 393,100 | 373,800 | 382,600 | 491,500 | ||||||||||||

| Estimated Units Sold from Distributors to Retailers | 397,800 | 343,500 | 354,300 | 411,200 | ||||||||||||

| Total Adjusted NICS Background Checks | 4,531,000 | 3,764,000 | 3,917,000 | 4,213,000 | ||||||||||||

| Average Unit Sales Price | $ | 378 | $ | 371 | $ | 366 | $ | 338 | ||||||||

| Units – Backlog | 647,300 | 884,400 | 962,600 | 1,094,600 | ||||||||||||

| Units – Company Inventory | 112,800 | 108,600 | 99,700 | 50,400 | ||||||||||||

| Units – Distributor Inventory (5) | 298,400 | 303,100 | 272,800 | 244,600 | ||||||||||||

| (5) | Distributor ending inventory as provided by the independent distributors of the Company’s products. |

(in millions except average sales price, net of Federal Excise Tax)

| 2023 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Orders Received | $ | 116.7 | $ | 58.8 | $ | 102.1 | $ | 156.2 | ||||||||

| Average Sales Price of Orders Received | $ | 369 | $ | 334 | $ | 396 | $ | 383 | ||||||||

| Ending Backlog | $ | 229.0 | $ | 234.8 | $ | 293.7 | $ | 327.3 | ||||||||

| Average Sales Price of Ending Backlog | $ | 522 | $ | 510 | $ | 496 | $ | 488 | ||||||||

| 2022 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Orders Received | $ | 81.0 | $ | 124.3 | $ | 98.9 | $ | 147.0 | ||||||||

| Average Sales Price of Orders Received | $ | 519 | $ | 421 | $ | 395 | $ | 385 | ||||||||

| Ending Backlog | $ | 314.4 | $ | 377.6 | $ | 389.6 | $ | 420.5 | ||||||||

| Average Sales Price of Ending Backlog | $ | 486 | $ | 427 | $ | 405 | $ | 384 | ||||||||

Fourth Quarter Net Sales and Gross Profit Analysis

Net sales, cost of products sold, and gross profit data for the three months ended (dollars in millions):

| December 31, 2023 |

December 31, 2022 |

Change | % Change | |||||||||||||

| Net firearms sales | $ | 129.6 | $ | 148.7 | $ | (19.1 | ) | (12.8 | )% | |||||||

| Net casting sales | 1.0 | 0.5 | 0.5 | 79.1 | % | |||||||||||

| Total net sales | 130.6 | 149.2 | (18.6 | ) | (12.5 | )% | ||||||||||

| Cost of products sold | 98.3 | 109.6 | (11.3 | ) | (10.3 | )% | ||||||||||

| Gross profit | $ | 32.3 | $ | 39.6 | $ | (7.3 | ) | (18.4 | )% | |||||||

| Gross margin | 24.7% | 26.5% | (1.8 | )% | (5.6 | )% |

Results of Operations - 2022

Year ended December 31, 2022, as compared to year ended December 31, 2021:

Annual Summary Unit Data

Firearms unit data for orders, production, shipments and ending inventory, and castings setups (a measure of foundry production) are as follows:

| 2022 | 2021 | 2020 | ||||||||||

| Units Ordered | 1,083,800 | 1,835,500 | 3,041,700 | |||||||||

| Units Produced | 1,733,200 | 2,154,600 | 1,659,100 | |||||||||

| Units Shipped | 1,641,000 | 2,142,900 | 1,717,700 | |||||||||

| Average Sales Price | $ | 362 | $ | 340 | $ | 329 | ||||||

| Units – Backlog | 647,300 | 1,204,500 | 1,511,900 | |||||||||

| Units – Company Inventory | 112,800 | 20,600 | 8,800 | |||||||||

| Units – Distributor Inventory (1) | 298,400 | 164,200 | 39,200 | |||||||||

| Castings Setups | 55,971 | 68,469 | 66,044 | |||||||||

Orders Received and Ending Backlog

(in millions except average sales price, net of Federal Excise Tax):

| 2022 | 2021 | 2020 | ||||||||||

| Orders Received | 451.2 | $ | 606.5 | $ | 992.9 | |||||||

| Average Sales Price of Orders Received (2) | $ | 416 | $ | 330 | $ | 326 | ||||||

| Ending Backlog | $ | 314.4 | $ | 429.7 | $ | 516.6 | ||||||

| Average Sales Price of Ending Backlog (2) | $ | 486 | $ | 357 | $ | 342 | ||||||

| (1) | Distributor ending inventory as provided by the independent distributors of the Company’s products. |

| (2) | Average sales price for orders received and ending backlog is net of Federal Excise Tax of 10% for handguns and 11% for long guns. |

Product Demand

The estimated sell-through of the Company’s products from the independent distributors to retailers in 2022 decreased 25% from 2021. For the same period, adjusted NICS decreased 11%. These decreases are attributable to decreased consumer demand for firearms from the unprecedented levels of the surge that began in 2020 and remained for most of 2021. The greater reduction in the sell-through of the Company’s products relative to adjusted NICS background checks may be attributable to the following:

| ● | More aggressive promotions, discounts, rebates, and the extension of payment terms offered by our competitors, |

| ● | An apparent increase in sales of used firearms at retail, which are included in the adjusted NICS checks, but are not distinguished from new gun sales, and |

| ● | Decreased retailer inventories as the anticipation of further discounting may be encouraging cautious buying behavior by retailers. |

Estimated sell-through from distributors to retailers and total adjusted NICS background checks:

| 2022 | 2021 | 2020 | ||||||||||

| Estimated Units Sold from Distributors to Retailers (1) | 1,506,800 | 2,017,800 | 1,948,900 | |||||||||

| Total Adjusted NICS Background Checks (2) | 16,425,000 | 18,515,000 | 21,084,000 | |||||||||

| (1) | The estimates for each period were calculated by taking the beginning inventory at the distributors, plus shipments from the Company to distributors during the period, less the ending inventory at distributors. These estimates are only a proxy for actual market demand as they: |

| ● | Rely on data provided by independent distributors that are not verified by the Company, |

| ● | Do not consider potential timing issues within the distribution channel, including goods-in-transit, and |

| ● | Do not consider fluctuations in inventory at retail. |

| (2) | NICS background checks are performed when the ownership of most firearms, either new or used, is transferred by a Federal Firearms Licensee. NICS background checks are also performed for permit applications, permit renewals, and other administrative reasons. |

The adjusted NICS data presented above was derived by the NSSF by subtracting NICS checks that are not directly related to the sale of a firearm, including checks used for concealed carry (“CCW”) permit application checks as well as checks on active CCW permit databases.

Adjusted NICS data can be impacted by changes in state laws and regulations and any directives and interpretations issued by governmental agencies.

Production

The Company reviews the estimated sell-through from the independent distributors to retailers, as well as inventory levels at the independent distributors and at the Company, to plan production levels and manage inventories. These reviews resulted in a decrease in total unit production of 20% in 2022 compared to 2021.

Inventories

The Company’s finished goods inventory increased by 92,200 units during 2022.

Distributor inventories of the Company’s products increased by 134,200 units during 2022, and approximate a reasonable level to support rapid fulfillment of retailer demand for most product families.

Inventory data follows:

| 2022 | 2021 | 2020 | ||||||||||

| Units – Company Inventory | 112,800 | 20,600 | 8,800 | |||||||||

| Units – Distributor Inventory (3) | 298,400 | 164,200 | 39,200 | |||||||||

| Total inventory (4) | 411,200 | 184,800 | 48,000 |

| (3) | Distributor ending inventory as provided by the independent distributors of the Company’s products. These numbers do not include goods-in-transit inventory that has been shipped from the Company but not yet received by the distributors. |

| (4) | This total does not include inventory at retailers. The Company does not have access to data on retailer inventories. |

Quarterly Summary Unit Data

To supplement the summary annual unit data and discussion above, the same data for the last eight quarters follows:

| 2022 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Units Ordered | 156,000 | 295,600 | 250,600 | 381,600 | ||||||||||||

| Units Produced | 397,300 | 382,800 | 431,800 | 521,300 | ||||||||||||

| Units Shipped | 393,100 | 373,800 | 382,600 | 491,500 | ||||||||||||

| Estimated Units Sold from Distributors to Retailers | 397,800 | 343,500 | 354,300 | 411,200 | ||||||||||||

| Total Adjusted NICS Background Checks | 4,531,000 | 3,764,000 | 3,917,000 | 4,213,000 | ||||||||||||

| Average Unit Sales Price | $ | 378 | $ | 371 | $ | 366 | $ | 338 | ||||||||

| Units – Backlog | 647,300 | 884,400 | 962,600 | 1,094,600 | ||||||||||||

| Units – Company Inventory | 112,800 | 108,600 | 99,700 | 50,400 | ||||||||||||

| Units – Distributor Inventory (5) | 298,400 | 303,100 | 272,800 | 244,600 | ||||||||||||

| 2021 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Units Ordered | 373,000 | 218,800 | 453,400 | 790,300 | ||||||||||||

| Units Produced | 512,100 | 525,200 | 575,400 | 541,900 | ||||||||||||

| Units Shipped | 502,300 | 524,800 | 580,800 | 535,000 | ||||||||||||

| Estimated Units Sold from Distributors to Retailers | 458,200 | 457,400 | 583,300 | 518,900 | ||||||||||||

| Total Adjusted NICS Background Checks | 4,763,000 | 3,971,000 | 4,298,000 | 5,483,000 | ||||||||||||

| Average Unit Sales Price | $ | 334 | $ | 338 | $ | 343 | $ | 343 | ||||||||

| Units – Backlog | 1,204,500 | 1,333,800 | 1,639,800 | 1,767,200 | ||||||||||||

| Units – Company Inventory | 20,600 | 10,900 | 10,400 | 15,700 | ||||||||||||

| Units – Distributor Inventory (5) | 164,200 | 120,100 | 52,800 | 55,300 | ||||||||||||

| (5) | Distributor ending inventory as provided by the independent distributors of the Company’s products. |

(in millions except average sales price, net of Federal Excise Tax)

| 2022 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Orders Received | $ | 81.0 | $ | 124.3 | $ | 98.9 | $ | 147.0 | ||||||||

| Average Sales Price of Orders Received | $ | 519 | $ | 421 | $ | 395 | $ | 385 | ||||||||

| Ending Backlog | $ | 314.4 | $ | 377.6 | $ | 389.6 | $ | 420.5 | ||||||||

| Average Sales Price of Ending Backlog | $ | 486 | $ | 427 | $ | 405 | $ | 384 | ||||||||

| 2021 | ||||||||||||||||

| Q4 | Q3 | Q2 | Q1 | |||||||||||||

| Orders Received | $ | 119.2 | $ | 61.1 | $ | 158.3 | $ | 267.9 | ||||||||

| Average Sales Price of Orders Received | $ | 320 | $ | 279 | $ | 349 | $ | 339 | ||||||||

| Ending Backlog | $ | 429.7 | $ | 471.7 | $ | 582.3 | $ | 612.3 | ||||||||

| Average Sales Price of Ending Backlog | $ | 357 | $ | 354 | $ | 355 | $ | 346 | ||||||||

Net Sales, Cost of Products Sold, and Gross Profit

Net sales, cost of products sold, and gross profit data for the year ended (dollars in millions):

| December 31, 2022 |

December 31, 2021 |

Change | % Change | |||||||||||||

| Net firearms sales | $ | 593.3 | $ | 728.1 | $ | (134.8) | (18.5 | )% | ||||||||

| Net casting sales | 2.5 | 2.6 | (0.1) | (1.6 | )% | |||||||||||

| Total net sales | 595.8 | 730.7 | (134.9) | (18.5 | )% | |||||||||||

| Cost of products sold | 415.7 | 451.2 | (35.5) | (7.8 | )% | |||||||||||

| Gross profit | $ | 180.1 | $ | 279.5 | $ | (99.4) | (35.6 | )% | ||||||||

| Gross margin | 30.2% | 38.3% | (8.1)% | (29.7 | )% |

Firearms sales and unit shipments decreased 18.5% and 23.4%, respectively, in 2022. New products represented $78.4 million or 14% of firearms sales in 2022, compared to $155.5 million or 22% of firearms sales in 2021. New product sales include only major new products that were introduced in the past two years. In 2022, new products included the MAX-9 pistol, LCP MAX, Marlin 1895 lever-action rifles, PC Charger, LC Carbine, and Small-Frame Autoloading Rifle.

The decreased gross profit for the year ended December 31, 2022 is attributable to the significant decrease in sales, as well as inflationary cost increases in materials, commodities, services, energy, fuel and transportation, which were partially offset by increased pricing.

The decrease in gross margin for the year ended December 31, 2022 is attributable to the aforementioned inflationary cost increases and unfavorable deleveraging of fixed costs resulting from decreased production and sales.

Selling, General and Administrative

Selling, general and administrative expenses were $76.6 million in 2022, a slight increase of $0.1 million from $76.5 million in 2021, and an increase from 10.5% of sales in 2021 to 12.9% of sales in 2022. The increase in these expenses was primarily attributable to increased shipping costs and to the resumption of trade show participation costs, travel expenditures, and advertising that had been deferred during the height of the COVID-19 restrictions, almost entirely offset by decreased incentive compensation expenses and decreased variable costs, such as shipping, as a result of the reduced sales volume.

Other Operating Income (Expense), Net

Other operating income (expense), net was de minimis in 2022 and an expense of $0.1 million in 2021.

Operating Income

Operating income was $103.5 million or 17.3% of sales in 2022. This is a decrease of $99.6 million from 2021 operating income of $203.1 million or 27.8% of sales.

Royalty Income

Royalty income was $0.8 million in 2022 and $2.0 million in 2021.

Interest Income

Interest income was $2.6 million in 2022, an increase from de minimis earnings in 2021, due to significantly increased interest rates earned on short-term investments beginning in the second quarter of 2022.

Interest Expense

Interest expense was $0.3 million in 2022 and $0.2 million and 2021.

Other Income, Net

Other income, net was $1.7 million in 2022, an increase of $0.1 million from $1.6 million in 2021.

Income Taxes and Net Income