UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

FORM

_________________

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported):

_______________________________

(Exact name of registrant as specified in its charter)

_______________________________

| (State or Other Jurisdiction of Incorporation) | (Commission File Number) | (I.R.S. Employer Identification No.) |

(Address of Principal Executive Offices) (Zip Code)

(

(Registrant's telephone number, including area code)

Not Applicable

(Former name or former address, if changed since last report)

_______________________________

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) | |

| Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) | |

| Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) | |

| Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

On July 15, 2026, Great Southern Bancorp, Inc. issued a press release reporting preliminary financial results for the quarter ended June 30, 2026. A copy of the press release, including unaudited financial information released as a part thereof, is attached as Exhibit 99.1 to this Current Report on Form 8-K and incorporated herein by reference.

(d) Exhibits

| Exhibit Number | Description | |||

| 99.1 | Press Release dated July 15, 2026 | |||

| 99.2 | Earnings Presentation | |||

| 99.3 | Loan Portfolio | |||

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document) |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| GREAT SOUTHERN BANCORP, INC. | ||

| Date: July 15, 2026 | By: | /s/ Joseph W. Turner |

| Joseph W. Turner | ||

| President and Chief Executive Officer | ||

EXHIBIT 99.1

Great Southern Bancorp, Inc. Reports Preliminary Second Quarter Earnings of $1.43 Per Diluted Common Share

Preliminary Financial Results and Business Update for the Quarter Ended June 30, 2026

SPRINGFIELD, Mo., July 15, 2026 (GLOBE NEWSWIRE) -- Great Southern Bancorp, Inc. (the “Company”) (NASDAQ:GSBC), the holding company for Great Southern Bank (the “Bank”), today reported that preliminary earnings for the three months ended June 30, 2026, were $1.43 per diluted common share ($15.8 million net income) compared to $1.72 per diluted common share ($19.8 million net income) for the three months ended June 30, 2025. The 2026 second quarter results were negatively impacted by non-recurring expenses recorded in the period related to the consolidation of certain banking centers and other operational areas, which are discussed below.

For the quarter ended June 30, 2026, annualized return on average common equity was 9.83%, annualized return on average assets was 1.12%, annualized net interest margin was 3.76% and the efficiency ratio was 67.21%, compared to 12.81%, 1.34%, 3.68% and 59.16%, respectively, for the quarter ended June 30, 2025.

Excluding the non-recurring expenses referenced above, for the quarter ended June 30, 2026, net income was $17.4 million, earnings per diluted common share were $1.57, annualized return on average common equity was 10.82%, annualized return on average assets was 1.24%, and the efficiency ratio was 63.47%. A reconciliation of these non-GAAP calculations is detailed in “Non-GAAP Financial Measures” below.

Key Results:

| 1 |

Certain Income and Expense Items Impacting Second Quarter 2026 Results: During the three months ended June 30, 2026, there were certain income and expense items that impacted the Company’s results of operations.

Selected Financial Data:

| Three Months Ended | ||||||||||

|

June 30, |

June 30, |

March 31, |

||||||||

|

2026 |

2025 |

2026 |

||||||||

| (Dollars in thousands, except per share data) | ||||||||||

| Net interest income | $ | 49,493 | $ | 50,963 | $ | 48,328 | ||||

| Provision (credit) for credit losses on loans and unfunded commitments | 8 | (110 | ) | (931 | ) | |||||

| Non-interest income | 7,375 | 8,212 | 7,029 | |||||||

| Non-interest expense | 38,222 | 35,005 | 34,792 | |||||||

| Provision for income taxes | 2,843 | 4,494 | 4,020 | |||||||

| Net income | $ | 15,795 | $ | 19,786 | $ | 17,476 | ||||

| Earnings per diluted common share | $ | 1.43 | $ | 1.72 | $ | 1.58 | ||||

Joseph W. Turner, President and CEO of Great Southern, commented: "Our second quarter performance reflects continued strong results within our core banking franchise. Throughout the quarter, we remained focused on the fundamentals that have consistently guided our long-term success, including sound credit underwriting, thoughtful balance sheet management, and prudent expense control. We reported preliminary net income of $15.8 million, or $1.43 per diluted common share, for the second quarter of 2026, compared to $19.8 million, or $1.72 per diluted common share, for the second quarter of 2025. As outlined above, our second quarter results were inclusive of one-time expenses associated with branch consolidation and workforce reduction initiatives. For the six months ended June 30, 2026, preliminary net income totaled $33.3 million, or $2.99 per diluted common share, compared to $36.9 million, or $3.18 per diluted common share, in the first half of 2025.”

| 2 |

Turner noted, "Net interest income remained strong in the quarter, a result of prudent asset-liability management and disciplined pricing on earning assets and funding sources. Our net interest margin was 3.76% in the quarter, compared to 3.68% in the second quarter of 2025. Our pricing discipline helped mitigate the absence of $2.0 million in quarterly interest income recorded in the prior year period from a previously terminated interest rate swap, as well as lower earning assets, given the loan balance decline in the second quarter of 2026. Though our prioritization of net interest income will remain, credit and pricing discipline may temper near-term earnings given our focus on long-term stockholder returns.”

Turner continued, “Turning to our balance sheet, and as discussed in the prior quarter, period-to-period loan trends are influenced significantly by loan repayments from our borrowers. Elevated payoff activity in the second quarter of 2026 led to a $148.9 million decline in loan balances, compared to balances at the end of the 2026 first quarter. Despite the increased payoff volume, we remain committed to an origination strategy anchored by conservative credit and underwriting standards. As it relates to funding, we were pleased to see continued expansion within our core non-interest-bearing checking portfolios, reflecting the strength of our long-standing customer relationships. Additionally, as total earning assets moderated during the quarter, we were able to reduce higher-cost wholesale funding. These actions supported the level of our net interest margin while preserving our balance sheet flexibility.”

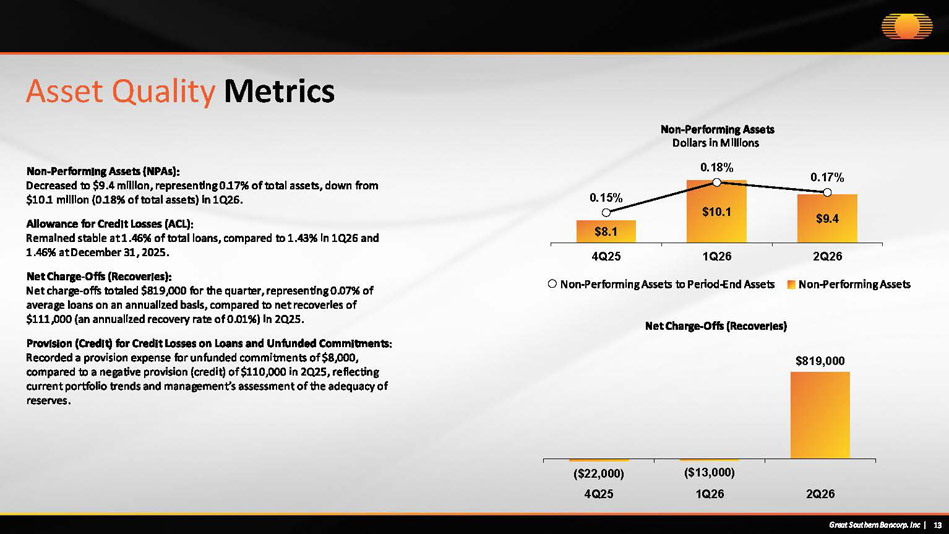

Turner added, "Asset quality remained very strong through the first half of 2026. Total non-performing assets were $9.4 million, or 0.17% of total assets, as of June 30, 2026. Included in this total is a $1.8 million multi-family loan transferred to foreclosed assets in the quarter. This loan experienced idiosyncratic issues which resulted in a $909,000 charge off upon its transfer to foreclosed assets.

Turner further commented, "As outlined above, we announced the consolidation of nine banking centers into other nearby locations along with the elimination of 66 positions across various divisions in the Company. Though these decisions resulted in the realization of several non-recurring expenses in the second quarter of 2026, we’re confident they will allow for better alignment with our customer base and improved returns for our stockholders, going forward. We expect the operational efficiencies created by these actions, the impact of which should begin to be realized in the fourth quarter of 2026, will produce an increase in annual pre-tax income of over $2 million.”

"Great Southern enters the second half of 2026 in a strong position, with robust capital and liquidity levels and a prudent balance sheet posture. As of June 30, 2026, tangible common equity was 11.47% of tangible assets and book value per common share increased to $58.95. Looking ahead, we remain focused on protecting asset quality, executing thoughtful operational improvements, and building long-term value for our stockholders," Turner concluded.

NET INTEREST INCOME

| Three Months Ended | ||||||||||||

| June 30, |

June

30, |

March

31, |

||||||||||

|

2026 |

2025 |

2026 |

||||||||||

| (Dollars in thousands) | ||||||||||||

| Interest Income | $ | 72,461 | $ | 80,975 | $ | 71,165 | ||||||

| Interest Expense | 22,968 | 30,012 | 22,837 | |||||||||

| Net Interest Income | $ | 49,493 | $ | 50,963 | $ | 48,328 | ||||||

| Net interest margin | 3.76 | % | 3.68 | % | 3.71 | % | ||||||

| Average interest-earning assets to average interest-bearing liabilities | 129.9 | % | 126.9 | % | 128.8 | % | ||||||

| 3 |

Net interest income for the second quarter of 2026 decreased $1.5 million (2.9%) to $49.5 million, compared to $51.0 million for the second quarter of 2025. This decrease was driven primarily by the $2.0 million net reduction in quarterly interest income associated with a previously terminated interest rate swap (income recognition ended on October 6, 2025). Additionally, compared to the year-ago quarter, interest income declined due to lower loan balances and lower market rates, which primarily impacted the interest rates on existing variable-rate loans and newly originated fixed-rate loans. Mostly offsetting the decrease in interest income was reduced interest expense, due to the strategic management of maturing/repricing brokered deposits and interest-bearing demand deposits. Also, there was no interest expense on subordinated notes in the quarter ended June 30, 2026, as those notes were redeemed in June 2025. Annualized net interest margin was 3.76% in the second quarter of 2026, compared to 3.68% in the same period of 2025 and 3.71% in the first quarter of 2026. The average interest rate spread was 3.24% for the three months ended June 30, 2026, compared to 3.09% for the three months ended June 30, 2025 and 3.20% for the three months ended March 31, 2026.

The average yield on total interest-earning assets decreased from 5.84% in the 2025 second quarter to 5.51% in the 2026 second quarter, with the average yield on loans decreasing 37 basis points, the average yield on investment securities increasing two basis points and the average yield on other interest earning assets (primarily funds held at the Federal Reserve Bank) decreasing 80 basis points. The average rate paid on total interest-bearing liabilities decreased from 2.75% in the 2025 second quarter to 2.27% in the 2026 second quarter, with the average rate paid on interest-bearing demand and savings deposits, time deposits and brokered deposits decreasing 22 basis points, 53 basis points and 61 basis points, respectively. The average rate paid on short-term borrowings decreased 67 basis points.

Market interest rates, primarily the federal funds rate and SOFR rates, declined in the fourth quarter of 2025, and remained lower through the first half of 2026. There were no federal funds rate cuts in the first half of 2026, but there were federal funds rate cuts in September, October, and December of 2025, totaling 75 basis points. This market rate decline reduced the average yield on loans, though the impact was tempered as cash flows from lower-rate fixed rate loans originated a few years ago were deployed into residential and commercial real estate loans with comparably higher rates of interest. The decline in market interest rates also resulted in lower average rates paid on deposits and borrowings, compared to the prior-year second quarter and the first quarter of 2026.

To mitigate exposure to the risk of fluctuations in future cash flows resulting from changes in interest rates (primarily related to falling interest rates), the Company has strategically utilized derivative financial instruments - primarily interest rate swaps - as part of its interest rate risk management strategy.

The following table presents, for the periods indicated, the effect of cash flow hedge accounting included in interest income in the consolidated statements of income:

| Three Months Ended | |||||||||||

|

June

30, |

June

30, |

March 31, | |||||||||

|

2026 |

2025 |

2026 |

|||||||||

| (In thousands) | |||||||||||

| Terminated interest rate swaps | $ | — | $ | 2,025 | $ | — | |||||

| Active interest rate swaps | (1,022 | ) | (1,757 | ) | (1,031 | ) | |||||

|

Increase (decrease) to interest income |

$ | (1,022 | ) | $ | 268 | $ | (1,031 | ) | |||

The Company entered into an interest rate swap in October 2018, which was terminated in March 2020. Upon termination, the Company received $45.9 million, inclusive of accrued but unpaid interest, from its swap counterparty. The net amount, after deducting accrued interest and deferred income taxes, was accreted to interest income on loans monthly until the originally scheduled termination date of October 6, 2025. With this date having passed, the Company no longer has the benefit of that income from the terminated swap. At June 30, 2026, the Company had two active interest rate swaps with a combined notional amount of $400 million. These swaps resulted in a reduction of interest income of $1.0 million and $1.8 million in the three months ended June 30, 2026 and 2025, respectively.

| 4 |

Market rates for time deposits for much of 2024 were elevated but have declined as the FOMC cut the federal funds rate by 100 basis points in late 2024, 25 basis points in the third quarter of 2025 and 50 basis points in the fourth quarter of 2025. As of June 30, 2026, time deposit maturities (including brokered time deposits) over the next 12 months were as follows: within three months — $630.7 million, with a weighted-average rate of 3.38%; within three to six months — $263.2 million, with a weighted-average rate of 3.10%; and within six to twelve months — $25.5 million, with a weighted-average rate of 1.40%. Based on time deposit market rates in June 2026, overall average replacement rates for maturing time deposits originated through our retail branch system are likely to be approximately 2.70 - 3.20%, depending on term. Brokered time deposit rates were generally at or above 3.90% at the end of June 2026.

NON-INTEREST INCOME

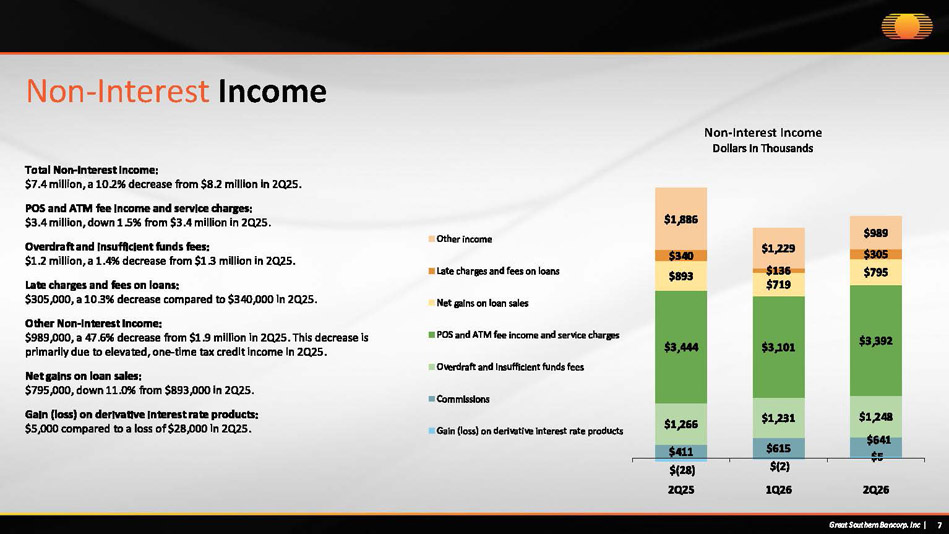

For the quarter ended June 30, 2026, non-interest income decreased $837,000, to $7.4 million, when compared to the quarter ended June 30, 2025, primarily as a result of the following items:

NON-INTEREST EXPENSE

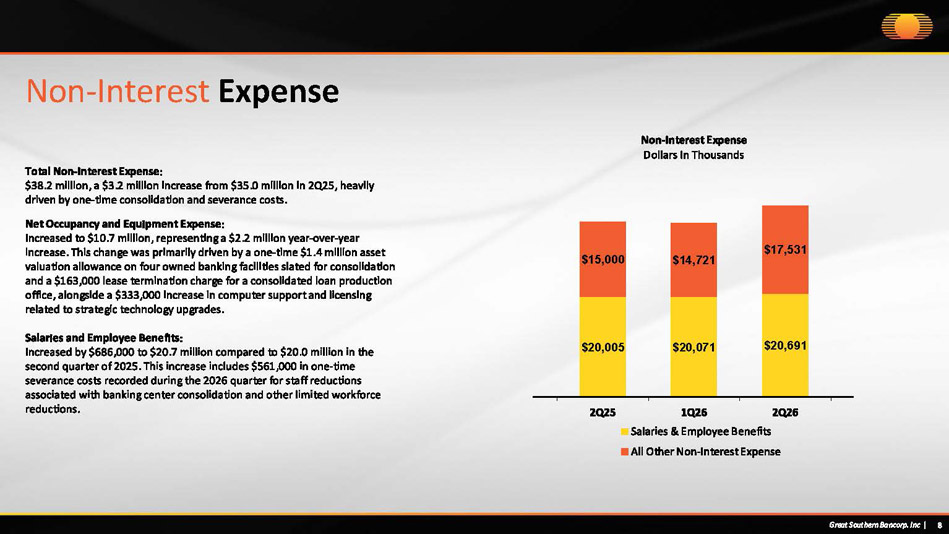

For the quarter ended June 30, 2026, non-interest expense increased $3.2 million, to $38.2 million, when compared to the quarter ended June 30, 2025, primarily as a result of the following items:

The Company’s efficiency ratio for the quarter ended June 30, 2026, was 67.21% compared to 59.16% for the same quarter in 2025. The Company’s ratio of non-interest expense to average assets was 2.72% for the three months ended June 30, 2026, compared to 2.37% for the three months ended June 30, 2025. These increased percentages were largely due to the one-time expenses previously discussed. Average assets for the three months ended June 30, 2026, decreased $298.6 million, or 5.0%, compared to the three months ended June 30, 2025, primarily due to the decline in the average balance of net loans.

| 5 |

INCOME TAXES

For the three months ended June 30, 2026 and 2025, the Company's effective tax rate was 15.3% and 18.5%, respectively. For the six months ended June 30, 2026 and 2025, the Company's effective tax rate was 17.1% and 19.2%, respectively. These effective rates were below the statutory federal tax rate of 21.0%, due primarily to the utilization of certain investment tax credits and the Company’s tax-exempt investments and tax-exempt loans, which reduced the Company’s effective tax rate. The effective rates in the 2026 periods also decreased due to a higher-than-normal level of deductions related to the significant amount of stock option exercises by the Company’s employees. The Company’s effective tax rate may fluctuate in future periods as it is impacted by the level and timing of the Company’s utilization of tax credits, the level of tax-exempt investments and loans, the amount of taxable income in various state jurisdictions and the overall level of pre-tax income. State tax expense estimates continually evolve as taxable income and apportionment between states are analyzed. The Company currently expects its effective tax rate (combined federal and state) will be approximately 18.0% to 19.5% in future periods.

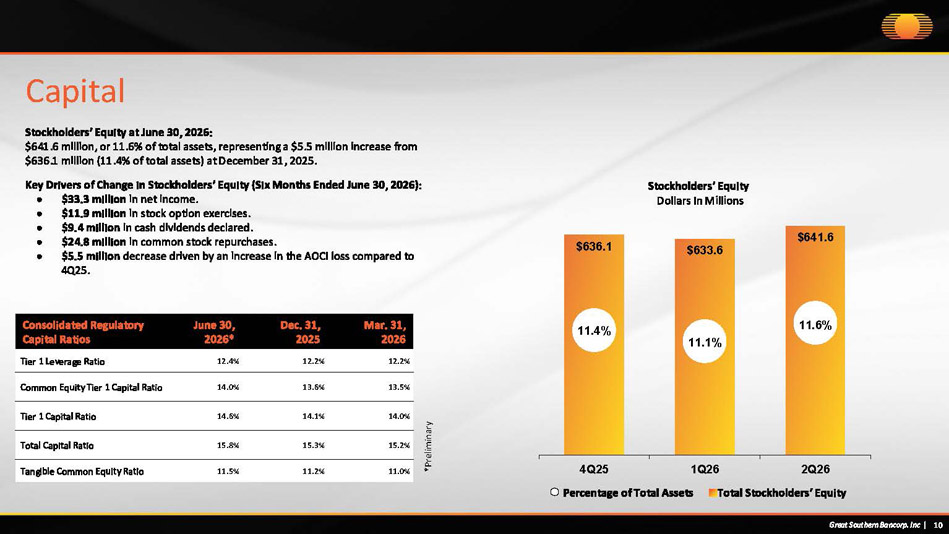

CAPITAL

| June 30, | December 31, | March 31, | |||||||

| 2026 | 2025 | 2026 | |||||||

| Consolidated Regulatory Capital Ratios | (Preliminary) | ||||||||

| Tier 1 Leverage Ratio | 12.4 | % | 12.2 | % | 12.2 | % | |||

| Common Equity Tier 1 Capital Ratio | 14.0 | % | 13.6 | % | 13.5 | % | |||

| Tier 1 Capital Ratio | 14.6 | % | 14.1 | % | 14.0 | % | |||

| Total Capital Ratio | 15.8 | % | 15.3 | % | 15.2 | % | |||

| Tangible Common Equity Ratio | 11.5 | % | 11.2 | % | 11.0 | % | |||

As of June 30, 2026, total stockholders’ equity was $641.6 million, representing 11.6% of total assets and a book value of $58.95 per common share. This compares to total stockholders’ equity of $636.1 million, or 11.4% of total assets, and a book value of $57.50 per common share at December 31, 2025. The $5.5 million increase in stockholders’ equity from December 31, 2025, was primarily driven by $33.3 million in net income and an $11.9 million increase from stock option exercises, partially offset by $9.4 million in cash dividends declared on the Company’s common stock, $24.8 million in common stock repurchases, and an increase in unrealized losses on investments and interest rate swaps. The increased unrealized losses on the Company’s available-for-sale investment securities and interest rate swaps, which totaled $37.7 million and $32.2 million (net of taxes) at June 30, 2026 and December 31, 2025, respectively, decreased stockholders’ equity by $5.5 million during the six months ended June 30, 2026. These net unrealized losses primarily resulted from increased intermediate-term market interest rates, which generally decreased the fair value of the investment securities and interest rate swaps. In 2026, market interest rates and interest rate expectations for future periods decreased early in the first quarter before increasing significantly since March to levels higher than those at December 31, 2025, ultimately resulting in decreases in the fair value of the Company’s investment securities and interest rate swaps during the six months ended June 30, 2026.

The Company had unrealized losses on its portfolio of held-to-maturity investment securities, which totaled $17.4 million and $16.6 million at June 30, 2026 and December 31, 2025, respectively, that were not included in its total capital balance. If unrealized losses on held-to-maturity securities were included in capital (net of taxes) at June 30, 2026 and December 31, 2025, they would have decreased total stockholder’s equity at those dates by $13.1 million and $12.5 million, respectively. These amounts were equal to 2.0% of total stockholders’ equity of $641.6 million at June 30, 2026 and $636.1 million at December 31, 2025.

In April 2025, the Company’s Board of Directors authorized the purchase, from time to time, of up to one million additional shares of the Company’s common stock. As of June 30, 2026, approximately 304,000 shares remained available under this stock repurchase authorization.

During the three months ended June 30, 2026, the Company repurchased 114,624 shares of its common stock at an average price of $68.39, and the Company’s Board of Directors declared a regular quarterly cash dividend of $0.43 per common share, which, combined, reduced stockholders’ equity by $12.5 million. During the three months ended June 30, 2026, the Company experienced stock option exercises of 125,221 shares of its common stock at an average price of $54.17, which increased stockholders’ equity by $7.3 million.

| 6 |

During the six months ended June 30, 2026, the Company repurchased 383,288 shares of its common stock at an average price of $64.29, and the Company’s Board of Directors declared regular quarterly cash dividends totaling $0.86 per common share, which, combined, reduced stockholders’ equity by $34.1 million. During the six months ended June 30, 2026, the Company experienced stock option exercises of 205,480 shares of its common stock at an average price of $52.89, which increased stockholders’ equity by $11.9 million.

LIQUIDITY AND DEPOSITS

Liquidity is a measure of the Company’s ability to generate sufficient cash to meet present and future financial obligations in a timely manner. The Company’s primary sources of funds are customer deposits, FHLBank advances, other borrowings, loan repayments, unpledged securities, proceeds from sales of loans and available-for-sale securities and funds provided from operations. The Company utilizes some or all of these sources of funds depending on the comparative costs and availability at the time. The Company has, from time to time, chosen not to pay rates on deposits as high as the rates paid by certain of its competitors and, at management’s discretion, supplements deposits with alternative sources of funds. Management believes that the Company maintains overall liquidity sufficient to satisfy its depositors’ requirements and meet its borrowers’ credit needs.

At June 30, 2026, the Company had the following available secured lines and on-balance sheet liquidity:

| June 30, 2026 | |

| Federal Home Loan Bank line | $1,234.0 million |

| Federal Reserve Bank line | 319.6 million |

| Cash and cash equivalents | 180.0 million |

| Unpledged securities – Available-for-sale | 339.9 million |

| Unpledged securities – Held-to-maturity | 23.4 million |

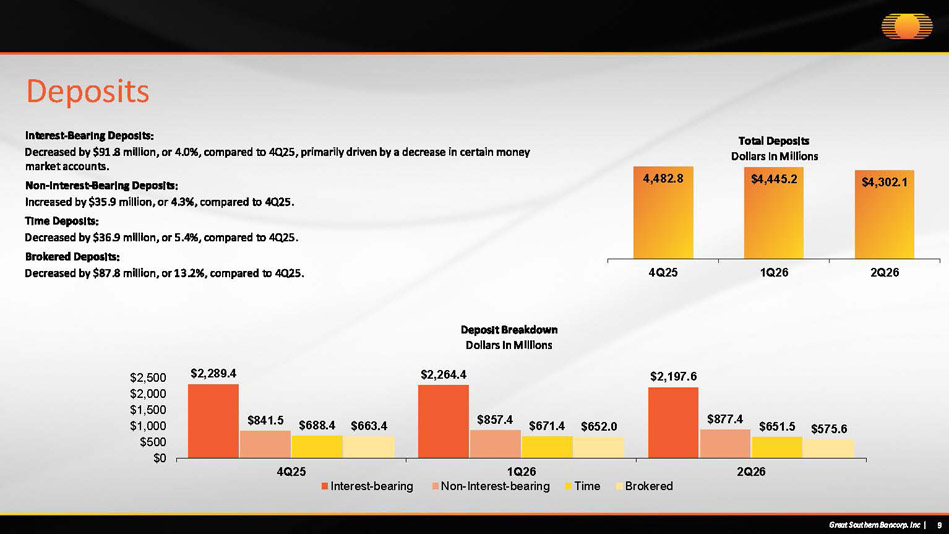

During the six months ended June 30, 2026, the Company’s total deposits decreased $180.7 million. Interest-bearing checking balances decreased $91.8 million (4.0%), primarily in certain money market accounts, and non-interest-bearing checking balances increased $35.9 million (4.3%). Time deposits generated through the Company’s banking center and corporate services networks decreased $36.9 million (5.4%). Brokered deposits, obtained through a variety of sources, decreased $87.8 million (13.2%). As total assets (primarily loans receivable) decreased, the Company elected not to replace some of its maturing brokered deposits. Most of this deposit decrease occurred in the second quarter of 2026, as total deposits decreased $143.1 million in the three months ended June 30, 2026.

At June 30, 2026, the Company had the following deposit balances:

| June 30, 2026 | |

| Interest-bearing checking | $2,197.6 million |

| Non-interest-bearing checking | 877.4 million |

| Time deposits | 651.5 million |

| Brokered deposits | 575.6 million |

At June 30, 2026, the Company estimated that its uninsured deposits, excluding deposit accounts of the Company’s consolidated subsidiaries, were approximately $665.6 million (15.5% of total deposits).

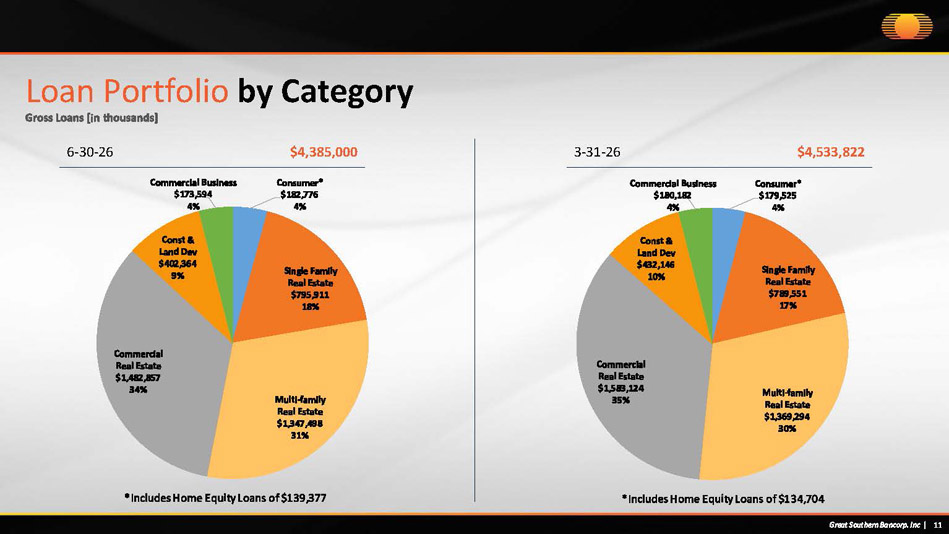

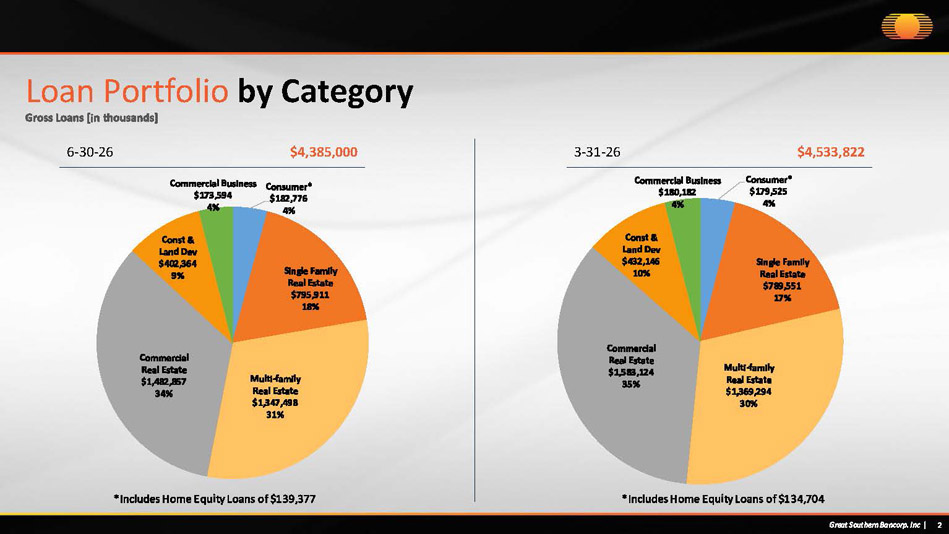

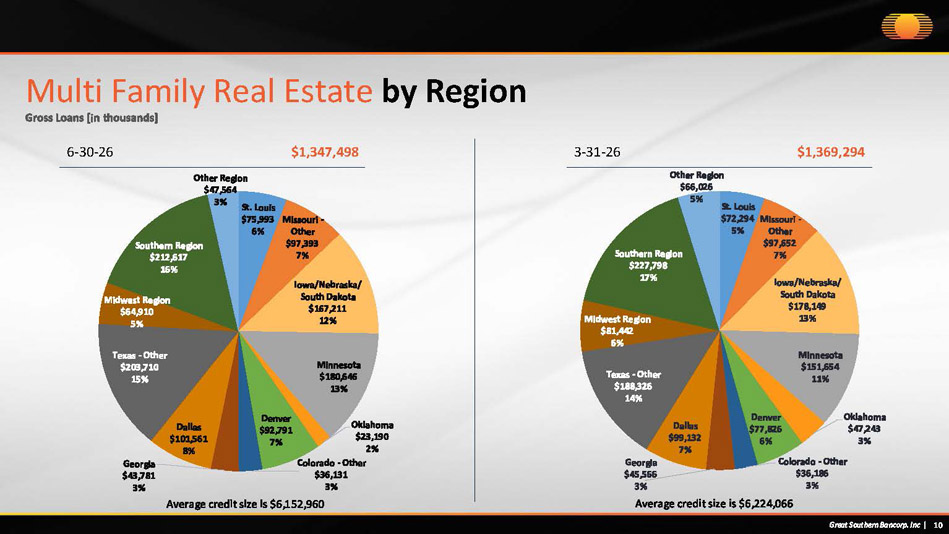

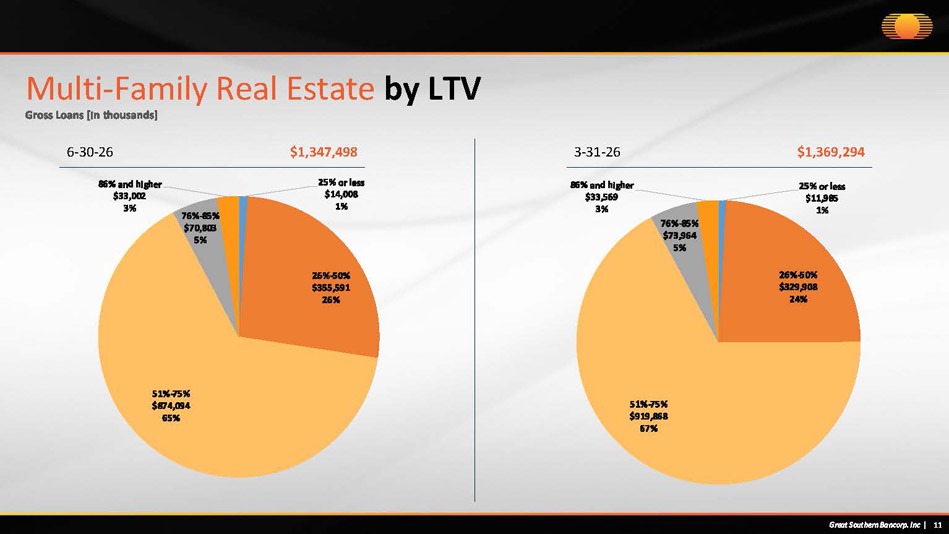

LOANS

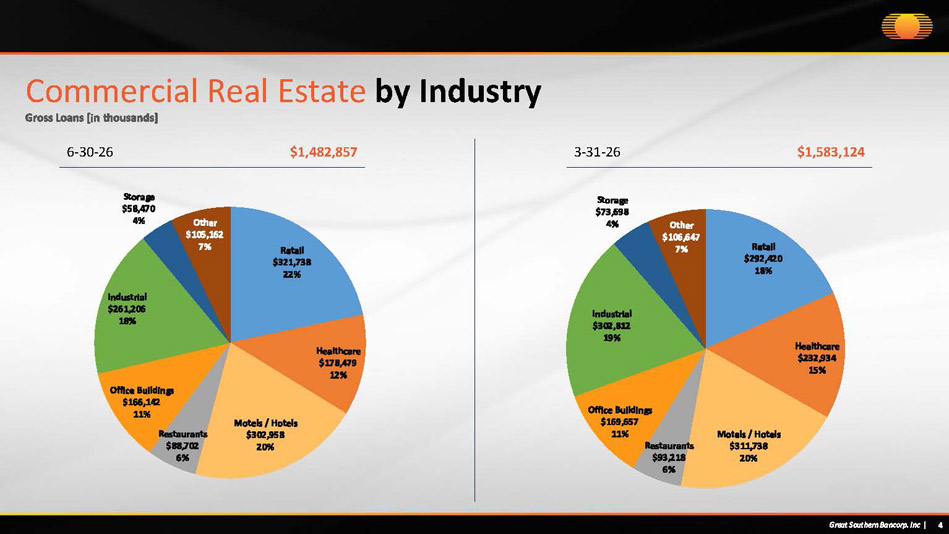

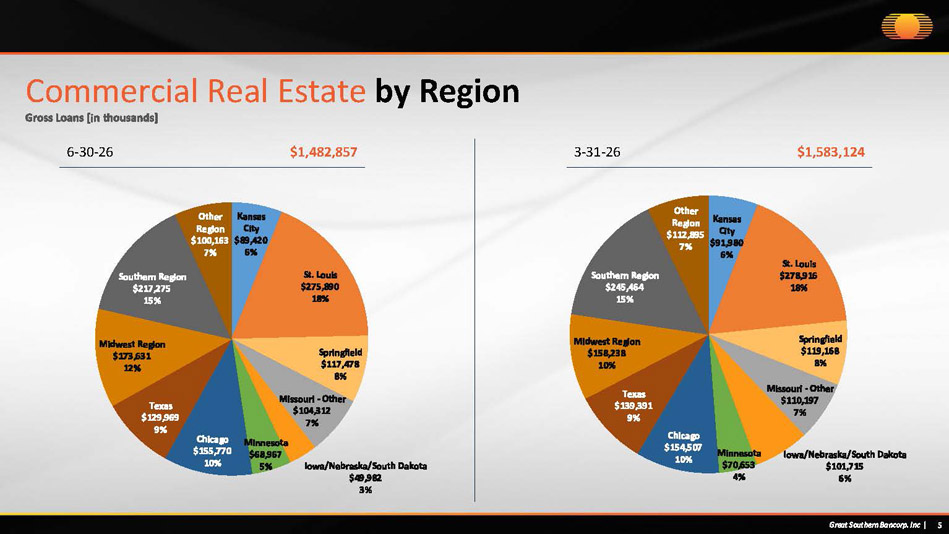

Total net loans, excluding mortgage loans held for sale, decreased $49.1 million, or 1.1%, from $4.36 billion at December 31, 2025 to $4.31 billion at June 30, 2026. This decrease was primarily driven by decreases in commercial real estate loans of $73.3 million and other residential (multi-family) loans of $39.9 million, partially offset by an increase in construction loans of $53.2 million. Compared to March 31, 2026, net loans decreased $148.9 million.

| 7 |

The pipeline of the unfunded portion of loans and formal loan commitments remained strong, with the largest portion of these unfunded balances consisting of the unfunded portion of outstanding construction loans ($531.5 million at June 30, 2026). See the table below.

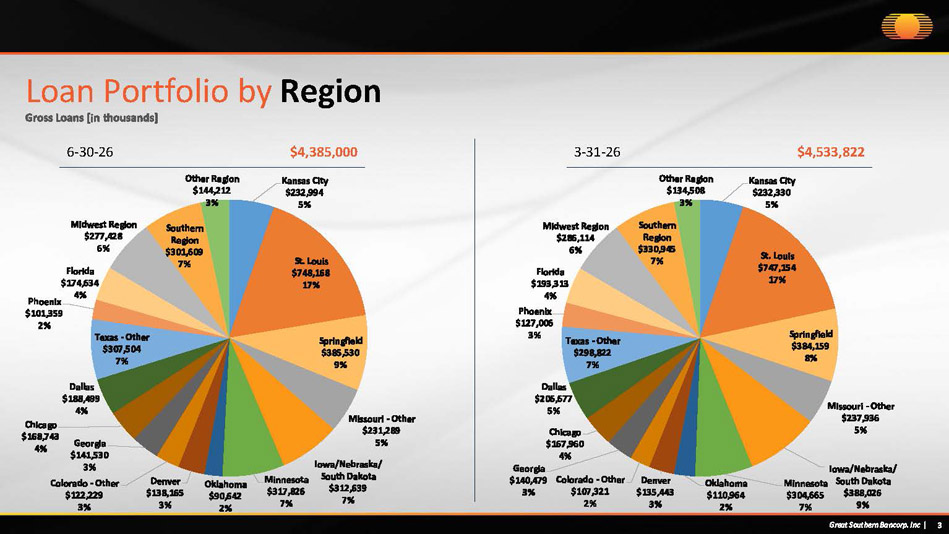

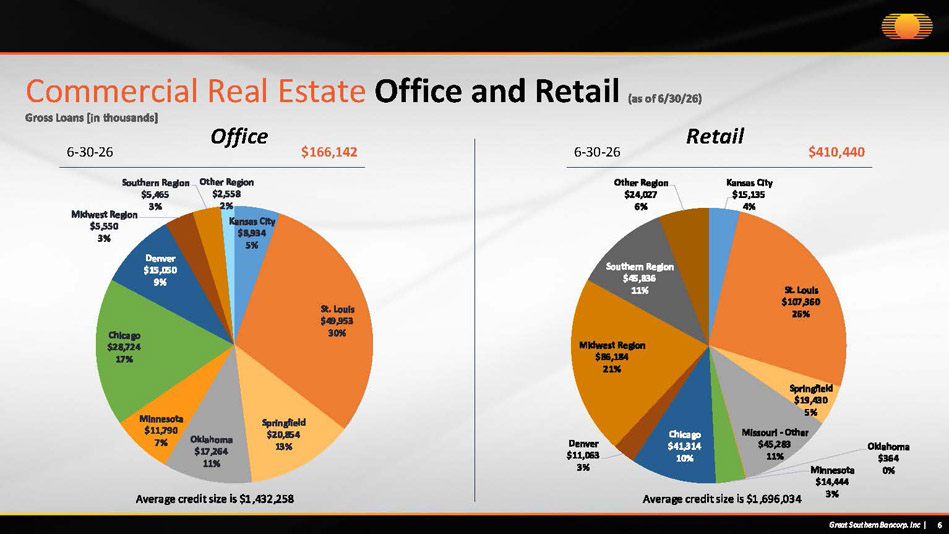

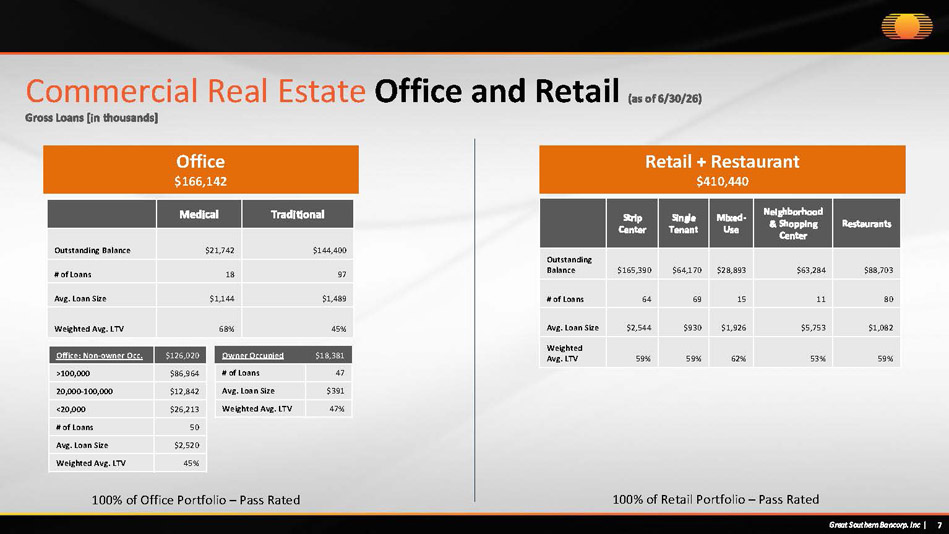

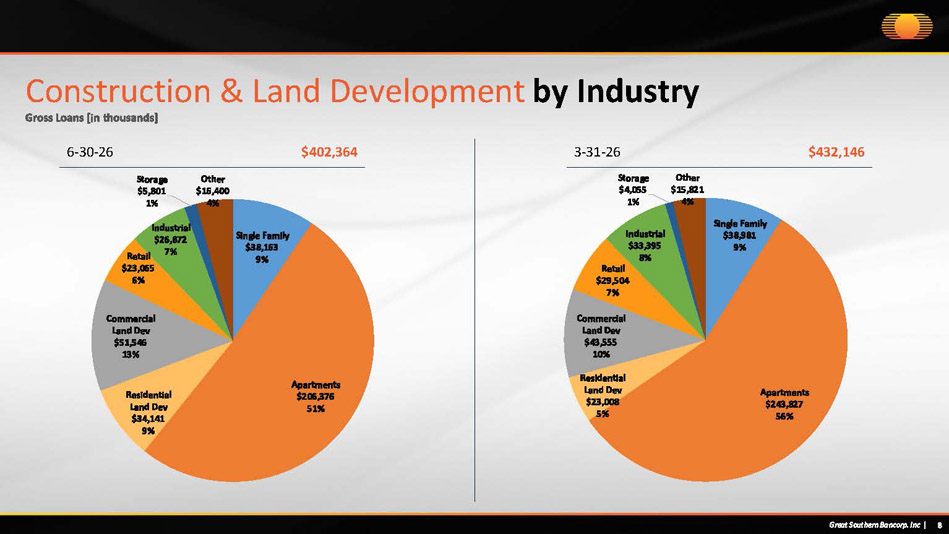

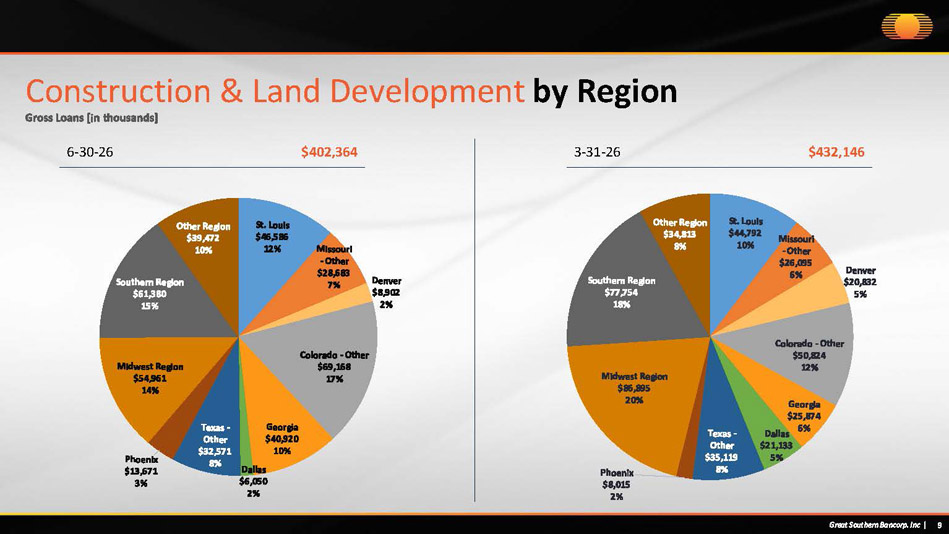

For additional details about the Company’s loan portfolio, please refer to the quarterly loan portfolio presentation available on the Company’s Investor Relations website under “Presentations.”

Loan commitments and the unfunded portion of loans at the dates indicated were as follows (in thousands):

| June

30, 2026 |

March

31, 2026 |

December

31, 2025 |

December

31, 2024 |

December

31, 2023 |

||||||

| Closed non-construction loans with unused available lines | ||||||||||

| Secured by real estate (one- to four-family) | $ | 214,597 | $ | 214,107 | $ | 208,229 | $ | 205,599 | $ | 203,964 |

| Secured by real estate (not one- to four-family) | — | — | — | — | — | |||||

| Not secured by real estate – commercial business | 106,290 | 106,024 | 114,568 | 106,621 | 82,435 | |||||

| Closed construction loans with unused available lines | ||||||||||

| Secured by real estate (one-to four-family) | 116,195 | 119,231 | 112,684 | 94,501 | 101,545 | |||||

| Secured by real estate (not one-to four-family) | 531,842 | 530,756 | 624,025 | 703,947 | 719,039 | |||||

| Loan commitments not closed | ||||||||||

| Secured by real estate (one-to four-family) | 22,937 | 19,194 | 14,113 | 14,373 | 12,347 | |||||

| Secured by real estate (not one-to four-family) | 49,139 | 24,053 | 19,412 | 53,660 | 48,153 | |||||

| Not secured by real estate – commercial business | 33,940 | 35,762 | 38,262 | 22,884 | 11,763 | |||||

| $ | 1,074,940 | $ | 1,049,127 | $ | 1,131,293 | $ | 1,201,585 | $ | 1,179,246 | |

PROVISION FOR CREDIT LOSSES AND ALLOWANCE FOR CREDIT LOSSES

During both the three months and six months ended June 30, 2026 and 2025, the Company did not record a provision expense on its portfolio of outstanding loans. Total net charge offs were $819,000 for the three months ended June 30, 2026, compared to total net recoveries of $111,000 during the same period in the prior year. Total net charge offs were $806,000 for the six months ended June 30, 2026, compared to total net recoveries of $55,000 during the same period in the prior year. During the quarter ended June 30, 2026, the Company recorded a provision for losses on unfunded commitments of $8,000, compared to a negative provision for losses on unfunded commitments of $110,000 for the same period in 2025. For the six months ended June 30, 2026, the Company recorded a negative provision for losses on unfunded commitments of $923,000, compared to a negative provision for losses on unfunded commitments of $458,000 for the same period in 2025.

The Bank’s allowance for credit losses as a percentage of total loans was 1.46% at both June 30, 2026 and December 31, 2025, compared to 1.43% at March 31, 2026. Management considers the allowance for credit losses adequate to cover losses inherent in the Bank’s loan portfolio at June 30, 2026, based on recent reviews of the portfolio and current economic conditions. However, if challenging economic conditions persist or worsen, or if management’s assessment of the loan portfolio changes, additional provisions for credit losses may be required, which could adversely impact the Company’s future financial performance.

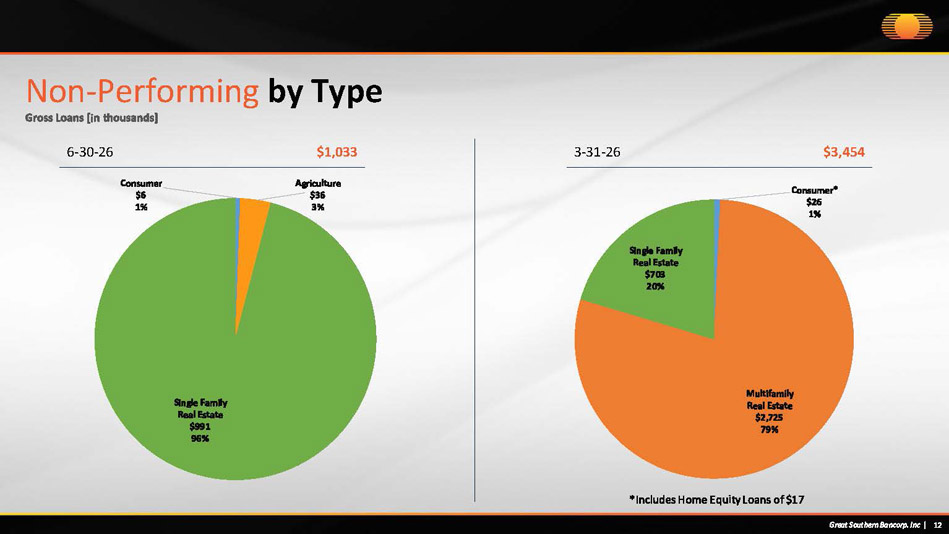

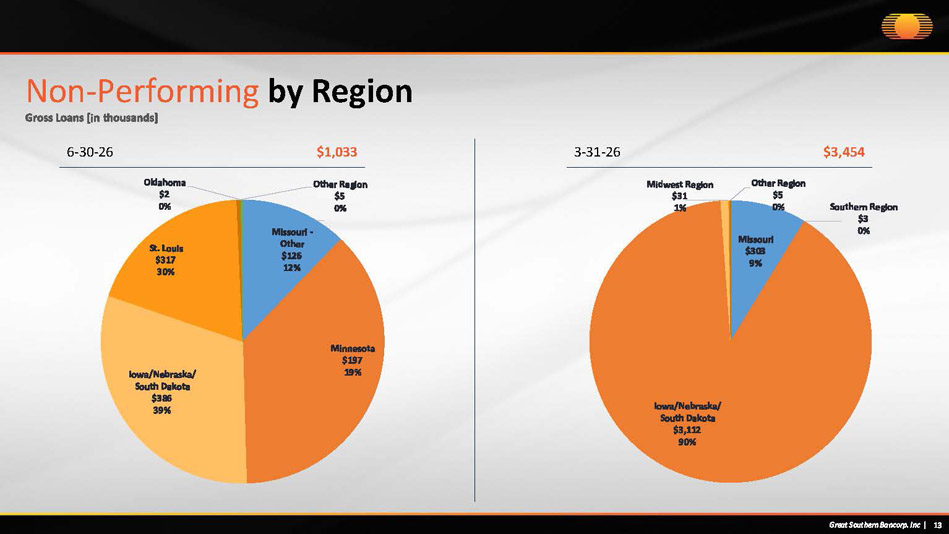

ASSET QUALITY

At June 30, 2026, non-performing assets were $9.4 million, an increase of $1.3 million from $8.1 million at December 31, 2025, and a decrease of $676,000 compared to March 31, 2026. Non-performing assets as a percentage of total assets were 0.17% at June 30, 2026, compared to 0.15% at December 31, 2025.

| 8 |

Activity in the non-performing loan categories during the quarter ended June 30, 2026, was as follows:

|

Beginning Balance, April 1 |

Additions to Non- Performing |

Removed from Non- Performing |

Transfers to Potential Problem Loans |

Transfers

to Foreclosed Assets and Repossessions |

Charge- Offs |

Payments |

Ending Balance, June 30 |

||||||||||||

| (In thousands) | |||||||||||||||||||

| One- to four-family construction | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | |||

| Subdivision construction | — | — | — | — | — | — | — | — | |||||||||||

| Land development | — | — | — | — | — | — | — | — | |||||||||||

| Commercial construction | — | — | — | — | — | — | — | — | |||||||||||

| One- to four-family residential | 703 | 368 | — | — | — | — | (81 | ) | 990 | ||||||||||

| Other residential (multi-family) | 2,725 | — | — | — | (1,807 | ) | (909 | ) | (9 | ) | — | ||||||||

| Commercial real estate | — | — | — | — | — | — | — | — | |||||||||||

| Commercial business | — | 36 | — | — | — | — | — | 36 | |||||||||||

| Consumer | 26 | — | — | — | — | (17 | ) | (2 | ) | 7 | |||||||||

| Total non-performing loans | $ | 3,454 | $ | 404 | $ | — | $ | — | $ | (1,807 | ) | $ | (926 | ) | $ | (92 | ) | $ | 1,033 |

| 9 |

Activity in the potential problem loans categories during the quarter ended June 30, 2026, was as follows:

|

Beginning Balance, April 1 |

Additions to Potential Problem |

Removed from Potential Problem |

Transfers to Non- Performing |

Transfers

to Foreclosed Assets and Repossessions |

Charge- Offs |

Loan Advances (Payments) |

Ending Balance, June 30 |

||||||||||||

| (In thousands) | |||||||||||||||||||

| One- to four-family construction | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | |||

| Subdivision construction | — | — | — | — | — | — | — | — | |||||||||||

| Land development | — | — | — | — | — | — | — | — | |||||||||||

| Commercial construction | — | — | — | — | — | — | — | — | |||||||||||

| One- to four-family residential | 943 | 25 | — | — | — | — | (112 | ) | 856 | ||||||||||

| Other residential (multi-family) | — | — | — | — | — | — | — | — | |||||||||||

| Commercial real estate | — | — | — | — | — | — | — | — | |||||||||||

| Commercial business | 14 | — | — | — | — | — | (2 | ) | 12 | ||||||||||

| Consumer | 281 | 47 | — | — | (5 | ) | (7 | ) | (27 | ) | 289 | ||||||||

| Total potential problem loans | $ | 1,238 | $ | 72 | $ | — | $ | — | $ | (5 | ) | $ | (7 | ) | $ | (141 | ) | $ | 1,157 |

Activity in the foreclosed assets and repossessions categories during the quarter ended June 30, 2026 was as follows:

|

Beginning Balance, April 1 |

Additions |

ORE

and Repossession Sales |

Capitalized Costs |

ORE and Repossession Write-Downs |

Ending Balance, June 30 |

||||||||

| (In thousands) | |||||||||||||

| One-to four-family construction | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | |

| Subdivision construction | — | — | — | — | — | — | |||||||

| Land development | — | — | — | — | — | — | |||||||

| Commercial construction | — | — | — | — | — | — | |||||||

| One- to four-family residential | 643 | — | (643 | ) | — | — | — | ||||||

| Other residential (multi-family) | — | 1,807 | — | — | — | 1,807 | |||||||

| Commercial real estate | 5,960 | — | — | 582 | — | 6,542 | |||||||

| Commercial business | — | — | — | — | — | — | |||||||

| Consumer | 12 | 12 | (13 | ) | — | — | 11 | ||||||

| Total foreclosed assets and repossessions | $ | 6,615 | $ | 1,819 | $ | (656 | ) | $ | 582 | $ | — | $ | 8,360 |

BUSINESS INITIATIVES

The Company maintains its focus on technology initiatives and advancements with its current core provider and key partners. These investments in both foundational projects and a heightened customer experience continue to foster an organizational emphasis on innovation and forward progress.

Great Southern launched a partnership with Greenlight, a debit card and financial learning app for kids and teens, in April 2026. The partnership offers a free Greenlight membership to Great Southern customers and is part of the Company’s ongoing efforts to expand both technology and family banking offerings.

Also in April, the Company’s fully redesigned website www.GreatSouthernBank.com, launched. The website, representative of Great Southern’s continued technology investments, offers customers and interested parties an improved online experience with up-to-date content, improved navigation, easier access to financial education information and more.

| 10 |

In June 2026 the Company decided, as part of its regular operational reviews, to consolidate nine banking centers into other Great Southern locations and eliminate a total of 66 positions across various Company divisions, including those at the impacted banking centers. These decisions were part of routine business maintenance as the organization evaluated products, services and workforce to align with changing market dynamics. Of the nine consolidating banking centers, one is in Arkansas, one is in Kansas, two are in Iowa and five are in Missouri (three in the Springfield metro area). Affected banking centers will close October 1, except for the Arkansas location, which will close September 25. All other consolidated staff positions outside of the banking centers have an effective date of September 30. As a result of these planned consolidations, certain expenses were required to be recorded in the 2026 second quarter financial statements. A list of the affected banking center locations is available on our website www.GreatSouthernBank.com.

The banking center consolidations and the workforce reductions are expected to result in approximately $2.3 - $2.7 million in annual pre-tax income improvement, beginning in the fourth quarter of 2026. This estimate incorporates compensation, facility and other non-interest expense savings, expected to be $4.4 - $4.8 million annually. This expense savings is expected to be partially offset by a projected amount of customer deposit attrition over time related to the branch closures, resulting in additional interest expense on alternative funding sources along with reduced non-interest income generated from these deposit accounts. If deposit account attrition is ultimately greater than our estimates, it may negatively impact our anticipated annual pre-tax income improvement. At June 30, 2026, total demand deposits at the nine banking centers were approximately $170 million and retail CD balances were approximately $25 million.

Also, as part of the organizational evaluation of products and services, Great Southern continues to expand its Live Teller ATM network with four new locations, including its first installations in the Des Moines, Iowa, market and a new Great Southern Express-branded location in Ozark, Mo.

The banking center located at 3839 Indian Hills Dr. in Sioux City, Iowa, temporarily closed July 3, 2026, for a complete remodel. This reinvestment will bring a fully refreshed banking center to the Bank’s Sioux City customers, including updated and brightened interiors, updated technology, and the installation of a drive-thru Live Teller ATM offering extended banking hours for customer convenience. During the temporary closure, customers are served by six additional banking centers in the greater Sioux City area, and 15 ATM locations.

Earnings Conference Call

The Company will host a conference call on Thursday, July 16, 2026, at 2:00 p.m. Central Time to discuss second quarter 2026 preliminary earnings. The call will be available live or in a recorded version at the Company’s Investor Relations website, http://investors.greatsouthernbank.com. Participants may register for the call at https://register-conf.media-server.com/register/BI1519b65fe3df412abf1fe40dfe95c397.

About Great Southern Bancorp, Inc.

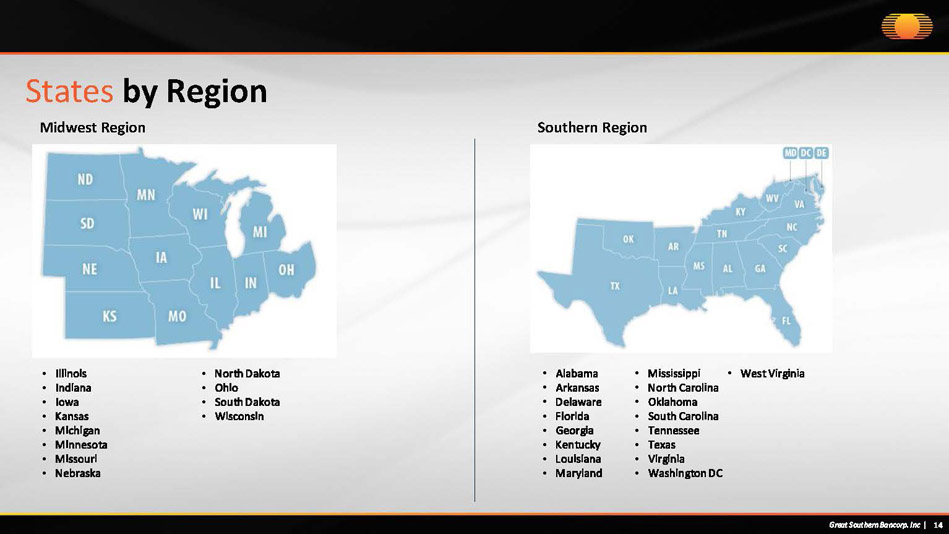

Headquartered in Springfield, Missouri, Great Southern offers a broad range of banking services to customers. The Company currently operates 87 retail banking centers in Missouri, Iowa, Kansas, Minnesota, Arkansas and Nebraska and commercial lending offices in Atlanta, Charlotte, Chicago, Dallas, Denver, Omaha, and Phoenix. The common stock of Great Southern Bancorp, Inc. is listed on the Nasdaq Global Select Market under the symbol “GSBC.”

www.GreatSouthernBank.com

| 11 |

Forward-Looking Statements

When used in this press release and in other documents filed or furnished by the Company with or to the Securities and Exchange Commission (the “SEC”), in the Company's other press releases or other public or stockholder communications, and in oral statements made with the approval of an authorized executive officer, the words or phrases “may,” “might,” “could,” “should,” "will likely result," "are expected to," "will continue," "is anticipated," “believe,” "estimate," "project," "intends" or similar expressions are intended to identify "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements also include, but are not limited to, statements regarding plans, objectives, expectations or consequences of announced transactions, known trends and statements about future performance, operations, products and services of the Company. The Company’s ability to predict results or the actual effects of future plans or strategies is inherently uncertain, and the Company’s actual results could differ materially from those contained in the forward-looking statements.

Factors that could cause or contribute to such differences include, but are not limited to: (i) expected revenues, cost savings, earnings accretion, synergies and other benefits from the Company's merger and acquisition activities might not be realized within the anticipated time frames or at all, and costs or difficulties relating to integration matters, including but not limited to customer and employee retention, might be greater than expected; (ii) changes in economic conditions, either nationally or in the Company's market areas; (iii) the effects of any new or continuing public health issues on general economic and financial market conditions; (iv) fluctuations in interest rates, the effects of inflation or a potential recession, whether caused by Federal Reserve actions or otherwise; (v) the impact of bank failures or adverse developments at other banks and related negative press about the banking industry in general on investor and depositor sentiment; (vi) slower or negative economic growth caused by tariffs, changes in energy prices, supply chain disruptions or other factors; (vii) the risks of lending and investing activities, including changes in the level and direction of loan delinquencies and write-offs and changes in estimates of the adequacy of the allowance for credit losses; (viii) the possibility of realized or unrealized losses on securities held in the Company's investment portfolio; (ix) the Company's ability to access cost-effective funding and maintain sufficient liquidity; (x) fluctuations in real estate values and both residential and commercial real estate market conditions; (xi) the ability to adapt successfully to technological changes to meet customers' needs and developments in the marketplace; (xii) the possibility that security measures implemented might not be sufficient to mitigate the risk of a cyber-attack or cyber theft, and that such security measures might not protect against systems failures or interruptions; (xiii) legislative or regulatory changes that adversely affect the Company's business; (xiv) changes in accounting policies and practices or accounting standards; (xv) results of examinations of the Company and the Bank by their regulators, including the possibility that the regulators may, among other things, require the Company to limit its business activities, change its business mix, increase its allowance for credit losses, write-down assets or increase its capital levels, or affect its ability to borrow funds or maintain or increase deposits, which could adversely affect its liquidity and earnings; (xvi) costs and effects of litigation, including settlements and judgments; (xvii) competition; and (xviii) natural disasters, war, terrorist activities or civil unrest and their effects on economic and business environments in which the Company operates. The Company wishes to advise readers that the factors listed above and other risks described in the Company’s most recent Annual Report on Form 10-K, including, without limitation, those described under “Item 1A. Risk Factors,” subsequent Quarterly Reports on Form 10-Q and other documents filed or furnished from time to time by the Company with the SEC (which are available on our website at www.greatsouthernbank.com and the SEC’s website at www.sec.gov), could affect the Company's financial performance and cause the Company's actual results for future periods to differ materially from any opinions or statements expressed with respect to future periods in any current statements.

The Company does not undertake-and specifically declines any obligation- to publicly release the result of any revisions which may

be made to any forward-looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence

of anticipated or unanticipated events.

| 12 |

The following tables set forth selected consolidated financial information of the Company at the dates and for the periods indicated. Financial data at all dates other than December 31, 2025, and for all periods is unaudited. In the opinion of management, all adjustments, which consist only of normal recurring accrual adjustments, necessary for a fair presentation of the results at and for such unaudited dates and periods have been included. The results of operations and other data for the three and six months ended June 30, 2026 and 2025, and the three months ended March 31, 2026, are not necessarily indicative of the results of operations which may be expected for any future period.

| June 30, | December 31, | ||||

| 2026 | 2025 | ||||

| (In thousands) | |||||

| Selected Financial Condition Data: | |||||

| Total assets | $ | 5,522,824 | $ | 5,598,606 | |

| Loans receivable, gross | 4,377,132 | 4,427,678 | |||

| Allowance for credit losses | 63,965 | 64,771 | |||

| Other real estate owned, net | 8,360 | 6,036 | |||

| Available-for-sale securities, at fair value | 503,795 | 523,831 | |||

| Held-to-maturity securities, at amortized cost | 175,264 | 179,200 | |||

| Deposits | 4,302,067 | 4,482,774 | |||

| Total borrowings | 511,247 | 405,169 | |||

| Total stockholders’ equity | 641,597 | 636,126 | |||

| Non-performing assets | 9,393 | 8,130 | |||

| Three Months Ended |

Six Months Ended |

Three Months Ended |

||||||||||||||||

| June 30, |

June 30, |

March 31, |

||||||||||||||||

| 2026 |

2025 |

2026 |

2025 |

2026 |

||||||||||||||

| (In thousands) | ||||||||||||||||||

| Selected Operating Data: | ||||||||||||||||||

| Interest income | $ | 72,461 | $ | 80,975 | $ | 143,626 | $ | 161,218 | $ | 71,165 | ||||||||

| Interest expense | 22,968 | 30,012 | 45,805 | 60,921 | 22,837 | |||||||||||||

| Net interest income | 49,493 | 50,963 | 97,821 | 100,297 | 48,328 | |||||||||||||

| Provision (credit) for credit losses on loans and unfunded commitments | 8 | (110 | ) | (923 | ) | (458 | ) | (931 | ) | |||||||||

| Non-interest income | 7,375 | 8,212 | 14,404 | 14,802 | 7,029 | |||||||||||||

| Non-interest expense | 38,222 | 35,005 | 73,014 | 69,827 | 34,792 | |||||||||||||

| Provision for income taxes | 2,843 | 4,494 | 6,863 | 8,784 | 4,020 | |||||||||||||

| Net income | $ | 15,795 | $ | 19,786 | $ | 33,271 | $ | 36,946 | $ | 17,476 | ||||||||

|

At or For the Three Months Ended |

At or For the Six Months Ended |

At or For the Three Months Ended | |||||||||||||||||

| June 30, | June 30, | March 31, | |||||||||||||||||

|

2026 |

2025 |

2026 |

2025 |

2026 |

|||||||||||||||

| (Dollars in thousands, except per share data) | |||||||||||||||||||

| Per Common Share: | |||||||||||||||||||

| Net income (fully diluted) | $ | 1.43 | $ | 1.72 | $ | 2.99 | $ | 3.18 | $ | 1.58 | |||||||||

| Book value | $ | 58.95 | $ | 54.61 | $ | 58.95 | $ | 54.61 | $ | 58.27 | |||||||||

| Earnings Performance Ratios: | |||||||||||||||||||

| Annualized return on average assets | 1.12 | % | 1.34 | % | 1.18 | % | 1.24 | % | 1.24 | % | |||||||||

| Annualized return on average common stockholders’ equity | 9.83 | % | 12.81 | % | 10.34 | % | 12.06 | % | 10.85 | % | |||||||||

| Net interest margin | 3.76 | % | 3.68 | % | 3.74 | % | 3.63 | % | 3.71 | % | |||||||||

| Average interest rate spread | 3.24 | % | 3.09 | % | 3.22 | % | 3.05 | % | 3.20 | % | |||||||||

| Efficiency ratio | 67.21 | % | 59.16 | % | 65.06 | % | 60.67 | % | 62.85 | % | |||||||||

| Non-interest expense to average total assets | 2.72 | % | 2.37 | % | 2.60 | % | 2.35 | % | 2.47 | % | |||||||||

| Asset Quality Ratios: | |||||||||||||||||||

| Allowance for credit losses to period-end loans | 1.46 | % | 1.41 | % | 1.46 | % | 1.41 | % | 1.43 | % | |||||||||

| Non-performing assets to period-end assets | 0.17 | % | 0.14 | % | 0.17 | % | 0.14 | % | 0.18 | % | |||||||||

| Non-performing loans to period-end loans | 0.02 | % | 0.04 | % | 0.02 | % | 0.04 | % | 0.08 | % | |||||||||

| Annualized net charge-offs (recoveries) to average loans | 0.07 | % | (0.01 | )% | 0.04 | % | 0.00 | % | 0.00 | % | |||||||||

| 13 |

|

Great Southern Bancorp, Inc. and Subsidiaries Consolidated Statements of Financial Condition (In thousands, except number of shares) |

|||||||||

|

June

30, 2026 |

December

31, 2025 |

March

31, 2026 |

|||||||

| Assets | |||||||||

| Cash | $ | 97,200 | $ | 109,833 | $ | 101,405 | |||

| Interest-bearing deposits in other financial institutions | 82,781 | 79,721 | 85,999 | ||||||

| Cash and cash equivalents | 179,981 | 189,554 | 187,404 | ||||||

| Available-for-sale securities | 503,795 | 523,831 | 513,846 | ||||||

| Held-to-maturity securities | 175,264 | 179,200 | 177,594 | ||||||

| Mortgage loans held for sale | 7,868 | 6,838 | 6,823 | ||||||

| Loans receivable, net of allowance for

credit losses of $63,965 – June 2026; $64,771 – December 2025; $64,784 – March 2026 |

4,307,712 | 4,356,853 | 4,456,639 | ||||||

| Interest receivable | 18,467 | 18,068 | 19,716 | ||||||

| Prepaid expenses and other assets | 123,005 | 128,615 | 124,023 | ||||||

| Other real estate owned and repossessions, net | 8,360 | 6,036 | 6,615 | ||||||

| Premises and equipment, net | 132,838 | 133,257 | 132,113 | ||||||

| Goodwill and other intangible assets | 9,444 | 9,660 | 9,552 | ||||||

| Federal Home Loan Bank stock and other interest-earning assets | 27,414 | 20,079 | 27,720 | ||||||

| Current and deferred income taxes | 28,676 | 26,615 | 25,277 | ||||||

| Total Assets | $ | 5,522,824 | $ | 5,598,606 | $ | 5,687,322 | |||

| Liabilities and Stockholders’ Equity | |||||||||

| Liabilities | |||||||||

| Deposits | $ | 4,302,067 | $ | 4,482,774 | $ | 4,445,161 | |||

| Securities sold under reverse repurchase agreements with customers | 39,913 | 48,467 | 37,198 | ||||||

| Short-term borrowings | 445,560 | 330,928 | 470,660 | ||||||

| Subordinated debentures issued to capital trust | 25,774 | 25,774 | 25,774 | ||||||

| Accrued interest payable | 3,080 | 3,612 | 3,250 | ||||||

| Advances from borrowers for taxes and insurance | 10,283 | 5,781 | 9,021 | ||||||

| Accounts payable and accrued expenses | 46,925 | 56,596 | 55,011 | ||||||

| Liability for unfunded commitments | 7,625 | 8,548 | 7,617 | ||||||

| Total Liabilities | 4,881,227 | 4,962,480 | 5,053,692 | ||||||

| Stockholders’ Equity | |||||||||

| Capital stock | |||||||||

| Preferred stock, $.01 par value; authorized 1,000,000 shares; issued and outstanding June 2026, December 2025 and March 2026 -0- shares | — | — | — | ||||||

| Common stock, $.01 par value; authorized 20,000,000 shares; issued and outstanding June 2026 – 10,884,444 shares; December 2025 – 11,062,252 shares; March 2026 – 10,873,847 shares | 83 | 111 | 83 | ||||||

| Additional paid-in capital | 59,278 | 54,120 | 56,126 | ||||||

| Retained earnings | 619,960 | 614,095 | 612,570 | ||||||

| Accumulated other comprehensive loss | (37,724 | ) | (32,200 | ) | (35,149 | ) | |||

| Total Stockholders’ Equity | 641,597 | 636,126 | 633,630 | ||||||

| Total Liabilities and Stockholders’ Equity | $ | 5,522,824 | $ | 5,598,606 | $ | 5,687,322 | |||

| 14 |

|

Great Southern Bancorp, Inc. and Subsidiaries Consolidated Statements of Income (In thousands, except per share data) |

|||||||||||||||||||

|

Three Months Ended |

Six Months Ended |

Three Months Ended |

|||||||||||||||||

|

June 30, |

June 30, |

March 31, |

|||||||||||||||||

|

2026 |

2025 |

2026 |

2025 |

2026 |

|||||||||||||||

| Interest Income | |||||||||||||||||||

| Loans | $ | 65,686 | $ | 73,830 | $ | 130,346 | $ | 146,901 | $ | 64,660 | |||||||||

| Investment securities and other | 6,775 | 7,145 | 13,280 | 14,317 | 6,505 | ||||||||||||||

| 72,461 | 80,975 | 143,626 | 161,218 | 71,165 | |||||||||||||||

| Interest Expense | |||||||||||||||||||

| Deposits | 17,861 | 24,368 | 36,198 | 48,968 | 18,337 | ||||||||||||||

| Securities sold under reverse repurchase agreements | 133 | 372 | 229 | 743 | 96 | ||||||||||||||

| Short-term borrowings, overnight FHLBank borrowings and other interest-bearing liabilities | 4,620 | 3,974 | 8,682 | 8,424 | 4,062 | ||||||||||||||

| Subordinated debentures issued to capital trust | 354 | 389 | 696 | 771 | 342 | ||||||||||||||

| Subordinated notes | — | 909 | — | 2,015 | — | ||||||||||||||

| 22,968 | 30,012 | 45,805 | 60,921 | 22,837 | |||||||||||||||

| Net Interest Income | 49,493 | 50,963 | 97,821 | 100,297 | 48,328 | ||||||||||||||

| Provision for Credit Losses on Loans | — | — | — | — | — | ||||||||||||||

| Provision (Credit) for Unfunded Commitments | 8 | (110 | ) | (923 | ) | (458 | ) | (931 | ) | ||||||||||

| Net Interest Income After Provision for Credit Losses and Provision (Credit) for Unfunded Commitments | 49,485 | 51,073 | 98,744 | 100,755 | 49,259 | ||||||||||||||

| Non-interest Income | |||||||||||||||||||

| Commissions | 641 | 411 | 1,256 | 673 | 615 | ||||||||||||||

| Overdraft and Insufficient funds fees | 1,248 | 1,266 | 2,479 | 2,481 | 1,231 | ||||||||||||||

| POS and ATM fee income and service charges | 3,392 | 3,444 | 6,493 | 6,678 | 3,101 | ||||||||||||||

| Net gains on loan sales | 795 | 893 | 1,514 | 1,494 | 719 | ||||||||||||||

| Late charges and fees on loans | 305 | 340 | 441 | 583 | 136 | ||||||||||||||

| Gain (loss) on derivative interest rate products | 5 | (28 | ) | 3 | (52 | ) | (2 | ) | |||||||||||

| Other income | 989 | 1,886 | 2,218 | 2,945 | 1,229 | ||||||||||||||

| 7,375 | 8,212 | 14,404 | 14,802 | 7,029 | |||||||||||||||

| Non-interest Expense | |||||||||||||||||||

| Salaries and employee benefits | 20,691 | 20,005 | 40,762 | 40,134 | 20,071 | ||||||||||||||

| Net occupancy and equipment expense | 10,683 | 8,435 | 19,547 | 16,968 | 8,864 | ||||||||||||||

| Postage | 889 | 825 | 1,814 | 1,756 | 925 | ||||||||||||||

| Insurance | 1,099 | 1,095 | 2,171 | 2,260 | 1,072 | ||||||||||||||

| Advertising | 836 | 705 | 1,208 | 995 | 372 | ||||||||||||||

| Office supplies and printing | 197 | 238 | 419 | 504 | 222 | ||||||||||||||

| Telephone | 705 | 705 | 1,390 | 1,411 | 685 | ||||||||||||||

| Legal, audit and other professional fees | 967 | 929 | 1,657 | 1,967 | 690 | ||||||||||||||

| Expense (income) on other real estate and repossessions | (85 | ) | (168 | ) | (31 | ) | (238 | ) | 54 | ||||||||||

| Intangible asset amortization | 108 | 108 | 216 | 216 | 108 | ||||||||||||||

| Other operating expenses | 2,132 | 2,128 | 3,861 | 3,854 | 1,729 | ||||||||||||||

| 38,222 | 35,005 | 73,014 | 69,827 | 34,792 | |||||||||||||||

| Income Before Income Taxes | 18,638 | 24,280 | 40,134 | 45,730 | 21,496 | ||||||||||||||

| Provision for Income Taxes | 2,843 | 4,494 | 6,863 | 8,784 | 4,020 | ||||||||||||||

| Net Income | $ | 15,795 | $ | 19,786 | $ | 33,271 | $ | 36,946 | $ | 17,476 | |||||||||

| Earnings Per Common Share | |||||||||||||||||||

| Basic | $ | 1.45 | $ | 1.73 | $ | 3.04 | $ | 3.20 | $ | 1.59 | |||||||||

| Diluted | $ | 1.43 | $ | 1.72 | $ | 2.99 | $ | 3.18 | $ | 1.58 | |||||||||

| Dividends Declared Per Common Share | $ | 0.43 | $ | 0.40 | $ | 0.86 | $ | 0.80 | $ | 0.43 | |||||||||

| 15 |

Average Balances, Interest Rates and Yields

The following table presents, for the periods indicated, the total dollar amounts of interest income from average interest-earning assets and the resulting yields, as well as the interest expense on average interest-bearing liabilities, expressed both in dollars and rates, and the net interest margin. Average balances of loans receivable include the average balances of nonaccrual loans for each period. Interest income on loans includes interest received on nonaccrual loans on a cash basis. Interest income on loans also includes the amortization of net loan fees, which were deferred in accordance with accounting standards. Net fees included in interest income were $1.2 million and $1.1 million for the three months ended June 30, 2026 and 2025, respectively. Net fees included in interest income were $2.0 million and $2.1 million for the six months ended June 30, 2026 and 2025, respectively. Tax-exempt income was not calculated on a tax equivalent basis. The table does not reflect any effect of income taxes.

| June 30, 2026 |

Three

Months Ended June 30, 2026 |

Three

Months Ended June 30, 2025 |

|||||||||||||||||||

| Average | Yield/ | Average | Yield/ | ||||||||||||||||||

| Yield/Rate | Balance | Interest | Rate | Balance | Interest | Rate | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||

| Interest-earning assets: | |||||||||||||||||||||

| Loans receivable: | |||||||||||||||||||||

| One- to four-family residential | 4.39 | % | $ | 785,845 | $ | 8,611 | 4.40 | % | $ | 822,283 | $ | 8,750 | 4.27 | % | |||||||

| Other residential | 6.23 | 1,319,178 | 20,688 | 6.29 | 1,565,447 | 27,281 | 6.99 | ||||||||||||||

| Commercial real estate | 6.02 | 1,538,995 | 23,199 | 6.05 | 1,489,015 | 23,082 | 6.22 | ||||||||||||||

| Construction | 6.21 | 469,176 | 7,433 | 6.35 | 480,254 | 8,617 | 7.20 | ||||||||||||||

| Commercial business | 5.81 | 178,472 | 3,023 | 6.79 | 208,119 | 3,517 | 6.78 | ||||||||||||||

| Other loans | 6.21 | 181,982 | 2,732 | 6.02 | 167,548 | 2,583 | 6.18 | ||||||||||||||

| Total loans receivable | 5.80 | 4,473,648 | 65,686 | 5.89 | 4,732,666 | 73,830 | 6.26 | ||||||||||||||

| Investment securities | 3.22 | 709,009 | 5,977 | 3.38 | 727,336 | 6,099 | 3.36 | ||||||||||||||

| Other interest-earning assets | 3.63 | 91,392 | 798 | 3.50 | 97,463 | 1,046 | 4.30 | ||||||||||||||

| Total interest-earning assets | 5.43 | 5,274,049 | 72,461 | 5.51 | 5,557,465 | 80,975 | 5.84 | ||||||||||||||

| Non-interest-earning assets: | |||||||||||||||||||||

| Cash and cash equivalents | 94,498 | 100,289 | |||||||||||||||||||

| Other non-earning assets | 247,571 | 256,923 | |||||||||||||||||||

| Total assets | $ | 5,616,118 | $ | 5,914,677 | |||||||||||||||||

| Interest-bearing liabilities: | |||||||||||||||||||||

| Interest-bearing demand and savings | 1.19 | $ | 2,182,530 | 6,423 | 1.18 | $ | 2,225,933 | 7,791 | 1.40 | ||||||||||||

| Time deposits | 2.95 | 659,741 | 4,802 | 2.92 | 757,608 | 6,521 | 3.45 | ||||||||||||||

| Brokered deposits | 3.83 | 684,484 | 6,636 | 3.89 | 895,340 | 10,056 | 4.50 | ||||||||||||||

| Total deposits | 1.97 | 3,526,755 | 17,861 | 2.03 | 3,878,881 | 24,368 | 2.52 | ||||||||||||||

| Securities sold under reverse repurchase agreements | 1.55 | 34,900 | 133 | 1.53 | 65,607 | 372 | 2.27 | ||||||||||||||

| Short-term borrowings, overnight FHLBank borrowings and other interest-bearing liabilities | 3.97 | 472,564 | 4,620 | 3.92 | 347,303 | 3,974 | 4.59 | ||||||||||||||

| Subordinated debentures issued to capital trust | 5.52 | 25,774 | 354 | 5.51 | 25,774 | 389 | 6.05 | ||||||||||||||

| Subordinated notes | — | — | — | — | 62,631 | 909 | 5.82 | ||||||||||||||

| Total interest-bearing liabilities | 2.21 | 4,059,993 | 22,968 | 2.27 | 4,380,196 | 30,012 | 2.75 | ||||||||||||||

| Non-interest-bearing liabilities: | |||||||||||||||||||||

| Demand deposits | 859,352 | 849,862 | |||||||||||||||||||

| Other liabilities | 53,725 | 66,585 | |||||||||||||||||||

| Total liabilities | 4,973,070 | 5,296,643 | |||||||||||||||||||

| Stockholders’ equity | 643,048 | 618,034 | |||||||||||||||||||

| Total liabilities and stockholders’ equity | $ | 5,616,118 | $ | 5,914,677 | |||||||||||||||||

| Net interest income: | $ | 49,493 | $ | 50,963 | |||||||||||||||||

| Interest rate spread | 3.22 | % | 3.24 | % | 3.09 | % | |||||||||||||||

| Net interest margin* | 3.76 | % | 3.68 | % | |||||||||||||||||

| Average interest-earning assets to average interest-bearing liabilities | 129.9 | % | 126.9 | % | |||||||||||||||||

___________________

*Defined as the Company’s net interest income divided by average total interest-earning assets.

| 16 |

| June 30, 2026 |

Six

Months Ended June 30, 2026 |

Six Months Ended June 30, 2025 |

||||||||||||||||||

| Average | Yield/ | Average | Yield/ | |||||||||||||||||

| Yield/Rate | Balance | Interest | Rate | Balance | Interest | Rate | ||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||

| Interest-earning assets: | ||||||||||||||||||||

| Loans receivable: | ||||||||||||||||||||

| One- to four-family residential | 4.39 | % | $ | 784,137 | $ | 16,996 | 4.37 | % | $ | 826,426 | $ | 17,318 | 4.23 | % | ||||||

| Other residential | 6.23 | 1,350,667 | 42,220 | 6.30 | 1,555,881 | 53,731 | 6.96 | |||||||||||||

| Commercial real estate | 6.02 | 1,544,527 | 45,988 | 6.00 | 1,499,665 | 46,096 | 6.20 | |||||||||||||

| Construction | 6.21 | 436,986 | 13,799 | 6.37 | 485,392 | 17,270 | 7.17 | |||||||||||||

| Commercial business | 5.81 | 178,149 | 5,987 | 6.78 | 209,944 | 7,339 | 7.05 | |||||||||||||

| Other loans | 6.21 | 178,909 | 5,356 | 6.04 | 166,989 | 5,147 | 6.22 | |||||||||||||

| Total loans receivable | 5.80 | 4,473,375 | 130,346 | 5.88 | 4,744,297 | 146,901 | 6.24 | |||||||||||||

| Investment securities | 3.22 | 715,891 | 11,709 | 3.30 | 732,699 | 12,173 | 3.35 | |||||||||||||

| Other interest-earning assets | 3.63 | 90,441 | 1,571 | 3.50 | 101,238 | 2,144 | 4.27 | |||||||||||||

| Total interest-earning assets | 5.43 | 5,279,707 | 143,626 | 5.48 | 5,578,234 | 161,218 | 5.83 | |||||||||||||

| Non-interest-earning assets: | ||||||||||||||||||||

| Cash and cash equivalents | 96,086 | 100,537 | ||||||||||||||||||

| Other non-earning assets | 247,025 | 259,692 | ||||||||||||||||||

| Total assets | $ | 5,622,818 | $ | 5,938,463 | ||||||||||||||||

| Interest-bearing liabilities: | ||||||||||||||||||||

| Interest-bearing demand and savings | 1.19 | $ | 2,216,555 | 13,154 | 1.20 | $ | 2,223,716 | 15,588 | 1.41 | |||||||||||

| Time deposits | 2.95 | 673,399 | 9,897 | 2.96 | 764,791 | 13,235 | 3.49 | |||||||||||||

| Brokered deposits | 3.83 | 682,760 | 13,147 | 3.88 | 893,983 | 20,145 | 4.54 | |||||||||||||

| Total deposits | 1.97 | 3,572,714 | 36,198 | 2.04 | 3,882,490 | 48,968 | 2.54 | |||||||||||||

| Securities sold under reverse repurchase agreements | 1.55 | 36,522 | 229 | 1.26 | 73,957 | 743 | 2.03 | |||||||||||||

| Short-term borrowings, overnight FHLBank borrowings and other interest-bearing liabilities | 3.97 | 446,007 | 8,682 | 3.93 | 369,849 | 8,424 | 4.59 | |||||||||||||

| Subordinated debentures issued to capital trust | 5.52 | 25,774 | 696 | 5.45 | 25,774 | 771 | 6.03 | |||||||||||||

| Subordinated notes | — | — | — | — | 68,741 | 2,015 | 5.91 | |||||||||||||

| Total interest-bearing liabilities | 2.21 | 4,081,017 | 45,805 | 2.26 | 4,420,811 | 60,921 | 2.78 | |||||||||||||

| Non-interest-bearing liabilities: | ||||||||||||||||||||

| Demand deposits | 847,290 | 835,888 | ||||||||||||||||||

| Other liabilities | 50,914 | 68,961 | ||||||||||||||||||

| Total liabilities | 4,979,221 | 5,325,660 | ||||||||||||||||||

| Stockholders’ equity | 643,597 | 612,803 | ||||||||||||||||||

| Total liabilities and stockholders’ equity | $ | 5,622,818 | $ | 5,938,463 | ||||||||||||||||

| Net interest income: | $ | 97,821 | $ | 100,297 | ||||||||||||||||

| Interest rate spread | 3.22 | % | 3.22 | % | 3.05 | % | ||||||||||||||

| Net interest margin* | 3.74 | % | 3.63 | % | ||||||||||||||||

| Average interest-earning assets to average interest-bearing liabilities | 129.4 | % | 126.2 | % | ||||||||||||||||

___________________

*Defined as the Company’s net interest income divided by average total interest-earning assets.

| 17 |

NON-GAAP FINANCIAL MEASURES

This document contains certain financial information determined by methods other than in accordance with accounting principles generally accepted in the United States (“GAAP”), including the ratio of tangible common equity to tangible assets and information excluding one-time branch consolidation and severance costs, specifically, net income, earnings per diluted common share, annualized return on average common equity, annualized return on average assets and efficiency ratio.

In calculating the ratio of tangible common equity to tangible assets, we subtract period-end intangible assets from common equity and from total assets. Management believes that the presentation of this measure excluding the impact of intangible assets provides useful supplemental information that is helpful in understanding our financial condition and results of operations, as it provides a method to assess management’s success in utilizing our tangible capital as well as our capital strength. Management also believes that providing a measure that excludes balances of intangible assets, which are subjective components of valuation, facilitates the comparison of our performance with the performance of our peers. In addition, management believes that this is a standard financial measure used in the banking industry to evaluate performance.

Management believes that the presentation of certain measures excluding one-time branch consolidation and severance costs provides useful supplemental information that is helpful in understanding our core operating performance when comparing periods.

These non-GAAP financial measurements are supplemental and not a substitute for any analysis based on GAAP financial measures. Because not all companies use the same calculation of non-GAAP measures, this presentation may not be comparable to other similarly titled measures as calculated by other companies.

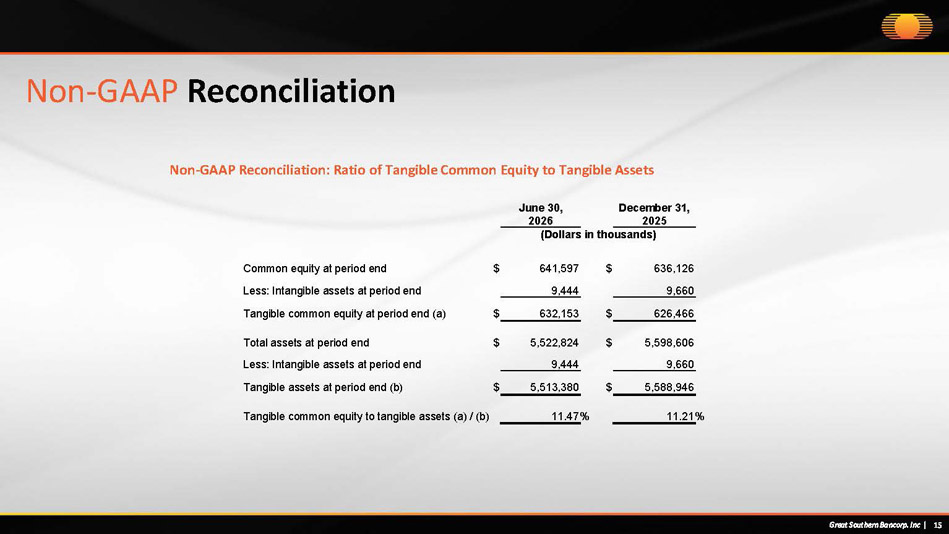

Non-GAAP Reconciliation: Ratio of Tangible Common Equity to Tangible Assets

| June 30, | December 31, | ||||||

| 2026 | 2025 | ||||||

| (Dollars in thousands) | |||||||

| Common equity at period end | $ | 641,597 | $ | 636,126 | |||

| Less: Intangible assets at period end | 9,444 | 9,660 | |||||

| Tangible common equity at period end (a) | $ | 632,153 | $ | 626,466 | |||

| Total assets at period end | $ | 5,522,824 | $ | 5,598,606 | |||

| Less: Intangible assets at period end | 9,444 | 9,660 | |||||

| Tangible assets at period end (b) | $ | 5,513,380 | $ | 5,588,946 | |||

| Tangible common equity to tangible assets (a) / (b) | 11.47 | % | 11.21 | % | |||

| 18 |

Non-GAAP Reconciliation: Exclusion of One-Time Branch Consolidation and Severance Costs

| Three Months Ended | ||||

| June 30, 2026 | ||||

| (Dollars in thousands) | ||||

| Reported net income at period end | $ | 15,795 | ||

| Plus: One-time consolidation and severance costs | 2,120 | |||

| Less: Tax adjustment related to consolidation and severance costs | (521 | ) | ||

| Non-GAAP net income | $ | 17,394 | ||

| Reported non-interest expense | $ | 38,222 | ||

| Less: One-time consolidation and severance costs | (2,120 | ) | ||

| Non-GAAP non-interest expense | $ | 36,102 | ||

| Non-GAAP annualized return on average common equity | ||||

| Definition: Non-GAAP net income (annualized) divided by average common equity | 10.82 | % | ||

| Non-GAAP annualized return on average assets | ||||

| Definition: Non-GAAP net income (annualized) divided by average total assets | 1.24 | % | ||

| Non-GAAP efficiency ratio | ||||

| Definition: Non-GAAP non-interest expense divided by the sum of net interest income and non-interest income | 63.47 | % | ||

| Non-GAAP earnings per common diluted share | ||||

| Definition: Non-GAAP net income divided by average diluted shares outstanding | $ | 1.57 | ||

CONTACT:

Kincade Ayers

Investor Relations

(616) 233-0500

19

EXHIBIT 99.2

Earnings Presentation July 2026 Great Southern Bancorp. Inc (NASDAQ: GSBC) Second Quarter Ended June 30, 2026

Forward - Looking Statements When used in this presentation and in other documents filed or furnished by the Company with or to the Securities and Exchange Commission (the “SEC”), in the Company's other press releases or other public or stockholder communications, and in oral statements made with the approval of an authorized executive officer, the words or phrases “may,” “might,” “could,” “should,” "will likely result," "are expected to," "will continue," "is anticipated," “believe,” "estimate," "project," "intends" or similar expressions are intended to identify "forward - looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Forward - looking statements also include, but are not limited to, statements regarding plans, objectives, expectations or consequences of announced transactions, known trends and statements about future performance, operations, products and services of the Company. The Company’s ability to predict results or the actual effects of future plans or strategies is inherently uncertain, and the Company’s actual results could differ materially from those contained in the forward - looking statements. Factors that could cause or contribute to such differences include, but are not limited to: (i) expected revenues, cost savings, earnings accretion, synergies and other benefits from the Company's merger and acquisition activities might not be realized within the anticipated time frames or at all, and costs or difficulties relating to integration matters, including but not limited to customer and employee retention, might be greater than expected; (ii) changes in economic conditions, either nationally or in the Company's market areas; (iii) the effects of any new or continuing public health issues on general economic and financial market conditions; (iv) fluctuations in interest rates, the effects of inflation or a potential recession, whether caused by Federal Reserve actions or otherwise; (v) the impact of bank failures or adverse developments at other banks and related negative press about the banking industry in general on investor and depositor sentiment; (vi) slower or negative economic growth caused by tariffs, changes in energy prices, supply chain disruptions or other factors; (vii) the risks of lending and investing activities, including changes in the level and direction of loan delinquencies and write - offs and changes in estimates of the adequacy of the allowance for credit losses; (viii) the possibility of realized or unrealized losses on securities held in the Company's investment portfolio; (ix) the Company's ability to access cost - effective funding and maintain sufficient liquidity; (x) fluctuations in real estate values and both residential and commercial real estate market conditions; (xi) the ability to adapt successfully to technological changes to meet customers' needs and developments in the marketplace; (xii) the possibility that security measures implemented might not be sufficient to mitigate the risk of a cyber - attack or cyber theft, and that such security measures might not protect against systems failures or interruptions; (xiii) legislative or regulatory changes that adversely affect the Company's business; (xiv) changes in accounting policies and practices or accounting standards; (xv) results of examinations of the Company and Great Southern Bank by their regulators, including the possibility that the regulators may, among other things, require the Company to limit its business activities, change its business mix, increase its allowance for credit losses, write - down assets or increase its capital levels, or affect its ability to borrow funds or maintain or increase deposits, which could adversely affect its liquidity and earnings; (xvi) costs and effects of litigation, including settlements and judgments; (xvii) competition; and (xviii) natural disasters, war, terrorist activities or civil unrest and their effects on economic and business environments in which the Company operates. The Company wishes to advise readers that the factors listed above and other risks described in the Company’s most recent Annual Report on Form 10 - K, including, without limitation, those described under “Item 1A. Risk Factors,” subsequent Quarterly Reports on Form 10 - Q and other documents filed or furnished from time to time by the Company with the SEC (which are available on our website at www.greatsouthernbank.com and the SEC’s website at www.sec.gov), could affect the Company's financial performance and cause the Company's actual results for future periods to differ materially from any opinions or statements expressed with respect to future periods in any current statements. The Company does not undertake - and specifically declines any obligation - to publicly release the result of any revisions which may be made to any forward - looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events. Great Southern Bancorp. Inc | 2

Executive Management Team Joseph W. Turner joined Great Southern in 1991 and became an officer of Bancorp in 1995. He was appointed to the Board of Directors of Bancorp and Great Southern in 1997 and has served as President and Chief Executive Officer since 2000. In this role, he has led the company’s strategic vision, financial growth, and operational execution, positioning Great Southern as a strong and competitive institution. Before joining Great Southern, Mr. Turner practiced law with Stinson LLP in Kansas City, Missouri, where he specialized in financial and corporate matters. His deep understanding of regulatory compliance, risk management, and corporate governance has been instrumental in guiding the bank’s financial strategy. Mr. Turner is the son of William V. Turner, Chairman of the Board, and the brother of Julie Turner Brown, a fellow director. He also serves on the board of CoxHealth, contributing expertise in financial oversight. His decades of leadership have driven Great Southern’s success, ensuring stability, disciplined management, and long - term value for shareholders. Joseph W. Turner President & Chief Executive Officer Rex A. Copeland Senior Vice President & Chief Financial Officer Rex A. Copeland has served as Senior Vice President, Chief Financial Officer, and Treasurer of Great Southern Bancorp, Inc. and Great Southern Bank since 2000. He oversees all financial functions of the company, including financial reporting, strategic planning, risk management, and capital allocation. With decades of experience in corporate finance, he has played a pivotal role in shaping financial policies, ensuring regulatory compliance, and optimizing efficiency. Before joining Great Southern, Mr. Copeland held financial leadership positions at Bank One Corporation, where he contributed to internal audit, financial strategy and corporate accounting. He began his career as an auditor with Forvis Mazars, LLP (formerly BKD, LLP), developing a strong foundation in financial reporting, internal controls, and audit procedures. Previously practicing as a Certified Public Accountant, he has expertise in financial management, corporate governance, and regulatory affairs. Mr. Copeland’s leadership has been instrumental in Great Southern’s stability and long - term growth. His financial expertise supports disciplined fiscal management and shareholder value. He remains active in industry organizations, offering insights on financial best practices and corporate strategy. Great Southern Bancorp. Inc | 3

Financial Performance Great Southern Bancorp. Inc (NASDAQ: GSBC) Quarter Ended June 30, 2026

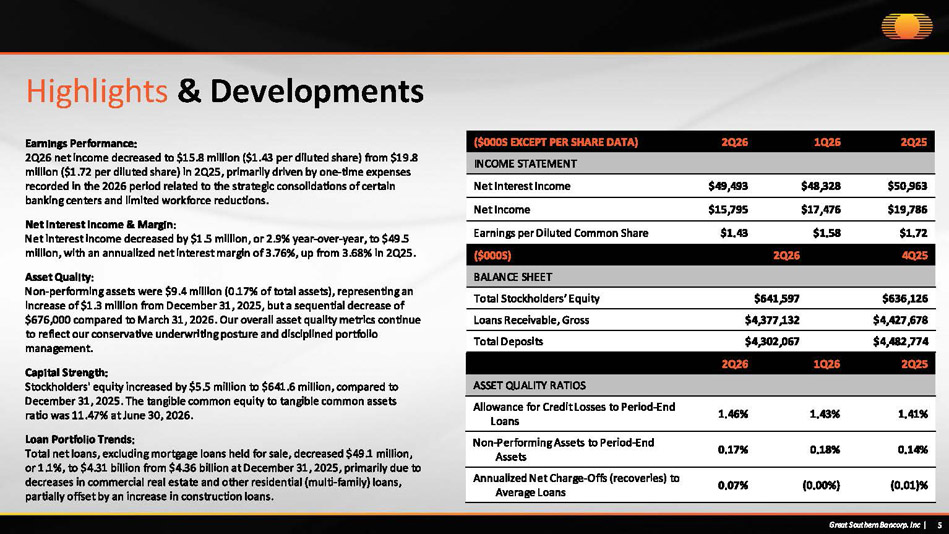

Highlights & Developments Great Southern Bancorp. Inc | 5 Earnings Performance: 2Q26 net income decreased to $15.8 million ($1.43 per diluted share) from $19.8 million ($1.72 per diluted share) in 2Q25, primarily driven by one - time expenses recorded in the 2026 period related to the strategic consolidations of certain banking centers and limited workforce reductions. Net Interest Income & Margin: Net interest income decreased by $1.5 million, or 2.9% year - over - year, to $49.5 million, with an annualized net interest margin of 3.76%, up from 3.68% in 2Q25. Asset Quality: Non - performing assets were $9.4 million (0.17% of total assets), representing an increase of $1.3 million from December 31, 2025, but a sequential decrease of $676,000 compared to March 31, 2026. Our overall asset quality metrics continue to reflect our conservative underwriting posture and disciplined portfolio management. Capital Strength : Stockholders' equity increased by $ 5 . 5 million to $ 641 . 6 million, compared to December 31 , 2025 . The tangible common equity to tangible common assets ratio was 11 . 47 % at June 30 , 2026 . Loan Portfolio Trends: Total net loans, excluding mortgage loans held for sale, decreased $49.1 million, or 1.1%, to $4.31 billion from $4.36 billion at December 31, 2025, primarily due to decreases in commercial real estate and other residential (multi - family) loans, partially offset by an increase in construction loans. 2Q25 1Q26 2Q26 ($000S EXCEPT PER SHARE DATA) INCOME STATEMENT $50,963 $48,328 $49,493 Net Interest Income $19,786 $17,476 $15,795 Net Income $1.72 $1.58 $1.43 Earnings per Diluted Common Share 4Q25 2Q26 ($000S) BALANCE SHEET $636,126 $641,597 Total Stockholders’ Equity $4,427,678 $4,377,132 Loans Receivable, Gross $4,482,774 $4,302,067 Total Deposits 2Q25 1Q26 2Q26 ASSET QUALITY RATIOS 1.41% 1.43% 1.46% Allowance for Credit Losses to Period - End Loans 0.14% 0.18% 0.17% Non - Performing Assets to Period - End Assets (0.01)% (0.00%) 0.07% Annualized Net Charge - Offs (recoveries) to Average Loans

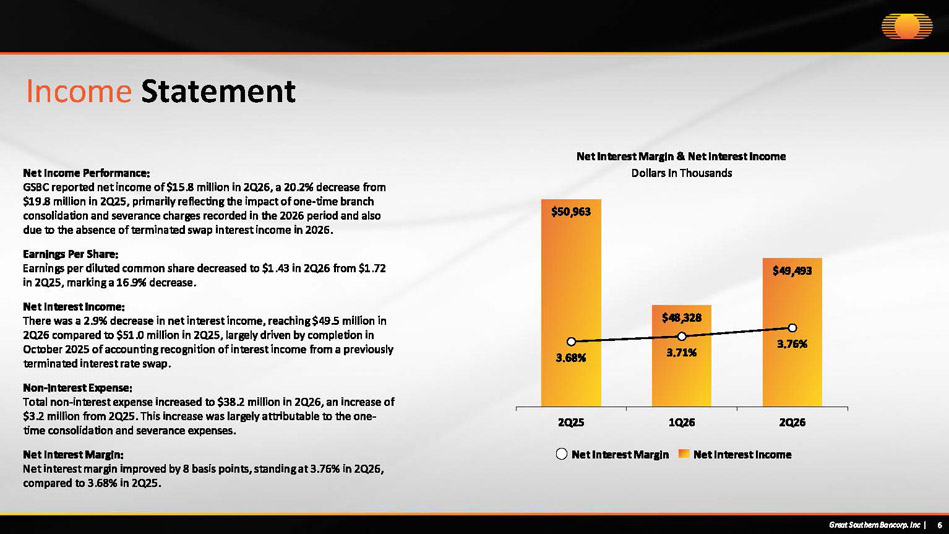

$50,963 $48,328 $49,493 3.68% 3.71% 3.76% 2Q25 1Q26 2Q26 Income Statement Net Income Performance: GSBC reported net income of $15.8 million in 2Q26, a 20.2% decrease from $19.8 million in 2Q25, primarily reflecting the impact of one - time branch consolidation and severance charges recorded in the 2026 period and also due to the absence of terminated swap interest income in 2026. Earnings Per Share: Earnings per diluted common share decreased to $1.43 in 2Q26 from $1.72 in 2Q25, marking a 16.9% decrease. Net Interest Income: There was a 2.9% decrease in net interest income, reaching $49.5 million in 2Q26 compared to $51.0 million in 2Q25, largely driven by completion in October 2025 of accounting recognition of interest income from a previously terminated interest rate swap. Non - interest Expense: Total non - interest expense increased to $38.2 million in 2Q26, an increase of $3.2 million from 2Q25. This increase was largely attributable to the one - time consolidation and severance expenses. Net Interest Margin: Net interest margin improved by 8 basis points, standing at 3.76% in 2Q26, compared to 3.68% in 2Q25. Net Interest Margin & Net Interest Income Dollars In Thousands Net Interest Margin Net Interest Income Great Southern Bancorp. Inc | 6